Item 1. Reports to Shareholders

Lehman Brothers

Income Funds

Investor Class Shares

Institutional Class Shares

Trust Class Shares

| Lehman Brothers Core Bond Fund | | Lehman Brothers New York Municipal Money Fund |

| Lehman Brothers High Income Bond Fund | | Lehman Brothers Short Duration Bond Fund |

| Lehman Brothers Municipal Money Fund | | Lehman Brothers Strategic Income Fund |

| Lehman Brothers Municipal Securities Trust | | Neuberger Berman Cash Reserves |

Annual Report

October 31, 2007

Contents

THE FUNDS

PORTFOLIO COMMENTARY

| Lehman Brothers Core Bond Fund | | | 2 | | |

|

| Lehman Brothers High Income Bond Fund | | | 5 | | |

|

| Lehman Brothers Municipal Money Fund | | | 8 | | |

|

| Lehman Brothers New York Municipal Money Fund | | | 8 | | |

|

| Lehman Brothers Municipal Securities Trust | | | 10 | | |

|

| Lehman Brothers Short Duration Bond Fund | | | 13 | | |

|

| Lehman Brothers Strategic Income Fund | | | 15 | | |

|

| Neuberger Berman Cash Reserves | | | 18 | | |

|

| FUND EXPENSE INFORMATION | | | 23 | | |

|

SCHEDULE OF INVESTMENTS

| Lehman Brothers Core Bond Fund | | | 26 | | |

|

| Lehman Brothers High Income Bond Fund | | | 32 | | |

|

| Lehman Brothers Municipal Money Fund | | | 37 | | |

|

| Lehman Brothers Municipal Securities Trust | | | 47 | | |

|

| Lehman Brothers New York Municipal Money Fund | | | 50 | | |

|

| Lehman Brothers Short Duration Bond Fund | | | 54 | | |

|

| Lehman Brothers Strategic Income Fund | | | 57 | | |

|

| Neuberger Berman Cash Reserves | | | 67 | | |

|

| FINANCIAL STATEMENTS | | | 74 | | |

|

The "Neuberger Berman" name and logo are registered service marks of Neuberger Berman, LLC. "Neuberger Berman Management Inc." and the individual fund names in this report are either service marks or registered service marks of Neuberger Berman Management Inc. ©2007 Neuberger Berman Management Inc. All rights reserved. ©2007 Lehman Brothers Asset Management LLC. All rights reserved.

FINANCIAL HIGHLIGHTS/PER SHARE DATA

| Lehman Brothers Core Bond Fund | | | 94 | | |

|

| Lehman Brothers High Income Bond Fund | | | 96 | | |

|

| Lehman Brothers Municipal Money Fund | | | 97 | | |

|

| Lehman Brothers Municipal Securities Trust | | | 98 | | |

|

| Lehman Brothers New York Municipal Money Fund | | | 99 | | |

|

| Lehman Brothers Short Duration Bond Fund | | | 100 | | |

|

| Lehman Brothers Strategic Income Fund | | | 102 | | |

|

| Neuberger Berman Cash Reserves | | | 104 | | |

|

| Reports of Independent Registered Public Accounting Firms | | | 107 | | |

|

| Directory | | | 109 | | |

|

| Trustees and Officers | | | 110 | | |

|

| Proxy Voting Policies and Procedures | | | 118 | | |

|

| Quarterly Portfolio Schedule | | | 118 | | |

|

| Notice to Shareholders | | | 118 | | |

|

| Board Consideration of the Management and Sub-Advisory Agreements | | | 119 | | |

|

The "Neuberger Berman" name and logo are registered service marks of Neuberger Berman, LLC. "Neuberger Berman Management Inc." and the individual fund names in this report are either service marks or registered service marks of Neuberger Berman Management Inc. ©2007 Neuberger Berman Management Inc. All rights reserved. ©2007 Lehman Brothers Asset Management LLC. All rights reserved.

Chairman's Letter

Dear Fellow Shareholder,

For much of the fiscal year ended October 31, 2007, bond investors enjoyed the fruits of a long "pause" in interest rate increases by the Federal Reserve. After ending its previous two-year monetary tightening cycle in June 2006, the Fed appeared to be successfully walking a fine line between moderating economic growth and limiting price inflation.

For its part, the fixed income market experienced a period of relatively low volatility and historically narrow spreads between Treasuries and other fixed income securities. Overall, bond investors appeared confident both that the economy was slowing and that the Fed's pause would turn out to be more permanent.

However, the placid environment did not last. Beginning in July, concern over the spreading impact of subprime mortgage defaults helped trigger a crisis environment in the credit markets. Investors moved rapidly to the safety of Treasury securities at the expense of other fixed income instruments, and many financial institutions became highly reluctant to lend to all but the safest borrowers.

Concerned that this "credit crunch" would drive the economy into recession, Federal Reserve Chairman Ben Bernanke showed that he was willing to employ the full array of policy tools at his disposal. The Fed injected liquidity into the banking system, lowered the Discount rate and accepted a wider range of collateral at the discount window before proceeding with cuts to its Fed Funds rate. When those cuts came, they were dramatic, starting with a 50 basis point reduction in September and another 25 basis point cut in October. Investors responded with some relief to these measures, as non-Treasury securities recovered somewhat through the end of the fiscal year, but the markets remained under stress.

Like the Fed chairman, our portfolio managers were willing to use all the tools available to them — to attempt to preserve principal, extract value and maintain risk control. In the midst of the summer volatility, strongly ingrained risk management techniques were decided advantages, while their focus on fundamental, ongoing credit research helped them maintain portfolios that they believe are positioned to weather ongoing credit concerns. In addition, an emphasis on economic forecasting enabled them to position duration effectively, while continued vigilance allowed them to react quickly and decisively during the tumultuous summer months and beyond.

Looking forward, the credit markets have not left all their problems in the rear view mirror. Subprime mortgage exposure remains a serious issue and tighter credit conditions suggest that a keen focus on research remains essential. There are, of course, no guarantees in the financial markets. However, you can be assured that your managers will continue to exercise sound judgment in navigating a still challenging environment.

Sincerely,

Peter Sundman

Chairman of the Board

Lehman Brothers Income Funds

1

Lehman Brothers Core Bond Fund Portfolio Commentary

For the fiscal year ended October 31, 2007, the Lehman Brothers Core Bond Fund generated a positive return but trailed its benchmark, the Lehman Brothers U.S. Aggregate Index.

After performing strongly throughout most of the year, the portfolio struggled in the last several months as portfolio holdings suffered price declines related to the credit crises that developed beginning in July. We remain confident that the issues we hold are fundamentally solid and we believe that we will recoup any value lost to date. In our view, this will happen either through principal repayment, as the cash flows on these securities are realized, or through price appreciation, when the market has time to discriminate regarding the quality of collateral and structural protection. However, we are probably going to have to endure further volatility over the balance of the year and into 2008 as the data on the economy, housing and subprime delinquencies/losses evolve.

The bond market rallied in late calendar 2006, with advances driven by a combination of slower economic growth (which encouraged bond investors) and an end to the Federal Reserve's two-year campaign to raise interest rates. The Fed remained on hold throughout most of fiscal 2007, with rates at 5.25%. The minutes from the Federal Open Market Committee's March meeting (released in April) indicated the Fed's reluctance to cut rates, given the level of inflation, despite the slowing of the economy.

However, reports in early July of the collapse of two mortgage-related hedge funds, combined with the downgrade of a number of subprime-related collateralized debt obligations, intensified investors' worries and prompted a flight to quality. In a six-week period from early July to mid-August, the two-year Treasury rose in price as its yield fell 100 basis points (or one percentage point) and spreads on some investment grade securities (compared to Treasury levels) widened 50 basis points or more, as price declines were exacerbated by the unwinding of leveraged positions by some investors. High yield spreads widened 180 basis points as prices on below-investment-grade securities declined while Treasury prices rose.

These severe conditions prompted the Fed to respond with all its policy tools, starting in mid-August with an infusion of new liquidity into the banking system and culminating in a 50 basis-point cut in the Fed Funds rate in mid-September and a further 25 basis-point cut in October. With these actions, non-Treasury sectors managed to recover modestly from mid-August through the end of the reporting period.

In terms of portfolio strategy, we made several duration moves throughout the period to take advantage of expectations for interest rates. We shortened portfolio duration (or sensitivity to interest rates) from neutral to a quarter-year below the benchmark in response to the late calendar 2006 rally, believing that the market's expectation for an imminent rate cut was overly optimistic. As the crisis intensified, we initiated a long duration position in advance of a seemingly unavoidable rate cut by the Federal Reserve. The portfolio is currently modestly longer than the benchmark.

