UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

| Investment Company Act file number | 811-04813 |

| | |

| | BNY Mellon Investment Funds I | |

| | (Exact name of Registrant as specified in charter) | |

| | | |

| | c/o BNY Mellon Investment Adviser, Inc. 240 Greenwich Street New York, New York 10286 | |

| | (Address of principal executive offices) (Zip code) | |

| | | |

| | Deirdre Cunnane, Esq. 240 Greenwich Street New York, New York 10286 | |

| | (Name and address of agent for service) | |

| |

| Registrant's telephone number, including area code: | (212) 922-6400 |

| | |

Date of fiscal year end: | 12/31 | |

| Date of reporting period: | 12/31/2023 | |

| | | | | | | |

The following N-CSR relates only to the Registrant's series listed below and does not relate to any series of the Registrant with a different fiscal year end and, therefore, different N-CSR reporting requirements. A separate N-CSR will be filed for any series with a different fiscal year end, as appropriate.

BNY Mellon Global Fixed Income Fund

FORM N-CSR

Item 1. Reports to Stockholders.

BNY Mellon Global Fixed Income Fund

| |

ANNUAL REPORT December 31, 2023 |

| |

|

| |

IMPORTANT NOTICE – UPCOMING CHANGES TO ANNUAL AND SEMI-ANNUAL REPORTS The Securities and Exchange Commission (the “SEC”) has adopted rule and form amendments that will result in changes to the design and delivery of annual and semi-annual fund reports (“Reports”). Beginning in July 2024, Reports will be streamlined to highlight key information. Certain information currently included in Reports, including financial statements, will no longer appear in the Reports but will be available online, delivered free of charge to shareholders upon request, and filed with the SEC. If you previously elected to receive the fund’s Reports electronically, you will continue to do so. Otherwise, you will receive paper copies of the fund’s re-designed Reports by USPS mail in the future. If you would like to receive the fund’s Reports (and/or other communications) electronically instead of by mail, please contact your financial advisor or, if you are a direct investor, please log into your mutual fund account at www.bnymellonim.com/us and select “E-Delivery” under the Profile page. You must be registered for online account access before you can enroll in E-Delivery. |

| |

Save time. Save paper. View your next shareholder report online as soon as it’s available. Log into www.im.bnymellon.com and sign up for eCommunications. It’s simple and only takes a few minutes. |

| |

The views expressed in this report reflect those of the portfolio manager(s) only through the end of the period covered and do not necessarily represent the views of BNY Mellon Investment Adviser, Inc. or any other person in the BNY Mellon Investment Adviser, Inc. organization. Any such views are subject to change at any time based upon market or other conditions and BNY Mellon Investment Adviser, Inc. disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a fund in the BNY Mellon Family of Funds are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any fund in the BNY Mellon Family of Funds. |

| |

Not FDIC-Insured • Not Bank-Guaranteed • May Lose Value |

Contents

T H E F U N D

F O R M O R E I N F O R M AT I O N

Back Cover

DISCUSSION OF FUND PERFORMANCE (Unaudited)

For the period from January 1, 2023, through December 31, 2023, as provided by Portfolio Managers Nathaniel Hyde, CFA, Brendan Murphy, CFA and Scott Zaleski, CFA, Adam Whiteley and Harvey Bradley of Insight North America, LLC, sub-adviser

Market and Fund Performance Overview

For the 12-month period ended December 31, 2023, BNY Mellon Global Fixed Income Fund (the “fund”) produced a total return of 7.45% for Class A shares, 6.62% for Class C shares, 7.78% for Class I shares and 7.84% for Class Y shares.1 In comparison, the Bloomberg Global Aggregate Index (Hedged) (the “Index”), the fund’s benchmark, produced a total return of 7.15% for the same period.2

Global bond markets gained ground during the period as yields remained at attractive levels, and the pace of interest-rate increases from the U.S. Federal Reserve (the “Fed”) slowed in the face of moderating inflationary pressures. The fund provided mixed performance relative to the Index, with relatively strong performance in some areas and relatively weak performance in others.

The Fund’s Investment Approach

The fund seeks to maximize total return, while realizing a market level of income consistent with preserving principal and liquidity. To pursue its goal, the fund normally invests at least 80% of its net assets, plus any borrowings for investment purposes, in U.S. dollar- and non-U.S. dollar-denominated, fixed-income securities of governments and companies located in various countries, including emerging markets. The fund invests principally in bonds, notes, mortgage-related securities, asset-backed securities, floating-rate loans (limited to up to 20% of the fund’s net assets) and other floating-rate securities, and Eurodollar and Yankee dollar instruments. The fund generally invests in eight or more countries, but always invests in at least three countries, one of which may be the United States. The fund may invest up to 25% of its assets in emerging markets, generally, and up to 7% of its net assets in any single emerging-markets country.

We focus on identifying undervalued government bond markets, currencies, sectors and securities and de-emphasize the use of interest-rate forecasting. We look for fixed-income securities with the potential for credit upgrades, unique structural characteristics or innovative features. We select securities by using fundamental economic research and quantitative analysis to allocate assets among countries and currencies, by focusing on sectors and individual securities that appear to be relatively undervalued, and by actively trading among sectors.

High Volatility Amid Shifting Interest-Rate Expectation

In the wake of a turbulent year in 2022, bond investors faced additional volatility in the first six months of 2023 as central banks continued to combat inflation, and the U.S. regional banking system experienced a crisis of confidence. The first two months of the reporting period saw a continuation of the risk-on, long-duration rally that characterized the last quarter of 2022, with a consistent downturn in credit spreads as interest rates increased in developed markets in response to high levels of inflation. (Credit spreads refer to the comparative yields of bonds of different credit quality but the same maturity.) The market

2

dynamic changed abruptly in March as rising interest rates led to failures of a few prominent U.S. regional banks, driving a significant rally in yields and a sell-off in spreads. However, the Fed stepped in quickly to calm markets and reduce the likelihood for further contagion. The second quarter of 2023 saw yields decline and spreads increase to pre-crisis levels, with inflation and the central bank’s interest-rate response once again driving the performance of fixed-income markets.

During the third quarter, trends generally resumed the direction set at the beginning of the year, with international bond markets largely following the U.S. lead. Hopes for near-term rate cuts by the Fed faded in the face of sustained hawkish rhetoric from the central bank, and expectations shifted to an acceptance that rates would stay higher for longer than previously contemplated. The back end of the yield curve came under particular pressure, with the 10-year U.S. Treasury yield rising much more sharply than the 2-year Treasury yield, although the curve remained inverted. Yields peaked in late October on renewed hopes for rate cuts, prompting strong gains in duration and risk assets. The Fed added fuel to the rally’s engine in December, signaling a likelihood of multiple rate cuts in 2024 and its view that a recession appeared unlikely given prevailing economic conditions.

A Balance of Positive and Negative Positions

A wide range of positive positions bolstered the fund’s performance relative to the Index during the period, with the strongest returns realized during the year-end rally. Credit exposure bolstered relative returns, largely due to security selection, which more than made up for the negative impact of the fund’s conservative credit allocation. The fund’s selection process identified particularly attractive credit opportunities among European financials and property names, which appeared more favorably priced than credits in other sectors and regions. In the inflation space, the fund added modest performance, using inflation swaps to position for higher 20-year break-even inflation in the United States and lower 30-year break-even inflation in Europe. Overweight exposure to local emerging markets enhanced returns, particularly during the first half of the year, while intra-European government bond positioning proved additive during the second and fourth quarters. Finally, overweight exposure to agency mortgage-backed securities (“MBS”), while a source of volatility, also contributed positively to relative performance on balance.

Conversely, underweight exposure to U.S. duration detracted from relative returns, as did overweight exposure to small-credit beta in March and active duration positions in May. While local emerging-markets exposure provided contributions for the period overall, the position undermined returns from August through October. Unlike 2022, when developed-markets duration drove positive performance for the fund, the position had little positive or negative impact on relative returns during 2023.

The fund used a wide range of derivative instruments to adopt various positions and hedge against various risks during the period, primarily interest-rate and credit-default swaps. In general, we used derivatives to isolate and reduce the risks associated with various positions taken by the fund. Accordingly, the performance of the fund in aggregate reflects, to a degree, the use of derivatives during the period.

3

DISCUSSION OF FUND PERFORMANCE (Unaudited) (continued)

Maintaining a Constructive View on Global Fixed Income

While we remain generally bullish on global fixed income, we hold a nuanced view of the market’s diverse risks and opportunities. Given prevailing expectations for aggressive rate cuts in 2024, which may not be fully realized, we take a cautious attitude toward duration in most developed markets, especially considering how rapidly the market repriced in November and December 2023. We see more value in peripheral international markets, such as Sweden and Australia, where curves still slope upward; long-duration positions carry positively; and room remains for the market to price in additional easing. In short, while we are tactically cautious on the outlook for U.S. and European duration, we see attractive opportunities to add alpha through active relative-value trading in the rate space.

As of December 31, 2023, the fund holds generally underweight duration exposure, particularly in Canada, Europe and, to a lesser degree, the United States, with overweight positions in a few specific markets (Australia, New Zealand, South Korea and Sweden). In terms of yield curve positioning, the fund holds overweight exposure to the 5-to-7-year part of the curve, and underweight exposure to the 20-plus-year bucket. The fund holds modestly overweight exposure to risk assets, with a skew toward European credits and an overweight position in U.S. agency MBS. The fund also holds a small, long position in the Japanese yen, reflecting our outlook for the Bank of Japan and the attractive valuation on offer when we entered into the trade.

January 16, 2024

1 Total return includes reinvestment of dividends and any capital gains paid and does not take into consideration the maximum initial sales charge in the case of Class A shares or the applicable contingent deferred sales charge imposed on redemptions in the case of Class C shares. Had these charges been reflected, returns would have been lower. Class I and Class Y are not subject to any initial or deferred sales charge. Past performance is no guarantee of future results. Share price and investment return fluctuate such that upon redemption, fund shares may be worth more or less than their original cost.

2 Source: FactSet. — The Bloomberg Global Aggregate Index (Hedged) is a flagship measure of global, investment grade debt from 24 local currency markets. This multi-currency benchmark includes treasury, government-related, corporate and securitized, fixed-rate bonds from both developed and emerging market issuers. Currency exposure is hedged to the U.S. dollar. Investors cannot invest directly in any index.

Bonds are subject generally to interest-rate, credit, liquidity and market risks, to varying degrees, all of which are more fully described in the fund’s prospectus. Generally, all other factors being equal, bond prices are inversely related to interest-rate changes, and rate increases can cause price declines.

Foreign bonds are subject to special risks, including exposure to currency fluctuations, changing political and economic conditions and potentially less liquidity. The fixed-income securities of issuers located in emerging markets can be more volatile and less liquid than those of issuers in more mature economies.

Investments in foreign currencies are subject to the risk that those currencies will decline in value relative to the U.S. dollar, or, in the case of hedged positions, that the U.S. dollar will decline relative to the currency being hedged. Currency rates in foreign countries may fluctuate significantly over short periods of time. A decline in the value of foreign currencies relative to the U.S. dollar will reduce the value of securities held by the fund and denominated in those currencies.

