UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number | 811-03940 | |||||

|

| |||||

| Strategic Funds, Inc. |

| ||||

| (Exact name of Registrant as specified in charter) |

| ||||

|

|

| ||||

|

c/o The Dreyfus Corporation 200 Park Avenue New York, New York 10166 |

| ||||

| (Address of principal executive offices) (Zip code) |

| ||||

|

|

| ||||

| Bennett A. MacDougall, Esq. 200 Park Avenue New York, New York 10166 |

| ||||

| (Name and address of agent for service) |

| ||||

| ||||||

Registrant's telephone number, including area code: | (212) 922-6000 | |||||

|

| |||||

Date of fiscal year end:

| 11/30 |

| ||||

Date of reporting period: | 11/30/15 |

| ||||

The following N-CSR relates only to the Registrant’s series listed below and does not affect the other series of the Registrant, which have different fiscal year ends and, therefore, different N-CSR reporting requirements. Separate N-CSR Forms will be filed for these series, as appropriate.

Dreyfus MLP Fund

Dreyfus Select Managers Small Cap Value Fund

Dreyfus U.S. Equity Fund

Global Stock Fund

International Stock Fund

FORM N-CSR

Item 1. Reports to Stockholders.

Dreyfus MLP Fund

| ANNUAL REPORT |

|

Save time. Save paper. View your next shareholder report online as soon as it’s available. Log into www.dreyfus.com and sign up for Dreyfus eCommunications. It’s simple and only takes a few minutes. |

The views expressed in this report reflect those of the portfolio manager only through the end of the period covered and do not necessarily represent the views of Dreyfus or any other person in the Dreyfus organization. Any such views are subject to change at any time based upon market or other conditions and Dreyfus disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Dreyfus fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Dreyfus fund. |

Not FDIC-Insured • Not Bank-Guaranteed • May Lose Value |

Contents

THE FUND

With Those of Other Funds | |

Sold Short | |

Public Accounting Firm | |

FOR MORE INFORMATION

Back Cover

| The Fund |

Dear Shareholder:

We are pleased to present this annual report for Dreyfus MLP Fund, covering the period from the commencement of operations on April 30, 2015, through November 30, 2015. For information about how the fund performed during the reporting period, as well as general market perspectives, we provide a Discussion of Fund Performance on the pages that follow.

Financial markets proved volatile over the reporting period amid choppy U.S. and global economic growth. Employment and housing market gains helped U.S. stocks advance over the reporting period’s first half, driving some broad measures of market performance to new record highs in the spring. Although those gains were erased over the summer when global economic instability undermined investor sentiment, a renewed rally in the fall enabled most stock indices to end the reporting period in mildly positive territory. In contrast, international stocks mostly provided negative results, but developed markets fared better than emerging markets amid falling commodity prices and depreciating currency values. U.S. bonds produced modestly positive total returns overall, with municipal bonds achieving higher returns, on average, than U.S. government securities and corporate-backed bonds.

We expect market volatility to persist over the near term until investors see greater clarity regarding domestic and global economic conditions. Our investment strategists and portfolio managers are monitoring developments carefully, keeping a close watch on credit spreads, currency values, commodity prices, corporate profits, economic trends in the emerging markets, and other developments that could influence investor sentiment. Over the longer term, we remain confident that markets are likely to benefit as investors increasingly recognize that inflation is likely to stay low, economic growth expectations are stabilizing, and monetary policies remain accommodative in most regions of the world. In our view, investors will continue to be well served under these circumstances by a long-term perspective and a disciplined investment approach.

Thank you for your continued confidence and support.

Sincerely,

J. Charles Cardona

President

The Dreyfus Corporation

December 17, 2015

2

DISCUSSION OF FUND PERFORMANCE

For the period of April 30, 2015, through November 30, 2015, as provided by Robert A. Nicholson and Zev D. Nijensohn, Portfolio Managers

Fund and Market Performance Overview

For the period between the fund’s inception on April 30, 2015, and the end of its fiscal year on November 30, 2015, Dreyfus MLP Fund’s Class A shares produced a total return of -32.66%, Class C shares returned -32.98%, Class I shares returned -32.58%, and Class Y shares returned -32.58%.1 In comparison, the fund’s benchmark, the Alerian MLP Index (“the Index”) produced a total return of -30.53% for the same period.2

The reporting period proved highly challenging for securities across the energy complex as significant declines in commodity prices, coupled with increased currency and rate volatility, triggered widespread risk aversion. Midstream companies, including master limited partnerships, correlated strongly with the rest of the sector.

The Fund’s Investment Approach

The fund seeks total return consisting of capital appreciation and income. To pursue it goal, the fund invests in master limited partnerships (“MLPs”), that own and operate assets that are used in the energy sector, including assets used in gathering, processing, storing, and transporting oil and gas, refined products, coal, electricity or alternative fuels, or that provide energy-related equipment or services. The fund intends to concentrate its investments, under normal circumstances, in the energy sector, primarily investing in “midstream” energy infrastructure MLPs. The fund typically maintains a concentrated portfolio of 15 to 20 positions. The fund may utilize leverage through borrowings, short sales, or derivative instruments.

We employ a bottom-up fundamental and event driven process to select MLP investments, in which we evaluate both fundamental drivers and financial structure drivers to identify catalysts that can impact cash flow growth and valuation throughout the MLP lifecycle.

Falling Commodity Prices Sparked Market Turmoil

The reporting period began following a sharp decline in prices of oil, natural gas, and natural gas liquids. Prices remained relatively stable through mid-June but resumed their downward spiral as global supply continued to outpace demand. Volatility accelerated in August against the backdrop of a debt crisis in Greece, poor Chinese economic data, U.S. dollar strength and fears of rate hikes from the Federal Reserve Board. This culminated in a disruption in capital markets access for the MLP sector.

In this tumultuous climate, the energy infrastructure MLPs in which the fund invests lost considerable value. Selling pressure among investors was broad-based, punishing a wide range of MLPs without regard to their underlying business fundamentals. While commodity prices clearly have altered the industry’s growth profile, the valuation loss has not been commensurate with the cash flow stability and asset quality of the majority of companies.

Widespread Industry Weakness Undermined Fund Results

Few energy infrastructure MLPs were spared from losses in the precipitously declining market environment. The fund held outsized exposure to growth-oriented MLPs and

3

DISCUSSION OF FUND PERFORMANCE (continued)

General Partners, which, although harboring relatively limited direct commodity exposure, were affected more directly by selling pressure. The significant losses suffered by the fund in Kinder Morgan and Tallgrass Energy GP fall in that category, as both have large inventories of projects (and dropdowns) that historically have been externally financed.

The fund benefited modestly from its exposure to NiSource, which announced a spin-off of its gas pipeline division and benefited from a flight-to-safety due to its regulated utility business model.

The fund maintained several short positions over the reporting period, primarily for hedging purposes.

Maintaining a Disciplined Approach

As noted, we have seen a material shift in near-term fundamentals and sentiment across the energy infrastructure sector. The ensuing selloff has been almost unprecedented in its breadth and severity, rivalling what we witnessed in the depths of the financial crisis. Despite recent liquidity-driven market declines, we remain encouraged by the underlying fundamentals of energy infrastructure MLPs in general and the fund’s holdings in particular. Our research shows that the hard assets contained in the fund’s holdings provide mission-critical services that are difficult for energy providers to replace, predominantly earn fee-based revenues through long-term contracts, and provide solid returns on invested capital.

Every cyclical downturn has its own unique characteristics, but it is worth pointing out that in its almost 20-year trading history, the Index has declined more than 10% in only three calendar years: 1999, 2002, and 2008. We firmly believe this downturn has sharply overshot, creating potentially attractive medium- to long-term investment opportunities for disciplined investors.

We have reacted to the current environment by eliminating or trimming positions with difficult-to-qualify near-term assumptions, especially related to capital access, and we have shifted more capital toward large, investment-grade, midstream MLPs with high yields and limited commodity sensitivity, which we believe provide cheap optionality to a recovery in oil prices. Finally, we have maintained a sizeable cash balance, which we believe will provide us with flexibility to respond to market dislocations.

