Forward Looking Statements In order for you to better understand the business of the Company – where we have been and where we want to go – our remarks today (those of the Company officers who will speak or respond to questions) will include forward looking statements related to anticipated financial performance, future operating results, business prospects, new products, and similar matters. These statements represent our best judgment, based upon present circumstances and the information now available to us, of what we think may occur in the future – and, of course, it is possible that actual results may differ materially from those we envision today. For a more complete discussion on the subject of forward looking statements, including a list of some of the risk factors that might adversely affect future operating results, we refer you to the section entitled “Forward Looking Statements” which appears in our annual report on Form 10-K as filed with the Securities and Exchange Commission 2

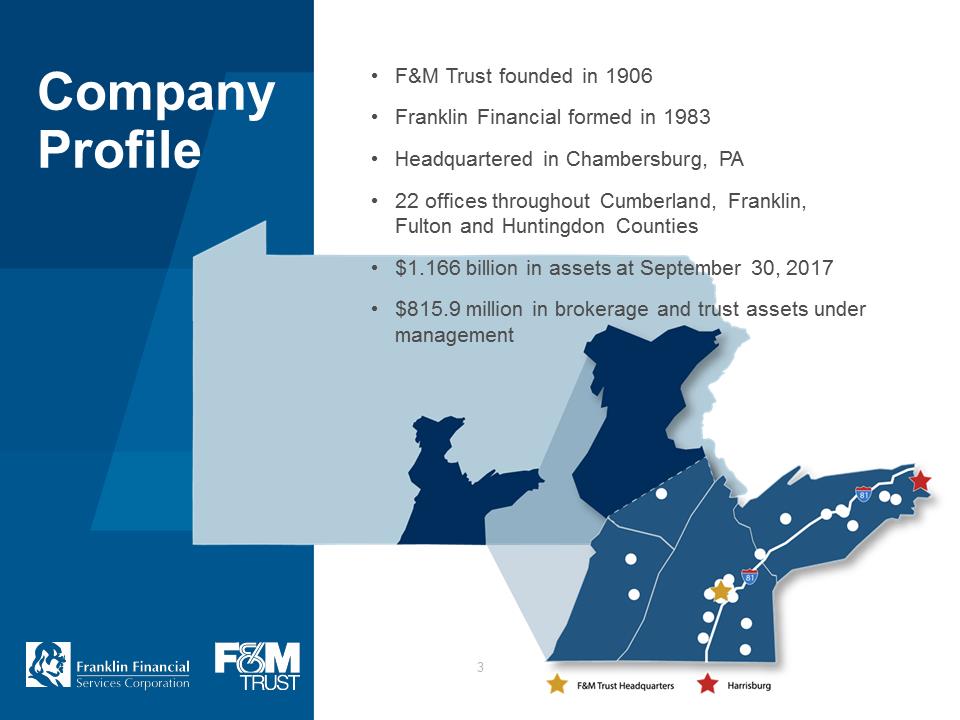

F&M Trust founded in 1906 Franklin Financial formed in 1983 Headquartered in Chambersburg, PA 22 offices throughout Cumberland, Franklin, Fulton and Huntingdon Counties $1.166 billion in assets at September 30, 2017 $815.9 million in brokerage and trust assets under management 3

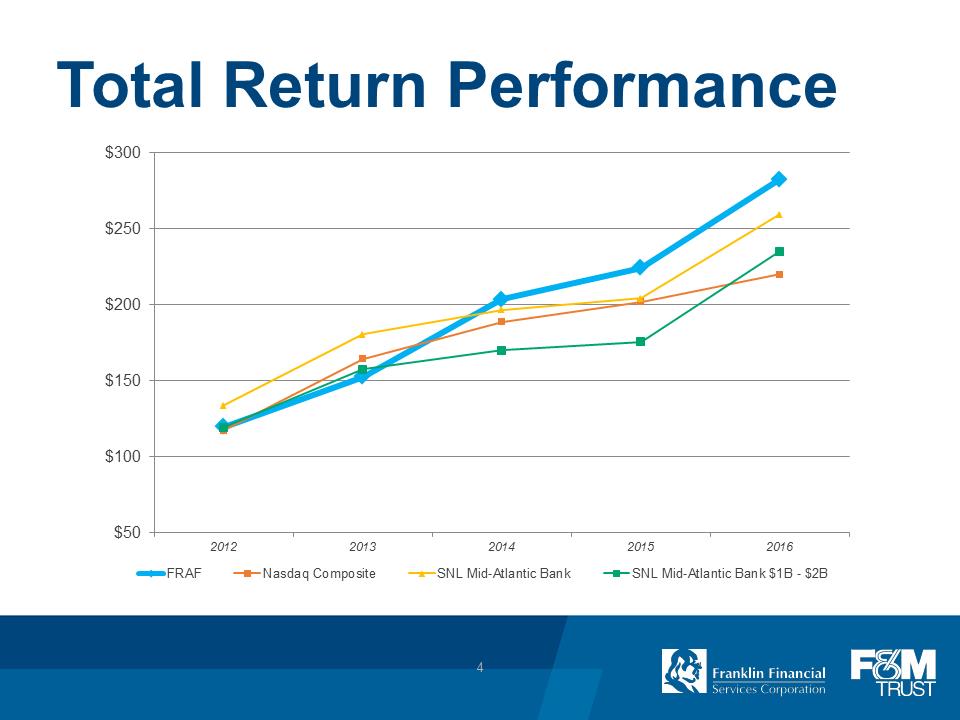

Total Return Performance $300 $250 $200 $150 $100 $50 2012 2013 2014 2015 2016FRAF Nasdaq Composite SNL Mid-Atlantic Bank SNL Mid-Atlantic Bank $1B - $2B 4

