Exhibit 99.1

1 PRESENTATION NAME TO GO HERE 201 7 INVESTOR MEETING

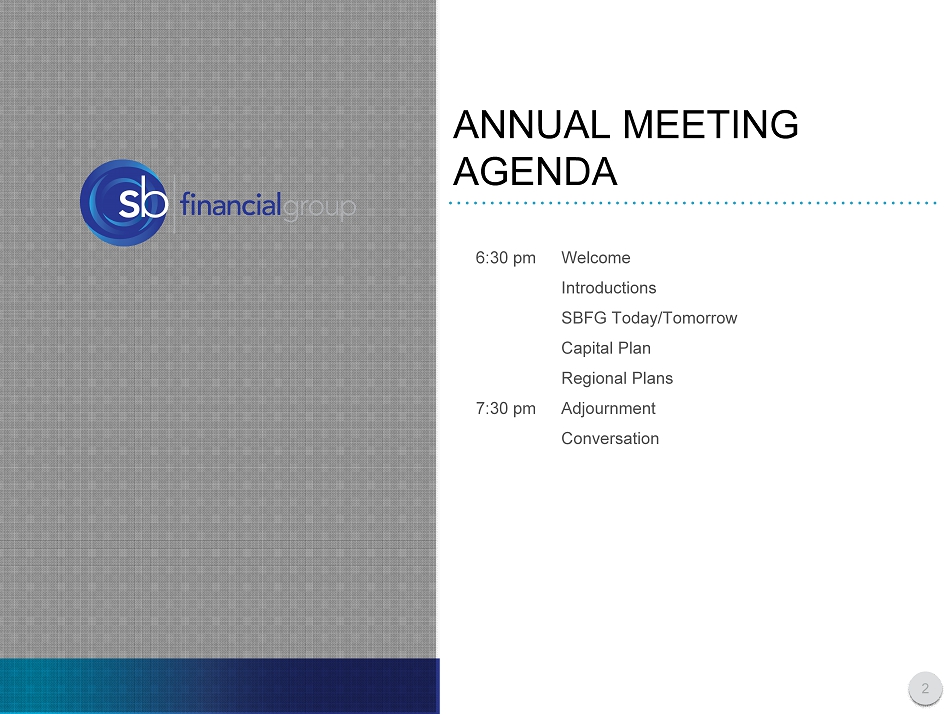

6:30 pm Welcome Introductions SBFG Today/Tomorrow Capital Plan Regional Plans 7:30 pm Adjournment Conversation ANNUAL MEETING AGENDA 2

B USINESS OVERVIEW BUILDING A HIGH - PERFORMANCE COMPANY 3

SAFE HARBOR STATEMENT SB FINANCIAL GROUP Certain statements within this document, which are not statements of historical fact, constitute forward - looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Forward - looking statements involve risks and uncertainties and actual results may differ materially from those predicted by the forward - looking statements. These risks and uncertainties include, but are not limited to, risks and uncertainties inherent in the national and regional banking, insurance and mortgage industries, competitive factors specific to markets in which SB Financial Group and its subsidiaries operate, future interest rate levels, legislative and regulatory actions, capital market conditions, general economic conditions, geopolitical events, the loss of key personnel and other factors. Additional factors that could cause results to differ from those described above can be found in the Company’s Annual Report on Form 10 - K and documents subsequently filed by SB Financial Group with the Securities and Exchange Commission. Forward - looking statements speak only as of the date on which they are made, and SB Financial Group undertakes no obligation to update any forward - looking statement to reflect events or circumstances after the date on which the statement is made except as required by law. All subsequent written and oral forward - looking statements attributable to SB Financial Group or any person acting on its behalf are qualified by these cautionary statements. 4

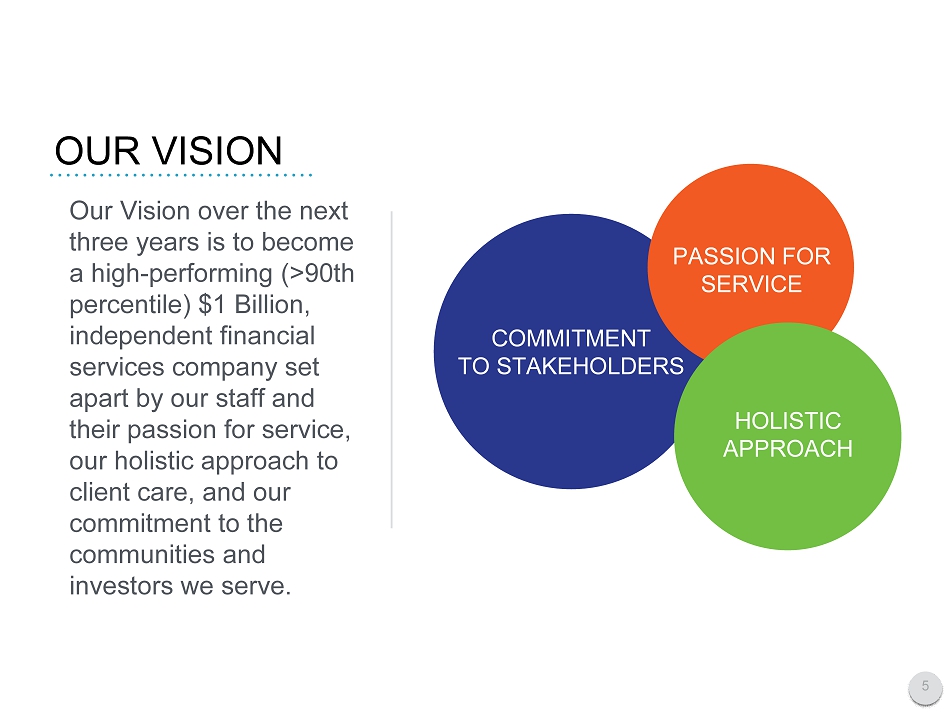

OUR VISION COMMITMENT TO S TAKEHOLDERS PASSION FOR SERVICE Our Vision over the next three years is to become a high - performing ( > 90th percentile) $1 Billion, independent financial services company set apart by our staff and their passion for service, our holistic approach to client care, and our commitment to the communities and investors we serve. HOLISTIC APPROACH 5

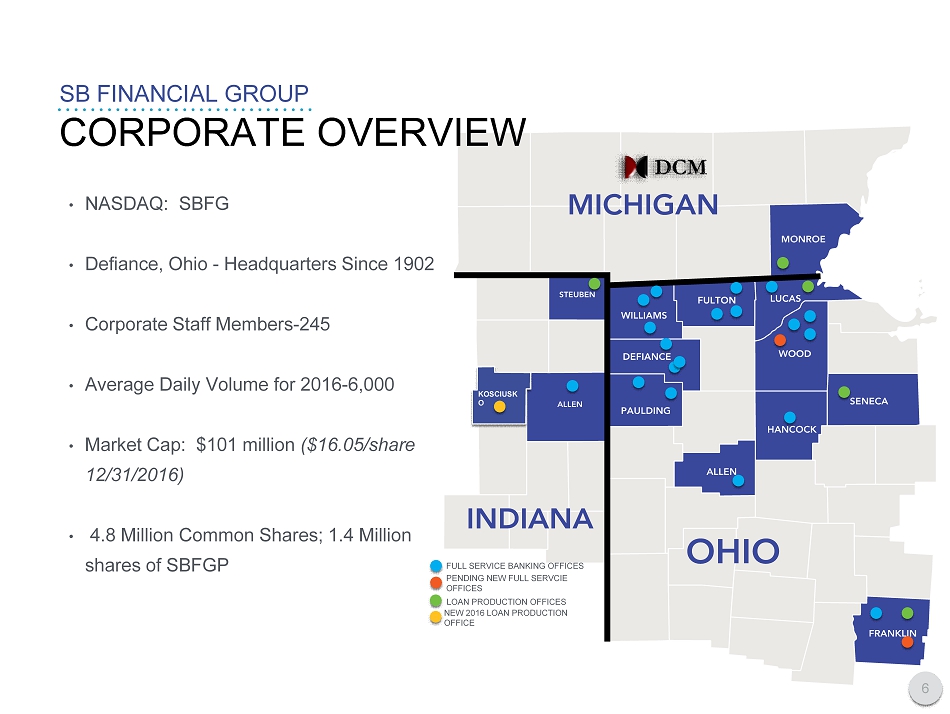

KOSCIUSK O • NASDAQ: SBFG • Defiance , Ohio - Headquarters Since 1902 • Corporate Staff Members - 245 • Average Daily Volume for 2016 - 6,000 • Market Cap: $101 million ($16.05/share 12/31/2016 ) • 4.8 Million Common Shares; 1.4 Million shares of SBFGP CORPORATE OVERVIEW SB FINANCIAL GROUP 6 FULL SERVICE BANKING OFFICES LOAN PRODUCTION OFFICES NEW 2016 LOAN PRODUCTION OFFICE PENDING NEW FULL SERVCIE OFFICES

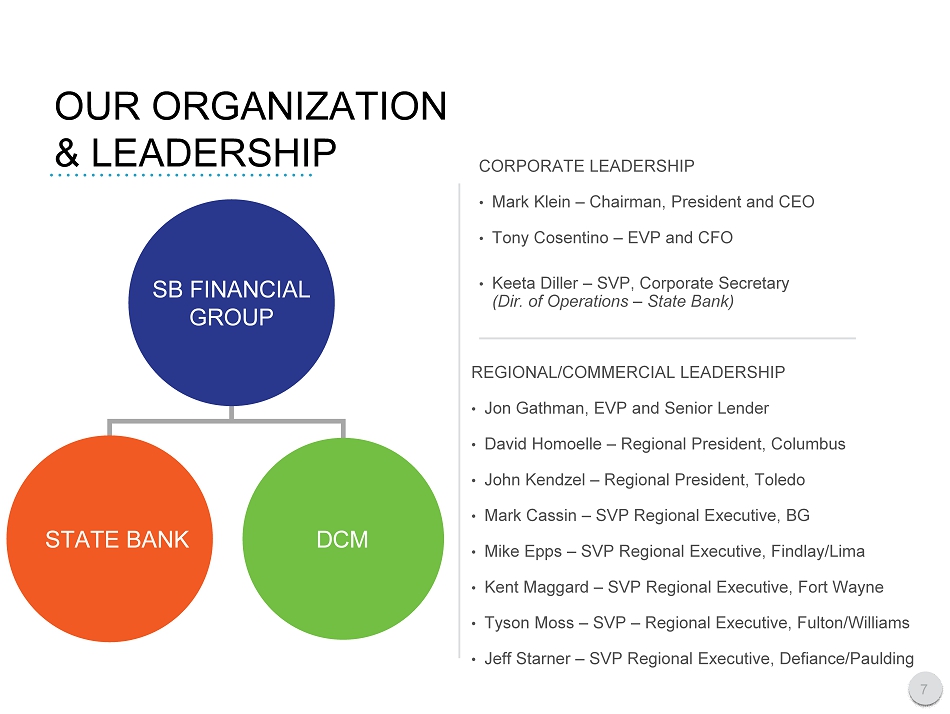

OUR ORGANIZATION & LEADERSHIP CORPORATE LEADERSHIP • Mark Klein – Ch airman, President and CEO • Tony Cosentino – EVP and CFO • Keeta Diller – SVP, Corporate Secretary (Dir. of Operations – State Bank) REGIONAL /COMMERCIAL LEADERSHIP • Jon Gathman, EVP and Senior Lender • David Homoelle – Regional President, Columbus • John Kendzel – Regional President, Toledo • Mark Cassin – SVP Regional Executive, BG • Mi ke Epps – SVP Regional Executive, Findlay/Lima • Kent Maggard – SVP Regional Executive, Fort Wayne • Tyson Moss – SVP – Regional Executive, Fulton/Williams • Jeff Starner – SVP Regional Executive, Defiance/Paulding SB FINANCIAL GROUP STATE BANK DCM 7

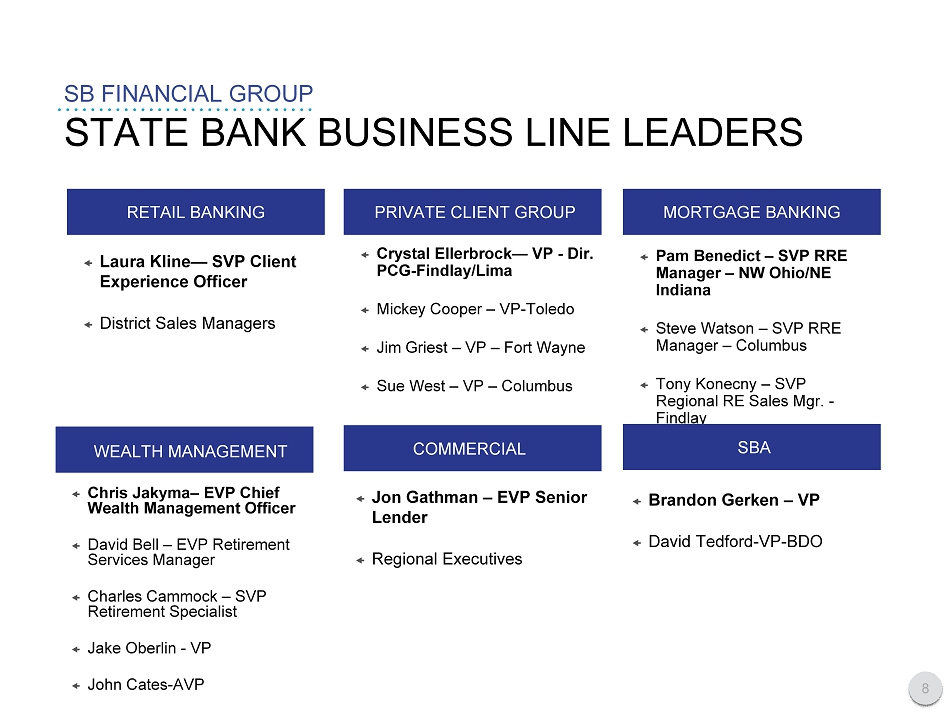

STATE BANK BUSINESS LINE LEADERS SB FINANCIAL GROUP RETAIL BANKING COMMERCIAL Chris Jakyma – EVP Chief Wealth Management Officer David Bell – EVP Retirement Services Manager Charles Cammock – SVP Retirement Specialist Jake Oberlin - VP John Cates - A VP PRIVATE CLIENT GROUP Crystal Ellerbrock — VP - Dir. PCG - Findlay/Lima Mickey Cooper – VP - Toledo Jim Griest – VP – Fort Wayne Sue West – VP – Columbus MORTGAGE BANKING Pam Benedict – SVP RRE Manager – NW Ohio/NE Indiana Steve Watson – SVP RRE Manager – Columbus Tony Konecny – S VP Regional RE Sales Mgr. - Findlay SBA Brandon Gerken – VP David Tedford - VP - BDO 8 WEALTH MANAGEMENT Jon Gathman – EVP Senior Lender Regional Executives Laura Kline — S VP Client Experience Officer District Sales Managers

