As filed with the Securities and Exchange Commission on January 5, 2009

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-3802

LEHMAN BROTHERS INCOME FUNDS

(Exact Name of the Registrant as Specified in Charter)

605 Third Avenue, 2nd Floor

New York, New York 10158-0180

(Address of Principal Executive Offices – Zip Code)

Registrant's telephone number, including area code: (212) 476-8800

Robert Conti, Chief Executive Officer

c/o Neuberger Berman Management LLC

Lehman Brothers Income Funds

605 Third Avenue, 2nd Floor

New York, New York 10158-0180

Arthur Delibert, Esq.

K&L Gates LLP

1601 K Street, N.W.

Washington, D.C. 20006-1600

(Names and Addresses of agents for service)

Date of fiscal year end: October 31, 2008

Date of reporting period: October 31, 2008

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Shareholders

Income Funds

Investor Class Shares

Institutional Class Shares

Reserve Class Shares

Trust Class Shares

Class A Shares

Class C Shares

Neuberger Berman California Tax-Free Money Fund

Neuberger Berman Core Bond Fund

Neuberger Berman Core Plus Bond Fund

Neuberger Berman High Income Bond Fund

Neuberger Berman Municipal Money Fund

Neuberger Berman Municipal Securities Trust

Neuberger Berman New York Municipal Money Fund

Neuberger Berman Short Duration Bond Fund

Neuberger Berman Strategic Income Fund

Neuberger Berman Cash Reserves

Annual Report

October 31, 2008

Contents

THE FUNDS

PORTFOLIO COMMENTARY

| Neuberger Berman California Tax-Free Money Fund | | | 2 | | |

|

| Neuberger Berman Municipal Money Fund | | | 2 | | |

|

| Neuberger Berman New York Municipal Money Fund | | | 3 | | |

|

| Neuberger Berman Core Bond Fund | | | 5 | | |

|

| Neuberger Berman Core Plus Bond Fund | | | 9 | | |

|

| Neuberger Berman High Income Bond Fund | | | 13 | | |

|

| Neuberger Berman Municipal Securities Trust | | | 15 | | |

|

| Neuberger Berman Short Duration Bond Fund | | | 18 | | |

|

| Neuberger Berman Strategic Income Fund | | | 21 | | |

|

| Neuberger Berman Cash Reserves | | | 25 | | |

|

| FUND EXPENSE INFORMATION | | | 32 | | |

|

SCHEDULE OF INVESTMENTS

| Neuberger Berman California Tax-Free Money Fund | | | 34 | | |

|

| Neuberger Berman Core Bond Fund | | | 35 | | |

|

| Neuberger Berman Core Plus Bond Fund | | | 40 | | |

|

| Neuberger Berman High Income Bond Fund | | | 43 | | |

|

| Neuberger Berman Municipal Money Fund | | | 48 | | |

|

| Neuberger Berman Municipal Securities Trust | | | 52 | | |

|

| Neuberger Berman New York Municipal Money Fund | | | 54 | | |

|

| Neuberger Berman Short Duration Bond Fund | | | 56 | | |

|

| Neuberger Berman Strategic Income Fund | | | 59 | | |

|

| Neuberger Berman Cash Reserves | | | 61 | | |

|

| FINANCIAL STATEMENTS | | | 66 | | |

|

The "Neuberger Berman" name and logo are registered service marks of Neuberger Berman, LLC. "Neuberger Berman Management LLC" and the individual fund names in this report are either service marks or registered service marks of Neuberger Berman Management LLC, formerly Neuberger Berman Management Inc. ©2008 Neuberger Berman Management LLC. All rights reserved. ©2008 Lehman Brothers Asset Management LLC. All rights reserved.

FINANCIAL HIGHLIGHTS/PER SHARE DATA

| Neuberger Berman California Tax-Free Money Fund | | | 92 | | |

|

| Neuberger Berman Core Bond Fund | | | 92 | | |

|

| Neuberger Berman Core Plus Bond Fund | | | 94 | | |

|

| Neuberger Berman High Income Bond Fund | | | 94 | | |

|

| Neuberger Berman Municipal Money Fund | | | 94 | | |

|

| Neuberger Berman Municipal Securities Trust | | | 94 | | |

|

| Neuberger Berman New York Municipal Money Fund | | | 96 | | |

|

| Neuberger Berman Short Duration Bond Fund | | | 96 | | |

|

| Neuberger Berman Strategic Income Fund | | | 96 | | |

|

| Neuberger Berman Cash Reserves | | | 98 | | |

|

| Reports of Independent Registered Public Accounting Firms | | | 102 | | |

|

| Directory | | | 104 | | |

|

| Trustees and Officers | | | 105 | | |

|

| Proxy Voting Policies and Procedures | | | 113 | | |

|

| Quarterly Portfolio Schedule | | | 113 | | |

|

| Notice to Shareholders | | | 113 | | |

|

| Board Consideration of the Management and Sub-Advisory Agreements | | | 114 | | |

|

The "Neuberger Berman" name and logo are registered service marks of Neuberger Berman, LLC. "Neuberger Berman Management LLC" and the individual fund names in this report are either service marks or registered service marks of Neuberger Berman Management LLC, formerly Neuberger Berman Management Inc. ©2008 Neuberger Berman Management LLC. All rights reserved. ©2008 Lehman Brothers Asset Management LLC. All rights reserved.

President's Letter

Dear Fellow Shareholder,

The last 12 months tested the resolve of novice and seasoned investors alike. The problems associated with the subprime mortgage market escalated, morphing into a global crisis as the period progressed. Stresses were particularly evident in September and October, as a series of truly remarkable events disrupted much of the financial marketplace.

During that two-month period, the U.S. Treasury essentially took over mortgage giants Fannie Mae and Freddie Mac, the government seized control of insurance leader AIG, Washington Mutual collapsed and was acquired by JP Morgan, Wachovia was taken over by Wells Fargo and a major money market fund "broke the buck," as its net asset value fell below $1.00 a share. The traditional idea of "Wall Street" also came to an end, as the March demise of Bear Stearns was followed in September by Lehman Brothers' bankruptcy filing, Bank of America's announced acquisition of Merrill Lynch and the decision by Goldman Sachs and Morgan Stanley to become bank holding companies subject to regulation by the Federal Reserve.

Governments in the U.S. and abroad took action in an attempt to stabilize the global financial system and restore investor confidence. In addition to coordinated interest rate cuts, certain central banks moved to directly invest in troubled financial organizations and institute other measures to unfreeze the credit markets. In October, the U.S. Congress approved the $700 billion Troubled Asset Relief Program (TARP), whose implementation continues to evolve.

During the fiscal year, the fixed income markets experienced periods of extreme volatility as the credit markets seized up and highly leveraged entities were forced to sell assets into an already illiquid market. Against this backdrop, investors looked to pare the risks in their portfolios by purchasing ultra-safe, short-term Treasuries. In contrast, the spreads (or yield over Treasuries) of corporate and other fixed income securities widened, in some cases reaching unprecedented — and in our view excessive — levels. Even securities with strong credit fundamentals performed poorly amid phases of indiscriminant selling.

Throughout this extremely challenging period, our portfolio managers adhered to their disciplined investment processes, which have proven reliable over a variety of market cycles. As in the past, they closely monitored the unfolding situation in the financial markets and conducted extensive research on existing and prospective Fund holdings. In our money market portfolios, managers heightened their emphasis on liquidity and reduced weighted average maturity, while in intermediate and longer strategies, they maintained asset mixes that we believe will benefit shareholders as markets resume more normal and fundamentals-driven performance patterns.

Looking ahead to the next fiscal year, we expect to see continued periods of heightened volatility in the financial markets. While it may be difficult to remain calm during these periods, we urge you to stay focused on the long term and avoid making emotion-based decisions that in our view could undermine your financial goals. Yes, challenges remain, but we believe that extensive and aggressive policy interventions by the U.S. and other governments will ultimately contribute to more normal market conditions and enhance opportunities for patient investors.

