Use these links to rapidly review the document

TABLE OF CONTENTS

PART IV

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10K

| | |

| (Mark One) | | |

ý |

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934 |

For the fiscal year ended February 1, 2014 |

OR |

o |

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934 |

For the transition period from to |

Commission file number 1-3381

The Pep Boys—Manny, Moe & Jack

(Exact name of registrant as specified in its charter)

| | |

Pennsylvania

(State or other jurisdiction of

incorporation or organization) | | 23-0962915

(I.R.S. employer

identification no.) |

3111 West Allegheny Avenue,

Philadelphia, PA

(Address of principal executive office) |

|

19132

(Zip code) |

215-430-9000

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| | |

| Title of each class | | Name of each exchange on which registered |

|---|

| Common Stock, $1.00 par value | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:None

Indicate by check mark whether the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No ý

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of "large accelerated filer," "accelerated filer," and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

| | | | | | |

| Large accelerated filer o | | Accelerated filer ý | | Non-accelerated filer o

(Do not check if a

smaller reporting company) | | Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act) Yes o No ý

As of the close of business on August 3, 2013 the aggregate market value of the voting stock held by non-affiliates of the registrant was approximately $652,232,000.

As of April 5, 2014, there were 53,237,793 shares of the registrant's common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant's definitive Proxy Statement to be delivered to shareholders in connection with the Annual Meeting of Shareholders to be held June 11, 2014 are incorporated by reference into Part III of this Annual Report.

Table of Contents

TABLE OF CONTENTS

| | | | | | |

| |

| | Page | |

|---|

PART I | | | | |

Item 1. | | Business | | | 1 | |

Item 1A. | | Risk Factors | | | 10 | |

Item 1B. | | Unresolved Staff Comments | | | 14 | |

Item 2. | | Properties | | | 15 | |

Item 3. | | Legal Proceedings | | | 15 | |

Item 4. | | Mine Safety Disclosures | | | 15 | |

PART II | | |

| |

Item 5. | | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | | | 16 | |

Item 6. | | Selected Financial Data | | | 18 | |

Item 7. | | Management's Discussion and Analysis of Financial Condition and Results of Operations | | | 19 | |

Item 7A. | | Quantitative and Qualitative Disclosures About Market Risk | | | 34 | |

Item 8. | | Financial Statements and Supplementary Data | | | 36 | |

Item 9. | | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | | | 76 | |

Item 9A. | | Controls and Procedures | | | 76 | |

Item 9B. | | Other Information | | | 79 | |

PART III | | |

| |

Item 10. | | Directors, Executive Officers and Corporate Governance | | | 79 | |

Item 11. | | Executive Compensation | | | 79 | |

Item 12. | | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | | | 79 | |

Item 13. | | Certain Relationships and Related Transactions and Director Independence | | | 79 | |

Item 14. | | Principal Accounting Fees and Services | | | 79 | |

PART IV | | |

| |

Item 15. | | Exhibits and Financial Statement Schedules | | | 80 | |

| | Signatures | | | 83 | |

i

Table of Contents

PART I

ITEM 1 BUSINESS

GENERAL

The Pep Boys—Manny, Moe & Jack and subsidiaries (the "Company") has been the best place to shop and care for your car since it began operations in 1921. Approximately 19,000 associates are focused on delivering the best customer service in the automotive aftermarket to our customers across our nearly 800 locations located throughout the United States and Puerto Rico. Pep Boys satisfies all of a customer's automotive needs through our unique offering of service, tires, parts and accessories.

Our stores are organized into a hub and spoke network consisting of Supercenters and Service & Tire Centers. Supercenters average approximately 20,000 square feet (our new Supercenter format is approximately 14,000 square feet) and combine do-it-for-me service labor, installed merchandise and tire offerings ("DIFM") with do-it-yourself parts and accessories ("DIY"). Most of our Supercenters also have a commercial sales program that delivers parts, tires and equipment to automotive repair shops and dealers. Service & Tire Centers, which average approximately 5,000 square feet, provide DIFM services in neighborhood locations that are conveniently located where our customers live or work. Service & Tire Centers are designed to capture market share and leverage our existing Supercenters and support infrastructure. We also operate a handful of legacy DIY only Pep Express stores.

The following table sets forth the percentage of total revenues from continuing operations contributed by each class of similar products or services for the Company and should be read in conjunction with the Consolidated Financial Statements and Notes thereto included elsewhere herein:

| | | | | | | | | | |

| | Year ended | |

|---|

| | February 1,

2014 | | February 2,

2013 | | January 28,

2012 | |

|---|

Parts and accessories | | | 59.9 | % | | 59.9 | % | | 61.0 | % |

Tires | | | 17.9 | | | 18.7 | | | 18.6 | |

| | | | | | | | |

| | | | | | | | | | | |

Total merchandise sales | | | 77.8 | | | 78.6 | | | 79.6 | |

Service labor | | | 22.2 | | | 21.4 | | | 20.4 | |

| | | | | | | | |

| | | | | | | | | | | |

Total revenues | | | 100.0 | % | | 100.0 | % | | 100.0 | % |

| | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | |

In fiscal 2013, we opened or acquired 40 new Service & Tire Centers and seven new Supercenters and converted two Supercenters into Service & Tire Centers. We also closed two Service & Tire Centers and four Supercenters. As of February 1, 2014, we operated 568 Supercenters, 225 Service & Tire Centers and six Pep Express stores located in 35 states and Puerto Rico. These locations consist of approximately 12,910,000 gross square feet of retail space, including over 7,500 service bays.

1

Table of Contents

The following table indicates, by state, the number of stores the Company had in operation at the end of each of the last four fiscal years, and the number of stores opened and closed by the Company during each of the last three fiscal years:

NUMBER OF STORES AT END OF FISCAL YEARS 2010 THROUGH 2013

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

State | | 2013

Year

End | | Opened | | Closed | | 2012

Year

End | | Opened | | Closed | | 2011

Year

End | | Opened | | Closed | | 2010

Year

End | |

|---|

Alabama | | | 39 | | | 1 | | | — | | | 38 | | | 1 | | | — | | | 37 | | | 36 | | | — | | | 1 | |

Arizona | | | 20 | | | — | | | 2 | | | 22 | | | — | | | — | | | 22 | | | — | | | — | | | 22 | |

Arkansas | | | 1 | | | — | | | — | | | 1 | | | — | | | — | | | 1 | | | — | | | — | | | 1 | |

California | | | 149 | | | 18 | | | — | | | 131 | | | 1 | | | — | | | 130 | | | 4 | | | 3 | | | 129 | |

Colorado | | | 7 | | | — | | | — | | | 7 | | | — | | | — | | | 7 | | | — | | | — | | | 7 | |

Connecticut | | | 7 | | | — | | | — | | | 7 | | | — | | | — | | | 7 | | | — | | | — | | | 7 | |

Delaware | | | 9 | | | — | | | — | | | 9 | | | 1 | | | — | | | 8 | | | 1 | | | — | | | 7 | |

Florida | | | 98 | | | 7 | | | — | | | 91 | | | 5 | | | 4 | | | 90 | | | 30 | | | — | | | 60 | |

Georgia | | | 47 | | | 1 | | | 3 | | | 49 | | | 3 | | | 1 | | | 47 | | | 22 | | | — | | | 25 | |

Illinois | | | 38 | | | 3 | | | — | | | 35 | | | 3 | | | — | | | 32 | | | 3 | | | — | | | 29 | |

Indiana | | | 7 | | | — | | | — | | | 7 | | | — | | | — | | | 7 | | | — | | | — | | | 7 | |

Kentucky | | | 4 | | | — | | | — | | | 4 | | | — | | | — | | | 4 | | | — | | | — | | | 4 | |

Louisiana | | | 8 | | | — | | | — | | | 8 | | | — | | | — | | | 8 | | | — | | | — | | | 8 | |

Maine | | | 1 | | | — | | | — | | | 1 | | | — | | | — | | | 1 | | | — | | | — | | | 1 | |

Maryland | | | 20 | | | — | | | — | | | 20 | | | — | | | — | | | 20 | | | 1 | | | — | | | 19 | |

Massachusetts | | | 7 | | | — | | | — | | | 7 | | | — | | | — | | | 7 | | | — | | | — | | | 7 | |

