UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File number: 811-04982

Heartland Group, Inc.

(Exact name of Registrant as specified in charter)

| 790 North Water Street, Suite 1200, Milwaukee, WI | | 53202 |

| (Address of principal executive offices) | | (Zip code) |

Nicole J. Best

Heartland Group, Inc., 790 North Water Street, Suite 1200, Milwaukee, WI 53202

(Name and address of agent for service)

Ellen Drought

Godfrey & Kahn, S.C., 833 East Michigan Street, Suite 1800, Milwaukee, WI 53202-5615

(With a copy to:)

Registrant’s telephone number, including area code: (414) 347-7777

Date of fiscal year end: December 31

Date of reporting period: June 30, 2023

Form N-CSR is to be used by management investment companies to file reports with the Commission, not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to the Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

| Item 1. | Reports to Stockholders. |

| A MESSAGE FROM OUR PRESIDENT AND CEO | 1 |

| | |

| HEARTLAND MID CAP VALUE FUND | |

| Management’s Discussion of Fund Performance | 2 |

| | |

| HEARTLAND VALUE PLUS FUND | |

| Management’s Discussion of Fund Performance | 4 |

| | |

| HEARTLAND VALUE FUND | |

| Management’s Discussion of Fund Performance | 6 |

| | |

| THE HEARTLAND FAMILY OF EQUITY FUNDS | |

| Additional Fund Characteristics | 8 |

| | |

| FINANCIAL STATEMENTS | |

| Schedules of Investments | 10 |

| Statements of Assets and Liabilities | 15 |

| Statements of Operations | 16 |

| Statements of Changes in Net Assets | 17 |

| Financial Highlights | 18 |

| Notes to Financial Statements | 21 |

| | |

| ADDITIONAL INFORMATION | |

| Expense Examples | 28 |

| Other Information | 28 |

| Definitions and Disclosures | 29 |

| Statement Regarding Liquidity Risk Management Program | 30 |

| Board Review of Investment Advisory Agreement | 31 |

| Information Regarding Executive Officers and Directors | 33 |

“The easiest way to solve a problem is to deny it exists.”

| Dear Fellow Shareholders, | —Issac Asimov |

Recently, risk-taking returned to the market in a big way. The tech-heavy NASDAQ Composite Index is up more than 30% year to date, driven in large part to the speculative frenzy over artificial intelligence stocks. Is this surprising, given that a series of bank failures in March seemed to scare investors straight earlier in the year? Not really. Denial is a natural phase in the investment cycle, coming after delusion but preceding capitulation and despair.

Yet denying that a problem exists does not actually make it go away. The truth is, there is a long list of nagging problems, including the Federal Reserve’s still-restrictive monetary policy, 6-month T-bills yielding 5.4% — tough competition for equities — and the 14th consecutive monthly decline in the Leading Economic Indicators.

These things will not disappear overnight even if the Federal Reserve is done raising rates, which remains a big if. Many of the effects of higher borrowing costs are already taking their toll, and there is a strong likelihood of further credit stress in the coming months. Banks are hunkering down, tightening their lending standards while cutting back on loan issuance.

Something else that cannot be denied is how narrow the breadth is in today’s market. So far this year, a smaller percentage of stocks are beating the benchmark than was the case in the run up to the global financial crisis, the dotcom crash, and the early ’80s recessions.

Percentage of S&P 500 Stocks that Outperformed the S&P 500

Source: Ned Davis Research, yearly data from 12/31/1973 to 12/31/2022 and partial year data from 1/1/2023 to 6/22/2023. This chart represents the percentage of S&P 500® stocks that outperformed the S&P 500® over the calendar year. All indices are unmanaged. It is not possible to invest directly in an index. Past performance does not guarantee future results.

Narrow markets have historically been associated with poor performance while wide breadth has correlated with strong price gains in the 12 months after the fact. The good news is, there is a corollary to this rule — one that signals hope for patient, value-minded investors like us who have a focus on small-cap names. Ned Davis Research examined past periods in which the market’s breadth narrowed—specifically, when fewer than 30% of the stocks in the S&P 500 were beating the benchmark. It found that in the 12 months following those instances, small stocks outperformed large stocks every time.

Source: Ned Davis Research, daily data from 3/27/1980 to 5/31/2023. This chart represents the Russell 2000® to 1000® ratio performance after the percent of S&P 500® stocks outperforming the index in last three months falls below 30%. All indices are unmanaged. It is not possible to invest directly in an index. Past performance does not guarantee future results.

In our opinion, the market’s advance, principally fueled by P/E expansion, the allure of AI stocks, and the hope for imminent Federal Reserve rate cuts, is destined to disappoint. Yet we believe this remains a constructive environment for value investors who are disciplined. We are focused on what the market is giving us and being extremely selective in identifying opportunities that can shine over the next the next market cycle, not just the coming quarter.

