UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number | 811-04813 |

| |

| Dreyfus Investment Funds | |

| (Exact name of Registrant as specified in charter) | |

| | |

| c/o The Dreyfus Corporation 200 Park Avenue New York, New York 10166 | |

| (Address of principal executive offices) (Zip code) | |

| | |

| Michael A. Rosenberg, Esq. 200 Park Avenue New York, New York 10166 | |

| (Name and address of agent for service) | |

|

Registrant's telephone number, including area code: | (212) 922-6000 |

| |

Date of fiscal year end: | 9/30 | |

Date of reporting period: | 3/31/2011 | |

| | | | | | | |

The following N-CSR relates only to the Registrant’s series listed below and does not affect the other series of the Registrant, which have a different fiscal year end and, therefore, different N-CSR reporting requirements. Separate N-CSR Forms will be filed for those series, as appropriate.

-Dreyfus/The Boston Company Emerging Markets Core Equity Fund

-Dreyfus/The Boston Company Large Cap Core Fund

-Dreyfus/The Boston Company Small Cap Growth Fund

-Dreyfus/The Boston Company Small Cap Tax-Sensitive Equity Fund

-Dreyfus/The Boston Company Small Cap Value Fund

-Dreyfus/The Boston Company Small/Mid Growth Fund

-Dreyfus/Standish Intermediate Tax Exempt Bond Fund

-Dreyfus/Newton International Equity Fund

FORM N-CSR

Item 1. Reports to Stockholders.

Save time. Save paper. View your next shareholder report online as soon as it’s available. Log into www.dreyfus.com and sign up for Dreyfus eCommunications. It’s simple and only takes a few minutes.

The views expressed in this report reflect those of the portfolio manager only through the end of the period covered and do not necessarily represent the views of Dreyfus or any other person in the Dreyfus organization. Any such views are subject to change at any time based upon market or other conditions and Dreyfus disclaims any responsibility to update such views.These views may not be relied on as investment advice and, because investment decisions for a Dreyfus fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Dreyfus fund.

Not FDIC-Insured • Not Bank-Guaranteed • May Lose Value

| | Contents |

| | THE FUND |

| 2 | A Letter from the Chairman and CEO |

| 3 | Discussion of Fund Performance |

| 6 | Understanding Your Fund’s Expenses |

| 6 | Comparing Your Fund’s Expenses With Those of Other Funds |

| 7 | Statement of Investments |

| 12 | Statement of Assets and Liabilities |

| 13 | Statement of Operations |

| 14 | Statement of Changes in Net Assets |

| 16 | Financial Highlights |

| 19 | Notes to Financial Statements |

| 32 | Information About the Renewal of the Fund’s Investment Advisory Agreement |

| | FOR MORE INFORMATION |

| | Back Cover |

Dreyfus/The Boston

Company Emerging

Markets Core Equity Fund

The Fund

A LETTER FROM THE CHAIRMAN AND CEO

Dear Shareholder:

We are pleased to present this semiannual report for Dreyfus/The Boston Company Emerging Markets Core Equity Fund, covering the six-month period from October 1, 2010, through March 31, 2011.

Equities throughout the world fared well over the past six months. International stock markets have rallied broadly since the fall of 2010, when new rounds of monetary stimulus from U.S. and foreign central banks gave investors confidence that the global economy was unlikely to slip back into recession. As a result, developed markets rebounded strongly from relatively depressed levels, while emerging markets added more moderately to their previous gains.Although political uprisings in the Middle East and the disasters in Japan injected some uncertainty into the investment climate, these events do not appear to have derailed the global market rally. Market sectors that tend to be sensitive to macroeconomic changes performed particularly well as commodity prices climbed and investors looked forward to better business conditions.

We currently expect most developed and emerging markets to adopt less stimulative fiscal and monetary policies over the remainder of 2011 as the global economy reaches the middle stages of its cycle. Moreover, in the wake of recent gains we believe that selectivity will become a more important determinant of investment success in international markets.We favor the core of Europe over more peripheral members of the European Union, and while we expect the emerging markets to grow faster than developed markets, the growth rate in China seems likely to moderate.As always, your financial advisor can help you align your investment portfolio with the opportunities and challenges that 2011 has in store.

For information about how the fund performed during the reporting period, as well as general market perspectives, we provide a Discussion of Fund Performance on the pages that follow.

Thank you for your continued confidence and support.

Jonathan R. Baum

Chairman and Chief Executive Officer

The Dreyfus Corporation

April 15, 2011

2

DISCUSSION OF FUND PERFORMANCE

For the period of October 1, 2010, through March 31, 2011, as provided by Sean P. Fitzgibbon, CFA, and Jay Malikowski, Portfolio Managers

Fund and Market Performance Overview

For the six-month period ended March 31, 2011, Dreyfus/The Boston Company Emerging Markets Core Equity Fund’s Class A shares produced a total return of 9.70%, Class C shares returned 9.19% and Class I shares returned 9.99%.1 In comparison, the fund’s benchmark, the Morgan Stanley Capital International Emerging Markets Index (the “MSCI EM Index”), produced a total return of 9.61% for the same period.2 Emerging-markets stocks generally rallied over the reporting period while the global economic recovery gathered momentum.The fund’s returns were roughly in line with its benchmark, as relative strength in the technology and energy sectors was balanced by weaker results in the consumer staples and industrials sectors.

The Fund’s Investment Approach

The fund seeks long-term growth of capital.To pursue this goal, the fund normally invests at least 80% of its assets in equity securities of companies that are located in foreign countries represented in the MSCI EM Index.The fund may invest up to 20% of its net assets in fixed income securities and may invest in preferred stocks of any credit quality if common stocks of the relevant company are not available. The fund employs a “bottom-up” investment approach, which emphasizes individual stock selection.

Greater Economic Confidence Supported Rallying Markets

The global economic recovery gained traction in the fall of 2010 after a new round of easing of monetary policy by major central banks alleviated investors’ economic worries. In addition, by October most European banks had passed a series of “stress tests,” corporate earnings climbed across a variety of regions and industry groups, mergers-and-acquisitions activity intensified and commodity prices surged higher. Greater clarity regarding fiscal and tax policies in the United States after the national midterm elections in November also supported global investor sentiment.

DISCUSSION OF FUND PERFORMANCE (continued)

The resulting rally in global equity markets persisted into February when political uprisings in the Middle East sparked a sharp increase in oil and gas prices, which investors worried might dampen global economic growth. In March, a devastating earthquake, tsunami and nuclear disaster in Japan gave investors cause for concern regarding the world’s second largest economy. However, investor sentiment proved resilient in light of more encouraging economic news in other regions of the world, and most markets had regained all of their lost ground by the reporting period’s end.

In a reversal of the trend over the past several years, emerging equity markets generally produced lower returns than more developed markets during the reporting period. Because most emerging markets were not as severely affected by the Great Recession in 2008 and 2009, their stock markets had less room to rally during the subsequent global economic recovery. In addition, scandals in some markets, most notably India, reminded investors of the risks inherent in investing in former third-world nations.

Stock Selections Produced Positive Results

Our security selection strategy proved effective during the reporting period, achieving especially attractive results in China, where automobile seller Great Wall Motor benefited from surging demand for car and trucks in many of the nation’s more remote cities. From a market sector perspective, the fund achieved above-average results in the information technology sector, where Taiwanese mobile handset maker HTC encountered robust sales of its Android-based phones.The energy sector ranked as the benchmark’s strongest segment and contributed positively to the fund’s relative performance, mainly due to gains in Russian oil giant Gazprom and South Africa’s Sasol.

On the other hand, disappointments during the reporting period included India, where an influence peddling scandal generally depressed investor sentiment. In addition, Indian building materials supplier Sintex Industries was hurt by concerns that the scandal might delay government approvals of some construction projects. Also in India, rising fuel costs hurt earnings of budget airline SpiceJet, which we sold during the reporting period. Finally, the fund suffered shortfalls in the consumer staples sector, as higher costs for raw materials weighed on the earnings of food companies. For example, China Agri-Industries Holdings lost value due to the rising price of soybeans.

4

Positioned for Greater Global Growth

We expect the global economic recovery to persist. Although inflationary pressures remain a concern in Latin America and Asia, some markets in Eastern Europe have so far proved relatively insensitive to rising commodity prices. Consequently, we have increased the fund’s holdings in Russia, where we expect a stock market dominated by energy producers to benefit from high oil prices.We have identified a number of attractively valued opportunities in India, where political risks appear to be easing. Conversely, we recently reduced the fund’s exposure to Indonesia, where stocks have become more richly valued. In our judgment, these strategies position the fund well as the global economic cycle moves to a more mature phase.

