Exhibit 99.1

Financial Summary

| | | | | | | | |

| | | 2011 | | | 2010 | |

For the Year | | | | | | | | |

Net interest income | | $ | 15,927,000 | | | $ | 16,245,000 | |

Provision for loan losses | | | 1,050,000 | | | | 1,375,000 | |

Non-interest income | | | 6,796,000 | | | | 7,207,000 | |

Non-interest expense | | | 17,312,000 | | | | 18,258,000 | |

Net income | | | 3,402,000 | | | | 3,098,000 | |

| | |

Per Share | | | | | | | | |

Basic earnings | | $ | 1.46 | | | $ | 1.34 | |

Diluted earnings | | | 1.46 | | | | 1.34 | |

Cash dividends declared | | | 0.22 | | | | 0.20 | |

| | |

At Year End | | | | | | | | |

Assets | | $ | 509,220,000 | | | $ | 493,880,000 | |

Gross loans | | | 332,804,000 | | | | 309,524,000 | |

Allowance for loan loss | | | 5,412,000 | | | | 5,694,000 | |

Deposits | | | 420,511,000 | | | | 409,901,000 | |

Other borrowings | | | 7,751,000 | | | | 10,079,000 | |

Shareholders' equity | | | 51,865,000 | | | | 47,843,000 | |

| | |

Ratios | | | | | | | | |

Return on average assets | | | 0.68 | % | | | 0.65 | % |

Return on average equity | | | 6.80 | % | | | 6.56 | % |

Total risk-based capital ratio | | | 13.67 | % | | | 13.69 | % |

ALLL as percentage of loans | | | 1.63 | % | | | 1.84 | % |

Southern Michigan Bancorp, Inc. is a bank holding company. The Company’s wholly-owned subsidiary, Southern Michigan Bank & Trust, offers individuals, businesses, institutions and governmental agencies a full range of commercial banking services primarily in the southwest Michigan communities in which they are located and in areas immediately surrounding these communities.

| | |

To Our Shareholders | | “Much of Southern's new business activity is attributable to our focus on personalized service as well as the attractiveness of Southern as a strong and stable community banking franchise.” —John H. Castle, Chairman and Chief Executive Officer |

I am pleased to announce that Southern Michigan Bancorp, Inc. reported net income for 2011 of $3.4 million, or $1.46 per share. This represents a 9.8 percent increase over net income of $3.1 million, or $1.34 per share, for 2010. Our net income for the year was bolstered by strong fourth quarter earnings in which Southern earned just over $1 million, an increase of 39 percent over the $723,000 earned for the fourth quarter of 2010.

Southern’s financial performance for 2011 was significantly impacted by continued improvements in the quality of our loan portfolio, successful implementation of strategies to reduce operating expenses, and loan growth of $23.3 million, principally in the fourth quarter of 2011, from year-end 2010 levels. Growth in the loan portfolio resulted in favorable improvement in our net interest margin with fourth quarter 2011 net interest income increasing by $123,000, or 3 percent, compared to 2010.

Key loan portfolio metrics reflected substantial improvements compared with 2010 results. Our loan portfolio at year-end 2011 totaled $332.8 million, and represented an increase of 7.5 percent over $309.5 million in loan totals at year end 2010. Provision for loan loss expense for 2011, which totaled $1.05 million, was reduced by more than 23 percent from provision for loan loss expense of $1.375 million for 2010. Net loan charge-offs for 2011 were at the lowest level in four years totaling $1.332 million, or .40 percent of loans, down from $1.756 million, or .55 percent of loans for 2010.

Total non-interest expense for 2011 decreased $946 thousand to $17.3 million, or 5.2 percent, as compared to 2010. This was accomplished by consolidating two offices, streamlining back-office operations and deploying new technologies to enhance customer service.

