UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-4395

Smith Barney Muni Funds

(Exact name of registrant as specified in charter)

125 Broad Street, New York, NY 10004

(Address of principal executive offices) (Zip code)

Robert I. Frenkel, Esq.

Smith Barney Fund Management LLC

300 First Stamford Place

Stamford, CT 06902

(Name and address of agent for service)

Registrant’s telephone number, including area code: (800) 451-2010

Date of fiscal year end: March 31

Date of reporting period: March 31, 2005

ITEM 1. REPORT TO STOCKHOLDERS.

The Annual Report to Stockholders is filed herewith.

SMITH BARNEY MUNI FUNDS

NEW YORK MONEY MARKET PORTFOLIO

NEW YORK PORTFOLIO

ANNUAL REPORT | MARCH 31, 2005

NOT FDIC INSURED • NOT BANK GUARANTEED • MAY LOSE VALUE

WHAT’S INSIDE

LETTER FROM THE CHAIRMAN

R. JAY GERKEN, CFA

Chairman, President and Chief Executive Officer

Dear Shareholder,

Despite rising interest rates, continued high oil prices, geopolitical concerns and uncertainties surrounding the U.S. Presidential election, the U.S. economy continued to expand during the period. Given the strength of the economy and surging energy prices, the Federal Reserve Board (“Fed”)i raised its federal funds rateii target seven times during the fiscal year in an attempt to ward off inflation. The Fed raised its target rate by an additional 0.25% to 3.00% at its May meeting, after the Fund’s reporting period.

This market environment can be a positive for short-term instruments such as money market securities. Rising rates result in higher levels of income offered by new short-term securities. Throughout the one-year period, money market yields rose as these securities closely tracked the rising fed funds target rate.

Regardless of the economic expansion and higher interest rates, the overall bond market posted a modest gain during the period. Municipal bond credit quality continued to improve, as municipalities benefited from higher tax revenues, driven by improving economic growth and fiscal discipline. This caused municipal credit quality spreads to tighten.

Please read on for a more detailed look at prevailing economic and market conditions during the Funds’ fiscal year and to learn how those conditions have affected Fund performance.

Information About Your Fund

As you may be aware, several issues in the mutual fund industry have recently come under the scrutiny of federal and state regulators. The Funds’ Adviser and some of its affiliates have received requests for information from various government regulators regarding market timing, late trading, fees, and other mutual fund issues in connection with various investigations. The regulators appear to be examining, among other things, the Funds’ response to market timing and shareholder exchange activity, including compliance with prospectus disclosure related to these subjects. The Funds have been informed that the Adviser and its affiliates are responding to those information requests, but are not in a position to predict the outcome of these requests and investigations.

1 Smith Barney Muni Funds | 2005 Annual Report

Important information concerning the Funds and its Adviser with regard to recent regulatory developments is contained in the “Additional Information” note in the Notes to the Financial Statements included in this report.

As always, thank you for your confidence in our stewardship of your assets. We look forward to helping you continue to meet your financial goals.

Sincerely,

R. Jay Gerken, CFA

Chairman, President and Chief Executive Officer

May 3, 2005

| i | The Federal Reserve Board is responsible for the formulation of a policy designed to promote economic growth, full employment, stable prices, and a sustainable pattern of international trade and payments. |

| ii | The federal funds rate is the interest rate that banks with excess reserves at a Federal Reserve district bank charge other banks that need overnight loans. |

2 Smith Barney Muni Funds | 2005 Annual Report

MANAGER OVERVIEW

JOSEPH P. DEANE

Vice President and Investment Officer

JULIE P. CALLAHAN, CFA

Vice President and Investment Officer

New York Money Market Portfolio

Performance Review

As of March 31, 2005, the seven-day current yield for Class A shares of the Smith Barney Muni Funds — New York Money Market Portfolio was 1.48% and its seven-day effective yield, which reflects compounding, was 1.49%.1

SMITH BARNEY MUNI FUNDS — NEW YORK MONEY MARKET PORTFOLIO

YIELDS AS OF MARCH 31, 2005

(unaudited)

| | | | |

| | | Seven-Day

Current Yield1 | | Seven-Day

Effective Yield1 |

| | | | | |

Class A Shares | | 1.48% | | 1.49% |

| | | | | |

Class Y Shares | | 1.61% | | 1.62% |

The performance shown represents past performance. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown above.

Yields will fluctuate and may reflect reimbursements and/or fee waivers, without which the performance would have been lower.

An investment is neither insured nor guaranteed by the Federal Deposit Insurance Corporation (“FDIC”) or any other government agency. Although the fund seeks to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in the fund.

Certain investors may be subject to the federal Alternative Minimum Tax, and state and local taxes may apply. Capital gains, if any, are fully taxable. Please consult your personal tax or legal adviser.

| 1 | The seven-day effective yield is calculated similarly to the seven-day current yield but, when annualized, the income earned by an investment in the fund is assumed to be reinvested. The effective yield typically will be slightly higher than the current yield because of the compounding effect of the assumed reinvestment. |

3 Smith Barney Muni Funds | 2005 Annual Report

Investment Approach

During the period, the Fund included a significant amount of municipal obligations backed by school districts and revenue bonds. Revenue bonds are issued to finance public works such as tunnels, sewer systems and bridges, and the issuers’ finances are supported directly by the operations of these systems. The Fund maintained a diversified mix of securities that included commercial paper, fixed-income notes and variable-rate demand notes.

Given the current rate environment and expectations that interest rates will continue to rise, we continued to maintain a cautious maturity stance in the municipal money market portfolio. While no one can say with any certainty where interest rates will head, as of the period’s close, we felt this strategy was prudent considering the close proximity of yields on shorter- and longer-term money market instruments given the recent economic environment.

Municipal Market Review

The U.S. economy was surprisingly resilient during the one year period ended March 31, 2005. Following a 3.3% gain in the second quarter of 2004, gross domestic product (“GDP”)i growth was a robust 4.0% in the third quarter and 3.8% in the fourth quarter. On April 28, after the reporting period ended, first quarter 2005 GDP growth estimates came in at 3.1%.

Given the overall strength of the economy, the Federal Reserve Board (“Fed”)ii moved to raise interest rates to head off inflation. As expected, the Fed increased its target for the federal funds rateiii by 0.25% to 1.25% on June 30, 2004 — the first rate hike in four years. The Fed again raised rates in 0.25% increments during its next six meetings, bringing the target for the federal funds rate from 1.00% to 2.75% by the end of March. The Fed raised its target rate by an additional 0.25% to 3.00% at its May meeting, after the Fund’s reporting period.

For much of the reporting period, the fixed income market confounded many investors as short-term interest rates rose in concert with the Fed rate tightening, while longer-term rates, surprisingly, remained fairly steady. However, this changed late in the period, coinciding with the Fed’s official statement accompanying its March rate hike. While the Fed continued to say it expected to raise rates at a “measured” pace, it made several adjustments to its statement, which some investors interpreted to mean larger rate hikes could be possible in the future. This subsequently caused longer-term interest rates to rise sharply.

For the period, the municipal bond market, represented by the Lehman Brothers Municipal Bond Index,iv rose 2.67% for the year. Like the other fixed income markets, longer maturity munis performed better than their shorter-term counterparts.

4 Smith Barney Muni Funds | 2005 Annual Report

Municipal money market yields rose during the fiscal year as a whole. This trend began in the second quarter of 2004, in anticipation of the first Fed rate increase. Monetary policy was viewed as being accommodative and the Fed was seen as needing to shift to a less stimulative stance.

Thank you for your investment in the Smith Barney Muni Funds — New York Money Market Portfolio. As ever, we appreciate that you have chosen us to manage your assets and we remain focused on achieving the Fund’s investment goals.

Sincerely,

| | |

| |  |

| Joseph P. Deane | | Julie P. Callahan, CFA |

Vice President and

Investment Officer | | Vice President and

Investment Officer |

May 3, 2005

The information provided is not intended to be a forecast of future events, a guarantee of future results or investment advice. Views expressed may differ from those of the firm as a whole.

RISKS: Certain Investors may be subject to the federal Alternative Minimum Tax, and state and local taxes will apply. Capital gains, if any, are fully taxable. An investment in a money market fund is neither insured nor guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Although the Fund seeks to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in the Fund.

All index performance reflects no deduction for fees, expenses or taxes. Please note that an investor cannot invest directly in an index.

| i | Gross domestic product is a market value of goods and services produced by labor and property in a given country. |

| ii | The Federal Reserve Board is responsible for the formulation of a policy designed to promote economic growth, full employment, stable prices, and a sustainable pattern of international trade and payments. |

| iii | The federal funds rate is the interest rate that banks with excess reserves at a Federal Reserve district bank charge other banks that need overnight loans. |

| iv | The Lehman Brothers Municipal Bond Index is a broad measure of the municipal bond market with maturities of at least one year. |

5 Smith Barney Muni Funds | 2005 Annual Report

MANAGER OVERVIEW

JOSEPH P. DEANE

Vice President and Investment Officer

DAVID T. FARE

Vice President and Investment Officer

New York Portfolio

Performance Review

For the 12 months ended March 31, 2005, Class A shares of the Smith Barney Muni Funds — New York Portfolio, excluding sales charges, returned 2.28%. These shares outperformed the Lipper New York Municipal Debt Funds Category Average,1 which was 2.07%. The Fund’s unmanaged benchmark,

PERFORMANCE SNAPSHOT

AS OF MARCH 31, 2005

(excluding sales charges)

(unaudited)

| | | | | | |

| | | 6 Months | | | 12 Months | |

| | | | | | | |

New York Portfolio — Class A Shares | | 1.00 | % | | 2.28 | % |

| | | | | | | |

Lehman Brothers Municipal Bond Index | | 1.21 | % | | 2.67 | % |

| | | | | | | |

Lipper New York Municipal Debt Funds Category Average | | 0.99 | % | | 2.07 | % |

The performance shown represents past performance. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown above. Principal value and investment returns will fluctuate and investors’ shares, when redeemed, may be worth more or less than their original cost. To obtain performance data current to the most recent month-end, please visit our website at www.citigroupam.com.

Performance figures may reflect reimbursements and/or fee waivers, without which the performance would have been lower.

Class A share returns assume the reinvestment of income dividends and capital gains distributions at net asset value and the deduction of all fund expenses. Returns have not been adjusted to include sales charges that may apply when shares are purchased or the deduction of taxes that a shareholder would pay on fund distributions. Excluding sales charges, Class B shares returned 0.73%, Class C shares returned 0.79% and Class Y shares returned 1.09% over the six months ended March 31, 2005. Excluding sales charges, Class B shares returned 1.72%, Class C shares returned 1.69% and Class Y shares returned 2.38% over the twelve months ended March 31, 2005.

