UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-4395

Smith Barney Muni Funds

(Exact name of registrant as specified in charter)

125 Broad Street, New York, NY 10004

(Address of principal executive offices) (Zip code)

Robert I. Frenkel, Esq.

C/o Citigroup Asset Management

300 First Stamford Place

Stamford, CT 06902

(Name and address of agent for service)

Registrant’s telephone number, including area code: (800) 451-2010

Date of fiscal year end: March 31

Date of reporting period: September 30, 2005

| ITEM 1. | REPORT TO STOCKHOLDERS. |

The Semi-Annual Report to Stockholders is filed herewith.

EXPERIENCE

Smith Barney Muni Funds –

Massachusetts Money

Market Portfolio

S E M I - A N N U A L

R E P O R T

SEPTEMBER 30, 2005

INVESTMENT PRODUCTS: NOT FDIC INSURED • NO BANK GUARANTEE • MAY LOSE VALUE

|

| Smith Barney Muni Funds – | ||

|

|

| ||

|

|

| ||

Semi-Annual • September 30, 2005 |

|

| ||

|

|

| ||

|

|

| ||

What’s |

|

|

|

|

| 1 |

| ||

| 4 |

| ||

| 5 |

| ||

| 7 |

| ||

| 13 |

| ||

|

| 14 |

| |

|

| 15 |

| |

|

| 16 |

| |

|

| 17 |

| |

Fund objective The Fund seeks to provide income exempt from both regular federal income tax and Massachusetts personal income tax from a portfolio of high quality short-term municipal obligations selected for liquidity and stability of principal. |

| 23 |

| |

| ||

R. JAY GERKEN, CFA

|

| Dear Shareholder, There was no shortage of potential threats to the U.S. economy during the reporting period. These included record high oil prices, rising short-term interest rates, the devastation inflicted by Hurricanes Katrina and Rita, geopolitical issues, and falling consumer confidence. However, the economy proved to be surprisingly resilient. First quarter 2005 gross domestic product (“GDP”)i growth was 3.8% and second quarter GDP growth was 3.3%, another solid advance. This marked nine consecutive quarters in which GDP grew 3.0% or more. The Federal Reserve Board (“Fed”)ii continued to raise interest rates in an attempt to ward off inflation. After raising rates seven times from June 2004 through March 2005, the Fed increased its target for the federal funds rateiii in 0.25% increments four additional times over the period. All told, the Fed’s 11 rate hikes have brought the target for the federal funds rate from 1.00% to 3.75%. This also represents the longest sustained Fed tightening cycle since 1977-1979. Following the end of the Fund’s reporting period, at its November meeting, the Fed once again raised the target rate by 0.25% to 4.00%. During much of the reporting period, the fixed income market confounded investors as short-term interest rates rose in concert with the Fed rate tightening, while longer-term rates, surprisingly, declined. When the period began, the federal funds target rate was 2.75% and the yield on the 10-year Treasury was 4.13%. When the reporting period ended, the federal funds rate rose to 3.75%. Due to a spike in September, the 10-year yield was 4.29% at that time, slightly higher than when the period began, but still lower than its yield of 4.62% when the Fed began its tightening cycle on June 30, 2004. This trend also occurred in the municipal bond market.

|

Smith Barney Muni Funds 2005 Semi-Annual Report | 1 |

|

| Performance Review As of September 30, 2005, the seven-day current yield for Class A shares of the Smith Barney Muni Funds– Massachusetts Money Market Portfolio was 2.05% and its seven-day effective yield, which reflects compounding, was 2.07%.1 |

Fund Performance as of September 30, 2005 (unaudited) | |||||

Seven-day current yield1 |

| 2.05% |

|

| |

Seven-day effective yield1 |

| 2.07% |

|

| |

The performance shown represents past performance. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown above. |

| ||||

|

| An investment in the Fund is neither insured nor guaranteed by the Federal Deposit Insurance Corporation (“FDIC”) or any other government agency. Although the Fund seeks to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in the Fund. Special Shareholder Notice On June 24, 2005, Citigroup Inc. (“Citigroup”) announced that it has signed a definitive agreement under which Citigroup will sell substantially all of its worldwide asset management business to Legg Mason, Inc. (“Legg Mason”). As part of this transaction, Smith Barney Fund Management LLC (the “Manager”), currently an indirect wholly owned subsidiary of Citigroup, would become an indirect wholly owned subsidiary of Legg Mason. The Manager is the investment manager to the Fund. The transaction is subject to certain regulatory approvals, as well as other customary conditions to closing. Subject to such approvals and the satisfaction of the other conditions, Citigroup expects the transaction to be completed later this year. Under the Investment Company Act of 1940, consummation of the transaction will result in the automatic termination of the investment management contract between the Fund and the Manager. Therefore the Trust’s Board of Trustees has approved a new investment management contract between the Fund and the Manager to become effective |

1 | The seven-day current yield reflects the amount of income generated by the investment during that seven-day period and assumes that the income is generated each week over a 365-day period. The yield is shown as a percentage of the investment. The seven-day effective yield is calculated similarly to the seven-day current yield but, when annualized, the income earned by an investment in the Fund is assumed to be reinvested. The effective yield typically will be slightly higher than the current yield because of the compounding effect of the assumed reinvestment. |

2 | Smith Barney Muni Funds 2005 Semi-Annual Report |

|

| upon the closing of the sale to Legg Mason. The new investment management contract has been presented to shareholders for their approval. Information About Your Fund As you may be aware, several issues in the mutual fund industry have recently come under the scrutiny of federal and state regulators. The Fund’s Manager and some of its affiliates have received requests for information from various government regulators regarding market timing, late trading, fees, and other mutual fund issues in connection with various investigations. The regulators appear to be examining, among other things, the Fund’s response to market timing and shareholder exchange activity, including compliance with prospectus disclosure related to these subjects. The Fund has been informed that the Manager and its affiliates are responding to those information requests, but are not in a position to predict the outcome of these requests and investigations. Important information concerning the Fund and its Manager with regard to recent regulatory developments is contained in the Notes to Financial Statements included in this report. As always, thank you for your confidence in our stewardship of your assets. We look forward to helping you continue to meet your financial goals. Sincerely, R. Jay Gerken, CFA November 11, 2005 |

The information provided is not intended to be a forecast of future events, a guarantee of future results or investment advice. Views expressed may differ from those of the firm as a whole. | |

RISKS: Certain investors may be subject to the Federal Alternative Minimum Tax (AMT), and state and local taxes may apply. Capital gains, if any, are fully taxable. An investment in a money market fund is neither insured nor guaranteed by the FDIC or any other government agency. Although the Fund seeks to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in the Fund. | |

i | Gross domestic product is a market value of goods and services produced by labor and property in a given country. |

ii | The Federal Reserve Board is responsible for the formulation of a policy designed to promote economic growth, full employment, stable prices, and a sustainable pattern of international trade and payments. |

iii | The federal funds rate is the interest rate that banks with excess reserves at a Federal Reserve district bank charge other banks that need overnight loans. |

Smith Barney Muni Funds 2005 Semi-Annual Report | 3 |

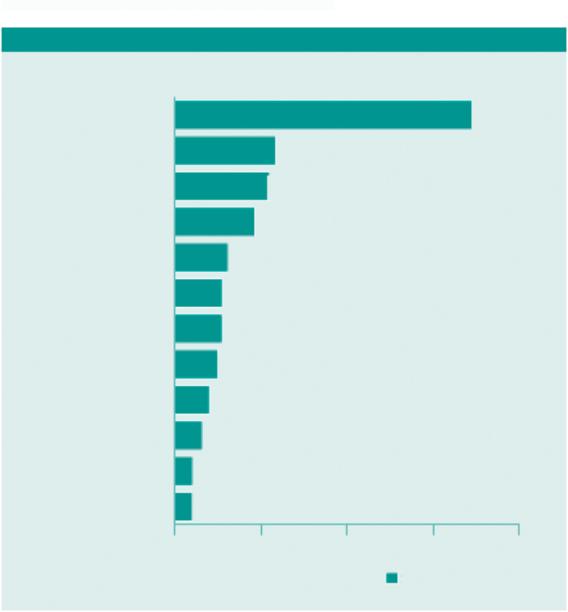

Education

Hospitals

Transportation

General Obligations

Miscellaneous

Life Care Systems

Water & Sewer

Solid Waste

Housing: Multi-Family

Industrial Development

Utilities

Housing: Single-Family

34.5%

11.7%

11.0%

9.3%

6.2%

5.5%

5.5%

5.0%

4.0%

3.2%

2.1%

2.0%

0.0%

10.0%

20.0%

30.0%

40.0%

September 30, 2005

As a Percent of Total Investments

Investment Breakdown

Investment Breakdown†

4 | Smith Barney Muni Funds 2005 Semi-Annual Report |

Example

As a shareholder of the Fund, you may incur two types of costs: (1) transaction costs and (2) ongoing costs, including management fees; distribution fees and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

This example is based on an investment of $1,000 invested on April 1, 2005 and held for the six months ended September 30, 2005.

