UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-03752

AMG Funds III

(Exact name of registrant as specified in charter)

800 Connecticut Avenue, Norwalk, Connecticut 06854

(Address of principal executive offices) (Zip code)

AMG Funds LLC

800 Connecticut Avenue, Norwalk, Connecticut 06854

(Name and address of agent for service)

Registrant’s telephone number, including area code: (203) 299-3500

Date of fiscal year end: May 31

Date of reporting period: June 1, 2014 – May 31, 2015

(Annual Shareholder Report)

Item 1. Reports to Shareholders

| | | | |

| | ANNUAL REPORT | | |

| | | | | | |

| | |

| | | AMG Funds |

| | | May 31, 2015 | | | | |

| | | AMG Managers Cadence Capital Appreciation Fund |

| | | Investor Class: MPAFX | | | Service Class: MCFYX | | | Institutional Class: MPCIX |

| | | AMG Managers Cadence Mid Cap Fund |

| | | Investor Class: MCMAX | | | Service Class: MCMYX | | | Institutional Class: MCMFX |

| | | AMG Managers Cadence Emerging Companies Fund |

| | | | | | Service Class: MECAX | | | Institutional Class:MECIX |

| | |

| | |

| | | |

| www.amgfunds.com | | AR065-0515 |

| | | | |

| | | | | |

| | | AMG Funds | | |

| | | Annual Report—May 31, 2015 | | |

| | | | | | |

| | | TABLE OF CONTENTS | | PAGE | |

| | | | |

| | | LETTER TO SHAREHOLDERS | | | 2 | |

| | | |

| | | ABOUT YOUR FUND’S EXPENSES | | | 3 | |

| | | |

| | | PORTFOLIO MANAGER’S COMMENTS, FUND SNAPSHOTS, AND SCHEDULES OF PORTFOLIO INVESTMENTS | | | | |

| | | |

| | | AMG Managers Cadence Capital Appreciation Fund | | | 4 | |

| | | AMG Managers Cadence Mid Cap Fund | | | 10 | |

| | | AMG Managers Cadence Emerging Companies Fund | | | 16 | |

| | | |

| | | NOTES TO SCHEDULES OF PORTFOLIO INVESTMENTS | | | 22 | |

| | | |

| | | FINANCIAL STATEMENTS | | | | |

| | | |

| | | Statement of Assets and Liabilities | | | 24 | |

| | | Balance sheets, net asset value (NAV) per share computations and cumulative undistributed amounts | | | | |

| | | |

| | | Statement of Operations | | | 26 | |

| | | Detail of sources of income, expenses, and realized and unrealized gains (losses) during the fiscal year | | | | |

| | | |

| | | Statements of Changes in Net Assets | | | 27 | |

| | | Detail of changes in assets for the past two fiscal years | | | | |

| | | |

| | | Financial Highlights | | | 28 | |

| | | Historical net asset values per share, distributions, total returns, income and expense ratios, turnover ratios and net assets | | | | |

| | | |

| | | Notes to Financial Highlights | | | 33 | |

| | | |

| | | Notes to Financial Statements | | | 34 | |

| | | Accounting and distribution policies, details of agreements and transactions with Fund management and affiliates, and descriptions of certain investment risks | | | | |

| | | |

| | | REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM | | | 42 | |

| | | |

| | | TRUSTEES AND OFFICERS | | | 43 | |

|

Nothing contained herein is to be considered an offer, sale or solicitation of an offer to buy shares of any series of the AMG Family of Funds. Such offering is made only by prospectus, which includes details as to offering price and other material information. |

| |

|

| | | | |

| | | | |

| | Letter to Shareholders | | |

| | | | |

DEAR SHAREHOLDER:

Overall, U.S. equity investors were rewarded with another strong period of returns for the fiscal year ended May 31, 2015. Despite the collapse of oil prices and its negative effects on energy stocks, the S&P 500 Index, a widely followed barometer of the U.S. equity market, rose nearly 12% during the past twelve months. Nine out of ten sectors of the S&P 500 were positive over the prior twelve months, led by health care. International stocks, by comparison, fell 1%, as measured by the MSCI ACWI ex USA Index (in U.S. Dollar terms). International investment returns in U.S. Dollar terms were impacted by the strengthening U.S. Dollar. The first quarter of 2015 also marked the six-year anniversary of the equity bull market. The first quarter of 2015 also marked 9 consecutive quarters of positive performance for the S&P 500. Continuing the trend from 2014, equity funds, particularly international funds, saw strong inflows in 2015.

The Barclays U.S. Aggregate Bond Index, a broad U.S. bond market benchmark, returned 3.0% for the fiscal year ended May 31, 2015. Interest rates fell throughout much of 2014, lending positive support to bond prices. However, interest rates have increased more recently, putting pressure on bond prices, driven by a combination of the strengthening U.S. economy along with market expectation of an eventual end, in the coming months, to the Federal Reserve’s zero interest rate policy.

Our foremost goal at AMG Funds is to provide investment solutions that help our shareholders successfully reach their long-term investment goals. By partnering with AMG’s affiliated investment boutiques, AMG Funds provide access to a distinctive array of actively managed, return oriented investment strategies. Additionally, we oversee and distribute a number of complementary open-architecture mutual funds subadvised by unaffiliated investment managers. We thank you for your continued confidence and investment in AMG Funds. You can rest assured that under all market conditions our team is focused on delivering excellent investment management services for your benefit.

Respectfully,

Jeffery Cerutti

President

AMG Funds

| | | | | | | | |

| Average Annual Total Returns | | Periods ended May 31, 2015 |

| Stocks: | | | | 1 Year | | 3 Years | | 5 Years |

| Large Caps | | (S&P 500 Index) | | 11.81% | | 19.67% | | 16.54% |

| | | | |

| Small Caps | | (Russell 2000® Index) | | 11.32% | | 19.45% | | 15.04% |

| | | | |

| International | | (MSCI All Country World Index ex USA Index) | | (0.90)% | | 12.61% | | 8.09% |

| Bonds: | | | | | | | | |

| Investment Grade | | (Barclays U.S. Aggregate Bond Index) | | 3.03% | | 2.21% | | 3.90% |

| | | | |

| High Yield | | (Barclays U.S. High Yield Bond Index) | | 1.95% | | 8.10% | | 9.21% |

| | | | |

| Tax-exempt | | (Barclays Municipal Bond Index) | | 3.18% | | 3.09% | | 4.53% |

| | | | |

| Treasury Bills | | (BofA Merrill Lynch 6-month U.S. Treasury Bill) | | 0.15% | | 0.17% | | 0.21% |

| | | | |

| | | | | |

| | | About Your Fund’s Expenses | | |

| | | | | |

|

As a shareholder of a Fund, you may incur two types of costs: (1) transaction costs, which may include sales charges (loads) on purchase payments; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution (12b-1) fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on $1,000 invested at the beginning of the period and held for the entire period as indicated below. ACTUAL EXPENSES The first line of the following table provides information about the actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period. HYPOTHETICAL EXAMPLE FOR COMPARISON PURPOSES The second line of the following table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed annual rate of return of 5% before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds by comparing this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds. Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. |

| | | | | | | | |

| Six Months Ended May 31, 2015 | | Expense

Ratio for

the Period | | Beginning

Account Value

12/01/14 | | Ending

Account Value

05/31/15 | | Expenses

Paid During

the Period* |

| AMG Managers Cadence Capital Appreciation Fund |

| Investor Class | | | | | | | | |

| Based on Actual Fund Return | | 1.12% | | $1,000 | | $1,056 | | $5.74 |

| Hypothetical (5% return before expenses) | | 1.12% | | $1,000 | | $1,019 | | $5.64 |

| Service Class | | | | | | | | |

| Based on Actual Fund Return | | 0.97% | | $1,000 | | $1,057 | | $4.97 |

| Hypothetical (5% return before expenses) | | 0.97% | | $1,000 | | $1,020 | | $4.89 |

| Institutional Class | | | | | | | | |

| Based on Actual Fund Return | | 0.72% | | $1,000 | | $1,058 | | $3.69 |

| Hypothetical (5% return before expenses) | | 0.72% | | $1,000 | | $1,021 | | $3.63 |

| AMG Managers Cadence Mid Cap Fund |

| Investor Class | | | | | | | | |

| Based on Actual Fund Return | | 1.12% | | $1,000 | | $1,054 | | $5.73 |

| Hypothetical (5% return before expenses) | | 1.12% | | $1,000 | | $1,019 | | $5.64 |

| Service Class | | | | | | | | |

| Based on Actual Fund Return | | 0.97% | | $1,000 | | $1,055 | | $4.97 |

| Hypothetical (5% return before expenses) | | 0.97% | | $1,000 | | $1,020 | | $4.89 |

| Institutional Class | | | | | | | | |

| Based on Actual Fund Return | | 0.72% | | $1,000 | | $1,056 | | $3.69 |

| Hypothetical (5% return before expenses) | | 0.72% | | $1,000 | | $1,021 | | $3.63 |

| AMG Managers Cadence Emerging Companies Fund |

| Service Class | | | | | | | | |

| Based on Actual Fund Return | | 1.67% | | $1,000 | | $1,117 | | $8.81 |

| Hypothetical (5% return before expenses) | | 1.67% | | $1,000 | | $1,017 | | $8.40 |

| Institutional Class | | |

| Based on Actual Fund Return | | 1.42% | | $1,000 | | $1,119 | | $7.50 |

| Hypothetical (5% return before expenses) | | 1.42% | | $1,000 | | $1,018 | | $7.14 |

| * | Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (182), then divided by 365. |