Michigan | | | 5 | | | — | | | — | | | 5 | | | — | | | — | | | 5 | | | — | | | — | | | 5 | |

Minnesota | | | 3 | | | — | | | — | | | 3 | | | — | | | — | | | 3 | | | — | | | — | | | 3 | |

Missouri | | | 1 | | | — | | | — | | | 1 | | | — | | | — | | | 1 | | | — | | | — | | | 1 | |

Nevada | | | 12 | | | — | | | — | | | 12 | | | — | | | — | | | 12 | | | — | | | — | | | 12 | |

New Hampshire | | | 4 | | | — | | | — | | | 4 | | | — | | | — | | | 4 | | | — | | | — | | | 4 | |

New Jersey | | | 43 | | | 4 | | | 1 | | | 40 | | | 4 | | | — | | | 36 | | | 4 | | | — | | | 32 | |

New Mexico | | | 8 | | | — | | | — | | | 8 | | | — | | | — | | | 8 | | | — | | | — | | | 8 | |

New York | | | 39 | | | 2 | | | — | | | 37 | | | 4 | | | — | | | 33 | | | 2 | | | — | | | 31 | |

North Carolina | | | 10 | | | 2 | | | — | | | 8 | | | — | | | — | | | 8 | | | — | | | — | | | 8 | |

Ohio | | | 12 | | | — | | | — | | | 12 | | | — | | | — | | | 12 | | | — | | | — | | | 12 | |

Oklahoma | | | 5 | | | — | | | — | | | 5 | | | — | | | — | | | 5 | | | — | | | — | | | 5 | |

Pennsylvania | | | 60 | | | 5 | | | — | | | 55 | | | 2 | | | — | | | 53 | | | 2 | | | — | | | 51 | |

Puerto Rico | | | 27 | | | — | | | — | | | 27 | | | — | | | — | | | 27 | | | — | | | — | | | 27 | |

Rhode Island | | | 2 | | | — | | | — | | | 2 | | | — | | | — | | | 2 | | | — | | | — | | | 2 | |

South Carolina | | | 6 | | | — | | | — | | | 6 | | | — | | | — | | | 6 | | | — | | | — | | | 6 | |

Tennessee | | | 7 | | | — | | | — | | | 7 | | | 1 | | | 1 | | | 7 | | | — | | | — | | | 7 | |

Texas | | | 61 | | | 4 | | | — | | | 57 | | | 1 | | | — | | | 56 | | | 7 | | | — | | | 49 | |

Utah | | | 6 | | | — | | | — | | | 6 | | | — | | | — | | | 6 | | | — | | | — | | | 6 | |

Virginia | | | 17 | | | — | | | — | | | 17 | | | — | | | — | | | 17 | | | 1 | | | — | | | 16 | |

Washington | | | 9 | | | — | | | — | | | 9 | | | — | | | — | | | 9 | | | 7 | | | — | | | 2 | |

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total | | | 799 | | | 47 | | | 6 | | | 758 | | | 26 | | | 6 | | | 738 | | | 120 | | | 3 | | | 621 | |

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

We are targeting a total of 30 new Service & Tire Centers and three new Supercenters in fiscal 2014. We expect to lease new Service & Tire Center and Supercenter locations, as we believe that there are sufficient existing available locations, including build to suit locations, in the marketplace with attractive lease terms to enable our expansion.

2

Table of Contents

INDUSTRY OVERVIEW

The automotive aftermarket industry is in the mature stage of its life cycle and while the DIY space is dominated by a small number of companies with large market shares, the DIFM or automotive service business is highly fragmented. Over the past decade, consumers have moved away from DIY toward DIFM due to increasing vehicle complexity and electronic content, as well as decreasing availability of diagnostic equipment and know-how. In addition, while this needs-based industry has a dedicated DIY customer base, the number of consumers that would prefer to have a professional fix their vehicle fluctuates with economic cycles. For example, a drop in disposable income during the recession forced some former DIFM consumers to work on their own vehicles, resulting in short-term growth in the DIY market. During this period, weak labor and credit markets depressed new vehicles sales, thereby increasing the average length of vehicle ownership. This increase in the average age of vehicles on the road also aided the short-term growth of the DIY industry as owners of older vehicles were more likely to work on their own vehicles. However, we believe that as the economy continues to gain steam, consumers will become more confident and invest in new vehicles, and once again shift away from DIY toward DIFM and will do so at increasing rates. Consistent with this long-term trend, we have adopted a long-term strategy of growing our automotive service business, while maintaining our DIY customer base by offering the newest and broadest product assortment in the automotive aftermarket.

BUSINESS STRATEGY

All of our efforts are focused on ensuring that Pep Boys is the best place to shop and care for your car. The legacy of our founders—Manny, Moe & Jack—has inspired us since 1921 to deliver passionate customer service. We are people taking care of people ... and their cars. More than just words, we continue to learn more from our growing set of customer data and to advance our customer centered business model. Over the past two years, we have reconstituted our senior executive team to help guide the development of our strategy around our target customer segments and the delivery of world-class customer service. The following strategies have been developed and prioritized to support our vision and, in turn, our ultimate goal as a public company of maximizing shareholder value.

Attract, develop and retain the best people. We need the best people to care for our customers and their cars. This process begins with their recruitment and continues throughout their tenure as Pep Boys associates. We are constantly reviewing and improving our hiring process to include updated core competency and positional profiles and pre-hire assessment screening. Once hired, a Pep Boys associate has the opportunity to participate in a variety of classroom, online skills, and leadership training to develop a career path with us. We also offer performance-based compensation programs designed to reward the delivery of the passionate customer service that is the centerpiece of our vision.

Grow where our target customers live, work and shop. We achieve this through both our physical locations and online presence. We have researched and developed proprietary customer segment targets that we believe allow us to maximize our profitability. Our store growth, and any rationalization of our store base, is designed to optimize the proximity of these locations to our target customers. Similarly, our omni-channel digital strategy, which we call e-SERVE, is developed around making it easier for our target customers to do business with us. pepboys.com (including our mobile device version) allows our customers to learn about the breadth and depth of our service and product offerings, price and schedule service appointments, and purchase products for in store or home delivery.

Deliver customer experiences that are "beyond expectations". We strive to be friendly, do it right, show compassion and keep promises with each and every customer. We have developed a new training program designed to teach our associates how to enhance the customer experience through building relationships with our customers. Before addressing a customer's immediate need, our associates are taught to build rapport with the customer that will not only lead to customer satisfaction with the

3

Table of Contents

current transaction, but ultimately to the customer choosing Pep Boys for all of their automotive needs in the future. Information gathered through our rewards program, customer surveys and focus groups helps us to understand the customer experience that our target customer segments expect and the services and products that will best meet their needs and desires.

Provide the best assortment and shopping experience in the automotive aftermarket. We begin by being a full service—tire, maintenance and repair—shop. Our full service capabilities, ASE (Automotive Service Excellence) certified technicians and continuous investment in training and equipment allow customers to rely on us for all of their automotive maintenance and repair needs—from replacing the oil in their engine to replacing the engine itself. By offering a broad assortment of branded and private label products, we enjoy a competitive advantage over many of our DIFM competitors.

The size of our Supercenters allows us to provide the highest level of replacement parts coverage and the broadest range of maintenance, performance and appearance products and accessories in the industry. We are able to leverage our Superhub stores, which have a larger assortment of product than our normal Supercenter, to satisfy customer needs for slow-moving product by delivering this product to requesting Supercenters on demand. We are also expanding our Speed Shops (106 as of the end of fiscal 2013), a store-in-a-store within existing Supercenters that creates a differentiated retail experience for automotive enthusiasts by stocking high-performance and specialty products. We are similarly focused on price optimization and inventory rationalization opportunities.

We are currently testing a new market concept that we call the "Road Ahead," which began in the first quarter of fiscal 2013 with a re-grand opening of our West Hillsboro, Florida location. Due to the success at this store we converted the balance of our Tampa, Florida market to this concept in the fourth quarter of fiscal 2013. The early results have also been encouraging and as a result we will convert an additional 20 Supercenters in three markets to this concept in the first half of fiscal 2014 and have initiated plans for an additional three markets for the back half of fiscal 2014, through the early part of fiscal 2015. Designed around the shopping habits of our target customer segments, this concept enhances the entire store—our people, the product assortment, its exterior and interior look and feel and the marketing programs—to learn how we can be successful in attracting more of these target customers and earn a greater share of their annual spend in the automotive aftermarket. Our Road Ahead strategy also allows us to use our retail business to drive the service business with free professional battery and wiper installations.

