UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act File Number 811-4946

THOMPSON PLUMB FUNDS, INC.

(Exact name of registrant as specified in charter)

918 Deming Way

Madison, Wisconsin 53717

(Address of principal executive offices)--(Zip code)

John W. Thompson

Chief Executive Officer and President

Thompson Plumb Funds, Inc.

918 Deming Way

Madison, Wisconsin 53717

(Name and address of agent for service)

With a copy to:

Fredrick G. Lautz, Esq.

Quarles & Brady LLP

411 East Wisconsin Avenue

Milwaukee, Wisconsin 53202

Registrant's telephone number, including area code: (608) 827-5700

Date of fiscal year end: November 30, 2010

Date of reporting period: May 31, 2010

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, N.W., Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Report to Stockholders.

|

Semi-Annual Report

May 31, 2010 Thompson Plumb Growth Fund Thompson Plumb MidCap Fund Thompson Plumb Bond Fund Telephone: 1-800-999-0887

www.thompsonplumb.com ___________________________________________ |

THOMPSON PLUMB FUNDS, INC.

SEMI-ANNUAL REPORT TO SHAREHOLDERS

NOTE ON FORWARD-LOOKING STATEMENTS

The matters discussed in this report may constitute forward-looking statements. These include any Advisor or portfolio manager predictions, assessments, analyses or outlooks for individual securities, industries, investment styles, market sectors, interest rates, economic trends and/or markets. These statements involve risks and uncertainties. In addition to the general risks described for each Fund in its current Prospectus, other factors bearing on these reports include the accuracy of the Advisor’s or portfolio manager’s forecasts and predictions, the appropriateness of the investment strategies designed by the Advisor or portfolio manager and the ability of the Advisor or portfolio manager to implement its strategies efficiently and successfully. Any one or more of these factors, as well as other risks affecting the securities markets generally, could cause the actual results of any Fund to differ materially as compared to its benchmarks.

2

THOMPSON PLUMB FUNDS, INC.

SEMI-ANNUAL REPORT TO SHAREHOLDERS

May 31, 2010

CONTENTS

| Page(s) |

| GROWTH FUND | |

| Investment review | 4-6 |

Schedule of investments | 7-8 |

| |

| MIDCAP FUND | |

Investment review | 9-11 |

Schedule of investments | 12-13 |

| |

| BOND FUND | |

Investment review | 14-16 |

Schedule of investments | 17-24 |

| |

| FUND EXPENSE EXAMPLES | 25 |

| |

| FINANCIAL STATEMENTS | |

Statements of assets and liabilities | 26 |

Statements of operations | 27 |

Statements of changes in net assets | 28 |

Notes to financial statements | 29-34 |

Financial highlights | 35-37 |

| |

| ADDITIONAL INFORMATION | 38 |

This report contains information for existing shareholders of Thompson Plumb Funds, Inc. It

does not constitute an offer to sell. This Semi-Annual Report is authorized for distribution to prospective investors

only when preceded or accompanied by a Fund Prospectus, which contains information about

the Funds’ objectives and policies, risks, management, expenses and other information.

A Prospectus can be obtained by calling 1-800-999-0887.

Please read your Prospectus carefully.

3

GROWTH FUND INVESTMENT REVIEW (Unaudited) |

| May 31, 2010 |

Portfolio Managers

James T. Evans, CFA

Jason L. Stephens, CFA

John W. Thompson, CFA

Performance

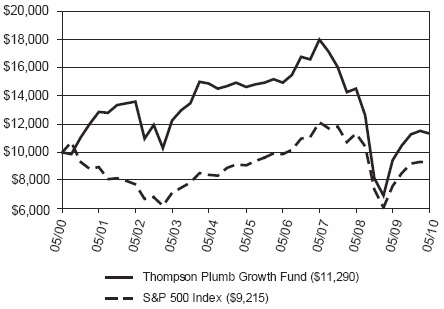

The Growth Fund produced a total return of 0.13% for the six-month period ended May 31, 2010, as compared to its benchmark, the S&P 500 Index, which returned 0.40%.

Comparison of Change in Value of a Hypothetical $10,000 Investment

| Average Annual Total Returns | |

| Through 05/31/10 | |

| 1 Year | | 3 Year | | 5 Year | | 10 Year | |

| Thompson Plumb Growth Fund | 19.49 | % | | -14.41 | % | | -5.00 | % | | 1.22 | % | |

| S&P 500 Index | 20.99 | % | | -8.69 | % | | 0.31 | % | | -0.82 | % | |

Gross Expense Ratio as of 3/31/10 was 1.54%.

Net Expense Ratio – Effective 12/01/09 – 1.40%*

* The Advisor has contractually agreed to waive management fees and/or reimburse expenses incurred by the Growth Fund through March 31, 2011.

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by calling 1-800-999-0887 or visiting www.thompsonplumb.com.

Results include the reinvestment of all dividends and capital gains distributions. Investment performance reflects all fee waivers that may be in effect. In the absence of such waivers, total return would be reduced. The performance information reflected in the graph and the table above does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares, nor does it imply future performance. The S&P 500 Index is an unmanaged index commonly used to measure the performance of U.S. stocks. You cannot directly invest in an index.

See Notes to Financial Statements.

4

GROWTH FUND INVESTMENT REVIEW (Unaudited) (Continued) |

| May 31, 2010 |

Management Commentary

The modest lag in the Fund’s performance relative to its benchmark during the first half of the fiscal year was attributable to both sector and issue selection, with the Health Care, Energy and Industrials sectors having the largest effect on overall relative performance. This positive impact was partially offset by the decision to overweight the Health Care sector as the sector performed the second worst overall among sectors in the S&P 500 during this period. Health Care had the largest overall positive impact on relative performance because of individual issue selection. Our decision to overweight Health Care stocks was based on a belief that the share prices of Fund holdings in that sector had been unfairly punished during the government health care debate, and that following the passage of a health-care reform bill these holdings would outperform their peers. We were correct about the attractiveness of many of the individual holdings in the Fund relative to other Health Care stocks, but overestimated the size of the bounce that the sector would receive. Going forward, if the sector rotates back into more widespread favor with investors, we feel the Fund is well positioned to take advantage of that change in sentiment.

Industrials and Energy were the two sectors that made the largest negative contribution to the Fund’s performance. Relative underperformance in the Energy sector was attributable to an overweight position that the Fund implemented roughly a month in advance of the Deepwater Horizon oil spill in the Gulf of Mexico. The sector sank after the spill began, dragging the Fund’s holdings in that sector with it. Aside from the individual companies directly involved in the Deepwater Horizon rig, we believe the long-term consequences of the spill will actually be positive for most Energy stocks as any resulting constraint in supply growth stemming from the spill would be likely to increase oil and gas prices. Within the Industrials sector, the Fund’s relative underperformance was largely attributable to issue selection, as the holdings of the Fund, which we view as more defensive, did not keep up with the names that we see as more cyclical within the S&P 500.

Over the remainder of the fiscal year we expect the economy to continue to recover, and have positioned the Fund to take advantage of such a continued recovery if our expectation proves to be correct. We believe a more modest recovery, as opposed to a sharp “V”-shaped bounce, remains the most likely path of future growth. While at the end of the last fiscal year there was no evidence to support a “V” outlook, we are beginning to see some signs that to us signal that growth could occur faster than our more modest expectations. These signs have not been significant enough to change our prediction of which type of recovery is most likely, but they have been enough to bear watching. Most importantly, we believe the odds of a double-dip recession have declined. As a result, we have structured the sector weightings of the Fund and even its individual holdings in a way that we believe would perform well in such a growth environment. As long as we perceive that the fundamental data supporting our investment decisions is continuing to improve and that stocks remain attractively valued, we will maintain a positive outlook for equity market returns.

Opinions expressed are subject to change, are not guaranteed and should not be considered investment advice.

Mutual fund investing involves risk. Principal loss is possible. Investments in smaller companies involve additional risks such as limited liquidity and greater volatility.

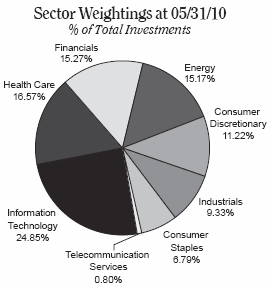

Please refer to the Schedule of Investments on page 7 of this report for holdings information. The management commentary above as well as Fund holdings and asset/sector allocations should not be considered a recommendation to buy or sell any security. In addition, please note that Fund holdings and asset/sector allocations are subject to change.

Current and future portfolio holdings are subject to risk.

See Notes to Financial Statements.

5

GROWTH FUND INVESTMENT REVIEW (Unaudited) (Continued) |

| May 31, 2010 |

| | Top 10 Equity Holdings at 05/31/10 |

| | | % of Fund’s |

| Company | Industry | Net Assets |

| Exxon Mobil Corp. | Oil & Gas Producers | 4.05% |

| Intel Corp. | Technology Hardware & | 2.60% |

| | Equipment | |

| Johnson & Johnson | Pharmaceuticals & | 2.46% |

| | Biotechnology | |

| Microsoft Corp. | Software & Computer | 2.41% |

| | Services | |

| General Electric Co. | General Industrials | 2.24% |

| St. Jude Medical, Inc. | Health Care Equipment & | 2.05% |

| | Services | |

| Bank of America Corp. | Banks | 2.00% |

| QUALCOMM Inc. | Technology Hardware & | 2.00% |

| | Equipment | |

| Hess Corp. | Oil & Gas Producers | 1.98% |

| Amgen Inc. | Pharmaceuticals & | 1.98% |

| | Biotechnology | |

| As of May 31, 2010, 99.9% of the Fund’s net assets were in equity, cash and short-term instruments. |

See Notes to Financial Statements.

