UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-02258

Eaton Vance Series Trust II

(Exact Name of Registrant as Specified in Charter)

Two International Place, Boston, Massachusetts 02110

(Address of Principal Executive Offices)

Maureen A. Gemma

Two International Place, Boston, Massachusetts 02110

(Name and Address of Agent for Services)

(617) 482-8260

(Registrant’s Telephone Number)

October 31

Date of Fiscal Year End

April 30, 2017

Date of Reporting Period

Item 1. Reports to Stockholders

Eaton Vance

Income Fund of Boston

Semiannual Report

April 30, 2017

Commodity Futures Trading Commission Registration. Effective December 31, 2012, the Commodity Futures Trading Commission (“CFTC”) adopted certain regulatory changes that subject registered investment companies and advisers to regulation by the CFTC if a fund invests more than a prescribed level of its assets in certain CFTC-regulated instruments (including futures, certain options and swap agreements) or markets itself as providing investment exposure to such instruments. The Fund has claimed an exclusion from the definition of the term “commodity pool operator” under the Commodity Exchange Act. Accordingly, neither the Fund nor the adviser with respect to the operation of the Fund is subject to CFTC regulation. Because of its management of other strategies, the Fund’s adviser is registered with the CFTC as a commodity pool operator and a commodity trading advisor.

Fund shares are not insured by the FDIC and are not deposits or other obligations of, or guaranteed by, any depository institution. Shares are subject to investment risks, including possible loss of principal invested.

This report must be preceded or accompanied by a current summary prospectus or prospectus. Before investing, investors should consider carefully the investment objective, risks, and charges and expenses of a mutual fund. This and other important information is contained in the summary prospectus and prospectus, which can be obtained from a financial advisor. Prospective investors should read the prospectus carefully before investing. For further information, please call 1-800-262-1122.

Semiannual Report April 30, 2017

Eaton Vance

Income Fund of Boston

Table of Contents

| | | | |

Performance | | | 2 | |

| |

Fund Profile | | | 2 | |

| |

Endnotes and Additional Disclosures | | | 3 | |

| |

Fund Expenses | | | 4 | |

| |

Financial Statements | | | 5 | |

| |

Board of Trustees’ Contract Approval | | | 41 | |

| |

Officers and Trustees | | | 45 | |

| |

Important Notices | | | 46 | |

Eaton Vance

Income Fund of Boston

April 30, 2017

Performance1,2

Portfolio Managers Michael W. Weilheimer, CFA and Stephen C. Concannon, CFA

| | | | | | | | | | | | | | | | | | | | | | | | |

| % Average Annual Total Returns | | Class

Inception Date | | | Performance

Inception Date | | | Six Months | | | One Year | | | Five Years | | | Ten Years | |

Class A at NAV | | | 06/15/1972 | | | | 06/15/1972 | | | | 4.79 | % | | | 10.26 | % | | | 6.11 | % | | | 6.28 | % |

Class A with 4.75% Maximum Sales Charge | | | — | | | | — | | | | –0.12 | | | | 4.99 | | | | 5.08 | | | | 5.77 | |

Class B at NAV | | | 06/20/2002 | | | | 06/15/1972 | | | | 4.40 | | | | 9.24 | | | | 5.32 | | | | 5.50 | |

Class B with 5% Maximum Sales Charge | | | — | | | | — | | | | –0.60 | | | | 4.24 | | | | 4.99 | | | | 5.50 | |

Class C at NAV | | | 06/21/2002 | | | | 06/15/1972 | | | | 4.22 | | | | 9.24 | | | | 5.28 | | | | 5.50 | |

Class C with 1% Maximum Sales Charge | | | — | | | | — | | | | 3.22 | | | | 8.24 | | | | 5.28 | | | | 5.50 | |

Class I at NAV | | | 07/01/1999 | | | | 06/15/1972 | | | | 4.91 | | | | 10.52 | | | | 6.37 | | | | 6.57 | |

Class R at NAV | | | 01/05/2004 | | | | 06/15/1972 | | | | 4.66 | | | | 9.98 | | | | 5.84 | | | | 6.03 | |

Class R6 at NAV | | | 07/01/2014 | | | | 06/15/1972 | | | | 4.96 | | | | 10.42 | | | | 6.42 | | | | 6.59 | |

BofA Merrill Lynch U.S. High Yield Index | | | — | | | | — | | | | 5.50 | % | | | 13.66 | % | | | 6.87 | % | | | 7.32 | % |

BofA Merrill Lynch U.S. High Yield Constrained Index | | | — | | | | — | | | | 5.49 | | | | 13.65 | | | | 6.87 | | | | 7.40 | |

| | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| % Total Annual Operating Expense Ratios3 | | Class A | | | Class B | | | Class C | | | Class I | | | Class R | | | Class R6 | |

| | | 0.99 | % | | | 1.75 | % | | | 1.74 | % | | | 0.74 | % | | | 1.24 | % | | | 0.66 | % |

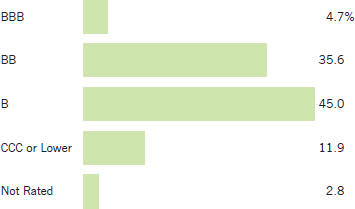

Fund Profile4

Credit Quality (% of bonds, loans and mortgage-backed securities)5

See Endnotes and Additional Disclosures in this report.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value (NAV) or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance less than or equal to one year is cumulative. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than quoted. Returns are before taxes unless otherwise noted. For performance as of the most recent month-end, please refer to eatonvance.com.

Eaton Vance

Income Fund of Boston

April 30, 2017

Endnotes and Additional Disclosures

| 1 | BofA Merrill Lynch U.S. High Yield Index is an unmanaged index of below-investment grade U.S. corporate bonds. BofA Merrill Lynch U.S. High Yield Constrained Index is an unmanaged index of below-investment grade U.S. corporate bonds, with issuer exposure capped at 2%. BofA Merrill Lynch® indices not for redistribution or other uses; provided “as is”, without warranties, and with no liability. Eaton Vance has prepared this report, BofAML does not endorse it, or guarantee, review, or endorse Eaton Vance’s products. Unless otherwise stated, index returns do not reflect the effect of any applicable sales charges, commissions, expenses, taxes or leverage, as applicable. It is not possible to invest directly in an index. |

| 2 | Total Returns at NAV do not include applicable sales charges. If sales charges were deducted, the returns would be lower. Total Returns shown with maximum sales charge reflect the stated maximum sales charge. Unless otherwise stated, performance does not reflect the deduction of taxes on Fund distributions or redemptions of Fund shares. |

| | Performance prior to the inception date of a class may be linked to the performance of an older class of the Fund. This linked performance is adjusted for any applicable sales charge, but is not adjusted for class expense differences. If adjusted for such differences, the performance would be different. Performance presented in the financial highlights included in the financial statements is not linked. In the performance table, the performance of Class R6 is linked to Class I. Performance since inception for an index, if presented, is the performance since the Fund’s or oldest share class’ inception, as applicable. |

| 3 | Source: Fund prospectus. The expense ratios for the current reporting period can be found in the Financial Highlights section of this report. |

| 4 | Fund invests in an affiliated investment company (Portfolio) with the same objective(s) and policies as the Fund. References to investments are to the Portfolio’s holdings. |

| 5 | Credit ratings are categorized using S&P. If S&P does not publish a rating, then the Moody’s rating is applied. Ratings, which are subject to change, apply to the creditworthiness of the issuers of the underlying securities and not to the Fund or its shares. Credit ratings measure the quality of a bond based on the issuer’s creditworthiness, with ratings ranging from AAA, being the highest, to D, being the lowest based on S&P’s measures. Ratings of BBB or higher by S&P or Baa or higher by Moody’s are considered to be investment-grade quality. Credit ratings are based largely on the ratings agency’s analysis at the time of rating. The rating assigned to any particular security is not necessarily a reflection of the issuer’s current financial condition and does not necessarily reflect its assessment of the volatility of a security’s market value or of the liquidity of an investment in the security. Holdings designated as “Not Rated” are not rated by the national ratings agencies stated above. |

| | Fund profile subject to change due to active management. |

Eaton Vance

Income Fund of Boston

April 30, 2017

Fund Expenses

Example: As a Fund shareholder, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchases and redemption fees (if applicable); and (2) ongoing costs, including management fees; distribution and/or service fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of Fund investing and to compare these costs with the ongoing costs of investing in other mutual funds. The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (November 1, 2016 – April 30, 2017).

Actual Expenses: The first section of the table below provides information about actual account values and actual expenses. You may use the information in this section, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first section under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes: The second section of the table below provides information about hypothetical account values and hypothetical expenses based on the actual Fund expense ratio and an assumed rate of return of 5% per year (before expenses), which is not the actual Fund return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in your Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) or redemption fees (if applicable). Therefore, the second section of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would be higher.

| | | | | | | | | | | | | | | | |

| | | Beginning Account Value (11/1/16) | | | Ending Account Value (4/30/17) | | | Expenses Paid During Period* (11/1/16 – 4/30/17) | | | Annualized Expense Ratio | |

| | | | |

| | | | | | | | | | | | | | | | |

Actual | | | | | | | | | | | | | | | | |

Class A | | $ | 1,000.00 | | | $ | 1,047.90 | | | $ | 5.13 | | | | 1.01 | % |

Class B | | $ | 1,000.00 | | | $ | 1,044.00 | | | $ | 8.92 | | | | 1.76 | % |

Class C | | $ | 1,000.00 | | | $ | 1,042.20 | | | $ | 8.91 | | | | 1.76 | % |

Class I | | $ | 1,000.00 | | | $ | 1,049.10 | | | $ | 3.86 | | | | 0.76 | % |

Class R | | $ | 1,000.00 | | | $ | 1,046.60 | | | $ | 6.39 | | | | 1.26 | % |

Class R6 | | $ | 1,000.00 | | | $ | 1,049.60 | | | $ | 3.40 | | | | 0.67 | % |

| | | | | | | | | | | | | | | | | |

| | | | |

| | | | | | | | | | | | | | | | |

Hypothetical | | | | | | | | | | | | | | | | |

(5% return per year before expenses) | | | | | | | | | | | | | | | | |

Class A | | $ | 1,000.00 | | | $ | 1,019.80 | | | $ | 5.06 | | | | 1.01 | % |

Class B | | $ | 1,000.00 | | | $ | 1,016.10 | | | $ | 8.80 | | | | 1.76 | % |

Class C | | $ | 1,000.00 | | | $ | 1,016.10 | | | $ | 8.80 | | | | 1.76 | % |

Class I | | $ | 1,000.00 | | | $ | 1,021.00 | | | $ | 3.81 | | | | 0.76 | % |

Class R | | $ | 1,000.00 | | | $ | 1,018.50 | | | $ | 6.31 | | | | 1.26 | % |

Class R6 | | $ | 1,000.00 | | | $ | 1,021.50 | | | $ | 3.36 | | | | 0.67 | % |

| * | Expenses are equal to the Fund’s annualized expense ratio for the indicated Class, multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period). The Example assumes that the $1,000 was invested at the net asset value per share determined at the close of business on October 31, 2016. The Example reflects the expenses of both the Fund and the Portfolio. |