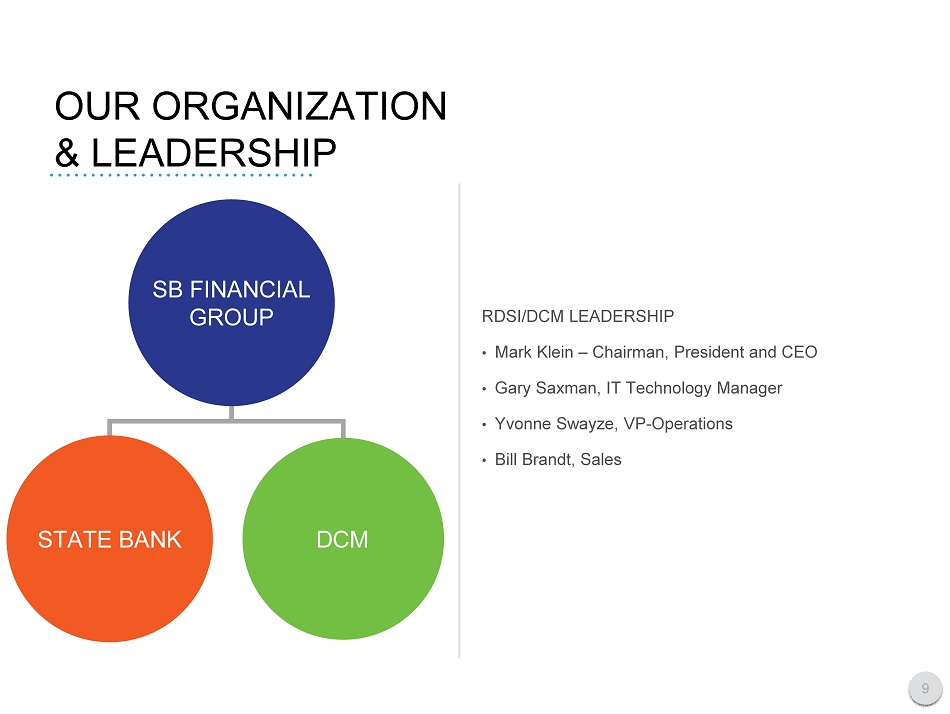

OUR ORGANIZATION & LEADERSHIP RDSI/DCM LEADERSHIP • Mark Klein – Chairman, President and CEO • Gary Saxman, IT Technology Manager • Yvonne Swayze, VP - Operations • Bill Brandt, Sales SB FINANCIAL GROUP STATE BANK DCM 9

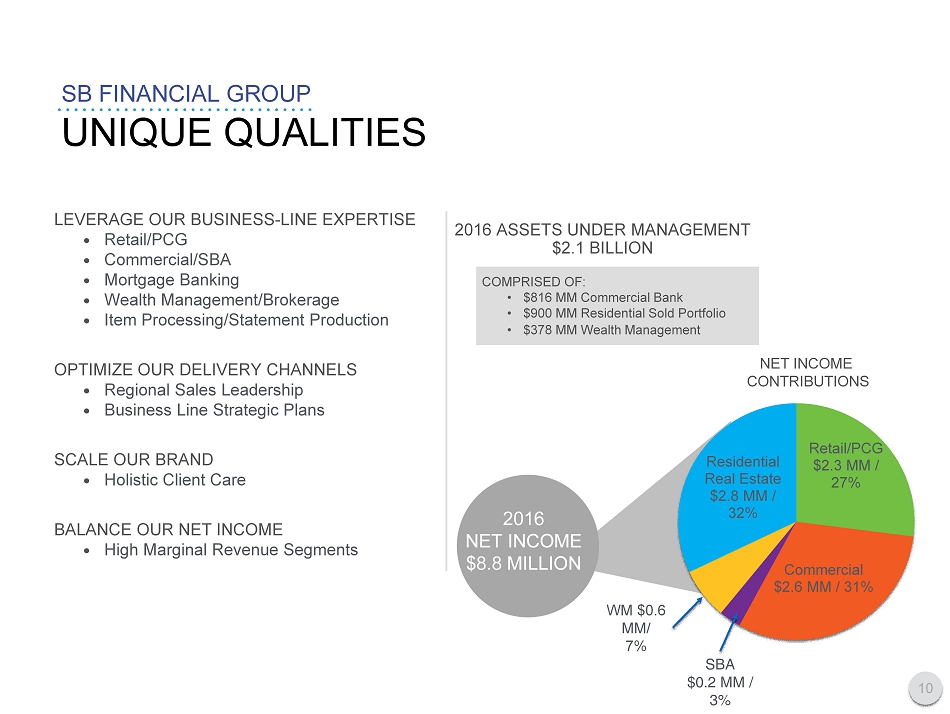

LEVERAG E OUR BUSINESS - LINE EXPERTISE • Retail/PCG • Commercial/SBA • Mortgage Banking • Wealth Management /Brokerage • Item Processing/Statement Production OPTIMIZ E OUR DELIVERY CHANNELS • Regional Sales Leadership • Business Line Strategic Plans SCALE OUR BRAND • Holistic Client Care BALANCE OUR NET INCOME • High Marginal Revenue Segments 201 6 NET INCOME $ 8.8 MILLION UNIQUE QUALITIES SB FINANCIAL GROUP Retail/PCG $2.3 MM / 27% Commercial $2.6 MM / 31% Residential Real Estate $2.8 MM / 32% 201 6 ASSETS UNDER MANAGEMENT $ 2.1 BILLION COMPRISED OF: • $ 816 MM Commercial Bank • $ 900 MM Residential Sold Portfolio • $3 78 MM Wealth Management 10 WM $0.6 MM/ 7% SBA $0.2 MM / 3% NET INCOME CONTRIBUTIONS

Become a Top - Decil e , Independent Financial Services Company KEY INITIATIVES 11 Increase profitability through ongoing diversification of revenue streams Strengthen penetration in all markets served Expand product service utilization by new and existing customers Deliver gains in operational excellence Sustain asset quality

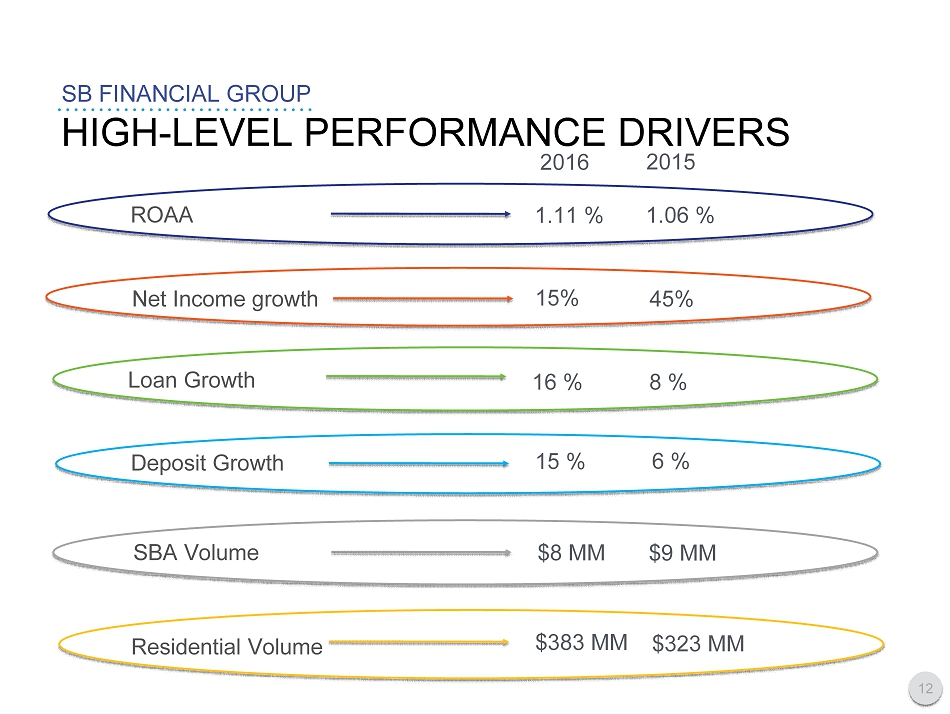

HIGH - LEVEL PERFORMANCE DRIVERS SB FINANCIAL GROUP 12 2016 2015 SBA Volume $8 MM $9 MM $383 MM $323 MM Residential Volume Deposit Growth 15 % 6 % Loan Growth 16 % 8 % 45% 15% Net Income growth 1.06 % 1.11 % ROAA

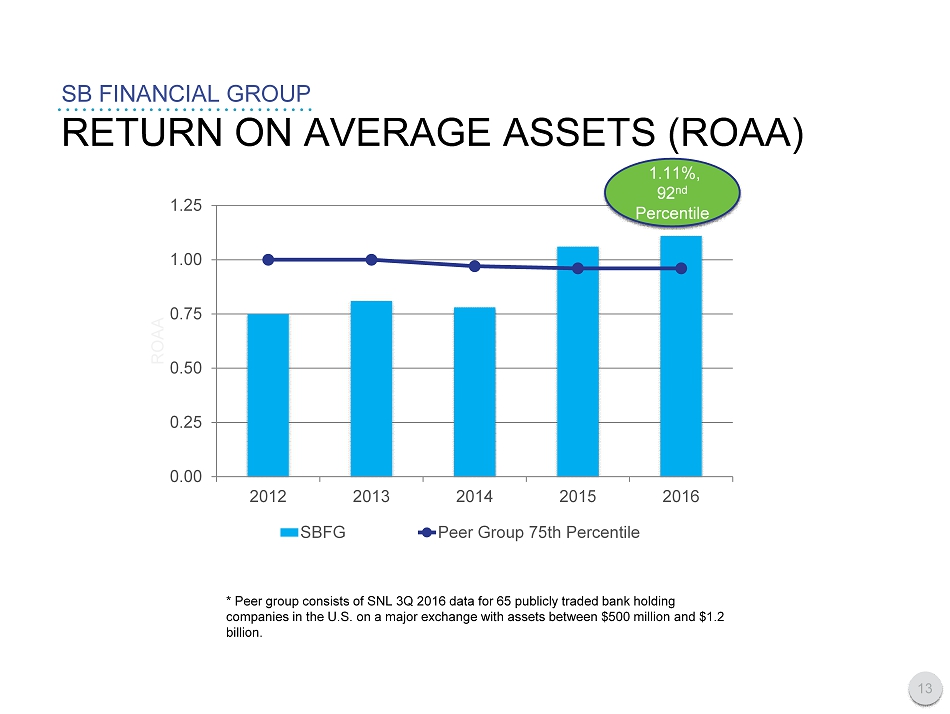

RETURN ON AVERAGE ASSETS (ROAA) SB FINANCIAL GROUP 0.00 0.25 0.50 0.75 1.00 1.25 2012 2013 2014 2015 2016 ROAA SBFG Peer Group 75th Percentile * Peer group consists of SNL 3Q 201 6 data for 65 publicly traded bank holding companies in the U.S. on a major exchange with assets between $500 million and $1. 2 billion. 13 1.11%, 92 nd Percentile

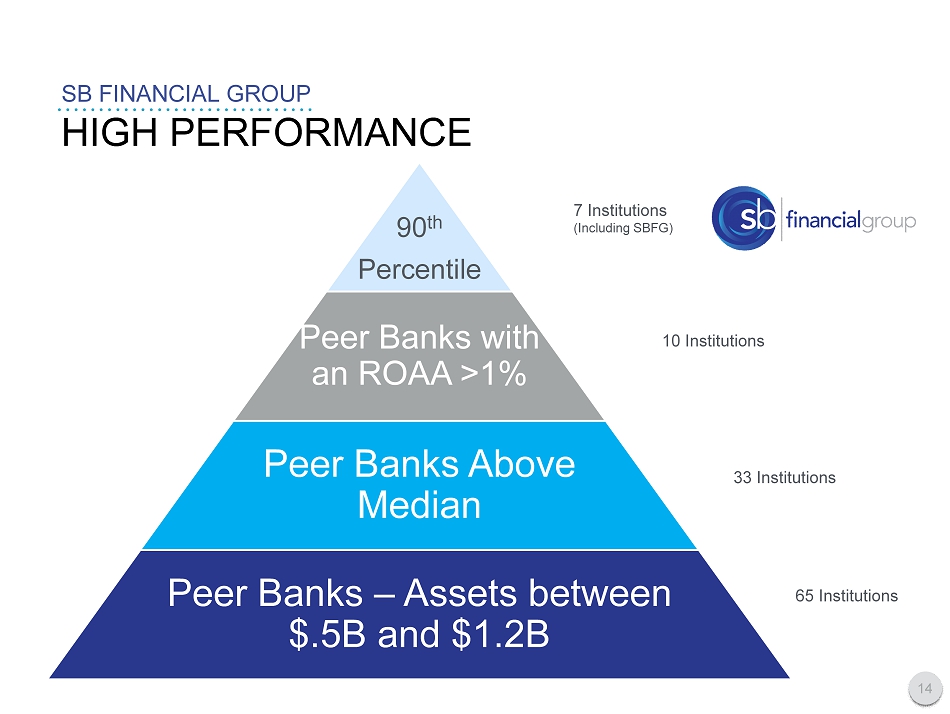

SB FINANCIAL GROUP 14 90 th Percentile Peer Banks with an ROAA >1% Peer Banks Above Median Peer Banks – Assets between $.5B and $1.2B HIGH PERFORMANCE 7 Institutions (Including SBFG) 10 Institutions 33 Institutions 65 Institutions

