UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C.

August 1, 2008

FORM 20-F

AMENDMENT NO. 1

(Mark One)

[ ]

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

[x]

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2007

OR

[ ]

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ……………………………… to ………………………………

Commission file number 013345

OR

[ ]

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Date of event requiring this shell company report ……………………………………………

CALEDONIA MINING CORPORATION

(Exact name of Registrant as specified in its charter)

Caledonia Mining Corporation is variously referred to in this Report

as “Caledonia”, “the Corporation” or “the Company”

Canada

(Jurisdiction of incorporation or organization)

24 Ninth Street, Lower Houghton, Johannesburg, Gauteng 2198, South Africa

(Address of principal executive offices)

Carl R. Jonsson, 1710-1177 West Hastings Street,

Vancouver, BC V6E 2L3, Canada; tel: (604) 640-6357; fax: (604) 681-0139

email: jonsson@securitieslaw.bc.ca

2

(Name, telephone, email and/or facsimile number and address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

(Title of Class)

(Title of Class)

Securities registered or to be registered pursuant to Section 12(g) of the Act

Title of each class

Name of each exchange on which registered

Common shares

Toronto Stock Exchange

London Stock Exchange Alternative Investment Market

NASD OTC Bulletin Board

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the closing of the period covered by the annual report

487,869,280

Indicate by check mark if the registration is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes

No x

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes

No x

Note – checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days

Yes

x

No

3

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer ______ Accelerated filer

Non-accelerated filer x

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

U.S. GAAP …… International Financial Reporting Standards as issued by the International Accounting Standards Board

Other:

Canadian GAAP

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow

Item 17

x

Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes

No

x

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

Yes

No

NOTE: All references to monies herein are to Canadian dollars unless otherwise specifically indicated

This Form 20-F Amendment, together with exhibits filed herewith, are being filed to clarify and expand on certain information contained in the original Form 20-F filed on May 9, 2008. This Amendment No. 1 amends and restates the original Form 20-F. Unless otherwise specifically noted herein, it does not bring the information up to date.

FORWARD LOOKING STATEMENTS

The Company cautions readers regarding forward looking statements found in this Annual Report and in any other statement made by, or on behalf of the Company, whether or not in future filings with the United States Securities Exchange Commission. Forward looking statements are statements not based on historical information and which relate to future operations, strategies, financial results or other developments. Forward looking statements are necessarily based upon estimates and assumptions that are inherently subject to significant business, economic and competitive uncertainties and contingencies, many of which are beyond the Company’s control and many of which, with respect to future business decisions,

4

are subject to change. See “Item 3. Key Information - D. Risk Factors”. These uncertainties and contingencies can affect actual results and could cause actual results to differ materially from those expressed in any forward looking statements made by or on behalf of the Company. The Company disclaims any obligation to update forward looking statements.

PART 1

1.

IDENTITY of DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not required as this is an “annual report under the Securities Exchange Act of 1934 (“Exchange Act”).

However, the information required above can readily be determined from Caledonia’s Proxy and Information Circular dated April 14, 2008 attached as Exhibit #14b..

2.

OFFER STATISTICS AND TIMETABLE

Not required as this is an “annual report under the Exchange Act”.

3.

KEY INFORMATION

Selected Financial Data

Table 3 A shows the applicable selected financial data for the 5-year period 2003 to 2007 in Canadian Generally Accepted Accounting Principles.

Table 3 A (i)shows the applicable selected financial data for the 5-year period 2003 to 2007 in United States Generally Accepted Accounting Principles.

Table 3 A (ii) shows the US$exchange rates against the Canadian $ for each of the 5-year periods indicated, for the period end and average exchange rate and the range of high and low rates for each year and the high and low exchange rates for the individual last six months ending March 31, 2008.

5

Table 3A - Selected Financial Information - Canadian Generally Accepted Accounting Principles

2007 | 2006(2) | 2005(2) | 2004(2) | 2003(1)(2) | |

Financial - $ Thousands Cdn except per share amounts |

|

|

| ||

Revenue from Operations | 10,039 | 13,586 | 6 | 3 | 58 |

Gross Profit (Loss) | 294 | 5,014 | (751) | (466) | (94) |

Expenses (General, Administration, Interest) Amortization) | 4,195 | 2,047 | 2,997 | 2,304 | 14,476 |

Net Income (Loss) for continuing operations | (3,906) | 2,315 | (3,748) | (2,770) | (4,811) |

Income(loss) from discontinued operations | (709) | (7,990) | (5,932) | (7,222) | (36) |

Net Income (Loss) for the Year after discontinued operations | (4,615) | (5,675) | (9,680) | (9,979) | (14,496) |

Cash | 76 | 1,252 | 1,076 | 6,470 | 4,179 |

Current Assets | 4,408 | 8,773 | 2,264 | 7,481 | 4,573 |

Total Assets | 29,492 | 31,456 | 22,338 | 23,666 | 19,530 |

Current Liabilities | 4,343 | 5,899 | 2,589 | 1,062 | 790 |

Long Term Liabilities | 1,054 | 1,221 | 377 | 423 | 1,089 |

Working Capital (Deficiency) | 65 | 2,874 | (325) | 6,419 | 3,783 |

Shareholders’ Equity | 24,095 | 24,336 | 19,372 | 22,181 | 17,651 |

Total Capital Expenditures (including Mineral Properties) | 3,250 | 3,579 | 5,284 | 3,813 | 2,279 |

Expenditures on Mineral Properties | 2,633 | 659 | 2,583 | 2,298 | 2,042 |

Financing Raised | 4,380 | 7,559 | 6,588 | 14,314 | 9,511 |

Dividends Declared | - | - | - | - | - |

Share Information

Market Capitalization ($ Thousands) | 53,666 | 45,798 | 42,632 | 39,145 | 105,955 |

Shares Outstanding (Thousands) | 487,869 | 457,981 | 370,715 | 301,112 | 252,274 |

Warrants & Options (Thousands) | 35,148 | 102,354 | 34,748 | 52,342 | 27,348 |

Earnings (Loss) per Share – continuing operations | (0.008) | 0.005 | (0.012) | (0.036) | (0.062) |

Earnings (Loss) per Share | (0.009) | (0.013) | (0.031) | (0.034) | (0.062) |

(1)

Restated for the adoption of the Asset Retirement Obligations change in accounting policy.

(2)

Presented to show the results of continuing and discounted operations due to the decision to sell the Barbrook and Eersteling Mines.

Table 3A (i) - Selected Financial Information - United States Generally Accepted Accounting Principles

| 2007 | 2006(1) | 2005(1) | 2004(1) | 2003(1) |

Revenue from Operations | 10,039 | 13,586 | 6 | 3 | 58 |

Gross Profit (Loss) | (2,339) | 4,355 | (2,791) | (872) | (8,987) |

Expenses (General and Administration, Interest and Amortization) | 4,195 | 2,047 | 2,997 | 2,304 | 14,605 |

Net Income (Loss) from continuing operations | (6,539) | 1,656 | (5,788) | (3,163) | (4,949) |

Net Income (Loss) from discontinued operations | (709) | (7,990) | (5,932) | (7,222) | (36) |

6

Net Income (Loss) | (7,248) | (6,334) | (11,720) | (10,385) | (4,985) |

Cash | 76 | 1,252 | 1,076 | 6,470 | 4,179 |

Current Assets | 4,408 | 8,773 | 2,264 | 7,481 | 4,573 |

Total Assets | 21,507 | 26,135 | 17,591 | 20,977 | 17,283 |

Current Liabilities | 4,343 | 5,899 | 2,589 | 1,062 | 790 |

Long Term Liabilities | 1,054 | 1,221 | 377 | 423 | 1,089 |

Working Capital (Deficiency) | 65 | 2,874 | (325) | 6,419 | 3,783 |

Shareholders’ Equity (Deficiency) | 16,110 | 19,015 | 14,625 | 19,492 | 15,404 |

Total Capital Expenditures (including Mineral Properties) | 617 | 2,920 | 3,244 | 3,407 | 1,601 |

Expenditures on Mineral Properties | - | - | 543 | 830 | 1,365 |

Financing Raised | 4,380 | 7,559 | 6,785 | 14,314 | 9,442 |

Deemed Dividends | 134 | - | 171 | - | - |

Share Information |

|

|

|

| |

Market Capitalization ($ Thousands) | 53,666 | 45,798 | 42,632 | 39,145 | 105,955 |

Shares Outstanding (Thousands) | 487,869 | 457,981 | 370,715 | 301,112 | 252,274 |

Warrants & Options (Thousands) | 35,148 | 102,354 | 34,748 | 52,342 | 27,348 |

Basic and Diluted Income (Loss) per share - continuing operations | (0.01) | 0.00 | (0.02) | (0.01) | (0.02) |

Basic and Diluted Income (Loss) per Share | (0.01) | (0.02) | (0.04) | (0.036) | (0.022) |

(1)

Presented to show the results of continuing and discontinued operations due to the decision to sell the Barbrook and Eersteling Mines.

Table 3A (ii) - Summary of Exchange Rates for the 5-year Period - 2003 to 2007

The following table sets forth, for each of the years indicated, the exchange rate of the United States dollar into Canadian currency at the end of such year, the average exchange rate during each such year and the range of high and low rates for each such year as supplied by the Bank of Canada.

Exchange Rate | 2007 | 2006 | 2005 | 2004 | 2003 |

Rate at the End of the Period(1) | 0.982 | 1.1654 | 1.1630 | 1.2020 | 1.2965 |

Average Rate (2) | 1.0744 | 1.342 | 1.2114 | 1.3000 | 1.4015 |

High Rate (1) | 1.185 | 1.1794 | 1.2585 | 1.3957 | 1.5777 |

Low Rate (1) | 0.9145 | 1.0948 | 1.1630 | 1.1759 | 1.2839 |

Notes:

(1)

The rate of exchange is the Bank of Canada closing rate for the period.

