As filed with the Securities and Exchange Commission on August 18, 2015

1933 Act Registration No. 333-205683

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-14

REGISTRATION STATEMENT UNDER

THE SECURITIES ACT OF 1933

Pre-Effective Amendment No. 2 ☒ Post-Effective Amendment No. ☐

(Check appropriate box or boxes)

Neuberger Berman Advisers Management Trust

(Exact name of Registrant as specified in charter)

605 Third Avenue

New York, New York 10158-0180

(Address of Principal Executive Offices) (Zip Code)

Registrant’s Telephone Number, including Area Code: (212) 476-8800

Robert Conti

Chief Executive Officer and President

Neuberger Berman Advisers Management Trust

605 Third Avenue, 2nd Floor

New York, New York 10158-0180

(Name and Address of Agent for Service)

With copies to:

Arthur C. Delibert, Esq.

K&L Gates LLP

1601 K Street, N.W.

Washington, D.C. 20006-1601

(Names and Addresses of Agents for Service of Process)

Approximate Date of Proposed Public Offering: As soon as practicable after this registration statement goes effective under the Securities Act of 1933, as amended.

Title of Securities being registered: Class I Shares and Class S Shares of Mid Cap Growth Portfolio.

No filing fee is due because of Registrant’s reliance on Section 24(f) of the Investment Company Act of 1940, as amended.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until such date as the Commission, acting pursuant to said Section 8(a), may determine that the Registration Statement shall become effective.

NEUBERGER BERMAN ADVISERS MANAGEMENT TRUST

FORM N-14

CONTENTS OF REGISTRATION STATEMENT ON FORM N-14

This Registration Statement consists of the following papers and documents:

Cover Sheet

Contents of Registration Statement on Form N-14

Letter to Shareholders

Notice of Special Meeting

Part A – Information Statement and Prospectus

Part B – Statement of Additional Information

Part C – Other Information

Signature Page

Exhibits

NEUBERGER BERMAN ADVISERS MANAGEMENT TRUST

Balanced Portfolio

Growth Portfolio

Small Cap Growth Portfolio

605 Third Avenue

New York, New York 10158-0180

August 18, 2015

Dear Valued Contractholder:

On June 24, 2015, the Board of Trustees (the “Board”) of the Neuberger Berman Advisers Management Trust (the “Trust”) approved three separate reorganizations of Balanced Portfolio, Growth Portfolio, and Small Cap Growth Portfolio (each, a “Merging Portfolio”) into Mid Cap Growth Portfolio (the “Surviving Portfolio,” and together with the Merging Portfolios, the “Portfolios”) (each a “Reorganization”). Each Reorganization is independent of the others, and the Reorganization of any Merging Portfolio may proceed even if the Reorganization of one or both of the other Merging Portfolios is postponed or cancelled. All Portfolios are series of the Trust:

Merging Portfolio will be reorganized into Surviving Portfolio |

| Balanced Portfolio - Class I | à | Mid Cap Growth Portfolio - Class I |

| Growth Portfolio - Class I | à | Mid Cap Growth Portfolio - Class I |

| Small Cap Growth Portfolio - Class S | à | Mid Cap Growth Portfolio - Class S |

Each Reorganization will take effect on or about November 6, 2015. No shareholder vote is required for any of the Reorganizations. We are not asking you for a proxy, and you are requested not to send us a proxy. Shares of each Portfolio are held directly by insurance companies or qualified plans that offer the Portfolio to contractholders as an investment vehicle. You are receiving this letter because, as of August 17, 2015, you were the indirect holder of one of the Merging Portfolios through your ownership of a variable annuity contract or qualified plan. At the time of each Reorganization, contractholders who are shareholders of a Merging Portfolio (indirectly through a separate account) automatically will become shareholders (again, indirectly through that separate account) of the Surviving Portfolio, receiving shares of the Surviving Portfolio having an aggregate net asset value equal to the contractholder’s shares in the Merging Portfolio.

Each Portfolio is managed by Neuberger Berman Management LLC (“NBM” or the “Manager”) and NBM retains Neuberger Berman LLC as subadviser to each Portfolio to provide research services. Each Portfolio has substantially similar investment objectives and identical fundamental investment limitations. (Fundamental investment limitations are those that cannot be changed without a vote of the shareholders.) Each Portfolio also has similar principal risks although there are differences in the principal risks, investment policies and strategies of the Portfolios and these differences are outlined herein. Accordingly, each Reorganization will result in no material changes to the Merging Portfolio’s investment objective or fundamental investment limitations, though certain of its principal risks, investment policies and strategies will change. Although each Portfolio has similar principal risks, an investment in the Surviving Portfolio potentially has or may present greater risks than an investment in a Merging Portfolio. The Surviving Portfolio has a potentially increased risk profile due to certain differences in investment strategy, policies and principal risks: the Balanced Portfolio normally allocates at least 25% of its net assets to investment grade bonds and other debt securities from U.S. government and corporate issuers and does not have a policy to invest in companies of any particular market capitalization while the Surviving Portfolio is not currently invested in investment grade bonds and other debt securities from US government and corporate issuers and has an 80% policy to invest in mid cap companies; and the Small Cap Growth Portfolio normally invests at least 80% of its net assets in small cap companies, is not currently invested in foreign securities and compares its performance to the Russell 2000 Growth Index while the Surviving Portfolio has an 80% policy to invest in mid cap companies, is permitted to invest in foreign securities and compares its performance to the Russell Midcap Growth Index. The attached Combined Prospectus and

Information Statement contains further information regarding each Reorganization and the Surviving Portfolio. Please read it carefully.

The Board believes that each Reorganization will benefit the Merging Portfolio and its contractholders as a result of the Surviving Portfolio’s larger asset base and the elimination of the smaller investment options that are less viable than the investment options available to the Surviving Portfolio. The Surviving Portfolio has identical contractual expense caps as Balanced Portfolio and Growth Portfolio, and lower contractual expense caps than Small Cap Growth Portfolio, which NBM has agreed to maintain until December 31, 2018. Currently, the Surviving Portfolio operates below its contractual expense cap and its annual fund operating expenses (“Net Expenses”) are lower than each Merging Portfolio’s Net Expenses after fee waiver and/or expense reimbursement. Further, no Reorganization is expected to result directly in any adverse tax consequences or changes in account values for shareholders or contractholders. No sales load, commission or other fee will be imposed on shareholders in connection with the tax-free exchange of their shares. Detailed information regarding each Reorganization is contained in the enclosed materials. If you have any questions regarding a Reorganization, please call the Manager toll-free at 800-366-6264 or 800-877-9700.

Sincerely,

/s/ Robert Conti

Robert Conti

President and Chief Executive Officer

Neuberger Berman Advisers Management Trust

IMPORTANT NOTICE REGARDING CHANGE IN INVESTMENT OBJECTIVE

AND INVESTMENT POLICY OR STRATEGY

Effective as of the closing of each Reorganization, shareholders of each Merging Portfolio will become shareholders of the Surviving Portfolio with the investment objective, investment strategies and investment policies of the Surviving Portfolio. The chart below outlines any differences between each Merging Portfolio’s current investment objective and any 80% investment policy or other material investment strategy (as articulated in the Portfolio’s principal investment strategy):

| Merging Portfolio | Merging Portfolio Investment Objective | Surviving Portfolio Investment Objective | Merging Portfolio 80% Policy or Material Investment Strategy | Surviving Portfolio 80% Policy |

Balanced Portfolio | Growth of capital | (same) | The Portfolio normally allocates between common stocks of mid-cap companies (defined as those with a total market cap within the market cap range of Russell Mid Cap) and investment grade bonds and other debt securities from US government and corporate issuers. Normally allocate 50% to 70% of net assets to stock investments, with balance allocated to debt securities (at least 25%) and operating cash. Although it may invest in securities of any maturity, the Portfolio normally seeks to maintain an average portfolio duration of two years or less. Compares its performance to the Russell Midcap Growth Index and the Barclays 1-3 Year U.S. Government/Credit Index. | To pursue its goal, the Portfolio normally invests at least 80% of its net assets in common stocks of mid-capitalization companies, which it defines as those with a total market capitalization within the market capitalization range of the Russell Midcap Index at the time of purchase. Compares its performance to the Russell Midcap Growth Index. |