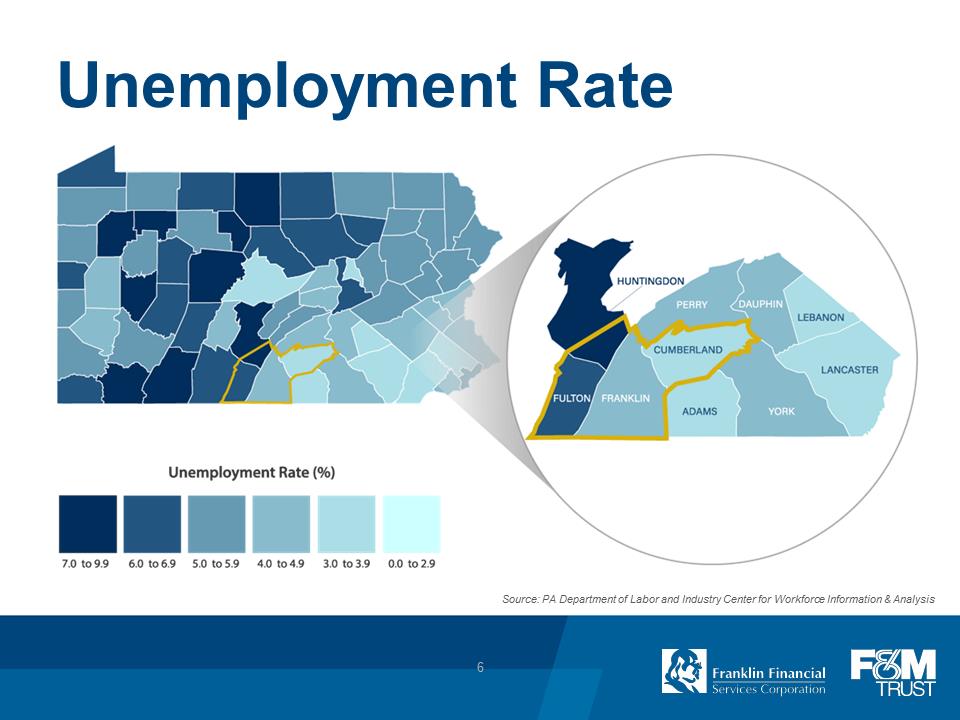

#1 Deposit Market Share in Chambersburg (47.6%) Share#1 Deposit Market Share in Franklin County (32.1%) #1 Deposit Market Share in Fulton County(35.0%) #7 Deposit Market Share in Carlisle (6.2%) #10 Deposit Market Share in Cumberland County (3.2%) 2016 Honorable Mention Source: SNL Financial; 2017 U.S. Financial Institutions Deposit Market Share 6

Management TeamTimothy G. Henry Mark R. Hollar Lorie Heckman Steven D. Butz Lise M. Shehan President & CEO CFO & Treasurer Risk Management Commercial Services Investment & Trust Services Patricia A. Hanks Ronald L. Cekovich Karen K. Carmack Matthew D. Weaver Retail Services Technology Services Human Resources Marketing & Corp. Comm. 8

Management Team Years of Banking Experience Joined F&M Trust Prior Experience Timothy G. Henry 35 2016 Fulton, Centra Bank, BlueRidge Bank, President and CEO Susquehanna Bank, BB&T Mark R. Hollar 29 1994 ValleyBank & Trust CFO and Treasurer Lorie Heckman 31 1986 _ Risk Management Steven D. Butz 322013 PNC, Waypoint, Sovereign, Graystone Commercial Services Tower, Susquehanna Bank Lise M. Shehan 29 2011 Corestates, Fulton, Hershey Trust Co. Investment and Trust Services Patricia A. Hanks 38 1999 Lebanon Valley National Retail Services Ronald L. Cekovich 33 2001 Frederick County National Bank Technology Services Karen K. Carmack 22 2000 ACNB Human Resources Matthew D. Weaver 172014 Susquehanna Bank, Marketing & Corporate Communications Clifton LarsonAllen, IMRE 9

2017 • Focus on Remaining Independent Strategic • Strategic Loan Growth Initiatives • Protection of Net Interest Margin • Expansion of Investment & Trust Services • Emphasis on Development and Utilization of Delivery Channels • Enhancing Our Sales and Service Culture • Development of Marketing Initiatives 10

Loan Portfolio • Focus on the Cumberland County and Capital Region markets • Strengthening of our commercial loan pipeline since April 2015 • Rotation out of loan participations • New additions to local commercial services team Source: The Central Penn Business Journal, February 2016 11

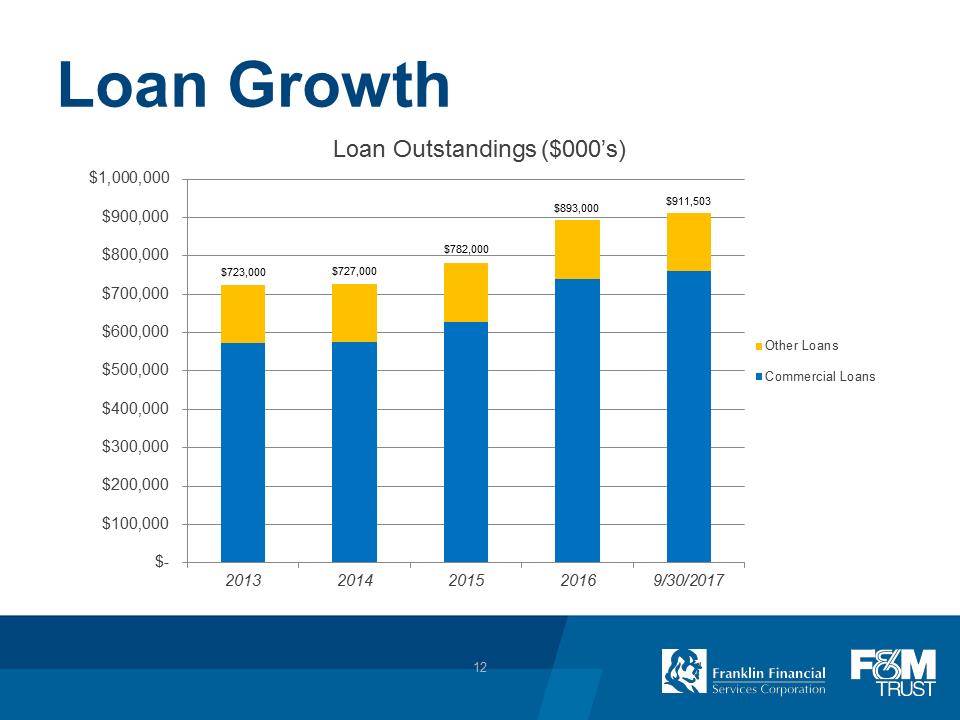

Loan Growth Loan Outstandings ($000’s) $1,000,000 $911,503 $893,000 $900,000 $800,000 $782,000 $723,000 $727,000 $700,000 $600,000Other Loans $500,000 Commercial Loans $400,000 $300,000 $200,000 $100,000 $- 2013 2014 2015 2016 9/30/2017 12