(2)

The average rate means the average of the exchange rates during the year.

The high and low rates of exchange for each of the 6 months from October 2007 to March 2008 are as follows:

| Oct. 2007 | Nov. 2007 | Dec. 2007 | Jan. 2008 | Feb. 2008 | March 2008 |

Closing | 0.9547 | 0.99 | 0.982 | 0.997 | 0.9788 | 1.0232 |

Average | 0.97673 | 0.9625 | 1.00151 | 1.01099 | 1.00203 | 1.00077 |

Hi | 0.9988 | 0.99 | 1.0193 | 1.0323 | 1.0161 | 1.0241 |

Low | 0.9547 | 0.9145 | 0.9807 | 0.982 | 0.9788 | 0.9785 |

7

C.

Risk Factors

An investment in the securities involves a high degree of risk. Investors need to carefully consider the following risk factors, in addition to the other information contained in this section “D” and the Exhibits hereto.

Industry Competition

The mining industry is a highly diverse and competitive international business. The selection of geographic areas of interest are only limited by the degree of risk a company is willing to accept by the acquisition of properties in emerging or developed markets and/or prospecting in explored or virgin territory. Mining by its nature, is a competitive business with the search for fresh ground with good exploration potential and the raising of the requisite capital to move projects forward to production. Globally the mining industry is prone to cyclical variations in the price of the commodities produced by it, as dictated by supply and demand factors, speculative factors and industry-controlled marketing cartels. Nature provides the ultimate uncertainty with geological and occasionally climatic surprises. Commensurate with the acceptance of this risk profile is the potential for high rewards.

Exploration and Development

The exploration, and development of, and the production from mineral deposits is potentially subject to a number of political, economic and other risks. Exploration, development and production activities are potentially subject to political, economic and other risks, including:

-

cancellation or renegotiation of contracts;

-

changes in local and foreign laws and regulations;

-

changes in tax laws;

-

delays or refusal in granting prospecting permissions, mining authorizations and work permits for foreign management staff;

-

environmental controls and permitting

-

expropriation or nationalization of property or assets;

-

foreign exchange controls;

government mandated social expenditures, such as comprehensive health care for HIV/AIDS infected employees and families;

-

import and export regulation, including restrictions on the sale of their production in foreign currencies;

-

industrial relations and the associated stability thereof;

-

inflation of cost that is not compensated for by a currency devaluation;

-

requirement that a foreign subsidiary or operating unit have a domestic joint venture partner, possibly which the foreign company must subsidize;

-

restrictions on the ability of local operating companies to sell their production for foreign currencies, and on the ability of such companies to hold these foreign currencies in offshore and/or local bank accounts;

-

restrictions on the ability of a foreign company to have management control of exploration and/or development and/or mining operations;

-

restrictions on the remittance of dividend and interest payments offshore;

-

retroactive tax or royalty claims;

-

risks of loss due to civil strife, acts of war, guerrilla activities, insurrection and terrorism;

-

royalties and tax increases or claims by governmental entities;

-

unreliable local infrastructure and services such as power, communications and transport links;

-

other risks arising out of foreign sovereignty over the areas in which Caledonia’s operations are conducted.

Such risks could potentially arise in any country in which Caledonia operates. However the risks are regarded as greater in South Africa and Zambia and particularly in Zimbabwe. In Southern Africa, Black Economic Empowerment Legislation and a number of economic and social issues may result in increased political and economic risks of operating in that area.

The President of the Republic of Zimbabwe brought the Indigenisation and Economic Empowerment Act into law through decree in March 2008. The law seeks to ensure that a majority stake (at least 51%) in all companies is held by Indigenous Zimbabweans. Additionally theMines and Minerals Amendment Bill was presented before the closure of the last session of Parliament but not passed into law, and has thus lapsed. The Mines and

8

Minerals Amendment Bill if enacted into law also seeks to ensure among other things that a majority stake is held in all mining companies by either indigenous Zimbabweans or the Government of Zimbabwe. Whilst neither the two pieces of legislation allow for compulsory acquisition, the Mines and Minerals Amendment Bill did provide for severe penalties in the form of extremely prohibitive taxes and potential withdrawal of mineral rights in the event of non voluntary compliance within certain time frames.

The Zambian government has announced the following proposed changes to their tax laws that will have a bearing on the Nama cobalt project if passed into law. The key changes are:

·

Increase in mineral royalty from 0.6% to 3%

·

Increase in profit tax rate from 25% to 30%

·

Introduction of variable profits tax of 15% for net profits above 8%

·

Introduction of a windfall profit tax for copper mines

·

Capital allowances reduced from 100% to 25%

These measures have been highly controversial with mining companies, many of which invested in the country under specific tax incentives and formalised their business models accordingly. Some mining companies are threatening legal recourse as they argue their businesses will become unviable. Proposed capital expenditure projects are being reconsidered. Various representations have been made by the mining companies through the Chamber of Mines to the government since the budget announcement at the end of January, however the government has taken a firm position, and we understand that the changes have been approved by parliament.

Consequently, Caledonia’s exploration, development and production activities may be substantially affected by factors beyond Caledonia’s control, any of which could materially adversely affect Caledonia’s financial position or results from operations. Furthermore, in the event of a dispute arising from such activities, Caledonia may be subject to exclusive jurisdiction of courts outside North America or may not be successful in subjecting persons to the jurisdiction of the courts in North America, which could adversely affect the outcome of a dispute.

History of Losses; Accumulated Deficit; No Assurance of Revenue or Operating Profit

Since inception from February 1992, Caledonia has recorded a loss in every year except 1994 and 2000. As at December 31, 2007, the consolidated accumulated deficit was $171.89 million.

Write-downs on capital assets and mineral properties are typical for the mining industry. Caledonia’s policy is to review the carrying value of assets relative to current market conditions on an annual basis.

Fluctuating Minerals Prices and Foreign Currency Exchange Rates

As Caledonia’s activities primarily relate to the exploration, development and production of minerals the fluctuating World prices for such minerals have a significant potential effect on the Company’s future activities and the potential profitability of any of its minerals production activities. There is never any assurance, when activities are undertaken, or production operations are commenced, that the World price of the minerals involved will continue at a sufficiently high price to justify the ongoing activities or the continuation of the production.

Most costs incurred by the Company in its exploration, development and production activities in southern Africa have to be paid in local currencies. However, mineral prices are generally quoted in United States dollars. The profitability of any production operations of the Company and the potential profitability of its exploration and development activities will therefore be seriously affected by adverse changes in the currency exchange rates.

Black Empowerment and Indigenization

The governments of the southern African countries in which the Company operates have, or are proposing, legislation (typically referred to as “black empowerment”) requiring companies to allow participation in their shareholdings and business enterprises by the indigenous (i.e. black) population. In not all instances is it assured that such interests will have to be paid for at full fair value. In Zimbabwe, when Caledonia purchased the Blanket Mine, it agreed to establish a trust for the benefit of the employees of the Blanket Mine, and the area in

9

which it is located, into which up to 30% of the issued shares of the wholly owned subsidiary which acquired and is operating the Blanket Mine would be placed - for no consideration. The ultimate terms and conditions of black empowerment arrangements forced on the Company - and the Zimbabwean trust when it is established - could seriously affect the profitability and economic prospects of the Company.

Need for Additional Funds

The Company’s plans for ongoing and increased activity - and the development, ultimately, of cobalt production operations in Zambia - will require funding in excess of the Company’s funds on hand. There is no assurance that all of the required additional funding can be raised and the Company may therefore have to reduce its ongoing activities.

The primary method by which the Company is seeking to finance the construction of, initially, a bulk sample pilot test plant - and ultimately production facilities - on its Zambian cobalt properties is to seek long-term agreements for future sales of cobalt concentrate to be produced from the property. These agreements have been secured during February and March 2008 whereby 51,560 tonnes of cobalt metal equivalent will be sold to four large Chinese refiners over the 5 year period ending in 2013.

Where possible the Company seeks, and will continue to seek, for new mineral property acquisitions or exploration activities joint venture agreements with other companies which will be required to supply all, or a significant portion, of the required funding.

Dependence upon Key Personnel

Caledonia’s success depends (i) on the continued contributions of its directors, executive officers, management and consultants, and (ii) on Caledonia’s ability to attract new personnel whenever Caledonia seeks to implement its business strategy. There is no assurance that the Company will always be able to locate and hire all of the personnel that it may consider that it requires. The Company, where it considers it appropriate, engages consulting and service companies to undertake some of the work function.

Mr. Harvey retired from his position as Technical Director in December 2005, but continues as a director, and James Johnstone retired from his position as Chief Operating Officer, but also continues as a Director.

Steven Curtis was appointed Vice President Finance and Chief Financial Officer in April 2006. In order to split the roles of the Chairman and the CEO Mr. Rupert Pardoe of Johannesburg, South Africa was appointed as Chairman of the Board of Directors of the Corporation in February 2005. Mr. Hayden stepped down as the Chairman at that time but continues as the Corporation’s President and CEO. Robert Liverant was appointed a Director and a member of the Audit Committee in January 2007, and Mr. Leigh Wilson was appointed a Director and a member of the Audit Committee in March 2008.

Absence of Dividends

The Company has never paid or declared any dividends.