April 15, 2011

| |

| | Equity funds are subject generally to market, market sector, market liquidity, issuer and investment |

| | style risks, among other factors, to varying degrees, all of which are more fully described in the |

| | fund’s prospectus. |

| | The fund’s performance will be influenced by political, social and economic factors affecting |

| | investments in foreign companies.These special risks include exposure to currency fluctuations, less |

| | liquidity, less developed or less efficient trading markets, lack of comprehensive company |

| | information, political instability and differing auditing and legal standards. Investments in foreign |

| | currencies are subject to the risk that those currencies will decline in value relative to the U.S. |

| | dollar, or, in the case of hedged positions, that the U.S. dollar will decline relative to the currency |

| | being hedged. |

| | Emerging markets tend to be more volatile than the markets of more mature economies, and |

| | generally have less diverse and less mature economic structures and less stable political systems than |

| | those of developed countries. |

| 1 | Total return includes reinvestment of dividends and any capital gains paid, and does not take into |

| | consideration the maximum initial sales charge in the case of Class A shares, or the applicable |

| | contingent deferred sales charges imposed on redemptions in the case of Class C shares. Had these |

| | charges been reflected, returns would have been lower. Past performance is no guarantee of future |

| | results. Share price and investment return fluctuate such that upon redemption, fund shares may be |

| | worth more or less than their original cost.The fund’s returns reflect the absorption of certain fund |

| | expenses by The Dreyfus Corporation pursuant to an agreement in effect through February 1, |

| | 2012, at which time it may be extended, terminated or modified. Had these expenses not been |

| | absorbed, the fund’s returns would have been lower. |

| 2 | SOURCE: LIPPER INC. – Reflects reinvestment of net dividends and, where applicable, |

| | capital gain distributions. The Morgan Stanley Capital International Emerging Markets Index |

| | is a free float-adjusted market capitalization weighted index that is designed to measure the |

| | equity performance in global emerging markets. The index consists of 26 MSCI emerging |

| | market national indices. MSCI Indices reflect investable opportunities for global investors by |

| | taking into account local market restrictions on share ownership by foreigners. Investors cannot |

| | invest directly in any index. |

UNDERSTANDING YOUR FUND’S EXPENSES (Unaudited)

As a mutual fund investor, you pay ongoing expenses, such as management fees and other expenses. Using the information below, you can estimate how these expenses affect your investment and compare them with the expenses of other funds.You also may pay one-time transaction expenses, including sales charges (loads) and redemption fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial adviser.

Review your fund’s expenses

The table below shows the expenses you would have paid on a $1,000 investment in Dreyfus/The Boston Company Emerging Markets Core Equity Fund from October 1, 2010 to March 31, 2011. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

| | | | | | |

| Expenses and Value of a $1,000 Investment | | | | |

| assuming actual returns for the six months ended March 31, 2011 | | |

| | | Class A | | Class C | | Class I |

| Expenses paid per $1,000† | $ | 11.76 | $ | 15.65 | $ | 7.85 |

| Ending value (after expenses) | $ | 1,097.00 | $ | 1,091.90 | $ | 1,099.90 |

|

| COMPARING YOUR FUND’S EXPENSES |

| WITH THOSE OF OTHER FUNDS (Unaudited) |

Using the SEC’s method to compare expenses

The Securities and Exchange Commission (SEC) has established guidelines to help investors assess fund expenses. Per these guidelines, the table below shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return. You can use this information to compare the ongoing expenses (but not transaction expenses or total cost) of investing in the fund with those of other funds.All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

| | | | | | |

| Expenses and Value of a $1,000 Investment | | | | |

| assuming a hypothetical 5% annualized return for the six months ended March 31, 2011 |

| | | Class A | | Class C | | Class I |

| Expenses paid per $1,000† | $ | 11.30 | $ | 15.03 | $ | 7.54 |

| Ending value (after expenses) | $ | 1,013.71 | $ | 1,009.97 | $ | 1,017.45 |

† Expenses are equal to the fund’s annualized expense ratio of 2.25% for Class A, 3.00% for Class C and 1.50% for Class I, multiplied by the average account value over the period, multiplied by 182/365 (to reflect the one-half year period).

6

STATEMENT OF INVESTMENTS

March 31, 2011 (Unaudited)

| | |

| Common Stocks—88.4% | Shares | Value ($) |

| Brazil—4.6% | | |

| Banco do Brasil | 10,600 | 191,854 |

| Fleury | 10,900 | 161,899 |

| Gafisa | 16,800 | 106,193 |

| Obrascon Huarte Lain Brasil | 2,300 | 87,202 |

| Porto Seguro | 5,000 | 84,525 |

| Rossi Residencial | 16,800 | 140,047 |

| | | 771,720 |

| China—9.7% | | |

| Changyou.com, ADR | 3,540 a | 113,988 |

| China Communications Construction, Cl. H | 167,000 | 159,302 |

| China Construction Bank, Cl. H | 340,000 | 318,646 |

| China Petroleum & Chemical, Cl. H | 230,000 | 230,634 |

| China Vanadium Titano-Magnetite Mining | 249,000 a | 107,237 |

| Evergrande Real Estate Group | 181,000 | 99,592 |

| Great Wall Motor, Cl. H | 102,750 | 189,951 |

| Industrial & Commercial Bank of China, Cl. H | 230,000 | 191,012 |

| Mongolian Mining | 104,000 | 132,899 |

| Weichai Power, Cl. H | 13,000 | 78,967 |

| | | 1,622,228 |

| Hong Kong—7.6% | | |

| China Agri-Industries Holdings | 190,481 | 213,535 |

| China Minsheng Bank, Cl. H | 207,500 | 190,733 |

| China Mobile | 37,500 | 345,421 |

| CNOOC | 105,000 | 264,574 |

| Country Garden Holdings | 214,000 | 93,539 |

| Guangdong Investment | 150,000 | 75,785 |

| Hutchison Whampoa | 8,000 | 94,722 |

| | | 1,278,309 |

| Hungary—2.0% | | |

| MOL Hungarian Oil and Gas | 1,690 a | 216,038 |

| OTP Bank | 4,050a | 119,845 |

| | | 335,883 |

| India—9.2% | | |

| Apollo Tyres | 82,250 | 128,276 |

| Chambal Fertilizers & Chemicals | 68,940 | 121,663 |

STATEMENT OF INVESTMENTS (Unaudited) (continued)

