OMB APPROVAL

OMB Number: 3235-0570

Expires: September 30, 2007

Estimated average burden hours per response...19.4

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-3616

Madison Mosaic Income Trust

(Exact name of registrant as specified in charter)

550 Science Drive, Madison, WI 53711

(Address of principal executive offices)(Zip code)

W. Richard Mason

Madison/Mosaic Legal and Compliance Department

8777 N. Gainey Center Drive, Suite 220

Scottsdale, AZ 85258

(Name and address of agent for service)

Registrant's telephone number, including area code: 608-274-0300

Date of fiscal year end: December 31

Date of reporting period: December 31, 2006

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspoection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. s 3507.

Item 1. Reports to Shareholders.

ANNUAL REPORT

December 31, 2006

Madison Mosaic Income Trust

- Intermediate Income Fund

- Government Fund

(logo) Madison Mosaic Funds (TM)

www.mosaicfunds.com

Contents

| Management's Discussion of Fund Performance | |

| Review of Period | 1 |

| Outlook | 1 |

| Fund Overview | 2 |

| Comparison of Changes in the Value of a $10,000 Investment | 4 |

| Report of Independent Registered Public Accounting Firm | 5 |

| Portfolio of Investments | |

| Government Fund | 6 |

| Intermediate Income Fund | 7 |

| Statements of Assets and Liabilities | 9 |

| Statements of Operations | 10 |

| Statements of Changes in Net Assets | 11 |

| Financial Highlights | 12 |

| Notes to Financial Statements | 13 |

| Management Information | 17 |

Madison Mosaic Income Trust December 31, 2006

Management's Discussion of Fund Performance

Review of Period

We saw strong economic growth in 2006. While some of the initial 2006 growth can be attributed to a snap-back from the hurricane depressed levels seen in the fourth quarter of 2005, the economy was still showing signs of strength at the end of the year.

Meanwhile, inflation pressures remained in place. Industrial commodity prices rose across the board, with inputs such as zinc and copper reaching new highs. Capacity utilization, which is a measure of how much slack exists in industrial production, moved above 82%, a level that has traditionally been inflationary. Rising input prices, higher capacity utilization and tighter labor markets are all classic signs of a maturing economic expansion.

One of the notable events of the period was the retirement of long-time Federal Reserve Chairman Alan Greenspan, and the beginning of the Bernanke era. Rates were raised twice in the first quarter under Greenspan. Under new Fed Chairman, Ben Bernanke, the Federal Reserve raised short-term rates two more times during the second quarter of 2006, bringing the period-end rate to 5.25%, and then held firm for the remainder of the year.

Although interest rates were little changed from start to finish in 2006, the path of the benchmark 10-year Treasury bond was hardly straight. Yields increased in the first half of the year as the Fed continued its policy of raising the Federal funds rate. However, once the Fed paused halfway through the year, the marketplace became "data dependent." As the economy showed signs of cooling, rates retraced their earlier rise. Fed Chairman Bernanke has proved his resolve to remain hawkish on inflation, but appears confident that if the economy slows, pricing pressures will ease. More recent data may prove a difficult test for the central bank as inflation pressures remain and economic data has shown signs of acceleration.

Outlook

Our research indicates that the economy is, in fact, slowing. However, we would note that GDP growth is slowing relative to the heady pace set in the post-hurricane first quarter of 2006. Since that quarter, readings have come in at a more trend-like pace. Much of the slowing has been driven by a weakening housing market and slumping auto sales.

The rest of the economy, however, has remained strong and real estate has shown signs of bottoming recently. Furthermore, stocks have shown solid gains, gasoline prices are lower, and mortgage rates are down. All of these are potential drivers of accelerated consumer spending going forward.

Herein lies the dilemma for the Federal Reserve. Although the economy showed signs of slowing in the third quarter and early in the fourth, they must now evaluate the pockets of strength. Primarily, the employment situation remains conducive to a healthy economy. Unemployment has been stuck in the 4.5% range and wages have risen approximately 4.2% year-over-year. Therefore, the Fed will need to evaluate how much the economy is actually cooling and whether or not it is enough to keep inflation tame.

Inflation remains the Fed's primary area of focus. Although commodity prices backed off early in the second half of the year, they have recently crept back up. Furthermore, the Consumer Price Index (both headline and core) continues to advance at a 2.5% pace. This is (and has been for some time) above the Fed's stated comfort level. In light of this and recent signs of strength, it appears the market has gotten ahead of itself. Continued signs of inflation and the market's recognition that the Fed will not be easing soon are the biggest risks to rates.

Madison Mosaic Income Trust 1

Management's Discussion of Fund Performance (continued)

Fund Overview

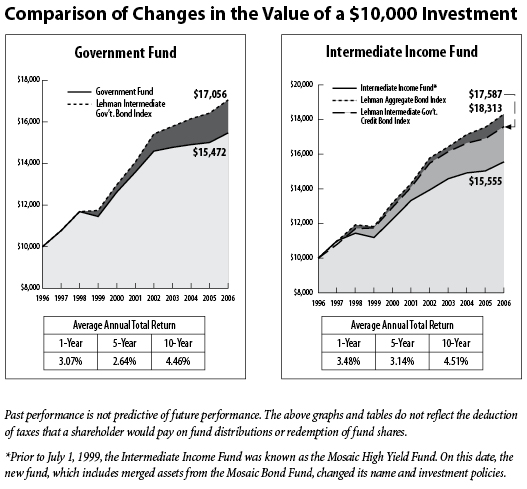

Madison Mosaic Government Fund

Madison Mosaic Government Fund returned 3.07% for the annual period ended December 31, 2006. This return trailed the fund's peers, as the Lipper Intermediate Government Fund Index rose 3.71%. The fund outperformed its peers over the first half of the year as rates rose and bond valuations fell, but trailed in the second half as investors began to look forward to Federal Reserve easing. These return differentials largely reflect management's defensive positioning of the portfolio. When interest rates rise, bond valuations fall, and shorter bonds typically retain their value far better than longer bonds. The fund's 30-day SEC yield at period end was 3.56 %, with an effective duration of 2.82 years, just slightly longer than the 2.79 years at the period's start.

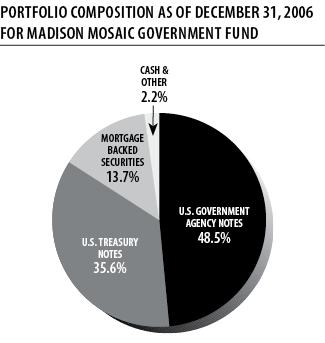

Madison Mosaic Government held 35.6% in Treasuries, 48.5% in government agency notes, with the remainder in mortgage-backed securities and cash. The fund's largest positions during this twelve-month period were short to intermediate duration bonds issued by the U.S. Treasury and Freddie Mac.

TOP TEN HOLDINGS AS OF DECEMBER 31, 2006 FOR MADISON MOSAIC GOVERNMENT FUND

% of net assets | |

| Freddie Mac, 5.5%, 9/15/11 | 10.05% |

| US Treasury Note, 4.75%, 11/15/08 | 8.99% |

| Freddie Mac, 5.75%, 4/15/08 | 8.25% |

| Freddie Mac, 5.125%, 10/15/08 | 8.20% |

| US Treasury Note, 4%, 6/15/09 | 7.24% |

| US Treasury Note, 4.25%, 8/15/14 | 6.67% |

| Federal Home Loan Bank, 4.1%, 6/13/08 | 6.46% |

| US Treasury Note, 4%, 3/15/10 | 5.61% |

| US Treasury Note, 5.125%, 6/30/11 | 5.49% |

| Freddie Mac, 5%, 10/18/10 | 5.08% |

Madison Mosaic Intermediate Income Fund

Madison Mosaic Intermediate Income Fund rose 3.48% for the twelve months ended December 31, 2006. Over the same period, the Lipper Intermediate Investment Grade Index rose 4.47%. The performance gap was due to our credit and yield curve strategy. During the year, the fund decreased the credit weighting due to valuation concerns, the aging of the economic cycle and a significant increase in shareholder friendly activity. The fund also increased the credit quality by buying higher rated assets as the credit curve continued to tighten.

2 Annual Report - December 31, 2006

Management's Discussion of Fund Performance (continued)

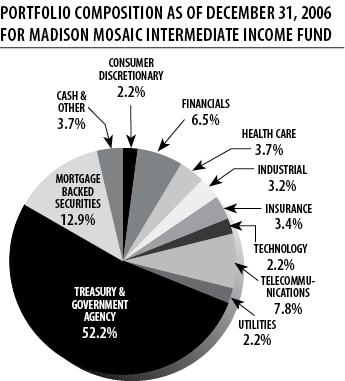

In addition, the fund began to reposition assets along the yield curve to take advantage of a steeper yield curve in 2007. These strategies had a negative impact on performance during the year. On a positive note, the duration or interest rate sensitivity of the fund was lower then the market, which protected investors as yields rose during the year. At periods end, the fund's duration was 4.04 years, while the 30-day SEC yield was 3.97%. The duration of the fund rose during the period, from a start point of 2.92 years. In addition, we are entering the late stages of the economic cycle and the Federal Reserve is likely to hold rates steady which means we are nearing the end of the rate cycle. The mortgaged-backed sector was also increased because valuations looked more attractive then the credit sector. We reduced the credit sector to 31.2% from 59.9% and increased our exposure to government and agency notes to 52.2%.

