| UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 |

| FORM N-CSR |

| CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES |

| Investment Company Act file number | 811-04813 |

| Dreyfus Investment Funds (Exact name of Registrant as specified in charter) |

| c/o The Dreyfus Corporation 200 Park Avenue New York, New York 10166 (Address of principal executive offices) (Zip code) |

| Michael A. Rosenberg, Esq. 200 Park Avenue New York, New York 10166 (Name and address of agent for service) |

| Registrant's telephone number, including area code: | (212) 922-6000 |

| Date of fiscal year end: | 12/31 | |

| Date of reporting period: | 12/31/2008 |

The following N-CSR relates only to the Registrant’s series listed below and does not affect the other series of the Registrant, which have a different fiscal year end and, therefore, different N-CSR reporting requirements. Separate N-CSR Forms will be filed for those series, as appropriate.

| Dreyfus/Standish Fixed Income Fund Dreyfus/Standish Global Fixed Income Fund Dreyfus/Standish International Fixed Income Fund |

| FORM N-CSR |

| Item 1. | Reports to Stockholders. |

| Dreyfus/Standish Fixed Income Fund |

| ANNUAL REPORT December 31, 2008 |

The views expressed in this report reflect those of the portfolio manager only through the end of the period covered and do not necessarily represent the views of Dreyfus or any other person in the Dreyfus organization. Any such views are subject to change at any time based upon market or other conditions and Dreyfus disclaims any responsibility to update such views.These views may not be relied on as investment advice and, because investment decisions for a Dreyfus fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Dreyfus fund.

| Contents | ||

| THE FUND | ||

| 2 | A Letter from the CEO | |

| 3 | Discussion of Fund Performance | |

| 6 | Fund Performance | |

| 7 | Understanding Your Fund’s Expenses | |

| 7 | Comparing Your Fund’s Expenses | |

| With Those of Other Funds | ||

| 8 | Statement of Investments | |

| 28 | Statement of Financial Futures | |

| 28 | Statement of Options Written | |

| 29 | Statement of Assets and Liabilities | |

| 30 | Statement of Operations | |

| 31 | Statement of Changes in Net Assets | |

| 32 | Financial Highlights | |

| 33 | Notes to Financial Statements | |

| 50 | Report of Independent Registered | |

| Public Accounting Firm | ||

| 51 | Information About the Review | |

| and Approval of the Fund’s | ||

| Investment Advisory Agreement | ||

| 60 | Board Members Information | |

| 62 | Officers of the Fund | |

| FOR MORE INFORMATION | ||

| Back Cover | ||

| Dreyfus/Standish Fixed Income Fund |

| The Fund |

| A LETTER FROM THE CEO Dear Shareholder: |

We present to you this annual report for Dreyfus/Standish Fixed Income Fund, covering the 12-month period from January 1, 2008, through December 31, 2008.

2008 was the most difficult year in decades for the financial markets. A credit crunch that began in 2007 exploded in mid-2008 into a global financial crisis, resulting in the failures of major financial institutions, a deep and prolonged recession and lower investment values across a broad range of asset classes. Governments and regulators throughout the world moved aggressively to curtail the damage, implementing unprecedented reductions of short-term interest rates, massive injections of liquidity into the banking system, government bailouts of struggling companies and plans for massive economic stimulus programs. U.S. government securities generally fared well in the ensuing “flight to quality,” but riskier bond market sectors suffered sharp price declines.

Although we expect the U.S. and global economies to remain weak until longstanding imbalances have worked their way out of the system, the financial markets currently appear to have priced in investors’ generally low expectations. In previous recessions, however, the markets have tended to anticipate economic improvement before it occurs, potentially leading to major rallies when few expected them. That’s why it makes sense to remain disciplined, maintain a long-term perspective and adopt a consistent asset allocation strategy that reflects one’s future goals and attitudes toward risk. As always, we urge you to consult with your financial advisor, who can recommend the course of action that is right for you.

For information about how the fund performed during the reporting period, as well as market perspectives, we have provided a Discussion of Fund Performance given by the fund’s Portfolio Managers.

Thank you for your continued confidence and support.

| Jonathan R. Baum Chief Executive Officer The Dreyfus Corporation January 15, 2009 |

2

DISCUSSION OF FUND PERFORMANCE

For the period of January 1, 2008, through December 31, 2008, as provided by David R. Bowser, CFA, and Peter Vaream, Co-Portfolio Managers

Fund and Market Performance Overview

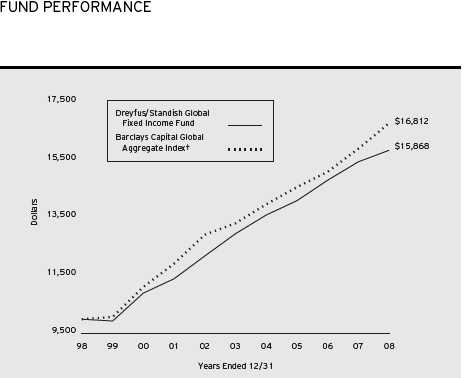

For the 12-month period ended December 31, 2008, Dreyfus/Standish Fixed Income Fund achieved a total return of –5.00% .1 In comparison, the Barclays Capital U.S.Aggregate Bond Index (the “Index”), the fund’s benchmark, achieved a total return of 5.24% for the same period.2

With the notable exception of U.S.Treasury securities,most sectors of the U.S. bond market suffered in 2008 as a financial crisis intensified, nearly leading to the collapse of the U.S. and global banking systems.The fund produced a lower return than its benchmark Index, due to its relative underweight position in U.S.Treasury securities and exposure to higher yielding bond market sectors that fared poorly in the downturn.

The Fund’s Investment Approach

The fund seeks to achieve a high level of current income, consistent with conserving principal and liquidity, and secondarily seeks capital appreciation when changes in interest rates or other economic conditions indicate that capital appreciation may be available without significant risk to principal.

To achieve this, the fund invests, under normal circumstances, at least 80% of net assets (including for this purpose borrowing for investment purposes) in fixed-income securities issued by U.S. and foreign governments and companies.The fund may invest up to 20% of assets in non-U.S. dollar-denominated securities of foreign issuers, including emerging-market issuers, and no more than 10% of assets in these foreign currency-denominated securities that have not been hedged back to the U.S. dollar. The fund may also invest in fixed-income futures contracts, options and swaps.

In terms of credit quality, the fund invests primarily in investment-grade securities, but may invest up to 15% of assets in below investment-grade securities, sometimes referred to as junk bonds.The fund will not invest in securities rated lower than B at the time of purchase. In this instance, we will attempt to select fixed-income securities that have the potential to be upgraded.

The Fund 3

| DISCUSSION OF FUND PERFORMANCE (continued) |

Global Financial Crisis Sparked Broad Declines

A credit crunch that began in the sub-prime mortgage market in 2007 developed into a full-blown global financial crisis over the summer of 2008, leading to the failures of several major financial institutions and sending repercussions throughout the world’s credit markets. As the crisis came close to spinning out of control in September, very difficult liquidity conditions in various markets, including the interbank lending market, nearly led to the collapse of the global banking system. Unprecedented interventions by government and monetary authorities, which pumped billions of dollars of liquidity into the system and rescued struggling corporations, helped thaw frozen credit markets by year-end.These efforts included approval of the Troubled Asset Relief Program (“TARP”) by the U.S. Congress and coordinated cuts of short-term interest rates by central banks, including the Federal Reserve Board, which reduced its target for the overnight federal funds rate to the unprecedented low level of 0% to 0.25% .

Meanwhile, slumping housing markets, rising unemployment and sharply lower consumer confidence exacerbated a downturn in the U.S. economy. Commodity prices that had soared over the first half of 2008 plummeted over the second half when demand abated for energy and construction materials worldwide. In November, the National Bureau of Economic Research officially declared that the U.S. economy has been mired in recession since late 2007.

As market conditions deteriorated, many highly leveraged institutional investors were forced to de-lever their portfolios, selling their more liquid investments to raise cash for margin calls and redemption requests. Consequently, selling pressure intensified even among fundamentally sound fixed-income securities, leading to broadly lower prices for corporate bonds, asset-backed securities, mortgage-backed securities and the sovereign debt of developing nations. Lower-rated bonds were particularly hard-hit. U.S.Treasury securities were a notable exception, gaining considerable value as risk-averse investors flocked to the relatively safe haven provided by U.S. government-backed investments.

Sector Allocation Strategies Weighed on Performance

The fund’s longstanding preference for higher yielding bond market sectors detracted from its relative performance in this challenging

4

environment. Relatively light exposure to U.S. Treasury securities, which we believe offered unappealing current yields, and an overweight position in investment-grade corporate bonds, commercial mortgage-backed securities and asset-backed securities with sound credit fundamentals weighed negatively on the fund’s total return performance despite generating high current yields.

On the other hand, the fund’s interest-rate strategies contributed positively to relative performance, as a “bulleted” emphasis on securities with three- to five-year maturities helped it benefit from widening yield differences along the bond market’s maturity range early in the year. Similarly, a modestly long average duration helped the portfolio participate more fully in the benefits of falling U.S. interest rates.

Anticipating a Return to Fundamentals

As of year-end, the financial crisis has persisted and the economic downturn has worsened. However, low expectations among investors for 2009 appear to have already been priced into bond prices, and unexpected good news could spark a market rally.Therefore, we have maintained the funds’s overweight exposure to market sectors that we believe have been punished too severely during the downturn.After extensive credit analysis, we have found what we believe to be particularly compelling values among certain commercial mortgage-backed securities and corporate bonds, which we expect to fare well in an eventual recovery.

January 15, 2009

| 1 | Total return includes reinvestment of dividends and any capital gains paid. Past performance is no guarantee of future results. Share price, yield and investment return fluctuate such that upon redemption, fund shares may be worth more or less than their original cost. Return figure provided reflects the absorption of certain fund expenses by The Dreyfus Corporation pursuant to a voluntary undertaking in effect, which may be extended, terminated or modified at any time. Had these expenses not been absorbed, the fund’s return would have been lower. |

| 2 | SOURCE: LIPPER INC. — Reflects reinvestment of dividends and, where applicable, capital gain distributions.The Barclays Capital U.S. Aggregate Bond Index is a widely accepted, unmanaged total return index of corporate, U.S. government and U.S. government agency debt instruments, mortgage-backed securities and asset-backed securities with an average maturity of 1-10 years.The Index does not include fees and expenses to which the fund is subject. |

The Fund 5

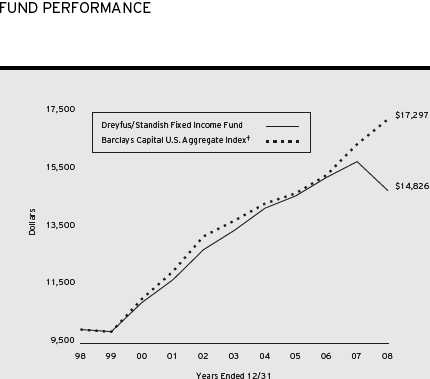

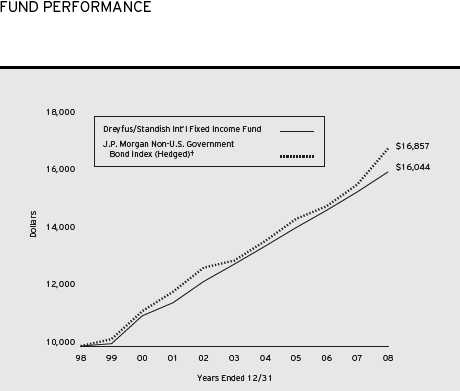

Comparison of change in value of $10,000 investment in Dreyfus/Standish Fixed Income Fund and the Barclays Capital U.S. Aggregate Index

| Average Annual Total Returns as of 12/31/08 | ||||||

| 1 Year | 5 Years | 10 Years | ||||

| Fund | (5.00)% | 2.28% | 4.17% |

† Source: Lipper Inc.