December 17, 2015

Master Limited Partnership (MLP) investments involve risks that differ from investments in common stock, including risks related to limited control and limited rights to vote on matters affecting the MLP, risks related to potential conflicts of interest between the MLP and the MLP’s general partner, cash flow risks, dilution risks and risks related to the general partner’s right to require unit-holders to sell their common units at an undesirable time or price. Under normal circumstances, the fund concentrates its investments in the energy sector, focusing on energy infrastructure MLPs, and may, therefore, be more susceptible to the risks affecting such sector and MLPs. In addition, the fund’s performance may be more vulnerable to changes in the market value than more broadly diversified funds.

Equity funds are subject generally to market, market sector, market liquidity, issuer, and investment style risks, among other factors, to varying degrees, all of which are more fully described in the fund’s prospectus.

Because the fund’s investments are concentrated in the energy and related sectors, the value of its shares will be affected by factors particular to those sectors and may fluctuate more widely than that of a fund which invests in a broad range of industries. The market value of these securities may be affected by numerous factors, including events occurring in nature, inflationary pressures, and domestic and international politics. Interest rates, commodity prices, economic, tax, energy developments, and government regulations may affect supply and demand dynamics and the share prices of companies in the sector.

Securities of companies within specific energy sectors can perform differently from the overall market. This may be due to changes in such things as the regulatory or competitive environment or to changes in investor perceptions regarding a sector. Because the fund may

4

allocate relatively more assets to certain energy sectors than others, the fund’s performance may be more sensitive to developments, which affect those sectors emphasized by the fund.

Small and midsize companies carry additional risks because their earnings and revenues tend to be less predictable, and their share prices more volatile than those of larger, more established companies.

MLP tax risk will depend on the MLPs being treated as partnerships for U.S. federal income tax purposes. Partnerships do not pay U.S. federal income tax at the partnership level. Rather, each partner is allocated a share of the partnership’s income, gains, losses, deductions and expenses. A change in current tax law, or a change in the business of a given MLP, could result in an MLP being treated as a corporation for U.S. federal income tax purposes, which would result in the MLP being required to pay U.S. federal income tax (as well as state and local income taxes) on its taxable income.

1 Total return includes reinvestment of dividends and any capital gains paid, and does not take into consideration the maximum initial sales charge in the case of Class A shares, or the applicable contingent deferred sales charge imposed on redemptions in the case of Class C shares. Had these charges been reflected, returns would have been lower. Past performance is no guarantee of future results. Share price and investment return fluctuate such that upon redemption, fund shares may be worth more or less than their original cost. Return figures provided reflect the absorption of certain fund expenses by The Dreyfus Corporation pursuant to an undertaking in effect through May 1, 2016, at which time it may be extended, terminated, or modified. Had these expenses not been absorbed, the fund’s returns would have been lower.

2 Lipper Inc. — Reflects reinvestment of dividends and, where applicable, capital gain distributions. The Alerian MLP Index is a float-adjusted, market capitalization weighted composite of 50 energy MLPs representing approximately 75% of the available market capitalization, with a median market capitalization of approximately $3.2 billion as of December 31, 2015. Investors cannot invest directly in any index.

5

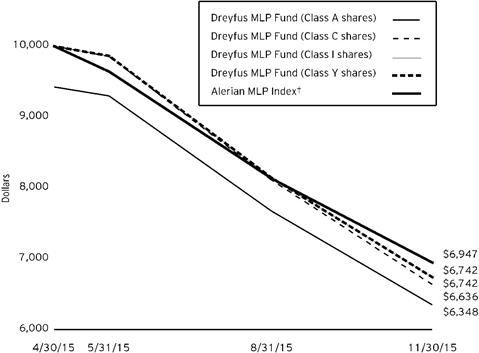

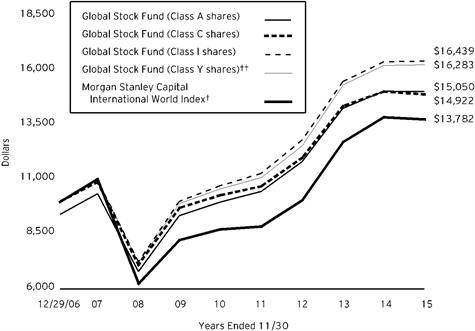

FUND PERFORMANCE

Comparison of change in value of $10,000 investment in Dreyfus MLP Fund Class A shares, Class C shares, Class I shares and Class Y shares, and the Alerian Dreyfus MLP Index

† Source: Lipper Inc.

Past performance is not predictive of future performance.

The above graph compares a $10,000 investment made in each of the Class A, Class C, Class I and Class Y shares of Dreyfus MLP Fund on 4/30/15 (inception date) to a $10,000 investment made in the Alerian MLP Index (the “Index”) on that date. All dividends and capital gain distributions are reinvested.

The fund invests at least 80% of its net assets, plus any borrowings for investment purposes, in master limited partnership (MLP) investments. MLPs in which the fund normally invests own and operate assets that are used in the energy sector, including assets used in exploring, developing, producing, generating, transporting, transmitting, terminalling, storing, gathering, processing, refining, distributing, mining or marketing of natural gas, natural gas liquids, crude oil, refined products, coal, electricity or alternative fuels, or that provide energy-related equipment or services. The Index is a float-adjusted, market capitalization weighted composite of 50 energy MLPs representing approximately 75% of the available market capitalization. The Index reflects the reinvestment of dividends and other distributions. These factors can contribute to the Index potentially outperforming or underperforming the fund. Unlike a mutual fund, the Index is not subject to charges, fees and other expenses. Investors cannot invest directly in any index. Further information relating to fund performance, including expense reimbursements, if applicable, is contained in the Financial Highlights section of the prospectus and elsewhere in this report.

6

Aggregate Total Returns as of 11/30/15 | |||||

Inception | From | ||||

Class A shares | |||||

with maximum sales charge (5.75%) | 4/30/15 | -36.52% | |||

without sales charge | 4/30/15 | -32.66% | |||

Class C shares | |||||

with applicable redemption charge† | 4/30/15 | -33.64% | |||

without redemption | 4/30/15 | -32.98% | |||

Class I shares | 4/30/15 | -32.58% | |||

Class Y shares | 4/30/15 | -32.58% | |||

Alerian MLP Index | 4/30/15 | -30.53% | |||

Past performance is not predictive of future performance. The fund’s performance shown in the graph and table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. In addition to the performance of Class A shares shown with and without a maximum sales charge, the fund’s performance shown in the table takes into account all other applicable fees and expenses on all classes.

† The maximum contingent deferred sales charge for Class C shares is 1% for shares redeemed within one year of the date of purchase.

7

UNDERSTANDING YOUR FUND’S EXPENSES (Unaudited)

As a mutual fund investor, you pay ongoing expenses, such as management fees and other expenses. Using the information below, you can estimate how these expenses affect your investment and compare them with the expenses of other funds. You also may pay one-time transaction expenses, including sales charges (loads) and redemption fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial adviser.

Review your fund’s expenses

The table below shows the expenses you would have paid on a $1,000 investment in Dreyfus MLP Fund from June 1, 2015 to November 30, 2015. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

Expenses and Value of a $1,000 Investment | ||||||||||||

assuming actual returns for the six months ended November 30, 2015 | ||||||||||||

|

|

|

| Class A | Class C | Class I | Class Y | |||||

Expenses paid per $1,000† |

| $ 8.52 |

| $ 11.54 |

| $ 7.43 |

| $ 7.39 | ||||

Ending value (after expenses) |

| $ 682.70 |

| $ 680.00 |

| $ 683.50 |

| $ 683.50 | ||||

COMPARING YOUR FUND’S EXPENSES

WITH THOSE OF OTHER FUNDS (Unaudited)

Using the SEC’s method to compare expenses

The Securities and Exchange Commission (SEC) has established guidelines to help investors assess fund expenses. Per these guidelines, the table below shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return. You can use this information to compare the ongoing expenses (but not transaction expenses or total cost) of investing in the fund with those of other funds. All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

Expenses and Value of a $1,000 Investment | |||||||||||

assuming a hypothetical 5% annualized return for the six months ended November 30, 2015 | |||||||||||

|

|

|

| Class A | Class C | Class I | Class Y | ||||

Expenses paid per $1,000† |

| $ 10.20 |

| $ 13.82 |

| $ 8.90 |

| $ 8.85 | |||

Ending value (after expenses) |

| $ 1,014.94 |

| $ 1,011.33 |

| $ 1,016.24 |

| $ 1,016.29 | |||

† Expenses are equal to the fund’s annualized expense ratio of 2.02% for Class A, 2.74% for Class C, 1.76% for Class I and 1.75% for Class Y, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period).

