Exhibit 1

| ASX Release 4 MAY 2020 Level 18, 275 Kent Street Sydney, NSW, 2000 Westpac 2020 Interim Financial Results Announcement (incorporating requirements of Appendix 4D) Westpac Banking Corporation (“Westpac”) today provides the attached Westpac 2020 Interim Financial Results Announcement (incorporating requirements of Appendix 4D). For further information: David LordingAndrew Bowden Group Head of Media RelationsHead of Investor Relations 0419 683 411T. (02) 8253 4008 (ext. 24008) M. 0438 284 863 This document has been authorised for release by Tim Hartin, Group Company Secretary. |

| 2020 Interim Financial Results For the six months ended 31 March 2020 Incorporating the requirements of Appendix 4D Westpac Banking Corporation ABN 33 007 457 141 A Westpac Little Ripper drone in flight above bushfire affected areas. A trial initiative supported by Westpac, in partnership with WIRES, is using innovative technology to assist with wildlife search and rescue. |

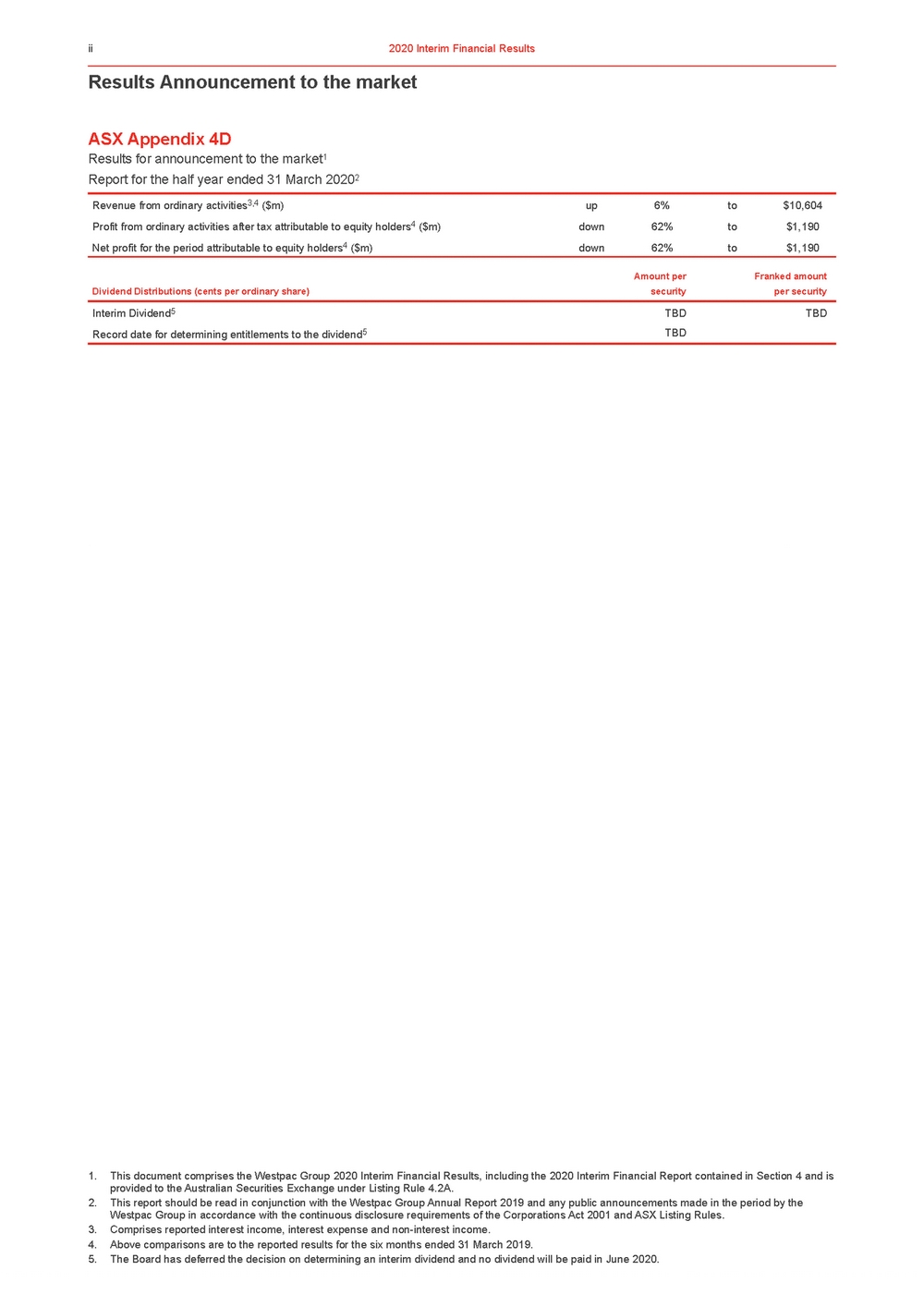

| Results Announcement to the market ASX Appendix 4D Results for announcement to the market1 Report for the half year ended 31 March 20202 1. This document comprises the Westpac Group 2020 Interim Financial Results, including the 2020 Interim Financial Report contained in Section 4 and is provided to the Australian Securities Exchange under Listing Rule 4.2A. 2. This report should be read in conjunction with the Westpac Group Annual Report 2019 and any public announcements made in the period by the Westpac Group in accordance with the continuous disclosure requirements of the Corporations Act 2001 and ASX Listing Rules. 3. Comprises reported interest income, interest expense and non-interest income. 4. Above comparisons are to the reported results for the six months ended 31 March 2019. 5. The Board has deferred the decision on determining an interim dividend and no dividend will be paid in June 2020. |

| Index 01 Group results11 1.1 Reported results1 1.2 Key financial information2 1.3 Cash earnings results3 1.4 Market share and system multiple metrics8 02 Review of Group operations9 2.1 Performance overview132 2.2 Review of earnings21 2.3 Credit quality33 2.4 Balance sheet and funding35 2.5 Capital and dividends40 2.6 Sustainability performance46 03 Divisional results52 3.1 Consumer533 3.2 Business57 3.3 Westpac Institutional Bank60 3.4 Westpac New Zealand62 3.5 Group Businesses65 04 2020 Interim Financial Report67 4.1 Directors’ report684 4.2 Consolidated income statement97 4.3 Consolidated statement of comprehensive income98 4.4 Consolidated balance sheet99 4.5 Consolidated statement of changes in equity100 4.6 Consolidated cash flow statement101 4.7 Notes to the consolidated financial statements102 4.8 Statutory statements1365 05 Cash earnings financial information139 06 Other information150 6.1 Disclosure regarding forward-looking statements150 6.2 References to websites151 6.3 Credit ratings151 6.4 Dividend reinvestment plan1516 6.5 Information on related entities151 6.6 Financial calendar and Share Registry details152 6.7 Exchange rates156 07 Glossary157 7 |

| Results Announcement to the market In this Interim Financial Results Announcement (Results Announcement) references to ‘Westpac’, ‘WBC’, ‘Westpac Group’, ‘the Group’, ‘we’, ‘us’ and ‘our’ are to Westpac Banking Corporation and its controlled entities, unless it clearly means just Westpac Banking Corporation. All references to $ in this Results Announcement are to Australian dollars unless otherwise stated. Financial calendar Interim Results Announcement released4 May 2020 Ex-dividend date for interim dividend1 TBD Record date for interim dividend (Sydney)1 TBD Interim dividend payable1 TBD Final Results Announcement (scheduled) 2 November 2020 1. The Board has deferred the decision on determining an interim dividend and no dividend will be paid in June 2020. |

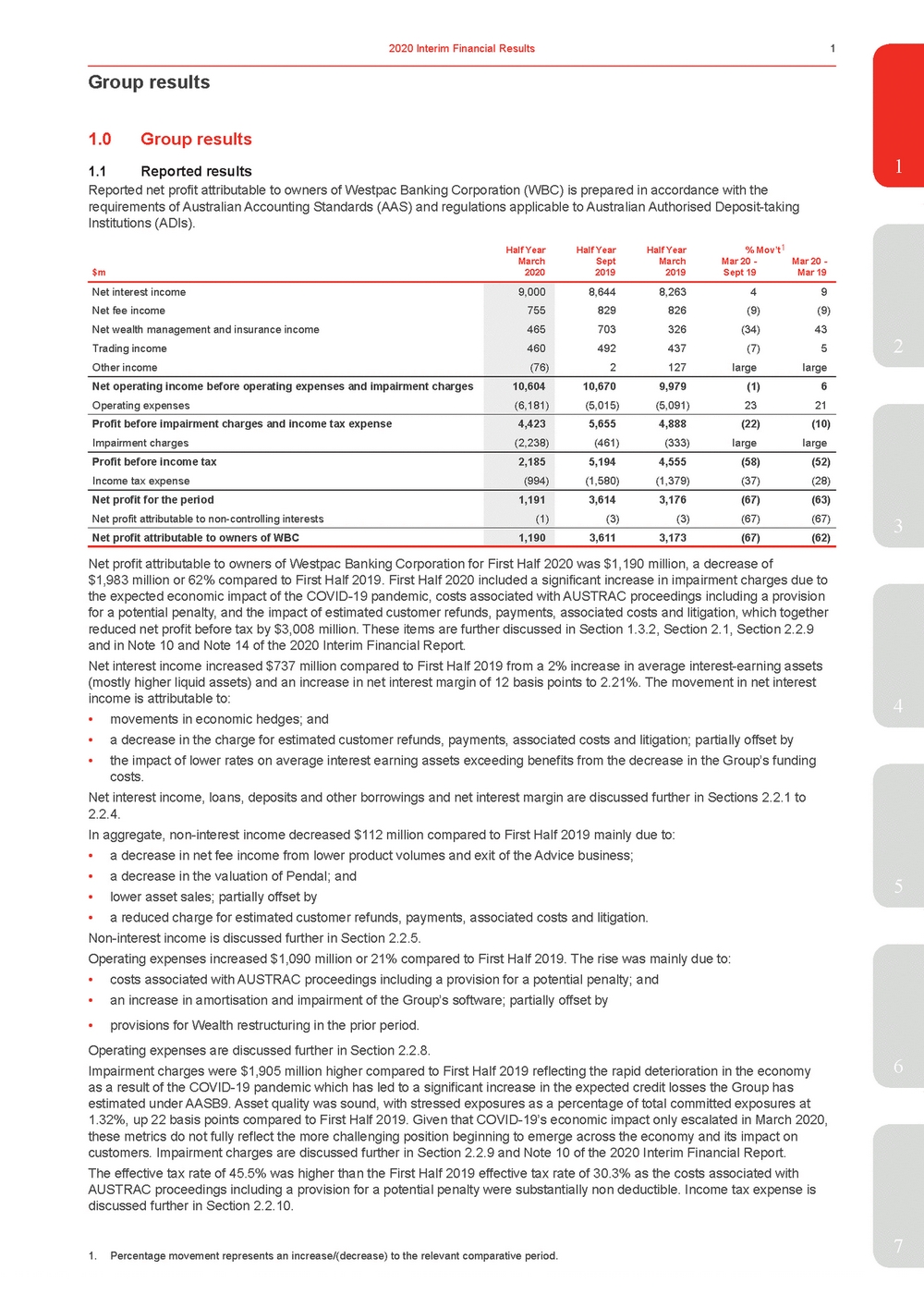

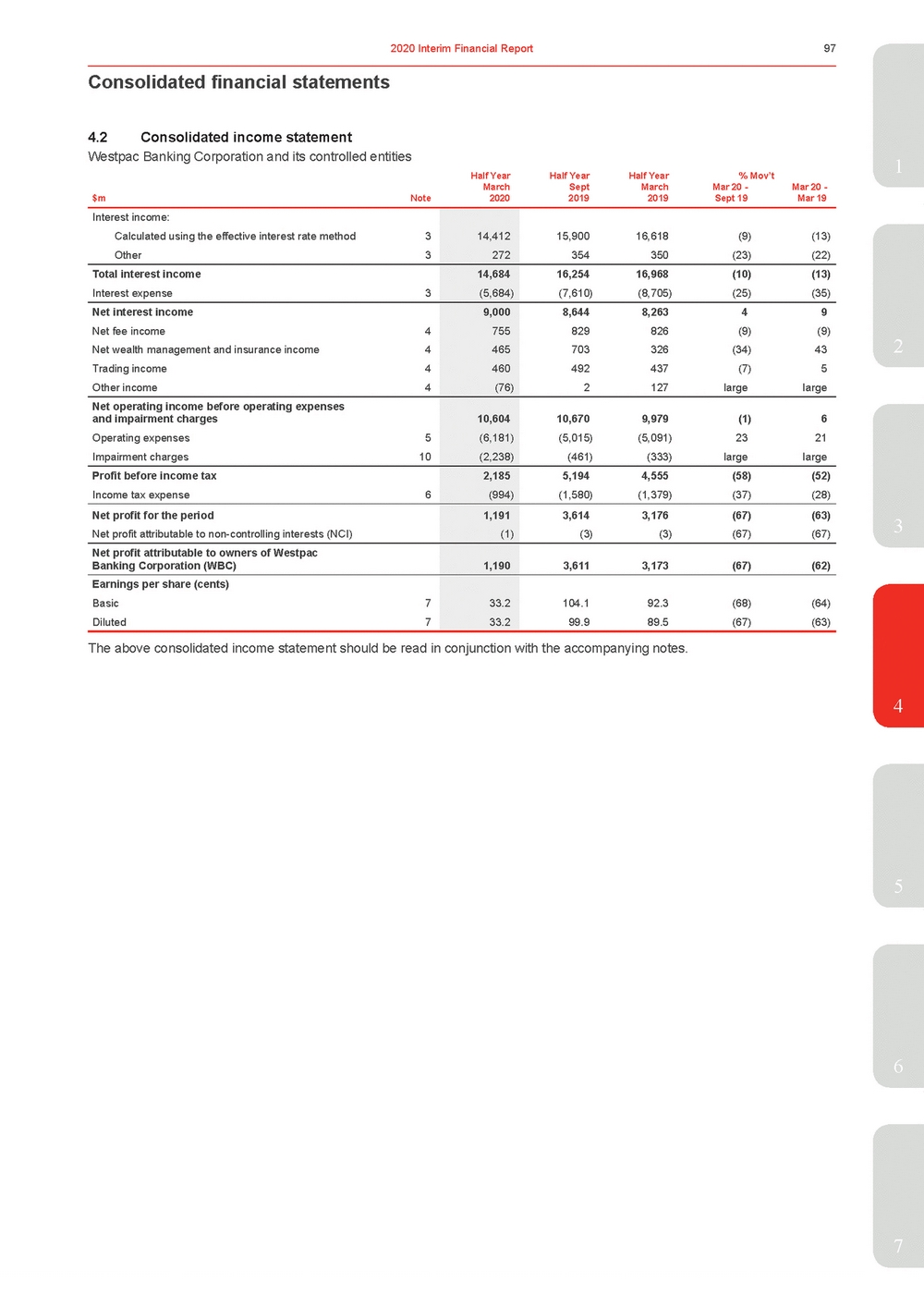

| 1.0Group results 1.1Reported results1 Reported net profit attributable to owners of Westpac Banking Corporation (WBC) is prepared in accordance with the requirements of Australian Accounting Standards (AAS) and regulations applicable to Australian Authorised Deposit-taking Institutions (ADIs). Half YearHalf YearHalf Year% Mov’t1 March $m2020 Sept 2019 March 2019 Mar 20 - Sept 19 Mar 20 - Mar 19 Net interest income Net fee income Net wealth management and insurance income Trading income Other income 9,000 755 465 460 (76) 8,6448,26349 829826(9)(9) 703326(34)43 492437(7)5 2127largelarge Net operating income before operating expenses and impairment charges Operating expenses 10,604 (6,181) 10,6709,979(1)6 (5,015)(5,091)2321 Profit before impairment charges and income tax expense Impairment charges 4,423 (2,238) 5,6554,888(22)(10) (461)(333)largelarge Profit before income tax Income tax expense 2,185 (994) 5,1944,555(58)(52) (1,580)(1,379)(37)(28) Net profit for the period Net profit attributable to non-controlling interests 1,191 (1) 3,6143,176(67)(63) (3)(3)(67)(67) Net profit attributable to owners of WBC 1,190 3,6113,173(67)(62) 3 Net profit attributable to owners of Westpac Banking Corporation for First Half 2020 was $1,190 million, a decrease of $1,983 million or 62% compared to First Half 2019. First Half 2020 included a significant increase in impairment charges due to the expected economic impact of the COVID-19 pandemic, costs associated with AUSTRAC proceedings including a provision for a potential penalty, and the impact of estimated customer refunds, payments, associated costs and litigation, which together reduced net profit before tax by $3,008 million. These items are further discussed in Section 1.3.2, Section 2.1, Section 2.2.9 and in Note 10 and Note 14 of the 2020 Interim Financial Report. Net interest income increased $737 million compared to First Half 2019 from a 2% increase in average interest-earning assets (mostly higher liquid assets) and an increase in net interest margin of 12 basis points to 2.21%. The movement in net interest income is attributable to:4 •movements in economic hedges; and •a decrease in the charge for estimated customer refunds, payments, associated costs and litigation; partially offset by •the impact of lower rates on average interest earning assets exceeding benefits from the decrease in the Group’s funding costs. Net interest income, loans, deposits and other borrowings and net interest margin are discussed further in Sections 2.2.1 to 2.2.4. In aggregate, non-interest income decreased $112 million compared to First Half 2019 mainly due to: •a decrease in net fee income from lower product volumes and exit of the Advice business; •a decrease in the valuation of Pendal; and 5 •lower asset sales; partially offset by •a reduced charge for estimated customer refunds, payments, associated costs and litigation. Non-interest income is discussed further in Section 2.2.5. Operating expenses increased $1,090 million or 21% compared to First Half 2019. The rise was mainly due to: •costs associated with AUSTRAC proceedings including a provision for a potential penalty; and •an increase in amortisation and impairment of the Group’s software; partially offset by •provisions for Wealth restructuring in the prior period. Operating expenses are discussed further in Section 2.2.8. Impairment charges were $1,905 million higher compared to First Half 2019 reflecting the rapid deterioration in the economy6 as a result of the COVID-19 pandemic which has led to a significant increase in the expected credit losses the Group has estimated under AASB9. Asset quality was sound, with stressed exposures as a percentage of total committed exposures at 1.32%, up 22 basis points compared to First Half 2019. Given that COVID-19’s economic impact only escalated in March 2020, these metrics do not fully reflect the more challenging position beginning to emerge across the economy and its impact on customers. Impairment charges are discussed further in Section 2.2.9 and Note 10 of the 2020 Interim Financial Report. The effective tax rate of 45.5% was higher than the First Half 2019 effective tax rate of 30.3% as the costs associated with AUSTRAC proceedings including a provision for a potential penalty were substantially non deductible. Income tax expense is discussed further in Section 2.2.10. 7 |

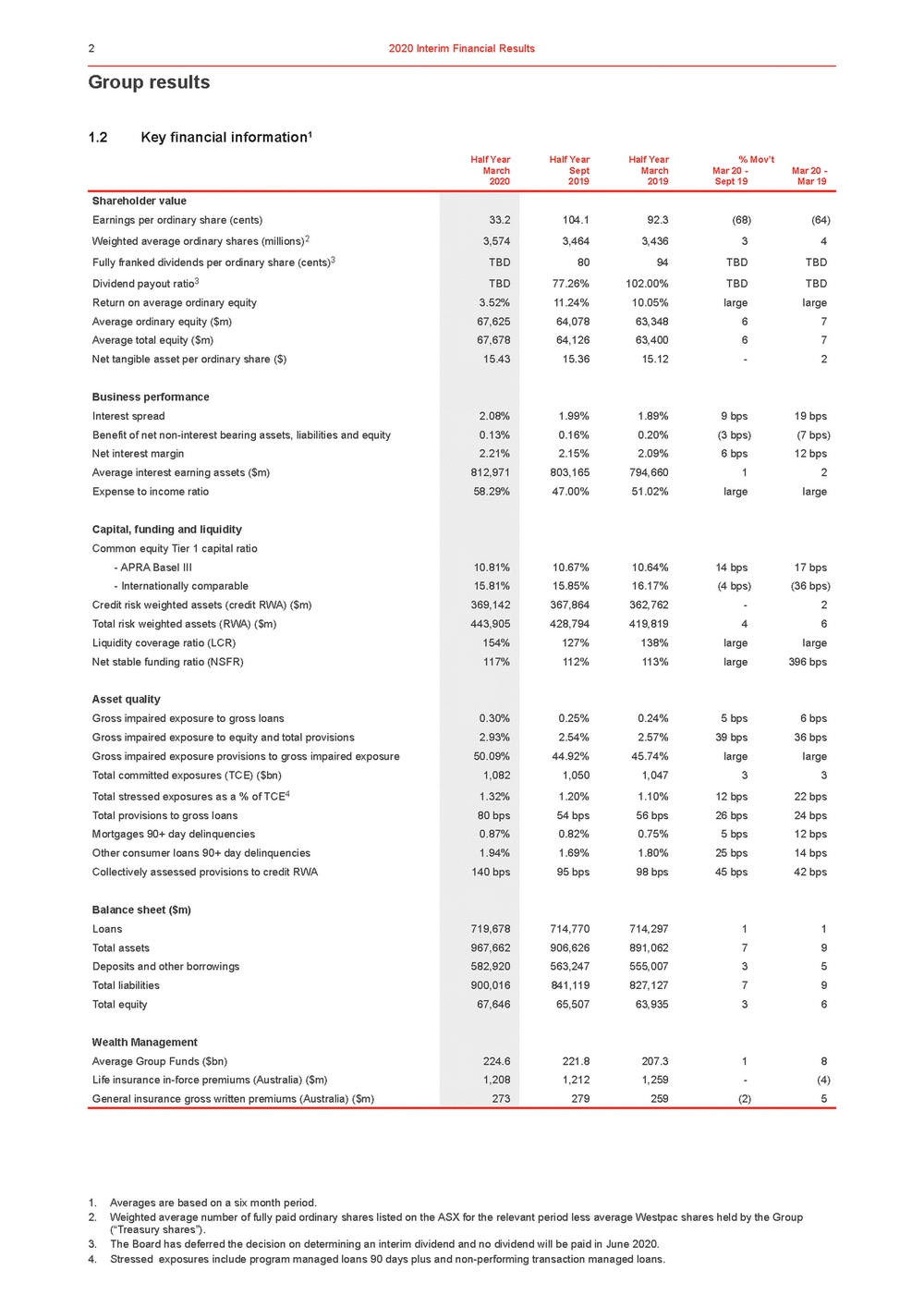

| Group results 1. Averages are based on a six month period. 2. Weighted average number of fully paid ordinary shares listed on the ASX for the relevant period less average Westpac shares held by the Group (“Treasury shares”). 3. The Board has deferred the decision on determining an interim dividend and no dividend will be paid in June 2020. 4. Stressed exposures include program managed loans 90 days plus and non-performing transaction managed loans. |

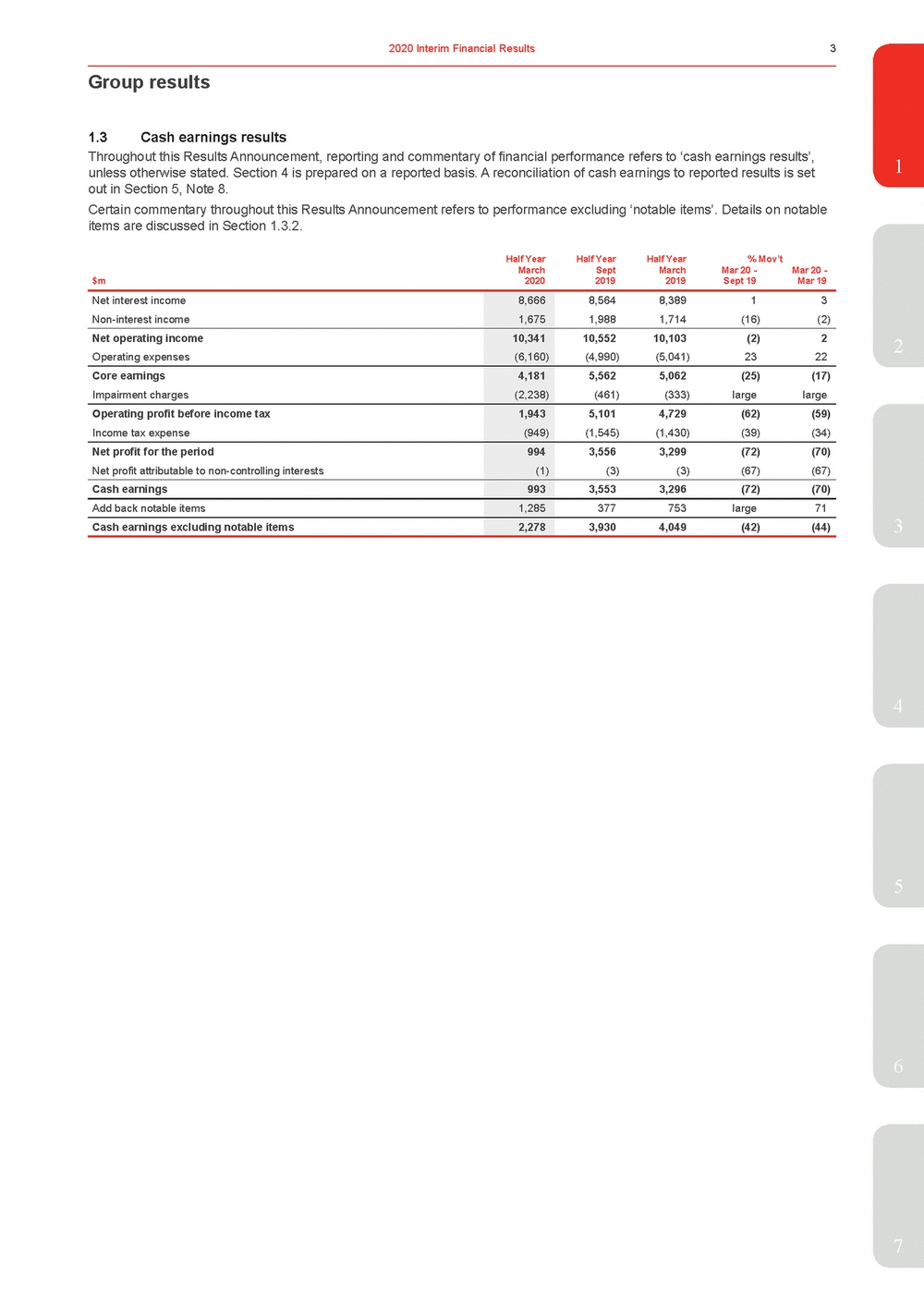

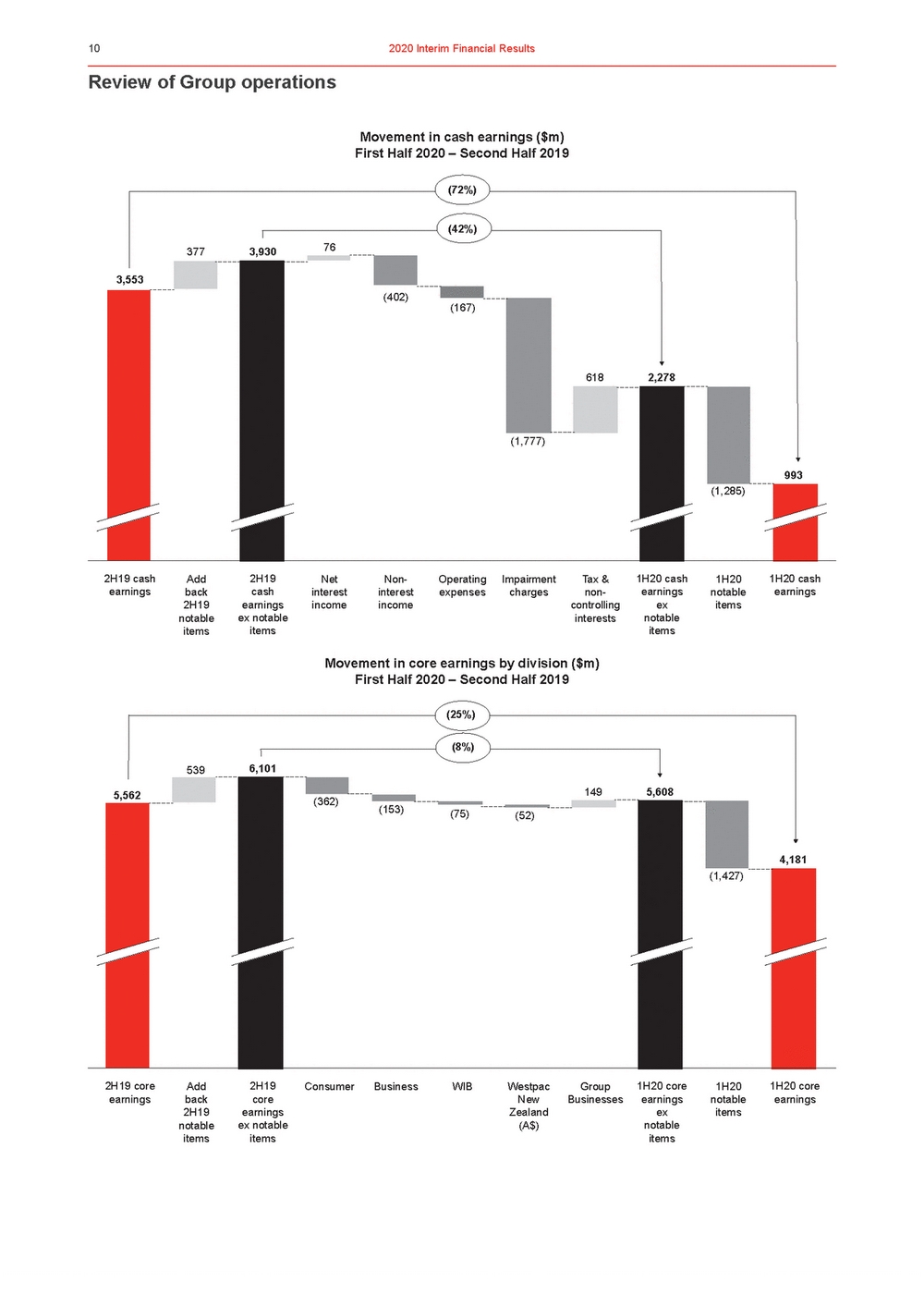

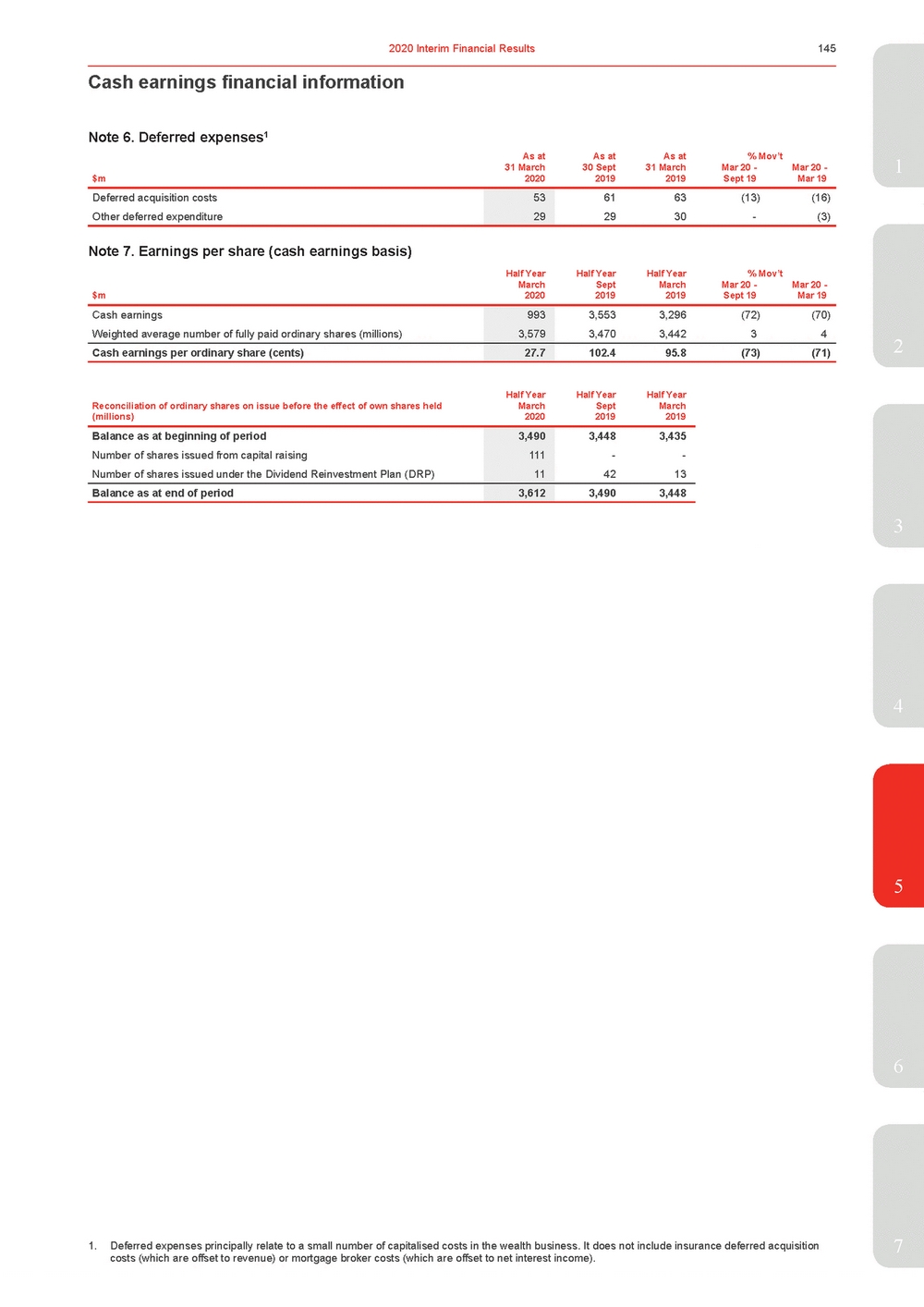

| 1.3 Cash earnings results 1 Certain commentary throughout this Results Announcement refers to performance excluding ‘notable items’. Details on notable items are discussed in Section 1.3.2. Half YearHalf YearHalf Year% Mov’t March $m2020 Sept 2019 March 2019 Mar 20 - Sept 19 Mar 20 - Mar 19 Net interest income Non-interest income 8,666 1,675 8,5648,38913 1,9881,714(16)(2) Net operating income Operating expenses 10,341 (6,160) 10,55210,103(2)2 (4,990)(5,041)2322 Core earnings Impairment charges 4,181 (2,238) 5,5625,062(25)(17) (461)(333)largelarge Operating profit before income tax Income tax expense 1,943 (949) 5,1014,729(62)(59) (1,545)(1,430)(39)(34) Net profit for the period Net profit attributable to non-controlling interests 994 (1) 3,5563,299(72)(70) (3)(3)(67)(67) Cash earnings 993 3,5533,296(72)(70) Add back notable items 1,285 377753large71 Cash earnings excluding notable items 2,278 3,9304,049(42)(44) 3 4 5 6 7 |

