Exhibit 13

2006 ANNUAL REPORT

Our Message to You… Our Valued Shareholders

Benjamin Disraeli once said, “The secret of success is constancy to purpose.” At MidWestOne Financial Group, Inc., our vision is to be the leading financial services provider in our communities. To attain this goal, we’ve defined our mission: Maximize shareholder value by a relentless focus on providing efficient service and support to our customers, employees and communities. Persistent determination toward fulfilling our mission and vision keep “success” in our realm.

One of our most significant accomplishments, the consolidation of our four banks, was attained in only nine months. While the consolidation was challenging, we are truly grateful to the efforts of each team member. Due to everyone’s dedication, the transition was complete January 1, 2006, and we have already started reaping the benefits. Many processes are no longer duplicated, creating more time to focus on the needs of our customers.

Not only did the consolidation create efficiencies, it has positioned us for current and future expansion. both in existing markets and into new ones. We have moved from our temporary location to our permanent banking office in historic downtown Davenport, Iowa. Locating downtown met the needs of both our bank and the community. This market, with immense potential, has already provided us with over $43 million in loans. With naming rights on the building just blocks from the Mississippi River, MidWestOne Bank will light up the Davenport skyline for years to come.

Additionally, in the fall of 2007, we’ll be opening a new location in Cedar Falls, Iowa. Our current offices in nearby Waterloo and Hudson already have customers from Cedar Falls who are anxiously awaiting the convenience of the new location. The combination of branches in Cedar Falls, Hudson and Waterloo will strategically position MidWestOne to effectively serve customers throughout the Cedar Valley area. leading to future growth.

In order for our company to be the leading financial services provider in our communities, we are committed to offering more than just banking services. Our investment and insurance firms, MidWestOne Investment Services, Inc. and Cook & Son Agency, Inc., work daily to integrate their services with those offered by the bank.

Steady growth in our existing markets led to strong portfolio growth in 2006. Total assets grew 10%, to end the year at $745 million. Net income increased $353,000, up 6% from 2005. The company earned $1.74 per share in 2006, compared to $1.63 in 2005. Additionally, MidWestOne share price grew 12.2%, with dividends up three cents per share over last year.

Our success in 2006 can be attributed to “constancy to purpose” – a relentless focus on our vision and mission. We invite you to peruse the next few pages for illustrations of our success and a glimpse through the eyes of the people that make it happen. our employees, community members and most importantly, our customers.

Charles S. Howard

Chairman, President & CEO, right

David A. Meinert

Executive Vice President & CFO, left

In 2006, Cook & Son Agency exceeded revenue and earnings goals by expanding its customer base.

MidWestOne Bank opened 16,087 new accounts in 2006.

Company-wide, MidWestOne employs 236 people.

Revenue generated from sales was up 89% for MidWestOne Investment Services in 2006.

