As filed with the Securities and Exchange Commission on January 4, 2018

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-03802

NEUBERGER BERMAN INCOME FUNDS

(Exact name of registrant as specified in charter)

c/o Neuberger Berman Investment Advisers LLC

1290 Avenue of the Americas

New York, New York 10104-0002

(Address of principal executive offices – Zip Code)

Registrant's telephone number, including area code: (212) 476-8800

Robert Conti

Chief Executive Officer and President

Neuberger Berman Income Funds

c/o Neuberger Berman Investment Advisers LLC

1290 Avenue of the Americas

New York, New York 10104-0002

Arthur C. Delibert, Esq.

K&L Gates LLP

1601 K Street, N.W.

Washington, D.C. 20006-1600

(Names and addresses of agents for service)

Date of fiscal year end: October 31

Date of reporting period: October 31, 2017

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940, as amended (“Act”) (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Report to Shareholders.

Following is a copy of the annual report transmitted to shareholders pursuant to Rule 30e-1 under the Act.

Neuberger Berman

Income Funds

Investor Class Shares

Trust Class Shares

Institutional Class Shares

Core Bond Fund

Core Plus Fund

Emerging Markets Debt Fund

Floating Rate Income Fund

High Income Bond Fund

Municipal High Income Fund

Class A Shares

Class C Shares

Class R3 Shares

Class R6 Shares

Municipal Intermediate Bond Fund

New York Municipal Income Fund

Short Duration Bond Fund

Short Duration High Income Fund

Strategic Income Fund

Unconstrained Bond Fund

Annual Report

October 31, 2017

Contents

THE FUNDS

PORTFOLIO COMMENTARY

Core Bond Fund | | | 2 | | |

Core Plus Fund | | | 5 | | |

Emerging Markets Debt Fund | | | 8 | | |

Floating Rate Income Fund | | | 12 | | |

High Income Bond Fund | | | 15 | | |

Municipal High Income Fund | | | 18 | | |

Municipal Intermediate Bond Fund | | | 21 | | |

New York Municipal Income Fund | | | 24 | | |

Short Duration Bond Fund | | | 27 | | |

Short Duration High Income Fund | | | 30 | | |

Strategic Income Fund | | | 33 | | |

Unconstrained Bond Fund | | | 36 | | |

FUND EXPENSE INFORMATION | | | 44 | | |

SCHEDULE OF INVESTMENTS

Core Bond Fund | | | 47 | | |

Core Plus Fund | | | 57 | | |

Emerging Markets Debt Fund | | | 65 | | |

Positions by Industry | | | 82 | | |

Floating Rate Income Fund | | | 94 | | |

High Income Bond Fund | | | 110 | | |

Municipal High Income Fund | | | 126 | | |

Municipal Intermediate Bond Fund | | | 134 | | |

New York Municipal Income Fund | | | 142 | | |

Short Duration Bond Fund | | | 145 | | |

Short Duration High Income Fund | | | 151 | | |

Strategic Income Fund | | | 164 | | |

Unconstrained Bond Fund | | | 199 | | |

FINANCIAL STATEMENTS | | | 218 | | |

FINANCIAL HIGHLIGHTS (ALL CLASSES)/PER SHARE DATA

Core Bond Fund | | | 264 | | |

Core Plus Fund | | | 264 | | |

Emerging Markets Debt Fund | | | 266 | | |

Floating Rate Income Fund | | | 268 | | |

High Income Bond Fund | | | 268 | | |

Municipal High Income Fund | | | 270 | | |

Municipal Intermediate Bond Fund | | | 272 | | |

New York Municipal Income Fund | | | 274 | | |

Short Duration Bond Fund | | | 274 | | |

Short Duration High Income Fund | | | 276 | | |

Strategic Income Fund | | | 278 | | |

Unconstrained Bond Fund | | | 280 | | |

Reports of Independent Registered Public Accounting Firms | | | 284 | | |

Directory | | | 286 | | |

Trustees and Officers | | | 287 | | |

Proxy Voting Policies and Procedures | | | 296 | | |

Quarterly Portfolio Schedule | | | 296 | | |

Board Consideration of the Management and Sub-Advisory Agreements | | | 296 | | |

Notice to Shareholders | | | 302 | | |

The "Neuberger Berman" name and logo and "Neuberger Berman Investment Advisers LLC" name are registered service marks of Neuberger Berman Group LLC. The individual Fund names in this piece are either service marks or registered service marks of Neuberger Berman Investment Advisers LLC, an affiliate of Neuberger Berman BD LLC, distributor, member FINRA. @2017 Neuberger Berman BD LLC, distributor. All rights reserved.

Dear Shareholder,

I am pleased to present this annual shareholder report for the Neuberger Berman Income Funds.

The U.S. economy, as measured by gross domestic product (GDP), continued to expand and the pace accelerated as the 12-month reporting period progressed. Against this backdrop, the U.S. Federal Reserve (Fed) raised interest rates on three occasions during the reporting period, with another rate hike possible before the end of December. Additionally, in a well telegraphed move, the Fed began reducing its balance sheet in October 2017. Elsewhere, growth outside the U.S. largely improved, although inflation remained relatively tame. Meanwhile, central banks outside the U.S. largely maintained their accommodative monetary policies.

After selling off following the U.S. election in November 2016, the U.S. government bond market stabilized and started to rebound in March 2017. This turnaround was triggered by a number of factors, including tempered expectations for fiscal stimulus in the U.S. and several geopolitical events that led to flights to quality.

All told, the Bloomberg Barclays U.S. Aggregate Bond Index gained 0.90% during the 12 months ended October 31, 2017. Investment grade corporate bonds produced positive excess returns relative to equal-duration Treasuries during the period, while securitized sectors generated mixed results. Investors who took on more risk were typically rewarded, as high yield bonds, bank loans and emerging market debt outperformed. For example, the ICE BofAML U.S. High Yield Constrained Index returned 9.14% during the reporting period.

The synchronous global expansion and buoyant markets have so far been able to withstand a number of crucial questions. Looking ahead, how will extreme levels of monetary policy accommodation eventually be unwound? What are the prospects for the reflationary, pro-growth elements of President Trump's agenda? When will a long forecasted increase in U.S. government bond yields materialize? What is the impact of wildcards such as North Korea or an unusually destructive hurricane season? As unsettling as it may be, we don't anticipate complete clarity on these questions in the near term, and we do think there may be some unexpected answers — including that the global economic upturn may nevertheless continue.

We believe the fundamentals for corporate credit, the securitized sectors and the municipal market remain supportive, although valuations have become less attractive. In terms of U.S. government bonds, we anticipate yields for U.S. Treasuries and other developed market sovereigns will drift higher in 2018. Pursuant to our long-term investment philosophy, we will actively manage our fixed income funds and adjust their portfolios given the evolving economic and investment backdrop.

Thank you for your continued support and trust. We look forward to continue serving your investment needs in the years to come.

Sincerely,

ROBERT CONTI

PRESIDENT AND CEO

NEUBERGER BERMAN MUTUAL FUNDS

1

Core Bond Fund Commentary (Unaudited)

Neuberger Berman Core Bond Fund Institutional Class generated a 0.95% total return for the 12 months ended October 31, 2017 and outperformed its benchmark, the Bloomberg Barclays U.S. Aggregate Bond Index, which provided a 0.90% total return for the same period. (Performance for all share classes is provided in the table immediately following this letter.)

The overall U.S. fixed income market generated a modest gain during the reporting period. Both short- and longer-term Treasury yields rose over the 12 months ended October 31, 2017. In general, short-term yields moved higher as the U.S. Federal Reserve (Fed) raised interest rates three times over the reporting period. The Fed also began reducing its balance sheet in October 2017. Meanwhile, longer-term Treasury yields fluctuated given changing expectations for economic growth in the U.S., uncertainties surrounding future fiscal policy, and a number of geopolitical events.

The Fund's allocation to non-agency mortgage-backed securities (MBS) benefited performance. A solid housing market led to ongoing improvement in mortgage creditworthiness, and a shrinking pool of existing securities was met by increasing investor demand. Security selection within investment grade corporate bonds also contributed to results. Corporate credit continued to benefit from solid investor risk appetite and supportive fundamentals. An allocation to U.S. Treasury Inflation-Protected Securities was beneficial as inflation expectations accelerated following the November 2016 U.S. elections. Conversely, the Fund's overall duration positioning and exposures to global sovereign bonds were both detractors from performance.

