UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-04521

| T. Rowe Price State Tax-Free Income Trust |

|

| (Exact name of registrant as specified in charter) |

| |

| 100 East Pratt Street, Baltimore, MD 21202 |

|

| (Address of principal executive offices) |

| |

| David Oestreicher |

| 100 East Pratt Street, Baltimore, MD 21202 |

|

| (Name and address of agent for service) |

Registrant’s telephone number, including area code: (410) 345-2000

Date of fiscal year end: February 28

Date of reporting period: February 28, 2015

Item 1. Report to Shareholders

| New York Tax-Free Money Fund | February 28, 2015 |

The views and opinions in this report were current as of February 28, 2015. They are not guarantees of performance or investment results and should not be taken as investment advice. Investment decisions reflect a variety of factors, and the managers reserve the right to change their views about individual stocks, sectors, and the markets at any time. As a result, the views expressed should not be relied upon as a forecast of the fund’s future investment intent. The report is certified under the Sarbanes-Oxley Act, which requires mutual funds and other public companies to affirm that, to the best of their knowledge, the information in their financial reports is fairly and accurately stated in all material respects.

REPORTS ON THE WEB

Sign up for our E-mail Program, and you can begin to receive updated fund reports and prospectuses online rather than through the mail. Log in to your account at troweprice.com for more information.

Manager’s Letter

Fellow Shareholders

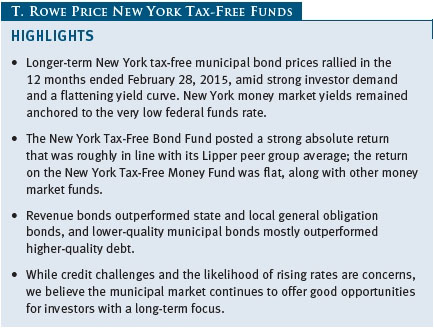

Longer-term New York tax-free municipal bond prices rallied in the 12 months ended February 28, 2015, amid strong investor demand and a flattening yield curve. The Federal Reserve ended its asset purchase program in October 2014 on the back of improvements in the labor market and other aspects of the economy, and investors have shifted their focus to the timing of the Fed’s first rate hike. Yields on shorter-term U.S. Treasury securities climbed as investors anticipated the Fed’s policy tightening—possibly beginning as early as mid-2015—while longer-term Treasury yields defied market expectations and moved lower. Tax-free and taxable money market rates remained close to 0.00%. Lower-quality, longer-maturity revenue bonds outperformed higher-quality, short-maturity issues and general obligation (GO) debt, as investors continued to seek attractive yields in the ongoing low-rate environment. By focusing primarily on revenue bonds, the New York Tax-Free Bond Fund delivered a strong positive return, roughly in line with its benchmark for both the 6- and 12-month periods. The return on the New York Tax-Free Money Fund was roughly flat for both periods, like most money funds.

ECONOMY AND INTEREST RATES

Data on the U.S. labor market and other aspects of the economy continued to improve during the reporting period, as the unemployment rate dropped to 5.5% as of February 2015 from 6.7% 12 months earlier. The federal government’s latest available estimate of gross domestic product growth for the fourth quarter of 2014 showed that the economy expanded at a respectable 2.2% annual rate. Although this represented a slowdown from the 5.0% third-quarter 2014 growth pace, it was still far stronger than the 2.1% contraction in the first quarter of last year, which most economists attributed to severe winter weather. Inflation trends, meanwhile, remained benign. Plummeting oil prices in the second half of 2014 led to falling inflation rates—the consumer price index (CPI) declined 0.1% in the 12 months through January 2015, marking the first negative 12-month CPI reading since October 2009. However, core CPI, which excludes food and energy, rose 1.6% in the 12 months through January.

The Federal Reserve ended its large-scale asset purchases in October 2014, and investors’ attention since then has been focused on when the central bank will make the initial increase in short-term lending rates. In her semiannual testimony before Congress in February, Fed Chair Janet Yellen said that the central bank will begin to evaluate an initial interest rate hike on a “meeting-by-meeting basis,” with policymakers basing their decision on the latest available economic data. While below-target inflation and global economic weakness could delay the Fed’s plans, central bank officials have repeatedly expressed their intent to begin tightening policy around midyear. However, we expect rate increases to occur at a measured pace and not necessarily at regular intervals. Absent a spike in Treasury yields, investor demand for tax-free income should continue to support municipal debt prices.

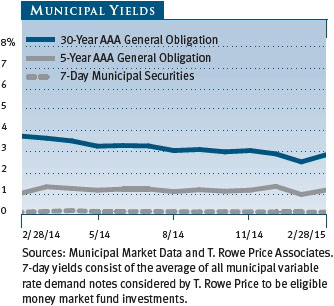

The difference between short- and long-term yields for both Treasuries and municipal debt decreased over the 12-month reporting period, flattening the yield curve for both asset classes amid benign inflation trends. In Treasuries, shorter-term yields climbed considerably, while yields on longer-term securities decreased even more significantly. For example, the yield on the 30-year Treasury “long bond” fell by 98 basis points in the reporting period. (One basis point equals 0.01 percentage points.) Municipal yields followed a similar pattern as yields climbed for shorter-term debt even as they decreased for long-maturity bonds. Money market yields remained anchored close to 0.00%. At the end of the reporting period, intermediate- and long-term municipal debt yielded more than comparable-maturity Treasuries, making them attractive as an alternative for taxable fixed income investors.

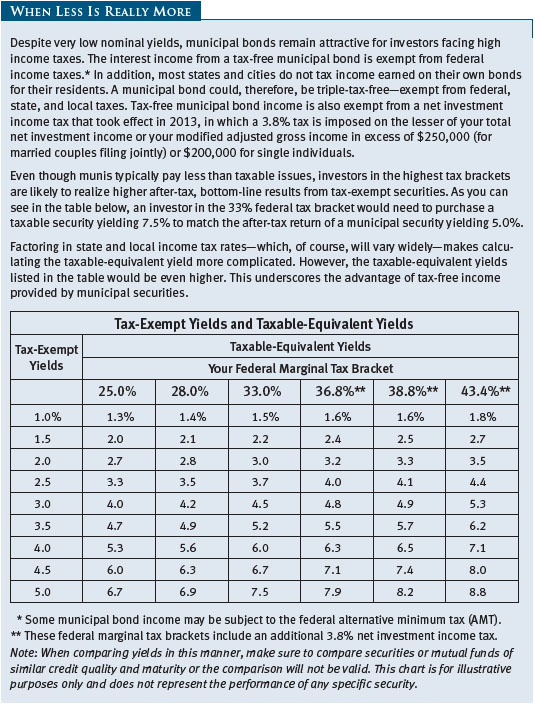

As an illustration of their relative attractiveness, on February 28, 2015, the 2.90% yield offered by a 30-year tax-free GO bond rated AAA was about 112% of the 2.60% pretax yield offered by a 30-year Treasury bond. Including the 3.8% net investment income tax that took effect in 2013 as part of the Affordable Care Act, the top marginal federal tax rate currently stands at 43.4%. An investor in this tax bracket would need to invest in a taxable bond yielding about 5.12% to receive the same after-tax income as that generated by the municipal bond. (To calculate a municipal bond’s taxable-equivalent yield, divide the yield by the quantity of 1.00 minus your federal tax bracket expressed as a decimal—in this case, 1.00 – 0.434, or 0.566.)

MUNICIPAL MARKET NEWS

Demand outstripped supply in the municipal bond market for much of 2014 and provided a strong technical backdrop that helped support bond prices. Toward the end of the year, supply picked up as municipalities took advantage of declining interest rates that made refinancing more attractive. In 2014, total municipal bond issuance exceeded $330 billion, according to The Bond Buyer, which was approximately the same as full-year 2013 issuance. In the first two months of 2015, the volume of supply picked up significantly from comparable periods in previous years, with refundings rising significantly and new-money bonds seeing small increases. Inflows into the asset class were robust, with high yield and intermediate-term portfolios experiencing the most demand. The broad municipal bond market posted positive returns in every month in 2014 as well as January 2015. However, that streak ended in February 2015 when elevated supply and a sell-off in Treasuries led to the first monthly loss for municipals since December 2013.

Municipal bond issuer fundamentals remain generally sound, as austerity-minded state and local government leaders have been conservative about adding to indebtedness since the financial crisis. According to data compiled by the Pew Charitable Trusts, total tax revenue collected by the 50 U.S. states has recovered from its steep decline following the financial crisis. However, while some states and localities have fared quite well, other states, such as Illinois, New Jersey, and Pennsylvania, are more challenged; Puerto Rico, a U.S. territory, is extremely challenged.