Intermediate Income can invest as much as 35% in lower-rated securities. Although high-yield bonds outperformed higher-grade bonds over the past year, we trimmed our exposure, in line with our general move from corporates to governments. The fund began the period with 11.1% of its assets in Ba/BB bonds, the highest rating among bonds in the high yield (or "junk bond") category, and ended the period with no exposure to bonds of this rating or lower. This reduction reflects our cautious outlook for corporate bonds in general, and a sense that the superior returns for low-quality bonds are near the end of a cycle.

TOP TEN HOLDINGS AS OF DECEMBER 31, 2006 FOR MADISON MOSAIC INTERMEDIATE INCOME FUND

% of net assets | |

| Federal Home Loan Bank, 4.1%, 6/13/08 | 10.70% |

| US Treasury Note, 5.125%, 6/30/11 | 8.83% |

| US Treasury Note, 4.25%, 1/15/11 | 8.54% |

| US Treasury Note, 4%, 3/15/10 | 7.97% |

| US Treasury Note, 4.25%, 8/15/14 | 5.37% |

| Freddie Mac, 5.5%, 9/15/11 | 5.22% |

| AT&T Broadband, 8.375%, 3/15/13 | 4.48% |

| United Healthcare Group, 5%, 8/15/14 | 3.69% |

| FNMA MBS #745275, 5%, 2/1/36 | 3.45% |

| Markel Corp., 6.8%, 2/15/13 | 3.38% |

Madison Mosaic Income Trust 3

Management's Discussion of Fund Performance (concluded)

4 Annual Report - December 31, 2006

Madison Mosaic Income Trust December 31, 2006

Report of Independent Registered Public Accounting Firm

To the Board of Trustees and Shareholders of Madison Mosaic Income Trust:

We have audited the accompanying statements of assets and liabilities, including the portfolios of investments of the Madison Mosaic Income Trust (the "Trust"), including the Government Fund and Intermediate Income Fund (collectively, the "Funds"), as of December 31, 2006 and the related statements of operations for the year then ended and the statements of changes in net assets for each of the two years in the period then ended and the financial highlights for each of the three years in the period then ended. These financial statements and financial highlights are the responsibility of the Trust's management. Our responsibility is to express an opinion on these financial statements based on our audits. The financial highlights for each of the two years in the period ended December 31, 2003, were audited by other auditors. Those auditors expressed an unqualified opinion on those financial highlights in their report dated February 14, 2004.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. The Trust is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audit included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Trust's internal control over financial reporting. Accordingly we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of December 31, 2006 by correspondence with the Funds' custodian and brokers. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of each of the Funds constituting the Trust as of December 31, 2006, and the results of their operations for the year then ended and the changes in their net assets for each of the two years in the period then ended and financial highlights for each of the three years in the period then ended, in conformity with accounting principles generally accepted in the United States of America.

Grant Thornton LLP

(signature)

Chicago, Illinois

February 2, 2007

Madison Mosaic Income Trust 5

Madison Mosaic Income Trust December 31, 2006

Government Fund - Portfolio of Investments

| CREDIT RATING* | PRINCIPAL AMOUNT | VALUE | ||

| MOODY'S | S&P | |||

| U.S. GOVERNMENT & AGENCY OBLIGATIONS: 97.8% of net assets | ||||

| U.S. GOVERNMENT AGENCY NOTES: 48.5% | ||||

| Aaa | AAA | Federal Home Loan Bank, 4.1%, 6/13/08 | $200,000 | $197,301 |

| Aaa | AAA | Fannie Mae, 6.625%, 11/15/10 | 105,000 | 111,296 |

| Aaa | AAA | Fannie Mae, 6%, 5/15/11 | 100,000 | 104,223 |

| Aaa | AAA | Fannie Mae, 6.125%, 3/15/12 | 100,000 | 105,411 |

| Aaa | AAA | Freddie Mac, 5.75%, 4/15/08 | 250,000 | 251,925 |

| Aaa | AAA | Freddie Mac, 5.125%, 10/15/08 | 250,000 | 250,426 |

| Aaa | AAA | Freddie Mac, 5%, 10/18/10 | 155,000 | 155,195 |

| Aaa | AAA | Freddie Mac, 5.5%, 9/15/11 | 300,000 | 307,032 |

| U.S. TREASURY NOTES: 35.6% | ||||

| Aaa | AAA | US Treasury Notes, 4.375%, 12/31/07 | 50,000 | 49,709 |

| Aaa | AAA | US Treasury Notes, 4.75%, 11/15/08 | 275,000 | 274,732 |

| Aaa | AAA | US Treasury Notes, 4%, 6/15/09 | 225,000 | 221,194 |

| Aaa | AAA | US Treasury Notes, 4%, 3/15/10 | 175,000 | 171,384 |

| Aaa | AAA | US Treasury Notes, 5.125%, 6/30/11 | 165,000 | 167,836 |

| Aaa | AAA | US Treasury Notes, 4.25%, 8/15/14 | 210,000 | 203,913 |

| MORTGAGE BACKED SECURITIES: 13.7% | ||||

| Aaa | AAA | Fannie Mae, Mortgage Pool #555345, 5.5%, 2/1/18 | 72,093 | 72,323 |

| Aaa | AAA | Fannie Mae, Mortgage Pool #555545, 5%, 6/1/18 | 117,370 | 115,679 |

| Aaa | AAA | Fannie Mae, Mortgage Pool #636758, 6.5%, 5/1/32 | 31,005 | 31,725 |

| Aaa | AAA | Fannie Mae, Mortgage Pool #254346, 6.5%, 6/1/32 | 26,478 | 27,093 |

| Aaa | AAA | Fannie Mae, Mortgage Pool #254405, 6%, 8/1/32 | 50,871 | 51,352 |

| Aaa | AAA | Freddie Mac, Mortgage Pool, Gold Pass Through Certificates #E57247, 6.5%, 3/1/09 | 17,344 | 17,590 |

| Aaa | AAA | Freddie Mac, Mortgage Pool, Gold Pass Through Certificates #E90778, 5.5%, 8/1/17 | 54,948 | 55,058 |

| Aaa | AAA | Freddie Mac, Mortgage Pool, Gold Pass Through Certificates #C01364, 6.5%, 6/1/32 | 29,571 | 30,245 |

| Aaa | AAA | Government National Mortgage Association II, Guaranteed Pass Through Certificates #2483, 7%, 9/20/27 | 15,487 | 15,964 |

| TOTAL U.S. GOVERNMENT & AGENCY OBLIGATIONS (Cost $3,028,553) | $2,988,606 | |||

| REPURCHASE AGREEMENT: 1.2% of net assetsWith Morgan Stanley and Company issued 12/29/06 at 4.65%, due 1/3/07, collateralized by $38,956 in United States Treasury Notes due 11/15/18. Proceeds at maturity are $38,025 (Cost $38,000). | $38,000 | |||

| TOTAL INVESTMENTS: 99.0% of net assets (Cost $3,066,553) | $3,026,606 | |||

| CASH AND RECEIVABLES LESS LIABILITIES: 1.0% of net assets | 28,756 | |||

| NET ASSETS: 100% | $3,055,362 | |||

The Notes to Financial Statements are an integral part of these statements.

6 Annual Report - December 31, 2006

Madison Mosaic Income Trust December 31, 2006

Intermediate Income Fund - Portfolio of Investments

| CREDIT RATING* | PRINCIPAL AMOUNT | VALUE | ||

| MOODY'S | S&P | |||

| CORPORATE DEBT SECURITIES: 31.2% of net assets | ||||

| CONSUMER DISCRETIONARY: 2.2% | ||||

| Aa2 | AA | Wal-Mart Stores Inc., 4.75%, 8/15/10 | $100,000 | $98,836 |

| FINANCIALS: 6.5% | ||||

| Aa3 | AA- | Goldman Sachs, 5.75%, 10/1/16 | 100,000 | 101,754 |

| Aa3 | AA- | HSBC Finance Corp., 5.5%, 1/19/16 | 100,000 | 100,649 |

| A1 | AA- | International Lease Finance, 4.875%, 9/1/10 | 100,000 | 98,371 |

| HEALTH CARE: 3.7% | ||||

| A3 | A | United Healthcare Group, 5%, 8/15/14 | 175,000 | 169,910 |

| INDUSTRIAL: 3.2% | ||||

| Baa3 | BBB- | Lubrizol Corp., 4.625%, 10/1/09 | 150,000 | 147,235 |

| INSURANCE: 3.4% | ||||

| Baa3 | BBB- | Markel Corp., 6.8%, 2/15/13 | 150,000 | 155,950 |

| TECHNOLOGY: 2.2% | ||||

| A1 | A+ | CISCO Systems, 5.5%, 2/22/16 | 100,000 | 100,242 |

| TELECOMMUNICATIONS: 7.8% | ||||

| Baa2 | BBB+ | AT&T Broadband, 8.375%, 3/15/13 | 181,000 | 206,424 |

| Baa1 | A | Verizon New England, 6.5%, 9/15/11 | 150,000 | 154,375 |

| UTILITIES: 2.2% | ||||

| Baa2 | BBB | Dominion Resources Inc., 5.7%, 9/17/12 | 75,000 | 75,942 |

| A2 | A- | Wisconsin Power & Light, 7.625%, 3/1/10 | 25,000 | 26,607 |

| TOTAL CORPORATE DEBT SECURITIES (Cost $1,418,308) | $1,436,295 | |||

The Notes to Financial Statements are an integral part of these statements.