Growth Portfolio | Growth of capital | (same) | To pursue its goal, the Portfolio normally invests in common stocks of mid-capitalization companies, which it defines as those with a total market capitalization within the market capitalization range of the Russell Midcap Index at the time of purchase. Compares its performance to the Russell Midcap Growth Index. | To pursue its goal, the Portfolio normally invests at least 80% of its net assets in common stocks of mid-capitalization companies, which it defines as those with a total market capitalization within the market capitalization range of the Russell Midcap Index at the time of purchase. Compares its performance to the Russell Midcap Growth Index. |

Small Cap Growth Portfolio | Long-term growth of capital | Growth of capital | To pursue its goal, the Portfolio normally invests at least 80% of its net assets in common stocks of small-capitalization companies, which it defines as those with a total market capitalization within the market capitalization range of the Russell 2000 Index at the time of initial purchase. Compares its performance to the Russell 2000 Growth Index. |

Questions and Answers

Q. What is happening? Why did I get this document?

A. The Board of Trustees, including the Trustees who are not “interested persons” (within the meaning of Section 2(a)(19) of the Investment Company Act of 1940, as amended (“1940 Act”)) of the Trust (the “Board”), of Neuberger Berman Advisers Management Trust (the “Trust”), has approved three separate reorganizations of Balanced Portfolio, Growth Portfolio, and Small Cap Growth Portfolio (each, a “Merging Portfolio”) into Mid Cap Growth Portfolio (the “Surviving Portfolio”) (each a “Reorganization”). Each Reorganization is independent of the others, and the Reorganization of any Merging Portfolio may proceed even if the Reorganization of one or both of the other Merging Portfolios is postponed or cancelled. Each Merging Portfolio and the Surviving Portfolio (collectively, the “Portfolios”) are each series of the Trust. Please see below for more information comparing the Portfolios’ investment objectives, strategies and policies.

You are receiving this document because, as of August 17, 2015, you were the indirect holder of one of the Merging Portfolios through your ownership of a variable annuity contract or qualified plan. Pursuant to a Plan of Reorganization and Dissolution adopted by the Board, upon closing of a Reorganization, your shares of the participating Merging Portfolio (which you own indirectly through a separate account) will convert to shares of the Surviving Portfolio with an aggregate net asset value (“NAV”) equal to those Merging Portfolio shares as of the close of business on the day of the closing of the Reorganization, which currently is expected to take place on or about November 6, 2015 (“Effective Date”). (For convenience, shares you own indirectly through a separate account are referred to below as though you owned them directly.)

Q. What is this document?

A. This document is a Combined Prospectus and Information Statement (“Information Statement”) for each Merging Portfolio and the Surviving Portfolio. This Information Statement contains information the shareholders of each Merging Portfolio should know prior to the Reorganization. You should retain this document for future reference.

Q. What are the Reorganizations?

A. Each Reorganization discussed in this Information Statement will reorganize a Merging Portfolio into the Surviving Portfolio on or about the Effective Date. The Portfolios have substantially similar investment objectives and identical fundamental investment limitations. Each Portfolio also has similar principal risks although there are differences in principal risks, investment policies and strategies of the Portfolios. Accordingly, the Reorganization will result in no material changes to the Merging Portfolio’s investment objective or fundamental investment limitations, though certain of its principal risks, investment policies and strategies will change. Although each Portfolio has similar principal risks, an investment in the Surviving Portfolio potentially has or may present greater risks than an investment in a Merging Portfolio. The Surviving Portfolio has a potentially increased risk profile due to certain differences in investment strategy, policies and principal risks: the Balanced Portfolio normally allocates at least 25% of its net assets to investment grade bonds and other debt securities from U.S. government and corporate issuers and does not have a policy to invest in companies of any particular market capitalization while the Surviving Portfolio is not currently invested in investment grade bonds and other debt securities from US government and corporate issuers and has an 80% policy to invest in mid cap companies; and the Small Cap Growth Portfolio normally invests at least 80% of its net assets in small cap companies, is not currently invested in foreign securities and compares its performance to the Russell 2000 Growth Index while the Surviving Portfolio has an 80% policy to invest in mid cap companies, is permitted to invest in foreign securities and compares its performance to the Russell Midcap Growth Index. Please see below for more information comparing the investment objectives, strategies, policies and principal risks of the Portfolios.

Q. Why did the Board Approve Each Reorganization?

A. NBM recommended to the Board that each Merging Portfolio be merged with the Surviving Portfolio. After considering the terms and conditions of each reorganization, the investment objectives, strategies and principal risks of each Portfolio, fees and expenses,

including the total annual expense ratios, of each Portfolio, and the relative performance of each Portfolio, the Board believes that reorganizing each Merging Portfolio into the Surviving Portfolio is in the best interests of each Portfolio and that the interests of each Portfolio's shareholders will not be diluted as a result of any reorganization. In reaching this conclusion, the Board determined that reorganizing each Merging Portfolio into the Surviving Fund, which also is managed by NBM and has a substantially similar investment objective and identical fundamental investment limitations as those of the Surviving Portfolio, offers potential benefits to Shareholders. These potential benefits include permitting Shareholders to pursue the same investment goals in a larger combined fund with a more viable long-term future that has a comparable performance record to that of each Merging Portfolio and is expected to have a lower total annual expense ratio than each Merging Portfolio.

Q. How will this affect me as a shareholder?

A. Shareholders of each Merging Portfolio will become shareholders of the Surviving Portfolio on the Effective Date. No sales charges or other fees, other than those described below, will be imposed in connection with any Reorganization. In addition, the Portfolios’ procedures for purchasing, redeeming and exchanging shares are identical.

If you own Class I shares or Class S shares, as applicable, of a Merging Portfolio, you will receive Class I shares or Class S shares, respectively, of the Surviving Portfolio. Class I shares and Class S shares do not have either a front-end sales charge or a contingent deferred sales charge (“CDSC”).

Q. After the Reorganization of my Portfolio, will I own the same number of shares?

A. The aggregate value of your investment will not change as a result of the Reorganization. It is likely, however, that the number of shares you own will change because your shares will be exchanged at the NAV per share of the Surviving Portfolio, which is likely to be different from the NAV per share of your Merging Portfolio.

Q. Do the Portfolio Managers who manage each Merging Portfolio also manage the Surviving Portfolio?

A. Not in each case. Kenneth Turek is the portfolio manager of the Surviving Portfolio, as well as Growth Portfolio. He is one of several portfolio managers of the Balanced Portfolio. The Small Cap Growth Portfolio has a different portfolio manager.

Q. Will my expenses increase pursuant to the Reorganization of my Portfolio?

A. No. Currently, the Surviving Portfolio’s annual fund operating expenses (“Net Expenses”) are lower than each Merging Portfolio’s Net Expenses after fee waiver and/or expense reimbursement.

Q. What are the tax consequences of the Reorganizations?

A. Each Reorganization is expected to be a tax-free transaction for federal income tax purposes.

Q. Can I still purchase shares of a Merging Portfolio until its Reorganization?

A. You may continue to purchase shares of a Merging Portfolio through November 4, 2015. As a result of each Reorganization, effective November 4, 2015, the Merging Portfolios will no longer accept purchases or exchanges of shares.

Q. What if I want to exchange my shares into another Neuberger Berman Portfolio prior to the Reorganization of my Portfolio?

A. You may exchange shares in each Merging Portfolio to another Neuberger Berman Portfolio prior to the Reorganization subject to the availability of another Neuberger Berman Portfolio in your insurance product or plan and further subject to any limitations in the prospectus for your variable contract or your qualified plan documentation. Additional information about your options for transferring your investment will be provided to you by your insurance company or other applicable financial intermediary.

Q. Who is paying the costs of each Reorganization?

A. NBM will pay the costs associated with each Reorganization. The Surviving Portfolio will pay any fees payable to governmental authorities for the registration or qualification of the Surviving Portfolio shares distributable to each Merging Portfolio’s shareholders pursuant to the Reorganization and all related transfer agency costs. Such fees and costs are not expected to be material to the operation of the Surviving Portfolio.

If you have any questions, please call the Neuberger Berman Family of Portfolios toll-free at 800-366-6264 or 800-877-9700.