Early in the fiscal year, we reduced our overall position in mortgage-backed securities, as mortgage spreads narrowed to 17-year lows but increased the position later in the period. As of fiscal year-end, mortgage-backed securities remain, at approximately 50%, a substantial part of the portfolio. After decreasing exposure to corporate debt and increasing exposure to U.S. Treasury securities throughout much of the period, we reversed this position as spreads widened, to end with holdings at close to the same levels of a year earlier, at approximately 18% and 9% of the portfolio, respectively. Portfolio holdings of U.S. government agency securities and asset-backed securities remained at approximately 9% and 11%, respectively, of the portfolio.

We continue to believe that the economy will avoid a recession, as the impact of housing on the overall economy is not as large as the bond market appears to think. Global growth, combined with the decline in the dollar, should provide enough balance and time for the U.S. to work through the problems presented by the mortgage market and current conditions in the credit markets.

RATING SUMMARY

AAA/Government/

Government Agency | | | 79.6 | % | |

| AA | | | 3.1 | | |

| A | | | 5.7 | | |

| BBB | | | 9.5 | | |

| BB | | | 0.4 | | |

| B | | | 0.0 | | |

| CCC | | | 0.0 | | |

| CC | | | 0.0 | | |

| C | | | 0.0 | | |

| D | | | 0.0 | | |

| Short Term | | | 1.7 | | |

2

In closing, we believe that our systematic approach to managing risk continues to contribute to the returns of the Fund, and we expect to be able to continue to provide value for our shareholders in the future.

Sincerely,

Richard W. Knee

Portfolio Manager

3

Core Bond Fund

AVERAGE ANNUAL TOTAL RETURN ENDED 10/31/072, 6, 10, 12

| | | Investor

Class | | Institutional

Class | | Lehman Brothers

U.S. Aggregate Index | |

| 1 Year | | | 3.67 | % | | | 4.08 | % | | | 5.38 | % | |

| 5 Year | | | 3.88 | % | | | 4.32 | % | | | 4.41 | % | |

| 10 Year | | | 5.05 | % | | | 5.47 | % | | | 5.91 | % | |

| Life of Fund | | | 5.34 | % | | | 5.72 | % | | | 6.21 | %13 | |

| Inception Date | | | 02/01/1997 | | | | 10/01/1995 | | | | | | |

Performance data quoted represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Results are shown on a "total return" basis and include reinvestment of all dividends and capital gain distributions. The composition, industries and holdings of the Fund are subject to change.

Current performance may be lower or higher than the performance data quoted. For performance data current to the most recent month end, please visit www.nb.com/performance.

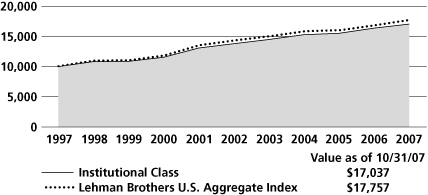

COMPARISON OF A $10,000 INVESTMENT

| | This chart shows the value of a hypothetical $10,000 investment in the Fund over the past 10 fiscal years. The graphs are based on the Institutional Class share only; performance of other classes will vary due to differences in fee structures (see Average Annual Total Return chart above). The result is compared with benchmarks, which may include a broad-based market index and/or a narrower index. Please note that market indices do not include expenses. All results include the reinvestment of dividends and capital gain distributions. Results represent past performance and do not indicate future results. The chart and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Please see Endnotes and Glossary of Indices for additional information.

The composition, industries and holdings of the Fund are subject to change.

For the period ending 10/31/07, the 30-day SEC yield of the Investor Class shares was 4.67%, and the Institutional Class shares was 5.08%. | |

|

4

Lehman Brothers High Income Bond Fund Portfolio Commentary

For the fiscal year ended October 31, 2007, the Lehman Brothers High Income Bond Fund generated a positive return, finishing just behind its benchmark, the Lehman Brothers U.S. Corporate High Yield 2% Issuer Cap Index.

High yield bonds materially outperformed Treasuries during the first seven months of the fiscal year. By the end of May 2007, this superior relative performance resulted in credit spreads (the difference in yield between comparable maturity U.S. Treasuries and high yield bonds) shrinking to 2.45%, near a historical low. However, high yield bond prices started to slide in June and retreated through August. This was largely due to investors' diminished appetite for risk caused in part by concerns about hedge funds' and financial institutions' exposure to subprime mortgage securities. At peaks in late July and early September, credit spreads reached almost 5%. The high yield market rallied in late September and remained stable in October, with credit spreads closing the fiscal year at 4.50%.

Investors' more risk-averse posture was clearly reflected in the new issue market. Prior to June, high yield investors were willing to support highly leveraged deals with structures beneficial to issuers such as toggle notes, which allow the issuer discretion to pay in cash or with additional notes. However, high yield investors' appetite for these types of transactions diminished significantly in June and several high profile bond offerings were pulled or restructured. We believe that the re-pricing of risk and structural improvements in the new issues market is positive for the longer term health of high yield securities. However, even with more reasonably priced and more conservatively structured new issues, we remain quite selective in our new issue purchases.

Longer term, we believe credit fundamentals are the most important factors in determining high yield bond performance. High yield fundamentals are directly linked to the health of the economy. We note that, despite the weak housing market and the credit crunch spawned by the sub-prime mortgage mess, the U.S. economy has remained strong. Third quarter GDP growth was initially reported at a robust 3.9% and later raised to 4.9%. Even if this figure is revised downward, it will likely exceed previous expectations by a wide margin. We suspect that fourth quarter GDP growth will be somewhat less impressive and, in the first half of 2008, we expect growth to slow to around 2%.

Still, even in a slower growth environment, we don't think that high yield default rates will increase to troubling levels. Interestingly, high yield default rates actually declined from 1.6% to 1.3% (near a record low) during the three months high yield bonds were retreating. Unless our economic forecasts are wrong and the economy slides into recession, we believe that high yield default rates will go no higher than 2% to 3% — still below the long-term historical average. We are confident that our commitment to high quality, in-house fundamental credit research will continue to help us effectively manage credit risk in the portfolio.

Over the course of fiscal 2007, security selection and overweights in the health care, services, energy, media and utilities sectors enhanced returns. The fact that we had almost no exposure to real estate or homebuilders was also a performance plus. Security selection in the food and beverage, and technology sectors detracted from returns. Anticipating more moderate economic growth, we have been gravitating to less economically sensitive industry groups, which historically enjoy more stable cash flows. Currently, the portfolio is overweight in health care, broadcasting, cable television, packaging, metals and publishing. The portfolio is underweight in more cyclical industries including energy, paper, homebuilders and capital goods.

The portfolio's weighted average maturity and duration (a standard measure of interest rate risk) fluctuated only modestly over the 12-month reporting period. This was a function of security selection rather than an attempt to anticipate interest rate trends. Our bias toward intermediate maturity securities, which we believe generally have more attractive risk/reward characteristics than longer maturity bonds, will usually result in weighted average maturity and duration that are slightly lower than benchmark levels. On the credit front, we increased our exposure to

RATING SUMMARY

AAA/Government/

Government Agency | | | 0.0 | % | |

| AA | | | 0.0 | | |

| A | | | 0.0 | | |

| BBB | | | 2.4 | | |

| BB | | | 36.3 | | |

| B | | | 46.6 | | |

| CCC | | | 14.1 | | |

| CC | | | 0.0 | | |

| C | | | 0.0 | | |

| D | | | 0.0 | | |

| Not Rated | | | 0.3 | | |

| Short Term | | | 0.3 | | |

5

BB rated securities (the highest rated securities in our investment universe) at attractive prices during the market volatility in September and the portfolio's present quality distribution stands in line with the benchmark.

Looking ahead, we expect the high yield bond market to remain relatively stable, producing moderate coupon-oriented returns in fiscal 2008.

Sincerely,

Ann H. Benjamin and Thomas P. O'Reilly

Portfolio Co-Managers

6

High Income Bond Fund

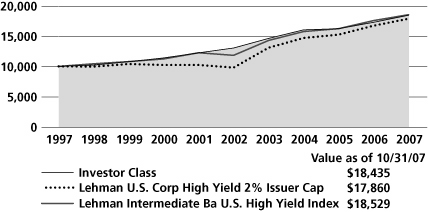

AVERAGE ANNUAL TOTAL RETURN ENDED 10/31/071, 6, 9, 12

| | | Investor

Class9 | | Lehman Brothers

US Corp High Yield 2%

Issuer Cap Index | | Lehman Brothers

Intermediate Ba

U.S. High Yield Index | |

| 1 Year | | | 6.73 | % | | | 6.88 | % | | | 5.55 | % | |

| 5 Year | | | 7.19 | % | | | 12.76 | % | | | 9.41 | % | |

| 10 Year | | | 6.31 | % | | | 5.97 | % | | | 6.36 | % | |

| Life of Fund | | | 7.77 | % | | | N/A | | | | 7.94 | %13 | |

| Inception Date | | | 02/01/1992 | | | | | | | | | | |

Performance data quoted represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Results are shown on a "total return" basis and include reinvestment of all dividends and capital gain distributions. The composition, industries and holdings of the Fund are subject to change.