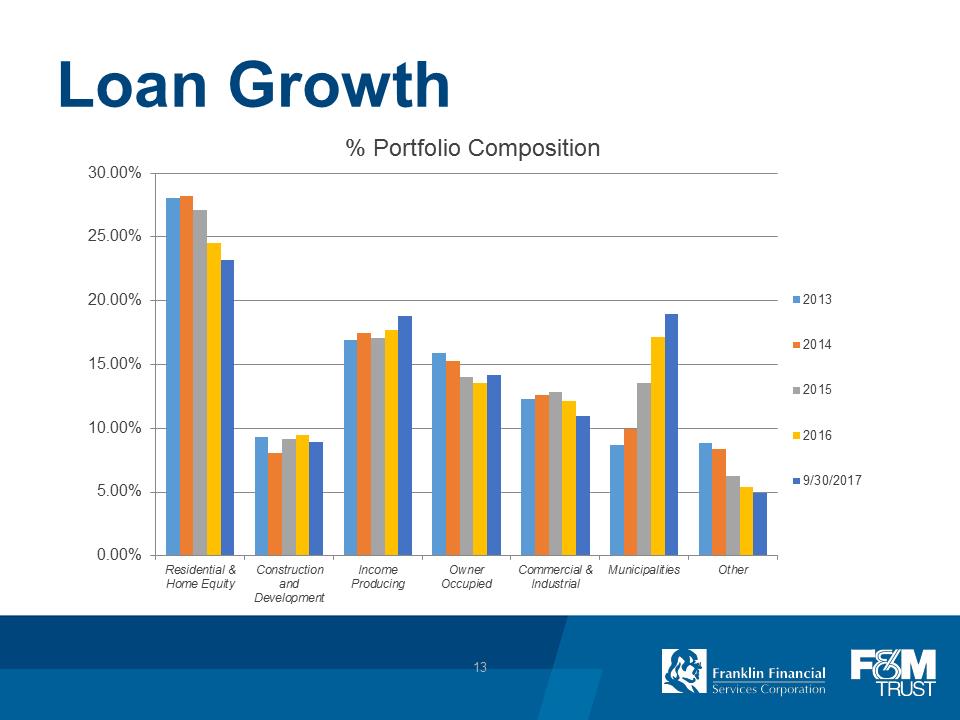

Loan Growth % Portfolio Composition 30.00% 25.00% 20.00 15.00% 10.00% 5.00% 0.00% 2013 2014 2015 2016 9/30/2017Residential & Construction Income Owner Commercial & Municipalities Other Home Equity and Producing Occupied Industrial Development 13

Net Interest Margin • Implementing strategies to improve deposit growth • Creation of Business Banking team with focus on core deposits • Restructured Treasury Management function to include additional resources in Cumberland County / Capital Region • Loan pricing discipline in a rising rate environment 14

Investment & Trust Services • Trust powers since our incorporation in 1906 • Fully integrated trust, investment, insurance and brokerage services, focused exclusively on client needs • Over 300 years of combined financial services experience among our professional staff members • Additional resources in Cumberland, Franklin and Fulton Counties to focus on portfolio expansion and new relationships • 42.8% of total non-interest income in 2016; 45.5% for the first nine months of 2017 15

Delivery Channels • Focus on evolution of online and mobile platforms as primary channel for engagement • Improvement of social networks through enhanced focus on the bank’s website, Facebook and Twitter presence • Growth in online engagement across generational lines (including Generations X, Y & Z) • Continuing to introduce Universal Banker concept to select Community Office locations 16

Delivery Channels “The office transformation not only provides a better experience for our consumer and business customers, but it also breaks down the barriers of traditional banking.” Boiling Springs Community Office and Waynesboro Community Office 17

Sales and Service Culture • Integrated process to continue building sales and service culture • Assessment of sales training program showing quantifiable results • Focus on initiative to improve service experience with external and internal customers • Working across organizational boundaries and breaking down “silos” between departments 18

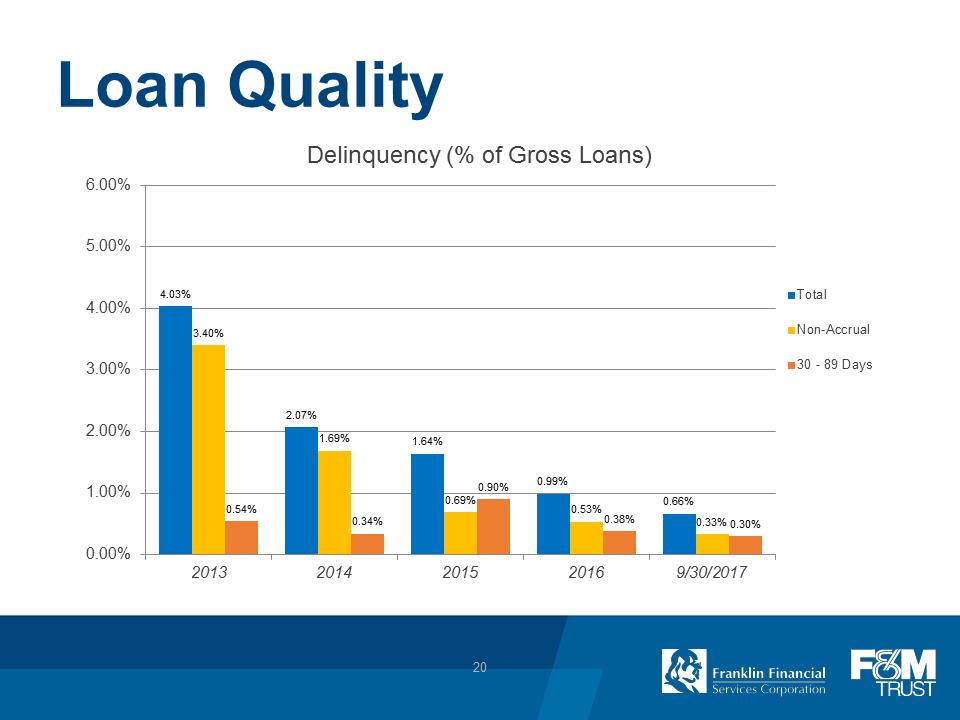

Loan Quality Delinquency (% of Gross Loans) Total Non-Accrual 30 - 89 Days 6.00% 5.00% 4.00% 3.00% 2.00% 1.00% 0.00% 4.03% 3.40% 0.54% 2.07% 1.69% 0.34% 1.64% 0.69% 0.90% 0.99% 0.53% 0.38% 0.66% 0.33% 0.30% 20 2013 2014 2015 2016 9/30/2017