Madison Mosaic Income Trust 7

Intermediate Income Fund - Portfolio of Investments - December 31, 2006 (concluded)

| CREDIT RATING* | PRINCIPAL AMOUNT | VALUE | ||

| MOODY'S | S&P | |||

| MORTGAGE BACKED SECURITIES: 12.9% of net assets | ||||

| Aaa | AAA | Federal National Mortgage Association, Mortgage Pool #636758, 6.5%, 5/1/32 | 41,340 | 42,300 |

| Aaa | AAA | Federal National Mortgage Association, Mortgage Pool #725341, 5%, 2/1/19 | 92,049 | 90,724 |

| Aaa | AAA | Federal National Mortgage Association, Mortgage Pool #745275, 5%, 2/1/36 | 164,794 | 159,200 |

| Aaa | AAA | Federal National Mortgage Association, Mortgage Pool #902070, 6%, 12/1/36 | 150,000 | 151,062 |

| Aaa | AAA | Federal National Mortgage Association, Mortgage Pool #903002, 6%, 12/1/36 | 149,870 | 150,932 |

| TOTAL MORTGAGE BACKED SECURITIES (Cost $597,590) | $594,218 | |||

| U.S. GOVERNMENT & AGENCY OBLIGATIONS: 52.2% of net assets | ||||

| Aaa | AAA | Federal Home Loan Bank, 4.1%, 6/13/08 | 500,000 | 493,253 |

| Aaa | AAA | Freddie Mac, 5%, 10/18/10 | 150,000 | 150,189 |

| Aaa | AAA | Freddie Mac, 5.5%, 9/15/11 | 235,000 | 240,508 |

| Aaa | AAA | US Treasury Note, 4.0%, 3/15/10 | 375,000 | 367,251 |

| Aaa | AAA | US Treasury Note, 4.25%, 1/15/11 | 400,000 | 393,500 |

| Aaa | AAA | US Treasury Note, 5.125%, 6/30/11 | 400,000 | 406,875 |

| Aaa | AAA | US Treasury Note, 4.25%, 8/15/14 | 255,000 | 247,609 |

| Aaa | AAA | US Treasury Note, 5.375%, 2/15/31 | 100,000 | 107,149 |

| TOTAL U.S. GOVERNMENT & AGENCY OBLIGATIONS (Cost $2,417,265) | $2,406,334 | |||

| REPURCHASE AGREEMENT: 0.2% of net assets | ||||

| With Morgan Stanley and Company issued 12/29/06 at 4.65%, due 1/3/07, collateralized by $10,252 in United States Treasury Notes due 11/15/18. Proceeds at maturity are $10,006 (Cost $10,000). | 10,000 | |||

| TOTAL INVESTMENTS: 96.5% of net assets (Cost $4,443,163) | $4,446,847 | |||

| CASH AND RECEIVABLES LESS LIABILITIES: 3.5% of net assets | 162,678 | |||

| NET ASSETS: 100% | $4,609,525 | |||

Notes to the Portfolio of Investments:

* – Unaudited; Moody's – Moody's Investor Services, Inc.; S&P – Standard & Poor's Corporation

The Notes to Financial Statements are an integral part of these statements.

8 Annual Report - December 31, 2006

Madison Mosaic Income Trust December 31, 2006

Statements of Assets and Liabilities

Government Fund | Intermediate Income Fund | |

| ASSETS | ||

| Investments, at value (Note 1 and 2) | ||

| Investment securities | $2,988,606 | $4,436,847 |

| Repurchase agreements | 38,000 | 10,000 |

| Total investments* | 3,026,606 | 4,446,847 |

| Cash | 812 | 807 |

| Receivables | ||

| Investment securities sold | -- | 757,167 |

| Interest | 30,976 | 65,437 |

| Total assets | 3,058,394 | 5,270,258 |

| LIABILITIES | ||

| Payables | ||

| Investment securities purchased | -- | 637,141 |

| Dividends | 1,042 | 1,647 |

| Capital shares redeemed | 107 | 19,349 |

| Independent trustee fees | 250 | 250 |

| Auditor fees | 1,633 | 2,346 |

| Total liabilities | 3,032 | 660,733 |

| NET ASSETS | $3,055,362 | $4,609,525 |

| Net assets consists of: | ||

| Paid in capital | $3,160,167 | $5,487,636 |

| Accumulated net realized losses | (64,858) | (881,795) |

| Net unrealized appreciation (depreciation) on investments | (39,947) | 3,684 |

| Net Assets | $3,055,362 | $4,609,525 |

| CAPITAL SHARES OUTSTANDING An unlimited number of capital shares, without par value, are authorized (Note 7) | 307,238 | 716,169 |

| NET ASSET VALUE PER SHARE | $9.94 | $6.44 |

| *INVESTMENT SECURITIES, AT COST | $3,066,553 | $4,443,163 |

The Notes to Financial Statements are an integral part of these statements.

Madison Mosaic Income Trust 9

Madison Mosaic Income Trust

Statements of Operations

For the year ended December 31, 2006

Government Fund | Intermediate Income Fund | |

| INVESTMENT INCOME (Note 1) | ||

| Interest income | $136,448 | $248,151 |

| EXPENSES (Notes 3 and 5) | ||

| Investment advisory fees | 19,828 | 32,363 |

| Other expenses: | ||

| Service agreement fees | 13,484 | 18,900 |

| Independent trustee fees | 1,000 | 1,000 |

| Auditor fees | 3,500 | 4,500 |

| Total other expenses | 17,984 | 24,400 |

| Total expenses | 37,812 | 56,763 |

| NET INVESTMENT INCOME | 98,636 | 191,388 |

| REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS | ||

| Net realized loss on investments | (14,010) | (29,087) |

| Change in net unrealized appreciation of investments | 13,457 | 11,788 |

| NET LOSS ON INVESTMENTS | (553) | (17,299) |

| TOTAL INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | $98,083 | $174,089 |

10 Annual Report - December 31, 2006

Madison Mosaic Income Trust

Statements of Changes in Net Assets

For the period indicated

Government Fund | Intermediate Income Fund | |||

Year Ended December 31, | Year Ended December 31, | |||

2006 | 2005 | 2006 | 2005 | |

| INCREASE (DECREASE) IN NET ASSETS RESULTING FROM OPERATIONS | ||||

| Net investment income | $98,636 | $104,422 | $191,388 | $205,476 |

| Net realized loss on investments | (14,010) | (33,374) | (29,087) | (19,269) |

| Net unrealized appreciation (depreciation) on investments | 13,457 | (60,384) | 11,788 | (144,338) |

| Total increase in net assets resulting from operations | 98,083 | 10,664 | 174,089 | 41,869 |

| DISTRIBUTION TO SHAREHOLDERS FROM NET INVESTMENT INCOME | (98,636) | (104,422) | (191,388) | (205,476) |

| CAPITAL SHARE TRANSACTIONS (Note 7) | (191,990) | (1,790,351) | (975,135) | (275,711) |

| TOTAL DECREASE IN NET ASSETS | (192,543) | (1,884,109) | (992,434) | (439,318) |

| NET ASSETS | ||||

| Beginning of period | $3,247,905 | $5,132,014 | $5,601,959 | $6,041,277 |

| End of period | $3,055,362 | $3,247,905 | $4,609,525 | $5,601,959 |

The Notes to Financial Statements are an integral part of these statements.

Madison Mosaic Income Trust 11

Madison Mosaic Income Trust

Financial Highlights

Selected data for a share outstanding for the periods indicated

GOVERNMENT FUND

Year Ended December 31, | |||||

2006 | 2005 | 2004 | 2003 | 2002 | |

| Net asset value, beginning of year | $9.95 | $10.16 | $10.36 | $10.58 | $10.24 |

| Investment operations: | |||||

| Net investment income | 0.31 | 0.28 | 0.29 | 0.35 | 0.41 |

| Net realized and unrealized gain (loss) on investments | (0.01) | (0.21) | (0.20) | (0.22) | 0.34 |

| Total from investment operations | 0.30 | 0.07 | 0.09 | 0.13 | 0.75 |

| Less distributions from net investment income | (0.31) | (0.28) | (0.29) | (0.35) | (0.41) |

| Net asset value, end of year | $9.94 | $9.95 | $10.16 | $10.36 | $10.58 |

| Total return (%) | 3.07 | 0.69 | 0.89 | 1.24 | 7.45 |

| Ratios and supplemental data | |||||

| Net assets, end of year (in thousands) | $3,055 | $3,248 | $5,132 | $5,356 | $5,939 |

| Ratio of expenses to average net assets (%) | 1.19 | 1.19 | 1.15 | 1.15 | 1.14 |

| Ratio of net investment income to average net assets (%) | 3.11 | 2.75 | 2.83 | 3.32 | 3.92 |

| Portfolio turnover (%) | 41 | 43 | 55 | 31 | 44 |

INTERMEDIATE INCOME FUND

Year Ended December 31, | |||||

2006 | 2005 | 2004 | 2003 | 2002 | |

| Net asset value, beginning of year | $6.46 | $6.64 | $6.71 | $6.66 | $6.67 |

| Investment operations: | |||||

| Net investment income | 0.24 | 0.23 | 0.22 | 0.25 | 0.30 |

| Net realized and unrealized gain (loss) on investments | (0.02) | (0.18) | (0.07) | 0.05 | (0.01) |

| Total from investment operations | 0.22 | 0.05 | 0.15 | 0.30 | 0.29 |

| Less distributions from net investment income | (0.24) | (0.23) | (0.22) | (0.25) | (0.30) |

| Net asset value, end of year | $6.44 | $6.46 | $6.64 | $6.71 | $6.66 |

| Total return (%) | 3.48 | 0.77 | 2.30 | 4.63 | 4.56 |

| Ratios and supplemental data | |||||

| Net assets, end of year (in thousands) | $4,610 | $5,602 | $6,041 | $6,428 | $6,839 |

| Ratio of expenses to average net assets (%) | 1.10 | 1.08 | 1.07 | 1.08 | 1.07 |

| Ratio of net investment income to average net assets (%) | 3.70 | 3.49 | 3.32 | 3.76 | 4.61 |

| Portfolio turnover (%) | 60 | 60 | 46 | 36 | 54 |

The Notes to Financial Statements are an integral part of these statements.