Many states and cities, for example, are grappling with underfunded pensions and other post-employment benefit (OPEB) obligations. In contrast with the past, where the market has typically overlooked this long-term risk, we believe pension risks will become increasingly priced into the market over time. Part of our thinking is based on new reporting rules from the Governmental Accounting Standards Board (GASB) that will bring more transparency to states’ funding gaps in the coming year. State and local municipalities will be required to report net liabilities directly on their balance sheets on a mark-to-market basis beginning in fiscal year 2015, as opposed to smoothing the value of plan assets over multiple years and relegating the number to financial statement footnotes.

Detroit and Puerto Rico are two municipal borrowers that have generated materially negative headlines at times over the last two years, but this had only a muted impact on the broad muni market in the reporting period. Market participants seemed to recognize that situations such as these are unique and that municipal bond market fundamentals were strong overall. In the case of Detroit, the U.S. Bankruptcy Court accepted the city’s plan to emerge from bankruptcy in November 2014. The plan calls for 74% and 34% recovery rates for Detroit’s unlimited tax and limited tax GO debt holders, respectively, while retiree pension benefits remain largely intact. Although Detroit GO debt only represents a small portion of the municipal bond market, we have longer-term concerns about the precedent of pension beneficiaries receiving more favorable treatment than bondholders in a bankruptcy. This reinforces our strong preference for single-project revenue bonds that are secured by specified revenue-generating assets or dedicated taxes and are more insulated from pension funding risks.

Meanwhile, Puerto Rico continued to struggle with its finances, and the territory’s economic outlook deteriorated. In June 2014, the territory enacted the Puerto Rico Corporations Debt Enforcement & Recovery Act (Recovery Act), which would have allowed Puerto Rico’s public corporations, including electric utility Puerto Rico Electric Power Authority, to restructure their debt. However, at the end of the reporting period, a federal judge struck down the Recovery Act as unconstitutional and ruled that Puerto Rico’s public corporations may not use the Recovery Act to restructure their debt. As Puerto Rico’s governmental issuers are not eligible to restructure their debts under Chapter 9 of the federal bankruptcy code, any negotiated settlement with creditors promises to be a chaotic process. Moody’s has since downgraded the commonwealth’s general GO to Caa1 from B2, with a negative outlook for all of Puerto Rico’s governmental and public corporation debt. The commonwealth is now seeking an appeal of the ruling, with arguments to be heard in May. We are closely following developments on the island as growing uncertainty and increasing pressure on the commonwealth’s GO debt could send ripples across the broader municipal market. We continue to have little or no direct exposure to Puerto Rico in the New York Tax-Free Funds. Events such as Detroit’s bankruptcy and the ongoing developments in Puerto Rico highlight the need for diligent credit research and careful bond selection.

In terms of sector performance, revenue bonds handily outperformed local and state GOs during the reporting period. We continue to favor bonds backed by a dedicated revenue stream over GOs, with a preference for higher-yielding health care and transportation bonds. Among revenue bonds, the hospital and industrial revenue segments were among the best-performing areas, as investors favored higher-yielding issues. Revenue debt in the special tax and leasing sectors also generated healthy returns but trailed the revenue bond leaders. In general, lower-quality municipal bonds outperformed higher-quality debt as higher yields attracted investors in the ongoing low-rate environment. Longer-maturity bonds also outperformed as the yield curve flattened over the reporting period.

NEW YORK MARKET NEWS

Moody’s Investors Service rates New York State GO debt Aa1, while Standard & Poor’s and Fitch both rate the bonds AA+. All three rating agencies maintain a stable outlook on New York State after upgrading its GO rating last year. Credit agency ratings for New York City are Aa2 from Moody’s, AA from S&P, and AA from Fitch, all with stable outlooks.

New York’s employment growth fell below that of the U.S. as a whole in 2014, and the statewide unemployment rate, at 5.7% in December 2014, was higher than the national rate of 5.6%. Employment in New York City grew at a significantly higher rate in 2014 than in the U.S. as a whole, but the city’s unemployment rate, at 6.4% in December 2014, continued to exceed state and national unemployment levels. The state’s 2013 per capita personal income was 122% of the national average, ranking it the fourth highest in the nation. We expect overall economic growth across the state to remain tepid.

The recovering economy has helped boost tax revenues and strengthen the state’s fiscal condition. Budgetary estimates for fiscal 2015 show a general fund cash balance of $7.8 billion, including a sizable $5.4 billion balance from financial settlements reached with several banks. Estimates also include $1.8 billion in “rainy day” reserves, which have been relatively stable for nearly a decade. The state’s budget for fiscal 2016 proposes allocating $4.6 billion of this balance to the Dedicated Infrastructure Investment Fund while setting aside $850 million as a cushion against future budgetary shortfalls.

According to Moody’s 2014 State Debt Medians Report, New York is the second most heavily indebted state, with $63 billion of net tax-supported debt, and ranks fifth among all states for debt per capita and sixth for debt as a percentage of personal income. Unlike many other states, however, New York’s pension funds are relatively well funded, with an aggregate funded ratio near 85% as of April 1, 2014. However, New York’s OPEB liability is high at $68 billion and primarily reflects health benefits for retired state and State University of New York employees. This liability was completely unfunded as of fiscal year 2015. The majority of New York’s debt is appropriation-backed, which means that the legislature must approve debt service payments on these obligations annually, and it has no legal requirement to continue consenting to these expenses.

New York City continues to demonstrate solid fiscal management, making multiyear financial plans and rolling forward budget surpluses from stronger years. Audited results for fiscal 2014 indicate that the city ended the year with a surplus of $4.6 billion (6.7% of expenditures), which it rolled forward to help balance fiscal 2015 and fiscal 2016. Property taxes remain the city’s largest revenue source and act as a stabilizing factor given the city’s practice of phasing in tax assessments over five years. The city’s projected budget gaps between fiscal 2017 and fiscal 2019 increased last year due to the settlement of long outstanding labor contracts. While this is negative, those projections remain well below levels seen during the recession. Of more concern is that New York City’s long-term liabilities are quite high. Per capita GO debt was just under $5,000 in fiscal 2014. The city’s pension plans were 73% funded at the end of fiscal year 2014 based upon new reporting standards from the GASB Statement No. 68. The net OPEB obligation is very high at $90 billion.

PORTFOLIO STRATEGIES

New York Tax-Free Money Fund

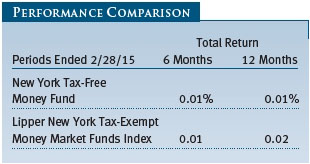

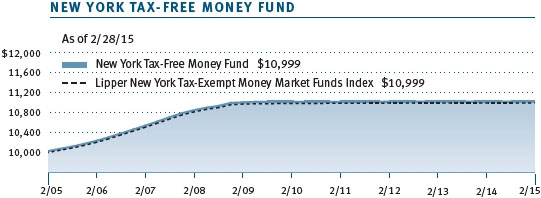

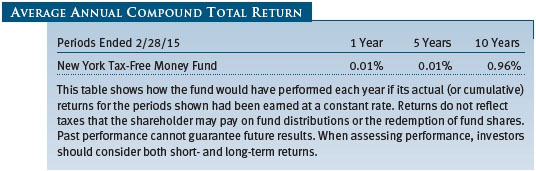

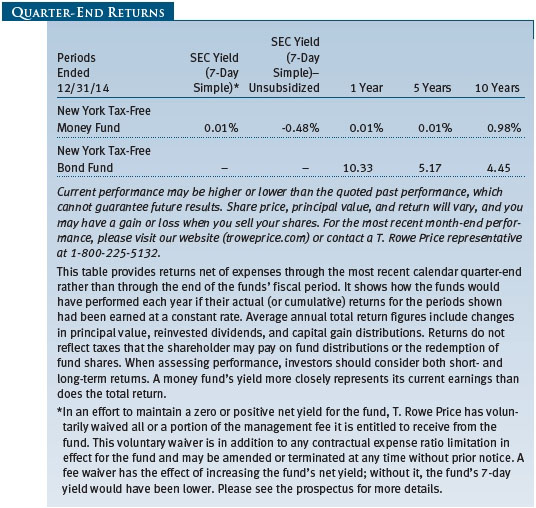

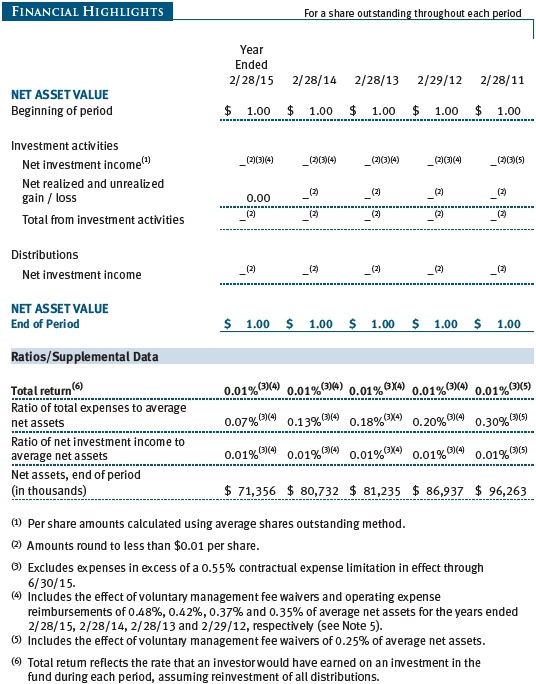

The New York Tax-Free Money Fund returned 0.01% for the 6- and 12-month periods ended February 28, 2015, and was roughly flat compared with the return for the Lipper New York Tax-Exempt Money Market Funds Index. All money market rates continue to be closely tied to the Federal Reserve’s fed funds target rate of 0.00% to 0.25%. While performance comparisons are difficult in this extremely low interest rate environment, the fund’s long-term record relative to its competitors remained favorable. (Based on cumulative total return, Lipper ranked the New York Tax-Free Money Fund 7 of 51, 17 of 51, 32 of 49, and 21 of 41 New York tax-exempt money market funds for the 1-, 3-, 5-, and 10-year periods ended February 28, 2015, respectively. Past performance cannot guarantee future results.)

