As filed with the Securities and Exchange Commission on June 24, 2020

Securities Act File No. 333-______

1940 Act Registration No. 811-4603

U.S. SECURITIES AND EXCHANGE

COMMISSION

WASHINGTON, D.C. 20549

FORM N-14

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

☐ Pre-Effective Amendment No._____

☐ Post-Effective Amendment No.____

(Check appropriate box or boxes)

THRIVENT SERIES FUND, INC.

(Exact Name of Registrant as Specified in Charter)

901 MARQUETTE AVENUE, SUITE 2500

MINNEAPOLIS, MINNESOTA 55402-3265

(Address of Principal Executive Offices)

612-844-7190

(Area Code and Telephone Number)

JOHN D. JACKSON

ASSISTANT SECRETARY

THRIVENT SERIES FUND, INC.

901 MARQUETTE AVENUE, SUITE 2500

MINNEAPOLIS, MINNESOTA 55402-3265

(Name and Address of Agent for Service)

Approximate Date of Proposed Public Offering: As soon as practicable after this registration statement becomes effective. It is proposed that this filing will become effective on July 24, 2020 pursuant to Rule 488 under the Securities Act of 1933.

Title of Securities Being Registered: Shares of beneficial interest, par value $.01 per share. The Registrant has registered an indefinite number of shares of beneficial interest pursuant to Section 24(f) of the Investment Company Act of 1940, as amended, and is in a continuous offering of such shares under an effective registration statement (File Nos. 33-3677 and 811-4603). No filing fee is due herewith because of reliance on Section 24(f) of the Investment Company Act of 1940, as amended.

LETTER FOR CONTRACTHOLDERS

Dear Contractholder:

The Board of Directors of Thrivent Series Fund, Inc. (the “Fund”) has scheduled a special meeting of contractholders for August 24, 2020 (the “Meeting”). At the Meeting, the contractholders of Thrivent Partner Growth Stock Portfolio (the “Target Portfolio”) will be asked to consider and approve an Agreement and Plan of Reorganization (an “Agreement”) providing for its reorganization into Thrivent Large Cap Growth Portfolio (the “Acquiring Portfolio”).

As further described in the Prospectus/Proxy Statement, Thrivent Financial for Lutherans is the direct shareholder of the Target Portfolio and sponsor of the variable life insurance contracts and variable annuity contracts (each, a “Variable Contract”). As the holder of a Variable Contract, you are being solicited for voting instructions so that shares of the Target Portfolio may be voted in proportion to the instructions received.

Due to COVID-19 health and safety concerns, the Meeting will be conducted online only on August 24, 2020 at 9:30 a.m. Central Time. You will not be able to attend the meeting in person.

You will be able to attend and participate in the Meeting online by visiting www.proxypush.com/THR, where you will be able to listen to the meeting live, submit questions and vote.

To be admitted to the Meeting and vote your shares, you must register in advance at www.proxypush.com/THR prior to the deadline of Thursday, August 20, 2020 at 4:00 p.m. Central Time and provide the control number as provided in the Notice, or proxy card, or voting instruction form at www.proxypush.com/THR. Upon completing your registration, you will receive further instructions via email, including unique links to access the Meeting and to submit questions in advance of the Meeting.

If you are not planning to attend the Meeting online, please vote before August 24 in one of the ways described below.

If the merger is approved, your investment in the Target Portfolio will automatically be transferred into the Acquiring Portfolio. We will send you a written confirmation after this takes place. This transfer is not expected to be a taxable event. (Of course, you may transfer your investment to a completely different series, which will not count as one of your permitted annual exchanges.)

Your vote counts! You may vote quickly and easily in any one of these ways:

| | • | | Internet: see the instructions on the enclosed proxy card. |

| | • | | Phone: see the instructions on the enclosed proxy card. |

| | • | | Mail: use the enclosed proxy card and postage-paid envelope. |

| | • | | Attend the virtual Meeting: attend the Meeting online on August 24. You can register to attend and vote at the Meeting online by following the instructions on the enclosed proxy card. |

Thank you for taking this matter seriously and participating in this important process.

Sincerely,

David S. Royal

President and Chief Investment Officer

Thrivent Series Fund, Inc.

Questions & Answers

For Contractholders of Thrivent Partner Growth Stock Portfolio

Although we recommend that you read the complete Prospectus/Proxy Statement, we have provided the following questions and answers to clarify and summarize the issues to be voted on.

Q: Why is a contractholder meeting being held?

A: A special meeting of contractholders (the “Meeting”) of Thrivent Partner Growth Stock Portfolio (the “Target Portfolio”) is being held to seek contractholder approval of a reorganization (the “Reorganization”) of the Target Portfolio into Thrivent Large Cap Growth Portfolio (the “Acquiring Portfolio”). Please refer to the Prospectus/Proxy Statement for a detailed explanation of the proposed Reorganization and for a more complete description of the Acquiring Portfolio.

Q: Why is the Reorganization being recommended?

A: After careful consideration, the Board of Directors (the “Board”) of Thrivent Series Fund, Inc. (the “Fund”) has determined that the Reorganization is in the best interests of the contractholders of the Target Portfolio and recommends that you cast your vote “FOR” the proposed Reorganization. The Target Portfolio and the Acquiring Portfolio both invest primarily in equity securities with growth characteristics and each is a series of the Company, an open-end investment company registered under the Investment Company Act of 1940. Thrivent Financial for Lutherans (“Thrivent Financial”) is the investment adviser for the Target Portfolio and the Acquiring Portfolio.

The Target Portfolio has generally underperformed relative to comparable growth equity funds since its current portfolio management took over in 2014. The Reorganization was approved by the Board on June 24, 2020. The Board considered the fact that as of March 31, 2020, the Target Portfolio was ranked in the bottom quartile of its Lipper peer group for the prior one-year and two-year periods and below median for the three-year and five-year periods. The Acquiring Portfolio has posted much more competitive results, ranking in the top quartile for the one-year and two-year time periods and above median for three-year and five-year periods. The current portfolio manager, Lauri Brunner, began managing the Acquiring Portfolio in September 2018.

The Board believes that the Reorganization would be in the best interests of the contractholders of the Target Portfolio because: (i) contractholders will become contractholders of a much larger combined portfolio with greater potential to increase asset size and achieve economies of scale; (ii) at the time of the Board’s approval on June 24, 2020, the Acquiring Portfolio had achieved better performance than the

1

Target Portfolio for the one-, two-, three- and five-year periods ended March 31, 2020, both in terms of Lipper peer group rankings and on an absolute basis, though there is no guarantee of future performance; (iii) Thrivent Financial believes that it can most effectively manage the assets currently in the Target Portfolio by combining such assets with the Acquiring Portfolio; and (iv) the Acquiring Portfolio has a lower gross expense ratio than the Target Portfolio and shareholders of the Target Portfolio will experience a lower net expense ratio in the Acquiring Portfolio following the Reorganization.

The Acquiring Portfolio anticipates selling approximately 47% of the market value of the Target Portfolio’s investments after the Reorganization. As of May 29, 2020, the Target Portfolio’s investments that the Acquiring Portfolio would anticipate selling have a market value of $130,403,977.46.

Q: Who can vote?

A: Owners of the variable life insurance contracts and variable annuity contracts (each a “Variable Contract” and such owners, “Contractholders”) as of July 10, 2020 funded by the Target Portfolio are entitled to vote at the Meeting. Thrivent Financial for Lutherans (“Thrivent Financial”) is the Target Portfolio’s investment adviser. Thrivent Financial (the “Shareholder”) is the sponsor of your Variable Contract. The Target Portfolio is currently an investment option in the separate accounts held directly by the Shareholder, which are used to fund the variable life insurance policies and variable annuity contracts sponsored by the Shareholder. Accordingly, Contractholders are being solicited to provide voting instructions to the direct Shareholder, which will in turn cast votes in accordance with instructions provided by the Contractholders.

If your voting instructions are not timely received, any shares of the Target Portfolio attributable to a Variable Contract will be voted by Thrivent Financial in proportion to the voting instructions received for all Variable Contracts participating in the proxy solicitation. This voting procedure may result in a relatively small number of Contractholders determining the outcome of the vote. If a proxy card is timely returned with no voting instructions, the shares of the Portfolio will be voted FOR the Reorganization.

