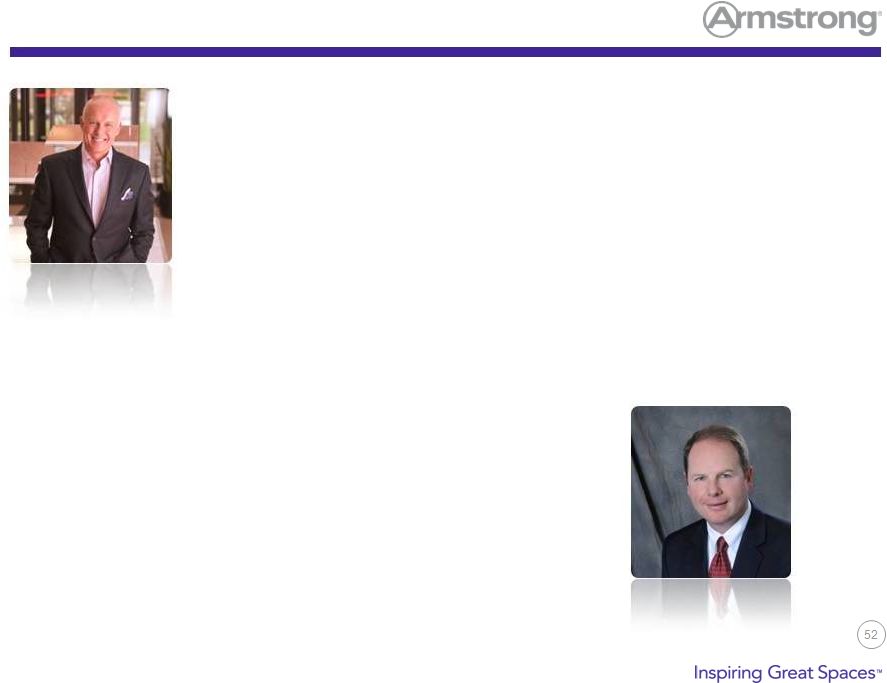

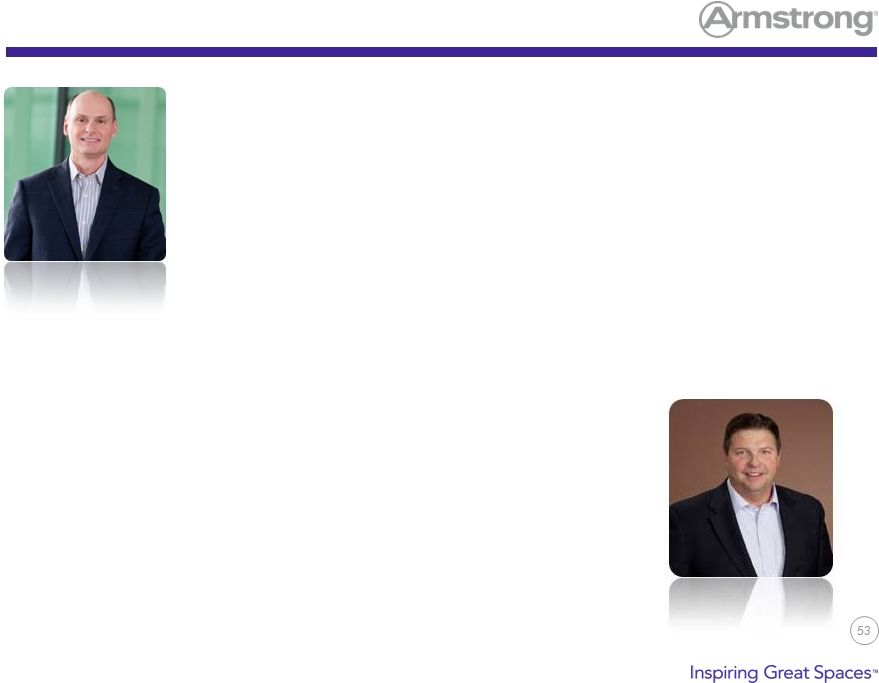

Matthew J. Espe, Chief Executive Officer and President In July 2010, Matthew J. Espe was appointed CEO of Armstrong World Industries, Inc., in Lancaster, Pennsylvania. Matt brings 30 years of experience in sales, marketing, distribution and management with global manufacturing businesses to Armstrong. In his previous role at Ricoh Americas Corporation, a subsidiary of Ricoh Company, Ltd., he served as chairman and CEO. Prior, he was chairman and CEO of IKON Office Solutions, Inc., a $4 billion office equipment distributor and services provider with 24,000 employees. Ricoh acquired IKON in 2008. Before joining IKON in 2002, Matt was president and CEO of GE Lighting. In a career that spanned 22 years there, he managed multiple business units as well as functions including sales, marketing, distribution and manufacturing. Along with a wealth of experience, he also brings a finely-tuned global perspective, having led businesses in Europe, Asia and North America. Matt is a former director of Unisys Corporation and Graphic Packaging, Inc. He currently serves on the advisory board at the College of Business and Economics at the University of Idaho and on the advisory council for Drexel University's Lebow College of Business, Center for Corporate Governance. Additionally, Matt is a member of the National Association of Corporate Directors (NACD) and the Wall Street Journal CEO Council. He graduated from the University of Idaho with a bachelor's degree in marketing, and received his MBA from Whittier College. David S. Schulz is senior vice president and CFO of Armstrong World Industries, Inc., in Lancaster, Pennsylvania. Mr. Schulz joined Armstrong in 2011 as vice president, finance for Armstrong Building Products. Prior, he served as CFO of Procter & Gamble Company’s Americas snacks division, and from 2008 to 2009 as the finance director for the Coffee business unit of the J.M. Smucker Co. following the merger of P&G’s Folgers Coffee Co. with Smucker. His experience covers a wide range of finance leadership positions encompassing operational finance, planning and analysis, mergers and acquisitions, and financial reporting. Well known as a strong business partner, Mr. Schulz actively engages with other functions to drive improvement. Prior to joining Procter & Gamble, Mr. Schulz was an officer in the United States Marine Corps. He earned his bachelor’s degree in finance from Villanova University in 1987 and a master’s degree in management from the U.S. Naval Postgraduate School in 1993. David S. Schulz, Senior Vice President and Chief Financial Officer |