UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-3896 | ||||||||

| |||||||||

FPA U.S. VALUE FUND, INC. | |||||||||

(Exact name of registrant as specified in charter) | |||||||||

| |||||||||

11601 WILSHIRE BLVD., STE. 1200 LOS ANGELES, CALIFORNIA |

| 90025 | |||||||

(Address of principal executive offices) |

| (Zip code) | |||||||

| |||||||||

J. RICHARD ATWOOD, PRESIDENT FPA U.S. VALUE FUND, INC. 11601 WILSHIRE BLVD., STE. 1200 LOS ANGELES, CALIFORNIA 90025 | Copy to:

MARK D. PERLOW, ESQ. DECHERT LLP ONE BUSH STREET, STE. 1600 SAN FRANCISCO, CA 94104 | ||||||||

(Name and address of agent for service) |

| ||||||||

| |||||||||

Registrant’s telephone number, including area code: | (310) 473-0225 |

| |||||||

| |||||||||

Date of fiscal year end: | December 31 |

| |||||||

| |||||||||

Date of reporting period: | December 31, 2016 |

| |||||||

Item 1: Report to Shareholders.

Annual Report

FPA U.S. Value Fund, Inc.

December 31, 2016

Distributor:

UMB DISTRIBUTION SERVICES, LLC

235 West Galena Street

Milwaukee, Wisconsin 53212

FPA U.S. VALUE FUND, INC.

LETTER TO SHAREHOLDERS

Dear Fellow Shareholders,

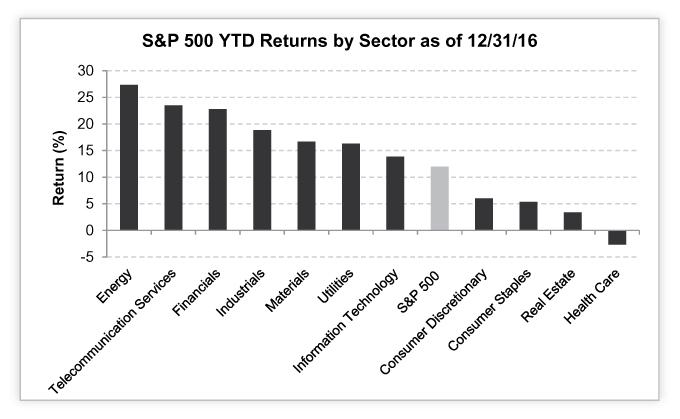

In the fourth quarter, FPA U.S. Value Fund (the "Fund") gained 4.12%. It outperformed the total return of the S&P 500 and the Morningstar Large Blend Fund Average by 0.30% and 0.26%, respectively. For calendar 2016, the Fund returned -2.00% compared to the S&P 500 and the Morningstar Large Blend Fund Average returns of 11.96% and 10.37%, respectively.1

While the Fund outperformed in the fourth quarter, it underperformed in 2016. This was largely driven by sector exposures. During 2016, the Fund had no exposure to Energy, Telecommunications Services, Materials and Utilities — four of the top-performing sectors. Additionally, the Fund was underweight Financials, Industrials and Information Technology — three other top-performing sectors. At the same time, the Fund was heavily overweight Consumer Discretionary and Healthcare — two of the worst-performing sectors in the market. Lastly, the Fund held approximately 10% of cash on average throughout the year.

Source: S&P Dow Jones Indices LLC.

1 Source: Morningstar.

1

FPA U.S. VALUE FUND, INC.

LETTER TO SHAREHOLDERS

(Continued)

Key Performers

It is worth re-emphasizing that the Fund's sector exposures are not driven by a top-down view. Rather, they are based on where I believe the market offers high-quality businesses within secularly healthy, growing industries at attractive valuations.

Within healthcare, the majority of the Fund's exposure is in the pharmaceutical services industry, which has been under pressure in part because of public criticism over the ever-increasing prices of branded drugs. For 2016, the healthcare services industry was down over 8%.

Source: Google Finance. Past performance is no guarantee of future results.

In 2016 and the three previous U.S. Presidential elections, the pharmaceutical supply chain underperformed the market in the year prior to the vote. However, in the year following the 2004, 2008 and 2012 U.S. Presidential elections, the industry enjoyed meaningful outperformance. Of course, past performance does not guarantee future results.

2

FPA U.S. VALUE FUND, INC.

LETTER TO SHAREHOLDERS

(Continued)

Sources: Bloomberg, J.P. Morgan

| Winners2 | Performance Contribution | Losers2 | Performance Contribution | ||||||||||||

Tempur Sealy International | 1.40 | % | McKesson | -1.07 | % | ||||||||||

Time Warner | 0.88 | % | CVS Health | -0.61 | % | ||||||||||

Twenty First Century Fox | 0.83 | % | Cardinal Health | -0.44 | % | ||||||||||

Anthem | 0.66 | % | Houghton Mifflin Harcourt | -0.40 | % | ||||||||||

CBS Corp | 0.61 | % | Walgreens Boots Alliance | -0.22 | % | ||||||||||

| YTD 2016 Winners2 | Performance Contribution | YTD 2016 Losers2 | Performance Contribution | ||||||||||||

Time Warner | 1.99 | % | Houghton Mifflin Harcourt | -2.03 | % | ||||||||||

CBS | 1.43 | % | McKesson | -1.85 | % | ||||||||||

Tempur Sealy International | 1.26 | % | CVS Health | -0.98 | % | ||||||||||

Whirlpool | 1.12 | % | Bayerische Motoren Werke | -0.81 | % | ||||||||||

Ingersoll-Rand | 0.81 | % | Cardinal Health | -0.71 | % | ||||||||||

The Fund's top five winners for the fourth quarter contributed approximately 4.37%, while its top five losers cost the Fund approximately 2.75%. For the calendar year 2016, the Fund's top five winners contributed approximately 6.61%, while its top five losers cost the Fund approximately 6.37%. Media helped the Fund's performance in the

2 Reflects the top contributors and top detractors to the Fund's performance based on contribution to return for the quarter. Contribution is presented as the gross of investment management fees, transactions costs, and Fund operating expenses, which if included, would reduce the returns presented.

3

FPA U.S. VALUE FUND, INC.

LETTER TO SHAREHOLDERS

(Continued)

fourth quarter and throughout 2016 with three and two of the top five winners, respectively. Conversely, pharmaceutical services exposure hurt the Fund's performance in the fourth quarter and throughout 2016 with four and three of the top five losers, respectively.

One of the Fund's biggest winners in Q4 and 2016 was Time Warner (NYSE: TWX). On October 22, 2016 AT&T announced it would acquire TWX in a 50% stock and 50% cash transaction valued at $107.50 per share. The transaction is expected to close by the end of 2017.

Initially, the market's reaction was one of great skepticism that this transaction would receive anti-trust approval. This was in part due to the political rhetoric prior to the Presidential election that saw the two leading candidates voice their objections to the deal. As a result, the stock traded at a significant discount to the offer price and languished in the mid- to high 80s in the three weeks following the deal's announcement. In mid-November, as the market began to focus more on the facts behind this vertical integration and to look to the precedent of the successful Comcast-NBC Universal merger in 2011, TWX rose to the low-90s and closed the year at $96.53. The stock still trades at more than a 10% discount to the acquisition price. While I believe there is a high probability that this transaction will close, the upside is now partially capped, so I trimmed the Fund's position size during the quarter.

One of the Fund's biggest losers in Q4 and 2016 was CVS Health (NYSE: CVS). On Nov. 8, 2016, CVS announced its Q3 results and provided a preliminary outlook for 2017 that was well below consensus estimates. This negative surprise largely stemmed from the decision by Tricare, the health care program for U.S. uniformed service members and their families, and Prime Therapeutics, the fourth-largest pharmacy benefits manager (PBM), to build a restricted pharmacy network with Walgreens as the cornerstone piece. CVS stores were excluded, and as a result, the company will lose more than 40 million prescriptions. Since these prescription losses are spread across many stores and geographic regions, there is not much in the way of variable expenses it can cut over the short-term to help offset the gross profit lost from these sales. As a result, CVS expects its 2017 EPS3 to only increase slightly compared to prior consensus expectations of double-digit growth.

While this was certainly disappointing news that impacted the stock price, it does not change CVS' enviable competitive position as the leading player in retail pharmacy, pharmacy benefits management, specialty pharmacy and infusion as well as institutional pharmacy. Its vertical integration provides it with unique competitive advantages that are practically impossible to replicate. Until this recent setback, CVS' PBM and retail pharmacy businesses had been gaining market share every year since 2011. Its fantastic run from 2011 onward came on the heels of a poor 2010 selling season that saw its PBM lose a significant amount of business because of poor customer service during a difficult merger integration with its retail pharmacy business.