Ginnie Maes and other securities backed by the full faith and credit of the United States Government are guaranteed only as to timely payment of interest and principal when held to maturity. The market prices for such securities are not guaranteed and will fluctuate. Privately issued mortgage related securities also are subject to credit

risks associated with the underlying mortgage properties. These securities may be more volatile and less liquid than more traditional, government backed debt securities.

High yield bonds are subject to increased credit risk and are considered speculative in terms of the issuer’s perceived ability to continue making interest payments on a timely basis and to repay principal upon maturity.

The fund may, but is not required to, use derivative instruments. A small investment in derivatives could have a potentially large impact on the fund’s performance. The use of derivatives involves risks different from, or possibly greater than, the risks associated with investing directly in the underlying assets.

4

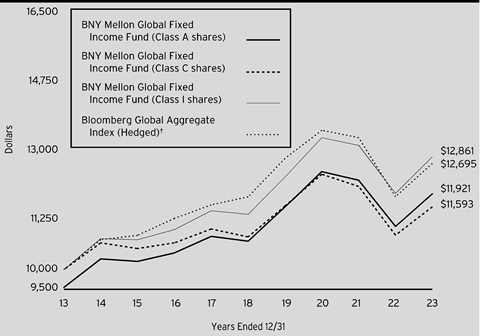

FUND PERFORMANCE (Unaudited)

Comparison of change in value of a $10,000 investment in Class A shares, Class C shares and Class I shares of BNY Mellon Global Fixed Income Fund with a hypothetical investment of $10,000 in the Bloomberg Global Aggregate Index (Hedged) (the “Index”).

† Source: FactSet

Past performance is not predictive of future performance.

The above graph compares a hypothetical $10,000 investment made in each of the Class A shares, Class C shares and Class I shares of BNY Mellon Global Fixed Income Fund on 12/31/13 to a hypothetical investment of $10,000 made in the Index on that date. All dividends and capital gain distributions are reinvested.

The fund’s performance shown in the line graph above takes into account the maximum initial sales charge on Class A shares and all other applicable fees and expenses of the applicable classes. The Index is a flagship measure of global investment-grade debt from 24 local currency markets. This multi-currency benchmark includes treasury, government-related, corporate and securitized fixed-rate bonds from both developed and emerging markets issuers. Currency exposure is hedged to the U.S. dollar. Unlike a mutual fund, the Index is not subject to charges, fees and other expenses. Investors cannot invest directly in any index. Further information relating to fund performance, including expense reimbursements, if applicable, is contained in the Financial Highlights section of the prospectus and elsewhere in this report.

5

FUND PERFORMANCE (Unaudited) (continued)

Comparison of change in value of a $1,000,000 investment in Class Y shares of BNY Mellon Global Fixed Income Fund with a hypothetical investment of $1,000,000 in the Bloomberg Global Aggregate Index (Hedged) (the “Index”).

† Source: FactSet

Past performance is not predictive of future performance.

The above graph compares a hypothetical $1,000,000 investment made in Class Y shares of BNY Mellon Global Fixed Income Fund on 12/31/13 to a hypothetical investment of $1,000,000 made in the Index on that date. All dividends and capital gain distributions are reinvested.

The fund’s performance shown in the line graph above takes into account all applicable fees and expenses of the fund’s Class Y shares. The Index is a flagship measure of global investment-grade debt from 24 local currency markets. This multi-currency benchmark includes treasury, government-related, corporate and securitized fixed-rate bonds from both developed and emerging markets issuers. Currency exposure is hedged to the U.S. dollar. Unlike a mutual fund, the Index is not subject to charges, fees and other expenses. Investors cannot invest directly in any index. Further information relating to fund performance, including expense reimbursements, if applicable, is contained in the Financial Highlights section of the prospectus and elsewhere in this report.

6

| | | | | | | |

Average Annual Total Returns as of 12/31/2023 |

| | 1 Year | 5 Years | 10 Years |

Class A shares | | | | | | |

with maximum sales charge (4.50%) | | 2.61% | 1.21% | | 1.77% | |

without sales charge | | 7.45% | 2.15% | | 2.24% | |

Class C shares | | | | | | |

with applicable redemption charge † | | 5.62% | 1.37% | | 1.49% | |

without redemption | | 6.62% | 1.37% | | 1.49% | |

Class I shares | | 7.78% | 2.44% | | 2.55% | |

Class Y shares | | 7.84% | 2.50% | | 2.61% | |

Bloomberg Global

Aggregate Index ( Hedged ) | | 7.15% | 1.40% | | 2.41% | |

† The maximum contingent deferred sales charge for Class C shares is 1% for shares redeemed within one year of the date of purchase.

The performance data quoted represents past performance, which is no guarantee of future results. Share price and investment return fluctuate and an investor’s shares may be worth more or less than original cost upon redemption. Current performance may be lower or higher than the performance quoted. Go to www.im.bnymellon.com for the fund’s most recent month-end returns.

The fund’s performance shown in the graphs and table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. In addition to the performance of Class A shares shown with and without a maximum sales charge, the fund’s performance shown in the table takes into account all other applicable fees and expenses on all classes.

7

UNDERSTANDING YOUR FUND’S EXPENSES (Unaudited)

As a mutual fund investor, you pay ongoing expenses, such as management fees and other expenses. Using the information below, you can estimate how these expenses affect your investment and compare them with the expenses of other funds. You also may pay one-time transaction expenses, including sales charges (loads) and redemption fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial adviser.

Review your fund’s expenses

The table below shows the expenses you would have paid on a $1,000 investment in BNY Mellon Global Fixed Income Fund from July 1, 2023 to December 31, 2023. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

| | | | | | | |

Expenses and Value of a $1,000 Investment | |

Assume actual returns for the six months ended December 31, 2023 | |

| | | | | | |

| | Class A | Class C | Class I | Class Y | |

Expenses paid per $1,000† | $4.38 | $8.28 | $2.79 | $2.43 | |

Ending value (after expenses) | $1,045.30 | $1,041.00 | $1,047.20 | $1,047.20 | |

COMPARING YOUR FUND’S EXPENSES WITH THOSE OF OTHER FUNDS (Unaudited)

Using the SEC’s method to compare expenses

The Securities and Exchange Commission (“SEC”) has established guidelines to help investors assess fund expenses. Per these guidelines, the table below shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return. You can use this information to compare the ongoing expenses (but not transaction expenses or total cost) of investing in the fund with those of other funds. All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

| | | | | | | |

Expenses and Value of a $1,000 Investment | |

Assuming a hypothetical 5% annualized return for the six months ended December 31, 2023 | |

| | | | | | |

| | Class A | Class C | Class I | Class Y | |

Expenses paid per $1,000† | $4.33 | $8.19 | $2.75 | $2.40 | |

Ending value (after expenses) | $1,020.92 | $1,017.09 | $1,022.48 | $1,022.84 | |

† | Expenses are equal to the fund’s annualized expense ratio of .85% for Class A, 1.61% for Class C, .54% for Class I and .47% for Class Y, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). |

8

STATEMENT OF INVESTMENTS

December 31, 2023

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity Date | | Principal Amount ($) | a | Value ($) | |

Bonds and Notes - 91.1% | | | | | |

Australia - .9% | | | | | |

Australia, Sr. Unscd. Bonds, Ser. 140 | AUD | 4.50 | | 4/21/2033 | | 26,725,000 | | 18,997,191 | |

Australia, Sr. Unscd. Bonds, Ser. 150 | AUD | 3.00 | | 3/21/2047 | | 5,240,000 | | 2,886,247 | |

| | 21,883,438 | |

Austria - .9% | | | | | |

Raiffeisen Bank International AG, Sr. Bonds | EUR | 4.75 | | 1/26/2027 | | 8,300,000 | b | 9,265,927 | |

Raiffeisen Bank International AG, Sr. Notes | EUR | 0.05 | | 9/1/2027 | | 900,000 | | 868,009 | |

Raiffeisen Bank International AG, Sub. Notes | EUR | 2.88 | | 6/18/2032 | | 7,600,000 | b | 7,565,863 | |

Raiffeisen Bank International AG, Sub. Notes | EUR | 7.38 | | 12/20/2032 | | 2,700,000 | b | 3,150,875 | |

| | 20,850,674 | |

Belgium - .5% | | | | | |

Belgium, Sr. Unscd. Bonds, Ser. 76 | EUR | 1.90 | | 6/22/2038 | | 11,200,000 | c | 10,922,866 | |

Bermuda - .1% | | | | | |

Athora Holding Ltd., Sr. Unscd. Bonds | EUR | 6.63 | | 6/16/2028 | | 1,652,000 | | 1,887,237 | |

Canada - 1.7% | | | | | |

Canada, Bonds | CAD | 1.75 | | 12/1/2053 | | 19,725,000 | | 11,186,853 | |

Canada, Bonds | CAD | 3.25 | | 9/1/2028 | | 17,600,000 | | 13,329,139 | |

CNH Capital Canada Receivables Trust, Ser. 2021-1A, Cl. A2 | CAD | 1.00 | | 11/16/2026 | | 3,455,585 | c | 2,513,641 | |

Ford Auto Securitization Trust II, Ser. 2022-AA, Cl. A3 | CAD | 5.40 | | 9/15/2028 | | 11,382,000 | c | 8,713,129 | |

MBarc Credit Canada, Inc., Ser. 2021-AA, Cl. A3 | CAD | 0.93 | | 2/17/2026 | | 1,943,492 | c | 1,464,458 | |

The Toronto-Dominion Bank, Sr. Unscd. Notes | EUR | 1.95 | | 4/8/2030 | | 2,741,000 | | 2,782,945 | |

| | 39,990,165 | |

Cayman Islands - .5% | | | | | |

Octagon 61 CLO, Ser. 2023-2A, Cl. A, (3 Month TSFR +1.85%) | | 7.27 | | 4/20/2036 | | 5,274,060 | c,d | 5,304,375 | |

Regatta XXV Funding Ltd. CLO, Ser. 2023-1A, Cl.A, (3 Month TSFR +1.90%) | | 7.15 | | 7/15/2036 | | 5,775,000 | c,d | 5,805,348 | |

| | 11,109,723 | |

China - 3.1% | | | | | |

China, Unscd. Bonds | CNY | 3.81 | | 9/14/2050 | | 438,050,000 | | 72,221,799 | |

Denmark - .1% | | | | | |

Denmark, Bonds | DKK | 4.50 | | 11/15/2039 | | 14,250,000 | | 2,697,637 | |

9

STATEMENT OF INVESTMENTS (continued)

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity Date | | Principal Amount ($) | a | Value ($) | |

Bonds and Notes - 91.1% (continued) | | | | | |

France - 5.3% | | | | | |

BNP Paribas SA, Sr. Notes | EUR | 3.63 | | 9/1/2029 | | 2,100,000 | b | 2,331,335 | |

Electricite de France SA, Jr. Sub. Notes | EUR | 2.63 | | 12/1/2027 | | 5,400,000 | e | 5,317,447 | |