Sincerely,

Robert Conti

President and CEO

Neuberger Berman Mutual Funds

1

California Tax-Free Money Fund Commentary

Municipal Money Fund Commentary

New York Municipal Money Fund Commentary

The fiscal year ended October 31, 2008 was remarkably difficult for investors. Over much of the period, the subprime mortgage meltdown worsened and financial institutions in the U.S. and overseas took further multi-billion-dollar write-downs of troubled fixed-income assets. Concerns over the resulting slowdown of credit markets spread worldwide and inflicted considerable punishment on companies with exposure to mortgages and assets with complex structures. Markets were further rocked by high profile failures of institutions holding toxic debt, which led to consolidations and the government bailouts of Fannie Mae, Freddie Mac and others, as well as an historic U.S. rescue package involving the potential purchase of subprime assets from financial companies. Investors fled many credits and sought safety in U.S. Treasuries, which briefly traded at a premium in September.

During the reporting period, the Fed acted aggressively to fend off a potential recession. It made seven cuts to the Fed Funds rate (which was reduced from 4.5% to just 1%), created a liquidity facility letting banks borrow more easily from the Fed, opened up its discount window to primary fixed income dealers, and facilitated the acquisition of Bear Stearns by JPMorgan Chase. Toward the end of the reporting period, the Fed worked to create alternate forms of liquidity, such as the new Commercial Paper Funding Facility (CPPF) and the Money Market Investor Funding Facility (MMIFF) — programs employing the Fed balance sheet to fill a current void in the marketplace.

During these difficult times, we focused on liquidity and safety by investing a substantial portion of the Funds' assets in variable rate demand notes, or VRDNs. We believe they are the safest and most liquid securities in the municipal money markets.

Looking forward, we expect increasing demand from VRDN securities to drive down yields. In September, the SIFMA Municipal Swap Index, which is a proxy for weekly VRDNs, rose, we believe, in reaction to the severe market disruptions. Yet, more recently, the market has experienced strong demand for floating rate paper and, during October, yields dropped from 7.96% to 1.82% as of month-end.

California Tax-Free Money Fund6,8,13,14

From inception on December 27, 2007 through October 31, 2008, Neuberger Berman California Tax-Free Money Fund (formerly Lehman Brothers California Tax-Free Money Fund) Investor Class and Reserve Class returned 1.43% and 1.64%, respectively. From January 1, 2008, Investor Class returned 1.38%, compared to the iMoneyNet Money Fund Report Tax-Free State-Specific Retail Average return of 1.50%, while Reserve Class returned 1.58% compared to the iMoneyNet Money Fund Report Tax-Free State-Specific Institutional Average return of 1.66%. The Investor and Reserve Class' seven-day tax equivalent current yields (assuming the highest federal and California state income tax bracket) were 2.36% and 2.82%, respectively, on October 31, 2008, while their seven-day tax-equivalent effective yields (also assuming the highest federal and California state income tax bracket) were 2.39% and 2.86%.* The weighted average maturity of the Fund was 4.8 day s on October 31, 2008.

Municipal Money Fund1,5,6,8,9,13

The Neuberger Berman Municipal Money Fund (formerly Lehman Brothers Municipal Money Fund) returned 2.12% for the fiscal year ended October 31, 2008, compared to the iMoneyNet Money Fund Report Tax-Free National Retail Average return of 2.06% for the same time period. Over the course of the fiscal year, the Fund's seven-day tax-equivalent current yield (assuming the highest federal income tax bracket) decreased from 4.52% to 2.20%. Its seven-day tax-equivalent effective yield (also assuming the highest federal tax bracket) went from 4.62% on October 31, 2007 to 2.22% on October 31, 2008.* During that time period, the Fund's weighted average maturity decreased from 24.6 days on October 31, 2007 to 12.8 days on October 31, 2008.

2

New York Municipal Money Fund5,6,8,9,13

The Neuberger Berman New York Municipal Money Fund (formerly Lehman Brothers New York Municipal Money Fund) returned 2.19% for the fiscal year ended October 31, 2008, compared to the 1.97% return of its iMoneyNet Money Fund Report Tax-Free State-Specific Retail Average benchmark. Over the course of the fiscal year, the Fund's seven-day tax-equivalent current yield (taxable at the highest federal, New York State and New York City income tax brackets) decreased from 5.21% on October 31, 2007 to 2.60% on October 31, 2008. Its seven-day tax-equivalent effective yield (also taxable at the highest federal, New York State and New York City income tax brackets) went from 5.35% to 2.63% during that timeframe.* During that time period, the Fund's weighted average maturity decreased from 17.5 days on October 31, 2007 to 8.4 days on October 31, 2008.

Sincerely,

William J. Furrer and Kristian J. Lind

Portfolio Co-Managers

* Current yield more closely reflects current earnings than does total return. Tax-equivalent yields are the taxable yields that an investor would have had to receive in order to realize the same level of yield after federal income taxes at the highest federal tax rate, currently 35%, assuming that all of a Fund's income is exempt from federal income taxes. For Neuberger Berman California Tax-Free Money Fund, tax equivalent yields are calculated based on federal and California State tax rates for a combined rate of 45.3%. For Neuberger Berman New York Municipal Money Fund, tax-equivalent yields are calculated based on federal, New York State, and New York City tax rates for a combined rate of 41.8%.

A portion of the income of Neuberger Berman Municipal Money Fund and Neuberger Berman New York Municipal Money Fund may be a tax preference item for purposes of the federal alternative minimum tax for certain investors.

An investment in each Fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Notwithstanding the preceding statement, Fund shareholders will be guaranteed to receive $1.00 net asset value for amounts that they held as of September 19, 2008 subject to the terms of the U.S. Treasury's Temporary Guarantee Program for Money Market Funds. The Program generally does not guarantee any new investments in the Fund made after September 19, 2008, and is scheduled to expire on December 18, 2008 (See the Funds' current prospectus as supplemented and Note I — U.S. Treasury Temporary Guarantee Program for Money Market Funds for more information about the Program's scope and limitations.) Although each Fund seeks to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in the Fund.

The composition, industries and holdings of each fund are subject to change. Investment return will fluctuate. Past performance is no guarantee of future results.

Unaudited performance data current to the most recent month-end are available at www.nb.com.

3

California Tax-Free Money Fund

Municipal Money Fund

New York Municipal Money Fund

TICKER SYMBOLS

CALIFORNIA TAX-FREE MONEY FUND

| Investor Class: | | LCIXX | |

| Reserve Class: | | LCRXX | |

TICKER SYMBOLS

MUNICIPAL MONEY FUND

TICKER SYMBOLS

NEW YORK MUNICIPAL MONEY FUND

NB CALIFORNIA TAX-FREE MONEY FUND

MATURITY DIVERSIFICATION

| (% by Maturity) | |

| 1 – 7 Days | | | 100.0 | % | |

| 8 – 30 Days | | | 0.0 | | |

| 31 – 90 Days | | | 0.0 | | |

| 91 – 180 Days | | | 0.0 | | |

| 181+ Days | | | 0.0 | | |

NB MUNICIPAL MONEY FUND

MATURITY DIVERSIFICATION

| (% by Maturity) | |

| 1 – 7 Days | | | 90.6 | % | |

| 8 – 30 Days | | | 0.2 | | |

| 31 – 90 Days | | | 3.0 | | |

| 91 – 180 Days | | | 5.0 | | |

| 181+ Days | | | 1.2 | | |

NB NEW YORK MUNICIPAL MONEY FUND

MATURITY DIVERSIFICATION

| (% by Maturity) | |

| 1 – 7 Days | | | 94.8 | % | |

| 8 – 30 Days | | | 0.0 | | |

| 31 – 90 Days | | | 0.4 | | |

| 91 – 180 Days | | | 0.0 | | |

| 181+ Days | | | 4.8 | | |

4

Core Bond Fund Commentary

For the fiscal year ended October 31, 2008, Neuberger Berman Core Bond Fund (formerly Lehman Brothers Core Bond Fund) posted a negative return and underperformed its benchmark, the Barclays Capital U.S. Aggregate Index.

The fiscal year was among the most challenging periods in the financial markets since the Great Depression. What began as a fairly contained problem in the subprime mortgage market escalated and eventually dragged down the equity and fixed income markets in the U.S. and abroad. Even in hindsight, it would have been difficult to predict the series of events that have unfolded over the last 12 months. Massive deleveraging, illiquidity, seizing credit markets, extreme volatility and the end of "Wall Street" as it was once known were just a few of the factors that triggered a massive flight to quality. This served to drive short-term Treasury yields sharply lower. At one point, the yield available from the three-month Treasury bill fell to around zero percent — meaning that investors were content to earn next to nothing just to access a government guarantee that they wouldn't lose money.