12 Annual Report - December 31, 2006

Madison Mosaic Income Trust December 31, 2006

Notes to Financial Statements

1. Summary of Significant Accounting Policies. Madison Mosaic Income Trust (the "Trust") is registered with the Securities and Exchange Commission under the Investment Company Act of 1940 as an open-end, diversified investment management company. This report contains information about two separate funds (the "Funds") whose objective is to receive and distribute bond income. The Government Fund invests in securities of the U.S. Government and its agencies. The Intermediate Income Fund invests in investment grade corporate, government and government agency fixed income securities. The Intermediate Income Fund may also invest a portion of its assets in securities rated as low as "B" by Moody's Investors Service, Inc. or Standard & Poor's Corporation. A third Trust portfolio, available to certain institutional investors (as defined in the fund's prospectus) presents its financial information in a separate report.

Securities Valuation: Repurchase agreements and other securities having maturities of 60 days or less are valued at amortized cost, which approximates market value. Securities having longer maturities, for which market quotations are readily available, are valued at the mean between their closing bid and ask prices. Securities for which market quotations are not readily available are valued at their fair value as determined in good faith under procedures approved by the Board of Trustees.

Investment Transactions: Investment transactions are recorded on a trade date basis. The cost of investments sold is determined on the identified cost basis for financial statement and federal income tax purposes.

Investment Income: Interest income is recorded on an accrual basis. Bond premium is amortized and original issue discount and market discount are accreted over the expected life of each applicable security using the effective interest method. Other income is accrued as earned.

Distribution of Income and Gains: Distributions are recorded on the ex-dividend date. Net investment income, determined as gross investment income less total expenses, is declared as a regular dividend and distributed to shareholders monthly. Capital gain distributions, if any, are declared and paid annually at year-end.

The tax character of distributions paid during 2006 and 2005 were as follows:

2006 | 2005 | |

| Government Fund: | ||

| Distributions paid from ordinary income | $98,636 | $104,422 |

| Intermediate Income Fund: | ||

| Distributions paid from ordinary income | $191,388 | $205,476 |

As of December 31, 2006, the components of distributable earnings on a tax basis were as follows:

| Government Fund: | |

| Accumulated net realized losses | $(64,729) |

| Net unrealized depreciation on investments | (40,076) |

$(104,805) | |

| Intermediate Income Fund: | |

| Accumulated net realized losses | $(875,091) |

| Net unrealized depreciation on investments | (3,020) |

$(878,111) |

Net realized gains or losses may differ for financial and tax reporting purposes as a result of loss deferrals related to wash sales and post-October transactions.

Income Tax: No provision is made for federal income taxes since it is the intention of the Trust to comply with the provisions of the Internal Revenue Code available to investment companies and to make the requisite distribution to shareholders of taxable income which will be sufficient to relieve it from all or substantially all federal income taxes. As of December 31, 2006, the Funds had available for

Madison Mosaic Income Trust 13

Notes to Financial Statements (continued)

federal income tax purposes the following unused capital loss carryovers:

| Expiration Date | Government Fund | Intermediate Income Fund |

| December 31, 2007 | $9,847 | $486,268 |

| December 31, 2008 | 5,458 | 89,747 |

| December 31, 2009 | -- | 12,901 |

| December 31, 2010 | -- | 243,364 |

| December 31, 2013 | 33,544 | 20,428 |

| December 31, 2014 | 15,880 | 22,383 |

Due to inherent differences in the recognition of income, expenses, and realized gains/losses under U.S. generally accepted accounting principles and federal income tax purposes, permanent differences between book and tax basis reporting for the 2006 fiscal year have been identified and appropriately reclassified. In the Intermediate Income Fund, permanent differences relating to the expiration of capital loss carryovers totaling $153,185 were reclassified from accumulated net realized losses to net paid in capital on shares of beneficial interest.

Use of Estimates: The preparation of the financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions. Such estimates affect the reported amounts of assets and liabilities and reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates.

2. Investments in Repurchase Agreements. When the Trust purchases securities under agreements to resell, the securities are held for safekeeping by the Trust's custodian bank as collateral. Should the market value of the securities purchased under such an agreement decrease below the principal amount to be received at the termination of the agreement plus accrued interest, the counterparty is required to place an equivalent amount of additional securities in safekeeping with the Trust's custodian bank. Pursuant to an Exemptive Order issued by the Securities and Exchange Commission, the Trust, along with other registered investment companies having Advisory and Services Agreements with the same advisor, transfers uninvested cash balances into a joint trading account. The aggregate balance in this joint trading account is invested in one or more consolidated repurchase agreements whose underlying securities are U.S. Treasury or federal agency obligations. As of December 31, 2006, the Government Fund had approximately a 0.1% interest and the Intermediate Income Fund had a less than 0.1% interest in the consolidated repurchase agreement of $27,381,000 collateralized by $28,069,660 in United States Treasury Notes. Proceeds at maturity were $27,398,684.

3. Investment Advisory Fees and Other Transactions with Affiliates. The investment advisor to the Trust, Madison Mosaic, LLC, a wholly owned subsidiary of Madison Investment Advisors, Inc. (collectively "the Advisor"), earns an advisory fee equal to 0.625% per annum of the average net assets of the Funds. The fees are accrued daily and are paid monthly.

4. Investment Transactions. Purchases and sales of securities (excluding short-term securities) for the year ended December 31, 2006 were as follows:

Purchases | Sales | |

| Government Fund: | ||

| U.S. Gov't securities | $1,254,478 | $1,289,054 |

| Other | -- | -- |

| Intermediate Income Fund: | ||

| U.S. Gov't securities | $2,494,414 | $1,577,537 |

| Other | 556,315 | 2,433,957 |

5. Other Expenses. Under a separate Services Agreement, the Advisor will provide or arrange for each Fund to have all other necessary operational and support services for a fee based on a percentage of average net assets. These fees are accrued daily and paid monthly. This percentage is 0.425% for the Government Fund and 0.365% for the Intermediate Income Fund.

The Funds also pay the expenses of the Funds' Independent Trustees and auditors directly. For the year ended December 31, 2006 these fees

14 Annual Report - December 31, 2006

Notes to Financial Statements (continued)

amounted to $1,000 and $3,500, respectively for the Government Fund and $1,000 and $4,500, respectively for the Intermediate Income Fund.

6. Aggregate Cost and Unrealized Appreciation (Depreciation). The aggregate cost for federal income tax purposes and the net unrealized appreciation (depreciation) are stated as follows as of December 31, 2006:

Government Fund | Intermediate Income Fund | |

| Aggregate Cost | $3,066,682 | $4,449,067 |

| Gross unrealized appreciation | 5,772 | 39,396 |

| Gross unrealized depreciation | (45,848) | (42,416) |

| Net unrealized depreciation | $(40,076) | $(3,020) |

7. Capital Share Transactions. An unlimited number of capital shares, without par value, are authorized. Transactions in capital shares for the following periods were:

Year Ended December 31, | ||

| Government Fund | 2006 | 2005 |

| In Dollars | ||

| Shares sold | $236,648 | $304,015 |

| Shares issued in reinvestment of dividends | 87,003 | 90,429 |

| Total shares issued | 323,651 | 394,444 |

| Shares redeemed | (515,641) | (2,184,795) |

| Net decrease | $(191,990) | $(1,790,351) |

| In Shares | ||

| Shares sold | 23,818 | 30,261 |

| Shares issued in reinvestment of dividends | 8,791 | 9,007 |

| Total shares issued | 32,609 | 39,268 |

| Shares redeemed | (51,921) | (217,768) |

| Net decrease | (19,312) | (178,500) |

| Intermediate Income Fund | Year Ended December 31, | |

2006 | 2005 | |

| In Dollars | ||

| Shares sold | $149,370 | $935,307 |

| Shares issued in reinvestment of dividends | 168,855 | 182,309 |

| Total shares issued | 318,225 | 1,117,616 |

| Shares redeemed | (1,293,360) | (1,393,327) |

| Net decrease | $(975,135) | $(275,711) |

| In Shares | ||

| Shares sold | 23,295 | 142,185 |

| Shares issued in reinvestment of dividends | 26,362 | 27,906 |

| Total shares issued | 49,657 | 170,091 |

| Shares redeemed | (201,330) | (212,454) |

| Net decrease | (151,673) | (42,363) |

8. Line of Credit. The Government Fund has a $1 million and the Intermediate Income Fund has a $1.25 million revolving credit facility with a bank for temporary emergency purposes, including the meeting of redemption requests that otherwise might require the untimely disposition of securities. The interest rate on the outstanding principal amount is equal to the prime rate less 1/2%. During the year ended December 31, 2006, neither Fund borrowed on their respective lines of credit.

