Use these links to rapidly review the document

TABLE OF CONTENTS

PART IV

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10K

| | |

| (Mark One) | | |

ý |

|

Annual Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the fiscal year ended January 31, 2009 |

OR |

o |

|

Transition Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the transition period from to |

Commission file number 1-3381

The Pep Boys—Manny, Moe & Jack

(Exact name of registrant as specified in its charter)

| | |

Pennsylvania

(State or other jurisdiction of

incorporation or organization) | | 23-0962915

(I.R.S. employer identification no.) |

3111 West Allegheny Avenue,

Philadelphia, PA

(Address of principal executive office) |

|

19132

(Zip code) |

215-430-9000

(Registrant's telephone number, including area code) |

Securities registered pursuant to Section 12(b) of the Act:

| | |

| Title of each class | | Name of each exchange on which registered |

|---|

| Common Stock, $1.00 par value | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark whether the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No ý

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of "large accelerated filer," "accelerated filer," and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

| | | | | | |

| Large accelerated filer o | | Accelerated filer ý | | Non-accelerated filer o

(Do not check if a smaller reporting company) | | Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act) Yes o No ý

As of the close of business on August 2, 2008 the aggregate market value of the voting stock held by non-affiliates of the registrant was approximately $308,971,231.

As of April 3, 2009, there were 52,265,326 shares of the registrant's common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant's definitive proxy statement, which will be filed with the Securities and Exchange Commission pursuant to Regulation 14A not later than 120 days after the end of the Company's fiscal year, for the Company's Annual Meeting of Shareholders 2009 are incorporated by reference into Part III of this Form 10-K.

TABLE OF CONTENTS

| | | | |

| |

| | Page |

|---|

PART I | | | | |

Item 1. | | Business | | 1 |

Item 1A. | | Risk Factors | | 8 |

Item 1B. | | Unresolved Staff Comments | | 12 |

Item 2. | | Properties | | 12 |

Item 3. | | Legal Proceedings | | 13 |

Item 4. | | Submission of Matters to a Vote of Security Holders | | 13 |

PART II | | �� | | |

Item 5. | | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | | 14 |

Item 6. | | Selected Financial Data | | 16 |

Item 7. | | Management's Discussion and Analysis of Financial Condition and Results of Operations | | 17 |

Item 7A. | | Quantitative and Qualitative Disclosures About Market Risk | | 34 |

Item 8. | | Financial Statements and Supplementary Data | | 36 |

Item 9. | | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | | 85 |

Item 9A. | | Controls and Procedures | | 85 |

Item 9B. | | Other Information | | 89 |

PART III | | | | |

Item 10. | | Directors, Executive Officers and Corporate Governance | | 89 |

Item 11. | | Executive Compensation | | 89 |

Item 12. | | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | | 89 |

Item 13. | | Certain Relationships and Related Transactions and Director Independence | | 89 |

Item 14. | | Principal Accounting Fees and Services | | 89 |

PART IV | | | | |

Item 15. | | Exhibits and Financial Statement Schedules | | 90 |

| | Signatures | | 94 |

Table of Contents

PART I

ITEM 1 BUSINESS

GENERAL

The Pep Boys—Manny, Moe & Jack and subsidiaries ("the Company") fiscal year ends on the Saturday nearest to January 31. Fiscal year 2008, which ended January 31, 2009, was comprised of 52 weeks; fiscal year 2007, which ended February 2, 2008, was comprised of 52 weeks; and fiscal year 2006, which ended February 3, 2007, was comprised of 53 weeks.

The Company is a leading automotive service and retail chain. The Company operates in one industry, the automotive aftermarket. The Company is engaged principally in automotive repair and maintenance and the sale of automotive tires, parts and accessories. The Company's primary operating unit is its SUPERCENTER format. As of January 31, 2009, the Company operated 562 stores consisting of 552 SUPERCENTERS and 1 SERVICE & TIRE CENTER, having an aggregate of 5,845 service bays, as well as 9 non-service/non-tire format PEP BOYS EXPRESS stores. The Company operates approximately 11,514,000 gross square feet of retail space, including service bays. The SUPERCENTERS average approximately 20,700 square feet and the PEP BOYS EXPRESS stores average approximately 9,500 square feet. The Company believes that its unique SUPERCENTER format offers the broadest capabilities in the industry and positions the Company to gain market share and increase its profitability by serving "do-it-for-me" DIFM (service labor, installed merchandise and tires) and "do-it-yourself" DIY (retail) customers with the highest quality service offerings and merchandise. In most of our stores we also have a commercial sales program that provides commercial credit and prompt delivery of tires, parts and other products to local, regional and national repair garages and dealers.

The following table sets forth the percentage of total revenues from continuing operations contributed by each class of similar products or services for the Company and should be read in conjunction with the Consolidated Financial Statements and Notes thereto included elsewhere herein:

| | | | | | | | | | |

| | Year ended | |

|---|

| | January 31,

2009 | | February 2,

2008 | | February 3,

2007 | |

|---|

Parts and Accessories | | | 65.1 | % | | 66.6 | % | | 68.5 | % |

Tires | | | 16.3 | | | 15.2 | | | 14.1 | |

| | | | | | | | |

Total Merchandise Sales | | | 81.4 | | | 81.8 | | | 82.6 | |

Service Labor | | | 18.6 | | | 18.2 | | | 17.4 | |

| | | | | | | | |

Total Revenues | | | 100.0 | % | | 100.0 | % | | 100.0 | % |

| | | | | | | | |

1

Table of Contents

As of January 31, 2009 the Company operated its stores in 35 states and Puerto Rico. The following table indicates, by state, the number of stores the Company had in operation at the end of each of the last five fiscal years, and the number of stores opened and closed by the Company during each of the last four fiscal years:

NUMBER OF STORES AT END OF FISCALS 2004 THROUGH 2008

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

State | | 2008

Year

End | | Closed | | Opened | | 2007

Year

End | | Closed | | Opened | | 2006

Year

End | | Closed | | Opened | | 2005

Year

End | | Closed | | Opened | | 2004

Year

End | |

|---|

Alabama | | | 1 | | | — | | | — | | | 1 | | | — | | | — | | | 1 | | | — | | | — | | | 1 | | | — | | | — | | | 1 | |

Arizona | | | 22 | | | — | | | — | | | 22 | | | 1 | | | 1 | | | 22 | | | — | | | — | | | 22 | | | — | | | — | | | 22 | |

Arkansas | | | 1 | | | — | | | — | | | 1 | | | — | | | — | | | 1 | | | — | | | — | | | 1 | | | — | | | — | | | 1 | |

California | | | 118 | | | — | | | — | | | 118 | | | 3 | | | — | | | 121 | | | — | | | — | | | 121 | | | 1 | | | — | | | 122 | |

Colorado | | | 7 | | | — | | | — | | | 7 | | | 1 | | | — | | | 8 | | | — | | | — | | | 8 | | | — | | | — | | | 8 | |

Connecticut | | | 7 | | | — | | | — | | | 7 | | | 1 | | | — | | | 8 | | | — | | | — | | | 8 | | | — | | | — | | | 8 | |

Delaware | | | 6 | | | — | | | — | | | 6 | | | — | | | — | | | 6 | | | — | | | — | | | 6 | | | — | | | — | | | 6 | |

Florida | | | 43 | | | — | | | — | | | 43 | | | — | | | — | | | 43 | | | — | | | — | | | 43 | | | — | | | — | | | 43 | |

Georgia | | | 22 | | | — | | | — | | | 22 | | | 3 | | | — | | | 25 | | | — | | | — | | | 25 | | | — | | | — | | | 25 | |

Illinois | | | 22 | | | — | | | — | | | 22 | | | 1 | | | — | | | 23 | | | — | | | — | | | 23 | | | — | | | — | | | 23 | |

Indiana | | | 7 | | | — | | | — | | | 7 | | | 2 | | | — | | | 9 | | | — | | | — | | | 9 | | | — | | | — | | | 9 | |

Kansas | | | — | | | — | | | — | | | — | | | 2 | | | — | | | 2 | | | — | | | — | | | 2 | | | — | | | — | | | 2 | |

Kentucky | | | 4 | | | — | | | — | | | 4 | | | — | | | — | | | 4 | | | — | | | — | | | 4 | | | — | | | — | | | 4 | |

Louisiana | | | 8 | | | — | | | — | | | 8 | | | 2 | | | — | | | 10 | ** | | — | | | — | | | 10 | ** | | — | | | — | | | 10 | |

Maine | | | 1 | | | — | | | — | | | 1 | | | — | | | — | | | 1 | | | — | | | — | | | 1 | | | — | | | — | | | 1 | |