France, Bonds | EUR | 0.75 | | 5/25/2028 | | 51,050,000 | | 52,937,879 | |

France, Bonds | EUR | 0.75 | | 5/25/2052 | | 12,800,000 | | 8,116,707 | |

France, Bonds | EUR | 4.00 | | 10/25/2038 | | 18,810,000 | | 23,788,000 | |

Kering SA, Sr. Unscd. Notes | EUR | 3.63 | | 9/5/2031 | | 5,100,000 | | 5,832,442 | |

Kering SA, Sr. Unscd. Notes | EUR | 3.88 | | 9/5/2035 | | 4,000,000 | | 4,641,492 | |

La Banque Postale SA, Sub. Notes | EUR | 5.50 | | 3/5/2034 | | 4,100,000 | b | 4,743,899 | |

Orano SA, Sr. Unscd. Notes | EUR | 5.38 | | 5/15/2027 | | 5,100,000 | | 5,899,998 | |

Suez SACA, Sr. Unscd. Notes | EUR | 2.38 | | 5/24/2030 | | 7,400,000 | | 7,714,531 | |

Suez SACA, Sr. Unscd. Notes | EUR | 5.00 | | 11/3/2032 | | 1,000,000 | | 1,222,979 | |

| | 122,546,709 | |

Germany - 2.6% | | | | | |

Bundesrepublik Deutschland Bundesanleihe, Bonds | EUR | 1.80 | | 8/15/2053 | | 21,650,000 | | 21,579,897 | |

Deutsche Bahn Finance GmbH, Gtd. Notes | EUR | 1.88 | | 5/24/2030 | | 2,490,000 | | 2,600,533 | |

Deutsche Bahn Finance GmbH, Gtd. Notes | EUR | 2.75 | | 3/19/2029 | | 6,210,000 | | 6,886,057 | |

Deutsche Bahn Finance GmbH, Gtd. Notes | EUR | 3.25 | | 5/19/2033 | | 1,956,000 | | 2,230,707 | |

LEG Immobilien SE, Sr. Unscd. Notes | EUR | 0.88 | | 1/17/2029 | | 400,000 | | 386,337 | |

Volkswagen Bank GmbH, Sr. Notes | EUR | 4.63 | | 5/3/2031 | | 7,200,000 | | 8,351,950 | |

Vonovia SE, Sr. Unscd. Notes | EUR | 0.63 | | 12/14/2029 | | 1,400,000 | | 1,277,867 | |

Vonovia SE, Sr. Unscd. Notes | EUR | 0.75 | | 9/1/2032 | | 12,000,000 | | 10,092,042 | |

Vonovia SE, Sr. Unscd. Notes | EUR | 1.00 | | 6/16/2033 | | 700,000 | | 589,779 | |

Vonovia SE, Sr. Unscd. Notes | EUR | 2.38 | | 3/25/2032 | | 6,300,000 | b | 6,108,395 | |

| | 60,103,564 | |

Greece - .2% | | | | | |

Hellenic Republic, Sr. Unscd. Notes | EUR | 4.38 | | 7/18/2038 | | 3,438,000 | c | 4,185,100 | |

Hungary - .3% | | | | | |

Hungary, Bonds, Ser. 32/A | HUF | 4.75 | | 11/24/2032 | | 2,699,850,000 | | 7,194,120 | |

Hungary, Sr. Unscd. Notes | | 6.75 | | 9/25/2052 | | 880,000 | c | 986,916 | |

| | 8,181,036 | |

Indonesia - .3% | | | | | |

Indonesia, Bonds, Ser. FR83 | IDR | 7.50 | | 4/15/2040 | | 93,430,000,000 | | 6,487,490 | |

Ireland - .8% | | | | | |

ESB Finance DAC, Gtd. Notes | EUR | 3.75 | | 1/25/2043 | | 6,270,000 | | 6,890,259 | |

Hammerson Ireland Finance DAC, Gtd. Notes | EUR | 1.75 | | 6/3/2027 | | 3,219,000 | | 3,260,709 | |

Permanent TSB Group Holdings PLC, Sr. Unscd. Notes | EUR | 6.63 | | 4/25/2028 | | 4,035,000 | | 4,706,149 | |

10

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity Date | | Principal Amount ($) | a | Value ($) | |

Bonds and Notes - 91.1% (continued) | | | | | |

Ireland - .8% (continued) | | | | | |

Permanent TSB Group Holdings PLC, Sub. Notes | EUR | 3.00 | | 8/19/2031 | | 4,102,000 | | 4,287,741 | |

| | 19,144,858 | |

Italy - 3.2% | | | | | |

Autostrade per L'Italia SpA, Sr. Unscd. Notes | EUR | 1.88 | | 9/26/2029 | | 2,340,000 | | 2,303,912 | |

Autostrade per L'Italia SpA, Sr. Unscd. Notes | EUR | 2.00 | | 12/4/2028 | | 12,900,000 | | 13,111,946 | |

Italy Buoni Poliennali Del Tesoro, Sr. Unscd. Bonds, Ser. 10Y | EUR | 4.40 | | 5/1/2033 | | 51,150,000 | | 60,178,960 | |

| | 75,594,818 | |

Japan - 2.9% | | | | | |

Japan (20 Year Issue), Bonds, Ser. 183 | JPY | 1.40 | | 12/20/2042 | | 4,358,900,000 | | 31,180,594 | |

Japan (20 Year Issue), Bonds, Ser. 184 | JPY | 1.10 | | 3/20/2043 | | 1,329,500,000 | | 9,014,780 | |

Japan (30 Year Issue), Bonds, Ser. 66 | JPY | 0.40 | | 3/20/2050 | | 1,074,200,000 | | 5,668,641 | |

Japan (30 Year Issue), Bonds, Ser. 69 | JPY | 0.70 | | 12/20/2050 | | 1,593,000,000 | | 9,052,911 | |

Japan (40 Year Issue), Bonds, Ser. 15 | JPY | 1.00 | | 3/20/2062 | | 1,032,100,000 | | 5,813,902 | |

Mizuho Financial Group, Inc., Sr. Unscd. Notes | EUR | 4.03 | | 9/5/2032 | | 4,767,000 | | 5,439,719 | |

OSCAR US Funding X LLC, Ser. 2019-1A, Cl. A4 | | 3.27 | | 5/10/2026 | | 509,423 | c | 508,132 | |

OSCAR US Funding XI LLC, Ser. 2019-2A, Cl. A4 | | 2.68 | | 9/10/2026 | | 1,811,561 | c | 1,801,745 | |

| | 68,480,424 | |

Jersey - .5% | | | | | |

Ballyrock 24 Ltd. CLO, Ser. 2023-24A, Cl. A1, (3 Month TSFR +1.77%) | | 7.03 | | 7/15/2036 | | 5,420,000 | c,d | 5,436,824 | |

Invesco US Ltd. CLO, Ser. 2023-3A, CI. A, (3 Month TSFR +1.80%) | | 7.22 | | 7/15/2036 | | 5,600,000 | c,d | 5,627,804 | |

| | 11,064,628 | |

Luxembourg - .8% | | | | | |

Logicor Financing Sarl, Gtd. Notes | EUR | 0.88 | | 1/14/2031 | | 10,680,000 | | 9,129,202 | |

Logicor Financing Sarl, Gtd. Notes | EUR | 1.63 | | 1/17/2030 | | 1,147,000 | | 1,085,902 | |

Logicor Financing Sarl, Gtd. Notes | EUR | 2.00 | | 1/17/2034 | | 1,095,000 | | 948,514 | |

Logicor Financing Sarl, Gtd. Notes | EUR | 3.25 | | 11/13/2028 | | 2,475,000 | | 2,603,553 | |

SELP Finance Sarl, Gtd. Bonds | EUR | 0.88 | | 5/27/2029 | | 1,996,000 | b | 1,879,628 | |

SELP Finance Sarl, Gtd. Notes | EUR | 3.75 | | 8/10/2027 | | 2,205,000 | | 2,438,973 | |

| | 18,085,772 | |

Mexico - 1.8% | | | | | |

Mexico, Bonds, Ser. M | MXN | 7.50 | | 5/26/2033 | | 798,700,000 | | 42,634,334 | |

Netherlands - 1.4% | | | | | |

Athora Netherlands NV, Sub. Notes | EUR | 2.25 | | 7/15/2031 | | 1,170,000 | | 1,153,245 | |

11

STATEMENT OF INVESTMENTS (continued)

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity Date | | Principal Amount ($) | a | Value ($) | |

Bonds and Notes - 91.1% (continued) | | | | | |

Netherlands - 1.4% (continued) | | | | | |

Athora Netherlands NV, Sub. Notes | EUR | 5.38 | | 8/31/2032 | | 9,541,000 | | 10,106,335 | |

ING Groep NV, Sr. Unscd. Notes | | 6.11 | | 9/11/2034 | | 2,188,000 | b | 2,297,532 | |

Sartorius Finance BV, Gtd. Notes | EUR | 4.50 | | 9/14/2032 | | 8,200,000 | | 9,457,928 | |

Stellantis NV, Sr. Unscd. Notes | EUR | 4.25 | | 6/16/2031 | | 3,210,000 | | 3,682,889 | |

Vonovia Finance BV, Gtd. Notes | EUR | 0.50 | | 9/14/2029 | | 1,700,000 | | 1,549,423 | |

WPC Eurobond BV, Gtd. Bonds | EUR | 2.25 | | 7/19/2024 | | 2,975,000 | | 3,245,201 | |

| | 31,492,553 | |

New Zealand - 3.5% | | | | | |

New Zealand, Unscd. Bonds, Ser. 433 | NZD | 3.50 | | 4/14/2033 | | 79,639,000 | | 47,211,387 | |

New Zealand, Unscd. Bonds, Ser. 532 | NZD | 2.00 | | 5/15/2032 | | 66,105,000 | | 35,117,656 | |

| | 82,329,043 | |

Peru - .7% | | | | | |

Peru Government Bond, Sr. Unscd. Bonds | PEN | 7.30 | | 8/12/2033 | | 61,075,000 | c | 17,319,565 | |

Portugal - .3% | | | | | |

Novo Banco SA, Sub. Notes | EUR | 9.88 | | 12/1/2033 | | 5,300,000 | b | 6,494,538 | |

Romania - .3% | | | | | |

Romania, Bonds | EUR | 3.62 | | 5/26/2030 | | 3,450,000 | c | 3,511,335 | |

Romania, Notes | EUR | 6.38 | | 9/18/2033 | | 2,072,000 | c | 2,423,520 | |

Romania, Sr. Unscd. Notes | EUR | 1.75 | | 7/13/2030 | | 771,000 | | 689,849 | |

| | 6,624,704 | |

Singapore - .4% | | | | | |

Pfizer Investment Enterprises Pte Ltd., Gtd. Notes | | 5.34 | | 5/19/2063 | | 2,250,000 | | 2,273,463 | |

Singapore, Bonds | SGD | 2.63 | | 5/1/2028 | | 9,000,000 | | 6,810,608 | |

| | 9,084,071 | |

South Africa - 1.6% | | | | | |

South Africa, Sr. Unscd. Bonds, Ser. 2044 | ZAR | 8.75 | | 1/31/2044 | | 912,536,000 | | 37,060,161 | |

South Korea - 4.2% | | | | | |

Korea, Bonds, Ser. 2812 | KRW | 2.38 | | 12/10/2028 | | 11,350,200,000 | | 8,488,577 | |

