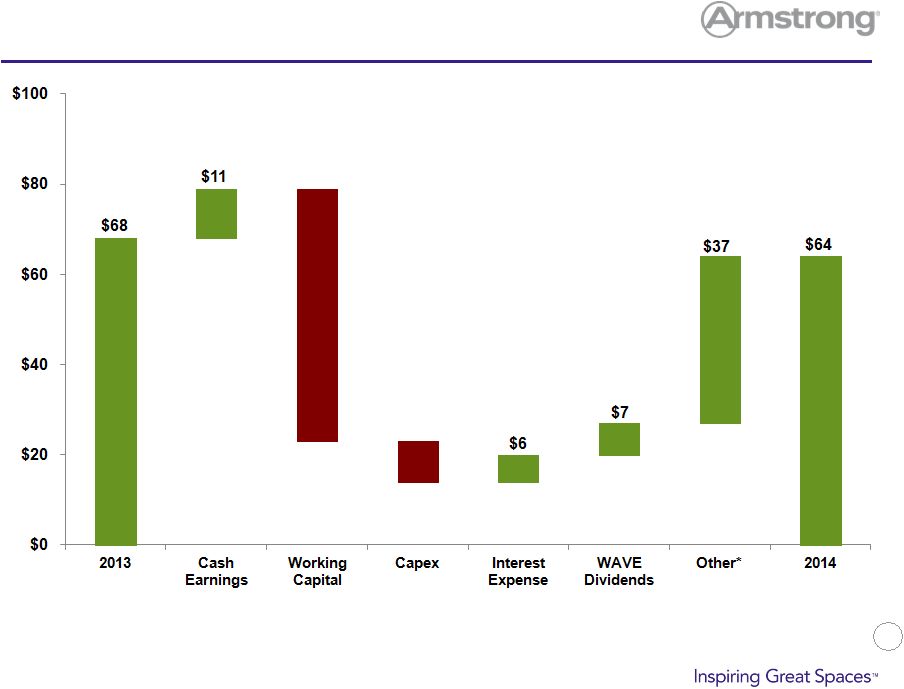

5 Creating Two Independent Industry Leaders [Armstrong World Industries] • Global commercial suspended ceiling solutions provider • #1 market position in all major geographies • Poised to deliver margin expansion driven by recovery in North American commercial • Recently completed investments in expanded sales and manufacturing capabilities • Attractive opportunities for enhanced growth and margins, including emerging markets • 23 year WAVE JV delivered $68M of cash dividends and $65M of equity earnings in 2014 Vic Grizzle Chief Executive Officer Key Statistics (2014 Year End) $1.3B (95/5) Revenue (% Commercial vs. Residential) $330M * Adjusted EBITDA ~3,400 Team Members Worldwide 22 Manufacturing Facilities in 8 Countries † 100+ Countries Have Armstrong Ceilings [Armstrong Flooring ] • Dedicated hard surface flooring products designer and manufacturer • Substantial margin expansion, driven by mix and operating leverage • Positioned to benefit from expected recovery in North American commercial • Significant growth opportunity in Asia • Well-positioned for both residential and non-residential cyclical recoveries Don Maier Chief Executive Officer Key Statistics (2014 Year End) $1.2B (35/65) Revenue (% Commercial vs. Residential) $114M * Adjusted EBITDA ~3,600 Team Members Worldwide 17 Manufacturing Facilities in 3 Countries 8,000,000+ Annual Visitors to Global Websites * Does not include unallocated corporate expense of $60 million †Including the WAVE JV |