9. New Accounting Pronouncements. In July 2006, the Financial Accounting Standards Board (FASB) issued FASB Interpretation No. 48, "Accounting for Uncertainty in Income Taxes – an Interpretation of FASB Statement No. 109" ("FIN 48"), which clarifies the accounting for uncertainty in tax positions taken or expected to be taken in a tax return. FIN 48 provides guidance on the measurement, recognition, classification and disclosure of tax positions, along with accounting for the related interest and penalties. FIN 48 is effective for fiscal years beginning after December 15, 2006, and is to be applied to all open tax years as of the date of effectiveness. The Fund is currently evaluating the impact, if any, of applying the various provisions of FIN 48.

Madison Mosaic Income Trust 15

Notes to Financial Statements (continued)

On September 15, 2006, the Financial Accounting Standards Board issued Standard No. 157, "Fair Value Measurements" ("FAS 157"). FAS 157 addresses how companies should measure fair value when specified assets and liabilities are measured at fair value for either recognition or disclosure purposes under generally accepted accounting principles (GAAP). FAS 157 is intended to make the measurement of fair value more consistent and comparable and improve disclosures about those measures. FAS 157 is effective for financial statements issued for fiscal years beginning after November 15, 2007. At this time, management believes the adoption of FAS 157 will have no material impact on the financial statements of the Fund.

Fund Expenses

Example: As a shareholder of the Funds, you incur two types of costs: (1) transaction costs and (2) ongoing costs, including Investment advisory fees and Other expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other mutual funds. See footnotes 3 and 5 above for an explanation of the types of costs charged by the Funds. This Example is based on an investment of $1,000 invested on July 1, 2006 and held for the six-months ended December 31, 2006.

Actual Expenses

The table below titled "Based on Actual Total Return" provides information about actual account values and actual expenses. You may use the information provided in this table, together with the amount you invested, to estimate the expenses that you paid over the period. To estimate the expenses you paid on your account, divide your ending account value by $1,000 (for example, an $8,500 ending account valued divided by $1,000 = 8.5), then multiply the result by the number under the heading entitled "Expenses Paid During the Period."

| Based on Actual Total Return1 | |||||

Actual Total Return2 | Beginning Account Value | Ending Account Value | Annualized Expense Ratio3 | Expenses Paid During the Period3 | |

| Government Fund | 3.21% | $1,000.00 | $1,032.07 | 1.19% | $6.14 |

| Intermediate Income Fund | 3.67% | $1,000.00 | $1,036.65 | 1.10% | $5.66 |

| 1For the six months ended December 31, 2006. 2Assumes reinvestment of all dividends and capital gains distributions, if any, at net asset value. 3Expenses are equal to the Funds' annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year, then divided by 365. | |||||

Hypothetical Example for Comparison Purposes

The table on the next page titled "Based on Hypothetical Total Return" provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio and an assumed rate of return of 5.00% per year before expenses, which is neither Fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use the information provided in this table to compare the ongoing costs of investing in either Fund and other funds. To do so, compare the 5.00% hypothetical example relating to the applicable Fund with the 5.00% hypothetical examples that appear in the shareholder reports of the other funds.

16 Annual Report - December 31, 2006

Notes to Financial Statements (concluded)

| Based on Hypothetical Total Return1 | |||||

Hypothetical Annualized Total Return | Beginning Account Value | Ending Account Value | Annualized Expense Ratio2 | Expenses Paid During the Period2 | |

| Government Fund | 5.00% | $1,000.00 | $1,025.47 | 1.19% | $6.09 |

| Intermediate Income Fund | 5.00% | $1,000.00 | $1,025.47 | 1.10% | $5.60 |

| 1For the six months ended December 31, 2006. 2Expenses are equal to the Funds' annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year, then divided by 365. | |||||

Madison Mosaic Income Trust December 31, 2006

Management Information

Independent Trustees

| Name, Address and Age | Position(s) Held with Fund | Term of Office and Length of Time Served | Principal Occupation(s) During Past 5 Years | Number of Portfolios in Fund Complex Overseen | Other Directorships Held |

| Philip E. Blake 550 Science Drive Madison, WI 53711 Born 1944 | Trustee | Indefinite Term since May 2001 | Retired investor; formerly Vice President - Publishing, Lee Enterprises Inc. | All 11 Madison Mosaic Funds and the Madison Strategic Sector Premium Fund. | Madison Newspapers, Inc. of Madison, WI; Trustee of the Madison Claymore Covered Call Fund; Nerites Corp. |

| James R. Imhoff, Jr. 550 Science Drive Madison, WI 53711 Born 1944 | Trustee | Indefinite Term since July 1996 | Chairman and CEO of First Weber Group, Inc. (real estate brokers) of Madison, WI. | All 11 Madison Mosaic Funds and the Madison Strategic Sector Premium Fund. | Trustee of the Madison Claymore Covered Call Fund; Park Bank, FSB. |

| Lorence D. Wheeler 550 Science Drive Madison, WI 53711 Born 1938 | Trustee | Indefinite Term since July 1996 | Retired investor; formerly Pension Specialist for CUNA Mutual Group (insurance) and President of Credit Union Benefits Services, Inc. (a provider of retirement plans and related services for credit union employees nationwide). | All 11 Madison Mosaic Funds and the Madison Strategic Sector Premium Fund. | Trustee of the Madison Claymore Covered Call Fund; Grand Mountain Bank, FSB. |

Madison Mosaic Income Trust 17

Management Information (concluded)

Interested Trustees*

| Frank E. Burgess 550 Science Drive Madison, WI 53711 Born 1942 | Trustee and Vice President | Indefinite Terms since July 1996 | Founder, President and Director of Madison Investment Advisors, Inc. | All 11 Madison Mosaic Funds and the Madison Strategic Sector Premium Fund. | Trustee of the Madison Claymore Covered Call Fund; Capitol Bank, FSB. |

| Katherine L. Frank 550 Science Drive Madison, WI 53711 Born 1960 | Trustee and President | Indefinite Terms President since July 1996, Trustee since May 2001 | Principal and Vice President of Madison Investment Advisors, Inc. and President of Madison Mosaic, LLC | President of all 11 Madison Mosaic Funds. Trustee of all Madison Mosaic Funds except Equity Trust; President and Trustee of the Madison Strategic Sector Premium Fund. | None |

Officers*

| Jay R. Sekelsky 550 Science Drive Madison, WI 53711 Born 1959 | Vice President | Indefinite Term since July 1996 | Principal and Vice President of Madison Investment Advisors, Inc. and Vice President of Madison Mosaic, LLC | All 11 Madison Mosaic Funds and the Madison Strategic Sector Premium Fund. | None |

| Christopher Berberet 550 Science Drive Madison, WI 53711 Born 1959 | Vice President | Indefinite Term since July 1996 | Principal and Vice President of Madison Investment Advisors, Inc. and Vice President of Madison Mosaic, LLC | All 11 Madison Mosaic Funds and the Madison Strategic Sector Premium Fund. | None |

| W. Richard Mason 8777 N. Gainey Center Drive, #220 Scottsdale, AZ 85258 Born 1960 | Secretary, General Counsel and Chief Compliance Officer | Indefinite Terms since November 1992 | Principal of Mosaic Funds Distributor, LLC; General Counsel and Chief Compliance Officer for Madison Investment Advisors, Madison Scottsdale, LC and Madison Mosaic, LLC; General Counsel for Concord Asset Management, LLC. | All 11 Madison Mosaic Funds and the Madison Strategic Sector Premium Fund. | None |

| Greg Hoppe 550 Science Drive Madison, WI 53711 Born 1969 | Chief Financial Officer | Indefinite Term since August 1999 | Vice President of Madison Mosaic, LLC | All 11 Madison Mosaic Funds and the Madison Strategic Sector Premium Fund. | None |

*All interested Trustees and Officers of the Trust are employees and/or owners of Madison Investment Advisors, Inc. Since Madison Investment Advisors, Inc. serves as the investment advisor to the Trust, each of these individuals is considered an "interested person" of the Trust as the term is defined in the Investment Company Act of 1940.

The Statement of Additional Information contains more information about the Trustees and is available upon request. To request a free copy, call Mosaic Funds at 1-800-368-3195.

18 Annual Report - December 31, 2006

Forward-Looking Statement Disclosure. One of our most important responsibilities as mutual fund managers is to communicate with shareholders in an open and direct manner. Some of our comments in our letters to shareholders are based on current management expectations and are considered "forward-looking statements." Actual future results, however, may prove to be different from our expectations. You can identify forward-looking statements by words such as "estimate," "may," "will," "expect," "believe," "plan" and other similar terms. We cannot promise future returns. Our opinions are a reflection of our best judgment at the time this report is compiled, and we disclaim any obligation to update or alter forward-looking statements as a result of new information, future events, or otherwise.

