OMB APPROVAL

OMB Number: 3235-0570

Expires: January 31, 2014

Estimated average burden

hours per response..... 20.6

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-3790

Pear Tree Funds

(Exact name of registrant as specified in charter)

55 Old Bedford Road, Lincoln, MA 01773

(Address of principal executive offices)

Willard L. Umphrey

Pear Tree Advisors, Inc.

55 Old Bedford Road, Lincoln, MA 01773

(Name and address of agent for service)

Registrant’s telephone number, including area code: (781) 676-5900

Date of fiscal year end: March 31

Date of reporting period: April 1, 2012 through September 30, 2012

ITEM 1. REPORTS TO SHAREOWNERS.

[Pear Tree Funds Logo]

PEAR TREE FUNDS

Pear Tree Columbia Small Cap Fund

Pear Tree Columbia Micro Cap Fund

Pear Tree Quality Fund

Pear Tree PanAgora Dynamic Emerging Markets Fund

Pear Tree Polaris Foreign Value Fund

Pear Tree Polaris Foreign Value Small Cap Fund

SEMI-ANNUAL REPORT

September 30, 2012

TABLE OF CONTENTS

President’s Letter 3

Fund Expenses 4

Portfolio Manager Commentaries 6

Pear Tree Columbia Small Cap Fund 6

Pear Tree Columbia Micro Cap Fund 9

Pear Tree Quality Fund 11

Pear Tree PanAgora Dynamic Emerging Markets Fund 13

Pear Tree Polaris Foreign Value Fund 15

Pear Tree Polaris Foreign Value Small Cap Fund 18

Schedules of Investments 21

Pear Tree Columbia Small Cap Fund 21

Pear Tree Columbia Micro Cap Fund 28

Pear Tree Quality Fund 33

Pear Tree PanAgora Dynamic Emerging Markets Fund 36

Pear Tree Polaris Foreign Value Fund 44

Pear Tree Polaris Foreign Value Small Cap Fund 47

Statements of Assets and Liabilities 52

Statements of Operations 56

Statements of Changes in Net Assets 58

Financial Highlights 64

Notes to Financial Statements 76

Information for Shareholders 92

Management Contract and Advisory Contract Approval 93

Service Providers inside back cover

This report must be preceded or accompanied by a current Pear Tree Funds prospectus for individuals who are not current shareholders of the Funds. If you are not a shareholder of a Pear Tree Fund, you should read the prospectus carefully before investing because it contains more complete information on the Pear Tree Funds’ investment objectives, risks, charges and expenses. Please consider this information carefully. For a prospectus and other information, visit www.peartreefunds.com or call (800) 326-2151.

NOT FDIC INSURED • MAY LOSE VALUE • NO BANK GUARANTEE

Neither Pear Tree Funds nor U.S. Boston Capital Corporation is a bank.

PEAR TREE FUNDS

Dear Fellow Shareholder,

We are pleased to provide you with the Pear Tree Funds’ Semi-Annual Report for the six month period ended September 30, 2012 and to update you on recent market conditions and the performance of the Pear Tree Funds.

For current performance information, please visit our website at www.peartreefunds.com. We thank you for your continued confidence in the Pear Tree Funds. Please feel free to e-mail us at feedback@peartreefunds.com or call us at 800-326-2151 with any questions or for assistance on your account.

Sincerely,

Willard Umphrey

President and Chairman

Any statements in this report regarding market or economic trends or the factors influencing the historical or future performance of the Pear Tree Funds are the views of Fund management as of the date of this report. These views are subject to change at any time based upon market and other conditions, and Fund management and the subadvisors to the Funds disclaim any responsibility to update such views. These views may not be relied upon as investment advice or as an indication of trading intent on behalf of any Pear Tree Fund. Any references to specific securities are not recommendations of such securities and may not be representative of any Pear Tree Fund’s current or future investments.

Past performance is no guarantee of future results, and there is no guarantee that market forecasts will be realized.

PEAR TREE FUNDS

FUND EXPENSES

We believe it’s important for Fund shareholders to have a clear understanding of fund expenses and the impact expenses have on investment returns. The following is important information about each Fund’s Expense Example, which appears below.

Expense Example

As a shareholder of a Fund, you incur two types of costs: (1) transaction costs, and (2) ongoing costs, including management fees, distribution (12b-1) fees (on Ordinary Shares) and other Fund expenses. The example is intended to help you understand your ongoing costs (in dollars) of investing in a Fund and to compare these costs with the ongoing costs of investing in other mutual funds. These examples are based on $1,000 invested at the beginning of the period and held for the entire period from April 1, 2012 to September 30, 2012.

Actual Expenses

The first line for each Share Class for each Fund provides information about actual account returns and actual expenses. You may use the information in this line, together with the amount you invested for that Fund and Share Class, to estimate the expenses that you paid over the period. To estimate the expenses you paid over the period, simply divide your account value by $1,000, then multiply the result by the number under the heading “Expenses Paid During the Period.”

Hypothetical Example for Comparison Purposes

The second line for each Share Class for each Fund shows you hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return.

The hypothetical account values and hypothetical expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing expenses of investing in the Fund with the ongoing expenses of other funds. To do so, compare the Fund’s 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

PEAR TREE FUNDS

Expense Example for the 6 months ended September 30, 2012

| Pear Tree Fund | Share Class | Total Return Description | Beginning Account Value 4/1/12 | Ending Account Value 9/30/2012 | Annualized Expense Ratio | Expenses Paid* 4/1/12 – 9/30/2012 |

| Small Cap | Ordinary | Actual | $1,000.00 | $990.70 | 1.65% | $8.23 |

| Hypothetical | $1,000.00 | $1,016.80 | 1.65% | $8.34 | ||

| Institutional | Actual | $1,000.00 | $992.20 | 1.40% | $7.00 | |

| Hypothetical | $1,000.00 | $1,018.04 | 1.40% | $7.09 | ||

| Quality | Ordinary | Actual | $1,000.00 | $1,040.50 | 1.48% | $7.57 |

| Hypothetical | $1,000.00 | $1,017.65 | 1.48% | $7.49 | ||

| Institutional | Actual | $1,000.00 | $1,042.80 | 1.00% | $5.14 | |

| Hypothetical | $1,000.00 | $1,020.03 | 1.00% | $5.08 | ||

| Emerging Markets | Ordinary | Actual | $1,000.00 | $992.10 | 1.80% | $9.01 |

| Hypothetical | $1,000.00 | $1,016.02 | 1.80% | $9.12 | ||

| Institutional | Actual | $1,000.00 | $993.50 | 1.53% | $7.66 | |

| Hypothetical | $1,000.00 | $1,017.39 | 1.53% | $7.75 | ||

| Foreign Value | Ordinary | Actual | $1,000.00 | $1,036.70 | 1.61% | $8.23 |

| Hypothetical | $1,000.00 | $1,016.98 | 1.61% | $8.15 | ||

| Institutional | Actual | $1,000.00 | $1,038.20 | 1.36% | $6.95 | |

| Hypothetical | $1,000.00 | $1,018.25 | 1.36% | $6.88 | ||

| Foreign Value | Ordinary | Actual | $1,000.00 | $1,023.30 | 1.70% | $8.60 |

| Small Cap | Hypothetical | $1,000.00 | $1,016.57 | 1.70% | $8.57 | |

| Institutional | Actual | $1,000.00 | $1,024.40 | 1.45% | $7.34 | |

| Hypothetical | $1,000.00 | $1,017.81 | 1.45% | $7.32 | ||

| Micro-Cap | Ordinary | Actual | $1,000.00 | $987.20 | 1.97% | $9.84 |

| Hypothetical | $1,000.00 | $1,014.60 | 1.97% | $9.98 | ||

| Institutional | Actual | $1,000.00 | $987.70 | 1.83% | $9.13 | |

| Hypothetical | $1,000.00 | $1,015.95 | 1.83% | $9.26 |

| * | “Expenses Paid” for each Fund share class relating to actual or hypothetical returns, is the amount equal to the product of (a) that Fund’s and Share Class’ average account value for the six-month period ended September 30, 2012, multiplied by (b) the corresponding “Annualized Expense Ratio” multiplied by (c) the fraction 183/366 (which reflects the six-month period covered by this report). |

PEAR TREE COLUMBIA SMALL CAP FUND

INVESTMENT PROFILE

All Data as of September 30, 2012

Investment Commentary

For the semi-annual period ended September 30, 2012 the Pear Tree Columbia Small Cap Fund’s Ordinary Shares (the “Fund”) underperformed its benchmark, the Russell 2000 Index. The Fund achieved a return of –0.93% at net asset value compared to 1.60% for the Index.

| Fund Information | ||

| Net Assets Under Management | $96.2 Million | |

| Number of Companies | 168 | |

| Price to Book Ratio | 2.7 | |

| Price to Earnings Ratio | 19.0 | |

| Ordinary | Institutional | |

| Total Expense Ratio (Net) | 1.65% | 1.40% |

| Ticker Symbol | USBNX | QBNAX |

Market Conditions and Investment Strategies

The past six months have been a rollercoaster ride for investors as equity markets fell in the first three months in response to concerns over the European debt crisis and the evolving economic slowdown in the U.S. and China. The markets then turned up over the next three months as investor sentiment reversed after central banks around the world took action to provide stimulus measures in order to stabilize and promote growth through monetary easing and lower interest rates. The net result for the period was a modest gain for the benchmark index.

Health Care and Utilities were the two best performing sectors in the Index over the past six months with gains of over 10% and 8% respectively, while Energy, which fell over 7%, and Information Technology, which lost over 6%, were the laggards during the period.

Analyzing our performance versus the Index for the quarter, the largest detractor to our performance was the Industrial sector, which cost us over 2.3% of return relative to the benchmark. This was primarily due to one of our largest and historically best performing holdings, Acacia Research Corp., which fell over 34% during the period. The company reported better than expected results for the second quarter but about half of the revenue came from one specific customer. Some seemed concerned that the growth of the business was tied to one time deals and might not be repeatable. Our view of the company leads us to believe that this is an erroneous interpretation so we added to our position and anticipate that this will be a strong performer in the quarters ahead.

We also underperformed the benchmark in the Financials sector due to stock selection which detracted over 2% of return versus the Index. Portfolio holdings Hersha Hospitality Trust, a Real Estate Investment Trust, and Green Dot Corp., an issuer of prepaid credit cards, both declined during the period, each costing over 0.3% of relative return.

Conversely, our best performance during past six months came in the Information Technology and Telecommunications Services sectors. In Technology, portfolio holdings Alliance Data Systems Corp., which provides customer loyalty solutions, and OSI Systems Inc., which markets security and inspection systems, both performed well adding 0.6% and 0.5% respectively to relative return for the period. In Telecom, our largest position, SBA Communications Corp., was the portfolio’s best contributor to performance gaining over 23% as secular trends continued to provide a very robust growth outlook for wireless tower operators.

