UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

Certified Shareholder Report of

Registered Management Investment Companies

Investment Company Act File Number: 811-04692

Emerging Markets Growth Fund, Inc.

(Exact Name of Registrant as Specified in Charter)

11100 Santa Monica Boulevard, 15th Floor

Los Angeles, California 90025

(Address of Principal Executive Offices)

Registrant's telephone number, including area code: (213) 486-9200

Date of fiscal year end: June 30

Date of reporting period: June 30, 2015

Laurie D. Neat

Emerging Markets Growth Fund, Inc.

333 South Hope Street, 55th Floor

Los Angeles, California 90071

(Name and Address of Agent for Service)

ITEM 1 – Reports to Stockholders

| Emerging Markets Growth FundSM Annual report for the year ended June 30, 2015 |

Emerging Markets Growth Fund seeks long-term growth of capital and invests primarily in common stock and other equity securities of issuers in developing countries.

Fund results shown in this report are for past periods and are not predictive of results for future periods. The results shown are before taxes on fund distributions and sale of fund shares. Current and future results may be lower or higher than those shown. Share prices and returns will vary, so investors may lose money. Investing for short periods makes losses more likely. Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value. For current information and month-end results, please call (800) 421-4989.

Investing in developing markets involves risks, such as significant currency and price fluctuations, political instability, differing securities regulations and periods of illiquidity, which are detailed in the fund’s prospectus. Investments in developing markets have been more volatile than investments in developed markets, reflecting the greater uncertainties of investing in less established economies. Individuals investing in developing markets should have a long-term perspective and be able to tolerate potentially sharp declines in the value of their investments.

Contents

| 1 | Letter to investors | |

| 2 | 20 largest equity holdings | |

| 8 | Investment portfolio | |

| 17 | Financial statements | |

| 19 | Notes to financial statements |

Emerging markets stocks lost ground as oil prices dropped in the second half of 2014, Russia grappled with its worst financial crisis since its 1998 default, and Brazil struggled in a weaker economic and political environment. The value of Emerging Markets Growth Fund fell 7.71% with distributions reinvested for the 12-month period, while its benchmark, the unmanaged MSCI Emerging Markets Investable Market Index (IMI) shed 4.41%. Most emerging markets currencies depreciated against the U.S. dollar, with many posting steep declines.

Equities gathered momentum in early 2015 amid more accommodative monetary policies in China and the implementation of reforms in several emerging markets countries. Financials stocks improved modestly overall, while health care companies rose sharply. Technology shares slipped, however, on the heels of robust gains and as increased competition for smartphones weighed on shares. Commodity-related stocks suffered the worst losses.

Market review

Equity returns varied dramatically by country. Weak oil prices hampered Russian equities late last year, as did worries about the impact of sanctions. Stocks sank in the last six months of 2014 as the country suffered its largest political and economic crisis in decades, sparked by military tensions with Ukraine. Russia’s central bank hiked interest rates sharply in late 2014 to help support the ailing ruble, but reversed course in 2015, taking the key interest rate down to 11.5% by the end of June. Stocks regained some ground in early 2015, but still lost 27.88%* for the period. The ruble dropped 39%. Meanwhile, Brazilian stocks fell 30.14%, weighed down by deteriorating economic conditions and the 29% depreciation of the real. A corruption scandal involving

| * | Unless otherwise noted, country and sector returns are based on MSCI EM IMI indices, expressed in U.S. dollars, and assume the reinvestment of dividends. Results reflect dividends net of withholding taxes. |

Results at a glance

For periods ended June 30, 2015, with distributions reinvested

| Cumulative total returns | Average annual total returns | |||||||||||||||||||||||

| 6 months | 1 year | 3 years | 5 years | 10 years | Lifetime1 | |||||||||||||||||||

| Emerging Markets Growth Fund | 2.36 | % | -7.71 | % | 2.63 | % | 1.02 | % | 8.02 | % | 13.91 | % | ||||||||||||

| MSCI Emerging Markets IMI2,3 | 3.64 | -4.41 | 4.24 | 3.87 | 8.40 | 10.81 | 4 | |||||||||||||||||

| MSCI Emerging Markets Index3,5 | 2.95 | -5.12 | 3.71 | 3.68 | 8.11 | 10.71 | 4 | |||||||||||||||||

| 1 | Since May 30, 1986. |

| 2 | Returns for the MSCI Emerging Markets Investable Market Index (IMI) were calculated using the MSCI Emerging Markets Index with dividends gross of withholding taxes from December 31, 1987, to December 31, 2000, and with dividends net of withholding taxes from January 1, 2001, to November 30, 2007, and using the MSCI Emerging Markets IMI with dividends net of withholding taxes thereafter. |

| 3 | The indices are unmanaged and, therefore, have no expenses. |

| 4 | The MSCI Emerging Markets Index did not start until December 31, 1987. As a result, the International Finance Corporation (IFC) Global Composite Index was used in lieu of the MSCI Emerging Markets Index from May 30, 1986, to December 31, 1987. |

| 5 | Results reflect dividends gross of withholding taxes through December 31, 2000, and dividends net of withholding taxes thereafter. |

The total annual fund operating expense ratio is 0.75% as of the most recent fiscal year-end, and is 0.80% including “Acquired Fund” fees and expenses.

| Emerging Markets Growth Fund | 1 |

| Percent of net assets as of 6/30/15 | Price change for the 12 months ended 6/30/15* | |||||||

| Bank of China | 2.8 | % | 45.2 | % | ||||

| Taiwan Semiconductor Manufacturing | 2.7 | 7.5 | ||||||

| China Overseas Land & Investment | 2.7 | 45.5 | ||||||

| AIA Group | 1.9 | 30.3 | ||||||

| China Mengniu Dairy | 1.8 | 7.8 | ||||||

| China Pacific Insurance Group | 1.8 | 36.0 | ||||||

| Bharti Airtel | 1.7 | 17.8 | ||||||

| Cemex | 1.5 | -28.0 | ||||||

| ICICI Bank | 1.5 | 3.8 | ||||||

| Hypermarcas | 1.4 | -16.5 | ||||||

| Samsonite International | 1.4 | 4.9 | ||||||

| Delta Electronics | 1.3 | -29.7 | ||||||

| Naspers | 1.3 | 32.3 | ||||||

| Housing Development Finance | 1.3 | 23.4 | ||||||

| Vale | 1.3 | -56.8 | ||||||

| Beijing Enterprises Holdings | 1.2 | -20.5 | ||||||

| China Everbright International | 1.2 | 25.4 | ||||||

| China Resources Land | 1.1 | 77.3 | ||||||

| Melco Crown Entertainment | 1.1 | -45.0 | ||||||

| Haitian International Holdings | 1.1 | .6 | ||||||

| Total | 32.1 | % | ||||||

| * | The percent change is reflected in U.S. dollars. The actual gain or loss on the total position in the fund may differ from the percentage shown. |

a major state-owned energy firm rocked the country’s equity market in 2015, raising concerns about the government’s involvement and the efficacy of reforms following President Dilma Rousseff’s re-election last October.

China’s market rallied despite signs of slowing economic growth. Chinese stocks climbed 25.05% as investors seemed reassured that looser monetary policies might help stabilize the economy. The People’s Bank of China surprised many observers by cutting interest rates for the first time in more than two years in November, followed by further reductions in February, May and June. Banks gained amid expectations that more supportive policies would help spur lending. Real estate shares also rebounded as Chinese authorities continued to ease mortgage lending restrictions. Among other major policy developments, the government launched the Shanghai-Hong Kong Stock Connect in late 2014, making mainland-listed stocks available to foreign investors.

Elsewhere in the region, Indian equities advanced 3.85% on the heels of a market rally last year. Stocks lost steam late in the period as exuberance over Prime Minister Narendra Modi’s historic election in May 2014 waned and investors appeared to take profits after gains. Several Southeast Asian markets moderated after a strong run, with Thai equities finishing the 12-month period in negative territory in the face of a sluggish economy. Indonesian equities dropped 10.18% amid disappointing economic data and more modest levels of enthusiasm about reforms following Joko Widodo’s presidential win last July. Technology stocks weighed on South Korean equities, which fell 9.38%, while Taiwanese shares ended nearly flat.

Portfolio review

The portfolio lost value, lagging the benchmark. Commodity stocks fell as the sharp slide in oil prices and reduced capital expenditures hurt several energy exploration and production firms as well as energy services companies. Stock selection in Russia further detracted from fund results as the country’s market tumbled.

The choice of consumer discretionary stocks also hindered fund returns. Hong Kong–listed casinos faltered as gambling revenue in Macau continued to fall, hampered by China’s anticorruption campaign and increased restrictions on VIP gambling. Managers maintained their investments in several of these stocks based on their expectations for

| 2 | Emerging Markets Growth Fund |

Where the fund’s assets were invested

| Value of holdings | ||||||||||||||||||||||||

| Percent of net assets | MSCI EM IMI1 | 6/30/15 | ||||||||||||||||||||||

| 6/30/13 | 6/30/14 | 12/31/14 | 6/30/15 | 6/30/15 | (in thousands) | |||||||||||||||||||

| Asia-Pacific | ||||||||||||||||||||||||

| China | 18.2 | % | 21.3 | % | 27.5 | % | 27.4 | % | 24.7 | % | $ | 1,264,372 | ||||||||||||