Become a Top - Dec ile , Independent Financial Services Company KEY INITIATIVES 15 Sustain asset quality Expand product service utilization by new and existing customers Strengthen penetration in all markets served Deliver gains in operational excellence Increase profitability through ongoing diversification of revenue streams

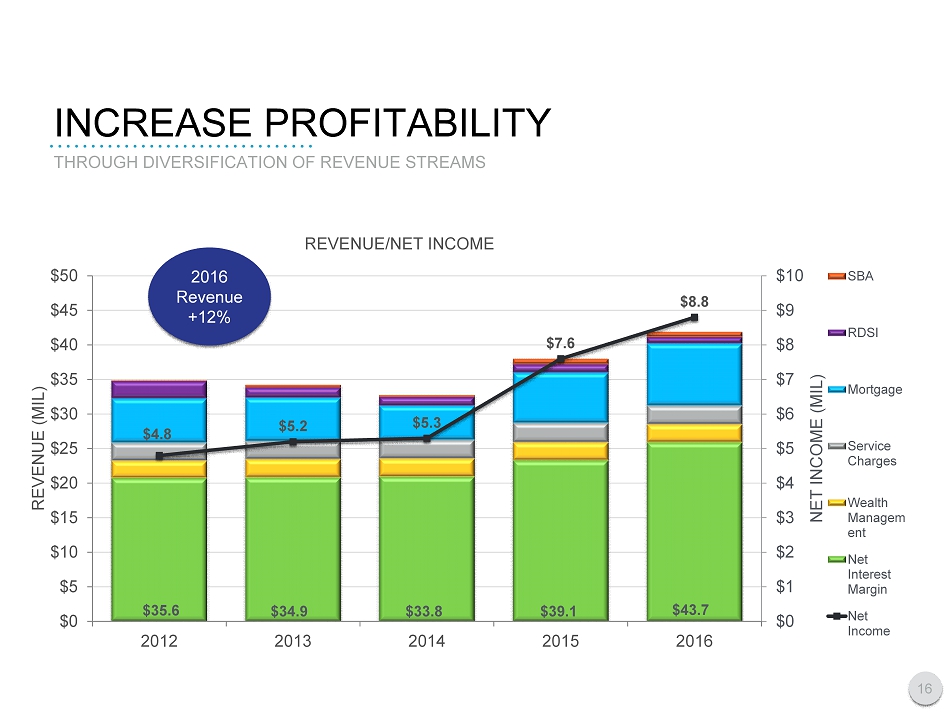

INCREASE PROFITABILITY $35.6 $34.9 $33.8 $39.1 $43.7 $4.8 $5.2 $5.3 $7.6 $8.8 $0 $1 $2 $3 $4 $5 $6 $7 $8 $9 $10 $0 $5 $10 $15 $20 $25 $30 $35 $40 $45 $50 2012 2013 2014 2015 2016 NET INCOME (MIL) REVENUE (MIL) REVENUE/NET INCOME SBA RDSI Mortgage Service Charges Wealth Managem ent Net Interest Margin Net Income THROUGH DIVERSIFICATION OF REVENUE STREAMS 16 2016 Revenue +12%

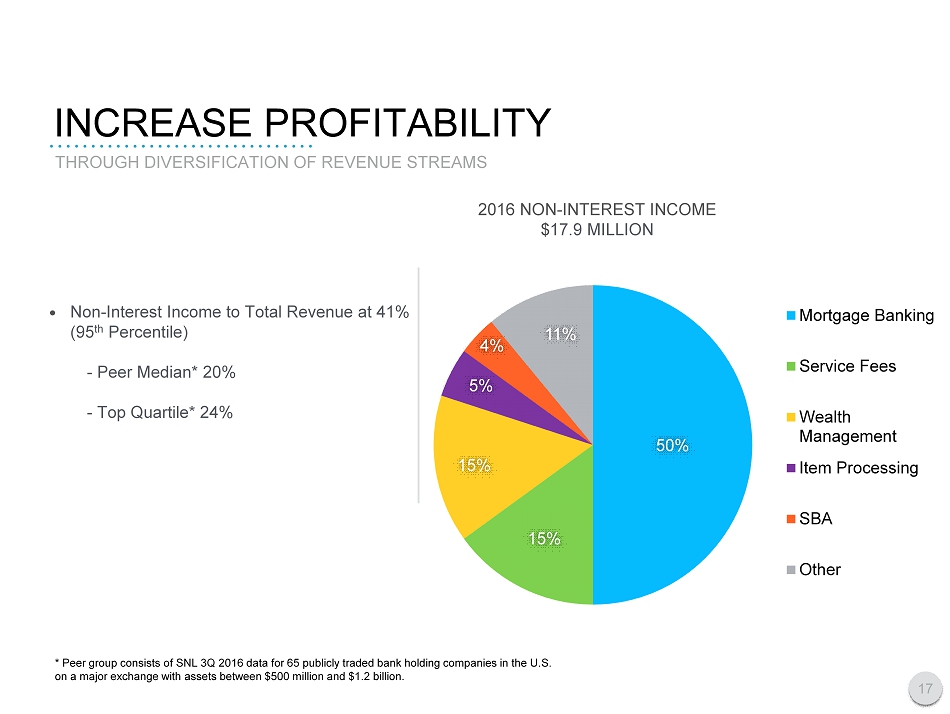

• Non - Interest Income to Total Revenue at 4 1 % (95 th Percentile) - Peer Median * 20 % - Top Quartile * 2 4 % INCREASE PROFITABILITY 201 6 NON - INTEREST INCOME $ 17.9 MILLION 50% 15% 15% 5% 4% 11% Mortgage Banking Service Fees Wealth Management Item Processing SBA Other THROUGH DIVERSIFICATION OF REVENUE STREAMS 17 * Peer group consists of SNL 3Q 201 6 data for 65 publicly traded bank holding companies in the U.S. on a major exchange with assets between $500 million and $1. 2 billion.

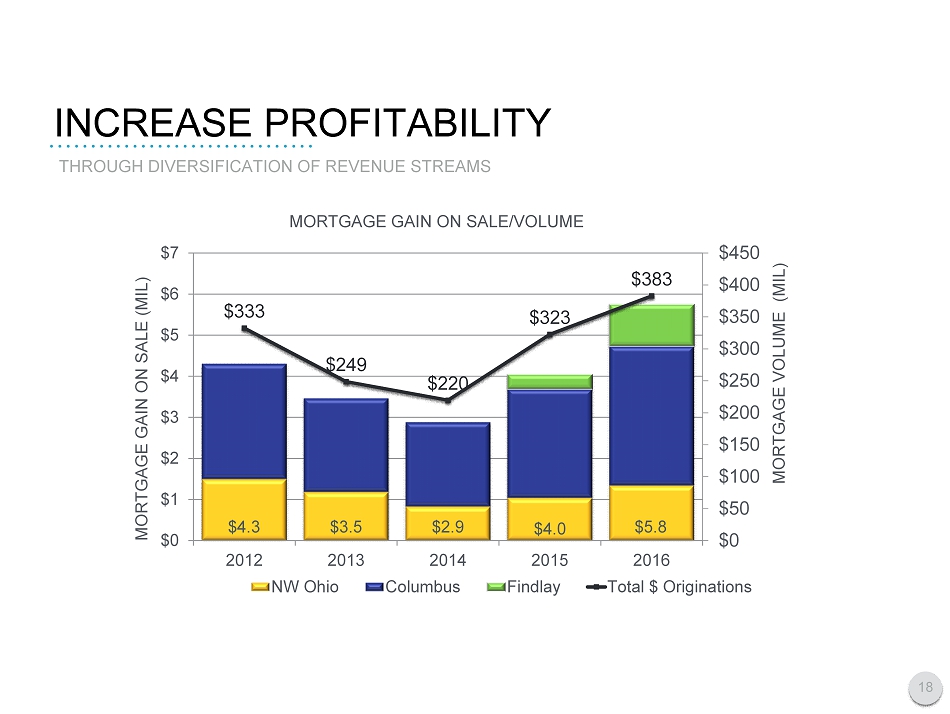

INCREASE PROFITABILITY $333 $249 $220 $323 $383 $0 $50 $100 $150 $200 $250 $300 $350 $400 $450 $0 $1 $2 $3 $4 $5 $6 $7 2012 2013 2014 2015 2016 MORTGAGE VOLUME (MIL) MORTGAGE GAIN ON SALE (MIL) MORTGAGE GAIN ON SALE/VOLUME NW Ohio Columbus Findlay Total $ Originations THROUGH DIVERSIFICATION OF REVENUE STREAMS 18 $3.5 $4.3 $2.9 $5.8 $4.0

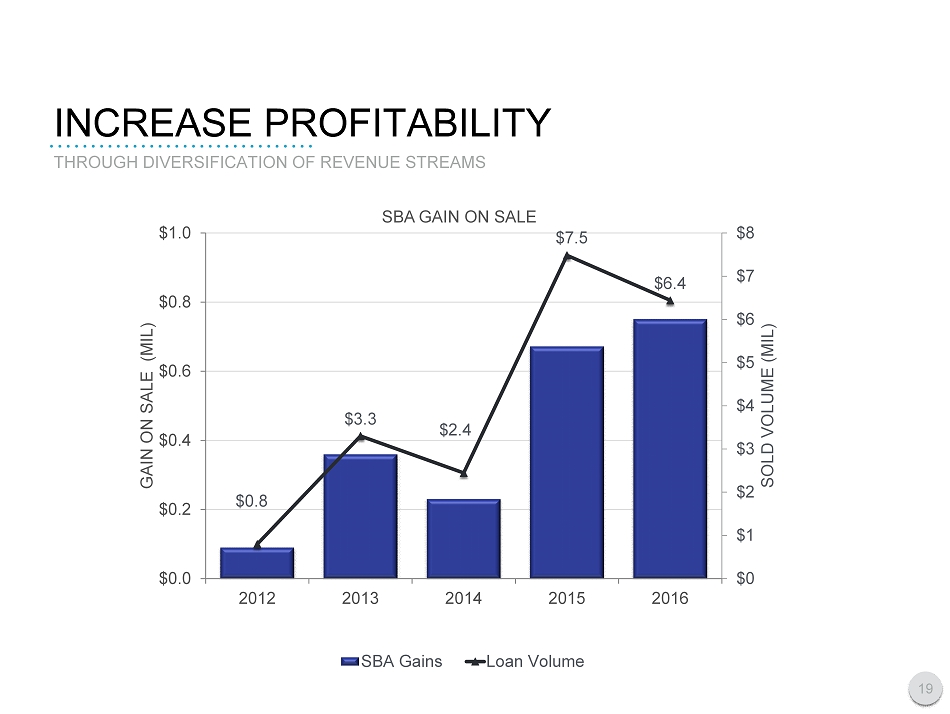

INCREASE PROFITABILITY $0.8 $3.3 $2.4 $7.5 $6.4 $0 $1 $2 $3 $4 $5 $6 $7 $8 $0.0 $0.2 $0.4 $0.6 $0.8 $1.0 2012 2013 2014 2015 2016 SOLD VOLUME (MIL) GAIN ON SALE (MIL) SBA GAIN ON SALE SBA Gains Loan Volume THROUGH DIVERSIFICATION OF REVENUE STREAMS 19

20 INCREASE PROFITABILITY • Expand Residential Real Estate Lending • Retain Servicing/Build Portfolio • Leverage SBA Business Line Expertise • Build Wealth Management Bench THROUGH DIVERSIFICATION OF REVENUE STREAMS

Strengthen penetration in all markets served Increase profitability through ongoing diversification of revenue streams Sustain asset quality Deliver gains in operational excellence Expand product service utilization by new and existing customers Become a Top - Deci le, Independent Financial Services Company KEY INITIATIVES 21

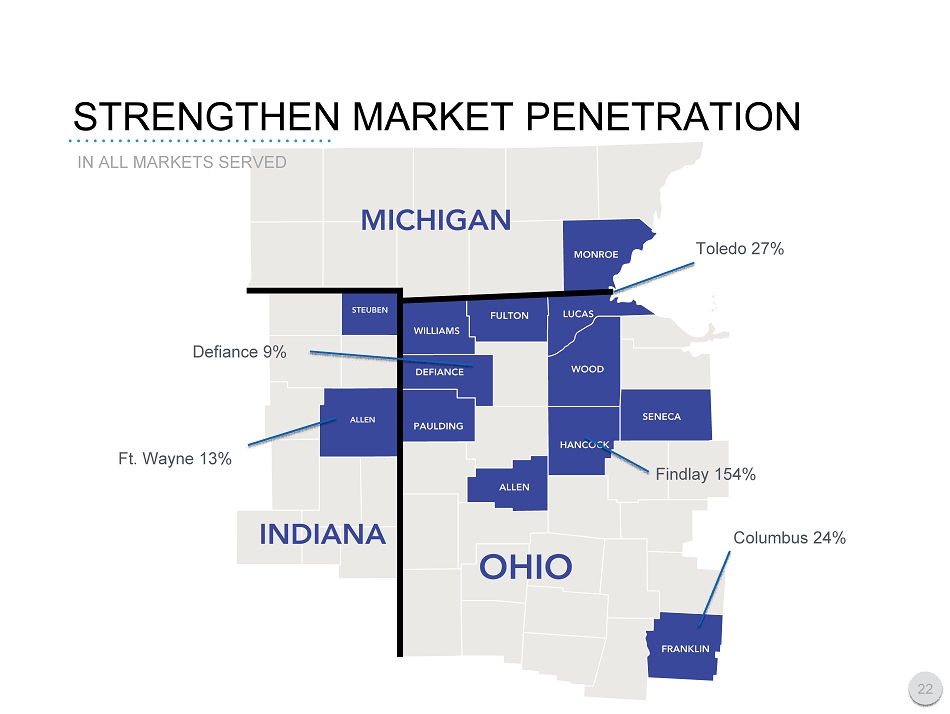

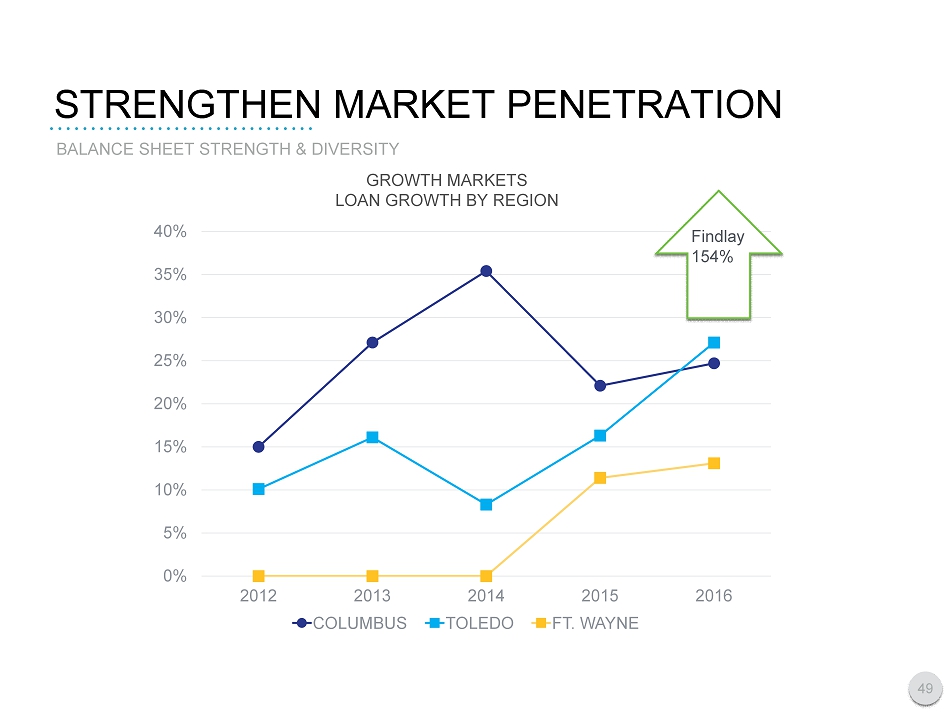

STRENGTHEN MARKET PENETRATION IN ALL MARKETS SERVED Toledo 27% Columbus 2 4 % Ft. Wayne 13 % 22 Defiance 9% Findlay 154 %

