OMB APPROVAL

OMB Number: 3235-0570

Expires: August 31, 2010

Estimated average burden hours per response...18.9

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-3616

Madison Mosaic Income Trust

(Exact name of registrant as specified in charter)

550 Science Drive, Madison, WI 53711

(Address of principal executive offices)(Zip code)

W. Richard Mason

Madison/Mosaic Legal and Compliance Department

8777 N. Gainey Center Drive, Suite 220

Scottsdale, AZ 85258

(Name and address of agent for service)

Registrant's telephone number, including area code: 608-274-0300

Date of fiscal year end: December 31

Date of reporting period: December 31, 2008

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspoection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. s 3507.

Item 1. Reports to Shareholders.

ANNUAL REPORT

December 31, 2008

Madison Mosaic Income Trust

- Core Bond Fund

- Government Fund

(logo) Madison Mosaic Funds (TM)

www.mosaicfunds.com

Contents

Management’s Discussion of Fund Performance | |

Market Review | 1 |

Outlook | 1 |

Fund Overview | 2 |

Comparison of Changes in the Value of a $10,000 Investment | 4 |

Report of Independent Registered Public Accounting Firm | 5 |

Portfolio of Investments | |

Government Fund | 6 |

Core Bond Fund | 8 |

Statements of Assets and Liabilities | 10 |

Statements of Operations | 11 |

Statements of Changes in Net Assets | 12 |

Financial Highlights | 13 |

Notes to Financial Statements | 14 |

Management Information | 18 |

Madison Mosaic Income Trust December 31, 2008

Management’s Discussion of Fund Performance

Market Review

Depending on where you were invested, the bond market of 2008 was the best or worst of times. Riskier bonds were hammered in the wake of a broad credit crunch, while a flight to safety lifted the returns of U.S. Treasury securities. As the year progressed, the problems that began in the subprime mortgage area bloomed into a full fledged credit crisis. The credit crisis sent unexpected shock waves into virtually all areas of the global economy, sparking a worldwide economic slowdown and eventually into global recession. As credit froze, highly leveraged investment firms began to spiral downward and many financial firms that are household names found themselves on the brink—or over the brink—of insolvency. Meanwhile, many investment vehicles with plain vanilla names like “core bond” or “short term bond” ended the year with large losses due to investments in toxic bonds or through investments in firms whose fates where linked with the securitized market.

Countering the crisis in the financial sector was a series of significant, even historically unprecedented, federal interventions. Beginning in January the Federal Reserve made the first of a series of rate cuts, which by the December cut lowered the target federal funds rate to a range of 0% to 0.25%, the lowest in modern history. In addition to rate cuts, the Federal government injected massive stimulus into the financial system in order to provide a solid base from which to repair balance sheets and normalize credit markets. These federal interventions were headlines throughout the year, including: the bailout of Bear Stearns; what amounted to a federal acquisition of mortgage companies Fannie Mae and Freddie Mac; and the Congressional creation of the $700 billion TARP program. An additional large stimulus package is expected under the new presidential administration.

At the same time, high-quality bonds, particularly those issued by the U.S. government, reaped the rewards as investors fled to the safest instruments available. Not only did Treasury securities have strong real returns, they looked tremendous compared to the losses that pummeled stock investors. The S&P 500 was down -37.0% for the year, while the major international market indices dropped more than -40% as well.

Within the bond market, there was a disparity in returns unlike any year in memory. For instance, the Barclays Capital indices (formerly Lehman Brothers indices) showed a gap from a 13.7% annual return for Treasury securities to -26.2% for high-yield bonds. Within corporate bonds, returns varied from 8.1% for AAA rated bonds to - -26.5% for bonds rated B and -44.3% for bonds rated one step lower at CAA. Many bond mutual funds stumbled as well, as the Lipper Indices showed average annual returns of - -4.7% for Intermediate Investment Grade Funds, -4.1% for Inflation Protected Treasury Bond Funds, -4.6% for Short Investment Grade Funds, and -2.3% for Intermediate Municipal Bond Funds.

Outlook

As we enter 2009, the U.S. economy, and most of the world, is mired in a severe recession. It is increasingly difficult to find reason for optimism in upcoming economic data. U.S. consumer confidence has fallen to generational lows. Manufacturers are paring back production and employment in anticipation of a prolonged recession. Unemployment rates are rising, and likely to rise further. Credit remains tight and is only available to the most worthy of borrowers.

The process of de-leveraging, begun in 2007, will likely continue well into 2009. The financial sector de-leveraging, while well-advanced, has more room to run. Private sector corporate de-leveraging will

Madison Mosaic Income Trust 1

Management's Discussion of Fund Performance (continued)

likely be a less troublesome issue, as non-financial corporate balance sheets remain in good shape. The process of consumer de-leveraging, we fear, is still in its early stages, and should only be magnified as the unemployment rate rises and the recession deepens.

There are bright spots, however. The monetary and fiscal stimulus brought to bear so far is staggering, and should eventually have its intended effect. Estimates of U.S. Government infusions into the banking industry alone are in the $1-$2 trillion range. And the $100 decline in the price of a barrel of crude could put up to $260 billion back into consumers’ pockets—a large stimulus in and of itself. After a gloomy first half, we expect the economy to begin to show modest signs of life in the second half of 2009.

Fund Overview

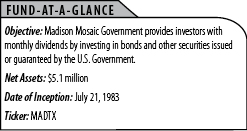

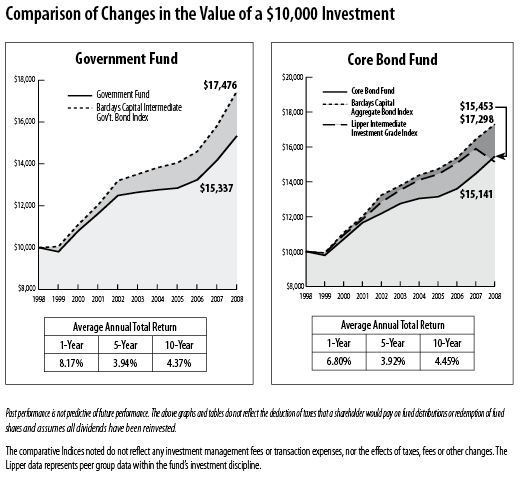

MOSAIC GOVERNMENT FUND

Mosaic Government Fund had an 8.17% return for the annual period ended December 31, 2008. This return was slightly ahead of its peers, as the Lipper Intermediate U.S. Government Fund Index rose 8.14%. The Fund’s 30-day SEC yield at period end was 1.34%, with an effective duration of 2.56 years. The Fund benefited from its duration positioning, as the yield curve steepened over the year, giving an advantage to the bonds in the intermediate sector. On the other hand, Treasury bonds outperformed all other sectors of the bond market, and our weighting in Government Agency bonds was a relative drag on performance. In the end, these two factors were in general balance, allowing us to perform in line with our peer group.

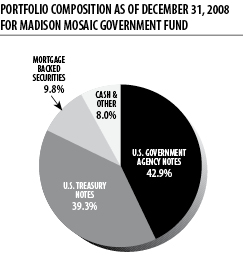

At year end, Mosaic Government held 39.3% in U.S. Treasury Notes, 42.9% in government agency notes, with the remainder in agency-backed mortgage securities and short-term notes. The Fund’s largest positions during this twelve-month period were short to intermediate duration bonds issued by the U.S. Treasury, Fannie Mae and Freddie Mac.

TOP TEN HOLDINGS AS OF DECEMBER 31, 2008

FOR MADISON MOSAIC GOVERNMENT FUND

% of net assets |

US Treasury Note, 5.125%, 6/30/11 | 7.97% |

US Treasury Note, 4%, 11/15/12 | 7.66% |

US Treasury Note, 4.75%, 5/31/12 | 6.62% |

Freddie Mac, 5.5%, 9/15/11 | 6.56% |

US Treasury Note, 4%, 3/15/10 | 6.18% |

US Treasury Note, 3.625%, 10/31/09 | 6.07% |

Fannie Mae, 4.625%, 10/15/13 | 4.35% |

Freddie Mac, 5%, 10/18/10 | 3.26% |

Freddie Mac, 4.5%, 7/15/13 | 3.22% |

Fannie Mae, 4.75%, 2/21/13 | 3.22% |

2 Annual Report • December 31, 2008

Management's Discussion of Fund Performance (continued)

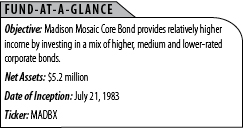

MOSAIC CORE BOND FUND

Mosaic Core Bond Fund (formerly Intermediate Income) rose 6.80% for the twelve months ended December 31, 2008. Over the same period, the Lipper Intermediate Investment Grade Index fell -4.71%. This performance gap was largely a quality and active management story, as the Fund’s preference for high-quality bonds and avoidance of problem issues made a dramatic difference. The gap in returns between Core Bond and its peers – more than 11% for the year—indicates just how important security selection was in 2008. While we believe many other fund managers may have chased yield and bought bonds which were backed by suspect mortgages, we avoided these issues due to concerns over the state of the housing market, even though many sported top ratings from third party raters. While Core Bond does own agency mortgages, these are conventional, conforming mortgages. It does not have, or has never had, direct exposure to low-quality bonds containing subprime loans. Another positive factor in performance was the timing of a number of trades which took advantage of some of the major interest rate moves in a year characterized by exceptional volatility.