Current performance may be lower or higher than the performance data quoted. For performance data current to the most recent month end, please visit www.nb.com/performance.

COMPARISON OF A $10,000 INVESTMENT

| | This chart shows the value of a hypothetical $10,000 investment in the Fund over the past 10 fiscal years. The result is compared with one or more benchmarks, which may include a broad-based market index and/or a narrower index. Please note that market indices do not include expenses. All results include the reinvestment of dividends and capital gain distributions. Results represent past performance and do not indicate future results. The chart and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Please see Endnotes and Glossary of Indices for additional information.

The composition, industries and holdings of the Fund are subject to change.

For the period ending 10/31/07, the 30-day SEC yield of the Investor Class shares was 7.78%. | |

|

7

Lehman Brothers Municipal Money Fund

Lehman Brothers New York Municipal Money Fund

Portfolio Commentary

The financial markets were relatively quiet during the first seven months of the fiscal year ended October 31, 2007. Then, investors became more concerned about the potential consequences that rising subprime mortgage defaults could have for the economy and financial institutions holding hard-to-value collateralized subprime mortgage debt. In response to subprime-related issues, the credit markets nearly seized up in July, sparking a flight to quality as investors waited until the depth and ultimate impact of the credit crunch could be evaluated. In response, the Federal Reserve injected liquidity into the financial system in August and subsequently cut the Federal Funds rate by 75 basis points in September and October. This temporarily calmed the financial markets, but they experienced additional turmoil toward the end of the 12-month reporting period.

The primary effect of subprime mortgage concerns late in the fiscal year was a strong flow of funds into short-term U.S. Treasuries and municipal money market funds. With demand for short-term U.S. Treasuries showing particular strength, municipal money funds provided relatively attractive after-tax yields.

Normally, when the Federal Reserve eases, the yield curve steepens (with longer maturity issues offering higher yields). As such, we would generally attempt to extend the Funds' weighted average maturity in such circumstances to lock in the higher yields of longer-term securities. This time around, however, the money market yield curve stayed inverted, with variable rate demand notes (VRDNs) — among the shortest maturity instruments in the market — providing higher yields than one-year securities. VDRNs also allow the Funds to be more liquid during periods of market stress. For these reasons, VRDNs, as of fiscal year-end, are by far our largest allocation and the Funds' weighted average maturity actually declined over the course of fiscal 2007.

Looking ahead, the Federal Reserve appears to be in a quandary. Should the subprime mortgage mess further damage the financial system and push the economy toward recession, we believe the Fed would reluctantly come to the rescue with additional rate cuts. However, further Fed easing would likely result in even more pressure on the already weak dollar and, with commodities prices rising (for oil, agricultural products, gold and industrial materials), possibly fan the flames of inflation.

We believe the Fed will sit on the fence as long as possible before making its next move. In the interim, as long as variable rate demand notes are priced so attractively, we will likely maintain the Funds' current weighted average maturities.

Lehman Brothers Municipal Money Fund1, 5, 7

Lehman Brothers Municipal Money Fund posted a positive total return for the fiscal year, surpassing its iMoneyNet Money Fund Report Tax-Free National Retail Average benchmark. Over the course of the fiscal year the Fund's seven-day tax-equivalent current yield* (taxable at the highest federal income tax bracket) decreased from 4.65% on October 31, 2006 to 4.52% on October 31, 2007. Its seven-day tax-equivalent effective yield (also taxable at the highest federal income tax bracket) went from 4.76% on October 31, 2006 to 4.62% on October 31, 2007.

MATURITY DIVERSIFICATION

| (% by Maturity) | |

| 1 - 7 Days | | | 86.4% | |

| 8 - 30 Days | | | 2.1 | | |

| 31 - 90 Days | | | 4.5 | | |

| 91 - 180 Days | | | 1.0 | | |

| 181+ Days | | | 6.0 | | |

8

Lehman Brothers New York Municipal Money Fund4, 5, 7

Lehman Brothers New York Municipal Money Fund posted a positive total return for the fiscal year, surpassing its iMoneyNet Money Fund Report Tax-Free State-Specific Retail Average benchmark. Over the course of the fiscal year, the Fund's seven-day tax-equivalent current yield* (taxable at the highest federal, New York State and New York City income tax brackets) decreased from 5.40% on October 31, 2006 to 5.21% on October 31, 2007. Its seven-day tax-equivalent effective yield (also taxable at the highest federal, New York State and New York City income tax brackets) went from 5.55% on October 31, 2006 to 5.35% on October 31, 2007.**

MATURITY DIVERSIFICATION

| (% by Maturity) | |

| 1 - 7 Days | | | 91.9% | |

| 8 - 30 Days | | | 4.2 | | |

| 31 - 90 Days | | | 0.0 | | |

| 91 - 180 Days | | | 0.0 | | |

| 181+ Days | | | 3.9 | | |

Sincerely,

William J. Furrer and Kristian Lind

Portfolio Co-Managers

* Current yield more closely reflects current earnings than does total return. Tax-equivalent yields are the taxable yields that an investor would have had to receive in order to realize the same level of yield after federal income taxes at the highest federal tax rate, currently 35%, assuming that all of a Fund's income is exempt from federal income taxes. For the Lehman Brothers New York Municipal Money Fund, tax-equivalent yields are is calculated based on federal, New York State, and New York City tax rates for a combined rate of 41.8%.

** The U.S. Supreme Court is considering a case from Kentucky involving the question of whether a state can give a tax deduction to holders of other states' bonds. Although it is not possible to predict how the court might decide the case, we will watch it carefully as it has the potential to affect single-state municipal funds.

A portion of the income of Lehman Brothers Municipal Money Fund and Lehman Brothers New York Municipal Money Fund may be a tax preference item for purposes of the federal alternative minimum tax for certain investors.

An investment in the Fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Although the Fund seeks to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in the Fund.

The composition, industries and holdings of the Fund are subject to change. Investment return will fluctuate. Past performance is no guarantee of future results.

Unaudited performance data current to the most recent month-end are available at www.lehmanam.com.

9

Lehman Brothers Municipal Securities Trust Portfolio Commentary

Lehman Brothers Municipal Securities Trust provided a modestly positive return for the fiscal year ended October 31, 2007, outperforming the Lipper Intermediate Municipal Debt Funds Average but lagging the Lehman Brothers 7-Year General Obligation Index.

The Fund got off to a good start with municipal securities prices firming as demand outpaced supply during the seasonally strong end of calendar 2006. However, starting in the first quarter of calendar 2007, new issuances surged on the way to what we expect will be a record year for municipal bonds. Although increased supply was absorbed by the market in an orderly fashion, it restrained municipal bond prices during the reporting period.

Credit spreads (the yield differential between higher and lower rated bonds), became tight relative to historical levels during the first half of the reporting period, a reflection of investors' willingness to assume risk. However, as problems with subprime mortgages and subprime mortgage-backed securities surfaced in July, investors became more risk averse and we saw a classic "flight to quality" to the relative safety of U.S. Treasury securities. Stocks and corporate bonds were hit hardest but municipal securities softened as well, in part due to the subprime mortgage problems facing hedge funds, which have been big buyers of municipal securities. Supported by an injection of liquidity by the Federal Reserve and two Fed Funds rate cuts, the financial markets stabilized in September and early October. However, toward the end of fiscal 2007, as prominent financial institutions began announcing large write-downs of the subprime mortgage backed securities in their portfolios, investors once again fled to Treasuries.

With credit spreads widening, some investors may have found it tempting to enhance portfolio yield by increasing exposure to lower rated investment grade municipal bonds. However, we believe that there are still sufficient uncertainties (the financial health of municipal bond insurers FGIC and Ambac being one of the marketplace's primary concerns), that we have decided to maintain the portfolio's AA+ average credit rating.

The Fed's monetary easing has resulted in a steeper yield curve (higher yields for longer maturity securities). Normally we would have extended the portfolio's weighted average maturity to lock in higher yields in the longer end of the market. However, concerns about hedge fund selling and inflationary pressures resulting from the Fed's rate cuts discouraged us from moving farther out on the yield curve. In addition, if the Fed continues to ease, we believe that short to intermediate maturity securities in the one- to seven-year range will benefit more than bonds in the longer end of the market.