Eaton Vance

Income Fund of Boston

April 30, 2017

Statement of Assets and Liabilities (Unaudited)

| | | | |

| Assets | | April 30, 2017 | |

Investment in Boston Income Portfolio, at value (identified cost, $6,040,597,499) | | $ | 6,250,785,620 | |

Receivable for Fund shares sold | | | 13,111,808 | |

Total assets | | $ | 6,263,897,428 | |

| |

| Liabilities | | | | |

Payable for Fund shares redeemed | | $ | 34,952,814 | |

Distributions payable | | | 1,502,837 | |

Payable to affiliates: | | | | |

Distribution and service fees | | | 496,430 | |

Trustees’ fees | | | 42 | |

Accrued expenses | | | 1,625,724 | |

Total liabilities | | $ | 38,577,847 | |

Net Assets | | $ | 6,225,319,581 | |

| |

| Sources of Net Assets | | | | |

Paid-in capital | | $ | 6,236,738,641 | |

Accumulated net realized loss from Portfolio | | | (205,657,488 | ) |

Accumulated distributions in excess of net investment income | | | (15,949,693 | ) |

Net unrealized appreciation from Portfolio | | | 210,188,121 | |

Total | | $ | 6,225,319,581 | |

| |

| Class A Shares | | | | |

Net Assets | | $ | 1,226,811,155 | |

Shares Outstanding | | | 211,324,373 | |

Net Asset Value and Redemption Price Per Share | | | | |

(net assets ÷ shares of beneficial interest outstanding) | | $ | 5.81 | |

Maximum Offering Price Per Share | | | | |

(100 ÷ 95.25 of net asset value per share) | | $ | 6.10 | |

| |

| Class B Shares | | | | |

Net Assets | | $ | 11,485,687 | |

Shares Outstanding | | | 1,977,099 | |

Net Asset Value and Offering Price Per Share* | | | | |

(net assets ÷ shares of beneficial interest outstanding) | | $ | 5.81 | |

| |

| Class C Shares | | | | |

Net Assets | | $ | 250,005,434 | |

Shares Outstanding | | | 43,001,083 | |

Net Asset Value and Offering Price Per Share* | | | | |

(net assets ÷ shares of beneficial interest outstanding) | | $ | 5.81 | |

| |

| Class I Shares | | | | |

Net Assets | | $ | 4,571,019,407 | |

Shares Outstanding | | | 786,959,663 | |

Net Asset Value, Offering Price and Redemption Price Per Share | | | | |

(net assets ÷ shares of beneficial interest outstanding) | | $ | 5.81 | |

| |

| Class R Shares | | | | |

Net Assets | | $ | 45,638,413 | |

Shares Outstanding | | | 7,859,371 | |

Net Asset Value, Offering Price and Redemption Price Per Share | | | | |

(net assets ÷ shares of beneficial interest outstanding) | | $ | 5.81 | |

| |

| Class R6 Shares | | | | |

Net Assets | | $ | 120,359,485 | |

Shares Outstanding | | | 20,721,868 | |

Net Asset Value, Offering Price and Redemption Price Per Share | | | | |

(net assets ÷ shares of beneficial interest outstanding) | | $ | 5.81 | |

On sales of $50,000 or more, the offering price of Class A shares is reduced.

| * | Redemption price per share is equal to the net asset value less any applicable contingent deferred sales charge. |

| | | | |

| | 5 | | See Notes to Financial Statements. |

Eaton Vance

Income Fund of Boston

April 30, 2017

Statement of Operations (Unaudited)

| | | | |

| Investment Income | | Six Months Ended April 30, 2017 | |

Interest and other income allocated from Portfolio | | $ | 195,407,519 | |

Dividends allocated from Portfolio | | | 2,799,277 | |

Expenses allocated from Portfolio | | | (19,563,809 | ) |

Total investment income from Portfolio | | $ | 178,642,987 | |

| |

| Expenses | | | | |

Distribution and service fees | | | | |

Class A | | $ | 1,916,300 | |

Class B | | | 63,128 | |

Class C | | | 1,240,679 | |

Class R | | | 111,002 | |

Trustees’ fees and expenses | | | 250 | |

Custodian fee | | | 29,824 | |

Transfer and dividend disbursing agent fees | | | 2,962,031 | |

Legal and accounting services | | | 84,721 | |

Printing and postage | | | 1,224,954 | |

Registration fees | | | 165,124 | |

Miscellaneous | | | 23,562 | |

Total expenses | | $ | 7,821,575 | |

| |

Net investment income | | $ | 170,821,412 | |

| |

| Realized and Unrealized Gain (Loss) from Portfolio | | | | |

Net realized gain (loss) — | | | | |

Investment transactions | | $ | (4,983,606 | ) |

Swap contracts | | | 346,310 | |

Foreign currency and forward foreign currency exchange contract transactions | | | 70,498 | |

Net realized loss | | $ | (4,566,798 | ) |

Change in unrealized appreciation (depreciation) — | | | | |

Investments | | $ | 130,894,357 | |

Swap contracts | | | (331,062 | ) |

Foreign currency and forward foreign currency exchange contracts | | | 12,340 | |

Net change in unrealized appreciation (depreciation) | | $ | 130,575,635 | |

| |

Net realized and unrealized gain | | $ | 126,008,837 | |

| |

Net increase in net assets from operations | | $ | 296,830,249 | |

| | | | |

| | 6 | | See Notes to Financial Statements. |

Eaton Vance

Income Fund of Boston

April 30, 2017

Statements of Changes in Net Assets

| | | | | | | | |

| Increase (Decrease) in Net Assets | | Six Months Ended April 30, 2017 (Unaudited) | | | Year Ended October 31, 2016 | |

From operations — | | | | | | | | |

Net investment income | | $ | 170,821,412 | | | $ | 324,197,086 | |

Net realized loss from investment transactions, swap contracts and foreign currency and forward foreign currency exchange contract transactions | | | (4,566,798 | ) | | | (63,758,211 | ) |

Net change in unrealized appreciation (depreciation) from investments, swap contracts, foreign currency and forward foreign currency exchange contracts | | | 130,575,635 | | | | 177,726,574 | |

Net increase in net assets from operations | | $ | 296,830,249 | | | $ | 438,165,449 | |

Distributions to shareholders — | | | | | | | | |

From net investment income | | | | | | | | |

Class A | | $ | (43,020,822 | ) | | $ | (76,522,676 | ) |

Class B | | | (307,044 | ) | | | (817,440 | ) |

Class C | | | (6,035,746 | ) | | | (11,861,202 | ) |

Class I | | | (129,741,251 | ) | | | (240,455,379 | ) |

Class R | | | (1,189,042 | ) | | | (2,307,025 | ) |

Class R6 | | | (2,525,512 | ) | | | (2,161,401 | ) |

Tax return of capital | | | | | | | | |

Class A | | | — | | | | (6,307,831 | ) |

Class B | | | — | | | | (64,280 | ) |

Class C | | | — | | | | (971,446 | ) |

Class I | | | — | | | | (20,189,526 | ) |

Class R | | | — | | | | (184,370 | ) |

Class R6 | | | — | | | | (190,795 | ) |

Total distributions to shareholders | | $ | (182,819,417 | ) | | $ | (362,033,371 | ) |

Transactions in shares of beneficial interest — | | | | | | | | |

Proceeds from sale of shares | | | | | | | | |

Class A | | $ | 168,912,828 | | | $ | 611,868,271 | |

Class B | | | 15,195 | | | | 282,185 | |

Class C | | | 14,772,191 | | | | 48,632,020 | |

Class I | | | 1,006,805,136 | | | | 2,516,434,506 | |

Class R | | | 7,958,121 | | | | 18,548,685 | |

Class R6 | | | 65,330,931 | | | | 44,004,485 | |

Net asset value of shares issued to shareholders in payment of distributions declared | | | | | | | | |

Class A | | | 41,170,187 | | | | 79,077,089 | |

Class B | | | 266,488 | | | | 764,599 | |

Class C | | | 5,497,750 | | | | 11,589,767 | |

Class I | | | 122,579,897 | | | | 246,393,677 | |

Class R | | | 1,080,868 | | | | 2,365,990 | |

Class R6 | | | 2,058,723 | | | | 1,207,909 | |

Cost of shares redeemed | | | | | | | | |

Class A | | | (695,914,594 | ) | | | (368,664,965 | ) |

Class B | | | (1,624,597 | ) | | | (4,782,172 | ) |

Class C | | | (27,768,032 | ) | | | (56,377,082 | ) |

Class I | | | (1,016,891,688 | ) | | | (2,192,072,233 | ) |

Class R | | | (8,124,640 | ) | | | (24,611,506 | ) |

Class R6 | | | (9,724,232 | ) | | | (8,608,103 | ) |

Net asset value of shares exchanged | | | | | | | | |

Class A | | | 1,287,119 | | | | 2,815,183 | |

Class B | | | (1,287,119 | ) | | | (2,815,183 | ) |

Net increase (decrease) in net assets from Fund share transactions | | $ | (323,599,468 | ) | | $ | 926,053,122 | |

| | |

Net increase (decrease) in net assets | | $ | (209,588,636 | ) | | $ | 1,002,185,200 | |

| | |

| Net Assets | | | | | | | | |

At beginning of period | | $ | 6,434,908,217 | | | $ | 5,432,723,017 | |

At end of period | | $ | 6,225,319,581 | | | $ | 6,434,908,217 | |

| | |

Accumulated distributions in excess of net investment income

included in net assets | | | | | | | | |

At end of period | | $ | (15,949,693 | ) | | $ | (3,951,688 | ) |

| | | | |

| | 7 | | See Notes to Financial Statements. |

Eaton Vance

Income Fund of Boston

April 30, 2017

Financial Highlights

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Class A | |

| | | Six Months Ended April 30, 2017 (Unaudited) | | | Year Ended October 31, | |

| | | | 2016 | | | 2015 | | | 2014 | | | 2013 | | | 2012 | |

Net asset value — Beginning of period | | $ | 5.700 | | | $ | 5.660 | | | $ | 6.020 | | | $ | 6.060 | | | $ | 5.920 | | | $ | 5.720 | |

| | | | | | |

| Income (Loss) From Operations | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment income(1) | | $ | 0.149 | | | $ | 0.302 | | | $ | 0.318 | | | $ | 0.331 | | | $ | 0.349 | | | $ | 0.355 | |

