UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-04920

WASATCH FUNDS TRUST

(Exact name of registrant as specified in charter)

505 Wakara Way, 3rd Floor

Salt Lake City, UT 84108

(Address of principal executive offices)(Zip code)

| | |

| (Name and Address of Agent for Service) | | Copy to: |

| |

Samuel S. Stewart, Jr. Wasatch Advisors, Inc. 505 Wakara Way, 3rd Floor Salt Lake City, UT 84108 | | Eric F. Fess, Esq. Chapman & Cutler LLP 111 West Monroe Street Chicago, IL 60603 |

Registrant’s telephone number, including area code: (801) 533-0777

Date of fiscal year end: September 30

Date of reporting period: September 30, 2017

Item 1. Report to Shareholders.

2017 Annual Report September 30, 2017 Equity Funds / Wasatch Core Fund Wasatch Emerging India Fund Wasatch Emerging Markets Select Fund Wasatch Emerging Markets Small Cap Fund Wasatch Frontier Emerging Small Countries Fund Wasatch Global Opportunities Fund Wasatch International Growth Fund Wasatch International Opportunities Fund Wasatch Large Cap Value Fund Wasatch Long/Short Fund Wasatch Micro Cap Fund Wasatch Micro Cap Value Fund Wasatch Small Cap Growth Fund Wasatch Small Cap Value Fund Wasatch Strategic Income Fund Wasatch Ultra Growth Fund Wasatch World Innovators Fund Bond Funds / Wasatch-1st Source Income Fund Wasatch-Hoisington U.S. Treasury Fund

WASATCH FUNDS

Salt Lake City, Utah

www.WasatchFunds.com

800.551.1700

This material must be accompanied or preceded by a prospectus.

Please read the prospectus carefully before you invest.

Wasatch Funds are distributed by ALPS Distributors, Inc.

1

| | |

| LETTERTO SHAREHOLDERS — THE CALM AMIDSTTHE STORMS | | |

|

|

|

| | |

Samuel S. Stewart, Jr. PhD, CFA President of

Wasatch Funds | | DEAR FELLOW SHAREHOLDERS: Hurricane Harvey came first, pummeling Texas on August 25th. Less than two weeks later, Irma battered the Caribbean and Florida. Jose and Maria soon followed, again striking the Caribbean and disabling much of Puerto Rico’s infrastructure. In less than a month, four storms (two rated Category 4 and two Category 5) left a trail of destruction — estimated in the hundreds of billions of dollars — that will take months, if not years, to repair. Yet the financial markets hardly blinked. Hurricanes weren’t the only storms. There were political storms over health care, the debt ceiling, the National Football League and the Russia investigation. A storm of words raged between North Korea’s supreme leader Kim Jong Un and President Donald Trump. The belated announcement of a data breach at Equifax, potentially affecting nearly one of every two Americans, unleashed a storm of concern about cybersecurity. The Trump Twitter storm was unrelenting. And yet the markets hardly blinked. So far at least, regardless of the perils that have dominated the news day after day, the economy and markets have continued to advance. Truly, it’s been the calm amidst the storms. Which, of course, begs the question: Can it last? Or, from an investor’s point of view, might this be the calm before the storm in the |

financial markets?

As you know from my prior letters, I’ve been cautiously optimistic regarding the market. Generally speaking, financial markets take their cues from the economy. While investors have been quick to complain about the economy’s slow growth rate, it’s that very same measured pace that so far has prevented the economy from developing the excesses that typically lead to recessions and market declines.

With the current economic expansion now in its 100th month, the third-longest run since 1854, it’s important to note that recessions don’t occur in response to a timetable. Rather, they result from problems in the economy, of which there appear to be few.

I’m reluctant to go on record with a letter supporting the continuation of a bull market without also making an argument for the onset of a bear market. My bear-market argument depends on an unexpected event/catalyst, possibly geopolitical in nature. I’m not predicting such an event, and I’m surprised that one of the events cited above didn’t lead to a market correction. Even so, I still regard an event as the likely cause of the next bear market.

MARKETS

Many of my recent letters have commented that stocks — particularly in the U.S. — are expensive. However, I must admit that stocks aren’t as expensive if we consider the level of interest rates. After all, the inverse of the price/earnings (P/E) ratio (the price paid for $1 of earnings) is termed the earnings yield or the return in earnings for $1 of investment in a stock. The interest rate on a bond is the return in cash for $1 invested in the bond. While I won’t argue that the earnings yield on a stock and the interest rate on a bond are equivalent, they are related.

Going back 35 years when interest rates were in double-digit territory, P/E ratios for stocks were in single digits, with the result that the earnings yield on stocks was in double digits. In comparison, stocks today look quite expensive, with multiples close to three times what they were back then. However, that comparison overlooks the fact that bond rates are now only about one-fifth of what they were then, making bonds five times more expensive today than they were 35 years ago.

Avoiding much of the detail about what makes our economy today different from that of 35 years ago (and ignoring the risk premium stocks must offer for providing investors with earnings instead of cash), I could argue that stocks today are inexpensive relative to bonds. So if bonds aren’t overly expensive, then neither are stocks.

This might lead one to ask: Are bonds expensive? Relative to recent history, bonds in the U.S. seem expensive. Bond yields have generally fallen from double-digit territory into low single-digit territory. Ten-year U.S. Treasury bonds currently yield about 2.3%. However, German and Japanese government bonds of the same maturity yield less than 0.5%. Moreover, five-year government bonds in Germany and Japan have negative yields. So U.S. government bonds certainly aren’t expensive on a relative basis.

In a sign that interest rates overseas may remain low, some countries have been issuing 100-year bonds. Austria, for example, recently issued bonds that won’t mature until 2117 and that yield just 2.1%. Other recent issuers of 100-year bonds include Argentina, Ireland and Mexico. Purchased mainly by institutional investors to meet long-term pension and insurance obligations, these bonds indicate that slow economic growth around the world may constrain future investment returns. Why else would an institutional investor tie up money for so long? As for interest rates in the U.S., I have to wonder how much they can rise when rates are so low overseas.

Why are interest rates so low? At the heart of this question are cyclical vs. secular forces. If rates are low because the economy is weak, then the cyclical forces of our strengthening economy should drive rates higher. The fact that this has failed to happen suggests secular forces may be at play. For example, changing demographics may be weighing on interest rates. As people get older, they’re less likely to build new homes. Instead, they’re more likely to be downsizing. The primary concern of most older people is having adequate savings to support themselves in retirement. This global flood of savings is likely playing a major role in keeping interest rates low.

2

| | |

| | SEPTEMBER 30, 2017 (UNAUDITED) |

|

|

|

If in fact secular forces are keeping interest rates low, these forces may also be keeping stock prices high. So while valuations are stretched relative to earnings, they may not be as stretched relative to interest rates. For this reason and for the reasons discussed above, I remain cautiously optimistic that the economy and markets, both in the U.S. and abroad, will continue to advance at a slow pace overall.

WASATCH

While U.S. equities are generally more expensive, we’re often finding better valuations and/or greater headroom for growth overseas — both in developed markets and in emerging markets. Indeed, Japan is one of our largest investment allocations to an international developed market and India is one of our largest allocations to an emerging market.

We readily acknowledge that for many years — particularly in the 1990s and 2000s — Japan’s economy was mired in deflation, creating a difficult investment environment. For many investors, the perception remains that it’s tough to make money in Japan. Moreover, it’s true that the Japanese population is shrinking, the country’s overall economic growth is slow, and there’s not much inflation on the horizon. Nonetheless, we think that investors who look no further than these issues are missing out on significant opportunities.

Known as Abenomics, the economic policies introduced by Prime Minister Shinzo Abe in 2012 appear to be taking hold. Over the past few years, based on our investment team’s frequent visits to Japan, we’ve seen the positive results of these policies — from improvements in corporate governance to efforts addressing the country’s labor shortage.

Because Japan is a global leader in innovation, it’s no surprise the country has a vibrant market for small-cap stocks. This indicates Japan has created an entrepreneurial environment that favors investment. Unlike in much of the developed world, there are fewer dominant industry players in Japan. That’s beginning to change, however, and we’re investing in companies that we believe can consolidate their industries and gain market share from competitors.

After investing in the country for over a decade, the members of our investment team are more excited than ever about the investment opportunities they’re finding in India. With its democratic government and strong institutions, India has avoided much of the political turmoil, massive borrowing, debt defaults and runaway inflation that have plagued other emerging-market countries over the past 30 years. India’s population of greater than 1.3 billion is among the youngest in the world. In addition, the country’s growing middle class, increasing urbanization and rapid household formation are driving domestic consumer demand. Moreover, reforms introduced by Prime Minister Narendra Modi are designed to further the country’s growth and development.

With sincere thanks for your continued investment and for your trust,

Sam Stewart

Information in this document regarding market or economic trends, or the factors influencing historical or future performance, reflects the opinions of management as of the date of this document. These statements should not be relied upon for any other purpose. Past performance is no guarantee of future results, and there is no guarantee that the market forecasts discussed will be realized.

CFA® is a trademark owned by CFA Institute.

Wasatch Advisors is the investment advisor to Wasatch Funds.