Persistently low rates continue to suppress income for investors in the New York Tax-Free Money Fund. However, for the first time in over six years, the possibility of higher rates looms on the investment horizon. The Fed, which has maintained a zero rate stance since the 2008 financial crisis, seems inclined to begin tightening monetary policy sometime in 2015. Most market observers feel that the U.S. economy is now strong enough—despite the absence of inflation—for the Fed to lift rates this summer.

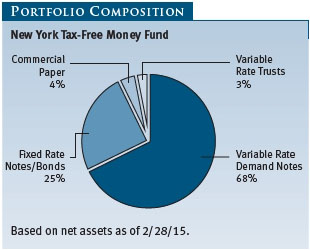

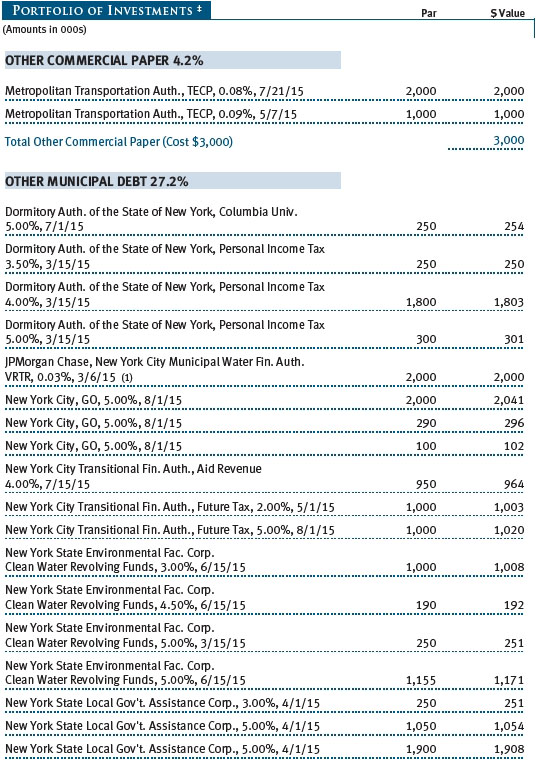

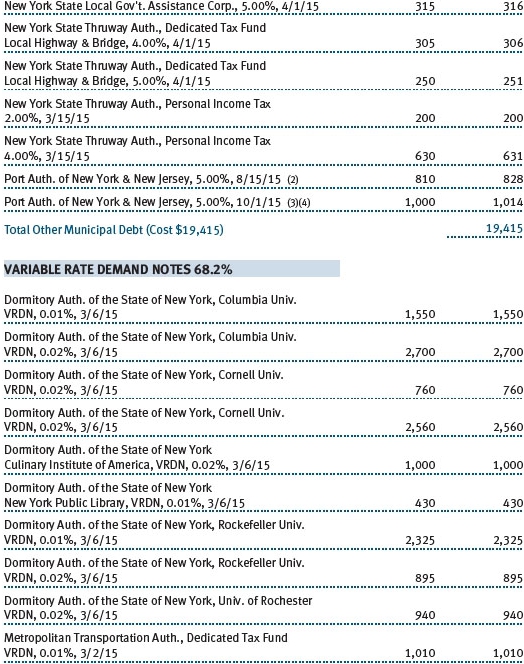

Municipal money markets have yet to price in this sentiment. After oscillating in a relatively narrow range during the first half of the year, the slope of the New York municipal money market yield curve steepened over the past six months as overnight and seven-day yields moved lower by two to three basis points to 0.02%, while the yield on one-year paper moved four basis points higher to 0.16%. Persistently strong demand for high-quality, short-maturity New York investments explains much of this move. As expectations build for a Fed liftoff, we would expect to see such sentiment affecting one-year yields, though front-end yields (one to three months) are likely to move only when a rate increase appears imminent. The low interest rates over the last few years continue to contribute to a supply/demand imbalance as issuers chose to borrow for longer periods to lock in favorable financing costs. We have discussed this concern in prior letters, and, at this time, we see no signs of abatement ahead. Net new issuance of variable rate demand notes (VRDNs)—which represent 68% of the portfolio—has been negative since 2008. For example, net new VRDN issuance was down nearly 9% in 2014 after dropping 14% in 2013 and 13% in 2012. With these reductions in supply, investors have been left to be price-takers with VRDN yields of 0.01% to 0.03%. With the Fed poised to raise interest rates later this year, investors seem inclined to take a wait-and-see approach by buying VRDNs and commercial paper with less than three-month maturities, anchoring the front-end of the yield curve.

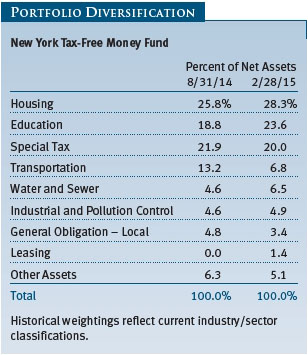

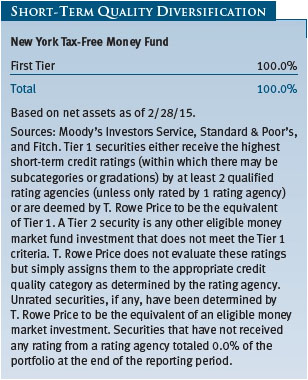

Credit quality in New York continues to rebound somewhat, as the improving economy benefits many municipal issuers primarily through higher tax revenues. Continuing our policy of only investing in the most highly rated debt, we have significant exposures to the housing, education, and revenue bond sectors. Some of our prominent positions in the portfolio include credits related to the New York City Housing Authority, Columbia University, and the New York State Local Government Assistance Corporation. Many of our VRDN issues continue to rely on higher-quality banks such as TD Bank and JP Morgan Chase for credit enhancement, while many of our housing bonds are backed by the Federal National Mortgage Association (Fannie Mae) and Federal Home Loan Mortgage Corporation. (Please refer to the fund’s portfolio of investments for a complete list of our holdings and the amount each represents in the portfolio.)

With a Fed rate liftoff on the investment horizon, we are less inclined to invest in longer-maturity bonds, the prices of which we believe do not reflect our interest rate expectations. As such, the fund’s weighted average maturity will move shorter until we believe the yield curve correctly prices in near-term rate increases. As always, we remain committed to managing a high-quality, diversified portfolio focused on liquidity and stability of principal, which we deem to be of the utmost importance to our shareholders.

Finally, as we discussed in our last shareholder letter, the Securities and Exchange Commission rule changes governing money market funds are expected to become effective in October 2016. T. Rowe Price is currently reviewing these rule changes and their ramifications for shareholders. For most shareholders, there will be minimal or no change to their investments. We intend to offer a full range of money market solutions for all shareholders, and we’ll write more on this very important topic as the situation unfolds.

New York Tax-Free Bond Fund

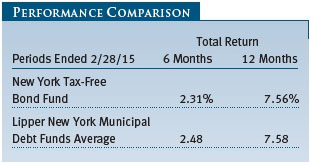

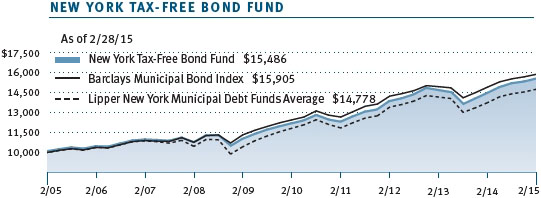

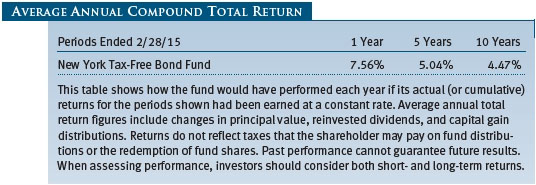

Your fund returned 2.31% and 7.56% for the 6- and 12-month periods ended February 28, 2015, respectively, and performed roughly in line with its Lipper peer group average for both time periods. The New York Tax-Free Bond Fund ranked in the top quintile of its Lipper peer group for the 3- and 10-year periods and also compares favorably in the five-year period. (Based on cumulative total return, Lipper ranked the New York Tax-Free Bond Fund 44 of 100, 18 of 89, 22 of 78, and 12 of 67 New York municipal debt funds for the 1-, 3-, 5-, and 10-year periods ended February 28, 2015, respectively. Past performance cannot guarantee future results.)