Over the course of fiscal 2007, the portfolio's allocation to revenue bonds (primarily essential purpose bonds) increased from 55.5% of assets to 66.5%. Concurrently, the allocation to general obligation bonds (GO's) declined from 35.6% of assets to 27.1%. Our bias toward essential purpose revenue bonds is based on the fact that historically they have outperformed GO's during periods when economic growth was slowing. In addition, we are concerned about the potentially negative impact declining home prices and a softer labor market will have on the municipal tax revenues that fund GO bond principal and interest payments. Finally, essential purpose revenue bonds are often structured with secure legal provisions that further protect bondholders.

Moving forward, all eyes are on the Federal Reserve, which in our opinion is in a very tough position. On the one hand, the Fed must be willing to ease if the credit crunch further threatens the health of the financial system and the economy appears headed into recession. On the other hand, inflation remains a legitimate concern. Clearly, the Fed is worried about the impact rising commodity prices (oil, gold, agricultural products, and industrial materials) could have on the inflationary front. In addition, the Fed also seems concerned about the impact further rate cuts would have on the already sagging dollar. Our best guess is that the Fed will sit on its hands hoping that the credit markets will survive the subprime mortgage mess so that it doesn't have to make additional rate cuts that could fan inflation and put more pressure on the dollar. With the Fed in

RATING SUMMARY

| AAA | | | 63.1 | % | |

| AA | | | 23.5 | | |

| A | | | 9.5 | | |

| BBB | | | 2.8 | | |

| BB | | | 0.0 | | |

| B | | | 0.0 | | |

| CCC | | | 0.0 | | |

| CC | | | 0.0 | | |

| C | | | 0.0 | | |

| D | | | 0.0 | | |

| Not Rated | | | 0.0 | | |

| Short Term | | | 1.1 | | |

10

limbo, we will likely maintain the portfolio's current weighted average maturity and duration, until something good or bad happens to give us confidence that monetary policy is likely to change.

In closing, today municipal securities appear to us attractively priced relative to Treasuries. With intermediate maturity municipal bonds yields on average about 90% of the 10-year Treasury bond yield as of fiscal year end, municipal securities provide a significant yield advantage for investors in the 35% income tax bracket.

Sincerely,

William J. Furrer and James L. Iselin

Portfolio Co-Managers

11

Municipal Securities Trust

AVERAGE ANNUAL TOTAL RETURN ENDED 10/31/071, 6, 8, 12

| | | Investor

Class | | Lehman Brothers

7-Year GO Index | |

| 1 Year | | | 2.61 | % | | | 3.60 | % | |

| 5 Year | | | 2.95 | % | | | 3.99 | % | |

| 10 Year | | | 4.23 | % | | | 4.98 | % | |

| Life of Fund | | | 5.33 | % | | | 6.15 | %13 | |

| Inception Date | | | 07/09/1987 | | | | | | |

Performance data quoted represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Results are shown on a "total return" basis and include reinvestment of all dividends and capital gain distributions. The composition, industries and holdings of the Fund are subject to change.

Current performance may be lower or higher than the performance data quoted. For performance data current to the most recent month end, please visit www.nb.com/performance.

COMPARISON OF A $10,000 INVESTMENT

| | This chart shows the value of a hypothetical $10,000 investment in the Fund over the past 10 fiscal years. The result is compared with one or more benchmarks, which may include a broad-based market index and/or a narrower index. Please note that market indices do not include expenses. All results include the reinvestment of dividends and capital gain distributions. Results represent past performance and do not indicate future results. The chart and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Please see Endnotes and Glossary of Indices for additional information.

The composition, industries and holdings of the Fund are subject to change.

For the period ending 10/31/07, the 30-day SEC yield of the Investor Class Shares was 3.63% and the tax equivalent yield was 5.58% for an investor in the highest federal income tax bracket (35%). | |

|

12

Lehman Brothers Short Duration Bond Fund Portfolio Commentary

For the fiscal year ended October 31, 2007, the Lehman Brothers Short Duration Bond Fund generated a positive return but modestly trailed its benchmark, the Merrill Lynch 1-3 Year Treasury Index.

The Fund's underperformance relative to the Treasury benchmark is the result of the flight to the safety of Treasury securities prompted by the credit crises in the last months of the fiscal year. The performance of the Fund relative to its peer group remains quite strong due to the high quality bias in the portfolio's structure.

The beginning of the fiscal year was characterized by relatively low volatility — U.S. Treasuries were range-bound and corporate bond spreads remained tight. Concerns regarding the subprime mortgage market began to emerge in February, and by July the collapse of two mortgage-related hedge funds combined with the downgrade of a number of subprime-related collateralized debt obligations intensified investors' worries, prompting a flight to quality. In a six-week period from early July to mid-August, the two-year Treasury note rose in price as its yield fell almost 100 basis points (or one percentage point) and spreads on some investment grade securities (compared to Treasury levels) widened 50 basis points or more, as price declines were exacerbated by the unwinding of positions by leveraged investors, such as hedge funds.

The resurgence of market volatility this year has provided us with several interesting relative value opportunities. We took advantage of market dislocations and reallocated assets from U.S. Agencies and corporate bonds into higher-yielding, AAA-rated asset-backed securities and AAA-rated mortgage-backed securities that are primarily backed by shorter duration adjustable rate mortgages. These transactions allowed us to increase the yield of the portfolio and also increase credit quality. We believe that our extensive fundamental credit research process, supported by our proprietary portfolio management tools, will enable us to continue to uncover undervalued assets that will contribute to returns.

Despite issues in the credit markets and the weakness in the housing sector, concerns remain that higher commodity prices and a weaker U.S. dollar will fuel inflation. Federal Reserve Chairman Ben Bernanke has stated that further Fed action will be data dependant. We have maintained a slightly defensive duration position, with portfolio duration shorter than that of the benchmark, as we monitor these factors. We expect to continue to maintain this posture until the risks to the economy and inflation become more balanced. In the meantime, our defensive positioning provides yield enhancement due to the inversion in the front end of the yield curve.

To protect principal, we have focused intently on credit quality, and are maintaining a high credit quality bias, with the bulk of the portfolio in AAA, AA and A rated securities, with only a small allocation to BBB rated securities. We are also maintaining a highly diversified portfolio in order to attempt to further reduce credit risk. We expect that the market will remain volatile as we move into the end of the calendar year, and we will continue to look for investment opportunities as they present themselves.

In closing, our disciplined investment process, proprietary fundamental credit research and keen focus on risk management have allowed us to provide our investors with consistent and secure returns, regardless of interest rates and market cycles.

Sincerely,

John Dugenske and Thomas Sontag

Portfolio Co-Managers

RATING SUMMARY

AAA/Government/

Government Agency | | | 81.1 | % | |

| AA | | | 7.0 | | |

| A | | | 4.2 | | |

| BBB | | | 5.6 | | |

| BB | | | 0.0 | | |

| B | | | 0.0 | | |

| CCC | | | 0.0 | | |

| CC | | | 0.0 | | |

| C | | | 0.0 | | |

| D | | | 0.0 | | |

| Not Rated | | | 0.0 | | |

| Short Term | | | 2.1 | | |

13

Short Duration Bond Fund

AVERAGE ANNUAL TOTAL RETURN ENDED 10/31/071, 6, 12

| | | Investor

Class | | Trust

Class | | Merrill Lynch 1–3 Year

Treasury Index | |

| 1 Year | | | 5.24 | % | | | 5.15 | % | | | 5.78 | % | |

| 5 Year | | | 2.98 | % | | | 2.86 | % | | | 2.85 | % | |

| 10 Year | | | 4.10 | % | | | 3.99 | % | | | 4.64 | % | |

| Life of Fund | | | 5.62 | % | | | 5.56 | % | | | 6.07 | %13 | |

| Inception Date | | | 06/09/1986 | | | | 08/30/1993 | | | | | | |

Performance data quoted represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Results are shown on a "total return" basis and include reinvestment of all dividends and capital gain distributions. The composition, industries and holdings of the Fund are subject to change.

Current performance may be lower or higher than the performance data quoted. For performance data current to the most recent month end, please visit www.nb.com/performance.

| | This chart shows the value of a hypothetical $10,000 investment in the Fund over the past 10 fiscal years. The graphs are based on the Investor Class shares only; performance of other classes will vary due to differences in fee structures (see Average Annual Total Returns chart above). The result is compared with one or more benchmarks, which may include a broad-based market index and/or a narrower index. Please note that market indices do not include expenses. All results include the reinvestment of dividends and capital gain distributions. Results represent past performance and do not indicate future results. The chart and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Please see Endnotes and Glossary of Indices for additional information.