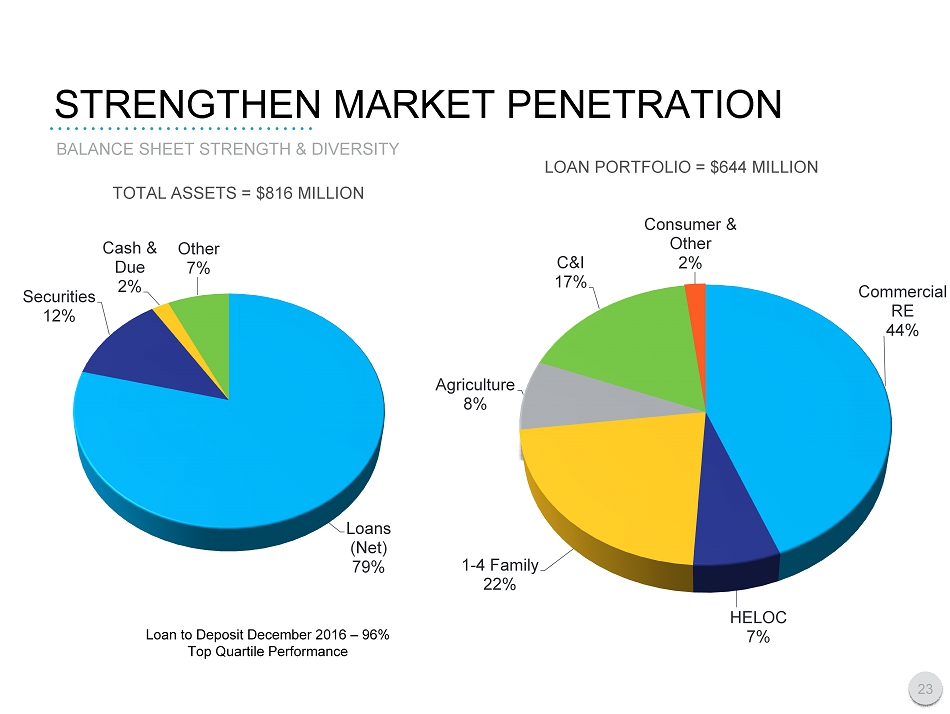

Loans (Net) 79% Securities 12% Cash & Due 2% Other 7% STRENGTHEN MARKET PENETRATION TOTAL ASSETS = $ 816 MILLION LOAN PORTFOLIO = $ 644 MILLION Loan to Deposit December 201 6 – 9 6 % Top Quartile Performance Commercial RE 44% HELOC 7% 1 - 4 Family 22% Agriculture 8% C&I 17% Consumer & Other 2% BALANCE SHEET STRENGTH & DIVERSITY 23

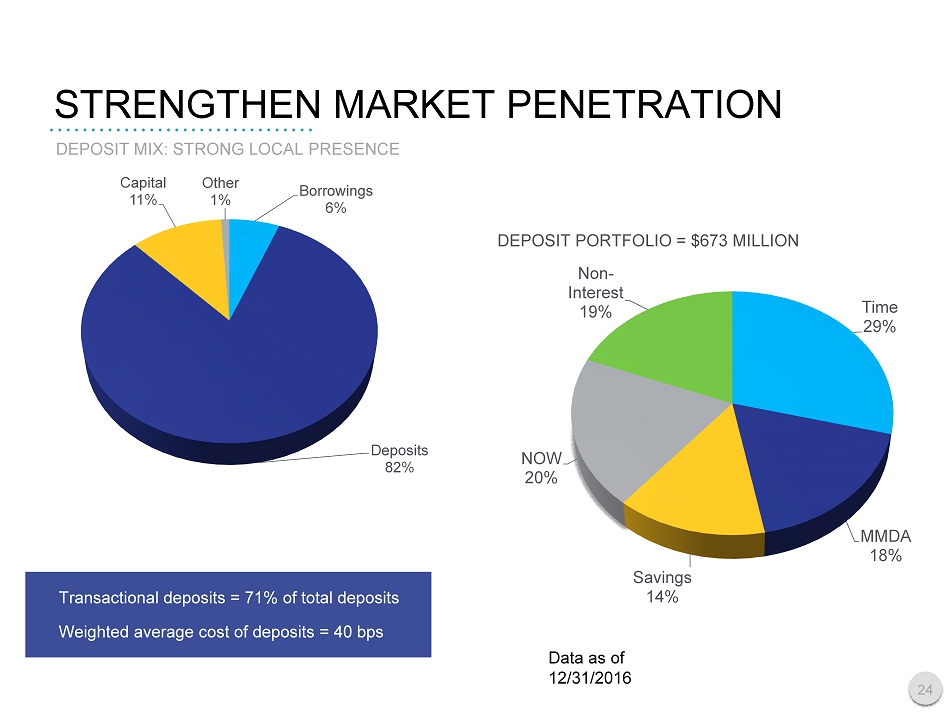

Borrowings 6% Deposits 82% Capital 11% Other 1% STRENGTHEN MARKET PENETRATION DEPOSIT PORTFOLIO = $673 MILLION Time 29% MMDA 18% Savings 14% NOW 20% Non - Interest 19% Data as of 12/31/201 6 Transactional deposits = 7 1 % of total deposits Weighted average cost of deposits = 4 0 bps DEPOSIT MIX: STRONG LOCAL PRESENCE 24

25 STRENGTHEN MARKET PENETRATION Goal is $1 Billion (Scale) • Expand “in - market” presence/resources • Organic entrance into contiguous “urban” markets • M&A opportunities • Household growth via Residential Business Line IN ALL MARKETS SERVED

Expand product service utilization by new and existing customers Increase profitability through ongoing diversification of revenue streams Sustain asset quality Deliver gains in operational excellence Strengthen penetration in all markets served Become a Top - Dec ile , Independent Financial Services Company KEY INITIATIVES 26

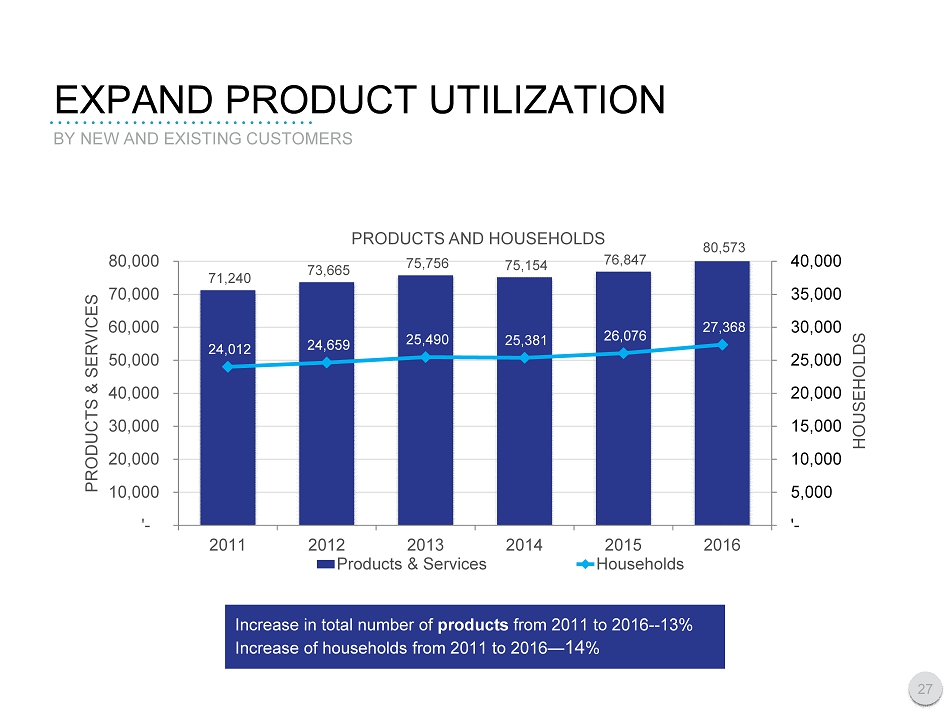

EXPAND PRODUCT U TILIZATION BY NEW AND EXISTING CUSTOMERS 71,240 73,665 75,756 75,154 76,847 80,573 24,012 24,659 25,490 25,381 26,076 27,368 '- 5,000 10,000 15,000 20,000 25,000 30,000 35,000 40,000 '- 10,000 20,000 30,000 40,000 50,000 60,000 70,000 80,000 2011 2012 2013 2014 2015 2016 HOUSEHOLDS PRODUCTS & SERVICES PRODUCTS AND HOUSEHOLDS Products & Services Households Increase in total number of products from 2011 to 201 6 - - 13 % Increase of households from 2011 to 201 6 — 14 % 27

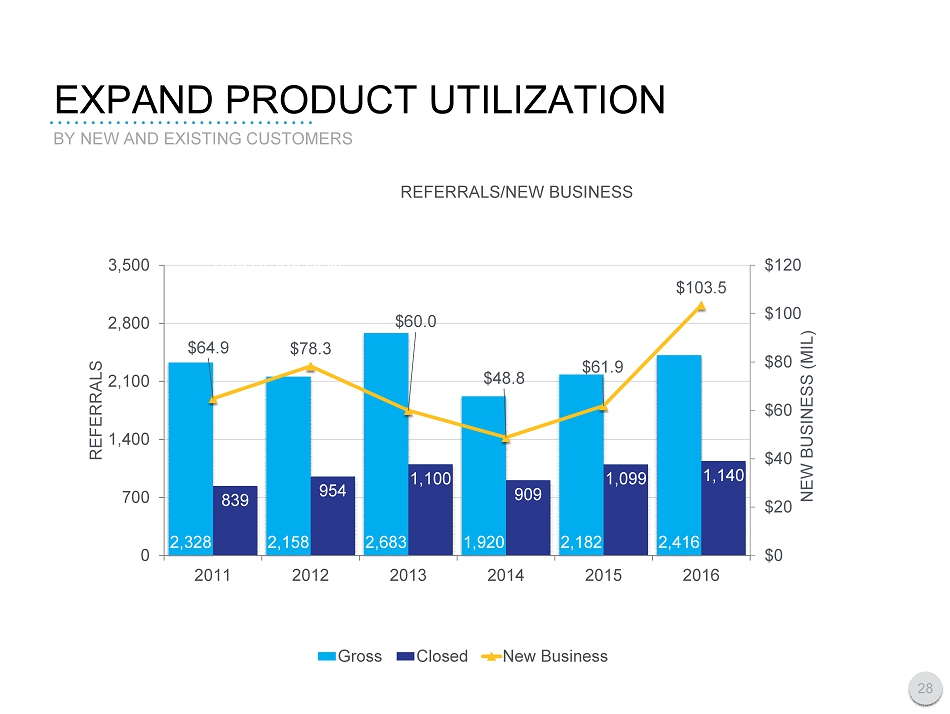

EXPAND PRODUCT U TILIZATION BY NEW AND EXISTING CUSTOMERS 2,328 2,158 2,683 1,920 2,182 2,416 839 954 1,100 909 1,099 1,140 $64.9 $78.3 $60.0 $48.8 $61.9 $103.5 $0 $20 $40 $60 $80 $100 $120 0 700 1,400 2,100 2,800 3,500 2011 2012 2013 2014 2015 2016 NEW BUSINESS (MIL) REFERRALS REFERRALS/NEW BUSINESS Gross Closed New Business 28 201 EMPLOYEE PARTICIPATION

29 EXPAND PRODUCT UTILIZATION More and Deeper Relationships (Scope) • Clients “for life” • Business Lines working “Interdependently” • Retail “on - boarding” Process • Holistic Client Care

Become a Top - Dec ile , Independent Financial Services Company KEY INITIATIVES 30 Deliver gains in operational excellence Increase profitability through ongoing diversification of revenue streams Sustain asset quality Expand product service utilization by new and existing customers Strengthen penetration in all markets served

