The Fund invests in fixed income securities whose value is derived from an underlying pool of mortgages or consumer loans. The value of these securities is sensitive to changes in economic conditions, including delinquencies and/or defaults, and may be adversely affected by shifts in the market’s perception of the issuers and changes in interest rates. Investors receive principal and interest payments as the underlying mortgages and consumer loans are paid back. Some of these securities are collateralized mortgage obligations (CMOs). CMOs are debt securities issued by U.S. government agencies or by financial institutions and other mortgage lenders, which are collateralized by a pool of mortgages held under an indenture. Prepayment of mortgages may shorten the stated maturity of the obligation and can result in a loss of premium, if any has been paid. Certain of these securities may be stripped (securities which provide only the principal or interest feature of the underlying security). The yield to maturity on an interest-only CMO is extremely sensitive not only to changes in prevailing interest rates, but also to the rate of principal payments (including prepayments) on the related underlying mortgage assets. A rapid rate of principal payments may have a material adverse effect on the Fund’s yield to maturity. If the underlying mortgage assets experience greater than anticipated prepayments of principal, the Fund may fail to fully recoup its initial investment in these securities even if the securities are rated in the highest rating categories.

The Fund may invest up to 15% of its net assets in illiquid securities, which may include securities with contractual restrictions on resale, securities exempt from registration under Rule 144A of the Securities Act of 1933, as amended, and other securities which may not be readily marketable. The relative illiquidity of these securities may impair the Fund from disposing of them in a timely manner and at a fair price when it is necessary or desirable to do so. While maintaining oversight, the Fund’s Board has delegated to DMC the day-to-day functions of determining whether individual securities are liquid for purposes of the Fund’s limitation on investments in illiquid assets. Securities eligible for resale pursuant to Rule 144A, which are determined to be liquid, are not subject to the Fund’s 15% limit on investments in illiquid securities. Rule 144A and illiquid securities have been identified on the statement of net assets.

The Fund enters into contracts in the normal course of business that contain a variety of indemnifications. The Fund’s maximum exposure under these arrangements is unknown. However, the Fund has not had prior claims or losses pursuant to these contracts. Management has reviewed the Fund’s existing contracts and expects the risk of loss to be remote.

On August 18, 2009, Lincoln National Corporation and Macquarie Group (“Macquarie”) entered into an agreement pursuant to which Delaware Investments, including DMC, DDLP and DSC, will be acquired by Macquarie, an Australia-based global provider of banking, financial, advisory, investment and funds management services (the “Transaction”). Upon completion of the Transaction, DMC, DDLP and DSC will be wholly-owned subsidiaries of Macquarie.

The Transaction will result in a change of control of DMC which, in turn, will cause the termination of the investment advisory agreement between DMC and the Fund. As a result, a Special Meeting of Shareholders (the “Meeting”) of the Fund will be scheduled for the purpose of asking shareholders to approve a new investment advisory agreement between DMC and the Fund (the “New Agreement”). If approved by shareholders, the New Agreement will take effect upon the closing of the Transaction, which is currently anticipated to occur in the fourth quarter of 2009. Shareholders of the Fund will receive proxy materials including more detailed information about the Meeting, the Transaction and the proposed New Agreement.

Amendment to Investment Advisory Fee — In addition to the expense cap described in footnote 2, effective September 11, 2009, DMC has agreed to voluntarily waive all or a portion of its investment advisory fees and/or pay/reimburse expenses (excluding any 12b-1 plan expenses, taxes, interest, inverse floater program expenses, brokerage fees, certain insurance costs, and nonroutine expenses) in order to prevent total annual fund operating expenses from exceeding, in an aggregate amount, 0.75% of the Fund’s average daily net assets until such time as the voluntary expense cap is discontinued. These fee waivers and expense reimbursements apply only to expenses paid directly by the Fund, and may be discontinued at any time because they are voluntary.

Effective July 31, 2009, the Fund adopted Financial Accounting Standards Board Statement of Financial Accounting Standards No. 165, Subsequent Events (FAS 165). In accordance with FAS 165, management has evaluated whether any events or transactions occurred subsequent to July 31, 2009 through September 21, 2009, the date of issuance of the Fund’s financial statements, and determined that there were no material events or transactions other than those already disclosed that would require recognition or disclosure in the Fund’s financial statements.

13. Tax Information (Unaudited)

The information set forth below is for the Fund’s fiscal year as required by federal income tax laws. Shareholders, however, must report distributions on a calendar year basis for income tax purposes, which may include distributions for portions of two fiscal years of a fund. Accordingly, the information needed by shareholders for income tax purposes will be sent to them in January of each year. Please consult your tax advisor for proper treatment of this information.

For the fiscal year ended July 31, 2009, the Fund designates distributions paid during the year as follows:

| (A) Long-Term Capital Gains Distributions (Tax Basis) | — |

| (B) Ordinary Income Distributions* (Tax Basis) | 100 | % |

| Total Distributions (Tax Basis) | 100 | % |

(A) and (B) are based on a percentage of the Fund’s total distributions.

For the fiscal year ended July 31, 2009, certain dividends paid by the Fund may be subject to a maximum tax rate of 15%, as provided for by the Jobs and Growth Tax Relief Reconciliation Act of 2003. The Fund intends to designate up to a maximum amount of $51,533 to be taxed at a maximum rate of 15%. Complete information will be computed and reported in conjunction with your 2009 Form 1099-DIV.

*For the fiscal year ended July 31, 2009, certain ordinary income paid by the Fund, determined to be Qualified Interest Income may be subject to relief from U.S. withholding for foreign shareholders, as provided by the American Jobs Creation Act of 2004. For the fiscal year ended July 31, 2009, the Fund has designated maximum Qualified Interest Income distributions of $4,207,497.

67

Report of independent

registered public accounting firm

To the Shareholders and Board of Trustees

Delaware Group Government Fund — Delaware Core Plus Bond Fund

We have audited the accompanying statement of net assets of Delaware Core Plus Bond Fund (one of the series constituting Delaware Group Government Fund) (the “Fund”) as of July 31, 2009, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. We were not engaged to perform an audit of the Fund’s internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements and financial highlights, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of July 31, 2009 by correspondence with the custodian and brokers or by other appropriate auditing procedures where replies from brokers were not received. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of the Delaware Core Plus Bond Fund series of Delaware Group Government Fund at July 31, 2009, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended, and its financial highlights for each of the five years in the period then ended, in conformity with U.S. generally accepted accounting principles.

Philadelphia, Pennsylvania

September 21, 2009

68

Other Fund information

(Unaudited)

Delaware Core Plus Bond Fund

Board Consideration of Delaware Core Plus Bond Fund Investment Advisory Agreement

At a meeting held on May 19-21, 2009 (the “Annual Meeting”), the Board of Trustees (the “Board”), including a majority of disinterested or independent Trustees, approved the renewal of the Investment Advisory Agreement for the Delaware Core Plus Bond Fund (the “Fund”). In making its decision, the Board considered information furnished specifically in connection with the renewal of the Investment Advisory Agreement with Delaware Management Company (“DMC”), which included materials provided by DMC and its affiliates (“Delaware Investments”) concerning, among other things, the nature, extent and quality of services provided to the Fund, the costs of such services to the Fund, economies of scale and the financial condition and profitability of Delaware Investments. Reference was made to information furnished at regular quarterly Board meetings, including reports detailing Fund performance, investment strategies and expenses, as well as information prepared specifically in connection with the renewal of the investment advisory and sub-advisory contracts. In addition, in connection with the Annual Meeting, reports were provided in February 2009 and included independent historical and comparative reports prepared by Lipper Inc. (“Lipper”), an independent statistical compilation organization. The Lipper reports compared the Fund’s investment performance and expenses with those of other comparable mutual funds. The independent Trustees reviewed and discussed the Lipper reports with counsel to the independent Trustees. The Board requested and received information regarding DMC’s policy with respect to advisory fee levels and its breakpoint philosophy; the structure of portfolio manager compensation; the investment manager’s profitability; and any constraints or limitations on the availability of securities in certain investment styles which had in the past year inhibited, or which were likely in the future to inhibit, DMC’s ability to invest fully in accordance with Fund policies.

In considering information relating to the approval of the Fund’s advisory agreement, the independent Trustees received assistance and advice from and met separately with counsel to the independent Trustees. Although the Board gave attention to all information furnished, the following discussion identifies, under separate headings, the primary factors taken into account by the Board during its contract renewal considerations.