Portfolio Changes

The Consumer Discretionary and Materials sector weightings increased during the period, while the Information Technology, Energy, and Telecommunications Services sectors declined. Changes in all other sectors were not material.

A Look Ahead

We remain committed to our philosophy of investing in high quality companies with unique positions of market leadership and competitive positions that can be sustained. We look for companies with strong and predictable earnings growth, positive earnings revisions and valuations that are not excessive. As we view the period ahead, we are optimistic that the recent market trend, which we believe has favored lower quality issues, will reverse and our focus on higher quality will allow us to achieve our goal of outperforming the benchmark index and our peers.

The Fund is co-managed by Robert von Pentz, CFA, and Rhys Williams, CFA of Columbia Partners, L.L.C. Investment Management.

PEAR TREE COLUMBIA SMALL CAP FUND

Top 10 Holdings

| Percentage of total net assets | 32.2% |

| Alliance Data Systems Corporation | 4.7% |

| Entertainment Properties Trust | 4.3% |

| Acacia Research Corporation—Acacia Technologies | 3.8% |

| Hersha Hospitality Trust | 3.7% |

| Core Laboratories N.V. | 3.5% |

| Catamaran Corporation | 3.0% |

| United Natural Foods, Inc. | 2.6% |

| Hain Celestial Group, Inc. | 2.3% |

| OSI Systems, Inc. | 2.2% |

| Gardner Denver, Inc. | 2.1% |

There is no guarantee that such securities will continue to be viewed favorably or held in the Fund’s portfolio.

Sector Allocation

| Percentage of total net assets | 100.0% |

| Financials | 22.8% |

| Consumer Discretionary | 17.8% |

| Information Technology | 14.6% |

| Industrials | 14.5% |

| Health Care | 10.6% |

| Consumer Staples | 8.3% |

| Energy | 4.5% |

| Telecommunication Services | 1.8% |

| Materials | 0.9% |

| CASH + other assets (net) | 4.2% |

Value of a $10,000 Investment

Pear Tree Columbia Small Cap (PTSC) Ordinary Shares vs. Russell 2000 Index

Average Annual Total Returns

| 3Q 2012 | Six Months | One Year | Five Year | Ten Year | Since Inception | Inception Date | |

| Ordinary Shares | 0.75% | –0.93% | 27.35% | –2.97% | 7.81% | 9.75% | 08/03/92 |

Institutional Shares1 | 0.80% | –0.78% | 27.72% | –2.73% | 8.21% | 9.05% | 01/06/93 |

Russell 20002 | 5.25% | 1.60% | 31.91% | 2.21% | 10.17% | 8.97% |

1 Institutional Shares may only be purchased by certain categories of investors and are not subject to sales charges or distribution fees.

2 The Russell 2000 Index is a market capitalization-weighted index of 2,000 small company stocks. It is widely recognized as representative of the general market for small company stocks. Index returns assume the reinvestment of dividends and, unlike Fund returns, do not reflect any fees or expenses. You cannot invest directly in an Index. The beginning date of the Index is 08/3/92.

Small company stocks may trade less frequently and in a limited volume, and their prices may fluctuate more than stocks of other companies. Small company stocks may therefore be more vulnerable to adverse developments than those of larger companies. The Fund may invest in the issuers in the real estate industry. Changes in real estate values or economic downturns can have a significant negative effect on these issuers.

PEAR TREE COLUMBIA MICRO CAP FUND

INVESTMENT PROFILE

All Data as of September 30, 2012

Investment Commentary

For the semi-annual period ended September 30, 2012 the Pear Tree Columbia Micro Cap Fund’s Ordinary Shares (the “Fund”) underperformed its benchmark, the Russell Microcap Index. The Fund achieved a return of –1.28% at net asset value compared to 3.82% for the Index.

| Fund Information | ||

| Net Assets Under Management | $4.6 Million | |

| Number of Companies | 100 | |

| Price to Book Ratio | 2.2 | |

| Price to Earnings Ratio | 16.2 | |

| Ordinary | Institutional | |

| Total Expense Ratio (Gross) | 1.98% | 2.07% |

| Total Expense Ratio (Net) | 1.98% | 1.83% |

| Ticker Symbol | PTFMX | MICRX |

Market Conditions and Investment Strategies

The equity markets over the past six months trended down initially as concerns over the European debt crisis and slowing global growth weighed on investors. After falling in May, stock markets bottomed in early June, traded sideways in July, moved higher in August, and continued their upward trajectory through the end of the period. This was somewhat surprising to us given the macro headwinds that confront global economies and businesses in this environment. In the end, investors concluded that the massive liquidity injected by the U.S. Federal Reserve and the European Central Bank offset weakening economies, gargantuan budget problems, and the inevitable inflationary consequence of “printing” money. The mantra for many years, “Don’t fight the Fed” has proved to be correct again, at least for the time being.

Health Care and Financials were the two best performing sectors in the Index over the past six months with gains of over 15% and 10% respectively, while Energy, which fell nearly 8%, and Information Technology, which lost almost 5%, were the laggards during the period.

Analyzing our performance versus the Index for the quarter, the largest detractor to our return was the Industrial sector, which cost us over 1.2% relative to the benchmark. This was due to stock selection and being overweight one of the poorer performing sectors in the Index. Portfolio holding MagneTek Inc., fell over 41% during the period, and detracted over 0.5% of relative return. We also underperformed in Information Technology, another negative performer for the benchmark, due to our stock selection during the period. Holding MEMSIC Inc., which fell over 34% in the period, cost over 0.3% of return versus the benchmark.

Conversely, our best performance during the past six months came in the Consumer Discretionary sector where we added nearly 0.7% of relative return due primarily to stock selection. Portfolio holding Overstock.com Inc., one of the best overall performers in the portfolio, gained over 97% during the period.

Portfolio Changes

The Industrials, Health Care and Materials sector weightings increased during the period, while the Information Technology, Consumer Staples and Energy sectors declined. Changes in all other sectors were not material.

A Look Ahead

Investor skepticism is at record highs, yet domestic equities are off to their best start in fifteen years. On the margin things appear to be improving. This can be attributed to lower input prices, global stimulus, and a resurgent U.S. housing market. Late-stage cyclicals that benefit from inflationary growth are particularly poised to outperform, explaining our increasing exposure to Materials and Industrials. Typically, when the business environment reaches a positive inflection point, microcaps benefit as they are more economically sensitive in nature.

The Fund is managed by Robert von Pentz, CFA, of Columbia Partners, L.L.C. Investment Management.

PEAR TREE COLUMBIA MICRO CAP FUND

Top 10 Holdings

| Percentage of total net assets | 12.9% |

| Overstock.com, Inc. | 1.4% |

| Alliance Healthcare Services, Inc. | 1.4% |

| Harris Interactive, Inc. | 1.3% |

| U.S. Concrete, Inc. | 1.3% |

| BioDelivery Sciences International, Inc. | 1.3% |

| NASB Financial, Inc. | 1.3% |

| Argan, Inc. | 1.3% |

| CECO Environmental Corp. | 1.2% |

| Homeowners Choice, Inc. | 1.2% |

| Smith & Wesson Holding Corporation | 1.2% |

There is no guarantee that such securities will continue to be viewed favorably or held in the Fund’s portfolio.

Sector Allocation

| Percentage of total net assets | 100.0% |

| Financials | 26.4% |

| Consumer Discretionary | 24.6% |

| Industrials | 16.1% |

| Information Technology | 11.4% |

| Health Care | 6.6% |

| Consumer Staples | 6.5% |

| Materials | 4.0% |

| Energy | 1.6% |

| Cash and Other Assets (Net) | 2.8% |

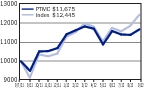

Value of a $10,000 Investment

Pear Tree Columbia Micro Cap (PTMC) Ordinary Shares vs. Russell Microcap Index

Average Annual Total Returns

| 3Q 2012 | Six Months | One Year | Five Year | Ten Year | Since Inception | Inception Date | |

| Ordinary Shares | 0.78% | –1.28% | 15.95% | 9/12/2011 | |||

Institutional Shares1 | 0.81% | –1.23% | 12.47% | 9/7/2011 | |||

Russell Microcap Index2 | 5.92% | 3.82% | 22.96% |

1 Institutional Shares may only be purchased by certain categories of investors and are not subject to sales charges or distribution fees.

2 The Russell Microcap Index measures the performance of the microcap segment of the U.S. equity market. Microcap stocks make up less than 3% of the U.S. equity market (by market cap) and consist of the smallest 1,000 securities in the small-cap Russell 2000®Index, plus the next smallest eligible securities by market cap. The Russell Microcap Index is constructed to provide a comprehensive and unbiased barometer for the microcap segment trading on national exchanges, while excluding lesser-regulated OTC bulletin board securities and pink-sheet stocks due to their failure to meet national exchange listing requirements. The Russell Microcap is completely reconstituted annually to ensure larger stocks do not distort performance and characteristics of the true microcap opportunity set.

Investing in foreign markets, particularly emerging markets, can be more volatile than the U.S. market due to increased risks of adverse issuer, political, regulatory, market or economic developments and can perform differently than the U.S. market.

PEAR TREE QUALITY FUND

INVESTMENT PROFILE

All Data as of September 30, 2012

Investment Commentary

For the semi-annual period ended September 30, 2012, the Pear Tree Quality Fund’s Ordinary Shares (the “Fund”) outperformed its benchmark, S&P 500 (the “Index”). The Fund achieved a return of 4.05% at net asset value compared to 3.43% for the Index.

| Fund Information | ||

| Net Assets Under Management | $97.8 Million | |

| Number of Companies | 62 | |

| Price to Book Ratio | 3.5 | |

| Price to Earnings Ratio | 13.5 | |

| Ordinary | Institutional | |

| Total Expense Ratio (Gross) | 1.63% | 1.37% |

| Total Expense Ratio (Net) | 1.48% | 1.00% |

| Ticker Symbol | USBOX | QGIAX |

Market Conditions and Investment Strategies

The Fund’s investment manager currently chooses securities for the Fund by periodically selecting a mutual fund (the “Target Portfolio”) and monitoring the Target Portfolio’s holdings. The Fund’s investment adviser, at the direction of the investment manager, rebalances the Fund’s portfolio to correspond to the Target Portfolio’s most recent holdings as publicly reported. From April 1, 2012 to September 30, 2012, the Fund’s Ordinary Shares, when compared to the Target Portfolio, had a tracking error of 0.23.