8

STATEMENT OF INVESTMENTS

November 30, 2015

Common Stocks - 13.6% | Shares | Value ($) | |||

Energy - 7.2% | |||||

Kinder Morgan | 45,474 | 1,071,822 | |||

Plains GP Holdings, Cl. A | 30,984 | 379,864 | |||

1,451,686 | |||||

Real Estate - 5.0% | |||||

InfraREIT | 50,026 | a | 1,009,024 | ||

Utilities - 1.4% | |||||

NiSource | 14,333 | 275,050 | |||

Total Common Stocks (cost $4,451,999) | 2,735,760 | ||||

Master Limited Partnerships - 73.5% | |||||

Energy - 70.0% | |||||

Buckeye Partners LP | 18,764 | b | 1,270,135 | ||

Cheniere Energy Partners LP | 54,135 | b | 1,391,270 | ||

Cone Midstream Partners LP | 95,625 | b | 1,079,606 | ||

Energy Transfer Equity LP | 35,466 | b | 671,726 | ||

Energy Transfer Partners LP | 23,291 | 889,949 | |||

EnLink Midstream Partners LP | 47,306 | 705,806 | |||

Enterprise Products Partners LP | 77,308 | 1,962,850 | |||

MPLX LP | 33,281 | 1,429,086 | |||

NuStar Energy LP | 9,063 | 362,701 | |||

Nustar GP Holdings LLC | 30,153 | 749,604 | |||

Southcross Energy Partners LP | 55,090 | 253,414 | |||

Tallgrass Energy GP LP | 72,606 | 1,594,428 | |||

Valero Energy Partners LP | 24,227 | 1,122,437 | |||

Western Gas Equity Partners LP | 13,432 | b | 560,383 | ||

Western Gas Partners LP | 1,456 | 69,917 | |||

14,113,312 | |||||

Materials - 3.5% | |||||

Westlake Chemical Partners LP | 45,557 | 709,778 | |||

Total Master Limited Partnerships (cost $18,224,381) | 14,823,090 | ||||

Warrants - .7% | Number of Warrants | Value ($) | |||

Energy - .7% | |||||

Kinder Morgan (5/25/17) | 503,786 | c | 151,136 | ||

9

STATEMENT OF INVESTMENTS (continued)

Other Investment - 11.8% | Shares | Value ($) | |||

Registered Investment Company; | |||||

Dreyfus Institutional Preferred Plus Money Market Fund | 2,387,402 | d | 2,387,402 | ||

Total Investments (cost $26,757,343) | 99.6% | 20,097,388 | |||

Cash and Receivables (Net) | 0.4% | 82,617 | |||

Net Assets | 100.0% | 20,180,005 | |||

LLC—Limited Liability Company

LP—Limited Partnership

aInvestment in real estate investment trust.

bHeld by a broker as collateral for open short positions.

cNon-income producing security.

dInvestment in affiliated money market mutual fund.

Portfolio Summary (Unaudited) † | Value (%) |

Energy | 77.9 |

Money Market Investment | 11.8 |

Real Estate | 5.0 |

Materials | 3.5 |

Utilities | 1.4 |

99.6 |

† Based on net assets.

See notes to financial statements.

10

STATEMENT OF SECURITIES SOLD SHORT

November 30, 2015

Common Stocks-12.7% | Shares | Value ($) | |||

Exchange-Traded Funds-12.7% | |||||

iShares 20+ Year Treasury Bond ETF | 15,468 | 1,878,589 | |||

iShares U.S. Real Estate ETF | 3,739 | 281,210 | |||

SPDR Barclays High Yield Bond ETF | 11,250 | 397,800 | |||

Total Common Stocks (proceeds $2,644,397) | 2,557,599 | ||||

Master Limited Partnerships-.9% | |||||

Energy-.9% | |||||

Spectra Energy Partners LP | 4,449 | 188,504 | |||

Total Securities Sold Short (proceeds $2,848,111) | 2,746,103 |

ETF—Exchange-Traded Fund

LP—Limited Partnership

Portfolio Summary (Unaudited) † | Value (%) |

Exchange-Traded Funds | 12.7 |

Energy | .9 |

13.6 |

† Based on net assets.

See notes to financial statements.

11

STATEMENT OF ASSETS AND LIABILITIES

November 30, 2015

|

|

|

|

|

|

|

|

|

| Cost |

| Value |

|

Assets ($): |

|

|

|

| ||

Investments in securities—See Statement of Investments: |

|

|

|

| ||

Unaffiliated issuers |

| 24,369,941 |

| 17,709,986 |

| |

Affiliated issuers |

| 2,387,402 |

| 2,387,402 |

| |

Receivable from brokers for proceeds on securities |

|

|

|

| 2,848,111 |

|

Dividends receivable |

|

|

|

| 160 |

|

Prepaid expenses |

|

|

|

| 86,073 |

|

|

|

|

|

| 23,031,732 |

|

Liabilities ($): |

|

|

|

| ||

Due to The Dreyfus Corporation and affiliates—Note 3(c) |

|

|

|

| 12,345 |

|

Securities sold short, at value (proceeds $2,848,111—See |

|

|

|

| 2,746,103 |

|

Due to broker |

|

|

|

| 2,285 |

|

Accrued expenses |

|

|

|

| 90,994 |

|

|

|

|

|

| 2,851,727 |

|

Net Assets ($) |

|

| 20,180,005 |

| ||

Composition of Net Assets ($): |

|

|

|

| ||

Paid-in capital |

|

|

|

| 28,848,936 |

|

Accumulated investment (loss)—net |

|

|

|

| (162,545) |

|

Accumulated net realized gain (loss) on investments |

|

|

|

| (1,948,439) |

|

Accumulated net unrealized appreciation (depreciation) |

|

|

|

| (6,557,947) |

|

Net Assets ($) |

|

| 20,180,005 |

| ||

Net Asset Value Per Share | Class A | Class C | Class I | Class Y |

|

Net Assets ($) | 3,835,933 | 667,271 | 7,907,466 | 7,769,335 |

|

Shares Outstanding | 461,252 | 80,587 | 949,349 | 932,731 |

|

Net Asset Value Per Share ($) | 8.32 | 8.28 | 8.33 | 8.33 |

|

See notes to financial statements.