Lipper, Inc. is a major independent mutual-fund tracking organization. Returns are based on the period ended March 31, 2005, including the reinvestment of dividends and capital gains distributions, if any, calculated among the 110 funds for the six-month period and among the 110 funds for the 12-month period in the Fund’s Lipper category and excluding sales charges.

| 1 | Lipper, Inc. is a major independent mutual-fund tracking organization. Returns are based on the 12-month period ended March 31, 2005, including the reinvestment of dividends and capital gains, if any, calculated among the 110 funds in the Fund’s Lipper category, and excluding sales charges. |

6 Smith Barney Muni Funds | 2005 Annual Report

the Lehman Brothers Municipal Bond Indexi, returned 2.67% for the same period.

Certain investors may be subject to the federal Alternative Minimum Tax, and state and local taxes may apply. Capital gains, if any, are fully taxable. Please consult your personal tax or legal adviser.

Investment Approach

Over the period, we maintained a lower-duration approach. This more defensive approach to interest rate risk resulted in a smoother ride for investors who held the fund over the period in comparison to longer-duration portfolios.

While rising interest rates are generally troublesome for longer-term fixed income securities, since bond prices decline as rates are expected to rise, rising rates result in higher levels of income on new bonds issued in the future. In the recent market and rate environment, we believe that this cautious approach to managing interest rate risk is more prudent than a longer-duration strategy. During the period, we maintained a focus on targeting issues with competitive coupons in a diverse cross-section of market segments that we believed would continue to offer favorable prospects on a risk/reward basis.

Municipal Market Review

The U.S. economy was surprisingly resilient during the one year period ended March 31, 2005. Following a 3.3% gain in the second quarter of 2004, gross domestic product (“GDP”)ii growth was a robust 4.0% in the third quarter and 3.8% in the fourth quarter. On April 28, after the reporting period ended, first quarter 2005 GDP growth estimates came in at 3.1%.

Given the overall strength of the economy, the Federal Reserve Board (“Fed”)iii moved to raise interest rates to head off inflation. As expected, the Fed increased its target for the federal funds rateiv by 0.25% to 1.25% on June 30, 2004 — the first rate hike in four years. The Fed again raised rates in 0.25% increments during its next six meetings, bringing the target for the federal funds rate from 1.00% to 2.75% by the end of March. The Fed raised its target rate by an additional 0.25% to 3.00% at its May meeting, after the Fund’s reporting period.

For much of the reporting period, the fixed income market confounded many investors as short-term interest rates rose in concert with the Fed rate tightening, while longer-term rates, surprisingly, remained fairly steady. However, this changed late in the period, coinciding with the Fed’s official statement accompanying its March rate hike. While the Fed continued to say it expected to raise rates at a “measured” pace, it made several adjustments to its statement, which some investors interpreted to mean larger rate hikes could be possible in the future. This subsequently caused longer-term interest rates to rise sharply.

7 Smith Barney Muni Funds | 2005 Annual Report

For the period, the municipal bond market, represented by the Lehman Brothers Municipal Bond Index, rose 2.67% for the year. Like the other fixed income markets, longer maturity munis performed better than their shorter-term counterparts.

Municipal money market yields rose during the fiscal year as a whole. This trend began in the second quarter of 2004, in anticipation of the first Fed rate increase. Monetary policy was viewed as being accommodative and the Fed was seen as needing to shift to a less stimulative stance.

Thank you for your investment in the Smith Barney Muni Funds — New York Portfolio. As ever, we appreciate that you have chosen us to manage your assets and we remain focused on achieving the Fund’s investment goals.

Sincerely,

| | |

| |  |

| Joseph P. Deane | | David T. Fare |

Vice President and

Investment Officer | | Vice President and

Investment Officer |

May 3, 2005

The information provided is not intended to be a forecast of future events, a guarantee of future results or investment advice. Views expressed may differ from those of the firm as a whole.

RISKS: Certain Investors may be subject to the federal Alternative Minimum Tax, and state and local taxes will apply. Capital gains, if any, are fully taxable. Keep in mind, that the Fund’s investments are subject to interest rate and credit risk. As interest rates rise, bond prices fall, reducing the value of the Fund’s share price. As a non-diversified fund, it can invest a larger percentage of its assets in fewer issues than a diversified fund. This may magnify the Fund’s losses from events affecting a particular issuer. The Fund may use derivatives, such as options and futures, which can be illiquid, may disproportionately increase losses, and have a potentially large impact on Fund performance.

All index performance reflects no deduction for fees, expenses or taxes. Please note an investor cannot invest directly in an index.

| i | The Lehman Brothers Municipal Bond Index is a broad measure of the municipal bond market with maturities of at least one year. |

| ii | Gross domestic product is a market value of goods and services produced by labor and property in a given country. |

| iii | The Federal Reserve Board is responsible for the formulation of a policy designed to promote economic growth, full employment, stable prices, and a sustainable pattern of international trade and payments. |

| iv | The federal funds rate is the interest rate that banks with excess reserves at a Federal Reserve district bank charge other banks that need overnight loans. |

8 Smith Barney Muni Funds | 2005 Annual Report

New York Money Market Portfolio

Fund at a Glance (unaudited)

9 Smith Barney Muni Funds | 2005 Annual Report

New York Money Market Portfolio

Fund Expenses (unaudited)

Example

As a shareholder of the Fund, you may incur two types of costs: (1) transaction costs, including front-end and back-end sales charges (loads) on purchase payments, reinvested dividends, or other distributions; and (2) ongoing costs, including management fees; distribution and/or service (12b-1) fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

This example is based on an investment of $1,000 invested on October 1, 2004 and held for the six months ended March 31, 2005.

Actual Expenses

The table below titled “Based on Actual Total Return” provides information about actual account values and actual expenses. You may use the information provided in this table, together with the amount you invested, to estimate the expenses that you paid over the period. To estimate the expenses you paid on your account, divide your ending account value by $1,000 (for example, an $8,600 ending account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled “Expenses Paid During the Period”.

Based on Actual Total Return(1)

| | | | | | | | | | | | | | | |

| | | Actual

Total

Return(2) | | | Beginning

Account

Value | | Ending Account

Value | | Annualized

Expense

Ratio | | | Expenses

Paid During

the Period(3) |

Class A | | 0.59 | % | | $ | 1,000.00 | | $ | 1,005.90 | | 0.60 | % | | $ | 3.00 |

|

Class Y | | 0.65 | | | | 1,000.00 | | | 1,006.50 | | 0.48 | | | | 2.40 |

|

| (1) | | For the six months ended March 31, 2005. |

| (2) | | Assumes reinvestment of all dividends and capital gain distributions, if any, at net asset value. Total return is not annualized, as it may not be representative of the total return for the year. Performance figures may reflect voluntary fee waivers and/or expense reimbursements. Past performance is no guarantee of future results. In the absence of voluntary fee waivers and/or expense reimbursements, the total return would have been lower. |

| (3) | | Expenses (net of voluntary fee waiver) are equal to each class’ respective annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year, then divided by 365. |

10 Smith Barney Muni Funds | 2005 Annual Report

New York Money Market Portfolio

Fund Expenses (unaudited) (continued)

Hypothetical Example for Comparison Purposes

The table below titled “Based on Hypothetical Total Return” provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio and an assumed rate of return of 5.00% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use the information provided in this table to compare the ongoing costs of investing in the Fund and other funds. To do so, compare the 5.00% hypothetical example relating to the Fund with the 5.00% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table below are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as front-end or back-end sales charges (loads). Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher.

Based on Hypothetical Total Return(1)

| | | | | | | | | | | | | | | |

| | | Hypothetical

Annualized

Total Return | | | Beginning

Account

Value | | Ending

Account

Value | | Annualized

Expense

Ratio | | | Expenses

Paid During

the Period(2) |

Class A | | 5.00 | % | | $ | 1,000.00 | | $ | 1,021.94 | | 0.60 | % | | $ | 3.02 |

|

Class Y | | 5.00 | | | | 1,000.00 | | | 1,022.54 | | 0.48 | | | | 2.42 |

|

| (1) | | For the six months ended March 31, 2005. |

| (2) | | Expenses (net of voluntary fee waiver) are equal to each class’ respective annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year, then divided by 365. |

11 Smith Barney Muni Funds | 2005 Annual Report

New York Portfolio

Fund at a Glance (unaudited)

12 Smith Barney Muni Funds | 2005 Annual Report

New York Portfolio

Fund Expenses (unaudited)

Example

As a shareholder of the Fund, you may incur two types of costs: (1) transaction costs, including front-end and back-end sales charges (loads) on purchase payments, reinvested dividends, or other distributions; and (2) ongoing costs, including management fees; distribution and/or service (12b-1) fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

This example is based on an investment of $1,000 invested on October 1, 2004 and held for the six months ended March 31, 2005.

Actual Expenses

The table below titled “Based on Actual Total Return” provides information about actual account values and actual expenses. You may use the information provided in this table, together with the amount you invested, to estimate the expenses that you paid over the period. To estimate the expenses you paid on your account, divide your ending account value by $1,000 (for example, an $8,600 ending account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled “Expenses Paid During the Period”.

Based on Actual Total Return(1)

| | | | | | | | | | | | | | | |

| | | Actual Total

Return Without Sales Charges(2) | | | Beginning

Account

Value | | Ending Account

Value | | Annualized

Expense

Ratio | | | Expenses

Paid During

the Period(3) |

Class A | | 1.00 | % | | $ | 1,000.00 | | $ | 1,010.00 | | 0.71 | % | | $ | 3.56 |

|

Class B | | 0.73 | | | | 1,000.00 | | | 1,007.30 | | 1.24 | | | | 6.21 |

|

Class C(4) | | 0.79 | | | | 1,000.00 | | | 1,007.90 | | 1.27 | | | | 6.36 |

|

Class Y | | 1.09 | | | | 1,000.00 | | | 1,010.90 | | 0.56 | | | | 2.81 |

|

| (1) | | For the six months ended March 31, 2005. |

| (2) | | Assumes reinvestment of dividends and capital gain distributions, if any, at net asset value and does not reflect the deduction of the applicable sales charge with respect to Class A shares or the applicable contingent deferred sales charges (“CDSC”) with respect to Class B and C shares. Total return is not annualized, as it may not be representative of the total return for the year. Performance figures may reflect voluntary fee waivers and/or expense reimbursements. Past performance is no guarantee of future results. In the absence of voluntary fee waivers and/or expense reimbursements, the total return would have been lower. |

| (3) | | Expenses (net of voluntary fee waiver) are equal to each class’ respective annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year, then divided by 365. |

| (4) | | On April 29, 2004, Class L shares were renamed as Class C shares. |

13 Smith Barney Muni Funds | 2005 Annual Report

New York Portfolio

Fund Expenses (unaudited) (continued)

Hypothetical Example for Comparison Purposes

The table below titled “Based on Hypothetical Total Return” provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio and an assumed rate of return of 5.00% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use the information provided in this table to compare the ongoing costs of investing in the Fund and other funds. To do so, compare the 5.00% hypothetical example relating to the Fund with the 5.00% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table below are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as front-end or back-end sales charges (loads). Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher.