Past performance is not predictive of future performance.The fund’s performance shown in the graph and table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

The above graph compares a $10,000 investment made in Dreyfus/Standish Fixed Income Fund on 12/31/98 to a $10,000 investment made in the Barclays Capital U.S. Aggregate Index (the “Index”) on that date. All dividends and capital gain distributions are reinvested.

Effective 12/1/08,The Dreyfus Corporation became the fund’s investment adviser and the name of Mellon Institutional Funds Investment Trust was changed to Dreyfus Investment Funds.The fund’s name was changed to Dreyfus/Standish Fixed Income Fund.

The fund’s performance shown in the line graph takes into account all applicable fees and expenses.The Index is a widely accepted, unmanaged total return index of corporate, U.S. government and U.S. government agency debt instruments, mortgage-backed securities and asset-backed securities with an average of maturity of 1-10 years. Unlike a mutual fund, the Index is not subject to charges, fees and other expenses. Investors cannot invest directly in any index. These factors can contribute to the Index potentially outperforming the fund. Further information relating to fund performance, including expense reimbursements, if applicable, is contained in the Financial Highlights section of the prospectus and elsewhere in this report.

6

UNDERSTANDING YOUR FUND’S EXPENSES (Unaudited)

As a mutual fund investor, you pay ongoing expenses, such as management fees and other expenses. Using the information below, you can estimate how these expenses affect your investment and compare them with the expenses of other funds.You also may pay one-time transaction expenses, including sales charges (loads) and redemption fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial adviser.

Review your fund’s expenses

The table below shows the expenses you would have paid on a $1,000 investment in Dreyfus/Standish Fixed Income Fund from July 1, 2008 to December 31, 2008. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

Expenses and Value of a $1,000 Investment assuming actual returns for the six months ended December 31, 2008

| Expenses paid per $1,000† | $ 2.31 | |

| Ending value (after expenses) | $953.70 |

COMPARING YOUR FUND’S EXPENSES WITH THOSE OF OTHER FUNDS (Unaudited)

Using the SEC’s method to compare expenses

The Securities and Exchange Commission (SEC) has established guidelines to help investors assess fund expenses. Per these guidelines, the table below shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return. You can use this information to compare the ongoing expenses (but not transaction expenses or total cost) of investing in the fund with those of other funds.All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

Expenses and Value of a $1,000 Investment assuming a hypothetical 5% annualized return for the six months ended December 31, 2008

| Expenses paid per $1,000† | $ 2.39 | |

| Ending value (after expenses) | $1,022.77 |

| † Expenses are equal to the fund’s annualized expense ratio of .47%, multiplied by the average account value over the period, multiplied by 184/366 (to reflect the one-half year period). |

The Fund 7

| STATEMENT OF INVESTMENTS | ||||||||||

| December 31, 2008 | ||||||||||

| Coupon | Maturity | Principal | ||||||||

| Bonds and Notes—123.7% | Rate (%) | Date | Amount ($)f | Value ($) | ||||||

| Asset Backed—9.2% | ||||||||||

| American Express Credit Account | ||||||||||

| Master Trust, Ser. 2007-6, Cl. C | 1.59 | 1/15/13 | 3,975,000 | a,b | 2,592,757 | |||||

| American Express Credit Account | ||||||||||

| Master Trust, Ser. 2004-C, Cl. C | 1.70 | 2/15/12 | 168,618 | a,b | 145,542 | |||||

| American General Mortgage Loan | ||||||||||

| Trust, Ser. 2006-1, Cl. A1 | 5.75 | 12/25/35 | 851 | a,b,c | 846 | |||||

| AmeriCredit Automobile Receivables | ||||||||||

| Trust, Ser. 2008-AF, Cl. A2A | 4.47 | 1/12/12 | 1,390,000 | c | 1,314,367 | |||||

| AmeriCredit Automobile Receivables | ||||||||||

| Trust, Ser. 2005-DA, Cl. A3 | 4.87 | 12/6/10 | 124,461 | 121,858 | ||||||

| AmeriCredit Automobile Receivables | ||||||||||

| Trust, Ser. 2006-BG, Cl. A3 | 5.21 | 10/6/11 | 1,368,567 | c | 1,332,073 | |||||

| AmeriCredit Prime Automobile | ||||||||||

| Receivables, Ser. 2007-2M, | ||||||||||

| Cl. A2B | 2.26 | 11/8/10 | 205,222 | b | 201,547 | |||||

| AmeriCredit Prime Automobile | ||||||||||

| Receivables Trust, | ||||||||||

| Ser. 2007-1, Cl. E | 6.96 | 1/8/11 | 916,044 | a | 526,725 | |||||

| Bank of America Credit Card Trust, | ||||||||||

| Ser. 2007-B1, Cl. B1 | 1.28 | 6/15/12 | 2,480,000 | b,c | 2,190,944 | |||||

| Bayview Financial Acquisition | ||||||||||

| Trust, Ser. 2005-B, Cl. 1A6 | 5.21 | 4/28/39 | 163,902 | b | 122,542 | |||||

| Capital Auto Receivables Asset | ||||||||||

| Trust, Ser. 2005-1, Cl. C | 4.73 | 9/15/10 | 925,000 | c | 906,435 | |||||

| Capital Auto Receivables Asset | ||||||||||

| Trust, Ser. 2004-2, Cl. D | 5.82 | 5/15/12 | 1,805,000 | a | 1,768,631 | |||||

| Capital One Auto Finance Trust, | ||||||||||

| Ser. 2007-A, Cl. A3B | 1.20 | 8/15/11 | 939,630 | b | 892,280 | |||||

| Capital One Auto Finance Trust, | ||||||||||

| Ser. 2006-C, Cl. A3A | 5.07 | 7/15/11 | 970,345 | c | 941,025 | |||||

| Capital One Auto Finance Trust, | ||||||||||

| Ser. 2007-C, Cl. A3A | 5.13 | 4/16/12 | 2,530,000 | c | 2,310,669 | |||||

| Capital One Auto Finance Trust, | ||||||||||

| Ser. 2006-A, Cl. A3 | 5.33 | 11/15/10 | 70,061 | c | 69,824 | |||||

| ChaseFlex Trust, | ||||||||||

| Ser. 2006-2, Cl. A1A | 5.59 | 9/25/36 | 155,119 | b,c | 149,204 | |||||

| Citibank Credit Card Issuance | ||||||||||

| Trust, Ser. 2007-B1, Cl. B1 | 4.13 | 4/2/12 | 70,000 | b | 60,429 | |||||

| Citicorp Residential Mortgage | ||||||||||

| Securities, Ser. 2006-2, Cl. A2 | 5.56 | 9/25/36 | 2,400,000 | b,c | 2,296,752 | |||||

8

| Coupon | Maturity | Principal | ||||||||

| Bonds and Notes (continued) | Rate (%) | Date | Amount ($)f | Value ($) | ||||||

| Asset Backed (continued) | ||||||||||

| Citigroup Mortgage Loan Trust, | ||||||||||

| Ser. 2005-WF1, Cl. A5 | 5.01 | 2/25/35 | 140,615 | b | 98,633 | |||||

| Citigroup Mortgage Loan Trust, | ||||||||||

| Ser. 2005-WF2, Cl. AF7 | 5.25 | 8/25/35 | 1,780,404 | b | 1,135,066 | |||||

| CS First Boston Mortgage | ||||||||||

| Securities, Ser. 2002-HE4, | ||||||||||

| Cl. MF1 | 6.94 | 8/25/32 | 332,741 | b,c | 146,762 | |||||

| Ford Credit Auto Owner Trust, | ||||||||||

| Ser. 2005-C, Cl. C | 4.72 | 2/15/11 | 700,000 | c | 667,729 | |||||

| Ford Credit Auto Owner Trust, | ||||||||||

| Ser. 2006-C, Cl. C | 5.47 | 9/15/12 | 490,000 | 330,042 | ||||||

| Ford Credit Auto Owner Trust, | ||||||||||

| Ser. 2007-A, Cl. D | 7.05 | 12/15/13 | 600,000 | a | 372,399 | |||||

| Green Tree Financial, | ||||||||||

| Ser. 1994-7, Cl. M1 | 9.25 | 3/15/20 | 313,384 | c | 271,167 | |||||

| GSAA Home Equity Trust, | ||||||||||

| Ser. 2006-7, Cl. AV1 | 1.48 | 3/25/46 | 378,770 | b,c | 351,789 | |||||

| Honda Auto Receivables Owner | ||||||||||

| Trust, Ser. 2006-1, Cl. A3 | 5.07 | 2/18/10 | 116,957 | 116,828 | ||||||

| Hyundai Auto Receivables Trust, | ||||||||||

| Ser. 2004-A, Cl. B | 3.46 | 8/15/11 | 11,790 | 11,767 | ||||||

| Hyundai Auto Receivables Trust, | ||||||||||

| Ser. 2007-A, Cl. A3A | 5.04 | 1/17/12 | 845,000 | c | 831,044 | |||||

| Hyundai Auto Receivables Trust, | ||||||||||

| Ser. 2006-B, Cl. C | 5.25 | 5/15/13 | 10,000 | 9,085 | ||||||

| JP Morgan Mortgage Acquisition, | ||||||||||

| Ser. 2007-HE1, Cl. AF1 | 0.57 | 4/1/37 | 1,649,576 | b,c | 1,303,537 | |||||

| Mastr Asset Backed Securities | ||||||||||

| Trust, Ser. 2006-AM1, Cl. A2 | 1.53 | 1/25/36 | 413,194 | b | 385,169 | |||||

| Nomura Asset Acceptance, | ||||||||||

| Ser. 2005-AP1, Cl. 2A5 | 4.86 | 2/25/35 | 39,129 | b | 24,037 | |||||

| Nomura Asset Acceptance, | ||||||||||

| Ser. 2005-WF1, Cl. 2A5 | 5.16 | 3/25/35 | 925,987 | b | 689,713 | |||||

| Origen Manufactured Housing, | ||||||||||

| Ser. 2004-B, Cl. A2 | 3.79 | 12/15/17 | 7,946 | c | 7,770 | |||||

| Origen Manufactured Housing, | ||||||||||

| Ser. 2005-B, Cl. A2 | 5.25 | 12/15/18 | 146,718 | c | 139,687 | |||||

| Origen Manufactured Housing | ||||||||||

| Ser. 2005-B, Cl. A3 | 5.61 | 5/15/22 | 100,000 | 81,988 | ||||||

The Fund 9

| STATEMENT OF INVESTMENTS (continued) |

| Coupon | Maturity | Principal | ||||||||

| Bonds and Notes (continued) | Rate (%) | Date | Amount ($)f | Value ($) | ||||||