6

GROWTH FUND SCHEDULE OF INVESTMENTS (Unaudited) |

| May 31, 2010 |

| Shares | | Value |

| COMMON STOCKS - 99.9% | | | | |

| Consumer Discretionary - 11.2% | | | | |

| Automobiles & Parts - 0.5% | | | | |

| LKQ Corp. (a) | 36,175 | | $ | 666,344 |

| |

| General Retailers - 5.2% | | | | |

| Abercrombie & Fitch Co. Class A | 16,800 | | | 601,944 |

| Bed Bath & Beyond Inc. (a) | 30,200 | | | 1,355,074 |

| Best Buy Co., Inc. | 32,225 | | | 1,361,506 |

| Kohl’s Corp. (a) | 19,450 | | | 987,088 |

| Office Depot, Inc. (a) | 92,250 | | | 535,050 |

| Target Corp. | 36,570 | | | 1,994,162 |

| | | | | 6,834,824 |

| Media - 5.0% | | | | |

| CBS Corp. Class B | 69,695 | | | 1,014,759 |

| Lions Gate | | | | |

| Entertainment Corp. (a) | 148,300 | | | 1,008,440 |

| The Walt Disney Co. | 30,250 | | | 1,010,955 |

| Time Warner Inc. | 44,975 | | | 1,393,775 |

| Viacom Inc. Class B (a) | 60,700 | | | 2,040,127 |

| | | | | 6,468,056 |

| Personal Goods - 0.5% | | | | |

| Hanesbrands, Inc. (a) | 24,775 | | | 675,862 |

| |

| Consumer Staples - 6.8% | | | | |

| Beverages - 1.2% | | | | |

| PepsiCo, Inc. | 25,850 | | | 1,625,707 |

| |

| Food & Drug Retailers - 4.3% | | | | |

| Sysco Corp. | 57,175 | | | 1,704,387 |

| Walgreen Co. | 58,575 | | | 1,876,743 |

| Wal-Mart Stores, Inc. | 39,200 | | | 1,981,952 |

| | | | | 5,563,082 |

| Household Goods & Home | | | | |

| Construction - 1.3% | | | | |

| The Procter & Gamble Co. | 27,375 | | | 1,672,339 |

| |

| Energy - 15.1% | | | | |

| Oil & Gas Producers - 11.3% | | | | |

| Anadarko Petroleum Corp. | 17,400 | | | 910,542 |

| Chevron Corp. | 18,045 | | | 1,332,984 |

| Devon Energy Corp. | 21,145 | | | 1,350,108 |

| Exxon Mobil Corp. | 87,570 | | | 5,294,482 |

| Hess Corp. | 48,750 | | | 2,593,500 |

| Marathon Oil Corp. | 42,775 | | | 1,329,875 |

| Murphy Oil Corp. | 24,950 | | | 1,331,831 |

| Petrohawk Energy Corp. (a) | 35,400 | | | 680,742 |

| | | | | 14,824,064 |

| Oil Equipment, Services & | | | | |

| Distribution - 3.8% | | | | |

| Helmerich & Payne, Inc. | 27,800 | | | 1,047,504 |

| Schlumberger Ltd. | 21,225 | | | 1,191,784 |

| Smith International, Inc. | 31,850 | | | 1,196,286 |

| Weatherford International Ltd. (a) | 109,350 | | | 1,544,022 |

| | | | | 4,979,596 |

| Financials - 15.3% | | | | |

| Banks - 8.9% | | | | |

| Associated Banc-Corp | 149,340 | | | 2,005,636 |

| Bank of America Corp. | 166,200 | | | 2,615,988 |

| First Horizon National Corp. (a) | 104,673 | | | 1,303,179 |

| JPMorgan Chase & Co. | 50,950 | | | 2,016,601 |

| Marshall & Ilsley Corp. | 86,900 | | | 708,235 |

| Northern Trust Corp. | 45,170 | | | 2,295,088 |

| PNC Financial Services Group, Inc. | 10,750 | | | 674,563 |

| | | | | 11,619,290 |

| Financial Services - 5.9% | | | | |

| American Express Co. | 33,800 | | | 1,347,606 |

| Discover Financial Services | 95,590 | | | 1,285,685 |

| Eaton Vance Corp. | 63,000 | | | 1,883,070 |

| State Street Corp. | 57,100 | | | 2,179,507 |

| T. Rowe Price Group Inc. | 19,250 | | | 953,260 |

| | | | | 7,649,128 |

| Insurance - 0.5% | | | | |

| Aflac, Inc. | 15,060 | | | 667,158 |

| |

| Health Care - 16.6% | | | | |

| Health Care Equipment & | | | | |

| Services - 10.1% | | | | |

| Baxter International Inc. | 39,450 | | | 1,665,973 |

| Henry Schein, Inc. (a) | 23,840 | | | 1,344,814 |

| Medco Health | | | | |

| Solutions, Inc. (a) | 35,505 | | | 2,046,863 |

| Medtronic, Inc. | 33,250 | | | 1,302,735 |

| Patterson Cos., Inc. | 34,155 | | | 1,014,745 |

| ResMed Inc. (a) | 15,225 | | | 957,500 |

| St. Jude Medical, Inc. (a) | 71,640 | | | 2,675,038 |

| TomoTherapy Inc. (a) | 51,644 | | | 162,679 |

| Waters Corp. (a) | 9,890 | | | 676,872 |

| Zimmer Holdings, Inc. (a) | 23,395 | | | 1,308,482 |

| | | | | 13,155,701 |

| Health Care Services - 1.0% | | | | |

| McKesson Corp. | 19,375 | | | 1,356,250 |

See Notes to Financial Statements.

7

GROWTH FUND SCHEDULE OF INVESTMENTS (Unaudited) (Continued) |

| May 31, 2010 |

| Shares | | Value |

| COMMON STOCKS (continued) | | | | | |

| Health Care (continued) | | | | | |

| Pharmaceuticals & | | | | | |

| Biotechnology - 5.5% | | | | | |

| Amgen Inc. (a) | | 50,050 | | $ | 2,591,589 |

| Johnson & Johnson | | 55,135 | | | 3,214,370 |

| Novartis AG ADR | | 29,275 | | | 1,317,668 |

| | | | | | 7,123,627 |

| |

| Industrials - 9.3% | | | | | |

| Aerospace & Defense - 1.0% | | | | | |

| Lockheed Martin Corp. | | 16,475 | | | 1,316,682 |

| |

| General Industrials - 3.5% | | | | | |

| General Electric Co. | | 178,975 | | | 2,926,241 |

| 3M Co. | | 20,570 | | | 1,631,407 |

| | | | | | 4,557,648 |

| Industrial Transportation - 1.0% | | | |

| FedEx Corp. | | 16,000 | | | 1,335,840 |

| |

| Support Services - 3.8% | | | | | |

| Cintas Corp. | | 51,350 | | | 1,335,100 |

| EnergySolutions | | 212,050 | | | 1,325,312 |

| Mobile Mini, Inc. (a) | | 41,800 | | | 668,800 |

| W.W. Grainger, Inc. | | 16,095 | | | 1,637,666 |

| | | | | | 4,966,878 |

| |

| Information Technology - 24.8% | | | | | |

| Computer Programs - 2.6% | | | | | |

| Activision Blizzard, Inc. | | 63,985 | | | 687,839 |

| Electronic Arts Inc. (a) | | 116,735 | | | 1,927,295 |

| Take-Two Interactive Software, | | | | | |

| Inc. (a) | | 61,825 | | | 715,315 |

| | | | | | 3,330,449 |

| Electronic & Electrical | | | | | |

| Equipment - 0.5% | | | | | |

| Flextronics International Ltd. (a) | | 99,295 | | | 651,375 |

| |

| Internet Programs & | | | | | |

| Services - 1.7% | | | | | |

| eBay Inc. (a) | | 106,255 | | | 2,274,920 |

| |

| IT Services - 1.5% | | | | | |

| Alliance Data Systems Corp. (a) | | 9,375 | | | 662,437 |

| Visa Inc. Class A | | 17,885 | | | 1,295,947 |

| | | | | | 1,958,384 |

| Software & Computer | | | | | |

| Services - 4.2% | | | | | |

| Adobe Systems Inc. (a) | | 31,425 | | | 1,008,114 |

| Google Inc. Class A (a) | | 2,720 | | | 1,319,690 |

| Microsoft Corp. | | 122,051 | | | 3,148,916 |

| | | | | | 5,476,720 |

| Technology Hardware & | | | | | |

| Equipment - 14.3% | | | | | |

| Altera Corp. | | 71,500 | | | 1,685,255 |

| Broadcom Corp. Class A | | 20,390 | | | 703,863 |

| Cisco Systems, Inc. (a) | | 110,915 | | | 2,568,791 |

| EMC Corp. (a) | | 73,700 | | | 1,372,294 |

| Hewlett-Packard Co. | | 14,450 | | | 664,844 |

| Intel Corp. | | 158,500 | | | 3,395,070 |

| JDS Uniphase Corp. (a) | | 118,610 | | | 1,364,015 |

| Linear Technology Corp. | | 48,320 | | | 1,351,027 |

| Maxim Integrated Products, Inc. | | 74,530 | | | 1,323,653 |

| QUALCOMM Inc. | | 73,530 | | | 2,614,727 |

| Xilinx, Inc. | | 69,375 | | | 1,696,219 |

| | | | | | 18,739,758 |

| |

| Telecommunication Services - 0.8% | | | |

| Mobile Telecommunications - 0.8% | | | |

| Vodafone Group Plc ADR | | 51,995 | | | 1,045,100 |

| |

| TOTAL COMMON STOCKS | | | | | |

| (COST $114,628,067) | | | | | 130,534,782 |

| |

| | Principal | | | |

| | Amount | | | |

| SHORT-TERM INVESTMENTS - 0.0% | | | | | |

| Variable-Rate Demand | | | | | |

| Notes - 0.0% | | | | | |

| American Family Financial | | | | | |

| Services, 0.100% | $ | 804 | | | 804 |

| |

| Total Variable-Rate Demand Notes | | | | | 804 |

| |

| TOTAL SHORT-TERM INVESTMENTS | | | |

| (COST $804) | | | | | 804 |

| |

| TOTAL INVESTMENTS - 99.9% | | | | | |

| (COST $114,628,871) | | | | | 130,535,586 |

| |

| NET OTHER ASSETS AND | | | | | |

| LIABILITIES - 0.1% | | | | | 134,717 |

| |

| NET ASSETS - 100.0% | | | | $ | 130,670,303 |

| | | | | | |

(a) Non-income producing security.

ADR: American Depository Receipt

See Notes to Financial Statements.

8

MIDCAP FUND INVESTMENT REVIEW (Unaudited) |

| May 31, 2010 |

Portfolio Managers

James T. Evans, CFA

Jason L. Stephens, CFA

John W. Thompson, CFA

Performance

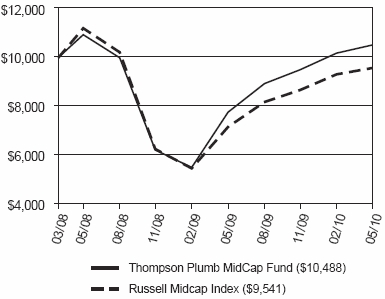

The MidCap Fund produced a total return of 10.89% for the six-month period ended May 31, 2010, as compared to its benchmark, the Russell Midcap Index, which returned 10.41%.

Comparison of Change in Value of a Hypothetical $10,000 Investment

| Average Annual Total Returns |

| Through 05/31/10 |

| | | Since | |

| | | Inception | |

| 1 Year | | (03/31/08) | |

| Thompson Plumb MidCap Fund | 35.40% | | 2.22% | |

| Russell Midcap Index | 33.93% | | -2.14% | |

Gross Expense Ratio as of 3/31/10 was 4.21%.

Net Expense Ratio after reimbursement was 1.30%.*

* The Advisor has contractually agreed to waive management fees and/or reimburse expenses incurred by the MidCap Fund through March 31, 2011.

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by calling 1-800-999-0887 or visiting www.thompsonplumb.com.

Results include the reinvestment of all dividends and capital gains distributions. Investment performance reflects all fee waivers that may be in effect. In the absence of such waivers, total return would be reduced. The performance information reflected in the graph and the table above does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares, nor does it imply future performance. The Russell Midcap Index measures the performance of the 800 smallest companies in the Russell 1000 Index based on total market capitalization. You cannot directly invest in an index.

See Notes to Financial Statements.

9

MIDCAP FUND INVESTMENT REVIEW (Unaudited) (Continued) |

| May 31, 2010 |

Management Commentary

The MidCap Fund outperformed its benchmark during the first half of the fiscal year as a result of overall sector selection coupled with individual issue selection within the Technology and Consumer Staples sectors. These areas of strength were enough to offset relatively underperforming issue selection within the Industrials sector. The positive relative sector selection mostly came from decisions to underweight the Fund’s Utilities holdings and overweight its Consumer Discretionary holdings relative to the Fund’s benchmark. Within the Technology sector, JDS Uniphase, Akamai Technologies and Heartland Payment Systems stood out, with returns of 55%, 65% and 74%, respectively, during the six-month period, while many other holdings outpaced the benchmark’s average return for that sector as well. The Fund’s performance in the Consumer Staples sector benefited from the acquisition of Bare Escentuals by Japanese firm Shiseido at a healthy premium to its share price prior to the announcement of the acquisition.