2006 Financial Highlights

Year Ended December 31 | ||||||||||||||||

(in thousands, except per share amounts) |

| 2006 |

| 2005 |

| 2004 |

| 2003 |

| 2002 |

| |||||

SUMMARY OF INCOME DATA | ||||||||||||||||

Interest income excluding loan pool participations | $ | 37,312 |

| 29,858 |

| 27,977 |

| 28,593 |

| 27,482 |

| |||||

Interest and discount on loan pool participations |

| 9,142 |

| 10,222 |

| 9,395 |

| 8,985 |

| 10,058 |

| |||||

Total interest income |

| 46,454 |

| 40,080 |

| 37,372 |

| 37,578 |

| 37,540 |

| |||||

Total interest expense |

| 21,209 |

| 15,426 |

| 13,370 |

| 14,767 |

| 17,027 |

| |||||

Net interest income |

| 25,245 |

| 24,654 |

| 24,002 |

| 22,811 |

| 20,513 |

| |||||

Provision for loan losses |

| 180 |

| 468 |

| 858 |

| 589 |

| 1,070 |

| |||||

Noninterest income |

| 5,928 |

| 4,428 |

| 4,276 |

| 4,358 |

| 3,787 |

| |||||

Noninterest expense |

| 21,459 |

| 19,415 |

| 18,513 |

| 17,387 |

| 14,426 |

| |||||

Income before income tax |

| 9,534 |

| 9,199 |

| 8,907 |

| 9,193 |

| 8,804 |

| |||||

Income tax expense |

| 3,093 |

| 3,111 |

| 3,078 |

| 3,267 |

| 3,015 |

| |||||

Net income | $ | 6,441 |

| 6,088 |

| 5,829 |

| 5,926 |

| 5,789 |

| |||||

PER SHARE DATA | ||||||||||||||||

Net income - basic | $ | 1.74 |

| 1.63 |

| 1.54 |

| 1.54 |

| 1.49 |

| |||||

Net income - diluted |

| 1.71 |

| 1.59 |

| 1.50 |

| 1.50 |

| 1.46 |

| |||||

Cash dividends declared |

| 0.71 |

| 0.68 |

| 0.68 |

| 0.64 |

| 0.64 |

| |||||

Book value |

| 16.83 |

| 15.77 |

| 15.18 |

| 14.84 |

| 14.17 |

| |||||

Net tangible book value |

| 12.92 |

| 11.81 |

| 11.32 |

| 11.08 |

| 11.53 |

| |||||

SELECTED FINANCIAL RATIOS | ||||||||||||||||

Net income to average assets |

| 0.92 | % | 0.93 | % | 0.92 | % | 0.98 | % | 1.07 | % | |||||

Net income to average equity |

| 10.65 | % | 10.49 | % | 10.23 | % | 10.52 | % | 10.91 | % | |||||

Dividend payout ratio |

| 40.80 | % | 41.72 | % | 44.16 | % | 41.56 | % | 42.95 | % | |||||

Total shareholders’ equity to total assets |

| 8.39 | % | 8.63 | % | 8.75 | % | 9.01 | % | 10.37 | % | |||||

Tangible shareholders’ equity to tangible assets |

| 6.57 | % | 6.59 | % | 6.67 | % | 6.88 | % | 8.60 | % | |||||

Tier 1 capital ratio |

| 10.01 | % | 10.38 | % | 10.88 | % | 11.20 | % | 14.67 | % | |||||

Net interest margin |

| 3.99 | % | 4.11 | % | 4.14 | % | 4.10 | % | 4.10 | % | |||||

Gross revenue of loan pools to total gross revenue |

| 17.45 | % | 22.97 | % | 22.17 | % | 21.42 | % | 24.34 | % | |||||

Allowance for loan losses to total loans |

| 1.13 | % | 1.16 | % | 1.19 | % | 1.29 | % | 1.30 | % | |||||

Non-performing loans to total loans |

| 1.15 | % | 0.77 | % | 0.73 | % | 0.83 | % | 0.86 | % | |||||

Net loans charged off (recovered) to average loans |

| (0.11 | %) | 0.05 | % | 0.25 | % | 0.08 | % | 0.15 | % | |||||

December 31 (in thousands) |

| 2006 |

| 2005 |

| 2004 |

| 2003 |

| 2002 |

| |||||

SELECTED BALANCE SHEET DATA | ||||||||||||||||

Total assets | $ | 744,911 |

| 676,332 |

| 650,564 |

| 623,306 |

| 537,026 |

| |||||

Total loans net of unearned discount |

| 503,832 |

| 433,437 |

| 398,854 |

| 377,017 |

| 306,024 |

| |||||

Total loan pool participations |

| 98,885 |

| 103,570 |

| 105,502 |

| 89,059 |

| 82,341 |

| |||||

Allowance for loan losses |

| 5,693 |

| 5,011 |

| 4,745 |

| 4,857 |

| 3,967 |

| |||||

Total deposits |

| 560,615 |

| 505,245 |

| 475,102 |

| 453,125 |

| 395,546 |

| |||||

Total shareholders’ equity |

| 62,533 |

| 58,386 |

| 56,930 |

| 56,144 |

| 55,698 |

|

OUR MISSION To maximize shareholder value by a relentless focus on…

…providing efficient service and support to our employees.