Any shares of the Target Portfolio held by Thrivent Financial or its affiliates for their own account will also be voted in proportion to the voting instructions received from all Contractholders participating in the proxy solicitation.

Q: How will the Reorganization affect me?

A: Assuming Contractholders approve the proposed Reorganization, the assets of the Target Portfolio will be combined with those of the Acquiring Portfolio. The shares of the Target Portfolio that fund your benefits under Variable Contracts automatically

2

would be exchanged for an equal dollar value of shares of the Acquiring Portfolio. The Reorganization would affect only the investments underlying Variable Contracts and would not otherwise affect Variable Contracts. Following the Reorganization, the Target Portfolio will dissolve.

Q: Will I have to pay any commission or other similar fee as a result of the Reorganization?

A: Contractholders will not pay any commissions or fees in connection with the Reorganization, although certain transaction costs such as trading commissions and custody transaction charges will be borne by the Target Portfolio and/or the Acquiring Portfolio.

Q: Will the total annual operating expenses that my portfolio investment bears increase as a result of the Reorganization?

A: No, they are likely to decrease. An unexpected increase in “Other Expenses” of the Acquiring Portfolio could cause them to increase. For more information about how fund expenses may change as a result of the Reorganization, please see the comparative and pro forma table and related disclosures in the COMPARISON OF THE PORTFOLIOS—Expenses section of the Prospectus/Proxy Statement.

Q: Will I have to pay any U.S. federal income taxes as a result of the Reorganization?

A: The Reorganization is expected to be tax-free for federal income tax purposes. The Target Portfolio will seek an opinion of counsel to this effect. Generally, neither Shareholders nor Contractholders will incur capital gains or losses on the exchange of Target Portfolio shares for Acquiring Portfolio shares as a result of the Reorganization. The cost basis on each investment will also remain the same. If you choose to make a total or partial surrender of your Variable Contract, you may be subject to taxes and other charges under your Variable Contract.

Q: Can I surrender or exchange my interests in the Target Portfolio for a different subaccount option of the Fund or surrender my contract before the Reorganization takes place?

A: Yes, but please refer to the most recent prospectus of your Variable Contract as certain charges and/or restrictions may apply to such exchanges and surrenders.

Q: If Contractholders of the Target Portfolio do not approve the Reorganization, what will happen to the Target Portfolio?

A: Thrivent Financial will reassess what changes it would like to make to a Target Portfolio, including a possible repurposing of the Target Portfolio’s principal investment strategies or recommending to the Board a liquidation of the Target Portfolio. It may ultimately decide to make no changes.

3

Q: Who pays the costs of the Reorganization?

A: If the Reorganization is approved, certain transaction costs such as trading commissions and custody transaction charges will be borne by the Target Portfolio and/or the Acquiring Portfolio. Other costs associated with the Reorganization, such as the costs of the Meeting, proxy expenses, legal fees, IT system changes, audit fees and filing fees, will be paid by Thrivent Financial and will not be borne by shareholders of the Target Portfolio, regardless of whether the Reorganization is completed.

Q: How can I vote?

A: Contractholders are invited to attend the online Meeting to cast their vote. Due to COVID-19 safety concerns, the Meeting will be conducted online only and Contractholders will not be able to attend in person.

You will be able to attend and participate in the Meeting online by visiting www.proxypush.com/THR, where you will be able to listen to the meeting live, submit questions and vote.

To be admitted to the Meeting and vote your shares, you must register in advance at www.proxypush.com/THR prior to the deadline of Thursday, August 20, 2020 at 4:00 p.m. Central Time and provide the control number as provided in the Notice, or proxy card, or voting instruction form at www.proxypush.com/THR. Upon completing your registration, you will receive further instructions via email, including unique links to access the Meeting and to submit questions in advance of the Meeting.

You may also vote by executing a proxy using one of three methods:

| | • | | Internet: Instructions for casting your vote via the Internet can be found in the enclosed proxy voting materials. The required control number is printed on your enclosed proxy card. If this feature is used, there is no need to mail the proxy card. |

| | • | | Phone: Instructions for casting your vote via phone can be found in the enclosed proxy voting materials. The toll-free number and required control number are printed on your enclosed proxy card. If this feature is used, there is no need to mail the proxy card. |

| | • | | Mail: If you vote by mail, please indicate your voting instructions on the enclosed proxy card, date and sign the card, and return it in the envelope provided, which is addressed for your convenience and needs no postage if mailed in the United States. |

Contractholders who execute proxies by Internet, phone or mail may revoke them at any time prior to the Meeting by filing with the Target Portfolio a written notice of revocation, by executing another proxy bearing a later date, by voting later by Internet or phone or by attending the online Meeting. Merely attending the online Meeting, however, will not revoke any previously submitted proxy.

4

Q: How do I attend the Meeting online?

A: There is no physical location for the Meeting. To attend the Meeting online, please visit www.proxypush.com/THR and follow the instruction as outlined on the website.

The Meeting will be a webcast that you can view on your browser with no plug-ins or downloads required. You can access the Meeting online using your computer, tablet or mobile device.

Access to the Meeting Online. A live audio webcast of the Meeting will begin promptly at 9:30 a.m. Central Time on August 24, 2020. Online access to the audio webcast will open approximately 15 minutes in advance of the meeting start time. You should ensure that you have a strong Wi-Fi connection wherever you intend to participate in the Meeting and give yourself plenty of time to log in and ensure that you can hear audio prior to the start of the Meeting.

Registration. To attend the Meeting online, you must register at www.proxypush.com/THR by 4:00 p.m. Central Time on August 20, 2020. You will receive an email confirming your registration, and you will receive a link with instructions on how to access the Meeting approximately one hour prior to its start time. However, you won’t be able to join the Meeting until 15 minutes before it is scheduled to start.

Q: When should I vote?

A: Every vote is important and the Board encourages you to record your vote as soon as possible. Voting your proxy now will ensure that the necessary number of votes is obtained, without the time and expense required for additional proxy solicitation.

Q: Who should I call if I have questions about the proposal in the Prospectus/Proxy Statement?

A: Call Mediant Communications at 888-441-3205 with your questions.

Q: How can I get more information about the Target and Acquiring Portfolios or my variable contract?

A: You may obtain (1) a prospectus, statement of additional information or annual/semiannual report for the Portfolios, (2) a prospectus or statement of additional information for your Variable Contract or (3) the statement of additional information regarding the Reorganization (request the “Reorganization SAI”) by:

| | • | | Phone—800-847-4836 and say “Variable Annuity” or “Variable Universal Life” |

5

| | • | | Mail—Thrivent Series Fund, Inc., 4321 North Ballard Road, Appleton, WI 54919 |

| | — | For a copy of a prospectus, a statement of additional information, and/or annual/semiannual report: |

| | • | | Variable Annuity Reference Center: https://www.thrivent.com/what-we-offer/insurance/annuities/variable-annuity-reference-center.html |

| | • | | Variable Universal Life Reference Center: https://www.thrivent.com/what-we-offer/insurance/variable-universal-life-reference-center.html |

| | • | | AdvisorFlex Variable Annuity Reference Center: https://www.thrivent.com/what-we-offer/insurance/annuities/thrivent-advisorflex-variable-annuity-reference-center.html |

| | — | For a copy of the Reorganization SAI: www.proxypush.com/THR |

6

Thrivent Partner Growth Stock Portfolio

a series of

THRIVENT SERIES FUND, INC.

901 Marquette Ave., Suite 2500

Minneapolis, Minnesota 55402

800-847-4836

Thrivent.com

NOTICE OF SPECIAL MEETING

OF CONTRACTHOLDERS

To be Held on August 24, 2020

NOTICE IS HEREBY GIVEN THAT a special meeting of contractholders (with any adjournments, the “Meeting”) of Thrivent Partner Growth Stock Portfolio (the “Target Portfolio”), a series of Thrivent Series Fund, Inc. (the “Fund”), will be held on August 24, 2020 at 9:30 a.m. Central Time. The Meeting will be held online only and Contractholders will not be able to attend the Meeting in person. To participate in the online Meeting, contractholders eligible to vote at the Meeting must register in advance at www.proxypush.com/THR prior to the deadline of Thursday, August 20, 2020 at 4:00 p.m. Central Time and provide the control number as provided in the Notice, or proxy card, or voting instruction form at www.proxypush.com/THR. Upon completing your registration, you will receive further instructions via email, including unique links to access the Meeting and to submit questions in advance of the Meeting.