Wasatch Funds are distributed by ALPS Distributors, Inc. (ADI). ADI is not affiliated with Wasatch Advisors or Wasatch Funds.

Abenomics refers to the economic policies advocated by Japanese Prime Minister Shinzo Abe after his December 2012 re-election to the post he last held in 2007. His aim was to revive the sluggish economy with “three arrows” — a massive fiscal stimulus, more aggressive monetary easing from the Bank of Japan, and structural reforms to boost Japan’s competitiveness.

A bull market is defined as a prolonged period in which investment prices rise faster than their historical average. Bull markets can happen as the result of an economic recovery, an economic boom, or investor psychology.

A bear market is generally defined as a drop of 20% or more in stock prices over at least a two-month period. Bears are investors who are pessimistic with regard to the stock market’s prospects.

The price/earnings (P/E) ratio, also known as the P/E multiple, is the price of a stock divided by its earnings per share.

Valuation is the process of determining the current worth of an asset or company.

3

| | |

| WASATCH CORE GROWTH FUND (WGROX / WIGRX) | | SEPTEMBER 30, 2017 (UNAUDITED) |

|

|

|

Management Discussion

The Wasatch Core Growth Fund is managed by a team of Wasatch portfolio managers led by JB Taylor, Paul Lambert and Mike Valentine.

| | | | |

JB Taylor Lead Portfolio Manager | |

Paul Lambert Portfolio Manager | |

Mike Valentine Portfolio Manager |

OVERVIEW

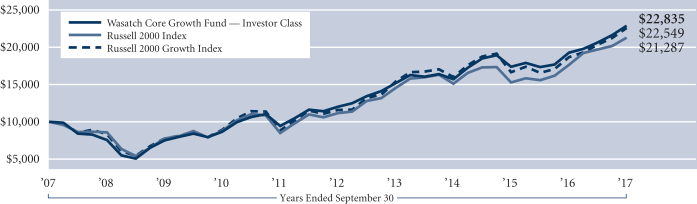

The Wasatch Core Growth Fund — Investor Class gained 18.69% for the 12 months ended September 30, 2017, lagging the 20.74% return of its benchmark, the Russell 2000 Index, and the 20.98% return of the Russell 2000 Growth Index.

The industrials and consumer-discretionary sectors were two of the strongest contributors to the Fund’s return during the 12-month period, outperforming the benchmark driven by stock selection. In addition, the Fund’s investments in the financials sector contributed significantly to results for the period.

The Fund’s strong showing in the industrials sector, particularly for the three months ended September 30, 2017, was also aided by an overweight position relative to the benchmark. Unlike the post-election “reflation trade” (or “Trump trade”) of the kind we avoided late last year, we recognize that the slow-growth economy is chugging along well enough now to favor a positive turn for the sector, which we believe bodes well for our industrial holdings.

DETAILSOFTHE YEAR

ICON plc, a global contract research organization providing drug development and other services to the pharmaceutical, biotechnology and medical-device industries, was a top contributor to the Fund’s performance for the 12-month period. ICON’s most-recent quarterly financial results were reported in July and showed an increase in net income of 10.7% and a rise in earnings per share of 14.9% compared to the same quarter a year ago. Given the company’s strong backlog of business, we believe ICON can continue to do well.

Another top contributor was online retailer Wayfair, Inc. Wayfair’s stock leapt higher as the company reported strong growth throughout the year. Wayfair’s growth stands in contrast to many traditional retailers that are experiencing a slowdown in business to the point of having to close stores. In fact, more retail store closings have been announced so far in the 2017 calendar year than in all of the previous year. We continue to like Wayfair’s ongoing growth prospects —

namely its focus on expanding share in the online marketplace for home furnishings.

Cornerstone OnDemand, Inc. was the leading detractor from the Fund’s performance for the fiscal year. Despite showing signs of strength midway through the period, management eventually reported numbers that didn’t wow investors, missing expectations on earnings even while reporting stronger sales. In addition, we viewed the company’s mix of new contracts as far from ideal. We see little room for error on management’s part at this point and so we sold our position.

Another leading detractor was MEDNAX, Inc., which struggled over the past several months. MEDNAX operates neonatal intensive care units (NICUs) in partnership with health-care organizations. The company’s net revenue for its most-recently reported quarter increased 9.2% driven largely by contributions from acquisitions completed since April 2016. While management said that operating results for the company’s second quarter were mostly in line with their expectations, trends remained challenging. Overall same-unit revenue fell 0.9% year-over-year due primarily to a decline in the number of days infants spent in NICUs and an increase in services reimbursed through government programs. We have chosen to monitor the challenges MEDNAX faces from the sidelines and have sold our position.

OUTLOOK

The economic scenario of the past year appears to be continuing in the U.S. with regard to sustained moderate growth, low inflation and rising asset prices. Looking forward, we don’t expect valuation tailwinds to continue. Company fundamentals will have to matter more to investors at some point, which we believe would bode well for the Fund. We believe we have a great team that learns from mistakes and the best culture for applying a disciplined investment approach. As valuations right-size to growth rates, we think our discipline will shine.

Fundamentals are certainly of more central importance to investors now than in the period after the presidential election, but there are distractions such as the extraordinary monetary accommodation by the Federal Reserve (Fed). Recently, the Fed announced its intention to start reducing bond holdings acquired during its quantitative-easing program. While it’s not exactly clear how quickly that will unfold, the announcement itself represents a step toward normalcy.

In the Fund, we’re especially focused at present on companies that seem poised to deliver long-term growth by benefiting from world-wide economic strength, industrial-production trends and increased capital expenditure by businesses. Our disciplined approach continues to turn up attractive prospects, such as in the industrials sector mentioned above. Elsewhere, too, we’re finding what we consider to be high-quality companies with outstanding long-term growth prospects. There’s no shortage of opportunities for the Fund’s investment style, although we always have to remain vigilant regarding valuations.

Thank you for the opportunity to manage your assets.

| | Current and future holdings are subject to risk. |

4

| | |

| WASATCH CORE GROWTH FUND (WGROX / WIGRX) | | SEPTEMBER 30, 2017 (UNAUDITED) |

|

|

|

Portfolio Summary

AVERAGE ANNUAL TOTAL RETURNS

| | | | | | | | | | | | | | | |

| | | 1 YEAR | | 5 YEARS | | 10 YEARS |

Core Growth (WGROX) — Investor | | | | 18.69% | | | | | 13.77% | | | | | 8.61% | |

Core Growth (WIGRX) — Institutional | | | | 18.87% | | | | | 13.88% | | | | | 8.67% | |

Russell 2000® Index | | | | 20.74% | | | | | 13.79% | | | | | 7.85% | |

Russell 2000® Growth Index | | | | 20.98% | | | | | 14.28% | | | | | 8.47% | |

Data shows past performance, which is not indicative of future performance. Current performance may be lower or higher than the performance quoted. To obtain the most recent month-end performance data available, please visit www.WasatchFunds.com. The Advisor may absorb certain Fund expenses, without which total return would have been lower. Investment returns and principal value will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

As of the September 1, 2017 prospectus, the Total Annual Fund Operating Expenses for the Wasatch Core Growth Fund are Investor Class: 1.21% / Institutional Class — Gross: 1.09%, Net: 1.05%. The expense ratio shown elsewhere in this report may be different. Net expenses are based on Fund expenses, net of waivers and reimbursements. See the prospectus for additional information regarding Fund expenses.

Wasatch Funds will deduct a 2.00% redemption proceeds fee on Fund shares held 60 days or less. Performance data does not reflect the deduction of fees, including sales charges, or the taxes you would pay on fund distributions or the redemption of fund shares. Fees and taxes, if reflected, would reduce the performance quoted. Wasatch does not charge any sales fees. For more complete information including charges, risks and expenses, read the prospectus carefully.

Performance for the Institutional Class prior to 1/31/2012 is based on the performance of the Investor Class. Performance of the Fund’s Institutional Class prior to 1/31/2012 uses the actual expenses of the Fund’s Investor Class without any adjustments. For any such period of time, the performance of the Fund’s Institutional Class would have been substantially similar to, yet higher than, the performance of the Fund’s Investor Class, because the shares of both classes are invested in the same portfolio of securities, but the classes bear different expenses.

Investing in small cap funds will be more volatile and loss of principal could be greater than investing in large cap or more diversified funds. Investing in foreign securities, especially in emerging markets, entails special risks, such as currency fluctuations and political uncertainties, which are described in more detail in the prospectus.