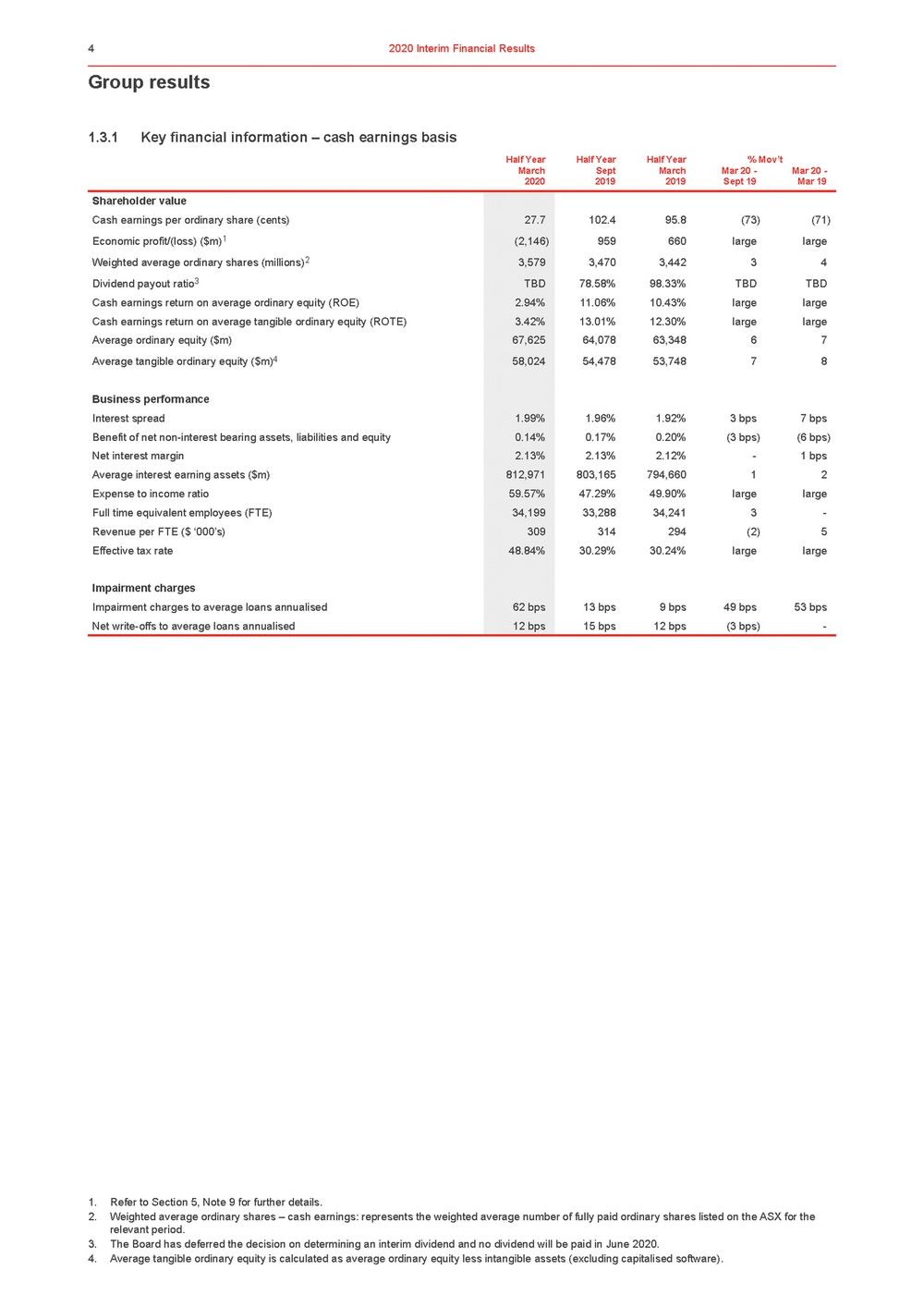

| Group results 1. Refer to Section 5, Note 9 for further details. 2. Weighted average ordinary shares – cash earnings: represents the weighted average number of fully paid ordinary shares listed on the ASX for the relevant period. 3. The Board has deferred the decision on determining an interim dividend and no dividend will be paid in June 2020. 4. Average tangible ordinary equity is calculated as average ordinary equity less intangible assets (excluding capitalised software). |

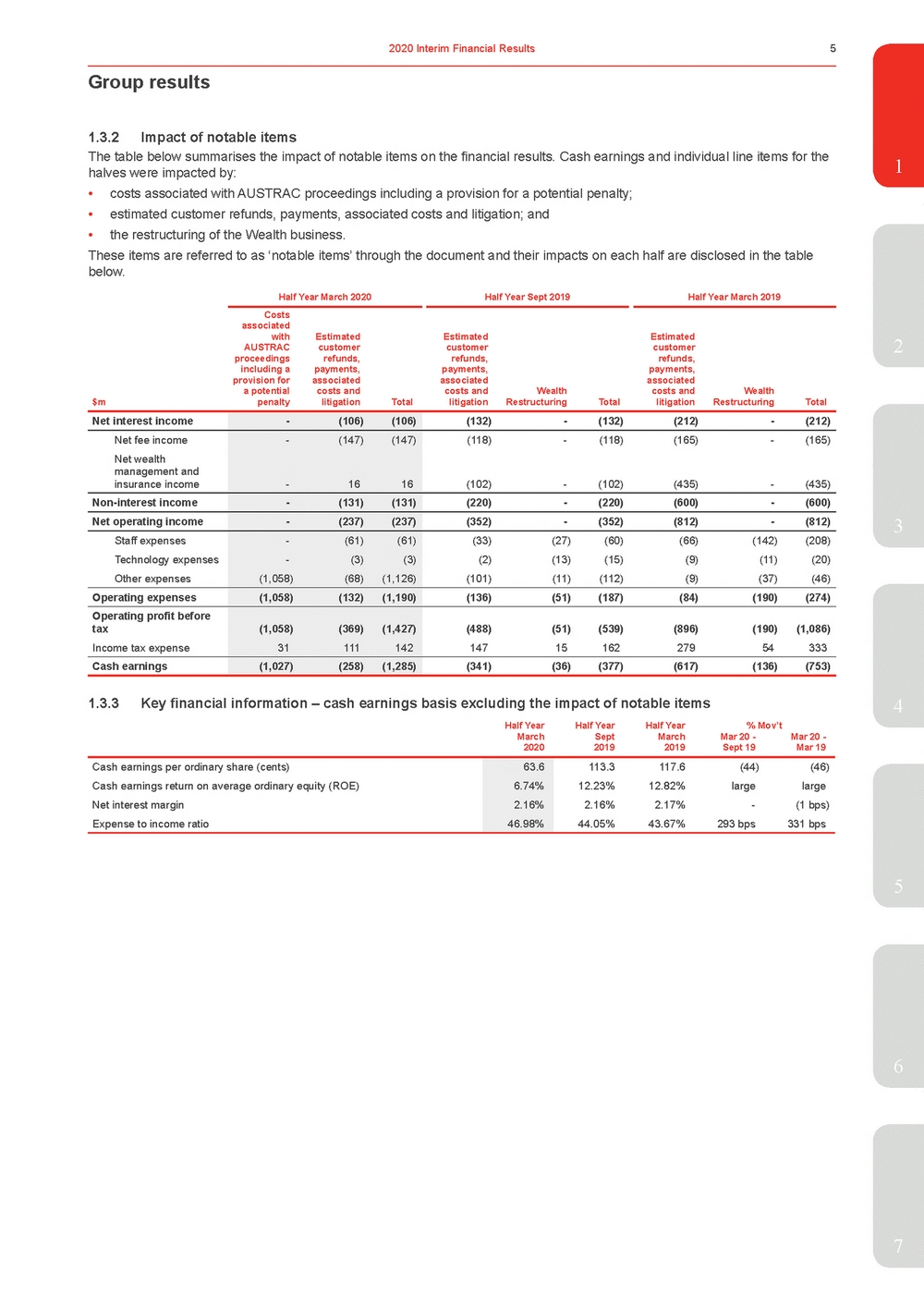

| 1 halves were impacted by: •costs associated with AUSTRAC proceedings including a provision for a potential penalty; •estimated customer refunds, payments, associated costs and litigation; and •the restructuring of the Wealth business. These items are referred to as ‘notable items’ through the document and their impacts on each half are disclosed in the table below. Half Year March 2020Half Year Sept 2019Half Year March 2019 Costs associated with Estimated Estimated Estimated AUSTRAC customer customer customer proceedings refunds, refunds, refunds, including a payments, payments, payments, provision for associated associated associated a potential costs and costs and Wealth costs and Wealth penalty litigation Total litigation Restructuring Total litigation Restructuring Total $m Net interest income -(106)(106) (132)-(132)(212)-(212) Net fee income Net wealth management and insurance income -(147)(147) -1616 (118)-(118)(165)-(165) (102)-(102)(435)-(435) Non-interest income -(131)(131) (220)-(220)(600)-(600) Net operating income -(237)(237) (352)-(352)(812)-(812) Staff expenses Technology expenses Other expenses -(61)(61) - (3)(3) (1,058)(68)(1,126) (33)(27) (60)(66)(142)(208) (2)(13)(15)(9) (11)(20) (101)(11)(112)(9)(37)(46) Operating expenses (1,058)(132)(1,190) (136)(51)(187)(84)(190)(274) Operating profit before tax Income tax expense (1,058)(369)(1,427) 31111142 (488)(51)(539)(896)(190)(1,086) 1471516227954333 Cash earnings (1,027)(258)(1,285) (341)(36)(377)(617)(136)(753) 1.3.3Key financial information – cash earnings basis excluding the impact of notable items4 Half YearHalf YearHalf Year% Mov’t 5 6 7 |

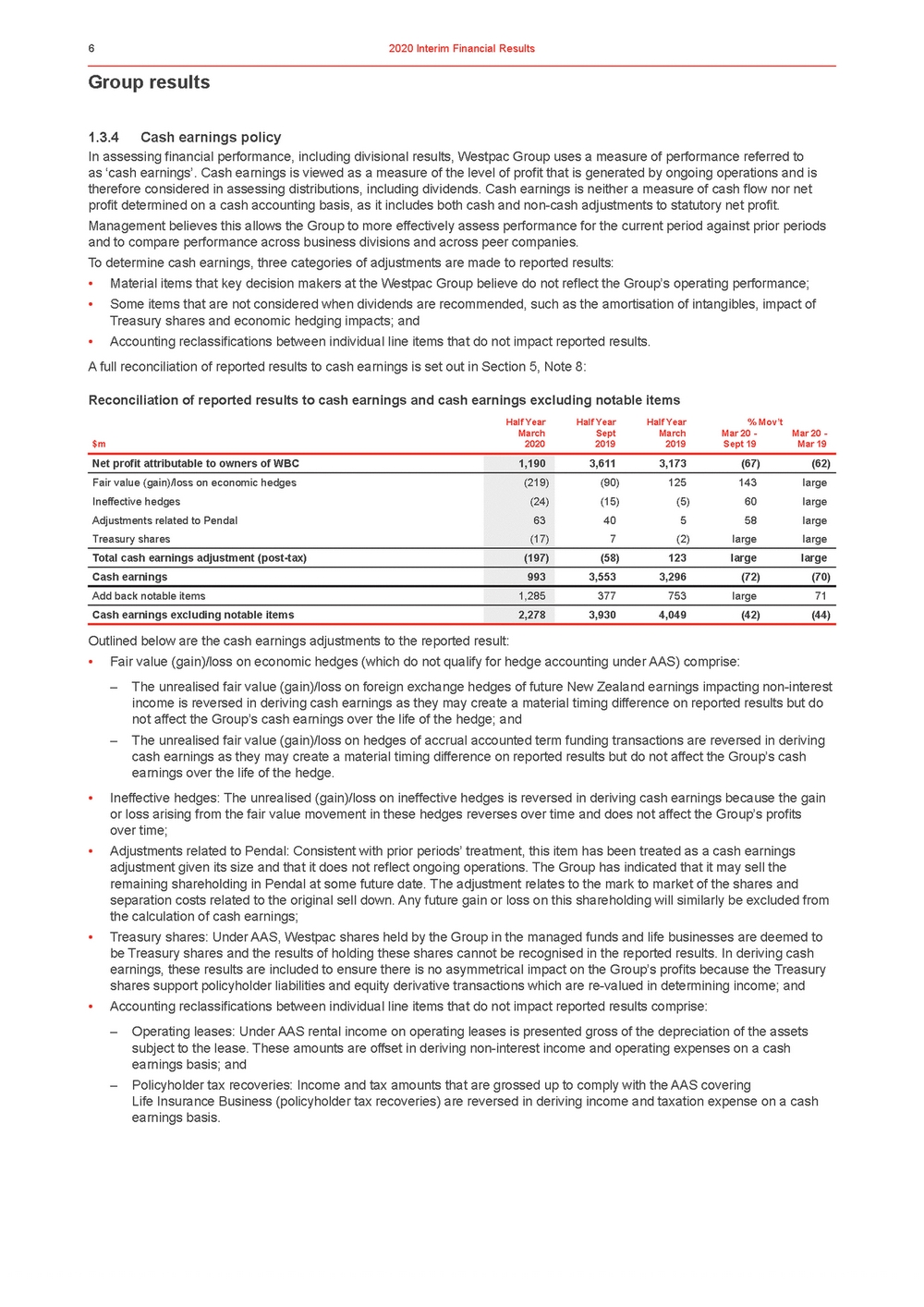

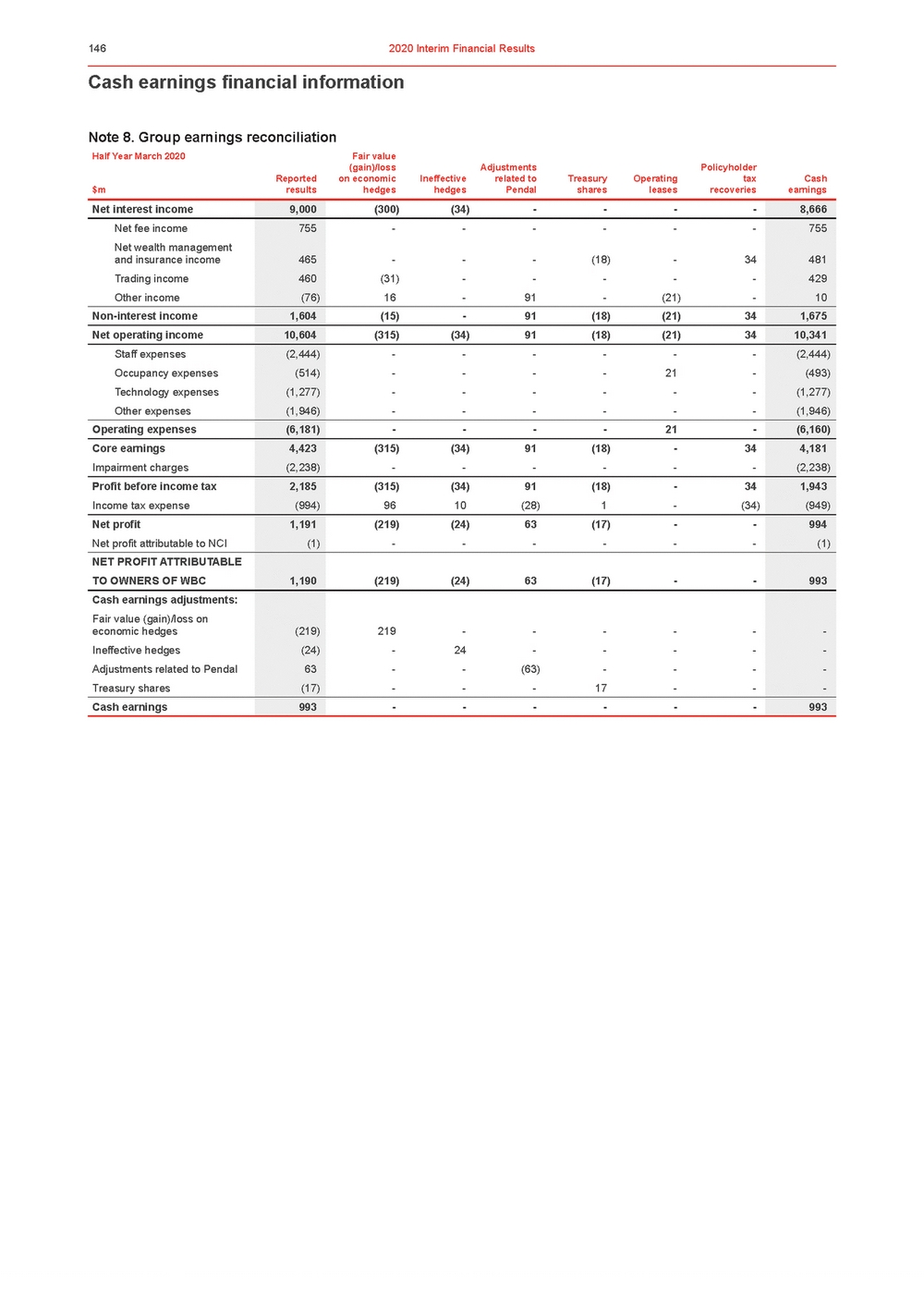

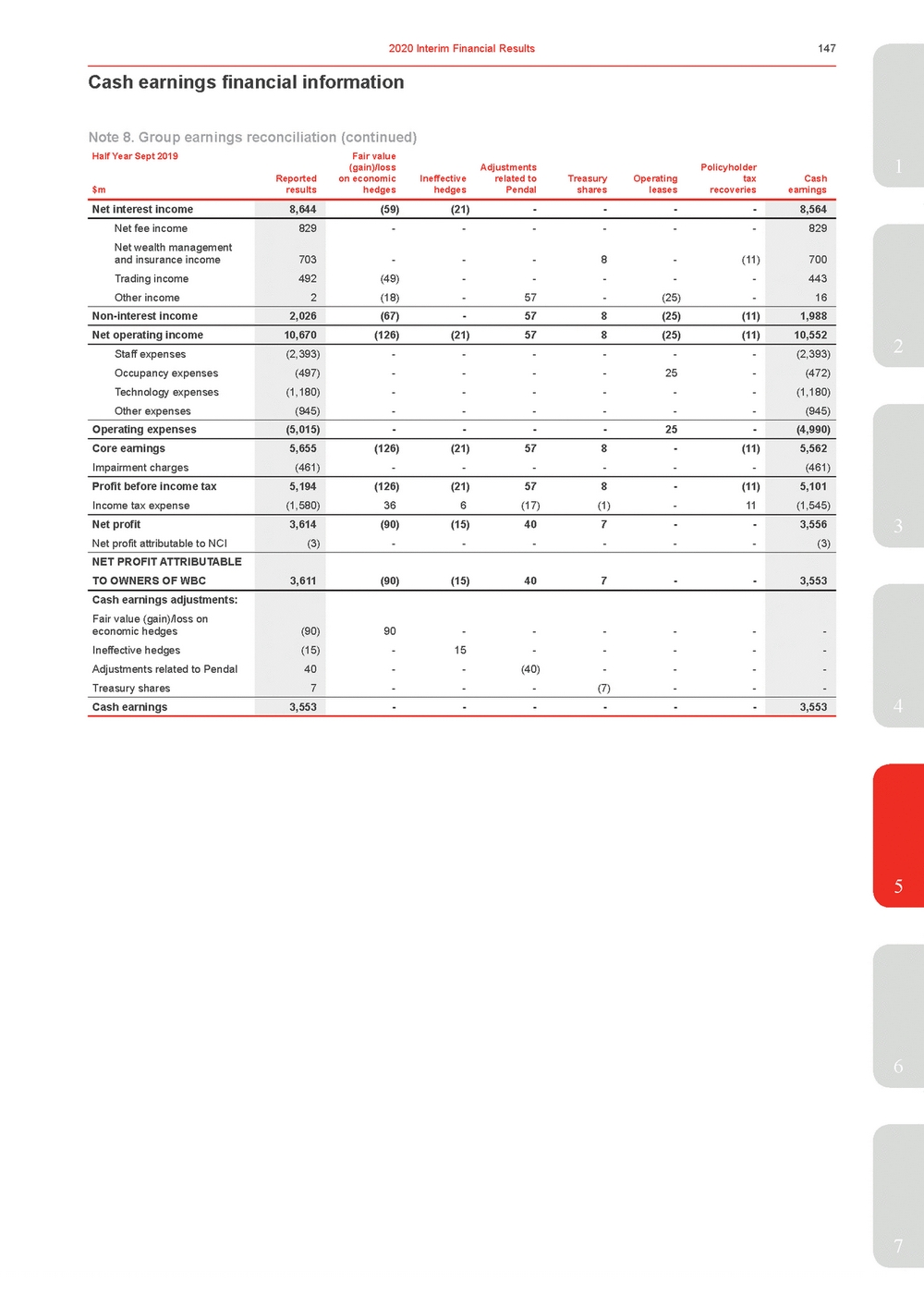

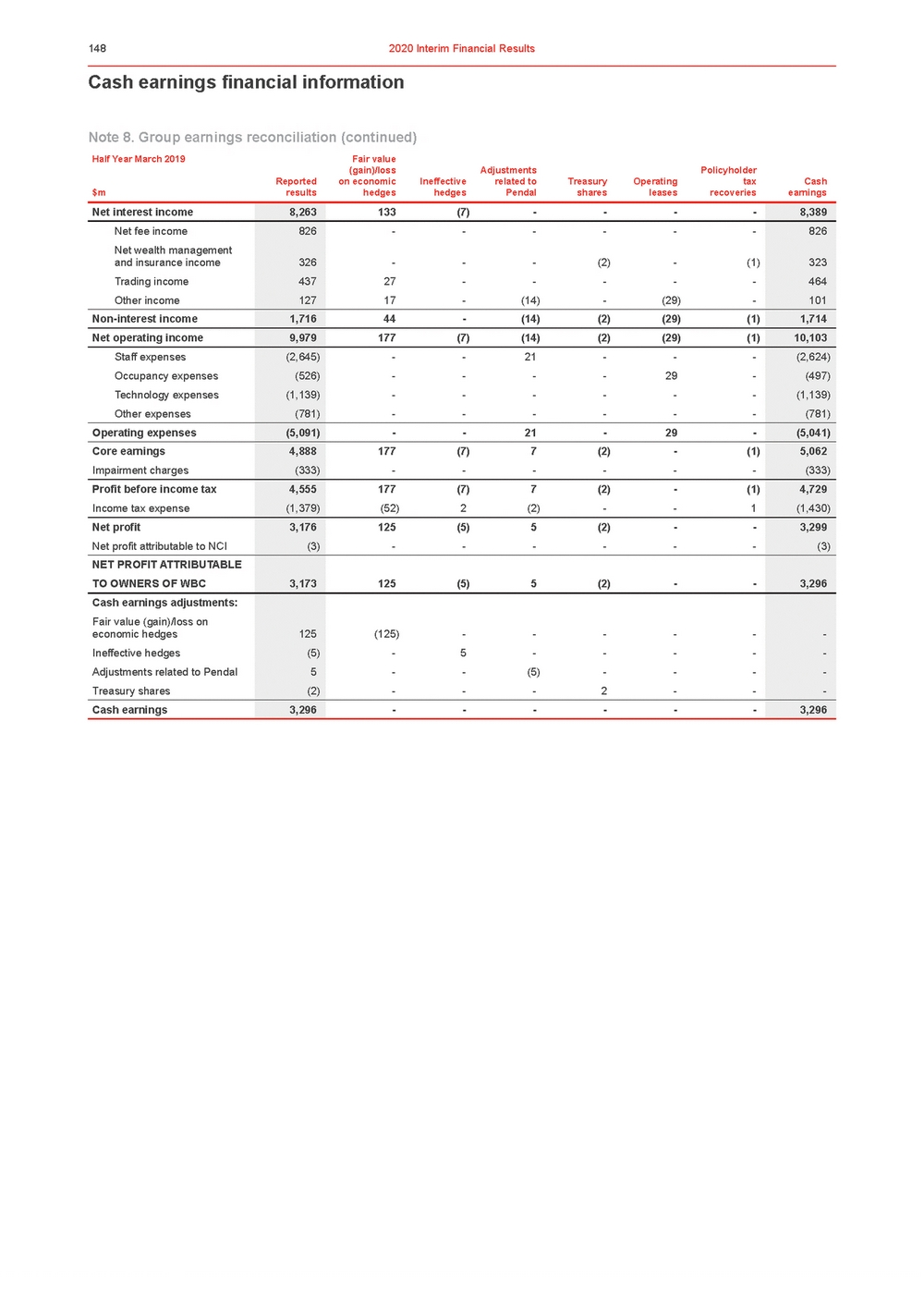

| Group results 1.3.4Cash earnings policy In assessing financial performance, including divisional results, Westpac Group uses a measure of performance referred to as ‘cash earnings’. Cash earnings is viewed as a measure of the level of profit that is generated by ongoing operations and is therefore considered in assessing distributions, including dividends. Cash earnings is neither a measure of cash flow nor net profit determined on a cash accounting basis, as it includes both cash and non-cash adjustments to statutory net profit. Management believes this allows the Group to more effectively assess performance for the current period against prior periods and to compare performance across business divisions and across peer companies. To determine cash earnings, three categories of adjustments are made to reported results: •Material items that key decision makers at the Westpac Group believe do not reflect the Group’s operating performance; •Some items that are not considered when dividends are recommended, such as the amortisation of intangibles, impact of Treasury shares and economic hedging impacts; and •Accounting reclassifications between individual line items that do not impact reported results. A full reconciliation of reported results to cash earnings is set out in Section 5, Note 8: Reconciliation of reported results to cash earnings and cash earnings excluding notable items Half YearHalf YearHalf Year% Mov’t March $m2020 Sept 2019 March 2019 Mar 20 - Sept 19 Mar 20 - Mar 19 Outlined below are the cash earnings adjustments to the reported result: •Fair value (gain)/loss on economic hedges (which do not qualify for hedge accounting under AAS) comprise: – The unrealised fair value (gain)/loss on foreign exchange hedges of future New Zealand earnings impacting non-interest income is reversed in deriving cash earnings as they may create a material timing difference on reported results but do not affect the Group’s cash earnings over the life of the hedge; and – The unrealised fair value (gain)/loss on hedges of accrual accounted term funding transactions are reversed in deriving cash earnings as they may create a material timing difference on reported results but do not affect the Group’s cash earnings over the life of the hedge. •Ineffective hedges: The unrealised (gain)/loss on ineffective hedges is reversed in deriving cash earnings because the gain or loss arising from the fair value movement in these hedges reverses over time and does not affect the Group’s profits over time; •Adjustments related to Pendal: Consistent with prior periods’ treatment, this item has been treated as a cash earnings adjustment given its size and that it does not reflect ongoing operations. The Group has indicated that it may sell the remaining shareholding in Pendal at some future date. The adjustment relates to the mark to market of the shares and separation costs related to the original sell down. Any future gain or loss on this shareholding will similarly be excluded from the calculation of cash earnings; •Treasury shares: Under AAS, Westpac shares held by the Group in the managed funds and life businesses are deemed to be Treasury shares and the results of holding these shares cannot be recognised in the reported results. In deriving cash earnings, these results are included to ensure there is no asymmetrical impact on the Group’s profits because the Treasury shares support policyholder liabilities and equity derivative transactions which are re-valued in determining income; and •Accounting reclassifications between individual line items that do not impact reported results comprise: – Operating leases: Under AAS rental income on operating leases is presented gross of the depreciation of the assets subject to the lease. These amounts are offset in deriving non-interest income and operating expenses on a cash earnings basis; and – Policyholder tax recoveries: Income and tax amounts that are grossed up to comply with the AAS covering Life Insurance Business (policyholder tax recoveries) are reversed in deriving income and taxation expense on a cash earnings basis. |

| 1 the Group’s overall results or balance sheet but impacts divisional results and balance sheets. Comparative divisional financial information has been restated for this change. The change realigned divisional earnings and balance sheet disclosures for Consumer and Business for customer migrations following a refinement to Westpac’s definition of a small to medium size enterprise customer. The change is aimed at providing a more tailored service to the customers, by aligning them with the division that is best able to meet their needs. The change moves approximately 49,000 customers from the Business to Consumer division. This Results Announcement is unaudited PricewaterhouseCoopers have reviewed the financial statements contained within Section 4 of this Results Announcement and have issued an unmodified review report. All other sections, including the Directors’ Report in Section 4 of the Results Announcement have not been subject to review by PricewaterhouseCoopers. The financial information contained in this Results2 Announcement includes information extracted from the reviewed financial statements together with information that has not been reviewed. The cash earnings disclosed as part of this Results Announcement have not been separately reviewed by PricewaterhouseCoopers. 3 4 5 6 7 |

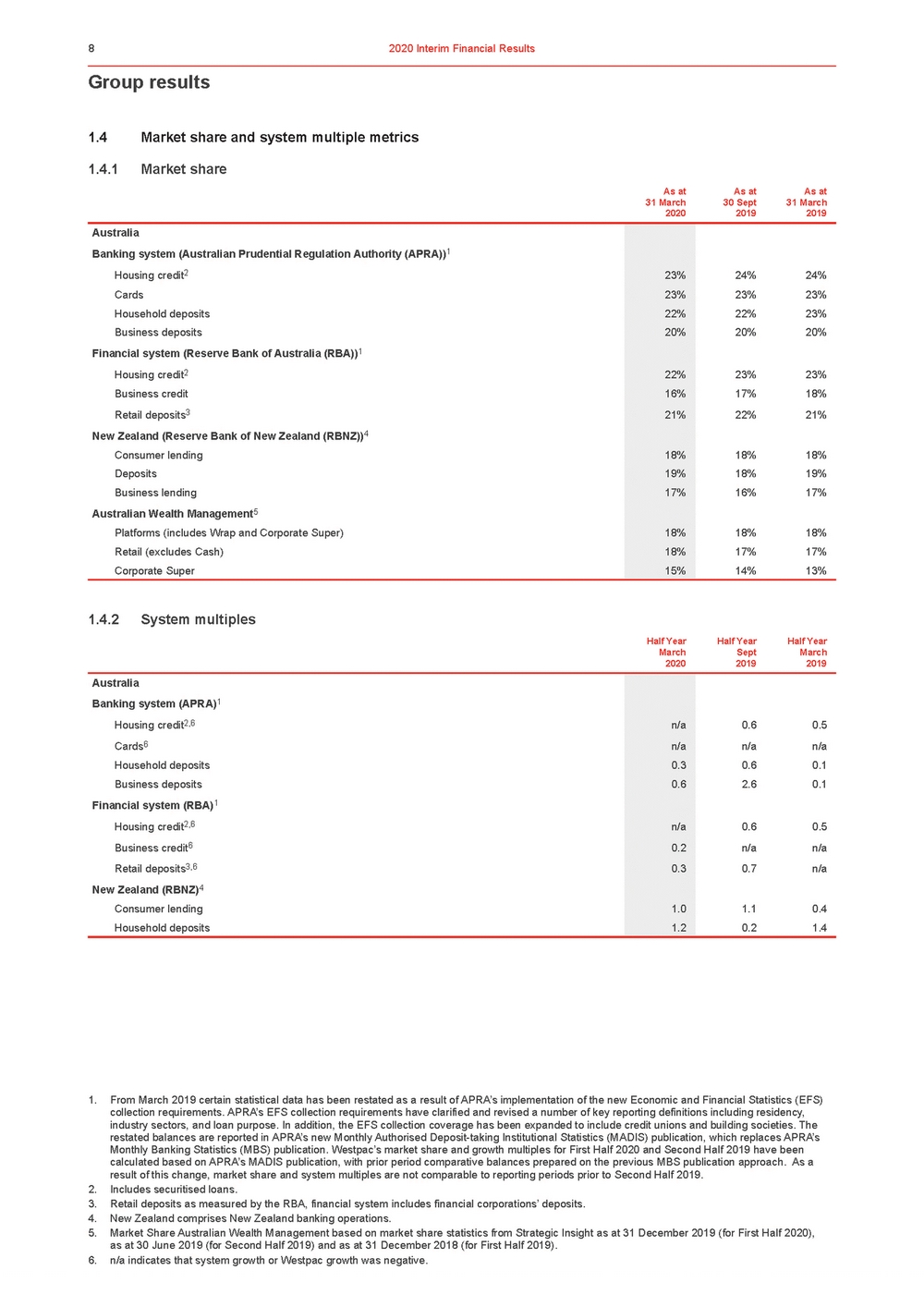

| Group results 1.4Market share and system multiple metrics 1.4.1Market share As atAs atAs at Australia Banking system (Australian Prudential Regulation Authority (APRA))1 31 March 2020 30 Sept 2019 31 March 2019 Financial system (Reserve Bank of Australia (RBA))1 Housing credit2 22% 23% 23% Business credit 16% 17% 18% Retail deposits3 21% 22% 21% New Zealand (Reserve Bank of New Zealand (RBNZ))4 1.4.2System multiples Half YearHalf YearHalf Year Australia Banking system (APRA)1 March 2020 Sept 2019 March 2019 Housing credit2,6 n/a0.60.5 Cards6 n/an/an/a Household deposits0.30.60.1 Business deposits0.62.60.1 Financial system (RBA)1 Housing credit2,6 n/a0.60.5 Business credit6 0.2n/an/a Retail deposits3,6 0.30.7n/a New Zealand (RBNZ)4 Consumer lending1.01.10.4 Household deposits1.20.21.4 1. From March 2019 certain statistical data has been restated as a result of APRA’s implementation of the new Economic and Financial Statistics (EFS) collection requirements. APRA’s EFS collection requirements have clarified and revised a number of key reporting definitions including residency, industry sectors, and loan purpose. In addition, the EFS collection coverage has been expanded to include credit unions and building societies. The restated balances are reported in APRA’s new Monthly Authorised Deposit-taking Institutional Statistics (MADIS) publication, which replaces APRA’s Monthly Banking Statistics (MBS) publication. Westpac’s market share and growth multiples for First Half 2020 and Second Half 2019 have been calculated based on APRA’s MADIS publication, with prior period comparative balances prepared on the previous MBS publication approach. As a result of this change, market share and system multiples are not comparable to reporting periods prior to Second Half 2019. 2. Includes securitised loans. 3. Retail deposits as measured by the RBA, financial system includes financial corporations’ deposits. 4. New Zealand comprises New Zealand banking operations. 5. Market Share Australian Wealth Management based on market share statistics from Strategic Insight as at 31 December 2019 (for First Half 2020), as at 30 June 2019 (for Second Half 2019) and as at 31 December 2018 (for First Half 2019). 6. n/a indicates that system growth or Westpac growth was negative. |