| Hong Kong | 3.5 | 7.5 | 7.6 | 7.3 | — | 337,556 | ||||||||||||||||||

| India | 9.0 | 12.6 | 14.1 | 11.5 | 8.0 | 532,943 | ||||||||||||||||||

| Indonesia | 2.0 | 1.8 | 1.8 | 2.0 | 2.3 | 93,146 | ||||||||||||||||||

| Malaysia | 3.7 | 3.1 | 2.5 | 2.2 | 3.2 | 99,230 | ||||||||||||||||||

| Philippines | .9 | .8 | 1.0 | .5 | 1.4 | 22,515 | ||||||||||||||||||

| Singapore | .7 | .9 | 1.0 | .9 | — | 41,055 | ||||||||||||||||||

| South Korea | 10.0 | 9.2 | 6.4 | 4.3 | 15.0 | 200,023 | ||||||||||||||||||

| Taiwan | 5.7 | 5.3 | 5.3 | 5.8 | 13.3 | 268,307 | ||||||||||||||||||

| Thailand | 2.0 | 2.1 | 1.8 | 1.3 | 2.5 | 59,667 | ||||||||||||||||||

| 55.7 | 64.6 | 69.0 | 63.2 | 70.4 | 2,918,814 | |||||||||||||||||||

| Latin America | ||||||||||||||||||||||||

| Argentina | — | .3 | .6 | .9 | — | 43,545 | ||||||||||||||||||

| Brazil | 7.1 | 6.9 | 5.2 | 6.4 | 6.9 | 292,774 | ||||||||||||||||||

| Chile | 1.3 | 1.1 | 1.2 | 1.1 | 1.2 | 52,044 | ||||||||||||||||||

| Colombia | .4 | — | — | — | .5 | — | ||||||||||||||||||

| Mexico | 3.5 | 3.4 | 3.5 | 4.8 | 4.2 | 220,487 | ||||||||||||||||||

| Peru | — | .1 | .1 | .1 | .4 | 3,187 | ||||||||||||||||||

| 12.3 | 11.8 | 10.6 | 13.3 | 13.2 | 612,037 | |||||||||||||||||||

| Eastern Europe and Middle East | ||||||||||||||||||||||||

| Czech Republic | — | — | — | — | .2 | — | ||||||||||||||||||

| Greece | — | .3 | .1 | — | 2 | .4 | 1,851 | |||||||||||||||||

| Hungary | — | — | — | — | .2 | — | ||||||||||||||||||

| Israel | .7 | .6 | .1 | .1 | — | 6,083 | ||||||||||||||||||

| Oman | .4 | .4 | .5 | .4 | — | 18,231 | ||||||||||||||||||

| Poland | .7 | — | — | — | 1.4 | — | ||||||||||||||||||

| Russia | 7.0 | 6.8 | 4.4 | 4.1 | 3.3 | 189,417 | ||||||||||||||||||

| Saudi Arabia | .1 | — | — | .8 | — | 37,313 | ||||||||||||||||||

| Turkey | .4 | — | — | .7 | 1.4 | 31,720 | ||||||||||||||||||

| United Arab Emirates | .2 | .3 | .5 | .9 | .7 | 40,862 | ||||||||||||||||||

| Qatar | — | — | — | — | .9 | — | ||||||||||||||||||

| 9.5 | 8.4 | 5.6 | 7.0 | 8.5 | 325,477 | |||||||||||||||||||

| Africa | ||||||||||||||||||||||||

| Egypt | — | — | — | — | .3 | — | ||||||||||||||||||

| Morocco | .1 | — | — | — | — | — | ||||||||||||||||||

| South Africa | 1.2 | 1.9 | 2.7 | 3.2 | 7.6 | 149,618 | ||||||||||||||||||

| 1.3 | 1.9 | 2.7 | 3.2 | 7.9 | 149,618 | |||||||||||||||||||

| Other markets3 | ||||||||||||||||||||||||

| Australia | 1.1 | 1.3 | 1.2 | .8 | 36,534 | |||||||||||||||||||

| Austria | .3 | .4 | .5 | .4 | 18,971 | |||||||||||||||||||

| Canada | 1.0 | 1.5 | 1.1 | .9 | 43,626 | |||||||||||||||||||

| Italy | .2 | .2 | .2 | .2 | 9,035 | |||||||||||||||||||

| Luxembourg | .8 | — | — | — | — | |||||||||||||||||||

| Netherlands | .6 | .7 | .3 | — | 2 | 1,788 | ||||||||||||||||||

| Switzerland | — | .6 | .7 | .7 | 32,929 | |||||||||||||||||||

| United Kingdom | 3.5 | 2.6 | 2.0 | 1.9 | 85,843 | |||||||||||||||||||

| United States of America | 3.1 | 2.3 | 2.3 | 2.9 | 131,608 | |||||||||||||||||||

| 10.6 | 9.6 | 8.3 | 7.8 | 360,334 | ||||||||||||||||||||

| Multinational | .4 | .4 | .4 | .4 | 19,190 | |||||||||||||||||||

| Other4 | 4.9 | — | — | — | — | |||||||||||||||||||

| Short-term securities and other assets less liabilities | 5.3 | 3.3 | 3.4 | 5.1 | 235,432 | |||||||||||||||||||

| Total net assets | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | $ | 4,620,902 | ||||||||||||||

| 1 | A dash indicates that the market is not included in the index. Source: MSCI. |

| 2 | Amount less than 0.1%. |

| 3 | Includes investments in companies incorporated in the region that have significant operations in emerging markets. |

| 4 | Includes securities in initial period of acquisition. |

| Emerging Markets Growth Fund | 3 |

longer term growth in the firms’ mass market divisions and their belief that the companies have solid business models.

A number of the fund’s investments in China were bright spots. The Chinese financial sector posted particularly strong gains amid looser policies. Bank of China shares climbed 45.2%. Property developers also rebounded, while China Pacific Insurance shares jumped 36.0%. Several industrials stocks in China rallied, supported by increased infrastructure spending, a major railway merger in early 2015 and the government’s continued focus on environmental reforms. A few health care stocks in China gained amid new policies, as well as increasing demand for health and wellness-related products.

Several investments in India also rose sharply, with ICICI Bank and HDFC Bank advancing as investors seemed to take comfort from signs of economic recovery. Strong global demand for pharmaceuticals also boosted shares of a few generic drug manufacturers in India, as did enthusiasm over the merger between Ranbaxy Laboratories and Sun Pharmaceutical Industries.

Outlook

Emerging markets continue to face a number of crosscurrents. Stocks may suffer from risk aversion in the coming months as the U.S. Federal Reserve initiates gradual interest rate hikes, though currencies may have already seen the brunt of depreciation in recent years. The global economy seems to be finding its footing, despite facing certain challenges. Countries around the world are at different phases of their business cycles and responding differently to deflation, weaker commodity prices and U.S. dollar strength. A strong U.S. dollar and depressed commodity prices have historically been a headwind for emerging markets, but fundamentals in some developing countries have improved as weaker oil prices have reduced current account deficits and contributed to lower inflation.

While the timing of an interest rate hike by the U.S. Federal Reserve remains uncertain, an increase seems imminent. Meanwhile, other central banks are pursuing accommodative policies, which should help support growth in several developed and developing economies. Europe has adopted a new quantitative easing program, Japan has maintained looser policies and China’s government appears committed to targeted stimulus measures and interest rate cuts to help maintain modest economic growth. China and several other Asian governments such as India seem dedicated to carrying out longer reforms even as markets face periods of potential volatility.

| 12 months ended 6/30/15 | 6 months ended 6/30/15 | |||||||||||||||

| Expressed in | Expressed in | Expressed in | Expressed in | |||||||||||||

| Percent change in key markets* | U.S. dollars | local currency | U.S. dollars | local currency | ||||||||||||

| Asia-Pacific | ||||||||||||||||

| China | 25.0 | % | 25.1 | % | 16.3 | % | 16.3 | % | ||||||||

| India | 3.9 | 10.0 | 1.4 | 2.3 | ||||||||||||

| Indonesia | -10.2 | 1.0 | -13.1 | -6.5 | ||||||||||||

| Malaysia | -21.0 | -7.2 | -8.4 | -1.1 | ||||||||||||

| Philippines | 7.3 | 10.8 | 2.2 | 3.1 | ||||||||||||

| South Korea | -9.4 | -.1 | 4.7 | 6.2 | ||||||||||||

| Taiwan | -.2 | 3.1 | 4.1 | 1.6 | ||||||||||||

| Thailand | -.2 | 3.9 | -.9 | 1.7 | ||||||||||||

| Latin America | ||||||||||||||||

| Brazil | -30.1 | -1.5 | -9.7 | 5.6 | ||||||||||||

| Chile | -14.9 | -1.8 | -3.8 | 1.4 | ||||||||||||

| Colombia | -40.8 | -18.1 | -16.2 | -8.4 | ||||||||||||

| Mexico | -12.6 | 5.8 | -2.0 | 4.3 | ||||||||||||

| Peru | -7.6 | -7.3 | -5.1 | -5.0 | ||||||||||||

| Eastern Europe and Middle East | ||||||||||||||||

| Czech Republic | -13.3 | 5.8 | -1.9 | 4.7 | ||||||||||||

| Hungary | -4.2 | 20.0 | 25.0 | 35.6 | ||||||||||||

| Poland | -19.3 | -.1 | -3.7 | 1.9 | ||||||||||||

| Russia | -27.9 | 7.1 | 27.9 | 20.6 | ||||||||||||

| Turkey | -16.1 | 6.0 | -14.5 | -2.0 | ||||||||||||

| Greece | -55.2 | -44.9 | -21.1 | -14.3 | ||||||||||||

| United Arab Emirates | .9 | 0.9 | 4.1 | 4.1 | ||||||||||||

| Qatar | 4.4 | 4.4 | -2.5 | -2.5 | ||||||||||||

| Africa | ||||||||||||||||

| Egypt | -5.4 | 0.7 | -12.2 | -6.6 | ||||||||||||

| South Africa | -1.6 | 12.2 | 1.9 | 6.9 | ||||||||||||

| Emerging Markets Growth Fund | -7.7 | % | 2.4 | % | ||||||||||||

| * | The market indices, compiled by MSCI, are unmanaged and, therefore, have no expenses. Country returns are based on MSCI EM IMI data and reflect dividends net of withholding taxes. |

| 4 | Emerging Markets Growth Fund |

On the whole, varying levels of economic health and divergent policies are likely to result in significant disparities in developing market country returns and valuations. Fund managers actively invest on a company-by-company basis across a wide array of sectors and industries. They continue to favor well-managed firms that are poised to benefit from a growing middle class and increased demand for consumer goods, financial services and health care as people strive for a better quality of life. Stocks in the consumer sectors make up 20% of the portfolio’s total assets combined. Financials stocks comprise more than 25% of fund assets, with an emphasis on Asian banks and insurance companies with strong long-term growth prospects.