TOP 10 EQUITY HOLDINGS*

| | | | |

| Company | | % of Net

Assets | |

| ICON plc (Ireland) | | | 3.2% | |

| Copart, Inc. | | | 3.1% | |

| Old Dominion Freight Line, Inc. | | | 2.6% | |

| Trex Co., Inc. | | | 2.6% | |

| Eagle Bancorp, Inc. | | | 2.5% | |

| | | | |

| Company | | % of Net

Assets | |

| Cimpress N.V. | | | 2.4% | |

| Tyler Technologies, Inc. | | | 2.4% | |

| Balchem Corp. | | | 2.4% | |

| Texas Capital Bancshares, Inc. | | | 2.4% | |

| Euronet Worldwide, Inc. | | | 2.3% | |

| * | As of September 30, 2017, there were 60 holdings in the Fund. Foreign currency contracts, written options and repurchase agreements, if any, are not included in the number of holdings. Portfolio holdings are subject to change at any time. References to specific securities should not be construed as recommendations by the Funds or their Advisor. Current and future holdings are subject to risk. |

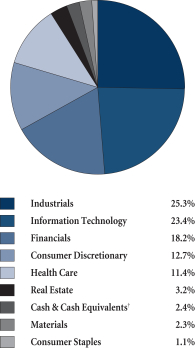

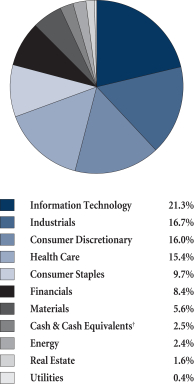

SECTOR BREAKDOWN**

| ** | Excludes securities sold short and options written, if any. |

| † | Also includes Other Assets & Liabilities. |

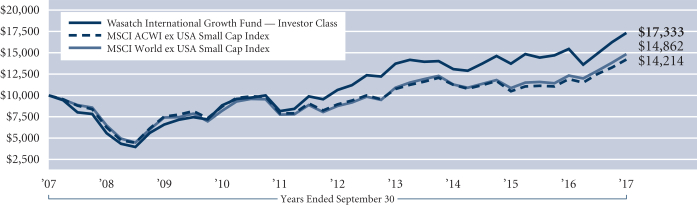

GROWTHOFA HYPOTHETICAL $10,000 INVESTMENT

Past performance does not predict future performance. The graph above does not reflect the deduction of fees, sales charges, or taxes that you would pay on fund distributions or the redemption of fund shares. Wasatch does not charge any sales fees. The Russell 2000 Index is an unmanaged total return index of the smallest 2,000 companies in the Russell 3000 Index, as ranked by total market capitalization. The Russell 2000 Index is widely regarded in the industry as accurately capturing the universe of small company stocks. The Russell 2000 Growth Index is an unmanaged total return index that measures the performance of those Russell 2000 Index companies with higher price-to-book ratios and higher forecasted growth values. You cannot invest directly in these or any indexes.

5

| | |

| WASATCH EMERGING INDIA FUND (WAINX / WIINX) | | SEPTEMBER 30, 2017 (UNAUDITED) |

|

|

|

Management Discussion

The Wasatch Emerging India Fund is managed by a team of Wasatch portfolio managers led by Ajay Krishnan and Matthew Dreith.

| | | | |

Ajay Krishnan, CFA Lead Portfolio Manager | |

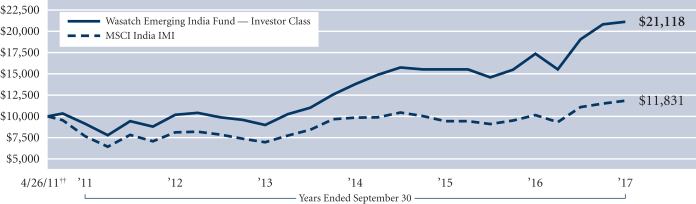

Matthew Dreith, CFA Associate Portfolio Manager | | OVERVIEW The Wasatch Emerging India Fund — Investor Class returned 21.65% during what was an eventful 12 months ended September 30, 2017. The Fund outpaced its benchmark, the |

MSCI India Investable Market Index (IMI), which rose 16.58%.

Soon after the fiscal year’s outset, Prime Minister Narendra Modi rattled investors by banning large-denomination banknotes from circulation in a surprise move designed to root out unaccounted wealth. Though the demonetization initiative fell short of its stated goals, it came to be viewed by many Indians as a victory for the common citizen over corrupt interests. Mr. Modi’s Bharatiya Janata Party (BJP) reaped the benefits in March when it scored landslide gains in elections to the state assembly of Uttar Pradesh, India’s most-populous province. The decisive win left Mr. Modi unchallenged as a national leader and raised optimism for additional reforms aimed at furthering India’s growth and development.

Those hopes were realized in July with the long-awaited replacement of India’s complex jumble of federal, state and interstate taxes. The newly implemented goods-and-services tax (GST) soon began speeding up the flow of goods throughout India by eliminating time-consuming stops at various checkpoints. By easing the burden of double taxation, streamlining compliance and eliminating other inefficiencies, GST is expected to lower the cost of doing business in India.

Fueled in part by an influx of banned currency into the country’s financial system, Indian stock prices rose for most of the past 12 months. The Modi government’s success at advancing its legislative agenda, meanwhile, attracted significant purchases from overseas investors. Trading was choppy during the final two months of the period, as heavy flooding and disruptions related to demonetization and GST appeared to weigh on India’s economy. According to an official report released in late August, India’s year-over-year gross-domestic-product (GDP) growth slowed to 5.7% during the April-to-June quarter from 6.1% growth during the previous quarter.

DETAILSOFTHE YEAR

Performance in the Fund was driven mainly by outsized gains in its consumer and financial stocks. Very low exposure to the poor-performing information-technology sector was another reason the Fund surpassed its benchmark by as much as it did. Underperformance in the materials sector

and lack of exposure to the strong energy sector were the Fund’s primary sources of weakness against the benchmark.

The strongest contributor to Fund performance for the year was Avenue Supermarts Ltd., which benefited from rising profits. The company operates a chain of supermarkets that offer items ranging from food to apparel and general merchandise. With retail distribution in India still largely dominated by small neighborhood stores called kiranas, we think opportunities abound for well-managed operators such as Avenue to formalize their industries and reap significant economies of scale.

Bajaj Finance Ltd. was the second-best contributor. A non-bank financial company, Bajaj offers a broad spectrum of lending services. The company’s stock price reached a 52-week high in September after its qualified institutional placement of equity shares was well-received by investors. Bajaj Finance has also profited from robust demand for credit.

The greatest detractor from Fund performance for the year was Divi’s Laboratories Ltd., a manufacturer of active pharmaceutical ingredients and intermediates. Shares of Divi’s tumbled after management announced that the U.S. Food and Drug Administration had issued an import alert for products manufactured at its Unit II facility in Visakhapatnam, Andhra Pradesh. Paring earlier losses, however, the stock rose sharply when the plant was reinspected in September. We increased the Fund’s position in Divi’s based on our positive assessment of its long-term prospects.

Second-largest detractor Amara Raja Batteries Ltd. makes lead-acid storage batteries for industrial and automotive applications. The company’s shares languished for most of the year as higher prices for lead impacted earnings. Looking forward, we think Amara Raja’s price increases will improve profit margins across its various business segments.

OUTLOOK

We don’t believe the disappointing GDP growth reported near the end of the period is anything to be overly concerned about and certainly don’t believe it signals a prolonged deceleration of India’s economy. We had been expecting India’s economic growth to slow for a few quarters as companies reduced inventories ahead of the July 1st rollout of GST. So, it’s not surprising to see a moderate downtick in growth during the quarter leading up to the GST launch date.

Much has been written about the likely impact on India and other emerging markets as central banks in developed countries prepare to unwind their quantitative-easing programs. Here again, we expect the effects to be limited and short-lived. Current circumstances are very different from 2013, when the prospect of U.S. monetary tightening chased investors out of higher-yielding emerging-market currencies. Recently, in fact, India’s central bank has struggled at times to prevent vast inflows of foreign capital from causing the rupee to appreciate too rapidly.

Longer term, we believe India’s improved political climate will underpin investor confidence as recent reforms work their way through the economy.

Thank you for the opportunity to manage your assets.

| | Current and future holdings are subject to risk. |

6

| | |

| WASATCH EMERGING INDIA FUND (WAINX / WIINX) | | SEPTEMBER 30, 2017 (UNAUDITED) |

|

|

|

Portfolio Summary

AVERAGE ANNUAL TOTAL RETURNS

| | | | | | | | | | | | | | | |

| | | 1 YEAR | | 5 YEARS | | SINCE INCEPTION

4/26/11 |

Emerging India (WAINX) — Investor | | | | 21.65% | | | | | 15.68% | | | | | 12.32% | |

Emerging India (WIINX) — Institutional | | | | 21.89% | | | | | 15.79% | | | | | 12.41% | |

MSCI India IMI | | | | 16.58% | | | | | 7.81% | | | | | 2.65% | |

Data shows past performance, which is not indicative of future performance. Current performance may be lower or higher than the performance quoted. To obtain the most recent month-end performance data available, please visit www.WasatchFunds.com. The Advisor may absorb certain Fund expenses, without which total return would have been lower. Investment returns and principal value will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

As of the September 1, 2017 prospectus, the Total Annual Fund Operating Expenses for the Wasatch Emerging India Fund are Investor Class — Gross: 1.87%, Net: 1.75% / Institutional Class — Gross: 2.00%, Net: 1.50%. The expense ratio shown elsewhere in this report may be different. Net expenses are based on Fund expenses, net of waivers and reimbursements. See the prospectus for additional information regarding Fund expenses.

Wasatch Funds will deduct a 2.00% redemption proceeds fee on Fund shares held 60 days or less. Performance data does not reflect the deduction of fees, including sales charges, or the taxes you would pay on fund distributions or the redemption of fund shares. Fees and taxes, if reflected, would reduce the performance quoted. Wasatch does not charge any sales fees. For more complete information including charges, risks and expenses, read the prospectus carefully.