On the other hand, the Fund’s relative underperformance in the Industrials sector was attributable to a combination of underperforming individual stocks, such as EnergySolutions and Alliant Techsystems, coupled with a deliberate choice to avoid firms that we view as highly cyclical. With many of the names we view as more aggressive trading at healthy multiples of their prior peak earnings levels (much less of their current earnings levels), we believed that their potential for upside was limited. During the first half of the Fund’s fiscal year, the market disagreed with our viewpoint, causing the lag.

We are encouraged by the level of recent merger and acquisition (M&A) activity involving midcap companies, including some companies that have been held by the MidCap Fund. One of the primary reasons behind our launch of the MidCap Fund was to target midcap stocks that we viewed as offering attractive growth opportunities at reasonable valuations. We hoped that the Fund would provide shareholders with the opportunity to own indirect stakes in faster-growing companies before those companies’ business models had matured or their larger brethren had acquired them.

During the first year and a half of the Fund’s existence, the contracting credit markets and difficult environment for private equity funds made the Fund’s performance more dependent on earnings growth and price-to-earnings expansion of companies in the Fund’s portfolio, and less dependent on M&A activity. Now that it appears that some larger firms as well as many private equity funds have regained enough confidence to consider entering into M&A deals, we believe an extra component of shareholder return may be available to Fund shareholders through the premium typically paid to targets in M&A deals.

The first half of the fiscal year has seen Bare Escentuals, Smith International and Virtual Radiologic enter into deals to be acquired, while Pactiv and Airgas have seen their stock prices jump as rumors about potential deals have swirled. The stocks of all of these companies were held by the Fund at the time the transactions were announced or rumors of them made the news. We are hopeful these deals will be precursors to others in the second half of the fiscal year, and we feel that this is likely to be the case as long as the economy continues to recover.

Opinions expressed are subject to change, are not guaranteed and should not be considered investment advice.

Mutual fund investing involves risk. Principal loss is possible. Midcap companies tend to have limited liquidity and greater volatility than large-capitalization companies.

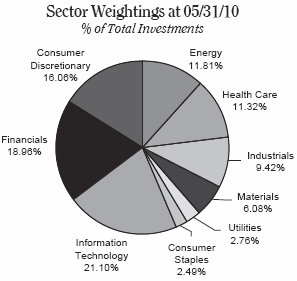

Please refer to the Schedule of Investments on page 12 of this report for holdings information. The management commentary above as well as Fund holdings and asset/sector allocations should not be considered a recommendation to buy or sell any security. In addition, please note that Fund holdings and asset/sector allocations are subject to change.

Current and future portfolio holdings are subject to risk.

Earnings Growth is a measure of growth in a company’s net income over a specific period, often one year.

Price to earnings (P/E) ratio is a common tool for comparing the prices of different common stocks and is calculated by dividing the current market price of a stock by the earnings per share.

See Notes to Financial Statements.

10

MIDCAP FUND INVESTMENT REVIEW (Unaudited) (Continued) |

| May 31, 2010 |

| | Top 10 Equity Holdings at 05/31/10 |

| | | | % of Fund’s |

| Company | Industry | Net Assets |

| Investment Technology Group, Inc. | Financial Services | 2.10% |

| | Maxim Integrated Products, Inc. | Technology Hardware | 2.02% |

| | & Equipment | |

| EnergySolutions | Support Services | 2.01% |

| Henry Schein, Inc. | Health Care Equipment | 2.00% |

| | & Services | |

| Murphy Oil Corp. | Oil & Gas Producers | 2.00% |

| Associated Banc-Corp | Banks | 1.99% |

| ResMed Inc. | Health Care Equipment | 1.99% |

| | & Services | |

| Electronic Arts Inc. | Computer Programs | 1.95% |

| JDS Uniphase Corp. | Technology Hardware | 1.93% |

| | & Equipment | |

| Weatherford International Ltd. | Oil Equipment, Services | 1.90% |

| | & Distribution | |

| As of May 31, 2010, 100.0% of the Fund’s net assets were in equity, cash and short-term instruments. |

See Notes to Financial Statements.

11

MIDCAP FUND SCHEDULE OF INVESTMENTS (Unaudited) |

| May 31, 2010 |

| Shares | | Value |

| COMMON STOCKS - 100.0% | | | | |

| Consumer Discretionary - 16.1% | | | | |

| Automobiles & Parts - 1.0% | | | | |

| LKQ Corp. (a) | 7,110 | | $ | 130,966 |

| |

| General Retailers - 5.3% | | | | |

| Abercrombie & Fitch Co. Class A | 5,260 | | | 188,466 |

| Bed Bath & Beyond Inc. (a) | 4,385 | | | 196,755 |

| Jos. A. Bank Clothiers, Inc. (a) | 1,597 | | | 96,906 |

| Nordstrom, Inc. | 3,340 | | | 132,598 |

| Office Depot, Inc. (a) | 11,629 | | | 67,448 |

| | | | | 682,173 |

| Household Products - 1.8% | | | | |

| Jarden Corp. | 4,610 | | | 134,197 |

| The Middleby Corp. (a) | 1,775 | | | 99,950 |

| | | | | 234,147 |

| Media - 2.5% | | | | |

| CBS Corp. Class B | 6,635 | | | 96,606 |

| Lions Gate | | | | |

| �� Entertainment Corp. (a) | 32,321 | | | 219,783 |

| | | | | 316,389 |

| Personal Goods - 3.7% | | | | |

| Coach, Inc. | 5,768 | | | 237,122 |

| Hanesbrands, Inc. (a) | 8,508 | | | 232,098 |

| | | | | 469,220 |

| Travel & Leisure - 1.8% | | | | |

| Darden Restaurants, Inc. | 5,371 | | | 230,416 |

| |

| Consumer Staples - 2.5% | | | | |

| Food Producers - 2.5% | | | | |

| McCormick & Co., Inc. | 5,083 | | | 196,051 |

| The J. M. Smucker Co. | 2,242 | | | 123,803 |

| | | | | 319,854 |

| |

| Energy - 11.8% | | | | |

| Mining - 0.3% | | | | |

| CONSOL Energy Inc. | 900 | | | 32,832 |

| |

Oil & Gas Producers - 7.2% | | | | |

| ATP Oil & Gas Corp. (a) | 4,765 | | | 50,700 |

| Bill Barrett Corp. (a) | 2,065 | | | 67,236 |

| Chesapeake Energy Corp. | 1,475 | | | 32,952 |

| Denbury Resources Inc. (a) | 2,000 | | | 32,900 |

| Forest Oil Corp. (a) | 1,275 | | | 33,966 |

| Murphy Oil Corp. | 4,811 | | | 256,811 |

| Noble Energy, Inc. | 2,563 | | | 152,473 |

| Petrohawk Energy Corp. (a) | 5,175 | | | 99,515 |

| Pioneer Natural Resources Co. | 550 | | | 35,035 |

| Quicksilver Resources Inc. (a) | 2,690 | | | 32,845 |

| Range Resources Corp. | 2,275 | | | 102,261 |

| Swift Energy Co. (a) | 1,120 | | | 30,968 |

| | | | | 927,662 |

| | | | | |

| Oil Equipment, Services & | | | | |

Distribution - 4.3% | | | | |

| Helmerich & Payne, Inc. | 3,690 | | | 139,039 |

| Smith International, Inc. | 4,590 | | | 172,400 |

| Weatherford International Ltd. (a) | 17,320 | | | 244,558 |

| | | | | 555,997 |

| |

| Financials - 18.9% | | | | |

| Banks - 7.1% | | | | |

| Associated Banc-Corp | 19,009 | | | 255,291 |

| First Horizon National Corp. (a) | 17,040 | | | 212,148 |

| Marshall & Ilsley Corp. | 19,981 | | | 162,845 |

| Northern Trust Corp. | 3,730 | | | 189,521 |

| Regions Financial Corp. | 4,250 | | | 32,428 |

| SunTrust Banks, Inc. | 1,175 | | | 31,666 |

| Zions Bancorporation | 1,380 | | | 33,051 |

| | | | | 916,950 |

| Financial Services - 5.7% | | | | |

| Discover Financial Services | 16,244 | | | 218,482 |

| Eaton Vance Corp. | 8,100 | | | 242,109 |

| Investment Technology | | | | |

| Group, Inc. (a) | 15,965 | | | 269,170 |

| | | | | 729,761 |

| Insurance - 6.1% | | | | |

| Cincinnati Financial Corp. | 6,025 | | | 163,820 |

| Genworth Financial Inc. | | | | |

| Class A (a) | 1,835 | | | 28,608 |

| StanCorp Financial Group, Inc. | 3,818 | | | 163,372 |

| Torchmark Corp. | 4,476 | | | 230,648 |

| Unum Group | 8,726 | | | 201,571 |

| | | | | 788,019 |

| |

| Health Care - 11.3% | | | | |

| Health Care Equipment & | | | | |

| Services - 9.5% | | | | |

| Henry Schein, Inc. (a) | 4,564 | | | 257,455 |

Lincare Holdings Inc. (a) | 1,486 | | | 69,575 |

Patterson Cos., Inc. | 7,505 | | | 222,974 |

ResMed Inc. (a) | 4,055 | | | 255,019 |

Virtual Radiologic Corp. (a) | 5,420 | | | 91,490 |

Waters Corp. (a) | 2,939 | | | 201,145 |

Zimmer Holdings, Inc. (a) | 2,275 | | | 127,241 |

| | | | | 1,224,899 |

See Notes to Financial Statements.