Nature, Extent and Quality of Service. The Board considered the services provided by Delaware Investments to the Fund and its shareholders. In reviewing the nature, extent and quality of services, the Board considered reports furnished to it throughout the year, which covered matters such as the relative performance of the Fund, compliance of portfolio managers with the investment policies, strategies and restrictions for the Fund, compliance by DMC and Delaware Distributors, L.P. (together, “Management”) personnel with the Code of Ethics adopted throughout the Delaware Investments Family of Funds complex and adherence to fair value pricing procedures as established by the Board. The Board was pleased with the current staffing of the Fund’s investment advisor and the emphasis placed on research in the investment process. The Board gave favorable consideration to DMC’s efforts to control expenditures while maintaining service levels committed to fund matters. The Board also considered the transfer agent and shareholder services provided to Fund shareholders by DMC’s affiliate, Delaware Service

69

Other Fund information

(Unaudited)

Delaware Core Plus Bond Fund

Board Consideration of Delaware Core Plus Bond Fund Investment Advisory Agreement (continued)

Company, Inc. (“DSC”), noting DSC’s high level of service. The Board noted that Management finished upgrading investment accounting functions through outsourcing to improve the quality and lower the cost of delivering investment accounting services to the Fund. The Board once again noted the benefits provided to Fund shareholders through each shareholder’s ability to exchange an investment in one Delaware Investments fund for the same class of shares in another Delaware Investments fund without a sales charge, to reinvest Fund dividends into additional shares of the Fund or into additional shares of other Delaware Investments funds and the privilege to combine holdings in other Delaware Investments funds to obtain a reduced sales charge. The Board was satisfied with the nature, extent and quality of the overall services provided by Delaware Investments.

Investment Performance. The Board placed significant emphasis on the investment performance of the Fund in view of its importance to shareholders. Although the Board gave appropriate consideration to performance reports and discussions with portfolio managers at Board meetings throughout the year, the Board gave particular weight to the Lipper reports furnished for the Annual Meeting. The Lipper reports prepared for the Fund showed the investment performance of its Class A shares in comparison to a group of similar funds as selected by Lipper (the “Performance Universe”). A fund with the best performance ranked first, and a fund with the poorest performance ranked last. The highest/best performing 25% of funds in the Performance Universe make up the first quartile; the next 25%, the second quartile; the next 25%, the third quartile; and the poorest/worst performing 25% of funds in the Performance Universe make up the fourth quartile. Comparative annualized performance for the Fund was shown for the past one-, three-, five- and ten-year periods ended December 31, 2008. The Board’s objective is that the Fund’s performance for the periods considered be at or above the median of its Performance Universe. The following paragraph summarizes the performance results for the Fund and the Board’s view of such performance.

The Performance Universe for the Fund consisted of the Fund and all retail and institutional intermediate investment-grade debt funds as selected by Lipper. The Lipper report comparison showed that the Fund’s total return for the one-, three- and five-year periods was in the second quartile of its Performance Universe. Although the Fund’s total return for the ten-year period was in the third quartile, the Board was satisfied with the recent performance.

Comparative Expenses. The Board considered expense comparison data for the Delaware Investments Family of Funds. Management provided the Board with information on pricing levels and fee structures for the Fund as of October 31, 2008 and, for comparative funds, information as of their respective fiscal year end occurring on or before August 31, 2008. The Board also focused on the comparative analysis of effective management fees and total expense ratios of the Fund versus effective management fees and expense ratios of a group of similar funds as selected by Lipper (the “Expense Group”). In reviewing comparative costs, the Fund’s contractual management fee and the actual management fee incurred by

70

the Fund were compared with the contractual management fees (assuming all funds in the Expense Group were similar in size to the Fund) and actual management fees (as reported by each fund) within the Expense Group, taking into account any applicable breakpoints and fee waivers. The Fund’s total expenses were also compared with those of its Expense Group. The Lipper total expenses, for comparative consistency, were shown by Lipper for Class A shares and comparative total expenses including 12b-1 and non 12b-1 service fees. The Board considered fees paid to Delaware Investments for nonmanagement services. The Board’s objective is to limit the Fund’s total expense ratio to be competitive with that of the Expense Group. The following paragraph summarizes the expense results for the Fund and the Board’s view of such expenses.

The expense comparisons for the Fund showed that its actual management fee was in the quartile with the lowest expenses of its Expense Group and its total expenses were in the quartile with the second lowest expenses of its Expense Group. The Board was satisfied with the management fee and total expenses of the Fund in comparison to those of its Expense Group as shown in the Lipper report.

Management Profitability. The Board considered the level of profits realized by Delaware Investments in connection with the operation of the Fund. In this respect, the Board reviewed the Investment Management Profitability Analysis that addressed the overall profitability of Delaware Investments’ business in providing management and other services to each of the individual funds and the Delaware Investments Family of Funds as a whole. Specific attention was given to the methodology followed in allocating costs for the purpose of determining profitability. Management stated that the level of profits of Delaware Investments, to a certain extent, reflect recent operational cost savings and efficiencies initiated by Delaware Investments. The Board considered Delaware Investments’ efforts to improve services provided to fund shareholders and to meet additional regulatory and compliance requirements resulting from recent industry-wide Securities and Exchange Commission initiatives. The Board also considered the extent to which Delaware Investments might derive ancillary benefits from fund operations, including the potential for procuring additional business as a result of the prestige and visibility associated with its role as service provider to the Delaware Investments Family of Funds and the benefits from allocation of fund brokerage to improve trading efficiencies. The Board found that the management fees were reasonable in light of the services rendered and the level of profitability of Delaware Investments.

Economies of Scale. The Trustees considered whether economies of scale are realized by Delaware Investments as the Fund’s assets increase and the extent to which any economies of scale are reflected in the level of management fees charged. The Trustees reviewed the standardized advisory fee pricing and structure, approved by the Board and shareholders, which includes breakpoints. Breakpoints in the advisory fee occur when the advisory fee rate is reduced on assets in excess of specified levels. Breakpoints result in a lower advisory fee than would otherwise be the case on all assets when the asset levels specified are exceeded. The Board noted that the fee under

71

Other Fund information

(Unaudited)

Delaware Core Plus Bond Fund

Board Consideration of Delaware Core Plus Bond Fund Investment Advisory Agreement (continued)

the Fund’s management contract fell within the standard structure. Although the Fund has not reached a size at which it can take advantage of breakpoints, the Board recognized that the fee was structured so that when the Fund grows, economies of scale may be shared.

Fund management

Paul Grillo, CFA

Senior Vice President, Co-Chief Investment Officer — Total Return Fixed Income Strategy

Paul Grillo is a member of the firm’s taxable fixed income portfolio management team with primary responsibility for portfolio construction and strategic asset allocation. He is also a member of the firm’s asset allocation committee, which is responsible for building and managing multi-asset class portfolios. He joined Delaware Investments in 1992 as a mortgage-backed and asset-backed securities analyst, assuming portfolio management responsibilities in the mid-1990s. Grillo serves as co-lead portfolio manager for the firm’s Diversified Income products and has been influential in the growth and distribution of the firm’s multisector strategies. Prior to joining Delaware Investments, Grillo served as a mortgage strategist and trader at Dreyfus Corporation. He also worked as a mortgage strategist and portfolio manager at Chemical Investment Group and as a financial analyst at Chemical Bank. Grillo holds a bachelor’s degree in business management from North Carolina State University and an MBA with a concentration in finance from Pace University.

Thomas H. Chow, CFA

Senior Vice President, Senior Portfolio Manager

Thomas H. Chow is a member of the firm’s taxable fixed income portfolio management team, with primary responsibility for portfolio construction and strategic asset allocation in investment grade credit exposures. He is the lead portfolio manager for Delaware Corporate Bond Fund and Delaware Extended Duration Bond Fund, as well as several institutional mandates. His experience includes significant exposure to asset liability management strategies and credit risk opportunities. Prior to joining Delaware Investments in 2001 as a portfolio manager working on the Lincoln General Account, he was a trader of high grade and high yield securities, and was involved in the portfolio management of collateralized bond obligations (CBOs) and insurance portfolios at SunAmerica/AIG from 1997 to 2001. Before that, he was an analyst, trader, and portfolio manager at Conseco Capital Management from 1989 to 1997. Chow received a bachelor’s degree in business analysis from Indiana University, and he is a Fellow of Life Management Institute.