| | | |

| Common Stocks (continued) | Shares | Value ($) |

| India (continued) | | |

| Hexaware Technologies | 100,860 | 149,158 |

| Oil & Natural Gas | 16,280 | 105,905 |

| Shree Renuka Sugars | 132,370 | 206,592 |

| Sintex Industries | 93,480 | 317,784 |

| Tata Consultancy Services | 5,940 | 157,508 |

| Tata Motors | 8,250 | 230,785 |

| Welspun | 25,680 | 118,855 |

| | | 1,536,526 |

| Indonesia—1.7% | | |

| Bank Mandiri | 125,500 | 98,007 |

| Bank Pembangunan Daerah Jawa Barat dan Banten | 444,500 | 64,831 |

| Indofood Sukses Makmur | 209,000 | 129,612 |

| | | 292,450 |

| Malaysia—2.9% | | |

| AMMB Holdings | 62,000 | 132,854 |

| Axiata Group | 80,800a | 127,786 |

| KNM Group | 108,500 | 98,873 |

| Tenaga Nasional | 57,875 | 119,428 |

| | | 478,941 |

| Mexico—2.4% | | |

| America Movil, ADR, Ser. L | 3,600 | 209,160 |

| Fomento Economico Mexicano, ADR | 3,240 | 190,188 |

| | | 399,348 |

| Poland—.8% | | |

| KGHM Polska Miedz | 2,230 | 141,515 |

| Russia—8.9% | | |

| Gazprom, ADR | 15,520 | 502,382 |

| LUKOIL, ADR | 6,550 | 469,308 |

| Magnitogorsk Iron & Steel Works, GDR | 5,030 b,c,d | 73,589 |

| MMC Norilsk Nickel, ADR | 6,432 | 170,062 |

| Sberbank of Russian, GDR | 650 | 269,444 |

| | | 1,484,785 |

| South Africa—6.5% | | |

| Aveng | 24,860 | 131,080 |

| Exxaro Resources | 6,980 | 170,719 |

8

| | |

| Common Stocks (continued) | Shares | Value ($) |

| South Africa (continued) | | |

| FirstRand | 47,580 | 141,369 |

| MTN Group | 16,744 | 338,023 |

| Sasol | 5,210 | 301,502 |

| | | 1,082,693 |

| South Korea—14.4% | | |

| BS Financial Group | 11,910 a | 172,632 |

| Chong Kun Dang Pharmaceutical | 2,320 | 53,085 |

| Daegu Bank | 8,440 | 138,493 |

| Daehan Steel | 4,690 | 43,182 |

| Hana Financial Group | 2,200 | 95,164 |

| Hyundai Mipo Dockyard | 906 | 154,448 |

| Hyundai Mobis | 1,284 | 383,345 |

| Korea Electric Power | 3,780a | 92,695 |

| KT | 3,090 | 109,578 |

| Kukdo Chemical | 1,100 | 56,858 |

| POSCO | 261 | 120,156 |

| Samsung Electronics | 645 | 548,010 |

| SK Holdings | 846 | 127,253 |

| SK Innovation | 722 | 138,878 |

| Woori Finance Holdings | 4,780 | 63,402 |

| Youngone | 5,916 | 56,089 |

| Youngone Holdings | 1,804 | 54,024 |

| | | 2,407,292 |

| Taiwan—10.6% | | |

| Advanced Semiconductor Engineering | 74,892 | 81,242 |

| Asia Cement | 53,168 | 59,756 |

| Catcher Technology | 17,000 | 84,114 |

| Chroma Ate | 21,000 | 67,842 |

| Chunghwa Telecom | 23,200 | 72,267 |

| CTCI | 102,000 | 116,199 |

| Fubon Financial Holding | 116,195 | 154,300 |

| Grand Pacific Petrochemical | 130,000 | 80,016 |

| HON HAI Precision Industry | 55,240 | 193,485 |

| HTC | 8,300 | 324,588 |

| Powertech Technology | 38,500 | 120,581 |

STATEMENT OF INVESTMENTS (Unaudited) (continued)

| | |

| Common Stocks (continued) | Shares | Value ($) |

| Taiwan (continued) | | |

| Taishin Financial Holdings | 233,463 | 132,187 |

| Taiwan Semiconductor Manufacturing, ADR | 24,439 | 297,667 |

| | | 1,784,244 |

| Thailand—2.9% | | |

| Asian Property Development | 338,700 | 67,836 |

| Bangchak Petroleum | 102,800 | 62,760 |

| Banpu | 3,600 | 83,184 |

| Kasikornbank | 30,900 | 128,712 |

| Krung Thai Bank | 103,500 | 62,229 |

| Krung Thai Bank | 135,300 | 82,312 |

| | | 487,033 |

| Turkey—4.2% | | |

| Arcelik | 17,860 | 82,588 |

| Ford Otomotiv Sanayi | 7,500 | 71,646 |

| Haci Omer Sabanci Holding | 21,587 | 100,382 |

| KOC Holding | 25,780 | 119,880 |

| Turk Telekomunikasyon | 43,670 | 219,474 |

| Turkiye Halk Bankasi | 13,800 | 106,804 |

| | | 700,774 |

| Total Common Stocks | | |

| (cost $11,330,097) | | 14,803,741 |

| |

| Preferred Stocks—11.4% | | |

| Brazil | | |

| Banco Bradesco | 16,575 | 338,576 |

| Banco do Estado do Rio Grande do Sul | 14,100 | 173,589 |

| Bradespar | 5,500 | 144,183 |

| Cia de Bebidas das Americas | 2,700 | 75,163 |

| Cia Paranaense de Energia, Cl. B | 9,000 | 245,031 |

| Itau Unibanco Holding | 3,924 | 93,494 |

| Petroleo Brasileiro | 14,100 | 246,220 |

| Usinas Siderurgicas de Minas Gerais, Cl. A | 4,350 | 52,622 |

| Vale, Cl. A | 18,900 | 548,600 |

| Total Preferred Stocks | | |

| (cost $1,169,478) | | 1,917,478 |

10

| | | |

| Investment of Cash Collateral | | |

| for Securities Loaned—.0% | Shares | Value ($) |

| Registered Investment Company; | | |

| Dreyfus Institutional Cash Advantage Fund | | |

| (cost $4,050) | 4,050e | 4,050 |

| Total Investments (cost $12,503,625) | 99.8% | 16,725,269 |

| Cash and Receivables (Net) | .2% | 28,198 |

| Net Assets | 100.0% | 16,753,467 |

|

| ADR—American Depository Receipts |

| GDR—Global Depository Receipts |

| a Non-income producing security. |

| b Security, or portion thereof, on loan.At March 31, 2011, the value of the fund’s security on loan was $4,389 and |

| the value of the collateral held by the fund was $4,050. |

| c The valuation of this security has been determined in good faith by management under the direction of the Board of |

| Trustees.At March 31, 2011, the value of this security amounted to $73,589 or 0.4% of net assets. |

| d Security exempt from registration under Rule 144A of the Securities Act of 1933.This security may be resold in |

| transactions exempt from registration, normally to qualified institutional buyers.At March 31, 2011, this security had |

| a value of $73,589 or 0.4% of net assets. |

| e Investment in affiliated money market mutual fund. |

| | | |

| Portfolio Summary (Unaudited)† | | |

| |

| | Value (%) | | Value (%) |

| Financial | 23.3 | Consumer Discretionary | 7.2 |

| Energy | 16.2 | Consumer Staples | 4.4 |

| Materials | 13.2 | Utilities | 3.2 |

| Information Technology | 12.8 | Health Care | 1.3 |

| Industrial | 9.7 | Money Market Investment | .0 |

| Telecommunication Services | 8.5 | | 99.8 |

| |

| † Based on net assets. | | | |

| See notes to financial statements. | | | |

|

| STATEMENT OF ASSETS AND LIABILITIES |

| March 31, 2011 (Unaudited) |

| | | | |

| | | Cost | Value |

| Assets ($): | | | |

| Investments in securities—See Statement of Investments (including | | |

| securities on loan, valued at $4,389)—Note 1(c): | | | |

| Unaffiliated issuers | | 12,499,575 | 16,721,219 |

| Affiliated issuers | | 4,050 | 4,050 |

| Cash | | | 8,239 |

| Cash denominated in foreign currencies | | 90,750 | 92,167 |

| Receivable for investment securities sold | | | 93,789 |

| Dividends and interest receivable | | | 23,503 |

| Unrealized appreciation on forward foreign | | | |

| currency exchange contracts—Note 4 | | | 494 |

| Prepaid expenses | | | 26,573 |

| | | | 16,970,034 |

| Liabilities ($): | | | |

| Due to The Dreyfus Corporation and affiliates—Note 3(c) | | 21,673 |

| Payable for investment securities purchased | | | 168,126 |

| Liability for securities on loan—Note 1(c) | | | 4,050 |

| Unrealized depreciation on forward foreign | | | |

| currency exchange contracts—Note 4 | | | 329 |

| Accrued expenses | | | 22,389 |

| | | | 216,567 |

| Net Assets ($) | | | 16,753,467 |

| Composition of Net Assets ($): | | | |

| Paid-in capital | | | 14,288,187 |

| Accumulated distributions in excess of investment income—net | | (116,302) |

| Accumulated net realized gain (loss) on investments | | | (1,641,646) |

| Accumulated net unrealized appreciation (depreciation) | | | |

| on investments and foreign currency transactions | | | 4,223,228 |

| Net Assets ($) | | | 16,753,467 |

| |

| |

| Net Asset Value Per Share | | | |

| | Class A | Class C | Class I |

| Net Assets ($) | 192,574 | 236,361 | 16,324,532 |

| Shares Outstanding | 6,524 | 8,216 | 556,194 |

| Net Asset Value Per Share ($) | 29.52 | 28.77 | 29.35 |

| |

| See notes to financial statements. | | | |

12

|

| STATEMENT OF OPERATIONS |

| Six Months Ended March 31, 2011 (Unaudited) |

| | |

| Investment Income ($): | |

| Income: | |

| Cash dividends (net of $11,494 foreign taxes withheld at source): | |

| Unaffiliated issuers | 95,927 |

| Affiliated issuers | 39 |

| Income from securities lending—Note 1(c) | 250 |

| Total Income | 96,216 |

| Expenses: | |

| Investment advisory fee—Note 3(a) | 90,612 |

| Custodian fees—Note 3(c) | 52,378 |

| Accounting and administrative fees—Note 3(a) | 22,500 |

| Auditing fees | 18,971 |

| Registration fees | 18,265 |

| Shareholder servicing costs—Note 3(c) | 12,030 |

| Prospectus and shareholders’ reports | 7,375 |

| Legal fees | 2,624 |

| Distribution fees—Note 3(b) | 931 |

| Trustees’ fees and expenses—Note 3(d) | 575 |

| Loan commitment fees—Note 2 | 22 |

| Miscellaneous | 11,184 |

| Total Expenses | 237,467 |

| Less—expense reimbursement from The Dreyfus | |

| Corporation due to undertaking—Note 3(a) | (111,279) |

| Less—reduction in fees due to earnings credits—Note 3(c) | (2) |

| Net Expenses | 126,186 |

| Investment (Loss)—Net | (29,970) |

| Realized and Unrealized Gain (Loss) on Investments—Note 4 ($): | |

| Net realized gain (loss) on investments and foreign currency transactions | 1,304,827 |