12

MIDCAP FUND SCHEDULE OF INVESTMENTS (Unaudited) (Continued) |

| May 31, 2010 |

| Shares | | Value |

| COMMON STOCKS (continued) | | | | | |

| Health Care Services - 1.8% | | | | | |

| McKesson Corp. | | 1,910 | | $ | 133,700 |

| MWI Veterinary Supply, Inc. (a) | | 1,933 | | | 94,736 |

| | | | | | 228,436 |

| |

| Industrials - 9.4% | | | | | |

| Aerospace & Defense - 1.6% | | | | | |

| Alliant Techsystems Inc. (a) | | 3,029 | | | 208,365 |

| |

| Industrial Engineering - 1.2% | | | | | |

| SPX Corp. | | 2,625 | | | 155,138 |

| |

| Support Services - 6.6% | | | | | |

| Cintas Corp. | | 8,895 | | | 231,270 |

| EnergySolutions | | 41,285 | | | 258,031 |

| Mobile Mini, Inc. (a) | | 8,250 | | | 132,000 |

| W.W. Grainger, Inc. | | 2,208 | | | 224,664 |

| | | | | | 845,965 |

| |

| Information Technology - 21.1% | | | | | |

| Computer Programs - 4.7% | | | | | |

| Activision Blizzard, Inc. | | 15,445 | | | 166,034 |

| Electronic Arts Inc. (a) | | 15,160 | | | 250,292 |

| Take-Two Interactive | | | | | |

| Software, Inc. (a) | | 16,060 | | | 185,814 |

| | | | | | 602,140 |

| Electronic & Electrical | | | | | |

| Equipment - 3.5% | | | | | |

| Celestica Inc. (a) | | 6,981 | | | 64,993 |

| Flextronics International Ltd. (a) | | 29,327 | | | 192,385 |

| Molex Inc. Class A | | 10,960 | | | 192,786 |

| | | | | | 450,164 |

| IT Services - 2.0% | | | | | |

| Alliance Data Systems Corp. (a) | | 1,875 | | | 132,487 |

| Fiserv, Inc. (a) | | 2,647 | | | 125,865 |

| | | | | | 258,352 |

| Software & Computer | | | | | |

| Services - 1.0% | | | | | |

| Akamai Technologies, Inc. (a) | | 3,325 | | | 132,069 |

| |

| Technology Hardware & | | | | | |

| Equipment - 9.9% | | | | | |

| Altera Corp. | | 8,300 | | | 195,631 |

| Broadcom Corp. Class A | | 4,000 | | | 138,080 |

| JDS Uniphase Corp. (a) | | 21,561 | | | 247,951 |

| Linear Technology Corp. | | 6,952 | | | 194,378 |

| Maxim Integrated Products, Inc. | | 14,601 | | | 259,314 |

| Xilinx, Inc. | | 9,511 | | | 232,544 |

| | | | | | 1,267,898 |

| Materials - 6.1% | | | | | |

| Chemicals - 2.7% | | | | | |

| Airgas, Inc. | | 2,097 | | | 131,000 |

| International Flavors & | | | | | |

| Fragrances Inc. | | 4,948 | | | 220,186 |

| | | | | | 351,186 |

| General Materials - 1.1% | | | | | |

| Pactiv Corp. (a) | | 4,950 | | | 141,471 |

| |

| Household Materials - 1.3% | | | | | |

| The Scotts Miracle-Gro Co. | | | | | |

| Class A | | 3,646 | | | 161,992 |

| |

| Industrial Materials - 1.0% | | | | | |

| Nalco Holding Co. | | 5,593 | | | 126,737 |

| |

| Utilities - 2.8% | | | | | |

| Electricity - 0.8% | | | | | |

| Pepco Holdings, Inc. | | 5,985 | | | 96,538 |

| |

| Gas, Water & Multiutilities - 2.0% | | | |

| MDU Resources Group, Inc. | | 8,547 | | | 159,829 |

| SCANA Corp. | | 2,689 | | | 97,584 |

| | | | | | 257,413 |

| |

| TOTAL COMMON STOCKS (COST | | | | | |

| $10,890,249) | | | | | 12,843,149 |

| |

| | Principal | | | |

| | Amount | | | |

| SHORT-TERM INVESTMENTS - 0.0% | | | | | |

| Variable-Rate Demand Notes - 0.0% | | | | |

| American Family Financial | | | | | |

| Services, 0.100% | $ | 130 | | | 130 |

| |

| Total Variable-Rate Demand Notes | | | | | 130 |

| |

| TOTAL SHORT-TERM INVESTMENTS | | | |

| (COST $130) | | | | | 130 |

| |

| TOTAL INVESTMENTS - 100.0% | | | | | |

| (COST $10,890,379) | | | | | 12,843,279 |

| |

| NET OTHER ASSETS AND | | | | | |

| LIABILITIES - 0.0% | | | | | 3,539 |

| |

| NET ASSETS - 100.0% | | | | $ | 12,846,818 |

| | | | | | |

(a) Non-income producing security.

See Notes to Financial Statements.

13

BOND FUND INVESTMENT REVIEW (Unaudited) |

| May 31, 2010 |

Portfolio Managers

James T. Evans, CFA

Jason L. Stephens, CFA

John W. Thompson, CFA

Performance

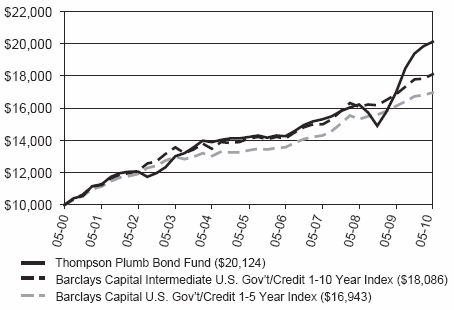

The Bond Fund produced a total return of 3.73% for the six-month period ended May 31, 2010, as compared to its benchmark, the Barclays Capital Intermediate U.S. Government/Credit 1-10 Year Index, which returned 1.65%, and as compared to the Barclays Capital U.S. Government/Credit 1-5 Year Index, which returned 1.18%.

Comparison of Change in Value of a Hypothetical $10,000 Investment

| Average Annual Total Returns |

| Through 05/31/10 |

| 1 Year | | 3 Year | | 5 Year | | 10 Year | |

| Thompson Plumb Bond Fund | 18.19% | | 9.56% | | 7.21% | | 7.24% | |

| Barclays Capital Intermediate U.S. Gov’t/Credit 1-10 Year Index | 7.33% | | 6.50% | | 5.06% | | 6.11% | |

| Barclays Capital U.S. Gov’t/Credit 1-5 Year Index | 5.00% | | 5.85% | | 4.81% | | 5.42% | |

Gross Expense Ratio as of 3/31/10 was 1.20%.

Net Expense Ratio after reimbursement was 0.80%.*

30-Day SEC Yield as of 05/31/10 was 3.10%.

30-Day SEC Yield (without reimbursement) as of 05/31/10 was 2.94%.

* The Advisor has contractually agreed to waive management fees and/or reimburse expenses incurred by the Bond Fund through March 31, 2011.

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by calling 1-800-999-0887 or visiting www.thompsonplumb.com.

Results include the reinvestment of all dividends and capital gains distributions. Investment performance reflects all fee waivers that may be in effect. In the absence of such waivers, total return would be reduced. The performance information reflected in the graph and the table above does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares, nor does it imply future performance. The Barclays Capital Intermediate U.S. Government/Credit 1-10 Year Index is a market-value-weighted index of all investment-grade bonds with maturities of more than one year and less than 10 years. The Barclays Capital U.S. Government/Credit 1-5 Year Index is a market-value-weighted index of all investment-grade bonds with maturities of more than one year and less than 5 years. You cannot directly invest in an index.

See Notes to Financial Statements.

14

BOND FUND INVESTMENT REVIEW (Unaudited) (Continued) |

| May 31, 2010 |

Management Commentary

The Bond Fund outperformed both its benchmark and the Barclays Capital U.S. Government/Credit 1-5 Year Index over the semi-annual period as a result of the Fund’s larger allocation to corporate bonds. This overweighting helped performance in two ways. First, the average spread between Treasury bonds and corporate bonds at the BBB quality tier narrowed by 31 basis points, which more than overcame the impact of the 5-10 basis point increase in Treasury bond yields during the period. As a result, the average corporate bond in the Fund appreciated in value while the average Treasury or Agency bond in the Fund’s benchmark and in the Barclays Capital U.S. Government/Credit 1-5 Year Index depreciated in value. Secondly, with a higher average yield than both Treasury and Agency bonds, corporate bonds simply spun off more return in the form of interest income than those alternate types of bonds. With more of the Fund allocated to this higher-yielding category, the overall return of the Fund was enhanced relative to the benchmark.

Despite the decrease of 31 basis points in corporate bond spreads during the semi-annual time period, the decline as of mid-April of this year was a much larger 95 basis points. It was after this point that worries about European sovereign debt, efforts by the Chinese government to slow China’s economy, and the Deepwater Horizon oil spill all conspired to create a flight to quality among investors. As a result, corporate bond spreads ended the period at 181 basis points, at the higher end of the historical “normal range” of 100-200 basis points. At these levels we believe owning corporate bonds is still an attractive alternative to owning Treasury or Agency debt, and will likely maintain our current allocation. The steepness of the yield curve is such that we feel it remains attractive to buy corporate debt with maturities of 4-5 years, and with the passage of time “ride” each bond down the maturity curve to a 1-2 year maturity. Thus we expect that the current “barbell” strategy of buying corporate debt with maturities of 4-5 years along with Treasury and Agency debt with maturities of 6 months or less is likely to remain in place for the immediate future.

Opinions expressed are subject to change, are not guaranteed and should not be considered investment advice.

Mutual fund investing involves risk. Principal loss is possible. Investments in debt securities typically decrease in value when interest rates rise. This risk is usually greater for longer-term debt securities. Investments in asset-backed and mortgage-backed securities involve additional risks such as credit risk, prepayment risk, possible illiquidity and default, and increased susceptibility to adverse economic developments.

Please refer to the Schedule of Investments on page 17 of this report for holdings information. The management commentary above as well as Fund holdings should not be considered a recommendation to buy or sell any security. In addition, please note that Fund holdings are subject to change.

Current and future portfolio holdings are subject to risk.

SEC Yield is a standardized yield computed by dividing the net investment income per share earned during the 30-day period prior to quarter-end and was created to allow for fairer comparisons among bond funds.

Basis point is a unit that is equal to 1/100th of 1%, and is used to denote the change in a financial instrument.

Yield is the income earned from a bond, which takes into account the sum of the interest payment, the redemption value at the bond’s maturity, and the initial purchase price of the bond.

See Notes to Financial Statements.

15

BOND FUND INVESTMENT REVIEW (Unaudited) (Continued) |

| May 31, 2010 |

Asset Allocation at 05/31/10

% of Total Investments

| Portfolio Concentration at 05/31/10 |

| (Includes cash and cash equivalents) |

| % of Total Investments |

| Quality |

| U.S. Government and Agency Issues | | 19.3% | |

| AA | | 5.4% | |

| A | | 16.8% | |

| BBB | | 51.2% | |

| BB and Below | | 4.3% | |

| Not Rated | | 0.1% | |

| Short-Term Investments | | 2.7% | |

| Common Stocks | | 0.2% | |

| | 100.0% | |

| | | | |

| Effective Maturity |

| Under 1 year | | 25.2% | |

| 1 to 3 years | | 11.7% | |

| 3 to 5 years | | 46.0% | |

| 5 to 10 years | | 16.1% | |

| Over 10 years | | 0.8% | |

| Common Stocks | | 0.2% | |

| | 100.0% | |

| | | | |

See Notes to Financial Statements.