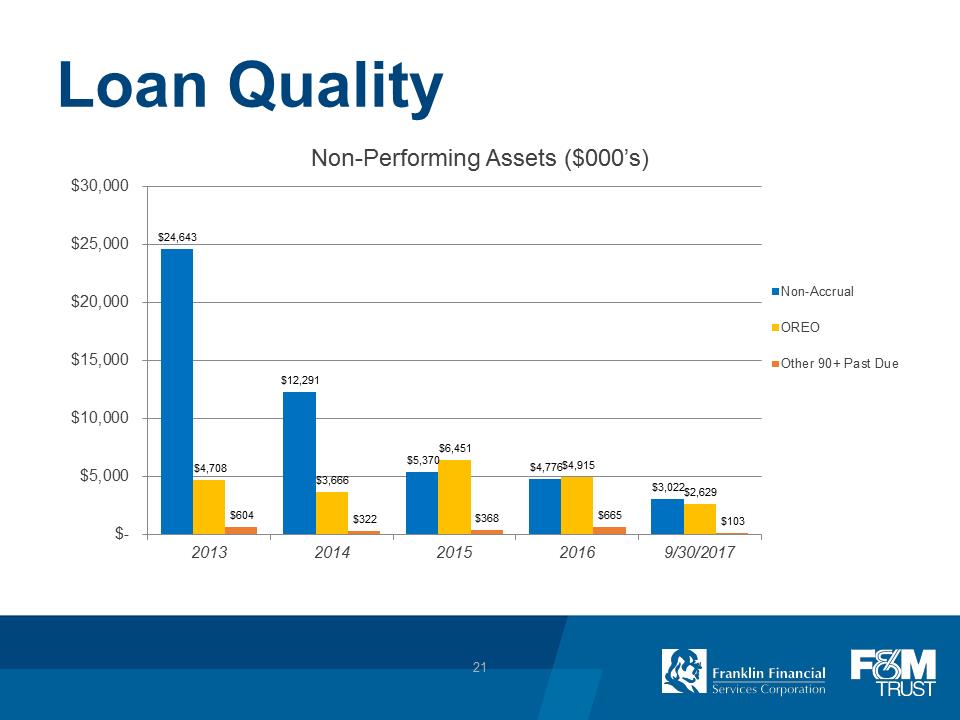

Loan Quality Non-Performing Assets ($000’s) $30,000 $25,000 $20,000 $15,000 $10,000 $5,000 $- $24,643 $4,708 $604 $12,291 $3,666 $322 $5,370 $6,451 $368 $4,776 $4,915 $665 $3,022 $2,629 $103 2013 2014 2015 2016 9/30/2017 21

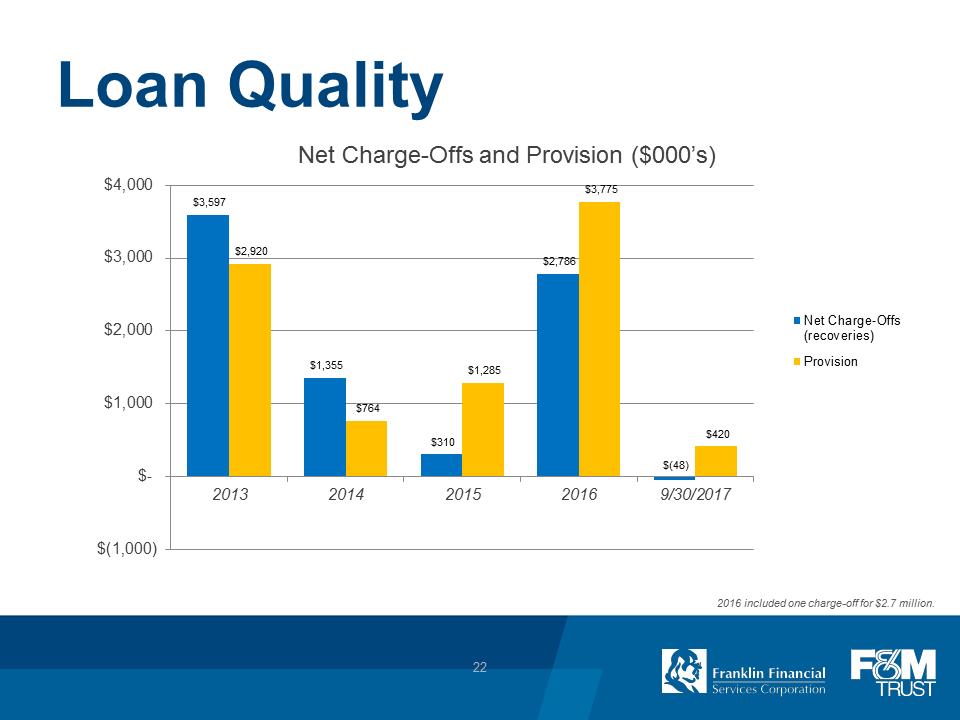

Loan Quality Net Charge-offs and Provision ($000’s) Net Charge-offs (recoveries) Provision $4,000 $3,000 $2,000 $1,000 $- $(1,000) $3,597 $2,920 $1,355 $764 $310 $1,285 $2,786 $3,775 $(48) $420 2013 2014 2015 2016 9/30/2017 2016 includes one charge-off for $2.7 million 22