The composition, industries and holdings of the Fund are subject to change.

For the period ending 10/31/07, the 30-day SEC yield of the Investor Class Shares was 4.93% and the Trust Class shares was 4.83%. | |

|

14

Lehman Brothers Strategic Income Fund Portfolio Commentary

Lehman Brothers Strategic Income Fund generated a positive return in the fiscal year ended October 31, 2007, surpassing its benchmark, the Lehman Brothers U.S. Aggregate Index.

In our opinion, the Fund's performance for the period reflects the benefits of investing in a diversified portfolio of income producing securities. The portfolio represents an attractive mix of such investments, overseen by an asset allocation committee whose primary responsibility is to adjust the portfolio's structure among several market sectors.

As of October 31, 2007, the Fund included 37.3% in corporate bonds, 22.3% in common and preferred securities (including real estate investment trusts or REITs), 19.9% in foreign bonds, 17.1% in Treasury issues, agency obligations and mortgage backed securities, 2.6% in convertible debt and 0.8% in cash.

REITs

The FTSE NAREIT Equity REITs Index enjoyed strong performance early in the fiscal year but declined substantially in June and July due, in our opinion, to several factors including: investors' concerns about the summer's credit crunch and its impact on the economy, a rotation out of yield-oriented sectors by some investors, selling pressure from hedge funds unwinding large REIT positions, and a drop-off in merger and acquisition activity. However, a rally during the fall helped trim REITs' losses, leaving the index with a modest gain for the reporting period.

During the fiscal year, the Fund's real estate holdings declined slightly, hindered by weakness in apartment, office and mixed use holdings. In contrast, health care and regional mall holdings had a positive impact on results.

We believe that REITs can deliver favorable returns in the coming fiscal year, supported by our expectations for above-average earnings growth and favorable yields. Although REITs are currently valued at the higher end of historical norms, they still trade at a roughly 10% discount to net asset value. Looking forward, we anticipate that a tight supply of credit will limit commercial real estate development, helping to preserve favorable supply/demand dynamics in many REIT sectors.

High Yield Securities

The high yield bond market outperformed Treasuries during the first seven months of the reporting period, but investors' aversion to risk later in the time period dragged down performance. The high yield portfolio earned positive returns, but slightly trailed the performance of the Lehman Brothers High Yield 2% Issuer Cap Index during the fiscal year.

Security selection in the food and beverage and technology sectors detracted from returns. Portfolio performance was enhanced, however, by our security selection and overweighting of health care, services, energy, media and utilities sectors. We also had virtually no exposure to real estate firms or homebuilders, which further enhanced performance.

We anticipate that economic growth will moderate. As such, we have been gravitating to less economically sensitive industry groups, such as health care, broadcasting, cable television, packaging, metals and publishing. At the same time, the portfolio is underweight in more cyclical industries, including energy, paper, homebuilders and capital goods.

Investment Grade Fixed Income

The bond market saw significant turbulence during the fiscal year. Early on, volatility levels were relatively low. U.S. Treasuries traded within a limited range and corporate bond spreads remained tight. However, with new concerns regarding the subprime mortgage market, investors initiated a flight to quality. In a six-week period from early July to mid-August, the two-year Treasury note rose in price as its yield fell almost 100 basis points (or one percentage point) and spreads on some investment grade securities (compared to Treasury levels) widened 50 basis points or more, as price declines were exacerbated by the unwinding of positions by leveraged investors, such as hedge funds.

ASSET DIVERSIFICATION

| Corporate Debt | | | 37.3 | % | |

| Convertible Debt | | | 2.6 | | |

| Foreign Securities | | | 19.9 | | |

| U.S. Government Agency Securities | | | 0.9 | | |

| Mortgage-Backed Securities | | | 12.8 | | |

| U.S. Treasury Securities | | | 3.4 | | |

| Preferred Stock | | | 0.9 | | |

| Common Stock | | | 21.4 | | |

| Short Term Investments | | | 0.7 | | |

| Cash, receivables and other assets, less liabilities | | | 0.1 | | |

15

During the period, the investment grade fixed income portfolio allocation, which has an average overall AA credit quality, benefited from our strong interest in bonds perceived to be in the safest and most liquid sectors. We have selectively increased our allocation to the BBB sector and have been able to take advantage of higher yields available due to the widening of credit spreads. The portfolio also benefited from the attractive yields of longer bonds due to the steepening of the yield curve.

Foreign Securities

As in the U.S., economic uncertainty prompted volatility throughout the global capital markets during the fiscal year. Looking forward to 2008, we believe that theme will continue. As credit conditions tighten and economic growth rates decline, in our view, to a sub-trend pace globally, interest rates should remain low for some time.

We believe expectations for lower interest rates in Europe will grow and that the U.S. dollar will recoup some of its losses relative to other currencies. Conversely, the yen should continue to exhibit strength against the dollar. If, as we expect, high risk asset classes begin to underperform due to higher volatility, tighter credit conditions, and a shift in market psychology, the yen is likely to strengthen as investors begin selling their long positions and buying back their yen denominated short positions (unwinding what is known as the "carry trade").

Income Oriented Equity Securities

The portion of the portfolio focusing on income producing equity securities substantially outperformed the S&P 500 during the 12-month reporting period.

Our performance benefited from our overweighting in Energy and Utilities holdings, as both of those sectors had strong returns. Within the Energy sector, rising oil prices during the performance period helped boost petroleum firms' profits. We also enhanced returns by investing in convertible securities and covered calls. While covered calls limit upside potential they also offer protection during market declines.

We continue to maintain positions in Canadian income trusts (CIT), which are focused on energy related companies. CITs are similar to U.S. real estate investment trusts in that they avoid tax at the corporate level and offer relatively high income yields to investors. We believe these securities are reasonably valued, but due to the potential for a change in their tax status in 2011, we continue to monitor them closely.

Sincerely,

Strategic Income Fund

Asset Allocation Committee

16

Strategic Income Fund

AVERAGE ANNUAL TOTAL RETURN ENDED 10/31/073, 6, 11, 12

| | | Institutional

Class | | Trust

Class | | Lehman Brothers

U.S. Aggregate Index | |

| 1 Year | | | 5.64 | % | | | 5.54 | % | | | 5.38 | % | |

| Life of Fund | | | 8.16 | % | | | 8.14 | % | | | 3.80 | %13 | |

| Inception Date | | 07/11/2003 | | 04/02/2007 | | | |

Performance data quoted represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed may be worth more or less than their original cost. Results are shown on a "total return" basis and include reinvestment of all dividends and capital gain distributions. The composition, industries and holdings of the Fund are subject to change.

Current performance may be higher or lower than the performance data quoted. For performance data current to the most recent month end, please visit www.nb.com/performance.

| | This chart shows the value of a hypothetical $10,000 investment in the Fund over the past 10 fiscal years, or since the Fund's inception, if it has not operated for 10 years. The graphs are based on the Institutional Class shares only; performance of other classes will vary due to differences in fee structures (see Average Annual Total Returns chart above).The result is compared with one or more benchmarks, which may include a broad-based market index and/or a narrower index. Please note that market indices do not include expenses. All results include the reinvestment of dividends and capital gain distributions. Results represent past performance and do not indicate future results. The chart and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Please see Endnotes and Glossary of Indices for additional information.

The composition, industries and holdings of the Fund are subject to change.

For the period ending 10/31/07, the 30-day SEC yield of the Institutional Class shares was 4.43% and the Trust Class Shares was 4.18%. | |

|

17

Neuberger Berman Cash Reserves Portfolio Commentary

We are pleased to report that Neuberger Berman Cash Reserves delivered positive returns and outperformed the iMoneyNet Money Fund Report Taxable First Tier Retail Average during the fiscal year ended October 31, 2007. The Fund closed the period with a seven-day effective yield of 4.80% and a seven-day current yield* of 4.69%.1, 5

The combination of slower economic growth and a continued pause in the Federal Reserve's two-year tightening campaign led to a rally in bonds early in the reporting period. The Fed remained on hold for much of this time, with the Fed Funds rate at 5.25%, as the central bank balanced concerns about inflation with indications of a slowing economy.

However, beginning in July, worries about reports of large losses at hedge funds in the subprime and collateralized debt space led to a flight-to-quality bid for Treasuries and a widening of risk premiums in the market. Investors became increasingly concerned about contagion to the broader market from the shakeout in subprime mortgages, leading to more investors taking refuge in Treasuries. The cost of borrowing increased dramatically, as the excesses of a prolonged period of liquidity began to be removed from the market.