16

BOND FUND SCHEDULE OF INVESTMENTS (Unaudited) |

| May 31, 2010 |

| | Shares or | | | |

| | Principal | | | |

| | Amount | | Value |

| COMMON STOCKS - 0.2% | | | | | | |

| Financials - 0.2% | | | | | | |

| Financial Services - 0.2% | | | | | | |

| CIT Group, Inc. (a) | | | 17,450 | | $ | 641,985 |

| | | | | | |

| TOTAL COMMON STOCKS | | | | | | |

| (COST $501,587) | | | | | | 641,985 |

| | | | | | |

| BONDS - 95.2% | | | | | | |

| Collateralized Mortgage | | | | | | |

| Obligations - 0.8% | | | | | | |

| General American Railcar II | | | | | | |

| 6.210% due 9/20/2017 | | $ | 2,421,166 | | | 2,475,846 |

| | | | | | |

| Total Collateralized Mortgage | | | | | | |

| Obligations | | | | | | 2,475,846 |

| | | | | | |

| Convertible Bonds - 1.3% | | | | | | |

| Amgen Inc. | | | | | | |

| 0.375% due 2/1/2013 | | | 782,000 | | | 771,248 |

| EMC Corp. | | | | | | |

| 1.750% due 12/1/2013 | | | 1,000,000 | | | 1,276,250 |

| Medtronic, Inc. | | | | | | |

| 1.625% due 4/15/2013 | | | 991,000 | | | 1,004,626 |

| NASDAQ OMX Group, Inc. | | | | | | |

| 2.500% due 8/15/2013 | | | 1,020,000 | | | 977,925 |

| | | | | | |

| Total Convertible Bonds | | | | | | 4,030,049 |

| | | | | | |

| Corporate Bonds - 73.9% | | | | | | |

| Alcoa Inc. | | | | | | |

| 6.000% due 7/15/2013 | | | 200,000 | | | 211,859 |

| American Express | | | | | | |

| 0.428% due 10/4/2010 (b) | | | 400,000 | | | 399,876 |

| 6.650% due 9/15/2015 | | | 90,000 | | | 98,787 |

| 6.900% due 9/15/2015 | | | 277,000 | | | 307,265 |

| American General Finance | | | | | | |

| 6.000% due 10/15/2014 | | | 1,000,000 | | | 852,660 |

| 6.000% due 12/15/2014 | | | 1,000,000 | | | 817,555 |

| 6.900% due 12/15/2017 | | | 1,000,000 | | | 795,000 |

| American Standard Cos., Inc. | | | | | | |

| 5.500% due 4/1/2015 | | | 25,000 | | | 26,721 |

| Amphenol Corp. | | | | | | |

| 4.750% due 11/15/2014 | | | 1,698,000 | | | 1,781,163 |

| Arden Realty LP | | | | | | |

| 5.250% due 3/1/2015 | | | 3,019,000 | | | 3,205,097 |

| Associated Banc-Corp | | | | | | |

| 6.750% due 8/15/2011 | | | 2,622,000 | | | 2,618,106 |

| Axis Capital Holdings | | | | | | |

| 5.750% due 12/1/2014 | | | 2,244,000 | | | 2,383,599 |

| Bank of America Corp. | | | | | | |

| 7.375% due 5/15/2014 | | | 866,000 | | | 956,210 |

| 5.375% due 6/15/2014 | | | 50,000 | | | 51,666 |

| 5.150% due 8/15/2015 | | | 34,000 | | | 34,087 |

| 5.350% due 9/15/2015 | | | 383,000 | | | 389,744 |

| 5.250% due 12/1/2015 | | | 333,000 | | | 333,137 |

| BB&T Corp. | | | | | | |

| 5.200% due 12/23/2015 | | | 769,000 | | | 820,292 |

| Bear Stearns Cos. LLC | | | | | | |

| 3.760% due 3/10/2014 (b) | | | 270,000 | | | 252,428 |

| 3.710% due 4/10/2014 (b) | | | 100,000 | | | 95,614 |

| Berkshire Hathaway | | | | | | |

| 4.200% due 12/15/2010 | | | 1,448,000 | | | 1,474,425 |

| Best Buy Co. | | | | | | |

| 6.750% due 7/15/2013 | | | 570,000 | | | 639,192 |

| Black Hills Corp. | | | | | | |

| 9.000% due 5/15/2014 | | | 2,442,000 | | | 2,838,796 |

| Boston Properties LP | | | | | | |

| 5.625% due 4/15/2015 | | | 331,000 | | | 355,885 |

| Boston Scientific Corp. | | | | | | |

| 5.450% due 6/15/2014 | | | 292,000 | | | 295,996 |

| 4.500% due 1/15/2015 | | | 3,072,000 | | | 2,988,190 |

| 6.250% due 11/15/2015 | | | 2,606,000 | | | 2,712,317 |

| Brinker International | | | | | | |

| 5.750% due 6/1/2014 | | | 5,372,000 | | | 5,591,102 |

| Capital One Bank | | | | | | |

| 6.500% due 6/13/2013 | | | 423,000 | | | 462,395 |

| Caterpillar Inc. | | | | | | |

| 4.300% due 6/1/2010 | | | 1,000,000 | | | 1,000,000 |

| CBS Corp. | | | | | | |

| 8.200% due 5/15/2014 | | | 967,000 | | | 1,131,442 |

| CenterPoint Energy, Inc. | | | | | | |

| 6.850% due 6/1/2015 | | | 192,000 | | | 215,941 |

| CIT Group, Inc. | | | | | | |

| 7.000% due 5/1/2013 | | | 202,759 | | | 195,156 |

| 7.000% due 5/1/2014 | | | 304,143 | | | 285,894 |

| 7.000% due 5/1/2015 | | | 304,143 | | | 280,572 |

| 7.000% due 5/1/2016 | | | 506,906 | | | 460,017 |

| 7.000% due 5/1/2017 | | | 709,672 | | | 640,479 |

| Citigroup, Inc. | | | | | | |

| 5.625% due 8/27/2012 | | | 250,000 | | | 258,498 |

| 5.000% due 9/15/2014 | | | 469,000 | | | 463,717 |

| Commercial Net Lease Realty, Inc. | | | | | | |

| 6.150% due 12/15/2015 | | | 426,000 | | | 438,876 |

See Notes to Financial Statements.

17

BOND FUND SCHEDULE OF INVESTMENTS (Unaudited) (Continued) |

| May 31, 2010 |

| | | Principal | | | |

| | | Amount | | Value |

| BONDS (continued) | | | | | | |

| | Corporate Bonds (continued) | | | | | | |

| CONSOL Energy Inc. | | | | | | |

| 7.875% due 3/1/2012 | | $ | 1,252,000 | | $ | 1,333,380 |

| Continental Corp. | | | | | | |

| 8.375% due 8/15/2012 | | | 150,000 | | | 162,883 |

| Corning Inc. | | | | | | |

| 6.050% due 6/15/2015 | | | 1,000,000 | | | 1,013,307 |

| 6.200% due 3/15/2016 | | | 428,000 | | | 475,190 |

| Countrywide Financial Corp. | | | | | | |

| 6.730% due 4/17/2013 | | | 93,000 | | | 98,344 |

| 6.250% due 5/15/2016 | | | 925,000 | | | 951,232 |

| Coventry Health Care, Inc. | | | | | | |

| 6.300% due 8/15/2014 | | | 2,944,000 | | | 3,119,094 |

| 6.125% due 1/15/2015 | | | 658,000 | | | 662,010 |

| Darden Restaurants | | | | | | |

| 7.125% due 2/1/2016 | | | 75,000 | | | 85,259 |

| Discover Financial Services | | | | | | |

| 0.786% due 6/11/2010 (b) | | | 500,000 | | | 499,898 |

| Dow Chemical Co. | | | | | | |

| 7.600% due 5/15/2014 | | | 1,688,000 | | | 1,933,773 |

| 4.300% due 12/15/2014 | | | 117,000 | | | 118,260 |

| 5.900% due 2/15/2015 | | | 650,000 | | | 700,374 |

| Duquesne Light Holdings Inc. | | | | | | |

| 5.500% due 8/15/2015 | | | 5,820,000 | | | 5,920,430 |

| Fidelity National Financial, Inc. | | | | | | |

| 5.250% due 3/15/2013 | | | 166,000 | | | 168,471 |

| Fifth Third Bancorp | | | | | | |

| 6.250% due 5/1/2013 | | | 1,356,000 | | | 1,464,439 |

| First Tennessee Bank | | | | | | |

| 4.500% due 5/15/2013 | | | 1,780,000 | | | 1,715,502 |

| 4.625% due 5/15/2013 | | | 2,126,000 | | | 2,058,857 |

| 5.050% due 1/15/2015 | | | 2,035,000 | | | 1,976,467 |

| 5.650% due 4/1/2016 | | | 270,000 | | | 259,826 |

| First Union National | | | | | | |

| 7.800% due 8/18/2010 | | | 80,000 | | | 81,061 |

| Fortune Brands, Inc. | | | | | | |

| 4.875% due 12/1/2013 | | | 450,000 | | | 473,455 |

| 6.375% due 6/15/2014 | | | 1,143,000 | | | 1,260,169 |

| 5.375% due 1/15/2016 | | | 54,000 | | | 57,506 |

| GE Capital Franchise Finance | | | | | | |

| 8.750% due 10/15/2010 | | | 208,000 | | | 213,432 |

| General Electric Capital Corp. | | | | | | |

| 4.875% due 10/21/2010 | | | 500,000 | | | 506,929 |

| 4.250% due 12/1/2010 | | | 62,000 | | | 62,882 |

| 6.000% due 10/26/2012 (c) | | | 69,000 | | | 69,834 |

| 5.900% due 5/13/2014 | | | 450,000 | | | 491,645 |

| 5.600% due 7/15/2014 | | | 500,000 | | | 523,845 |

| 4.500% due 5/15/2015 | | | 60,000 | | | 59,933 |

| 5.250% due 6/15/2015 | | | 25,000 | | | 25,881 |

| 5.400% due 6/15/2015 | | | 59,000 | | | 61,463 |

| 5.500% due 8/15/2015 | | | 30,000 | | | 31,449 |

| 5.000% due 4/15/2016 | | | 40,000 | | | 40,236 |

| Genworth Life Insurance Co. | | | | | | |

| 5.875% due 5/3/2013 (e) | | | 1,365,000 | | | 1,422,338 |

| GMAC LLC | | | | | | |

| 7.000% due 10/15/2011 | | | 200,000 | | | 197,053 |

| 7.250% due 8/15/2012 | | | 100,000 | | | 98,011 |

| 7.000% due 11/15/2012 | | | 50,000 | | | 48,145 |

| 7.100% due 1/15/2013 | | | 32,000 | | | 30,988 |

| 6.000% due 7/15/2013 | | | 60,000 | | | 54,942 |

| 0.000% due 6/15/2015 (d) | | | 1,250,000 | | | 796,875 |

| 6.350% due 2/15/2016 (c) | | | 75,000 | | | 65,194 |

| 6.500% due 2/15/2016 (c) | | | 100,000 | | | 87,576 |

| 6.500% due 9/15/2016 (c) | | | 87,000 | | | 75,296 |

| 7.250% due 9/15/2017 | | | 259,000 | | | 228,161 |

| Harley-Davidson | | | | | | |

| 5.250% due 12/15/2012 (e) | | | 1,675,000 | | | 1,752,822 |

| 15.000% due 2/1/2014 | | | 500,000 | | | 658,157 |

| 5.750% due 12/15/2014 (e) | | | 3,800,000 | | | 3,924,199 |

| Hartford Financial Services | | | | | | |

| 3.410% due 6/15/2010 (b) | | | 500,000 | | | 499,565 |

| 7.900% due 6/15/2010 | | | 50,000 | | | 50,115 |

| 5.250% due 10/15/2011 | | | 305,000 | | | 313,636 |

| 4.625% due 7/15/2013 | | | 750,000 | | | 770,200 |

| 5.050% due 7/15/2013 | | | 35,000 | | | 35,248 |

| 4.750% due 3/1/2014 | | | 825,000 | | | 845,569 |

| HCP, Inc. | | | | | | |

| 5.650% due 12/15/2013 | | | 1,368,000 | | | 1,437,564 |

| 6.000% due 3/1/2015 | | | 3,216,000 | | | 3,397,228 |

| 7.072% due 6/8/2015 | | | 531,000 | | | 585,036 |

| Hospitality Properties Trust | | | | | | |

| 6.750% due 2/15/2013 | | | 512,000 | | | 544,038 |

| 7.875% due 8/15/2014 | | | 2,543,000 | | | 2,795,108 |

| 5.125% due 2/15/2015 | | | 1,493,000 | | | 1,460,718 |

| HRPT Properties Trust | | | | | | |

| 5.750% due 11/1/2015 | | | 150,000 | | | 154,560 |

| HSBC Finance Corp. | | | | | | |

| 8.000% due 7/15/2010 | | | 306,000 | | | 308,280 |

| 5.700% due 7/15/2012 | | | 125,000 | | | 130,425 |

| 6.000% due 4/15/2013 | | | 621,000 | | | 661,494 |

| 4.400% due 5/15/2013 | | | 100,000 | | | 99,859 |

| 4.790% due 9/15/2013 (b) | | | 156,000 | | | 151,705 |

| 4.650% due 10/10/2013 (b) | | | 131,000 | | | 125,312 |

| 4.430% due 1/10/2014 (b) | | | 206,000 | | | 202,815 |

See Notes to Financial Statements.