Aside from government securities, every sector of the fixed income market posted a negative return during the reporting period. Investor risk aversion and a rapidly declining faith in our financial system even caused securities with strong underlying fundamentals to perform poorly. In this environment, fixed income mutual funds that held spread product (non-Treasuries) were likely to generate weak performance.

Indeed, while the Fund was defensively positioned and, overall, maintained a high quality portfolio, this was not enough to overcome its exposure to spread product. Compared to the benchmark, which contains a roughly 24% allocation to Treasuries, about 5% of the Fund's portfolio was invested in Treasuries during the reporting period. While this positioning was detrimental to the Fund's recent performance, we continue to believe that an overweight to spread product is essential to meet the Fund's objective of generating high total return through a combination of income and capital appreciation.

Looking more closely at the Fund's performance, its mortgage-related holdings, whether residential or commercial mortgage-backed securities, were the largest drag on results. While the Fund's overweight in the corporate sector hurt its absolute performance, security selection offset a portion of these losses. In particular, the Fund's exposure to large, highly diversified banks and brokerage companies held up fairly well. The Fund's interest rate positioning was also a modest contributor to performance. In January, we shortened the Fund's duration, reducing its sensitivity to interest rate fluctuations, relative to its benchmark. Since then, the Fund's duration has been tactically adjusted and relatively neutral versus that of the benchmark.

Given the market's gyrations, it may be tempting to "jump ship" and follow the herd into short-term Treasuries. We strongly believe this would be precisely the wrong action to take at this time. Such a course would call for selling into distressed and illiquid markets, locking in losses, and allocating whatever proceeds we can garner into low-yielding Treasuries with limited upside potential. In contrast, we believe spread sectors have indiscriminately widened to extreme levels, often with little regard to underlying fundamentals. More than ever, we believe this dislocation will lead to very attractive opportunities for disciplined, patient investors. In addition, we are optimistic that our disciplined investment approach and exposure to spread sectors exhibiting solid credit fundamentals will be rewarded. We would also like to point out that, as of October 31, 2008, the Fund has a significant yield advantage versus its benchmark.

5

In our view, a key catalyst for a turnaround will be the outcome of the aggressive financial intervention that has been implemented by the Federal Reserve and U.S. Treasury. In the short-term, we expect to see continued volatility in the financial markets given the uncertainties surrounding the outcome of the government's massive policy intervention and the depth and breadth of the economic recession.

Sincerely,

Richard W. Knee, Thanos Bardas, David Brown and Thomas Sontag

Portfolio Co-Managers

6

Core Bond Fund

TICKER SYMBOL

| Investor Class | | LBCNX | |

| Institutional Class | | LBCLX | |

| Class A | | LBIAX | |

| Class C | | LBICX | |

RATING SUMMARY

| (% by Ratings) | |

| AAA/Government/Government Agency | | | 76.6 | % | |

| AA | | | 3.5 | | |

| A | | | 8.8 | | |

| BBB | | | 10.2 | | |

| BB | | | 0.5 | | |

| B | | | 0.4 | | |

| CCC | | | 0.0 | | |

| Not Rated | | | 0.0 | | |

AVERAGE ANNUAL TOTAL RETURN ENDED 10/31/082,7,11,13

| | | Inception

Date | | 1 Year | | 5 Years | | 10 Years | | Life of

Fund15 | |

| At NAV | | | | | | | | | | | | | | | | | | | |

| Investor Class | | 02/01/1997 | | | (7.72 | %) | | | 1.33 | % | | | 3.42 | % | | | 4.28 | % | |

| Institutional Class | | 10/01/1995 | | | (7.34 | %) | | | 1.73 | % | | | 3.84 | % | | | 4.66 | % | |

| Class A | | 12/20/2007 | | | (7.68 | %) | | | 1.66 | % | | | 3.80 | % | | | 4.63 | % | |

| Class C | | 12/20/2007 | | | (8.29 | %) | | | 1.52 | % | | | 3.73 | % | | | 4.58 | % | |

| With Sales Charge | | | | | | | | | | | | | | | | | | | |

| Class A | | | | | (11.60 | %) | | | 0.78 | % | | | 3.35 | % | | | 4.29 | % | |

| Class C | | | | | (9.18 | %) | | | 1.52 | % | | | 3.73 | % | | | 4.58 | % | |

| Barclays Capital U.S. Aggregate Index | | | | | 0.30 | % | | | 3.48 | % | | | 5.00 | % | | | 5.75 | % | |

Performance data quoted represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Results are shown on a "total return" basis and include reinvestment of all dividends and capital gain distributions. The composition, industries and holdings of the Fund are subject to change.

Current performance may be lower or higher than the performance data quoted. For performance data current to the most recent month end, please visit www.nb.com/performance.

Class A and Class C of Neuberger Berman Core Bond Fund each commenced operations on December 20, 2007. The performance information for Class A and Class C prior to the class' commencement of operations is for the Institutional Class of Neuberger Berman Core Bond Fund. Because the Institutional Class has lower expenses, its performance typically would have been better than that of Class A or Class C.

For the period ending October 31, 2008, the 30-day SEC yield was 4.79%, 4.24%, 5.42% and 5.00% for Class A, Class C, Institutional Class and Investor Class shares, respectively.

As stated in the Fund's most recent prospectus, the total annual fund operating expense ratios for fiscal year 2007 were 1.18%, 1.93%, 0.84% and 1.31% for Class A, Class C, Institutional Class and Investor Class shares, respectively (prior to any fee waivers or expense reimbursements). The net expense ratios are 0.86%, 1.61%, 0.46% and 0.86% for Class A, Class C, Institutional Class and Investor Class shares, respectively. Neuberger Berman Management LLC has contractually agreed to limit certain expenses of the Fund through 10/31/2018 for Class A, Class C, Institutional Class and Investor Class shares.

Total Returns shown with a sales charge reflect the deduction of current maximum initial sales charge of 4.25% for Class A shares and the applicable contingent deferred sales charges (CDSC) for Class C shares. The maximum CDSC for Class C shares is 1%, which is reduced to 0% after 1 year. The performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses. The performance information shown with a sales charge for Class A and Class C has been adjusted to reflect the appropriate sales charge applicable to Class A and Class C shares, but has not been adjusted to take into account differences in class specific operating expenses (such as Rule 12b-1 fees). Please see the prospectus for more information about sales charge structures, if any, and class expenses for your share class.

7

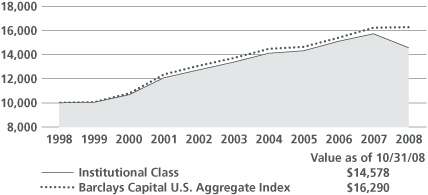

Core Bond Fund

COMPARISON OF A $10,000 INVESTMENT

This chart shows the value of a hypothetical $10,000 investment in the Fund over the past 10 fiscal years, or since the Fund's inception, if it has not operated for 10 years. The graphs are based on the Institutional Class shares only; performance of other classes will vary due to differences in fee structures (see Average Annual Total Returns chart above). The result is compared with benchmarks, which may include a broad-based market index and/or a narrower index. Please note that market indices do not include expenses. All results include the reinvestment of dividends and capital gain distributions. Results represent past performance and do not indicate future results. The chart and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Please see Endnotes and Glossary of Indices for additional information.

8

Core Plus Bond Fund Commentary

For the reporting period from its inception on May 1, 2008 through October 31, 2008, Neuberger Berman Core Plus Bond Fund (formerly Lehman Brothers Core Plus Bond Fund) posted a negative return and underperformed its benchmark, the Barclays Capital U.S. Aggregate Index. However, the Fund outperformed its peers as represented by the Lipper General Bond Funds Average.

