| | |

| UNITED STATES

SECURITIES AND EXCHANGE COMMISSION |

| | |

| CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

|

| | |

| Investment Company Act file number: | (811-03897) |

| | |

| Exact name of registrant as specified in charter: | Putnam U.S. Government Income Trust |

| | |

| Address of principal executive offices: | One Post Office Square, Boston, Massachusetts 02109 |

| | |

| Name and address of agent for service: | Robert T. Burns, Vice President

One Post Office Square

Boston, Massachusetts 02109 |

| | |

| Copy to: | Bryan Chegwidden, Esq.

Ropes & Gray LLP

1211 Avenue of the Americas

New York, New York 10036 |

| | |

| Registrant's telephone number, including area code: | (617) 292-1000 |

| | |

| Date of fiscal year end: | September 30, 2017 |

| | |

| Date of reporting period : | October 1, 2016 — September 30, 2017 |

| | |

|

Item 1. Report to Stockholders: | |

| | |

| The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940: | |

Putnam

U.S. Government

Income Trust

Annual report

9 | 30 | 17

Consider these risks before investing: Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk and the risk that they may increase in value less than other bonds when interest rates decline and decline in value more than other bonds when interest rates rise. Bond investments are subject to interest-rate risk (the risk of bond prices falling if interest rates rise) and credit risk (the risk of an issuer defaulting on interest or principal payments). Interest-rate risk is greater for longer-term bonds, and credit risk is greater for below-investment-grade bonds. Risks associated with derivatives include increased investment exposure (which may be considered leverage) and, in the case of over-the-counter instruments, the potential inability to terminate or sell derivatives positions and the potential failure of the other party to the instrument to meet its obligations. Unlike bonds, funds that invest in bonds have fees and expenses. Bond prices may fall or fail to rise over time for several reasons, including general financial market conditions, changing market perceptions (including perceptions about the risk of default and expectations about monetary policy or interest rates), changes in government intervention in the financial markets, and factors related to a specific issuer or industry. These and other factors may lead to periods of increased volatility and reduced liquidity in the fund’s portfolio holdings. You can lose money by investing in the fund.

Message from the Trustees

November 10, 2017

Dear Fellow Shareholder:

A fair amount of investor optimism has helped keep financial markets on a steady course throughout 2017. Global stock markets have generally made solid advances with low volatility, while bond market performance has been a bit more uneven. As we approach the closing weeks of the year, it is important to note that a number of macroeconomic and geopolitical risks around the world could disrupt market momentum.

In all market environments, we believe investors should remain focused on time-tested strategies: maintain a well-diversified portfolio, think about long-term goals, and speak regularly with your financial advisor. In the following pages, you will find an overview of your fund’s performance for the reporting period as well as an outlook for the coming months.

We would like to take this opportunity to recognize and thank Robert J. Darretta, John A. Hill, and W. Thomas Stephens, who recently retired from your fund’s Board of Trustees. We are grateful for their years of work on behalf of you and your fellow shareholders, and we wish them well in their future endeavors.

Thank you for investing with Putnam.

Home ownership is the most common way to invest in the real estate market, but it is not the only way. It is also possible for individuals to invest in the mortgages used to finance homes and businesses through instruments called mortgage-backed securities (MBS).

Since 1984, Putnam U.S. Government Income Trust has invested in some of the highest-quality MBS with the goal of seeking as high a level of current income as Putnam believes is consistent with preservation of capital. However, investing in MBS carries certain risks. As a result, your fund’s team of experienced analysts uses proprietary models to seek out investment opportunities, while striving to maintain an appropriate amount of risk for the fund.

MBS are essentially securities that represent a stake in the principal from, and interest paid on, a collection of mortgages. Most MBS are created when government agencies or government-sponsored

|

| 2 U.S. Government Income Trust |

entities, including Fannie Mae, Ginnie Mae, and Freddie Mac, buy mortgages from financial institutions, such as banks or credit unions, and package them together by the thousands. These pools of mortgages act as collateral for the MBS that government-sponsored entities sell to different investors, including Putnam U.S. Government Income Trust.

By seeking opportunities among MBS, your fund’s manager seeks higher returns than Treasuries can typically offer, but with less volatility than stocks.

Data are historical. Past performance is not a guarantee of future results.

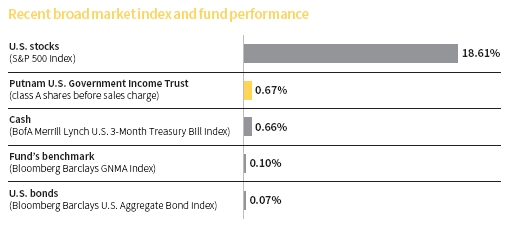

Indexes are unmanaged and are not available for direct investment. The Standard & Poor’s 500 Index is an unmanaged index of common stock performance. The Bloomberg Barclays GNMA Index is an unmanaged index of Government National Mortgage Association bonds.

Understanding mortgage-related securities

MBS (Mortgage-backed securities)

MBS are pools of mortgages used as collateral for issuing a security. These securities represent claims on the principal and interest payments made by the borrowers whose loans are in the pool.

Fannie Mae (Federal National Mortgage Association) and Freddie Mac (Federal Home Loan Mortgage Corporation)

Formerly public companies, Fannie Mae and Freddie Mac were placed under conservatorship by the U.S. government in September 2008 and are now controlled by the Federal Housing Finance Agency. Both companies buy mortgages from primary lenders (savings and loans, commercial banks, credit unions, and housing finance agencies) and develop MBS.

Ginnie Mae (Government National Mortgage Association)

Ginnie Mae is a government-owned corporation established in 1968 whose MBS are backed by the full faith and credit of the U.S. government.

CMOs (Collateralized mortgage obligations)

CMOs are structured mortgage-backed securities that use pools of MBS, or mortgage loans themselves, as collateral and carve the cash flows into different classes to meet the needs of various investors.

|

| U.S. Government Income Trust 3 |

Current performance may be lower or higher than the quoted past performance, which cannot guarantee future results. Share price, principal value, and return will fluctuate, and you may have a gain or a loss when you sell your shares. Performance of class A shares assumes reinvestment of distributions and does not account for taxes. Fund returns in the bar chart do not reflect a sales charge of 4.00%; had they, returns would have been lower. See below and pages 10–12 for additional performance information. For a portion of the periods, the fund had expense limitations, without which returns would have been lower. To obtain the most recent month-end performance, visit putnam.com.

This comparison shows your fund’s performance in the context of broad market indexes for the 12 months ended 9/30/17. See above and pages 10–12 for additional fund performance information. Index descriptions can be found on page 16.

|

| 4 U.S. Government Income Trust |

Mike is a Co-Head of Fixed Income at Putnam. He has a B.A. from Cornell University. Mike joined Putnam in 1997 and has been in the investment industry since 1989.

In addition to Mike, your fund is managed by Jatin Misra, Ph.D., CFA. Jatin has a Ph.D. from the Massachusetts Institute of Technology and a Bachelor of Technology from the Indian Institute of Technology. He has been in the investment industry since he joined Putnam in 2004.

Mike, what was the fund’s investment environment like during the reporting period?

Overall, it was a generally supportive environment for riskier assets. By contrast, rising interest rates and investor preference for the higher yields offered by taking more risk weighed on the performance of U.S. Treasuries and other government securities.

Looking first at the economic backdrop, the U.S. economy posted solid growth in the second half of 2016, then registered lower-than-expected results in the first quarter of 2017. Growth rebounded in 2017’s second quarter, repeating a pattern we’ve seen over the past two years: weak growth in the winter followed by stronger growth in the spring and summer.

Second-quarter 2017 U.S. gross domestic product was revised upward to an annual rate of 3.1% — the strongest reading since the first quarter of 2015. Despite economic disruption in Texas and Florida caused by Hurricanes Harvey and Irma, the unemployment rate dropped to 4.2% in September, a level not seen since early 2001.

|

| U.S. Government Income Trust 5 |

Allocations are shown as a percentage of the fund’s net assets as of 9/30/17. Cash and net other assets, if any, represent the market value weights of cash, derivatives, short-term securities, and other unclassified assets in the portfolio. Summary information may differ from the portfolio schedule included in the financial statements due to the inclusion of derivative securities, any interest accruals, the use of different classifications of securities for presentation purposes, and rounding. Allocations may not total 100% because the table includes the notional value (non-cash investments) of certain derivatives (the economic value for purposes of calculating periodic payment obligations), including to-be-announced (TBA) commitments, if any, in addition to the market value of securities. Holdings and allocations may vary over time.