18

BOND FUND SCHEDULE OF INVESTMENTS (Unaudited) (Continued) |

| May 31, 2010 |

| | | | | Principal | | | |

| | | | | | Amount | | Value |

| BONDS (continued) | | | | | | |

| Corporate Bonds (continued) | | | | | | |

| | HSBC Finance Corp. (continued) | | | | | | |

| | | 5.600% due 4/15/2014 | | $ | 75,000 | | $ | 78,550 |

| | | 5.500% due 7/15/2014 | | | 30,000 | | | 30,700 |

| | | 5.500% due 8/15/2014 | | | 45,000 | | | 45,112 |

| | | 6.000% due 8/15/2014 | | | 553,000 | | | 576,406 |

| | | 6.000% due 8/15/2014 | | | 67,000 | | | 69,805 |

| | | 5.800% due 9/15/2014 | | | 153,000 | | | 159,032 |

| | | 5.850% due 9/15/2014 | | | 90,000 | | | 93,682 |

| | | 5.650% due 10/15/2014 | | | 30,000 | | | 30,996 |

| | | 5.750% due 10/15/2014 | | | 274,000 | | | 285,807 |

| | | 5.350% due 11/15/2014 | | | 25,000 | | | 25,688 |

| | | 5.300% due 11/15/2016 | | | 82,000 | | | 80,491 |

| | Ingersoll-Rand | | | | | | |

| | | 9.500% due 4/15/2014 | | | 1,026,000 | | | 1,260,084 |

| | International Bank for | | | | | | |

| | | Reconstruction and | | | | | | |

| | | Development | | | | | | |

| | | 0.000% due 8/15/2010 (d) | | | 79,000 | | | 78,888 |

| | International Lease Finance Corp. | | | | | | |

| | | 5.000% due 6/15/2010 | | | 300,000 | | | 299,789 |

| | ITT Hartford Group | | | | | | |

| | | 7.300% due 11/1/2015 | | | 416,000 | | | 463,159 |

| | Jefferson-Pilot Corp. | | | | | | |

| | | 4.750% due 1/30/2014 | | | 3,739,000 | | | 3,839,344 |

| | John Hancock Life Ins. Co. | | | | | | |

| | | 5.450% due 9/15/2015 | | | 201,000 | | | 212,046 |

| | | 5.450% due 10/15/2015 | | | 29,000 | | | 30,529 |

| | | 5.500% due 11/15/2015 | | | 75,000 | | | 78,975 |

| | | 5.250% due 12/15/2015 | | | 25,000 | | | 26,231 |

| | | 5.500% due 12/15/2015 | | | 25,000 | | | 26,536 |

| | | 5.000% due 4/15/2016 | | | 60,000 | | | 61,769 |

| | Johnson Controls, Inc. | | | | | | |

| | | 5.250% due 1/15/2011 | | | 1,035,000 | | | 1,053,667 |

| | Lexmark International, Inc. | | | | | | |

| | | 5.900% due 6/1/2013 | | | 2,556,000 | | | 2,706,827 |

| | Lincoln National Corp. | | | | | | |

| | | 4.750% due 2/15/2014 | | | 1,638,000 | | | 1,679,980 |

| | Manufacturers & Traders Trust Co. | | | | | | |

| | | 5.585% due 12/28/2020 (b) | | | 1,347,000 | | | 1,257,132 |

| | Marriott International, Inc. | | | | | | |

| | | 5.810% due 11/10/2015 | | | 373,000 | | | 403,402 |

| | Marshall & Ilsley Bank | | | | | | |

| | | 5.350% due 4/1/2011 | | | 1,219,000 | | | 1,230,911 |

| | | 6.375% due 9/1/2011 | | | 2,694,000 | | | 2,729,504 |

| | | 5.300% due 9/8/2011 | | | 757,000 | | | 760,533 |

| | | 5.150% due 2/22/2012 | | | 561,000 | | | 553,264 |

| | | 4.900% due 3/15/2012 | | | 15,000 | | | 14,844 |

| | | 5.500% due 7/15/2012 | | | 10,000 | | | 9,968 |

| | | 5.250% due 9/4/2012 | | | 1,640,000 | | | 1,623,595 |

| | | 5.200% due 2/16/2017 | | | 50,000 | | | 44,614 |

| | Masco Corp. | | | | | | |

| | | 5.875% due 7/15/2012 | | | 1,558,000 | | | 1,612,271 |

| | | 7.125% due 8/15/2013 | | | 2,981,000 | | | 3,142,209 |

| | | 4.800% due 6/15/2015 | | | 500,000 | | | 479,932 |

| | | 6.125% due 10/3/2016 | | | 715,000 | | | 701,276 |

| | Maytag Corp. | | | | | | |

| | | 5.000% due 5/15/2015 | | | 50,000 | | | 50,500 |

| | MBNA Corp. | | | | | | |

| | | 7.500% due 3/15/2012 | | | 100,000 | | | 107,712 |

| | | 6.625% due 6/15/2012 | | | 75,000 | | | 80,071 |

| | | 5.000% due 6/15/2015 | | | 455,000 | | | 459,346 |

| | Merrill Lynch & Co. | | | | | | |

| | | 5.450% due 2/5/2013 | | | 500,000 | | | 521,707 |

| | | 6.150% due 4/25/2013 | | | 455,000 | | | 481,501 |

| | | 0.000% due 8/30/2013 (d) | | | 65,000 | | | 56,832 |

| | | 5.000% due 2/3/2014 | | | 138,000 | | | 139,664 |

| | | 5.450% due 7/15/2014 | | | 1,032,000 | | | 1,063,675 |

| | | 5.000% due 1/15/2015 | | | 143,000 | | | 141,030 |

| | | 5.300% due 9/30/2015 | | | 1,512,000 | | | 1,538,448 |

| | Met Life | | | | | | |

| | | 4.625% due 8/19/2010 (e) | | | 50,000 | | | 50,324 |

| | Montpelier Re Holdings Ltd. | | | | | | |

| | | 6.125% due 8/15/2013 | | | 6,681,000 | | | 6,921,877 |

| | Morgan Stanley | | | | | | |

| | | 4.143% due 6/1/2011 (b) | | | 500,000 | | | 491,050 |

| | | 4.750% due 4/1/2014 | | | 4,268,000 | | | 4,236,895 |

| | | 6.000% due 4/28/2015 | | | 3,440,000 | | | 3,547,417 |

| | | 5.375% due 10/15/2015 | | | 714,000 | | | 704,510 |

| | Nabisco, Inc. | | | | | | |

| | | 7.550% due 6/15/2015 | | | 50,000 | | | 58,587 |

| | National City Corp. | | | | | | |

| | | 0.427% due 6/16/2010 (b) | | | 1,000,000 | | | 999,924 |

| | | 4.900% due 1/15/2015 | | | 1,000,000 | | | 1,068,045 |

| | | 4.250% due 7/1/2018 | | | 200,000 | | | 191,627 |

| | National Rural Utilities | | | | | | |

| | | 7.200% due 10/1/2015 | | | 30,000 | | | 34,616 |

| | NationsBank Corp. | | | | | | |

| | | 0.000% due 8/15/2013 (d) | | | 91,000 | | | 79,512 |

| | | 7.750% due 8/15/2015 | | | 187,000 | | | 209,016 |

| | NiSource Finance Corp. | | | | | | |

| | | 5.400% due 7/15/2014 | | | 215,000 | | | 230,708 |

| | | 10.750% due 3/15/2016 | | | 600,000 | | | 769,543 |

See Notes to Financial Statements.