At period end, the Fund’s duration was 3.20 years, while its 30-day SEC yield was 4.36%. The duration of the Fund fell during the period, from a start point of 4.01 years, as we continue to pursue what we feel are conservative, sound management decisions which can produce strong returns without undue risk.

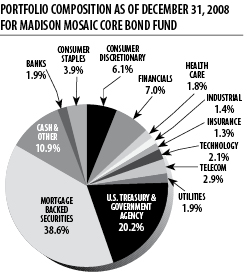

The Fund began the period with 27.0% invested in corporate bonds. Over the course of the year this was increased to 30.3%. At period end, the Fund had 20.2% of its assets in government and government agency bonds, and 38.6% in higher quality agency mortgage-backed securities.

TOP TEN HOLDINGS AS OF DECEMBER 31, 2008

FOR MADISON MOSAIC CORE BOND FUND

% of net assets |

US Treasury Note, 3.875%, 5/15/18 | 5.83% |

Freddie Mac, 5.5%, 9/15/11 | 5.02% |

FNMA MBS #745275, 5%, 2/1/36 | 4.69% |

FNMA MBS #905805, 6%, 1/1/37 | 4.10% |

FHLMC MBS #A51727, 6%, 8/1/36 | 4.07% |

US Treasury Note, 5.375%, 2/15/31 | 3.97% |

FHLMC MBS #G11911, 5%, 2/1/21 | 3.26% |

Freddie Mac, 5%, 10/18/10 | 3.08% |

FNMA MBS #256514, 6%, 12/1/36 | 2.96% |

FHLMC MBS #C02660, 6.5%, 11/1/36 | 2.65% |

Madison Mosaic Income Trust 3

Management's Discussion of Fund Performance (concluded)

4 Annual Report • December 31, 2008

Madison Mosaic Income Trust December 31, 2008

Report of Independent Registered Public Accounting Firm

To the Board of Trustees and Shareholders of Madison Mosaic Income Trust

We have audited the accompanying statements of assets and liabilities, including the portfolios of investments of the Madison Mosaic Income Trust (the “Trust”), including the Government Fund and Core Bond Fund (collectively, the “Funds”), as of December 31, 2008 and the related statement of operations for the year then ended and the statements of changes in net assets for each of the two years in the period then ended and the financial highlights for each of the five years in the period then ended. These financial statements and financial highlights are the responsibility of the Trust’s management. Our responsibility is to express an opinion on these financial statements based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. The Trust is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Trust’s internal control over financial reporting. Accordingly we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of December 31, 2008 by correspondence with the Funds’ custodian and brokers. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of each of the Funds constituting the Trust as of December 31, 2008, and the results of their operations for the year then ended and the changes in their net assets for each of the two years in the period then ended and financial highlights for each of the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America.

(signature)

Grant Thornton, LLP

Chicago, Illinois

February 20, 2009

Madison Mosaic Income Trust 5

Madison Mosaic Income Trust December 31, 2008

Government Fund - Portfolio of Investments

CREDIT RATING* | | PRINCIPAL AMOUNT |

VALUE

|

MOODY’S | S&P | |

| | US GOVERNMENT & AGENCY OBLIGATIONS: 92.0% of net assets | | |

| | US GOVERNMENT AGENCY NOTES: 42.9% | | |

Aaa | AAA | Federal Home Loan Bank, 4%, 9/6/13 | $150,000 | $160,269 |

Aaa | AAA | Fannie Mae, 6.625%, 11/15/10 | 105,000 | 115,706 |

Aaa | AAA | Fannie Mae, 3.15%, 4/1/11 | 150,000 | 150,889 |

Aaa | AAA | Fannie Mae, 6%, 5/15/11 | 100,000 | 110,590 |

Aaa | AAA | Fannie Mae, 6.125%, 3/15/12 | 100,000 | 113,661 |

Aaa | AAA | Fannie Mae, 4.875%, 5/18/12 | 100,000 | 108,982 |

Aaa | AAA | Fannie Mae, 3.625%, 2/12/13 | 150,000 | 158,900 |

Aaa | AAA | Fannie Mae, 4.75%, 2/21/13 | 150,000 | 163,210 |

Aaa | AAA | Fannie Mae, 4.375%, 7/17/13 | 150,000 | 161,928 |

Aaa | AAA | Fannie Mae, 4.625%, 10/15/13 | 200,000 | 220,387 |

Aaa | AAA | Freddie Mac, 5%, 10/18/10 | 155,000 | 165,085 |

Aaa | AAA | Freddie Mac, 3.125%, 10/25/10 | 50,000 | 51,782 |

Aaa | AAA | Freddie Mac, 5.5%, 9/15/11 | 300,000 | 332,771 |

Aaa | AAA | Freddie Mac, 4.5%, 7/15/13 | 150,000 | 163,361 |

| | US TREASURY NOTES: 39.3% | | |

Aaa | AAA | US Treasury Note, 4%, 6/15/09 | 50,000 | 50,863 |

Aaa | AAA | US Treasury Note, 3.625%, 10/31/09 | 300,000 | 307,992 |

Aaa | AAA | US Treasury Note, 4%, 3/15/10 | 300,000 | 313,641 |

Aaa | AAA | US Treasury Note, 5.125%, 6/30/11 | 365,000 | 404,095 |

Aaa | AAA | US Treasury Note, 4.75%, 5/31/12 | 300,000 | 335,883 |

Aaa | AAA | US Treasury Note, 4%, 11/15/12 | 350,000 | 388,637 |

Aaa | AAA | US Treasury Note, 4.5%, 2/15/16 | 75,000 | 88,313 |

Aaa | AAA | US Treasury Note, 4.5%, 5/15/17 | 90,000 | 105,637 |

| | MORTGAGE BACKED SECURITIES: 9.8% | | |

Aaa | AAA | Fannie Mae, Mortgage Pool #555345, 5.5%, 2/1/18 | 46,415 | 48,148 |

Aaa | AAA | Fannie Mae, Mortgage Pool #555545, 5%, 6/1/18 | 81,388 | 84,032 |

Aaa | AAA | Fannie Mae, Mortgage Pool #636758, 6.5%, 5/1/32 | 20,233 | 21,115 |

Aaa | AAA | Fannie Mae, Mortgage Pool #254346, 6.5%, 6/1/32 | 18,571 | 19,380 |

Aaa | AAA | Fannie Mae, Mortgage Pool #254405, 6%, 8/1/32 | 36,789 | 38,021 |

Aaa | AAA | Fannie Mae, Mortgage Pool #953589, 5.5%, 1/1/38 | 90,923 | 93,323 |

Aaa | AAA | Freddie Mac, Mortgage Pool #E57247, 6.5%, 3/1/09 | 840 | 840 |

Aaa | AAA | Freddie Mac, Mortgage Pool #E90778, 5.5%, 8/1/17 | 37,741 | 39,067 |

Aaa | AAA | Freddie Mac, Mortgage Pool #C01364, 6.5%, 6/1/32 | 21,281 | 22,208 |

Aaa | AAA | Government National Mortgage Association, Mortgage Pool #2483, 7%, 9/20/27 | 10,821 | 11,415 |

Aaa | AAA | Government National Mortgage Association, Mortgage Pool #676516, 6%, 2/15/38 | 114,808 | 118,681 |

| | TOTAL US GOVERNMENT & AGENCY OBLIGATIONS (Cost $4,465,468) | | $4,668,812 |

| | | | |

The Notes to Financial Statements are an integral part of these statements.

6 Annual Report • December 31, 2008

Government Fund • Portfolio of Investments • December 31, 2008 (concluded)

| | PRINCIPAL AMOUNT |

VALUE

|

| | |

| | REPURCHASE AGREEMENT: 7.2% of net assets | | |

| | With U.S. Bank National Association issued 12/31/08 at 0.01%, due 1/2/09, collateralized by $370,311 in Freddie Mac MBS #E99430 due 9/1/18. Proceeds at maturity are $363,032. (Cost $363,032) | | $363,032 |

| | | | |

| | TOTAL INVESTMENTS: 99.2% of net assets (Cost $4,828,500) | | $5,031,844 |

| | | | |

| | CASH AND RECEIVABLES LESS LIABILITIES: 0.8% of net assets | | 39,487 |

| | | | |

| | NET ASSETS: 100% | | $5,071,331 |

The Notes to Financial Statements are an integral part of these statements.