Combined Prospectus and Information Statement

August 18, 2015

Reorganization of the Assets and Liabilities of each of the

BALANCED PORTFOLIO

GROWTH PORTFOLIO

SMALL CAP GROWTH PORTFOLIO

each a series of Neuberger Berman Advisers Management Trust

By and in Exchange for Shares of and Assumption of Liabilities by the

MID CAP GROWTH PORTFOLIO,

a series of Neuberger Berman Advisers Management Trust

605 Third Avenue

New York, New York 10158-0180

800-366-6264

800-877-9700

This Combined Prospectus and Information Statement (“Information Statement”) contains information you should know about a Plan of Reorganization and Dissolution (“Plan”) adopted by the Board of Trustees, including the Trustees who are not “interested persons” (within the meaning of Section 2(a)(19) of the Investment Company Act of 1940, as amended (“1940 Act”)) of the Trust (the “Board”), of Neuberger Berman Advisers Management Trust (“Trust”) relating to three separate reorganizations of Balanced Portfolio, Growth Portfolio, and Small Cap Growth Portfolio (each, a “Merging Portfolio”) into Mid Cap Growth Portfolio (the “Surviving Portfolio”) (each a “Reorganization”). The Merging Portfolios and the Surviving Portfolio (collectively, the “Portfolios”) are series of the Trust. The Trust is a Delaware statutory trust and is a registered, open-end management investment company. The investment objective of Balanced Portfolio and Growth Portfolio, as well as the Surviving Portfolio, is to seek growth of capital, and the investment objective of Small Cap Growth Portfolio is to seek long-term growth of capital. You should carefully read this Information Statement, which contains important information you should know, and keep it for future reference.

Upon completion of the Reorganization of your Merging Portfolio you, as the owner of a variable annuity contract and/or a variable life insurance policy issued by an insurance company that participates in that Merging Portfolio through the investment divisions of a separate account or accounts established by that company (each, a “Separate Account”), will become a shareholder of the Surviving Portfolio through that Separate Account. (For convenience, shares you own indirectly through a Separate Account are referred to throughout this Information Statement as though you owned them directly.) You will receive shares of the Surviving Portfolio with an aggregate net asset value (“NAV”) equal to the aggregate NAV of the shares of your Merging Portfolio that you hold as of the close of business on the day of the closing of the Reorganization, which is expected to be November 6, 2015 (“Effective Date”). The shares of the Surviving Portfolio that you receive will be of the same class as the shares of the Merging Portfolio that you currently hold. When each Reorganization is completed, the respective Merging Portfolio will be liquidated and dissolved.

This Combined Prospectus and Information Statement sets forth important information that you should know regarding each Reorganization. You should read and retain this Combined Prospectus and Information Statement for future reference. The following documents have been

filed with the Securities and Exchange Commission (“SEC”) and are incorporated by reference into this Information Statement:

| 1. | The registration statement for the Trust (File Nos. 811-04255 and 002-88566) contains a prospectus for each Merging Portfolio and the Surviving Portfolio dated May 1, 2015. You should review the prospectus for your respective Merging Portfolio and the Surviving Portfolio. |

| | |

| 2. | The combined Statement of Additional Information for the Portfolios dated May 1, 2015. |

| | |

| 3. | The audited financial statements included in the Surviving Portfolio’s and your respective Merging Portfolio’s Annual Report to shareholders for the fiscal year ended December 31, 2014, and the unaudited financial statements and financial highlights included in the corresponding Semi-Annual Reports to shareholders of the Portfolios for the six-month period ended June 30, 2015. |

Each Portfolio previously sent its Annual Report and Semi-Annual Report to its shareholders. For a free copy of these reports or any of the other documents listed above, you may call 800-366-6264 or 800-877-9700, send an email to fundinquiries@nb.com, or write to a Portfolio at:

Neuberger Berman Management LLC

605 Third Avenue

New York, New York 10158-0180

800-366-6264

800-877-9700

You also may obtain many of these documents by accessing the Internet site for the Portfolios at www.nb.com. Text-only versions of all the Portfolios’ documents can be viewed online or downloaded from the EDGAR database on the SEC’s Internet site at www.sec.gov. The Trust is subject to the informational requirements of the Securities Exchange Act of 1934, as amended. Accordingly, it must file certain reports and other information with the SEC. You can review and copy information regarding the Portfolios by visiting the SEC’s Public Reference Room, Room 1580, 100 F Street NE, Washington, D.C. 20549. You can obtain copies, upon payment of a duplicating fee, by sending an e-mail request to publicinfo@sec.gov or by writing the Public Reference Room at the address above. Information on the operations of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

The SEC has not approved or disapproved these securities or determined if this Information Statement is truthful or complete. Any representation to the contrary is a criminal offense.

We are not asking you for a proxy or written consent, and you are requested not to send us a proxy or written consent.

Shares of each Portfolio are not deposits or obligations of, or guaranteed or endorsed by, any bank and are not insured by the Federal Deposit Insurance Corporation, the Federal Reserve Board or any other agency, and are subject to investment risks, including possible loss of principal.

No person has been authorized to give any information or to make any representation other than those in this Information Statement, and, if given or made, such other information or representation must not be relied upon as having been authorized by any Portfolio or the Trust.

| ABOUT EACH REORGANIZATION | 8 |

| Summary | 8 |

| Considerations Regarding each Reorganization | 9 |

Comparison of Investment Objectives, Strategies and Policies and Information about Adviser/Subadviser and Portfolio Managers | 11 |

| Comparison of Fundamental Investment Limitations and Non-Fundamental Policies | 12 |

| Comparison of Principal Risks | 15 |

| Comparison of Fees and Expenses | 19 |

| Example of Portfolio Expenses | 22 |

| Comparative Performance Information | 25 |

| Capitalization | 30 |

| Information Regarding the Plan of Reorganization and Dissolution | 30 |

| Reasons for the Reorganizations | 32 |

| Description of the Securities to be Issued | 33 |

| Federal Income Tax Considerations | 34 |

| ADDITIONAL INFORMATION ABOUT THE SURVIVING PORTFOLIO | |

| OTHER INFORMATION | 35 |

| Investment Adviser, Subadviser, and Portfolio Managers | 41 |

| Legal Matters | 42 |

| Control Persons | 42 |

| Experts | 44 |

| Additional Information | 44 |

| FINANCIAL HIGHLIGHTS | 45 |

| APPENDIX A PLAN OF REORGANIZATION AND DISSOLUTION | A-1 |

| APPENDIX B FINANCIAL HIGHLIGHTS | B-1 |

ABOUT EACH REORGANIZATION

Summary

The following is a summary of certain information relating to each Reorganization and is qualified in its entirety by reference to the more complete information contained elsewhere in the Information Statement. Due primarily to concerns over asset levels and limited prospects for future growth, Neuberger Berman Management LLC (“NBM” or the “Manager”), the investment manager of each Merging Portfolio, recommended to the Board of Trustees of the Trust, the separate reorganization of each Merging Portfolio into the Surviving Portfolio.

After careful consideration of a number of factors, the Board of Trustees, including the Trustees who are not “interested persons” (within the meaning of Section 2(a)(19) of the Investment Company Act of 1940, as amended (“1940 Act”)) of the Trust (the “Board”), voted unanimously to approve the reorganization of each Merging Portfolio into the Surviving Portfolio and the Plan with respect to each Reorganization. In each Reorganization, the Surviving Portfolio would acquire all of the assets of each Merging Portfolio in exchange solely for the assumption of all the liabilities of the Merging Portfolio and the issuance of shares of the Surviving Portfolio to be distributed pro rata by the Merging Portfolio to its shareholders in complete liquidation and dissolution of the Merging Portfolio. As a result of each Reorganization, each shareholder of a Merging Portfolio would become the owner of the Surviving Portfolio’s shares having a total aggregate value equal to the total aggregate value of his or her holdings in the Merging Portfolio on the Effective Date. Each Reorganization is independent of the others, and the Reorganization of any Merging Portfolio may proceed even if the Reorganization of one or both of the other Merging Portfolios is postponed or cancelled.

The Surviving Portfolio offers both Class I and Class S shares. Balanced Portfolio and Growth Portfolio each offer Class I shares and Small Cap Growth Portfolio offers Class S shares. Each Merging Portfolio shareholder would receive shares of the same class of the Surviving Portfolio having the same aggregate value as such shareholder currently owns. Each Merging Portfolio’s respective class of shares has the same purchase, distribution, exchange and redemption procedures as the corresponding class of shares of the Surviving Portfolio.