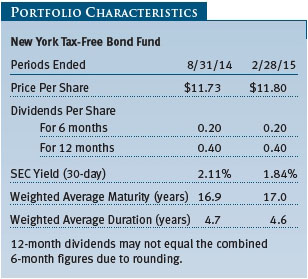

Over the past six months, we have managed the fund’s duration (a measure of its interest rate sensitivity) in a narrow range compared with the Barclays Municipal Bond Index, keeping it relatively unchanged at 4.6 years (down 0.3 from one year ago). We also held the fund’s weighted average maturity steady near 17 years, reflecting our view that the Fed is likely to slowly increase interest rates to more normal levels.

We nudged the fund’s yield curve positioning slightly toward longer maturities, maintaining an overweight to bonds with maturities of 15 years and longer compared with the Barclays index to benefit from the higher yield. This aided performance as the difference between short- and longer-maturity yields decreased over the period. Also, in the second half of the period, we reduced our cash position to purchase longer-maturity bonds as short-term rates were generally paltry and added little to overall returns.

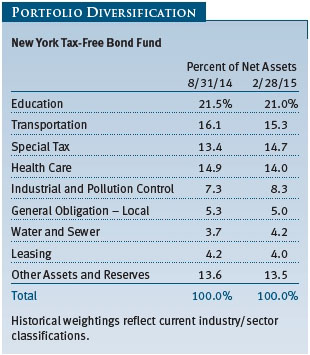

Overall, the fund’s sector weightings saw slight shifts, reflecting our participation in the new issue market. The education sector continued to be the largest weighting in the fund, followed by transportation. In the special tax sector, we added to holdings backed by New York State’s personal income taxes. While New York issuance is heavily dominated by a handful of large issuers mainly concentrated in the New York City region, we took the opportunity to invest in some bonds from issuers that rarely sell tax-exempt debt while also adding diversification. In the industrial and pollution control sector, we added Pratt Paper bonds offering attractive yields. Other new names in the fund included Molloy College and 3 World Trade Center. We continue to favor revenue over GOs, reflecting our longer-term concern that many state and local governments will face fiscal challenges related to pension and health care liabilities. (Please refer to the fund’s portfolio of investments for a complete list of our holdings and the amount each represents in the portfolio.)

The fund’s best performers for the 12-month period were chiefly longer-duration, longer-maturity, and lower-rated securities. These holdings benefited as credit spreads narrowed and longer-term interest rates declined and as investors continued to pursue higher yields. Strong performance contributors included hospital and life care holdings. For example, Amsterdam Harborside, a retirement community and distressed issuer that we have been adding incrementally, contributed to relative returns as a turnaround in the issuer’s financial condition heightened demand and boosted valuations. The fund’s small exposure to tobacco bonds backed by state Master Settlement Agreement payments also outperformed the general market. On the other hand, returns on high-quality, shorter-maturity holdings lagged the broad market, offering little yield and little upside.

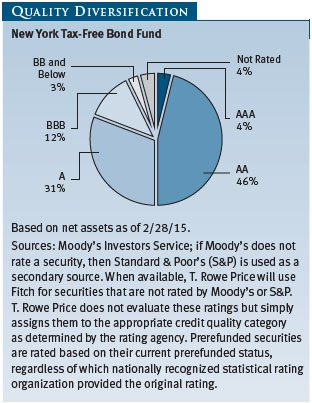

During the last six months, we made minimal shifts in the portfolio’s quality diversification. High-quality AAA and AA holdings, which compose 50% of the fund, were little changed. The fund’s allocation to A rated holdings, the next-largest quality category, decreased slightly to 31%. Our exposure to nonrated securities increased to 4%, reflecting purchases in the higher-yielding names discussed earlier. Of note, the fund continues to hold little or no direct debt from the Commonwealth of Puerto Rico.

OUTLOOK

We believe that the municipal bond market remains a high-quality market that offers good opportunities for long-term investors seeking tax-free income. While fundamentals are sound overall and technical support should persist, there could be hurdles in 2015. In particular, with the Fed preparing to tighten monetary policy, we are mindful that rising rates would likely weaken the appetite for bonds with higher interest rate risk.

In addition, while we believe that many states deserve high credit ratings and will be able to continue servicing their debts, we have some longer-term concerns about significant funding shortfalls for pensions and OPEB obligations in some jurisdictions. These funding gaps stem from investment losses during the financial crisis, insufficient plan contributions, and unrealistic return projections. Although few large plans are at risk of insolvency in the near term, the magnitude of unfunded liabilities is becoming more conspicuous in a few states.

History has shown that when negative headlines spark a broad muni sell-off, cheap valuations tend to be short-lived. Investors quickly return to take advantage of more attractive taxable-equivalent yields and the opportunity to purchase high-quality securities at a discount. We believe this resilience will endure, but it is critical to possess the fundamental research prowess to avoid the deteriorating credits at the center of any storm. Ultimately, we believe T. Rowe Price’s independent credit research is our greatest strength and will remain an asset for our investors as we navigate the current market environment. As always, we focus on finding attractively valued bonds issued by municipalities with good long-term fundamentals—an investment strategy that we believe will continue to serve our investors well.

Thank you for investing with T. Rowe Price.

Respectfully submitted,

Joseph K. Lynagh

Chairman of the Investment Advisory Committee

New York Tax-Free Money Fund

Konstantine B. Mallas

Chairman of the Investment Advisory Committee

New York Tax-Free Bond Fund

March 13, 2015

The committee chairmen have day-to-day responsibility for managing the portfolios and work with committee members in developing and executing the funds’ investment programs.

RISKS OF FIXED INCOME INVESTING

Since money market funds are managed to maintain a constant $1.00 share price, there should be little risk of principal loss. However, there is no assurance the fund will avoid principal losses if fund holdings default or are downgraded or if interest rates rise sharply in an unusually short period. In addition, the fund’s yield will vary; it is not fixed for a specific period like the yield on a bank certificate of deposit. An investment in the fund is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. Although a money market fund seeks to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in it. Bonds are subject to interest rate risk (the decline in bond prices that usually accompanies a rise in interest rates) and credit risk (the chance that any fund holding could have its credit rating downgraded or that a bond issuer will default by failing to make timely payments of interest or principal), potentially reducing the fund’s income level and share price.

GLOSSARY

Barclays Municipal Bond Index: A broadly diversified index of tax-exempt bonds.

Basis point: One one-hundredth of one percentage point, or 0.01%.

Credit spreads: The amount of additional yield demanded by bond investors in exchange for buying riskier assets.

Duration: A measure of a bond fund’s sensitivity to changes in interest rates. For example, a fund with a duration of five years would fall about 5% in price in response to a one-percentage-point rise in interest rates, and vice versa.

Federal funds rate: The interest rate charged on overnight loans of reserves by one financial institution to another in the United States. The Federal Reserve sets a target federal funds rate to affect the direction of interest rates.

General obligation (GO) debt: A government’s strongest pledge that obligates its full faith and credit, including, if necessary, its ability to raise taxes.

Gross domestic product: The total market value of all goods and services produced in a country in a given year.

Investment grade: High-quality bonds as measured by one of the major credit rating agencies. For example, Standard & Poor’s designates the bonds in its top four categories (AAA to BBB) as investment grade.

Lipper averages: The averages of available mutual fund performance returns for specified time periods in categories defined by Lipper, Inc.

Lipper indexes: Fund benchmarks that consist of a small number (10 to 30) of the largest mutual funds in a particular category as tracked by Lipper Inc.

Other post-employment benefits (OPEBs): Benefits paid to an employee after retirement, such as premiums for life and health insurance.

Prerefunded bond: A bond that originally may have been issued as a general obligation or revenue bond but that is now secured by an escrow fund consisting entirely of direct U.S. government obligations that are sufficient for paying the bondholders.

Revenue (or revenue-backed) bond: A bond issued to fund specific projects, such as airports, bridges, hospitals, and toll roads, where a portion of the revenue generated is used to service the interest payments on the bond.