The Fund's use of futures contracts detracted from performance during the reporting period.

There were several adjustments made to the portfolio during the reporting period. Although we ended the 12 month period higher than we began it, we tactically adjusted the Fund's duration, first increasing duration following the November 2016 U.S. election sell-off and then subsequently reducing duration. Over the period, we decreased holdings in U.S. Treasuries. We initially increased the Fund's allocation to investment grade corporate bonds then later pared this allocation as valuations became less attractive after a strong rally. Within securitized sectors, we increased the Fund's holdings of asset-backed securities and, to lesser extents, commercial MBS and non-agency MBS.

Looking ahead, the long-awaited sell-off in government bond yields may continue to prove elusive. Investors seem to doubt whether the Fed will hike rates meaningfully and seem to expect the Fed's balance sheet exit may be a non-event. Compare today's mindset to the "taper tantrum" of 2013 when former Fed Chair Bernanke's mere mention of a potential future tapering of asset purchases sparked a major sell-off and volatility spike. As of the period end, the Fed actually started reducing holdings — which is arguably more significant than tapering — and it anticipates to continue hiking rates. Nevertheless, Treasury yields and interest rate volatility remain stubbornly low. We believe there's certainly a chance it plays out calmly and predictably, but the bond market's current stance may prove to be overly complacent. We believe reducing central bank balance sheet holdings — quantitative tightening — should add to volatility in fixed income markets just as adding to central bank balance sheets — quantitative easing — had previously reduced volatility.

Sincerely,

THANOS BARDAS, DAVID M. BROWN, ANDREW A. JOHNSON, THOMAS J. MARTHALER AND BRADLEY C. TANK

PORTFOLIO MANAGERS

Information about principal risks of investing in the Fund is set forth in the prospectus and statement of additional information.

The portfolio composition, industries and holdings of the Fund are subject to change without notice.

The opinions expressed are those of the Fund's portfolio managers. The opinions are as of the date of this report and are subject to change without notice.

2

Core Bond Fund (Unaudited)

TICKER SYMBOLS

Investor Class | | NCRIX | |

Institutional Class | | NCRLX | |

Class A | | NCRAX | |

Class C | | NCRCX | |

PORTFOLIO BY TYPE OF SECURITY

(as a % of Total Net Assets) | |

Asset-Backed Securities | | | 11.9 | % | |

Corporate Bonds | | | 26.9 | | |

Developed Markets Ex- U.S. | | | 1.3 | | |

Foreign Government Security | | | 0.8 | | |

Mortgage-Backed Securities | | | 33.8 | | |

U.S. Government Agency Securities | | | 2.1 | | |

U.S. Treasury Obligations | | | 30.9 | | |

Short-Term Investment | | | 1.8 | | |

Liabilities Less Other Assets | | | (9.5 | )* | |

Total | | | 100.0 | % | |

* Includes the impact of the Fund's open positions in derivatives, if any.

PERFORMANCE HIGHLIGHTS2,18

| | | Inception | | Average Annual Total Return

Ended 10/31/2017 | |

| | | Date | | 1 Year | | 5 Years | | 10 Years | | Life of Fund | |

At NAV | | | | | | | | | | | | | | | | | | | | | |

| Investor Class3 | | 02/01/1997 | | | 0.54 | % | | | 1.50 | % | | | 4.14 | % | | | 4.79 | % | |

| Institutional Class3 | | 10/01/1995 | | | 0.95 | % | | | 1.92 | % | | | 4.58 | % | | | 5.20 | % | |

| Class A4 | | 12/20/2007 | | | 0.54 | % | | | 1.51 | % | | | 4.14 | % | | | 5.00 | % | |

| Class C4 | | 12/20/2007 | | | -0.21 | % | | | 0.76 | % | | | 3.38 | % | | | 4.65 | % | |

With Sales Charge | | | | | | | | | | | | | | | | | | | |

| Class A4 | | | | | | | -3.76 | % | | | 0.63 | % | | | 3.68 | % | | | 4.79 | % | |

| Class C4 | | | | | | | -1.19 | % | | | 0.76 | % | | | 3.38 | % | | | 4.65 | % | |

Index | | | | | | | | | | | | | | | | | | | | | |

Bloomberg Barclays U.S. Aggregate

Bond Index1,14 | | | | | | | 0.90 | % | | | 2.04 | % | | | 4.19 | % | | | 5.29 | % | |

The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For performance data current to the most recent month-end, please visit www.nb.com/performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares.

The investment return and principal value of an investment will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

Returns would have been lower if Neuberger Berman Investment Advisers LLC ("Management") had not reimbursed certain expenses and/or waived a portion of the investment management fees during certain of the periods shown. Repayment by a class (of expenses previously reimbursed and/or fees previously waived by Management) will decrease the class's returns. Please see Note B in the Notes to Financial Statements for specific information regarding expense reimbursement and/or fee waiver arrangements.

For the period ended October 31, 2017, the 30-day SEC yields were 2.14%, 2.54%, 2.14% and 1.40% for Investor Class, Institutional Class, Class A and Class C shares, respectively. Absent expense reimbursements and/or fee waivers, the 30-day SEC yields would have been 2.04%, 2.57%, 2.20% and 1.46% for Investor Class, Institutional Class, Class A and Class C shares, respectively.

As stated in the Fund's most recent prospectus, the total annual operating expense ratios for fiscal year 2016 were 1.15%, 0.60%, 0.98% and 1.72% for Investor Class, Institutional Class, Class A and Class C shares, respectively (before expense reimbursements and/or fee waivers, if any). The expense ratios were 0.86%, 0.46%, 0.86% and 1.61% for Investor Class, Institutional Class, Class A and Class C shares, respectively, after expense reimbursements and/or fee waivers. The expense ratios for the annual period ended October 31, 2017 can be found in the Financial Highlights section of this report.

Returns shown with a sales charge reflect the deduction of the current maximum initial sales charge of 4.25% for Class A shares and the contingent deferred sales charge (CDSC) for Class C shares. The CDSC for Class C shares is 1%, which is reduced to 0% after 1 year. The performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses. Please see the prospectus for more information about sales charge structures, if any, and class expenses for your share class.

3

Core Bond Fund (Unaudited)

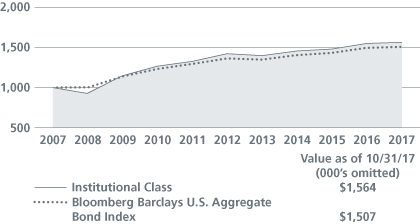

COMPARISON OF A $1,000,000 INVESTMENT

(000's omitted)

This graph shows the change in value of a hypothetical $1,000,000 investment in the Fund over the past 10 fiscal years, or since the Fund's inception if it has not operated for 10 years. The graph is based on the Institutional Class shares only; the performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses (see Performance Highlights chart on previous page). The result is compared with benchmarks, which include a broad-based market index and may include a more narrowly based index. Market indices have not been reduced to reflect any of the fees and costs of investing. The results shown in the graph reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares. Results represent past performance and do not indicate future results.

4

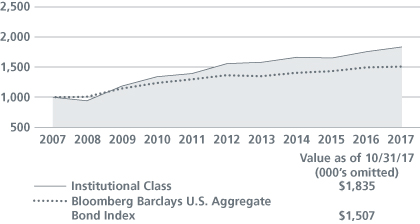

Core Plus Fund Commentary (Unaudited)

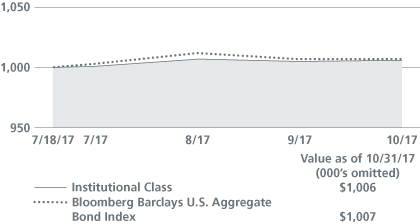

Neuberger Berman Core Plus Fund Institutional Class generated a 0.63% total return from its inception on July 18, 2017 through October 31, 2017 (the "reporting period") and underperformed its benchmark, the Bloomberg Barclays U.S. Aggregate Bond Index, which provided a 0.72% total return for the same period. (Performance for all share classes is provided in the table immediately following this letter.)

The overall U.S. fixed income market, as measured by the Bloomberg Barclays U.S. Aggregate Bond Index, generated a modest gain during 2017. Both short- and longer-term Treasury yields rose during the reporting period. In general, short-term yields moved higher in anticipation of further U.S. Federal Reserve (Fed) interest rate hikes. In addition, the Fed began reducing its balance sheet in October 2017. Meanwhile, longer-term Treasury yields fluctuated given changing expectations for economic growth in the U.S., uncertainties surrounding future fiscal policy, and a number of geopolitical events.

