UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

[ X ] ANNUAL REPORT PURSUANT TO SECTION 13 or 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2006

or

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

Commission File Number 001-11663

COMMUNITY BANKS, INC.

(Exact name of registrant as specified in its charter)

Pennsylvania | | 23-2251762 |

(State of Incorporation) | | (I.R.S. Employer Identification No.) |

| | | |

777 East Park Drive, Harrisburg, PA | | 17111 |

(Address of principal executive offices) | | (Zip Code) |

Registrant’s telephone number, including area code: (717) 920-5800

Securities registered pursuant to Section 12 (b) of the Act:

Title of Each Class | | Name of Each Exchange on Which Registered |

Common Stock, par value $5 per share | | NASDAQ Global Select Market |

Securities registered pursuant to Section 12 (g) of the Act: None

| Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. | Yes | | | No | X |

| Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. | Yes | | | No | X |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for shorter period that the registrant was required to file such reports), and (2) has been subject to

| such filing requirements for the past 90 days. | Yes | X | | No | |

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of the Form 10-K or any amendments to this Form 10-K. [X ]

| Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and larger accelerated filer” in Rule 12b-2 of the Exchange Act. |

| Large accelerated filer | | | Accelerated filer | X | | Non-accelerated filer | |

| Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). | Yes | | | No | X |

Aggregate market value of the Common Stock, $5 par value, held by non-affiliates, computed by reference to the closing price on June 30, 2006: $576,000,000

Number of shares of the Common Stock, $5 par value, outstanding as of the close of business on February 28, 2007: 23,541,000 shares.

Documents Incorporated by Reference:

Portions of the Proxy Statement for the 2007 Annual Meeting of Shareholders of Community Banks, Inc., have been incorporated by reference into Part III.

(This page intentionally blank)

COMMUNITY BANKS, INC.

FORM 10-K

INDEX

PART I | | Page |

| | | |

| Item 1 | | 4 - 10 |

| Item 1A | | 10 - 12 |

| Item 1B | | 13 |

| Item 2 | | 13 |

| Item 3 | | 13 |

| Item 4 | | 13 |

| | | |

| | | |

PART II | | |

| | | |

| Item 5 | | 14 - 15 |

| Item 6 | | 16 |

| Item 7 | | 17 - 54 |

| Item 7A | | 55 - 57 |

| Item 8 | | 58 - 90 |

| Item 9 | | 91 |

| Item 9A | | 91 |

| Item 9B | | 91 |

| | | |

| | | |

PART III | | |

| | | |

| Item 10 | | 94 |

| Item 11 | | 94 |

| Item 12 | | 94 |

| Item 13 | | 94 |

| Item 14 | | 94 |

| | | |

| | | |

PART IV | | |

| | | |

| Item 15 | | 95 - 96 |

| | | |

| | | |

| | 97 - 98 |

| | | |

| | | |

PART I

General

Business Overview

Community Banks, Inc., (the “Corporation” or “Community”) is a financial holding company that was formed as a Pennsylvania corporation in 1982. Community directly owns 100% of its operating subsidiaries. Its major operating entity is its wholly-owned banking subsidiary, referred to in this report as CommunityBanks (or the “Bank”), and includes several other subsidiaries of both the holding company and the Bank, each of which was formed to facilitate delivery of non-banking services to its customers and the Bank. Community’s banking subsidiary has nearly $3.5 billion in assets and aggregate annual revenues exceeding $140 million at December 31, 2006. The executive offices of Community are located at 777 East Park Drive, Harrisburg, Pennsylvania 17111. Community provides its services primarily through its community banking offices that are located throughout the central portion of Pennsylvania stretching from the Pocono Mountains in northeastern Pennsylvania to just over the Pennsylvania border in Carroll County, Maryland.

The common stock of Community is listed on the Global Select Market Tier of the Nasdaq Stock Market under the symbol CMTY. Community’s internet address is www.communitybanks.com. Electronic copies of Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q and Current Reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act, are available through the “Investor Relations” section of Community’s website as soon as reasonably practicable after filing such material with, or furnishing it to, the Securities and Exchange Commission. Copies of such reports are also available at no charge.

Community conducts a traditional and full service commercial and retail banking business and also provides trust services through 74 retail banking offices located throughout Pennsylvania and Maryland. The delivery of customer services has been constructed around a regional operating and management structure which emphasizes local delivery of customer services combined with centralized support functions. Currently, the Bank operates six individual regions. Community conducts its business within 11 counties in Pennsylvania and Maryland. The following is a summary of the number of offices operating in each county of Community’s market, presented in the order of the highest deposit balances per county. This information is provided pursuant to a formal request of the Federal Deposit Insurance Corporation (“FDIC”) as of June 30th of each year.

Pennsylvania Counties | | Number of Offices | | Deposits at June 30, 2006 | |

| | | | | | | (in thousands) | |

| York | | | 20 | | $ | 595,412 | |

| Lancaster | | | 12 | | | 547,810 | |

| Dauphin | | | 11 | | | 293,887 | |

| Berks | | | 6 | | | 286,328 | |

| Schuylkill | | | 7 | | | 195,910 | |

| Adams | | | 3 | | | 132,978 | |

| Luzerne | | | 3 | | | 109,338 | |

| Cumberland | | | 5 | | | 78,208 | |

| Northumberland | | | 2 | | | 68,581 | |

| Chester | | | 2 | | | 63,075 | |

| Snyder | | | 1 | | | 17,736 | |

| | | | | | | | |

Maryland Counties | | | | | | | |

| | | | | | | | |

| Carroll | | | 2 | | $ | 25,105 | |

The Bank operates in a geographic market that is home to a wide range of construction, manufacturing, distribution, health care, and agricultural industries and also includes various other service industry components. The Corporation’s headquarters is located in Harrisburg Pennsylvania, which is the state capital of Pennsylvania, and is the hub of the Commonwealth’s various governmental departments, units, and agencies. The Bank offers a wide range of personal banking services, including a variety of checking and savings products, time deposits and individual retirement accounts. Retail customers are also served by a product line that includes secured loan products, such as home equity loans and lines of credit, construction loans and residential mortgage loans. Residential loans are generally underwritten based on secondary market standards and the vast majority of originations are sold in the secondary market. Consumer loan products also include automobile loans, personal lines of credit and a checking account overdraft protection service.

Commercial banking services are provided to small and medium-sized businesses almost all of which are operated within Community’s footprint. Commercial lending offerings include commercial, commercial real estate, commercial construction and agricultural loans. Commercial loans, by their nature carry higher risk than credit extensions to individual consumers. Ongoing changes in a commercial borrowers’ financial condition and cash flow, plus the potential for volatility in the value of collateral has an inherently higher risk profile. The Corporation also offers letters of credit, traditional deposit products, and cash management services.

Non-banking subsidiaries

Over the years, Community has formed various special purpose wholly-owned subsidiaries, including companies formed to provide specialized services to its customers. All of these subsidiaries are engaged in activities related to the business of banking. In addition to the Bank, the financial services holding company maintains two special purpose subsidiaries, which include CommunityBanks Investments, Inc. (CBII), an investment holding company and Community Banks Life Insurance Company, Inc. (CBLIC), a credit life reinsurance company. In addition to its traditional business banking, retail banking and trust services offered through the Bank, the Bank itself operates additional specialized subsidiaries to facilitate delivery of non-banking services to customers. Banking subsidiaries include: Community Banks Insurance Services LLC, which offers property and casualty and personal insurance lines to businesses and consumers; and Community Settlement, LLC, which provides title and real estate settlement services. Other non-bank subsidiaries have been formed to facilitate operations of the Bank and include UDNB Inc., an investment holding company; CB Services LLC, a payroll services provider and PSB Realty Company, a real estate holding company. On July 1, 2005, Community acquired Blue Ball National Bank (“Blue Ball”) through its acquisition of PennRock Financial Services Corp. (“PennRock”). Blue Ball, which was PennRock’s major operating subsidiary, was merged into the Bank and now operates as a separate division in the Lancaster, Berks and Chester County segments of the franchise.