Fundamentally Yours,

Will Nasgovitz

President and Chief Executive Officer

1

| PORTFOLIO MANAGEMENT TEAM |

Colin P. McWey, CFA

Will R. Nasgovitz

Troy W. McGlone, CFA | MANAGEMENT REPORT After taking risk off the table earlier in the year, investors scrambled back during the second quarter, sparked by better-than-expected inflation data, the resolution of the debt ceiling crisis in Washington, and newfound hope that the Federal Reserve might be done tightening. As a result, Growth outperformed Value in the first half of the year, and speculative Growth did even better. Our Mid Cap Value Fund Investor Class gained 8.0% for the first six months, leading the Russell Midcap® Value Index, which was up 5.23%. Our outperformance was driven by stock selection, particularly in the Technology, Consumer Discretionary, Real Estate, and Utilities sectors. We remain confident that effective stock selection will provide opportunities for good relative performance, and potentially downside protection, in a market where many uncertainties remain. We also believe Value will have an advantage going forward. That said, we do not rely on top-down forecasts to pick stocks. We build our portfolio through bottom-up stock selection, relying on our 10 Principles of Value Investing™ within a two-bucket approach. Among Value investors, there are those who prefer owning high-quality companies trading at decent bargains (“value") and others who focus on deeply discounted companies that have produced poor economic returns over time (“deep value”). Just as Growth and Value tend to take turns outperforming, these two styles within value investing also tend to alternate market leadership. Within the mid-cap space, choosing one while ignoring the other does not seem prudent, as this can cause a top-down bet to be introduced into the portfolio. In the Value bucket, Hasbro (HAS) is one of the world’s leading toy and game manufacturers with key franchises such as Peppa Pig, Play-Doh, My Little Pony, and Playskool. For several years, Hasbro’s returns on invested capital have been going the wrong way. That said, we believe the shares possess compelling turnaround and self-help potential. The company has made progress working down excess inventory at retailers. This progress comes in front of an impressive slate of new products and entertainment releases, including movies, which should help catalyze better sales. Hasbro is streamlining operations and strategic focus across its products/gaming/entertainment segments by allocating more resources to growing its larger brands, while simultaneously de-emphasizing smaller brands that have created unnecessary distraction in recent years. Additionally, we expect management to complete a partial divestiture of noncore assets in its entertainment segment to reduce expenses and relieve the burden of inefficiently deployed capital. Furthermore, we are encouraged by Hasbro’s undertaking of a $250-300 million multi-year cost-saving initiative and a necessary supply chain management overhaul. Our purchase of Hasbro shares was motivated by these operational/strategic changes, our confidence in the company’s ability to significantly expand operating margins, and compelling multiples of earnings, cashflow and invested capital. Also in value, Centene Corporation (CNC) is one of the largest managed health care insurance providers in the U.S. and the largest player in Medicaid. The stock has underperformed this year, as CNC faces reimbursement headwinds including a reduction in its 2024 Medicare Advantage premiums and higher healthcare utilization from the return of elective procedures. Investors also fear a potential loss of insured lives when Medicaid eligibility, which was expanded during the pandemic, gets redetermined in 2023-2024. CNC’s historical results have lacked the consistency demonstrated by premier large managed care companies. However, since 2021, the company has steadily upgraded its leadership ranks from the CEO on down through the executive ranks and line-of-business leaders. CNC’s executive leadership is comprised of industry veterans with a demonstrated record of success. Their executive compensation is clearly aligned with shareholder value creation, and they recently bought large amounts of CNC stock personally in the open market, demonstrating confidence in their prospects. Self-help initiatives are well underway and include noncore divestitures, material expense streamlining, improved digital capabilities, improved provider contracting, and meaningful share repurchases. In our estimation, the market is too focused on near-term overhangs that will prove temporary and disregards the substantial value creation opportunities that lie ahead. CNC trades at just 10X 2023 earnings compared to peers valued at mid/upper teens P/E ratios. After a brief pause caused by the reimbursement headwinds in 2024, we expect CNC to resume its 12-15% EPS growth rate, comparable to leading industry operators. This should help close the valuation gap. In the deep value bucket, Stericycle (SRCL) is the largest medical waste disposal and compliance company in the U.S. Over the past few years, the company has transformed itself from an aggressive, acquisition-driven company to one focused on organic growth, integrating core assets, reducing debt, and expanding profit margins. Toward that end, the company has undertaken several self-help strategies. This includes divesting non-core operations in order to focus on its core businesses of medical waste disposal and document destruction in the U.S. and Europe. Today, SRCL is largely complete with this portfolio reshaping and has successfully reduced debt to target levels. The critical action items left for the company pertain to integrating technology systems and demonstrating further progress in operational execution. In summary, SRCL is morphing from a “holding company” into an “operating company,” with the latter offering far better prospects of rewarding shareholders. Candidly, this is not our first time owning SRCL. The first time around, we became shareholders far too early in the company’s turnaround efforts and exited the position. However, we continue to monitor the progress made under a much-improved management team and expect a better outcome for shareholders going forward. Regulated waste companies with leading market shares and secular growth, like SRCL, trade at far more expensive multiples of EBITDA and free cash flow. Additionally, the company is significantly underearning its potential. As this dynamic changes, we can envision a virtuous circle where the company earns progressively higher trading multiples on higher earnings power. We remain focused on bottom-up stock selection because that is something that is within our control, unlike the stock market. We also believe this will remain a key determinant of success for our shareholders. CFA® is a registered trademark owned by the CFA Institute. |

2

FUND SUMMARY

| Average Annual Total Returns as of June 30, 2023 | Inception Date | Year to Date* | One Year | Three Years | Five Years | Since Inception |

| Investor Class (HRMDX) | 10/31/14 | 8.00% | 15.08% | 20.18% | 10.11% | 9.29% |

| Institutional Class (HNMDX) | 10/31/14 | 8.12% | 15.34% | 20.47% | 10.36% | 9.56% |

| Russell Midcap® Value Index | - | 5.23% | 10.50% | 15.04% | 6.84% | 7.33% |

Index Source: FactSet Research Systems, Inc., and Russell®.

* Not annualized.

In the prospectus dated 5/1/23, the Net Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement for the Investor and Institutional Class are 1.10% and 0.85%, respectively. The Advisor has contractually agreed to waive its management fees and/or reimburse expenses of the Fund to ensure that Net Annual Operating Expenses do not exceed 1.10% of the Fund's average daily net assets for the Investor Class and 0.85% for the Institutional Class, through at least 4/5/2025, and subject thereafter to annual reapproval of the agreement by the Board of Directors. Without such waiver and/or reimbursements, the Gross Fund Operating Expenses would be 1.16% and 1.04% for the Investor and Institutional Class, respectively.

Past performance does not guarantee future results. Performance represents past performance; current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. All returns reflect reinvested dividends and capital gains distributions, but do not reflect the deduction of taxes that an investor would pay on distributions or redemptions. Subject to certain exceptions, shares of a Fund redeemed or exchanged within 10 days of purchase are subject to a 2% redemption fee. Performance does not reflect this fee, which if deducted would reduce an individual’s return. To obtain performance through the most recent month end, call 800-432-7856, or visit www.heartlandadvisors.com.

HYPOTHETICAL GROWTH OF $10,000 SINCE INCEPTION - 10/31/14 - INVESTOR CLASS SHARES

SECTOR ALLOCATION - % OF EQUITY INVESTMENTS

Sector and Industry classifications are sourced from GICS®. The Global Industry Classification Standard (GICS®) is the exclusive intellectual property of MSCI Inc. (“MSCI”) and S&P Global Market Intelligence (“S&P”). Neither MSCI, S&P, their affiliates, nor any of their third party providers (“GICS Parties”) makes any representations or warranties, express or implied, with respect to GICS or the results to be obtained by the use thereof, and expressly disclaims all warranties, including warranties of accuracy, completeness, merchantability, and fitness for a particular purpose. The GICS Parties shall not have any liability for any direct, indirect, special, punitive, consequential, or any other damages (including lost profits) even if notified of such damages.

INVESTMENT GOAL

The Fund seeks long-term capital appreciation and modest current income.

INVESTMENT STRATEGY/DISTINGUISHING CHARACTERISTIC

The Fund seeks long-term capital appreciation. It invests in mid-size, dividend paying companies with a market cap range defined by the Russell Midcap® Index. The Fund utilizes Heartland's disciplined and time-tested 10 Principles of Value Investing™, designed to capture upside potential while minimizing downside risk.

INVESTMENT CONSIDERATIONS

The Fund invests in a smaller number of stocks (generally 40 to 60) than the average mutual fund. The performance of these holdings generally will increase the volatility of the Fund's returns. The Fund also invests in mid-sized companies on a value basis. Mid-sized securities generally are more volatile and less liquid than those of larger companies. There is no assurance that dividend-paying stocks will mitigate volatility. Value investments are subject to the risk that their intrinsic value may not be recognized by the broad market.