The Meeting is being held for the following purposes:

| | 1. | To approve an Agreement and Plan of Reorganization pursuant to which the Target Portfolio would (i) transfer all of its assets to Thrivent Large Cap Growth Portfolio (the “Acquiring Portfolio”), a series of the Fund, in exchange for Shares of the Acquiring Portfolio, (ii) distribute such Shares of the Acquiring Portfolio to contractholders of the Target Portfolio, and (iii) dissolve. |

| | 2. | To transact such other business as may properly be presented at the Meeting or any adjournment thereof. |

The Board of Directors of the Fund (the “Board”) has fixed the close of business on July 10, 2020 as the record date for the determination of contractholders (“Contractholders”) entitled to notice of, and to vote at, the Meeting and all adjournments thereof.

Thrivent Financial for Lutherans is the direct shareholder of the Target Portfolio and sponsor of the variable life insurance contracts and variable annuity contracts (each, a “Variable Contract”). As the holder of a Variable Contract, you are being solicited for voting instructions so that shares of the Target Portfolio may be voted in proportion to the instructions received.

1

Contractholders are invited to attend the online Meeting to cast their vote. Due to COVID-19 safety concerns, the Meeting will be conducted online only and Contractholders will not be able to attend in person.

You may also vote by executing a proxy using one of three methods:

| | • | | Internet—Instructions for casting your vote via the Internet can be found in the enclosed proxy voting materials. The required control number is printed on your enclosed proxy card. If this feature is used, there is no need to mail the proxy card. |

| | • | | Phone—Instructions for casting your vote via phone can be found in the enclosed proxy voting materials. The toll-free number and required control number are printed on your enclosed proxy card. If this feature is used, there is no need to mail the proxy card. |

| | • | | Mail—If you vote by mail, please indicate your voting instructions on the enclosed proxy card, date and sign the card, and return it in the envelope provided, which is addressed for your convenience and needs no postage if mailed in the United States. |

Contractholders who execute proxies by Internet, phone, or mail may revoke them at any time prior to the Meeting by filing with the Target Portfolio a written notice of revocation, by executing another proxy bearing a later date, or by attending the online Meeting. Merely attending the online Meeting, however, will not revoke any previously submitted proxy.

The Board recommends that you cast your vote FOR the proposed Reorganization as described in the Prospectus/Proxy Statement.

YOUR VOTE IS IMPORTANT

Please return your proxy card or record your voting instructions promptly no matter how many shares you own. In order to avoid the additional expense of further solicitation, we ask that you mail your proxy card or record your voting instructions by Internet or phone promptly regardless of whether you plan to attend the online Meeting.

Date: [ ], 2020

John D. Jackson

Assistant Secretary

Thrivent Series Fund, Inc.

2

COMBINED PROSPECTUS/PROXY STATEMENT

THRIVENT PARTNER GROWTH STOCK PORTFOLIO

a series of

THRIVENT SERIES FUND, INC.

901 Marquette Ave., Suite 2500

Minneapolis, Minnesota 55402

800-847-4836

[ ], 2020

This Prospectus/Proxy Statement is furnished to you as a contractholder of Thrivent Partner Growth Stock Portfolio (the “Target Portfolio”), a series of Thrivent Series Fund, Inc. (the “Fund”). A special meeting of shareholders of the Target Portfolio will be held on August 24, 2020 (the “Meeting”) to consider the items that are described below and discussed in greater detail elsewhere in this Prospectus/Proxy Statement. The Board of Directors of the Fund (the “Board”) requests that you vote your shares by completing and returning the enclosed proxy card or by recording your voting instructions by Internet or phone regardless of whether you plan to attend the Meeting online in order to avoid the additional expense of further solicitation.

The Acquiring Portfolio and the Target Portfolio are sometimes referred to herein individually as a “Portfolio” or collectively as the “Portfolios.” Each of the Acquiring Portfolio and the Target Portfolio is organized as a series of the Fund, an open-end investment company registered under the Investment Company Act of 1940, as amended (the “1940 Act”). The Target Portfolio is a diversified company and the Acquiring Portfolio is non-diversified company, each as defined under the 1940 Act.

The Board has fixed the close of business on July 10, 2020 as the record date (“Record Date”) for the determination of contractholders (“Contractholders”) entitled to notice of, and to vote at, the Meeting and all adjournments thereof. For ease of reference, the term “Shareholders” will be used in this Prospectus/Proxy Statement and the accompanying materials to refer collectively to both record owners and beneficial owners of shares of the Target Portfolio and Acquiring Portfolio (i.e., owners of variable life insurance contracts and variable annuity contracts (each, a “Variable Contract”) funded by the Portfolios and shareholders of the Portfolios) as of the Record Date.

This Prospectus/Proxy Statement sets forth concisely the information shareholders of the Target Portfolio ought to know before voting on the Reorganization. Please read it carefully and retain it for future reference.

The following documents, each having been filed with the Securities and Exchange Commission (the “SEC”), are incorporated herein by reference:

| | • | | The Thrivent Series Fund, Inc. Prospectus, dated April 30, 2020 (the “Fund Prospectus”) with SEC file number 033-03677. |

1

| | • | | A Statement of Additional Information, dated [ ], 2020, relating to this Combined Prospectus/Proxy Statement (the “Reorganization SAI”) with SEC file number [ ]; |

| | • | | The Thrivent Series Fund, Inc. Statement of Additional Information, dated April 30, 2020 (the “Fund SAI”) with SEC file number 033-03677. |

Copies of the foregoing may be obtained without charge by calling or writing the Portfolio as set forth below. If you wish to request the Reorganization SAI, please ask for the “Reorganization SAI.”

In addition, each Portfolio will furnish, without charge, a copy of its most recent annual report and subsequent semi-annual report, if any, to a Contractholder upon request.

Copies of each Portfolio’s most recent prospectus, statement of additional information, annual report and semi-annual report can be obtained at Thrivent.com as follows:

| | • | | Variable Annuity Reference Center: https://www.thrivent.com/what-we-offer/insurance/annuities/variable-annuity-reference-center.html |

| | • | | Variable Universal Life Reference Center: https://www.thrivent.com/what-we-offer/insurance/variable-universal-life-reference-center.html |

| | • | | AdvisorFlex Variable Annuity Reference Center: https://www.thrivent.com/what-we-offer/insurance/annuities/thrivent-advisorflex-variable-annuity-reference-center.html |

Requests for these documents can also be made by calling 800-847-4836 or writing Thrivent Series Fund, Inc., 4321 North Ballard Road, Appleton, WI 54919. A copy of the Reorganization SAI can also be obtained from Mediant Communications at www.proxypush.com/THR.

The Portfolios file reports and other information with the SEC. Information filed by the Portfolios with the SEC can be reviewed on the EDGAR database on the SEC’s internet site (https://www.sec.gov). You can also request copies of these materials, upon payment of a duplicating fee, by electronic request at the SEC’s e-mail address (publicinfo@sec.gov).

The Board knows of no business other than that discussed above that will be presented for consideration at the Meeting. If any other matter is properly presented, it is the intention of the persons named in the enclosed proxy to vote in accordance with their best judgment.

2

No person has been authorized to give any information or make any representation not contained in this Prospectus/Proxy Statement and, if so given or made, such information or representation must not be relied upon as having been authorized. This Prospectus/Proxy Statement does not constitute an offer to sell or a solicitation of an offer to buy any securities in any jurisdiction in which, or to any person to whom, it is unlawful to make such offer or solicitation.

Neither the Securities and Exchange Commission nor any state regulator has approved or disapproved of these shares or passed upon the adequacy of this Prospectus/Proxy Statement. A representation to the contrary is a crime.

The date of this Prospectus/Proxy Statement is [ ], 2020. The Prospectus/Proxy Statement will be sent to Contractholders on or around [ ], 2020.