The fund also has considerable exposure to the health care sector, particularly in China, as demand for medical services and health-related products continues to grow. Managers favor a few smaller companies that make pharmaceuticals and wellness products as well as firms that are likely to benefit from reforms and the privatization of hospitals.

Managers are also attracted to select industrials firms as several governments have demonstrated an increased commitment to infrastructure development in their respective countries. Industrials make up a substantial portion of the portfolio at 11% of total net assets. Among commodity-related investments, the fund has limited exposure to larger emerging markets energy firms, especially against the backdrop of weaker oil prices and reduced capital expenditures, but managers have identified companies that should be supported by more environmentally friendly policies in China. They also favor company-specific opportunities in the materials sector, including low-cost producers of iron ore, copper and diamonds.

We believe that the emerging markets universe offers a wide range of compelling investment options, and we look forward to reporting to you again in another six months.

Sincerely,

Victor D. Kohn

President

August 17, 2015

| Emerging Markets Growth Fund | 5 |

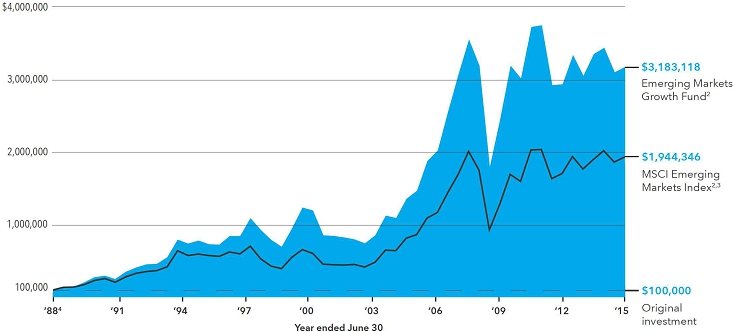

The value of a long-term investment

How a $100,000 investment has grown

While notable for their volatility in recent years, financial markets have tended to reward investors over the long term. Active management — bolstered by experience and careful research — can add even more value. This chart shows how a $100,0001 investment in Emerging Markets Growth Fund (EMGF) grew from December 31, 1987 — the inception of the MSCI Emerging Markets (EM) Index — through June 30, 2015, the end of the fund’s latest fiscal year.

As you can see, the $100,000 would have grown to $3,183,118. This is significantly more than the $1,944,346 generated by the unmanaged MSCI EM Index.

Total returns (with all distributions reinvested for periods ended June 30, 2015)

| Cumulative total returns | Average annual total returns | |||||||

| 1 year | -7.71 | % | -7.71 | % | ||||

| 5 years | 5.22 | 1.02 | ||||||

| 10 years | 116.33 | 8.02 | ||||||

Results are for past periods and are not predictive of results for future periods. The results shown are before taxes on fund distributions and sale of fund shares. Current and future results may be lower or higher than those shown. Share prices and returns will vary, so investors may lose money. Investing for short periods makes losses more likely. For current information and month-end results, please call (800) 421-4989.

| 1 | The minimum initial investment for EMGF is $100,000. |

| 2 | Values are based on a $100,000 investment with distributions reinvested. |

| 3 | Returns for the MSCI Emerging Markets Index were calculated using the MSCI Emerging Markets Index with gross dividends from December 31, 1987, to December 31, 2000, and with net dividends from January 1, 2001, to November 30, 2007, and using the MSCI EM IMI with net dividends thereafter. The indices are unmanaged and, therefore, have no expenses. |

| 4 | For the period December 31, 1987 (inception of the MSCI EM Index), through June 30, 1988. EMGF began operations on May 30, 1986. |

| 6 | Emerging Markets Growth Fund |

About the fund and its adviser

Emerging Markets Growth Fund was organized in 1986 by the International Finance Corporation (IFC), an affiliate of the World Bank, as a vehicle for investing in the securities of companies based in developing countries. The premise behind the formation of the fund was that rapid growth in these countries could create very attractive investment opportunities. It also was felt that the availability of equity capital would stimulate the development of capital markets and encourage countries to liberalize their investment regulations.

Capital International, Inc., the fund’s investment adviser, is part of The Capital Group Companies,SM Inc. one of the world’s most experienced investment advisory organizations, with roots dating back to 1931. The fund has been managed by Capital International or an affiliate since 1986. Capital Group employs a research-driven approach to investing and has a global investment research network spanning three continents. This network of analysts and portfolio managers travel the world scrutinizing thousands of companies and keeping a close watch on industry trends and government actions.

Capital Group has devoted substantial resources to the task of evaluating and managing investments in developing countries. It is an intensive effort that combines company and industry analysis with broader political and macroeconomic views. We believe that our extensive worldwide research capabilities and integrated global investment process continue to provide Emerging Markets Growth Fund with a competitive edge.

| Emerging Markets Growth Fund | 7 |

Investment portfolio June 30, 2015

| Sector diversification | unaudited | |||||||||||||||

| Equity securities | ||||||||||||||||

| Common stocks | Convertible stocks | Bonds & notes | Percent of net assets | |||||||||||||

| Financials | 25.2 | % | — | % | — | %* | 25.2 | % | ||||||||

| Consumer discretionary | 11.9 | — | — | * | 11.9 | |||||||||||

| Industrials | 10.8 | — | — | 10.8 | ||||||||||||

| Information technology | 8.8 | — | — | 8.8 | ||||||||||||

| Consumer staples | 8.3 | — | .1 | 8.4 | ||||||||||||

| Materials | 8.1 | — | — | 8.1 | ||||||||||||

| Health care | 5.6 | — | * | — | 5.6 | |||||||||||

| Telecommunication services | 5.3 | — | — | 5.3 | ||||||||||||

| Energy | 4.3 | — | — | 4.3 | ||||||||||||

| Utilities | 3.8 | — | — | 3.8 | ||||||||||||

| Other | 2.2 | — | — | 2.2 | ||||||||||||

| Government | — | — | .5 | .5 | ||||||||||||

| 94.3 | % | — | %* | .6 | % | 94.9 | ||||||||||

| Short-term securities | 4.1 | |||||||||||||||

| Other assets less liabilities | 1.0 | |||||||||||||||

| Net assets | 100.0 | % | ||||||||||||||

*Amount rounds to less than .1%.

| Equity securities | Shares | Value (000) | ||||||

| Asia-Pacific 63.2% | ||||||||

| China 27.4% | ||||||||

| Anhui Conch Cement Co. Ltd. | 4,404,254 | $ | 15,235 | |||||

| Anhui Conch Cement Co. Ltd. (Hong Kong) | 3,500 | 12 | ||||||

| Bank of China Ltd. (Hong Kong) | 195,926,724 | 127,390 | ||||||

| Beijing Enterprises Holdings Ltd. (Hong Kong) | 7,421,500 | 55,866 | ||||||

| China Everbright International Ltd. (Hong Kong) | 30,255,000 | 54,253 | ||||||

| China High Speed Transmission Equipment Group Co., Ltd. (Hong Kong)1 | 13,034,600 | 11,317 | ||||||

| China Longyuan Power Group Corp., Ltd. (Hong Kong) | 9,706,000 | 10,793 | ||||||

| China Mengniu Dairy Co. (Hong Kong) | 17,140,000 | 85,462 | ||||||

| China Merchants Bank Co., Ltd. (Hong Kong) | 6,987,000 | 20,371 | ||||||

| China Modern Dairy Holdings Ltd. (Hong Kong) | 88,258,000 | 31,767 | ||||||

| China Overseas Grand Oceans Group, Ltd. (Hong Kong) | 9,390,100 | 4,761 | ||||||

| China Overseas Land & Investment Ltd. (Hong Kong) | 35,606,000 | 125,630 | ||||||

| China Pacific Insurance (Group) Co., Ltd. (Hong Kong) | 17,361,600 | 83,319 | ||||||

| China Resources Land Ltd. (Hong Kong) | 15,895,937 | 51,575 | ||||||

| China Shineway Pharmaceutical Group Ltd. (Hong Kong) | 3,765,000 | 5,625 | ||||||

| China Unicom (Hong Kong) Ltd. | 5,430,836 | 8,547 | ||||||

| China Vanke Co. Ltd.1 | 791,100 | 1,852 | ||||||

| China Vanke Co. Ltd. (Hong Kong) | 7,769,200 | 19,124 | ||||||

| CRRC Corp. Ltd. (Hong Kong)1 | 8,804,000 | 13,516 | ||||||

| 8 | Emerging Markets Growth Fund |

| Equity securities (continued) | Shares | Value (000) | ||||||

| Asia-Pacific (continued) | ||||||||

| China (continued) | ||||||||

| EVA Precision Industrial Holdings Ltd. (Hong Kong) | 41,940,000 | $ | 12,336 | |||||

| Goodbaby International Holdings Ltd. (Hong Kong)1 | 24,688,000 | 10,319 | ||||||

| Great Wall Motor Co., Ltd. (Hong Kong) | 2,559,500 | 12,547 | ||||||

| Guangdong Investment Ltd. (Hong Kong) | 2,886,000 | 4,043 | ||||||

| Haitian International Holdings Ltd. (Hong Kong) | 20,649,000 | 48,535 | ||||||

| Honghua Group Ltd. (Hong Kong)1 | 17,991,000 | 1,950 | ||||||

| Huaneng Power International, Inc. (Hong Kong) | 34,220,000 | 47,678 | ||||||

| Industrial and Commercial Bank of China Ltd. (Hong Kong) | 38,171,708 | 30,334 | ||||||

| Jiangsu Hengli Highpressure Oil Cylinder Co., Ltd. | 7,316,586 | 21,510 | ||||||