Providing efficient service and support to our customers and communities stems from the dedication and efforts of our employees. It is a mission that cannot be fulfilled by only one person, but the team as a whole.

“Every customer deserves access to comprehensive wealth management, and that vision from MidWestOne leadership sets the agenda for our growing investment services division. Eventually, we’d like to see a financial adviser on-site at every location. We offer advice for every stage of our customers’ financial planning: asset accumulation, income distribution and strategic planning for future wealth transfers. After ten years in large corporate settings, I welcome the caring family atmosphere of MidWestOne and I appreciate our accessible leaders.”

- Mike Roozeboom, President, MidWestOne Investment Services, Pella

“As we open new offices, we’re committed to hiring upbeat, positive self-starters who work well with one another—individuals whose overall outlook creates a ripple effect throughout the rest of the staff and customer base. I was hired with extensive management experience so I notice the talents of the people who work for an organization, as well as the quality of the training provided. MidWestOne sends every new employee to a comprehensive orientation focused on how we cater to our customers. It is so impressive. and Charlie Howard is there to meet everyone. Having an opportunity to get to know the CEO is a real team-builder and is so refreshing!”

- Wendy Terronez, Branch Manager/Consumer Loan Officer, Davenport

“Right out of college, I started as a teller at another bank and worked my way up. Coming home to Waterloo in April 2005 to work for MidWestOne was a great move. Banking is so much more than calculations, charts or crunching numbers. Here, it’s about people. As a community bank, we are empowered to make decisions based on our knowledge of our customers’ needs, their businesses and the overall business climate. Best of all, I like how all of us, staff as well as customers, feel like family.”

- Luke Lesyshen, Commercial Loan Officer, Waterloo

Mike

Wendy

Luke

At MidWestOne,our timeless values - demonstrating we care, listening to needs, being proactive and taking that extra step—provide endless possibilities, not only to our customers, but also to our communities and shareholders.

As we’ve ventured into metropolitan areas, it’s become evident that the community-feel offered by MidWestOne is truly valued. Starting from nothing, the Davenport office has grown to $43 million in assets in a little over a year. Brian Cornwell, market president in Davenport, said, “Our growth has been tremendous. There are banks that have been in town for over 50 years whose book of business is only three to four times the size of what we’ve done so far.”

David Meinert, MidWestOne’s executive vice president and CFO, mentioned, “Markets like Davenport and Waterloo/Cedar Falls have tremendous growth potential. It is incredible to enter new communities with absolutely no presence and be able to make such an impact.” MidWestOne seems to be well received because of personalized service and community spirit put forth. “We take pride that our employees serve on civic boards, coordinate fundraisers and volunteer to help kids in the community. Our presence in all of our markets is much more than simply financial.”

…providing efficient service and support

“By building a new location, we’re showing we are committed to the community. committed to expanding, growing and investing here.” - Jim Chizek, Market President in the Cedar Valley

Waterloo and Cedar Falls are similar to Davenport in the fact that together they have a large population, yet there is still the desire for community banking. “Anyone can make a loan, but not all banks have relationships with their customers,” said Jim Chizek, market president in the Cedar Valley. “Banking is a win/win partnership that means we succeed if they succeed. My customers are my friends. We are partners.”

to our communities.

“It matters to us that MidWestOne has made the commitment to our region by joining our momentum for revitalization. Welcome to Davenport!”

- Dan Huber, former President, DavenportOne

Theodore Roosevelt once said, “Far and away the best prize that life offers is the chance to work hard at work worth doing.” At MidWestOne, we not only believe our services make a difference, our customers affirm it.

“Jim, my banker at MidWestOne, knows me, my business and our community. Not only has he given me sound advice, he’s actually saved me money and even stopped me when I was about to make a costly decision that wasn’t best for business. Best of all, when I walk into MidWestOne, everyone knows my name, welcomes me and is genuinely eager to help me achieve my goals.”