| Asset Backed (continued) | ||||||||||

| Residential Asset Mortgage | ||||||||||

| Products, Ser. 2004-RS12, | ||||||||||

| Cl. AI6 | 4.55 | 12/25/34 | 72,888 | 50,618 | ||||||

| Residential Funding Mortgage | ||||||||||

| Securities, Ser. 2005-HI3, | ||||||||||

| Cl. A4 | 5.49 | 9/25/35 | 100,000 | 94,861 | ||||||

| Specialty Underwriting & | ||||||||||

| Residential Finance, | ||||||||||

| Ser. 2006-BC2 Cl. A2B | 5.57 | 2/25/37 | 289,431 | b,c | 196,753 | |||||

| Terwin Mortgage Trust, | ||||||||||

| Ser. 2006-9HGA Cl. A1 | 0.55 | 10/25/37 | 148,932 | a,b | 135,800 | |||||

| Vanderbilt Mortgage Finance, | ||||||||||

| Ser. 1999-A, Cl. 1A6 | 6.75 | 3/7/29 | 1,030,000 | b | 828,211 | |||||

| Wachovia Auto Loan Owner Trust, | ||||||||||

| Ser. 2007-1, Cl. D | 5.65 | 2/20/13 | 1,725,000 | c | 821,548 | |||||

| Wells Fargo Mortgage Backed | ||||||||||

| Securities Trust, Ser. 2003-1, | ||||||||||

| Cl. 2A9 | 5.75 | 2/25/33 | 193,516 | c | 150,764 | |||||

| WFS Financial Owner Trust, | ||||||||||

| Ser. 2005-3, Cl. B | 4.50 | 5/17/13 | 580,000 | c | 556,446 | |||||

| WFS Financial Owner Trust, | ||||||||||

| Ser. 2005-2, Cl. B | 4.57 | 11/19/12 | 891,000 | c | 876,766 | |||||

| 28,630,429 | ||||||||||

| Banks—9.6% | ||||||||||

| Bank of America, | ||||||||||

| Jr. Sub. Bonds | 8.00 | 12/29/49 | 2,470,000 | b,e | 1,779,190 | |||||

| Barclays Bank, | ||||||||||

| Jr. Sub. Bonds | 5.93 | 12/15/49 | 1,300,000 | a,b | 478,598 | |||||

| Barclays Bank, | ||||||||||

| Sub. Bonds | 7.70 | 4/25/49 | 625,000 | a,b | 414,177 | |||||

| Capital One Financial, | ||||||||||

| Sr. Unscd. Notes | 2.47 | 9/10/09 | 2,425,000 | b | 2,310,278 | |||||

| Chevy Chase Bank, | ||||||||||

| Sub. Notes | 6.88 | 12/1/13 | 1,322,000 | 1,065,862 | ||||||

| Chuo Mitsui Trust & Banking, | ||||||||||

| Jr. Sub. Notes | 5.51 | 12/29/49 | 1,335,000 | a,b | 919,776 | |||||

| Citigroup, | ||||||||||

| Sr. Unscd. Notes | 5.50 | 4/11/13 | 4,865,000 | 4,741,400 | ||||||

| City National of Beverly Hills | ||||||||||

| California, Sr. Notes | 5.13 | 2/15/13 | 595,000 | 510,058 | ||||||

10

| Coupon | Maturity | Principal | ||||||||||

| Bonds and Notes (continued) | Rate (%) | Date | Amount ($)f | Value ($) | ||||||||

| Banks (continued) | ||||||||||||

| Colonial Bank, | ||||||||||||

| Sub. Notes | 6.38 | 12/1/15 | 1,100,000 | 734,478 | ||||||||

| HSBC Finance Capital Trust IX, | ||||||||||||

| Gtd. Notes | 5.91 | 11/30/35 | 3,135,000 | b | 1,313,164 | |||||||

| Industrial Bank of Korea, | ||||||||||||

| Sub. Notes | 4.00 | 5/19/14 | 280,000 | a,b | 257,534 | |||||||

| Manufacturers & Traders Trust, | ||||||||||||

| Sub. Notes | 5.59 | 12/28/20 | 625,000 | b | 449,045 | |||||||

| Marshall & Ilsley Bank, | ||||||||||||

| Sub. Notes, Ser. BN | 2.48 | 12/4/12 | 4,745,000 | b,c | 3,716,170 | |||||||

| MUFG Capital Finance I, | ||||||||||||

| Bank Gtd. Bonds | 6.35 | 7/29/49 | 710,000 | b | 495,345 | |||||||

| NB Capital Trust IV, | ||||||||||||

| Bank Gtd. Cap. Secs | 8.25 | 4/15/27 | 265,000 | 219,686 | ||||||||

| Royal Bank of Scotland Group, | ||||||||||||

| Jr. Sub. Bonds | 6.99 | 10/5/49 | 1,360,000 | a,b | 636,651 | |||||||

| Sovereign Bancorp, | ||||||||||||

| Sr. Unscd. Notes | 1.73 | 3/23/10 | 1,235,000 | b | 1,096,921 | |||||||

| Sovereign Bancorp, | ||||||||||||

| Sr. Unscd. Notes | 2.46 | 3/1/09 | 46,000 | b | 45,233 | |||||||

| Sovereign Bancorp, | ||||||||||||

| Sr. Unscd. Notes | 4.80 | 9/1/10 | 1,085,000 | 973,602 | ||||||||

| St. George Bank, | ||||||||||||

| Sub. Notes | 5.30 | 10/15/15 | 871,000 | a | 839,670 | |||||||

| Sumitomo Mitsui Banking, | ||||||||||||

| Sub. Notes | EUR | 4.38 | 7/15/49 | 550,000 | b | 442,890 | ||||||

| Sumitomo Mitsui Banking, | ||||||||||||

| Sub. Notes | �� | 5.63 | 7/29/49 | 845,000 | a,b | 626,601 | ||||||

| SunTrust Preferred Capital I, | ||||||||||||

| Bank, Gtd. Notes | 5.85 | 12/31/49 | 1,205,000 | b | 651,075 | |||||||

| Wachovia, | ||||||||||||

| Sub. Notes | 6.38 | 1/15/09 | 990,000 | 988,290 | ||||||||

| Wells Fargo & Co., | ||||||||||||

| Sub. Notes | 6.38 | 8/1/11 | 785,000 | 801,736 | ||||||||

| Wells Fargo Capital XIII, | ||||||||||||

| Bank Gtd. Secs | 7.70 | 12/29/49 | 3,035,000 | b | 2,506,946 | |||||||

| Western Financial Bank, | ||||||||||||

| Sub. Debs | 9.63 | 5/15/12 | 905,000 | 892,241 | ||||||||

| 29,906,617 | ||||||||||||

The Fund 11

| STATEMENT OF INVESTMENTS (continued) |

| Coupon | Maturity | Principal | ||||||||

| Bonds and Notes (continued) | Rate (%) | Date | Amount ($)f | Value ($) | ||||||

| Basic Materials—.5% | ||||||||||

| Alcoa, | ||||||||||

| Sr. Unscd. Notes | 6.00 | 7/15/13 | 345,000 | 312,242 | ||||||

| Cabot Finance, | ||||||||||

| Sr. Unscd. Notes | 5.25 | 9/1/13 | 890,000 | a | 938,366 | |||||

| Enterprise Products Operating, | ||||||||||

| Gtd. Notes, Ser. B | 4.63 | 10/15/09 | 230,000 | 222,806 | ||||||

| 1,473,414 | ||||||||||

| Collateralized Mortgage | ||||||||||

| Obligations—6.7% | ||||||||||

| Banc of America Mortgage | ||||||||||

| Securities, Ser. 2004-F, Cl. 2A7 | 4.15 | 7/25/34 | 22,349 | b,c | 21,535 | |||||

| Countrywide Home Loan Mortgage | ||||||||||

| Pass-Through Trust, | ||||||||||

| Ser. 2005-31, Cl. 2A1 | 5.47 | 1/25/36 | 2,536,621 | b,c | 1,822,116 | |||||

| Federal National Mortgage | ||||||||||

| Association, Grantor Trust, | ||||||||||

| Ser. 2001-T11, Cl. B | 5.50 | 9/25/11 | 20,000 | g | 21,442 | |||||

| Government National Mortgage | ||||||||||

| Association, Ser. 2004-57, Cl. A | 3.02 | 1/16/19 | 689,929 | c | 686,995 | |||||

| Government National Mortgage | ||||||||||

| Association, Ser. 2004-97, Cl. AB | 3.08 | 4/16/22 | 1,493,815 | c | 1,486,134 | |||||

| Government National Mortgage | ||||||||||

| Association, Ser. 2007-46, Cl. A | 3.14 | 11/16/29 | 1,117,936 | c | 1,114,883 | |||||

| Government National Mortgage | ||||||||||

| Association, Ser. 2004-25, Cl. AC | 3.38 | 1/16/23 | 488,997 | c | 488,306 | |||||

| Government National Mortgage | ||||||||||

| Association, Ser. 2004-77, Cl. A | 3.40 | 3/16/20 | 289,247 | c | 288,837 | |||||

| Government National Mortgage | ||||||||||

| Association, Ser. 2004-67, Cl. A | 3.65 | 9/16/17 | 222,915 | c | 222,744 | |||||

| Government National Mortgage | ||||||||||

| Association, Ser. 2005-90, Cl. A | 3.76 | 9/16/28 | 1,323,710 | c | 1,326,589 | |||||

| Government National Mortgage | ||||||||||

| Association, Ser. 2005-29, Cl. A | 4.02 | 7/16/27 | 935,041 | c | 940,356 | |||||

| Government National Mortgage | ||||||||||

| Association, Ser. 2005-9, Cl. A | 4.03 | 5/16/22 | 1,078,676 | c | 1,075,481 | |||||

| Government National Mortgage | ||||||||||

| Association, Ser. 2004-51, Cl. A | 4.15 | 2/16/18 | 1,032,410 | c | 1,036,792 | |||||

| Government National Mortgage | ||||||||||

| Association, Ser. 2006-9, Cl. A | 4.20 | 8/16/26 | 2,216,646 | c | 2,233,869 | |||||

12

| Coupon | Maturity | Principal | ||||||||

| Bonds and Notes (continued) | Rate (%) | Date | Amount ($)f | Value ($) | ||||||

| Collateralized Mortgage | ||||||||||

| Obligations (continued) | ||||||||||

| Government National Mortgage | ||||||||||

| Association, Ser. 2006-3, Cl. A | 4.21 | 1/16/28 | 1,654,042 | c | 1,667,663 | |||||

| Government National Mortgage | ||||||||||

| Association, Ser. 2006-55, Cl. A | 4.25 | 7/16/29 | 2,028,534 | c | 2,047,563 | |||||

| Government National Mortgage | ||||||||||

| Association, Ser. 2005-32, Cl. B | 4.39 | 8/16/30 | 1,230,540 | c | 1,242,015 | |||||

| Government National Mortgage | ||||||||||

| Association, Ser. 2005-87, Cl. A | 4.45 | 3/16/25 | 1,052,394 | c | 1,063,746 | |||||

| Structured Asset Mortgage | ||||||||||

| Investments, Ser. 1998-2, Cl. B | 5.63 | 4/30/30 | 30,005 | b,c | 23,689 | |||||

| WaMu Mortgage Pass Through | ||||||||||

| Certificates, Ser. 2004-AR7, | ||||||||||

| Cl. A6 | 3.94 | 7/25/34 | 241,000 | b,c | 236,266 | |||||

| WaMu Mortgage Pass Through | ||||||||||

| Certificates, Ser. 2004-AR9, | ||||||||||

| Cl. A7 | 4.14 | 8/25/34 | 1,342,000 | b,c | 1,290,430 | |||||

| WaMu Mortgage Pass-Through | ||||||||||

| Certificates, | ||||||||||

| Ser. 2005-AR4, Cl. A4B | 4.67 | 4/25/35 | 656,000 | b,c | 612,018 | |||||

| 20,949,469 | ||||||||||

| Commercial Mortgage | ||||||||||

| Pass-Through Ctfs.—8.8% | ||||||||||

| Banc of America Commercial | ||||||||||

| Mortgage, Ser. 2002-2, Cl. A3 | 5.12 | 7/11/43 | 560,000 | c | 520,565 | |||||

| Bayview Commercial Asset Trust, | ||||||||||

| Ser. 2004-1, Cl. A | 0.83 | 4/25/34 | 290,628 | a,b | 211,846 | |||||

| Bayview Commercial Asset Trust, | ||||||||||

| Ser. 2003-2, Cl. A | 1.05 | 12/25/33 | 283,858 | a,b | 235,997 | |||||

| Bayview Commercial Asset Trust, | ||||||||||

| Ser. 2005-3A, Cl. B1 | 1.57 | 11/25/35 | 115,364 | a,b | 61,120 | |||||

| Bayview Commercial Asset Trust, | ||||||||||

| Ser. 2006-SP1, Cl. A1 | 1.67 | 4/25/36 | 153,111 | a,b | 120,958 | |||||

| Bayview Commercial Asset Trust, | ||||||||||

| Ser. 2006-SP2, Cl. A | 1.68 | 1/25/37 | 1,010,897 | a,b | 774,650 | |||||

| Bayview Commercial Asset Trust, | ||||||||||

| Ser. 2006-2A, Cl. B2 | 2.87 | 7/25/36 | 345,105 | a,b | 173,898 | |||||

| Bayview Commercial Asset Trust, | ||||||||||

| Ser. 2006-1A, Cl. B2 | 3.10 | 4/25/36 | 181,887 | a,b | 87,142 | |||||

The Fund 13

| STATEMENT OF INVESTMENTS (continued) |

| Coupon | Maturity | Principal | ||||||||

| Bonds and Notes (continued) | Rate (%) | Date | Amount ($)f | Value ($) | ||||||

