Exhibit 13

OUR BOARD OF DIRECTORS

Richard R. Donohue

TD&T Financial Group

John P. Pothoven

President & CEO,

MidWestOne Bank

Charles S. Howard

Chairman, President & CEO

James G. Wake

Smith-Wake Ag Services

Barbara J. Kniff

KLK Construction

Michael R. Welter

General Contractor

David A. Meinert

Executive Vice President & CFO

Edward C. Whitham

Financial Management

Accounting, Inc.

OUR CORPORATE OFFICERS

Charles S. Howard

Chairman, President & CEO

[GRAPHIC]

David A. Meinert

Executive Vice President & CFO

Karen K. Binns

Secretary/Treasurer

Bryce C. Abbas

Auditor

Jeffrey D. Richards

Loan Review Officer

Jeffrey L. Rhoads

Vice President/Finance

OUR LOCATIONS

MidWestOne Bank

www.midwestonebank.com

Oskaloosa • Belle Plaine • Burlington

Davenport • Fairfield • Fort Madison

Hudson • North English • Ottumwa • Pella

Sigourney • Wapello • Waterloo

MidWestOne Investment Services, Inc.

Pella • Burlington • Fairfield • Oskaloosa

Ottumwa • Sigourney

Cook & Son Agency, Inc.

Pella

[GRAPHIC]

[GRAPHIC]

All Kinds of People

One Common Goal

[GRAPHIC]

2005 Annual Report

[GRAPHIC]

BOARD OF DIRECTORS

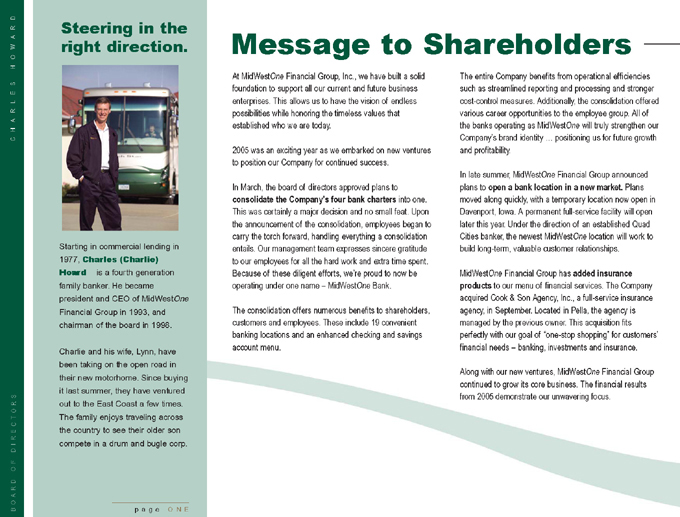

CHARLES HOWARD

Steering in the right direction.

[GRAPHIC]

Starting in commercial lending in 1977, Charles (Charlie) Howard is a fourth generation family banker. He became president and CEO of MidWestOne Financial Group in 1993, and chairman of the board in 1998.

Charlie and his wife, Lynn, have been taking on the open road in their new motorhome. Since buying it last summer, they have ventured out to the East Coast a few times. The family enjoys traveling across the country to see their older son compete in a drum and bugle corp.

Message to Shareholders

At MidWestOne Financial Group, Inc., we have built a solid foundation to support all our current and future business enterprises. This allows us to have the vision of endless possibilities while honoring the timeless values that established who we are today.

2005 was an exciting year as we embarked on new ventures to position our Company for continued success.

In March, the board of directors approved plans to consolidate the Company’s four bank charters into one. This was certainly a major decision and no small feat. Upon the announcement of the consolidation, employees began to carry the torch forward, handling everything a consolidation entails. Our management team expresses sincere gratitude to our employees for all the hard work and extra time spent. Because of these diligent efforts, we’re proud to now be operating under one name – MidWestOne Bank.

The consolidation offers numerous benefits to shareholders, customers and employees. These include 19 convenient banking locations and an enhanced checking and savings account menu.

The entire Company benefits from operational efficiencies such as streamlined reporting and processing and stronger cost-control measures. Additionally, the consolidation offered various career opportunities to the employee group. All of the banks operating as MidWestOne will truly strengthen our Company’s brand identity … positioning us for future growth and profitability.

In late summer, MidWestOne Financial Group announced plans to open a bank location in a new market. Plans moved along quickly, with a temporary location now open in Davenport, lowa. A permanent full-service facility will open later this year. Under the direction of an established Quad Cities banker, the newest MidWestOne location will work to build long-term, valuable customer relationships.

MidWestOne Financial Group has added insurance products to our menu of financial services. The Company acquired Cook & Son Agency, Inc., a full-service insurance agency, in September. Located in Pella, the agency is managed by the previous owner. This acquisition fits perfectly with our goal of “one-stop shopping” for customers’ financial needs – banking, investments and insurance.

Along with our new ventures, MidWestOne Financial Group continued to grow its core business. The financial results from 2005 demonstrate our unwavering focus.