Over the previous six months, the Healthcare sector was the largest positive contributor to the Fund’s performance. The fact that the Fund has no holdings in the Financial sector also provided strong outperformance relative to the benchmark. The Fund’s large overweight position in Consumer Staples also contributed to outperformance.

The greatest detractor to performance came from the Telecom Services sector where the underweighting negatively affected relative performance. Other detractors were sector allocation in the Consumer Discretionary and Energy sectors.

Portfolio Changes

We expect the Fund to have a relatively low turnover rate given the historical stability and relatively low turnover rate of the current Target Portfolio.

For the six month period ending September 30, 2012, the Fund rebalanced the holdings twice to replicate the publicly disclosed holdings of the current target portfolio. The two rebalances resulted in the sale of six positions, four healthcare companies and two consumer staple positions. Also as a result of the rebalances, the Fund opened a new position in one Consumer Staple company.

A Look Ahead

For the foreseeable future, the Fund’s investment manager expects the Target Portfolio to remain the same. For more information on the selection of the Target Portfolio(s), please see the Fund’s Prospectus.

The Fund’s target portfolio is GMO Quality Fund III (GQETX) and the Fund is managed by Robert von Pentz, CFA of Columbia Partners, L.L.C. Investment Management.

PEAR TREE QUALITY FUND

Top 10 Holdings

| Percentage of total net assets | 43.8% |

| Johnson & Johnson | 5.5% |

| Oracle Corporation | 5.2% |

| Philip Morris International, Inc. | 4.8% |

| Pfizer Inc. | 4.5% |

| Coca-Cola Company (The) | 4.5% |

| Apple, Inc. | 4.3% |

| Google, Inc. | 4.3% |

| Microsoft Corporation | 4.1% |

| Chevron Corporation | 3.3% |

| Wal-Mart Stores, Inc. | 3.3% |

There is no guarantee that such securities will continue to be viewed favorably or held in the Fund’s portfolio.

Sector Allocation

| Percentage of total net assets | 100.0% |

| Information Technology | 30.0% |

| Consumer Staples | 28.4% |

| Health Care | 26.7% |

| Energy | 8.4% |

| Consumer Discretionary | 4.6% |

| Industrials | 0.8% |

| Telecommunication Services | 0.6% |

| CASH + other assets (net) | 0.5% |

Value of a $10,000 Investment

Pear Tree Quality (PTQ) Ordinary Shares vs. S&P 500 Index

Average Annual Total Returns

| 3Q 2012 | Six Months | One Year | Five Year | Ten Year | Since Inception | Inception Date | |

| Ordinary Shares | 5.89% | 4.05% | 25.69% | –2.02% | 5.19% | 8.82% | 05/06/85 |

Institutional Shares1 | 5.98% | 4.28% | 26.34% | –1.93% | 5.49% | 7.27% | 03/25/91 |

S&P 5002 | 6.35% | 3.43% | 30.20% | 1.05% | 8.01% | 10.28% |

1 Institutional Shares may only be purchased by certain categories of investors and are not subject to sales charges or distribution fees.

2 The S&P 500 Index is an unmanaged index of stocks chosen to their size industry characteristics. It is widely recognized as representative of stocks in the United States. Index returns assume the reinvestment of dividends and, unlike Fund returns, do not reflect any fees or expenses. You cannot invest directly in the Index. The beginning date for the Index is 05/29/85.

Investing in foreign markets can be more volatile than the U.S. market due to increased risks of adverse issuer, political, regulatory, market or economic developments and can perform differently than the U.S. market.

PEAR TREE PANAGORA DYNAMIC EMERGING MARKETS FUND

INVESTMENT PROFILE

All Data as of September 30, 2012

Investment Commentary

For the semi-annual period ended September 30, 2012, the Pear Tree Panagora Dynamic Emerging Markets Fund’s Ordinary Shares (the “Fund”) outperformed its benchmark, MSCI Emerging Markets Index (the Index”). The Fund achieved a return of –0.79% at net asset value compared to

–1.59% for the Index.

| Fund Information | ||

| Net Assets Under Management | $151.1 Million | |

| Number of Companies | 197 | |

| Price to Book Ratio | 1.4 | |

| Price to Earnings Ratio | 9.2 | |

| Ordinary | Institutional | |

| Total Expense Ratio (Net) | 1.80% | 1.53% |

| Ticker Symbol | QFFOX | QEMAX |

Market Conditions and Investment Strategies

On a country basis, the largest contributors were South Korea (+1.07%) and Brazil (+0.60%). Among holdings in South Korea, the largest contributor was an overweight to Korea Zinc while among holdings in Brazil, the largest contributor was not holding OGX Petroleo e Gas Participacoes. The largest detractors were China (–0.40%) and India (–0.31%). Among holdings in China the largest detractor was an overweight to Dongfeng Motor Group Co while among holdings in India the largest detractor was not holding Hdfc Bank.

On a sector basis, the largest contributors were Materials (+0.73%) and Consumer Discretionary (+0.72%). Among the holdings in Materials the largest contributor was an overweight to Kghm Polska Miedz while among holdings in Consumer Discretionary the largest contributor was an overweight to Great Wall Motor Company. The largest detractors were Financials (–0.28%) and Health Care (–0.12%). Among holdings in Financials the largest detractor was an overweight to Banco Estado Rio Grande while among holdings in Health Care the largest detractor was not holding Sun Pharmaceuticals.

During the semi-annual period that ended September 2012, our proprietary Dynamic Alpha model performed well — our high-ranked alpha stocks outperformed the worst ranked alpha stocks. Our proprietary Valuation composite performed well — stocks with attractive valuations outperformed their more expensive peers. Our proprietary Quality composite performed well — stocks with strong business and management quality metrics outperformed lower quality peers. Our proprietary Momentum composite performed well — stocks with positive market sentiment outperformed stocks with poor earnings and price momentum.

Portfolio Changes

There were no significant portfolio changes during the semi-annual period ended September 30, 2012.

A Look Ahead

As a quantitative investment firm, we tend not to provide strategy-specific forward looking commentary. We believe that our systematic investment approach ensures that we deliver a portfolio of our highest conviction of ideas to all of our clients.

The Fund’s portfolio is managed by a team of portfolio managers at PanAgora Asset Management, Inc.

PEAR TREE PANAGORA DYNAMIC EMERGING MARKETS FUND

Top 10 Holdings

| Percentage of total net assets | 21.7% |

| Samsung Electronics Co., Ltd. | 4.9% |

| China Construction Bank Corporation | 2.2% |

| China Mobile Limited | 2.2% |

| Vale SA | 2.0% |

| Petroleo Brasileiro SA | 1.9% |

| CNOOC Limited | 1.9% |

| Taiwan Semiconductor Manufacturing Co., Ltd. | 1.7% |

| LUKoil | 1.7% |

| Hyundai Motor Co. | 1.6% |

| Bank of China Ltd. | 1.6% |

There is no guarantee that such securities will continue to be viewed favorably or held in the Fund’s portfolio.

Sector Allocation

| Percentage of total net assets | 100.0% |

| Financials | 23.4% |

| Information Technology | 15.3% |

| Energy | 14.4% |

| Consumer Discretionary | 10.0% |

| Materials | 9.6% |

| Consumer Staples | 9.3% |

| Industrials | 8.6% |

| Telecommunication Services | 6.6% |

| Utilities | 2.2% |

| Health Care | 0.4% |

| CASH + other assets (net) | 0.2% |

Top 10 Country Allocations

| Percentage of total net assets | 83.2% |

| South Korea | 17.3% |

| Taiwan | 12.0% |

| Brazil | 10.9% |

| China | 10.6% |

| South Africa | 7.3% |

| Hong Kong | 6.9% |

| Russia | 5.0% |

| India | 4.9% |

| Malaysia | 4.5% |

| Mexico | 3.8% |

Value of a $10,000 Investment

Pear Tree PanAgora Dynamic Emerging Markets (PTEM) Ordinary Shares vs. MSCI EM Index

PEAR TREE PANAGORA DYNAMIC EMERGING MARKETS FUND

Average Annual Total Returns

| 3Q 2012 | Six Months | One Year | Five Year | Ten Year | Since Inception | Inception Date | |

| Ordinary Shares | 8.28% | –0.79% | 17.27% | –4.49% | 17.16% | 6.32% | 09/30/94 |

Institutional Shares1 | 8.36% | –0.65% | 17.58% | –4.26% | 17.54% | 8.21% | 04/02/96 |

MSCI EM2 | 7.89% | –1.59% | 17.33% | –0.98% | 17.37% | 5.70% |

1 Institutional Shares may only be purchased by certain categories of investors and are not subject to sales charges or distribution fees.

2 The Morgan Stanley Capital International Emerging Markets (“MSCI EM”) Index is an unmanaged index comprised of stocks located in countries other than the United States. It is widely recognized as representative of the general market for emerging markets. Index returns assume the reinvestment of dividends and, unlike Fund returns, do not reflect fees or expenses. You cannot invest directly in an Index. The beginning date for the Index is 09/30/94.

Investing in foreign markets, particularly emerging markets, can be more volatile than the U.S. market due to increased risks of adverse issuer, political, regulatory, market or economic developments and can perform differently than the U.S. market.

PEAR TREE POLARIS FOREIGN VALUE FUND

INVESTMENT PROFILE

All Data as of September 30, 2012

Investment Commentary

For the semi-annual period ended September 30, 2012, the Pear Tree Polaris Foreign Value Fund’s Ordinary Shares (the “Fund”) outperformed its benchmark, the MSCI EAFE Index (the “Index”). The Fund achieved a return of 3.67% at net asset value compared to –0.35% for the Index.

| Fund Information | ||

| Net Assets Under Management | $576.7 Million | |

| Number of Companies | 42 | |

| Price to Book Ratio | 1.7 | |

| Price to Earnings Ratio | 15.8 | |

| Ordinary | Institutional | |

| Total Expense Ratio (Net) | 1.62% | 1.36% |

| Ticker Symbol | QFVOX | QFVIX |

Market Conditions and Investment Strategies

Strong portfolio performance stemmed from returns in eight of 10 sectors, with only Information Technology and Materials in absolute negative territory. Consumer Discretionary stocks were the top contributors, with Barratt Developments and Persimmon, plc posting double digit returns. The performance of both British homebuilders was helped by their continued focus on margins over volumes (i.e. buying lower priced land, and building more houses at higher prices than apartments).

Japanese brewery Asahi Group, dairy supplier Meiji and refrigerated food storage and transport company Nichirei propelled the performance of the Consumer Staples sector. All three experienced a recovery in operations following the March 2011 earthquake, highlighted by stronger sales and operating profits. Asahi posted an extraordinary gain on a change in equity in Chinese soft drink affiliate, Tingyi-Asahi Beverages, which entered a strategic alliance with PepsiCo. Nichirei continued to see stable demand for its convenience foods and food logistics services.