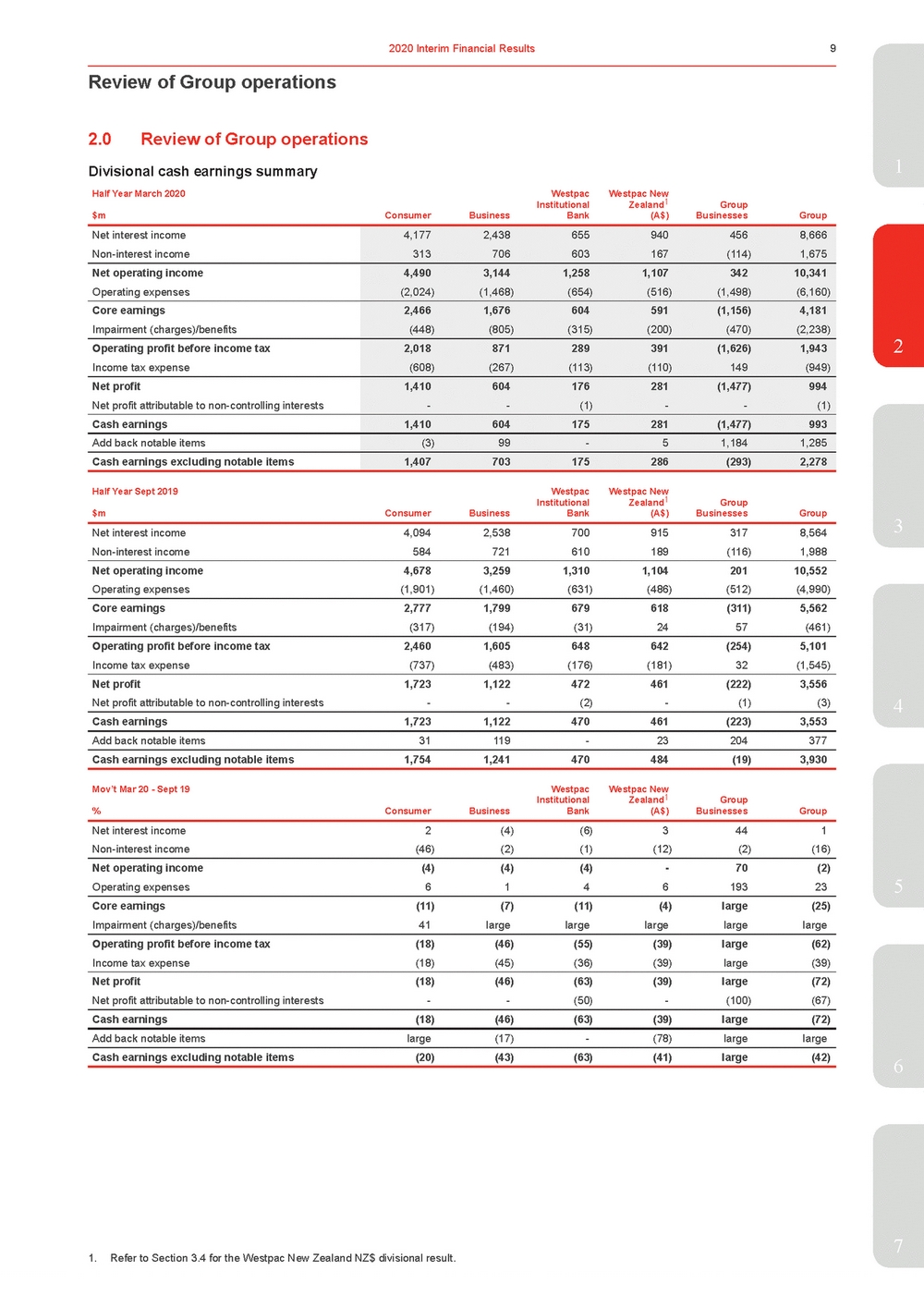

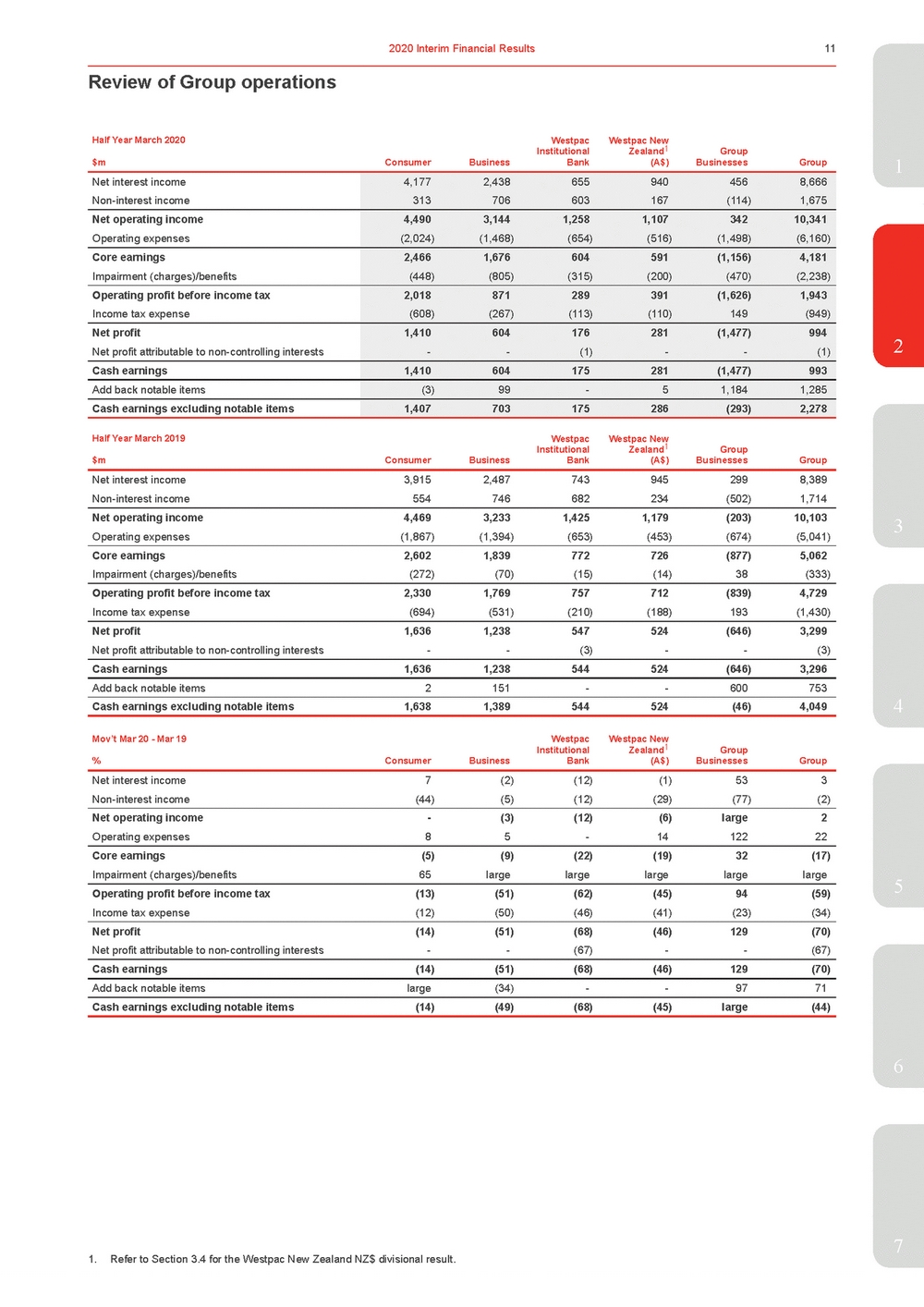

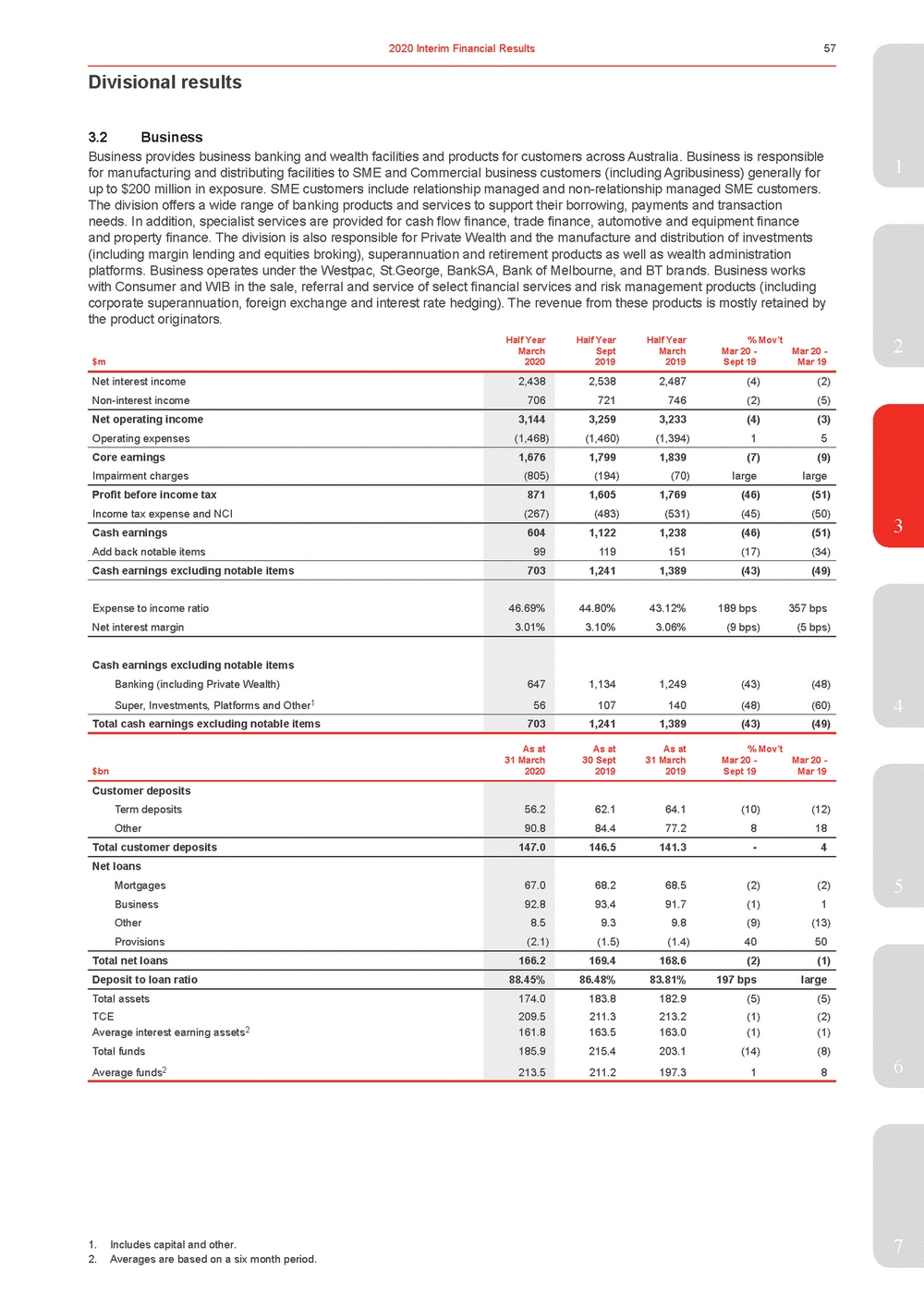

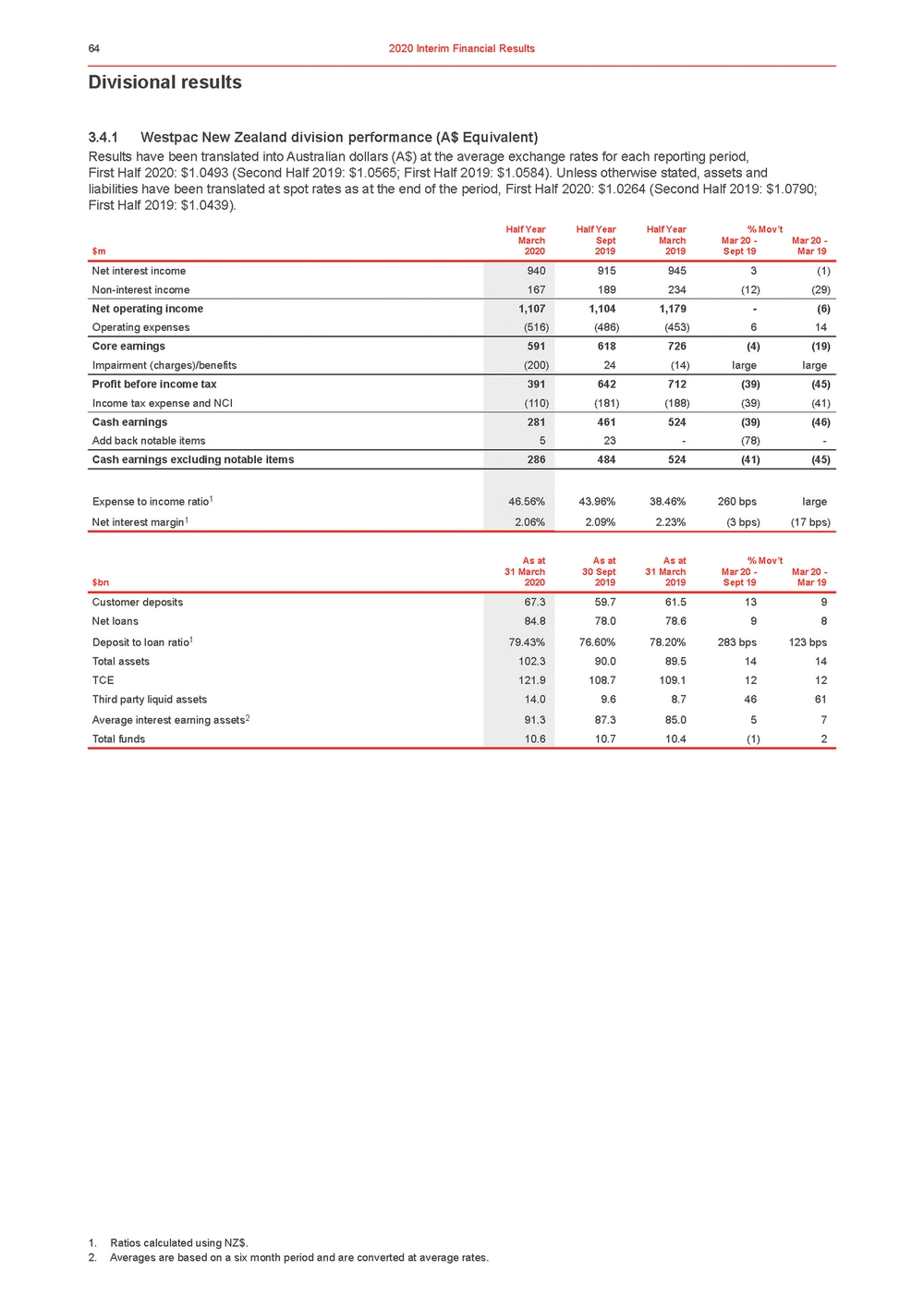

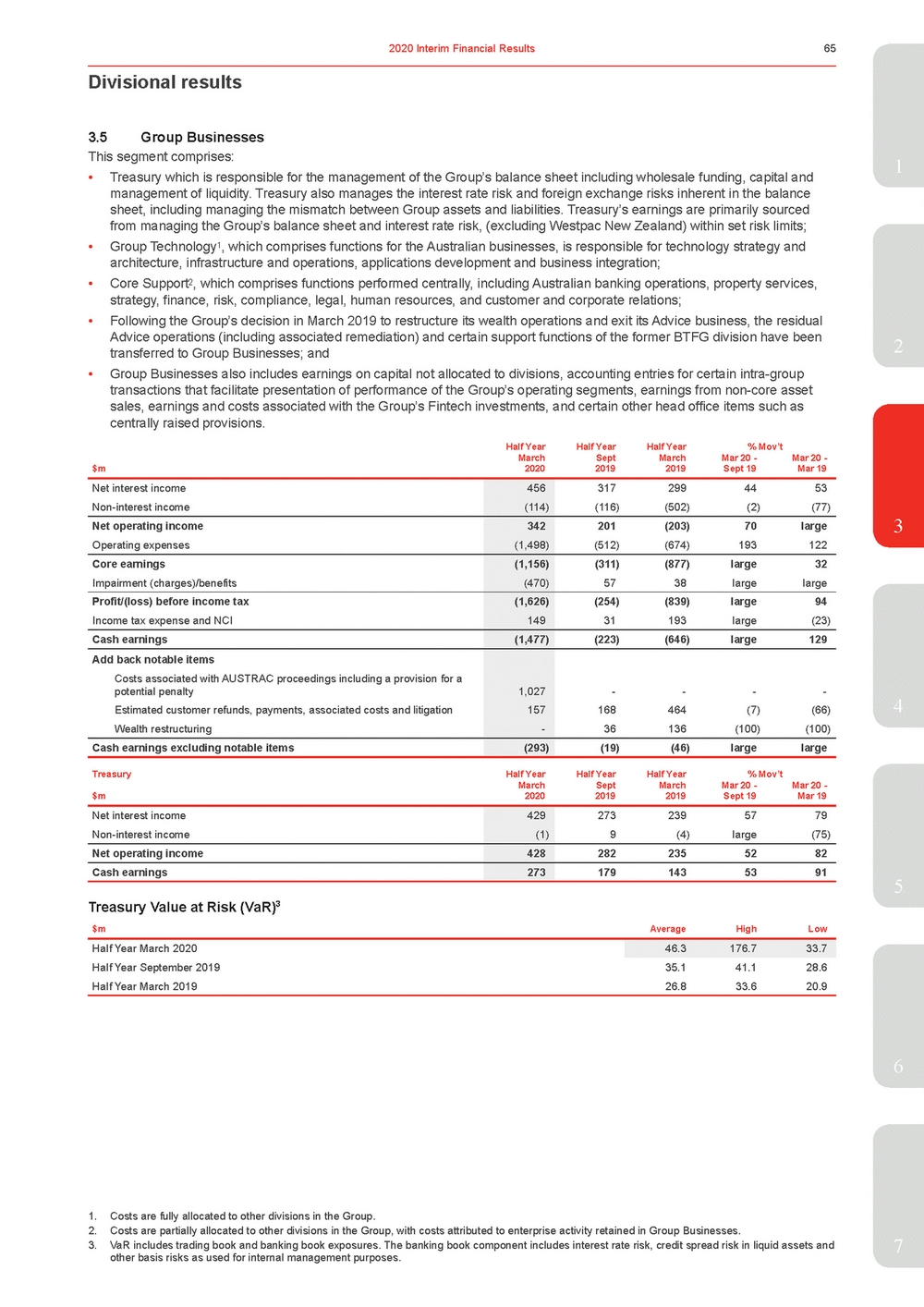

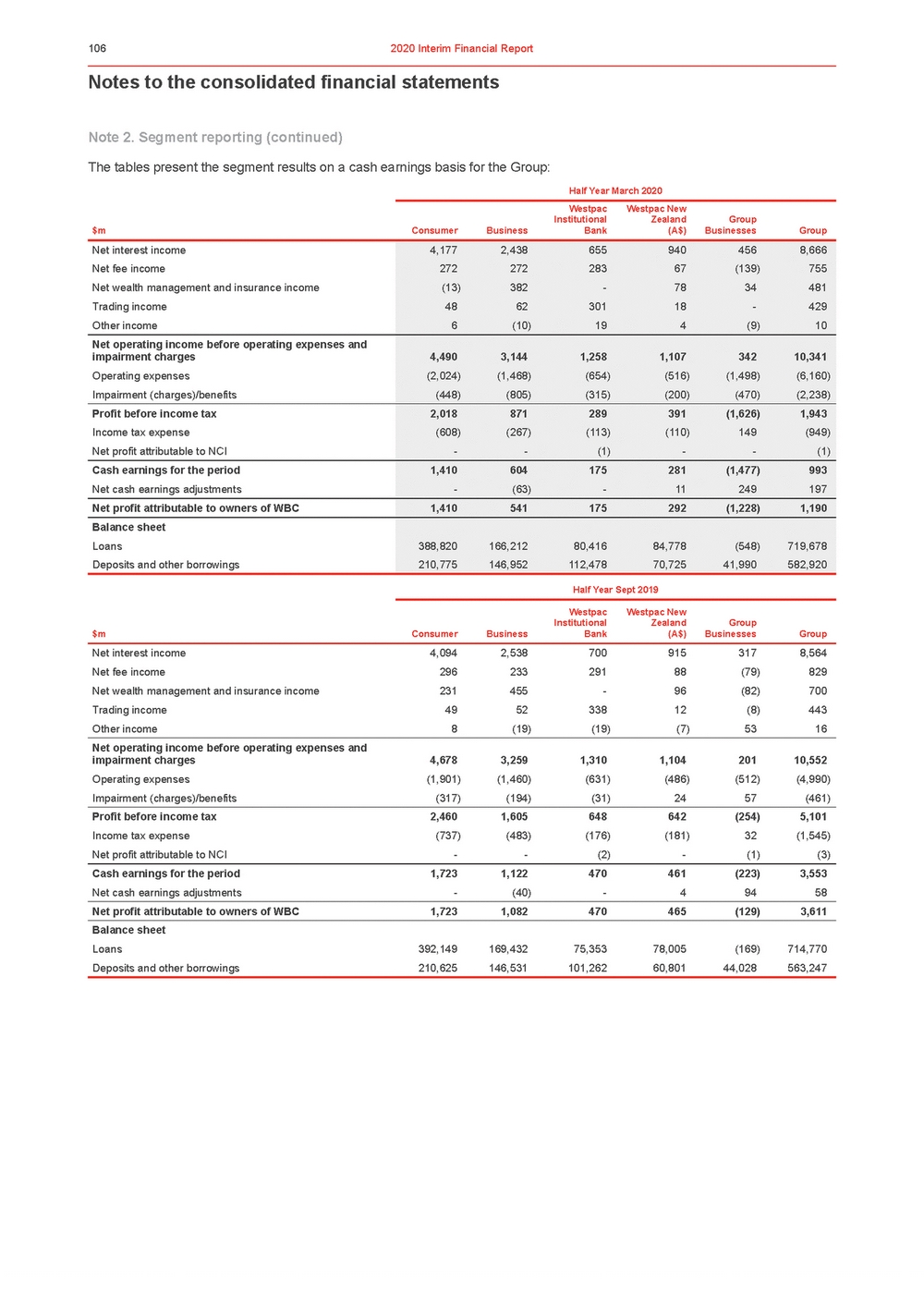

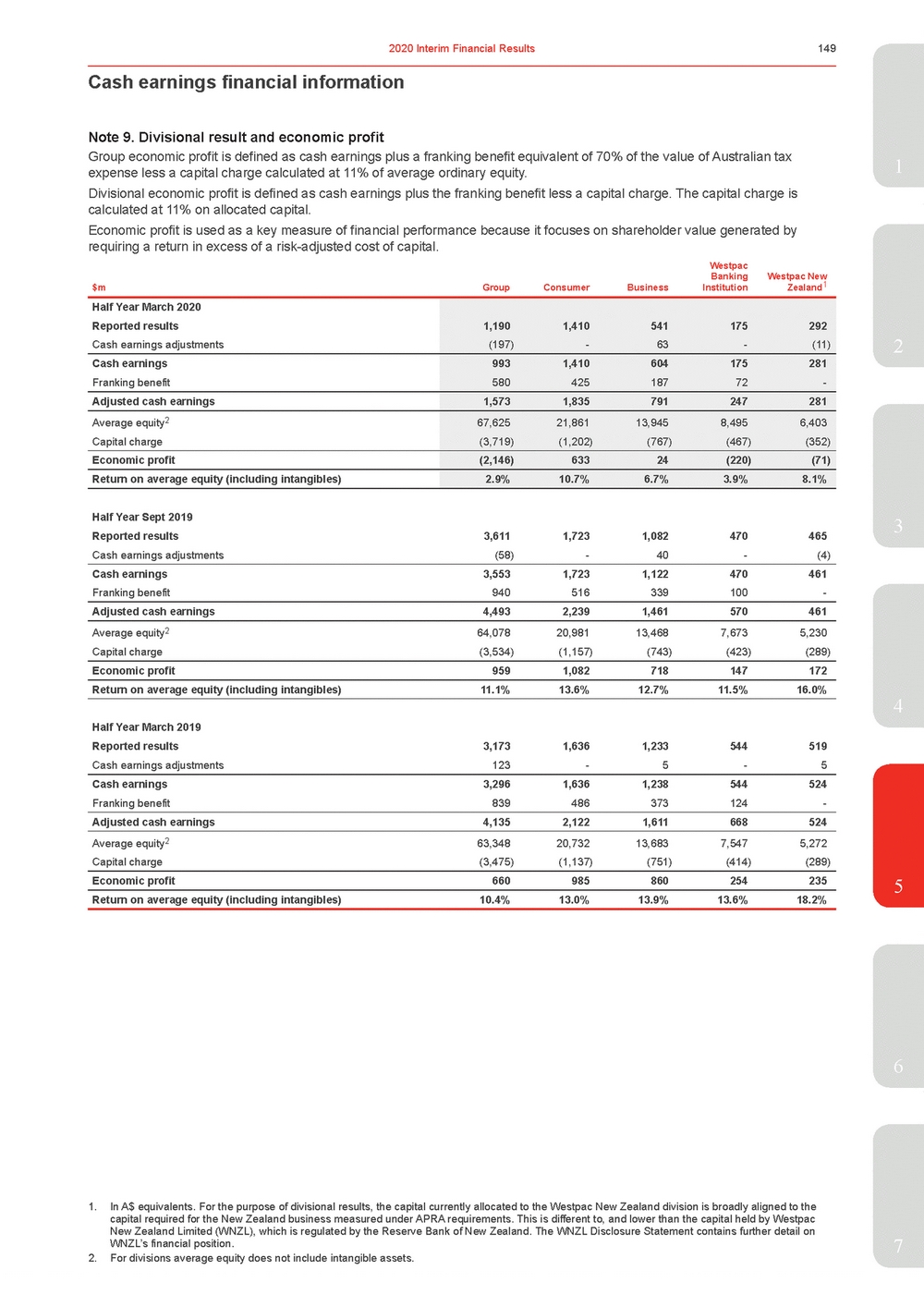

| 2.0Review of Group operations Divisional cash earnings summary1 Half Year March 2020 $m ConsumerBusiness Westpac Institutional Bank Westpac New Zealand1 (A$) Group BusinessesGroup Net interest income Non-interest income 4,1772,438 313706 655940 603167 4568,666 (114)1,675 Net operating income Operating expenses 4,4903,144 (2,024)(1,468) 1,2581,107 (654)(516) 34210,341 (1,498)(6,160) Core earnings Impairment (charges)/benefits 2,4661,676 (448)(805) 604591 (315)(200) (1,156)4,181 (470)(2,238) Operating profit before income tax Income tax expense 2,018871 (608)(267) 289391 (113)(110) (1,626)1,943 149(949) Net profit Net profit attributable to non-controlling interests 1,410604 --176281 (1)-(1,477)994 -(1) Cash earnings 1,410604 175281 (1,477)993 Add back notable items (3)99 -5 1,1841,285 Cash earnings excluding notable items 1,407703 175286 (293)2,278 Half Year Sept 2019 $m ConsumerBusiness Westpac Institutional Bank Westpac New Zealand1 (A$) Group BusinessesGroup Net interest income4,0942,5387009153178,5643 Non-interest income584721610189(116)1,988 Net operating income4,6783,2591,3101,10420110,552 Operating expenses(1,901)(1,460)(631)(486)(512)(4,990) Core earnings2,7771,799679618(311)5,562 Impairment (charges)/benefits(317)(194)(31)2457(461) Operating profit before income tax2,4601,605648642(254)5,101 Income tax expense(737)(483)(176)(181)32(1,545) Net profit1,7231,122472461(222)3,556 Net profit attributable to non-controlling interests--(2)-(1)(3)4 Cash earnings1,7231,122470461(223)3,553 Add back notable items31119-23204377 Cash earnings excluding notable items1,7541,241470484(19)3,930 Mov’t Mar 20 - Sept 19 % ConsumerBusiness Westpac Institutional Bank Westpac New Zealand1 (A$) Group BusinessesGroup Net interest income2(4)(6)3441 Non-interest income(46)(2)(1)(12)(2)(16) Net operating income(4)(4)(4)-70(2) Operating expenses6146193235 Core earnings (11)(7) (11)(4)large(25) Impairment (charges)/benefits 41largelargelarge largelarge Operating profit before income tax (18) (46) (55) (39)large(62) Income tax expense (18) (45) (36) (39) large(39) Net profit (18) (46) (63) (39)large(72) Net profit attributable to non-controlling interests-- (50) - (100)(67) Cash earnings (18) (46) (63) (39)large(72) Add back notable itemslarge (17)-(78) largelarge Cash earnings excluding notable items (20) (43) (63) (41)large(42) 7 1. Refer to Section 3.4 for the Westpac New Zealand NZ$ divisional result. |

| Review of Group operations Movement in cash earnings ($m) First Half 2020 – Second Half 2019 (72%) 3773,93076 (42%) 3,553 (402) (167) 6182,278 (1,777) (1,285) 993 Movement in core earnings by division ($m) First Half 2020 – Second Half 2019 (25%) 5,562 5396,101 (362) (8%) (153)(75)(52) 1495,608 (1,427) 4,181 |

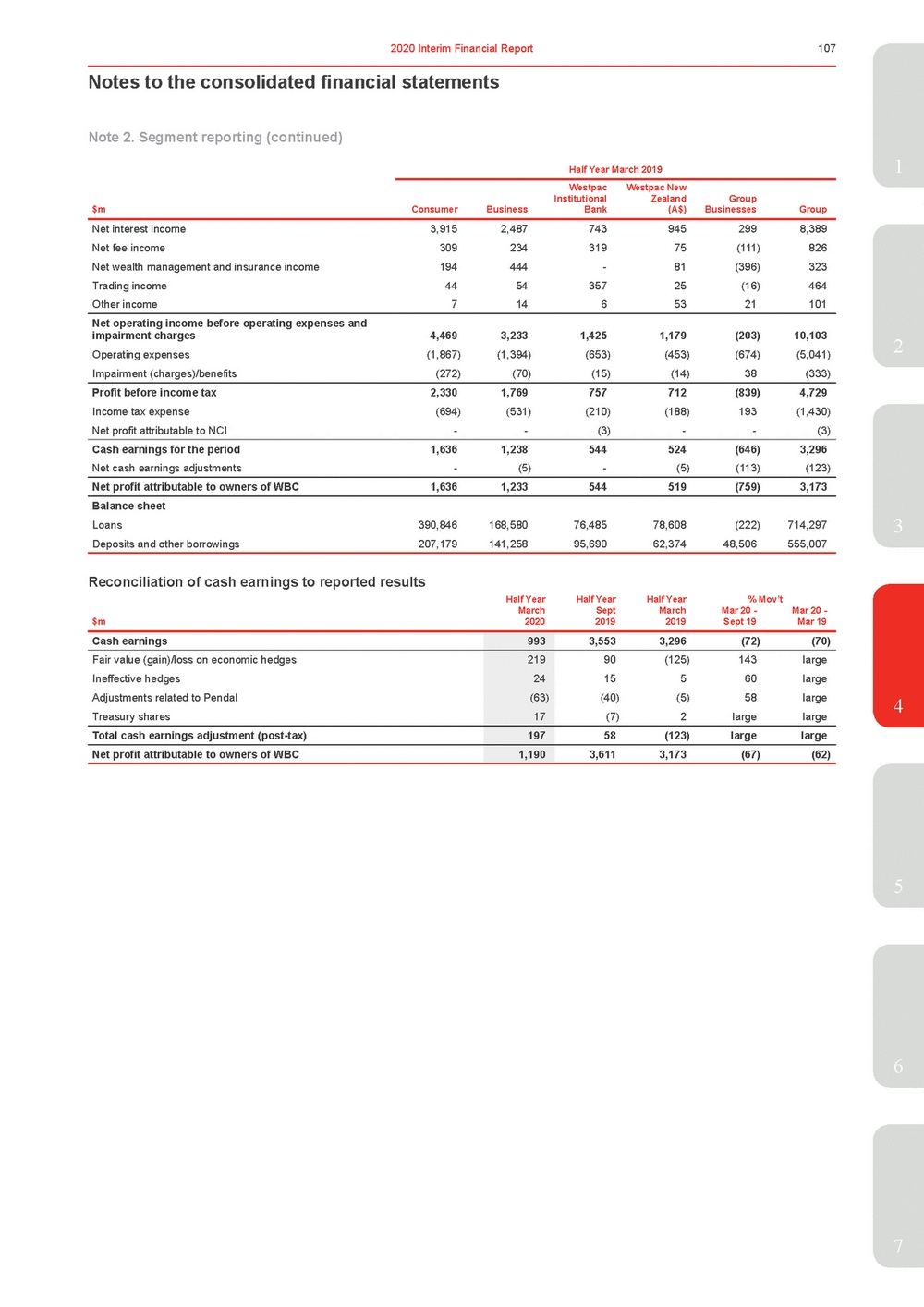

| Net interest income Non-interest income 4,1772,438 313706 655940 603167 4568,666 (114)1,675 Net operating income Operating expenses 4,4903,144 (2,024)(1,468) 1,2581,107 (654)(516) 34210,341 (1,498)(6,160) Core earnings Impairment (charges)/benefits 2,4661,676 (448)(805) 604591 (315)(200) (1,156)4,181 (470)(2,238) Operating profit before income tax Income tax expense 2,018871 (608)(267) 289391 (113)(110) (1,626)1,943 149(949) Net profit Net profit attributable to non-controlling interests 1,410604 --176281 (1)-(1,477)994 -(1) Cash earnings 1,410604 175281 (1,477)993 Add back notable items (3)99 -5 1,1841,285 Cash earnings excluding notable items 1,407703 175286 (293)2,278 Half Year March 2020 Westpac Westpac New $m Consumer Business Institutional Bank Zealand1 (A$) Group Businesses Group 2 Half Year March 2019 Westpac Institutional Westpac New Zealand1 Group $m Consumer Business Bank (A$) Businesses Group Net interest income 3,915 2,487 743 945 299 8,389 Non-interest income 554 746 682 234 (502) 1,714 Net operating income 4,469 3,233 1,425 1,179 (203) 10,103 Operating expenses (1,867) (1,394) (653) (453) (674) (5,041) Core earnings 2,602 1,839 772 726 (877) 5,062 Impairment (charges)/benefits (272) (70) (15) (14) 38 (333) Operating profit before income tax 2,330 1,769 757 712 (839) 4,729 Income tax expense (694) (531) (210) (188) 193 (1,430) Net profit 1,636 1,238 547 524 (646) 3,299 Net profit attributable to non-controlling interests - - (3) - - (3) Cash earnings 1,636 1,238 544 524 (646) 3,296 Add back notable items 2 151 - - 600 753 Cash earnings excluding notable items 1,638 1,389 544 524 (46) 4,049 Mov’t Mar 20 - Mar 19 Westpac Institutional Westpac New Zealand1 Group % Consumer Business Bank (A$) Businesses Group Net interest income 7 (2) (12) (1) 53 3 Non-interest income (44) (5) (12) (29) (77) (2) Net operating income - (3) (12) (6) large 2 Operating expenses 8 5 - 14 122 22 Core earnings (5) (9) (22) (19) 32 (17) Impairment (charges)/benefits 65 large large large large large Operating profit before income tax (13) (51) (62) (45) 94 (59) Income tax expense (12) (50) (46) (41) (23) (34) Net profit (14) (51) (68) (46) 129 (70) Net profit attributable to non-controlling interests - - (67) - - (67) Cash earnings (14) (51) (68) (46) 129 (70) Add back notable items large (34) - - 97 71 Cash earnings excluding notable items (14) (49) (68) (45) large (44) 4 5 6 7 1. Refer to Section 3.4 for the Westpac New Zealand NZ$ divisional result. |