Total assets as of December 31, 2011 were $509.2 million, a record high level in Southern's history, compared with $493.9 million as of December 31, 2010. Our annualized return on average assets for 2011 and 2010 was 0.68 percent and 0.65 percent, respectively. The annualized return on average equity was 6.80 percent for 2011 compared to 6.56 percent for 2010.

Southern's financial results for 2011 reflect steady improvement across most operating areas of the bank. We are now approaching levels of performance attained prior to the onset of the economic downturn that began about four years ago. As a result we were able to increase the fourth quarter 2011 dividend to $.07 per share, or $.28 annualized, an increase of $.02 per share over our October 2011 cash dividend payment. As our financial performance improves and greater certainty emerges within regulatory and economic environments, we will continue to evaluate alternative dividend payment options and strategies.

Signs of economic improvement are slowly beginning to emerge locally and regionally. Our pipeline for new loans is at the highest level in several years. Much of Southern's new business activity is attributable to our focus on personalized service as well as the attractiveness of Southern as a strong and stable community banking franchise. We have been successful in growing the loan portfolio while maintaining our conservative discipline that has always been an important part of our credit culture.

2011 2 Annual Report

All banks, including Southern, are operating in an unprecedented environment of historically low interest rates that, according to the Federal Reserve, are likely to remain in effect for some time. As a result our net interest margins, the difference between what we pay for deposits and what we charge for loans, are expected to continue to be narrow. In addition, the full effect of new bank regulations, including the Dodd-Frank Act, has yet to be reflected in our operating cost structure. Although we are satisfied with our accomplishments attained during 2011 and over the past four years, we remain cautious due to the many uncertainties likely to have a profound impact on community banks in Michigan and throughout the United States. Future earnings growth will come from selective retention of new clients and from identifying strategies to lower operating expenses without sacrificing our traditionally high standards of customer service.

During 2012 and beyond, we expect to further adapt emerging technologies to our core banking services. Our customers' use of mobile and internet banking, ATMs, debit cards, remote deposit capture and other technologically-based services and delivery channels is growing at double digit rates. At the same time, routine banking transactions completed in our branches are flat or declining despite increases in overall customer relationships. Over the next several years, our branch network will take on a greater role involving consultative selling and managing more complex banking transactions.

Uncertainties associated with a slow economic recovery, persistently high unemployment, changes in tax policies, rising health care costs and costly new regulations will provide imposing challenges to many community banks. Southern remains in an enviable position to take advantage of growth and other expansion opportunities that may be presented to us in the future.

In closing, our successes achieved last year were the product of effective planning by our Board of Directors and strategic execution by our management group and staff. Many opportunities and challenges lie ahead for 2012. We remain focused on Southern’s core mission to create value for our shareholders.

Thank you for your continued support of Southern.