Tell our story internally and externally. It is essential to our success that our associates and consumers understand our vision and brand position. As consumers had come to understand the breadth and depth of our offerings and gave us credit for our value proposition, in fiscal 2013 we turned our attention to focusing our message on the customer experience that we believe our target customer segments desire but have been unable to find in the automotive aftermarket. Consistent with our strategy described above, our TRUST THE BOYS TO GET YOU THERE brand positioning shifted from a more promotional message to a more customer service oriented message. This message is conveyed to our associates through corporate communications and leadership training, while tailored marketing plans including TV and radio promotions, digital media, direct marketing, grass-roots and print campaigns deliver the message to our target customer segments.

STORE IMPROVEMENTS

In fiscal 2013, our capital expenditures totaled approximately $65.0 million which included the acquisition of 18 Service and Tire Centers in Southern California. Our fiscal 2013 capital expenditures also included the addition of 29 new locations, the conversion of 11 Supercenters into Superhubs, the addition of 63 Speed Shops within existing Supercenters and required expenditures for existing stores, offices and distribution centers. Our fiscal 2014 capital expenditures are expected to be approximately

4

Table of Contents

$80.0 million, which includes the planned addition of 30 Service & Tire Centers, three Supercenters, and the conversion of 41 stores to the new "Road Ahead" format. These expenditures are expected to be funded from cash on hand and net cash generated from operating activities. Additional capacity, if needed, exists under our revolving credit facility.

SERVICES AND PRODUCTS

As of February 1, 2014, we operated a total of 7,520 service bays in 793 of our 799 locations. Each service location performs a full range of automotive maintenance and repair services (except body work) and installs tires, parts and accessories.

Each Pep Boys Supercenter carries a similar product line, with variations based on the number and type of cars in the market where the store is located. A Pep Boys Service & Tire Center carries tires and a limited selection of our products. A full complement of inventory at a typical Supercenter includes an average of approximately 29,000 items, while Service & Tire Centers average approximately 2,000 items. Our product lines include: tires; batteries; new and remanufactured parts for domestic and import vehicles; chemicals and maintenance items; fashion, electronic, and performance accessories; and select non-automotive merchandise that appeals to our target customer segments.

In addition to offering a wide variety of high quality name brand products, we sell an array of high quality products under various private label names. We sell tires under the names DEFINITY, FUTURA® and CORNELL®, and batteries under the name PROSTART®. We also sell wheel covers under the name FUTURA®; air filters, anti-freeze, chemicals, cv axles, hub assemblies, lubricants, oil, oil filters, oil treatments, transmission fluids, custom wheels and wiper blades under the name PROLINE®; alternators, battery booster packs, alkaline type batteries and starters under the name PROSTART®; power steering hoses, chassis parts and power steering pumps under the name PROSTEER®; brakes under the name PROSTOP® and brakes, batteries, starters, ignitions and chassis under the name VALUEGRADE. All products sold by the Company under various private label names were approximately 20% of our merchandise sales in fiscal 2013, 24% in 2012, and 26% in 2011. The year over year decreases are the result of our introduction of additional brand name tires.

Our commercial automotive parts delivery program, branded PEP EXPRESS PARTS®, is designed to increase our market share with the professional installer and to leverage our inventory investment. The program satisfies the commercial customer's automotive inventory needs by taking advantage of the breadth and quality of Pep Boys' parts inventory as well as its experience supplying its own service bays and mechanics. As of February 1, 2014, approximately 79%, or 454, of our 574 Supercenters and Pep Express stores provided commercial parts delivery as compared to approximately 80%, or 458 stores, at the end of fiscal 2012.

We have a point-of-sale system in all of our stores, which gathers sales and inventory data by stock-keeping unit from each store on a daily basis. This information is then used to formulate pricing, inventory, marketing and merchandising strategies. We have an electronic parts catalog that allows our associates to efficiently look up the parts that our customers need and to provide complete job solutions, advice and information for customers' vehicles. We have an electronic work order system in all service centers. This system creates a service history for each vehicle, provides customers with a comprehensive sales document and enables us to maintain a service customer database.

We use a competitive pricing strategy, setting prices based on market forces and then complementing them with promotions. We believe that targeted advertising and promotions play important roles in succeeding in today's environment. We are constantly working to understand our target customer segments' needs and desires so that we can deliver outstanding customer service and build long-lasting, loyal relationships with them. We utilize advertising, promotions and a loyalty card program (Rewards) to convey our commitment to customer service and to promote our service and repair capabilities and product offerings. We are committed to an effective multi-media promotional

5

Table of Contents

schedule supplemented by extensive direct marketing, grass-roots campaigns and occasional print campaigns. Finally, we utilize in-store signage and creative product placement to help educate customers about services and products that fit their needs.

Through our desktop and mobile website at www.pepboys.com, we strive to empower customers to make informed product and service purchase decisions for their automotive projects and vehicle maintenance needs. We focus on providing dependable product and service information, online buying guides and how-to advice, customer product ratings and reviews, product videos and clear repair service details in a convenient 24/7 online experience. Through our website, customers can learn more about the Pep Boys brand and our products and services, purchase and schedule installation of tires with our TreadSmart application, schedule automotive maintenance and repair services with our eServe application, keep track of maintenance and service records through our online Glovebox application, and purchase automotive parts and accessories through several delivery methods, including buying online and shipping to home or picking up in store, as well as the convenience to reserve items online and pay in store.

This year we have continued to improve the stability of our online infrastructure through a platform migration upgrade and continued vigilance of Payment Card Industry (PCI) standards and compliance to ensure our overall security and customer privacy. We maintain a dedicated online customer service team who provides direct support, including answering any order, product or service questions, assistance in ordering and basic technical support to customers who contact them via phone, live chat, email or webform. We are committed to the continued improvement of our online presence with a focus on providing a seamless omni-channel customer experience that builds trust and enriches the personal connection between our customers and our brand.

STORE OPERATIONS AND MANAGEMENT

Most Pep Boys stores are open seven days a week. Most Supercenters have a Retail Manager and Service Manager (Service & Tire Centers only have a Service Manager) who report to geographic-specific Area Directors and Divisional or Assistant Divisional Vice Presidents. The Divisional or Assistant Divisional Vice Presidents report to one of the Vice President—Supercenters, East US, the Vice President—Supercenters, West US or the Vice President—Service & Tire Centers who, in turn, report to the Senior Vice President—Store Operations, who, in turn, reports to the President & Chief Executive Officer. As of February 1, 2014, the average length of service with Pep Boys for a Retail Manager and a Service Manager is approximately 11.0 and 7.5 years, respectively.

Supervision and control over individual stores is facilitated by Area Directors and Divisional or Assistant Divisional Vice Presidents who make regular visits to stores and utilize the Company's computer system and operational handbooks. All of our advertising, accounting, purchasing, information technology and most administrative functions are conducted at our corporate headquarters in Philadelphia, Pennsylvania. Certain administrative functions for our regional operations are performed at various regional offices. See "Item 2 Properties."

INVENTORY CONTROL AND DISTRIBUTION

Most of our merchandise is distributed to our stores from our warehouses by dedicated and contract carriers. Target levels of inventory for products are established for each warehouse and store based upon prior shipment history, sales trends and seasonal demand. Inventory on hand is compared to target levels on a weekly basis at each warehouse, potentially triggering re-ordering of merchandise from suppliers. In addition, each Pep Boys store has an automated inventory replenishment system that orders additional inventory, generally from a warehouse, when a store's inventory on-hand falls below the target level. We also consolidate certain slow-moving hard parts inventory into our centrally-located

6

Table of Contents

Indianapolis warehouse that can service each of our stores with overnight delivery of these parts when necessary.