| Jiangsu Hengrui Medicine Co., Ltd. | 5,095,990 | 36,603 | ||||||

| Lenovo Group Ltd. (Hong Kong) | 24,764,000 | 34,311 | ||||||

| Longfor Properties Co., Ltd. (Hong Kong) | 13,915,268 | 22,152 | ||||||

| MicroPort Scientific Corp. (Hong Kong)1 | 5,325,404 | 2,624 | ||||||

| Minth Group Ltd. (Hong Kong) | 17,888,000 | 40,015 | ||||||

| New Oriental Education & Technology Group, Inc. (ADR)1 | 60,900 | 1,493 | ||||||

| Nine Dragons Paper (Holdings) Ltd. (Hong Kong) | 5,318,300 | 4,652 | ||||||

| Sany Heavy Equipment International Holdings Co., Ltd. (Hong Kong)1 | 39,996,000 | 11,093 | ||||||

| Shandong Weigao Group Medical Polymer Co., Ltd. (Hong Kong) | 1,086,800 | 812 | ||||||

| Shanghai Fosun Pharmaceutical (Group) Co., Ltd. (Hong Kong) | 6,892,500 | 25,564 | ||||||

| Shanghai Jahwa United Co., Ltd. | 3,040,841 | 21,282 | ||||||

| Shanghai Pharmaceutical (Group) Co., Ltd. (Hong Kong) | 10,479,600 | 29,202 | ||||||

| Shenguan Holdings Group Ltd. (Hong Kong) | 42,642,000 | 10,947 | ||||||

| Sino Biopharmaceutical Ltd. (Hong Kong) | 28,956,000 | 33,620 | ||||||

| Sinofert Holdings Ltd. (Hong Kong) | 103,544,000 | 23,777 | ||||||

| Tencent Holdings Ltd. (Hong Kong) | 363,500 | 7,254 | ||||||

| Want Want China Holdings Ltd. (Hong Kong) | 4,527,000 | 4,789 | ||||||

| Weichai Power Co., Ltd. (Hong Kong) | 782,177 | 2,608 | ||||||

| Whirlpool China Co., Ltd.1 | 5,399,904 | 13,837 | ||||||

| Zhongsheng Group Holdings Ltd. (Hong Kong) | 293,269 | 206 | ||||||

| Zhuzhou CSR Times Electric Co., Ltd. (Hong Kong) | 2,917,000 | 21,864 | ||||||

| 1,264,372 | ||||||||

| Hong Kong 7.3% | ||||||||

| AIA Group Ltd. | 13,142,200 | 86,043 | ||||||

| Cheung Kong Infrastructure Holdings Ltd. | 4,640,000 | 36,035 | ||||||

| Chow Sang Sang Holdings International Ltd. | 1,821,235 | 3,656 | ||||||

| Galaxy Entertainment Group Ltd. | 6,632,000 | 26,437 | ||||||

| Hilong Holding Ltd. | 12,984,000 | 3,769 | ||||||

| Jardine Matheson Holdings Ltd. | 122,800 | 6,969 | ||||||

| Melco Crown Entertainment Ltd. (ADR) | 2,505,600 | 49,185 | ||||||

| MGM China Holdings Ltd. | 4,094,800 | 6,698 | ||||||

| Samsonite International SA | 18,046,300 | 62,393 | ||||||

| Stella International Holdings Ltd. | 1,954,000 | 4,663 | ||||||

| VTech Holdings Ltd. | 301,600 | 4,004 | ||||||

| Wynn Macau, Ltd. | 28,576,400 | 47,704 | ||||||

| 337,556 |

| Emerging Markets Growth Fund | 9 |

| Equity securities (continued) | Shares | Value (000) | ||||||

| Asia-Pacific (continued) | ||||||||

| India 11.5% | ||||||||

| Apollo Hospitals Enterprise Ltd. | 807,844 | $ | 16,694 | |||||

| Apollo Hospitals Enterprise Ltd. (GDR)2 | 239,100 | 4,941 | ||||||

| Bharat Electronics Ltd. | 159,496 | 8,431 | ||||||

| Bharti Airtel Ltd. | 12,025,119 | 79,321 | ||||||

| CRISIL Ltd. | 104,294 | 3,170 | ||||||

| Emami Ltd. | 209,279 | 3,811 | ||||||

| Glenmark Pharmaceuticals Ltd. | 1,491,755 | 23,289 | ||||||

| Godrej Consumer Products Ltd. | 332,339 | 6,457 | ||||||

| HDFC Bank Ltd.1 | 2,522,019 | 48,319 | ||||||

| Housing Development Finance Corp. Ltd. | 2,890,450 | 58,846 | ||||||

| ICICI Bank Ltd. | 4,771,283 | 23,077 | ||||||

| ICICI Bank Ltd. (ADR) | 4,336,800 | 45,190 | ||||||

| Info Edge (India) Ltd. | 1,288,951 | 17,287 | ||||||

| Infosys Ltd. | 1,747,850 | 27,018 | ||||||

| ITC Ltd. | 2,034,894 | 10,071 | ||||||

| Just Dial Ltd. | 162,393 | 3,236 | ||||||

| Kotak Mahindra Bank Ltd. | 687,914 | 15,070 | ||||||

| Larsen & Toubro Ltd. | 267,488 | 7,489 | ||||||

| Lupin Ltd. | 409,249 | 12,121 | ||||||

| Steel Authority of India Ltd. | 31,507,763 | 30,404 | ||||||

| Sun Pharmaceutical Industries Ltd. | 2,073,078 | 28,472 | ||||||

| Tata Steel Ltd. | 3,916,406 | 18,733 | ||||||

| Tech Mahindra Ltd. | 1,814,133 | 13,612 | ||||||

| Thermax Ltd. | 331,403 | 5,442 | ||||||

| Torrent Power Ltd. | 2,000,288 | 4,398 | ||||||

| United Spirits Ltd.1 | 47,240 | 2,508 | ||||||

| VA Tech Wabag Ltd. | 1,336,254 | 15,536 | �� | |||||

| 532,943 | ||||||||

| Indonesia 2.0% | ||||||||

| Agung Podomoro Land Tbk PT | 170,161,500 | 4,812 | ||||||

| Bank Mandiri (Persero) Tbk PT, Series B | 16,312,192 | 12,296 | ||||||

| Bank Rakyat Indonesia (Persero) Tbk PT | 17,726,800 | 13,761 | ||||||

| Elang Mahkota Teknologi Tbk PT | 44,456,400 | 37,012 | ||||||

| Matahari Department Store Tbk PT | 5,449,700 | 6,765 | ||||||

| Surya Citra Media Tbk PT | 85,792,100 | 18,500 | ||||||

| 93,146 | ||||||||

| Malaysia 2.2% | ||||||||

| Bumi Armada Bhd. | 49,528,130 | 14,965 | ||||||

| CIMB Group Holdings Bhd. | 13,381,261 | 19,400 | ||||||

| Genting Bhd. | 4,990,100 | 10,660 | ||||||

| Genting Bhd., warrants, expire 20181 | 1,716,975 | 482 | ||||||

| IHH Healthcare Bhd.1 | 19,524,400 | 29,289 | ||||||

| IJM Corp. Bhd. | 13,044,154 | 22,541 | ||||||

| Naim Cendera Holdings Bhd. | 3,173,700 | 1,893 | ||||||

| 99,230 |

| 10 | Emerging Markets Growth Fund |

| Equity securities (continued) | Shares | Value (000) | ||||||

| Asia-Pacific (continued) | ||||||||

| Philippines 0.5% | ||||||||

| International Container Terminal Services, Inc. | 7,388,598 | $ | 18,058 | |||||

| SM Investments Corp. | 224,580 | 4,457 | ||||||

| 22,515 | ||||||||

| Singapore 0.9% | ||||||||

| CapitaLand Retail China Trust | 4,232,560 | 5,468 | ||||||

| KrisEnergy Ltd.1 | 10,391,000 | 3,472 | ||||||

| Olam International Ltd. | 7,185,868 | 10,031 | ||||||

| Olam International Ltd., warrants, expires 20181 | 447,230 | 86 | ||||||

| Yoma Strategic Holdings Ltd.1 | 69,713,483 | 21,998 | ||||||

| 41,055 | ||||||||

| South Korea 4.3% | ||||||||

| Daum Kakao Corp. | 81,608 | 9,233 | ||||||

| Hana Financial Group Inc. | 90,623 | 2,360 | ||||||

| Hankook Tire Co., Ltd. | 242,000 | 9,112 | ||||||

| Hyundai Engineering & Construction Co., Ltd. | 134,407 | 4,946 | ||||||

| HYUNDAI MOBIS Co., Ltd. | 107,546 | 20,440 | ||||||

| Hyundai Motor Co. | 273,359 | 33,329 | ||||||

| Hyundai Motor Co., Series 2 preference | 66,197 | 6,231 | ||||||

| LG Household & Health Care Ltd. | 33,877 | 23,507 | ||||||

| LG Uplus Corp. | 4,287,370 | 37,898 | ||||||

| Orion Corp. | 11,369 | 10,681 | ||||||

| Samsung Electronics Co., Ltd. (GDR)2 | 61,409 | 35,034 | ||||||

| Shinhan Financial Group Co., Ltd. | 194,675 | 7,252 | ||||||

| 200,023 | ||||||||

| Taiwan 5.8% | ||||||||

| Advantech Co., Ltd. | 654,000 | 4,494 | ||||||

| AirTAC International Group | 4,032,850 | 25,291 | ||||||

| CTCI Corp. | 17,099,000 | 27,654 | ||||||

| Delta Electronics, Inc. | 12,159,348 | 62,266 | ||||||

| Ginko International Co., Ltd. | 846,000 | 10,652 | ||||||

| Merida Industry Co., Ltd. | 197,300 | 1,279 | ||||||

| Taiwan Semiconductor Manufacturing Co., Ltd. | 27,807,568 | 126,625 | ||||||

| Yungtay Engineering Co., Ltd. | 5,227,000 | 10,046 | ||||||

| 268,307 | ||||||||

| Thailand 1.3% | ||||||||

| Bangkok Bank PCL, nonvoting depository receipt | 6,221,900 | 32,790 | ||||||

| Central Pattana PCL | 2,683,900 | 3,774 | ||||||

| KASIKORNBANK PCL | 1,635,300 | 9,151 | ||||||

| PTT PCL | 1,312,600 | 13,952 | ||||||

| 59,667 | ||||||||

| Total Asia-Pacific | 2,918,814 |

| Emerging Markets Growth Fund | 11 |

| Equity securities (continued) | Shares | Value (000) | ||||||

| Latin America 12.7% | ||||||||

| Argentina 0.9% | ||||||||

| Grupo Financiero Galicia SA, Class B | 5 | $ | — | |||||

| YPF Sociedad Anónima, Class D (ADR) | 1,587,500 | 43,545 | ||||||

| 43,545 | ||||||||

| Brazil 5.8% | ||||||||

| Banco Bradesco SA, preferred nominative (ADR) | 2,125,956 | 19,474 | ||||||

| BM&FBOVESPA SA – Bolsa de Valores, Mercadorias e Futuros, ordinary nominative | 11,416,300 | 43,035 | ||||||