page ONE

BOARD OF DIRECTORS

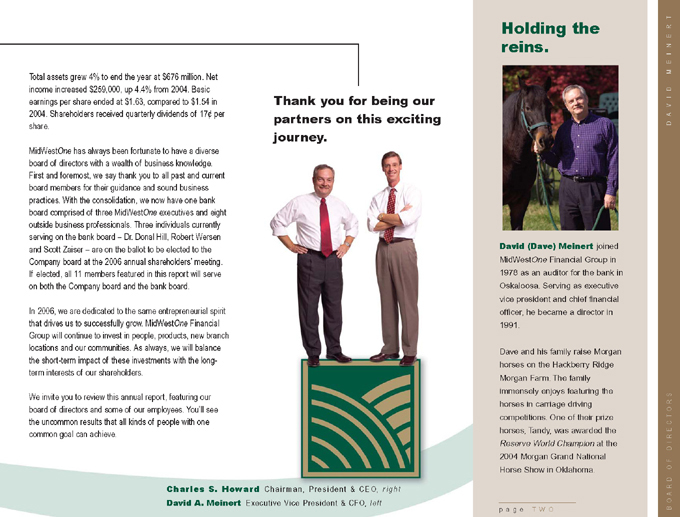

DAVID MEINERT

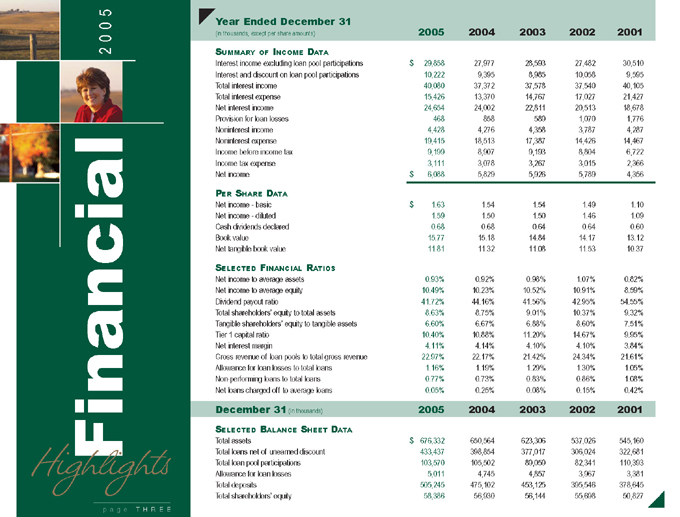

Total assets grew 4% to end the year at $676 million. Net income increased $259,000, up 4.4% from 2004. Basic earnings per share ended at $1.63, compared to $1.54 in 2004. Shareholders received quarterly dividends of 17¢ per share.

MidWestOne has always been fortunate to have a diverse board of directors with a wealth of business knowledge. First and foremost, we say thank you to all past and current board members for their guidance and sound business practices. With the consolidation, we now have one bank board comprised of three MidWestOne executives and eight outside business professionals. Three individuals currently serving on the bank board – Dr. Donal Hill, Robert Wersen and Scott Zaiser – are on the ballot to be elected to the Company board at the 2006 annual shareholders’ meeting. If elected, all 11 members featured in this report will serve on both the Company board and the bank board.

In 2006, we are dedicated to the same entrepreneurial spirit that drives us to successfully grow. MidWestOne Financial Group will continue to invest in people, products, new branch locations and our communities. As always, we will balance the short-term impact of these investments with the long-term interests of our shareholders.

We invite you to review this annual report, featuring our board of directors and some of our employees. You’ll see the uncommon results that all kinds of people with one common goal can achieve.

Thank you for being our partners on this exciting journey.

[GRAPHIC]

Charles S. Howard Chairman, President & CEO, right

David A. Meinert Executive Vice President & CFO, left

Holding the reins.

[GRAPHIC]

David (Dave) Meinert joined MidWestOne Financial Group in 1978 as an auditor for the bank in Oskaloosa. Serving as executive vice president and chief financial officer, he became a director in 1991.

Dave and his family raise Morgan horses on the Hackberry Ridge Morgan Farm. The family immensely enjoys featuring the horses in carriage driving competitions. One of their prize horses, Tandy, was awarded the Reserve World Champion at the 2004 Morgan Grand National Horse Show in Oklahoma.

page TWO

Highlights Financial 2005

[GRAPHIC]

Year Ended December 31

(in thousands, except per share amounts)

2005

2004

2003

2002

2001

Summary of Income Data

Interest income excluding loan pool participations

$29,858

27,977

28,593

27,482

30,510

Interest and discount on loan pool participations

10,222

9,395

8,985

10,058

9,595

Total interest income

40,080

37,372

37,578

37,540

40,105

Total interest expense

15,426

13,370

14,767

17,027

21,427

Net interest income

24,654

24,002

22,811

20,513

18,678

Provision for loan losses

468

858

589

1,070

1,776

Noninterest income

4,428

4,276

4,358

3,787

4,287

Noninterest expense

19,415

18,513

17,387

14,426

14,467

Income before income tax

9,199

8,907

9,193

8,804

6,722

Income tax expense

3,111

3,078

3,267

3,015

2,366

Net income

$6,088

5,829

5,926

5,789

4,356

Per Share Data

Net income—basic

$1.63

1.54

1.54

1.49

1.10

Net income—diluted

1.59

1.50

1.50

1.46

1.09

Cash dividends declared

0.68

0.68

0.64

0.64

0.60

Book value

15.77

15.18

14.84

14.17

13.12

Net tangible book value

11.81

11.32

11.08

11.53

10.37

Selected Financial Ratios

Net income to average assets

0.93%

0.92%

0.98%

1.07%

0.82%

Net income to average equity

10.49%

10.23%

10.52%

10.91%

8.59%

Dividend payout ratio

41.72%

44.16%

41.56%

42.95%

54.55%

Total shareholders’ equity to total assets

8.63%

8.75%

9.01%

10.37%

9.32%

Tangible shareholders’ equity to tangible assets

6.60%

6.67%

6.88%

8.60%

7.51%

Tier 1 capital ratio

10.40%

10.88%

11.20%

14.67%

9.95%

Net interest margin

4.11%

4.14%

4.10%

4.10%

3.84%

Gross revenue of loan pools to total gross revenue

22.97%

22.17%

21.42%

24.34%

21.61%

Allowance for loan losses to total loans

1.16%

1.19%

1.29%

1.30%

1.05%

Non-performing loans to total loans

0.77%

0.73%

0.83%

0.86%

1.08%

Net loans charged off to average loans

0.05%

0.25%

0.08%

0.15%

0.42%

December 31(in thousands)

2005

2004

2003

2002

2001

Selected Balance Sheet Data

Total assets

$676,332

650,564

623,306

537,026

545,160

Total loans net of unearned discount

433,437

398,854

377,017

306,024

322,681

Total loan pool participations

103,570

105,502

89,059

82,341

110,393

Allowance for loan losses

5,011

4,745

4,857

3,967

3,381

Total deposits

505,245

475,102

453,125

395,546

378,645

Total shareholders’ equity

58,386

56,930

56,144

55,698

50,827

page THREE

All kinds of people. In different communities.

With one common goal.

Whether it’s the voice greeting them on the phone or the person opening their account, customers experience a consistent level of service throughout all MidWestOne locations for their banking, investment and insurance needs.

“We have a group of dedicated people with unique talents and skills always reaching out to help,” comments Charles Howard, MidWestOne Financial Group CEO. “Our employee team holds true the timeless values that provide endless possibilities for all customers. We’re proud to feature a select few in this annual report.”