12

STATEMENT OF OPERATIONS

From April 30, 2015 (commencement of operations) to November 30, 2015

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Investment Income ($): |

|

|

|

| ||

Income: |

|

|

|

| ||

Distributions from Master Limited Partnerships |

|

| 521,471 |

| ||

Less return of capital on distributions from Master |

|

| (521,471) |

| ||

Cash dividends: |

|

|

|

| ||

Unaffiliated issuers |

|

| 79,069 |

| ||

Affiliated issuers |

|

| 1,907 |

| ||

Total Income |

|

| 80,976 |

| ||

Expenses: |

|

|

|

| ||

Management fee—Note 3(a) |

|

| 131,812 |

| ||

Professional fees |

|

| 155,168 |

| ||

Dividends on securities sold short |

|

| 52,968 |

| ||

Registration fees |

|

| 42,439 |

| ||

Interest on securities sold short |

|

| 15,358 |

| ||

Shareholder servicing costs—Note 3(c) |

|

| 7,494 |

| ||

Prospectus and shareholders’ reports |

|

| 6,730 |

| ||

Distribution fees—Note 3(b) |

|

| 3,676 |

| ||

Custodian fees—Note 3(c) |

|

| 1,805 |

| ||

Directors’ fees and expenses—Note 3(d) |

|

| 1,047 |

| ||

Loan commitment fees—Note 2 |

|

| 74 |

| ||

Miscellaneous |

|

| 14,918 |

| ||

Total Expenses, before income taxes |

|

| 433,489 |

| ||

Less—reduction in expenses due to undertaking—Note 3(a) |

|

| (189,967) |

| ||

Less—reduction in fees due to earnings credits—Note 3(c) |

|

| (1) |

| ||

Net Expenses, before income taxes |

|

| 243,521 |

| ||

Income Taxes |

|

| 0 |

| ||

Investment (Loss)—Net |

|

| (162,545) |

| ||

Realized and Unrealized Gain (Loss) on Investments—Note 4 ($): |

|

| ||||

Net realized gain (loss) on investments: |

|

| ||||

Long transactions |

|

| (1,907,307) |

| ||

Short sale transactions |

|

| (19,100) |

| ||

Net realized gain (loss) on options transactions |

|

| (22,032) |

| ||

Net Realized Gain (Loss) |

|

| (1,948,439) |

| ||

Net unrealized appreciation (depreciation) on investments |

|

| (6,659,955) |

| ||

Net unrealized appreciation (depreciation) on securities sold short |

|

| 102,008 |

| ||

Net Unrealized Appreciation (Depreciation) |

|

| (6,557,947) |

| ||

Net Realized and Unrealized Gain (Loss) on Investments |

|

| (8,506,386) |

| ||

Net (Decrease) in Net Assets Resulting from Operations |

| (8,668,931) |

| |||

See notes to financial statements.

13

STATEMENT OF CHANGES IN NET ASSETS

From April 30, 2015 (commencement of operations) to November 30, 2015

|

|

|

| ||||||||||

|

|

|

|

|

|

|

| ||||||

Operations ($): |

|

|

|

|

|

|

| ||||||

Investment (loss)—net |

|

| (162,545) |

|

|

|

| ||||||

Net realized gain (loss) on investments |

| (1,948,439) |

|

|

|

| |||||||

Net unrealized appreciation (depreciation) |

| (6,557,947) |

|

|

|

| |||||||

Net Increase (Decrease) in Net Assets | (8,668,931) |

|

|

|

| ||||||||

Distributions to Shareholders from ($): |

|

|

|

|

|

|

| ||||||

Tax return of capital: |

|

|

|

|

|

|

| ||||||

Class A |

|

| (35,733) |

|

|

|

| ||||||

Class C |

|

| (7,890) |

|

|

|

| ||||||

Class I |

|

| (93,424) |

|

|

|

| ||||||

Class Y |

|

| (89,989) |

|

|

|

| ||||||

Total Distributions |

|

| (227,036) |

|

|

|

| ||||||

Capital Stock Transactions ($): |

|

|

|

|

|

|

| ||||||

Net proceeds from shares sold: |

|

|

|

|

|

|

| ||||||

Class A |

|

| 5,499,418 |

|

|

|

| ||||||

Class C |

|

| 1,005,119 |

|

|

|

| ||||||

Class I |

|

| 11,506,962 |

|

|

|

| ||||||

Class Y |

|

| 11,375,000 |

|

|

|

| ||||||

Dividends reinvested: |

|

|

|

|

|

|

| ||||||

Class A |

|

| 4,173 |

|

|

|

| ||||||

Class I |

|

| 14,323 |

|

|

|

| ||||||

Cost of shares redeemed: |

|

|

|

|

|

|

| ||||||

Class A |

|

| (250,606) |

|

|

|

| ||||||

Class I |

|

| (78,417) |

|

|

|

| ||||||

Increase (Decrease) in Net Assets | 29,075,972 |

|

|

|

| ||||||||

Total Increase (Decrease) in Net Assets | 20,180,005 |

|

|

|

| ||||||||

Net Assets ($): |

|

|

|

|

|

|

| ||||||

Beginning of Period |

|

| - |

|

|

|

| ||||||

End of Period |

|

| 20,180,005 |

|

|

|

| ||||||

Accumulated investment (loss)—net | (162,545) |

|

|

|

| ||||||||

Capital Share Transactions (Shares): |

|

|

|

|

|

|

| ||||||

Class A |

|

|

|

|

|

|

| ||||||

Shares sold |

|

| 488,525 |

|

|

|

| ||||||

Shares issued for dividends reinvested |

|

| 496 |

|

|

|

| ||||||

Shares redeemed |

|

| (27,769) |

|

|

|

| ||||||

Net Increase (Decrease) in Shares Outstanding | 461,252 |

|

|

|

| ||||||||

Class C |

|

|

|

|

|

|

| ||||||

Shares sold |

|

| 80,587 |

|

|

|

| ||||||

Class I |

|

|

|

|

|

|

| ||||||

Shares sold |

|

| 956,452 |

|

|

|

| ||||||

Shares issued for dividends reinvested |

|

| 1,703 |

|

|

|

| ||||||

Shares redeemed |

|

| (8,806) |

|

|

|

| ||||||

Net Increase (Decrease) in Shares Outstanding | 949,349 |

|

|

|

| ||||||||

Class Y |

|

|

|

|

|

|

| ||||||

Shares sold |

|

| 932,731 |

|

|

|

| ||||||

See notes to financial statements.

14

FINANCIAL HIGHLIGHTS

The following table describes the performance for each share class for the period from April 30, 2015 (commencement of operations) to November 30, 2015. All information (except portfolio turnover rate) reflects financial results for a single fund share. Total return shows how much your investment in the fund would have increased (or decreased) during the period, assuming you had reinvested all dividends and distributions. These figures have been derived from the fund’s financial statements.

Class A Shares | Class C Shares | Class I Shares | Class Y Shares | ||||||

Per Share Data ($): | |||||||||

Net asset value, beginning of period | 12.50 | 12.50 | 12.50 | 12.50 | |||||

Investment Operations: | |||||||||

Investment (loss)—neta | (.08) | (.13) | (.07) | (.07) | |||||

Net realized and unrealized | (4.00) | (3.99) | (4.00) | (4.00) | |||||

Total from Investment Operations | (4.08) | (4.12) | (4.07) | (4.07) | |||||

Distributions: | |||||||||

Tax return of capital | (.10) | (.10) | (.10) | (.10) | |||||

Net asset value, end of period | 8.32 | 8.28 | 8.33 | 8.33 | |||||

Total Return (%)b | (32.66)c | (32.98)c | (32.58) | (32.58) | |||||

Ratios/Supplemental Data (%): | |||||||||

Ratio of total expenses to average net assetsd | 3.47 | 4.22 | 3.21 | 3.20 | |||||

Ratio of net expenses to average net assetsd | 2.03 | 2.76 | 1.77 | 1.76 | |||||

Ratio of net investment (loss) | (1.38) | (2.16) | (1.16) | (1.15) | |||||

Portfolio Turnover Rateb | 57.76 | 57.76 | 57.76 | 57.76 | |||||

Net Assets, end of period ($ x 1,000) | 3,836 | 667 | 7,907 | 7,769 | |||||

a Based on average shares outstanding.

b Not annualized.

c Exclusive of sales charge.

d Annualized.

See notes to financial statements.

15

NOTES TO FINANCIAL STATEMENTS

NOTE 1—Significant Accounting Policies:

Dreyfus MLP Fund (the “fund”) is a separate non-diversified series of Strategic Funds, Inc. (the “Company”), which is registered under the Investment Company Act of 1940, as amended (the “Act”), as an open-end management investment company and operates as a series company currently offering ten series, including the fund. The fund’s investment objective is to seek total return, consisting of capital appreciation and income. The Dreyfus Corporation (the “Manager” or “Dreyfus”), a wholly-owned subsidiary of The Bank of New York Mellon Corporation (“BNY Mellon”), serves as the fund’s investment adviser. The Boston Company Asset Management, LLC (“TBCAM”), a wholly-owned subsidiary of BNY Mellon and an affiliate of Dreyfus, serves as the fund’s sub-investment adviser.