|

| Sincerely, |

|

|

| John H. Castle |

| Chairman and Chief Executive Officer |

2011 3 Annual Report

2011 4 Annual Report

| | |

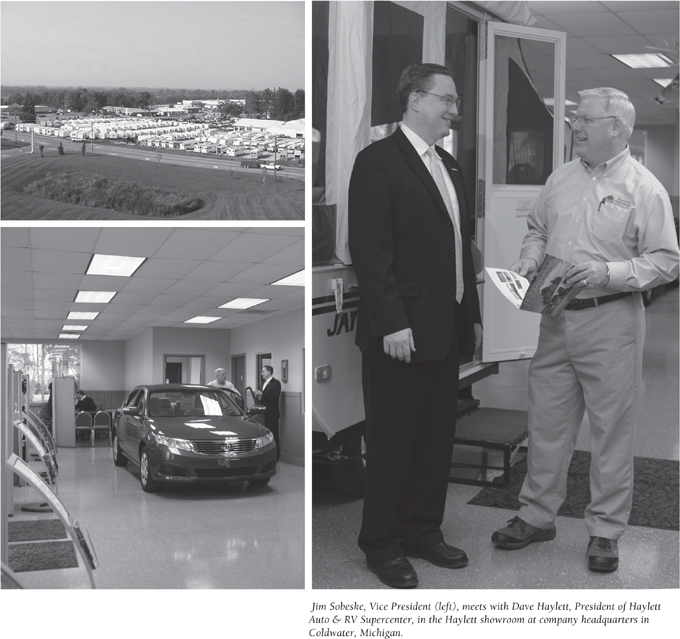

Client Profile: HAYLETT AUTO & RV SUPERCEIMTER | | “...They are a first class team. When you become a customer of Southern Michigan Bank & Trust, you gain a business partner with a vast amount of knowledge and experience.” — Dave Haylett, President, Haylett Auto & RV Supercenter |

Relationships are important to Dave Haylett. “There’s a confidence and security in working with people you know,” says Dave. Relationships are what got Dave into the car business in the first place. As a child, he mowed lawn for retired Dodge dealer Leonard Pierce in Coldwater and spent hours listening to his “war stories” about the business. As a teenager, Dave worked at Dick Johnson’s local Chevrolet dealership washing Bell Telephone trucks on Saturdays. “I loved the atmosphere. I didn't know it at the time, but I was certainly being groomed for my lifetime passion.”

After spending many successful years as General Sales Manager of Battle Creek Ford, he ventured out on his own in 1989. Three of the people who worked for Dave in Battle Creek work for him today, 22 years later, at Haylett Auto & RV Supercenter. “I’m so proud of the fact we've maintained great relationships with our employees, with our vendors, and with our customers. I've been in this business long enough to have had the pleasure of seeing generations come back as customers—first a husband and wife, then their children, and now grandchildren. I think that says a lot about the way we do business."

In the early 1990s, Dave identified the growing potential of the recreational vehicle (RV) market and added a full service RV dealership to his business. “Starting a dealership in this area turned out to be a major plus for us," Dave recalls. “I was able to get access to the top lines of reputable RV manufacturers because they were not being effectively represented in this region. I wouldn't have had this opportunity in a metropolitan area.” This strategic move, coupled with the Haylett reputation and service culture, have propelled Haylett Auto & RV Supercenter to be recognized as a “Jayco Gold Dealer” (the top 8% of dealers in the country); Haylett Auto & RV Supercenter is ranked 6th in the state of Michigan in travel trailer sales. Dave is a longstanding board member of the Michigan Association of Recreational Vehicles & Campgrounds (MARVAC). His business has dealings worldwide, from Coldwater, Michigan to Canada and to Europe.

“The landscape of this business is constantly changing; if you don't move with it, you could be gone,” Dave observes. The Haylett business has evolved into a company offering brokerage, RV, trailer and vehicle sales, parts and accessories, and service. When Dave saw another opportunity to increase his business, he turned to Southern Michigan Bank & Trust. “I’ve known the team at Southern for years, so I decided to rely on the relationships I’ve had with those individuals to see if they would be willing to work with me.” Not only was Southern Michigan Bank & Trust willing and able to work with Dave, they were also knowledgeable of his operations and had a presence in the area in which he was looking to expand.

“It sounds cliche, but Southern Michigan Bank & Trust truly is big enough to serve you, yet small enough to know you. They are a first class team. When you become a customer of Southern Michigan Bank & Trust, you gain a business partner with a vast amount of knowledge and experience. We deal with so many aspects running our various operations, and Southern Michigan Bank & Trust can handle them all—from cash management and electronic banking to ACH and financing.” With the help of vice president of commercial lending, Jim Sobeske, and Electronic Services Officer Jamie Tobalske, the phenomenal undertaking of transitioning from one financial institution to another went smoothly. "I'm so excited about the next chapter of this business, and I'm looking forward to a long relationship with Southern Michigan Bank & Trust."

“We are well aware that Dave has many banking options available and honored that he chose Southern Michigan Bank & Trust as his bank. We are proud to be associated with him and his team,” Sobeske added. “We share with Dave the high value placed on relationships and what it takes to earn and maintain that level of trust.”