Possible Volatility of Share Price

Market prices for mining company securities, by their nature, are volatile. Factors, such as rapidly changing commodity prices, political unrest globally and in countries where Caledonia operates, speculative interest in mining stocks etc. are but a few factors affecting the volatility of the share price. Caledonia listed its shares on the London Stock Exchange’s Alternative Investment Market (“AIM”) in June 2005 and is trying to attract more institutional and stock analyst coverage of its shares.

4

INFORMATION ON THE COMPANY

The purpose of this standard is to provide information about the company’s business operations, the products it makes or the services it provides, and the factors that affect the business. The standard also is intended to provide information regarding the adequacy and suitability of the company’s properties, plants and equipment, as well as its plans for future increases or decreases in such capacity.

10

A.

History and Development of Caledonia

Caledonia was incorporated, effective February 05, 1992, by the amalgamation pursuant to the laws of the Province of British Columbia, Canada of two "public" companies and one "private" company. The two public companies were Golden North Resource Corporation ("Golden North"), a British Columbia company and Thorco Resources Inc. ("Thorco"), an Ontario company. The private company was Doelcam Mining Corporation ("Doelcam"), an Ontario company. Such three companies being herein variously referred to as the "Amalgamating Companies".

The amalgamation of companies under the British Columbia Company Act was, in effect a merger of the Amalgamating Companies into a single new corporate entity, which replaces the original Amalgamating Companies. As a result of the amalgamation, Caledonia became possessed of all the assets and assumed responsibility for all of the liabilities, of the Amalgamating Companies.

As a result of the amalgamation, all of the issued and outstanding shares of the Amalgamating Companies were exchanged for fully paid and non-assessable common shares in the capital of Caledonia.

Following the amalgamation, the shares of Caledonia were listed for trading on the Toronto Stock Exchange and quoted on the NASDAQ small caps market. In 1997, NASDAQ put Caledonia on notice that new listing requirements were in the process of being implemented. A minimum bid price of US$1.00 per share for a period of ten consecutive trade days is required for Caledonia to regain compliance with the new listing requirements. Caledonia was unable to regain compliance and on October 16th 1998, Caledonia announced that NASDAQ would no longer quote Caledonia’s securities for trading. In addition to trading on the Toronto Stock Exchange, Caledonia’s common stock commenced trading on NASDAQ’s OTC Bulletin Board system under the same symbol, CALVF, immediately after removal from the NASDAQ National Market. In June 2005 Caledonia was admitted to the London Stock Exchange’s AIM market under the ticker sy mbol “CMCL”.

In March 1995, Caledonia decided to de-register as a Corporation under the laws of the Province of British Columbia, and simultaneously, was registered as a Canadian Corporation under the provisions of the Canadian Business Corporations Act(CBCA).

The addresses and telephone numbers of Caledonia’s two principal offices are:

Head Office - South Africa

Representational Office - Canada

Greenstone Management Services

67 Yonge Street, Suite 1201

24, 9th Street, Lower Houghton

Toronto, Ontario, Canada

Johannesburg, Gauteng, 2198

M5E 1J8

South Africa

(416) 369-9507

(27) 11 447 2499

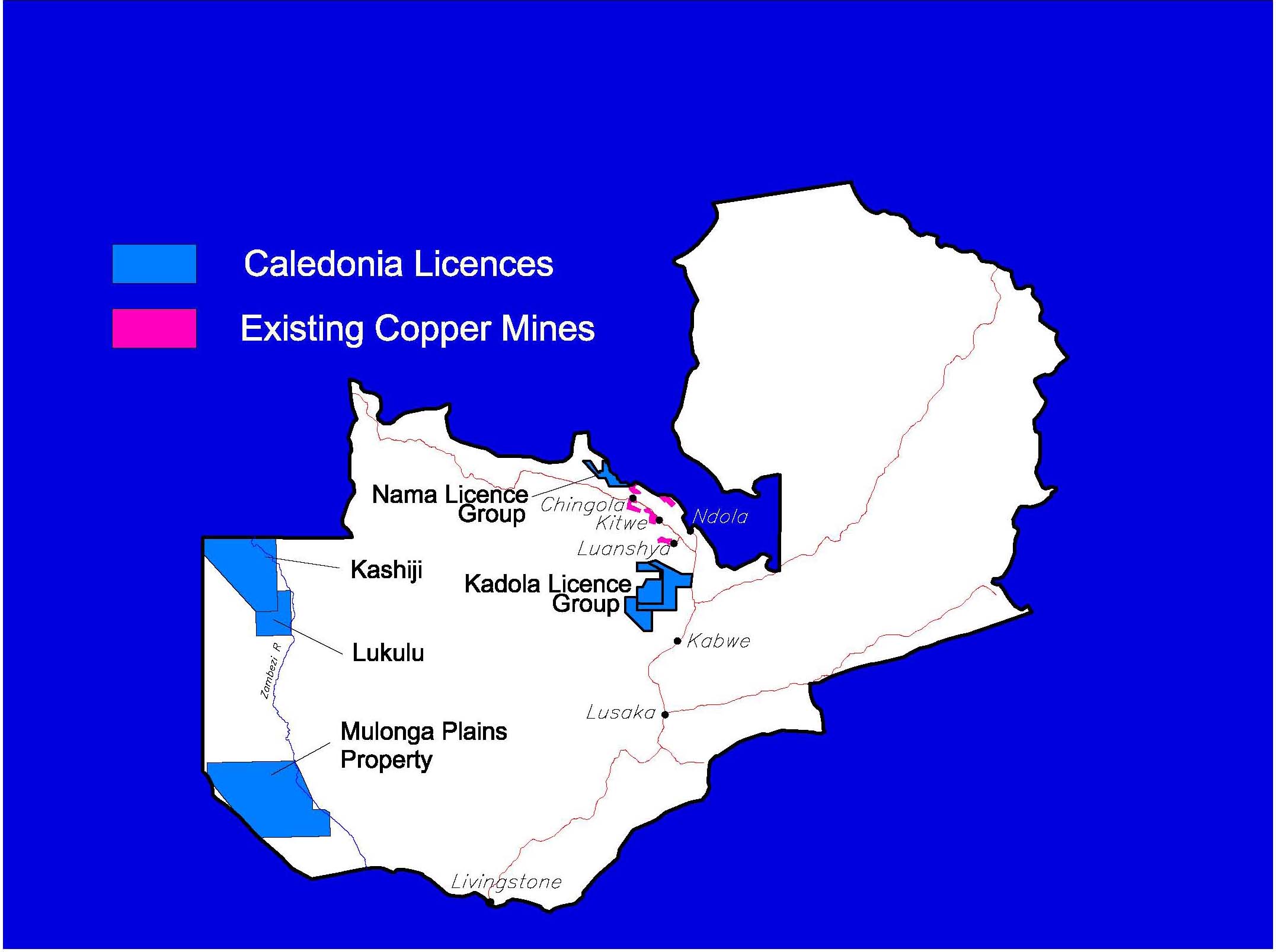

In August 2000, Caledonia was notified by its joint venture partner on its Mulonga Plain properties in Zambia that it had expended more than US$ 3 million on exploration on the properties and as such had earned a 60% interest in that property. The joint venture partner has continued work on the Mulonga Plain properties in 2004 - 2006 in its search for diamondiferous kimberlite pipes but has not yet announced further exploration work for the 2007 exploration season.

In August 2005 the joint venture partners, Motapa Exploration Limited and Caledonia Western Limited, a fully owned subsidiary of Caledonia, formed Motapa Mining Limited, a Zambian company, to hold and maintain the licences of the Mulonga Plain JV on behalf of the JV partners. At present Caledonia holds 40% of Mulonga Mining Limited, Motapa Exploration Limited holds the other 60%. Motapa Exploration Limited has given the Corporation notice that it intends withdrawing from the joint venture and intends to transfer all rights in and title to the properties to the Corporation for a nominal amount.

The Corporation has applied for a retention license over the properties managed under the joint venture.

11

In August 2000, Caledonia concluded a deal with a major mining company whereby the company would spend a total of $750,000 over a 3-year period on Caledonia’s Kikerk Lake diamond property in northern Canada to earn a 52.5% interest in the property from Caledonia who at that time held a 70% interest. By the end of 2002 the mining group had spent in excess of $750,000 on the Kikerk property and had earned a 52.5% interest. The joint venture parties signed a 3-way joint venture exploration agreement in early 2002. The operator of the joint venture did approximately $2,440,000 of work on the property in the 2002 – 2004 period. Cost of exploration at Kikerk Lake in 2005 totalled $530,000. At the date of this report, the operator has not reported the cost of its 2006 work. During 2007 Caledonia has written down its investment in Kikerk Lake by $750,000 to a nil balance.

In August 2000, Caledonia signed a heads of agreement with a major mining group over Caledonia’s Nama group licences in Zambia – the “Kalimba project”. The mining group undertook to spend US$ 2,500,000 over a 4-year period to earn a 30% interest in the property by funding all of the exploration work on the Kalimba project. The mining group carried out exploration work on the Kalimba project between 2000 and March 2002 when it withdrew from the joint venture as part of its overall cutback in worldwide exploration. The property is again fully owned by Caledonia. Caledonia collected a 10-tonne bulk sample from Nama during the3rd quarter of 2004 and conducted metallurgical tests to produce a concentrate and confirm whether or not the specifications required by the smelter can be met. The tests continued into 2006. Letters of intent have been signed with potential purchasers for the long term supply of Cobalt concent rate. Long terms supply discussions are ongoing with a number of large users of Cobalt

In 1995 the Company acquired ownership of the shares of the now-subsidiary companies which owned the Barbrook and Eersteling Mines in South Africa. Actually the original acquisition was of only 96.4% of the issued shares of Eersteling Gold Mining Company Ltd. - with the remaining 3.6% being acquired in mid 2004.

