Table of Contents

Exhibit 13.1

NOTICE & PROXY STATEMENT

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934 (Amendment No. )

Filed by the Registrant x

Filed by a Party other than the Registrant ¨

Check the appropriate box:

¨ Preliminary Proxy Statement | ¨ CONFIDENTIAL, FOR USE OF THE COMMISSION ONLY (AS PERMITTED BY RULE 14A-6(E)(2)) |

x Definitive Proxy Statement

¨ Definitive Additional Materials

¨ Soliciting Material Pursuant to Section 240.14a-11(c) or Section 240.14a-12

MidwestOne Financial Group, Inc.

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| x | No fee required |

| ¨ | Fee computed on table below per Exchange Act Rules 14a-6(i)(4) and 0-11. |

| (1) | Title of each class of securities to which transaction applies: |

| (2) | Aggregate number of securities to which transaction applies: |

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (Set forth the amount on which the filing fee is calculated and state how it was determined): |

| (4) | Proposed maximum aggregate value of transaction: |

| (5) | Total fee paid: |

| ¨ | Fee paid previously with preliminary materials. |

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form of Schedule and the date of its filing. |

| (1) | Amount Previously Paid: |

| (2) | Form, Schedule or Registration Statement No.: |

| (3) | Filing Party: |

| (4) | Date Filed: |

Table of Contents

NOTICE OF ANNUAL MEETING OF SHAREHOLDERS TO BE HELD APRIL 29, 2005

To The Shareholders Of MidWestOne Financial Group, Inc.:

The Annual Meeting of Shareholders of MidWestOne Financial Group, Inc. will be held at the Elmhurst Country Club, 2214 South 11th Street, Oskaloosa, Iowa, on Friday, April 29, 2005, at 10:30 a.m., for the following purposes:

| 1. | To elect directors to serve until the Annual Meeting of Shareholders at which their term expires and until their successors shall have been elected and qualified; |

| 2. | To ratify the appointment of KPMG LLP as independent auditors for the current fiscal year; and |

| 3. | To transact such other business as may properly come before the meeting or any adjournment thereof. |

* * * * *

The Board of Directors has fixed the close of business on February 25, 2005, as the record date for the determination of shareholders entitled to receive notice of and to vote at the Annual Meeting or any adjournment thereof.

To be sure that your shares are represented at the meeting, please either complete and promptly mail the enclosed proxy card in the envelope provided for this purpose or vote through the telephone or Internet voting procedures described on the proxy card. If your shares are registered in the name of a bank or brokerage firm, telephone or Internet voting will be available to you only if offered by your bank or broker and such procedures are described on the voting form sent to you.

By Order of the Board of Directors

Charles S. Howard, Chairman of the Board

Oskaloosa, Iowa

March 21, 2005

Table of Contents

PROXY STATEMENT

MidWestOne Financial Group, Inc.

222 First Avenue East

Oskaloosa, Iowa 52577

INTRODUCTION

The enclosed Proxy is solicited by the Board of Directors of MidWestOne Financial Group, Inc., an Iowa corporation (the “Company”), for use at the Annual Meeting of Shareholders to be held on April 29, 2005, and at any adjournment thereof. The Proxy may be revoked at any time before it is exercised by submitting a later dated Proxy, by giving notice of such revocation to the Company in writing, or by attending and requesting such revocation at the Annual Meeting. Attendance at the Annual Meeting will not in and of itself constitute the revocation of the Proxy. If the Proxy is not revoked, the shares represented thereby will be voted in the manner specified in the Proxy. A Proxy properly executed and received prior to the Annual Meeting which does not give specific voting instructions will be voted FOR the election of the nominees to the Board of Directors set forth herein and FOR the ratification of the appointment of KPMG LLP as independent auditors for the current fiscal year and as the persons designated as proxies on the enclosed proxy card determine is in the best interests of the Company in any other business that may properly come before the meeting or any adjournment thereof. Abstentions will be treated as shares present and entitled to vote for purposes of determining whether a quorum is present, but not voted for purposes of determining the approval of any matter submitted to the shareholders for a vote. If a Proxy returned by a broker indicates that the broker does not have discretionary authority to vote some or all of the shares covered thereby for any matter submitted to the shareholders for a vote (broker non-votes), such shares will be considered to be present for the purpose of determining whether a quorum is present, but will not be considered as entitled to vote at the Annual Meeting of Shareholders.

For participants in the MidWestOne Financial Group, Inc. Employee Stock Ownership Plan and Trust (the “ESOP”), the proxy card will also serve as a voting instruction card for MidWestOne Bank & Trust, the trustee of the ESOP (the “Trustee”), with respect to shares held in the participants’ accounts. A participant cannot direct the voting of shares allocated to the participant’s account in the ESOP unless the proxy card is signed and returned. If proxy cards representing shares in the ESOP are not returned, those shares will be voted by the Trustee in the same proportion as the shares for which signed proxy cards are returned by the other participants in the ESOP.

The cost of preparing, assembling, and mailing this Proxy Statement, the Notice of Annual Meeting of Shareholders, and the accompanying Proxy is being borne by the Company. In addition to the solicitation by mail, officers, directors, and regular employees of the Company may solicit Proxies by telephone or personal interview. Such persons will receive no additional compensation for such services. Brokerage houses, nominees, fiduciaries, and other custodians will be requested to forward soliciting material to the beneficial owners of shares held of record by them and will be reimbursed by the Company for their reasonable expenses.

The record date for shareholders entitled to vote at the meeting is the close of business on February 25, 2005, at which time the Company had issued and outstanding 3,769,166 shares of Common Stock, and all of those shares are eligible to vote at the Annual Meeting of Shareholders. Holders of Common Stock are entitled to one vote per share on any matter that may properly come before the meeting.

This Proxy Statement, the enclosed Proxy, and the attached Notice were first sent to shareholders on approximately March 21, 2005.

3

Table of Contents

PROPOSAL 1

Election Of Directors

Four directors are to be elected at the Annual Meeting of Shareholders by holders of Common Stock to serve until the Annual Meeting of Shareholders at which their respective term expires and until their respective successor has been elected and qualified. The Articles of Incorporation and Bylaws of the Company state that the Board of Directors of the Company shall set the size of the Board of Directors in a range of not less than five directors nor greater than fifteen directors. The Board of Directors set the size for the current Board of Directors at nine individuals. The Nominating Committee and the Board of Directors have identified Barbara J. Kniff to fill the vacancy on the Board caused by the retirement of William D. Hassel effective March 31, 2004. A non-management director recommended Ms. Kniff to the Nominating Committee. Because of the retirement of John W. N. Steddom effective December 31, 2004, there will be one vacancy on the Board for which the Nominating Committee and the Board of Directors have not identified a qualified nominee as of the date of this Proxy Statement. The Board of Directors has no present intention to fill this vacancy at the Annual Meeting; however, under the Company’s Articles of Incorporation and Bylaws, the Board of Directors may fill such vacancy at any time. At the date of this Proxy Statement, the Board does not have any arrangement, understanding or commitment to any person concerning nomination or election to the Board, other than those persons listed under the caption “Election of Directors” herein.

Each shareholder of record shall be entitled to as many votes as the total of the number of shares of Common Stock, $5.00 par value per share, held of record by such shareholder. Proxies cannot be voted for a greater number of persons than the number of nominees named. The Company does not have cumulative voting.

Under applicable provisions of Iowa law and the Bylaws of the Company, a majority of the outstanding shares of the Company entitled to vote, represented in person or by Proxy, constitute a quorum. If a quorum is present, the affirmative vote of a majority of the shares represented at the meeting and entitled to vote on the election of directors in the manner set forth above will be required to elect directors.

In the absence of instructions to the contrary, the Proxies solicited by the Board of Directors will be voted in favor of the election of the nominees identified in the following table, all of whom are members of the present Board of Directors other than Barbara J. Kniff.

The nominees and the directors of the Company whose terms continue beyond the 2005 Annual Meeting of Shareholders are identified in the following table. The term for which nominees Charles S. Howard, David A. Meinert, and James G. Wake are nominated will expire at the 2008 Annual Meeting of Shareholders, and the term for which nominee Barbara J. Kniff is nominated will expire at the 2006 Annual Meeting of Shareholders. Except as may be otherwise expressly stated, the nominees for director have been employed in the capacities indicated for more than five years. Additional information regarding these nominees and each director as of February 25, 2005, is set forth in the following table. The number of shares of Common Stock of the Company beneficially owned by each of the nominees and directors as of February 25, 2005, is set forth on pages 12and 13.