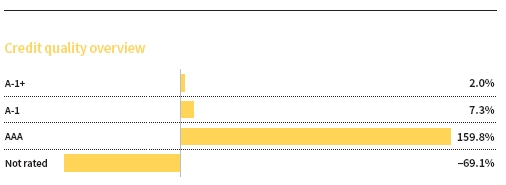

Credit qualities are shown as a percentage of the fund’s net assets as of 9/30/17. A bond rated BBB or higher (A-3 or higher, for short-term debt) is considered investment grade. This chart reflects the highest security rating provided by one or more of Standard & Poor’s, Moody’s, and Fitch. To-be-announced (TBA) mortgage commitments, if any, are included based on their issuer ratings. Ratings may vary over time.

Cash, derivative instruments, and net other assets are shown in the not-rated category. Payables and receivables for TBA mortgage commitments are included in the not-rated category and may result in negative weights. The fund itself has not been rated by an independent rating agency.

|

| 6 U.S. Government Income Trust |

Turning to interest rates, the yield on the benchmark 10-year U.S. Treasury spiked in November and December 2016, as many investors viewed then-President-elect Donald Trump’s economic agenda as stimulative and potentially inflationary. Yields were also influenced by the Federal Reserve’s decision to raise policy interest rates. Longer-term yields declined slightly in the first half of 2017, even though the Fed raised rates in June for the third time in as many quarters. Investors accepted the reality that changes in tax, health care, and fiscal policies would take time to develop and implement.

At its mid-September 2017 policy meeting, the Fed left the target for short-term interest rates unchanged at a range of 1% to 1.25%. However, the 10-year Treasury yield moved higher, as the central bank indicated that it still saw the potential for raising rates once more this year and three times in 2018. The board also announced that in October 2017 it would begin to shrink its massive portfolio of Treasuries and agency mortgage-backed securities [MBS] that it accumulated after the 2008 financial crisis.

For the period as a whole, the 10-year Treasury yield rose from 1.59% to 2.33%.

The fund outpaced its benchmark and Lipper peer group average for the 12-month period. Which strategies and holdings fueled its favorable relative performance?

Our holdings of agency interest-only collateralized mortgage obligations [IO CMOs] were the biggest contributor versus the benchmark. A combination of rising mortgage rates and lending that continued to be constrained by stringent bank underwriting standards resulted in a subdued rate of mortgage refinancing. As a result, prepayment speeds on the mortgages underlying our IO CMO positions stayed below market expectations.

Our interest-rate and yield-curve positioning also aided relative performance. The fund’s duration — a key measure of interest-rate sensitivity — was shorter than that of the benchmark, which worked well during a period when bond yields rose.

Within IO CMOs, we focused on securities backed by mortgage pools that we believed would be less sensitive to refinancing risk. These included securities structured from jumbo loans and reverse mortgages.

A jumbo mortgage is a home loan for an amount that exceeds conforming loan limits established by regulation. The jumbo loan limit is $417,000 in most of the United States. The limit on jumbo loans is $625,500 in the highest-cost areas.

A reverse mortgage allows a homeowner to borrow money against the value of his or her home. Normally, the mortgage does not have to be repaid until the borrower dies or the home is sold. As a result, unlike conventional home mortgages, reverse mortgages are generally insensitive to the direction of interest rates. In an effort to find investment opportunities that are less susceptible to refinancing risk, Putnam has developed the capability to identify what we believe are attractive opportunities among IO CMOs backed by reverse mortgages.

Our holdings of reverse-mortgage interest-only securities posted strong returns late in the period after the Department of Housing and Urban Development [HUD] announced changes that we think reduce the incentives for holders of existing reverse mortgages to refinance.

What detracted versus the benchmark?

Adverse results from our “mortgage basis” positioning — which is a strategy that seeks to exploit the yield differential between current-coupon, 30-year agency pass-throughs and 30-year Treasuries — partially detracted from the overall positive performance of our prepayment strategies.

|

| U.S. Government Income Trust 7 |

How did you use derivatives during the period?

We used interest-rate swaps and options to hedge the risks inherent in the fund’s duration and yield-curve positioning, to isolate the prepayment risk associated with our CMO holdings, and to help manage overall downside risk. We also employed futures to help manage the fund’s yield-curve strategies. Lastly, we used total return swaps to hedge the fund’s sector exposures and to gain access to specific areas of the market.

What is your outlook for the months ahead?

The Fed had signaled for months that it was planning to begin reducing its $4.5 trillion bond portfolio, and in September 2017, announced that it would start the process in October 2017. The Fed’s plan is to allow a specific amount of securities to mature each month (or pay down, in the case of MBS): $6 billion in Treasuries and $4 billion in MBS. It would then allow the amount of maturities to increase each quarter, ultimately reaching a maximum of $30 billion per month for Treasuries and $20 billion per month for agency MBS. We expect that the Fed will reduce its holdings in a gradual and predictable manner in an effort to avoid interest-rate spikes or other market strains.

The Fed stopped adding to its investments more than three years ago, but it has been reinvesting the proceeds of maturing bonds to keep its holdings steady. These reinvestments have helped to keep a lid on long-term interest rates, and letting securities mature without reinvesting could put upward pressure on rates. That said, we think the incremental nature of the plan suggests that rate volatility may be limited, at least initially.

Turning to bond yields, we think yields are too low given generally favorable global economic conditions. Although we don’t believe yields are likely to rise significantly this year, partly due to strong global demand for U.S. bonds, we do think they’ll be higher by the end of 2018. There are a lot of unknowns: potentially significant changes to the Fed’s Board of Governors in 2018; the timing of when the European Central Bank will begin to taper its bond-purchase program; the possibility of tax reform in the United States; potentially tighter monetary policy in other countries, such as Canada and the United Kingdom; and the ongoing potential for geopolitical flare-ups. So, while there are a variety of crosscurrents that could impact the trajectory of bond yields both in the United States and overseas, we think the overall trend will be for yields to rise next year.

This chart illustrates the fund’s composition by maturity, showing the percentage of holdings in different maturity ranges and how the composition has changed over the past six months. Holdings and maturity ranges may vary over time. A negative number represents cash to be allocated to to-be-announced (TBA) agency pass-through mortgage-backed securities, which the fund has agreed to purchase.

|

| 8 U.S. Government Income Trust |

Given this outlook, how do you plan to position the fund?

As of September 30, the fund’s duration was modestly shorter than that of the benchmark. We plan to keep it that way for now, given our expectations for moderately higher interest rates in the months ahead.

We also plan to take a tactical approach toward our mortgage-basis positioning. We think the Fed’s plan for reducing its bond portfolio has been well telegraphed, and therefore we believe the market impact for MBS is likely to be minimal.

We think IO CMOs remain attractive, since relatively tight mortgage-lending standards may continue to curb refinancing activity.

Lastly, we continue to like reverse-mortgage IOs. In addition to broadening the fund’s diversification, we think they offer a combination of reduced rate sensitivity, reasonable liquidity [ease of trading at favorable bid/ask spreads], and attractive yield spreads.

Thanks for your time and for bringing us up to date, Mike.

The views expressed in this report are exclusively those of Putnam Management and are subject to change. They are not meant as investment advice.

Please note that the holdings discussed in this report may not have been held by the fund for the entire period. Portfolio composition is subject to review in accordance with the fund’s investment strategy and may vary in the future. Current and future portfolio holdings are subject to risk.

ABOUT DERIVATIVES

Derivatives are an increasingly common type of investment instrument, the performance of which is derived from an underlying security, index, currency, or other area of the capital markets. Derivatives employed by the fund’s managers generally serve one of two main purposes: to implement a strategy that may be difficult or more expensive to invest in through traditional securities, or to hedge unwanted risk associated with a particular position.

For example, the fund’s managers might use currency forward contracts to capitalize on an anticipated change in exchange rates between two currencies. This approach would require a significantly smaller outlay of capital than purchasing traditional bonds denominated in the underlying currencies. In another example, the managers may identify a bond that they believe is undervalued relative to its risk of default, but may seek to reduce the interest-rate risk of that bond by using interest-rate swaps, a derivative through which two parties “swap” payments based on the movement of certain rates.