Based on Hypothetical Total Return(1)

| | | | | | | | | | | | | | | |

| | | Hypothetical

Annualized

Total Return | | | Beginning

Account

Value | | Ending

Account

Value | | Annualized

Expense

Ratio | | | Expenses

Paid During

the Period(2) |

Class A | | 5.00 | % | | $ | 1,000.00 | | $ | 1,021.39 | | 0.71 | % | | $ | 3.58 |

|

Class B | | 5.00 | | | | 1,000.00 | | | 1,018.75 | | 1.24 | | | | 6.24 |

|

Class C(3) | | 5.00 | | | | 1,000.00 | | | 1,018.60 | | 1.27 | | | | 6.39 |

|

Class Y | | 5.00 | | | | 1,000.00 | | | 1,022.14 | | 0.56 | | | | 2.82 |

|

| (1) | | For the six months ended March 31, 2005. |

| (2) | | Expenses (net of voluntary fee waiver) are equal to each class’ respective annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year, then divided by 365. |

| (3) | | On April 29, 2004, Class L shares were renamed as Class C shares. |

14 Smith Barney Muni Funds | 2005 Annual Report

New York Portfolio

Average Annual Total Returns(1) (unaudited)

| | | | | | | | | | | | |

| |

| | | Without Sales Charges(2)

| |

| | | Class A | | | Class B | | | Class C(3) | | | Class Y | |

Twelve Months Ended 3/31/05 | | 2.28 | % | | 1.72 | % | | 1.69 | % | | 2.38 | % |

|

|

Five Years Ended 3/31/05 | | 5.61 | | | 5.05 | | | 5.01 | | | N/A | |

|

|

Ten Years Ended 3/31/05 | | 5.75 | | | 5.19 | | | 5.15 | | | N/A | |

|

|

Inception* through 3/31/05 | | 6.47 | | | 5.96 | | | 5.17 | | | 4.55 | |

|

|

| |

| | | With Sales Charges(4)

| |

| | | Class A | | | Class B | | | Class C(3) | | | Class Y | |

Twelve Months Ended 3/31/05 | | (1.85 | )% | | (2.68 | )% | | 0.71 | % | | 2.38 | % |

|

|

Five Years Ended 3/31/05 | | 4.76 | | | 4.89 | | | 5.01 | | | N/A | |

|

|

Ten Years Ended 3/31/05 | | 5.32 | | | 5.19 | | | 5.15 | | | N/A | |

|

|

Inception* through 3/31/05 | | 6.23 | | | 5.96 | | | 5.17 | | | 4.55 | |

|

|

Cumulative Total Returns(1) (unaudited)

| | | |

| | | Without Sales Charges(2) | |

Class A (3/31/95 through 3/31/05) | | 74.89 | % |

|

|

Class B (3/31/95 through 3/31/05) | | 65.89 | |

|

|

Class C(3) (3/31/95 through 3/31/05) | | 65.21 | |

|

|

Class Y (Inception* through 3/31/05) | | 20.75 | |

|

|

| (1) | | All figures represent past performance and are not a guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Performance figures may reflect voluntary fee waivers and/or expense reimbursements. In the absence of voluntary fee waivers and/or expense reimbursements, the total return would have been lower. |

| (2) | | Assumes reinvestment of all dividends and capital gain distributions, if any, at net asset value and does not reflect the deduction of the applicable sales charge with respect to Class A shares or the applicable contingent deferred sales charges (“CDSC”) with respect to Class B and C shares. |

| (3) | | On April 29, 2004, Class L shares were renamed as Class C shares. |

| (4) | | Assumes reinvestment of all dividends and capital gain distributions, if any, at net asset value. In addition, Class A shares reflect the deduction of the maximum sales charge of 4.00%; Class B shares reflect the deduction of a 4.50% CDSC, which applies if shares are redeemed within one year from purchase payment. This CDSC declines by 0.50% the first year after purchase payment and thereafter by 1.00% per year until no CDSC is incurred. Class C shares reflect the deduction of a 1.00% CDSC, which applies if shares are redeemed within one year from purchase payment. |

| * | | Inception dates for Class A, B, C and Y shares are January 16, 1987, November 11, 1994, January 8, 1993 and January 4, 2001, respectively. |

15 Smith Barney Muni Funds | 2005 Annual Report

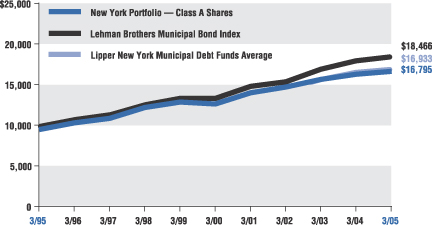

Historical Performance (unaudited)

Value of $10,000 Invested in Class A Shares of

the New York Portfolio vs.

the Lehman Brothers Municipal Bond Index and

Lipper New York Municipal Debt Funds Average†

March 1995 — March 2005

| † | Hypothetical illustration of $10,000 invested in Class A shares on March 31, 1995, assuming the reinvestment of dividends and capital gains, if any, at net asset value through March 31, 2005. The Lehman Brothers Municipal Bond Index is a broad measure of the municipal bond market with maturities of at least one year. The Index is unmanaged and is not subject to the same management and trading expenses of a mutual fund. Please note that an investor cannot invest directly in an index. The Lipper New York Municipal Debt Funds Average is composed of the Fund’s peer group of mutual funds (110 funds as of March 31, 2005). The performance of the Fund’s other classes may be greater or less than the Class A shares’ performance indicated on this chart, depending on whether greater or lesser sales charges and fees were incurred by shareholders investing in the other classes. |

All figures represent past performance and are not a guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Performance figures may reflect voluntary fee waivers and/or expense reimbursements. In the absence of voluntary fee waivers and/or expense reimbursements, the total return would have been lower.

16 Smith Barney Muni Funds | 2005 Annual Report

| | |

| Schedules of Investments | | March 31, 2005 |

NEW YORK MONEY MARKET PORTFOLIO

| | | | | | | |

FACE

AMOUNT | | RATING(a) | | SECURITY | | VALUE |

| Education — 7.9% | | | | | |

| | | | | Albany IDA Civic Facilities University at Albany | | | |

| | | | | AMBAC-Insured: | | | |

| $ 4,950,000 | | A-1 | | Series A 2.30% VRDO | | $ | 4,950,000 |

| 13,870,000 | | A-1 | | Series B 2.30% VRDO | | | 13,870,000 |

| 11,035,000 | | A-1 | | Series C 2.30% VRDO | | | 11,035,000 |

| 15,725,000 | | A-1 | | Series D 2.30% VRDO | | | 15,725,000 |

| 5,625,000 | | A-1+ | | Dutchess County IDA Marist College Series 98A

2.30% VRDO | | | 5,625,000 |

| | | | | New York State Dormitory Authority: | | | |

| | | | | Columbia University: | | | |

| 2,000,000 | | A-1+ | | Series C 2.02% due 5/2/05 | | | 2,000,000 |

| 2,000,000 | | A-1+ | | Series SGA 132 PART 2.26% VRDO | | | 2,000,000 |

| | | | | Cornell University TECP: | | | |

| 15,000,000 | | A-1+ | | 2.03% due 6/2/05 | | | 15,000,000 |

| 15,000,000 | | A-1+ | | 2.03% due 6/6/05 | | | 15,000,000 |

| 500,000 | | Aaa* | | Leake & Watts Services MBIA-Insured

3.00% due 7/1/05 | | | 501,237 |

| 7,460,000 | | VMIG1* | | Oxford University Press Inc. 2.23% VRDO | | | 7,460,000 |

| 1,665,000 | | A-1+ | | Rockefeller University Series A 2.23% VRDO | | | 1,665,000 |

| 7,842,500 | | VMIG1* | | State Personal Income Tax Revenue Series 821

FGIC-Insured PART 2.30% VRDO | | | 7,842,500 |

| 9,945,000 | | A-1 | | State University Series PA 622 PART 2.34% VRDO | | | 9,945,000 |

| | | | | Puerto Rico Industrial Tourist Education Medical & Environmental Control Facilities MBIA-Insured PART: | | | |

| 16,380,000 | | A-1+ | | Series 235 2.29% VRDO | | | 16,380,000 |

| 9,320,000 | | VMIG 1* | | Series 464 1.85% VRDO | | | 9,320,000 |

| 7,500,000 | | VMIG 1* | | Tompkins County IDA Ithaca College Project XLCA-Insured 2.30% VRDO | | | 7,500,000 |

| 6,500,000 | | A-1+ | | Troy IDA Rensselaer Polytech Institute Series E

2.27% VRDO | | | 6,500,000 |

|

| | | | | | | | 152,318,737 |

|

| Escrowed to Maturity — 0.5% | | | |

| 9,170,000 | | A-1 | | New York State Environmental Facilities Corp. Clean Water and Drinking Series PT-409 PART 2.30% VRDO (Escrowed to maturity with U.S. government securities) | | | 9,170,000 |

|

| Finance — 12.0% | | | |

| 35,525,000 | | A-1+ | | Nassau County IFA Sales Tax Revenue FSA-Insured Series B 2.21% VRDO | | | 35,525,000 |

| 4,200,000 | | AAA | | New York City Municipal Assistance Corp. Series E

6.00% due 7/1/05 | | | 4,242,850 |

| | | | | New York City TFA: | | | |

| | | | | Future Tax Secured: | | | |

| 45,300,000 | | A-1+ | | Series A-2 2.23% VRDO | | | 45,300,000 |

| 2,460,000 | | A-1+ | | Series C-4 2.29% VRDO | | | 2,460,000 |

See Notes to Financial Statements.