4

Table of Contents

Name and Principal Occupation for the last five years | First Became a Director | Present Term Expires at Annual Meeting | Age | |||

Nominees: | ||||||

Charles S. Howard | 1988 | 2005 | 49 | |||

Chairman of the Company since January 1998 and President and Chief Executive Officer of the Company since June 1993; previously Executive Vice President of the Company; Chairman of Central Valley Bank(1) from June 1994 to January 2000; Vice Chairman of MidWestOne Bank & Trust since January 1996; Chairman of Pella State Bank(1) since November 1997; Chairman of MIC Financial, Inc.(1) since January 1998; Chairman of MidWestOne Investment Services, Inc.(1) since October 2004 | ||||||

David A. Meinert | 1991 | 2005 | 51 | |||

Executive Vice President of the Company since June 1993 and Chief Financial Officer since September 1984; President of Central Valley Bank from June 1994 to January 1997; Chairman of Central Valley Bank from January 2000; President of MIC Financial, Inc. since March 2000; Executive Vice President and Treasurer of MidWestOne Investment Services, Inc. since October 2004 | ||||||

James G. Wake | 2000 | 2005 | 65 | |||

General Manager, Smith-Wake Ag Group, Oskaloosa, Iowa. This is an agri business involved in feed, grain, and livestock production. | ||||||

Barbara J. Kniff | 48 | |||||

Chairman and Secretary/Treasurer of KLK Construction, Inc., Pella, Iowa, doing underground utility work. Member in ViewPointe, LLC, a land development company. Member in Phantom Partners, LLC d/b/a Culver’s of Colorado Springs. | ||||||

Other Directors: | ||||||

Richard R. Donohue | 1999 | 2007 | 55 | |||

Managing Partner, Theobald, Donohue & Thompson, Oskaloosa, Iowa. This is a certified public accounting firm in which he is involved in all phases of the practice. | ||||||

John P. Pothoven | 1994 | 2007 | 62 | |||

President and, since January 1998, Chairman of MidWestOne Bank & Trust(1) | ||||||

Michael R. Welter | 2000 | 2006 | 54 | |||

President of M&M Enterprises, Sigourney, Iowa, doing general commercial contracting work in Southeast Iowa, and President of Sigourney Fast Stop, a convenience store located in Sigourney, Iowa | ||||||

Edward C. Whitham | 2000 | 2006 | 65 | |||

President, Financial Management Accounting, Inc., Burlington, Iowa. This is an accounting, tax preparation, and pension administration firm in which he is involved in all phases of the practice. | ||||||

| (1) | MidWestOne Bank & Trust, MidWestOne Bank, Central Valley Bank, Pella State Bank, MIC Financial, Inc., and MidWestOne Investment Services, Inc. are subsidiaries of the Company (all located in Iowa). |

5

Table of Contents

INFORMATION ABOUT THE BOARD AND ITS COMMITTEES

Board Meetings

Twelve regularly scheduled meetings of the Board of Directors of the Company were held during 2004. Each director other than John W. N. Steddom attended at least 75 percent of the Board meetings and any meetings of committees on which he served. Mr. Steddom retired from the Board of Directors as of December 31, 2004 due to health reasons. Mr. Steddom was able to attend six meetings of the Board of Directors, two meetings of the Compensation Committee, and two meetings of the Nominating Committee during 2004. The Board has an Audit Committee, a Compensation Committee, and a Nominating Committee. To promote open discussion among the independent directors (those directors who are not officers or employees of the Company), the independent directors meet in executive session a minimum of two times per year. The Company strongly encourages all Board members to attend the Annual Meeting of Shareholders. All Board members other than Mr. Steddom attended the Annual Meeting of Shareholders held in 2004.

Committee Membership and Meetings

The Audit Committee consists of Richard R. Donohue, as Chairperson, Michael R. Welter, and Edward C. Whitham, all of whom are independent directors under criteria established by the Securities and Exchange Commission and NASDAQ. Based on the attributes, education and experience requirements required by NASD Rule 4350(d)(2)(A), the requirements set forth in Section 407 of the Sarbanes-Oxley Act of 2002 and associated regulations, the Board of Directors has identified Richard R. Donohue as an “Audit Committee Financial Expert” as defined under Item 401(h) of Regulation S-K and has determined him to be “independent.” The Audit Committee recommends independent auditors to the Board, reviews with the independent auditors the plan, scope and results of the auditors’ services, approves their fees and reviews the Company’s financial reporting and internal control functions. The Audit Committee also performs the duties set forth in its written charter, which has been adopted by the Board of Directors. A copy of the Audit Committee Charter is attached to this Proxy Statement as Exhibit A. The Committee is also prepared to meet privately at any time at the request of the independent public accountants or members of management to review any special situation arising on any of the above subjects. Reference is made to the “Report of the Audit Committee.” The Audit Committee met five times during 2004. None of the Audit Committee members serve on any other audit committee of a listed company.

During 2004, the Compensation Committee consisted of John W. N. Steddom, as Chairperson, Richard R. Donohue, James G. Wake, Michael R. Welter, and Edward C. Whitham, all of whom are independent directors under criteria established by the Securities and Exchange Commission and NASDAQ. The Compensation Committee reviews the Company’s compensation and benefit policies, including the individual salaries of the executive officers and makes recommendations to the Board of Directors as to the salary of the Chief Executive Officer and the Executive Vice President. The Compensation Committee also performs the duties set forth in its Report of Executive Compensation. Reference is made to the “Report of the Compensation Committee.” The Compensation Committee also performs the duties set forth in its written charter, which was adopted by the Compensation Committee in December 2004. A copy of the Compensation Committee Charter is attached to this Proxy Statement as Exhibit B. The Compensation Committee met two times during 2004.

The Company’s Nominating Committee was established during early 2004. The Committee consisted of Edward C. Whitham, as Chairperson, Richard R. Donohue, John W. N. Steddom, James G. Wake, and Michael R. Welter, all of whom are independent directors under criteria established by the Securities and Exchange Commission and NASDAQ. This Committee makes recommendations to the Board of Directors regarding the composition and structure of the Board and nominations for election of directors. This Committee recommended to the Board the director-nominees proposed in this Proxy Statement for election by the shareholders. It reviews the qualifications of, and recommends to the Board, candidates to fill Board vacancies that occur during the year. The Nominating Committee also performs the duties set forth in its written charter, a copy of which was attached to the Proxy filed in 2004. The Charter, among other things, contains information regarding the composition of

6

Table of Contents

the Board of Directors and selection criteria used by the Committee. This Committee will consider, as part of its nomination process, any director candidate recommended by a shareholder of the Company who follows the procedures shown under the heading “2006 Shareholder Proposals.” When identifying and evaluating nominees to the Company’s board of directors, the Nominating Committee reviews current directors of the Company, reviews current directors of the Company’s banking subsidiaries, solicits input from existing directors and executive officers, and reviews submissions from shareholders, if any. The Nominating Committee met four times in 2004.

Directors’ Compensation

From January 1, 2004 through March 31, 2004, non-employee directors of the Company were paid a quarterly fee in advance based upon an annual retainer of $2,500, plus a fee for meetings attended. From April 1, 2004 through December 31, 2004, non-employee directors of the Company were paid a quarterly fee in advance based upon an annual retainer of $3,000, plus a fee for meetings attended. From January 1, 2004 through March 31, 2004, each non-employee director was paid $350 per regular and special meeting for directors’ meetings attended and $50 per meeting for committee meetings attended. From April 1, 2004 through December 31, 2004, each non-employee director was paid $450 per regular and special meeting for directors’ meetings attended and $150 per meeting for committee meetings attended. No employee directors are paid directors’ fees. After one year of service as a director, non-employee directors are also entitled to annual option grants under the Company’s 1998 Stock Incentive Plan pursuant to a formula based on the financial performance of the Company for the fiscal year. On April 30, 2004, each non-employee director of MidWestOne Financial Group, Inc. and its subsidiaries was granted a non-qualified stock option for 1,379 shares at an exercise price of $18.52 per share. The number of shares to be awarded pursuant to non-qualified stock options for non-employee directors is determined by dividing the fair market value (the bid price) of the underlying shares on the date of grant of the options into five percent of the pre-tax profits of the Company for the previous fiscal year. The number of shares so determined is then allocated equally among the eligible non-employee directors on the date of grant of the options (the date of the Annual Meeting of Shareholders of the Company).