Ultimately, the power of CVS' vertically integrated model proved itself a success, which can be seen in its robust EPS growth of ~13% per annum since then. I believe 2017 will likely be another speed bump on a long road of further market share gains across its various pharmacy-related businesses, which serve a growing market fueled by aging U.S. demographics. Beyond 2017, management expects EPS can rise at an approximate 10% CAGR4. This will be accomplished through a combination of organic revenue growth, expense reductions, share repurchases and strategic acquisitions.

3 EPS (Earnings Per Share) is the portion of a company's profit allocated to each outstanding share of common stock. It serves as an indicator of a company's profitability.

4 CAGR is the compound annual growth rate.

4

FPA U.S. VALUE FUND, INC.

LETTER TO SHAREHOLDERS

(Continued)

CVS trades at an undemanding 13.5x forward EPS. Management's guidance for 2017 EPS is based on a ~39% effective tax rate. This is because CVS earns all of its profits in the U.S. Should there be some kind of U.S. corporate tax reform that reduces tax rates to ~25%, CVS would be trading at just ~11x forward EPS. Compare this to Walgreens Boots Alliance (NYSE: WBA), which trades at 16.6x forward EPS and already has an effective tax rate of ~25% thanks in part to its large non-U.S. business. After integrating Rite Aid (assuming Federal Trade Commission approval), I believe WBA's long-term EPS growth rate should approximate CVS' ~10%. Therefore, I expect the valuation of both companies to converge over time.

Portfolio Activity

Performance disparities within certain sectors provided opportunities to continue to reallocate capital to better values in the market to maximize the Fund's long-term, risk-adjusted returns.

For example, because of WBA's growing valuation premium compared to CVS and the big three distributors (MCK, CAH and ABC), I sold WBA and allocated more capital to those four companies. In addition, I bought back Allergan (NYSE: AGN) and added HCA Holdings (NYSE: HCA) and Rite Aid (NYSE: RAD) to the portfolio. Overall, disclosed healthcare-related exposure increased less than 1%.

Including media, the portfolio's disclosed exposure to the Consumer Discretionary sector increased ~9.3% during Q4. Within media, as the valuation of TWX and CBS Corporation (NYSE: CBS) expanded, those positions were trimmed, while Twenty-First Century Fox, Inc. (NASDAQ: FOXA) grew by appreciation. At the same time, I added Disney (NYSE: DIS), AMC Entertainment (NASDAQ: AMCX) and Discovery Communications (NASDAQ: DISCK) to the Fund. Overall, disclosed exposure to media increased by about 4%.

Existing positions in Tempur Sealy International, Inc. (NYSE: TPX), The Madison Square Garden Company (NYSE: MSG) and Whirlpool Corporation (NYSE: WHR) increased, which accounted for a little over 5% of the added exposure in the Consumer Discretionary sector. In addition, I established new positions in Dollar General (NYSE: DG) and sold Norwegian Cruise Line Holdings Ltd. (NASDAQ: NCLH), which nearly offset each other.

Since the Presidential election, two of the strongest-performing sectors have been Financials and Industrials, where valuations have expanded meaningfully. A majority of the Fund's disclosed exposure to Financials has been eliminated, as Invesco Ltd. (NYSE: IVZ) and Ameriprise Financial Inc. (NYSE: AMP) were sold and partially replaced with a small position in Citigroup (NYSE: C). At the same time, disclosed exposure to Industrials was reduced by ~2.4%. I sold Spirit Airlines (NASDAQ: SAVE) and Ingersoll-Rand Plc (NYSE: IR), and trimmed the Southwest Airlines Co. (NYSE: LUV) position. However, a new position in Regus plc (LSE: IWG), the largest global office outsourcing services company, was established.

Lastly, one of the weaker-performing sectors right after the election was Information Technology. During that sell-off, the Fund added to its investment in Alphabet Inc. (NASDAQ: GOOG) and bought back Apple Inc. (NASDAQ: AAPL).

Cash and equivalents declined by approximately 2.5% to end the quarter at nearly 8% of the portfolio.

In terms of disclosed sector exposures at the end of 2016 compared to 2015, there were some notable changes. The industries where I continue to find the most value, several of which underperformed the market in 2016, have become bigger weights in the portfolio. Consumer Discretionary has increased from 39.0% to 42.9% while Health Care increased from 25.3% to 28.1% of the portfolio. A couple of the stronger performing sectors the Fund had some exposure to such as Industrials and Financials had their weights reduced. Industrials were reduced from 10.8% to 6.4% while Financials decreased from 11.4% to 1.2% of the portfolio. Two sectors the

5

FPA U.S. VALUE FUND, INC.

LETTER TO SHAREHOLDERS

(Continued)

Fund had no exposure to at the end of 2015, Information Technology and Consumer Staples, at the end of 2016 made up 7.1% and 6.8% of the portfolio, respectively. Lastly, what remained the same at the end of 2016 versus 2015: the Fund continues to have no exposure to Energy, Utilities, Real Estate, Materials and Telecommunication Services.

Portfolio Profile

At the end of the quarter, the Fund had 25 disclosed positions, compared to 21 at the end of the third quarter. Since I continue to find the most value in large-cap companies, the weighted average market capitalization of the Fund's disclosed holdings was approximately $77 billion at quarter-end compared to approximately $56 billion at the end of the third quarter. However, the median market cap was approximately $28 billion.

The top 10 positions accounted for about 59% of the portfolio as of Dec. 31, 2016. As of that date, approximately 66% of disclosed investments were in large-cap companies, 19% in mid-cap and 7% in mega-cap. The Fund's exposure to U.S. equities was 90%, with just one non-U.S. domiciled investment, Regus plc, making up approximately 2% of the portfolio. However, it is worth noting that the U.S. is Regus' largest market and makes up nearly half of its business.

The investment portfolio ended the fourth quarter priced at an approximate 23% discount to my estimate of its intrinsic value, which is down from a 27% discount at the end of the third quarter. This assumes no change to the U.S. corporate tax rate. However, given the portfolio's large exposure to U.S. businesses paying at or close to a full effective tax rate, corporate tax reform that lowers the U.S. tax rate to ~25% would have a positive impact on portfolio companies' earnings.

Based on consensus estimates for 2017, at the end of the fourth quarter, the portfolio had a forward-weighted average P/E5 of 13.9x and a forecasted EPS growth rate of 11.5% over the next two years. The consensus estimates do not appear to include any benefit from potential corporate tax reform.

The Fund's investment objective is long-term growth of capital, with current income as a secondary consideration. The Fund seeks to deliver returns in excess of the S&P 500 Index over full market cycles. By design, the portfolio is unique in its construct in order to achieve this. As of Dec. 31, approximately 19% of the disclosed portfolio was invested in six companies that are not in the S&P 500. About 73% of the disclosed portfolio was invested in 19 companies that comprise approximately 10% of the S&P 500. Approximately 59% of the Fund's exposure resides within four industries.

Given the Fund's composition, investors should expect that over any given quarter, year, or years, the Fund could have highly divergent results compared to the market. However, I believe the philosophy of focusing investments in high-quality companies within secularly healthy, growing industries at cheap valuations best positions the Fund to deliver on its stated objective and goal.

Conclusion

I remain enthusiastic about the Fund's investments and their prospective returns over the long term. Compared to the broader market, I believe our portfolio is of higher quality, has greater potential for earnings growth, and is less financially levered. Even better, based on consensus estimates, our portfolio's securities, in the aggregate, trade at a sizable discount to the S&P 500's forward P/E and to my estimate of their intrinsic value.

5 P/E (Price-to-Earnings Ratio) is a ratio for valuing a company that measures its current share price relative to its per-share earnings.

6

FPA U.S. VALUE FUND, INC.

LETTER TO SHAREHOLDERS

(Continued)

I look forward to delivering value for shareholders over the coming years. Your confidence and continued support is truly appreciated.

Respectfully submitted,

Gregory R. Nathan

Portfolio Manager

January 2017

The discussions of Fund investments represent the views of the Fund's managers at the time of this report and are subject to change without notice. References to individual securities are for informational purposes only and should not be construed as recommendations to purchase or sell individual securities. While the Fund's managers believe that the Fund's holdings are value stocks, there can be no assurance that others will consider them as such. Further, investing in value stocks presents the risk that value stocks may fall out of favor with investors and underperform growth stocks during given periods.

FORWARD LOOKING STATEMENT DISCLOSURE

As mutual fund managers, one of our responsibilities is to communicate with shareholders in an open and direct manner. Insofar as some of our opinions and comments in our letters to shareholders are based on our current expectations, they are considered "forward-looking statements" which may or may not prove to be accurate over the long term. While we believe we have a reasonable basis for our comments and we have confidence in our opinions, actual results may differ materially from those we anticipate. You can identify forward-looking statements by words such as "believe," "expect," "may," "anticipate," and other similar expressions when discussing prospects for particular portfolio holdings and/or the markets, generally. We cannot, however, assure future results and disclaim any obligation to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise. Further, information provided in this report should not be construed as a recommendation to purchase or sell any particular security.