Finnish industrial companies Kone OYJ and Konecranes OYJ produced strong returns for the six-month period, benefitting from new product developments, higher orders and healthy backlog. Italian ground engineering services company Trevi Finanziaria announced positive earnings, followed by news of international orders in Thailand, West Africa and Venezuela.

More than 65% of the Fund’s stocks achieved absolute positive returns; those that fared worse included French exploration and production company Maurel et Prom, German ATM manufacturer Wincor Nixdorf and Japanese chemical company Showa Denko. Growth in its retail point of sale outlets sustained Wincor Nixdorf, which has seen slower bank branch ATM sales due to reduced capital spending by stressed European banks. Showa Denko suffered from slowing demand in both of its product lines — petrochemicals and hard disc media.

Portfolio Changes

In early April, the Fund purchased Italy’s Lottomatica, a provider of video lottery terminals and other lottery programs. During difficult macro-economic times, lotteries are in high demand as governments rely on the higher reserves from consistent ticket sales. State Bank of India was sold during the period, as significant headwinds faced the company: Indian GDP is decreasing, while inflation, interest rates and non-performing assets are rising. We believe State Bank of India remains a good value; however, our concern to protect against declines led us to sell the company.

A Look Ahead

International markets experienced a healthy rebound, with four of the past six months in positive territory. However, guarded optimism must prevail, as stagnant macro-economic activity and slow global trade will likely persist. China GDP growth is slowing and export sales to Europe are lessening. In India, a lack of government productivity is holding back project development. With the Brazilian currency especially strong, the export of the country’s products is down, thereby threatening recession. Among developed countries, the U.S. economy will continue to experience fits and starts, benefitting from low cost energy and service sectors, offset by a still weak housing market and mixed job reports. With uncertainty comes volatility that can create market inefficiencies. We will continue our efforts to conduct bottom-up research to pinpoint some of the most fundamentally-strong, but undervalued companies worldwide.

The Fund’s lead portfolio manager is Bernard R. Horn, Jr., of Polaris Capital Management, LLC

PEAR TREE POLARIS FOREIGN VALUE FUND

Top 10 Holdings

| Percentage of total net assets | 25.1% |

| Samsung Electronics Company Ltd. | 3.4% |

| Taylor Wimpey plc | 2.7% |

| Smurfit Kappa Group plc | 2.6% |

| Kone OYJ, Class B | 2.5% |

| Barratt Developments plc | 2.5% |

| Persimmon plc | 2.4% |

| Konecranes OYJ | 2.3% |

| Imerys S.A. | 2.3% |

| Teva Pharmaceuticals SP | 2.2% |

| Sasol Ltd. | 2.2% |

There is no guarantee that such securities will continue to be viewed favorably or held in the Fund’s portfolio.

Sector Allocation

| Percentage of total net assets | 100.0% |

| Materials | 18.4% |

| Consumer Discretionary | 15.3% |

| Financials | 10.4% |

| Industrials | 8.7% |

| Consumer Staples | 8.1% |

| Information Technology | 7.5% |

| Energy | 5.9% |

| Health Care | 4.4% |

| Telecommunication Services | 3.9% |

| Utilities | 1.4% |

| Cash and Other Assets (Net) | 16.0% |

Top 10 Country Allocations

| Percentage of total net assets | 66.7% |

| Germany | 12.1% |

| United Kingdom | 10.5% |

| Japan | 9.8% |

| Finland | 6.8% |

| Ireland | 6.7% |

| France | 6.1% |

| Sweden | 5.9% |

| South Korea | 3.4% |

| Italy | 3.2% |

| Israel | 2.2% |

Value of a $10,000 Investment

Pear Tree Polaris Foreign Value (PTFV) Ordinary Shares vs. MSCI EAFE Index

PEAR TREE POLARIS FOREIGN VALUE FUND

Average Annual Total Returns

| 3Q 2012 | Six Months | One Year | Five Year | Ten Year | Since Inception | Inception Date | |

| Ordinary Shares | 10.30% | 3.67% | 21.03% | –3.22% | 10.89% | 5.91% | 05/15/98 |

Institutional Shares1 | 10.37% | 3.82% | 21.37% | –3.03% | 11.15% | 7.72% | 12/18/98 |

MSCI EAFE2 | 6.98% | –0.35% | 14.33% | –4.77% | 8.69% | 3.53% |

1 Institutional Shares may only be purchased by certain categories of investors and are not subject to sales charges or distribution fees.

2 The Morgan Stanley Capital International Europe, Australia, and Far East (“MSCI EAFE”) Index is an unmanaged index comprised of stocks located in countries other than the United States. It is widely recognized as representative of the general market for emerging markets. Index returns assume the reinvestment of dividends and, unlike Fund returns, do not reflect fees or expenses. You cannot invest directly in an Index. The beginning date for the Index is 05/29/98.

Investing in foreign markets, particularly emerging markets, can be more volatile than the U.S. market due to increased risks of adverse issuer, political, regulatory, market or economic developments and can perform differently than the U.S. market.

PEAR TREE POLARIS FOREIGN VALUE SMALL CAP FUND

INVESTMENT PROFILE

All Data as of September 30, 2012

Investment Commentary

For the semi-annual period ended September 30, 2012, the Pear Tree Polaris Foreign Value Small Cap Fund’s Ordinary Shares (the “Fund”) outperformed its benchmark, the S&P EPAC Small Cap Index (the “Index”). The Fund achieved a return of 2.33% at net asset value compared to

–0.85% for the Index.

| Fund Information | ||

| Net Assets Under Management | $92.3 Million | |

| Number of Companies | 67 | |

| Price to Book Ratio | 1.9 | |

| Price to Earnings Ratio | 18.5 | |

| Ordinary | Institutional | |

| Total Expense Ratio (Net) | 1.70% | 1.45% |

| Ticker Symbol | QUSOX | QUSIX |

Market Conditions and Investment Strategies

Stocks in the defensive sectors (i.e. Utilities, Consumer Staples and Healthcare) were among the top performers for the quarter, while cyclical stock contributed to a lesser extent. Absolute positive returns were achieved in eight of 10 sectors, with only Materials and Energy in negative territory.

United Drug, the Ireland-based pharmaceutical and healthcare services, was the top contributor to performance for the six month period. The company continued its growth through acquisition strategy, delivering strong earnings and margins. United Drug’s efforts to delist from the Irish stock exchange in favor of the London market were also met with resounding support.

British information technology company CSR added to the period’s returns, after selling its handset operations to Samsung Electronics for $310 million. The capital from this sale will be used to focus on CSR’s other high margin businesses.

Public water utility, Manila Water Company, posted strong gains as it experienced rising water connections in the Philippines. The company also benefitted from a tariff adjustment.

U.K. homebuilder Galliford Try also added to returns for the period. After a 2009 capital raise, the company purchased large parcels of inexpensive land in Southern England during the economic downturn, targeting significant improvement in production volumes and profitability metrics. It has successfully delivered on its target.

Materials sector stocks were among the underperformers for the six month period, with weak returns from India’s USHA Martin and Japan’s Chugoku Marine Paints. Chugoku suffered under high priced oil, which is the main raw material of the company’s paints. USHA Martin experienced falling auto demand and is dealing with a dispute at one of its coal mines. Textile and clothing maker Texwinca Holdings suffered margin contraction due to significantly higher cotton prices in China than in the international market.

Portfolio Changes

During the six-month period, the Fund purchased shares of SpareBank 1 SR Bank ASA of Norway, the Fund’s third purchase of a regional bank in Norway. All three have similar business models, with strong balance sheets, limited downside risks and good market positioning, but are defined by different geographic reach. The Fund’s position in Scandinavian gas station chain operator Statoil Fuel & Retail was sold at a profit, as a result of a friendly buyout from Canada’s Alimentation Couche-Tard.

A Look Ahead

International markets have experienced a healthy rebound in recent months. However, guarded optimism must prevail, as stagnant macro-economic activity and slow global trade will likely persist. China GDP growth is slowing and export sales to Europe are lessening. In India, a lack of government productivity could potentially slow project development. With the Brazilian currency especially strong, the export of the country’s products could become less profitable. Among developed countries, the U.S. economy should continue to experience fits and starts, benefitting from low cost energy and service sectors, offset by a weak housing market and mixed job reports. With uncertainty comes volatility that can create market inefficiencies. We will continue our efforts to conduct bottom-up research to pinpoint some of the most fundamentally-strong, but undervalued small-cap companies worldwide.

The Fund’s lead portfolio manager is Bernard R. Horn, Jr., of Polaris Capital Management, LLC

PEAR TREE POLARIS FOREIGN VALUE SMALL CAP FUND

Top 10 Holdings

| Percentage of total net assets | 24.6% |

| Manila Water Company, Inc. | 2.9% |

| United Drug plc | 2.8% |

| Dockwise Ltd. | 2.7% |

| Equatorial Energia S.A. | 2.6% |

| Galliford Try plc | 2.5% |

| M1 Ltd. | 2.4% |

| Freenet AG | 2.3% |

| DaiichiKosho Co., Ltd. | 2.2% |

| Thai Union Frozen Products PCL | 2.1% |

| BML, Inc. | 2.1% |

There is no guarantee that such securities will continue to be viewed favorably or held in the Fund’s portfolio.

Sector Allocation

| Percentage of total net assets | 100.0% |

| Consumer Discretionary | 23.0% |

| Consumer Staples | 13.0% |

| Financials | 11.7% |

| Information Technology | 11.6% |

| Industrials | 10.6% |

| Utilities | 7.6% |

| Health Care | 6.8% |

| Telecommunication Services | 6.5% |

| Materials | 5.5% |

| Energy | 2.7% |

| Cash and Other Assets (Net) | 1.0% |

Top 10 Country Allocations

| Percentage of total net assets | 74.6% |

| United Kingdom | 16.5% |

| Japan | 11.5% |

| India | 8.7% |

| Ireland | 8.2% |

| Hong Kong | 6.2% |

| Norway | 5.7% |

| Thailand | 5.7% |

| Sweden | 4.2% |

| Germany | 4.1% |

| Singapore | 3.8% |

Value of a $10,000 Investment

Pear Tree Polaris Foreign Value Small Cap (PTFVSC) Ordinary Shares vs. S&P EPAC Small Cap Index

PEAR TREE POLARIS FOREIGN VALUE SMALL CAP FUND

Average Annual Total Returns

| 3Q 2012 | Six Months | One Year | Five Year | Ten Year | Since Inception | Inception Date | |

| Ordinary Shares | 8.97% | 2.33% | 15.26% | 2.36% | 5/1/2008 | ||

Institutional Shares1 | 8.95% | 2.44% | 15.48% | 2.58% | 5/1/2008 | ||

S&P/EPAC Small Cap Index2 | 7.86% | –0.85% | 13.92% | –1.79% |

1 Institutional Shares may only be purchased by certain categories of investors and are not subject to sales charges or distribution fees.