The Company offers the option to the directors to defer receipt of all or a portion of the cash that would have been paid as directors’ fees. The deferred fees are invested by the Company, and the director is an unsecured general creditor of the Company. At the time the deferral election is made, the director specifies the amount of the fees to be deferred and the duration of the deferral. The deferred fees are credited with interest based upon the return on average tangible equity of the Company based upon an average of the last three fiscal years.

7

Table of Contents

MANAGEMENT

Executive Officers

Name | Age | Position with the Company | ||

Charles S. Howard | 49 | Chairman, President and Chief Executive Officer | ||

David A. Meinert | 51 | Executive Vice President and Chief Financial Officer | ||

John P. Pothoven | 62 | Chairman and President of MidWestOne Bank & Trust |

Charles S. Howard and David A. Meinert were elected by the Board of Directors of the Company in April 2004 to the positions described above for a term of one year or until their successors are duly elected and qualified. John P. Pothoven was elected by the MidWestOne Bank & Trust Board of Directors in January 2005 to the positions described above for a term of one year or until his successor is duly elected and qualified. The responsibilities and experience of each executive officer are described below.

Charles S. Howard has been a director of the Company since 1988 and a director of MidWestOne Bank & Trust since 1993. He was elected President and Chief Executive Officer of the Company in June 1993 and elected Chairman of the Company in January 1998. Mr. Howard was elected Vice Chairman of MidWestOne Bank & Trust in January 1996. Mr. Howard served as Chairman of Central Valley Bank from June 1994 until January 2000 and served as a director of Central Valley Bank from June 1994 to January 2004. He has also served as Chairman and as a director of Pella State Bank since November 1997. He has also been a director of MidWestOne Bank since October 1999. Mr. Howard was elected as Chairman and as a director of MidWestOneInvestment Services, Inc. in October 2004. Prior thereto, he served as Executive Vice President and Chief Operating Officer of the Company.

David A. Meinert, C.P.A., has been a director of the Company since 1991. He also serves as Executive Vice President and Chief Financial Officer of the Company. Mr. Meinert was elected as Chairman of Central Valley Bank in January 2000, has served as a director of Central Valley Bank since 1994, and served as President of Central Valley Bank from June 1994 to January 1997. He has also been a director of MidWestOne Bank since October 1999. Mr. Meinert was a director of Pella State Bank from November 1997 to January 2004. Mr. Meinert was elected as President of MIC Financial, Inc. effective March 1, 2000. Mr. Meinert was elected as Executive Vice President and Treasurer and as a director of MidWestOne Investment Services, Inc. in October 2004.

John P. Pothoven has been a director of the Company since 1994 and a director of MidWestOne Bank & Trust since 1976. He has served as President and Chief Executive Officer of MidWestOne Bank & Trust since 1984 and as Chairman of MidWestOne Bank & Trust since January 1998. Mr. Pothoven joined MidWestOne Bank & Trust in 1976 as a Vice President and was promoted to Executive Vice President in 1978.

Executive Compensation

The following table sets forth information concerning the annual and long-term compensation of those persons who were at December 31, 2004, the Chairman, President, and Chief Executive Officer of the Company, the Executive Vice President and Chief Financial Officer of the Company, and the Chairman and President of MidWestOne Bank & Trust for the last three fiscal years ended December 31, 2004. The Company has no other executive officers as defined by SEC regulations.

8

Table of Contents

Summary Compensation Table

Year | Annual Compensation | Long Term Compensation Securities Underlying Options | All Other Compensation(2) | ||||||||||

Name and Principal Position | Salary(1) | Bonus | |||||||||||

Charles S. Howard, | 2004 | $ | 236,080 | $ | 26,985 | 7,000 | $ | 21,796 | |||||

Chairman, President and | 2003 | 227,000 | 34,991 | 7,350 | 18,411 | ||||||||

Chief Executive Officer | 2002 | 219,250 | 31,731 | 7,000 | 18,709 | ||||||||

David A. Meinert, | 2004 | $ | 173,264 | $ | 19,805 | 7,000 | $ | 19,974 | |||||

Executive Vice President and | 2003 | 166,600 | 25,680 | 7,350 | 17,079 | ||||||||

Chief Financial Officer | 2002 | 158,000 | 24,494 | 7,000 | 15,963 | ||||||||

John P. Pothoven, | 2004 | $ | 163,400 | $ | 13,000 | 5,000 | $ | 98,228 | |||||

Chairman and President, | 2003 | 163,400 | 22,979 | 5,250 | 100,841 | ||||||||

MidWestOne Bank & Trust | 2002 | 164,650 | 26,300 | 5,000 | 68,279 | ||||||||

| (1) | Amounts include director compensation of $7,600 from MidWestOneFinancial Group, Inc., $7,050 from MidWestOne Bank & Trust, and $4,400 from Pella State Bank for 2002 to Charles S. Howard; $7,600 from MidWestOne Financial Group, Inc. and $4,400 from Pella State Bank for 2002 to David A. Meinert; $7,600 from MidWestOne Financial Group, Inc. and $7,050 from MidWestOne Bank & Trust for 2002 to John P. Pothoven. For 2002, David A. Meinert elected to defer $7,600 of director’s fees under the Deferred Compensation Plan for directors and John P. Pothoven elected to defer $7,050 of director’s fees under such plan. |

| (2) | Amounts include the following: |

Name | Year | Salary Continuation | ESOP Contribution | 401(k) Match | Group Term Life Insurance | |||||||||

Charles S. Howard | 2004 | $ | 4,543 | $ | 10,843 | $ | 5,980 | $ | 430 | |||||

| 2003 | 4,113 | 7,790 | 5,980 | 528 | ||||||||||

| 2002 | 3,723 | 10,454 | 4,004 | 528 | ||||||||||

David A. Meinert | 2004 | $ | 5,618 | $ | 7,958 | $ | 5,968 | $ | 430 | |||||

| 2003 | 5,085 | 5,733 | 5,733 | 528 | ||||||||||

| 2002 | 4,603 | 6,452 | 4,380 | 528 | ||||||||||

John P. Pothoven | 2004 | $ | 84,672 | $ | 7,466 | $ | 5,660 | $ | 430 | |||||

| 2003 | 90,100 | 5,141 | 5,072 | 528 | ||||||||||

| 2002 | 56,276 | 6,557 | 4,918 | 528 | ||||||||||

Charles S. Howard is entitled to receive $110,000 per year for 15 years starting at age 65 pursuant to the salary continuation plan. David A. Meinert is entitled to receive $95,000 per year for 15 years starting at age 65 pursuant to the salary continuation plan. John P. Pothoven is entitled to receive $85,000 per year for 15 years starting at age 65 pursuant to the salary continuation plan. The Company matches 50 percent of employee contributions to the 401(k) Plan up to a maximum employee contribution of 6 percent of compensation.

Stock Options

The following table sets forth information concerning the grant of stock options under the Company’s 1998 Stock Incentive Plan during the last fiscal year.