3

TABLE OF CONTENTS

4

SUMMARY

The following is a summary of certain information contained elsewhere in this Prospectus/Proxy Statement and is qualified in its entirety by reference to the more complete information contained in this Prospectus/Proxy Statement. Contractholders should read the entire Prospectus/Proxy Statement carefully.

The Reorganization

The Board, including the directors who are not “interested persons” (as defined in the 1940 Act) of each Portfolio (the “Independent Directors”), has unanimously approved an Agreement and Plan of Reorganization (the “Reorganization Agreement”) on behalf of each Portfolio, subject to Target Portfolio Contractholder approval. The Reorganization Agreement provides for:

| | • | | the transfer of all of the assets of the Target Portfolio to the Acquiring Portfolio in exchange for shares of the Acquiring Portfolio; |

| | • | | the distribution by the Target Portfolio of such Acquiring Portfolio shares to Target Portfolio shareholders; and |

| | • | | the dissolution of the Target Portfolio. |

When the Reorganization is complete, Target Portfolio shareholders will hold Acquiring Portfolio shares. The aggregate value of the Acquiring Portfolio shares a Target Portfolio shareholder will receive in the Reorganization will equal the aggregate value of the Target Portfolio shares owned by such shareholder immediately prior to the Reorganization, but the overall number of shares held by Target Portfolio shareholders may change. After the Reorganization, the Acquiring Portfolio will continue to operate with the investment objective and investment policies set forth in this Prospectus/Proxy Statement. The Reorganization will not affect your Variable Contract.

As discussed in more detail elsewhere in this Prospectus/Proxy Statement, the Board believes that the Reorganization would be in the best interests of the Target Portfolio’s Contractholders because: (i) Contractholders will become contractholders of a larger combined portfolio with greater potential to increase asset size and achieve economies of scale; (ii) the Acquiring Portfolio has achieved better performance than the Target Portfolio for the one-, two- and three-year periods ended December 31, 2019, though there is no guarantee of future performance; (iii) Thrivent Financial, the Portfolios’ investment adviser, believes that it can most effectively manage the assets currently in the Target Portfolio by combining such assets with the Acquiring Portfolio; and (iv) the Acquiring Portfolio has a lower gross expense ratio than the Target Portfolio and shareholders of the Target Portfolio will experience a lower net expense ratio in the Acquiring Portfolio following the Reorganization.

5

In addition, the Board, when determining whether to approve the Reorganization, considered, among other things, the future growth prospects of each of the Target Portfolio and the Acquiring Portfolio, the fact that the Target Portfolio Contractholders would not experience any diminution in contractholder services as a result of the Reorganization, and the fact that the Reorganization is expected to be a tax-free reorganization for federal income tax purposes.

Background and Reasons for the Reorganization

The Target Portfolio and the Acquiring Portfolio have similar investment objectives to seek long-term growth of capital, but the Target Portfolio has a secondary objective to increase dividend income while the Acquiring Portfolio does not.

The two Portfolios also have some similarities and some differences in their principal investment strategies, which are described in more detail in the COMPARISON OF THE PORTFOLIOS—Investment Objective and Principal Strategies section of the Prospectus/Proxy Statement. Both Portfolios invest in equity securities of domestic and international companies with potential above average earnings growth. The Target Portfolio also seeks investments in companies that have the ability to pay increasing dividends through strong cash flow. The Acquiring Portfolio focuses mainly on the equity securities of large domestic and international companies which have market capitalizations equivalent to those included in widely known indices such as the Russell 1000 Growth Index, S&P 500 Index, or the large company market capitalization classifications published by Lipper, Inc. These companies typically have a market capitalization of approximately $8 billion or more.

In determining whether to recommend approval of the Reorganization Agreement to Target Portfolio Contractholders, the Board considered a number of factors, including, but not limited to: (i) the expenses and advisory fees applicable to the Portfolios before the proposed Reorganization and the estimated expense ratios of the combined portfolio after the proposed Reorganization; (ii) the comparative investment performance of the Portfolios; (iii) the future growth prospects of each Portfolio; (iv) the terms and conditions of the Reorganization Agreement; (v) whether the Reorganization would result in the dilution of Contractholder interests; (vi) the compatibility of the Portfolios’ investment objectives, policies, risks and restrictions; (vii) that the proposed Reorganization was expected to be a tax-free reorganization for federal income tax purposes; (viii) the compatibility of the Portfolios’ service features available to Contractholders; and (ix) the estimated costs of the Reorganization, which, except for transaction costs, would be borne by Thrivent Financial for Lutherans (“Thrivent Financial” or the “Adviser”), the investment adviser of the Portfolios. The Board concluded that these factors supported a determination to approve the Reorganization Agreement.

6

The Board has determined that the Reorganization is in the best interests of the Target Portfolio and that the interests of the Target Portfolio’s Contractholders will not be diluted as a result of the Reorganization. In addition, the Board has determined that the Reorganization is in the best interests of the Acquiring Portfolio and that the interests of the Acquiring Portfolio Contractholders will not be diluted as a result of the Reorganization.

The Board is asking Contractholders of the Target Portfolio to approve the Reorganization at the Meeting to be held on August 24, 2020. If Contractholders of the Target Portfolio approve the proposed Reorganization, it is expected that the closing date of the transaction (the “Closing Date”) will be after the close of business on or about August 31, 2020, but it may be at a different time as described herein.

Effect if Contractholders do not Approve the Reorganization of the Target Portfolio

If Contractholders of the Target Portfolio do not approve the proposed Reorganization, the Board will consider alternatives, including repurposing the Target Portfolio’s principal strategies.

The Board recommends that you vote “FOR” the Reorganization.

7

COMPARISON OF THE PORTFOLIOS

Investment Objective and Principal Strategies

Investment Objective. The Target Portfolio and the Acquiring Portfolio have similar investment objectives to seek long-term growth of capital, but the Target Portfolio has a secondary objective to increase dividend income while the Acquiring Portfolio does not.

Principal Strategies. Both Portfolios invest in equity securities of domestic and international companies with potential above average earnings growth. The Target Portfolio also seeks investments in companies that have the ability to pay increasing dividends through strong cash flow. The Acquiring Portfolio focuses mainly on the equity securities of large domestic and international companies which have market capitalizations equivalent to those included in widely known indices such as the Russell 1000 Growth Index, S&P 500 Index, or the large company market capitalization classifications published by Lipper, Inc. These companies typically have a market capitalization of approximately $8 billion or more.

The Target Fund is managed by a subadviser, T. Rowe Price Associates, Inc. The Acquiring Fund is managed by the Adviser.

Portfolio Holdings. A description of the Portfolios’ policies and procedures with respect to the disclosure of the Portfolios’ portfolio securities is available on the Portfolios’ website.

The following table provides a side-by-side comparison of the investment objectives and principal strategies of the Target Portfolio and the Acquiring Portfolio.

| | | | |

| | | |

| | | Target Portfolio | | Acquiring Portfolio |

Investment

Objective | | The investment objective of the Target Portfolio is to seek long-term growth of capital and, secondarily, increase dividend income. | | The investment objective of the Acquiring Portfolio is to seek long-term growth of capital. |