MBSC Securities Corporation (the “Distributor”), a wholly-owned subsidiary of Dreyfus, is the distributor of the fund’s shares. The fund is authorized to issue 100 million shares of $.001 par value Common Stock in each of the following classes of shares: Class A, Class C, Class I and Class Y. Class A shares generally are subject to a sales charge imposed at the time of purchase. Class C shares are subject to a contingent deferred sales charge (“CDSC”) imposed on Class C shares redeemed within one year of purchase. Class I and Class Y shares are sold at net asset value per share generally to institutional investors. Other differences between the classes include the services offered to and the expenses borne by each class, the allocation of certain transfer agency costs, and certain voting rights. Income, expenses (other than expenses attributable to a specific class), and realized and unrealized gains or losses on investments are allocated to each class of shares based on its relative net assets.

As of November 30, 2015, MBC Investments Corp., an indirect subsidiary of BNY Mellon, held 320,000 Class A, 80,000 Class C, 800,000 Class I and 800,000 Class Y shares of the fund.

The Company accounts separately for the assets, liabilities and operations of each series. Expenses directly attributable to each series are charged to that series’ operations; expenses which are applicable to all series are allocated among them on a pro rata basis.

The Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) is the exclusive reference of authoritative U.S. generally accepted accounting principles (“GAAP”) recognized by the FASB to be applied by nongovernmental entities. Rules and interpretive

16

releases of the Securities and Exchange Commission (“SEC”) under authority of federal laws are also sources of authoritative GAAP for SEC registrants. The fund’s financial statements are prepared in accordance with GAAP, which may require the use of management estimates and assumptions. Actual results could differ from those estimates.

The Company enters into contracts that contain a variety of indemnifications. The fund’s maximum exposure under these arrangements is unknown. The fund does not anticipate recognizing any loss related to these arrangements.

(a) Portfolio valuation: The fair value of a financial instrument is the amount that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date (i.e., the exit price). GAAP establishes a fair value hierarchy that prioritizes the inputs of valuation techniques used to measure fair value. This hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurements) and the lowest priority to unobservable inputs (Level 3 measurements).

Additionally, GAAP provides guidance on determining whether the volume and activity in a market has decreased significantly and whether such a decrease in activity results in transactions that are not orderly. GAAP requires enhanced disclosures around valuation inputs and techniques used during annual and interim periods.

Various inputs are used in determining the value of the fund’s investments relating to fair value measurements. These inputs are summarized in the three broad levels listed below:

Level 1—unadjusted quoted prices in active markets for identical investments.

Level 2—other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, credit risk, etc.).

Level 3—significant unobservable inputs (including the fund’s own assumptions in determining the fair value of investments).

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

Changes in valuation techniques may result in transfers in or out of an assigned level within the disclosure hierarchy. Valuation techniques used to value the fund’s investments are as follows:

17

NOTES TO FINANCIAL STATEMENTS (continued)

Investments in securities are valued at the last sales price on the securities exchange or national securities market on which such securities are primarily traded. Securities listed on the National Market System for which market quotations are available are valued at the official closing price or, if there is no official closing price that day, at the last sales price. For open short positions, asked prices are used for valuation purposes. Bid price is used when no asked price is available. Registered investment companies that are not traded on an exchange are valued at their net asset value. All of the preceding securities are generally categorized within Level 1 of the fair value hierarchy.

Securities not listed on an exchange or the national securities market, or securities for which there were no transactions, are valued at the average of the most recent bid and asked prices. These securities are generally categorized within Level 2 of the fair value hierarchy.

Fair valuing of securities may be determined with the assistance of a pricing service using calculations based on indices of domestic securities and other appropriate indicators, such as prices of relevant American Depository Receipts and financial futures. Utilizing these techniques may result in transfers between Level 1 and Level 2 of the fair value hierarchy.

When market quotations or official closing prices are not readily available, or are determined not to reflect accurately fair value, such as when the value of a security has been significantly affected by events after the close of the exchange or market on which the security is principally traded (for example, a foreign exchange or market), but before the fund calculates its net asset value, the fund may value these investments at fair value as determined in accordance with the procedures approved by the Company’s Board of Directors (the “Board”). Certain factors may be considered when fair valuing investments such as: fundamental analytical data, the nature and duration of restrictions on disposition, an evaluation of the forces that influence the market in which the securities are purchased and sold, and public trading in similar securities of the issuer or comparable issuers. These securities are either categorized within Level 2 or 3 of the fair value hierarchy depending on the relevant inputs used.

For restricted securities where observable inputs are limited, assumptions about market activity and risk are used and are generally categorized within Level 3 of the fair value hierarchy.

Options, which are traded on an exchange, are valued at the last sales price on the securities exchange on which such securities are primarily traded or at the last sales price on the national securities market on each business day and are generally categorized within Level 1 of the fair value hierarchy.

18

Options traded over-the-counter (“OTC”) are valued at the mean between the bid and asked price and are generally categorized within Level 2 of the fair value hierarchy.

The following is a summary of the inputs used as of November 30, 2015 in valuing the fund’s investments:

Level 1 - Unadjusted Quoted Prices | Level 2 - Other Significant Observable Inputs | Level 3 -Significant Unobservable Inputs | Total | ||

Assets ($) | |||||

Investments in Securities: | |||||

Equity Securities - Domestic Common Stocks† | 2,735,760 | — | — | 2,735,760 | |

Master Limited Partnership Shares† | 14,823,090 | — | — | 14,823,090 | |

Mutual Funds | 2,387,402 | — | — | 2,387,402 | |

Warrants† | 151,136 | — | — | 151,136 | |

Liabilities ($) | |||||

Securities Sold Short: | |||||

Master Limited Partnership Shares†† | (188,504) | — | — | (188,504) | |

Exchange-Traded Funds†† | (2,557,599) | — | — | (2,557,599) | |

† See Statement of Investments for additional detailed categorizations.

†† See Statement of Securities Sold Short for additional detailed categorizations.

(b) Securities transactions and investment income: Securities transactions are recorded on a trade date basis. Realized gains and losses from securities transactions are recorded on the identified cost basis. Dividend income is recognized on the ex-dividend date and interest income, including, where applicable, accretion of discount and amortization of premium on investments, is recognized on the accrual basis.

(c) Affiliated issuers: Investments in other investment companies advised by Dreyfus are defined as “affiliated” under the Act. Investments in affiliated investment companies during the period ended November 30, 2015 were as follows:

19

NOTES TO FINANCIAL STATEMENTS (continued)

Affiliated Investment Company | Value | Purchases ($) | Sales ($) | Value | Net |

Dreyfus Institutional Preferred Plus Money Market Fund | — | 37,143,688 | 34,756,286 | 2,387,402 | 11.8 |

(d) Risk: The fund invests primarily in Master Limited Partnerships (“MLPs”). MLPs and MLP-related investments comprise a minimum of 80% of investable assets of the fund. The majority of MLPs operate in the energy and/or natural resources sector. MLPs are generally organized under state law as limited partnerships or limited liability companies. An MLP consists of at least one general partner and one or more limited partners. The general partner controls the operations and management of the MLP and has an ownership stake in the MLP. The limited partners, through their ownership of limited partner interests, contribute capital to the entity, have a limited role in the operation and management of the entity and receive cash distributions.

MLPs are subject to certain risks, such as supply and demand risk, depletion and exploration risk, commodity pricing risk, acquisition risk, and the risk associated with the hazards inherent in midstream energy industry activities. A substantial portion of the cash flow received by the fund is derived from investments in equity securities of MLPs. The amount of cash that MLPs have available for distributions, and the tax character of such distributions, are dependent upon the amount of cash generated by the MLP’s operations.

(e) Distributions to shareholders: The fund currently anticipates making quarterly distributions to its shareholders of substantially all of the fund’s distributable cash flow received as cash distributions from MLPs, interest payments received on debt securities owned by the fund, and other payments on or derived from securities owned by the fund.

The fund intends to pay out a consistent dividend that over time approximates the distributions received from the fund’s portfolio investments based on, among other considerations, distributions the fund actually receives from portfolio investments and estimated future cash flows. Because the fund’s policy will be to pay consistent dividends based on estimated income from investments and future cash flows, the fund’s dividends may exceed the amount the fund actually receives from its portfolio investments.