9

Table of Contents

Option Grants in Last Fiscal Year

| Individual Grants | ||||||||||||||||

Name | Number of Shares Underlying Options Granted | % of Total Options Granted to Employees in Fiscal Year | Exercise ($/Sh) | Expiration Date | Potential Realizable Value at Assumed Annual Rates of Stock Price Appreciation for Option Term(1) | |||||||||||

| 5% | 10% | |||||||||||||||

Charles S. Howard | 7,000 | 8.57 | % | $ | 20.84 | 12/31/14 | $ | 91,743 | $ | 232,495 | ||||||

David A. Meinert | 7,000 | 8.57 | % | $ | 20.84 | 12/31/14 | $ | 91,743 | $ | 232,495 | ||||||

John P. Pothoven | 5,000 | 6.12 | % | $ | 20.84 | 12/31/14 | $ | 65,531 | $ | 166,068 | ||||||

| (1) | The amounts set forth represent the value that would be received by the Named Executive Officers upon exercise of the option on the date before the expiration date of the option based upon assumed annual growth rates in the market value of the Company’s shares of 5 percent and 10 percent, rates prescribed by applicable SEC rules. Actual gains, if any, on stock option exercises are dependent on the future performance of the Company’s shares and other factors such as the general condition of the stock market and the timing of the exercise of the options. |

Aggregated Option Exercises In Last Fiscal Year

And Fiscal Year-End Option Values

Name | Shares Acquired on Exercise | Value Realized | Number of Securities Underlying Unexercised Options at FY-End(#) Exercisable/Unexercisable | Value of Unexercised In-The-Money | ||||||

Charles S. Howard | 0 | $ | 0 | 36,037/14,305 | $ | 174,848/$23,456 | ||||

David A. Meinert | 16,550 | 165,353 | 62,446/14,305 | $ | 498,797/$23,456 | |||||

John P. Pothoven | 0 | 0 | 32,782/ 5,218 | $ | 208,279/$16,155 | |||||

Employment Contracts and Termination of Employment and Change-In-Control Arrangements

The Company presently has no employment contracts with the named executive officers of the Company. The Company does maintain a salary continuation plan for the named executive officers of the Company. The benefits provided pursuant to such salary continuation plan are listed in the section “Executive Compensation” in Footnote 2. The salary continuation plan contains a change-in-control provision which applies in the event that there is both a change in control of the Company and the employment of the particular named executive officer is terminated with the Company within 24 months after such change in control. In such event, the change-in-control benefit is paid to the employee in a lump sum within 90 days following termination of employment. The amount of the change-in-control benefit is determined by vesting the employee in 100 percent of the normal retirement benefit the employee would otherwise have been entitled to receive pursuant to the salary continuation plan.

REPORT ON EXECUTIVE COMPENSATION FOR MIDWESTONE FINANCIAL GROUP, INC.

Compensation Committee Interlocks and Insider Participation

The Compensation Committee of the Board of Directors of the Company reviews and approves the Company’s executive compensation policies and evaluates the performance of the executive officers. In 2004, the Compensation Committee consisted of Richard R. Donohue, John W. N. Steddom, James G. Wake, Michael R. Welter, and Edward C. Whitham. All members of the Committee attended the two meetings held during the fiscal year. All members of the Compensation Committee are independent directors and there are no Compensation Committee interlocks.

10

Table of Contents

Compensation Philosophy

The philosophy of the Compensation Committee in setting its compensation policies for executive officers is to maximize stockholder value over time. The Compensation Committee believes that executive compensation should be directly linked to continuous improvements in corporate performance and increases in stockholder value. In this regard, the Compensation Committee has adopted the following guidelines for compensation decisions:

| • | Provide a competitive total compensation package that enables the Company to attract and retain key executive talent. |

| • | Align executive compensation programs with the Company’s annual and long-term business strategies and objectives. |

| • | Provide variable compensation opportunities that are directly linked to the performance of the Company and the performance of the individual employee. |

The Compensation Committee focuses primarily on the following three components in forming the total compensation package for its executive officers:

| • | Base salary |

| • | Annual incentive bonus |

| • | Long-term incentives |

Base Salary

The Compensation Committee intends to compensate the executive officers competitively within the industry. In order to evaluate the Company’s competitive posture in the industry, the Compensation Committee reviews and analyzes the compensation packages, including base salary levels, offered by its peer group. In addition, the Compensation Committee, together with the Board of Directors, subjectively evaluates the level of performance of each executive officer in order to determine current and future appropriate base pay levels.

The Compensation Committee reviewed the compensation of the President and Executive Vice President and recommended an increase of four percent in the base salary of the President and an increase of four percent in the base salary of the Executive Vice President. The recommendations for the President and Executive Vice President were based upon peer review data, levels of responsibility, breadth of knowledge, prior experience, management recommendations for other employees, cost of living, and performance.

Annual Incentive Bonus

The Company uses a “Performance Compensation Plan” (the “Plan”) for employees of the Company and its subsidiaries. The Plan is designed to assist the Board of Directors and management in communicating to the employees the goal of profitable growth.

Each employee participating in the Plan is eligible to be considered to receive an annual bonus based upon pre-tax profits. At the bank subsidiary level, the Plan focuses on pre-tax profits at the individual bank plus the overall profitability of the Company. At the holding company level, the Plan focuses on consolidated budgeted pre-tax profits for the holding company. For the employees of the holding company, the Plan provides that a bonus pool will be created in the amount of 2 percent of the consolidated budgeted pre-tax profits for the Company. The size of the pool is then adjusted by a formula upward or downward depending upon how actual profits compared to budget. The amount of the pool is then allocated among three groups by the designated percentage amounts and leaves 20 percent to be allocated at the discretion of the Committee. The President and the Executive Vice President receive an aggregate of 25 percent of the pool, which is allocated proportionately between them based upon base compensation. Additionally, the Board of Directors retains the discretion to

11

Table of Contents

deviate from the Plan if warranted. The Compensation Committee recommended payment of the annual incentive bonus to the President and the Executive Vice President pursuant to the Plan formula. The Committee did not recommend that any of the discretionary pool be awarded for 2004.

Long-term Incentives

The Company provides its executive officers with long-term incentive compensation through grants of stock options. The Compensation Committee is responsible for determining the individuals to whom grants should be made, the timing of grants, the exercise price per share, and the number of shares subject to each option. Other than the stock options, the Compensation Committee made no other long-term performance awards during the last fiscal year. The stock option grants are discretionary grants by the Compensation Committee. The Compensation Committee takes into consideration the profits of the Company during the most recent fiscal year, the profit trend line of the Company, the position of the employee, peer review of similar companies, and the total compensation package of the eligible employees in determining the amount of the grants.

The Compensation Committee believes that stock options provide the Company’s executive officers with the opportunity to purchase and maintain an equity interest in the Company and to share in the appreciation of the value of the stock. The Compensation Committee believes that stock options directly motivate an executive to maximize long-term stockholder value and help align the focus of the executive officers with the interests of the shareholders. The options also utilize vesting periods in order to encourage key employees to continue in the employ of the Company. All options to executive officers to date have been granted at the fair market value of the Company’s common stock determined on the basis of the bid price of the stock. All options for 2004 were granted at the bid price of the stock on December 31, 2004. The amount of the stock option awards is reflected in the compensation table for the executive officers.

Summary

The Compensation Committee believes that its executive compensation philosophy of paying its executive officers well by means of competitive base salaries, annual bonuses, and long-term incentives, as described in this report, serves the interests of the Company and the Company’s stockholders.

Richard R. Donohue

James G. Wake

Michael R. Welter

Edward C. Whitham

12

Table of Contents

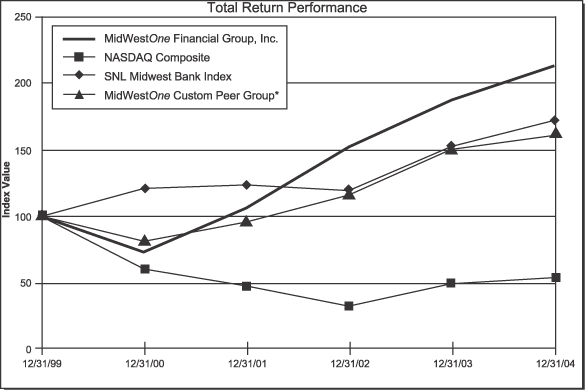

Financial Performance

The following graph illustrates the cumulative total return (assuming the reinvestment of dividends) experienced by the Company’s shareholders since December 31, 1999, through December 31, 2004, compared to the NASDAQ Composite, SNL Midwest Bank Index, and the MidWestOne Custom Peer Group.

MIDWESTONE FINANCIAL GROUP, INC.