8

| | | | |

| | | |

| | | Target Portfolio | | Acquiring Portfolio |

Principal

Strategies | | The Portfolio’s principal strategy for achieving its investment objectives under normal circumstances is to invest at least 80% of net assets (plus the amount of any borrowing for investment purposes) in common stocks. Should the Adviser determine that the Portfolio would benefit from reducing the percentage of its assets invested in common stocks from 80% to a lesser amount, it will notify you at least 60 days prior to such a change. The Portfolio concentrates its investments in growth companies. The Portfolio’s subadviser, T. Rowe Price Associates, Inc. (“T. Rowe Price”), seeks investments in companies that have the ability to pay increasing dividends through strong cash flow. The subadviser generally looks for companies with an above-average rate of earnings growth and a lucrative niche in the economy that gives them the ability to sustain earnings momentum even during times of slow economic growth. T. Rowe Price believes that when a company increases its earnings faster than both inflation and the overall economy, the market will eventually reward it with a higher stock price. The Portfolio may at times invest significantly in certain sectors, such as the information technology sector. In pursuing the Portfolio’s investment objectives, T. Rowe Price has the discretion to purchase some securities that do not meet its normal investment criteria, as described above, when it believes such purchase will provide an opportunity for substantial appreciation. These situations might arise when T. Rowe Price believes a security could increase in value for a variety of reasons including a change in management, an extraordinary corporate event, a new product introduction or innovation, or a favorable competitive development. While the Portfolio invests primarily (at least 80%) in common stocks, it may also invest in foreign stocks (up to 30% of total assets), and futures and options to obtain investment exposure or for hedging, in keeping with the Portfolio’s objectives. The Portfolio may sell securities for a variety of reasons, such as to secure gains, limit losses, or reposition assets into more promising opportunities. | | Under normal circumstances, the Portfolio invests at least 80% of its net assets (plus the amount of any borrowing for investment purposes) in equity securities of large companies. The Adviser focuses mainly on the equity securities of large domestic and international companies which have market capitalizations equivalent to those included in widely known indices such as the Russell 1000 Growth Index, S&P 500 Index, or the large company market capitalization classifications published by Lipper, Inc. These companies typically have a market capitalization of approximately $8 billion or more. Should the Adviser change the investments used for purposes of this 80% threshold, you will be notified at least 60 days prior to the change. The Portfolio seeks to achieve its investment objective by investing in common stocks. The Adviser uses fundamental, quantitative, and technical investment research techniques and focuses on stocks of companies that it believes have demonstrated and will sustain above-average earnings growth over time, or which are expected to develop rapid sales and earnings growth in the future when compared to the economy and stock market as a whole. Many such companies are in the technology sector and the Portfolio may at times have a higher concentration in this industry. The Portfolio may sell securities for a variety of reasons, such as to secure gains, limit losses, or reposition assets into more promising opportunities. |

9

Principal Risks

The Portfolios are subject to similar principal risks, with a few differences. Shares of each Portfolio will rise and fall in value and there is a risk that you could lose money by investing in each Portfolio. The table below compares the principal risks of an investment in each Portfolio. The risks are listed alphabetically and each risk is described below the table.

| | | | | | | | |

Risk | | Target

Portfolio | | | Acquiring

Portfolio | |

Derivatives Risk | | | X | | | | | |

Equity Security Risk | | | X | | | | X | |

Foreign Securities Risk | | | X | | | | X | |

Growth Investing Risk | | | X | | | | X | |

Health Crisis Risk | | | X | | | | X | |

Investment Adviser Risk | | | X | | | | X | |

Issuer Risk | | | X | | | | X | |

Large Cap Risk | | | | | | | X | |

Market Risk | | | X | | | | X | |

Non-Diversified Risk | | | | | | | X | |

Technology-Oriented Companies Risk | | | X | | | | X | |

Principal risks to which both Portfolios are subject

Equity Security Risk. Equity securities held by the Portfolio may decline significantly in price, sometimes rapidly or unpredictably, over short or extended periods of time, and such declines may occur because of declines in the equity market as a whole, or because of declines in only a particular country, company, industry, or sector of the market. From time to time, the Portfolio may invest a significant portion of its assets in companies in one or more related sectors or industries which would make the Portfolio more vulnerable to adverse developments affecting such sectors or industries. Equity securities are generally more volatile than most debt securities.

Foreign Securities Risk. Foreign securities generally carry more risk and are more volatile than their domestic counterparts, in part because of potential for higher political and economic risks, lack of reliable information and fluctuations in currency exchange rates where investments are denominated in currencies other than the U.S. dollar. Certain events in foreign markets may adversely affect foreign and domestic issuers, including interruptions in the global supply chain, natural disasters and outbreak of infectious diseases. The Portfolio’s investment in any country could be subject to governmental actions such as capital or currency controls, nationalizing a company or industry, expropriating assets, or imposing punitive taxes that would have an adverse effect on security prices, and impair the Portfolio’s ability to repatriate capital or income. Foreign securities may also be more difficult to resell than comparable U.S. securities because the markets for foreign securities are often less liquid. Even when a foreign security increases in price in its local currency, the appreciation may be diluted by adverse changes in exchange rates when the security’s value is converted to U.S. dollars. Foreign withholding taxes also may apply and errors and delays may occur in the settlement process for foreign securities.

10

Growth Investing Risk. Growth style investing includes the risk of investing in securities whose prices historically have been more volatile than other securities, especially over the short term. Growth stock prices reflect projections of future earnings or revenues and, if a company’s earnings or revenues fall short of expectations, its stock price may fall dramatically.

Health Crisis Risk. The global pandemic outbreak of the novel coronavirus known as COVID-19 has resulted in substantial market volatility and global business disruption. The duration and full effects of the outbreak are uncertain and may result in trading suspensions and market closures, limit liquidity and the ability of the Portfolio to process shareholder redemptions, and negatively impact Portfolio performance. The COVID-19 outbreak and future pandemics could affect the global economy in ways that cannot be foreseen and may exacerbate other types of risks, negatively impacting the value of the Portfolio.

Investment Adviser Risk. The Portfolio is actively managed and the success of its investment strategy depends significantly on the skills of the Adviser in assessing the potential of the investments in which the Portfolio invests. This assessment of investments may prove incorrect, resulting in losses or poor performance, even in rising markets. There is also no guarantee that the Adviser will be able to effectively implement the Portfolio’s investment objective.

Issuer Risk. Issuer risk is the possibility that factors specific to an issuer to which the Portfolio is exposed will affect the market prices of the issuer’s securities and therefore the value of the Portfolio.

Market Risk. Over time, securities markets generally tend to move in cycles with periods when security prices rise and periods when security prices decline. The value of the Portfolio’s investments may move with these cycles and, in some instances, increase or decrease more than the applicable market(s) as measured by the Portfolio’s benchmark index(es). The securities markets may also decline because of factors that affect a particular industry or due to impacts from the spread of infectious illness, public health threats or similar issues.

Technology-Oriented Companies Risk. Common stocks of companies that rely extensively on technology, science or communications in their product development or operations may be more volatile than the overall stock market and may or may not move in tandem with the overall stock market. Technology, science and communications are rapidly changing fields, and stocks of these companies, especially of smaller or unseasoned companies, may be subject to more abrupt or erratic market movements than the stock market in general. There are significant competitive pressures among technology-oriented companies and the products or operations of such companies may become obsolete quickly. In addition, these companies may have limited product lines, markets or financial resources and the management of such companies may be more dependent upon one or a few key people.

11

Additional principal risk to which only the Target Portfolio is subject

Derivatives Risk. The use of derivatives (such as futures and options) involves additional risks and transaction costs which could leave the Portfolio in a worse position than if it had not used these instruments. The Portfolio utilizes equity futures in order to increase or decrease its exposure to various asset classes at a lower cost than trading stocks directly. The use of derivatives can lead to losses because of adverse movements in the price or value of the underlying asset, index or rate, which may be magnified by certain features of the contract. Changes in the value of the derivative may not correlate as intended with the underlying asset, rate or index, and the Portfolio could lose much more than the original amount invested. Derivatives can be highly volatile, illiquid and difficult to value. Certain derivatives may also be subject to counterparty risk, which is the risk that the other party in the transaction will not fulfill its contractual obligations due to its financial condition, market events, or other reasons.

Additional principal risks to which only the Acquiring Portfolio is subject

Large Cap Risk. Large-sized companies may be unable to respond quickly to new competitive challenges such as changes in technology. They may also not be able to attain the high growth rate of successful smaller companies, especially during extended periods of economic expansion.

Non-Diversified Risk. The Portfolio is not “diversified” within the meaning of the 1940 Act. That means the Portfolio may invest a greater percentage of its assets in the securities of any single issuer compared to other funds. A non-diversified portfolio is generally more susceptible than a diversified portfolio to the risk that events or developments affecting a particular issuer or industry will significantly affect the Portfolio’s performance.

The Target Portfolio is a diversified company as defined under the 1940 Act.

Management of the Portfolios

The Board. The Board has oversight responsibilities for each Portfolio and performs its fiduciary duties imposed on the directors of investment companies by the 1940 Act and under applicable state law.