| Commercial Mortgage | ||||||||||

| Pass-Through Ctfs. (continued) | ||||||||||

| Bayview Commercial Asset Trust, | ||||||||||

| Ser. 2005-3A, Cl. B3 | 3.47 | 11/25/35 | 230,727 | a,b | 115,202 | |||||

| Bayview Commercial Asset Trust, | ||||||||||

| Ser. 2005-4A, Cl. B3 | 4.90 | 1/25/36 | 80,044 | a,b | 24,013 | |||||

| Bear Stearns Commercial Mortgage | ||||||||||

| Securities, Ser. 2003-T12, Cl. A3 | 4.24 | 4/13/12 | 2,073,000 | b,c | 2,017,718 | |||||

| Bear Stearns Commercial Mortgage | ||||||||||

| Securities, Ser. 2005-T18 Cl. A2 | 4.56 | 2/13/42 | 105,000 | b,c | 99,253 | |||||

| Bear Stearns Commercial Mortgage | ||||||||||

| Securities, Ser. 2006-PW12, | ||||||||||

| Cl. AAB | 5.69 | 9/11/38 | 875,000 | b | 716,529 | |||||

| Bear Stearns Commercial Mortgage | ||||||||||

| Securities, Ser. 1998-C1, Cl. A2 | 6.44 | 6/16/30 | 2,477 | c | 2,469 | |||||

| Credit Suisse Mortgage Capital | ||||||||||

| Certificate, Ser. 2006-C1, Cl. A2 | 5.51 | 2/15/39 | 45,000 | b | 40,332 | |||||

| Credit Suisse/Morgan Stanley | ||||||||||

| Commercial Mortgage Certificates, | ||||||||||

| Ser. 2006-HC1A, Cl. A1 | 1.39 | 5/15/23 | 1,121,936 | a,b,c | 900,216 | |||||

| Crown Castle Towers, | ||||||||||

| Ser. 2006-1A, Cl. AFX | 5.24 | 11/15/36 | 2,725,000 | a,c | 2,265,946 | |||||

| Crown Castle Towers, | ||||||||||

| Ser. 2006-1A, Cl. B | 5.36 | 11/15/36 | 620,000 | a,c | 452,600 | |||||

| Crown Castle Towers, | ||||||||||

| Ser. 2006-1A, Cl. C | 5.47 | 11/15/36 | 1,555,000 | a,c | 1,093,289 | |||||

| Crown Castle Towers, | ||||||||||

| Ser. 2005-1A, Cl. D | 5.61 | 6/15/35 | 610,000 | a,c | 428,879 | |||||

| Crown Castle Towers, | ||||||||||

| Ser. 2006-1A, Cl. D | 5.77 | 11/15/36 | 950,000 | a,c | 598,500 | |||||

| CS First Boston Mortgage | ||||||||||

| Securities, Ser. 2005-C4, Cl. AAB | 5.07 | 8/15/38 | 1,050,000 | b | 859,530 | |||||

| DLJ Commercial Mortgage | ||||||||||

| Ser. 1998-CF2, Cl. B1 | 7.02 | 11/12/31 | 224,885 | b,c | 224,345 | |||||

| Federal National Mortgage | ||||||||||

| Association, Grantor Trust, | ||||||||||

| Ser. 2002-T11, Cl. A | 4.77 | 4/25/12 | 16,472 | c,g | 16,821 | |||||

| Federal National Mortgage | ||||||||||

| Association, Grantor Trust, | ||||||||||

| Ser. 2002-T3, Cl. A | 5.14 | 12/25/11 | 491,138 | c,g | 510,893 | |||||

14

| Coupon | Maturity | Principal | ||||||||

| Bonds and Notes (continued) | Rate (%) | Date | Amount ($)f | Value ($) | ||||||

| Commercial Mortgage | ||||||||||

| Pass-Through Ctfs. (continued) | ||||||||||

| Federal National Mortage | ||||||||||

| Association, Grantor Trust, | ||||||||||

| Ser. 2001-T6, Cl. B, | 6.09 | 5/25/11 | 146,000 | c,g | 157,499 | |||||

| Global Signal Trust, | ||||||||||

| Ser. 2006-1, Cl. C | 5.71 | 2/15/36 | 875,000 | a,c | 656,250 | |||||

| Global Signal Trust, | ||||||||||

| Ser. 2006-1, Cl. D | 6.05 | 2/15/36 | 1,105,000 | a,c | 800,849 | |||||

| Global Signal Trust, | ||||||||||

| Ser. 2006-1, Cl. E | 6.50 | 2/15/36 | 425,000 | a | 290,292 | |||||

| GMAC Commercial Mortgage | ||||||||||

| Securities, Ser. 2003-C3, Cl. A2 | 4.22 | 4/10/40 | 78,130 | c | 75,427 | |||||

| Goldman Sachs Mortgage Securities | ||||||||||

| Corporation II, Ser. 2007-EOP, | ||||||||||

| Cl. B | 2.13 | 3/20/20 | 2,965,000 | a,b,c | 1,908,510 | |||||

| Goldman Sachs Mortgage Securities | ||||||||||

| Corporation II, Ser. 2007-EOP, | ||||||||||

| Cl. E�� | 2.32 | 3/20/20 | 1,120,000 | a,b,c | 720,546 | |||||

| Goldman Sachs Mortgage Securities | ||||||||||

| Corporation II, Ser. 2007-EOP, | ||||||||||

| Cl. F | 2.36 | 3/20/20 | 50,000 | a,b,c | 30,197 | |||||

| Goldman Sachs Mortgage Securities | ||||||||||

| Corporation II, Ser. 2007-EOP, | ||||||||||

| Cl. G | 2.40 | 3/20/20 | 25,000 | a,b,c | 15,094 | |||||

| Goldman Sachs Mortgage Securities | ||||||||||

| Corporation II, Ser. 2007-EOP, | ||||||||||

| Cl. K | 2.93 | 3/20/20 | 650,000 | a,b | 391,895 | |||||

| Goldman Sachs Mortgage Securities | ||||||||||

| Corporation II, Ser. 2007-EOP, | ||||||||||

| Cl. L | 3.18 | 3/20/20 | 35,000 | a,b | 21,000 | |||||

| Impac CMB Trust, | ||||||||||

| Ser. 2005-8, Cl. 2M2 | 1.22 | 2/25/36 | 111,208 | b,c | 55,815 | |||||

| Impac CMB Trust, | ||||||||||

| Ser. 2005-8, Cl. 2M3 | 1.97 | 2/25/36 | 88,199 | b,c | 35,774 | |||||

| Impac Secured Assets CMN Owner | ||||||||||

| Trust, Ser. 2006-1, Cl. 2A1 | 0.82 | 5/25/36 | 587,944 | b,c | 418,651 | |||||

| JP Morgan Chase Commercial | ||||||||||

| Mortgage Securities, | ||||||||||

| Ser. 2004-C1, Cl. A2 | 4.30 | 1/15/38 | 1,960,000 | c | 1,806,771 | |||||

The Fund 15

| STATEMENT OF INVESTMENTS (continued) |

| Coupon | Maturity | Principal | ||||||||

| Bonds and Notes (continued) | Rate (%) | Date | Amount ($)f | Value ($) | ||||||

| Commercial Mortgage | ||||||||||

| Pass-Through Ctfs. (continued) | ||||||||||

| JP Morgan Chase Commercial | ||||||||||

| Mortgage Securities, | ||||||||||

| Ser. 2005-LDP5, Cl. A2 | 5.20 | 12/15/44 | 1,485,000 | c | 1,332,494 | |||||

| LB Commercial Conduit Mortgage | ||||||||||

| Trust, Ser. 1999-C1, Cl. B | 6.93 | 6/15/31 | 62,000 | c | 61,758 | |||||

| Merrill Lynch Mortgage Trust, | ||||||||||

| Ser. 2005-CKI1, Cl. A2 | 5.22 | 11/12/37 | 350,000 | b,c | 316,733 | |||||

| Merrill Lynch Mortgage Trust, | ||||||||||

| Ser. 2002-MW1, Cl. A3 | 5.40 | 7/12/34 | 1,508,495 | c | 1,471,605 | |||||

| Morgan Stanley Capital I, | ||||||||||

| Ser. 2005-HQ5, Cl. A2 | 4.81 | 1/14/42 | 1,407,836 | c | 1,365,116 | |||||

| Morgan Stanley Dean Witter Capital | ||||||||||

| I, Ser. 2001-PPM, Cl. A2 | 6.40 | 2/15/31 | 16,427 | 16,202 | ||||||

| Morgan Stanley Dean Witter Capital | ||||||||||

| I, Ser. 2001-PPM, Cl. A3 | 6.54 | 2/15/31 | 20,065 | 19,825 | ||||||

| SBA CMBS Trust, | ||||||||||

| Ser. 2006-1A, Cl. D | 5.85 | 11/15/36 | 375,000 | a,c | 266,250 | |||||

| Sovereign Commercial Mortgage | ||||||||||

| Securities Trust, | ||||||||||

| Ser. 2007-C1, Cl. D | 5.78 | 7/22/30 | 780,000 | a,b | 82,305 | |||||

| TIAA Seasoned Commercial Mortgage | ||||||||||

| Trust, Ser. 2007-C4, Cl. A3 | 6.09 | 8/15/39 | 940,000 | b | 812,296 | |||||

| Wachovia Bank Commercial Mortgage | ||||||||||

| Trust, Ser. 2005-C16, Cl. A2 | 4.38 | 10/15/41 | 990,245 | c | 937,018 | |||||

| Wachovia Bank Commercial Mortgage | ||||||||||

| Trust, Ser. 2005-C19, Cl. A5 | 4.66 | 5/15/44 | 740,000 | 649,048 | ||||||

| 27,267,931 | ||||||||||

| Communications—4.0% | ||||||||||

| AT & T, | ||||||||||

| Sr. Unscd. Notes | 5.60 | 5/15/18 | 1,670,000 | 1,703,380 | ||||||

| AT & T, | ||||||||||

| Gtd. Notes | 7.30 | 11/15/11 | 975,000 | c | 1,013,642 | |||||

| Comcast, | ||||||||||

| Gtd. Notes | 5.50 | 3/15/11 | 335,000 | c | 328,077 | |||||

| Comcast, | ||||||||||

| Gtd. Notes | 6.30 | 11/15/17 | 1,265,000 | 1,233,526 | ||||||

| Cox Communications, | ||||||||||

| Notes | 6.25 | 6/1/18 | 1,125,000 | a | 1,000,246 | |||||

16

| Coupon | Maturity | Principal | ||||||||

| Bonds and Notes (continued) | Rate (%) | Date | Amount ($)f | Value ($) | ||||||

