If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with section 8(a) of the Securities Act of 1933 or until this registration statement shall become effective on such date as the Commission, acting pursuant to said section 8(a), may determine.

This Post-Effective Amendment No. 1 (“PEA”) to the Form S-3 Registration Statement No. 333-267670 (“Registration Statement”) of The Lincoln National Life Insurance Company is being filed for the purpose of including in the Registration Statement the additions/modifications reflected in the Supplement. A new crediting method and several new Indexed Accounts are being added to the Registration Statement. Part II has also been updated pursuant to the requirements of Form S-3. This PEA does not amend any other part of the Registration Statement except as specifically noted herein.

THE LINCOLN NATIONAL LIFE INSURANCE COMPANY

Lincoln Level Advantage 2SM B-Share Index-Linked Annuity

Lincoln Level Advantage 2SM Access Index-Linked Annuity

Lincoln Level Advantage 2SM Advisory Index-Linked Annuity

Lincoln Level Advantage 2SM Advisory Class Index-Linked Annuity

Lincoln Level Advantage 2SM Select Index-Linked Annuity

Supplement dated _______, 2023 to the Prospectus dated February 1, 2023

This supplement describes changes to the prospectus for your Lincoln Level Advantage 2SM Index-Linked Annuity contract. It is for informational purposes and requires no action on your part. All other provisions in your prospectus remain unchanged.

OVERVIEW

Several new Indexed Accounts will be available on new contracts beginning ____, 2023. Each account offers a 1-year Indexed Term, a 10% Protection Level, and a Dual Performance Trigger Rate. You can find complete details about all the features of your contract in your prospectus.

DESCRIPTION OF CHANGES

The following Indexed Accounts are available for new contractowners beginning _____, 2023:

1-Year Dual Performance Trigger Rate Indexed Account with Protection Level

| • | S&P 500® Dual Performance Trigger, 10% Protection |

| • | Russell 2000® Dual Performance Trigger, 10% Protection |

| • | Capital Strength Net Fee IndexSM Dual Performance Trigger, 10% Protection |

| • | First Trust American Leadership IndexTM Dual Performance Trigger, 10% Protection |

| • | iShares® MSCI ACWI ETF Dual Performance Trigger, 10% Protection |

The following is a discussion describing changes that are now incorporated into the sections of your prospectus as specified.

Special Terms – The following term is added to the Special Terms section:

Dual Performance Trigger Rate –The rate used to determine the Performance Rate for an Indexed Segment at the end of an Indexed Term if the Index performance is positive, negative, or equal to zero.

Risk Factors – In addition to those Risk Factors outlined in Risks of Investing in the Indexed Accounts section, the following potential risk is associated with Dual Performance Trigger Rate Indexed Accounts and is added to the Risks of Investing in the Indexed Accounts section.

| • | Gains in your Indexed Segment are limited by any applicable Dual Performance Trigger Rate. If the performance of the Index is zero, positive, or negative, a specified rate is used to determine the Segment Ending Value. The Dual Performance Trigger Rate may be lower than the actual performance of the Index, which means that your return could be lower than if you had invested directly in a fund based on the applicable Index. The Dual Performance Trigger Rate applies for the full term of the Indexed Segment. The Dual Performance Trigger Rate will be lower for contracts with the Guarantee of Principal Death Benefit. Dual Performance Trigger Rates for new Segments will be declared at least 5 business days in advance of the beginning of a Segment. |

The Investments of the Indexed Accounts section is changed as follows:

The following Indexed Accounts are added to the list of available Indexed Accounts, noted as being available to new contracts beginning ______, 2023:

Indexed Accounts with Dual Performance Trigger Rates:

1-Year Dual Performance Trigger Rate Indexed Account with Protection Level

| • | S&P 500® Dual Performance Trigger, 10% Protection |

| • | Russell 2000® Dual Performance Trigger, 10% Protection |

| • | Capital Strength Net Fee IndexSM Dual Performance Trigger, 10% Protection |

| • | First Trust American Leadership IndexTM Dual Performance Trigger, 10% Protection |

| • | iShares® MSCI ACWI ETF Dual Performance Trigger, 10% Protection |

The following line item is added to the chart in the Crediting Methods and Protection Levels section:

Dual Performance Trigger Rate •1-Year Dual Performance Trigger Rate – 1.00% minimum rate | You receive the Dual Performance Trigger Rate 1) if the Index performance is zero, positive, or negative within the Protection Level; or 2) if the percentage change in the Index Value is down more than the Protection Level the Dual Performance Trigger Rate is used to offset loss, which may provide a positive return. |

The following section is added as a new section immediately prior to the Protection Levels section:

Dual Performance Trigger Rates – The

Dual Performance Trigger Rate is a rate of return for an Index Segment that we declare at the beginning of the Indexed Term. It is used to determine the Segment Ending Value if the Index return for the Indexed Term is zero, positive, or negative. The Dual Performance Trigger Rate will not change during the Indexed Term unless

Secure Lock+

SM feature is elected.