- Robert Klein, Co-Owner of B.K. Tile, MidWestOne Bank customer, Cedar Falls

“From the determination of my line of credit, to the lot purchase and groundbreaking, to project completion was an extraordinary relationship. I give many thanks to the professional staff at MidWestOne. They went above and beyond to see to it the financials were done correctly and promptly. I felt like my project was their only one. Not having to worry about banking details allowed me to stay focused on being a doctor and put my remaining time and energy into overlooking the construction itself. Having a bank like MidWestOne made building a new facility much easier than I ever imagined.”

- Dr. Anthony D. Bailey, MidWestOne Bank customer, Cedar Falls

…providing efficient service and support

“ It’s a very people thing! I bank with MidWestOne because I know, trust and appreciate their entire team. expert advice has facilitated years of our growth and success.”

- Robert Klein, MidWestOne Bank customer, Cedar Falls

Jim

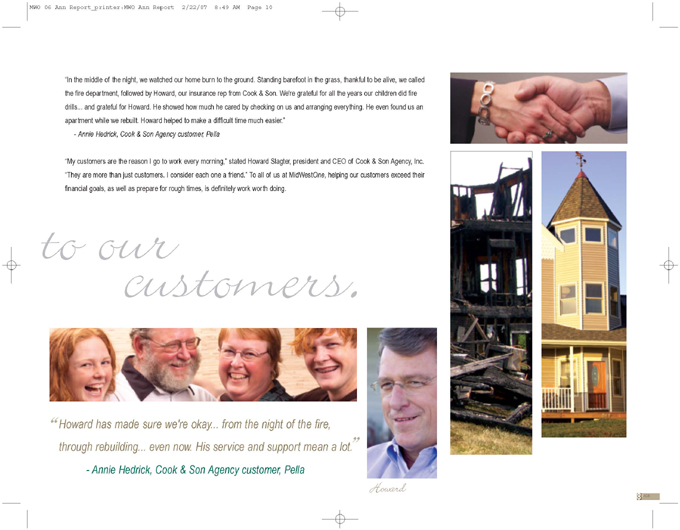

“In the middle of the night, we watched our home burn to the ground. Standing barefoot in the grass, thankful to be alive, we called the fire department, followed by Howard, our insurance rep from Cook & Son. We’re grateful for all the years our children did fire drills. and grateful for Howard. He showed how much he cared by checking on us and arranging everything. He even found us an apartment while we rebuilt. Howard helped to make a difficult time much easier.”

-Annie Hedrick, Cook & Son Agency customer, Pella

“My customers are the reason I go to work every morning,” stated Howard Slagter, president and CEO of Cook & Son Agency, Inc. “They are more than just customers. I consider each one a friend.” To all of us at MidWestOne, helping our customers exceed their financial goals, as well as prepare for rough times, is definitely work worth doing.

to our customers.

“Howard has made sure we’re okay. from the night of the fire, through rebuilding. even now. His service and support mean a lot.”

- Annie Hedrick, Cook & Son Agency customer, Pella

Howard

OUR VISION

To be the leading financial services provider…

…in our communities.

Today, financial services encompass so much more than simply offering checking and savings accounts. Members of MidWestOne Financial Group work together to provide comprehensive financial and fiscal management, through banking, investments and insurance.

Sue and John Doty, who are enjoying retirement in their charming condo in downtown Pella, Iowa, can attest to the importance of sound financial planning. “John plays golf almost every day and I enjoy just not working,” commented Sue. Not only has the couple utilized the advisers at MidWestOne Investment Services, they have had a long-time banking relationship at MidWestOne Bank. Their financial adviser helped Sue and John manage their 401(k)s and profit sharing plans in such a way that when John retired at 62, Sue could retire too, even though she was only 55. “We’ve always appreciated working with a company we know and trust. Employees are friendly, knowledgeable and go the extra step to make sure we are meeting our financial goals, whether it is banking or investments.”