2 The S&P/Europe Pacific Asia Composite Small Cap (“S&P/EPAC”) Index measures the bottom 20% of institutionary investable capital of developed and emerging (after 09/30/1994) countries, selected by the index sponsor outside of the United States. It is widely recognized as representative of the general market for foreign markets. Index returns assume the reinvestment of dividends and, unlike Fund returns, do not reflect any fees or expenses. You cannot invest directly in an Index. The Index was established in 1989.

Investing in foreign markets, particularly emerging markets, can be more volatile than the U.S. market due to increased risks of adverse issuer, political, regulatory, market or economic developments and can perform differently than the U.S. market.

PEAR TREE COLUMBIA SMALL CAP FUND

SCHEDULE OF INVESTMENTS

September 30, 2012 (Unaudited)

Common Stock—95.8%

| Shares | Value | |

| AIR FREIGHT & LOGISTICS—0.0% | ||

| Echo Global Logistics, Inc. (a) | 1,882 | $32,276 |

| AIRLINES—0.7% | ||

| Spirit Airlines, Inc. (a) | 42,243 | 721,510 |

| BANKS—6.1% | ||

| BBX Capital Corporation (a) | 6,176 | 39,897 |

| Berkshire Bancorp, Inc. (a) | 3,884 | 31,965 |

| CoBiz Financial, Inc. | 91,266 | 638,862 |

| Codorus Valley Bancorp, Inc. | 2,526 | 36,337 |

| FBR & Co. (a) | 12,396 | 38,304 |

| F.N.B. Corporation | 159,469 | 1,787,647 |

| Guaranty Bancorp (a) | 15,675 | 31,664 |

| Intervest Bancshares Corporation (a) | 9,223 | 35,047 |

| Macatawa Bank Corporation (a) | 10,311 | 32,067 |

| NASB Financial, Inc. (a) | 1,795 | 44,588 |

| Pacific Mercantile Bancorp (a) | 4,788 | 31,314 |

| Pinnacle Financial Partners, Inc. (a) | 60,718 | 1,173,072 |

| Popular, Inc. (a) | 43,340 | 755,416 |

| Preferred Bank (a) | 2,481 | 35,181 |

| Republic First Bancorp, Inc. (a) | 17,220 | 35,645 |

| Susquehanna Bancshares, Inc. | 56,684 | 592,915 |

| Taylor Capital Group, Inc. (a) | 2,151 | 36,825 |

| United Bankshares, Inc. (b) | 16,595 | 413,381 |

| Wilshire Bancorp, Inc. (a) | 6,344 | 39,967 |

| 5,830,094 | ||

| BEVERAGES—1.7% | ||

| SodaStream International Ltd. (a)(b) | 42,457 | 1,663,041 |

| BIOTECHNOLOGY—0.0% | ||

| BioDelivery Sciences International, Inc. (a) | 7,062 | 44,632 |

| BUILDING PRODUCTS—1.6% | ||

| Builders FirstSource, Inc. (a) | 6,509 | 33,782 |

| NCI Building Systems, Inc. (a) | 41,898 | 420,237 |

| PGT, Inc. (a) | 11,204 | 36,749 |

| Trex Company, Inc. (a) | 30,684 | 1,046,938 |

| 1,537,706 | ||

| CHEMICALS—0.1% | ||

| Penford Corporation (a) | 3,854 | 28,828 |

| TPC Group, Inc. (a) | 890 | 36,321 |

| 65,149 |

The accompanying notes are an integral part of these financial statements.

| COMMERCIAL SERVICES & SUPPLIES—8.2% | ||

| Acacia Research Corporation—Acacia Technologies (a) | 133,228 | 3,651,780 |

| CECO Environmental Corp. | 4,510 | 44,063 |

| Core-Mark Holding Company, Inc. | 720 | 34,639 |

| Heartland Payment Systems, Inc. | 41,997 | 1,330,465 |

| Hudson Global, Inc. (a) | 8,940 | 32,452 |

| Intersections, Inc. | 2,145 | 22,608 |

| Kforce, Inc. (a) | 125,682 | 1,481,791 |

| Move, Inc. (a) | 3,691 | 31,816 |

| StarTek, Inc. (a) | 11,423 | 34,269 |

| Sypris Solutions, Inc. | 4,835 | 34,522 |

| Waste Connections, Inc. | 38,805 | 1,173,851 |

| 7,872,256 | ||

| COMMUNICATIONS EQUIPMENT—1.8% | ||

| Ambient Corporation (a) | 4,868 | 25,606 |

| Boingo Wireless, Inc. (a) | 3,000 | 23,820 |

| CalAmp Corp. (a) | 4,557 | 37,413 |

| NICE-Systems Ltd. (a)(c) | 41,569 | 1,380,922 |

| Ubiquiti Networks, Inc. (a)(b) | 21,431 | 255,029 |

| 1,722,790 | ||

| CONSTRUCTION MATERIALS—0.0% | ||

| U.S. Concrete, Inc. (a) | 7,076 | 45,852 |

| CONTAINERS & PACKAGING—0.0% | ||

| Myers Industries, Inc. | 2,019 | 31,537 |

| DISTRIBUTORS—0.0% | ||

| AMCON Distributing Company | 583 | 37,837 |

| DIVERSIFIED FINANCIALS—4.8% | ||

| CIFC Corp. (a) | 4,889 | 35,787 |

| First Cash Financial Services, Inc. (a) | 35,595 | 1,637,726 |

| FirstCity Financial Corporation (a) | 3,936 | 31,606 |

| ICG Group, Inc. (a) | 122,762 | 1,247,262 |

| Medley Capital Corporation | 92,602 | 1,302,910 |

| Meta Financial Group, Inc. | 1,753 | 42,510 |

| MicroFinancial, Inc. | 4,186 | 38,302 |

| NGP Capital Resources Co. | 4,889 | 36,472 |

| Nicholas Financial, Inc. | 2,718 | 35,090 |

| QC Holdings, Inc. | 8,505 | 30,448 |

| Tree.Com, Inc. (a) | 7,896 | 123,730 |

| White River Capital, Inc. | 1,524 | 34,427 |

| 4,596,270 | ||

| ELECTRICAL EQUIPMENT—0.0% | ||

| Magnetek, Inc. (a) | 2,337 | 26,315 |

| ELECTRONIC EQUIPMENT & INSTRUMENTS—3.0% | ||

| Finisar Corporation (a) | 48,132 | 688,287 |

| OSI Systems, Inc. (a) | 27,419 | 2,134,295 |

| TESSCO Technologies, Inc. | 1,534 | 32,475 |

| 2,855,057 |

The accompanying notes are an integral part of these financial statements.

| ENERGY EQUIPMENT & SERVICES—4.4% | ||

| Core Laboratories N.V. | 27,354 | 3,322,964 |

| Dawson Geophysical Company (a) | 17,547 | 443,237 |

| Hornbeck Offshore Services, Inc. (a) | 14,426 | 528,713 |

| 4,294,914 | ||

| FOOD & DRUG RETAILING—2.8% | ||

| Pantry, Inc. (The) (a) | 2,276 | 33,116 |

| PetMed Express, Inc. | 2,858 | 28,694 |

| United Natural Foods, Inc. (a) | 43,296 | 2,530,651 |

| Village Super Market, Inc., Class A | 1,023 | 37,606 |

| 2,630,067 | ||

| FOOD PRODUCTS—3.7% | ||

| Andersons, Inc. (The) | 35,287 | 1,328,908 |

| Chefs’ Warehouse, Inc. (The) (a) | 1,920 | 31,450 |

| Hain Celestial Group, Inc. (a) | 34,838 | 2,194,794 |

| John B. Sanfilippo & Son, Inc. (a) | 1,862 | 24,243 |

| 3,579,395 | ||

| HEALTH CARE EQUIPMENT & SUPPLIES—3.9% | ||

| Accuray Incorporated (a) | 123,924 | 877,382 |

| Natus Medical, Inc. (a) | 92,350 | 1,207,014 |

| Solta Medical, Inc. (a) | 281,034 | 882,447 |

| Syneron Medical Ltd. (a) | 77,833 | 758,872 |

| 3,725,715 | ||

| HEALTH CARE PROVIDERS & SERVICES—5.9% | ||

| Alliance Healthcare Services, Inc. (a) | 34,956 | 49,288 |

| Bio-Reference Laboratories, Inc. (a) | 39,913 | 1,140,714 |

| Catamaran Corporation (a) | 29,088 | 2,849,751 |

| Henry Schein, Inc. (a) | 19,172 | 1,519,764 |

| Psychemedics Corporation | 3,295 | 40,034 |

| U.S. Physical Therapy, Inc. | 1,341 | 37,052 |

5,636,603 | ||

| HOTELS, RESTAURANTS & LEISURE—1.2% | ||

| AFC Enterprises, Inc. (a) | 1,475 | 36,285 |

| Ark Restaurants Corp. | 2,462 | 41,300 |

| Einstein Noah Restaurant Group, Inc. | 2,023 | 35,787 |

| Jamba, Inc. (a) | 15,675 | 34,955 |

| Kona Grill, Inc. (a) | 4,018 | 35,961 |

| Multimedia Games Holding Company, Inc. (a) | 2,271 | 35,723 |

| Nathan’s Famous, Inc. (a) | 1,165 | 36,639 |

| National CineMedia, Inc. | 55,659 | 911,138 |

| 1,167,788 | ||

| HOUSEHOLD DURABLES—2.2% | ||

| Emerson Radio Corp. (a) | 17,305 | 35,735 |

| M.D.C. Holdings, Inc. | 18,119 | 697,763 |

| Standard Pacific Corporation (a) | 200,968 | 1,358,544 |

| U.S. Home Systems, Inc. | 3,454 | 43,071 |

| 2,135,113 |

The accompanying notes are an integral part of these financial statements.