Korea, Bonds, Ser. 3212 | KRW | 4.25 | | 12/10/2032 | | 94,239,600,000 | | 79,093,022 | |

Korea, Bonds, Ser. 5209 | KRW | 3.13 | | 9/10/2052 | | 5,180,000,000 | | 4,089,293 | |

Korea, Bonds, Ser. 5303 | KRW | 3.25 | | 3/10/2053 | | 7,778,000,000 | | 6,303,518 | |

| | 97,974,410 | |

Spain - 2.3% | | | | | |

Banco de Credito Social Cooperativo SA, Sub. Notes | EUR | 5.25 | | 11/27/2031 | | 7,200,000 | | 7,412,032 | |

Cellnex Finance Co. SA, Gtd. Notes | EUR | 2.00 | | 9/15/2032 | | 5,500,000 | | 5,207,725 | |

Cellnex Telecom SA, Sr. Unscd. Notes | EUR | 1.75 | | 10/23/2030 | | 8,000,000 | b | 7,759,665 | |

Cellnex Telecom SA, Sr. Unscd. Notes | EUR | 1.88 | | 6/26/2029 | | 1,500,000 | | 1,513,302 | |

Ibercaja Banco SA, Sub. Notes | EUR | 2.75 | | 7/23/2030 | | 6,600,000 | b | 6,990,219 | |

12

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity Date | | Principal Amount ($) | a | Value ($) | |

Bonds and Notes - 91.1% (continued) | | | | | |

Spain - 2.3% (continued) | | | | | |

Spain, Sr. Unscd. Bonds | EUR | 0.70 | | 4/30/2032 | | 27,750,000 | c | 25,877,057 | |

| | 54,760,000 | |

Supranational - .2% | | | | | |

JBS USA LUX SA/JBS USA Food Co./JBS USA Finance, Inc., Gtd. Notes | | 3.63 | | 1/15/2032 | | 5,915,000 | | 5,076,385 | |

Sweden - .2% | | | | | |

Sweden, Bonds, Ser. 1056 | SEK | 2.25 | | 6/1/2032 | | 37,450,000 | | 3,789,477 | |

Switzerland - 1.8% | | | | | |

Switzerland, Bonds | CHF | 0.50 | | 6/27/2032 | | 10,775,000 | | 12,626,025 | |

UBS Group AG, Sr. Unscd. Notes | EUR | 0.65 | | 1/14/2028 | | 3,780,000 | | 3,818,362 | |

UBS Group AG, Sr. Unscd. Notes | EUR | 0.88 | | 11/3/2031 | | 14,469,000 | | 12,931,420 | |

UBS Group AG, Sr. Unscd. Notes | EUR | 2.88 | | 4/2/2032 | | 12,330,000 | | 12,742,398 | |

| | 42,118,205 | |

Thailand - .3% | | | | | |

Thailand, Sr. Unscd. Bonds | THB | 3.39 | | 6/17/2037 | | 193,725,000 | | 6,014,043 | |

United Kingdom - 4.6% | | | | | |

BAT International Finance PLC, Gtd. Notes | EUR | 2.25 | | 1/16/2030 | | 5,700,000 | | 5,610,052 | |

Brass No. 10 PLC, Ser. 10-A, Cl. A1 | | 0.67 | | 4/16/2069 | | 1,108,943 | c | 1,076,996 | |

British American Tobacco PLC, Sub. Notes, Ser. 5.25 | EUR | 3.00 | | 12/27/2026 | | 6,500,000 | e | 6,433,021 | |

Gemgarto PLC, Ser. 2021-1A, Cl. A, (3 Month SONIO +0.59%) | GBP | 5.81 | | 12/16/2067 | | 2,409,736 | c,d | 3,070,541 | |

International Distributions Services PLC, Gtd. Notes | EUR | 5.25 | | 9/14/2028 | | 1,130,000 | | 1,295,722 | |

Thames Water Utilities Finance PLC, Sr. Scd. Notes | EUR | 1.25 | | 1/31/2032 | | 1,257,000 | | 1,048,277 | |

Thames Water Utilities Finance PLC, Sr. Scd. Notes | EUR | 4.38 | | 1/18/2031 | | 3,447,000 | | 3,607,735 | |

Tower Bridge Funding PLC, Ser. 2021-2, CI. A, (3 Month SONIO +0.78%) | GBP | 6.00 | | 11/20/2063 | | 2,426,769 | d | 3,092,362 | |

United Kingdom Gilt, Bonds | GBP | 1.25 | | 7/31/2051 | | 26,900,000 | | 18,261,834 | |

United Kingdom Gilt, Bonds | GBP | 3.25 | | 1/31/2033 | | 29,500,000 | | 36,787,524 | |

United Kingdom Gilt, Bonds | GBP | 3.75 | | 7/22/2052 | | 3,175,000 | | 3,801,320 | |

United Kingdom Gilt, Bonds | GBP | 4.50 | | 6/7/2028 | | 17,500,000 | | 23,253,279 | |

| | 107,338,663 | |

United States - 42.8% | | | | | |

A&D Mortgage Trust, Ser. 2023-NQM2, Cl. A1 | | 6.13 | | 5/25/2068 | | 4,728,040 | c | 4,729,037 | |

Aligned Data Centers Issuer LLC, Ser. 2023-1A, Cl. A2 | | 6.00 | | 8/17/2048 | | 3,914,000 | c | 3,883,742 | |

American Homes 4 Rent Trust, Ser. 2014-SFR3, Cl. A | | 3.68 | | 12/17/2036 | | 3,755,238 | c | 3,683,333 | |

13

STATEMENT OF INVESTMENTS (continued)

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity Date | | Principal Amount ($) | a | Value ($) | |

Bonds and Notes - 91.1% (continued) | | | | | |

United States - 42.8% (continued) | | | | | |

AmeriCredit Automobile Receivables Trust, Ser. 2020-1, Cl. C | | 1.59 | | 10/20/2025 | | 3,232,545 | | 3,207,904 | |

AMSR Trust, Ser. 2019-SFR1, Cl. B | | 3.02 | | 1/19/2039 | | 4,925,000 | c | 4,568,625 | |

AT&T, Inc., Sr. Unscd. Notes | | 4.50 | | 5/15/2035 | | 1,400,000 | | 1,327,196 | |

Avis Budget Rental Car Funding AESOP LLC, Ser. 2023-4A, Cl. A | | 5.49 | | 6/20/2029 | | 3,643,000 | c | 3,676,676 | |

Avis Budget Rental Car Funding AESOP LLC, Ser. 2023-8A, Cl. A | | 6.02 | | 2/20/2030 | | 2,831,000 | c | 2,921,798 | |

Berkshire Hathaway Finance Corp., Gtd. Notes | EUR | 1.50 | | 3/18/2030 | | 6,540,000 | | 6,559,895 | |

Bristol-Myers Squibb Co., Sr. Unscd. Notes | | 6.25 | | 11/15/2053 | | 3,051,000 | | 3,494,555 | |

Bristol-Myers Squibb Co., Sr. Unscd. Notes | | 6.40 | | 11/15/2063 | | 3,211,000 | | 3,723,895 | |

BXHPP Trust, Ser. 2021-FILM, Cl. B, (1 Month TSFR +1.01%) | | 6.38 | | 8/15/2036 | | 9,620,000 | c,d | 8,850,584 | |

CAMB Commercial Mortgage Trust, Ser. 2019-LIFE, Cl. A, (1 Month TSFR +1.12%) | | 6.73 | | 12/15/2037 | | 8,350,000 | c,d | 8,298,823 | |

Capital One Financial Corp., Sr. Unscd. Notes | | 7.62 | | 10/30/2031 | | 9,905,000 | | 10,893,818 | |

Carrier Global Corp., Sr. Unscd. Notes | EUR | 4.50 | | 11/29/2032 | | 3,829,000 | c | 4,529,189 | |

Carrier Global Corp., Sr. Unscd. Notes | | 5.90 | | 3/15/2034 | | 1,863,000 | b,c | 2,015,774 | |

Carrier Global Corp., Sr. Unscd. Notes | | 6.20 | | 3/15/2054 | | 1,346,000 | c | 1,557,549 | |

Carvana Auto Receivables Trust, Ser. 2021-N2, Cl. C | | 1.07 | | 3/10/2028 | | 1,309,299 | | 1,226,659 | |

Celanese US Holdings LLC, Gtd. Bonds | EUR | 5.34 | | 1/19/2029 | | 7,801,000 | b | 9,045,963 | |

Charter Communications Operating LLC/Charter Communications Operating Capital, Sr. Scd. Notes | | 5.25 | | 4/1/2053 | | 7,583,000 | | 6,360,976 | |

COLT Mortgage Loan Trust, Ser. 2023-2, Cl. A1 | | 6.60 | | 7/25/2068 | | 3,121,030 | c | 3,164,975 | |

COLT Mortgage Loan Trust, Ser. 2023-4, Cl. A1 | | 7.16 | | 10/25/2068 | | 7,266,935 | c | 7,457,278 | |

Columbia Pipelines Operating Co. LLC, Sr. Unscd. Notes | | 5.93 | | 8/15/2030 | | 6,623,000 | c | 6,853,430 | |

Columbia Pipelines Operating Co. LLC, Sr. Unscd. Notes | | 6.04 | | 11/15/2033 | | 3,441,000 | c | 3,605,367 | |

CVS Health Corp., Sr. Unscd. Notes | | 5.05 | | 3/25/2048 | | 3,200,000 | | 2,995,758 | |

CyrusOne Data Centers Issuer I LLC, Ser. 2023-1A, Cl. B | | 5.45 | | 4/20/2048 | | 1,263,887 | c | 1,129,472 | |

14

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity Date | | Principal Amount ($) | a | Value ($) | |

Bonds and Notes - 91.1% (continued) | | | | | |

United States - 42.8% (continued) | | | | | |

CyrusOne Data Centers Issuer I LLC, Ser. 2023-2A, Cl. A2 | | 5.56 | | 11/20/2048 | | 4,454,000 | c | 4,252,391 | |

Digital Euro Finco LLC, Gtd. Bonds | EUR | 2.63 | | 4/15/2024 | | 5,814,000 | | 6,382,121 | |

Domino's Pizza Master Issuer LLC, Ser. 2021-1A, Cl. A2I | | 2.66 | | 4/25/2051 | | 5,484,375 | c | 4,861,272 | |

Energy Transfer LP, Sr. Unscd. Notes | | 6.40 | | 12/1/2030 | | 3,053,000 | b | 3,267,745 | |

Energy Transfer LP, Sr. Unscd. Notes | | 6.55 | | 12/1/2033 | | 3,218,000 | | 3,496,824 | |

Ent Auto Receivables Trust, Ser. 2023-1A, Cl. A3 | | 6.24 | | 1/16/2029 | | 2,112,000 | c | 2,152,925 | |

Exelon Corp., Sr. Unscd. Notes | | 5.60 | | 3/15/2053 | | 4,480,000 | | 4,565,154 | |

Federal Agricultural Mortgage Corp. Mortgage Trust, Ser. 2021-1, CI. A | | 2.18 | | 1/25/2051 | | 5,713,322 | c | 4,710,291 | |