72

Roger A. Early, CPA, CFA, CFP

Senior Vice President, Co-Chief Investment Officer — Total Return Fixed Income Strategy

Roger A. Early rejoined Delaware Investments in March 2007 as a member of the firm’s taxable fixed income portfolio management team, with primary responsibility for portfolio construction and strategic asset allocation. During his previous time at the firm, from 1994 to 2001, he was a senior portfolio manager in the same area, and he left Delaware Investments as head of its U.S. investment grade fixed income group. In recent years, Early was a senior portfolio manager at Chartwell Investment Partners and Rittenhouse Financial and served as the chief investment officer for fixed income at Turner Investments. Prior to joining Delaware Investments in 1994, he worked for more than 10 years at Federated Investors where he managed more than $25 billion in mutual fund and institutional portfolios in the short-term and investment grade markets. He left the firm as head of institutional fixed income management. Earlier in his career, he held management positions with the Federal Reserve Bank, PNC Financial, Touche Ross, and Rockwell International. Early earned his bachelor’s degree in economics from The Wharton School of the University of Pennsylvania and an MBA with concentrations in finance and accounting from the University of Pittsburgh. He is a member of the CFA Society of Philadelphia.

Kevin P. Loome, CFA

Senior Vice President, Senior Portfolio Manager, Head of High Yield Investments

Kevin P. Loome is head of the High Yield fixed income team, responsible for portfolio construction and strategic asset allocation of all high yield fixed income assets. Prior to joining Delaware Investments in August 2007 in his current position, Loome spent 11 years at T. Rowe Price, starting as an analyst and leaving the firm as a portfolio manager. He began his career with Morgan Stanley as a corporate finance analyst in the New York and London offices. Loome received his bachelor’s degree in commerce from the University of Virginia and earned an MBA from the Tuck School of Business at Dartmouth.

73

Board of trustees/directors and officers addendum

Delaware Investments® Family of Funds

A mutual fund is governed by a Board of Trustees/Directors (“Trustees”), which has oversight responsibility for the management of a fund’s business affairs. Trustees establish procedures and oversee and review the performance of the investment manager, the distributor, and others who perform services for the fund. The independent fund trustees, in particular, are advocates

| Name, Address, | | Position(s) | | Length of |

| and Birth Date | | Held with Fund(s) | | Time Served |

| Interested Trustees | | | | |

| | | | |

| Patrick P. Coyne1 | | Chairman, President, | | Chairman and Trustee |

| 2005 Market Street | | Chief Executive Officer, | | since August 16, 2006 |

| Philadelphia, PA 19103 | | and Trustee | | |

| April 1963 | | | | President and |

| | | | Chief Executive Officer |

| | | | since August 1, 2006 |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| Independent Trustees | | | | |

| | | | |

| Thomas L. Bennett | | Trustee | | Since March 2005 |

| 2005 Market Street | | | | |

| Philadelphia, PA 19103 | | | | |

| October 1947 | | | | |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

1 Patrick P. Coyne is considered to be an “Interested Trustee” because he is an executive officer of the Fund’s(s’) investment advisor.

74

for shareholder interests. Each trustee has served in that capacity since he or she was elected to or appointed to the Board of Trustees, and will continue to serve until his or her retirement or the election of a new trustee in his or her place. The following is a list of the Trustees and Officers with certain background and related information.

| | Number of Portfolios in | | |

| Principal Occupation(s) | | Fund Complex Overseen | | Other Directorships |

| During Past 5 Years | | by Trustee or Officer | | Held by Trustee or Officer |

| | | | |

| | | | |

| Patrick P. Coyne has served in | | 80 | | Director |

| various executive capacities | | | | Kaydon Corp. |

| at different times at | | | | (July 2007–Present) |

| Delaware Investments.2 | | | | |

| | | | Board of Governors Member |

| | | | Investment Company |

| | | | Institute (ICI) |

| | | | (2007–Present) |

| | | | |

| | | | Member of Investment Committee |

| | | | Cradle of Liberty Council, BSA |

| | | | (November 2007–Present) |

| | | | |

| | | | Finance Committee Member |

| | | | St. John Vianney |

| | | | Roman Catholic Church |

| | | | (2007–Present) |

| | | | |

| | | | |

| | | | |

| Private Investor | | 80 | | Director |

| (March 2004–Present) | | | | Bryn Mawr Bank Corp. (BMTC) |

| | | | (April 2007–Present) |

| Investment Manager | | | | |

| Morgan Stanley & Co. | | | | Chairman of |

| (January 1984–March 2004) | | | | Investment Committee |

| | | | Pennsylvania Academy of |

| | | | Fine Arts (2007–Present) |

| | | | Trustee (2004–Present) |

| |

2 Delaware Investments is the marketing name for Delaware Management Holdings, Inc. and its subsidiaries, including the Fund’s(s’) investment advisor, principal underwriter, and its transfer agent.

75

Board of trustees/directors and officers addendum

Delaware Investments® Family of Funds

| Name, Address, | Position(s) | Length of |

| and Birth Date | Held with Fund(s) | Time Served |

| Independent Trustees (continued) | | |

| | | |

| Thomas L. Bennett | | |

| (continued) | | |

| |

| |

| |

| |

| |

| John A. Fry | Trustee | Since January 2001 |

| 2005 Market Street | | |

| Philadelphia, PA 19103 | | |

| May 1960 | | |

| | | |

| | | |

| | | |

| |

| Anthony D. Knerr | Trustee | Since April 1990 |

| 2005 Market Street | | |

| Philadelphia, PA 19103 | | |

| December 1938 | | |

| |

| |

| Lucinda S. Landreth | Trustee | Since March 2005 |

| 2005 Market Street | | |

| Philadelphia, PA 19103 | | |

| June 1947 | | |

| |

| Ann R. Leven | Trustee | Since October 1989 |

| 2005 Market Street | | |

| Philadelphia, PA 19103 | | |

| November 1940 | | |

| |

| Thomas F. Madison | Trustee | Since May 19973 |

| 2005 Market Street | | |

| Philadelphia, PA 19103 | | |

| February 1936 | | |

| |

| |

| |

3 In 1997, several funds managed by Voyageur Fund Managers, Inc. (the “Voyageur Funds”) were incorporated into the Delaware Investments Family of Funds. Mr. Madison served as a director of the Voyageur Funds from 1993 until 1997.

76

| | Number of Portfolios in | | |

| Principal Occupation(s) | | Fund Complex Overseen | | Other Directorships |

| During Past 5 Years | | by Trustee or Officer | | Held by Trustee or Officer |

| |

| | | | | |

| | | | Investment Committee and |

| | | | Governance Committee |

| | | | Member |

| | | | Pennsylvania Horticultural |

| | | | Society |

| | | | (February 2006–Present) |

| |

| President | | 80 | | Director |

| Franklin & Marshall College | | | | Community Health Systems |

| (June 2002–Present) | | | | |

| | | | Director |

| Executive Vice President | | | | Ecore International |

| University of Pennsylvania | | | | |

| (April 1995–June 2002) | | | | |

| |

| Founder and | | 80 | | None |

| Managing Director | | | | |

| Anthony Knerr & Associates | | | | |

| (Strategic Consulting) | | | | |

| (1990–Present) | | | | |

| |

| Chief Investment Officer | | 80 | | None |

| Assurant, Inc. (Insurance) | | | | |

| (2002–2004) | | | | |

| |

| |

| Consultant | | 80 | | None |

| ARL Associates | | | | |

| (Financial Planning) | | | | |

| (1983–Present) | | | | |

| |

| President and | | 80 | | Director and Chair of |

| Chief Executive Officer | | | | Compensation Committee, |

| MLM Partners, Inc. | | | | Governance Committee |

| (Small Business Investing | | | | Member |

| and Consulting) | | | | CenterPoint Energy |

| (January 1993–Present) | | | | |

| |

77

Board of trustees/directors and officers addendum

Delaware Investments® Family of Funds

| Name, Address, | | Position(s) | | Length of |

| and Birth Date | | Held with Fund(s) | | Time Served |

| Independent Trustees (continued) | | | | |

| |

| Thomas F. Madison | | | | |

| (continued) | | | | |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| Janet L. Yeomans | | Trustee | | Since April 1999 |