Performance for the Institutional Class prior to 2/1/2016 is based on the performance of the Investor Class. Performance of the Fund’s Institutional Class prior to 2/1/2016 uses the actual expenses of the Fund’s Investor Class without any adjustments. For any such period of time, the performance of the Fund’s Institutional Class would have been substantially similar to, yet higher than, the performance of the Fund’s Investor Class, because the shares of both classes are invested in the same portfolio of securities, but the classes bear different expenses.

Investing in small cap funds will be more volatile and loss of principal could be greater than investing in large cap or more diversified funds. Investing in foreign securities, especially in emerging markets, entails special risks, such as unstable currencies, highly volatile securities markets and political and social instability, which are described in more detail in the prospectus.

TOP 10 EQUITY HOLDINGS*

| | | | |

| Company | | % of Net

Assets | |

| Bajaj Finance Ltd. (India) | | | 5.7% | |

| HDFC Bank Ltd. ADR (India) | | | 5.0% | |

| Housing Development Finance Corp. Ltd. (India) | | | 4.8% | |

| Avenue Supermarts Ltd. (India) | | | 4.7% | |

| MakeMyTrip Ltd. (India) | | | 3.7% | |

| | | | |

| Company | | % of Net

Assets | |

| AU Small Finance Bank Ltd. (India) | | | 3.6% | |

| Divi’s Laboratories Ltd. (India) | | | 3.4% | |

| Endurance Technologies Ltd. (India) | | | 3.0% | |

| Quess Corp. Ltd. (India) | | | 3.0% | |

| V-Mart Retail Ltd. (India) | | | 2.9% | |

| * | As of September 30, 2017, there were 53 holdings in the Fund. Foreign currency contracts, written options and repurchase agreements, if any, are not included in the number of holdings. Portfolio holdings are subject to change at any time. References to specific securities should not be construed as recommendations by the Funds or their Advisor. Current and future holdings are subject to risk. |

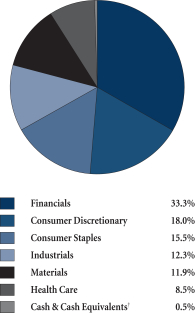

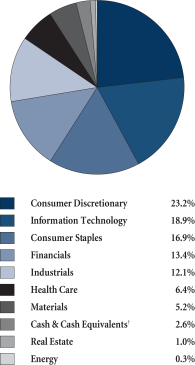

SECTOR BREAKDOWN**

| ** | Excludes securities sold short and options written, if any. |

| † | Also includes Other Assets & Liabilities. |

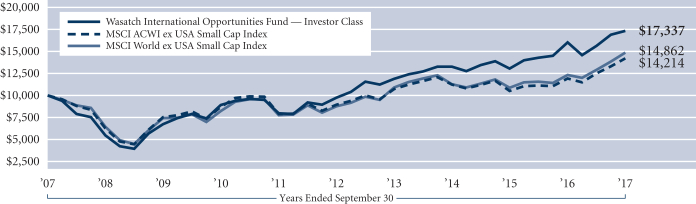

GROWTHOFA HYPOTHETICAL $10,000 INVESTMENT

Past performance does not predict future performance. The graph above does not reflect the deduction of fees, sales charges, or taxes that you would pay on fund distributions or the redemption of fund shares. Wasatch does not charge any sales fees. ††Inception: April 26, 2011. The MSCI India IMI (Investable Market Index) is designed to measure the performance of the large-, mid- and small-cap segments of the Indian market. The Index covers approximately 99% of the free-float adjusted market capitalization of the Indian equity universe. You cannot invest directly in this or any index.

7

| | |

| WASATCH EMERGING MARKETS SELECT FUND (WAESX / WIESX) | | SEPTEMBER 30, 2017 (UNAUDITED) |

|

|

|

Management Discussion

The Wasatch Emerging Markets Select Fund is managed by a team of Wasatch portfolio managers led by Ajay Krishnan, Roger Edgley and Scott Thomas.

| | | | |

Ajay Krishnan, CFA Lead Portfolio Manager | |

Roger Edgley, CFA Portfolio Manager | |

Scott Thomas, CFA Associate Portfolio

Manager |

OVERVIEW

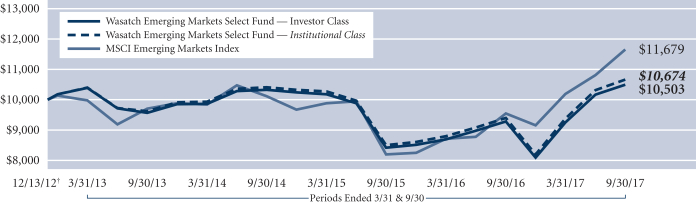

Rich valuations in developed countries and improving fundamentals across a number of emerging economies helped push emerging-market equities higher during the 12 months ended September 30, 2017. The Wasatch Emerging Markets Select Fund — Investor Class returned 13.33% during the period. Outpacing the Fund, the benchmark MSCI Emerging Markets Index rose 22.46%.

Initial strength in the U.S. dollar gave way to a sustained slide that underpinned support for emerging markets for most of the fiscal year. Against a basket of major rivals, the greenback slipped -2.5% during the period. By making assets in other currencies more appealing to international investors, a weaker dollar encourages financial flows into developing nations. In so doing, the weak dollar has loosened global financial conditions by making it easier for governments and companies outside the U.S. to issue securities.

Korea was the largest among several sources of Fund underperformance. Markets reacted negatively when China clamped down on tourism to Korea in retaliation for its deployment of the United States’ Terminal High Altitude Area Defense (THAAD) anti-missile defense system. As investors sought the perceived safety of larger Korean companies, small and mid-cap stocks — such as those held in the Fund — were hurt the most.

The Fund’s substantial weighting in Mexican stocks also impacted performance as equity returns in Mexico lagged stronger gains in other countries. Although the Fund’s Mexican holdings posted a healthy double-digit return, they underperformed the benchmark’s Mexican component.

Bright spots for the Fund included South Africa and the United Arab Emirates, two countries in which the Fund handily outgained its benchmark. Though our underweight exposure to China was a headwind to Fund performance, we significantly increased the Fund’s investments in China as the year progressed.

DETAILSOFTHE YEAR

The strongest contributor to Fund performance for the year was Bajaj Finance Ltd. An Indian non-bank financial company, Bajaj offers a broad spectrum of lending services.

The company’s stock price reached a 52-week high in September after its qualified institutional placement of equity shares was well-received by investors.

The Fund’s second-largest contributor was MercadoLibre, Inc., a Latin American e-commerce company that generates approximately half its sales in Brazil. Originally a provider of auction-type platforms that connect buyers with sellers, MercadoLibre has been increasing its fulfillment capabilities.

Key additions to the Fund included Alibaba Group Holding Ltd. and Tencent Holdings Ltd., two Chinese companies increasingly viewed by international investors as proxies for China’s growing middle class.

The greatest detractor from Fund performance for the year was Divi’s Laboratories Ltd., an Indian manufacturer of active pharmaceutical ingredients and intermediates. Shares of Divi’s tumbled after it announced that the U.S. Food and Drug Administration had issued an import alert for products manufactured at its Unit II facility in Visakhapatnam, Andhra Pradesh. We sold the stock to seek better opportunities elsewhere.

Second-largest detractor GT Capital Holdings, Inc. is based in the Philippines. GT Capital’s interests include lending, car distribution and insurance. The company’s stock came under pressure amid mounting fears that the Duterte government’s overhaul of the country’s vehicle excise tax would depress sales of automobiles. With the stock languishing and sentiment continuing to deteriorate, we moved on.

OUTLOOK

Much has been written about the likely implications for emerging markets as central banks in developed countries prepare to unwind their quantitative-easing programs. For our part, we expect any negative effects to be limited and short-lived. Current circumstances are very different from 2013, when the prospect of U.S. monetary tightening chased investors out of higher-yielding emerging-market currencies. Today, fiscal and current-account balances in most countries are stronger, foreign-exchange reserves are generally higher, and investor sentiment is better.

During the period from December 31, 2015 through September 30, 2017 the Fund returned approximately 24%, while the MSCI Emerging Markets Index climbed about 43% on a total-return basis. Despite its recent strong run, the Index has been essentially flat since its peak in the fall of 2007, and price-to-book ratios in most emerging markets remain below their long-term averages.

Moreover, greater than one-fourth of the 43% move in the Index over the past seven quarters was delivered by just four mega-cap information-technology stocks. We believe large-cap outperformance on that scale is unsustainable, and future gains are likely to be more broadly based. With economic fundamentals in countries such as Mexico, India, Brazil and Russia stabilizing or improving, we think stocks of well-situated small and mid-size companies in emerging markets may begin to close the gap in recent performance compared to larger peers.