September brought the release of August payroll figures — the first negative numbers in four years — as well as a sharp revision to the prior two months' data, which were seen as proof that the employment situation appears to be worsening. (August payroll figures were adjusted upward in October.) This, coupled with a housing market that continued to see declining prices and higher inventories, heightened the Fed's interest in preempting any material effects on economic growth.

As a result, the Fed reduced the Fed Funds rate by 50 basis points at its September meeting, marking its first rate reduction since 2003. The move to 4.75% was only the second time in the last 20 years that an easing cycle had commenced with a 50 basis-point reduction. This was followed by a further 25 basis-point cut in October. In taking rates lower, the Federal Open Market Committee commented that the action was "intended to help forestall some of the adverse effects on the broader economy that might otherwise arise from the disruptions in the financial markets." The committee added that it was prepared to "act as needed to foster price stability and sustainable economic growth."

Throughout the period, we maintained the bulk of the portfolio's holdings in corporate commercial paper and floating rate medium term corporate/bank notes, which ended the period at 56.3% and 28.6% of portfolio holdings, respectively. We also had a small percentage, 4.9% of the portfolio in repurchase agreements at the end of the fiscal year. The weighted average maturity of the portfolio ended the fiscal year at 44.5 days — almost exactly where it was a year prior, after reaching a high of 66 days in March, and a low of 26.8 days in the middle of October, prior to a second rate cut by the Federal Reserve.

The U.S. economy has been extremely resilient thus far. However, we anticipate that further deterioration in the housing market will start to take its toll on the consumer and ultimately business investment. The market is suffering from a crisis of confidence, and while the Fed remains reluctant to take rates lower, we believe that the easing cycle may continue. As always, we will seek to provide consistent and secure returns to our shareholders.

Sincerely,

John C. Donohue and Scott F. Riecke

Portfolio Co-Managers

* Current yield more closely reflects current earnings than does total return.

MATURITY DIVERSIFICATION

| (% by Maturity) | |

| 1 - 7 Days | | | 30.2% | | |

| 8 - 30 Days | | | 29.0 | | |

| 31 - 90 Days | | | 27.9 | | |

| 91 - 180 Days | | | 6.4 | | |

| 181+ Days | | | 6.5 | | |

18

Endnotes

1 Neuberger Berman Management Inc. ("Management") has contractually undertaken to forgo current payment of fees and/or expenses reimburse the following Funds so that the total annual operating expenses (exclusive of taxes, interest, brokerage commissions and extraordinary expenses) are limited to 0.65% for Neuberger Berman Cash Reserves (Investor Class), 1.00% for Lehman Brothers High Income Bond Fund (Investor Class), 0.70% for Lehman Brothers Short Duration Bond Fund (Investor Class), 0.80% for Lehman Brothers Short Duration Bond Fund (Trust Class), 0.65% for Lehman Brothers Municipal Securities Trust (Investor Class) and 0.59% for Lehman Brothers Municipal Money Fund (Investor Class) of average daily net assets. Each undertaking lasts until October 31, 2010. Absent such forgone fees and/or reimbursements, the performance of each listed c lass of each Fund except for Lehman Brothers High Income Bond Fund and Neuberger Berman Cash Reserves would have been less.

Each of these Funds has contractually undertaken to repay Management for fees and expenses forgone and/or its excess expenses paid by Management, provided the repayments do not cause its total annual operating expenses (exclusive of taxes, interest, brokerage commissions and extraordinary expenses) to exceed the above stated expense limitation and the repayments are made within three years after the year that Management incurred the expense. For the year ended October 31, 2007, there were no repayments of expenses to Management.

2 Management has contractually undertaken to forgo current payment of fees and/or reimburse Lehman Brothers Core Bond Fund so that total annual operating expenses (exclusive of taxes, interest, brokerage commissions and extraordinary expenses) of the Fund are limited to 0.85% and 0.45% of average daily net assets for the Investor Class and Institutional Class, respectively. The undertakings last until October 31, 2017. The Fund has contractually undertaken to repay Management for fees and expenses forgone and/or its excess expenses paid by Management, provided the repayments do not cause total annual operating expenses (exclusive of taxes, interest, brokerage commissions, and extraordinary expenses) to exceed the above-stated expense limitation and the repayments are made within three years after the year that Management incurred the expense. Absent such forgone fees and/or reimbursements, the performance of each class would have been lower. Management has voluntarily agreed to waive its management fee in the amount of 0.25% (0.20% prior to March 1, 2006) of the Fund's average daily net assets through October 31, 2007. Management has agreed to continue this voluntary waiver after this date. If this voluntary waiver was not in place, performance would be lower for the Fund.

3 Management has contractually undertaken to forgo current payment of fees and/or reimburse Lehman Brothers Strategic Income Fund so that total annual operating expenses (exclusive of taxes, interest, brokerage commissions and extraordinary expenses) of the Fund are limited to 1.10% and 0.85% of average daily net assets for the Trust Class and Institutional Class, respectively. The undertaking lasts until October 31, 2010 and October 31, 2017 for the Trust Class and Institutional Class, respectively. The Fund has contractually undertaken to repay Management for fees and expenses forgone and/or its excess expenses paid by Management, provided the repayments do not cause its total annual operating expenses (exclusive of taxes, interest, brokerage commissions, and extraordinary expenses) to exceed the above stated expense limitation and the re payments are made within three years after the year that Management incurred the expense. Absent such forgone fees and/or reimbursements, the performance of the Fund would have been lower.

4 Management has contractually undertaken to forgo current payment of fees and/or reimburse the Investor Class of Lehman Brothers New York Municipal Money Fund so that the total annual operating expenses (exclusive of taxes, interest, brokerage commissions and extraordinary expenses) of the Fund are limited to 0.59% of average daily net assets. The undertaking lasts until October 31, 2010. Absent such forgone fees and/or reimbursements, the performance of the Investor Class of the Fund would have been less. The Fund has contractually undertaken to repay Management for fees and expenses forgone and/or its excess expenses paid by Management, provided the repayments do not cause its total annual operating expenses (exclusive of taxes, interest, brokerage commissions and extraordinary expenses) to exceed the above stated expense limitation and the repayments are made within

19

three years after the year that Management incurred the expense. For the year ended October 31, 2007, there were no repayments of expenses to Management.

Effective June 5, 2006, Management voluntarily agreed to waive certain expenses of the Investor Class of New York Municipal Money, so that the total annual operating expenses (exclusive of taxes, interest, brokerage commissions and extraordinary expenses) of the Class are limited to 0.52% of the average daily net assets. In addition, effective January 17, 2007, Management voluntarily agreed to waive certain expenses of the Investor Class of the Fund, so that the total annual operating expenses (exclusive of taxes, interest, brokerage commissions and extraordinary expenses) of the Class are limited to 0.47% of the average daily net assets. Absent such waivers, the performance of the Investor Class of the Fund would have been less.

5 "Current yield" of a money market fund refers to the income generated by an investment in a Fund over a recent 7-day period. This income is then "annualized." The "effective yield" is calculated similarly but, when annualized, the income earned by an investment in the Fund is assumed to be reinvested. The "effective yield" will be slightly higher than the "current yield" because of the compounding effect of this assumed reinvestment. Yields of a money market fund will fluctuate and past performance is not a guarantee of future results.

6 Annual total returns are for the period end October 31, 2007. Returns are shown on a "total return" basis and assume reinvestment of all dividends and capital gain distributions.

7 Tax-equivalent effective yield is the taxable effective yield that an investor would have had to receive in order to realize the same level of yield after federal income taxes at the highest federal tax rate, currently 35%, assuming that all of a Fund's income is exempt from federal income taxes. For Lehman Brothers New York Municipal Money Fund, tax-equivalent yield is calculated based on federal, New York State, and New York City tax rates for a combined rate of 41.8%.

8 A portion of the income of Lehman Brothers Municipal Securities Trust may be a tax preference item for purposes of the federal alternative minimum tax for certain investors.

9 This Fund is the successor to the Lipper High Income Bond Fund ("Lipper Fund"). The total return data for the periods prior to September 7, 2002, are those of the Lipper High Income Bond Fund Premier Class. The data reflect performance of the Lipper Fund for the period April 1, 1996, through September 6, 2002. The investment policies, objectives, guidelines and restrictions of the Fund are in all material respects equivalent to those of the Lipper Fund. Returns would have been lower if the manager of the Lipper Fund had not waived certain of its fees during the periods shown.

10 The Fund is the successor to Ariel Premier Bond Fund ("Ariel Bond Fund"). The total return data for the periods prior to June 13, 2005 are those of the Ariel Bond Fund Investor Class and Institutional Class. The data reflects performance of Ariel Bond Fund Investor Class for the period February 1, 1997 through June 10, 2005 and the performance of Ariel Bond Fund Institutional Class for the period October 1, 1995 (date of inception) through January 31, 1997. The investment policies, guidelines and restrictions of the Fund are in all respects equivalent to Ariel Bond Fund. Ariel Bond Fund Institutional Class had lower expenses and typically higher returns than Ariel Bond Fund Investor Class. Returns would have been lower if the manager of Ariel Bond Fund had not waived certain of its fees during the periods shown.