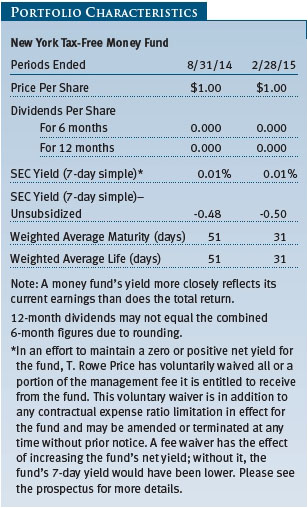

SEC yield (7-day simple): A method of calculating a money fund’s yield by annualizing the fund’s net investment income for the last seven days of each period divided by the fund’s net asset value at the end of the period. Yield will vary and is not guaranteed.

SEC yield (30-day): A method of calculating a fund’s yield that assumes all securities are held until maturity. Yield will vary and is not guaranteed.

Variable rate demand note (VRDN): Generally, a debt security that requires the issuer to redeem at the holder’s discretion on a specified date or dates prior to maturity. Upon redemption, the issuer pays par to the holder who loses future coupon payments that might otherwise be due. The VRDN might be especially attractive at times of rising rates to protect against interest rate risk by redeeming at par value and reinvesting the proceeds in a new bond.

Weighted average life: A measure of a fund’s credit quality risk. In general, the longer the average life, the greater the fund’s credit quality risk. The average life is the dollar-weighted average maturity of a portfolio’s individual securities without taking into account interest rate readjustment dates. Money funds must maintain a weighted average life of less than 120 days.

Weighted average maturity (WAM): A measure of a fund’s interest rate sensitivity. In general, the longer the average maturity, the greater the fund’s sensitivity to interest rate changes. The weighted average maturity may take into account the interest rate readjustment dates for certain securities. Money funds must maintain a weighted average maturity of less than 60 days.

Yield curve: A graph depicting the relationship between yields and maturity dates for a set of similar securities. These curves are in constant flux. One of the key activities in managing any fixed income portfolio is to study the trends reflected by yield curves.

Performance and Expenses

This chart shows the value of a hypothetical $10,000 investment in the fund over the past 10 fiscal year periods or since inception (for funds lacking 10-year records). The result is compared with benchmarks, which may include a broad-based market index and a peer group average or index. Market indexes do not include expenses, which are deducted from fund returns as well as mutual fund averages and indexes.

This chart shows the value of a hypothetical $10,000 investment in the fund over the past 10 fiscal year periods or since inception (for funds lacking 10-year records). The result is compared with benchmarks, which may include a broad-based market index and a peer group average or index. Market indexes do not include expenses, which are deducted from fund returns as well as mutual fund averages and indexes.

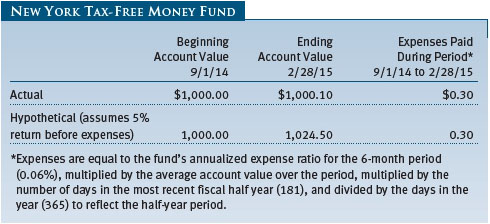

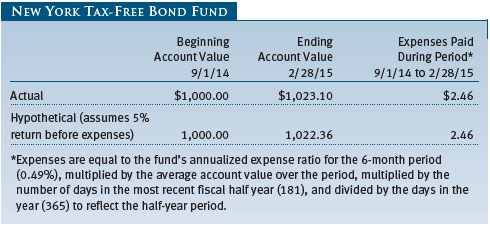

As a mutual fund shareholder, you may incur two types of costs: (1) transaction costs, such as redemption fees or sales loads, and (2) ongoing costs, including management fees, distribution and service (12b-1) fees, and other fund expenses. The following example is intended to help you understand your ongoing costs (in dollars) of investing in the fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the most recent six-month period and held for the entire period.

Actual Expenses

The first line of the following table (Actual) provides information about actual account values and expenses based on the fund’s actual returns. You may use the information on this line, together with your account balance, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number on the first line under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The information on the second line of the table (Hypothetical) is based on hypothetical account values and expenses derived from the fund’s actual expense ratio and an assumed 5% per year rate of return before expenses (not the fund’s actual return). You may compare the ongoing costs of investing in the fund with other funds by contrasting this 5% hypothetical example and the 5% hypothetical examples that appear in the shareholder reports of the other funds. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period.

Note: T. Rowe Price charges an annual account service fee of $20, generally for accounts with less than $10,000. The fee is waived for any investor whose T. Rowe Price mutual fund accounts total $50,000 or more; accounts electing to receive electronic delivery of account statements, transaction confirmations, prospectuses, and shareholder reports; or accounts of an investor who is a T. Rowe Price Preferred Services, Personal Services, or Enhanced Personal Services client (enrollment in these programs generally requires T. Rowe Price assets of at least $100,000). This fee is not included in the accompanying table. If you are subject to the fee, keep it in mind when you are estimating the ongoing expenses of investing in the fund and when comparing the expenses of this fund with other funds.

You should also be aware that the expenses shown in the table highlight only your ongoing costs and do not reflect any transaction costs, such as redemption fees or sales loads. Therefore, the second line of the table is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. To the extent a fund charges transaction costs, however, the total cost of owning that fund is higher.

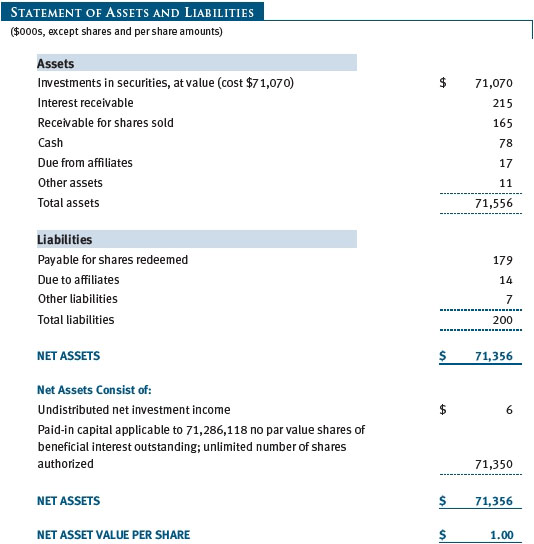

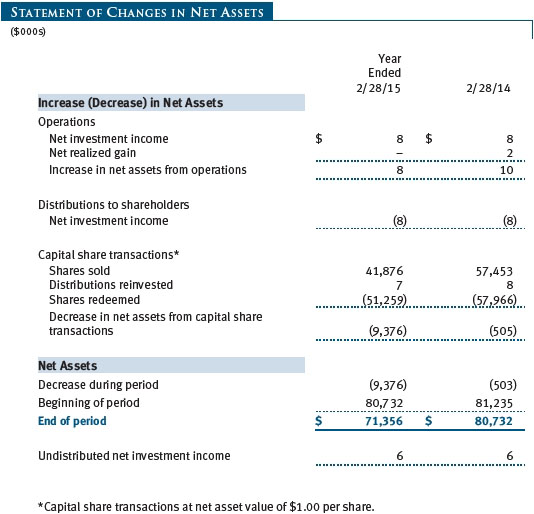

The accompanying notes are an integral part of these financial statements.

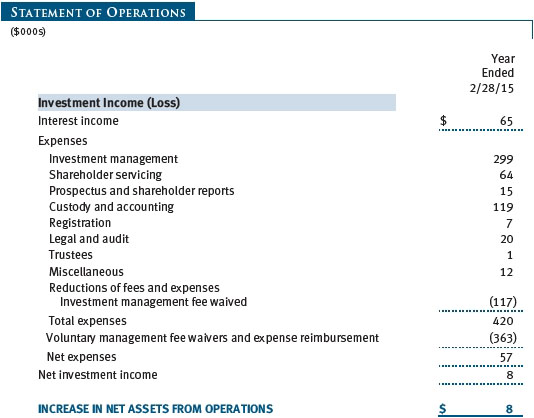

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

| Notes to Financial Statements |

T. Rowe Price State Tax-Free Income Trust (the trust), is registered under the Investment Company Act of 1940 (the 1940 Act). The New York Tax-Free Money Fund (the fund) is a diversified, open-end management investment company established by the trust. The fund commenced operations on August 28, 1986. The fund seeks to provide preservation of capital, liquidity, and, consistent with these objectives, the highest level of income exempt from federal, New York state, and New York City income taxes.

NOTE 1 - SIGNIFICANT ACCOUNTING POLICIES

Basis of Preparation The fund is an investment company and follows accounting and reporting guidance in the Financial Accounting Standards Board (FASB) Accounting Standards Codification Topic 946 (ASC 946). The accompanying financial statements were prepared in accordance with accounting principles generally accepted in the United States of America (GAAP), including but not limited to ASC 946. GAAP requires the use of estimates made by management. Management believes that estimates and valuations are appropriate; however, actual results may differ from those estimates, and the valuations reflected in the accompanying financial statements may differ from the value ultimately realized upon sale or maturity.

Investment Transactions, Investment Income, and Distributions Income and expenses are recorded on the accrual basis. Premiums and discounts on debt securities are amortized for financial reporting purposes. Income tax-related interest and penalties, if incurred, would be recorded as income tax expense. Investment transactions are accounted for on the trade date. Realized gains and losses are reported on the identified cost basis. Distributions to shareholders are recorded on the ex-dividend date. Income distributions are declared daily and paid monthly.