Subsidiary trusts, which are not consolidated in the financial statements in accordance with provisions of Financial Accounting Standards Board (FASB) Interpretation No. 46, “Consolidation of Variable Interest Entities, An Interpretation of ARB No. 51,” have been formed to execute trust preferred issuances: CMTY Capital Trust I in December, 2002, for a pooled issuance of $15 million and CMTY Statutory Capital Trust II in December, 2003, for an issuance of $15 million. In January, 2006, Community formed CMTY Statutory Capital Trust III and CMTY Statutory Capital Trust IV for pooled issuances of $10 million each.

At December 31, 2006 no single non-banking subsidiary had net income exceeding 5% of consolidated net income.

Operating Segments

All of the operations of Community operate and are reported under its one reportable segment, community banking.

Employees

At December 31, 2006, Community had 993 full-time equivalent employees and Community considers its employee relations to be satisfactory.

History and Pending Acquisitions

The current charter for the Bank’s primary predecessor bank was originally granted in 1911. Community was formed from several predecessor banks pursuant to mergers that took place over a number of years prior to the advent of interstate banking. These historical mergers were subject to geographical limitations imposed by state and federal banking regulations that significantly limited bank merger activity until the 1980’s. In 1998, Community entered into a benchmark merger agreement that provided the foundation for the current organization. At that time, People’s State Bank, a state-chartered bank with offices throughout Pennsylvania’s York and Adams county region and Community Banks, N.A, a federally-chartered bank with headquarters in Dauphin County, Pennsylvania were merged as subsidiaries of Community Banks, Inc. These two banks would eventually come together under a common management team and under the common identity of “CommunityBanks”. The consolidation of these two banks was designed to facilitate the aforementioned regional operating focus, ease regulatory burdens and, at the same time, sustain an operating philosophy that adhered to a philosophy of local decision-making.

Subsequent to the 1998 merger, management focused on continuing to build the franchise through smaller banking mergers, the formation or acquisition of specialized financial services businesses, and de novo office expansion. The Corporation’s most recent transformational merger occurred on July 1, 2005, when Community completed its acquisition of PennRock. At the time of the announcement of the merger, Community had nearly $2 billion of assets and $1.3 billion in deposits. The acquisition of PennRock, and its primary operating subsidiary, Blue Ball Bank, added $1.2 billion in assets, $880 million in deposits, and extended Community’s banking market into the vibrant Lancaster, Berks and Chester counties of southeastern Pennsylvania. At the time of the merger, Blue Ball was legally merged into the Bank but continues to operate as a separate division within its core markets.

During 2006, Community completed two smaller mergers: the Wiley Agency, an insurance agency located in Lancaster County, Pennsylvania and; Sentry Trust, a separate trust services division of a competitor bank. Each of these acquisitions was designed to leverage existing platforms of the insurance and trust segments of the Corporation’s existing businesses.

In the third quarter of 2006, Community announced mergers of BUCS Financial Corp (BUCS) and East Prospect State Bank (East Prospect). BUCS is a former credit union that now operates as BUCS Federal Bank. BUCS has four offices that are located just north of the Baltimore, Maryland beltway, in Baltimore and Howard Counties. At the time of the announcement BUCS had just over $140 million in assets and will serve as Community’s first significant entry into the northern Maryland market. East Prospect is a single unit bank with approximately $45 million of deposits and operates within the heart of Community’s York county market. East Prospect will be operated as a retail office within Community’s York County region. Each of the acquired banks will be merged into the Bank and both mergers are expected to be completed in the second quarter of 2007.

Competition

There are approximately 1,265 offices of commercial and savings banks operating within the market area in which Community competes. The following presentation provides an indication of Community’s share of the market at June 30, 2006, in each of the counties in which it operates:

Pennsylvania Counties | | Branches of Other Institutions Located in County | | Total Deposits within County (in thousands) | | Community’s Share of Market (%) | | Rank within Market | |

| | | | | | | | | | |

| York | | | 156 | | $ | 5,888,860 | | | 10 | | | 4 | |

| Lancaster | | | 203 | | | 8,103,302 | | | 7 | | | 5 | |

| Dauphin | | | 105 | | | 4,272,070 | | | 7 | | | 9 | |

| Berks | | | 144 | | | 6,864,002 | | | 4 | | | 7 | |

| Schuylkill | | | 73 | | | 1,860,886 | | | 11 | | | 4 | |

| Adams | | | 32 | | | 1,170,286 | | | 11 | | | 4 | |

| Luzerne | | | 130 | | | 5,218,371 | | | 2 | | | 11 | |

| Cumberland | | | 104 | | | 3,682,476 | | | 2 | | | 11 | |

| Northumberland | | | 34 | | | 1,172,803 | | | 6 | | | 9 | |

| Chester | | | 201 | | | 8,638,784 | | | 1 | | | 21 | |

| Snyder | | | 20 | | | 500,042 | | | 4 | | | 6 | |

Maryland Counties | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| Carroll | | | 63 | | $ | 2,585,676 | | | 1 | | | 14 | |

The banking and financial services industries are highly competitive, particularly in the region in which Community’s office network is located. Competition comes from a variety of competitors ranging in size from small unit banks, de novo banks, large regional banks and, finally, from banks which operate on a national level. Many of the Corporation’s competitors are significantly larger than Community and therefore have greater lending limits, larger branch networks, greater resources, and a wider array of banking and other financial services.

In addition to the competition from traditional financial institutions, Community has been subjected to competition from credit unions, brokerage firms, money market funds, consumer finance and credit card companies and other companies providing financial services and credit to consumers. The competition is especially fierce with the credit union industry, particularly in certain segments of Community’s markets. The expansion of credit union activity, now permitted by so-called “community-based” charters, continues to create mounting competitive pressure. The expansion of “fields of membership” is thought by most banks to be contributing to an increasingly unfair competitive situation, largely because of the tax-exempt status afforded credit unions. Initiatives to further expand the powers of credit unions to conduct business in areas that go far beyond the original intent of credit union charters continue to be pressed at both the state and federal levels.

Concentrations, Seasonality

No portions of Community’s businesses are dependent on a single or limited number of customers, the loss of which would have a material adverse effect on our business. No substantial portions of loans or investments are concentrated within a single industry or group of related industries, although a significant amount of loans are secured by real estate located in south central Pennsylvania. Community’s businesses are not seasonal in nature.

Environmental Compliance

Community’s compliance with federal, state and local environmental protection laws had no material effect on capital expenditures, earnings or competitive position in 2006, and is not expected to have a material effect on such expenditures, earnings or competitive position in 2007.

Supervision and Regulation

The banking industry is subject to extensive state and federal regulation. Proposals to change laws and regulations governing the banking industry are frequently raised in Congress, in state legislatures, and within the various bank regulatory agencies. The likelihood and timing that such changes may have on Community are difficult to determine with any certainty. Changes in laws or regulations, or changes in the interpretation of laws or regulations, may have a material impact on the business, operations and earnings of Community.

Regulation of the Holding Company

Community Banks, Inc. is registered as a financial holding company with the Federal Reserve Board in accordance with the requirements of the Gramm-Leach-Bliley Act. The Gramm-Leach-Bliley Act enables broad-scale consolidation among banks, securities firms and insurance companies for eligible bank holding companies that have elected and maintain “financial holding company” status. Financial holding companies can offer virtually any type of financial service, including banking, securities underwriting, insurance (both agency and underwriting) and merchant banking. If a bank holding company does not become a financial holding company, it will be limited to those activities previously determined by the Federal Reserve Board to be permissible; i.e., “closely related to banking” under the standard set forth in the Bank Holding Company Act. In order to become a financial holding company, all of a bank holding company’s bank subsidiaries must be well capitalized and well managed and have a rating under the Community Reinvestment Act of at least “satisfactory.” The Corporation is subject to the ongoing oversight of the Federal Reserve Board, which requires regular reports from Community and is authorized to make regular examinations of Community and its subsidiaries.

