Exhibit 3

| ASX Release 17 February 2025 WESTPAC 1Q25 INVESTOR DISCUSSION PACK For further information: Hayden Cooper Justin McCarthy Group Head of Media Relations General Manager, Investor Relations 0402 393 619 0422 800 321 This document has been authorised for release by Tim Hartin, Company Secretary. Level 18, 275 Kent Street Sydney, NSW, 2000 Following are Westpac’s 1Q25 slides covering financial performance, capital, credit quality and funding for the three months ended 31 December 2024. |

| 1Q25 INVESTOR DISCUSSION PACK FOR THE 3 MONTHS ENDED 31 DECEMBER 2024 © Westpac Banking Corporation ABN 33 007 457 141 This document should be read in conjunction with Westpac’s December 2024 Pillar 3 Report. All amounts are in Australian dollars. |

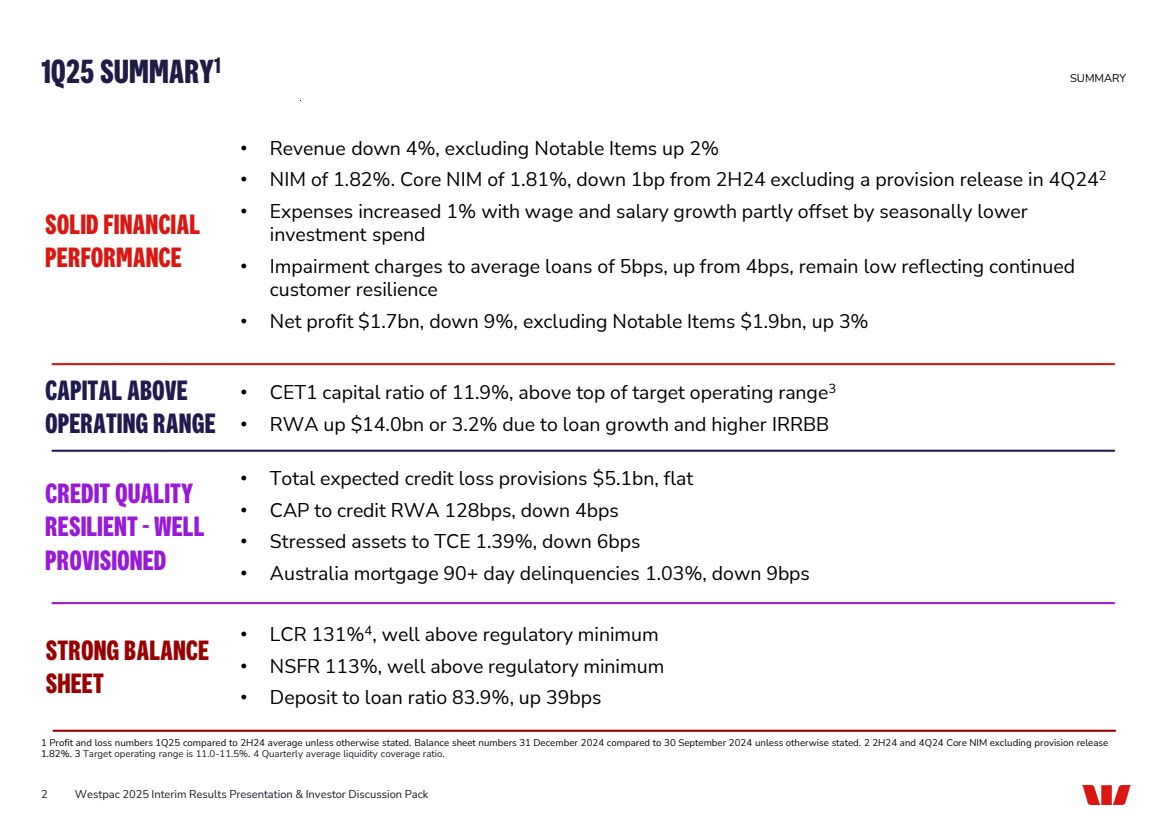

| 1Q25 SUMMARY1 2 • Revenue down 4%, excluding Notable Items up 2% • NIM of 1.82%. Core NIM of 1.81%, down 1bp from 2H24 excluding a provision release in 4Q242 • Expenses increased 1% with wage and salary growth partly offset by seasonally lower investment spend • Impairment charges to average loans of 5bps, up from 4bps, remain low reflecting continued customer resilience • Net profit $1.7bn, down 9%, excluding Notable Items $1.9bn, up 3% Westpac 2025 Interim Results Presentation & Investor Discussion Pack SUMMARY SOLID FINANCIAL PERFORMANCE CAPITAL ABOVE OPERATING RANGE • CET1 capital ratio of 11.9%, above top of target operating range3 • RWA up $14.0bn or 3.2% due to loan growth and higher IRRBB CREDIT QUALITY RESILIENT - WELL PROVISIONED • Total expected credit loss provisions $5.1bn, flat • CAP to credit RWA 128bps, down 4bps • Stressed assets to TCE 1.39%, down 6bps • Australia mortgage 90+ day delinquencies 1.03%, down 9bps STRONG BALANCE SHEET • LCR 131%4, well above regulatory minimum • NSFR 113%, well above regulatory minimum • Deposit to loan ratio 83.9%, up 39bps 1 Profit and loss numbers 1Q25 compared to 2H24 average unless otherwise stated. Balance sheet numbers 31 December 2024 compared to 30 September 2024 unless otherwise stated. 2 2H24 and 4Q24 Core NIM excluding provision release 1.82%. 3 Target operating range is 11.0-11.5%. 4 Quarterly average liquidity coverage ratio. |