| INDUSTRIAL CONGLOMERATES—0.5% | ||

| Lydall, Inc. (a) | 2,570 | 36,211 |

| Polypore International, Inc. (a)(b) | 12,180 | 430,563 |

| 466,774 | ||

| INSURANCE—0.1% | ||

| Homeowners Choice, Inc. | 1,868 | 43,898 |

| Imperial Holdings, Inc. (a) | 8,827 | 30,100 |

| 73,998 | ||

| INTERNET & CATALOG RETAIL—0.2% | ||

| 1-800-Flowers.com, Inc., Class A (a) | 9,737 | 36,319 |

| Nutrisystem, Inc. | 2,993 | 31,516 |

| Overstock.com, Inc. (a)(b) | 4,930 | 51,075 |

| 118,910 | ||

| INTERNET SOFTWARE & SERVICES—2.4% | ||

| Ancestry.com, Inc. (a)(b) | 47,090 | 1,416,467 |

| LivePerson (a) | 48,771 | 883,243 |

| 2,299,710 | ||

| IT CONSULTING & SERVICES—6.2% | ||

| Alliance Data Systems Corporation (a) | 32,190 | 4,569,371 |

| Computer Task Group, Inc. (a) | 2,458 | 39,770 |

| Hackett Group, Inc. (The) (a) | 6,633 | 27,726 |

| Industrial Services of America, Inc. (a) | 7,361 | 26,941 |

| InterNAP Network Services Corporation (a) | 166,656 | 1,174,925 |

| Lionbridge Technologies, Inc. (a) | 10,992 | 38,692 |

| Wayside Technology Group, Inc. | 2,833 | 35,327 |

| 5,912,752 | ||

| LEISURE EQUIPMENT & PRODUCTS—4.1% | ||

| Arctic Cat, Inc. (a) | 33,987 | 1,409,101 |

| Callaway Golf Company | 69,377 | 425,975 |

| Glu Mobile, Inc. (a)(b) | 187,403 | 867,676 |

| Nautilus, Inc. (a) | 10,132 | 26,546 |

| Smith & Wesson Holding Corporation (a) | 108,481 | 1,194,375 |

| 3,923,673 | ||

| MACHINERY—3.2% | ||

| Actuant Corporation | 19,296 | 552,252 |

| Argan, Inc. (a) | 2,552 | 44,532 |

| Gardner Denver, Inc. | 33,284 | 2,010,686 |

| Supreme Industries, Inc. (a) | 8,423 | 30,744 |

| Titan International, Inc. (b) | 22,331 | 394,366 |

| 3,032,580 | ||

| MEDIA—6.1% | ||

| Ballantyne Strong, Inc. | 5,855 | 24,357 |

| Cinemark Holdings, Inc. | 82,132 | 1,842,221 |

| Harris Interactive, Inc. (a) | 31,778 | 46,396 |

| IMAX Corporation (a) | 74,390 | 1,481,105 |

| Regal Entertainment Group, Class A | 117,014 | 1,646,387 |

| TiVo, Inc. (a) | 80,648 | 841,158 |

| 5,881,624 |

The accompanying notes are an integral part of these financial statements.

| METALS & MINING—0.8% | ||

| Silver Standard Resources, Inc. (a) | 45,534 | 729,910 |

| MULTILINE RETAIL—0.0% | ||

| Gordmans Stores, Inc. (a) | 1,986 | 36,642 |

| OFFICE ELECTRONICS—0.0% | ||

| PAR Technology Corporation (a) | 6,991 | 38,101 |

| OIL & GAS—0.1% | ||

| Adams Resources & Energy, Inc. | 813 | 24,797 |

| VAALCO Energy, Inc. (a) | 3,919 | 33,507 |

58,304 | ||

| PERSONAL PRODUCTS—0.1% | ||

| Female Health Company (The) | 5,730 | 40,970 |

| United-Guardian, Inc. | 1,904 | 35,985 |

| 76,955 | ||

| PHARMACEUTICALS—0.8% | ||

| Obagi Medical Products, Inc. (a) | 2,255 | 27,985 |

| Par Pharmaceutical Companies, Inc. (a) | 14,429 | 721,161 |

| POZEN, Inc. (a) | 5,163 | 34,231 |

| 783,377 | ||

| REAL ESTATE—11.8% | ||

| AG Mortgage Investment Trust, Inc. | 1,617 | 39,018 |

| American Campus Communities, Inc. | 30,684 | 1,346,414 |

| Apollo Commercial Real Estate Finance, Inc. | 2,133 | 36,986 |

| Brandywine Realty Trust | 83,586 | 1,018,913 |

| Dynex Capital, Inc. | 3,394 | 36,486 |

| Education Realty Trust, Inc. | 45,188 | 492,549 |

| Entertainment Properties Trust | 94,022 | 4,177,398 |

| Extra Space Storage, Inc. | 21,075 | 700,744 |

| Hersha Hospitality Trust | 722,381 | 3,539,667 |

| 11,388,175 | ||

| ROAD & RAIL—0.3% | ||

| Old Dominion Freight Line (a) | 7,309 | 220,439 |

| Pacer International, Inc. (a) | 6,122 | 24,366 |

| Saia, Inc. (a) | 1,626 | 32,748 |

| Universal Truckload Services, Inc. | 2,378 | 37,976 |

| 315,529 | ||

| SEMICONDUCTOR EQUIPMENT & PRODUCTS—0.4% | ||

| inTEST Corporation (a) | 10,251 | 27,165 |

| MIPS Technologies, Inc. (a) | 48,624 | 359,332 |

| Ultra Clean Holdings, Inc. (a) | 5,361 | 30,611 |

| 417,108 | ||

| SOFTWARE—0.8% | ||

| Majesco Entertainment Company (a) | 17,305 | 21,804 |

| MedAssets, Inc. (a) | 22,277 | 396,531 |

| Verint Systems, Inc. (a) | 12,561 | 344,674 |

| 763,009 |

The accompanying notes are an integral part of these financial statements.

| SPECIALTY RETAIL—2.7% | ||

| Destination Maternity Corporation | 1,572 | 29,396 |

| Fifth & Pacific Companies, Inc. (a) | 84,246 | 1,076,664 |

| Hot Topic, Inc. | 3,582 | 31,163 |

| PC Connection, Inc. | 3,080 | 35,451 |

| Pier 1 Imports, Inc. | 72,117 | 1,351,473 |

| Winmark Corporation | 606 | 32,773 |

| 2,556,920 | ||

| TEXTILES & APPAREL—1.3% | ||

| dELiA*s, Inc. (a) | 23,942 | 33,279 |

| DGSE Companies, Inc. (a) | 4,693 | 4,693 |

| Vera Bradley, Inc. (a)(b) | 51,574 | 1,230,040 |

| 1,268,012 | ||

| WIRELESS TELECOMMUNICATION SERVICES—4.8% | ||

| SBA Communications Corp., Class A (a) | 27,868 | 1,752,897 |

| TOTAL COMMON STOCK | ||

| (Cost $71,750,009) | 92,146,877 | |

Short Term Investments—5.8% | ||

| Par Value | Value | |

| State Street Bank & Trust Co., Repurchase Agreement .01%, 10/01/12, (Dated 09/28/12), Collateralized by $5,720,000 par U.S. Treasury Note-.375% due 04/15/2015, Market Value $5,741,347, Repurchase Proceeds $5,623,927 (Cost $5,623,922) | $5,623,922 | 5,623,922 |

TOTAL INVESTMENTS (EXCLUDING INVESTMENTS PURCHASED WITH CASH COLLATERAL FROM SECURITIES LOANED)—101.6% (Cost $77,373,931) | 97,770,799 | |

INVESTMENTS PURCHASED WITH CASH COLLATERAL FROM SECURITIES LOANED—6.2% | ||

| Money Market—6.2% | ||

| Western Asset Institutional Cash Reserves—Inst. | ||

| (Cost $5,971,584) | 5,971,584 | 5,971,584 |

TOTAL INVESTMENTS—107.8% (Cost $83,345,515) | 103,742,383 | |

| OTHER ASSETS & LIABILITIES (NET)—(7.8%) | (7,543,228) | |

| NET ASSETS—100% | $96,199,155 |

| (a) | Non-income producing security |

| (b) | All or a portion of this security was out on loan. |

| (c) | ADR—American Depositary Receipts |

The accompanying notes are an integral part of these financial statements.

PEAR TREE COLUMBIA MICRO CAP FUND

SCHEDULE OF INVESTMENTS

September 30, 2012 (Unaudited)

Common Stock—97.2%

| Shares | Value | |

| AIR FREIGHT & LOGISTICS—0.9% | ||

| Echo Global Logistics, Inc. (a) | 2,410 | $ 41,332 |

| BANKS—13.2% | ||

| BBX Capital Corporation (a) | 7,908 | 51,086 |

| Berkshire Bancorp, Inc. (a) | 4,973 | 40,928 |

| Codorus Valley Bancorp, Inc. | 3,234 | 46,521 |

| FBR & Co. (a) | 15,873 | 49,048 |

| Guaranty Bancorp (a) | 20,072 | 40,545 |

| Intervest Bancshares Corporation (a) | 11,810 | 44,878 |

| Macatawa Bank Corporation (a) | 13,204 | 41,064 |

| NASB Financial, Inc. (a) | 2,299 | 57,107 |

| Pacific Mercantile Bancorp (a) | 6,132 | 40,103 |

| Preferred Bank (a) | 3,177 | 45,050 |

| Republic First Bancorp, Inc. (a) | 22,050 | 45,644 |

| Taylor Capital Group, Inc. (a) | 2,754 | 47,148 |

| Wilshire Bancorp, Inc. (a) | 8,124 | 51,181 |

| 600,303 | ||

| BIOTECHNOLOGY—1.3% | ||

| BioDelivery Sciences International, Inc. (a) | 9,043 | 57,152 |

| BUILDING PRODUCTS—2.0% | ||

| Builders FirstSource, Inc. (a) | 8,335 | 43,259 |

| PGT, Inc. (a) | 14,346 | 47,055 |

| 90,314 | ||

| CHEMICALS—1.8% | ||

| Penford Corporation (a) | 4,935 | 36,914 |

| TPC Group, Inc. (a) | 1,140 | 46,523 |

| 83,437 | ||

| COMMERCIAL SERVICES & SUPPLIES—6.6% | ||

| CECO Environmental Corp. | 5,776 | 56,432 |

| Core-Mark Holding Company, Inc. | 922 | 44,357 |

| Hudson Technologies, Inc. (a) | 11,448 | 41,556 |

| Intersections, Inc. | 2,746 | 28,943 |

| Move, Inc. (a) | 4,727 | 40,747 |

| StarTek, Inc. (a) | 14,628 | 43,884 |

| Sypris Solutions, Inc. | 6,191 | 44,204 |

| 300,123 | ||

| COMMUNICATIONS EQUIPMENT—2.5% | ||

| Ambient Corporation (a) | 6,234 | 32,791 |

| Boingo Wireless, Inc. (a) | 3,842 | 30,505 |

| CalAmp Corp. (a) | 5,836 | 47,914 |

| 111,210 |

The accompanying notes are an integral part of these financial statements.