The short time since the Fund's inception has included some of the greatest upheaval in the financial markets since the Great Depression. What had earlier been a fairly contained problem in the subprime mortgage market expanded during the period and dragged the global equity and fixed income markets lower. Even in hindsight, it would have been difficult to predict the series of events that have unfolded over the last five months. Massive deleveraging, illiquidity, seizing credit markets, extreme volatility and the end of "Wall Street" as it was once known were just a few of the factors that triggered a massive flight to quality. This served to drive short-term Treasury yields sharply lower. At one point, the yield available from the three-month Treasury bill fell to around zero percent — meaning that investors were content to earn next to nothing just to access a government guarantee that they wouldn't lose money.

Aside from government securities, virtually every sector of the fixed income market posted a negative return during the reporting period. Investor risk aversion and a rapidly declining faith in our financial system even caused securities with strong underlying fundamentals to perform poorly. In this environment, any fixed income mutual fund that held spread product (non-Treasuries) was destined to generate weak performance.

Indeed, while the Fund was defensively positioned and, overall, maintained a high quality portfolio, this was not enough to overcome its exposure to spread product. Compared to the benchmark, which contains a roughly 24% allocation to Treasuries, less than 1% of the Fund's portfolio was invested in Treasuries during the reporting period. While this positioning was detrimental to the Fund's performance, we continue to believe that an overweight to spread product is essential to meet the Fund's objective of generating high total return through a combination of income and capital appreciation.

Looking more closely at the Fund's performance, its residential mortgage-backed securities were the largest drag on results for the reporting period. While the Fund's overweights in investment grade and high yield corporate bonds hurt its absolute performance, security selection offset a portion of these losses. In the investment grade space, the Fund's exposure to large, highly diversified banks and brokerage companies held up fairly well. In the high yield sector, underweighting more speculative CCC rated securities, maintaining an emphasis on companies with superior cash flow stability and avoiding cyclical issues added value. In terms of the Fund's duration, it was tactically adjusted and relatively neutral versus that of its benchmark during the reporting period.

Given the market's gyrations, it may be tempting to "jump ship" and follow the herd into short-term Treasuries. We strongly believe this would be precisely the wrong action to take at this time. Such a course would call for selling into distressed and illiquid markets, locking in losses, and allocating whatever proceeds we can garner into low-yielding Treasuries with limited upside potential. In contrast, we believe spread sectors have indiscriminately widened to extreme levels, often with little regard to underlying fundamentals. More than ever, we believe this dislocation will lead to very attractive opportunities for disciplined, patient investors. In addition, we are optimistic that our disciplined investment approach and exposure to spread sectors exhibiting solid credit fundamentals will be rewarded. We would also like to point out that as of October 31, 2008, the Fund has a significant yield advantage versus its benchmark .

9

In our view, a key catalyst for a turnaround will be the outcome of the aggressive financial intervention that has been implemented by the Federal Reserve and U.S. Treasury. In the short-term, we expect to see continued volatility in the financial markets given the uncertainties surrounding the outcome of the government's massive policy intervention and the depth and breadth of the economic recession.

Sincerely,

Richard W. Knee, Thanos Bardas, David Brown and Thomas Sontag

Portfolio Co-Managers

10

Core Plus Bond Fund

TICKER SYMBOL

| Institutional Class | | LBPIX | |

| Class A | | LBPAX | |

| Class C | | LBPCX | |

RATING SUMMARY

| (% by Ratings) | |

| AAA/Government/Government Agency | | | 74.0 | % | |

| AA | | | 3.3 | | |

| A | | | 8.7 | | |

| BBB | | | 9.2 | | |

| BB | | | 1.0 | | |

| B | | | 3.8 | | |

| CCC | | | 0.0 | | |

| Not Rated | | | 0.0 | | |

CUMULATIVE TOTAL RETURN ENDED 10/31/083,7,13

| | | Inception

Date | | Life of

Fund15 | |

| At NAV | | | | | | | |

| Institutional Class | | 05/01/2008 | | | (8.09 | %) | |

| Class A | | 05/01/2008 | | | (8.26 | %) | |

| Class C | | 05/01/2008 | | | (8.61 | %) | |

| With Sales Charge | | | | | | | |

| Class A | | | | | (12.13 | %) | |

| Class C | | | | | (9.50 | %) | |

| Barclays Capital U.S. Aggregate Index | | | | | (3.63 | %) | |

Performance data quoted represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Results are shown on a "total return" basis and include reinvestment of all dividends and capital gain distributions. The composition, industries and holdings of the Fund are subject to change.

Current performance may be lower or higher than the performance data quoted. For performance data current to the most recent month end, please visit www.nb.com/performance.

For the period ending October 31, 2008, the 30-day SEC yield was 5.73%, 4.95% and 6.11% for Class A, Class C and Institutional Class shares, respectively.

As stated in the Fund's most recent prospectus, the total annual fund operating expense ratios were 1.50%, 1.25%, and 0.94% for Class A, Class C and Institutional Class shares, respectively (prior to any fee waivers or expense reimbursements). The net expense ratios are 0.82%, 1.57% and 0.46% for Class A, Class C and Institutional Class Class shares, respectively. Neuberger Berman Management LLC has contractually agreed to limit certain expenses of the Fund through 10/31/2018 for Class A, Class C and Institutional Class shares.

Total Returns shown with a sales charge reflect the deduction of current maximum initial sales charge of 4.25% for Class A shares and the applicable contingent deferred sales charges (CDSC) for Class C shares. The maximum CDSC for Class C shares is 1%, which is reduced to 0% after 1 year. The performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses. The performance information shown with a sales charge for Class A and Class C has been adjusted to reflect the appropriate sales charge applicable to Class A and Class C shares, but has not been adjusted to take into account differences in class specific operating expenses (such as Rule 12b-1 fees). Please see the prospectus for more information about sales charge structures, if any, and class expenses for your share class.

11

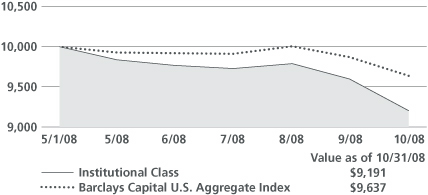

Core Plus Bond Fund

COMPARISON OF A $10,000 INVESTMENT

This chart shows the value of a hypothetical $10,000 investment in the Fund over the past 10 fiscal years, or since the Fund's inception, if it has not operated for 10 years. The graphs are based on the Institutional Class shares only; performance of other classes will vary due to differences in fee structures (see Cumulative Total Returns chart above). The result is compared with benchmarks, which may include a broad-based market index and/or a narrower index. Please note that market indices do not include expenses. All results include the reinvestment of dividends and capital gain distributions. Results represent past performance and do not indicate future results. The chart and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Please see Endnotes and Glossary of Indices for additional information.

12

High Income Bond Fund Commentary

For the fiscal year ended October 31, 2008, Neuberger Berman High Income Bond Fund (formerly Lehman Brothers High Income Bond Fund) posted a negative return in a difficult market environment. However, the Fund significantly outperformed its benchmark, the Barclays Capital U.S. Corporate High Yield 2% Issuer Cap Index.

Despite several rallies during the reporting period, high yield bonds ultimately fell victim to the turmoil in the financial markets, the weakening economy and heightened investor risk aversion. As the fiscal year began in November 2007, the spread on high yield bonds (or the difference between comparable maturity U.S. Treasuries and high yield issues) was 417 basis points (4.17%). While spreads had risen from their all-time low of 238 basis points in May 2007, they were still well below their 10-year average of roughly 500 basis points. High yield spreads then widened — and the bonds' prices fell — in November, as the fallout from the subprime mortgage market intensified and investors looked to shed riskier assets. After stabilizing somewhat, given better-than-expected economic data, spreads widened to 815 basis points in March 2008, coinciding with the collapse of Bear Stearns.

Hopes that this would represent the bottom of the high yield market's descent proved to be premature. While high yield prices rallied in April and early May — with spreads moving as low as 615 basis points — they again weakened in June and then largely tread water in July and August. This turned out to be the calm before the storm, as the financial markets then experienced a two-month period that often rivaled the tumultuous events of the Great Depression. This period was characterized by high profile corporate bankruptcies, plunging stock prices, stalled credits markets, forced deleveraging, illiquidity and massive government intervention that sought to stabilize the financial markets.