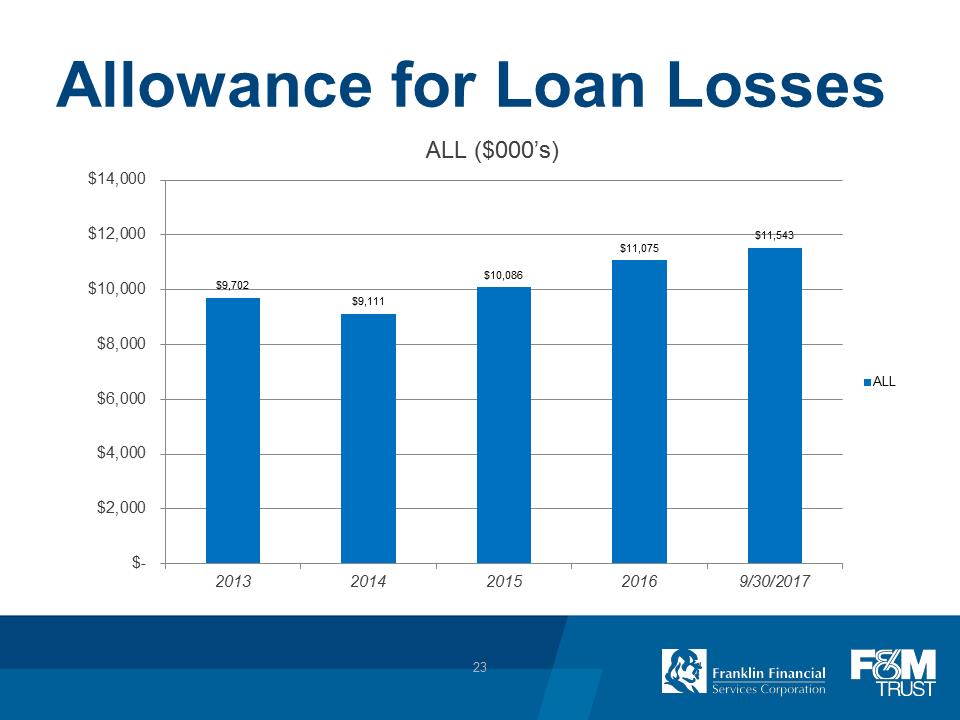

Allowance for Loan Losses ALL ($000’s) $14,000 $12,000 $10,000 $8,000 $6,000 $4,000 $2,000 $- $9,702 $9,111 $10,086 $11,075 $11,543 2013 2014 2015 2016 9/30/2017 23

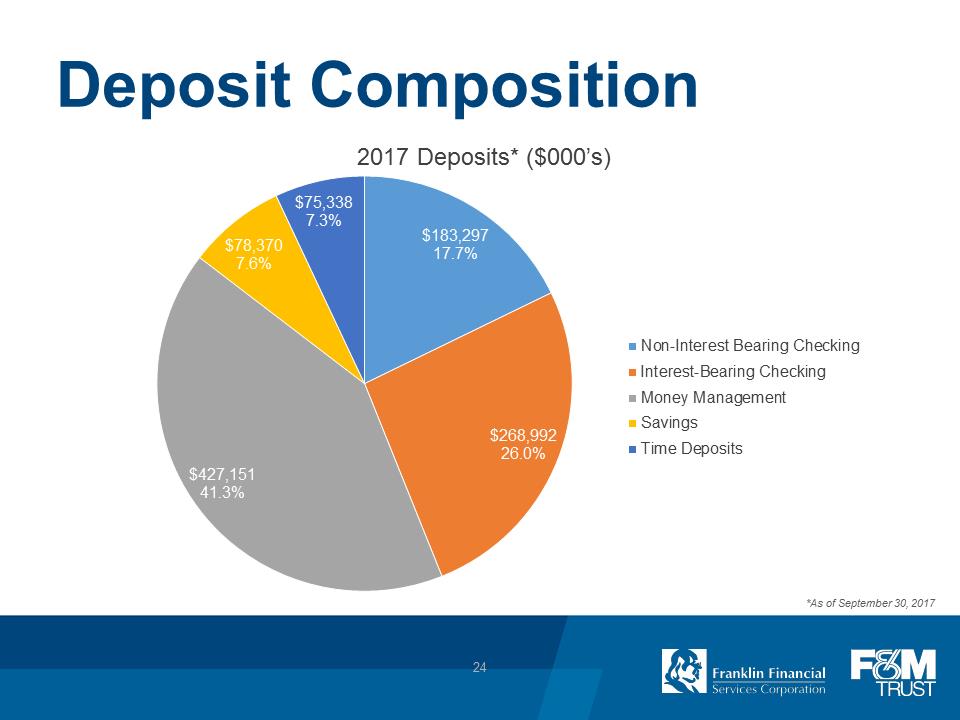

Deposit composition 2017 Deposits* ($000’s) $427,151 41.3% Money Management $268,992 26.0% Interest-bearing Checking $183,297 17.7% Non-interest bearing Checking $78,370 7.6% Savings $75,338 7.3% Time Deposits 24