Thank you for the opportunity to manage your assets.

| | Current and future holdings are subject to risk. |

8

| | |

| WASATCH EMERGING MARKETS SELECT FUND (WAESX / WIESX) | | SEPTEMBER 30, 2017 (UNAUDITED) |

|

|

|

Portfolio Summary

AVERAGE ANNUAL TOTAL RETURNS

| | | | | | | | | | | | | | | |

| | | 1 YEAR | | 5 YEARS | | SINCE INCEPTION 12/13/12 |

Emerging Markets Select (WAESX) — Investor | | | | 13.33% | | | N/A | | | | 1.03% | |

Emerging Markets Select (WIESX) — Institutional | | | | 13.73% | | | N/A | | | | 1.37% | |

MSCI Emerging Markets Index | | | | 22.46% | | | N/A | | | | 3.29% | |

Data shows past performance, which is not indicative of future performance. Current performance may be lower or higher than the performance quoted. To obtain the most recent month-end performance data available, please visit www.WasatchFunds.com. The Advisor may absorb certain Fund expenses, without which total return would have been lower. Investment returns and principal value will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

As of the September 1, 2017 prospectus, the Total Annual Fund Operating Expenses for the Wasatch Emerging Markets Select Fund are Investor Class — Gross: 1.88%, Net: 1.51% / Institutional Class — Gross: 1.52%, Net: 1.21%. The expense ratio shown elsewhere in this report may be different. Net expenses are based on Fund expenses, net of waivers and reimbursements. See the prospectus for additional information regarding Fund expenses.

Wasatch Funds will deduct a 2.00% redemption proceeds fee on Fund shares held 60 days or less. Performance data does not reflect the deduction of fees, including sales charges, or the taxes you would pay on fund distributions or the redemption of fund shares. Fees and taxes, if reflected, would reduce the performance quoted. Wasatch does not charge any sales fees. For more complete information including charges, risks and expenses, read the prospectus carefully.

Investing in foreign securities, especially in emerging markets, entails special risks, such as currency fluctuations and political uncertainties, which are described in more detail in the prospectus. Investing in small cap funds will be more volatile and loss of principal could be greater than investing in large cap or more diversified funds.

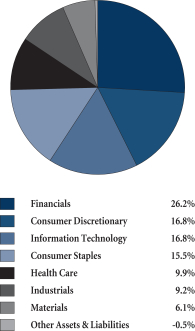

TOP 10 EQUITY HOLDINGS*

| | | | |

| Company | | % of Net

Assets | |

| Bajaj Finance Ltd. (India) | | | 5.9% | |

| Alibaba Group Holding Ltd. ADR (China) | | | 5.9% | |

| MercadoLibre, Inc. (Brazil) | | | 5.8% | |

| Tencent Holdings Ltd. (China) | | | 5.1% | |

| Ctrip.com International Ltd. ADR (China) | | | 4.6% | |

| | | | |

| Company | | % of Net

Assets | |

| NMC Health plc (United Arab Emirates) | | | 4.5% | |

| Medytox, Inc. (Korea) | | | 4.4% | |

| Raia Drogasil S.A. (Brazil) | | | 4.4% | |

| Naspers Ltd., Class N (South Africa) | | | 3.8% | |

| BGF Retail Co. Ltd. (Korea) | | | 3.5% | |

| * | As of September 30, 2017, there were 37 holdings in the Fund. Foreign currency contracts, written options and repurchase agreements, if any, are not included in the number of holdings. Portfolio holdings are subject to change at any time. References to specific securities should not be construed as recommendations by the Funds or their Advisor. Current and future holdings are subject to risk. |

SECTOR BREAKDOWN**

| ** | Excludes securities sold short and options written, if any. |

GROWTHOFA HYPOTHETICAL $10,000 INVESTMENT

Past performance does not predict future performance. The graph above does not reflect the deduction of fees, sales charges, or taxes that you would pay on fund distributions or the redemption of fund shares. Wasatch does not charge any sales fees. †Inception: December 13, 2012. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index designed to measure the equity market performance of emerging markets. You cannot invest directly in this or any index.

9

| | |

| WASATCH EMERGING MARKETS SMALL CAP FUND (WAEMX / WIEMX) | | SEPTEMBER 30, 2017 (UNAUDITED) |

|

|

|

Management Discussion

The Wasatch Emerging Markets Small Cap Fund is managed by a team of Wasatch portfolio managers led by Roger Edgley, Andrey Kutuzov and Scott Thomas.

| | | | |

Roger Edgley, CFA Lead Portfolio Manager | |

Andrey Kutuzov, CFA Associate Portfolio Manager | |

Scott Thomas, CFA Associate Portfolio Manager |

OVERVIEW

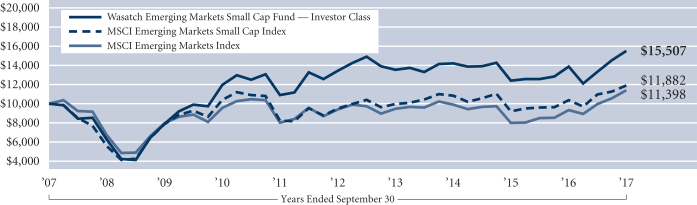

The Wasatch Emerging Markets Small Cap Fund — Investor Class gained 11.99% for the 12 months ended September 30, 2017 and underperformed the benchmark MSCI Emerging Markets Small Cap Index, which returned 14.89%.

Strong country fundamentals, firming commodity prices and a sagging U.S. dollar underpinned stock markets in developing nations for most of the 12-month period. Emerging markets continued to perform well based on optimism over economic growth and returning investment. Emerging-market currencies appear to have stabilized and are more competitive, current-account balances have improved for the majority of emerging markets and company valuations are still below their long-term averages.

Over the course of the period, we became more constructive on China and increased the Fund’s weight. China was the Fund’s top-contributing country for the 12 months. However, we recognize that challenges unique to the Chinese market remain. As a result, the Fund’s is underweight versus the benchmark in China. One holding in the United Arab Emirates (UAE) drove that country’s outperformance of its benchmark peer. Brazil was also a top-contributing country driven by one of our newer holdings.

The Fund’s substantial exposure to India hurt performance during the period. Indian stocks lost ground after soft economic data appeared to spook international investors. Largely the side effect of recent reforms, the slowdown in our view is short-term in nature. One of these reforms was the long-awaited replacement of India’s previous complex array of federal, state and interstate taxes with a nationwide goods-and-services tax (GST). Initial confusion over certain compliance issues has offset some of GST’s benefits in the short term, especially for small businesses. We think growth in India will pick up again once the reforms have worked their way through the country’s economy. Taiwan was also a significant detractor due primarily to company-specific factors. In Mexico, a significant overweight relative to the benchmark hindered the Fund’s results.

DETAILSOFTHE YEAR

The Fund’s top contributor for the period came from China. Sunny Optical Technology Group Co. Ltd., whose stock is listed in Hong Kong, designs and manufactures optical-related products. Sunny Optical continues to gain business in high-end product lines like multi-cameras in smartphones and cars.

The Fund’s second-best contributor was Magazine Luiza S.A., which operates consumer-electronics stores in Brazil. The company has put in place strong information-technology infrastructure to make the business an e-commerce player using its stores as showrooms and mini distribution centers. In Brazil, we believe the fundamentals of the country are improving as interest rates are coming down, inflation is decreasing, and the current-account situation has improved. Further, company earnings are improving after two years of decline. We are confident in the Fund’s positioning in Brazil.

The third-best contributor was NMC Health plc, the largest private health-care provider in the UAE. Health care has been an investment theme in the Fund, as emerging markets seek to build out their health-care infrastructure. NMC has been benefiting from new insurance rules that remove or reduce certain copayments and restrictions for holders of the UAE’s Thiqa medical-insurance card.

Several holdings in Taiwan were among the Fund’s largest detractors for the year. We sold our positions in PChome Online, Inc., a Chinese language internet company that offers e-commerce, advertising and portal services along with digital content, and Tung Thih Electronic Co. Ltd., which sells sensors to auto manufacturers. PChome was sold due to earnings weakness as we saw better opportunities elsewhere. We sold our shares of Tung Thih as the company’s core products faced increased competition and it was becoming less clear how Tung Thih’s new products would offset the slowing growth of core products. Poya International Co. Ltd. operates retail stores selling cosmetics, fashion accessories and groceries. Poya’s stock was down due to negative same-store-sales growth numbers. In our estimation, Poya is a high-quality business, as demonstrated by stable growth, cash generation and margin expansion.

OUTLOOK

We remain positive on the investment outlook for a majority of the emerging markets in our universe, and we are confident in the Fund’s positioning. In fact, we have been struggling to make space for the attractive new investments we have been finding. Emerging-market macro environments continue to improve, and we are finding numerous growth companies that we consider high quality with outstanding investment potential.

Wasatch is confident on the outlook for emerging markets. We see increasing innovation and significant improvement in the earnings of our portfolio companies and ongoing and sustainable economic development of emerging economies. We think these factors are likely to provide tailwinds for equities of well-positioned, high-quality businesses.