The turmoil triggered a massive flight to quality into short-term Treasuries; meanwhile virtually every spread (non-Treasury) sector performed poorly. Nowhere was this more evident than in the high yield bond market. After posting its worst monthly performance ever in September — with spreads reaching 997 basis points — the high yield market fell even further in October, as spreads soared to 1,492 basis points. During September and October, the overall high yield market, as measured by the Barclays Capital U.S. Corporate High Yield 2% Issuer Cap Index, fell 7.68% and 16.09%, respectively. As one would expect in this environment, more speculative CCC rated bonds significantly underperformed their BB rated counterparts (the highest rated securities in the non-investment grade universe).

While not much of a consolation, given the high yield market's decline, the Fund outperformed its benchmark (as noted above) during the reporting period. This was due to our relatively defensive positioning, which included underweighting CCC rated securities and overweighting BB rated issues. We also maintained an emphasis on companies with superior cash flow stability and avoided those cyclical issues that we believed were likely to be hurt by both a recession and weaker consumer spending. From an industry perspective, overweight positions and security selection in energy, cable, utilities, packaging and metals/mining contributed positively to relative performance. In contrast, security selection in non-cable media, retail and chemicals detracted from relative results.

Looking ahead, our analysis suggests that the high yield market will continue to face headwinds, which causes us to maintain our defensive positioning. In addition to the issues that triggered the sharp decline in September and October 2008, we believe that volatility is likely to persist in light of poor liquidity in the capital markets, continued deleveraging and uncertainties regarding the new administration's economic plans. We also expect to see rising default levels for high yield bonds given the weakening economy. Against this backdrop, we believe that our commitment to internally generated research, with a concentrated focus on assessing company and industry fundamentals, will be paramount as we seek to generate high total returns consistent with capital preservation.

Sincerely,

Ann Benjamin and Thomas R. O'Reilly

Portfolio Co-Managers

13

High Income Bond Fund

TICKER SYMBOL

RATING SUMMARY

| (% by Ratings) | |

| AAA/Government/Government Agency | | | 0.0 | % | |

| AA | | | 0.0 | | |

| A | | | 0.0 | | |

| BBB | | | 6.4 | | |

| BB | | | 53.1 | | |

| B | | | 31.0 | | |

| CCC | | | 5.7 | | |

| CC | | | 0.0 | | |

| Not Rated | | | 1.0 | | |

| Short Term | | | 2.8 | | |

AVERAGE ANNUAL TOTAL RETURN ENDED 10/31/081,7,10,13

| | | Inception

Date | | 1 Year | | 5 Years | | 10 Years | | Life of

Fund15 | |

| Investor Class | | | 02/01/1992 | | | | (20.86 | %) | | | (0.03 | %) | | | 3.63 | % | | | 5.80 | % | |

Barclays Capital U.S. Corp

High Yield 2% Issuer Cap Index | | | | | | | (25.41 | %) | | | 0.37 | % | | | 2.95 | % | | | N/A | | |

Performance data quoted represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Results are shown on a "total return" basis and include reinvestment of all dividends and capital gain distributions. The composition, industries and holdings of the Fund are subject to change.

Current performance may be lower or higher than the performance data quoted. For performance data current to the most recent month end, please visit www.nb.com/performance.

For the period ending October 31, 2008, the 30-day SEC Yield of the Fund's Investor Class shares was 12.55%.

As stated in the Fund's most recent prospectus, the total annual fund operating expense ratio for fiscal year 2007 was 0.93% for Investor Class shares (prior to any fee waivers or expense reimbursements).

COMPARISON OF A $10,000 INVESTMENT

This chart shows the value of a hypothetical $10,000 investment in the Fund over the past 10 fiscal years. The result is compared with one or more benchmarks, which may include a broad-based market index and/or a narrower index. Please note that market indices do not include expenses. All results include the reinvestment of dividends and capital gain distributions. Results represent past performance and do not indicate future results. The chart and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Please see Endnotes and Glossary of Indices for additional information.

14

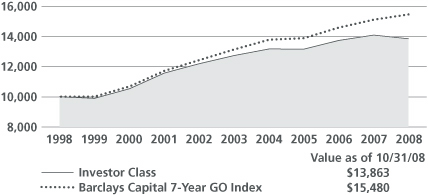

Municipal Securities Trust Commentary

For the fiscal year ended October 31, 2008, Neuberger Berman Municipal Securities Trust (formerly Lehman Brothers Municipal Securities Trust) posted a negative total return versus a gain for its Barclays Capital 7-Year General Obligation Index benchmark. However, the Fund outperformed its peers as represented by the Lipper Intermediate Municipal Debt Funds Index and the Lipper Intermediate Municipal Debt Funds Average.

Although the credit crunch did not impact the municipal securities market as directly or severely as it did the stock market and corporate bond market, municipal securities sustained collateral damage, most notably price erosion resulting from the forced liquidation of highly leveraged hedge funds' large municipal securities positions. The municipal bond market also faced challenges posed by a breakdown in its auction rate securities market as well as varying degrees of credit erosion to all seven of the once AAA rated municipal bond insurers. Finally, in September, demand for municipal securities was further undermined as sharp equity declines and unprecedented U.S. government intervention designed to support the ailing financial system sent investors rushing to the safe haven of U.S. Treasury securities.

During the darkest days of September, we saw investment grade municipal securities yields reach an almost unprecedented 125% to 150% of comparable maturity U.S. Treasury yields. This helped bring retail investors back into the market in early October and even attracted the attention of non-traditional municipal bond buyers such as foreign banks looking for high credit quality securities with higher yields than Treasuries. We also note that in October, California Governor Arnold Schwarzenegger indicated to the U.S. Treasury that California may have to borrow funds to meet the state's annual cash flow needs. That same month, a $4 billion issuance of California Revenue Anticipation Notes was over-subscribed by approximately 25%. Our conclusion is that investors never lost confidence in the municipal securities market, but rather temporarily withdrew until the all the financial dust settled.

In this challenging environment, we continued to focus on monitoring the credit quality of the securities in the portfolio and to diligently evaluate the credit worthiness and relative value of any new investment candidates. Rather than relying exclusively on the bond rating agencies, our research staff independently evaluates credit quality, helping us avoid securities vulnerable to credit downgrades and identify issues with the potential for credit upgrades. Also, as evidence mounted that the economy might be headed toward recession, we began eliminating positions in revenue bonds of more economically sensitive issuers and bolstering positions in securities with high debt service coverage and strong legal covenants protecting revenue streams. We also maintained high credit quality standards, closing fiscal year 2008 with a portfolio average credit quality of AA.

Over the course of the year, we maintained a neutral portfolio duration approximating 4.8 years. However, the fact that portfolio holdings were distributed over the one- to 15-year maturity range rather than concentrated in the better-performing six- to eight-year range of the Fund's index benchmark resulted in lagging relative performance.

In the year ahead, lower property, income and sales tax receipts, along with rising unemployment may reduce revenues for many municipal entities, which would exacerbate existing budget deficits. Municipal issuance is expected to be supported by a lack of "pay as you go" financing and pent-up demand for capital projects. Judging by the municipal securities market's late October rally, we expect still historically high yields relative to U.S. Treasuries to continue to support healthy demand. We also believe that hedge fund deleveraging will be more muted in the months ahead, providing additional support for municipal securities prices.

Moving forward, we will continue to focus on credit quality in an effort to avoid any of the potential potholes in the municipal securities market. We may also respond to the currently steep yield curve by taking advantage of evolving opportunities in longer maturity securities.

15

In closing, although we cannot rule out additional shocks to the financial system or the possibility of a prolonged global recession, we are hopeful that the relatively aggressive response by global monetary authorities to the financial crisis and additional fiscal stimulus here and abroad will eventually prove effective.

Sincerely,

William J. Furrer and James L. Iselin

Portfolio Co-Managers

16

Municipal Securities Trust

TICKER SYMBOL

RATING SUMMARY

| (% by Ratings) | |

| AAA/Government/Government Agency | | | 19.3 | % | |

| AA | | | 69.7 | | |

| A | | | 8.1 | | |

| BBB | | | 2.9 | | |

| BB | | | 0.0 | | |

| B | | | 0.0 | | |

| CCC | | | 0.0 | | |

| Not Rated | | | 0.0 | | |

| Short Term | | | 0.0 | | |

AVERAGE ANNUAL TOTAL RETURN ENDED 10/31/081,7,9,13

| | | Inception

Date | | 1 Year | | 5 Years | | 10 Years | | Life of

Fund15 | |

| Investor Class | | | 07/09/1987 | | | | (1.74 | %) | | | 1.69 | % | | | 3.32 | % | | | 4.99 | % | |

Barclays Capital

7-Year GO Index | | | | | | | 2.33 | % | | | 3.33 | % | | | 4.47 | % | | | 5.97 | % | |

Performance data quoted represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Results are shown on a "total return" basis and include reinvestment of all dividends and capital gain distributions. The composition, industries and holdings of the Fund are subject to change.