The Board has concluded that each Reorganization would be in the best interests of each Merging Portfolio and its existing shareholders and that the interests of each Merging Portfolio’s shareholders would not be diluted as a result of the transactions contemplated by each Reorganization. Among other things, each Reorganization would give each Merging Portfolio’s shareholders the opportunity to participate in a larger Portfolio, with a substantially similar investment objective and principal investment risks (although with certain differing investment strategies and policies as outlined herein). Although each Portfolio has similar principal risks, an investment in the Surviving Portfolio potentially has or may present greater risks than an investment in a Merging Portfolio. The Surviving Portfolio has a potentially increased risk profile due to certain differences in investment strategy, policies and principal risks: the Balanced Portfolio normally allocates at least 25% of its net assets to investment grade bonds and other debt securities from U.S. government and corporate issuers and does not have a policy to invest in companies of any particular market capitalization while the Surviving Portfolio is not currently invested in investment grade bonds and other debt securities from US government and corporate issuers and has an 80% policy to invest in mid cap companies; and the Small Cap Growth Portfolio normally invests at least 80% of its net assets in small cap companies, is not currently invested in foreign securities and compares its performance to the Russell 2000 Growth Index while the Surviving Portfolio has an 80% policy to invest in mid cap companies, is permitted to invest in foreign securities and compares its performance to the Russell Midcap Growth Index. The Surviving Portfolio has identical or lower contractual expense caps as each Merging Portfolio, which NBM has agreed to maintain until December 31, 2018. Currently, the Surviving Portfolio is operating below its contractual expense cap and its annual operating expenses (“Net Expenses”) are lower than each Merging Portfolio’s Net Expenses after fee waiver and/or expense reimbursement.

As a condition to each Reorganization, the Trust will receive an opinion of counsel that the Reorganization will be considered a tax-free reorganization under applicable provisions of the Internal Revenue Code of 1986, as amended (the “Code”), so that neither the Merging Portfolio participating therein nor the Surviving Portfolio or their shareholders will recognize any gain or

loss as a result of the Reorganization. See “Federal Income Tax Considerations” below for further information.

Considerations Regarding each Reorganization

Please note the following information regarding each Reorganization:

| ● | The Surviving Portfolio pursues a substantially similar investment objective as each Merging Portfolio. The investment objective of Balanced Portfolio and Growth Portfolio, as well as the Surviving Portfolio, is to seek growth of capital, and the investment objective of Small Cap Growth Portfolio is to seek long-term growth of capital. Each Portfolio, with the exception of Small Cap Growth Portfolio, invests in equity securities of mid-capitalization companies, while Small Cap Growth Portfolio invests in equity securities of small-capitalization companies. In addition, Balanced Portfolio invests between 30-50% of its assets in investment grade bonds and other debt securities from the U.S. government and corporate issuers. |

| | |

| | ● | The Surviving Portfolio has substantially similar investment objectives and identical fundamental investment limitations as each Merging Portfolio. Each Portfolio also has similar principal risks although there are differences in principal risks, investment policies and strategies. Accordingly, each Reorganization will result in no material changes to each Merging Portfolio’s investment objective and no changes to its fundamental investment limitations, though certain of its principal risks, investment policies and strategies will change. Although each Portfolio has similar principal risks, an investment in the Surviving Portfolio potentially has or may present greater risks than an investment in a Merging Portfolio. The Surviving Portfolio has a potentially increased risk profile due to certain differences in investment strategy, policies and principal risks: the Balanced Portfolio normally allocates at least 25% of its net assets to investment grade bonds and other debt securities from U.S. government and corporate issuers and does not have a policy to invest in companies of any particular market capitalization while the Surviving Portfolio is not currently invested in investment grade bonds and other debt securities from US government and corporate issuers and has an 80% policy to invest in mid cap companies; and the Small Cap Growth Portfolio normally invests at least 80% of its net assets in small cap companies, is not currently invested in foreign securities and compares its performance to the Russell 2000 Growth Index while the Surviving Portfolio has an 80% policy to invest in mid cap companies, is permitted to invest in foreign securities and compares its performance to the Russell Midcap Growth Index. See “Comparison of Investment Objectives, Strategies and Policies” below for further information. |

| | | |

| | ● | NBM is each Portfolio’s investment adviser. Kenneth Turek is the portfolio manager of the Surviving Portfolio, as well as Growth Portfolio. He is one of several portfolio managers of the Balanced Portfolio. The Small Cap Growth Portfolio has a different portfolio manager. |

| | | |

| | ● | NBM has reviewed the Portfolios’ current portfolio holdings and determined that each Merging Portfolio’s holdings generally are compatible with the Surviving Portfolio’s investment objective and policies. As a result, NBM believes that all or substantially all of each Merging Portfolio’s assets could be transferred to and held by the Surviving Portfolio. See “Comparison of Investment Objectives, Strategies and Policies” below for further information. |

| | | |

| | ● | The Class I shares of the Surviving Portfolio and Class I shares of Growth Portfolio have had very similar performance for the year-to-date period through June 30, 2015. |

| | ● | The Class I shares of the Surviving Portfolio outperformed the Class I shares of the Balanced Portfolio for the year-to-date period through June 30, 2015. |

| | | |

| | ● | The Class S shares of the Surviving Portfolio outperformed the Class S shares of the Small Cap Growth Portfolio for the year-to-date period through June 30, 2015. |

| | | |

| | ● | The Class I shares and Class S shares of the Surviving Portfolio outperformed the corresponding class of shares of each Merging Portfolio for each of the one-year, three-year, five-year, ten-year, and since inception periods (except for the three-year period for Small Cap Growth Portfolio). The following table provides each Portfolio’s performance record for these periods. |

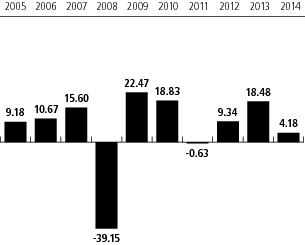

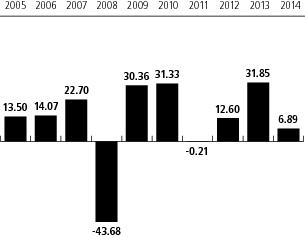

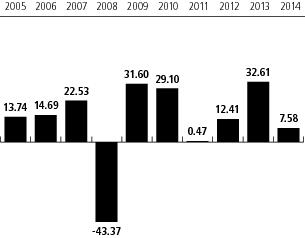

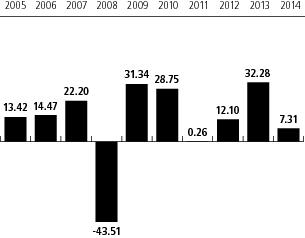

AVERAGE ANNUAL TOTAL RETURNS

(For the periods ended June 30, 2015)

| Portfolio Name | Class | YTD (through 6/30/15) | 1 Year | 3 Year | 5 Year | 10 Year | Since Inception |

| SURVIVING PORTFOLIO | | | | | | | |

| Mid Cap Growth Portfolio | I | 10.08% | 15.78% | 17.44% | 18.11% | 10.32% | 9.57% |

| Russell Midcap Growth Index | | 4.18% | 9.45% | 19.24% | 18.69% | 9.69% | 8.08% |

| Russell Midcap Index | | 2.35% | 6.63% | 19.26% | 18.23% | 9.40% | 9.58% |

| | | | | | | | |

| Mid Cap Growth Portfolio | S | 9.96% | 15.51% | 17.14% | 17.82% | 10.05% | 9.38% |

| Russell Midcap Growth Index | | 4.18% | 9.45% | 19.24% | 18.69% | 9.69% | 8.08% |

| Russell Midcap Index | | 2.35% | 6.63% | 19.26% | 18.23% | 9.40% | 9.58% |

| |

| MERGING PORTFOLIOS | | | | | | | |

| Balanced Portfolio | I | 6.81% | 9.98% | 10.46% | 10.98% | 5.75% | 6.98% |

| Russell Midcap Growth Index | | 4.18% | 9.45% | 19.24% | 18.69% | 9.69% | 10.92% |

| Barclays U.S. 1-3 Yr Govt/Credit Bond Index | | 0.72% | 0.93% | 0.94% | 1.17% | 2.83% | 5.02% |

| Russell Midcap Index | | 2.35% | 6.63% | 19.26% | 18.23% | 9.40% | 11.88% |

| |

| Growth Portfolio | I | 10.21% | 15.50% | 17.06% | 17.85% | 10.13% | 9.66% |

| Russell Midcap Growth Index | | 4.18% | 9.45% | 19.24% | 18.69% | 9.69% | N/A |

| Russell Midcap Index | | 2.35% | 6.63% | 19.26% | 18.23% | 9.40% | 12.66% |

| |

| Small Cap Growth Portfolio | S | 7.70% | 14.10% | 17.69% | 17.37% | 5.73% | 6.80% |

| Russell 2000 Growth Index | | 8.74% | 12.34% | 20.11% | 19.33% | 9.86% | 11.20% |

| Russell 2000 Index | | 4.75% | 6.49% | 17.81% | 17.08% | 8.40% | 10.30% |

Comparison of Investment Objectives, Strategies and Policies and Information about