| | | | |

| | | | | |

| | | AMG Managers Cadence Capital Appreciation Fund | | |

| | | Portfolio Manager’s Comments | | |

| | | | | | | | |

For the fiscal year ended May 31, 2015, the AMG Managers Cadence Capital Appreciation Fund (Institutional Class) (the “Fund”) returned 13.6%, lagging its benchmark, the Russell 1000® Growth Index, which returned 14.7%. U.S. stocks continued their ascent during the fiscal year ended May 31, 2015, with the broad S&P 500 Index returning 11.8%. This performance followed the S&P’s strong gain of 20.5% for the prior 12 months ended May 31, 2014, challenging many strategists who argued that rising stock prices in the face of slowing global economic growth were a recipe for investment disappointment. Despite the economic and market cross currents, the Fund posted a positive return, but modestly underperformed the Russell 1000 Growth Index. The Fund performed well for the fiscal year in the consumer staples, financials, materials and industrials sectors, adding value versus the Russell 1000 Growth Index through a combination of stock selection and sector allocation. In contrast, the Fund underperformed the benchmark in health care, information technology, consumer discretionary and energy. Health care has been among the market’s best performing sectors since 2011, powered by increased utilization, innovation in new drugs and medical devices, a powerful IPO market and a robust M&A environment. The Fund benefitted from these tailwinds with portfolio gains exceeding 30% in the fiscal year. Conversely, energy was the weakest sector over the last year, as crude oil prices collapsed by over 50%. Energy stocks in the Russell 1000 Growth Index declined by nearly 16%, and Fund holdings experienced declines that averaged nearly 27%. To emphasize the rotational nature of the equity market, energy was the Russell 1000 Growth’s strongest performing sector in the fiscal year ended May 31, 2014, returning over 35%. | | | | THE YEAR IN REVIEW The fiscal year started on a strong note, with the S&P 500 hitting eight new all-time highs in June, 2014. The employment picture and consumer spending, while far from robust, suggested the economic recovery, which started in June 2009 (essentially six years ago), was still intact, although growing at a slower pace than normal. The U.S. Federal Reserve (the “Fed”) maintained an accommodative monetary stance, fearful of policy mistakes at this stage of the recovery. However, talk of economic decoupling became increasingly loud during the summer months. While the U.S. continued to recover, Europe and the developing markets began to show signs of economic deceleration. China, which had been the primary economic engine of both the developed and the developing markets, showed clear signs of slowing, with some expressing fears of a hard landing. Copper and iron ore prices, as well as other industrial metals, all of which were closely linked with China’s growth, started to collapse. Crude oil prices peaked in late June and by the end of 2014 had fallen by over 50%. As the summer continued, economists described the Euro Zone as increasingly fragile and the foreign backdrop as the biggest threat to the U.S. economy. Economic weakness and declining commodity prices awakened fears of deflation. Central banks around the globe embarked on monetary easing programs to fuel growth and halt the spread of deflationary forces. Interest rates fell to historically low levels – including negative rates in some cases. As 2014 came to a close, the U.S. was the symbol of strength and stability, and the U.S. Dollar started one of its sharpest rises of the recent past. Dollar strength, however, posed a dual threat – U.S. exports became increasingly expensive relative to other countries, and currency translation impacted the reported sales and earnings of U.S. multinational companies. On top | | | | of these macroeconomic headwinds, the West Coast dock strike, bitter temperatures and historic snowfalls paralyzed parts of the country. Despite the many negative macroeconomic and geopolitical worries, stocks managed to look through the current fog and discount an improved future. OUTLOOK To quote John Kenneth Galbraith, “The only function of economic forecasting is to make astrology look respectable.” While this tongue-in-cheek statement could be applied to all types of forecasts, equity portfolio management demands an opinion or expectation about the future. Absent an unexpected geopolitical event or policy mistake, we continue to believe that U.S. and international economic recovery will continue, given that economies respond with a lag to economic stimulus. For example, it may take from six months to a year for the effects of central bank accommodation to work its way through the global economy. This is stimulus that, along with lower energy prices, improving labor conditions, increased household formation and improved consumer confidence, can propel the economy for years. The Fed will ultimately move off its zero interest rate policy. The only unknown variables are the timing of the initial rate increase, and the rate of further increases. The Fed has maintained that its actions will be data-dependent, which is interpreted to mean measured and gradual. (As this is being written, the timing for the initial rate increase is as early as September, and possibly December.) We know that most financial assets are not cheap by historical standards, with bonds being among the most richly valued alternatives. Stock and bond |

| | | | |

| | | | | |

| | | AMG Managers Cadence Capital Appreciation Fund | | |

| | | Portfolio Manager’s Comments (continued) | | |

| | | | | | | | |

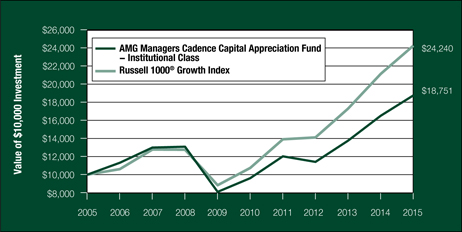

valuations are influenced by inflationary expectations and interest rate policy. We know that U.S. investors have been divesting their domestic mutual fund holdings for five or more years, seeking higher return or less risky or less correlated alternatives. The bull market that started in March, 2009, has been the least respected advance in memory. While select health care and biotechnology stocks, and some individual themes in information technology, have evidence of froth, it is hard to make the case of the market being as overvalued as last seen in March 2000. Given the above, we believe that stocks still offer the most attractive combination of risk and prospective return. Benign inflation benefits stocks over bonds, as businesses have greater flexibility navigating modestly higher costs. Bull markets never die of old age, as the old adage goes. They end when central bankers and policy makers raise interest rates to reduce the threat of rising inflationary expectations. When the yield curve inverts and short-term rates exceed long-term rates, it is only a matter of time before the bull market ends. This | | | | is not to say that the road ahead will be forever smooth – stocks reflect the fear and greed of investors with varied investment styles and objectives. Price volatility is an expression of investor sentiment that frequently arises at times when least expected. Cadence seeks to avoid these traps by following our time-tested investment approach. We seek growing, profitable companies selling at prices that make sense. Our research identifies stocks with improving sales and earnings, upward estimate revisions, and attractive relative valuations. We structure diversified portfolios, mindful that even the best managed businesses hit a pot hole on occasion. Thank you for your investment in the AMG Managers Cadence Capital Appreciation Fund. We appreciate your trust and look forward to rewarding your continued confidence in the year ahead. This commentary reflects the viewpoints of the Cadence Capital Management, LLC. as of May 31, | | | | 2015 and is not intended as a forecast or guarantee of future results. CUMULATIVE TOTAL RETURN PERFORMANCE AMG Managers Cadence Capital Appreciation Fund’s cumulative total return is based on the daily change in net asset value (NAV), and assumes that all dividends and distributions were reinvested. This graph compares a hypothetical $10,000 investment made in AMG Managers Cadence Capital Appreciation Fund’s Institutional Class on May 31, 2005, compared to a $10,000 investment made in the Russell 1000® Growth Index for the same time period. The graph and table do not reflect the deduction of taxes that a shareholder would pay on a Fund distribution or redemption of shares. The listed returns for the Fund are net of expenses and the returns for the index exclude expenses. Total returns would have been lower had certain expenses not been reduced. |

| | | | |

| | | | | |

| | | AMG Managers Cadence Capital Appreciation Fund | | |

| | | Portfolio Manager’s Comments (continued) | | |

CUMULATIVE TOTAL RETURN PERFORMANCE (continued)

The table below shows the average annual total returns for the AMG Managers Cadence Capital Appreciation Fund and the Russell 1000® Growth Index for the same time periods ended May 31, 2015.

| | | | | | | | | | | | |

| Average Annual Total Returns1 | | One

Year | | | Five

Years | | | Ten

Years | |

AMG Managers Cadence Capital Appreciation Fund 2,3,4,5 | | | | | | | | | | | | |

Investor Class | | | 13.16 | % | | | 13.85 | % | | | 6.07 | % |

Service Class | | | 13.41 | % | | | 14.03 | % | | | 6.23 | % |

Institutional Class | | | 13.62 | % | | | 14.29 | % | | | 6.49 | % |

Russell 1000® Growth Index 6 | | | 14.73 | % | | | 17.67 | % | | | 9.26 | % |

The performance data shown represents past performance. Past performance is not a guarantee of future results. Current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

Investors should carefully consider the Fund’s investment objectives, risks, charges, and expenses before investing. For performance information through the most recent month end, current net asset values per share for the Fund and other information, please call (800) 835-3879 or visit our website at www.amgfunds.com for a free prospectus. Read it carefully before investing or sending money.