Current performance may be lower or higher than the performance data quoted. For performance data current to the most recent month end, please visit www.nb.com/performance.

For the period ending October 31, 2008, the 30-day SEC yield of the Fund's Investor Class shares was 4.25% and the tax-equivalent yield was 6.54% for an investor in the highest federal income tax bracket (35%).

As stated in the Fund's most recent prospectus, the total annual fund operating expense ratio for fiscal year 2007 was 1.18% for Investor Class shares (prior to any fee waivers or expense reimbursements). The net expense ratio was 0.65%. Neuberger Berman Management LLC has contractually agreed to limit certain expenses of the Fund through 10/31/2011 for Investor Class shares.

COMPARISON OF A $10,000 INVESTMENT

This chart shows the value of a hypothetical $10,000 investment in the Fund over the past 10 fiscal years. The result is compared with one or more benchmarks, which may include a broad-based market index and/or a narrower index. Please note that market indices do not include expenses. All results include the reinvestment of dividends and capital gain distributions. Results represent past performance and do not indicate future results. The chart and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Please see Endnotes and Glossary of Indices for additional information.

17

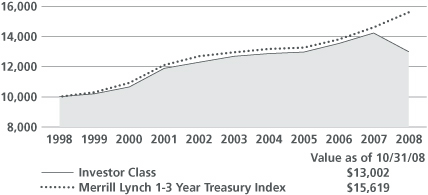

Short Duration Bond Fund Commentary

For the fiscal year ended October 31, 2008, Neuberger Berman Short Duration Bond Fund (formerly Lehman Brothers Short Duration Bond Fund) posted a negative return and underperformed its benchmark, the Merrill Lynch 1-3 Year Treasury Index.

The reporting period was characterized by periods of extreme volatility and upheaval in the financial markets. These factors, combined with a lack of liquidity and the rapidly weakening economy, served to undermine investor confidence and led to periods of extreme risk aversion. As is typical during times of stress, investors flocked to ultra-safe short-term Treasuries, driving their yields lower and their prices higher. During the fiscal year, the yield on the two-year Treasury fell from 3.94% to 1.56%. However, fixed income sectors that, in normal times, are considered safe havens saw their spreads widen dramatically relative to Treasuries. Even securities with strong underlying credit fundamentals were punished during periods of indiscriminate selling.

Given this backdrop, the Fund's relative underperformance was not unexpected, as its benchmark, the Merrill Lynch 1-3 Year Treasury Index, is comprised entirely of Treasury securities. In contrast, less than 2% of the Fund's portfolio was invested in Treasuries during the reporting period. As is typically the case, the majority of the Fund's assets were in spread product (non-Treasury securities), such as mortgage-related securities and corporate bonds.

During the reporting period, the Fund's mortgage securities were among its weakest performers. A constant drumbeat of bad news within the residential housing market extended to the commercial mortgage market as the period progressed. This was, in part, due to the weakening economy and fears that commercial mortgages would also be adversely affected. Even the Fund's highly rated investment grade corporate bonds were not immune to the market's sell-off. Toward the end of the reporting period, spreads on these securities widened to all-time records versus Treasuries. While the Fund's corporate holdings were not immune to this weakness, our emphasis on larger, highly diversified banks and brokerage companies held up relatively well. This was partially due to Treasury's direct capital infusion into certain financial institutions through the Troubled Asset Relief Program (TARP).

While we are disappointed with the Fund's performance over the reporting period, we remain confident in our disciplined investment process. In addition, we believe the securities the Fund holds are appropriate given its investment objective of generating the highest available current income, consistent with liquidity and low risk to principal.

We would also like to assure shareholders that we maintained the Fund's high quality bias throughout the 12-month reporting period, with our portfolio holdings rated AA+ on average. We also continued the Fund's diversification among a wide array of fixed-income securities. Prior to purchasing any security for the Fund, we conduct our own extensive fundamental research so that we can be confident in its quality rating and valuation. Risk management is also paramount in constructing and actively managing the portfolio.

At this point, the U.S. is in a recession. How prolonged and deep the recession will be is subject to conjecture. While the Federal Reserve and U.S. Treasury have been extremely aggressive in their policy response to the ongoing credit crisis, it will take time to determine the success of their actions. It will also take time for the Fed's recent interest rate cuts to work through the financial system. Finally, it is difficult to project the actions of the new Presidential administration. Collectively, we believe these factors will likely result in continued periods of elevated financial market volatility.

We remain confident in the holdings within the Fund's portfolio. With regard to the Fund's structured products, our extensive analysis indicates that there is a substantial amount of debt within the structures that is subordinate to our holdings and offers us some measure of protection. It is our belief that these holdings, which have been hurt by deleveraging and a lack of liquidity, are currently mispriced. We continue to receive principal payments at par (face value) on a monthly basis on these securities and feel that their prices will recover once the deleveraging in the financial system is complete. Looking at the investment grade corporate bond market, we believe certain industries are extremely attractive

18

given what we believe to be overly pessimistic default expectations and unsustainably wide spread levels. To seek to capitalize on this situation, we will continue to conduct extensive research to identify individual securities that have compelling valuations and solid credit fundamentals.

Sincerely,

Thomas Sontag, Michael Foster and Richard Grau

Portfolio Co-Managers

19

Short Duration Bond Fund

TICKER SYMBOL

| Investor Class | | LBSDX | |

| Trust Class | | LBDBX | |

RATING SUMMARY

| (% by Ratings) | |

| AAA/Government/Government Agency | | | 86.5 | % | |

| AA | | | 5.9 | | |

| A | | | 0.2 | | |

| BBB | | | 3.3 | | |

| BB | | | 0.0 | | |

| B | | | 0.0 | | |

| CCC | | | 0.0 | | |

| CC | | | 0.0 | | |

| Not Rated | | | 2.4 | | |

| Short Term | | | 1.7 | | |

AVERAGE ANNUAL TOTAL RETURN ENDED 10/31/081,7,13

| | | Inception

Date | | 1 Year | | 5 Years | | 10 Years | | Life of

Fund15 | |

| Investor Class | | 06/09/1986 | | | (8.70 | %) | | | 0.48 | % | | | 2.66 | % | | | 4.93 | % | |

| Trust Class | | 08/30/1993 | | | (8.76 | %) | | | 0.40 | % | | | 2.56 | % | | | 4.88 | % | |

| Merrill Lynch 1-3 Year Treasury Index | | | | | 6.85 | % | | | 3.81 | % | | | 4.56 | % | | | 6.10 | % | |

Performance data quoted represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Results are shown on a "total return" basis and include reinvestment of all dividends and capital gain distributions. The composition, industries and holdings of the Fund are subject to change.

Current performance may be lower or higher than the performance data quoted. For performance data current to the most recent month end, please visit www.nb.com/performance.

For the period ending October 31, 2008, the 30-day SEC Yield was 5.66% and 5.55% for Investor Class and Trust Class shares, respectively.

As stated in the Fund's most recent prospectus, the total annual Fund operating expense ratios for fiscal year 2007 were 0.91% and 1.18% for Investor Class and Trust Class shares, respectively. The net expense ratio was 0.70% and 0.80% for Investor Class and Trust Class shares, respectively. Neuberger Berman Management LLC has contractually agreed to limit certain expenses of the Fund through 10/31/2011 for Investor Class and Trust Class shares.

COMPARISON OF A $10,000 INVESTMENT

This chart shows the value of a hypothetical $10,000 investment in the Fund over the past 10 fiscal years. The graphs are based on the Investor Class shares only; performance of other classes will vary due to differences in fee structures (see Average Annual Total Returns chart above). The result is compared with one or more benchmarks, which may include a broad-based market index and/or a narrower index. Please note that market indices do not include expenses. All results include the reinvestment of dividends and capital gain distributions. Results represent past performance and do not indicate future results. The chart and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Please see Endnotes and Glossary of Indices for additional information.