We thank you for the opportunity to manage your assets.

| | Current and future holdings are subject to risk. |

10

| | |

| WASATCH EMERGING MARKETS SMALL CAP FUND (WAEMX / WIEMX) | | SEPTEMBER 30, 2017 (UNAUDITED) |

|

|

|

Portfolio Summary

AVERAGE ANNUAL TOTAL RETURNS

| | | | | | | | | | | | | | | |

| | | 1 YEAR | | 5 YEARS | | 10 YEARS |

Emerging Markets Small Cap (WAEMX) — Investor | | | | 11.99% | | | | | 2.95% | | | | | 4.49% | |

Emerging Markets Small Cap (WIEMX) — Institutional | | | | 12.36% | | | | | 3.01% | | | | | 4.52% | |

MSCI Emerging Markets Small Cap Index | | | | 14.89% | | | | | 4.60% | | | | | 1.74% | |

MSCI Emerging Markets Index | | | | 22.46% | | | | | 3.99% | | | | | 1.32% | |

Data shows past performance, which is not indicative of future performance. Current performance may be lower or higher than the performance quoted. To obtain the most recent month-end performance data available, please visit www.WasatchFunds.com. The Advisor may absorb certain Fund expenses, without which total return would have been lower. Investment returns and principal value will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

As of the September 1, 2017 prospectus, the Total Annual Fund Operating Expenses for the Wasatch Emerging Markets Small Cap Fund are Investor Class: 1.96% / Institutional Class: 1.81%. The expense ratio shown elsewhere in this report may be different. See the prospectus for additional information regarding Fund expenses.

Wasatch Funds will deduct a 2.00% redemption proceeds fee on Fund shares held 60 days or less. Performance data does not reflect the deduction of fees, including sales charges, or the taxes you would pay on fund distributions or the redemption of fund shares. Fees and taxes, if reflected, would reduce the performance quoted. Wasatch does not charge any sales fees. For more complete information including charges, risks and expenses, read the prospectus carefully.

Performance for the Institutional Class prior to 2/1/2016 is based on the performance of the Investor Class. Performance of the Fund’s Institutional Class prior to 2/1/2016 uses the actual expenses of the Fund’s Investor Class without any adjustments. For any such period of time, the performance of the Fund’s Institutional Class would have been substantially similar to, yet higher than, the performance of the Fund’s Investor Class, because the shares of both classes are invested in the same portfolio of securities, but the classes bear different expenses.

Investing in foreign securities, especially in emerging markets, entails special risks, such as currency fluctuations and political uncertainties, which are described in more detail in the prospectus. Investing in small cap funds will be more volatile and loss of principal could be greater than investing in large cap or more diversified funds.

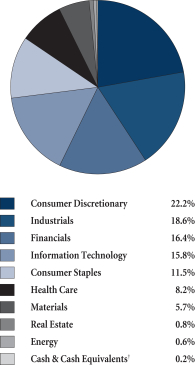

TOP 10 EQUITY HOLDINGS*

| | | | |

| Company | | % of Net

Assets | |

| Magazine Luiza S.A. (Brazil) | | | 3.1% | |

| Sunny Optical Technology Group Co. Ltd. (China) | | | 2.7% | |

| 51job, Inc. ADR (China) | | | 2.6% | |

| China Yongda Automobiles Services Holdings Ltd. (China) | | | 2.4% | |

| Clicks Group Ltd. (South Africa) | | | 2.4% | |

| | | | |

| Company | | % of Net

Assets | |

| Medytox, Inc. (Korea) | | | 2.2% | |

| ASPEED Technology, Inc. (Taiwan) | | | 2.1% | |

| Raia Drogasil S.A. (Brazil) | | | 2.0% | |

| Silergy Corp. (Taiwan) | | | 1.9% | |

| NMC Health plc (United Arab Emirates) | | | 1.8% | |

| * | As of September 30, 2017, there were 95 holdings in the Fund. Foreign currency contracts, written options and repurchase agreements, if any, are not included in the number of holdings. Portfolio holdings are subject to change at any time. References to specific securities should not be construed as recommendations by the Funds or their Advisor. Current and future holdings are subject to risk. |

SECTOR BREAKDOWN**

| ** | Excludes securities sold short and options written, if any. |

| † | Also includes Other Assets & Liabilities. |

GROWTHOFA HYPOTHETICAL $10,000 INVESTMENT

Past performance does not predict future performance. The graph above does not reflect the deduction of fees, sales charges, or taxes that you would pay on fund distributions or the redemption of fund shares. Wasatch does not charge any sales fees. The MSCI Emerging Markets and Emerging Markets Small Cap indexes are free float-adjusted market capitalization indexes designed to measure the equity market performance of emerging markets. You cannot invest directly in these or any indexes.

11

| | |

| WASATCH FRONTIER EMERGING SMALL COUNTRIES FUND (WAFMX / WIFMX) | | SEPTEMBER 30, 2017 (UNAUDITED) |

|

|

|

Management Discussion

The Wasatch Frontier Emerging Small Countries Fund is managed by a team of Wasatch portfolio managers led by Roger Edgley, Jared Whatcott and Scott Thomas.

| | | | |

Roger Edgley, CFA Lead Portfolio Manager | |

Jared Whatcott, CFA Portfolio Manager | |

Scott Thomas, CFA Portfolio Manager |

OVERVIEW

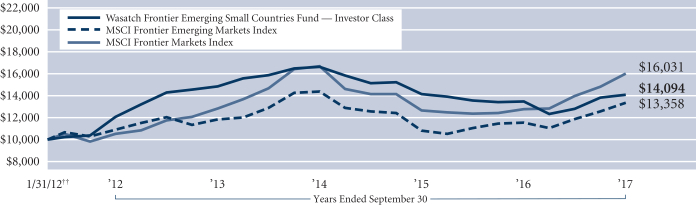

The Wasatch Frontier Emerging Small Countries Fund — Investor Class gained 4.56% for the 12 months ended September 30, 2017 and underperformed its benchmark, the MSCI Frontier Emerging Markets Index, which was up 15.53%.

Performance in frontier markets has been strong, and Wasatch is increasingly optimistic for many frontier and emerging small countries where we see improving macro conditions after a multi-year period of difficult adjustments. Frontier economies have now fiscally adjusted to weaker commodity prices, and depreciating currencies relative to a strong U.S. dollar. What’s more, domestic demand appears to have troughed and many economies appear poised for a continued cyclical recovery.

In the first six months of the period, due to lower oil prices, Nigerian stocks were pressured by economic and currency issues and we opted to sell our holdings and monitor conditions from the sidelines. As a result, the Fund did not participate when the Nigerian equity market subsequently rebounded. Nigeria ended the 12-month period as one of the best-performing markets in the benchmark and as the Fund’s largest detractor on a country basis. During the year, Pakistan faced some significant challenges — which, while not likely to be repeated, resulted in Pakistan being one of the benchmark’s weakest-performing markets. Although the Fund’s overweight position in Pakistan detracted from performance relative to the benchmark, we remain confident in the growth prospects of our holdings. Conversely, Kuwait was one of the benchmark’s best-performing markets; therefore, the Fund’s underweight position was detrimental.

On the positive side, we were well-positioned in Argentina as our stocks outperformed their benchmark counterparts. The Fund also benefited from investments in the United Arab Emirates (UAE), which is not in the benchmark.

DETAILSOFTHE YEAR

The top contributor to the Fund’s performance for the year was NMC Health plc, a hospital operator in the UAE, whose stock is listed on the London Stock Exchange. Since NMC Health’s initial public offering in 2012, the company

has rapidly grown its hospital network and now has nearly 1,600 beds. Further, as the Emirate of Dubai fully rolls out mandatory health insurance, we estimate that the value of the health-care market in Dubai could double.

Transportadora de Gas del Sur S.A., the exclusive pipeline company for the Southern Argentina region, and the largest in Argentina today, was the Fund’s second-best contributor. The company currently transports approximately two-thirds of the country’s natural gas and operates over half the installed natural gas liquids production capacity. We continue to believe tariff reforms will provide a boost to the company’s revenues and profits and put in place the right incentives to spur increased production.

The third-best contributor was MercadoLibre, an online e-commerce company focused on Latin America. Originally a provider of auction-type platforms that connect buyers with sellers, MercadoLibre has been increasing its fulfillment capabilities and recently introduced free shipping to customers in Brazil, Colombia and Chile. While this strategy pressures margins in the short-term, we believe it increases user satisfaction, business scale and further strengthens barriers to entry against would-be competitors.

In addition to the Fund’s Nigerian holdings, which were plagued by currency pressure and sold earlier in the year, our Egyptian holdings were also affected by currency adjustments. Egypt moved to a fully floating foreign exchange policy and the currency depreciated 50% in November 2016. The currency depreciation caused two of our names — Commercial International Bank S.A.E. and Global Telecom Holding S.A.E. — to be significant detractors in U.S. dollar terms for the 12-month period.

Olympic Industries Ltd., Bangladesh’s largest biscuit and confectionery manufacturer, was also a significant detractor. Growth of the company’s main biscuits segment slowed and other new products have yet to make up the difference. In addition, the stock fell from peak levels, reflecting softening of customers’ purchasing power. We expect these conditions to be temporary, and remain confident in Olympic Industries’ management and future business opportunities.

OUTLOOK

We have seen significant improvement in the outlook for our portfolio companies, and we are starting to see a rebound in earnings growth. This accelerating growth combined with reasonable valuations, and low correlations relative to developed and larger emerging markets continue to give us confidence in the Fund’s holdings in frontier and emerging small countries.