Madison Mosaic Income Trust 7

Madison Mosaic Income Trust December 31, 2008

Core Bond Fund - Portfolio of Investments

CREDIT RATING* | | PRINCIPAL AMOUNT |

VALUE

|

MOODY’S | S&P | |

| | CORPORATE DEBT SECURITIES: 30.3% of net assets | | |

| | | | |

| | BANKS: 1.9% | | |

Aa2 | AA- | Wells Fargo & Co., 4.95%, 10/16/13 | $100,000 | $97,731 |

| | | | |

| | CONSUMER DISCRETIONARY: 6.1% | | |

A2 | A | Costco Wholesale Corp., 5.5%, 3/15/17 | 100,000 | 106,464 |

A3 | A | McDonald’s Corp., 5.35%, 3/1/18 | 100,000 | 104,066 |

Aa2 | AA | Wal-Mart Stores, Inc., 4.75%, 8/15/10 | 100,000 | 103,869 |

| | | | |

| | CONSUMER STAPLES: 3.9% | | |

A1 | A+ | Sysco Corp., 5.25%, 2/12/18 | 100,000 | 101,540 |

A2 | A+ | Walgreen Co., 4.875%, 8/1/13 | 100,000 | 103,091 |

| | | | |

| | FINANCIALS: 7.0% | | |

A1 | A+ | American Express Co., 5.875%, 5/2/13 | 100,000 | 96,087 |

A1 | A | Goldman Sachs, 5.75%, 10/1/16 | 100,000 | 93,849 |

Aa3 | AA- | HSBC Finance Corp., 5.5%, 1/19/16 | 100,000 | 95,106 |

Baa1 | A- | International Lease Finance, 4.875%, 9/1/10 | 100,000 | 78,417 |

| | | | |

| | HEALTH CARE: 1.8% | | |

Baa1 | A- | UnitedHealth Group, 5%, 8/15/14 | 100,000 | 92,096 |

| | | | |

| | INDUSTRIAL: 1.4% | | |

Baa2 | BBB | Lubrizol Corp., 4.625%, 10/1/09 | 75,000 | 73,681 |

| | | | |

| | INSURANCE: 1.3% | | |

Baa2 | BBB | Markel Corp., 6.8%, 2/15/13 | 75,000 | 66,323 |

| | | | |

| | TECHNOLOGY: 2.1% | | |

A1 | A+ | Cisco Systems, Inc., 5.5%, 2/22/16 | 100,000 | 106,074 |

| | | | |

| | TELECOMMUNICATIONS: 2.9% | | |

Baa2 | BBB+ | AT&T Broadband, 8.375%, 3/15/13 | 75,000 | 77,657 |

Baa2 | A | Verizon New England, 6.5%, 9/15/11 | 75,000 | 74,496 |

| | | | |

| | UTILITIES: 1.9% | | |

Baa2 | A- | Dominion Resources Inc., 5.7%, 9/17/12 | 75,000 | 74,325 |

A2 | A- | Wisconsin Power & Light, 7.625%, 3/1/10 | 25,000 | 25,586 |

| | | | |

| | TOTAL CORPORATE DEBT SECURITIES (Cost $1,603,992) | | $1,570,458 |

The Notes to Financial Statements are an integral part of these statements.

8 Annual Report • December 31, 2008

Core Bond Fund • Portfolio of Investments • December 31, 2008 (concluded)

CREDIT RATING* | | PRINCIPAL AMOUNT |

VALUE

|

MOODY’S | S&P | |

| | MORTGAGE BACKED SECURITIES: 38.6% of net assets | | |

Aaa | AAA | Freddie Mac, Mortgage Pool #G11911, 5%, 2/1/21 | 164,491 | 169,319 |

Aaa | AAA | Freddie Mac, Mortgage Pool #A51727, 6%, 8/1/36 | 204,724 | 211,163 |

Aaa | AAA | Freddie Mac, Mortgage Pool #C02660, 6.5%, 11/1/36 | 132,341 | 137,634 |

Aaa | AAA | Fannie Mae, Mortgage Pool #725341, 5%, 2/1/19 | 64,320 | 66,409 |

Aaa | AAA | Fannie Mae, Mortgage Pool #745406, 6%, 3/1/21 | 102,580 | 106,826 |

Aaa | AAA | Fannie Mae, Mortgage Pool #837199, 5.5%, 3/1/21 | 118,572 | 122,351 |

Aaa | AAA | Fannie Mae, Mortgage Pool #636758, 6.5%, 5/1/32 | 26,978 | 28,154 |

Aaa | AAA | Fannie Mae, Mortgage Pool #745275, 5%, 2/1/36 | 237,792 | 243,152 |

Aaa | AAA | Fannie Mae, Mortgage Pool #745516, 5.5%, 5/1/36 | 114,610 | 117,641 |

Aaa | AAA | Fannie Mae, Mortgage Pool #256514, 6%, 12/1/36 | 148,713 | 153,297 |

Aaa | AAA | Fannie Mae, Mortgage Pool #902070, 6%, 12/1/36 | 116,849 | 120,451 |

Aaa | AAA | Fannie Mae, Mortgage Pool #903002, 6%, 12/1/36 | 119,926 | 123,623 |

Aaa | AAA | Fannie Mae, Mortgage Pool #905805, 6%, 1/1/37 | 206,977 | 212,451 |

Aaa | AAA | Fannie Mae, Mortgage Pool #953589, 5.5%, 1/1/38 | 90,923 | 93,323 |

Aaa | AAA | Fannie Mae, Mortgage Pool #965649, 6%, 1/1/38 | 93,752 | 96,637 |

| | | | |

| | TOTAL MORTGAGE BACKED SECURITIES (Cost $1,940,573) | | $2,002,431 |

| | | | |

| | US GOVERNMENT & AGENCY OBLIGATIONS: 20.2% of net assets | | |

Aaa | AAA | Freddie Mac, 5%, 10/18/10 | 150,000 | 159,760 |

Aaa | AAA | Freddie Mac, 5.5%, 9/15/11 | 235,000 | 260,670 |

Aaa | AAA | US Treasury Note, 3.875%, 5/15/18 | 265,000 | 302,266 |

Aaa | AAA | US Treasury Note, 4.25%, 11/15/17 | 100,000 | 116,524 |

Aaa | AAA | US Treasury Note, 5.375%, 2/15/31 | 150,000 | 206,156 |

| | | | |

| | TOTAL US GOVERNMENT & AGENCY OBLIGATIONS (Cost $911,711) | | $1,045,376 |

| | | | |

| | REPURCHASE AGREEMENT: 8.5% of net assets | | |

| | With U.S. Bank National Association issued 12/31/08 at 0.01%, due 1/2/09, collateralized by $451,978 in Freddie Mac MBS #E99430 due 9/1/18. Proceeds at maturity are $443,093. (Cost $443,093) | | 443,093 |

| | | | |

| | TOTAL INVESTMENTS: 97.6% of net assets (Cost $4,899,369) | | $5,061,358 |

| | | | |

| | LIABILITIES LESS CASH AND RECEIVABLES: 2.4% of net assets | | 126,179 |

| | | | |

| | NET ASSETS: 100% | | $5,187,537 |

Notes to the Portfolio of Investments: * – Unaudited; Moody’s – Moody’s Investor Services, Inc.; S&P – Standard & Poor’s Corporation

The Notes to Financial Statements are an integral part of these statements.

Madison Mosaic Income Trust 9

Madison Mosaic Income Trust December 31, 2008

Statements of Assets and Liabilities

| Government

Fund | Core Bond

Fund |

ASSETS | | |

Investments, at value (Notes 1 and 2) | | |

Investment securities | $4,668,812 | $4,618,265 |

Repurchase agreements | 363,032 | 443,093 |

Total investments* | 5,031,844 | 5,061,358 |

Receivables | | |

Interest | 39,562 | 48,275 |

Capital shares sold | 2,000 | 83,505 |

Total assets | 5,073,406 | 5,193,138 |

| | |

LIABILITIES | | |

Payables | | |

Dividends | 503 | 1,877 |

Capital shares redeemed | 322 | 1,474 |

Independent trustee fees | 250 | 250 |

Auditor fees | 1,000 | 2,000 |

Total liabilities | 2,075 | 5,601 |

| | |

NET ASSETS | $5,071,331 | $5,187,537 |

| | |

Net assets consists of: | | |

Paid in capital | $4,883,571 | $5,324,657 |

Accumulated net realized losses | (15,584) | (299,109) |

Net unrealized appreciation on investments | 203,344 | 161,989 |

Net Assets | $5,071,331 | $5,187,537 |

| | |

CAPITAL SHARES OUTSTANDING | | |

An unlimited number of capital shares, without par value, are authorized. (Note 7) | 469,072 | 770,036 |

| | |

NET ASSET VALUE PER SHARE | $10.81 | $6.74 |

*INVESTMENT SECURITIES, AT COST | $4,828,500 | $4,899,369 |

The Notes to Financial Statements are an integral part of these statements.

10 Annual Report • December 31, 2008

Madison Mosaic Income Trust December 31, 2008

Statements of Operations

For the year ended December 31, 2008

| Government

Fund | Core Bond

Fund |

INVESTMENT INCOME (Note 1) | | |

Interest income | $139,542 | $226,778 |

| | |

EXPENSES (Notes 3 and 5) | | |

Investment advisory fees | 16,588 | 20,768 |

Other expenses: | | |

Service agreement fees | 7,380 | 10,009 |

Independent trustee fees | 1,000 | 1,000 |

Auditor fees | 3,500 | 4,500 |

Line of credit interest and fees | 250 | 250 |

Total other expenses | 12,130 | 15,759 |

Total expenses | 28,718 | 36,527 |

| | |

NET INVESTMENT INCOME | 110,824 | 190,251 |

| | |

REALIZED AND UNREALIZED GAIN ON INVESTMENTS | | |

Net realized gain on investments | 39,402 | 30,122 |

Change in net unrealized appreciation of investments | 140,133 | 80,212 |

| | |

NET GAIN ON INVESTMENTS | 179,535 | 110,334 |

| | |

TOTAL INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | $290,359 | $300,585 |

The Notes to Financial Statements are an integral part of these statements.