Distributed by AMG Distributors, Inc., member FINRA/SIPC.

| 1 | Total return equals income yield plus share price change and assumes reinvestment of all dividends and capital gain distributions. Returns are net of fees and may reflect offsets of Fund expenses as described in the prospectus. No adjustment has been made for taxes payable by shareholders on their reinvested dividends and capital gain distributions. Returns for periods greater than one year are annualized. The listed returns on the Fund are net of expenses and based on the published NAV as of May 31, 2015. All returns are in U.S. dollars ($). |

|

2 From time to time, the Fund’s advisor has waived its fees and/or absorbed Fund expenses, which has resulted in higher returns. 3 The Fund invests in growth stocks, which may be more sensitive to market movements because their prices tend to reflect future investor expectations rather than just current profits. Growth stocks may underperform value stocks during given periods. 4 The Fund invests in large-capitalization companies that may underperform other stock funds (such as funds that focus on small- and medium-capitalization companies) when stocks of large-capitalization companies are out of favor. 5 The Fund is subject to special risk considerations similar to those associated with the direct ownership of real estate. Real estate valuations may be subject to factors such as changing general and local economic, financial, competitive, and environmental conditions. 6 The Russell 1000® Growth Index is a market capitalization weighted index that measures the performance of those Russell 1000 companies with higher price-to-book ratios and higher forecasted growth values. Unlike the Fund, the Russell 1000® Growth Index is unmanaged, is not available for investment and does not incur expenses. The Russell 1000® Growth Index is a registered trademark of Russell Investments. Russell® is a trademark of Russell Investments. Not FDIC insured, nor bank guaranteed. May lose value. |

| | | | |

| | | AMG Managers Cadence Capital Appreciation Fund | | |

| | | Fund Snapshots (unaudited) | | |

| | | May 31, 2015 | | |

PORTFOLIO BREAKDOWN

| | | | | | | | | | | | | | |

| | | Sector | | AMG Managers

Cadence Capital

Appreciation Fund** | | Russell 1000®

Growth Index | | |

| | | Information Technology | | | | 27.0 | % | | | | 29.1 | % | | |

| | | Consumer Discretionary | | | | 22.2 | % | | | | 18.8 | % | | |

| | | Health Care | | | | 16.9 | % | | | | 14.4 | % | | |

| | | Industrials | | | | 11.6 | % | | | | 11.4 | % | | |

| | | Consumer Staples | | | | 7.3 | % | | | | 10.4 | % | | |

| | | Financials | | | | 6.8 | % | | | | 5.1 | % | | |

| | | Energy | | | | 5.3 | % | | | | 4.6 | % | | |

| | | Materials | | | | 2.3 | % | | | | 4.0 | % | | |

| | | Utilities | | | | 0.7 | % | | | | 0.1 | % | | |

| | | Telecommunication Services | | | | 0.0 | % | | | | 2.1 | % | | |

| | | Other Assets and Liabilities | | | | (0.1 | )% | | | | 0.0 | % | | |

| | | ** As a percentage of net assets. | | | |

TOP TEN HOLDINGS

| | | | |

| Security Name | | | | % of Net Assets |

Apple, Inc.* | | | | 6.2% |

Microsoft Corp.* | | | | 3.3 |

Gilead Sciences, Inc.* | | | | 2.9 |

The Walt Disney Co.* | | | | 2.4 |

Facebook, Inc., Class A* | | | | 2.4 |

Visa, Inc., Class A | | | | 2.4 |

Google, Inc., Class A* | | | | 2.0 |

Biogen, Inc. | | | | 2.0 |

The Boeing Co.* | | | | 1.9 |

Hanesbrands, Inc. | | | | 1.8 |

| | | | |

Top Ten as a Group | | | | 27.3% |

| | | | |

* Top Ten Holding as of November 30, 2014. |

Because a fund’s strategy may result in multiple investments in particular sectors of the economy, its performance may depend on the performance of those sectors and may fluctuate more widely than investments diversified across more sectors. For additional information on these and other risk considerations, please see the Fund’s prospectus.

Any sectors, industries, or securities discussed should not be perceived as investment recommendations. Mention of a specific security should not be considered a recommendation to buy or solicitation to sell that security. Specific securities mentioned in this report may have been sold from the Fund’s portfolio of investments by the time you receive this report.