| 2005 Market Street | | | | |

| Philadelphia, PA 19103 | | | | |

| July 1948 | | | | |

| |

| |

| |

| |

| J. Richard Zecher | | Trustee | | Since March 2005 |

| 2005 Market Street | | | | |

| Philadelphia, PA 19103 | | | | |

| July 1940 | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| |

78

| Number of Portfolios in | |

| Principal Occupation(s) | Fund Complex Overseen | Other Directorships |

| During Past 5 Years | by Trustee or Officer | Held by Trustee or Officer |

| |

| | |

| | Lead Director and Chair of |

| | Audit and Governance |

| | Committees, Member of |

| | Compensation Committee |

| | Digital River, Inc. |

| | |

| | Director and Chair of |

| | Governance Committee, |

| | Audit Committee |

| | Member |

| | Rimage Corporation |

| | |

| | Director and Chair of |

| | the Compensation Committee |

| | Spanlink Communications |

| | |

| | Lead Director and Member of |

| | Compensation and |

| | Governance Committees |

| | Valmont Industries, Inc. |

| |

| Vice President and Treasurer | 80 | Director |

| (January 2006–Present) | | Okabena Company |

| Vice President — Mergers & Acquisitions | | |

| (January 2003–January 2006), and | | |

| Vice President | | |

| (July 1995–January 2003) | | |

| 3M Corporation | | |

| |

| Founder | 80 | Director and Audit |

| Investor Analytics | | Committee Member |

| (Risk Management) | | Investor Analytics |

| (May 1999–Present) | | |

| |

| Founder | | |

| Sutton Asset Management | | |

| (Hedge Fund) | | |

| (September 1996–Present) | | |

| |

79

Board of trustees/directors and officers addendum

Delaware Investments® Family of Funds

| Name, Address, | | Position(s) | | Length of |

| and Birth Date | | Held with Fund(s) | | Time Served |

| Officers | | | | |

| | | | | |

| David F. Connor | | Vice President, | | Vice President since |

| 2005 Market Street | | Deputy General | | September 2000 |

| Philadelphia, PA 19103 | | Counsel, and Secretary | | and Secretary since |

| December 1963 | | | | October 2005 |

| |

| |

| Daniel V. Geatens | | Vice President | | Treasurer |

| 2005 Market Street | | and Treasurer | | since October 25, 2007 |

| Philadelphia, PA 19103 | | | | |

| October 1972 | | | | |

| |

| David P. O’Connor | | Senior Vice President, | | Senior Vice President, |

| 2005 Market Street | | General Counsel, | | General Counsel, and |

| Philadelphia, PA 19103 | | and Chief Legal Officer | | Chief Legal Officer |

| February 1966 | | | | since October 2005 |

| |

| Richard Salus | | Senior Vice President | | Chief Financial Officer |

| 2005 Market Street | | and Chief Financial Officer | | since November 2006 |

| Philadelphia, PA 19103 | | | | |

| October 1963 | | | | |

| |

4 David F. Connor, Daniel V. Geatens, David P. O’Connor, and Richard Salus serve in similar capacities for the six portfolios of the Optimum Fund Trust, which have the same investment advisor, principal underwriter, and transfer agent as the registrant.

80

| | Number of Portfolios in | | |

| Principal Occupation(s) | | Fund Complex Overseen | | Other Directorships |

| During Past 5 Years | | by Trustee or Officer | | Held by Trustee or Officer |

| |

| |

| David F. Connor has served as | | 80 | | None4 |

| Vice President and Deputy | | | | |

| General Counsel of | | | | |

| Delaware Investments | | | | |

| since 2000. | | | | |

| |

| Daniel V. Geatens has served | | 80 | | None4 |

| in various capacities at | | | | |

| different times at | | | | |

| Delaware Investments. | | | | |

| |

| David P. O’Connor has served in | | 80 | | None4 |

| various executive and legal | | | | |

| capacities at different times | | | | |

| at Delaware Investments. | | | | |

| |

| Richard Salus has served in | | 80 | | None4 |

| various executive capacities | | | | |

| at different times at | | | | |

| Delaware Investments. | | | | |

| |

The Statement of Additional Information for the Fund(s) includes additional information about the Trustees and Officers and is available, without charge, upon request by calling 800 523-1918.

81

About the organization

Board of trustees | | | |

| | | | |

Patrick P. Coyne

Chairman, President, and

Chief Executive Officer

Delaware Investments®

Family of Funds

Philadelphia, PA Thomas L. Bennett

Private Investor

Rosemont, PA John A. Fry

President

Franklin & Marshall

College

Lancaster, PA | Anthony D. Knerr

Founder and Managing

Director

Anthony Knerr &

Associates

New York, NY Lucinda S. Landreth

Former Chief Investment

Officer

Assurant, Inc.

Philadelphia, PA | Ann R. Leven

Consultant

ARL Associates

New York, NY Thomas F. Madison

President and

Chief Executive Officer

MLM Partners, Inc.

Minneapolis, MN | Janet L. Yeomans

Vice President and

Treasurer

3M Corporation

St. Paul, MN J. Richard Zecher

Founder

Investor Analytics

Scottsdale, AZ |

| | | | |

| Affiliated officers | | | |

| | | | |

David F. Connor

Vice President, Deputy

General Counsel, and

Secretary

Delaware Investments

Family of Funds

Philadelphia, PA | Daniel V. Geatens

Vice President and

Treasurer

Delaware Investments

Family of Funds

Philadelphia, PA | David P. O’Connor

Senior Vice President,

General Counsel,

and Chief Legal Officer

Delaware Investments

Family of Funds

Philadelphia, PA | Richard Salus

Senior Vice President and

Chief Financial Officer

Delaware Investments

Family of Funds

Philadelphia, PA |

This annual report is for the information of Delaware Core Plus Bond Fund shareholders, but it may be used with prospective investors when preceded or accompanied by a current prospectus for Delaware Core Plus Bond Fund and the Delaware Investments Fund profile for the most recently completed calendar quarter. These documents are available at www.delawareinvestments.com. The prospectus sets forth details about charges, expenses, investment objectives, and operating policies of the investment company. You should read the prospectus carefully before you invest. The figures in this report represent past results that are not a guarantee of future results. The return and principal value of an investment in the investment company will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. |

Delaware Investments is the marketing name of Delaware Management Holdings, Inc. and its subsidiaries. The Fund files its complete schedule of portfolio holdings with the Securities and Exchange Commission for the first and third quarters of each fiscal year on Form N-Q. The Fund’s Forms N-Q, as well as a description of the policies and procedures that the Fund uses to determine how to vote proxies (if any) relating to portfolio securities are available without charge (i) upon request, by calling 800 523-1918; and (ii) on the Commission’s Web site at www.sec.gov. In addition, a description of the policies and procedures that the Fund uses to determine how to vote proxies (if any) relating to portfolio securities and the Fund’s Schedule of Investments are available without charge on the Fund’s Web site at www.delawareinvestments.com. The Fund’s Forms N-Q may be reviewed and copied at the Commission’s Public Reference Room in Washington, D.C.; information on the operation of the Public Reference Room may be obtained by calling 800 SEC-0330. Information (if any) regarding how the Fund voted proxies relating to portfolio securities during the most recently disclosed 12-month period ended June 30 is available without charge (i) through the Fund’s Web site at www.delawareinvestments.com; and (ii) on the Commission’s Web site at www.sec.gov. |

82

| |

| |

|

|

|

| | |

| | |

Annual report Delaware Inflation Protected Bond Fund July 31, 2009 Fixed income mutual fund |

This annual report is for the information of Delaware Inflation Protected Bond Fund shareholders, but it may be used with prospective investors when preceded or accompanied by a current prospectus for Delaware Inflation Protected Bond Fund. The figures in the annual report for Delaware Inflation Protected Bond Fund represent past results, which are not a guarantee of future results. The return and principal value of an investment in the investment company will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. You should consider the investment objectives, risks, charges, and expenses of the investment company carefully before investing. The Delaware Inflation Protected Bond Fund prospectus contains this and other important information about the investment company. Prospectuses for all open-end funds in the Delaware Investments® Family of Funds are available from your financial advisor, online at www.delawareinvestments.com, or by phone at 800 523-1918. Please read the prospectus carefully before you invest or send money. |

You can obtain shareholder reports and prospectuses online instead of in the mail.

Visit www.delawareinvestments.com/edelivery. |

Experience Delaware Investments

Delaware Investments is committed to the pursuit of consistently superior asset management and unparalleled client service. We believe in our investment processes, which seek to deliver consistent results, and in convenient services that help add value for our clients.

If you are interested in learning more about creating an investment plan, contact your financial advisor.

You can learn more about Delaware Investments or obtain a prospectus for Delaware Inflation Protected Bond Fund at www.delawareinvestments.com.

Manage your investments online |

- 24-hour access to your account information

- Obtain share prices

- Check your account balance and recent transactions

- Request statements or literature

- Make purchases and redemptions

|

Contact information

Investment manager

Delaware Management Company, a series of Delaware Management Business Trust

National distributor

Delaware Distributors, L.P.