| Communications (continued) | ||||||||||

| News America, | ||||||||||

| Gtd. Notes | 6.15 | 3/1/37 | 1,385,000 | 1,296,395 | ||||||

| News America, | ||||||||||

| Gtd. Notes | 6.65 | 11/15/37 | 515,000 | 511,348 | ||||||

| News America Holdings, | ||||||||||

| Gtd. Notes | 7.70 | 10/30/25 | 945,000 | 905,146 | ||||||

| TCI Communications, | ||||||||||

| Sr. Unscd. Bonds | 7.88 | 2/15/26 | 765,000 | 795,684 | ||||||

| Time Warner, | ||||||||||

| Gtd. Notes | 5.88 | 11/15/16 | 2,590,000 | 2,325,431 | ||||||

| Time Warner Cable, | ||||||||||

| Gtd. Notes | 5.85 | 5/1/17 | 1,295,000 | 1,184,943 | ||||||

| 12,297,818 | ||||||||||

| Consumer Cyclical—.1% | ||||||||||

| Daimler Finance North America, | ||||||||||

| Gtd. Notes | 2.35 | 3/13/09 | 80,000 | b | 79,963 | |||||

| DaimlerChrysler North America, | ||||||||||

| Gtd. Notes | 2.43 | 3/13/09 | 150,000 | b | 144,631 | |||||

| Macy’s, | ||||||||||

| Gtd. Notes | 4.80 | 7/15/09 | 30,000 | 28,439 | ||||||

| 253,033 | ||||||||||

| Consumer Noncyclical—.8% | ||||||||||

| Kraft Foods, | ||||||||||

| Sr. Unscd. Notes | 6.00 | 2/11/13 | 285,000 | 289,885 | ||||||

| Kroger, | ||||||||||

| Gtd. Notes | 6.15 | 1/15/20 | 1,165,000 | 1,151,689 | ||||||

| Safeway, | ||||||||||

| Sr. Unscd. Notes | 6.35 | 8/15/17 | 1,165,000 | 1,153,710 | ||||||

| 2,595,284 | ||||||||||

| Energy—.4% | ||||||||||

| Amerada Hess, | ||||||||||

| Sr. Unscd. Notes | 6.65 | 8/15/11 | 1,025,000 | 1,025,199 | ||||||

| ANR Pipeline, | ||||||||||

| Sr. Unscd. Notes | 7.00 | 6/1/25 | 10,000 | 10,046 | ||||||

| Chesapeake Energy, | ||||||||||

| Gtd. Notes | 7.50 | 6/15/14 | 255,000 | 216,750 | ||||||

| 1,251,995 | ||||||||||

The Fund 17

| STATEMENT OF INVESTMENTS (continued) |

| Coupon | Maturity | Principal | ||||||||

| Bonds and Notes (continued) | Rate (%) | Date | Amount ($)f | Value ($) | ||||||

| Financials—13.4% | ||||||||||

| Ace INA Holdings, | ||||||||||

| Gtd. Notes | 5.80 | 3/15/18 | 745,000 | 671,618 | ||||||

| Allstate, | ||||||||||

| Jr. Sub. Debs | 6.50 | 5/15/57 | 510,000 | b | 287,399 | |||||

| American Express Credit, | ||||||||||

| Sr. Unscd. Notes | 1.93 | 11/9/09 | 990,000 | b,c | 920,822 | |||||

| Ameriprise Financial, | ||||||||||

| Jr. Sub. Notes | 7.52 | 6/1/66 | 610,000 | b | 330,710 | |||||

| Amvescap, | ||||||||||

| Gtd. Notes | 5.38 | 2/27/13 | 595,000 | 528,947 | ||||||

| Amvescap, | ||||||||||

| Gtd. Notes | 5.63 | 4/17/12 | 80,000 | 73,251 | ||||||

| Arden Realty, | ||||||||||

| Sr. Unscd. Notes | 5.20 | 9/1/11 | 760,000 | 730,064 | ||||||

| Boeing Capital, | ||||||||||

| Sr. Unscd. Notes | 7.38 | 9/27/10 | 975,000 | c | 1,018,149 | |||||

| Boston Properties, | ||||||||||

| Sr. Unscd. Notes | 5.63 | 4/15/15 | 645,000 | 430,067 | ||||||

| Capmark Financial Group, | ||||||||||

| Gtd. Notes | 5.88 | 5/10/12 | 1,665,000 | 568,080 | ||||||

| Commercial Net Realty, | ||||||||||

| Sr. Unscd. Notes | 6.15 | 12/15/15 | 565,000 | 416,817 | ||||||

| Countrywide Home Loans, | ||||||||||

| Gtd. Notes | 4.13 | 9/15/09 | 590,000 | 583,184 | ||||||

| Duke Realty, | ||||||||||

| Sr. Notes | 7.75 | 11/15/09 | 859,000 | 800,468 | ||||||

| ERAC USA Finance, | ||||||||||

| Notes | 3.72 | 4/30/09 | 320,000 | a,b,c | 305,290 | |||||

| ERAC USA Finance, | ||||||||||

| Gtd. Notes | 6.38 | 10/15/17 | 1,425,000 | a | 990,460 | |||||

| ERAC USA Finance, | ||||||||||

| Notes | 7.95 | 12/15/09 | 1,008,000 | a,c | 964,439 | |||||

| Federal Realty Investment Trust, | ||||||||||

| Sr. Unscd. Bonds | 5.65 | 6/1/16 | 705,000 | 463,955 | ||||||

| Federal Realty Investment Trust, | ||||||||||

| Sr. Unscd. Notes | 6.00 | 7/15/12 | 380,000 | 304,571 | ||||||

| General Electric Capital, | ||||||||||

| Sr. Unscd. Notes | 4.52 | 10/21/10 | 2,755,000 | b,c | 2,558,825 | |||||

| Goldman Sachs Capital II, | ||||||||||

| Gtd. Bonds | 5.79 | 5/8/49 | 945,000 | b | 363,502 | |||||

18

| Coupon | Maturity | Principal | ||||||||

| Bonds and Notes (continued) | Rate (%) | Date | Amount ($)f | Value ($) | ||||||

| Financials (continued) | ||||||||||

| Goldman Sachs Group, | ||||||||||

| Sub. Notes | 5.63 | 1/15/17 | 390,000 | 335,558 | ||||||

| Goldman Sachs Group, | ||||||||||

| Sub. Notes | 6.75 | 10/1/37 | 925,000 | 753,062 | ||||||

| HRPT Properties Trust, | ||||||||||

| Sr. Unscd. Notes | 2.52 | 3/16/11 | 541,000 | b,c | 397,491 | |||||

| International Lease Finance, | ||||||||||

| Sr. Unscd. Notes | 2.37 | 5/24/10 | 40,000 | b | 31,894 | |||||

| International Lease Finance, | ||||||||||

| Sr. Unscd. Notes | 6.38 | 3/25/13 | 895,000 | 608,481 | ||||||

| J.P. Morgan & Co., | ||||||||||

| Sub. Notes | 6.25 | 1/15/09 | 30,000 | 30,015 | ||||||

| Jackson National Life Global, | ||||||||||

| Sr. Scd. Notes | 5.38 | 5/8/13 | 785,000 | a | 710,083 | |||||

| Janus Capital Group, | ||||||||||

| Sr. Unscd. Notes | 6.25 | 6/15/12 | 1,045,000 | 837,356 | ||||||

| Jefferies Group, | ||||||||||

| Sr. Unscd. Notes | 7.75 | 3/15/12 | 1,890,000 | 1,583,325 | ||||||

| JPMorgan Chase & Co., | ||||||||||

| Sr. Unscd. Notes | 6.40 | 5/15/38 | 1,230,000 | 1,460,294 | ||||||

| Kingsway America, | ||||||||||

| Sr. Notes | 7.50 | 2/1/14 | 45,000 | a | 36,417 | |||||

| Leucadia National, | ||||||||||

| Sr. Unscd. Notes | 7.00 | 8/15/13 | 1,185,000 | 948,000 | ||||||

| Leucadia National, | ||||||||||

| Sr. Unscd. Notes | 7.13 | 3/15/17 | 950,000 | 710,125 | ||||||

| Liberty Property, | ||||||||||

| Sr. Unscd. Notes | 5.50 | 12/15/16 | 535,000 | 318,840 | ||||||

| Lincoln National, | ||||||||||

| Sr. Unscd. Notes | 2.18 | 3/12/10 | 1,285,000 | b,c | 1,128,894 | |||||

| Lincoln National, | ||||||||||

| Jr. Sub. Bonds | 6.05 | 4/20/67 | 2,870,000 | b | 1,149,415 | |||||

| Mack-Cali Realty, | ||||||||||

| Sr. Unscd. Notes | 5.05 | 4/15/10 | 485,000 | 427,807 | ||||||

| Mack-Cali Realty, | ||||||||||

| Sr. Unscd. Notes | 5.13 | 1/15/15 | 581,000 | 366,061 | ||||||

| Mack-Cali Realty, | ||||||||||

| Sr. Unscd. Notes | 5.25 | 1/15/12 | 830,000 | 644,826 | ||||||

| Mack-Cali Realty, | ||||||||||

| Sr. Unscd. Notes | 5.80 | 1/15/16 | 595,000 | e | 385,738 | |||||

The Fund 19

| STATEMENT OF INVESTMENTS (continued) |

| Coupon | Maturity | Principal | ||||||||||

| Bonds and Notes (continued) | Rate (%) | Date | Amount ($)f | Value ($) | ||||||||

| Financials (continued) | ||||||||||||

| MassMutual Global Funding II, | ||||||||||||

| Notes | 3.80 | 4/15/09 | 637,000 | a | 637,182 | |||||||

| MBNA, | ||||||||||||

| Sr. Unscd. Notes | 6.13 | 3/1/13 | 1,470,000 | 1,420,423 | ||||||||

| Merrill Lynch & Co., | ||||||||||||

| Sub. Notes | 5.70 | 5/2/17 | 1,970,000 | 1,748,123 | ||||||||

| Merrill Lynch & Co., | ||||||||||||

| Sr. Unscd. Notes | 6.05 | 8/15/12 | 1,700,000 | 1,678,524 | ||||||||

| MetLife, | ||||||||||||

| Sr. Unscd. Notes | 5.00 | 6/15/15 | 2,078,000 | 1,949,066 | ||||||||

| Morgan Stanley, | ||||||||||||

| Sr. Unscd. Notes | 5.75 | 8/31/12 | 680,000 | 634,549 | ||||||||

| Morgan Stanley, | ||||||||||||

| Sr. Unscd. Notes | 6.60 | 4/1/12 | 805,000 | 778,821 | ||||||||

| Nippon Life Insurance, | ||||||||||||

| Notes | 4.88 | 8/9/10 | 1,000,000 | a | 979,577 | |||||||

| NYSE Euronext, | ||||||||||||

| Sr. Unscd. Notes | 4.80 | 6/28/13 | 895,000 | 868,970 | ||||||||

| Pacific Life Global Funding, | ||||||||||||

| Notes | 3.75 | 1/15/09 | 40,000 | a | 40,006 | |||||||

| Regency Centers, | ||||||||||||

| Gtd. Notes | 5.25 | 8/1/15 | 409,000 | 271,402 | ||||||||

| Regency Centers, | ||||||||||||

| Gtd. Notes | 5.88 | 6/15/17 | 330,000 | 209,296 | ||||||||

| Simon Property Group, | ||||||||||||

| Sr. Unscd. Notes | 5.00 | 3/1/12 | 836,000 | 660,972 | ||||||||

| Simon Property Group, | ||||||||||||

| Sr. Unscd. Notes | 5.75 | 5/1/12 | 776,000 | 620,769 | ||||||||

| SLM, | ||||||||||||

| Sr. Unscd. Notes, Ser. A | 4.00 | 1/15/09 | 2,745,000 | 2,732,483 | ||||||||

| Willis North America, | ||||||||||||

| Gtd. Notes | 6.20 | 3/28/17 | 440,000 | 305,269 | ||||||||

| 41,709,732 | ||||||||||||

| Foreign/Governmental—.1% | ||||||||||||

| Brazilian Government, | ||||||||||||

| Unsub. Bonds | BRL | 12.50 | 1/5/16 | 1,000,000 | 451,329 | |||||||

20

| Coupon | Maturity | Principal | ||||||||

| Bonds and Notes (continued) | Rate (%) | Date | Amount ($)f | Value ($) | ||||||