Implementation of the Superhub concept enables local expansion of our auto parts product assortment in a cost effective manner. We are now able to satisfy customer needs for slow-moving auto parts by carrying limited amounts of this product at Superhub locations. These Superhubs then deliver this product to requesting Supercenters to fulfill customer demand. Superhubs are generally replenished from distribution centers multiple times per week. As of February 1, 2014, we operated 53 Superhubs within existing Supercenters, with plans to convert an additional 10 Superhubs in fiscal 2014. These Superhubs, including our additional conversions in 2014, will provide approximately 550 of our stores with an expanded auto parts assortment. We also maintain one free standing tire hub warehouse in the Philadelphia market that offers an expanded assortment of tires and batteries for same day delivery to our stores in order to satisfy customer demand directly rather than from tire distributors. In fiscal 2014, we have plans to test three additional tire hubs within existing Supercenters.

SUPPLIERS

During fiscal 2013, our ten largest suppliers accounted for approximately 45% of the merchandise purchased. Only one of our suppliers accounted for more than 10% of our purchases. We have one long-term contract under which we are required to purchase merchandise. We believe that the relationships that we have established with our suppliers are generally good.

In the past, we have not experienced difficulty in obtaining satisfactory sources of supply and we believe that adequate alternative sources of supply exist, at similar cost, for the types of merchandise sold in our stores.

COMPETITION

We operate in a highly competitive environment. We encounter competition from national and regional chains, automotive dealerships and from local independent service providers and merchants. Our competitors include general, full range and discount department stores and online retailers which carry automotive parts and accessories and/or have automotive service centers, as well as specialized automotive retailers. Generally, the specialized automotive retailers focus on either DIFM or DIY. We believe that our operation in both DIFM and DIY differentiates us from most of our competitors. However, certain competitors are larger in terms of sales volume and/or number of stores. Therefore, these competitors have access to greater capital and management resources and have either been operating longer or have more stores in particular geographic areas. The principal methods of competition in our industry include store location, customer service, product offerings, quality and price.

REGULATION

We are subject to various federal, state and local laws and governmental regulations relating to the operation of our business, including those governing the handling, storage and disposal of hazardous substances contained in the products that we sell and use in our service bays, the recycling of batteries, tires and used lubricants, the sale of small engine merchandise and the ownership and operation of real property.

7

Table of Contents

EMPLOYEES

At February 1, 2014, the Company employed 18,914 persons as follows:

| | | | | | | | | | | | | | | | | | | |

Description | | Full-time | | % | | Part-time | | % | | Total | | % | |

|---|

Retail | | | 4,045 | | | 29.1 | | | 3,108 | | | 61.6 | | | 7,153 | | | 37.8 | |

Service center | | | 8,404 | | | 60.6 | | | 1,863 | | | 37.0 | | | 10,267 | | | 54.3 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

Store total | | | 12,449 | | | 89.7 | | | 4,971 | | | 98.6 | | | 17,420 | | | 92.1 | |

Warehouses | | | 584 | | | 4.2 | | | 63 | | | 1.3 | | | 647 | | | 3.4 | |

Offices | | | 841 | | | 6.1 | | | 6 | | | 0.1 | | | 847 | | | 4.5 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

Total employees | | | 13,874 | | | 100.0 | | | 5,040 | | | 100.0 | | | 18,914 | | | 100.0 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

We had no union employees as of February 1, 2014. At February 2, 2013, we employed 13,886 full-time and 5,555 part-time employees.

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

Certain statements contained herein, including in "Item 1 Business" and "Item 7 Management's Discussion and Analysis of Financial Condition and Results of Operations", constitute "forward-looking statements" within the meaning of The Private Securities Litigation Reform Act of 1995. The words "guidance", "expect", "anticipate", "estimates", "targets", "forecasts" and similar expressions are intended to identify such forward-looking statements. Forward-looking statements include management's expectations regarding implementation of its long-term strategic plan, future financial performance, automotive aftermarket trends, levels of competition, business development activities, future capital expenditures, financing sources and availability and the effects of regulation and litigation. Although we believe that the expectations reflected in such forward-looking statements are based on reasonable assumptions, we can give no assurance that our expectations will be achieved. Our actual results may differ materially from the results discussed in the forward-looking statements due to factors beyond our control, including the strength of the national and regional economies, retail and commercial consumers' ability to spend, the health of the various sectors of the automotive aftermarket, the weather in geographical regions with a high concentration of our stores, competitive pricing, the location and number of competitors' stores, product and labor costs and the additional factors described in our filings with the Securities and Exchange Commission ("SEC"). See "Item 1A Risk Factors." Forward-looking statements speak only as of the date they are made. We assume no obligation to update or supplement forward-looking statements that become untrue because of subsequent events.

SEC REPORTING

We electronically file certain documents with, or furnish such documents to, the SEC, including annual reports on Form 10-K, quarterly reports on Form 10-Q, and current reports on Form 8-K, along with any related amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934. From time-to-time, we may also file registration and related statements pertaining to equity or debt offerings. The SEC maintains an Internet website at www.sec.gov that contains reports, proxy and information statements, and other information regarding issuers that file or furnish documents electronically with the SEC. All our filings can be accessed through the Securities and Exchange Commission website at www.sec.gov and searching with our ticker symbol "PBY".

We provide free electronic access to our annual, quarterly and current reports (and all amendments to these reports) on our Internet website, www.pepboys.com, under the Investor Relations/Financial Information/SEC Filings link. These reports are available on our website as soon as

8

Table of Contents

reasonably practicable after we electronically file or furnish such materials with or to the SEC. Information on our website does not constitute part of this Annual Report, and any references to our website herein are intended as inactive textual references only.

Copies of our SEC reports are also available free of charge. Please call our investor relations department at 215-430-9105 or write Pep Boys, Investor Relations, 3111 West Allegheny Avenue, Philadelphia, PA 19132 to request copies.

EXECUTIVE OFFICERS OF THE COMPANY

The following table indicates the name, age, tenure with the Company and position (together with the year of election to such position) of the executive officers of the Company:

| | | | | | | |

Name | | Age | | Tenure with

Company

as of April 2014 | | Position with the Company and Date of Election to Position |

|---|

Michael R. Odell | | | 50 | | 7 years | | President & Chief Executive Officer since June 2010 |

David R. Stern | | | 47 | | 2 years | | Executive Vice President—Chief Financial Officer since September 2012 |

Christopher J. Adams | | | 46 | | 1 year | | Senior Vice President—Store Operations since March 2013 |

Thomas J. Carey | | | 56 | | 2 years | | Senior Vice President—Chief Customer Officer since August 2012 |

Joseph A. Cirelli | | | 55 | | 37 years | | Senior Vice President—Business Development since November 2007 |

James F. Flanagan | | | 53 | | 7 months | | Senior Vice President—Chief Human Resources Officer since August 2013 |

John J. Kelly | | | 56 | | 1 month | | Senior Vice President—Merchandising since March 2014 |

Brian D. Zuckerman | | | 44 | | 15 years | | Senior Vice President—General Counsel & Secretary since March 2009 |

Michael R. Odell was named Chief Executive Officer on September 22, 2008, after serving as Interim Chief Executive Officer since April 23, 2008. Mr. Odell received the additional title of President on June 17, 2010. Mr. Odell joined Pep Boys in September 2007 as Executive Vice President—Chief Operating Officer, after having most recently served as the Executive Vice President and General Manager of Sears Retail & Specialty Stores. Mr. Odell joined Sears in its finance department in 1994 where he served until he joined Sears operations team in 1998. There he served in various executive operations positions of increasing seniority, including as Vice President, Stores—Sears Automotive Group.

David R. Stern joined Pep Boys in September 2012 after having most recently served as Executive Vice President, Chief Administrative Officer and Chief Financial Officer of A.C. Moore Arts and Crafts. From 2007 until 2009, Mr. Stern held roles at Coldwater Creek, including Vice President, Financial Planning and Analysis and Corporate Controller. From 2000 to 2007, Mr. Stern was the Chief Financial Officer of Petro Services. Mr. Stern began his career as an internal auditor and gained experience as a financial analyst, accounting manager and corporate controller at several companies, including Delhaize America, before joining Petro Services.