The Dual Performance Trigger Rate may vary depending on the Death Benefit option, the Index, the Term, and the Protection Level.

The initial Dual Performance Trigger Rate applies to the initial Indexed Term. Indexed Segments with a Guarantee of Principal Death Benefit will have lower Dual Performance Trigger Rates than Indexed Segments with the Account Value Death Benefit. The Company will declare, at its discretion, a Dual Performance Trigger Rate for each subsequent Indexed Term. Subsequent Dual Performance Trigger Rates may differ from the Dual Performance Trigger Rate used for new Contracts or for other Contracts issued at different times.

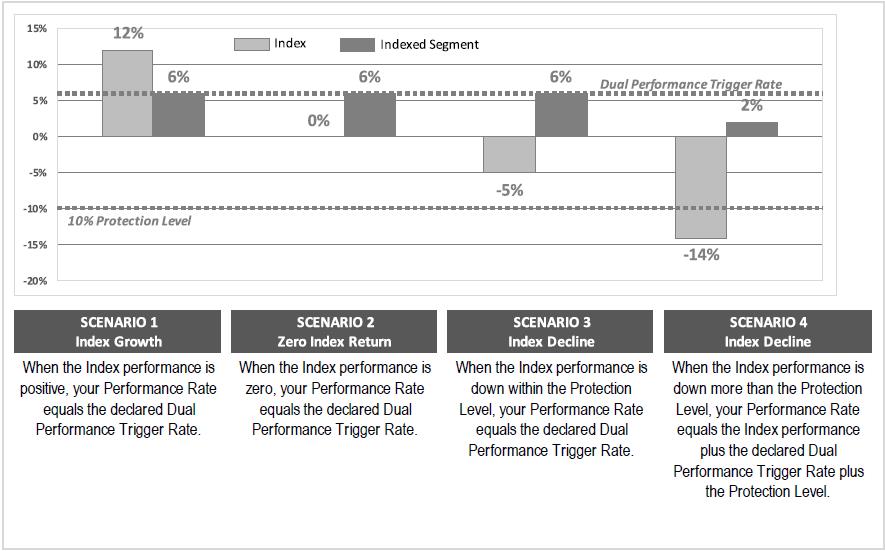

The Performance Rate is the percentage change in the Index Value from the Start Date to the End Date, adjusted by the Protection Level and the Dual Performance Trigger Rate. The Performance Rate can be positive, negative, or zero. The percentage change in the Index Value is calculated by subtracting the Index Value on the Start Date from the Index Value on the End Date, with the difference then divided by the Index Value on the Start Date. The daily Index Value is posted on the Index’s website. If an Index Value is not published for a particular day, we will use the Index Value at the close of the next Valuation Date the Index is published.

If the percentage change of the Index Value is greater than or equal to zero on the End Date, the Performance Rate is equal to the Dual Performance Trigger Rate. If the percentage change in the Index Value is less than zero, but the percent decline is not greater than the amount of the Protection Level, the Performance Rate is equal to the Dual Performance Trigger Rate. If the percentage change in the Index Value is less than zero, and the percent decline is greater than the amount of the Protection Level, the Performance Rate is the percentage change in the Index Value, plus the Dual Performance Trigger Rate, plus the Protection Level.

The amount credited to or deducted from the Indexed Segment is equal to the Performance Rate multiplied by the Indexed Crediting Base on the End Date. This will be used to determine the Segment Ending Value as set forth below. The Indexed Crediting Base is the amount that you allocated to the Indexed Segment, less any reallocations and withdrawals during the Indexed Term deducted proportionately by the amount that the reallocation or withdrawal reduced the Interim Value. Withdrawals include any applicable surrender charge, Interest Rate Adjustments, premium tax or rider fees and charges. If the Performance Rate is positive, the value of your Indexed Segment will increase. If the Performance Rate is negative (after calculation including the Protection Level), the value of your Indexed Segment will be reduced. If the Performance Rate is zero, the value of your Indexed Segment will not change.

