As filed with the Securities and Exchange Commission on , 2012

Securities Act File No. 333-

U.S. SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-14

| REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 |

| ¨ Pre-Effective Amendment No. |

| ¨ Post-Effective Amendment No. |

| (Check appropriate box or boxes) |

Thrivent Series Fund, Inc.

(Exact Name of Registrant as Specified in Declaration of Trust)

625 Fourth Avenue South

Minneapolis, Minnesota 55415

(Address of Principal Executive Offices)

(612) 844-5168

(Area Code and Telephone Number)

Rebecca A. Paulzine

Thrivent Mutual Funds

625 Fourth Avenue South

Minneapolis, Minnesota 55415

(Name and Address of Agent for Service)

Approximate Date of Proposed Public Offering: As soon as practicable after this registration statement becomes effective. It is proposed that this filing will become effective on pursuant to Rule 488 under the Securities Act of 1933.

Title of Securities Being Registered: Shares of beneficial interest, par value $.01 per share. The Registrant has registered an indefinite number of shares of beneficial interest pursuant to Section 24(f) of the Investment Company Act of 1940, as amended, and is in a continuous offering of such shares under an effective registration statement (File Nos. 33- and 811- ). No filing fee is due herewith because of reliance on Section 24(f) of the Investment Company Act of 1940, as amended.

LETTER FOR MEMBERS

Dear Member:

The Board of Directors of Thrivent Series Fund, Inc. (the “Fund”) has scheduled special meetings of contractholders for July 13, 2012, to seek approval of five mergers. At the meetings, the contractholders for each of the series of the Fund listed in the first column below (each a “Target Portfolio”) will be asked to consider and approve an Agreement and Plan of Reorganization (an “Agreement”) providing for its reorganization into the Fund series listed in the second column below (each an “Acquiring Portfolio”).

TARGET PORTFOLIO | ACQUIRING PORTFOLIO | |

Thrivent Partner Utilities Portfolio | Thrivent Diversified Income Plus Portfolio | |

Thrivent Partner Socially Responsible Bond Portfolio | Thrivent Income Portfolio | |

Thrivent Partner International Stock Portfolio | Thrivent Partner Worldwide Allocation Portfolio | |

Thrivent Large Cap Growth Portfolio II | Thrivent Large Cap Growth Portfolio | |

Thrivent Mid Cap Growth Portfolio II | Thrivent Mid Cap Growth Portfolio |

If you are not planning to attend the meeting in person, please vote before July 13th in one of the ways described below.

If a merger is approved, your investment in the Target Portfolio will automatically be transferred into the corresponding Acquiring Portfolio listed above. We will send you a written confirmation after this takes place. This transfer is not considered a taxable event. (Of course, you may transfer your investment to a completely different series, which will not count as one of your permitted annual exchanges.)

Your vote counts! You may vote quickly and easily in any one of these ways:

| • | Via internet: see the instructions on the enclosed proxy card. |

| • | Via telephone: see the instructions on the enclosed proxy card. |

| • | Via mail: use the enclosed proxy card and postage-paid envelope. |

| • | In person: attend the shareholder meeting on July 13 at the Thrivent Financial corporate office in Minneapolis. |

If you’d like more information about the Portfolios, you may order a statement of additional information to the Portfolios’ prospectuses, a shareholder report or the statement of additional information regarding the proposed Portfolio reorganizations (request the “Reorganization SAI”) by:

| • | Telephone: 1-800-THRIVENT (1-800-847-4836) |

| • | Mail: Thrivent Series Fund, Inc., 625 Fourth Avenue South, Minneapolis, MN 55415 |

| • | Internet: www.thrivent.com |

Thank you for taking this matter seriously and participating in this important process.

Sincerely,

Russell W. Swansen, President

EXPLANATORY NOTE

This Registration Statement is organized as follows:

| Page | ||||

Thrivent Partner Utilities Portfolio | 2 | |||

• Questions & Answers for Contractholders of Thrivent Partner Utilities Portfolio | ||||

• Notice of Special Meeting of Contractholders of Thrivent Partner Utilities Portfolio | ||||

• Prospectus/Proxy Statement Regarding Proposed Reorganization | ||||

Thrivent Partner Socially Responsible Bond Portfolio | 34 | |||

• Questions & Answers for Contractholders of Thrivent Partner Socially Responsible Bond Portfolio | ||||

• Notice of Special Meeting of Contractholders of Thrivent Partner Socially Responsible Bond Portfolio | ||||

• Prospectus/Proxy Statement Regarding Proposed Reorganization | ||||

Thrivent Partner International Stock Portfolio | 65 | |||

• Questions & Answers for Contractholders of Thrivent Partner International Stock Portfolio | ||||

• Notice of Special Meeting of Contractholders of Thrivent Partner International Stock Portfolio | ||||

• Prospectus/Proxy Statement Regarding Proposed Reorganization | ||||

Thrivent Large Cap Growth Portfolio II | 99 | |||

• Questions & Answers for Contractholders of Thrivent Large Cap Growth Portfolio II | ||||

• Notice of Special Meeting of Contractholders of Thrivent Large Cap Growth Portfolio II | ||||

• Prospectus/Proxy Statement Regarding Proposed Reorganization | ||||

Thrivent Mid Cap Growth Portfolio II | 127 | |||

• Questions & Answers for Contractholders of Thrivent Mid Cap Growth Portfolio II | ||||

• Notice of Special Meeting of Contractholders of Thrivent Mid Cap Growth Portfolio II | ||||

• Prospectus/Proxy Statement Regarding Proposed Reorganization | ||||

Statement of Additional Information Regarding the Proposed Reorganizations | ||||

Part C Information | ||||

Exhibits | ||||

Questions & Answers

For Contractholders of Thrivent Partner Utilities Portfolio

Although we recommend that you read the complete Prospectus/Proxy Statement, we have provided the following questions and answers to clarify and summarize the issues to be voted on.

Q: Why is a contractholder meeting being held?

A: A special meeting of contractholders (the “Meeting”) of Thrivent Partner Utilities Portfolio (the “Target Portfolio”) is being held to seek contractholder approval of a reorganization (the “Reorganization”) of the Target Portfolio into Thrivent Diversified Income Plus Portfolio (the “Acquiring Portfolio”), a fund that pursues a similar investment objective as the Target Portfolio. Please refer to the Prospectus/Proxy Statement for a detailed explanation of the proposed Reorganization and for a more complete description of the Acquiring Portfolio.

Q: Why is the Reorganization being recommended?

A: After careful consideration, the Board of Directors (the “Board”) of Thrivent Series Fund, Inc. (the “Fund”) has determined that the Reorganization will benefit the Target Portfolio’s contractholders and recommends that you cast your vote “FOR” the proposed Reorganization. The Target Portfolio and the Acquiring Portfolio have similar investment objectives, and each is a diversified series of the Fund, an open-end investment company registered under the Investment Company Act of 1940. Thrivent Financial for Lutherans (“Thrivent Financial”) is the investment adviser for the Target Portfolio and the Acquiring Portfolio.

The Board believes that the Reorganization would be in the best interests of the Target Portfolio’s contractholders because: (i) the advisory fee that these contractholders bear will decrease as a result of the Reorganization; (ii) the operating expenses that these contractholders bear will likely decrease as a result of the Reorganization; and (iii) contractholders will become contractholders in a larger combined portfolio, which increase the potential of realizing economies of scale whereby certain administrative costs may be spread across the combined portfolio’s larger asset base and, therefore, may increase the combined portfolio’s overall efficiency in the long term.

Q: Who can vote?

A: Owners of the variable contracts funded by the Target Portfolio and shareholders of the Target Portfolio (e.g., mutual funds affiliated with Thrivent Financial) are entitled to vote. Thrivent Financial and Thrivent Life Insurance Company (“Thrivent Life”), the sponsors of your variable contracts, will cast your votes according to your voting instructions. If no timely voting instructions are

2

received, any shares of the Target Portfolio attributable to a variable contract will be voted by Thrivent Financial or Thrivent Life in proportion to the voting instructions received for all variable contracts participating in the proxy solicitation. If a voting instruction form is returned with no voting instructions, the shares of the Target Portfolio to which the form relates will be voted FOR all the Reorganization.