2011 5 Annual Report

2011 6 Annual Report

| | |

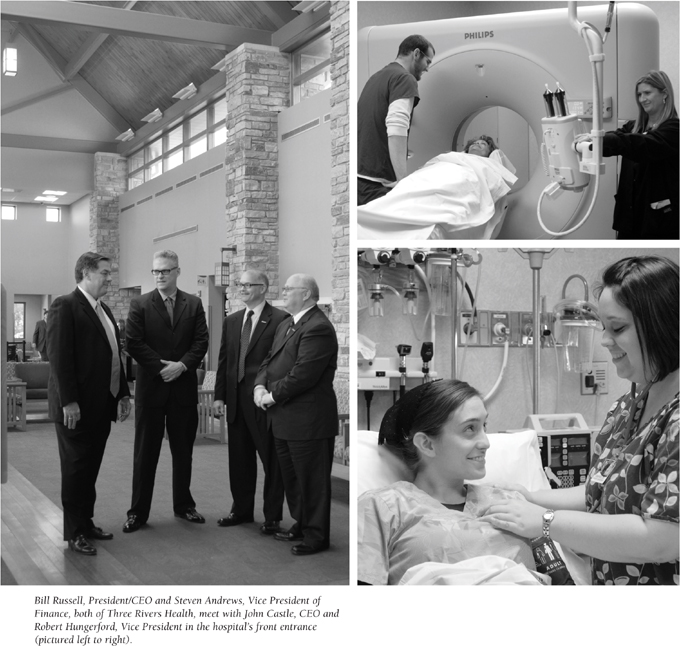

Client Profile: THREE RIVERS HEALTH | | “... They are large enough to support our needs, and they were able to develop an extremely complex financing solution.” — Bill Russell, President/CEO, Three Rivers Health |

“The difference between providing health care services in the city versus rural communities is simple. In the city they take care of patients. In rural communities we take care of family and friends,” states Three Rivers Health President/CEO Bill Russell.

Three Rivers Health employees, medical staff and volunteers are dedicated to providing high quality health care services to communities in Southwestern Michigan. Its vision is to improve the health of these residents by offering, in connection with an impressive network of providers, excellence and value in healthcare services, primarily through educating and promoting wellness and preventative services. With 300 employees, it is one of the largest employers in St. Joseph County.

The Three Rivers Health Authority Board (TRHAB) understood that the financial losses experienced in 2008 and 2009 could not continue, and major changes needed to be made in order for this important community health care provider to remain viable. TRHAB retained a new CEO, Bill Russell, in July of 2009 and together they made some painful, but essential changes. Steven Andrews, vice president of finance, confirmed that as a direct result of their actions, the hospital's operating results improved dramatically from losing $3.1 million in 2008 to generating a net profit of $504,000 in 2011.

The TRHAB also identified the need to explore financing alternatives, not only to lower its borrowing costs, but also to obtain new funding to invest in strategic initiatives that would ensure that future health care demands would be met. It was ultimately decided that for the hospital to remain a viable operation, it needed to change its organizational structure and become a nonprofit, tax-exempt corporation. Southern Michigan Bank & Trust supported the idea of making this change while remaining a community owned entity, offering counsel to hospital officials regarding financial and

organizational options. The new organizational structure was then placed on a ballot proposal, and in November 2011, an unprecedented 85% of voters said, “yes” to the proposed change. Robert Hungerford, vice president and commercial lender at Southern states, "Having been a part of this community the past 25 years, I have seen firsthand how our local hospital has responded to the needs of the community, and we were pleased to be able to help the hospital with attractive financing alternatives.”