Effective April 1, 2006 the Company purchased 100% of the issued shares of the Zimbabwean company “Blanket Mine (1983) (Private) Limited, the owner of the operating Blanket Gold Mine. The purchase consideration was $1,000,000 (U.S.) and the issuance to the vendor of 20,000,000 shares in the capital of Caledonia. Because the Company bought the shares of the company owning the Blanket Mine it thereby acquired all of the assets of that company and assumed all of its liabilities.

Caledonia has not been involved in any significant reorganization, mergers, receiverships or bankruptcies.

From time to time Caledonia receives mineral property and business proposals from third parties for review as potential investment opportunities. The Board of Directors or the officers of Caledonia reviews and evaluates those opportunities of merit and interest to Caledonia.

With the potential of improved political conditions in other Southern African countries, Caledonia is reviewing mining opportunities in certain of these countries. These activities are and will be undertaken through joint ventures or direct exploration expenditures.

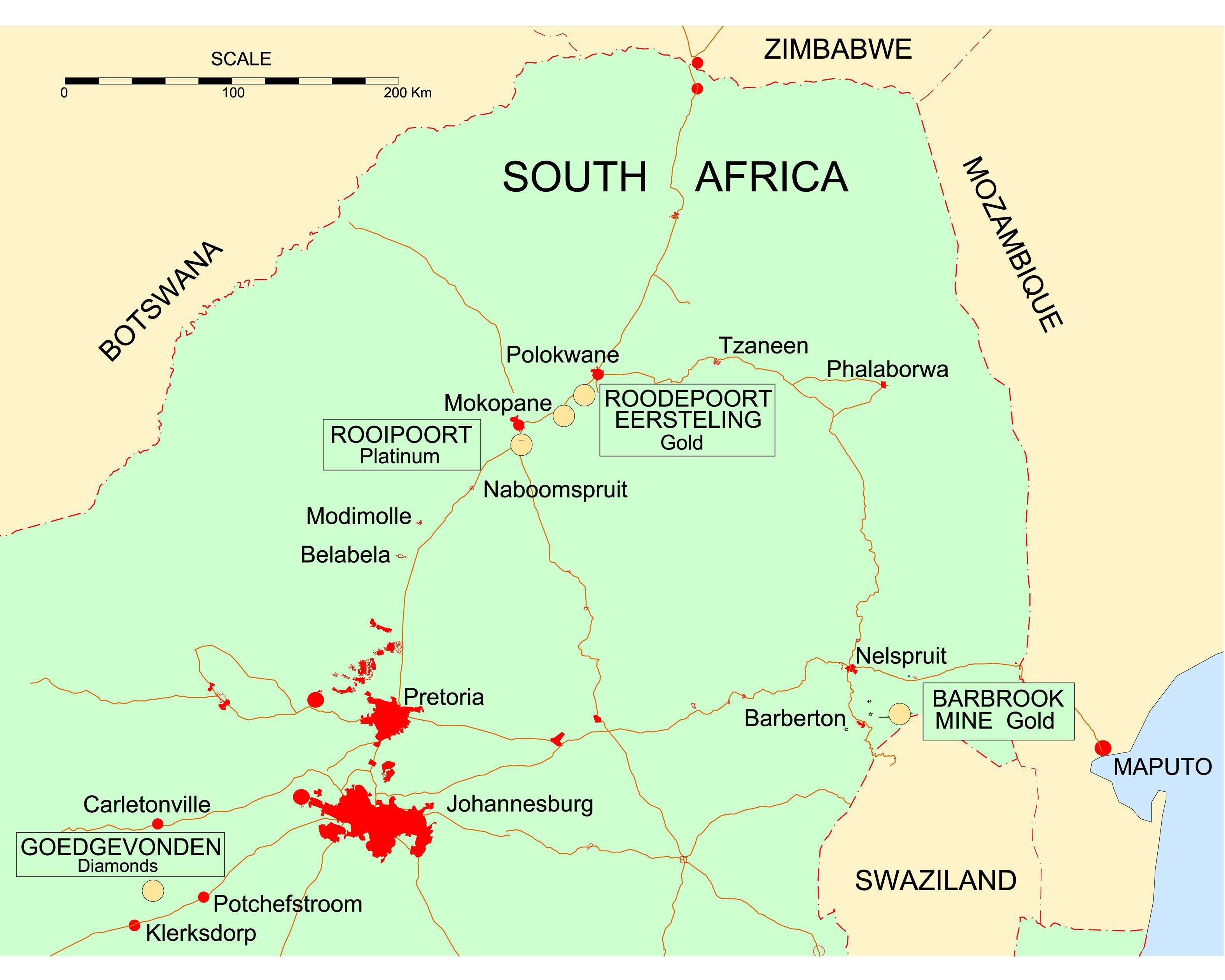

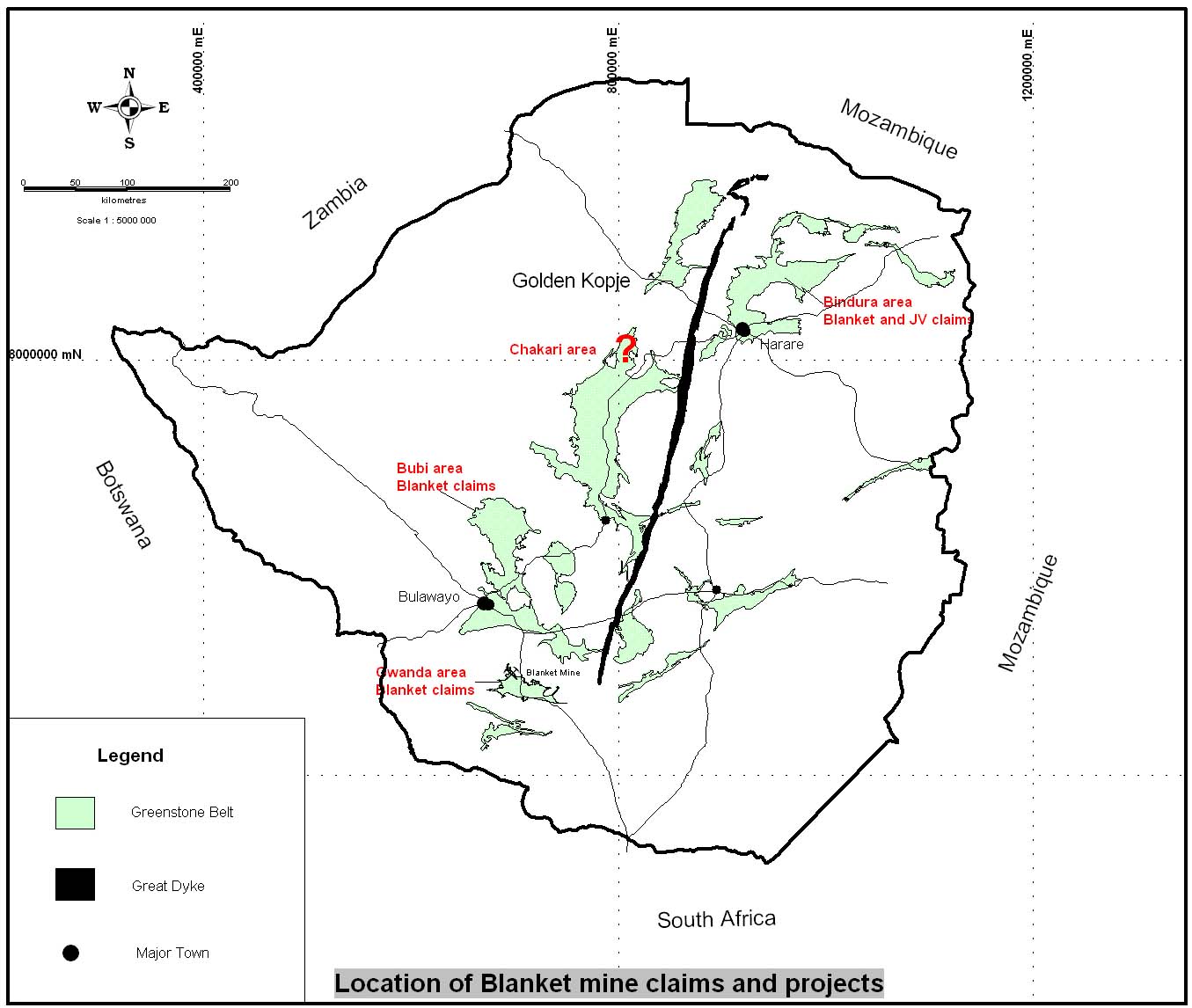

Pages 12, 13 and 14 are maps respectively of northern South Africa, Zimbabwe and Zambia – which show the locations of the Company’s properties in those countries.

B.

Business Overview

Mining and Exploration Activities:

Gold Production

Blanket Mine – Zimbabwe

Safety, Health and Environment

·

The mine recorded four lost time injuries, including one fatality, and four restricted work activity cases during the period. This is compared to the same period in 2006 which recorded three lost time and 7 restricted work activity cases. With the exception of the single fatality, the reduction in incidents in restricted work activity cases was attributable to the intensive safety training undertaken under the National Occupational Safety Association (“NOSA”).

12

·

An occupational health centre has been established and all employees were screened for occupational ailments. There were no occupational health illnesses detected during the year. HIV/AIDS continues to be an area of concern and management has put in place awareness programs to educate workers. The prevalence of medical retirees is increasing due to the HIV/AIDS pandemic.