The Fund's security selection within investment grade corporate bonds contributed to results as did an allocation to high yield corporates. After widening in early August, credit spreads subsequently recovered due to higher oil prices, diminished geopolitical risk and supportive corporate earnings. Allocations to hard currency emerging markets debt were also beneficial as the sector has seen ongoing investor inflows and improving fundamentals. Elsewhere, the Fund's duration positioning, particularly an overweight in U.S. interest rate sensitivity, detracted from performance as yields moved higher. Additionally, exposure to Italian sovereign yields was modestly unfavorable.

The Fund's aggregate use of futures and swap contracts detracted from performance during the reporting period.

The Fund was launched during the reporting period. We initiated a neutral weight in investment grade corporate bonds and an overweight in high yield corporates as well as hard currency emerging markets debt. To a lesser extent, the Fund also established overweight positions in asset-backed securities and credit risk transfer securities (collateralized mortgage obligations). Counterbalancing these allocations, the Fund has greater interest rate sensitivity than the benchmark and an overweight to agency mortgage-backed securities, both of which we believe may serve as a ballast in a risk-off market for credit.

Looking ahead, the long-awaited sell-off in government bond yields may continue to prove elusive. Investors seem to doubt whether the Fed will hike rates meaningfully and seem to expect the Fed's balance sheet exit may be a non-event. Compare today's mindset to the "taper tantrum" of 2013 when former Fed Chair Bernanke's mere mention of a potential future tapering of asset purchases sparked a major sell-off and volatility spike. As of the period end, the Fed actually started to reduce holdings — which is arguably more significant than tapering — and anticipates to continue hiking rates. Nevertheless, Treasury yields and interest rate volatility remain stubbornly low. We believe there's certainly a chance it plays out calmly and predictably, but the bond market's current stance may prove to be overly complacent. We believe reducing central bank balance sheet holdings — quantitative tightening — should add to volatility in fixed income markets just as adding to central bank balance sheets — quantitative easing — had previously reduced volatility.

Sincerely,

THANOS BARDAS, ASHOK BHATIA, DAVID M. BROWN, ANDREW A. JOHNSON, NATHAN KUSH,

THOMAS J. MARTHALER AND BRADLEY C. TANK

PORTFOLIO MANAGERS

Information about principal risks of investing in the Fund is set forth in the prospectus and statement of additional information.

The portfolio composition, industries and holdings of the Fund are subject to change without notice.

The opinions expressed are those of the Fund's portfolio managers. The opinions are as of the date of this report and are subject to change without notice.

5

Core Plus Fund (Unaudited)

TICKER SYMBOLS

Institutional Class | | NCPIX | |

Class A | | NCPAX | |

Class C | | NCPCX | |

Class R6 | | NCPRX | |

PORTFOLIO BY TYPE OF SECURITY

(as a % of Total Net Assets) | |

Asset-Backed Securities | | | 7.4 | % | |

Corporate Bonds | | | 31.1 | | |

Foreign Government Securities | | | 8.9 | | |

Mortgage-Backed Securities | | | 38.4 | | |

U.S. Treasury Obligations | | | 31.6 | | |

Short-Term Investment | | | 0.4 | | |

Liabilities Less Other Assets | | | (17.8 | )* | |

Total | | | 100.0 | % | |

* Includes the impact of the Fund's open positions in derivatives, if any.

PERFORMANCE HIGHLIGHTS

| | | Inception

Date | | Cumulative Total Return

Ended 10/31/2017

Life of Fund | |

At NAV | | | | | |

Institutional Class | | 07/18/2017 | | | 0.63 | % | |

Class A | | 07/18/2017 | | | 0.52 | % | |

Class C | | 07/18/2017 | | | 0.31 | % | |

Class R6 | | 07/18/2017 | | | 0.65 | % | |

With Sales Charge | | | | | |

Class A | | | | | -3.71 | % | |

Class C | | | | | -0.69 | % | |

Index | | | | | |

Bloomberg Barclays U.S. Aggregate

Bond Index1,14 | | | | | 0.72 | % | |

The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For performance data current to the most recent month-end, please visit www.nb.com/performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares.

The investment return and principal value of an investment will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

Returns would have been lower if Neuberger Berman Investment Advisers LLC ("Management") had not reimbursed certain expenses and/or waived a portion of the investment management fees during certain of the periods shown. Repayment by a class (of expenses previously reimbursed and/or fees previously waived by Management) will decrease the class's returns. Please see Note B in the Notes to Financial Statements for specific information regarding expense reimbursement and/or fee waiver arrangements.

For the period ended October 31, 2017, the 30-day SEC yields were 2.73%, 2.36%, 1.61% and 2.80% for Institutional Class, Class A, Class C and Class R6 shares, respectively. Absent expense reimbursements and/or fee waivers, the 30-day SEC yields would have been -2.94%, -3.35%, -4.08% and -2.88% for Institutional Class, Class A, Class C and Class R6 shares, respectively. A negative 30-day SEC yield results when a fund's accrued expenses exceed its income for the relevant period. Please note, in such instances the 30-day SEC yield may not equal the Fund's actual rate of income earned and distributed by the Fund and, therefore, a per share distribution may still be paid to shareholders.

As stated in the Fund's most recent prospectus, the estimated total annual operating expense ratios for fiscal year 2017 are 1.30%, 1.67%, 2.42% and 1.23% for Institutional Class, Class A, Class C and Class R6 shares, respectively (before expense reimbursements and/or fee waivers, if any). The estimated total annual operating expense ratios for the current fiscal year are 0.46%, 0.83%, 1.58% and 0.39% for Institutional Class, Class A, Class C and Class R6 shares, respectively, after expense reimbursements and/or fee waivers. The expense ratios for the annual period ended October 31, 2017 can be found in the Financial Highlights section of this report.

Returns shown with a sales charge reflect the deduction of the current maximum initial sales charge of 4.25% for Class A shares and the contingent deferred sales charge (CDSC) for Class C shares. The CDSC for Class C shares is 1%, which is reduced to 0% after 1 year. The performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses. Please see the prospectus for more information about sales charge structures, if any, and class expenses for your share class.

6

Core Plus Fund (Unaudited)

COMPARISON OF A $1,000,000 INVESTMENT

(000's omitted)

This graph shows the change in value of a hypothetical $1,000,000 investment in the Fund over the past 10 fiscal years, or since the Fund's inception if it has not operated for 10 years. The graph is based on the Institutional Class shares only; the performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses (see Performance Highlights chart on previous page). The result is compared with benchmarks, which include a broad-based market index and may include a more narrowly based index. Market indices have not been reduced to reflect any of the fees and costs of investing. The results shown in the graph reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares. Results represent past performance and do not indicate future results.

7

Emerging Markets Debt Fund Commentary (Unaudited)

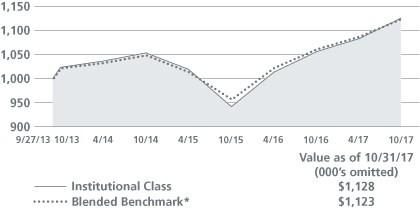

Neuberger Berman Emerging Markets Debt Fund Institutional Class generated a 6.77% total return for the 12 months ended October 31, 2017 and outperformed its benchmark, a custom blend consisting of 25% J.P. Morgan Emerging Markets Bond Index — Global Diversified, 25% J.P. Morgan Corporate Emerging Markets Bond Index — Diversified and 50% J.P. Morgan Government Bond Index — Emerging Markets Global Diversified, which provided a 5.75% total return for the same period. (Performance for all share classes is provided in the table immediately following this letter.)

Emerging markets (EM) experienced a turbulent start to the period, with markets selling-off sharply after the November 2016 U.S. elections followed by a recovery that extended through the end of the reporting period. Global economic activity surprised on the upside while inflation slowed, creating a "goldilocks" environment for EM debt and leading to a continuation of strong inflows. The recovery of commodity prices supported commodity producing and exporting economies. Further, reported Chinese growth remained at the higher end of our expectations, in spite of government measures to slow down credit growth. Additionally, exports from EM ex-China improved, reflecting healthier global demand. Finally, absent any indications of overheating in developed markets, core global monetary policy was expected to turn less accommodative only slowly. This, along with the historically low EM inflation, allowed EM central banks to cut rates and support further growth.