Adviser/Subadviser and Portfolio Managers

Each Merging Portfolio and the Surviving Portfolio have substantially similar investment objectives but pursue these objectives via different strategies. Accordingly, the Reorganizations will result in no material changes to any Merging Portfolio’s investment objective and no changes to fundamental investment limitations, though certain of its principal risks and investment strategies and policies will change. Although each Portfolio has similar principal risks, an investment in the Surviving Portfolio potentially has or may present greater risks than an investment in a Merging Portfolio. The Surviving Portfolio has a potentially increased risk profile due to certain differences in investment strategy, policies and principal risks: the Balanced Portfolio normally allocates at least 25% of its net assets to investment grade bonds and other debt securities from U.S. government and corporate issuers and does not have a policy to invest in companies of any particular market capitalization while the Surviving Portfolio is not currently invested in investment grade bonds and other debt securities from US government and corporate issuers and has an 80% policy to invest in mid cap companies; and the Small Cap Growth Portfolio normally invests at least 80% of its net assets in small cap companies, is not currently invested in foreign securities and compares its performance to the Russell 2000 Growth Index while the Surviving Portfolio has an 80% policy to invest in mid cap companies, is permitted to invest in foreign securities and compares its performance to the Russell Midcap Growth Index. The Portfolios’ investment objectives, strategies and policies are described below. The investment strategy described below does not reflect the complete strategies of each Portfolio, for more information please see the Principal Investment Strategies section of the prospectus for your Merging Portfolio and the Surviving Portfolio.

NBM, the investment adviser of each Merging Portfolio, has reviewed each Merging Portfolio’s current portfolio holdings and determined that those holdings generally are compatible with the Surviving Portfolio’s investment objective and policies. As a result, NBM believes that all or substantially all of each Merging Portfolio’s assets could be transferred to and held by the Surviving Portfolio. Nevertheless, in executing the Surviving Portfolio’s investment strategy, the portfolio manager may determine to sell some or a substantial portion of the assets of a Merging Portfolio after the completion of its Reorganization.

| | MERGING PORTFOLIOS | | SURVIVING PORTFOLIO |

| | BALANCED | GROWTH | SMALL CAP GROWTH | MID CAP GROWTH |

| Investment Objective | Growth of capital | Growth of capital | Long-term growth of capital | Growth of capital |

| Investment Strategy | Allocates between common stocks of mid-cap companies (defined as those with a total market cap within the market cap range of Russell Mid Cap) and investment grade bonds and other debt securities from US government and corporate issuers. Normally allocate 50% to 70% of net assets to stock investments, with balance allocated to debt securities (at least 25%) and operating cash. May invest up to 10% in below investment grade securities. Although it may invest in securities of any maturity, the Portfolio normally seeks to maintain an average portfolio duration of two years or less. | Normally invests in common stocks of mid-cap companies (defined as those with a total market cap within the market cap range of Russell Mid Cap) | Normally invests at least 80% of net assets in common stock of small-capitalization companies (defined as those with a total market cap within the market cap range of the Russell 2000) | Normally invests at least 80% of its net assets in common stocks of mid-cap companies (defined as those with a total market cap within the market cap range of Russell Mid Cap) |

| | MERGING PORTFOLIOS | | SURVIVING PORTFOLIO |

Investment Adviser/ Subadviser | Investment Adviser: Neuberger Berman Management LLC Subadviser: Neuberger Berman LLC | Investment Adviser: Neuberger Berman Management LLC Subadviser: Neuberger Berman LLC | Investment Adviser: Neuberger Berman Management LLC Subadviser: Neuberger Berman LLC | Investment Adviser: Neuberger Berman Management LLC Subadviser: Neuberger Berman LLC |

| Portfolio Managers | Kenneth J. Turek Thomas Sontag Michael Foster | Kenneth J. Turek | David H. Burshtan | Kenneth J. Turek |

Comparison of Fundamental Investment Limitations and Non-Fundamental Policies

The fundamental investment limitations for each Portfolio are the same. The table below summarizes the Portfolios’ fundamental investment limitations and non-fundamental policies. The fundamental investment limitations of each Portfolio may not be changed without a vote of the majority of the outstanding securities of the Portfolio. The Portfolios’ investment limitations and policies may be found in their combined Statement of Additional Information (“Combined SAI”). Except with respect to borrowing money, if a percentage limitation is adhered to at the time of the investment, a later increase or decrease in the percentage resulting from any change in value of net assets will not result in a violation of such restriction.

In addition to the policies noted below, the Surviving Portfolio has a non-fundamental policy that it shall normally invest at least 80% of its net assets, plus 80% of any borrowings for investment purposes, in mid-capitalization companies. The Surviving Portfolio will not alter this policy without providing at least 60 days’ prior notice to shareholders. The Small Cap Growth Portfolio, one of the Merging Portfolios, has a non-fundamental policy that it shall normally invest at least 80% of its net assets, plus 80% of any borrowings for investment purposes, in small-capitalization companies. The Small Cap Growth Portfolio will not alter this policy without providing at least 60 days’ prior notice to shareholders.

| Investment Restriction | All Portfolios |

| FUNDAMENTAL LIMITATIONS |

| Borrowing | Each Fund may not borrow money, except that a Fund may (i) borrow money from banks for temporary or emergency purposes and not for leveraging or investment and (ii) enter into reverse repurchase agreements for any purpose; provided that (i) and (ii) in combination do not exceed 33-1/3% of the value of its total assets (including the amount borrowed) less liabilities (other than borrowings). If at any time borrowings exceed 33-1/3% of the value of a Fund’s total assets, the Fund will reduce its borrowings within three days (excluding Sundays and holidays) to the extent necessary to comply with the 33-1/3% limitation. |

| Commodities | Each Fund may not purchase physical commodities or contracts thereon, unless acquired as a result of the ownership of securities or instruments, but this restriction shall not prohibit a Fund from purchasing futures contracts or options (including options on futures and foreign currencies and forward contracts but excluding options or futures contracts on physical commodities) or from investing in securities of any kind. |

| Concentration | Each Fund may not purchase any security if, as a result, 25% or more of its total assets (taken at current value) would be invested in the securities of issuers having their principal business activities in the same industry. This limitation does not apply to purchases of (i) securities issued or guaranteed by the U.S. Government and Agency Securities, or (ii) investments by all Funds in certificates of deposit or bankers’ acceptances issued by domestic branches of U.S. banks. |

| Lending | Each Fund may not lend any security or make any other loan if, as a result, more than 33-1/3% of its total assets (taken at current value) would be lent to other parties, except in accordance with its investment objective, policies, and limitations, (i) through the purchase of a portion of an issue of debt securities or (ii) by engaging in repurchase agreements. |

| Investment Restriction | All Portfolios |

| Real Estate | Each Fund may not purchase real estate unless acquired as a result of the ownership of securities or instruments, but this restriction shall not prohibit a Fund from purchasing securities issued by entities or investment vehicles that own or deal in real estate or interests therein, or instruments secured by real estate or interests therein. |

| Senior Securities | Each Fund may not issue senior securities, except as permitted under the 1940 Act. |

| Underwriting | Each Fund may not underwrite securities of other issuers, except to the extent that a Fund, in disposing of portfolio securities, may be deemed to be an underwriter within the meaning of the Securities Act of 1933, as amended (“1933 Act”). |

| Investment through a Master/Feeder Structure | Notwithstanding any other investment policy, each Fund may invest all of its net investable assets (cash, securities and receivables relating to securities) in an open-end management investment company having substantially the same investment objective, policies and limitations as the Fund. Currently, the Funds do not utilize this policy. Rather, each Fund invests directly in securities. |

| NON-FUNDAMENTAL POLICIES |

| Borrowing | Each Fund may not purchase securities if outstanding borrowings, including any reverse repurchase agreements, exceed 5% of its total assets. |