Actual Expenses

The table below titled “Based on Actual Total Return” provides information about actual account values and actual expenses. You may use the information provided in this table, together with the amount you invested, to estimate the expenses that you paid over the period. To estimate the expenses you paid on your account, divide your ending account value by $1,000 (for example, an $8,600 ending account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled “Expenses Paid During the Period”.

Based on Actual Total Return(1) | ||||||||||||||||||||

|

|

|

| Beginning |

| Ending |

| Annualized |

| Expenses |

| |||||||||

Class A |

|

| 0.91% |

| $ | 1,000.00 |

| $ | 1,009.10 |

|

| 0.66% |

| $ | 3.32 |

|

| |||

(1) | For the six months ended September 30, 2005. | |||||||||||||||||||

(2) | Assumes reinvestment of all distributions, including returns of capital, if any, at net asset value. Total return is not annualized, as it may not be representative of the total return for the year. Performance figures may reflect voluntary fee waivers and/or expense reimbursements. Past performance is no guarantee of future results. In the absence of voluntary fee waivers and/or expense reimbursements, the total return would have been lower. | |||||||||||||||||||

(3) | Expenses are equal to Class A’s annualized expense ratio the number of days in the most recent fiscal half-year, then divided by 365. | |||||||||||||||||||

Smith Barney Muni Funds 2005 Semi-Annual Report | 5 |

Fund Expenses (unaudited) (continued)

Hypothetical Example for Comparison Purposes

The table below titled “Based on Hypothetical Total Return” provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio and an assumed rate of return of 5.00% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use the information provided in this table to compare the ongoing costs of investing in the Fund and other funds. To do so, compare the 5.00% hypothetical example relating to the Fund with the 5.00% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table below are meant to highlight your ongoing costs only and do not reflect any transactional costs. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher.

Based on Hypothetical Total Return(1) | ||||||||||||||||||

|

|

|

| Beginning |

| Ending |

| Annualized |

| Expenses |

| |||||||

Class A |

| 5.00 | % |

| $1,000.00 |

|

| $1,021.76 |

| 0.66 | % |

| $3.35 |

|

| |||

(1) | For the six months ended September 30, 2005. |

(2) | Expenses are equal to Class A’s annualized expense ratio the number of days in the most recent fiscal half-year, then divided by 365. |

6 | Smith Barney Muni Funds 2005 Semi-Annual Report |

| Face |

| Rating‡ |

| Security |

| Value |

| |

Education — 34.7% |

|

|

| ||||||

$ | 5,120,000 |

| VMIG1(a) |

| Massachusetts State College Building Authority MERLOT, PART, Series B-11, |

|

|

|

|

|

|

|

|

| AMBAC-Insured, BPA-Wachovia Bank, 2.760%, 10/5/05 (b) |

| $ | 5,120,000 |

|

|

|

|

|

| Massachusetts State DFA: |

|

|

|

|

|

|

|

|

| Boston University: |

|

|

|

|

| 1,000,000 |

| A-1+ |

| Series R-1, XLCA-Insured, BPA-Societe Generale, 2.650%, 10/6/05 (b) |

|

| 1,000,000 |

|

| 1,400,000 |

| A-1+ |

| Series R-2, XLCA-Insured, BPA-Societe Generale, 2.900%, 10/3/05 (b) |

|

| 1,400,000 |

|

| 3,000,000 |

| A-1+ |

| Series R-3, XLCA-Insured, BPA-Societe Generale, 2.650%, 10/6/05 (b) |

|

| 3,000,000 |

|

| 1,500,000 |

| A-1+ |

| Clark University, Series A, AMBAC-Insured, BPA-Bank of America, 2.750%, |

|

|

|

|

|

|

|

|

| 10/5/05 (b) |

|

| 1,500,000 |

|

| 8,300,000 |

| A-1+ |

| Phillips Academy, BPA-Bank of New York, 2.750%, 10/6/05 (b) |

|

| 8,300,000 |

|

| 5,700,000 |

| A-1+ |

| Smith College Project, 2.730%, 10/6/05 (b) |

|

| 5,700,000 |

|

| 3,900,000 |

| VMIG1(a) |

| St. Mark’s School, LOC-Bank of America, 2.760%, 10/6/05 (b) |

|

| 3,900,000 |

|

| 2,515,000 |

| VMIG1(a) |

| Wentworth Institute, AMBAC-Insured, BPA-State Street Bank & Trust Co., |

|

|

|

|

|

|

|

|

| 2.750%, 10/6/05 (b) |

|

| 2,515,000 |

|

|

|

|

|

| Massachusetts State HEFA: |

|

|

|

|

|

|

|

|

| Amherst College: |

|

|

|

|

| 1,900,000 |

| A-1+ |

| Series F, 2.650%, 10/5/05 (b) |

|

| 1,900,000 |

|

| 2,500,000 |

| A-1+ |

| Series H, 2.700%, 4/3/06 |

|

| 2,500,000 |

|

| 1,500,000 |

| A-1+ |

| Bentley College, Issue K, LOC-Bank of America, 2.790%, 10/5/05 (b) |

|

| 1,500,000 |

|

| 3,000,000 |

| A-1 |

| Berklee College of Music, Series 385, MBIA-Insured, LIQ-Morgan Stanley, |

|

|

|

|

|

|

|

|

| 2.770%, 10/6/05 (b) |

|

| 3,000,000 |

|

|

|

|

|

| Harvard University, Series EE, TECP: |

|

|

|

|

| 2,000,000 |

| A-1+ |

| 2.600%, 10/4/05 |

|

| 2,000,000 |

|

| 2,000,000 |

| A-1+ |

| 2.640%, 10/18/05 |

|

| 2,000,000 |

|

| 3,000,000 |

| A-1+ |

| Massachusetts Institute of Technology, Series J-2, 2.650%, 10/6/05 (b) |

|

| 3,000,000 |

|

| 2,390,000 |

| VMIG1(a) |

| Simmons College, MERLOT, PART Series T, AMBAC-Insured, BPA- |

|

|

|

|

|

|

|

|

| Wachovia Bank, 2.760%, 10/5/05 (b) |

|

| 2,390,000 |

|

| 2,500,000 |

| A-1+ |

| University of Massachusetts, Series A, LOC-Dexia CLF 2.700%, 10/5/05 (b) |

|

| 2,500,000 |

|

| 1,995,000 |

| A-1+ |

| Wellesley College, Issue E, 2.750%, 10/5/05 (b) |

|

| 1,995,000 |

|

|

|

|

|

| Williams College: |

|

|

|

|

| 3,800,000 |

| A-1+ |

| 2.730%, 10/6/05 (b) |

|

| 3,800,000 |

|

| 4,400,000 |

| A-1+ |

| Series E, 2.760%, 10/5/05 (b) |

|

| 4,400,000 |

|

| 3,000,000 |

| VMIG1(a) |

| Massachusetts State IFA, Education Buckingham Browne Nichols, LOC-State |

|

|

|

|

|

|

|

|

| Street Bank, 2.750%, 10/6/05 (b) |

|

| 3,000,000 |

|

|

|

|

|

| Total Education |

|

| 66,420,000 |

|

See Notes to Financial Statements.