Any shares of the Target Portfolio held by Thrivent Financial, Thrivent Life or any of their affiliates for their own account and any shares held in an asset allocation portfolio managed by Thrivent Financial will also be voted in proportion to the voting instructions received for all variable contracts participating in the proxy solicitation.

Q: How will the Reorganization affect me?

A: Assuming contractholders approve the proposed Reorganization, the assets and liabilities of the Target Portfolio will be combined with those of the Acquiring Portfolio. The shares of the Target Portfolio that fund your benefits under variable contracts automatically would be exchanged for an equal dollar value of shares of the Acquiring Portfolio. The Reorganization would affect only the investments underlying variable contracts and would not otherwise affect variable contracts. Following the Reorganization, the Target Portfolio will dissolve.

Q: Will I have to pay any commission or other similar fee as a result of the Reorganization?

A: No. You will not pay any commissions or other similar fees as a result of the Reorganization.

Q: Will the total annual operating expenses that my portfolio investment bears increase as a result of the Reorganization?

A: No, they will likely decrease, and the investment management fee, which comprises a portion of the annual operating expenses, will decrease. For more information about how fund expenses may change as a result of the Reorganization, please see the comparative and pro forma table and related disclosures in the COMPARISON OF THE PORTFOLIOS—Expenses section of the prospectus/proxy statement.

Q: Will I have to pay any U.S. federal income taxes as a result of the Reorganization?

A: The Reorganization is expected to be tax-free for federal income tax purposes. The Target Portfolio will seek an opinion of counsel to this effect. It is expected that neither the shareholders of record (Thrivent Financial and Thrivent Life) nor contractholders will incur capital gains or losses on the exchange of Target Portfolio shares for Acquiring Portfolio shares as a result of the Reorganization. The cost basis on each investment will also remain the same. If you choose to make a total or partial surrender of your contract, you may be subject to taxes and other charges under your contract.

3

Q: Can I surrender or exchange my interests in the Target Portfolio for a different subaccount option under my contract or surrender my contract before the Reorganization takes place?

A: Yes, but please refer to the most recent prospectus of your variable contract as certain charges and/or restrictions may apply to such exchanges and surrenders.

Q: If contractholders do not approve the Reorganization, what will happen to the Target Portfolio?

A: Thrivent Financial for Lutherans and the Board will have to re-assess what changes it would like to make to the Target Portfolio, including a possible repurposing of the Portfolio’s principal investment strategies. It is possible that no changes would be made.

Q: Who pays the costs of the Reorganization?

A: The expenses of the Reorganization, including the costs of the Meeting, will be paid by Thrivent Financial.

Q: How can I vote?

A: Contractholders are invited to attend the Meeting and to vote in person. You may also vote by executing a proxy using one of three methods:

| • | By Internet: Instructions for casting your vote via the Internet can be found in the enclosed proxy voting materials. The required control number is printed on your enclosed proxy card. If this feature is used, there is no need to mail the proxy card. |

| • | By Telephone: Instructions for casting your vote via telephone can be found in the enclosed proxy voting materials. The toll-free number and required control number are printed on your enclosed proxy card. If this feature is used, there is no need to mail the proxy card. |

| • | By Mail: If you vote by mail, please indicate your voting instructions on the enclosed proxy card, date and sign the card, and return it in the envelope provided, which is addressed for your convenience and needs no postage if mailed in the United States. |

Contractholders who execute proxies by Internet, telephone or mail may revoke them at any time prior to the Meeting by filing with the Target Portfolio a written notice of revocation, by executing another proxy bearing a later date, by voting later by Internet or telephone or by attending the Meeting and voting in person. Merely attending the Meeting, however, will not revoke any previously submitted proxy.

4

Q: When should I vote?

A: Every vote is important and the Board encourages you to record your vote as soon as possible. Voting your proxy now will ensure that the necessary number of votes is obtained, without the time and expense required for additional proxy solicitation.

Q: Who should I call if I have questions about a Proposal in the proxy statement?

A: Call 1-800-847-4836 with your questions.

Q: How can I get more information about the Target and Acquiring Portfolios or my variable contract?

A: You may obtain (1) a prospectus, statement of additional information or annual/semiannual report for the Portfolios, (2) a prospectus or statement of additional information for your variable contract or (3) the Statement of Additional Information regarding the Reorganization (request the “Reorganization SAI”) by:

| • | Telephone—1-800-THRIVENT (1-800-847-4836) and say [“ ”] |

| • | Mail—Thrivent Series Fund, Inc., 4321 North Ballard Road, Appleton, WI 54919 |

| • | Internet— |

5

Thrivent Partner Utilities Portfolio

a series of

THRIVENT SERIES FUND, INC.

625 Fourth Avenue South

Minneapolis, Minnesota 55415

(800) 847-4836

www.thrivent.com

NOTICE OF SPECIAL MEETING

OF SHAREHOLDERS

to be Held on July 13, 2012

NOTICE IS HEREBY GIVEN THAT a special meeting of contractholders (the “Meeting”) of Thrivent Partner Utilities Portfolio (the “Target Fund”), a series of Thrivent Series Fund, Inc. (the “Fund”), will be held at the offices of Thrivent Financial for Lutherans, 625 Fourth Avenue South, Minneapolis, Minnesota 55415 on July 13, 2012 at 9:00 a.m. Central time for the following purposes:

| 1. | To approve an Agreement and Plan of Reorganization pursuant to which the Target Portfolio would (i) transfer all of its assets and liabilities to Thrivent Diversified Income Plus Portfolio (the “Acquiring Portfolio”), a series of the Fund, in exchange for Shares of the Acquiring Portfolio, (ii) distribute such Shares of the Acquiring Portfolio to shareholders of the Target Portfolio, and (iii) dissolve. |

| 2. | To transact such other business as may properly be presented at the Meeting or any adjournment thereof. |

The Board of Directors of the Trust (the “Board”) has fixed the close of business on May 16, 2012 as the record date for the determination of contractholders entitled to notice of, and to vote at, the Meeting and all adjournments thereof.

Contractholders are invited to attend the Meeting and to vote in person. You may also vote by executing a proxy using one of three methods:

| (i) | By internet—Instructions for casting your vote via the Internet can be found in the enclosed proxy voting materials. The required control number is printed on your enclosed proxy card. If this feature is used, there is no need to mail the proxy card. |

| (ii) | By telephone—Instructions for casting your vote via telephone can be found in the enclosed proxy voting materials. The toll-free number and required control number are printed on your enclosed proxy card. If this feature is used, there is no need to mail the proxy card. |

6

| (iii) | By mail—If you vote by mail, please indicate your voting instructions on the enclosed proxy card, date and sign the card, and return it in the envelope provided, which is addressed for your convenience and needs no postage if mailed in the United States. |

Contractholders who execute proxies by Internet, telephone or mail may revoke them at any time prior to the Meeting by filing with the Target Portfolio a written notice of revocation, by executing another proxy bearing a later date or by attending the Meeting and voting in person. Merely attending the Meeting, however, will not revoke any previously submitted proxy.

The Board recommends that you cast your vote FOR the proposed Reorganization as described in the Prospectus/Proxy Statement.

YOUR VOTE IS IMPORTANT

Please return your proxy card or record your voting instructions by telephone or via the Internet promptly no matter how many shares you own. In order to avoid the additional expense of further solicitation, we ask that you mail your proxy card or record your voting instructions by telephone or via the Internet promptly regardless of whether you plan to be present in person at the Meeting.

Date: , 2012

|

| David S. Royal |

| Secretary |

7

SUMMARY

The following is a summary of certain information contained elsewhere in this Prospectus/Proxy Statement and is qualified in its entirety by reference to the more complete information contained in this Prospectus/Proxy Statement. Contractholders should read the entire Prospectus/Proxy Statement carefully.

The Reorganization

The Board, including the directors who are not “interested persons” (as defined in the 1940 Act) of each Portfolio, has unanimously approved the Reorganization Agreement on behalf of each Portfolio, subject to Target Portfolio contractholder approval. The Reorganization Agreement provides for:

| • | the transfer of all of the assets and liabilities of the Target Portfolio to the Acquiring Portfolio in exchange for shares of the Acquiring Portfolio; |

| • | the distribution by the Target Portfolio of such Acquiring Portfolio shares to Target Portfolio shareholders; and |

| • | the dissolution of the Target Portfolio. |

When the Reorganization is complete, Target Portfolio shareholders will hold Acquiring Portfolio shares. The aggregate value of the Acquiring Portfolio shares a Target Portfolio shareholder will receive in the Reorganization will equal the aggregate value of the Target Portfolio shares owned by such shareholder immediately prior to the Reorganization. After the Reorganization, the Acquiring Portfolio will continue to operate with the investment objective and investment policies set forth in this Prospectus/Proxy Statement. The Reorganization will not affect your variable contract.