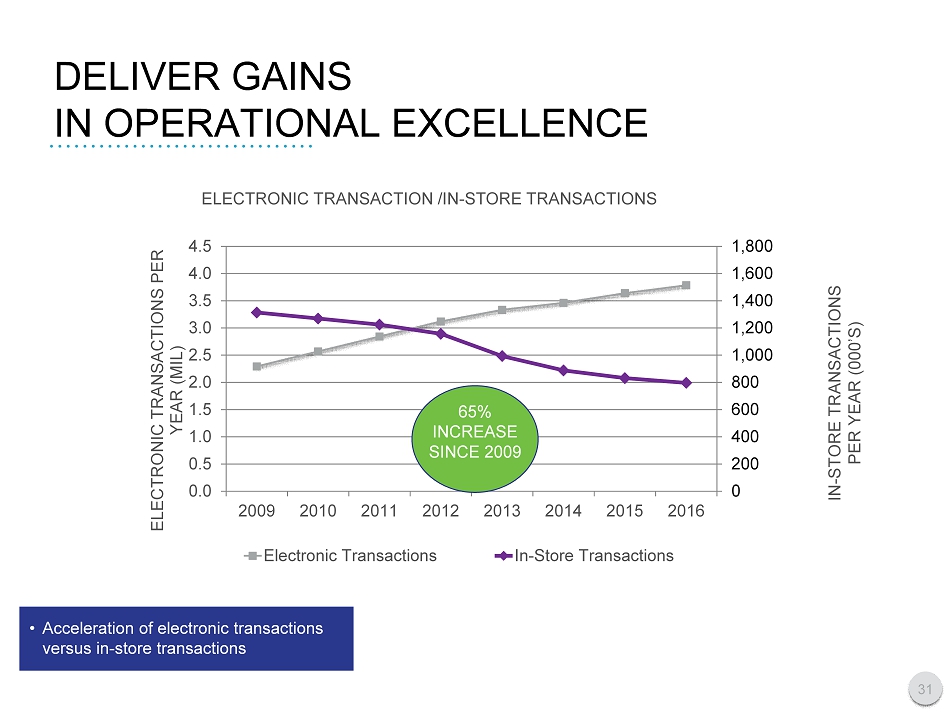

• Acceleration of electronic transactions versus in - store transactions DELIVER GAINS IN OPERATIONAL EXCELLENCE 0 200 400 600 800 1,000 1,200 1,400 1,600 1,800 0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 2009 2010 2011 2012 2013 2014 2015 2016 ELECTRONIC TRANSACTIONS PER YEAR (MIL) ELECTRONIC TRANSACTION /IN - STORE TRANSACTIONS Electronic Transactions In-Store Transactions 65 % INCREASE SINCE 2009 IN - STORE TRANSACTIONS PER YEAR (000’S) 31

DELIVER GAINS IN OPERATIONAL EXCELLENCE $528 $606 $666 $773 $900 3,988 4,549 4,950 5,632 6,414 0 1,500 3,000 4,500 6,000 7,500 $0 $200 $400 $600 $800 $1,000 2012 2013 2014 2015 2016 NUMBER OF LOANS $ OF LOANS ($MIL) MORTGAGE SERVICING PORTFOLIO Servicing Portfolio Number of Loans Serviced 32

33 DELIVER GAINS IN OPERATIONAL EXCELLENCE Operations as a Competitive Advantage • Client Contact Preference • Transactions/Interactions • Benchmark “High - Performing Bank” metrics • Technology Deployment (24/7) • Inspect/Expect

Increase profitability through ongoing diversification of revenue streams Deliver gains in operational excellence Expand product service utilization by new and existing customers Strengthen penetration in all markets served Sustain asset quality Become a Top - Dec ile , Independent Financial Services Company KEY INITIATIVES 34

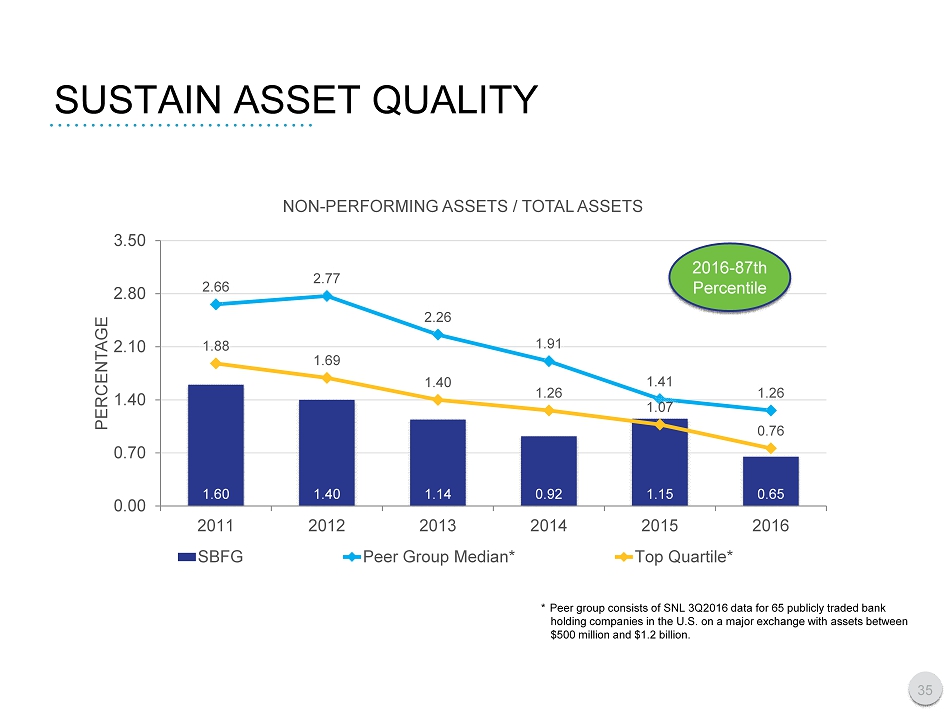

SUSTAIN ASSET Q UALITY 1.60 1.40 1.14 0.92 1.15 0.65 2.66 2.77 2.26 1.91 1.41 1.26 1.88 1.69 1.40 1.26 1.07 0.76 0.00 0.70 1.40 2.10 2.80 3.50 2011 2012 2013 2014 2015 2016 PERCENTAGE NON - PERFORMING ASSETS / TOTAL ASSETS SBFG Peer Group Median* Top Quartile* 2016 - 87th Percentile * Peer group consists of SNL 3Q2016 data for 65 publicly traded bank holding companies in the U.S. on a major exchange with assets between $500 million and $1. 2 billion. 35

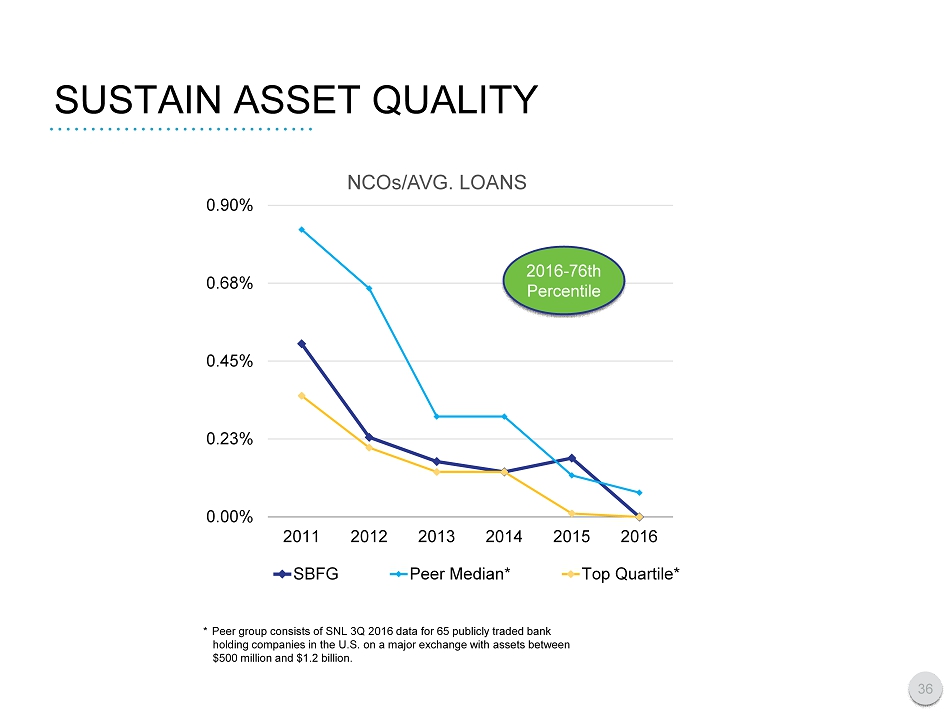

SUSTAIN ASSET Q UALITY * Peer group consists of SNL 3Q 201 6 data for 65 publicly traded bank holding companies in the U.S. on a major exchange with assets between $500 million and $1. 2 billion. 0.00% 0.23% 0.45% 0.68% 0.90% 2011 2012 2013 2014 2015 2016 NCOs/AVG. LOANS SBFG Peer Median* Top Quartile* 2016 - 76th Percentile 36

37 SUSTAIN ASSET QUALITY Solid Foundation • Experienced Lenders/Shared Values • Conscious Prospecting • Robust Loan Reviews • Decisive Collections

Become a Top - Dec ile , Independent Financial Services Company KEY INITIATIVES 38 Increase profitability through ongoing diversification of revenue streams Strengthen penetration in all markets served Expand product service utilization by new and existing customers Deliver gains in operational excellence Sustain asset quality

ANTHONY V. COSENTINO – EVP & CFO SB FINANCIAL GROUP, INC. 39

OUR VISION COMMITMENT TO S TAKEHOLDERS PASSION FOR SERVICE Our Vision over the next three years is to become a high - performing ( > 90th percentile) $1 Billion, independent financial services company set apart by our staff and their passion for service, our holistic approach to client care, and our commitment to the communities and investors we serve. HOLISTIC APPROACH 40

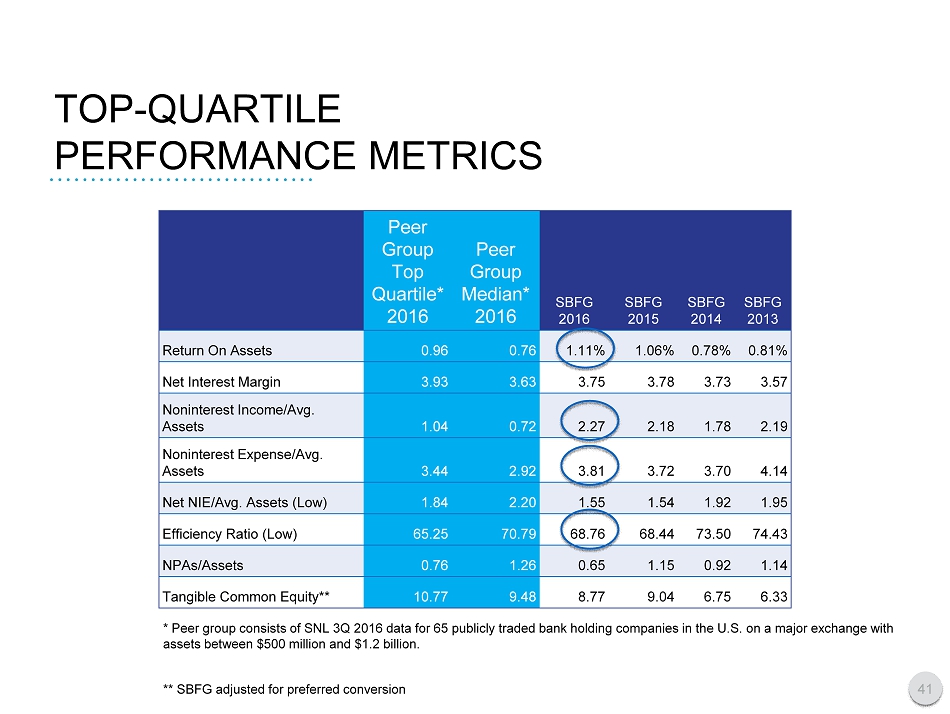

TOP - QUARTILE PERFORMANCE METRICS * Peer group consists of SNL 3Q 201 6 data for 65 publicly traded bank holding companies in the U.S. on a major exchange with assets between $500 million and $1. 2 billion. ** SBFG adjusted for preferred conversion Peer Group Top Quartile* 2016 Peer Group Median* 2016 SBFG 2016 SBFG 2015 SBFG 2014 SBFG 2013 Return On Assets 0.96 0.76 1.11% 1.06% 0.78% 0.81% Net Interest Margin 3.93 3.63 3.75 3.78 3.73 3.57 Noninterest Income/Avg. Assets 1.04 0.72 2.27 2.18 1.78 2.19 Noninterest Expense/Avg. Assets 3.44 2.92 3.81 3.7 2 3.70 4.14 Net NIE/Avg. Assets (Low) 1.84 2.20 1.55 1.5 4 1.92 1.95 Efficiency Ratio (Low) 65.25 70.79 68.76 68.44 73.50 74.43 NPAs/Assets 0.76 1.26 0.65 1.15 0.92 1.14 Tangible Common Equity ** 10.77 9.48 8.77 9.04 6.75 6.33 41

Become a Top - Dec ile , Independent Financial Services Company KEY INITIATIVES 42 Sustain asset quality Expand product service utilization by new and existing customers Strengthen penetration in all markets served Deliver gains in operational excellence Increase profitability through ongoing diversification of revenue streams

HEALTH OF THE BANKING INDUSTRY 43

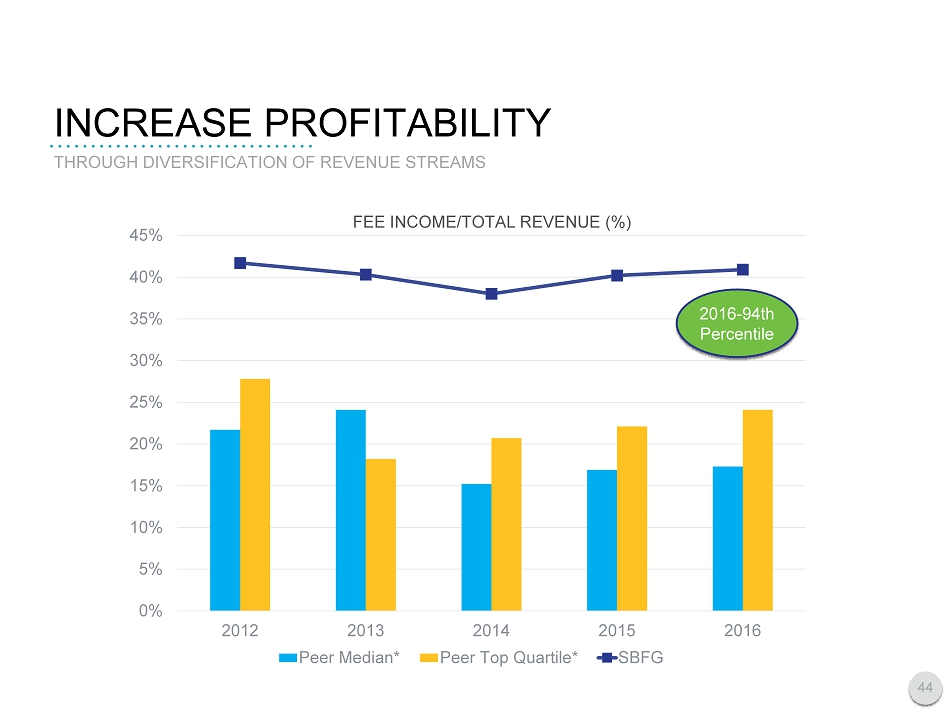

INCREASE PROFITABILITY THROUGH DIVERSIFICATION OF REVENUE STREAMS 44 0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 2012 2013 2014 2015 2016 Peer Median* Peer Top Quartile* SBFG FEE INCOME/TOTAL REVENUE (%) 2016 - 94th Percentile