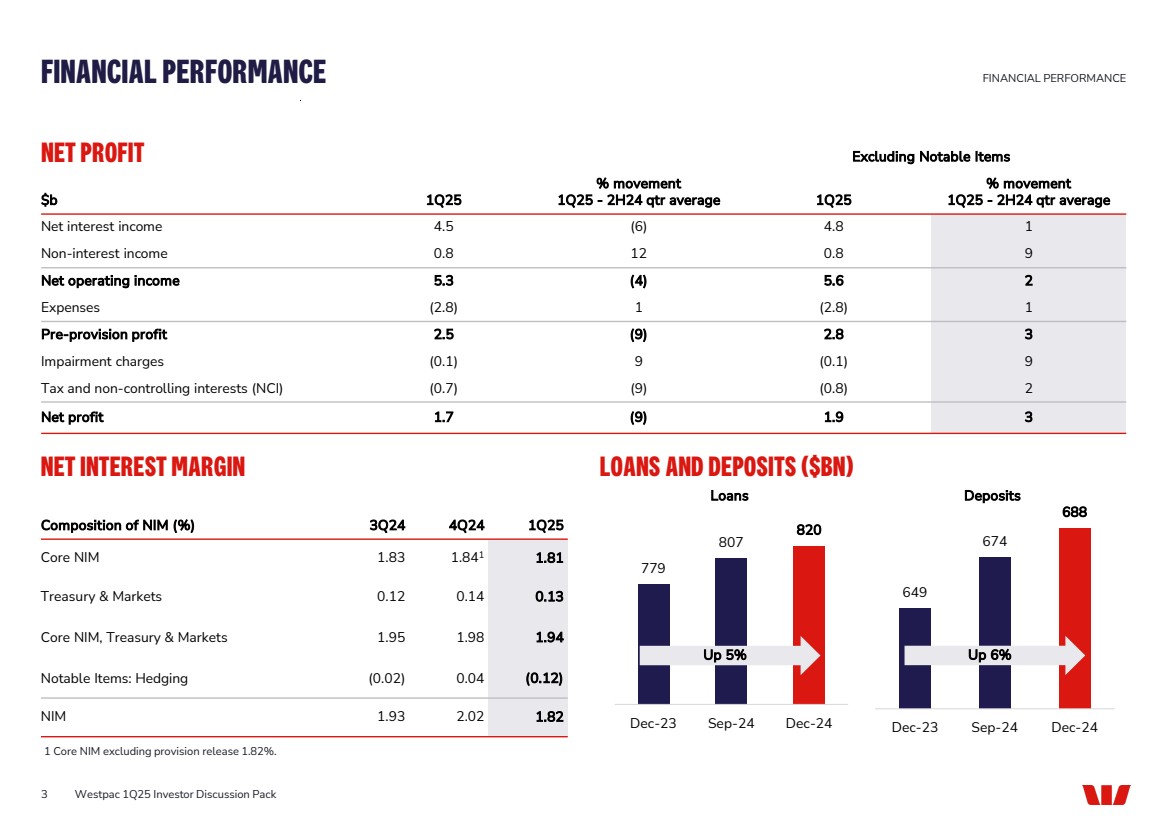

| Excluding Notable Items $b 1Q25 % movement 1Q25 - 2H24 qtr average 1Q25 % movement 1Q25 - 2H24 qtr average Net interest income 4.5 (6) 4.8 1 Non-interest income 0.8 12 0.8 9 Net operating income 5.3 (4) 5.6 2 Expenses (2.8) 1 (2.8) 1 Pre-provision profit 2.5 (9) 2.8 3 Impairment charges (0.1) 9 (0.1) 9 Tax and non-controlling interests (NCI) (0.7) (9) (0.8) 2 Net profit 1.7 (9) 1.9 3 NET INTEREST MARGIN LOANS AND DEPOSITS ($BN) Westpac 1Q25 Investor Discussion Pack FINANCIAL PERFORMANCE 1 Core NIM excluding provision release 1.82%. Composition of NIM (%) 3Q24 4Q24 1Q25 Core NIM 1.83 1.841 1.81 Treasury & Markets 0.12 0.14 0.13 Core NIM, Treasury & Markets 1.95 1.98 1.94 Notable Items: Hedging (0.02) 0.04 (0.12) NIM 1.93 2.02 1.82 779 807 820 Dec-23 Sep-24 Dec-24 Up 5% 649 674 688 Dec-23 Sep-24 Dec-24 FINANCIAL PERFORMANCE Up 6% Loans Deposits 3 NET PROFIT |

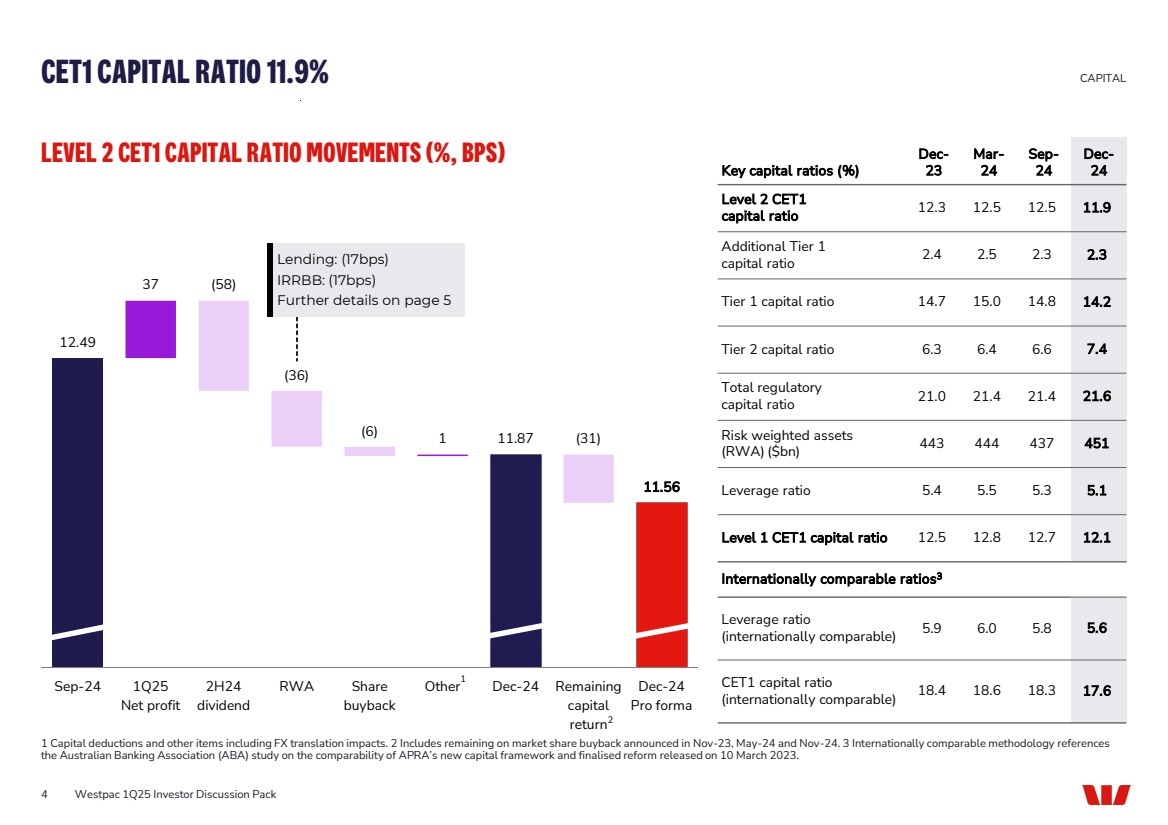

| 12.49 37 1 11.87 11.56 (58) (36) (6) (31) Sep-24 1Q25 Net profit 2H24 dividend RWA Share buyback Other Dec-24 Remaining capital return Dec-24 Pro forma Key capital ratios (%) Dec-23 Mar-24 Sep-24 Dec-24 Level 2 CET1 capital ratio 12.3 12.5 12.5 11.9 Additional Tier 1 capital ratio 2.4 2.5 2.3 2.3 Tier 1 capital ratio 14.7 15.0 14.8 14.2 Tier 2 capital ratio 6.3 6.4 6.6 7.4 Total regulatory capital ratio 21.0 21.4 21.4 21.6 Risk weighted assets (RWA) ($bn) 443 444 437 451 Leverage ratio 5.4 5.5 5.3 5.1 Level 1 CET1 capital ratio 12.5 12.8 12.7 12.1 Internationally comparable ratios3 Leverage ratio (internationally comparable) 5.9 6.0 5.8 5.6 CET1 capital ratio (internationally comparable) 18.4 18.6 18.3 17.6 LEVEL 2 CET1 CAPITAL RATIO MOVEMENTS (%, BPS) CET1 CAPITAL RATIO 11.9% CAPITAL 1 Capital deductions and other items including FX translation impacts. 2 Includes remaining on market share buyback announced in Nov-23, May-24 and Nov-24. 3 Internationally comparable methodology references the Australian Banking Association (ABA) study on the comparability of APRA’s new capital framework and finalised reform released on 10 March 2023. 1 Lending: (17bps) IRRBB: (17bps) Further details on page 5 4 Westpac 1Q25 Investor Discussion Pack 2 |