| Lending | Except for the purchase of debt securities and engaging in repurchase agreements, each Fund may not make any loans other than securities loans. |

| Margin Transactions | Each Fund may not purchase securities on margin from brokers or other lenders except that a Fund may obtain such short-term credits as are necessary for the clearance of securities transactions. For all Funds, margin payments in connection with transactions in futures contracts and options on futures contracts shall not constitute the purchase of securities on margin and shall not be deemed to violate the foregoing limitation. |

| Illiquid Securities | Each Fund may not purchase any security if, as a result, more than 15% of its net assets would be invested in illiquid securities. Generally, illiquid securities include securities that cannot be expected to be sold or disposed of within seven days in the ordinary course of business for approximately the amount at which the Fund has valued the securities, such as repurchase agreements maturing in more than seven days. |

| Investment Restriction | All Portfolios |

| Investments in Any One Issuer | At the close of each quarter of the Fund’s taxable year, (i) no more than 25% of the value of its total assets will be invested in the securities of a single issuer, and (ii) with regard to 50% of its total assets, no more than 5% of the value of its total assets will be invested in the securities of a single issuer. These limitations do not apply to U.S. government securities, as defined for federal tax purposes, or securities of another “regulated investment company” (as defined in section 851(a) of the Internal Revenue Code of 1986, as amended (“Code”)) (“RIC”). |

| Foreign Securities | The Funds may not invest more than 10% (20% in case of Mid Cap Growth Portfolio) of the value of their total assets in securities of foreign issuers, provided that this limitation shall not apply to foreign securities denominated in U.S. dollars, including American Depositary Receipts (“ADRs”). |

Comparison of Principal Risks

The principal risks of investing in the Surviving Portfolio and each Merging Portfolio are listed in the chart below and summarized in the text following the chart. The Portfolios are subject to substantially similar principal risks in most cases and the Balanced Portfolio is subject to additional risks that are not principal risks of the other Portfolios. Although each Portfolio has similar principal risks, an investment in the Surviving Portfolio potentially has or may present greater risks than an investment in a Merging Portfolio. The Surviving Portfolio has a potentially increased risk profile due to certain differences in investment strategy, policies and principal risks: the Balanced Portfolio normally allocates at least 25% of its net assets to investment grade bonds and other debt securities from U.S. government and corporate issuers and does not have a policy to invest in companies of any particular market capitalization while the Surviving Portfolio is not currently invested in investment grade bonds and other debt securities from US government and corporate issuers and has an 80% policy to invest in mid cap companies; and the Small Cap Growth Portfolio normally invests at least 80% of its net assets in small cap companies, is not currently invested in foreign securities and compares its performance to the Russell 2000 Growth Index while the Surviving Portfolio has an 80% policy to invest in mid cap companies, is permitted to invest in foreign securities and compares its performance to the Russell Midcap Growth Index. Historically, most of each Portfolios’ performance has depended on what happened in the markets. The markets’ behavior can be difficult to predict, particularly in the short term. There can be no guarantee that a Portfolio will achieve its goal. A Portfolio may take temporary defensive and cash management positions; in such a case, it will not be pursuing its principal investment strategies.

| Risk | Balanced | Growth | Small Cap Growth | Mid Cap Growth |

| Market Volatility | X | X | X | X |

| Issuer Specific Risk | X | X | X | X |

| Mid-Cap Stock Risk | X | X | | X |

| Small and Mid-Cap Stock Risk | | | X | |

| Growth Stock Risk | X | X | X | X |

| Sector Risk | X | X | X | X |

| Foreign Exposure Risk | X | X | | X |

| Risk Management Risk | X | X | X | X |

| Redemption Risk | X | X | X | X |

| Recent Market Conditions | X | X | X | X |

| Risk of Increase in Expenses | X | X | X | X |

| High Portfolio Turnover | | | X | |

| Interest Rate Risk | X | | | |

| Prepayment and Extension Risk | X | | | |

| Call Risk | X | | | |

| Credit Risk | X | | | |

| US Government Securities Risk | X | | | |

| Lower-Rated Debt Securities Risk | X | | | |

| Restricted Securities Risk | X | | | |

| Illiquid Investments Risk | X | | | |

The Portfolios are each subject to the following principal risks (unless noted otherwise):

Market Volatility. Markets may be volatile and values of individual securities and other investments may decline significantly in response to adverse issuer, political, regulatory, market, economic or other developments that may cause broad changes in market value, public perceptions concerning these developments, and adverse investor sentiment. If the Fund sells a portfolio position before it reaches its market peak, it may miss out on opportunities for better performance.

Issuer-Specific Risk. An individual security or particular type of security may be more volatile, and may perform differently, than the market as a whole.

Mid-Cap Stock Risk (All Portfolios except Small Cap Growth Portfolio). At times, mid-cap companies may be out of favor with investors. Compared to larger companies, mid-cap companies may depend on a more limited management group, may have a shorter history of operations, and may have limited product lines, markets or financial resources. The stocks of mid-cap companies are often more volatile and less liquid than the stocks of larger companies and may be more volatile and less liquid than the stocks of larger companies and may be more affected than other types of stocks by the underperformance of a sector or during market downturns.

Small- and Mid-Cap Stock Risk (Small Cap Growth Portfolio). At times, small- and mid-cap companies may be out of favor with investors. Compared to larger companies, small- and mid-cap companies may depend on a more limited management group, may have a shorter history of operations, and may have limited product lines, markets or financial resources. The stocks of small- and mid-cap companies are often more volatile and less liquid than the stocks of larger companies and may be more affected than other types of stocks by the underperformance of a sector or during market downturns. To the extent the Fund holds stocks of mid-cap companies, the Fund will be subject to their risks.

Growth Stock Risk. Because the prices of most growth stocks are based on future expectations, these stocks tend to be more sensitive than value stocks to bad economic news and negative earnings surprises. Bad economic news or changing investor perceptions may adversely affect growth stocks across several sectors and industries simultaneously.

Sector Risk. To the extent the Fund invests more heavily in particular sectors, its performance will be especially sensitive to developments that significantly affect those sectors. Individual sectors may be more volatile, and may perform differently, than the broader market. The

industries that constitute a sector may all react in the same way to economic, political or regulatory events.

Foreign Exposure Risk (All Portfolios except Small Cap Growth Portfolio). Securities issued by U.S. entities with substantial foreign operations may involve additional risks relating to political, economic, or regulatory conditions in foreign countries.

Risk Management. Risk is an essential part of investing. No risk management program can eliminate the Fund’s exposure to adverse events; at best, it may only reduce the possibility that the Fund will be affected by such events, and especially those risks that are not intrinsic to the Fund’s investment program.

Redemption Risk. The Fund may experience periods of heavy redemptions that could cause the Fund to sell assets at inopportune times or at a loss or depressed value. Redemption risk is heightened during periods of declining or illiquid markets. Heavy redemptions could hurt the Fund’s performance.

Recent Market Conditions. The financial crisis that started in 2008 continues to affect the U.S. and many foreign economies. The crisis and its after-effects have resulted, and may continue to result, in an unusually high degree of volatility in the financial markets, both domestic and foreign. In addition, global economies and financial markets are becoming increasingly interconnected, which increases the possibilities that conditions in one country or region might adversely impact issuers in a different country or region. The severity or duration of adverse economic conditions may also be affected by policy changes made by governments or quasi-governmental organizations. In addition, political events within the U.S. and abroad may affect investor and consumer confidence and may adversely impact financial markets and the broader economy, perhaps suddenly and to a significant degree. High public debt in the U.S. and other countries creates ongoing systemic and market risks and policymaking uncertainty. Because the impact on the markets has been widespread, it may be difficult to identify both risks and opportunities using past models of the interplay of market forces, or to predict the duration of these market conditions. In addition, there is a risk that the prices of goods and services in the U.S. and many foreign economies may decline over time, known as deflation (the opposite of inflation). Deflation may have an adverse effect on stock prices and creditworthiness and may make defaults on debt more likely.

Risk of Increase in Expenses. A decline in the Fund’s average net assets during the current fiscal year due to market volatility or other factors could cause the Fund’s expense ratios for the current fiscal year to be higher than the expense information presented in “Fees and Expenses.”

High Portfolio Turnover (Small Cap Growth Portfolio). The Fund may engage in active and frequent trading and may have a high portfolio turnover rate, which may increase the Fund’s transaction costs and may adversely affect the Fund’s performance.