Regulation of the Bank

The wholly-owned banking subsidiary, CommunityBanks, is subject to supervision and regulation, and is examined regularly, by the Federal Deposit Insurance Corporation (FDIC) and the state banking departments in the states in which it operates, which thus far has been limited to examinations conducted under the auspices of Pennsylvania Department of Banking. To the extent that the Bank’s subsidiaries are licensed to engage in the sale of insurance or the mortgage brokerage business, the subsidiaries are subject to examination by the respective licensing authorities. Community and its direct non-banking subsidiaries are affiliates, within the meaning of applicable banking laws and regulations of the Bank and its subsidiaries. As a result, the Bank and its subsidiaries are subject to restrictions on loans or extensions of credit to, purchase of assets from, investments in, and transactions with Community and its direct non-banking subsidiaries and on certain other transactions with them or involving their securities.

FDIC Insurance Assessment

The Bank is subject to deposit insurance assessments by the FDIC. These assessments are designed to fund both the Bank Insurance Fund (“BIF”) for banks and the Savings Association Insurance Fund (“SAIF”) for savings associations. The assessments by the FDIC for deposit insurance are based upon the risk classifications of depository institutions. Insurance premiums assessed for the last several years have not had a significant impact on operations.

In 2006, the FDIC announced a substantial increase in deposit insurance assessment rates to be effective January 1, 2007. At the same time, the FDIC also announced a One-Time Assessment Credit for those institutions that were in existence at December 31, 1996, and had paid a deposit insurance assessment prior to that date. Based upon the most current information available from the FDIC, it is expected that the annual assessment increase for the Bank will be in excess of $1 million per year at announced rates. For 2007, virtually all of the increase should be offset by the one-time credit. For years beyond 2007, anticipated rate changes are expected to increase the annual assessment expense, subject to any changes in prospective assessments that may be announced by the FDIC at some future date.

Capital Adequacy

The Federal Reserve Board and the FDIC have adopted risk-based capital adequacy guidelines for financial holding companies and banks under their supervision. Under these guidelines, “Tier 1 capital” and “Total capital” as a percentage of risk-weighted assets and certain off-balance sheet instruments must be at least 4% and 8%, respectively. The regulators have also imposed a leverage standard, which focuses on the institution’s ratio of Tier 1 capital to average total assets, adjusted for goodwill and certain other items, to supplement their risk-based ratios. This minimum leverage ratio was set at 3% and would apply only to those banking organizations receiving a regulatory composite 1 rating. Most banking organizations will be required to maintain a leverage ratio ranging from 1 to 2 percentage points above the minimum standard.

Community and the Bank are subject to various regulatory capital requirements administered by federal and state banking agencies. Failure to meet minimum capital requirements can initiate certain mandatory and possibly additional discretionary actions by regulators that, if undertaken, could have a direct material effect on Community’s financial statements. Under capital adequacy guidelines and the regulatory framework for prompt corrective action, each subsidiary bank must meet specific capital guidelines that involve quantitative measures of assets, liabilities, and certain off-balance sheet items as calculated under regulatory accounting practices. The capital amounts and classification are also subject to qualitative judgments by the regulators about the risk weightings of components, and other factors.

Quantitative measures established by regulation to ensure capital adequacy require Community to maintain minimum amounts and ratios of Total and Tier 1 capital to risk-weighted assets and of Tier 1 capital to average assets. Management believes, as of December 31, 2006, that Community and the Bank have met all capital adequacy requirements to which they are subject. For tables presenting Community’s capital ratios, see “Notes to Consolidated Financial Statements - Regulatory Matters” included in Part II, Item 8.

Monetary and Fiscal Policy

Community and the Bank are significantly affected by the monetary and fiscal policies of government authorities, including the Federal Reserve Board (FRB), which regulates the national money supply in order to manage recessionary and inflationary pressures. Among the instruments of monetary policy used by the FRB are open-market operations in U.S. Government securities and federal funds, changes in the discount rate on member bank borrowings, and changes in reserve requirements against member bank deposits. These techniques are used in varying combinations to influence the overall level of bank loans, investments and deposits, and the interest rates charged on loans and paid for deposits. The interest rate environment during 2006 was particularly challenging for most banks, particularly since the middle of the year. For most of 2006, Community and other banks operated in a flat yield curve environment which served to compress net returns from intermediation activities, which remains as the industry’s largest source of revenue. During the later half of the year, the curve remained in an inverted position, which has further compressed intermediation income and created an unprecedented competitive environment for the interest rates charged on loans and received on deposits. For additional discussion of the interest rate environment and its impact on operating results see the section entitled “2006 Economic Conditions and Yield Curve Dynamics” in Part II, Item 7 for further information.

The monetary policies of the FRB have had a significant effect on the operating results of banking institutions in the past and are expected to continue to do so in the future. The nature of future changes in monetary and fiscal policies, or the effect which they may have on Community’s business and earnings, cannot be predicted.

Compliance with Legislation

In addition to the ongoing supervision and regulation of the various bank regulatory authorities, Community has recently been subject to other forms of broader legislation which has had a profound effect on the operations of the Corporation in recent years. Two of the most significant have been the Sarbanes-Oxley Act of 2002 and the USA Patriot Act.

Sarbanes-Oxley Act of 2002

The Sarbanes-Oxley Act of 2002 (Sarbanes-Oxley) implemented a broad range of corporate governance, accounting, and reporting measures for companies that have securities registered under the Securities Exchange Act of 1934, including Community. Sarbanes-Oxley and its various promulgated regulations, established, among other things: (i) increased responsibility for Chief Executive Officers and Chief Financial Officers with respect to the content of filings with the SEC; (ii) enhanced requirements for audit committees, including independence and disclosure of expertise; (iii) enhanced requirements for auditor independence and the types of non-audit services that auditors can provide; (iv) accelerated filing requirements for SEC reports; (v) increased disclosure and reporting obligations for companies, their directors and their executive officers; and (vi) new and increased civil and criminal penalties for violation of securities laws.

Section 404 of Sarbanes-Oxley requires management to issue a report on the effectiveness of its internal controls over financial reporting. In addition, a reporting company’s independent registered public accountants are required to issue an opinion on management’s assessment and an opinion on the effectiveness of the reporting company’s internal control over financial reporting as of the end of the year. These reports for Community for 2006 can be found in Item 8, “Financial Statements and Supplementary Information.” Certifications of the Chief Executive Officer and the Chief Financial Officer as required by Sarbanes-Oxley and the resulting SEC rules can be found in the “Exhibits” section of this report.

USA Patriot Act

The United and Strengthening America by Providing Appropriate Tools Required to Intercept and Obstruct Terrorism Act of 2001 (the USA Patriot Act) imposed additional obligations on financial institutions, including the Bank, to implement and maintain polices, procedures and controls which are reasonably designed to detect and report instances of money laundering and the financing of terrorism. It also substantially broadened the scope of federal anti-money laundering laws and regulations by imposing significant new compliance and due diligence policies. Failure to comply with the Patriot Act’s requirements could have serious legal, financial, and reputation consequences for Community. Community has approved policies and procedures that are believed to be compliant with the Patriot Act and will continue to revise and update policies, procedures, and controls to reflect changes required, as necessary.

Community’s operations and financial results are subject to any number of both internal and external risk factors. This presentation will serve to highlight those risks that management believes are most relevant to Community’s current operating environment. The list is not exhaustive and may not capture all risks associated with Community’s business. Community is subject to a broad array of risks that affect the overall health of the economy and the banking industry as a whole. Consequently, there may be unidentified risks not discussed herein that have the potential to negatively impact Community’s liquidity, financial position or results of operations.

The presentation of risk factors should be read in conjunction with Community’s financial results presented in Part II, Item 7. The following risk factors should also be considered along with the other information concerning risk that is contained in this document. Risk factors contained herein have particular relevance when read in connection with any forward-looking statement presented throughout this Form 10-K. Please refer to the section entitled “Forward-Looking Statements” included in Part II, Item 7.

Future loan losses may exceed Community’s allowance for loan losses.