PORTFOLIO STATISTICS

| Number of holdings (excludes cash equivalents) | 42 |

| Net assets | $501.3 mil. |

| NAV (Investor Class) | $13.37 |

| NAV (Institutional Class) | $13.45 |

| Median market cap | $11.4 bil. |

| Weighted average market cap | $16.9 bil. |

TOP TEN HOLDINGS - % OF NET ASSETS (EXCLUDES CASH EQUIVALENTS)

| NOV, Inc. | 4.9 % |

| Teradata Corp. | 4.6 |

| Centene Corp. | 4.1 |

| PPG Industries, Inc. | 4.0 |

| FirstEnergy Corp. | 3.8 |

| Essex Property Trust, Inc. | 3.8 |

| CarMax, Inc. | 3.7 |

| Equity Commonwealth. | 3.4 |

| Qorvo, Inc. | 3.3 |

| Quest Diagnostics, Inc. | 3.1 |

Portfolio holdings, statistics, and manager views are subject to change without notice, and discussions of portfolio holdings are intended as illustrations of investment strategy, not as recommendations. Index definitions and investment terms are found on the page titled “Definitions and Disclosures.” All indices are unmanaged. It is not possible to invest directly in an index. All information, unless otherwise indicated, is as of 6/30/2023.

3

| PORTFOLIO MANAGEMENT TEAM |

Brad A. Evans, CFA

Andrew J. Fleming, CFA | MANAGEMENT REPORT At the start of the year, investors were scrambling for well-managed businesses with strong balance sheets, as the banking crisis refocused the market’s attention on fundamentals. But in the second quarter, the market’s appetite for risk taking returned in a big way and the types of financially sound companies we embrace — with consistent free cash flow generation to self-finance their organic growth and raise dividends over time — were largely ignored. As a result, this has proved to be a challenging market. Heartland Value Plus Fund Investor Class was up 0.27% in the first six months, versus a gain of 2.5% for the Russell 2000 Value Index. Factors we gravitate toward — such as low volatility, low leverage, and dividends — have not been working lately. While stock selection has been a leading driver of our performance over the long run, our selection effect was negative this year as the market has moved away from high-quality names with strong balance sheets. The new narrative in the market seems to indicate that the Federal Reserve may not simply be done tightening; it may be close to cutting rates shortly. It is not surprising, then, that speculative, low-quality stocks outperformed in the second quarter, since those types of equities led in the previous easing cycles. Underlying this line of thinking is the hope that the Federal Reserve has threaded the proverbial needle and is about to engineer a quick takeoff for the economy after achieving a ‘soft landing.’ While we do not view this as an impossibility, the chances of this occurring seem slim. By contrast, we think there is a high likelihood of some form of stagflation weighing on the economy going forward, and we continue to be positioned for this scenario. That said, we outperformed our benchmark in Consumer Staples, Utilities, Real Estate, and Industrials, where our stock selection added positive value. An example in industrials is Healthcare Services Group (HCSG), the leading provider of housekeeping and culinary services to skilled nursing facilities. As those healthcare providers scale, it makes sense for them to outsource ancillary services, yet currently only around 30% of skilled nursing facilities do so. The stock has come under pressure in recent years, as occupancy levels at their clients’ facilities plummeted during the global pandemic. Meanwhile, inflation in the aftermath of the pandemic disadvantaged HCSG’s contract pricing, meaning they were taking a hit on both revenues and costs. We believe those headwinds have abated. Not only is occupancy improving, the company’s two-year self-help strategy of renegotiating all contracts with all customers to include more dynamic pricing is finally starting to pay off. The company’s EBITDA margins fell to 4-4.5%, but our projections show them improving to 6.5% this year and 7.5% in 2024 on their way to a target of 10%. Today, the stock trades at 0.6 times enterprise value to sales. Yet when it was at this level of profitability in the past, the stock traded at 1.5 times EV/Sales. With more credit stress likely to come in this slow-growing economy, from our perspective, now is not the time to be distracted by all the bright, shiny objects that have garnered the market’s attention. It also seems more important than ever to have conviction about the companies we own. This means doing the work to assess the financial strength of every company under consideration, while confirming that each company’s self-help strategies remain intact and compelling. In our assessment, we hold many such names that are currently flying under the market’s radar. We see them as small kernels ready to pop. That may not happen in the coming weeks or months. But our goal is not to win the quarter; it is aligning the portfolio to outperform in the long run. CFA® is a registered trademark owned by the CFA Institute. |

4

FUND SUMMARY

| Average Annual Total Returns as of June 30, 2023 | Inception Date | Year to Date* | One Year | Three Years | Five Years | Ten Years | Fifteen Years | Twenty Years | Twenty-Five Years | Since Inception |

| Investor Class (HRVIX) | 10/26/93 | 0.27% | 7.77% | 15.15% | 6.43% | 7.20% | 7.17% | 9.11% | 8.24% | 9.71% |

| Institutional Class (HNVIX) | 5/1/08 | 0.41% | 8.04% | 15.43% | 6.68% | 7.44% | 7.44% | 9.31% | 8.40% | 9.84% |

| Russell 2000® Value Index | - | 2.50% | 6.01% | 15.43% | 3.54% | 7.29% | 7.72% | 8.29% | 7.62% | 9.09% |

Index Source: FactSet Research Systems, Inc., and Russell®.

* Not annualized.

In the prospectus dated 5/1/23, the Gross Fund Operating Expenses for the Investor and Institutional Class are 1.22% and 1.01%, respectively. The Advisor has voluntarily agreed to waive fees and/or reimburse expenses with respect to the Institutional Class, to the extent necessary to maintain the Institutional Class' Net Annual Operating Expenses at a ratio not to exceed 0.99% of average daily net assets. This voluntary waiver/reimbursement may be discontinued at any time. Without such waivers and/or reimbursements, total returns may have been lower.

Past performance does not guarantee future results. Performance for the Institutional Class prior to its initial offering is based on the performance of the Investor Class. Performance represents past performance; current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. All returns reflect reinvested dividends and capital gains distributions, but do not reflect the deduction of taxes that an investor would pay on distributions or redemptions. Subject to certain exceptions, shares of a Fund redeemed or exchanged within 10 days of purchase are subject to a 2% redemption fee. Performance does not reflect this fee, which if deducted would reduce an individual’s return. To obtain performance through the most recent month end, call 800-432-7856, or visit www.heartlandadvisors.com.

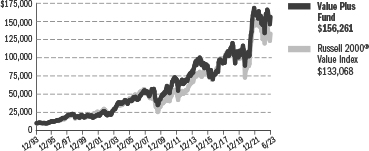

HYPOTHETICAL GROWTH OF $10,000 SINCE INCEPTION - 10/26/93 - INVESTOR CLASS SHARES

SECTOR ALLOCATION - % OF EQUITY INVESTMENTS

Sector and Industry classifications are sourced from GICS®. The Global Industry Classification Standard (GICS®) is the exclusive intellectual property of MSCI Inc. (“MSCI”) and S&P Global Market Intelligence (“S&P”). Neither MSCI, S&P, their affiliates, nor any of their third party providers (“GICS Parties”) makes any representations or warranties, express or implied, with respect to GICS or the results to be obtained by the use thereof, and expressly disclaims all warranties, including warranties of accuracy, completeness, merchantability, and fitness for a particular purpose. The GICS Parties shall not have any liability for any direct, indirect, special, punitive, consequential, or any other damages (including lost profits) even if notified of such damages.