Interest Rate Risk (Balanced Portfolio). In general, the value of investments with interest rate risk, such as debt securities, will move in the direction opposite to movements in interest rates. If interest rates rise, the value of such securities may decline. Typically, the longer the maturity or duration of a debt security, the greater the effect a change in interest rates could have on the security’s price. Thus, the sensitivity of the Fund’s debt securities to interest rate risk will increase with any increase in the duration of those securities.

Prepayment and Extension Risk (Balanced Portfolio). The Fund’s performance could be affected if borrowers pay back principal on certain debt securities, such as mortgage- or asset-backed securities, before or after the market anticipates such payments, shortening or lengthening their duration. Due to a decline in interest rates or an excess in cash flow, a debt security might be called or otherwise converted, prepaid or redeemed before maturity. As a result, the Fund may have to reinvest the proceeds in an investment offering a lower yield, may not benefit from any increase in value that might otherwise result from declining interest rates and may lose any premium it paid to acquire the security. Higher interest rates generally result in slower payoffs, which effectively increase duration, heighten interest rate risk, and increase the potential for price declines.

Call Risk (Balanced Portfolio). When interest rates are low, issuers will often repay the obligation underlying a “callable security” early, in which case the Fund may have to reinvest the proceeds in an investment offering a lower yield and may not benefit from any increase in value that might otherwise result from declining interest rates.

Credit Risk (Balanced Portfolio). Credit risk is the risk that issuers may fail, or become less able, to pay interest and/or principal when due. A downgrade or default affecting any of the Fund’s securities could affect the Fund’s performance.

U.S. Government Securities Risk (Balanced Portfolio). Although the Fund may hold securities that carry U.S. government guarantees, these guarantees do not extend to shares of the Fund itself and do not guarantee the market prices of the securities. Furthermore, not all securities issued by the U.S. government and its agencies and instrumentalities are backed by the full faith and credit of the U.S. Treasury.

Lower-Rated Debt Securities Risk (Balanced Portfolio). Lower-rated debt securities (commonly known as “junk bonds”) involve greater risks than investment grade debt securities. Lower-rated debt securities may fluctuate more widely in price and yield and may fall in price during times when the economy is weak or is expected to become weak. Lower-rated debt securities are considered by the major rating agencies to be predominantly speculative with respect to the issuer’s continuing ability to pay principal and interest and carry a greater risk that the issuer of such securities will default in the timely payment of principal and interest. Issuers of securities that are in default or have defaulted may fail to resume principal or interest payments, in which case the Fund may lose its entire investment.

Restricted Securities Risk (Balanced Portfolio). Restricted securities may not be listed on an exchange and may have no active trading market. Restricted securities may be illiquid, and the Fund may be unable to sell them at a time when it may otherwise be desirable to do so or may be able to sell them only at prices that are less than what the Fund regards as their fair market value. Transaction costs may be higher for restricted securities. In addition, the Fund may get only limited information about the issuer of a restricted security.

Illiquid Investments Risk (Balanced Portfolio). Illiquid investments may be more difficult to purchase or sell at an advantageous price or time, and there is a greater risk that the investments may not be sold for the price at which the Fund is carrying them.

Comparison of Fees and Expenses

The following tables show the fees and expenses of each class of shares of the Merging Portfolios and the Surviving Portfolio and the pro forma fees and expenses of each class of shares of the Surviving Portfolio after giving effect to each proposed Reorganization. Expenses for each Portfolio are based on the operating expenses incurred by each class of their shares for the twelve-month period ended December 31, 2014. The pro forma of each class of shares of the Surviving Portfolio assumes that all three Reorganizations take place as expected, that the Surviving Portfolios net assets are approximately equal to the combined net assets of the Portfolios as they currently stand, and that the Reorganizations had been in effect for the same period. This information does not reflect variable contract or qualified plan fees and expenses. If such fees and expenses were reflected, returns would be less than those shown. Please refer to the prospectus for your variable contract or your qualified plan documentation for information on their separate fees and expenses. These comparisons assume that each Reorganization was in effect for the period ended June 30, 2015.

Shareholder Fees (fees paid directly from your investment)

Not Applicable

Annual Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment)

| Balanced | | Mid Cap Growth | Mid Cap Growth After Reorganization (pro forma) |

| | Class I | | Class I | Class I |

Annual Fund Operating Expenses | | | |

| Management fees | 0.85 | 0.85 | 0.85 |

| Distribution (12b-1 fees) | None | None | None |

| Other expenses | 1.20 | 0.15 | 0.13 |

| Total annual operating expenses | 2.05 | 1.00 | 0.98 |

| Fee Waiver and/or expense reimbursement | 0.20 | | |

| Total annual operating expenses after fee waiver and/or expense reimbursement | 1.851 | | |

1 NBM has contractually undertaken to waive and/or reimburse certain fees and expenses of Class I so that total annual operating expenses (excluding the compensation of NBM, interest, taxes, transaction costs, brokerage commissions, dividend and interest expenses relating to short sales, acquired fund fees and expenses and extraordinary expenses, if any) are limited to 1.00% of average net asset value. These fee waivers and/or expense reimbursement are subject to recoupment by NBM within three years. This undertaking lasts until 12/31/2018 and may not be terminated during its term without the consent of the Board of Trustees. The Fund has agreed that Class I

will repay NBM for fees and expenses waived or reimbursed for the class provided that repayment does not cause annual operating expenses to exceed 1.00% of the class’ average net assets. Any such repayment must be made within three years after the year in which NBM incurred the expense.

| | Growth | | Mid Cap Growth | Mid Cap Growth After Reorganization (pro forma) |

| | Class I | | Class I | Class I |

Annual Fund Operating Expenses | | | |

| Management fees | 0.85 | 0.85 | 0.85 |

| Distribution (12b-1 fees) | None | None | None |

| Other expenses | 1.47 | 0.15 | 0.13 |

| Total annual operating expenses | 2.32 | 1.00 | 0.98 |

| Fee Waiver and/or expense reimbursement | 0.47 | | |

| Total annual operating expenses after fee waiver and/or expense reimbursement | 1.851 | | |

1 NBM has contractually undertaken to waive and/or reimburse certain fees and expenses of Class I so that total annual operating expenses (excluding the compensation of NBM, interest, taxes, transaction costs, brokerage commissions, dividend and interest expenses relating to short sales, acquired fund fees and expenses and extraordinary expenses, if any) are limited to 1.00% of average net asset value. These fee waivers and/or expense reimbursement are subject to recoupment by NBM within three years. This undertaking lasts until 12/31/2018 and may not be terminated during its term without the consent of the Board of Trustees. The Fund has agreed that Class I will repay NBM for fees and expenses waived or reimbursed for the class provided that repayment does not cause annual operating expenses to exceed 1.00% of the class’ average net assets. Any such repayment must be made within three years after the year in which NBM incurred the expense.

| | Small Cap Growth | | Mid Cap Growth | Mid Cap Growth After Reorganization (pro forma) |

| | Class S | | Class S | Class S |

Annual Fund Operating Expenses | | | |

| Management fees | 1.15 | 0.85 | 0.85 |

| Distribution (12b-1 fees) | 0.25 | 0.25 | 0.25 |

| Other expenses | 0.68 | 0.151 | 0.13 |

| Total annual operating expenses | 2.08 | 1.25 | 1.23 |

| Fee Waiver and/or expense reimbursement | 0.67 | | |

| Total annual operating expenses after fee waiver and/or expense reimbursement | 1.412 | | |

1 NBM has contractually undertaken to waive and/or reimburse certain fees and expenses of Class S so that total annual operating expenses (excluding interest, taxes, transaction costs, brokerage commissions, dividend and interest expenses related to short sales, acquired fund fees and expenses and extraordinary expenses, if any) are limited to 1.25% of average net asset value. These fee waivers and/or expense reimbursement are subject to recoupment by NBM within three years. This undertaking lasts until 12/31/2018 and may not be terminated during its term without the consent of the Board of Trustees. The Fund has agreed that Class S will repay NBM for fees and expenses waived or reimbursed for the class provided that repayment does not cause annual operating expenses to exceed 1.25% of the class’ average net assets. Any such repayment must be made within three years after the year in which NBM incurred the expense.