The Indexed Crediting Base is used only to calculate the performance of Indexed Accounts on the End Date, to calculate the Interim Value, and to calculate any Interest Rate Adjustment that may apply. This amount is not available for surrender, withdrawal, reallocation, annuitization, or as a Death Benefit.

Depending on market conditions, subsequent Dual Performance Trigger Rates may be higher or lower than the initial Dual Performance Trigger Rate. Subsequent Dual Performance Trigger Rates may differ from the Dual Performance Trigger Rate used for new contracts or for other contracts issued at different times. The Company will determine new Dual Performance Trigger Rates on a basis that does not discriminate unfairly within any class of contracts.

The following bullet is added to the Crediting Methods Considerations section:

| • | If you choose an Indexed Segment with a Dual Performance Trigger Rate, and there is positive performance, the Performance Rate on the Indexed Segment End Date could be lower, possibly significantly lower, than the actual index return. |

The Protection Level Considerations section is re-stated as follows:

Protection Level Considerations. You should choose a level of protection that is consistent with your risk tolerance and investment objectives.

| • | For accounts with a Performance Cap, Participation Rate, Performance Trigger Rate, or Spread Rate, if there is negative index performance, we absorb the first portion of the negative performance up to the stated percentage and you bear the risk of loss after your chosen Protection Level, including the loss of any previously credited amount. |

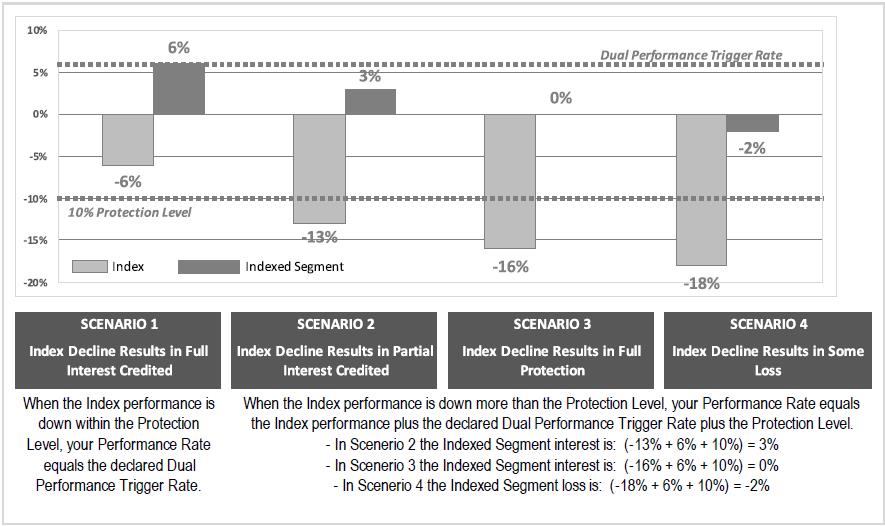

| • | For accounts with a Dual Performance Trigger Rate, if there is negative index performance, we absorb the first portion of the negative performance up to the stated percentage of the Protection Level. If there is negative index performance beyond the Protection Level, we continue to absorb the portion of the negative performance up to the stated percentage of the Dual Performance Trigger Rate. For example, if the Dual Performance Trigger Rate is 5%, we would absorb the first 5% of loss beyond the Protection Level. You bear the risk of loss thereafter, including the loss of any previously credited amount. |

The following disclosure is added in the Protection Levels section:

For the Dual Performance Trigger Indexed Accounts, the Protection Level is used to determine the Performance Rate on the End Date of the Segment when there is negative Index performance. If the percentage change in the Index Value is less than zero, but the percent decline is not greater than the amount of the Protection Level, the Performance Rate is equal to the Dual Performance Trigger Rate. However, if the percentage change in the Index Value has decreased by a greater percentage than the Protection Level then the amount of your investment in the Indexed Segment may be reduced. The Performance Rate would equal the percentage change in the Index Value, plus the Dual Performance Trigger Rate, plus the Protection Level. The amount of loss or gain is dependent on the percentage change in the Index Value, the Dual Performance Trigger Rate and the Protection Level on the Indexed Segment.