Credit risk is, perhaps, the single most significant risk to a community bank. Community is subject to credit risk, which is the risk of losing principal or interest due to borrowers’ failure to repay loans in accordance with their terms. A downturn in the economy or the real estate market in our market areas or a rapid change in interest rates could have a negative effect on collateral values and borrowers’ ability to repay. This deterioration in economic conditions could result in losses to Community in excess of loan loss allowances. To the extent loans are not paid timely, the loans are placed on non-accrual, thereby reducing interest income. To the extent loan charge-offs exceed our estimates, increased amounts charged to the provision for loan losses would reduce income.

Rapidly changing interest rate environments could reduce Community’s net interest margin, net interest income, fee income and net income.

Interest and fees on loans and securities, net of interest paid on deposits and borrowings, comprise the major source of revenue for Community. Interest rates are key drivers of net interest margin and subject to many factors beyond the control of management. For most of 2006, the banking industry experienced the impact of a “flat” or “inverted” yield curve, which significantly hampered efforts to expand net interest income in the second half of the year. The shape of the yield curve influences the interest rates that can be charged on loans or paid on deposits. The prolonged presence of a flat or inverted yield curve could significantly impact the potential for sustaining or improving net interest income in ensuing years or until the yield curve returns to a more normal position. Additionally, unexpected increases in interest rates in the future could result in interest expense increasing faster than interest income because of mismatches in financial instrument maturities. Further, substantially higher interest rates generally reduce loan demand and may result in slower loan growth. Decreases or increases in interest rates could have a negative effect on the spreads between the interest rates earned on assets and the rates of interest paid on liabilities, and therefore decrease net interest income.

The interest rate environment and the shape of the yield curve took on increased importance for the banking industry in 2006 and beyond. Although management believes it has implemented effective asset and liability management strategies to reduce the potential effects of changes in interest rates on Community’s results of operations, any substantial, unexpected, or prolonged deviations in market interest rates could have a significant effect on Community’s operations and its financial results. For a more complete description of the risks associated with interest rates and changes in rates, please refer to the section entitled “Net Interest Income” of Part II, Item 7.

Community’s profitability depends significantly on economic conditions in its local markets.

Community’s success depends primarily on the general economic conditions in its local markets of central Pennsylvania and northern Maryland. The local economic conditions in these areas have a significant impact on the demand for Community’s products and services as well as the ability of Community’s customers to repay loans, the value of the collateral securing loans and the stability of Community’s deposit funding sources. A significant decline in general economic conditions, caused by inflation, recession, acts of terrorism, outbreak of hostilities or other international or domestic occurrences, unemployment, changes in securities markets or other factors could impact these local economic conditions and, in turn, have a significant effect on Community’s operations and its financial results.

The financial services industry is very competitive

Community faces competition in attracting and retaining deposits, making loans, and providing other financial services throughout its market area. Competitors include other community banks, larger banking institutions, and a wide range of other financial institutions such as credit unions, government-sponsored enterprises, mutual fund companies, insurance companies and other non-bank businesses. Many of these competitors are national in scope and have substantially greater resources with which to service their customers.

Supervision, Regulation and Compliance

Community is subject to extensive state and federal laws and regulations governing the banking industry, in particular, and public companies, in general. Changes in those laws and regulations, or the degree of Community’s compliance with those laws and regulations as judged by any of several regulators that oversee Community, could have a significant effect on Community’s operations and its financial results.

Acquisitions

Over the last several years, the Corporation has entered into a number of mergers or acquisitions of both banks and other financial services companies. In connection with these transactions, estimates and assumptions were used to assess whether expense savings and other synergies could be realized from the merger and were considered in the determination of the acquisition price. The Corporation’s single largest merger was its acquisition of PennRock

Financial Services Corp. and its primary subsidiary, Blue Ball National Bank (Blue Ball) on July 1, 2005. Additionally, Community currently has pending mergers of two smaller financial institutions that are expected to be completed in the second quarter of 2007.

The success of these mergers, and all future mergers, is largely dependent on the level of efficiencies gained from a number of standard initiatives, including: the reconfiguration of duplicate internal operations; the removal of certain administrative functions; the elimination of redundant external contractual services and; the convergence and standardization of various retirement, bonus, and incentive programs. Each transaction includes risks that these expected savings, efficiencies, or synergies will not be fully realized or may take longer than estimated to be realized and could have a significant effect on Community’s operations and its financial results. Furthermore, a failure to realize these efficiencies, expense savings and other synergies in any single merger transaction may affect Community’s ability to acquire complementary businesses in future periods and, consequently, could seriously impact its ability to expand its franchise through acquisitions.

Goodwill Impairment

Current accounting standards require that the purchase method of accounting be used for all business combinations. Under purchase accounting, if the consideration exchanged in the acquisition of a company exceeds the fair market value of the net identifiable assets of that company, the excess amount must be reflected on the records of the acquirer as goodwill. At the end of 2006, Community had recorded approximately $246 million of goodwill, the majority of which was recognized in connection with the merger of PennRock. Under purchase accounting, the Corporation is required to evaluate goodwill for impairment on an annual basis. Recognition of any impairment in the carrying amount of goodwill must be included in the results of operations in the period in which a determination of impairment has been made. Based upon its most recent analysis, management has determined that the carrying amount of goodwill has not been impaired as of December 31, 2006. The carrying amount of goodwill will continue to be analyzed in subsequent periods and there is no assurance that goodwill or some portion thereof will not be considered impaired pursuant to an evaluation conducted at a future date.

Ability to Pay Dividends

Community’s ability to pay dividends depends, to a large extent, on its receipt of dividends from its direct or indirect subsidiaries. Currently, the Corporation’s primary source of dividends for distribution to shareholders is dependent upon the receipt of dividends from its primary banking subsidiary, CommunityBanks. The ability of the Bank to pay dividends to the Corporation is subject to its profitability, financial condition, and other cash flow requirements. There is no absolute assurance that the Bank or any of the other subsidiaries of the Corporation will be able to pay dividends in the future or that the Corporation will generate adequate cash flow to pay dividends in the future. Community’s failure to pay dividends on its common stock could have a material adverse effect on the market price of its stock.

Community’s stock price can be volatile.

The market price of Community common stock may fluctuate significantly in response to a number of other factors, including changes in securities analysts’ estimates of financial performance, volatility of stock market prices and volumes, rumors or erroneous information, changes in market valuations of similar companies and changes in accounting policies or procedures as may be required by the Financial Accounting Standards Board or other regulatory agencies.

None.

Community Banks, Inc., does not own or lease any property. As of December 31, 2006, the Bank owns 42 unencumbered properties and leases 40 other properties. Community’s other direct and indirect subsidiaries own 6 unencumbered properties and lease 4 properties. Five properties owned by Community’s indirect subsidiary, PSB Realty, are leased to the Bank.

The principal office of Community is located at 777 East Park Drive, Harrisburg Pennsylvania 17111. The principal office of the Bank is owned and located at 150 Market Square, Millersburg Pennsylvania 17061, with executive and administrative offices at 777 East Park Drive, Harrisburg PA 17111.

The Bank currently has 74 branch offices located in Adams, Berks, Chester, Cumberland, Dauphin, Lancaster, Luzerne, Northumberland, Schuylkill, Snyder, and York counties, Pennsylvania, and in Carroll County, Maryland. The Bank owns or leases 88 automated teller machines located throughout these counties.

From time to time, the Bank also acquires real estate by virtue of foreclosure proceedings, and such real estate is disposed of in the usual and ordinary course of business as expeditiously as is prudently possible.

Various actions and proceedings are presently pending to which Community and/or one or more of its subsidiaries is a party. These actions and proceedings arise out of routine operations and, in management’s opinion, will not have a material adverse effect on Community’s consolidated financial position or results of operations. Community is not required to make any disclosures pursuant to Section 6707A(e) of the Internal Revenue Code.

No matters were submitted to a vote of security holders during the fourth quarter of 2006.