Net realized and unrealized gain (loss) | | | 0.120 | | | | 0.076 | | | | (0.323 | ) | | | (0.014 | ) | | | 0.156 | | | | 0.252 | |

| | | | | | |

Total income (loss) from operations | | $ | 0.269 | | | $ | 0.378 | | | $ | (0.005 | ) | | $ | 0.317 | | | $ | 0.505 | | | $ | 0.607 | |

| | | | | | |

| Less Distributions | | | | | | | | | | | | | | | | | | | | | | | | |

From net investment income | | $ | (0.159 | ) | | $ | (0.312 | ) | | $ | (0.329 | ) | | $ | (0.357 | ) | | $ | (0.365 | ) | | $ | (0.394 | ) |

Tax return of capital | | | — | | | | (0.026 | ) | | | (0.026 | ) | | | — | | | | — | | | | (0.013 | ) |

| | | | | | |

Total distributions | | $ | (0.159 | ) | | $ | (0.338 | ) | | $ | (0.355 | ) | | $ | (0.357 | ) | | $ | (0.365 | ) | | $ | (0.407 | ) |

| | | | | | |

Net asset value — End of period | | $ | 5.810 | | | $ | 5.700 | | | $ | 5.660 | | | $ | 6.020 | | | $ | 6.060 | | | $ | 5.920 | |

| | | | | | |

Total Return(2) | | | 4.79 | %(3) | | | 7.02 | % | | | (0.10 | )% | | | 5.34 | % | | | 8.75 | % | | | 11.00 | % |

| | | | | | |

| Ratios/Supplemental Data | | | | | | | | | | | | | | | | | | | | | | | | |

Net assets, end of period (000’s omitted) | | $ | 1,226,811 | | | $ | 1,686,369 | | | $ | 1,349,462 | | | $ | 1,551,838 | | | $ | 1,830,909 | | | $ | 1,997,735 | |

Ratios (as a percentage of average daily net assets):(4) | | | | | | | | | | | | | | | | | | | | | | | | |

Expenses(5) | | | 1.01 | %(6) | | | 0.99 | % | | | 1.00 | % | | | 1.00 | % | | | 1.00 | % | | | 1.02 | % |

Net investment income | | | 5.24 | %(6) | | | 5.43 | % | | | 5.43 | % | | | 5.45 | % | | | 5.80 | % | | | 6.12 | % |

Portfolio Turnover of the Portfolio | | | 24 | %(3) | | | 34 | % | | | 36 | % | | | 43 | % | | | 56 | % | | | 64 | % |

| (1) | Computed using average shares outstanding. |

| (2) | Returns are historical and are calculated by determining the percentage change in net asset value with all distributions reinvested and do not reflect the effect of sales charges. |

| (4) | Includes the Fund’s share of the Portfolio’s allocated expenses. |

| (5) | Excludes the effect of custody fee credits, if any, of less than 0.005%. Effective September 1, 2015, custody fee credits, which were earned on cash deposit balances, were discontinued by the custodian. |

| | | | |

| | 8 | | See Notes to Financial Statements. |

Eaton Vance

Income Fund of Boston

April 30, 2017

Financial Highlights — continued

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Class B | |

| | | Six Months Ended April 30, 2017 (Unaudited) | | | Year Ended October 31, | |

| | | | 2016 | | | 2015 | | | 2014 | | | 2013 | | | 2012 | |

Net asset value — Beginning of period | | $ | 5.700 | | | $ | 5.660 | | | $ | 6.020 | | | $ | 6.070 | | | $ | 5.930 | | | $ | 5.720 | |

| | | | | | |

| Income (Loss) From Operations | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment income(1) | | $ | 0.128 | | | $ | 0.261 | | | $ | 0.276 | | | $ | 0.286 | | | $ | 0.303 | | | $ | 0.317 | |

Net realized and unrealized gain (loss) | | | 0.120 | | | | 0.075 | | | | (0.326 | ) | | | (0.023 | ) | | | 0.158 | | | | 0.257 | |

| | | | | | |

Total income (loss) from operations | | $ | 0.248 | | | $ | 0.336 | | | $ | (0.050 | ) | | $ | 0.263 | | | $ | 0.461 | | | $ | 0.574 | |

| | | | | | |

| Less Distributions | | | | | | | | | | | | | | | | | | | | | | | | |

From net investment income | | $ | (0.138 | ) | | $ | (0.274 | ) | | $ | (0.288 | ) | | $ | (0.313 | ) | | $ | (0.321 | ) | | $ | (0.352 | ) |

Tax return of capital | | | — | | | | (0.022 | ) | | | (0.022 | ) | | | — | | | | — | | | | (0.012 | ) |

| | | | | | |

Total distributions | | $ | (0.138 | ) | | $ | (0.296 | ) | | $ | (0.310 | ) | | $ | (0.313 | ) | | $ | (0.321 | ) | | $ | (0.364 | ) |

| | | | | | |

Net asset value — End of period | | $ | 5.810 | | | $ | 5.700 | | | $ | 5.660 | | | $ | 6.020 | | | $ | 6.070 | | | $ | 5.930 | |

| | | | | | |

Total Return(2) | | | 4.40 | %(3) | | | 6.20 | % | | | (0.87 | )% | | | 4.40 | % | | | 7.96 | % | | | 10.38 | % |

| | | | | | |

| Ratios/Supplemental Data | | | | | | | | | | | | | | | | | | | | | | | | |

Net assets, end of period (000’s omitted) | | $ | 11,486 | | | $ | 13,891 | | | $ | 20,491 | | | $ | 30,329 | | | $ | 39,996 | | | $ | 56,321 | |

Ratios (as a percentage of average daily net assets):(4) | | | | | | | | | | | | | | | | | | | | | | | | |

Expenses(5) | | | 1.76 | %(6) | | | 1.75 | % | | | 1.75 | % | | | 1.75 | % | | | 1.75 | % | | | 1.77 | % |

Net investment income | | | 4.48 | %(6) | | | 4.72 | % | | | 4.70 | % | | | 4.70 | % | | | 5.04 | % | | | 5.48 | % |

Portfolio Turnover of the Portfolio | | | 24 | %(3) | | | 34 | % | | | 36 | % | | | 43 | % | | | 56 | % | | | 64 | % |

| (1) | Computed using average shares outstanding. |

| (2) | Returns are historical and are calculated by determining the percentage change in net asset value with all distributions reinvested and do not reflect the effect of sales charges. |

| (4) | Includes the Fund’s share of the Portfolio’s allocated expenses. |

| (5) | Excludes the effect of custody fee credits, if any, of less than 0.005%. Effective September 1, 2015, custody fee credits, which were earned on cash deposit balances, were discontinued by the custodian. |

| | | | |

| | 9 | | See Notes to Financial Statements. |

Eaton Vance

Income Fund of Boston

April 30, 2017

Financial Highlights — continued

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Class C | |

| | | Six Months Ended April 30, 2017 (Unaudited) | | | Year Ended October 31, | |

| | | | 2016 | | | 2015 | | | 2014 | | | 2013 | | | 2012 | |

Net asset value — Beginning of period | | $ | 5.710 | | | $ | 5.660 | | | $ | 6.030 | | | $ | 6.070 | | | $ | 5.930 | | | $ | 5.720 | |

| | | | | | |

| Income (Loss) From Operations | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment income(1) | | $ | 0.128 | | | $ | 0.260 | | | $ | 0.274 | | | $ | 0.286 | | | $ | 0.303 | | | $ | 0.313 | |

Net realized and unrealized gain (loss) | | | 0.110 | | | | 0.086 | | | | (0.334 | ) | | | (0.013 | ) | | | 0.158 | | | | 0.261 | |

| | | | | | |

Total income (loss) from operations | | $ | 0.238 | | | $ | 0.346 | | | $ | (0.060 | ) | | $ | 0.273 | | | $ | 0.461 | | | $ | 0.574 | |

| | | | | | |

| Less Distributions | | | | | | | | | | | | | | | | | | | | | | | | |

From net investment income | | $ | (0.138 | ) | | $ | (0.274 | ) | | $ | (0.288 | ) | | $ | (0.313 | ) | | $ | (0.321 | ) | | $ | (0.352 | ) |

Tax return of capital | | | — | | | | (0.022 | ) | | | (0.022 | ) | | | — | | | | — | | | | (0.012 | ) |

| | | | | | |

Total distributions | | $ | (0.138 | ) | | $ | (0.296 | ) | | $ | (0.310 | ) | | $ | (0.313 | ) | | $ | (0.321 | ) | | $ | (0.364 | ) |

| | | | | | |

Net asset value — End of period | | $ | 5.810 | | | $ | 5.710 | | | $ | 5.660 | | | $ | 6.030 | | | $ | 6.070 | | | $ | 5.930 | |

| | | | | | |

Total Return(2) | | | 4.22 | %(3) | | | 6.39 | % | | | (1.04 | )% | | | 4.57 | % | | | 7.95 | % | | | 10.37 | % |

| | | | | | |

| Ratios/Supplemental Data | | | | | | | | | | | | | | | | | | | | | | | | |

Net assets, end of period (000’s omitted) | | $ | 250,005 | | | $ | 252,990 | | | $ | 247,325 | | | $ | 295,436 | | | $ | 308,296 | | | $ | 318,029 | |

Ratios (as a percentage of average daily net assets):(4) | | | | | | | | | | | | | | | | | | | | | | | | |

Expenses(5) | | | 1.76 | %(6) | | | 1.74 | % | | | 1.75 | % | | | 1.75 | % | | | 1.75 | % | | | 1.77 | % |

Net investment income | | | 4.48 | %(6) | | | 4.69 | % | | | 4.68 | % | | | 4.70 | % | | | 5.04 | % | | | 5.39 | % |

Portfolio Turnover of the Portfolio | | | 24 | %(3) | | | 34 | % | | | 36 | % | | | 43 | % | | | 56 | % | | | 64 | % |

| (1) | Computed using average shares outstanding. |

| (2) | Returns are historical and are calculated by determining the percentage change in net asset value with all distributions reinvested and do not reflect the effect of sales charges. |

| (4) | Includes the Fund’s share of the Portfolio’s allocated expenses. |

| (5) | Excludes the effect of custody fee credits, if any, of less than 0.005%. Effective September 1, 2015, custody fee credits, which were earned on cash deposit balances, were discontinued by the custodian. |

| | | | |

| | 10 | | See Notes to Financial Statements. |

Eaton Vance

Income Fund of Boston

April 30, 2017

Financial Highlights — continued

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Class I | |

| | | Six Months Ended April 30, 2017

(Unaudited) | | | Year Ended October 31, | |

| | | | 2016 | | | 2015 | | | 2014 | | | 2013 | | | 2012 | |

Net asset value — Beginning of period | | $ | 5.700 | | | $ | 5.660 | | | $ | 6.020 | | | $ | 6.070 | | | $ | 5.930 | | | $ | 5.720 | |

| | | | | | |

| Income (Loss) From Operations | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment income(1) | | $ | 0.156 | | | $ | 0.315 | | | $ | 0.330 | | | $ | 0.345 | | | $ | 0.363 | | | $ | 0.367 | |