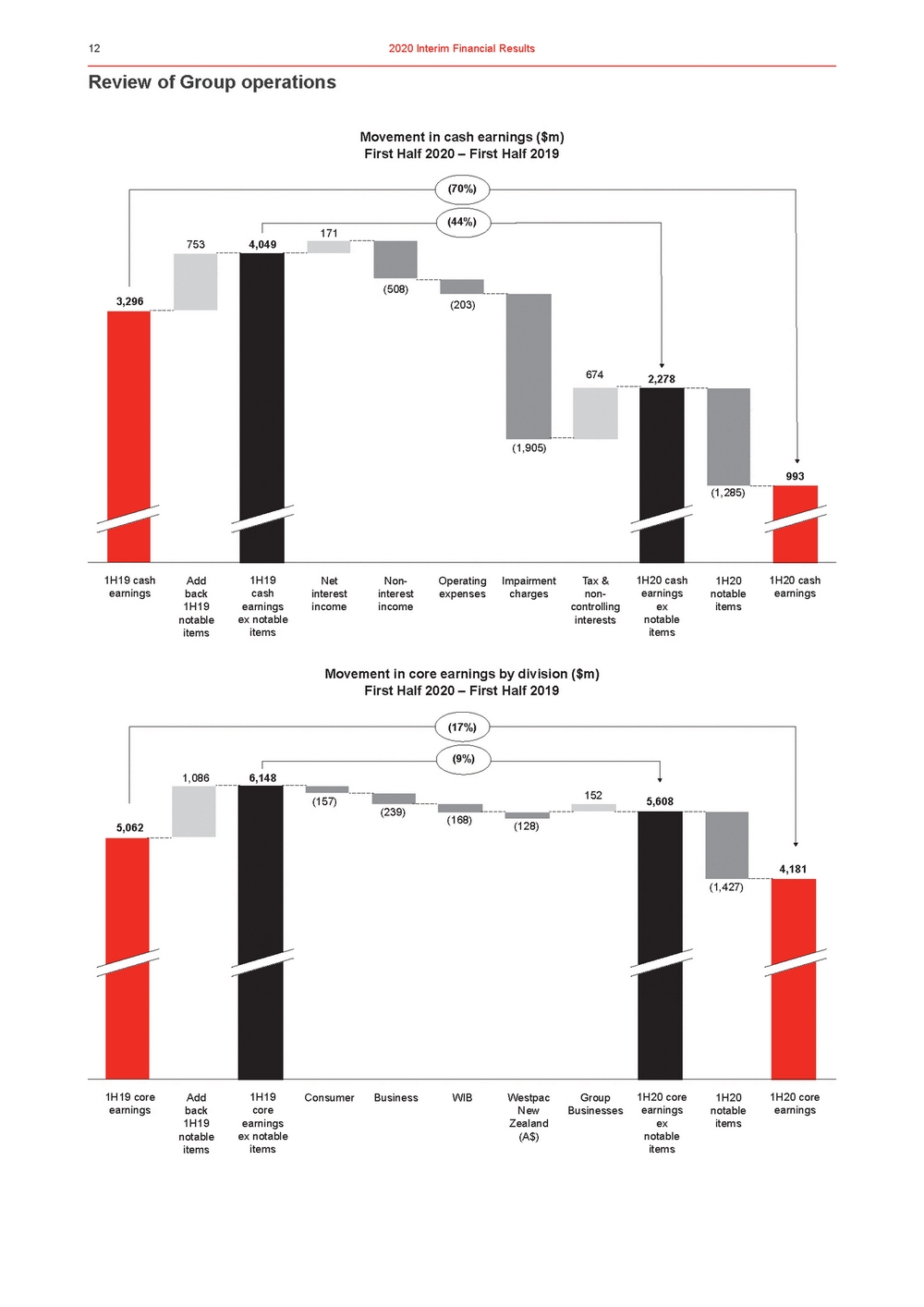

| Review of Group operations Movement in cash earnings ($m) First Half 2020 – First Half 2019 (70%) 7534,049 171 (44%) 3,296 (508) (203) 6742,278 (1,905) (1,285) 993 Movement in core earnings by division ($m) First Half 2020 – First Half 2019 (17%) 5,062 1,0866,148 (157) (239) (9%) (168)(128) 1525,608 (1,427) 4,181 |

| 2.1Performance overview Overview1 Westpac’s performance in First Half 2020 was significantly impacted by the COVID-19 pandemic, including its effect on employees, customers and the broader economy. Westpac’s coordinated approach to the crisis is focused on the safety of its people, support for customers and helping the economy through this challenging time. Westpac’s First Half 2020 financial results were considerably lower over both the prior half and prior corresponding period due to the immediate and expected flow-on impacts of COVID-19 on impairment charges, along with two other major factors outlined below. The first is the provisions and costs related to the Australian Transaction Reports and Analysis Centre’s (AUSTRAC) civil proceedings against Westpac in relation to alleged contraventions of the Anti-Money Laundering and Counter-Terrorism Financing Act. These civil proceedings contributed to Board and management changes and led to a provision for a potential penalty along with additional costs, including from the Group’s Response Plan. In aggregate, these costs reduced cash earnings2 in First Half 2020 by over $1 billion. Other impacts of the AUSTRAC civil proceedings are set out below. Secondly, the financial services sector, including Westpac, has continued to respond to the recommendations from the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry (Royal Commission), as well as governance, culture and accountability self-assessments. For Westpac, implementing these recommendations and putting things right for customers where the Group got it wrong has contributed to higher regulatory and compliance costs and additional provisions for estimated customer refunds, payments, associated costs and litigation. These provisions reduced cash earnings in First Half 2020 by $258 million. Prior to the emergence of COVID-19, the sector had been impacted by a slowing in GDP growth, continued low wages growth, subdued business and consumer sentiment and lower interest rates. For financial services companies, this resulted in relatively modest demand for lending, further pressure on net interest margins and increased competition, particularly from new and smaller players. The housing market on the other hand had shown some signs of recovery with house prices generally3 improving in major markets through the half. However, given recent events this recovery is unlikely to be sustained. COVID-19 The largest financial impact of COVID-19 on performance in First Half 2020 has been a material increase in impairment charges linked to the changed economic outlook. Slower activity, together with falls in asset values, have also contributed to the write-down of certain assets and capitalised software. While other aspects of Westpac’s operations were impacted by the effects of COVID-19, as the crisis emerged late in the period, the financial impact was relatively modest. Additional effects are expected to emerge in Second Half 2020, the size of which will depend on a range of factors including the duration of the crisis, the impact of stimulus measures and how consumers and businesses respond. Over the last two centuries, Westpac has supported its people, customers, and the community more broadly through recessions,4 depressions and a range of crises. Westpac will continue to do so through the COVID-19 pandemic. Some examples of Westpac’s actions include the following: Protecting employees The physical and mental wellbeing of employees is paramount, and the Group has enhanced policies, practices and procedures to keep our people safe, assist them to work effectively and continue supporting customers and the community, including: •Supporting around 22,000 employees working from home in Australia, with around 4,000 employees remaining in corporate sites to deliver essential banking services; •Over 300,000 hours of video conferencing in March 2020 compared to 42,000 hours 12 months ago; 5 •Actively changed work arrangements to deal with increased customer demand for assistance, a decline in branch visits and lockdowns experienced by some offshore service providers; and •Special paid leave for employees (including casuals) required to self-isolate. Supporting consumers Helping consumers to bank safely and manage their finances effectively, including: •A range of initiatives to reduce personal contact by helping customers set up internet banking, encouraging self-serve and increasing the use of electronic and contactless channels; •Remaining open for business with over 94% of Australian branches open, and ATM availability exceeding 98% through6 March 2020; •Supporting consumers with a range of special assistance packages including principal and interest deferral for mortgages (6 months) and cards/personal loans (3 months); •Around 120,000 assistance packages for mortgages have been approved; •Special interest rates for term deposits, fixed rate home loans for 1, 2 and 3 year terms; and •Increased limits on tap-and-go transactions to $200 from $100 and increased limits on digital cheque deposits. 7 |

| Review of Group operations Supporting businesses Helping businesses manage their finances through these challenging times, including: •Payment deferral options for businesses with certain loans of up to $10 million; •Seconding certain of the Group’s business specialists into contact centres to support businesses manage their cash flow; •Approved over 31,000 assistance packages; •Providing unsecured loans of up to $0.25 million for 3 years for businesses with turnover <$50 million (50% guaranteed by the Federal Government); •Providing temporary funding to businesses waiting for JobKeeper payments; •Working closely with large corporates and institutions to support liquidity needs with WIB supporting a $5 billion increase in lending late in First Half 2020; and •Special interest rates and fees: 200 basis point discount on overdrafts, 100 basis point discount on cash-based loans, fees waived on merchant terminal rentals for up to 3 months, no establishment fee for equipment finance loans. Supporting the economy and community As one of Australia’s and New Zealand’s major banks, Westpac plays a critical role in supporting the economy and the communities in which it operates, including: •Materially improving system stability and resilience, with a 48% reduction in high severity incidents while keeping our systems and data safe from external hacks; •Supporting State governments with debt purchases and data insights on the impacts of the COVID-19 on consumers and businesses; •Updating the Group’s employee matching gifts program to support certain COVID-19 related causes; •With their major sponsor impacted by the effects of COVID-19, St.George Bank stepped in to help fund Little Wings which provides a free service to help rural families travel to the Sydney Children’s Hospital to receive vital medical treatment; •Working constructively with government and the industry to develop effective support mechanisms for customers. Through First Half 2020, Westpac responded to the severe bushfires that impacted much of eastern Australia by setting up practical, on-the-ground support for customers, our people and for those caring for affected communities. Some of the initiatives included: allocating $3.8 million for emergency cash grants for consumers and businesses, making mortgage payments for one year for those losing their principal residence and providing low interest rates on loans to help businesses rebuild. Additional community support included funds for financial counselling along with donations to the Salvation Army’s Disaster Appeal, state bushfire appeals and to various volunteer services. For our people, Westpac provided uncapped paid leave to emergency services volunteers in bushfire affected areas along with grants of $5,000 to employees needing emergency relief. CEO priorities Following his appointment as CEO, Peter King announced some changes to the Group’s priorities which reflect Westpac’s immediate regulatory and compliance needs, responding to the more challenging operating environment and actions to improve Westpac’s performance focus. These priorities also reaffirm the Group’s customer focus and its service orientation. The four priorities are: 1. Customer Franchise – in the short term, support customers through the COVID-19 crisis. Longer term, grow the customer base and deepen relationships through superior service; 2. Performance Discipline – simplify the portfolio and drive improved execution across the Group’s banking businesses; 3. Digital Transformation – build a common and upgraded technology platform, and migrate more activity to digital; and 4. Risk Management – build a stronger risk culture driven from the first line. Implement recommendations of the Group’s Culture, Governance and Accountability (CGA) self-assessment and the Royal Commission and respond to AUSTRAC matters, including implementing the response plan. Financial performance summary With this backdrop, cash earnings for First Half 2020 were $993 million, down $2,560 million or 72% on Second Half 2019 and $2,303 million lower (or 70%) than First Half 2019. The result was significantly affected by higher impairment charges along with AUSTRAC related costs and other notable items. The notable items help to explain Westpac’s performance and include estimated customer refunds, payments, associated costs and litigation and are explained later in this overview with more information in Sections 1.3.2 and Section 4.7, Note 14. The cash earnings impact of notable items was $1,285 million in First Half 2020 (compared to $377 million in Second Half 2019 and $753 million in First Half 2019). Excluding notable items, cash earnings were $2,278 million, down $1,652 million or 42% over Second Half 2019 and down 44% compared to First Half 2019 with most of that decline due to the significant increase in impairment charges. Earnings excluding notable items are summarised later in this overview. |