| Health Care—.6% | ||||||||||

| Community Health Systems, | ||||||||||

| Gtd. Notes | 8.88 | 7/15/15 | 585,000 | 541,125 | ||||||

| Coventry Health Care, | ||||||||||

| Sr. Unscd. Notes | 5.88 | 1/15/12 | 450,000 | 330,660 | ||||||

| Coventry Health Care, | ||||||||||

| Sr. Unscd. Notes | 5.95 | 3/15/17 | 695,000 | 362,823 | ||||||

| Wellpoint, | ||||||||||

| Sr. Unscd. Notes | 5.88 | 6/15/17 | 715,000 | 651,796 | ||||||

| 1,886,404 | ||||||||||

| Industrials—5.8% | ||||||||||

| Atlas Copco, | ||||||||||

| Sr. Unscd. Bonds | 5.60 | 5/22/17 | 535,000 | a | 503,402 | |||||

| Ball, | ||||||||||

| Gtd. Notes | 6.88 | 12/15/12 | 305,000 | 303,475 | ||||||

| British Sky Broadcasting, | ||||||||||

| Gtd. Notes | 6.88 | 2/23/09 | 133,000 | c | 133,614 | |||||

| British Sky Broadcasting, | ||||||||||

| Sr. Notes | 8.20 | 7/15/09 | 975,000 | c | 991,257 | |||||

| BSKYB Finance UK, | ||||||||||

| Gtd. Notes | 6.50 | 10/15/35 | 1,250,000 | a | 920,549 | |||||

| Crown Americas, | ||||||||||

| Gtd. Notes | 7.63 | 11/15/13 | 720,000 | 716,400 | ||||||

| Healthcare Realty Trust, | ||||||||||

| Sr. Unscd. Notes | 8.13 | 5/1/11 | 575,000 | 453,945 | ||||||

| John Deere Capital, | ||||||||||

| Sr. Unscd. Notes | 2.24 | 9/1/09 | 657,000 | b,c | 640,210 | |||||

| KPN, | ||||||||||

| Sr. Unscd. Notes | 8.00 | 10/1/10 | 335,000 | c | 338,218 | |||||

| Lubrizol, | ||||||||||

| Gtd. Notes | 4.63 | 10/1/09 | 860,000 | 844,875 | ||||||

| Masco, | ||||||||||

| Sr. Unscd. Notes | 2.40 | 3/12/10 | 720,000 | b,c | 563,031 | |||||

| Mohawk Industries, | ||||||||||

| Sr. Unscd. Notes | 5.75 | 1/15/11 | 970,000 | 890,600 | ||||||

| Pearson Dollar Finance Two, | ||||||||||

| Gtd. Notes | 6.25 | 5/6/18 | 1,240,000 | a | 1,046,582 | |||||

The Fund 21

| STATEMENT OF INVESTMENTS (continued) |

| Coupon | Maturity | Principal | ||||||||

| Bonds and Notes (continued) | Rate (%) | Date | Amount ($)f | Value ($) | ||||||

| Industrials (continued) | ||||||||||

| Philip Morris International, | ||||||||||

| Sr. Unscd Notes | 5.65 | 5/16/18 | 1,615,000 | 1,603,881 | ||||||

| Prologis, | ||||||||||

| Sr. Unscd. Notes | 6.63 | 5/15/18 | 1,230,000 | 589,138 | ||||||

| Reed Elsevier Capital, | ||||||||||

| Gtd. Notes | 4.63 | 6/15/12 | 1,970,000 | 1,734,565 | ||||||

| Republic Service, | ||||||||||

| Sr. Unscd. Notes | 7.13 | 5/15/09 | 20,000 | 20,244 | ||||||

| Republic Services, | ||||||||||

| Sr. Unscd. Notes | 6.75 | 8/15/11 | 190,000 | c | 186,468 | |||||

| Telecom Italia Capital, | ||||||||||

| Gtd. Notes | 5.25 | 11/15/13 | 1,130,000 | 862,494 | ||||||

| Telecom Italia Capital, | ||||||||||

| Gtd. Notes | 7.72 | 6/4/38 | 880,000 | 724,525 | ||||||

| Telefonica Emisiones, | ||||||||||

| Gtd. Notes | 1.83 | 6/19/09 | 700,000 | b | 677,753 | |||||

| Union Pacific, | ||||||||||

| Sr. Unscd. Notes | 3.88 | 2/15/09 | 1,295,000 | c | 1,297,422 | |||||

| USA Waste Services, | ||||||||||

| Sr. Unscd. Notes | 7.00 | 7/15/28 | 596,000 | 495,557 | ||||||

| Waste Management, | ||||||||||

| Sr. Unscd. Notes | 7.38 | 8/1/10 | 260,000 | 263,578 | ||||||

| WEA Finance, | ||||||||||

| Sr. Notes | 7.13 | 4/15/18 | 1,225,000 | a | 870,322 | |||||

| Xerox, | ||||||||||

| Sr. Unscd. Notes | 5.50 | 5/15/12 | 235,000 | 197,085 | ||||||

| Xerox, | ||||||||||

| Sr. Unscd. Notes | 5.65 | 5/15/13 | 335,000 | 263,176 | ||||||

| 18,132,366 | ||||||||||

| Municipals—2.7% | ||||||||||

| Clark County, | ||||||||||

| GO (Bond Bank) | ||||||||||

| (Insured; MBIA, Inc.) | 5.25 | 6/1/20 | 310,000 | h | 347,637 | |||||

| Clark County School District, | ||||||||||

| Limited Tax GO (Insured; FSA) | 5.50 | 6/15/17 | 330,000 | h | 365,026 | |||||

| Clark County School District, | ||||||||||

| Limited Tax GO (Insured; FSA) | 5.50 | 6/15/18 | 220,000 | h | 243,351 | |||||

22

| Coupon | Maturity | Principal | ||||||||

| Bonds and Notes (continued) | Rate (%) | Date | Amount ($)f | Value ($) | ||||||

| Municipals (continued) | ||||||||||

| Cypress-Fairbanks Independent | ||||||||||

| School District, GO, Ser. A | ||||||||||

| (Schoolhouse) (Insured; PSF-GTD) | 5.25 | 2/15/22 | 280,000 | h | 292,667 | |||||

| Delaware Housing Authority, | ||||||||||

| Senior SFMR | 5.80 | 7/1/16 | 895,000 | 920,266 | ||||||

| Erie Tobacco Asset Securitization | ||||||||||

| Corporation, Tobacco | ||||||||||

| Settlement Asset-Backed Bonds | 6.00 | 6/1/28 | 925,000 | 649,766 | ||||||

| Michigan Tobacco Settlement | ||||||||||

| Finance Authority, Tobacco | ||||||||||

| Settlement Asset-Backed Bonds | 7.31 | 6/1/34 | 4,605,000 | 2,677,854 | ||||||

| Tobacco Settlement Authority of | ||||||||||

| Iowa, Tobacco Settlement | ||||||||||

| Asset-Backed Bonds | 6.50 | 6/1/23 | 3,073,000 | 2,223,899 | ||||||

| Williamson County, | ||||||||||

| Combination Tax and Revenue | ||||||||||

| Certificates of Obligation | ||||||||||

| (Insured; FSA) | 6.00 | 8/15/14 | 220,000 | h | 236,658 | |||||

| Wisconsin, | ||||||||||

| GO (Insured; MBIA, Inc.) | 5.00 | 5/1/15 | 380,000 | h | 426,269 | |||||

| 8,383,393 | ||||||||||

| Services—.8% | ||||||||||

| CVS Caremark, | ||||||||||

| Sr. Unscd. Notes | 5.75 | 8/15/11 | 400,000 | 401,623 | ||||||

| Donnelley (R.R.) and Sons, | ||||||||||

| Sr. Unscd. Notes | 5.63 | 1/15/12 | 1,280,000 | c | 1,139,119 | |||||

| Lowe’s Companies, | ||||||||||

| Sr. Unscd. Notes | 5.60 | 9/15/12 | 340,000 | 345,399 | ||||||

| Norfolk Southern, | ||||||||||

| Sr. Unscd. Notes | 6.75 | 2/15/11 | 312,000 | 315,776 | ||||||

| Ryder System, | ||||||||||

| Sr. Unscd. Notes | 3.50 | 3/15/09 | 145,000 | c | 144,024 | |||||

| 2,345,941 | ||||||||||

| Telecommunication Services—.2% | ||||||||||

| Verizon Communications, | ||||||||||

| Sr. Unscd. Notes | 8.95 | 3/1/39 | 500,000 | 647,840 | ||||||

The Fund 23

| STATEMENT OF INVESTMENTS (continued) |

| Principal | ||||

| Bonds and Notes (continued) | Amount ($)f | Value ($) | ||

| U.S. Government Agencies/ | ||||

| Mortgage-Backed—45.2% | ||||

| Federal Home Loan Mortgage Corp. | ||||

| 5.50% | 11,025,000 g,i | 11,313,503 | ||

| 6.00%, 1/15/29 | 9,140,000 g,i | 9,415,626 | ||

| 3.50%, 9/1/10 | 271,757 g | 269,313 | ||

| 4.00%, 10/1/09 | 305,150 g | 304,688 | ||

| 4.50%, 10/1/09—4/1/10 | 46,522 g | 46,795 | ||

| 5.00%, 12/1/35—6/1/37 | 7,148,637 g | 7,316,488 | ||

| 5.50%, 1/1/34—11/1/38 | 7,279,681 g | 7,460,424 | ||

| 6.00%, 6/1/22—11/1/37 | 413,537 g | 427,455 | ||

| 7.00%, 11/1/31 | 206,612 g | 217,194 | ||

| Federal National Mortgage Association | ||||

| 4.50% | 12,470,000 g,i | 12,532,350 | ||

| 5.00% | 14,335,000 g,i | 14,648,245 | ||

| 5.50%, 12/1/32 | 39,635,000 g,i | 40,632,058 | ||

| 6.00% | 8,080,000 g,i | 8,379,210 | ||

| 3.53%, 7/1/10 | 1,220,840 g | 1,221,121 | ||

| 4.00%, 5/1/10 | 1,046,336 g | 1,045,506 | ||

| 4.06%, 6/1/13 | 48,000 g | 47,609 | ||

| 4.50%, 11/1/14 | 13,773 g | 14,126 | ||

| 4.90%, 1/1/14 | 402,401 g | 410,969 | ||

| 5.00%, 10/1/11—1/1/36 | 3,608,004 g | 3,690,827 | ||

| 5.14%, 1/1/16 | 69,199 g | 71,290 | ||

| 5.50%, 11/1/24—6/1/38 | 13,559,539 g | 13,927,179 | ||

| 6.00%, 7/1/17—1/1/38 | 6,373,752 g | 6,569,901 | ||

| 6.50%, 12/1/15—11/1/37 | 173,898 g | 180,844 | ||

| 7.00%, 11/1/31—6/1/32 | 36,175 g | 38,290 | ||

| 7.50%, 2/1/29—11/1/29 | 8,084 g | 8,585 | ||

| 8.50%, 6/1/12 | 3,666 g | 3,911 | ||

| Government National Mortgage Association I | ||||

| 6.00%, 1/15/32 | 2,758 | 2,856 | ||

| 6.50%, 7/15/32 | 4,471 | 4,700 | ||

| 8.00%, 8/15/25—11/15/26 | 28,750 | 30,604 | ||

| 9.00%, 2/15/21 | 13,813 | 14,792 | ||

| 140,246,459 | ||||

| U.S. Government Securities—8.1% | ||||

| U.S. Treasury Bonds | ||||

| 5.00%, 5/15/37 | 2,975,000 | 4,311,427 | ||

| U.S. Treasury Notes | ||||

| 3.50%, 5/31/13 | 2,328,000 | 2,550,617 | ||

| 4.75%, 8/15/17 | 5,460,000 | 6,529,821 | ||

| 4.88%, 4/30/11 | 10,780,000 c | 11,821,790 | ||

| 25,213,655 |

24

| Coupon | Maturity | Principal | ||||||||

| Bonds and Notes (continued) | Rate (%) | Date | Amount ($)f | Value ($) | ||||||