PART II

Market Information

The shares of Community are traded on the Global Select Market Tier of the Nasdaq Stock Market under the symbol CMTY and are transferred through local and regional brokerage houses. Community had approximately 5,450 shareholders of record as of December 31, 2006. The following table sets forth dividends declared per share and the high and low closing prices for Community common stock as reported on the Nasdaq during the periods indicated.

| | 2006 | | 2005 |

| | Price Per Share | Dividends | | Price Per Share | Dividends |

| | Low | High | Declared | | Low | High | Declared |

| | | | | | | | |

| First Quarter | $25.67 | $27.85 | $0.19 | | $22.57 | $27.15 | $0.16 |

| Second Quarter | $24.38 | $27.39 | $0.20 | | $21.94 | $25.24 | $0.18 |

| Third Quarter | $24.58 | $27.29 | $0.20 | | $25.39 | $27.48 | $0.18 |

| Fourth Quarter | $25.74 | $28.48 | $0.20 | | $23.90 | $28.42 | $0.19 |

Holders of the common stock of Community are entitled to such dividends as may be declared from time to time by the Board of Directors out of funds legally available. Community currently expects that it will continue to pay comparable dividends in the future, subject to regulatory requirements, Community’s financial condition and requirements, future prospects, business conditions and other factors deemed relevant by the Board of Directors. As noted in “Capital Adequacy” in Part I, Item 1, Community is subject to various regulatory capital requirements that limit the amount of capital available for dividends.

The market prices listed above are based on historical market quotations and have been restated to reflect stock dividends and splits. Information concerning securities authorized for issuance under equity compensation plans is set forth in Note 14 to the Consolidated Financial Statements included in this report at Item 8 and is incorporated herein by reference.

Issuer Purchases of Equity Securities

During the fourth quarter of 2006, Community repurchased the following shares of its common stock pursuant to its employee benefit plans. During this period, Community did not purchase any shares pursuant to its Share Repurchase Program. Community did not sell any unregistered securities during the fourth quarter of 2006.

| | | Total Number of Shares Purchased | | Average Price Paid Per Share | | Total Number of Shares Purchased as part of Publicly Announced Plans or Programs | | Capacity to Purchase More Shares Under Repurchase Program | |

| | | | | | | | | | |

| 10/1/06-10/31/06 | | | 1,963 | | $ | 27.06 | | | 1,963 | | | 53,900 | |

| 11/1/06-11/30/06 | | | 450 | | $ | 27.16 | | | 450 | | | 53,900 | |

| 12/1/06-12/31/06 | | | 299 | | $ | 28.34 | | | 299 | | | 53,900 | |

| 1. | In July 2003, Community registered 50,000 shares of its common stock for purchase by employees pursuant to the 401(k) savings plan and the Board of Directors authorized the repurchase of shares of Community common stock to fund the plan. No timetable was set for these repurchases. |

| 2. | In the fourth quarter of 2005, Community announced a plan to repurchase 787,500 (restated for 5% stock dividend in 2006) of its shares. No expiration date was given for the repurchase. As of December 31, 2006, 53,900 shares remain to be purchased pursuant to this plan. |

| 3. | During the fourth quarter of 2006, no plan or program expired and Community did not determine to terminate any repurchase program. |

STOCK PERFORMANCE GRAPH

The following graph shows the yearly percentage change in Community’s cumulative total shareholder return on its common stock from December 31, 2001, to December 31, 2006, compared with the cumulative total return of the Nasdaq Stock Market (U.S. Companies), and a self-determined peer group consisting of thirteen bank holding companies. The bank holding companies in the peer group are Bryn Mawr Bank Corporation, Citizens & Northern Corporation, Comm Bancorp, Inc., Community Bank System, Inc., FNB Financial Corporation, Harleysville National Corporation, KNBT Bancorp, Inc., Leesport Financial Corp., National Penn Bancshares, Inc., Omega Financial Corporation, S&T Bancorp, Inc., Sandy Spring Bancorp, Inc., and Sterling Financial Corporation. Community selected these companies because they conduct a community banking business in similar markets and they are similar to Community in asset size and market capitalization.

| | | At or for the Year Ended December 31, | |

| | | 2006 | | 2005 * | | 2004 | | 2003 | | 2002 | |

| | | (dollars in thousands except for per share data) | |

BALANCE SHEET DATA | | | | | | | | | | | |

| At Period End: | | | | | | | | | | | | | | | | |

Investment securities | | $ | 659,136 | | $ | 628,585 | | $ | 619,110 | | $ | 646,961 | | $ | 667,801 | |

Total loans | | | 2,370,889 | | | 2,237,065 | | | 1,217,456 | | | 1,084,678 | | | 916,051 | |

Total assets | | | 3,496,370 | | | 3,332,430 | | | 1,954,799 | | | 1,861,063 | | | 1,680,362 | |

Total deposits | | | 2,513,182 | | | 2,294,367 | | | 1,305,537 | | | 1,230,685 | | | 1,132,913 | |

Long-term debt | | | 315,079 | | | 430,719 | | | 404,662 | | | 411,422 | | | 320,533 | |

Stockholders’ equity | | | 486,161 | | | 476,673 | | | 152,341 | | | 143,406 | | | 129,162 | |

| Average: | | | | | | | | | | | | | | | | |

Total assets | | | 3,403,421 | | | 2,668,605 | | | 1,941,096 | | | 1,780,679 | | | 1,580,046 | |

Total stockholders’ equity | | | 475,710 | | | 318,768 | | | 145,750 | | | 135,773 | | | 119,352 | |

| | | | | | | | | | | | | | | | | |

EARNINGS DATA: | | | | | | | | | | | | | | | | |

| Net interest income | | | 106,900 | | | 82,645 | | | 56,557 | | | 52,514 | | | 50,488 | |

| Provision for loan losses | | | 2,050 | | | 2,300 | | | 3,100 | | | 2,500 | | | 3,350 | |

| Net interest income after provision for loan losses | | | 104,850 | | | 80,345 | | | 53,457 | | | 50,014 | | | 47,138 | |

| Other income | | | 34,967 | | | 26,437 | | | 23,213 | | | 20,463 | | | 13,975 | |

| Other expense | | | 84,885 | | | 75,069 | | | 49,993 | | | 45,718 | | | 39,300 | |

| Provision for income taxes | | | 13,901 | | | 6,072 | | | 4,879 | | | 4,359 | | | 3,367 | |

| Net income | | | 41,031 | | | 25,641 | | | 21,798 | | | 20,400 | | | 18,446 | |

| | | | | | | | | | | | | | | | �� | |

PER SHARE DATA: | | | | | | | | | | | | | | | | |

| Basic earnings per share | | | 1.74 | | | 1.38 | | | 1.70 | | | 1.59 | | | 1.45 | |

| Diluted earnings per share | | | 1.72 | | | 1.35 | | | 1.65 | | | 1.54 | | | 1.42 | |

| Cash dividends declared | | | 0.79 | | | 0.71 | | | 0.64 | | | 0.60 | | | 0.52 | |

| Book value | | | 20.67 | | | 19.81 | | | 11.86 | | | 11.17 | | | 10.16 | |

| Average diluted shares outstanding | | | 23,918,486 | | | 18,975,425 | | | 13,203,653 | | | 13,122,240 | | | 13,115,886 | |

| | | | | | | | | | | | | | | | | |

PROFITABILITY RATIOS: | | | | | | | | | | | | | | | | |

| Return on average assets | | | 1.21 | % | | 0.96 | % | | 1.12 | % | | 1.15 | % | | 1.17 | % |

| Return on average stockholders’ equity | | | 8.63 | % | | 8.04 | % | | 14.96 | % | | 15.03 | % | | 15.46 | % |

| Net interest margin (FTE) | | | 3.88 | % | | 3.76 | % | | 3.44 | % | | 3.50 | % | | 3.78 | % |

| Efficiency ratio | | | 57.33 | % | | 57.51 | % | | 60.42 | % | | 60.59 | % | | 56.92 | % |