The Fund's positive performance was driven by country allocation and bottom-up security selection across the underlying sleeves in the portfolio. The tactical asset allocation detracted from performance, however the Fund's duration hedging was positive, making the top-down positioning positive for the reporting period. Tactically, we started with an overweight in local currency funded by an underweight in corporates, and a neutral position in hard currency. We moved to cash after the November 2016 U.S. elections and rotated from local to hard currency as EM faced uncertainty surrounding the new U.S. Administration's trade rhetoric. As the sentiment improved, supported by attractive valuations, we added to the EM foreign currencies (EMFX) overlay in EM high yielders. As EM growth continued to recover, we added back to the foreign currency (FX) overlay and moved to an overweight in local currency, while maintaining the overweight to hard currency and underweight to corporates.

In hard currency, the significant contributors to performance were security selection in Argentina, Malaysia and Indonesia, an underweight position in the Philippines, and overweights in Argentina and frontier countries including Mongolia, Iraq and Ghana. The underweight exposure to Hungary and Zambia detracted from performance as well as security selection in Venezuela. In the corporate space we benefitted from overweights in Argentina and Brazil and underweights in low beta countries, such as Hong Kong, Singapore, Israel and Korea, as the market rallied. Security selection in India was also positive though this was offset somewhat by security selection in Brazil and Colombia. By sector, positions in metals & mining, consumer, and utilities were positive, while oil & gas created a drag on relative performance. In local currency, local rates positioning drove outperformance. Key contributors were Central and Eastern Europe, the Middle East and Africa, and positions in Russia and the Czech Republic, while Hungary detracted from the Fund's performance. In Latin America, rates position in Colombia was positive, but was offset by exposure in Brazil. A new rates position in Sri Lanka was also additive, while the contribution from FX was negative in the reporting period. FX exposure to Russia, Colombia, Korea and Taiwan detracted from the EMFX returns. This was mitigated by positive returns from Czech Republic, Brazil and Mexico.

The Fund's aggregate use of futures, forward foreign currency and swap contracts contributed positively to performance during the reporting period.

In our view, the fundamental outlook for EM continues to be positive. We think external vulnerabilities have receded considerably and several countries have lately been in a position of rebuilding FX reserves and easing monetary policy. Both export growth data and domestic macro indicators such as retail sales have been showing strength across the EM world.

8

Corporates and consumers, China aside, have deleveraged and adjusted to lower commodity prices. Absent any indications of overheating in developed markets, core global monetary policy is expected to gradually move tighter only slowly, allowing EM central banks to cut rates and support growth further. We believe this, along with historically low EM inflation, if they continue, should be supportive of lower bond yields and EM currencies.

Sincerely,

ROB DRIJKONINGEN, GORKY URQUIETA, BART VAN DER MADE, RAOUL LUTTIK,

JENNIFER GORGOLL, VERA KARTSEVA AND NISH POPAT

PORTFOLIO CO-MANAGERS

Information about principal risks of investing in the Fund is set forth in the prospectus and statement of additional information.

The portfolio composition, industries and holdings of the Fund are subject to change without notice.

The opinions expressed are those of the Fund's portfolio managers. The opinions are as of the date of this report and are subject to change without notice.

9

Emerging Markets Debt Fund (Unaudited)

TICKER SYMBOLS

Institutional Class | | NERIX | |

Class A | | NERAX | |

Class C | | NERCX | |

PERFORMANCE HIGHLIGHTS

| | | Inception | | Average Annual Total Return

Ended 10/31/2017 | |

| | | Date | | 1 Year | | Life of Fund | |

At NAV | | | | | | | |

Institutional Class | | 09/27/2013 | | | 6.77 | % | | | 2.99 | % | |

Class A | | 09/27/2013 | | | 6.26 | % | | | 2.58 | % | |

Class C | | 09/27/2013 | | | 5.47 | % | | | 1.82 | % | |

With Sales Charge | | | | | | | |

Class A | | | | | 1.69 | % | | | 1.51 | % | |

Class C | | | | | 4.47 | % | | | 1.82 | % | |

Index | | | | | | | |

| Blended Benchmark*1,14 | | | | | 5.75 | % | | | 2.88 | % | |

* Blended benchmark is composed of 50% J.P. Morgan Government Bond Index (GBI) — Emerging Markets Global Diversified, 25% J.P. Morgan Emerging Markets Bond Index (EMBI) — Global Diversified, and 25% J.P. Morgan Corporate Emerging Markets Bond Index (CEMBI) — Diversified, and is rebalanced monthly.

The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For performance data current to the most recent month-end, please visit www.nb.com/performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares.

The investment return and principal value of an investment will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

Returns would have been lower if Neuberger Berman Investment Advisers LLC ("Management") had not reimbursed certain expenses and/or waived a portion of the investment management fees during certain of the periods shown. Repayment by a class (of expenses previously reimbursed and/or fees previously waived by Management) will decrease the class's returns. Please see Note B in the Notes to Financial Statements for specific information regarding expense reimbursement and/or fee waiver arrangements.

For the period ended October 31, 2017, the 30-day SEC yields were 5.38%, 5.01% and 4.24% for Institutional Class, Class A and Class C shares, respectively. Absent expense reimbursements and/or fee waivers, the 30-day SEC yields would have been 5.35%, 4.84% and 4.24% for Institutional Class, Class A and Class C shares, respectively.

As stated in the Fund's most recent prospectus, the total annual operating expense ratios for fiscal year 2016 were 1.21%, 1.74% and 2.37% for Institutional Class, Class A and Class C shares, respectively (before expense reimbursements and/or fee waivers, if any). The expense ratios were 0.79%, 1.16% and 1.91% for Institutional Class, Class A and Class C shares, respectively, after expense reimbursements and/or fee waivers. The expense ratios for the annual period ended October 31, 2017 can be found in the Financial Highlights section of this report.

Returns shown with a sales charge reflect the deduction of the current maximum initial sales charge of 4.25% for Class A shares and the contingent deferred sales charge (CDSC) for Class C shares. The CDSC for Class C shares is 1%, which is reduced to 0% after 1 year. The performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses. Please see the prospectus for more information about sales charge structures, if any, and class expenses for your share class.

10

Emerging Markets Debt Fund (Unaudited)

COMPARISON OF A $1,000,000 INVESTMENT

(000's omitted)

This graph shows the change in value of a hypothetical $1,000,000 investment in the Fund over the past 10 fiscal years, or since the Fund's inception if it has not operated for 10 years. The graph is based on the Institutional Class shares only; the performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses (see Performance Highlights chart on previous page). The result is compared with benchmarks, which include a broad-based market index and may include a more narrowly based index. Market indices have not been reduced to reflect any of the fees and costs of investing. The results shown in the graph reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares. Results represent past performance and do not indicate future results.

* Blended benchmark is composed of 50% J.P. Morgan Government Bond Index (GBI) — Emerging Markets Global Diversified, 25% J.P. Morgan Emerging Markets Bond Index (EMBI) — Global Diversified, and 25% J.P. Morgan Corporate Emerging Markets Bond Index (CEMBI) — Diversified, and is rebalanced monthly.

11

Floating Rate Income Fund Commentary (Unaudited)

Neuberger Berman Floating Rate Income Fund Institutional Class generated a 4.14% total return for the 12 months ended October 31, 2017 and underperformed its benchmark, the S&P/LSTA Leveraged Loan Index, which provided a 5.06% total return for the same period. (Performance for all share classes is provided in the table immediately following this letter.)

The senior floating rate bank loan market posted positive results during the reporting period. Supporting the asset class were generally solid fundamentals, relatively low defaults and indications from the U.S. Federal Reserve that it would continue to take a measured approach in terms of raising interest rates. For the 12 months ended October 31, 2017, securities rated B in the S&P/LSTA Leveraged Loan Index returned 5.13%, whereas BB rated and CCC rated securities returned 3.97% and 15.22%, respectively.

The Fund tactically adjusted its position in non-floating rate securities during the reporting period. We have the flexibility to allocate up to 20% of the portfolio in these securities, usually fixed-rate senior bonds. Relative value between floating rate loans and bonds fluctuated during the reporting period given the increase in volatility. Against this backdrop, the Fund's non-floating rate allocation ended the reporting period at approximately 7.9%.