Bill Russell is excited about the future of Three Rivers Health and partnering with Southern: “I was impressed with Southern Michigan Bank & Trust as a regional bank. They are large enough to support our needs, and they were able to develop an extremely complex financing solution. Banking with them will allow us to reduce operating overhead, begin generating cash from operations, reinvest more in our facility in order to strengthen our balance sheet, and sustain and advance our mission while creating a better opportunity to survive in an ever-changing, unpredictable health care environment.”

In describing the hospital’s confidence in Southern Michigan Bank & Trust, Bill Russell said, “Many years ago I was given the sage advice to find good people to work with and then get out of their way to let them do what they're good at doing. Southern Michigan Bank & Trust is just that—good people who are good at what they do. They are our partner in this venture, and I'm happy to let them do what they're good at doing so we can continue to take care of the health of our friends and family.”

2011 7 Annual Report

2011 8 Annual Report

| | |

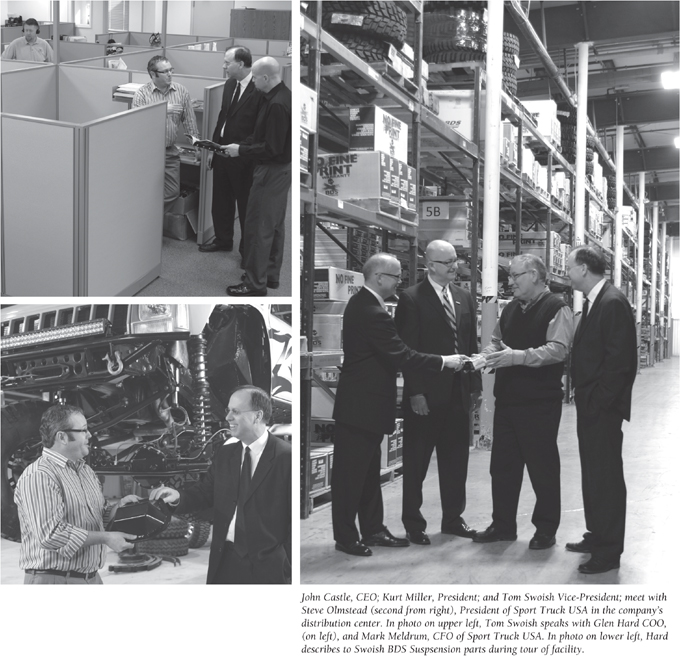

Client Profile: SPORT TRUCK USA | | “Southern has always been there for us; they are competitive, have quick response times, and they know and understand our business.” — Mark Meldrum, CFO, Sport Truck USA |

“We’re different and we want our customers to know it right off the bat. The standard warranty in our industry is two paragraphs long, complex and designed to get the company out of backing their product. We don't operate that way; we never have," says Steve Olmstead, President of Sport Truck USA. Our warranty reads, "If you are the original purchaser of any BDS product and it breaks, we will give you a new part. Period.”

Standing apart from the crowd and having a simple “do what's right” attitude has served the company well as it has transformed into a major player in the suspension and off-road products market. After observing an industry that was unwilling to stand behind their products and put the best interests of the customer at the forefront of their business, the company developed its own line of suspension products under the name BDS Suspension. Seeking out distributors and shop owners with the same philosophy of top-notch customer service has also helped to enable national and international growth. Bealing with local vendors and suppliers has always been a priority for BDS. “Ninety-nine percent of our parts are made in the US. A majority are made within 150 miles of Coldwater,” states Olmstead. “When a part is ordered it ships the same day, and if a product is in our catalog or on the website, it is in stock.”

Sport Truck USA d/b/a Truckmaster Bistributing is a full service, globally recognized distributor of aftermarket vehicle accessories offering over 100,000 warehoused parts to the United States and Canada. Its emphasis is suspension products and it is regarded as an industry expert in this specialized area. It is also the exclusive distributor to subsidiaries BBS Suspension, Zone Offroad Products and 4x4 Posi-Lok. Under the guidance of a skilled management team, this company has evolved into a major player with annual sales more than doubling over the past three years. Sport Truck is also unique in that it is completely employee-owned and continues to be based in Coldwater, Michigan, all while maintaining its position as an industry leader.