Net realized and unrealized gain (loss) | | | 0.120 | | | | 0.077 | | | | (0.320 | ) | | | (0.023 | ) | | | 0.157 | | | | 0.265 | |

| | | | | | |

Total income from operations | | $ | 0.276 | | | $ | 0.392 | | | $ | 0.010 | | | $ | 0.322 | | | $ | 0.520 | | | $ | 0.632 | |

| | | | | | |

| Less Distributions | | | | | | | | | | | | | | | | | | | | | | | | |

From net investment income | | $ | (0.166 | ) | | $ | (0.325 | ) | | $ | (0.343 | ) | | $ | (0.372 | ) | | $ | (0.380 | ) | | $ | (0.409 | ) |

Tax return of capital | | | — | | | | (0.027 | ) | | | (0.027 | ) | | | — | | | | — | | | | (0.013 | ) |

| | | | | | |

Total distributions | | $ | (0.166 | ) | | $ | (0.352 | ) | | $ | (0.370 | ) | | $ | (0.372 | ) | | $ | (0.380 | ) | | $ | (0.422 | ) |

| | | | | | |

Net asset value — End of period | | $ | 5.810 | | | $ | 5.700 | | | $ | 5.660 | | | $ | 6.020 | | | $ | 6.070 | | | $ | 5.930 | |

| | | | | | |

Total Return(2) | | | 4.91 | %(3) | | | 7.28 | % | | | 0.15 | % | | | 5.42 | % | | | 9.01 | % | | | 11.46 | % |

| | | | | | |

| Ratios/Supplemental Data | | | | | | | | | | | | | | | | | | | | | | | | |

Net assets, end of period (000’s omitted) | | $ | 4,571,019 | | | $ | 4,376,959 | | | $ | 3,744,639 | | | $ | 2,903,827 | | | $ | 2,113,533 | | | $ | 2,224,443 | |

Ratios (as a percentage of average daily net assets):(4) | | | | | | | | | | | | | | | | | | | | | | | | |

Expenses(5) | | | 0.76 | %(6) | | | 0.74 | % | | | 0.75 | % | | | 0.75 | % | | | 0.75 | % | | | 0.77 | % |

Net investment income | | | 5.48 | %(6) | | | 5.67 | % | | | 5.64 | % | | | 5.68 | % | | | 6.04 | % | | | 6.32 | % |

Portfolio Turnover of the Portfolio | | | 24 | %(3) | | | 34 | % | | | 36 | % | | | 43 | % | | | 56 | % | | | 64 | % |

| (1) | Computed using average shares outstanding. |

| (2) | Returns are historical and are calculated by determining the percentage change in net asset value with all distributions reinvested. |

| (4) | Includes the Fund’s share of the Portfolio’s allocated expenses. |

| (5) | Excludes the effect of custody fee credits, if any, of less than 0.005%. Effective September 1, 2015, custody fee credits, which were earned on cash deposit balances, were discontinued by the custodian. |

| | | | |

| | 11 | | See Notes to Financial Statements. |

Eaton Vance

Income Fund of Boston

April 30, 2017

Financial Highlights — continued

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Class R | |

| | | Six Months Ended April 30, 2017

(Unaudited) | | | Year Ended October 31, | |

| | | | 2016 | | | 2015 | | | 2014 | | | 2013 | | | 2012 | |

Net asset value — Beginning of period | | $ | 5.700 | | | $ | 5.660 | | | $ | 6.020 | | | $ | 6.060 | | | $ | 5.920 | | | $ | 5.720 | |

| | | | | | |

| Income (Loss) From Operations | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment income(1) | | $ | 0.142 | | | $ | 0.288 | | | $ | 0.301 | | | $ | 0.316 | | | $ | 0.333 | | | $ | 0.342 | |

Net realized and unrealized gain (loss) | | | 0.120 | | | | 0.076 | | | | (0.321 | ) | | | (0.014 | ) | | | 0.157 | | | | 0.251 | |

| | | | | | |

Total income (loss) from operations | | $ | 0.262 | | | $ | 0.364 | | | $ | (0.020 | ) | | $ | 0.302 | | | $ | 0.490 | | | $ | 0.593 | |

| | | | | | |

| Less Distributions | | | | | | | | | | | | | | | | | | | | | | | | |

From net investment income | | $ | (0.152 | ) | | $ | (0.299 | ) | | $ | (0.315 | ) | | $ | (0.342 | ) | | $ | (0.350 | ) | | $ | (0.381 | ) |

Tax return of capital | | | — | | | | (0.025 | ) | | | (0.025 | ) | | | — | | | | — | | | | (0.012 | ) |

| | | | | | |

Total distributions | | $ | (0.152 | ) | | $ | (0.324 | ) | | $ | (0.340 | ) | | $ | (0.342 | ) | | $ | (0.350 | ) | | $ | (0.393 | ) |

| | | | | | |

Net asset value — End of period | | $ | 5.810 | | | $ | 5.700 | | | $ | 5.660 | | | $ | 6.020 | | | $ | 6.060 | | | $ | 5.920 | |

| | | | | | |

Total Return(2) | | | 4.66 | %(3) | | | 6.75 | % | | | (0.36 | )% | | | 5.08 | % | | | 8.48 | % | | | 10.73 | % |

| | | | | | |

| Ratios/Supplemental Data | | | | | | | | | | | | | | | | | | | | | | | | |

Net assets, end of period (000’s omitted) | | $ | 45,638 | | | $ | 43,902 | | | $ | 47,575 | | | $ | 37,575 | | | $ | 34,457 | | | $ | 36,971 | |

Ratios (as a percentage of average daily net assets):(4) | | | | | | | | | | | | | | | | | | | | | | | | |

Expenses(5) | | | 1.26 | %(6) | | | 1.24 | % | | | 1.25 | % | | | 1.25 | % | | | 1.25 | % | | | 1.27 | % |

Net investment income | | | 4.98 | %(6) | | | 5.20 | % | | | 5.15 | % | | | 5.19 | % | | | 5.54 | % | | | 5.90 | % |

Portfolio Turnover of the Portfolio | | | 24 | %(3) | | | 34 | % | | | 36 | % | | | 43 | % | | | 56 | % | | | 64 | % |

| (1) | Computed using average shares outstanding. |

| (2) | Returns are historical and are calculated by determining the percentage change in net asset value with all distributions reinvested. |

| (4) | Includes the Fund’s share of the Portfolio’s allocated expenses |

| (5) | Excludes the effect of custody fee credits, if any, of less than 0.005%. Effective September 1, 2015, custody fee credits, which were earned on cash deposit balances, were discontinued by the custodian. |

| | | | |

| | 12 | | See Notes to Financial Statements. |

Eaton Vance

Income Fund of Boston

April 30, 2017

Financial Highlights — continued

| | | | | | | | | | | | | | | | |

| | | Class R6 | |

| | | Six Months Ended April 30, 2017

(Unaudited) | | | Year Ended October 31, | | | Period Ended October 31, 2014(1) | |

| | | | 2016 | | | 2015 | | |

Net asset value — Beginning of period | | $ | 5.700 | | | $ | 5.660 | | | $ | 6.020 | | | $ | 6.160 | |

| | | | |

| Income (Loss) From Operations | | | | | | | | | | | | | | | | |

Net investment income(2) | | $ | 0.158 | | | $ | 0.319 | | | $ | 0.326 | | | $ | 0.114 | |

Net realized and unrealized gain (loss) | | | 0.121 | | | | 0.078 | | | | (0.311 | ) | | | (0.129 | ) |

| | | | |

Total income (loss) from operations | | $ | 0.279 | | | $ | 0.397 | | | $ | 0.015 | | | $ | (0.015 | ) |

| | | | |

| Less Distributions | | | | | | | | | | | | | | | | |

From net investment income | | $ | (0.169 | ) | | $ | (0.330 | ) | | $ | (0.348 | ) | | $ | (0.125 | ) |

Tax return of capital | | | — | | | | (0.027 | ) | | | (0.027 | ) | | | — | |

| | | | |

Total distributions | | $ | (0.169 | ) | | $ | (0.357 | ) | | $ | (0.375 | ) | | $ | (0.125 | ) |

| | | | |

Net asset value — End of period | | $ | 5.810 | | | $ | 5.700 | | | $ | 5.660 | | | $ | 6.020 | |

| | | | |

Total Return(3) | | | 4.96 | %(4) | | | 7.38 | % | | | 0.24 | % | | | (0.23 | )%(4) |

| | | | |

| Ratios/Supplemental Data | | | | | | | | | | | | | | | | |

Net assets, end of period (000’s omitted) | | $ | 120,359 | | | $ | 60,797 | | | $ | 23,230 | | | $ | 1,173 | |

Ratios (as a percentage of average daily net assets):(5) | | | | | | | | | | | | | | | | |

Expenses(6) | | | 0.67 | %(7) | | | 0.66 | % | | | 0.66 | % | | | 0.69 | %(7) |

Net investment income | | | 5.56 | %(7) | | | 5.71 | % | | | 5.62 | % | | | 5.67 | %(7) |

Portfolio Turnover of the Portfolio | | | 24 | %(4) | | | 34 | % | | | 36 | % | | | 43 | %(8) |

| (1) | For the period from the commencement of operations, July 1, 2014, to October 31, 2014. |

| (2) | Computed using average shares outstanding. |

| (3) | Returns are historical and are calculated by determining the percentage change in net asset value with all distributions reinvested. |

| (5) | Includes the Fund’s share of the Portfolio’s allocated expenses. |

| (6) | Excludes the effect of custody fee credits, if any, of less than 0.005%. Effective September 1, 2015, custody fee credits, which were earned on cash deposit balances, were discontinued by the custodian. |

| (8) | For the Portfolio’s year ended October 31, 2014. |

| | | | |

| | 13 | | See Notes to Financial Statements. |

Eaton Vance

Income Fund of Boston

April 30, 2017

Notes to Financial Statements (Unaudited)

1 Significant Accounting Policies

Eaton Vance Income Fund of Boston (the Fund) is a diversified series of Eaton Vance Series Trust II (the Trust). The Trust is a Massachusetts business trust registered under the Investment Company Act of 1940, as amended (the 1940 Act), as an open-end management investment company. The Fund offers six classes of shares. Class A shares are generally sold subject to a sales charge imposed at time of purchase. Class B and Class C shares are sold at net asset value and are generally subject to a contingent deferred sales charge (see Note 5). Class I, Class R and Class R6 shares are sold at net asset value and are not subject to a sales charge. Class B shares automatically convert to Class A shares eight years after their purchase as described in the Fund’s prospectus. Beginning January 1, 2012, Class B shares are only available for purchase upon exchange from another Eaton Vance fund or through reinvestment of distributions. Each class represents a pro-rata interest in the Fund, but votes separately on class-specific matters and (as noted below) is subject to different expenses. Realized and unrealized gains and losses are allocated daily to each class of shares based on the relative net assets of each class to the total net assets of the Fund. Net investment income, other than class-specific expenses, is allocated daily to each class of shares based upon the ratio of the value of each class’s paid shares to the total value of all paid shares. Sub-accounting, recordkeeping and similar administrative fees payable to financial intermediaries, which are a component of transfer and dividend disbursing agent fees on the Statement of Operations, are not allocated to Class R6 shares. Each class of shares differs in its distribution plan and certain other class-specific expenses. The Fund invests all of its investable assets in interests in Boston Income Portfolio (the Portfolio), a Massachusetts business trust, having the same investment objectives and policies as the Fund. The value of the Fund’s investment in the Portfolio reflects the Fund’s proportionate interest in the net assets of the Portfolio (99.9% at April 30, 2017). The performance of the Fund is directly affected by the performance of the Portfolio. The financial statements of the Portfolio, including the portfolio of investments, are included elsewhere in this report and should be read in conjunction with the Fund’s financial statements.