| | | | |

| | | AMG Managers Cadence Capital Appreciation Fund | | |

| | | Schedule of Portfolio Investments | | |

| | | May 31, 2015 | | |

| | | | | | | | |

| | | | Shares | | | | Value | |

Common Stocks - 100.1% | | | | | | | | |

Consumer Discretionary - 22.2% | | | | | | | | |

Aramark | | | 43,411 | | | | $1,360,935 | |

Delphi Automotive PLC | | | 20,067 | | | | 1,745,428 | |

Foot Locker, Inc. | | | 26,910 | | | | 1,700,712 | |

Genuine Parts Co. | | | 13,876 | | | | 1,255,362 | |

Hanesbrands, Inc. | | | 74,420 | | | | 2,371,021 | |

Harman International Industries, Inc. | | | 13,295 | | | | 1,602,313 | |

Hilton Worldwide Holdings, Inc.* | | | 49,572 | | | | 1,435,605 | |

Macy’s, Inc. | | | 28,885 | | | | 1,933,851 | |

Nordstrom, Inc. | | | 15,310 | | | | 1,112,118 | |

Omnicom Group, Inc.1 | | | 20,334 | | | | 1,515,493 | |

O’Reilly Automotive, Inc.* | | | 9,362 | | | | 2,055,240 | |

The Priceline Group, Inc.* | | | 1,522 | | | | 1,783,845 | |

Scripps Networks Interactive, Inc., Class A | | | 17,448 | | | | 1,169,191 | |

Starbucks Corp. | | | 42,000 | | | | 2,182,320 | |

The TJX Cos., Inc. | | | 25,058 | | | | 1,613,234 | |

VF Corp. | | | 18,586 | | | | 1,309,012 | |

The Walt Disney Co. | | | 28,447 | | | | 3,139,695 | |

Total Consumer Discretionary | | | | | | | 29,285,375 | |

Consumer Staples - 7.3% | | | | | | | | |

The Clorox Co. | | | 10,030 | | | | 1,079,830 | |

Colgate-Palmolive Co. | | | 22,648 | | | | 1,512,660 | |

Constellation Brands, Inc., Class A | | | 13,903 | | | | 1,639,025 | |

CVS Health Corp. | | | 21,519 | | | | 2,203,115 | |

Mondelez International, Inc., Class A | | | 29,991 | | | | 1,247,326 | |

Philip Morris International, Inc. | | | 24,202 | | | | 2,010,460 | |

Total Consumer Staples | | | | | | | 9,692,416 | |

Energy - 5.3% | | | | | | | | |

Anadarko Petroleum Corp. | | | 11,910 | | | | 995,795 | |

EOG Resources, Inc. | | | 18,687 | | | | 1,657,350 | |

Halliburton Co. | | | 34,208 | | | | 1,553,043 | |

Kinder Morgan, Inc. | | | 37,983 | | | | 1,575,915 | |

National Oilwell Varco, Inc. | | | 13,082 | | | | 643,504 | |

Whiting Petroleum Corp.* | | | 17,373 | | | | 573,135 | |

Total Energy | | | | | | | 6,998,742 | |

Financials - 6.8% | | | | | | | | |

American Tower Corp. | | | 21,095 | | | | 1,957,405 | |

JPMorgan Chase & Co. | | | 29,126 | | | | 1,915,908 | |

Marsh & McLennan Cos., Inc. | | | 28,059 | | | | 1,633,876 | |

| | | | | | | | |

| | | | Shares | | | | Value | |

T. Rowe Price Group, Inc. | | | 17,380 | | | | $1,402,392 | |

Wells Fargo & Co. | | | 36,463 | | | | 2,040,469 | |

Total Financials | | | | | | | 8,950,050 | |

Health Care - 16.9% | | | | | | | | |

Abbott Laboratories | | | 40,267 | | | | 1,956,976 | |

Aetna, Inc. | | | 10,956 | | | | 1,292,479 | |

Biogen, Inc.* | | | 6,571 | | | | 2,608,621 | |

Cardinal Health, Inc. | | | 18,150 | | | | 1,600,286 | |

Gilead Sciences, Inc.* | | | 33,763 | | | | 3,790,572 | |

Johnson & Johnson | | | 17,863 | | | | 1,788,801 | |

Mallinckrodt PLC* | | | 15,800 | | | | 2,045,152 | |

Medtronic PLC | | | 24,601 | | | | 1,877,548 | |

Mylan N.V.* | | | 27,325 | | | | 1,984,615 | |

Stryker Corp. | | | 19,586 | | | | 1,882,802 | |

Zoetis, Inc. | | | 29,660 | | | | 1,476,178 | |

Total Health Care | | | | | | | 22,304,030 | |

Industrials - 11.6% | | | | | | | | |

Alaska Air Group, Inc. | | | 23,882 | | | | 1,543,732 | |

American Airlines Group, Inc. | | | 29,648 | | | | 1,256,186 | |

The Boeing Co. | | | 17,934 | | | | 2,520,086 | |

Honeywell International, Inc. | | | 22,122 | | | | 2,305,112 | |

Illinois Tool Works, Inc. | | | 16,924 | | | | 1,587,979 | |

Ingersoll-Rand PLC | | | 22,134 | | | | 1,522,377 | |

Rockwell Automation, Inc. | | | 11,696 | | | | 1,437,321 | |

United Parcel Service, Inc.,

Class B | | | 18,238 | | | | 1,809,574 | |

WABCO Holdings, Inc.* | | | 11,010 | | | | 1,391,884 | |

Total Industrials | | | | | | | 15,374,251 | |

Information Technology - 27.0% | | | | | | | | |

Accenture PLC, Class A | | | 22,238 | | | | 2,135,738 | |

Adobe Systems, Inc.* | | | 16,497 | | | | 1,304,748 | |

Apple, Inc. | | | 62,392 | | | | 8,128,430 | |

Avago Technologies, Ltd. | | | 12,960 | | | | 1,918,987 | |

Facebook, Inc., Class A* | | | 39,593 | | | | 3,135,370 | |

Google, Inc., Class A* | | | 4,906 | | | | 2,675,340 | |

Google, Inc., Class C* | | | 4,117 | | | | 2,190,697 | |

Intuit, Inc. | | | 16,870 | | | | 1,757,011 | |

MasterCard, Inc., Class A | | | 25,316 | | | | 2,335,654 | |

Microsoft Corp. | | | 91,781 | | | | 4,300,858 | |

Red Hat, Inc.* | | | 20,582 | | | | 1,590,371 | |

Splunk, Inc.* | | | 14,782 | | | | 999,559 | |

|

|

| The accompanying notes are an integral part of these financial statements. |

| 8 |

| | | | |

| | | | | |

| | | AMG Managers Cadence Capital Appreciation Fund | | |

| | | Schedule of Portfolio Investments (continued) | | |

| | | | | | | | |

| | | Shares | | | Value | |

Information Technology - 27.0% (continued) | | | | | |

Visa, Inc., Class A | | | 45,536 | | | | $3,127,412 | |

Total Information Technology | | | | | | | 35,600,175 | |

Materials - 2.3% | | | | | | | | |

CF Industries Holdings, Inc. | | | 3,487 | | | | 1,101,474 | |

Sealed Air Corp. | | | 39,849 | | | | 1,940,646 | |

Total Materials | | | | | | | 3,042,120 | |

Utilities - 0.7% | | | | | | | | |

ITC Holdings Corp. | | | 25,391 | | | | 896,048 | |

Total Common Stocks

(cost $101,740,084) | | | | | | | 132,143,207 | |

| | | | | | | | |

| | | | | | | | |

| | | Principal Amount | | | Value | |

Short-Term Investments - 0.9% | | | | | |

Repurchase Agreements - 0.9%2 | | | | | |

Cantor Fitzgerald Securities, Inc., dated 05/29/15, due 06/01/15, 0.110%, total to be received $1,000,009 (collateralized by various U.S. Government Agency Obligations, 0.000% - 8.000%, 07/15/15 - 04/20/65, totaling $1,020,000) | | | $1,000,000 | | | | $1,000,000 | |

Nomura Securities International, Inc., dated 05/29/15, due 06/01/15, 0.110%, total to be received $174,254 (collateralized by various U.S. Government Agency Obligations, 0.000% - 9.500%, 06/15/15 - 04/20/65, totaling $177,737) | | | 174,252 | | | | 174,252 | |

Total Repurchase Agreements | | | | 1,174,252 | |

Total Short-Term Investments

(cost $1,174,252) | | | | 1,174,252 | |

Total Investments - 101.0%

(cost $102,914,336) | | | | 133,317,459 | |

Other Assets, less Liabilities - (1.0)% | | | | (1,347,990 | ) |

Net Assets - 100.0% | | | | | | | $131,969,469 | |

| | | | | | | | |

|

|

| The accompanying notes are an integral part of these financial statements. |

| 9 |

| | | | |

| | | | | |

| | | AMG Managers Cadence Mid Cap Fund | | |

| | | Portfolio Manager’s Comments | | |

| | | | | | | | |

For the fiscal year ended May 31, 2015, the AMG Managers Cadence Mid Cap Fund (Institutional Class) (the “Fund”) returned 15.6%, outperforming its benchmark, the Russell Midcap® Growth Index, which returned 14.7%. U.S. stocks continued their ascent during the fiscal year ended May 31, 2015, with the broad S&P 500 Index returning 11.8% and the Russell Midcap Growth Index returning 14.7%. This performance followed the S&P’s strong gain of 20.5% for the prior 12 months ended May 31, 2014, challenging many strategists who argued that rising stock prices in the face of slowing global economic growth were a recipe for investment disappointment. Despite the economic and market cross currents, the Fund posted a strong positive return and modestly outperformed the benchmark. The Fund performed well for the fiscal year in information technology, consumer staples, financials and materials, adding value versus the Russell Midcap Growth Index through a combination of stock selection and sector allocation. Fund holdings had average returns that ranged from 21.4% for financials to 37.1% for information technology, outperforming both the Index and the corresponding sectors of the Index. In contrast, the Fund underperformed the benchmark in consumer discretionary, with average gains of 2.6% compared with the sector’s gains of 14.5%. Health care has been among the market’s best performing sectors since 2011, powered by increased utilization, innovation in new drugs and medical devices, a powerful IPO market and a robust M&A environment. The Fund benefitted from these tailwinds with portfolio gains exceeding 42% in the fiscal year. Conversely, energy was the Fund’s weakest sector in absolute terms over the last year, as crude oil prices collapsed by over 50%. While our holdings lagged the Index’s energy stocks, the Fund’s underweight position in the sector added value relative to the benchmark. To emphasize the rotational nature of | | | | the equity market, energy was among the Russell Midcap Growth’s strongest performing sectors in the fiscal year ended May 31, 2014, returning over 26%. THE YEAR IN REVIEW The fiscal year started on a strong note, with the S&P 500 hitting eight new all-time highs in June, 2014. The employment picture and consumer spending, while far from robust, suggested the economic recovery, which started in June 2009 (essentially six years ago), was still intact, although growing at a slower pace than normal. The U.S. Federal Reserve (the “Fed”) maintained an accommodative monetary stance, fearful of policy mistakes at this stage of the recovery. However, talk of economic decoupling became increasingly loud during the summer months. While the U.S. continued to recover, Europe and the developing markets began to show signs of economic deceleration. China, which had been the primary economic engine of both the developed and the developing markets, showed clear signs of slowing, with some expressing fears of a hard landing. Copper and iron ore prices, as well as other industrial metals, all of which were closely linked with China’s growth, started to collapse. Crude oil prices peaked in late June and by the end of 2014 had fallen by over 50%. As the summer continued, economists described the Euro Zone as increasingly fragile and the foreign backdrop as the biggest threat to the U.S. economy. Economic weakness and declining commodity prices awakened fears of deflation. Central banks around the globe embarked on monetary easing programs to fuel growth and halt the spread of deflationary forces. Interest rates fell to historically low levels – including negative rates in some cases. As 2014 came to a close, the U.S. was the symbol of strength and stability, and the U.S. Dollar started one of its sharpest rises of the recent past. Dollar strength, however, posed a dual threat – U.S. exports became increasingly expensive relative to other countries, and currency | | | | translation impacted the reported sales and earnings of U.S. multinational companies. On top of these macroeconomic headwinds, the West Coast dock strike, bitter temperatures and historic snowfalls paralyzed parts of the country. Despite the many negative macroeconomic and geopolitical worries, stocks managed to look through the current fog and discount an improved future. OUTLOOK To quote John Kenneth Galbraith, “The only function of economic forecasting is to make astrology look respectable.” While this tongue-in-cheek statement could be applied to all types of forecasts, equity portfolio management demands an opinion or expectation about the future. Absent an unexpected geopolitical event or policy mistake, we continue to believe that U.S. and international economic recovery will continue, given that economies respond with a lag to economic stimulus. For example, it may take from six months to a year for the effects of central bank accommodation to work its way through the global economy. This is stimulus that, along with lower energy prices, improving labor conditions, increased household formation and improved consumer confidence, can propel the economy for years. The Fed will ultimately move off its zero-interest rate policy. The only unknown variables are the timing of the initial rate increase, and the rate of further increases. The Fed has maintained that its actions will be data-dependent, which is interpreted to mean measured and gradual. (As this is being written, the timing for the initial rate increase is as early as September, and possibly December.) We know that most financial assets are not cheap by historical standards, with bonds being among the most richly valued alternatives. Stock and bond valuations are influenced by inflationary |

| | | | |

| | | | | |

| | | AMG Managers Cadence Mid Cap Fund | | |

| | | Portfolio Manager’s Comments (continued) | | |

| | | | | | | | |

expectations and interest rate policy. We know that U.S. investors have been divesting their domestic mutual fund holdings for five or more years, seeking higher return or less risky or less correlated alternatives. The bull market that started in March, 2009, has been the least respected advance in memory. While select health care and biotechnology stocks, and some individual themes in information technology, have evidence of froth, it is hard to make the case of the market being as overvalued as last seen in March 2000. Given the above, we believe that stocks still offer the most attractive combination of risk and prospective return. Benign inflation benefits stocks over bonds, as businesses have greater flexibility navigating modestly higher costs. Bull markets never die of old age, as the old adage goes. They end when central bankers and policy makers raise interest rates to reduce the threat of rising inflationary expectations. When the yield curve inverts and short-term rates exceed long-term rates, it is only a matter of time before the bull market ends. This | | | | is not to say that the road ahead will be forever smooth – stocks reflect the fear and greed of investors with varied investment styles and objectives. Price volatility is an expression of investor sentiment that frequently arises at times when least expected. Cadence seeks to avoid these traps by following our time-tested investment approach. We seek growing, profitable companies selling at prices that make sense. Our research identifies stocks with improving sales and earnings, upward estimate revisions and attractive relative valuations. We structure diversified portfolios, mindful that even the best managed businesses hit a pot hole on occasion. Thank you for your investment in the AMG Managers Cadence Mid Cap Fund. We appreciate your trust and look forward to rewarding your continued confidence in the year ahead. This commentary reflects the viewpoints of the Cadence Capital Management, LLC. as of May 31, | | | | 2015 and is not intended as a forecast or guarantee of future results. CUMULATIVE TOTAL RETURN PERFORMANCE AMG Managers Cadence Mid Cap Fund’s cumulative total return is based on the daily change in net asset value (NAV), and assumes that all dividends and distributions were reinvested. This graph compares a hypothetical $10,000 investment made in AMG Managers Cadence Mid Cap Fund’s Institutional Class on May 31, 2005, compared to a $10,000 investment made in the Russell Midcap® Growth Index for the same time period. The graph and table do not reflect the deduction of taxes that a shareholder would pay on a Fund distribution or redemption of shares. The listed returns for the Fund are net of expenses and the returns for the index exclude expenses. Total returns would have been lower had certain expenses not been reduced. |

| | | | |

| | | | | |

| | | AMG Managers Cadence Mid Cap Fund | | |

| | | Portfolio Manager’s Comments (continued) | | |

CUMULATIVE TOTAL RETURN PERFORMANCE (continued)

