Table of Contents

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-K

FOR ANNUAL AND TRANSITION REPORTS

PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2002

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 0-14549

UNITED SECURITY BANCSHARES, INC.

(Exact Name of Registrant as Specified in Its Charter)

Delaware | 63-0843362 | |

(State or Other Jurisdiction of | (I.R.S. Employer | |

Incorporation or Organization) | Identification No.) | |

131 West Front Street | ||

Post Office Box 249 | ||

Thomasville, Alabama | 36784 | |

(Address of Principal Executive Offices) | (Zip Code) |

Registrant’s telephone number, including area code (334) 636-5424

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Name of Each Exchange on Which Registered | |

None | None |

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, Par Value $0.01 per share

(Title of class)

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether registrant is an accelerated filer (as defined in Exchange Act 12b-2). Yes x No ¨

Shares of common stock ($0.01 par value) outstanding as of March 3, 2003: 3,216,137

The aggregate market value of the voting stock held by non-affiliates of the registrant on June 28, 2002 was $80,924,827.

DOCUMENTS INCORPORATED BY REFERENCE.

Portions of the registrant’s definitive proxy statement for the 2003 annual meeting of its shareholders are incorporated by reference into Part III.

Table of Contents

United Security Bancshares, Inc.

Annual Report on Form 10-K

for the fiscal year ended

December 31, 2002

Part | Item | Caption | Sequential Page No. | |||

I | 1 | 2 | ||||

2 | 11 | |||||

3 | 11 | |||||

4 | 12 | |||||

II | 5 | Market for Registrant’s Common Equity and Related Stockholder Matters | 12 | |||

6 | 14 | |||||

7 | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 15 | ||||

7A | 41 | |||||

8 | 42 | |||||

9 | Changes In and Disagreements With Accountants on Accounting and Financial Disclosure | 71 | ||||

III | 10 | 71 | ||||

11 | 71 | |||||

12 | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 72 | ||||

13 | 72 | |||||

14 | 73 | |||||

IV | 15 | Exhibits, Financial Statement Schedules and Reports on Form 8-K | 73 | |||

78 | ||||||

80 | ||||||

Exhibits | ||||||

1

Table of Contents

PART I

General

United Security Bancshares, Inc. (“Bancshares”) is a Delaware corporation organized in 1999, as a successor by merger with United Security Bancshares, Inc., an Alabama corporation. Bancshares is a bank holding company registered under the Bank Holding Company Act of 1956, as amended, and it operates one banking subsidiary, First United Security Bank (the “Bank”). The Bank owns all of the stock of Acceptance Loan Company, Inc. (“ALC”), a finance company organized for the purpose of making consumer loans and purchasing consumer loans from vendors. Bancshares owns all the stock of First Security Courier Corporation (“First Security”), an Alabama corporation organized for the purpose of providing certain bank courier services. The Bank’s wholly-owned Arizona subsidiary, FUSB Reinsurance, Inc. (“FUSB Reinsurance”), reinsures or “underwrites” credit life and credit accident and health insurance policies sold to the Bank’s consumer loan customers. FUSB Reinsurance is responsible for the first level of risk on these policies up to a specified maximum amount, and the primary third-party insurer retains the remaining risk. The third-party insurer and/or a third-party administrator is responsible for performing most of the administrative functions of FUSB Reinsurance on a contract basis.

The Bank has seventeen banking offices, which are located in Thomasville, Coffeeville, Fulton, Gilbertown, Grove Hill, Butler, Jackson, Brent, Centreville, Woodstock, Bucksville, Calera and Harpersville, Alabama, and its market area includes portions of Bibb, Chilton, Clarke, Choctaw, Hale, Jefferson, Marengo, Monroe, Perry, Shelby, Sumter, Tuscaloosa, Washington and Wilcox Counties in Alabama, as well as Clarke, Lauderdale and Wayne Counties in Mississippi.

2

Table of Contents

The Bank conducts a general commercial banking business and offers banking services such as the receipt of demand, savings and time deposits, personal and commercial loans, credit card and safe deposit box services and the purchase and sale of government securities.

As of December 31, 2002, the Bank had 183 full-time equivalent employees, ALC had 97 full-time equivalent employees and Bancshares had no employees, other than the executive officers of Bancshares who are indicated in Part III, Item 10 of this report.

Competition

Bancshares and its subsidiaries encounter strong competition in making loans, acquiring deposits and attracting customers for investment services. Competition among financial institutions is based upon interest rates offered on deposit accounts, interest rates charged on loans, other credit and service charges relating to loans, the quality and scope of the services rendered, the convenience of banking facilities and, in the case of loans to commercial borrowers, relative lending limits. The Bank competes with other commercial banks (including at least ten in its service area), savings and loan associations, credit unions, finance companies, mutual funds, insurance companies, brokerage and investment banking companies and other financial intermediaries operating in Alabama and elsewhere. Many of these competitors, some of which are affiliated with large bank holding companies, have substantially greater resources and lending limits. In addition, many of the Bank’s non-bank competitors are not subject to the same extensive federal regulations that govern bank holding companies and federally-insured banks.

The Gramm-Leach-Bliley Act (the “GLB Act”), which became effective March 11, 2000, permits bank holding companies to become financial holding companies and thereby affiliate with securities firms and insurance companies and engage in other activities that are financial in nature. See “Supervision and Regulation.”Under the GLB Act, securities firms and insurance companies

3

Table of Contents

that elect to become financial holding companies may acquire banks and other financial institutions. The GLB Act, which represents the most sweeping reform of financial services regulation in over sixty years, may significantly change the competitive environment in which Bancshares and the Bank conduct business. At this time, however, it is not possible to predict the full effect that the GLB Act will have on Bancshares. One consequence may be increased competition from large financial services companies that will be permitted to provide many types of financial services, including bank products, to their customers.

The financial services industry is also likely to become more competitive as further technological advances enable more companies to provide financial services. These technological advances may diminish the importance of depository institutions and other financial intermediaries in the transfer of funds among parties.

The Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994 (the “IBBEA”) authorized bank holding companies to acquire banks and other bank holding companies without geographic limitations beginning September 30, 1995, which has increased further the competitiveness of the banking industry.

In addition, beginning on June 1, 1997, the IBBEA authorized interstate mergers and consolidations of existing banks, provided that neither bank’s home state had opted out of interstate branching by May 31, 1997. The State of Alabama opted in with respect to interstate branching. Once a bank has established branches in a state through an interstate merger, the bank may establish and acquire additional branches at any location in the state where any bank involved in the interstate merger could have established or acquired branches under applicable federal or state law.

Under the IBBEA, Alabama banks may also establish branches or offices in any other state, any territory of the United States or any foreign country, provided that the branch or office is

4

Table of Contents

established in compliance with federal law and the law of the proposed location and is approved by the Alabama Superintendent of Banks. Under former law, Alabama banks could not establish a branch in any location other than its principal place of business, except as authorized by local laws or general laws of local application. These more liberal branching laws have increased and are likely to continue increasing competition within the State of Alabama among banking institutions located in Alabama and from those located outside of Alabama, many of which are larger than Bancshares. Size gives the larger banks certain advantages in competing for business from large corporations. These advantages include higher lending limits and the ability to offer services in other areas of Alabama and the Southeastern United States.

Supervision and Regulation

Bancshares and the Bank are subject to state and federal banking laws and regulations which impose specific requirements and restrictions on, and provide for general regulatory oversight with respect to, virtually all aspects of operations. These laws and regulations are generally intended to protect depositors, not shareholders. To the extent that the following summary describes statutory or regulatory provisions, it is qualified in its entirety by reference to the particular statutory and regulatory provisions. Any change in applicable laws or regulations may have a material effect on the business and prospects of Bancshares.

Beginning with the enactment of the Financial Institutions Reform, Recovery and Enforcement Act of 1989 and following in 1991 with the Federal Deposit Insurance Corporation Act (“FDICIA”), numerous additional regulatory requirements have been placed on the banking industry in the past fifteen years, and additional changes have been proposed. The operations of Bancshares and the Bank may be affected by legislative changes and the policies of various regulatory authorities. Bancshares is unable to predict the nature or the extent of the effect on its business and

5

Table of Contents

earnings that fiscal or monetary policies, economic control or new federal or state legislation may have in the future.

As a bank holding company, Bancshares is subject to the regulation and supervision of the Board of Governors of the Federal Reserve System (the “Board of Governors”). Bancshares is required to file with the Board of Governors an annual report and such additional information as the Board of Governors may require. The Board of Governors may also conduct examinations of Bancshares and each of its subsidiaries.

The Bank Holding Company Act (“the Act”) imposes numerous restrictions on Bancshares. In particular, the Act requires a bank holding company to obtain the prior approval of the Board of Governors before it may acquire substantially all of the assets of any bank or control of any voting shares of any bank, if, after such acquisition, it would own or control, directly or indirectly, more than 5% of the voting shares of such bank. The Board of Governors may not approve an acquisition by Bancshares of substantially all the assets or the voting shares of any bank located outside Alabama unless such acquisition is specifically authorized by the laws of the state in which the bank to be acquired is located.