| Utilities—6.4% | ||||||||||

| AES, | ||||||||||

| Sr. Unscd. Notes | 7.75 | 10/15/15 | 1,150,000 | 971,750 | ||||||

| Cleveland Electric Illumination, | ||||||||||

| Sr. Unscd. Notes | 5.70 | 4/1/17 | 1,390,000 | 1,128,695 | ||||||

| Consolidated Edison of NY, | ||||||||||

| Sr. Unscd. Debs., Ser. 06-D | 5.30 | 12/1/16 | 1,060,000 | 1,038,202 | ||||||

| Consolidated Edison of NY, | ||||||||||

| Sr. Unscd. Debs., Ser. 08-A | 5.85 | 4/1/18 | 720,000 | 726,313 | ||||||

| Consumers Energy, | ||||||||||

| First Mortgage Bonds, Ser. O | 5.00 | 2/15/12 | 70,000 | 68,478 | ||||||

| Consumers Energy, | ||||||||||

| First Mortgage Bonds, Ser. B | 5.38 | 4/15/13 | 1,065,000 | 1,049,082 | ||||||

| Enel Finance International, | ||||||||||

| Gtd. Notes | 5.70 | 1/15/13 | 550,000 | a | 506,784 | |||||

| Enel Finance International, | ||||||||||

| Gtd. Bonds | 6.25 | 9/15/17 | 1,825,000 | a | 1,543,589 | |||||

| Energy Future Holdings, | ||||||||||

| Gtd. Notes | 10.88 | 11/1/17 | 2,400,000 | a | 1,716,000 | |||||

| FirstEnergy, | ||||||||||

| Sr. Unscd. Notes, Ser. B | 6.45 | 11/15/11 | 1,090,000 | 1,030,984 | ||||||

| FPL Group Capital, | ||||||||||

| Gtd. Debs | 5.63 | 9/1/11 | 2,120,000 | c | 2,151,225 | |||||

| National Grid, | ||||||||||

| Unsub. Notes | 6.30 | 8/1/16 | 1,595,000 | 1,391,815 | ||||||

| Nevada Power, | ||||||||||

| Mortgage Notes | 6.50 | 8/1/18 | 775,000 | 749,516 | ||||||

| Nevada Power, | ||||||||||

| Mortgage Notes, Ser. R | 6.75 | 7/1/37 | 745,000 | 668,493 | ||||||

| NiSource Finance, | ||||||||||

| Gtd. Notes | 2.72 | 11/23/09 | 775,000 | b,c | 698,462 | |||||

| NiSource Finance, | ||||||||||

| Gtd. Notes | 5.25 | 9/15/17 | 760,000 | 461,401 | ||||||

| Pacific Gas & Electric, | ||||||||||

| Sr. Unscd. Bonds | 3.60 | 3/1/09 | 525,000 | c | 523,564 | |||||

| Pacific Gas & Electric, | ||||||||||

| Sr. Unscd. Notes | 6.35 | 2/15/38 | 760,000 | 834,111 | ||||||

| Pepco Holdings, | ||||||||||

| Sr. Unscd. Notes | 2.83 | 6/1/10 | 25,000 | b | 24,772 | |||||

| Sierra Pacific Power, | ||||||||||

| Mortgage Notes, Ser. P | 6.75 | 7/1/37 | 370,000 | 332,003 | ||||||

The Fund 25

| STATEMENT OF INVESTMENTS (continued) |

| Coupon | Maturity | Principal | ||||||||

| Bonds and Notes (continued) | Rate (%) | Date | Amount ($)f | Value ($) | ||||||

| Utilities (continued) | ||||||||||

| Southern Co., | ||||||||||

| Sr. Unscd. Notes, Ser. A | 5.30 | 1/15/12 | 825,000 | c | 833,653 | |||||

| Veolia Environnement, | ||||||||||

| Sr. Unscd. Notes | 5.25 | 6/3/13 | 1,220,000 | 1,132,487 | ||||||

| Windsor Financing, | ||||||||||

| Sr. Scd. Notes | 5.88 | 7/15/17 | 214,938 | a | 227,157 | |||||

| 19,808,536 | ||||||||||

| Yankee—.3% | ||||||||||

| Rio Tinto Finance, | ||||||||||

| Gtd. Notes | 5.88 | 7/15/13 | 945,000 | 753,410 | ||||||

| Shinsei Finance II, | ||||||||||

| Unscd. Bonds | 7.16 | 7/1/49 | 420,000 | a,b | 87,675 | |||||

| 841,085 | ||||||||||

| Total Bonds and Notes | ||||||||||

| (cost $422,469,242) | 384,292,730 | |||||||||

| Face Amount | ||||||||||

| Covered by | ||||||||||

| Options—.0% | Contracts ($) | Value ($) | ||||||||

| Call Options | ||||||||||

| 3-Month Floor USD Libor-BBA | ||||||||||

| Interest Rate, January 2009 @ 2.5 | ||||||||||

| (cost $66,912) | 26,250,000 j | 0 | ||||||||

| Principal | ||||||||||

| Short-Term Investments—2.1% | Amount ($) | Value ($) | ||||||||

| U.S. Government Agency—1.7% | ||||||||||

| Federal Home Loan Mortgage Corp, | ||||||||||

| 0.50%, 1/13/09 | 5,000,000 g | 5,000,040 | ||||||||

| U.S. Treasury Bills—.4% | ||||||||||

| 0.44%, 1/2/09 | 1,380,000 c | 1,380,000 | ||||||||

| Total Short-Term Investments | ||||||||||

| (cost $6,379,150) | 6,380,040 | |||||||||

| Other Investment—5.4% | Shares | Value ($) | ||||||||

| Registered Investment Company; | ||||||||||

| Dreyfus Institutional Preferred | ||||||||||

| Plus Money Market Fund | ||||||||||

| (cost $16,906,203) | 16,906,203 k | 16,906,203 | ||||||||

26

| Investment of Cash Collateral | ||||

| for Securities Loaned—.7% | Shares | Value ($) | ||

| BlackRock Cash Strategies L.L.C | 1,983,334 d,l | 1,983,334 | ||

| Registered Investment Company; | ||||

| Dreyfus Institutional Cash Advantage Fund | 240,666 k,l | 240,666 | ||

| Total Investment of Cash Collateral | ||||

| for Securities Loaned | ||||

| (cost $2,224,000) | 2,224,000 | |||

| Total Investments (cost $448,045,507) | 131.9% | 409,802,973 | ||

| Liabilities, Less Cash and Receivables | (31.9%) | (99,061,326) | ||

| Net Assets | 100.0% | 310,741,647 | ||

| FSA—Financial Security Assurance GO—General Obligation LIBOR-BBA—London Interbank Offered Rate British Bankers’ Association MBIA—Municipal Bond Investors Assurance Insurance Corporation PSF-GTD—Permanent School Fund Guaranteed SFMR—Single Family Mortgage Revenue |

| a | Securities exempt from registration under Rule 144A of the Securities Act of 1933.These securities may be resold in transactions exempt from registration, normally to qualified institutional buyers. At December 31, 2008, these securities amounted to $36,467,277 or 11.7% of net assets. |

| b | Variable rate security—interest rate subject to periodic change. |

| c | Denotes all or part of security segregated as collateral for delayed securities, futures and swap contracts. |

| d | Illiquid security. At the period end, the value of these securities amounted to $1,983,334 or 0.6% of net assets.The valuation of this security has been determined in good faith under the Board of Trustees. |

| e | All or a portion of these securities are on loan. At December 31, 2008, the total market value of the fund’s securities on loan is $2,121,710 and the total market value of the collateral held by the fund is $2,224,000. |

| f | Principal amount stated in U.S. Dollars unless otherwise noted. BRL—Brazilian Real EUR—Euro. |

| g | On September 7, 2008, the Federal Housing Finance Agency (FHFA) placed Federal National Mortgage Association and Federal Home Loan Mortgage Corporation into conservatorship with FHFA as the conservator. As such, the FHFA will oversee the continuing affairs of these companies. |

| h | These securities are prerefunded; the date shown represents the prerefunded date. Bonds which are prerefunded are collateralized by U.S. Government securities which are held in escrow and are used to pay principal and interest on the municipal issue and to retire the bonds in full at the earliest refunding date. |

| i | Purchased on a forward commitment basis. |

| j | Non-income producing security. |

| k | Investment in affiliated money market mutual fund. |

| l | Investment of security lending cash collateral. |

| Portfolio Summary (Unaudited)† | ||||||

| Value (%) | Value (%) | |||||

| U.S. Government & Agencies | 53.3 | Municipals | 2.7 | |||

| Corporate Bonds | 52.1 | Foreign/Governmental | .1 | |||

| Asset/Mortgage-Backed | 15.5 | Options | .0 | |||

| Short-Term/Money Market Investments | 8.2 | 131.9 | ||||

| † Based on net assets. | ||||||

| See notes to financial statements. | ||||||

The Fund 27

STATEMENT OF FINANCIAL FUTURES

December 31, 2008

| Unrealized | ||||||||

| Market Value | Appreciation | |||||||

| Covered by | (Depreciation) | |||||||

| Contracts | Contracts ($) | Expiration | at 12/31/2008 ($) | |||||

| Financial Futures Long | ||||||||

| 10 Year Long Gilt | 53 | 9,408,523 | March 2009 | 559,974 | ||||

| U.S. Long Bonds | 172 | 23,744,063 | March 2009 | 2,218,542 | ||||

| U.S. Treasury 5 Year Notes | 80 | 9,524,375 | March 2009 | 157,536 | ||||

| U.S. Treasury 10 Year Notes | 43 | 5,407,250 | March 2009 | 114,141 | ||||

| Financial Futures Short | ||||||||

| U.S. Treasury 2 Year Notes | 180 | (39,251,250) | March 2009 | (347,020) | ||||

| 2,703,173 | ||||||||

| See notes to financial statements. | ||||||||

STATEMENT OF OPTIONS WRITTEN

December 31, 2008

| Face Amount | ||||||

| Covered by | ||||||

| Contracts | Contracts ($) | Value ($) | ||||

| Call Options: | ||||||

| U.S. Treasury 5 Year Notes, | ||||||

| January 2009 @ 118.5 | 54 | 54,000 | (65,812) | |||

| U.S. Treasury 10 Year Notes, | ||||||

| January 2009 @ 127.5 | 28 | 28,000 | (24,938) | |||

| Put Options: | ||||||

| U.S. Treasury 5 Year Notes, | ||||||

| January 2009 @ 118.5 | 54 | 54,000 | (35,859) | |||

| U.S. Treasury 10 Year Notes, | ||||||

| January 2009 @ 127.5 | 28 | 28,000 | (73,938) | |||

| (Premiums received $237,699) | (200,547) |

| See notes to financial statements. |

28

STATEMENT OF ASSETS AND LIABILITIES

December 31, 2008

| Cost | Value | |||

| Assets ($): | ||||

| Investments in securities—See Statement of Investments (including | ||||

| securities on loan, valued at $2,121,710)—Note 1(c): | ||||

| Unaffiliated issuers | 430,898,638 | 392,656,104 | ||

| Affiliated issuers | 17,146,869 | 17,146,869 | ||

| Cash | 3,087,128 | |||

| Cash denominated in foreign currencies | 9 | 9 | ||

| Receivable for investment securities sold | 17,568,232 | |||

| Dividends and interest receivable | 3,130,501 | |||

| Unrealized appreciation on forward currency exchange contracts—Note 4 | 461,812 | |||