Like any other investment, derivatives may not appreciate in value and may lose money. Derivatives may amplify traditional investment risks through the creation of leverage and may be less liquid than traditional securities. And because derivatives typically represent contractual agreements between two financial institutions, derivatives entail “counterparty risk,” which is the risk that the other party is unable or unwilling to pay. Putnam monitors the counterparty risks we assume. For example, Putnam often enters into collateral agreements that require the counterparties to post collateral on a regular basis to cover their obligations to the fund. Counterparty risk for exchange-traded futures and centrally cleared swaps is mitigated by the daily exchange of margin and other safeguards against default through their respective clearinghouses.

|

| U.S. Government Income Trust 9 |

Your fund’s performance

This section shows your fund’s performance, price, and distribution information for periods ended September 30, 2017, the end of its most recent fiscal year. In accordance with regulatory requirements for mutual funds, we also include expense information taken from the fund’s current prospectus. Performance should always be considered in light of a fund’s investment strategy. Data represent past performance. Past performance does not guarantee future results. More recent returns may be less or more than those shown. Investment return and principal value will fluctuate, and you may have a gain or a loss when you sell your shares. Performance information does not reflect any deduction for taxes a shareholder may owe on fund distributions or on the redemption of fund shares. For the most recent month-end performance, please visit the Individual Investors section at putnam.com or call Putnam at 1-800-225-1581. Class R and Y shares are not available to all investors. See the Terms and Definitions section in this report for definitions of the share classes offered by your fund.

Fund performance Total return for periods ended 9/30/17

| | | | | | | | |

| | Annual | | | | | | | |

| | average | | Annual | | Annual | | Annual | |

| | (life of fund) | 10 years | average | 5 years | average | 3 years | average | 1 year |

| Class A (2/8/84) | | | | | | | | |

| Before sales charge | 6.25% | 52.64% | 4.32% | 6.06% | 1.18% | 2.11% | 0.70% | 0.67% |

| After sales charge | 6.12 | 46.53 | 3.89 | 1.81 | 0.36 | –1.97 | –0.66 | –3.35 |

| Class B (4/27/92) | | | | | | | | |

| Before CDSC | 6.01 | 44.17 | 3.73 | 2.29 | 0.45 | –0.05 | –0.02 | –0.07 |

| After CDSC | 6.01 | 44.17 | 3.73 | 0.41 | 0.08 | –2.88 | –0.97 | –4.95 |

| Class C (7/26/99) | | | | | | | | |

| Before CDSC | 5.44 | 40.94 | 3.49 | 2.16 | 0.43 | –0.16 | –0.05 | –0.09 |

| After CDSC | 5.44 | 40.94 | 3.49 | 2.16 | 0.43 | –0.16 | –0.05 | –1.07 |

| Class M (2/6/95) | | | | | | | | |

| Before sales charge | 5.94 | 49.46 | 4.10 | 4.72 | 0.93 | 1.37 | 0.46 | 0.41 |

| After sales charge | 5.84 | 44.60 | 3.76 | 1.32 | 0.26 | –1.92 | –0.64 | –2.85 |

| Class R (1/21/03) | | | | | | | | |

| Net asset value | 5.96 | 47.89 | 3.99 | 4.78 | 0.94 | 1.39 | 0.46 | 0.41 |

| Class Y (4/11/94) | | | | | | | | |

| Net asset value | 6.43 | 56.09 | 4.55 | 7.40 | 1.44 | 2.90 | 0.96 | 0.89 |

Current performance may be lower or higher than the quoted past performance, which cannot guarantee future results. After-sales-charge returns for class A and M shares reflect the deduction of the maximum 4.00% and 3.25% sales charge, respectively, levied at the time of purchase. Class B share returns after contingent deferred sales charge (CDSC) reflect the applicable CDSC, which is 5% in the first year, declining over time to 1% in the sixth year, and is eliminated thereafter. Class C share returns after CDSC reflect a 1% CDSC for the first year that is eliminated thereafter. Class R and Y shares have no initial sales charge or CDSC. Performance for class B, C, M, R, and Y shares before their inception is derived from the historical performance of class A shares, adjusted for the applicable sales charge (or CDSC) and the higher operating expenses for such shares, except for class Y shares, for which 12b-1 fees are not applicable.

For a portion of the periods, the fund had expense limitations, without which returns would have been lower.

Class B share performance reflects conversion to class A shares after eight years.

|

| 10 U.S. Government Income Trust |

Comparative index returns For periods ended 9/30/17

| | | | | | | | |

| | Annual | | | | | | | |

| | average | | Annual | | Annual | | Annual | |

| | (life of fund) | 10 years | average | 5 years | average | 3 years | average | 1 year |

| Bloomberg Barclays | | | | | | | | |

| GNMA Index | 7.25% | 50.44% | 4.17% | 8.45% | 1.64% | 6.54% | 2.14% | 0.10% |

| Lipper GNMA Funds | | | | | | | | |

| category average* | 6.52 | 44.67 | 3.75 | 5.28 | 1.03 | 4.26 | 1.40 | –0.28 |

Index and Lipper results should be compared with fund performance before sales charge, before CDSC, or at net asset value.

* Over the 1-year, 3-year, 5-year, 10-year, and life-of-fund periods ended 9/30/17, there were 58, 53, 51, 41, and 4 funds, respectively, in this Lipper category.

Past performance does not indicate future results. At the end of the same time period, a $10,000 investment in the fund’s class B and C shares would have been valued at $14,417 and $14,094, respectively, and no contingent deferred sales charges would apply. A $10,000 investment in the fund’s class M shares ($9,675 after sales charge) would have been valued at $14,460. A $10,000 investment in the fund’s class R and Y shares would have been valued at $14,789 and $15,609, respectively.

|

| U.S. Government Income Trust 11 |

Fund price and distribution information For the 12-month period ended 9/30/17

| | | | | | | | |

| Distributions | Class A | Class B | Class C | Class M | Class R | Class Y |

| Number | 12 | 12 | 12 | 12 | 12 | 12 |

| Income | $0.396 | $0.300 | $0.297 | $0.362 | $0.361 | $0.432 |

| Capital gains | — | — | — | — | — | — |

| Total | $0.396 | $0.300 | $0.297 | $0.362 | $0.361 | $0.432 |

| | Before | After | Net | Net | Before | After | Net | Net |

| | sales | sales | asset | asset | sales | sales | asset | asset |

| Share value | charge | charge | value | value | charge | charge | value | value |

| 9/30/16 | $13.20 | $13.75 | $13.14 | $13.08 | $13.26 | $13.71 | $13.07 | $13.08 |

| 9/30/17 | 12.89 | 13.43 | 12.83 | 12.77 | 12.95 | 13.39 | 12.76 | 12.76 |

| | Before | After | Net | Net | Before | After | Net | Net |

| Current rate | sales | sales | asset | asset | sales | sales | asset | asset |

| (end of period) | charge | charge | value | value | charge | charge | value | value |

| Current dividend rate1 | 3.07% | 2.95% | 2.34% | 2.35% | 2.78% | 2.69% | 2.82% | 3.39% |

| Current 30-day | | | | | | | | |

| SEC yield2 | N/A | 2.75 | 2.14 | 2.11 | N/A | 2.54 | 2.61 | 3.11 |

The classification of distributions, if any, is an estimate. Before-sales-charge share value and current dividend rate for class A and M shares, if applicable, do not take into account any sales charge levied at the time of purchase. After-sales-charge share value, current dividend rate, and current 30-day SEC yield, if applicable, are calculated assuming that the maximum sales charge (4.00% for class A shares and 3.25% for class M shares) was levied at the time of purchase. Final distribution information will appear on your year-end tax forms.

1 Most recent distribution, including any return of capital and excluding capital gains, annualized and divided by share price before or after sales charge at period-end.

2 Based only on investment income and calculated using the maximum offering price for each share class, in accordance with SEC guidelines.

|

| 12 U.S. Government Income Trust |

Your fund’s expenses

As a mutual fund investor, you pay ongoing expenses, such as management fees, distribution fees (12b-1 fees), and other expenses. In the most recent six-month period, your fund’s expenses were limited; had expenses not been limited, they would have been higher. Using the following information, you can estimate how these expenses affect your investment and compare them with the expenses of other funds. You may also pay one-time transaction expenses, including sales charges (loads) and redemption fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial representative.

Expense ratios

| | | | | | |

| | Class A | Class B | Class C | Class M | Class R | Class Y |

| Total annual operating expenses for the | | | | | | |

| fiscal year ended 9/30/16* | 0.89% | 1.62% | 1.64% | 1.13% | 1.14% | 0.64% |

| Annualized expense ratio for the | | | | | | |

| six-month period ended 9/30/17† | 0.90% | 1.63% | 1.65% | 1.14% | 1.15% | 0.65% |

Fiscal-year expense information in this table is taken from the most recent prospectus, is subject to change, and may differ from that shown for the annualized expense ratio and in the financial highlights of this report.

Expenses are shown as a percentage of average net assets.

* Restated to reflect current fees resulting from a change to the fund’s investor servicing arrangements effective 9/1/16.