The table below shows the average annual total returns for the AMG Managers Cadence Mid Cap Fund and the Russell Midcap® Growth Index for the same time periods ended May 31, 2015.

| | | | | | | | | | | | |

| Average Annual Total Returns 1 | | One

Year | | | Five

Years | | | Ten

Years | |

AMG Managers Cadence Mid Cap Fund 2,3,4,5 | | | | | | | | | | | | |

Investor Class | | | 15.14 | % | | | 15.11 | % | | | 7.42 | % |

Service Class | | | 15.34 | % | | | 15.29 | % | | | 7.59 | % |

Institutional Class | | | 15.62 | % | | | 15.58 | % | | | 7.85 | % |

Russell Midcap® Growth Index 6 | | | 14.72 | % | | | 17.52 | % | | | 10.07 | % |

The performance data shown represents past performance. Past performance is not a guarantee of future results. Current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

Investors should carefully consider the Fund’s investment objectives, risks, charges and expenses before investing. For performance information through the most recent month end, current net asset values per share for the Fund and other information, please call (800) 835-3879 or visit our website at www.amgfunds.com for a free prospectus. Read it carefully before investing or sending money.

Distributed by AMG Distributors, Inc., member FINRA/SIPC.

| 1 | Total return equals income yield plus share price change and assumes reinvestment of all dividends and capital gain distributions. Returns are net of fees and may reflect offsets of Fund expenses as described in the prospectus. No adjustment has been made for taxes payable by shareholders on their reinvested dividends and capital gain distributions. Returns for periods greater than one year are annualized. The listed returns on the Fund are net of expenses and based on the published NAV as of May 31, 2015. All returns are in U.S. dollars ($). |

| | |

| | | 2 From time to time, the Fund’s advisor has waived its fees and/or absorbed Fund expenses, which has resulted in higher returns. 3 The Fund invests in growth stocks, which may be more sensitive to market movements because their prices tend to reflect future investor expectations rather than just current profits. Growth stocks may underperform value stocks during given periods. 4 The Fund is subject to risks associated with investments in mid-capitalization companies such as erratic earnings patterns, competitive conditions, limited earnings history, and a reliance on one or a limited number of products. 5 The Fund is subject to special risk considerations similar to those associated with the direct ownership of real estate. Real estate valuations may be subject to factors such as changing general and local economic, financial, competitive, and environmental conditions. 6 The Russell Midcap® Growth Index measures the performance of the Russell Midcap companies with higher price-to-book ratios and higher forecasted growth values. The stocks are also members of the Russell 1000® Growth Index. Unlike the Fund, the Index is unmanaged, is not available for investment, and does not incur expenses. The Russell Midcap® Growth Index is a registered trademark of Russell Investments. Russell® is a trademark of Russell Investments. Not FDIC insured, nor bank guaranteed. May lose value. |

| | | | |

| | | AMG Managers Cadence Mid Cap Fund | | |

| | | Fund Snapshots (unaudited) | | |

| | | May 31, 2015 | | |

PORTFOLIO BREAKDOWN

| | | | | | | | | | | | | | |

| | | Sector | | AMG Managers

Cadence Mid

Cap Fund** | | Russell Midcap®

Growth Index | | |

| | | Consumer Discretionary | | | | 20.5 | % | | | | 22.9 | % | | |

| | | Information Technology | | | | 20.2 | % | | | | 18.7 | % | | |

| | | Health Care | | | | 17.8 | % | | | | 14.3 | % | | |

| | | Consumer Staples | | | | 15.4 | % | | | | 8.0 | % | | |

| | | Industrials | | | | 9.3 | % | | | | 15.5 | % | | |

| | | Financials | | | | 7.9 | % | | | | 9.6 | % | | |

| | | Energy | | | | 4.7 | % | | | | 5.1 | % | | |

| | | Materials | | | | 3.9 | % | | | | 4.8 | % | | |

| | | Telecommunication Services | | | | 0.0 | % | | | | 0.9 | % | | |

| | | Utilities | | | | 0.0 | % | | | | 0.2 | % | | |

| | | Other Assets and Liabilities | | | | 0.3 | % | | | | 0.0 | % | | |

| | | ** As a percentage of net assets. | | | |

TOP TEN HOLDINGS

| | | | |

| Security Name | | | | % of Net Assets |

The WhiteWave Foods Co. | | | | 2.6% |

Constellation Brands, Inc., Class A | | | | 2.4 |

Skyworks Solutions, Inc.* | | | | 2.2 |

Moody’s Corp.* | | | | 2.2 |

Sealed Air Corp.* | | | | 2.1 |

Mallinckrodt PLC | | | | 2.1 |

Avago Technologies, Ltd. | | | | 2.1 |

Tableau Software, Inc., Class A | | | | 2.1 |

Zoetis, Inc. | | | | 2.1 |

Hanesbrands, Inc.* | | | | 2.0 |

| | | | |

Top Ten as a Group | | | | 21.9% |

| | | | |

* Top Ten Holding as of November 30, 2014. |

Because a fund’s strategy may result in multiple investments in particular sectors of the economy, its performance may depend on the performance of those sectors and may fluctuate more widely than investments diversified across more sectors. For additional information on these and other risk considerations, please see the Fund’s prospectus.

Any sectors, industries, or securities discussed should not be perceived as investment recommendations. Mention of a specific security should not be considered a recommendation to buy or solicitation to sell that security. Specific securities mentioned in this report may have been sold from the Fund’s portfolio of investments by the time you receive this report.