Smith Barney Muni Funds 2005 Semi-Annual Report | 7 |

Schedule of Investments (September 30, 2005) (unaudited) (continued) | |||||||||

| Face |

| Rating‡ |

| Security |

| Value |

| |

General Obligations — 9.4% |

|

|

| ||||||

$ | 4,510,000 |

| MIG1(a) |

| Dover & Sherborn Regional School District, BAN 3.000%, 11/10/05 |

| $ | 4,513,806 |

|

|

|

|

|

| Massachusetts State: |

|

|

|

|

| 1,550,000 |

| A-1+ |

| Central Artery, Series A, SPA, BPA-Landesbank Baden-Wurttemberg, 2.830%, |

|

|

|

|

|

|

|

|

| 10/3/05 (b) |

|

| 1,550,000 |

|

| 4,000,000 |

| A-1 |

| MSTC, PART, Series 2002-209, Class A, FSA-Insured, LIQ-Bear Stearns, |

|

|

|

|

|

|

|

|

| 2.800%, 10/5/05 |

|

| 4,000,000 |

|

| 3,000,000 |

| A-1+ |

| Refunding, Series B, BPA-Depfa Bank Plc, 2.780%, 10/6/05 (b) |

|

| 3,000,000 |

|

| 4,901,000 |

| MIG1(a) |

| Newburyport, MA, BAN, 4.000%, due 4/28/06 |

|

| 4,934,407 |

|

|

|

|

|

| Total General Obligations |

|

| 17,998,213 |

|

Hospitals (b) — 11.7% |

|

|

| ||||||

| 9,000,000 |

| VMIG1(a) |

| Massachusetts State DFA, Notre Dame Health Care Center, LOC-KBC Bank NV, |

|

|

|

|

|

|

|

|

| 2.840%, 10/6/05 |

|

| 9,000,000 |

|

|

|

|

|

| Massachusetts State HEFA: |

|

|

|

|

| 2,500,000 |

| A-1 |

| Bay State Medical Center, Series 834, FGIC-Insured, PART, LIQ- Morgan |

|

|

|

|

|

|

|

|

| Stanley, 2.770%, 10/6/05 |

|

| 2,500,000 |

|

|

|

|

|

| Capital Asset Program: |

|

|

|

|

| 700,000 |

| VMIG1(a) |

| Series E, LOC-Bank of America, 2.820%, 10/3/05 |

|

| 700,000 |

|

| 820,000 |

| A-1+ |

| Series M-2, LOC-Bank of America, 2.710%, 10/6/05 |

|

| 820,000 |

|

| 1,100,000 |

| VMIG1(a) |

| Harvard Vanguard Medical Associates, LOC-Bank of America, 2.750%, 10/6/05 |

|

| 1,100,000 |

|

|

|

|

|

| Partners Healthcare: |

|

|

|

|

| 1,500,000 |

| A-1+ |

| Series D-4, BPA- JPMorgan Chase & Co., 2.740%, 10/6/05 |

|

| 1,500,000 |

|

| 1,000,000 |

| A-1+ |

| Series D-6, 2.820%, 10/3/05 |

|

| 1,000,000 |

|

| 2,400,000 |

| A-1+ |

| Series P-2, FSA-Insured, BPA- JPMorgan Chase & Co. & Bayerische |

|

|

|

|

|

|

|

|

| Landesbank, 2.750%, 10/5/05 |

|

| 2,400,000 |

|

| 3,475,000 |

| A-1+ |

| Systems P-1, FSA-Insured, BPA- JPMorgan Chase & Co. & Bayerische |

|

|

|

|

|

|

|

|

| Landesbank, 2.750%, 10/5/05 |

|

| 3,475,000 |

|

|

|

|

|

| Total Hospitals |

|

| 22,495,000 |

|

Housing: Multi-Family (b) — 5.0% |

|

|

| ||||||

| 2,600,000 |

| VMIG1(a) |

| Massachusetts State DFA, MFH, Archstone Readstone, Series A, LOC-PNC Bank, |

|

|

|

|

|

|

|

|

| 2.790%, 10/5/05 (c) |

|

| 2,600,000 |

|

|

|

|

|

| Massachusetts State HFA: |

|

|

|

|

| 5,000,000 |

| A-1+ |

| Housing Revenue, Series F, FSA-Insured, LIQ-Dexia CLF, 2.760%, 10/5/05 |

|

| 5,000,000 |

|

| 2,000,000 |

| VMIG1(a) |

| MFH, Princeton Crossing, Series A, LIQ-FNMA, 2.840%, 10/6/05 (c) |

|

| 2,000,000 |

|

|

|

|

|

| Total Housing: Multi-Family |

|

| 9,600,000 |

|

Housing: Single Family (b) — 2.0% |

|

|

| ||||||

| 3,864,000 |

| VMIG1(a) |

| Massachusetts State HFA, Single Family, Clipper Tax Exempt Trust, Series 98- |

|

|

|

|

|

|

|

|

| 8, PART, AMBAC-Insured, BPA-State Street Bank & Trust Co., 2.780%, 10/6/05 |

|

| 3,864,000 |

|

See Notes to Financial Statements.

8 | Smith Barney Muni Funds 2005 Semi-Annual Report |

Schedule of Investments (September 30, 2005) (unaudited) (continued) | ||||||||||||

| Face | Rating‡ |

| Security |

| Value |

| |||||

Industrial Development (b) — 3.2% |

| |||||||||||

Massachusetts State DFA: | ||||||||||||

$ | 1,845,000 | A-1+ | Ahead Headgear Inc., LOC-Citizen Bank, 2.780%, 10/5/05 (c) | $ | 1,845,000 | |||||||

700,000 | A-1+ | Cider Mills Farms Co.Inc., LOC-Bank of America 2.800%, 10/5/05 (c) |

| 700,000 | ||||||||

2,710,000 | NR | Epichem Inc. Project, LOC-Wachovia Bank, 2.890%, 10/6/05 (c) |

| 2,710,000 | ||||||||

| Massachusetts State IFA: |

|

| |||||||||

500,000 | A-1+ | 420 Newburyport Turnpike, Series 1998, LOC-Bank of America, |

|

| ||||||||

| 2.780%, 10/5/05 |

| 500,000 | |||||||||

400,000 | NR | Peterson American Corp. Project, LOC-JPMorgan Chase & Co., 2.930%, |

|

| ||||||||

| 10/5/05 (c) |

| 400,000 | |||||||||

|

| Total Industrial Development |

| 6,155,000 |

| |||||||

Life Care Systems (b) — 5.5% |

|

| ||||||||||

Massachusetts State DFA: |

|

| ||||||||||

| 3,000,000 | A-1 | Brooksby Village Inc. Project, LOC-LaSalle Bank, 2.730%, 10/6/05 |

| 3,000,000 | |||||||

4,000,000 | A-1+ | Whalers Cove Project, Series A, LOC-Wachovia Bank NA, 2.790%, 10/6/05 (c) |

| 4,000,000 | ||||||||

3,590,000 | VMIG1(a) | Massachusetts State HEFA, CIL Realty of Massachusetts Inc., |

|

| ||||||||

| LOC-Dexia CLF, 2.750%, 10/5/05 |

| 3,590,000 | |||||||||

|

| Total Life Care Systems |

| 10,590,000 |

| |||||||

Miscellaneous — 6.3% |

| |||||||||||

Massachusetts State DFA: |

|

| ||||||||||

| 1,920,000 | A-1+ | Decas Cranberry Products Inc., LOC-Bank of America, 2.800%, 10/5/05 (b)(c) |

| 1,920,000 | |||||||

3,700,000 | A-1+ | Draper Laboratory Issue, MBIA-Insured, LIQ-JP Morgan Chase |

|

| ||||||||

| & Co., 2.710%,10/5/05 (b) |

| 3,700,000 | |||||||||

2,670,000 | A-1+ | Horner Millwork Corp., LOC-Bank of America, 2.800%, 10/5/05 (b)(c) |

| 2,670,000 | ||||||||

3,000,000 | A-1 | RAN, TECP, LOC-Wachovia Bank, 2.730%, 11/28/05 |

| 3,000,000 | ||||||||

800,000 | VMIG1(a) | Massachusetts State IFA, Whitehead Institute Biomed Research, |

|

| ||||||||

| BPA-Bank of America, 2.700%, 10/5/05 (b) |

| 800,000 | |||||||||

|

| Total Miscellaneous |

| 12,090,000 |

| |||||||

Solid Waste — 4.1% |

|

| ||||||||||

Massachusetts State DFA, Solid Waste Disposal Revenue, Newark Group Project: |

|

| ||||||||||

| 500,000 | A-1+ | Series A, LOC- JPMorgan Chase & Co., 2.780%, 10/5/05 (b)(c) |

| 500,000 | |||||||

7,300,000 | A-1+ | Series C, LOC- JPMorgan Chase & Co., 2.780%, 10/5/05 (b)(c) |

| 7,300,000 | ||||||||

|

| Total Solid Waste |

| 7,800,000 |

| |||||||

Transportation — 11.0% |

|

| ||||||||||

Massachusetts Bay Transportation Authority: |

|

| ||||||||||

| 4,700,000 | A-1+ | General Transportation Systems, LOC-Westdeutsche Landesbank, |

|

| |||||||

|

| 2.750%, 10/5/05 (b) |

| 4,700,000 | ||||||||

See Notes to Financial Statements.