Maryland | | | 18 | | | — | | | — | | | 18 | | | 1 | | | — | | | 19 | | | — | | | — | | | 19 | | | — | | | — | | | 19 | |

Massachusetts | | | 6 | | | — | | | — | | | 6 | | | 1 | | | — | | | 7 | | | — | | | — | | | 7 | | | — | | | — | | | 7 | |

Michigan | | | 5 | | | — | | | — | | | 5 | | | 2 | | | — | | | 7 | | | — | | | — | | | 7 | | | — | | | — | | | 7 | |

Minnesota | | | 3 | | | — | | | — | | | 3 | | | — | | | — | | | 3 | | | — | | | — | | | 3 | | | — | | | — | | | 3 | |

Missouri | | | 1 | | | — | | | — | | | 1 | | | — | | | — | | | 1 | | | — | | | — | | | 1 | | | — | | | — | | | 1 | |

Nevada | | | 12 | | | — | | | — | | | 12 | | | — | | | — | | | 12 | | | — | | | — | | | 12 | | | — | | | — | | | 12 | |

New Hampshire | | | 4 | | | — | | | — | | | 4 | | | — | | | — | | | 4 | | | — | | | — | | | 4 | | | — | | | — | | | 4 | |

New Jersey | | | 29 | | | — | | | — | | | 29 | | | — | | | 1 | | | 28 | | | — | | | — | | | 28 | | | — | | | — | | | 28 | |

New Mexico | | | 8 | | | — | | | — | | | 8 | | | — | | | — | | | 8 | | | — | | | — | | | 8 | | | — | | | — | | | 8 | |

New York | | | 29 | | | — | | | — | | | 29 | | | — | | | — | | | 29 | | | — | | | — | | | 29 | | | — | | | — | | | 29 | |

North Carolina | | | 8 | | | — | | | — | | | 8 | | | 2 | | | — | | | 10 | | | — | | | — | | | 10 | | | — | | | — | | | 10 | |

Ohio | | | 10 | | | — | | | — | | | 10 | | | 2 | | | — | | | 12 | | | — | | | — | | | 12 | | | — | | | — | | | 12 | |

Oklahoma | | | 5 | | | — | | | — | | | 5 | | | 1 | | | — | | | 6 | | | — | | | — | | | 6 | | | — | | | — | | | 6 | |

Pennsylvania | | | 42 | | | — | | | — | | | 42 | | | — | | | — | | | 42 | | | — | | | — | | | 42 | | | — | | | — | | | 42 | |

Puerto Rico | | | 27 | | | — | | | — | | | 27 | | | — | | | ��� | | | 27 | | | — | | | — | | | 27 | | | — | | | — | | | 27 | |

Rhode Island | | | 2 | | | — | | | — | | | 2 | | | 1 | | | — | | | 3 | | | — | | | — | | | 3 | | | — | | | — | | | 3 | |

South Carolina | | | 6 | | | — | | | — | | | 6 | | | — | | | — | | | 6 | | | — | | | — | | | 6 | | | — | | | — | | | 6 | |

Tennessee | | | 7 | | | — | | | — | | | 7 | | | — | | | — | | | 7 | | | — | | | — | | | 7 | | | — | | | — | | | 7 | |

Texas | | | 47 | | | — | | | — | | | 47 | | | 7 | | | — | | | 54 | | | — | | | — | | | 54 | | | 1 | | | — | | | 55 | |

Utah | | | 6 | | | — | | | — | | | 6 | | | — | | | — | | | 6 | | | — | | | — | | | 6 | | | — | | | — | | | 6 | |

Virginia | | | 16 | | | — | | | — | | | 16 | | | — | | | — | | | 16 | | | — | | | — | | | 16 | | | — | | | — | | | 16 | |

Washington | | | 2 | | | — | | | — | | | 2 | | | — | | | — | | | 2 | | | — | | | — | | | 2 | | | — | | | — | | | 2 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total | | | 562 | | | — | | | — | | | 562 | | | 33 | * | | 2 | | | 593 | | | — | | | — | | | 593 | | | 2 | | | — | | | 595 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

- *

- As more fully described in Note 7—Store Closures and Asset Impairments of the notes to the Consolidated Financial Statements included in Item 8, the Company closed 31 stores during the fourth quarter of fiscal 2007.

- **

- Due to damage sustained as a result of Hurricane Katrina in August 2005, two stores were temporarily closed at fiscal 2005 year end. One store was reopened in fiscal 2006 and the other store was reopened in fiscal 2007.

2

Table of Contents

BUSINESS STRATEGY

Our vision for Pep Boys is to take what we believe to be our industry-leading position in automotive services and accessories and become the automotive solutions provider of choice for the value-oriented customer. Our brand positioning—"Pep Boys Does Everything. For Less." is designed to convey to the consumer the breadth of the automotive services and merchandise that we offer and our value proposition. We will lead with our service business and grow through service spokes. We will create a differentiated retail experience by creating the automotive superstore. We will leverage our supercenters and service spokes to provide a complete offering for our commercial customers.

To achieve this vision, our business strategy focuses on four key areas; operational execution, merchandise assortment, marketing programs and store growth.

- •

- Operational Execution. In a highly competitive marketplace, we strive for operational excellence in order to provide a differentiated customer experience. We are investing in our associates through the development of incentive-based compensation programs, "best-in-class" store operating standards and procedures and sales training programs, all of which are designed to improve customer service and sales.

- •

- Merchandise Assortment. We spent much of 2008 clearing non-core inventory, updating our hard parts assortments and re-merchandising our stores as evidence of our commitment to carry the broadest assortment of automotive aftermarket merchandise available for service, retail and commercial consumers.

- •

- Marketing Programs. Taking our learnings from extensive testing conducted in 2008, we have developed a specific tailored marketing plan for each of our markets to maximize our reach and efficiencies. The cornerstone of our 2009 marketing program is TV and radio promotions, scheduled around traditional shopping holidays, that focus on the most frequently needed services—tires, oil changes and brakes. These promotions will be supplemented by extensive direct marketing and grass-roots campaigns and occasional print campaigns.

- •

- Store Growth. Our store plans are centered on a "hub and spoke" model, which calls for adding smaller neighborhood service shops to our existing SUPERCENTER store base in order to further leverage our existing inventories, distribution network, operations infrastructure and advertising spend. We are targeting 30 new spokes per year with a range of 20 to 40.

STORE IMPROVEMENTS

In fiscal year 2008, the Company's capital expenditures totaled $151,883,000. Of this amount, $117,121,000 was used to purchase 29 properties that were previously leased under a master operating lease. The balance of the capital expenditures of $34,762,000 was used for remodeling stores and for other store and corporate improvements. During fiscal year 2008, the Company did not open or close any stores. Our fiscal year 2009 capital expenditures are expected to be approximately $50,000,000 which includes the addition of 20 to 40 service only "spoke" shops and the general improvement of our existing stores. These expenditures are expected to be funded from net cash generated from operating activities and the Company's existing line of credit.

SERVICES AND PRODUCTS

The Company operates 5,845 service bays in 553 of its 562 locations. Each service location performs a full range of automotive repair and maintenance service (except body work) and installs tires, hard parts and accessories.

Each Pep Boys SUPERCENTER and PEP BOYS EXPRESS store carries a similar product line, with variations based on the number and type of cars in the markets where the store is located. A full

3

Table of Contents

complement of inventory at a typical SUPERCENTER includes an average of approximately 23,000 items (approximately 21,000 items at a PEP BOYS EXPRESS store). The Company's product lines include: tires (not stocked at PEP BOYS EXPRESS stores); batteries; new and remanufactured parts for domestic and import vehicles; chemicals and maintenance items; fashion, electronic, and performance accessories; and a limited amount of select non-automotive merchandise that appeals to automotive "Do-It-Yourself" customers, such as generators, power tools, personal transportation products, and canopies.

In addition to offering a wide variety of high quality name brand products, the Company sells an array of high quality products under various private label names. The Company sells tires under the names CORNELL®, FUTURA® and DEFINITY; and batteries under the name PROSTART®. The Company also sells wheel covers under the name FUTURA®; water pumps and cooling system parts under the name PROCOOL®; air filters, anti-freeze, chemicals, cv axles, lubricants, oil, oil filters, oil treatments, transmission fluids and wiper blades under the name PROLINE®; power tools under the name ALLEGHENY; alternators, battery booster packs, alkaline type batteries and starters under the name PROSTART®; power steering hoses and power steering pumps under the name PROSTEER®; brakes under the name PROSTOP® and brakes, starters and ignition under the name VALUEGRADE. All products sold by the Company under various private label names were approximately 28%, 27% and 24% of the Company's merchandise sales in fiscal years 2008, 2007 and 2006, respectively.