Federal Home Loan Mortgage Corp. Multifamily Structured Credit Risk, Ser. 2021-MN1, Cl. M1, (1 Month SOFR +2.00%) | | 7.34 | | 1/25/2051 | | 1,057,933 | c,d,f | 1,028,393 | |

Federal Home Loan Mortgage Corp. Multifamily Structured Pass Through Certificates, Ser. KC02, Cl. A2 | | 3.37 | | 7/25/2025 | | 5,541,473 | f | 5,411,074 | |

Federal Home Loan Mortgage Corp. Multifamily Structured Pass Through Certificates, Ser. KL3W, Cl. AFLW, (1 Month SOFR +0.56%) | | 5.90 | | 8/25/2025 | | 3,827,732 | d,f | 3,832,470 | |

Federal Home Loan Mortgage Corp. Seasoned Credit Risk Transfer Trust, Ser. 2017-4, Cl. M45T | | 4.50 | | 6/25/2057 | | 2,187,360 | f | 2,079,361 | |

Federal Home Loan Mortgage Corp. Seasoned Credit Risk Transfer Trust, Ser. 2018-4, Cl. M55D | | 4.00 | | 3/25/2058 | | 3,186,025 | f | 2,960,069 | |

Federal Home Loan Mortgage Corp. Seasoned Credit Risk Transfer Trust, Ser. 2019-3, Cl. M55D | | 4.00 | | 10/25/2058 | | 2,347,140 | f | 2,182,386 | |

Federal Home Loan Mortgage Corp. Seasoned Credit Risk Transfer Trust, Ser. 2020-3, Cl. TTU | | 2.50 | | 5/25/2060 | | 2,110,197 | f | 1,911,142 | |

Federal Home Loan Mortgage Corp. Seasoned Loans Structured Transaction Trust, Ser. 2018-2, Cl. A1 | | 3.50 | | 11/25/2028 | | 4,552,145 | f | 4,341,165 | |

Federal Home Loan Mortgage Corp. Seasoned Loans Structured Transaction Trust, Ser. 2019-1, Cl. A2 | | 3.50 | | 5/25/2029 | | 5,000,000 | f | 4,638,685 | |

15

STATEMENT OF INVESTMENTS (continued)

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity Date | | Principal Amount ($) | a | Value ($) | |

Bonds and Notes - 91.1% (continued) | | | | | |

United States - 42.8% (continued) | | | | | |

Federal Home Loan Mortgage Corp. Seasoned Loans Structured Transaction Trust, Ser. 2019-2, Cl. A1C | | 2.75 | | 9/25/2029 | | 4,019,507 | f | 3,712,010 | |

Federal Home Loan Mortgage Corp. Seasoned Loans Structured Transaction Trust, Ser. 2019-3, Cl. A2C | | 2.75 | | 11/25/2029 | | 6,425,000 | f | 5,676,550 | |

Federal National Mortgage Association Grantor Trust, Ser. 2017-T1, Cl. A | | 2.90 | | 6/25/2027 | | 7,633,049 | f | 7,226,457 | |

General Motors Financial Co., Inc., Sr. Unscd. Notes | | 5.85 | | 4/6/2030 | | 2,444,000 | b | 2,522,344 | |

Helios Issuer LLC, Ser. 2023-GRID1, Cl. 1A | | 5.75 | | 12/20/2050 | | 829,377 | c | 851,978 | |

Honeywell International, Inc., Sr. Unscd. Bonds | EUR | 4.13 | | 11/2/2034 | | 5,980,000 | | 7,026,911 | |

Honeywell International, Inc., Sr. Unscd. Notes | EUR | 3.75 | | 5/17/2032 | | 2,386,000 | | 2,736,122 | |

Life Mortgage Trust, Ser. 2021-BMR, Cl. A, (1 Month TSFR +0.81%) | | 6.18 | | 3/15/2038 | | 4,275,920 | c,d | 4,185,880 | |

Mosaic Solar Loan Trust, Ser. 2023-2A, Cl. A | | 5.36 | | 9/22/2053 | | 2,417,447 | c | 2,387,385 | |

Nasdaq, Inc., Sr. Unscd. Notes | | 6.10 | | 6/28/2063 | | 6,664,000 | b | 7,212,229 | |

National Grid North America, Inc., Sr. Unscd. Notes | EUR | 1.05 | | 1/20/2031 | | 7,340,000 | | 6,863,094 | |

New Residential Mortgage Loan Trust, Ser. 2022-NQM1, CI. A1 | | 2.28 | | 4/25/2061 | | 5,471,947 | c | 4,678,745 | |

Purewest Funding LLC, Ser. 2021-1, Cl. A1 | | 4.09 | | 12/22/2036 | | 2,544,904 | c | 2,445,497 | |

Realty Income Corp., Sr. Unscd. Notes | EUR | 4.88 | | 7/6/2030 | | 6,834,000 | b | 7,999,370 | |

Realty Income Corp., Sr. Unscd. Notes | EUR | 5.13 | | 7/6/2034 | | 1,288,000 | | 1,575,141 | |

Retained Vantage Data Centers Issuer LLC, Ser. 2023-1A, Cl. A2A | | 5.00 | | 9/15/2048 | | 5,630,000 | c | 5,300,403 | |

SBA Tower Trust, Asset Backed Notes | | 1.88 | | 1/15/2026 | | 6,860,000 | c | 6,368,947 | |

SBA Tower Trust, Asset Backed Notes | | 2.59 | | 10/15/2031 | | 6,340,000 | c | 5,115,489 | |

SBA Tower Trust, Asset Backed Notes | | 2.84 | | 1/15/2025 | | 8,030,000 | c | 7,757,387 | |

SpringCastle America Funding LLC, Ser. 2020-AA, Cl. A | | 1.97 | | 9/25/2037 | | 2,554,306 | c | 2,358,400 | |

Stack Infrastructure Issuer LLC, Ser. 2023-1A, CI. A2 | | 5.90 | | 3/25/2048 | | 1,430,000 | c | 1,410,249 | |

Tapestry, Inc., Sr. Unscd. Notes | | 7.70 | | 11/27/2030 | | 3,247,000 | | 3,420,766 | |

16

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity Date | | Principal Amount ($) | a | Value ($) | |

Bonds and Notes - 91.1% (continued) | | | | | |

United States - 42.8% (continued) | | | | | |

Tapestry, Inc., Sr. Unscd. Notes | | 7.85 | | 11/27/2033 | | 3,403,000 | | 3,631,897 | |

Tesla Auto Lease Trust, Ser. 2021-A, CI. C | | 1.18 | | 3/20/2025 | | 1,496,145 | c | 1,491,419 | |

The PNC Financial Services Group, Inc., Sr. Unscd. Notes | | 5.94 | | 8/18/2034 | | 11,280,000 | | 11,733,614 | |

The PNC Financial Services Group, Inc., Sr. Unscd. Notes | | 6.04 | | 10/28/2033 | | 4,385,000 | | 4,583,864 | |

Tricon American Homes Trust, Ser. 2019-SFR1, Cl. A | | 2.75 | | 3/17/2038 | | 7,428,760 | c | 7,057,511 | |

TRP LLC, Ser. 2021-1, Cl. A | | 2.07 | | 6/19/2051 | | 6,559,756 | c | 5,810,757 | |

TRP LLC, Ser. 2021-2, Cl. A | | 2.15 | | 6/19/2051 | | 6,634,061 | c | 5,928,599 | |

Truist Financial Corp., Sr. Unscd. Notes | | 5.12 | | 1/26/2034 | | 3,648,000 | | 3,535,092 | |

Truist Financial Corp., Sr. Unscd. Notes | | 5.87 | | 6/8/2034 | | 8,175,000 | | 8,344,974 | |

Truist Financial Corp., Sr. Unscd. Notes | | 6.12 | | 10/28/2033 | | 859,000 | | 892,410 | |

Truist Financial Corp., Sr. Unscd. Notes | | 7.16 | | 10/30/2029 | | 2,399,000 | b | 2,592,731 | |

U.S. Bancorp, Sr. Unscd. Notes | | 5.84 | | 6/12/2034 | | 5,801,000 | | 5,986,446 | |

U.S. Bancorp, Sr. Unscd. Notes | | 5.85 | | 10/21/2033 | | 4,612,000 | | 4,754,225 | |

U.S. Treasury Bonds | | 3.63 | | 2/15/2053 | | 10,650,000 | | 9,837,105 | |

U.S. Treasury Bonds | | 4.13 | | 8/15/2053 | | 30,000,000 | g | 30,332,812 | |

U.S. Treasury Notes | | 3.13 | | 11/15/2028 | | 59,400,000 | | 57,392,930 | |

U.S. Treasury Notes | | 3.88 | | 12/31/2029 | | 10,275,000 | g | 10,259,748 | |

U.S. Treasury Notes | | 4.00 | | 7/31/2030 | | 49,220,800 | g | 49,499,590 | |

U.S. Treasury Notes | | 4.38 | | 8/31/2028 | | 79,050,000 | | 80,752,972 | |

U.S. Treasury Notes | | 4.63 | | 9/30/2030 | | 61,950,000 | | 64,594,974 | |

Upstart Securitization Trust, Ser. 2021-4, Cl. A | | 0.84 | | 9/20/2031 | | 248,336 | c | 247,541 | |

Vantage Data Centers Issuer LLC, Ser. 2023-1A, CI. A2 | | 6.32 | | 3/16/2048 | | 5,716,000 | c | 5,724,814 | |

Verizon Communications, Inc., Sr. Unscd. Bonds | EUR | 4.25 | | 10/31/2030 | | 2,900,000 | | 3,399,508 | |

Verus Securitization Trust, Ser. 2023-4, CI. A1 | | 5.81 | | 5/25/2068 | | 2,851,219 | c | 2,849,940 | |

Verus Securitization Trust, Ser. 2023-5, CI. A1 | | 6.48 | | 6/25/2068 | | 3,251,477 | c | 3,285,146 | |

Volkswagen Group of America Finance LLC, Gtd. Notes | | 6.45 | | 11/16/2030 | | 5,456,000 | c | 5,812,653 | |

WEA Finance LLC, Gtd. Notes | | 2.88 | | 1/15/2027 | | 2,764,000 | | 2,461,365 | |

WEA Finance LLC, Gtd. Notes | | 2.88 | | 1/15/2027 | | 3,410,000 | c | 3,036,633 | |

WEA Finance LLC, Gtd. Notes | | 4.13 | | 9/20/2028 | | 2,326,000 | c | 2,073,756 | |

WEA Finance LLC, Gtd. Notes | | 4.63 | | 9/20/2048 | | 379,000 | c | 256,277 | |

17

STATEMENT OF INVESTMENTS (continued)

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity Date | | Principal Amount ($) | a | Value ($) | |

Bonds and Notes - 91.1% (continued) | | | | | |

United States - 42.8% (continued) | | | | | |

WEA Finance LLC/Westfield UK & Europe Finance PLC, Gtd. Notes | | 4.75 | | 9/17/2044 | | 6,752,000 | c | 4,835,449 | |

Wells Fargo & Co., Sr. Unscd. Notes | | 5.39 | | 4/24/2034 | | 3,670,000 | | 3,688,082 | |