17 Smith Barney Muni Funds | 2005 Annual Report

| | |

| Schedules of Investments (continued) | | March 31, 2005 |

NEW YORK MONEY MARKET PORTFOLIO

| | | | | | | | | | |

FACE

AMOUNT | | RATING(a) | | SECURITY | | VALUE | | |

| | Finance — 12.0% (continued) | | | | | |

| $ | 14,920,000 | | A-1 | | MSTC Series 122 PART 2.26% VRDO | | $ | 14,920,000 | | |

| | | | | | New York City Recovery: | | | | | |

| | 14,100,000 | | A-1+ | | Series 2D 2.22% VRDO | | | 14,100,000 | | |

| | 6,775,000 | | A-1+ | | Series 3B 2.32% VRDO | | | 6,775,000 | | |

| | | | | | New York State LGAC: | | | | | |

| | 60,435,000 | | A-1+ | | Series 93A 2.22% VRDO | | | 60,435,000 | | |

| | 26,000 | | A-1+ | | Series C 2.15% VRDO | | | 26,000 | | |

| | 4,350,000 | | A-1+ | | Series SGA 59 AMBAC-Insured 2.30% VRDO | | | 4,350,000 | | |

| | | | | | Puerto Rico IFA MSTC PART: | | | | | |

| | 19,995,000 | | A-1 | | Series 103 2.23% VRDO | | | 19,995,000 | | |

| | 19,995,000 | | A-1 | | Series 106 2.23% VRDO | | | 19,995,000 | | |

| | 4,850,000 | | A-1 | | Puerto Rico MFA Series PA-610 FSA-Insured PART

2.28% VRDO | | | 4,850,000 | | |

|

|

| | | | | | | | | 232,973,850 | | |

|

|

| | General Obligation — 15.9% | | | | | |

| | | | | | Allegany County NY GO: | | | | | |

| | 6,250,000 | | MIG 1* | | BAN 3.50% due 12/8/05 | | | 6,305,510 | | |

| | 2,000,000 | | MIG 1* | | TAN 3.50% due 12/8/05 | | | 2,017,763 | | |

| | 475,000 | | AAA | | Dover UFSD GO Series B FSA-Insured 3.00% due 9/1/05 | | | 476,415 | | |

| | 16,500,000 | | MIG 1* | | Middle County CSD GO TAN 3.00% due 6/30/05 | | | 16,554,015 | | |

| | 12,500,000 | | MIG 1* | | Miller Place UFSD GO TAN 3.00% due 6/30/05 | | | 12,539,375 | | |

| | 507,764 | | AAA | | Monroe-Woodbury CSD GO FSA-Insured

2.00% due 4/15/05 | | | 507,928 | | |

| | 4,750,000 | | NR† | | Mount Sinai UFSD GO TAN 3.00% due 6/24/05 | | | 4,762,877 | | |

| | 500,000 | | AAA | | Nassau County GO General Improvement Series A

4.25% due 6/1/05 | | | 502,186 | | |

| | | | | | New York City GO: | | | | | |

| | 33,000,000 | | A-1+ | | Series A-3 2.23% VRDO | | | 33,000,000 | | |

| | 10,000,000 | | A-1+ | | Series C-2 2.23% VRDO | | | 10,000,000 | | |

| | 4,500,000 | | A-1+ | | Series H-4 2.28% VRDO | | | 4,500,000 | | |

| | 4,000,000 | | A-1+ | | Series H-5 94 MBIA-Insured 1.95% due 4/7/05 TECP | | | 4,000,000 | | |

| | 4,300,000 | | A-1 | | Series H-7 2.28% VRDO | | | 4,300,000 | | |

| | 7,500,000 | | A-1+ | | Series J-2 2.28% VRDO | | | 7,500,000 | | |

| | 5,995,000 | | A-1 | | Series PA 624 AMBAC-Insured PART 2.31% VRDO | | | 5,995,000 | | |

| | 600,000 | | A-1+ | | Series SGB 35 AMBAC-Insured PART 2.26% VRDO | | | 600,000 | | |

| | 3,400,000 | | A-1+ | | Sub-series H-3 2.28% VRDO | | | 3,400,000 | | |

| | 10,000,000 | | A-1+ | | Sub-series J-3 2.28% VRDO | | | 10,000,000 | | |

| | | | | | New York State GO: | | | | | |

| | 52,900,000 | | A-1+ | | Series 1998A 2.00% due 6/6/05 TECP | | | 52,900,000 | | |

| | 24,605,000 | | A-1+ | | Series A 1.80% due 10/7/05 | | | 24,605,000 | | |

| | 305,000 | | Aaa* | | North Salem CSD GO MBIA-Insured Series B

3.00% due 6/15/05 | | | 305,928 | | |

See Notes to Financial Statements.

18 Smith Barney Muni Funds | 2005 Annual Report

| | |

| Schedules of Investments (continued) | | March 31, 2005 |

NEW YORK MONEY MARKET PORTFOLIO

| | | | | | | | | | |

FACE

AMOUNT | | RATING(a) | | SECURITY | | VALUE | | |

| | General Obligation — 15.9% (continued) | | | | | |

| | | | | | Puerto Rico GDB TECP: | | | | | |

| $ | 17,718,000 | | A-1 | | 2.02% due 5/6/05 | | $ | 17,718,000 | | |

| | 15,000,000 | | A-1 | | 1.95% due 5/13/05 | | | 15,000,000 | | |

| | 8,000,000 | | A-1 | | 2.10% due 5/24/05 | | | 8,000,000 | | |

| | 14,675,000 | | A-1 | | 2.08% due 6/8/05 | | | 14,675,000 | | |

| | 4,855,000 | | A-1 | | 2.08% due 6/9/05 | | | 4,855,000 | | |

| | 7,980,000 | | VMIG 1* | | Puerto Rico GO MERLOT Series A44 FGIC-Insured PART 2.32% VRDO | | | 7,980,000 | | |

| | 23,000,000 | | MIG 1* | | South Country CSD GO TAN 2.75% due 6/21/05 | | | 23,050,633 | | |

| | 350,000 | | AA+ | | Southampton Town GO 3.00% due 5/1/05 | | | 350,288 | | |

| | 5,000,000 | | MIG 1* | | Suffolk County GO TAN 3.00% due 9/8/05 | | | 5,025,269 | | |

| | 5,000,000 | | MIG 1* | | Syracuse GO RAN Series E 3.00% due 6/30/05 | | | 5,014,450 | | |

| | | | | | Warwick CSD GO FGIC-Insured: | | | | | |

| | 255,000 | | Aaa* | | Series A 3.00% due 6/15/06 | | | 255,456 | | |

| | 435,000 | | Aaa* | | Series B 2.50% due 1/15/06 | | | 435,668 | | |

| | 315,000 | | Aaa* | | Westhill CSD GO MBIA-Insured 2.00% due 6/15/05 | | | 315,223 | | |

|

|

| | | | | | | | | 307,446,984 | | |

|

|

| | Government Facilities — 3.2% | | | | | |

| | | | | | Jay Street Development Corp. Court Facilities Lease Revenue: | | | | | |

| | 1,900,000 | | A-1+ | | Series A 2.28% VRDO | | | 1,900,000 | | |

| | 28,625,000 | | A-1+ | | Series A-3 2.23% VRDO | | | 28,625,000 | | |

| | 2,500,000 | | A-1+ | | Series A-4 2.28% VRDO | | | 2,500,000 | | |

| | | | | | New York State Urban Development Corp. PART: | | | | | |

| | 8,000,000 | | VMIG 1* | | MERLOT Series N AMBAC-Insured 2.32% VRDO | | | 8,000,000 | | |

| | 21,300,000 | | A-1+ | | Putter 313 2.30% VRDO | | | 21,300,000 | | |

|

|

| | | | | | | | | 62,325,000 | | |

|

|

| | Hospitals — 6.1% | | | | | |

| | 15,000,000 | | A-1+ | | Nassau County Health Care Corp. Series C-1 FSA-Insured 2.23% VRDO | | | 15,000,000 | | |

| | 2,495,000 | | VMIG 1* | | New York City IDA IDR Peninsula Hospital Center Project 2.35% VRDO | | | 2,495,000 | | |

| | | | | | New York State Dormitory Authority: | | | | | |

| | 6,035,000 | | A-1+ | | Glen Eddy Inc. 2.24% VRDO | | | 6,035,000 | | |

| | | | | | Mental Health Services: | | | | | |

| | 8,780,000 | | A-1+ | | Series D-2B FSA-Insured 2.25% VRDO | | | 8,780,000 | | |

| | 40,000,000 | | A-1+ | | Series D-2E 2.23% VRDO | | | 40,000,000 | | |

| | 15,000,000 | | A-1+ | | Series D-2G 2.23% VRDO | | | 15,000,000 | | |

| | 22,300,000 | | A-1+ | | Series D-2H 2.23% VRDO | | | 22,300,000 | | |

| | 8,000,000 | | VMIG 1* | | Ontario County IDR Frederick Ferris Thompson Hospital 2.28% VRDO | | | 8,000,000 | | |

|

|

| | | | | | | | | 117,610,000 | | |

|

|

See Notes to Financial Statements.

19 Smith Barney Muni Funds | 2005 Annual Report

| | |

| Schedules of Investments (continued) | | March 31, 2005 |

NEW YORK MONEY MARKET PORTFOLIO

| | | | | | | | | | |

FACE

AMOUNT | | RATING(a) | | SECURITY | | VALUE | | |

| | Housing: Multi-Family — 9.6% | | | | | |

| | | | | | New York City HDC MFH: | | | | | |

| $ | 42,300,000 | | A-1+ | | 2 Gold Street Series A 2.25% VRDO | | $ | 42,300,000 | | |

| | 18,500,000 | | A-1+ | | 90 West Street Series A 2.25% VRDO | | | 18,500,000 | | |

| | 14,600,000 | | A-1+ | | Atlantic Court Apartments 2.28% VRDO AMT | | | 14,600,000 | | |

| | | | | | New York State HFA: | | | | | |

| | 20,800,000 | | VMIG 1* | | 20 River Terrace FNMA 2.28% VRDO | | | 20,800,000 | | |

| | 3,000,000 | | VMIG 1* | | 240 East 39th Street FNMA 2.31% VRDO AMT | | | 3,000,000 | | |

| | 12,800,000 | | VMIG 1* | | 750 Sixth Avenue Series A FNMA 2.31% VRDO AMT | | | 12,800,000 | | |

| | 6,000,000 | | VMIG 1* | | Biltmore Tower Housing Series A FNMA 2.31% VRDO | | | 6,000,000 | | |

| | 2,300,000 | | VMIG 1* | | Historic Front Street Series A 2.30% VRDO | | | 2,300,000 | | |