The Company's commercial automotive parts delivery program, branded PEP EXPRESS PARTS®, is designed to increase the Company's market share with the professional installer and to leverage its inventory investment. The program satisfies the installed merchandise customer by taking advantage of the breadth and quality of the Company's parts inventory as well as its experience supplying its own service bays and mechanics. As of January 31, 2009, approximately 76% or 425 of the Company's stores provided commercial parts delivery.

The Company has a point-of-sale system in all of its stores, which gathers sales and inventory data by stock-keeping unit from each store on a daily basis. This information is then used by the Company to help formulate its pricing, inventory, marketing and merchandising strategies. The Company has an electronic parts catalog and an electronic commercial invoicing system in all of its stores. The Company has an electronic work order system in all of its service centers. This system creates a service history for each vehicle, provides customers with a comprehensive sales document and enables the Company to maintain a service customer database.

The Company primarily uses an "Everyday Low Price" (EDLP) strategy in establishing its selling prices. Management believes that EDLP provides better value to its customers on a day-to-day basis, helps level customer demand and allows more efficient management of inventories. On a periodic basis, the Company employs a promotional pricing strategy on select items to drive increased customer traffic.

The Company uses various forms of advertising to promote its service and merchandise offerings, its service and repair capabilities and its commitment to customer service and satisfaction. The Company is committed to an effective promotional schedule with TV and radio promotions, scheduled around traditional shopping holidays throughout the year that focus on the most frequently needed services—tires, oil changes and brakes. These promotions will be supplemented by extensive direct marketing and grass-roots campaigns and occasional print campaigns. The Company is also piloting and expects to roll out in fiscal year 2009, a loyalty program designed to reward these customers who make Pep Boys their first choice for all of their automotive aftermarket purchases.

The Company maintains and is constantly upgrading a website located at www.pepboys.com. Pepboys.com is a multifaceted tool for connecting with existing and potential customers. It serves as an important portal to our Company, allowing consumers the freedom and convenience to access more information about the organization, our stores and our service, tires, parts and accessories offerings online. The site helps to establish Pep Boys as an automotive authority by providing consumers with

4

Table of Contents

general and seasonal car care tips, do-it-yourself vehicle maintenance and light repair guidance and safe driving pointers. Exclusive online coupons give site visitors who share with us their e-mail addresses access to special discounts on services and products at their local Pep Boys.

In fiscal year 2008, approximately 37% of the Company's total revenues were cash transactions with the remainder being co-branded credit card, other credit and debit card transactions and commercial credit accounts.

The Company does not experience significant seasonal fluctuation in the generation of its revenues.

STORE OPERATIONS AND MANAGEMENT

All Pep Boys stores are open seven days a week. Each SUPERCENTER has a Retail Manager and Service Manager (PEP BOYS EXPRESS STORES only have a Retail Manager) who report to geographic-specific Area Directors and Division Vice Presidents. The Divisional Vice Presidents report to the Senior Vice President of Stores who in turn reports to the Chief Executive Officer. As of January 31, 2009, a Retail Manager's and a Service Manager's average length of service with the Company is approximately 7.8 and 5.1 years, respectively.

Supervision and control over individual stores is facilitated by means of the Company's computer system, operational handbooks and regular visits to stores by Area Directors and Divisional Vice Presidents. All of the Company's advertising, accounting, purchasing, management information systems, and most of its administrative functions are conducted at its corporate headquarters in Philadelphia, Pennsylvania. Certain administrative functions for the Company's regional operations are performed at various regional offices of the Company. See "Item 2 Properties."

INVENTORY CONTROL AND DISTRIBUTION

Most of the Company's merchandise is distributed to its stores from its warehouses primarily by dedicated and contract carriers. Target levels of inventory for each product are established for each of the Company's warehouses and stores and are based upon prior shipment history, sales trends and seasonal demand. Inventory on hand is compared to the target levels on a weekly basis at each warehouse, potentially triggering re-ordering of merchandise from its suppliers.

Each Pep Boys store has an automatic inventory replenishment system that automatically orders additional inventory, generally from a warehouse, when a store's inventory on hand falls below the target levels. In addition, the Company's centralized buying system, coupled with continued advancement in its warehouse and distribution systems, has enhanced the Company's ability to control its inventory.

SUPPLIERS

During fiscal year 2008, the Company's ten largest suppliers accounted for approximately 48% of the merchandise purchased by the Company. No single supplier accounted for more than 20% of the Company's purchases. The Company has no long-term contracts under which it is required to purchase merchandise except for a contract to purchase bulk oil for use in the Company's service bays, which expires in 2011. Management believes that the relationships the Company has established with its suppliers are generally good.

In the past, the Company has not experienced difficulty in obtaining satisfactory sources of supply and believes that adequate alternative sources of supply exist, at substantially similar cost, for the types of merchandise sold in its stores.

5

Table of Contents

COMPETITION

The business of the Company is highly competitive. The Company encounters competition from nationwide and regional chains and from local independent merchants. The Company's competitors include general, full range, discount or traditional department stores which carry automotive parts and accessories and/or have automotive service centers, as well as specialized automotive retailers. Generally, the specialized automotive retailers focus on either the "do-it-yourself" or "do-it-for-me" areas of the business. The Company believes that its operation in both the "do-it-for-me" and "do-it-yourself" areas of the business positively differentiates it from most of its competitors. However, certain competitors are larger in terms of sales volume, store size, and/or number of stores. Therefore, these competitors have access to greater capital and management resources and have been operating longer or have more stores in particular geographic areas than the Company. The principal methods of competition in our industry include store location, availability of product, customer service and product offerings, quality and price.

The Company believes that the warranty policies in connection with the higher priced items it sells, such as tires, batteries, brake linings and other major automotive parts and accessories, are comparable or superior to those of its competitors.

REGULATION

The Company is subject to various federal, state and local laws and governmental regulations relating to the operation of its business, including those governing the handling, storage and disposal of hazardous substances contained in the products it sells and uses in its service bays, the recycling of batteries, tires and used lubricants, and the ownership and operation of real property.

EMPLOYEES

At January 31, 2009, the Company employed 18,458 persons as follows:

| | | | | | | | | | | | | | | | | | | |

Description | | Full-time | | % | | Part-time | | % | | Total | | % | |

|---|

Retail | | | 3,891 | | | 32.0 | | | 4,551 | | | 72.4 | | | 8,442 | | | 45.7 | |

Service Center | | | 7,008 | | | 57.6 | | | 1,676 | | | 26.6 | | | 8,684 | | | 47.1 | |

| | | | | | | | | | | | | | |

STORE TOTAL | | | 10,899 | | | 89.6 | | | 6,227 | | | 99.0 | | | 17,126 | | | 92.8 | |

Warehouses | | | 555 | | | 4.5 | | | 54 | | | 0.9 | | | 609 | | | 3.3 | |

Offices | | | 715 | | | 5.9 | | | 8 | | | 0.1 | | | 723 | | | 3.9 | |

| | | | | | | | | | | | | | |

TOTAL EMPLOYEES | | | 12,169 | | | 100.0 | | | 6,289 | | | 100.0 | | | 18,458 | | | 100.0 | |

| | | | | | | | | | | | | | |

The Company had no union employees as of January 31, 2009. At February 2, 2008, the Company employed approximately 12,070 full-time and 6,494 part-time employees.

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

Certain statements contained herein, including in "Item 1 Business" and "Item 7 Management's Discussion and Analysis of Financial Condition and Results of Operations", constitute "forward-looking statements" within the meaning of The Private Securities Litigation Reform Act of 1995. The words "guidance," "expects," "anticipates," "estimates," "forecasts" and similar expressions are intended to identify these forward-looking statements. Forward-looking statements include management's expectations regarding implementation of its long-term strategic plan, future financial performance, automotive aftermarket trends, levels of competition, business development activities, future capital expenditures, financing sources and availability and the effects of regulation and litigation. Although we believe that the expectations reflected in these forward-looking statements are based on reasonable assumptions, we can give no assurance that our expectations will be achieved. Our actual results may

6

Table of Contents

differ materially from the results discussed in the forward-looking statements due to factors beyond our control, including the strength of the national and regional economies, retail and commercial consumers' ability to spend, the health of the various sectors of the automotive aftermarket, the weather in geographical regions with a high concentration of our stores, competitive pricing, the location and number of competitors' stores, product and labor costs and the additional factors described in our filings with the Securities and Exchange Commission ("SEC"). See "Item 1A Risk Factors." We assume no obligation to update or supplement forward-looking statements that become untrue because of subsequent events.