The following is a summary of significant accounting policies of the Fund. The policies are in conformity with accounting principles generally accepted in the United States of America (U.S. GAAP). The Fund is an investment company and follows accounting and reporting guidance in the Financial Accounting Standards Board (FASB) Accounting Standards Codification Topic 946.

A Investment Valuation — Valuation of securities by the Portfolio is discussed in Note 1A of the Portfolio’s Notes to Financial Statements, which are included elsewhere in this report.

B Income — The Fund’s net investment income or loss consists of the Fund’s pro-rata share of the net investment income or loss of the Portfolio, less all actual and accrued expenses of the Fund.

C Federal Taxes — The Fund’s policy is to comply with the provisions of the Internal Revenue Code applicable to regulated investment companies and to distribute to shareholders each year substantially all of its net investment income, and all or substantially all of its net realized capital gains. Accordingly, no provision for federal income or excise tax is necessary.

As of April 30, 2017, the Fund had no uncertain tax positions that would require financial statement recognition, de-recognition, or disclosure. The Fund files a U.S. federal income tax return annually after its fiscal year-end, which is subject to examination by the Internal Revenue Service for a period of three years from the date of filing.

D Expenses — The majority of expenses of the Trust are directly identifiable to an individual fund. Expenses which are not readily identifiable to a specific fund are allocated taking into consideration, among other things, the nature and type of expense and the relative size of the funds.

E Use of Estimates — The preparation of the financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of income and expense during the reporting period. Actual results could differ from those estimates.

F Indemnifications — Under the Trust’s organizational documents, its officers and Trustees may be indemnified against certain liabilities and expenses arising out of the performance of their duties to the Fund. Under Massachusetts law, if certain conditions prevail, shareholders of a Massachusetts business trust (such as the Trust) could be deemed to have personal liability for the obligations of the Trust. However, the Trust’s Declaration of Trust contains an express disclaimer of liability on the part of Fund shareholders and the By-laws provide that the Trust shall assume the defense on behalf of any Fund shareholders. Moreover, the By-laws also provide for indemnification out of Fund property of any shareholder held personally liable solely by reason of being or having been a shareholder for all loss or expense arising from such liability. Additionally, in the normal course of business, the Fund enters into agreements with service providers that may contain indemnification clauses. The Fund’s maximum exposure under these arrangements is unknown as this would involve future claims that may be made against the Fund that have not yet occurred.

G Other — Investment transactions are accounted for on a trade date basis.

H Interim Financial Statements — The interim financial statements relating to April 30, 2017 and for the six months then ended have not been audited by an independent registered public accounting firm, but in the opinion of the Fund’s management, reflect all adjustments, consisting only of normal recurring adjustments, necessary for the fair presentation of the financial statements.

Eaton Vance

Income Fund of Boston

April 30, 2017

Notes to Financial Statements (Unaudited) — continued

2 Distributions to Shareholders and Income Tax Information

The Fund declares dividends daily to shareholders of record at the time of declaration. Distributions are generally paid monthly. Distributions of realized capital gains (reduced by available capital loss carryforwards) are made at least annually. Distributions are declared separately for each class of shares. Shareholders may reinvest income and capital gain distributions in additional shares of the same class of the Fund at the net asset value as of the reinvestment date or, at the election of the shareholder, receive distributions in cash. Distributions to shareholders are determined in accordance with income tax regulations, which may differ from U.S. GAAP. As required by U.S. GAAP, only distributions in excess of tax basis earnings and profits are reported in the financial statements as a return of capital. Permanent differences between book and tax accounting relating to distributions are reclassified to paid-in capital. For tax purposes, distributions from short-term capital gains are considered to be from ordinary income.

At October 31, 2016, the Fund, for federal income tax purposes, had capital loss carryforwards of $45,934,301 and deferred capital losses of $134,521,398 which would reduce its taxable income arising from future net realized gains on investment transactions, if any, to the extent permitted by the Internal Revenue Code, and thus would reduce the amount of distributions to shareholders, which would otherwise be necessary to relieve the Fund of any liability for federal income or excise tax. Such capital loss carryforwards will expire on October 31, 2017 ($43,883,291) and October 31, 2019 ($2,051,010) and their character is short-term. Under tax regulations, capital losses incurred in taxable years beginning after December 2010 are considered deferred capital losses and are treated as arising on the first day of the Fund’s next taxable year, retaining the same short-term or long-term character as when originally deferred. Deferred capital losses are required to be used prior to capital loss carryforwards, which carry an expiration date. As a result of this ordering rule, capital loss carryforwards may be more likely to expire unused. Of the deferred capital losses at October 31, 2016, $20,903,743 are short-term and $113,617,655 are long-term.

3 Transactions with Affiliates

Eaton Vance Management (EVM) serves as the administrator of the Fund, but receives no compensation. The Portfolio has engaged Boston Management and Research (BMR), a subsidiary of EVM, to render investment advisory services. See Note 2 of the Portfolio’s Notes to Financial Statements which are included elsewhere in this report. EVM provides sub-transfer agency and related services to the Fund pursuant to a Sub-Transfer Agency Support Services Agreement. For the six months ended April 30, 2017, EVM earned $48,096 from the Fund pursuant to such agreement, which is included in transfer and dividend disbursing agent fees on the Statement of Operations. The Fund was informed that Eaton Vance Distributors, Inc. (EVD), an affiliate of EVM and the Fund’s principal underwriter, received $54,231 as its portion of the sales charge on sales of Class A shares for the six months ended April 30, 2017. EVD also received distribution and service fees from Class A, Class B, Class C and Class R shares (see Note 4) and contingent deferred sales charges (see Note 5).

Trustees and officers of the Fund who are members of EVM’s or BMR’s organizations receive remuneration for their services to the Fund out of the investment adviser fee. Certain officers and Trustees of the Fund and the Portfolio are officers of the above organizations.

4 Distribution Plans

The Fund has in effect a distribution plan for Class A shares (Class A Plan) pursuant to Rule 12b-1 under the 1940 Act. Pursuant to the Class A Plan, the Fund pays EVD a distribution and service fee of 0.25% per annum of its average daily net assets attributable to Class A shares for distribution services and facilities provided to the Fund by EVD, as well as for personal services and/or the maintenance of shareholder accounts. Distribution and service fees paid or accrued to EVD for the six months ended April 30, 2017 amounted to $1,916,300 for Class A shares. The Fund also has in effect distribution plans for Class B shares (Class B Plan), Class C shares (Class C Plan) and Class R shares (Class R Plan) pursuant to Rule 12b-1 under the 1940 Act. Pursuant to the Class B and Class C Plans, the Fund pays EVD amounts equal to 0.75% per annum of its average daily net assets attributable to Class B and Class C shares for providing ongoing distribution services and facilities to the Fund. For the six months ended April 30, 2017, the Fund paid or accrued to EVD $47,346 and $930,509 for Class B and Class C shares, respectively. The Class R Plan requires the Fund to pay EVD an amount up to 0.50% per annum of its average daily net assets attributable to Class R shares for providing ongoing distribution services and facilities to the Fund. The Trustees of the Trust have currently limited Class R distribution payments to 0.25% per annum of the average daily net assets attributable to Class R shares. For the six months ended April 30, 2017, the Fund paid or accrued to EVD $55,501 for Class R shares.

Pursuant to the Class B, Class C and Class R Plans, the Fund also makes payments of service fees to EVD, financial intermediaries and other persons in amounts equal to 0.25% per annum of its average daily net assets attributable to that class. Service fees paid or accrued are for personal services and/or the maintenance of shareholder accounts. They are separate and distinct from the sales commissions and distribution fees payable to EVD. Service fees paid or accrued for the six months ended April 30, 2017 amounted to $15,782, $310,170 and $55,501 for Class B, Class C and Class R shares, respectively.

Distribution and service fees are subject to the limitations contained in the Financial Industry Regulatory Authority Rule 2341(d) and for Class B, are further limited to a 5% maximum sales charge as determined in accordance with such rule.

Eaton Vance

Income Fund of Boston

April 30, 2017

Notes to Financial Statements (Unaudited) — continued

5 Contingent Deferred Sales Charges

A contingent deferred sales charge (CDSC) generally is imposed on redemptions of Class B shares made within six years of purchase and on redemptions of Class C shares made within one year of purchase. Class A shares may be subject to a 1% CDSC if redeemed within 18 months of purchase (depending on the circumstances of purchase). Generally, the CDSC is based upon the lower of the net asset value at date of redemption or date of purchase. No charge is levied on shares acquired by reinvestment of dividends or capital gain distributions. The CDSC for Class B shares is imposed at declining rates that begin at 5% in the case of redemptions in the first and second year after purchase, declining one percentage point each subsequent year. Class C shares are subject to a 1% CDSC if redeemed within one year of purchase. For the six months ended April 30, 2017, the Fund was informed that EVD received approximately $20,000, $1,000 and $7,000 of CDSCs paid by Class A, Class B and Class C shareholders, respectively.

6 Investment Transactions

For the six months ended April 30, 2017, increases and decreases in the Fund’s investment in the Portfolio aggregated $319,680,311 and $849,521,459, respectively.