Madison Mosaic Income Trust 11

Madison Mosaic Income Trust December 31, 2008

Statements of Changes in Net Assets

For the period indicated

| Government Fund | Core Bond Fund |

| Year Ended December 31, | Year Ended December 31, |

| 2008 | 2007 | 2008 | 2007 |

INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | | | | |

Net investment income | $110,824 | $98,925 | $190,251 | $183,286 |

Net realized gain on investments | 39,402 | 25 | 30,122 | 18,781 |

Net unrealized appreciation (depreciation) on investments | 140,133 | 103,158 | 80,212 | 78,093 |

Total increase in net assets resulting from operations | 290,359 | 202,108 | 300,585 | 280,160 |

| | | | |

DISTRIBUTION TO SHAREHOLDERS FROM NET INVESTMENT INCOME | (110,824) | (98,925) | (190,251) | (183,286) |

| | | | |

CAPITAL SHARE TRANSACTIONS (Note 7) | 1,905,512 | (172,261) | 554,376 | (183,572) |

| | | | |

TOTAL INCREASE (DECREASE) IN NET ASSETS | 2,085,047 | (69,078) | 664,710 | (86,698) |

| | | | |

NET ASSETS | | | | |

Beginning of period | $2,986,284 | $3,055,362 | $4,522,827 | $4,609,525 |

End of period | $5,071,331 | $2,986,284 | $5,187,537 | $4,522,827 |

The Notes to Financial Statements are an integral part of these statements.

12 Annual Report • December 31, 2008

Madison Mosaic Income Trust

Financial Highlights

Selected data for a share outstanding for the periods indicated

GOVERNMENT FUND

| Year Ended December 31, |

| 2008 | 2007 | 2006 | 2005 | 2004 |

Net asset value, beginning of period | $10.30 | $9.94 | $9.95 | $10.16 | $10.36 |

Investment operations: | | | | | |

Net investment income | 0.32 | 0.33 | 0.31 | 0.28 | 0.29 |

Net realized and unrealized gain (loss) on investments | 0.51 | 0.36 | (0.01) | (0.21) | (0.20) |

Total from investment operations | 0.83 | 0.69 | 0.30 | 0.07 | 0.09 |

Less distributions from net investment income | (0.32) | (0.33) | (0.31) | (0.28) | (0.29) |

Net asset value, end of period | $10.81 | $10.30 | $9.94 | $9.95 | $10.16 |

Total return (%) | 8.17 | 7.10 | 3.07 | 0.69 | 0.89 |

Ratios and supplemental data | | | | | |

Net assets, end of period (in thousands) | $5,071 | $2,986 | $3,055 | $3,248 | $5,132 |

Ratio of expenses to average net assets (%) | 0.78 | 1.15 | 1.19 | 1.19 | 1.15 |

Ratio of net investment income to average net assets (%) | 3.00 | 3.30 | 3.11 | 2.75 | 2.83 |

Portfolio turnover (%) | 67 | 18 | 41 | 43 | 55 |

CORE BOND FUND

| Year Ended December 31, |

| 2008 | 2007 | 2006 | 2005 | 2004 |

Net asset value, beginning of period | $6.58 | $6.44 | $6.46 | $6.64 | $6.71 |

Investment operations: | | | | | |

Net investment income | 0.27 | 0.26 | 0.24 | 0.23 | 0.22 |

Net realized and unrealized gain (loss) on investments | 0.16 | 0.14 | (0.02) | (0.18) | (0.07) |

Total from investment operations | 0.43 | 0.40 | 0.22 | 0.05 | 0.15 |

Less distributions from net investment income | (0.27) | (0.26) | (0.24) | (0.23) | (0.22) |

Net asset value, end of period | $6.74 | $6.58 | $6.44 | $6.46 | $6.64 |

Total return (%) | 6.80 | 6.41 | 3.48 | 0.77 | 2.30 |

Ratios and supplemental data | | | | | |

Net assets, end of period (in thousands) | $5,188 | $4,523 | $4,610 | $5,602 | $6,041 |

Ratio of expenses to average net assets (%) | 0.80 | 1.12 | 1.10 | 1.08 | 1.07 |

Ratio of net investment income to average net assets (%) | 4.18 | 4.05 | 3.70 | 3.49 | 3.32 |

Portfolio turnover (%) | 36 | 41 | 60 | 60 | 46 |

The Notes to Financial Statements are an integral part of these statements.

Madison Mosaic Income Trust 13

Madison Mosaic Income Trust

Notes to Financial Statements

1. Summary of Significant Accounting Policies. Madison Mosaic Income Trust (the “Trust”) is registered with the Securities and Exchange Commission under the Investment Company Act of 1940 as an open-end, diversified investment management company. This report contains information about two separate funds (the “Funds”) each of whose objective is to receive and distribute bond income. The Government Fund invests in securities of the U.S. Government and its agencies. The Core Bond Fund invests in investment grade corporate, government and government agency fixed income securities. The Core Bond Fund may also invest a portion of its assets in securities rated as low as “B” by Moody’s Investors Service, Inc. or Standard & Poor’s Corporation. Two additional Trust portfolios present their financial information in a separate report.

Securities Valuation: Repurchase agreements and other securities having maturities of 60 days or less are valued at amortized cost, which approximates market value. Securities having longer maturities, for which market quotations are readily available, are valued at the mean between their closing bid and ask prices. Securities for which market quotations are not readily available are valued at their fair value as determined in good faith under procedures approved by the Board of Trustees.

The Funds adopted Financial Accounting Standards Board Statement No. 157, Fair Value Measurements (FAS 157) effective January 1, 2008. In accordance with FAS 157, fair value is defined as the price that the Funds would receive to sell an investment or pay to transfer a liability in an orderly transaction with an independent buyer in the principal market, or in the absence of a principal market the most advantageous market for the investment or liability. FAS 157 establishes a three-tier hierarchy to distinguish between (1) inputs that reflect the assumptions market participants would use in pricing an asset or liability developed based on market data obtained from sources independent of the reporting entity (observable inputs) and (2) inputs that reflect the reporting entity’s own assumptions about the assumptions market participants would use in pricing an asset or liability developed based on the best information available in the circumstances (unobservable inputs) and to establish classification of fair value measurements for disclosure purposes.

Various inputs as noted above are used in determining the value of the Funds’ investments and other financial instruments. These inputs are summarized in the three broad levels listed below.

- Level 1: Quoted prices in active markets for identical securities

- Level 2: Other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.)

- Level 3: Significant unobservable inputs (including the Funds’ own assumptions in determining the fair value of investments)

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

The following is a summary of the inputs used to value the Funds’ assets as of December 31, 2008:

| Investments in Securities |

Valuation Inputs | Government

Fund | Core Bond

Fund |

Level 1: Quoted prices | $-- | $-- |

Level 2: Other significant observable inputs | $5,031,844 | $5,061,358 |

Level 3: Significant unobservable inputs | -- | -- |

Total | $5,031,844 | $5,061,358 |

Investment Transactions: Investment transactions are recorded on a trade date basis. The cost of investments sold is determined on the identified cost basis for financial statement and federal income tax purposes.

Investment Income: Interest income is recorded on an accrual basis. Bond premium is amortized and original issue discount and market discount are accreted over the expected life of each applicable security using the effective interest method. Other income is accrued as earned.

Distribution of Income and Gains: Distributions are recorded on the ex-dividend date. Net investment income, determined as gross investment income less total expenses, is declared as a regular dividend and distributed to shareholders monthly. Capital gain distributions, if any, are declared and paid annually at year-end.

The tax character of distributions paid during 2008 and 2007 were as follows:

14 Annual Report • December 31, 2008

Notes to Financial Statements (continued)

| 2008 | 2007 |

Government Fund: | | |

Distributions paid from ordinary income | $110,824 | $98,925 |

Core Bond Fund: | | |

Distributions paid from ordinary income | $190,251 | $183,286 |

As of December 31, 2008, the components of distributable earnings on a tax basis were as follows:

Government Fund: | |

Accumulated net realized losses | $(15,405) |

Net unrealized appreciation on investments | 203,165 |

| $187,760 |

Core Bond Fund: | |

Accumulated net realized losses | $(299,076) |

Net unrealized appreciation on investments | 161,956 |

| $(137,120) |

Net realized gains or losses may differ for financial and tax reporting purposes as a result of loss deferrals related to wash sales and post-October transactions.

Income Tax: No provision is made for federal income taxes since it is the intention of the Trust to comply with the provisions of Subchapter M of the Internal Revenue Code available to investment companies and to make the requisite distribution to shareholders of taxable income which will be sufficient to relieve it from all or substantially all federal income taxes.

The Funds adopted the provisions of Financial Accounting Standards Board Interpretation No. 48 (“FIN 48”), “Accounting for Uncertainty in Income Taxes.” The implementation of FIN 48 resulted in no material liability for unrecognized tax benefits and no material change to the beginning net asset value of the funds.

As of and during the year ended December 31, 2008, the Funds did not have a liability for any unrecognized tax benefits. The funds recognize interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the statement of operations. During the period, the Funds did not incur any interest or penalties.