| BRF SA, ordinary nominative | 75 | 1 | ||||||

| BRF SA, ordinary nominative (ADR) | 246,000 | 5,144 | ||||||

| BTG Pactual Group, units | 156,200 | 1,436 | ||||||

| CCR SA, ordinary nominative | 3,980,800 | 19,090 | ||||||

| Gerdau SA (ADR) | 809,300 | 1,950 | ||||||

| Hypermarcas SA, ordinary nominative1 | 8,653,700 | 62,987 | ||||||

| Itaú Unibanco Holding SA, preferred nominative (ADR) | 1,958,314 | 21,444 | ||||||

| QGEP Participações SA, ordinary nominative | 5,779,200 | 12,584 | ||||||

| TIM Participações SA, ordinary nominative | 1,128,500 | 3,717 | ||||||

| TIM Participações SA, ordinary nominative (ADR) | 71,900 | 1,176 | ||||||

| Usinas Siderúrgicas de Minas Gerais SA – Usiminas, Class A, preferred nominative | 2,296,700 | 3,044 | ||||||

| Vale SA, Class A, preferred nominative | 2,280,870 | 11,430 | ||||||

| Vale SA, Class A, preferred nominative (ADR) | 4,401,200 | 22,226 | ||||||

| Vale SA, ordinary nominative (ADR) | 4,262,800 | 25,108 | ||||||

| Wilson Sons Ltd. (BDR) | 1,334,100 | 13,345 | ||||||

| 267,191 | ||||||||

| Chile 1.1% | ||||||||

| Enersis SA | 9,689,523 | 3,080 | ||||||

| Enersis SA (ADR) | 1,739,750 | 27,540 | ||||||

| Inversiones La Construcción SA | 1,901,502 | 21,424 | ||||||

| 52,044 | ||||||||

| Mexico 4.8% | ||||||||

| América Móvil, SAB de CV, Series L (ADR) | 4,104,200 | 87,461 | ||||||

| CEMEX, SAB de CV, ordinary participation certificates, units (ADR)1 | 7,709,588 | 70,620 | ||||||

| Fibra Uno Administracion, SA de CV | 10,042,800 | 23,839 | ||||||

| Grupo Comercial Chedraui, SAB de CV, Class B | 2,180,000 | 6,190 | ||||||

| Grupo Sanborns, SAB de CV, Series B1 | 3,682,600 | 5,588 | ||||||

| Impulsora del Desarrollo y el Empleo en América Latina, SA de CV, Series B11 | 12,661,244 | 24,763 | ||||||

| Minera Frisco, SAB de CV, ordinary participation certificate, Series A11 | 2,645,366 | 1,976 | ||||||

| Urbi Desarrollos Urbanos, SA de CV (Mexico)1 | 1,046,737 | 50 | ||||||

| 220,487 | ||||||||

| Peru 0.1% | ||||||||

| Graña y Montero SAA (ADR) | 454,000 | 3,187 | ||||||

| Total Latin America | 586,454 |

| 12 | Emerging Markets Growth Fund |

| Equity securities (continued) | Shares | Value (000) | ||||||

| Eastern Europe and Middle East 7.0% | ||||||||

| Greece 0.0% | ||||||||

| Jumbo SA | 261,972 | $ | 1,851 | |||||

| Israel 0.1% | ||||||||

| Shufersal Ltd.1 | 2,567,201 | 6,083 | ||||||

| Oman 0.4% | ||||||||

| bank muscat SAOG | 12,046,501 | 17,211 | ||||||

| Russia 4.1% | ||||||||

| ALROSA OJSC | 28,618,091 | 32,671 | ||||||

| Baring Vostok Private Equity Fund, LP (acquired 12/15/00, cost: $5,514,000)1,3,4,5,6 | 11,783,118 | 15,569 | ||||||

| Baring Vostok Private Equity Fund III, LP (acquired 3/30/05, cost: $18,511,000)3,4,5,6 | 24,142,754 | 22,397 | ||||||

| Baring Vostok Private Equity Fund IV, LP (acquired 4/25/07, cost: $19,108,000)1,3,4,5,6 | 21,106,994 | 13,656 | ||||||

| Baring Vostok Fund IV Supplemental Fund, LP (acquired 10/8/07, cost: $34,972,000)1,3,4,5,6 | 37,951,580 | 26,263 | ||||||

| Globaltrans Investment PLC (GDR)1 | 249,985 | 1,187 | ||||||

| Magnit PJSC | 20,509 | 4,236 | ||||||

| Magnit PJSC (GDR) | 177,810 | 9,897 | ||||||

| Mobile TeleSystems OJSC (ADR) | 1,452,100 | 14,202 | ||||||

| Moscow Exchange MICEX-RTS PJSC | 9,164,906 | 11,596 | ||||||

| New Century Capital Partners, LP (acquired 12/7/95, cost: $686,000)3,5 | 5,247,900 | 2,292 | ||||||

| Rosneft Oil Company OJSC (GDR) | 731,291 | 3,013 | ||||||

| Sberbank of Russia | 5,989,268 | 7,852 | ||||||

| Surgutneftegas OJSC, preference | 8,674,425 | 6,704 | ||||||

| Yandex NV, Class A1 | 1,174,900 | 17,882 | ||||||

| 189,417 | ||||||||

| Saudi Arabia 0.8% | ||||||||

| Saudi Basic Industries Corp., warrants, expire 20162 | 1,159,188 | 29,393 | ||||||

| Savola Group Co., warrants, expire 20172 | 433,760 | 7,920 | ||||||

| 37,313 | ||||||||

| Turkey 0.7% | ||||||||

| Akbank TAS | 10,969,592 | 31,720 | ||||||

| Aktaş Elektrik Ticaret AŞ1 | 4,273 | — | ||||||

| 31,720 | ||||||||

| United Arab Emirates 0.9% | ||||||||

| DP World Ltd. | 1,133,619 | 24,259 | ||||||

| First Gulf Bank PJSC | 4,011,860 | 16,603 | ||||||

| 40,862 | ||||||||

| Total Eastern Europe and Middle East | 324,457 | |||||||

| Africa 3.2% | ||||||||

| South Africa 3.2% | ||||||||

| Barloworld Ltd. | 1,038,638 | 8,238 | ||||||

| Discovery Ltd. | 2,695,298 | 28,019 | ||||||

| Mr Price Group Ltd. | 240,639 | 4,955 | ||||||

| MTN Group Ltd. | 251,515 | 4,729 | ||||||

| Naspers Ltd., Class N | 389,453 | 60,662 | ||||||

| Shoprite Holdings Ltd. | 2,427,900 | 34,624 |

| Emerging Markets Growth Fund | 13 |

| Equity securities (continued) | Shares | Value (000) | ||||||

| Africa (continued) | �� | |||||||

| South Africa (continued) | ||||||||

| Telkom SA SOC Ltd.1 | 1,591,800 | $ | 8,391 | |||||

| Total Africa | 149,618 | |||||||

| Other markets 7.8% | ||||||||

| Australia 0.8% | ||||||||

| Oil Search Ltd. | 6,641,111 | 36,534 | ||||||

| Austria 0.4% | ||||||||

| Vienna Insurance Group AG | 552,924 | 18,971 | ||||||

| Canada 0.9% | ||||||||

| Centerra Gold Inc. | 2,328,300 | 13,235 | ||||||

| First Quantum Minerals Ltd. | 2,324,433 | 30,391 | ||||||

| 43,626 | ||||||||

| Italy 0.2% | ||||||||

| Tenaris SA (ADR) | 334,400 | 9,035 | ||||||

| Netherlands 0.0% | ||||||||

| Fugro NV, depository receipts1 | 81,589 | 1,788 | ||||||

| Switzerland 0.7% | ||||||||

| Dufry AG1 | 236,460 | 32,929 | ||||||

| United Kingdom 1.9% | ||||||||

| Glencore PLC1 | 2,273,464 | 9,120 | ||||||

| Global Ports Investments PLC (GDR) | 2,368,003 | 11,698 | ||||||

| Lonmin PLC1 | 11,008,279 | 19,355 | ||||||

| PZ Cussons PLC | 3,571,058 | 20,301 | ||||||

| SABMiller PLC | 113,603 | 5,898 | ||||||

| Sedibelo Platinum Mines Ltd.1 | 16,963,500 | 9,925 | ||||||

| Tullow Oil PLC | 1,788,518 | 9,546 | ||||||

| 85,843 | ||||||||

| United States of America 2.9% | ||||||||

| AES Corp. | 2,094,500 | 27,773 | ||||||

| Alibaba Group Holding Ltd. (ADR)1 | 75,500 | 6,211 | ||||||

| Arcos Dorados Holdings, Inc., Class A | 2,383,628 | 12,538 | ||||||

| Cobalt International Energy, Inc.1 | 3,781,593 | 36,719 | ||||||

| Ctrip.com International, Ltd. (ADR)1 | 135,773 | 9,860 | ||||||

| MercadoLibre, Inc. | 178,000 | 25,223 | ||||||

| Xoom Corp.1 | 630,900 | 13,284 | ||||||

| 131,608 | ||||||||

| Total other markets | 360,334 | |||||||

| Multinational 0.4% | ||||||||

| Capital International Private Equity Fund IV, LP (acquired 3/29/05, cost: $16,190,000)3,4,5,6 | 50,724,946 | 18,114 | ||||||