| | | | | | Service Contract Revenue: | | | | | |

| | 37,500,000 | | A-1+ | | Series A 2.23% VRDO | | | 37,500,000 | | |

| | 9,500,000 | | A-1+ | | Series C 2.23% VRDO | | | 9,500,000 | | |

| | 3,100,000 | | VMIG 1* | | Union Square South 2.26% VRDO AMT | | | 3,100,000 | | |

| | 4,800,000 | | VMIG 1* | | West 43rd Street Housing FNMA 2.25% VRDO AMT | | | 4,800,000 | | |

| | 10,000,000 | | VMIG 1* | | Worth Street Series A FNMA 2.25% VRDO AMT | | | 10,000,000 | | |

|

|

| | | | | | | | | 185,200,000 | | |

|

|

| | Housing: Single-Family — 2.0% | | | | | |

| | | | | | New York State Mortgage Agency Revenue: | | | | | |

| | 20,000,000 | | VMIG 1* | | 2.31% VRDO AMT | | | 20,000,000 | | |

| | 19,000,000 | | VMIG 1* | | Series 122 2.26% VRDO AMT | | | 19,000,000 | | |

|

|

| | | | | | | | | 39,000,000 | | |

|

|

| | Industrial Development — 6.6% | | | | | |

| | 1,650,000 | | VMIG 1* | | Erie County IDA Rosina Food Products Inc. 2.30% VRDO | | | 1,650,000 | | |

| | 2,600,000 | | A-1+ | | Genesee County IDR RJ Properties Project

2.34% VRDO AMT | | | 2,600,000 | | |

| | 2,670,000 | | A-1+ | | Lancaster IDA Sealing Devices Inc. 2.30% VRDO AMT | | | 2,670,000 | | |

| | 3,000,000 | | A-1+ | | Lewis County IDA Climax Manufacturing Co. Project

2.34% VRDO AMT | | | 3,000,000 | | |

| | 305,000 | | A-1+ | | Monroe County IDA JADA Precision | | | | | |

| | | | | | Plastic Project Series 97 2.34% VRDO AMT | | | 305,000 | | |

| | 2,805,000 | | A-1+ | | Nassau County IDA Rubbies Costume Co. Project

2.34% VRDO | | | 2,805,000 | | |

| | | | | | New York City IDA IDR: | | | | | |

| | | | | | 1 Bryant Park LLC: | | | | | |

| | 21,000,000 | | A-1+ | | Series A 2.32% VRDO | | | 21,000,000 | | |

| | 21,900,000 | | A-1+ | | Series B 2.32% VRDO | | | 21,900,000 | | |

| | 3,875,000 | | VMIG 1* | | Ahava Food Corp. Project 2.35% VRDO AMT | | | 3,875,000 | | |

| | 5,600,000 | | A-1+ | | Children’s Oncology Society 2.28% VRDO | | | 5,600,000 | | |

| | 3,600,000 | | A-1+ | | Gary Plastic Packaging Corp. Series 98

2.40% VRDO AMT | | | 3,600,000 | | |

See Notes to Financial Statements.

20 Smith Barney Muni Funds | 2005 Annual Report

| | |

| Schedules of Investments (continued) | | March 31, 2005 |

NEW YORK MONEY MARKET PORTFOLIO

| | | | | | | | | | |

FACE

AMOUNT | | RATING(a) | | SECURITY | | VALUE | | |

| | Industrial Development — 6.6% (continued) | | | | | |

| $ | 1,600,000 | | A-1 | | Linear Lighting Corp. Project 2.50% VRDO AMT | | $ | 1,600,000 | | |

| | 4,750,000 | | F-1+** | | Planned Parenthood Project 2.30% VRDO | | | 4,750,000 | | |

| | 1,495,000 | | A-1+ | | PS Bibbs Inc. 2.40% VRDO AMT | | | 1,495,000 | | |

| | 8,250,000 | | A-1+ | | Stock Exchange Project B 2.30% VRDO | | | 8,250,000 | | |

| | 1,500,000 | | A-1+ | | Oneida County IDR Harden Furniture Series 98

2.34% VRDO | | | 1,500,000 | | |

| | | | | | Onondaga County IDA: | | | | | |

| | 3,355,000 | | A-1+ | | Syracuse Executive Air 2.34% VRDO AMT | | | 3,355,000 | | |

| | 5,410,000 | | A-1+ | | Syracuse Research Corp. 2.25% VRDO | | | 5,410,000 | | |

| | 1,815,000 | | A-1+ | | Ontario County IDR Dixit Enterprises Series B

2.30% VRDO AMT | | | 1,815,000 | | |

| | 2,525,000 | | A-1+ | | Oswego County IDR Fulton Thermal Corp.

2.34% VRDO AMT | | | 2,525,000 | | |

| | 4,110,000 | | P-1* | | Rotterdam IDA IDR Rotterdam Park Project 2.30% VRDO | | | 4,110,000 | | |

| | 1,830,000 | | P-1* | | Schenectady County IDR Scotia Industrial Park Project

Series 98A 2.30% VRDO | | | 1,830,000 | | |

| | 3,380,000 | | A-1+ | | St. Lawrence County IDA United Helpers Independent Living Corp. 2.30% VRDO | | | 3,380,000 | | |

| | 4,060,000 | | A-1+ | | Suffolk County IDR JBC Realty 2.34% VRDO | | | 4,060,000 | | |

| | 4,895,000 | | A-1+ | | Westchester County IDA Boys & Girls Club Project

2.30% VRDO | | | 4,895,000 | | |

| | 2,225,000 | | A-1+ | | Yates IDR Coach & Equipment Manufacturing Corp.

2.34% VRDO AMT | | | 2,225,000 | | |

| | | | | | Yonkers IDA Consumers Union Facilities: | | | | | |

| | 2,300,000 | | VMIG 1* | | 2.30% VRDO | | | 2,300,000 | | |

| | 5,890,000 | | A-1+ | | AMBAC-Insured 2.30% VRDO | | | 5,890,000 | | |

|

|

| | | | | | | | | 128,395,000 | | |

|

|

| | Life Care Systems — 0.1% | | | | | |

| | 1,400,000 | | VMIG 1* | | Monroe County IDA St. Ann’s Home for the Aged Project 2.28% VRDO | | | 1,400,000 | | |

|

|

| | Miscellaneous — 3.0% | | | | | |

| | 58,925,000 | | A-1+ | | Oneida Indian Nation Series 2002 2.28% VRDO | | | 58,925,000 | | |

|

|

| | Pollution Control — 0.5% | | | | | |

| | 8,700,000 | | A-1+ | | New York State Environmental Facilities Corp., Clean Water and Drinking, Series 1997-A

2.00% due 7/13/05 TECP | | | 8,700,000 | | |

|

|

| | Public Facilities — 2.9% | | | | | |

| | | | | | New York City Trust for Cultural Resources: | | | | | |

| | 3,035,000 | | VMIG 1* | | American Museum of Natural History Series 162 AMBAC-Insured PART 2.30% VRDO | | | 3,035,000 | | |

| | 45,000 | | VMIG 1* | | Asia Society 2.24% VRDO | | | 45,000 | | |

| | 21,600,000 | | A-1+ | | Pierpont Morgan Library 2.28% VRDO | | | 21,600,000 | | |

See Notes to Financial Statements.

21 Smith Barney Muni Funds | 2005 Annual Report

| | |

| Schedules of Investments (continued) | | March 31, 2005 |

NEW YORK MONEY MARKET PORTFOLIO

| | | | | | | | | | |

FACE

AMOUNT | | RATING(a) | | SECURITY | | VALUE | | |

| | Public Facilities — 2.9% (continued) | | | | | |

| $ | 30,000 | | VMIG 1* | | Soloman R. Guggenheim Museum Series B

2.30% VRDO | | $ | 30,000 | | |

| | | | | | New York State Dormitory Authority: | | | | | |

| | | | | | Metropolitan Museum of Art: | | | | | |

| | 12,455,000 | | A-1+ | | Series A 2.23% VRDO | | | 12,455,000 | | |

| | 4,240,000 | | A-1+ | | Series B 2.23% VRDO | | | 4,240,000 | | |

| | | | | | New York Public Library MBIA-Insured: | | | | | |

| | 5,730,000 | | A-1 | | Series 99A 2.23% VRDO | | | 5,730,000 | | |

| | 9,285,000 | | A-1 | | Series B 2.23% VRDO | | | 9,285,000 | | |

|

|

| | | | | | | | | 56,420,000 | | |

|

|

| | Transportation — 13.7% | | | | | |

| | | | | | Metropolitan Transportation Authority: | | | | | |

| | 10,000,000 | | A-1+ | | BAN Series CP-1A Sub-series A 2.05% due 6/1/05 TECP | | | 10,000,000 | | |

| | 69,100,000 | | A-1+ | | FSA-Insured Series A-3 XLCA-Insured 2.23% VRDO | | | 69,100,000 | | |

| | | | | | New York State Thruway Authority: | | | | | |

| | 21,750,000 | | A-1+ | | 2.02% due 5/2/05 TECP | | | 21,750,000 | | |

| | 3,765,000 | | SP-1+ | | 2.25% due 10/6/05 | | | 3,775,131 | | |

| | 8,845,000 | | A-1 | | MSTC Series 120 FGIC-Insured PART 2.26% VRDO | | | 8,845,000 | | |

| | 5,000,000 | | A-1+ | | Series SGA 66 PART 2.26% VRDO | | | 5,000,000 | | |

| | | | | | Port Authority of New York & New Jersey: | | | | | |

| | 7,860,000 | | A-1+ | | Putter Series 177 MBIA-Insured PART 2.33% VRDO | | | 7,860,000 | | |

| | 3,500,000 | | NR† | | Series 98-1 Equipment Notes 2.42% VRDO AMT | | | 3,500,000 | | |

| | 3,500,000 | | NR† | | Series 98-2 Equipment Notes 2.32% VRDO | | | 3,500,000 | | |

| | 4,755,000 | | A-1 | | Series 646 FSA-Insured PART 2.28% VRDO | | | 4,755,000 | | |

| | 4,540,000 | | A-1+ | | Series 2000A 2.05% due 5/11/05 TECP AMT | | | 4,540,000 | | |

| | | | | | Series B TECP: | | | | | |

| | 1,820,000 | | A-1+ | | 1.83% due 4/6/05 | | | 1,820,000 | | |

| | 14,990,000 | | A-1+ | | 2.03% due 6/2/05 | | | 14,990,000 | | |

| | | | | | Versatile Structure Obligation: | | | | | |

| | 2,300,000 | | A-1+ | | Series 95-3 2.30% VRDO | | | 2,300,000 | | |

| | 2,800,000 | | A-1+ | | Series 96-5 2.30% VRDO | | | 2,800,000 | | |

| | | | | | Puerto Rico Commonwealth Highway & Transportation Authority: | | | | | |

| | 11,550,000 | | A-1+ | | Series A AMBAC-Insured 2.23% VRDO | | | 11,550,000 | | |

| | 3,475,000 | | VMIG 1* | | Series FFF 2.32% MBIA-Insured VRDO | | | 3,475,000 | | |

| | | | | | Triborough Bridge & Tunnel Authority: | | | | | |

| | 17,520,000 | | AAA | | Series 72 MBIA-Insured PART 2.26% VRDO | | | 17,520,000 | | |

| | 13,135,000 | | VMIG 1* | | Series 109 PART 2.30% VRDO | | | 13,135,000 | | |

| | 11,170,000 | | A-1+ | | Series A FSA-Insured 2.23% VRDO | | | 11,170,000 | | |

| | 19,200,000 | | A-1+ | | Series C AMBAC-Insured 2.23% VRDO | | | 19,200,000 | | |

| | 25,000,000 | | A-1+ | | Series F 2.28% VRDO | | | 25,000,000 | | |

|

|

| | | | | | | | | 265,585,131 | | |

|

|

See Notes to Financial Statements.