In terms of the Fund's quality biases, an underweight to CCC rated issues and security selection within B rated issues detracted from performance. Conversely, security selection of BB rated issues contributed to performance.

From a sector perspective, security selection within oil & gas, business equipment & services, and electronics-electrical detracted the most from performance during the reporting period. In contrast, security selection within retailers, financial intermediaries, and drugs were the largest contributors to performance.

We continue to believe that the floating rate loan market is compensating investors for default risk. We think defaults may have peaked in 2016 and could remain below 2% in both 2017 and 2018 as revenue and leverage ratios improve. While volatility has failed to emerge in the non-investment grade space, as it has in most risk markets, we believe the potential remains for a spike in volatility over the balance of the year given ongoing policy uncertainty in the U.S., various geopolitical flashpoints, and the possibility that the improvement in global economic growth could wane.

Sincerely,

THOMAS P. O'REILLY, JOSEPH P. LYNCH, STEPHEN J. CASEY AND DANIEL DOYLE

PORTFOLIO MANAGERS

Information about principal risks of investing in the Fund is set forth in the prospectus and statement of additional information.

The portfolio composition, industries and holdings of the Fund are subject to change without notice.

The opinions expressed are those of the Fund's portfolio managers. The opinions are as of the date of this report and are subject to change without notice.

The loan ratings noted above represent segments of the S&P/LSTA Leveraged Loan Index, which are determined based on the ratings issued by Standard & Poor's.

12

Floating Rate Income Fund (Unaudited)

TICKER SYMBOLS

Institutional Class | | NFIIX | |

Class A | | NFIAX | |

Class C | | NFICX | |

PORTFOLIO BY MATURITY DISTRIBUTION

(as a % of Total Investments*) | |

One to less than Five Years | | | 36.1 | % | |

Five to less than Ten Years | | | 62.7 | | |

Ten Years or Greater | | | 1.2 | | |

Total | | | 100.0 | % | |

* Does not include Short-Term Investments or the impact of the Fund's open positions in derivatives, if any.

PERFORMANCE HIGHLIGHTS

| | | Inception | | Average Annual Total Return

Ended 10/31/2017 | |

| | | Date | | 1 Year | | 5 Years | | Life of Fund | |

At NAV | | | | | | | | | |

| Institutional Class5 | | 12/30/2009 | | | 4.14 | % | | | 3.41 | % | | | 4.47 | % | |

Class A | | 12/29/2009 | | | 3.76 | % | | | 3.03 | % | | | 4.07 | % | |

| Class C5 | | 12/30/2009 | | | 2.99 | % | | | 2.26 | % | | | 3.32 | % | |

With Sales Charge | | | | | | | | | |

Class A | | | | | -0.66 | % | | | 2.15 | % | | | 3.51 | % | |

| Class C5 | | | | | 1.99 | % | | | 2.26 | % | | | 3.32 | % | |

Index | | | | | | | | | |

| S&P/LSTA Leveraged Loan Index1,14 | | | | | 5.06 | % | | | 4.15 | % | | | 5.23 | % | |

The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For performance data current to the most recent month-end, please visit www.nb.com/performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares.

The investment return and principal value of an investment will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

Returns would have been lower if Neuberger Berman Investment Advisers LLC ("Management") had not reimbursed certain expenses and/or waived a portion of the investment management fees during certain of the periods shown. Repayment by a class (of expenses previously reimbursed and/or fees previously waived by Management) will decrease the class's returns. Please see Note B in the Notes to Financial Statements for specific information regarding expense reimbursement and/or fee waiver arrangements.

For the period ended October 31, 2017, the 30-day SEC yields were 3.79%, 3.42% and 2.68% for Institutional Class, Class A and Class C shares, respectively. Absent expense reimbursements and/or fee waivers, the 30-day SEC yields would have been 3.41% and 2.67% for Class A and Class C shares, respectively.

As stated in the Fund's most recent prospectus, the total annual operating expense ratios for fiscal year 2016 were 0.92%, 1.32% and 2.05% for Institutional Class, Class A and Class C shares, respectively (before expense reimbursements and/or fee waivers, if any). The expense ratios were 0.71%, 1.08% and 1.83% for Institutional Class, Class A and Class C shares, respectively, after expense reimbursements and/or fee waivers. The expense ratios for the annual period ended October 31, 2017 can be found in the Financial Highlights section of this report.

Returns shown with a sales charge reflect the deduction of the current maximum initial sales charge of 4.25% for Class A shares and the contingent deferred sales charge (CDSC) for Class C shares. The CDSC for Class C shares is 1%, which is reduced to 0% after 1 year. The performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses. Please see the prospectus for more information about sales charge structures, if any, and class expenses for your share class.

13

Floating Rate Income Fund (Unaudited)

COMPARISON OF A $1,000,000 INVESTMENT

(000's omitted)

This graph shows the change in value of a hypothetical $1,000,000 investment in the Fund over the past 10 fiscal years, or since the Fund's inception if it has not operated for 10 years. The graph is based on the Institutional Class shares only; the performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses (see Performance Highlights chart on previous page). The result is compared with benchmarks, which include a broad-based market index and may include a more narrowly based index. Market indices have not been reduced to reflect any of the fees and costs of investing. The results shown in the graph reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares. Results represent past performance and do not indicate future results.

14

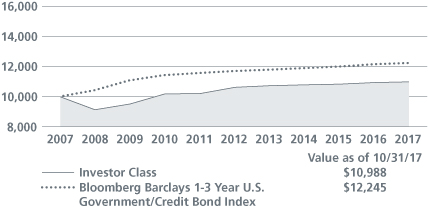

High Income Bond Fund Commentary (Unaudited)

Neuberger Berman High Income Bond Fund Investor Class generated a 6.84% total return for the 12 months ended October 31, 2017 and underperformed its benchmark, the ICE BofAML U.S. High Yield Constrained Index, which provided a 9.14% total return for the same period. (Performance for all share classes is provided in the table immediately following this letter.)

The overall high yield market, as measured by the ICE BofAML U.S. High Yield Constrained Index, generated strong results during the reporting period. After a weak start in November 2016, the high yield market rallied over nine of the last 11 months of the reporting period. This was driven by a number of factors, including overall strong corporate earnings, low defaults, improving global growth, and rising oil prices. Against this backdrop, investor demand was generally robust as investors looked to generate incremental yield in the low interest rate environment. Within the benchmark index, securities rated CCC and lower (relatively lower ratings) and securities rated BB (a higher rating) returned 13.72% and 7.78%, respectively.*

From a sector perspective, an underweight to energy, as well as security selection within support services and banking detracted the most from performance. In contrast, security selection within utilities, an underweight to super retail and security selection within gaming contributed the most to results.

In terms of the Fund's quality biases, security selection within BB and B rated securities was negative for its performance, as was our underweight to CCC rated securities.

We made several adjustments to the portfolio during the reporting period. The Fund's allocation to BBB and BB rated securities was reduced. We also increased our allocation to B rated bonds, reducing our underweight to slightly above 1% from 6%. From a sector perspective, the Fund increased its allocation to diversified financial services securities, while reducing its gas distribution and health care exposure.

Looking ahead, it is widely anticipated that the U.S. Federal Reserve (Fed) will raise interest rates again following its mid-December meeting, which would be the third hike of 2017. All in all, we believe the Fed's measured approach to policy normalization represents a constructive scenario for high yield bonds, which historically have performed well during rising-rate environments. We continue to believe that the high yield market is compensating investors for default risk. We anticipate high yield defaults will remain below historical averages for the remainder of 2017 and 2018 if the U.S. economic expansion continues. While volatility has failed to emerge in the non-investment grade space, as it has in most risk markets, the potential remains for a spike in volatility over the balance of the year given ongoing policy uncertainty in the U.S., various geopolitical flashpoints, and the possibility that the improvement in global economic growth could wane. We don't believe lower-quality high yield securities at current levels are compensating investors for these risks, which is one of the reasons why we increased our allocation to B rated bonds as noted above.

Sincerely,

THOMAS P. O'REILLY, RUSS COVODE, DANIEL DOYLE, AND PATRICK FLYNN

PORTFOLIO CO-MANAGERS

* The performance of certain rated bonds within the benchmark, as noted above, represent issues that are rated Ba1/BB+ through Ba3/BB- and CCC+/Caa1 or lower, based on an average of Moody's, S&P and Fitch, as calculated by ICE BofAML.