| | | | |

| | | AMG Managers Cadence Mid Cap Fund | | |

| | | Schedule of Portfolio Investments | | |

| | | May 31, 2015 | | |

| | | | | | | | |

| | | | Shares | | | | Value | |

Common Stocks - 99.7% | | | | | | | | |

Consumer Discretionary - 20.5% | | | | | | | | |

Aramark | | | 86,790 | | | | $2,720,867 | |

Dillard’s, Inc., Class A | | | 14,470 | | | | 1,678,665 | |

DISH Network Corp., Class A* | | | 11,780 | | | | 833,906 | |

Domino’s Pizza, Inc. | | | 11,210 | | | | 1,218,079 | |

Foot Locker, Inc. | | | 44,110 | | | | 2,787,752 | |

Hanesbrands, Inc. | | | 102,440 | | | | 3,263,738 | |

Harman International Industries, Inc. | | | 19,350 | | | | 2,332,062 | |

Hilton Worldwide Holdings, Inc.* | | | 94,730 | | | | 2,743,381 | |

Leggett & Platt, Inc. | | | 44,420 | | | | 2,100,178 | |

Macy’s, Inc. | | | 26,350 | | | | 1,764,133 | |

Restaurant Brands International, Inc.1 | | | 76,745 | | | | 2,967,729 | |

Six Flags Entertainment Corp. | | | 34,610 | | | | 1,691,045 | |

Ulta Salon Cosmetics & Fragrance, Inc.* | | | 20,780 | | | | 3,171,444 | |

Under Armour, Inc., Class A*,1 | | | 38,310 | | | | 3,003,887 | |

VF Corp. | | | 22,880 | | | | 1,611,438 | |

Total Consumer Discretionary | | | | | | | 33,888,304 | |

Consumer Staples - 15.4% | | | | | | | | |

Church & Dwight Co., Inc. | | | 24,660 | | | | 2,070,700 | |

Constellation Brands, Inc., Class A | | | 33,710 | | | | 3,974,072 | |

Dr. Pepper Snapple Group, Inc. | | | 39,130 | | | | 2,998,923 | |

The Hain Celestial Group, Inc.* | | | 46,300 | | | | 2,929,401 | |

The Kroger Co. | | | 29,120 | | | | 2,119,936 | |

Mead Johnson Nutrition Co. | | | 16,800 | | | | 1,634,640 | |

Molson Coors Brewing Co., Class B | | | 40,370 | | | | 2,962,351 | |

Monster Beverage Corp.* | | | 18,530 | | | | 2,358,498 | |

The WhiteWave Foods Co.* | | | 89,820 | | | | 4,314,055 | |

Total Consumer Staples | | | | | | | 25,362,576 | |

Energy - 4.7% | | | | | | | | |

Cabot Oil & Gas Corp. | | | 49,360 | | | | 1,676,266 | |

Cameron International Corp.* | | | 28,160 | | | | 1,445,453 | |

Helmerich & Payne, Inc.1 | | | 8,890 | | | | 648,881 | |

Western Refining, Inc. | | | 55,550 | | | | 2,443,089 | |

Whiting Petroleum Corp.* | | | 45,817 | | | | 1,511,503 | |

Total Energy | | | | | | | 7,725,192 | |

Financials - 7.9% | | | | | | | | |

Extra Space Storage, Inc. | | | 41,510 | | | | 2,906,945 | |

Marsh & McLennan Cos., Inc. | | | 42,480 | | | | 2,473,610 | |

McGraw Hill Financial, Inc. | | | 22,280 | | | | 2,311,550 | |

| | | | | | | | |

| | | | Shares | | | | Value | |

Moody’s Corp. | | | 33,060 | | | | $3,573,786 | |

Sovran Self Storage, Inc. | | | 19,930 | | | | 1,817,815 | |

Total Financials | | | | | | | 13,083,706 | |

Health Care - 17.8% | | | | | | | | |

Agios Pharmaceuticals, Inc.*,1 | | | 13,260 | | | | 1,617,985 | |

Alkermes PLC* | | | 49,120 | | | | 3,001,232 | |

AmerisourceBergen Corp. | | | 24,900 | | | | 2,802,744 | |

Cardinal Health, Inc. | | | 33,590 | | | | 2,961,630 | |

Centene Corp.* | | | 31,400 | | | | 2,365,676 | |

HCA Holdings, Inc.* | | | 18,170 | | | | 1,486,851 | |

Laboratory Corp. of America Holdings* | | | 13,640 | | | | 1,608,838 | |

Mallinckrodt PLC* | | | 26,880 | | | | 3,479,347 | |

Mettler-Toledo International, Inc.* | | | 7,490 | | | | 2,431,853 | |

Mylan N.V.* | | | 33,540 | | | | 2,436,010 | |

Vertex Pharmaceuticals, Inc.* | | | 13,570 | | | | 1,740,895 | |

Zoetis, Inc. | | | 68,620 | | | | 3,415,217 | |

Total Health Care | | | | | | | 29,348,278 | |

Industrials - 9.3% | | | | | | | | |

AerCap Holdings N.V.* | | | 34,260 | | | | 1,652,702 | |

Alaska Air Group, Inc. | | | 46,090 | | | | 2,979,258 | |

Cintas Corp. | | | 24,670 | | | | 2,123,840 | |

The Dun & Bradstreet Corp. | | | 13,000 | | | | 1,663,090 | |

The Middleby Corp.* | | | 16,080 | | | | 1,747,896 | |

RR Donnelley & Sons Co. | | | 85,400 | | | | 1,637,972 | |

Snap-on,, Inc. | | | 11,590 | | | | 1,801,086 | |

Verisk Analytics, Inc.* | | | 23,720 | | | | 1,721,598 | |

Total Industrials | | | | | | | 15,327,442 | |

Information Technology - 20.2% | | | | | | | | |

Akamai Technologies, Inc.* | | | 34,920 | | | | 2,663,348 | |

Avago Technologies, Ltd. | | | 23,200 | | | | 3,435,224 | |

Check Point Software Technologies, Ltd.* | | | 32,310 | | | | 2,737,303 | |

Equinix, Inc. | | | 10,540 | | | | 2,825,458 | |

FireEye, Inc.*,1 | | | 66,840 | | | | 3,112,739 | |

IPG Photonics Corp.*,1 | | | 17,940 | | | | 1,701,430 | |

NVIDIA Corp. | | | 75,470 | | | | 1,670,151 | |

NXP Semiconductors N.V.* | | | 18,030 | | | | 2,023,868 | |

Sabre Corp. | | | 112,570 | | | | 2,936,951 | |

Skyworks Solutions, Inc. | | | 32,740 | | | | 3,580,446 | |

SolarWinds, Inc.* | | | 38,660 | | | | 1,834,417 | |

Splunk, Inc.* | | | 22,212 | | | | 1,501,975 | |

|

|

| The accompanying notes are an integral part of these financial statements. |

| 14 |

| | | | |

| | | | | |

| | | AMG Managers Cadence Mid Cap Fund | | |

| | | Schedule of Portfolio Investments (continued) | | |

| | | | | | | | |

| | | Shares | | | Value | |

Information Technology - 20.2% (continued) | | | | | |

Tableau Software, Inc., Class A* | | | 30,300 | | | | $3,430,263 | |

Total Information Technology | | | | | | | 33,453,573 | |

Materials - 3.9% | | | | | | | | |

Axalta Coating Systems , Ltd.* | | | 39,630 | | | | 1,357,328 | |

International Paper Co. | | | 30,760 | | | | 1,594,291 | |

Sealed Air Corp. | | | 72,020 | | | | 3,507,374 | |

Total Materials | | | | | | | 6,458,993 | |

Total Common Stocks

(cost $137,221,706) | | | | | | | 164,648,064 | |

| | |

| | | Principal

Amount | | | | |

Short-Term Investments - 4.2% | | | | | |

Repurchase Agreements - 4.0%2 | | | | | |

Cantor Fitzgerald Securities, Inc., dated 05/29/15, due 06/01/15, 0.110%, total to be received $1,592,796 (collateralized by various U.S. Government Agency Obligations, 0.000% - 8.000%, 07/15/15 - 04/20/65, totaling $1,624,637) | | | $1,592,781 | | | | 1,592,781 | |

Citigroup Global Markets, Inc., dated 05/29/15, due 06/01/15, 0.100%, total to be received $335,312 (collateralized by various U.S. Government Agency Obligations, 0.084% - 4.375%, 04/30/16 - 11/15/39, totaling $342,015) | | | 335,309 | | | | 335,309 | |

Daiwa Capital Markets America, dated 05/29/15, due 06/01/15, 0.140%, total to be received $1,592,800 (collateralized by various U.S. Government Agency Obligations, 0.000% - 8.000%, 08/19/15 - 03/01/48, totaling $1,624,637) | | | 1,592,781 | | | | 1,592,781 | |

| | | | | | | | |

| | | Principal Amount | | | Value | |

HSBC Securities USA, Inc., dated 05/29/15, due 06/01/15, 0.080%, total to be received $1,592,792 (collateralized by various U.S. Government Agency Obligations, 0.000% - 9.375%, 07/15/15 - 07/15/32, totaling $1,624,643) | | | $1,592,781 | | | | $1,592,781 | |

Nomura Securities International, Inc., dated 05/29/15, due 06/01/15, 0.110%, total to be received $1,592,796 (collateralized by various U.S. Government Agency Obligations, 0.000% - 9.500%, 06/15/15 - 04/20/65 totaling $1,624,637) | | | 1,592,781 | | | | 1,592,781 | |

Total Repurchase Agreements | | | | 6,706,433 | |

| | |

| | | Shares | | | | |

Other Investment Companies - 0.2%3 | | | | | |

Dreyfus Institutional Cash Advantage Fund, Institutional Class Shares, 0.08% | | | 282,994 | | | | 282,994 | |

Total Short-Term Investments

(cost $6,989,427) | | | | 6,989,427 | |

Total Investments - 103.9%

(cost $144,211,133) | | | | 171,637,491 | |

Other Assets, less Liabilities - (3.9)% | | | | (6,470,357 | ) |

Net Assets - 100.0% | | | | | | | $165,167,134 | |

|

|

| The accompanying notes are an integral part of these financial statements. |

| 15 |

| | | | |

| | | | | |

| | | AMG Managers Cadence Emerging Companies Fund | | |

| | | Portfolio Manager’s Comments | | |

| | | | | | | | |

For the fiscal year ended May 31, 2015, the AMG Managers Cadence Emerging Companies Fund (Institutional Class) (the “Fund”) returned 15.3%, lagging its benchmark, the Russell Microcap® Growth Index, which returned 18.5%. U.S. stocks continued their ascent during the fiscal year ended May 31, 2015, with the broad S&P 500 Index returning 11.8%, the Russell 2000® Index returning 11.3% and the Russell Microcap Growth Index gaining 18.5%. This performance followed the S&P’s strong gain of 20.5% for the prior 12 months ended May 31, 2014, challenging many strategists who argued that rising stock prices in the face of slowing global economic growth were a recipe for investment disappointment. Despite the economic and market cross currents, the Fund posted a positive return, but underperformed the Index, largely attributable to underweighting the top-performing biotechnology industry. The Fund performed well for the fiscal year in consumer discretionary, consumer staples and materials, adding value versus the Russell Microcap Growth Index through a combination of stock selection and sector allocation. In contrast, the Fund underperformed the benchmark in health care, information technology and industrials. Health care has been among the market’s best performing sectors since 2011, powered by increased utilization, innovation in new drugs and medical devices, a powerful IPO market and a robust M&A environment. The sector, which represented an average of 40.4% of the Index, accounted for most of the Index’s total return for the fiscal year, with average gains of 40.8%. Within health care, micro-cap biotechnology stocks powered the sector, with average returns of 55.6%. This performance, coupled with the industry’s 20.7% average weighting in the Index, contributed over half of the Index’s total return for the full fiscal year. The Fund benefitted from these tailwinds with portfolio gains exceeding 40% in the sector and average returns of nearly 85% for the biotechnology holdings. The Fund has historically underweighted the biotechnology industry due to | | | | many companies’ loss-making financial profile and risky business models dependent on scientific advancement, regulatory uncertainty and narrow product profiles. Conversely, energy was the market’s and the Fund’s weakest sector on an absolute basis over the last year, as crude oil prices collapsed by over 50%. The Fund’s holdings essentially matched the weighting and the performance of the Index, which resulted in minimal impact on relative performance. To emphasize the rotational nature of the equity market, energy was the Russell Microcap Growth’s strongest performing sector in the year ended May 31, 2014, returning nearly 44%. THE YEAR IN REVIEW The fiscal year started on a strong note, with the S&P 500 hitting eight new all-time highs in June, 2014. The employment picture and consumer spending, while far from robust, suggested the economic recovery, which started in June 2009 (essentially six years ago), was still intact, although growing at a slower pace than normal. The U.S. Federal Reserve (the “Fed”) maintained an accommodative monetary stance, fearful of policy mistakes at this stage of the recovery. However, talk of economic decoupling became increasingly loud during the summer months. While the U.S. continued to recover, Europe and the developing markets began to show signs of economic deceleration. China, which had been the primary economic engine of both the developed and the developing markets, showed clear signs of slowing, with some expressing fears of a hard landing. Copper and iron ore prices, as well as other industrial metals, all of which were closely linked with China’s growth, started to collapse. Crude oil prices peaked in late June and by the end of 2014 had fallen by over 50%. As the summer continued, economists described the Euro Zone as increasingly fragile and the foreign backdrop as the biggest threat to the U.S. economy. Economic weakness and declining commodity prices awakened fears of deflation. Central banks around the globe embarked on | | | | monetary easing programs to fuel growth and halt the spread of deflationary forces. Interest rates fell to historically low levels – including negative rates in some cases. As 2014 came to a close, the U.S. was the symbol of strength and stability, and the U.S Dollar started one of its sharpest rises of the recent past. Dollar strength, however, posed a dual threat – U.S. exports became increasingly expensive relative to other countries, and currency translation impacted the reported sales and earnings of U.S. multinational companies. On top of these macroeconomic headwinds, the West Coast dock strike, bitter temperatures and historic snowfalls paralyzed parts of the country. Despite the many negative macroeconomic and geopolitical worries, stocks managed to look through the current fog and discount an improved future. OUTLOOK To quote John Kenneth Galbraith, “The only function of economic forecasting is to make astrology look respectable.” While this tongue-in-cheek statement could be applied to all types of forecasts, equity portfolio management demands an opinion or expectation about the future. Absent an unexpected geopolitical event or policy mistake, we continue to believe that U.S. and international economic recovery will continue, given that economies respond with a lag to economic stimulus. For example, it may take from six months to a year for the effects of central bank accommodation to work its way through the global economy. This is stimulus that, along with lower energy prices, improving labor conditions, increased household formation and improved consumer confidence, can propel the economy for years. The Fed will ultimately move off its zero interest rate policy. The only unknown variables are the timing of the initial rate increase, and the rate of further increases. The Fed has maintained that its actions will be data-dependent, which is interpreted to mean measured and gradual. (As this is being written, the timing for the initial rate ncrease is as early as September, and possibly December.) |