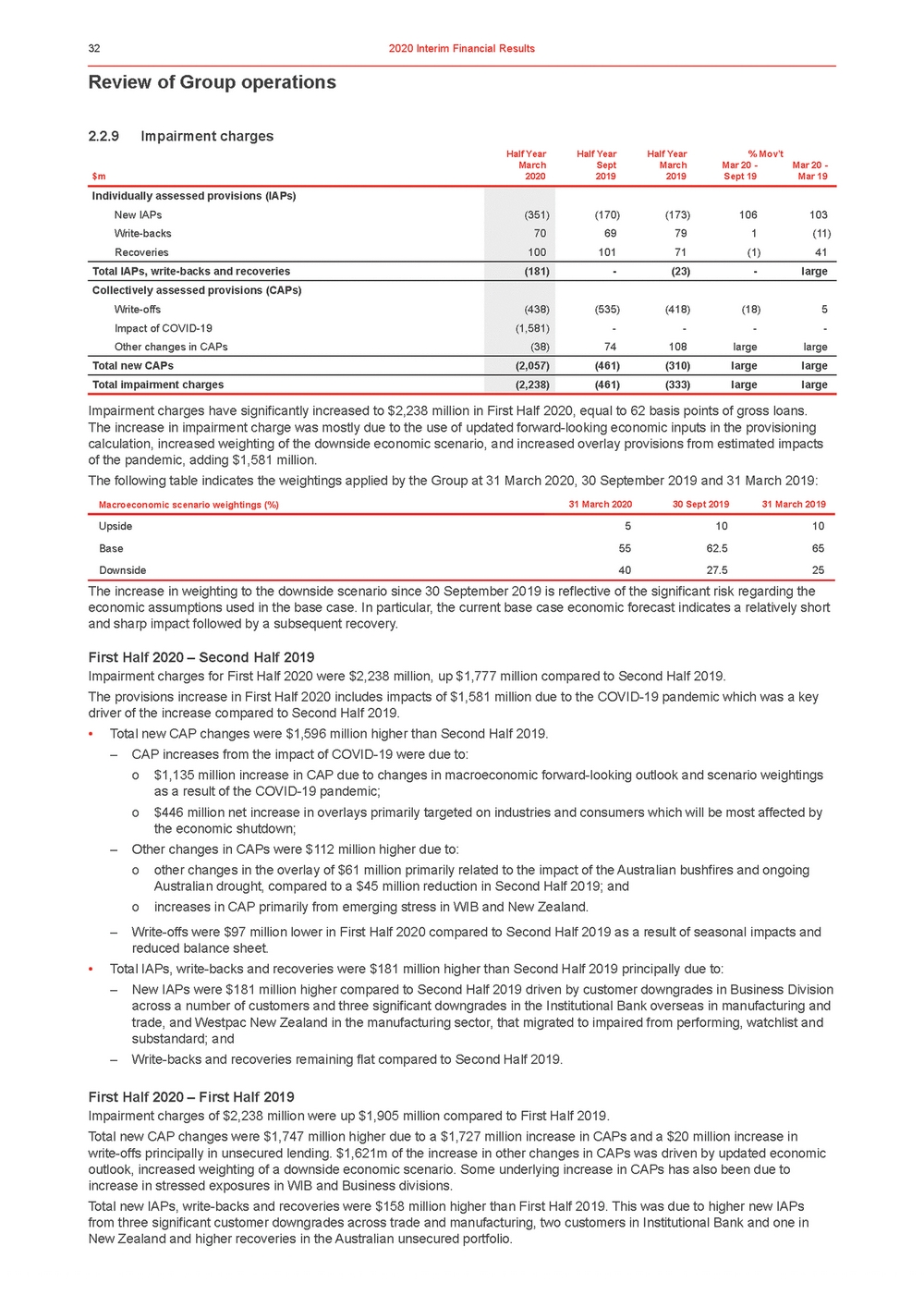

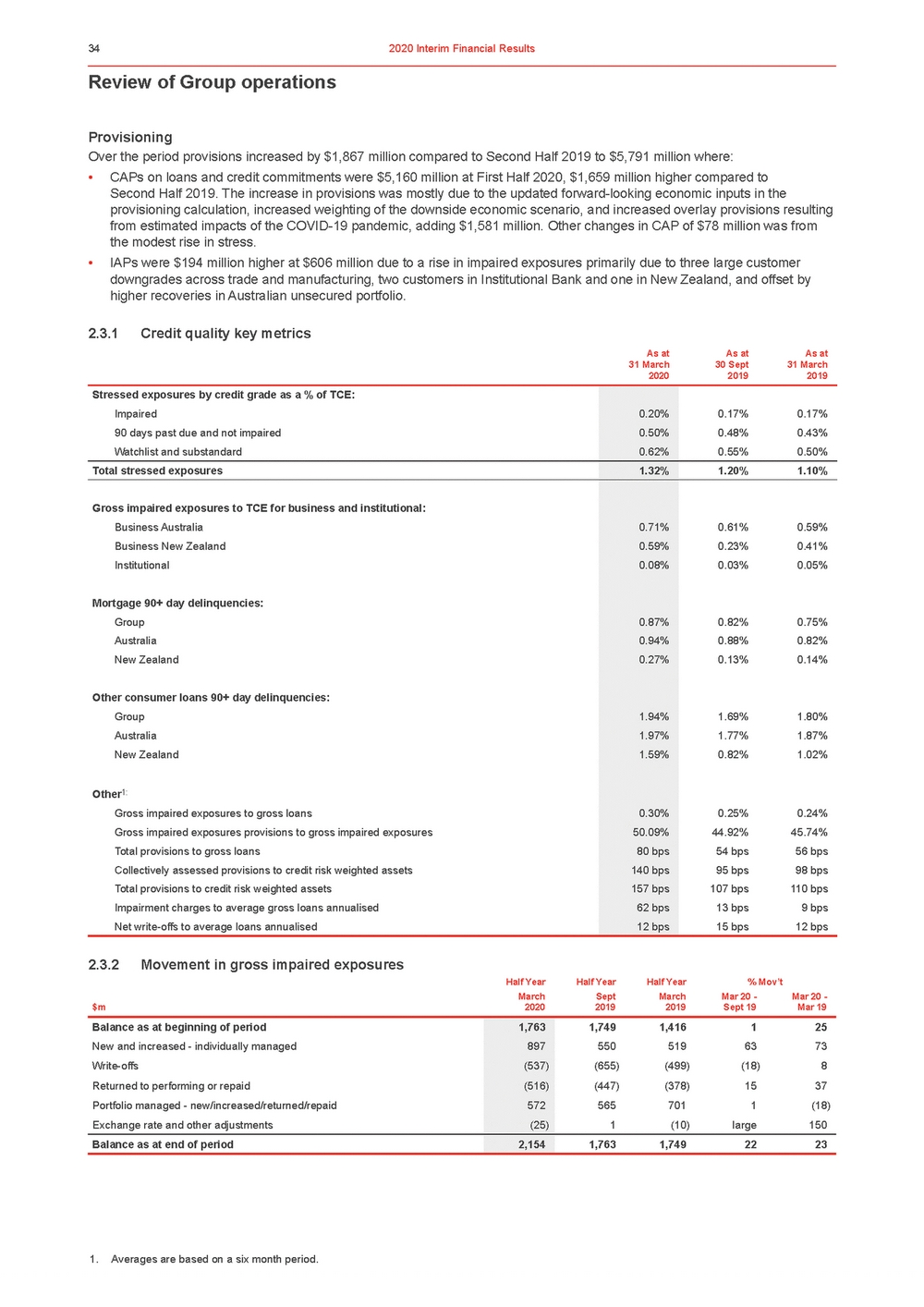

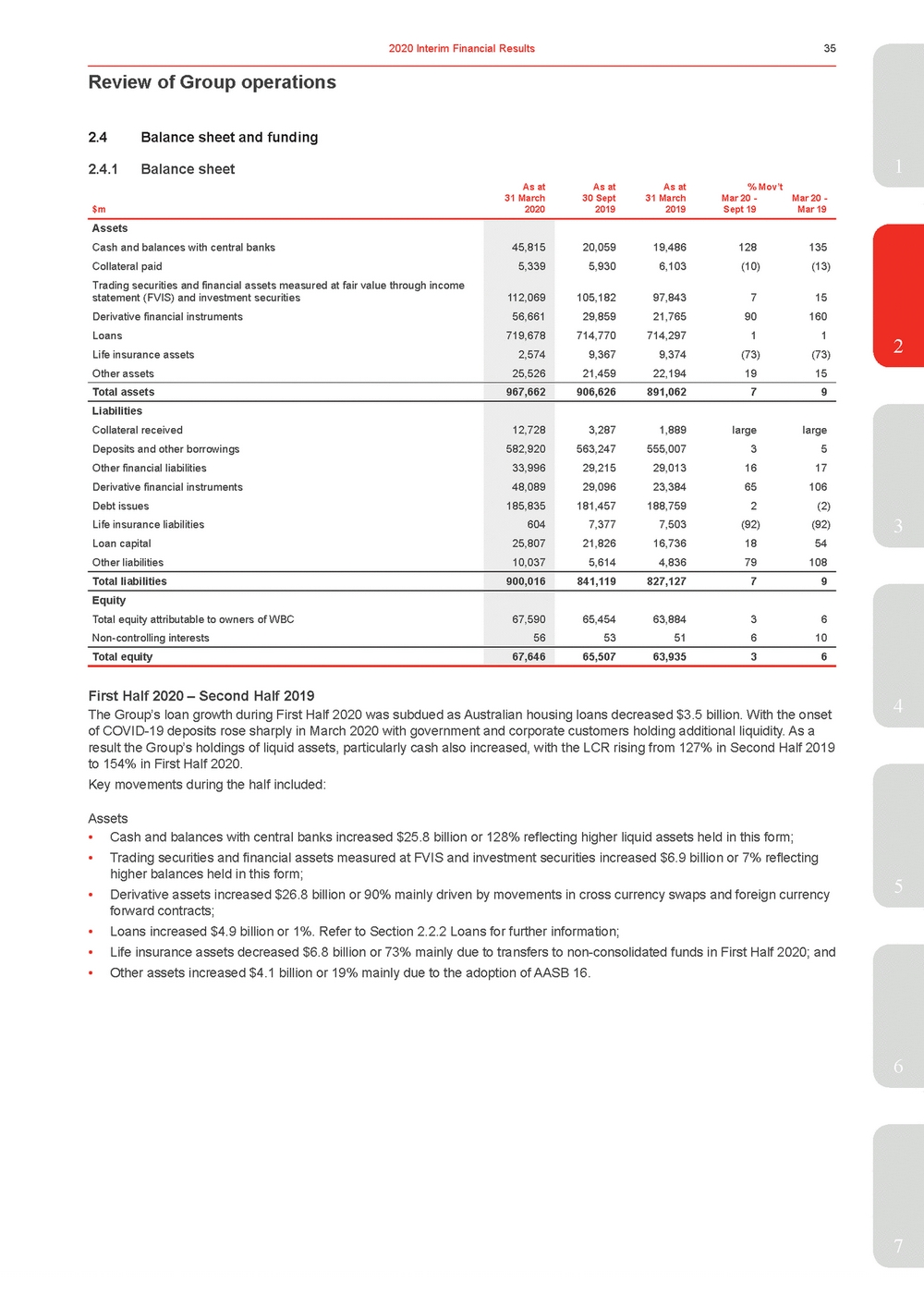

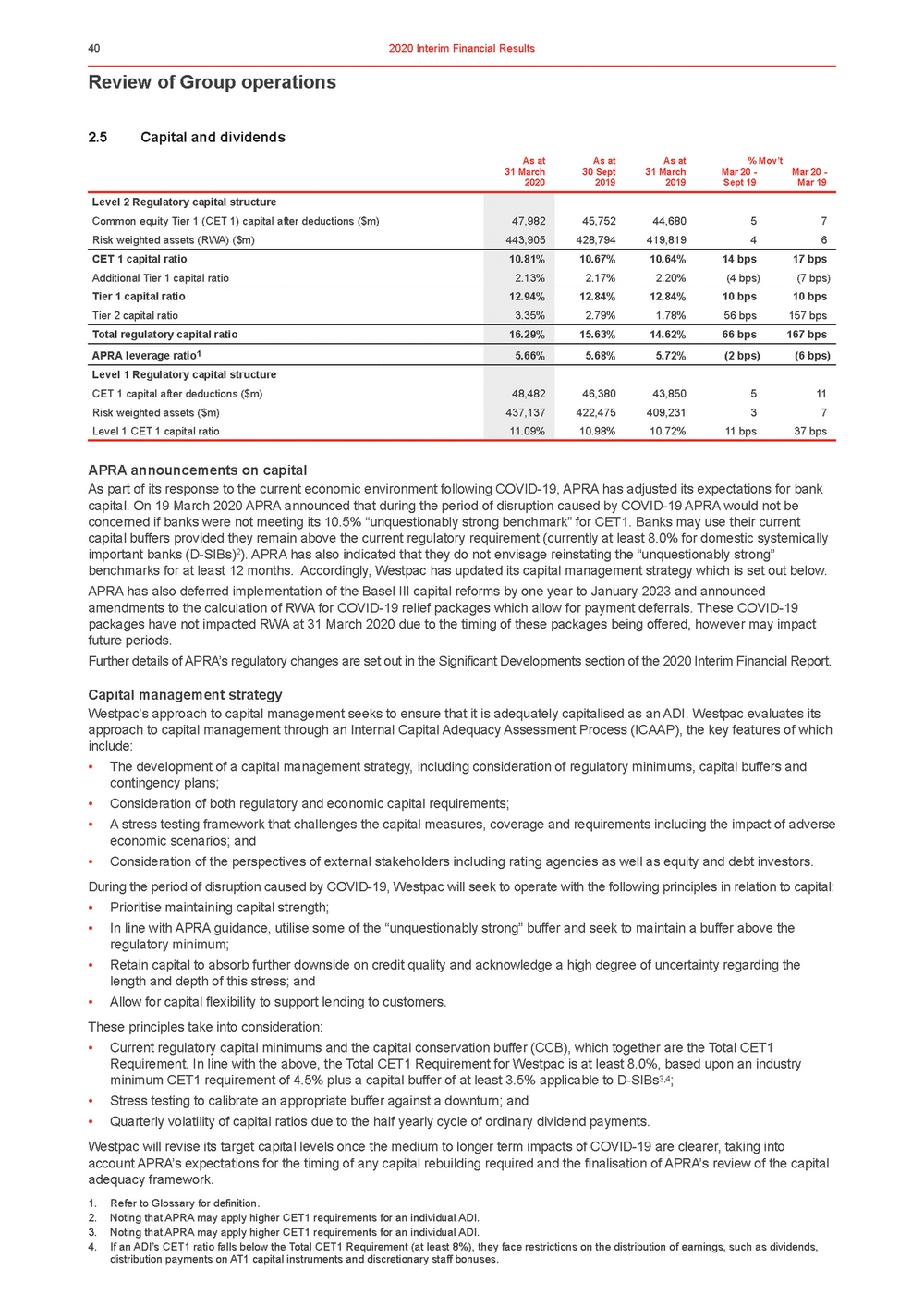

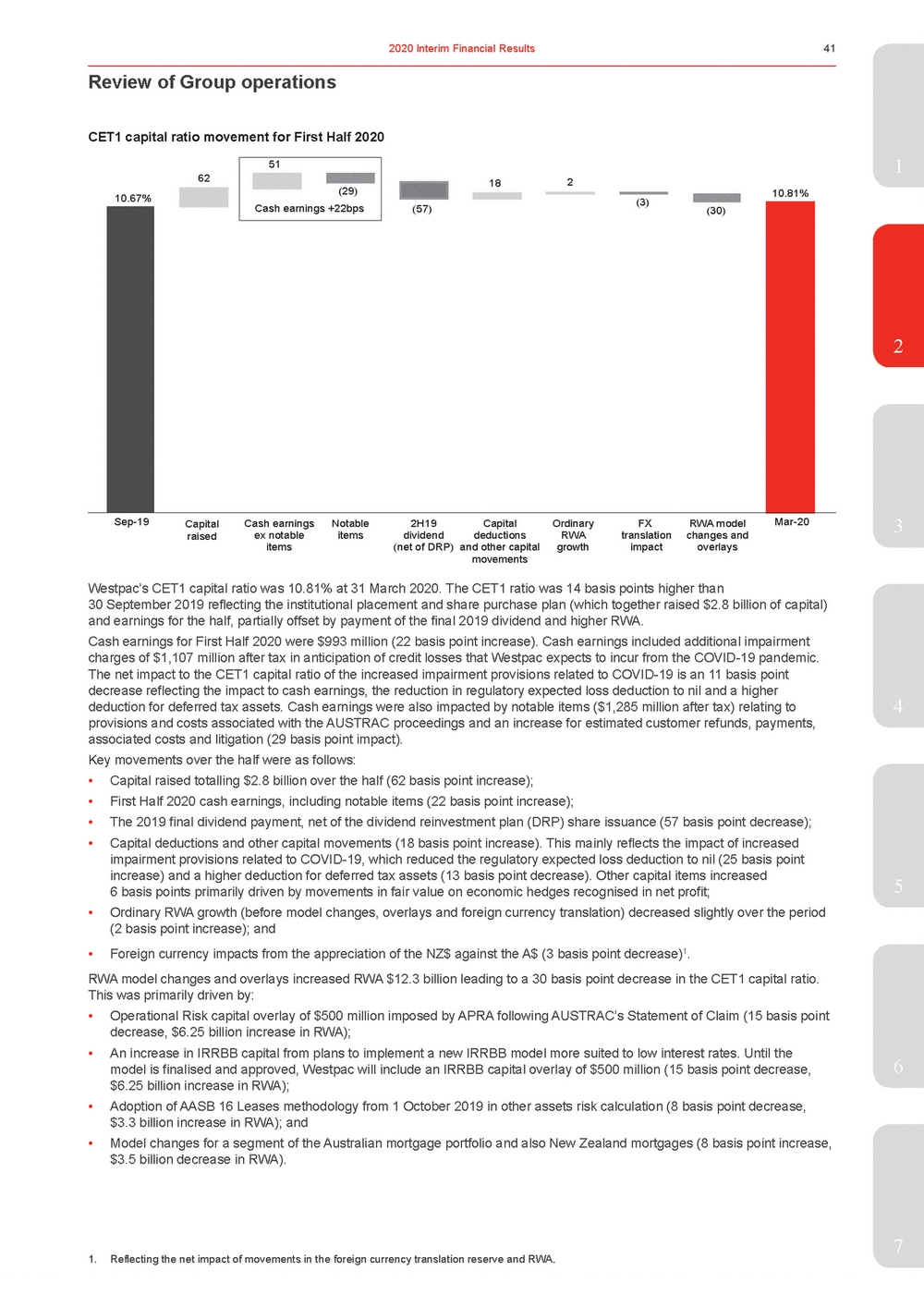

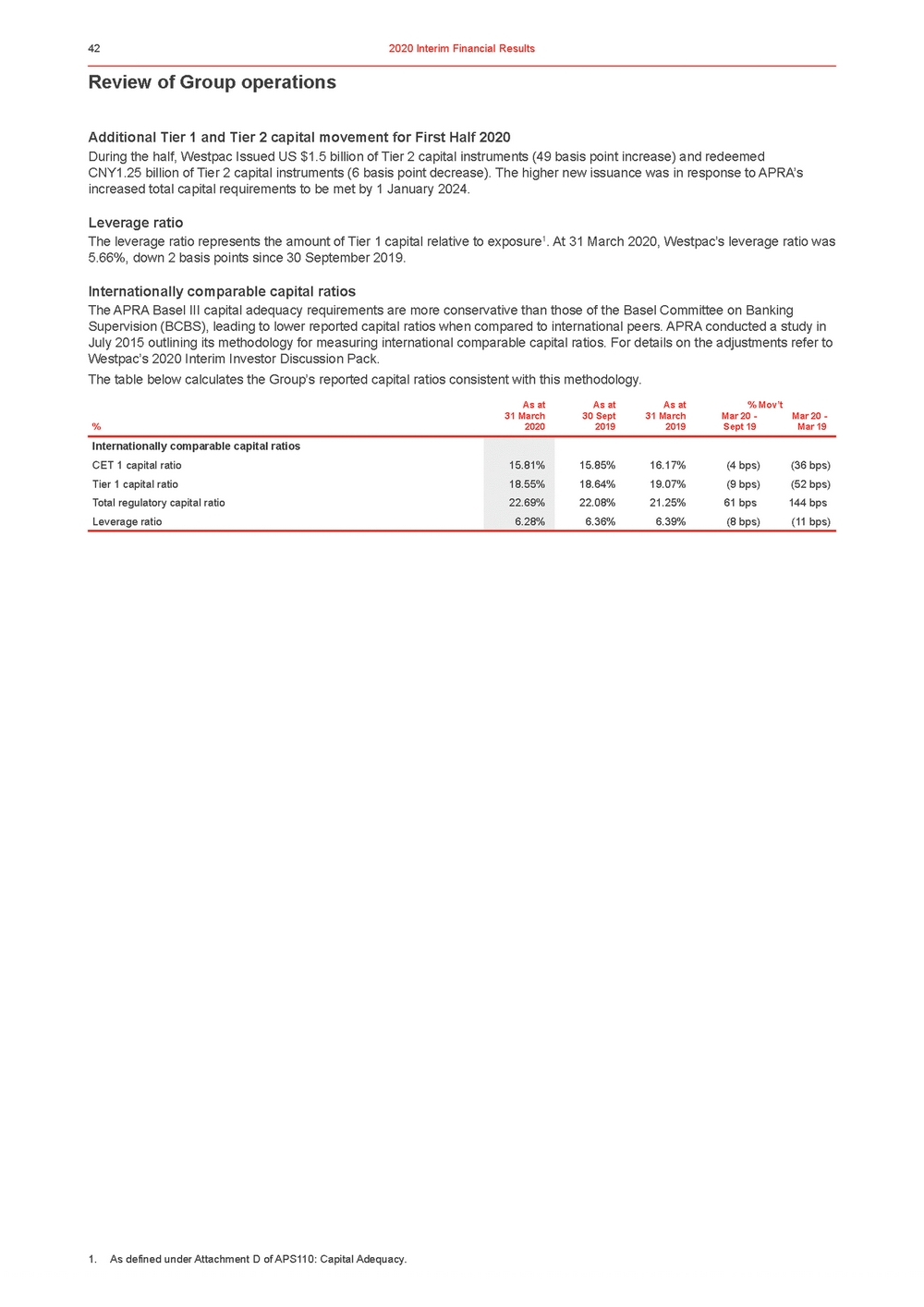

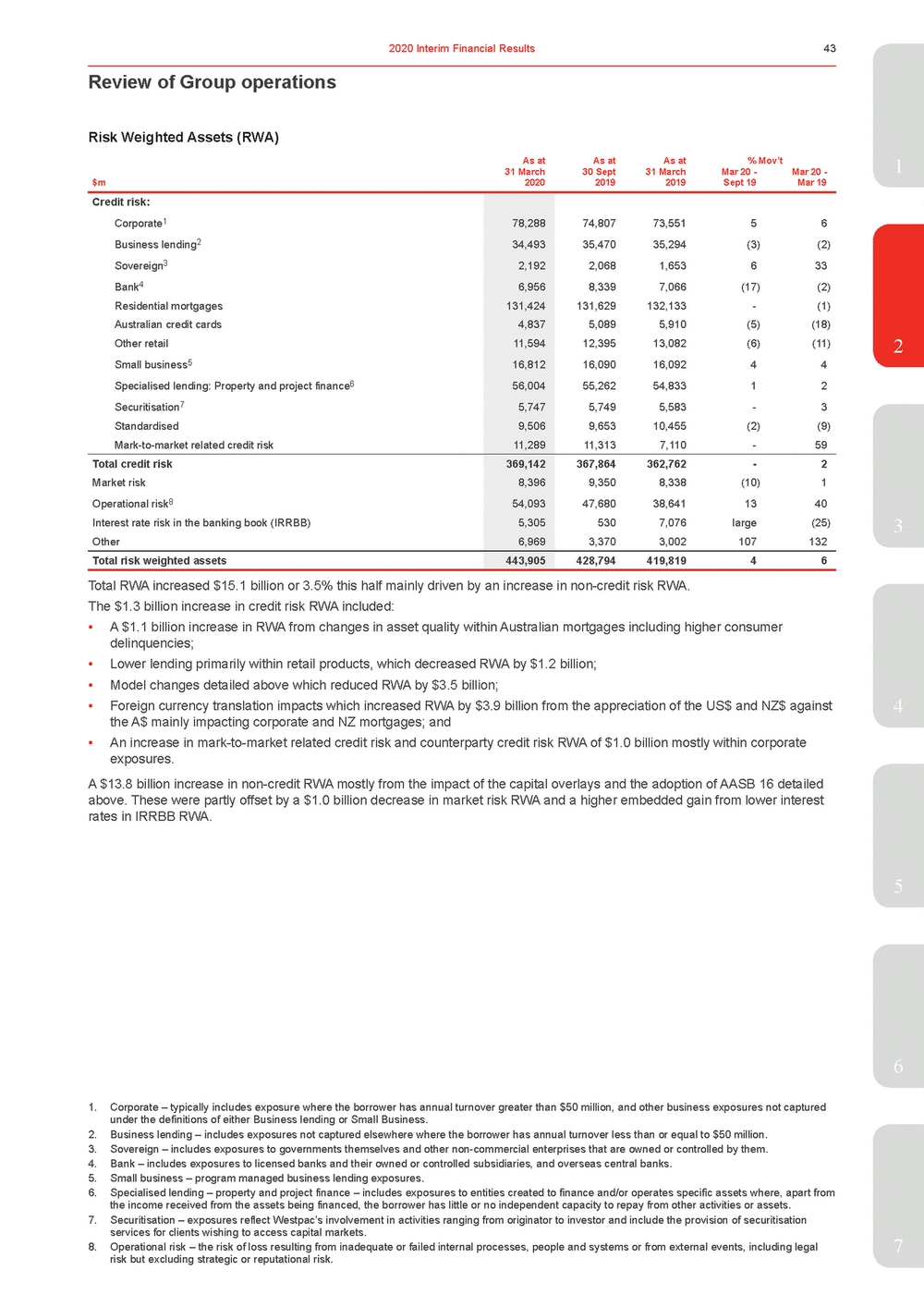

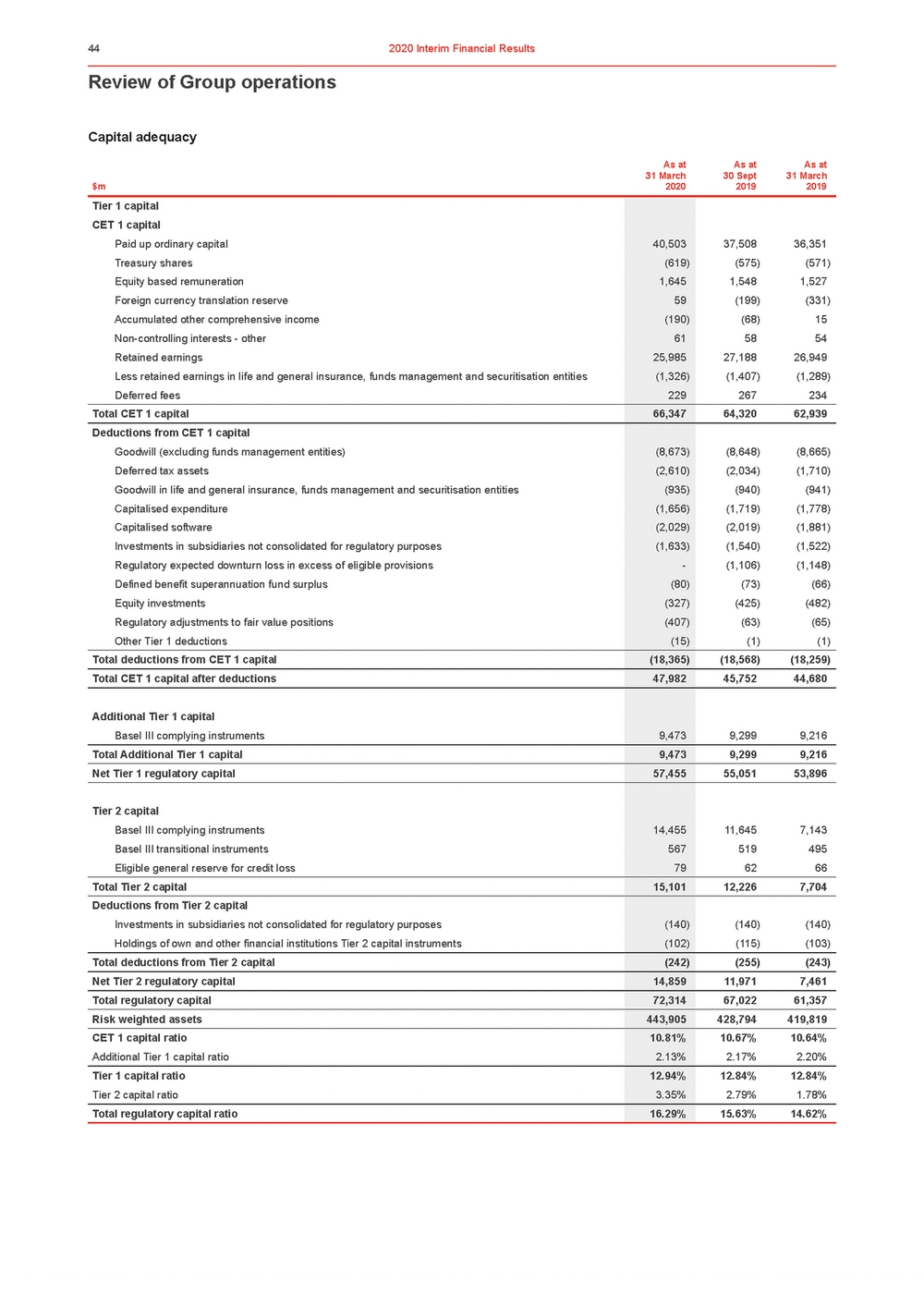

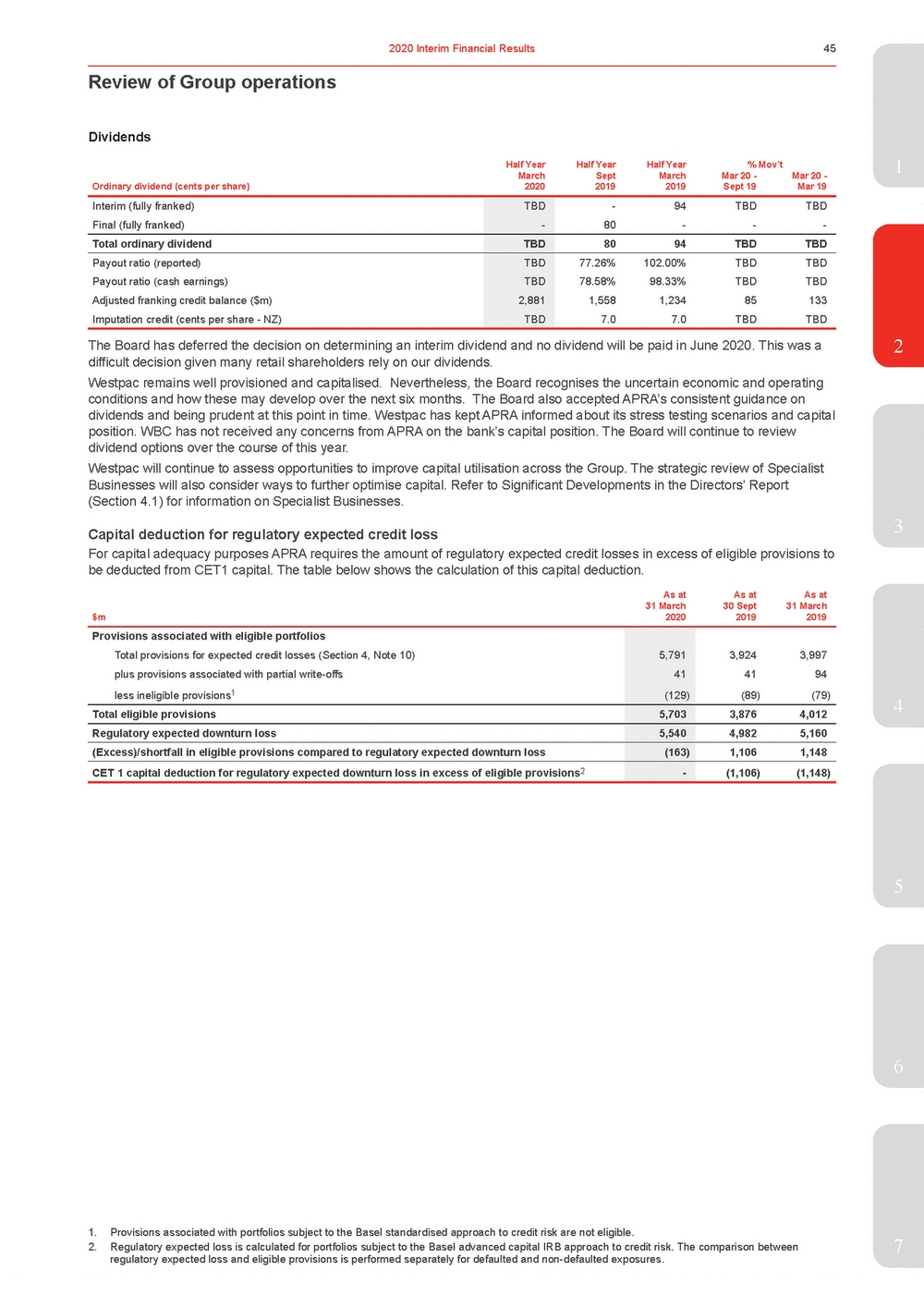

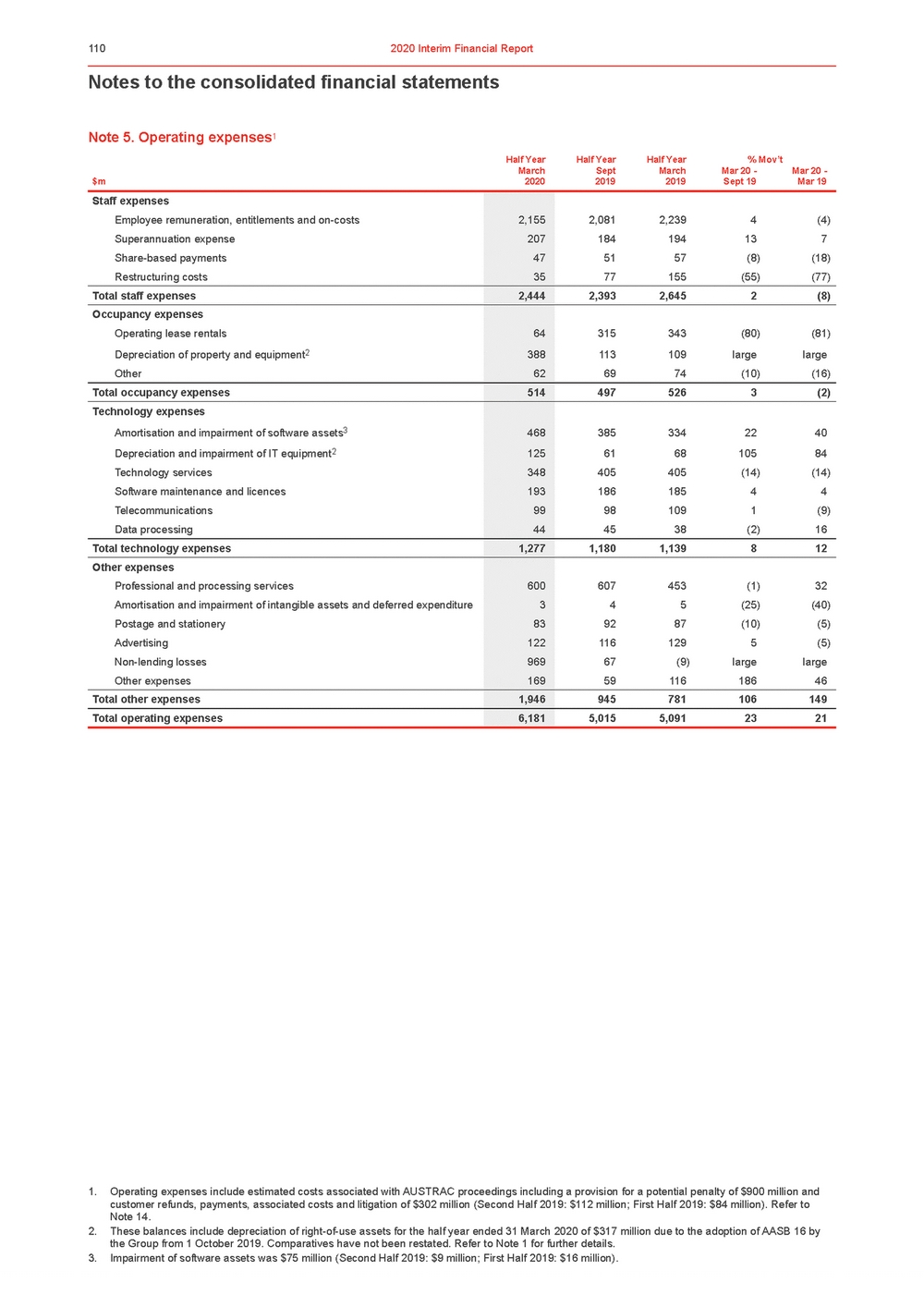

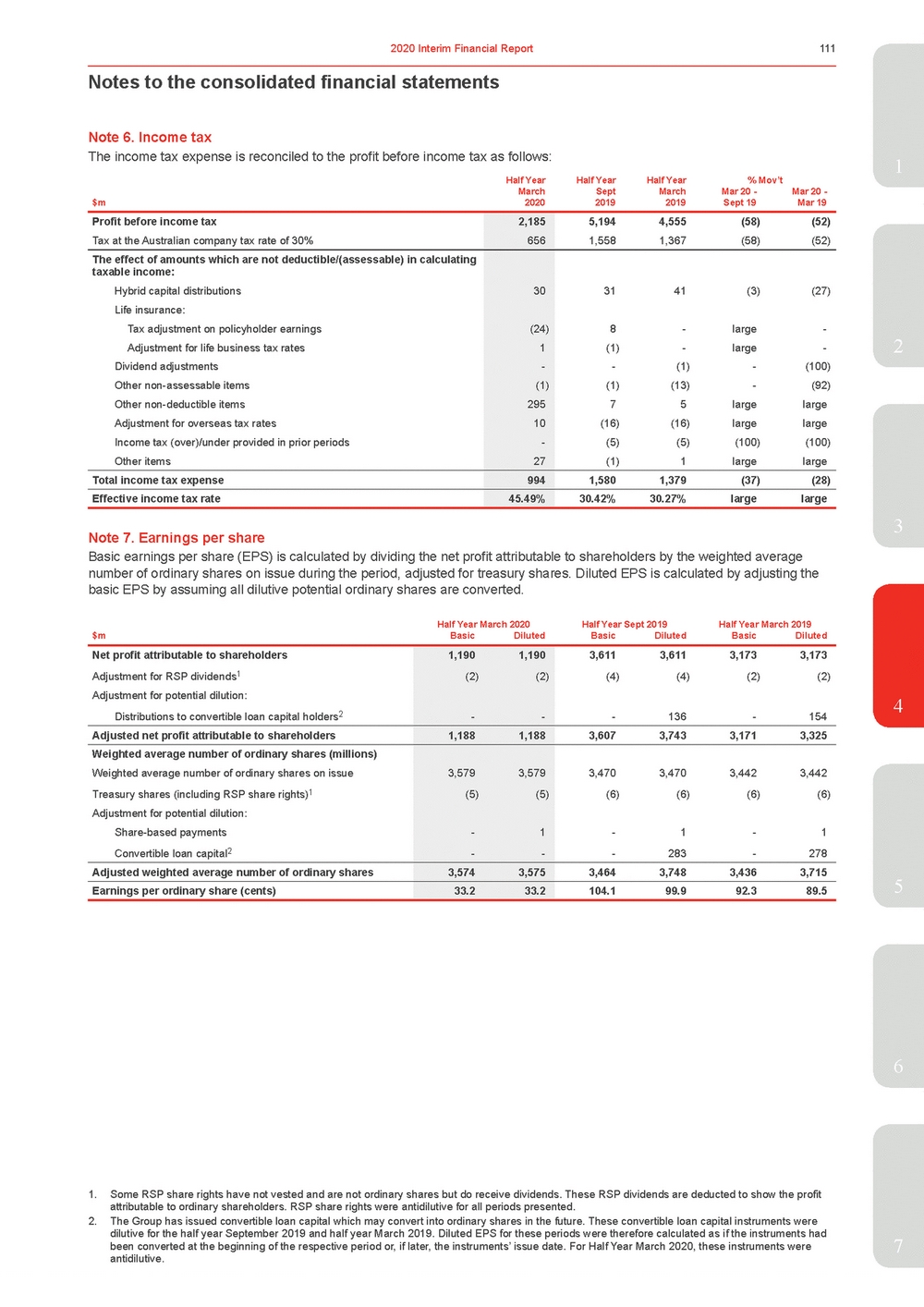

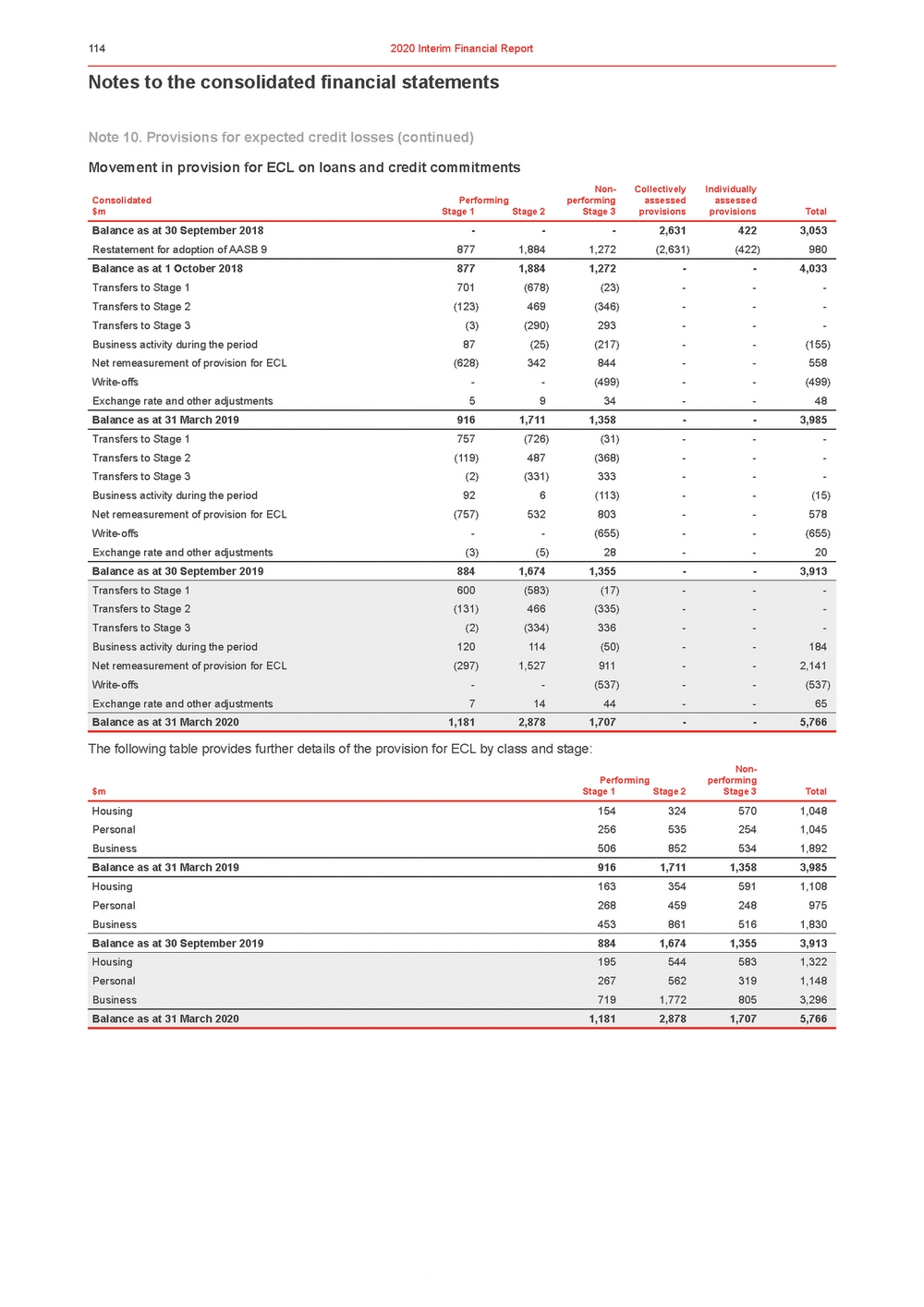

| margins. Balance sheet growth was relatively modest for most of First Half 2020 although a flight to quality and higher demand for liquidity saw loans and customer deposits end First Half 2020 up 1% and 4% respectively.1 The decline in non-interest income in First Half 2020 of 16% was mostly due to higher insurance claims from severe storms and bushfires while wealth income was also lower. Expenses were higher, up 23% over the prior half, with most of the increase due to AUSTRAC related costs. Excluding this and other notable items, expenses were 3% higher reflecting increased risk and compliance costs, some asset write-downs and higher software amortisation. Asset quality metrics were sound over First Half 2020 with impaired exposures to gross loans of 30 basis points at 31 March 2020 compared to 25 basis points at 30 September 2019. Stressed exposures to total committed exposures ended the half at 1.32% compared to 1.20% at 30 September 2019. Given the effects of COVID-19 only began to escalate in March, these metrics do not reflect the more difficult position beginning to emerge across the economy and its impact on customers. While there was a small rise in stressed exposures at March 2020, a significant change in the economic and industry outlook related to the COVID-19 pandemic has led to impairment charges of $2,238 million in First Half 2020, up $1,777 million over the2 prior half and up $1,905 million over the prior corresponding period. Assessing the likely impact of the COVID-19 outbreak was the main contributor to the increased impairment charges in First Half 2020. The increase in impairment charges lifted impairment provisions and provision coverage ratios with the ratio of collectively assessed provisions to credit risk weighted assets of 1.40% at 31 March 2020 up from 0.95% at 30 September 2019. The lower cash earnings, combined with capital raised in the half, translated to a decline in return and per share metrics. The cash earnings return on equity was 2.9% in First Half 2020 down from 11.1% in Second Half 2019. Cash earnings per ordinary share were 27.7 cents in First Half 2020, down around 73% over both the prior half and prior corresponding period. Excluding notable items, cash earnings per share were 63.6 cents. Cash earnings were lower across all divisions with a decline in core earnings and higher impairment charges across the Group. Reviewing movements on the prior corresponding period, in First Half 2020 cash earnings were 70% lower than First Half 2019.3 Excluding notable items, First Half 2020 cash earnings were 44% lower than First Half 2019. Most of this decline was from the increase in impairment charges and higher notable items. On capital, Westpac completed an institutional share placement and a retail share purchase plan in the half, raising $2.8 billion. These lifted capital levels and contributed to a 3.5% increase in shares on issue. As a result, the Group reported a common equity tier 1 (CET1) capital ratio of 10.8% at 31 March 2020 compared to 10.7% at 30 September 2019 and 10.6% at 31 March 2019. The higher capital ratio was achieved while absorbing higher risk weighted assets (RWA) from an additional $500 million operational risk capital overlay from APRA associated with the AUSTRAC matter, and payment of the final 2019 dividend. Interest rate risk in the banking book RWA was also higher, including from a $500 million capital overlay that will apply until a new IRRBB model is finalised and approved. Net tangible assets per share were $15.43 at 31 March 2020 compared to $15.36 at 30 September 2019.4 The Group’s funding and liquidity was strong over the half with liquidity ratios remaining comfortably above regulatory minimums. Higher customer deposit growth relative to loan growth lifted the deposit to loan ratio to over 75% while the liquidity coverage ratio (LCR) and the net stable funding ratio (NSFR) ended the half at 154% and 117% respectively. Dividends The Board has deferred the decision on determining an interim dividend and no dividend will be paid in June 2020. This was a difficult decision given many retail shareholders rely on our dividends. Westpac remains well provisioned and capitalised. Nevertheless, the Board recognises the uncertain economic and operating conditions and how these may develop over the next six months. The Board also accepted APRA’s consistent guidance on dividends and being prudent at this point in time. Westpac has kept APRA informed about its stress testing scenarios and capital position. WBC has not received any concerns from APRA on the bank’s capital position. The Board will continue to review5 dividend options over the course of this year. Westpac will continue to assess opportunities to improve capital utilisation across the Group. The strategic review of Specialist Businesses will also consider ways to further optimise capital. Refer to Significant Developments in the Directors’ Report (Section 4.1) for information on Specialist Businesses. Bank Levy Despite the lower earnings, the Government’s Bank Levy cost $196 million in First Half 2020, similar to the $198 million in Second Half 2019. The Bank Levy in First Half 2020 was equal to 20% of cash earnings and is equivalent to 4 cents per share and is included in net interest income where it reduced net interest margin by 5 basis points. In aggregate, taxes paid along with the Bank Levy give Westpac an adjusted effective tax rate of 50.8%.6 7 |

| Review of Group operations AUSTRAC Civil Proceedings On 20 November 2019, AUSTRAC launched civil proceedings against Westpac in the Federal Court of Australia, lodging a Statement of Claim with the Court. Westpac had previously disclosed that it had self-reported to AUSTRAC a failure to report a large number of international funds transfer instructions (IFTIs) and that AUSTRAC was also investigating a number of other areas relating to Westpac’s processes, procedures and monitoring. Commencement of the civil proceedings has significantly impacted Westpac and has contributed to: •The stepping down of the CEO, Brian Hartzer, and the appointment of Peter King as CEO; •The Chairman Lindsay Maxsted bringing forward his retirement and the subsequent appointment of John McFarlane as Westpac Chairman (from April 2020); •Cancellation of the annual short-term incentives for the CEO and the Group Executives for Full Year 2020. •The commencement of a detailed response plan to immediately lift the Group’s financial crime standards and protect people from online child exploitation; •A provision for a potential penalty of $900 million (not tax deductible) relating to AUSTRAC’s civil proceedings along with additional costs associated with the response plan (earnings impact of $127 million after tax); •Additional investigations by the corporate regulator (ASIC) and the prudential regulator (APRA), along with APRA imposing an additional operational risk capital overlay equal to $500 million; and •The launch of shareholder class actions in Australia and in the United States. Since the civil proceedings were launched, Westpac has been in discussions and mediation with AUSTRAC seeking to agree a Statement of Agreed Facts and Admissions along with a proposed penalty that could be put to the Court on a joint basis with AUSTRAC. At the case management hearing on 30 March 2020, the Court ordered that the parties file a Statement of Agreed Facts and Admissions with the Court by 8 May 2020, and that Westpac file a Defence in relation to the remaining matters by 15 May 2020. Westpac considered the available information and has made a provision of $900 million for a potential penalty in relation to AUSTRAC’s 20 November 2019 Statement of Claim. The provision has been taken in circumstances where there remains considerable uncertainty on the approach the Court might take in assessing the appropriate penalty and where there remains a prospect that Westpac and AUSTRAC could agree a penalty which could be recommended to the Court on a joint basis (which the Court would have regard to but not be obliged to accept). The Court’s decision on the appropriate penalty will likely involve balancing many different competing and complex factors and the exercise of discretion. Accordingly, the actual penalty paid by Westpac may be materially higher or lower than the current provision. Further details on this provision can be found in Section 4.7, Note 14. On 24 November 2019 Westpac announced a detailed response plan to the AUSTRAC proceedings. This response plan included three elements and progress over the half included: Response plan elementsProgress Immediate fixes•Reported outstanding IFTIs to AUSTRAC. •Closed relevant Australasian Cash Management and LitePay products. Lifting our standards•Established a new Board Financial Crime Committee. •Appointed Promontory to provide assurance over Westpac’s assessment of management accountability in relation to the issues raised in the AUSTRAC proceedings and the adequacy of Westpac’s Financial Crime Program. •Established an independent Advisory Panel to review Board risk governance and Board accountability in relation to the issues raised in the AUSTRAC proceedings. •Updated transaction monitoring rules and implemented enhanced oversight of the processes. Protecting people•Investing to reduce human impact of financial crime, including partnerships with International Justice Mission and Save the Children. •Established the Safer Children, Safer Communities Roundtable to guide investments for a program of work to support the prevention of online child exploitation. Further details on the AUSTRAC matter can be found in Significant Developments and Risk Factors in the Directors’ Report (Section 4.1) and in Section 4.7, Note 14. |

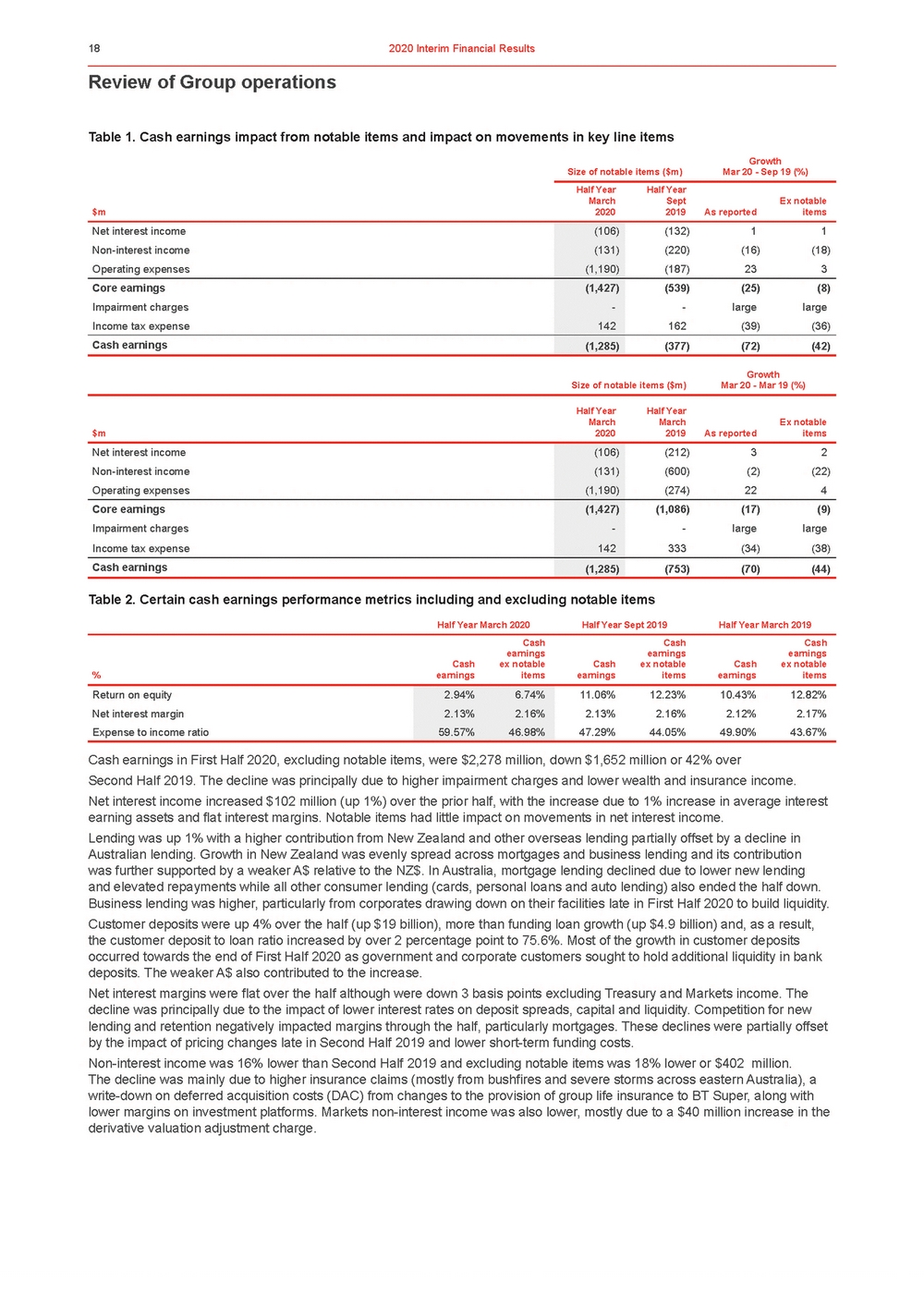

| 1 In First Half 2020, and following the AUSTRAC Statement of Claim, APRA requested that Westpac reassess its CGA remediation plan to determine whether it is ‘fit for purpose’. The reassessment is underway and due to be completed by 30 June 2020. In parallel with the reassessment, Westpac is continuing to implement recommendations from its various programs of work, including: •Royal Commission: Of the 49 Royal Commission recommendations relevant to Westpac, 13 are implemented, 22 are being implemented, and 14 are awaiting further regulatory clarity; and •CGA self-assessment: Implementing the CGA remediation plan, with 67% of recommendations implemented for design2 effectiveness as at 31 March 2020. Customer remediation Through its ‘get it right, put it right’ initiatives, products, processes and policies have continued to be reviewed to identify where the Group may not have got it right for customers. Where problems have been identified, the Group has committed to fix them and refund customers. These initiatives identified a number of issues that have required remediation. The Group booked an after-tax cost of $258 million for provisions for estimated customer refunds and payments, associated costs and litigation in First Half 2020. The cost of major items in First Half 2020 related to: •Provisions for estimated refunds to certain business customers who were provided with business loans where they should3 have been provided with loans covered by the National Consumer Credit Protection Act and the National Credit Code; •Provisions for estimated compensation to customers on the Group’s platforms who were not advised of certain corporate actions. As these customers may have missed out on value associated with these actions a compensating payment is being made; and •Provisions for estimated refunds to some BT customers where certain wealth fees were inadequately disclosed. Management of the Group’s key customer remediation programs have been centralised in the Group’s remediation hub and over 600,000 customers have now received over $350 million in refunds. Financial performance First Half 2020 – Second Half 20191 Cash earnings of $993 million, were down $2,560 million or 72% over Second Half 2019. The decline in cash earnings was4 principally due to higher impairment charges and higher charges for notable items. To help explain Westpac’s performance, certain major items in this result are described as ‘notable items’. These include: •Provisions for estimated customer refunds and payments, associated costs, and litigation; •Restructuring costs associated with the reset of Westpac’s wealth strategy in 2019; •A provision for a potential penalty relating to AUSTRAC’s civil proceedings; and •Costs associated with Westpac’s AUSTRAC response plan. Throughout this Results Announcement, the term ‘notable items’ refers only to these items. Notable items are also discussed further in Section 1.3.2 and Section 4.7, Note 14. Notable items impact cash earnings, the major income statement line items and certain performance metrics. The following5 tables present the quantum of these items and their impact on movements in the income statement (Table 1) and certain performance metrics (Table 2) over the last three halves. 6 7 1. Unless otherwise stated. |

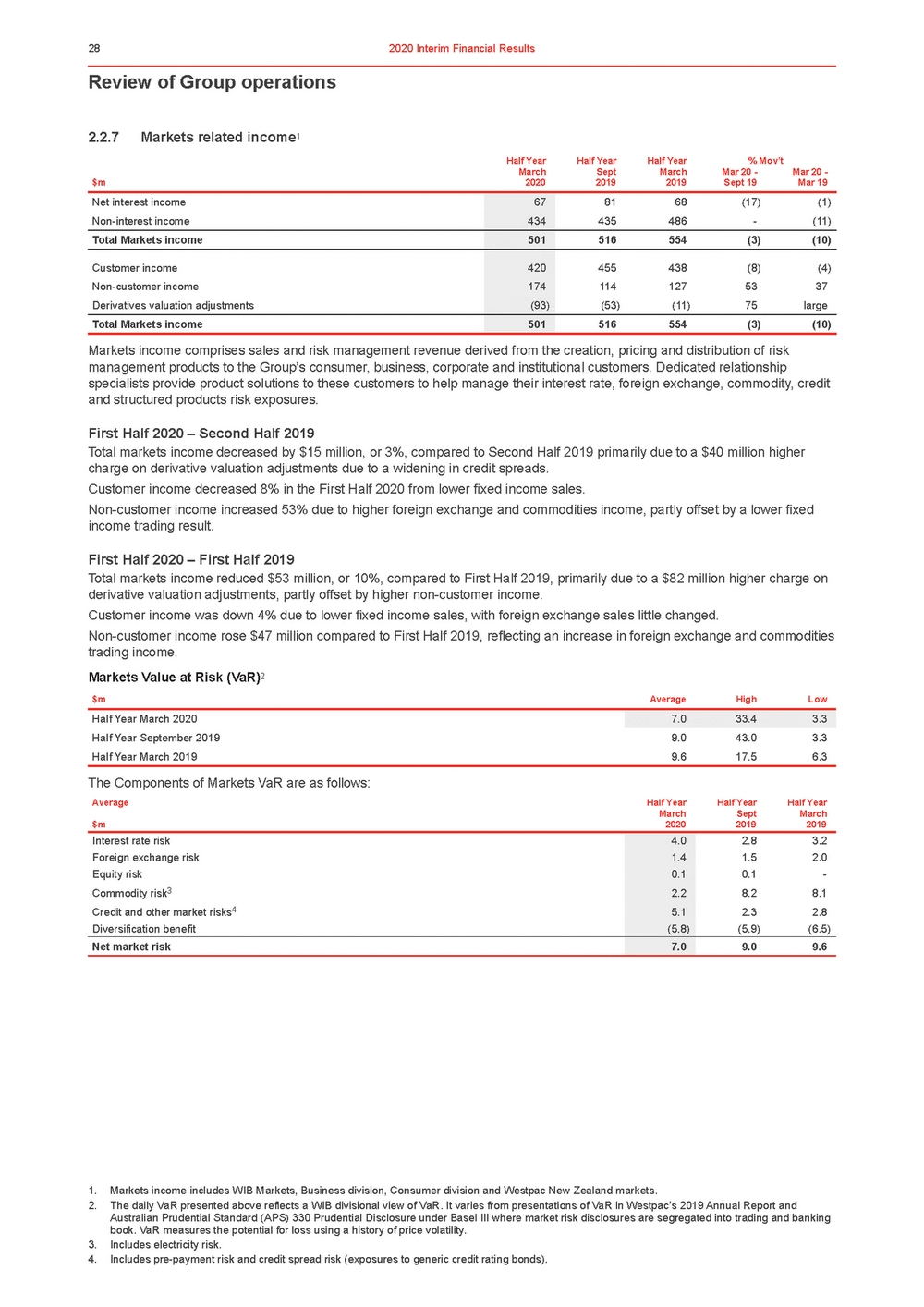

| Review of Group operations Table 1. Cash earnings impact from notable items and impact on movements in key line items Size of notable items ($m) Half YearHalf Year Growth Mar 20 - Sep 19 (%) March $m2020 Sept 2019 As reported Ex notable items Size of notable items ($m) Growth Mar 20 - Mar 19 (%) Half YearHalf Year March $m2020 March 2019 As reported Ex notable items Table 2. Certain cash earnings performance metrics including and excluding notable items Half Year March 2020Half Year Sept 2019Half Year March 2019 Cash earnings in First Half 2020, excluding notable items, were $2,278 million, down $1,652 million or 42% over Second Half 2019. The decline was principally due to higher impairment charges and lower wealth and insurance income. Net interest income increased $102 million (up 1%) over the prior half, with the increase due to 1% increase in average interest earning assets and flat interest margins. Notable items had little impact on movements in net interest income. Lending was up 1% with a higher contribution from New Zealand and other overseas lending partially offset by a decline in Australian lending. Growth in New Zealand was evenly spread across mortgages and business lending and its contribution was further supported by a weaker A$ relative to the NZ$. In Australia, mortgage lending declined due to lower new lending and elevated repayments while all other consumer lending (cards, personal loans and auto lending) also ended the half down. Business lending was higher, particularly from corporates drawing down on their facilities late in First Half 2020 to build liquidity. Customer deposits were up 4% over the half (up $19 billion), more than funding loan growth (up $4.9 billion) and, as a result, the customer deposit to loan ratio increased by over 2 percentage point to 75.6%. Most of the growth in customer deposits occurred towards the end of First Half 2020 as government and corporate customers sought to hold additional liquidity in bank deposits. The weaker A$ also contributed to the increase. Net interest margins were flat over the half although were down 3 basis points excluding Treasury and Markets income. The decline was principally due to the impact of lower interest rates on deposit spreads, capital and liquidity. Competition for new lending and retention negatively impacted margins through the half, particularly mortgages. These declines were partially offset by the impact of pricing changes late in Second Half 2019 and lower short-term funding costs. Non-interest income was 16% lower than Second Half 2019 and excluding notable items was 18% lower or $402 million. The decline was mainly due to higher insurance claims (mostly from bushfires and severe storms across eastern Australia), a write-down on deferred acquisition costs (DAC) from changes to the provision of group life insurance to BT Super, along with lower margins on investment platforms. Markets non-interest income was also lower, mostly due to a $40 million increase in the derivative valuation adjustment charge. |