| Net realized gain (loss) on forward foreign currency exchange contracts | (1,545) |

| Net Realized Gain (Loss) | 1,303,282 |

| Net unrealized appreciation (depreciation) on | |

| investments and foreign currency transactions | 288,177 |

| Net unrealized appreciation (depreciation) on | |

| forward foreign currency exchange contracts | 165 |

| Net Unrealized Appreciation (Depreciation) | 288,342 |

| Net Realized and Unrealized Gain (Loss) on Investments | 1,591,624 |

| Net Increase in Net Assets Resulting from Operations | 1,561,654 |

| |

| See notes to financial statements. | |

STATEMENT OF CHANGES IN NET ASSETS

| | | | |

| | Six Months Ended | |

| | March 31, 2011 | Year Ended |

| | (Unaudited) | September 30, 2010 |

| Operations ($): | | |

| Investment income (loss)—net | (29,970) | 117,960 |

| Net realized gain (loss) on investments | 1,303,282 | 2,659,677 |

| Net unrealized appreciation | | |

| (depreciation) on investments | 288,342 | 103,765 |

| Net Increase (Decrease) in Net Assets | | |

| Resulting from Operations | 1,561,654 | 2,881,402 |

| Dividends to Shareholders from ($): | | |

| Investment income—net: | | |

| Class A Shares | (603) | — |

| Class C Shares | — | (2,360) |

| Class I Shares | (62,615) | (218,041) |

| Total Dividends | (63,218) | (220,401) |

| Beneficial Interest Transactions ($): | | |

| Net proceeds from shares sold: | | |

| Class A Shares | 81,709 | 127,583 |

| Class C Shares | 6,117 | 53,392 |

| Class I Shares | 145,503 | 1,420,351 |

| Dividends reinvested: | | |

| Class A Shares | 512 | — |

| Class C Shares | — | 2,139 |

| Class I Shares | 4,708 | 137,480 |

| Cost of shares redeemed: | | |

| Class A Shares | (57,369) | (13,885) |

| Class C Shares | (48,724) | (8,496) |

| Class I Shares | (1,265,104) | (4,780,001) |

| Increase (Decrease) in Net Assets from | | |

| Beneficial Interest Transactions | (1,132,648) | (3,061,437) |

| Total Increase (Decrease) in Net Assets | 365,788 | (400,436) |

| Net Assets ($): | | |

| Beginning of Period | 16,387,679 | 16,788,115 |

| End of Period | 16,753,467 | 16,387,679 |

| Accumulated distributions in excess of | | |

| investment income—net | (116,302) | (23,114) |

14

| | | | |

| | Six Months Ended | |

| | March 31, 2011 | Year Ended |

| | (Unaudited) | September 30, 2010 |

| Capital Share Transactions: | | |

| Class A | | |

| Shares sold | 2,869 | 5,107 |

| Shares issued for dividends reinvested | 18 | — |

| Shares redeemed | (2,012) | (553) |

| Net Increase (Decrease) in Shares Outstanding | 875 | 4,554 |

| Class C | | |

| Shares sold | 217 | 2,190 |

| Shares issued for dividends reinvested | — | 89 |

| Shares redeemed | (1,778) | (369) |

| Net Increase (Decrease) in Shares Outstanding | (1,561) | 1,910 |

| Class I | | |

| Shares sold | 5,181 | 59,386 |

| Shares issued for dividends reinvested | 169 | 5,719 |

| Shares redeemed | (45,495) | (200,276) |

| Net Increase (Decrease) in Shares Outstanding | (40,145) | (135,171) |

| See notes to financial statements. | | |

FINANCIAL HIGHLIGHTS

The following tables describe the performance for each share class for the fiscal periods indicated.All information (except portfolio turnover rate) reflects financial results for a single fund share.Total return shows how much your investment in the fund would have increased (or decreased) during each period, assuming you had reinvested all dividends and distributions.These figures have been derived from the fund’s financial statements.

| | | | | |

| | Six Months Ended | | |

| | March 31, 2011 | Year Ended September 30, |

| Class A Shares | (Unaudited) | 2010 | 2009a |

| Per Share Data ($): | | | |

| Net asset value, beginning of period | 26.99 | 22.70 | 13.55 |

| Investment Operations: | | | |

| Investment income (loss)—netb | (.16) | .17 | .14 |

| Net realized and unrealized | | | |

| gain (loss) on investments | 2.77 | 4.12 | 9.01 |

| Total from Investment Operations | 2.61 | 4.29 | 9.15 |

| Distributions: | | | |

| Dividends from investment income—net | (.08) | — | — |

| Net asset value, end of period | 29.52 | 26.99 | 22.70 |

| Total Return (%)c | 9.70d | 18.85 | 67.60d |

| Ratios/Supplemental Data (%): | | | |

| Ratio of total expenses | | | |

| to average net assets | 3.71e | 3.69 | 11.21e |

| Ratio of net expenses | | | |

| to average net assets | 2.25e | 2.25 | 2.00e |

| Ratio of net investment income | | | |

| (loss) to average net assets | (1.09)e | .71 | 1.56e |

| Portfolio Turnover Rate | 32.96d | 102.30 | 157.45 |

| Net Assets, end of period ($ x 1,000) | 193 | 152 | 25 |

| |

| a | From March 31, 2009 (commencement of initial offering) to September 30, 2009. |

| b | Based on average shares outstanding at each month end. |

| c | Exclusive of sales charge. |

| d | Not annualized. |

| e | Annualized. |

| See notes to financial statements. |

16

| | | | | | |

| | Six Months Ended | | |

| | March 31, 2011 | Year Ended September 30, |

| Class C Shares | (Unaudited) | 2010 | 2009a |

| Per Share Data ($): | | | |

| Net asset value, beginning of period | 26.36 | 22.62 | 13.55 |

| Investment Operations: | | | |

| Investment (loss)—netb | (.25) | (.13) | (.03) |

| Net realized and unrealized | | | |

| gain (loss) on investments | 2.66 | 4.17 | 9.10 |

| Total from Investment Operations | 2.41 | 4.04 | 9.07 |

| Distributions: | | | |

| Dividends from investment income—net | — | (.30) | — |

| Net asset value, end of period | 28.77 | 26.36 | 22.62 |

| Total Return (%)c | 9.19d | 17.95 | 66.94d |

| Ratios/Supplemental Data (%): | | | |

| Ratio of total expenses | | | |

| to average net assets | 3.96e | 4.18 | 3.80e |

| Ratio of net expenses | | | |

| to average net assets | 3.00e | 3.00 | 2.75e |

| Ratio of net investment (loss) | | | |

| to average net assets | (1.84)e | (.57) | (.35)e |

| Portfolio Turnover Rate | 32.96d | 102.30 | 157.45 |

| Net Assets, end of period ($ x 1,000) | 236 | 258 | 178 |

| |

| a | From March 31, 2009 (commencement of initial offering) to September 30, 2009. |

| b | Based on average shares outstanding at each month end. |

| c | Exclusive of sales charge. |

| d | Not annualized. |

| e | Annualized. |

| See notes to financial statements. |

FINANCIAL HIGHLIGHTS (continued)

| | | | | | | | | | | | |

| Six Months Ended | | | | | |

| March 31, 2011 | | Year Ended September 30, | |

| Class I Shares | (Unaudited) | 2010 | 2009a | 2008 | 2007 | 2006b |

| Per Share Data ($): | | | | | | |

| Net asset value, | | | | | | |

| beginning of period | 26.79 | 22.67 | 21.33 | 33.24 | 20.55 | 20.00 |

| Investment Operations: | | | | | | |

| Investment income (loss)—netc | (.05) | .18 | .24 | .35 | .31 | .06 |

| Net realized and unrealized | | | | | | |

| gain (loss) on investments | 2.72 | 4.26 | 2.21 | (8.86) | 12.62 | .49 |

| Total from Investment Operations | 2.67 | 4.44 | 2.45 | (8.51) | 12.93 | .55 |

| Distributions: | | | | | | |

| Dividends from | | | | | | |

| investment income—net | (.11) | (.32) | (.26) | (.26) | (.24) | — |

| Dividends from net realized | | | | | | |

| gain on investments | — | — | (.85) | (3.14) | — | — |

| Total Distributions | (.11) | (.32) | (1.11) | (3.40) | (.24) | — |

| Net asset value, end of period | 29.35 | 26.79 | 22.67 | 21.33 | 33.24 | 20.55 |

| Total Return (%) | 9.99d | 19.73 | 14.90 | (28.51) | 63.25 | 2.75d |

| Ratios/Supplemental Data (%): | | | | | | |

| Ratio of total expenses | | | | | | |

| to average net assets | 2.86e | 3.07 | 3.50 | 2.74 | 3.18 | 8.64e |

| Ratio of net expenses | | | | | | |

| to average net assets | 1.50e | 1.50 | 1.43 | 1.45 | 1.45 | 1.45e |

| Ratio of net investment income | | | | | | |

| (loss) to average net assets | (.33)e | .75 | 1.43 | 1.21 | 1.15 | 1.31e |

| Portfolio Turnover Rate | 32.96d | 102.30 | 157.45 | 128 | 76 | 31d |

| Net Assets, end of period | | | | | | |

| ($ x 1,000) | 16,325 | 15,978 | 16,585 | 15,328 | 13,671 | 5,693 |

| |

| a | The fund commenced offering three classes of shares on March 31, 2009.The existing shares were redesignated as |

| | Class I shares. |

| b | From July 10, 2006 (commencement of operations) to September 30, 2006. |

| c | Based on average shares outstanding at each month end. |

| d | Not annualized. |

| e | Annualized. |

| See notes to financial statements. |

18

NOTES TO FINANCIAL STATEMENTS (Unaudited)