The GLB Act permits bank holding companies to become financial holding companies and thereby affiliate with securities firms and insurance companies and engage in other activities that are financial in nature. A bank holding company may become a financial holding company by filing a declaration if each of its subsidiary banks is well capitalized under the FDICIA prompt corrective action provisions, is well managed and has at least a satisfactory rating under the Community Reinvestment Act (“CRA”). No regulatory approval will be required for a financial holding company to acquire a company, other than a bank or savings association, engaged in activities that

6

Table of Contents

are financial in nature or incidental to activities that are financial in nature, as determined by the Board of Governors.

The GLB Act defines “financial in nature” to include securities underwriting; dealing and market making; sponsoring mutual funds and investment companies; insurance underwriting and agency; and activities that the Board of Governors has determined to be closely related to banking. A national bank also may engage, subject to limitations on investment, in activities that are financial in nature (other than insurance underwriting, insurance company portfolio investment, merchant banking, real estate development and real estate investment) through a financial subsidiary of the bank, if the bank is well capitalized, well managed and has at least a satisfactory CRA rating. Subsidiary banks of a financial holding company or national banks with financial subsidiaries must continue to be well capitalized and well managed in order to continue to engage in activities that are financial in nature without regulatory actions or restrictions, which could include divestiture of the financial subsidiary or subsidiaries. In addition, a financial holding company or a bank may not acquire a company that is engaged in activities that are financial in nature unless each of the subsidiary banks of the financial holding company or the bank at issue has a CRA rating of satisfactory or better.

The GLB Act preserves the role of the Board of Governors as the umbrella supervisor for holding companies while at the same time incorporating a system of functional regulation designed to take advantage of the strengths of the various federal and state regulators. In particular, the GLB Act replaces the broad exemption from Securities and Exchange Commission regulation that banks previously enjoyed with more limited exemptions, and it reaffirms that states are the regulators for the insurance activities of all persons, including federally-chartered banks.

7

Table of Contents

The GLB Act also establishes a minimum federal standard of financial privacy. In general, the applicable regulations issued by the various federal regulatory agencies prohibit affected financial institutions (including banks, insurance agencies and broker/dealers) from sharing information about their customers with non-affiliated third parties unless (1) the financial institution has first provided a privacy notice to the customer; (2) the financial institution has given the customer an opportunity to opt out of the disclosure; and (3) the customer has not opted out after being given a reasonable opportunity to do so.

Subsidiary banks of a bank holding company are subject to certain restrictions on extensions of credit to the bank holding company or any of its non-bank subsidiaries, on investments in the stock or other securities thereof, and on the acceptance of such stocks or securities as collateral for loans to any borrower. Among other requirements, transactions between a bank and its affiliates must be on an arm’s-length basis.

The Bank is subject to extensive supervision and regulation by the Alabama State Banking Department and the Federal Deposit Insurance Corporation (the “FDIC”). Among other things, these agencies have the authority to prohibit the Bank from engaging in any activity (such as paying dividends) that, in the opinion of the agency, would constitute an unsafe or unsound practice. The Bank is also subject to various requirements and restrictions under federal and state law. Areas subject to regulation include dividend payments, reserves, investments, loans (including loans to insiders and significant shareholders), mergers, issuance of securities, establishment of branches and other aspects of operation, including compliance with truth-in-lending laws, usury laws and other consumer protection laws. The GLB Act establishes minimum federal standards of financial privacy pursuant to which financial institutions will be required to institute written privacy policies that must be disclosed to customers at certain required intervals. In addition to the impact of regulation,

8

Table of Contents

commercial banks are affected significantly by the actions of the Board of Governors as it attempts to control the money supply and credit availability in order to influence the economy.

There are a number of obligations and restrictions imposed on bank holding companies and their depository institution subsidiaries by federal law and regulatory policy that are designed to reduce potential loss exposure to the depositors of such depository institutions and to the FDIC insurance fund in the event the depository institution becomes in danger of default or is in default. For example, under a policy of the Board of Governors with respect to bank holding company operations, a bank holding company is required to serve as a source of financial strength to its subsidiary depository institutions and commit resources to support such institutions in circumstances where it might not do so absent such policy. In addition, the “cross-guarantee” provisions of federal law require insured depository institutions under common control to reimburse the FDIC for any loss suffered or reasonably anticipated as a result of the default of a commonly controlled insured depository institution or for any assistance provided by the FDIC to a commonly controlled insured depository institution in danger of default. Although the FDIC’s claim is junior to the claims of non-affiliated depositors, holders of secured liabilities, general creditors and subordinated creditors, it is superior to the claims of shareholders.

The federal banking agencies have broad powers under current federal law to take prompt corrective action to resolve problems of insured depository institutions. The extent of these powers depends upon whether the institutions in question are “well capitalized,” “adequately capitalized,” “undercapitalized,” “significantly undercapitalized” or “critically undercapitalized” as such terms are defined under regulations issued by the federal banking agencies. In general, the agencies measure capital adequacy within a framework that makes capital requirements sensitive to the risk profiles of individual banking companies. The guidelines define capital as either Tier 1 (primarily common

9

Table of Contents

shareholders’ equity) or Tier 2 (certain debt instruments and a portion of the allowance for loan losses). Bancshares and the Bank are subject to a minimum Tier 1 capital ratio (Tier 1 capital to risk-weighted assets) of 4%, total capital ratio (Tier 1 plus Tier 2 to risk-weighted assets) of 8% and Tier 1 leverage ratio (Tier 1 to average quarterly assets) of 3%. To be considered a “well capitalized” institution, the Tier 1 capital ratio, the total capital ratio and the Tier 1 leverage ratio must equal or exceed 6%, 10% and 5%, respectively.

The CRA requires that, in connection with examinations of a financial institution such as the Bank, the FDIC must evaluate the record of the financial institution in meeting the credit needs of its local communities, including low and moderate income neighborhoods, consistent with the safe and sound operation of those institutions. The CRA does not establish specific lending requirements or programs for financial institutions nor does it limit an institution’s discretion to develop the types of products and services that it believes are best suited to its particular community. These factors are considered in evaluating mergers, acquisitions and applications to open a branch or facility. The CRA also requires all institutions to make public disclosure of their CRA ratings. The Bank received a satisfactory rating in its most recent evaluation.

From time to time, various bills are introduced in the United States Congress with respect to the regulation of financial institutions. Certain of these proposals, if adopted, could significantly change the regulation of banks and the financial services industry. Bancshares cannot predict whether any of these proposals will be adopted or, if adopted, how these proposals would affect Bancshares.

FDIC regulations require that management report on its responsibility for preparing its institution’s financial statements and for establishing and maintaining an internal control structure

10

Table of Contents

and procedures for financial reporting and compliance with designated laws and regulations concerning safety and soundness.

Supervision, regulation and examination of banks by the bank regulatory agencies are intended primarily for the protection of depositors rather than for holders of Bancshares common stock.

Available Information

The Bank’s website address is http://www.firstusbank.com (Bancshares does not maintain a website). Bancshares’ annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) of the Exchange Act are not currently available on the Bank’s website; however, Bancshares is currently assessing the expense associated with implementing this feature. Bancshares will provide paper copies of these reports free of charge upon written request, and these reports are available on the Securities and Exchange Commission’s website, http://www.sec.gov.

Bancshares owns no property and does not expect to own any property. The business of Bancshares is conducted from the seventeen offices of the Bank. The Bank owns all of its offices in fee without encumbrances. ALC leases office space throughout Alabama but owns no property. During 2002, the aggregate annual rental payments for office space for ALC totaled approximately $364,467.34.

Bancshares and the Bank, because of the nature of their businesses, are subject at various times to numerous legal actions, threatened or pending. In the opinion of Bancshares, based on review and consultation with legal counsel, the outcome of any legal proceedings presently pending

11

Table of Contents

against Bancshares or the Bank will not have a material effect on Bancshares’ consolidated financial statements or results of operations.

Item 4.Submission of Matters to a Vote of Security Holders.

Not applicable.

PART II

Item 5.Market For Registrant’s Common Equity and Related Stockholder Matters.

There were 3,658,780 shares of Bancshares common stock issued and 3,216,137 shares outstanding as of March 3, 2003. As of March 3, 2003, there were approximately 983 shareholders of Bancshares.

Bancshares’ common stock trades under the symbol “USBI” on The Nasdaq SmallCap Market. The sales price range for Bancshares’ common stock during each calendar quarter of 2001 and 2002 is shown below. The market prices represent sales prices as reported in the Nasdaq Historical Quotes.