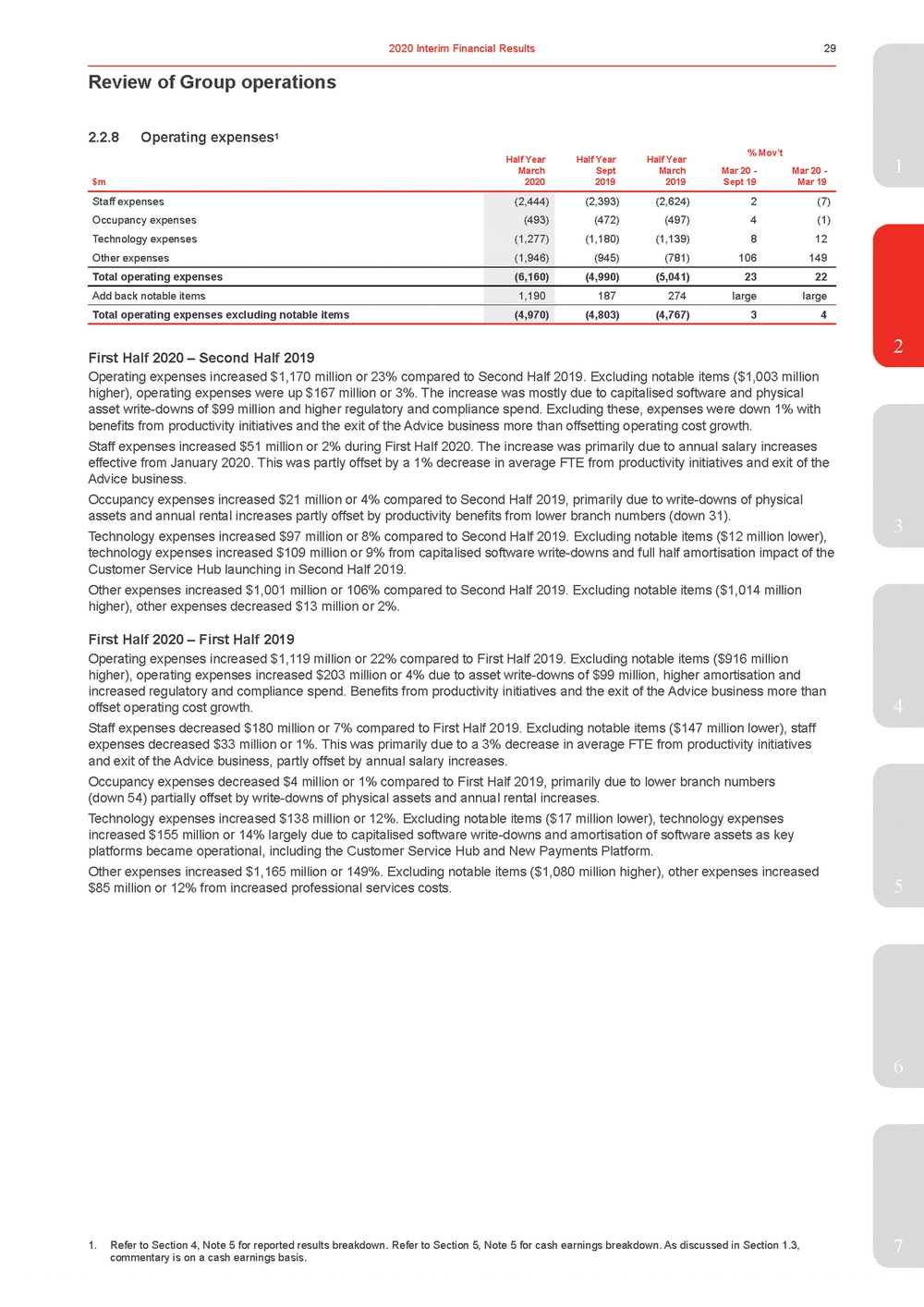

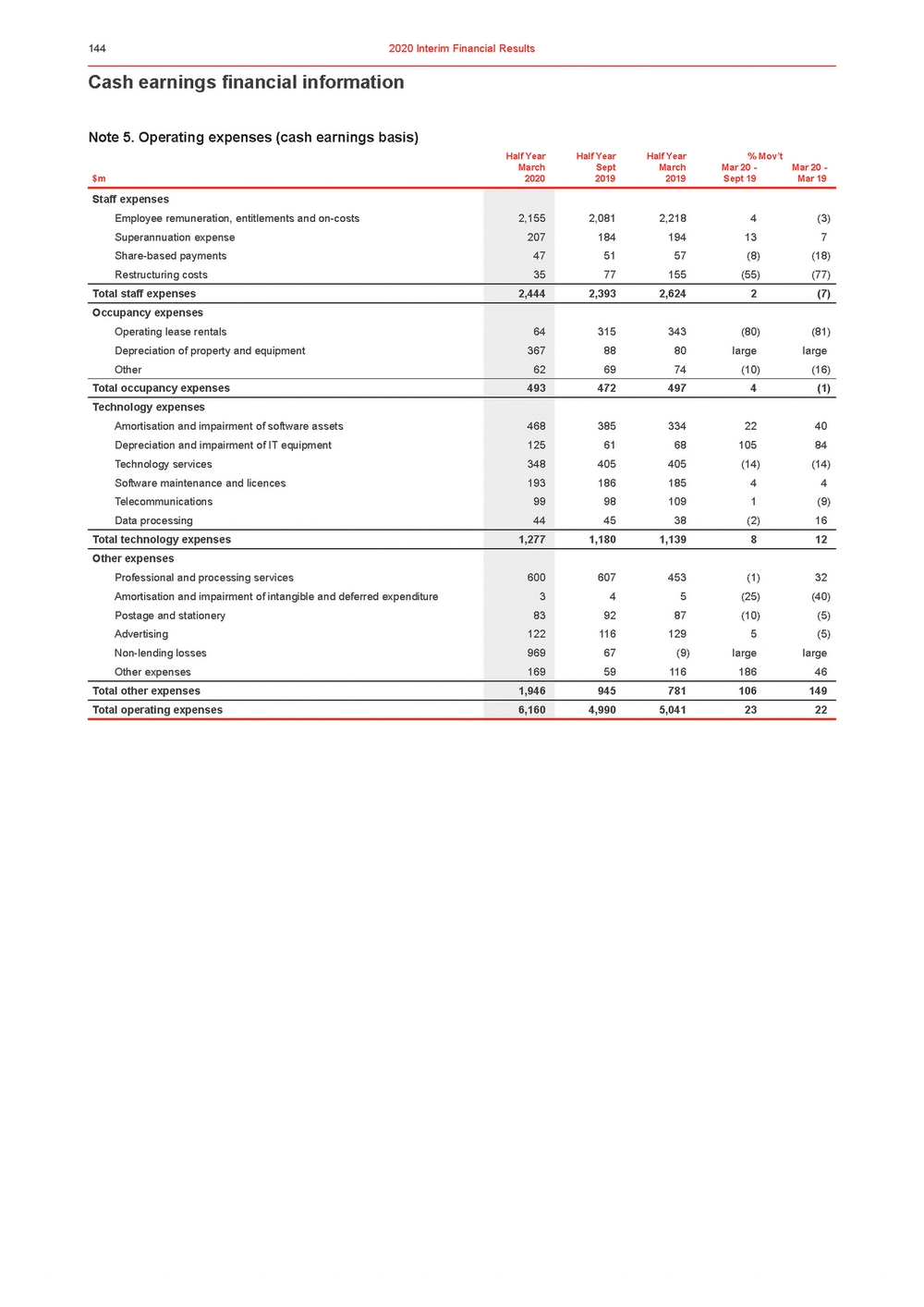

| items, expenses were 3% higher with an increase in regulatory and compliance related spending, and a write-down of certain assets, including capitalised software. Ordinary expenses increased $167 million over the half more than offset by $188 million1 in productivity savings, including a further reduction of 31 branches and the full period impact from the reset of the Group’s wealth business. Asset quality was sound at 31 March 2020, although most asset quality metrics experienced some deterioration later in the half. That deterioration reflected higher new impaired exposures and increased customer hardship following the bushfires and severe storms experienced through summer. It also reflects a reallocation of resources to work on assessing COVID-19 hardship applications rather than managing existing delinquencies. Mortgage 90+ day delinquencies were up 5 basis points over the half while 30+ day mortgage delinquencies were 23 basis points higher. In both instances, the rise largely occurred in March 2020. The Group has also seen a significant rise in mortgage hardship which increased by over 50%. Other consumer 90+ day delinquencies were also higher, up 25 basis points over the half. The full impact of COVID-19 is expected to emerge in future periods.2 As part of the industry-wide response to COVID-19, the Group has seen many consumers and small businesses apply for principal and interest deferrals. Customers approved for these deferrals will not be recorded in traditional stress metrics while part of these packages but will nevertheless be monitored closely, particularly once the deferral period ends. Reflecting the trends in asset quality, along with a deterioration in the economic and industry outlook, impairment charges were materially higher over the half, up $1,777 million. In aggregate, COVID-19 related impairment charges were $1,581 million. The increase in impairment charges has seen a lift in provision coverage with the ratio of collectively assessed provisions to credit risk weighted assets of 1.40% at 31 March 2020 up from 0.95% at 30 September 2019. Westpac’s tax rate was 48.8% for First Half 2020 well above Australia’s corporate tax rate of 30%. Excluding the impact of the non-deductible AUSTRAC penalty provision the effective tax rate would have been 33.4%. 3 Financial performance summary First Half 2020 – First Half 2019 Cash earnings of $993 million, was down $2,303 million or 70% over First Half 2019. The decline was principally due to higher impairment charges and higher expenses related to the AUSTRAC response plan. Excluding notable items, cash earnings of $2,278 million were $1,771 million lower. Net interest income was 3% higher than the prior corresponding half, principally due to lower notable items and higher average interest earning assets. Excluding notable items, net interest income was 2% higher. Total lending was 1% higher over the year (up $5 billion) with a $6 billion contribution from NZ lending and a $1.7 billion contribution from offshore lending (mostly FX related). The increase was partially offset by lower Australian lending (down $2.5 billion). The decline in Australian lending was due to lower consumer lending and higher provisions, partially offset by increased corporate loan balances. Customer deposits were higher over the year with strong growth in late March 2020 as customers increased liquidity in response to COVID-19. Net interest margins were higher over the year from lower notable items. Excluding notable items, the margin excluding4 Treasury and Markets was down 5 basis points. Lower interest rates and strong competition were behind the decline. Non-interest income was lower over the year, down 22% excluding notable items. The fall was due to lower insurance income from higher claims and a DAC write-down, lower advice income, a decline in card fees, lower syndication activity and a higher derivative valuation adjustment charge. Asset sales were also lower. Expenses were much higher, up 22% from higher notable items. Excluding notable items and expenses were up 4%. The rise was due to higher regulatory and compliance spending and an increase in software amortisation. Ordinary expenses increased $144 million over the half partially offset by $188 million in productivity savings. Asset quality deteriorated modestly over the half from the weaker operating environment and from bushfires and severe weather events. The COVID-19 outbreak only had a small impact on asset quality metrics in First Half 2020. Impairment charges were significantly higher, up $1,905 million to $2,238 million reflecting the rise in stress and the COVID-195 related provisions. 6 7 |

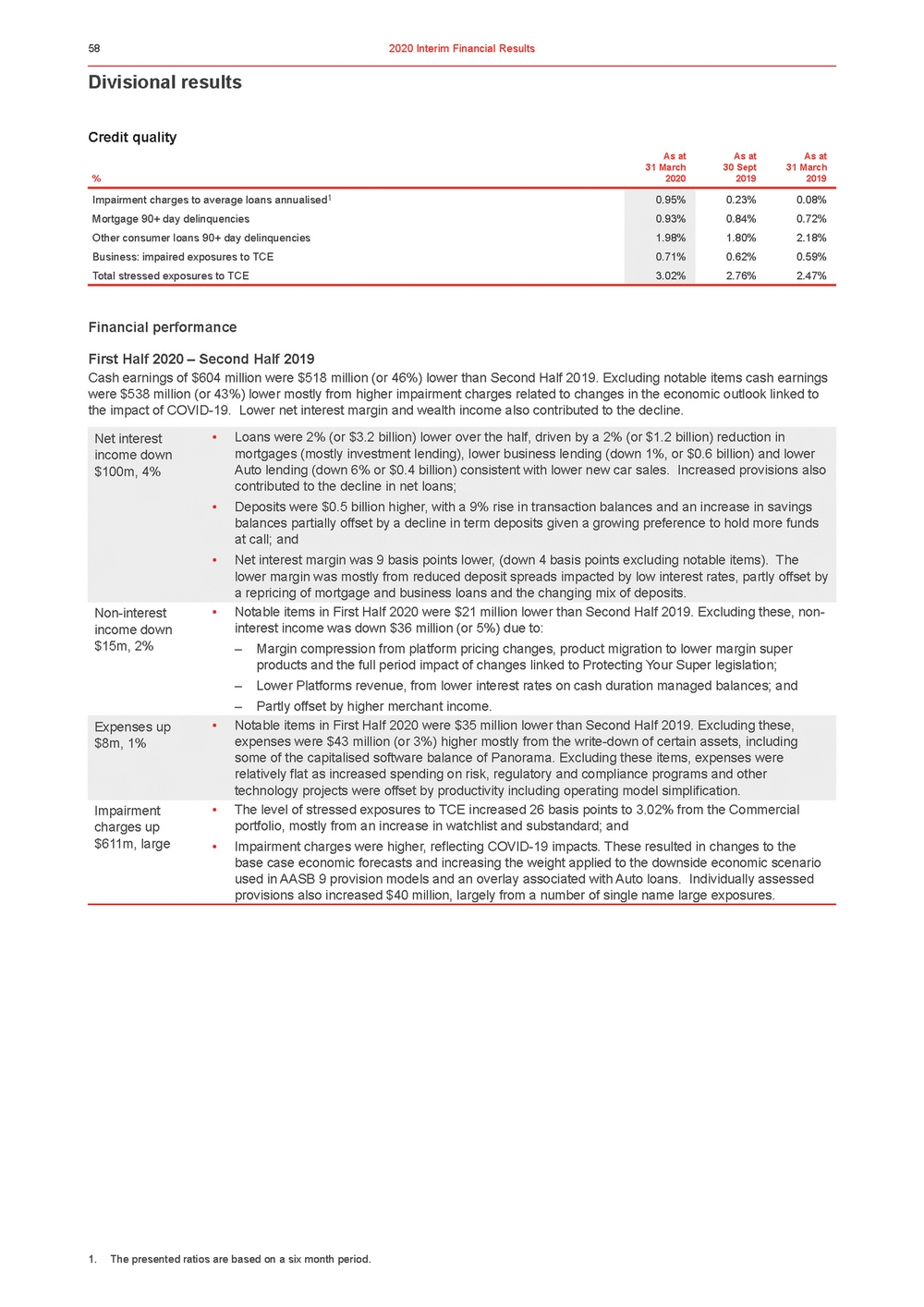

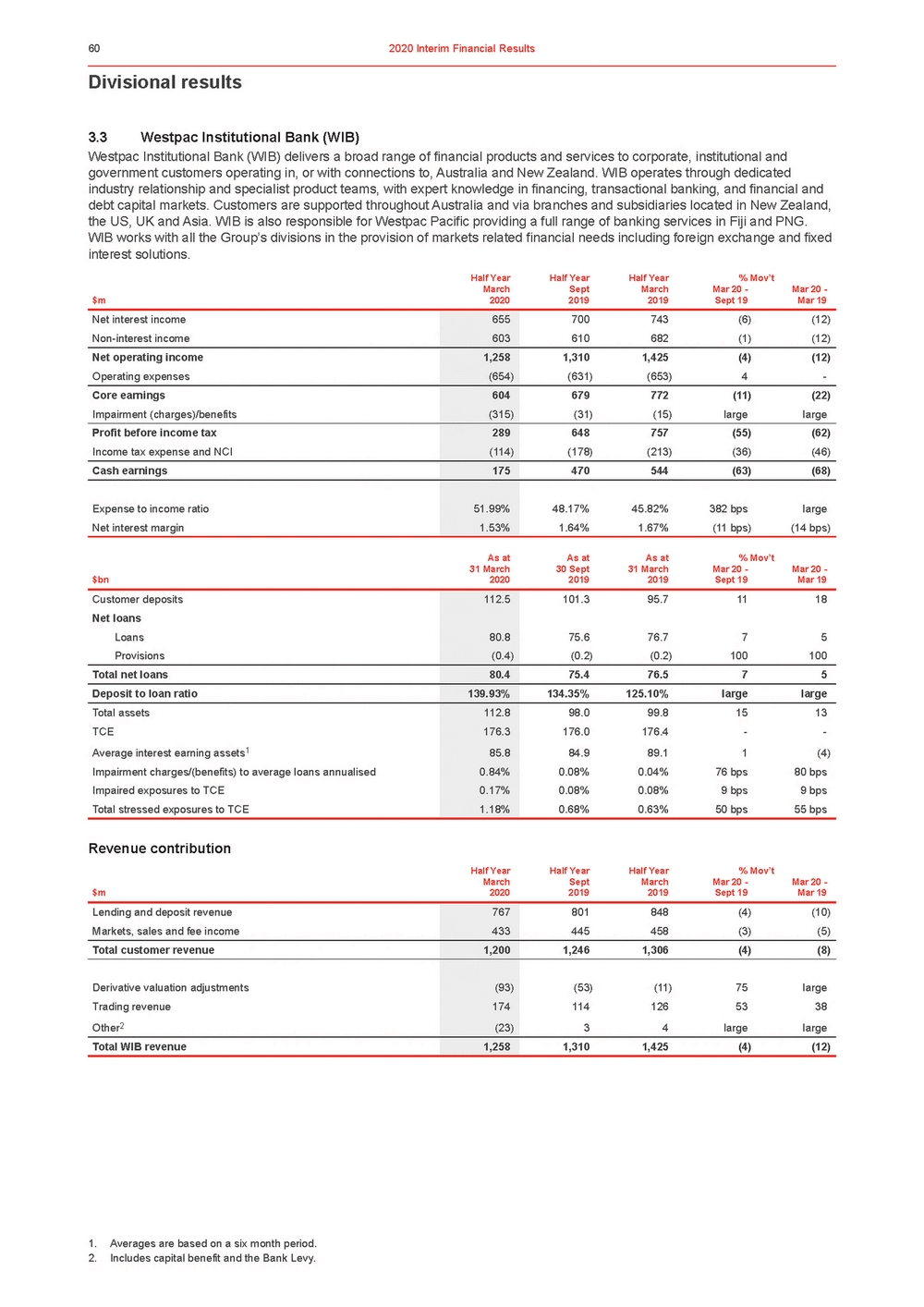

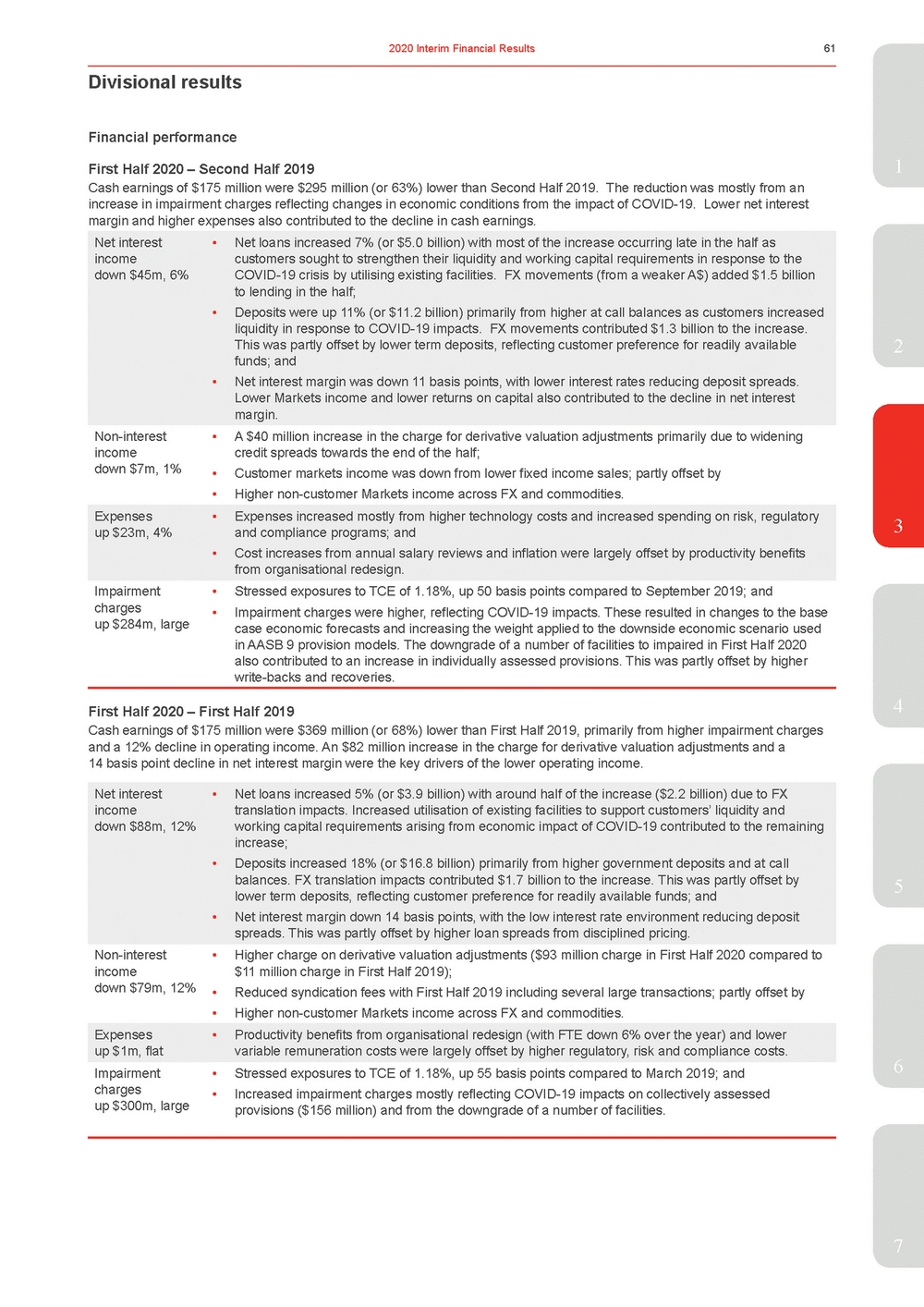

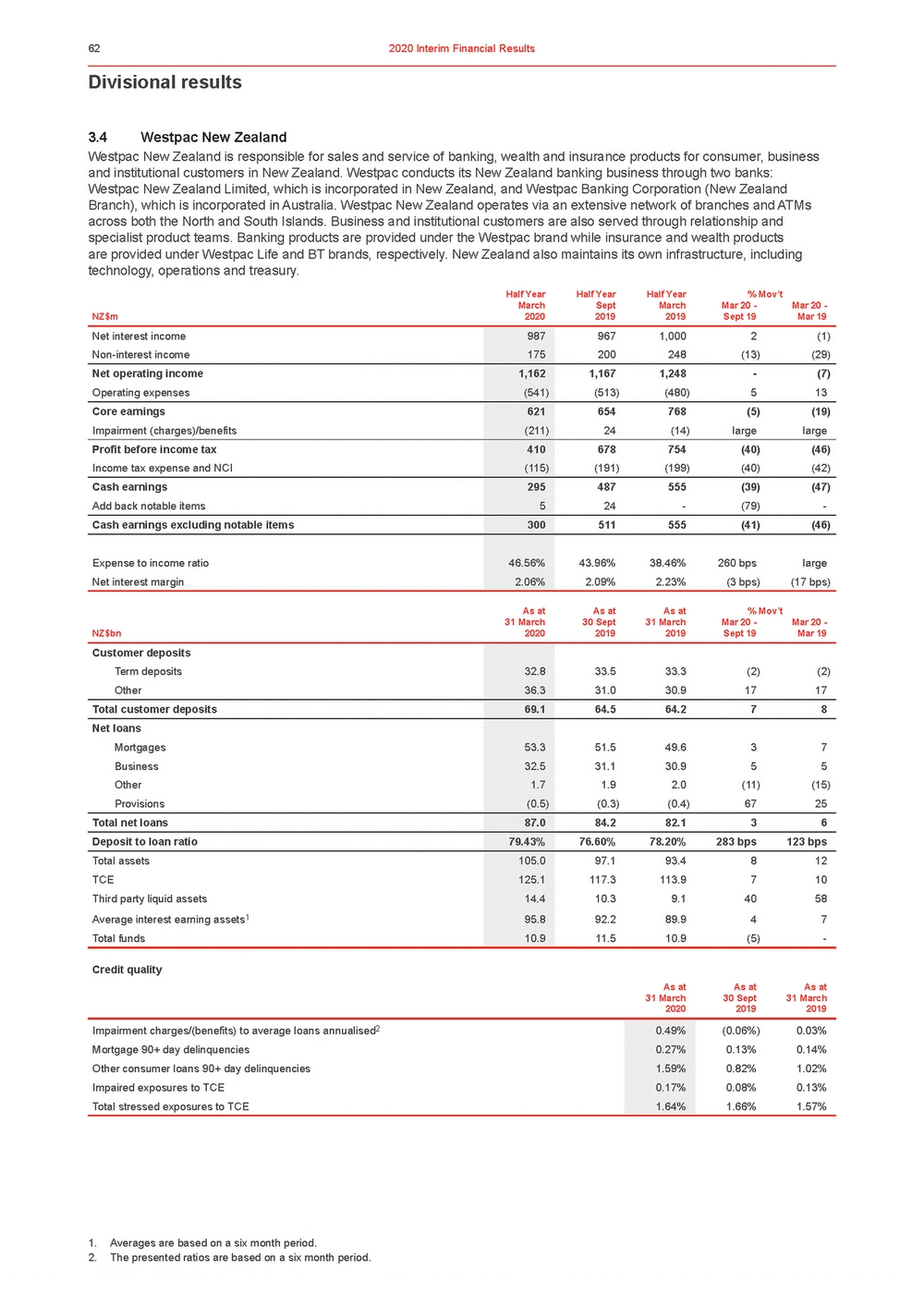

| Review of Group operations Divisional performance summary The performance of each division is based on First Half 2020 compared to Second Half 2019 and is discussed below. Consumer Cash earnings of $1,410 million were $313 million (or 18%) lower than Second Half 2019 from an increase in insurance claims associated with bushfires and severe weather events, the write-down of certain assets (including a DAC write-down related to group life insurance), and from higher impairment charges. Lending declined over the prior half, particularly in mortgages as new flows slowed and run-off increased. Other personal lending also declined (6%) as customers sought to use other forms of short-term finance. Interest margins were higher principally due to pricing changes late in 2019 although margins subsequently eased through the half. Expenses were higher as the division invested more in both risk and compliance activities and from the continued roll-out of the Group’s Customer Service Hub. Impairment charges were higher, mostly reflecting COVID-19 impacts. Business Cash earnings of $604 million were $518 million (or 46%) lower than Second Half 2019. Excluding notable items, cash earnings were $538 million (or 43%) lower from higher impairment charges, lower net interest margins and a decline in wealth income. Excluding notable items, net interest income was lower, from a 2% decline in loans (across most forms of lending) and a 4 basis point decline in margins. The decline in net interest margins was primarily due to lower spreads on deposits from lower interest rates. Non-interest income was also down, mostly from lower fees on a range of wealth and super products. Expenses excluding notable items increased $43 million from the write-down of certain assets, including some of the capitalised software costs of Panorama. Technology expenses and regulatory and compliance costs were also higher, as were salaries although these were largely offset by productivity initiatives implemented early in the period. Higher impairment charges mostly reflecting COVID-19 impacts. Westpac Institutional Bank Cash earnings of $175 million were $295 million (or 63%) lower than Second Half 2019. The reduction was mostly from an increase in impairment charges reflecting higher impaired exposures and changes in economic scenarios from the impact of COVID-19. Lower net interest margins and higher expenses also contributed to the decline in cash earnings. Net interest income declined by 6%, mostly from an 11 basis point decline in margins from reduced deposit spreads. Non-interest income also fell, including from a $40 million increase in the charge for derivative valuation adjustments partially offset by higher Markets income. Expenses were higher as the division invested in its financial crime capabilities. Westpac New Zealand Cash earnings of NZ$295 million were NZ$192 million (or 39%) lower than Second Half 2019. The decline was due to higher impairment charges, lower non-interest income from further fee simplification initiatives and a 5% increase in expenses including from higher risk, regulatory and compliance costs along with a rise in expenses associated with improving work arrangements. Net interest income was little changed over the prior half with a 3% increase in lending (mostly mortgages and small business lending) offset by a 3 basis point decline in margins, mostly from lower deposit spreads as interest rates eased. Impairment charges were higher reflecting COVID-19 impacts. Group Businesses Group Businesses recorded a loss of $1,477 million in First Half 2020 compared to a $223 million loss in Second Half 2019. This was mostly due to a $900 million (non-deductible) provision for a potential penalty related to the AUSTRAC proceedings and a $470 million impairment charge related to COVID-19. These impacts were partly offset by higher Treasury income, lower expenses related to the exit of the Advice business and lower restructuring expenses. |