NOTE 1—Significant Accounting Policies:

Dreyfus/The Boston Company Emerging Markets Core Equity Fund (the “fund”) is a separate diversified series of Dreyfus Investment Funds (the “Trust”), which is registered under the Investment Company Act of 1940, as amended (the “Act”), as an open-end management investment company and operates as a series company currently offering eleven series, including the fund.The fund’s investment objective is to seek long-term growth of capital. The Dreyfus Corporation (the “Manager” or “Dreyfus”), a wholly-owned subsidiary of The Bank of New York Mellon Corporation (“BNY Mellon”), serves as the fund’s investment adviser.

MBSC Securities Corporation (the “Distributor”), a wholly-owned subsidiary of the Manager, is the distributor of the fund’s shares.The fund is authorized to issue an unlimited number of $.001 par value shares of Beneficial Interest in each of the following classes of shares: Class A, Class C and Class I. Class A shares are subject to a sales charge imposed at the time of purchase. Class C shares are subject to a contingent deferred sales charge (“CDSC”) on Class C shares redeemed within one year of purchase. Class I shares are sold primarily to bank trust departments and other financial service providers (including The Bank of NewYork Mellon, a subsidiary of BNY Mellon and an affiliate of Dreyfus), acting on behalf of customers having a qualified trust or investment account or relationship at such institution, and bear no distribution or shareholder services fees. Class I shares are offered without a front-end sales charge or CDSC. Other differences between the classes include the services offered to, the expenses borne by each class, the allocation of certain transfer agency costs and certain voting rights. Income, expenses (other than expenses attributable to a specific class), and realized and unrealized gains or losses on investments are allocated to each class of shares based on its relative net assets.

The Trust accounts separately for the assets, liabilities and operations of each series. Expenses directly attributable to each series are charged to that series’ operations; expenses which are applicable to all series are allocated among them on a pro rata basis.

NOTES TO FINANCIAL STATEMENTS (Unaudited) (continued)

The Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) is the exclusive reference of authoritative U.S. generally accepted accounting principles (“GAAP”) recognized by the FASB to be applied by nongovernmental entities. Rules and interpretive releases of the Securities and Exchange Commission (“SEC”) under authority of federal laws are also sources of authoritative GAAP for SEC registrants. The fund’s financial statements are prepared in accordance with GAAP, which may require the use of management estimates and assumptions.Actual results could differ from those estimates.

(a) Portfolio valuation: Investments in securities are valued at the last sales price on the securities exchange or national securities market on which such securities are primarily traded. Securities listed on the National Market System for which market quotations are available are valued at the official closing price or, if there is no official closing price that day, at the last sales price. Securities not listed on an exchange or the national securities market, or securities for which there were no transactions, are valued at the average of the most recent bid and asked prices, except for open short positions, where the asked price is used for valuation purposes. Bid price is used when no asked price is available. Registered investment companies that are not traded on an exchange are valued at their net asset value.When market quotations or official closing prices are not readily available, or are determined not to reflect accurately fair value, such as when the value of a security has been significantly affected by events after the close of the exchange or market on which the security is principally traded (for example, a foreign exchange or market), but before the fund calculates its net asset value, the fund may value these investments at fair value as determined in accordance with the procedures approved by the Board of Trustees. Fair valuing of securities may be determined with the assistance of a pricing service using calculations based on indices of domestic securities and other appropriate indicators, such as prices of relevant ADRs and futures contracts. For other securities that are fair valued by the Board of Trustees, certain factors may be considered such as: funda-

20

mental analytical data, the nature and duration of restrictions on disposition, an evaluation of the forces that influence the market in which the securities are purchased and sold, and public trading in similar securities of the issuer or comparable issuers. Investments denominated in foreign currencies are translated to U.S. dollars at the prevailing rates of exchange. Forward foreign currency exchange contracts (“forward contracts”) are valued at the forward rate.

The fair value of a financial instrument is the amount that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date (i.e. the exit price). GAAP establishes a fair value hierarchy that prioritizes the inputs of valuation techniques used to measure fair value.This hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurements) and the lowest priority to unobservable inputs (Level 3 measurements).

Additionally, GAAP provides guidance on determining whether the volume and activity in a market has decreased significantly and whether such a decrease in activity results in transactions that are not orderly. GAAP requires enhanced disclosures around valuation inputs and techniques used during annual and interim periods.

Various inputs are used in determining the value of the fund’s investments relating to fair value measurements.These inputs are summarized in the three broad levels listed below:

Level 1—unadjusted quoted prices in active markets for identical investments.

Level 2—other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, credit risk, etc.).

Level 3—significant unobservable inputs (including the fund’s own assumptions in determining the fair value of investments).

NOTES TO FINANCIAL STATEMENTS (Unaudited) (continued)

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

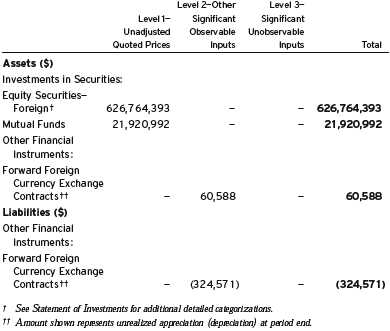

The following is a summary of the inputs used as of March 31, 2011 in valuing the fund’s investments:

| | | | | | | |

| | | | Level 2—Other | | Level 3— | | |

| | | Level 1— | Significant | | Significant | | |

| | | Unadjusted | Observable | | Unobservable | | |

| | | Quoted Prices | Inputs | | Inputs | Total | |

| Assets ($) | | | | | | |

| Investments in Securities: | | | | | |

| Equity Securities— | | | | | | |

| | Foreign† | 16,647,630 | 73,589 | | — | 16,721,219 | |

| Mutual Funds | 4,050 | — | | — | 4,050 | |

| Forward Foreign | | | | | | |

| | Currency Exchange | | | | | | |

| | Contracts†† | — | 494 | | — | 494 | |

| Liabilities ($) | | | | | | |

| Other Financial | | | | | | |

| | Instruments: | | | | | | |

| Forward Foreign | | | | | | |

| | Currency Exchange | | | | | | |

| | Contracts†† | — | (329 | ) | — | (329 | ) |

| |

| † | See Statement of Investments for additional detailed categorizations. | | |

| †† | Amount shown represents unrealized appreciation (depreciation) at period end. | | |

In January 2010, FASB issued Accounting Standards Update (“ASU”) No. 2010-06 “Improving Disclosures about FairValue Measurements”. The portions of ASU No. 2010-06 which require reporting entities to prepare new disclosures surrounding amounts and reasons for significant transfers in and out of Level 1 and Level 2 fair value measurements as well as inputs and valuation techniques used to measure fair value for both recurring and nonrecurring fair value measurements that fall in either Level 2 or Level 3 have been adopted by the fund. No significant transfers between Level 1 or Level 2 fair value measurements occurred at March 31, 2011.

(b) Foreign currency transactions: The fund does not isolate that portion of the results of operations resulting from changes in foreign exchange rates on investments from the fluctuations arising from changes

22

in market prices of securities held. Such fluctuations are included with the net realized and unrealized gain or loss on investments.

Net realized foreign exchange gains or losses arise from sales of foreign currencies, currency gains or losses realized on securities transactions between trade and settlement date and the difference between the amounts of dividends, interest, and foreign withholding taxes recorded on the fund’s books and the U.S. dollar equivalent of the amounts actually received or paid. Net unrealized foreign exchange gains and losses arise from changes in the value of assets and liabilities other than investments resulting from changes in exchange rates. Foreign currency gains and losses on investments are included with net realized and unrealized gain or loss on investments.