| | | | | | | | | | | | | | | | | |

CAPITAL AND LIQUIDITY RATIOS: | | | | | | | | | | | | |

| Stockholders’ equity to total assets | | | 13.90 | % | | 14.30 | % | | 7.79 | % | | 7.71 | % | | 7.69 | % |

| Average equity to average assets | | | 13.98 | | | 11.95 | % | | 7.51 | % | | 7.62 | % | | 7.55 | % |

| Dividend payout ratio | | | 45.52 | | | 52.42 | % | | 37.69 | % | | 37.35 | % | | 36.07 | % |

| Net loans to assets | | | 67.13 | % | | 66.36 | % | | 61.47 | % | | 57.25 | % | | 53.10 | % |

| | | | | | | | | | | | | | | | | |

ASSET QUALITY RATIOS: | | | | | | | | | | | | | | | | |

| Allowance for loan losses to total loans outstanding | | | 1.00 | % | | 1.03 | % | | 1.18 | % | | 1.22 | % | | 1.35 | % |

| Allowance for loan losses to non-accrual loans | | | 188 | % | | 253 | % | | 266 | % | | 162 | % | | 131 | % |

| Non-accrual loans to total loans outstanding | | | 0.53 | % | | 0.41 | % | | 0.45 | % | | 0.76 | % | | 1.04 | % |

| Non-performing assets to total assets | | | 0.36 | % | | 0.32 | % | | 0.38 | % | | 0.70 | % | | 0.63 | % |

| Net charge-offs to average loans outstanding | | | 0.06 | % | | 0.05 | % | | 0.16 | % | | 0.17 | % | | 0.35 | % |

* 2005 amounts include the impact of the July 1, 2005 merger with PennRock Financial Services Corp.

INTRODUCTION

Purpose of this Presentation

This presentation has been designed to provide a narrative explanation of the financial statements of Community Banks, Inc. (“Community” or “the Corporation”). The purpose of this presentation is to enhance 2006 financial disclosures and to provide a framework for evaluating the extent to which historical performance can be relied upon to assess prospects for future performance.

Presentation Format

Throughout this presentation, net interest income and yields on earning assets have been presented on a fully-tax equivalent basis. Unless otherwise indicated, balances represent average daily balances, earnings per share are presented on a fully-diluted basis, and all dollar amounts are presented in thousands.

Background

The July 1, 2005, merger with PennRock Financial Services Corp (“PennRock”) represented a milestone in the expansion of the Community franchise. As required under generally accepted accounting principles (“GAAP”), the merger was accounted for under the purchase method of accounting for business combinations (“purchase accounting”). Prior to the merger, PennRock’s financial performance was derived principally from activities of its primary operating subsidiary, Blue Ball National Bank (“Blue Ball”).

For 2006, annual results reflected “combined” operating activities of Community and the former Blue Ball for the entire year. In 2005, operating results of historical Community were combined with the operating results of the former Penn Rock beginning on July 1, 2005, to form the newly-combined Community. In accordance with GAAP, financial results for the six month period prior to the July 1, 2005, merger date did not include Blue Ball-related financial activity and reflected only the pre-merger financial results for historical Community. Consequently, presentations of annual results for the twelve month period ended December 31, 2005, reflect a “hybrid” presentation consisting of six months of pre-merger Community activity and six months of post-merger combined results.

Virtually all comparisons of full year 2006 financial results to the hybrid results of 2005 will reflect distortions owing to the hybrid presentation of 2005 financial statements. Similarly, all financial presentations prior to 2005 are exclusively those of pre-merger, historical Community and will also yield distortions when compared to both the 2006 combined results and the 2005 hybrid results.

To the extent practical, alternate presentations of financial information will be made in order to make comparative results more meaningful to the reader. Such information will be clearly defined and labeled so as to provide consistent and comparable presentations, despite the inherent limitations of comparability resulting from the merger. As an intuitive baseline, the addition of Blue Ball activities would ordinarily be expected to increase combined operations by 50% for full year comparisons, based upon the comparative size of the separate companies prior to the merger. Because of the mid-year 2005 consummation date, however, increases from 2005 to 2006 would be expected to reflect general increases of half that amount, or 25%, exclusive of the effects of operational improvements and organic balance sheet growth.

GAAP REPORTING ISSUES

This section of the presentation will summarize the salient GAAP reporting issues associated with presentations of financial information for Community, including: forward-looking statements; critical accounting policies; and GAAP versus “non-GAAP” presentations.

Forward-Looking Statements

Periodically, Community has made, and will continue to make, assertions that may include forward-looking information. Community cautions that forward-looking information disseminated through financial presentations should not be construed as guarantees of future performance. Furthermore, actual results may differ from expectations contained in such forward-looking information as a result of factors that are not predictable. Financial performance can be affected by any number of factors that are not predictable or are out of management’s direct control. Examples include: the effect of prevailing economic conditions; unforeseen or dramatic changes in the general interest rate environment; actions or changes in policies of the Federal Reserve Board and other government agencies; the risk associated with global instability; business risk associated with the management of the credit extension function and fiduciary activities. Each of these factors could affect estimates, assumptions, uncertainties and risk used to develop forward-looking information, and could cause actual results to differ materially from management’s expectations regarding future performance.

Critical Accounting Policies

The identification of those accounting policies which are deemed to be critical to the application of GAAP on reported results of Community is an important facet of this presentation. Management has identified the applicable promulgations of GAAP that have particular relevance in connection with reported results:

| § | Allowance for Loan Losses: Adequacy of Allowance |

| § | Purchase Accounting for Business Combinations |

| § | “Other than Temporary” Impairment of Investment Securities |

Management believes that the application of its accounting policies and procedures for each of the above items should be considered to be a critical accounting policy to ensure the fair presentation of Community’s financial statements.

Community applies a systemic methodology in order to estimate the allowance for loan losses. This methodology incorporates management’s judgments about the credit quality of the loan portfolio and a disciplined, regimented methodology that is consistently applied. This process requires that a detailed analysis of the loan portfolio be performed on a quarterly basis. This analysis includes a specific individual loan review for any and all loans that meet specific materiality criteria. Such loans are evaluated for impairment under the provisions of Statement of Financial Accounting Standards (“SFAS”) No. 114, “Accounting by Creditors for Impairment of a Loan.” The portfolio is further stratified to analyze groups of homogeneous loans with similar risk characteristics. Such loans are evaluated under the provisions of SFAS No. 5 “Accounting for Contingencies.”

Management considers all known relevant internal and external factors that may affect loan collectibility, as well as particular risks indigenous to specific types of lending. The process is further designed to consolidate the aggregate loss estimates and to ensure that the allowance for loan losses is recorded in accordance with generally accepted accounting principles. The final results are reviewed and approved by executive management. Results are regularly validated by a review of trends associated with loan volume, delinquencies, potential concentrations, or other factors that may influence the methodology used to estimate the allowance for loan losses.

| · | Purchase Accounting for Business Combinations |

In June of 2001, the Financial Accounting Standards Board (“FASB”) issued SFAS No. 141, “Business Combinations,” and SFAS No. 142, “Goodwill and Other Intangible Assets.” These standards eliminated the pooling-of-interests method of accounting (“pooling”) in favor of purchase accounting. Further, these standards were promulgated to ensure that post-merger financial statements of combined entities are prepared in a manner that best represents the underlying economics of a business combination.

These standards necessitate the application of accounting policies and procedures that entail the use of assumptions, estimates, and judgments that are critical to the presentation of financial information, including the ongoing valuation of intangibles. The ultimate responsibility for the application of these standards and the adequacy of disclosures related thereto rests with management. While Community has applied these standards to other business combinations completed since 2001, the magnitude of the PennRock merger on Community’s consolidated results suggests that the application of these standards since the date of that merger is substantially more critical to the presentation of financial information.

| · | Other than Temporary Impairment of Investment Securities |

Investment securities are written down to their net realizable value when there is impairment in value that is considered to be other than temporary. The determination of whether or not other than temporary impairment exists is a matter of judgment. Management reviews its investment securities portfolio regularly for possible impairment that is other than temporary by analyzing the facts and circumstances of each investment and the expectations for that investment’s performance.