7

FPA U.S. VALUE FUND, INC.

HISTORICAL PERFORMANCE

(Unaudited)

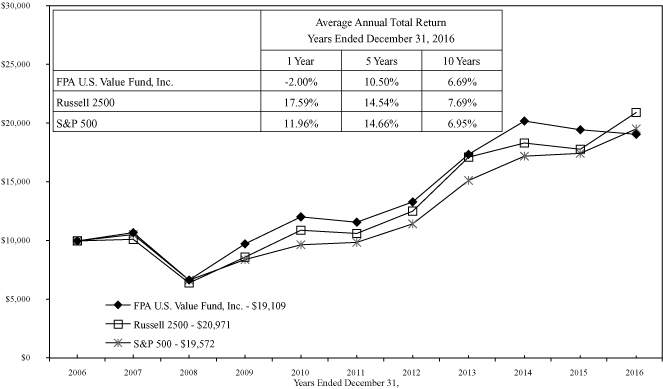

Change in Value of a $10,000 Investment in FPA U.S. Value Fund, Inc. vs. Russell 2500 Index and S&P 500 for the Ten Years Ended December 31, 2016

The Russell 2500 Index consists of the 2,500 smallest companies in the Russell 3000 total capitalization universe. This index is considered a measure of small to medium capitalization stock performance. The Standard & Poor's 500 Composite Index (S&P 500) is an unmanaged index that is generally representative of the U.S. stock market. The indexes do not reflect any commissions, fees or other expenses of investing which would be incurred by an investor purchasing the stocks it represents. The performance of the Fund and of the Indexes is computed on a total return basis which includes reinvestment of all distributions. It is not possible to invest directly in an index.

A new strategy for FPA U.S. Value Fund, Inc. was implemented beginning on September 1, 2015. The returns above include performance of the previous managers prior to that date.

Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown. This data represents past performance and investors should understand that investment returns and principal values fluctuate, so that when you redeem your investment may be worth more or less than its original cost. Current month-end performance data can be obtained by visiting the website at www.fpafunds.com or by calling toll-free, 1-800-982-4372. Information regarding the Fund's expense ratio and redemption fees can be found on pages 13 and 16. The Prospectus details the Fund's objective and policies, sales charges, and other matters of interest to prospective investors. Please read the Prospectus carefully before investing. The Prospectus may be obtained by visiting the website at www.fpafunds.com, by email at crm@fpafunds.com, toll-free by calling 1-800-982-4372 or by contacting the Fund in writing.

8

FPA U.S. VALUE FUND, INC.

PORTFOLIO SUMMARY

December 31, 2016

Common Stocks | 92.4 | % | |||||||||

Entertainment Content | 21.7 | % | |||||||||

Health Care Supply Chain | 19.2 | % | |||||||||

Home & Office Furnishings | 7.1 | % | |||||||||

Food & Drug Stores | 6.8 | % | |||||||||

Internet Media | 5.5 | % | |||||||||

Entertainment Facilities | 5.0 | % | |||||||||

Managed Care | 4.8 | % | |||||||||

Home Improvement | 4.4 | % | |||||||||

Airlines | 4.1 | % | |||||||||

Specialty Pharma | 3.1 | % | |||||||||

Mass Merchants | 2.6 | % | |||||||||

Professional Services | 2.2 | % | |||||||||

Publishing & Broadcasting | 2.0 | % | |||||||||

Communications Equipment | 1.6 | % | |||||||||

Diversified Banks | 1.2 | % | |||||||||

Health Care Facilities | 1.1 | % | |||||||||

Call Options Written | (0.2 | )% | |||||||||

Short-Term Investments | 7.9 | % | |||||||||

Other Assets and Liabilities, Net | (0.1 | )% | |||||||||

Net Assets | 100.0 | % | |||||||||

9

FPA U.S. VALUE FUND, INC.

PORTFOLIO OF INVESTMENTS

December 31, 2016

COMMON STOCKS | Shares | Fair Value | |||||||||

ENTERTAINMENT CONTENT — 21.7% | |||||||||||

AMC Networks, Inc. (Class A)* | 35,200 | $ | 1,842,368 | ||||||||

CBS Corporation (Class B) | 97,440 | 6,199,133 | |||||||||

Discovery Communications, Inc. (Class C)* | 44,500 | 1,191,710 | |||||||||

Time Warner, Inc. | 67,380 | 6,504,191 | |||||||||

Twenty-First Century Fox, Inc. (Class A) | 229,500 | 6,435,180 | |||||||||

Walt Disney Co. (The) | 22,763 | 2,372,360 | |||||||||

$ | 24,544,942 | ||||||||||

HEALTH CARE SUPPLY CHAIN — 19.2% | |||||||||||

AmerisourceBergen Corporation | 99,510 | $ | 7,780,687 | ||||||||

Cardinal Health, Inc. | 98,560 | 7,093,363 | |||||||||

McKesson Corporation | 48,300 | 6,783,735 | |||||||||

$ | 21,657,785 | ||||||||||

HOME & OFFICE FURNISHINGS — 7.1% | |||||||||||

Tempur Sealy International, Inc.* | 117,300 | $ | 8,009,244 | ||||||||

FOOD & DRUG STORES — 6.8% | |||||||||||

CVS Health Corporation | 79,260 | $ | 6,254,407 | ||||||||

Rite Aid Corporation* | 169,000 | 1,392,560 | |||||||||

$ | 7,646,967 | ||||||||||

INTERNET MEDIA — 5.5% | |||||||||||

Alphabet, Inc. (Class C)* | 7,973 | $ | 6,153,721 | ||||||||

ENTERTAINMENT FACILITIES — 5.0% | |||||||||||

Madison Square Garden Co. (The) (Class A)* | 32,950 | $ | 5,651,254 | ||||||||

MANAGED CARE — 4.8% | |||||||||||

Anthem, Inc. | 37,700 | $ | 5,420,129 | ||||||||

HOME IMPROVEMENT — 4.4% | |||||||||||

Whirlpool Corporation | 27,625 | $ | 5,021,396 | ||||||||

AIRLINES — 4.1% | |||||||||||

Delta Air Lines, Inc. | 52,500 | $ | 2,582,475 | ||||||||

Southwest Airlines Co. | 41,850 | 2,085,804 | |||||||||

$ | 4,668,279 | ||||||||||

10

FPA U.S. VALUE FUND, INC.

PORTFOLIO OF INVESTMENTS (Continued)

December 31, 2016

COMMON STOCKS — Continued | Shares | Fair Value | |||||||||

SPECIALTY PHARMA — 3.1% | |||||||||||

Allergan plc* | 16,500 | $ | 3,465,165 | ||||||||

MASS MERCHANTS — 2.6% | |||||||||||

Dollar General Corporation | 40,000 | $ | 2,962,800 | ||||||||

PROFESSIONAL SERVICES — 2.2% | |||||||||||

IWG plc (Switzerland) | 824,000 | $ | 2,498,124 | ||||||||

PUBLISHING & BROADCASTING — 2.0% | |||||||||||

Houghton Mifflin Harcourt Co.* | 205,000 | $ | 2,224,250 | ||||||||

COMMUNICATIONS EQUIPMENT — 1.6% | |||||||||||

Apple, Inc. | 15,600 | $ | 1,806,792 | ||||||||

DIVERSIFIED BANKS — 1.2% | |||||||||||

Citigroup, Inc. | 23,150 | $ | 1,375,805 | ||||||||

HEALTH CARE FACILITIES — 1.1% | |||||||||||

HCA Holdings, Inc.* | 16,500 | $ | 1,221,330 | ||||||||

| TOTAL COMMON STOCKS — 92.4% (Cost $101,541,707) | $ | 104,327,983 | |||||||||

CALL OPTIONS WRITTEN — (0.2)% | |||||||||||

| Rite Aid Corporation, Call-Strike $7.00; expires 01/20/17, 169,000* (Link Brokers Derivatives Corp. Counterparty) (Premiums received $117,147) | (169,000 | ) | $ | (253,500 | ) | ||||||

| TOTAL INVESTMENT SECURITIES — 92.2% (Cost $101,424,560) | $ | 104,074,483 | |||||||||

11

FPA U.S. VALUE FUND, INC.