“Our companies share the same culture of being customer service driven,” states Kurt Miller, President of Southern Michigan Bank & Trust. “We are proud of our longstanding relationship with Sport Truck USA and the ability to support its banking needs as this company continues to grow.” Sport Truck makes good use of a wide range of Southern’s cash management and electronic services; from direct deposit of payroll and Health Savings Accounts, to wire transfers, account reconciliations and electronic statements. In October 2011, Tom Swoish, vice president and commercial loan officer, closed on a specialized loan arrangement to Sport Truck's Employee Stock Ownership Program to purchase the remaining shares of outstanding stock and become 100% employee-owned. Olmstead states, “We were in a unique situation. We weren't borrowing money to buy more parts or build a warehouse. We were borrowing to finance the purchase of company stock.”

Although Sport Truck USA has been a long-time customer of Southern Michigan Bank & Trust, there were other financial institutions “courting” the business. “Southern has always been there for us; they are competitive, have quick response times, and they know and understand our business,” said CFO Mark Meldrum. Olmstead added, “They’ve always allowed us to pursue our company goals without worrying about adequate funding. We believe in staying local whenever it’s possible. A relationship with someone in your own backyard has a tendency to last through the many ups and downs of the business cycle.”

2011 9 Annual Report

Southern Michigan Bancorp, Inc.

Board of Directors

| | | | |

Dean Calhoun | | Nolan E. (Rick) Hooker | | Thomas D. Meyer |

Coldwater Veneer, Inc. | | Hooker Oil / Best American | | Meyer Ventures, LLC |

| | Car Washes | | |

John S. Carton | | | | Kurt G. Miller |

Retired Business Executive | | Gregory J. Hull | | President of SMB, Inc. and |

| | Farmer | | SMB&T |

John H. Castle | | | | |

Chairman & CEO of SMB, Inc. | | Thomas E. Kolassa | | Freeman E. Riddle |

and SMB&T | | HUB International, Inc. | | Spoor-Parlin, Inc. |

| | |

H. Kenneth Cole Hillsdale College | | Donald J. Labrecque Labrecque Management | | |

| | |

Gary H. Hart | | | | |

Infmisource, Inc. | | Brian P. McConnell | | |

| | Burr Oak Tool, Inc. | | |

Executive Officers of

Southern Michigan Bancorp. lnc.