A Committed Citizen

Service is truly a meaningful word to Tim Brcka, market president for MidWestOne Bank in Ottumwa. After college graduation, he began working in the financial services industry in Ottumwa. Tim started as vice president at Central Valley Bank in 1998, was promoted to executive vice president in 2004 and now serves as market president.

More than 20 years since his college graduation, Tim is still dedicated to his career in the Ottumwa community. “From helping loan customers to volunteering for various organizations, Tim always strives to do his best,” states Tom Campbell, MidWestOne north regional president. “He takes a thoughtful approach to ensure that everyone’s needs are met. I appreciate the time and energy he devotes to his customers and the community.”

Tim began his career working with agricultural customers and now also focuses on the financial needs of small businesses. He understands that a strong business climate is crucial to a healthy community and will do whatever he can to support that. Tim is an active participant in a variety of economic and civic organizations.

“I have been a member of the Noon Lions Club for over 15 years and make it a priority to get involved,” Tim comments. “We sponsor the annual pro balloon races … a major event in Ottumwa that’s been going on for over 25 years. It draws a lot of spectators and groups raise funds for worthwhile causes.”

The list of Tim’s commitments continues with the YMCA board, area development corporation, bank trade associations and more. He is a prime example of the caliber of people serving customers at MidWestOne.

Tim Brcka serves as chairman of the Ottumwa Pro Balloon Race Committee.

[GRAPHIC]

page FOUR

BOARD OF DIRECTORS

MICHAEL WELTER

Building on success.

[GRAPHIC]

Michael (Mike) Welter has been a director of the Company for the last five years. He started M&M Enterprises, a general contracting company, in 1976. The construction company specializes in concrete work. Employee numbers for M&M Enterprises fluctuate based on seasonal work and the scope of projects. For example, the company employed over 200 individuals while working on the Cargill facility in Eddyville, Iowa.

A resident of Sigourney, Iowa, Mike has been active in economic development and understands the needs of local business owners. He also owns and manages the Fast Stop Convenience Store in Sigourney.

Cheryl Washington (left) and Sandy Bailey (right) enjoy visiting at a coffeehouse in Oskaloosa.

[GRAPHIC]

A Concerned Companion

Sandy Bailey, vice president/retail banking at MidWestOne Bank in Oskaloosa, gives new meaning to the term personal banking. Sandy started her banking career over 15 years ago as a personal banker, and was promoted to vice president in 2003. She assists customers with a variety of deposit services. Last fall, Sandy encountered a unique experience while helping a customer open a checking account. “As I was opening the account, I noticed Cheryl’s driver’s license was from the New Orleans area,” recalls Sandy.

page FIVE

BOARD OF DIRECTORS

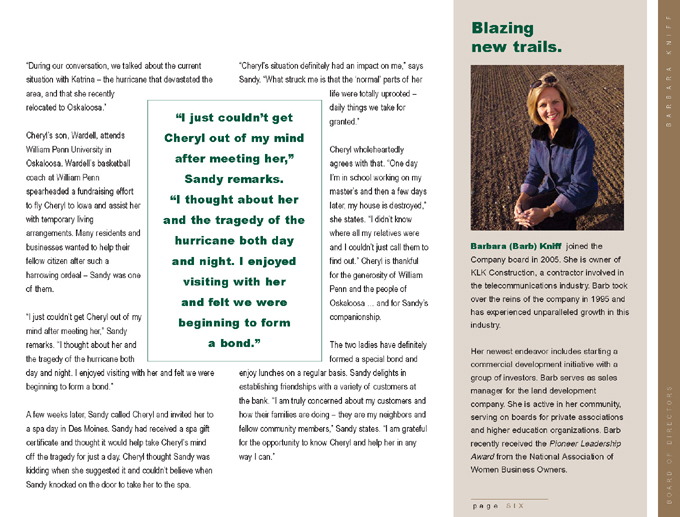

BARBARA KNIFF

“During our conversation, we talked about the current situation with Katrina – the hurricane that devastated the area, and that she recently relocated to Oskaloosa.”

Cheryl’s son, Wardell, attends William Penn University in Oskaloosa. Wardell’s basketball coach at William Penn spearheaded a fundraising effort to fly Cheryl to Iowa and assist her with temporary living arrangements. Many residents and businesses wanted to help their fellow citizen after such a harrowing ordeal – Sandy was one of them.

“I just couldn’t get Cheryl out of my mind after meeting her,” Sandy remarks. “I thought about her and the tragedy of the hurricane both day and night. I enjoyed visiting with her and felt we were beginning to form a bond.”

A few weeks later, Sandy called Cheryl and invited her to a spa day in Des Moines. Sandy had received a spa gift certificate and thought it would help take Cheryl’s mind off the tragedy for just a day. Cheryl thought Sandy was kidding when she suggested it and couldn’t believe when Sandy knocked on the door to take her to the spa.

“Cheryl’s situation definitely had an impact on me,” says Sandy. “What struck me is that the ‘normal’ parts of her life were totally uprooted –daily things we take for granted.”

Cheryl wholeheartedly agrees with that. “One day I’m in school working on my master’s and then a few days later, my house is destroyed,” she states. “I didn’t know where all my relatives were and I couldn’t just call them to find out.” Cheryl is thankful for the generosity of William Penn and the people of Oskaloosa … and for Sandy’s companionship.

The two ladies have definitely formed a special bond and enjoy lunches on a regular basis. Sandy delights in establishing friendships with a variety of customers at the bank. “I am truly concerned about my customers and how their families are doing – they are my neighbors and fellow community members,” Sandy states. “I am grateful for the opportunity to know Cheryl and help her in any way I can.”

“I just couldn’t get Cheryl out of my mind after meeting her,” Sandy remarks. “I thought about her and the tragedy of the hurricane both day and night. I enjoyed visiting with her and felt we were beginning to form a bond.”

Blazing new trails.

[GRAPHIC]

Barbara (Barb) Kniff joined the Company board in 2005. She is owner of KLK Construction, a contractor involved in the telecommunications industry. Barb took over the reins of the company in 1995 and has experienced unparalleled growth in this industry.

Her newest endeavor includes starting a commercial development initiative with a group of investors. Barb serves as sales manager for the land development company. She is active in her community, serving on boards for private associations and higher education organizations. Barb recently received the Pioneer Leadership Award from the National Association of Women Business Owners.

page SIX

BOARD OF DIRECTORS

RICHARD DONOHUE

Giving 110 percent.