Proxy Voting Information. The Trust only invests in non-voting securities. Nevertheless, the Trust adopted policies that provide guidance and set forth parameters for the voting of proxies relating to securities held in the Trust's portfolios. Additionally, information regarding how the Trust voted proxies related to portfolio securities for the period ended December 31, 2006 is available. These policies and voting information are available to you upon request and free of charge by writing to Madison Mosaic Funds, 550 Science Drive, Madison, WI 53711 or by calling toll-free at 1-800-368-3195. The Trust's proxy voting policies and voting information may also be obtained by visiting the Securities and Exchange Commission web site at www.sec.gov. The Trust will respond to shareholder requests for copies of our policies and voting information within two business days of request by first-class mail or other means designed to ensure prompt delivery.

N-Q Disclosure. The Trust files its complete schedule of portfolio holdings with the U.S. Securities and Exchange Commission (the "Commission") for the first and third quarters of each fiscal year on Form N-Q. The Trust's Forms N-Q are available on the Commission's website. The Trust's Forms N-Q may be reviewed and copied at the Commission's Public Reference Room in Washington, DC. Information about the operation of the Public Reference Room may be obtained by calling the Commission at 1-202-551-8090. Form N-Q and other information about the Trust are available on the EDGAR Database on the Commission's Internet site at http://www.sec.gov. Copies of this information may also be obtained, upon payment of a duplicating fee, by electronic request at the following email address: publicinfo@sec.gov, or by writing the Commission's Public Reference Section, Washington, DC 20549-0102. Finally, you may call Madison Mosaic at 800-368-3195 if you would like a copy of Form N-Q and we will mail one to you at no charge.

Discussion of Contract Renewal (Unaudited)

The Trustees considered a number of factors when the Board most recently approved the advisory contract between us and the Trust in July 2006. Rather than providing you with a list of factors or conclusory statements that explained the Board's decisionmaking process, the following discussion is designed to describe what you would have seen and heard if you had been at the Trust's Board meeting when it most recently approved the advisory contract:

With regard to the nature, extent and quality of the services to be provided by the Advisor, the Board reviewed the biographies and tenure of the personnel involved in fund management, including the recent growth of both the fixed and equity portfolio management teams. They recognized the wide array of investment professionals employed by the firm. Ms. Frank and Mr. Burgess discussed the firm's ongoing investment philosophies and strategies intended to provide superior performance consistent with each funds' investment objectives under various market scenarios. The Trustees also noted their familiarity with the Advisor due to the Advisor's history of providing advisory services to the Trusts.

The Board also discussed with the Advisor the quality of services provided to the Trusts by the transfer agent, US Bancorp Fund Services, LLC. The Advisor reported that the transfer agent has routinely ranked at or near the top in customer service surveys for third party transfer agents.

Madison Mosaic Income Trust 19

With regard to the investment performance of each fund and the investment advisor, the Board reviewed current performance information for each fund. They discussed the reasons for both outperformance and underperformance compared with peer groups and applicable indices. In particular, the Board recognized that as of the date of the meeting, most funds were underperforming their peer groups for the year ended June 30, 2006. With regard to fixed-income performance, the Advisor explained its active bond management style and its goal of protecting shareholders during periods of rising interest rates. The Advisor explained that, in the long-term, it believes this philosophy is in the best interest of fixed-income fund shareholders and is in accordance with applicable prospectus disclosures of investment objectives and policies for such funds. The Board engaged in a comprehensive discussion of fund performance and market conditions with representatives of the Advisor. The Advisor was optimistic about future performance and the direction of the markets.

The Board reviewed the Advisor's methodology for arriving at the peer groups and indices used for performance comparisons. The Board reviewed both short-term and long-term standardized performance, i.e. one, five and ten year (or since inception) average annual total returns for each fund and comparable funds, as well as standardized yields for fixed income funds.

With regard to the costs of the services to be provided and the profits to be realized by the investment advisor and its affiliates from the relationship with each fund, the Board reviewed the expense ratios for each Madison Mosaic fund compared with funds with similar investment objectives and of similar size. The Board reviewed such comparisons based on a variety of peer group comparisons from data extracted from industry databases including comparison to funds with similar investment objectives based on their broad asset category, total asset size and distribution method, e.g. whether the comparison included or did not include comparable no-load funds, as well as from data provided directly by funds that most resembled each Trust portfolio's asset size and investment objective for the last year. The Board reviewed the objective manner by which Madison Mosaic fees were compared to fees in the industry.

The Trustees recognized that each Madison Mosaic fund's fee structure should be reviewed based on total fund expense ratio rather than simply comparing advisory fees to other advisory fees in light of the simple expense structure maintained by the Trusts (i.e. a single advisory and a single services fee, with only the fixed fees of the Independent Trustees and auditors paid separately). As such, the Board focused its attention on the total expense ratios paid by other funds of similar size and category when considering the individual components of the expense ratios. The Board also recognized that investors are often required to pay distribution fees (loads) over and above the amounts identified in the expense ratio comparison reviewed by the Board, whereas no such fees are paid by Madison Mosaic shareholders.

The Trustees sought to ensure that fees were adequate so that the Advisor did not neglect its management responsibilities for the Trusts in favor of more "profitable" accounts. At the same time, the Trustees sought to ensure that compensation paid to the Advisor was not unreasonably high. With these considerations in mind, the Board compared the Advisor's fee schedule for separately managed accounts with the fees paid by the Trusts. The Trustees recognized that the Advisor provides vastly more services to the Trusts than it does for separately managed accounts. The Board also reviewed materials demonstrating that although the Advisor is compensated for a variety of the administrative services it provides or arranges to provide pursuant to its Services Agreements with the Trusts, such compensation generally does not cover all costs due to the relatively small size of the funds in the Madison Mosaic family. Administrative, operational, regulatory and compliance fees and costs in excess of the Services Agreement fees are paid by the Advisor from its investment advisory fees earned. For these reasons, the Trustees recognized that examination of the Trusts' total expense ratios

20 Annual Report - December 31, 2006

compared to those of other investment companies was more meaningful than a simple comparison of basic "investment management only" fee schedules.

In reviewing costs and profits, the Trustees recognized that Madison Mosaic Funds are to a certain extent "subsidized" by the greater Madison Investment Advisors, Inc. organization because the salaries of all portfolio management personnel, trading desk personnel, corporate accounting personnel and employees of the Advisor who served as Trust officers, as well as facility costs (rent), could not be supported by fees received from the Trusts alone. However, although Madison Mosaic represents approximately $400 million out of the approximately $8 billion managed by the Madison Investment Advisors, Inc. organization in Wisconsin at the time of the meeting, the Trusts are profitable to the Advisor because such salaries and fixed costs are already paid from revenue generated by management of the remaining assets. The Trustees noted that total Madison managed assets, including subsidiaries, exceeded $10 billion at the time of the meeting. As a result, although the fees paid by the Trusts at their present size might not be sufficient to profitably support a stand alone mutual fund complex, they are reasonably profitable to the Advisor as part of its larger, diversified organization. The Trustees also recognized that Madison Mosaic's reputation benefited the Advisor's reputation in attracting separately managed accounts and other investment advisory business. In sum, the Trustees recognized that Madison Mosaic Funds are important to the Advisor, are managed with the attention given to other firm clients and are not treated as "loss leaders."

With regard to the extent to which economies of scale would be realized as a fund grows, the Trustees recognized that Madison Mosaic Funds, both individually and as a complex, remain small and that economies of scale would likely be addressed after funds see assets grow significantly beyond their current levels. In light of their size, the Trustees noted that at current asset levels, it was premature to discuss economies of scale beyond the existing breakpoint schedules now in effect for the largest of the funds in the family.

Finally, the Board reviewed the role of Mosaic Funds Distributor, LLC. They noted that the Advisor pays all distribution expenses of Madison Mosaic Funds because the Trusts do not pay distribution fees. Such expenses include NASD regulatory fees and "blue sky" fees charged by state governments in order to permit the funds to be offered in the various United States jurisdictions.

Based on all of the material factors explained above, plus a number of other matters that the Trustees are generally required to consider under guidelines developed by the Securities and Exchange Commission, the Trustees concluded that our contract should be renewed for another year.

Madison Mosaic Income Trust 21

The Madison Mosaic Family of Mutual Funds

Madison Mosaic Equity Trust

Investors Fund

Balanced Fund

Mid-Cap Fund

Foresight Fund

Madison Institutional Equity Option Fund

Madison Mosaic Income Trust

Government Fund

Intermediate Income Fund

Institutional Bond Fund

Madison Mosaic Tax-Free Trust

Virginia Tax-Free Fund

Tax-Free National Fund

Madison Mosaic Government Money Market

For more complete information on any Madison Mosaic fund, including charges and expenses, request a prospectus by calling 1-800-368-3195. Read it carefully before you invest or send money. This document does not constitute an offering by the distributor in any jurisdiction in which such offering may not be lawfully made. Mosaic Funds Distributor, LLC.

TRANSER AGENT

Mosaic Funds

c/o US Bancorp Fund Services, LLC

P.O. Box 701

Milwaukee, WI 53201-0701

TELEPHONE NUMBERS

Shareholder Service

Toll-free nationwide: 888-670-3600

550 Science Drive

Madison, Wisconsin 53711

Madison Mosaic Funds

www.mosaicfunds.com

SEC File Number 811-3616

ANNUAL REPORT

December 31, 2006

Madison Mosaic

Income Trust

Institutional Bond Fund

(logo) Madison Mosaic Funds (TM)

www.mosaicfunds.com

Contents

| Management's Discussion of Fund Performance | |

| Review of Period | 1 |

| Outlook | 1 |

| Fund Overview | 2 |

| Report of Independent Registered Public Accounting Firm | 4 |

| Portfolio of Investments | 5 |

| Statement of Assets and Liabilities | 6 |

| Statement of Operations | 7 |

| Statements of Changes in Net Assets | 7 |

| Financial Highlights | 8 |

| Notes to Financial Statements | 9 |

| Management Information | 14 |

Madison Mosaic Institutional Bond Fund December 31, 2006

Management's Discussion of Fund Performance

Review of Period

We saw strong economic growth in 2006. While some of the initial 2006 growth can be attributed to a snap-back from the hurricane depressed levels seen in the fourth quarter of 2005, the economy was still showing signs of strength at the end of the year.