As of December 31, 2008, the Funds had available for federal income tax purposes the following unused capital loss carryovers:

Expiration Date | Government

Fund | Core Bond

Fund |

December 31, 2009 | -- | 12,901 |

December 31, 2010 | -- | 243,364 |

December 31, 2013 | -- | 20,428 |

December 31, 2014 | 15,301 | 22,383 |

December 31, 2015 | 104 | -- |

Due to inherent differences in the recognition of income, expenses, and realized gains/losses under U.S. generally accepted accounting principles and federal income tax purposes, permanent differences between book and tax basis reporting for the 2008 fiscal year have been identified and appropriately reclassified. In the Core Bond Fund, permanent differences relating to the expiration of capital loss carryovers totaling $59,592 was reclassified from accumulated net realized losses to net paid in capital on shares of beneficial interest.

Use of Estimates: The preparation of the financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions. Such estimates affect the reported amounts of assets and liabilities and reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates.

2. Investments in Repurchase Agreements. When the Trust purchases securities under agreements to resell, the securities are held for safekeeping by the Trust’s custodian bank as collateral. Should the market value of the securities purchased under such an agreement decrease below the principal amount to be received at the termination of the agreement plus accrued interest, the counterparty is required to place an equivalent amount of additional securities in safekeeping with the Trust’s custodian bank. Pursuant to an Exemptive Order issued by the Securities and Exchange Commission, the Trust, along with other registered investment companies having Advisory and Services Agreements with the same advisor, transfers uninvested cash balances into a joint trading account. The aggregate balance in this joint trading account is invested in one or more consolidated repurchase agreements whose underlying securities are U.S. Treasury or federal agency obligations. As of December 31, 2008, the Government Fund had a 5.0% interest and the Core Bond Fund had a 6.1% interest in the consolidated repurchase agreement of $7,263,519 collateralized by $7,409,165 in Freddie Mac Mortgaged Backed Security Notes. Proceeds at maturity were $7,263,523.

Madison Mosaic Income Trust 15

Notes to Financial Statements (continued)

3. Investment Advisory Fees and Other Transactions with Affiliates. The investment advisor to the Trust, Madison Mosaic, LLC, a wholly owned subsidiary of Madison Investment Advisors, Inc. (collectively “the Advisor”), earned an advisory fee equal to 0.625% per annum of the average net assets of the Funds through April 30, 2008. Effective May 1, 2008, this fee was reduced to 0.40% for the Funds. The fees are accrued daily and are paid monthly.

4. Investment Transactions. Purchases and sales of securities (excluding short-term securities) for the year ended December 31, 2008 were as follows:

| Purchases | Sales |

Government Fund: | | |

U.S. Gov’t securities | $3,827,607 | $2,235,090 |

Other | -- | -- |

Core Bond Fund: | | |

U.S. Gov’t securities | $1,244,171 | $1,522,395 |

Other | 400,845 | -- |

5. Other Expenses. Under a separate Services Agreement, the Advisor will provide or arrange for each Fund to have all other necessary operational and support services for a fee based on a percentage of average net assets. These fees are accrued daily and paid monthly. This percentage was 0.365% for both the Government Fund and the Core Bond Fund, respectively through April 30, 2008. Effective May 1, 2008, this fee was reduced to 0.28% for the Government Fund and 0.30% for the Core Bond Fund, respectively. The direct expenses paid by the Funds and referenced below come out of this fee.

The Funds pay the expenses of the Funds’ Independent Trustees and auditors directly. For the year ended December 31, 2008, these fees amounted to $1,000 and $3,500, respectively for the Government Fund and $1,000 and $4,500, respectively for the Core Bond Fund.

6. Aggregate Cost and Unrealized Appreciation (Depreciation). The aggregate cost for federal income tax purposes and the net unrealized appreciation (depreciation) are stated as follows as of December 31, 2008:

| Government

Fund | Core Bond

Fund |

Aggregate Cost | $4,828,679 | $4,899,402 |

Gross unrealized appreciation | 204,298 | 225,476 |

Gross unrealized depreciation | (1,133) | (63,520) |

Net unrealized appreciation | $203,165 | $161,956 |

7. Capital Share Transactions. An unlimited number of capital shares, without par value, are authorized. Transactions in capital shares for the following periods were:

| Year Ended December 31, |

Government Fund | 2008 | 2007 |

In Dollars | | |

Shares sold | $4,267,608 | $119,646 |

Shares issued in reinvestment of dividends | 101,420 | 87,325 |

Total shares issued | 4,369,028 | 206,971 |

Shares redeemed | (2,463,516) | (379,232) |

Net increase (decrease) | $1,905,512 | $(172,261) |

| | |

In Shares | | |

Shares sold | 405,160 | 11,925 |

Shares issued in reinvestment of dividends | 9,693 | 8,700 |

Total shares issued | 414,853 | 20,625 |

Shares redeemed | (235,724) | (37,920) |

Net increase (decrease) | 179,129 | (17,295) |

| Year Ended December 31, |

Core Bond Fund | 2008 | 2007 |

In Dollars | | |

Shares sold | $1,090,514 | $201,762 |

Shares issued in reinvestment of dividends | 170,361 | 163,019 |

Total shares issued | 1,260,875 | 364,781 |

Shares redeemed | (706,499) | (548,353) |

Net increase (decrease) | $554,376 | $(183,572) |

| | |

In Shares | | |

Shares sold | 166,397 | 31,266 |

Shares issued in reinvestment of dividends | 23,720 | 25,251 |

Total shares issued | 190,117 | 56,517 |

Shares redeemed | (107,709) | (85,058) |

Net increase (decrease) | 82,408 | (28,541) |

8. Line of Credit. The Government Fund has a $1 million and the Core Bond Fund has a $1.25 million revolving credit facility with a bank for temporary emergency purposes, including the meeting of redemption requests that otherwise might require the untimely disposition of securities. The interest rate on the outstanding principal amount is equal to the prime rate less 1/2%.

16 Annual Report • December 31, 2008

Notes to Financial Statements (concluded)

Each Fund paid $250 for the year to maintain its line of credit. During the year ended December 31, 2008, neither Fund borrowed on their respective lines of credit.

9. Accounting Pronouncements. On March 19, 2008, Financial Accounting Standards Board released Statement of Financial Accounting Standards No. 161, Disclosures about Derivative Instruments and Hedging Activities (FAS 161). FAS 161 requires qualitative disclosures about objectives and strategies for using derivatives, quantitative disclosures about fair value amounts of and gains and losses on derivative instruments and disclosures about credit-risk-related contingent features in derivative agreements. The application of FAS 161 is required for fiscal years and interim periods beginning after November 15, 2008. At this time, management is evaluating the implications of FAS 161 and its impact on the financial statements has not yet been determined.

Fund Expenses (unaudited)

Example: As a shareholder of the Funds, you incur two types of costs: (1) transaction costs and (2) ongoing costs, including Investment advisory fees and Other expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other mutual funds. See Notes 3 and 5 above for an explanation of the types of costs charged by the Funds. This Example is based on an investment of $1,000 invested on July 1, 2008 and held for the six-months ended December 31, 2008.

Actual Expenses

The table below titled “Based on Actual Total Return” provides information about actual account values and actual expenses. You may use the information provided in this table, together with the amount you invested, to estimate the expenses that you paid over the period. To estimate the expenses you paid on your account, divide your ending account value by $1,000 (for example, an $8,500 ending account valued divided by $1,000 = 8.5), then multiply the result by the number under the heading entitled “Expenses Paid During the Period.”

Based on Actual Total Return1 |

| Beginning

Account Value | Ending

Account Value | Annualized

Expense Ratio | Expenses Paid

During the Period2 |

Government Fund | $1,000.00 | $1,061.95 | 0.78% | $4.00 |

Core Bond Fund | $1,000.00 | $1,052.98 | 0.80% | $4.07 |

1For the six-months ended December 31, 2008.

2Expenses are equal to the Funds’ annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year, then divided by 366. |

Hypothetical Example for Comparison Purposes

The table on the next page titled “Based on Hypothetical Total Return” provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio and an assumed rate of return of 5.00% per year before expenses, which is neither Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use the information provided in this table to compare the ongoing costs of investing in either Fund and other funds. To do so, compare the 5.00% hypothetical example relating to the applicable Fund with the 5.00% hypothetical examples that appear in the shareholder reports of the other funds.

Madison Mosaic Income Trust 17

Based on Hypothetical Total Return1 |

| Beginning

Account Value | Ending

Account Value | Annualized

Expense Ratio | Expenses Paid

During the Period2 |

Government Fund | $1,000.00 | $1,025.40 | 0.78% | $3.96 |

Core Bond Fund | $1,000.00 | $1,025.40 | 0.80% | $4.09 |

1For the six-months ended December 31, 2008. |

2Expenses are equal to the Funds’ annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year, then divided by 366. |

Management Information

Independent Trustees

Name, Address and Age | Position(s) Held with Fund | Term of Office and Length of Time Served | Principal Occupation(s) During Past 5 Years | Number of Portfolios in Fund Complex Overseen | Other Directorships Held |

Philip E. Blake

550 Science Drive

Madison, WI 53711

Born 1944 | Trustee | Indefinite Term since May 2001 | Retired investor; formerly Vice President - Publishing, Lee Enterprises Inc. | All 13 Madison Mosaic Funds and the Madison Strategic Sector Premium Fund. | Madison Newspapers, Inc. of Madison, WI; Trustee of the Madison Claymore Covered Call and Equity Strategy Fund; Nerites Corp. |

James R. Imhoff, Jr.