High | Low | |||||

2001 | ||||||

First Quarter | $ | 30.50 | $ | 20.50 | ||

Second Quarter |

| 27.00 |

| 19.00 | ||

Third Quarter |

| 29.50 |

| 26.10 | ||

Fourth Quarter |

| 28.62 |

| 28.00 | ||

2002 | ||||||

First Quarter | $ | 29.30 | $ | 28.00 | ||

Second Quarter |

| 30.33 |

| 26.70 | ||

Third Quarter |

| 30.01 |

| 27.00 | ||

Fourth Quarter |

| 31.50 |

| 28.75 | ||

12

Table of Contents

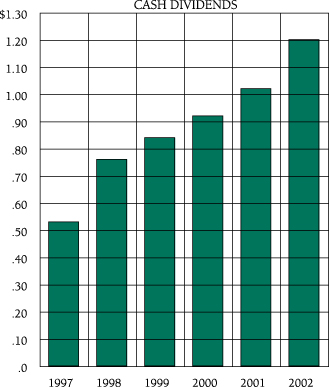

Bancshares has declared dividends on its common stock on a quarterly basis in the past two years as follows:

Dividends Declared | |||

2001 | |||

First Quarter | $ | 0.25 | |

Second Quarter |

| 0.25 | |

Third Quarter |

| 0.25 | |

Fourth Quarter |

| 0.27 | |

2002 | |||

First Quarter | $ | 0.30 | |

Second Quarter |

| 0.30 | |

Third Quarter |

| 0.30 | |

Fourth Quarter |

| 0.30 | |

As a holding company, Bancshares, except under extraordinary circumstances, will not generate earnings of its own, but will rely solely on dividends paid to it by the Bank as the source of income to meet its expenses and pay dividends. Under normal circumstances, Bancshares’ ability to pay dividends will depend entirely on the ability of the Bank to pay dividends to Bancshares.

The Bank is a state banking corporation, and the payment of dividends by the Bank is governed by the Alabama Banking Code. The Alabama Banking Code imposes certain restrictions on banks regarding the payment of dividends. The Bank is required by Alabama law to obtain approval of the Superintendent of the State Banking Department of Alabama (the “Superintendent”) prior to the payment of dividends if the total of all dividends declared by the Bank in any calendar year will exceed the total of (a) the Bank’s net earnings (as defined by statute) for that year plus (b) its retained net earnings for the preceding two years, less any required transfers to surplus. Also, no dividends may be paid from the Bank’s surplus without the prior written approval of the Superintendent.

13

Table of Contents

Item 6.Selected Financial Data.

UNITED SECURITY BANCSHARES, INC. AND SUBSIDIARIES

SELECTED FINANCIAL INFORMATION

Year Ended December 31, | ||||||||||||||||||||

2002 | 2001 | 2000 | 1999 | 1998 | ||||||||||||||||

(In Thousands of Dollars, Except Per Share Amounts) | ||||||||||||||||||||

RESULTS OF OPERATIONS | ||||||||||||||||||||

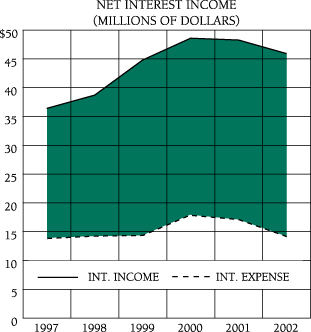

Interest Revenue | $ | 45,752 |

| $ | 47,776 |

| $ | 48,323 |

| $ | 44,919 |

| $ | 43,255 |

| |||||

Interest Expense |

| 14,134 |

|

| 18,419 |

|

| 18,292 |

|

| 15,365 |

|

| 15,518 |

| |||||

Net Interest Revenue |

| 31,618 |

|

| 29,357 |

|

| 30,031 |

|

| 29,554 |

|

| 27,737 |

| |||||

Provision for Loan Losses |

| 3,859 |

|

| 5,255 |

|

| 6,837 |

|

| 4,305 |

|

| 3,187 |

| |||||

Non-Interest Revenue |

| 5,069 |

|

| 4,730 |

|

| 4,883 |

|

| 4,747 |

|

| 4,558 |

| |||||

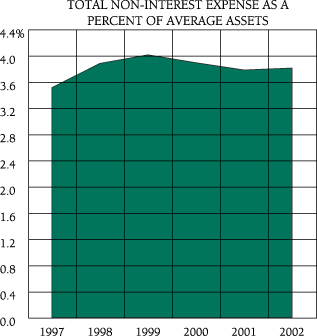

Non-Interest Expense |

| 20,032 |

|

| 19,493 |

|

| 19,106 |

|

| 18,534 |

|

| 17,008 |

| |||||

Income Before Income Taxes |

| 12,796 |

|

| 9,339 |

|

| 8,971 |

|

| 11,462 |

|

| 12,100 |

| |||||

Income Taxes |

| 3,621 |

|

| 2,552 |

|

| 2,193 |

|

| 3,302 |

|

| 3,521 |

| |||||

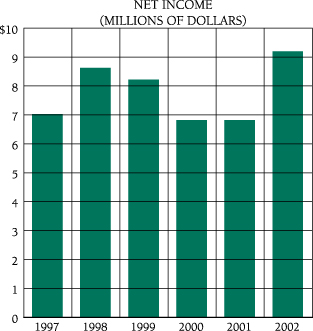

Net Income Before Cumulative Effect of a Change in Accounting Principle | $ | 9,175 |

| $ | 6,787 |

| $ | 6,778 |

| $ | 8,160 |

| $ | 8,579 |

| |||||

Cumulative Effect of a Change in Accounting Principle | $ | 0 |

| $ | (200 | ) |

| 0 |

| $ | 0 |

| $ | 0 |

| |||||

Net Income After Cumulative Effect of a Change in Accounting Principle | $ | 9,175 |