John H. Castle

Chairman & Chief Executive Officer

Kurt G. Miller

President

Danice L. Chartrand

Senior Vice President /

Chief Financial Officer

2011 10 Annual Report

Officers of

Southern Michigan Bank & Trust

EXECUTIVE OFFICERS OF SOUTHERN MICHIGAN BANK & TRUST

John H. Castle

Chairman & Chief Executive Officer

Kurt G. Miller

President

Danice L. Chartrand

Senior Vice President / Chief Financial Officer

COMMERCIAL LOANS

David Clow

Senior Vice President / Head of Commercial Lending

Deborah Davis

Vice President

Nick Grabowski

Vice President

Sarah Headley

Vice President

Robert Hungerford

Vice President

Doug Kiessling

Vice President

James Sobeske

Vice President

Tom Swoish

Vice President

Joan Trenary

Vice President

Jason Williams

Vice President

RESIDENTIAL & CONSUMER LOANS

Jamie Smoker

Senior Vice President / Head of Residential & Consumer Lending

Rick Feller

Vice President / Lending and Sr. Collections Administrator

Phyllis Wingate

Vice President /

Head of Retail Loan Operations

Jeremiah Ervans

Assistant Vice President / Retail Loan Officer

Tim Fox

Assistant Vice President / Retail Loan Officer

DeAnne Hawley

Assistant Vice President / Retail Loan Officer

Shari Kline

Assistant Vice President / Retail Loan Officer

Diane Krimmel

Assistant Vice President / Retail Loan Officer

Lori Lemmon

Assistant Vice President / Retail Loan Officer

Tammy Malatok

Assistant Vice President / Retail Loan Officer

Gregory Mallar

Assistant Vice President / Retail Loan Officer

Cassidy Munn

Assistant Vice President / Retail Loan Officer

Desiree Kauffman

Retail Loan Offidcer

Connie Swain-Caudill

Assistant Vice President / Senior Collections Manager

LOAN REVIEW

Trisha Pawloski

Assistant Vice President / Loan Review Officer

TRUST DEPARTMENT

Mary Guthrie

Senior Vice President / Senior Trust Officer

R. David Rumsey

Vice President / Senior Investment Officer

Jean Winans

Vice President / Senior Trust Officer

Susan White

Vice President / Trust Officer

INVESTMENTS

Melissa Barlow

Vice President / Senior Investment Officer

RETAIL BANKING SERVICES

Eric Anfflin

First Vice President / Retail Banking Services / Chief Deposit Officer

COLD WATER MAIN &EAST CHICAGOBRANCHES

Abby Austin

Assistant Vice President / Branch Manager

BATTLE CREEK & MARSHALL BRANCHES

Claudia Murch

Assistant Vice President / Regional Branch Manager

HILLSDALE AND CAMDENBRANCHES

Lori Neill

Assistant Vice President / Regional Branch Manager

UNION CITY BRANCH

Ken Brooks

Vice President / Regional Branch Manager

TEKONSHA BRANCH

Dawn Copas

Branch Manager

WESTERN REGION

Sally Cotton

First Vice President / Regional Manager

MENDON BRANCH

Doreen Tobin

Assistant Vice President / Regional Branch Manager

CENTREVILLE BRANCH

Paul Harker

Branch Manager

THREE RIVERS MAIN BRANCH

Sharon Bachinski

Assistant Vice President / Regional Branch Manager

THREE RIVERS WESTLAND BRANCH

Lynette Lorenz

Assistant Vice President / Branch Manager

ACCOUNTING

Sara Herrmann

Vice President / Finance

OPERATIONS / INFORMATION SYSTEMS

Dave McKinley

First Vice President / Head of Operations

Paul Mahle

Assistant Vice President / Senior Data Processing Officer

Becky Omo

Assistant Vice President / Operations Representative

Angie Smith

Assistant Vice President / Operations Manager

Jamie Tobalske

Assistant Vice President /

e-Services Officer

Jeff Kiersey

Systems Solutions Officer

Vikki Kline

Project / Research Officer

COMPLIANCE

Christine Hagaman

Vice President / Compliance Officer

MARKETING

Patty Parker

Vice President

2011 11 Annual Report

Shareholder Information

Annual Meeting

The annual meeting of Southern Michigan Bancorp, Inc. will be held on May 10, 2012 at 4:00 p.m. at the Dearth Community Center on the Branch County Fairgrounds in Coldwater, Michigan.

Market Information

The Trust Department of Southern Michigan Bank & Trust acts as the transfer and dividend paying agent for the Company's stock. For information concerning the Company's stock, call the Trust Department at (517) 279-5503 or (800) 379-7628.

Market Makers

Boenning & Scattergood

Powell, Ohio

(866) 326-8113

Howe Barnes Investments, Inc.

Chicago, Illinois

(312) 655-2954 or

(800) 800-4693

Stifel, Nicolaus & Company, Inc.

Grand Rapids, Michigan

(800) 676-0477

Milliard Lyons, Inc.

Coldwater, Michigan

(517) 278-4333 or

(800) 211-5257

Robert Baird & Company

Grand Rapids, Michigan

(616) 459-4491 or

(800) 888-6200

Royal Securities Company

Grand Rapids, Michigan

(616) 459-2844 or

(888) 804-8891

2011 12 Annual Report