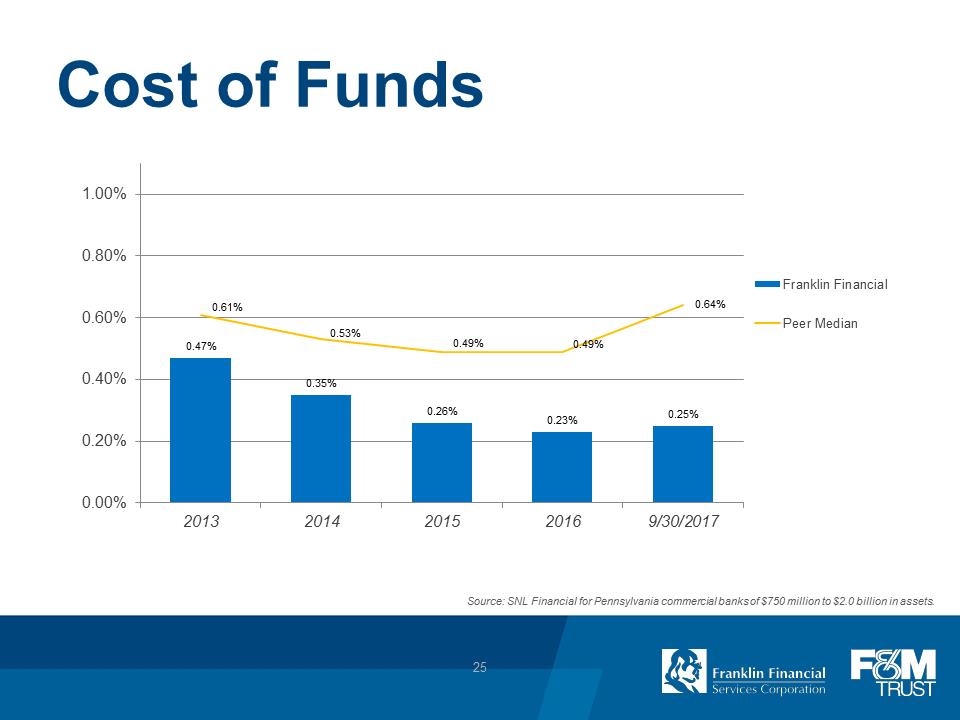

Cost of Funds 1.00% 0.80% 0.60% 0.40% 0.20% 0.00% 0.47% 0.35% 0.26% 0.23% 0.25% 0.61% 0.53% 0.49% .64% 2013 2014 2015 2016 9/30/2017 Franklin Financial Peer Median Source: SNL Financial for Pennsylvania commercial banks of $750 million to $2 billion in assets 25

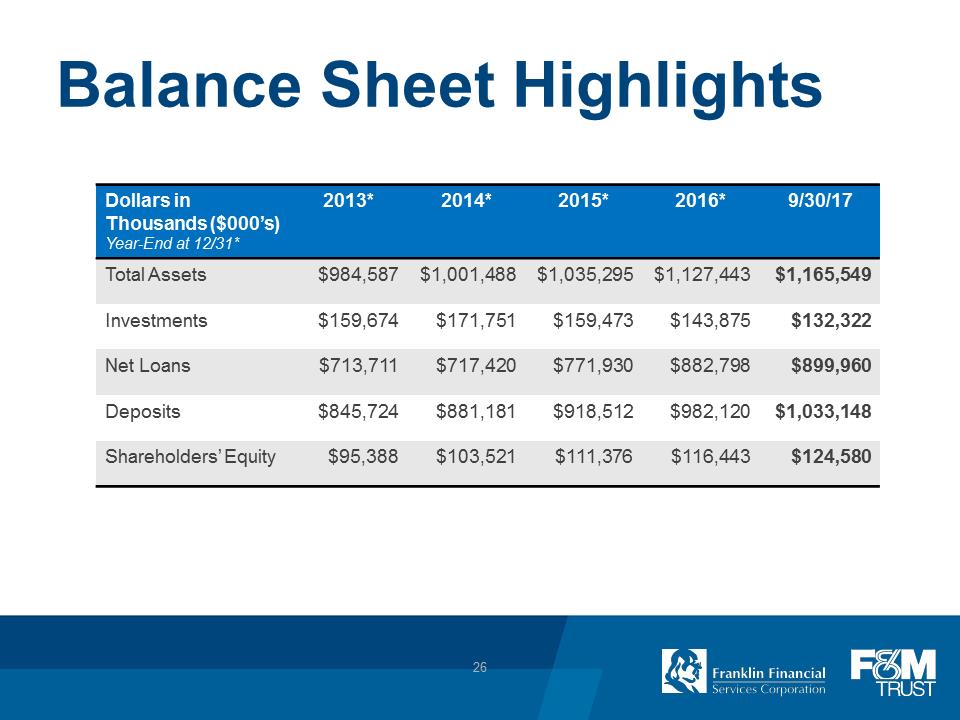

Balance Sheet Highlights Dollars in 2013* 2014* 2015* 2016* 9/30/17 Thousands ($000’s) Year-End at 12/31* Total Assets $984,587 $1,001,488 $1,035,295 $1,127,443 $1,165,549 Investments $159,674 $171,751 $159,473 $143,875 $132,322 Net Loans $713,711 $717,420 $771,930 $882,798 $899,960 Deposits $845,724 $881,181 $918,512 $982,120 $1,033,148 Shareholders’ Equity $95,388 $103,521 $111,376 $116,443 $124,580 26

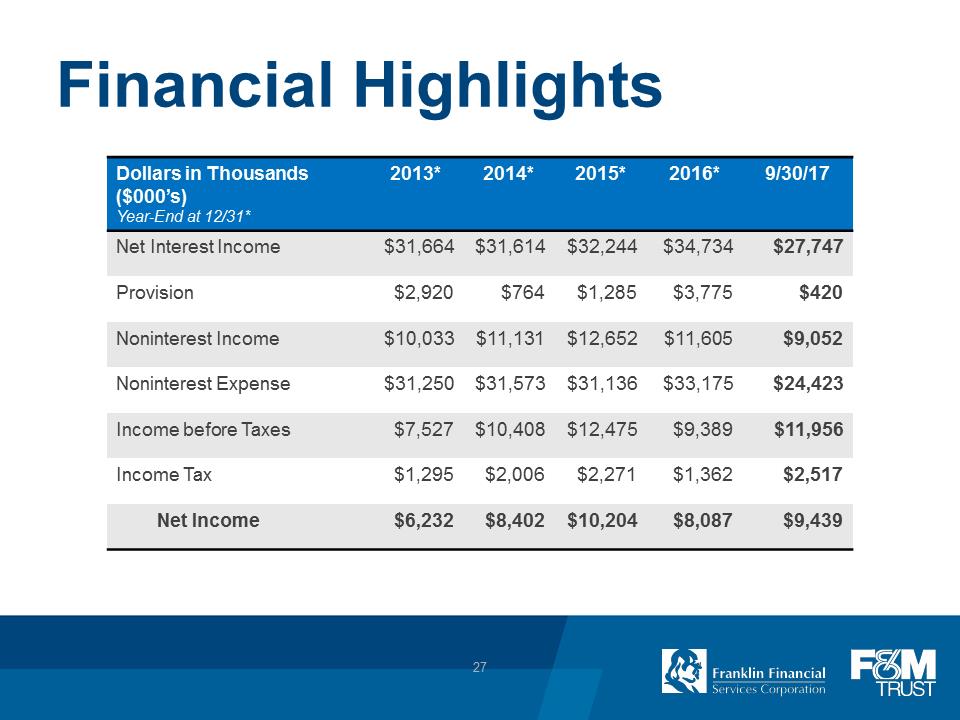

Financial Highlights Dollars in Thousands 2013* 2014* 2015* 2016* 9/30/17 ($000’s) Year-End at 12/31* Net Interest Income $31,664 $31,614 $32,244 $34,734 $27,747 Provision $2,920 $764 $1,285 $3,775 $420 Noninterest Income $10,033 $11,131 $12,652 $11,605 $9,052 Noninterest Expense $31,250 $31,573 $31,136 $33,175 $24,423 Income before Taxes $7,527 $10,408 $12,475 $9,389 $11,956 Income Tax $1,295 $2,006 $2,271 $1,362 $2,517 Net Income $6,232 $8,402 $10,204 $8,087 $9,439 27