Stock Price Performance

| Period Ending | ||||||||||||

Index | 12/31/99 | 12/31/00 | 12/31/01 | 12/31/02 | 12/31/03 | 12/31/04 | ||||||

MidWestOne Financial Group, Inc. | 100.00 | 73.15 | 106.37 | 152.55 | 187.83 | 213.76 | ||||||

NASDAQ Composite | 100.00 | 60.82 | 48.16 | 33.11 | 49.93 | 54.49 | ||||||

SNL Midwest Bank Index | 100.00 | 121.10 | 123.76 | 119.39 | 152.82 | 172.44 | ||||||

MidWestOne Custom Peer Group* | 100.00 | 81.18 | 95.68 | 116.02 | 150.47 | 161.19 | ||||||

| * | MidWestOne Custom Peer Group consists of Midwest commercial banks with total assets between $500 million and $1 billion that are headquartered in Iowa, Illinois, Indiana, Kansas, Kentucky, Michigan, Missouri, North Dakota, Ohio, and Wisconsin. |

13

Table of Contents

Loans to Officers and Directors and Other Transactions With Officers and Directors

During 2004, MidWestOne Bank & Trust, MidWestOne Bank, Central Valley Bank, and Pella State Bank made loans or loan commitments, in the ordinary course of business, to directors and officers of the Company and to corporations or partnerships with which one or more of the officers or directors of the Company were associated. In the opinion of management of the Company, all such loans and loan commitments were made on substantially the same terms, including interest rates and collateral, as those prevailing at the time for comparable transactions with other persons, and did not involve more than the normal risk of collectibility or present other unfavorable features.

Ownership of Securities by Certain Beneficial Owners

The following table sets forth certain information as of February 25, 2005, with respect to the Common Stock beneficially owned by each existing director of the Company, by each nominee, by all executive officers and directors as a group and by each shareholder known by the Company to be the beneficial owner of more than five percent of the Common Stock.

Name | Amount and Nature of Beneficial Ownership(1) | Percent of Class(1) | |||

Richard R. Donohue(2) | 4,550 | * | |||

Charles S. Howard(3) | 259,203 | 6.8 | % | ||

Barbara J. Kniff | 0 | * | |||

David A. Meinert(4) | 114,374 | 3.0 | % | ||

John P. Pothoven(5) | 102,281 | 2.7 | % | ||

James G. Wake(6) | 6,051 | * | |||

Michael R. Welter(7) | 8,293 | * | |||

Edward C. Whitham(8) | 4,683 | * | |||

Executive Officers and Directors as a group | 499,435 | 12.8 | % | ||

MidWestOne Financial Group, Inc. Employee Stock Ownership Plan (ESOP)(10)(11) | 533,657 | 14.2 | % | ||

Jeffrey L. Gendell(12) | 211,081 | 6.7 | % | ||

| * | Less than 1%. |

| (1) | Except as described in the following notes, each person or group owns the shares directly and has sole voting and investment power with respect to such shares. The shares listed include shares subject to options exercisable within sixty days of February 25, 2005. |

| (2) | Such shares include 1,616 shares owned by his spouse, 19 shares held by a partnership, and 2,375 shares subject to currently exercisable options. |

| (3) | Such shares include 51,039 shares owned by his spouse, 3,500 shares owned jointly with his spouse, a total of 2,450 shares owned as custodian for his two minor children, 57,503 shares in Howard Partners, L.P., in which Mr. Howard is a one-third partner, 36,037 shares subject to currently exercisable options, and 37,305 shares allocated to his ESOP account. |

| (4) | Such shares include 17,088 shares owned jointly with his spouse, a total of 532 shares owned as custodian for his two minor children, 62,446 shares subject to currently exercisable options, and 34,308 shares allocated to his ESOP account. Excludes the remaining 499,349 ESOP shares with respect to which Mr. Meinert shares dispositive power as an ESOP Administrator. |

14

Table of Contents

| (5) | Such shares include 4,117 shares held in an IRA, 32,782 shares subject to currently exercisable options, and 43,035 shares allocated to his ESOP account. Excludes the remaining 490,622 ESOP shares with respect to which Mr. Pothoven shares dispositive power as an ESOP Administrator. |

| (6) | Such shares include 223 shares owned by his spouse, 380 shares owned by a corporation of which Mr. Wake has control, and 5,099 shares subject to currently exercisable options. |

| (7) | Such shares include 7,138 shares owned jointly with his spouse, 655 shares held in an IRA, 500 shares owned by a corporation of which Mr. Welter has control. |

| (8) | Such shares include 570 shares held in a profit sharing plan, 578 shares held in his spouse’s IRA, 220 shares held in his spouse’s profit sharing plan, 217 shares held in spouse’s money purchase pension plan, and 1,276 shares subject to currently exercisable options. |

| (9) | Such shares include a total of 114,648 ESOP shares allocated to the accounts of directors and executive officers and a total of 140,015 shares subject to currently exercisable options. |

| (10) | The Company’s ESOP holds shares of the Company’s Common Stock pursuant to the terms of the ESOP. The Trustee of the ESOP, the Trust Department of MidWestOne Bank & Trust, has the power to dispose of ESOP shares in accordance with the terms of the ESOP and votes any unallocated ESOP shares at the direction of the Committee acting as ESOP Administrators. The ESOP Administrators are Thomas W. Campbell, President of Central Valley Bank, Jerry D. Krause, President of MidWestOne Bank, Michael T. Patrick, President of Pella State Bank, Fred L. Koogler, President of MidWestOne Investment Services, Inc., David A. Meinert, and John P. Pothoven. Shares allocated to participants’ accounts are voted by the respective participants. Shares not voted by a participant will be voted by the Trustee in the same proportion as the shares for which signed proxy cards are returned by the other participants in the ESOP. The Trustee disclaims beneficial ownership of all of the shares, and the ESOP Administrators disclaim beneficial ownership of all shares other than those allocated to their respective accounts held by the ESOP. The amount of beneficial ownership shown for the ESOP includes those shares allocated to accounts of directors and executive officers of the Company, which shares are also reflected in the individual’s respective beneficial ownership as indicated in the footnotes above. |

| (11) | The address of the ESOP Administrators is 222 First Avenue East, Oskaloosa, IA 52577. |

| (12) | The Company has received a Schedule 13F from Jeffrey L. Gendell, 55 Railroad Avenue, 3rd Floor, Greenwich, CT 06830. Mr. Gendell indicates that he has sole voting power over 211,081 shares in his capacity as an institutional investment manager. |

15

Table of Contents

PROPOSAL 2

Ratification Of Auditors’ Appointment

The Board of Directors of the Company, at the recommendation of the Audit Committee, has approved the accounting firm of KPMG LLP, independent certified public accountants, as the principal accountant for the Company to conduct the audit examination of the Company and its subsidiaries for the 2005 fiscal year. KPMG LLP was also the principal accountant and performed the audit for the 2004 fiscal year.

A representative from KPMG LLP is anticipated to be present at the Annual Meeting of Shareholders. He will have the opportunity to make a statement if he desires to do so and is expected to be available to respond to appropriate questions from shareholders.

The Board recommends that shareholders vote FOR the ratification of the appointment of KPMG LLP as independent auditors for the 2005 fiscal year. In the absence of instructions to the contrary, proxies solicited by the Board of Directors will be voted FOR ratification of the appointment of KPMG LLP as independent auditors.

Independent Public Accountants

Fees

The following table presents fees for professional audit services rendered by KPMG LLP for the audit of the Company’s annual financial statements for the fiscal years ended December 31, 2004 and 2003, and fees billed for other services rendered by KPMG LLP:

| 2004 | 2003 | |||||

Audit Fees (1) | $ | 118,500 | $ | 109,700 | ||

Audit-Related Fees (2) | 10,400 | 37,668 | ||||

Tax Fees (3) | 44,000 | 60,800 | ||||

All Other Fees (4) | 0 | 14,500 | ||||

Total | $ | 172,900 | $ | 222,668 | ||

| 1. | Audit Fees represent fees for professional services provided for the audit of the Company’s annual financial statements and review of the Company’s quarterly financial statements in connection with the filing of current and periodic reports. |

| 2. | Audit-Related Fees represent assurance and related services that are reasonably related to the performance of the audit or review of the Company’s financial statements. Such services related primarily to internal control examinations pursuant to the Statement of Auditing Standards No. 70, audits of employee benefit plans and other attestation services. Included for 2003 was $27,968 in fees for loan review in connection with the 2002 year-end audit. |

| 3. | Tax Fees represent fees for professional services related to tax compliance, which included preparation of tax returns, tax advice and tax planning. |

| 4. | All other fees represent services provided for the acquisition of Belle Plaine Service Corp. in 2003. |

Independence

The Audit Committee has considered whether the non-audit services provided by KPMG LLP to the Company are compatible with maintaining the independence of KPMG LLP and concluded that the independence of KPMG LLP is not compromised by providing such services.

The Audit Committee pre-approves all auditing services and permitted non-audit services, including the fees and terms of those services, to be performed for the Company by its independent auditor prior to engagement.