† Expense ratios for each class are for the fund’s most recent fiscal half year. As a result of this, ratios may differ from expense ratios based on one-year data in the financial highlights.

Expenses per $1,000

The following table shows the expenses you would have paid on a $1,000 investment in each class of the fund from 4/1/17 to 9/30/17. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

| | | | | | |

| | Class A | Class B | Class C | Class M | Class R | Class Y |

| Expenses paid per $1,000*† | $4.53 | $8.19 | $8.29 | $5.74 | $5.79 | $3.27 |

| Ending value (after expenses) | $1,007.60 | $1,004.60 | $1,004.60 | $1,006.90 | $1,007.00 | $1,009.10 |

* Expenses for each share class are calculated using the fund’s annualized expense ratio for each class, which represents the ongoing expenses as a percentage of average net assets for the six months ended 9/30/17. The expense ratio may differ for each share class.

† Expenses are calculated by multiplying the expense ratio by the average account value for the period; then multiplying the result by the number of days in the period; and then dividing that result by the number of days in the year.

|

| U.S. Government Income Trust 13 |

Estimate the expenses you paid

To estimate the ongoing expenses you paid for the six months ended 9/30/17, use the following calculation method. To find the value of your investment on 4/1/17, call Putnam at 1-800-225-1581.

Compare expenses using the SEC’s method

The Securities and Exchange Commission (SEC) has established guidelines to help investors assess fund expenses. Per these guidelines, the following table shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return. You can use this information to compare the ongoing expenses (but not transaction expenses or total costs) of investing in the fund with those of other funds. All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

| | | | | | |

| | Class A | Class B | Class C | Class M | Class R | Class Y |

| Expenses paid per $1,000*† | $4.56 | $8.24 | $8.34 | $5.77 | $5.82 | $3.29 |

| Ending value (after expenses) | $1,020.56 | $1,016.90 | $1,016.80 | $1,019.35 | $1,019.30 | $1,021.81 |

* Expenses for each share class are calculated using the fund’s annualized expense ratio for each class, which represents the ongoing expenses as a percentage of average net assets for the six months ended 9/30/17. The expense ratio may differ for each share class.

† Expenses are calculated by multiplying the expense ratio by the average account value for the six-month period; then multiplying the result by the number of days in the six-month period; and then dividing that result by the number of days in the year.

|

| 14 U.S. Government Income Trust |

Terms and definitions

Important terms

Total return shows how the value of the fund’s shares changed over time, assuming you held the shares through the entire period and reinvested all distributions in the fund.

Before sales charge, or net asset value, is the price, or value, of one share of a mutual fund, without a sales charge. Before-sales-charge figures fluctuate with market conditions, and are calculated by dividing the net assets of each class of shares by the number of outstanding shares in the class.

After sales charge is the price of a mutual fund share plus the maximum sales charge levied at the time of purchase. After-sales-charge performance figures shown here assume the 4.00% maximum sales charge for class A shares and 3.25% for class M shares.

Contingent deferred sales charge (CDSC) is generally a charge applied at the time of the redemption of class B or C shares and assumes redemption at the end of the period. Your fund’s class B CDSC declines over time from a 5% maximum during the first year to 1% during the sixth year. After the sixth year, the CDSC no longer applies. The CDSC for class C shares is 1% for one year after purchase.

Share classes

Class A shares are generally subject to an initial sales charge and no CDSC (except on certain redemptions of shares bought without an initial sales charge).

Class B shares are closed to new investments and are only available by exchange from another Putnam fund or through dividend and/or capital gains reinvestment. They are not subject to an initial sales charge and may be subject to a CDSC.

Class C shares are not subject to an initial sales charge and are subject to a CDSC only if the shares are redeemed during the first year.

Class M shares have a lower initial sales charge and a higher 12b-1 fee than class A shares and no CDSC.

Class R shares are not subject to an initial sales charge or CDSC and are available only to employer-sponsored retirement plans.

Class Y shares are not subject to an initial sales charge or CDSC, and carry no 12b-1 fee. They are generally only available to corporate and institutional clients and clients in other approved programs.

Fixed-income terms

Current rate is the annual rate of return earned from dividends or interest of an investment. Current rate is expressed as a percentage of the price of a security, fund share, or principal investment.

Mortgage-backed security (MBS), also known as a mortgage “pass-through,” is a type of asset-backed security that is secured by a mortgage or collection of mortgages. The following are types of MBSs:

• Agency credit-risk transfer security (CRT) is backed by a reference pool of agency mortgages. Unlike a regular agency pass-through, the principal invested in a CRT is not backed by a U.S. government agency. To compensate investors for this risk, a CRT typically offers a higher yield than conventional pass-through securities. Similar to a CMBS, a CRT is structured into various tranches for investors, offering different levels of risk and yield based on the underlying reference pool.

• Agency “pass-through” has its principal and interest backed by a U.S. government agency, such as the Federal National Mortgage Association (Fannie Mae), Government National Mortgage Association (Ginnie Mae), and Federal Home Loan Mortgage Corporation (Freddie Mac).

|

| U.S. Government Income Trust 15 |

• Collateralized mortgage obligation (CMO) represents claims to specific cash flows from pools of home mortgages. The streams of principal and interest payments on the mortgages are distributed to the different classes of CMO interests in “tranches.” Each tranche may have different principal balances, coupon rates, prepayment risks, and maturity dates. A CMO is highly sensitive to changes in interest rates and any resulting change in the rate at which homeowners sell their properties, refinance, or otherwise prepay loans. CMOs are subject to prepayment, market, and liquidity risks.

• Interest-only (IO) security is a type of CMO in which the underlying asset is the interest portion of mortgage, Treasury, or bond payments.

• Non-agency residential mortgage-backed security (RMBS) is an MBS not backed by Fannie Mae, Ginnie Mae, or Freddie Mac. One type of RMBS is an Alt-A mortgage-backed security.

• Commercial mortgage-backed security (CMBS) is secured by the loan on a commercial property.

Yield curve is a graph that plots the yields of bonds with equal credit quality against their differing maturity dates, ranging from shortest to longest. It is used as a benchmark for other debt, such as mortgage or bank lending rates.

Comparative indexes

Bloomberg Barclays GNMA Index is an unmanaged index of Government National Mortgage Association bonds.

Bloomberg Barclays U.S. Aggregate Bond Index is an unmanaged index of U.S. investment-grade fixed-income securities.

BofA Merrill Lynch U.S. 3-Month Treasury Bill Index is an unmanaged index that seeks to measure the performance of U.S. Treasury bills available in the marketplace.

S&P 500 Index is an unmanaged index of common stock performance.

Indexes assume reinvestment of all distributions and do not account for fees. Securities and performance of a fund and an index will differ. You cannot invest directly in an index.

Merrill Lynch, Pierce, Fenner & Smith Incorporated (“BofAML”), used with permission. BofAML permits use of the BofAML indices and related data on an “as is” basis, makes no warranties regarding same, does not guarantee the suitability, quality, accuracy, timeliness, and/or completeness of the BofAML indices or any data included in, related to, or derived therefrom, assumes no liability in connection with the use of the foregoing, and does not sponsor, endorse, or recommend Putnam Investments, or any of its products or services.

Lipper is a third-party industry-ranking entity that ranks mutual funds. Its rankings do not reflect sales charges. Lipper rankings are based on total return at net asset value relative to other funds that have similar current investment styles or objectives as determined by Lipper. Lipper may change a fund’s category assignment at its discretion. Lipper category averages reflect performance trends for funds within a category.

|

| 16 U.S. Government Income Trust |

Other information for shareholders

Proxy voting

Putnam is committed to managing our mutual funds in the best interests of our shareholders. The Putnam funds’ proxy voting guidelines and procedures, as well as information regarding how your fund voted proxies relating to portfolio securities during the 12-month period ended June 30, 2017, are available in the Individual Investors section of putnam.com, and on the Securities and Exchange Commission (SEC) website, www.sec.gov. If you have questions about finding forms on the SEC’s website, you may call the SEC at 1-800-SEC-0330. You may also obtain the Putnam funds’ proxy voting guidelines and procedures at no charge by calling Putnam’s Shareholder Services at 1-800-225-1581.

Fund portfolio holdings

The fund will file a complete schedule of its portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. Shareholders may obtain the fund’s Form N-Q on the SEC’s website at www.sec.gov. In addition, the fund’s Form N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, D.C. You may call the SEC at 1-800-SEC-0330 for information about the SEC’s website or the operation of the Public Reference Room.