No matter the community, you will find many different people with many different financial needs. Whether it is a young child, a college student, a couple that just got married or someone looking to retire, our mission is to help them every step along the way.

“ We love retirement. Thanks to our financial planning adviser, we were able to retire early!”

- Sue Doty, MidWestOne Investment Services customer, Pella

CONSOLIDATED Balance SHEETS

December 31 (in thousands) |

| 2006 |

| 2005 |

| ||

ASSETS | |||||||

Cash and due from banks | $ | 20,279 |

| 13,103 |

| ||

Interest-bearing deposits in banks |

| 447 |

| 417 |

| ||

Cash and cash equivalents |

| 20,726 |

| 13,520 |

| ||

Investment securities: | |||||||

Available for sale |

| 70,743 |

| 74,506 |

| ||

Held to maturity (fair value of $12,168 in 2006 and $12,925 in 2005) |

| 12,220 |

| 12,986 |

| ||

Loans |

| 503,832 |

| 433,437 |

| ||

Allowance for loan losses |

| (5,693 | ) | (5,011 | ) | ||

Net loans |

| 498,139 |

| 428,426 |

| ||

Loan pool participations |

| 98,885 |

| 103,570 |

| ||

Premises and equipment, net |

| 12,327 |

| 10,815 |

| ||

Accrued interest receivable |

| 6,587 |

| 5,334 |

| ||

Goodwill |

| 13,405 |

| 13,405 |

| ||

Other intangible assets |

| 1,128 |

| 1,417 |

| ||

Other assets |

| 10,751 |

| 12,353 |

| ||

Total assets | $ | 744,911 |

| 676,332 |

| ||

LIABILITIES AND SHAREHOLDERS ‘E QUITY | |||||||

Deposits: | |||||||

Demand | $ | 64,291 |

| 50,309 |

| ||

Interest-bearing checking accounts |

| 65,482 |

| 65,435 |

| ||

Savings |

| 101,443 |

| 115,218 |

| ||

Certificates of deposit |

| 329,399 |

| 274,283 |

| ||

Total deposits |

| 560,615 |

| 505,245 |

| ||

Federal funds purchased |

| 465 |

| 7,575 |

| ||

Federal Home Loan Bank advances |

| 99,100 |

| 83,100 |

| ||

Notes payable |

| 4,050 |

| 6,100 |

| ||

Long-term debt |

| 10,310 |

| 10,310 |

| ||

Accrued interest payable |

| 2,804 |

| 1,672 |

| ||

Other liabilities |

| 5,034 |

| 3,944 |

| ||

Total liabilities |

| 682,378 |

| 617,946 |

| ||

SHAREHOLDERS’ EQUITY | |||||||

Common stock, $5 par value; authorized 20,000,000 shares;issued 4,912,849 as of December 31, 2006 and December 31, 2005 |

| 24,564 |

| 24,564 |

| ||

Capital surplus |

| 13,076 |

| 12,886 |

| ||

Treasury stock at cost; 1,197,418 and 1,211,462 shares as of December 31, 2006 and December 31, 2005, respectively |