16

Table of Contents

REPORT OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS

The incorporation by reference of this Proxy Statement into any document filed with the Securities and Exchange Commission shall not be deemed to include the following report unless such report is specifically stated to be incorporated by reference into such document.

The Audit Committee of the Board of Directors of the Company serves as the representative of the Board for general oversight of the Company’s financial accounting and reporting process, systems of internal controls regarding finance, accounting and legal compliance and monitoring the independence and performance of the Company’s independent auditors and internal auditing department. The Company’s management has primary responsibility for preparing the Company’s financial statements and the Company’s financial reporting process. The Company’s independent accountants, KPMG LLP, are responsible for expressing an opinion on the conformity of the Company’s audited financial statements to generally accepted accounting principles.

As part of its responsibilities, the Audit Committee hereby reports as follows:

| 1. | The Audit Committee has reviewed and discussed the audited financial statements for the year ended December 31, 2004, with the Company’s management. |

| 2. | The Audit Committee has discussed with KPMG LLP the matters required to be discussed by the Statement on Auditing Standards No. 61 (Communication with Audit Committees). |

| 3. | The Audit Committee has received the written disclosures and the letter from KPMG LLP required by Independence Standards Board Standard No. 1 (Independence Discussions with Audit Committees) and has discussed with KPMG LLP the independence of KPMG LLP. |

| 4. | Based on the review and discussions referred to in paragraphs 1 through 3 above, the Audit Committee recommended to the Board of Directors of the Company, and the Board has approved, that the audited financial statements be included in the Company’s annual report on Form 10-K for the fiscal year ended December 31, 2004, for filing with the Securities and Exchange Commission. |

| 5. | The Board has adopted an Audit Committee Charter, which is attached to this Proxy Statement as Exhibit A. |

Each of the members of the Audit Committee is independent as defined under the listing standards of the NASD/AMEX exchange. The undersigned members of the Audit Committee have submitted this Report.

Richard R. Donohue

Michael R. Welter

Edward C. Whitham

17

Table of Contents

GENERAL MATTERS

Financial Statements

The Company’s 2004 Annual Report to Shareholders has accompanied the mailing of this Proxy Statement.

The Company will provide without charge to each shareholder solicited, upon the written request of any such shareholder, a copy of its annual report on Form 10-K as filed with the Securities and Exchange Commission, including the financial statements, for the fiscal year ended December 31, 2004. Such written request should be directed to Karen K. Binns, Secretary/Treasurer, MidWestOne Financial Group, Inc., P. O. Box 1104, Oskaloosa, Iowa 52577-1104. It is also available on the Securities and Exchange Commission’s Internet web site at http://www.sec.gov/cgi-bin/srch-edgar.

Section 16(a) Beneficial Ownership Reporting Compliance

Section 16(a) of the Securities Exchange Act of 1934 requires that the Company’s directors and executive officers and persons who own more than 10 percent of the Company’s Common Stock file initial reports of ownership and reports of changes of ownership with the Securities and Exchange Commission and NASDAQ. Specific due dates for these reports have been established, and the Company is required to disclose in its Proxy Statement any failure to file by these dates during the Company’s 2004 fiscal year.

All the applicable filing requirements were satisfied by the officers, directors and 10 percent owners during 2004. In making this statement, the Company is relying upon written representations of its incumbent officers, directors, and 10 percent owners and copies of applicable reports furnished to the Company.

Shareholder Communications

The Company provides for a process for stockholders to send communications to the Board of Directors. Stockholders may send communications to the Board of Directors by contacting the Company’s Chief Financial Officer in one of the following ways:

In writing at 222 First Avenue East, Oskaloosa, Iowa, 52577;

By email atdmeinert@mwofg.com.

The Chief Financial Officer will submit each communication received to the Board of Directors at the next regular meeting.

2006 Shareholder Proposals

In order for any proposals of shareholders pursuant to the procedures prescribed in Rule 14a-8 under the Securities Exchange Act of 1934 to be presented as an item of business at the Annual Meeting of Shareholders of the Company to be held in 2006, the proposal must be received at the Company’s principal executive offices no later than November 22, 2005 and must be limited to 500 words. To be included in the Company’s proxy statement, the shareholder must be a holder of record or beneficial owner of at least $2,000 in market value or one percent (1%) of the Company’s shares entitled to be voted on the proposal and have held the shares for at least one year and shall continue to hold the shares through the date of the Annual Meeting. Either you, or your representative who is qualified under state law to present the proposal on your behalf, must attend the meeting to present the proposal. Shareholders may not submit more than one proposal. A shareholder proposal submitted outside the procedures described in Rule 14a-8 shall be considered untimely unless received no later than February 6, 2006.

18

Table of Contents

Shareholders wishing to recommend names of individuals for possible nomination to the Company’s Board of Directors may do so according to the following procedures established by the Board:

| 1. | Contact the Secretary of the Company to obtain the Board Membership Criteria established by the Board of Directors. |

| 2. | Make typewritten submission to the Secretary of the Company naming the proposed candidate and specifically noting how the candidate meets the criteria set forth by the Board. |

| 3. | Submission must be received by the Company 120 days prior to the expected mailing date of the proxy. |

| 4. | Person making submission must prove they are a shareholder of the Company and that they own shares with a market value of at least $2,000 and have held those shares for at least one year at the time the submission is made. |

| 5. | If the person being submitted is aware of the submission, he or she must sign a statement indicating such. |

| 6. | If the person being submitted is not aware of the submission, the submitter must explain why. |

The written submission must be mailed to:

Corporate Secretary

MidWestOne Financial Group, Inc.

222 First Avenue East

Oskaloosa, Iowa 52577

Other Matters

Management does not know of any other matters to be presented at the meeting, but should other matters properly come before the meeting, the proxies will vote on such matters in accordance with their best judgment.

By Order of the Board of Directors

Karen K. Binns, Secretary

March 21, 2005

19

Table of Contents

Exhibit A

MIDWESTONE FINANCIAL GROUP, INC.

AUDIT COMMITTEE CHARTER

I. Audit Committee Purpose

The Audit Committee is appointed by the Board of Directors to assist the Board in oversight responsibilities. The Audit Committee’s primary duties and responsibilities are to:

| • | Monitor the integrity of the Company’s financial reporting process and systems of internal controls regarding finance, accounting, and legal compliance. |

| • | Monitor the independence and performance of the Company’s independent auditors and internal auditing department. |

| • | Monitor compliance by the Company with applicable legal and regulatory requirements. |

| • | Provide an avenue of communication among the independent auditors, management, the internal auditing department, and the Board of Directors. |

II. Audit Committee Composition and Meetings

Audit Committee members shall meet the requirements of the NASDAQ/AMEX Exchange. The Audit Committee shall be comprised of three or more directors as determined by the Board, each of whom shall be independent directors, free from any relationship that would interfere with the exercise of his or her independent judgment. All members of the Committee shall have a basic understanding of finance and accounting and be able to read and understand fundamental financial statements, and at least one member of the Committee shall be an “audit committee financial expert” as defined by the Securities and Exchange Commission.

Audit Committee members shall be appointed by the Board. If an Audit Committee Chair is not designated or present, the members of the Committee may designate a Chair by majority vote of the Committee membership.

The Committee shall meet at least four times annually, or more frequently as circumstances dictate. The Audit Committee Chair shall prepare and/or approve an agenda in advance of each meeting. The Committee should meet privately in executive session at least annually with management, the director of the internal auditing department, the independent auditor, and as a committee to discuss any matters that the Committee or each of these groups believe should be discussed. In addition, the Committee, or at least its Chair, should communicate with management and the independent auditors quarterly to review the Company’s financial statements and significant findings based upon the auditor’s limited review procedures.