INVESTMENT GOAL

The Fund seeks long-term capital appreciation and modest current income.

INVESTMENT STRATEGY/DISTINGUISHING CHARACTERISTIC

The Fund seeks to capture the long-term capital appreciation of small-cap stocks, while potentially mitigating volatility by focusing on dividend-paying companies. The Fund utilizes Heartland's disciplined and time-tested 10 Principles of Value Investing™, designed to capture upside potential while minimizing downside risk.

INVESTMENT CONSIDERATIONS

The Fund invests in small companies that are generally less liquid and more volatile than large companies. The Fund also invests in a smaller number of stocks (generally 40 to 70) than the average mutual fund. The performance of these holdings generally will increase the volatility of the Fund's returns. Value investments are subject to the risk that their intrinsic value may not be recognized by the broad market.

PORTFOLIO STATISTICS

| Number of holdings (excludes cash equivalents) | 42 |

| Net assets | $440.2 mil. |

| NAV (Investor Class) | $36.97 |

| NAV (Institutional Class) | $36.73 |

| Median market cap | $1.7 bil. |

| | |

| Weighted average market cap | $2.3 bil. |

TOP TEN HOLDINGS - % OF NET ASSETS (EXCLUDES CASH EQUIVALENTS)

| Powell Industries, Inc. | 4.8% |

| PotlatchDeltic Corp. | 4.1 |

| Texas Capital Bancshares, Inc. | 3.7 |

| TreeHouse Foods, Inc. | 3.4 |

| Haemonetics Corp. | 3.4 |

| Carter's, Inc. | 3.3 |

| Comstock Resources, Inc. | 3.3 |

| Avanos Medical, Inc. | 3.2 |

| Granite Construction, Inc. | 2.9 |

| The Hanover Insurance Group, Inc. | 2.8 |

Portfolio holdings, statistics, and manager views are subject to change without notice, and discussions of portfolio holdings are intended as illustrations of investment strategy, not as recommendations. Index definitions and investment terms are found on the page titled “Definitions and Disclosures.” All indices are unmanaged. It is not possible to invest directly in an index. All information, unless otherwise indicated, is as of 6/30/2023.

5

| PORTFOLIO MANAGEMENT TEAM |

Bill J. Nasgovitz

Will R. Nasgovitz | MANAGEMENT REPORT “The easiest way to solve a problem is to deny it exists.” —Isaac Asimov It was not surprising that risk-taking returned to the market, just a few months after a series of bank failures in March seemed to scare investors straight. Denial is a natural phase in the investment cycle, coming after delusion but preceding capitulation and despair. It helped propel the NASDAQ Composite Index, a beneficiary of the recent frenzy over artificial intelligence stocks, up more than 30% for the first six months. By contrast, the Russell 2000® Value Index gained just 2.50% in the first six months. The Heartland Value Fund Investor Class outperformed the benchmark with a return of 5.97%. Stock selection provided a boost in the first six months, particularly in Financials, Health Care, Consumer Discretionary, Real Estate, Materials, and Utilities — sectors where we outpaced the small cap value index. Yet denying problems exist — such as the Federal Reserve’s still-restrictive monetary policy, 5.4% yields on 6-month T-bills that are tough competition for equities, and 14 consecutive monthly declines in the Leading Economic Indicators — does not make them go away. We believe investors will begin recognizing this once the markets price in growing credit and solvency risks. Our approach in these moments is to be patient and add to holdings with attractive risk/reward characteristics that fit our 10 Principles of Value Investing™. We remain focused on uncovering businesses with strong leadership and resilient balance sheets offering compelling valuations. Mohawk (MHK), a new position, is a perfect example of a stock that has “come to us.” A leading manufacturer of flooring including carpets, tiles, and wood and vinyl products for the residential and commercial markets, Mohawk ran into stiff headwinds in recent years owing to high inflation in its source materials. This compressed their margins, and the stock price was nearly cut in half between June 2021 and early 2023. We believe the worst of those pricing pressures are largely behind the business, which stands to benefit from several trends, including ongoing growth in home remodeling; the anticipated reacceleration of existing home sales once rates begin to stabilize; and office space conversions as the commercial real estate market struggles with hybrid work. We purchased the shares when they were selling at around 6 times our estimated 2024 earnings, even though the stock has historically traded at a P/E of 15. Electronic manufacturing services companies, like Benchmark Electronics (BHE), tend to do well in terms of profit and sales growth when things are good but poorly when times are bad, owing in part to their significant fixed cost overhead. Though management has shifted its production mix away from lower-margin and slower-growth segments (like advanced computing) and toward more profitable areas (like semi-cap equipment), BHE’s margins failed to deliver during the recent downturn in the semiconductor cycle. Moreover, recent moves to expand capacity to help customers “re-shore” manufacturing were not fully scaled, further weighing on profitability. This short-term disappointment caused the stock to sell-off sharply and approach our downside target, creating a compelling entry point. We believe management has now positioned the business in segments that will allow for above-average industry growth and margin expansion. BHE trades at 12 times 2023 earnings and 10 times 2024 profits. By comparison, industry peers with similar growth and margin expansion opportunities are trading at P/E ratios (based on 2024 earnings) in the low- to mid-teens. Healthcare Services Group (HCSG) manages housekeeping, laundry, dining, and nutritional services within the healthcare market. The stock has come under pressure in recent years, as occupancy levels at their clients’ skilled nursing facilities (SNFs) plummeted during the COVID shutdowns. Meanwhile, inflation in the aftermath of the pandemic disadvantaged HCSG’s contract pricing. We believe those headwinds have abated, as occupancy is improving, and the company is restructuring its agreements to include more dynamic pricing. There is also a significant opportunity to gain market share, as only 30% of SNFs currently outsource their housekeeping. Management’s efforts have guided EBITDA margins back to 6%. Today, HCSG sports a balance sheet that exceeds our expectations with net cash and strong free cash flow and trades at 0.6X enterprise value to sales. Yet when it was at this level of profitability in the past, the business was priced at 1.5X EV/Sales. Despite the speculative nature of this year’s rally, we believe this remains a constructive environment for value investors who are disciplined. We are focused on what the market is giving us, being extremely selective in identifying opportunities that can shine over the next market cycle, not just the coming quarters. |

| 6 | | |

FUND SUMMARY

| Average Annual Total Returns as of June 30, 2023 | | Inception Date | | | Year to Date* | | | One Year | | | Three Years | | | Five Years | | | Ten Years | | | Fifteen Years | | | Twenty Years | | | Twenty-Five Years | | | Since Inception | |

| Investor Class (HRTVX) | | | 12/28/84 | | | | 5.97 | % | | | 11.13 | % | | | 15.98 | % | | | 5.37 | % | | | 6.61 | % | | | 5.93 | % | | | 7.39 | % | | | 7.85 | % | | | 10.96 | % |

| Institutional Class (HNTVX) | | | 5/1/08 | | | | 6.06 | % | | | 11.27 | % | | | 16.14 | % | | | 5.51 | % | | | 6.77 | % | | | 6.11 | % | | | 7.53 | % | | | 7.96 | % | | | 11.04 | % |

| Russell 2000® Value Index | | | - | | | | 2.50 | % | | | 6.01 | % | | | 15.43 | % | | | 3.54 | % | | | 7.29 | % | | | 7.72 | % | | | 8.29 | % | | | 7.62 | % | | | 10.33 | % |

Index Source: FactSet Research Systems, Inc., and Russell®.