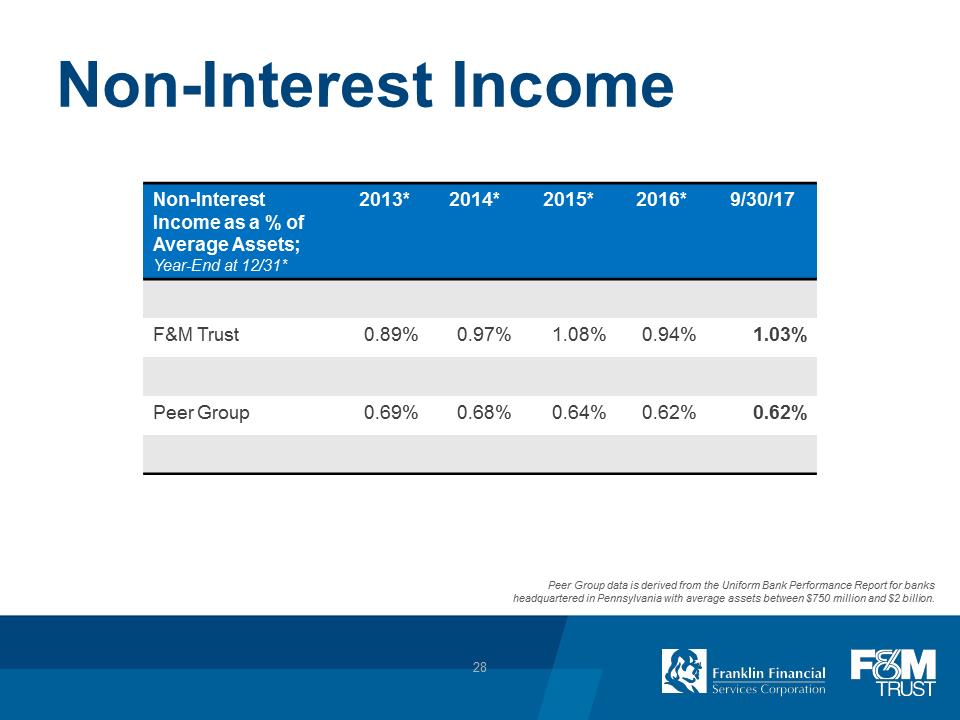

Non-Interest Income Non-Interest 2013* 2014* 2015* 2016* 9/30/17 Income as a % of Average Assets; Year-End at 12/31* F&M Trust 0.89% 0.97% 1.08% 0.94% 1.03% Peer Group 0.69% 0.68% 0.64% 0.62% 0.62% Peer Group data is derived from the Uniform Bank Performance Report for banks headquartered in Pennsylvania with average assets between $750 million and $2 billion. 28

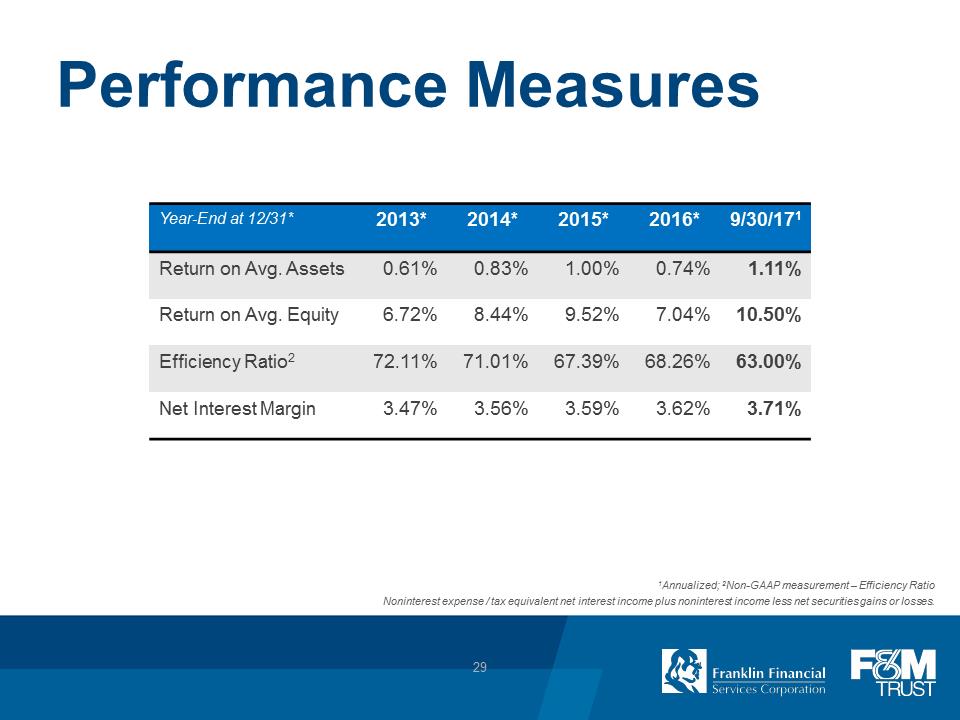

Performance Measures Year-End at 12/31* 2013* 2014* 2015* 2016* 9/30/171 Return on Avg. Assets 0.61% 0.83% 1.00% 0.74% 1.11% Return on Avg. Equity 6.72% 8.44% 9.52% 7.04% 10.50% Efficiency Ratio2 72.11% 71.01% 67.39% 68.26% 63.00% Net Interest Margin 3.47% 3.56% 3.59% 3.62% 3.71% Annualized; Non-GAAP measurement – Efficiency Ratio Noninterest expense / tax equivalent net interest income plus noninterest income less net securities gains or losses. 29