| (17,099 | ) | (16,951 | ) | ||

Retained earnings |

| 42,447 |

| 38,630 |

| ||

Accumulated other comprehensive loss |

| (455 | ) | (743 | ) | ||

Total shareholders’ equity |

| 62,533 |

| 58,386 |

| ||

Total liabilities and shareholders’ equity | $ | 744,911 |

| 676,332 |

|

CONSOLIDATED STATEMENTS OF Income

Year Ended December 31 | ||||||||

(in thousands, except per share amounts) |

| 2006 |

| 2005 | 2004 | |||

INTEREST INCOME | ||||||||

Interest and fees on loans | $ | 33,897 |

| 26,518 | 23,885 | |||

Interest income and discount on loan pool participations |

| 9,142 |

| 10,222 | 9,395 | |||

Interest on bank deposits |

| 32 |

| 9 | 4 | |||

Interest on federal funds sold |

| 84 |

| 13 | 50 | |||

Interest on investment securities: | ||||||||

Available for sale |

| 2,809 |

| 2,829 | 3,589 | |||

Held to maturity |

| 490 |

| 489 | 449 | |||

Total interest income |

| 46,454 |

| 40,080 | 37,372 | |||

INTEREST EXPENSE | ||||||||

Interest on deposits: | ||||||||

Interest-bearing checking accounts |

| 347 |

| 321 | 239 | |||

Savings |

| 2,818 |

| 1,677 | 1,328 | |||

Certificates of deposit |

| 11,880 |

| 7,891 | 6,770 | |||

Interest on federal funds purchased |

| 418 |

| 272 | 82 | |||

Interest on Federal Home Loan Bank advances |

| 4,446 |

| 3,933 | 3,975 | |||

Interest on notes payable |

| 373 |

| 583 | 428 | |||

Interest on long-term debt |

| 927 |

| 749 | 548 | |||

Total interest expense |

| 21,209 |

| 15,426 | 13,370 | |||

Net interest income |

| 25,245 |

| 24,654 | 24,002 | |||

Provision for loan losses |

| 180 |

| 468 | 858 | |||

Net interest income after provision for loan losses |

| 25,065 |

| 24,186 | 23,144 | |||

NONINTEREST INCOME | ||||||||

Service charges and fees |

| 2,831 |

| 2,309 | 2,292 | |||

Brokerage commissions |

| 995 |

| 564 | 326 | |||

Insurance commissions |

| 705 |

| 218 | 85 | |||

Data processing income |

| 219 |

| 203 | 209 | |||

Mortgage origination fees |

| 580 |

| 443 | 455 | |||

Other operating income |

| 810 |

| 663 | 683 | |||

Gains (losses) on sale of available for sale securities |

| (212 | ) | 28 | 226 | |||

Total noninterest income |

| 5,928 |

| 4,428 | 4,276 | |||

NONINTEREST EXPENSE | ||||||||

Salaries and employee benefits expense |

| 12,546 |

| 10,830 | 10,539 | |||

Net occupancy expense |

| 3,491 |

| 3,468 | 3,222 | |||

Professional fees |

| 656 |

| 975 | 854 | |||

Other intangible asset amortization |

| 289 |

| 305 | 308 | |||

Other operating expense |

| 4,477 |

| 3,837 | 3,590 | |||

Total noninterest expense |

| 21,459 |

| 19,415 | 18,513 | |||

Income before income tax expense |

| 9,534 |

| 9,199 | 8,907 | |||

Income tax expense |

| 3,093 |

| 3,111 | 3,078 | |||

Net income | $ | 6,441 |

| 6,088 | 5,829 | |||

Net income per share - basic | $ | 1.74 |

| 1.63 | 1.54 | |||

Net income per share - diluted | $ | 1.71 |

| 1.59 | 1.50 |

CONSOLIDATED Statements OF CHANGES IN SHAREHOLDERS’ EQUITY AND COMPREHENSIVE INCOME (LOSS)

(in thousands, except per share amounts) | | Common | Capital | | Treasury | | Retained | | Accumulated | | Total |