(c) Securities transactions and investment income: Securities transactions are recorded on a trade date basis. Realized gains and losses from securities transactions are recorded on the identified cost basis. Dividend income is recognized on the ex-dividend date and interest income, including, where applicable, accretion of discount and amortization of premium on investments, is recognized on the accrual basis.

Pursuant to a securities lending agreement with The Bank of New York Mellon, the fund may lend securities to qualified institutions. It is the fund’s policy that, at origination, all loans are secured by collateral of at least 102% of the value of U.S. securities loaned and 105% of the value of foreign securities loaned. Collateral equivalent to at least 100% of the market value of securities on loan is maintained at all times. Collateral is either in the form of cash, which can be invested in certain money market mutual funds managed by the Manager, U.S. Government and Agency securities or letters of credit. The fund is entitled to receive all income on securities loaned, in addition to income earned as a result of the lending transaction. Although each security loaned is fully collateralized, the fund bears the risk of delay in recovery of, or loss of rights in, the securities loaned should a borrower fail to return the securities in a timely manner. During the

NOTES TO FINANCIAL STATEMENTS (Unaudited) (continued)

period ended March 31, 2011, The Bank of New York Mellon earned $135 from lending portfolio securities, pursuant to the securities lending agreement.

Investing in foreign markets may involve special risks and considerations not typically associated with investing in the U.S. These risks include revaluation of currencies, high rates of inflation, repatriation restrictions on income and capital, and adverse political and economic developments. Moreover, securities issued in these markets may be less liquid, subject to government ownership controls and delayed settlements, and their prices may be more volatile than those of comparable securities in the U.S.

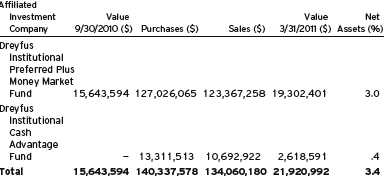

(d) Affiliated issuers: Investments in other investment companies advised by Dreyfus are defined as “affiliated” in the Act.

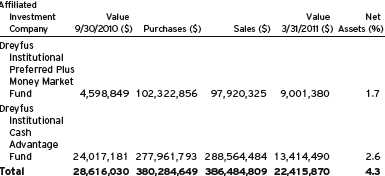

The fund may invest in shares of certain affiliated investment companies also advised or managed by Dreyfus. Investments in affiliated investment companies for the period ended March 31, 2011 were as follows:

| | | | | | | |

| Affiliated | | | | | | | |

| Investment | Value | | | | Value | | Net |

| Company | 9/30/2010 | ($) | Purchases ($) | Sales ($) | 3/31/2011 | ($) | Assets (%) |

| Dreyfus | | | | | | | |

| Institutional | | | | | | | |

| Preferred Plus | | | | | | |

| Money Market | | | | | | |

| Fund | — | | 1,462,494 | 1,462,494 | — | | — |

| Dreyfus | | | | | | | |

| Institutional | | | | | | | |

| Cash Advantage | | | | | | |

| Fund | 144,550 | | 2,259,658 | 2,400,158 | 4,050 | | — |

| Total | 144,550 | | 3,722,152 | 3,862,652 | 4,050 | | — |

(e) Dividends to shareholders: Dividends are recorded on the ex-dividend date. Dividends from investment income-net and dividends from net realized capital gains, if any, are normally declared and paid annually, but the fund may make distributions on a more frequent basis to comply with the distribution requirements of the Internal Revenue Code of 1986, as amended (the “Code”).To the extent that net realized capital gains can be offset by capital loss carryovers, it is the policy

24

of the fund not to distribute such gains. Income and capital gain distributions are determined in accordance with income tax regulations, which may differ from GAAP.

(f) Federal income taxes: It is the policy of the fund to continue to qualify as a regulated investment company, if such qualification is in the best interests of its shareholders, by complying with the applicable provisions of the Code, and to make distributions of taxable income sufficient to relieve it from substantially all federal income and excise taxes.

As of and during the period ended March 31, 2011, the fund did not have any liabilities for any uncertain tax positions.The fund recognizes interest and penalties, if any, related to uncertain tax positions as income tax expense in the Statement of Operations. During the period, the fund did not incur any interest or penalties.

Each of the tax years in the three-year period ended September 30, 2010 remains subject to examination by the Internal Revenue Service and state taxing authorities.

The fund has an unused capital loss carryover of $2,045,216 available for federal income tax purposes to be applied against future net securities profits, if any, realized subsequent to September 30, 2010. If not applied, $1,300,051 of the carryover expires in fiscal 2017 and $745,165 expires in fiscal 2018.

Under the recently enacted Regulated Investment Company Modernization Act of 2010, the fund will be permitted to carry forward capital losses incurred in taxable years beginning after December 22, 2010 for an unlimited period. However, any losses incurred during those future taxable years will be required to be utilized prior to the losses incurred in pre-enactment taxable years.As a result of this ordering rule, pre-enactment capital loss carryovers may be more likely to expire unused.

The tax character of distributions paid to shareholders during the fiscal year ended September 30, 2010 was as follows: ordinary income $220,401.The tax character of current year distributions will be determined at the end of the current fiscal year.

NOTES TO FINANCIAL STATEMENTS (Unaudited) (continued)

NOTE 2—Bank Lines of Credit:

The fund participates with other Dreyfus-managed funds in a $225 million unsecured credit facility led by Citibank, N.A. and a $300 million unsecured credit facility provided by The Bank of New York Mellon (each, a “Facility”), each to be utilized primarily for temporary or emergency purposes, including the financing of redemptions. In connection therewith, the fund has agreed to pay its pro rata portion of commitment fees for each Facility. Interest is charged to the fund based on rates determined pursuant to the terms of the respective Facility at the time of borrowing. During the period ended on March 31, 2011, the fund did not borrow under the Facilities.

NOTE 3—Investment Advisory Fee and Other Transactions with Affiliates:

(a) Pursuant to an investment advisory agreement with the Manager, the investment advisory fee is computed at the annual rate of 1.10% of the value of the fund’s average daily net assets and is payable monthly. The Manager has agreed, until February 1, 2012, to waive receipt of its fees and/or assume the expenses of the fund so that the direct expenses of Class A, Class C and Class I shares (excluding Rule 12b-1 fees, shareholder services fees, taxes, interest, brokerage commissions, acquired fund fees and extraordinary expenses) do not exceed 2.00%, 2.00% and 1.50%, respectively, of the value of such class’ average daily net assets. The expense reimbursement, pursuant to the undertaking, amounted to $111,279 during the period ended March 31, 2011.

During the period, the Trust had an agreement with The Bank of New York Mellon pursuant to whichThe Bank of NewYork Mellon provided administration and fund accounting services for the fund. For these services, the fund pays The Bank of NewYork Mellon a fixed fee plus asset and transaction based fees, as well as out-of-pocket expenses. Pursuant to this agreement, the fund was charged $22,500 during the period ended March 31, 2011 for administration and fund accounting services.

26

At a Board Meeting of the Trust held on February 15-16, 2011, the Board of Trustees of the Trust terminated the agreement with The Bank of New York Mellon and, on behalf of the Trust, entered into a Fund Accounting and Administration Agreement (the “Administration Agreement”) with Dreyfus, effective May 1, 2011, whereby Dreyfus will perform administrative, accounting and recordkeeping services for the fund. The fund has agreed to compensate Dreyfus for providing accounting services, administration, compliance monitoring, regulatory and shareholder reporting, as well as related facilities, equipment and clerical help.The fee is based on the fund’s average daily net assets and computed at the following annual rates: .10% of the first $500 million, .065% of the next $500 million and .02% in excess of $1 billion.

In addition, after applying any expense limitations or fee waivers that reduce the fees paid to Dreyfus for this service, Dreyfus has contractually agreed in writing to waive any remaining fees for this service to the extent that they exceed both Dreyfus’ costs in providing these services and a reasonable allocation of the costs incurred by Dreyfus and its affiliates related to the support and oversight of these services.

The fund also will reimburse Dreyfus for the out-of-pocket expenses incurred by it in performing this service for the fund.

(b) Under the Distribution Plan (the “Plan”) adopted pursuant to Rule 12b-1 under the Act, Class C shares pay the Distributor for distributing its shares at an annual rate of .75% of the value of the average daily net assets of Class C shares. During the period ended March 31, 2011, Class C shares were charged $931 pursuant to the Plan.