550 Science Drive

Madison, WI 53711

Born 1944 | Trustee | Indefinite Term since July 1996 | Chairman and CEO of First Weber Group, Inc. (real estate brokers) of Madison, WI. | All 13 Madison Mosaic Funds and the Madison Strategic Sector Premium Fund. | Trustee of the Madison Claymore Covered Call and Equity Strategy Fund; Park Bank, FSB. |

Lorence D. Wheeler

550 Science Drive

Madison, WI 53711

Born 1938 | Trustee | Indefinite Term since July 1996 | Retired investor; formerly Pension Specialist for CUNA Mutual Group (insurance) and President of Credit Union Benefits Services, Inc. (a provider of retirement plans and related services for credit union employees nationwide). | All 13 Madison Mosaic Funds and the Madison Strategic Sector Premium Fund. | Trustee of the Madison Claymore Covered Call and Equity Strategy Fund; Grand Mountain Bank, FSB; Grand Mountain Bancshares, Inc. |

Interested Trustees*

Frank E. Burgess

550 Science Drive

Madison, WI 53711

Born 1942 | Trustee and Vice President | Indefinite Terms since July 1996 | Founder, President and Director of Madison Investment Advisors, Inc. | All 13 Madison Mosaic Funds and the Madison Strategic Sector Premium Fund. | Trustee of the Madison Claymore Covered Call and Equity Strategy Fund; Capitol Bank, FSB; American Riviera Bank. |

Katherine L. Frank

550 Science Drive

Madison, WI 53711

Born 1960 | Trustee and President | Indefinite Terms President since July 1996, Trustee since May 2001 | Principal and Vice President of Madison Investment Advisors, Inc. and President of Madison Mosaic, LLC | President of all 13 Madison Mosaic Funds. Trustee of all Madison Mosaic Funds except Equity Trust; President and Trustee of the Madison Strategic Sector Premium Fund. | None |

18 Annual Report • December 31, 2008

Management Information (concluded)

Officers*

Jay R. Sekelsky

550 Science Drive

Madison, WI 53711

Born 1959 | Vice President | Indefinite Term since July 1996 | Principal and Vice President of Madison Investment Advisors, Inc. and Vice President of Madison Mosaic, LLC | All 13 Madison Mosaic Funds and the Madison Strategic Sector Premium Fund. | None |

Christopher Berberet

550 Science Drive

Madison, WI 53711

Born 1959 | Vice President | Indefinite Term since July 1996 | Principal and Vice President of Madison Investment Advisors, Inc. and Vice President of Madison Mosaic, LLC | All 13 Madison Mosaic Funds and the Madison Strategic Sector Premium Fund. | None |

W. Richard Mason

8777 N. Gainey Center Drive, #220

Scottsdale, AZ 85258

Born 1960 | Secretary, General Counsel and Chief Compliance Officer | Indefinite Terms since November 1992 | Principal of Mosaic Funds Distributor, LLC; General Counsel and Chief Compliance Officer for Madison Investment Advisors, Madison Scottsdale, LC and Madison Mosaic, LLC; General Counsel for Concord Asset Management, LLC. | All 13 Madison Mosaic Funds and the Madison Strategic Sector Premium Fund. | None |

Greg Hoppe

550 Science Drive

Madison, WI 53711

Born 1969 | Chief Financial Officer | Indefinite Term since August 1999 | Vice President of Madison Mosaic, LLC | All 13 Madison Mosaic Funds and the Madison Strategic Sector Premium Fund. | None |

*All interested Trustees and Officers of the Trust are employees and/or owners of Madison Investment Advisors, Inc. Since Madison Investment Advisors, Inc. serves as the investment advisor to the Trust, each of these individuals is considered an “interested person” of the Trust as the term is defined in the Investment Company Act of 1940.

The Statement of Additional Information contains more information about the Trustees and is available upon request. To request a free copy, call Mosaic Funds at 1-800-368-3195.

Forward-Looking Statement Disclosure. One of our most important responsibilities as mutual fund managers is to communicate with shareholders in an open and direct manner. Some of our comments in our letters to shareholders are based on current management expectations and are considered “forward-looking statements.” Actual future results, however, may prove to be different from our expectations. You can identify forward-looking statements by words such as “estimate,” “may,” “will,” “expect,” “believe,” “plan” and other similar terms. We cannot promise future returns. Our opinions are a reflection of our best judgment at the time this report is compiled, and we disclaim any obligation to update or alter forward-looking statements as a result of new information, future events, or otherwise.

Proxy Voting Information. The Trust only invests in non-voting securities. Nevertheless, the Trust adopted policies that provide guidance and set forth parameters for the voting of proxies relating to securities held in the Trust’s portfolios. Additionally, information regarding how the Trust voted proxies related to portfolio securities for the period ended June 30, 2008 is available. These policies and voting information are available to you upon request and free of charge by writing to Madison Mosaic Funds, 550 Science Drive, Madison, WI 53711 or by calling toll-free at 1-800-368-3195. The Trust’s proxy voting policies and voting information may also be obtained by visiting the Securities and Exchange Commission web site at www.sec.gov. The Trust will respond to shareholder requests for copies of our policies and voting information within

Madison Mosaic Income Trust 19

two business days of request by first-class mail or other means designed to ensure prompt delivery.

N-Q Disclosure. The Trust files its complete schedule of portfolio holdings with the U.S. Securities and Exchange Commission (the “Commission”) for the first and third quarters of each fiscal year on Form N-Q. The Trust’s Forms N-Q are available on the Commission’s website. The Trust’s Forms N-Q may be reviewed and copied at the Commission’s Public Reference Room in Washington, DC. Information about the operation of the Public Reference Room may be obtained by calling the Commission at 1-202-551-8090. Form N-Q and other information about the Trust are available on the EDGAR Database on the Commission’s Internet site at http://www.sec.gov. Copies of this information may also be obtained, upon payment of a duplicating fee, by electronic request at the following email address: publicinfo@sec.gov, or by writing the Commission’s Public Reference Section, Washington, DC 20549-0102. Finally, you may call Madison Mosaic at 800-368-3195 if you would like a copy of Form N-Q and we will mail one to you at no charge.

Discussion of Contract Renewal (Unaudited)

The Trustees considered a number of factors when the Board most recently approved the advisory contract between the Advisor and the Trust in July 2008. Rather than providing you with a list of factors or conclusory statements that explained the Board’s decisionmaking process, the following discussion is designed to describe what you would have seen and heard if you had been at the Trust’s Board meeting when it most recently approved the advisory contract:

With regard to the nature, extent and quality of the services to be provided by the Advisor, the Board reviewed the biographies and tenure of the personnel involved in fund management. They recognized the wide array of investment professionals employed by the firm. The officers of the investment advisor discussed the firm’s ongoing investment philosophies and strategies intended to provide superior performance consistent with each funds’ investment objectives under various market scenarios. The Trustees also noted their familiarity with the Advisor due to the Advisor’s history of providing advisory services to the Madison Mosaic family.

The Board also discussed the quality of services provided by the transfer agent, US Bancorp Fund Services, LLC. The Advisor reported that the transfer agent has routinely ranked at or near the top in customer service surveys for third party transfer agents. The Independent Trustees noted that they had just completed a satisfactory on-site review of the transfer agent’s facilities and operations, including its main operations in Milwaukee, Wisconsin and its emergency recovery center located in West Allis, Wisconsin.

With regard to the investment performance of each fund and the investment Advisor, the Board reviewed current performance information. They discussed the reasons for both outperformance and underperformance compared with peer groups and applicable indices. With regard to Madison Mosaic Income Trust fund performance, the Advisor explained its active bond management style and its goal of protecting shareholders during periods of rising interest rates. The Advisor explained that, in the long-term, it believes this philosophy is in the best interest of fixed-income fund shareholders and is in accordance with applicable prospectus disclosures of investment objectives and policies for the Trust’s funds. The Advisor reported to the Board that these funds were performing in accordance with their stated investment objectives and policies.

The Board engaged in a comprehensive discussion of fund performance and market conditions.

The officers of the Advisor also discussed the Advisor’s methodology for arriving at the peer groups and indices used for performance comparisons. The Board reviewed both short-term and long-term standardized performance, i.e. one, five and ten year (or since inception) average annual total returns for each fund and comparable funds, as well as standardized yields for fixed income funds.

With regard to the costs of the services to be provided and the profits to be realized by the investment Advisor and its affiliates from the relationship with each Mosaic fund, the Board reviewed the expense ratios for each Madison Mosaic fund compared with funds with similar investment objectives and of similar size. The Board reviewed such comparisons based on a variety of peer group comparisons from data extracted from industry databases including comparison to funds with similar investment objectives based on their broad asset category and total asset size, as well as from data provided directly by funds that most resembled each portfolio’s asset size and investment objective for the last year. The Advisor discussed the objective manner by which Madison Mosaic fees were compared to fees in the industry.