| International Hospital Corp. Holding NV, Class A (acquired 9/25/97, cost: $8,011,000)1,3,4 | 609,873 | 402 | ||||||

| International Hospital Corp. Holding NV, Class B, cumulative, convertible preferred (acquired 2/12/07, cost: $3,504,000)1,3,4 | 622,354 | 411 | ||||||

| Pan-African Investment Partners II Ltd., Class A, preferred (acquired 6/20/08, cost: $7,142,000)1,3,4,5 | 3,800 | 263 | ||||||

| Total Multinational | 19,190 | |||||||

| Total equity securities (cost: $3,702,553,000) | 4,358,867 |

| 14 | Emerging Markets Growth Fund |

| Bonds & notes | Principal amount (000) | Value (000) | ||||||

| Latin America 0.6% | ||||||||

| Brazil 0.6% | ||||||||

| Brazil (Federal Republic of), Series B, 6.00% 20507 | BRL | 27 | $ | 23,280 | ||||

| Marfrig Holdings (Europe) BV 8.375%, 2018 | $ | 985 | 997 | |||||

| Marfrig Overseas Ltd. 9.50%, 2020 | 1,272 | 1,306 | ||||||

| Total Latin America | 25,583 | |||||||

| Asia-Pacific 0.0% | ||||||||

| China 0.0% | ||||||||

| Fu Ji Food and Catering Services Holdings Ltd. 0.00% convertible, 20208 | CNY | 93,400 | — | |||||

| Eastern Europe and Middle East 0.0% | ||||||||

| Oman 0.0% | ||||||||

| bank muscat (SAOG) 3.50% convertible, 2018 | OMR | 1,598 | 411 | |||||

| bank muscat (SAOG) 4.50% convertible, 2016 | 144 | 40 | ||||||

| bank muscat (SAOG) 4.50% convertible, 2017 | 2,148 | 569 | ||||||

| Total Eastern Europe and Middle East | 1,020 | |||||||

| Total bonds & notes (cost: $33,391,000) | 26,603 | |||||||

| Short-term securities | ||||||||

| Corporate short-term notes 4.1% | ||||||||

| Bank of Tokyo-Mitsubishi UFJ Ltd. 0.10% due 7/7/2015 | $ | 33,500 | 33,499 | |||||

| General Electric Co. 0.06% due 7/1/2015 | 32,300 | 32,300 | ||||||

| Sumitomo Mitsui Banking Corp. 0.14% due 7/14/20152 | 60,000 | 59,996 | ||||||

| Victory Receivables Corp. 0.12% due 7/6/20152 | 61,300 | 61,298 | ||||||

| Total short-term securities (cost: $187,096,000) | 187,093 | |||||||

| Total investment securities (cost: $3,923,040,000) | 4,572,563 | |||||||

| Other assets less liabilities | 48,339 | |||||||

| Net assets | $ | 4,620,902 | ||||||

Forward currency contracts

The fund has entered into over-the-counter (“OTC”) forward currency contracts as shown in the following table. The average notional amount of open OTC forward currency contracts was $164,799,000 over the prior 12-month period.

| Unrealized | ||||||||||||

| Notional amount | (depreciation)/ appreciation | |||||||||||

| Receive | Deliver | at 6/30/2015 | ||||||||||

| Settlement date | Counterparty | (000) | (000) | (000) | ||||||||

| Sales: | ||||||||||||

| Brazilian reais | 7/20/2015 | UBS AG | $21,743 | BRL68,168 | $ (37 | ) | ||||||

| Euros | 7/31/2015 | Bank of America | 18,362 | EUR16,377 | 97 | |||||||

| $ 60 | ||||||||||||

| Emerging Markets Growth Fund | 15 |

Investment in affiliates

If the fund owns more than 5% of the outstanding voting securities of an issuer, the fund’s investment in that issuer represents an investment in an affiliate as defined in the Investment Company Act of 1940. In addition, Capital International Private Equity Fund IV, LP is considered an affiliate since this issuer has the same investment adviser as the fund. A summary of the fund’s transactions in the securities of affiliated issuers during the year ended June 30, 2015, is as follows (dollars in thousands):

| Dividend | Value of | |||||||||||||||||||||||

| Beginning | Ending | and interest | affiliates at | |||||||||||||||||||||

| Issuer | shares | Additions | Reductions | shares | income | 6/30/2015 | ||||||||||||||||||

| Baring Vostok Private Equity Fund* | 11,783,118 | — | — | 11,783,118 | $ | — | $ | 15,569 | ||||||||||||||||

| Baring Vostok Private Equity Fund III* | 23,512,961 | 629,793 | — | 24,142,754 | 653 | 22,397 | ||||||||||||||||||

| Baring Vostok Capital Partners IV* | 53,863,990 | 5,194,584 | — | 59,058,574 | — | 39,919 | ||||||||||||||||||

| Capital International Private Equity Fund IV* | 50,616,424 | 108,522 | — | 50,724,946 | 9 | 18,114 | ||||||||||||||||||

| International Hospital | 1,232,227 | — | — | 1,232,227 | — | 813 | ||||||||||||||||||

| Pan-African Investment Partners II | 3,800 | — | — | 3,800 | — | 263 | ||||||||||||||||||

| $ | 662 | $ | 97,075 | |||||||||||||||||||||

| * | For private equity funds structured as limited partnerships, shares are not applicable and therefore the fund’s interest in the partnerships is reported. |

| 1 | Security did not produce income during the last 12 months. |

| 2 | Acquired in a transaction exempt from registration under Rule 144A or section 4(2) of the Securities Act of 1933 (not including purchases of securities that were publicly offered in the primary local market but were not registered under U.S. securities laws). May be resold in the U.S. in transactions exempt from registration, normally to qualified institutional buyers. The total value of all such securities was $198,582,000, which represented 4.30% of the net assets of the fund. |

| 3 | Acquired through a private placement transaction exempt from registration under the Securities Act of 1933. These securities, acquired at a cost of $113,638,000, may be subject to legal or contractual restrictions on resale. The total value of all such securities was $99,367,000, which represented 2.15% of the net assets of the fund. |

| 4 | This issuer represents investment in an affiliate as defined in the Investment Company Act of 1940. This definition includes, but is not limited to, issuers in which the fund owns more than 5% of the outstanding voting securities. Capital International Private Equity Fund IV, LP is also considered an affiliate since this issuer has the same investment adviser as the fund. |

| 5 | Cost and market value do not include prior distributions to the fund from income or proceeds realized from securities held by the private equity fund. Therefore, the cost and market value may not be indicative of the private equity fund’s performance. For private equity funds structured as limited partnerships, shares are not applicable and therefore the fund’s interest in the partnerships is reported. |

| 6 | Excludes an unfunded capital commitment representing an agreement which obligates the fund to meet capital calls in the future. Capital calls can only be made if and when certain requirements have been fulfilled; thus, the timing and the amount of such capital calls cannot readily be determined. |

| 7 | Index-linked bond whose principal amount moves with a government retail price index. |

| 8 | Scheduled interest and/or principal payment was not received. |

Key to abbreviations

ADR — American Depositary Receipts

BDR — Brazilian Depositary Receipts

GDR — Global Depositary Receipts

BRL — Brazilian reais

CNY — Chinese yuan

EUR — Euros

OMR — Omani rials

See Notes to Financial Statements

| 16 | Emerging Markets Growth Fund |

Statement of assets and liabilities

| at June 30, 2015 | (dollars in thousands, except per-share amounts) |

| Assets: | ||||||||

| Investment securities, at value: | ||||||||

| Unaffiliated issuers (cost: $3,810,088) | $ | 4,475,488 | ||||||

| Affiliated issuers (cost: $112,952) | 97,075 | $ | 4,572,563 | |||||

| Cash | 184 | |||||||

| Cash denominated in non-U.S. currency (cost: $4,059) | 4,061 | |||||||

| Unrealized appreciation on open forward currency contracts | 97 | |||||||

| Receivables for: | ||||||||

| Sales of investments | 30,360 | |||||||

| Sales of fund’s shares | 902 | |||||||

| Dividends and interest | 24,474 | |||||||

| Non-U.S. taxes | 1,995 | 57,731 | ||||||

| 4,634,636 | ||||||||

| Liabilities: | ||||||||

| Unrealized depreciation on open forward currency contracts | 37 | |||||||

| Payables for: | ||||||||

| Purchases of investments | 5,951 | |||||||

| Investment advisory services | 2,680 | |||||||

| Directors’ compensation | 1,864 | |||||||

| Repurchase of fund’s shares | 2,780 | |||||||

| Other accrued expenses | 422 | 13,697 | ||||||

| 13,734 | ||||||||

| Net assets at June 30, 2015: | ||||||||

| Equivalent to $6.94 per share on 666,010,466 shares of $0.01 par value capital stock outstanding (authorized capital stock – 2,000,000,000 shares) | $ | 4,620,902 | ||||||

| Net assets consist of: | ||||||||

| Capital paid in on shares of stock | $ | 4,049,899 | ||||||

| Undistributed net investment income | 17,567 | |||||||

| Accumulated net realized loss | (95,968 | ) | ||||||

| Net unrealized appreciation | 649,404 | |||||||

| Net assets at June 30, 2015 | $ | 4,620,902 |

See Notes to Financial Statements

| Emerging Markets Growth Fund | 17 |

Statement of operations

| for the year ended June 30, 2015 | (dollars in thousands) |

| Investment income: | ||||||||

| Income: | ||||||||

| Dividends (net of non-U.S. withholding tax of $7,429; also includes $653 from affiliates) | $ | 98,466 | ||||||