7 Shares of Beneficial Interest

The Fund’s Declaration of Trust permits the Trustees to issue an unlimited number of full and fractional shares of beneficial interest (without par value). Such shares may be issued in a number of different series (such as the Fund) and classes. Transactions in Fund shares were as follows:

| | | | | | | | |

| Class A | | Six Months Ended April 30, 2017

(Unaudited) | | | Year Ended October 31, 2016 | |

| | |

Sales | | | 29,523,082 | | | | 109,009,587 | |

Issued to shareholders electing to receive payments of distributions in Fund shares | | | 7,159,483 | | | | 14,241,169 | |

Redemptions | | | (121,404,404 | ) | | | (66,482,062 | ) |

Exchange from Class B shares | | | 223,929 | | | | 509,078 | |

| | |

Net increase (decrease) | | | (84,497,910 | ) | | | 57,277,772 | |

| | |

| | | | | | | | |

| Class B | | Six Months Ended April 30, 2017

(Unaudited) | | | Year Ended October 31, 2016 | |

| | |

Sales | | | 2,638 | | | | 50,735 | |

Issued to shareholders electing to receive payments of distributions in Fund shares | | | 46,341 | | | | 137,985 | |

Redemptions | | | (283,351 | ) | | | (865,634 | ) |

Exchange to Class A shares | | | (223,647 | ) | | | (508,621 | ) |

| | |

Net decrease | | | (458,019 | ) | | | (1,185,535 | ) |

| | |

| | | | | | | | |

| Class C | | Six Months Ended April 30, 2017

(Unaudited) | | | Year Ended October 31, 2016 | |

| | |

Sales | | | 2,570,334 | | | | 8,769,444 | |

Issued to shareholders electing to receive payments of distributions in Fund shares | | | 954,202 | | | | 2,085,190 | |

Redemptions | | | (4,837,716 | ) | | | (10,209,560 | ) |

| | |

Net increase (decrease) | | | (1,313,180 | ) | | | 645,074 | |

Eaton Vance

Income Fund of Boston

April 30, 2017

Notes to Financial Statements (Unaudited) — continued

| | | | | | | | |

| Class I | | Six Months Ended April 30, 2017

(Unaudited) | | | Year Ended October 31, 2016 | |

| | |

Sales | | | 175,697,150 | | | | 456,925,142 | |

Issued to shareholders electing to receive payments of distributions in Fund shares | | | 21,303,094 | | | | 44,312,211 | |

Redemptions | | | (177,481,246 | ) | | | (395,530,956 | ) |

| | |

Net increase | | | 19,518,998 | | | | 105,706,397 | |

| | |

| | | | | | | | |

| Class R | | Six Months Ended April 30, 2017

(Unaudited) | | | Year Ended October 31, 2016 | |

| | |

Sales | | | 1,390,441 | | | | 3,343,505 | |

Issued to shareholders electing to receive payments of distributions in Fund shares | | | 187,865 | | | | 427,031 | |

Redemptions | | | (1,418,583 | ) | | | (4,479,655 | ) |

| | |

Net increase (decrease) | | | 159,723 | | | | (709,119 | ) |

| | |

| | | | | | | | |

| Class R6 | | Six Months Ended April 30, 2017

(Unaudited) | | | Year Ended October 31, 2016 | |

| | |

Sales | | | 11,399,685 | | | | 7,877,244 | |

Issued to shareholders electing to receive payments of distributions in Fund shares | | | 357,261 | | | | 215,395 | |

Redemptions | | | (1,694,701 | ) | | | (1,538,095 | ) |

| | |

Net increase | | | 10,062,245 | | | | 6,554,544 | |

Boston Income Portfolio

April 30, 2017

Portfolio of Investments (Unaudited)

| | | | | | | | |

| Corporate Bonds & Notes — 87.3% | |

| | |

| | | | | | | | |

| Security | | Principal Amount (000’s omitted) | | | Value | |

| | | | | | | | |

|

Aerospace — 0.8% | |

Booz Allen Hamilton, Inc.,

5.125%, 5/1/25(1) | | $ | 2,495 | | | $ | 2,535,544 | |

Huntington Ingalls Industries, Inc., 5.00%, 11/15/25(1) | | | 7,605 | | | | 8,042,287 | |

Orbital ATK, Inc., 5.25%, 10/1/21 | | | 6,870 | | | | 7,127,625 | |

Orbital ATK, Inc., 5.50%, 10/1/23 | | | 1,945 | | | | 2,027,663 | |

TransDigm, Inc., 6.00%, 7/15/22 | | | 15,200 | | | | 15,694,000 | |

TransDigm, Inc., 6.375%, 6/15/26 | | | 295 | | | | 297,950 | |

TransDigm, Inc., 6.50%, 7/15/24 | | | 14,665 | | | | 15,104,950 | |

| | | | | | | | | |

| | | | | | $ | 50,830,019 | |

| | | | | | | | | |

|

Air Transportation — 0.2% | |

VistaJet Malta Finance PLC/VistaJet Co. Finance, LLC, 7.75%, 6/1/20(1) | | $ | 12,880 | | | $ | 10,529,400 | |

| | | | | | | | | |

| | | | | | $ | 10,529,400 | |

| | | | | | | | | |

|

Automotive & Auto Parts — 1.0% | |

American Axle & Manufacturing, Inc., 5.125%, 2/15/19 | | $ | 3,205 | | | $ | 3,241,300 | |

American Axle & Manufacturing, Inc., 6.25%, 4/1/25(1) | | | 6,190 | | | | 6,174,525 | |

American Axle & Manufacturing, Inc., 6.50%, 4/1/27(1) | | | 5,085 | | | | 5,059,575 | |

American Tire Distributors, Inc., 10.25%, 3/1/22(1) | | | 12,310 | | | | 12,694,687 | |

General Motors Financial Co., Inc., 3.25%, 5/15/18 | | | 1,780 | | | | 1,803,662 | |

General Motors Financial Co., Inc., 4.75%, 8/15/17 | | | 1,955 | | | | 1,971,459 | |

General Motors Financial Co., Inc., 6.75%, 6/1/18 | | | 4,760 | | | | 5,003,246 | |

Navistar International Corp., 8.25%, 11/1/21 | | | 15,215 | | | | 15,481,262 | |

ZF North America Capital, Inc., 4.00%, 4/29/20(1) | | | 6,150 | | | | 6,426,750 | |

ZF North America Capital, Inc., 4.50%, 4/29/22(1) | | | 3,680 | | | | 3,877,800 | |

ZF North America Capital, Inc., 4.75%, 4/29/25(1) | | | 3,245 | | | | 3,387,196 | |

| | | | | | | | | |

| | | | | | $ | 65,121,462 | |

| | | | | | | | | |

|

Banks & Thrifts — 0.9% | |

Ally Financial, Inc., 3.50%, 1/27/19 | | $ | 16,565 | | | $ | 16,813,475 | |

Ally Financial, Inc., 6.25%, 12/1/17 | | | 5,890 | | | | 6,044,613 | |

Ally Financial, Inc., 8.00%, 12/31/18 | | | 2,500 | | | | 2,712,500 | |

CIT Group, Inc., 5.375%, 5/15/20 | | | 13,300 | | | | 14,347,375 | |

CIT Group, Inc., 5.50%, 2/15/19(1) | | | 2,601 | | | | 2,753,809 | |

JPMorgan Chase & Co., Series S, 6.75% to 2/1/24(2)(3) | | | 9,210 | | | | 10,400,392 | |

| | | | | | | | | |

| | | | | | $ | 53,072,164 | |

| | | | | | | | | |

|

Broadcasting — 1.3% | |

CBS Radio, Inc., 7.25%, 11/1/24(1) | | $ | 11,190 | | | $ | 12,197,100 | |

EW Scripps Co. (The), 5.125%, 5/15/25(1) | | | 2,495 | | | | 2,566,731 | |

iHeartCommunications, Inc., 11.25%, 3/1/21 | | | 10,550 | | | | 8,149,875 | |

| | | | | | | | |

| Security | | Principal Amount (000’s omitted) | | | Value | |

| | | | | | | | |

|

Broadcasting (continued) | |

Netflix, Inc., 5.50%, 2/15/22 | | $ | 8,685 | | | $ | 9,336,375 | |

Netflix, Inc., 5.875%, 2/15/25 | | | 5,730 | | | | 6,231,375 | |

Sirius XM Radio, Inc., 6.00%, 7/15/24(1) | | | 25,438 | | | | 27,282,255 | |

Tribune Media Co., 5.875%, 7/15/22 | | | 6,235 | | | | 6,581,167 | |

Univision Communications, Inc., 5.125%, 5/15/23(1) | | | 6,190 | | | | 6,313,800 | |

| | | | | | | | | |

| | | | | | $ | 78,658,678 | |

| | | | | | | | | |

|

Building Materials — 1.6% | |

Brundage-Bone Concrete Pumping, Inc., 10.375%, 9/1/21(1) | | $ | 6,215 | | | $ | 6,494,675 | |

Builders FirstSource, Inc.,

5.625%, 9/1/24(1) | | | 7,620 | | | | 7,934,325 | |

Builders FirstSource, Inc.,

10.75%, 8/15/23(1) | | | 5,199 | | | | 6,095,828 | |

FBM Finance, Inc., 8.25%, 8/15/21(1) | | | 10,650 | | | | 11,541,831 | |

HD Supply, Inc., 5.25%, 12/15/21(1) | | | 7,870 | | | | 8,332,363 | |

HD Supply, Inc., 5.75%, 4/15/24(1) | | | 8,750 | | | | 9,318,750 | |

Hillman Group, Inc. (The), 6.375%, 7/15/22(1) | | | 14,330 | | | | 13,720,975 | |

Rexel S.A., 5.25%, 6/15/20(1) | | | 9,191 | | | | 9,426,007 | |

Standard Industries, Inc.,

5.50%, 2/15/23(1) | | | 12,035 | | | | 12,546,487 | |

Standard Industries, Inc., 6.00%, 10/15/25(1) | | | 14,595 | | | | 15,653,137 | |

USG Corp., 5.50%, 3/1/25(1) | | | 1,695 | | | | 1,786,106 | |

| | | | | | | | | |

| | | | | | $ | 102,850,484 | |

| | | | | | | | | |

|

Cable / Satellite TV — 6.8% | |

Altice Financing S.A., 6.50%, 1/15/22(1) | | $ | 1,405 | | | $ | 1,477,006 | |

Altice Financing S.A., 6.625%, 2/15/23(1) | | | 13,855 | | | | 14,703,619 | |

Altice Luxembourg S.A.,

7.625%, 2/15/25(1) | | | 6,140 | | | | 6,577,475 | |

Altice Luxembourg S.A.,

7.75%, 5/15/22(1) | | | 27,860 | | | | 29,670,900 | |

Altice US Finance I Corp., 5.375%, 7/15/23(1) | | | 4,030 | | | | 4,221,425 | |

Altice US Finance I Corp.,

5.50%, 5/15/26(1) | | | 14,955 | | | | 15,497,119 | |

Cablevision Systems Corp., 5.875%, 9/15/22 | | | 12,265 | | | | 12,617,619 | |

Cablevision Systems Corp., 7.75%, 4/15/18 | | | 10,805 | | | | 11,331,744 | |

Cablevision Systems Corp., 8.00%, 4/15/20 | | | 12,960 | | | | 14,507,165 | |

CCO Holdings, LLC/CCO Holdings Capital Corp., 5.25%, 9/30/22 | | | 12,245 | | | | 12,734,800 | |