(c) Under the Shareholder Services Plan, Class A and Class C shares pay the Distributor at the annual rate of .25% of the value of their average daily net assets for the provision of certain services.The services provided may include personal services relating to shareholder accounts, such as answering shareholder inquiries regarding the fund and providing reports and other information, and services related to the maintenance

NOTES TO FINANCIAL STATEMENTS (Unaudited) (continued)

of shareholder accounts.The Distributor may make payments to Service Agents (a securities dealer, financial institution or other industry professional) in respect of these services. The Distributor determines the amounts to be paid to Service Agents. During the period ended March 31, 2011, Class A and Class C shares were charged $246 and $310, respectively, pursuant to the Shareholder Services Plan.

The fund compensates Dreyfus Transfer, Inc., a wholly-owned subsidiary of the Manager, under a transfer agency agreement for providing personnel and facilities to perform transfer agency services for the fund. During the period ended March 31, 2011, the fund was charged $818 pursuant to the transfer agency agreement, which is included in Shareholder servicing costs in the Statement of Operations.

The fund has arrangements with the custodian and cash management bank whereby the fund may receive earnings credits when positive cash balances are maintained, which are used to offset custody and cash management fees. For financial reporting purposes, the fund includes net earnings credits as an expense offset in the Statement of Operations.

The fund compensates The Bank of New York Mellon under cash management agreements for performing cash management services related to fund subscriptions and redemptions. During the period ended March 31, 2011, the fund was charged $80 pursuant to the cash management agreements, which is included in Shareholder servicing costs in the Statement of Operations. These fees were partially offset by earnings credits of $2.

The fund also compensates The Bank of New York Mellon under a custody agreement for providing custodial services for the fund. During the period ended March 31, 2011, the fund was charged $52,378 pursuant to the custody agreement.

During the period ended March 31, 2011, the fund was charged $3,146 for services performed by the Chief Compliance Officer.

The components of “Due to The Dreyfus Corporation and affiliates” in the Statement of Assets and Liabilities consist of: investment advisory fees

28

$15,865, Rule 12b-1 distribution plan fees $155, shareholder services plan fees $96, custodian fees $25,038, chief compliance officer fees $1,957 and transfer agency per account fees $257, which are offset against an expense reimbursement currently in effect in the amount of $21,695.

(d) Each Trustee who is not an “interested person” of the Trust (as defined in the Act) receives $60,000 per annum, plus $7,000 per joint Board meeting of the Trust, The Dreyfus/Laurel Funds, Inc., The Dreyfus/Laurel Funds Trust, The Dreyfus/Laurel Tax-Free Municipal Funds and Dreyfus Funds, Inc. (collectively, the “Board Group Open-End Funds”) attended, $2,500 for separate in-person committee meetings attended which are not held in conjunction with a regularly scheduled Board meeting and $2,000 for Board meetings and separate committee meetings attended that are conducted by telephone. The Board Group Open-End Funds also reimburse eachTrustee who is not an “interested person” of theTrust (as defined in the Act) for travel and out-of-pocket expenses. With respect to Board meetings, the Chairman of the Board receives an additional 25% of such compensation (with the exception of reimbursable amounts).The Chair of each of the Board’s committees, unless the Chair also serves as Chair of the Board, receives $1,350 per applicable committee meeting. In the event that there is an in-person joint committee meeting or a joint telephone meeting of the Board Group Open-End Funds and Dreyfus High Yield Strategies Fund, the $2,500 or $2,000 fee, as applicable, is allocated between the Board Group Open-End Funds and Dreyfus High Yield Strategies Fund.These fees and expenses are charged and allocated to each series based on net assets.

(e) A 2% redemption fee is charged and retained by the fund on certain shares redeemed within sixty days following the date of issuance, subject to exceptions, including redemptions made through the use of the fund’s exchange privilege. During the period ended March 31, 2011, redemption fees charged and retained by the fund amounted to $475.

NOTES TO FINANCIAL STATEMENTS (Unaudited) (continued)

NOTE 4—Securities Transactions:

The aggregate amount of purchases and sales of investment securities, excluding short-term securities and forward contracts, during the period ended March 31, 2011, amounted to $5,378,411 and $6,511,697, respectively.

Forward Foreign Currency Exchange Contracts: The fund enters into forward contracts in order to hedge its exposure to changes in foreign currency exchange rates on its foreign portfolio holdings, to settle foreign currency transactions or as a part of its investment strategy. When executing forward contracts, the fund is obligated to buy or sell a foreign currency at a specified rate on a certain date in the future. With respect to sales of forward contracts, the fund incurs a loss if the value of the contract increases between the date the forward contract is opened and the date the forward contract is closed.The fund realizes a gain if the value of the contract decreases between those dates.With respect to purchases of forward contracts, the fund incurs a loss if the value of the contract decreases between the date the forward contract is opened and the date the forward contract is closed.The fund realizes a gain if the value of the contract increases between those dates. Any realized gain or loss which occurred during the period is reflected in the Statement of Operations.The fund is exposed to foreign currency risk as a result of changes in value of underlying financial instruments. The fund is also exposed to credit risk associated with counterparty nonperformance on these forward contracts, which is typically limited to the unrealized gain on each open contract.The following summarizes open forward contracts at March 31, 2011:

| | | | | |

| | Foreign | | | Unrealized |

| Forward Foreign Currency | Currency | | | Appreciation |

| Exchange Contracts | Amounts | Cost ($) | Value ($) | (Depreciation) ($) |

| Purchases: | | | | |

| Taiwan Dollar, | | | | |

| Expiring 4/1/2011 | 4,760,000 | 162,147 | 161,869 | (278) |

| Turkish Lira, | | | | |

| Expiring 4/1/2011 | 7,414 | 4,798 | 4,801 | 3 |

30

| | | | | |

| | Foreign | | | Unrealized |

| Forward Foreign Currency | Currency | | | Appreciation |

| Exchange Contracts | Amounts | Proceeds ($) | Value ($) | (Depreciation) ($) |

| Sales: | | | | |

| Brazilian Real, | | | | |

| Expiring 4/5/2011 | 66,110 | 40,983 | 40,492 | 491 |

| South Korean Won, | | | | |

| Expiring 4/4/2011 | 53,510,328 | 48,730 | 48,781 | (51) |

| Gross Unrealized | | | | |

| Appreciation | | | | 494 |

| Gross Unrealized | | | | |

| Depreciation | | | | (329) |

The following summarizes the average market value of derivatives outstanding for the period ended March 31, 2011:

| |

| | Average Market Value ($) |

| Forward contracts | 49,829 |

At March 31, 2011, accumulated net unrealized appreciation on investments was $4,221,644, consisting of $4,380,364 gross unrealized appreciation and $158,720 gross unrealized depreciation.

At March 31, 2011, the cost of investments for federal income tax purposes was substantially the same as the cost for financial reporting purposes (see the Statement of Investments).

|

| INFORMATION ABOUT THE RENEWAL OF THE FUND’S |

| INVESTMENT ADVISORY AGREEMENT (Unaudited) |

At a meeting of the fund’s Board of Trustees held on February 15 and 16, 2011, the Board considered the renewal of the fund’s Investment Advisory Agreement pursuant to which Dreyfus provides the fund with investment advisory services (the “Agreement”).The Board also considered the approval of a new Fund Accounting and Administrative Services Agreement (the “Administration Agreement” and together with the Agreement, the “Agreements”) pursuant to which Dreyfus would provide the fund with administrative services.1 The Board members, none of whom are “interested persons” (as defined in the Investment Company Act of 1940, as amended) of the fund, were assisted in their review by independent legal counsel and met with counsel in executive session separate from representatives of Dreyfus. In considering the renewal of the Agreement and the approval of the Administration Agreement, the Board considered all factors that it believed to be relevant, including those discussed below.The Board did not identify any one factor as dispositive, and each Board member may have attributed different weights to the factors considered.

Analysis of Nature, Extent, and Quality of Services Provided to the Fund.The Board members considered information previously provided to them in presentations from representatives of Dreyfus regarding the nature, extent, and quality of the services provided to funds in the Dreyfus fund complex, and representatives of Dreyfus confirmed that there had been no material changes in this information. Dreyfus provided the number of open accounts in the fund, the fund’s asset size and the allocation of fund assets among distribution channels. Dreyfus also had previously provided information regarding the diverse intermediary relationships and distribution channels of funds in the Dreyfus fund complex and Dreyfus’ corresponding need for broad, deep, and diverse resources to be able to provide ongoing shareholder services to each distribution channel, including the distribution channel(s) for the fund.

The Board members also considered research support available to, and portfolio management capabilities of, the fund’s portfolio management personnel and that Dreyfus also would provide oversight of day-to-day fund operations, including fund accounting and administration and

32

assistance in meeting legal and regulatory requirements.The Board members also considered Dreyfus’ extensive administrative, accounting, and compliance infrastructures.The Board also considered portfolio management’s brokerage policies and practices (including policies and practices regarding soft dollars) and the standards applied in seeking best execution.