20

Strategic Income Fund Commentary

For the fiscal year ended October 31, 2008, Neuberger Berman Strategic Income Fund (formerly Lehman Brothers Strategic Income Fund) posted a negative return and underperformed its benchmark, the Barclays Capital U.S. Aggregate Index.

Neuberger Berman, LLC, the holder of shares representing a majority of the voting power of the Fund, approved changes to the Fund's fundamental investment policy on industry concentration during the reporting period. Effective February 28, 2008, the two of us assumed responsibility for the management of the Fund, which was previously managed by an asset allocation committee. In addition, the Fund's investment approach, which had included dividend-paying equities and real estate investment trust ("REIT") securities, was amended to seek high current income solely through investments in fixed income securities.

In brief, our investment process starts with a macro, or top-down, point of view that leads to strategic allocations across fixed income sectors. Once the sector strategy is set, we seek to purchase what we believe are the most attractive securities for the Fund. In evaluating both the sectors and the securities that comprise them, we rely on intensive research and proprietary analytical tools to help us identify what we believe are the best opportunities in the market. As such, we know our holdings well, which allows us to maintain our investment discipline even as market volatility negatively affects the prices of the Fund's holdings.

The fiscal year was among the most challenging periods in the financial markets since the Great Depression. What began as a fairly contained problem in the subprime mortgage market escalated and eventually dragged down the equity and fixed income markets in the U.S. and abroad. Even in hindsight, it would have been difficult to predict the series of events that have unfolded over the last 12 months. Massive deleveraging, illiquidity, seizing credit markets, extreme volatility and the end of "Wall Street" as it was once known were just a few of the factors that triggered a massive flight to quality. This served to drive short-term Treasury yields sharply lower. At one point, the yield available from the three-month Treasury bill fell to around zero percent — meaning that investors were content to earn next to nothing just to access a government guarantee that they wouldn't lose money.

Aside from government securities, every sector of the fixed income market posted a negative return during the reporting period. Investor risk aversion and a rapidly declining faith in our financial system even caused securities with strong underlying fundamentals to perform poorly. In this environment, any fixed income mutual fund that held spread product (non-Treasuries) was destined to generate weak performance.

Indeed, while the Fund was defensively positioned, this was not enough to overcome its exposure to spread product. Compared to the benchmark, which contains a roughly 24% allocation to Treasuries, about 2% of the Fund's portfolio was invested in Treasuries during the reporting period. While this positioning was detrimental to the Fund's performance, we continue to believe that an overweight to spread product is essential to meet the Fund's objective of generating high total return through a combination of income and capital appreciation.

Looking more closely at the Fund's performance, its overweights in investment grade and high yield corporate bonds were the largest drag on its absolute results. However, security selection offset a portion of these losses. For example, in the investment grade space, the Fund's exposure to large, highly diversified banks and brokerage companies held up fairly well. Within the high yield sector, underweighting more speculative CCC rated securities, maintaining an emphasis on companies with superior cash flow stability and avoiding cyclical issues added value.

Given the market's gyrations, it may be tempting to "jump ship" and follow the herd into short-term Treasuries. We strongly believe this would be precisely the wrong action to take at this time. Such a course would call for selling into distressed and illiquid markets, locking in losses, and allocating whatever proceeds we can garner into low-yielding Treasuries with limited upside potential. In contrast, we believe spread sectors have indiscriminately widened to extreme levels, often with little regard to underlying fundamentals. More than ever, we believe this dislocation will lead to very attractive opportunities for disciplined, patient investors. In addition, we are optimistic that our disciplined investment

21

approach and exposure to spread sectors exhibiting solid credit fundamentals will be rewarded. We would also like to point out that, as of October 31, 2008, the Fund has a significant yield advantage versus its benchmark.

In our view, a key catalyst for a turnaround will be the outcome of the aggressive financial intervention that has been implemented by the Federal Reserve and U.S. Treasury. In the short-term, we expect to see continued volatility in the financial market given the uncertainties surrounding the outcome of the government's massive policy intervention and the depth and breadth of the economic recession.

Sincerely,

Bradley C. Tank and Richard W. Knee

Portfolio Co-Managers

22

Strategic Income Fund

TICKER SYMBOL

| Institutional Class | | LBSIX | |

| Trust Class | | LBSTX | |

| Class A | | LBBAX | |

| Class C | | LBBCX | |

RATING SUMMARY

| (% by Ratings) | |

| AAA/Government/Government Agency | | | 56.5 | % | |

| AA | | | 3.9 | | |

| A | | | 11.1 | | |

| BBB | | | 10.6 | | |

| BB | | | 0.0 | | |

| B | | | 16.8 | | |

| CCC | | | 0.0 | | |

| Not Rated | | | 1.1 | | |

AVERAGE ANNUAL TOTAL RETURN ENDED 10/31/084,7,12,13

| | | Inception

Date | | 1 Year | | 5 Years | | Life of

Fund15 | |

| At NAV | | | | | | | | | | | | | | | |

| Institutional Class | | 07/11/2003 | | | (6.09 | %) | | | 5.26 | % | | | 5.32 | % | |

| Trust Class | | 04/02/2007 | | | (6.54 | %) | | | 5.14 | % | | | 5.21 | % | |

| Class A | | 12/20/2007 | | | (6.39 | %) | | | 5.19 | % | | | 5.26 | % | |

| Class C | | 12/20/2007 | | | (6.96 | %) | | | 5.06 | % | | | 5.14 | % | |

| With Sales Charge | | | | | | | | | | | | | | | |

| Class A | | | | | (10.37 | %) | | | 4.28 | % | | | 4.40 | % | |

| Class C | | | | | (7.80 | %) | | | 5.06 | % | | | 5.14 | % | |

| Barclays Capital U.S. Aggregate Index | | | | | 0.30 | % | | | 3.48 | % | | | 3.13 | % | |

Performance data quoted represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed may be worth more or less than their original cost. Results are shown on a "total return" basis and include reinvestment of all dividends and capital gain distributions.

Current performance may be higher or lower than the performance data quoted. For performance data current to the most recent month end, please visit www.nb.com/performance.

For the period ending October 31, 2008, the 30-day SEC yield was 5.93%, 5.56%, 6.49% and 6.17% for Class A, Class C, Institutional Class and Trust Class shares, respectively.

As stated in the Fund's most recent prospectus, the total annual fund operating expense ratios for fiscal year 2007 were 1.78%, 2.53%, 2.69% and 4.77% for Class A, Class C, Institutional Class and Trust Class shares, respectively (prior to any fee waivers or expense reimbursements). The net expense ratios are 1.16%, 1.86%, 0.76% and 1.11% for Class A, Class C, Institutional Class and Trust Class shares, respectively. Neuberger Berman Management LLC has contractually agreed to limit certain expenses of the Fund through 10/31/2018 for Class A, Class C and Institutional Class and through 10/31/2011 for Trust Class shares.

Total Returns shown with a sales charge reflect the deduction of current maximum initial sales charge of 4.25% for Class A shares and the applicable contingent deferred sales charges (CDSC) for Class C shares. The maximum CDSC for Class C shares is 1%, which is reduced to 0% after 1 year. The performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses. The performance information shown with a sales charge for Class A and Class C has been adjusted to reflect the appropriate sales charge applicable to Class A and Class C shares, but has not been adjusted to take into account differences in class specific operating expenses (such as Rule 12b-1 fees). Please see the prospectus for more information about sales charge structures, if any, and class expenses for your share class.

23

Strategic Income Fund

COMPARISON OF A $10,000 INVESTMENT

This chart shows the value of a hypothetical $10,000 investment in the Fund over the past 10 fiscal years, or since the Fund's inception, if it has not operated for 10 years. The graphs are based on the Institutional Class shares only; performance of other classes will vary due to differences in fee structures (see Average Annual Total Returns chart above).The result is compared with one or more benchmarks, which may include a broad-based market index and/or a narrower index. Please note that market indices do not include expenses. All results include the reinvestment of dividends and capital gain distributions. Results represent past performance and do not indicate future results. The chart and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Please see Endnotes and Glossary of Indices for additional information.

