Market Overview

Investor sentiment, marked by pessimism throughout much of the period, shifted to optimism toward the end of the calendar year. This transformation was fueled by indications of a possible soft landing for the U.S. economy and signals from the U.S. Federal Reserve ("Fed") about potential interest rate reductions in 2024. Positive reports on consumer spending, employment, rising personal income, and decreasing inflation further bolstered this improved outlook.

By the period's end, GDP growth stood at 4.9%, slightly revised down from the initially reported 5.2%. Both consumer spending and personal income showed increases, reflecting a relatively healthy consumer environment. While bond yields generally ended the period where they started, the bond market experienced several notable events. In October, U.S. Treasury 10-year yields reached levels unseen since 2007 as investors began to accept the Fed's resolve to maintain higher rates for longer. Yields sharply declined in December after the Fed, responding to encouraging inflation data, hinted at potential future rate reductions.

Equities gained broadly after falling earlier in the period, as previously overlooked market segments saw positive returns as rate expectations took hold. Small caps returned 8.6%, with small value outpacing small growth. While large caps added to yearly gains, posting a 9.7% return for the six-month period, according to the Russell family of indices.

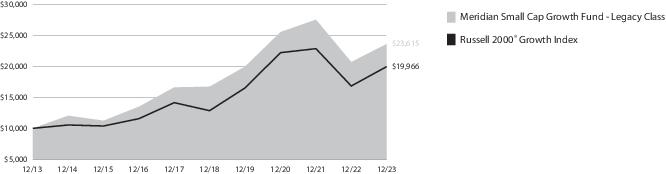

Fund Performance (as of December 31, 2023)

The Meridian Hedged Equity Fund (the “Fund”) Legacy Class Shares advanced 7.45% (net) for the six-month period ended December 31, 2023, underperforming its benchmark, the S&P 500® Index, which gained 8.04%. Additionally, the Fund outperformed its secondary benchmark the CBOE S&P Buy Write Index, which returned 1.23%.

Global equity volatility fell sharply in 2023 to levels last seen before the pandemic. However, we believe there are reasons to expect volatility to be biased higher in 2024 between lingering macro uncertainty, a continued risk of recession, and volatility historically tracking interest rates with a lag.

Our investment strategy prioritizes the management of downside risks over chasing excess returns. Over time, we expect the preservation of capital in down markets to be a quiet and powerful contributor to the long-term compounding of returns.

Our goal is to build and maintain a durable portfolio capable of minimizing losses during market downturns while participating in upswings. To achieve this, we focus on high-quality businesses with attractive valuations, substantial competitive advantages, strong balance sheets, robust cash flow, and limited volatility.

We focus on quality as a central tenet of our strategy. We own long positions in high-quality companies for growth potential, and when conditions warrant, we hedge select positions through call options in an attempt to enhance safety, generate income, and mitigate downside risks. We underpin this approach with thorough fundamental analysis that seeks to balance risks with the potential for long-term growth.

Leading individual contributors included Vistra Corp., Sally Beauty Holdings, Inc., and Zoom Communications, Inc.

Vistra Corp. is a leading integrated retail electricity and power generation company, primarily focused on the deregulated electricity market. The company provides a range of energy and utility services, including electricity generation, sales, and distribution to residential, commercial, and industrial customers. Vistra's business model combines efficient power generation with a robust retail platform. We believe the recent outperformance of the stock is attributable to a combination of strategic decisions and favorable market conditions. Firstly, the acquisition of Energy Harbor strategically expanded Vistra's portfolio, enhancing its focus on sustainable energy sources like nuclear and renewables. We believe this move aligns with the growing global emphasis on cleaner energy and positions Vistra favorably for future market trends. Secondly, we believe Vistra's strong financial performance, marked by robust free cash flow and increased EBITDA, reflects operational efficiency and sound management. The company's effective hedging strategies have provided stability against commodity price volatility. Additionally, Vistra's shareholder-friendly policies, including substantial share buybacks and attractive dividends, have significantly contributed to the stock's appreciation. We continued to hold Vistra in the Fund during the period.

Sally Beauty Holdings, Inc. is a global distributor of retail and professional beauty products and is the largest in the U.S. by store count. Its operations are divided into two main segments: Sally Beauty Supply, catering to retail consumers, and Beauty Systems Group, serving the needs of salons and stylists. The recent increase in the company's stock price can be attributed