The Adviser. Thrivent Financial is the investment adviser for each Portfolio and manages each Portfolio on a day-to-day basis. Thrivent Financial and its investment advisory affiliate, Thrivent Asset Management, LLC, have been in the investment advisory business since 1986 and managed approximately $132 billion in assets as of December 31, 2019, including approximately $55 billion in mutual fund assets. These advisory entities are located at 901 Marquette Avenue, Suite 2500, Minneapolis, Minnesota 55402.

12

The Portfolios’ annual report to Contractholders discusses the basis for the Board approving the investment advisory agreement during the period covered by the report.

Portfolio Management. Thrivent Financial has engaged T. Rowe Price, 100 East Pratt Street, Baltimore, Maryland 21202, as investment subadviser for the Target Portfolio. T. Rowe Price and its affiliates had approximately $1.21 trillion in total assets under management as of December 31, 2019. Joseph B. Fath, CPA is primarily responsible for the day-to-day management of the Target Portfolio. Mr. Fath has served as the portfolio manager of the Target Portfolio since April 2014. He currently serves as Chairman of the Portfolio’s Investment Advisory Committee. Mr. Fath joined T. Rowe Price in 2002. He joined as an equity research analyst and, since 2008, has assisted other T. Rowe Price portfolio managers in managing the Firm’s U.S. large-cap growth strategies.

Lauri Brunner is primarily responsible for the day-to-day management of the Acquiring Portfolio, and she has served as portfolio manager of the Acquiring Portfolio since September 2018. Ms. Brunner has been with Thrivent Financial since 2007 and currently is a Senior Portfolio Manager. Ms. Brunner will continue to manage the Acquiring Portfolio following the Reorganization.

The Fund SAI provides information about the portfolio managers’ compensation, other accounts managed by the portfolio managers, and the portfolio managers’ ownership of shares of the Portfolios.

Advisory and Other Fees

Advisory Fees. Each Portfolio pays an annual investment advisory fee to the Adviser. The advisory contract between the Adviser and the Fund provides for the following advisory fees for each Portfolio, expressed as an annual rate of average daily net assets:

Target Portfolio

0.650% of average daily net assets up to $250 million

0.625% of average daily net assets greater than $250 million up to $500 million

0.600% of average daily net assets greater than $500 million up to $1 billion

0.550% of average daily net assets over $1 billion

Acquiring Portfolio

0.400% for all assets

During the twelve-months ended December 31, 2019, the contractual advisory fees for the Target Portfolio were 0.650% of the Target Portfolio’s average daily net assets.

13

During the twelve-months ended December 31, 2019, the contractual advisory fees for the Acquiring Portfolio were 0.400% of the Acquiring Portfolio’s average daily net assets.

For a complete description of each Portfolio’s advisory services, see the section of the Portfolio Prospectus entitled “Management” and the section of the Fund SAI entitled “Investment Adviser, Investment Subadvisers, and Portfolio Managers.”

Expenses

The table below sets forth the fees and expenses that investors may pay to buy and hold shares of each of the Target Portfolio and the Acquiring Portfolio, including (i) the fees and expenses paid by the Target Portfolio for the twelve-month period ended December 31, 2019, (ii) the fees and expenses paid by the Acquiring Portfolio for the twelve-month period ended December 31, 2019, and (iii) pro forma fees and expenses for the Acquiring Portfolio for the twelve-month period ended December 31, 2019, assuming the Reorganization had been completed as of the beginning of such period. If you own a Variable Contract, you will have additional expenses, including mortality and expense risk charges. These additional contract-level expenses are not reflected in the table below.

| | | | | | | | | | | | |

| | | Actual | | | Pro Forma | |

| | | Target

Portfolio | | | Acquiring

Portfolio | | | Acquiring

Portfolio

(assuming

merger with

Target Portfolio) | |

Shareholder Fees (fees directly paid from your investment) | | | | | | | | | | | | |

Maximum Sales Charge (Load) | | | N/A | | | | N/A | | | | N/A | |

Maximum Deferred Sales Charge (Load) | | | N/A | | | | N/A | | | | N/A | |

| | | |

Annual Fund Operating Expenses as a Percentage of Average Net Assets (expenses that you pay each year as a percentage of the value of your investment) | | | | | | | | | | | | |

Management Fees | | | 0.65 | % | | | 0.40 | % | | | 0.40 | % |

Other Expenses | | | 0.09 | % | | | 0.04 | % | | | 0.04 | % |

Total Annual Operating Expenses | | | 0.74 | % | | | 0.44 | % | | | 0.44 | % |

Example

The following example, using the actual and pro forma operating expenses for the twelve-month period ended December 31, 2019, is intended to help you compare the costs of investing in the Acquiring Portfolio pro forma after the Reorganization with the costs of investing in each of the Target Portfolio and the Acquiring Portfolio without the Reorganization. The example assumes that you invest $10,000 in each

14

Portfolio for the time period indicated and that you redeem all of your shares at the end of each period. The example also assumes that your investments have a 5% return each year and that each Portfolio’s operating expenses remain the same each year. Although your actual returns may be higher or lower, based on these assumptions your costs would be:

| | | | | | | | | | | | |

| | | Actual | | | Pro Forma | |

| | | Target

Portfolio | | | Acquiring

Portfolio | | | Acquiring

Portfolio

(assuming

merger with the

Target Portfolio) | |

Total operating expenses assuming redemption at the end of the period | | | | | | | | | | | | |

One Year | | $ | 76 | | | $ | 45 | | | $ | 45 | |

Three Years | | $ | 237 | | | $ | 141 | | | $ | 141 | |

Five Years | | $ | 411 | | | $ | 246 | | | $ | 246 | |

Ten Years | | $ | 918 | | | $ | 555 | | | $ | 555 | |

Portfolio Turnover

Each Portfolio pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Portfolio shares are held in a taxable account. These costs, which are not reflected in Total Annual Operating Expenses or in the Example, affect the Portfolios’ performance. During the fiscal year ended December 31, 2019, the Acquiring Portfolio’s and the Target Portfolio’s portfolio turnover rates were 58% and 29%, respectively, of the average value of their portfolios.

Pricing of Portfolio Shares

The price of a Portfolio’s shares is based on the Portfolio’s net asset value (“NAV”). Each Portfolio generally determines its NAV once daily at the close of regular trading on the New York Stock Exchange (“NYSE”), which is normally 4:00 p.m. Eastern Time. If the NYSE has an unscheduled early close but certain other markets remain open until their regularly scheduled closing time, the NAV may be determined as of the regularly scheduled closing time of the NYSE. If the NYSE and/or certain other markets close early due to extraordinary circumstances (e.g., weather, terrorism, etc.), the NAV may be calculated as of the early close of the NYSE and/or other markets. The NAV generally will not be determined on days when, due to extraordinary circumstances, the NYSE and/or certain other markets do not open for trading. The Portfolios generally do not determine NAV on holidays observed by the NYSE or on any other day when the NYSE is closed. The NYSE is regularly closed on Saturdays and Sundays, New Year’s Day, Martin Luther King, Jr. Day, Presidents’ Day, Good Friday, Memorial Day, Independence Day, Labor Day, Thanksgiving Day and Christmas Day.

15

Each Portfolio determines its NAV by adding the value of Portfolio assets, subtracting the Portfolio’s liabilities, and dividing the result by the number of outstanding shares. To determine the NAV, the other Portfolios generally value their securities at current market value using readily available market prices. If market prices are not available or if the Adviser determines that they do not accurately reflect fair value for a security, the Board has authorized the Adviser to make fair valuation determinations pursuant to policies approved by the Board. Fair valuation of a particular security is an inherently subjective process, with no single standard to utilize when determining a security’s fair value. In each case where a security is fair valued, consideration is given to the facts and circumstances relevant to the particular situation. This consideration includes a review of various factors set forth in the pricing policies adopted by the Board. For any portion of a Portfolio’s assets that are invested in other mutual funds, the NAV is calculated based upon the NAV of the mutual funds in which the Portfolio invests, and the prospectuses for those mutual funds explain the circumstances under which they will use fair value pricing and the effects of such a valuation.