New Accounting Guidance In June 2014, FASB issued Accounting Standards Update (ASU) No. 2014-11, Transfers and Servicing (Topic 860), Repurchase-to-Maturity Transactions, Repurchase Financings, and Disclosures. The ASU changes the accounting for certain repurchase agreements and expands disclosure requirements related to repurchase agreements, securities lending, repurchase-to-maturity and similar transactions. The ASU is effective for interim and annual reporting periods beginning after December 15, 2014. Adoption will have no effect on the fund’s net assets or results of operations.

NOTE 2 - VALUATION

The fund’s financial instruments are valued and its net asset value (NAV) per share is computed at the close of the New York Stock Exchange (NYSE), normally 4 p.m. ET, each day the NYSE is open for business. The fund’s financial instruments are reported at fair value, which GAAP defines as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. The T. Rowe Price Valuation Committee (the Valuation Committee) has been established by the fund’s Board of Trustees (the Board) to ensure that financial instruments are appropriately priced at fair value in accordance with GAAP and the 1940 Act. Subject to oversight by the Board, the Valuation Committee develops and oversees pricing-related policies and procedures and approves all fair value determinations.

Various valuation techniques and inputs are used to determine the fair value of financial instruments. GAAP establishes the following fair value hierarchy that categorizes the inputs used to measure fair value:

Level 1 – quoted prices (unadjusted) in active markets for identical financial instruments that the fund can access at the reporting date

Level 2 – inputs other than Level 1 quoted prices that are observable, either directly or indirectly (including, but not limited to, quoted prices for similar financial instruments in active markets, quoted prices for identical or similar financial instruments in inactive markets, interest rates and yield curves, implied volatilities, and credit spreads)

Level 3 – unobservable inputs

Observable inputs are developed using market data, such as publicly available information about actual events or transactions, and reflect the assumptions market participants would use to price the financial instrument. Unobservable inputs are those for which market data are not available and are developed using the best information available about the assumptions that market participants would use to price the financial instrument. GAAP requires valuation techniques to maximize the use of relevant observable inputs and minimize the use of unobservable inputs. Input levels are not necessarily an indication of the risk or liquidity associated with financial instruments at that level but rather the degree of judgment used in determining those values. For example, securities held by a money market fund are generally high quality and liquid; however, they are reflected as Level 2 because the inputs used to determine fair value are not quoted prices in an active market.

In accordance with Rule 2a-7 under the 1940 Act, the fund values its securities at amortized cost, which approximates fair value. Securities for which amortized cost is deemed not to reflect fair value are stated at fair value as determined in good faith by the Valuation Committee. On February 28, 2015, all of the fund’s financial instruments were classified as Level 2 in the fair value hierarchy.

NOTE 3 - OTHER INVESTMENT TRANSACTIONS

Consistent with its investment objective, the fund engages in the following practices to manage exposure to certain risks and/or to enhance performance. The investment objective, policies, program, and risk factors of the fund are described more fully in the fund’s prospectus and Statement of Additional Information.

Restricted Securities The fund may invest in securities that are subject to legal or contractual restrictions on resale. Prompt sale of such securities at an acceptable price may be difficult and may involve substantial delays and additional costs.

NOTE 4 - FEDERAL INCOME TAXES

No provision for federal income taxes is required since the fund intends to continue to qualify as a regulated investment company under Subchapter M of the Internal Revenue Code and distribute to shareholders all of its income and gains. Distributions determined in accordance with federal income tax regulations may differ in amount or character from net investment income and realized gains for financial reporting purposes. Financial reporting records are adjusted for permanent book/tax differences to reflect tax character but are not adjusted for temporary differences.

The fund files U.S. federal, state, and local tax returns as required. The fund’s tax returns are subject to examination by the relevant tax authorities until expiration of the applicable statute of limitations, which is generally three years after the filing of the tax return but which can be extended to six years in certain circumstances. Tax returns for open years have incorporated no uncertain tax positions that require a provision for income taxes.

Reclassifications to paid-in capital relate primarily to undistributed income on which the fund paid tax. For the year ended February 28, 2015, the following reclassifications were recorded to reflect tax character (there was no impact on results of operations or net assets):

Distributions during the years ended February 28, 2015 and February 28, 2014, totaled $8,000 and $8,000, respectively, and were characterized as tax-exempt income for tax purposes. At February 28, 2015, the tax-basis cost of investments and components of net assets were as follows:

NOTE 5 - RELATED PARTY TRANSACTIONS

The fund is managed by T. Rowe Price Associates, Inc. (Price Associates), a wholly owned subsidiary of T. Rowe Price Group, Inc. (Price Group). The investment management agreement between the fund and Price Associates provides for an annual investment management fee, which is computed daily and paid monthly. The fee consists of an individual fund fee, equal to 0.10% of the fund’s average daily net assets, and a group fee. The group fee rate is calculated based on the combined net assets of certain mutual funds sponsored by Price Associates (the group) applied to a graduated fee schedule, with rates ranging from 0.48% for the first $1 billion of assets to 0.275% for assets in excess of $400 billion. The fund’s group fee is determined by applying the group fee rate to the fund’s average daily net assets. At February 28, 2015, the effective annual group fee rate was 0.29%.

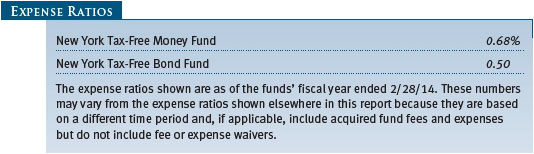

The fund is also subject to a contractual expense limitation through June 30, 2015. During the limitation period, Price Associates is required to waive its management fee and reimburse the fund for any expenses, excluding interest, taxes, brokerage commissions, and extraordinary expenses, that would otherwise cause the fund’s ratio of annualized total expenses to average net assets (expense ratio) to exceed its expense limitation of 0.55%. For a period of three years after the date of any reimbursement or waiver, the fund may repay Price Associates for expenses previously reimbursed and management fees waived to the extent its net assets grow or expenses decline sufficiently to allow repayment without causing the fund’s expense ratio to exceed its expense limitation. Such repayment is subject to shareholder approval. Pursuant to this agreement, management fees in the amount of $117,000 were waived during the year ended February 28, 2015. Including these amounts, management fees waived in the amount of $321,000 remain subject to repayment by the fund at February 28, 2015.

Price Associates may voluntarily waive all or a portion of its management fee and reimburse operating expenses to the extent necessary for the fund to maintain a zero or positive net yield (voluntary waiver). This voluntary waiver is in addition to the contractual expense limit in effect for the fund. Any amounts waived or reimbursed under this voluntary agreement are not subject to repayment by the fund. Price Associates may amend or terminate this voluntary arrangement at any time without prior notice. For the year ended February 28, 2015, management fees waived and operating expenses reimbursed totaled $363,000.

In addition, the fund has entered into service agreements with Price Associates and a wholly owned subsidiary of Price Associates (collectively, Price). Price Associates computes the daily share price and provides certain other administrative services to the fund. T. Rowe Price Services, Inc., provides shareholder and administrative services in its capacity as the fund’s transfer and dividend-disbursing agent. For the year ended February 28, 2015, expenses incurred pursuant to these service agreements were $95,000 for Price Associates and $48,000 for T. Rowe Price Services, Inc. The total amount payable at period-end pursuant to these service agreements is reflected as Due to Affiliates in the accompanying financial statements.

| Report of Independent Registered Public Accounting Firm |

To the Board of Trustees of T. Rowe Price State Tax-Free Income Trust and

Shareholders of New York Tax-Free Money Fund

In our opinion, the accompanying statement of assets and liabilities, including the portfolio of investments, and the related statements of operations and of changes in net assets and the financial highlights present fairly, in all material respects, the financial position of the New York Tax-Free Money Fund (one of the portfolios comprising T. Rowe Price State Tax-Free Income Trust, hereafter referred to as the “Fund”) at February 28, 2015, the results of its operations, the changes in its net assets and the financial highlights for each of the periods indicated therein, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits, which included confirmation of securities at February 28, 2015 by correspondence with the custodian, provide a reasonable basis for our opinion.

PricewaterhouseCoopers LLP

Baltimore, Maryland

April 15, 2015

| Tax Information (Unaudited) for the Tax Year Ended 2/28/15 |

We are providing this information as required by the Internal Revenue Code. The amounts shown may differ from those elsewhere in this report because of differences between tax and financial reporting requirements.

The fund’s distributions to shareholders included $8,000 which qualified as exempt-interest dividends.

| Information on Proxy Voting Policies, Procedures, and Records |

A description of the policies and procedures used by T. Rowe Price funds and portfolios to determine how to vote proxies relating to portfolio securities is available in each fund’s Statement of Additional Information. You may request this document by calling 1-800-225-5132 or by accessing the SEC’s website, sec.gov.