Wells Fargo & Co., Sr. Unscd. Notes | | 5.56 | | 7/25/2034 | | 6,900,000 | | 7,028,550 | |

Wells Fargo Commercial Mortgage Trust, Ser. 2021-SAVE, Cl. A, (1 Month TSFR +1.26%) | | 6.63 | | 2/15/2040 | | 2,877,544 | c,d | 2,802,991 | |

Federal Home Loan Mortgage Corp.: | | | |

2.00%, 8/1/2051-4/1/2052 | | | 44,200,319 | f | 36,495,142 | |

2.50%, 10/1/2050 | | | 18,424,733 | f | 15,953,909 | |

3.50%, 6/1/2052 | | | 23,325,511 | f | 21,403,419 | |

5.00%, 7/1/2052 | | | 24,551,467 | f | 24,330,383 | |

5.50%, 9/1/2053 | | | 15,458,784 | f | 15,754,623 | |

Federal National Mortgage Association: | | | |

2.00%, 1/1/2051-11/1/2051 | | | 32,761,625 | f | 26,990,463 | |

2.50%, 9/1/2050-4/1/2052 | | | 44,649,473 | f | 38,588,457 | |

3.00%, 6/1/2050 | | | 36,534,147 | f | 32,929,023 | |

4.00%, 5/1/2052-6/1/2052 | | | 14,463,826 | f | 13,688,372 | |

4.50%, 6/1/2052 | | | 48,291,920 | f | 46,845,482 | |

5.00%, 7/1/2052 | | | 26,223,318 | f | 25,963,063 | |

| | 996,125,804 | |

Total Bonds and Notes

(cost $2,111,124,223) | | 2,121,673,894 | |

Description /Number of Contracts/Counterparty | Exercise

Price | | Expiration Date | | Notional Amount ($) | a | Value ($) | |

Options Purchased - .0% | | | | | |

Call Options - .0% | | | | | |

Japanese Yen, Contracts N/A, Goldman Sachs & Co. LLC | | 149.10 | | 1/25/2024 | | 5,620,000 | | 875 | |

Japanese Yen Cross Currency, Contracts N/A, Goldman Sachs & Co. LLC | EUR | 159.35 | | 1/4/2024 | | 5,891,000 | | 253 | |

Japanese Yen Cross Currency, Contracts N/A, Goldman Sachs & Co. LLC | GBP | 185.20 | | 1/2/2024 | | 2,896,000 | | 2 | |

| | 1,130 | |

Put Options - .0% | | | | | |

Japanese Yen, Contracts N/A, HSBC Securities (USA) Inc. | JPY | 141.70 | | 1/16/2024 | | 1,669,048,500 | | 67,905 | |

Total Options Purchased

(cost $249,324) | | 69,035 | |

18

| | | | | | | | | | |

| |

Description | | | | | Shares | | Value ($) | |

Exchange-Traded Funds - 6.4% | | | | | |

United States - 6.4% | | | | | |

iShares Broad USD Investment Grade Corporate Bond ETF | | | | | | 2,084,280 | b | 106,840,193 | |

iShares iBoxx Investment Grade Corporate Bond ETF | | | | | | 372,152 | b | 41,182,340 | |

Total Exchange-Traded Funds

(cost $140,195,593) | | 148,022,533 | |

| | 1-Day

Yield (%) | | | | | | | |

Investment Companies - .1% | | | | | |

Registered Investment Companies - .1% | | | | | |

Dreyfus Institutional Preferred Government Plus Money Market Fund, Institutional Shares

(cost $2,036,558) | | 5.43 | | | | 2,036,558 | h | 2,036,558 | |

19

STATEMENT OF INVESTMENTS (continued)

| | | | | | | | | | |

| |

Description | 1-Day

Yield (%) | | | | Shares | | Value ($) | |

Investment of Cash Collateral for Securities Loaned - 2.1% | | | | | |

Registered Investment Companies - 2.1% | | | | | |

Dreyfus Institutional Preferred Government Plus Money Market Fund, Institutional Shares

(cost $48,722,829) | | 5.43 | | | | 48,722,829 | h | 48,722,829 | |

Total Investments (cost $2,302,328,527) | | 99.7% | 2,320,524,849 | |

Cash and Receivables (Net) | | 0.3% | 8,025,950 | |

Net Assets | | 100.0% | 2,328,550,799 | |

ETF—Exchange-Traded Fund

SOFR—Secured Overnight Financing Rate

SONIA—Sterling Overnight Index Average

TSFR—Term Secured Overnight Financing Rate Reference Rates

AUD—Australian Dollar

CAD—Canadian Dollar

CHF—Swiss Franc

CNY—Chinese Yuan Renminbi

DKK—Danish Krone

EUR—Euro

GBP—British Pound

HUF—Hungarian Forint

IDR—Indonesian Rupiah

JPY—Japanese Yen

KRW—South Korean Won

MXN—Mexican Peso

NZD—New Zealand Dollar

PEN—Peruvian Nuevo Sol

SEK—Swedish Krona

SGD—Singapore Dollar

THB—Thai Baht

ZAR—South African Rand

a Amount stated in U.S. Dollars unless otherwise noted above.

b Security, or portion thereof, on loan. At December 31, 2023, the value of the fund’s securities on loan was $58,281,571 and the value of the collateral was $60,197,325, consisting of cash collateral of $48,722,829 and U.S. Government & Agency securities valued at $11,474,496. In addition, the value of collateral may include pending sales that are also on loan.

c Security exempt from registration pursuant to Rule 144A under the Securities Act of 1933. These securities may be resold in transactions exempt from registration, normally to qualified institutional buyers. At December 31, 2023, these securities were valued at $288,554,122 or 12.39% of net assets.

d Variable rate security—interest rate resets periodically and rate shown is the interest rate in effect at period end. Security description also includes the reference rate and spread if published and available.

e Security is a perpetual bond with no specified maturity date. Maturity date shown is next reset date of the bond.

f The Federal Housing Finance Agency (“FHFA”) placed the Federal Home Loan Mortgage Corporation and Federal National Mortgage Association into conservatorship with FHFA as the conservator. As such, the FHFA oversees the continuing affairs of these companies.

g Held by a broker as collateral for open over-the-counter derivative contracts.

h Investment in affiliated issuer. The investment objective of this investment company is publicly available and can be found within the investment company’s prospectus.

20

| | |

Portfolio Summary (Unaudited) † | Value (%) |

Foreign Governmental | 34.3 |

U.S. Treasury Securities | 13.0 |

U.S. Government Agencies Mortgage-Backed | 12.9 |

Investment Companies | 8.6 |

Banks | 6.5 |

Real Estate | 4.0 |

Commercial Mortgage Pass-Through Certificates | 2.9 |

Asset-Backed Certificates | 2.3 |

U.S. Government Agencies Collateralized Mortgage Obligations | 1.7 |

Utilities | 1.6 |

Asset-Backed Certificates/Auto Receivables | 1.2 |

Collateralized Loan Obligations Debt | 1.0 |

Health Care | .9 |

Automobiles & Components | .9 |

Insurance | .8 |

Diversified Financials | .8 |

Consumer Durables & Apparel | .8 |

Energy | .7 |

Commercial & Professional Services | .7 |

Industrial | .6 |

Transportation | .6 |

Agriculture | .5 |

U.S. Government Agencies Collateralized Municipal-Backed Securities | .4 |

Electronic Components | .4 |

Chemicals | .4 |

Building Materials | .3 |

Media | .3 |

Metals & Mining | .3 |

Food Products | .2 |

Telecommunication Services | .2 |

Options Purchased | .0 |

| | 99.8 |

† Based on net assets.

See notes to financial statements.

21

STATEMENT OF INVESTMENTS (continued)

| | | | | | | |

Affiliated Issuers | | | |

Description | Value ($) 12/31/2022 | Purchases ($)† | Sales ($) | Value ($) 12/31/2023 | Dividends/

Distributions ($) | |

Registered Investment Companies - .1% | | |

Dreyfus Institutional Preferred Government Plus Money Market Fund, Institutional Shares - .1% | 2,332,190 | 1,329,316,583 | (1,329,612,215) | 2,036,558 | 1,528,005 | |

Investment of Cash Collateral for Securities Loaned - 2.1%†† | | |

Dreyfus Institutional Preferred Government Plus Money Market Fund, Institutional Shares - 2.1% | - | 461,461,681 | (412,738,852) | 48,722,829 | 73,457 | ††† |

Dreyfus Institutional Preferred Government Plus Money Market Fund, SL Shares - .0% | 64,109,388 | 195,085,768 | (259,195,156) | - | 171,311 | ††† |

Total - 2.2% | 66,441,578 | 1,985,864,032 | (2,001,546,223) | 50,759,387 | 1,772,773 | |

† Includes reinvested dividends/distributions.

†† Effective July 3, 2023, cash collateral for securities lending was transferred from Dreyfus Institutional Preferred Government Plus Money Market Fund, SL Shares to Dreyfus Institutional Preferred Government Plus Money Market Fund, Institutional Shares.

††† Represents securities lending income earned from the reinvestment of cash collateral from loaned securities, net of fees and collateral investment expenses, and other payments to and from borrowers of securities.

See notes to financial statements.

| | | | | | | |

Futures | | | |

Description | Number of

Contracts | Expiration | Notional

Value ($) | Market

Value ($) | Unrealized Appreciation (Depreciation) ($) | |

Futures Long | | |

Australian 10 Year Bond | 1,972 | 3/15/2024 | 152,141,360a | 156,777,658 | 4,636,298 | |

Euro BTP Italian Government Bond | 487 | 3/7/2024 | 61,762,638a | 64,057,858 | 2,295,220 | |

U.S. Treasury 2 Year Notes | 22 | 3/28/2024 | 4,485,293 | 4,530,109 | 44,816 | |

U.S. Treasury 5 Year Notes | 139 | 3/28/2024 | 15,083,898 | 15,119,508 | 35,610 | |

22

| | | | | | | |

Futures (continued) | | | |

Description | Number of

Contracts | Expiration | Notional

Value ($) | Market

Value ($) | Unrealized Appreciation (Depreciation) ($) | |

Futures Short | | |

Canadian 10 Year Bond | 2,292 | 3/19/2024 | 205,561,183a | 214,799,864 | (9,238,681) | |

Euro 30 Year Bond | 332 | 3/7/2024 | 48,016,235a | 51,941,996 | (3,925,761) | |

Euro-Bobl | 2,130 | 3/7/2024 | 276,252,178a | 280,476,602 | (4,224,424) | |

Euro-Bond | 252 | 3/7/2024 | 37,979,128a | 38,173,973 | (194,845) | |

Euro-Schatz | 176 | 3/7/2024 | 20,651,182a | 20,701,182 | (50,000) | |

Long Term French Government Future | 50 | 3/7/2024 | 7,005,614a | 7,259,023 | (253,409) | |

U.S. Treasury 10 Year Notes | 107 | 3/19/2024 | 11,914,924 | 12,079,297 | (164,373) | |

U.S. Treasury Ultra Long Bond | 320 | 3/19/2024 | 39,454,386 | 42,750,000 | (3,295,614) | |

Ultra 10 Year U.S. Treasury Notes | 213 | 3/19/2024 | 24,018,728 | 25,137,329 | (1,118,601) | |

Gross Unrealized Appreciation | | 7,011,944 | |

Gross Unrealized Depreciation | | (22,465,708) | |

a Notional amounts in foreign currency have been converted to USD using relevant foreign exchange rates.