| $ | 6,587 |

| $ | 6,778 |

| $ | 8,160 |

| $ | 8,579 |

| |||||

Net Income Per Share: | ||||||||||||||||||||

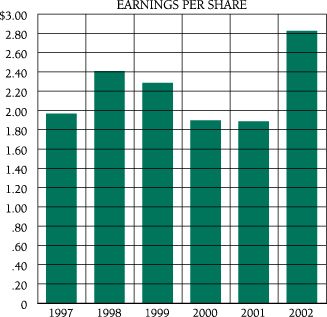

Basic | $ | 2.82 |

| $ | 1.89 |

|

| 1.90 |

| $ | 2.29 |

| $ | 2.42 |

| |||||

Diluted | $ | 2.82 |

| $ | 1.88 |

|

| 1.89 |

| $ | 2.28 |

| $ | 2.40 |

| |||||

Average Number of Shares Outstanding (000) |

| 3,253 |

|

| 3,494 |

|

| 3,570 |

|

| 3,561 |

|

| 3,543 |

| |||||

PERIOD END STATEMENT OF CONDITION | ||||||||||||||||||||

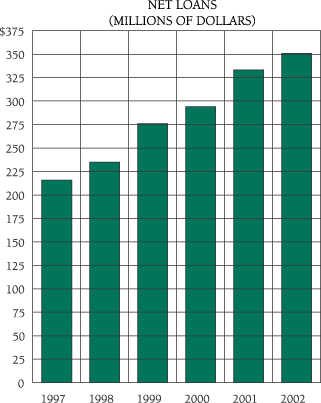

Total Assets | $ | 535,318 |

| $ | 523,112 |

| $ | 509,165 |

| $ | 476,599 |

| $ | 450,073 |

| |||||

Loans, Net |

| 351,434 |

|

| 332,994 |

|

| 296,941 |

|

| 276,172 |

|

| 235,060 |

| |||||

Deposits |

| 353,100 |

|

| 354,815 |

|

| 338,156 |

|

| 326,751 |

|

| 326,645 |

| |||||

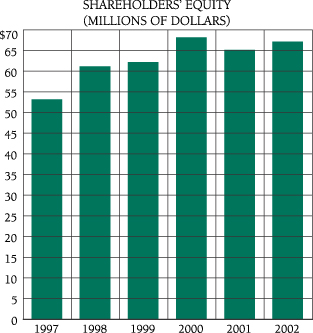

Shareholders’ Equity |

| 67,032 |

|

| 65,206 |

|

| 67,628 |

|

| 61,671 |

|

| 60,568 |

| |||||

AVERAGE BALANCES | ||||||||||||||||||||

Total Assets | $ | 532,409 |

| $ | 516,305 |

| $ | 491,580 |

| $ | 459,922 |

| $ | 439,080 |

| |||||

Average Earning Assets |

| 498,868 |

|

| 486,615 |

|

| 454,055 |

|

| 424,074 |

|

| 408,506 |

| |||||

Loans, Net |

| 345,374 |

|

| 318,453 |

|

| 295,394 |

|

| 256,192 |

|

| 231,792 |

| |||||

Deposits |

| 357,539 |

|

| 345,919 |

|

| 331,877 |

|

| 328,263 |

|

| 320,958 |

| |||||

Shareholders’ Equity |

| 65,309 |

|

| 67,736 |

|

| 63,604 |

|

| 61,140 |

|

| 57,409 |

| |||||

PERFORMANCE RATIOS | ||||||||||||||||||||

Net Income to: | ||||||||||||||||||||

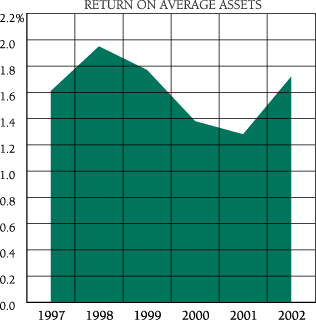

Average Total Assets |

| 1.72 | % |

| 1.28 | % |

| 1.38 | % |

| 1.77 | % |

| 1.95 | % | |||||

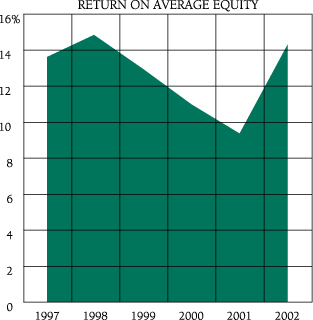

Average Shareholders’ Equity |

| 14.05 | % |

| 9.72 | % |

| 10.66 | % |

| 13.35 | % |

| 14.94 | % | |||||

Average Shareholders’ Equity to: | ||||||||||||||||||||

Average Total Assets |

| 12.27 | % |

| 13.12 | % |

| 12.94 | % |

| 13.29 | % |

| 13.07 | % | |||||

Dividend Payout Ratio |

| 42.35 | % |

| 53.98 | % |

| 48.47 | % |

| 36.67 | % |

| 31.40 | % | |||||

14

Table of Contents

Item 7.Management’s Discussion and Analysis of Financial Condition and Results of Operations.

MANAGEMENT’S DISCUSSION AND ANALYSIS OF

FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Introduction

The following discussion and financial information are presented to aid in an understanding of the current financial position and results of operations of United Security Bancshares, Inc. (“United Security” or the “Company”), and should be read in conjunction with the Audited Financial Statements and Notes thereto included herein. The emphasis of this discussion will be on the years 2002, 2001, and 2000. All yields presented and discussed herein are based on the accrual basis and not on the tax-equivalent basis, unless otherwise indicated.

United Security is the parent holding company of First United Security Bank (the “Bank”). The Bank operates a finance company, Acceptance Loan Company, Inc. (“ALC”), that currently has twenty-six offices in Alabama and Southeast Mississippi. The Bank also owns a reinsurance company, FUSB Reinsurance, Inc. United Security also operates a courier company as a subsidiary, First Security Courier Corporation, which is in the business of delivering checks and documents to the Federal Reserve to aid in check clearing. This courier company performs courier services for the Bank as well as other companies in our market area.

At December 31, 2002, United Security had consolidated assets of approximately $535.3 million and operated seventeen banking locations in five counties. These seventeen locations contributed approximately $8.0 million to consolidated net income in 2002. The Bank’s sole business is banking; therefore, loans and investments are its principal sources of income.

Discussions of certain matters contained in this Annual Report on Form 10-K may contain certain forward-looking statements within the meaning of such term in the Private Securities Litigation Reform Act of 1995 with respect to the financial condition, results of operations and business of United Security and the Bank related to, among other things:

| A. | Trends or uncertainties in economic and business conditions which will impact future operating results, liquidity and capital resources and the relationship among those trends or uncertainties and nonperforming loans and other loans; |

| B. | The diversification of product production among timber-related entities and the effect of that diversification on the Bank’s concentration of loans to timber-related entities; |

| C. | The composition of United Security’s derivative securities portfolio and its interest rate hedging strategies and volatility caused by uncertainty over the economy, inflation and future interest rate trends; |

| D. | The effect of the market’s perception of future inflation and real returns and the monetary policies of the Federal Reserve Board on short- and long-term interest rates; |

| E. | The effect of interest rate changes on liquidity and interest rate sensitivity management; |

| F. | The amount of anticipated (i) net loan charge-offs, (ii) loans on a non-accrual basis, and (iii) derivative income; and |

| G. | The expectations, beliefs, and plans of management as set forth in the letter to shareholders contained in this Annual Report. |

These forward-looking statements involve certain risks and uncertainties. Factors that may cause actual results to differ materially from those contemplated by such forward-looking statements include, among others, the following possibilities:

| 1) | The perceived diversification in product production when the timber industry fails to protect the Bank from its concentration of loans to the timber industry as a result of, for example, the emergence of technological developments or market difficulties that affect the timber industry as a whole; |

| 2) | Periods of lower interest rates continue to accelerate the rate at which the underlying obligations of mortgage-backed securities and collateralized mortgage obligations are prepaid, thereby affecting the yield on such securities held by the Bank; |

15

Table of Contents

| 3) | Inflation grows at a greater-than-expected rate with a material adverse effect on interest rate spreads and the assumptions management of United Security has used in its interest rate hedging strategies and interest rate sensitivity gap strategies; |

| 4) | Rising interest rates adversely affect the demand for consumer credit; |

| 5) | General economic conditions, either nationally or in Alabama and Mississippi, are less favorable than expected; and |

| 6) | The effects of, and changes in, federal and state laws, regulations and policies affecting banking, insurance and monetary and financial matters. |

Critical Accounting Policies

The accounting principles followed by the Company and the methods of applying these principles conform with accounting principles generally accepted in the United States and with general practices within the banking industry. Critical accounting policies relate to securities, loans, allowance for loan losses, accounting estimates, derivatives and hedging. A description of these policies, which significantly affect the determination of financial position, results of operations and cash flows, are summarized in Note 2, “Summary of Significant Accounting Policies” in the “Notes to Consolidated Financial Statements.”

Financial Condition

United Security’s financial condition depends primarily on the quality and nature of the Bank’s assets, liabilities, capital structure, the quality of its personnel, and prevailing market and economic conditions.

The majority of the assets and liabilities of a financial institution are monetary and, therefore, differ greatly from most commercial and industrial companies that have significant investments in fixed assets and inventories. Inflation has an important impact on the growth of total assets in the banking industry, resulting in the need to increase equity capital at rates greater than the applicable inflation rate in order to maintain an appropriate equity to asset ratio. Also, the category of other expenses tends to rise during periods of general inflation.

The Bank owns all of the stock of Acceptance Loan Company, Inc. (“ALC”), an Alabama corporation. ALC is a finance company with twenty-six offices organized for the purpose of making consumer loans. The Bank is ALC’s only source of funds, which amounts to approximately $84.7 million. ALC reported a net income of $1.2 million for the year ended December 31, 2002. This is an improvement over the $1.4 million loss in 2001.

Management believes the most significant factor in producing quality financial results is the Bank’s ability to react properly and in a timely manner to changes in interest rates. Management, therefore, continues to maintain a more balanced position between interest-sensitive assets and liabilities in order to protect against wide interest rate fluctuations. The following table reflects the distribution of average assets, liabilities, and shareholders’ equity for each of the three years ended December 31, 2002, 2001, and 2000.

16

Table of Contents

Distribution of Assets, Liabilities, and Shareholders’ Equity, with

Interest Rates and Interest Differentials

December 31, | |||||||||||||||||||||||||||

2002 | 2001 | 2000 | |||||||||||||||||||||||||

Average Balance | Interest | Yield/ Rate % | Average Balance | Interest | Yield/ Rate % | Average Balance | Interest | Yield/ Rate % | |||||||||||||||||||

(In Thousands of Dollars, Except Percentages) | |||||||||||||||||||||||||||

ASSETS | |||||||||||||||||||||||||||

Interest Earning Assets: | |||||||||||||||||||||||||||

Loans (Note A) | $ | 345,374 | $ | 37,478 | 10.85 | % | $ | 318,453 | $ | 37,230 | 11.69 | % | $ | 295,394 | $ | 37,069 | 12.55 | % | |||||||||

Taxable Investments (Note B) |

| 136,149 |

| 7,261 | 5.33 | % |

| 143,795 |

| 9,164 | 6.37 | % |

| 132,650 |

| 9,604 | 7.24 | % | |||||||||

Non-Taxable Investments |

| 17,027 |

| 1,007 | 5.91 | % |

| 21,082 |

| 1,270 | 6.02 | % |

| 22,780 |

| 1,445 | 6.34 | % | |||||||||

Federal Funds Sold |

| 318 |

| 6 | 1.89 | % |

| 3,285 |

| 112 | 3.41 | % |

| 3,231 |

| 205 | 6.34 | % | |||||||||

Total Interest-Earning Assets |

| 498,868 |

| 45,752 | 9.17 | % |

| 486,615 |

| 47,776 | 9.82 | % |

| 454,055 |

| 48,323 | 10.64 | % | |||||||||

Non-Interest Earning Assets: | |||||||||||||||||||||||||||

Other Assets |

| 33,541 |

| 29,690 |

| 37,525 | |||||||||||||||||||||

Total | $ | 532,409 | $ | 516,305 | $ | 491,580 | |||||||||||||||||||||

LIABILITIES AND SHAREHOLDERS’ EQUITY | |||||||||||||||||||||||||||

Interest-Bearing Liabilities: | |||||||||||||||||||||||||||

Demand Deposits | $ | 66,969 | $ | 700 | 1.05 | % | $ | 60,615 | $ | 1,002 | 1.65 | % | $ | 58,732 | $ | 1,182 | 2.01 | % | |||||||||