INCREASE PROFITABILITY THROUGH DIVERSIFICATION OF REVENUE STREAMS 45 $0 $1,000 $2,000 $3,000 $4,000 $5,000 $6,000 $7,000 $8,000 $9,000 $10,000 2012 2013 2014 2015 2016 RRE SBA FSA Revenue from Sale of Loans Revenue ($000’s) $6,549 $5,651 $4,548 $7,210 $9,151

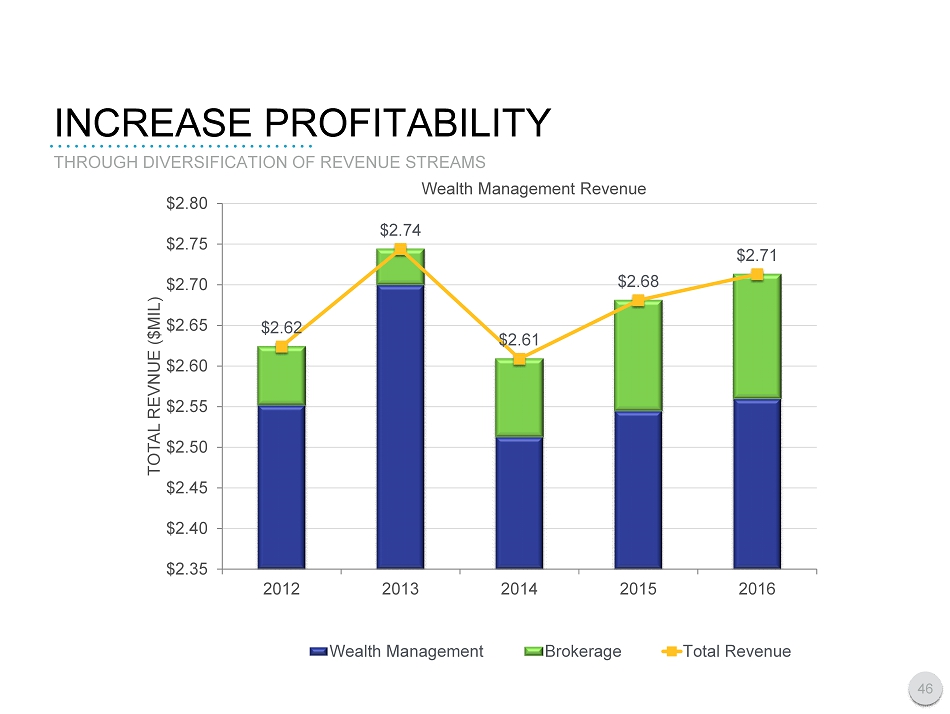

INCREASE PROFITABILITY $2.62 $2.74 $2.61 $2.68 $2.71 $2.35 $2.40 $2.45 $2.50 $2.55 $2.60 $2.65 $2.70 $2.75 $2.80 2012 2013 2014 2015 2016 TOTAL REVNUE ($MIL) Wealth Management Revenue Wealth Management Brokerage Total Revenue THROUGH DIVERSIFICATION OF REVENUE STREAMS 46

Strengthen penetration in all markets served Increase profitability through ongoing diversification of revenue streams Sustain asset quality Deliver gains in operational excellence Expand product service utilization by new and existing customers Become a Top - Deci le, Independent Financial Services Company KEY INITIATIVES 47

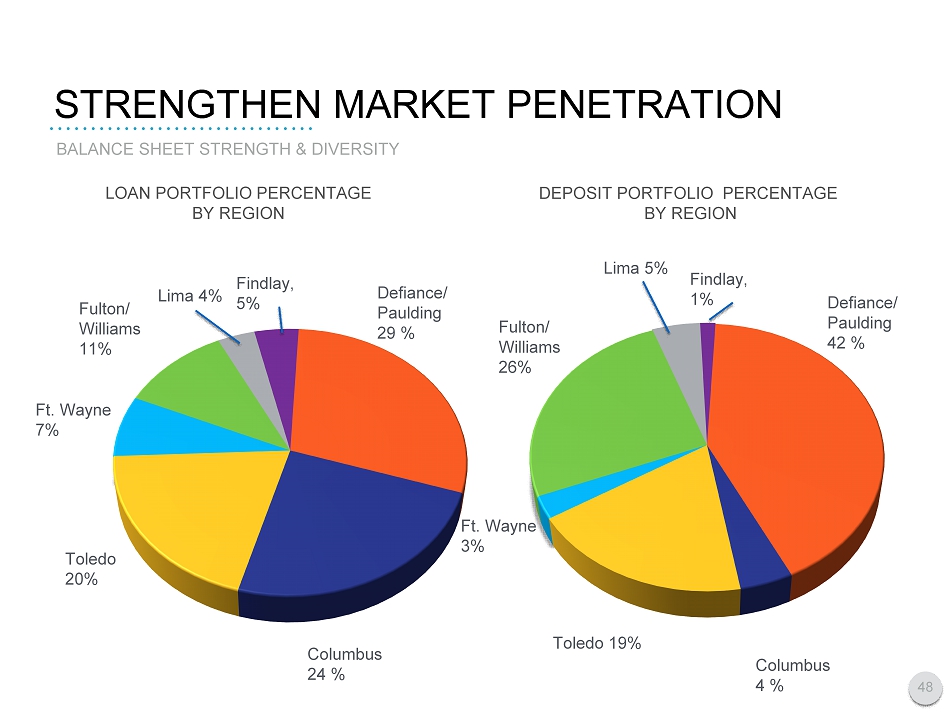

STRENGTHEN MARKET PENETRATION LOAN PORTFOLIO PERCENTAGE BY REGION DEPOSIT PORTFOLIO PERCENTAGE BY REGION Columbus 4 % BALANCE SHEET STRENGTH & DIVERSITY 48 Fulton/ Williams 11% Ft. Wayne 7% Findlay, 5% Lima 4% Defiance/ Paulding 29 % Columbus 24 % Toledo 20% Defiance/ Paulding 42 % Toledo 19% Ft. Wayne 3 % Fulton/ Williams 26% Lima 5% Findlay, 1%

STRENGTHEN MARKET PENETRATION BALANCE SHEET STRENGTH & DIVERSITY 49 Columbus 24 % Defiance/ Paulding 42 % 0% 5% 10% 15% 20% 25% 30% 35% 40% 2012 2013 2014 2015 2016 COLUMBUS TOLEDO FT. WAYNE GROWTH MARKETS LOAN GROWTH BY REGION Findlay 154%

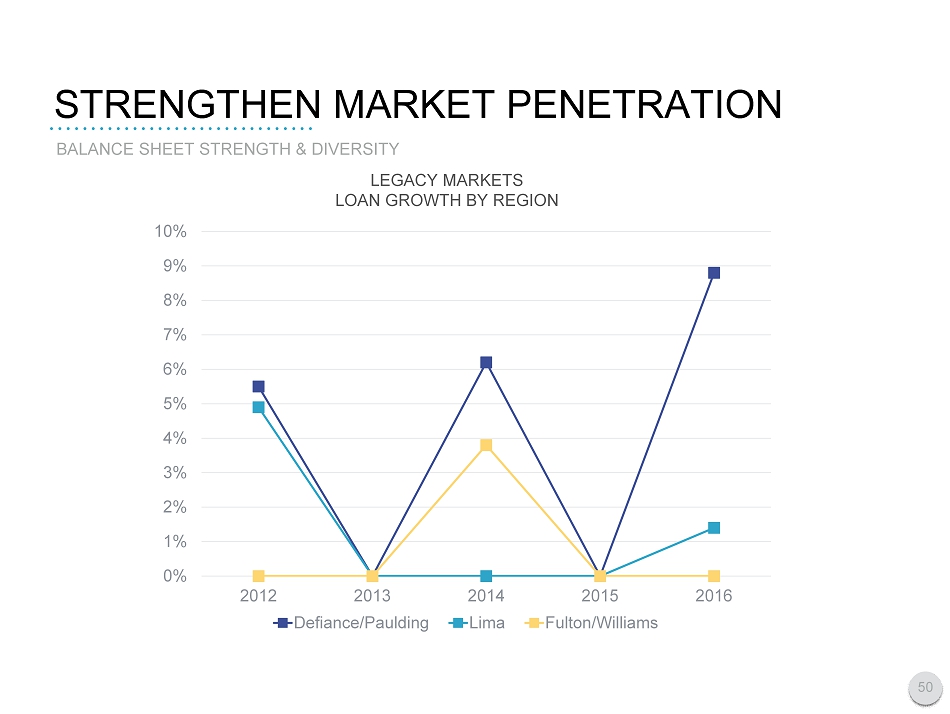

STRENGTHEN MARKET PENETRATION BALANCE SHEET STRENGTH & DIVERSITY 50 Columbus 24 % Defiance/ Paulding 42 % 0% 1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 2012 2013 2014 2015 2016 Defiance/Paulding Lima Fulton/Williams LEGACY MARKETS LOAN GROWTH BY REGION

Expand product service utilization by new and existing customers Increase profitability through ongoing diversification of revenue streams Sustain asset quality Deliver gains in operational excellence Strengthen penetration in all markets served Become a Top - Dec ile , Independent Financial Services Company KEY INITIATIVES 51

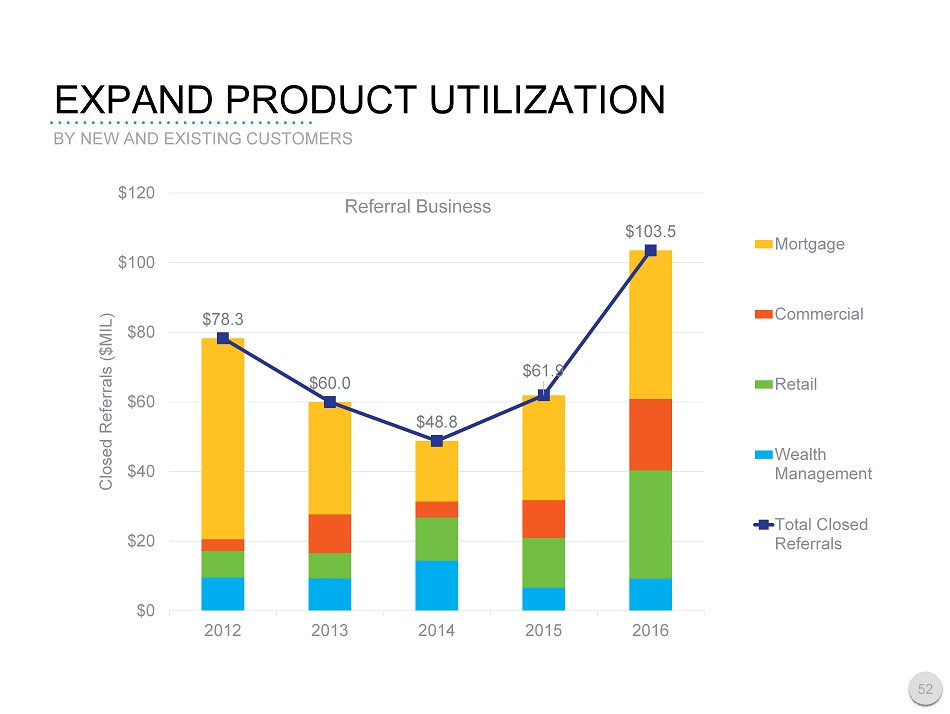

EXPAND PRODUCT U TILIZATION BY NEW AND EXISTING CUSTOMERS Increase in total number of products from 2011 to 201 6 - - 13 % Increase of households from 2011 to 201 6 — 14 % 52 $78.3 $60.0 $48.8 $61.9 $103.5 $0 $20 $40 $60 $80 $100 $120 2012 2013 2014 2015 2016 Closed Referrals ($MIL) Referral Business Mortgage Commercial Retail Wealth Management Total Closed Referrals

Become a Top - Dec ile , Independent Financial Services Company KEY INITIATIVES 53 Deliver gains in operational excellence Increase profitability through ongoing diversification of revenue streams Sustain asset quality Expand product service utilization by new and existing customers Strengthen penetration in all markets served

DELIVER GAINS IN OPERATIONAL EXCELLENCE $528 $606 $666 $773 $900 $1,149 $1,444 $1,577 $1,793 $2,079 0 500 1,000 1,500 2,000 2,500 $0 $200 $400 $600 $800 $1,000 2012 2013 2014 2015 2016 REVENUE ($000’s) $ OF LOANS ($MIL) MORTGAGE SERVICING PORTFOLIO Servicing Portfolio Income from Servicing 54