22 Smith Barney Muni Funds | 2005 Annual Report

| | |

| Schedules of Investments (continued) | | March 31, 2005 |

NEW YORK MONEY MARKET PORTFOLIO

| | | | | | | |

FACE

AMOUNT | | RATING(a) | | SECURITY | | VALUE |

| Utilities — 8.8% | | | |

| | | | | Long Island Power Authority: | | | |

| $25,000,000 | | A-1+ | | Series 1A 2.28% VRDO | | $ | 25,000,000 |

| 1,530,000 | | A-1+ | | Series 1B 2.28% VRDO | | | 1,530,000 |

| 8,000,000 | | A-1+ | | Series 2B 2.28% VRDO | | | 8,000,000 |

| 8,900,000 | | A-1+ | | Series 7B MBIA-Insured 2.23% VRDO | | | 8,900,000 |

| 13,100,000 | | A-1+ | | Series H FSA-Insured 2.23% VRDO | | | 13,100,000 |

| 13,280,000 | | VMIG 1* | | New York State Energy Research & Development Authority Long Island Lighting Co. Series A

2.31% VRDO AMT | | | 13,280,000 |

| | | | | New York State Power Authority TECP: | | | |

| 28,900,000 | | A-1 | | Series 1 1.93% due 5/11/05 | | | 28,900,000 |

| | | | | Series 2: | | | |

| 19,600,000 | | A-1 | | 2.05% due 5/2/05 | | | 19,600,000 |

| 7,400,000 | | A-1 | | 2.05% due 5/3/05 | | | 7,400,000 |

| 16,000,000 | | A-1 | | 2.05% due 5/10/05 | | | 16,000,000 |

| 15,750,000 | | A-1+ | | 2.15% due 9/1/05 | | | 15,750,000 |

| | | | | Puerto Rico Electric Power Authority MBIA-Insured PART: | | | |

| 10,500,000 | | A-1+ | | Series SGA 43 2.23% VRDO | | | 10,500,000 |

| 2,900,000 | | A-1+ | | Series SGA 44 2.23% VRDO | | | 2,900,000 |

|

| | | | | | | | 170,860,000 |

|

| Water & Sewer — 5.8% | | | |

| | | | | New York City Municipal Water Finance Authority: | | | |

| 15,000,000 | | A-1+ | | Series 1 2.15% due 7/8/05 TECP | | | 15,000,000 |

| 20,000,000 | | A-1+ | | Series 5B 2.15% due 7/14/05 TECP | | | 20,000,000 |

| 20,000,000 | | A-1+ | | Series 6 2.13% due 7/14/05 TECP | | | 20,000,000 |

| 2,200,000 | | A-1+ | | Series A FGIC-Insured 2.25% VRDO | | | 2,200,000 |

| 2,075,000 | | A-1+ | | Series C 2.29% VRDO | | | 2,075,000 |

| 5,000,000 | | A-1 | | Series C-2 2.22% VRDO | | | 5,000,000 |

| 1,100,000 | | A-1+ | | Series C-3 2.28% VRDO | | | 1,100,000 |

| 10,000,000 | | A-1+ | | Series F-1 2.28% VRDO | | | 10,000,000 |

| 7,200,000 | | A-1+ | | Series F-2 2.29% VRDO | | | 7,200,000 |

| 5,025,000 | | A-1+ | | Series G FGIC-Insured 2.28% VRDO | | | 5,025,000 |

| | | | | New York State Environmental Facilities Corp. | | | |

| | | | | Clean Water and Drinking: | | | |

| 9,990,000 | | A-1 | | MSTC Series 9040 PART 2.27% VRDO | | | 9,990,000 |

| | | | | Series B: | | | |

| 7,080,000 | | AAA | | 5.50% due 6/15/05 | | | 7,206,620 |

| 6,695,000 | | AAA | | 5.60% due 6/15/05 | | | 6,816,101 |

| 1,400,000 | | AAA | | Pollution Control Revenue MBIA-Insured

5.50% due 6/15/05 | | | 1,410,088 |

|

| | | | | | | | 113,022,809 |

|

| | | | | TOTAL INVESTMENTS — 98.6%

(Cost — $1,909,352,511***) | | | 1,909,352,511 |

| | | | | Other Assets in Excess of Liabilities — 1.4% | | | 26,418,977 |

|

| | | | | TOTAL NET ASSETS — 100.0% | | $ | 1,935,771,488 |

|

See Notes to Financial Statements.

23 Smith Barney Muni Funds | 2005 Annual Report

| | |

| Schedules of Investments (continued) | | March 31, 2005 |

| (a) | | All ratings are by Standard & Poor’s Ratings Service (“Standard & Poor’s”) except for those identified by an asterisk (*) which are rated by Moody’s Investors Service (“Moody’s”) and those identified by a double asterisk (**) are rated by Fitch Ratings (“Fitch”). All ratings are unaudited. |

| † | | Security has not been rated by either Standard & Poor’s, Moody’s or Fitch. However, the Board of Trustees has determined that the security presents minimal credit risk. |

| *** | | Aggregate cost for federal income tax purposes is substantially the same. |

See pages 33 through 35 for definitions of ratings and certain abbreviations.

See Notes to Financial Statements.

24 Smith Barney Muni Funds | 2005 Annual Report

| | |

| Schedules of Investments (continued) | | March 31, 2005 |

| | | | | | | | |

NEW YORK PORTFOLIO |

FACE AMOUNT | | RATING(a) | | SECURITY | | VALUE |

| | Education — 28.0% | | | |

| $ | 2,755,000 | | Aaa* | | Albany IDA, Civic Facility Revenue, (St. Rose Project), Series A,

AMBAC-Insured, 5.375% due 7/1/31 | | $ | 2,931,816 |

| | | | | | Amherst IDA, Civic Facilities Revenue, University of Buffalo

Foundation Faculty-Student Housing, Series B,

AMBAC-Insured: | | | |

| | 1,000,000 | | AAA | | 5.125% due 8/1/20 | | | 1,077,230 |

| | 3,615,000 | | AAA | | 5.250% due 8/1/31 | | | 3,819,211 |

| | | | | | Madison County IDA, Civic Facilities Revenue, (Colgate

University Project), Series B: | | | |

| | 2,250,000 | | AA- | | 5.000% due 7/1/23 | | | 2,342,295 |

| | 2,000,000 | | AA- | | 5.000% due 7/1/33 | | | 2,051,440 |

| | | | | | New York State Dormitory Authority Revenue: | | | |

| | | | | | City University Systems: | | | |

| | 16,925,000 | | AAA | | 3rd Generation, Series 1, FGIC-Insured,

5.250% due 7/1/25 (b) | | | 17,835,226 |

| | | | | | 4th Generation, Series A: | | | |

| | 6,000,000 | | AA- | | Call 7/1/11 @ 100, 5.250% due 7/1/31 (c) | | | 6,601,260 |

| | 2,840,000 | | AA- | | MBIA/IBC-Insured, (Call 7/1/08 @ 101),

5.000% due 7/1/28 (c) | | | 3,044,281 |

| | 1,660,000 | | AA- | | MBIA/IBC-Insured, (Call 7/1/08 @ 101),

5.000% due 7/1/28 (c) | | | 1,779,404 |

| | | | | | Series A, FGIC-Insured: | | | |

| | 5,825,000 | | AAA | | 5.625% due 7/1/16 (d) | | | 6,674,751 |

| | 14,000,000 | | AAA | | 2nd Generation, 5.000% due 7/1/16 (b) | | | 14,801,360 |

| | 7,000,000 | | AAA | | Series B, FSA-Insured, 6.000% due 7/1/14 | | | 8,009,470 |

| | 2,500,000 | | A3* | | Series C, 7.500% due 7/1/10 | | | 2,771,725 |

| | 2,000,000 | | AAA | | Columbia University, 5.000% due 7/1/18 | | | 2,111,400 |

| | | | | | Court Facilities, City of New York Issue: | | | |

| | 5,000,000 | | A | | 6.000% due 5/15/39 | | | 5,455,100 |

| | 3,000,000 | | AAA | | AMBAC-Insured, 5.750% due 5/15/30 | | | 3,299,940 |

| | 2,000,000 | | AA- | | Department of Education, 5.000% due 7/1/24 | | | 2,074,780 |

| | 5,000,000 | | AAA | | New School University, MBIA-Insured, 5.000% due 7/1/29 | | | 5,120,650 |

| | 10,260,000 | | AAA | | Rockefeller University, 5.000% due 7/1/28 (b) | | | 10,566,877 |

| | 1,000,000 | | AA- | | School Improvement Program, 5.000% due 7/1/18 | | | 1,038,690 |

| | 1,150,000 | | AAA | | St. John’s University, MBIA-Insured, 5.250% due 7/1/25 | | | 1,211,847 |

| | | | | | State University Dormitory Facility, FGIC-Insured,

(Call 7/1/11 @ 100): | | | |

| | 1,000,000 | | AAA | | 5.500% due 7/1/26 (c) | | | 1,114,130 |

| | 1,000,000 | | AAA | | 5.500% due 7/1/27 (c) | | | 1,114,130 |

| | 12,000,000 | | AAA | | 5.100% due 7/1/31 (b)(c) | | | 13,102,200 |

| | | | | | State University Educational Facility: | | | |

| | | | | | Series A: | | | |

| | 12,750,000 | | AAA | | FGIC-Insured, (Call 5/15/12 @ 101),

5.000% due 5/15/27 (b)(c) | | | 13,925,933 |

See Notes to Financial Statements.