Savings Deposits |

| 43,665 |

| 645 | 1.48 | % |

| 40,292 |

| 899 | 2.23 | % |

| 39,591 |

| 1,020 | 2.58 | % | |||||||||

Time Deposits |

| 205,039 |

| 7,936 | 3.87 | % |

| 206,128 |

| 11,537 | 5.60 | % |

| 193,157 |

| 11,065 | 5.73 | % | |||||||||

Other Liabilities |

| 102,292 |

| 4,852 | 4.74 | % |

| 96,837 |

| 4,982 | 5.14 | % |

| 86,470 |

| 5,025 | 5.81 | % | |||||||||

Total Interest-Bearing Liabilities |

| 417,965 |

| 14,133 | 3.38 | % |

| 403,872 |

| 18,420 | 4.56 | % |

| 377,950 |

| 18,292 | 4.84 | % | |||||||||

Non-Interest Bearing Liabilities: | |||||||||||||||||||||||||||

Demand Deposits |

| 41,866 |

| 38,884 |

| 40,397 | |||||||||||||||||||||

Other Liabilities |

| 7,269 |

| 5,813 |

| 9,629 | |||||||||||||||||||||

Shareholders’ Equity |

| 65,309 |

| 67,736 |

| 63,604 | |||||||||||||||||||||

Total | $ | 532,409 | $ | 516,305 | $ | 491,580 | |||||||||||||||||||||

Net-Interest Income (Note C) | $ | 31,619 | $ | 29,356 | $ | 30,031 | |||||||||||||||||||||

Net Yield on Interest-Earning Assets | 6.33 | % | 6.03 | % | 6.61 | % | |||||||||||||||||||||

Note A | — | For the purpose of these computations, non-accruing loans are included in the average loan amounts outstanding. | ||

Note B | — | Taxable investments include all held-to-maturity, available-for-sale, and trading account securities. | ||

Note C | — | Loan fees of $2,821,752, $2,932,596, and $2,513,817 for 2002, 2001, and 2000, respectively, are included in interest income amounts above. |

17

Table of Contents

Loans and Allowances for Loan Losses

Total loans outstanding increased by $18.5 million in 2002 with $358.1 million outstanding at year-end. Loans represent 71.9% of the Company’s earning assets and provide 81.9% of interest income.

Real estate loans make up 66.3% of total gross loans at year-end 2002, up from 62.7% last year. These loans consist of construction loans to both businesses and individuals on residential and commercial development, commercial buildings and apartment complexes, with most of this activity being commercial. Real estate loans also consist of other loans secured by real estate, such as one-to-four family dwellings, including mobile homes, loans on land only, multi-family dwellings, non-farm non-residential real estate and home equity loans.

Commercial loans totaled $40.1 million at year-end 2002. These loans decreased $5.2 million or 11.5% from year-end 2001 to year-end 2002. While these loans decreased last year, they have grown 13.3% over the last five years. This decrease over the past year is due to decreased loan demand as a result of a sluggish economy.

Consumer loans are the second largest group of loans which represents 22.7% of total loans outstanding. They amount to $82.6 million at year-end 2002, a 1.4% decline from 2001. These loans include loans to individuals for

household, family and other personal expenditures, including credit cards and other related credit plans. 49.1% of these loans are originated at ALC. Consumer loans at ALC declined 4.6% from 2001 to 2002, due primarily to the sale of two production offices located in the State of Florida. Consumer loans at the Bank grew $2.8 million, or 9.2% from year-end 2001 to 2002.

The allowance for loan losses is maintained at a level, which, in management’s judgment, is adequate to absorb credit losses inherent in the loan portfolio. The amount of the allowance is based on management’s evaluation of the collectibility of the loan portfolio, including the nature of the portfolio and changes in its risk profile, credit concentrations, historical trends, and economic conditions. This evaluation also considers the balance of impaired loans. Losses on individually identified impaired loans are measured based on the present value of expected future cash flows discounted at each loan’s original effective market interest rate. As a practical expedient, impairment may be measured based on the loan’s observable market price or the fair value of the collateral if the loan is collateral dependent. When the measure of the impaired loan is less than the recorded investment in the loan, the impairment is recorded through the provision added to the allowance for loan losses. One-to-four family residential mortgages and consumer installment loans are subjected to a collective evaluation for impairment, considering delinquency and repossession statistics, historical loss experience, and other factors. Though management believes the allowance for loan losses to be adequate, ultimate losses may vary from their estimates. However, estimates are reviewed periodically, and as adjustments become necessary they are reported in earnings during periods they become known.

The Bank’s loan policy requires immediate recognition of a loss if significant doubt exists as to the repayment of the principal balance of a loan. Consumer installment loans at the Bank and ALC are generally recognized as losses if they become 90 days and 120 days delinquent, respectively. The only exception to this policy occurs when the underlying value of the collateral or the customer’s financial position makes a loss unlikely.

A credit review of the Bank’s individual loans is conducted periodically by branch and by loan officer. A risk rating is assigned to each loan and is reviewed at least annually. In assigning risk, management takes into consideration the capacity of the borrower to repay, collateral values, current economic conditions and other factors.

18

Table of Contents

Loan officers and other personnel handling loan transactions undergo frequent training dedicated to improving the credit quality as well as the yield of the loan portfolio. The Bank utilizes a written loan policy, which attempts to guide lending personnel in maintaining consistent underwriting standards. This policy is intended to aid loan officers and lending personnel in making sound credit decisions and to assure compliance with state and federal regulations.

In order to better manage credit risk, ALC oversees its portfolio through formal underwriting standards, monitoring of customer payments and active follow-up. ALC assesses the adequacy of the allowance for loan losses on an aggregate level based upon recent delinquency status and estimates of inherent loss from historical experience within these portfolios. ALC concentrates more on loans secured by real estate and places less emphasis on automobile loans.

The following table shows the Company’s loan distribution as of December 31, 2002, 2001, 2000, 1999, and 1998.

December 31, | |||||||||||||||

2002 | 2001 | 2000 | 1999 | 1998 | |||||||||||

(In Thousands of Dollars) | |||||||||||||||

Commercial, Financial and Agricultural | $ | 40,145 | $ | 45,345 | $ | 41,507 | $ | 39,996 | $ | 35,444 | |||||

Real Estate |

| 241,668 |

| 216,979 |

| 180,627 |

| 156,979 |

| 123,264 | |||||

Installment |

| 82,570 |

| 83,783 |

| 87,713 |

| 90,599 |

| 86,282 | |||||

Less: Unearned Interest, Commissions & Fees |

| 6,326 |

| 6,523 |

| 6,377 |

| 5,823 |

| 4,941 | |||||

Total | $ | 358,057 | $ | 339,584 | $ | 303,470 | $ | 281,751 | $ | 240,049 | |||||

The amounts of total loans (excluding installment loans) outstanding at December 31, 2002, which, based on the remaining scheduled repayments of principal, are due in (1) one year or less, (2) more than one year but within five years, and (3) more than five years, are shown in the following table.

Maturing | ||||||||||||

Within | After One | After | Total | |||||||||

(In Thousands of Dollars) | ||||||||||||

Commercial, Financial, and Agricultural | $ | 29,758 | $ | 8,496 | $ | 1,891 | $ | 40,145 | ||||

Real Estate—Mortgage |

| 94,563 |

| 65,523 |

| 81,582 |

| 241,668 | ||||

Total | $ | 124,321 | $ | 74,019 | $ | 83,473 | $ | 281,813 | ||||

Variable rate loans totaled approximately $55.5 million and are included in the one-year category.

The Bank and ALC ended the year with an allowance for loan losses of $6.6 million, the same as December 31, 2001. Total loans charged off in 2002 totaled $4.9 million. Recoveries on loans previously charged off totaled $1.1 million, resulting in net charge-offs of $3.8 million. Net charge-offs for 2001 totaled $5.2 million. Management charged to operations $3.9 million in 2002 as an addition to the allowance for loan losses. This compares to $5.3 million charged to operations for 2001. Of the 2002 net charge-offs of $3.8 million, $2.4 million represents charge-offs from ALC loans and $1.4 million from the Bank. Net loan charge-offs as a percentage of average loans decreased from 1.63% in 2001 to 1.11% in 2002 primarily due to improved credit quality related to ALC’s portfolio.

19

Table of Contents

Non-Performing Assets

The following table presents information on non-performing loans and real estate acquired in settlement of loans.