* Not annualized.

In the prospectus dated 5/1/23, the Gross Fund Operating Expenses for the Investor and Institutional Class are 1.09% and 0.98%, respectively.

Past performance does not guarantee future results. Performance for the Institutional Class prior to its initial offering is based on the performance of the Investor Class. Performance represents past performance; current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. All returns reflect reinvested dividends and capital gains distributions, but do not reflect the deduction of taxes that an investor would pay on distributions or redemptions. Subject to certain exceptions, shares of a Fund redeemed or exchanged within 10 days of purchase are subject to a 2% redemption fee. Performance does not reflect this fee, which if deducted would reduce an individual’s return. To obtain performance through the most recent month end, call 800-432-7856, or visit www.heartlandadvisors.com.

HYPOTHETICAL GROWTH OF $10,000 SINCE INCEPTION –

12/28/84 - INVESTOR CLASS SHARES

SECTOR ALLOCATION - % OF EQUITY INVESTMENTS

Sector and Industry classifications are sourced from GICS®. The Global Industry Classification Standard (GICS®) is the exclusive intellectual property of MSCI Inc. (“MSCI”) and S&P Global Market Intelligence (“S&P”). Neither MSCI, S&P, their affiliates, nor any of their third party providers (“GICS Parties”) makes any representations or warranties, express or implied, with respect to GICS or the results to be obtained by the use thereof, and expressly disclaims all warranties, including warranties of accuracy, completeness, merchantability, and fitness for a particular purpose. The GICS Parties shall not have any liability for any direct, indirect, special, punitive, consequential, or any other damages (including lost profits) even if notified of such damages.

INVESTMENT GOAL

The Fund seeks long-term capital appreciation through investing in small companies.

INVESTMENT STRATEGY/DISTINGUISHING CHARACTERISTIC

The Fund seeks to capture long-term capital appreciation by investing in micro- and smallcap companies. The micro- and small-cap segment of the stock market is robust with thousands of publicly traded issues, many of which lack traditional Wall Street research coverage. Thus, we believe this market is often inefficient, mispricing businesses and offering opportunities for fundamental research-minded investors such as Heartland. The Fund utilizes Heartland's disciplined and time-tested 10 Principles of Value Investing™, designed to capture upside potential while minimizing downside risk.

INVESTMENT CONSIDERATIONS

The Fund invests primarily in small companies selected on a value basis. Such securities generally are more volatile and less liquid than those of larger companies. Value investments are subject to the risk that their intrinsic value may not be recognized by the broad market.

| PORTFOLIO STATISTICS | | | |

| Number of holdings (excludes cash equivalents) | | | 86 | |

| Net assets | $662.8 mil. | |

| NAV (Investor Class) | | $ | 42.97 | |

| NAV (Institutional Class) | | $ | 44.10 | |

| Median market cap | | | $1.1 bil. | |

| Weighted average market cap | | | $2.3 bil. | |

| TOP TEN HOLDINGS - % OF NET ASSETS (EXCLUDES CASH EQUIVALENTS) | | | |

| Encompass Health Corp. | | | 2.5 | % |

| Century Communities, Inc. | | | 2.3 | |

| Capital City Bank Group, Inc. | | | 2.3 | |

| Perrigo Co. PLC | | | 2.3 | |

| Radian Group, Inc. | | | 2.2 | |

| Texas Capital Bancshares, Inc. | | | 2.1 | |

| NOV, Inc. | | | 2.1 | |

| National Fuel Gas Co. | | | 1.9 | |

| Lincoln Educational Services Corp. | | | 1.9 | |

| Northwest Pipe Co. | | | 1.8 | |

Portfolio holdings, statistics, and manager views are subject to change without notice, and discussions of portfolio holdings are intended as illustrations of investment strategy, not as recommendations Index definitions and investment terms are found on the page titled “Definitions and Disclosures.” All indices are unmanaged. It is not possible to invest directly in an index. All information, unless otherwise indicated, is as of 6/30/2023.

7

| SECTOR ALLOCATION - % OF TOTAL INVESTMENTS |

The following table summarizes the sector classifications of each of the Heartland Funds as of June 30, 2023. These sectors represent groupings of industry classifications.

| | MID CAP VALUE FUND | VALUE PLUS FUND | VALUE FUND |

| Communication Services | 3.0% | 2.1% | 0.4% |

| Consumer Discretionary | 9.0 | 7.0 | 11.5 |

| Consumer Staples | 3.2 | 9.2 | 2.5 |

| Energy | 7.2 | 7.4 | 5.1 |

| Financials | 13.2 | 13.6 | 23.4 |

| Health Care | 13.3 | 12.6 | 11.6 |

| Industrials | 14.0 | 23.5 | 15.5 |

| Information Technology | 12.7 | 4.1 | 4.2 |

| Materials | 10.3 | 9.5 | 8.0 |

| Real Estate | 7.2 | 6.9 | 8.2 |

| Utilities | 6.3 | 2.7 | 5.9 |

| Short-Term Investments | 0.6 | 1.4 | 3.7 |

| Total | 100.0% | 100.0% | 100.0% |

Portfolio holdings, statistics, and manager views are subject to change without notice and discussions of portfolio holdings are intended as illustrations of investment strategy, not as recommendations.

8

THIS PAGE INTENTIONALLY LEFT BLANK

9

| HEARTLAND MID CAP VALUE FUND | SCHEDULE OF INVESTMENTS |

June 30, 2023 (Unaudited)