| Interest (also includes $9 from affiliates) | 3,117 | $ | 101,583 | |||||

| Fees and expenses: | ||||||||

| Investment advisory services | 36,932 | |||||||

| Custodian | 1,765 | |||||||

| Registration statement and prospectus | 35 | |||||||

| Auditing and legal | 509 | |||||||

| Reports to shareholders | 11 | |||||||

| Directors’ compensation | 582 | |||||||

| Other | 1,015 | |||||||

| Total fees and expenses before expense reduction | 40,849 | |||||||

| Less custodian expense reduction | 2 | |||||||

| Total fees and expenses after expense reduction | 40,847 | |||||||

| Net investment income | 60,736 | |||||||

| Net realized gain and unrealized depreciation: | ||||||||

| Net realized gain (loss) on: | ||||||||

| Investments (includes $9,462 gain from affiliates) | 185,211 | |||||||

| Forward currency contracts | 28,723 | |||||||

| Currency transactions | (1,496 | ) | 212,438 | |||||

| Net unrealized (depreciation) appreciation on: | ||||||||

| Investments | (721,495 | ) | ||||||

| Forward currency contracts | 1,842 | |||||||

| Currency translations | (178 | ) | (719,831 | ) | ||||

| Net realized gain and unrealized depreciation | (507,393 | ) | ||||||

| Net decrease in net assets resulting from operations | $ | (446,657 | ) |

Statements of changes in net assets

(dollars in thousands)

| Year ended June 30 | ||||||||

| 2015 | 2014 | |||||||

| Operations: | ||||||||

| Net investment income | $ | 60,736 | $ | 76,309 | ||||

| Net realized gain | 212,438 | 97,797 | ||||||

| Net unrealized (depreciation) appreciation | (719,831 | ) | 879,393 | |||||

| Net (decrease) increase in net assets resulting from operations | (446,657 | ) | 1,053,499 | |||||

| Dividends and distributions paid to shareholders: | ||||||||

| Dividends from net investment income | (97,584 | ) | (114,887 | ) | ||||

| Distributions from net realized gain on investments | (182,621 | ) | (344,660 | ) | ||||

| Total dividends and distributions paid to shareholders | (280,205 | ) | (459,547 | ) | ||||

| Capital share transactions: | ||||||||

| Proceeds from shares sold: 30,603,677 and 53,493,672 shares, respectively | 221,712 | 412,002 | ||||||

| Proceeds from shares issued in reinvestment of net investment income dividends and net realized gain distributions: 39,626,363 and 58,008,358 shares, respectively | 266,289 | 447,825 | ||||||

| Cost of shares repurchased: 223,467,957 and 366,368,599 shares, respectively | (1,666,691 | ) | (2,875,510 | ) | ||||

| Cost of shares repurchased in connection with in-kind redemption for the year ended June 30, 2014: 210,008,947 shares | — | (1,615,760 | ) | |||||

| Net decrease in net assets resulting from capital share transactions | (1,178,690 | ) | (3,631,443 | ) | ||||

| Total decrease in net assets | (1,905,552 | ) | (3,037,491 | ) | ||||

| Net assets: | ||||||||

| Beginning of year | 6,526,454 | 9,563,945 | ||||||

| End of year (including undistributed net investment income: $17,567 and $17,760, respectively) | $ | 4,620,902 | $ | 6,526,454 | ||||

See Notes to Financial Statements

| 18 | Emerging Markets Growth Fund |

1. Organization

Emerging Markets Growth Fund, Inc. (the “fund”) is registered under the Investment Company Act of 1940 as an open-end, diversified management investment company. The fund seeks long-term growth of capital and invests primarily in common stock and other equity securities of issuers in developing countries.

On October 22, 2014, shareholders approved the elimination of certain fundamental policies in order to allow the fund to convert from an open-end interval fund to an open-end, daily valued fund on October 31, 2014. Shareholders also approved updates to and the elimination of certain fundamental investment policies of the fund.

2. Significant accounting policies

The fund is an investment company that applies the accounting and reporting guidance issued in Topic 946 by the U.S. Financial Accounting Standards Board. The fund’s financial statements have been prepared to comply with U.S. generally accepted accounting principles (“U.S. GAAP”). These principles require management to make estimates and assumptions that affect reported amounts and disclosures. Actual results could differ from those estimates. Subsequent events, if any, have been evaluated through the date of issuance in the preparation of the financial statements. The fund follows the significant accounting policies described below, as well as the valuation policies described in the next section on valuation.

Security transactions and related investment income — Security transactions are recorded by the fund as of the date the trades are executed with brokers. Realized gains and losses from security transactions are determined based on the specific identified cost of the securities. In the event a security is purchased with a delayed payment date, the fund will segregate liquid assets sufficient to meet its payment obligations. Dividend income is recognized on the ex-dividend date and interest income is recognized on an accrual basis. Market discounts, premiums and original issue discounts on fixed-income securities are amortized daily over the expected life of the security.

Dividends and distributions to shareholders — Dividends and distributions to shareholders are recorded on the ex-dividend date.

Currency translation — Assets and liabilities, including investment securities, denominated in currencies other than U.S. dollars are translated into U.S. dollars at the exchange rates supplied by one or more pricing vendors on the valuation date. Purchases and sales of investment securities and income and expenses are translated into U.S. dollars at the exchange rates on the dates of such transactions. The effects of changes in exchange rates on investment securities are included with the net realized gain or loss and net unrealized appreciation or depreciation on investments on the fund’s statement of operations. The realized gain or loss and unrealized appreciation or depreciation resulting from all other transactions denominated in currencies other than U.S. dollars are disclosed separately.

Shares issued and redeemed — The fund intends to issue shares in exchange for cash and redeem shares in cash, however, the investment adviser, at its discretion, may accept securities in exchange of fund shares or pay a redemption in whole or in part by a distribution of the fund’s portfolio securities. An issuance or redemption of shares “in-kind” is based upon the closing value of the securities as of the trade date. Realized gains/losses, if any, resulting from redemptions of shares in-kind are reflected separately in the statement of operations.

3. Valuation

Capital International, Inc., the fund’s investment adviser, values the fund’s investments at fair value as defined by U.S. GAAP. The net asset value of the fund is generally determined as of approximately 4:00 p.m. New York time each day the New York Stock Exchange is open. Prior to October 31, 2014, the net asset value of the fund was only determined on the last business day of each week and month except on any day on which the New York Stock Exchange was closed for trading.

Methods and inputs — The fund’s investment adviser uses the following methods and inputs to establish the fair value of the fund’s assets and liabilities. Use of particular methods and inputs may vary over time based on availability and relevance as market and economic conditions evolve.

| Emerging Markets Growth Fund | 19 |

Equity securities are generally valued at the official closing price of, or the last reported sale price on, the exchange or market on which such securities are traded, as of the close of business on the day the securities are being valued or, lacking any sales, at the last available bid price. Prices for each security are taken from the principal exchange or market on which the security trades.

Fixed-income securities, including short-term securities, are generally valued at prices obtained from one or more pricing vendors. Vendors value such securities based on one or more of the inputs described in the following table. The table provides examples of inputs that are commonly relevant for valuing particular classes of fixed-income securities in which the fund is authorized to invest. However, these classifications are not exclusive and any of the inputs may be used to value any other class of fixed-income security.

| Fixed-income class | Examples of standard inputs | |

| All | Benchmark yields, transactions, bids, offers, quotations from dealers and trading systems, new issues, spreads and other relationships observed in the markets among comparable securities; and proprietary pricing models such as yield measures calculated using factors such as cash flows, financial or collateral performance and other reference data (collectively referred to as “standard inputs”) | |

| Corporate bonds & notes; convertible securities | Standard inputs and underlying equity of the issuer | |

| Bonds & notes of governments & government agencies | Standard inputs and interest rate volatilities |

When the fund’s investment adviser deems it appropriate to do so (such as when vendor prices are unavailable or not deemed to be representative), fixed-income securities will be valued in good faith at the mean quoted bid and ask prices that are reasonably and timely available (or bid prices, if ask prices are not available) or at prices for securities of comparable maturity, quality and type.

Securities with both fixed-income and equity characteristics, or equity securities traded principally among fixed-income dealers, are generally valued in the manner described for either equity or fixed-income securities, depending on which method is deemed most appropriate by the fund’s investment adviser. Forward currency contracts are valued at the mean of representative quoted bid and ask prices, generally based on prices supplied by one or more pricing vendors.

Securities and other assets for which representative market quotations are not readily available or are considered unreliable by the fund’s investment adviser are fair valued as determined in good faith under fair valuation guidelines adopted by authority of the fund’s board of directors as further described. The investment adviser follows fair valuation guidelines, consistent with U.S. Securities and Exchange Commission rules and guidance, to consider relevant principles and factors when making fair value determinations. The investment adviser considers relevant indications of value that are reasonably and timely available to it in determining the fair value to be assigned to a particular security, such as the type and cost of the security; contractual or legal restrictions on resale of the security; relevant financial or business developments of the issuer; actively traded similar or related securities; conversion or exchange rights on the security; related corporate actions; significant events occurring after the close of trading in the security; and changes in overall market conditions. In addition, the closing prices of equity securities that trade in markets outside U.S. time zones may be adjusted to reflect significant events that occur after the close of local trading but before the net asset value of the fund is determined. Fair valuations and valuations of investments that are not actively trading involve judgment and may differ materially from valuations that would have been used had greater market activity occurred.

Processes and structure — The fund’s board of directors has delegated authority to the fund’s investment adviser to make fair value determinations, subject to board oversight. The investment adviser has established a Joint Fair Valuation Committee (the “Fair Valuation Committee”) to administer, implement and oversee the fair valuation process, and to make fair value decisions. The Fair Valuation Committee regularly reviews its own fair value decisions, as well as decisions made under its standing instructions to the investment adviser’s valuation teams. The Fair Valuation Committee reviews changes in fair value measurements from period to period and may, as deemed appropriate, update the fair valuation guidelines to better reflect the results of back testing and address new or evolving issues. The Fair Valuation Committee reports any changes to the fair valuation guidelines to the audit committee with supplemental information to support the changes. The fund’s audit committee also regularly reviews reports that describe fair value determinations and methods.

| 20 | Emerging Markets Growth Fund |

The fund’s investment adviser has also established a Fixed-Income Pricing Review Group to administer and oversee the fixed-income valuation process, including the use of fixed-income pricing vendors. This group regularly reviews pricing vendor information and market data. Pricing decisions, processes and controls over security valuation are also subject to additional internal reviews, including an annual control self-evaluation program facilitated by the investment adviser’s compliance group.