Financial intermediary wholesaler

Lincoln Financial Distributors, L.P.

Shareholder servicing, dividend disbursing, and transfer agent

Delaware Service Company, Inc.

Mailing address

2005 Market Street

Philadelphia, PA 19103-7094

Shareholder assistance by phone

800 523-1918, weekdays from 8 a.m. to 7 p.m. Eastern time

For securities dealers and financial institutions representatives only

800 362-7500

Table of contents | |

| Portfolio management review | 1 |

| Performance summary | 4 |

| Disclosure of Fund expenses | 8 |

| Security type and credit quality breakdown | 10 |

| Statement of net assets | 11 |

| Statement of operations | 20 |

| Statements of changes in net assets | 22 |

| Financial highlights | 24 |

| Notes to financial statements | 32 |

| Report of independent registered public accounting firm | 49 |

| Other Fund information | 50 |

| Board of trustees/directors and officers addendum | 54 |

| About the organization | 62 |

Views expressed herein are current as of July 31, 2009, and are subject to change.

Funds are not FDIC insured and are not guaranteed. It is possible to lose the principal amount invested.

Mutual fund advisory services provided by Delaware Management Company, a series of Delaware Management Business Trust, which is a registered investment advisor. Delaware Investments is the marketing name of Delaware Management Holdings, Inc. and its subsidiaries. Lincoln Financial Group is the marketing name for Lincoln National Corporation and its affiliates.

© 2009 Delaware Distributors, L.P.

All third-party trademarks cited are the property of their respective owners.

| Portfolio management review | |

| Delaware Inflation Protected Bond Fund | Aug. 11, 2009 |

| Performance preview (for the period ended July 31, 2009) | | | | |

| Delaware Inflation Protected Bond Fund (Class A shares) | | 1-year return | | +1.12% |

| Barclays Capital U.S. Treasury Inflation-Protected Securities (TIPS) Index, formerly Lehman Brothers U.S. Treasury Inflation-Protected (TIPS) Index (benchmark) | | 1-year return | | -0.54% |

Past performance is not a guarantee of future results.

For complete, annualized performance for Delaware Inflation Protected Bond Fund, please see the table on page 4.

The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions. |

The fiscal year ended July 31, 2009, was a time of extraordinary volatility across virtually all financial markets. The period began with inflation ranking as one of many investors’ most pressing concerns. Commodities central to industry, agriculture, and economic sectors were richly priced, in part because of robust demand from emerging markets such as China and India.

However, during the last five months of 2008, U.S. economic growth reversed abruptly, turning significantly negative. As the flow of credit dried up, tapped-out consumers slashed their spending. Meanwhile, the credit crisis that had started in the subprime mortgage market spread like wildfire, engulfing such marquee financial companies as Merrill Lynch, Washington Mutual, Wachovia, American International Group (AIG), Fannie Mae, Freddie Mac, and Lehman Brothers, the last of which was forced to declare bankruptcy in September 2008. Lehman’s bankruptcy accelerated the economic downturn and heightened the sense of panic already gripping the financial markets. In December, the National Bureau of Economic Research declared that the U.S. economy was in recession during 2008.

As the U.S. economy slumped and economies in other developed nations followed suit, investors’ outlook for inflation shifted dramatically. At the beginning of the period,

The fiscal year ended July 31, 2009, was a time of extraordinary volatility across virtually all financial markets.

- The period began with inflation ranking as one of many investors’ most pressing concerns.

- However, during the last five months of 2008, U.S. economic growth reversed abruptly, turning significantly negative.

- During the first calendar quarter of 2009, many deflationary fears were replaced by hopeful statements about the economy and expectations of inflation growth stemming from the significant amounts of liquidity being pumped into the financial system.

Data for this portfolio management review were provided by Bloomberg unless otherwise noted. | | 1 |

Portfolio management review

Delaware Inflation Protected Bond Fund

the prices of Treasury inflation-protected securities (TIPS) reflected an expected inflation rate of somewhere between 3% and 5%.

By the end of 2008, the TIPS market was anticipating an extended period of deflation, or declining prices. The shift to a deflationary outlook was reflected in negative returns both for the Fund and its benchmark during the final five months of 2008. These losses occurred despite sharply falling yields in the Treasury market, which were spurred by a flight to quality and which, on balance, tend to be advantageous for fixed income investments. During this turn of events, the yields of short-term TIPS actually exceeded those of comparable Treasurys for a brief time, a relatively rare occurrence.

The new year ushered in a much friendlier environment for TIPS. A massive fiscal stimulus program signed into law by President Obama in February, coupled with the Federal Reserve Board commitment to keeping short-term interest rates historically low, and a variety of government initiatives designed to restore liquidity and boost confidence in the financial markets, resulted in renewed investor willingness to accept risk. Beginning in March 2009, stocks embarked on a sustained rally, while in the fixed income markets, credit spreads — which reflect the premium anticipated for the increased risk of non-Treasury investments — narrowed substantially. At the same time, many deflationary fears were replaced by hopeful statements about the economy and expectations of inflation growth stemming from the significant amounts of liquidity being pumped into the financial system. This shift was beneficial to the TIPS market, producing positive returns for our benchmark and the Fund during the first seven months of 2009, even in the face of rising yields in the Treasury market.

Fund performance

For its fiscal year ended July 31, 2009, Delaware Inflation Protected Bond Fund returned +1.12% for Class A shares at net asset value and -3.44% at maximum offer price. Both figures reflect all distributions reinvested. During the same period, the Fund’s benchmark, the Barclays Capital U.S. TIPS Index, returned -0.54% (source: Barclays Capital). For the complete, annualized performance of the Fund, please see the table on page 4.

Our decision to overweight longer-maturity TIPS benefited the Fund’s results relative to our benchmark early in the period. This same position later hurt Fund performance when deflationary expectations gave way to renewed fears of inflation, particularly during the first quarter of 2009. This change took place because investors continued to look for inflationary conditions over the longer term even while their short-term outlook called for deflation. Consequently, longer-maturity TIPS held up better when TIPS prices were falling; longer-maturity TIPS did not gain nearly as much during the substantial first-quarter rally. Our overweight position in longer-maturity TIPS was the greatest detractor to the Fund’s return as compared with the benchmark. The single most significant factor holding back the Fund’s results during the rally was our relative underweight in shorter-maturity TIPS during that rally.

Alternatively, Fund performance benefited from some of our allocation decisions among non-TIPS asset classes. At the beginning of the period, for example, roughly 20% of the Fund’s assets was jointly allocated to Treasury securities and agency securities. These positions aided the Fund’s performance during the latter part of 2008, as sharply falling Treasury yields caused their prices

2

to soar. Near the end of 2008, with the yields of investment grade corporate bonds approaching double digits, we sold most of our Treasury and agency positions and shifted that capital into the corporate sector due to the historic valuations we believed existed at that time. That shift proved to be a timely decision, as bond yields in the corporate sector fell, and prices subsequently surged higher when investors’ confidence in corporate balance sheets and earnings prospects recovered.

Inflation on the near-term horizon?

At the end of the fiscal year, in our view, many investors began to presume that the huge amount of money being used to stimulate the U.S. economy and bail out troubled corporations would produce higher inflation in relatively short order. We believe these concerns about inflation could be somewhat premature. Over the longer term, when economies here and in other developed nations begin to regain traction, inflation could indeed become a problem. As of the end of the reporting period, however, U.S. unemployment was approaching 10% and was still climbing. The demand for goods and services also was considerably short of the nation’s productive capacity. These conditions (high unemployment and a production gap) do not typically correlate with inflation. As a result, we believe inflationary pressures in the United States could remain relatively subdued for longer than many investors expect.

Prior to the current recession, many U.S. consumers seemed to spend freely, relying on rising home and stock prices to fund their purchases and running up a substantial amount of debt. As a result of the current credit crisis and the accompanying crash in both home and stock prices, consumers have retrenched in a major way. Savings rates have increased notably and spending remains muted as consumers attempt to pay down debt and stockpile cash. In our view, this situation is not likely to change significantly anytime soon. As a result, we believe that the prices of short-term TIPS may have gotten ahead of themselves and that the longer end of the TIPS market offers better value.

Given the entrenched nature of inflation in the U.S. economy since World War II, we remain convinced that most portfolios may generally benefit from an allocation to TIPS as a way to hedge against potential longer-term inflationary pressures.