ADDITIONAL INFORMATION – Information Incorporated by Reference. The second paragraph of this section of the prospectus is re-stated as follows:

Lincoln Life files reports and other information with the SEC, as required under the Securities Exchange Act of 1934 (“the Exchange Act”). Lincoln Life’s annual report on Form 10-K for the year ended December 31, 2022, as well as Lincoln Life’s quarterly reports filed on Form 10-Q, for the periods ending March 31, 2023 (TBD), respectively, are incorporated by reference into this prospectus. Lincoln Life’s annual reports contain information about Lincoln Life, including its consolidated audited financial statements for Lincoln Life’s latest fiscal year. Lincoln Life files its Exchange Act documents and reports (including annual reports on Form 10-K, quarterly reports on Form 10-Q, and current reports on Form 8-K) electronically with the SEC under File No. 000-55871. In addition, all documents subsequently filed by Lincoln Life pursuant to sections 13(a), 13(c), 14 or 15(d) of the Exchange Act prior to the termination of this offering are also incorporated by reference into this prospectus. We are not incorporating by reference, in any case, any documents or information deemed to have been furnished and not filed in accordance with SEC rules.

APPENDIX A – The following example is added to Appendix A of your prospectus.

Interim Value for Indexed Segment(s) with Dual Performance Trigger Rates and Protection Level

The Interim Value of a Segment is equal to the sum of (1) and (2), where:

(1) is the value of the fixed income asset proxy of a Segment on the Valuation Date the Interim Value is calculated. It is determined for a Segment as C x [1 + (D x (E - 1))] where:

C = the Crediting Base of the Segment on the Valuation Date of the calculation.

D = the ask price of the derivative asset proxy as a percentage of the Crediting Base on the Start Date of the Segment.

If an election to lock and reset a Segment is exercised during a Term:

D = the ask price of the derivative asset proxy on the most recent Valuation Date that the Segment was reset as a percentage of the Crediting Base.

E = the total days elapsed in the Term divided by the total days in the Term.

If an election to lock and reset a Segment is exercised during the Term:

E = the total days elapsed in the Term since the most recent Valuation Date that the Segment was reset divided by the total days in the Term. The total days in the Term is measured from the most recent Valuation Date that the Segment was reset to the End Date of the Term.

(2) is the fair value of the derivative asset proxy, determined solely by Us, on any Valuation Date that the Interim Value is calculated for a Segment.

The Derivative Asset Proxy section of Appendix A is restated as follows:

2. Derivative Asset Proxy. This is meant to represent the fair market value methodology we use to value the replicating portfolio of derivatives that support the Indexed Accounts.

For each Segment, we solely designate and value derivatives, each of which is tied to the performance of the index associated with the Segment and consider the Crediting Method and Protection Level of the Segment. These are used to estimate the gain or loss on the market value of the derivative portfolio replicating the Segment on a given Valuation Date and considers the cost of exiting the portfolio prior to the End Date of the Segment.

The valuation of the derivatives is based on standard, market consistent methodologies and inputs from recognized market data service providers. The methodology used to value these derivatives is determined solely by us and may vary, higher or lower, from other estimated valuations or the actual selling price of identical derivatives. Any variance between our estimated fair value price and other estimated or actual prices may be different from Segment type to Segment type and may also change from day to day. Additionally, inputs obtained from these outside market data service providers may vary over time based on market conditions and changes in valuation standards.

If any of the values used to calculate the derivative asset proxy are delayed and prevent us from calculating the Interim Value on a particular Valuation Date, we will use the prior business day’s value to calculate the Interim Value.

The options or other instruments valued for each Indexed Account type are as follows:

| A. | At-the money call option: This represents the market value of the potential to receive an amount equal to the percentage growth in the Index during the Indexed Term. |

| B. | Out-of-the-money call option: This represents the market value of the potential for gain in excess of the Performance Cap rate or Spread Rate, as applicable. |

| C. | Digital option: This represents the market value of the option to provide the Performance Trigger Rate under zero or positive Index returns. |

| D. | Out-of-the-money put option: This represents the market value of the potential to receive an amount equal to the excess loss beyond the Protection Level. |

| E. | U.S. Treasury bond: This represents the market value of the bond to provide the Dual Performance Trigger Rate. |

Note: Put option D will always reduce the Interim Value even if the Index has increased during the Indexed Term.

For each Segment with a Performance Cap Rate and Protection Level,

the replicating portfolio of derivatives is equal to: A minus B minus D.

For each Segment with a Participation Rate and Protection Level, the replicating portfolio of derivatives is equal to: A multiplied by the Participation Rate minus D.

For each Segment with a Performance Trigger Rate and Protection Level, the replicating portfolio of derivatives is equal to: C minus D.

For each Segment with a Spread Rate and Protection Level, the replicating portfolio of derivatives is equal to: B minus D.

For each Segment with a Dual Performance Trigger Rate and Protection Level, the replicating portfolio of derivatives is equal to: E minus D.