As discussed in more detail elsewhere in this prospectus/proxy statement, the Board believes that the Reorganization would be in the best interests of the Target Portfolio’s contractholders because: (i) the advisory fee that these contractholders bear will decrease as a result of the Reorganization; (ii) the operating expenses that these contractholders bear will likely decrease as a result of the Reorganization; and (iii) contractholders will become contractholders in a larger combined portfolio, which increase the potential of realizing economies of scale whereby certain administrative costs may be spread across the combined portfolio’s larger asset base and, therefore, may increase the combined portfolio’s overall efficiency in the long term. In addition, the Board, when determining whether to approve the Reorganization, considered, among other things, the future growth prospects of each of the Target Portfolio and the Acquiring Portfolio, the comparative performance of the two Portfolios, and that the Reorganization is expected to be a tax-free reorganization for federal income tax purposes.

8

Background and Reasons for the Reorganization

The Target Portfolio and the Acquiring Portfolio have similar investment objectives. The Target Portfolio seeks capital appreciation and current income; the Acquiring Portfolio seeks to maximize income while maintaining prospects for capital appreciation.

Despite this similarity, there are significant differences between the two Portfolios’ principal investment strategies, which are described in more detail in the COMPARISON OF THE PORTFOLIOS—Investment Objective and Principal Strategies section of the prospectus/proxy statement. Under normal circumstances, the Target Portfolio invests at least 80% of its assets in equity and debt securities issued by domestic and foreign utilities companies. It invests primarily, however, in equity securities, but it may change its allocation among equity and debt investments as it deems appropriate to achieve its objective. The Acquiring Portfolio is not subject to an 80% investment requirement. Under normal circumstances, it invests in a diversified portfolio of income-producing debt and equity securities.

Further, the Acquiring Portfolio, unlike the Target Portfolio, invests in junk bonds, mortgage-backed securities (including commercially-backed ones) and asset-backed securities. Investing in these asset classes has specific risks, which are described in more detail in the COMPARISON OF THE PORTFOLIOS—Principal Risks section of the prospectus/proxy statement. In addition, the Acquiring Portfolio, unlike the Target Portfolio, does not concentrate its investments in securities of companies in the utilities industry.

In determining whether to recommend approval of the Reorganization Agreement to Target Portfolio contractholders, the Board considered a number of factors, including, but not limited to: (i) the Adviser currently manages the assets of each Portfolio; (ii) the expenses and advisory fees applicable to the Portfolios before the proposed Reorganization and the estimated expense ratios of the combined portfolio after the proposed Reorganization; (iii) the comparative investment performance of the Portfolios; (vi) the future growth prospects of each Portfolio; (iv) whether the Reorganization would result in the dilution of contractholder interests; (v) the compatibility of the Portfolios’ investment objectives, policies, risks and restrictions; (vi) the anticipated tax consequences of the proposed Reorganization; (vii) the fact that Thrivent Financial would bear the costs of the Reorganization. The Board concluded that these factors supported a determination to approve the Reorganization Agreement.

The Board has determined that the Reorganization is in the best interests of the Target Portfolio and that the interests of the Target Portfolio’s contractholders will not be diluted as a result of the Reorganization. In addition, the Board has determined that the Reorganization is in the best interests of the Acquiring Portfolio and that the

9

interests of the Acquiring Portfolio contractholders will not be diluted as a result of the Reorganization.

The Board is asking contractholders of the Target Portfolio to approve the Reorganization at the Meeting to be held on July 13, 2012. If contractholders of the Target Portfolio approve the proposed Reorganization, it is expected that the closing date of the transaction (the “Closing Date”) will be after the close of business on or about July 27, 2012, but it may be at a different time as described herein. If contractholders of the Target Portfolio do not approve the proposed Reorganization, the Board will consider alternatives, including repurposing the Target Portfolio’s investment objective(s) and principal strategies.

The Board recommends that you vote “FOR” the Reorganization.

10

COMPARISON OF THE PORTFOLIOS

Investment Objective and Principal Strategies

Investment Objective. The Target Portfolio seeks capital appreciation and current income; the Acquiring Portfolio seeks to maximize income while maintaining prospects for capital appreciation. There are risks inherent in all investments in securities; accordingly, there can be no assurance that either of the Portfolios will achieve its investment objectives.

Principal Strategies. Under normal circumstances, the Target Portfolio invests at least 80% of its assets in equity and debt securities issued by domestic and foreign utilities companies. Utilities companies are those that are primarily engaged in the ownership or operation of facilities used to generate, transmit or distribute electricity, telecommunications, gas or water. The Target Portfolio concentrates its investments in the securities of companies in the utilities industry. The Acquiring Portfolio is not subject to any 80% investment requirement nor does it concentrate its investments in securities of companies in any particular industry.

The Target Portfolio invests primarily in equity securities, but it may change its allocation among equity and debt investments as it deems appropriate to achieve its objective. The Acquiring Portfolio, under normal circumstances, invests in a diversified portfolio of income-producing debt and equity securities.

The debt securities in which the Target Portfolio invests generally are limited to those rated investment grade. A security is investment grade when assigned a credit quality rating of at least “Baa” by Moody’s Investors Service, “BBB” by Standard & Poor’s Ratings Services (“S&P”) or, if unrated, considered to be of comparable credit quality by the Portfolio’s adviser. The debt securities in which the Acquiring Portfolio invests may be of any maturity or credit quality, including high yield, high risk bonds, notes, debentures and other debt obligations commonly known as “junk bonds.” At the time of purchase, these high-yield securities are rated within or below the “BB” major rating category by S&P or the “Ba” major rating category by Moody’s or are unrated but considered to be of comparable quality by the Acquiring Portfolio’s investment adviser. The Acquiring Portfolio may also invest in mortgage-backed securities (including commercially backed ones) and asset-backed securities.

The foreign securities in which the Target Portfolio invests may be issued by companies located in both developed and emerging markets. There are no limits on the geographic allocation of the Portfolio investments. The adviser anticipates, however, that the Portfolio’s investments will focus primarily on securities issued by utilities companies in the U.S. and that the investments in securities issued by foreign companies will focus on companies in Canada and Western Europe and other developed markets. The Acquiring Portfolio may invest in foreign securities but does not do so as a principal strategy.

11

Portfolio Holdings. A description of the Portfolios’ policies and procedures with respect to the disclosure of the Portfolios’ portfolio securities is available on the Portfolios’ website.

Principal Risks

The Portfolios are subject to similar principal risks, including Market Risk, Issuer Risk, Volatility Risk, Credit Risk, Interest Rate Risk and Investment Adviser Risk. The Acquiring Portfolio is also subject to High Yield Risk, Liquidity Risk and Mortgage-Related and Other Asset-Backed Securities Risk. The Target Portfolio, unlike the Acquiring Portfolio, is subject to Utility Industry Risk, Foreign Securities Risk and Emerging Markets Risk. These risks are described below.

It is important to note that, in the event that the high-yield or mortgage-related and other asset-backed markets were to perform poorly or the utilities sector or foreign securities markets were to perform well, the Target Portfolio, if it were still in existence, may outperform the combined portfolio.

Principal risks to which both Portfolios are subject

Market Risk. Over time, securities markets generally tend to move in cycles with periods when security prices rise and periods when security prices decline. The value of the Portfolio’s investments may move with these cycles and, in some instances, increase or decrease more than the applicable market(s) as measured by the Portfolio’s benchmark index(es). The securities markets may also decline because of factors that affect a particular industry.

Issuer Risk. Issuer risk is the possibility that factors specific to a company, to which the Portfolio’s portfolio is exposed, will affect the market prices of the company’s securities and therefore the value of the Portfolio. Some factors affecting the performance of a company include demand for the company’s products or services, the quality of management of the company and brand recognition and loyalty. Common stock of a company is subordinate to other securities issued by the company. If a company becomes insolvent, interests of investors owning common stock will be subordinated to the interests of other investors in, and general creditors of, the company.