The Mine continues to monitor the ground water in the ground-water pumping wells downstream of the tailings impoundment. Results continue to be well within the Governmental Environmental Management Agent (“EMA”) minimum levels. Re-grassing of the slopes on Dam B was undertaken and is ongoing. As a result of management’s continuing efforts to improve pollution control measures at Blanket Mine, the EMA has now upgraded the slimes dam from the red to the yellow category and management intends to strive for achievement of the highest (“green”) safety category.

Capital Projects

Number 4 Shaft Expansion Project

Projects at Blanket focused mainly on the expansion program which involved the upgrading of the No. 4 shaft and the crushing/milling section of the plant. Shaft equipping of the No. 4 shaft continued throughout the year and was completed at the end of October. Work remaining to complete the shaft upgrade includes the equipping of loading and ore bin arrangements at the shaft bottom as well as the installation of a crusher and conveyor system to reduce the size of the ore prior to hoisting.

This expansion project is designed to facilitate the increase in underground production from the current 600 tonnes per day (“tpd”) to 1,000 tpd. This should enable the total gold recovered to increase from 25,000 oz to 40,000 oz per annum.

Operations

Contrary to the project plan, Blanket suffered a prolonged unplanned No4 shaft closure from February to the end of July which was beyond Management’s control and was due mainly to a lack of power supply and severely restricted foreign currency receipts from the RBZ. During July, production was halted and the mine put on care and maintenance to save costs as the high grade sands being processed during this period were depleted and the contractor cost of transporting the sands to the plant escalated to an uneconomic level. In order to gain rapid access to the new mid-shaft loading bins underground, the decision was taken to speed up equipping of the No. 4 shaft by operating around the clock when power availability allowed. This decision paid some dividends, as Blanket was able to partially commission the No. 4 shaft to haul from 14 level at the end of July, thereby allowing the resumption of some underground operations building up to the planned produc tion level of up to 600 tonnes per day. However recurring power outages continued to cause major disruptions to the final quarter operations, but these were eventually resolved by the mine undertaking to pay the Zimbabwe Electricity Supply Authority (“ZESA”) in foreign currency for its power supply. Absenteeism, power supply problems, and the consistent withholding of foreign currency by the RBZ so severely limited Blanket’s ability to restore production to the 600 tpd level that it was unachievable. The RBZ controls all foreign currency needed by Blanket which includes US Dollars from gold sales proceeds and payments to ZESA and certain suppliers, and also South African Rand required for certain supplier payments. Gold production has averaged 1,000 ounces per month since underground mining operations were resumed in July 2007 compared to the pre-shaft expansion target of 2,100 ounces per month.

Frequent power disruptions during the last two quarters of the year allowed the shafts and metallurgical plant to operate for only 86% of the available time, processing 100,082 tonnes instead of a forecast 178,000 tonnes. Both the nearly completed No. 4 shaft expansion and the plant are currently running well although foreign currency shortages are beginning to affect the plant availability, in particular the crushing and screening plant and the carbon in leach (C.I.L) sections due to the inability to purchase critical wear parts due to the foreign currency delays. Discussions are ongoing with RBZ to try to improve the receipt of US Dollars for gold delivered.

13

Production results for year to December 2007 | 2007 | 2008 Jan.- Feb. | |

Ore mined | tonnes | 100,082 | 17,165 |

Development advance (ROM) | meters | 669 | 85 |

Development advance (Capital) | meters | 504 | 26 |

Ore milled | Tonnes | 100,082 | 17,285 |

Ore Gold Grade milled | grams/tonne | 3.58 | 3.51 |

Ore – Gold Recovered | ounces | 9,885 | 1,719 |

Sands Processed | tonnes | 125,137 | - |

Sands Grade | grams/tonne | 1.29 | - |

Sands Gold Recovered | ounces | 3,414 | - |

Gold produced | ounces | 13,299 | 1,719 |

Gold Sold | ounces | 13,985 | 1,876 |

Outlook

The aims and objectives of Blanket Mine for 2008, subject to the return of reliable payment procedures for gold sales proceeds by the RBZ, are:

·

To complete the No. 4 shaft project in order to realize the planned increase in ore production to 1,000 tonnes per day and gold production to 3,330 ounces of gold per month.

·

To intensify underground development initiatives in order to open up sufficient reserves to sustain the planned increase in ore production.

·

To explore ways of controlling input costs in a hyperinflationary environment (such as off-shore purchasing).

·

To explore ways of retaining key staff in a hyperinflationary economy.

·

To formulate a development strategy for the exploration properties in the Gwanda Greenstone Belt.

·

To focus employee and management attention and effort on issues of safety, health and environment.

·

To focus on off-mine exploration to supply additional ore to the plant

7.2 Exploration and Project Development

COBALT AND BASE METALS

Nama Cobalt Project – Zambia

Property

Caledonia Nama Limited (“Nama”), a wholly owned subsidiary of the Corporation, holds a Retention License in northern Zambia on which near-surface cobalt/copper mineralization has been discovered. This area lies immediately northwest of the operating Konkola Copper mine and adjoins the extensive land holdings of Teal Mining and Exploration Limited. This Retention License covers an area of 80,625 hectares and is valid for two years.

Work Completed

The 2001/2002 soil sampling program carried out jointly by Nama and BHP Billiton was completed over the remainder of the original license areas not covered by Nama in its 1995 and 1996 soil sampling and drilling program. The 1995/1996 programs identified a number of high priority anomalous targets (anomalies A, B, C, D and E) within the required geological setting. Reverse Circulation (“RC”) drilling was carried out on anomalies A, B, C, and D to a depth of at least 150 meters. The 2001/2002 soil sampling program results identified an additional 11 anomalous areas for further investigation including anomalies F to P. These targets have not yet been followed up in the search for copper/cobalt oxide and sulphide bodies.

In the second quarter of 2004, a mini bulk sample of 30 tonnes was excavated at Nama A (Discovery) site and underwent successful screening tests and heavy media/gravity separation tests in South Africa. Following

14

encouraging results, a further one tonne sample were sent for additional test work to fine tune the extraction process for the cobalt oxide.

During 2006 metallurgical test work provided a metallurgical flow-sheet. Two further bulk samples were taken from Anomaly A to enhance and refine the metallurgical processes and cost parameters for producing a marketable and economically viable cobalt product.

In 2006/2007 a Technical Report, compliant with NI 43-101 was prepared for Anomaly A at Nama by Mr. David Grant, C.Geol., FGS, Pr.Sci.Nat., an independent consultant who is the “Independent Qualified Person” for Nama’s resources as required by NI 43-101 of the Canadian Securities Administrators.

In his report, which has been filed on SEDAR and is available on the Corporation’s website, Mr. Grant estimates the Indicated Resources at Anomaly A as 43,656,000 tonnes grading 0.055% Co, 0.099% Cu and 0.011%Ni. Mr. Grant subsequently re-evaluated the data for Anomaly C and prepared an update to the previous Technical Report which included the following additional Indicated Resources for Anomaly C; 78,218,000 tonnes grading 0.043% Co, 0.012% Cu and 0.019% Ni. The combined resource is therefore 121,874,000 tonnes grading 0.047% Co, 0.043% Cu and 0.016% Ni. This second NI 43-101 report has been filed on Sedar and is available on the Corporation website.

Mr. Grant also states that Anomalies F through Q inclusive are worthy of further investigation.

Nama continued exploration on the Nama Retention License area during the 2007 field season. During the year $2,470 was spent on exploration consisting mainly of drilling diamond and reverse circulation holes. The results of the exploration activities will be released as soon as available.

Diamond drill core holes were drilled for both geological and bulk density measurement purposes. Bulk density measurements are required in order to determine ore volumes and tonnages for mining purposes with an acceptable level of accuracy. The bulk density drill holes were sited so as to provide information of a geological nature in critical areas and thereby provide the added benefit of improving the definition and understanding of the ore bodies.

A total of 4,099 meters of Diamond drilling was completed during the 2007 exploration field season, and the breakdown per anomaly area is as follows:

Anomaly | Diamond Drill Holes | Meters Drilled | Comment |

A | 7 | 1,769 | Geological and assay data |

A | 4 | 320 | Bulk Density & Geological data |

C | 3 | 770 | Geological and assay data |

C | 8 | 640 | Bulk Density & Geological data |

D | 6 | 600 | Bulk Density & Geological data |

Total | 28 | 4,099 |

|

A total of 5,560 meters of Reverse Circulation drilling was completed during the 2007 exploration season and the breakdown per ore body area is as follows:

Anomaly | RC Drill Holes | Meters Drilled |

A | 2 | 160 |

C | 23 | 1,309 |

D | 51 | 4,091 |

Total | 76 | 5,560 |

The earlier than usual onset of the rains in early November made it impossible to drill some outstanding areas of Anomaly D and Anomaly Q which is a prominent but untested geochemical target. In order to obtain at least some geological information on Anomaly Q in early 2008, a shallow pit and trench sampling program has been implemented.

The diamond drill core was logged and split on site prior to dispatch to an accredited analytical laboratory in Kalulushi, Zambia for analysis of cobalt, copper, nickel and zinc, amongst others. Quality Control and Quality Assurance control procedures were put in place to verify the accuracy of the drill core splitting and handling and the laboratory results.

15

All assay data has been received and is currently being verified and consolidated into the project database. The resource modelling and re-evaluation of the various anomalies is in progress and a revised independent Technical Report compliant with NI 43-101 standards will be issued once this work is completed.

The metallurgical testing to establish the likely product specification of the cobalt hydroxide product has been completed. Based on this metallurgical test work the cobalt hydroxide specification has been discussed with, and is acceptable, to the refiners who have signed purchase agreements for the cobalt hydroxide product.