See notes to financial statements.

| | | | | | | |

Options Written | | | |

Description/ Contracts/ Counterparties | Exercise Price | Expiration Date | Notional Amount ($) | a | Value ($) | |

Call Options: | | | | | | |

Japanese Yen,

Contracts N/A, HSBC Securities (USA) Inc. | 138.79 | 1/16/2024 | 1,669,048,500 | JPY | (50,544) | |

Japanese Yen,

Contracts N/A, Goldman Sachs & Co. LLC | 153.00 | 1/25/2024 | 5,620,000 | | (97) | |

Japanese Yen Cross Currency,

Contracts N/A, Goldman Sachs & Co. LLC | 162.00 | 1/4/2024 | 5,891,000 | EUR | (5) | |

Japanese Yen Cross Currency,

Contracts N/A, Goldman Sachs & Co. LLC | 188.00 | 1/2/2024 | 2,896,000 | GBP | - | |

Put Options: | | | | | | |

Japanese Yen,

Contracts N/A, Goldman Sachs & Co. LLC | 143.90 | 1/25/2024 | 5,620,000 | | (151,533) | |

Japanese Yen,

Contracts N/A, HSBC Securities (USA) Inc. | 145.50 | 1/16/2024 | 1,669,048,500 | JPY | (6,346) | |

Japanese Yen Cross Currency,

Contracts N/A, Goldman Sachs & Co. LLC | 155.65 | 1/4/2024 | 5,891,000 | EUR | (27,420) | |

23

STATEMENT OF INVESTMENTS (continued)

| | | | | | | |

Options Written (continued) | | | |

Description/ Contracts/ Counterparties | Exercise Price | Expiration Date | Notional Amount ($) | a | Value ($) | |

Put Options: (continued) | | | | | | |

Japanese Yen Cross Currency,

Contracts N/A, Goldman Sachs & Co. LLC | 180.00 | 1/2/2024 | 2,896,000 | GBP | (16,663) | |

Total Options Written (premiums received $246,713) | | | | (252,608) | |

a Notional amount stated in U.S. Dollars unless otherwise indicated.

EUR—Euro

GBP—British Pound

JPY—Japanese Yen

See notes to financial statements.

| | | | | | |

Forward Foreign Currency Exchange Contracts | |

Counterparty/ Purchased

Currency | Purchased Currency

Amounts | Currency

Sold | Sold

Currency

Amounts | Settlement Date | Unrealized Appreciation (Depreciation) ($) |

Barclays Capital, Inc. |

United States Dollar | 60,202,077 | Japanese Yen | 8,803,440,000 | 1/19/2024 | (2,439,768) |

United States Dollar | 94,121,755 | South Korean Won | 123,371,973,000 | 1/19/2024 | (1,792,084) |

BNP Paribas Corp. |

United States Dollar | 913,381 | British Pound | 729,000 | 1/19/2024 | (15,951) |

Euro | 3,203,685 | Australian Dollar | 5,254,000 | 1/19/2024 | (43,122) |

United States Dollar | 1,358,726 | Euro | 1,243,000 | 1/19/2024 | (14,672) |

Citigroup Global Markets Inc. |

Japanese Yen | 4,857,741,000 | United States Dollar | 34,350,630 | 1/19/2024 | 215,160 |

Goldman Sachs & Co. LLC |

United States Dollar | 5,857,532 | Taiwan Dollar | 178,479,000 | 1/19/2024 | 26,505 |

United States Dollar | 6,573,148 | Singapore Dollar | 8,795,000 | 1/19/2024 | (97,842) |

United States Dollar | 34,725,272 | Canadian Dollar | 47,095,000 | 1/19/2024 | (827,538) |

United States Dollar | 15,061,283 | Swiss Franc | 13,099,000 | 1/19/2024 | (548,298) |

Mexican Peso | 30,284,000 | United States Dollar | 1,733,188 | 1/19/2024 | 43,785 |

United States Dollar | 2,136,244 | Mexican Peso | 37,405,000 | 1/19/2024 | (58,567) |

United States Dollar | 17,424,645 | Peruvian Nuevo Sol | 65,555,000 | 1/19/2024 | (284,706) |

24

| | | | | | |

Forward Foreign Currency Exchange Contracts (continued) | |

Counterparty/ Purchased

Currency | Purchased Currency

Amounts | Currency

Sold | Sold

Currency

Amounts | Settlement Date | Unrealized Appreciation (Depreciation) ($) |

Goldman Sachs & Co. LLC (continued) |

United States Dollar | 2,044,175 | Swedish Krona | 21,381,000 | 1/19/2024 | (77,546) |

United States Dollar | 2,527,879 | Danish Krone | 17,434,000 | 1/19/2024 | (56,773) |

United States Dollar | 76,540,567 | New Zealand Dollar | 124,292,000 | 1/19/2024 | (2,036,897) |

United States Dollar | 1,751,545 | Australian Dollar | 2,669,000 | 1/19/2024 | (68,543) |

Swedish Krona | 13,901,000 | United States Dollar | 1,361,267 | 1/19/2024 | 18,184 |

United States Dollar | 36,886,109 | South African Rand | 700,012,000 | 1/19/2024 | (1,310,942) |

Euro | 4,120,000 | United States Dollar | 4,492,801 | 1/19/2024 | 59,411 |

United States Dollar | 7,836,197 | Euro | 7,126,000 | 1/19/2024 | (37,362) |

United States Dollar | 6,553,762 | Hungarian Forint | 2,315,987,000 | 1/19/2024 | (101,595) |

HSBC Securities (USA) Inc. |

Canadian Dollar | 5,420,000 | United States Dollar | 4,081,920 | 1/19/2024 | 9,729 |

United States Dollar | 1,209,336 | Swedish Krona | 12,098,000 | 1/19/2024 | 8,804 |

United States Dollar | 5,513,271 | Thai Baht | 193,625,000 | 1/19/2024 | (170,385) |

Euro | 6,465,000 | United States Dollar | 7,055,553 | 1/19/2024 | 87,664 |

United States Dollar | 175,639,934 | Euro | 162,323,000 | 1/19/2024 | (3,711,704) |

United States Dollar | 6,862,320 | Indonesian Rupiah | 106,229,675,000 | 1/19/2024 | (35,618) |

United States Dollar | 2,328,523 | South Korean Won | 3,009,732,000 | 1/19/2024 | (11,352) |

Euro | 4,222,408 | British Pound | 3,640,000 | 1/19/2024 | 25,079 |

British Pound | 5,436,000 | Euro | 6,244,386 | 1/19/2024 | 30,373 |

United States Dollar | 70,866,537 | Chinese Yuan Renminbi | 506,016,625 | 1/19/2024 | (251,852) |

British Pound | 1,397,700 | United States Dollar | 1,751,331 | 1/19/2024 | 30,462 |

United States Dollar | 357,951 | British Pound | 280,000 | 1/19/2024 | 1,006 |

United States Dollar | 2,548,941 | New Zealand Dollar | 4,101,000 | 1/19/2024 | (43,713) |

Japanese Yen | 2,219,746,000 | United States Dollar | 15,625,504 | 1/19/2024 | 169,342 |

25

STATEMENT OF INVESTMENTS (continued)

| | | | | | |

Forward Foreign Currency Exchange Contracts (continued) | |

Counterparty/ Purchased

Currency | Purchased Currency

Amounts | Currency

Sold | Sold

Currency

Amounts | Settlement Date | Unrealized Appreciation (Depreciation) ($) |

J.P. Morgan Securities LLC |

United States Dollar | 3,373,141 | Swedish Krona | 35,340,000 | 1/19/2024 | (133,787) |

United States Dollar | 3,728,312 | Australian Dollar | 5,500,000 | 1/19/2024 | (22,337) |

Canadian Dollar | 3,747,000 | United States Dollar | 2,760,136 | 1/19/2024 | 68,537 |

Morgan Stanley & Co. LLC |

Euro | 3,536,000 | United States Dollar | 3,871,335 | 1/19/2024 | 35,612 |

United States Dollar | 171,226,726 | Euro | 158,302,000 | 1/19/2024 | (3,682,086) |

British Pound | 729,000 | United States Dollar | 913,969 | 1/19/2024 | 15,363 |

United States Dollar | 90,969,050 | British Pound | 72,158,000 | 1/19/2024 | (1,018,215) |

United States Dollar | 19,070,932 | Australian Dollar | 28,953,000 | 1/19/2024 | (673,167) |

RBC Capital Markets, LLC |

United States Dollar | 40,406,211 | Mexican Peso | 701,986,000 | 1/19/2024 | (784,188) |

United States Dollar | 183,126,088 | Euro | 169,165,000 | 1/19/2024 | (3,785,316) |

Canadian Dollar | 3,965,000 | United States Dollar | 2,920,281 | 1/19/2024 | 72,964 |

Gross Unrealized Appreciation | | | 917,980 |

Gross Unrealized Depreciation | | | (24,135,926) |

See notes to financial statements.

| | | | | | | |

Centrally Cleared Interest Rate Swaps |

Received

Reference

Entity | Paid

Reference

Entity | Maturity Date | Notional

Amount ($) | Market

Value ($) | Upfront

Payments/

Receipts ($) | Unrealized Appreciation(Depreciation) ($) |

SEK - 12 Month Fixed at 3.70% | SEK - 3 Month STIBOR at 4.06% | 10/3/2028 | 138,466,992 | 9,208,192 | 540,958 | 8,667,234 |

EUR Fixed at 2.80% at Maturity | EUR - Eurostat Eurozone HICP Ex Tobacco Unrevised NSA at Maturity | 7/28/2053 | 40,476,327 | 4,647,118 | 2,556,216 | 2,090,902 |

26

| | | | | | | | |

Centrally Cleared Interest Rate Swaps (continued) |

Received

Reference

Entity | Paid

Reference

Entity | Maturity Date | Notional

Amount ($) | Market

Value ($) | Upfront

Payments/

Receipts ($) | Unrealized Appreciation(Depreciation) ($) |

USD - US CPI Urban Consumers NSA at Maturity | USD Fixed at 2.53% at Maturity | 7/28/2053 | 55,615,000 | (1,590,050) | 996,599 | (2,586,649) |

USD - US CPI Urban Consumers NSA at Maturity | USD Fixed at 2.45% at Maturity | 12/7/2053 | 48,869,000 | (746,362) | 52,359 | (798,721) |

EUR Fixed at 2.50% at Maturity | EUR - Eurostat Eurozone HICP Ex Tobacco Unrevised NSA at Maturity | 12/7/2053 | 36,187,481 | 645,911 | 779,839 | (133,928) |

GBP - 12 Month Sterling Overnight Interbank Average at 5.19% | GBP 12 Month Fixed at 3.45% | 12/21/2028 | 127,465,000 | (330,344) | 100,434 | (430,778) |