GAAP versus Non-GAAP

Like many financial institutions, Community had accounted for virtually all of its business combinations using the pooling method of accounting prior to 2002. Under pooling, historical pre-merger financial information of the combined companies was restated “as if” the combination had occurred prior to the earliest period presented. This approach was advantageous in that it allowed for year-over-year financial performance comparisons that were prepared on a consistent basis. Under purchase accounting, financial statements for any periods prior to the date of the merger are not restated, creating the potential for comparisons that, in some respects, are inherently inconsistent.

Like most other financial institutions that have made large acquisitions since the mandate of purchase accounting, Community is now providing certain non-GAAP information to assist investors in their understanding of the effect of acquisition activity on reported results. Many of these disclosures have been designed to overcome comparability issues related to the influence of intangibles (principally goodwill) created in mergers. Such information is not presented as a substitute for traditional GAAP measurements, but is provided as a supplemental enhancement to improve comparability and investor understanding.

Community has augmented its traditional GAAP presentation by providing an extensive reconciliation of relevant GAAP and non-GAAP measures to enhance its disclosures of comparative financial performance. The reconciliation appears at the end of Part II, Item 7, of this filing. Below is a summary of critical GAAP measurements along with a brief description of the adjustments necessary to produce comparable non-GAAP measurements.

Traditional GAAP Measures | | Adjustments | | Comparable Non-GAAP Measures |

| | | | | |

Balance Sheet: | | | | |

| Average Assets | | Excludes Intangible Assets from Assets | | Average “Tangible” Assets |

| Average Equity | | Excludes Intangible Assets from Equity | | Average “Tangible” Equity |

| Equity to Assets | | Excludes Intangible Assets from Equity and Assets | | “Tangible” Equity to Assets |

| Book Value per Share | | Excludes Intangible Assets from Equity | | “Tangible” Book Value per Share |

| | | | | |

Performance: | | | | |

| Net Income / EPS | | Excludes After-Tax Effect of Mergers & Acquisitions (M&A) Expense and Other Special Charges | | “Core” Net Income / EPS |

| Net Income / EPS | | Excludes After-Tax Effect of CDI Amortization, M&A Expense, and Other Special Charges | | “Tangible” or “Operating” Income / EPS |

| Return on Average Assets (ROA) | | “Tangible” Net Income divided by Average “Tangible” Assets | | Operating Return on Average “Tangible” Assets (ROTA) |

| Return on Average Equity (ROE) | | “Tangible” Net Income divided by Average “Tangible” Equity | | Operating Return on Average “Tangible” Equity (ROTE) |

2006 PERFORMANCE OVERVIEW AND SUMMARY

Executive Overview

In the first full year of combined operations with Blue Ball, Community reported 2006 net income of $41 million and earnings per share of $1.72. Results for the year improved dramatically from 2005 when net income and earnings per share were $25.6 million and $1.35, respectively. While 2006 earnings per share grew 27% from 2005, performance in the previous year had been adversely affected by $8.2 million in pre-tax merger, conversion, and restructuring expenses that had been recorded prior to the consummation of the 2005 mid-year merger with Blue Ball. On July 1, 2005, Community completed the acquisition of Blue Ball and, as required under GAAP, combined Blue Ball’s operating activities for only the last six months of that year. The addition of the Blue Ball Division has facilitated Community’s ongoing transformation to a more strategically relevant franchise in the Mid-Atlantic region.

During the third quarter of 2006, Community announced two pending mergers with future banking partners when it revealed its plans to acquire BUCS Financial Corp and East Prospect State Bank. These two combinations are expected to be completed in the second quarter of 2007 and will provide an important market extension into the desirable, adjacent Central Maryland region and will bolster Community’s existing position in the vibrant York County, Pennsylvania, market. Earlier in 2006, Community completed a smaller acquisition of an insurance agency operating within its Blue Ball market and then subsequently acquired the trust business of a competing financial institution. Each of these acquisitions were fully absorbed by Community by the end of 2006 and will allow the Corporation to further leverage the existing infrastructure that was designed to serve the specialized needs of these customers.

By the end of 2006, Community’s operating footprint boasted assets of $3.5 billion and 74 banking offices that extend throughout the center of Pennsylvania from the Pocono region to just over the Maryland border. Blue Ball operates as a separate division in the attractive Lancaster, Berks and Chester county markets of south-central Pennsylvania. Community is the 8th largest financial services holding company headquartered in Pennsylvania and the largest financial institution headquartered in its capital city of Harrisburg. The pending mergers will add 5 offices and approximately $200 million in assets upon completion.

2006 Economic Conditions and Yield Curve Dynamics

The dominant economic theme for the banking industry throughout 2006 was the ongoing influence of “yield curve dynamics.” The primary source of revenue for most financial institutions, particularly community banks, is derived from intermediation activities. Intermediation activities are defined as the net revenues generated from the process of gathering deposits, combined with the facilitation of credit extension to retail and commercial customers. Banks must maintain a constant vigilance on monitoring and managing the effects of interest rate changes on this essential source of revenue production. Much of this effort focuses on future expectations regarding the shape of the yield curve, or yield curve dynamics, and its impact on pricing activities.

Yield curve dynamics begins with the notion that current interest rate offerings on various maturities of U. S. Treasury securities provide the fundamental indicator of the prevailing interest rate profile and, simultaneously, act as a guidepost for incremental loan and deposit pricing decisions. The traditional, or “normal” yield curve, has some level of slope and is typified by steadily increasing rate offerings on instruments with longer maturities. The slope of the yield curve is driven primarily by expectations for both inflationary trends and the implied future interest rate expectations for these instruments. Generally speaking, a yield curve with a steeper degree of slope provides more opportunity for banks to increase the spread between earning asset yields and funding costs. A steeper yield curve, when combined with growth in earning assets and deposits, can be expected to yield expanded revenue performance.

Since the beginning of 2004, the Federal Reserve executed a series of rate hikes that created a yield curve that was considered essentially “flat” by the end of 2005. By explanation, a flat yield curve is characterized by a negligible disparity between interest rate offerings across the maturity spectrum of the yield curve. By the middle of 2006, the yield curve had actually reached an “inverted” condition. An inverted yield curve is characterized by key short-term interest rates that are higher than the rate offerings on instruments with longer maturities; the opposite condition of a normal yield curve. This phenomenon, which is infrequent in occurrence, is normally unsustainable for more than a short period of time. Uncharacteristically, during the entire second half of 2006, the yield curve remained in an inverted position. For banks, the presence of a flat or inverted yield curve for a prolonged or sustained period can measurably reduce future opportunities to expand revenue from intermediation activities.

During the course of 2006, yield curve conditions contributed to a gradual compression in net interest margins and net interest income growth for Community, the two key metrics for top-line revenue expansion. The prolonged presence of an inverted yield curve presented special earnings challenges for Community, as well as throughout the banking industry, as rising deposit funding costs, which are influenced primarily by short-term interest rate trends, have experienced continuous increases. Alternatively, the portion of the earning asset base whose rates are derived from the longer end of the curve, most notably the investment portfolio and loans with fixed long-term maturities, have not kept pace with the increased cost of funding. Additionally, Community has been increasingly reluctant to extend credit maturities without a rate premium commensurate with the incremental interest rate risk associated with longer-term loans. This confluence of conditions was particularly apparent during the fourth quarter of 2006 when, for the first time in recent history, net interest income experienced a slight decline. Consequently, it is believed that the entire banking industry faces a meaningful challenge in the form of further net interest margin compression absent favorable and timely changes in yield curve dynamics in the coming year.

2006 Performance Summary

The four major components of operating performance are net interest income; the provision for credit losses; non-interest income; and non-interest expenses.

Net interest income, which remains Community’s single largest revenue source, grew to $115 million 2006 versus $90 million in 2005, an increase of 28%. Growth was attributed primarily to the full year addition of Blue Ball activity in 2006.