We believe that bottom-up analysis and travel to the regions in which we invest is critical, as economic growth, political structures and willingness to reform vary widely in developing markets. We continue to travel extensively and are excited about the future of frontier and emerging small countries and their expanding role in the global economy.

Thank you for the opportunity to manage your assets.

| | Current and future holdings are subject to risk. |

12

| | |

| WASATCH FRONTIER EMERGING SMALL COUNTRIES FUND (WAFMX / WIFMX) | | SEPTEMBER 30, 2017 (UNAUDITED) |

|

|

|

Portfolio Summary

AVERAGE ANNUAL TOTAL RETURNS

| | | | | | | | | | | | | | | |

| | | 1 YEAR | | 5 YEARS | | SINCE INCEPTION 1/31/12 |

Frontier Emerging Small Countries (WAFMX) — Investor | | | | 4.56% | | | | | 3.10% | | | | | 6.24% | |

Frontier Emerging Small Countries (WIFMX) — Institutional | | | | 4.55% | | | | | 3.17% | | | | | 6.31% | |

MSCI Frontier Emerging Markets Index | | | | 15.53% | | | | | 4.13% | | | | | 5.24% | |

MSCI Frontier Markets Index | | | | 25.47% | | | | | 8.73% | | | | | 8.68% | |

Data shows past performance, which is not indicative of future performance. Current performance may be lower or higher than the performance quoted. To obtain the most recent month-end performance data available, please visit www.WasatchFunds.com. The Advisor may absorb certain Fund expenses, without which total return would have been lower. Investment returns and principal value will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

As of the September 1, 2017 prospectus, the Total Annual Fund Operating Expenses for the Wasatch Frontier Emerging Small Countries Fund are Investor Class — Gross: 2.39%, Net: 2.25% / Institutional Class: 2.06%. The expense ratio shown elsewhere in this report may be different. Net expenses are based on Fund expenses, net of waivers and reimbursements. See the prospectus for additional information regarding Fund expenses.

Wasatch Funds will deduct a 2.00% redemption proceeds fee on Fund shares held 60 days or less. Performance data does not reflect the deduction of fees, including sales charges, or the taxes you would pay on fund distributions or the redemption of fund shares. Fees and taxes, if reflected, would reduce the performance quoted. Wasatch does not charge any sales fees. For more complete information including charges, risks and expenses, read the prospectus carefully.

Performance for the Institutional Class prior to 2/1/2016 is based on the performance of the Investor Class. Performance of the Fund’s Institutional Class prior to 2/1/2016 uses the actual expenses of the Fund’s Investor Class without any adjustments. For any such period of time, the performance of the Fund’s Institutional Class would have been substantially similar to, yet higher than, the performance of the Fund’s Investor Class, because the shares of both classes are invested in the same portfolio of securities, but the classes bear different expenses.

Investing in small cap funds will be more volatile and loss of principal could be greater than investing in large cap or more diversified funds. Investing in foreign securities, especially in frontier and emerging markets, entails special risks, such as currency fluctuations and political uncertainties, which are described in more detail in the prospectus.

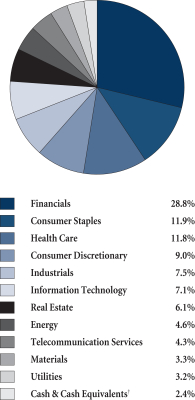

TOP 10 EQUITY HOLDINGS*

| | | | |

| Company | | % of Net

Assets | |

| NMC Health plc (United Arab Emirates) | | | 5.2% | |

| Transportadora de Gas del Sur S.A. ADR (Argentina) | | | 4.6% | |

| Philippine Seven Corp. (Philippines) | | | 4.3% | |

| Aramex PJSC (United Arab Emirates) | | | 4.2% | |

| Vietnam Dairy Products JSC (Vietnam) | | | 4.1% | |

| | | | |

| Company | | % of Net

Assets | |

| MercadoLibre, Inc. (Brazil) | | | 4.1% | |

| Ayala Land, Inc. (Philippines) | | | 4.0% | |

| Banco Davivienda S.A. (Colombia) | | | 3.6% | |

| Credicorp Ltd. (Peru) | | | 3.4% | |

| Naspers Ltd., Class N (South Africa) | | | 3.2% | |

| * | As of September 30, 2017, there were 48 holdings in the Fund. Foreign currency contracts, written options and repurchase agreements, if any, are not included in the number of holdings. Portfolio holdings are subject to change at any time. References to specific securities should not be construed as recommendations by the Funds or their Advisor. Current and future holdings are subject to risk. |

SECTOR BREAKDOWN**

| ** | Excludes securities sold short and options written, if any. |

| † | Also includes Other Assets & Liabilities. |

GROWTHOFA HYPOTHETICAL $10,000 INVESTMENT

Past performance does not predict future performance. The graph above does not reflect the deduction of fees, sales charges, or taxes that you would pay on fund distributions or the redemption of fund shares. Wasatch does not charge any sales fees. ††Inception: January 31, 2012. The MSCI Frontier Emerging Markets and MSCI Frontier Markets indexes are free float-adjusted market capitalization indexes designed to measure the equity market performance of the global frontier and emerging markets. You cannot invest directly in these or any indexes.

13

| | |

| WASATCH GLOBAL OPPORTUNITIES FUND (WAGOX / WIGOX) | | SEPTEMBER 30, 2017 (UNAUDITED) |

|

|

|

Management Discussion

The Wasatch Global Opportunities Fund is managed by a team of Wasatch portfolio managers led by JB Taylor and Ajay Krishnan.

| | | | |

JB Taylor Lead Portfolio Manager | |

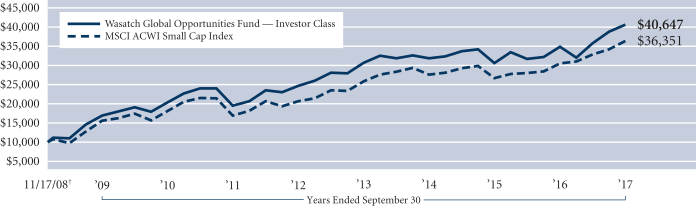

Ajay Krishnan, CFA Lead Portfolio Manager | | OVERVIEW On the strength of stock selection, the health-care, financials and consumer-discretionary sectors made strong contributions as the Wasatch Global Opportunities Fund — Investor Class |

| gained 16.61% for the 12 months ended September 30, 2017. The Fund also benefited from a significant underweighting versus the benchmark in the real-estate sector. The Fund lagged its benchmark, the MSCI ACWI Small Cap Index, which rose 19.23%. |

Among all countries, the U.S. was the top contributor to the Fund’s performance for the 12-month period driven by strong stock selection. Overseas, India was the leading contributor to the Fund’s absolute performance on a country basis, despite a pullback in the last three months of the period. India’s new goods-and-services tax (GST), introduced in July, resulted in trade disruptions that adversely affected the country’s equity market. We believe the volatility will be short-lived, and that GST will ultimately prove to be beneficial over time, a pattern similar to that which ensued following last year’s demonetization program. We believe India’s economy will continue to improve under the direction of the Modi government, and we remain positive on the outlook for our Indian holdings.

DETAILSOFTHE YEAR

Exact Sciences Corp. was the top contributor to the Fund’s performance for the 12-month period. The molecular-diagnostics company has an innovative test for colon cancer. Named Cologuard,® the test avoids the high cost and invasiveness of a colonoscopy by screening a stool sample for cancerous cells. Shares of Exact Sciences began climbing in late April after accelerating demand for Cologuard produced better-than-expected revenues and earnings.

MercadoLibre, Inc. was also a top contributor to performance for the period. This $10.4 billion market-cap company is engaged in online e-commerce focused on Latin America. The company has benefited both from strong regional growth and from the continuing migration of retail sales from brick-and-mortar stores to the online environment.

Another leading contributor during the period, Trex Co., Inc. is an industrial company that has been benefiting from growth in the housing market. The company has established leadership in composite decking, railing and other outdoor-living products. The firm’s current management team, we believe, is especially strong and able to take advantage of homeowners’ preference for the durability, maintenance and

environmental benefits that composite products provide over wood-based competitors. With mortgage rates still attractive, we expect the company to maintain its strong growth rate and competitive advantage.

Cornerstone OnDemand, Inc. was the leading detractor from the Fund’s performance for the period. Despite showing signs of strength midway through the period, management eventually reported numbers that didn’t wow investors, missing expectations on earnings even while reporting stronger sales. In addition, we viewed the company’s mix of new contracts as far from ideal. We see little room for error on management’s part at this point and so we sold our position.

Another detractor was Gurunavi, Inc., a Japanese company that operates an internet portal for ordering food from restaurants online. We like the company’s dominant market position and its opportunity to offer more services and products to customers. Gurunavi has been investing heavily to grow its business. As a result, the company’s recent financial results missed analysts’ expectations.

Australia’s Domino’s Pizza Enterprises Ltd. also detracted. Domino’s has seen growth slow in 2017 and also had negative press surrounding how some franchises pay their employees. Our investment team was in Australia during September, and we remain impressed with the quality of Domino’s management and their use of data and information technology to make their business better.