| | | SHARES | | | VALUE | |

| COMMON STOCKS (98.4%) | | |

| Automobiles (1.1%) | | | | | | |

| Thor Industries, Inc. | | | 52,798 | | | $ | 5,464,593 | |

| | | | | | | | | |

| Banks (3.8%) | | | | | | | | |

| PNC Financial Services Group, Inc. | | | 97,797 | | | | 12,317,532 | |

| Texas Capital Bancshares, Inc.(a) | | | 135,002 | | | | 6,952,603 | |

| | | | | | | | 19,270,135 | |

| Building Products (1.2%) | | | | | | | | |

| A.O. Smith Corp. | | | 83,083 | | | | 6,046,781 | |

| | | | | | | | | |

| Capital Markets (4.4%) | | | | | | | | |

| Interactive Brokers Group, Inc. | | | 134,390 | | | | 11,163,777 | |

| Northern Trust Corp. | | | 148,417 | | | | 11,003,637 | |

| | | | | | | | 22,167,414 | |

| Chemicals (6.7%) | | | | | | | | |

| FMC Corp. | | | 127,191 | | | | 13,271,109 | |

| PPG Industries, Inc. | | | 135,561 | | | | 20,103,696 | |

| | | | | | | | 33,374,805 | |

| Commercial Services & Supplies (1.6%) | | | | | | | | |

| Stericycle, Inc.(a) | | | 171,519 | | | | 7,965,342 | |

| | | | | | | | | |

| Containers & Packaging (3.5%) | | | | | | | | |

| Ball Corp. | | | 104,406 | | | | 6,077,473 | |

| Packaging Corp. of America | | | 87,238 | | | | 11,529,374 | |

| | | | | | | | 17,606,847 | |

| Electric Utilities (6.3%) | | | | | | | | |

| Constellation Energy Corp. | | | 135,263 | | | | 12,383,327 | |

| FirstEnergy Corp. | | | 491,719 | | | | 19,118,035 | |

| | | | | | | | 31,501,362 | |

| Electronic Equipment, Instruments & Components (1.1%) | | | | | | | | |

| TE Connectivity Ltd. | | | 37,919 | | | | 5,314,727 | |

| | | | | | | | | |

| Energy Equipment & Services (4.9%) | | | | | | | | |

| NOV, Inc. | | | 1,537,093 | | | | 24,654,972 | |

| Entertainment (1.6%) | | | | | | | | |

| Activision Blizzard, Inc. | | | 96,119 | | | | 8,102,832 | |

| Food Products (3.2%) | | | | | | | | |

| Conagra Brands, Inc. | | | 216,534 | | | | 7,301,527 | |

| Ingredion, Inc. | | | 82,752 | | | | 8,767,574 | |

| | | | | | | | 16,069,101 | |

| Ground Transportation (2.3%) | | | | | | | | |

| JB Hunt Transport | | | | | | | | |

| Services, Inc. | | | 64,879 | | | | 11,745,045 | |

| | | SHARES | | | VALUE | |

| Health Care Equipment & Supplies (2.0%) | | | | | | | | |

| DENTSPLY SIRONA, Inc. | | | 248,296 | | | $ | 9,936,806 | |

| Health Care Providers & Services (8.3%) | | | | | | | | |

| Centene Corp.(a) | | | 303,024 | | | | 20,438,969 | |

| Encompass Health Corp. | | | 80,758 | | | | 5,468,124 | |

| Quest Diagnostics, Inc. | | | 110,756 | | | | 15,567,863 | |

| | | | | | | | 41,474,956 | |

| Household Durables (2.4%) | | | | | | | | |

| Mohawk Industries, Inc.(a) | | | 117,779 | | | | 12,150,082 | |

| Insurance (4.7%) | | | | | | | | |

| First American Financial Corp. | | | 217,493 | | | | 12,401,451 | |

| Markel Group, Inc.(a) | | | 3,021 | | | | 4,178,587 | |

| Old Republic International Corp. | | | 287,439 | | | | 7,234,839 | |

| | | | | | | | 23,814,877 | |

| Leisure Products (1.7%) | | | | | | | | |

| Hasbro, Inc. | | | 134,544 | | | | 8,714,415 | |

| Machinery (5.1%) | | | | | | | | |

| Flowserve Corp. | | | 341,313 | | | | 12,679,778 | |

| Kennametal, Inc. | | | 452,150 | | | | 12,836,538 | |

| | | | | | | | 25,516,316 | |

| Marine Transportation (2.0%) | | | | | | | | |

| Kirby Corp.(a) | | | 133,584 | | | | 10,279,289 | |

| Media (1.4%) | | | | | | | | |

| Cable One, Inc. | | | 10,401 | | | | 6,834,289 | |

| Office REITs (3.4%) | | | | | | | | |

| Equity Commonwealth | | | 832,187 | | | | 16,860,109 | |

| | | | | | | | | |

| Oil, Gas & Consumable Fuels (2.2%) | | | | | | | | |

| Pioneer Natural Resources Co. | | | 53,326 | | | | 11,048,081 | |

| | | | | | | | | |

| Pharmaceuticals (2.9%) | | | | | | | | |

| Perrigo Co. PLC | | | 424,262 | | | | 14,403,695 | |

| Residential REITs (3.8%) | | | | | | | | |

| Essex Property Trust, Inc. | | | 81,006 | | | | 18,979,706 | |

| | | | | | | | | |

| Semiconductors & Semiconductor Equipment (6.9%) | | | | | | | | |

| Micron Technology, Inc. | | | 157,045 | | | | 9,911,110 | |

| Qorvo, Inc.(a) | | | 161,355 | | | | 16,463,051 | |

| Skyworks Solutions, Inc. | | | 73,755 | | | | 8,163,941 | |

| | | | | | | | 34,538,102 | |

| | | SHARES | | | VALUE | |

| Software (4.6%) | | | | | | |

| Teradata Corp.(a) | | | 431,662 | | | $ | 23,055,067 | |

| | | | | | | | | |

| Specialty Retail (3.7%) | | | | | | | | |

| CarMax, Inc.(a) | | | 220,973 | | | | 18,495,440 | |

| | | | | | | | | |

| Trading Companies & Distributors (1.6%) | | | | | | | | |

| Watsco, Inc. | | | 20,605 | | | | 7,860,189 | |

| TOTAL COMMON STOCKS |

| (Cost $452,470,200) | | $ | 493,245,375 | |

| | | INTEREST RATE | | | PAR AMOUNT | | | VALUE | |

| SHORT-TERM INVESTMENTS (0.6%) | | | | | | | | | |

| Time Deposits (0.6%) | | | | | | | | | |

| Citibank (New York) 07/03/2023(b) | | | 4.42 | % | | $ | 2,938,127 | | | $ | 2,938,127 | |

| TOTAL SHORT-TERM INVESTMENTS | | | | | |

| (Cost $2,938,127) | | | $ | 2,938,127 | |

| TOTAL INVESTMENTS - (99.0%) | | | | | |

| (Cost $455,408,327) | | | $ | 496,183,502 | |

| OTHER ASSETS AND LIABILITIES, NET - (1.0%) | | | | 5,098,083 | |

| TOTAL NET ASSETS - (100.0%) | | | $ | 501,281,585 | |

| The accompanying Notes to Financial Statements are an integral part of these Statements. |