Information about principal risks of investing in the Fund is set forth in the prospectus and statement of additional information.

The portfolio composition, industries and holdings of the Fund are subject to change without notice.

The opinions expressed are those of the Fund's portfolio managers. The opinions are as of the date of this report and are subject to change without notice.

15

High Income Bond Fund (Unaudited)

TICKER SYMBOLS

Investor Class | | NHINX | |

Institutional Class | | NHILX | |

Class A | | NHIAX | |

Class C | | NHICX | |

Class R3 | | NHIRX | |

Class R6 | | NRHIX | |

PORTFOLIO BY MATURITY DISTRIBUTION

(as a % of Total Investments*) | |

Less than One Year | | | 3.2 | % | |

One to less than Five Years | | | 32.5 | | |

Five to less than Ten Years | | | 57.0 | | |

Ten Years or Greater | | | 7.3 | | |

Total | | | 100.0 | % | |

* Does not include Short-Term Investments or the impact of the Fund's open positions in derivatives, if any.

PERFORMANCE HIGHLIGHTS6,19

| | | Inception | | Average Annual Total Return

Ended 10/31/2017 | |

| | | Date | | 1 Year | | 5 Years | | 10 Years | | Life of Fund | |

At NAV | | | | | | | | | | | |

| Investor Class7 | | 02/01/1992 | | | 6.84 | % | | | 5.01 | % | | | 7.28 | % | | | 7.58 | % | |

| Institutional Class8 | | 05/27/2009 | | | 6.82 | % | | | 5.13 | % | | | 7.43 | % | | | 7.63 | % | |

| Class A8 | | 05/27/2009 | | | 6.49 | % | | | 4.73 | % | | | 7.06 | % | | | 7.49 | % | |

| Class C8 | | 05/27/2009 | | | 5.77 | % | | | 3.98 | % | | | 6.42 | % | | | 7.24 | % | |

| Class R38 | | 05/27/2009 | | | 6.20 | % | | | 4.47 | % | | | 6.85 | % | | | 7.41 | % | |

| Class R68 | | 03/15/2013 | | | 7.03 | % | | | 5.22 | % | | | 7.39 | % | | | 7.62 | % | |

With Sales Charge | |

| Class A8 | | | | | 1.91 | % | | | 3.83 | % | | | 6.60 | % | | | 7.31 | % | |

| Class C8 | | | | | 4.77 | % | | | 3.98 | % | | | 6.42 | % | | | 7.24 | % | |

Index | |

ICE BofAML U.S. High Yield

Constrained Index^1,14 | | | | | 9.14 | % | | | 6.30 | % | | | 7.78 | % | | | N/A | | |

^ Effective October 20, 2017, the BofA Merrill Lynch U.S. High Yield Master II Constrained Index changed its name to the ICE BofAML U.S. High Yield Constrained Index.

The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For performance data current to the most recent month-end, please visit www.nb.com/performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares.

The investment return and principal value of an investment will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

Returns would have been lower if Neuberger Berman Investment Advisers LLC ("Management") had not reimbursed certain expenses and/or waived a portion of the investment management fees during certain of the periods shown. Repayment by a class (of expenses previously reimbursed and/or fees previously waived by Management) will decrease the class's returns. Please see Note B in the Notes to Financial Statements for specific information regarding expense reimbursement and/or fee waiver arrangements.

For the period ended October 31, 2017, the 30-day SEC yields were 4.39%, 4.53%, 4.03%, 3.41%, 3.89% and 4.62% for Investor Class, Institutional Class, Class A, Class C, Class R3 and Class R6 shares, respectively. Absent expense reimbursement and/or fee waiver, the 30-day SEC yield would have been 3.88% for Class A shares.

As stated in the Fund's most recent prospectus, the total annual operating expense ratios for fiscal year 2016 were 0.85%, 0.71%, 1.08%, 1.82%, 1.41% and 0.62% for Investor Class, Institutional Class, Class A, Class C, Class R3 and Class R6 shares, respectively (before expense reimbursements and/or fee waivers, if any). The expense ratio was 1.38% for Class R3 after expense reimbursements and/or fee waivers. The expense ratios for the annual period ended October 31, 2017 can be found in the Financial Highlights section of this report.

Returns shown with a sales charge reflect the deduction of the current maximum initial sales charge of 4.25% for Class A shares and the contingent deferred sales charge (CDSC) for Class C shares. The CDSC for Class C shares is 1%, which is reduced to 0% after 1 year. The performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses. Please see the prospectus for more information about sales charge structures, if any, and class expenses for your share class.

16

High Income Bond Fund (Unaudited)

COMPARISON OF A $10,000 INVESTMENT

This graph shows the change in value of a hypothetical $10,000 investment in the Fund over the past 10 fiscal years, or since the Fund's inception if it has not operated for 10 years. The graph is based on the Investor Class shares only; the performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses (see Performance Highlights chart on previous page). The result is compared with benchmarks, which include a broad-based market index and may include a more narrowly based index. Market indices have not been reduced to reflect any of the fees and costs of investing. The results shown in the graph reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares. Results represent past performance and do not indicate future results.

17

Municipal High Income Fund Commentary (Unaudited)

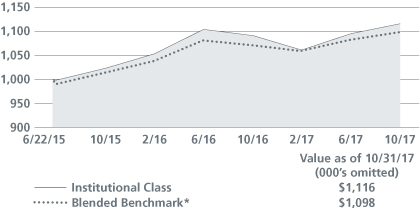

Neuberger Berman Municipal High Income Fund Institutional Class generated a 2.24% total return for the 12 months ended October 31, 2017 and underperformed its benchmark, a custom blend consisting of 65% Bloomberg Barclays Municipal Bond Index and 35% Bloomberg Barclays Municipal High Yield Index, which provided a 2.48% total return for the same period. (Performance for all share classes is provided in the table immediately following this letter.)

The municipal bond market outperformed the taxable bond market during the reporting period. Municipal securities were supported by generally positive fundamentals, solid demand, and more moderate supply than a year earlier. Both short- and longer-term Treasury yields rose over the 12 months ended October 31, 2017. Short-term yields generally moved higher as the U.S. Federal Reserve (Fed) raised interest rates three times over the reporting period and began reducing its balance sheet in October 2017. Meanwhile, longer-term Treasury yields fluctuated given changing expectations for economic growth in the U.S., uncertainties surrounding future fiscal policy and a number of geopolitical events. All told, the Bloomberg Barclays Municipal Bond Index gained 2.19% for the 12 months ended October 31, 2017, whereas the overall taxable bond market, as measured by the Bloomberg Barclays U.S. Aggregate Bond Index, returned 0.90%.

We tactically adjusted the Fund's duration during the reporting period. Having a duration that was longer than the Fund's benchmark initially detracted from results as rates moved sharply higher in December 2016. Duration positioning then benefited results as rates subsequently declined. As the reporting period progressed, we moved to reduce the Fund's duration. Overall, duration positioning was a headwind for results.

The Fund's credit biases were beneficial for results. In particular, having an overweight to securities rated BBB and below was additive for returns as they outperformed their higher rated counterparts. From a sector perspective, an underweight to tobacco securitization bonds detracted from performance. In addition, having no allocation to securities issued by Puerto Rico contributed to results. On the downside, our small diversified exposure to the Virgin Islands detracted from performance as they were negatively impacted by Hurricane Maria.

Given the slow but steady economic growth backdrop and subdued but stable level of inflation, we see no reason to doubt the Fed's intention of taking a measured approach to future monetary policy tightening. That being said, changes in fiscal policy or potential volatility caused by the withdrawal of monetary accommodation might cause adjustments to that forecast. Specific to the municipal bond market, technicals continue to look promising for the remainder of the year, in our opinion. As was characteristic of most of 2017, we believe reduced new issue supply should provide a firm bid for municipal product. We will keep a close eye on both tax reform and infrastructure investment legislation, but we believe that several months may pass before any legislation becomes a reality. We continue to execute on our research based, bottom-up investment process in the effort to find attractive buying opportunities for our investors.

Sincerely,

JAMES L. ISELIN, S. BLAKE MILLER AND ERIC J. PELIO

PORTFOLIO MANAGERS

Information about principal risks of investing in the Fund is set forth in the prospectus and statement of additional information.

The portfolio composition, industries and holdings of the Fund are subject to change without notice.

The opinions expressed are those of the Fund's portfolio managers. The opinions are as of the date of this report and are subject to change without notice.