PORTFOLIO OF INVESTMENTS (Continued)

December 31, 2016

| Principal Amount | Fair Value | ||||||||||

SHORT-TERM INVESTMENTS — 7.9% | |||||||||||

| State Street Bank Repurchase Agreement — 0.03% 1/3/2017 (Dated 12/30/2016, repurchase price of $8,972,030, collateralized by $9,180,000 principal amount U.S. Treasury Note — 1.50% 2020, fair value $9,152,644) | $ | 8,972,000 | $ | 8,972,000 | |||||||

| TOTAL SHORT-TERM INVESTMENTS (Cost $8,972,000) | $ | 8,972,000 | |||||||||

| TOTAL INVESTMENTS — 100.1% (Cost $110,396,560) | $ | 113,046,483 | |||||||||

Other Assets and Liabilities, net — (0.1)% | (114,340 | ) | |||||||||

NET ASSETS — 100.0% | $ | 112,932,143 | |||||||||

* Non-income producing security.

See notes to financial statements.

12

FPA U.S. VALUE FUND, INC.

STATEMENT OF ASSETS AND LIABILITIES

December 31, 2016

ASSETS | |||||||

Investment securities — at fair value (identified cost $101,541,707) | $ | 104,327,983 | |||||

Short-term investments — at amortized cost (maturities 60 days or less) | 8,972,000 | ||||||

Cash | 825 | ||||||

Due from broker — OTC derivatives collateral | 250,000 | ||||||

Receivable for: | |||||||

Dividends and interest | 213,502 | ||||||

Capital Stock sold | 78,890 | ||||||

Prepaid expenses and other assets | 2,477 | ||||||

Total assets | 113,845,677 | ||||||

LIABILITIES | |||||||

Written options, at value (premiums received $117,147) | 253,500 | ||||||

Payable for: | |||||||

Capital Stock repurchased | 516,973 | ||||||

Advisory fees | 21,474 | ||||||

Accrued expenses and other liabilities | 121,587 | ||||||

Total liabilities | 913,534 | ||||||

NET ASSETS | $ | 112,932,143 | |||||

SUMMARY OF SHAREHOLDERS' EQUITY | |||||||

| Capital Stock — par value $0.01 per share; authorized 25,000,000 shares; 12,422,816 outstanding shares | $ | 124,228 | |||||

Additional Paid-in Capital | 112,590,680 | ||||||

Accumulated net realized loss on investments | (2,948,940 | ) | |||||

| Undistributed net investment income | 527,031 | ||||||

Unrealized appreciation of investments | 2,639,144 | ||||||

NET ASSETS | $ | 112,932,143 | |||||

NET ASSET VALUE | |||||||

Offering and redemption price per share | $ | 9.09 | |||||

See notes to financial statements.

13

FPA U.S. VALUE FUND, INC.

STATEMENT OF OPERATIONS

For the Year Ended December 31, 2016

INVESTMENT INCOME | |||||||

Dividends (net of foreign taxes withheld of $92,437) | $ | 2,089,657 | |||||

Interest | 4,374 | ||||||

Total investment income | 2,094,031 | ||||||

EXPENSES | |||||||

Advisory fees | 948,488 | ||||||

Legal fees | 179,994 | ||||||

Transfer agent fees and expenses | 129,249 | ||||||

Director fees and expenses | 104,412 | ||||||

Reports to shareholders | 100,016 | ||||||

Audit and tax services fees | 53,981 | ||||||

Filing fees | 53,311 | ||||||

Custodian fees | 12,316 | ||||||

Professional fees | 5,882 | ||||||

Administrative services fees | 5,460 | ||||||

Other | 62,063 | ||||||

Total expenses | 1,655,172 | ||||||

Reimbursement from Adviser | (119,215 | ) | |||||

Net expenses | 1,535,957 | ||||||

Net investment income | 558,074 | ||||||

NET REALIZED AND UNREALIZED GAIN (LOSS) | |||||||

Net realized gain (loss) on: | |||||||

Investments | (2,592,431 | ) | |||||

Written options | 403,271 | ||||||

Foreign currency transactions | (3,419 | ) | |||||

Net change in unrealized appreciation (depreciation) of: | |||||||

Investments | (2,236,920 | ) | |||||

Written options | (136,353 | ) | |||||

Translation of foreign currency denominated amounts | (2,643 | ) | |||||

Net realized and unrealized loss | (4,568,495 | ) | |||||

NET DECREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | (4,010,421 | ) | ||||

See notes to financial statements.

14

FPA U.S. VALUE FUND, INC.

STATEMENTS OF CHANGES IN NET ASSETS

| Year Ended December 31, 2016 | Year Ended December 31, 2015 | ||||||||||

INCREASE (DECREASE) IN NET ASSETS | |||||||||||

Operations: | |||||||||||

Net investment income (loss) | $ | 558,074 | $ | (90,302 | ) | ||||||

Net realized gain (loss) | (2,192,579 | ) | 188,436,374 | ||||||||

Net change in unrealized depreciation | (2,375,916 | ) | (201,901,424 | ) | |||||||

Net decrease in net assets resulting from operations | (4,010,421 | ) | (13,555,352 | ) | |||||||

Distributions to shareholders from: | |||||||||||

Net realized capital gains | (1,226,393 | ) | (186,046,273 | ) | |||||||

Total distributions | (1,226,393 | ) | (186,046,273 | ) | |||||||

Capital Stock transactions: | |||||||||||

Proceeds from Capital Stock sold | 16,995,453 | 30,648,612 | |||||||||

| Proceeds from shares issued to shareholders upon reinvestment of dividends and distributions | 1,026,355 | 175,645,775 | |||||||||

Cost of Capital Stock repurchased | (66,488,439 | )* | (176,950,134 | )* | |||||||

Net increase (decrease) from Capital Stock transactions | (48,466,631 | ) | 29,344,253 | ||||||||

Total change in net assets | (53,703,445 | ) | (170,257,372 | ) | |||||||

NET ASSETS | |||||||||||

Beginning of Year | 166,635,588 | 336,892,960 | |||||||||

End of Year | $ | 112,932,143 | $ | 166,635,588 | |||||||

CHANGE IN CAPITAL STOCK OUTSTANDING | |||||||||||

Shares of Capital Stock sold | 1,933,917 | 1,678,809 | |||||||||

| Shares issued to shareholders upon reinvestment of dividends and distributions | 117,029 | 19,876,715 | |||||||||

Shares of Capital Stock repurchased | (7,441,302 | ) | (10,039,239 | ) | |||||||

Change in Capital Stock outstanding | (5,390,356 | ) | 11,516,285 | ||||||||

* Net of redemption fees of $5,272 and $39,215 for the year ended December 31, 2016 and year ended December 31, 2015, respectively.

See notes to financial statements.

15

FPA U.S. VALUE FUND, INC.

FINANCIAL HIGHLIGHTS

Selected Data for Each Share of Capital Stock Outstanding Throughout Each Year

Year Ended December 31, | |||||||||||||||||||||||

2016 | 2015 | 2014 | 2013 | 2012 | |||||||||||||||||||

Per share operating performance: | |||||||||||||||||||||||

Net asset value at beginning of year | $ | 9.36 | $ | 53.50 | $ | 49.53 | $ | 41.09 | $ | 36.36 | |||||||||||||

Income from investment operations: | |||||||||||||||||||||||

Net investment income (loss)* | $ | 0.04 | $ | (0.01 | ) | $ | (0.08 | ) | — | $ | 0.02 | ||||||||||||

| Net realized and unrealized gain (loss) on investment securities | (0.23 | ) | (4.38 | ) | 8.08 | $ | 11.98 | 5.35 | |||||||||||||||

Total from investment operations | $ | (0.19 | ) | $ | (4.39 | ) | $ | 8.00 | $ | 11.98 | $ | 5.37 | |||||||||||

Less distributions: | |||||||||||||||||||||||

| Dividends from net investment income | — | — | — | $ | (0.02 | ) | — | ||||||||||||||||

| Distributions from net realized capital gains | $ | (0.08 | ) | $ | (39.75 | ) | $ | (4.03 | ) | (3.52 | ) | $ | (0.64 | ) | |||||||||

Total distributions | $ | (0.08 | ) | $ | (39.75 | ) | $ | (4.03 | ) | $ | (3.54 | ) | $ | (0.64 | ) | ||||||||

Redemption fees | — | ** | — | ** | — | ** | — | ** | — | ** | |||||||||||||

Net asset value at end of year | $ | 9.09 | $ | 9.36 | $ | 53.50 | $ | 49.53 | $ | 41.09 | |||||||||||||

Total investment return*** | (2.00 | )% | (3.68 | )% | 16.38 | % | 30.46 | % | 14.96 | % | |||||||||||||

Ratios/supplemental data: | |||||||||||||||||||||||

Net assets, end of year (in $000's) | $ | 112,932 | $ | 166,636 | $ | 336,893 | $ | 310,921 | $ | 255,084 | |||||||||||||

Ratio of expenses of average net assets: | |||||||||||||||||||||||

Before reimbursement from Adviser | 1.20 | % | 0.97 | % | 0.94 | % | 0.96 | % | 1.02 | % | |||||||||||||

After reimbursement from Adviser | 1.11 | % | 0.97 | % | 0.94 | % | 0.96 | % | 1.02 | % | |||||||||||||

| Ratio of net investment income (loss) to average net assets: | |||||||||||||||||||||||

Before reimbursement from Adviser | 0.32 | % | (0.03 | )% | (0.16 | )% | (0.22 | )% | 0.04 | % | |||||||||||||

After reimbursement from Adviser | 0.40 | % | (0.03 | )% | (0.16 | )% | (0.22 | )% | 0.04 | % | |||||||||||||

Portfolio turnover rate | 115 | % | 109 | % | 5 | % | 8 | % | 2 | % | |||||||||||||

* Per share amount is based on average shares outstanding.