Classifications — The fund’s investment adviser classifies the fund’s assets and liabilities into three levels based on the inputs used to value the assets or liabilities. Level 1 values are based on quoted prices in active markets for identical securities. Level 2 values are based on significant observable market inputs, such as quoted prices for similar securities and quoted prices in inactive markets. Certain securities trading outside the U.S. may transfer between Level 1 and Level 2 due to valuation adjustments resulting from significant market movements following the close of local trading. Level 3 values are based on significant unobservable inputs that reflect the investment adviser’s determination of assumptions that market participants might reasonably use in valuing the securities. The valuation levels are not necessarily an indication of the risk or liquidity associated with the underlying investment. For example, U.S. government securities are reflected as Level 2 because the inputs used to determine fair value may not always be quoted prices in an active market. The following tables present the fund’s valuation levels as of June 30, 2015 (dollars in thousands):

| Investment securities | ||||||||||||||||

| Level 1 | Level 21 | Level 31 | Total | |||||||||||||

| Assets: | ||||||||||||||||

| Equity securities: | ||||||||||||||||

| Asia-Pacific | $ | 2,901,326 | $ | 4,941 | $ | 12,547 | $ | 2,918,814 | ||||||||

| Latin America | 586,404 | — | 50 | 586,454 | ||||||||||||

| Eastern Europe and Middle East | 205,116 | 39,164 | 80,177 | 324,457 | ||||||||||||

| Other markets | 500,027 | — | 29,115 | 529,142 | ||||||||||||

| Bonds & notes | — | 26,603 | — | 26,603 | ||||||||||||

| Short-term securities | — | 187,093 | — | 187,093 | ||||||||||||

| Total | $ | 4,192,873 | $ | 257,801 | $ | 121,889 | $ | 4,572,563 | ||||||||

| Other investments2 | ||||||||||||||||

| Level 1 | Level 2 | Level 3 | Total | |||||||||||||

| Assets: | ||||||||||||||||

| Unrealized appreciation on open forward currency contracts | $ | — | $ | 97 | $ | — | $ | 97 | ||||||||

| Liabilities: | ||||||||||||||||

| Unrealized depreciation on open forward currency contracts | — | (37 | ) | — | (37 | ) | ||||||||||

| Total | $ | — | $ | 60 | $ | — | $ | 60 | ||||||||

| 1 | Level 2 and Level 3 include securities with an aggregate value of $165,994,000, which represented 3.59% of the net assets of the fund, that were fair valued under guidelines adopted by authority of the fund’s board of directors. |

| 2 | Forward currency contracts are not included in the investment portfolio. |

The following table reconciles the valuation of the fund’s Level 3 investment securities and related transactions during the year ended June 30, 2015 (dollars in thousands):

| Beginning | Gross | Net | Net | Gross | Ending | |||||||||||||||||||||||||||

| value at | transfers | realized | unrealized | transfers out | value at | |||||||||||||||||||||||||||

| 7/1/2014 | into Level 33 | Purchases | Sales | gain/(loss)4 | depreciation4 | of Level 33 | 6/30/2015 | |||||||||||||||||||||||||

| Private equity funds | $ | 171,104 | $ | — | $ | 5,933 | $ | (11,565 | ) | $ | 9,462 | $ | (76,380 | ) | $ | — | $ | 98,554 | ||||||||||||||

| Other securities5 | 11,569 | 17,994 | 9,691 | (10,164 | ) | (1,994 | ) | (3,761 | ) | — | 23,335 | |||||||||||||||||||||

| Total | $ | 182,673 | $ | 17,994 | $ | 15,624 | $ | (21,729 | ) | $ | 7,468 | $ | (80,141 | ) | $ | — | $ | 121,889 | ||||||||||||||

| Net unrealized depreciation during the period on Level 3 investment securities held at June 30, 2015 (dollars in thousands): | $ | (87,145 | ) | |||||||||||||||||||||||||||||

| 3 | Transfers into and out of Level 3 are based on the beginning market value of the quarter in which they occurred. |

| 4 | Net realized gain/(loss) and unrealized depreciation are included in the related amounts on investments in the statement of operations. |

| 5 | Represents less than 1% of portfolio securities as of June 30, 2015. |

| Emerging Markets Growth Fund | 21 |

The fund owns an interest in multiple private equity funds, which are considered alternative investments and are classified as Level 3 investment securities. The private equity funds are fair valued using the net asset value based on the fund’s financial statements adjusted for known company or market events, updated market pricing for underlying securities, and/or fund transactions (i.e., drawdowns and distributions) and may include other unobservable inputs.

The other unobservable inputs used in the fair value measurements of the fund’s private equity investments are directional adjustments based on relevant market data (such as significant movement of a country-specific exchange-traded fund or index after the financial statement date of the private equity fund). Significant increases (decreases) of these inputs could result in significantly higher (lower) fair valuation. There were no other unobservable inputs as of June 30, 2015.

The following table lists the characteristics of the alternative investments held by the fund as of June 30, 2015 (dollars in thousands):

| Investment type | Investment strategy | Fair value | Unfunded commitment* | Remaining life† | Redemption terms | |||||

| Private equity funds | Primarily private sector equity investments (i.e., expansion capital, buyouts) in emerging markets | $98,554 | $10,869 | ≤1 to 3 years | Redemptions are not permitted. These funds distribute proceeds from the liquidation of underlying assets of the funds. |

| * | Unfunded capital commitments represent agreements which obligate the fund to meet capital calls in the future. Payment would be made when a capital call is requested. Capital calls can only be made if and when certain requirements have been fulfilled; thus, the timing of such capital calls cannot readily be determined. |

| † | Represents the remaining life of the fund term or the estimated period of liquidation. |

4. Risk factors

Investing in the fund may involve certain risks including, but not limited to, those described below.

Market conditions — The prices of, and the income generated by, the common stocks and other securities held by the fund may decline — sometimes rapidly or unpredictably — due to various factors, including events or conditions affecting the general economy or particular industries; overall market changes; local, regional or global political, social or economic instability; governmental or governmental agency responses to economic conditions; and currency exchange rate, interest rate and commodity price fluctuations.

Issuer risks — The prices of, and the income generated by, securities held by the fund may decline in response to various factors directly related to the issuers of such securities, including reduced demand for an issuer’s goods or services, poor management performance and strategic initiatives such as mergers, acquisitions or dispositions, and the market response to any such initiatives.

Investing in growth-oriented stocks — Growth-oriented common stocks and other equity-type securities (such as preferred stocks, convertible preferred stocks and convertible bonds) may involve larger price swings and greater potential for loss than other types of investments.

Investing outside the United States — Securities of issuers domiciled outside the United States, or with significant operations or revenues outside the United States, may lose value because of adverse political, social, economic or market developments (including social instability, regional conflicts, terrorism and war) in the countries or regions in which the issuers operate or generate revenue. These securities may also lose value due to changes in foreign currency exchange rates against the U.S. dollar and/or currencies of other countries. Issuers of these securities may be more susceptible to actions of foreign governments, such as the imposition of price controls or punitive taxes, that could adversely impact revenues. Securities markets in certain countries may be more volatile and/or less liquid than those in the United States. Investments outside the United States may also be subject to different accounting practices and different regulatory, legal and reporting standards and practices, and may be more difficult to value, than those in the United States. In addition, the value of investments outside the United States may be reduced by foreign taxes, including foreign withholding taxes on interest and dividends. Further, there may be increased risks of delayed settlement of securities purchased or sold by the fund. The risks of investing outside the United States may be heightened in connection with investments in developing countries.

Investing in developing countries — Investing in countries with developing economies and/or markets may involve risks in addition to and greater than those generally associated with investing in developed countries. For instance, developing countries may have less developed legal and accounting systems than those in developed countries. The governments of these countries

| 22 | Emerging Markets Growth Fund |

may be less stable and more likely to impose capital controls, nationalize a company or industry, place restrictions on foreign ownership and on withdrawing sale proceeds of securities from the country, and/or impose punitive taxes that could adversely affect the prices of securities. In addition, the economies of these countries may be dependent on relatively few industries that are more susceptible to local and global changes. Securities markets in these countries can also be relatively small and have substantially lower trading volumes. As a result, securities issued in these countries may be more volatile and less liquid, and may be more difficult to value, than securities issued in countries with more developed economies and/or markets. Less certainty with respect to security valuations may lead to additional challenges and risks in calculating the fund’s net asset value. Additionally, there may be increased settlement risks for transactions in local securities.

Management — The investment adviser to the fund actively manages the fund’s investments. Consequently, the fund is subject to the risk that the methods and analyses employed by the investment adviser in this process may not produce the desired results. This could cause the fund to lose value or its investment results to lag relevant benchmarks or other funds with similar objectives.

5. Certain investment techniques

Forward currency contracts — The fund has entered into OTC forward currency contracts, which represent agreements to exchange currencies on specific future dates at predetermined rates. The fund’s investment adviser uses forward currency contracts to manage the fund’s exposure to changes in exchange rates. Upon entering into these contracts, risks may arise from the potential inability of counterparties to meet the terms of their contracts and from possible movements in exchange rates.

On a daily basis, forward currency contracts are valued and unrealized appreciation or depreciation for open forward currency contracts is recorded in the fund’s statement of assets and liabilities. Realized gains or losses are recorded at the time the forward currency contract is closed or offset by another contract with the same broker for the same settlement date and currency.

Closed forward currency contracts that have not reached their settlement date are included in the respective receivables or payables for closed forward currency contracts in the fund’s statement of assets and liabilities. Net realized gains or losses from closed forward currency contracts and net unrealized appreciation or depreciation from open forward currency contracts are recorded in the fund’s statement of operations and statements of changes in net assets.