| Unrealized appreciation on swap contracts—Note 4 | 241,234 | |||

| Prepaid expenses | 1,291 | |||

| 434,293,180 | ||||

| Liabilities ($): | ||||

| Due to The Dreyfus Corporation and affiliates—Note 3(c) | 155,569 | |||

| Due to Administrator—Note 3(a) | 6,168 | |||

| Payable for investment securities purchased | 113,473,696 | |||

| Dividend payable | 4,500,000 | |||

| Liability for securities on loan—Note 1(c) | 2,224,000 | |||

| Payable for shares of Capital Stock redeemed | 1,230,246 | |||

| Other liabilities | 652,015 | |||

| Payable for futures variation margin—Note 4 | 639,598 | |||

| Unrealized depreciation on forward currency exchange contracts—Note 4 | 368,271 | |||

| Outstanding options written, at value (premiums received $237,699) | 200,547 | |||

| Accrued expenses | 101,423 | |||

| 123,551,533 | ||||

| Net Assets ($) | 310,741,647 | |||

| Composition of Net Assets ($): | ||||

| Paid-in capital | 398,099,136 | |||

| Accumulated undistributed investment income—net | 1,061,417 | |||

| Accumulated net realized gain (loss) on investments | (53,246,276) | |||

| Accumulated net unrealized appreciation (depreciation) on investments, | ||||

| options transactions, swap transactions and foreign currency transactions | ||||

| (including $2,703,173 net unrealized appreciation on financial futures) | (35,172,630) | |||

| Net Assets ($) | 310,741,647 | |||

| Shares Outstanding | ||||

| (unlimited number of $.001 par value shares of Beneficial Interest authorized) | 17,733,737 | |||

| Net Asset Value, offering and redemption price per share ($) | 17.52 | |||

| See notes to financial statements. | ||||

The Fund 29

| STATEMENT OF OPERATIONS | ||

| Year Ended December 31, 2008 | ||

| Investment Income ($): | ||

| Income: | ||

| Interest | 23,731,942 | |

| Dividends: | ||

| Unaffiliated issuers | 4,293 | |

| Affiliated issuers | 218,008 | |

| Income from securities lending | 287,750 | |

| Total Income | 24,241,993 | |

| Expenses: | ||

| Advisory fee—Note 3(a) | 1,746,896 | |

| Administration fee—Note 3(a) | 107,484 | |

| Custodian fees—Note 3(c) | 193,703 | |

| Professional fees | 160,658 | |

| Directors’ fees and expenses—Note 3(d) | 64,046 | |

| Shareholder servicing costs—Note 3(c) | 33,517 | |

| Administrative service fees— Note 3(b) | 14,917 | |

| Loan commitment fees—Note 2 | 6,945 | |

| Registration fees | 1,926 | |

| Miscellaneous | 88,411 | |

| Total Expenses | 2,418,503 | |

| Less—reduction in advisory fee | ||

| due to undertaking—Note 3(a) | (81,289) | |

| Less—reduction in fees due to earnings credits—Note 1(c) | (192) | |

| Net Expenses | 2,337,022 | |

| Investment Income—Net | 21,904,971 | |

| Realized and Unrealized Gain (Loss) on Investments—Note 4 ($): | ||

| Net realized gain (loss) on investments | (12,081,968) | |

| Net realized gain (loss) on options written transactions | (246,683) | |

| Net realized gain (loss) on financial futures | 480,175 | |

| Net realized gain (loss) on swap transactions | 762,264 | |

| Net realized gain (loss) on forward currency exchange contracts | (215,806) | |

| Net Realized Gain (Loss) | (11,302,018) | |

| Net unrealized appreciation (depreciation) on investments, options | ||

| transactions, swap transactions and foreign currency transactions | ||

| (including $2,398,116 net unrealized appreciation on financial futures) | (29,080,065) | |

| Net Realized and Unrealized Gain (Loss) on Investments | (40,382,083) | |

| Net (Decrease) in Net Assets Resulting from Operations | (18,477,112) | |

| See notes to financial statements. | ||

30

STATEMENT OF CHANGES IN NET ASSETS

| Year Ended December 31, | ||||

| 2008 | 2007 | |||

| Operations ($): | ||||

| Investment income—net | 21,904,971 | 28,004,037 | ||

| Net realized gain (loss) on investments | (11,302,018) | (3,472,829) | ||

| Net unrealized appreciation | ||||

| (depreciation) on investments | (29,080,065) | (4,425,132) | ||

| Net Increase (Decrease) in Net Assets | ||||

| Resulting from Operations | (18,477,112) | 20,106,076 | ||

| Dividends to Shareholders from ($): | ||||

| Investment income—net | (19,851,849) | (28,878,320) | ||

| Beneficial Interest Transactions ($): | ||||

| Net proceeds from shares sold | 23,413,889 | 125,494,967 | ||

| Dividends reinvested | 13,684,047 | 19,716,752 | ||

| Cost of shares redeemed | (253,599,379)a | (130,439,783) | ||

| Increase (Decrease) in Net Assets from | ||||

| Beneficial Interest Transactions | (216,501,443) | 14,771,936 | ||

| Total Increase (Decrease) in Net Assets | (254,830,404) | 5,999,692 | ||

| Net Assets ($): | ||||

| Beginning of Period | 565,572,051 | 559,572,359 | ||

| End of Period | 310,741,647 | 565,572,051 | ||

| Undistributed (Distributions in excess) | ||||

| investment income—net | 1,061,417 | (655,864) | ||

| Capital Share Transactions (shares): | ||||

| Shares sold | 1,228,451 | 6,411,187 | ||

| Shares issued for dividends reinvested | 735,348 | 1,016,283 | ||

| Shares redeemed | (13,516,112) | (6,670,212) | ||

| Net Increase (Decrease) in Shares Outstanding | (11,552,313) | 757,258 | ||

| a Includes redemption-in-kind amounting to $26,531,547. | ||||

| See notes to financial statements. | ||||

The Fund 31

FINANCIAL HIGHLIGHTS

The following table describes the performance for the fiscal periods indicated. Total return shows how much your investment in the fund would have increased (or decreased) during each period, assuming you had reinvested all dividends and distributions.These figures have been derived from the fund’s financial statements.

| Year Ended December 31, | ||||||||||

| 2008 | 2007 | 2006 | 2005 | 2004 | ||||||

| Per Share Data ($): | ||||||||||

| Net asset value, beginning of period | 19.31 | 19.61 | 19.66 | 20.08 | 20.08 | |||||

| Investment Operations: | ||||||||||

| Investment income—neta | .88 | .96 | .93 | .82 | .77 | |||||

| Net realized and unrealized | ||||||||||

| gain (loss) on investments | (1.81) | (.26) | (.10) | (.23) | .36 | |||||

| Total from Investment Operations | (.93) | .70 | .83 | .59 | 1.13 | |||||

| Distributions: | ||||||||||

| Dividends from investment income—net | (.86) | (1.00) | (.88) | (1.01) | (1.13) | |||||

| Net asset value, end of period | 17.52 | 19.31 | 19.61 | 19.66 | 20.08 | |||||

| Total Return (%) | (5.00) | 3.64 | 4.38 | 2.96 | 5.74 | |||||

| Ratios/Supplemental Data (%): | ||||||||||

| Ratio of total expenses | ||||||||||

| to average net assets | .52 | .51b | .50b | .49b | .48b | |||||

| Ratio of net expenses | ||||||||||

| to average net assets | .50 | .50 | .50 | .49 | .48 | |||||

| Ratio of net investment income | ||||||||||

| to average net assets | 4.72 | 4.93 | 4.75 | 4.09 | 3.77 | |||||

| Portfolio Turnover Ratec,d | 443 | 430 | 382 | 380 | 301 | |||||

| Net Assets, end of period ($ x 1,000) | 310,742 | 565,572 | 559,572 | 455,891 | 463,307 | |||||

| a | Based on average shares outstanding at each month end. |

| b | Includes the fund’s share of the The Standish Mellon Fixed Income Portfolio’s (the “Portfolio”) allocated expenses. |

| c | On October 25, 2007, the fund, which owned 100% of the Portfolio on such date, withdrew entirely from the Portfolio and received the Portfolio’s securties and cash in exchange for its interests in the Portfolio. Effective October 26, 2007, the fund began investing directly in the securities in which the Portfolio had invested. Portfolio turnover represents activity of both the fund and the Portfolio for the year.The amounts shown for 2004-2006 are ratios for the Portfolio. |

| d | The portfolio turnover rates excluding mortgage dollar roll transactions for the periods ended December 31, 2008, 2007, 2006, 2005 and 2004 were 72%, 166%, 139%, 106% and 98%, respectively. |

| See notes to financial statements. |

32

NOTES TO FINANCIAL STATEMENTS

NOTE 1—Significant Accounting Policies:

Dreyfus/Standish Fixed Income Fund (the “fund”) is a separate diversified series of Dreyfus Investment Funds (the “Trust”), which is registered under the Investment Company Act of 1940, as amended (the “Act”), as an open-end management investment company and operates as a series company currently offering fourteen series, including the fund.The fund’s investment objective is to achieve a high level of current income while preserving principal and maintaining liquidity. Prior to December 1, 2008, Standish Mellon Asset Management Company LLC, a wholly-owned subsidiary of The Bank of NewYork Mellon Corporation (“BNY Mellon”), served as the fund’s investment adviser. After December 1, 2008, The Dreyfus Corporation (the “Manager” or “Dreyfus”), a wholly-owned subsidiary of BNY Mellon, serves as the fund’s investment adviser. MBSC Securities Corporation (the “Distributor”), a wholly-owned subsidiary of the Manager, is the distributor of the fund’s shares, which are sold to the public without a sales charge.

At a meeting of the fund’s Board of Trustees held on August 27, 2008, the Board approved, effective December 1, 2008, a proposal to change the names of the Trust and the fund from “Mellon Institutional Funds Investment Trust” and “Standish Mellon Fixed Income Fund” to “Dreyfus Investment Funds” and “Dreyfus/Standish Fixed Income Fund,” respectively.

Effective July 1, 2008, BNY Mellon reorganized and consolidated a number of its banking and trust company subsidiaries.As a result of the reorganization, any services previously provided to the fund by Mellon Bank, N.A. or Mellon Trust of New England, N.A. are now provided by The Bank of NewYork Mellon (formerly,The Bank of NewYork).

The Trust accounts separately for the assets, liabilities and operations of each series. Expenses directly attributable to each series are charged to that series’ operations; expenses which are applicable to all series are allocated among them on a pro rata basis.

The Fund 33

| NOTES TO FINANCIAL STATEMENTS (continued) |

The fund’s financial statements are prepared in accordance with U.S. generally accepted accounting principles, which may require the use of management estimates and assumptions. Actual results could differ from those estimates.

The fund enters into contracts that contain a variety of indemnifica-tions.The fund’s maximum exposure, if any, under these arrangements is unknown.The fund does not anticipate recognizing any loss related to these arrangements.