CCO Holdings, LLC/CCO Holdings Capital Corp., 5.375%, 5/1/25(1) | | | 13,405 | | | | 14,008,225 | |

CCO Holdings, LLC/CCO Holdings Capital Corp., 5.75%, 1/15/24 | | | 1,625 | | | | 1,714,375 | |

CCO Holdings, LLC/CCO Holdings Capital Corp., 5.75%, 2/15/26(1) | | | 11,655 | | | | 12,408,845 | |

CCO Holdings, LLC/CCO Holdings Capital Corp., 5.875%, 4/1/24(1) | | | 20,085 | | | | 21,541,162 | |

Cequel Communications Holdings I, LLC/Cequel Capital Corp., 5.125%, 12/15/21(1) | | | 8,884 | | | | 9,128,310 | |

Cequel Communications Holdings I, LLC/Cequel Capital Corp., 6.375%, 9/15/20(1) | | | 1,365 | | | | 1,410,222 | |

| | | | |

| | 18 | | See Notes to Financial Statements. |

Boston Income Portfolio

April 30, 2017

Portfolio of Investments (Unaudited) — continued

| | | | | | | | |

| Security | | Principal Amount (000’s omitted) | | | Value | |

| | | | | | | | |

|

Cable / Satellite TV (continued) | |

CSC Holdings, LLC, 5.25%, 6/1/24 | | $ | 1,900 | | | $ | 1,927,303 | |

CSC Holdings, LLC, 6.75%, 11/15/21 | | | 12,915 | | | | 14,238,787 | |

CSC Holdings, LLC, 8.625%, 2/15/19 | | | 4,385 | | | | 4,841,259 | |

CSC Holdings, LLC, 10.125%, 1/15/23(1) | | | 17,855 | | | | 20,756,437 | |

CSC Holdings, LLC, 10.875%, 10/15/25(1) | | | 20,770 | | | | 25,001,887 | |

DISH DBS Corp., 5.875%, 7/15/22 | | | 12,425 | | | | 13,192,741 | |

DISH DBS Corp., 5.875%, 11/15/24 | | | 1,805 | | | | 1,899,763 | |

DISH DBS Corp., 6.75%, 6/1/21 | | | 14,092 | | | | 15,360,280 | |

DISH DBS Corp., 7.75%, 7/1/26 | | | 10,115 | | | | 11,872,481 | |

SFR Group S.A., 6.00%, 5/15/22(1) | | | 23,425 | | | | 24,508,406 | |

SFR Group S.A., 6.25%, 5/15/24(1) | | | 2,925 | | | | 3,038,344 | |

SFR Group S.A., 7.375%, 5/1/26(1) | | | 12,495 | | | | 13,197,844 | |

Unitymedia GmbH, 6.125%, 1/15/25(1) | | | 3,975 | | | | 4,263,625 | |

Unitymedia Hessen GmbH & Co. KG/Unitymedia NRW GmbH, 5.50%, 1/15/23(1) | | | 13,345 | | | | 13,945,525 | |

UPCB Finance IV, Ltd.,

5.375%, 1/15/25(1) | | | 4,740 | | | | 4,846,650 | |

Virgin Media Finance PLC, 5.75%, 1/15/25(1) | | | 9,450 | | | | 9,674,438 | |

Virgin Media Finance PLC, 6.375%, 4/15/23(1) | | | 3,265 | | | | 3,440,494 | |

Virgin Media Secured Finance PLC, 5.25%, 1/15/26(1) | | | 12,495 | | | | 12,698,044 | |

Virgin Media Secured Finance PLC, 5.50%, 8/15/26(1) | | | 7,835 | | | | 8,021,081 | |

VTR Finance B.V., 6.875%, 1/15/24(1) | | | 8,330 | | | | 8,871,450 | |

Ziggo Bond Finance B.V., 5.875%, 1/15/25(1) | | | 6,220 | | | | 6,414,375 | |

Ziggo Bond Finance B.V.,

6.00%, 1/15/27(1) | | | 13,180 | | | | 13,476,550 | |

Ziggo Secured Finance B.V., 5.50%, 1/15/27(1) | | | 6,485 | | | | 6,679,550 | |

| | | | | | | | | |

| | | | | | $ | 425,717,325 | |

| | | | | | | | | |

|

Capital Goods — 0.6% | |

Anixter, Inc., 5.50%, 3/1/23 | | $ | 9,930 | | | $ | 10,563,038 | |

Welbilt, Inc., 9.50%, 2/15/24 | | | 20,975 | | | | 24,331,000 | |

| | | | | | | | | |

| | | | | | $ | 34,894,038 | |

| | | | | | | | | |

|

Chemicals — 1.9% | |

Alpha 3 B.V./Alpha US Bidco, Inc., 6.25%, 2/1/25(1) | | $ | 5,350 | | | $ | 5,457,000 | |

CF Industries, Inc., 4.95%, 6/1/43 | | | 7,920 | | | | 6,689,786 | |

Chemours Co. (The), 7.00%, 5/15/25 | | | 4,665 | | | | 5,148,994 | |

Platform Specialty Products Corp., 6.50%, 2/1/22(1) | | | 19,885 | | | | 20,481,550 | |

Platform Specialty Products Corp., 10.375%, 5/1/21(1) | | | 6,445 | | | | 7,194,231 | |

PQ Corp., 6.75%, 11/15/22(1) | | | 3,150 | | | | 3,425,594 | |

SPCM S.A., 4.875%, 9/15/25(1) | | | 4,070 | | | | 4,125,963 | |

Tronox Finance, LLC, 6.375%, 8/15/20 | | | 26,130 | | | | 26,685,262 | |

Tronox Finance, LLC, 7.50%, 3/15/22(1) | | | 10,220 | | | | 10,731,000 | |

Valvoline, Inc., 5.50%, 7/15/24(1) | | | 2,810 | | | | 2,978,600 | |

Versum Materials, Inc., 5.50%, 9/30/24(1) | | | 9,540 | | | | 9,933,525 | |

W.R. Grace & Co., 5.125%, 10/1/21(1) | | | 9,590 | | | | 10,321,237 | |

| | | | | | | | |

| Security | | Principal Amount (000’s omitted) | | | Value | |

| | | | | | | | |

|

Chemicals (continued) | |

W.R. Grace & Co., 5.625%, 10/1/24(1) | | $ | 2,500 | | | $ | 2,721,875 | |

| | | | | | | | | |

| | | | | | $ | 115,894,617 | |

| | | | | | | | | |

|

Consumer Products — 1.7% | |

CBC Ammo, LLC/CBC FinCo, Inc., 7.25%, 11/15/21(1) | | $ | 13,610 | | | $ | 13,780,125 | |

Central Garden & Pet Co., 6.125%, 11/15/23 | | | 15,080 | | | | 16,173,300 | |

HRG Group, Inc., 7.875%, 7/15/19 | | | 26,940 | | | | 28,024,335 | |

Scotts Miracle-Gro Co. (The), 6.00%, 10/15/23 | | | 4,115 | | | | 4,418,481 | |

Spectrum Brands, Inc., 5.75%, 7/15/25 | | | 15,435 | | | | 16,622,106 | |

Tempur Sealy International, Inc., 5.50%, 6/15/26 | | | 3,015 | | | | 3,007,463 | |

Tempur Sealy International, Inc., 5.625%, 10/15/23 | | | 8,905 | | | | 9,145,435 | |

Vista Outdoor, Inc., 5.875%, 10/1/23 | | | 14,965 | | | | 14,965,000 | |

| | | | | | | | | |

| | | | | | $ | 106,136,245 | |

| | | | | | | | | |

|

Containers — 2.7% | |

ARD Finance S.A., 7.125%, 9/15/23(1)(4) | | $ | 8,590 | | | $ | 8,933,600 | |

Ardagh Packaging Finance PLC/Ardagh Holdings USA, Inc., 4.25%, 9/15/22(1) | | | 5,600 | | | | 5,721,520 | |

Ardagh Packaging Finance PLC/Ardagh Holdings USA, Inc.,

4.625%, 5/15/23(1) | | | 13,015 | | | | 13,340,375 | |

Ardagh Packaging Finance PLC/Ardagh Holdings USA, Inc., 6.00%, 6/30/21(1) | | | 3,900 | | | | 4,056,000 | |

Ardagh Packaging Finance PLC/Ardagh Holdings USA, Inc., 6.00%, 2/15/25(1) | | | 19,270 | | | | 19,968,537 | |

Ardagh Packaging Finance PLC/Ardagh Holdings USA, Inc., 7.25%, 5/15/24(1) | | | 28,090 | | | | 30,688,325 | |

Berry Plastics Corp., 6.00%, 10/15/22 | | | 10,130 | | | | 10,801,113 | |

BWAY Holding Co., 5.50%, 4/15/24(1) | | | 14,980 | | | | 15,185,975 | |

BWAY Holding Co., 7.25%, 4/15/25(1) | | | 15,260 | | | | 15,279,075 | |

Owens-Brockway Glass Container, Inc., 5.875%, 8/15/23(1) | | | 19,975 | | | | 21,410,703 | |

Owens-Brockway Glass Container, Inc., 6.375%, 8/15/25(1) | | | 4,160 | | | | 4,531,800 | |

Reynolds Group Issuer, Inc./Reynolds Group Issuer, LLC, 5.125%, 7/15/23(1) | | | 8,925 | | | | 9,315,469 | |

Reynolds Group Issuer, Inc./Reynolds Group Issuer, LLC, 6.875%, 2/15/21 | | | 4,171 | | | | 4,290,661 | |

Reynolds Group Issuer, Inc./Reynolds Group Issuer, LLC, 7.00%, 7/15/24(1) | | | 7,115 | | | | 7,670,859 | |

| | | | | | | | | |

| | | | | | $ | 171,194,012 | |

| | | | | | | | | |

|

Diversified Financial Services — 2.3% | |

Aircastle, Ltd., 5.00%, 4/1/23 | | $ | 4,955 | | | $ | 5,301,850 | |

Alliance Data Systems Corp., 5.875%, 11/1/21(1) | | | 14,975 | | | | 15,536,562 | |