SEC REPORTING

We electronically file certain documents with, or furnish such documents to, the SEC, including annual reports on Form 10-K, quarterly reports on Form 10-Q, and current reports on Form 8-K, along with any related amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act. From time-to-time, we may also file registration and related statements pertaining to equity or debt offerings. You may read and copy any materials we file with the SEC at the SEC's Office of Filings and Information Services at 100 F Street, NE, Washington, DC 20549. You may obtain information regarding the Office of Filings and Information Services by calling the SEC at 1-800-SEC-0330. In addition, the SEC maintains an Internet website at www.sec.gov that contains reports, proxy and information statements, and other information regarding issuers that file or furnish documents electronically with the SEC.

We provide free electronic access to our annual, quarterly and current reports (and all amendments to these reports) on our Internet website, www.pepboys.com. These reports are available on our website as soon as reasonably practicable after we electronically file or furnish such materials with or to the SEC. Information on our website does not constitute part of this Annual Report, and any references to our website herein are intended as inactive textual references only.

Copies of our SEC reports are also available free of charge from our investor relations department. Please call 215-430-9720 or write Pep Boys, Investor Relations, 3111 West Allegheny Avenue, Philadelphia, PA 19132.

EXECUTIVE OFFICERS OF THE COMPANY

The following table indicates the names, ages and tenures with the Company and positions (together with the year of election to such positions) of the executive officers of the Company:

| | | | | | | |

Name | | Age | | Tenure

with

Company

as of

April 16, 2009 | | Position with the Company and Date of Election to Position |

|---|

| Michael R. Odell | | | 45 | | 19 months | | Chief Executive Officer—since September 2008 |

| Raymond L. Arthur | | | 50 | | 11 months | | Executive Vice President—Chief Financial Officer since May 2008 |

| Joseph A. Cirelli | | | 50 | | 32 years | | Senior Vice President—Business Development since November 2007 |

| Troy E. Fee | | | 40 | | 21 months | | Senior Vice President—Human Resources since July 2007 |

| Scott A. Webb | | | 45 | | 19 months | | Senior Vice President—Merchandising & Marketing since September 2007 |

| William Shull | | | 50 | | 7 months | | Senior Vice President—Stores since September 2008 |

| Brian D. Zuckerman | | | 39 | | 10 years | | Senior Vice President—General Counsel & Secretary—since March 2009 |

7

Table of Contents

Michael R. Odell was named Chief Executive Officer on September 22, 2008, after serving as Interim Chief Executive Officer since April 23, 2008. Mr. Odell joined the Company in September 2007 as Executive Vice President—Chief Operating Officer, after having most recently served as the Executive Vice President and General Manager of Sears Retail & Specialty Stores. Mr. Odell joined Sears in its finance department in 1994 where he served until he joined Sears operations team in 1998. There he served in various executive operations positions of increasing seniority, including as Vice President, Stores—Sears Automotive Group.

Raymond L. Arthur joined Pep Boys in April 2008 after serving as Executive Vice President and Chief Financial Officer of Toys "R" Us Inc., from 2004 to 2006, where he oversaw its strategic review and restructuring of company-wide operations, as well as managing the leveraged buy-out of the company. During his seven year tenure at Toys "R" Us, Mr. Arthur also served as President and Chief Financial Officer of toysrus.com from 2000 to 2003 and as Corporate Controller of Toys "R" Us from 1999 to 2000. Prior to that, he worked in a variety of roles of increasing responsibility for General Signal, American Home Products, American Cyanamid and in public accounting.

Joseph A. Cirelli was named Senior Vice President—Corporate Development in November 2007. Since March 1977, Mr. Cirelli has served the Company in positions of increasing seniority, including Senior Vice President—Service, Vice President—Real Estate and Development, Vice President—Operations Administration, and Vice President—Customer Satisfaction.

Troy E. Fee, Senior Vice President—Human Resources, joined the Company in July 2007, after having most recently served as the Senior Vice President of Human Resources Shared Services for TBC Corporation, then the parent company of Big O Tires, Tire Kingdom and National Tire & Battery. Mr. Fee has over 20 years experience in operations and human resources in the tire and automotive service and repair business.

Scott A. Webb, Senior Vice President—Merchandising & Marketing, joined the Company in September 2007 after having most recently served as the Vice President, Merchandising and Customer Satisfaction of AutoZone. Mr. Webb joined AutoZone in 1986 where he began his service in field management before transitioning, in 1992, to the Merchandising function.

William Shull joined the Company in September 2008 as Senior Vice President—Stores. Over the last 25 years Mr. Shull has held several senior management positions where his focus was on building and integrating store management teams into successfully profitable and cohesive units. Some of his executive positions include SVP—Sales at The Wiz; SVP—Mall Operations of TransWorld Entertainment; SVP—Operations of Hollywood Entertainment; and in his 13 years at AutoZone he was instrumental in building the foundation of the retail chain in 4 geographic regions and responsible for store communications, training, and served on several strategic initiative committees. He was also a principal and the COO of a small, high-end custom electronics firm in Memphis TN, selling his stake in 2005.

Brian D. Zuckerman was named Senior Vice President—General Counsel & Secretary on March 1, 2009 after having most recently served as Vice President—General Counsel & Secretary since 2003. Mr. Zuckerman joined the Company as a staff attorney in 1999. Prior to joining Pep Boys, Mr. Zuckerman practiced corporate and securities law with two firms in Philadelphia.

Each of the officers serves at the pleasure of the Board of Directors of the Company.

ITEM 1A RISK FACTORS

Our business faces significant risks. The risks described below may not be the only risks we face. If any of the events or circumstances described as risks below actually occurs, our business, results of operations and or financial condition could be materially and adversely affected. The following section discloses all known material risks that we face. However, it does not include risks that may arise in the

8

Table of Contents

future that are yet unknown nor existing risks that we do not judge material to the presentation of our financial statements.

Risks Related to Pep Boys

We may not be able to successfully implement our business strategy, which could adversely affect our business, financial condition, results of operations and cash flows.

In fiscal year 2007, we adopted our long-term strategic plan, which includes numerous initiatives to increase sales, enhance our margins and increase our return on invested capital in order to increase our earnings and cash flow. If these initiatives are unsuccessful, or if we are unable to implement the initiatives efficiently and effectively, our business, financial condition, results of operations and cash flows could be adversely affected.

Successful implementation of our business strategy also depends on factors specific to the retail automotive aftermarket industry, many of which may be beyond our control (See "Risks Related to Our Industry").

If we are unable to generate sufficient cash flows from our operations, our liquidity will suffer and we may be unable to satisfy our obligations.

We require significant capital to fund our business. While we believe we have the ability to sufficiently fund our planned operations and capital expenditures for the next year, circumstances could arise that would materially affect our liquidity. For example, cash flows from our operations could be affected by changes in consumer spending habits or the failure to maintain favorable vendor payment terms or our inability to successfully implement sales growth initiatives. We may be unsuccessful in securing alternative financing when needed, on terms that we consider acceptable, or at all.

The degree to which we are leveraged could have important consequences to your investment in our securities, including the following risks:

- •

- our ability to obtain additional financing for working capital, capital expenditures, acquisitions or general corporate purposes may be impaired in the future;

- •

- a substantial portion of our cash flow from operations must be dedicated to the payment of rent and the principal and interest on our debt, thereby reducing the funds available for other purposes;

- •

- our failure to comply with financial and operating restrictions placed on us and our subsidiaries by our credit facilities could result in an event of default that, if not cured or waived, could have a material adverse effect on our business or our prospects; and

- •

- if we are substantially more leveraged than some of our competitors, we might be at a competitive disadvantage to those competitors that have lower debt service obligations and significantly greater operating and financial flexibility than we do.

We depend on our relationships with our vendors and a disruption of these relationships or of our vendors' operations could have a material adverse effect on our business and results of operations.

Our business depends on developing and maintaining productive relationships with our vendors. Many factors outside our control may harm these relationships. For example, financial difficulties that some of our vendors may face may increase the cost of the products we purchase from them or may interrupt our source of supply. In addition, our failure to promptly pay, or order sufficient quantities of inventory from our vendors may increase the cost of products we purchase or may lead to vendors refusing to sell products to us at all. A disruption of our vendor relationships or a disruption in our vendors' operations could have a material adverse effect on our business and results of operations.

9

Table of Contents

We depend on our senior management team and our other personnel, and we face substantial competition for qualified personnel.