Volatility Risk. Volatility risk is the risk that certain types of securities shift in and out of favor depending on market and economic conditions as well as investor sentiment. The value of the Portfolio’s shares may be affected by weak equity markets or changes in interest rate or bond yield levels. As a result, the value of the Portfolio’s shares may fluctuate significantly in the short term.

Credit Risk. Credit risk is the risk that an issuer of a bond held by the Portfolio to which the Portfolio’s portfolio is exposed may no longer be able to pay its debt. As a result of such an event, the bond may decline in price and affect the value of the Portfolio.

12

Interest Rate Risk. Interest rate risk is the risk that bond prices decline in value when interest rates rise for bonds that pay a fixed rate of interest. Bonds with longer durations or maturities tend to be more sensitive to changes in interest rates than bonds with shorter durations or maturities.

Investment Adviser Risk. The Portfolio is actively managed and the success of its investment strategy depends significantly on the skills of the adviser(s) in assessing the potential of the investments in which the Portfolio invests. This assessment of investments may prove incorrect, resulting in losses or poor performance, even in rising markets.

Additional principal risks to which only Acquiring Portfolio is subject

High Yield Risk. High yield securities, to which the Portfolio’s portfolio is exposed, are considered predominantly speculative with respect to the issuer’s continuing ability to make principal and interest payments. If the issuer of the security is in default with respect to interest or principal payments, the value of the Portfolio will be negatively affected.

Liquidity Risk. Liquidity risk is the ability to sell a security relatively quickly for a price that most closely reflects the actual value of the security. High-yield bonds have a less liquid resale market. As a result, the Portfolio may have difficulty selling or disposing of securities quickly in certain markets or may only be able to sell the holdings at prices substantially less than what the Portfolio believes they are worth.

Mortgage-Related and Other Asset-Backed Securities Risk. The value of mortgage-related and asset-backed securities will be influenced by the factors affecting the housing market and the assets underlying such securities. As a result, during periods of declining asset value, difficult or frozen credit markets, swings in interest rates, or deteriorating economic conditions, mortgage-related and asset-backed securities may decline in value, face valuation difficulties, become more volatile and/or become illiquid.

Additional principal risks to which only Target Portfolio is subject

Utility Industry Risk. As a sector fund that invests primarily in utilities companies, the Portfolio is subject to the risks associated with this sector. The Portfolio therefore is more vulnerable to price changes of utilities companies’ securities and factors that affect the utilities industry than a more broadly diversified fund. The prices of securities issued by utilities companies historically have changed more in response to interest rate movements than other stocks. Generally, when interest rates go up, the value of securities issued by utilities companies goes down. There is no guarantee that this relationship will continue in the future.

Foreign Securities Risk. To the extent the Portfolio’s portfolio is exposed to foreign securities, it is subject to various risks associated with such securities. Foreign

13

securities are generally more volatile than their domestic counterparts, in part because of higher political and economic risks, lack of reliable information and fluctuations in currency exchange rates. Foreign securities also may be more difficult to resell than comparable U.S. securities because the markets for foreign securities are often less liquid. Even when a foreign security increases in price in its local currency, the appreciation may be diluted by adverse changes in exchange rates when the security’s value is converted to U.S. dollars. Foreign withholding taxes also may apply and errors and delays may occur in the settlement process for foreign securities.

Emerging Markets Risk. The economic and political structures of developing nations, in most cases, do not compare favorably with the U.S. or other developed countries in terms of wealth and stability, and their financial markets often lack liquidity. Portfolio performance will likely be negatively affected by portfolio exposure to nations in the midst of, among other things, hyperinflation, currency devaluation, trade disagreements, sudden political upheaval or interventionist government policies. Significant buying or selling actions by a few major investors may also heighten the volatility of emerging markets. These factors make investing in emerging market countries significantly riskier than in other countries and events in any one country could cause the Portfolio’s share price to decline.

Management of the Portfolios

The Board. The Board is responsible for the overall supervision of the operations of each Portfolio and performs the various duties imposed on the directors of investment companies by the 1940 Act and under applicable state law.

The Adviser. The Adviser, Thrivent Financial for Lutherans (“Thrivent Financial” or the “Adviser”), is the investment adviser for each Portfolio. Thrivent Financial and its investment advisory affiliate, Thrivent Asset Management, LLC, have been in the investment advisory business since 1986 and managed approximately $76 billion in assets as of December 31, 2011, including approximately $34 billion in mutual fund assets. These advisory entities are located at 625 Fourth Avenue South, Minneapolis, Minnesota 55415.

The Adviser and the Fund received an exemptive order from the SEC that permits the Adviser and the Portfolios, with the approval of the Board, to retain one or more subadvisers for the Portfolios, or subsequently change a subadviser, without submitting the respective investment subadvisory agreements, or material amendments to those agreements, to a vote of the contractholders of the applicable Portfolio. The Adviser will notify contractholders of a Portfolio if there is a new subadviser for that Portfolio.

The Portfolios’ annual and semiannual reports to contractholders discuss the basis for the Board approving any investment advisory agreement or investment subadvisory agreement during the period covered by the report.

14

Portfolio Management. Darren M. Bagwell, CFA has served as portfolio manager of the Target Portfolio since 2011. He has been with Thrivent Financial since 2002 in an investment management capacity and currently is the firm’s Director of Equity Research.

Mark L. Simenstad, CFA, David R. Spangler, CFA, Kevin R. Brimmer, FSA and Paul J. Ocenasek, CFA have served as portfolio managers of the Acquiring Portfolio since the respective years of 2006, 2007, 2007 and 2004. Mr. Simenstad is Vice President of Fixed Income Mutual Funds and Separate Accounts and has been with Thrivent Financial since 1999. Mr. Spangler has been with Thrivent Financial since 2002 and was Director of Investment Product Management from 2002 to 2006. Mr. Brimmer has been with Thrivent Financial since 1985 and has been a portfolio manager since 2002. Mr. Ocenasek has been with Thrivent Financial since 1987 and, since 1997, has served as portfolio manager to other Thrivent mutual funds.

Advisory and Other Fees

Advisory Fees. Each Portfolio pays an annual investment advisory fee to the Adviser. The advisory contract between the Adviser and the Fund provides for the following advisory fees for each class of shares of a Portfolio, expressed as an annual rate of average daily net assets:

| Target Portfolio |

0.750% on the first $50 million of average daily net assets |

0.725% of average daily net assets over $50 million |

| Acquiring Portfolio |

0.400% of average daily net assets |

During the twelve-months ended December 31, 2011, the contractual advisory fees for the Target Portfolio were 0.75% of the Target Portfolio’s average daily net assets.

During the twelve-months ended December 31, 2011, the contractual advisory fees for the Acquiring Portfolio were 0.40% of the Acquiring Portfolio’s average daily net assets.

The Adviser may from time to time voluntarily waive all or a portion of its management fee or reimburse a Portfolio for all or a portion of its other expenses. Any voluntary fee waivers and/or expense reimbursements generally may be discontinued by the Adviser at any time.

With respect to the Target Portfolio, the Adviser has contractually agreed, through at least April 30, 2013, to waive certain fees and/or reimburse certain expenses associated with the shares of the Target Portfolio in order to limit the net annual

15

portfolio operating expenses (excluding acquired (underlying) portfolio fees and expenses, if any) to an annual rate of 0.90% of the average daily net assets of the shares of the Target Portfolio. This contractual provision, however, may be terminated before the indicated termination date upon the mutual agreement between the Independent Directors and the Adviser.

For a complete description of each Portfolio’s advisory services, see the section of the Portfolio Prospectus entitled “Management” and the section of the Fund SAI entitled “Investment Adviser, Investment Subadvisers, and Portfolio Managers.”