Richard (Dick) Donohue has been a director of MidWestOne Financial Group since 1999. A certified public accountant, Dick is managing partner in the firm of TD&T Financial Group. The firm’s entities specialize in accounting, financial services and technology solutions.

TD&T Financial Group is comprised of nine offices throughout eastern Iowa. Residing in Oskaloosa since 1973, Dick now travels to Cedar Rapids to manage the firm’s newest office.

Dick is a strong community supporter. He has served as Chamber president, was on an economic development board and also coached Little League. Additionally, he owns a recreational facility in Oskaloosa.

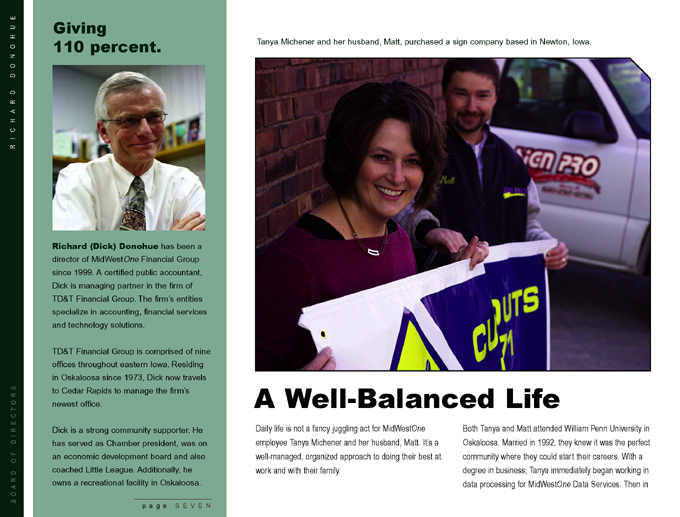

Tanya Michener and her husband, Matt, purchased a sign company based in Newton, Iowa.

[GRAPHIC]

A Well-Balanced Life

Daily life is not a fancy juggling act for MidWestOne employee Tanya Michener and her husband, Matt. It’s a well-managed, organized approach to doing their best at work and with their family.

Both Tanya and Matt attended William Penn University in Oskaloosa. Married in 1992, they knew it was the perfect community where they could start their careers. With a degree in business, Tanya immediately began working in data processing for MidWestOne Data Services. Then in

page SEVEN

BOARD OF DIRECTORS

SCOTT ZAISER

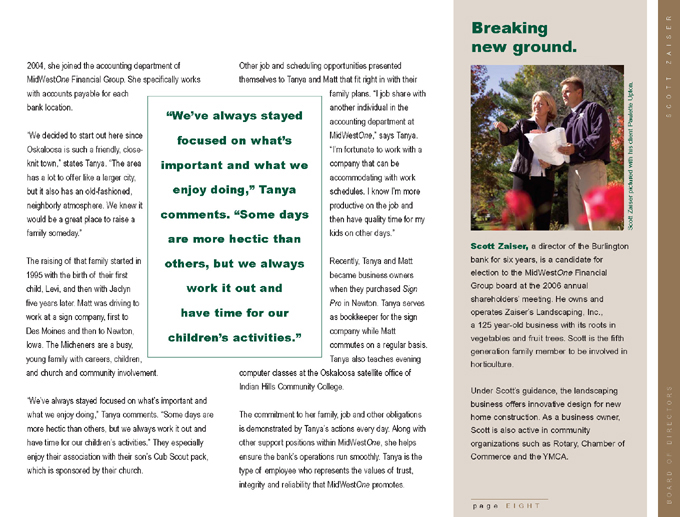

2004, she joined the accounting department of MidWestOne Financial Group. She specifically works with accounts payable for each bank location.

“We decided to start out here since Oskaloosa is such a friendly, close-knit town,” states Tanya. “The area has a lot to offer like a larger city, but it also has an old-fashioned, neighborly atmosphere. We knew it would be a great place to raise a family someday.”

The raising of that family started in 1995 with the birth of their first child, Levi, and then with Jaclyn five years later. Matt was driving to work at a sign company, first to Des Moines and then to Newton, Iowa. The Micheners are a busy, young family with careers, children, and church and community involvement.

“We’ve always stayed focused on what’s important and what we enjoy doing,” Tanya comments. “Some days are more hectic than others, but we always work it out and have time for our children’s activities.” They especially enjoy their association with their son’s Cub Scout pack, which is sponsored by their church.

Other job and scheduling opportunities presented themselves to Tanya and Matt that fit right in with their family plans. “I job share with another individual in the accounting department at MidWestOne,” says Tanya. “I’m fortunate to work with a company that can be accommodating with work schedules. I know I’m more productive on the job and then have quality time for my kids on other days.”

Recently, Tanya and Matt became business owners when they purchased Sign Pro in Newton. Tanya serves as bookkeeper for the sign company while Matt commutes on a regular basis. Tanya also teaches evening computer classes at the Oskaloosa satellite office of Indian Hills Community College.

The commitment to her family, job and other obligations is demonstrated by Tanya’s actions every day. Along with other support positions within MidWestOne, she helps ensure the bank’s operations run smoothly. Tanya is the type of employee who represents the values of trust, integrity and reliability that MidWestOne promotes.

“We’ve always stayed focused on what’s important and what we enjoy doing,” Tanya comments. “Some days are more hectic than others, but we always work it out and have time for our children’s activities.”

Breaking new ground.

[GRAPHIC]

Scott Zaiser pictured with his client Paulette Upton.

Scott Zaiser, a director of the Burlington bank for six years, is a candidate for election to the MidWestOne Financial Group board at the 2006 annual shareholders’ meeting. He owns and operates Zaiser’s Landscaping, Inc., a 125 year-old business with its roots in vegetables and fruit trees. Scott is the fifth generation family member to be involved in horticulture.

Under Scott’s guidance, the landscaping business offers innovative design for new home construction. As a business owner, Scott is also active in community organizations such as Rotary, Chamber of Commerce and the YMCA.

page EIGHT

BOARD OF DIRECTORS

JOHN POTHOVEN

Raising the bar.

[GRAPHIC]

John Pothoven with Marie Ware, director of MCRF.

Working in banking for 30 years, John Pothoven is president and CEO of the newly consolidated MidWestOne Bank. He has served on the Company board since 1994.