Christopher J. Adams joined Pep Boys in March 2013 after having most recently served as Chief Operating Officer of CarGroup Holdings LLC d/b/a webuyanycar.com since November 2010. From July 2008 to September 2010, Mr. Adams served as Chief Operating Officer of The BabyPlus Company, a manufacturer and distributor of a prenatal education system. From November 2006 to July 2008, Mr. Adams served as Chief Operating Officer of Holland Partners, a developer and manager of

9

Table of Contents

multifamily communities. Mr. Adams began his career at Enterprise Rent-A-Car in September 1989 where through July 2006 he progressed from a management trainee to become one of the executives selected to open up and lead Enterprise's U.K. operations.

Thomas J. Carey joined Pep Boys in August 2012 after having most recently served as Senior Vice President and Chief Marketing Officer for Orchard Supply Hardware Stores. From March 2003 to June 2007, Mr. Carey served as Senior Vice President, Chief Marketing Officer, of West Marine, Inc. Prior to joining West Marine, Mr. Carey served in various marketing leadership positions of increasing seniority with several national retailers, including Sunglass Hut, Bloomingdale's and Builders Square. Mr. Carey also has agency experience with, among others, Ogilvy & Mather and Young & Rubicam.

Joseph A. Cirelli was named Senior Vice President—Corporate Development in November 2007. Since March 1977, Mr. Cirelli has served the Company in positions of increasing seniority, including Senior Vice President—Service, Vice President—Real Estate and Development, Vice President—Operations Administration, and Vice President—Customer Satisfaction.

James F. Flanagan joined Pep Boys in August 2013 after having most recently served as the Senior Vice President of Human Resources for Procurian, a comprehensive procurement solution company. From 2004 to 2012, Mr. Flanagan served as Executive President, Human Resources of GSI Commerce. Mr. Flanagan's 20+ years of human resources leadership experience also included positions at Starbucks, Starwood Hotels, Sheraton Hotels, Bank of America and homegrocer.com. Mr. Flanagan began his career as a labor and employment attorney.

John J. Kelly joined Pep Boys in March 2014 after having most recently served as President of Decible, a start-up electronics joint-venture, since June 2013. From April 2009 to May 2013, Mr. Kelly served as Vice President of Home Merchandising of QVC. Prior to joining QVC, Mr. Kelly served as Chief Merchandising Officer of Circuit City Stores. Mr. Kelly's 30+ years of merchandising leadership experience also included positions at Sharp Electronics and Macy's.

Brian D. Zuckerman was named Senior Vice President—General Counsel & Secretary on March 1, 2009 after having most recently served as Vice President—General Counsel & Secretary since 2003. Mr. Zuckerman joined the Company as a staff attorney in 1999. Prior to joining Pep Boys, Mr. Zuckerman practiced corporate and securities law with two firms in Philadelphia.

Each of the executive officers serves at the pleasure of the Board of Directors of the Company.

ITEM 1A RISK FACTORS

The following section discloses all known material risks that we face. However, it does not include risks that may arise in the future that are yet unknown nor existing risks that we do not judge material to the presentation of our financial statements. If any of the events or circumstances described as risk below actually occurs, our business, results of operations and/or financial condition could be materially and adversely affected.

Risks Related to Pep Boys

We may not be able to successfully implement our business strategy, which could adversely affect our business, financial condition, results of operations and cash flows.

Our long-term strategic plan, which we update annually, includes numerous initiatives including our "Road Ahead" remodels and store growth programs to increase sales, enhance our margins and increase our return on invested capital in order to increase our earnings and cash flow. If these initiatives are unsuccessful, or if we are unable to implement the initiatives efficiently and effectively, our business, financial condition, results of operations and cash flows could be adversely affected.

10

Table of Contents

Successful implementation of our business strategy also depends on factors specific to the automotive aftermarket industry, many of which may be beyond our control (see "Risks Related to Our Industry").

If we are unable to generate sufficient cash flows from our operations, our liquidity will suffer and we may be unable to satisfy our obligations.

We require significant capital to fund our business. While we believe we have the ability to sufficiently fund our planned operations and capital expenditures for the next fiscal year, circumstances could arise that would materially affect our liquidity. For example, cash flows from our operations could be affected by changes in consumer spending habits or the failure to maintain favorable supplier payment terms or our inability to successfully implement sales growth initiatives. We may be unsuccessful in securing alternative financing when needed, on terms that we consider acceptable, or at all.

The degree to which we are leveraged could have important consequences on investments in our securities, including the following risks:

- •

- our ability to obtain additional financing for working capital, capital expenditures, acquisitions or general corporate purposes may be impaired in the future;

- •

- a substantial portion of our cash flow from operations must be dedicated to the payment of rent and the principal and interest on our debt, thereby reducing the funds available for other purposes;

- •

- our failure to comply with financial and operating restrictions placed on us and our subsidiaries by our credit facilities could result in an event of default that, if not cured or waived, could have a material adverse effect on our business or our prospects; and

- •

- if we are substantially more leveraged than some of our competitors, we might be at a competitive disadvantage to those competitors that have lower debt service obligations and significantly greater operating and financial flexibility than we do.

We depend on our relationships with our suppliers and a disruption of these relationships or of our suppliers' operations could have a material adverse effect on our business and results of operations.

Our business depends on developing and maintaining productive relationships with our suppliers. Many factors outside our control may harm these relationships. For example, financial difficulties that some of our suppliers may face could increase the cost of the products we purchase from them or might interrupt our source of supply. In addition, our failure to promptly pay or order sufficient quantities of inventory from our suppliers may increase the cost of products we purchase or could lead to suppliers refusing to sell products to us at all.

A disruption of our supplier relationships or a disruption in our suppliers' operations could have a material adverse effect on our business and results of operations.

We depend on our senior management team and our other personnel, and we face substantial competition for qualified personnel.

Our success depends in part on the efforts of our senior management team. Our continued success will also depend on our ability to retain existing, and attract additional, qualified field personnel to meet our needs. We face substantial competition, both from within and outside of the automotive aftermarket, to retain and attract qualified personnel. In addition, we believe that the number of qualified automotive service technicians in the industry is generally insufficient to meet demand.

11

Table of Contents

We are subject to environmental laws and may be subject to environmental liabilities that could have a material adverse effect on us in the future.

We are subject to various federal, state and local environmental laws and governmental regulations relating to the operation of our business, including those governing the handling, storage and disposal of hazardous substances contained in the products we sell and use in our service bays, the recycling of batteries, tires and used lubricants, the ownership and operation of real property and the sale of small engine merchandise. When we acquire or dispose of real property or enter into financings secured by real property, we undertake investigations that may reveal soil and/or groundwater contamination at the subject real property. All such known contamination has either been remediated, or is in the process of being remediated. Any costs expected to be incurred related to such contamination are either covered by insurance or financial reserves provided for in the consolidated financial statements. However, there exists the possibility of additional soil and/or groundwater contamination on our real property where we have not undertaken an investigation. A failure by us to comply with environmental laws and regulations could have a material adverse effect on us.

A breach of our security could compromise customer, employee or Company information and could harm our reputation, lead to substantial additional costs, or possible litigation.

In the course of business, personal information about our customers and employees is stored both electronically and physically. We have taken reasonable and appropriate steps to safeguard this information. If this information is compromised, however, our reputation could be damaged resulting in lost business, we could incur additional costs in remediating the issue, or we could face possible regulatory action. The regulatory environment related to information security and privacy is constantly evolving, and compliance with those requirements could result in additional costs. There is no guarantee that the procedures we have implemented are adequate to safeguard all confidential information, and a breach of this information could potentially have a negative impact on our results of operations and financial condition.

Business interruptions may negatively impact our store hours, operability of our computer systems and the availability and cost of merchandise which may adversely impact our sales and profitability.

War or acts of terrorism, hurricanes, tornadoes, earthquakes or other natural disasters, or the threat of any of these calamities or others, may have a negative impact on our ability to obtain merchandise to sell in our stores, result in certain of our stores being closed for an extended period of time, negatively affect the lives of our customers or associates, or otherwise negatively impact our operations. Some of our merchandise is imported from other countries. If imported goods become difficult or impossible to import into the United States, and if we cannot obtain such merchandise from other sources at similar costs, our sales and profit margins may be negatively affected.