19

BOND FUND SCHEDULE OF INVESTMENTS (Unaudited) (Continued) |

| May 31, 2010 |

| | | | | Principal | | | |

| | | | | | Amount | | Value |

| BONDS (continued) | | | | | | |

| Corporate Bonds (continued) | | | | | | |

| | Nordstrom, Inc. | | | | | | |

| | | 6.250% due 1/15/2018 | | $ | 1,200,000 | | $ | 1,345,531 |

| | Owens Corning | | | | | | |

| | | 6.500% due 12/1/2016 | | | 840,000 | | | 882,412 |

| | PNC Funding Corp. | | | | | | |

| | | 5.250% due 11/15/2015 | | | 352,000 | | | 375,069 |

| | PPL Energy Supply, LLC | | | | | | |

| | | 6.500% due 5/1/2018 | | | 1,000,000 | | | 1,089,944 |

| | Principal Financial Group | | | | | | |

| | | 7.875% due 5/15/2014 | | | 2,750,000 | | | 3,149,900 |

| | | 4.023% due 4/1/2016 (b) | | | 50,000 | | | 47,075 |

| | Progressive Corp. | | | | | | |

| | | 7.000% due 10/1/2013 | | | 25,000 | | | 27,491 |

| | Protective Life Corp. | | | | | | |

| | | 4.300% due 6/1/2013 | | | 350,000 | | | 354,653 |

| | | 4.875% due 11/1/2014 | | | 820,000 | | | 824,457 |

| | Prudential Financial, Inc. | | | | | | |

| | | 4.750% due 4/1/2014 | | | 5,000 | | | 5,226 |

| | | 5.100% due 9/20/2014 | | | 225,000 | | | 238,508 |

| | | 6.200% due 1/15/2015 | | | 1,100,000 | | | 1,210,374 |

| | | 5.000% due 3/16/2015 | | | 140,000 | | | 143,897 |

| | R.R. Donnelley & Sons Co. | | | | | | |

| | | 4.950% due 4/1/2014 | | | 4,488,000 | | | 4,574,080 |

| | | 5.500% due 5/15/2015 | | | 911,000 | | | 923,954 |

| | Simon Property Group, LP | | | | | | |

| | | 5.300% due 5/30/2013 | | | 1,000,000 | | | 1,072,657 |

| | | 5.750% due 12/1/2015 | | | 1,089,000 | | | 1,184,129 |

| | | 6.100% due 5/1/2016 | | | 1,000,000 | | | 1,096,414 |

| | SLM Corp. | | | | | | |

| | | 5.400% due 10/25/2011 | | | 132,000 | | | 132,345 |

| | | 3.623% due 3/15/2012 (b) | | | 145,000 | | | 131,370 |

| | | 3.643% due 6/15/2012 (b) | | | 106,000 | | | 96,505 |

| | | 3.793% due 6/15/2012 (b) | | | 66,000 | | | 60,568 |

| | | 5.125% due 8/27/2012 | | | 491,000 | | | 481,507 |

| | | 3.793% due 9/15/2012 (b) | | | 65,000 | | | 58,937 |

| | | 3.693% due 12/15/2012 (b) | | | 90,000 | | | 80,592 |

| | | 4.500% due 12/15/2012 | | | 25,000 | | | 23,693 |

| | | 4.500% due 12/15/2012 | | | 87,000 | | | 82,430 |

| | | 5.375% due 1/15/2013 | | | 395,000 | | | 386,319 |

| | | 4.500% due 3/15/2013 | | | 25,000 | | | 23,195 |

| | | 4.700% due 6/15/2013 | | | 10,000 | | | 8,985 |

| | | 4.750% due 6/15/2013 | | | 24,000 | | | 21,596 |

| | | 4.800% due 6/15/2013 | | | 25,000 | | | 23,155 |

| | | 4.593% due 9/15/2013 (b) | | | 91,000 | | | 80,171 |

| | | 5.000% due 10/1/2013 | | | 945,000 | | | 891,630 |

| | | 4.300% due 12/15/2013 | | | 1,000 | | | 920 |

| | | 5.150% due 12/15/2013 | | | 60,000 | | | 56,174 |

| | | 5.250% due 12/15/2013 | | | 30,000 | | | 28,492 |

| | | 4.293% due 1/1/2014 (b) | | | 591,000 | | | 500,807 |

| | | 4.263% due 1/31/2014 (b) | | | 125,000 | | | 102,298 |

| | | 4.700% due 3/15/2014 | | | 25,000 | | | 23,000 |

| | | 4.950% due 3/15/2014 | | | 15,000 | | | 13,829 |

| | | 5.150% due 3/15/2014 | | | 10,000 | | | 9,347 |

| | | 3.763% due 4/1/2014 (b) | | | 1,125,000 | | | 952,616 |

| | | 3.943% due 4/1/2014 (b) | | | 155,000 | | | 128,286 |

| | | 3.843% due 5/1/2014 (b) | | | 500,000 | | | 405,725 |

| | | 5.375% due 5/15/2014 | | | 692,000 | | | 633,524 |

| | | 4.523% due 6/2/2014 (b) | | | 70,000 | | | 58,313 |

| | | 5.100% due 6/15/2014 (c) | | | 20,000 | | | 18,428 |

| | | 5.150% due 6/15/2014 (c) | | | 26,000 | | | 24,000 |

| | | 5.050% due 11/14/2014 | | | 35,000 | | | 30,619 |

| | | 3.893% due 12/15/2014 (b) | | | 444,000 | | | 336,592 |

| | | 6.500% due 12/15/2014 (b) | | | 250,000 | | | 216,238 |

| | | 5.000% due 4/15/2015 | | | 225,000 | | | 195,750 |

| | | 4.093% due 9/15/2015 (b) | | | 90,000 | | | 70,646 |

| | | 5.000% due 9/15/2015 | | | 55,000 | | | 49,029 |

| | | 5.000% due 9/15/2015 | | | 45,000 | | | 40,083 |

| | | 5.000% due 9/15/2015 | | | 25,000 | | | 22,268 |

| | | 4.193% due 12/15/2015 (b) | | | 128,000 | | | 97,763 |

| | | 4.393% due 5/3/2019 (b) | | | 217,000 | | | 153,671 |

| | | 7.000% due 6/15/2021 (c) | | | 79,000 | | | 64,893 |

| | | 5.400% due 4/25/2023 (c) | | | 50,000 | | | 34,543 |

| | StanCorp Financial Group | | | | | | |

| | | 6.875% due 10/1/2012 | | | 505,000 | | | 531,275 |

| | Staples, Inc. | | | | | | |

| | | 9.750% due 1/15/2014 | | | 750,000 | | | 918,500 |

| | Steelcase, Inc. | | | | | | |

| | | 6.500% due 8/15/2011 | | | 2,013,000 | | | 2,046,853 |

| | Sunoco, Inc. | | | | | | |

| | | 4.875% due 10/15/2014 | | | 1,470,000 | | | 1,503,253 |

| | | 9.625% due 4/15/2015 | | | 3,666,000 | | | 4,377,813 |

| | SunTrust Bank | | | | | | |

| | | 5.000% due 9/1/2015 | | | 4,525,000 | | | 4,581,671 |

| | Textron Financial Corp. | | | | | | |

| | | 5.400% due 4/28/2013 | | | 635,000 | | | 656,611 |

| | Time Warner, Inc. | | | | | | |

| | | 6.875% due 5/1/2012 | | | 170,000 | | | 185,262 |

| | Torchmark Corp. | | | | | | |

| | | 7.375% due 8/1/2013 | | | 1,320,000 | | | 1,425,790 |

| | | 6.375% due 6/15/2016 | | | 1,017,000 | | | 1,046,326 |

| | | 7.875% due 5/15/2023 | | | 1,000,000 | | | 1,116,292 |

| | Transamerica Finance Corp. | | | | | | |

| | | 0.000% due 9/1/2012 (d) | | | 100,000 | | | 89,990 |

See Notes to Financial Statements.

20

BOND FUND SCHEDULE OF INVESTMENTS (Unaudited) (Continued) |

| May 31, 2010 |

| | | | | Principal | | | |

| | | | | | Amount | | Value |

| BONDS (continued) | | | | | | |

| Corporate Bonds (continued) | | | | | | |

| | Transatlantic Holdings, Inc. | | | | | | |

| | | 5.750% due 12/14/2015 | | $ | 2,590,000 | | $ | 2,643,199 |

| | Tyco Electronics Group | | | | | | |

| | | 6.000% due 10/1/2012 | | | 395,000 | | | 425,974 |

| | | 5.950% due 1/15/2014 | | | 792,000 | | | 866,758 |

| | UBS PaineWebber Group Inc. | | | | | | |

| | | 7.625% due 2/15/2014 | | | 50,000 | | | 55,533 |

| | UDR, Inc. | | | | | | |

| | | 5.500% due 4/1/2014 | | | 2,386,000 | | | 2,467,644 |

| | | 5.250% due 1/15/2015 | | | 690,000 | | | 708,072 |

| | Unitrin, Inc. | | | | | | |

| | | 4.875% due 11/1/2010 | | | 1,150,000 | | | 1,156,625 |

| | Unum Group | | | | | | |

| | | 7.625% due 3/1/2011 | | | 154,000 | | | 158,975 |

| | | 7.125% due 9/30/2016 | | | 3,200,000 | | | 3,579,984 |

| | UnumProvident Group | | | | | | |

| | | 6.850% due 11/15/2015 (e) | | | 1,900,000 | | | 2,045,567 |

| | Verizon New York | | | | | | |

| | | 6.875% due 4/1/2012 | | | 250,000 | | | 270,539 |

| | Viacom, Inc. | | | | | | |

| | | 5.625% due 8/15/2012 | | | 1,535,000 | | | 1,619,789 |

| | | 6.250% due 4/30/2016 | | | 365,000 | | | 409,737 |

| | Wachovia Bank | | | | | | |

| | | 4.375% due 6/1/2010 | | | 50,000 | | | 50,000 |

| | | 4.800% due 11/1/2014 | | | 1,550,000 | | | 1,615,895 |

| | | 4.875% due 2/1/2015 | | | 500,000 | | | 523,006 |

| | | 5.000% due 8/15/2015 | | | 1,750,000 | | | 1,820,884 |

| | | 5.600% due 3/15/2016 | | | 50,000 | | | 52,678 |

| | | 5.625% due 10/15/2016 | | | 200,000 | | | 212,560 |

| | Wells Fargo & Co. | | | | | | |

| | | 7.550% due 6/21/2010 | | | 89,000 | | | 89,326 |

| | | 4.625% due 8/9/2010 | | | 75,000 | | | 75,502 |

| | | 5.750% due 5/16/2016 | | | 200,000 | | | 215,221 |

| | Westinghouse Credit | | | | | | |

| | | 8.875% due 6/14/2014 | | | 47,000 | | | 54,035 |

| | Wilmington Trust Corp. | | | | | | |

| | | 4.875% due 4/15/2013 | | | 25,000 | | | 24,526 |

| | Wyeth | | | | | | |

| | | 5.500% due 2/1/2014 | | | 1,000,000 | | | 1,111,685 |

| | Wyndham Worldwide | | | | | | |

| | | 9.875% due 5/1/2014 | | | 5,835,000 | | | 6,448,107 |

| | XL Capital | | | | | | |

| | | 6.500% due 1/15/2012 | | | 250,000 | | | 263,837 |

| | | 5.250% due 9/15/2014 | | | 3,678,000 | | | 3,874,424 |

| | Yum! Brands, Inc. | | | | | | |

| | | 6.250% due 4/15/2016 | | | 791,000 | | | 888,087 |

| | Zions Bancorporation | | | | | | |

| | | 5.000% due 11/7/2012 | | | 500,000 | | | 496,571 |

| | | 5.650% due 5/15/2014 | | | 1,700,000 | | | 1,590,471 |

| | | 7.750% due 9/23/2014 | | | 4,313,000 | | | 4,340,970 |

| | | | | | | | | |

| | Total Corporate Bonds | | | | | | 227,968,829 |

| | | | | | | | | |

| Federal Agency Mortgage- | | | | | | |

| | Backed Securities - 0.6% | | | | | | |

| | Fannie Mae | | | | | | |

| | | 6.000% due 10/1/2037, | | | | | | |

| | | Pool #88-8736 | | | 519,958 | | | 557,127 |

| | | 6.000% due 3/1/2038, | | | | | | |

| | | Pool #25-7134 | | | 975,638 | | | 1,045,382 |

| | Ginnie Mae | | | | | | |

| | | 7.000% due 5/15/2033, | | | | | | |

| | | Pool #78-2071 | | | 89,049 | | | 100,437 |

| | | | | | | | | |

| | Total Federal Agency Mortgage- | | | | | | |

| | | Backed Securities | | | | | | 1,702,946 |

| | | | | | | | | |

| United States Government and | | | | | | |

| | Agency Issues - 18.6% | | | | | | |

| | Chattanooga Valley Corp. (TVA) | | | | | | |

| | | 0.000% due 7/1/2010 (d) | | | 305,000 | | | 304,738 |

| | Fannie Mae | | | | | | |

| | | 4.500% due 6/1/2010 | | | 180,000 | | | 180,000 |

| | | 4.625% due 6/1/2010 | | | 215,000 | | | 215,000 |

| | | 3.375% due 6/10/2010 | | | 50,000 | | | 50,038 |

| | | 7.125% due 6/15/2010 | | | 712,000 | | | 713,918 |

| | | 4.625% due 6/16/2010 | | | 25,000 | | | 25,045 |

| | | 4.375% due 6/21/2010 | | | 10,000 | | | 10,022 |

| | | 3.270% due 6/30/2010 | | | 120,000 | | | 120,283 |

| | | 5.125% due 7/6/2010 (c) | | | 330,000 | | | 331,533 |

| | | 3.000% due 7/12/2010 | | | 797,000 | | | 799,502 |

| | | 5.125% due 7/13/2010 (c) | | | 105,000 | | | 105,584 |

| | | 0.000% due 7/15/2010 (d) | | | 41,000 | | | 40,958 |

| | | 4.700% due 7/28/2010 | | | 65,000 | | | 65,447 |

| | | 5.000% due 7/28/2010 (c) | | | 165,000 | | | 166,213 |

| | | 4.750% due 8/2/2010 | | | 60,000 | | | 60,447 |

| | | 0.000% due 8/7/2010 (d) | | | 246,000 | | | 245,626 |

| | | 4.875% due 8/11/2010 | | | 50,000 | | | 50,380 |

| | | 0.000% due 8/12/2010 (d) | | | 35,000 | | | 34,943 |

| | | 3.250% due 8/12/2010 | | | 5,000 | | | 5,030 |

| | | 0.000% due 8/15/2010 (d) | | | 40,000 | | | 39,932 |

| | | 4.250% due 8/15/2010 | | | 671,000 | | | 676,524 |

| | | 4.300% due 8/18/2010 | | | 35,000 | | | 35,297 |

| | | 5.000% due 8/24/2010 | | | 157,000 | | | 158,691 |

See Notes to Financial Statements.