Smith Barney Muni Funds 2005 Semi-Annual Report | 9 |

Schedule of Investments (September 30, 2005) (unaudited) (continued) | |||||||||||

| Face | Rating‡ |

| Security |

| Value |

| ||||

Transportation — 11.0% (continued) | |||||||||||

Massachusetts Port Authority, TECP, LOC-Westdeutsche Landesbank: | |||||||||||

$ | 2,000,000 | A-1+ | 2.480%, 10/6/05 | $ | 2,000,000 | ||||||

1,000,000 | A-1+ | 2.500%, 10/6/05 (c) | 1,000,000 | ||||||||

2,000,000 | A-1+ | 2.690%, 11/1/05 (c) | 2,000,000 | ||||||||

4,000,000 | A-1+ | 2.550%, 11/7/05 | 4,000,000 | ||||||||

Massachusetts State Turnpike Authority: | |||||||||||

3,999,000 | VMIG1(a) | Clipper Tax Exempt Trust, PART, Series 00-2, MBIA-Insured, LIQ- | |||||||||

State Street Bank & Trust Co., 2.900%, 2/2/06 | 3,999,000 | ||||||||||

3,400,000 | VMIG1(a) | PART, Series 334, MBIA-Insured, LIQ-Morgan Stanley, | |||||||||

2.770%, 10/6/05 (b) | 3,400,000 | ||||||||||

|

|

|

| Total Transportation |

| 21,099,000 | |||||

Utilities — 2.1% | |||||||||||

4,000,000 | VMIG1(a) | Massachusetts State DFA, ISO New England Inc., | |||||||||

| LOC-Key Bank, 2.770%, 10/6/05 (b) | 4,000,000 | |||||||||

Water & Sewer (b) — 5.5% | |||||||||||

2,800,000 | A-1+ | Boston, MA, Water and Sewer Community Revenue, General Senior | |||||||||

| Series A, LOC-State Street Bank & Trust Co., 2.650%, 10/6/05 | 2,800,000 | |||||||||

Massachusetts State Water Resources, Authority, Multi-Modal, | |||||||||||

General Subordinated: | |||||||||||

Series B: | |||||||||||

1,930,000 | A-1+ | AMBAC-Insured, LIQ-Bank of Nova Scotia, 2.750%, 10/5/05 | 1,930,000 | ||||||||

1,720,000 | A-1+ | FGIC-Insured, LIQ-Bayerische Landesbank, 2.750%, 10/5/05 | 1,720,000 | ||||||||

1,000,000 | A-1+ | Series C, FGIC-Insured, LIQ-Bayerische Landesbank, 2.750%, 10/5/05 | 1,000,000 | ||||||||

3,100,000 | A-1+ | Series D, FGIC-Insured, LIQ-Dexia CLF, 2.750%, 10/5/05 | 3,100,000 | ||||||||

|

|

|

| Total Water & Sewer |

| 10,550,000 | |||||

TOTAL INVESTMENTS — 100.5% | |||||||||||

|

|

| (Cost — $192,661,213#) | 192,661,213 | |||||||

|

|

| Liabilities in Excess of Other Assets — (0.5)% | (1,036,880 | ) | ||||||

|

|

|

| TOTAL NET ASSETS — 100.0% |

| $ | 191,624,333 | ||||

‡ | All ratings are by Standard & Poor’s Ratings Service, unless otherwise footnoted. All ratings are unaudited. |

(a) | Rating by Moody’s Investors Service. All ratings are unaudited. |

(b) | Variable rate demand obligations have a demand feature under which the Fund could tender them back to the issuer on no more than 7 days notice. Coupon rates disclosed are those which are in effect at September 30, 2005. Date shown is the date of the next interest rate change. |

(c) | Income from this issue is considered a preference item for purposes of calculating the alternative minimum tax (AMT). |

# | Aggregate cost for federal income tax purposes is substantially the same. |

See pages 11 through 12 for certain abbreviations and definitions of ratings. |

See Notes to Financial Statements.

10 | Smith Barney Muni Funds 2005 Semi-Annual Report |

Schedule of Investments (September 30, 2005) (unaudited) (continued) |

Abbreviations used in this schedule: | ||

AMBAC | – Ambac Assurance Corporation | |

BAN | – Bond Anticipation Notes | |

BPA | – Bond Purchase Agreement | |

CIL | – Corporation for Independent Living | |

DFA | – Development Finance Agency | |

FGIC | – Financial Guaranty Insurance Company | |

FNMA | – Federal National Mortgage Association | |

FSA | – Financial Security Assurance | |

HEFA | – Health & Educational Facilities Authority | |

HFA | – Housing Finance Authority | |

IFA | – Industrial Finance Agency | |

ISO | – Independent System Operator | |

LIQ | – Liquidity Facility | |

LOC | – Letter of Credit | |

MBIA | – Municipal Bond Investors Assurance Corporation | |

MERLOT | – Municipal Exempt Receipts Liquidity Optional Tender | |

MFH | – Multi-Family Housing | |

MSTC | – Municipal Securities Trust Certificates | |

PART | – Partnership Structure | |

RAN | – Revenue Anticipation Notes | |

SPA | – Standby Bond Purchase Agreement | |

TECP | – Tax Exempt Commercial Paper | |

XLCA | – XL Capital Assurance | |

See Notes to Financial Statements.

Smith Barney Muni Funds 2005 Semi-Annual Report | 11 |

Short-Term Security Ratings (unaudited)

The definitions of the applicable ratings symbols are set forth below:

SP-1 | — |

| Standard & Poor’s highest rating indicating very strong or strong capacity to pay principal and interest; those issues determined to possess overwhelming safety characteristics are denoted with a plus (+) sign. |

A-1 | — |

| Standard & Poor’s highest commercial paper and variable-rate demand obligation (VRDO) rating indicating that the degree of safety regarding timely payment is either overwhelming or very strong; those issues determined to possess overwhelming safety characteristics are denoted with a plus (+) sign. |

VMIG 1 | — |

| Moody’s highest rating for issues having a demand feature- VRDO. |

MIG1 | — |

| Moody’s highest rating for short-term municipal obligations. |

P-1 | — |

| Moody’s highest rating for commercial paper and for VRDO prior to the advent of the VMIG 1 rating. |

NR | — |

| Indicates that the bond is not rated by Standard & Poor’s or Moody’s. |

12 | Smith Barney Muni Funds 2005 Semi-Annual Report |

See Notes to Financial Statements.

Smith Barney Muni Funds 2005 Semi-Annual Report | 13 |

See Notes to Financial Statements.

14 | Smith Barney Muni Funds 2005 Semi-Annual Report |

For the six months ended September 30, 2005 (unaudited) |

|

|

|

|

| ||

|

| September 30 |

| March 31 |

| ||

OPERATIONS: |

|

|

|

|

|

|

|

Net investment income |

|

| $ 1,694,317 |

| $ | 1,628,062 |

|

DISTRIBUTIONS TO SHAREHOLDERS FROM (NOTE 1): |

|

|

|

|

|

|

|

Net investment income |

|

| (1,694,317 | ) |

| (1,628,062 | ) |

Decrease in Net Assets From Distributions to Shareholders |

|

| (1,694,317 | ) |

| (1,628,062 | ) |

FUND SHARE TRANSACTIONS (NOTE 3): |

|

|

|

|

|

|

|

Net proceeds from sale of shares |

|

| 481,262,718 |

|

| 801,144,776 |

|

Reinvestment of distributions |

|

| 1,591,492 |

|

| 1,523,195 |

|

Cost of shares repurchased |

|

| (474,280,359 | ) |

| (842,227,262 | ) |

Increase (Decrease) in Net Assets From Fund Share Transactions |

|

| 8,573,851 |

|

| (39,559,291 | ) |

Increase (Decrease) in Net Assets |

|

| 8,573,851 |

|

| (39,559,291 | ) |

NET ASSETS: |

|

|

|

|

|

|

|

Beginning of period |

|

| 183,050,482 |

|

| 222,609,773 |

|

End of period |

|

| $ 191,624,333 |

| $ | 183,050,482 |

|

See Notes to Financial Statements.