** Rounds to less than $0.01 per share.

*** Return is based on net asset value per share, adjusted for reinvestment of distributions, and does not reflect deduction of the sales charge.

See notes to financial statements.

16

FPA U.S. VALUE FUND, INC.

NOTES TO FINANCIAL STATEMENTS

December 31, 2016

NOTE 1 — Significant Accounting Policies

FPA U.S. Value Fund, Inc. (the "Fund") is registered under the Investment Company Act of 1940, as a diversified, open-end, management investment company. The Fund's primary investment objective is long-term growth of capital. Current income is a secondary consideration. The Fund qualifies as an investment company pursuant to Financial Accounting Standard Board (FASB) Accounting Standards Codification (ASC) No. 946, Financial Services — Investment Companies. The following is a summary of significant accounting policies consistently followed by the Fund in the preparation of its financial statements.

A. Security Valuation

The Fund's investments are reported at fair value as defined by accounting principles generally accepted in the United States of America, ("U.S. GAAP"). The Fund generally determines its net asset value as of approximately 4:00 p.m. New York time each day the New York Stock Exchange is open. Further discussion of valuation methods, inputs and classifications can be found under Disclosure of Fair Value Measurements.

B. Securities Transactions and Related Investment Income

Securities transactions are accounted for on the date the securities are purchased or sold. Dividend income and distributions to shareholders are recorded on the ex-dividend date. Interest income and expenses are recorded on an accrual basis. The books and records of the Fund are maintained in U.S. dollars as follows: (1) the foreign currency market value of investment securities, and other assets and liabilities stated in foreign currencies, are translated using the daily spot rate; and (2) purchases, sales, income and expenses are translated at the rate of exchange prevailing on the respective dates of such transactions. The resultant exchange gains and losses are included in net realized or net unrealized gain (loss) in the statement of operations.

C. Use of Estimates

The preparation of the financial statements in accordance with U.S. GAAP requires management to make estimates and assumptions that affect the amounts reported. Actual results could differ from those estimates.

D. Recent Accounting Pronouncement

In December 2016, the FASB released an accounting standard update ("ASU") 2016-19 that makes technical changes to various section of the ASC, including Topic 820, Fair Value Measurement. The changes to Topic 820 are intended to clarify the difference between a valuation approach and a valuation technique. The changes to ASC 820-10-50-2 require a reporting entity to disclose, for Level 2 and Level 3 fair value measurements, a change in either or both a valuation approach and a valuation technique and the reason(s) for the changes. The changes to Topic 820 are effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2016. At this time, management is evaluating the implications of the ASU and has not yet determined its impact on the financial statements and disclosures.

E. New and Amended Financial Reporting Rules and Forms

On October 13, 2016, the U.S. Securities Exchange Commission ("SEC") adopted new rules and forms, and amended existing rules and forms. The new and amended rules and forms are intended to modernize the reporting of information provided by funds and to improve the quality and type of information that funds provide to the SEC and investors. The new and amended rules and forms will be effective for the Fund for reporting periods beginning on and after June 1, 2018. Management is evaluating the new and amended rules and forms to determine the impact to the Fund.

17

FPA U.S. VALUE FUND, INC.

NOTES TO FINANCIAL STATEMENTS

Continued

NOTE 2 — Risk Considerations

Investing in the Fund may involve certain risks including, but not limited to, those described below.

Market Risk: Because the values of the Fund's investments will fluctuate with market conditions, so will the value of your investment in the Fund. You could lose money on your investment in the Fund or the Fund could underperform other investments.

Common Stocks and Other Securities: The prices of common stocks and other securities held by the Fund may decline in response to certain events taking place around the world, including; those directly involving companies whose securities are owned by the Fund; conditions affecting the general economy; overall market changes; local, regional or global political, social or economic instability; and currency, interest rate and commodity price fluctuations. In addition, the Adviser's emphasis on a value-oriented investment approach generally results in the Fund's portfolio being invested primarily in medium or smaller sized companies. Smaller companies may be subject to a greater degree of change in earnings and business prospects than larger, more established companies, and smaller companies are often more reliant on key products or personnel than larger companies. The Fund's foreign investments are subject to additional risks such as, foreign markets could go down or prices of the Fund's foreign investments could go down because of unfavorable changes in foreign currency exchange rates, foreign government actions, social, economic or political instability or other factors that can adversely affect investments in foreign countries. These factors can also make foreign securities less liquid, more volatile and harder to value than U.S. securities. In light of these characteristics of smaller companies and their securities, the Fund may be subjected to greater risk than that assumed when investing in the equity securities of larger companies.

Repurchase Agreements: Repurchase agreements permit the Fund to maintain liquidity and earn income over periods of time as short as overnight. Repurchase agreements held by the Fund are fully collateralized by U.S. Government securities, or securities issued by U.S. Government agencies, or securities that are within the three highest credit categories assigned by established rating agencies (Aaa, Aa, or A by Moody's or AAA, AA or A by Standard & Poor's) or, if not rated by Moody's or Standard & Poor's, are of equivalent investment quality as determined by the Adviser. Such collateral is in the possession of the Fund's custodian. The collateral is evaluated daily to ensure its market value equals or exceeds the current market value of the repurchase agreements including accrued interest. In the event of default on the obligation to repurchase, the Fund has the right to liquidate the collateral and apply the proceeds in satisfaction of the obligation.

The Fund may enter into repurchase agreements, under the terms of a Master Repurchase Agreement ("MRA"). The MRA permits the Fund, under certain circumstances including an event of default (such as bankruptcy or insolvency), to offset payables and/or receivables under the MRA with collateral held and/or posted to the counterparty and create one single net payment due to or from the Fund. However, bankruptcy or insolvency laws of a particular jurisdiction may impose restrictions on or prohibitions against such a right of offset in the event of a MRA counterparty's bankruptcy or insolvency. Pursuant to the terms of the MRA, the Fund receives securities as collateral with a market value in excess of the repurchase price to be received by the Fund upon the maturity of the repurchase transaction. Upon a bankruptcy or insolvency of the MRA counterparty, the Fund recognizes a liability with respect to such excess collateral to reflect the Fund's obligation under bankruptcy law to return the excess to the counterparty. Repurchase agreements outstanding at the end of the period are listed in the Fund's Portfolio of Investments.

NOTE 3 — Purchases and Sales of Investment Securities

Cost of purchases of investment securities (excluding short-term investments) aggregated $142,667,547 for the year ended December 31, 2016. The proceeds and cost of securities sold resulting in net realized losses of

18

FPA U.S. VALUE FUND, INC.

NOTES TO FINANCIAL STATEMENTS

Continued

$2,592,431 aggregated $184,391,448 and $186,983,879, respectively, for the year ended December 31, 2016. Realized gains or losses are based on the specific identification method.

NOTE 4 — Federal Income Tax

No provision for federal income tax is required because the Fund has elected to be taxed as a "regulated investment company" under the Internal Revenue Code (the "Code") and intends to maintain this qualification and to distribute each year to its shareholders, in accordance with the minimum distribution requirements of the Code, its taxable net investment income and taxable net realized gains on investments.

Distributions paid to shareholders are based on net investment income and net realized gains determined on a tax reporting basis, which may differ from financial reporting. For federal income tax purposes, the Fund had the following components of distributable earnings at December 31, 2016:

Undistributed Ordinary Income | $ | 527,031 | |||||

Capital Loss Carryforward | (1,832,721 | ) | |||||

Unrealized Appreciation | 1,522,925 | ||||||

The tax status of distributions paid during the fiscal years ended December 31, 2016 and 2015 were as follows:

2016 | 2015 | ||||||||||

Dividends from ordinary income | $ | 1,140,666 | — | ||||||||

Distributions from long-term capital gains | $ | 85,727 | $ | 186,046,273 | |||||||

The cost of investment securities held at December 31, 2016, was $102,657,926 for federal income tax purposes. Gross unrealized appreciation and depreciation for all investments (excluding short-term investments) at December 31, 2016, for federal income tax purposes was $8,352,182 and $6,682,125, respectively resulting in net unrealized appreciation of $1,670,057. As of and during the year ended December 31, 2016, the Fund did not have any liability for unrecognized tax benefits. The Fund recognizes interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the Statement of Operations. During the year, the Fund did not incur any interest or penalties. The Fund is not subject to examination by U.S. federal tax authorities for years ended on or before December 31, 2013 or by state tax authorities for years ended on or before December 31, 2012.