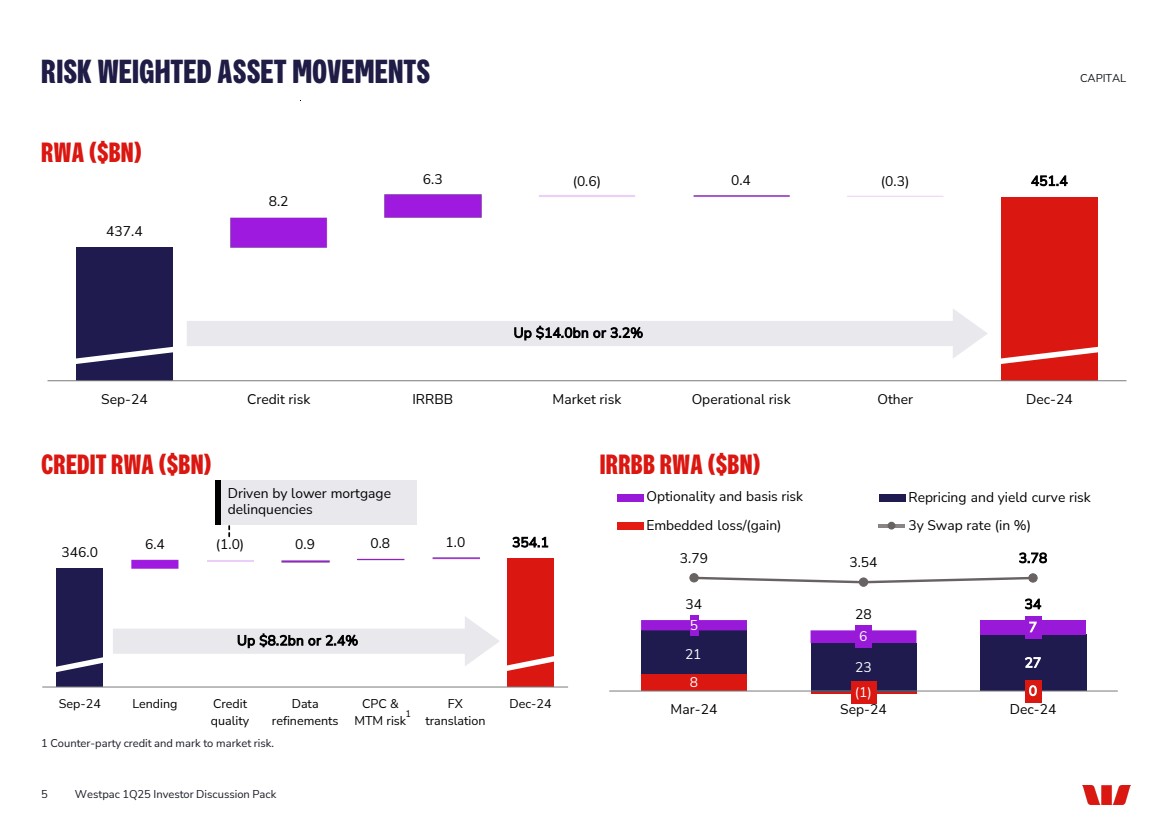

| (0.6) (0.3) 437.4 8.2 6.3 0.4 451.4 Sep-24 Credit risk IRRBB Market risk Operational risk Other Dec-24 RWA ($BN) CREDIT RWA ($BN) IRRBB RWA ($BN) 8 (1) 0 21 23 27 5 6 7 34 28 34 3.79 3.54 3.78 -4 -3 -2 -1 0 1 2 3 4 -10 0 10 20 30 40 50 60 Mar-24 Sep-24 Dec-24 RISK WEIGHTED ASSET MOVEMENTS CAPITAL 1 Counter-party credit and mark to market risk. 346.0 6.4 (1.0) 0.9 0.8 1.0 354.1 Sep-24 Lending Credit quality Data refinements CPC & MTM risk FX translation Dec-24 Up $8.2bn or 2.4% Up $14.0bn or 3.2% 1 5 Westpac 1Q25 Investor Discussion Pack Driven by lower mortgage delinquencies Optionality and basis risk Embedded loss/(gain) Repricing and yield curve risk 3y Swap rate (in %) |

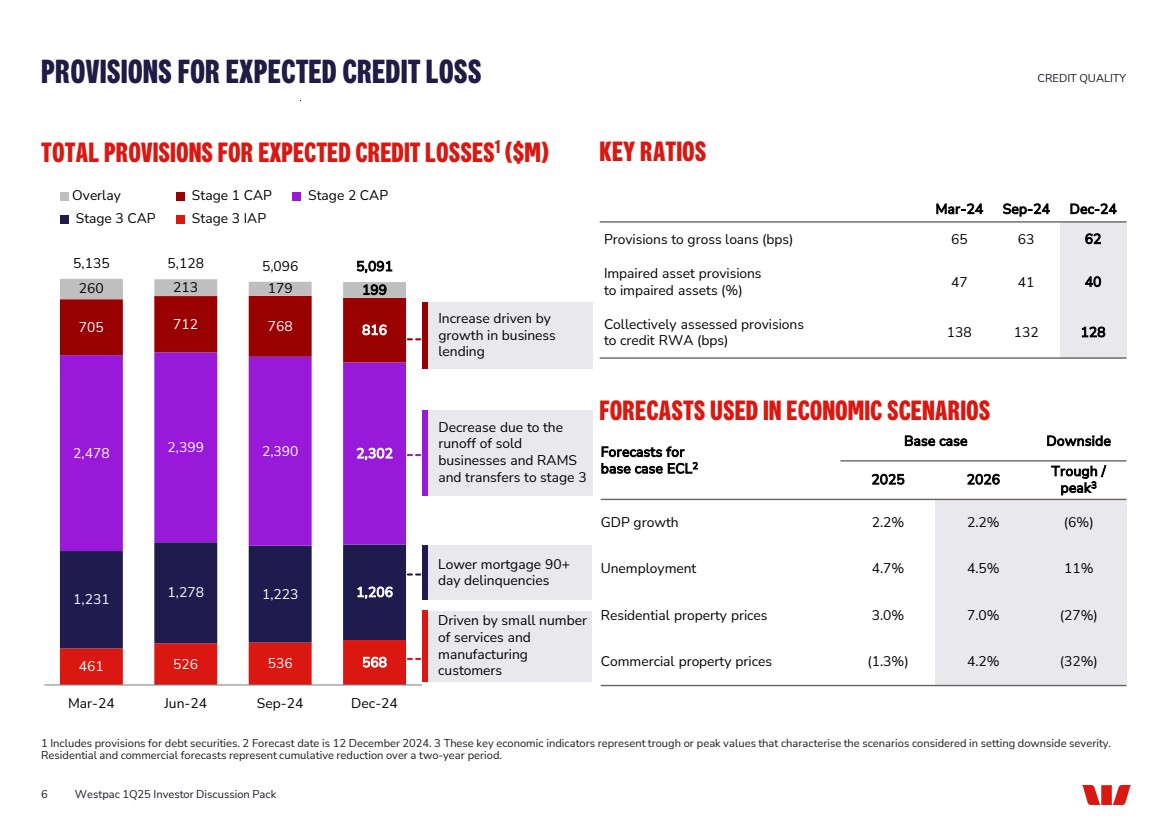

| 461 526 536 568 1,231 1,278 1,223 1,206 2,478 2,399 2,390 2,302 705 712 768 816 260 213 179 199 5,135 5,128 5,096 5,091 Mar-24 Jun-24 Sep-24 Dec-24 Overlay Stage 1 CAP Stage 2 CAP Stage 3 CAP Stage 3 IAP Lower mortgage 90+ day delinquencies Forecasts for base case ECL2 Base case Downside 2025 2026 Trough / peak3 GDP growth 2.2% 2.2% (6%) Unemployment 4.7% 4.5% 11% Residential property prices 3.0% 7.0% (27%) Commercial property prices (1.3%) 4.2% (32%) TOTAL PROVISIONS FOR EXPECTED CREDIT LOSSES KEY RATIOS 1 ($M) PROVISIONS FOR EXPECTED CREDIT LOSS CREDIT QUALITY 1 Includes provisions for debt securities. 2 Forecast date is 12 December 2024. 3 These key economic indicators represent trough or peak values that characterise the scenarios considered in setting downside severity. Residential and commercial forecasts represent cumulative reduction over a two-year period. Driven by small number of services and manufacturing customers Decrease due to the runoff of sold businesses and RAMS and transfers to stage 3 Mar-24 Sep-24 Dec-24 Provisions to gross loans (bps) 65 63 62 Impaired asset provisions to impaired assets (%) 47 41 40 Collectively assessed provisions to credit RWA (bps) 138 132 128 6 Westpac 1Q25 Investor Discussion Pack FORECASTS USED IN ECONOMIC SCENARIOS Increase driven by growth in business lending |