Smith Barney Muni Funds 2005 Semi-Annual Report | 15 |

For a share of beneficial interest outstanding throughout each year ended March 31, unless otherwise noted:

Class A |

| 2005(1) |

| 2005 |

| 2004 |

| 2003 |

| 2002 |

| 2001 |

| ||||||

Net Asset Value, Beginning of Period |

| $ | 1.000 |

| $ | 1.000 |

| $ | 1.000 |

| $ | 1.000 |

| $ | 1.000 |

| $ | 1.000 |

|

Income From Operations: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net investment income and net realized gain |

|

| 0.009 |

|

| 0.008 |

|

| 0.004 |

|

| 0.008 |

|

| 0.018 |

|

| 0.034 |

|

Less Distributions From: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net investment income and net realized gain |

|

| (0.009 | ) |

| (0.008 | ) |

| (0.004 | ) |

| (0.008 | ) |

| (0.018 | ) |

| (0.034 | ) |

Net Asset Value, End of Period |

| $ | 1.000 |

| $ | 1.000 |

| $ | 1.000 |

| $ | 1.000 |

| $ | 1.000 |

| $ | 1.000 |

|

Total Return(2) |

|

| 0.91 | % |

| 0.81 | % |

| 0.44 | % |

| 0.78 | % |

| 1.81 | % |

| 3.46 | % |

Net Assets, End of Period (millions) |

| $ | 192 |

| $ | 183 |

| $ | 223 |

| $ | 254 |

| $ | 300 |

| $ | 336 |

|

Ratios to Average Net Assets: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Gross expenses |

|

| 0.66 | %(3) |

| 0.64 | % |

| 0.61 | % |

| 0.65 | % |

| 0.66 | % |

| 0.66 | % |

Net expenses(4) |

|

| 0.66 | (3) |

| 0.64 | (5) |

| 0.61 |

|

| 0.65 |

|

| 0.65 | (5) |

| 0.65 | (5) |

Net investment income |

|

| 1.80 | (3) |

| 0.79 |

|

| 0.43 |

|

| 0.78 |

|

| 1.80 |

|

| 3.36 |

|

(1) | For the six months ended September 30, 2005 (unaudited). |

(2) | Performance figures may reflect voluntary fee waivers and/or expense reimbursements. Past performance is no guarantee of future results. In the absence of voluntary fee waivers and/or expense reimbursements, the total return would have been lower. Total returns for periods of less than one year are not annualized. |

(3) | Annualized. |

(4) | As a result of a voluntary expense limitation, the ratio of expenses to average net assets of the Fund will not exceed 0.80%. |

(5) | The investment manager voluntarily waived a portion of its management fee. |

See Notes to Financial Statements.

16 | Smith Barney Muni Funds 2005 Semi-Annual Report |

Notes to Financial Statements (unaudited)

1. Organization and Significant Accounting Policies

The Massachusetts Money Market Portfolio (the “Fund”), is a separate investment fund of Smith Barney Muni Funds (“Trust”), a Massachusetts business trust, registered under the Investment Company Act of 1940 (“1940 Act”), as amended, as an open-end management investment company.

The following are significant accounting policies consistently followed by the Fund and are in conformity with U.S. generally accepted accounting principles (“GAAP”). Estimates and assumptions are required to be made regarding assets, liabilities and changes in net assets resulting from operations when financial statements are prepared. Changes in the economic environment, financial markets and any other parameters used in determining these estimates could cause actual results to differ.

(a) Investment Valuation. Money market instruments are valued at amortized cost, in accordance with Rule 2a-7 under the 1940 Act, which approximates market value. This method involves valuing a portfolio security at its cost and thereafter assuming a constant amortization to maturity of any discount or premium. The Fund’s use of amortized cost is subject to its compliance with certain conditions as specified under Rule 2a-7 of the 1940 Act.

(b) Fund Concentration. Since the Fund invests primarily in obligations of issuers within Massachusetts, it is subject to possible concentration risks associated with the economic, political, or legal developments or industrial or regional matters specifically affecting Massachusetts.

(c) Security Transactions and Investment Income. Security transactions are accounted for on a trade date basis. Interest income, adjusted for amortization of premium and accretion of discount, is recorded on the accrual basis. The cost of investments sold is determined by use of the specific identification method. To the extent any issuer defaults on an expected interest payment, the Fund’s policy is to generally halt any additional interest income accruals and consider the realizability of interest accrued up to the date of default.

(d) Distributions to Shareholders. Distributions from net investment income on the shares of the Fund are declared each business day to shareholders of record, and are paid monthly. The Fund intends to satisfy conditions that will enable interest from municipal securities, which is exempt from federal and certain state income taxes, to retain such tax-exempt status when distributed to the shareholders of the Fund. Distributions of net realized gains, if any, are declared at least annually. Distributions are recorded on the ex-dividend date and are determined in accordance with income tax regulations, which may differ from GAAP.

(e) Federal and Other Taxes. It is the Fund’s policy to comply with the federal income and excise tax requirements of the Internal Revenue Code of 1986, as amended, applicable to regulated investment companies. Accordingly, the Fund intends to distribute substantially all of its taxable income and net realized gains on investments, if any, to shareholders each year. Therefore, no federal income tax provision is required in the Fund’s financial statements.

Smith Barney Muni Funds 2005 Semi-Annual Report | 17 |

Notes to Financial Statements (unaudited) (continued)

(f) Reclassification. GAAP requires that certain components of net assets be adjusted to reflect permanent differences between financial and tax reporting. These reclassifications have no effect on net assets or net asset values per share.

2. Management Agreement and Other Transactions with Affiliates

Smith Barney Fund Management LLC (“SBFM”), an indirect wholly-owned subsidiary of Citigroup Inc. (“Citigroup”), acts as investment manager to the Fund. As compensation for its services, the Fund pays SBFM a management fee calculated at an annual rate of 0.475% on the first $1 billion of the Fund’s average daily net assets; 0.450% on the next $1 billion; 0.425% on the next $3 billion; 0.400% on the next $5 billion and 0.375% on the Fund’s average daily net assets in excess of $10 billion. This fee is calculated daily and paid monthly. Effective October 1, 2005, the Fund’s management fee will be calculated daily and payable monthly, in accordance with the following breakpoint schedule:

Average Daily Net Assets | New Rate | |||

First $1 billion |

| 0.450 | % |

|

Next $1 billion |

| 0.425 |

|

|

Next $3 billion |

| 0.400 |

|

|

Next $5 billion |

| 0.375 |

|

|

Over $10 billion |

| 0.350 |

|

|

During the six months ended September 30, 2005, the Fund’s Class A shares had a voluntary expense limitation in place of 0.80%. This expense limitation can be terminated at any time by SBFM.

Citicorp Trust Bank, fsb. (“CTB”), another subsidiary of Citigroup, acts as the Fund’s transfer agent. PFPC Inc. (“PFPC”) acts as the Fund’s sub-transfer agent. CTB receives account fees and asset-based fees that vary according to the size and type of account. PFPC is responsible for shareholder recordkeeping and financial processing for all shareholder accounts and is paid by CTB. For the six months ended September 30, 2005, the Fund paid transfer agent fees of $14,919 to CTB.

Citigroup Global Markets Inc. (“CGM”), another indirect wholly-owned subsidiary of Citigroup, acts as the Fund’s distributor.

Pursuant to a Distribution Plan, the Fund pays a distribution fee with respect to its Class A shares calculated at the annual rate of 0.10% of the average daily net assets of that class. For the six months ended September 30, 2005, total distribution fees, which are accrued daily and paid monthly, were $93,991.

The Fund has adopted a non-qualified deferred compensation plan (the “Plan”), which allows non-interested trustees (“Trustee”) to defer the receipt of all or a portion of their fees until a later date specified by the Trustee. Under the Plan, deferred fees are considered an obligation of the Fund and any payments made pursuant to the Plan will be made from the Fund’s assets.

As of September 30, 2005, the Fund has accrued $1,562, as deferred compensation payable.

18 | Smith Barney Muni Funds 2005 Semi-Annual Report |

Notes to Financial Statements (unaudited) (continued)

Certain officers and one Trustee of the Trust are employees of Citigroup or its affiliates and do not receive compensation from the Trust.