| | | | |

| | | | | |

| | | AMG Managers Cadence Emerging Companies Fund | | |

| | | Portfolio Manager’s Comments (continued) | | |

| | | | | | | | |

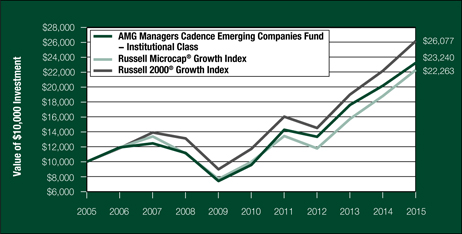

We know that most financial assets are not cheap by historical standards, with bonds being among the most richly valued alternatives. Stock and bond valuations are influenced by inflationary expectations and interest rate policy. We know that U.S. investors have been divesting their domestic mutual fund holdings for five or more years, seeking higher return or less risky or less correlated alternatives. The bull market that started in March, 2009, has been the least respected advance in memory. While select health care and biotechnology stocks, and some individual themes in information technology, have evidence of froth, it is hard to make the case of the market being as overvalued as last seen in March 2000. Given the above, we believe that stocks still offer the most attractive combination of risk and prospective return. Benign inflation benefits stocks over bonds, as businesses have greater flexibility navigating modestly higher costs. Bull markets never die of old age, as the old adage goes. They end when central bankers and policy makers raise interest rates to reduce the threat of rising inflationary | | | | expectations. When the yield curve inverts and short-term rates exceed long-term rates, it is only a matter of time before the bull market ends. This is not to say that the road ahead will be forever smooth – stocks reflect the fear and greed of investors with varied investment styles and objectives. Price volatility is an expression of investor sentiment that frequently arises at times when least expected. Cadence seeks to avoid these traps by following our time-tested investment approach. We seek growing, profitable companies selling at prices that make sense. Our research identifies stocks with improving sales and earnings, upward estimate revisions and attractive relative valuations. We structure diversified portfolios, mindful that even the best managed businesses hit a pot hole on occasion. Thank you for your investment in the AMG Managers Cadence Emerging Companies Fund. We appreciate your trust and look forward to rewarding your continued confidence in the year ahead. This commentary reflects the viewpoints of the Cadence Capital Management, LLC as of May 31, | | | | 2015 and is not intended as a forecast or guarantee of future results. CUMULATIVE TOTAL RETURN PERFORMANCE AMG Managers Cadence Emerging Companies Fund’s cumulative total return is based on the daily change in net asset value (NAV), and assumes that all dividends and distributions were reinvested. This graph compares a hypothetical $10,000 investment made in AMG Managers Cadence Emerging Companies Fund’s Institutional Class on May 31, 2005, to a $10,000 investment made in the Russell Microcap® Growth Index and the Russell 2000® Growth Index for the same time period. The graph and table do not reflect the deduction of taxes that a shareholder would pay on a Fund distribution or redemption of shares. The listed returns for the Fund are net of expenses and the returns for the index exclude expenses. Total returns would have been lower had certain expenses not been reduced. |

| | | | |

| | | | | |

| | | AMG Managers Cadence Emerging Companies Fund | | |

| | | Portfolio Manager’s Comments (continued) | | |

CUMULATIVE TOTAL RETURN PERFORMANCE (continued)

The table below shows the average annual total returns for the AMG Managers Cadence Emerging Companies Fund and the Russell Microcap® Growth Index and the Russell 2000® Growth Index for the same time periods ended May 31, 2015.

| | | | | | | | | | | | |

| | | One | | | Five | | | Ten | |

| Average Annual Total Returns1 | | Year | | | Years | | | Years | |

AMG Managers Cadence Emerging Companies Fund 2,3,4,5,6 | | | | | | | | | | | | |

Service Class | | | 14.95% | | | | 19.14% | | | | 8.53% | |

Institutional Class | | | 15.27% | | | | 19.44% | | | | 8.80% | |

| |

Russell Microcap® Growth Index7 | | | 18.51% | | | | 17.43% | | | | 8.33% | |

Russell 2000® Growth Index8 | | | 17.73% | | | | 17.37% | | | | 10.06% | |

|

| |

The performance data shown represents past performance. Past performance is not a guarantee of future results. Current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

Investors should carefully consider the Fund’s investment objectives, risks, charges and expenses before investing. For performance information through the most recent month end, current net asset values per share for the Fund and other information, please call (800) 835-3879 or visit our website at www.amgfunds.com for a free prospectus. Read it carefully before investing or sending money.

Distributed by AMG Distributors, Inc., member FINRA/SIPC.

| 1 | Total return equals income yield plus share price change and assumes reinvestment of all dividends and capital gain distributions. Returns are net of fees and may reflect offsets of Fund expenses as described in the prospectus. No adjustment has been made for taxes payable by shareholders on their reinvested dividends and capital gain distributions. Returns for periods greater than one year are annualized. The listed returns on the Fund are net of expenses and based on the published NAV as of May 31, 2015. All returns are in U.S. dollars ($). |

| | |

| | | 2 From time to time, the Fund’s advisor has waived its fees and/or absorbed Fund expenses, which has resulted in higher returns. 3 The Fundinvests in growth stocks, which may be more sensitive to market movements because their prices tend to reflect future investor expectations rather than just current profits. Growth stocks may underperform value stocks during given periods. 4 The Fund is subject to risks associated with investments in small-capitalization companies such as erratic earnings patterns, competitive conditions, limited earnings history, and a reliance on one or a limited number of products. 5 The Fund is subject to special risk considerations similar to those associated with the direct ownership of real estate. Real estate valuations may be subject to factors such as changing general and local economic, financial, competitive, and environmental conditions. 6 The Fund is subject to the special risks associated with investments in micro-cap companies, such as relatively short earnings history, competitive conditions, less publicly available corporate information and reliance on a limited number of products. 7 The Russell Microcap® Growth Index measures the performance of the micro-cap growth segment of the U.S. equity market. It includes those Russell Microcap Index companies with higher price-to-book ratios and higher forecasted growth values. Unlike the Fund, the Index is unmanaged, is not available for investment, and does not incur expenses. 8 The Russell 2000® Growth Index measures the performance of the Russell 2000 companies with higher price-to-book ratios and higher forecasted growth values. Unlike the Fund, the Index is unmanaged, is not available for investment, and does not incur expenses. The Russell Microcap® Growth Index and Russell 2000® Growth Index are registered trademarks of Russell Investments. Russell® is a trademark of Russell Investments. Not FDIC insured, nor bank guaranteed. May lose value. |

| | | | |

| | | AMG Managers Cadence Emerging Companies Fund | | |

| | | Fund Snapshots (unaudited) | | |

| | | May 31, 2015 | | |

PORTFOLIO BREAKDOWN

| | | | | | | | | | | | | | | | | |

| | | Sector | | AMG Managers Cadence Emerging

Companies Fund* | | Russell

Microcap®

Growth Index | | Russell

2000®

Growth

Index |

| | | Health Care | | | | 33.1 | % | | | | 45.4 | % | | | | 25.7 | % |

| | | Information Technology | | | | 19.2 | % | | | | 17.8 | % | | | | 26.0 | % |

| | | Consumer Discretionary | | | | 19.1 | % | | | | 10.9 | % | | | | 15.3 | % |

| | | Industrials | | | | 8.5 | % | | | | 10.2 | % | | | | 13.7 | % |

| | | Financials | | | | 7.9 | % | | | | 5.4 | % | | | | 7.5 | % |

| | | Consumer Staples | | | | 3.0 | % | | | | 2.4 | % | | | | 3.5 | % |

| | | Energy | | | | 2.3 | % | | | | 2.4 | % | | | | 3.1 | % |

| | | Telecommunication Services | | | | 1.9 | % | | | | 2.5 | % | | | | 0.7 | % |