| 10 | www.heartlandadvisors.com |

| HEARTLAND VALUE PLUS FUND | SCHEDULE OF INVESTMENTS |

| | June 30, 2023 (Unaudited) |

| | | SHARES | | | VALUE | |

| COMMON STOCKS (98.7%) | | | | | | |

| Aerospace & Defense (2.7%) | | | | | | |

| Park Aerospace Corp. | | | 855,000 | | | $ | 11,799,000 | |

| Banks (8.4%) | | | | | | | | |

| Glacier Bancorp, Inc. | | | 275,000 | | | | 8,571,750 | |

| Seacoast Banking Corp. of Florida | | | 550,000 | | | | 12,155,000 | |

| Texas Capital Bancshares, Inc.(a) | | | 315,000 | | | | 16,222,500 | |

| | | | | | | | 36,949,250 | |

| Capital Markets (2.5%) | | | | | | | | |

| Artisan Partners Asset | | | | | | | | |

| Management, Inc. (Class A) | | | 275,000 | | | | 10,810,250 | |

| | | | | | | | | |

| Chemicals (4.7%) | | | | | | | | |

| American Vanguard Corp. | | | 660,000 | | | | 11,794,200 | |

| Sensient Technologies Corp. | | | 125,000 | | | | 8,891,250 | |

| | | | | | | | 20,685,450 | |

| Commercial Services & Supplies (4.9%) | | | | | | | | |

| CoreCivic, Inc.(a) | | | 700,000 | | | | 6,587,000 | |

| Healthcare Services Group, Inc. | | | 700,000 | | | | 10,451,000 | |

| Stericycle, Inc.(a) | | | 100,000 | | | | 4,644,000 | |

| | | | | | | | 21,682,000 | |

| Construction & Engineering (2.9%) | | | | | | | | |

| Granite Construction, Inc. | | | 325,000 | | | | 12,928,500 | |

| | | | | | | | | |

| Diversified Telecommunication Services (2.1%) | | | | | | | | |

| ATN International, Inc. | | | 250,000 | | | | 9,150,000 | |

| | | | | | | | | |

| Electric Utilities (2.7%) | | | | | | | | |

| Portland General Electric Co. | | | 250,000 | | | | 11,707,500 | |

| | | | | | | | | |

| Electrical Equipment (5.6%) | | | | | | | | |

| Powell Industries, Inc. | | | 345,000 | | | | 20,903,550 | |

| Vicor Corp. | | | 70,000 | | | | 3,780,000 | |

| | | | | | | | 24,683,550 | |

| Electronic Equipment, Instruments & Components (4.1%) | | | | | | | | |

| Knowles Corp.(a) | | | 500,000 | | | | 9,030,000 | |

| Methode Electronics, Inc. | | | 275,000 | | | | 9,218,000 | |

| | | | | | | | 18,248,000 | |

| Energy Equipment & Services (4.1%) | | | | | | | | |

| ChampionX Corp. | | | 225,000 | | | | 6,984,000 | |

| Dril-Quip, Inc.(a) | | | 475,000 | | | | 11,053,250 | |

| | | | | | | | 18,037,250 | |

| | SHARES | | | VALUE | |

| Food Products (3.4%) | | | | | | |

| TreeHouse Foods, Inc.(a) | | | 300,000 | | | $ | 15,114,000 | |

| Ground Transportation (2.0%) | | | | | | | | |

| Heartland Express, Inc. | | | 550,000 | | | | 9,025,500 | |

| Health Care Equipment & Supplies (7.6%) | | | | | | | | |

| AngioDynamics, Inc.(a) | | | 450,000 | | | | 4,693,500 | |

| Avanos Medical, Inc.(a) | | | 550,000 | | | | 14,058,000 | |

| Haemonetics Corp.(a) | | | 175,000 | | | | 14,899,500 | |

| | | | | | | | 33,651,000 | |

| Health Care Technology (2.8%) | | | | | | | | |

| HealthStream, Inc. | | | 495,000 | | | | 12,157,200 | |

| Household Durables (1.6%) | | | | | | | | |

| MDC Holdings, Inc. | | | 150,000 | | | | 7,015,500 | |

| Household Products (5.8%) | | | | | | | | |

| Oil-Dri Corp. of America | | | 205,000 | | | | 12,092,950 | |

| Reynolds Consumer Products, Inc. | | | 125,000 | | | | 3,531,250 | |

| Spectrum Brands Holdings, Inc. | | | 125,000 | | | | 9,756,250 | |

| | | | | | | | 25,380,450 | |

| Insurance (2.8%) | | | | | | | | |

| The Hanover Insurance Group, Inc. | | | 110,000 | | | | 12,433,300 | |

| | | | | | | | | |

| Machinery (5.3%) | | | | | | | | |

| Astec Industries, Inc. | | | 175,000 | | | | 7,952,000 | |

| Douglas Dynamics, Inc. | | | 175,000 | | | | 5,229,000 | |

| Enerpac Tool Group Corp. (Class A) | | | 375,000 | | | | 10,125,000 | |

| | | | | | | | 23,306,000 | |

| Metals & Mining (4.8%) | | | | | | | | |

| Royal Gold, Inc. | | | 105,000 | | | | 12,051,900 | |

| Schnitzer Steel Industries, Inc. (Class A) | | | 310,000 | | | | 9,296,900 | |

| | | | | | | | 21,348,800 | |

| Oil, Gas & Consumable Fuels (3.3%) | | | | | | | | |

| Comstock Resources, Inc. | | | 1,250,000 | | | | 14,500,000 | |

| Pharmaceuticals (2.2%) | | | | | | | | |

| Phibro Animal Health Corp. (Class A) | | | 700,000 | | | | 9,590,000 | |

| Specialized REITs (6.9%) | | | | | | | | |

| Farmland Partners, Inc. | | | 600,000 | | | | 7,326,000 | |

| Lamar Advertising Co. (Class A) | | | 50,000 | | | | 4,962,500 | |

| PotlatchDeltic Corp. | | | 340,000 | | | | 17,969,000 | |

| | | | | | | | 30,257,500 | |

| | | SHARES | | | VALUE | |

| Specialty Retail (2.2%) | | | | | | |

| Monro, Inc. | | 235,000 | | $ | 9,548,050 | |

| Textiles, Apparel & Luxury Goods (3.3%) | | | | | | | | |

| Carter's, Inc. | | | 200,000 | | | | 14,520,000 | |

| TOTAL COMMON STOCKS | | | | | | | | |

| (Cost $409,007,904) | | | | | | $ | 434,528,050 | |

| | | INTEREST RATE | | | PAR AMOUNT | | | VALUE | |

| SHORT-TERM INVESTMENTS (1.5%) | | | | | | | | | |

| Time Deposits (1.5%) | | | | | | | | | |

| Citibank (New York) 07/03/2023(b) | | | 4.42 | % | | $ | 6,298,046 | | | $ | 6,298,046 | |

| TOTAL SHORT-TERM INVESTMENTS | | | | | |

| (Cost $6,298,046) | | | $ | 6,298,046 | |

| TOTAL INVESTMENTS - (100.2%) | | | | | |

| (Cost $415,305,950) | | | $ | 440,826,096 | |

| OTHER ASSETS AND LIABILITIES, NET - (-0.2%) | | | | (675,002 | ) |

| TOTAL NET ASSETS - (100.0%) | | | $ | 440,151,094 | |

| The accompanying Notes to Financial Statements are an integral part of these Statements. |