Five year supply agreements have been finalized with four large Chinese refiners to supply a total of 51,560 tonnes of cobalt metal equivalent over a five year period commencing in 2009. Nerin China (Nanchang Engineering and Research Institute of Nonferrous Metals) has been commissioned to produce a Feasibility Study in accordance with the Regulations and Preparation Basis of a Project Feasibility Study Report for the Nonferrous Metals Industry, and related Chinese specifications and standards.

During the year the Nama Environmental Impact Assessment (EIA) covering the new access road and power line routes to the proposed Nama Plant Site was completed, and has been submitted to the Environmental Council of Zambia for their final approval. This EIA study is currently being expanded to cover the anticipated future mining operations at Nama.

Rooipoort PGE/Ni/Cu Project (including Grasvally) - South Africa

Property

In 2002, Eersteling Gold Mining Company Limited (“EGM”) acquired the Rooipoort property, containing platinum group elements (PGE), nickel (Ni) and copper (Cu), from Rustenburg Platinum, owned by Anglo Platinum Limited. The property is located approximately 30 km southwest of the Eersteling Gold Mine property in an area that is presently undergoing a surge in platinum group metal exploration along a well-mineralized feature known as the “Platreef”. An additional 342 hectares on the farm Grasvally, immediately adjacent to, and south of, the Rooipoort property was optioned in 2004, and over which the Company was granted a New Order Prospecting Right in May 2005 (3 year period). A further 43 hectare portion was granted in April 2006 (5 year period).

Application for conversion of the Rooipoort property into a New Order Right in terms of the Mineral and Petroleum Development Act (“MPRDA”) was granted in November 2006.

In March 2006, the Company concluded an agreement, with Falconbridge Ventures of Africa (Pty) Ltd (“Falconbridge”) to acquire a 100% interest in Falconbridge’s prospecting rights covering a total area of 4,315.81 hectares contiguous with the Rooipoort property which effectively doubles the area of the Rooipoort Project property underlain by Bushveld Complex rocks with PGE potential. The Falconbridge properties were granted New Order Prospecting Rights in April 2006 (3,099 hectares, for a period of 5 years) and September 2006 (1,217 hectares, for a period of 5 years). The total area of EGM’s New Order Prospecting Rights in the Rooipoort PGE/Ni/Cu properties is now 8473.39 hectares.

EGM’s rights to the Rooipoort Project, together with the Falconbridge agreement are in the process of being transferred to Maid O’ The Mist (Pty) Ltd, a 100% South African registered subsidiary of the Corporation.

Exploration

To date, the Company has diamond-drilled a total of 18,450 meters in 54 holes on the Rooipoort PGE/Ni/Cu Exploration Project. This drilling covers the full 6 km strike length that makes up the project area.

Falconbridge drilled a total of 7,393 meters in 22 holes on the portions of Grasvally and the farms Jaagbaan and Moorddrift that comprise most of the property purchased from Falconbridge.

At the end of 2004, very preliminary, flotation amenability test work was performed at the SGS Lakefield laboratories in Johannesburg, South Africa on mineralized composite samples from 5 lithological units prepared from the early diamond drill-hole cores to verify the flotation amenability of the ore. The tests included milling and basic flotation to produce a flotation concentrate. The tests indicated that from each of the five mineralized zones, a re-cleaner flotation concentrate of low mass recovery can be produced that contains medium to high

16

recovery of platinum, palladium, gold, copper and nickel. This initial test work indicates that a relatively simple metallurgical process route could possibly produce a flotation concentrate from high-tonnage, low-grade feed material.

In September 2005, an independent resource estimate was calculated and incorporated into a NI 43-101 - compliant report by RSG Global of Australia. The results of this estimate are:

Inferred Resource: At 0.5g/t 2PGE+Au and 200m below surface (900m base)

Zone | Average True Width (m) | Tonnes | 2PGE+Au (g/t) | Pt (g/t) | Pd (g/t) | Au (g/t) | Ni % | Cu % |

M2 | 1.8 | 12,791,200 | 1.34 | 0.42 | 0.83 | 0.10 | 0.20 | 0.12 |

L3 | 1.3 | 5,337,154 | 1.15 | 0.59 | 0.51 | 0.05 | 0.15 | 0.10 |

The resource estimate is the work of Dr. Julian Verbeek supported by Mr. Ken Lomberg, both of RSG Global.

During 2007, field work consisting of geochemical sampling was conducted over the land acquired from Falconbridge. A total of 37.37 line kilometers was sampled during this phase of the work and 1500 samples submitted for assay for Ni, Cu and PGMs. Based on the results of this sampling, the drilling program for the coming 2008 drilling season will be laid out.

Maps and drill logs for the Rooipoort PGE/Ni/Cu Exploration Project shown on the Corporation’s website provide an overview of the exploration activity that has been carried out on the Rooipoort property. The Project Status Report and the full RSG NI 43-101 Technical Report are available on the Corporation’s website. As a result of the work done to date, additional target areas have been identified on the west and north-west of the property, and these are identified in the Project Status Report on the website.

Discussions with a suitable Joint Venture partner regarding a “farming-in” arrangement are currently underway.

GOLD

Zimbabwe Exploration - Gold

The Corporation’s exploration activities in Zimbabwe are conducted by the Blanket Mine’s exploration department. Blanket’s current exploration title holdings in the form of registered mining claims in the Gwanda Greenstone Belt total 78 claims, including a small number under option, covering a total area of 2,500 hectares. 47 claims of these claims are registered as precious metal (gold) blocks covering 415 hectares and 31 claims were pegged and are registered as base metal (Cu, Ni, As) blocks covering a total area of 2,085hectares

Blanket’s efforts were focused in certain key areas in the Gwanda Greenstone Belt (that are within trucking distance of the Blanket plant) such as GG and Mbudzane where it is believed there is the greatest chance of success. A drilling program initiated in late 2005 to probe for down-dip and strike extension mineralization associated with the GG prospect was continued into 2007 with 281 meters of drilling completed. The assay results establish the presence of two zones of potentially economic gold mineralization. The main exploration activities involved diamond core drilling and the development of a prospect shaft down to the first level aimed at exposing the ore body and providing a bulk sample for metallurgical testing.

The Bubi Greenstone Belt ground holding portfolio comprises a total of 27 base metal claims covering a combined total area of 2,820 hectares. Reconnaissance exploration work by soil, sampling and geological mapping has been completed in all the claims areas. In 2008 the focus will mainly be directed to conduct additional follow-up work to define drill targets on potentially prospective metal-in-soil anomalies so far identified in the area. The work in the Sandy Claims constitutes part of this detailed follow-up exploration work.

During the first quarter of 2008, and assuming the availability of funds, Blanket’s exploration focus is centered on the Gwanda area with the main emphasis being delineation of a potentially economic ore resource at the GG prospect and Mbudzane. At GG, this will be achieved through continued core drilling from the surface to establish the strike extent of established economic mineralization as well as by deepening the prospect shaft and extending underground development. At Mbudzane, a second phase core-drilling program has been planned to follow up on several highly prospective deep seated IP-anomalies generated in 2006.

In addition, Blanket is conducting basic reconnaissance exploration work on the Bunny’s Luck claims, the target being to determine the potential strike length of a 1m to 1.5m wide shear zone hosted quartz vein so far mapped over a strike length of 300m. Blanket needs to formulate a development strategy for its outside properties in the

17

Gwanda area, in particular, and elsewhere in general, in order to prevent forfeiture under the current indigenization proposals.

DIAMONDS

Kikerk Lake – Canada

The Kikerk Lake property consists of 5 mineral leases covering 12,912.5 acres (5,225.5 hectares). In 2001 and 2002, the Corporation announced the discovery of two diamondiferous kimberlites, “Potentilla” and “Stellaria”, on the Kikerk Lake property in Nunavut Canada, by its joint venture partner and operator of the property, Ashton Mining of Canada Inc. (“Ashton”), a wholly owned subsidiary of Stornoway Diamond Corporation (“Stornoway”). The two kimberlite pipes are approximately 700 meters apart. In 2005, Ashton collected 108 heavy mineral samples to follow up on previous anomalous results. These samples were sent to Ashton’s laboratory and results were received in the first quarter of 2007.

Ashton reported that approximately 24 line-kilometers of ground magnetic survey were conducted over a structural trend line, but there were no new magnetic features noted that would be indicative of kimberlite emplacement.

Four diamond drill holes, totaling 382 meters were drilled to test the Stellaria kimberlite and a possible source of kimberlite indicator minerals east of Stellaria. Results confirm that the Stellaria body has a steep dip to the north-west and limited width.

The Corporation’s 17.5% share of this program is funded by Ashton. Ashton holds a 52.5% interest, having incurred in excess of $750,000 in exploration expenditures on the property. This interest can be increased to 59.5% if Ashton funds the Corporation’s share of the costs through to a completed feasibility study. The remaining 30% interest is held by Stornoway. Recently Stornoway has amalgamated with Ashton.

Due to a lack of recent activity on this joint venture the carrying value of $750,000 has been written off.

Mulonga Plain – Zambia

Work Completed

Motapa Diamonds has given the Corporation notice that it intends withdrawing from the joint venture and intends to transfer all rights in and title to the properties to the Corporation for a nominal amount.

The Corporation has applied for a retention license over the properties managed under the joint venture.

The Mulonga Plain License area is located in Western Zambia, between the Zambezi River and the Angolan border. The Company has identified discrete areas within the license area. An airborne gravity survey was completed on the easternmost of these in late 2004.