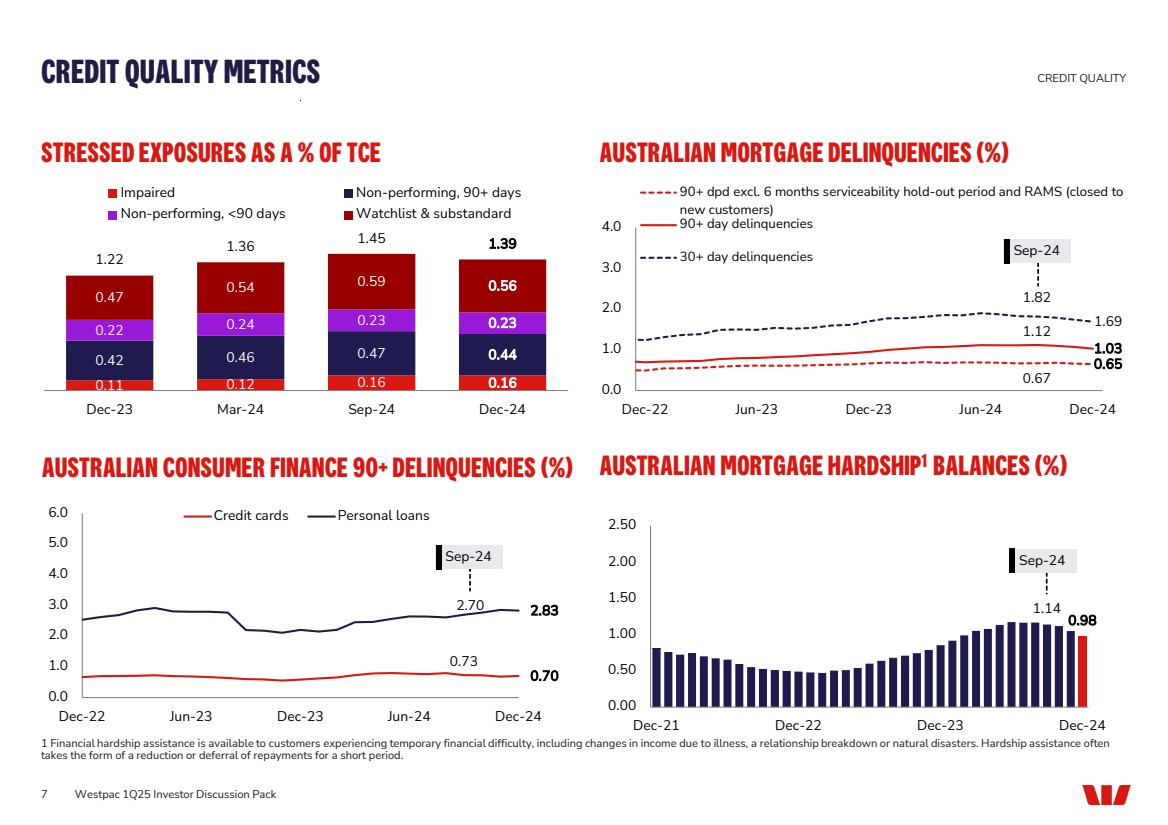

| 1.14 0.98 0.00 0.50 1.00 1.50 2.00 2.50 Dec-21 Dec-22 Dec-23 Dec-24 0.73 0.70 2.70 2.83 0.0 1.0 2.0 3.0 4.0 5.0 6.0 Dec-22 Jun-23 Dec-23 Jun-24 Dec-24 Credit cards Personal loans 0.11 0.12 0.16 0.16 0.42 0.46 0.47 0.44 0.22 0.24 0.23 0.23 0.47 0.54 0.59 0.56 1.22 1.36 1.45 1.39 Dec-23 Mar-24 Sep-24 Dec-24 Impaired Non-performing, 90+ days Non-performing, <90 days Watchlist & substandard AUSTRALIAN MORTGAGE DELINQUENCIES (%) AUSTRALIAN CONSUMER FINANCE 90+ DELINQUENCIES (%) STRESSED EXPOSURES AS A % OF TCE CREDIT QUALITY METRICS CREDIT QUALITY 1 Financial hardship assistance is available to customers experiencing temporary financial difficulty, including changes in income due to illness, a relationship breakdown or natural disasters. Hardship assistance often takes the form of a reduction or deferral of repayments for a short period. 7 Westpac 1Q25 Investor Discussion Pack 0.67 0.65 1.12 1.03 1.82 1.69 0.0 1.0 2.0 3.0 4.0 Dec-22 Jun-23 Dec-23 Jun-24 Dec-24 90+ dpd excl. 6 months serviceability hold-out period and RAMS (closed to new customers) 90+ day delinquencies 30+ day delinquencies AUSTRALIAN MORTGAGE HARDSHIP1 BALANCES (%) Sep-24 Sep-24 Sep-24 |

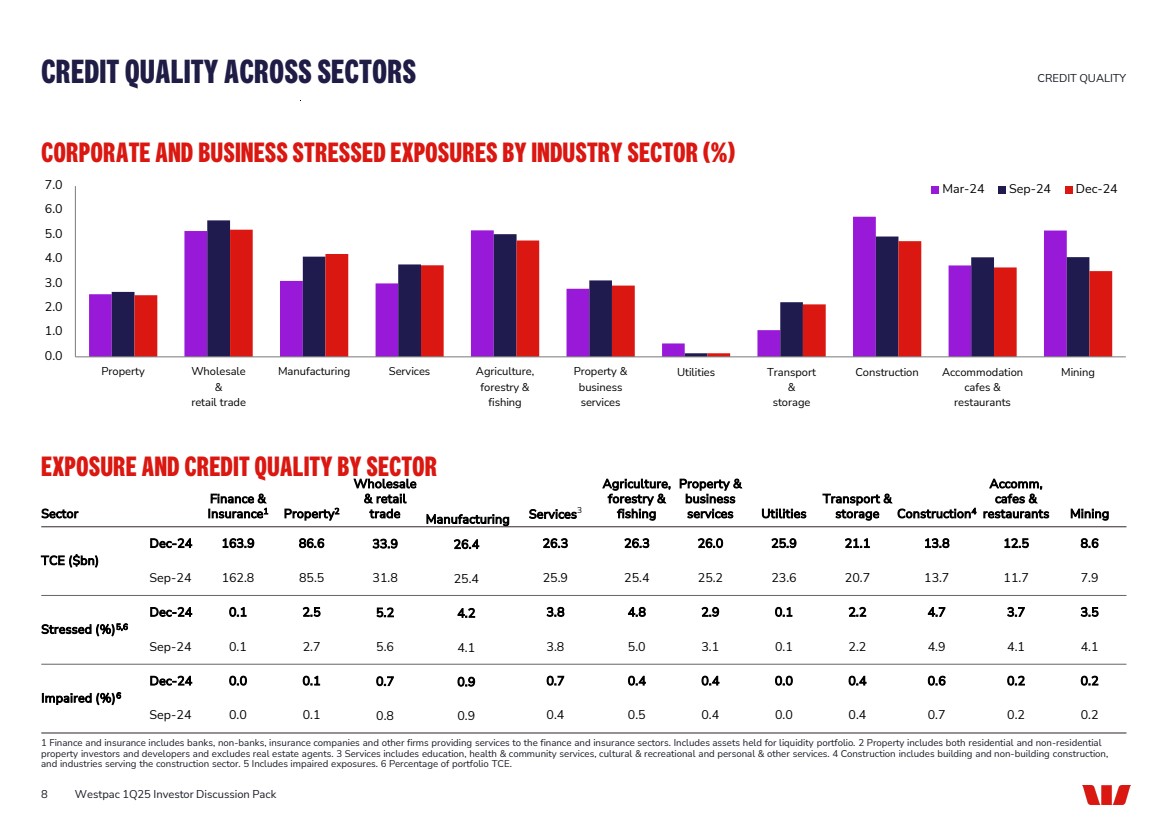

| 0.0 1.0 2.0 3.0 4.0 5.0 6.0 7.0 Property Wholesale & retail trade Manufacturing Services Agriculture, forestry & fishing Property & business services Utilities Transport & storage Construction Accommodation cafes & restaurants Mining Mar-24 Sep-24 Dec-24 CORPORATE AND BUSINESS STRESSED EXPOSURES BY INDUSTRY SECTOR (%) EXPOSURE AND CREDIT QUALITY BY SECTOR Sector Finance & Insurance1 Property2 Wholesale & retail trade Manufacturing Services3 Agriculture, forestry & fishing Property & business services Utilities Transport & storage Construction4 Accomm, cafes & restaurants Mining TCE ($bn) Dec-24 163.9 86.6 33.9 26.4 26.3 26.3 26.0 25.9 21.1 13.8 12.5 8.6 Sep-24 162.8 85.5 31.8 25.4 25.9 25.4 25.2 23.6 20.7 13.7 11.7 7.9 Stressed (%)5,6 Dec-24 0.1 2.5 5.2 4.2 3.8 4.8 2.9 0.1 2.2 4.7 3.7 3.5 Sep-24 0.1 2.7 5.6 4.1 3.8 5.0 3.1 0.1 2.2 4.9 4.1 4.1 Impaired (%)6 Dec-24 0.0 0.1 0.7 0.9 0.7 0.4 0.4 0.0 0.4 0.6 0.2 0.2 Sep-24 0.0 0.1 0.8 0.9 0.4 0.5 0.4 0.0 0.4 0.7 0.2 0.2 CREDIT QUALITY ACROSS SECTORS CREDIT QUALITY 1 Finance and insurance includes banks, non-banks, insurance companies and other firms providing services to the finance and insurance sectors. Includes assets held for liquidity portfolio. 2 Property includes both residential and non-residential property investors and developers and excludes real estate agents. 3 Services includes education, health & community services, cultural & recreational and personal & other services. 4 Construction includes building and non-building construction, and industries serving the construction sector. 5 Includes impaired exposures. 6 Percentage of portfolio TCE. 8 Westpac 1Q25 Investor Discussion Pack |