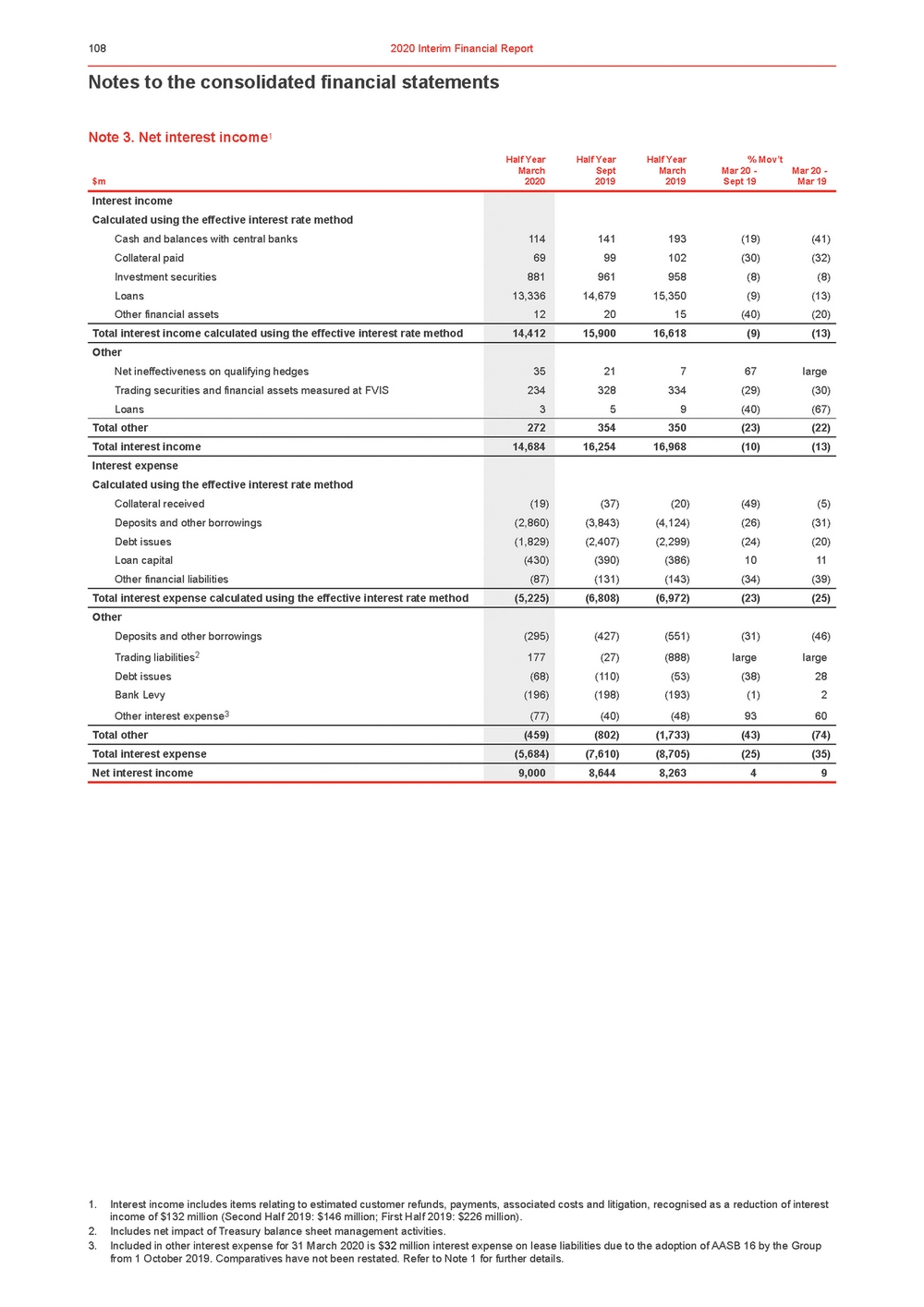

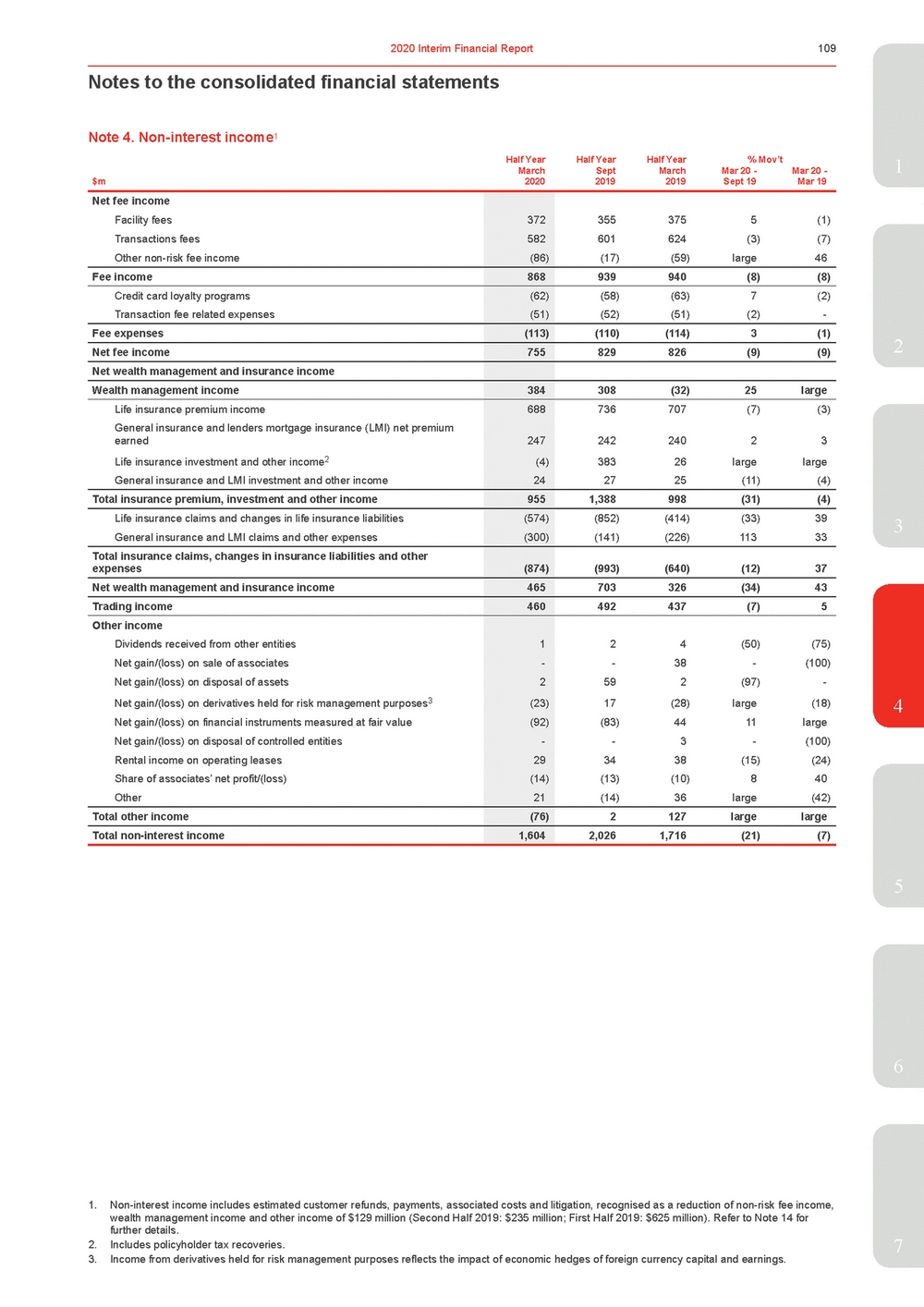

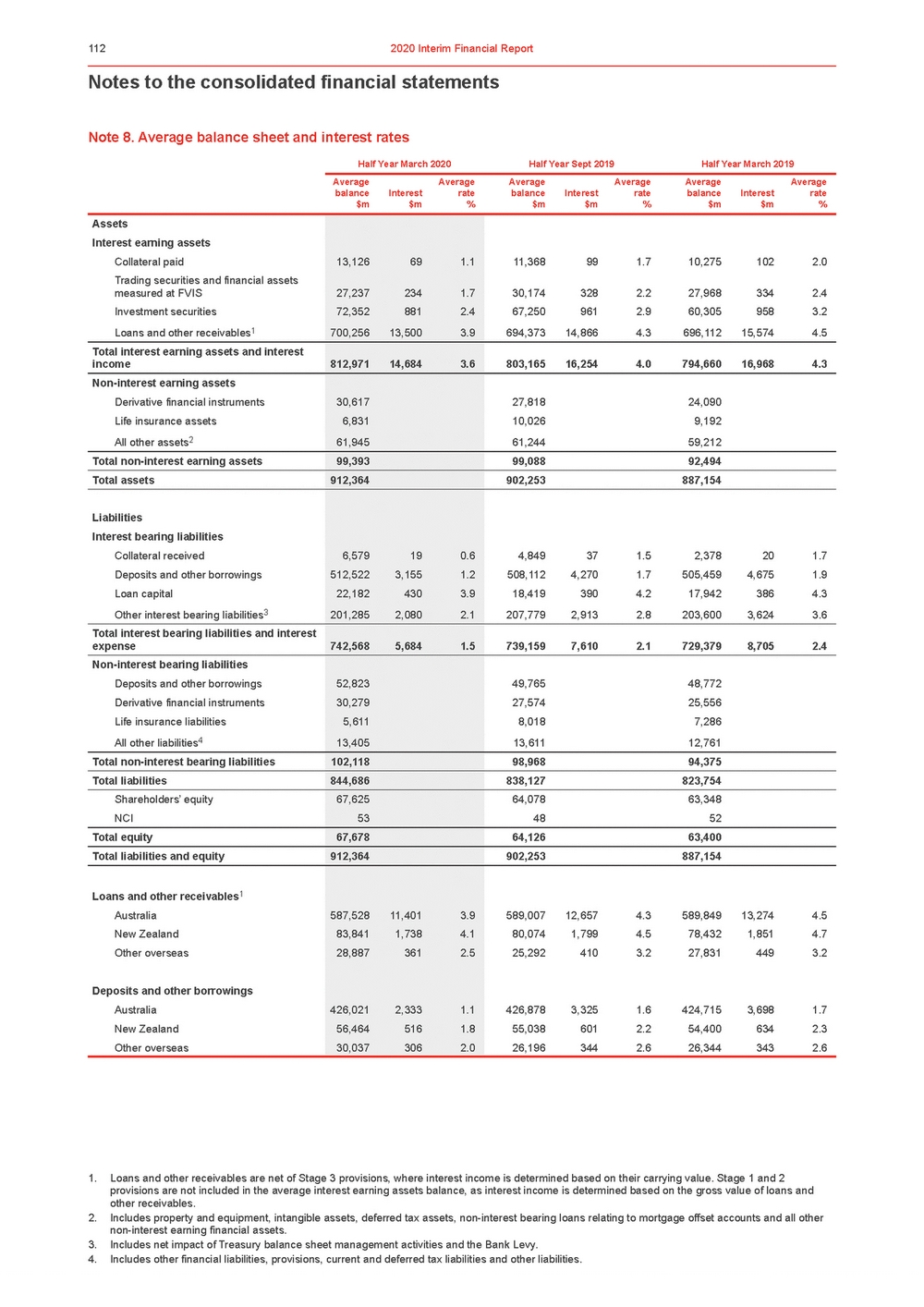

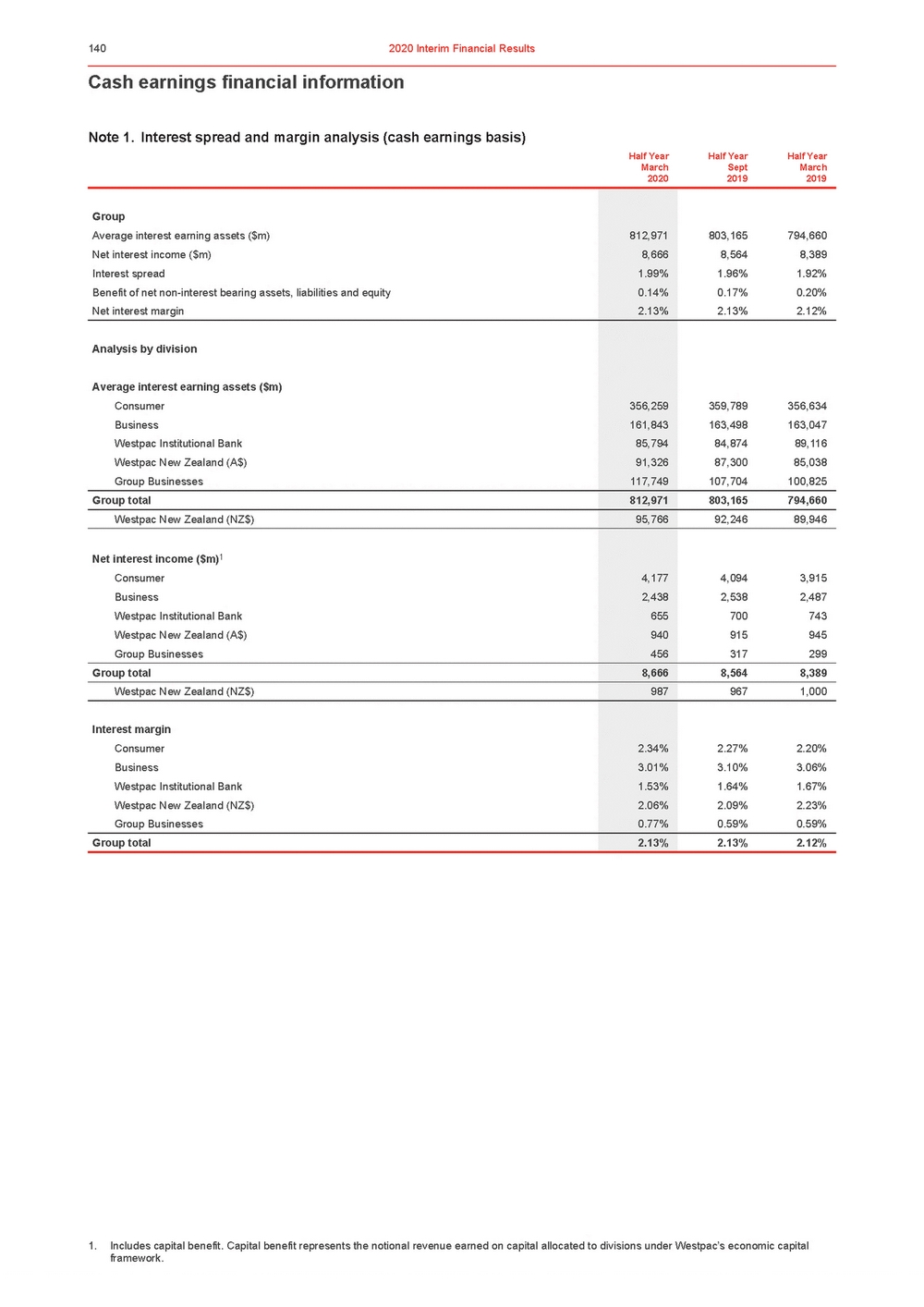

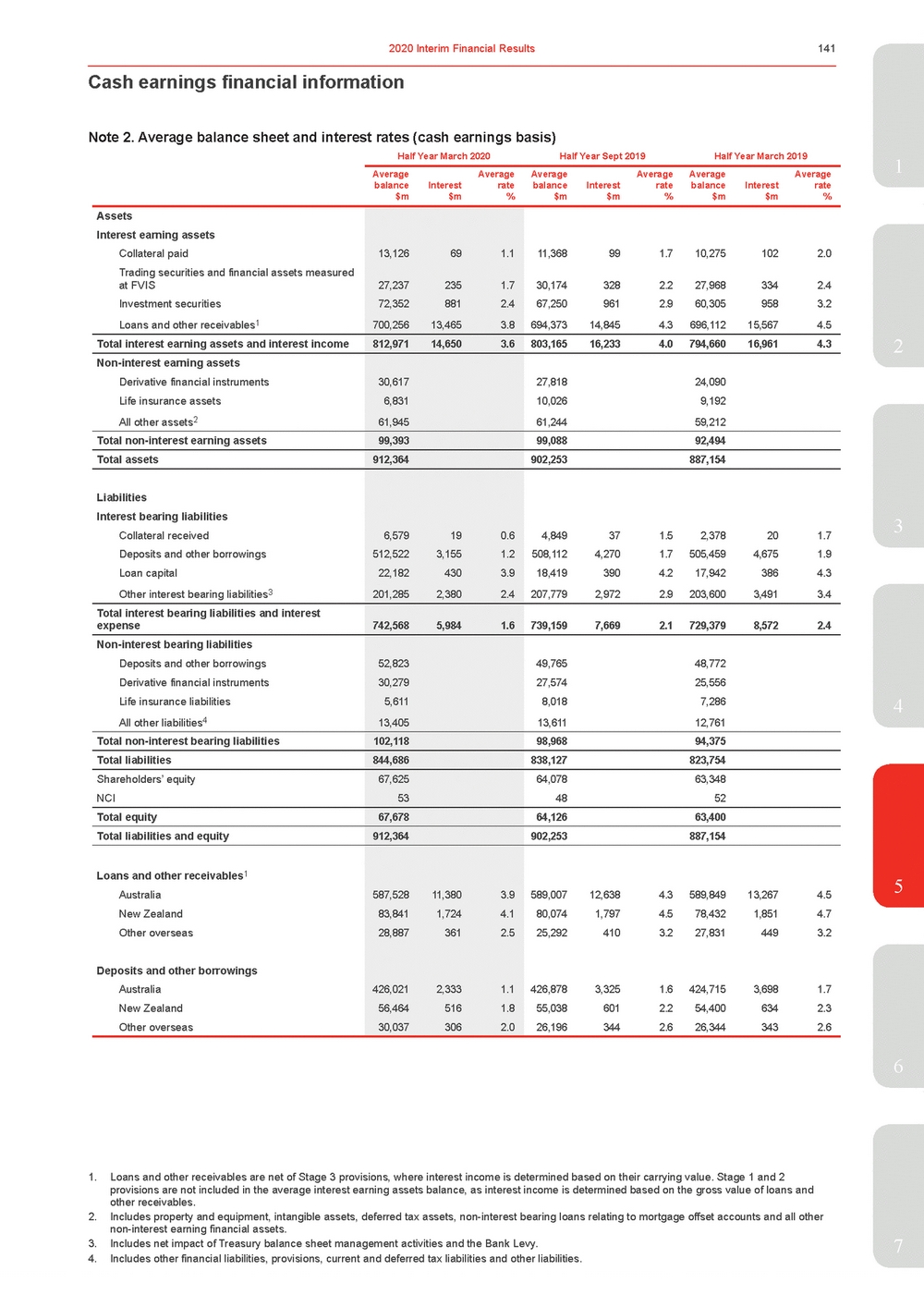

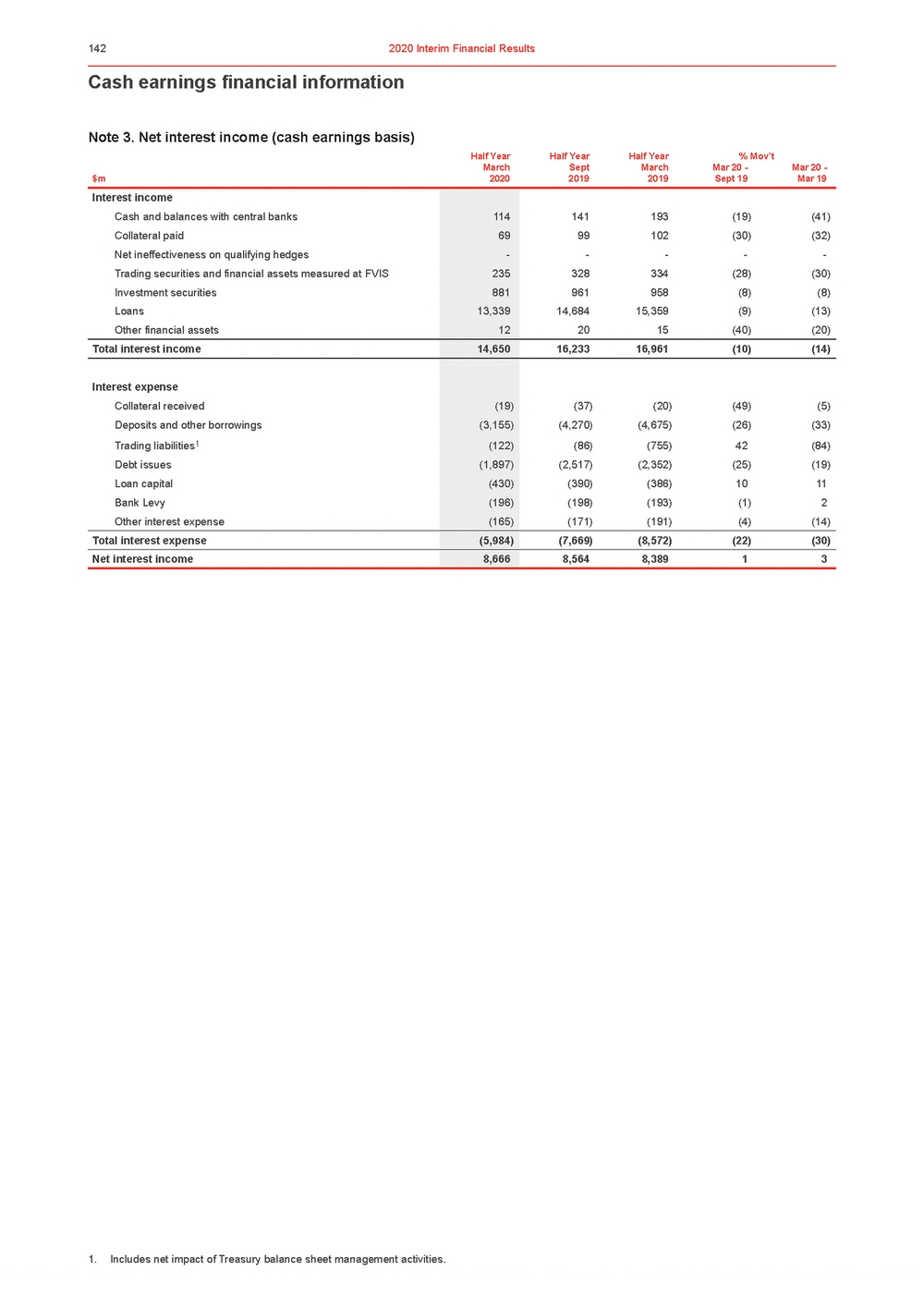

| 2.2.1Net interest income11 Half YearHalf YearHalf Year% Mov’t March 2020 Sept 2019 March 2019 Mar 20 - Sept 19 Mar 20 - Mar 19 Net interest Income ($m) Net interest income excluding Treasury & Markets Treasury net interest income2 Markets net interest income 8,155 444 67 8,2108,081(1)1 2732406385 8168(17)(1) Net interest income Add back notable items 8,666 106 8,5648,38913 132212(20)(50) Net interest income excluding notable items 8,772 8,6968,60112 Average interest earning assets ($m) Loans Third party liquid assets3 Other interest earning assets 675,273 115,771 21,927 675,756674,159--107,78697,222719 19,62323,27912(6) Average interest earning assets 812,971 803,165794,66012 Net interest margin (%) Group net interest margin Group net interest margin excluding Treasury & Markets4 2.13% 2.01% 2.13%2.12%-1 bps 2.04%2.04%(3 bps)(3 bps) Excluding notable items (%) Group net interest margin Group net interest margin excluding Treasury & Markets4 2.16% 2.04% 2.16%2.17%-(1 bps) 2.07%2.09%(3 bps)(5 bps) 3 First Half 2020 – Second Half 2019 Net interest income increased $102 million or 1% compared to Second Half 2019. Key features include: •A 1% increase in average interest earning assets primarily from New Zealand lending and higher holdings of third party liquid assets, partially offset by a reduction in Australian mortgage balances; •Group net interest margin was flat at 2.13%. Group net interest margin excluding Treasury and Markets, and notable items decreased 3 basis points. The decline was primarily due to lower interest rates impacting customer deposit spreads and4 income earned on capital, along with higher holdings of third party liquid assets. These were partially offset by pricing changes on Australian variable rate mortgages. Refer to section 2.2.4 for further details on net interest margin; and •Treasury and Markets net interest income increased $157 million or 44%, with higher Treasury revenue primarily driven by positioning for interest rate changes, partially offset by lower markets net interest income. First Half 2020 – First Half 2019 Net interest income increased $277 million or 3% compared to First Half 2019. Key features include: •A 2% growth in average interest earning assets, primarily from New Zealand mortgages and higher holdings of third party liquid assets, partially offset by lower institutional bank lending; •Group net interest margin increased 1 basis point to 2.13%. Group net interest margin excluding Treasury and Markets, and5 notable items decreased 5 basis points. The decline was primarily due to lower interest rates impacting customer deposit spreads and income earned on capital, along with higher holdings of third party liquid assets. These were partially offset by lower short term funding costs and pricing changes on Australian variable rate mortgages. Refer to section 2.2.4 for further details on net interest margin; and •The contribution from Treasury and Markets increased $203 million or 66%, with higher Treasury revenue primarily driven by positioning for interest rate changes. 6 1. Refer to Section 4, Note 3 for reported results breakdown. Refer to Section 5, Note 3 for cash earnings results breakdown. As discussed in Section 1.3, commentary is reflected on a cash earnings basis. 2. Treasury net interest income excludes capital benefit. 3. Refer Glossary for definition.7 4Calculated by dividing net interest income excluding Treasury and Markets by total average interest earning assets. |

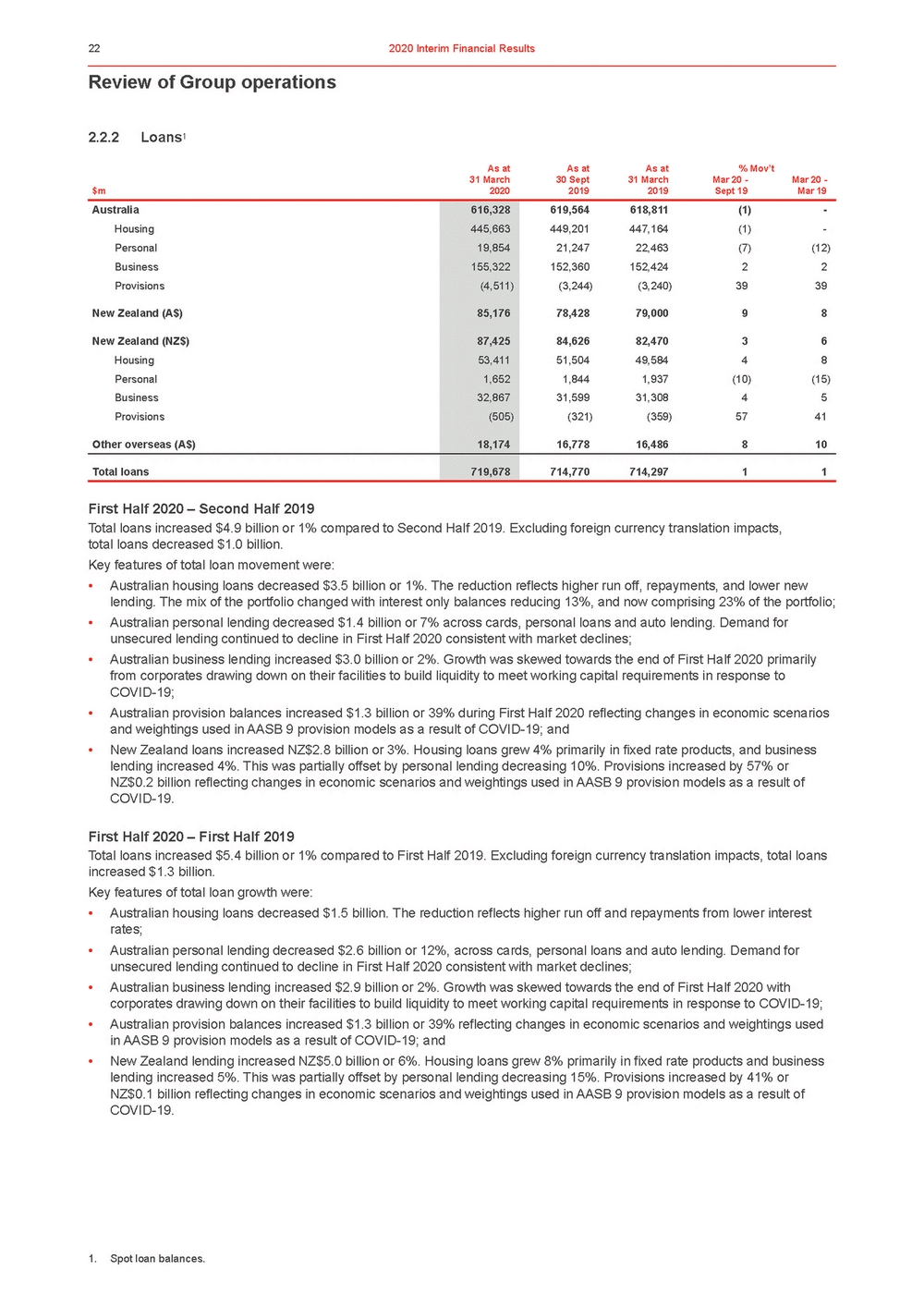

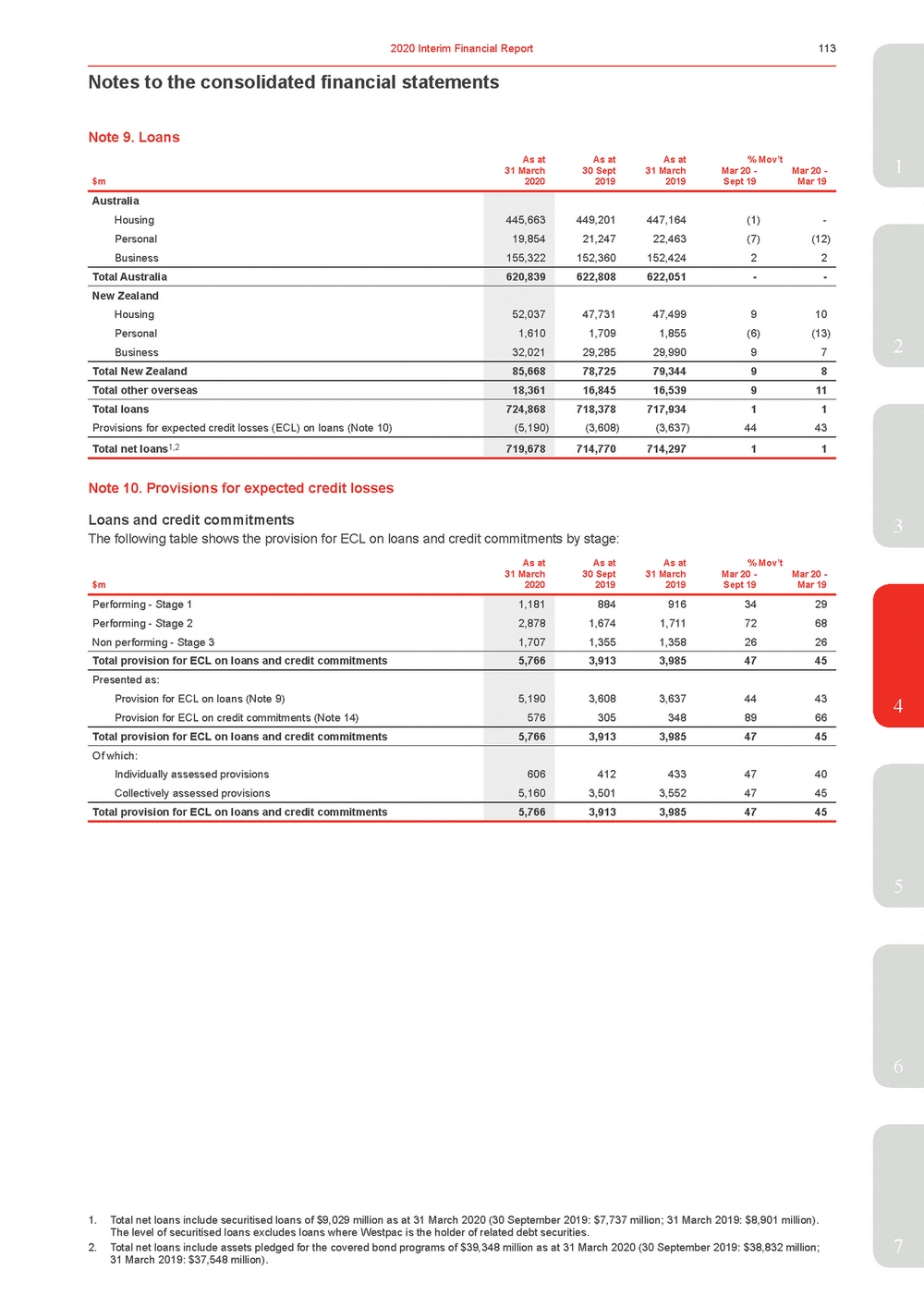

| Review of Group operations 2.2.2Loans1 As atAs atAs at% Mov’t 31 March $m2020 30 Sept 2019 31 March 2019 Mar 20 - Sept 19 Mar 20 - Mar 19 First Half 2020 – Second Half 2019 Total loans increased $4.9 billion or 1% compared to Second Half 2019. Excluding foreign currency translation impacts, total loans decreased $1.0 billion. Key features of total loan movement were: •Australian housing loans decreased $3.5 billion or 1%. The reduction reflects higher run off, repayments, and lower new lending. The mix of the portfolio changed with interest only balances reducing 13%, and now comprising 23% of the portfolio; •Australian personal lending decreased $1.4 billion or 7% across cards, personal loans and auto lending. Demand for unsecured lending continued to decline in First Half 2020 consistent with market declines; •Australian business lending increased $3.0 billion or 2%. Growth was skewed towards the end of First Half 2020 primarily from corporates drawing down on their facilities to build liquidity to meet working capital requirements in response to COVID-19; •Australian provision balances increased $1.3 billion or 39% during First Half 2020 reflecting changes in economic scenarios and weightings used in AASB 9 provision models as a result of COVID-19; and •New Zealand loans increased NZ$2.8 billion or 3%. Housing loans grew 4% primarily in fixed rate products, and business lending increased 4%. This was partially offset by personal lending decreasing 10%. Provisions increased by 57% or NZ$0.2 billion reflecting changes in economic scenarios and weightings used in AASB 9 provision models as a result of COVID-19. First Half 2020 – First Half 2019 Total loans increased $5.4 billion or 1% compared to First Half 2019. Excluding foreign currency translation impacts, total loans increased $1.3 billion. Key features of total loan growth were: •Australian housing loans decreased $1.5 billion. The reduction reflects higher run off and repayments from lower interest rates; •Australian personal lending decreased $2.6 billion or 12%, across cards, personal loans and auto lending. Demand for unsecured lending continued to decline in First Half 2020 consistent with market declines; •Australian business lending increased $2.9 billion or 2%. Growth was skewed towards the end of First Half 2020 with corporates drawing down on their facilities to build liquidity to meet working capital requirements in response to COVID-19; •Australian provision balances increased $1.3 billion or 39% reflecting changes in economic scenarios and weightings used in AASB 9 provision models as a result of COVID-19; and •New Zealand lending increased NZ$5.0 billion or 6%. Housing loans grew 8% primarily in fixed rate products and business lending increased 5%. This was partially offset by personal lending decreasing 15%. Provisions increased by 41% or NZ$0.1 billion reflecting changes in economic scenarios and weightings used in AASB 9 provision models as a result of COVID-19. 1. Spot loan balances. |