The bond ratings noted above represent segments of the Bloomberg Barclays Municipal Bond Index and Bloomberg Barclays Municipal High Yield Index, which are determined based on the average ratings issued by Standard & Poor's, Moody's and Fitch.

18

Municipal High Income Fund (Unaudited)

TICKER SYMBOLS

Institutional Class | | NMHIX | |

Class A | | NMHAX | |

Class C | | NMHCX | |

PORTFOLIO BY STATE AND TERRITORY

(as a % of Total Net Assets) | |

Alabama | | | 1.0 | % | |

Alaska | | | 3.7 | | |

American Samoa | | | 0.2 | | |

Arizona | | | 5.3 | | |

California | | | 7.5 | | |

Colorado | | | 3.4 | | |

Connecticut | | | 1.0 | | |

District of Columbia | | | 0.5 | | |

Florida | | | 5.3 | | |

Georgia | | | 1.0 | | |

Hawaii | | | 0.8 | | |

Illinois | | | 9.3 | | |

Indiana | | | 0.8 | | |

Iowa | | | 0.9 | | |

Kansas | | | 0.3 | | |

Kentucky | | | 1.5 | | |

Louisiana | | | 1.7 | | |

Maine | | | 0.7 | | |

Massachusetts | | | 1.2 | | |

Michigan | | | 4.0 | | |

Minnesota | | | 0.8 | | |

Mississippi | | | 2.7 | | |

Missouri | | | 1.6 | | |

Nevada | | | 0.5 | | |

New Jersey | | | 7.1 | | |

New Mexico | | | 0.5 | | |

New York | | | 2.9 | | |

North Carolina | | | 0.7 | | |

North Dakota | | | 1.1 | | |

Ohio | | | 1.9 | | |

Oregon | | | 0.5 | | |

Pennsylvania | | | 5.1 | | |

Rhode Island | | | 2.9 | | |

South Carolina | | | 0.6 | | |

Tennessee | | | 0.7 | | |

Texas | | | 7.8 | | |

Utah | | | 0.5 | | |

Vermont | | | 1.4 | | |

Virgin Islands | | | 0.4 | | |

Virginia | | | 0.6 | | |

Washington | | | 1.1 | | |

West Virginia | | | 0.9 | | |

Wisconsin | | | 5.6 | | |

Other Assets Less Liabilities | | | 2.0 | * | |

Total | | | 100.0 | % | |

* Includes the impact of the Fund's open positions in derivatives, if any.

PERFORMANCE HIGHLIGHTS10

| | | Inception | | Average Annual Total Return

Ended 10/31/2017 | |

| | | Date | | 1 Year | | Life of Fund | |

At NAV | | | | | | | |

Institutional Class | | 06/22/2015 | | | 2.24 | % | | | 4.74 | % | |

Class A | | 06/22/2015 | | | 1.87 | % | | | 4.36 | % | |

Class C | | 06/22/2015 | | | 1.20 | % | | | 3.63 | % | |

With Sales Charge | | | | | | | |

Class A | | | | | -2.44 | % | | | 2.47 | % | |

Class C | | | | | 0.23 | % | | | 3.63 | % | |

Index | |

| Blended Benchmark*1,14 | | | | | 2.48 | % | | | 4.03 | % | |

* Blended benchmark is composed of 65% Bloomberg Barclays Municipal Bond Index and 35% Bloomberg Barclays Municipal High Yield Index and is rebalanced monthly.

The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For performance data current to the most recent month-end, please visit www.nb.com/performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares.

The investment return and principal value of an investment will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

Returns would have been lower if Neuberger Berman Investment Advisers LLC ("Management") had not reimbursed certain expenses and/or waived a portion of the investment management fees during certain of the periods shown. Repayment by a class (of expenses previously reimbursed and/or fees previously waived by Management) will decrease the class's returns. Please see Note B in the Notes to Financial Statements for specific information regarding expense reimbursement and/or fee waiver arrangements.

For the period ended October 31, 2017, the 30-day SEC yields were 3.10%, 2.72% and 1.98% for Institutional Class, Class A and Class C shares, respectively. The tax-equivalent yields were 5.48%, 4.81% and 3.50% for Institutional Class, Class A and Class C shares, respectively, for a shareholder in the highest federal income tax bracket (39.6% plus 3.8% Medicare contribution tax).9 Absent expense reimbursements and/or fee waivers, the 30-day SEC yields would have been 2.97%, 2.51% and 1.85% for Institutional Class, Class A and Class C shares, respectively.

As stated in the Fund's most recent prospectus, the total annual operating expense ratios for fiscal year 2016 were 0.93%, 1.47% and 2.15% for Institutional Class, Class A and Class C shares, respectively (before expense reimbursements and/or fee waivers, if any). The expense ratios were 0.50%, 0.87% and 1.62% for Institutional Class, Class A and Class C shares, respectively, after expense reimbursements and/or fee waivers. The expense ratios for the annual period ended October 31, 2017 can be found in the Financial Highlights section of this report.

Returns shown with a sales charge reflect the deduction of the current maximum initial sales charge of 4.25% for Class A shares and the contingent deferred sales charge (CDSC) for Class C shares. The CDSC for Class C shares is 1%, which is reduced to 0% after 1 year. The performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses. Please see the prospectus for more information about sales charge structures, if any, and class expenses for your share class.

19

Municipal High Income Fund (Unaudited)

COMPARISON OF A $1,000,000 INVESTMENT

(000's omitted)

This graph shows the change in value of a hypothetical $1,000,000 investment in the Fund over the past 10 fiscal years, or since the Fund's inception if it has not operated for 10 years. The graph is based on the Institutional Class shares only; the performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses (see Performance Highlights chart on previous page). The result is compared with benchmarks, which include a broad-based market index and may include a more narrowly based index. Market indices have not been reduced to reflect any of the fees and costs of investing. The results shown in the graph reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares. Results represent past performance and do not indicate future results.

* Blended benchmark is composed of 65% Bloomberg Barclays Municipal Bond Index and 35% Bloomberg Barclays Municipal High Yield Index and is rebalanced monthly.

20

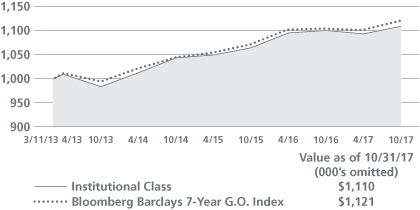

Municipal Intermediate Bond Fund Commentary (Unaudited)

Neuberger Berman Municipal Intermediate Bond Fund Investor Class generated a 1.28% total return for the 12 months ended October 31, 2017 and underperformed its benchmark, the Bloomberg Barclays 7-Year G.O. Index, which provided a 1.50% total return for the same period. (Performance for all share classes is provided in the table immediately following this letter.)

The municipal bond market outperformed the taxable bond market during the reporting period. Municipal securities were supported by generally positive fundamentals, solid demand, and more moderate supply than a year earlier. Both short- and longer-term Treasury yields rose over the 12 months ended October 31, 2017. Short-term yields generally moved higher as the U.S. Federal Reserve (Fed) raised interest rates three times over the reporting period and began reducing its balance sheet in October 2017. Meanwhile, longer-term Treasury yields fluctuated given changing expectations for economic growth in the U.S., uncertainties surrounding future fiscal policy, and a number of geopolitical events. All told, the Bloomberg Barclays Municipal Bond Index gained 2.19% for the 12 months ended October 31, 2017, whereas the overall taxable bond market, as measured by the Bloomberg Barclays U.S. Aggregate Bond Index, returned 0.90%.

Throughout the reporting period, the Fund maintained a barbell approach (investing in shorter and longer maturities). In contrast, the Fund's benchmark, the Bloomberg Barclays 7-Year G.O. Index, is concentrated in the six- to eight-year portion of the curve. This positioning modestly detracted from results as the five- to seven-year portion of the municipal curve outperformed over the 12-month period as a whole.

The Fund's credit biases were additive for results. In particular, having overweights to BBB rated and A rated securities benefited results as lower rated issues outperformed their higher rated counterparts. From a sector perspective, an overweight to revenue bonds added to results as they largely outperformed general obligation bonds.

A number of changes were made to the Fund during the reporting period. We tactically adjusted the Fund's duration, initially allowing it to drift shorter in anticipation of increased volatility, higher rates, and seasonal headwinds. As the period progressed, we increased the Fund's duration and ended the period slightly longer than the benchmark. Elsewhere, we opportunistically purchased certain lesser grade securities, which was beneficial for performance.