December 31, | ||||||||||||||||||||

2002 | 2001 | 2000 | 1999 | 1998 | ||||||||||||||||

(In Thousands of Dollars) | ||||||||||||||||||||

Non-Performing Assets: | ||||||||||||||||||||

Loans Accounted for on a Non-Accrual Basis | $ | 6,228 |

| $ | 2,595 |

| $ | 2,104 |

| $ | 1,725 |

| $ | 3,460 |

| |||||

Accruing Loans Past Due 90 Days or More |

| 1,433 |

|

| 2,346 |

|

| 2,237 |

|

| 1,347 |

|

| 1,610 |

| |||||

Real Estate Acquired in Settlement of Loans |

| 1,296 |

|

| 1,342 |

|

| 860 |

|

| 286 |

|

| 215 |

| |||||

Total | $ | 8,957 |

| $ | 6,283 |

| $ | 5,201 |

| $ | 3,358 |

| $ | 5,285 |

| |||||

Percent of Net Loans and Other Real Estate |

| 2.50 | % |

| 1.84 | % |

| 1.75 | % |

| 1.21 | % |

| 2.25 | % | |||||

Accruing loans past due 90 days or more at December 31, 2002, totaled $1.4 million. These loans are secured, and, taking into consideration the collateral value and the financial strength of the borrowers, management believes there will be no loss in these accounts and allowed the loans to continue accruing. Loans past due 90 days or more and originated by ALC totaled $1.0 million at December 31, 2002, or 71.4% of all loans past due 90 days and more and still accruing.

At December 31, 2002 and 2001, the recorded investment in loans that were considered to be impaired was $3,815,189 and $335,317, respectively, all of which were on a non-accrual basis at year-end. There was approximately $573,161 and $167,658 at December 31, 2002 and 2001, respectively, in the allowance for loan lossses specifically allocated to these impaired loans. The average recorded investment in impaired loans was approximately $2,402,336 and $360,317 at December 31, 2002 and 2001, respectively. No material amount of interest income was recognized in impaired loans for the years ended December 31, 2002 and 2001.

Non-performing assets as a percentage of net loans and other real estate was 2.5% at December 31, 2002. This increase from 1.84% is due primarily to four loans. Management reviews these loans and reports to the Board of Directors monthly. Management has set a goal to reduce the 2.5% to 1.5% or lower during 2003. Loans past due 90 days or more and still accruing are reviewed closely by management and are allowed to continue accruing only when underlying collateral values and management’s belief that the financial strength of the borrowers is sufficient to protect the Bank from loss. If at any time management determines there may be a loss of interest or principal, these loans will be changed to non-accrual and their asset value downgraded.

The Bank discontinues the accrual of interest on a loan when management has reason to believe the financial condition of the borrower has deteriorated so that the collection of interest is in doubt. When a loan is placed on non-accrual, all unpaid accrued interest is reversed against current income unless the collateral securing the loan is sufficient to cover the accrued interest. Interest received on non-accrual loans is generally either applied against the principal or recognized on a cash basis, according to management’s judgment as to whether the borrower can ultimately repay the loan. A loan may be restored to accrual status if the obligation is brought current, performs in accordance with the contract for a reasonable period, and if management determines that the repayment of the total debt is no longer in doubt.

Summarized below is information concerning the income on those loans with deferred interest or principal payments resulting from deterioration in the financial condition of the borrower.

December 31, | |||||||||

2002 | 2001 | 2000 | |||||||

(In Thousands of Dollars) | |||||||||

Total Loans Accounted for on a Non-Accrual Basis | $ | 6,228 | $ | 2,595 | $ | 2,104 | |||

Interest Income that Would Have Been Recorded Under Original Terms | $ | 367 | $ | 214 | $ | 194 | |||

Interest Income Reported and Recorded During The Year | $ | 98 | $ | 64 | $ | 30 | |||

At December 31, 2002, non-accrual loans totaled $6.2 million or 1.8% of loans, compared to $2.6 million or 0.8% of loans at December 31, 2001. This increase in non-accrual loans at December 31, 2001, was primarily due to increased levels of commercial and real estate loans being placed on non-accrual status. Three large commercial real estate loans totaling approximately $3.2 million account for substantially all of the increase. The majority of the loans in this category are in the process of liquidation or management has commitments from the principals involved for reduction during the year. Under - -

20

Table of Contents

lying collateral values support those loans which are not already in liquidation. Management continues to emphasize asset quality and believes that at December 31, 2002, it has adequate reserves for losses inherent in this portion of the portfolio.

Lending officers and other personnel involved in the lending process receive ongoing training in compliance as well as asset quality. The Bank has no foreign loans. The Bank does not make loans on commercial property outside its market area without prior approval of the Board of Directors or the Directors’ Loan Committee.

Allocation of Allowance for Loan Losses

The following table shows an allocation of the allowance for loan losses for each of the five years indicated.

December 31, | ||||||||||||||||||||||||||||||

2002 | 2001 | 2000 | 1999 | 1998 | ||||||||||||||||||||||||||

Allowance Allocation | Percent of Loans in Each Category to Total Loans | Allowance Allocation | Percent of Loans in Each Category to Total Loans | Allowance Allocation | Percent of Loans in Each Category to Total Loans | Allowance Allocation | Percent of Loans in Each Category to Total Loans | Allowance Allocation | Percent of Loans in Each Category to Total Loans | |||||||||||||||||||||

(In Thousands of Dollars) | ||||||||||||||||||||||||||||||

Commercial, Financial, and Agricultural | $ | 1,090 | 11 | % | $ | 587 | 13 | % | $ | 980 | 14 | % | $ | 837 | 14 | % | $ | 748 | 15 | % | ||||||||||

Real Estate |

| 3,114 | 66 | % |

| 973 | 63 | % |

| 653 | 59 | % |

| 558 | 55 | % |

| 499 | 50 | % | ||||||||||

Installment |

| 2,419 | 23 | % |

| 5,030 | 24 | % |

| 4,896 | 27 | % |

| 4,184 | 31 | % |

| 3,742 | 35 | % | ||||||||||

Total | $ | 6,623 | 100 | % | $ | 6,590 | 100 | % | $ | 6,529 | 100 | % | $ | 5,579 | 100 | % | $ | 4,989 | 100 | % | ||||||||||

The allowance for loan losses is established by risk group as follows:

| • | Large classified loans, non-accrual loans, and impaired loans are evaluated individually with specific reserves allocated based on management’s review. |

| • | Smaller non-accrual and adversely classified loans are assigned a portion of the allowance based on loan grading. Smaller past due loans are assigned a portion of the allowance using a formula that is based on the severity of the delinquency. |

| • | The remainder of the portfolio is also allocated a portion of the allowance based on past loss experience and the economic conditions for the particular loan portfolio. Allocation weights are assigned based on the Bank’s historical loan loss experience in each category, although a higher allocation weight may be used if current conditions indicate that the loan losses may exceed historical experience. While the total allowance is described as consisting of the portions described above, all portions are available to support inherent losses in the loan portfolio. |

Net charge-offs as shown in the “Summary of Loan Loss Experience” table below indicates the trend for the last five years.

21

Table of Contents

Summary of Loan Loss Experience

This table summarizes the Bank’s loan loss experience for each of the five years indicated.

December 31, | ||||||||||||||||||||

2002 | 2001 | 2000 | 1999 | 1998 | ||||||||||||||||

(In Thousands of Dollars) | ||||||||||||||||||||

Balance of Allowance for Loan Loss at Beginning of Period | $ | 6,590 |

| $ | 6,529 |

| $ | 5,579 |

| $ | 4,989 |

| $ | 4,046 |

| |||||

Charge-Offs: | ||||||||||||||||||||

Commercial, Financial, and Agricultural |

| (826 | ) |

| (413 | ) |

| (89 | ) |

| (94 | ) |

| (94 | ) | |||||

Real Estate—Mortgage |

| (501 | ) |

| (303 | ) |

| (199 | ) |

| (116 | ) |

| (111 | ) | |||||

Installment |

| (3,562 | ) |

| (5,307 | ) |

| (6,170 | ) |

| (4,232 | ) |

| (2,373 | ) | |||||

Credit Cards |

| (22 | ) |

| (27 | ) |

| (23 | ) |

| (30 | ) |

| (11 | ) | |||||

| (4,911 | ) |

| (6,050 | ) |

| (6,481 | ) |

| (4,472 | ) |

| (2,589 | ) | ||||||

Recoveries: | ||||||||||||||||||||

Commercial, Financial, and Agricultural |

| 111 |

|

| 29 |

|

| 20 |

|

| 66 |

|

| 20 |

| |||||

Real Estate—Mortgage |

| 35 |

|

| 21 |

|

| 7 |

|

| 21 |

|

| 15 |

| |||||

Installment |

| 924 |

|

| 798 |

|

| 554 |

|

| 418 |

|

| 305 |

| |||||

Credit Cards |

| 15 |

|

| 8 |

|

| 13 |

|

| 9 |

|

| 5 |

| |||||

| 1,085 |

|

| 856 |

|

| 594 |

|

| 514 |

|

| 345 |

| ||||||

Net Charge-Offs (Deduction) |

| (3,826 | ) |

| (5,194 | ) |

| (5,887 | ) |

| (3,958 | ) |

| (2,244 | ) | |||||

Additions Charged to Operations |

| 3,859 |

|

| 5,255 |

|

| 6,837 |

|

| 4,305 |

|

| 3,187 |

| |||||

Allowances Acquired |

| 0 |

|

| 0 |

|

| 0 |

|

| 243 | * |

| 0 |

| |||||

Balance of Allowance for Loan Loss at End of Period | $ | 6,623 |

| $ | 6,590 |

| $ | 6,529 |

| $ | 5,579 |

| $ | 4,989 |

| |||||

Ratio of Net Charge-Offs During Period to Average Loans Outstanding |

| 1.11 | % |

| 1.63 | % |

| 1.99 | % |

| 1.54 | % |

| 0.97 | % | |||||

* Acquisitions by ALC in 1999.