Our success depends in part on the efforts of our senior management team. Our continued success will also depend upon our ability to retain existing, and attract additional, qualified field personnel to meet our needs. We face substantial competition, both from within and outside of the automotive aftermarket to retain and attract qualified personnel. In addition, we believe that the number of qualified automotive service technicians in the industry is generally insufficient to meet demand.

We are subject to environmental laws and may be subject to environmental liabilities that could have a material adverse effect on us in the future.

We are subject to various federal, state and local environmental laws and governmental regulations relating to the operation of our business, including those governing the handling, storage and disposal of hazardous substances contained in the products we sell and use in our service bays, the recycling of batteries, tires and used lubricants, the ownership and operation of real property and the sale of small engine merchandise. When we acquire or dispose of real property or enter into financings secured by real property, we undertake investigations that may reveal soil and/or groundwater contamination at the subject real property. All such known contamination has either been remediated, or is in the process of being remediated. Any costs expected to be incurred related to such contamination are either covered by insurance or financial reserves or provided for in the consolidated financial statements. Any failure by us to comply with environmental laws and regulations could have a material adverse effect on us. However, there exists the possibility of additional soil and/or groundwater contamination on our real property where we have not undertaken an investigation.

Risks Related to Our Industry

Our industry is highly competitive, and price competition in some categories of the automotive aftermarket or a loss of trust in our participation in the "do-it-for-me" market, could cause a material decline in our revenues and earnings.

The automotive aftermarket retail and service industry is highly competitive and subjects us to a wide variety of competitors. We compete primarily with the following types of businesses in each category of the automotive aftermarket:

Do-It-Yourself

Retail

- •

- automotive parts and accessories stores;

- •

- automobile dealers that supply manufacturer replacement parts and accessories; and

- •

- mass merchandisers and wholesale clubs that sell automotive products and select non-automotive merchandise that appeals to automotive "Do-It-Yourself" customers, such as generators, power tools and canopies.

Do-It-For-Me

Service Labor

- •

- regional and local full service automotive repair shops;

- •

- automobile dealers that provide repair and maintenance services;

- •

- national and regional (including franchised) tire retailers that provide additional automotive repair and maintenance services; and

10

Table of Contents

Tire Sales

- •

- national and regional (including franchised) tire retailers; and

- •

- mass merchandisers and wholesale clubs that sell tires.

A number of our competitors have more financial resources, are more geographically diverse or have better name recognition than we do, which might place us at a competitive disadvantage to those competitors. Because we seek to offer competitive prices, if our competitors reduce their prices we may also be forced to reduce our prices, which could cause a material decline in our revenues and earnings.

With respect to the service labor category, the majority of consumers are unfamiliar with their vehicle's mechanical operation and, as a result, often select a service provider based on trust. Potential occurrences of negative publicity associated with the Pep Boys brand, the products we sell or installation or repairs performed in our service bays, whether or not factually accurate, could cause consumers to lose confidence in our products and services in the short or long term, and cause them to choose our competitors for their automotive service needs.

Vehicle miles driven may decrease, resulting in a decline of our revenues and negatively affecting our results of operations.

Our industry depends on the number of vehicle miles driven. Factors that may cause the number of vehicle miles and our revenues and our results of operations to decrease include:

- •

- the weather—as vehicle maintenance may be deferred during periods of inclement weather;

- •

- the economy—as during periods of poor economic conditions, customers may defer vehicle maintenance or repair, and during periods of good economic conditions, consumers may opt to purchase new vehicles rather than service the vehicles they currently own and replace worn or damaged parts;

- •

- gas prices—as increases in gas prices may deter consumers from using their vehicles; and

- •

- travel patterns—as changes in travel patterns may cause consumers to rely more heavily on mass transportation.

Economic Factors affecting consumer spending habits may continue, resulting in a decline in revenues and may negatively impact our business.

Many economic and other factors outside our control, including consumer confidence, consumer spending levels, employment levels, consumer debt levels and inflation, as well as the availability of consumer credit, affect consumer spending habits. A significant deterioration in the global financial markets and economic environment, recessions or an uncertain economic outlook could adversely affect consumer spending habits and can result in lower levels of economic activity. The domestic and international political situation also affects consumer confidence. Any of these events and factors could cause consumers to curtail spending, especially with respect to our more discretionary merchandise offerings, such as automotive accessories, tools and personal transportation products.

11

Table of Contents

During fiscal year 2008, there was significant deterioration in the global financial markets and economic environment, which negatively impacted consumer spending and our revenues. If these adverse trends in economic conditions continue or worsen, or if our efforts to counteract the impacts of these trends are not sufficiently effective, our revenues would continue to decline, negatively affecting our results of operations.

Consolidation among our competitors may negatively impact our business.

Recently some of our competitors have merged. If this trend continues or if they are able to achieve efficiencies in their mergers, the Company may face greater competitive pressures in the market in which they operate.

ITEM 1B UNRESOLVED STAFF COMMENTS

None.

ITEM 2 PROPERTIES

The Company owns its five-story, approximately 300,000 square foot corporate headquarters in Philadelphia, Pennsylvania. The Company also owns the following administrative regional offices—approximately 4,000 square feet of space in each of Melrose Park, Illinois and Bayamon, Puerto Rico as well as a 1,700 square foot space in Whitemarsh, Maryland. The Company also leases administrative regional offices of approximately 4,000 square feet of space in each of Decatur, Georgia and Carrollton, Texas. The Company owns a three-story, approximately 60,000 square foot structure in Los Angeles, California in which it occupies 7,200 square feet and sublets the remaining square footage to tenants.

Of the 562 store locations operated by the Company at January 31, 2009, 235 are owned and 327 are leased. As of January 31, 2009, 97 of the 235 stores owned by the Company are currently used as collateral under our Senior Secured Term Loan due October, 2013.

The following table sets forth certain information regarding the owned and leased warehouse space utilized by the Company to replenish its store locations at January 31, 2009:

| | | | | | | | | | | | |

Warehouse Locations | | Products

Warehoused | | Square

Footage | | Owned or

Leased | | Stores

Serviced | | States Serviced |

|---|

| San Bernardino, CA | | All | | | 600,000 | | Leased | | | 161 | | AZ, CA, NM, NV, UT, WA |

| McDonough, GA | | All | | | 392,000 | | Owned | | | 127 | | AL, FL, GA, LA, NC, PR, SC, TN, VA |

| Mesquite, TX | | All | | | 244,000 | | Owned | | | 69 | | AR, CO, LA, MO, NM, OK, TX |

| Plainfield, IN | | All | | | 403,000 | | Owned | | | 64 | | IL, IN, KY, MI, MN, OH, PA, TN |

| Chester, NY | | All | | | 400,400 | | Owned | | | 141 | | CT, DE, MA, MD, ME, NH, NJ, NY, PA, RI, VA |

| McDonough, GA | | All except tires | | | 30,000 | | Leased | | | — | | This facility does not ship directly to stores |

| | | | | | | | | | | |

| Total | | | | | 2,069,400 | | | | | 562 | | |

| | | | | | | | | | | |

In addition to the above distribution centers, the Company operates four satellite warehouses. These satellite warehouses stock approximately 32,000 SKUs and serve an average of 10-30 stores, in addition to having retail capabilities. These locations were leased and comprised 78,700 square feet. The Company anticipates that its existing and future warehouse space and its access to outside storage

12

Table of Contents

will accommodate inventory necessary to support future store expansion and any increase in stock-keeping units through the end of fiscal year 2009.

ITEM 3 LEGAL PROCEEDINGS

In September 2006, the United States Environmental Protection Agency ("EPA") requested certain information from the Company as part of an investigation to determine whether the Company had violated, and is in violation of, the Clean Air Act and its non-road engine regulations. The information requested concerned certain generator and personal transportation merchandise offered for sale by the Company. In the fourth quarter of 2008, the EPA informed the Company that it believed that the Company had violated the Clean Air Act by virtue of the fact that certain of this merchandise did not conform to their corresponding EPA Certificates of Conformity and that unless the EPA and the Company were able to reach a settlement, the EPA was prepared to commence a civil action. The Company is currently engaged in settlement discussions with the EPA that would call for the payment of a civil penalty by the Company and certain injunctive relief. As a result of these discussions, the Company has accrued an amount equal to its estimate of the civil penalty that the Company is prepared to pay to settle the matter and has temporarily restricted from sale, and taken a partial asset impairment against certain related inventory. If the Company is not able to reach a settlement with the EPA on mutually acceptable terms, the Company is prepared to vigorously defend any civil action filed.

The Company is also party to various other actions and claims arising in the normal course of business.