Expenses

The table below sets forth the fees and expenses that investors may pay to buy and hold shares of each of the Target Portfolio and the Acquiring Portfolio, including (i) the fees and expenses paid by the Target Portfolio for the twelve-month period ended December 31, 2011, (ii) the fees and expenses paid by the Acquiring Portfolio for the twelve-month period ended December 31, 2011, and (iii) pro forma fees and expenses for the Acquiring Portfolio for the twelve-month period ended December 31, 2011, assuming the Reorganization had been completed as of the beginning of such period. If you own a variable annuity contract or a variable life insurance contract, you will have additional expenses, including mortality and expense risk charges. These additional contract-level expenses are not reflected in the table below.

| Actual | Pro Forma | |||||||||||

| Target Portfolio | Acquiring Portfolio | Acquiring Portfolio | ||||||||||

Shareholder Fees (fees paid directly from your investment) | ||||||||||||

Maximum Sales Charge (Load) | N/A | N/A | N/A | |||||||||

Maximum Deferred Sales Charge (Load) | N/A | N/A | N/A | |||||||||

Annual Portfolio Operating Expenses As a Percentage of Net Assets (expenses that you pay each year as a percentage of the value of your investment) | ||||||||||||

Management Fees | 0.75 | % | 0.40 | % | 0.40 | % | ||||||

Other Expenses | 1.30 | % | 0.15 | % | 0.14 | % | ||||||

Acquired (Underlying) Portfolio Fees and Expenses | — | 0.12 | % | 0.11 | % | |||||||

Total Annual Operating Expenses | 2.05 | % | 0.67 | % | 0.65 | % | ||||||

Less Expense Reimbursement | 1.15 | %(1) | — | — | ||||||||

Net Annual Portfolio Operating Expenses | 0.90 | % | 0.67 | % | 0.65 | % | ||||||

| (1) | The Adviser has contractually agreed, through at least April 30, 2013, to waive certain fees and/or reimburse certain expenses associated with the shares of the Target Portfolio in order to limit the Net Annual Portfolio Operating Expenses to an annual rate of 0.90% of the average daily net assets of the shares. |

16

Example

The following example, using the actual and pro forma operating expenses for the twelve-month period ended December 31, 2011, is intended to help you compare the costs of investing in the Acquiring Portfolio pro forma after the Reorganization with the costs of investing in each of the Target Portfolio and the Acquiring Portfolio without the Reorganization. The example assumes that you invest $10,000 in each Portfolio for the time period indicated and that you redeem all of your shares at the end of each period. The example also assumes that your investments have a 5% return each year and that each Portfolio’s operating expenses remain the same each year. Although your actual returns may be higher or lower, based on these assumptions your costs would be:

| Actual | Pro Forma | |||||||||||

| Target Portfolio | Acquiring Portfolio | Acquiring Portfolio | ||||||||||

Total operating expenses assuming redemption at the end of the period | ||||||||||||

One Year | $ | 92 | $ | 68 | $ | 66 | ||||||

Three Years | $ | 531 | $ | 214 | $ | 208 | ||||||

Five Years | $ | 997 | $ | 373 | $ | 362 | ||||||

Ten Years | $ | 2,287 | $ | 835 | $ | 810 | ||||||

Portfolio Turnover

Each Portfolio pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Portfolio shares are held in a taxable account. These costs, which are not reflected in Total Annual Operating Expenses or in the Example, affect the Portfolios’ performance. During the fiscal year ended December 31, 2011, the Acquiring Portfolio’s and the Target Portfolio’s portfolio turnover rates were 127% and 92%, respectively, of the average value of their portfolios.

The Separate Accounts and the Retirement Plans

Shares in the Fund are currently sold, without sales charges, only to: (1) separate accounts of Thrivent Financial and Thrivent Life Insurance Company (“Thrivent Life”), a subsidiary of Thrivent Financial, which are used to fund benefits of variable life insurance and variable annuity contracts (each a “variable contract”) issued by Thrivent Financial and Thrivent Life; (2) other portfolios of Fund; and (3) retirement plans sponsored by Thrivent Financial.

A Prospectus for the variable contract describes how the premiums and the assets relating to the variable contract may be allocated among one or more of the

17

subaccounts that correspond to the portfolios of the Fund. Participants in the retirement plans should consult retirement plan documents for information on how to invest.

The Fund serves as the underlying investment vehicle for variable annuity contracts and variable life insurance policies that are funded through separate accounts established by Thrivent Financial. It is possible that in the future, it may not be advantageous for variable life insurance separate accounts and variable annuity separate accounts to invest in the portfolios at the same time. Although neither Thrivent Financial nor the Fund currently foresees any such disadvantage, the Fund’s Board monitors events in order to identify any material conflicts between such policy owners and contract owners. Material conflict could result from, for example, (1) changes in state insurance laws, (2) changes in federal income tax law, (3) changes in the investment management of a portfolio, or (4) differences in voting instructions between those given by policy owners and those given by contract owners. Should it be necessary, the Board would determine what action if any, should be taken on response to any such conflicts.

As a result of differences in tax treatment and other considerations, a conflict could arise between the interests of the variable life insurance contract owners, variable annuity contract owners, and plan participants with respect to their investments in the Fund. The Fund’s Board will monitor events in order to identify the existence of any material irreconcilable conflicts and to determine what action if any, should be taken in response to any such conflicts.

Pricing of Portfolio Shares

The price of a Portfolio’s shares is based on the Portfolio’s net asset value (“NAV”). The Portfolios determine their NAV once daily at the close of trading on the New York Stock Exchange (“NYSE”), which is normally 4:00 p.m. Eastern Time. The Portfolios do not determine NAV on holidays observed by the NYSE or on any other day when the NYSE is closed. The NYSE is regularly closed on Saturdays and Sundays, New Year’s Day, Martin Luther King, Jr. Day, Presidents Day, Good Friday, Memorial Day, Independence Day, Labor Day, Thanksgiving Day and Christmas Day.

Each Portfolio determines its NAV by adding the value of Portfolio assets, subtracting the Portfolio’s liabilities, and dividing the result by the number of outstanding shares. To determine the NAV, the Portfolios generally value their securities at current market value using readily available market quotations. If market prices are not available or if the Adviser determines that they do not accurately reflect fair value for a security, the Board of Directors has authorized the Adviser to make fair valuation determinations pursuant to policies approved by the Board of Directors. Fair valuation of a particular security is an inherently subjective process, with no single standard to utilize when determining a security’s fair value. In each case where a security is fair valued, consideration is given to the facts and circumstances relevant to the particular situation. This consideration includes a review of various factors set forth in the pricing policies adopted by the Board of Directors.

18

Because many foreign markets close before the U.S. markets, significant events may occur between the close of the foreign market and the close of the U.S. markets, when the Portfolio’s assets are valued, that could have a material impact on the valuation of foreign securities (i.e., available price quotations for these securities may not necessarily reflect the occurrence of the significant event). The Fund, subject to oversight by the Board of Directors, evaluates the impact of these significant events and adjusts the valuation of foreign securities to reflect the fair value as of the close of the U.S. markets to the extent that the available price quotations do not, in the Adviser’s opinion, adequately reflect the occurrence of the significant events.

The Fund has authorized Thrivent Financial and one or more other entities to accept orders from participants in the retirement plans. The separate accounts and the retirement plans each place an order to buy or sell shares of a respective Portfolio each business day. The amount of the order is based on the aggregate instructions from owners of the variable annuity contracts or the participants in the retirement plans. Orders placed before the close of the NYSE on a given day by the separate accounts, the retirement plans, or participants in the retirement plans result in share purchases and redemptions at the NAV calculated as of the close of the NYSE that day.

Please note that the Target Portfolio and the Acquiring Portfolio have identical valuation policies. As a result, there will be no material change to the value of the Target Portfolio’s assets because of the Reorganization.

Capitalization

The following table sets forth the capitalization of the Target Portfolio and the Acquiring Portfolio, as of December 31, 2011, and the pro forma capitalization of the Acquiring Portfolio as if the Reorganization occurred on that date. These numbers may differ as of the Closing Date.

| Actual | Pro Forma* | |||||||||||

| Target Portfolio | Acquiring Portfolio | Acquiring Portfolio | ||||||||||

Net assets | ||||||||||||

Portfolio Net Assets | $ | 11,118,547 | $ | 118,392,924 | $ | 129,511,471 | ||||||

Total | $ | 11,118,547 | $ | 118,392,924 | $ | 129,511,471 | ||||||

Net asset value per share | ||||||||||||

Net asset value | $ | 8.65 | $ | 6.56 | $ | 6.56 | ||||||

Shares outstanding | ||||||||||||

Portfolio Shares | 1,285,525 | 18,055,186 | 19,750,784 | |||||||||

Total | 1,285,525 | 18,055,186 | 19,750,784 | |||||||||

The pro forma shares outstanding reflect the issuance by the Acquiring Portfolio of approximately 1.7 million shares, reflecting the exchange of the assets and liabilities of the Target Portfolio for newly issued shares of the Acquiring Portfolio at the pro forma net asset value per share. The aggregate value of the Acquiring Portfolio

19

shares that a Target Portfolio contractholder receives in the Reorganization will equal the aggregate value of the Target Portfolio shares owned immediately prior to the Reorganization.