In the event that commercial transportation is curtailed or substantially delayed, our business may be adversely impacted, as we may have difficulty receiving merchandise from our suppliers and shipping it to our stores.

Terrorist attacks, war in the Middle East, or insurrection involving any oil producing country would likely result in an abrupt increase in the price of crude oil, gasoline, diesel fuel and other types of energy. Such price increases would increase the cost of doing business for us and our suppliers, and also would negatively impact our customers' disposable income and have an adverse impact on our business, sales, profit margins and results of operations.

We rely extensively on our computer systems and the systems of our business partners to manage inventory, process transactions and report results. Any such systems are subject to damage or interruption from power outages, telecommunication failures, computer viruses, security breaches and catastrophic events. If our computer systems or those of our business partners fail we may experience

12

Table of Contents

loss of critical data and interruptions or delays in our ability to process transactions and manage inventory. Any such loss, if widespread or extended, could adversely affect the operation of our business and our results of operations.

Risks Related to Our Industry

Our industry is highly competitive, and price competition in some segments of the automotive aftermarket, or a loss of trust in our participation in the "do-it-for-me" market, could cause a material decline in our revenues and earnings.

The automotive aftermarket retail and service industry is highly competitive and subjects us to a wide variety of competitors. We compete primarily with the following types of businesses in each segment of the automotive aftermarket:

Retail

Do-It-Yourself

- •

- automotive parts and accessories stores;

- •

- automobile dealers that supply manufacturer replacement parts and accessories;

- •

- mass merchandisers and wholesale clubs that sell automotive products and select non-automotive merchandise that appeals to automotive "Do-It-Yourself" customers, such as generators, power tools and canopies; and

- •

- online retailers

Commercial

- •

- mass merchandisers, wholesalers and jobbers (some of which are associated with national parts distributors or associations).

Service

Do-It-For-Me

- •

- regional and local full service automotive repair shops;

- •

- automobile dealers that provide repair and maintenance services;

- •

- national and regional (including franchised) tire retailers that provide additional automotive repair and maintenance services; and

- •

- national and regional (including franchised) specialized automotive (such as oil change, brake and transmission) repair facilities that provide additional automotive repair and maintenance services.

Tires

- •

- national and regional (including franchised) tire retailers; and

- •

- mass merchandisers and wholesale clubs that sell tires.

A number of our competitors have more financial resources, are more geographically diverse, have a higher geographic market concentration or have better name recognition than we do, which might place us at a competitive disadvantage to those competitors. Because we seek to offer competitive prices, if our competitors reduce their prices we may also be forced to reduce our prices, which could cause a material decline in our revenues and earnings.

13

Table of Contents

With respect to the service labor category, the majority of consumers are unfamiliar with their vehicle's mechanical operation and, as a result, often select a service provider based on trust. Potential occurrences of negative publicity associated with the Pep Boys brand, the products we sell or installation or repairs performed in our service bays, whether or not factually accurate, could cause consumers to lose confidence in our products and services in the short or long term, and cause them to choose our competitors for their automotive service needs.

Vehicle miles driven may decrease, resulting in a decline of our revenues and negatively affect our results of operations.

Our industry is significantly influenced by the number of vehicle miles driven. Factors that may cause the number of vehicle miles and our revenues and our results of operations to decrease include:

- •

- the weather—as vehicle maintenance may be deferred during periods of inclement weather;

- •

- the economy—as during periods of poor economic conditions, customers may defer vehicle maintenance or repair and drive less due to unemployment, and during periods of good economic conditions, consumers may opt to purchase new vehicles rather than service the vehicles they currently own and replace worn or damaged parts;

- •

- gas prices—as increases in gas prices may deter consumers from using their vehicles; and

- •

- travel patterns—as changes in travel patterns may cause consumers to rely more heavily on mass transportation.

Economic factors affecting consumer spending habits may continue, resulting in a decline in revenues and could negatively impact our business.

Many economic and other factors outside our control, including consumer confidence, consumer spending levels, employment levels, consumer debt levels and inflation, as well as the availability of consumer credit, affect consumer spending habits. A significant deterioration in the global financial markets and economic environment, recessions or an uncertain economic outlook could adversely affect consumer spending habits and result in lower levels of economic activity. The domestic and international political situation also affects consumer confidence. Any of these events and factors could cause consumers to curtail spending, especially with respect to our more discretionary merchandise offerings, such as automotive accessories, tools and personal transportation products.

During fiscal 2009, there was significant deterioration in the global financial markets and economic environment, which negatively impacted consumer spending and our revenues. While the economic climate improved somewhat in fiscal 2012, consumer spending has not returned to pre-recession levels. If the economy does not continue to strengthen, or if our efforts to counteract the impacts of these trends are not sufficiently effective, our revenues could decline, negatively affecting our results of operations.

Consolidation among our competitors may negatively impact our business.

Our industry has experienced consolidation over time. If this trend continues or if our competitors are able to achieve efficiencies in their mergers, the Company may face greater competitive pressures in the markets in which we operate.

ITEM 1B UNRESOLVED STAFF COMMENTS

None.

14

Table of Contents

ITEM 2 PROPERTIES

The Company owns its five-story, approximately 300,000 square foot corporate headquarters in Philadelphia, Pennsylvania. The Company also owns the following administrative regional offices—approximately 4,000 square feet of space in each of Melrose Park, Illinois and Bayamon, Puerto Rico. The Company leases an administrative regional office of approximately 3,500 square feet in Los Angeles, California.

Of the 799 store locations operated by the Company at February 1, 2014, 228 are owned and 571 are leased. As of February 1, 2014, 142 of the 228 stores owned by the Company are currently used as collateral under our Senior Secured Term Loan, due October 2018.

The following table sets forth certain information regarding the owned and leased warehouse space utilized by the Company to replenish its store locations at February 1, 2014:

| | | | | | | | | | | | |

Warehouse Locations | | Products

Warehoused | | Approximate

Square

Footage | | Owned

or

Leased | | Stores

Serviced | | States Serviced |

|---|

San Bernardino, CA | | All | | | 600,000 | | Leased | | | 196 | | AZ, CA, NV, UT, WA |

McDonough, GA | | All | | | 392,000 | | Owned | | | 244 | | AL, FL, GA, LA, NC, PR, SC, TN |

Mesquite, TX | | All | | | 244,000 | | Owned | | | 82 | | AR, CO, LA, MO, NM, OK, TX |

Plainfield, IN | | All | | | 403,000 | | Owned | | | 80 | | IL, IN, KY, MI, MN, OH, PA |

Chester, NY | | All | | | 402,000 | | Owned | | | 197 | | CT, DE, MA, MD, ME, NH, NJ, NY, PA, RI, VA |

Philadelphia, PA | | Tires & Batteries | | | 74,000 | | Leased | | | 70 | | DE, NJ, PA, VA, MD |

| | | | | | | | | | | | |

| | | | | | | | | | | | | |

Total | | | | | 2,115,000 | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | | |

The Company anticipates that its existing and future warehouse space and its access to outside storage will accommodate inventory necessary to support future store expansion and any increase in SKUs through the end of fiscal 2014.

ITEM 3 LEGAL PROCEEDINGS

The Company is party to a consent decree, effective July 15, 2010, with the United States Environmental Protection Agency ("EPA") that, among other things, required the Company to implement a formal compliance program with respect to certain small gasoline engine merchandise sold by the Company. In the fourth quarter of fiscal 2013, the EPA alleged, in writing, that the Company had violated certain inspection, testing and reporting requirements of the Consent Decree and made an aggregated stipulated penalty demand of $2.3 million as a result thereof. The Company is currently engaged in settlement negotiations with the EPA with respect thereto. The Company has accrued an amount that it believes is sufficient to resolve those violations for which it believes it is liable. If the Company is unable to resolve all of the violations with the EPA through its settlement negotiations, the Company intends to invoke formal dispute resolution procedures with the EPA under the terms of the Consent Decree.

The Company is also party to various actions and claims arising in the normal course of business. The Company believes that amounts accrued for awards or assessments in connection with all such matters are adequate and that the ultimate resolution of these matters will not have a material adverse effect on the Company's financial position. However, there exists a possibility of loss in excess of the amounts accrued, the amount of which cannot currently be estimated. While the Company does not believe that the amount of such excess loss will be material to the Company's financial position, any such loss could have a material adverse effect on the Company's results of operations in the period(s) during which the underlying matters are resolved.