Industry Concentration Factors

The Bank’s trade area includes Clarke, Choctaw, Bibb, Tuscaloosa, and Shelby Counties in Alabama, and parts of Chilton, Hale, Jefferson, Marengo, Monroe, Perry, Washington, Sumter and Wilcox Counties in Alabama as well as parts of Clarke, Lauderdale and Wayne Counties in Mississippi. There are several major paper mills in our trade area including the Alabama River Companies, Boise Cascade, Georgia Pacific and Weyerhauser. In addition, there are several sawmills, lumber companies, and pole and piling producers. The table below shows the dollar amount of loans made to timber and timber-related companies as of December 31, 2002. The amount of timber-related loans decreased from $30.7 million in 2001 to $26.7 million in 2002. The percentage of timber-related loans to gross loans decreased from 9.22% in 2001 to 7.46% in 2002.

Timber- Related Loans | Total | Percentage of | ||

$26.7 million | $358.1 million | 7.46% |

Management realizes that the Company is reasonably dependent on the economic health of the timber-related industries. Accordingly, this represents a concentration of loans in timber and timber-related industries. We continue to feel these risks are reduced by the diversification of product production within these industries. Some of the mills and industries specialize in paper and pulp, some in lumber and plywood, some in poles and pilings, and others in wood and veneer. We do not believe that this concentration is excessive or that it represents a trend which might materially impact future earnings, liquidity, or capital resources of the Company. Historically, the Company has benefited from the industries engaged in the growing, harvesting, processing and marketing of timber and timber-related products. The majority of the land in our trade area is used to grow pine and hardwood timber.

22

Table of Contents

Investments in Limited Partnerships

The Bank invests in limited partnerships that operate qualified affordable housing projects to receive tax benefits in the form of tax deductions from operating losses and tax credits. The Bank accounts for the investments under either the equity or the cost method based on the percentage ownership and influence over operations. The Bank’s interest in these partnerships was $3.9 million and $4.7 million for 2002 and 2001, respectively. Changes to earnings associated with the partnerships carried under the equity method amounted to approximately $826,000, $535,000, and $176,000 for 2002, 2001, and 2000, respectively. Management analyzes these investments annually for impairment. The assets and liabilities of these partnerships consist primarily of apartment complexes and related mortgages. The Bank’s carrying value approximates cost or its underlying equity in the net assets of the partnerships. The Bank had no remaining cash commitments to these partnerships at December 31, 2002. Although these investments are considered non-earning assets, they do contribute to the bottom line in the form of Federal income tax credits. These credits amounted to $701,000 in 2001 and are estimated to be approximately $700,000 for 2002. Also, operating losses related to these partnerships are available as deductions for taxes on the Bank’s books.

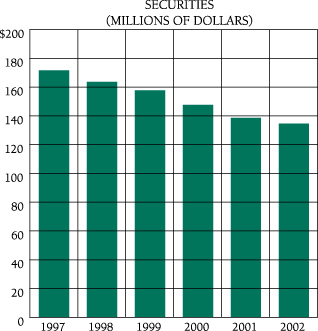

Investment Securities Available-for-Sale and Derivative Instruments

Investment securities available-for-sale included mortgage-backed securities of $113.3 million, state, county and municipal securities of $14.7 million, and other securities of $6.5 million. The securities portfolio is carried at fair value, and it decreased $4.3 million from December 31, 2001, to December 31, 2002, as a result of an overall decrease in investments, net of increases in unrealized gains due to changes in the rate environment.

At December 31, 2002, approximately $19.2 million in collateral mortgage obligations (“CMO”) held by the Bank had floating interest rates which reprice monthly, and $46.9 million had fixed interest rates.

Because of their liquidity, credit quality and yield characteristics, the majority of the purchases of taxable securities has been purchases of agency guaranteed mortgage-backed obligations and collateralized mortgage obligations. The mortgage-backed obligations in which the Bank invests represent an undivided interest in a pool of residential mortgages or may be collateralized by a pool of residential mortgages (“mortgage-backed securities”). Mortgage-backed securities have yield and maturity characteristics corresponding to the underlying mortgages and are subject to principal prepayment, refinancing, or foreclosure of the underlying mortgages. Although maturities of the underlying mortgage loans may range up to 30 years, scheduled principal and normal prepayments substantially shorten the effective maturities. As of December 31, 2002, the investment portfolio had an estimated average effective maturity of 3.4 years.

Interest rate risk contained in the overall securities portfolio is formally monitored on a monthly basis. Management assesses each month how risk levels in the investment portfolio affect overall company-wide interest rate risk. Expected changes in forecasted yield, earnings and market value of the bond portfolio are generally attributable to fluctuations in interest rates, as well as volatility caused by general uncertainty over the economy, inflation, and future interest rate trends. Mortgage-backed securities and CMOs present some degree of additional risk in that mortgages collateralizing these securities can be prepaid, thereby affecting the yield and market value of the portfolio.

The composition of the Bank’s investment portfolio reflects the Bank’s investment strategy of maximizing portfolio yields commensurate with risk and liquidity considerations. The primary objectives of the Bank’s investment strategy are to maintain an appropriate level of liquidity and provide a tool to assist in controlling the Bank’s interest rate position while at the same time producing adequate levels of interest income.

Fair market values of securities vary significantly as interest rates change. The gross unrealized gains and losses in the

23

Table of Contents

securities portfolio are not expected to have a material impact on liquidity or other funding needs. There were net unrealized gains, net of taxes, of $2.2 million in the securities portfolio on December 31, 2002, versus net unrealized gains, net of taxes, of $1.3 million one year ago.

The Bank has used certain derivative products for hedging purposes. These include interest rate swaps and caps. The use and detail regarding these products are fully discussed under “Liquidity and Interest Rate Sensitivity Management” and in Note 2 in the “Notes to Consolidated Financial Statements.” The Bank adopted the provisions of Statement of Financial Accounting Standards No. 133, as amended, effective January 1, 2001, as required by the Financial Accounting Standards Board. On that date, the Bank reassessed and designated derivative instruments used for risk management as fair value hedges, cash flow hedges and derivatives not qualifying for hedge accounting treatment, as appropriate. On January 1, 2001, the Bank had derivatives with a notional value of $69 million. In conjunction with the adoption of Statement of Financial Accounting Standards No. 133, the Bank recorded a transition adjustment of $24,000, net of taxes, to accumulated other comprehensive income and recorded a cumulative effect adjustment to earnings of $200,000 to reflect the fair value of such instruments on January 1, 2001.

Investment Securities Available-for-Sale

The following table sets forth the amortized costs of investment securities as well as their fair value and related unrealized gains or losses at the dates indicated.

December 31, | |||||||||

2002 | 2001 | 2000 | |||||||

(In Thousands of Dollars) | |||||||||

Investment Securities Available-for-Sale: | |||||||||

U.S. Treasury and Agency Securities | $ | 114 | $ | 3,027 | $ | 4,774 | |||

Obligations of States, Counties, and Political Subdivisions |

| 14,113 |

| 19,402 |

| 21,687 | |||

Mortgage-Backed Securities |

| 110,389 |

| 108,693 |

| 115,568 | |||

Other Securities |

| 6,352 |

| 5,606 |

| 5,017 | |||

Total Book Value |

| 130,968 |

| 136,728 |

| 147,046 | |||

Net Unrealized Gains/Losses |

| 3,562 |

| 2,114 |

| 1,072 | |||

Total Market Value | $ | 134,530 | $ | 138,842 | $ | 148,118 | |||

Investment Securities Available-for-Sale Maturity Schedule

Stated Maturity | ||||||||||||||||||||

Within | After One | After Five | After | |||||||||||||||||

Amount | Yield | Amount | Yield | Amount | Yield | Amount | Yield | |||||||||||||

(In Thousands of Dollars, Except Yields) | ||||||||||||||||||||

Investment Securities Available-for-Sale: | ||||||||||||||||||||

U.S. Treasury and Agency Securities | $ | 114 | 5.88% | $ | 0 | 0.00% | $ | 0 | 0.00% | $ | 0 | 0.00% | ||||||||

State, County and Municipal Obligations |

| 311 | 13.29% |

| 1,880 | 15.59% |

| 2,638 | 9.00% |

| 9,884 | 7.85% | ||||||||

Mortgage-Backed Securities |

| 0 | 0.00% |

| 897 | 5.96% |

| 24,129 | 4.93% |

| 88,242 | 5.19% | ||||||||

Preferred Stock |

| 0 | 0.00% |

| 0 | 0.00% |

| 0 | 0.00% |

| 632 | 5.70% | ||||||||

Total | $ | 425 | 11.30% | $ | 2,777 | 12.49% | $ | 26,767 | 5.33% | $ | 98,758 | 5.46% | ||||||||

Total Securities With Stated Maturity | $ | 128,727 | 5.60% | |||||||||||||||||

Equity Securities |

| 5,803 | 5.26% | |||||||||||||||||

| TOTAL | $ | 134,530 | 5.59% | ||||||||||||||||

Available-for-Sale Securities are stated at Market Value and Tax Equivalent Market Yields.