As of December 31, 2016, the Fund has $1,832,721 of short-term capital loss carryforwards which can be carried forward indefinitely.

During the year ended December 31, 2016, the Fund reclassified $35,780 from Accumulated Net Investment Income to Accumulated Net Realized Gain to align financial reporting with tax reporting. These permanent differences are primarily due to differing book and tax treatment of foreign currency gains and losses and non-taxable dividend adjustments.

NOTE 5 — Advisory Fees and Other Affiliated Transactions

Pursuant to an Investment Advisory Agreement (the "Agreement"), advisory fees were paid by the Fund to First Pacific Advisors, LLC (the "Adviser"). Under the terms of this Agreement, the Fund pays the Adviser a monthly fee calculated at the annual rate of 0.75% of the first $50 million of the Fund's average daily net assets and 0.65% of the average daily net assets in excess of $50 million. The Agreement obligates the Adviser to reduce its fee to the extent necessary to reimburse the Fund for any annual expenses (exclusive of interest, taxes, the cost of brokerage and research services, legal expenses related to portfolio securities, and extraordinary expenses such as litigation) in excess of 11/2% of the first $30 million and 1% of the remaining average net assets of the Fund for the year.

19

FPA U.S. VALUE FUND, INC.

NOTES TO FINANCIAL STATEMENTS

Continued

For the year ended December 31, 2016, the Fund paid aggregate fees and expenses of $104,412 to all Directors who are not affiliated persons of the Adviser.

NOTE 6 — Redemption Fees

A redemption fee of 2% applies to redemptions within 90 days of purchase. For the year ended December 31, 2016, the Fund collected $5,272 in redemption fees. The impact of these fees is less than $0.01 per share.

NOTE 7 — Disclosure of Fair Value Measurements

The Fund uses the following methods and inputs to establish the fair value of its assets and liabilities. Use of particular methods and inputs may vary over time based on availability and relevance as market and economic conditions evolve.

Equity securities are generally valued each day at the official closing price of, or the last reported sale price on, the exchange or market on which such securities principally are traded, as of the close of business on that day. If there have been no sales that day, equity securities are generally valued at the last available bid price. Securities that are unlisted and fixed-income and convertible securities listed on a national securities exchange for which the over-the-counter ("OTC") market more accurately reflects the securities' value in the judgment of the Fund's officers, are valued at the most recent bid price. Short-term corporate notes with maturities of 60 days or less at the time of purchase are valued at amortized cost.

Securities for which representative market quotations are not readily available or are considered unreliable by the Adviser are valued as determined in good faith under procedures adopted by the authority of the Fund's Board of Directors. Various inputs may be reviewed in order to make a good faith determination of a security's value. These inputs include, but are not limited to, the type and cost of the security; contractual or legal restrictions on resale of the security; relevant financial or business developments of the issuer; actively traded similar or related securities; conversion or exchange rights on the security; related corporate actions; significant events occurring after the close of trading in the security; and changes in overall market conditions. Fair valuations and valuations of investments that are not actively trading involve judgment and may differ materially from valuations of investments that would have been used had greater market activity occurred.

The Fund classifies its assets based on three valuation methodologies. Level 1 values are based on quoted market prices in active markets for identical assets. Level 2 values are based on significant observable market inputs, such as quoted prices for similar assets and quoted prices in inactive markets or other market observable inputs as noted above including spreads, cash flows, financial performance, prepayments, defaults, collateral, credit enhancements, and interest rate volatility. Level 3 values are based on significant unobservable inputs that reflect the Fund's determination of assumptions that market participants might reasonably use in valuing the assets. The valuation levels are not necessarily an indication of the risk associated with investing in those securities. The following table presents the valuation levels of the Fund's investments as of December 31, 2016:

Investments | Level 1 | Level 2 | Level 3 | Total | |||||||||||||||

Common Stocks | |||||||||||||||||||

Entertainment Content | $ | 24,544,942 | — | — | $ | 24,544,942 | |||||||||||||

Health Care Supply Chain | 21,657,785 | — | — | 21,657,785 | |||||||||||||||

Home & Office Furnishings | 8,009,244 | — | — | 8,009,244 | |||||||||||||||

Food & Drug Stores | 7,646,967 | — | — | 7,646,967 | |||||||||||||||

Internet Media | 6,153,721 | — | — | 6,153,721 | |||||||||||||||

Entertainment Facilities | 5,651,254 | — | — | 5,651,254 | |||||||||||||||

Managed Care | 5,420,129 | — | — | 5,420,129 | |||||||||||||||

20

FPA U.S. VALUE FUND, INC.

NOTES TO FINANCIAL STATEMENTS

Continued

Investments | Level 1 | Level 2 | Level 3 | Total | |||||||||||||||

Home Improvement | $ | 5,021,396 | — | — | $ | 5,021,396 | |||||||||||||

Airlines | 4,668,279 | — | — | 4,668,279 | |||||||||||||||

Specialty Pharma | 3,465,165 | — | — | 3,465,165 | |||||||||||||||

Mass Merchants | 2,962,800 | — | — | 2,962,800 | |||||||||||||||

Professional Services | 2,498,124 | — | — | 2,498,124 | |||||||||||||||

Publishing & Broadcasting | 2,224,250 | — | — | 2,224,250 | |||||||||||||||

Communications Equipment | 1,806,792 | — | — | 1,806,792 | |||||||||||||||

Diversified Banks | 1,375,805 | — | — | 1,375,805 | |||||||||||||||

Health Care Facilities | 1,221,330 | — | — | 1,221,330 | |||||||||||||||

Short-Term Investment | — | $ | 8,972,000 | — | 8,972,000 | ||||||||||||||

$ | 104,327,983 | $ | 8,972,000 | — | $ | 113,299,983 | |||||||||||||

Equity Options (equity risk) | $ | — | $ | (253,500 | ) | — | $ | (253,500 | ) | ||||||||||

Transfers of investments between different levels of the fair value hierarchy are recorded at market value as of the end of the reporting period. There were no transfers between Levels 1, 2, or 3 during the year ended December 31, 2016.

NOTE 8 — Collateral Requirements

FASB Accounting Standards Update No. 2011-11, Disclosures about Offsetting Assets and Liabilities requires disclosures to make financial statements that are prepared under U.S. GAAP more comparable to those prepared under International Financial Reporting Standards. Under this guidance the Fund discloses both gross and net information about instruments and transactions eligible for offset such as instruments and transactions subject to an agreement similar to a master netting arrangement. In addition, the Fund discloses collateral received and posted in connection with master netting agreements or similar arrangements.

The following table presents the Fund's OTC derivative assets and master repurchase agreements by counterparty net of amounts available for offset under an ISDA Master agreement or similar agreements and net of the related collateral received or pledged by the Fund as of December 31, 2016:

Counterparty | Gross Assets (Liabilities) in the Statement of Assets and Liabilities | Collateral Received (Pledged) | Assets (Liabilities) Available for Offset | Net Amount of Assets (Liabilities)* | |||||||||||||||

| State Street Bank and Trust Company: Repurchase Agreement | $ | 8,972,000 | $ | 8,972,000 | ** | — | — | ||||||||||||

| Link Brokers Derivatives Corp.: Call Option Written | (253,500 | ) | (250,000 | ) | — | $ | (3,500 | ) | |||||||||||

* Represents the net amount receivable (payable) from the counterparty in the event of default.

** Collateral with a value of $9,152,644 has been received in connection with a master repurchase agreement. Excess of collateral received from the individual master repurchase agreement is not shown for financial reporting purposes.

21

FPA U.S. VALUE FUND, INC.

REPORT OF INDEPENDENT REGISTERED

PUBLIC ACCOUNTING FIRM

TO THE SHAREHOLDERS

AND BOARD OF DIRECTORS OF FPA U.S. VALUE FUND, INC.

We have audited the accompanying statement of assets and liabilities of FPA U.S. Value Fund, Inc. (the "Fund"), including the portfolio of investments, as of December 31, 2016, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended. These financial statements and financial highlights are the responsibility of the Fund's management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. The Fund is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund's internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of December 31, 2016, by correspondence with the custodian and brokers; when replies were not received from brokers, we performed other auditing procedures. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, such financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of FPA U.S. Value Fund, Inc. as of December 31, 2016, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America.

Los Angeles, California

February 21, 2017

22

FPA U.S. VALUE FUND, INC.