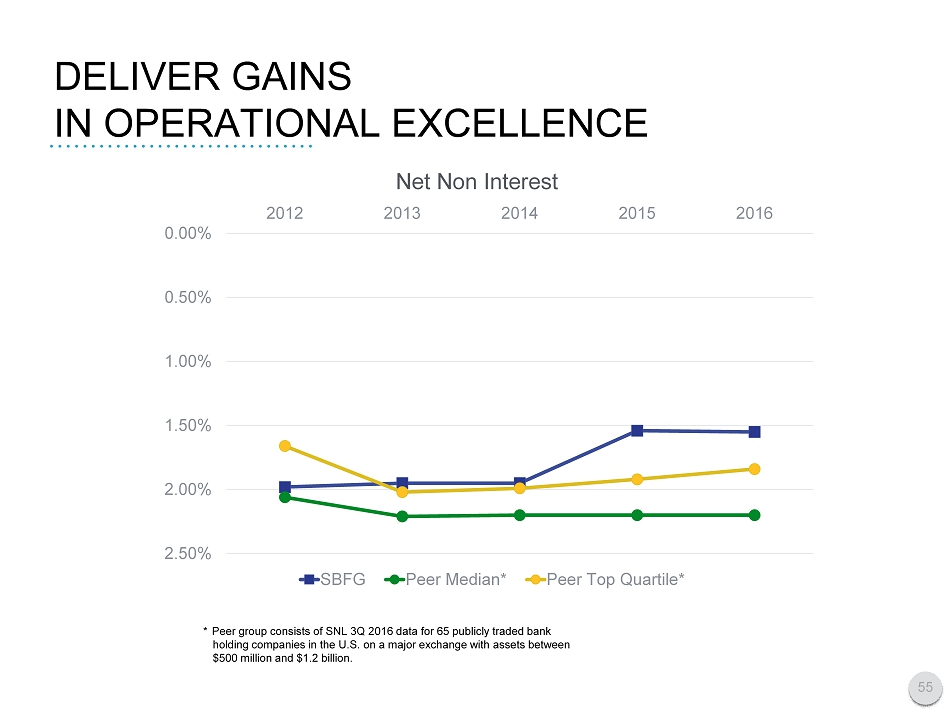

DELIVER GAINS IN OPERATIONAL EXCELLENCE 55 0.00% 0.50% 1.00% 1.50% 2.00% 2.50% 2012 2013 2014 2015 2016 SBFG Peer Median* Peer Top Quartile* * Peer group consists of SNL 3Q 201 6 data for 65 publicly traded bank holding companies in the U.S. on a major exchange with assets between $500 million and $1. 2 billion. Net Non Interest

Increase profitability through ongoing diversification of revenue streams Deliver gains in operational excellence Expand product service utilization by new and existing customers Strengthen penetration in all markets served Sustain asset quality Become a Top - Dec ile , Independent Financial Services Company KEY INITIATIVES 56

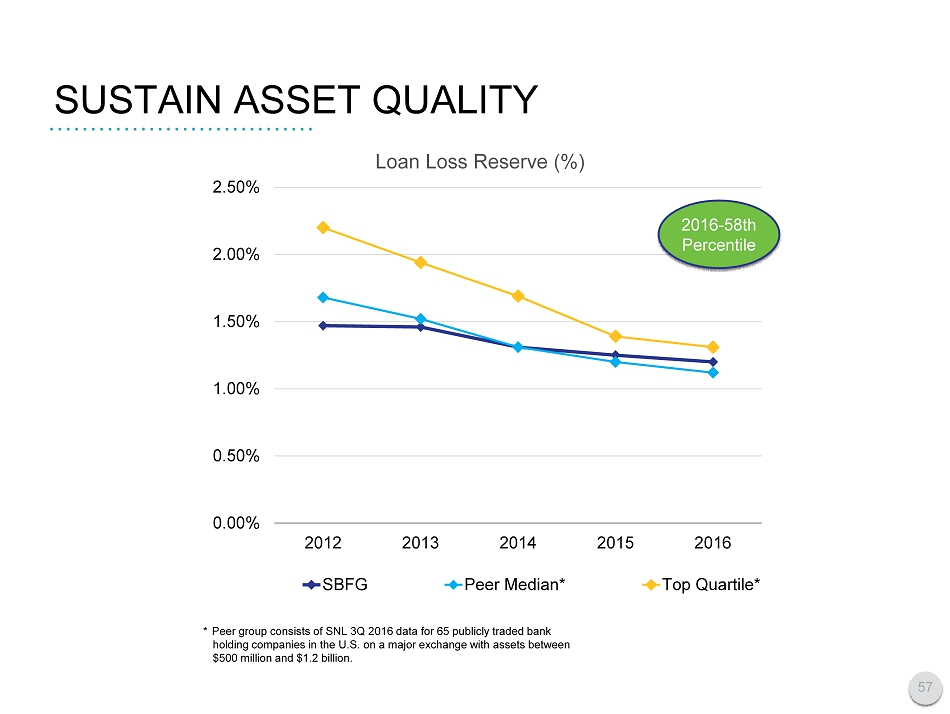

SUSTAIN ASSET Q UALITY * Peer group consists of SNL 3Q 201 6 data for 65 publicly traded bank holding companies in the U.S. on a major exchange with assets between $500 million and $1. 2 billion. 0.00% 0.50% 1.00% 1.50% 2.00% 2.50% 2012 2013 2014 2015 2016 Loan Loss Reserve (%) SBFG Peer Median* Top Quartile* 2016 - 58th Percentile 57

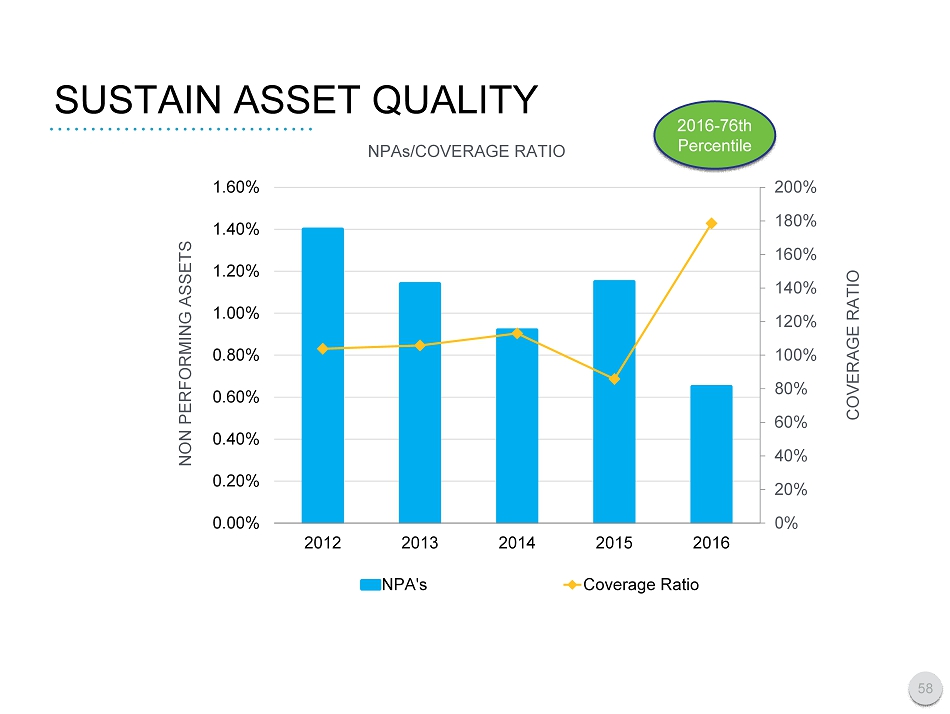

SUSTAIN ASSET Q UALITY 0% 20% 40% 60% 80% 100% 120% 140% 160% 180% 200% 0.00% 0.20% 0.40% 0.60% 0.80% 1.00% 1.20% 1.40% 1.60% 2012 2013 2014 2015 2016 NPA's Coverage Ratio 58 NON PERFORMING ASSETS COVERAGE RATIO NPAs/COVERAGE RATIO 2016 - 76th Percentile

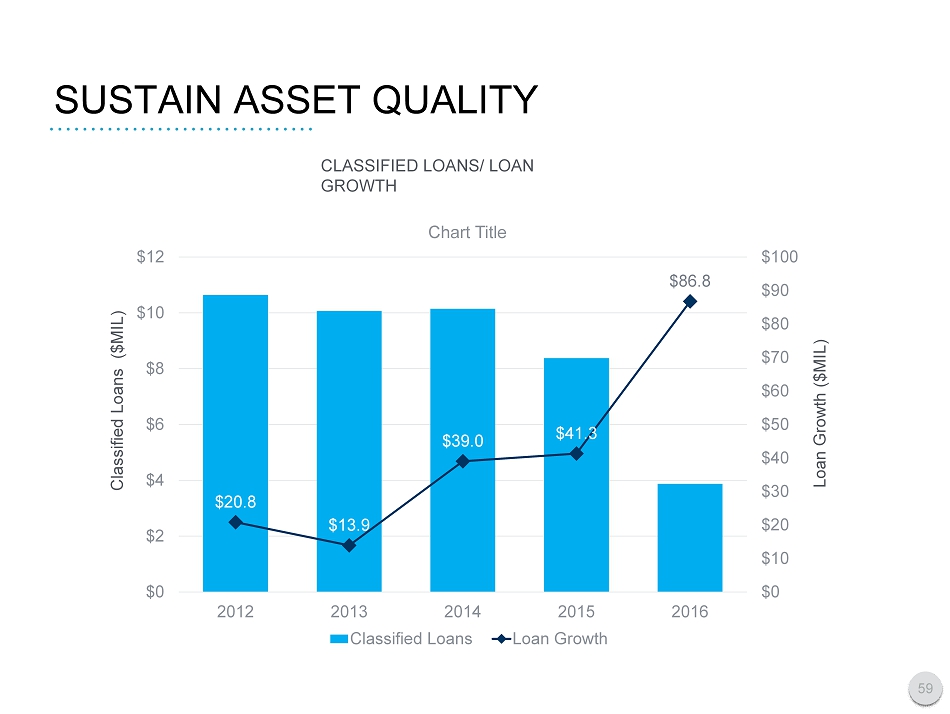

SUSTAIN ASSET Q UALITY 59 $20.8 $13.9 $39.0 $41.3 $86.8 $0 $10 $20 $30 $40 $50 $60 $70 $80 $90 $100 2012 2013 2014 2015 2016 $0 $2 $4 $6 $8 $10 $12 Chart Title Classified Loans Loan Growth Classified Loans ($MIL) Loan Growth ($MIL) CLASSIFIED LOANS/ LOAN GROWTH

Become a Top - Dec ile , Independent Financial Services Company KEY INITIATIVES 60 Increase profitability through ongoing diversification of revenue streams Strengthen penetration in all markets served Expand product service utilization by new and existing customers Deliver gains in operational excellence Sustain asset quality

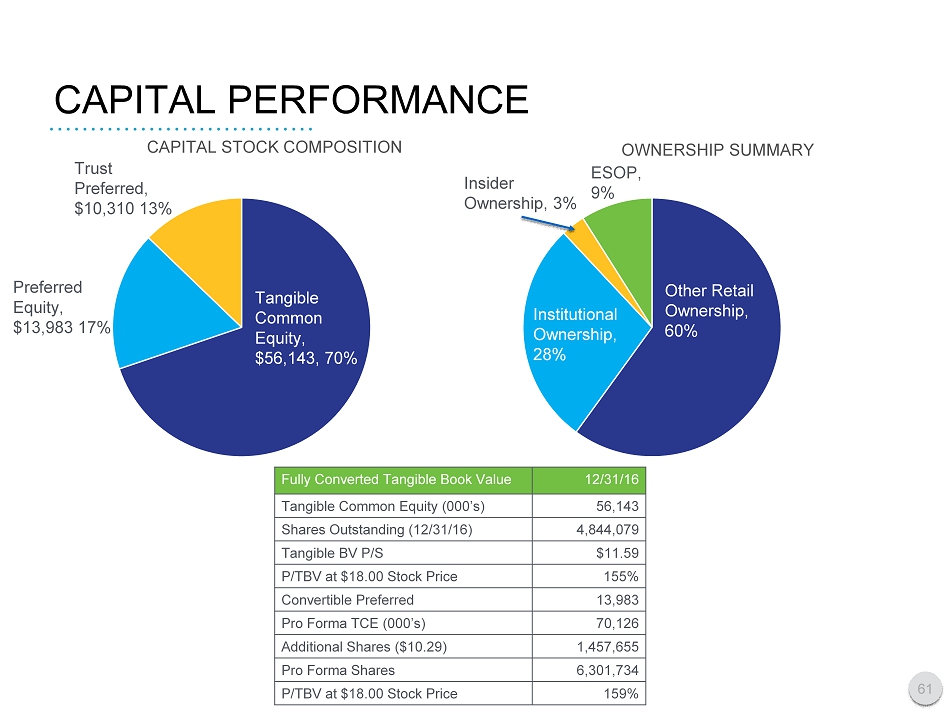

CAPITAL PERFORMANCE 61 CAPITAL STOCK COMPOSITION OWNERSHIP SUMMARY Fully Converted Tangible Book Value 12/31/16 Tangible Common Equity (000’s) 56,143 Shares Outstanding (12/31/16) 4,844,079 Tangible BV P/S $11.59 P/TBV at $18.00 Stock Price 155% Convertible Preferred 13,983 Pro Forma TCE (000’s) 70,126 Additional Shares ($10.29) 1,457,655 Pro Forma Shares 6,301,734 P/TBV at $18.00 Stock Price 159% Trust Preferred, $10,310 13% Preferred Equity, $13,983 17% Tangible Common Equity, $56,143, 70% Insider Ownership, 3% ESOP, 9% Other Retail Ownership, 60% Institutional Ownership, 28%

CAPITAL MARKET OPPORTUNITY 62 • Capital markets are active for community banks • Excellent time for SBFG to raise capital • Increased institutional ownership will help to increase liquidity • Need to fund organic growth and to build a currency for M&A • Future milestones include preferred conversion and likely entrance into Russell index