3

| Performance summary | |

| Delaware Inflation Protected Bond Fund | July 31, 2009 |

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Please obtain the performance data for the most recent month end by calling 800 523-1918 or visiting our Web site at www.delawareinvestments.com/performance. Current performance may be lower or higher than the performance data quoted.

You should consider the investment objectives, risks, charges, and expenses of the investment company carefully before investing. The Delaware Inflation Protected Bond Fund prospectus contains this and other important information about the investment company. Please request a prospectus through your financial advisor or by calling 800 523-1918 or visiting our Web site at www.delawareinvestments.com. Read the prospectus carefully before you invest or send money.

A rise or fall in interest rates can have a significant impact on bond prices and the net asset value (NAV) of the Fund. Funds that invest in bonds can lose their value as interest rates rise, and an investor can lose principal. Interest payments on inflation-protected debt securities will vary as the principal and/or interest is adjusted for inflation.

| Fund performance | Average annual total returns through July 31, 2009 |

| 1 year | | 3 years | | Lifetime |

| Class A (Est. Dec. 1, 2004) | | | | | |

| Excluding sales charge | +1.12% | | +5.69% | | +4.57% |

| Including sales charge | -3.44% | | +4.08% | | +3.55% |

| Class B (Est. Dec. 1, 2004) | | | | | |

| Excluding sales charge | +0.39% | | +4.90% | | +3.86% |

| Including sales charge | -3.55% | | +4.22% | | +3.58% |

| Class C (Est. Dec. 1, 2004) | | | | | |

| Excluding sales charge | +0.39% | | +4.90% | | +3.86% |

| Including sales charge | -0.60% | | +4.90% | | +3.86% |

| Institutional Class (Est. Dec. 1, 2004) | | | | | |

| Excluding sales charge | +1.36% | | +5.95% | | +4.81% |

| Including sales charge | +1.36% | | +5.95% | | +4.81% |

Returns reflect the reinvestment of all distributions and any applicable sales charges as noted in the following paragraphs.

Performance for Class B and C shares, excluding sales charges, assumes either that contingent deferred sales charges did not apply or that the investment was not redeemed.

Expense limitations were in effect for certain classes during the periods shown in the Fund performance chart and in the “Performance of a $10,000 investment” chart. The current expenses for each class are listed on the “Fund expenses” chart. (Note that all charts and graphs referred to in the “Performance summary” section of this report are found on pages 4 through 6.) Performance would have been lower had the expense limitations not been in effect.

4

The Fund offers Class A, B, C, and Institutional Class shares. Class A shares are sold with a maximum front-end sales charge of up to 4.50%, and have an annual distribution and service fee of up to 0.25% of average daily net assets.

Class B shares may be purchased only through dividend reinvestment and certain permitted exchanges as described in the prospectus. Please see the prospectus for additional information on Class B purchase and sales charges. Class B shares have a contingent deferred sales charge that declines from 4.00% to zero depending on the period of time the shares are held.

Class B shares will automatically convert to Class A shares on a quarterly basis approximately eight years after purchase. They are also subject to an annual distribution and service fee of up to 1.00% of average daily net assets.

Class C shares are sold with a contingent deferred sales charge of 1.00% if redeemed during the first 12 months. They are also subject to an annual distribution and service fee of 1.00% of average daily net assets.

Institutional Class shares were first made available Dec. 1, 2004, and are available without sales or asset-based distribution charges only to certain eligible institutional accounts.

Inflation-protected debt securities tend to react to changes in interest rates, and the expected impact of inflation on interest rates. In general, the price of an inflation-protected debt security can fall when interest rates fall and rise when interest rates rise. Interest payments on inflation-protected debt securities will vary as the principal and/or interest is adjusted for inflation. The Fund may experience portfolio turnover in excess of 100%, which could result in higher transaction costs and tax liability for investors.

The Fund may invest in derivatives, which may involve additional expenses and are subject to risk, including the risk that an underlying security or securities index moves in the opposite direction from what the portfolio manager anticipated. A derivative transaction depends upon the counterparties’ ability to fulfill their contractual obligations.

The “Fund performance” table and the “Performance of a $10,000 investment” graph do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

The Fund’s expense ratios, as described in the most recent prospectus, are disclosed in the following “Fund expense ratios” table. Delaware Investments has agreed to reimburse certain expenses and/or waive certain fees from Dec. 1, 2008, through Nov. 30, 2009. Please see the most recent prospectus for additional information on these fee waivers and/or reimbursements.

| Fund expense ratios | Class A | | Class B | | Class C | | Institutional Class |

| Total annual operating expenses | 0.94% | | 1.69% | | 1.69% | | 0.69% |

| (without fee waivers) | | | | | | | |

| Net expenses | 0.75% | | 1.50% | | 1.50% | | 0.50% |

| (including fee waivers, if any) | | | | | | | |

| Type of waiver | Contractual | | Contractual | | Contractual | | Contractual |

5

Performance summary

Delaware Inflation Protected Bond Fund

Performance of a $10,000 investment

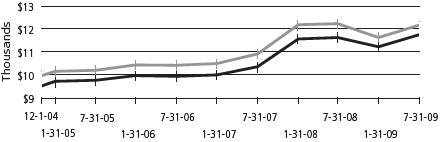

Average annual total returns from Dec. 1, 2004 (Fund’s inception), through July 31, 2009

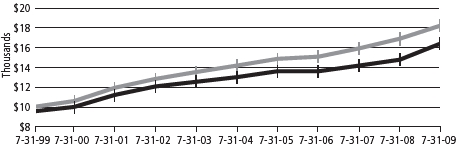

| For period beginning Dec. 1, 2004, through July 31, 2009 | Starting value | Ending value |

| | Barclays Capital U.S. Treasury Inflation-Protected Securities (TIPS) Index | $10,000 | $12,172 |

| | Delaware Inflation Protected Bond Fund — Class A shares | $9,550 | $11,766 |

The chart assumes $10,000 invested in the Fund on Dec. 1, 2004, and includes the effect of a 4.50% front-end sales charge and the reinvestment of all distributions. Please note additional details on these fees in the “Performance summary” section of this report, which includes pages 4 through 6.

The chart also assumes $10,000 invested in the Barclays Capital U.S. TIPS Index as of Dec. 1, 2004. The Barclays Capital U.S. TIPS Index, formerly the Lehman Brothers U.S. TIPS Index, measures the total return performance of the market for inflation-protected securities issued by the U.S. Treasury.

An index is unmanaged and does not reflect the costs of operating a mutual fund, such as the costs of buying, selling, and holding securities. You cannot invest directly in an index.

Performance of other Fund classes will vary due to different charges and expenses.

The “Fund performance” chart and the “Performance of a $10,000 investment” graph do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

| Stock symbols and CUSIP numbers |

| | | Nasdaq symbols | | CUSIPs | |

| Class A | | | DIPAX | | | 246094882 | |

| Class B | | | DIPBX | | | 246094874 | |

| Class C | | | DIPCX | | | 246094866 | |

| Institutional Class | | | DIPIX | | | 246094858 | |

6

Disclosure of Fund expenses

For the period February 1, 2009 to July 31, 2009

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, or other distributions; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution and/or service (12b-1) fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period February 1, 2009 to July 31, 2009.

Actual expenses

The first section of the table shown, “Actual Fund Return,” provides information about actual account values and actual expenses. You may use the information in this section of the table, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first section under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical example for comparison purposes

The second section of the table shown, “Hypothetical 5% Return,” provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second section of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher. The Fund’s expenses shown in the table reflect fee waivers in effect. The expenses shown in the table assume reinvestment of all dividends and distributions.

8

Delaware Inflation Protected Bond Fund

Expense analysis of an investment of $1,000

| | Beginning | | Ending | | | | Expenses |

| | Account Value | | Account Value | | Annualized | | Paid During Period |

| | 2/1/09 | | 7/31/09 | | Expense Ratio | | 2/1/09 to 7/31/09* |

| Actual Fund return |

| Class A | | $1,000.00 | | $1,046.70 | | 0.75% | | $3.81 | |

| Class B | | 1,000.00 | | 1,042.70 | | 1.50% | | 7.60 | |

| Class C | | 1,000.00 | | 1,042.70 | | 1.50% | | 7.60 | |

| Institutional Class | | 1,000.00 | | 1,047.70 | | 0.50% | | 2.54 | |

| Hypothetical 5% return (5% return before expenses) |

| Class A | | $1,000.00 | | $1,021.08 | | 0.75% | | $3.76 | |

| Class B | | 1,000.00 | | 1,017.36 | | 1.50% | | 7.50 | |

| Class C | | 1,000.00 | | 1,017.36 | | 1.50% | | 7.50 | |

| Institutional Class | | 1,000.00 | | 1,022.32 | | 0.50% | | 2.51 | |

*“Expenses Paid During Period” are equal to the Fund’s annualized expense ratio, multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period).