The Company accrued $5,700,000 in the fourth quarter of fiscal year 2008 for awards or assessments in connection with all such matters. The company believes that these amounts are adequate and that the ultimate resolution of these matters will not have a material adverse effect on the Company's financial position. However, there exists a reasonable possibility of loss in excess of the amounts accrued, the amount of which cannot currently be estimated. While the Company does not believe that the amount of such excess loss could be material to the Company's financial position, any such loss could have a material adverse effect on the Company's results of operations in the period(s) during which the underlying matters are resolved

ITEM 4 SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS

No matters were submitted to a vote of security holders, through the solicitation of proxies or otherwise, during the fourth quarter of the fiscal year ended January 31, 2009.

13

Table of Contents

PART II

ITEM 5 MARKET FOR THE REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

The common stock of The Pep Boys—Manny, Moe & Jack is listed on the New York Stock Exchange under the symbol "PBY". There were 5,261 registered shareholders as of April 3, 2009. The following table sets forth for the periods listed, the high and low sale prices and the cash dividends paid on the Company's common stock.

MARKET PRICE PER SHARE

| | | | | | | | | | |

| | Market Price Per Share | |

| |

|---|

| | Cash

Dividends

Per Share | |

|---|

| | High | | Low | |

|---|

Fiscal year ended January 31, 2009 | | | | | | | | | | |

Fourth Quarter | | $ | 5.31 | | $ | 2.62 | | $ | 0.0675 | |

Third Quarter | | | 9.49 | | | 3.00 | | | 0.0675 | |

Second Quarter | | | 10.36 | | | 6.40 | | | 0.0675 | |

First Quarter | | | 12.56 | | | 8.59 | | | 0.0675 | |

Fiscal year ended February 2, 2008 | | | | | | | | | | |

Fourth Quarter | | $ | 15.14 | | $ | 8.25 | | $ | 0.0675 | |

Third Quarter | | | 17.97 | | | 13.50 | | | 0.0675 | |

Second Quarter | | | 22.49 | | | 15.90 | | | 0.0675 | |

First Quarter | | | 19.93 | | | 14.73 | | | 0.0675 | |

On March 12, 2009, the Board of Directors reduced the quarterly cash dividend to $0.03 per share. It is the present intention of the Board of Directors to continue to pay this quarterly cash dividend; however, the declaration and payment of future dividends will be determined by the Board of Directors in its sole discretion and will depend upon the earnings, financial condition and capital needs of the Company and other factors which the Board of Directors deems relevant.

On September 7, 2006, the Company renewed its share repurchase program and reset the authority back to $100,000,000 for repurchases to be made from time to time in the open market or in privately negotiated transactions. During the first quarter of fiscal year 2007, the Company repurchased 2,702,460 shares of Common Stock for $50,841,000. The Company also disbursed during the first quarter of fiscal year 2007, $7,311,000 for 494,800 shares of Common Stock repurchased during the fourth quarter of fiscal year 2006. This program expired on September 30, 2007.

EQUITY COMPENSATION PLANS

The following table sets forth the Company's shares authorized for issuance under its equity compensation plans at January 31, 2009:

| | | | | | | | | | |

| | Number of securities

to be issued upon

exercise of

outstanding options,

warrants and rights

(a) | | Weighted average exercise price

of outstanding options,

warrants and rights

(b) | | Number of securities

remaining available for

future issuance under

equity compensation

plans (excluding securities

reflected in column (a)

(c) | |

|---|

Equity compensation plans approved by security holders | | | 1,293,952 | | $ | 9.34 | | | 1,638,118 | |

Equity compensation plans not approved by security holders | | | — | | | — | | | 500,000 | |

| | | | | | | | |

Total | | | 1,293,952 | | $ | 9.34 | | | 2,138,118 | |

| | | | | | | | |

14

Table of Contents

STOCK PRICE PERFORMANCE

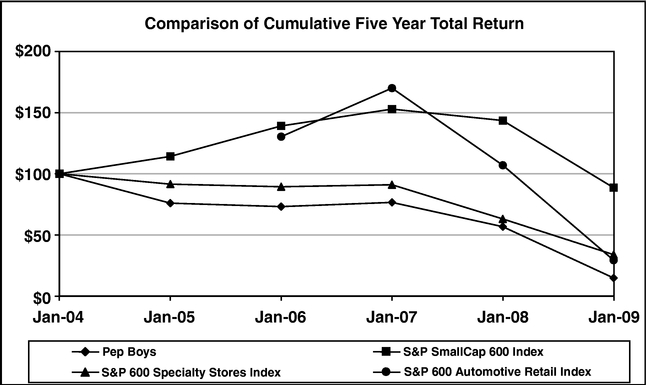

The following graph compares the cumulative total return on shares of Pep Boys Stock over the past five years with the cumulative total return on shares of companies in (1) the Standard & Poor's SmallCap 600 Index, (2) the S&P 600 Specialty Stores Index and (3) the S&P 600 Automotive Retail Index. Pep Boys moved from the S&P 600 Specialty Stores Index to the S&P 600 Automotive Retail Index upon its formation in May 2005. Until such time as the S&P 600 Automotive Retail index has five years of history, Pep Boys will show a comparison to both peer group indexes. The comparison assumes that $100 was invested in January 2004 in Pep Boys Stock and in each of the indices and assumes reinvestment of dividends. The companies currently comprising the S&P 600 Automotive Retail Index are: Group 1 Automotive, Inc.; Lithia Motors, Inc.; Midas, Inc.; Sonic Automotive, Inc.; and The Pep Boys—Manny, Moe & Jack.

| | | | | | | | | | | | | | | | | | | |

Company/Index | | Jan. 2004 | | Jan. 2005 | | Jan. 2006 | | Jan. 2007 | | Jan. 2008 | | Jan. 2009 | |

|---|

Pep Boys | | $ | 100 | | $ | 75.95 | | $ | 73.13 | | $ | 76.57 | | $ | 56.70 | | $ | 14.73 | |

S&P SmallCap 600 Index | | $ | 100 | | $ | 114.20 | | $ | 139.12 | | $ | 152.90 | | $ | 143.55 | | $ | 88.59 | |

S&P 600 Specialty Stores Index | | $ | 100 | | $ | 91.49 | | $ | 89.38 | | $ | 91.01 | | $ | 63.04 | | $ | 33.83 | |

S&P 600 Automotive Retail Index* | | | | | $ | 100 | | $ | 130.35 | | $ | 170.07 | | $ | 106.98 | | $ | 29.30 | |

- *

- The S&P 600 Automotive Retail Index was created in May 2005. Therefore, the total return for January 2006 is for the period from May 2005 through January 2006.

15

Table of Contents

ITEM 6 SELECTED FINANCIAL DATA

The following tables set forth the selected financial data for the Company and should be read in conjunction with the Consolidated Financial Statements and Notes thereto included elsewhere herein.

| | | | | | | | | | | | | | | | | |

Fiscal Year ended | | Jan. 31,

2009 | | Feb. 2,

2008 | | Feb. 3,

2007 | | Jan. 28,

2006 | | Jan. 29,

2005 | |

|---|

| | (dollar amounts are in thousands, except share data)

| |

|---|

STATEMENT OF OPERATIONS DATA(5) | | | | | | | | | | | | | | | | |

Merchandise sales | | $ | 1,569,664 | | $ | 1,749,578 | | $ | 1,853,077 | | $ | 1,830,632 | | $ | 1,838,258 | |

Service revenue | | | 358,124 | | | 388,497 | | | 390,778 | | | 378,342 | | | 404,101 | |

Total revenues | | | 1,927,788 | | | 2,138,075 | | | 2,243,855 | | | 2,208,974 | | | 2,242,359 | |

Gross profit from merchandise sales(6) | | | 440,502 | (1) | | 443,626 | (2) | | 533,276 | | | 470,019 | | | 510,583 | |

Gross profit from service revenue(6) | | | 24,930 | (1) | | 42,611 | (2) | | 33,004 | | | 32,276 | | | 92,245 | |

Total gross profit | | | 465,432 | (1) | | 486,237 | (2) | | 566,280 | | | 502,295 | | | 602,828 | |

Selling, general and administrative expenses | | | 485,044 | | | 518,373 | | | 546,399 | | | 519,600 | (3) | | 542,228 | (4) |

Net gain (loss) from disposition of assets | | | 9,716 | | | 15,151 | | | 8,968 | | | 4,826 | | | 11,848 | |

Operating (loss) profit | | | (9,896 | ) | | (16,985 | ) | | 28,849 | | | (12,479) | (3) | | 72,448 | (4) |

Non-operating income | | | 1,967 | | | 5,246 | | | 7,023 | | | 3,897 | | | 1,824 | |

Interest expense | | | 27,048 | | | 51,293 | | | 49,342 | | | 49,040 | | | 35,965 | |