Given the slow but steady economic growth backdrop and subdued but stable level of inflation, we see no reason to doubt the Fed's intention of taking a measured approach to future monetary policy tightening. That being said, changes in fiscal policy or potential volatility caused by the withdrawal of monetary accommodation might cause adjustments to that forecast. Specific to the municipal bond market, technicals continue to look promising for the remainder of the year, in our opinion. As was characteristic of most of 2017, we believe reduced new issue supply should provide a firm bid for municipal product. We will keep a close eye on both tax reform and infrastructure investment legislation, but we believe that several months may pass before any legislation becomes a reality. We continue to execute on our research based, bottom-up investment process in the effort to find attractive buying opportunities for our investors.

Sincerely,

JAMES L. ISELIN AND S. BLAKE MILLER

PORTFOLIO MANAGERS

Information about principal risks of investing in the Fund is set forth in the prospectus and statement of additional information.

The portfolio composition, industries and holdings of the Fund are subject to change without notice.

The opinions expressed are those of the Fund's portfolio managers. The opinions are as of the date of this report and are subject to change without notice.

The bond ratings noted above represent segments of the Bloomberg Barclays 7-Year G.O. Index, which are determined based on the average ratings issued by Standard & Poor's, Moody's and Fitch.

21

Municipal Intermediate Bond Fund (Unaudited)

TICKER SYMBOLS

Investor Class | | NMUIX | |

Institutional Class | | NMNLX | |

Class A | | NMNAX | |

Class C | | NMNCX | |

PORTFOLIO BY STATE AND TERRITORY

(as a % of Total Net Assets) | |

Alabama | | | 0.1 | % | |

Alaska | | | 3.4 | | |

Arizona | | | 0.8 | | |

Arkansas | | | 0.3 | | |

California | | | 10.2 | | |

Colorado | | | 0.8 | | |

Connecticut | | | 1.4 | | |

District of Columbia | | | 0.4 | | |

Florida | | | 5.9 | | |

Georgia | | | 2.6 | | |

Illinois | | | 5.4 | | |

Indiana | | | 3.6 | | |

Iowa | | | 0.6 | | |

Kentucky | | | 1.6 | | |

Louisiana | | | 0.5 | | |

Maryland | | | 3.8 | | |

Massachusetts | | | 1.1 | | |

Michigan | | | 0.9 | | |

Minnesota | | | 2.5 | | |

Mississippi | | | 3.3 | | |

Nevada | | | 0.4 | | |

New Jersey | | | 6.5 | | |

New York | | | 10.4 | | |

North Carolina | | | 4.0 | | |

Ohio | | | 1.2 | | |

Oklahoma | | | 1.4 | | |

Pennsylvania | | | 9.5 | | |

Rhode Island | | | 1.5 | | |

South Carolina | | | 1.6 | | |

Tennessee | | | 0.5 | | |

Texas | | | 10.2 | | |

Utah | | | 0.8 | | |

Vermont | | | 0.3 | | |

Virginia | | | 1.9 | | |

Washington | | | 3.7 | | |

Wisconsin | | | 0.7 | | |

Liabilities Less Other Assets | | | (3.8 | )* | |

Total | | | 100.0 | % | |

* Includes the impact of the Fund's open positions in derivatives, if any.

PERFORMANCE HIGHLIGHTS10

| | | Inception | | Average Annual Total Return

Ended 10/31/2017 | |

| | | Date | | 1 Year | | 5 Years | | 10 Years | | Life of Fund | |

At NAV | | | | | | | | | | | |

Investor Class | | 07/09/1987 | | | 1.28 | % | | | 2.14 | % | | | 3.55 | % | | | 4.74 | % | |

| Institutional Class11 | | 06/21/2010 | | | 1.43 | % | | | 2.30 | % | | | 3.66 | % | | | 4.78 | % | |

| Class A11 | | 06/21/2010 | | | 0.96 | % | | | 1.90 | % | | | 3.37 | % | | | 4.68 | % | |

| Class C11 | | 06/21/2010 | | | 0.30 | % | | | 1.16 | % | | | 2.81 | % | | | 4.49 | % | |

With Sales Charge | |

| Class A11 | | | | | -3.32 | % | | | 1.01 | % | | | 2.92 | % | | | 4.53 | % | |

| Class C11 | | | | | -0.69 | % | | | 1.16 | % | | | 2.81 | % | | | 4.49 | % | |

Index | |

Bloomberg Barclays

7-Year G.O. Index1,14 | | | | | 1.50 | % | | | 2.31 | % | | | 4.38 | % | | | 5.56 | % | |

The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For performance data current to the most recent month-end, please visit www.nb.com/performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares.

The investment return and principal value of an investment will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

Returns would have been lower if Neuberger Berman Investment Advisers LLC ("Management") had not reimbursed certain expenses and/or waived a portion of the investment management fees during certain of the periods shown. Repayment by a class (of expenses previously reimbursed and/or fees previously waived by Management) will decrease the class's returns. Please see Note B in the Notes to Financial Statements for specific information regarding expense reimbursement and/or fee waiver arrangements.

For the period ended October 31, 2017, the 30-day SEC yields were 1.37%, 1.52%, 1.15% and 0.41% for Investor Class, Institutional Class, Class A and Class C shares, respectively. The tax-equivalent yields were 2.42%, 2.69%, 2.03% and 0.72% for Investor Class, Institutional Class, Class A and Class C shares, respectively, for a shareholder in the highest federal income tax bracket (39.6% plus 3.8% Medicare contribution tax).9 Absent repayments, the 30-day SEC yields would have been 1.50%, 1.68%, 1.31% and 0.56% for Investor Class, Institutional Class, Class A and Class C shares, respectively.

As stated in the Fund's most recent prospectus, the total annual operating expense ratios for fiscal year 2016 were 0.84%, 0.65%, 1.03% and 1.78% for Investor Class, Institutional Class, Class A and Class C shares, respectively (before expense reimbursements and/or fee waivers, if any). The expense ratios were 0.65%, 0.50%, 0.87% and 1.62% for Investor Class, Institutional Class, Class A and Class C shares, respectively, after expense reimbursements and/or fee waivers. The expense ratios for the annual period ended October 31, 2017 can be found in the Financial Highlights section of this report.

Returns shown with a sales charge reflect the deduction of the current maximum initial sales charge of 4.25% for Class A shares and the contingent deferred sales charge (CDSC) for Class C shares. The CDSC for Class C shares is 1%, which is reduced to 0% after 1 year. The performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses. Please see the prospectus for more information about sales charge structures, if any, and class expenses for your share class.

22

Municipal Intermediate Bond Fund (Unaudited)

COMPARISON OF A $10,000 INVESTMENT

This graph shows the change in value of a hypothetical $10,000 investment in the Fund over the past 10 fiscal years, or since the Fund's inception if it has not operated for 10 years. The graph is based on the Investor Class shares only; the performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses (see Performance Highlights chart on previous page). The result is compared with benchmarks, which include a broad-based market index and may include a more narrowly based index. Market indices have not been reduced to reflect any of the fees and costs of investing. The results shown in the graph reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares. Results represent past performance and do not indicate future results.

23

New York Municipal Income Fund Commentary (Unaudited)

Neuberger Berman New York Municipal Income Fund Institutional Class generated a 0.84% total return for the 12 months ended October 31, 2017 and underperformed its benchmark, the Bloomberg Barclays 7-Year G.O. Index, which provided a 1.50% total return for the same period.

The municipal bond market outperformed the taxable bond market during the reporting period. Municipal securities were supported by generally positive fundamentals, solid demand, and more moderate supply than a year earlier. Both short- and longer-term Treasury yields rose over the 12 months ended October 31, 2017. Short-term yields generally moved higher as the U.S. Federal Reserve (Fed) raised interest rates three times over the period and began reducing its balance sheet in October 2017. Meanwhile, longer-term Treasury yields fluctuated given changing expectations for economic growth in the U.S., uncertainties surrounding future fiscal policy, and a number of geopolitical events. All told, the Bloomberg Barclays Municipal Bond Index gained 2.19% for the 12 months ended October 31, 2017, whereas the overall taxable bond market, as measured by the Bloomberg Barclays U.S. Aggregate Bond Index, returned 0.90%.