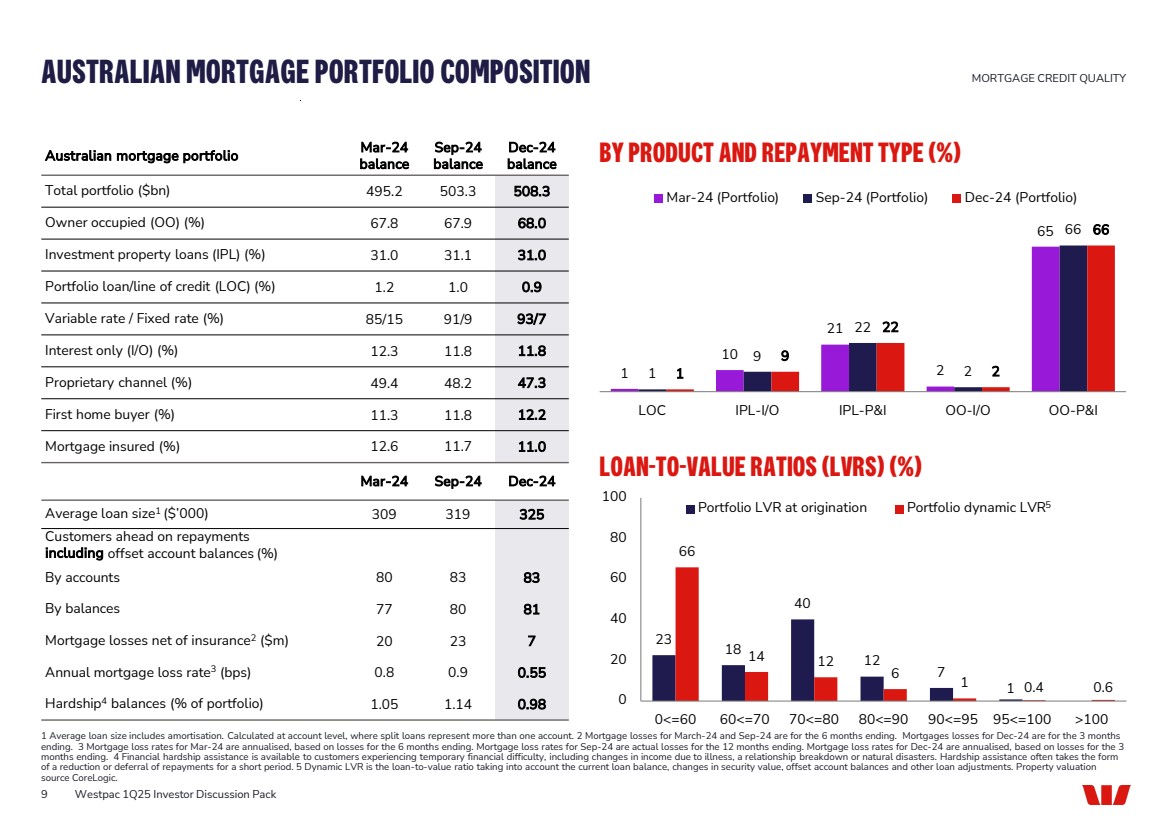

| Australian mortgage portfolio Mar-24 balance Sep-24 balance Dec-24 balance Total portfolio ($bn) 495.2 503.3 508.3 Owner occupied (OO) (%) 67.8 67.9 68.0 Investment property loans (IPL) (%) 31.0 31.1 31.0 Portfolio loan/line of credit (LOC) (%) 1.2 1.0 0.9 Variable rate / Fixed rate (%) 85/15 91/9 93/7 Interest only (I/O) (%) 12.3 11.8 11.8 Proprietary channel (%) 49.4 48.2 47.3 First home buyer (%) 11.3 11.8 12.2 Mortgage insured (%) 12.6 11.7 11.0 Mar-24 Sep-24 Dec-24 Average loan size1 ($’000) 309 319 325 Customers ahead on repayments including offset account balances (%) By accounts 80 83 83 By balances 77 80 81 Mortgage losses net of insurance2 ($m) 20 23 7 Annual mortgage loss rate3 (bps) 0.8 0.9 0.55 Hardship4 balances (% of portfolio) 1.05 1.14 0.98 AUSTRALIAN MORTGAGE PORTFOLIO COMPOSITION MORTGAGE CREDIT QUALITY 1 Average loan size includes amortisation. Calculated at account level, where split loans represent more than one account. 2 Mortgage losses for March-24 and Sep-24 are for the 6 months ending. Mortgages losses for Dec-24 are for the 3 months ending. 3 Mortgage loss rates for Mar-24 are annualised, based on losses for the 6 months ending. Mortgage loss rates for Sep-24 are actual losses for the 12 months ending. Mortgage loss rates for Dec-24 are annualised, based on losses for the 3 months ending. 4 Financial hardship assistance is available to customers experiencing temporary financial difficulty, including changes in income due to illness, a relationship breakdown or natural disasters. Hardship assistance often takes the form of a reduction or deferral of repayments for a short period. 5 Dynamic LVR is the loan-to-value ratio taking into account the current loan balance, changes in security value, offset account balances and other loan adjustments. Property valuation source CoreLogic. 9 Westpac 1Q25 Investor Discussion Pack BY PRODUCT AND REPAYMENT TYPE (%) LOAN-TO-VALUE RATIOS (LVRS) (%) 1 10 21 2 65 1 9 22 2 66 1 9 22 2 66 LOC IPL-I/O IPL-P&I OO-I/O OO-P&I Mar-24 (Portfolio) Sep-24 (Portfolio) Dec-24 (Portfolio) 23 18 40 12 7 1 66 14 12 6 1 0.4 0.6 0 20 40 60 80 100 0<=60 60<=70 70<=80 80<=90 90<=95 95<=100 >100 Portfolio LVR at origination Portfolio dynamic LVR5 |