3. Shares of Beneficial Interest

At September 30, 2005, the Trust had an unlimited number of shares of beneficial interest authorized with a par value of $0.001 per share.

Transactions in shares of the Fund were as follows:

Six Months Ended | Year Ended | |||||||

Class A | ||||||||

Shares sold | 481,262,718 | 801,144,776 | ||||||

Shares issued on reinvestment | 1,591,492 | 1,523,195 | ||||||

Shares repurchased | (474,280,359 | ) | (842,227,262 | ) | ||||

Net Increase (Decrease) | 8,573,851 | (39,559,291 | ) | |||||

4. Regulatory Matters

On May 31, 2005, the U.S. Securities and Exchange Commission (“SEC”) issued an order in connection with the settlement of an administrative proceeding against SBFM and CGM relating to the appointment of an affiliated transfer agent for the Smith Barney family of mutual funds (the “Funds”).

The SEC order finds that SBFM and CGM willfully violated Section 206(1) of the Investment Advisers Act of 1940 (“Advisers Act”). Specifically, the order finds that SBFM and CGM knowingly or recklessly failed to disclose to the boards of the Funds in 1999 when proposing a new transfer agent arrangement with an affiliated transfer agent that: First Data Investors Services Group (“First Data”), the Funds’ then-existing transfer agent, had offered to continue as transfer agent and do the same work for substantially less money than before; and that Citigroup Asset Management (“CAM”), the Citigroup business unit that includes the fund’s investment manager and other investment advisory companies, had entered into a side letter with First Data under which CAM agreed to recommend the appointment of First Data as sub-transfer agent to the affiliated transfer agent in exchange, among other things, for a guarantee by First Data of specified amounts of asset management and investment banking fees to CAM and CGM. The order also finds that SBFM and CGM willfully violated Section 206(2) of the Advisers Act by virtue of the omissions discussed above and other misrepresentations and omissions in the materials provided to the Funds’ boards, including the failure to make clear that the affiliated transfer agent would earn a high profit for performing limited functions while First Data continued to perform almost all of the transfer agent functions, and the suggestion that the proposed arrangement was in the Funds’ best interests and that no viable alternatives existed. SBFM and CGM do not admit or deny any wrongdoing or liability. The settlement does not establish wrongdoing or liability for purposes of any other proceeding.

The SEC censured SBFM and CGM and ordered them to cease and desist from violations of Sections 206(1) and 206(2) of the Advisers Act. The order requires

Smith Barney Muni Funds 2005 Semi-Annual Report | 19 |

Notes to Financial Statements (unaudited) (continued)

Citigroup to pay $208.1 million, including $109 million in disgorgement of profits, $19.1 million in interest, and a civil money penalty of $80 million. Approximately $24.4 million has already been paid to the Funds, primarily through fee waivers. The remaining $183.7 million, including the penalty, has been paid to the U.S. Treasury and will be distributed pursuant to a plan prepared by Citigroup and submitted for approval by the SEC. The order also requires that transfer agency fees received from the Funds since December 1, 2004 less certain expenses be placed in escrow and provides that a portion of such fees may be subsequently distributed in accordance with the terms of the order.

The order requires SBFM to recommend a new transfer agent contract to the Fund boards within 180 days of the entry of the order; if a Citigroup affiliate submits a proposal to serve as transfer agent or sub-transfer agent, an independent monitor must be engaged at the expense of SBFM and CGM to oversee a competitive bidding process. Under the order, Citigroup also must comply with an amended version of a vendor policy that Citigroup instituted in August 2004. That policy, as amended, among other things, requires that when requested by a Fund board, CAM will retain at its own expense an independent consulting expert to advise and assist the board on the selection of certain service providers affiliated with Citigroup.

At this time, there is no certainty as to how the proceeds of the settlement will be distributed, to whom such distributions will be made, the methodology by which such distributions will be allocated, and when such distributions will be made. Although there can be no assurance, Citigroup does not believe that this matter will have a material adverse effect on the Fund.

5. Legal Matters

Beginning in August 2005, five class action lawsuits alleging violations of federal securities laws and state law were filed against CGM and SBFM, (collectively, the “Defendants”) based on the May 31, 2005 settlement order issued against the Defendants by the SEC described in Note 4. The complaints seek injunctive relief and compensatory and punitive damages, removal of SBFM as the adviser for the Smith Barney family of funds, rescission of the Funds’ management and other contracts with SBFM, recovery of all fees paid to SBFM pursuant to such contracts, and an award of attorneys’ fees and litigation expenses.

On October 5, 2005, a motion to consolidate the five actions and any subsequently filed, related action was filed. That motion contemplates that a consolidated amended complaint alleging substantially similar causes of action will be filed in the future.

As of the date of this report, CAM believes that resolution of the pending lawsuit will not have a material effect on the financial position or results of operations of the Funds or the ability of the Advisers and their affiliates to continue to render services to the Funds under their respective contracts.

* * *

Beginning in June, 2004, class action lawsuits alleging violations of the federal securities laws were filed against CGM and a number of its affiliates, including SBFM and Salomon Brothers Asset Management Inc (the “Advisers”), substantially all of the mutual funds managed by the Advisers, including the Fund (the “Funds”), and directors or trustees of

20 | Smith Barney Muni Funds 2005 Semi-Annual Report |

Notes to Financial Statements (unaudited) (continued)

the Funds (collectively, the “Defendants”). The complaints alleged, among other things, that CGM created various undisclosed incentives for its brokers to sell Smith Barney and Salomon Brothers funds. In addition, according to the complaints, the Advisers caused the Funds to pay excessive brokerage commissions to CGM for steering clients towards proprietary funds. The complaints also alleged that the defendants breached their fiduciary duty to the Funds by improperly charging Rule 12b-1 fees and by drawing on fund assets to make undisclosed payments of soft dollars and excessive brokerage commissions. The complaints also alleged that the Funds failed to adequately disclose certain of the allegedly wrongful conduct. The complaints sought injunctive relief and compensatory and punitive damages, rescission of the Funds’ contracts with the Advisers, recovery of all fees paid to the Advisers pursuant to such contracts and an award of attorneys’ fees and litigation expenses.

On December 15, 2004, a consolidated amended complaint (the “Complaint”) was filed alleging substantially similar causes of action. While the lawsuit is in its earliest stages, to the extent that the Complaint purports to state causes of action against the Funds, CAM believes the Funds have significant defenses to such allegations, which the Funds intend to vigorously assert in responding to the Complaint.

Additional lawsuits arising out of these circumstances and presenting similar allegations and requests for relief may be filed against the Defendants in the future.

As of the date of this report, CAM and the Funds believe that the resolution of the pending lawsuit will not have a material effect on the financial position or results of operations of the Funds or the ability of the Advisers and their affiliates to continue to render services to the Funds under their respective contracts.

The Defendants have moved to dismiss the complaint. Those motions are pending before the court.

6. Other Matters

On June 24, 2005, Citigroup announced that it has signed a definitive agreement under which Citigroup will sell substantially all of its worldwide asset management business to Legg Mason, Inc. (“Legg Mason”).

As part of this transaction, SBFM (the “Manager”), currently an indirect wholly owned subsidiary of Citigroup, would become an indirect wholly owned subsidiary of Legg Mason. The Manager is the investment manager to the Fund.

The transaction is subject to certain regulatory approvals, as well as other customary conditions to closing. Subject to such approvals and the satisfaction of the other conditions, Citigroup expects the transaction to be completed later this year.

Under the 1940 Act, consummation of the transaction will result in the automatic termination of the Fund’s investment management with the Manager. Therefore, the Trust’s Board of Trustees has approved a new investment management contract between the Fund and the Manager to become effective upon the closing of the sale to Legg Mason. The new investment management contract has been presented to the shareholders of the Fund for their approval.

Smith Barney Muni Funds 2005 Semi-Annual Report | 21 |

Notes to Financial Statements (unaudited) (continued)

The Fund has received information from CAM concerning SBFM, an investment advisory company that is part of CAM. The information received from CAM is as follows:

On September 16, 2005, the staff of the Securities and Exchange Commission (the “Commission”) informed CFM that the staff is considering recommending that the Commission institute administrative proceedings against CFM for alleged violations of Sections 19(a) and 34(b) of the 1940 Act (and related Rule 19a-1). The notification is a result of an industry wide inspection undertaken by the Commission and is based upon alleged deficiencies in disclosures regarding dividends and distributions paid to shareholders of certain funds. In connection with the contemplated proceedings, the staff may seek a cease and desist order and/or monetary damages from SBFM.