20

The fund’s distributions will be treated for U.S. federal income tax purposes as (i) first, taxable dividends to the extent of a shareholder’s allocable share of the fund’s earnings and profits, (ii) second, on-taxable returns of capital to the extent of a shareholder’s tax basis in their shares of the fund (for the portion of those distributions that exceed the fund’s earnings and profits) and (iii) third, taxable gains (for the balance of those distributions). Dividend income will be treated as “qualified dividends” for federal income tax purposes, subject to favorable capital gain tax rates, provided that certain requirements are met. Unlike a regulated investment company under Sub-Chapter M of the Internal Revenue Code, the fund will not be able to pass-through the character of its recognized net capital gain by paying “capital gain dividends.” Cash distributions from an MLP to the fund that exceed the fund’s allocable share of such MLP’s net taxable income will reduce the fund’s adjusted tax basis in the equity securities of the MLP.

(f) Return of capital estimates: Distributions received from the fund’s investments in MLPs generally are comprised of income and return of capital. The fund records investment income and return of capital based on estimates made at the time such distributions are received. Such estimates are based on historical information available from each MLP and other industry sources. These estimates may subsequently be revised based on information received from MLPs after the tax reporting periods are concluded. During the period ended November 30, 2015, fund distributions are expected to be comprised of 100% return of capital and are recorded as such.

(g) Federal income taxes: The fund is treated as a regular corporation for U.S. federal and state income tax purposes, and will pay federal and state income tax on its taxable income. Currently, the maximum marginal regular federal income tax rate for a corporation is 35%. The fund may be subject to a 20% alternative minimum tax on its federal alternative minimum taxable income to the extent that its alternative minimum tax exceeds its regular federal income tax. The fund is currently using an estimated rate of 34% for federal income tax and 2% for state and local tax, net of federal tax benefit.

The fund invests primarily in MLPs, which generally are intended to be treated as partnerships for federal income tax purposes. As a partner in the MLPs, the fund must report its allocable share of the MLPs’ taxable income or loss in computing the fund’s taxable income or loss, regardless of the extent (if any) to which the MLPs make distributions.

The fund’s income tax expense or benefit is included in the Statement of Operations based on the components of income or gains (losses) to which

21

NOTES TO FINANCIAL STATEMENTS (continued)

such expense or benefit relates. Deferred income taxes reflect the net tax effects of temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for income tax purposes. Such temporary differences are principally: (i) taxes on unrealized gains (losses), which are attributable to the temporary difference between fair market value and tax basis, (ii) the net tax effects of temporary differences between the carrying amounts of assets and liabilities for financial reporting and income tax purposes and (iii) the net deferred tax benefit of accumulated net operating losses and capital loss carryforwards. During the period ended November 30, 2015, the fund had no income tax expense or benefit.

Deferred tax assets and liabilities are measured using effective tax rates expected to apply to taxable income in the years such temporary differences are realized or otherwise settled. To the extent the fund has a deferred tax asset, consideration is given to whether or not a valuation allowance is required. A valuation allowance is required if, based on the evaluation criterion provided by ASC 740, it is more-likely-than-not that some portion or the entire deferred tax asset will not be realized. The factors considered in assessing the fund’s valuation allowance are the nature, frequency and severity of current and cumulative losses, forecasts of future profitability, the duration of the statutory carryforward periods and the associated risks that operating and capital loss carryforwards may expire unused.

At November 30, 2015, the components of the fund’s deferred tax assets and liabilities were as follows:

Deferred tax assets: | ||||

Net operating loss carryforwards | $ (78,922) | |||

Capital loss carryforwards | (575,507) | |||

Unrealized losses on investment securities | (2,486,792) | |||

Total deferred tax assets, before valuation allowance | (3,141,221) | |||

Valuation allowance | 3,141,221 | |||

Net deferred tax assets, after valuation allowance | $ 0 |

Unexpected significant decreases in cash distributions from the fund’s MLP investments or significant declines in the fair value of its investments may change the fund’s assessment regarding the recoverability of its deferred tax assets and may result in a valuation allowance. If a valuation allowance is required to reduce any deferred tax asset in the future, it could have a material impact on the fund’s net asset value and results of operations. At November 30, 2015, the valuation allowance for deferred

22

tax assets was deemed necessary because Dreyfus believes it is more-likely-than-not that the fund will not be able to recognize deferred tax assets through future taxable income.

Net operating loss carryforwards and capital loss carryforwards are available to offset future taxable income. The fund’s net operating loss carryforward of $219,229 will expire on November 30, 2035 and the capital loss carryforward of $1,598,631 will expire on November 30, 2020.

The fund may rely, to some extent, on information provided by the MLPs, which may not be available on a timely basis, to estimate taxable income allocable to MLP shares held in its portfolio, and to estimate its associated deferred tax liability or assets. Such estimates are made in good faith. From time to time, as new information becomes available, the fund may modify its estimates or assumptions regarding its tax liability or asset.

The fund files income tax returns in the U.S. federal jurisdiction and various states. The fund has reviewed all major jurisdictions and concluded that there is no significant impact on the fund’s net assets and no tax liability resulting from unrecognized tax benefits or expenses relating to uncertain tax positions expected to be taken on its tax returns.

NOTE 2—Bank Lines of Credit:

The fund participates with other Dreyfus-managed funds in a $480 million unsecured credit facility led by Citibank, N.A. and a $300 million unsecured credit facility provided by The Bank of New York Mellon, a subsidiary of BNY Mellon and an affiliate of Dreyfus (each, a “Facility”), each to be utilized primarily for temporary or emergency purposes, including the financing of redemptions. Prior to October 7, 2015, the unsecured credit facility with Citibank, N.A. was $430 million. In connection therewith, the fund has agreed to pay its pro rata portion of commitment fees for each Facility. Interest is charged to the fund based on rates determined pursuant to the terms of the respective Facility at the time of borrowing. During the period ended November 30, 2015, the fund did not borrow under the Facilities.

NOTE 3—Management Fee, Sub-Investment Advisory Fee and Other Transactions with Affiliates:

(a) Pursuant to a management agreement with Dreyfus, the management fee is computed at the annual rate of 1.00% of the value of the fund’s average daily net assets and is payable monthly. Dreyfus has contractually agreed, from April 30, 2015 through May 1, 2016, to waive receipt of its fees and/or assume the expenses of the fund, so that the expenses of none of the classes (excluding Rule 12b-1 Distribution Plan fees, Shareholder

23

NOTES TO FINANCIAL STATEMENTS (continued)

Services Plan fees, dividend and interest expense on securities sold short, taxes, such as deferred tax expenses, brokerage commissions and extraordinary expenses) exceed 1.25% of the value of the fund’s average daily net assets. The reduction in expenses, pursuant to the undertaking, amounted to $189,967 during the period ended November 30, 2015.

Pursuant to a sub-investment advisory agreement between Dreyfus and TBCAM, TBCAM serves as the fund’s sub-investment adviser responsible for the day-to-day management of the fund’s portfolio. Dreyfus pays TBCAM a monthly fee at an annual percentage of the value of the fund’s average daily net assets. Dreyfus has obtained an exemptive order from the SEC (the “Order”), upon which the fund may rely, to use a manager of managers approach that permits Dreyfus, subject to certain conditions and approval by the Board, to enter into and materially amend sub-investment advisory agreements with one or more sub-investment advisers who are either unaffiliated with Dreyfus or are wholly-owned subsidiaries (as defined under the Act) of Dreyfus’ ultimate parent company, BNY Mellon, without obtaining shareholder approval. The Order also allows the fund to disclose the sub-investment advisory fee paid by Dreyfus to any unaffiliated sub-investment adviser in the aggregate with other unaffiliated sub-investment advisers in documents filed with the SEC and provided to shareholders. In addition, pursuant to the Order, it is not necessary to disclose the sub-investment advisory fee payable by Dreyfus separately to a sub-investment adviser that is a wholly-owned subsidiary of BNY Mellon in documents filed with the SEC and provided to shareholders; such fees are to be aggregated with fees payable to Dreyfus. Dreyfus has ultimate responsibility (subject to oversight by the Board) to supervise any sub-investment adviser and recommend the hiring, termination, and replacement of any sub-investment adviser to the Board.