The key inputs, including but not limited to the following, are also incorporated into the models:

| (1) | Implied Volatility of the Index—This input varies with (i) how much time remains until the Segment End Date, which is determined by using an expiration date for the designated derivative that corresponds to that time remaining and (ii) the relationship between the strike price of that derivative and the level of the Index at the time of the calculation. |

This relationship is referred to as the “moneyness” of the derivative described above, and is calculated as the ratio of current price to the strike price. Direct market data for these inputs for any given early withdrawal is generally not available. This is because derivatives on the Index that actually trade in the market have specific maturity dates and moneyness values that are unlikely to precisely match the Segment End Date and moneyness of the designated derivative that we use in our calculations. Accordingly, we interpolate between the implied volatility quotes that are based on the actual maturities and moneyness values.

(2) Interest Rate—We use interest rates, as applicable for each instrument, obtained from information provided by independent third parties which are recognized financial reporting vendors. Interest rates are obtained for maturities adjacent to the actual time remaining in the Segment at the time of the early withdrawal. We use linear interpolation to derive the exact remaining duration rate needed as the input.

(3) Index Dividend Yield—On a daily basis, we use the projected annual dividend yield across the entire Index obtained from information provided by independent third-party financial institutions. This value is a widely used assumption and is readily available from recognized financial reporting vendors. In addition, when we calculate the Interim Value, we obtain market values of derivatives each business day from outside vendors. Inputs obtained from these outside vendors may vary over time based on market conditions and changes in valuation standards. If we are delayed in receiving these values, we will use the prior business day’s values to calculate the Interim Value.

The following examples are added to the Examples section of Appendix A.

The following examples demonstrate how the Interim Value is calculated in different scenarios for Indexed Segments with Dual Performance Trigger Rates and Protection Levels.

| | | 1 Year | | | 1 Year | |

| Indexed Term length …………………………………………………………. | | 12 months | | | 12 months | |

| Months since Indexed Term Start Date ……………………………………. | | | 9 | | | | 3 | |

| Indexed Crediting Base ……………………………………………………… | | $ | 1,000 | | | $ | 1,000 | |

| Protection Level ………………………………………………………………. | | | 10 | % | | | 10 | % |

| Dual Performance Trigger Rate…………………………………………….. | | | 6 | % | | | 6 | % |

| Months to End Date ………………………………………………………….. | | | 3 | | | | 9 | |

| Change in Index Value is -15% | | 1 Year | | | 1 Year | |

| 1. Fair Value of Indexed Crediting Base …………….…………………… | | $ | 1,023 | | | $ | 996 | |

| 2. Fair Value of Replicating Portfolio of Options………………………….. | | $ | (40 | ) | | $ | (40 | ) |

| A. Sum of 1 + 2 …………………………………………………………….. | | $ | 983 | | | $ | 956 | |

| Account Interim Value ………………………..…………………………….. | | $ | 983 | | | $ | 956 | |

| Change in Index Value is -5% | | 1 Year | | | 1 Year | |

| 1. Fair Value of Indexed Crediting Base …………….…………………… | | $ | 1,023 | | | $ | 996 | |

| 2. Fair Value of Replicating Portfolio of Options………………………….. | | $ | 8 | | | $ | 3 | |

| A. Sum of 1 + 2 …………………………………………………………….. | | $ | 1,031 | | | $ | 999 | |

| Account Interim Value ……………………….…………………………….. | | $ | 1,031 | | | $ | 999 | |

| Change in Index Value is 10% | | 1 Year | | | 1 Year | |

| 1. Fair Value of Indexed Crediting Base …………….…………………… | | $ | 1,023 | | | $ | 996 | |

| 2. Fair Value of Replicating Portfolio of Options………………………….. | | $ | 27 | | | $ | 31 | |

| A. Sum of 1 + 2 …………………………………………………………….. | | $ | 1,050 | | | $ | 1,027 | |

| Account Interim Value ……………………………………………………….. | | $ | 1,050 | | | $ | 1,027 | |

| Change in Index Value is 20% | | 1 Year | | | 1 Year | |

| 1. Fair Value of Indexed Crediting Base …………….…………………… | | $ | 1,023 | | | $ | 996 | |

| 2. Fair Value of Replicating Portfolio of Options………………………….. | | $ | 30 | | | $ | 39 | |

| A. Sum of 1 + 2 …………………………………………………………….. | | $ | 1,053 | | | $ | 1,035 | |

| Account Interim Value ……………………….…………………………….. | | $ | 1,053 | | | $ | 1,035 | |