The maturities and weighted average yields of the investment securities available-for-sale at the end of 2002 are presented in the preceding table based on stated maturity. While the average stated maturity of the mortgage-backed securities (excluding CMOs) was 16.4 years, the average life expected was 2.7 years. The average stated maturity of the CMO portion of the portfolio was 18.1 years, and the average expected life was 1.4 years. The average expected life of investment securities available-for-sale was 3.4 years with an average tax equivalent yield of 5.59 percent.

24

Table of Contents

Condensed Portfolio Maturity Schedule

Maturity Summary | Dollar Amount | Portfolio Percentage | ||||

Maturing in 3 months or less | $ | 115,829 | 0.09 | % | ||

Maturing in 3 months to 1 year |

| 309,388 | 0.24 |

| ||

Maturing in 1 to 3 years |

| 1,076,678 | 0.84 |

| ||

Maturing in 3 to 5 years |

| 1,700,216 | 1.32 |

| ||

Maturing in 5 to 15 years |

| 51,006,076 | 39.62 |

| ||

Maturing in over 15 years |

| 74,518,788 | 57.89 |

| ||

Total | $ | 128,726,975 | 100.00 | % | ||

The following marketable equity securities have been excluded from the above Maturity Summary due to no stated maturity date.

Federal Home Loan Bank Stock | $5,619,900 | |

Mutual Funds | $ 10,226 | |

Other Marketable Equity Securities | $ 172,726 |

Condensed Portfolio Repricing Schedule

Repricing Summary | Dollar | Portfolio Percentage | ||||

Repricing in 30 days or less | $ | 19,182,873 | 14.90 | % | ||

Repricing in 31 days to 1 year |

| 309,388 | 0.24 |

| ||

Repricing in 1 to 3 years |

| 1,076,678 | 0.84 |

| ||

Repricing in 3 to 5 years |

| 1,503,249 | 1.17 |

| ||

Repricing in 5 to 15 years |

| 47,915,764 | 37.22 |

| ||

Repricing in over 15 years |

| 58,739,023 | 45.63 |

| ||

Total | $ | 128,726,975 | 100.00 | % | ||

Repricing in 30 days or less does not include: | ||||||

Mutual Funds |

| $ 10,226 | ||||

Repricing in 31 days to 1 year does not include: | ||||||

Federal Home Loan Bank Stock |

| $ 5,619,900 | ||||

Other Marketable Equity Securities |

| $ 172,726 | ||||

The tables above reflect all securities at market value on December 31, 2002.

Security Gains and Losses

Non-interest income from securities transactions and trading account transactions decreased in 2002 compared to 2001, as can be seen in the table below. The profits realized in 2002 were generated through the sale of investment securities. Gains in this area occurred in connection with the Bank’s asset and liability management activities and strategies.

The table below shows the associated net gains or (losses) for the periods 2002, 2001, and 2000.

2002 | 2001 | 2000 | ||||||||

Investment Securities | $ | 198,064 | $ | 178,634 |

| $ | 15,330 | |||

Trading Account |

| 0 |

| (12,650 | ) |

| 112,003 | |||

Total | $ | 198,064 | $ | 165,984 |

| $ | 127,333 | |||

Volume of sales as well as other information on securities is further discussed in Note 3 in the “Notes to Consolidated Financial Statements.”

25

Table of Contents

Deposits

Average total deposits increased 3.4% in 2002 compared to increases of 4.2% and 1.1% in 2001 and 2000, respectively. Management believes this deposit level continues to be affected by the competitive interest rate environment, and the availability of other low cost funding sources for the Bank.

Average non-interest bearing demand deposits have increased 3.6% over the last three years and increased 7.7% in 2002. The ratio of average non-interest bearing deposits to average total deposits remained relatively steady in 2002 at 11.7% from 11.2% in 2001 and 12.2% in 2000.

Average interest-bearing transaction accounts have increased 14.0% during the last three years. Interest-bearing transaction accounts continue to be an important source of funds for the Bank, accounting for 18.7% of average total deposits in 2002.

Average time deposits decreased by 0.5% in 2002, compared to an increase of 6.7% in 2001. The decrease is due to the lower rate environment. Average time deposits represented 57.3% of the total average deposits in 2002 compared to 59.6% in 2001 and 58.2% in 2000.

Average savings deposits have increased 10.3% since 2000. Average savings increased 8.4% in 2002 compared to 2001. The ratio of average savings to average total deposits increased to 12.2% in 2002 compared to 11.6% in 2001 and 11.9% in 2000.

The Bank’s deposit base remains the primary source of funding for the Bank. These deposits represented 71.7% of the average earning assets in 2002 and 71.1% of the average earning assets in 2001. As seen in the table below, overall rates on the deposits decreased to 2.6% in 2002, compared to 3.9% in 2001 and 4.0% in 2000. Emphasis continues to be placed on attracting consumer deposits.

The sensitivity of the Bank’s deposit rates to changes in market interest rates is reflected in its average interest rate paid on interest-bearing deposits. During 2002, market interest rates continued to decline dramatically throughout the year. The Bank’s average interest rate paid on interest-bearing deposits followed this trend.

Management, as part of an overall program to emphasize the growth of transaction accounts, continues to promote “on-line” banking and a bill paying program as well as enhancing the telephone banking product and the employee incentive plan. In addition, an increased effort is being placed on deposit promotions, direct-mail campaigns and cross-selling efforts.

Other Interest-Bearing Liabilities:Other interest-bearing liabilities include all interest-bearing liabilities except deposits, such as federal funds purchased and Federal Home Loan Bank (“FHLB”) advances. This category continues to be more fully utilized as an alternative source of funds as evidenced by the $5.5 million, or 5.6%, increase in average borrowing during 2002. The increase was due to a 3.7% increase in average long-term advances from the FHLB. The advances from the FHLB are an alternative to funding sources with similar maturities such as certificates of deposit. These advances generally offer more attractive rates when compared to other mid-term financing options. Average federal funds purchased and securities sold under agreements to repurchase increased from $0 in 2001 to $1.8 million in 2002. For additional information and discussion of these borrowings, refer to “Notes to Consolidated Financial Statements.”

26

Table of Contents

Average Daily Amount of Deposits and Rates

The average daily amount of deposits and rates paid on such deposits is summarized for the periods in the following table.

December 31, | ||||||||||||||||||

2002 | 2001 | 2000 | ||||||||||||||||

Amount | Rate | Amount | Rate | Amount | Rate | |||||||||||||

(In Thousands of Dollars, Except Percentages) | ||||||||||||||||||

Non-Interest Bearing DDA | $ | 41,866 | $ | 38,884 | $ | 40,397 | ||||||||||||

Interest-Bearing DDA |

| 66,969 | 1.05 | % |

| 60,615 | 1.65 | % |

| 58,732 | 2.01 | % | ||||||

Savings Deposits |

| 43,665 | 1.48 | % |

| 40,292 | 2.23 | % |

| 39,591 | 2.58 | % | ||||||

Time Deposits |

| 205,039 | 3.87 | % |

| 206,128 | 5.60 | % |

| 193,157 | 5.73 | % | ||||||

Total | $ | 357,539 | 2.60 | % | $ | 345,919 | 3.88 | % | $ | 331,877 | 4.00 | % | ||||||

Maturities of time certificates of deposit and other time deposits of $100,000 or more outstanding at December 31, 2002, are summarized as follows:

Maturities | Time Certificates of Deposit | Other | Total | ||||||

3 Months or Less | $ | 13,037,250 | $ | 7,664,967 | $ | 20,702,217 | |||

Over 3 Through 6 Months |

| 9,814,824 |

| 0 |

| 9,814,824 | |||

Over 6 Through 12 Months |

| 6,848,057 |

| 0 |

| 6,848,057 | |||

Over 12 Months |

| 22,454,463 |

| 0 |

| 22,454,463 | |||

Total | $ | 52,154,594 | $ | 7,664,967 | $ | 59,819,561 | |||

27

Table of Contents

Short-Term Borrowings