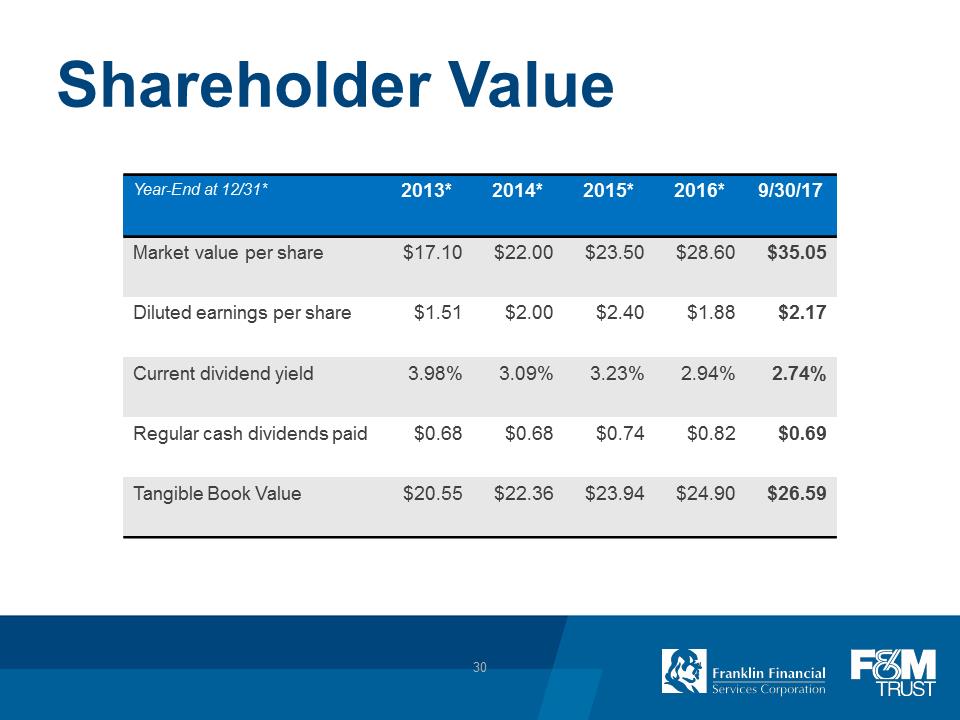

Shareholder Value Year-End at 12/31* 2013* 2014* 2015* 2016* 9/30/17 Market value per share $17.10 $22.00 $23.50 $28.60 $35.05 Diluted earnings per share $1.51 $2.00 $2.40 $1.88 $2.17 Current dividend yield 3.98% 3.09% 3.23% 2.94% 2.74% Regular cash dividends paid $0.68 $0.68 $0.74 $0.82 $0.69 Tangible Book Value $20.55 $22.36 $23.94 $24.90 $26.59 30

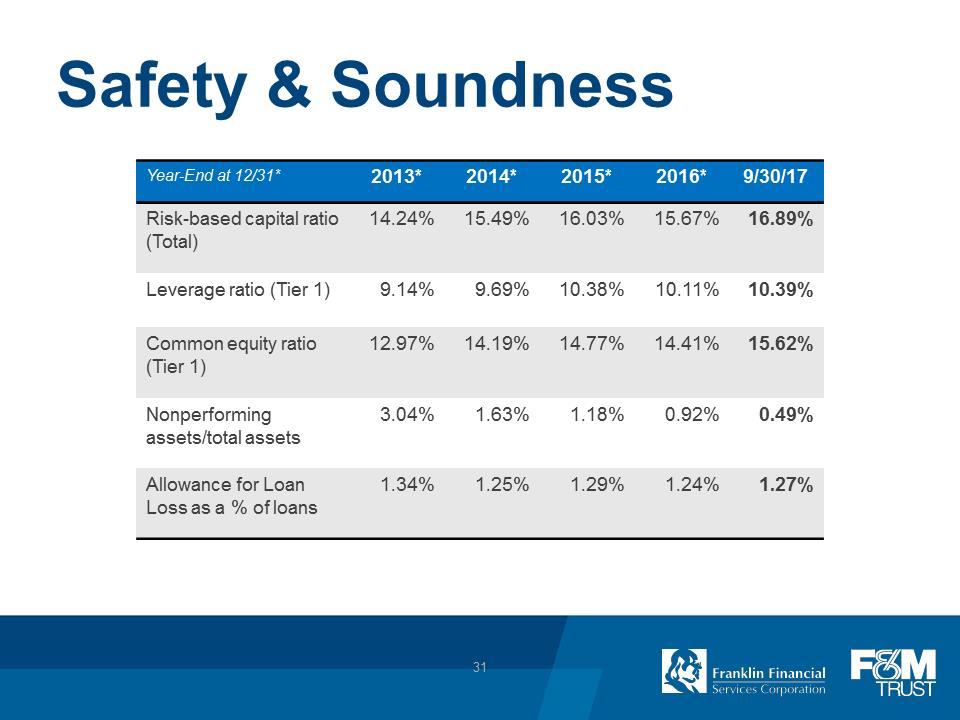

Safety & Soundness Year-End at 12/31* 2013* 2014* 2015* 2016* 9/30/17 Risk-based capital ratio (Total) 14.24% 15.49% 16.03% 15.67% 16.89% Leverage ratio (Tier 1) 9.14% 9.69% 10.38% 10.11% 10.39% Common equity ratio (Tier 1) 12.97% 14.19% 14.77% 14.41% 15.62% Nonperforming assets/total assets 3.04% 1.63% 1.18% 0.92% 0.49% Allowance for Loan Loss as a % of loans 1.34% 1.25% 1.29% 1.24% 1.27% 31

Liquidity • Federal Home Loan Bank – Excess Borrowing $310,000,000 • Federal Reserve Bank – Discount Window $20,000,000 • Correspondent Bank – Line of Credit $6,000,000 32

Stock Symbol: FRAF (OTCQX) www.franklinfin.com www.fmtrustonline.com 33