Trustee and employee fund ownership

Putnam employees and members of the Board of Trustees place their faith, confidence, and, most importantly, investment dollars in Putnam mutual funds. As of September 30, 2017, Putnam employees had approximately $509,000,000 and the Trustees had approximately $90,000,000 invested in Putnam mutual funds. These amounts include investments by the Trustees’ and employees’ immediate family members as well as investments through retirement and deferred compensation plans.

|

| U.S. Government Income Trust 17 |

Important notice regarding Putnam’s privacy policy

In order to conduct business with our shareholders, we must obtain certain personal information such as account holders’ names, addresses, Social Security numbers, and dates of birth. Using this information, we are able to maintain accurate records of accounts and transactions.

It is our policy to protect the confidentiality of our shareholder information, whether or not a shareholder currently owns shares of our funds. In particular, it is our policy not to sell information about you or your accounts to outside marketing firms. We have safeguards in place designed to prevent unauthorized access to our computer systems and procedures to protect personal information from unauthorized use.

Under certain circumstances, we must share account information with outside vendors who provide services to us, such as mailings and proxy solicitations. In these cases, the service providers enter into confidentiality agreements with us, and we provide only the information necessary to process transactions and perform other services related to your account. Finally, it is our policy to share account information with your financial representative, if you’ve listed one on your Putnam account.

|

| 18 U.S. Government Income Trust |

Trustee approval of management contract

General conclusions

The Board of Trustees of The Putnam Funds oversees the management of each fund and, as required by law, determines annually whether to approve the continuance of your fund’s management contract with Putnam Investment Management, LLC (“Putnam Management”) and the sub-management contract with respect to your fund between Putnam Management and its affiliate, Putnam Investments Limited (“PIL”). The Board, with the assistance of its Contract Committee, requests and evaluates all information it deems reasonably necessary under the circumstances in connection with its annual contract review. The Contract Committee consists solely of Trustees who are not “interested persons” (as this term is defined in the Investment Company Act of 1940, as amended (the “1940 Act”)) of The Putnam Funds (“Independent Trustees”).

At the outset of the review process, members of the Board’s independent staff and independent legal counsel discussed with representatives of Putnam Management the annual contract review materials furnished to the Contract Committee during the course of the previous year’s review, identifying possible changes in these materials that might be necessary or desirable for the coming year. Following these discussions and in consultation with the Contract Committee, the Independent Trustees’ independent legal counsel requested that Putnam Management and its affiliates furnish specified information, together with any additional information that Putnam Management considered relevant, to the Contract Committee. Over the course of several months ending in June 2017, the Contract Committee met on a number of occasions with representatives of Putnam Management, and separately in executive session, to consider the information that Putnam Management provided. Throughout this process, the Contract Committee was assisted by the members of the Board’s independent staff and by independent legal counsel for The Putnam Funds and the Independent Trustees.

In May 2017, the Contract Committee met in executive session to discuss and consider its recommendations with respect to the continuance of the contracts. At the Trustees’ June 2017 meeting, the Contract Committee met in executive session with the other Independent Trustees to review a summary of the key financial, performance and other data that the Contract Committee considered in the course of its review. The Contract Committee then presented its written report, which summarized the key factors that the Committee had considered and set forth its recommendations. The Contract Committee recommended, and the Independent Trustees approved, the continuance of your fund’s management and sub-management contracts, effective July 1, 2017. (Because PIL is an affiliate of Putnam Management and Putnam Management remains fully responsible for all services provided by PIL, the Trustees have not attempted to evaluate PIL as a separate entity, and all subsequent references to Putnam Management below should be deemed to include reference to PIL as necessary or appropriate in the context.)

The Independent Trustees’ approval was based on the following conclusions:

• That the fee schedule in effect for your fund represented reasonable compensation in light of the nature and quality of the services being provided to the fund, the fees paid by competitive funds, the costs incurred by Putnam Management in providing services to the fund, and the continued application of certain reductions and waivers noted below; and

• That the fee schedule in effect for your fund represented an appropriate sharing between fund shareholders and Putnam Management of such economies of scale as may exist in the management of the fund at current asset levels.

These conclusions were based on a comprehensive consideration of all information provided to the Trustees and were not the result of any single factor. Some of the factors that figured particularly in the Trustees’ deliberations and how the Trustees considered these factors are described below, although individual Trustees may have evaluated the information presented differently, giving different weights to various factors. It is also important to recognize that the management arrangements for your fund and the other Putnam funds are the result of many years of review and discussion between the Independent Trustees and Putnam Management, that some aspects of the arrangements may receive greater scrutiny in some years than others, and that the Trustees’ conclusions may be based, in part, on their consideration of fee arrangements in previous

|

| U.S. Government Income Trust 19 |

years. For example, with some minor exceptions, the funds’ current fee arrangements under the management contracts were first implemented at the beginning of 2010 following extensive review by the Contract Committee and discussions with representatives of Putnam Management, as well as approval by shareholders.

Management fee schedules and total expenses

The Trustees reviewed the management fee schedules in effect for all Putnam funds, including fee levels and breakpoints. The Trustees also reviewed the total expenses of each Putnam fund, recognizing that in most cases management fees represented the major, but not the sole, determinant of total costs to fund shareholders. (In a few instances, funds have implemented so-called “all-in” management fees covering substantially all routine fund operating costs.)

In reviewing fees and expenses, the Trustees generally focus their attention on material changes in circumstances — for example, changes in assets under management, changes in a fund’s investment strategy, changes in Putnam Management’s operating costs or profitability, or changes in competitive practices in the mutual fund industry — that suggest that consideration of fee changes might be warranted. The Trustees concluded that the circumstances did not indicate that changes to the management fee structure for your fund would be appropriate at this time.

Under its management contract, your fund has the benefit of breakpoints in its management fee schedule that provide shareholders with economies of scale in the form of reduced fee rates as assets under management in the Putnam family of funds increase. The Trustees concluded that the fee schedule in effect for your fund represented an appropriate sharing of economies of scale between fund shareholders and Putnam Management.

As in the past, the Trustees also focused on the competitiveness of each fund’s total expense ratio. In order to support the effort to have fund expenses meet competitive standards, the Trustees and Putnam Management have implemented certain expense limitations that were in effect during your fund’s fiscal year ending in 2016. These expense limitations were: (i) a contractual expense limitation applicable to specified retail open-end funds, including your fund, of 25 basis points (until September 1, 2016, this limitation was 32 basis points) on investor servicing fees and expenses and (ii) a contractual expense limitation applicable to specified open-end funds, including your fund, of 20 basis points on so-called “other expenses” (i.e., all expenses exclusive of management fees, distribution fees, investor servicing fees, investment-related expenses, interest, taxes, brokerage commissions, acquired fund fees and expenses and extraordinary expenses). These expense limitations attempt to maintain competitive expense levels for the funds. Most funds, including your fund, had sufficiently low expenses that these expense limitations were not operative during their fiscal years ending in 2016. Putnam Management has agreed to maintain the 25 basis points expense limitation until at least August 31, 2018 and to maintain the 20 basis points expense limitation until at least January 30, 2019. Putnam Management’s support for these expense limitation arrangements was an important factor in the Trustees’ decision to approve the continuance of your fund’s management and sub-management contracts.

The Trustees reviewed comparative fee and expense information for a custom group of competitive funds selected by Broadridge Financial Solutions, Inc. (“Broadridge”). This comparative information included your fund’s percentile ranking for effective management fees and total expenses (excluding any applicable 12b-1 fee), which provides a general indication of your fund’s relative standing. In the custom peer group, your fund ranked in the first quintile in effective management fees (determined for your fund and the other funds in the custom peer group based on fund asset size and the applicable contractual management fee schedule) and in the third quintile in total expenses (excluding any applicable 12b-1 fees) as of December 31, 2016. The first quintile represents the least expensive funds and the fifth quintile the most expensive funds. The fee and expense data reported by Broadridge as of December 31, 2016 reflected the most recent fiscal year-end data available in Broadridge’s database at that time.

In connection with their review of fund management fees and total expenses, the Trustees also reviewed the costs of the services provided and the profits realized by Putnam Management and its affiliates from their contractual relationships with the funds. This information included trends in revenues, expenses and profitability of Putnam Management and its affiliates relating to the investment management, investor servicing and

|

| 20 U.S. Government Income Trust |

distribution services provided to the funds. In this regard, the Trustees also reviewed an analysis of Putnam Management’s revenues, expenses and profitability, allocated on a fund-by-fund basis, with respect to the funds’ management, distribution, and investor servicing contracts. For each fund, the analysis presented information about revenues, expenses and profitability for each of the agreements separately and for the agreements taken together on a combined basis. The Trustees concluded that, at current asset levels, the fee schedules in place represented reasonable compensation for the services being provided and represented an appropriate sharing between fund shareholders and Putnam Management of such economies of scale as may exist in the management of the Putnam funds at that time.