John’s forte is fundraising for many community projects and endeavors. Serving as treasurer for the Mahaska Community Recreation Foundation (MCRF), he has played a vital role in promoting recreation. This includes the current development of the Lacey Complex ball fields, soccer facilities and a 15-mile recreation trail – all for enjoyment by community members.

Kris Andre serves meals to fellow parishioners at her church in Pella.

[GRAPHIC]

The Real Deal

It’s easy to see how Kris Andre’s pleasant nature complements the character of the community she calls home. A native of Pella, Iowa, Kris is service representative for MidWestOne Investment Services. “My husband and I married while attending Central College here in Pella,” states Kris. “He was from New Jersey so we moved there after college. During a trip back to visit family, my husband was offered a job. We were both excited to move back to my hometown. He became familiar with this special community during college, and I always knew it’s where I wanted to live.”

page NINE

BOARD OF DIRECTORS

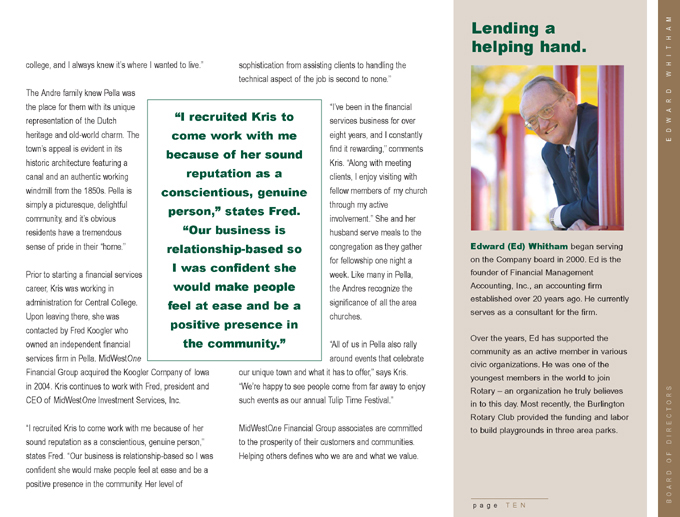

EDWARD WHITHAM

The Andre family knew Pella was the place for them with its unique representation of the Dutch heritage and old-world charm. The town’s appeal is evident in its historic architecture featuring a canal and an authentic working windmill from the 1850s. Pella is simply a picturesque, delightful community, and it’s obvious residents have a tremendous sense of pride in their “home.”

Prior to starting a financial services career, Kris was working in administration for Central College. Upon leaving there, she was contacted by Fred Koogler who owned an independent financial services firm in Pella. MidWestOne

Financial Group acquired the Koogler Company of Iowa in 2004. Kris continues to work with Fred, president and CEO of MidWestOne Investment Services, Inc.

“I recruited Kris to come work with me because of her sound reputation as a conscientious, genuine person,” states Fred. “Our business is relationship-based so I was confident she would make people feel at ease and be a positive presence in the community. Her level of sophistication from assisting clients to handling the technical aspect of the job is second to none.”

“I’ve been in the financial services business for over eight years, and I constantly find it rewarding,” comments Kris. “Along with meeting clients, I enjoy visiting with fellow members of my church through my active involvement.” She and her husband serve meals to the congregation as they gather for fellowship one night a week. Like many in Pella, the Andres recognize the significance of all the area churches.

“All of us in Pella also rally around events that celebrate our unique town and what it has to offer,” says Kris. “We’re happy to see people come from far away to enjoy such events as our annual Tulip Time Festival.”

MidWestOne Financial Group associates are committed to the prosperity of their customers and communities. Helping others defines who we are and what we value.

“I recruited Kris to come work with me because of her sound reputation as a conscientious, genuine person,” states Fred. “Our business is relationship-based so I was confident she would make people feel at ease and be a positive presence in the community.”

Lending a helping hand.

[GRAPHIC]

Edward (Ed) Whitham began serving on the Company board in 2000. Ed is the founder of Financial Management Accounting, Inc., an accounting firm established over 20 years ago. He currently serves as a consultant for the firm.

Over the years, Ed has supported the community as an active member in various civic organizations. He was one of the youngest members in the world to join Rotary – an organization he truly believes in to this day. Most recently, the Burlington Rotary Club provided the funding and labor to build playgrounds in three area parks.

page TEN

BOARD OF DIRECTORS

DR. DONAL HILL

Calling the shots.

[GRAPHIC]

Dr. Donal Hill is a candidate for election to MidWestOne Financial Group’s board of directors at the 2006 annual shareholders’ meeting. He served on the Central Valley Bank board for 10 years. Dr. Hill is an associate with the Medical Arts Clinic, P.C. in Fairfield, Iowa.

A native of Fairfield, Dr. Hill returned home to practice after serving as an intern in Des Moines. He retains staff privileges at many area hospitals and serves as deputy coroner for Jefferson County in Iowa. Dr. Hill has been active on various medical boards and associated with numerous private and civic organizations. He was named Physician of the Year by the Iowa Osteopathic Medical Association in 1998.

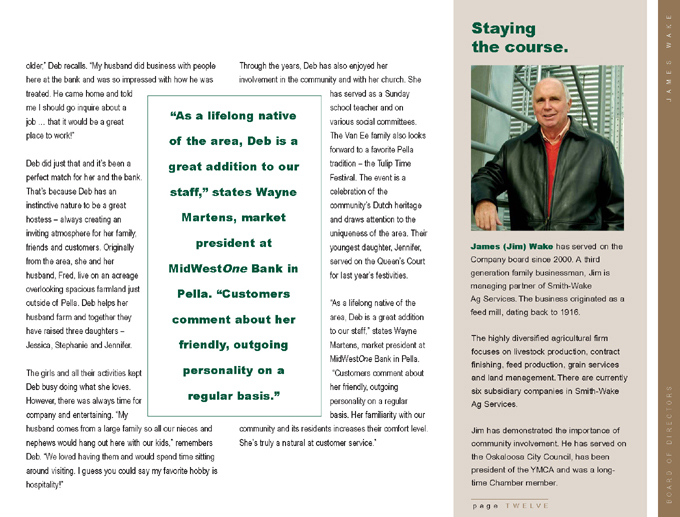

Deb Van Ee and her husband, Fred, enjoy rural life on an acreage just outside of Pella.