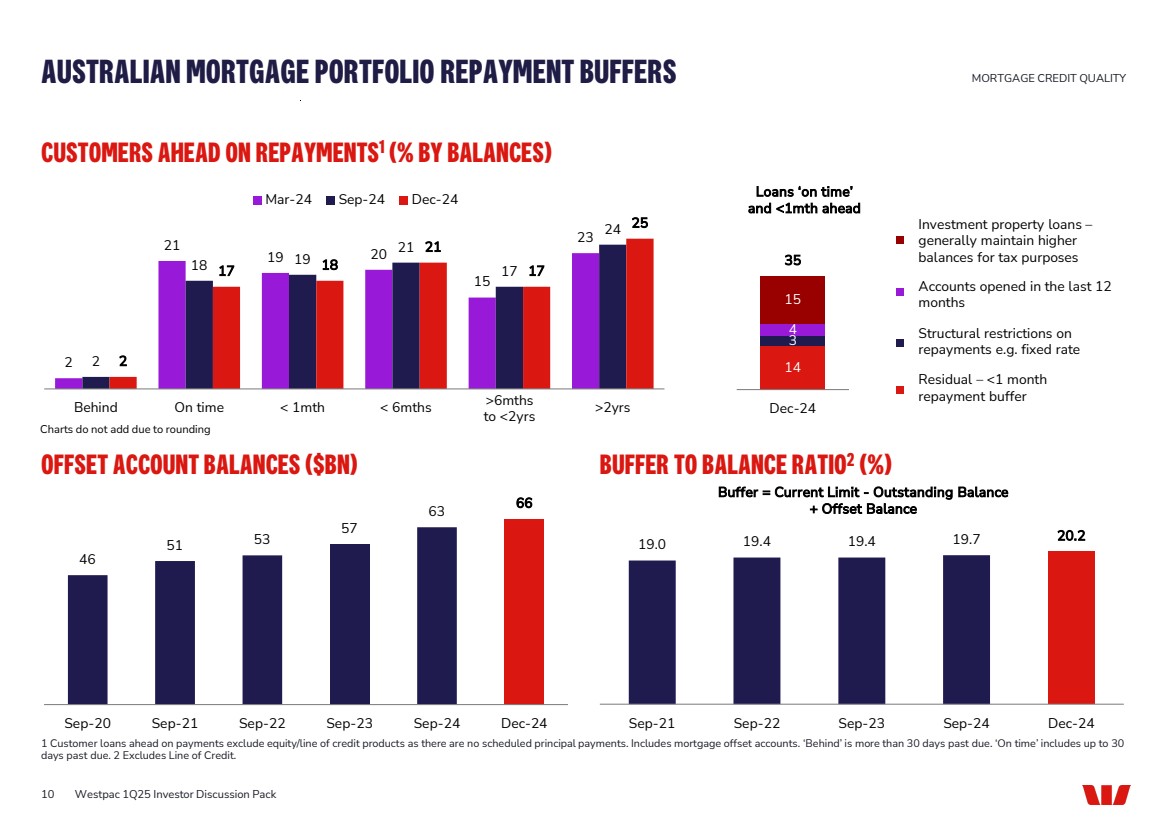

| 10 CUSTOMERS AHEAD ON REPAYMENTS1 (% BY BALANCES) OFFSET ACCOUNT BALANCES ($BN) BUFFER TO BALANCE RATIO2 (%) Westpac 1Q25 Investor Discussion Pack AUSTRALIAN MORTGAGE PORTFOLIO REPAYMENT BUFFERS MORTGAGE CREDIT QUALITY 1 Customer loans ahead on payments exclude equity/line of credit products as there are no scheduled principal payments. Includes mortgage offset accounts. ‘Behind’ is more than 30 days past due. ‘On time’ includes up to 30 days past due. 2 Excludes Line of Credit. 14 3 4 15 35 Dec-24 Investment property loans – generally maintain higher balances for tax purposes Accounts opened in the last 12 months Structural restrictions on repayments e.g. fixed rate Residual – <1 month repayment buffer Charts do not add due to rounding Loans ‘on time’ and <1mth ahead 19.0 19.4 19.4 19.7 20.2 Sep-21 Sep-22 Sep-23 Sep-24 Dec-24 Buffer = Current Limit - Outstanding Balance + Offset Balance 46 51 53 57 63 66 Sep-20 Sep-21 Sep-22 Sep-23 Sep-24 Dec-24 2 21 19 20 15 23 2 18 19 21 17 24 2 17 18 21 17 25 Behind On time < 1mth < 6mths >2yrs Mar-24 Sep-24 Dec-24 >6mths to <2yrs |

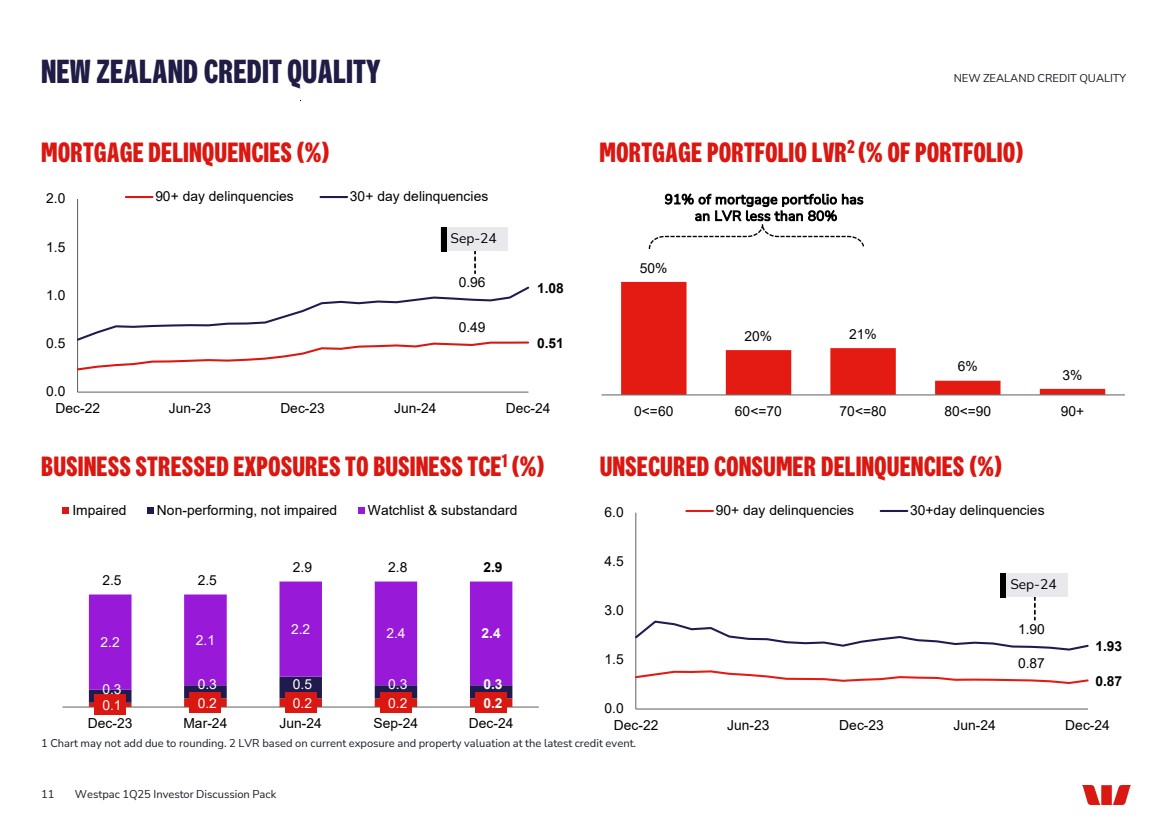

| MORTGAGE DELINQUENCIES (%) MORTGAGE PORTFOLIO LVR2 (% OF PORTFOLIO) BUSINESS STRESSED EXPOSURES TO BUSINESS TCE1 (%) UNSECURED CONSUMER DELINQUENCIES (%) NEW ZEALAND CREDIT QUALITY NEW ZEALAND CREDIT QUALITY 1 Chart may not add due to rounding. 2 LVR based on current exposure and property valuation at the latest credit event. 0.49 0.51 0.96 1.08 0.0 0.5 1.0 1.5 2.0 Dec-22 Jun-23 Dec-23 Jun-24 Dec-24 90+ day delinquencies 30+ day delinquencies 50% 20% 21% 6% 3% 0<=60 60<=70 70<=80 80<=90 90+ 0.1 0.2 0.2 0.2 0.2 0.3 0.3 0.5 0.3 0.3 2.2 2.1 2.2 2.4 2.4 2.5 2.5 2.9 2.8 2.9 Dec-23 Mar-24 Jun-24 Sep-24 Dec-24 Impaired Non-performing, not impaired Watchlist & substandard 0.87 0.87 1.90 1.93 0.0 1.5 3.0 4.5 6.0 Dec-22 Jun-23 Dec-23 Jun-24 Dec-24 90+ day delinquencies 30+day delinquencies 91% of mortgage portfolio has an LVR less than 80% 11 Westpac 1Q25 Investor Discussion Pack Sep-24 Sep-24 |