9

| Security type and credit quality breakdown | |

| Delaware Inflation Protected Bond Fund | As of July 31, 2009 |

Sector designations may be different than the sector designations presented in other Fund materials. The sector designations may represent the investment manager’s internal sector classifications, which may result in the sector designations for one Fund being different than another Fund’s sector designations.

| Security type | Percentage of net assets |

| Agency Asset-Backed Security | 0.00 | % |

| Agency Mortgage-Backed Security | 0.00 | % |

| Commercial Mortgage-Backed Security | 0.20 | % |

| Corporate Bonds | 17.44 | % |

| Banking | 2.23 | % |

| Basic Industry | 0.92 | % |

| Brokerage | 0.88 | % |

| Capital Goods | 0.49 | % |

| Communications | 4.45 | % |

| Consumer Cyclical | 1.32 | % |

| Consumer Non-Cyclical | 2.36 | % |

| Electric | 0.72 | % |

| Energy | 1.83 | % |

| Financials | 1.68 | % |

| Insurance | 0.56 | % |

| Foreign Agency | 0.05 | % |

| Non-Agency Asset-Backed Securities | 0.18 | % |

| Non-Agency Collateralized Mortgage Obligations | 0.03 | % |

| U.S. Treasury Obligations | 80.25 | % |

| Discount Note | 0.32 | % |

| Total Value of Securities | 98.47 | % |

| Receivables and Other Assets Net of Liabilities | 1.53 | % |

| Total Net Assets | 100.00 | % |

| Credit quality breakdown (as a % of fixed income investments)* | | |

| AAA | 82.27 | % |

| AA | 1.32 | % |

| A | 3.81 | % |

| BBB | 3.72 | % |

| BB | 6.57 | % |

| B | 1.74 | % |

| CCC | 0.57 | % |

| Total | 100.00 | % |

*Bond ratings are determined by independent, nationally recognized statistical rating organizations. |

10

| Statement of net assets | |

| Delaware Inflation Protected Bond Fund | July 31, 2009 |

| | Principal amount | | Value (U.S. $) |

| Agency Asset-Backed Security – 0.00% | | | | | | | |

| | Fannie Mae Whole Loan Series | | | | | | | |

| 2001-W2 AS5 6.473% 10/25/31 | | $ | 6,128 | | | $ | 6,100 |

| Total Agency Asset-Backed Security | | | | | | | |

| | (cost $6,113) | | | | | | | 6,100 |

| | | | | | | | |

| Agency Mortgage-Backed Security – 0.00% | | | | | | | |

| Freddie Mac S.F. 30 yr 8.00% 5/1/31 | | | 3,895 | | | | 4,402 |

| Total Agency Mortgage-Backed Security | | | | | | | |

| (cost $4,207) | | | | | | | 4,402 |

| | | | | | | | |

| Commercial Mortgage-Backed Security – 0.20% | | | | | | | |

| # | Crown Castle Towers Series 2006-1A B 144A | | | | | | | |

| 5.362% 11/15/36 | | | 450,000 | | | | 441,000 |

| Total Commercial Mortgage-Backed Security | | | | | | | |

| (cost $373,500) | | | | | | | 441,000 |

| | | | | | | | |

| Corporate Bonds – 17.44% | | | | | | | |

| Banking – 2.23% | | | | | | | |

| Bank of America 5.30% 3/15/17 | | | 1,000,000 | | | | 912,116 |

| JPMorgan Chase Capital XXV 6.80% 10/1/37 | | | 265,000 | | | | 242,968 |

| ·# | Rabobank Nederland 144A 11.00% 12/29/49 | | | 1,035,000 | | | | 1,208,976 |

| · | USB Capital IX 6.189% 10/29/49 | | | 2,360,000 | | | | 1,688,013 |

| · | Wells Fargo Capital XIII 7.70% 12/29/49 | | | 1,000,000 | | | | 870,659 |

| | | | | | | | 4,922,732 |

| Basic Industry – 0.92% | | | | | | | |

| ArcelorMittal 6.125% 6/1/18 | | | 1,000,000 | | | | 967,465 |

| Freeport-McMoRan Copper & Gold 8.375% 4/1/17 | | | 235,000 | | | | 249,453 |

| # | Georgia-Pacific 144A 8.25% 5/1/16 | | | 220,000 | | | | 228,800 |

| # | Teck Resources 144A | | | | | | | |

| 10.25% 5/15/16 | | | 130,000 | | | | 147,875 |

| 10.75% 5/15/19 | | | 375,000 | | | | 438,281 |

| | | | | | | | 2,031,874 |

11

Statement of net assets

Delaware Inflation Protected Bond Fund

| | | Principal amount | | Value (U.S. $) |

| Corporate Bonds (continued) | | | | | | | |

| Brokerage – 0.88% | | | | | | | |

| LaBranche 11.00% 5/15/12 | | $ | 575,000 | | | $ | 533,313 |

| Morgan Stanley | | | | | | | |

| ·1.463% 3/5/18 | | | 500,000 | | | | 398,750 |

| 5.375% 10/15/15 | | | 1,000,000 | | | | 1,003,595 |

| | | | | | | | 1,935,658 |

| Capital Goods – 0.49% | | | | | | | |

| Allied Waste North America 5.75% 2/15/11 | | | 634,000 | | | | 657,222 |

| Graphic Packaging International 9.50% 8/15/13 | | | 210,000 | | | | 210,263 |

| # | Owens-Brockway Glass Container 144A | | | | | | | |

| 7.375% 5/15/16 | | | 210,000 | | | | 208,950 |

| | | | | | | | 1,076,435 |

| Communications – 4.45% | | | | | | | |

| American Tower 7.125% 10/15/12 | | | 590,000 | | | | 601,800 |

| AT&T Wireless 8.125% 5/1/12 | | | 865,000 | | | | 982,551 |

| Cincinnati Bell 7.00% 2/15/15 | | | 245,000 | | | | 233,363 |

| Citizens Utilities 7.125% 3/15/19 | | | 615,000 | | | | 570,413 |

| # | Cricket Communications 144A 7.75% 5/15/16 | | | 350,000 | | | | 350,000 |

| Crown Castle International 9.00% 1/15/15 | | | 625,000 | | | | 663,281 |

| CSC Holdings | | | | | | | |

| 6.75% 4/15/12 | | | 590,000 | | | | 590,000 |

| #144A 8.50% 4/15/14 | | | 56,000 | | | | 57,960 |

| EchoStar DBS 7.125% 2/1/16 | | | 650,000 | | | | 633,750 |

| Inmarsat Finance II 10.375% 11/15/12 | | | 620,000 | | | | 651,000 |

| Intelsat Jackson Holdings 11.25% 6/15/16 | | | 90,000 | | | | 96,300 |

| # | Interpublic Group 144A 10.00% 7/15/17 | | | 215,000 | | | | 225,750 |

| # | Qwest 144A 8.375% 5/1/16 | | | 205,000 | | | | 211,150 |

| Sprint Capital 8.375% 3/15/12 | | | 854,000 | | | | 868,945 |

| Telecom Italia Capital 5.25% 10/1/15 | | | 1,000,000 | | | | 1,019,615 |

| Time Warner Cable | | | | | | | |

| 6.75% 7/1/18 | | | 120,000 | | | | 133,605 |

| 7.50% 4/1/14 | | | 650,000 | | | | 741,746 |

| # | Videotron 144A 9.125% 4/15/18 | | | 315,000 | | | | 328,388 |

| # | Wind Acquisition Finance 144A 11.75% 7/15/17 | | | 825,000 | | | | 886,875 |