(Loss) earnings from continuing operations before income taxes and cumulative effect of change in accounting principle | | | (34,977 | )(1) | | (63,032 | )(2) | | (13,470 | ) | | (57,622) | (3) | | 38,307 | (4) |

Net (loss) earnings from continuing operations before cumulative effect of change in accounting principle | | | (28,838 | ) | | (37,438 | ) | | (7,071 | ) | | (36,595) | (3) | | 23,991 | (4) |

Discontinued operations, net of tax | | | (1,591) | (1) | | (3,601) | (2) | | 4,333 | | | 1,088 | | | (412 | ) |

Cumulative effect of change in accounting principle net of tax | | | — | | | — | | | 189 | | | (2,021 | ) | | — | |

Net (loss) earnings | | | (30,429 | ) | | (41,039 | ) | | (2,549 | ) | | (37,528 | ) | | 23,579 | |

BALANCE SHEET DATA | | | | | | | | | | | | | | | | |

Working capital | | $ | 179,233 | | $ | 195,343 | | $ | 163,960 | | $ | 247,526 | | $ | 180,651 | |

Current ratio | | | 1.33 to 1 | | | 1.35 to 1 | | | 1.27 to 1 | | | 1.43 to 1 | | | 1.27 to 1 | |

Merchandise inventories | | $ | 564,931 | | $ | 561,152 | | $ | 607,042 | | $ | 616,292 | | $ | 602,760 | |

Property and equipment-net | | | 740,331 | | | 780,779 | | | 906,247 | | | 947,389 | | | 945,031 | |

Total assets | | | 1,552,389 | | | 1,583,920 | | | 1,767,199 | | | 1,821,753 | | | 1,867,023 | |

Long-term debt (includes all convertible debt) | | | 352,382 | | | 400,016 | | | 535,031 | | | 586,239 | | | 471,682 | |

Total stockholders' equity | | | 423,156 | | | 470,712 | | | 567,755 | | | 594,565 | | | 653,456 | |

DATA PER COMMON SHARE | | | | | | | | | | | | | | | | |

Basic (loss) earnings from continuing operations before cumulative effect of change in accounting principle | | $ | (0.55 | ) | $ | (0.72 | ) | $ | (0.13 | ) | $ | (0.67) | (3) | $ | 0.43 | (4) |

Basic (loss) earnings | | | (0.58 | ) | | (0.79 | ) | | (0.05 | ) | | (0.69) | (3) | | 0.42 | (4) |

Diluted (loss) earnings from continuing operations before cumulative effect of change in accounting principal | | | (0.55 | ) | | (0.72 | ) | | (0.13 | ) | | (0.67) | (3) | | 0.42 | (4) |

Diluted net (loss) earnings | | | (0.58 | ) | | (0.79 | ) | | (0.05 | ) | | (0.69) | (3) | | 0.41 | (4) |

Cash dividends declared | | | 0.27 | | | 0.27 | | | 0.27 | | | 0.27 | | | 0.27 | |

Book value per share | | | 8.10 | | | 9.10 | | | 10.53 | | | 10.97 | | | 11.87 | |

Common share price range: | | | | | | | | | | | | | | | | |

| | High | | | 12.56 | | | 22.49 | | | 16.55 | | | 18.80 | | | 29.37 | |

| | Low | | | 2.62 | | | 8.25 | | | 9.33 | | | 11.75 | | | 11.83 | |

OTHER STATISTICS | | | | | | | | | | | | | | | | |

Return on average stockholders' equity(7) | | | (6.8 | )% | | (7.9 | )% | | (0.4 | )% | | (6.0 | )% | | 3.9 | % |

Common shares issued and outstanding | | | 52,237,750 | | | 51,752,677 | | | 53,934,084 | | | 54,208,803 | | | 55,056,641 | |

Capital expenditures | | $ | 151,883 | (8) | $ | 41,953 | | $ | 53,903 | | $ | 92,083 | | $ | 103,766 | |

Number of retail outlets | | | 562 | | | 562 | | | 593 | | | 593 | | | 595 | |

Number of service bays | | | 5,845 | | | 5,845 | | | 6,162 | | | 6,162 | | | 6,181 | |

- (1)

- Includes an aggregate pretax charge of $5,353 for asset impairment, of which $2,779 was charged to merchandise cost of sales, $648 was charged to service cost of sales and $1,926 (pretax) was charged to discontinued operations.

- (2)

- Includes an aggregate pretax charge of $10,963 for the asset impairment and closure of 31 stores, of which $5,350 was charged to merchandise cost of sales, $1,849 was charged to service cost of sales and $3,764 (pretax) was charged to discontinued operations. In addition we recorded a pretax $32,803 inventory impairment charge to cost of merchandise sales for the discontinuance of certain product offerings.

- (3)

- Includes a pretax charge of $4,200 related to an asset impairment charge reflecting the remaining value of a commercial sales software asset, which was included in selling, general and administrative expenses.

- (4)

- Includes a pretax charge of $6,911 related to certain executive severance obligations.

- (5)

- Statement of operations data reflects 53 weeks for the fiscal year ended February 3, 2007 while the other years reflect 52 weeks.

- (6)

- Gross Profit from Merchandise Sales includes the cost of products sold, buying, warehousing and store occupancy costs. Gross Profit from Service Revenue includes the cost of installed products sold, buying, warehousing, service payroll and related employee benefits and occupancy costs. Occupancy costs include utilities, rents, real estate and property taxes, repairs and maintenance and depreciation and amortization expenses. Our gross profit may not be comparable to those of our competitors due to differences in industry practice regarding the classification of certain costs.

- (7)

- Return on average stockholders' equity is calculated by taking the net (loss) earnings for the period divided by average stockholders' equity for the year.

- (8)

- Includes the purchase of master lease assets for $117,121.

16

Table of Contents

ITEM 7 MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

OVERVIEW

Introduction

Pep Boys is a leader in the automotive aftermarket, with 562 locations, housing 5,845 service bays, located throughout 35 states and Puerto Rico. All of our stores feature the nationally recognized Pep Boys brand name, established through more than 85 years of providing high-quality automotive merchandise and services, and are company-owned, ensuring chain-wide consistency for our customers. We are the only national chain offering automotive service, accessories, tires and parts under one roof, positioning us to achieve our goal of becoming the automotive solutions provider of choice for the value-oriented customer. In most of our stores we also have a commercial sales program that provides commercial credit and prompt delivery of tires, parts and other products to local, regional and national repair garages and dealers.

Of our 562 stores, 552 are what we refer to as SUPERCENTERS, which feature an average of 11 state-of-the-art service bays, with an average of more than 20,000 square feet per SUPERCENTER. Our store size allows us to display and sell a more complete offering of merchandise in a wider array of categories than our competitors, with a comprehensive tire offering. We leverage this investment in inventory through our ability to install what we sell in our service bays and by offering this merchandise to both commercial and retail customers.

Our fiscal year ends on the Saturday nearest January 31, which results in an extra week every six years. Our fiscal year ended January 31, 2009 was a 52-week year with the fourth quarter including 13 weeks. Fiscal year 2006 included 53 weeks including 14 weeks in the fourth quarter. All other years included in this report are 52 weeks.

During fiscal 2008, we continued to focus on the key drivers of our long-term strategic plan—improving operational execution, expanding our hard parts assortment and developing a service center growth strategy. We continued to reinforce the importance of improving the customer shopping experience by focusing on continuous training on product knowledge, leadership and customer satisfaction. We made progress on our category management initiatives by completing our store remodel program, updating category line reviews and expanding our parts assortment. We also conducted extensive marketing tests to develop a tailored marketing plan for each of our markets in 2009 to maximize our reach and efficiencies. We also announced plans to add 20 to 40 service only "spokes" in fiscal year 2009 to complement our existing SUPERCENTER store base.

Our net loss per share for the fiscal year ended January 31, 2009 was $0.58 per share or a $0.21 per share improvement over the $0.79 loss per share recorded in fiscal year 2007 (See "Results of Operations").

In addition we continued our real estate monetization program by completing additional sale leaseback transactions on 63 properties in the first half of fiscal year 2008 for net proceeds of $211,470,000. The proceeds from these transactions were used to further reduce overall indebtedness, to satisfy our obligation under the master operating lease and for other capital expenditures.

CAPITAL & LIQUIDITY

Capital Resources and Needs

Our cash requirements arise principally from the purchase of inventory, capital expenditures related to existing and new stores, offices and distribution centers, debt service and contractual obligations.