Because many foreign markets close before the U.S. markets, significant events may occur between the close of the foreign market and the close of the U.S. markets, when the Portfolio’s assets are valued, that could have a material impact on the valuation of foreign securities (i.e., available price quotations for these securities may not necessarily reflect the occurrence of the significant event). The Fund, subject to oversight by the Board, evaluates the impact of these significant events and adjusts the valuation of foreign securities to reflect the fair value as of the close of the U.S. markets to the extent that the available price quotations do not, in the Adviser’s opinion, adequately reflect the occurrence of the significant events.

The separate accounts place an order to buy or sell shares of a respective Portfolio each business day. The amount of the order is based on the aggregate instructions from owners of the variable annuity contracts. Orders placed before the close of the NYSE on a given day by the separate accounts result in share purchases and redemptions at the NAV calculated as of the close of the NYSE that day.

Please note that the Target Portfolio and the Acquiring Portfolio have identical valuation policies. As a result, there will be no material change to the value of the Target Portfolio’s assets because of the Reorganization.

Also, the Target Portfolio and the Acquiring Portfolio have identical policies with respect to frequent purchases and redemptions and standing allocation orders (for more information, please see Policy Regarding Frequent Purchases and Redemptions and Standing Allocation Order disclosures in the Acquiring Portfolio’s Prospectus—these disclosures are incorporate herein by reference). The Reorganization will not affect these policies.

16

Capitalization

The following table sets forth the capitalization of the Target Portfolio and the Acquiring Portfolio, as of May 29, 2020, and the pro forma capitalization of the Acquiring Portfolio as if the Reorganization occurred on that date. These numbers may differ as of the Closing Date.

| | | | | | | | | | | | |

| | | Actual | | | Pro Forma | |

| | | Target

Portfolio | | | Acquiring

Portfolio | | | Acquiring

Portfolio

(assuming

merger with

the Target

Portfolio) | |

Net assets | | | | | | | | | | | | |

Portfolio Net Assets | | $ | 279,453,778 | | | $ | 1,637409,818 | | | $ | 1,916,863,595 | |

| | | |

Net asset value per share | | | | | | | | | | | | |

Net asset value | | $ | 29.62 | | | $ | 45.07 | | | $ | 45.07 | |

| | | |

Shares outstanding | | | | | | | | | | | | |

Portfolio Shares | | | 9,434,991 | | | | 36,329,407 | | | | 42,529,681 | |

The pro forma shares outstanding reflect the issuance by the Acquiring Portfolio of approximately 6,200,274 shares. Such issuance reflects the exchange of the assets of the Target Portfolio for newly issued shares of the Acquiring Portfolio at the pro forma net asset value per share. The aggregate value of the Acquiring Portfolio shares that a Target Portfolio shareholder receives in the Reorganization will equal the aggregate value of the Target Portfolio shares owned immediately prior to the Reorganization.

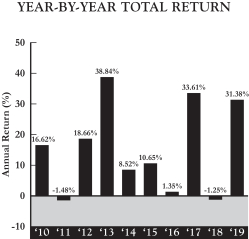

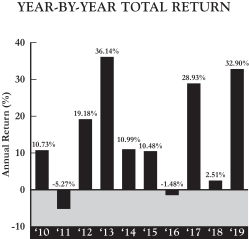

Annual Performance Information

The following chart shows the annual returns of the Target Portfolio since its inception and the Acquiring Portfolio for the past ten calendar years. The bar charts include the effects of each Portfolio’s expenses, but not charges or deductions against your Variable Contract. If these charges and deductions were included, returns would be lower than those shown.

17

Target Portfolio

Acquiring Portfolio

As a result of market activity, current performance may vary from the figures shown.

The Target Portfolio’s total return for the three-month period from January 1, 2020 to March 31, 2020 was-14.73%. The Acquiring Portfolio’s total return for the three-month period from January 1, 2020 to March 31, 2020 was -11.15%. During the past 10 years, the Target Portfolio’s highest quarterly return was 18.98% (for the quarter ended March 31, 2012) and its lowest quarterly return was -14.56% (for the

18

quarter ended September 30, 2011). During the past 10 years, the Acquiring Portfolio’s highest quarterly return was 16.67% (for the quarter ended March 31, 2012) and its lowest quarterly return was -17.08% (for the quarter ended September 30, 2011).

Comparative Performance Information

As a basis for evaluating each Portfolio’s performance and risks, the following table shows how each Portfolio’s performance compares with broad-based market indices that the Adviser believes are appropriate benchmarks for such Portfolio. Both Portfolios compare their performance against the Russell 1000 Growth Index, an unmanaged market capitalization-weighted index of growth-oriented stocks of the largest companies that are included in the Russell 1000 Index, and the S&P 500 Growth Index, which measures the performance of the growth stocks in the S&P 500 Index. Further, the table includes the effects of each Portfolio’s expenses, but not charges or deductions against your Variable Contract. If these charges and deductions were included, returns would be lower than those shown.

Average annual total returns are shown below for each Portfolio for the periods ended December 31, 2019 (the most recently completed calendar year prior to the date of this Prospectus/Proxy Statement). Remember that past performance of a Portfolio is not indicative of its future performance.

Average Annual Total Returns for the Period ended December 31, 2019

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Target Portfolio | | | Acquiring Portfolio | |

| | | Past 1

Year | | | Past 5

Years | | | Since

Inception

(4/30/08) | | | Past 1

Year | | | Past 5

Years | | | Past 10

Years | |

Applicable Portfolio | | | 31.38 | % | | | 14.22 | % | | | 14.85 | % | | | 32.90 | % | | | 13.84 | % | | | 13.70 | % |

Russell 1000 Growth Index (reflects no deduction for fees, expenses or taxes) | | | 36.39 | % | | | 14.63 | % | | | 15.22 | % | | | 36.39 | % | | | 14.63 | % | | | 15.22 | % |

S&P 500® Growth Index (reflects no deduction for fees, expenses or taxes) | | | 31.13 | % | | | 13.52 | % | | | 14.78 | % | | | 31.13 | % | | | 13.52 | % | | | 14.78 | % |

Financial Highlights

The Acquiring Portfolio’s and the Target Portfolio’s financial highlights for the fiscal year ended December 31, 2019, which are included in the Funds’ Prospectus and incorporated herein by reference, have been audited by PricewaterhouseCoopers LLP, independent registered public accounting firm, whose report thereon is included in the Annual Report to Shareholders. The financial highlights audited by PricewaterhouseCoopers LLP have been incorporated by reference in reliance on their reports given on their authority as experts in auditing and accounting.

19

Other Service Providers

Thrivent Financial, 901 Marquette Avenue, Suite 2500, Minneapolis, Minnesota 55402, provides administrative personnel and services necessary to operate the Portfolios and receives an administration fee from the Portfolios. The custodian for the Portfolios is State Street Bank and Trust Company, One Lincoln Street, Boston, Massachusetts 02111. PricewaterhouseCoopers LLP, 45 South Seventh Street, Suite 3400, Minneapolis, MN 55402, serves as the Fund’s independent registered public accounting firm.

Governing Law

The Fund is an open-end management investment company registered under the Investment Company Act of 1940 (the “1940 Act”) and was organized as a Minnesota corporation on February 24, 1986. The Fund is made up of 33 separate series or “Portfolios.” Each Portfolio of the Fund, other than Thrivent Large Cap Growth Portfolio and Thrivent Partner Healthcare Portfolio, is diversified within the meaning of the 1940 Act. Each Portfolio is in effect a separate investment fund, and a separate class of capital stock of the Fund is issued with respect to each Portfolio.

The Fund’s organizational documents are filed as part of the Fund’s registration statement with the SEC, and Contractholders may obtain copies of such documents as described on the first page of this Prospectus/Proxy Statement and in the Questions and Answers preceding this Prospectus/Proxy Statement.

Payments to Broker-Dealers and Other Financial Intermediaries

If you purchase a Portfolio through a broker-dealer or other financial intermediary (such as an insurance company), the Portfolio and its related companies may pay the intermediary for the sale of Portfolio shares and related services. These payments may create a conflict of interest by influencing the broker-dealer or other intermediary and your salesperson to recommend the Portfolio over another investment. Ask your salesperson or visit your financial intermediary’s website for more information.