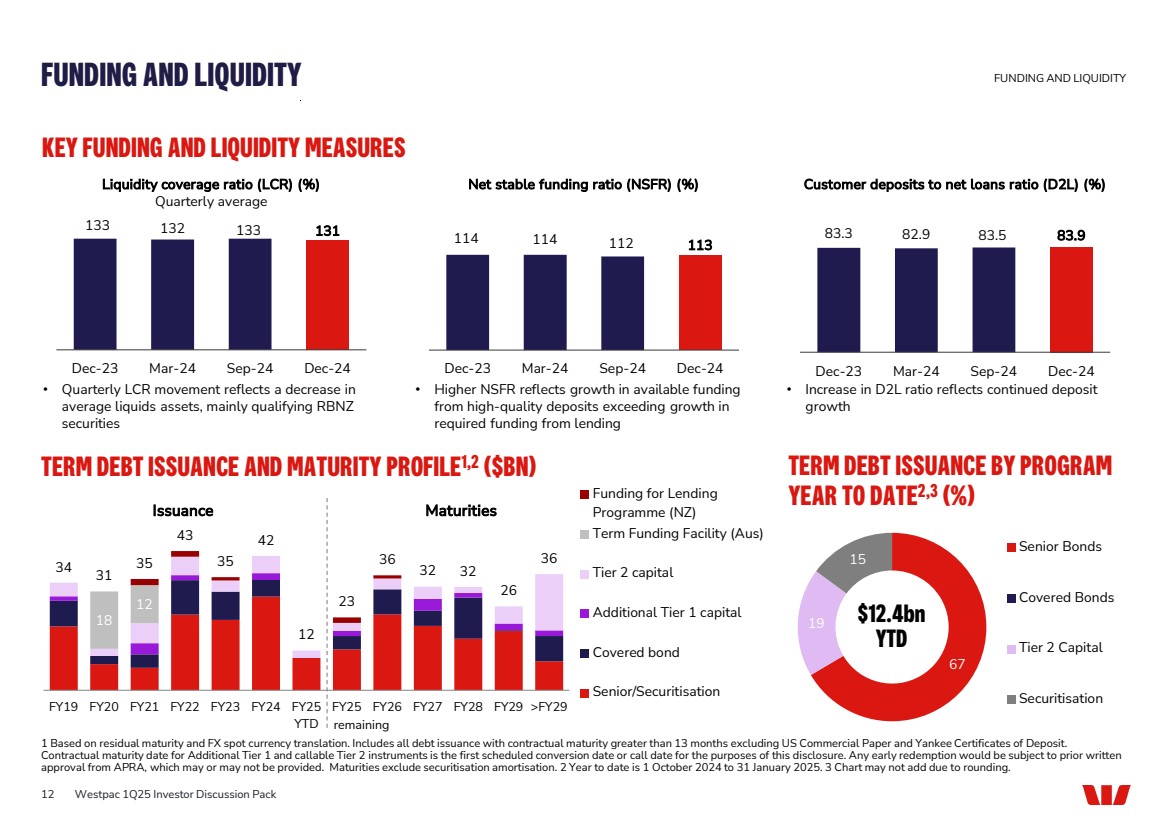

| TERM DEBT ISSUANCE AND MATURITY PROFILE1,2 ($BN) FUNDING AND LIQUIDITY FUNDING AND LIQUIDITY 1 Based on residual maturity and FX spot currency translation. Includes all debt issuance with contractual maturity greater than 13 months excluding US Commercial Paper and Yankee Certificates of Deposit. Contractual maturity date for Additional Tier 1 and callable Tier 2 instruments is the first scheduled conversion date or call date for the purposes of this disclosure. Any early redemption would be subject to prior written approval from APRA, which may or may not be provided. Maturities exclude securitisation amortisation. 2 Year to date is 1 October 2024 to 31 January 2025. 3 Chart may not add due to rounding. KEY FUNDING AND LIQUIDITY MEASURES Liquidity coverage ratio (LCR) (%) Quarterly average Net stable funding ratio (NSFR) (%) Customer deposits to net loans ratio (D2L) (%) • Quarterly LCR movement reflects a decrease in average liquids assets, mainly qualifying RBNZ securities • Increase in D2L ratio reflects continued deposit growth • Higher NSFR reflects growth in available funding from high-quality deposits exceeding growth in required funding from lending TERM DEBT ISSUANCE BY PROGRAM YEAR TO DATE2,3 (%) 12 Westpac 1Q25 Investor Discussion Pack 133 132 133 131 Dec-23 Mar-24 Sep-24 Dec-24 114 114 112 113 Dec-23 Mar-24 Sep-24 Dec-24 83.3 82.9 83.5 83.9 Dec-23 Mar-24 Sep-24 Dec-24 67 19 15 Senior Bonds Covered Bonds Tier 2 Capital Securitisation $12.4bn YTD 18 12 34 31 35 43 35 42 12 23 36 32 32 26 36 FY19 FY20 FY21 FY22 FY23 FY24 FY25 YTD FY25 FY26 FY27 FY28 FY29 >FY29 Funding for Lending Programme (NZ) Term Funding Facility (Aus) Tier 2 capital Additional Tier 1 capital Covered bond Senior/Securitisation Issuance Maturities remaining |

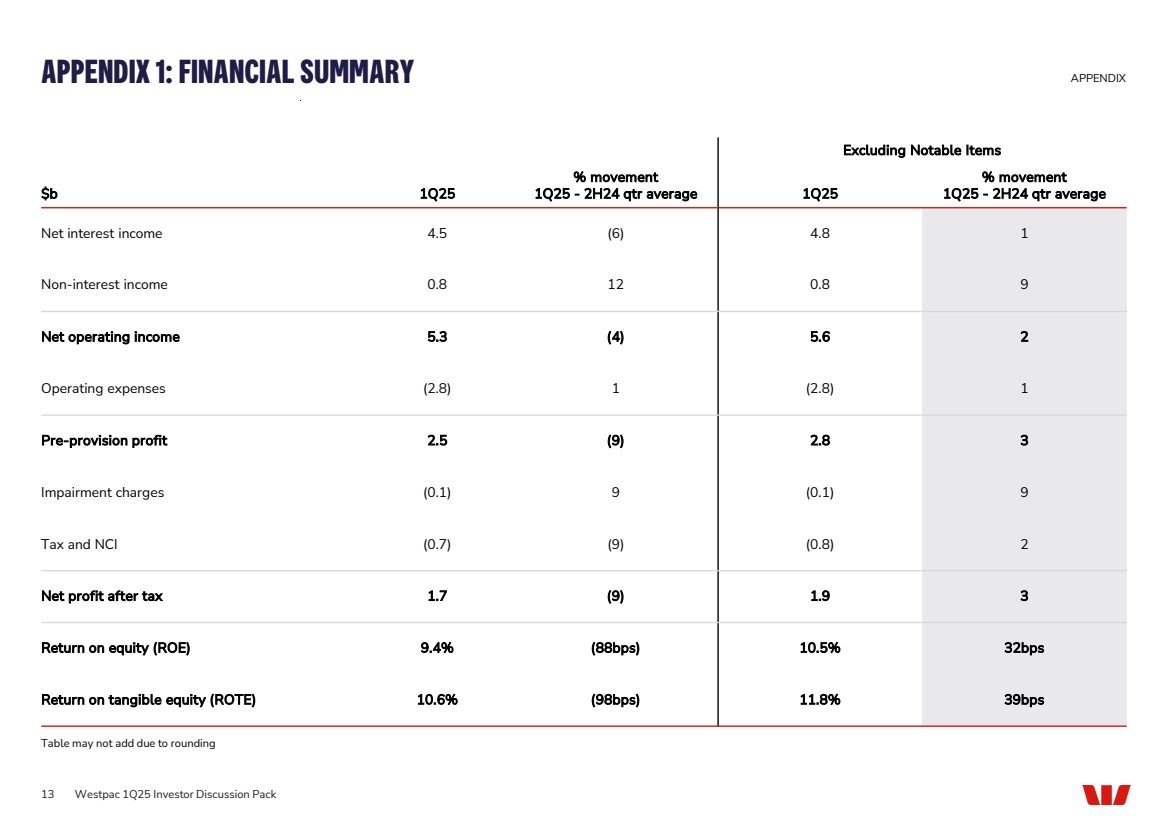

| Table may not add due to rounding APPENDIX 1: FINANCIAL SUMMARY APPENDIX Excluding Notable Items $b 1Q25 % movement 1Q25 - 2H24 qtr average 1Q25 % movement 1Q25 - 2H24 qtr average Net interest income 4.5 (6) 4.8 1 Non-interest income 0.8 12 0.8 9 Net operating income 5.3 (4) 5.6 2 Operating expenses (2.8) 1 (2.8) 1 Pre-provision profit 2.5 (9) 2.8 3 Impairment charges (0.1) 9 (0.1) 9 Tax and NCI (0.7) (9) (0.8) 2 Net profit after tax 1.7 (9) 1.9 3 Return on equity (ROE) 9.4% (88bps) 10.5% 32bps Return on tangible equity (ROTE) 10.6% (98bps) 11.8% 39bps 13 Westpac 1Q25 Investor Discussion Pack |