25 Smith Barney Muni Funds | 2005 Annual Report

| | |

| Schedules of Investments (continued) | | March 31, 2005 |

NEW YORK PORTFOLIO

| | | | | | | | | | |

FACE AMOUNT | | RATING(a) | | SECURITY | | VALUE | | |

| | Education — 28.0% (continued) | | | | | |

| $ | 12,110,000 | | AAA | | FSA-Insured, 5.875% due 5/15/17 (d) | | $ | 14,183,111 | | |

| | 7,030,000 | | AAA | | MBIA-Insured, 5.000% due 5/15/16 | | | 7,428,952 | | |

| | | | | | Series B: | | | | | |

| | 676,000 | | AA- | | 7.500% due 5/15/11 | | | 766,050 | | |

| | 5,000,000 | | AAA | | FGIC-Insured, 5.250% due 5/15/19 | | | 5,565,750 | | |

| | 5,000,000 | | AAA | | FSA-Insured, (Call 5/15/10 @ 101),

5.500% due 5/15/30 (c) | | | 5,573,100 | | |

| | | | | | University of Rochester, Series A, MBIA-Insured: | | | | | |

| | 3,915,000 | | AAA | | 5.000% due 7/1/16 | | | 4,139,055 | | |

| | 2,300,000 | | AAA | | 5.000% due 7/1/27 | | | 2,352,992 | | |

| | | | | | Rensselaer County IDA, Civic Facilities Revenue, (Polytechnic Institute Dormitory Project): | | | | | |

| | 5,430,000 | | A+ | | Series A, 5.125% due 8/1/29 | | | 5,602,077 | | |

| | 5,820,000 | | A+ | | Series B, 5.125% due 8/1/27 | | | 6,032,314 | | |

| | | | | | Schenectady IDA, Civic Facilities Revenue, (Union College Project), Series A, AMBAC-Insured: | | | | | |

| | 2,000,000 | | Aaa* | | 5.375% due 12/1/19 | | | 2,181,980 | | |

| | 1,725,000 | | Aaa* | | 5.000% due 7/1/22 | | | 1,809,128 | | |

| | 3,000,000 | | Aaa* | | 5.450% due 12/1/29 | | | 3,243,480 | | |

| | 2,390,000 | | Aaa* | | 5.625% due 7/1/31 | | | 2,621,615 | | |

| | | | | | Taconic Hills School District at Craryville, FGIC-Insured, State Aid Withholding: | | | | | |

| | 1,420,000 | | Aaa* | | 5.000% due 6/15/25 | | | 1,481,756 | | |

| | 700,000 | | Aaa* | | 5.000% due 6/15/26 | | | 729,120 | | |

| | 3,000,000 | | Aaa* | | Teachers College, MBIA-Insured, 5.000% due 7/1/22 | | | 3,131,160 | | |

|

|

| | | | | | | | | 200,716,786 | | |

|

|

| | Finance — 7.7% | | | | | |

| | | | | | New York City TFA Revenue: | | | | | |

| | 2,000,000 | | AAA | | Series 3, Sub-series 3-H, 2.280% due 4/1/05 (e) | | | 2,000,000 | | |

| | 10,000,000 | | AAA | | Series C, (Call 5/1/10 @ 101), 5.500% due 11/1/29 (b)(c) | | | 11,138,900 | | |

| | | | | | New York State LGAC: | | | | | |

| | 21,400,000 | | AAA | | Series 4-V, 2.260% due 4/6/05 (e) | | | 21,400,000 | | |

| | | | | | Series B: | | | | | |

| | 7,741,000 | | AA- | | 2.200% due 4/6/05 (e) | | | 7,741,000 | | |

| | 5,000,000 | | AAA | | MBIA-Insured, 4.875% due 4/1/20 | | | 5,136,600 | | |

| | 225,000 | | BBB+ | | New York State Municipal Bond Bank Agency, Special Revenue Program, City of Buffalo, Series A, 6.875% due 3/15/06 | | | 225,837 | | |

| | | | | | Puerto Rico Public Financial Corp., Series E: | | | | | |

| | 1,260,000 | | BBB+ | | 5.500% due 8/1/29 | | | 1,353,895 | | |

| | 3,740,000 | | BBB+ | | Call 2/1/12 @ 100, 5.500% due 8/1/29 (c) | | | 4,156,711 | | |

| | 2,000,000 | | AA- | | Tobacco Settlement Financing Corp., Series C-1

5.500% due 6/1/21 | | | 2,169,240 | | |

|

|

| | | | | | | | | 55,322,183 | | |

|

|

See Notes to Financial Statements.

26 Smith Barney Muni Funds | 2005 Annual Report

| | |

| Schedules of Investments (continued) | | March 31, 2005 |

NEW YORK PORTFOLIO

| | | | | | | |

FACE AMOUNT | | RATING(a) | | SECURITY | | VALUE |

General Obligation — 1.5% | | | |

| | | | | New York City GO: | | | |

| $ 500,000 | | AA- | | Series A-7, 2.280% due 4/1/05 (e) | | $ | 500,000 |

| 1,300,000 | | AA+ | | Series E-3, 2.280% due 4/1/05 (e) | | | 1,300,000 |

| 200,000 | | AA | | Series E-4, 2.280% due 4/1/05 (e) | | | 200,000 |

| 2,750,000 | | AA | | New York State GO, 9.875% due 11/15/05 | | | 2,871,578 |

| 4,505,000 | | Aaa* | | North Hempstead GO, Series A, FGIC-Insured,

5.000% due 9/1/22 | | | 4,675,289 |

| 1,000,000 | | AAA | | Yonkers GO, Series C, State Aid Withholding, FGIC-Insured,

5.000% due 6/1/19 | | | 1,049,900 |

|

| | | | | | | | 10,596,767 |

|

Government Facilities — 7.8% | | | |

| | | | | New York State Urban Development Corp. Revenue: | | | |

| 20,000,000 | | AA- | | Correctional & Youth Facilities, Series A, | | | |

| | | | | 5.500% due 1/1/17 (b) | | | 21,758,600 |

| 3,050,000 | | AAA | | Correctional Capital Facilities, MBIA-Insured,

5.000% due 1/1/20 | | | 3,203,293 |

| | | | | Correctional Facilities Service Contract: | | | |

| 6,600,000 | | AAA | | Series C, AMBAC-Insured, (Call 1/1/09 @ 101),

6.000% due 1/1/29 (c) | | | 7,341,642 |

| 18,400,000 | | AAA | | Series D, FSA-Insured, (Call 1/1/11 @ 100),

5.250% due 1/1/30 (b)(c) | | | 20,170,264 |

| 3,000,000 | | AA- | | State Facilities, 5.700% due 4/1/20 | | | 3,456,900 |

|

| | | | | | | | 55,930,699 |

|

Hospitals — 7.7% | | | |

| 1,620,000 | | AAA | | East Rochester, Housing Authority Revenue, (North Park Nursing Home), GNMA, 5.200% due 10/20/24 | | | 1,707,691 |

| 5,000,000 | | AAA | | Nassau Health Care Corp., Health System Revenue, FSA-Insured, (Call 8/1/09 @ 102), 5.500% due 8/1/19 (c) | | | 5,549,850 |

| | | | | New York City Health & Hospital Corp. Revenue, Health System, Series A: | | | |

| 3,000,000 | | AAA | | AMBAC-Insured, 5.000% due 2/15/20 | | | 3,149,550 |

| | | | | FSA-Insured: | | | |

| 1,110,000 | | AAA | | 5.000% due 2/15/22 | | | 1,153,013 |

| 3,750,000 | | AAA | | 5.125% due 2/15/23 | | | 3,922,875 |

| | | | | New York State Dormitory Authority Revenue: | | | |

| 5,000,000 | | AAA | | Maimonides Medical Center, FHA-Insured,

5.000% due 8/1/24 | | | 5,192,200 |

| | | | | Mental Health Services Facilities: | | | |

| | | | | Series B: | | | |

| 40,000 | | AA- | | 5.000% due 2/15/18 | | | 41,374 |

| 4,180,000 | | AA- | | 5.625% due 2/15/21 | | | 4,381,183 |

| 2,820,000 | | AA- | | Call 2/15/07 @ 102, 5.625% due 2/15/21 (c) | | | 3,019,600 |

| 2,460,000 | | AA- | | Call 2/15/08 @ 102, 5.000% due 2/15/18 (c) | | | 2,646,788 |

See Notes to Financial Statements.

27 Smith Barney Muni Funds | 2005 Annual Report

| | |

| Schedules of Investments (continued) | | March 31, 2005 |

NEW YORK PORTFOLIO

| | | | | | | |

FACE AMOUNT | | RATING(a) | | SECURITY | | VALUE |

| Hospitals — 7.7% (continued) | | | |

| | | | | Series D, FSA-Insured: | | | |

| $ 190,000 | | AAA | | 5.250% due 8/15/30 | | $ | 196,984 |

| 2,410,000 | | AAA | | Call 8/15/10 @ 100, 5.250% due 8/15/30 (c) | | | 2,640,323 |

| 324,000 | | AA- | | Series B, (Partially Pre-refunded with U.S. government securities to various call dates and prices), 7.500% due 5/15/11 | | | 380,794 |

| 3,000,000 | | AA | | St. Luke’s Home, Residential Health, FHA-Insured,

6.375% due 8/1/35 | | | 3,089,910 |

| 2,450,000 | | AAA | | St. Vincent’s Hospital & Medical Center, FHA-Insured,

7.400% due 8/1/30 | | | 2,460,388 |

| 1,500,000 | | AAA | | United Cerebral Palsy, AMBAC-Insured, 5.125% due 7/1/21 | | | 1,603,245 |

| 2,000,000 | | AAA | | Victory Memorial Hospital, MBIA-Insured, 5.375% due 8/1/25 | | | 2,109,400 |

| 2,500,000 | | AAA | | Willow Towers Inc. Project, GNMA, 5.400% due 2/1/34 | | | 2,630,850 |

| | | | | New York State Medical Care Facilities, | | | |

| | | | | Finance Agency Revenue: | | | |

| 2,500,000 | | B | | Central Suffolk Hospital Mortgage Project, Series A, 6.125% due 11/1/16 | | | 2,349,400 |

| 955,000 | | Aa1* | | Health Center Projects, Secured Mortgage Program, SONYMA-Insured, 6.375% due 11/15/19 | | | 991,424 |

| | | | | Series B: | | | |

| 910,000 | | AA | | Hospital & Nursing Home Insured Mortgage, FHA-Insured, 7.000% due 8/15/32 | | | 913,585 |