Comparative Analysis of the Fund’s Performance and Management Fee and Expense Ratio.The Board members reviewed reports prepared by Lipper, Inc. (“Lipper”), an independent provider of investment company data, which included information comparing (1) the fund’s performance with the performance of a group of comparable funds (the “Performance Group”) and with a broader group of funds (the “Performance Universe”), all for various periods ended December 31, 2010, and (2) the fund’s actual and contractual management fees and total expenses with those of a group of comparable funds (the “Expense Group”) and with a broader group of funds (the “Expense Universe”), the information for which was derived in part from fund financial statements available to Lipper as of September 30, 2010. Dreyfus previously had furnished the Board with a description of the methodology Lipper used to select the Performance Group and Performance Universe and the Expense Group and Expense Universe.

Dreyfus representatives stated that the usefulness of performance comparisons may be affected by a number of factors, including different investment limitations that may be applicable to the fund and comparison funds.They also noted that performance generally should be considered over longer periods of time, although it is possible that long-term performance can be adversely affected by even one period of significant underperformance so that a single investment decision or theme has the ability to affect disproportionately long-term performance. The Board members discussed the results of the comparisons and noted that the fund’s total return performance was variously above, at and below the Performance Group and Performance Universe medians. Dreyfus also provided a comparison of the fund’s calendar year total returns to the returns of the fund’s benchmark index.

|

| INFORMATION ABOUT THE RENEWAL OF THE FUND’S |

| INVESTMENT ADVISORY AGREEMENT (Unaudited) (continued) |

The Board members also reviewed the range of actual and contractual management fees and total expenses of the Expense Group and Expense Universe funds and discussed the results of the comparisons.They noted that the fund’s contractual management fee was at the Expense Group median, the fund’s actual management fee was below the Expense Group and Expense Universe medians and the fund’s total expenses were at the Expense Group median and above the Expense Universe median.

A representative of Dreyfus noted that Dreyfus has contractually agreed to waive receipt of its fees and/or assume the expenses of the fund, until February 1, 2012, so that annual direct fund operating expenses of Class A, Class C and Class I shares (excluding Rule 12b-1 fees, shareholder services fees, taxes, interest, brokerage commissions, acquired fund fees and extraordinary expenses) do not exceed 2.00%, 2.00% and 1.50%, respectively, of the fund’s average daily net assets. A representative of Dreyfus also noted that, in connection with the Administration Agreement and its related fees, Dreyfus contractually agreed to waive any fees to the extent that such fees exceed Dreyfus’ costs in providing the services contemplated under the Administration Agreement.

Representatives of Dreyfus reviewed with the Board members the management or investment advisory fees (1) paid by funds advised or administered by Dreyfus that are in the same Lipper category as the fund and (2) paid to Dreyfus or the Dreyfus-affiliated primary employer of the fund’s primary portfolio manager for advising any separate accounts and/or other types of client portfolios that are considered to have similar investment strategies and policies as the fund (the “Similar Clients”), and explained the nature of the Similar Clients.They discussed differences in fees paid and the relationship of the fees paid in light of any differences in the services provided and other relevant factors.The Board members considered the relevance of the fee information provided for the Similar Clients to evaluate the appropriateness and reasonableness of the fund’s management fee.

Analysis of Profitability and Economies of Scale. Dreyfus’ representatives reviewed the expenses allocated and profit received by Dreyfus and the resulting profitability percentage for managing the fund, and the method

34

used to determine the expenses and profit. The Board concluded that the profitability results were not unreasonable, given the services rendered, or to be rendered, and service levels provided, or to be provided, by Dreyfus.The Board also noted the expense limitation arrangement and its effect on Dreyfus’ profitability. The Board previously had been provided with information prepared by an independent consulting firm regarding Dreyfus’ approach to allocating costs to, and determining the profitability of, individual funds and the entire Dreyfus fund complex. The consulting firm also had analyzed where any economies of scale might emerge in connection with the management of a fund.

The Board’s counsel stated that the Board members should consider the profitability analysis (1) as part of their evaluation of whether the fees under the Agreements bear a reasonable relationship to the mix of services provided by Dreyfus, including the nature, extent and quality of such services, and (2) in light of the relevant circumstances for the fund and the extent to which economies of scale would be realized if the fund grows and whether fee levels reflect these economies of scale for the benefit of fund shareholders. Dreyfus representatives noted that a discussion of economies of scale is predicated on a fund having achieved a substantial size with increasing assets and that, if a fund’s assets had been stable or decreasing, the possibility that Dreyfus may have realized any economies of scale would be less. They also noted that, as a result of shared and allocated costs among funds in the Dreyfus funds complex, the extent of economies of scale could depend substantially on the level of assets in the complex as a whole, so that increases and decreases in complex-wide assets can affect potential economies of scale in a manner that is disproportionate to, or even in the opposite direction from, changes in the fund’s asset level. The Board members also considered potential benefits to Dreyfus from acting as investment adviser and noted the soft dollar arrangements in effect for trading the fund’s investments.

At the conclusion of these discussions, the Board agreed that it had been furnished with sufficient information to make an informed business decision with respect to the renewal of the Agreement and

|

| INFORMATION ABOUT THE RENEWAL OF THE FUND’S |

| INVESTMENT ADVISORY AGREEMENT (Unaudited) (continued) |

the approval of the Administration Agreement. Based on the discussions and considerations as described above, the Board concluded and determined as follows.

The Board concluded that the nature, extent and quality of the services provided by Dreyfus are adequate and appropriate.

The Board generally was satisfied with the fund’s overall perfor- mance, in light of the considerations described above.

The Board concluded that the fees payable to Dreyfus were reason- able in light of the considerations described above.

The Board determined that the economies of scale which may accrue to Dreyfus and its affiliates in connection with the management of the fund had been adequately considered by Dreyfus in connection with the fee rate charged to the fund pursuant to the Agreements and that, to the extent in the future it were determined that material economies of scale had not been shared with the fund, the Board would seek to have those economies of scale shared with the fund.

The Board members considered these conclusions and determinations, along with information received on a routine and regular basis throughout the year. In addition, it should be noted that the Board’s consideration of the contractual fee arrangements for this fund had the benefit of a number of years of reviews of similar agreements during which lengthy discussions took place between the Board members and Dreyfus representatives. Certain aspects of the arrangements may receive greater scrutiny in some years than in others, and the Board members’ conclusions may be based, in part, on their consideration of the same or similar arrangements in prior years. The Board members determined that renewal of the Agreement and approval of the Administration Agreement was in the best interests of the fund and its shareholders.

| 1 | Until May 1, 2011, administrative services were provided pursuant to a Custody,Administration and Accounting Services Agreement with The Bank of NewYork Mellon. |

36

Save time. Save paper. View your next shareholder report online as soon as it’s available. Log into www.dreyfus.com and sign up for Dreyfus eCommunications. It’s simple and only takes a few minutes.

The views expressed in this report reflect those of the portfolio manager only through the end of the period covered and do not necessarily represent the views of Dreyfus or any other person in the Dreyfus organization. Any such views are subject to change at any time based upon market or other conditions and Dreyfus disclaims any responsibility to update such views.These views may not be relied on as investment advice and, because investment decisions for a Dreyfus fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Dreyfus fund.

Not FDIC-Insured • Not Bank-Guaranteed • May Lose Value

| | Contents |

| | THE FUND |

| 2 | A Letter from the Chairman and CEO |

| 3 | Discussion of Fund Performance |

| 6 | Understanding Your Fund’s Expenses |

| 6 | Comparing Your Fund’s Expenses With Those of Other Funds |

| 7 | Statement of Investments |

| 11 | Statement of Assets and Liabilities |

| 12 | Statement of Operations |

| 13 | Statement of Changes in Net Assets |

| 15 | Financial Highlights |

| 18 | Notes to Financial Statements |

| 28 | Information About the Renewal of the Fund’s Investment Advisory Agreement |

| | FOR MORE INFORMATION |

| | Back Cover |

Dreyfus/The Boston

Company Large Cap

Core Fund

The Fund

A LETTER FROM THE CHAIRMAN AND CEO

Dear Shareholder:

We are pleased to present this semiannual report for Dreyfus/The Boston Company Large Cap Core Fund, covering the six-month period from October 1, 2010, through March 31, 2011.

Equities have fared quite well over the past year despite heightened market volatility in the spring and summer of 2010 stemming from a subpar U.S. economic recovery and developments in overseas markets. The U.S. stock market has rallied consistently since the fall, when a new round of monetary stimulus gave investors confidence that the economy was unlikely to slip back into recession. Market sectors that tend to be sensitive to macroeconomic changes performed particularly well, while traditionally defensive industry groups generally lagged market averages. Small- and midcap stocks typically gained more value, on average, than their larger, better established counterparts as investors looked forward to better business conditions for growing companies.