Ten, out of an original eleven, airborne gravity and magnetic targets were drill tested during 2005 and one hole was abandoned due to poor drilling conditions. Basalt basement was intersected in each of the holes at depths ranging from 87 meters to 173 meters with no kimberlite intercepts reported from any of the holes. Motapa has defined four prospective regions within the extensive Mulonga Plain anomaly through prior heavy mineral sampling, airborne magnetics and reconnaissance drilling. The 2005 drill program was designed to test the easternmost of these prospective regions and followed on from completion and interpretation of an airborne gravity survey in late 2004. A Falcon airborne survey was flown and the results interpreted in 2006.

Commenting on the 2005 results, Motapa’s CEO Dr. Larry Ott noted: “The extensive Mulonga Plain diamond and kimberlite indicator mineral anomaly remains highly prospective for discovery. This program has provided an initial drill test of one of four well defined indicator mineral dispersions. The remaining three areas, in the central and western portions of the Mulonga Plain remain essentially untested and results of this program should add considerably to our understanding of kimberlite indicator mineral dispersion within the Mulonga Plain and better constrain likely source kimberlite areas.” No further work was carried out in 2006 and 2007 as Motapa prioritized other areas of their property portfolio over Mulonga.

18

Kashiji Plain - Zambia

This license area is located in northwest Zambia, adjacent to the Angolan border. Prior work by Motapa has recovered 22 micro diamonds in association with numerous kimberlitic ilmenites. Work in 2005 focused on interpretation of results from the field work of 2004 in two discrete areas of anomalous kimberlite indicator mineral and diamond recoveries. No further field work was carried out on the Kashiji or Lukulu licenses in 2006 and 2007. This license is due to expire in June 2008, however as stated above the Corporation has also applied for retention licenses covering the Kashiji and Lukulu areas.

Goedgevonden - South Africa

The Corporation holds prospecting rights over the Goedgevonden diamond bearing kimberlite pipe and surrounding area. This property is located approximately 20km north of the Stilfontein gold mine in the Klerksdorp district of the North West Province in South Africa and 200km south west of Johannesburg.

In April 2005 an application for conversion of these rights was submitted in terms of the Mineral and Petroleum Resources Development Act (“MPRDA”) and the rights were granted in December 2006. An additional application for New Order Prospecting rights was submitted over an adjoining farm, Eleazar in June 2005. It is expected that this application will be granted shortly as soon as documentary proof of BEE participation has been presented.

Previous prospecting activities carried out in the mid 1970’s on Goedgevonden indicate that the pipe is oval in shape and covers a surface area of approximately 0.27 hectares. This work also confirms that the pipe was drill intersected at a depth of 425 meters, and that further down-dip extensions remain undefined. Previous drilling reported an average diamond content of 35 to 45 carats per hundred tonnes of material (“cpht”), with one hole yielding 65 cpht. The Corporation has not completed the work necessary to estimate a resource in terms of NI 43-101 for the Goedgevonden property.

A preliminary drilling program conducted in 2002 consisted of 7”, 8” and 12” diameter reverse circulation drill holes, followed by the collection of the drill samples and diamond recovery. Four holes were drilled in the centre of the pipe, three to a depth of 150 meters, and the other to 120 meters. The three remaining holes were drilled to delineate the pipe in more detail. All of the seven holes drilled entered the kimberlite at a depth of about 6 meters, and the four centrally-located holes were stopped whilst still in the kimberlite. A total of about 56 tonnes of drilling sample was collected and processed through a Van Eck and Lurie dense-media separation (“DMS”) plant and wet Sortex machine. From the diamond recoveries it was confirmed that the Goedgevonden pipe was diamondiferous, and sufficient gem-quality diamonds were recovered to warrant a larger bulk sample. Geological interpretive work as well as detailed ground gravity and magnetometer surveys were completed during 2003 but there was no further exploration activity on this property as corporate resources were concentrated on the Corporation’s other projects which were considered to be of higher priority in adding shareholder value.

Granting of the New Order Prospecting Rights (not yet signed) gives the Company security of tenure. Discussions are in progress with other parties with a view to realizing value by joint venture or disposal of the properties in the Goedgevonden Diamond Project.

Outlook

The outlook for the aforementioned exploration properties, except for Nama,is difficult to quantify. Exploration by its nature is speculative with a high degree of risk accompanied by the potential for high returns. The Corporation manages this risk by using well-qualified exploration professionals, senior mining company joint venture partners and by exploring in areas which are considered as having a better than average potential for discovery. The recent increases in the prices of precious and base metals should improve exploration expenditures of the major mining companies and could improve the likelihood of the Corporation negotiating joint venture agreements for its remaining wholly-owned exploration properties.

The Corporation intends to continue to focus its exploration activities of prospective properties by developing the properties through strategic alliances where possible with senior mining companies and metal producers.

In terms of the South Africa Minerals and Petroleum Resources Development Act (No 28 of 2002) (“MPRDA”) and implemented May 1, 2004, all “old order” mineral rights in South Africa are required to be converted to

19

“new order” rights, by a process of re-applying for these rights. Holders of all inactive prospecting and mining rights (immediately preceding May 1, 2004) were required to apply for conversion by April 30, 2005. Active prospecting right conversion applications closed on April 30, 2006 and active mining right conversions close on April 30, 2009.

Apart from various technical requirements for conversion, the new legislation requires that companies give attention to the requirements of theMPRDA as defined in Section 2(d) as well the Mining Charter as “substantially and meaningfully expand opportunities for historically disadvantaged persons, including women, to enter the mineral and petroleum industries and to benefit from the exploitation of the nation’s mineral and petroleum resources. The Mining Charter was formulated in negotiations between the government, the mining industry as largely represented by the Chamber of Mines of South Africa, and organized labour.

The Mining Charter seeks to address the implementation of section 2(d) in practical and measurable terms. Lack of clarity as to the status of prospecting under the Mining Charter has led to considerable debate and confusion in terms of the ability of companies involved in early stage prospecting work to meet or even indicate their commitment to meeting the terms of the Mining Charter, even before any sort of mineral resource has been established. This in part has been the cause of considerable delays in processing of the thousands of applications submitted as part of this process. However, there has recently been an apparent relaxing of the attitude of the South African authorities in respect of New Order Prospecting Rights and many companies, including the Corporation have received these new rights in recent months.

The Zimbabwe economy continues to be depressed and inflation is rampant. The survival of the mining industry is a high priority of the Government as its ability to generate foreign currency is of paramount importance. Management’s focus is to complete the No 4 shaft expansion and to bring production up to the 1000 tpd level. Cash flow management is critical to ensure the mining operations are protected, as much as possible, from the effects of local inflation by the utilization of foreign currency proceeds to fund operations. Management is also continuing with exploration in the areas near the Blanket mine to enable Blanket to expand its operation should economic improvements in Zimbabwe occur.

The President of the Republic of Zimbabwe brought the Indigenisation and Economic Empowerment Act into law through decree in March 2008. The law seeks to ensure that a majority stake (at least 51%) in all companies is held by Indigenous Zimbabweans. Additionally the Mines and Minerals Amendment Bill was presented before the closure of the last session of Parliament but not passed into law, and has thus lapsed. The Mines and Minerals Amendment Bill if enacted into law also seeks to ensure among other things that a majority stake is held in all mining companies by either indigenous Zimbabweans or the Government of Zimbabwe. Whilst neither the two pieces of legislation allow for compulsory acquisition, the Mines and Minerals Amendment Bill did provide for severe penalties in the form of extremely prohibitive taxes and potential withdrawal of mineral rights in the event of non voluntary compliance within certain time frames.

The Zambian government has announced the following proposed changes to their tax laws that will have a bearing on the Nama cobalt project if passed into law. The key changes are:

·

Increase in mineral royalty from 0.6% to 3%

·

Increase in profit tax rate from 25% to 30%

·

Introduction of variable profits tax of 15% for net profits above 8%

·

Introduction of a windfall profit tax for copper mines

·

Capital allowances reduced from 100% to 25%

These measures have been highly controversial with mining companies, many of which invested in the country under specific tax incentives and formalised their business models accordingly. Some mining companies are threatening legal recourse as they argue their businesses will become unviable. Proposed capital expenditure projects are being reconsidered. Various representations have been made by the mining companies through the Chamber of Mines to the government since the budget announcement at the end of January, however the government has taken a firm position, and we understand that the changes have been approved by parliament.

20

21

22

23

3.

General Comments

Caledonia’s activities are centered in Southern and Central Africa and in Northern Canada. Generally, in the gold mining industry the work is not seasonable except where heavy seasonal rainfall can affect surface mining or exploration. Caledonia is not dependent, to any material extent, on patents, licenses, contracts, specialized equipment or new manufacturing processes at this time. However, there may be occasions that Caledonia may wish to adopt such patents, licenses, specialized equipment, etc. if these are economically beneficial to its operations.

All mining and exploration activities are conducted under the various Economic, Mining and Environmental Regulations of the country where the operations are being carried out. It is always Caledonia’s standard that these regulations are complied with by Caledonia otherwise its activities risk being suspended.

(C)

Organizational Structure - Subsidiaries

Caledonia Mining Corporation owns 100% of the shares of the following incorporated subsidiary companies:

Zambia:

- Caledonia Mining (Zambia) Limited

- Caledonia Western Limited

- Caledonia Nama Limited

- Caledonia Kadola Limited

South Africa:

- Eersteling Gold Mining Company Limited

- Barbrook Mines Limited -

- Greenstone Management Services Limited

- Fintona Investments (Proprietary) Ltd

- Maid O’Mist (Proprietary) Limited

Barbados:

- Blanket (Barbados) Holdings Limited

- Caledonia Holdings (Africa) Limited

Zimbabwe:

- Blanket Mine (1983) (Private) Limited

- Caledonia Holdings Zimbabwe Limited

- Caledonia Mining Services Limited

Panama:

- Dunhill Enterprises Inc.