Meanwhile, inflation pressures remained in place. Industrial commodity prices rose across the board, with inputs such as zinc and copper reaching new highs. Capacity utilization, which is a measure of how much slack exists in industrial production, moved above 82%, a level that has traditionally been inflationary. Rising input prices, higher capacity utilization and tighter labor markets are all classic signs of a maturing economic expansion.

One of the notable events of the period was the retirement of long-time Federal Reserve Chairman Alan Greenspan, and the beginning of the Bernanke era. Rates were raised twice in the first quarter under Greenspan. Under new Fed Chairman, Ben Bernanke, the Federal Reserve raised short-term rates two more times during the second quarter of 2006, bringing the period-end rate to 5.25%, and then held firm for the remainder of the year.

Although interest rates were little changed from start to finish in 2006, the path of the benchmark 10-year Treasury bond was hardly straight. Yields increased in the first half of the year as the Fed continued its policy of raising the Federal funds rate. However, once the Fed paused halfway through the year, the marketplace became "data dependent." As the economy showed signs of cooling, rates retraced their earlier rise. Fed Chairman Bernanke has proved his resolve to remain hawkish on inflation, but appears confident that if the economy slows, pricing pressures will ease. More recent data may prove a difficult test for the central bank as inflation pressures remain and economic data has shown signs of acceleration.

Outlook

Our research indicates that the economy is, in fact, slowing. However, we would note that GDP growth is slowing relative to the heady pace set in the post-hurricane first quarter of 2006. Since that quarter, readings have come in at a more trend-like pace. Much of the slowing has been driven by a weakening housing market and slumping auto sales.

The rest of the economy, however, has remained strong and real estate has shown signs of bottoming recently. Furthermore, stocks have shown solid gains, gasoline prices are lower, and mortgage rates are down. All of these are potential drivers of accelerated consumer spending going forward.

Herein lies the dilemma for the Federal Reserve. Although the economy showed signs of slowing in the third quarter and early in the fourth, they must now evaluate the pockets of strength. Primarily, the employment situation remains conducive to a healthy economy. Unemployment has been stuck in the 4.5% range and wages have risen approximately 4.2% year-over-year. Therefore, the Fed will need to evaluate how much the economy is actually cooling and whether or not it is enough to keep inflation tame.

Inflation remains the Fed's primary area of focus. Although commodity prices backed off early in the second half of the year, they have recently crept back up. Furthermore, the Consumer Price Index (both headline and core) continues to advance at a 2.5% pace. This is (and has been for some time) above the Fed's stated comfort level. In light of this and recent signs of strength, it appears the market has gotten ahead of itself. Continued signs of inflation and the market's recognition that the Fed will not be easing soon are the biggest risks to rates.

Madison Mosaic Institutional Bond Fund 1

Management's Discussion of Fund Performance (continued)

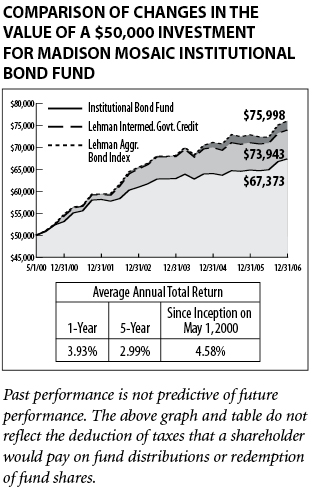

Fund Overview

Madison Mosaic Institutional Bond Fund (the "Fund") returned 3.93% for the annual period ended December 31, 2006. This return trailed the Fund's peers, as the Lipper Intermediate Investment Grade Index rose 4.47%. The Fund outperformed its peers over the first half of the year as rates rose and bond valuations fell, but trailed in the second half as investors began to look forward to Federal Reserve easing. These return differentials largely reflect management's defensive positioning of the portfolio. When interest rates rise, bond valuations fall, and shorter bonds typically retain their value far better than longer bonds. The Fund's 30-day SEC yield at period end was 4.40 %, with an effective duration of 2.91 years, slightly longer than the 2.80 years at the period's start.

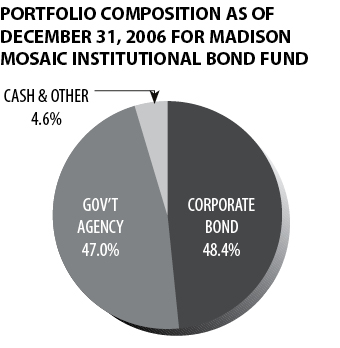

The Fund held 29.6% in Treasuries, 17.4% in government agency notes, and 48.4% in high-quality corporate bonds (as a percentage of net assets) with the remainder in cash and equivalents. The Fund's largest positions during this twelve-month period were short to intermediate duration bonds issued by the U.S. Treasury, Freddie Mac and Fannie Mae.

TOP TEN HOLDINGS AS OF DECEMBER 31, 2006 FOR MADISON MOSAIC INSTITUTIONAL BOND FUND

% of net assets | |

| US Treasury Note, 3.625%, 1/15/10 | 10.42% |

| Freddie Mac, 4.5%, 7/15/13 | 8.24% |

| Fannie Mae, 5.25%, 4/15/07 | 6.15% |

| US Treasury Note, 4.5%, 2/28/11 | 5.34% |

| US Treasury Note, 4.25%, 8/15/14 | 4.70% |

| US Treasury Note, 4.75%, 11/15/08 | 3.84% |

| US Treasury Note, 4.875%, 2/15/12 | 3.10% |

| MGIC Investment Corp., 6%, 3/15/07 | 3.07% |

| Freddie Mac, 3.625%, 9/15/08 | 3.00% |

| National Rural Utilities, 4.75%, 3/1/14 | 2.97% |

2 Annual Report - December 31, 2006

Management's Discussion of Fund Performance (concluded)

Madison Mosaic Institutional Bond Fund 3

Madison Mosaic Institutional Bond Fund December 31, 2006

Report of Independent Registered Public Accounting Firm

To the Board of Trustees and Shareholders of Madison Mosaic Income Trust:

We have audited the accompanying statements of assets and liabilities, including the portfolio of investments of the Madison Mosaic Institutional Bond Fund (the "Fund"), as of December 31, 2006 and the related statements of operations for the year then ended and the statements of changes in net assets for each of the two years in the period then ended and the financial highlights for each of the three years in the period then ended. These financial statements and financial highlights are the responsibility of the Fund's management. Our responsibility is to express an opinion on these financial statements based on our audits. The financial highlights for each of the two years in the period ended December 31, 2003, were audited by other auditors. Those auditors expressed an unqualified opinion on those financial highlights in their report dated February 14, 2004.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. The Fund is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audit included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund's internal control over financial reporting. Accordingly we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of December 31, 2006 by correspondence with the Fund's custodian and brokers. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of the Fund as of December 31, 2006, and the results of its operations for the year then ended and the changes in their net assets for each of the two years in the period then ended and financial highlights for each of the three years in the period then ended, in conformity with accounting principles generally accepted in the United States of America.

(signature)

Grant Thornton LLP

Chicago, Illinois

February 2, 2007

4 Annual Report - December 31, 2006

Madison Mosaic Institutional Bond Fund December 31, 2006

Portfolio of Investments

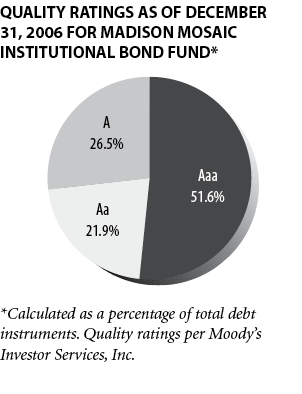

| CREDIT RATING* | PRINCIPAL AMOUNT | VALUE | ||

| MOODY'S | S&P | |||

| DEBT INSTRUMENTS: 95.4% of net assets | ||||

| Corporate Obligations: 48.4% | ||||

| A1 | A+ | American Express, 4.75%, 6/17/09 | $175,000 | $173,713 |

| Aa2 | AA- | Bank of America, 4.875%, 9/15/12 | 150,000 | 147,183 |

| A2 | A | CIT Group Inc, 4.125%, 11/03/09 | 150,000 | 145,565 |

| Aa1 | AA- | Citigroup Inc, 4.25%, 7/29/09 | 150,000 | 146,879 |

| A1 | A- | CONOCO Inc, 6.35%, 10/15/11 | 150,000 | 156,978 |

| A3 | A | Countrywide Home Loan, 5.625%, 5/15/07 | 175,000 | 175,149 |

| Aaa | AAA | General Electric Capital Corp, 4.25%, 6/15/12 | 150,000 | 143,013 |