(b) Under the Distribution Plan adopted pursuant to Rule 12b-1 under the Act, Class C shares pay the Distributor for distributing its shares at an annual rate of .75% of the value of its average daily net assets. During the period ended November 30, 2015, Class C shares were charged $3,676 pursuant to the Distribution Plan.

(c) Under the Shareholder Services Plan, Class A and Class C shares pay the Distributor at an annual rate of .25% of the value of their average daily net assets for the provision of certain services. The services provided may include personal services relating to shareholder accounts, such as answering shareholder inquiries regarding the fund and providing reports and other information, and services related to the maintenance of shareholder accounts. The Distributor may make payments to Service Agents (securities dealers, financial institutions or other industry

24

professionals) with respect to these services. The Distributor determines the amounts to be paid to Service Agents. During the period ended November 30, 2015, Class A and Class C shares were charged $5,431 and $1,225, respectively, pursuant to the Shareholder Services Plan.

The fund has arrangements with the transfer agent and the custodian whereby the fund may receive earnings credits when positive cash balances are maintained, which are used to offset transfer agency and custody fees. For financial reporting purposes, the fund includes net earnings credits as an expense offset in the Statement of Operations.

The fund compensates Dreyfus Transfer, Inc., a wholly-owned subsidiary of Dreyfus, under a transfer agency agreement for providing transfer agency and cash management services for the fund. The majority of transfer agency fees are comprised of amounts paid on a per account basis, while cash management fees are related to fund subscriptions and redemptions. During the period ended November 30, 2015, the fund was charged $598 for transfer agency services and $11 for cash management services. These fees are included in Shareholder servicing costs in the Statement of Operations. Cash management fees were partially offset by earnings credits of $1.

The fund compensates The Bank of New York Mellon under a custody agreement for providing custodial services for the fund. These fees are determined based on net assets, geographic region and transaction activity. During the period ended November 30, 2015, the fund was charged $1,805 pursuant to the custody agreement.

During the period ended November 30, 2015, the fund was charged $11,020 for services performed by the Chief Compliance Officer and his staff.

The components of “Due to The Dreyfus Corporation and affiliates” in the Statement of Assets and Liabilities consist of: management fees $16,926, Distribution Plan fees $420, Shareholder Services Plan fees $949, custodian fees $1,800, Chief Compliance Officer fees $1,765 and transfer agency fees $146, which are offset against an expense reimbursement currently in effect in the amount of $9,661.

(d) Each Board member also serves as a Board member of other funds within the Dreyfus complex. Annual retainer fees and attendance fees are allocated to each fund based on net assets.

25

NOTES TO FINANCIAL STATEMENTS (continued)

NOTE 4—Securities Transactions:

The aggregate amount of purchases and sales of investment securities and securities sold short, excluding short-term securities and options transactions, during the period ended November 30, 2015 were as follows:

|

| Purchases ($) | Sales ($) |

Long transactions | 38,217,935 | 11,419,216 | |

Short sale transactions | 841,296 | 3,670,307 | |

Total | 39,059,231 | 15,089,523 |

Short Sales: The fund is engaged in short-selling which obligates the fund to replace the security borrowed by purchasing the security at current market value. The fund incurs a loss if the price of the security increases between the date of the short sale and the date on which the fund replaces the borrowed security. The fund realizes a gain if the price of the security declines between those dates. Until the fund replaces the borrowed security, the fund will maintain daily a segregated account with a broker or custodian of permissible liquid assets sufficient to cover its short positions. Securities Sold Short at November 30, 2015 and their related market values and proceeds, are set forth in the Statement of Securities Sold Short.

The fund is liable for any dividends payable on securities while those securities are in a short position. Dividends declared on short positions are recorded on the ex-dividend date and recorded as an expense in the Statement of Operations. The fund is charged a securities loan fee in connection with short sale transactions which is recorded as interest on securities sold short in the Statement of Operations.

Derivatives: A derivative is a financial instrument whose performance is derived from the performance of another asset. The fund enters into International Swaps and Derivatives Association, Inc. Master Agreements or similar agreements (collectively, “Master Agreements”) with its OTC derivative contract counterparties in order to, among other things, reduce its credit risk to counterparties. Master Agreements include provisions for general obligations, representations, collateral and events of default or termination. Under a Master Agreement, the fund may offset with the counterparty certain derivative financial instrument’s payables and/or receivables with collateral held and/or posted and create one single net payment in the event of default or termination.

Each type of derivative instrument that was held by the fund during the period ended November 30, 2015 is discussed below.

26

Options Transactions: The fund purchases and writes (sells) put and call options to hedge against changes in or as a substitute for an investment. The fund is subject to market risk in the course of pursuing its investment objectives through its investments in options contracts. A call option gives the purchaser of the option the right (but not the obligation) to buy, and obligates the writer to sell, the underlying financial instrument at the exercise price at any time during the option period, or at a specified date. Conversely, a put option gives the purchaser of the option the right (but not the obligation) to sell, and obligates the writer to buy the underlying financial instrument at the exercise price at any time during the option period, or at a specified date.

As a writer of call options, the fund receives a premium at the outset and then bears the market risk of unfavorable changes in the price of the financial instrument underlying the option. Generally, the fund realizes a gain, to the extent of the premium, if the price of the underlying financial instrument decreases between the date the option is written and the date on which the option is terminated. Generally, the fund incurs a loss if the price of the financial instrument increases between those dates.

As a writer of put options, the fund receives a premium at the outset and then bears the market risk of unfavorable changes in the price of the financial instrument underlying the option. Generally, the fund realizes a gain, to the extent of the premium, if the price of the underlying financial instrument increases between the date the option is written and the date on which the option is terminated. Generally, the fund incurs a loss if the price of the financial instrument decreases between those dates.

As a writer of an option, the fund has no control over whether the underlying financial instrument may be sold (call) or purchased (put) and as a result bears the market risk of an unfavorable change in the price of the financial instrument underlying the written option. There is a risk of loss from a change in value of such options which may exceed the related premiums received. This risk is mitigated by Master Agreements between the fund and the counterparty and the posting of collateral, if any, by the counterparty to the fund to cover the fund’s exposure to the counterparty. The Statement of Operations reflects any unrealized gains or losses which occurred during the period as well as any realized gains or losses which occurred upon the expiration or closing of the option transaction. At November 30, 2015, there were no options written outstanding.

The following summarizes the average market value of derivatives outstanding during the period ended November 30, 2015:

27

NOTES TO FINANCIAL STATEMENTS (continued)

Average Market Value ($) | ||||

Equity options contracts | 200 |

At November 30, 2015, the cost of investments for federal income tax purposes was $27,107,151; accordingly, accumulated net unrealized depreciation on investments was $7,009,763, consisting of $47,532 gross unrealized appreciation and $7,057,295 gross unrealized depreciation.

28

REPORT OF INDEPENDENT REGISTERED

PUBLIC ACCOUNTING FIRM

Shareholders and Board of Directors

Dreyfus MLP Fund

We have audited the accompanying statement of assets and liabilities, including the statements of investments and securities sold short, of Dreyfus MLP Fund (one of the series comprising Strategic Funds, Inc.) as of November 30, 2015, and the related statements of operations and changes in net assets and the financial highlights for the period from April 30, 2015 (commencement of operations) to November 30, 2015. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audit.

We conducted our audit in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. We were not engaged to perform an audit of the Fund’s internal control over financial reporting. Our audit included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements and financial highlights, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of November 30, 2015 by correspondence with the custodian and others. We believe that our audit provides a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of Dreyfus MLP Fund at November 30, 2015, and the results of its operations, the changes in its net assets and the financial highlights for the period from April 30, 2015 to November 30, 2015, in conformity with U.S. generally accepted accounting principles.