APPROVAL OF INVESTMENT ADVISORY AGREEMENT

(Unaudited)

Approval of the Advisory Agreement. At a meeting of the Board of Directors held on August 8, 2016, the Directors approved the continuation of the advisory agreement between the Fund and the Adviser for an additional one-year period through September 30, 2017, on the recommendation of the Independent Directors, who met in executive session on August 8, 2016 prior to the Board meeting to review and discuss the proposed continuation of the advisory agreement. The following paragraphs summarize the material information and factors considered by the Board and the Independent Directors, as well as the Directors' conclusions relative to such factors.

Nature, Extent and Quality of Services. The Board and the Independent Directors considered information provided by the Adviser in response to their requests, as well as information provided throughout the year regarding the Adviser and its staffing in connection with the Fund, including the Fund's portfolio managers and the senior analysts on their team, the scope of services supervised and provided by the Adviser, and the absence of any significant service problems reported to the Board. The Board and the Independent Directors discussed with the Adviser the change in portfolio management to Gregory Nathan and related changes to the Fund's investment strategy effective September 1, 2015. The Adviser also discussed the name change from FPA Perennial Fund, Inc. to FPA U.S. Value Fund, Inc. and the changes to the Fund's investment strategy. It was noted that as a result of the change in investment strategy the Fund added the S&P 500 as an index, in addition to the Russell 2500 Index, since it is generally representative of the U.S. stock market. The Board and the Independent Directors then acknowledged the length of service of the Fund's portfolio manager, Gregory Nathan, who joined the Adviser in 2003 and has managed the Fund since 2015. After discussion, the Board and the Independent Directors concluded that the nature, extent and quality of services provided by the Adviser have benefited and should continue to benefit the Fund and its shareholders.

Investment Performance. The Board and the Independent Directors reviewed the overall investment performance of the Fund. The Directors also received information from an independent consultant, Morningstar, regarding the Fund's performance relative to a peer group of midcap core funds selected by Morningstar (the "Peer Group"). The Board and the Independent Directors recognized that the new strategy is less than 1-year old and has not yet had time to develop a meaningful, long term track record. However, given the Fund's and the Adviser's long history, the Board and the Independent Directors noted the Adviser's experience and track record, as well as the Fund's long-term investment performance. The Board and the Independent Directors noted the Fund underperformed its Peer Group for the one-, three- and five-year periods ending March 31, 2016 but outperformed its Peer Group for the ten-year period ending March 31, 2016. In addition, the Fund outperformed the Fund's benchmark, Russell 2500 Index for the one-, three-, five- and ten-year periods ending March 31, 2016 but underperformed the S&P 500 Index for the one-, three-, and five- periods ending March 31, 2016, but outperformed the S&P 500 Index for the ten-year period ending March 31, 2016. The Board and the Independent Directors concluded that the Adviser's continued management of the Fund should benefit the Fund and its shareholders.

Advisory Fees and Fund Expenses; Comparison with Peer Group and Institutional Fees. The Board and the Independent Directors considered information provided by the Adviser regarding the Fund's advisory fees and total expense levels. The Board and the Independent Directors reviewed comparative information regarding fees and expenses for the Peer Group. The Board and the Independent Directors noted that the Fund's advisory fees were above the median of those for the Peer Group and that the overall expense ratio of the Fund was above the median of that of the Peer Group. In addition, the Directors noted that the fee rate charged to the Fund is currently lower than the fee rate charged by the Adviser on the institutional account managed in a similar style by the portfolio managers. The Board and the Independent Directors concluded that the continued payment

23

FPA U.S. VALUE FUND, INC.

APPROVAL OF INVESTMENT ADVISORY AGREEMENT

(Unaudited) Continued

of advisory fees and expenses by the Fund to the Adviser was fair and reasonable and should continue to benefit the Fund and its shareholders.

Adviser Profitability and Costs. The Board and the Independent Directors considered information provided by the Adviser regarding the Adviser's costs in providing services to the Fund, the profitability of the Adviser and the benefits to the Adviser from its relationship to the Fund. They reviewed and considered the Adviser's representations regarding its assumptions and methods of allocating certain costs, such as personnel costs, which constitute the Adviser's largest operating cost, over-head and trading costs with respect to the provision of investment advisory services. The Independent Directors discussed with the Adviser the general process through which individuals' compensation is determined and then reviewed by the management committee of the Adviser, as well as the Adviser's methods for determining that the compensation levels are at appropriate levels to attract and retain the personnel necessary to provide high quality professional investment advice. In evaluating the Adviser's profitability, they excluded certain distribution and marketing-related expenses. The Board and the Independent Directors recognized that the Adviser is entitled under the law to earn a reasonable level of profits for the services that it provides to the Fund. The Board and the Independent Directors concluded that the Adviser's level of profitability from its relationship with the Fund did not indicate that the Adviser's compensation was unreasonable or excessive.

Economies of Scale and Sharing of Economies of Scale. The Board and the Independent Directors considered whether there have been economies of scale with respect to the management of the Fund, whether the Fund has appropriately benefited from any economies of scale, and whether the fee rate is reasonable in relation to the Fund's asset levels and any economies of scale that may exist. The Board and the Independent Directors considered the Adviser's representation that its internal costs of providing investment management services to the Fund have significantly increased in recent years as a result of a number of factors, including new or increased administrative expenses resulting from recent legislative and regulatory requirements. The Board and the Independent Directors considered quantitative and qualitative information regarding the Adviser's representation that it has also made significant investments in: (1) the portfolio manager, traders and other investment personnel who assist with the management of the Fund; (2) new compliance, operations, and administrative personnel; (3) information technology, portfolio accounting and trading systems; and (4) office space, each of which enhances the quality of services provided to the Fund. The Board and the Independent Directors also considered that the Adviser had foregone the reimbursement for providing certain financial services that it had previously received from the Fund. The Board and the Independent Directors also considered the Adviser's willingness to close funds to new investors when it believed that a fund may have limited capacity to grow or that it otherwise would benefit fund shareholders. The Board and the Independent Directors also noted that asset levels of the Fund are currently lower than they were seven years ago.

The Independent Directors noted that the fee rate contained a breakpoint as the Fund's assets increased. They considered that many mutual funds have breakpoints in the advisory fee structure as a means by which to share in the benefits of potential economies of scale as a fund's assets grow. They also considered that not all funds have breakpoints in their fee structures and that breakpoints are not the exclusive means of sharing potential economies of scale. The Board and the Independent Directors considered the Adviser's statement that it believes that additional breakpoints would not be appropriate for the Fund at this time given the ongoing investments the Adviser is making in its business for the benefit of the Fund, uncertainties regarding the direction of the economy, rising inflation, increasing costs for personnel and systems, and growth or contraction in the Fund's assets, all of which could negatively impact the profitability of the Adviser. The Board and the Independent Directors concluded

24

FPA U.S. VALUE FUND, INC.

APPROVAL OF INVESTMENT ADVISORY AGREEMENT

(Unaudited) Continued

that the Fund is benefitting from the ongoing investments made by the Adviser in its team of personnel serving the Fund and in the Adviser's service infrastructure, and that in light of these investments, additional breakpoints in the Fund's advisory fee structure were not warranted at current asset levels.

Ancillary Benefits. The Board and the Independent Directors considered other actual and potential benefits to the Adviser from managing the Fund, including the acquisition and use of research services with commissions generated by the Fund, in concluding that the contractual advisory and other fees are fair and reasonable for the Fund. They noted that the Adviser does not have any affiliates that benefit from the Adviser's relationship to the Fund.

Conclusions. The Board and the Independent Directors determined that the Fund continues benefitted from the services of the Adviser's highly experienced investment management team, which has produced competitive long-term returns, as well as their expectation that the new portfolio management team can also produce competitive long-term returns. In addition, the Board and the Independent Directors agreed that the Fund continues to receive high quality services from the Adviser. The Board and the Independent Directors concluded that the current advisory fee rate is reasonable and fair to the Fund and its shareholders in light of the nature and quality of the services provided by the Adviser and the Adviser's profitability and costs. The Board and the Independent Directors also noted their intention to continue monitoring the factors relevant to the Adviser's compensation, such as changes in the Fund's asset levels, changes in portfolio management personnel and the cost and quality of the services provided by the Adviser to the Fund. On the basis of the foregoing, and without assigning particular weight to any single factor, none of which was dispositive, the Board and the Independent Directors concluded that it would be in the best interests of the Fund to continue to be advised and managed by the Adviser and determined to approve the continuation of the current Advisory Agreement for another one-year period through September 30, 2017.

25

FPA U.S. VALUE FUND, INC.

SHAREHOLDER EXPENSE EXAMPLE

December 31, 2016 (Unaudited)

Fund Expenses

Mutual fund shareholders generally incur two types of costs: (1) transaction costs, and (2) ongoing costs, including advisory and administrative fees; shareholder service fees; and other Fund expenses. The Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The Example is based on an investment of $1,000 invested at the beginning of the year and held for the entire year.