Alliance Data Systems Corp., 6.375%, 4/1/20(1) | | | 12,725 | | | | 12,979,500 | |

| | | | |

| | 19 | | See Notes to Financial Statements. |

Boston Income Portfolio

April 30, 2017

Portfolio of Investments (Unaudited) — continued

| | | | | | | | |

| Security | | Principal Amount (000’s omitted) | | | Value | |

| | | | | | | | |

|

Diversified Financial Services (continued) | |

Icahn Enterprises, L.P./Icahn Enterprises Finance Corp., 6.00%, 8/1/20 | | $ | 7,115 | | | $ | 7,381,813 | |

Icahn Enterprises, L.P./Icahn Enterprises Finance Corp., 6.25%, 2/1/22(1) | | | 9,255 | | | | 9,648,338 | |

MSCI, Inc., 5.75%, 8/15/25(1) | | | 5,390 | | | | 5,834,675 | |

Navient Corp., 4.875%, 6/17/19 | | | 1,245 | | | | 1,288,451 | |

Navient Corp., 5.50%, 1/15/19 | | | 12,170 | | | | 12,672,012 | |

Navient Corp., 6.50%, 6/15/22 | | | 10,105 | | | | 10,458,675 | |

Navient Corp., 7.25%, 1/25/22 | | | 1,240 | | | | 1,325,250 | |

Navient Corp., 8.00%, 3/25/20 | | | 10,785 | | | | 11,890,462 | |

Park Aerospace Holdings, Ltd., 5.25%, 8/15/22(1) | | | 30,525 | | | | 32,356,500 | |

Park Aerospace Holdings, Ltd., 5.50%, 2/15/24(1) | | | 17,915 | | | | 18,989,900 | |

| | | | | | | | | |

| | | | | | $ | 145,663,988 | |

| | | | | | | | | |

|

Diversified Media — 1.1% | |

Clear Channel Worldwide Holdings, Inc., Series A, 6.50%, 11/15/22 | | $ | 6,075 | | | $ | 6,226,875 | |

Clear Channel Worldwide Holdings, Inc., Series B, 6.50%, 11/15/22 | | | 11,805 | | | | 12,291,956 | |

Clear Channel Worldwide Holdings, Inc., Series A, 7.625%, 3/15/20 | | | 2,005 | | | | 1,999,988 | |

IAC/InterActiveCorp, 4.875%, 11/30/18 | | | 10,598 | | | | 10,749,021 | |

MDC Partners, Inc., 6.50%, 5/1/24(1) | | | 24,130 | | | | 23,647,400 | |

National CineMedia, LLC, 6.00%, 4/15/22 | | | 8,240 | | | | 8,507,800 | |

Nielsen Co. Luxembourg S.a.r.l. (The), 5.50%, 10/1/21(1) | | | 5,585 | | | | 5,815,381 | |

| | | | | | | | | |

| | | | | | $ | 69,238,421 | |

| | | | | | | | | |

|

Energy — 13.6% | |

AmeriGas Partners, L.P./AmeriGas Finance Corp., 5.50%, 5/20/25 | | $ | 11,360 | | | $ | 11,530,400 | |

AmeriGas Partners, L.P./AmeriGas Finance Corp., 5.625%, 5/20/24 | | | 2,720 | | | | 2,781,200 | |

AmeriGas Partners, L.P./AmeriGas Finance Corp., 5.75%, 5/20/27 | | | 6,660 | | | | 6,709,950 | |

AmeriGas Partners, L.P./AmeriGas Finance Corp., 5.875%, 8/20/26 | | | 5,505 | | | | 5,615,100 | |

Antero Midstream Partners L.P./Antero Midstream Finance Corp., 5.375%, 9/15/24(1) | | | 8,495 | | | | 8,728,612 | |

Antero Resources Corp., 5.375%, 11/1/21 | | | 16,185 | | | | 16,771,706 | |

Antero Resources Corp., 5.625%, 6/1/23 | | | 13,015 | | | | 13,454,256 | |

Blue Racer Midstream, LLC/Blue Racer Finance Corp., 6.125%, 11/15/22(1) | | | 3,580 | | | | 3,682,925 | |

Canbriam Energy, Inc.,

9.75%, 11/15/19(1) | | | 19,215 | | | | 20,271,825 | |

Cheniere Corpus Christi Holdings, LLC, 5.875%, 3/31/25(1) | | | 15,580 | | | | 16,651,125 | |

| | | | | | | | |

| Security | | Principal Amount (000’s omitted) | | | Value | |

| | | | | | | | |

|

Energy (continued) | |

Cheniere Corpus Christi Holdings, LLC, 7.00%, 6/30/24(1) | | $ | 17,635 | | | $ | 19,793,171 | |

Chesapeake Energy Corp., 8.00%, 12/15/22(1) | | | 4,500 | | | | 4,758,750 | |

Concho Resources, Inc., 5.50%, 4/1/23 | | | 27,330 | | | | 28,474,444 | |

Continental Resources, Inc., 4.50%, 4/15/23 | | | 8,720 | | | | 8,632,800 | |

CrownRock, L.P./CrownRock Finance, Inc., 7.125%, 4/15/21(1) | | | 14,435 | | | | 14,958,269 | |

CrownRock, L.P./CrownRock Finance, Inc., 7.75%, 2/15/23(1) | | | 12,150 | | | | 13,061,250 | |

CVR Refining, LLC/Coffeyville Finance, Inc., 6.50%, 11/1/22 | | | 18,895 | | | | 19,272,900 | |

Denbury Resources, Inc., 5.50%, 5/1/22 | | | 3,545 | | | | 2,658,750 | |

Denbury Resources, Inc.,

9.00%, 5/15/21(1) | | | 16,725 | | | | 17,728,500 | |

Diamondback Energy, Inc.,

4.75%, 11/1/24(1) | | | 3,690 | | | | 3,717,675 | |

Diamondback Energy, Inc., 5.375%, 5/31/25(1) | | | 10,360 | | | | 10,774,400 | |

Endeavor Energy Resources, L.P./EER Finance, Inc., 7.00%, 8/15/21(1) | | | 20,580 | | | | 21,506,100 | |

Endeavor Energy Resources, L.P./EER Finance, Inc., 8.125%, 9/15/23(1) | | | 16,191 | | | | 17,324,370 | |

Energy Transfer Equity, L.P., 5.875%, 1/15/24 | | | 17,880 | | | | 19,355,100 | |

Energy Transfer Equity, L.P., 7.50%, 10/15/20 | | | 7,970 | | | | 9,021,044 | |

EP Energy, LLC/Everest Acquisition Finance, Inc., 8.00%, 11/29/24(1) | | | 6,610 | | | | 6,948,762 | |

EP Energy, LLC/Everest Acquisition Finance, Inc., 8.00%, 2/15/25(1) | | | 6,860 | | | | 6,139,700 | |

Extraction Oil & Gas Holdings, LLC/Extraction Finance Corp., 7.875%, 7/15/21(1) | | | 13,112 | | | | 13,800,380 | |

Great Western Petroleum, LLC/Great Western Finance Corp., 9.00%, 9/30/21(1) | | | 15,380 | | | | 15,995,200 | |

Gulfport Energy Corp., 6.00%, 10/15/24(1) | | | 21,885 | | | | 21,666,150 | |

Gulfport Energy Corp., 6.625%, 5/1/23 | | | 14,100 | | | | 14,346,750 | |

Halcon Resources Corp., 6.75%, 2/15/25(1) | | | 15,460 | | | | 14,918,900 | |

Holly Energy Partners, L.P./Holly Energy Finance Corp., 6.00%, 8/1/24(1) | | | 3,935 | | | | 4,180,938 | |

Matador Resources Co., 6.875%, 4/15/23 | | | 18,470 | | | | 19,578,200 | |

Murphy Oil Corp., 6.875%, 8/15/24 | | | 3,725 | | | | 3,976,438 | |

Newfield Exploration Co., 5.375%, 1/1/26 | | | 3,090 | | | | 3,256,088 | |

Newfield Exploration Co., 5.625%, 7/1/24 | | | 6,100 | | | | 6,477,468 | |

Noble Holding International, Ltd., 7.75%, 1/15/24 | | | 10,525 | | | | 9,656,687 | |

Oasis Petroleum, Inc., 6.50%, 11/1/21 | | | 3,205 | | | | 3,253,075 | |

Oasis Petroleum, Inc., 6.875%, 3/15/22 | | | 3,085 | | | | 3,138,988 | |

Oasis Petroleum, Inc., 6.875%, 1/15/23 | | | 16,210 | | | | 16,453,150 | |

Parsley Energy, LLC/Parsley Finance Corp., 5.25%, 8/15/25(1) | | | 5,135 | | | | 5,199,188 | |

Parsley Energy, LLC/Parsley Finance Corp., 5.375%, 1/15/25(1) | | | 9,390 | | | | 9,530,850 | |

| | | | |

| | 20 | | See Notes to Financial Statements. |

Boston Income Portfolio

April 30, 2017

Portfolio of Investments (Unaudited) — continued

| | | | | | | | |

| Security | | Principal Amount (000’s omitted) | | | Value | |

| | | | | | | | |

|

Energy (continued) | |

Parsley Energy, LLC/Parsley Finance Corp., 6.25%, 6/1/24(1) | | $ | 10,105 | | | $ | 10,736,562 | |

PBF Holding Co., LLC/PBF Finance Corp., 7.00%, 11/15/23 | | | 11,400 | | | | 11,628,000 | |

PBF Holding Co., LLC/PBF Finance Corp., 8.25%, 2/15/20 | | | 12,485 | | | | 12,797,125 | |

PBF Logistics, L.P./PBF Logistics Finance Corp., 6.875%, 5/15/23 | | | 14,565 | | | | 15,001,950 | |

PDC Energy, Inc., 6.125%, 9/15/24(1) | | | 2,630 | | | | 2,708,900 | |

Precision Drilling Corp., 6.50%, 12/15/21 | | | 1,700 | | | | 1,729,750 | |

Precision Drilling Corp., 6.625%, 11/15/20 | | | 1,163 | | | | 1,186,368 | |

Precision Drilling Corp., 7.75%, 12/15/23(1) | | | 695 | | | | 740,175 | |

Resolute Energy Corp., 8.50%, 5/1/20 | | | 5,050 | | | | 5,163,625 | |

Rice Energy, Inc., 7.25%, 5/1/23 | | | 8,095 | | | | 8,783,075 | |

RSP Permian, Inc., 6.625%, 10/1/22 | | | 22,005 | | | | 23,297,794 | |

Seven Generations Energy, Ltd., 6.75%, 5/1/23(1) | | | 32,610 | | | | 34,729,650 | |

Seven Generations Energy, Ltd., 6.875%, 6/30/23(1) | | | 6,520 | | | | 6,943,800 | |