Gross Unrealized Appreciation | 10,758,136 |

Gross Unrealized Depreciation | (3,950,076) |

EUR—Euro

GBP—British Pound

SEK—Swedish Krona

USD—United States Dollar

See notes to financial statements.

| | | | | | |

OTC Total Return Swaps | |

Received

Reference

Entity | Paid

Reference

Entity | Counterparties | Maturity Date | Notional

Amount ($) | Unrealized Appreciation (Depreciation) ($) |

EUR - Markit iBoxx € Corporates at Maturity | EUR - 3 Month Euribor at 3.94% | Goldman Sachs & Co. LLC | 3/20/24 | 122,675,705 | 2,242,471 |

USD - Markit iBoxx $ Investment Grade Corporate Bond ETF at Maturity | USD - 3 Month Secured Overnight Financing Rate at 5.35% | Morgan Stanley & Co. LLC | 3/20/24 | 16,826,837 | 497,748 |

27

STATEMENT OF INVESTMENTS (continued)

| | | | | | |

OTC Total Return Swaps (continued) | |

Received

Reference

Entity | Paid

Reference

Entity | Counterparties | Maturity Date | Notional

Amount ($) | Unrealized Appreciation (Depreciation) ($) |

EUR - 3 Month Euribor at 3.94% | EUR - Markit iBoxx € Liquid High Yield Index at Maturity | Goldman Sachs & Co. LLC | 3/20/24 | 82,413,078 | (1,956,603) |

EUR - Markit iBoxx € Corporates at Maturity | EUR - 3 Month Euribor at 3.94% | J.P. Morgan Securities LLC | 3/20/24 | 48,366,479 | 226,348 |

EUR - Markit iBoxx € Corporates at Maturity | EUR - Euribor at 3.94% at Maturity | Goldman Sachs & Co. LLC | 3/20/24 | 10,066,422 | 7,291 |

EUR - Euribor at 3.94% at Maturity | EUR - Markit iBoxx € Liquid High Yield Index at Maturity | Goldman Sachs & Co. LLC | 3/20/24 | 4,555,237 | (23,102) |

Gross Unrealized Appreciation | 2,973,858 |

Gross Unrealized Depreciation | (1,979,705) |

See notes to financial statements.

| | | | | | |

OTC Credit Default Swaps | |

Reference

Obligation/

Counterparty | Maturity

Date | Notional

Amount ($)1 | Market

Value ($) | Upfront

Payments/

Receipts ($) | Unrealized Appreciation($) |

Sold Contracts:2 | |

J.P. Morgan Securities LLC | | |

UPC Holding, 5.50%, 1/15/2028 Received 3 Month Fixed Rate of 5.00% | 12/20/2028 | 4,404,760 | 285,952 | 44,682 | 241,270 |

Gross Unrealized Appreciation | 241,270 |

1 The maximum potential amount the fund could be required to pay as a seller of credit protection or receive as a buyer of credit protection if a credit event occurs as defined under the terms of the swap agreement.

2 If the fund is a seller of protection and a credit event occurs, as defined under the terms of the swap agreement, the fund will either (i) pay to the buyer of protection an amount equal to the notional amount of the swap and take delivery of the reference obligation or (ii) pay a net settlement amount in the form of cash or securities equal to the notional amount of the swap less the recovery value of the reference obligation.

See notes to financial statements.

28

| | | | | | |

Centrally Cleared Credit Default Swaps | |

Reference

Obligation | Maturity

Date | Notional

Amount ($) | Market

Value ($) | Upfront

Payments/

Receipts ($) | Unrealized (Depreciation) ($) |

Purchased Contracts:1 | |

Markit iTraxx Europe Crossover Index Series 40, Paid 3 Month Fixed Rate of 5.00% | 12/20/2028 | 4,448,918 | (361,816) | (72,797) | (289,019) |

Markit iTraxx Europe Senior Financial Index Series 40, Paid 3 Month Fixed Rate of 1.00% | 12/20/2028 | 229,351,132 | (3,568,007) | (1,212,338) | (2,355,669) |

Markit iTraxx Europe Index Series 40, Paid 3 Month Fixed Rate of 1.00% | 12/20/2028 | 112,233,077 | (2,217,203) | (1,577,510) | (639,693) |

Markit CDX North America Investment Grade Index Series 41, Paid 3 Month Fixed Rate of 1.00% | 12/20/2028 | 244,765,000 | (4,829,337) | (4,118,785) | (710,552) |

Gross Unrealized Depreciation | (3,994,933) |

1 If the fund is a buyer of protection and a credit event occurs, as defined under the terms of the swap agreement, the fund will either (i) receive from the seller of protection an amount equal to the notional amount of the swap and deliver the reference obligation or (ii) receive a net settlement amount in the form of cash or securities equal to the notional amount of the swap less the recovery value of the reference obligation.

See notes to financial statements.

29

STATEMENT OF ASSETS AND LIABILITIES

December 31, 2023

| | | | | | | |

| | | | | | |

| | | Cost | | Value | |

Assets ($): | | | | |

Investments in securities—See Statement of Investments

(including securities on loan, valued at $58,281,571)—Note 1(c): | | | |

Unaffiliated issuers | 2,251,569,140 | | 2,269,765,462 | |

Affiliated issuers | | 50,759,387 | | 50,759,387 | |

Cash denominated in foreign currency | | | 5,947,319 | | 6,019,156 | |

Cash collateral held by broker—Note 4 | | 52,102,733 | |

Dividends, interest and securities lending income receivable | | 20,705,158 | |

Unrealized appreciation on over-the-counter swap agreements—Note 4 | | 3,215,128 | |

Receivable for shares of Beneficial Interest subscribed | | 3,156,002 | |

Receivable for futures variation margin—Note 4 | | 992,429 | |

Unrealized appreciation on forward foreign

currency exchange contracts—Note 4 | | 917,980 | |

Over-the-counter swap upfront payments—Note 4 | | 44,682 | |

Tax reclaim receivable—Note 1(b) | | 16,676 | |

Prepaid expenses | | | | | 107,011 | |

| | | | | 2,407,801,804 | |

Liabilities ($): | | | | |

Due to BNY Mellon Investment Adviser, Inc. and affiliates—Note 3(c) | | 809,307 | |

Liability for securities on loan—Note 1(c) | | 48,722,829 | |

Unrealized depreciation on forward foreign

currency exchange contracts—Note 4 | | 24,135,926 | |

Payable for shares of Beneficial Interest redeemed | | 2,268,248 | |

Unrealized depreciation on over-the-counter swap agreements—Note 4 | | 1,979,705 | |

Payable for swap variation margin—Note 4 | | 658,555 | |

Outstanding options written, at value

(premiums received $246,713)—Note 4 | | 252,608 | |

Trustees’ fees and expenses payable | | 57,081 | |

Other accrued expenses | | | | | 366,746 | |

| | | | | 79,251,005 | |

Net Assets ($) | | | 2,328,550,799 | |

Composition of Net Assets ($): | | | | |

Paid-in capital | | | | | 2,539,929,764 | |

Total distributable earnings (loss) | | | | | (211,378,965) | |

Net Assets ($) | | | 2,328,550,799 | |

| | | | | | |

Net Asset Value Per Share | Class A | Class C | Class I | Class Y | |

Net Assets ($) | 142,091,141 | 11,280,419 | 1,997,947,753 | 177,231,486 | |

Shares Outstanding | 7,216,062 | 593,597 | 100,514,638 | 8,895,959 | |

Net Asset Value Per Share ($) | 19.69 | 19.00 | 19.88 | 19.92 | |

| | | | | |

See notes to financial statements. | | | | | |

30

STATEMENT OF OPERATIONS

Year Ended December 31, 2023

| | | | | | | |

| | | | | | |

| | | | | | |

Investment Income ($): | | | | |

Income: | | | | |

Interest (net of $439,470 foreign taxes withheld at source) | | | 84,073,035 | |

Dividends: | |

Unaffiliated issuers | | | 1,286,483 | |

Affiliated issuers | | | 1,528,005 | |

Income from securities lending—Note 1(c) | | | 244,768 | |

Total Income | | | 87,132,291 | |

Expenses: | | | | |

Management fee—Note 3(a) | | | 8,742,702 | |

Shareholder servicing costs—Note 3(c) | | | 1,885,298 | |

Custodian fees—Note 3(c) | | | 345,714 | |

Trustees’ fees and expenses—Note 3(d) | | | 302,249 | |

Administration fee—Note 3(a) | | | 259,309 | |

Professional fees | | | 202,166 | |

Registration fees | | | 131,221 | |

Prospectus and shareholders’ reports | | | 125,778 | |

Distribution fees—Note 3(b) | | | 103,049 | |

Loan commitment fees—Note 2 | | | 46,219 | |

Chief Compliance Officer fees—Note 3(c) | | | 21,143 | |

Interest expense—Note 2 | | | 1,384 | |

Miscellaneous | | | 53,844 | |

Total Expenses | | | 12,220,076 | |

Less—reduction in fees due to earnings credits—Note 3(c) | | | (37,738) | |

Net Expenses | | | 12,182,338 | |

Net Investment Income | | | 74,949,953 | |

Realized and Unrealized Gain (Loss) on Investments—Note 4 ($): | | |

Net realized gain (loss) on investments and foreign currency transactions | (82,775,902) | |

Net realized gain (loss) on futures | 21,650,152 | |

Net realized gain (loss) on options transactions | 3,267,820 | |

Net realized gain (loss) on forward foreign currency exchange contracts | 5,428,824 | |

Net realized gain (loss) on swap agreements | (4,559,108) | |

Net Realized Gain (Loss) | | | (56,988,214) | |

Net change in unrealized appreciation (depreciation) on investments

and foreign currency transactions | 181,198,940 | |

Net change in unrealized appreciation (depreciation) on futures | (29,280,147) | |

Net change in unrealized appreciation (depreciation) on

options transactions | (600,668) | |

Net change in unrealized appreciation (depreciation) on

forward foreign currency exchange contracts | (9,397,924) | |

Net change in unrealized appreciation (depreciation) on swap agreements | 3,983,684 | |

Net Change in Unrealized Appreciation (Depreciation) | | | 145,903,885 | |

Net Realized and Unrealized Gain (Loss) on Investments | | | 88,915,671 | |

Net Increase from Payment by Affiliate—Note 5 | | | 235,235 | |

Net Increase in Net Assets Resulting from Operations | | 164,100,859 | |

| | | | | | |

See notes to financial statements. | | | | | |

31

STATEMENT OF CHANGES IN NET ASSETS

| | | | | | | | | | |

| | | | Year Ended December 31, |

| | | | 2023 | | 2022 | |

Operations ($): | | | | | | | | |

Net investment income | | | 74,949,953 | | | | 46,424,947 | |

Net realized gain (loss) on investments | | (56,988,214) | | | | (137,178,958) | |

Net change in unrealized appreciation

(depreciation) on investments | | 145,903,885 | | | | (157,315,484) | |

Net increase from payment by affiliate—Note 5 | | 235,235 | | | | - | |

Net Increase (Decrease) in Net Assets

Resulting from Operations | 164,100,859 | | | | (248,069,495) | |

Distributions ($): | |

Distributions to shareholders: | | | | | | | | |

Class A | | | (2,491,119) | | | | (3,898,168) | |