[GRAPHIC]

A True Hostess

It’s all about making customers feel welcome and at ease when Deb Van Ee is helping them with their financial needs. Deb is a personal banker at MidWestOne Bank in Pella. She started as a teller just five years ago and now assists customers with checking and savings accounts, certificates of deposit and daily management of their money.

“I had been a stay-at-home wife and mother and wanted to work outside the home as my children were getting

page ELEVEN

BOARD OF DIRECTORS

JAMES WAKE

older,” Deb recalls. “My husband did business with people here at the bank and was so impressed with how he was treated. He came home and told me I should go inquire about a job … that it would be a great place to work!”

Deb did just that and it’s been a perfect match for her and the bank. That’s because Deb has an instinctive nature to be a great hostess – always creating an inviting atmosphere for her family, friends and customers. Originally from the area, she and her husband, Fred, live on an acreage overlooking spacious farmland just outside of Pella. Deb helps her husband farm and together they have raised three daughters –Jessica, Stephanie and Jennifer.

The girls and all their activities kept Deb busy doing what she loves. However, there was always time for company and entertaining. “My husband comes from a large family so all our nieces and nephews would hang out here with our kids,” remembers Deb. “We loved having them and would spend time sitting around visiting. I guess you could say my favorite hobby is hospitality!”

Through the years, Deb has also enjoyed her involvement in the community and with her church. She has served as a Sunday school teacher and on various social committees. The Van Ee family also looks forward to a favorite Pella tradition – the Tulip Time Festival. The event is a celebration of the community’s Dutch heritage and draws attention to the uniqueness of the area. Their youngest daughter, Jennifer, served on the Queen’s Court for last year’s festivities.

“As a lifelong native of the area, Deb is a great addition to our staff,” states Wayne Martens, market president at MidWestOne Bank in Pella. “Customers comment about her friendly, outgoing personality on a regular basis. Her familiarity with our community and its residents increases their comfort level. She’s truly a natural at customer service.”

“As a lifelong native of the area, Deb is a great addition to our staff,” states Wayne Martens, market president at MidWestOne Bank in Pella. “Customers comment about her friendly, outgoing personality on a regular basis.”

Staying the course.

[GRAPHIC]

James (Jim) Wake has served on the Company board since 2000. A third generation family businessman, Jim is managing partner of Smith-Wake Ag Services. The business originated as a feed mill, dating back to 1916.

The highly diversified agricultural firm focuses on livestock production, contract finishing, feed production, grain services and land management. There are currently six subsidiary companies in Smith-Wake Ag Services.

Jim has demonstrated the importance of community involvement. He has served on the Oskaloosa City Council, has been president of the YMCA and was a long-time Chamber member.

page TWELVE

BOARD OF DIRECTORS

ROBERT WERSEN

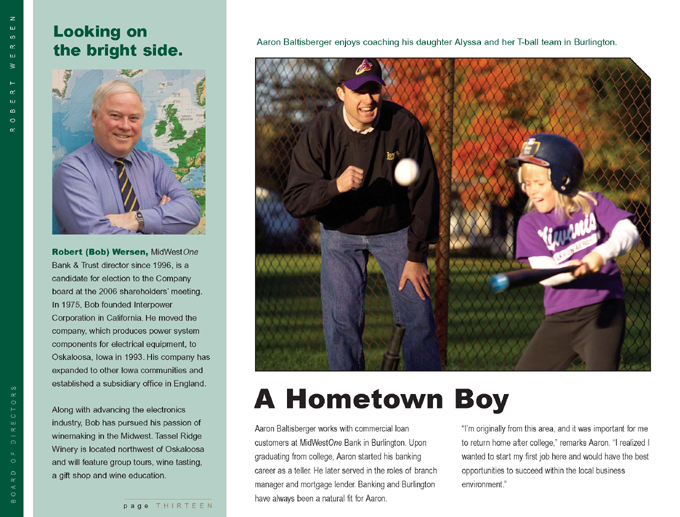

Looking on the bright side.

[GRAPHIC]

Robert (Bob) Wersen, MidWestOne Bank & Trust director since 1996, is a candidate for election to the Company board at the 2006 shareholders’ meeting. In 1975, Bob founded Interpower Corporation in California. He moved the company, which produces power system components for electrical equipment, to Oskaloosa, Iowa in 1993. His company has expanded to other Iowa communities and established a subsidiary office in England.

Along with advancing the electronics industry, Bob has pursued his passion of winemaking in the Midwest. Tassel Ridge Winery is located northwest of Oskaloosa and will feature group tours, wine tasting, a gift shop and wine education.

Aaron Baltisberger enjoys coaching his daughter Alyssa and her T-ball team in Burlington.

[GRAPHIC]

A Hometown Boy

Aaron Baltisberger works with commercial loan customers at MidWestOne Bank in Burlington. Upon graduating from college, Aaron started his banking career as a teller. He later served in the roles of branch manager and mortgage lender. Banking and Burlington have always been a natural fit for Aaron.

“I’m originally from this area, and it was important for me to return home after college,” remarks Aaron. “I realized I wanted to start my first job here and would have the best opportunities to succeed within the local business environment.”

page THIRTEEN

Aaron’s commitment to Burlington is a true testament to the types of communities served by MidWestOne Bank. Located along the scenic Mississippi River, Burlington is a city where its rich history is the driving force for the community’s prosperity today. Pioneer settlers were able to attract water and rail traffic and capitalize on these transportation assets to develop industry and growth. Now, over 150 years later, Burlington residents still build community camaraderie around the city’s assets. And Aaron shares the same sentiment to bolster his hometown.

“I knew everything Burlington had to offer growing up here,” reminisces Aaron. “I was ready to be actively involved in groups and events that bring out what is best about living here. I appreciate the bank encouraging our involvement as it really matters to all local residents and businesses.”

Aaron’s first commitment is his family. Married to his high school sweetheart, he and Gwen have two daughters –Alyssa and Katie. He especially enjoys coaching Alyssa’s T-ball team. The Baltisbergers also dedicate time to the local Girl Scouts.

Among the many civic organizations in Burlington, Aaron belongs to Kiwanis, which has a consistent focus on helping local children. He also participates in Junior Achievement – teaching middle school students about banking and financial topics. Aaron supports the business community as a Chamber ambassador.

Warmer weather brings entertaining events such as Steamboat Days – an American music festival on the riverfront. The regional event draws over 50,000 visitors to the area every year. Aaron has served as treasurer for the event and works consistently through the year on fundraising activities.