(D) Property, Plant and Equipment

(a)

South Africa:

The Barbrook and Eersteling gold mines, which are indirectly owned by the Company through its ownership of 100% of the shares of Barbrook Mines Limited and Eersteling Gold Mining Company Limited, are essentially fully equipped mines with all of the underground and surface equipment needed

24

to conduct mining operations and the treatment and concentration of ore mined from the properties. Due to the lengthy period of care and maintenance at Eersteling there has been some deterioration in the surface facilities which will require rehabilitation work before operations can be recommenced. The underground workings at Eersteling were allowed to flood and will require dewatering before mining access can be resumed. Because the Company is currently attempting to sell these mines it has no plans to expend further amounts on plant or equipment for them or to in any way expand or improve the facilities.

On February 21, 2008 the Corporation accepted an offer from Eastern Goldfields to purchase the entire issued share capital in Barbrook Mines Limited, its debts to the Corporation, and its payables of approximately $1,440,000 for approximately $9,100,000.

On March 3, 2008 the Corporation signed an Interim Agreement with a private Canadian company to purchase the entire issued share capital in Eersteling Gold Mining Company Limited (“EGM”) for $3,810,000 excluding the Rooipoort platinum exploration assets currently held by EGM which are in the process of being transferred to Maid O’ The Mist, a 100% held South African subsidiary of the Corporation.

(b)

Zimbabwe:

The Blanket Mine, in Zimbabwe, which the Company indirectly owns through its ownership of 100% of the shares of Blanket Mine (1983) (Private) Limited, the owner and operator of the Mine, is a fully equipped mine with all of the necessary plant and equipment to conduct mining operations and the concentration of ore mined from the Mine. As is noted above the Company is currently involved in expanding production from the Mine and expanding the capacity of the ore concentrator plant. To February 28, 2008 the Company had expended approximately the equivalent of $4,500,000 (Cdn.) on the Mine and plant expansion. It is estimated that, to complete the Mine plant expansion according to the present plans, will require the expenditure of approximately the equivalent of an additional $2,200,000 (Cdn.). Because of the political instability of Zimbabwe the Company is not attempting to seek either equity or debt financing for the expansion w ork and is, instead, funding it from the cashflow from the Blanket Mine. It is presently anticipated that the expanded production from the No. 4 shaft, and the treatment of that expanded production in the expanded concentrator plant facilities, will only be achieved when foreign currency owed to Blanket Mine for gold sales is paid by the Reserve Bank of Zimbabwe.

4A UNRESOLVED STAFF COMMENTS

The Company does not have any unresolved Securities and Exchange Commission Staff comments.

5

OPERATING AND FINANCIAL REVIEW AND PROSPECTS

A

Operating Results

SELECTED ANNUAL INFORMATION -

The following information is given for the last three fiscal year-ends of the Corporation:

C$000’s except for earnings per share amounts. | December 31, 2007 | December 31, 2006 (1) | December 31, 2005 (1) |

Net sales or total revenues | 10,039 | 13,586 | 6 |

Net (loss) or income before discontinued items or extraordinary items: - per share undiluted - per share diluted | (3,906) ($0.008) ($0.008) | 2,315 $0.005 $0.005 | (3,748) ($0.012) ($0.012) |

Discontinued Operations | (709) | (7,990) | (5,932) |

Net (loss) | (4,615) | (5,675) | (9,680) |

25

- per share undiluted - per share diluted | ($0.009) ($0.009) | ($0.013) ($0.013) | ($0.031) ($0.031) |

Comprehensive (loss) | (4,703) | (5,675) | (9,680) |

Total assets | 29,492 | 31,456 | 22,338 |

Total long-term financial liabilities | 1,054 | 1,221 | 377 |

Cash dividends declared per share | Nil | Nil | Nil |

(1) Figures have been reclassified to reflect Barbrook and Eersteling Mines under Discontinued Operations.

The above data was prepared in accordance with Canadian Generally Accepted Accounting Principles.

The results for 2007 and prior years have been presented on the basis that Barbrook and Eersteling Mines are discontinued operations and are classified as assets for sale. Neither sale transaction was concluded by December 31, 2007 but subsequent Sale Agreements for the purchase of the entire share capital of Barbrook Gold Mines Limited and Eersteling Gold Mining Company were signed with two independent buyers. The price for Barbrook is approximately $9,100,000 and for Eersteling is $3,810,000.

The above results for 2007 include Blanket Mine’s results for the 12 months ending December 2007 and for 6 months in 2006. During 2007 gold production at Blanket was disrupted by the shaft expansion project from February until the end of July. The delays were caused by a combination of frequent power cuts and the irregular and partial payment of US Dollars for gold delivered. During this period production was focused on processing sands as underground operations were curtailed by the shaft closure for equipping. Due to the economic climate in Zimbabwe, Blanket did not receive the full US Dollar proceeds for gold sales and thus the completion of the shaft expansion project was not possible. Entirely as a result of these factors Blanket has not been able to achieve and sustain gold production even at the levels achieved prior to the shaft expansion.

For the year ended December 31, 2007, the Corporation recorded a net loss after taxes, before discontinued operations, of $3,906,000 ($2,315,000 income in 2006 and a $3,748,000 loss in 2005), of which Blanket Mine contributed a loss of $510,000. Included in the 2007 loss is a foreign exchange loss of $1,012,000 ($143,000 gain in 2006 and a $50,000 loss in 2005). Blanket Mine reported an unrealized loss on foreign exchange of $1,203,000 during 2007. During 2007 the gross income from operations (before discontinued operations) was $294,000 ($5,014,000 income in 2006 and a $751,000 loss in 2005).

During 2007 the carrying value of $750,000 of the Kikerk Lake venture was written off leading to a total asset write-down of $750,000 ($nil in 2006 and $152,000 in 2005 of other mineral properties). The income tax expense of $5,000 relates to withholding taxes paid by Blanket Mine. The operating income of $294,000 includes an amortization charge of $18,000 ($40,000 in 2006 and $27,000 in 2005).

Blanket Mine recorded revenue for the 12 months of $10,001,000 from the 13,985 ounces of gold sold. During 2007 the RBZ (RBZ) stipulated various possible payment methods for gold sales. The methods varied from “65% of revenue in USD and 35% of revenue in Zimbabwean dollars (“Z$”) to 100% revenue received in Z$ if gold is sold at the gold support price. During the same period, the official exchange rate in Zimbabwe changed from Z$250 per US$1 to Z$30,000 per US$1.

The changes in the gold support price and the effective exchange rate received are shown in the table below

| Jan | Feb | Mar | Apr | May | June |

Ave gold price USD/oz | 631 | 665 | 655 | 679 | 667 | 655 |

Z$ Gold support price per gm | 16,000 | 16,000 | 16,000 | 16,000 | 350,000 | 1,000,000 |

Effective Z$:USD exchange rate | 789 | 748 | 760 | 733 | 16,322 | 47,489 |

Old Mutual Implied Rate– Z$’s per US$1 | 3,508 | 5,735 | 16,646 | 17,618 | 26,794 | 126,828 |

Effective discount to gold price based on buying power of the Z$ | 78% | 87% | 95% | 96% | 39% | 63% |

| ||||||

| Jul | Aug | Sept | Oct | Nov | Dec |

Ave gold price USD/oz | 665 | 665 | 713 | 755 | 806 | 803 |

26

Z$ Gold support price per gm | 3,000,000 | 3,500,000 | 4,000,000 | 5,000,000 | 7,500,000 | 10,000,000 |

Effective Z$:USD exchange rate | 140,324 | 163,712 | 174,503 | 205,995 | 289,440 | 387,362 |

Old Mutual Implied Rate– Z$’s per US$1 | 139,747 | 141,164 | 298,371 | 884,062 | 2,545,416 | 4,422,203 |

Effective discount to gold price based on buying power of the Z$ | 0% | 0% | 42% | 77% | 89% | 91% |

In January 2008 the gold support price was increased to Z$100 million per gram and in March 2008 was further increased to Z$700 million per gram.

During the year, the quarterly results (“Q”) of Blanket Mine have been translated into C$ using the rates of exchange (“ROE”) per the table below.

Z$’s per C$1 | Q4 ROE | Q3 ROE | Q2 ROE | Q1 ROE |

Sales revenue | 275,926 | 156,590 | 14,220 | 713 |

Other income statement items | 260,870 | 150,507 | 21,070 | 758 |

Monetary assets and liabilities | 378,644 | 168,645 | 47,451 | 758 |

All other assets and liabilities | 101.19 | 101.19 | 101.19 | 101.19 |

The rates are determined as follows:

Sales Revenue | The actual rate of exchange received on gold sales depending on the sale method chosen |

Other income statement items | The average effective rate of exchange determined by the gold support price during the quarter |

Monetary assets and liabilities | The quarter end effective rate of exchange determined by the gold support price during the quarter |

All other assets and liabilities | Historic rate determined at July 1, 2006 |

During 2007, the Corporation invested $3,250,000 in capital assets and mineral properties ($3,579,000 in 2006 and $5,284,000 in 2005). Of the amount invested in 2007, Blanket Mine spent $616,000 Nama spent $2,470,000 and Rooipoort spent $141,000. During the year $4,380,000 was raised from private placements, and the exercise of warrants and options, ($7,559,000 in 2006 and $6,588,000 in 2005) all net of issue costs.

The basic net income/ (loss) per share, for continuing operations, of ($0.008) in 2007, ($0.005 in 2006 and ($0.012) in 2005) has been calculated using a weighted average number of shares of 477,930,290 (423,838,628 for 2006 and 313,565,142 for 2005).