21

BOND FUND SCHEDULE OF INVESTMENTS (Unaudited) (Continued) |

| May 31, 2010 |

| | | | | Principal | | | |

| | | | | | Amount | | Value |

| BONDS (continued) | | | | | | |

| United States Government and | | | | | | |

| | Agency Issues (continued) | | | | | | |

| | | Fannie Mae (continued) | | | | | | |

| | | | 4.375% due 9/13/2010 | | $ | 382,000 | | $ | 386,492 |

| | | | 0.000% due 9/23/2010 (d) | | | 30,000 | | | 29,921 |

| | | | 0.000% due 10/8/2010 (d) | | | 58,000 | | | 57,825 |

| | | | 2.875% due 10/12/2010 | | | 645,000 | | | 651,177 |

| | | | 0.000% due 10/15/2010 (d) | | | 50,000 | | | 49,840 |

| | | | 0.000% due 11/15/2010 (d) | | | 31,000 | | | 30,876 |

| | | | 6.625% due 11/15/2010 | | | 1,160,000 | | | 1,193,922 |

| | | | 4.750% due 12/15/2010 | | | 1,848,000 | | | 1,893,280 |

| | | | 6.080% due 12/15/2010 | | | 80,000 | | | 82,400 |

| | | | 6.250% due 2/1/2011 | | | 495,000 | | | 514,122 |

| | Farmer Mac | | | | | | |

| | | 4.875% due 8/27/2010 | | | 100,000 | | | 101,106 |

| | | 4.625% due 10/12/2010 | | | 2,000 | | | 2,032 |

| | | Federal Farm Credit Banks | | | | | | |

| | | | 0.500% due 6/1/2010 | | | 50,000 | | | 50,000 |

| | | | 2.000% due 6/11/2010 | | | 100,000 | | | 100,046 |

| | | | 3.050% due 6/18/2010 | | | 50,000 | | | 50,066 |

| | | | 5.250% due 6/24/2010 | | | 50,000 | | | 50,160 |

| | | | 2.250% due 7/1/2010 | | | 150,000 | | | 150,251 |

| | | | 4.000% due 7/6/2010 | | | 25,000 | | | 25,091 |

| | | | 5.930% due 7/6/2010 | | | 315,000 | | | 316,740 |

| | | | 4.500% due 7/7/2010 | | | 70,000 | | | 70,298 |

| | | | 5.330% due 8/3/2010 | | | 80,000 | | | 80,700 |

| | | | 4.400% due 8/4/2010 | | | 111,000 | | | 111,807 |

| | | | 1.125% due 8/6/2010 | | | 150,000 | | | 150,264 |

| | | | 4.300% due 8/13/2010 | | | 15,000 | | | 15,122 |

| | | | 5.125% due 8/23/2010 | | | 10,000 | | | 10,109 |

| | | | 4.650% due 8/25/2010 | | | 55,000 | | | 55,565 |

| | | | 4.750% due 8/25/2010 | | | 155,000 | | | 156,629 |

| | | | 4.450% due 8/27/2010 | | | 531,000 | | | 536,334 |

| | | | 6.900% due 9/1/2010 | | | 115,000 | | | 116,847 |

| | | | 3.200% due 9/2/2010 | | | 250,000 | | | 251,772 |

| | | | 2.330% due 9/3/2010 | | | 50,000 | | | 50,267 |

| | | | 1.250% due 9/9/2010 | | | 5,000 | | | 5,014 |

| | | | 5.250% due 9/13/2010 | | | 671,000 | | | 680,221 |

| | | | 6.890% due 9/13/2010 | | | 15,000 | | | 15,284 |

| | | | 5.000% due 9/21/2010 | | | 15,000 | | | 15,218 |

| | | | 4.180% due 9/22/2010 | | | 75,000 | | | 75,910 |

| | | | 4.350% due 9/22/2010 | | | 61,000 | | | 61,772 |

| | | | 4.000% due 9/24/2010 | | | 145,000 | | | 146,709 |

| | | | 1.200% due 9/27/2010 | | | 10,000 | | | 10,031 |

| | | | 4.260% due 9/30/2010 | | | 50,000 | | | 50,664 |

| | | | 4.500% due 10/4/2010 | | | 25,000 | | | 25,363 |

| | | | 6.320% due 10/12/2010 | | | 185,000 | | | 189,088 |

| | | | 4.700% due 10/20/2010 | | | 332,000 | | | 337,710 |

| | | | 4.750% due 11/1/2010 | | | 55,000 | | | 56,029 |

| | | | 5.000% due 11/2/2010 | | | 10,000 | | | 10,199 |

| | | | 4.180% due 11/5/2010 | | | 290,000 | | | 294,853 |

| | | | 6.700% due 11/22/2010 | | | 167,000 | | | 172,095 |

| | | | 3.750% due 12/6/2010 | | | 250,000 | | | 254,308 |

| | | | 5.150% due 12/6/2010 | | | 120,000 | | | 122,948 |

| | | | 6.135% due 12/13/2010 | | | 150,000 | | | 154,587 |

| | | | 4.375% due 12/20/2010 | | | 30,000 | | | 30,654 |

| | | | 6.300% due 12/20/2010 | | | 36,000 | | | 37,176 |

| | | | 6.030% due 12/29/2010 | | | 120,000 | | | 123,879 |

| | | | 0.450% due 1/4/2011 | | | 75,000 | | | 74,996 |

| | | | 5.750% due 1/18/2011 | | | 243,000 | | | 251,112 |

| | | | 5.050% due 2/1/2011 | | | 25,000 | | | 25,758 |

| | Federal Home Loan Banks | | | | | | |

| | | 0.500% due 6/1/2010 | | | 25,000 | | | 25,000 |

| | | 3.000% due 6/11/2010 | | | 2,670,000 | | | 2,672,045 |

| | | 4.250% due 6/11/2010 | | | 695,000 | | | 695,773 |

| | | 5.250% due 6/11/2010 | | | 770,000 | | | 771,070 |

| | | 4.400% due 6/15/2010 | | | 30,000 | | | 30,048 |

| | | 2.750% due 6/18/2010 | | | 200,000 | | | 200,237 |

| | | 4.500% due 6/21/2010 | | | 175,000 | | | 175,414 |

| | | 0.560% due 6/22/2010 | | | 40,000 | | | 40,007 |

| | | 4.500% due 6/22/2010 | | | 20,000 | | | 20,050 |

| | | 5.000% due 6/30/2010 (c) | | | 100,000 | | | 100,381 |

| | | 1.000% due 7/6/2010 | | | 500,000 | | | 500,326 |

| | | 1.000% due 7/7/2010 | | | 50,000 | | | 50,038 |

| | | 4.570% due 7/7/2010 | | | 25,000 | | | 25,108 |

| | | 5.000% due 7/12/2010 (c) | | | 100,000 | | | 100,541 |

| | | 0.500% due 7/13/2010 | | | 15,000 | | | 15,003 |

| | | 1.060% due 7/13/2010 | | | 1,000,000 | | | 1,000,956 |

| | | 4.375% due 7/13/2010 | | | 135,000 | | | 135,650 |

| | | 4.500% due 7/13/2010 | | | 160,000 | | | 160,794 |

| | | 4.320% due 7/14/2010 | | | 50,000 | | | 50,243 |

| | | 3.500% due 7/16/2010 | | | 3,705,000 | | | 3,720,313 |

| | | 0.550% due 7/20/2010 | | | 500,000 | | | 500,210 |

| | | 3.750% due 7/22/2010 | | | 75,000 | | | 75,372 |

| | | 0.550% due 7/28/2010 | | | 440,000 | | | 440,216 |

| | | 1.300% due 7/30/2010 | | | 65,000 | | | 65,100 |

| | | 4.000% due 7/30/2010 | | | 35,000 | | | 35,215 |

| | | 0.550% due 8/4/2010 | | | 50,000 | | | 50,027 |

| | | 1.000% due 8/5/2010 | | | 35,000 | | | 35,047 |

| | | 4.550% due 8/6/2010 | | | 405,000 | | | 408,058 |

| | | 4.516% due 8/10/2010 | | | 210,000 | | | 211,666 |

| | | 4.700% due 8/10/2010 | | | 35,000 | | | 35,289 |

| | | 3.375% due 8/13/2010 | | | 65,000 | | | 65,412 |

| | | 4.125% due 8/13/2010 | | | 865,000 | | | 871,712 |

| | | 4.750% due 8/13/2010 | | | 1,515,000 | | | 1,528,649 |

See Notes to Financial Statements.

22

BOND FUND SCHEDULE OF INVESTMENTS (Unaudited) (Continued) |

| May 31, 2010 |

| | | | | Principal | | | |

| | | | | | Amount | | Value |

| BONDS (continued) | | | | | | |

| United States Government and | | | | | | |

| | Agency Issues (continued) | | | | | | |

| | | Federal Home Loan Banks (continued) | | | | | | |

| | | | 6.875% due 8/13/2010 | | $ | 570,000 | | $ | 577,543 |

| | | | 4.710% due 8/16/2010 | | | 20,000 | | | 20,186 |

| | | | 4.875% due 8/16/2010 | | | 160,000 | | | 161,543 |

| | | | 1.300% due 8/24/2010 | | | 25,000 | | | 25,061 |

| | | | 4.785% due 8/26/2010 | | | 155,000 | | | 156,661 |

| | | | 1.300% due 8/27/2010 | | | 130,000 | | | 130,329 |

| | | | 1.375% due 8/27/2010 | | | 80,000 | | | 80,217 |

| | | | 5.000% due 9/1/2010 | | | 515,000 | | | 521,121 |

| | | | 1.400% due 9/2/2010 | | | 25,000 | | | 25,073 |

| | | | 1.350% due 9/3/2010 | | | 290,000 | | | 290,822 |

| | | | 1.375% due 9/3/2010 | | | 530,000 | | | 531,535 |

| | | | 0.700% due 9/8/2010 | | | 25,000 | | | 25,031 |

| | | | 3.000% due 9/10/2010 | | | 260,000 | | | 261,971 |

| | | | 3.050% due 9/10/2010 | | | 25,000 | | | 25,193 |

| | | | 3.375% due 9/10/2010 | | | 115,000 | | | 115,990 |

| | | | 4.500% due 9/10/2010 | | | 255,000 | | | 257,948 |