| CONSTRUCTION MATERIALS—1.3% | ||

| U.S. Concrete, Inc. (a) | 9,061 | 58,715 |

| CONTAINERS & PACKAGING—0.9% | ||

| Myers Industries, Inc. | 2,586 | 40,393 |

| DISTRIBUTORS—1.1% | ||

| AMCON Distributing Company | 746 | 48,415 |

| DIVERSIFIED FINANCIALS—8.0% | ||

| CIFC Corp. (a) | 6,260 | 45,823 |

| FirstCity Financial Corporation (a) | 5,041 | 40,479 |

| Meta Financial Group, Inc. | 2,245 | 54,441 |

| MicroFinancial, Inc. | 5,361 | 49,053 |

| NGP Capital Resources Co. | 6,260 | 46,700 |

| Nicholas Financial, Inc. | 3,481 | 44,940 |

| QC Holdings, Inc. | 10,891 | 38,990 |

| White River Capital, Inc. | 1,951 | 44,073 |

| 364,499 | ||

| ELECTRICAL EQUIPMENT—0.8% | ||

| Magnetek, Inc. (a) | 2,992 | 33,690 |

| ELECTRONIC EQUIPMENT & INSTRUMENTS—0.9% | ||

| TESSCO Technologies, Inc. | 1,964 | 41,578 |

| FOOD & DRUG RETAILING—2.8% | ||

| Pantry, Inc. (The) (a) | 2,914 | 42,399 |

| PetMed Express, Inc. | 3,660 | 36,746 |

| Village Super Market, Inc., Class A | 1,310 | 48,156 |

| 127,301 | ||

| FOOD PRODUCTS—1.6% | ||

| Chefs’ Warehouse, Inc. (The) (a) | 2,458 | 40,262 |

| John B. Sanfilippo & Son, Inc. (a) | 2,385 | 31,053 |

| 71,315 | ||

| HEALTH CARE PROVIDERS & SERVICES—3.6% | ||

| Alliance Healthcare Services, Inc. (a) | 44,761 | 63,113 |

| Psychemedics Corporation | 4,219 | 51,261 |

| U.S. Physical Therapy, Inc. | 1,718 | 47,468 |

| 161,842 | ||

| HOTELS, RESTAURANTS & LEISURE—7.2% | ||

| AFC Enterprises, Inc. (a) | 1,889 | 46,469 |

| Ark Restaurants Corp. | 3,152 | 52,875 |

| Einstein Noah Restaurant Group, Inc. | 2,590 | 45,817 |

| Jamba, Inc. (a) | 20,072 | 44,761 |

| Kona Grill, Inc. (a) | 5,145 | 46,048 |

| Multimedia Games Holding Company, Inc. (a) | 2,908 | 45,743 |

| Nathan’s Famous, Inc. (a) | 1,492 | 46,923 |

| 328,636 |

The accompanying notes are an integral part of these financial statements.

| HOUSEHOLD DURABLES—2.2% | ||

| Emerson Radio Corp. (a) | 22,159 | 45,758 |

| U.S. Home Systems, Inc. | 4,423 | 55,155 |

| 100,913 | ||

| INDUSTRIAL CONGLOMERATES—1.0% | ||

| Lydall, Inc. (a) | 3,291 | 46,370 |

| INSURANCE—2.1% | ||

| Homeowners Choice, Inc. | 2,392 | 56,212 |

| Imperial Holdings, Inc. (a) | 11,303 | 38,543 |

| 94,755 | ||

| INTERNET & CATALOG RETAIL—3.4% | ||

| 1-800-Flowers.com, Inc., Class A (a) | 12,468 | 46,505 |

| Nutrisystem, Inc. | 3,832 | 40,351 |

| Overstock.com, Inc. (a) | 6,313 | 65,403 |

| 152,259 | ||

| IT CONSULTING & SERVICES—4.7% | ||

| Computer Task Group, Inc. (a) | 3,148 | 50,935 |

| Hackett Group, Inc. (The) (a) | 8,493 | 35,501 |

| Industrial Services of America, Inc. (a) | 9,425 | 34,496 |

| Lionbridge Technologies, Inc. (a) | 14,076 | 49,548 |

| Wayside Technology Group, Inc. | 3,627 | 45,229 |

| 215,707 | ||

| LEISURE EQUIPMENT & PRODUCTS—3.0% | ||

| Artic Cat, Inc. (a) | 1,155 | 47,886 |

| Nautilus, Inc. (a) | 12,974 | 33,992 |

| Smith & Wesson Holding Corporation (a) | 5,058 | 55,689 |

| 137,567 | ||

| MACHINERY—2.1% | ||

| Argan, Inc. (a) | 3,267 | 57,009 |

| Supreme Industries, Inc. (a) | 10,786 | 39,369 |

| 96,378 | ||

| MEDIA—2.0% | ||

| Ballantyne Strong, Inc. | 7,498 | 31,192 |

| Harris Interactive, Inc. (a) | 40,691 | 59,409 |

| 90,601 | ||

| MULTILINE RETAIL—1.0% | ||

| Gordmans Stores, Inc. (a) | 2,543 | 46,918 |

| OFFICE ELECTRONICS—1.1% | ||

| PAR Technology Corporation (a) | 8,952 | 48,788 |

| OIL & GAS—1.7% | ||

| Adams Resources & Energy, Inc. | 1,040 | 31,720 |

| VAALCO Energy, Inc. (a) | 5,018 | 42,904 |

| 74,624 |

The accompanying notes are an integral part of these financial statements.

| PERSONAL PRODUCTS—2.1% | ||

| Female Health Company (The) | 7,338 | 52,467 |

| United-Guardian, Inc. | 2,438 | 46,078 |

| 98,545 | ||

| PHARMACEUTICALS—1.7% | ||

| Obagi Medical Products, Inc. (a) | 2,888 | 35,840 |

| POZEN, Inc. (a) | 6,612 | 43,838 |

| 79,678 | ||

| REAL ESTATE—3.1% | ||

| AG Mortgage Investment Trust, Inc. | 2,070 | 49,949 |

| Apollo Commercial Real Estate Finance, Inc. | 2,731 | 47,355 |

| Dynex Capital, Inc. | 4,346 | 46,720 |

| 144,024 | ||

| ROAD & RAIL—2.7% | ||

| Pacer International, Inc. (a) | 7,839 | 31,199 |

| Saia, Inc. (a) | 2,082 | 41,931 |

| Universal Truckload Services, Inc. | 3,045 | 48,629 |

| 121,759 | ||

| SEMICONDUCTOR EQUIPMENT & PRODUCTS—1.6% | ||

| inTEST Corporation (a) | 13,126 | 34,784 |

| Ultra Clean Holdings, Inc. (a) | 6,865 | 39,199 |

| 73,983 | ||

| SOFTWARE—0.6% | ||

| Majesco Entertainment Company (a) | 22,159 | 27,920 |

| SPECIALTY RETAIL—3.6% | ||

| Destination Maternity Corporation | 2,013 | 37,643 |

| Hot Topic, Inc. | 4,586 | 39,898 |

| PC Connection, Inc. | 3,944 | 45,396 |

| Winmark Corporation | 776 | 41,966 |

| 164,903 | ||

| TEXTILES & APPAREL—1.1% | ||

| dELiA*s, Inc. (a) | 30,658 | 42,615 |

| DGSE Companies, Inc. (a) | 5,810 | 5,810 |

| 48,425 | ||

| TOTAL COMMON STOCK | ||

| (Cost $3,966,352) | 4,424,372 | |

Short Term Investments—2.8% | ||

| Par Value | Value | |

State Street Bank & Trust Co., Repurchase Agreement .01%, 10/01/12, (Dated 09/28/12), Collateralized by $130,000 par U.S. Treasury Note-.375% due 04/15/2015, Market Value $130,485, Repurchase Proceeds $127,250 (Cost $127,250) | $127,250 | 127,250 |

| TOTAL INVESTMENTS—100.0% | ||

| (Cost $4,402,782) | 4,551,622 | |

| OTHER ASSETS & LIABILITIES (NET)—0.0% | 1,908 | |

| NET ASSETS—100% | $4,553,530 |

| (a) | Non-income producing security |

The Portfolio is actively managed and holdings are subject to change.

There is no guarantee the Fund will continue to invest in the securities referenced.

Reference to specific securities or holdings should not be considered recommendations for action by investors.

The accompanying notes are an integral part of these financial statements.

PEAR TREE QUALITY FUND

SCHEDULE OF INVESTMENTS

September 30, 2012 (Unaudited)

Common Stock—99.5%

| Shares | Value | |

| AEROSPACE & DEFENSE—0.0% | ||

| United Technologies Corporation | 19 | $1,488 |

| BEVERAGES—5.7% | ||

| Anheuser-Busch InBev SA (b) | 9,143 | 785,475 |

| Coca-Cola Company (The) | 116,871 | 4,432,917 |

| Monster Beverage Corporation (a) | 6,995 | 378,849 |

| 5,597,241 | ||

| COMMUNICATIONS EQUIPMENT—1.3% | ||

| QUALCOMM Incorporated | 20,284 | 1,267,547 |

| COMPUTERS & PERIPHERALS—8.5% | ||

| Apple, Inc. (a) | 6,356 | 4,241,104 |

| Hewlett-Packard Company | 110,882 | 1,891,647 |

| International Business Machines | 10,711 | 2,221,997 |

| 8,354,748 | ||

| FOOD PRODUCTS—3.2% | ||

| Nestle, S.A. (b) | 28,201 | 1,782,585 |

| Unilever N.V. | 39,119 | 1,387,942 |

| 3,170,527 | ||

| FOOD STAPLES & DRUG RETAILING—7.4% | ||

| PepsiCo, Inc. | 38,437 | 2,720,186 |

| SYSCO Corporation | 15,330 | 479,369 |

| Tesco PLC (a)(b) | 39,393 | 637,379 |

| Wal-Mart Stores, Inc. | 44,277 | 3,267,643 |

| Walgreen Co. | 1,915 | 69,783 |

| 7,174,360 | ||

| HEALTH CARE EQUIPMENT & SERVICES—6.2% | ||

| Baxter International Inc. | 28 | 1,687 |

| Express Scripts, Inc. (a) | 36,128 | 2,264,142 |

| Intuitive Surgical, Inc. (a) | 56 | 27,755 |

| Medtronic, Inc. | 24,699 | 1,065,021 |

| UnitedHealth Group, Inc. | 24,939 | 1,381,870 |

| Zimmer Holdings, Inc. (a) | 18,872 | 1,276,125 |

| 6,016,600 | ||

| HEALTH CARE PROVIDERS & SERVICES—0.7% | ||

| Henry Schein, Inc. (a) | 703 | 55,727 |

| Laboratory Corporation of America Holdings (a) | 2,077 | 192,060 |

| Quest Diagnostics Incorporated | 6,701 | 425,044 |

| 672,831 | ||

| HOTELS, RESTAURANTS & LEISURE—1.1% | ||

| McDonald’s Corporation | 11,385 | 1,044,574 |

The accompanying notes are an integral part of these financial statements.