| ||||||

Balance at December 31, 2003 | $ | 24,564 | 12,976 |

| (14,589 | ) | 31,832 |

| 1,361 |

| 56,144 |

| ||||||

Comprehensive income: | ||||||||||||||||||

Net income |

| – | – |

| – |

| 5,829 |

| – |

| 5,829 |

| ||||||

Unrealized losses arising during the year on securities available for sale |

| – | – |

| – |

| – |

| (1,256 | ) | (1,256 | ) | ||||||

Less realized gains on securities available for sale, net of tax |

| – | – |

| – |

| – |

| (140 | ) | (140 | ) | ||||||

Total comprehensive income |

| – | – |

| – |

| 5,829 |

| (1,396 | ) | 4,433 |

| ||||||

Dividends paid ($.68 per share) |

| – | – |

| – |

| (2,576 | ) | – |

| (2,576 | ) | ||||||

Treasury stock reissued for the purchase of intangible assets (6,601 shares) |

| – | 27 |

| 88 |

| – |

| – |

| 115 |

| ||||||

Stock options exercised (77,456 shares) |

| – | (129 | ) | 1,005 |

| – |

| – |

| 876 |

| ||||||

Treasury stock purchased (115,379 shares) |

| – | – |

| (2,144 | ) | – |

| – |

| (2,144 | ) | ||||||

ESOP shares allocated |

| – | 82 |

| – |

| – |

| – |

| 82 |

| ||||||

Balance at December 31, 2004 |

| 24,564 | 12,956 |

| (15,640 | ) | 35,085 |

| (35 | ) | 56,930 |

| ||||||

Comprehensive income: | ||||||||||||||||||

Net income |

| – | – |

| – |

| 6,088 |

| – |

| 6,088 |

| ||||||

Unrealized losses arising during the year on securities available for sale |

| – | – |

| – |

| – |

| (687 | ) | (687 | ) | ||||||

Less realized gains on securities available for sale, net of tax |

| – | – |

| – |

| – |

| (21 | ) | (21 | ) | ||||||

Total comprehensive income |

| – | – |

| – |

| 6,088 |

| (708 | ) | 5,380 |

| ||||||

Dividends paid ($.68 per share) |

| – | – |

| – |

| (2,543 | ) | – |

| (2,543 | ) | ||||||

Treasury stock reissued for the purchase of nonbank subsidiary (4,393 shares) |

| – | 21 |

| 61 |

| – |

| – |

| 82 |

| ||||||

Stock options exercised (73,405 shares) |

| – | (160 | ) | 1,002 |

| – |

| – |

| 842 |

| ||||||

Treasury stock purchased (127,797 shares) |

| – | – |

| (2,374 | ) | – |

| – |

| (2,374 | ) | ||||||

ESOP shares allocated |

| – | 69 |

| – |

| – |

| – |

| 69 |

| ||||||

Balance at December 31, 2005 |

| 24,564 | 12,886 |

| (16,951 | ) | 38,630 |

| (743 | ) | 58,386 |

| ||||||

Comprehensive income: | ||||||||||||||||||

Net income |

| – | – |

| – |

| 6,441 |

| – |

| 6,441 |

| ||||||

Unrealized gains arising during the year on securities available for sale |

| – | – |

| – |

| – |

| 155 |

| 155 |

| ||||||

Less realized losses on securities available for sale, net of tax |

| – | – |

| – |

| – |

| 133 |

| 133 |

| ||||||

Total comprehensive income |

| – | – |

| – |

| 6,441 |

| 288 |

| 6,729 |

| ||||||

Dividends paid ($.71 per share) |

| – | – |

| – |

| (2,624 | ) | – |

| (2,624 | ) | ||||||

Stock-based compensation |

| – | 81 |

| 178 |

| – |

| – |

| 259 |

| ||||||

Stock options exercised (68,469 shares) |

| – | (16 | ) | 972 |

| – |

| – |

| 956 |

| ||||||

Treasury stock purchased (67,050 shares) |

| – | – |

| (1,298 | ) | – |

| – |

| (1,298 | ) | ||||||

ESOP shares allocated |

| – | 125 |

| – |

| – |

| – |

| 125 |

| ||||||

Balance at December 31, 2006 | $ | 24,564 | 13,076 |

| (17,099 | ) | 42,447 |

| (455 | ) | 62,533 |

|

INFORMATION Company

MidWestOne Financial Group, Inc. Common Stock trades on the NASDAQ Global Market and the quotations are furnished by the NASDAQ system. There were 412 shareholders of record on December 31, 2006 and an estimated 1,200 additional beneficial holders whose stock was held in street name by brokerage houses.