III. Audit Committee Responsibilities and Duties

General

| 1. | The Audit Committee shall be directly responsible for the appointment, termination, compensation and oversight of the work of the independent auditor (including resolution of disagreements between management and the independent auditor regarding financial reporting) for the purpose of preparing or issuing an audit report or related work. The independent auditor shall report directly to the Audit Committee. |

| 2. | The Audit Committee shall pre-approve all audit and any permitted non-audit services provided to the Company by the independent auditors and the fees to be paid for those services. The Audit Committee may form and delegate authority to subcommittees consisting of one or more members when appropriate, including the authority to grant pre-approvals of certain audit and permitted non-audit |

E-1

Table of Contents

services, provided that decisions of such subcommittee to grant pre-approvals shall be presented to the full Audit Committee at its next scheduled meeting. |

| 3. | The Audit Committee shall have the authority, to the extent it deems necessary or appropriate, to retain special legal, accounting or other consultants to advise the Committee. The Company shall provide for appropriate funding, as determined by the Audit Committee, for payment of compensation to the independent auditor for the purpose of rendering or issuing an audit report or performing other permitted services and to any consultants engaged by the Audit Committee. |

| 4. | The Audit Committee shall make regular reports to the Board. The Audit Committee shall review and reassess the adequacy of this Charter annually and recommend any proposed changes to the Board for approval. The Audit Committee shall annually review the Audit Committee’s own performance. |

Specific Tasks

The Audit Committee shall:

| 1. | Review and discuss with management and the independent auditor the annual audited and quarterly financial statements, including disclosures made in management’s discussion and analysis, earnings press releases and any earnings guidance provided to analysts and rating agencies, prior to the release of quarterly and annual earnings results. |

| 2. | Discuss with management and the independent auditor significant financial reporting issues and judgments made in connection with the preparation of the Company’s financial statements, including any significant changes in the Company’s selection or application of accounting principles and the adequacy of the Company’s internal controls. |

| 3. | Review and discuss with the independent auditors: |

| (i) | the scope, planning and staffing of the audit; |

| (ii) | any problems or difficulties encountered in the course of the audit, including any restrictions on the scope of the independent auditors’ activities or on access to requested information and management’s response, and any significant disagreements with management; |

| (iii) | any report by the independent auditor as required by Section 10A of the Exchange Act, including any report related to critical accounting policies and practices to be used, all alternative treatments of financial information within generally accepted accounting principles that have been discussed with management, ramifications of the use of such alternative disclosures and treatments, and the treatment preferred by the independent auditor, and other material written communications between the independent auditor and management; |

| (iv) | the matters required to be discussed by Statement on Auditing Standards No. 61 relating to the conduct of the audit, including any difficulties encountered in the course of the audit work. |

| 4. | Discuss with management the Company’s major financial risk exposures and the steps management has taken to monitor and control such exposures, including the Company’s risk assessment and risk management policies. |

| 5. | Review any disclosures made to the Audit Committee by the Company’s CEO and CFO during their certification process for the Form 10-K and Form 10-Q about any significant deficiencies in the design or operation of internal controls or material weaknesses therein and any fraud involving management or other employees who have a significant role in the Company’s internal controls. |

| 6. | Obtain and review a report from the independent auditor at least annually regarding (i) the independent auditor’s internal quality-control procedures, (ii) any material issues raised by the most recent internal quality-control review, or peer review, of the firm, or by any inquiry or investigation by governmental |

E-2

Table of Contents

or professional authorities within the preceding five years respecting one or more independent audits carried out by the firm, (iii) any steps taken to deal with any such issues, and (iv) all relationships between the independent auditor and the Company. |

| 7. | Evaluate the qualifications, performance and independence of the independent auditor, including considering whether the auditor’s quality controls are adequate and the provision of permitted non-audit services is compatible with maintaining the auditor’s independence, and taking into account the opinions of management and internal auditors. |

| 8. | Review and evaluate the lead partner of the independent auditor team and ensure the rotation of the lead (or coordinating) audit partner having primary responsibility for the audit and the audit partner responsible for reviewing the audit as required by law. |

| 9. | Discuss with the independent auditor and management the Company’s internal audit function and the responsibilities of those performing the internal audit, the internal audit budget, the staffing of the internal audit, and any recommended changes in the scope of the internal audit function. |

| 10. | Establish procedures for (i) the receipt, retention and treatment of complaints received by the Company regarding accounting, internal accounting controls or auditing matters, and (ii) the confidential, anonymous submission by employees of concerns regarding questionable accounting or auditing matters. Such procedures may be amended from time to time by the Audit Committee. |

| 11. | Discuss with management and the independent auditor any correspondence with regulators or governmental agencies and any published reports which raise material issues regarding the Company’s financial statements or accounting policies. |

| 12. | Obtain advice and assistance from the Company’s counsel as to matters that may have a material impact on the financial statements or the Company’s compliance policies. |

| 13. | Review and approve all “related party transactions.” The term “related party transactions” shall refer to transactions required to be disclosed pursuant to Item 404 of SEC Regulation S-K. |

Limitation

While the Audit Committee has the responsibilities, duties and powers set forth in this Charter, it is not the duty of the Audit Committee to plan or conduct audits or to determine that the Company’s financial statements and disclosures are complete and accurate and are in accordance with generally accepted accounting principles and applicable rules and regulations. These are the responsibilities of management and the independent auditor.

E-3

Table of Contents

Exhibit B

MIDWESTONE FINANCIAL GROUP, INC.

COMPENSATION COMMITTEE CHARTER

A. Purpose and Scope

The primary function of the Compensation Committee (the “Committee”) is to assist the Board of Directors (the “Board”) in fulfilling its responsibilities and duties by making recommendations to the Board with respect to the compensation of the Company’s Chief Executive Officer (“CEO”) and its executive officers.

B. Composition and Meetings

The Committee shall be comprised of a minimum of three members of the Board, as appointed by the Board, each of whom shall meet the applicable independence requirements promulgated by the Securities and Exchange Commission (the “SEC”) and the National Association of Securities Dealers (“NASD”).

The members of the Committee shall be elected by the Board and shall serve until their successors shall be duly elected and qualified or until their earlier resignation or removal. Unless a Chair of the Committee is elected by the full Board, the members of the Committee may designate a Chair by majority vote of the full Committee membership. A majority of the number of Committee members shall constitute a quorum for the transaction of business.

The Committee shall meet as often as necessary, but at least once each year, to enable it to fulfill its responsibilities and duties as set forth herein. The Committee shall report its actions to the Board and keep written minutes of its meetings, which shall be recorded and filed with the books and records of the Company.

C. Responsibilities and Duties

To fulfill its responsibilities and duties, the Committee shall:

| 1. | Produce an annual report on executive compensation for inclusion in the Company’s proxy statement. |

| 2. | Annually review and approve corporate goals and objectives relevant to the CEO’s compensation, evaluate the CEO’s performance in light of these goals and objectives, and recommend to the Board the CEO’s compensation level based on this evaluation. The CEO shall not be present during the voting or any deliberations concerning the CEO’s compensation. |

| 3. | Annually recommend to the Board the compensation of executive officers of the Company. The CEO may participate in such deliberations, but shall not vote to approve or recommend any form of compensation for such executive officers. |

| 4. | Make awards of stock options to the CEO, the executive officers, and other key employees under any Company employee stock option or stock-related plans now or from time to time hereafter in effect, and exercise such other power and authority as may be permitted or required under such plans. |

| 5. | Make recommendations to the Board with respect to incentive compensation plans and equity-based plans, and employment agreements between the Company and the CEO and other executive officers. |

| 6. | From time to time review and make recommendations to the Board with respect to the compensation of directors. |

| 7. | Make regular reports to the Board. |

| 8. | Review committee member qualifications; committee member appointment and removal; committee structure and operations (including authority to delegate to subcommittees); and committee reporting to the Board. |

E-4

Table of Contents

| 9. | Have sole authority to retain and terminate any compensation consultant used to assist in the evaluation or development of compensation arrangements between the Company and its directors, CEO and other executive officers, and shall have sole authority to approve the firm’s fees and other retention terms. |

| 10. | Have sole authority to obtain advice and assistance from internal or external legal, financial, or other advisors. |

| 11. | Review and assess the adequacy of this Charter periodically as conditions dictate, but at least annually, and recommend any modifications to this Charter if and when appropriate to the Board for its approval. |

| 12. | Annually review the Committee’s own performance. |

E-5

Table of Contents

MIDWESTONE FINANCIAL GROUP, INC.

APPENDIX TO THE PROXY STATEMENT

FISCAL YEAR 2004

Contents

| A-1 | ||

| F-1 | ||

| F-2 | ||

Consolidated Statements of Changes in Shareholders’ Equity and Comprehensive Income | F-3 | |

| F-4 | ||

| F-5 | ||

| F-30 | ||

Table of Contents

MIDWESTONE FINANCIAL GROUP, INC.