The description of our proxy voting policies and procedures is also available on our website, troweprice.com. To access it, click on the words “Social Responsibility” at the top of our corporate homepage. Next, click on the words “Conducting Business Responsibly” on the left side of the page that appears. Finally, click on the words “Proxy Voting Policies” on the left side of the page that appears.

Each fund’s most recent annual proxy voting record is available on our website and through the SEC’s website. To access it through our website, follow the above directions to reach the “Conducting Business Responsibly” page. Click on the words “Proxy Voting Records” on the left side of that page, and then click on the “View Proxy Voting Records” link at the bottom of the page that appears.

| How to Obtain Quarterly Portfolio Holdings |

The fund files a complete schedule of portfolio holdings with the Securities and Exchange Commission for the first and third quarters of each fiscal year on Form N-Q. The fund’s Form N-Q is available electronically on the SEC’s website (sec.gov); hard copies may be reviewed and copied at the SEC’s Public Reference Room, 100 F St. N.E., Washington, DC 20549. For more information on the Public Reference Room, call 1-800-SEC-0330.

| About the Fund’s Trustees and Officers |

Your fund is overseen by a Board of Trustees (Board) that meets regularly to review a wide variety of matters affecting or potentially affecting the fund, including performance, investment programs, compliance matters, advisory fees and expenses, service providers, and business and regulatory affairs. The Board elects the fund’s officers, who are listed in the final table. At least 75% of the Board’s members are independent of T. Rowe Price Associates, Inc. (T. Rowe Price), and its affiliates; “inside” or “interested” trustees are employees or officers of T. Rowe Price. The business address of each trustee and officer is 100 East Pratt Street, Baltimore, Maryland 21202. The Statement of Additional Information includes additional information about the fund trustees and is available without charge by calling a T. Rowe Price representative at 1-800-638-5660.

| Independent Trustees | | |

| |

| Name | | |

| (Year of Birth) | | |

| Year Elected* | | |

| [Number of T. Rowe Price | | Principal Occupation(s) and Directorships of Public Companies and |

| Portfolios Overseen] | | Other Investment Companies During the Past Five Years |

| | | |

| William R. Brody, M.D., Ph.D. | | President and Trustee, Salk Institute for Biological Studies (2009 to |

| (1944) | | present); Director, BioMed Realty Trust (2013 to present); Director, |

| 2009 | | Novartis, Inc. (2009 to 2014); Director, IBM (2007 to present) |

| [165] | | |

| | | |

| Anthony W. Deering | | Chairman, Exeter Capital, LLC, a private investment firm (2004 to |

| (1945) | | present); Director, Brixmor Real Estate Investment Trust (2012 to |

| 1986 | | present); Director and Advisory Board Member, Deutsche Bank North |

| [165] | | America (2004 to present); Director, Under Armour (2008 to present); |

| | Director, Vornado Real Estate Investment Trust (2004 to 2012) |

| | | |

| Donald W. Dick, Jr. | | Principal, EuroCapital Partners, LLC, an acquisition and management |

| (1943) | | advisory firm (1995 to present) |

| 2001 | | |

| [165] | | |

| | | |

| Bruce W. Duncan | | President, Chief Executive Officer and Director, First Industrial |

| (1951) | | Realty Trust, an owner and operator of industrial properties |

| 2013 | | (2009 to present); Chairman of the Board (2005 to present) and |

| [165] | | Director (1999 to present), Starwood Hotels & Resorts, a hotel and |

| | leisure company |

| | | |

| Robert J. Gerrard, Jr. | | Chairman of Compensation Committee and Director, Syniverse |

| (1952) | | Holdings, Inc., a provider of wireless voice and data services for |

| 2013 | | telecommunications companies (2008 to 2011); Advisory Board |

| [165] | | Member, Pipeline Crisis/Winning Strategies, a collaborative working |

| | to improve opportunities for young African Americans (1997 |

| | to present) |

| | | |

| Karen N. Horn | | Limited Partner and Senior Managing Director, Brock Capital Group, |

| (1943) | | an advisory and investment banking firm (2004 to present); Director, |

| 2003 | | Eli Lilly and Company (1987 to present); Director, Simon Property |

| [165] | | Group (2004 to present); Director, Norfolk Southern (2008 to present) |

| | | |

| Paul F. McBride | | Former Company Officer and Senior Vice President, Human |

| (1956) | | Resources and Corporate Initiatives, Black & Decker Corporation |

| 2013 | | (2004 to 2010) |

| [165] | | |

| | | |

| Cecilia E. Rouse, Ph.D. | | Dean, Woodrow Wilson School (2012 to present); Professor and |

| (1963) | | Researcher, Princeton University (1992 to present); Director, MDRC, |

| 2013 | | a nonprofit education and social policy research organization |

| [165] | | (2011 to present); Member, National Academy of Education (2010 |

| | to present); Research Associate, National Bureau of Economic |

| | Research’s Labor Studies Program (2011 to present); Member, |

| | President’s Council of Economic Advisers (2009 to 2011); Chair |

| | of Committee on the Status of Minority Groups in the Economic |

| | Profession, American Economic Association (2012 to present) |

| | | |

| John G. Schreiber | | Owner/President, Centaur Capital Partners, Inc., a real estate |

| (1946) | | investment company (1991 to present); Cofounder and Partner, |

| 1992 | | Blackstone Real Estate Advisors, L.P. (1992 to present); Director, |

| [165] | | General Growth Properties, Inc. (2010 to 2013); Director, Blackstone |

| | Mortgage Trust, a real estate financial company (2012 to present); |

| | Director and Chairman of the Board, Brixmor Property Group, Inc. |

| | (2013 to present); Director, Hilton Worldwide (2013 to present); |

| | Director, Hudson Pacific Properties (2014 to present) |

| | | |

| Mark R. Tercek | | President and Chief Executive Officer, The Nature Conservancy (2008 |

| (1957) | | to present) |

| 2009 | | |

| [165] | | |

| |

| *Each independent trustee serves until retirement, resignation, or election of a successor. |

| Inside Trustees | | |

| |

| Name | | |

| (Year of Birth) | | |

| Year Elected* | | |

| [Number of T. Rowe Price | | Principal Occupation(s) and Directorships of Public Companies and |

| Portfolios Overseen] | | Other Investment Companies During the Past Five Years |

| | | |

| Edward C. Bernard | | Director and Vice President, T. Rowe Price; Vice Chairman of the |

| (1956) | | Board, Director, and Vice President, T. Rowe Price Group, Inc.; |

| 2006 | | Chairman of the Board, Director, and President, T. Rowe Price |

| [165] | | Investment Services, Inc.; Chairman of the Board and Director, |

| | T. Rowe Price Retirement Plan Services, Inc., and T. Rowe Price |

| | Services, Inc.; Chairman of the Board, Chief Executive Officer, |

| | Director, and President, T. Rowe Price International and T. Rowe |

| | Price Trust Company; Chairman of the Board, all funds |

| | | |

| Edward A. Wiese, CFA | | Director and Vice President, T. Rowe Price Trust Company; |

| (1959) | | Vice President, T. Rowe Price, T. Rowe Price Group, Inc., and T. Rowe |

| 2015 | | Price International; Vice President, State Tax-Free Income Trust |

| [54] | | |

| |

| *Each inside trustee serves until retirement, resignation, or election of a successor. |

| Officers | | |

| |

| Name (Year of Birth) | | |

| Position Held With State Tax-Free Income Trust | | Principal Occupation(s) |

| | | |

| Austin Applegate (1974) | | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President | | Group, Inc.; formerly, Senior Municipal Credit |

| | Research Analyst, Barclays (to 2011) |

| | | |

| R. Lee Arnold, Jr., CFA, CPA (1970) | | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President | | Group, Inc. |

| | | |

| Darrell N. Braman (1963) | | Vice President, Price Hong Kong, Price |

| Vice President | | Singapore, T. Rowe Price, T. Rowe Price Group, |

| | Inc., T. Rowe Price International, T. Rowe Price |

| | Investment Services, Inc., and T. Rowe Price |

| | Services, Inc. |

| | | |

| M. Helena Condez (1962) | | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President | | Group, Inc. |

| | | |

| G. Richard Dent (1960) | | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President | | Group, Inc. |

| | | |

| Charles E. Emrich (1961) | | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President | | Group, Inc. |

| | | |

| Sarah J. Engle (1979) | | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President | | Group, Inc.; formerly, Program Examiner and |

| | Policy Analyst, Office of Management & Budget |

| | (to 2012); Analyst, Moody’s Investor Service |

| | (to 2010) |

| | | |

| John R. Gilner (1961) | | Chief Compliance Officer and Vice President, |

| Chief Compliance Officer | | T. Rowe Price; Vice President, T. Rowe Price |

| | Group, Inc., and T. Rowe Price Investment |

| | Services, Inc. |

| | | |

| Charles B. Hill, CFA (1961) | | Vice President, T. Rowe Price and T. Rowe Price |