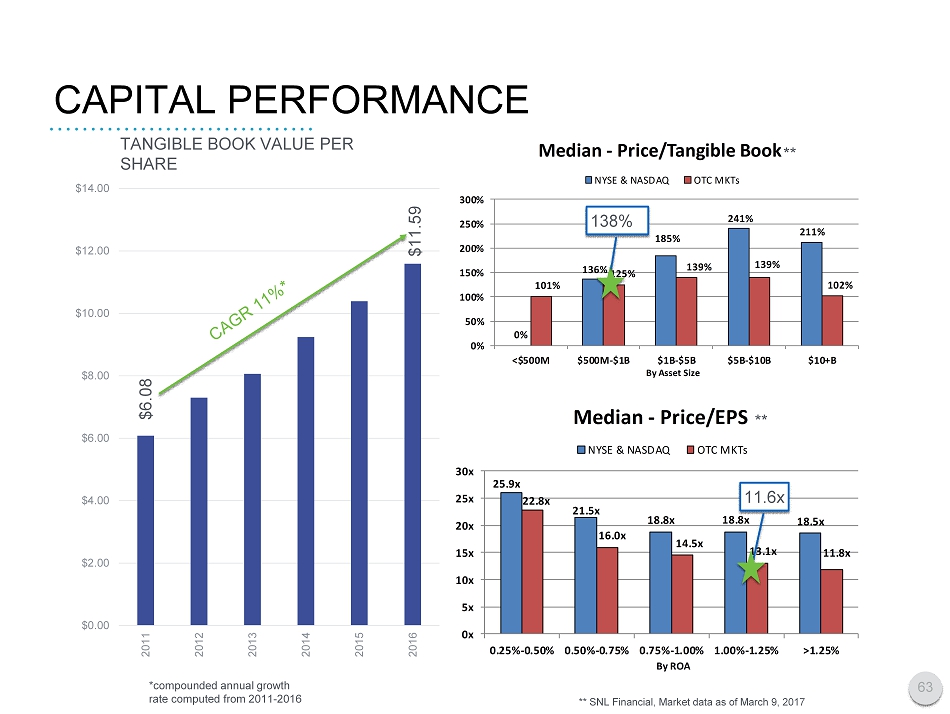

CAPITAL PERFORMANCE 63 0% 136% 185% 241% 211% 101% 125% 139% 139% 102% 0% 50% 100% 150% 200% 250% 300% <$500M $500M-$1B $1B-$5B $5B-$10B $10+B Median - Price/Tangible Book NYSE & NASDAQ OTC MKTs By Asset Size 25.9x 21.5x 18.8x 18.8x 18.5x 22.8x 16.0x 14.5x 13.1x 11.8x 0x 5x 10x 15x 20x 25x 30x 0.25%-0.50% 0.50%-0.75% 0.75%-1.00% 1.00%-1.25% >1.25% Median - Price/EPS NYSE & NASDAQ OTC MKTs By ROA $0.00 $2.00 $4.00 $6.00 $8.00 $10.00 $12.00 $14.00 2011 2012 2013 2014 2015 2016 *compounded annual growth rate computed from 2011 - 2016 TANGIBLE BOOK VALUE PER SHARE $6.08 $11.59 138% 11.6x ** SNL Financial, Market data as of March 9, 2017 ** **

MARK A. KLEIN – CHAIRMAN, PRESIDENT AND CEO SB FINANCIAL GROUP, INC. 64

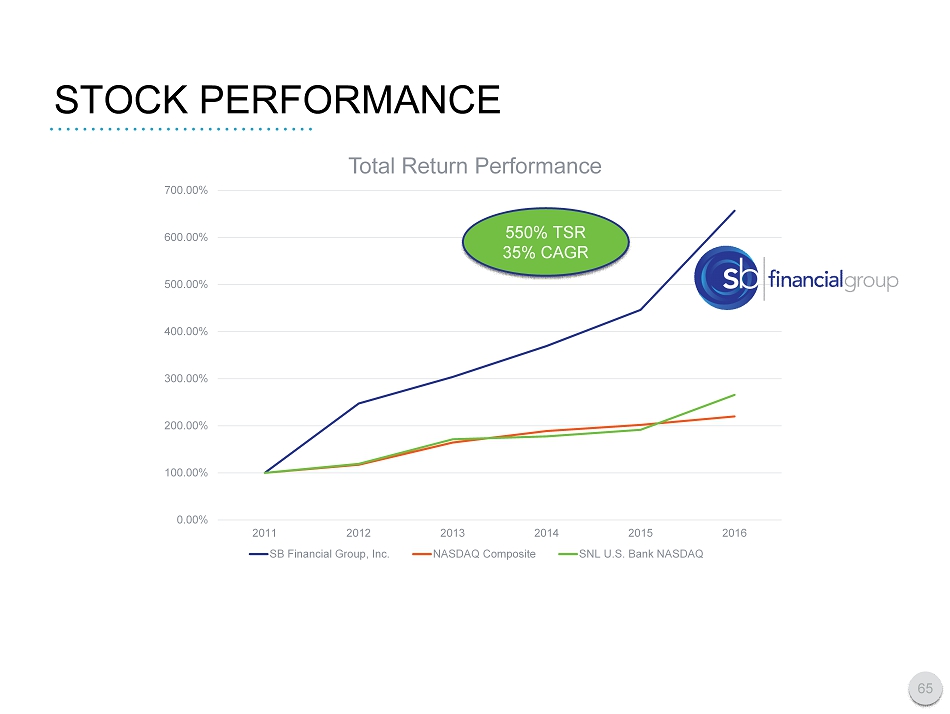

STOCK PERFORMANCE 65 Other Retail Ownership, 60% Institutional Ownership, 28% 0.00% 100.00% 200.00% 300.00% 400.00% 500.00% 600.00% 700.00% 2011 2012 2013 2014 2015 2016 Total Return Performance SB Financial Group, Inc. NASDAQ Composite SNL U.S. Bank NASDAQ 550% TSR 35% CAGR

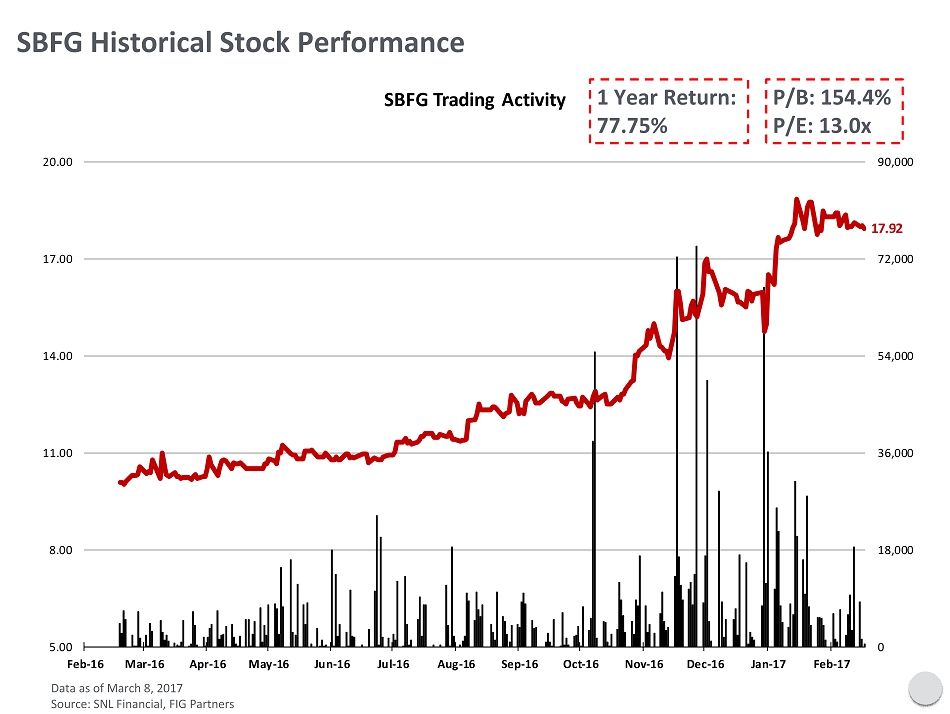

17.92 0 18,000 36,000 54,000 72,000 90,000 5.00 8.00 11.00 14.00 17.00 20.00 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16 Oct-16 Nov-16 Dec-16 Jan-17 Feb-17 SBFG Trading Activity SBFG Historical Stock Performance Data as of March 8, 2017 Source: SNL Financial, FIG Partners 1 Year Return: 77.75% P/B: 154.4% P/E: 13.0x

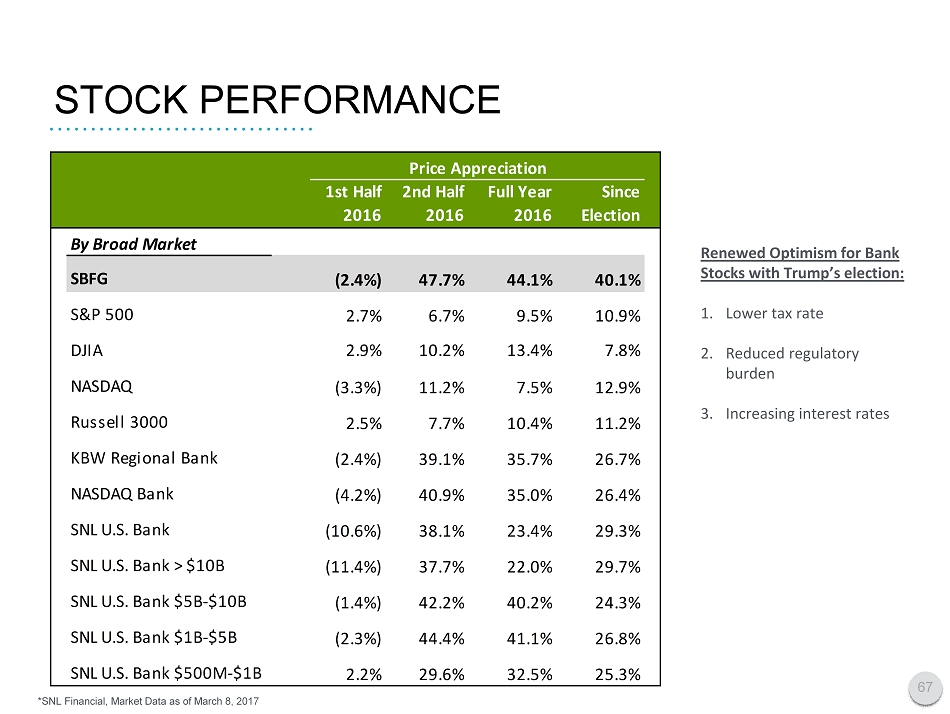

STOCK PERFORMANCE 67 Other Retail Ownership, 60% Institutional Ownership, 28% 1st Half 2016 2nd Half 2016 Full Year 2016 Since Election By Broad Market SBFG (2.4%) 47.7% 44.1% 40.1% S&P 500 2.7% 6.7% 9.5% 10.9% DJIA 2.9% 10.2% 13.4% 7.8% NASDAQ (3.3%) 11.2% 7.5% 12.9% Russell 3000 2.5% 7.7% 10.4% 11.2% KBW Regional Bank (2.4%) 39.1% 35.7% 26.7% NASDAQ Bank (4.2%) 40.9% 35.0% 26.4% SNL U.S. Bank (10.6%) 38.1% 23.4% 29.3% SNL U.S. Bank > $10B (11.4%) 37.7% 22.0% 29.7% SNL U.S. Bank $5B-$10B (1.4%) 42.2% 40.2% 24.3% SNL U.S. Bank $1B-$5B (2.3%) 44.4% 41.1% 26.8% SNL U.S. Bank $500M-$1B 2.2% 29.6% 32.5% 25.3% Price Appreciation Renewed Optimism for Bank Stocks with Trump’s election: 1. Lower tax r ate 2. Reduced regulatory burden 3. Increasing interest rates *SNL Financial, Market Data as of March 8, 2017

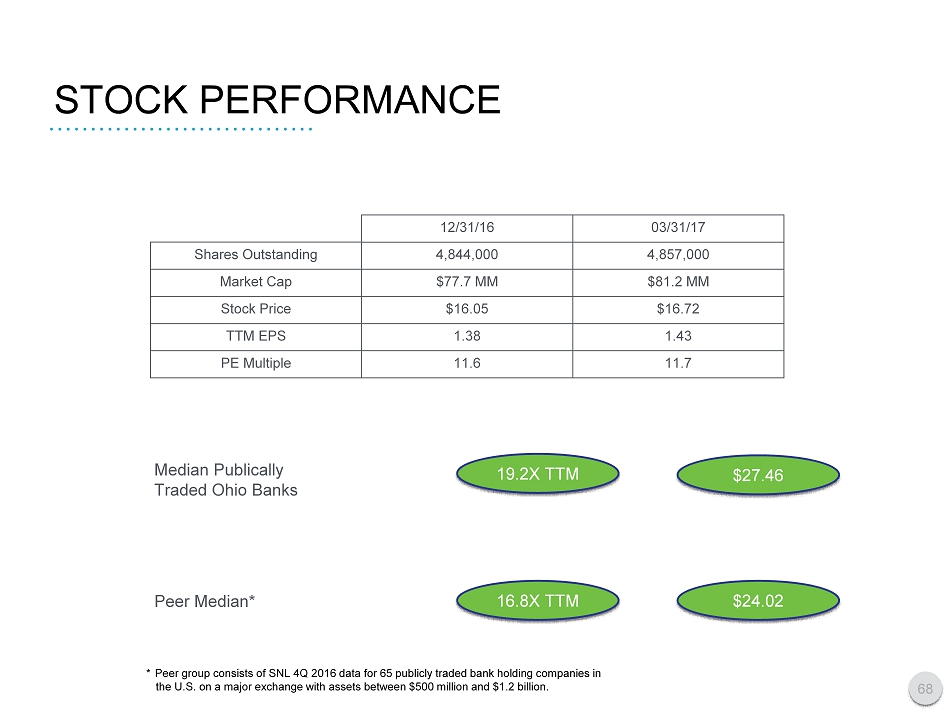

STOCK PERFORMANCE 68 Tangible Common Equity, $56,143, 70% Other Retail Ownership, 60% Institutional Ownership, 28% 12/31/16 03/31/17 Shares Outstanding 4,844,000 4,857,000 Market Cap $77.7 MM $81.2 MM Stock Price $16.05 $16.72 TTM EPS 1.38 1.43 PE Multiple 11.6 11.7 Median Publically Traded Ohio Banks Peer Median* * Peer group consists of SNL 4Q 2016 data for 65 publicly traded bank holding companies in the U.S. on a major exchange with assets between $500 million and $1.2 billion. 19.2X TTM 16.8X TTM $27.46 $24.02

MARK A. KLEIN\ – CHAIRMAN, PRESIDENT AND CEO ANTHONY V. COSENTINO – EVP & CFO SB FINANCIAL GROUP, INC. 69