Although there can be no assurance, SBFM believes that this matter is not likely to have a material adverse effect on the Fund or SBFM’s ability to perform investment advisory services relating to the Fund.

The Commission staff ‘s recent notification will not affect the sale by Citigroup of substantially all of CAM’s worldwide business to Legg Mason, which Citigroup continues to expect will occur in the fourth quarter of this year.

22 | Smith Barney Muni Funds 2005 Semi-Annual Report |

Board Approval of Management Agreement (unaudited)

Background

The members of the Board of Smith Barney Muni Funds – Massachusetts Money Market Portfolio (the “Fund”), including the Fund’s independent, or non-interested, Board members (the “Independent Board Members”), received information from the Fund’s manager (the “Manager”) to assist them in their consideration of the Fund’s management agreement (the “Management Agreement”). The Board received and considered a variety of information about the Manager and the Fund’s distributor(s), as well as the advisory and distribution arrangements for the Fund and other funds overseen by the Board, certain portions of which are discussed below.

The presentation made to the Board encompassed the Fund and all the funds for which the Board has responsibility. Some funds overseen by the Board have an investment advisory agreement and an administration agreement and some funds have an investment management agreement that encompasses both functions. The discussion below covers both advisory and administrative functions being rendered by the Manager whether a fund has a single agreement in place or both an advisory and administration agreement. The terms “Management Agreement”, “Contractual Management Fee” and “Actual Management Fee” are used in a similar manner to refer to both advisory and administration agreements and their related fees whether a fund has a single agreement or separate agreements in place.

Board Approval of Management Agreement

In approving the Management Agreement, the Fund’s Board, including the Independent Board Members, considered the following factors:

Nature, Extent and Quality of the Services under the Management Agreement

The Board received and considered information regarding the nature, extent and quality of services provided to the Fund by the Manager under the Management Agreement during the past year. The Board also received a description of the administrative and other services rendered to the Fund and its shareholders by the Manager. The Board noted information received at regular meetings throughout the year related to the services rendered by the Manager about the management of the Fund’s affairs and the Manager’s role in coordinating the activities of the Fund’s other service providers. The Board’s evaluation of the services provided by the Manager took into account the Board’s knowledge and familiarity gained as Board members of funds in the Citigroup Asset Management (“CAM”) fund complex, including the scope and quality of the Manager’s investment management and other capabilities and the quality of its administrative and other services. The Board observed that the scope of services provided by the Manager had expanded over time as a result of regulatory and other developments, including maintaining and monitoring its own and the Fund’s expanded compliance programs. The Board also considered the Manager’s response to recent regulatory compliance issues affecting it and the CAM fund complex. The Board reviewed information received from the Manager

Smith Barney Muni Funds 2005 Semi-Annual Report | 23 |

Board Approval of Management Agreement (unaudited) (continued)

regarding the implementation to date of the Fund’s compliance policies and procedures established pursuant to Rule 38a-1 under the Investment Company Act of 1940.

The Board reviewed the qualifications, backgrounds and responsibilities of the Fund’s senior personnel and the portfolio management team primarily responsible for the day-to-day portfolio management of the Fund. The Board also considered the degree to which the Manager implemented organizational changes to improve investment results and the services provided to the CAM fund complex. The Board noted that the Manager’s Office of the Chief Investment Officer, composed of the senior officers of the investment teams managing the funds in the CAM complex, participates in reporting to the Board on investment matters. The Board also considered, based on its knowledge of the Manager and its affiliates, the financial resources available to CAM and its parent organization, Citigroup Inc.

The Board also considered the Manager’s brokerage policies and practices, the standards applied in seeking best execution, the Manager’s policies and practices regarding soft dollars, the use of a broker affiliated with the Manager and the existence of quality controls applicable to brokerage allocation procedures. In addition, management also reported to the Board on, among other things, its business plans, recent organizational changes and portfolio manager compensation plan.

At the Board’s request following the conclusion of the 2004 contract continuance discussions, the Manager prepared and provided to the Board in connection with the 2005 discussions an analysis of complex-wide management fees, which, among other things, set out a proposed framework of fees based on asset classes. The Board engaged the services of independent consultants to assist it in evaluating the Fund’s fees generally and within the context of the framework.

The Board concluded that, overall, the nature, extent and quality of services provided (and expected to be provided) under the Management Agreement were acceptable.

Fund Performance

The Board received and considered performance information for the Fund as well as for a group of funds (the “Performance Universe”) selected by Lipper, Inc. (“Lipper”), an independent provider of investment company data. The Board was provided with a description of the methodology Lipper used to determine the similarity of the Fund with the funds included in the Performance Universe. The Board also noted that it had received and discussed with management information throughout the year at periodic intervals comparing the Fund’s performance against its benchmark(s).

The information comparing the Fund’s performance to that of its Performance Universe, consisting of all retail and institutional funds classified as “Massachusetts tax-exempt money market funds” by Lipper, showed that the Fund’s performance for the 1- and 3-year periods was below the median and for the 5-year period was within the median range. Notwithstanding this and based on their review, the Board continues to retain confidence in the Manager to seek to achieve the Fund’s investment objective and carry out its investment strategies.

24 | Smith Barney Muni Funds 2005 Semi-Annual Report |

Board Approval of Management Agreement (unaudited) (continued)

Management Fees and Expense Ratios

The Board reviewed and considered the contractual management fee (the “Contractual Management Fee”) payable by the Fund to the Manager in light of the nature, extent and quality of the management services provided by the Manager. The Board also reviewed and considered whether fee waiver and/or expense reimbursement arrangements are currently in place for the Fund and considered the actual fee rate (after taking any waivers and reimbursements into account) (the “Actual Management Fee”) and whether any fee waivers and reimbursements could be discontinued.

Additionally, the Board received and considered information comparing the Fund’s Contractual Management Fees and Actual Management Fee and the Fund’s overall expenses with those of funds in both the relevant expense group and a broader group of funds, each selected and provided by Lipper. The Board also reviewed information regarding fees charged by the Manager to other U.S. clients investing primarily in an asset class similar to that of the Fund including, where applicable, separate accounts. The Manager reviewed with the Board the significant differences in scope of services provided to the Fund and to these other clients, noting that the Fund is provided with administrative services, office facilities, Fund officers (including the Fund’s chief executive, chief financial and chief compliance officers), and that the Manager coordinates and oversees the provision of services to the Fund by other Fund providers. The Board considered the fee comparisons in light of the differences required to manage these different types of accounts. The Board received an analysis of complex-wide management fees provided by the Manager, which, among other things, set out a proposed framework of fees based on asset classes.

Management also discussed with the Board the Fund’s distribution arrangements. The Board was provided with information concerning revenues received by and certain expenses incurred by the Fund’s affiliated distributors and how the amounts received by the distributors are paid.

The information comparing the Fund’s Class A shares’ Contractual and Actual Management Fees as well as its actual total expense ratio to its Expense Group, consisting of 8 retail no-load funds (including the Fund) classified as “Massachusetts tax-exempt money market funds” by Lipper, showed that the Fund’s Contractual and Actual Management Fees were within the range of management fees paid by the other funds in the Expense Group and, indeed, the Contractual Management Fees were better than the median. The Board noted that the Fund’s actual total expense ratio was also better than the median. After discussion with the Board, the Manager offered to and will reduce the Contractual Management Fees with the effect of reducing fees by 0.025%.

Taking all of the above into consideration, the Board determined that the Management Fee was reasonable in light of the nature, extent and quality of the services provided to the Fund under the Management Agreement.

Smith Barney Muni Funds 2005 Semi-Annual Report | 25 |

Board Approval of Management Agreement (unaudited) (continued)

Manager Profitability

The Board received and considered a profitability analysis of the Manager and its affiliates in providing services to the Fund. The Board also received profitability information with respect to the CAM fund complex as a whole. In addition, the Board received information with respect to the Manager’s allocation methodologies used in preparing this profitability data as well as a report from an outside consultant that had reviewed the Manager’s methodology. The Manager’s profitability was considered not excessive in light of the nature, extent and quality of the services provided to the Fund.

Economies of Scale

The Board received and discussed information concerning whether the Manager realizes economies of scale as the Fund’s assets grow beyond current levels. However, because of the nature of the Manager’s business, the Board could not reach definitive conclusions as to whether the Manager might realize economies of scale or how great they may be.