| Executive Vice President | | Group, Inc. |

| | | |

| Gregory K. Hinkle, CPA (1958) | | Vice President, T. Rowe Price, T. Rowe Price |

| Treasurer | | Group, Inc., and T. Rowe Price Trust Company |

| | | |

| Dylan Jones, CFA (1971) | | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President | | Group, Inc. |

| | | |

| Marcy M. Lash (1963) | | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President | | Group, Inc. |

| | | |

| Alan D. Levenson, Ph.D. (1958) | | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President | | Group, Inc. |

| | | |

| Patricia B. Lippert (1953) | | Assistant Vice President, T. Rowe Price and |

| Secretary | | T. Rowe Price Investment Services, Inc. |

| | | |

| Joseph K. Lynagh, CFA (1958) | | Vice President, T. Rowe Price, T. Rowe Price |

| Executive Vice President | | Group, Inc., and T. Rowe Price Trust Company |

| | | |

| Konstantine B. Mallas (1963) | | Vice President, T. Rowe Price and T. Rowe Price |

| Executive Vice President | | Group, Inc. |

| | | |

| Hugh D. McGuirk, CFA (1960) | | Vice President, T. Rowe Price and T. Rowe Price |

| President | | Group, Inc. |

| | | |

| James M. Murphy, CFA (1967) | | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President | | Group, Inc. |

| | | |

| Linda A. Murphy (1959) | | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President | | Group, Inc. |

| | | |

| Alexander S. Obaza (1981) | | Vice President, T. Rowe Price, T. Rowe Price |

| Vice President | | Group, Inc., and T. Rowe Price Trust Company |

| | | |

| David Oestreicher (1967) | | Director, Vice President, and Secretary, T. Rowe |

| Vice President | | Price Investment Services, Inc., T. Rowe Price |

| | Retirement Plan Services, Inc., T. Rowe |

| | Price Services, Inc., and T. Rowe Price Trust |

| | Company; Chief Legal Officer, Vice President, |

| | and Secretary, T. Rowe Price Group, Inc.; Vice |

| | President and Secretary, T. Rowe Price and |

| | T. Rowe Price International; Vice President, |

| | Price Hong Kong and Price Singapore |

| | | |

| John W. Ratzesberger (1975) | | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President | | Group, Inc.; formerly, North American Head of |

| | Listed Derivatives Operation, Morgan Stanley |

| | (to 2013) |

| | | |

| Deborah D. Seidel (1962) | | Vice President, T. Rowe Price, T. Rowe Price |

| Vice President | | Group, Inc., T. Rowe Price Investment Services, |

| | Inc., and T. Rowe Price Services, Inc. |

| | | |

| Chen Shao (1980) | | Assistant Vice President, T. Rowe Price |

| Assistant Vice President | | |

| | | |

| Douglas D. Spratley, CFA (1969) | | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President | | Group, Inc. |

| | | |

| Timothy G. Taylor, CFA (1975) | | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President | | Group, Inc. |

| | | |

| Jeffrey T. Zoller (1970) | | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President | | Trust Company |

| |

| Unless otherwise noted, officers have been employees of T. Rowe Price or T. Rowe Price International for at least 5 years. |

Item 2. Code of Ethics.

The registrant has adopted a code of ethics, as defined in Item 2 of Form N-CSR, applicable to its principal executive officer, principal financial officer, principal accounting officer or controller, or persons performing similar functions. A copy of this code of ethics is filed as an exhibit to this Form N-CSR. No substantive amendments were approved or waivers were granted to this code of ethics during the period covered by this report.

Item 3. Audit Committee Financial Expert.

The registrant’s Board of Directors/Trustees has determined that Mr. Bruce W. Duncan qualifies as an audit committee financial expert, as defined in Item 3 of Form N-CSR. Mr. Duncan is considered independent for purposes of Item 3 of Form N-CSR.

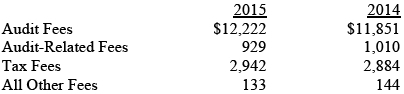

Item 4. Principal Accountant Fees and Services.

(a) – (d) Aggregate fees billed for the last two fiscal years for professional services rendered to, or on behalf of, the registrant by the registrant’s principal accountant were as follows:

Audit fees include amounts related to the audit of the registrant’s annual financial statements and services normally provided by the accountant in connection with statutory and regulatory filings. Audit-related fees include amounts reasonably related to the performance of the audit of the registrant’s financial statements and specifically include the issuance of a report on internal controls and, if applicable, agreed-upon procedures related to fund acquisitions. Tax fees include amounts related to services for tax compliance, tax planning, and tax advice. The nature of these services specifically includes the review of distribution calculations and the preparation of Federal, state, and excise tax returns. All other fees include the registrant’s pro-rata share of amounts for agreed-upon procedures in conjunction with service contract approvals by the registrant’s Board of Directors/Trustees.

(e)(1) The registrant’s audit committee has adopted a policy whereby audit and non-audit services performed by the registrant’s principal accountant for the registrant, its investment adviser, and any entity controlling, controlled by, or under common control with the investment adviser that provides ongoing services to the registrant require pre-approval in advance at regularly scheduled audit committee meetings. If such a service is required between regularly scheduled audit committee meetings, pre-approval may be authorized by one audit committee member with ratification at the next scheduled audit committee meeting. Waiver of pre-approval for audit or non-audit services requiring fees of a de minimis amount is not permitted.

(2) No services included in (b) – (d) above were approved pursuant to paragraph (c)(7)(i)(C) of Rule 2-01 of Regulation S-X.

(f) Less than 50 percent of the hours expended on the principal accountant’s engagement to audit the registrant’s financial statements for the most recent fiscal year were attributed to work performed by persons other than the principal accountant’s full-time, permanent employees.

(g) The aggregate fees billed for the most recent fiscal year and the preceding fiscal year by the registrant’s principal accountant for non-audit services rendered to the registrant, its investment adviser, and any entity controlling, controlled by, or under common control with the investment adviser that provides ongoing services to the registrant were $2,042,000 and $1,862,000, respectively.

(h) All non-audit services rendered in (g) above were pre-approved by the registrant’s audit committee. Accordingly, these services were considered by the registrant’s audit committee in maintaining the principal accountant’s independence.

Item 5. Audit Committee of Listed Registrants.

Not applicable.

Item 6. Investments.

(a) Not applicable. The complete schedule of investments is included in Item 1 of this Form N-CSR.

(b) Not applicable.

Item 7. Disclosure of Proxy Voting Policies and Procedures for Closed-End Management Investment Companies.

Not applicable.

Item 8. Portfolio Managers of Closed-End Management Investment Companies.

Not applicable.

Item 9. Purchases of Equity Securities by Closed-End Management Investment Company and Affiliated Purchasers.

Not applicable.

Item 10. Submission of Matters to a Vote of Security Holders.

Not applicable.

Item 11. Controls and Procedures.

(a) The registrant’s principal executive officer and principal financial officer have evaluated the registrant’s disclosure controls and procedures within 90 days of this filing and have concluded that the registrant’s disclosure controls and procedures were effective, as of that date, in ensuring that information required to be disclosed by the registrant in this Form N-CSR was recorded, processed, summarized, and reported timely.

(b) The registrant’s principal executive officer and principal financial officer are aware of no change in the registrant’s internal control over financial reporting that occurred during the registrant’s second fiscal quarter covered by this report that has materially affected, or is reasonably likely to materially affect, the registrant’s internal control over financial reporting.

Item 12. Exhibits.

(a)(1) The registrant’s code of ethics pursuant to Item 2 of Form N-CSR is attached.

(2) Separate certifications by the registrant's principal executive officer and principal financial officer, pursuant to Section 302 of the Sarbanes-Oxley Act of 2002 and required by Rule 30a-2(a) under the Investment Company Act of 1940, are attached.

(3) Written solicitation to repurchase securities issued by closed-end companies: not applicable.

(b) A certification by the registrant's principal executive officer and principal financial officer, pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 and required by Rule 30a-2(b) under the Investment Company Act of 1940, is attached.

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

T. Rowe Price State Tax-Free Income Trust

| By | /s/ Edward C. Bernard |

| | Edward C. Bernard |

| | Principal Executive Officer |

| | |

| Date April 17, 2015 | | |

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, this report has been signed below by the following persons on behalf of the registrant and in the capacities and on the dates indicated.

| By | /s/ Edward C. Bernard |

| | Edward C. Bernard |

| | Principal Executive Officer |

| | |

| Date April 17, 2015 | | |

| | |

| |

| | By | /s/ Gregory K. Hinkle |

| | Gregory K. Hinkle |

| | Principal Financial Officer |

| | |

| Date April 17, 2015 | | |