ITEM 4 MINE SAFETY DISCLOSURES

Not applicable.

15

Table of Contents

PART II

ITEM 5 MARKET FOR THE REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

The common stock of The Pep Boys—Manny, Moe & Jack is listed on the New York Stock Exchange under the symbol "PBY." There were 3,935 registered shareholders as of April 5, 2014. Since January 29, 2012 we have not paid a dividend on our common stock. The following table sets forth for the periods listed, the high and low sale prices of the Company's common stock, as reported by the New York Stock Exchange:

| | | | | | | |

| | Market Price

Per Share | |

|---|

| | High | | Low | |

|---|

Fiscal 2013 | | | | | | | |

Fourth quarter | | $ | 13.86 | | $ | 11.36 | |

Third quarter | | | 13.05 | | | 11.01 | |

Second quarter | | | 12.94 | | | 11.14 | |

First quarter | | | 12.14 | | | 10.29 | |

Fiscal 2012 | | | | | | | |

Fourth quarter | | $ | 11.16 | | $ | 9.48 | |

Third quarter | | | 10.57 | | | 8.76 | |

Second quarter | | | 14.93 | | | 8.67 | |

First quarter | | | 15.46 | | | 14.90 | |

On December 12, 2012, the Company's Board of Directors authorized a program to repurchase up to $50.0 million of the Company's common stock to be made from time to time in the open market or in privately negotiated transactions, with no expiration date.

The Company repurchased 238,000 shares of common stock for $2.8 million in Fiscal 2013. There were no shares repurchased in the fourth quarter of 2013. The Company repurchased 35,000 shares of common stock for $0.3 million in Fiscal 2012 and no shares were repurchased in Fiscal 2011. The repurchased shares are included in the Company's treasury stock.

EQUITY COMPENSATION PLANS

The following table sets forth the Company's shares authorized for issuance under its equity compensation plans at February 1, 2014:

| | | | | | | | | | |

| | Number of securities

to be issued upon

exercise of

outstanding options,

warrants and rights (a) | | Weighted average

exercise price of

outstanding options,

warrants and rights (b) | | Number of securities

remaining available for

future issuance under

equity compensation

plans (excluding

securities reflected

in the first column (a)) | |

|---|

Equity compensation plans approved by security holders | | | 2,738,100 | | $ | 5.26 | | | 2,831,084 | |

The Company maintains an Employee Stock Purchase Plan with an authorized aggregate share limit of 2,000,000 shares of Pep Boys' Common Stock. Eligible employees can elect to have up to 10 percent of compensation deducted for purchase of Company stock at a discount under the Plan. For fiscal 2013, 2012, and 2011, respectively, the total number of shares sold to employees was 62,547; 39,552; and 20,963. As of February 1, 2014, the total remaining for purchase was 1,875,753 shares.

16

Table of Contents

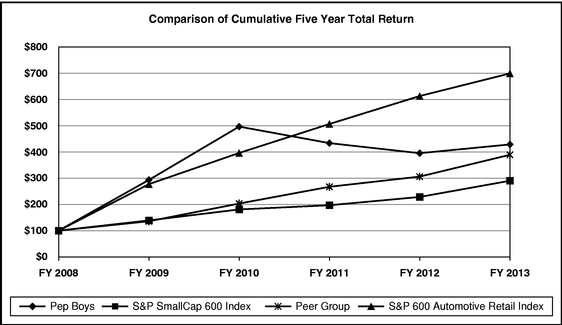

STOCK PRICE PERFORMANCE

The following graph compares the cumulative total return on shares of Pep Boys stock over the past five years with the cumulative total return on shares of companies in (1) the Standard & Poor's SmallCap 600 Index, (2) the S&P 600 Automotive Retail Index and (3) an index of peer and comparable companies as determined by the Company. The comparison assumes that $100 was invested in January 2009 in Pep Boys Stock and in each of the indices and assumes reinvestment of dividends. The S&P 600 Automotive Retail Index consists of companies in the S&P SmallCap 600 index that meet the definition of the automotive retail classification, and is currently comprised of: Group 1 Automotive, Inc.; Lithia Motors, Inc.; Monro Muffler Brake, Inc.; Sonic Automotive, Inc.; and The Pep Boys—Manny, Moe & Jack. The companies currently comprising the Peer Group are: Aaron's, Inc.; Advance Auto Parts, Inc.; AutoZone, Inc.; Big 5 Sporting Goods Corp.; Cabelas, Inc.; Conn's, Inc.; Dick's Sporting Goods, Inc.; HHGregg, Inc.; Midas, Inc. (included through FYE 2012); Monro Muffler Brake, Inc.; O'Reilly Automotive, Inc.; PetSmart, Inc.; RadioShack Corp.; Rent-A-Center, Inc.; Tractor Supply Co.; West Marine, Inc.

| | | | | | | | | | | | | | | | | | | |

Company/Index | | Jan. 2009 | | Jan. 2010 | | Jan. 2011 | | Jan. 2012 | | Jan. 2013 | | Jan. 2014 | |

|---|

Pep Boys | | $ | 100.00 | | $ | 293.18 | | $ | 496.44 | | $ | 433.48 | | $ | 395.08 | | $ | 428.45 | |

S&P SmallCap 600 Index | | | 100.00 | | | 138.97 | | | 180.75 | | | 196.79 | | | 228.32 | | | 290.04 | |

Peer Group | | | 100.00 | | | 135.79 | | | 203.21 | | | 267.11 | | | 305.86 | | | 388.99 | |

S&P 600 Automotive Retail Index | | | 100.00 | | | 277.11 | | | 396.02 | | | 506.34 | | | 612.87 | | | 698.89 | |

17

Table of Contents

ITEM 6 SELECTED FINANCIAL DATA

The following tables set forth the selected financial data for the Company and should be read in conjunction with the Consolidated Financial Statements and Notes thereto included elsewhere herein.

| | | | | | | | | | | | | | | | |

Fiscal Year Ended | | Feb. 1, 2014

(52 weeks) | | Feb. 2, 2013

(53 weeks) | | Jan. 28,

2012

(52 weeks) | | Jan. 29,

2011

(52 weeks) | | Jan. 30,

2010

(52 weeks) | |

|---|

| | (dollar amounts are in thousands, except per share data)

| |

|---|

STATEMENT OF OPERATIONS DATA | | | | | | | | | | | | | | | | |

Merchandise sales | | $ | 1,608,697 | | $ | 1,643,948 | | $ | 1,642,757 | | $ | 1,598,168 | | $ | 1,533,619 | |

Service revenue | | | 457,871 | | | 446,782 | | | 420,870 | | | 390,473 | | | 377,319 | |

Total revenues | | | 2,066,568 | | | 2,090,730 | | | 2,063,627 | | | 1,988,641 | | | 1,910,938 | |

Costs of merchandise sales | | | 1,108,359 | | | 1,159,994 | | | 1,154,322 | | | 1,110,380 | | | 1,084,804 | |

Cost of service revenue | | | 470,832 | | | 439,236 | | | 399,776 | | | 355,909 | | | 340,027 | |

Gross profit from merchandise sales(10) | | | 500,338 | (1) | | 483,954 | (3) | | 488,435 | (5) | | 487,788 | (7) | | 448,815 | (8) |

Gross (loss) profit from service revenue(10) | | | (12,961 | )(1) | | 7,546 | (3) | | 21,094 | (5) | | 34,564 | (7) | | 37,292 | (8) |

Total gross profit | | | 487,377 | (1) | | 491,500 | (3) | | 509,529 | (5) | | 522,352 | (7) | | 486,107 | (8) |

Selling, general and administrative expenses | | | 464,852 | | | 463,416 | | | 443,986 | | | 442,239 | | | 430,261 | |

Pension settlement expense | | | — | | | 17,753 | | | — | | | — | | | — | |

Net (loss) gain from disposition of assets | | | (227 | ) | | 1,323 | | | 27 | | | 2,467 | | | 1,213 | |

Operating profit | | | 22,298 | | | 11,654 | | | 65,570 | | | 82,580 | | | 57,059 | |