| 1,860,000 | | AAA | | Long-Term Healthcare, FSA-Insured, 6.450% due 11/1/14 | | | 1,866,454 |

| 3,140,000 | | AA | | Mortgage Project, FHA-Insured, 6.100% due 2/15/15 | | | 3,230,118 |

|

| | | | | | | | 55,226,999 |

|

| Housing: Multi-Family — 3.1% | | | |

| 35,000 | | NR | | Battery Park City Authority, Housing Revenue, FHA-Insured,

(Call 6/1/05 @ 100), 8.625% due 6/1/23 (c) | | | 35,348 |

| | | | | New York City HDC: | | | |

| 1,262,563 | | NR | | Cadman Project, 6.500% due 11/15/18 | | | 1,329,466 |

| 1,019,529 | | NR | | Kelly Project, 6.500% due 2/15/18 | | | 1,074,971 |

| 5,000,000 | | AA | | Series A, 5.100% due 11/1/24 | | | 5,127,600 |

| | | | | New York State Dormitory Authority Revenue, Park Ridge Housing Inc., FNMA: | | | |

| 1,000,000 | | AAA | | 6.375% due 8/1/20 (d) | | | 1,132,180 |

| 1,470,000 | | AAA | | 6.500% due 8/1/25 | | | 1,662,452 |

| | | | | New York State Housing Finance Agency Revenue, Secured Mortgage Program: | | | |

| | | | | Series A, SONYMA-Insured: | | | |

| 500,000 | | Aa1* | | 7.000% due 8/15/12 (g) | | | 502,890 |

See Notes to Financial Statements.

28 Smith Barney Muni Funds | 2005 Annual Report

| | |

| Schedules of Investments (continued) | | March 31, 2005 |

NEW YORK PORTFOLIO

| | | | | | | |

FACE AMOUNT | | RATING(a) | | SECURITY | | VALUE |

| Housing: Multi-Family — 3.1% (continued) | | | |

| $ 2,000,000 | | Aa1* | | 6.200% due 8/15/15 (g) | | $ | 2,050,880 |

| 500,000 | | Aa1* | | 7.050% due 8/15/24 (g) | | | 503,000 |

| 6,870,000 | | Aa1* | | Series B, SONYMA-Insured, 6.250% due 8/15/29 (g) | | | 7,113,267 |

| 985,000 | | AAA | | Series C, FHA-Insured, 6.500% due 8/15/24 | | | 991,225 |

| 640,000 | | A1* | | Rensselaer Housing Authority, MFH Mortgage Revenue, Rensselaer Elderly Apartments, Series A, 7.750% due 1/1/11 | | | 641,715 |

|

| | | | | | | | 22,164,994 |

|

| Housing: Single-Family — 2.0% | | | |

| | | | | New York State Mortgage Agency Revenue, Homeowner Mortgage: | | | |

| 2,950,000 | | Aa1* | | Series 65, 5.850% due 10/1/28 (g) | | | 3,010,593 |

| 4,775,000 | | Aa1* | | Series 67, 5.800% due 10/1/28 (g) | | | 4,893,802 |

| 6,000,000 | | Aa1* | | Series 71, 5.350% due 10/1/18 (g) | | | 6,100,800 |

|

| | | | | | | | 14,005,195 |

|

| Industrial Development — 1.9% | | | |

| 2,250,000 | | BBB | | Essex County IDA Revenue, Solid Waste, (International Paper Co. Project), Series A, 6.150% due 4/1/21(g) | | | 2,337,885 |

| 435,000 | | NR | | Monroe County IDA Revenue, Public Improvement, Canal Ponds Park, Series A, 7.000% due 6/15/13 | | | 435,583 |

| | | | | Onondaga County, IDA: | | | |

| 750,000 | | AA- | | Civic Facilities Revenue, (Syracuse Home Association Project), LOC-HSBC Bank USA, 5.200% due 12/1/18 | | | 796,965 |

| 8,000,000 | | A+ | | Sewer Facilities Revenue, (Bristol-Myers Squibb Co. Project), 5.750% due 3/1/24 (b)(g) | | | 8,905,280 |

| 1,410,000 | | AA | | Rensselaer County IDA, Albany International Corp.,

7.550% due 7/15/07 | | | 1,519,557 |

|

| | | | | | | | 13,995,270 |

|

| Life Care Systems — 1.8% | | | |

| | | | | New York State Dormitory Authority Revenue Bonds,

FHA-Insured: | | | |

| 3,815,000 | | AA | | Hebrew Nursing Home, 6.125% due 2/1/37 | | | 3,994,419 |

| 1,395,000 | | AAA | | Jewish Geriatric Center, 7.150% due 8/1/14 (b)(d) | | | 1,428,606 |

| 1,500,000 | | AAA | | Menorah Campus Nursing Home, 6.100% due 2/1/37 | | | 1,605,750 |

| 1,390,000 | | AA | | Niagara Frontier Home, Mortgage Revenue,

6.200% due 2/1/15 | | | 1,426,752 |

| 3,330,000 | | AA | | Wesley Garden Nursing Home, 6.125% due 8/1/35 | | | 3,525,538 |

| 1,250,000 | | AAA | | Syracuse IDA Revenue, James Square Association, FHA-Insured, 7.000% due 8/1/25 | | | 1,255,050 |

|

| | | | | | | | 13,236,115 |

|

See Notes to Financial Statements.

29 Smith Barney Muni Funds | 2005 Annual Report

| | |

| Schedules of Investments (continued) | | March 31, 2005 |

NEW YORK PORTFOLIO

| | | | | | | |

FACE AMOUNT | | RATING(a) | | SECURITY | | VALUE |

Pollution Control — 0.5% | | | |

| | | | | New York State Environmental Facilities Corp., State Water Revolving Fund, Series A: | | | |

| $ 190,000 | | AAA | | 7.500% due 6/15/12 | | $ | 191,959 |

| 805,000 | | AAA | | GIC-Societe General, 7.250% due 6/15/10 | | | 808,856 |

| 1,000,000 | | AAA | | North Country Development Authority, Solid Waste Management System Revenue, FSA-Insured,

6.000% due 5/15/15 | | | 1,137,310 |

| 1,710,000 | | CCC | | Puerto Rico Industrial, Medical & Environmental Facilities, Finance Authority Revenue, American Airlines Inc., Series A,

6.450% due 12/1/25 | | | 1,211,962 |

|

| | | | | | | | 3,350,087 |

|

Public Facilities — 2.1% | | | |

| | | | | New York City Trust Cultural Resource Revenue, AMBAC-Insured: | | | |

| 1,655,000 | | AAA | | American Museum of Natural History, Series A,

5.250% due 7/1/17 | | | 1,764,164 |

| | | | | Museum of Modern Art: | | | |

| 3,100,000 | | AAA | | Series A, 5.000% due 4/1/23 | | | 3,231,688 |

| 9,000,000 | | AAA | | Series D, 5.125% due 7/1/31 (b) | | | 9,354,870 |

| 570,000 | | AA- | | New York State COP, (Hanson Redevelopment Project),

8.375% due 5/1/08 | | | 601,031 |

|

| | | | | | | | 14,951,753 |

|

Transportation — 19.8% | | | |

| 750,000 | | BBB+ | | Albany, Parking Authority Revenue, Series A, 5.625% due 7/15/25 | | | 801,743 |

| | | | | Metropolitan Transportation Authority: | | | |

| | | | | Dedicated Tax Fund, Series A: | | | |

| 11,000,000 | | AAA | | FGIC-Insured, 5.250% due 11/15/23 (b) | | | 12,120,130 |

| | | | | FSA-Insured, (Call 10/1/14 @ 100): | | | |

| 2,290,000 | | AAA | | 5.125% due 4/1/19 (c) | | | 2,525,985 |

| 4,500,000 | | AAA | | 5.250% due 4/1/23 (c) | | | 5,008,140 |

| | | | | Transit Facilities Revenue, Series A: | | | |

| 5,000,000 | | AAA | | Call 7/1/09 @ 100, 6.000% due 7/1/19 (c) | | | 5,563,150 |

| 10,000,000 | | AAA | | MBIA-Insured, (Call 7/1/07 @ 101.50),

5.625% due 7/1/25 (b)(c) | | | 10,753,900 |

| | | | | Triborough Bridge & Tunnel Authority: | | | |

| | | | | Series A: | | | |

| 3,500,000 | | AA- | | Call 1/1/22 @ 100, 5.250% due 1/1/28 (c) | | | 3,933,895 |

| 5,200,000 | | AAA | | MBIA/IBC-Insured, 5.250% due 11/15/30 | | | 5,506,072 |

| | | | | Series B: | | | |

| 4,200,000 | | AAA | | Call 1/1/16 @ 100, 5.375% due 1/1/19 (c) | | | 4,727,268 |

| 10,125,000 | | AAA | | Call 1/1/22 @ 100, 5.500% due 1/1/30 (b)(c) | | | 11,588,062 |

| | | | | Triborough Bridge COP, AMBAC-Insured: | | | |

| 2,595,000 | | AAA | | Call 1/1/10 @ 101, 5.875% due 1/1/30 (c) | | | 2,916,495 |

| 20,000,000 | | AAA | | Series A, (Call 1/1/10 @ 101), 5.250% due 1/1/29 (b)(c) | | | 21,932,800 |

See Notes to Financial Statements.

30 Smith Barney Muni Funds | 2005 Annual Report

| | |

| Schedules of Investments (continued) | | March 31, 2005 |

NEW YORK PORTFOLIO

| | | | | | | |

FACE AMOUNT | | RATING(a) | | SECURITY | | VALUE |

Transportation — 19.8% (continued) | | | |

| | | | | New York State Thruway Authority: | | | |

| $ 5,000,000 | | AA- | | General Revenue, Series E, 5.000% due 1/1/25 | | $ | 5,115,450 |

| | | | | Highway & Bridge Toll Revenue Fund, FGIC-Insured: | | | |

| | | | | Series A: | | | |

| 3,410,000 | | AAA | | 5.000% due 4/1/19 | | | 3,586,365 |

| 2,000,000 | | AAA | | 5.000% due 4/1/20 | | | 2,097,260 |

| 2,500,000 | | AAA | | 5.000% due 4/1/21 | | | 2,613,875 |

| 15,000,000 | | AAA | | Series B, 5.000% due 4/1/19 (b) | | | 15,715,650 |

| 4,000,000 | | AAA | | Series B-1, 5.500% due 4/1/18 | | | 4,345,240 |

| | | | | Port Authority New York & New Jersey: | | | |