At MidWestOne, taking a local interest comes effortlessly.

Whether it’s our time or a financial donation, when something makes the communities we care about grow and prosper, it deserves our support.

“I was ready to be actively involved in groups and events that bring out what is best about living here. I appreciate the bank encouraging our involvement as it really matters to all local residents and businesses.”

[GRAPHIC]

page FOURTEEN

[GRAPHIC]

Consolidated Balance SHEETS

December 31 (in thousands)

2005

2004

Assets

Cash and due from banks

$13,103

14,117

Interest-bearing deposits in banks

417

368

Federal funds sold

—

930

Cash and cash equivalents

13,520

15,415

Investment securities:

Available for sale

74,506

87,795

Held to maturity (fair value of $12,925 in 2005 and $9,486 in 2004)

12,986

9,190

Loans

433,437

398,854

Allowance for loan losses

(5,011)

(4,745)

Net loans

428,426

394,109

Loan pool participations

103,570

105,502

Premises and equipment, net

10,815

10,492

Accrued interest receivable

5,334

4,573

Goodwill

13,268

13,156

Other intangible assets

1,417

1,318

Other assets

12,490

9,014

Total assets

$676,332

650,564

Liabilities And S Hareholders’ Equity

Deposits:

Demand

$50,309

46,016

Interest-bearing checking accounts

65,435

67,993

Savings

115,218

125,247

Certificates of deposit

274,283

235,846

Total deposits

505,245

475,102

Federal funds purchased

7,575

2,090

Federal Home Loan Bank advances

83,100

91,874

Notes payable

6,100

9,700

Long-term debt

10,310

10,310

Other liabilities

5,616

4,558

Total liabilities

617,946

593,634

Shareholders’ Equity

Common stock, $5 par value; authorized 20,000,000 shares; issued 4,912,849 as of December 31, 2005 and December 31, 2004

24,564

24,564

Capital surplus

12,886

12,956

Treasury stock at cost, 1,211,462 and 1,161,463 shares as of December 31, 2005 and December 31, 2004, respectively

(16,951)

(15,640)

Retained earnings

38,630

35,085

Accumulated other comprehensive loss

(743)

(35) |

|

Total shareholders’ equity

58,386

56,930

Total liabilities and shareholders’ equity

$676,332

650,564

pageFIFTEEN

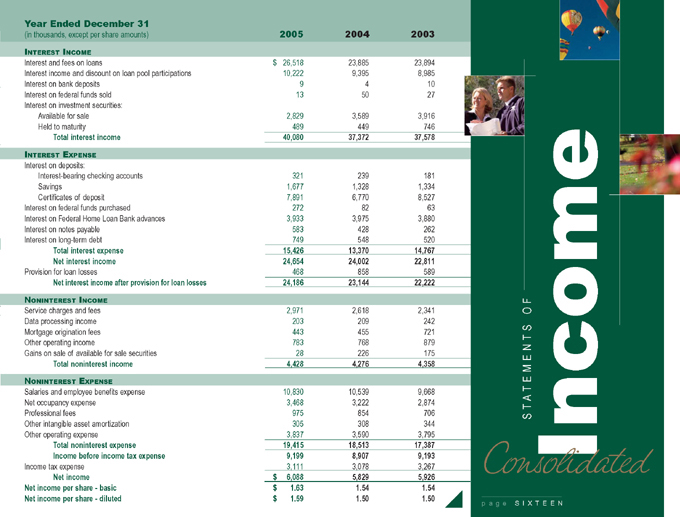

Consolidated Income STATEMENTS OF

Year Ended December 31

(in thousands, except per share amounts)

2005

2004

2003

Interest Income

Interest and fees on loans

$26,518

23,885

23,894

Interest income and discount on loan pool participations

10,222

9,395

8,985

Interest on bank deposits

9

4 |

|

10

Interest on federal funds sold

13

50

27

Interest on investment securities:

Available for sale

2,829

3,589

3,916

Held to maturity

489

449

746

Total interest income

40,080

37,372

37,578

Interest Expense

Interest on deposits:

Interest-bearing checking accounts

321

239

181

Savings

1,677

1,328

1,334

Certificates of deposit

7,891

6,770

8,527

Interest on federal funds purchased

272

82

63

Interest on Federal Home Loan Bank advances

3,933

3,975

3,880

Interest on notes payable

583

428

262

Interest on long-term debt

749

548

520

Total interest expense

15,426

13,370

14,767

Net interest income

24,654

24,002

22,811

Provision for loan losses

468

858

589

Net interest income after provision for loan losses

24,186

23,144

22,222

Noninterest Income

Service charges and fees

2,971

2,618

2,341

Data processing income

203

209

242

Mortgage origination fees

443

455

721

Other operating income

783

768

879

Gains on sale of available for sale securities

28

226

175

Total noninterest income

4,428

4,276

4,358

Noninterest Expense

Salaries and employee benefits expense

10,830

10,539

9,668

Net occupancy expense

3,468

3,222

2,874

Professional fees

975

854

706

Other intangible asset amortization

305

308

344

Other operating expense

3,837

3,590

3,795

Total noninterest expense

19,415

18,513

17,387

Income before income tax expense

9,199

8,907

9,193

Income tax expense

3,111

3,078

3,267

Net income

$6,088

5,829

5,926

Net income per share—basic

$1.63

1.54

1.54

Net income per share—diluted

$1.59

1.50

1.50

[GRAPHIC]

page SIXTEEN

[GRAPHIC]

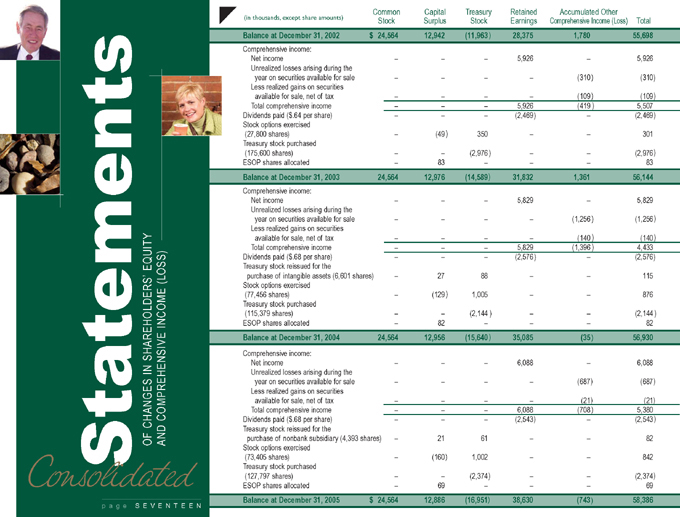

Consolidated Statements

OF CHANGES IN SHAREHOLDERS’ EQUITY AND COMPREHENSIVE INCOME (LOSS)