Actual Expenses

The information in the table under the heading "Actual Performance" provides information about actual account values and actual expenses. You may use the information in this column, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000= 8.6), then multiply the result by the number in the first column in the row entitled "Expenses Paid During Period" to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The information in the table under the heading "Hypothetical Performance (5% return before expenses)" provides information about hypothetical account values and hypothetical expenses based on the Fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund

and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs. Therefore, the information under the heading "Hypothetical Performance (5% return before expenses)" is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher. Even though the Fund does not charge transaction fees, if you purchase shares through a broker, the broker may charge you a fee. You should evaluate other mutual funds' transaction fees and any applicable broker fees to assess the total cost of ownership for comparison purposes.

| Actual Performance | Hypothetical Performance (5% return before expenses) | ||||||||||

| Beginning Account Value June 30, 2016 | $ | 1,000.00 | $ | 1,000.00 | |||||||

| Ending Account Value December 31, 2016 | $ | 1,041.20 | $ | 1,019.50 | |||||||

| Expenses Paid During Period* | $ | 5.76 | $ | 5.69 | |||||||

* Expenses are equal to the Fund's annualized expense ratio of 1.12%, multiplied by the average account value over the period and prorated for the six-months ended December 31, 2016 (184/366 days).

26

FPA U.S. VALUE FUND, INC.

DIRECTOR AND OFFICER INFORMATION

(Unaudited)

| Name and Year of Birth | Position(s) With Fund Years Served | Principal Occupation(s) During the Past 5 Years | Portfolios in Fund Complex Overseen | Other Directorships | |||||||||||||||

Allan M. Rudnick – 1940† | Director and Chairman* Years Served: 4 | Private Investor. Formerly Co-Founder, Chief Executive Officer, Chairman and Chief Investment Officer of Kayne Anderson Rudnick Investment Management from 1989 to 2007. | 7 | ||||||||||||||||

Sandra Brown – 1955† | Director* Years Served: <1 | Consultant. Formerly, CEO and President of Transamerica Financial Advisers, Inc., 1999 to 2009; President, Transamerica Securities Sales Corp. 1998 to 2009; VP, Bank of America Mutual Fund Administration 1990 to 1998. | 7 | ||||||||||||||||

Mark L. Lipson – 1949† | Director* Years Served: 1 | Consultant. ML2Advisors, LLC. Former member of the Management Committee and Western Region Head at Bessemer Trust Company from 2007 to 2014. | 7 | ||||||||||||||||

Alfred E. Osborne, Jr. – 1944† | Director* Years Served: 2 | Senior Associate Dean of the John E. Anderson School of Management at UCLA. | 7 | Wedbush, Inc., Nuverra Environmental Solutions, Inc., and Kaiser Aluminun, Inc. | |||||||||||||||

A. Robert Pisano – 1943† | Director* Years Served: 4 | Consultant. Formerly President and Chief Operating Officer of the Motion Picture Association of America, Inc. from 2005 to 2011. | 7 | Entertainment Partners, and Resources Global Professionals | |||||||||||||||

Patrick B. Purcell – 1943† | Director* Years Served: 4 | Retired. Formerly Executive Vice President, Chief Financial and Administrative Officer of Paramount Pictures from 1983 to 1998. | 7 | ||||||||||||||||

J. Richard Atwood – 1960 | Director* and President Years Served: 19 | Managing Partner of the Adviser. | 7 | ||||||||||||||||

Gregory Nathan – 1981 | Vice President & Portfolio Manager Years Served: 1 | Managing Director of the Adviser since 2015 Formerly Vice President of the Adviser from 2007 to 2015. | |||||||||||||||||

Leora R. Weiner – 1970 | Chief Compliance Officer Years Served: 2 | Managing Director and General Counsel of the Adviser since 2014. Formerly Managing Director, General Counsel and Chief Compliance Officer of Tradewinds Global Investors, LLC from 2008 to 2014. | |||||||||||||||||

E. Lake Setzler – 1967 | Treasurer Years Served: 10 | Senior Vice President and Controller of the Adviser. | |||||||||||||||||

Francine S. Hayes – 1967 | Secretary Years Served: 1 | Vice President and Senior Counsel of State Street Bank and Trust Company | |||||||||||||||||

* Directors serve until their resignation, removal or retirement.

† Audit Committee member

The Statement of Additional Information includes additional information about the Directors and is available, without charge, upon request by calling (800) 982-4372.

27

(This page has been left blank intentionally.)

FPA U.S. VALUE FUND, INC.

INVESTMENT ADVISER

First Pacific Advisors, LLC

11601 Wilshire Boulevard, Suite 1200

Los Angeles, CA 90025

TRANSFER & SHAREHOLDER SERVICE AGENT

UMB Fund Services, Inc.

P.O. Box 2175

Milwaukee, WI 53201-2175

or

235 West Galena Street

Milwaukee, WI 53212-3948

(800) 638-3060

CUSTODIAN AND ADMINISTRATOR

State Street Bank and Trust Company

Boston, Massachusetts

TICKER SYMBOL: FPPFX

CUSIP: 302548102

DISTRIBUTOR

UMB Distribution Services, LLC

235 West Galena Street

Milwaukee, Wisconsin 53212-3948

LEGAL COUNSEL

Dechert LLP

San Francisco, California

INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

Deloitte & Touche LLP

Los Angeles, California

This report has been prepared for the information of shareholders of FPA U.S. VALUE FUND, INC., and is not authorized for distribution to prospective investors unless preceded or accompanied by an effective prospectus.

The Fund's complete proxy voting record for the 12 months ended June 30, 2016 is available without charge, upon request by calling (800) 982-4372 and on the SEC's website at www.sec.gov.

The Fund's schedule of portfolio holdings, filed the first and third quarter of the Fund's fiscal year on Form N-Q with the SEC, is available on the SEC's website at www.sec.gov. Form N-Q is available at the SEC's Public Reference Room in Washington, D.C., and information on the operations of the Public Reference Room may be obtained by calling (202) 551-8090. To obtain Form N-Q from the Fund, shareholders can call (800) 982-4372.

Additional information about the Fund is available online at www.fpafunds.com. This information includes, among other things, holdings, top sectors, and performance, and is updated on or about the 15th business day after the end of each quarter.

Item 2. Code of Ethics.

(a) The registrant has adopted a code of ethics that applies to the registrant’s principal executive and financial officers.

(b) Not applicable.

(c) During the period covered by this report, there were no amendments to the provisions of the code of ethics adopted in 2(a) above.

(d) During the period covered by this report, there were not any implicit or explicit waivers to the provisions of the code of ethics adopted in 2(a).

(e) Not Applicable

(f) A copy of the registrant’s code of ethics is filed as an exhibit to this Form N-CSR.

Item 3. Audit Committee Financial Expert.

The registrant’s board of directors has determined that Patrick B. Purcell, a member of the registrant’s audit committee and board of directors, is an “audit committee financial expert” and is “independent,” as those terms are defined in this Item. This designation will not increase the designee’s duties, obligations or liability as compared to his duties, obligations and liability as a member of the audit committee and of the board of directors. This designation does not affect the duties, obligations or liability of any other member of the audit committee or the board of directors.

Item 4. Principal Accountant Fees and Services.

|

| 2015 |

| 2016 |

| ||

(a) Audit Fees |

| $ | 39,500 |

| $ | 40,883 |

|

(b) Audit Related Fees |

| $ | -0- |

| $ | -0- |

|

(c) Tax Fees(1) |

| $ | 8,700 |

| $ | 9,005 |

|

(d) All Other Fees |

| $ | -0- |

| $ | -0- |

|

(1) Tax fees are for the preparation of the registrant’s tax return(s).

(e)(1) The audit committee shall pre-approve all audit and permissible non-audit services that the committee considers compatible with maintaining the independent auditors’ independence. The pre-approval requirement will extend to all non-audit services provided to the registrant, the adviser, and any entity controlling, controlled by, or under common control with the adviser that provides ongoing services to the registrant, if the engagement relates directly to the operations and financial reporting of the registrant; provided, however, that an engagement of the registrant’s independent auditors to perform attest services for the registrant, the adviser or its affiliates required by generally accepted auditing standards to complete the examination of the registrant’s financial statements (such as an examination conducted in accordance with Statement on Standards for Attestation Engagements Number 16, or a Successor Statement, issued by the American Institute of Certified Public Accountants), will be deem pre-approved if:

(i) the registrant’s independent auditors inform the audit committee of the engagement,

(ii) the registrant’s independent auditors advise the audit committee at least annually that the performance of this engagement will not impair the independent auditor’s independence with respect to the registrant, and

(iii) the audit committee receives a copy of the independent auditor’s report prepared in connection with such services. The committee may delegate to one or more committee members the authority to review and pre-approve audit and permissible non-audit services. Actions taken under any such delegation will be reported to the full committee at its next meeting.