11 Lehman Brothers Strategic Income Fund Trust Class commenced operations on April 2, 2007. The performance information for the Fund prior to its commencement of operations is for the Institutional Class.

12 Unaudited performance data current to the most recent month-end are available at www.nb.com.

13 The date used to calculate Life of Fund performance for the index is the inception date of the oldest share class.

20

Glossary of Indices

| Merrill Lynch 1-3 Year Treasury Index: | | An unmanaged total return market value index consisting of all coupon-bearing U.S. Treasury publicly placed debt securities with maturities between 1 and 3 years. | |

| |

| Lehman Brothers 7-Year General Obligation Index: | | An unmanaged total return performance benchmark for the intermediate-term, 7-year, investment grade General Obligations (State and Local) tax-exempt bond market. | |

| |

| Lehman Brothers Intermediate Ba U.S. High Yield Index: | | An unmanaged index comprised of BB-rated bonds with maturities of less than 10 years. | |

| |

| Lehman Brothers U.S. Aggregate Index: | | An unmanaged index that represents the U.S. domestic investment grade bond market. It is comprised of the Lehman Brothers Government/Corporate Bond Index, Mortgage-Backed Securities Index, and Asset-Backed Securities Index, including securities that are of investment-grade quality or better, have at least one year to maturity, and have an outstanding par value of at least $100 million. | |

| |

| Lehman Brothers U.S. Corporate High Yield 2% Issuer Cap Index: | | An unmanaged sub-index of the Lehman Brothers U.S. Corporate High Yield Index (which includes all U.S. dollar-denominated, taxable, fixed rate, non-investment grade debt), capped such that no single issuer accounts for more than 2% of the index weight. | |

| |

| Lipper Intermediate Municipal Debt Funds Average: | | Measures the performance of mutual funds that invest in municipal debt issues with dollar-weighted average maturities of five to ten years, as tracked by Lipper. | |

| |

| iMoneyNet Money Fund Report Tax-Free National Institutional Average: | | Measures all national tax-free and municipal institutional funds. Portfolio holdings of tax-free funds include Rated and Unrated Demand Notes, Rated and Unrated General Market Notes, Commercial Paper, Put Bonds — 6 months or less, Put Bonds — over 6 months, AMT Paper, and Other Tax-Free holdings. | |

| |

| iMoneyNet Money Fund Report Taxable First Tier Retail Average: | | Measures the performance of retail money market mutual funds which hold "First Tier" securities as defined by Rule 2a-7 of the Investment Company Act of 1940 (not including Second Tier Commercial Paper). First Tier securities are those rated in the highest short-term rating category by two or more nationally recognized statistical ratings organizations or one, if only one has rated the security. | |

| |

| iMoneyNet Money Fund Report Tax-Free National Retail Average: | | Measures all national tax-free and municipal retail funds. Portfolio holdings of tax-free funds include Rated and Unrated Demand Notes, Rated and Unrated General Market Notes, Commercial Paper, Put Bonds — 6 months or less, Put Bonds — over 6 months, AMT Paper, and Other Tax-Free holdings. | |

| |

| iMoneyNet Money Fund Report Tax-Free State-Specific Retail Average: | | Measures the performance of retail state-specific tax-free and municipal money mutual funds. Portfolio holdings of tax-free funds include Rated and Unrated Demand Notes, Rated and Unrated General Market Notes, Commercial Paper, Put Bonds — 6 months or less, Put Bonds — over 6 months, AMT Paper, and Other Tax-Free holdings. | |

|

21

| FTSE NAREIT Equity REITs Index: | | FTSE NAREIT Equity REITs Index tracks the performance of all Equity REITs currently listed on the New York Stock Exchange, the NASDAQ National Market System and the American Stock Exchange. REITs are classified as Equity if 75% or more of their gross invested book assets are invested directly or indirectly in equity of commercial properties. | |

| |

| S&P 500 Index: | | The S&P 500 Index is widely regarded as the standard for measuring the performance of large-cap stocks traded on U.S.markets and includes a representative sample of leading companies in leading industries. | |

| |

Please note that indices do not take into account any fees and expenses or any tax consequences of investing in the individual securities that they track and that investors cannot invest directly in any index or average. Data about the performance of each index or average are prepared or obtained by Management and include reinvestment of all dividends and capital gain distributions. Each Fund may invest in securities not included in its respective index.

22

Information About Your Fund's Expenses

These tables are designed to provide information regarding costs related to your investments. All mutual funds incur operating expenses, which include management fees, fees for administrative services and cost of shareholder reports, among others. The following examples are based on an investment of $1,000 made at the beginning of the six month period ended October 31, 2007 and held for the entire period. The tables illustrate the fund's costs in two ways:

| Actual Expenses and Performance: | | The first section of the tables provide information about actual account values and actual expenses in dollars, based on the fund's actual performance during the period. You may use the information in this line, together with the amount you invested, to estimate the expenses you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first section of the table under the heading entitled "Expenses Paid During the Period" to estimate the expenses you paid over the period. | |

|

| Hypothetical Example for Comparison Purposes: | | The second section of the tables provide information about hypothetical account values and hypothetical expenses based on the fund's actual expense ratio and an assumed rate of return at 5% per year before expenses. This return is not the fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in these funds versus other funds. To do so, compare the expenses shown in this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds. | |

|

23

Expense Information as of 10/31/07 (Unaudited)

LEHMAN BROTHERS CORE BOND FUND

| Actual | | Beginning Account

Value

5/1/07 | | Ending Account

Value

10/31/07 | | Expenses Paid During

the Period*

5/1/07 - 10/31/07 | | Expense

Ratio | |

| Investor Class | | $ | 1,000.00 | | | $ | 1,009.40 | | | $ | 4.31 | | | | .85 | % | |

| Institutional Class | | $ | 1,000.00 | | | $ | 1,011.40 | | | $ | 2.28 | | | | .45 | % | |

| Hypothetical (5% annual return before expenses)** | |

| Investor Class | | $ | 1,000.00 | | | $ | 1,020.92 | | | $ | 4.33 | | | | .85 | % | |

| Institutional Class | | $ | 1,000.00 | | | $ | 1,022.94 | | | $ | 2.29 | | | | .45 | % | |

LEHMAN BROTHERS HIGH INCOME BOND FUND

| Actual | | Beginning Account

Value

5/1/07 | | Ending Account

Value

10/31/07 | | Expenses Paid During

the Period*

5/1/07 - 10/31/07 | | Expense

Ratio | |

| Investor Class | | $ | 1,000.00 | | | $ | 997.50 | | | $ | 4.73 | | | | .94 | % | |

| Hypothetical (5% annual return before expenses)** | |

| Investor Class | | $ | 1,000.00 | | | $ | 1,020.47 | | | $ | 4.79 | | | | .94 | % | |

LEHMAN BROTHERS MUNICIPAL MONEY FUND

| Actual | | Beginning Account

Value

5/1/07 | | Ending Account

Value

10/31/07 | | Expenses Paid During

the Period*

5/1/07 - 10/31/07 | | Expense

Ratio | |

| Investor Class | | $ | 1,000.00 | | | $ | 1,016.10 | | | $ | 2.95 | | | | .58 | % | |

| Hypothetical (5% annual return before expenses)** | |

| Investor Class | | $ | 1,000.00 | | | $ | 1,022.28 | | | $ | 2.96 | | | | .58 | % | |

LEHMAN BROTHERS MUNICIPAL SECURITIES TRUST

| Actual | | Beginning Account

Value

5/1/07 | | Ending Account

Value

10/31/07 | | Expenses Paid During

the Period*

5/1/07 - 10/31/07 | | Expense

Ratio | |

| Investor Class | | $ | 1,000.00 | | | $ | 1,014.80 | | | $ | 3.30 | | | | .65 | % | |

| Hypothetical (5% annual return before expenses)** | |

| Investor Class | | $ | 1,000.00 | | | $ | 1,021.93 | | | $ | 3.31 | | | | .65 | % | |

24

Expense Information as of 10/31/07 cont'd (Unaudited)