| HOUSEHOLD PRODUCTS—4.7% | ||

| Church & Dwight Co., Inc. | 6,624 | 357,630 |

| Colgate-Palmolive Company | 19,290 | 2,068,274 |

| Procter & Gamble Company | 31,015 | 2,151,200 |

| 4,577,104 | ||

| INDUSTRIAL CONGLOMERATES—0.8% | ||

| 3M Company | 8,428 | 778,916 |

| MULTILINE RETAIL—2.6% | ||

| Target Corporation | 40,639 | 2,579,357 |

| OIL & GAS—8.4% | ||

| BP plc (b) | 23,445 | 993,130 |

| Chevron Corporation | 28,046 | 3,269,042 |

| Exxon Mobil Corporation | 19,053 | 1,742,396 |

| Royal Dutch Shell plc (b) | 15,766 | 1,094,318 |

| TOTAL S.A. (b) | 21,826 | 1,093,483 |

| 8,192,369 | ||

| PHARMACEUTICALS & BIOTECHNOLOGY—19.8% | ||

| Abbott Laboratories | 39,975 | 2,740,686 |

| Amgen, Inc. | 8,497 | 716,467 |

| AstraZeneca PLC (b) | 11,519 | 551,299 |

| Bristol-Myers Squibb Company | 38 | 1,283 |

| Eli Lilly and Company | 390 | 18,490 |

| GlaxoSmithKline plc (b) | 23,028 | 1,064,815 |

| Johnson & Johnson | 78,314 | 5,396,618 |

| Merck & Co., Inc. | 14,235 | 641,998 |

| Novartis AG (b) | 20,443 | 1,252,338 |

| Pfizer, Inc. | 178,745 | 4,441,813 |

| Roche Holding Ltd (b) | 25,562 | 1,201,159 |

| Sanofi-Aventis (b) | 25,206 | 1,085,370 |

| Takeda Pharmaceutical Company Limited (b) | 11,683 | 269,760 |

| 19,382,096 | ||

| SOFTWARE & SERVICES—20.2% | ||

| Cisco Systems, Inc. | 166,625 | 3,180,871 |

| Google, Inc. (a) | 5,557 | 4,192,757 |

| MasterCard Incorporated | 2,372 | 1,070,911 |

| Microsoft Corporation | 135,090 | 4,022,980 |

| Oracle Corporation (a) | 160,076 | 5,040,793 |

| SAP AG (b) | 12,618 | 900,042 |

| Visa, Inc. | 10,019 | 1,345,351 |

| Yahoo! Inc. (a) | 444 | 7,093 |

| 19,760,798 | ||

| SPECIALTY RETAIL—0.5% | ||

| Lowe’s Companies, Inc. | 17,127 | 517,921 |

| TEXTILES & APPAREL—0.4% | ||

| Nike, Inc. | 3,871 | 367,397 |

The accompanying notes are an integral part of these financial statements.

| TOBACCO—7.4% | ||

| British American Tobacco p.l.c. (b) | 12,899 | 1,323,953 |

| Lorillard, Inc. | 10,637 | 1,238,679 |

| Philip Morris International, Inc. | 51,720 | 4,651,697 |

| 7,214,329 | ||

| WIRELESS TELECOMMUNICATIONS—0.6% | ||

| NTT DOCOMO, Inc. (b) | 40,066 | 647,467 |

TOTAL COMMON STOCK (Cost $85,541,497) | 97,317,670 | |

TOTAL INVESTMENTS 99.5% (Cost $85,541,497) | $97,317,670 | |

| OTHER ASSETS & LIABILITIES (NET)—0.5% | 454,667 | |

| NET ASSETS—100% | $97,772,337 |

| (a) | Non-Income producing security |

| (b) | ADR—American Depositary Receipts |

The accompanying notes are an integral part of these financial statements.

PEAR TREE PANAGORA DYNAMIC EMERGING MARKETS FUND

SCHEDULE OF INVESTMENTS

September 30, 2012 (Unaudited)

Common Stock—96.2%

| Shares | Value | |

| BRAZIL—7.4% | ||

| Banco do Brasil SA | 142,212 | $ 1,738,996 |

| BM&F Bovespa SA | 321,824 | 1,943,861 |

| Companhia de Bebidas das Americas (c) | 43,066 | 1,648,136 |

| Embraer S.A. (c) | 7,764 | 206,678 |

| EZ TEC Empreendimentos e Participacoes SA | 60,035 | 745,368 |

| Obrascon Huarte Lain Brasil SA | 25,100 | 230,196 |

| Oi SA (c) | 11,298 | 56,038 |

| Petroleo Brasileiro SA | 89,183 | 1,024,586 |

| Petroleo Brasileiro SA (c) | 84,344 | 1,861,472 |

| Sao Martinho SA | 14,418 | 170,050 |

| Sul America SA | 72,612 | 537,044 |

| Vale SA | 57,653 | 1,037,305 |

| 11,199,730 | ||

| CHILE—1.6% | ||

| Banco Santander Chile (c) | 8,079 | 591,706 |

| Compania Cervecerias Unidas SA (c) | 6,660 | 475,058 |

| Enersis SA (c) | 40,692 | 666,942 |

| LATAM Airlines Group SA (b)(c) | 25,927 | 655,434 |

| 2,389,140 | ||

| CHINA—10.6% | ||

| Bank of China Ltd., Class H | 6,366,392 | 2,430,281 |

| China Communications Construction Co., Ltd., Class H | 656,680 | 530,998 |

| China Construction Bank Corporation | 4,837,422 | 3,356,353 |

| China Petroleum & Chemical Corporation | 2,015,239 | 1,881,640 |

| China Shenhua Energy Co., Ltd. | 208,105 | 805,147 |

| China Yuchai International Ltd. | 17,977 | 229,207 |

| Dongfeng Motor Group Company Limited | 780,881 | 909,377 |

| Giant Interactive Group, Inc. (b)(c) | 106,939 | 555,013 |

| Great Wall Motor Co., Ltd. (b) | 601,980 | 1,591,503 |

| Harbin Electric Company Limited | 444,945 | 341,998 |

| Industrial & Commercial Bank of China Ltd. | 2,208,911 | 1,304,713 |

| Inner Mongolia Yitai Coal Co., Ltd., Class B | 40,848 | 219,436 |

| PetroChina Company Limited | 1,383,778 | 1,816,710 |

| Tencent Holdings Limited | 1,600 | 54,681 |

| 16,027,057 | ||

| COLOMBIA—0.7% | ||

| Ecopetrol S.A. (b)(c) | 17,581 | 1,036,048 |

| CZECH REPUBLIC—0.5% | ||

| CEZ AS | 18,425 | 687,747 |

The accompanying notes are an integral part of these financial statements.

| HONG KONG—6.9% | ||

| Central China Real Estate Ltd. | 297,371 | 72,866 |

| Champion Real Estate Investment Trust | 595,000 | 272,406 |

| China Mobile Limited | 290,779 | 3,232,524 |

| China Zhongwang Holdings Limited (a)(b) | 278,800 | 105,349 |

| Chongqing Rural Commercial Bank Co. | 1,034,687 | 406,987 |

| CNOOC Limited | 1,396,218 | 2,859,401 |

| COSCO International Holdings Ltd. | 205,193 | 80,976 |

| Dairy Farm International Holdings Limited | 10,800 | 119,988 |

| Giordano International Limited (b) | 402,000 | 338,022 |

| KWG Property Holding Limited | 395,919 | 218,535 |

| Lenovo Group Limited | 1,267,489 | 1,054,327 |

| Skyworth Digital Holdings Limited (b) | 1,786,000 | 845,316 |

| Soho China Limited (b) | 1,220,979 | 751,100 |

| Yuexiu Real Estate Investment Trust | 215,088 | 105,130 |

| 10,462,927 | ||

| HUNGARY—0.3% | ||

| EGIS Pharmaceuticals PLC | 1,899 | 150,483 |

| Richter Gedeon Nyrt. | 1,411 | 246,495 |

| 396,978 | ||

| INDIA—4.9% | ||

| Allahabad Bank | 29,921 | 83,219 |

| Andhra Bank | 253,412 | 542,185 |

| Bajaj Holdings & Investment Limited | 14,136 | 211,055 |

| Bank of Baroda | 19,608 | 295,914 |

| Chambal Fertilizers & Chemicals Ltd. | 379,300 | 530,711 |

| Gitanjali Gems Limited | 87,208 | 572,155 |

| Grasim Industries Limited | 10,406 | 654,407 |

| Gujarat State Fertilisers & Chemicals Limited | 31,990 | 48,551 |

| Hexaware Technologies Limited | 145,863 | 337,383 |

| Indiabulls Financial Services Limited | 172,508 | 699,909 |

| Indian Bank | 140,982 | 515,869 |

| Oil and Natural Gas Corp. Limited | 140,610 | 746,703 |

| Oil India Limited | 19,730 | 184,227 |

| Rural Electrification Corporation Limited | 172,142 | 711,479 |

| South Indian Bank Limited | 458,831 | 198,338 |

| Syndicate Bank | 166,229 | 343,520 |

| Tata Chemicals Ltd. | 34,131 | 207,135 |

| TVS Motor Company Ltd. | 155,385 | 125,204 |

| UCO Bank | 319,644 | 466,331 |

| 7,474,295 |

The accompanying notes are an integral part of these financial statements.

| INDONESIA—2.4% | ||

| PT AKR Corporindo Tbk | 1,296,078 | 575,583 |

| PT Aneka Tambang Tbk | 2,183,989 | 308,086 |

| PT Astra Agro Lestari Tbk | 230,648 | 529,020 |

| PT Bank Bukopin Tbk | 3,526,000 | 235,804 |

| PT Holcim Indonesia Tbk | 522,500 | 155,603 |

| PT Indo Tambangraya Megah Tbk | 29,620 | 130,458 |

| PT Indofood CBP Sukses Makmur Tbk | 312,500 | 207,354 |

| PT PP London Sumatra Indonesia Tbk | 2,762,340 | 707,182 |

| PT Sampoerna Agro Tbk | 452,953 | 137,259 |

| PT Telekomunikasi Indonesia Tbk | 616,958 | 609,222 |

| 3,595,571 | ||

| ISRAEL—0.8% | ||