24

Cash Reserves Commentary1,6,13

We are pleased to report that Neuberger Berman Cash Reserves returned 2.94% for the fiscal year ended October 31, 2008, compared to the iMoneyNet Money Fund Report Taxable First Tier Retail Average return of 2.64%. The Fund closed the period with a seven-day current yield of 0.97% and a seven-day effective yield of 0.97%.*

The fiscal year was remarkably difficult for investors. Over much of the period, the subprime mortgage meltdown worsened and financial institutions in the U.S. and overseas took further multi-billion-dollar write-downs of troubled fixed-income assets. Concerns over the resulting slowdown of credit markets spread worldwide and inflicted considerable punishment on companies with exposure to mortgages and assets with complex structures. Markets were further rocked by high profile failures of institutions holding toxic debt, which led to consolidations and the government bailouts of Fannie Mae, Freddie Mac and others, as well as to an historic U.S. rescue package involving the potential purchase of subprime assets from financial companies. Investors fled many credits and sought safety in U.S. Treasuries.

During the reporting period, the Fed acted aggressively to fend off a potential recession. It made seven cuts to the Fed Funds rate (which was reduced from 4.5% to just 1%), created a liquidity facility letting banks borrow more easily from the Fed, opened up its discount window to primary fixed income dealers, and facilitated the acquisition of Bear Stearns by JPMorgan Chase. Toward the end of the reporting period, the Fed worked to create alternate forms of liquidity, such as the new Commercial Paper Funding Facility (CPPF) and the Money Market Investor Funding Facility (MMIFF) — programs employing the Fed balance sheet to fill a current void in the marketplace.

Throughout the period, we maintained the bulk of the Fund's holdings in highly rated commercial paper and certificates of deposits. As of October 31, 2008, the majority of the Fund's assets are allocated to commercial paper of high quality issuers coupled with overnight repurchase agreements which are over-collateralized by government agency securities. In terms of credit quality, roughly 86% of the portfolio is invested in A-1+ securities, and all securities are top tier. The portfolio remains highly liquid with no securities having a maturity date longer than 90 days and with a majority of the portfolio invested in overnight securities.

The Fund started the reporting period with a weighted average maturity (WAM) of 44.5 days. Due to ongoing liquidity strains in the credit markets, we shortened WAM throughout the fiscal year. Despite the aggressive easing cycle of the Federal Reserve, the portfolio continues to have a short WAM (9.1 days at fiscal year-end) and to be highly liquid. In our view, the state of the credit markets remains unprecedented and merits our already stringent focus on capital preservation and daily liquidity. Our fundamental outlook is that the market could remain strained well into 2009. We believe that current positioning leaves us with flexibility to purchase longer maturity securities in the event that the yield curve steepens and the credit markets return to a more traditional, functioning environment.

Sincerely,

John C. Donohue and Scott F. Riecke

Portfolio Co-Managers

* Current and effective yield more closely reflect current earnings than does total return.

An investment in the Fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Notwithstanding the preceding statement, Fund shareholders will be guaranteed to receive $1.00 net asset value for amounts that they held as of September 19, 2008 subject to the terms of the U.S. Treasury's Temporary Guarantee Program for Money Market Funds. The Program generally does not guarantee any new investments in the Fund made after September 19, 2008, and is scheduled to expire on December 18, 2008 (See the Funds' current prospectus as supplemented and Note I — U.S. Treasury Temporary Guarantee Program for Money Market Funds for more information about the Program's scope and limitations.)

Although the Fund seeks to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in the Fund.

The composition, industries and holdings of the Fund are subject to change. Investment return will fluctuate. Past performance is no guarantee of future results.

Unaudited performance data current to the most recent month-end are available at www.nb.com.

25

Cash Reserves

TICKER SYMBOL

MATURITY DIVERSIFICATION

| (% by Maturity) | |

| 1 - 7 Days | | | 75.8 | % | |

| 8 - 30 Days | | | 17.1 | | |

| 31 - 90 Days | | | 7.1 | | |

| 91 - 180 Days | | | 0.0 | | |

| 181+ Days | | | 0.0 | | |

26

Endnotes

1 Neuberger Berman Management LLC ("Management") has contractually agreed to forgo current payment of fees and/or reimburse expenses of the following Funds so that the total annual operating expenses (exclusive of taxes, interest, brokerage commissions and extraordinary expenses) are limited to 0.65% for Neuberger Berman Cash Reserves (Investor Class), 1.00% for Neuberger Berman High Income Bond Fund (Investor Class), 0.70% for Neuberger Berman Short Duration Bond Fund (Investor Class), 0.80% for Neuberger Berman Short Duration Bond Fund (Trust Class), 0.65% for Neuberger Berman Municipal Securities Trust (Investor Class) and 0.59% for Neuberger Berman Municipal Money Fund (Investor Class) of average daily net assets. Each undertaking lasts until October 31, 2011. Absent such forgone fees and/or reimbursements, the performance of each liste d class of each Fund would have been lower. Each of these Funds has contractually agreed to repay Management for fees and expenses forgone and/or its excess expenses paid by Management, provided the repayments do not cause its total annual operating expenses (exclusive of taxes, interest, brokerage commissions and extraordinary expenses) to exceed the above stated expense limitation and the repayments are made within three years after the year that Management incurred the expense. For the year ended October 31, 2008, the Investor Class of Neuberger Berman Municipal Money Fund repaid expenses to Management.

2 Management has contractually agreed to forgo current payment of fees and/or reimburse Neuberger Berman Core Bond Fund so that total annual operating expenses (exclusive of taxes, interest, brokerage commissions and extraordinary expenses) of the Fund are limited to 0.85%, 0.45%, 0.85% and 1.60% of average daily net assets for the Investor Class, Institutional Class, Class A and Class C, respectively. The undertakings last until October 31, 2018. The Fund has contractually undertaken to repay Management for fees and expenses forgone and/or its excess expenses paid by Management, provided the repayments do not cause total annual operating expenses (exclusive of taxes, interest, brokerage commissions, and extraordinary expenses) to exceed the above-stated expense limitation and the repayments are made within three years after the year that M anagement incurred the expense. Absent such forgone fees and/or reimbursements, the performance of each class of the Fund would have been lower. Management has voluntarily agreed to waive its management fee in the amount of 0.25% (0.20% prior to March 1, 2006) of the Fund's average daily net assets through October 31, 2008. Management has agreed to continue this voluntary waiver after this date but may, at its sole discretion, modify or terminate this voluntary waiver at any time without notice to the Fund. If this voluntary waiver was not in place, performance would be lower for the Fund. For the year ended October 31, 2008, there were no repayment of expenses to Management.

3 Management has contractually agreed to forgo current payment of fees and/or reimburse Neuberger Berman Core Plus Bond Fund so that total annual operating expenses (exclusive of taxes, interest, brokerage commissions and extraordinary expenses) of the Fund are limited to 0.45%, 0.82% and 1.57% of average daily net assets for the Institutional Class, Class A and Class C, respectively. The undertakings last until October 31, 2018 for Institutional Class and until October 31, 2011 for Class A and C. The Fund has contractually agreed to repay Management for fees and expenses forgone and/or its excess expenses paid by Management, provided the repayments do not cause total annual operating expenses (exclusive of taxes, interest, brokerage commissions, and extraordinary expenses) to exceed the above-stated expense limitation and the repayments ar e made within three years after the year that Management incurred the expense. Absent such forgone fees and/or reimbursements, the performance of each class of the Fund would have been lower. Management has voluntarily agreed to waive its management fee in the amount of 0.25% (0.20% prior to March 1, 2006) of the Fund's average daily net assets through October 31, 2008. Management has agreed to continue this voluntary waiver after this date but may, at its sole discretion, modify or terminate this voluntary waiver at any time without notice to the Fund. If this voluntary waiver was not in place, performance would be lower for the Fund. For the year ended October 31, 2008, there were no repayment of expenses to Management.

4 Management has contractually agreed to forgo current payment of fees and/or reimburse Neuberger Berman Strategic Income Fund so that total annual operating expenses (exclusive of taxes, interest, brokerage commissions and extraordinary expenses) of the Fund are limited to 1.10%, 0.85%, (through February 28, 2008, and 0.75%

27