As in past years, the Trustees recognized that each Madison Mosaic fund’s fee structure should be reviewed based on total fund expense ratio rather than simply comparing advisory fees to other advisory fees in light of the simple expense structure (i.e. a single advisory and a single services fee, with only the fixed fees of the Independent Trustees and auditors paid separately). As such, the Board focused its attention on the total expense ratios paid by other funds of similar size and category when considering the individual components of the expense ratios. The Board also recognized that investors are often required to pay distribution fees (loads) over and above the amounts identified in the expense ratio

20 Annual Report • December 31, 2008

comparison reviewed by the Board, whereas no such fees are paid by Madison Mosaic shareholders.

The Trustees sought to ensure that fees were adequate so that the Advisor did not neglect its management responsibilities for the Trusts in favor of more “profitable” accounts. At the same time, the Trustees sought to ensure that compensation paid to the Advisor was not unreasonably high. The Board reviewed materials demonstrating that although the Advisor is compensated for a variety of the administrative services it provides or arranges to provide pursuant to its Services Agreements, such compensation generally does not cover all costs due to the relatively small size of the funds in the Madison Mosaic family. Administrative, operational, regulatory and compliance fees and costs in excess of the Services Agreement fees are paid by the Advisor from its investment advisory fees earned. For these reasons, the Trustees recognized that examination of total expense ratios compared to those of other investment companies was more meaningful than a simple comparison of basic “investment management only” fee schedules.

In reviewing costs and profits, the Trustees recognized that Madison Mosaic Funds are to a certain extent “subsidized” by the greater Madison Investment Advisors, Inc. organization because the salaries of all portfolio management personnel, trading desk personnel, corporate accounting personnel and employees of the Advisor who served as officers of the funds, as well as facility costs (rent), could not be supported by fees received from the funds alone. However, although Madison Mosaic represents only a few hundred million dollars of assets out of the multiple billions of assets managed by the Madison Investment Advisors, Inc. organization in Wisconsin at the time of the meeting, the Madison Mosaic family is profitable to the Advisor at the margin because such salaries and fixed costs are proportionately paid from revenue generated by management of the remaining assets. The Trustees reviewed a profitability analysis of the funds and recognized that, as explained above, full salaries of all portfolio managers had not been factored into the analyses. As a result, although the fees paid by each respective Madison Mosaic fund at its present size might not be sufficient to profitably support a “stand-alone” mutual fund complex, the funds are reasonably profitable to the Advisor as part of its larger, diversified organization. The Trustees also recognized that Madison Mosaic’s reputation benefited the Advisor’s reputation in attracting separately managed accounts and other investment advisory business. In sum, the Trustees recognized that Madison Mosaic Funds are important to the Advisor, are managed with the attention given to other firm clients and are not treated as “loss leaders.”

The Board engaged in a general and detailed discussion regarding fees. The Trustees recognized that the Advisor had materially lowered fees in connection with the Core Bond and Government Funds in order to help make them more competitive with larger funds. As part of the Board’s review of the costs of services and the profits to be realized by the Advisor, the Board considered the reasonableness and propriety of the securities research and so-called “soft dollar” benefits, if any, that the Advisor receives in connection with brokerage transactions. The Trustees recognized that “soft-dollar” benefits were not generated by fixed-income transactions.

With regard to the extent to which economies of scale would be realized as a fund grows, the Trustees recognized that Madison Mosaic Funds, both individually and as a complex, remain small and that economies of scale would likely be addressed after funds see assets grow significantly beyond their current levels. In light of their size, the Trustees noted that at current asset levels, it was premature to discuss additional economies of scale.

Finally, the Board reviewed the role of Mosaic Funds Distributor, LLC. They noted that the Advisor pays all distribution expenses of Madison Mosaic Funds because the funds themselves do not pay distribution fees. Such expenses include FINRA regulatory fees and “blue sky” fees charged by state governments in order to permit the funds to be offered in the various United States jurisdictions.

Based on all of the material factors explained above, plus a number of other matters that the Trustees are generally required to consider under guidelines developed by the Securities and Exchange Commission, the Trustees concluded that the Advisor’s contract should be renewed for another year.

Madison Mosaic Income Trust 21

The Madison Mosaic Family of Mutual Funds

Madison Mosaic Equity Trust

Investors Fund

Balanced Fund

Mid-Cap Fund

Disciplined Equity Fund

Small/Mid-Cap Fund

Madison Institutional Equity Option Fund

Madison Mosaic Income Trust

Government Fund

Core Bond Fund

Institutional Bond Fund

Corporate Income Shares (COINS) Fund

Madison Mosaic Tax-Free Trust

Virginia Tax-Free Fund

Tax-Free National Fund

Madison Mosaic Government Money Market

For more complete information on any Madison Mosaic fund, including charges and expenses, request a prospectus by calling 1-800-368-3195. Read it carefully before you invest or send money. This document does not constitute an offering by the distributor in any jurisdiction in which such offering may not be lawfully made. Mosaic Funds Distributor, LLC.

TRANSER AGENT

Mosaic Funds

c/o US Bancorp Fund Services, LLC

P.O. Box 701

Milwaukee, WI 53201-0701

TELEPHONE NUMBERS

Shareholder Service

Toll-free nationwide: 888-670-3600

550 Science Drive

Madison, Wisconsin 53711

Madison Mosaic Funds

www.mosaicfunds.com

SEC File Number 811-3616

ANNUAL REPORT

December 31, 2008

Madison Mosaic

Income Trust

Institutional Bond Fund

Corporate Income Shares (COINS) Fund

(logo) Madison Mosaic Funds (TM)

www.mosaicfunds.com

Contents

Management’s Discussion of Fund Performance | |

Market Review | 1 |

Outlook | 1 |

Fund Overview | 2 |

Comparison of Changes in the Value of an Investment | 4 |

Report of Independent Registered Public Accounting Firm | 5 |

Portfolio of Investments | |

Institutional Bond Fund | 6 |

Corporate Income Shares (COINS) Fund | 8 |

Statements of Assets and Liabilities | 10 |

Statements of Operations | 11 |

Statements of Changes in Net Assets | 12 |

Financial Highlights | 13 |

Notes to Financial Statements | 14 |

Management Information | 18 |

Madison Mosaic Income Trust December 31, 2008

Management’s Discussion of Fund Performance

Market Review

Depending on where you were invested, the bond market of 2008 was the best or worst of times. Riskier bonds were hammered in the wake of a broad credit crunch, while a flight to safety lifted the returns of Treasuries. As the year progressed, the problems that began in the subprime mortgage area bloomed into a full fledged credit crisis. The credit crisis sent unexpected shock waves into virtually all areas of the global economy, sparking a worldwide economic slowdown eventually leading into global recession. As credit froze, highly leveraged investment firms began to spiral downward, and many financial firms that are household names found themselves on the brink—or over the brink—of insolvency. Meanwhile, many investment vehicles with plain vanilla names like “core bond” or “short term bond” ended the year with large losses due to investments in toxic bonds or through investments in firms whose fates where linked with the securitized market.

Countering the crisis in the financial sector was a series of significant, even historically unprecedented, federal interventions. Beginning in January the Federal Reserve made the first of a series of rate cuts, which by the December cut lowered the target federal funds rate to a range of 0% to 0.25%, the lowest in modern history. In addition to rate cuts, the Federal government injected massive stimulus into the financial system in order to provide a solid base from which to repair balance sheets and normalize credit markets. These federal interventions were headlines throughout the year, including: the bailout of Bear Stearns; what amounted to a federal acquisition of mortgage companies Fannie Mae and Freddie Mac; and the Congressional creation of the $700 billion TARP program. An additional large stimulus package is expected under the new presidential administration.

At the same time, high-quality bonds, particularly those issued by the U.S. government, reaped the rewards as investors fled to the safest instruments available. Not only did Treasuries have strong real returns, they looked tremendous compared to the losses that pummeled stock investors. The S&P 500 was down -37.0% for the year, while the major international market indices dropped more than -40% as well.

Within the bond market, there was a disparity in returns unlike any year in memory. For instance, the Barclays Capital indices (formerly Lehman Brothers indices) showed a gap from a 13.7% annual return for Treasuries to -26.2% for high-yield bonds. Within corporate bonds, returns varied from 8.1% for AAA rated bonds to -26.5% for bonds rated B and -44.3% for bonds rated one step lower at CAA. Many bond mutual funds stumbled as well, as the Lipper Indices showed average annual returns of -4.7% for Intermediate Investment Grade Funds, -4.1% for Inflation Protected Treasury Bond Funds, - -4.6% for Short Investment Grade Funds, and -2.3% for Intermediate Municipal Bond Funds.

Outlook

As we enter 2009, the U.S. economy, and most of the world, is mired in a severe recession. It is increasingly difficult to find reason for optimism in upcoming economic data. U.S. consumer confidence has fallen to generational lows. Manufacturers are paring back production and employment in anticipation of a prolonged recession. Unemployment rates are rising, and likely to rise further. Credit remains tight and is only available to the most worthy of borrowers.

The process of de-leveraging, begun in 2007, will likely continue well into 2009. The financial sector de-leveraging, while well-advanced, has more room to run. Private sector corporate de-leveraging will likely be a less troublesome issue, as non-financial corporate balance sheets remain in good shape. The process of consumer de-leveraging, we fear, is still in its early stages, and should only be magnified

Madison Mosaic Income Trust 1

Management's Discussion of Fund Performance (continued)

as the unemployment rate rises and the recession deepens.