Merger termination fees, net | | | — | | | 42,816 | (2) | | — | | | — | | | — | |

Non-operating income | | | 1,789 | | | 2,012 | | | 2,324 | | | 2,609 | | | 2,261 | |

Interest expense | | | 14,797 | | | 33,982 | (4) | | 26,306 | | | 26,745 | | | 21,704 | (9) |

Earnings from continuing operations before income taxes and discontinued operations | | | 9,290 | | | 22,500 | | | 41,588 | | | 58,444 | | | 37,616 | |

Income tax expense | | | 2,237 | | | 9,345 | | | 12,460 | (6) | | 21,273 | (6) | | 13,503 | |

Earnings from continuing operations before discontinued operations | | | 7,053 | | | 13,155 | | | 29,128 | | | 37,171 | | | 24,113 | |

Discontinued operations, net of tax | | | (188 | ) | | (345 | ) | | (225 | ) | | (540 | ) | | (1,077 | )(8) |

Net earnings | | | 6,865 | | | 12,810 | | | 28,903 | | | 36,631 | | | 23,036 | |

BALANCE SHEET DATA | | | | | | | | | | | | | | | | |

Working capital | | $ | 131,029 | | $ | 126,505 | | $ | 166,627 | | $ | 203,367 | | $ | 205,525 | |

Current ratio | | | 1.19 to 1 | | | 1.18 to 1 | | | 1.27 to 1 | | | 1.36 to 1 | | | 1.40 to 1 | |

Merchandise inventories | | $ | 672,354 | | $ | 641,208 | | $ | 614,136 | | $ | 564,402 | | $ | 559,118 | |

Property and equipment-net | | $ | 625,525 | | $ | 657,270 | | $ | 696,339 | | $ | 700,981 | | $ | 706,450 | |

Total assets | | $ | 1,605,481 | | $ | 1,603,949 | | $ | 1,633,779 | | $ | 1,556,672 | | $ | 1,499,086 | |

Long-term debt, excluding current maturities | | $ | 199,500 | | $ | 198,000 | | $ | 294,043 | | $ | 295,122 | | $ | 306,201 | |

Total stockholders' equity | | $ | 548,065 | | $ | 537,572 | | $ | 504,329 | | $ | 478,460 | | $ | 443,295 | |

DATA PER COMMON SHARE | | | | | | | | | | | | | | | | |

Basic earnings from continuing operations before discontinued operations | | $ | 0.13 | | $ | 0.25 | | $ | 0.55 | | $ | 0.71 | | $ | 0.46 | |

Basic earnings | | | 0.13 | | | 0.24 | | | 0.54 | | | 0.70 | | | 0.44 | |

Diluted earnings from continuing operations before discontinued operations | | | 0.13 | | | 0.24 | | | 0.54 | | | 0.70 | | | 0.46 | |

Diluted earnings | | | 0.13 | | | 0.24 | | | 0.54 | | | 0.69 | | | 0.44 | |

Cash dividends declared | | | — | | | — | | | 0.12 | | | 0.12 | | | 0.12 | |

Book value | | | 10.30 | | | 10.12 | | | 9.56 | | | 9.10 | | | 8.46 | |

Common share price range: | | | | | | | | | | | | | | | | |

High | | | 13.86 | | | 15.46 | | | 14.70 | | | 15.96 | | | 10.83 | |

Low | | | 10.29 | | | 8.67 | | | 8.18 | | | 7.86 | | | 2.76 | |

OTHER STATISTICS | | | | | | | | | | | | | | | | |

Return on average stockholders' equity(11) | | | 1.3 | % | | 2.4 | % | | 5.8 | % | | 7.9 | % | | 5.3 | % |

Common shares issued and outstanding | | | 53,198,169 | | | 53,125,743 | | | 52,753,719 | | | 52,585,131 | | | 52,392,967 | |

Capital expenditures | | $ | 53,982 | | $ | 54,696 | | $ | 74,746 | | $ | 70,252 | | $ | 43,214 | |

Number of stores | | | 799 | | | 758 | | | 738 | | | 621 | | | 587 | |

Number of service bays | | | 7,520 | | | 7,303 | | | 7,182 | | | 6,259 | | | 6,027 | |

- (1)

- Includes an aggregate pretax charge of $7.7 million for asset impairment, of which $2.4 million was charged to merchandise cost of sales, $5.3 million was charged to service cost of sales.

- (2)

- In fiscal 2012, we recorded settlement proceeds, net of merger related costs of $42.8 million, resulting from the termination of the "go private" transaction.

18

Table of Contents

- (3)

- Includes an aggregate pretax charge of $10.6 million for asset impairment, of which $5.1 million was charged to merchandise cost of sales, $5.5 million was charged to service cost of sales.

- (4)

- Includes $11.2 million of fees associated with debt refinancing.

- (5)

- Includes an aggregate pretax charge of $1.6 million for asset impairment, of which $0.6 million was charged to merchandise cost of sales, $1.0 million was charged to service cost of sales.

- (6)

- Includes a tax benefit of $3.6 million and $2.2 million in Fiscal 2011 and Fiscal 2010, respectively, due to the release of valuation allowances on state net operating loss carryforwards and credits.

- (7)

- Includes a pretax benefit of $5.9 million due to the reduction in reserve for excess inventory which reduced merchandise cost of sales and an aggregate pretax charge of $1.0 million for asset impairment, of which $0.8 million was charged to merchandise cost of sales and $0.2 million was charged to service cost of sales.

- (8)

- Includes an aggregate pretax charge of $3.1 million for asset impairment, of which $2.2 million was charged to merchandise cost of sales, $0.7 million was charged to service cost of sales and $0.2 million (pretax) was charged to discontinued operations.

- (9)

- Includes a gain from debt retirement of $6.2 million.

- (10)

- Gross profit from merchandise sales includes the cost of products sold, buying, warehousing and store occupancy costs. Gross profit from service revenue includes the cost of installed products sold, buying, warehousing, service payroll and related employee benefits and occupancy costs. Occupancy costs include utilities, rents, real estate and property taxes, repairs and maintenance and depreciation and amortization expenses. Our gross profit may not be comparable to those of our competitors due to differences in industry practice regarding the classification of certain costs.

- (11)

- Return on average stockholders' equity is calculated by dividing net earnings (loss) for the period by average stockholders' equity for the year.

ITEM 7 MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

OVERVIEW

The following discussion and analysis explains the results of our operations for fiscal 2013 and 2012 and developments affecting our financial condition as of February 1, 2014. This discussion and analysis below should be read in conjunction with Item 6 "Selected Consolidated Financial Data," and our consolidated financial statements and the notes included elsewhere in this report. The discussion and analysis contains "forward looking statements" within the meaning of The Private Securities Litigation Reform Act of 1995. Forward looking statements include management's expectations regarding implementation of its long-term strategic plan, future financial performance, automotive aftermarket trends, levels of competition, business development activities, future capital expenditures, financing sources and availability and the effects of regulation and litigation. Actual results may differ materially from the results discussed in the forward looking statements due to a number of factors beyond our control, including those set forth under the section entitled "Item 1A Risk Factors" elsewhere in this report.

Introduction

The Pep Boys—Manny, Moe & Jack and subsidiaries (the "Company") has been the best place to shop and care for your car since it began operations in 1921. Approximately 19,000 associates are focused on delivering the best customer service in the automotive aftermarket to our customers across our nearly 800 locations located throughout the United States and Puerto Rico. Pep Boys satisfies all of a customer's automotive needs through our unique offering of service, tires, parts and accessories.

Our stores are organized into a hub and spoke network consisting of Supercenters and Service & Tire Centers. Supercenters average approximately 20,000 square feet (our new Supercenter format is approximately 14,000 square feet) and combine do-it-for-me service labor, installed merchandise and tire offerings ("DIFM") with do-it-yourself parts and accessories ("DIY"). Most of our Supercenters

19

Table of Contents

also have a commercial sales program that delivers parts, tires and equipment to automotive repair shops and dealers. Service & Tire Centers, which average approximately 5,000 square feet, provide DIFM services in neighborhood locations that are conveniently located where our customers live or work. Service & Tire Centers are designed to capture market share and leverage our existing Supercenters and support infrastructure. We also operate a handful of legacy DIY only Pep Express stores.