New York, New York

January 28, 2016

29

BOARD MEMBERS INFORMATION (Unaudited)

INDEPENDENT BOARD MEMBERS

Chairman of the Board (1995)

Principal Occupation During Past 5 Years:

· Corporate Director and Trustee (1995-present)

Other Public Company Board Memberships During Past 5 Years:

· CBIZ (formerly, Century Business Services, Inc.), a provider of outsourcing functions for small and medium size companies, Director (1997-present)

No. of Portfolios for which Board Member Serves: 140

———————

Joni Evans (73)

Board Member (2006)

Principal Occupation During Past 5 Years:

· Chief Executive Officer, www.wowOwow.com an online community dedicated to women’s conversations and publications (2007-present)

· Principal, Joni Evans Ltd. (publishing) (2006-present)

No. of Portfolios for which Board Member Serves: 24

———————

Ehud Houminer (75)

Board Member (1994)

Principal Occupation During Past 5 Years:

· Executive-in-Residence at the Columbia Business School, Columbia

University (1992-present)

Other Public Company Board Memberships During Past 5 Years:

· Avnet, Inc., an electronics distributor, Director (1993-2012)

No. of Portfolios for which Board Member Serves: 61

———————

Hans C. Mautner (78)

Board Member (1980)

Principal Occupation During Past 5 Years:

· President-International Division and an Advisory Director of Simon Property Group, a

real estate investment company (1998-2010)

· Chairman and Chief Executive Officer of Simon Global Limited, a real estate company (1999-2010)

No. of Portfolios for which Board Member Serves: 24

———————

30

Robin A. Melvin (52)

Board Member (1995)

Principal Occupation During Past 5 Years:

· Co-chairman, Illinois Mentoring Partnership, non-profit organization dedicated to increasing the quantity and quality of mentoring services in Illinois; (2014-present; a board member since 2013)

· Director, Boisi Family Foundation, a private family foundation that supports

youth-serving organizations that promote the self sufficiency of youth from

disadvantaged circumstances (1995-2012)

No. of Portfolios for which Board Member Serves: 111

———————

Burton N. Wallack (65)

Board Member (2006)

Principal Occupation During Past 5 Years:

· President and Co-owner of Wallack Management Company, a real estate management

company (1987-present)

No. of Portfolios for which Board Member Serves: 24

———————

Gordon J. Davis (74)

Board Member (2006)

Principal Occupation During Past 5 Years:

· Partner in the law firm of Venable LLP (2012-present)

· Partner in the law firm of Dewey & LeBoeuf LLP (1994-2012)

Other Public Company Board Memberships During Past 5 Years:

· Consolidated Edison, Inc., a utility company, Director (1997-2014)

· The Phoenix Companies, Inc., a life insurance company, Director (2000-2014)

No. of Portfolios for which Board Member Serves: 60

Gordon J. Davis is deemed to be an “interested person” (as defined under the Act) of the Company as a result of his affiliation with Venable LLP, which provides legal services to the Company.

———————

Once elected all Board Members serve for an indefinite term, but achieve Emeritus status upon reaching age 80. The address of the Board Members and Officers is c/o The Dreyfus Corporation, 200 Park Avenue, New York, New York 10166. Additional information about the Board Member is available in the fund’s Statement of Additional Information which can be obtained from Dreyfus free of charge by calling this toll free number: 1-800-DREYFUS.

William Hodding Carter III, Emeritus Board Member

Arnold S. Hiatt, Emeritus Board Member

31

OFFICERS OF THE FUND (Unaudited)

BRADLEY J. SKAPYAK, President since January 2010.

Chief Operating Officer and a director of the Manager since June 2009, Chairman of Dreyfus Transfer, Inc., an affiliate of the Manager and the transfer agent of the funds, since May 2011 and Executive Vice President of the Distributor since June 2007. From April 2003 to June 2009, Mr. Skapyak was the head of the Investment Accounting and Support Department of the Manager. He is an officer of 66 investment companies (comprised of 140 portfolios) managed by the Manager. He is 57 years old and has been an employee of the Manager since February 1988.

BENNETT A. MACDOUGALL, Chief Legal Officer since October 2015

Chief Legal Officer of the Manager since June 2015; from June 2005 to June 2015, Director and Associate General Counsel of Deutsche Bank – Asset & Wealth Management Division, and Chief Legal Officer of Deutsche Investment Management Americas Inc. He is an officer of 67 investment companies (comprised of 165 portfolios) managed by the Manager. He is 44 years old and has been an employee of the Manager since June 2015.

JANETTE E. FARRAGHER, Vice President and Secretary since December 2011.

Assistant General Counsel of BNY Mellon, and an officer of 67 investment companies (comprised of 165 portfolios) managed by the Manager. She is 52 years old and has been an employee of the Manager since February 1984.

JAMES BITETTO, Vice President and Assistant Secretary since August 2005.

Managing Counsel of BNY Mellon and Secretary of the Manager, and an officer of 67 investment companies (comprised of 165 portfolios) managed by the Manager. He is 49 years old and has been an employee of the Manager since December 1996.

JONI LACKS CHARATAN, Vice President and Assistant Secretary since August 2005.

Managing Counsel of BNY Mellon, and an officer of 67 investment companies (comprised of 165 portfolios) managed by the Manager. She is 60 years old and has been an employee of the Manager since October 1988.

JOSEPH M. CHIOFFI, Vice President and Assistant Secretary since August 2005.

Managing Counsel of BNY Mellon, and an officer of 67 investment companies (comprised of 165 portfolios) managed by the Manager. He is 54 years old and has been an employee of the Manager since June 2000.

JOHN B. HAMMALIAN, Vice President and Assistant Secretary since August 2005.

Senior Managing Counsel of BNY Mellon, and an officer of 67 investment companies (comprised of 165 portfolios) managed by the Manager. He is 52 years old and has been an employee of the Manager since February 1991.

MAUREEN E. KANE, Vice President and Assistant Secretary since April 2015.

Managing Counsel of BNY Mellon since July 2014; from October 2004 until July 2014, General Counsel, and from May 2009 until July 2014, Chief Compliance Officer of Century Capital Management. She is an officer of 67 investment companies (comprised of 165 portfolios) managed by the Manager. She is 53 years old and has been an employee of the Manager since July 2014.

SARAH S. KELLEHER, Vice President and Assistant Secretary since April 2014.

Senior Counsel of BNY Mellon, and an officer of 67 investment companies (comprised of 165 portfolios) managed by the Manager; from August 2005 to March 2013, Associate General Counsel of Third Avenue Management. She is 40 years old and has been an employee of the Manager since March 2013.

JEFF PRUSNOFSKY, Vice President and Assistant Secretary since August 2005.

Senior Managing Counsel of BNY Mellon, and an officer of 67 investment companies (comprised of 165 portfolios) managed by the Manager. He is 50 years old and has been an employee of the Manager since October 1990.

JAMES WINDELS, Treasurer since November 2001.

Director – Mutual Fund Accounting of the Manager, and an officer of 67 investment companies (comprised of 165 portfolios) managed by the Manager. He is 57 years old and has been an employee of the Manager since April 1985.

32

RICHARD CASSARO, Assistant Treasurer since December 2005.

Senior Accounting Manager – Money Market and Municipal Bond Funds of the Manager, and an officer of 67 investment companies (comprised of 165 portfolios) managed by the Manager. He is 56 years old and has been an employee of the Manager since September 1982.

GAVIN C. REILLY, Assistant Treasurer since December 2005.

Tax Manager of the Investment Accounting and Support Department of the Manager, and an officer of 67 investment companies (comprised of 165 portfolios) managed by the Manager. He is 47 years old and has been an employee of the Manager since April 1991.

ROBERT S. ROBOL, Assistant Treasurer since August 2003.

Senior Accounting Manager – Fixed Income Funds of the Manager, and an officer of 67 investment companies (comprised of 165 portfolios) managed by the Manager. He is 51 years old and has been an employee of the Manager since October 1988.

ROBERT SALVIOLO, Assistant Treasurer since July 2007.

Senior Accounting Manager – Equity Funds of the Manager, and an officer of 67 investment companies (comprised of 165 portfolios) managed by the Manager. He is 48 years old and has been an employee of the Manager since June 1989.

ROBERT SVAGNA, Assistant Treasurer since August 2005.

Senior Accounting Manager – Equity Funds of the Manager, and an officer of 67 investment companies (comprised of 165 portfolios) managed by the Manager. He is 48 years old and has been an employee of the Manager since November 1990.

JOSEPH W. CONNOLLY, Chief Compliance Officer since October 2004.