MANAGEMENT’S DISCUSSION & ANALYSIS OF

RESULTS OF OPERATIONS AND FINANCIAL CONDITION

The following discussion and analysis is intended as a review of significant factors affecting the financial condition and results of operation of MidWestOne Financial Group, Inc. and subsidiaries (the “Company”) for the periods indicated. The discussion should be read in conjunction with the consolidated financial statements and the notes thereto.

“Safe Harbor” Statement Under the Private Securities Litigation Reform Act

With the exception of the historical information contained in this report, the matters described herein contain forward-looking statements that involve risk and uncertainties that individually or mutually impact the matters herein described, including but not limited to financial projections, product demand and market acceptance, the effect of economic conditions, the impact of competitive products and pricing, governmental regulations, results of litigation, technological difficulties and/or other factors outside the control of the Company, which are detailed from time to time in the Company’s SEC reports. The Company disclaims any intent or obligation to update these forward-looking statements. The Company’s actual results could differ significantly from those anticipated in these forward-looking statements.

Overview

The Company’s principal business is conducted by its four subsidiary banks and consists of full service community-based commercial and retail banking. In 2004, the Company enhanced its non-banking service offering through the addition of a retail brokerage and financial planning subsidiary. Additionally, the Company derives a substantial portion of its operating revenue from its investments in pools of performing and nonperforming loans referred to as loan pool participations. The profitability of the Company depends primarily on its net interest income, provision for loan losses, other income, and operating expenses.

Net interest income is the difference between total interest income and total interest expense. Interest income is earned by the Company on its loans made to customers, the investment securities it holds in its portfolio, and the interest and discount recovery generated from its loan pool participations. The interest expense incurred by the Company results from the interest paid on customer deposits and borrowed funds. Fluctuations in net interest income can result from the changes in volumes of assets and liabilities as well as changes in market interest rates. The provision for loan losses reflects the cost of credit risk in the Company’s loan portfolio and is dependent on increases in the loan portfolio and management’s assessment of the collectibility of the loan portfolio under current economic conditions. Other income consists of service charges on deposit accounts, fees received for data processing services provided to nonaffiliated banks, mortgage loan origination fees, other fees and commissions, and realized security gains or losses. Operating expenses include salaries and employee benefits, occupancy and equipment expenses, professional fees, other noninterest expenses, and the amortization of goodwill and other intangible assets. These operating expenses are significantly influenced by the growth of operations, with additional employees necessary to staff new banking centers.

Acquisition of Koogler Company of Iowa

On July 30, 2004, the Company acquired Koogler Company of Iowa (“KCI”), a sole proprietorship, which was a retail brokerage and financial planner. The identifiable intangible asset acquired was a customer list, with the remainder of the purchase price allocated to goodwill. The acquisition was part cash and part stock, and was accounted for as a purchase transaction. The Company formed a new wholly-owned subsidiary called MidWestOne Investment Services, Inc. to provide retail brokerage and financial planning services throughout the banking offices of the Company. Revenues and expenses related to the new activity were reflected on the Company’s books from August 1, 2004 forward.

A-1

Table of Contents

Acquisition of Belle Plaine Service Corp.

On February 1, 2003, the Company acquired the Belle Plaine Service Corp. (“BPSC”) and its wholly-owned subsidiary Citizens Bank & Trust (“CB&T”) of Hudson, Iowa in a 100 percent cash transaction. The acquisition was accounted for as a purchase transaction with revenues and expenses reflected on the Company’s books from February 1, 2003 forward. As of February 1, 2003, BPSC had total assets of $77,602,000, loans totaling $61,010,000, and deposits of $62,940,000. The Company’s results of operation for the year ended December 31, 2002 does not include any income or expense related to BPSC. CB&T was subsequently merged with another of the Company’s subsidiary banks on June 14, 2003.

Performance Summary

For the year ended December 31, 2004, the Company recorded net income of $5,829,000, or $1.54 per share basic and $1.50 per share diluted. This compares with $5,926,000, or $1.54 per share basic and $1.50 per share diluted, for the year ended December 31, 2003. Net income was $97,000 or 2 percent lower in 2004. An increase in net interest income was offset by greater loan loss provision, a reduction in noninterest income and increased noninterest expense.

Total assets of the Company increased $27,258,000 or 4 percent to a year-end 2004 total of $650,564,000 compared with a 2003 total of $623,306,000. The Company’s total loans outstanding increased $21,837,000 or 6 percent in 2004 to $398,854,000 at December 31, 2004. Loan pool participations as of December 31, 2004 totaled $105,502,000, an increase of 18 percent from the year-end 2003 balance of $89,059,000. Deposits increased $21,977,000 or 5 percent to $475,102,000 as of December 31, 2004.

Return on average assets is a measure of profitability that indicates how effectively a financial institution utilizes its assets. It is calculated by dividing net income by average total assets. The Company’s return on average assets was .92 percent for 2004, .98 percent for 2003 and 1.07 percent for 2002. Net income for 2004 was slightly lower while average assets increased during the year, thus reducing the return on average assets in 2004. Return on average equity indicates what the Company earned on its shareholders’ investment and is calculated by dividing net income by average total shareholders’ equity. The return on average equity for the Company was 10.23 percent for 2004, 10.52 percent for 2003 and 10.91 percent for 2002. Return on average equity declined in 2004 reflecting the lower earnings of the Company and an increase in average total shareholders’ equity.

A-2

Table of Contents

Results of Operations

2004 Compared to 2003

Net Interest Income. Net interest income is the total of interest income less interest expense. Net interest income increased $1,191,000 or 5 percent in 2004 to $24,002,000 compared with $22,811,000 in 2003. The net interest spread, which is the difference between the yield earned on assets and the rate paid on liabilities, increased to 3.84 percent in 2004 from 3.77 percent in 2003. Net interest margin is a measurement of the net return on interest-earning assets and is computed by dividing net interest income on a tax-equivalent basis for the year by the annual average balance of all interest-earning assets. The net interest margin on a tax-equivalent basis (FTE) for 2004 was 4.13 percent compared to 4.10 percent for 2003. The following table presents a comparison of the average balance of earning assets, interest-bearing liabilities, interest income and expense, and average yields and costs for the years 2004 and 2003.

MIDWESTONE FINANCIAL GROUP

CONSOLIDATED NET INTEREST EARNINGS ANALYSIS (FTE)

| Year ended December 31, | ||||||||||||||

| 2004 | 2003 | |||||||||||||

(in thousands) | Average Balance | Interest | Average Rate | Average Balance | Interest | Average Rate | ||||||||

Average earning assets: | ||||||||||||||

Loans | 391,131 | 23,885 | 6.11 | % | 366,754 | 23,894 | 6.52 | % | ||||||

Loan pool participations | 89,430 | 9,395 | 10.50 | % | 85,959 | 8,985 | 10.45 | % | ||||||

Interest-bearing deposits | 498 | 4 | 0.84 | % | 1,638 | 10 | 0.62 | % | ||||||

Investment securities | 102,454 | 4,038 | 3.94 | % | 106,210 | 4,662 | 4.39 | % | ||||||

Federal funds sold | 3,329 | 50 | 1.49 | % | 2,295 | 27 | 1.19 | % | ||||||

Total earning assets | 586,842 | 37,372 | 6.37 | % | 562,856 | 37,578 | 6.68 | % | ||||||

Average interest-bearing liabilities: | ||||||||||||||

Interest-bearing demand deposits | 64,203 | 239 | 0.37 | % | 56,194 | 181 | 0.32 | % | ||||||

Savings deposits | 124,106 | 1,328 | 1.07 | % | 115,042 | 1,334 | 1.16 | % | ||||||

Certificates of deposit | 232,373 | 6,770 | 2.91 | % | 243,073 | 8,527 | 3.51 | % | ||||||

Total deposits | 420,682 | 8,337 | 1.98 | % | 414,309 | 10,042 | 2.42 | % | ||||||

Federal funds purchased | 5,578 | 82 | 1.47 | % | 4,763 | 63 | 1.32 | % | ||||||

Federal Home Loan Bank advances | 82,250 | 3,975 | 4.83 | % | 70,631 | 3,880 | 5.49 | % | ||||||

Notes payable | 10,108 | 428 | 4.23 | % | 7,725 | 262 | 3.38 | % | ||||||

Long-term debt | 10,310 | 548 | 5.32 | % | 10,310 | 520 | 5.05 | % | ||||||