Annual Performance Information

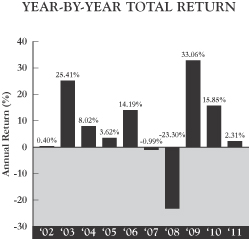

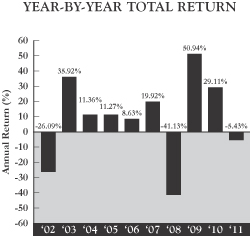

The following chart shows the annual returns of the Target Portfolio since its inception and the Acquiring Portfolio for its past ten fiscal years. On April 30, 2004, the Acquiring Portfolio became the successor by merger with the High Yield Bond Portfolio of AAL Variable Product Series Fund, Inc. Prior to this merger, the Acquiring Portfolio had no assets or liabilities. The performance presented for the period prior to the merger is for the High Yield Bond Portfolio, which commenced operations on March 2, 1998. In addition, on June 30, 2006, the Acquiring Portfolio’s investment objective and principal strategies were changed, which had the effect of converting the Acquiring Portfolio from one which invested at least 80% of its assets in high-yield securities to one that invest in a diversified portfolio of income-producing securities. The performance presented for the period after the April 30, 2004 merger but before the June 30, 2006 conversion reflects the performance of an investment portfolio that was materially different from the Acquiring Portfolio. Further, the bar charts include the effects of each Portfolio’s expenses, but not charges or deductions against your variable contract. If these charges and deductions were included, returns would be lower than those shown.

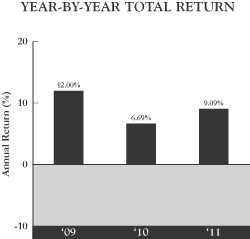

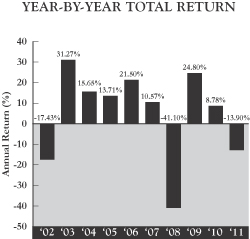

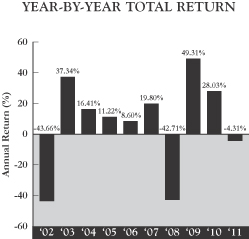

Thrivent Partner Utilities Portfolio

20

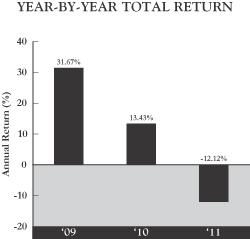

Thrivent Diversified Income Plus Portfolio

As a result of market activity, current performance may vary from the figures shown.

Since its inception, the Target Portfolio’s highest quarterly return was 11.87% (for the quarter ended September 30, 2010) and its lowest quarterly return was -10.01% (for the quarter ended March 31, 2009). Since its inception, the Acquiring Portfolio’s highest quarterly return was 15.49% (for the quarter ended June 30, 2009) and its lowest quarterly return was -16.46% (for the quarter ended December 31, 2008).

Comparative Performance Information

As a basis for evaluating each Portfolio’s performance and risks, the following table shows how each Portfolio’s performance compares with broad-based market indices that the Adviser believes are appropriate benchmarks for such Portfolio. The Target Portfolio’s benchmarks are the S&P 500 Telecommunications Services Index, which is a capitalization-weighted index of telecommunications sector securities, and the S&P 500 Utilities Index, which is a capitalization-weighted index of utilities sector securities. The Acquiring Portfolio’s benchmarks are the S&P 500 Dividend Aristocrats Index and the Barclays Capital Aggregate Bond Index. The former measures the performance of large-cap companies within the S&P 500 index that have followed a managed-dividends policy of consistently increasing dividends every year for at least 25 years. This index also has both capital growth and dividend income characteristics. The latter index measures the performance of U.S. investment grade bonds. Further, the table includes the effects of each Portfolio’s expenses, but not charges or deductions against your variable contract. If these charges and deductions were included, returns would be lower than those shown.

21

Average annual total returns are shown below for each Portfolio for the periods ended December 31, 2011 (the most recently completed calendar year prior to the date of this Prospectus/Proxy Statement). Remember that past performance of a Portfolio is not indicative of its future performance.

Average Annual Total Returns for the Period ended December 31, 2011

| Target Portfolio | Acquiring Portfolio | |||||||||||||||||||

| Past 1 Year | Since Inception (4/30/08) | Past 1 Year | Past 5 Years | Past 10 Years | ||||||||||||||||

Applicable Portfolio | 9.09% | -2.30% | 2.31% | 3.69% | 6.79% | |||||||||||||||

S&P 500 Telecommunications Services Index (reflects no deductions for fees, expenses or taxes) | 6.27% | 1.57% | — | — | — | |||||||||||||||

S&P 500 Utilities Index (reflects no deductions for fees, expenses or taxes) | 19.91% | 1.60% | — | — | — | |||||||||||||||

S&P 500 Dividend Aristocrats Index (reflects no deductions for fees, expenses or taxes) | — | — | 8.33% | 4.59% | 7.10% | |||||||||||||||

Barclays Capital Aggregate Bond Index (reflects no deductions for fees, expenses or taxes) | — | — | 7.84% | 6.50% | 5.78% | |||||||||||||||

S&P 500 Index (reflects no deductions for fees, expenses or taxes) | — | — | 2.11% | -0.25% | 2.92% | |||||||||||||||

Barclays Capital U.S. Corporate High Yield Bond Index (reflects no deductions for fees, expenses or taxes) | — | — | 4.98% | 7.54% | 8.85% | |||||||||||||||

Barclays Capital U.S. Corporate Investment Grade Index (reflects no deductions for fees, expenses or taxes) | — | — | 8.15% | 6.82% | 6.36% | |||||||||||||||

Other Service Providers

Thrivent Financial for Lutherans, 625 Fourth Avenue South, Minneapolis, Minnesota 55415, provides administrative personnel and services necessary to operate the Portfolios and receives an administration fee from the Portfolios. The custodian for the Portfolios is State Street Bank and Trust Company, 225 Franklin Street, Boston, Massachusetts 02110. PricewaterhouseCoopers LLP, 225 South Sixth Street, Suite 1400, Minneapolis, MN 55402, serves as the Fund’s independent registered public accounting firm.

22

Governing Law

The Fund is an open-end management investment company registered under the Investment Company Act of 1940 (the “1940 Act”) and was organized as a Minnesota corporation on February 24, 1986. The Fund is made up of 41 separate series or “Portfolios.” Each Portfolio of the Fund, other than the Thrivent Aggressive Allocation Portfolio, the Thrivent Moderately Aggressive Allocation Portfolio, the Thrivent Moderate Allocation Portfolio, the Thrivent Moderately Conservative Allocation Portfolio, the Thrivent Partner Healthcare Portfolio, the Thrivent Partner Natural Resources Portfolio and the Thrivent Partner Socially Responsible Bond Portfolio, is diversified. Each Portfolio is in effect a separate investment fund, and a separate class of capital stock of the Fund is issued with respect to each Portfolio.

The Fund’s organizational documents are filed as part of the Fund’s registration statement with the SEC, and shareholders may obtain copies of such documents as described on page viii of this Prospectus/Proxy Statement.

23

INFORMATION ABOUT THE REORGANIZATION

General

Under the Reorganization Agreement, the Target Portfolio will transfer all of its assets and liabilities to the Acquiring Portfolio in exchange for shares of the Acquiring Portfolio. The Acquiring Portfolio shares issued to the Target Portfolio will have an aggregate value equal to the aggregate value of the Target Portfolio’s net assets immediately prior to the Reorganization. Upon receipt by the Target Portfolio of Acquiring Portfolio Shares, the Target Portfolio will distribute such shares of the Acquiring Portfolio to Target Portfolio shareholders. Then, as soon as practicable after the Closing Date of the Reorganization, the Target Portfolio will dissolve under applicable state law.