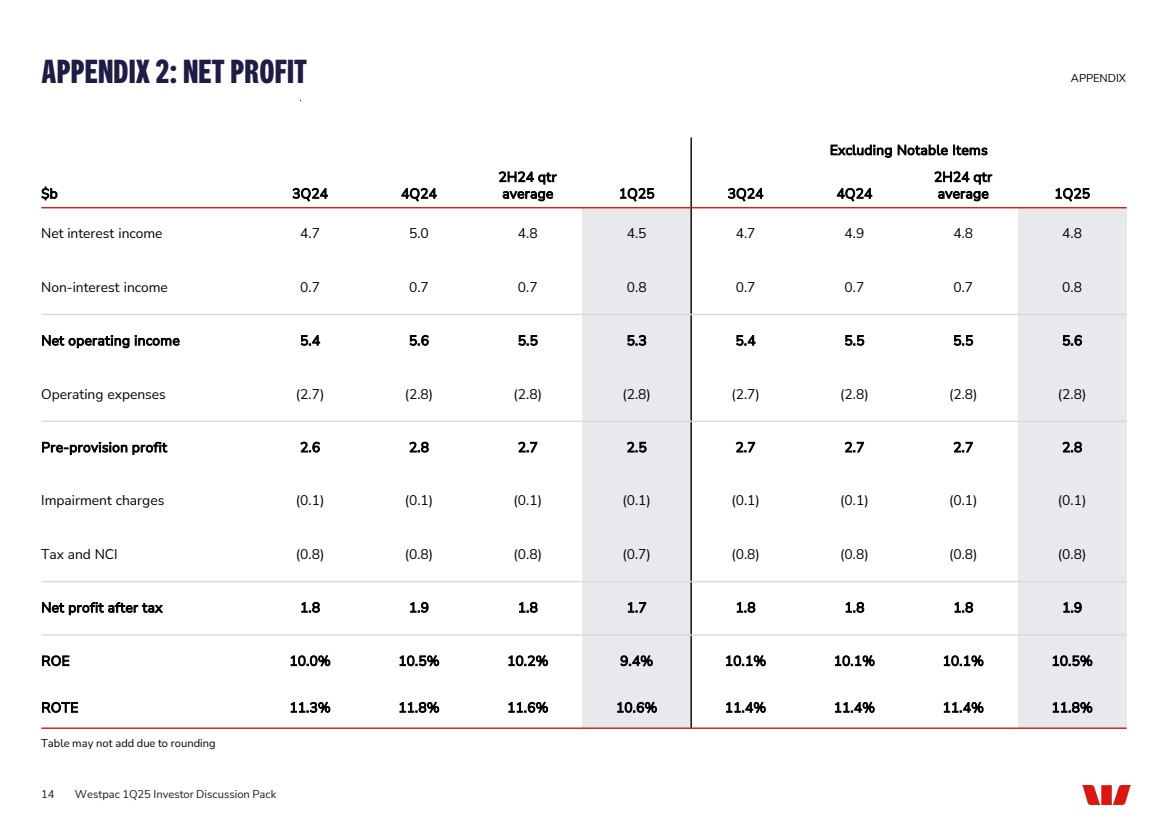

| Table may not add due to rounding APPENDIX 2: NET PROFIT APPENDIX Excluding Notable Items $b 3Q24 4Q24 2H24 qtr average 1Q25 3Q24 4Q24 2H24 qtr average 1Q25 Net interest income 4.7 5.0 4.8 4.5 4.7 4.9 4.8 4.8 Non-interest income 0.7 0.7 0.7 0.8 0.7 0.7 0.7 0.8 Net operating income 5.4 5.6 5.5 5.3 5.4 5.5 5.5 5.6 Operating expenses (2.7) (2.8) (2.8) (2.8) (2.7) (2.8) (2.8) (2.8) Pre-provision profit 2.6 2.8 2.7 2.5 2.7 2.7 2.7 2.8 Impairment charges (0.1) (0.1) (0.1) (0.1) (0.1) (0.1) (0.1) (0.1) Tax and NCI (0.8) (0.8) (0.8) (0.7) (0.8) (0.8) (0.8) (0.8) Net profit after tax 1.8 1.9 1.8 1.7 1.8 1.8 1.8 1.9 ROE 10.0% 10.5% 10.2% 9.4% 10.1% 10.1% 10.1% 10.5% ROTE 11.3% 11.8% 11.6% 10.6% 11.4% 11.4% 11.4% 11.8% 14 Westpac 1Q25 Investor Discussion Pack |

| NIM Net interest margin CET1 capital ratio Common equity tier one capital ratio RWA Risk weighted assets CAP Collectively assessed provisions TCE Total committed exposures LCR Liquidity coverage ratio NSFR Net stable funding ratio ROE Return on average equity ROTE Return on average tangible equity APPENDIX 3: ABBREVIATIONS 15 Westpac Group 2024 Full Year Results Presentation & Investor Discussion Pack APPENDIX |

| INVESTOR RELATIONS TEAM – CONTACT US CONTACT US INVESTOR RELATIONS CONTACT SHARE REGISTRY CONTACT For all shareholding enquiries relating to: • Address details and communication preferences • Updating bank account details, and participation in the dividend reinvestment plan For all matters relating to Westpac’s strategy, performance and results 1800 804 255 westpac@cm.mpms.mufg.com au.investorcentre.mpms.mufg.com +61 2 9178 2977 investorrelations@westpac.com.au westpac.com.au/investorcentre 16 Westpac 1Q25 Investor Discussion Pack Lucy Wilson Head of Corporate Reporting and ESG Catherine Garcia Head of Investor Relations, Institutional Arthur Petratos Manager, Shareholder Services Laura Babaic Graduate, Investor Relations Jacqueline Boddy Head of Debt Investor Relations Justin McCarthy General Manager, Investor Relations James Wibberley Manager, Investor Relations Nathan Fontyne Senior Analyst, Investor Relations |

| DISCLAIMER The material contained in this presentation is intended to be general background information on Westpac Banking Corporation (Westpac) and its activities. The information is supplied in summary form and is therefore not necessarily complete. It is not intended that it be relied upon as advice to investors or potential investors, who should consider seeking independent professional advice depending upon their specific investment objectives, financial situation or particular needs. The material contained in this presentation may include information derived from publicly available sources that have not been independently verified. No representation or warranty is made as to the accuracy, completeness or reliability of the information. All amounts are in Australian dollars unless otherwise indicated. This presentation contains statements that constitute “forward-looking statements” within the meaning of Section 21E of the US Securities Exchange Act of 1934. Forward-looking statements are statements that are not historical facts. Forward-looking statements appear in a number of places in this presentation and include statements regarding our intent, belief or current expectations with respect to our business and operations, macro and micro economic and market conditions, results of operations and financial condition, capital adequacy, liquidity and risk management, including, without limitation, future loan loss provisions and financial support to certain borrowers, forecasted economic indicators and performance metric outcomes, indicative drivers, climate- and other sustainability-related statements, commitments, targets, projections and metrics, and other estimated and proxy data. We use words such as ‘will’, ‘may’, ‘expect’, ‘intend’, ‘seek’, ‘would’, ‘should’, ‘could’, ‘continue’, ‘plan’, ‘estimate’, ‘anticipate’, ‘believe’, ‘probability’, ‘indicative’, ‘risk’, ‘aim’, ‘outlook’, ‘forecast’, ‘f’cast’, ‘f’, ‘assumption’, ‘projection’, ‘target’, ‘goal’, ‘guidance’, ‘ambition’, ‘objective’ or other similar words to identify forward-looking statements, or otherwise identify forward-looking statements. These forward-looking statements reflect our current views on future events and are subject to change, certain known and unknown risks, uncertainties and assumptions and other factors which are, in many instances, beyond our control (and the control of our officers, employees, agents and advisors), and have been made based on management’s expectations or beliefs concerning future developments and their potential effect upon us. Forward-looking statements may also be made, verbally or in writing, by members of Westpac’s management or Board in connection with this presentation. Such statements are subject to the same limitations, uncertainties, assumptions and disclaimers set out in this presentation. There can be no assurance that future developments or performance will align with our expectations or that the effect of future developments on us will be those anticipated. Actual results could differ materially from those we expect or which are expressed or implied in forward-looking statements, depending on various factors including, but not limited to, those described in the sections titled ‘Our Operating Environment’ and ‘Risk Management' in our 2024 Annual Report, as well as the document titled ‘2024 Risk Factors’ (each available at www.westpac.com.au). When relying on forward-looking statements to make decisions with respect to us, investors and others should carefully consider such factors and other uncertainties and events. Except as required by law, we assume no obligation to revise or update any forward-looking statements contained in this presentation, whether from new information, future events, conditions or otherwise, after the date of this presentation. We also make statements about our processes and policies (including what they are designed to do) as well as the availability of our systems or product features. Systems, processes and product features can be subject to disruption, and may not always work as intended, so these statements are limited by the factors described in the section titled ‘Risk Management’ in our 2024 Annual Report, as well as the 2024 Risk Factors document. DISCLAIMER 17 Westpac 1Q25 Investor Discussion Pack |