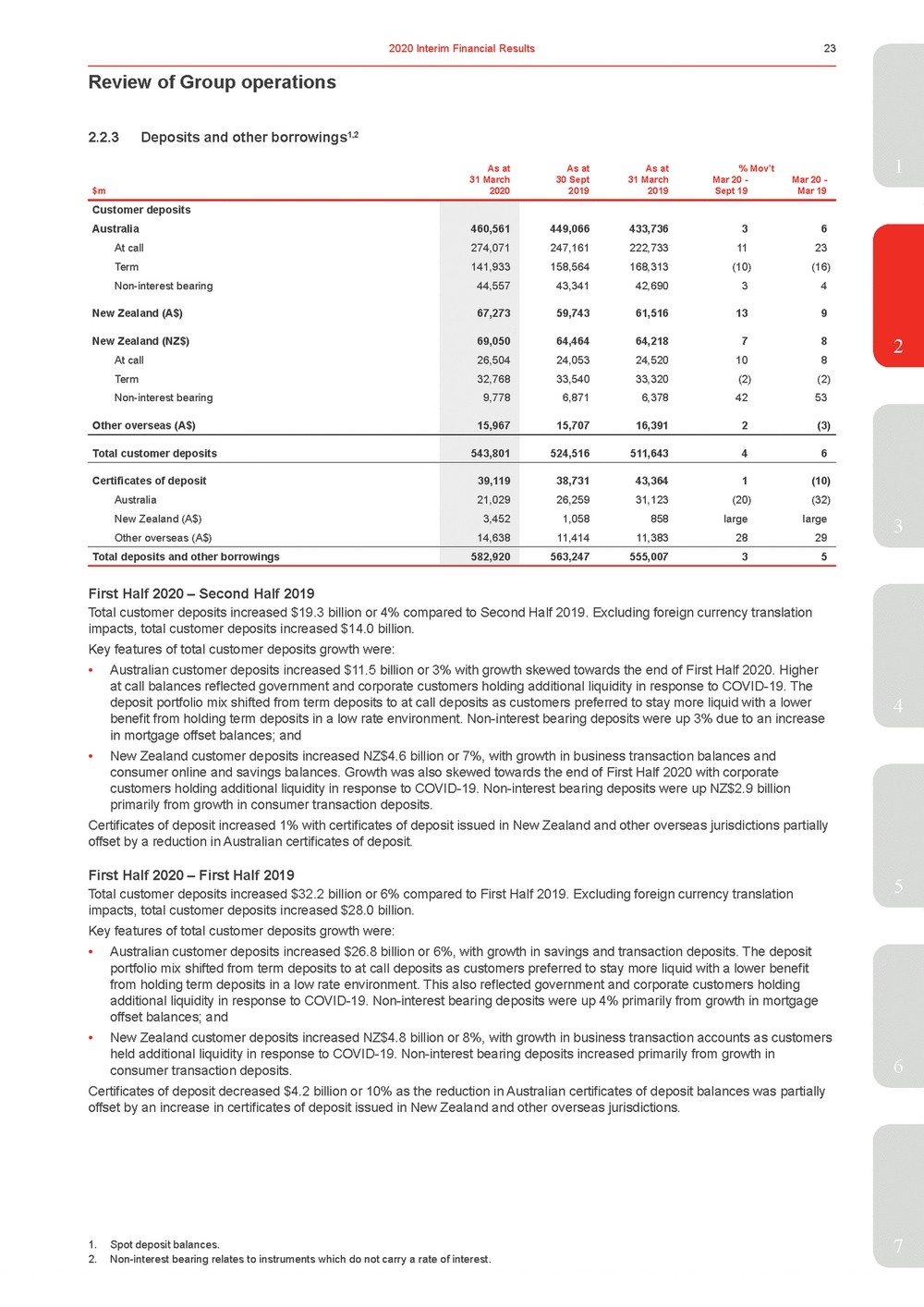

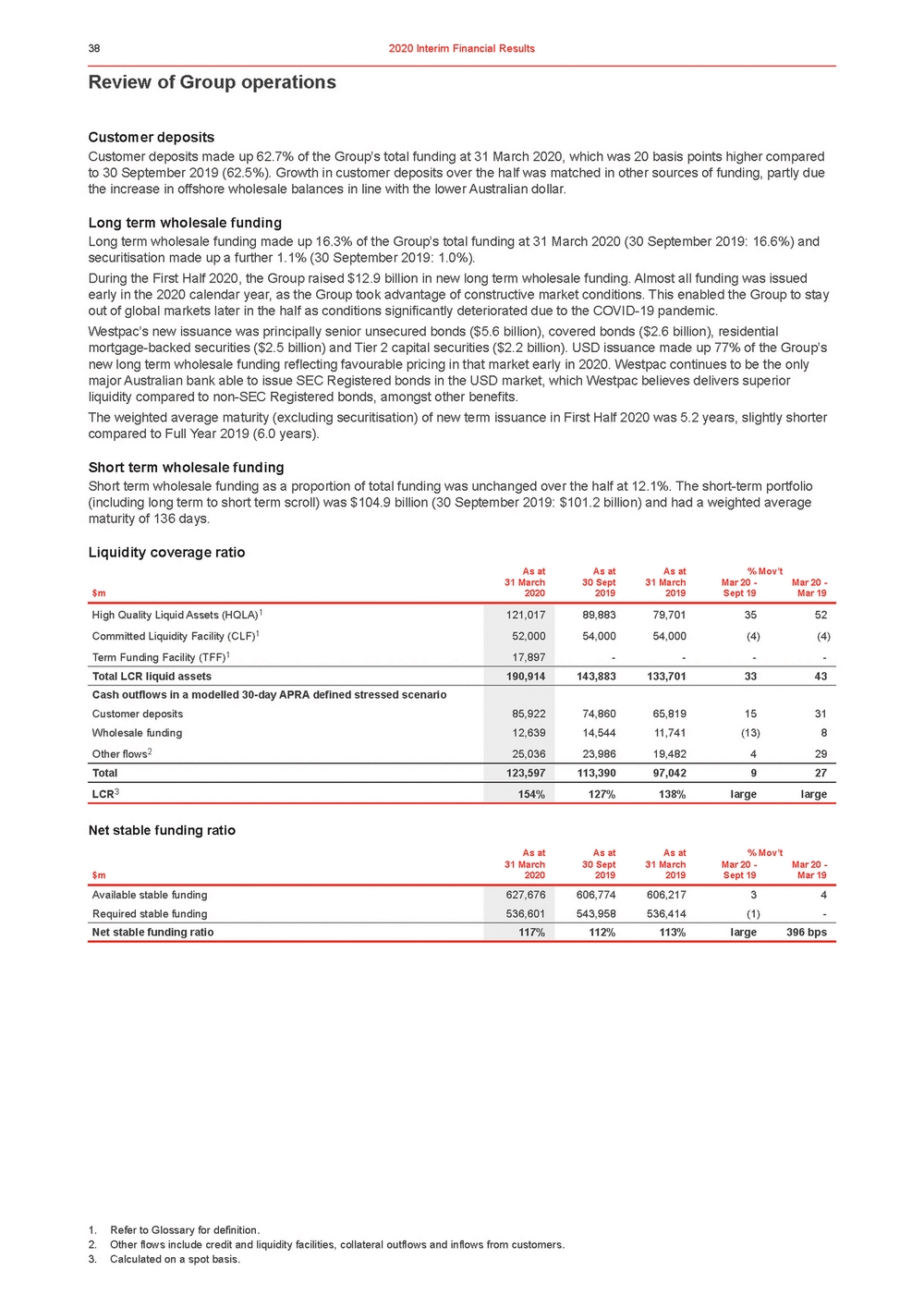

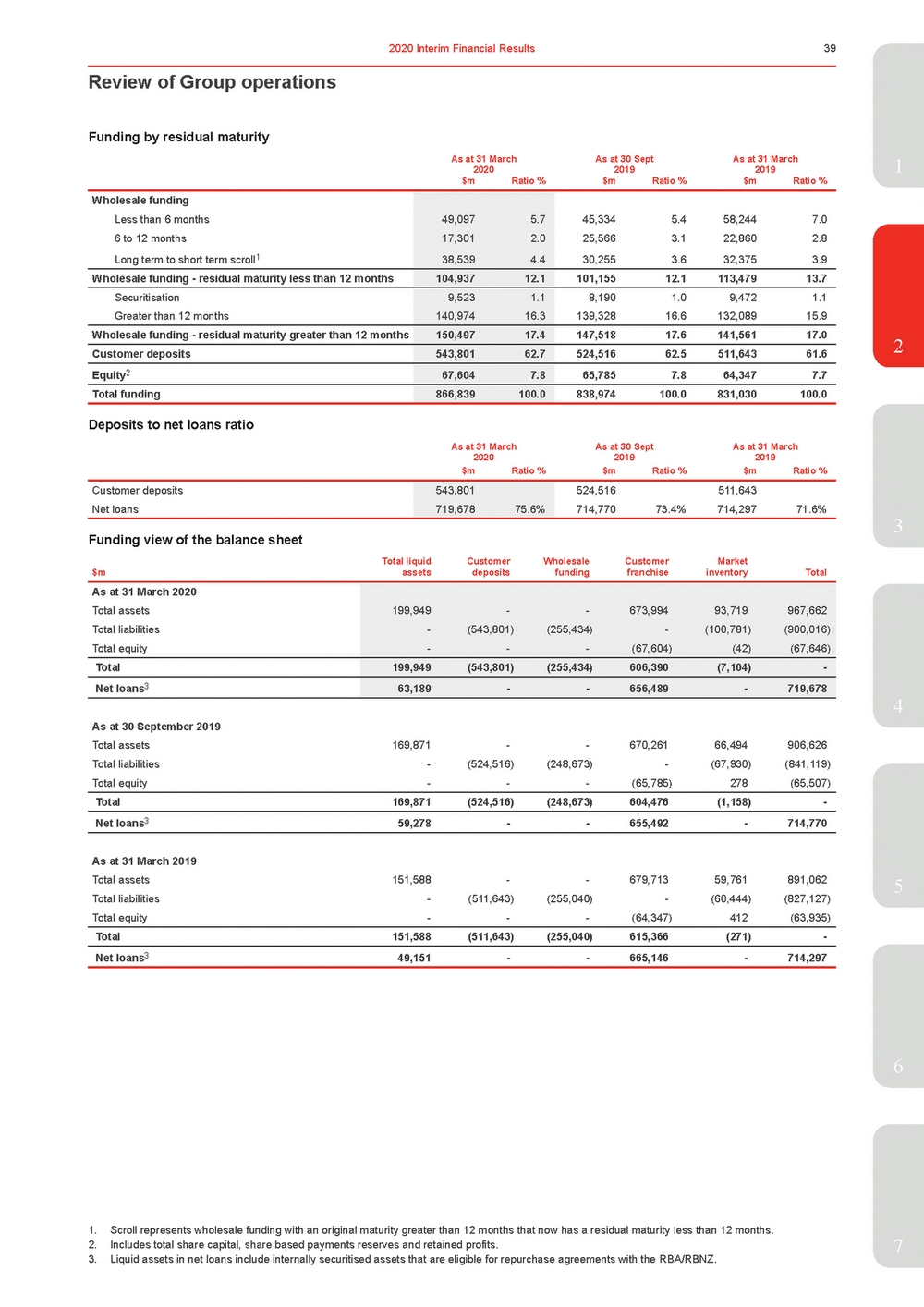

| 2.2.3Deposits and other borrowings1,2 As atAs atAs at% Mov’t1 31 March $m2020 30 Sept 2019 31 March 2019 Mar 20 - Sept 19 Mar 20 - Mar 19 Customer deposits Australia At call Term Non-interest bearing New Zealand (A$) New Zealand (NZ$) At call Term Non-interest bearing Other overseas (A$) 460,561 274,071 141,933 44,557 67,273 69,050 26,504 32,768 9,778 15,967 449,066433,73636 247,161222,7331123 158,564168,313(10)(16) 43,34142,69034 59,74361,516139 64,46464,21878 24,05324,520108 33,54033,320(2)(2) 6,8716,3784253 15,70716,3912(3) Total customer deposits 543,801 524,516511,64346 Certificates of deposit Australia New Zealand (A$) Other overseas (A$) 39,119 21,029 3,452 14,638 38,73143,3641(10) 26,25931,123(20)(32) 1,058858largelarge 11,41411,3832829 Total deposits and other borrowings 582,920 563,247555,00735 3 First Half 2020 – Second Half 2019 Total customer deposits increased $19.3 billion or 4% compared to Second Half 2019. Excluding foreign currency translation impacts, total customer deposits increased $14.0 billion. Key features of total customer deposits growth were: •Australian customer deposits increased $11.5 billion or 3% with growth skewed towards the end of First Half 2020. Higher at call balances reflected government and corporate customers holding additional liquidity in response to COVID-19. The deposit portfolio mix shifted from term deposits to at call deposits as customers preferred to stay more liquid with a lower4 benefit from holding term deposits in a low rate environment. Non-interest bearing deposits were up 3% due to an increase in mortgage offset balances; and •New Zealand customer deposits increased NZ$4.6 billion or 7%, with growth in business transaction balances and consumer online and savings balances. Growth was also skewed towards the end of First Half 2020 with corporate customers holding additional liquidity in response to COVID-19. Non-interest bearing deposits were up NZ$2.9 billion primarily from growth in consumer transaction deposits. Certificates of deposit increased 1% with certificates of deposit issued in New Zealand and other overseas jurisdictions partially offset by a reduction in Australian certificates of deposit. First Half 2020 – First Half 2019 Total customer deposits increased $32.2 billion or 6% compared to First Half 2019. Excluding foreign currency translation5 impacts, total customer deposits increased $28.0 billion. Key features of total customer deposits growth were: •Australian customer deposits increased $26.8 billion or 6%, with growth in savings and transaction deposits. The deposit portfolio mix shifted from term deposits to at call deposits as customers preferred to stay more liquid with a lower benefit from holding term deposits in a low rate environment. This also reflected government and corporate customers holding additional liquidity in response to COVID-19. Non-interest bearing deposits were up 4% primarily from growth in mortgage offset balances; and •New Zealand customer deposits increased NZ$4.8 billion or 8%, with growth in business transaction accounts as customers held additional liquidity in response to COVID-19. Non-interest bearing deposits increased primarily from growth in consumer transaction deposits.6 Certificates of deposit decreased $4.2 billion or 10% as the reduction in Australian certificates of deposit balances was partially offset by an increase in certificates of deposit issued in New Zealand and other overseas jurisdictions. 1. Spot deposit balances.7 2. Non-interest bearing relates to instruments which do not carry a rate of interest. |

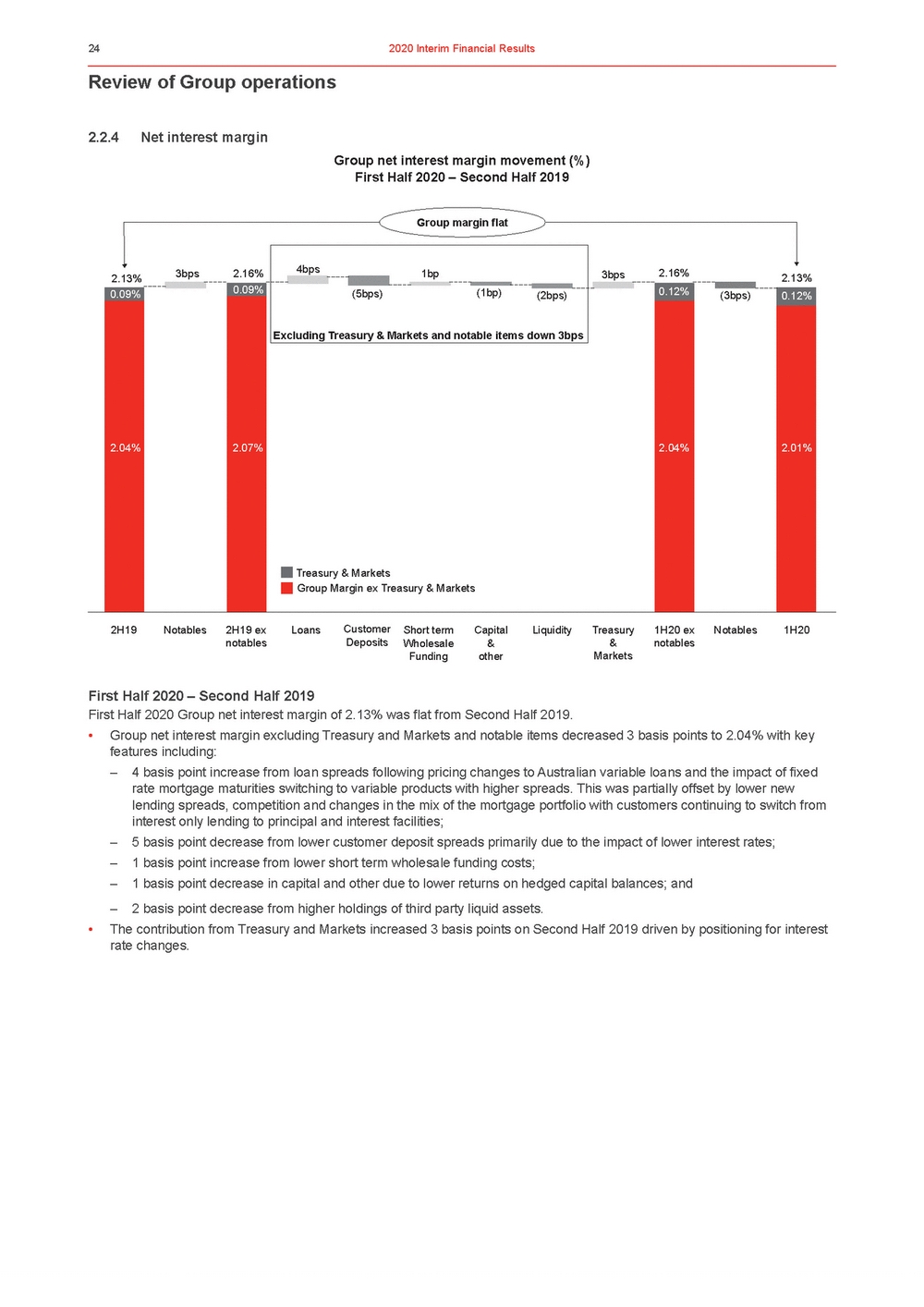

| Review of Group operations 2.2.4Net interest margin Group net interest margin movement (%) First Half 2020 – Second Half 2019 Group margin flat 2.13% 3bps 2.16%4bps1bp3bps 2.16% 2.13% 0.09% 0.09% (5bps)(1bp)(2bps) 0.12% (3bps) 0.12% Excluding Treasury & Markets and notable items down 3bps 2.04% 2.07%2.04% 2.01% Treasury & Markets Group Margin ex Treasury & Markets First Half 2020 – Second Half 2019 First Half 2020 Group net interest margin of 2.13% was flat from Second Half 2019. •Group net interest margin excluding Treasury and Markets and notable items decreased 3 basis points to 2.04% with key features including: – 4 basis point increase from loan spreads following pricing changes to Australian variable loans and the impact of fixed rate mortgage maturities switching to variable products with higher spreads. This was partially offset by lower new lending spreads, competition and changes in the mix of the mortgage portfolio with customers continuing to switch from interest only lending to principal and interest facilities; – 5 basis point decrease from lower customer deposit spreads primarily due to the impact of lower interest rates; – 1 basis point increase from lower short term wholesale funding costs; – 1 basis point decrease in capital and other due to lower returns on hedged capital balances; and – 2 basis point decrease from higher holdings of third party liquid assets. •The contribution from Treasury and Markets increased 3 basis points on Second Half 2019 driven by positioning for interest rate changes. |

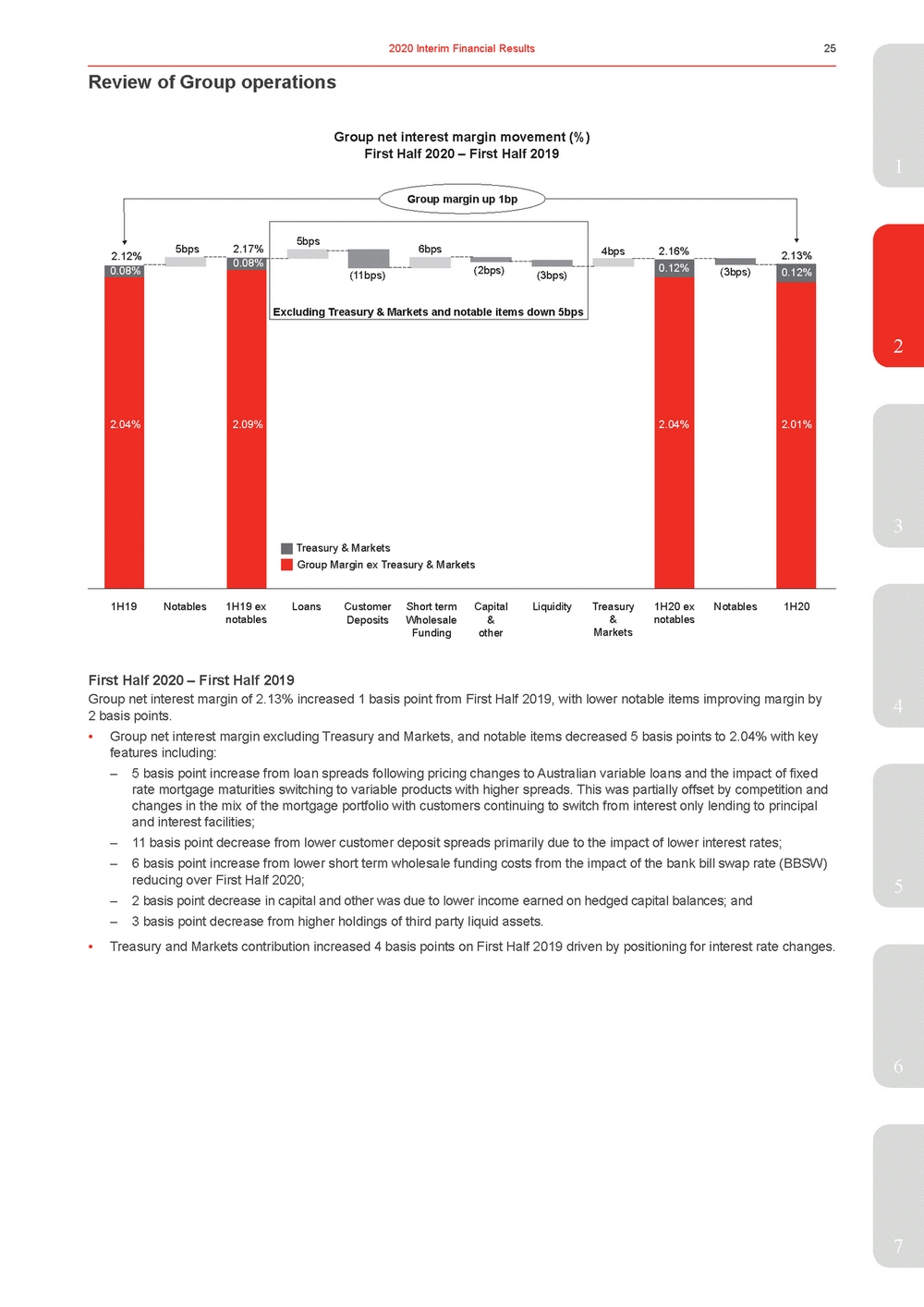

| Group net interest margin movement (%) First Half 2020 – First Half 2019 1 Group margin up 1bp 2.12% 0.08% 5bps 2.17% 0.08% 5bps 6bps4bps (11bps)(2bps)(3bps) 2.16% 0.12% (3bps) 2.13% 0.12% Excluding Treasury & Markets and notable items down 5bps 2 2.04% 2.09%2.04% 2.01% 3 Treasury & Markets Group Margin ex Treasury & Markets First Half 2020 – First Half 2019 4 2 basis points. •Group net interest margin excluding Treasury and Markets, and notable items decreased 5 basis points to 2.04% with key features including: – 5 basis point increase from loan spreads following pricing changes to Australian variable loans and the impact of fixed rate mortgage maturities switching to variable products with higher spreads. This was partially offset by competition and changes in the mix of the mortgage portfolio with customers continuing to switch from interest only lending to principal and interest facilities; – 11 basis point decrease from lower customer deposit spreads primarily due to the impact of lower interest rates; – 6 basis point increase from lower short term wholesale funding costs from the impact of the bank bill swap rate (BBSW) reducing over First Half 2020;5 – 2 basis point decrease in capital and other was due to lower income earned on hedged capital balances; and – 3 basis point decrease from higher holdings of third party liquid assets. •Treasury and Markets contribution increased 4 basis points on First Half 2019 driven by positioning for interest rate changes. 6 7 |

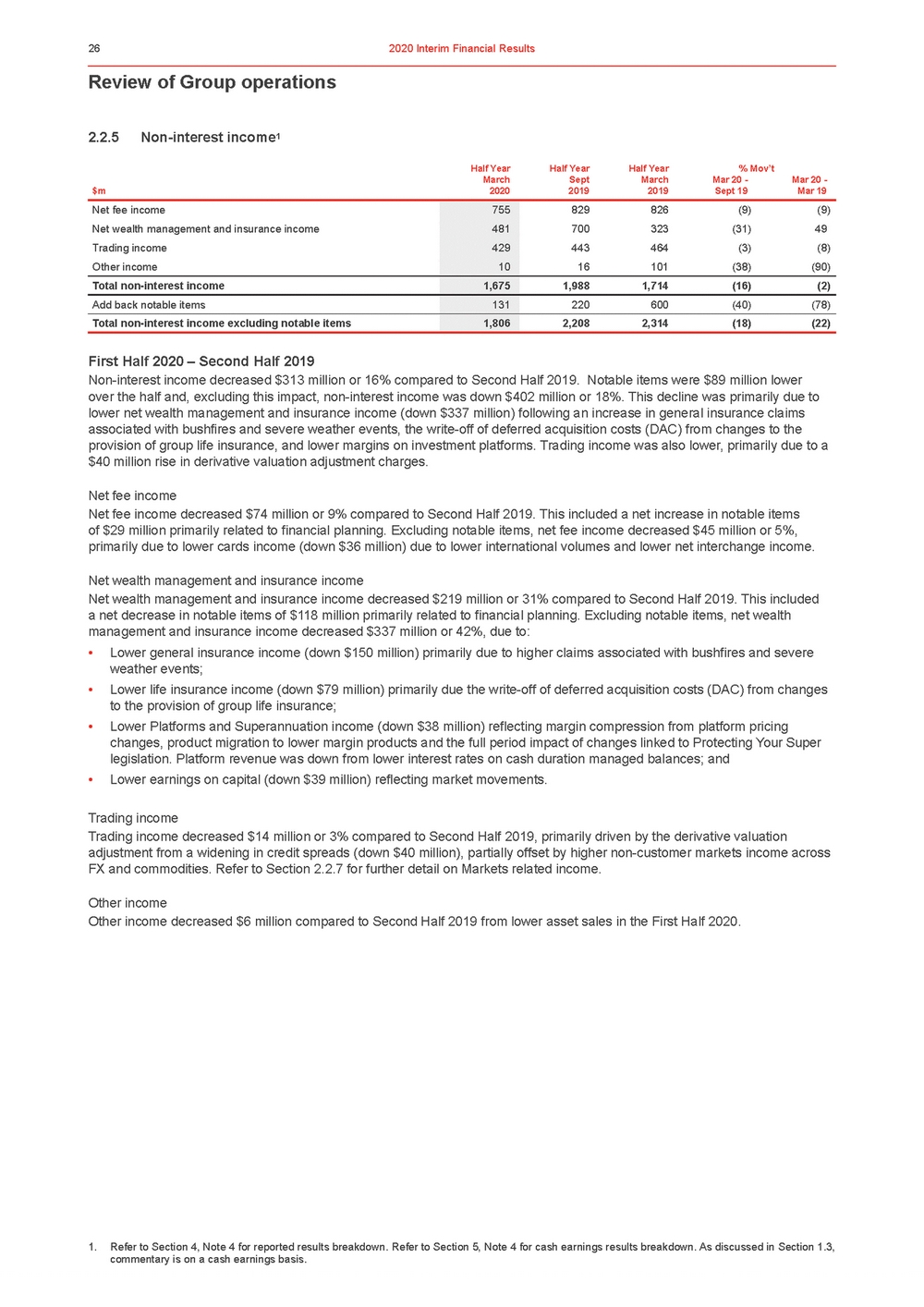

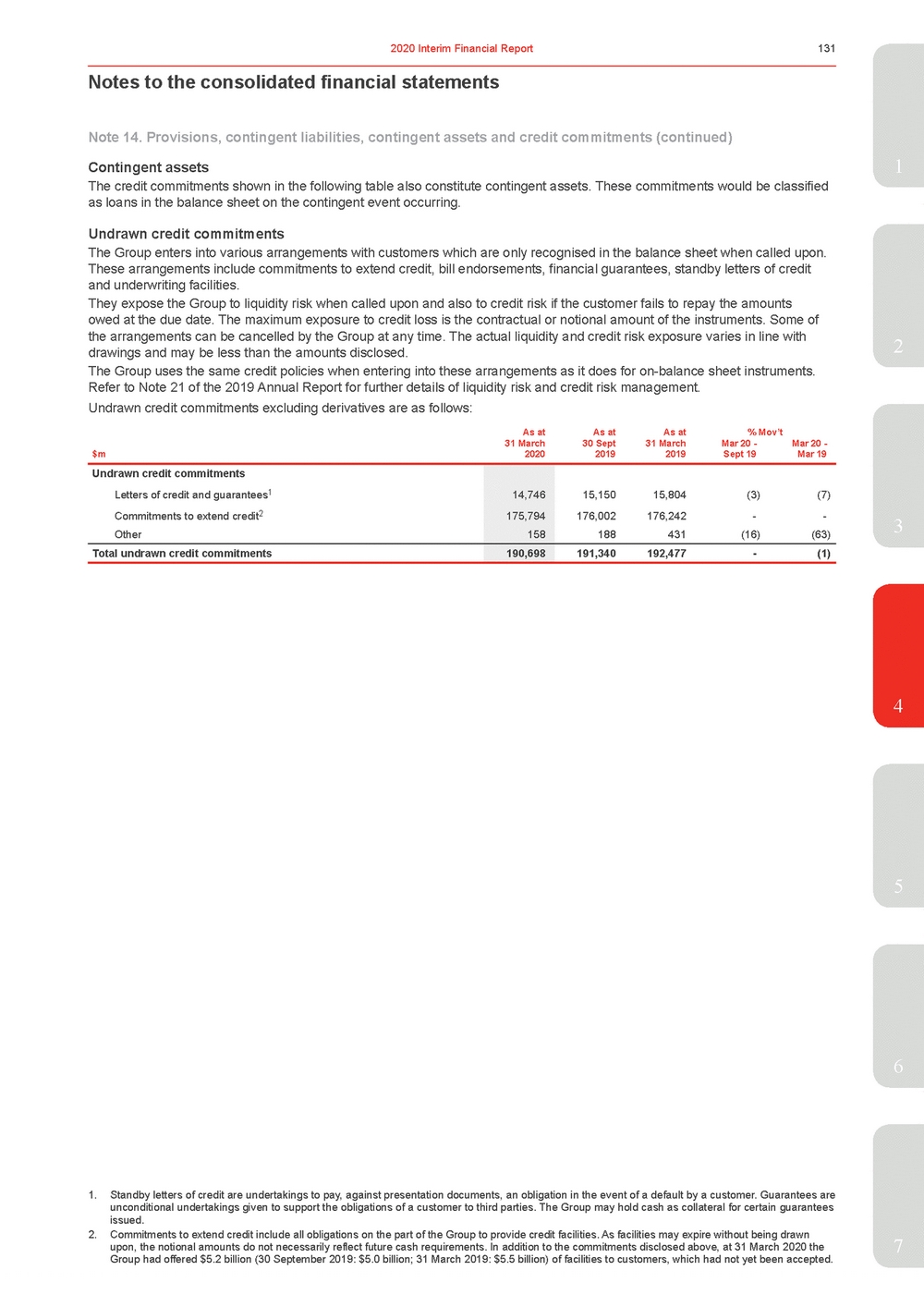

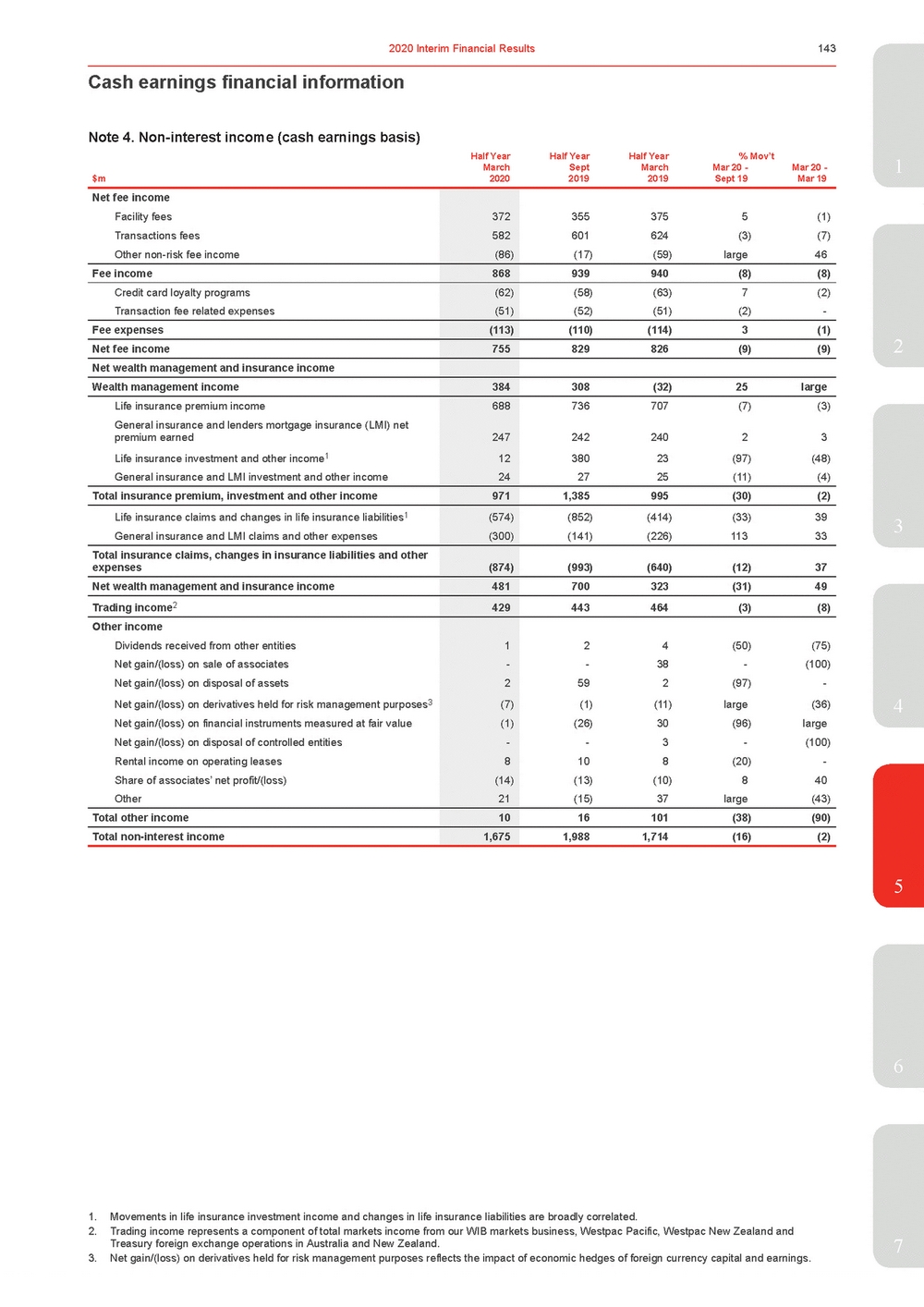

| Review of Group operations 2.2.5Non-interest income1 Half YearHalf YearHalf Year% Mov’t March $m2020 Sept 2019 March 2019 Mar 20 - Sept 19 Mar 20 - Mar 19 First Half 2020 – Second Half 2019 Non-interest income decreased $313 million or 16% compared to Second Half 2019. Notable items were $89 million lower over the half and, excluding this impact, non-interest income was down $402 million or 18%. This decline was primarily due to lower net wealth management and insurance income (down $337 million) following an increase in general insurance claims associated with bushfires and severe weather events, the write-off of deferred acquisition costs (DAC) from changes to the provision of group life insurance, and lower margins on investment platforms. Trading income was also lower, primarily due to a $40 million rise in derivative valuation adjustment charges. Net fee income Net fee income decreased $74 million or 9% compared to Second Half 2019. This included a net increase in notable items of $29 million primarily related to financial planning. Excluding notable items, net fee income decreased $45 million or 5%, primarily due to lower cards income (down $36 million) due to lower international volumes and lower net interchange income. Net wealth management and insurance income Net wealth management and insurance income decreased $219 million or 31% compared to Second Half 2019. This included a net decrease in notable items of $118 million primarily related to financial planning. Excluding notable items, net wealth management and insurance income decreased $337 million or 42%, due to: •Lower general insurance income (down $150 million) primarily due to higher claims associated with bushfires and severe weather events; •Lower life insurance income (down $79 million) primarily due the write-off of deferred acquisition costs (DAC) from changes to the provision of group life insurance; •Lower Platforms and Superannuation income (down $38 million) reflecting margin compression from platform pricing changes, product migration to lower margin products and the full period impact of changes linked to Protecting Your Super legislation. Platform revenue was down from lower interest rates on cash duration managed balances; and •Lower earnings on capital (down $39 million) reflecting market movements. Trading income Trading income decreased $14 million or 3% compared to Second Half 2019, primarily driven by the derivative valuation adjustment from a widening in credit spreads (down $40 million), partially offset by higher non-customer markets income across FX and commodities. Refer to Section 2.2.7 for further detail on Markets related income. Other income Other income decreased $6 million compared to Second Half 2019 from lower asset sales in the First Half 2020. 1. Refer to Section 4, Note 4 for reported results breakdown. Refer to Section 5, Note 4 for cash earnings results breakdown. As discussed in Section 1.3, commentary is on a cash earnings basis. |

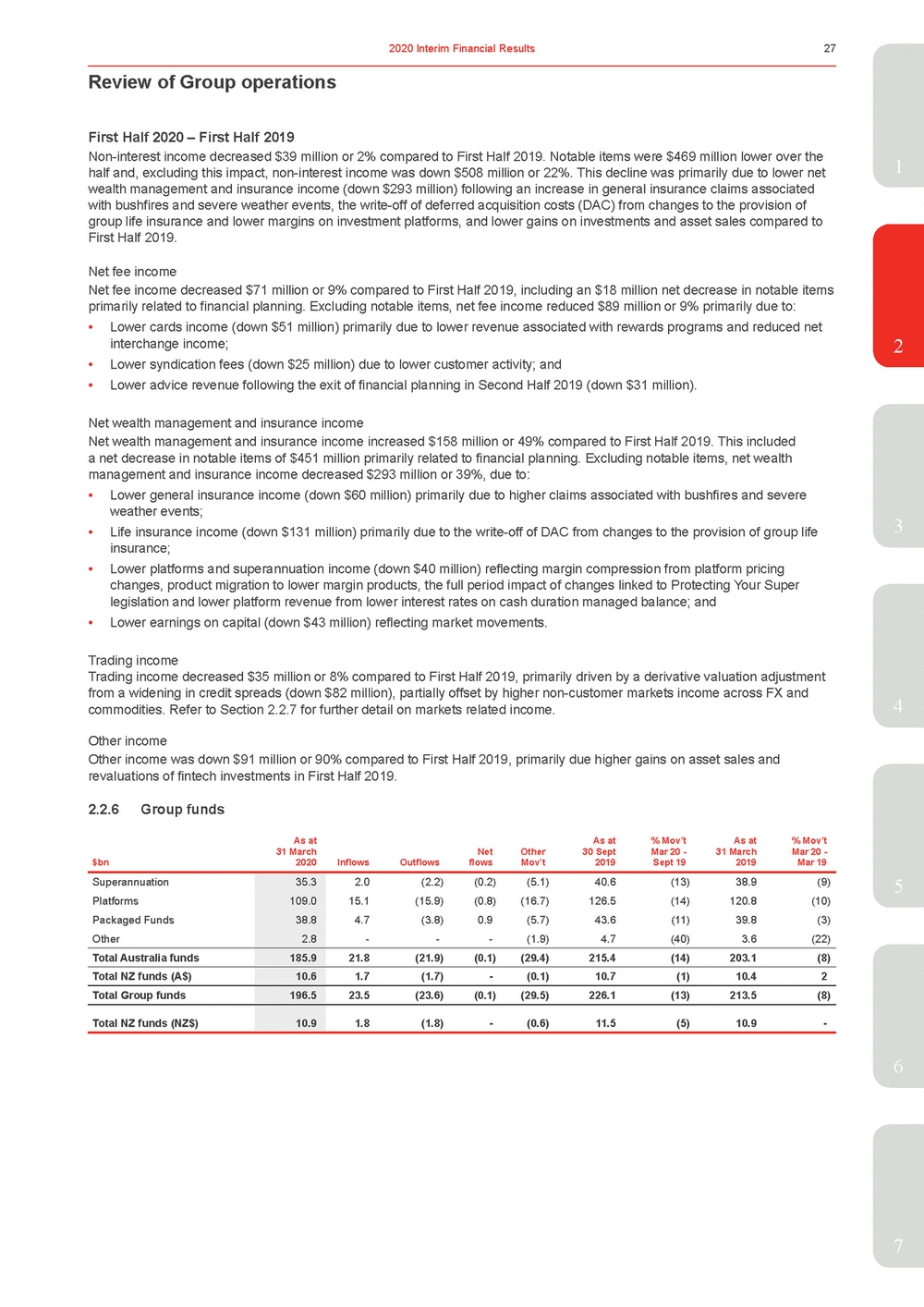

| First Half 2020 – First Half 2019 1 Net fee income Net fee income decreased $71 million or 9% compared to First Half 2019, including an $18 million net decrease in notable items primarily related to financial planning. Excluding notable items, net fee income reduced $89 million or 9% primarily due to: •Lower cards income (down $51 million) primarily due to lower revenue associated with rewards programs and reduced net interchange income;2 •Lower syndication fees (down $25 million) due to lower customer activity; and •Lower advice revenue following the exit of financial planning in Second Half 2019 (down $31 million). Net wealth management and insurance income Net wealth management and insurance income increased $158 million or 49% compared to First Half 2019. This included a net decrease in notable items of $451 million primarily related to financial planning. Excluding notable items, net wealth management and insurance income decreased $293 million or 39%, due to: •Lower general insurance income (down $60 million) primarily due to higher claims associated with bushfires and severe weather events; •Life insurance income (down $131 million) primarily due to the write-off of DAC from changes to the provision of group life3 insurance; •Lower platforms and superannuation income (down $40 million) reflecting margin compression from platform pricing changes, product migration to lower margin products, the full period impact of changes linked to Protecting Your Super legislation and lower platform revenue from lower interest rates on cash duration managed balance; and •Lower earnings on capital (down $43 million) reflecting market movements. Trading income Trading income decreased $35 million or 8% compared to First Half 2019, primarily driven by a derivative valuation adjustment from a widening in credit spreads (down $82 million), partially offset by higher non-customer markets income across FX and commodities. Refer to Section 2.2.7 for further detail on markets related income.4 Other income Other income was down $91 million or 90% compared to First Half 2019, primarily due higher gains on asset sales and revaluations of fintech investments in First Half 2019. 2.2.6Group funds As at As at % Mov’t As at % Mov’t 31 March Net Other 30 Sept Mar 20 - 31 March Mar 20 - 2020 Inflows Outflows flows Mov’t 2019 Sept 19 2019 Mar 19 Superannuation Platforms Packaged Funds Other 35.3 109.0 38.8 2.8 2.0(2.2)(0.2)(5.1)40.6(13)38.9(9) 15.1(15.9)(0.8)(16.7)126.5(14)120.8(10) 4.7(3.8)0.9(5.7)43.6(11)39.8(3) ---(1.9)4.7(40)3.6(22) Total Australia funds 185.9 21.8(21.9)(0.1)(29.4)215.4(14)203.1(8) Total NZ funds (A$) 10.6 1.7(1.7)-(0.1)10.7(1)10.42 Total Group funds 196.5 23.5(23.6)(0.1)(29.5)226.1(13)213.5(8) Total NZ funds (NZ$) 10.9 1.8(1.8)-(0.6)11.5(5)10.9-6 7 |