20

INFORMATION ABOUT THE REORGANIZATION

General

Under the Reorganization Agreement, the Target Portfolio will transfer all of its assets to the Acquiring Portfolio in exchange for shares of the Acquiring Portfolio. The Acquiring Portfolio shares issued to the Target Portfolio will have an aggregate value equal to the aggregate value of the Target Portfolio’s net assets immediately prior to the Reorganization. Upon receipt by the Target Portfolio of Acquiring Portfolio shares, the Target Portfolio will distribute such shares of the Acquiring Portfolio to Target Portfolio shareholders. Then, as soon as practicable after the Closing Date of the Reorganization, the Target Portfolio will dissolve under applicable state law. The Acquiring Portfolio anticipates selling approximately 47% of the market value of the Target Portfolio’s investments after the Reorganization. As of May 29, 2020, the Target Portfolio’s investments that the Acquiring Portfolio would anticipate selling have a market value of $130,403,977.46.

The Target Portfolio will distribute the Acquiring Portfolio shares received by it pro rata to Target Portfolio shareholders of record in exchange for their interest in shares of the Target Portfolio. Accordingly, as a result of the Reorganization, each Target Portfolio shareholder would own Acquiring Portfolio shares that would have an aggregate value immediately after the Reorganization equal to the aggregate value of that shareholder’s Target Portfolio shares immediately prior to the Reorganization. The interests of each of the Target Portfolio’s shareholders will not be diluted as a result of the Reorganization. However, as a result of the Reorganization, a shareholder of the Target Portfolio or the Acquiring Portfolio will hold a reduced percentage of ownership in the larger combined portfolio than the shareholder did in either of the separate Portfolios.

The Acquiring Portfolio will be the accounting survivor of the Reorganization.

No sales charge or fee of any kind will be assessed to Target Portfolio shareholders in connection with their receipt of Acquiring Portfolio shares in the Reorganization.

Approval of the Reorganization will constitute approval of amendments to any of the fundamental investment restrictions of the Target Portfolio that might otherwise be interpreted as impeding the Reorganization, but solely for the purpose of and to the extent necessary for consummation of the Reorganization.

Terms of the Reorganization Agreement

The following is a summary of the material terms of the Reorganization Agreement. The form of Reorganization Agreement is attached as Appendix A to the Reorganization SAI.

21

Pursuant to the Reorganization Agreement, the Acquiring Portfolio will acquire all of the assets of the Target Portfolio on the Closing Date in exchange for shares of the Acquiring Portfolio. Subject to the Target Portfolio’s Contractholders approving the Reorganization, the Closing Date shall occur on August 31, 2020 or such other date as determined by an officer of the Fund.

On the Closing Date, the Target Portfolio will transfer to the Acquiring Portfolio all of its assets. The Acquiring Portfolio will in turn transfer to the Target Portfolio a number of its shares equal in value to the value of the net assets of the Target Portfolio transferred to the Acquiring Portfolio as of the Closing Date, as determined in accordance with the valuation method described in the Acquiring Portfolio’s then current prospectus. In order to minimize any potential for undesirable federal income and excise tax consequences in connection with the Reorganization, the Target Portfolio will distribute on or before the Closing Date all or substantially all of its undistributed net investment income (including net capital gains) as of such date.

The Target Portfolio expects to distribute shares of the Acquiring Portfolio received by the Target Portfolio to Contractholders of the Target Portfolio promptly after the Closing Date and then dissolve.

The Acquiring Portfolio and the Target Portfolio have made certain standard representations and warranties to each other regarding their capitalization, status and conduct of business. Unless waived in accordance with the Reorganization Agreement, the obligations of the parties to the Reorganization Agreement are conditioned upon, among other things:

| | • | | the approval of the Reorganization by the Target Portfolio’s Contractholders; |

| | • | | the absence of any rule, regulation, order, injunction or proceeding preventing or seeking to prevent the consummation of the transactions contemplated by the Reorganization Agreement; |

| | • | | the receipt of all necessary approvals, registrations and exemptions under federal and state laws; |

| | • | | the truth in all material respects as of the Closing Date of the representations and warranties of the parties and performance and compliance in all material respects with the parties’ agreements, obligations and covenants required by the Reorganization Agreement; |

| | • | | the effectiveness under applicable law of the registration statement of the Acquiring Portfolio of which this Prospectus/Proxy Statement forms a part and the absence of any stop orders under the Securities Act of 1933, as amended, pertaining thereto; and |

| | • | | the receipt of an opinion of counsel relating to the characterization of the Reorganization as a tax-free reorganization for federal income tax purposes (as further described herein under the heading “Material Federal Income Tax Consequences of the Reorganization”). |

22

The Reorganization Agreement may be terminated or amended by the mutual consent of the parties either before or after approval thereof by the Contractholders of the Target Portfolio, provided that no such amendment after such approval shall be made if it would have a material adverse effect on the interests of such Target Portfolio’s Contractholders. The Reorganization Agreement also may be terminated by the non-breaching party if there has been a material misrepresentation, material breach of any representation or warranty, material breach of contract or failure of any condition to closing.

Reasons for the Proposed Reorganization

In determining whether to recommend approval of the Reorganization Agreement to Target Portfolio Contractholders, the Board considered a number of factors, including, but not limited to: (i) the expenses and advisory fees applicable to the Portfolios before the proposed Reorganization and the estimated expense ratios of the combined portfolio after the proposed Reorganization; (ii) the comparative investment performance of the Portfolios; (iii) the future growth prospects of each Portfolio; (iv) the terms and conditions of the Reorganization Agreement; (v) whether the Reorganization would result in the dilution of Contractholder interests; (vi) the compatibility of the Portfolios’ investment objectives, policies, risks and restrictions; (vii) that the proposed Reorganization was expected to be a tax-free reorganization for federal income tax purposes; (viii) the compatibility of the Portfolios’ service features available to Contractholders; and (ix) the estimated costs of the Reorganization, which, except for transaction costs, would be borne by the Adviser. The Board considered all factors presented to it, including any adverse factors as described above, and after due consideration concluded that these factors supported a determination to approve the Reorganization Agreement.

The Board believes that the Reorganization would be in the best interests of the Target Portfolio’s Contractholders because: (i) Contractholders will become Contractholders of a larger combined portfolio with greater potential to increase asset size and achieve economies of scale; (ii) the Acquiring Portfolio has achieved better performance than the Target Portfolio for the one-, two- and three-year periods ended December 31, 2019, though there is no guarantee of future performance; (iii) Thrivent Financial, the Portfolios’ investment adviser, believes that it can most effectively manage the assets currently in the Target Portfolio by combining such assets with the Acquiring Portfolio; and (iv) the Acquiring Portfolio has a lower gross expense ratio than the Target Portfolio and shareholders of the Target Portfolio will experience a lower net expense ratio in the Acquiring Portfolio following the Reorganization.

The Board has determined that the Reorganization is in the best interests of the Target Portfolio and that the interests of the Target Portfolio’s Contractholders will not be diluted as a result of the Reorganization. In addition, the Board has determined that

23

the Reorganization is in the best interests of the Acquiring Portfolio and that the interests of the Acquiring Portfolio Contractholders will not be diluted as a result of the Reorganization.

Material Federal Income Tax Consequences of the Reorganization

The following is a general summary of the material anticipated U.S. federal income tax consequences of the Reorganization. This discussion is based upon the Internal Revenue Code of 1986, as amended (the “Code”), Treasury regulations, court decisions, published positions of the Internal Revenue Service (“IRS”) and other applicable authorities, all as in effect on the date hereof and all of which are subject to change or differing interpretations (possibly with retroactive effect). This discussion is limited to U.S. persons who hold shares of the Target Portfolio as capital assets for U.S. federal income tax purposes on the date of the exchange. For federal income tax purposes, the Contractholders are not the shareholders of the Target Portfolio. Rather, Thrivent Financial and its separate accounts are the shareholders.

This summary does not address all of the U.S. federal income tax consequences that may be relevant to a particular Contractholder or to Contractholders who may be subject to special treatment under U.S. federal income tax laws. No assurance can be given that the IRS would not assert or that a court would not sustain a position contrary to any of the tax aspects described below. Contractholders should consult their own tax advisers as to the U.S. federal income tax consequences of the Reorganization to them, as well as the effects of state, local and non-U.S. tax laws.