The Target Portfolio will distribute the Acquiring Portfolio shares received by it pro rata to Target Portfolio shareholders of record in exchange for their interest in shares of the Target Portfolio. Accordingly, as a result of the Reorganization, each Target Portfolio shareholder would own Acquiring Portfolio shares that would have an aggregate value immediately after the Reorganization equal to the aggregate value of that shareholder’s Target Portfolio shares immediately prior to the Reorganization. The interests of each of the Target Portfolio’s shareholders will not be diluted as a result of the Reorganization. However, as a result of the Reorganization, a shareholder of the Target Portfolio or the Acquiring Portfolio will hold a reduced percentage of ownership in the larger combined portfolio than the shareholder did in either of the separate Portfolios.

No sales charge or fee of any kind will be assessed to Target Portfolio shareholders in connection with their receipt of Acquiring Portfolio shares in the Reorganization.

Approval of the Reorganization will constitute approval of amendments to any of the fundamental investment restrictions of the Target Portfolio that might otherwise be interpreted as impeding the Reorganization, but solely for the purpose of and to the extent necessary for consummation of the Reorganization.

Terms of the Reorganization Agreement

The following is a summary of the material terms of the Reorganization Agreement. This summary is qualified in its entirety by reference to the form of Reorganization Agreement, a form of which is attached as Appendix A to the Reorganization SAI.

Pursuant to the Reorganization Agreement, the Acquiring Portfolio will acquire all of the assets and the liabilities of the Target Portfolio on the Closing Date in exchange for Shares of the Acquiring Portfolio. Subject to the Target Portfolio’s contractholders approving the Reorganization, the Closing Date shall occur on July 27, 2012 or such other date as determined by an officer of the Fund.

24

On the Closing Date, the Target Portfolio will transfer to the Acquiring Portfolio all of its assets and liabilities. The Acquiring Portfolio will in turn transfer to the Target Portfolio a number of its Shares equal in value to the value of the net assets of the Target Portfolio transferred to the Acquiring Portfolio as of the Closing Date, as determined in accordance with the valuation method described in the Acquiring Portfolio’s then current prospectus. In order to minimize any potential for undesirable federal income and excise tax consequences in connection with the Reorganization, the Target Portfolio will distribute on or before the Closing Date all or substantially all of its undistributed net investment income (including net capital gains) as of such date.

The Target Portfolio expects to distribute Shares of the Acquiring Portfolio received by the Target Portfolio to contractholders of the Target Portfolio promptly after the Closing Date and then dissolve.

The Acquiring Portfolio and the Target Portfolio have made certain standard representations and warranties to each other regarding their capitalization, status and conduct of business. Unless waived in accordance with the Reorganization Agreement, the obligations of the parties to the Reorganization Agreement are conditioned upon, among other things:

| • | the approval of the Reorganization by the Target Portfolio’s contractholders; |

| • | the absence of any rule, regulation, order, injunction or proceeding preventing or seeking to prevent the consummation of the transactions contemplated by the Reorganization Agreement; |

| • | the receipt of all necessary approvals, registrations and exemptions under federal and state laws; |

| • | the truth in all material respects as of the Closing Date of the representations and warranties of the parties and performance and compliance in all material respects with the parties’ agreements, obligations and covenants required by the Reorganization Agreement; |

| • | the effectiveness under applicable law of the registration statement of the Acquiring Portfolio of which this Prospectus/Proxy Statement forms a part and the absence of any stop orders under the Securities Act of 1933, as amended, pertaining thereto; and |

| • | the receipt of an opinion of counsel relating to the tax free nature of the Reorganization (as further described herein under the heading “Material Federal Income Tax Consequences of the Reorganization”). |

The Reorganization Agreement may be terminated or amended by the mutual consent of the parties either before or after approval thereof by the contractholders of the Target Portfolio, provided that no such amendment after such approval shall be made if it would have a material adverse effect on the interests of such Target Portfolio’s contractholders. The Reorganization Agreement also may be terminated by

25

the non-breaching party if there has been a material misrepresentation, material breach of any representation or warranty, material breach of contract or failure of any condition to closing.

Reasons for the Proposed Reorganization

In determining whether to recommend approval of the Reorganization Agreement to Target Portfolio contractholders, the Board considered a number of factors, including, but not limited to: (i) the Adviser currently manages the assets of each Portfolio; (ii) the expenses and advisory fees applicable to the Portfolios before the proposed Reorganization and the estimated expense ratios of the combined portfolio after the proposed Reorganization; (iii) the comparative investment performance of the Portfolios; (vi) the future growth prospects of each Portfolio; (iv) the terms and conditions of the Reorganization Agreement and whether the Reorganization would result in the dilution of contractholder interests; (v) the compatibility of the Portfolios’ investment objectives, policies, risks and restrictions; (vi) the anticipated tax consequences of the proposed Reorganization; (vii) the compatibility of the Portfolios’ service features available to contractholders, including exchange privileges; and (viii) the estimated costs of the Reorganization. The Board concluded that these factors supported a determination to approve the Reorganization Agreement.

After careful consideration, the Board believes that the Reorganization would be in the best interests of the Target Portfolio’s contractholders because: (i) the advisory fee that these contractholders bear will decrease as a result of the Reorganization; (ii) the operating expenses that these contractholders bear will likely decrease as a result of the Reorganization; and (iii) contractholders will become contractholders in a larger combined portfolio, which increase the potential of realizing economies of scale whereby certain administrative costs may be spread across the combined portfolio’s larger asset base and, therefore, may increase the combined portfolio’s overall efficiency in the long term.

The Board has determined that the Reorganization is in the best interests of the Target Portfolio and that the interests of the Target Portfolio’s contractholders will not be diluted as a result of the Reorganization. In addition, the Board has determined that the Reorganization is in the best interests of the Acquiring Portfolio and that the interests of the Acquiring Portfolio contractholders will not be diluted as a result of the Reorganization.

Material Federal Income Tax Consequences of the Reorganization

The following is a general summary of the material anticipated U.S. federal income tax consequences of the Reorganization. This discussion is based upon the Internal Revenue Code of 1986, as amended (the “Code”), Treasury regulations, court decisions, published positions of the Internal Revenue Service (“IRS”) and other applicable authorities, all as in effect on the date hereof and all of which are subject to

26

change or differing interpretations (possibly with retroactive effect). This discussion is limited to U.S. persons who hold shares of the Target Portfolio as capital assets for U.S. federal income tax purposes. For federal income tax purposes, the contractholders are not the shareholders of the Target Portfolio. Rather, Thrivent Financial and Thrivent Life and their separate accounts are the shareholders.

This summary does not address all of the U.S. federal income tax consequences that may be relevant to a particular contractholder or to contractholders who may be subject to special treatment under U.S. federal income tax laws. No assurance can be given that the IRS would not assert or that a court would not sustain a position contrary to any of the tax aspects described below. Contractholders should consult their own tax advisers as to the U.S. federal income tax consequences of the Reorganization to them, as well as the effects of state, local and non-U.S. tax laws.

The Reorganization is expected to be a tax-free reorganization for U.S. federal income tax purposes. It is a condition to closing the Reorganization that the Target Portfolio and the Acquiring Portfolio receive an opinion from Skadden, Arps, Slate, Meagher & Flom LLP, special counsel to each Portfolio (“Skadden Arps”), dated as of the Closing Date, to the effect that on the basis of existing provisions of the Code, the Treasury regulations promulgated thereunder, current administrative rules and court decisions, generally for U.S. federal income tax purposes, except as noted below:

| • | the Reorganization will constitute a reorganization within the meaning of Section 368(a) of the Code, and the Target Portfolio and the Acquiring Portfolio will each be a “party to a reorganization” within the meaning of Section 368(b) of the Code; |

| • | under Section 361 of the Code, no gain or loss will be recognized by the Target Portfolio upon the transfer of its assets to the Acquiring Portfolio in exchange for Acquiring Portfolio shares and the assumption by the Acquiring Portfolio of the Target Portfolio’s liabilities, or upon the distribution of Acquiring Portfolio shares by the Target Portfolio to its contractholders in liquidation; |

| • | under Section 1032 of the Code, no gain or loss will be recognized by the Acquiring Portfolio upon receipt of the assets transferred to the Acquiring Portfolio in exchange for Acquiring Portfolio shares and the assumption by the Acquiring Portfolio of the liabilities of the Target Portfolio; |

| • | under Section 362(b) of the Code, the Acquiring Portfolio’s tax basis in the assets that the Acquiring Portfolio receives from the Target Portfolio will be the same as the Target Portfolio’s tax basis in such assets immediately prior to such exchange; |

| • | under Section 1223(2) of the Code, the Acquiring Portfolio’s holding periods in such assets will include the Target Portfolio’s holding periods in such assets; |