The information examined by the Trustees in connection with their annual contract review for the Putnam funds included information regarding fees charged by Putnam Management and its affiliates to institutional clients, including defined benefit pension and profit-sharing plans, charities, college endowments, foundations, sub-advised third-party mutual funds, state, local and non-U.S. government entities, and corporations. This information included, in cases where an institutional product’s investment strategy corresponds with a fund’s strategy, comparisons of those fees with fees charged to the Putnam funds, as well as an assessment of the differences in the services provided to these different types of clients as compared to the services provided to the Putnam Funds. The Trustees observed that the differences in fee rates between these clients and the Putnam funds are by no means uniform when examined by individual asset sectors, suggesting that differences in the pricing of investment management services to these types of clients may reflect, among other things, historical competitive forces operating in separate markets. The Trustees considered the fact that in many cases fee rates across different asset classes are higher on average for mutual funds than for institutional clients, as well as the differences between the services that Putnam Management provides to the Putnam funds and those that it provides to its other clients. The Trustees did not rely on these comparisons to any significant extent in concluding that the management fees paid by your fund are reasonable.

Investment performance

The quality of the investment process provided by Putnam Management represented a major factor in the Trustees’ evaluation of the quality of services provided by Putnam Management under your fund’s management contract. The Trustees were assisted in their review of the Putnam funds’ investment process and performance by the work of the investment oversight committees of the Trustees, which meet on a regular basis with the funds’ portfolio teams and with the Chief Investment Officers and other senior members of Putnam Management’s Investment Division throughout the year. In addition, in response to a request from the Independent Trustees, Putnam Management provided the Trustees with in-depth presentations regarding each of the equity and fixed income investment teams, including the operation of the teams and their investment approaches. The Trustees concluded that Putnam Management generally provides a high-quality investment process — based on the experience and skills of the individuals assigned to the management of fund portfolios, the resources made available to them, and in general Putnam Management’s ability to attract and retain high-quality personnel — but also recognized that this does not guarantee favorable investment results for every fund in every time period.

The Trustees considered that 2016 was a challenging year for the performance of the Putnam funds, with generally disappointing results for the international and global equity funds and taxable fixed income funds, mixed results for small-cap equity, Spectrum, global asset allocation, equity research and tax exempt fixed income funds, but generally strong results for U.S. equity funds. The Trustees noted, however, that they were encouraged by the positive performance trend since mid-year 2016 across most Putnam Funds. In particular, from May 1, 2016 through April 30, 2017, 51% of Putnam Fund assets were in the top quartile and 87% were above the median of the Putnam Funds’ competitive industry rankings. They noted that the longer-term performance of the Putnam funds generally continued to be strong, exemplified by the fact that the Putnam funds were ranked by the Barron’s/Lipper Fund Families survey as the 5th-best performing mutual fund complex out of 54 complexes for the five-year period ended December 31, 2016. In addition, while the survey ranked the Putnam Funds 52nd out of 61 mutual fund complexes for the one-year period ended 2016, the Putnam Funds have ranked 1st or 2nd

|

| U.S. Government Income Trust 21 |

in the survey for the one-year period three times since 2009 (most recently in 2013). They also noted, however, the disappointing investment performance of some funds for periods ended December 31, 2016 and considered information provided by Putnam Management regarding the factors contributing to the underperformance and actions being taken to improve the performance of these particular funds. The Trustees indicated their intention to continue to monitor closely the performance of those funds, including the effectiveness of any efforts Putnam Management has undertaken to address underperformance and whether additional actions to address areas of underperformance are warranted.

For purposes of the Trustees’ evaluation of the Putnam Funds’ investment performance, the Trustees generally focus on a competitive industry ranking of each fund’s total net return over a one-year, three-year and five-year period. For a number of Putnam funds with relatively unique investment mandates for which Putnam Management informed the Trustees that meaningful competitive performance rankings are not considered to be available, the Trustees evaluated performance based on their total gross and net returns and, in most cases, comparisons of those returns with the returns of selected investment benchmarks. In the case of your fund, the Trustees considered that its class A share cumulative total return performance at net asset value was in the following quartiles of its Lipper Inc. (“Lipper”) peer group (Lipper GNMA Funds) for the one-year, three-year and five-year periods ended December 31, 2016 (the first quartile representing the best-performing funds and the fourth quartile the worst-performing funds):

| |

| One-year period | 4th |

| Three-year period | 3rd |

| Five-year period | 2nd |

Over the one-year, three-year and five-year periods ended December 31, 2016, there were 62, 58 and 54 funds, respectively, in your fund’s Lipper peer group. (When considering performance information, shareholders should be mindful that past performance is not a guarantee of future results.)

The Trustees expressed concern about your fund’s fourth quartile performance over the one-year period ended December 31, 2016 and considered the circumstances that may have contributed to this disappointing performance. The Trustees considered Putnam Management’s observation that the fund’s underperformance over the one-year period was largely attributable to the fund’s relative emphasis on shorter duration investments (which reduced the fund’s sensitivity to interest rate changes but detracted from performance, particularly during January and February 2016). The Trustees also noted Putnam Management’s view that some of the fund’s mortgage-related investments were negatively impacted by market reactions to the unexpected outcomes of the U.K.’s vote to leave the European Union and the U.S. elections.

The Trustees considered that during the second half of 2016 and into 2017, the fund’s emphasis on shorter duration investments had been beneficial and the fund had delivered top decile returns for the period July 2016 through January 2017; and that Putnam Management remained confident in the fund’s portfolio managers. The Trustees also considered Putnam Management’s continued efforts to support fund performance through the appointment of an additional portfolio manager in February 2017 and through initiatives including structuring compensation for portfolio managers and research analysts to enhance accountability for fund performance, emphasizing accountability in the portfolio management process, and affirming its commitment to a fundamental-driven approach to investing. The Trustees noted further that Putnam Management continued to strengthen its fundamental research capabilities by adding new investment personnel.

As a general matter, the Trustees believe that cooperative efforts between the Trustees and Putnam Management represent the most effective way to address investment performance concerns that may arise from time to time. The Trustees noted that investors in the Putnam funds have, in effect, placed their trust in the Putnam organization, under the oversight of the funds’ Trustees, to make appropriate decisions regarding the management of the funds. Based on Putnam Management’s willingness to take appropriate measures to address fund performance issues and Putnam Management’s responsiveness to Trustee concerns about investment performance, the Trustees concluded that it continues to be advisable to seek change within Putnam Management to address performance shortcomings. In the Trustees’ view, the alternative of engaging a new investment adviser for an underperforming fund would entail significant disruptions and would not likely provide any greater assurance of improved investment performance.

|

| 22 U.S. Government Income Trust |

Brokerage and soft-dollar allocations; investor servicing

The Trustees considered various potential benefits that Putnam Management may receive in connection with the services it provides under the management contract with your fund. These include benefits related to brokerage allocation and the use of soft dollars, whereby a portion of the commissions paid by a fund for brokerage may be used to acquire research services that are expected to be useful to Putnam Management in managing the assets of the fund and of other clients. Subject to policies established by the Trustees, soft dollars generated by these means are used predominantly to acquire brokerage and research services (including third-party research and market data) that enhance Putnam Management’s investment capabilities and supplement Putnam Management’s internal research efforts. However, the Trustees noted that a portion of available soft dollars continues to be used to pay fund expenses. The Trustees indicated their continued intent to monitor regulatory and industry developments in this area with the assistance of their Brokerage Committee, including any developments with respect to the European Union’s updated Markets in Financial Instruments Directive and its potential impact on PIL’s use of client commissions to obtain investment research. The Trustees also indicated their continued intent to monitor the allocation of the Putnam funds’ brokerage in order to ensure that the principle of seeking best price and execution remains paramount in the portfolio trading process.

Putnam Management may also receive benefits from payments that the funds make to Putnam Management’s affiliates for investor or distribution services. In conjunction with the annual review of your fund’s management and sub-management contracts, the Trustees reviewed your fund’s investor servicing agreement with Putnam Investor Services, Inc. (“PSERV”) and its distributor’s contracts and distribution plans with Putnam Retail Management Limited Partnership (“PRM”), both of which are affiliates of Putnam Management. The Trustees concluded that the fees payable by the funds to PSERV and PRM, as applicable, for such services are fair and reasonable in relation to the nature and quality of such services, the fees paid by competitive funds, and the costs incurred by PSERV and PRM, as applicable, in providing such services. Furthermore, the Trustees were of the view that the services provided were required for the operation of the funds, and that they were of a quality at least equal to those provided by other providers.

|

| U.S. Government Income Trust 23 |

Financial statements

These sections of the report, as well as the accompanying Notes, preceded by the Report of Independent Registered Public Accounting Firm, constitute the fund’s financial statements.