(in thousands, except share amounts)

Common Stock

Capital Surplus

Treasury Stock

Retained Earnings

Accumulated Other Comprehensive Income (Loss)

Total

Balance at December 31, 2002

$24,564

12,942

(11,963)

28,375

1,780

55,698

Comprehensive income:

Net income

—

—

—

5,926

—

5,926

Unrealized losses arising during the year on securities available for sale

—

—

—

—

(310)

(310)

Less realized gains on securities available for sale, net of tax

—

—

—

—

(109)

(109)

Total comprehensive income

—

—

—

5,926

(419)

5,507

Dividends paid ($.64 per share)

—

—

—

(2,469)

—

(2,469)

Stock options exercised (27,800 shares)

—

(49) |

|

350

—

—

301

Treasury stock purchased (175,600 shares)

—

—

(2,976)

—

—

(2,976)

ESOP shares allocated

—

83

—

—

—

83

Balance at December 31, 2003

24,564

12,976

(14,589)

31,832

1,361

56,144

Comprehensive income:

Net income

—

—

—

5,829

—

5,829

Unrealized losses arising during the year on securities available for sale

—

—

—

—

(1,256)

(1,256)

Less realized gains on securities available for sale, net of tax

—

—

—

—

(140)

(140)

Total comprehensive income

—

—

—

5,829

(1,396)

4,433

Dividends paid ($.68 per share)

—

—

—

(2,576)

—

(2,576)

Treasury stock reissued for the purchase of intangible assets (6,601 shares)

—

27

88

—

—

115

Stock options exercised (77,456 shares)

—

(129)

1,005

—

—

876

Treasury stock purchased (115,379 shares)

—

—

(2,144)

—

—

(2,144)

ESOP shares allocated

—

82

—

—

—

82

Balance at December 31, 2004

24,564

12,956

(15,640)

35,085

(35) |

|

56,930

Comprehensive income:

Net income

—

—

—

6,088

—

6,088

Unrealized losses arising during the year on securities available for sale

—

—

—

—

(687)

(687)

Less realized gains on securities available for sale, net of tax

—

—

—

—

(21) |

|

(21) |

|

Total comprehensive income

—

—

—

6,088

(708)

5,380

Dividends paid ($.68 per share)

—

—

—

(2,543)

—

(2,543)

Treasury stock reissued for the purchase of nonbank subsidiary (4,393 shares)

—

21

61

—

—

82

Stock options exercised (73,405 shares)

—

(160)

1,002

—

—

842

Treasury stock purchased (127,797 shares)

—

—

(2,374)

—

—

(2,374)

ESOP shares allocated

—

69

—

—

—

69

Balance at December 31, 2005

$24,564

12,886

(16,951)

38,630

(743)

58,386

page SEVENEEN

[GRAPHIC]

Information Company

AUDITOR’S

Report

Report of Independent Registered Public Accounting Firm

To the Board of Directors of MidWestOne Financial Group, Inc.:

We have audited, in accordance with the standards of the Public Company Accounting Oversight Board (United States), the consolidated balance sheets of MidWestOne Financial Group, Inc. as of December 31, 2005 and 2004, and the related consolidated statements of income, changes in shareholders’ equity and comprehensive income and cash flows for each of the years in the three year period ended December 31, 2005 (not presented herein); and in our report dated March 10, 2006, we expressed an unqualified opinion on those consolidated financial statements.

In our opinion, the information set forth in the condensed consolidated financial information appearing on pages 15 through 17 is fairly presented, in all material respects, in relation to the consolidated financial statements from which it has been derived.

[GRAPHIC]

KPMG LLP

Des Moines, Iowa

March 10, 2006

MidWest One Financial Group, Inc. Common Stock trades on the Nasdaq National Market and the quotations are furnished by the Nasdaq system. There were 414 shareholders of record on December 31, 2005 and an estimated 1,100 additional beneficial holders whose stock was held in street name by brokerage houses.

Nasdaq Symbol OSKY

Corporate Headquarters

222 First Avenue East

P.O. Box 1104

Oskaloosa, IA 52577

(641) 673-8448

www.midwestonefinancial.com

Annual Shareholders’ Meeting

April 28, 2006, 10:30 a.m.

Elmhurst Country Club

2214 South 11th Street

Oskaloosa, IA 52577

Wall Street Journal and Other Newspapers

MdWstOneFnl or MdWsOnFn

Transfer Agent/Dividend Disbursing Agent

Illinois Stock Transfer Company

209 West Jackson Boulevard

Suite 903

Chicago, IL 60606

(312) 427-2953

(800) 757-5755

Independent Auditor

KPMG LLP

2500 Ruan Center

Des Moines, IA 50309

The following table sets forth the quarterly high and low closing price per share for the Company’s stock during 2005 and 2004.

‘05 Quarter Ended

High

Low

March 31

$20.26

$17.48

June 30

18.90

17.50

September 30

19.24

18.38

December 31

18.74

17.25

‘04 Quarter Ended

High

Low

March 31

$19.10

$18.25

June 30

18.95

17.65

September 30

18.36

17.20

December 31

20.96

17.68

As of December 31, 2005, the Company had 3,701,387 shares of Common Stock outstanding. On December 31, 2004, there were 3,751,386 shares outstanding. The Company has declared per share cash dividends with respect to its Common Stock as follows:

Quarter

1st

2nd

3rd

4th

2005

$.17

$.17

$.17

$.17

2004

$.17

$.17

$.17

$.17

FORM 10-K

Copies of the MidWestOne Financial Group, Inc. Annual Report to the Securities and Exchange Commission on Form 10-K will be mailed without charge to shareholders upon written request to Karen K. Binns, Secretary/Treasurer, at the corporate headquarters. It is also available on the Securities and Exchange Commission’s Internet website at: www.sec.gov/cgi-bin/srch-edgar.