2 NBM has contractually undertaken to waive and/or reimburse certain fees and expenses of Class S so that total annual operating expenses (excluding interest, taxes, transaction costs, brokerage commissions, dividend and interest expenses relating to short sales, acquired fund fees and expenses and extraordinary expenses, if any) are limited to 1.40% of average net asset value. These fee waivers and/or expense reimbursement are subject to recoupment by NBM within three years. This undertaking lasts until 12/31/2018 and may not be terminated during its term without the consent of the Board of Trustees. The Fund has agreed that Class S will repay NBM for fees and expenses waived or reimbursed for the class provided that repayment does not cause annual operating expenses to exceed 1.40% of the class’ average net assets. Any such repayment must be made within three years after the year in which NBM incurred the expense.

| | Balanced | Growth | Small Cap Growth | | Mid Cap Growth | Mid Cap Growth Assuming Consummation of All Three Reorganizations (pro forma) |

| | Class I | Class I | Class S | | Class I | Class S | Class I | Class S |

Annual Fund Operating Expenses | | | | | | | |

| Management fees | 0.85 | 0.85 | 1.15 | 0.85 | 0.85 | 0.85 | 0.85 |

| Distribution (12b-1 fees) | None | None | 0.25 | None | 0.25 | None | 0.25 |

| Other expenses | 1.20 | 1.47 | 0.68 | 0.15 | 0.15 | 0.12 | 0.12 |

| Total annual operating expenses | 2.05 | 2.32 | 2.08 | 1.00 | 1.251 | 0.97 | 1.22 |

| Fee Waiver and/or expense reimbursement | 0.20 | 0.47 | 0.67 | | |

| Total annual operating expenses after fee waiver and/or expense reimbursement | 1.852 | 1.853 | 1.414 | | |

1 NBM has contractually undertaken to waive and/or reimburse certain fees and expenses of Class S so that total annual operating expenses (excluding interest, taxes, transaction costs, brokerage commissions, dividend and interest expenses related to short sales, acquired fund fees and expenses and extraordinary expenses, if any) are limited to 1.25% of average net asset value. These fee waivers and/or expense reimbursement are subject to recoupment by NBM within three years. This undertaking lasts until 12/31/2018 and may not be terminated during its term without the consent of the Board of Trustees. The Fund has agreed that Class S will repay NBM for fees and expenses waived or reimbursed for the class provided that repayment does not cause annual operating expenses to

exceed 1.25% of the class’ average net assets. Any such repayment must be made within three years after the year in which NBM incurred the expense.

2 NBM has contractually undertaken to waive and/or reimburse certain fees and expenses of Class I so that total annual operating expenses (excluding the compensation of NBM, interest, taxes, transaction costs, brokerage commissions, dividend and interest expenses relating to short sales, acquired fund fees and expenses and extraordinary expenses, if any) are limited to 1.00% of average net asset value. These fee waivers and/or expense reimbursement are subject to recoupment by NBM within three years. This undertaking lasts until 12/31/2018 and may not be terminated during its term without the consent of the Board of Trustees. The Fund has agreed that Class I will repay NBM for fees and expenses waived or reimbursed for the class provided that repayment does not cause annual operating expenses to exceed 1.00% of the class’ average net assets. Any such repayment must be made within three years after the year in which NBM incurred the expense.

3 NBM has contractually undertaken to waive and/or reimburse certain fees and expenses of Class I so that total annual operating expenses (excluding the compensation of NBM, interest, taxes, transaction costs, brokerage commissions, dividend and interest expenses relating to short sales, acquired fund fees and expenses and extraordinary expenses, if any) are limited to 1.00% of average net asset value. These fee waivers and/or expense reimbursement are subject to recoupment by NBM within three years. This undertaking lasts until 12/31/2018 and may not be terminated during its term without the consent of the Board of Trustees. The Fund has agreed that Class I will repay NBM for fees and expenses waived or reimbursed for the class provided that repayment does not cause annual operating expenses to exceed 1.00% of the class’ average net assets. Any such repayment must be made within three years after the year in which NBM incurred the expense.

4 NBM has contractually undertaken to waive and/or reimburse certain fees and expenses of Class S so that total annual operating expenses (excluding interest, taxes, transaction costs, brokerage commissions, dividend and interest expenses relating to short sales, acquired fund fees and expenses and extraordinary expenses, if any) are limited to 1.40% of average net asset value. These fee waivers and/or expense reimbursement are subject to recoupment by NBM within three years. This undertaking lasts until 12/31/2018 and may not be terminated during its term without the consent of the Board of Trustees. The Fund has agreed that Class S will repay NBM for fees and expenses waived or reimbursed for the class provided that repayment does not cause annual operating expenses to exceed 1.40% of the class’ average net assets. Any such repayment must be made within three years after the year in which NBM incurred the expense.

Example of Portfolio Expenses

This example can help you compare costs between each Merging Portfolio and the Surviving Portfolio and the pro forma costs for the Surviving Portfolio after giving effect to the Reorganization. The example assumes that you invested $10,000 for the periods shown, that you earned a hypothetical 5% total return each year, and that the Portfolios’ expenses were those in the table above. Your costs would be the same whether you sold your shares or continued to hold them at the end of each period. Actual performance and expenses may be higher or lower. These examples do not take into account any fees or expenses that your insurance company or other financial intermediary may impose.

Reorganization of Balanced Into Mid Cap Growth including Proformas

| Year 1 |

| | Balanced | Mid Cap Growth | Mid Cap Growth (pro forma) |

| Class I | $188 | $102 | $100 |

| Year 3 |

| | Balanced | Mid Cap Growth | Mid Cap Growth (pro forma) |

| Class I | $582 | $318 | $312 |

| Year 5 |

| | Balanced | Mid Cap Growth | Mid Cap Growth (pro forma) |

| Class I | $1,045 | $552 | $542 |

| Year 10 |

| | Balanced | Mid Cap Growth | Mid Cap Growth (pro forma) |

| Class I | $2,328 | $1,225 | $1201 |

Reorganization of Growth Into Mid Cap Growth including Proformas

| Year 1 |

| | Growth | Mid Cap Growth | Mid Cap Growth (pro forma) |

| Class I | $188 | $102 | $100 |

| Year 3 |

| | Growth | Mid Cap Growth | Mid Cap Growth (pro forma) |

| Class I | $582 | $318 | $312 |

| Year 5 |

| | Growth | Mid Cap Growth | Mid Cap Growth (pro forma) |

| Class I | $1,105 | $552 | $542 |

| Year 10 |

| | Growth | Mid Cap Growth | Mid Cap Growth (pro forma) |

| Class I | $2,540 | $1,225 | $1201 |

Reorganization of Small Cap Growth Into Mid Cap Growth including Proformas

| Year 1 |

| | Small Cap Growth | Mid Cap Growth | Mid Cap Growth (pro forma) |

| Class S | $144 | $127 | $125 |

| Year 3 |

| | Small Cap Growth | Mid Cap Growth | Mid Cap Growth (pro forma) |

| Class S | $446 | $397 | $390 |

| Year 5 |

| | Small Cap Growth | Mid Cap Growth | Mid Cap Growth (pro forma) |

| Class S | $922 | $686 | $676 |

| Year 10 |

| | Small Cap Growth | Mid Cap Growth | Mid Cap Growth (pro forma) |

| Class S | $2,239 | $1,511 | $1489 |

Consummation of All Three Reorganizations including Proformas

| Year 1 |

| | Balanced | Growth | Small Cap Growth | Mid Cap Growth | Mid Cap Growth (pro forma) |

| Class I | $188 | $188 | - | $102 | $99 |

| Class S | - | - | $144 | $127 | $124 |

| Year 3 |

| | Balanced | Growth | Small Cap Growth | Mid Cap Growth | Mid Cap Growth (pro forma) |

| Class I | $582 | $582 | - | $318 | $309 |

| Class S | - | - | $446 | $397 | $387 |

| Year 5 |

| | Balanced | Growth | Small Cap Growth | Mid Cap Growth | Mid Cap Growth (pro forma) |

| Class I | $1,045 | $1,105 | - | $552 | $536 |

| Class S | - | - | $922 | $686 | $670 |

| Year 10 |

| | Balanced | Growth | Small Cap Growth | Mid Cap Growth | Mid Cap Growth (pro forma) |

| Class I | $2,328 | $2,540 | - | $1,225 | $1190 |

| Class S | - | - | $2,239 | $1,511 | $1477 |

Comparative Performance Information