The Board noted that the Fund’s asset level exceeded the breakpoints (or would exceed any proposed breakpoints) and, as a result, the Fund and its shareholders realized or would realize the benefit of a lower total expense ratio than if no breakpoints had been in place. The Board also noted that as the Fund’s assets have increased over time, it has realized other economies of scale as certain expenses, such as fees for Board members, auditors and legal fees, become a smaller percentage of overall assets.

The Board noted that Management Fee effective on October 1, 2005 will be 0.45% of the first $1 billion of assets; 0.425% of the next $1 billion of assets; 0.40% of the next $3 billion of assets; 0.375% of the next $5 billion of assets and 0.35% of assets over $10 billion.

Other Benefits to the Manager

The Board considered other benefits received by the Manager and its affiliates as a result of their relationship with the Fund, including soft dollar arrangements, receipt of brokerage and the opportunity to offer additional products and services to Fund shareholders.

In light of the costs of providing investment management and other services to the Fund and the Manager’s ongoing commitment to the Fund, the profits and other ancillary benefits that the Manager and its affiliates received were considered reasonable.

In light of all of the foregoing, the Board approved the Management Agreement to continue for another year.

No single factor reviewed by the Board was identified by the Board as the principal factor in determining whether to approve the Management Agreement. The Independent Board Members were advised by separate independent legal counsel throughout the process. The Board discussed the proposed continuance of the Management Agreement in a private session with their independent legal counsel at which no representatives of the Manager were present.

26 | Smith Barney Muni Funds 2005 Semi-Annual Report |

(This page intentionally left blank.)

(This page intentionally left blank.)

|

| Smith Barney Muni Funds – |

| ||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| TRUSTEES |

| INVESTMENT MANAGER |

|

|

| Lee Abraham |

| Smith Barney Fund |

|

|

| Jane F. Dasher |

| Management LLC |

|

|

| Donald R. Foley |

|

|

|

|

| R. Jay Gerken, CFA |

| DISTRIBUTOR |

|

|

| Chairman |

| Citigroup Global Markets Inc. |

|

|

| Richard E. Hanson, Jr. |

|

|

|

|

| Paul Hardin |

| CUSTODIAN |

|

|

| Roderick C. Rasmussen |

| State Street Bank and |

|

|

| John P. Toolan |

| Trust Company |

|

|

|

|

|

|

|

|

| OFFICERS |

| TRANSFER AGENT |

|

|

| R. Jay Gerken, CFA |

| Citigroup Trust Bank, fsb. |

|

|

| President and |

| 125 Broad Street, 11th Floor |

|

|

| Chief Executive Officer |

| New York, New York 10004 |

|

|

|

|

|

|

|

|

| Andrew B. Shoup |

| SUB-TRANSFER AGENT |

|

|

| Senior Vice President and |

| PFPC Inc. |

|

|

| Chief Administrative Officer |

| P.O. Box 9699 |

|

|

|

|

| Providence, Rhode Island |

|

|

| Robert J. Brault |

| 02940-9699 |

|

|

| Chief Financial Officer |

|

|

|

|

| and Treasurer |

| INDEPENDENT |

|

|

|

|

| REGISTERED PUBLIC |

|

|

| Julie P. Callahan, CFA |

| ACCOUNTING FIRM |

|

|

| Vice President and |

| KPMG LLP |

|

|

| Investment Officer |

| 345 Park Avenue |

|

|

|

|

| New York, NY 10154 |

|

|

| Joseph P. Deane |

|

|

|

|

| Vice President and |

|

|

|

|

| Investment Officer |

|

|

|

|

|

|

|

|

|

|

| Andrew Beagley |

|

|

|

|

| Chief Anti-Money Laundering |

|

|

|

|

| Compliance Officer and |

|

|

|

|

| Chief Compliance Officer |

|

|

|

|

|

|

|

|

|

|

| Robert I. Frenkel |

|

|

|

|

| Secretary and |

|

|

|

|

| Chief Legal Officer |

|

|

|

|

|

|

|

|

|

Smith Barney Muni Funds –

Massachusetts Money

Market Portfolio

The Fund is a separate investment fund of the Smith Barney Muni Funds, a Massachusetts business trust.

SMITH BARNEY MUNI FUNDS

Smith Barney Mutual Funds

125 Broad Street

10th Floor, MF-2

New York, New York 10004

The Fund files its complete schedule of portfolio holdings with the Securities and Exchange Commission for the first and third quarters of each fiscal year on Form N-Q. The Fund’s Forms N-Q are available on the Commission’s website at www.sec.gov. The Fund’s Forms N-Q may be reviewed and copied at the Commission’s Public Reference Room in Washington, D.C., and information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330. To obtain information on Form N-Q from the Fund, shareholders can call 1-800-451-2010.

Information on how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30 and a description of the policies and procedures that the Fund uses to determine how to vote proxies relating to portfolio securities is available (1) without charge, upon request, by calling

1-800-451-2010, and (2) on the Fund’s website at www.citigroupam.com and (3) on the SEC’s website at www.sec.gov.

This report is submitted for the general information of the shareholders of Smith Barney Muni Funds – Massachusetts Money Market Portfolio and is not intended for use by the general public.

This report must be

preceded or accompanied

by a free prospectus.

Investors should consider the Fund’s investment objectives, risks, charges and expenses carefully before investing. The prospectus contains this and other important information about the Fund. Please read the prospectus carefully before investing.

www.citigroupam.com

©2005 Citigroup Global Markets Inc. Member NASD, SIPC

FD01908 11/05 05-9298

| ITEM 2. | CODE OF ETHICS. |

| Not Applicable. |

| ITEM 3. | AUDIT COMMITTEE FINANCIAL EXPERT. |

| Not Applicable. |

| ITEM 4. | PRINCIPAL ACCOUNTANT FEES AND SERVICES. |

| Not Applicable. |

| ITEM 5. | AUDIT COMMITTEE OF LISTED REGISTRANTS. |

| Not Applicable. |

| ITEM 6. | SCHEDULE OF INVESTMENTS. |

| Not Applicable. |

| ITEM 7. | DISCLOSURE OF PROXY VOTING POLICIES AND PROCEDURES FOR CLOSED-END MANAGEMENT INVESTMENT COMPANIES. |

| Not Applicable. |

| ITEM 8. | [RESERVED] |

| ITEM 9. | PURCHASES OF EQUITY SECURITIES BY CLOSED-END MANAGEMENT INVESTMENT COMPANY AND AFFILIATED PURCHASERS. |

| Not Applicable. |

| ITEM 10. | SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS. |

| Not Applicable. |

| ITEM 11. | CONTROLS AND PROCEDURES. |

| (a) | The registrant’s principal executive officer and principal financial officer have concluded that the registrant’s disclosure controls and procedures (as defined in Rule 30a- 3(c) under the Investment Company Act of 1940, as amended (the “1940 Act”)) are effective as of a date within 90 days of the filing date of this report that includes the disclosure required by this paragraph, based on their evaluation of the disclosure controls and procedures required by Rule 30a-3(b) under the 1940 Act and 15d-15(b) under the Securities Exchange Act of 1934. |

| (b) | There were no changes in the registrant’s internal control over financial reporting (as defined in Rule 30a-3(d) under the 1940 Act) that occurred during the registrant’s last fiscal half-year (the registrant’s second fiscal half-year in the case of an annual report) that have materially affected, or are likely to materially affect the registrant’s internal control over financial reporting. |

| ITEM 12. | EXHIBITS. |

| (a) | Not applicable. |

| (b) | Attached hereto. |

| Exhibit 99.CERT | Certifications pursuant to section 302 of the Sarbanes-Oxley Act of 2002 |

| Exhibit 99.906CERT | Certifications pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, the registrant has duly caused this Report to be signed on its behalf by the undersigned, there unto duly authorized.

Smith Barney Muni Fund

| By: | /s/ R. Jay Gerken R. Jay Gerken Chief Executive Officer of Smith Barney Muni Funds |

| Date: | December 7, 2005 |

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, this report has been signed below by the following persons on behalf of the registrant and in the capacities and on the dates indicated.

| By: | /s/ R. Jay Gerken R. Jay Gerken Chief Executive Officer of Smith Barney Muni Funds. |

| Date: | December 7, 2005 |

| By: | /s/ Robert J. Brault Robert J. Brault Chief Financial Officer of Smith Barney Muni Funds |

| Date: | December 7, 2005 |