LEHMAN BROTHERS NEW YORK MUNICIPAL MONEY FUND

| Actual | | Beginning Account

Value

5/1/07 | | Ending Account

Value

10/31/07 | | Expenses Paid During

the Period*

5/1/07- 10/31/07 | | Expense

Ratio | |

| Investor Class | | $ | 1,000.00 | | | $ | 1,016.60 | | | $ | 2.34 | | | | .46 | % | |

| Hypothetical (5% annual return before expenses)** | |

| Investor Class | | $ | 1,000.00 | | | $ | 1,022.89 | | | $ | 2.35 | | | | .46 | % | |

LEHMAN BROTHERS SHORT DURATION BOND FUND

| Actual | | Beginning Account

Value

5/1/07 | | Ending Account

Value

10/31/07 | | Expenses Paid During

the Period*

5/1/07 - 10/31/07 | | Expense

Ratio | |

| Investor Class | | $ | 1,000.00 | | | $ | 1,026.20 | | | $ | 3.57 | | | | .70 | % | |

| Trust Class | | $ | 1,000.00 | | | $ | 1,025.80 | | | $ | 4.08 | | | | .80 | % | |

| Hypothetical (5% annual return before expenses)** | |

| Investor Class | | $ | 1,000.00 | | | $ | 1,021.68 | | | $ | 3.57 | | | | .70 | % | |

| Trust Class | | $ | 1,000.00 | | | $ | 1,021.17 | | | $ | 4.08 | | | | .80 | % | |

LEHMAN BROTHERS STRATEGIC INCOME FUND

| Actual | | Beginning Account

Value

5/1/07 | | Ending Account

Value

10/31/07 | | Expenses Paid During

the Period*

5/1/07 - 10/31/07 | | Expense

Ratio | |

| Institutional Class | | $ | 1,000.00 | | | $ | 1,011.90 | | | $ | 4.31 | | | | .85 | % | |

| Trust Class | | $ | 1,000.00 | | | $ | 1,010.90 | | | $ | 5.58 | | | | 1.10 | % | |

| Hypothetical (5% annual return before expenses)** | |

| Institutional Class | | $ | 1,000.00 | | | $ | 1,020.92 | | | $ | 4.33 | | | | .85 | % | |

| Trust Class | | $ | 1,000.00 | | | $ | 1,019.66 | | | $ | 5.60 | | | | 1.10 | % | |

NEUBERGER BERMAN CASH RESERVES

| Actual | | Beginning Account

Value

5/1/07 | | Ending Account

Value

10/31/07 | | Expenses Paid During

the Period*

5/1/07 - 10/31/07 | | Expense

Ratio | |

| Investor Class | | $ | 1,000.00 | | | $ | 1,024.70 | | | $ | 2.65 | | | | .52 | % | |

| Hypothetical (5% annual return before expenses)** | |

| Investor Class | | $ | 1,000.00 | | | $ | 1,022.58 | | | $ | 2.65 | | | | .52 | % | |

* For each class of the Fund, expenses are equal to the annualized expense ratio for the class, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period shown).

** Hypothetical 5% annual return before expenses is calculated by multiplying the number of days in the most recent period divided by 365.

25

Schedule of Investments Lehman Brothers Core Bond Fund

| PRINCIPAL AMOUNT | | | | RATING§ | | VALUE† | |

| (000's omitted) | | | | Moody's | | S&P | | (000's omitted) | |

U.S. Treasury Securities-Backed by the Full Faith and Credit of

the U.S. Government (8.8%) | | | |

| $ | 445 | | | U.S. Treasury Bonds, 8.13%, due 8/15/19 | | TSY | | TSY | | $ | 584 | | |

| | 1,435 | | | U.S. Treasury Bonds, 6.00%, due 2/15/26 | | TSY | | TSY | | | 1,643 | ØØ | |

| | 4,685 | | | U.S. Treasury Notes, 4.38%, due 8/15/12 | | TSY | | TSY | | | 4,745 | ØØ | |

| | 625 | | | U.S. Treasury Strips, due 8/15/14 & 2/15/25 | | TSY | | TSY | | | 362 | | |

Total U.S. Treasury Securities-Backed by the Full

Faith and Credit of the U.S. Government (Cost $7,236) | | | | | | 7,334 | |

| U.S. Government Agency Securities (9.0%) | | | |

| | 850 | | | Fannie Mae, Notes, 5.25%, due 1/29/09 & 9/15/16 | | AGY | | AGY | | | 862 | | |

| | 1,320 | | | Fannie Mae, Notes, 4.30%, due 3/9/09 | | AGY | | AGY | | | 1,318 | | |

| | 660 | | | Fannie Mae, Notes, 5.38%, due 7/15/16 | | AGY | | AGY | | | 682 | | |

| | 725 | | | Fannie Mae, Notes, 5.00%, due 5/11/17 | | AGY | | AGY | | | 728 | | |

| | 200 | | | Federal Home Loan Bank, Bonds, 5.00%, due 11/17/17 | | AGY | | AGY | | | 202 | | |

| | 280 | | | Federal Home Loan Bank, Bonds, 5.50%, due 7/15/36 | | AGY | | AGY | | | 291 | | |

| | 700 | | | Federal Home Loan Bank, Bonds, 5.13%, due 6/18/08 | | AGY | | AGY | | | 702 | | |

| | 2,450 | | | Freddie Mac, Notes, 4.75%, due 1/18/11 | | AGY | | AGY | | | 2,473 | | |

| | 200 | | | Freddie Mac, Notes, 5.13%, due 7/15/12 | | AGY | | AGY | | | 204 | | |

| Total U.S. Government Agency Securities (Cost $7,412) | | | | | | 7,462 | |

Mortgage-Backed Securities (84.4%)

Adjustable Rate Mortgages (41.6%) | | | |

| | 60 | | | ACE Securities Corp., Ser. 2006-FM1, Class A2A, 4.91%, due 11/25/07 | | Aaa | | AAA | | | 60 | µØØ | |

| | 205 | | | ACE Securities Corp., Ser. 2006-FM1, Class A2B, 4.96%, due 11/25/07 | | Aaa | | AAA | | | 200 | µØØ | |

| | 171 | | | ACE Securities Corp., Ser. 2005-HE6, Class A2B, 5.07%, due 11/25/07 | | Aaa | | AAA | | | 171 | µØØ | |

| | 1,075 | | | Advanta Business Card Master Trust, Ser. 2001-A, Class A, 5.30%, due 11/20/07 | | Aaa | | AAA | | | 1,076 | µ | |

| | 209 | | | Asset Backed Securities Corp. Home Equity, Ser. 2005-HE6, Class A2B,

5.12%, due 11/25/07 | | Aaa | | AAA | | | 208 | µØØ | |

| | 570 | | | Bank of America Credit Card Trust, Ser. 2007-A7, Class A7,

5.09%, due 11/15/07 | | Aaa | | AAA | | | 567 | µØØ | |

| | 800 | | | Bank of America Credit Card Trust, Ser. 2007-A13, Class A13,

5.33%, due 11/15/07 | | Aaa | | AAA | | | 800 | µØØ | |

| | 92 | | | Banc of America Funding Corp., Ser. 2006-G, Class 2A2,

5.08%, due 11/20/07 | | Aaa | | AAA | | | 91 | µØØ | |

| | 116 | | | Banc of America Funding Corp., Ser. 2006-G, Class 2A1,

5.22%, due 11/20/07 | | Aaa | | AAA | | | 115 | µØØ | |

| | 327 | | | Banc of America Funding Corp., Ser. 2005-F, Class 4A1,

5.35%, due 11/20/07 | | Aaa | | AAA | | | 328 | µ | |

| | 386 | | | Banc of America Funding Corp., Ser. 2006-A, Class 3A2,

5.88%, due 11/20/07 | | | | AAA | | | 388 | µ | |

| | 800 | | | Bank One Issuance Trust, Ser. 2003-A3, Class A3, 5.20%, due 11/15/07 | | Aaa | | AAA | | | 800 | µØØ | |

| | 800 | | | Bank One Issuance Trust, Ser. 2003-A1, Class A1, 5.21%, due 11/15/07 | | Aaa | | AAA | | | 800 | µØØ | |

| | 164 | | | Bear Stearns ALT-A Trust, Ser. 2006-4, Class 32A1,

6.48%, due 7/25/36 | | Aaa | | AAA | | | 167 | | |

| | 406 | | | Bear Stearns ALT-A Trust, Ser. 2007-2, Class 2A1,

5.61%, due 11/25/07 | | Aaa | | AAA | | | 408 | µ | |

| | 330 | | | Carrington Mortgage Loan Trust, Ser. 2006-NC3, Class A3, 5.02%, due 11/25/07 | | Aaa | | AAA | | | 311 | µØØ | |

| | 220 | | | Carrington Mortgage Loan Trust, Ser. 2006-NC4, Class M2, 5.19%, due 11/25/07 | | Aa2 | | AA | | | 166 | µØØ | |