Exhibit 99.2

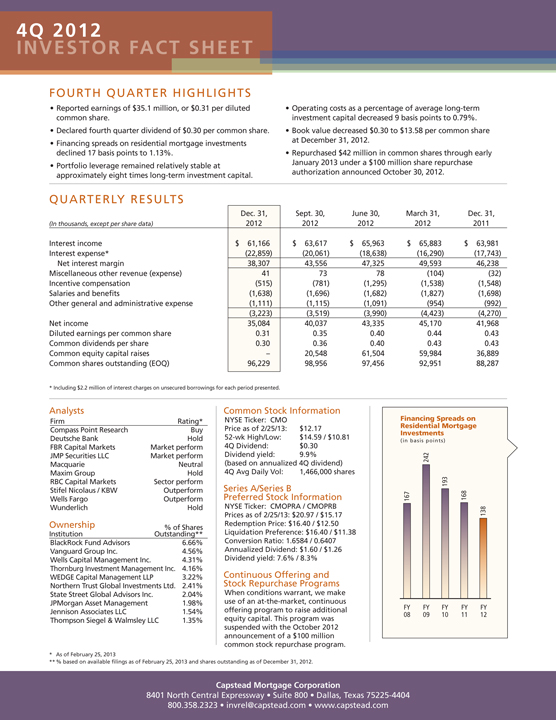

Portfolio Leverage*

Capstead Mortgage Corporation

8401 North Central Expressway Suite 800

Dallas,

$1.60

billion

$12.78

billion

Portfolio Leverage

Repurchase Arrangements

and Similar Borrowings

divided by Long-Term

Investment Capital

8.00:1

Long-Term

Investment Capital

(in millions)

Long-termUnsecured Borrowings, net

Preferred Stock, recorded amount

Common Stock

08 09 10 11 12*

$860

$1,114

Total Assets

(in millions)

08 09 10 11 12* $7,729 $8,629 $8,999 $1,127 $12,845 $14,469 $1,393 $1,597 $100

$189 $1,308

Capstead is based in Dallas, Texas and is listed on the New York Stock

Exchange (symbol CMO). Having been formed in 1985, we hold the

distinction of being the oldest of the publicly-traded mortgage REITs.

We invest in a leveraged portfolio of residential adjustable-rate

mortgage (“ARM”) securities issued and guaranteed by Fannie Mae,

Freddie Mac or Ginnie Mae.

Our investment strategy of focusing on agency-guaranteed ARM

securities differentiates us fromour peers because ARMsecurities reset

to more current interest rates within a relatively short period of time

allowing for:

the recovery of financing spreads diminished during periods of rising

interest rates, and

smaller fluctuations in portfolio values, and therefore book value,

caused by changes in interest rates compared to fixed-rate

mortgage securities.

Quality Assets

Agency-guaranteed residential mortgage securities are considered to

have little, if any, credit risk, particularly given federal government

support for FannieMae and FreddieMac. Thesemortgage investments

are highly liquid and can be financed with multiple funding providers

through standard repurchase arrangements.

Conservatively Financed

We prudently leverage our portfolio to provide financial flexibility

needed to successfully manage through periods of changing market

conditions, and we have long-standing relationships with numerous

lending counterparties. Further, our use of two-year term interest rate

swap agreements helps furthermitigate the effects of rising short-term

interest rates.

Experienced Management in a Stockholder Friendly Structure

Our management team has over 85 years of combined mortgage

finance industry experience.We are self-managed with low operating

costs and rely heavily on performance-based compensation. This

structure greatly enhances the alignment of management interests

with those of our stockholders.

ABOUT US

*As of December 31, 2012

Capstead Mortgage Corporation

8401 2012

Financing Spreads on

Residential Mortgage

Investments

(in basis points)

FY FY FY FY FY

08 09 10 11 12

138167168

Analysts

Firm Rating*Compass Point Research BuyDeutsche Bank Hold

FBR Capital Markets Market performJMP Securities LLC Market performMacquarie NeutralMaxim Group HoldRBC Capital Markets Sector performStifel Nicolaus / KBW OutperformWells Fargo Outperform

Wunderlich HoldOwnership %of SharesInstitution Outstanding**BlackRock Fund Advisors 6.66%Vanguard Group Inc. 4.56%Wells Capital Management Inc. 4.31%Thornburg Investment Management Inc. 4.16%WEDGE Capital Management LLP 3.22%Northern Trust Global Investments Ltd. 2.41%State Street Global Advisors Inc. 2.04%JPMorgan Asset Management 1.98%Jennison Associates LLC 1.54%

Thompson Siegel &Walmsley LLC 1.35%

Common Stock Information

NYSE Ticker: CMOPrice as of 2/25/13: $12.1752-wk High/Low: $14.59 / $10.814Q Dividend: $0.30

Dividend yield: 9.9%(based on annualized 4Q dividend)

4Q Avg Daily Vol: 1,466,000 shares

Series A/Series B

Preferred Stock Information

NYSE Ticker: CMOPRA / CMOPRBPrices as of 2/25/13: $20.97 / $15.17Redemption Price: $16.40 / $12.50

Liquidation Preference: $16.40 / $11.38Conversion Ratio: 1.6584 / 0.6407Annualized Dividend: $1.60 / $1.26

Dividend yield: 7.6% / 8.3%

Continuous Offering and

Stock Repurchase Programs

When conditions warrant, we makeuse of an at-the-market, continuousoffering program to raise additional

equity capital. This program wassuspended with the October 2012

announcement of a $100 millioncommon stock repurchase program.

* As of February 25, 2013**% based on available filings as of February 25, 2013 and shares outstanding as of December 31, 2012.

242193 Reported earnings of $35.1 million, or $0.31 per dilutedcommon share.

Declared fourth quarter dividend of $0.30 per common share.

Financing spreads on residential mortgage investmentsdeclined 17 basis points to 1.13%.

Portfolio leverage remained relatively stable atapproximately eight times long-term investment capital.

Operating costs as a percentage of average long-terminvestment capital decreased 9 basis points to 0.79%.

Book value decreased $0.30 to $13.58 per common shareat December 31, 2012.

Repurchased $42 million in common shares through earlyJanuary 2013 under a $100 million share repurchaseauthorization announced October 30, 2012.

FOURTH QUARTER HIGHLIGHTS

QUARTERLY RESULTS

Dec. 31, Sept. 30, June 30, March 31, Dec. 31,(In thousands, except per share data) 2012 2012 2012 2012 2011

Interest income $ 61,166 $ 63,617 $ 65,963 $ 65,883 $ 63,981Interest expense* (22,859) (20,061) (18,638) (16,290) (17,743)Net interest margin 38,307 43,556 47,325 49,593 46,238Miscellaneous other revenue (expense) 41 73 78 (104) (32)Incentive compensation (515) (781) (1,295) (1,538) (1,548)Salaries and benefits (1,638) (1,696) (1,682) (1,827) (1,698)Other general and administrative expense (1,111) (1,115) (1,091) (954) (992)(3,223) (3,519) (3,990) (4,423) (4,270)Net income 35,084 40,037 43,335 45,170 41,968Diluted earnings per common share 0.31 0.35 0.40 0.44 0.43Common dividends per share 0.30 0.36 0.40 0.43 0.43

Common equity capital raises – 20,548 61,504 59,984 36,889Common shares outstanding (EOQ) 96,229 98,956 97,456 92,951 88,287* Including $2.2 million of interest charges on unsecured borrowings for each period presented.