The fund’s portfolio lists all the fund’s investments and their values as of the last day of the reporting period. Holdings are organized by asset type and industry sector, country, or state to show areas of concentration and diversification.

Statement of assets and liabilities shows how the fund’s net assets and share price are determined. All investment and non-investment assets are added together. Any unpaid expenses and other liabilities are subtracted from this total. The result is divided by the number of shares to determine the net asset value per share, which is calculated separately for each class of shares. (For funds with preferred shares, the amount subtracted from total assets includes the liquidation preference of preferred shares.)

Statement of operations shows the fund’s net investment gain or loss. This is done by first adding up all the fund’s earnings — from dividends and interest income — and subtracting its operating expenses to determine net investment income (or loss). Then, any net gain or loss the fund realized on the sales of its holdings — as well as any unrealized gains or losses over the period — is added to or subtracted from the net investment result to determine the fund’s net gain or loss for the fiscal year.

Statement of changes in net assets shows how the fund’s net assets were affected by the fund’s net investment gain or loss, by distributions to shareholders, and by changes in the number of the fund’s shares. It lists distributions and their sources (net investment income or realized capital gains) over the current reporting period and the most recent fiscal year-end. The distributions listed here may not match the sources listed in the Statement of operations because the distributions are determined on a tax basis and may be paid in a different period from the one in which they were earned.

Financial highlights provide an overview of the fund’s investment results, per-share distributions, expense ratios, net investment income ratios, and portfolio turnover in one summary table, reflecting the five most recent reporting periods. In a semiannual report, the highlights table also includes the current reporting period.

|

| 24 U.S. Government Income Trust |

Report of Independent Registered Public Accounting Firm

The Board of Trustees and Shareholders

Putnam U.S. Government Income Trust:

We have audited the accompanying statement of assets and liabilities of Putnam U.S. Government Income Trust (the fund), including the fund’s portfolio, as of September 30, 2017, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years in the five-year period then ended. These financial statements and financial highlights are the responsibility of the fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of September 30, 2017, by correspondence with the custodian and brokers or by other appropriate auditing procedures. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of Putnam U.S. Government Income Trust as of September 30, 2017, the results of its operations for the year then ended, the changes in its net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years in the five-year period then ended, in conformity with U.S. generally accepted accounting principles.

Boston, Massachusetts

November 10, 2017

|

| U.S. Government Income Trust 25 |

The fund’s portfolio 9/30/17

| | |

| U.S. GOVERNMENT AND AGENCY | Principal | |

| MORTGAGE OBLIGATIONS (164.8%)* | amount | Value |

| U.S. Government Guaranteed Mortgage Obligations (103.7%) | | |

| Government National Mortgage Association Adjustable Rate Mortgages | | |

| 1 Yr Monthly Treasury Average CMT Index + 1.50%, 2.125%, 7/20/26 | $12,620 | $12,866 |

| Government National Mortgage Association Pass-Through Certificates | | |

| 8.50%, 12/15/19 | 1,150 | 1,174 |

| 7.50%, 10/20/30 | 49,806 | 59,254 |

| 5.50%, 8/15/35 | 323 | 362 |

| 5.00%, TBA, 10/1/47 | 52,000,000 | 55,696,878 |

| 4.50%, with due dates from 6/20/34 to 4/20/46 | 31,367,812 | 33,956,648 |

| 4.50%, TBA, 10/1/47 | 38,000,000 | 40,511,564 |

| 4.00%, with due dates from 9/15/39 to 5/20/46 | 84,071,864 | 90,306,688 |

| 4.00%, TBA, 10/1/47 | 86,000,000 | 90,555,317 |

| 3.500%, 04/20/46 i | 518,516 | 541,066 |

| 3.50%, with due dates from 7/15/42 to 7/20/47 | 174,251,186 | 182,215,774 |

| 3.50%, TBA, 10/1/47 | 118,000,000 | 122,673,909 |

| 3.00%, with due dates from 3/20/43 to 10/20/44 | 2,597,615 | 2,642,690 |

| 3.00%, TBA, 10/1/47 | 238,000,000 | 241,328,287 |

| | | 860,502,477 |

| U.S. Government Agency Mortgage Obligations (61.1%) | | |

| Federal Home Loan Mortgage Corporation Pass-Through Certificates | | |

| 4.50%, with due dates from 7/1/44 to 3/1/45 | 806,665 | 875,330 |

| 4.00%, 9/1/45 | 1,584,336 | 1,680,795 |

| 3.50%, with due dates from 4/1/42 to 1/1/47 | 3,331,229 | 3,449,162 |

| 3.50%, TBA, 10/1/47 | 3,000,000 | 3,093,281 |

| 3.00%, with due dates from 3/1/43 to 6/1/46 | 4,032,973 | 4,068,660 |

| 3.00%, 10/1/46 ## | 7,493,622 | 7,537,530 |

| Federal National Mortgage Association Pass-Through Certificates | | |

| 6.00%, with due dates from 2/1/36 to 5/1/41 | 3,567,397 | 4,049,529 |

| 6.00%, TBA, 10/1/47 | 5,000,000 | 5,628,963 |

| 5.50%, 2/1/35 | 769,496 | 858,245 |

| 5.50%, TBA, 10/1/47 | 44,000,000 | 48,688,750 |

| 5.50%, TBA, 9/1/47 | 5,000,000 | 5,538,672 |

| 4.50%, with due dates from 4/1/41 to 10/1/46 | 4,001,687 | 4,345,761 |

| 4.50%, TBA, 11/1/47 | 37,000,000 | 39,666,601 |

| 4.50%, TBA, 10/1/47 | 49,000,000 | 52,590,779 |

| 4.00%, with due dates from 5/1/43 to 7/1/56 | 28,100,743 | 29,922,462 |

| 4.00%, 8/1/47 ## | 2,995,624 | 3,160,968 |

| 4.00%, TBA, 10/1/47 | 80,000,000 | 84,218,752 |

| 3.50%, with due dates from 6/1/42 to 6/1/56 | 30,458,378 | 31,632,349 |

| 3.50%, 5/1/56 ## | 1,887,678 | 1,950,355 |

| 3.00%, with due dates from 9/1/42 to 3/1/47 | 42,232,303 | 42,596,445 |

| 3.00%, TBA, 11/1/47 | 8,000,000 | 8,012,500 |

| 3.00%, TBA, 10/1/47 | 61,000,000 | 61,190,625 |

| 2.50%, 3/1/43 | 63,829,228 | 62,303,314 |

| | | 507,059,828 |

| Total U.S. government and agency mortgage obligations (cost $1,367,408,252) | $1,367,562,305 |