| | | | | | | | 9,846,492 |

12

| | | Principal amount | | Value (U.S. $) |

| Corporate Bonds (continued) | | | | | | | |

| Consumer Cyclical – 1.32% | | | | | | | |

| Ford Motor Credit 8.00% 6/1/14 | | $ | 1,250,000 | | | $ | 1,155,674 |

| Goodyear Tire & Rubber 10.50% 5/15/16 | | | 260,000 | | | | 280,150 |

| # | Invista 144A 9.25% 5/1/12 | | | 175,000 | | | | 168,875 |

| | Macy’s Retail Holdings | | | | | | | |

| 8.875% 7/15/15 | | | 105,000 | | | | 108,866 |

| 10.625% 11/1/10 | | | 700,000 | | | | 714,373 |

| # | MGM MIRAGE 144A | | | | | | | |

| 10.375% 5/15/14 | | | 80,000 | | | | 86,200 |

| 11.125% 11/15/17 | | | 105,000 | | | | 116,025 |

| 13.00% 11/15/13 | | | 155,000 | | | | 175,538 |

| Ryland Group 8.40% 5/15/17 | | | 120,000 | | | | 118,200 |

| | | | | | | | 2,923,901 |

| Consumer Non-Cyclical – 2.36% | | | | | | | |

| # | Anheuser-Busch InBev Worldwide 144A | | | | | | | |

| 7.20% 1/15/14 | | | 800,000 | | | | 890,018 |

| ARAMARK 8.50% 2/1/15 | | | 465,000 | | | | 470,813 |

| # | Bio-Rad Laboratories 144A 8.00% 9/15/16 | | | 110,000 | | | | 112,750 |

| Community Health Systems 8.875% 7/15/15 | | | 835,000 | | | | 864,225 |

| Corrections Corporation of America 7.75% 6/1/17 | | | 220,000 | | | | 221,650 |

| HCA 9.25% 11/15/16 | | | 870,000 | | | | 909,150 |

| Inverness Medical Innovations 9.00% 5/15/16 | | | 205,000 | | | | 205,513 |

| Quest Diagnostics 5.45% 11/1/15 | | | 1,000,000 | | | | 988,689 |

| Select Medical 7.625% 2/1/15 | | | 105,000 | | | | 91,350 |

| SUPERVALU 7.50% 11/15/14 | | | 480,000 | | | | 466,800 |

| | | | | | | | 5,220,958 |

| Electric – 0.72% | | | | | | | |

| # | AES 144A 8.75% 5/15/13 | | | 285,000 | | | | 292,125 |

| # | Calpine Construction Finance 144A 8.00% 6/1/16 | | | 315,000 | | | | 318,150 |

| Illinois Power 9.75% 11/15/18 | | | 10,000 | | | | 12,022 |

| IPALCO Enterprises 8.125% 11/14/11 | | | 45,000 | | | | 46,463 |

| w | Mirant Mid Atlantic Pass Through Trust A | | | | | | | |

| 8.625% 6/30/12 | | | 486,437 | | | | 491,300 |

| NRG Energy 7.375% 2/1/16 | | | 455,000 | | | | 441,350 |

| | | | | | | | 1,601,410 |

13

Statement of net assets

Delaware Inflation Protected Bond Fund

| | | Principal amount | | Value (U.S. $) |

| Corporate Bonds (continued) | | | | | | | |

| Energy – 1.83% | | | | | | | |

| Chesapeake Energy 9.50% 2/15/15 | | $ | 855,000 | | | $ | 911,643 |

| El Paso 7.00% 6/15/17 | | | 425,000 | | | | 410,465 |

| Enterprise Products Operating 9.75% 1/31/14 | | | 270,000 | | | | 324,149 |

| Kinder Morgan Energy Partners | | | | | | | |

| 5.95% 2/15/18 | | | 100,000 | | | | 104,029 |

| 9.00% 2/1/19 | | | 120,000 | | | | 146,376 |

| Massey Energy 6.875% 12/15/13 | | | 960,000 | | | | 931,199 |

| Noble Energy 8.25% 3/1/19 | | | 615,000 | | | | 730,682 |

| PetroHawk Energy 9.125% 7/15/13 | | | 140,000 | | | | 145,950 |

| Range Resources 8.00% 5/15/19 | | | 235,000 | | | | 240,288 |

| Talisman Energy 7.75% 6/1/19 | | | 80,000 | | | | 93,736 |

| | | | | | | | 4,038,517 |

| Financials – 1.68% | | | | | | | |

| Capital One Bank 8.80% 7/15/19 | | | 1,045,000 | | | | 1,135,417 |

| | FTI Consulting 7.625% 6/15/13 | | | 615,000 | | | | 616,538 |

| General Electric Capital 5.625% 9/15/17 | | | 1,000,000 | | | | 1,010,209 |

| International Lease Finance | | | | | | | |

| 5.625% 9/20/13 | | | 625,000 | | | | 436,536 |

| 5.875% 5/1/13 | | | 375,000 | | | | 261,362 |

| 6.625% 11/15/13 | | | 370,000 | | | | 256,360 |

| | | | | | | | 3,716,422 |

| Insurance – 0.56% | | | | | | | |

| MetLife 6.817% 8/15/18 | | | 750,000 | | | | 804,365 |

| # | Metropolitan Life Global Funding I 144A | | | | | | | |

| 5.125% 4/10/13 | | | 170,000 | | | | 173,469 |

| · | Prudential Financial 0.62% 6/10/15 | | | 400,000 | | | | 267,688 |

| | | | | | | | 1,245,522 |

| Total Corporate Bonds (cost $35,567,761) | | | | | | | 38,559,921 |

| | | | | | | | |

| Foreign Agency – 0.05%D | | | | | | | |

| Republic of Korea – 0.05% | | | | | | | |

| Korea Development Bank 5.30% 1/17/13 | | | 120,000 | | | | 118,848 |

| Total Foreign Agency (cost $120,743) | | | | | | | 118,848 |

14

| | | Principal amount | | Value (U.S. $) |

| Non-Agency Asset-Backed Securities – 0.18% | | | | | | | |

| Caterpillar Financial Asset Trust | | | | | | | |

| Series 2007-A A3A 5.34% 6/25/12 | | $ | 63,723 | | | $ | 65,066 |

| | Series 2008-A A3 4.94% 4/25/14 | | | 150,000 | | | | 150,330 |

| · | Ford Credit Auto Owner Trust | | | | | | | |

| Series 2008-A A3B 1.088% 4/15/12 | | | 150,000 | | | | 149,814 |

| John Deere Owner Trust | | | | | | | |

| Series 2007-A A3 5.04% 7/15/11 | | | 21,797 | | | | 21,928 |

| Total Non-Agency Asset-Backed Securities | | | | | | | |

| (cost $371,798) | | | | | | | 387,138 |

| | | | | | | | | |

| Non-Agency Collateralized Mortgage Obligations – 0.03% | | | | | | | |

| · | Bank of America Mortgage Securities | | | | | | | |

| Series 2002-K 2A1 4.683% 10/20/32 | | | 8,055 | | | | 7,266 |

| · | Wells Fargo Mortgage Backed Securities Trust | | | | | | | |

| Series 2004-EE 3A1 4.474% 12/25/34 | | | 64,529 | | | | 60,833 |

| Total Non-Agency Collateralized Mortgage | | | | | | | |

| Obligations (cost $71,092) | | | | | | | 68,099 |

| | | | | | | | | |

| U.S. Treasury Obligations – 80.25% | | | | | | | |

| U.S. Treasury Inflation Index Bond 2.375% 1/15/25 | | | 17,936,919 | | | | 18,329,289 |

| U.S. Treasury Inflation Index Notes | | | | | | | |

| ¥1.625% 1/15/15 | | | 31,023,612 | | | | 30,946,053 |

| 2.00% 1/15/14 | | | 15,549,535 | | | | 15,875,111 |

| 2.00% 7/15/14 | | | 10,664,582 | | | | 10,887,877 |

| 2.00% 1/15/16 | | | 32,755,392 | | | | 33,308,139 |

| 2.375% 1/15/17 | | | 19,406,235 | | | | 20,291,644 |

| 3.00% 7/15/12 | | | 19,744,206 | | | | 20,873,338 |

| 3.375% 1/15/12 | | | 17,656,211 | | | | 18,726,619 |

| 3.50% 1/15/11 | | | 4,054,842 | | | | 4,230,976 |

| U.S. Treasury Notes | | | | | | | |

| 2.625% 7/31/14 | | | 2,210,000 | | | | 2,220,195 |

| 3.125% 5/15/19 | | | 1,820,000 | | | | 1,764,259 |

| Total U.S. Treasury Obligations | | | | | | | |

| (cost $170,250,000) | | | | | | | 177,453,500 |

15

Statement of net assets

Delaware Inflation Protected Bond Fund

| Principal amount | | Value (U.S. $) | |

| ¹Discount Note – 0.32% | | | | | | | | |

| Federal Home Loan Bank 0.09% 8/3/09 | | $ | 717,006 | | | $ | 717,002 | |

| Total Discount Note (cost $717,002) | | | | | | | 717,002 | |

| | | | | | | | | |