OUTLOOK

As the 12-month period drew to a close, Japanese Prime Minister Shinzo Abe called for a general election to be held on October 22nd. For years, many investors have avoided Japan and thus may have little interest in the outcome. But with our substantial commitment to Japanese equities — the country represents one of our largest non-U.S. allocations — we think the vote, which can be viewed as a referendum on Abenomics, is significant.

Prior to Abe’s reforms, Japan’s economy had been stagnating. Today, there are many indications that the country’s economy is improving. For example, Japan’s gross domestic product (GDP) has now expanded in the last six quarters, the longest sustained period of growth since before the global financial crisis. With unemployment at a multi-decade low of 2.8%, we’re starting to see modest wage inflation in some parts of the economy.

One factor contributing to our positive view is that Japanese companies are underfollowed. Nearly half the listed companies in Japan have just two or fewer analysts researching them. With an investment approach that includes frequent company visits, we think we have an advantage over other investors. Japan’s small-cap market, one of the most vibrant we’ve found anywhere, is another factor contributing to the country’s reputation as a leading global innovator.

Although our research focus isn’t macro-oriented, we’re aware of economic and geopolitical issues. Overall, we’re optimistic regarding investment opportunities available around the globe.

Thank you for the opportunity to manage your assets.

| | Current and future holdings are subject to risk. |

14

| | |

| WASATCH GLOBAL OPPORTUNITIES FUND (WAGOX / WIGOX) | | SEPTEMBER 30, 2017 (UNAUDITED) |

|

|

|

Portfolio Summary

AVERAGE ANNUAL TOTAL RETURNS

| | | | | | | | | | | | | | | |

| | | 1 YEAR | | 5 YEARS | | SINCE INCEPTION 11/17/08 |

Global Opportunities (WAGOX) — Investor | | | | 16.61% | | | | | 10.48% | | | | | 17.13% | |

Global Opportunities (WIGOX) — Institutional | | | | 16.92% | | | | | 10.54% | | | | | 17.16% | |

MSCI ACWI Small Cap Index | | | | 19.23% | | | | | 11.94% | | | | | 15.66% | |

Data shows past performance, which is not indicative of future performance. Current performance may be lower or higher than the performance quoted. To obtain the most recent month-end performance data available, please visit www.WasatchFunds.com. The Advisor may absorb certain Fund expenses, without which total return would have been lower. Investment returns and principal value will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

As of the September 1, 2017 prospectus, the Total Annual Fund Operating Expenses for the Wasatch Global Opportunities Fund are Investor Class: 1.53% / Institutional Class — Gross: 2.32%, Net: 1.35%. The expense ratio shown elsewhere in this report may be different. Net expenses are based on Fund expenses, net of waivers and reimbursements. See the prospectus for additional information regarding Fund expenses.

Wasatch Funds will deduct a 2.00% redemption proceeds fee on Fund shares held 60 days or less. Performance data does not reflect the deduction of fees, including sales charges, or the taxes you would pay on fund distributions or the redemption of fund shares. Fees and taxes, if reflected, would reduce the performance quoted. Wasatch does not charge any sales fees. For more complete information including charges, risks and expenses, read the prospectus carefully.

Performance for the Institutional Class prior to 2/1/2016 is based on the performance of the Investor Class. Performance of the Fund’s Institutional Class prior to 2/1/2016 uses the actual expenses of the Fund’s Investor Class without any adjustments. For any such period of time, the performance of the Fund’s Institutional Class would have been substantially similar to, yet higher than, the performance of the Fund’s Investor Class, because the shares of both classes are invested in the same portfolio of securities, but the classes bear different expenses.

Investing in small and micro cap funds will be more volatile and loss of principal could be greater than investing in large cap or more diversified funds. Investing in foreign securities, especially in emerging markets, entails special risks, such as currency fluctuations and political uncertainties, which are described in more detail in the prospectus.

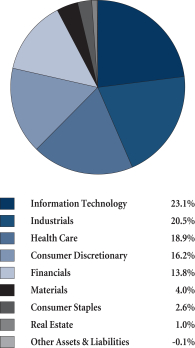

TOP 10 EQUITY HOLDINGS*

| | | | |

| Company | | % of Net

Assets | |

| MercadoLibre, Inc. (Brazil) | | | 3.1% | |

| Medytox, Inc. (Korea) | | | 2.9% | |

| Cavium, Inc. | | | 2.8% | |

| Trex Co., Inc. | | | 2.7% | |

| HealthEquity, Inc. | | | 2.5% | |

| | | | |

| Company | | % of Net

Assets | |

| MakeMyTrip Ltd. (India) | | | 2.3% | |

| Knight-Swift Transportation Holdings, Inc. | | | 2.2% | |

| Copart, Inc. | | | 2.0% | |

| Somany Ceramics Ltd. (India) | | | 2.0% | |

| Ollie’s Bargain Outlet Holdings, Inc. | | | 2.0% | |

| * | As of September 30, 2017, there were 81 holdings in the Fund. Foreign currency contracts, written options and repurchase agreements, if any, are not included in the number of holdings. Portfolio holdings are subject to change at any time. References to specific securities should not be construed as recommendations by the Funds or their Advisor. Current and future holdings are subject to risk. |

SECTOR BREAKDOWN**

| ** | Excludes securities sold short and options written, if any. |

GROWTHOFA HYPOTHETICAL $10,000 INVESTMENT

Past performance does not predict future performance. The graph above does not reflect the deduction of fees, sales charges, or taxes that you would pay on fund distributions or the redemption of fund shares. Wasatch does not charge any sales fees. †Inception: November 17, 2008. The MSCI ACWI (All Country World Index) Small Cap Index is a free float-adjusted market capitalization index designed to measure the performance of small capitalization securities in developed and emerging markets. You cannot invest directly in this or any index.

15

| | |

| WASATCH INTERNATIONAL GROWTH FUND (WAIGX / WIIGX) | | SEPTEMBER 30, 2017 (UNAUDITED) |

|

|

|

Management Discussion

The Wasatch International Growth Fund is managed by a team of Wasatch portfolio managers led by Roger Edgley, Ken Applegate and Linda Lasater.

| | | | |

Roger Edgley, CFA Lead Portfolio Manager | |

Ken Applegate, CFA Portfolio Manager | |

Linda Lasater, CFA Associate Portfolio Manager |

OVERVIEW

The Wasatch International Growth Fund — Investor Class gained 12.04% for the 12 months ended September 30, 2017 and underperformed its benchmark, the MSCI ACWI ex USA Small Cap Index, which gained 19.19%.

Late in 2016, value stocks dramatically outperformed growth stocks. High-quality (based on returns on equity) growth stocks were among the weakest performers. That began to change in 2017. Throughout the first nine months of the year, investors in developed markets became refocused on quality and growth stocks. Although the Fund outperformed its benchmark for the first nine months of calendar year 2017, the underperformance that occurred in the last quarter of 2016 hindered the Fund’s results relative to the Index for the 12-month period.

Among developed international markets, European corporate earnings have been recovering after years of underinvestment and economic indicators have continued to improve. In the United Kingdom (U.K.), Brexit still clouds the future. Most of the Fund’s U.K. investments derive a meaningful portion of their revenue from outside the country, and so have been benefiting from increased global economic activity. We have seen signs that Brexit is weakening Britain’s domestic consumers. Since the referendum in June 2016, we have reduced our exposure to U.K. domestic focused companies.

During the last five years we have identified a number of positive changes in Japan, many of which have been sparked by policies introduced by Prime Minister Shinzo Abe. These changes have opened up more interesting and attractive investment opportunities, and we have been increasing our weighting in Japan.

Emerging markets continued to perform well based on optimism over growth and returning investment. India was a strong-performing market for the 12-month period. However, Indian stocks experienced volatility as the Modi government’s reforms, including last year’s demonetization of large-denomination bank notes and the nationwide goods-and-services tax initiated in June, continue to work their way through the economy. Although the Fund’s Indian holdings trailed those in the Index for the period, we continue to like their growth prospects.

DETAILSOFTHE YEAR

The Fund’s top contributor for the 12-month period was Ipsen S.A., a French pharmaceutical company that has transitioned into a global supplier of oncology products and is leveraging its global sales force to sell an increasing number of products.

Nihon M&A Center, Inc., a Japanese company that connects sellers and buyers of small businesses, was the Fund’s second-best contributor. Nihon M&A has been benefiting from the demographic trends of baby boomers retiring and looking to sell their businesses. Management has enhanced the company’s market position by hosting informational seminars for sellers, and by building relationships with banks, accounting firms and other lead-generating sources.

Another Japanese holding, Seria Co. Ltd., was the Fund’s third-best contributor. Seria, which operates a chain of 100-yen stores (essentially dollar stores), continued to generate strong earnings growth.

The greatest detractor from performance for the year was also from Japan. Gurunavi, Inc. operates an internet portal for ordering food from restaurants online. We like the company’s dominant market position and its opportunity to offer more services and products to customers. Gurunavi has been investing heavily to grow its business. As a result, the company’s recent financial results missed analysts’ expectations.

NCC Group plc, which provides security software and consulting services, was the Fund’s second-largest detractor. The U.K.-based company issued a second profit warning early in 2017 and the CEO stepped down. Our conviction regarding the company’s long-term prospects waned, and we sold our shares.