|

| 26 U.S. Government Income Trust |

| | |

| | Principal | |

| U.S. TREASURY OBLIGATIONS (—%)* | amount | Value |

| U.S. Treasury Notes 1.500%, 01/31/22 i | $186,000 | $183,703 |

| Total U.S. treasury obligations (cost $183,703) | | $183,703 |

| |

| | Principal | |

| MORTGAGE-BACKED SECURITIES (29.9%)* | amount | Value |

| Agency collateralized mortgage obligations (29.9%) | | |

| Federal Home Loan Mortgage Corporation | | |

| IFB Ser. 3408, Class EK (-4.024 x 1 Month US LIBOR) + 25.793%, | | |

| 20.826%, 4/15/37 | $207,017 | $317,252 |

| IFB Ser. 2976, Class LC (-3.667 x 1 Month US LIBOR) + 24.42%, | | |

| 19.894%, 5/15/35 | 1,423,190 | 2,074,510 |

| IFB Ser. 3072, Class SM (-3.667 x 1 Month US LIBOR) + 23.796%, | | |

| 19.27%, 11/15/35 | 624,422 | 904,391 |

| IFB Ser. 3249, Class PS (-3.3 x 1 Month US LIBOR) + 22.275%, | | |

| 18.201%, 12/15/36 | 205,887 | 286,924 |

| IFB Ser. 3065, Class DC (-3 x 1 Month US LIBOR) + 19.86%, | | |

| 16.157%, 3/15/35 | 2,518,260 | 3,632,965 |

| IFB Ser. 2990, Class LB (-2.556 x 1 Month US LIBOR) + 16.945%, | | |

| 13.791%, 6/15/34 | 1,396,396 | 1,666,978 |

| IFB Ser. 4136, Class ES, IO (-1 x 1 Month US LIBOR) + 6.25%, | | |

| 5.016%, 11/15/42 | 5,096,673 | 690,462 |

| IFB Ser. 4436, Class SC, IO (-1 x 1 Month US LIBOR) + 6.15%, | | |

| 4.916%, 2/15/45 | 11,187,023 | 1,972,295 |

| Ser. 4122, Class TI, IO, 4.50%, 10/15/42 | 4,437,932 | 840,109 |

| Ser. 4024, Class PI, IO, 4.50%, 12/15/41 | 3,660,685 | 645,459 |

| Ser. 4018, Class DI, IO, 4.50%, 7/15/41 | 2,393,456 | 334,475 |

| Ser. 4546, Class PI, IO, 4.00%, 12/15/45 | 12,564,526 | 1,857,502 |

| Ser. 4601, Class IC, IO, 4.00%, 12/15/45 | 9,169,972 | 1,364,804 |

| Ser. 4530, Class HI, IO, 4.00%, 11/15/45 | 7,127,582 | 1,062,901 |

| Ser. 4500, Class GI, IO, 4.00%, 8/15/45 | 5,529,940 | 1,005,122 |

| Ser. 4425, IO, 4.00%, 1/15/45 | 7,454,821 | 1,220,727 |

| Ser. 4452, Class QI, IO, 4.00%, 11/15/44 | 6,172,828 | 1,234,380 |

| Ser. 4116, Class MI, IO, 4.00%, 10/1/42 | 10,860,691 | 2,049,630 |

| Ser. 4019, Class JI, IO, 4.00%, 5/15/41 | 5,655,031 | 782,176 |

| Ser. 3996, Class IK, IO, 4.00%, 3/15/39 | 6,680,314 | 458,607 |

| Ser. 4015, Class GI, IO, 4.00%, 3/15/27 | 4,855,431 | 541,069 |

| FRB Ser. 57, Class 2A1, 3.576%, 7/25/43 W | 19,185 | 20,663 |

| Ser. 4621, Class QI, IO, 3.50%, 10/15/46 | 21,862,380 | 3,495,357 |

| Ser. 4165, Class AI, IO, 3.50%, 2/15/43 | 3,907,684 | 640,509 |

| Ser. 4136, Class IQ, IO, 3.50%, 11/15/42 | 6,820,256 | 894,408 |

| Ser. 4199, Class CI, IO, 3.50%, 12/15/37 | 5,752,932 | 458,152 |

| FRB Ser. 59, Class 2A1, 3.332%, 10/25/43 | 12,129 | 11,977 |

| Ser. 4150, Class DI, IO, 3.00%, 1/15/43 | 7,614,596 | 956,584 |

| Ser. 4141, Class PI, IO, 3.00%, 12/15/42 | 7,266,531 | 831,727 |

| Ser. 4158, Class TI, IO, 3.00%, 12/15/42 | 11,164,226 | 1,141,319 |

| Ser. 4165, Class TI, IO, 3.00%, 12/15/42 | 13,462,798 | 1,335,186 |

| Ser. 4171, Class NI, IO, 3.00%, 6/15/42 | 8,003,213 | 815,047 |

| Ser. 4183, Class MI, IO, 3.00%, 2/15/42 | 5,767,152 | 533,462 |

| Ser. 4201, Class JI, IO, 3.00%, 12/15/41 | 7,284,033 | 615,939 |

| FRB Ser. 8, Class A9, IO, 0.456%, 11/15/28 W | 1,444,234 | 19,858 |

|

| U.S. Government Income Trust 27 |

| | |

| | Principal | |

| MORTGAGE-BACKED SECURITIES (29.9%)* cont. | amount | Value |

| Agency collateralized mortgage obligations cont. | | |

| Federal Home Loan Mortgage Corporation | | |

| FRB Ser. 59, Class 1AX, IO, 0.274%, 10/25/43 W | $3,909,622 | $38,639 |

| Ser. 48, Class A2, IO, 0.212%, 7/25/33 W | 5,927,153 | 43,529 |

| Ser. 315, PO, zero %, 9/15/43 | 8,677,640 | 7,155,367 |

| Ser. 3369, Class BO, PO, zero %, 9/15/37 | 6,276 | 5,255 |

| Ser. 3391, PO, zero %, 4/15/37 | 22,087 | 18,875 |

| Ser. 3300, PO, zero %, 2/15/37 | 60,713 | 52,688 |

| Ser. 3314, PO, zero %, 11/15/36 | 13,987 | 13,722 |

| Ser. 3206, Class EO, PO, zero %, 8/15/36 | 4,916 | 4,334 |

| Ser. 3175, Class MO, PO, zero %, 6/15/36 | 57,269 | 48,200 |

| Ser. 3210, PO, zero %, 5/15/36 | 4,174 | 3,805 |

| Ser. 3326, Class WF, zero %, 10/15/35 W | 24,613 | 18,490 |

| FRB Ser. 3117, Class AF, zero %, 2/15/36 | 13,250 | 10,094 |

| Federal National Mortgage Association | | |

| IFB Ser. 06-62, Class PS (-6 x 1 Month US LIBOR) + 39.90%, | | |

| 32.477%, 7/25/36 | 346,917 | 629,958 |

| IFB Ser. 05-74, Class NK (-5 x 1 Month US LIBOR) + 27.50%, | | |

| 21.314%, 5/25/35 | 1,240,215 | 1,722,515 |

| IFB Ser. 06-8, Class HP (-3.667 x 1 Month US LIBOR) + 24.566%, | | |

| 20.03%, 3/25/36 | 452,001 | 694,933 |

| IFB Ser. 07-53, Class SP (-3.667 x 1 Month US LIBOR) + 24.20%, | | |

| 19.664%, 6/25/37 | 542,991 | 797,477 |

| IFB Ser. 05-122, Class SE (-3.5 x 1 Month US LIBOR) + 23.10%, | | |

| 18.77%, 11/25/35 | 358,416 | 482,413 |

| IFB Ser. 08-24, Class SP (-3.667 x 1 Month US LIBOR) + 23.283%, | | |

| 18.747%, 2/25/38 | 2,032,484 | 2,744,815 |

| IFB Ser. 05-75, Class GS (-3 x 1 Month US LIBOR) + 20.25%, | | |

| 16.538%, 8/25/35 | 209,520 | 272,055 |

| IFB Ser. 05-106, Class JC (-3.101 x 1 Month US LIBOR) + 20.124%, | | |

| 16.288%, 12/25/35 | 764,641 | 1,117,492 |

| IFB Ser. 05-83, Class QP (-2.6 x 1 Month US LIBOR) + 17.394%, | | |

| 14.177%, 11/25/34 | 193,911 | 235,565 |

| IFB Ser. 11-4, Class CS (-2 x 1 Month US LIBOR) + 12.90%, | | |

| 10.426%, 5/25/40 | 1,151,007 | 1,324,777 |

| IFB Ser. 11-123, Class KS, IO (-1 x 1 Month US LIBOR) + 6.60%, | | |

| 5.363%, 10/25/41 | 1,293,214 | 205,699 |

| FRB Ser. 03-W11, Class A1, 4.426%, 6/25/33 W | 800 | 837 |

| FRB Ser. 04-W7, Class A2, 4.176%, 3/25/34 W | 6,815 | 7,592 |

| Ser. 12-118, Class PI, IO, 4.00%, 6/25/42 | 5,891,365 | 997,011 |

| Ser. 12-62, Class MI, IO, 4.00%, 3/25/41 | 4,195,912 | 508,691 |

| Ser. 12-104, Class HI, IO, 4.00%, 9/25/27 | 7,807,953 | 911,221 |

| FRB Ser. 03-W14, Class 2A, 3.911%, 1/25/43 W | 20,378 | 21,517 |

| FRB Ser. 03-W3, Class 1A4, 3.515%, 8/25/42 W | 35,285 | 37,706 |

| Ser. 16-70, Class QI, IO, 3.50%, 10/25/46 | 24,317,637 | 3,774,827 |

| Ser. 15-10, Class AI, IO, 3.50%, 8/25/43 | 8,770,627 | 1,219,776 |

| Ser. 12-124, Class JI, IO, 3.50%, 11/25/42 | 2,516,672 | 312,118 |

| Ser. 13-22, Class PI, IO, 3.50%, 10/25/42 | 6,399,423 | 1,179,292 |

| Ser. 12-114, Class NI, IO, 3.50%, 10/25/41 | 11,157,862 | 1,657,622 |