NASDAQ Symbol OSKY

Corporate Headquarters

222 First Avenue East P.O. Box 1104 Oskaloosa, IA 52577 (641) 673-8448 www.midwestonefinancial.com

Annual Shareholders’ Meeting

April 26, 2007, 10:30 a.m. The Peppertree 2274 Highway 63 Oskaloosa, IA 52577

Wall Street Journal and Other Newspapers

MdWstOneFnl or MdWsOnFn

Transfer Agent/Dividend Disbursing Agent

Illinois Stock Transfer Company

209 West Jackson Boulevard, Suite 903 Chicago, IL 60606 (312) 427-2953 (800) 757-5755

Independent Auditor

KPMG LLP 2500 Ruan Center Des Moines, IA 50309

The following table sets forth the quarterly high and low closing price per share for the Company’s stock during 2006 and 2005.

‘06 Quarter Ended |

| High |

| Low | ||

March 31 | $ | 19.80 | $ | 17.50 | ||

June 30 |

| 19.70 |

| 18.75 | ||

September 30 |

| 19.86 |

| 18.80 | ||

December 31 |

| 20.55 |

| 18.85 | ||

‘05 Quarter Ended |

| High |

| Low | ||

March 31 | $ | 20.26 | $ | 17.48 | ||

June 30 |

| 18.90 |

| 17.50 | ||

September 30 |

| 19.24 |

| 18.38 | ||

December 31 |

| 18.74 |

| 17.25 |

As of December 31, 2006, the Company had 3,715,431 shares of Common Stock outstanding. On December 31, 2005, there were 3,701,387 shares outstanding. The Company has declared per share cash dividends with respect to its Common Stock as follows:

Quarter |

| 1st |

| 2nd |

| 3rd |

| 4th | ||||

2006 | $ | .17 | $ | .18 | $ | .18 | $ | .18 | ||||

2005 | $ | .17 | $ | .17 | $ | .17 | $ | .17 |

FORM 10-K

Copies of the MidWestOne Financial Group, Inc. Annual Report to the Securities and Exchange Commission on Form 10-K will be mailed without charge to shareholders upon written request to Karen K. Binns, Secretary/Treasurer, at the corporate headquarters. It is also available on the Securities and Exchange Commission’s Internet website at: www.sec.gov/cgi-bin/srch-edgar.

20% of employees have worked for MidWestOne for more than 10 years.

All of our branches contribute to charitable causes in their communities.

OUR Corporate OFFICERS

Charles S. Howard, Chairman, President & CEO David A. Meinert, Executive Vice President & CFO Jeffrey L. Rhoads, Vice President/Finance Karen K. Binns, Secretary/Treasurer

Bryce C. Abbas, Auditor

Jeffrey D. Richards, Loan Review Officer

OUR Board OF DIRECTORS

Richard R. Donohue, TD&T Financial Group, P.C. • Dr. Donal D. Hill, Medical Arts Clinic, P.C.

Charles S. Howard,Chairman, President & CEO • Barbara J. Kniff-McCulla, KLK Construction Corp.

David A. Meinert, Executive Vice President & CFO • John P. Pothoven, President & CEO, MidWestOne Bank James G. Wake, Smith-Wake Ag Services • Michael R. Welter, M & M Enterprises Robert D. Wersen, Interpower Corporation • Edward C. Whitham, Financial Management Accounting, Inc. R. Scott Zaiser, Zaiser’s Landscaping, Inc.

OUR Locations

MidWestOne Bank www.midwestonebank.com

Oskaloosa • Belle Plaine • Burlington Davenport • Fairfield • Fort Madison Hudson • North English • Ottumwa • Pella Sigourney • Wapello • Waterloo

MidWestOne Investment Services, Inc.

Pella • Burlington • Fairfield • Oskaloosa Ottumwa • Sigourney

Cook & Son Agency, Inc. - Pella

Waterloo Hudson

Belle Plaine

North English

Davenport

Pella

Wapello

Oskaloosa

Sigourney

Ottumwa

Fairfield Burlington

Fort Madison