In addition to the yield curve dynamics and associated interest rate trends previously discussed, expansion of net interest income was hampered by constrained loan demand that began to emerge in the third quarter of 2006. Additionally, the presence of a flat or inverted yield curve minimized the opportunities to expand investment yields commensurate with the rise in funding costs. On the funding side, Community experienced both a measurable shift in consumer preference for time deposits and a lack of growth in lower-cost core deposit balances. During the course of the year, rates paid on short-term time deposits rose at levels commensurate with the general rise in short-term interest rates. The upward pressure on short-term rates influenced time deposit pricing for Community and its competitors. The differential in rates between core deposit balances and retail time deposits precluded any opportunity to increase lower-cost core deposit balances and, simultaneously, increased Community’s mix of higher-cost, short-term certificate of deposit balances. All of these factors influenced an increase in funding costs.

Despite these conditions, Community was able to avoid any meaningful deterioration in net interest income performance throughout most of the year. Late in the third and into the fourth quarter of 2006, Community experienced trends that, absent future changes in yield curve trends, are likely to dampen meaningful revenue expansion from intermediation activities in the near term.

| · | Provision for Credit Losses |

Community’s credit profile remained largely unchanged from 2005 as most vital metrics remained stable. Credit quality metrics have been stellar for the last three years and reflect an overall industry trend. The provision for credit losses was $2.1 million for 2006 versus $2.3 million for 2005. The 2006 provision exceeded net charge-offs for the year, which reached $1.4 million, or 0.06% of loans. The comparable numbers in 2005 were $0.8 million and 0.05% of loans.

Non-interest income, which included the additional fees from the acquired insurance and trust businesses, grew to $35.0 million in 2006 (inclusive of modest security gains), versus $26.4 million in 2005, a growth rate of 32%. The growth rate in this important source of revenues exceeded expectations beyond the incremental Blue Ball contribution, due partially to the favorable influence of the fees from acquired businesses. Expenses associated with these acquired operations were similarly influenced. Other fees, including retail investment sales and consolidated overdraft program fees, also experienced steady improvements. The various non-interest income sources of revenue now provide 23% of aggregate corporate revenues.

Non-interest expenses for the year reached $84.9 million versus $75.1 million in 2005. Exclusive of merger, conversion and restructuring expenses totaling $8.2 million related to the Blue Ball merger, 2005 expenses would have totaled $66.9 million. Expenses in 2006 grew nearly 27% from the adjusted 2005 expense total. The growth rate was substantially attributed to the full year addition of Blue Ball operations and, to a far lesser extent, to the comparatively modest additions from the acquired businesses. The efficiency ratio for 2006 was 57.33%. While Community was able to achieve substantial efficiencies from combining core operating activities of pre-merger Community and Blue Ball, more significant reductions were precluded by continued investments in organic office expansion efforts.

| · | Comparative Performance Measures |

Important traditional measures of relative financial performance between financial institutions include return on average assets (ROA) and return on average equity (ROE), which were 1.21% and 8.63%, respectively, for 2006. Comparable measures in 2005 were 0.96% and 8.04%. The 2005 GAAP measures of relative performance were inclusive of the merger, conversion and restructuring expenses that suppressed 2005 performance. Additionally, the relative magnitude of the acquisition of PennRock to Community’s historical franchise has distorted any comparisons to Community’s pre-merger performance prior to 2005.

Since the consummation of the PennRock merger, Community has been providing certain non-GAAP measures designed to assist investors in their understanding of the effect of acquisition activity on reported results. The comparable non-GAAP measures to traditional ROA and ROE metrics exclude certain non-cash expenses, unusual charges and certain intangible assets from the computation, and have been designated as “operating return on tangible assets” (ROTA) and “operating return on tangible equity” (ROTE). ROTA and ROTE increased to 1.36% and 19.57%, respectively, compared to 1.27% and 17.09% for the year ago period.

PERFORMANCE COMPONENTS

The purpose of this section of the presentation is to provide a more in-depth comparative analysis of the four major components of performance during 2006.

Net Interest Income

As with most financial institutions, Community’s major source of revenue is derived from intermediation activities and is reported as net interest income. Net interest income is defined as the difference between interest income on earning assets and interest expense on deposits and borrowed funds. Net interest margin is a relative measure of a financial institution’s ability to efficiently deliver net interest income from a given level of earning assets. Both net interest income and net interest margin are influenced by the frequency, velocity, and extent of interest rate changes, including the slope of the yield curve, and by the composition and absolute volumes of earning assets and funding sources.

The following table compares net interest income and net interest margin components between 2005 and 2006 (in thousands):

| | | 2006 | | 2005 | | Change | |

| | | Amount | | Yield / Rate | | Amount | | Yield / Rate | | Amount | | Yield / Rate | |

| | | | | | | | | | | | | | | | | | | | |

| Interest income | | $ | 205,436 | | | 6.95 | % | $ | 149,456 | | | 6.26 | % | $ | 55,980 | | | 0.69 | % |

| Interest expense | | | 90,734 | | | 3.56 | % | | 59,648 | | | 2.90 | % | | 31,086 | | | 0.66 | % |

| Net interest income | | $ | 114,702 | | | | | $ | 89,808 | | | | | $ | 24,894 | | | | |

| | | | | | | | | | | | | | | | | | | | |

| Interest spread | | | | | | 3.39 | % | | | | | 3.36 | % | | | | | 0.03 | % |

| Impact of non-interest funds | | | | | | 0.49 | % | | | | | 0.40 | % | | | | | 0.09 | % |

| | | | | | | | | | | | | | | | | | | | |

| Net interest margin | | | | | | 3.88 | % | | | | | 3.76 | % | | | | | 0.12 | % |

| · | Overview--2006 versus 2005 |

Comparisons of net interest income and net interest margin for 2005 and 2006 were disproportionately influenced by the fact that only six months of Blue Ball activity is included in 2005 results, while 2006 included the combined twelve months’ results. The majority of the volume increases in both interest income and interest expense can be attributed to the additional six months of Blue Ball activity included in 2006 results.

Quarterly presentations of asset yields, cost of funds, net interest margin, net interest income and other key metrics provide a more meaningful analysis of underlying trends in this component of performance. These trends, when observed in combination with yield curve movements, provide insight into the increases in annual results shown above. To begin this analysis, it is important to take an historical view of the interdependency of incremental pricing decisions and the influence of yield curve dynamics over the last several years.

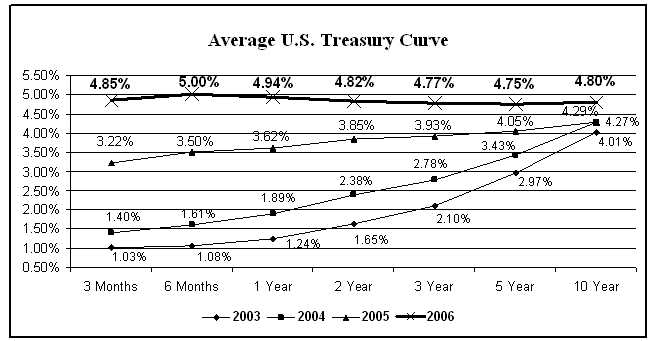

| · | Yield Curve Dynamics: Quantitative Comparisons |

The following presentation of the yield curve at the end of the past four years provides a dramatic illustration of two primary issues that have affected interest rate trends since 2003. First, overall interest rates have increased, although

such increases have been most significant at the short end of the curve, with little or no change in the longer maturities. These increases coincided with the series of interest rate increases in the benchmark Fed Funds rate that the Federal Reserve commenced at the beginning of 2004. Secondly, the yield curves at the end of both 2005 and 2006 had remarkably less slope than the previous two year ends. This dynamic forced the yield curve into a nearly flat position by the end of 2005 and into an inverted position by the end of 2006. This is illustrated in the following table:

The above presentation provides an array of interest rates in place at discrete points in time. While useful, this comparison may exaggerate rate trend movements because it displays interest rates at specific points in time. Rates displayed at discrete points in time are vulnerable to one-day swings and variations, and may not be indicative of general or average trends.