There are bright spots, however. The monetary and fiscal stimulus brought to bear so far is staggering, and should eventually have its intended effect. Estimates of U.S. Government infusions into the banking industry alone are in the $1-$2 trillion range. And the $100 decline in the price of a barrel of crude could put up to $260 billion back in consumers’ pockets—a large stimulus in and of itself. After a gloomy first half, we expect the economy to begin to show modest signs of life in the second half of 2009.

Fund Overview

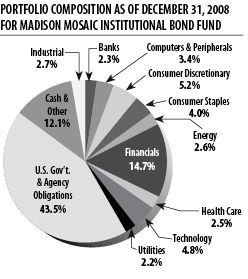

Institutional Bond Fund

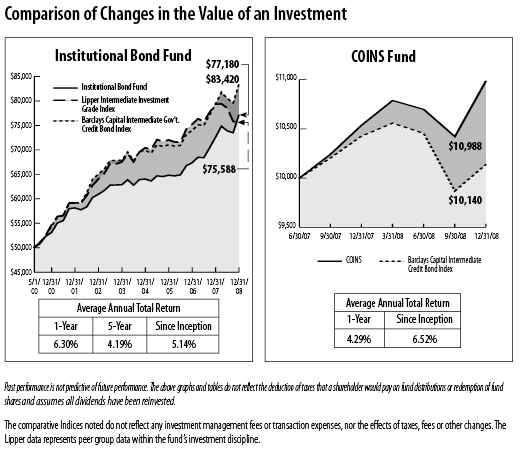

Mosaic Institutional Bond Fund had a 6.30% return for the annual period ended December 31, 2008. Over the same period, the Lipper Intermediate Investment Grade Index fell -4.71%. This performance gap was largely a quality and active management story, as the fund’s preference for high-quality bonds and avoidance of problem issues made a dramatic difference. The gap in returns between Institutional Bond and its peers—more than 11% for the year—indicates just how important security selection was in 2008. While many fund managers chased yield and bought bonds which were backed by suspect mortgages, we avoided these issues due to concerns over the state of the housing market, even though many sported top ratings from third party raters. Another positive factor in performance was the timing of a number of trades which took advantage of some of the major interest rate moves in a year characterized by exceptional volatility.

At period end, the Fund’s duration was 3.23 years, while its 30-day SEC yield was 3.12%. The duration of the Fund ended close to the 3.53 years where we started as we continue to pursue what we feel are conservative, sound management decisions which can produce strong returns without undue risk. The Fund began the period with 46.3% invested in investment-grade corporate bonds and ended the year with 44.4%. At period end, the Fund had 32.1% of the fund in Treasuries, and 11.4% in agency bonds. The fund’s largest holdings were in Treasury notes maturing between 2011 and 2017 and intermediate bonds issued by Freddie Mac and Fannie Mae.

TOP TEN HOLDINGS AS OF DECEMBER 31, 2008

FOR MADISON MOSAIC INSTITUTIONAL BOND FUND

% of net assets |

US Treasury Note, 4.875%, 2/15/12 | 6.49% |

US Treasury Note, 4.5%, 2/28/11 | 6.27% |

US Treasury Note, 4.5%, 5/15/17 | 5.45% |

US Treasury Note, 4.25%, 8/15/14 | 5.34% |

US Treasury Note, 4%, 11/15/12 | 4.12% |

Freddie Mac, 4.5%, 7/15/13 | 3.79% |

US Treasury Note, 3.625%, 1/15/10 | 3.60% |

Fannie Mae, 4.625%, 10/15/14 | 3.10% |

Freddie Mac, 5.125%, 7/15/12 | 2.82% |

United Parcel, 5.5%, 1/15/18 | 2.73% |

2 Annual Report • December 31, 2008

Management's Discussion of Fund Performance (continued)

Corporate Income Shares (COINS) Fund

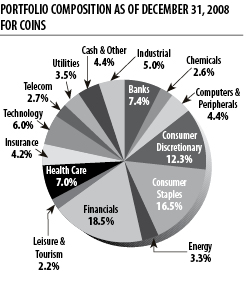

COINS is a corporate bond portfolio designed for exclusive use within separately managed accounts. COINS had a return of 4.29% for the one-year period ended December 31, 2008. This compares to the -2.76% return of the Barclays Capital Intermediate Credit Bond Index. This outperformance was largely a matter of security selection and quality, as COINS held significantly less exposure to lower-rated triple-B bonds than its benchmark and avoided problem issuers. The managers of COINS also kept exposure to longer-term and troubled financial bonds at a minimum. At the end of the period, the portfolio held a diversified portfolio of 39 corporate bonds with a composite quality rating of AA1 by Moody’s. The portfolio had an effective duration of 3.20 years, down from the period’s start 3.81 years, with a yield-to-maturity of 4.15%, compared to the period start of 4.61%. More than ninety-five percent of the portfolio was rated A or higher by Standard and Poor’s, with approximately 4.3% rated triple-B.

TOP TEN HOLDINGS AS OF DECEMBER 31, 2008

FOR COINS FUND

% of net assets |

Abbott Laboratories, 5.875%, 5/15/16 | 2.86% |

Coca-Cola Co., 5.35%, 11/15/17 | 2.85% |

Cisco Systems, Inc., 5.5%, 2/22/16 | 2.80% |

3M Company, 4.5%, 11/1/11 | 2.79% |

Sysco Corp., 5.25%, 2/12/18 | 2.68% |

General Electric Capital Corp., 5.4%, 2/15/17 | 2.63% |

Du Pont, 4.75%, 11/15/12 | 2.61% |

Household Finance Co., 6.375%, 10/15/11 | 2.60% |

Natl Rural Utilities, 4.75%, 3/1/14 | 2.45% |

American Express Co., 4.875%, 7/15/13 | 2.45% |

Madison Mosaic Income Trust 3

Management's Discussion of Fund Performance (concluded)

4 Annual Report • December 31, 2008

Madison Mosaic Income Trust December 31, 2008

Report of Independent Registered Public Accounting Firm

To the Board of Trustees and Shareholders of Madison Mosaic Income Trust:

We have audited the accompanying statements of assets and liabilities, including the portfolio of investments of the Madison Mosaic Income Trust (the “Trust”) including the Institutional Bond Fund and Corporate Income Shares Fund (COINS Fund) (the “Funds”), as of December 31, 2008 and the related statement of operations for the year then ended and the statements of changes in net assets for each of the two years in the period then ended and for the period from July 1, 2007 (commencement of operations) through December 31, 2008 for the COINS Fund, and the financial highlights for each of the five years in the period then ended and for the period from July 1, 2007 (commencement of operations) through December 31, 2008 for the COINS Fund. These financial statements and financial highlights are the responsibility of the Trust’s management. Our responsibility is to express an opinion on these financial statements based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. The Trust is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Trust’s internal control over financial reporting. Accordingly we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of December 31, 2008 by correspondence with the Funds’ custodian and brokers. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of the Funds as of December 31, 2008, and the results of their operations for the year then ended and the changes in their net assets for each of the two years in the period then ended and for the period from July 1, 2007 (commencement of operations) through December 31, 2008 for the COINS Fund, and financial highlights for each of the five years in the period then ended and for the period from July 1, 2007 (commencement of operations) through December 31, 2008 for the COINS Fund, in conformity with accounting principles generally accepted in the United States of America.

(signature)

Grant Thornton LLP

Chicago, Illinois

February 20, 2009

Madison Mosaic Income Trust 5

Madison Mosaic Income Trust December 31, 2008

Institutional Bond Fund - Portfolio of Investments

CREDIT RATING* | | PRINCIPAL AMOUNT | VALUE |

MOODY’S | S&P | |

| | CORPORATE DEBT SECURITIES: 44.4% of net assets | | |

| | | | |

| | BANKS: 2.3% | | |

Aa2 | A+ | Bank of America, 4.875%, 9/15/12 | $50,000 | $49,380 |

| | | | |

| | COMPUTERS & PERIPHERAL: 3.4% | | |

A2 | A | Hewlett-Packard Co., 5.25%, 3/1/12 | 35,000 | 36,190 |

A1 | A+ | IBM Corp, 4.75%, 11/29/12 | 35,000 | 36,180 |

| | | | |

| | CONSUMER DISCRETIONARY: 5.2% | | |

A2 | A+ | Target Corp., 5.875%, 3/1/12 | 55,000 | 55,875 |

Aa2 | AA | Wal-Mart Stores, Inc., 4.55%, 5/1/13 | 55,000 | 56,999 |

| | | | |

| | CONSUMER STAPLES: 4.0% | | |

Aa2 | A+ | Pepsico Inc., 4.65%, 2/15/13 | 50,000 | 51,457 |

A1 | A+ | Sysco Corp., 5.25%, 2/12/18 | 35,000 | 35,539 |

| | | | |

| | ENERGY: 2.6% | | |

A1 | A | Conoco Funding Co., 6.35%, 10/15/11 | 35,000 | 36,844 |

Aa1 | AA | Texaco Capital Inc., 5.5%, 1/15/09 | 20,000 | 19,991 |

| | | | |

| | FINANCIALS: 14.7% | | |