17

Table of Contents

Cash flows realized through the sale of automotive parts, accessories and services is our primary source of liquidity. Net cash used in operating activities was $39,507,000 in fiscal year 2008 while net cash provided by operating activities was $52,784,000 in fiscal year 2007 and $92,430,000 in fiscal year 2006. The $92,291,000 decrease in cash flows from operating activities in fiscal year 2008 as compared to fiscal year 2007 resulted from a $31,143,000 increase in our net loss (net of non-cash adjustments), and $58,244,000 in unfavorable changes in our operating assets and liabilities. The change in operating assets and liabilities was primarily due to an unfavorable change in merchandise inventory of $16,865,000. The inventory change is a result of our decision to exit certain non-core inventory in the fiscal year 2007 compounded by a decision to expand our hard parts assortment in fiscal year 2008. The change in accounts payable of $13,017,000 was primarily attributable to the timing of our accounts payable cycle. In addition, we expended approximately $5,000,000 to convert our vacation plan to a paid time off plan, satisfied approximately $19,918,000 of liabilities associated with our defined benefits executive supplemental retirement plan ($14,441,000 of the payment was to terminate the SERP) and paid $4,539,000 in connection with reducing the notional value on an interest rate swap by $55,000,000.

In fiscal years 2008 and 2007, we generated $78,726,000 and $149,262,000, respectively, of cash flows from investing activities, while in fiscal year 2006 we used $57,339,000 of cash in investing activities. Fiscal years 2008 and 2007 included positive cash flow due to the sale lease back transactions of 63 and 34 stores, respectively, for $211,470,000 and $162,918,000 in net proceeds. The proceeds in fiscal year 2008 were used to satisfy a $117,121,000 purchase obligation under a master operating lease, to fund other capital expenditures and to retire $26,528,000 of senior subordinated notes. The proceeds in fiscal year 2007 were used to prepay a portion of the Company's Senior Secured Term Loan. In fiscal years 2008 and 2007, we also cancelled certain company-owned life insurance policies for net proceeds of $15,588,000 and $30,045,000, respectively. The proceeds from these non-core assets were used to satisfy our obligations under the Company's defined benefit executive supplemental retirement plan in the current year and to repay borrowings under our revolving credit facility and for general corporate purposes in the prior year.

Our primary capital requirements are for new stores and for maintenance capital expenditures related to, and the remodeling of, our existing stores, offices and distribution centers. Capital expenditures in fiscal years 2008, 2007 and 2006 were $34,762,000 (excluding the purchase of assets under the master lease), $43,116,000 and $49,391,000, respectively. Capital expenditures in fiscal year 2008 were lower than fiscal year 2007 as a result of fewer store remodels. At the end of fiscal year 2008, we had no material capital expenditure commitments. Our fiscal year 2009 capital expenditures are expected to be approximately $50,000,000 which includes the addition of 20 to 40 service only "spoke" shops and the general maintenance of our existing stores. These expenditures are expected to be funded from net cash generated from operating activities and the Company's existing line of credit.

In fiscal years 2008, 2007 and 2006 we used cash of $38,813,000; $203,004,000 and $61,488,000, respectively, in financing activities to reduce our overall indebtedness. In fiscal year 2008, we expended $6,754,000 for financing costs associated with our new $300,000,000 credit facility. In fiscal 2007, we repurchased $50,841,000 of our common shares and paid an additional $7,311,000 to settle shares of our common stock repurchased in the fourth quarter of fiscal year 2006.

We anticipate that cash provided by operating activities, our existing line of credit and cash on hand will exceed our expected cash requirements in fiscal 2009. We expect to have excess availability under our existing line of credit during the entirety of fiscal 2009. We also have substantial owned real estate which we believe we can monetize, if necessary, through additional sale leaseback or other financing transactions.

Our working capital was $179,233,000 at January 31, 2009; $195,343,000 at February 2, 2008 and $163,960,000 at February 3, 2007. Our long-term debt, as a percentage of its total capitalization, was 45% at January 31, 2009; 46% at February 2, 2008 and 49% at February 3, 2007. As of January 31,

18

Table of Contents

2009, we had a $300,000,000 line of credit, with an availability of approximately $182,115,000. Our current portion of long term debt was $1,453,000 at January 31, 2009.

The following chart represents our total contractual obligations and commercial commitments as of January 31, 2009:

| | | | | | | | | | | | | | | | |

Contractual Obligations | | Total | | Due in less

than 1 year | | Due in

1 - 3 years | | Due in

3 - 5 years | | Due after

5 years | |

|---|

| | (dollars in thousands)

| |

|---|

Long-term debt(1) | | $ | 349,191 | | $ | 1,078 | | $ | 2,156 | | $ | 147,560 | | $ | 198,397 | |

Operating leases | | | 777,957 | | | 77,103 | | | 146,357 | | | 135,940 | | | 418,557 | |

Expected scheduled interest payments on all long-term debt, capital leases and lease finance obligations | | | 134,318 | | | 25,256 | | | 50,235 | | | 47,919 | | | 10,908 | |

Capital and lease financing obligations(1) | | | 4,644 | | | 375 | | | 527 | | | 575 | | | 3,167 | |

Other long-term obligations(2) | | | 22,156 | | | 1,711 | | | — | | | — | | | — | |

| | | | | | | | | | | | |

Total contractual obligations | | $ | 1,288,266 | | $ | 105,523 | | $ | 199,275 | | $ | 331,994 | | $ | 631,029 | |

| | | | | | | | | | | | |

- (1)

- Long-term debt, capital leases and lease financing obligations include current maturities.

- (2)

- Primarily includes pension obligation of $9,304, FIN 48 liabilities and asset retirement obligations. We made voluntary contributions of $19,918; $440 and $504, to our pension plans in fiscal 2008, 2007 and 2006, respectively. Future plan contributions are dependent upon actual plan asset returns and interest rates. See Note 10 of Notes to Consolidated Financial Statements in "Item 8 Financial Statements and Supplementary Data" for further discussion of our pension plans. The above table does not reflect the timing of projected settlements for our recorded asset disposal costs of $7,130 and our FIN 48 liabilities of $3,429 because we cannot make a reliable estimate of the timing of the related cash payments.

| | | | | | | | | | | | | | | | |

Commercial Commitments | | Total | | Due in less

than 1 year | | Due in

1 - 3 years | | Due in

3 - 5 years | | Due after

5 years | |

|---|

| | (dollar amounts in thousands)

| |

|---|

Import letters of credit | | $ | 354 | | $ | 354 | | $ | — | | $ | — | | $ | — | |

Standby letters of credit | | | 86,502 | | | 46,502 | | | 40,000 | | | — | | | — | |

Surety bonds | | | 9,235 | | | 9,195 | | | 40 | | | — | | | — | |

Purchase obligations(1)(2) | | | 14,633 | | | 13,920 | | | 594 | | | 119 | | | — | |

| | | | | | | | | | | | |

Total commercial commitments | | $ | 110,724 | | $ | 69,971 | | $ | 40,634 | | $ | 119 | | $ | — | |

| | | | | | | | | | | | |

- (1)

- Our open purchase orders are based on current inventory or operational needs and are fulfilled by our vendors within short periods of time. We currently do not have minimum purchase commitments under our vendor supply agreements and generally our open purchase orders (orders that have not been shipped) are not binding agreements. Those purchase obligations that are in transit from our vendors at January 31, 2009 are considered to be a commercial commitment.

- (2)

- In the first quarter of fiscal 2005, we entered into a commercial commitment to purchase approximately $4,800 of products over a six-year period. The commitment for years two through five is approximately $950 per year, while the final year's commitment is approximately half that amount. Following year two, we are obligated to pay the vendor a per unit fee if there is a shortfall between our cumulative purchases during the two year period and the minimum purchase requirement. For years three through six, we are obligated to pay the vendor a per unit fee for any

19

Table of Contents

annual shortfall. The maximum annual obligation under any shortfall is approximately $950. At January 31, 2009, we expect to meet the cumulative minimum purchase requirements under this contract.

Long-term Debt

Senior Secured Term Loan Facility due October, 2013

On January 27, 2006 we entered into a $200,000,000 Senior Secured Term Loan facility due January 27, 2011. This facility is secured by a collateral pool consisting of real property and improvements associated with our stores, which is adjusted periodically based upon real estate values and borrowing levels. Interest at the rate of London Interbank Offered Rate (LIBOR) plus 3.0% on this facility was payable starting in February 2006. Proceeds from this facility were used to satisfy and discharge our then outstanding $43,000,000 6.88% Medium Term Notes due March 6, 2006 and $100,000,000 6.92% Term Enhanced Remarketable Securities (TERMS) due July 7, 2016 and to reduce borrowings under our line of credit by approximately $39,000,000.