| Aa3 | AA- | Goldman Sachs, 6.65%, 5/15/09 | 150,000 | 154,945 |

| A3 | A- | Hewlett-Packard Co, 5.5%, 7/1/07 | 150,000 | 150,182 |

| Aa3 | AA- | Household Finance Co, 7.875%, 3/1/07 | 150,000 | 150,576 |

| A1 | A+ | IBM Corp, 4.75%, 11/29/12 | 150,000 | 146,625 |

| A1 | AA- | International Lease Finance, 4.875%, 9/1/10 | 150,000 | 147,556 |

| Aa3 | AA- | Merrill Lynch, 7%, 1/15/07 | 150,000 | 150,189 |

| A1 | A | MGIC Investment Corp, 6.0%, 3/15/07 | 200,000 | 200,168 |

| Aa3 | A+ | Morgan Stanley Dean Witter, 3.625%, 4/1/08 | 170,000 | 166,610 |

| A1 | A+ | National Rural Utilities, 4.75%, 3/1/14 | 200,000 | 193,241 |

| Aa2 | AA | Texaco Capital Inc, 5.5%, 1/15/09 | 150,000 | 151,388 |

| Aa2 | AA- | US Bancorp, 5.1%, 7/15/07 | 150,000 | 149,734 |

| Aa2 | AA | Wal-Mart Stores Inc, 4.55%, 5/1/13 | 150,000 | 144,777 |

| A1 | A | WPS Resources Corp, 7%, 11/1/09 | 150,000 | 156,126 |

| U.S. Government & Agency Obligations: 47.0% | ||||

| Aaa | AAA | Fannie Mae, 5.25%, 4/15/07 | 400,000 | 400,110 |

| Aaa | AAA | Freddie Mac, 3.625%, 9/15/08 | 200,000 | 195,460 |

| Aaa | AAA | Freddie Mac, 4.50%, 7/15/13 | 550,000 | 536,162 |

| Aaa | AAA | US Treasury Note, 4.75%,11/15/08 | 250,000 | 249,756 |

| Aaa | AAA | US Treasury Note, 3.625%, 1/15/10 | 700,000 | 678,618 |

| Aaa | AAA | US Treasury Note, 4.5%, 2/28/11 | 350,000 | 347,525 |

| Aaa | AAA | US Treasury Note, 4.875%, 2/15/12 | 200,000 | 201,891 |

| Aaa | AAA | US Treasury Note, 4.25%, 8/15/14 | 315,000 | 305,870 |

| Aaa | AAA | US Treasury Note, 4.5%, 2/15/16 | 150,000 | 147,658 |

| TOTAL DEBT INSTRUMENTS (Cost $6,255,982) | $6,213,647 | |||

| REPURCHASE AGREEMENT: 3.2% of net assets With Morgan Stanley and Company issued 12/29/06 at 4.65%, due 1/3/07, collateralized by $211,181 in United States Treasury Notes due 11/15/18. Proceeds at maturity are $206,133 (Cost $206,000). |

| 206,000 | ||

| TOTAL INVESTMENTS: 98.6% of net assets (Cost $6,461,982) | $6,419,647 | |||

| CASH AND RECEIVABLES LESS LIABILITIES: 1.4% of net assets | 91,108 | |||

| NET ASSETS: 100% | $6,510,755 | |||

Notes to the Portfolio of Investments:

* – Unaudited; Moody's – Moody's Investor Services, Inc.; S&P – Standard & Poor's Corporation

The Notes to Financial Statements are an integral part of these statements.

Madison Mosaic Institutional Bond Fund 5

Madison Mosaic Institutional Bond Fund December 31, 2006

Statement of Assets and Liabilities

| ASSETS | |

| Investments, at value (Note 1 and 2) | |

| Investment securities | $6,213,647 |

| Repurchase agreements | 206,000 |

| Total investments* | 6,419,647 |

| Cash | 415 |

| Interest receivable | 93,289 |

| Total assets | 6,513,351 |

| LIABILITIES | |

| Independent trustee fees | 250 |

| Auditor fees | 2,346 |

| Total liabilities | 2,596 |

| NET ASSETS | $6,510,755 |

| Net assets consists of: | |

| Paid in capital | 6,629,560 |

| Accumulated net realized losses | (76,470) |

| Net unrealized depreciation on investments | (42,335) |

| Net Assets | $6,510,755 |

| CAPITAL SHARES OUTSTANDING An unlimited number of capital shares, without par value, are authorized (Note 7) | 645,613 |

| NET ASSET VALUE PER SHARE | $10.08 |

| *INVESTMENT SECURITIES, AT COST | $6,461,982 |

The Notes to Financial Statements are an integral part of these statements.

6 Annual Report - December 31, 2006

Madison Mosaic Institutional Bond Fund

Statement of Operations

For the year ended December 31, 2006

| INVESTMENT INCOME (Note 1) | |

| Interest income | $309,932 |

| EXPENSES (Notes 3 and 5) | |

| Investment advisory fees | 21,006 |

| Other expenses: | |

| Service agreement fees | 5,601 |

| Independent trustee fees | 1,000 |

| Auditor fees | 4,500 |

| Total other expenses | 11,101 |

| Total Expenses | 32,107 |

| NET INVESTMENT INCOME | 277,825 |

| REALIZED AND UNREALIZED LOSS ON INVESTMENTS | |

| Net realized loss on investments | (66,536) |

| Change in net unrealized appreciation of investments | 40,369 |

| NET LOSS ON INVESTMENTS | (26,167) |

| TOTAL INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | $251,658 |

Madison Mosaic Institutional Bond Fund

Statements of Changes in Net Assets

Year Ended Dec. 31, | ||

2006 | 2005 | |

| INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | ||

| Net investment income | $277,825 | $266,275 |

| Net realized loss on investments | (66,536) | (1,669) |

| Net unrealized appreciation (depreciation) on investments | 40,369 | (166,002) |

| Total increase in net assets resulting from operations | 251,658 | 98,604 |

| DISTRIBUTIONS TO SHAREHOLDERS FROM NET INVESTMENT INCOME | (277,825) | (266,275) |

| CAPITAL SHARE TRANSACTIONS (Note 7) | (1,135,478) | 332,519 |

| TOTAL INCREASE (DECREASE) IN NET ASSETS | (1,161,645) | 164,848 |

| NET ASSETS | ||

| Beginning of year | $7,672,400 | $7,507,552 |

| End of year | $6,510,755 | $7,672,400 |

The Notes to Financial Statements are an integral part of these statements.

Madison Mosaic Institutional Bond Fund 7

Madison Mosaic Institutional Bond Fund

Financial Highlights

Selected data for a share outstanding throughout each period indicated

Year Ended December 31, | |||||

2006 | 2005 | 2004 | 2003 | 2002 | |

| Net asset value, beginning of period | $10.11 | $10.34 | $10.50 | $10.54 | $10.54 |

| Investment operations: | |||||

| Net investment income | 0.41 | 0.36 | 0.35 | 0.37 | 0.45 |

| Net realized and unrealized gain (loss) on investments | (0.03) | (0.23) | (0.16) | (0.04) | 0.04 |

| Total from investment operations | 0.38 | 0.13 | 0.19 | 0.33 | 0.49 |

| Less distributions: | |||||

| From net investment income | (0.41) | (0.36) | (0.35) | (0.37) | (0.45) |

| From net capital gains | -- | -- | -- | -- | (0.04) |

| Total distributions | (0.41) | (0.36) | (0.35) | (0.37) | (0.49) |

| Net asset value, end of period | $10.08 | $10.11 | $10.34 | $10.50 | $10.54 |

| Total return (%) | 3.93 | 1.24 | 1.84 | 3.18 | 4.79 |

| Ratios and supplemental data | |||||

| Net assets, end of period (in thousands) | $6,511 | $7,672 | $7,508 | $7,488 | $6,998 |

| Ratio of expenses to average net assets (%) | 0.46 | 0.45 | 0.45 | 0.45 | 0.45 |

| Ratio of net investment income to average net assets (%) | 3.97 | 3.48 | 3.35 | 3.53 | 4.28 |

| Portfolio turnover (%) | 34 | 39 | 24 | 38 | 30 |

The Notes to Financial Statements are an integral part of these statements.

8 Annual Report - December 31, 2006

Madison Mosaic Institutional Bond Fund December 31, 2006

Notes to Financial Statements

1. Summary of Significant Accounting Policies. Madison Mosaic Income Trust (the "Trust") is registered with the Securities and Exchange Commission under the Investment Company Act of 1940 as an open-end, diversified investment management company. The Trust currently offers three portfolios, each of which is a diversified mutual fund. This report contains information about one of these portfolios, the Madison Mosaic Institutional Bond Fund (the "Fund"), which commenced operations May 1, 2000. Its objectives and strategies are detailed in its prospectus. The remaining two Trust portfolios present their financial information in a separate report.

Securities Valuation: Repurchase agreements and other securities having maturities of 60 days or less are valued at amortized cost, which approximates market value. Securities having longer maturities, for which quotations are readily available, are valued at the mean between their closing bid and ask prices. Securities for which current market quotations are not readily available are valued at their fair value as determined in good faith under procedures approved by the Board of Trustees.

Investment Transactions: Investment transactions are recorded on a trade date basis. The cost of investments sold is determined on the identified cost basis for financial statement and federal income tax purposes.

Investment Income: Interest income is recorded on an accrual basis. Bond premium is amortized and original issue discount and market discount are accreted over the expected life of each applicable security using the effective interest method. Other income is accrued as earned.