| | | Materials | | | | 1.0 | % | | | | 2.6 | % | | | | 4.2 | % |

| | | Utilities | | | | 0.0 | % | | | | 0.4 | % | | | | 0.3 | % |

| | | Other Assets and Liabilities | | | | 4.0 | % | | | | 0.0 | % | | | | 0.0 | % |

| | | * As a percentage of net assets. | |

TOP TEN HOLDINGS

| | | | | | | | | | | | |

| | | | | | | |

| | | | | | | |

| | | Security Name | | | | % of Net Assets |

| | | Bluebird Bio, Inc. | | | | | | 2.0% | |

| | | Receptos, Inc. | | | | | | 1.7 | |

| | | Chimerix, Inc. | | | | | | 1.6 | |

| | | Alliance Fiber Optic Products, Inc. | | | | | | 1.4 | |

| | | LSI Industries, Inc. | | | | | | 1.4 | |

| | | AtriCure, Inc. | | | | | | 1.4 | |

| | | AMAG Pharmaceuticals, Inc. | | | | | | 1.4 | |

| | | RealD, Inc. | | | | | | 1.3 | |

| | | Capital Senior Living Corp. | | | | | | 1.3 | |

| | | Cascade Microtech, Inc. | | | | | | 1.3 | |

| | | | | | | | | | | |

| | | Top Ten as a Group | | | | | | 14.8% | |

| | | | | | | | | | | |

Because a fund’s strategy may result in multiple investments in particular sectors of the economy, its performance may depend on the performance of those sectors and may fluctuate more widely than investments diversified across more sectors. For additional information on these and other risk considerations, please see the Fund’s prospectus.

Any sectors, industries, or securities discussed should not be perceived as investment recommendations. Mention of a specific security should not be considered a recommendation to buy or solicitation to sell that security. Specific securities mentioned in this report may have been sold from the Fund’s portfolio of investments by the time you receive this report.

| | | | |

| | | AMG Managers Cadence Emerging Companies Fund | | |

| | | Schedule of Portfolio Investments | | |

| | | May 31, 2015 | | |

| | | | | | | | |

| | | | Shares | | | | Value | |

Common Stocks - 96.0% | | | | | | | | |

Consumer Discretionary - 19.1% | | | | | | | | |

Bassett Furniture Industries, Inc. | | | 12,345 | | | | $350,104 | |

Carmike Cinemas, Inc.* | | | 14,730 | | | | 409,936 | |

Carriage Services, Inc.1 | | | 18,680 | | | | 464,758 | |

Cavco Industries, Inc.* | | | 5,870 | | | | 425,751 | |

Cherokee, Inc. | | | 9,980 | | | | 238,522 | |

Escalade, Inc. | | | 21,930 | | | | 400,880 | |

Good Times Restaurants, Inc.* | | | 24,407 | | | | 224,056 | |

Haverty Furniture Cos., Inc. | | | 16,950 | | | | 356,120 | |

Installed Building Products, Inc.* | | | 19,240 | | | | 412,506 | |

Kona Grill, Inc.* | | | 14,340 | | | | 291,389 | |

Malibu Boats, Inc., Class A* | | | 19,400 | | | | 406,818 | |

Martha Stewart Living Omnimedia, Inc., Class A* | | | 68,320 | | | | 355,264 | |

Nautilus, Inc.* | | | 17,696 | | | | 373,740 | |

Nutrisystem, Inc. | | | 16,660 | | | | 379,182 | |

Overstock.com, Inc.*,1 | | | 16,660 | | | | 360,356 | |

Papa Murphy’s Holdings, Inc.* | | | 9,903 | | | | 170,134 | |

Stoneridge, Inc.* | | | 29,740 | | | | 354,798 | |

Superior Uniform Group, Inc. | | | 24,270 | | | | 458,703 | |

Tower International, Inc.* | | | 13,020 | | | | 358,180 | |

Winnebago Industries, Inc.1 | | | 9,270 | | | | 201,437 | |

Zoe’s Kitchen, Inc.*,1 | | | 5,990 | | | | 189,763 | |

Total Consumer Discretionary | | | | | | | 7,182,397 | |

Consumer Staples - 3.0% | | | | | | | | |

Calavo Growers, Inc. | | | 8,030 | | | | 405,114 | |

Lifeway Foods, Inc.* | | | 15,791 | | | | 282,027 | |

Primo Water Corp.*,1 | | | 70,095 | | | | 442,299 | |

Total Consumer Staples | | | | | | | 1,129,440 | |

Energy - 2.3% | | | | | | | | |

Abraxas Petroleum Corp.* | | | 119,090 | | | | 348,934 | |

Penn Virginia Corp.* | | | 49,240 | | | | 228,966 | |

Synergy Resources Corp.* | | | 25,320 | | | | 291,433 | |

Total Energy | | | | | | | 869,333 | |

Financials - 7.9% | | | | | | | | |

Atlas Financial Holdings, Inc.* | | | 22,790 | | | | 428,680 | |

Bryn Mawr Bank Corp. | | | 13,910 | | | | 401,721 | |

Eagle Bancorp, Inc.* | | | 9,590 | | | | 381,586 | |

Heritage Insurance Holdings, Inc.* | | | 16,880 | | | | 354,480 | |

Preferred Bank | | | 13,280 | | | | 366,262 | |

| | | | | | | | |

| | | | Shares | | | | Value | |

QTS Realty Trust, Inc., Class A | | | 10,150 | | | | $377,884 | |

Silvercrest Asset Management Group, Inc., Class A | | | 30,369 | | | | 394,797 | |

UMH Properties, Inc. | | | 29,080 | | | | 287,020 | |

Total Financials | | | | | | | 2,992,430 | |

Health Care - 33.1% | | | | | | | | |

Addus HomeCare Corp.* | | | 13,708 | | | | 383,961 | |

Albany Molecular Research, Inc.*,1 | | | 22,590 | | | | 455,189 | |

AMAG Pharmaceuticals, Inc.*,1 | | | 7,340 | | | | 510,717 | |

ANI Pharmaceuticals, Inc.*,1 | | | 3,390 | | | | 170,788 | |

AtriCure, Inc.* | | | 22,310 | | | | 511,791 | |

BioSpecifics Technologies Corp.* | | | 2,457 | | | | 117,051 | |

BioTelemetry, Inc.* | | | 42,468 | | | | 409,816 | |

Bluebird Bio, Inc.* | | | 3,920 | | | | 761,460 | |

Cambrex Corp.* | | | 10,390 | | | | 415,808 | |

Capital Senior Living Corp.* | | | 18,710 | | | | 481,970 | |

Cardiovascular Systems, Inc.* | | | 10,000 | | | | 279,800 | |

Chimerix, Inc.* | | | 14,570 | | | | 609,755 | |

Cross Country Healthcare, Inc.* | | | 19,460 | | | | 206,665 | |

Emergent Biosolutions, Inc.* | | | 13,909 | | | | 443,141 | |

Enanta Pharmaceuticals, Inc.*,1 | | | 5,220 | | | | 213,394 | |

Harvard Bioscience, Inc.* | | | 67,930 | | | | 380,408 | |

Heska Corp.* | | | 12,385 | | | | 392,604 | |

Icad, Inc.* | | | 37,486 | | | | 165,313 | |

Inogen, Inc.* | | | 11,160 | | | | 417,161 | |

Insys Therapeutics, Inc.*,1 | | | 6,210 | | | | 370,116 | |

Juniper Pharmaceuticals, Inc.* | | | 24,810 | | | | 199,224 | |

Ligand Pharmaceuticals, Inc.* | | | 4,450 | | | | 392,089 | |

MacroGenics, Inc.* | | | 7,430 | | | | 240,360 | |

Misonix, Inc.* | | | 28,932 | | | | 315,359 | |

POZEN, Inc.* | | | 53,850 | | | | 347,332 | |

The Providence Service Corp.* | | | 3,880 | | | | 186,473 | |

Psychemedics Corp. | | | 8,150 | | | | 120,131 | |

PTC Therapeutics, Inc.* | | | 4,190 | | | | 243,397 | |

Receptos, Inc.* | | | 3,825 | | | | 630,704 | |

Sangamo BioSciences, Inc.* | | | 28,220 | | | | 345,695 | |

SciClone Pharmaceuticals, Inc.* | | | 40,295 | | | | 373,132 | |

Sharps Compliance Corp.* | | | 60,235 | | | | 339,123 | |

Simulations Plus, Inc. | | | 55,937 | | | | 330,028 | |

SurModics, Inc.* | | | 14,360 | | | | 354,405 | |

|

|

| The accompanying notes are an integral part of these financial statements. |

| 20 |

| | | | |

| | | | | |

| | | AMG Managers Cadence Emerging Companies Fund | | |

| | | Schedule of Portfolio Investments (continued) | | |

| | | | | | | | |

| | | | Shares | | | | Value | |

Health Care - 33.1% (continued) | | | | | | | | |

U.S. Physical Therapy, Inc. | | | 7,580 | | | | $377,939 | |

Total Health Care | | | | | | | 12,492,299 | |

Industrials - 8.5% | | | | | |

Argan, Inc. | | | 10,540 | | | | 377,121 | |

CRA International, Inc.* | | | 10,751 | | | | 297,050 | |

Hawaiian Holdings, Inc.* | | | 18,730 | | | | 453,641 | |

Hill International, Inc.* | | | 87,799 | | | | 465,335 | |