27

| • | under Section 354 of the Code, no gain or loss will be recognized by contractholders of the Target Portfolio on the distribution of Acquiring Portfolio shares to them in exchange for their shares of the Target Portfolio; |

| • | under Section 358 of the Code, the aggregate tax basis of the Acquiring Portfolio shares that the Target Portfolio’s contractholders receive in exchange for their Target Portfolio shares will be the same as the aggregate tax basis of the Target Portfolio shares exchanged therefor; |

| • | under Section 1223(1) of the Code, a Target Portfolio contractholder’s holding period for the Acquiring Portfolio shares received in the Reorganization will be determined by including the holding period for the Target Portfolio shares exchanged therefor, provided that the contractholder held the Target Portfolio shares as a capital asset on the date of the exchange; and |

| • | under Section 381 of the Code, the Acquiring Portfolio will succeed to and take into account the items of the Target Portfolio described in Section 381(c) of the Code, subject to the conditions and limitations specified in Section 381, 382, 383 and 384 of the Code and the Treasury regulations thereunder. |

The opinion will be based on certain factual certifications made by the officers of the Trust and will also be based on customary assumptions such as the assumption that the Reorganization will be consummated in accordance with the Reorganization Agreement. The opinion is not a guarantee that the tax consequences of the Reorganization will be as described above. There is no assurance that the IRS or a court would agree with the opinion.

The Acquiring Portfolio intends to continue to be taxed under the rules applicable to regulated investment companies as defined in Section 851 of the Code which are the same rules currently applicable to Target Portfolio and its contractholders. In connection with the Reorganization, on or before the Closing Date, the Target Portfolio will declare to its contractholders a dividend which, together with all of its previous distributions, will have the effect of distributing to contractholders all of its investment company taxable income (computed without regard to the deduction for dividends paid), net tax-exempt interest income and net capital gains for the period beginning on January 1, 2012 and ending on the Closing Date.

A regulated investment company is permitted to carry forward net capital losses; however, net capital losses incurred in taxable years beginning on or before December 22, 2010 can be carried forward for eight taxable years only. Additionally capital losses incurred in taxable years beginning on or before December 22, 2010 cannot be utilized to offset capital gains until all net capital losses arising in tax years beginning after December 22, 2010 have been utilized. As a result, some net capital loss carryovers incurred on or before December 22, 2010 may expire unused.

28

Immediately prior to the Reorganization, the Target Portfolio will have unutilized capital loss carry forwards of approximately $1 million. The final amount of unutilized capital loss carry forwards for the Target Portfolio is subject to change and will not be determined until the Closing Date.

Generally, the Acquiring Portfolio will succeed to the capital loss carry forwards of the Target Portfolio, subject to the limitations described below. If the Target Portfolio has capital loss carry forwards, such capital losses would, in the absence of the Reorganization, generally be available to offset Target Portfolio capital gains, thereby reducing the amount of capital gain net income that must be distributed to the Target portfolio contractholders.

Under Sections 382 and 383 of the Code, an “equity structure shift” arising as a result of a reorganization under Section 368(a)(1) of the Code can result in limitations on the post-reorganization Portfolio’s use of capital loss carry forwards of the participating Portfolios. An “equity structure shift” can trigger limitations on capital loss carry forwards where there is a more than 50% change in the ownership of a Portfolio.

Because the Reorganization is not expected to result in a more than 50% change in ownership of the Target Portfolio or the Acquiring Portfolio, it is anticipated that the capital loss carryovers of the Target Portfolio will not be subject to an annual limitation and none of the Target Portfolio’s $1 million capital loss carry forward is expected to expire unutilized as a result of the Reorganization.

This summary of the U.S. federal income tax consequences of the Reorganization is made without regard to the particular facts and circumstances of any contractholder. Contractholders are urged to consult their own tax advisors as to the specific consequences to them of the Reorganization, including the applicability and effect of state, local, non-U.S. and other tax laws.

Expenses of the Reorganization

The expenses of the Reorganization will be paid by the Adviser or an affiliate and will not be borne by shareholders of the Target Portfolio.

Reorganization expenses include, but are not limited to: all costs related to the preparation and distribution of materials distributed to the Board; all expenses incurred in connection with the preparation of the Reorganization Agreement and a registration statement on Form N-14; SEC and state securities commission filing fees and legal and audit fees in connection with each Reorganization; the costs of printing and distributing this Prospectus/Proxy Statement; legal fees incurred preparing materials for the Boards attending the Board meetings and preparing the Board minutes; auditing fees associated with the Portfolio’s financial statements; portfolio transfer taxes (if any); and any similar expenses incurred in connection with the Reorganization.

29

Management of the Portfolios estimates the total cost of the Reorganization to be approximately $90,000. If the Reorganization is not approved by contractholders, the Adviser will still bear the costs of the proposed Reorganization.

Legal Matters

Certain legal matters concerning the federal income tax consequences of the Reorganization and the issuance of Shares of the Acquiring Portfolio will be passed on by Skadden Arps.

Contractholder Approval

The Board has unanimously approved the Reorganization, subject to shareholder approval. Approval of the Reorganization requires the affirmative vote of a “Majority of the Outstanding Voting Securities” of the Target Portfolio, which is, under the 1940 Act, the lesser of (1) 67% or more of the shares of the Portfolio present at the Meeting if the holders of more than 50% of the outstanding shares of the Portfolio are present or represented by proxy, or (2) more than 50% of the outstanding shares of the Portfolio.

Board Recommendation

The Board recommends voting “FOR” the proposed Reorganization.

CONTRACTHOLDER INFORMATION

Shareholder Information

At the close of business on the Record Date, the Acquiring Portfolio had outstanding shares. As of , 2012, the directors and officers of the Acquiring Portfolio as a group owned less than 1% of the shares of the Acquiring Portfolio. As of , 2012, no person was known by the Acquiring Portfolio to own beneficially or of record as much as 5% of the Acquiring Portfolio shares except as follows:

Name | Shares Outstanding | Approximate Percentage of Ownership | ||

At the close of business on the Record Date, the Target Portfolio had outstanding shares. As of , 2012, the directors and officers of the Target Portfolio as a group owned less than 1% of the shares of the Target Portfolio. As of , 2012, no person was known by the Target Portfolio to own beneficially or of record as much as 5% of the shares of the Target Portfolio except as follows:

Name | Shares Outstanding | Approximate Percentage of Ownership | ||

30

Annual Meeting of Shareholders

There will be no annual or further special meetings of shareholders of the Fund unless required by applicable law or called by the Board in its discretion. Shareholders wishing to submit proposals for inclusion in a proxy statement for a subsequent shareholder meeting should send their written proposals to the Secretary of the Fund, 625 Fourth Avenue South, Minneapolis, Minnesota 55415. Shareholder proposals should be received in a reasonable time before the solicitation is made.

VOTING INFORMATION AND REQUIREMENTS

General

Approval of the Reorganization requires the affirmative vote of a “Majority of the Outstanding Voting Securities” of the Target Portfolio, which is, under the 1940 Act, the lesser of (1) 67% or more of the shares of the Target Portfolio present at the Meeting if the holders of more than 50% of the outstanding shares of the Target Portfolio are present or represented by proxy, or (2) more than 50% of the outstanding shares of the Target Portfolio. Thrivent Financial and Thrivent Life, the sponsors of your variable contracts, are the shareholders of record of the shares of the Target Portfolio. Contractholders with investments in the Target Portfolio are entitled to provide proxy cards to Thrivent Financial and Thrivent Life for the shares related to their investments.

Record Date

The Board has fixed the close of business on May 16, 2012 as the Record Date for the determination of shareholders entitled to notice of, and to vote at, the Meeting. Target Portfolio shareholders on the Record Date are entitled to one vote for each share held, with no shares having cumulative voting rights. Contractholders with investments in the Target Portfolio as of the record date are entitled to submit proxy cards.

Quorum

A majority of the shares of the Target Portfolio entitled to vote at the Meeting represented in person or by proxy constitutes a quorum. Thrivent Financial and Thrivent Life together are the record owners of a majority of the shares of the Target Portfolio. The representation of Thrivent Financial and Thrivent Life at the Meeting will therefore assure the presence of a quorum.

Proxies