| Semi-Annual Report | June 30, 2023 | 11 |

| HEARTLAND VALUE FUND | SCHEDULE OF INVESTMENTS |

| | June 30, 2023 (Unaudited) |

| | | SHARES | | | VALUE | |

| COMMON STOCKS (96.9%) | | | | | | |

| Aerospace & Defense (1.6%) | | | | | | |

| BWX Technologies, Inc. | | | 150,000 | | | $ | 10,735,500 | |

| Automobile Components (1.0%) | | | | | | | | |

| Linamar Corp. (CAD)(c) | | | 120,000 | | | | 6,306,397 | |

| Automobiles (1.2%) | | | | | | | | |

| Thor Industries, Inc. | | | 80,000 | | | | 8,280,000 | |

| Banks (10.9%) | | | | | | | | |

| Associated Banc-Corp | | | 400,000 | | | | 6,492,000 | |

| Canadian Western Bank (CAD)(c) | | | 500,000 | | | | 9,330,062 | |

| Capital City Bank Group, Inc. | | | 500,000 | | | | 15,320,000 | |

| First Internet Bancorp | | | 250,000 | | | | 3,712,500 | |

| First Interstate | | | | | | | | |

| BancSystem, Inc. (Class A) | | | 150,000 | | | | 3,576,000 | |

| Glacier Bancorp, Inc. | | | 200,000 | | | | 6,234,000 | |

| Heritage Financial Corp. | | | 400,000 | | | | 6,468,000 | |

| Texas Capital Bancshares, Inc.(a) | | | 275,000 | | | | 14,162,500 | |

| TriCo Bancshares | | | 200,000 | | | | 6,640,000 | |

| | | | | | | | 71,935,062 | |

| | | | | | | | | |

| Beverages (1.3%) | | | | | | | | |

| Primo Water Corp. | | | 700,000 | | | | 8,778,000 | |

| | | | | | | | | |

| Chemicals (2.5%) | | | | | | | | |

| Core Molding | | | | | | | | |

| Technologies, Inc.(a) | | | 200,000 | | | | 4,550,000 | |

| Nufarm, Ltd. (AUD)(c)(d) | | | 2,000,000 | | | | 6,810,111 | |

| Orion SA | | | 250,000 | | | | 5,305,000 | |

| | | | | | | | 16,665,111 | |

| | | | | | | | | |

| Commercial Services & Supplies (2.7%) | | | | | | | | |

| CECO Environmental Corp.(a) | | | 550,000 | | | | 7,348,000 | |

| Healthcare Services Group, Inc. | | | 350,000 | | | | 5,225,500 | |

| Perma-Fix Environmental Services, Inc.(a) | | | 500,000 | | | | 5,490,000 | |

| | | | | | | | 18,063,500 | |

| | | | | | | | | |

| Communications Equipment (0.1%) | | | | | | | | |

| AudioCodes, Ltd. | | | 100,000 | | | | 913,000 | |

| | | | | | | | | |

| Construction & Engineering (1.8%) | | | | | | | | |

| Northwest Pipe Co.(a) | | | 395,000 | | | | 11,944,800 | |

| | | | | | | | | |

| Construction Materials (0.7%) | | | | | | | | |

| Knife River Corp.(a) | | | 100,000 | | | | 4,350,000 | |

| | | SHARES | | | VALUE | |

| Consumer Finance (1.0%) | | | | | | | | |

| Ezcorp, Inc. (Class A)(a) | | | 800,000 | | | $ | 6,704,000 | |

| | | | | | | | | |

| Containers & Packaging (1.3%) | | | | | | | | |

| Westrock Co. | | | 300,000 | | | | 8,721,000 | |

| | | | | | | | | |

| Diversified Consumer Services (2.9%) | | | | | | | | |

| Carriage Services, Inc. | | | 200,000 | | | | 6,494,000 | |

| Lincoln Educational Services Corp.(a)(e) | | | 1,850,000 | | | | 12,469,000 | |

| | | | | | | | 18,963,000 | |

| | | | | | | | | |

| Diversified REITs (1.0%) | | | | | | | | |

| Alpine Income Property Trust, Inc. | | | 400,000 | | | | 6,500,000 | |

| | | | | | | | | |

| Electric Utilities (1.7%) | | | | | | | | |

| ALLETE, Inc. | | | 200,000 | | | | 11,594,000 | |

| | | | | | | | | |

| Electrical Equipment (1.4%) | | | | | | | | |

| Orion Energy Systems, Inc.(a) | | | 900,000 | | | | 1,467,000 | |

| Thermon Group Holdings, Inc.(a) | | | 300,000 | | | | 7,980,000 | |

| | | | | | | | 9,447,000 | |

| | | | | | | | | |

| Electronic Equipment, Instruments & Components (1.3%) | | | | | | | | |

| Advanced Energy Industries, Inc. | | | 25,000 | | | | 2,786,250 | |

| Benchmark Electronics, Inc. | | | 225,000 | | | | 5,811,750 | |

| | | | | | | | 8,598,000 | |

| | | | | | | | | |

| Energy Equipment & Services (2.8%) | | | | | | | | |

| Dril-Quip, Inc.(a) | | | 200,000 | | | | 4,654,000 | |

| NOV, Inc. | | | 850,000 | | | | 13,634,000 | |

| | | | | | | | 18,288,000 | |

| | | | | | | | | |

| Financial Services (8.4%) | | | | | | | | |

| Cantaloupe, Inc.(a) | | | 900,000 | | | | 7,164,000 | |

| Cass Information Systems, Inc. | | | 225,682 | | | | 8,751,948 | |

| EVERTEC, Inc. | | | 200,000 | | | | 7,366,000 | |

| I3 Verticals, Inc. (Class A)(a) | | | 450,000 | | | | 10,287,000 | |

| MGIC Investment Corp. | | | 500,000 | | | | 7,895,000 | |

| Radian Group, Inc. | | | 565,395 | | | | 14,293,185 | |

| | | | | | | | 55,757,133 | |

| | | | | | | | | |

| Food Products (1.1%) | | | | | | | | |

| MamaMancini's Holdings, Inc.(a) | | | 950,000 | | | | 2,869,000 | |

| SunOpta, Inc.(a) | | | 700,000 | | | | 4,683,000 | |

| | | | | | | | 7,552,000 | |

| | | | | | | | | |

| Gas Utilities (1.9%) | | | | | | | | |

| National Fuel Gas Co. | | | 250,000 | | | | 12,840,000 | |

| | | SHARES | | | VALUE | |

| Ground Transportation (0.5%) | | | | | | |

| Marten Transport, Ltd. | | | 150,000 | | | $ | 3,225,000 | |

| | | | | | | | | |

| Health Care Equipment & Supplies (3.5%) | | | | | | | | |

| Accuray, Inc.(a) | | | 2,000,000 | | | | 7,740,000 | |

| Haemonetics Corp.(a) | | | 100,000 | | | | 8,514,000 | |

| Integer Holdings Corp.(a) | | | 75,000 | | | | 6,645,750 | |

| | | | | | | | 22,899,750 | |

| | | | | | | | | |

| Health Care Providers & Services (4.8%) | | | | | | | | |

| Encompass Health Corp. | | | 240,000 | | | | 16,250,400 | |

| InfuSystem Holdings, Inc.(a) | | | 425,000 | | | | 4,092,750 | |

| Patterson Cos., Inc. | | | 350,000 | | | | 11,641,000 | |

| | | | | | | | 31,984,150 | |

| | | | | | | | | |

| Health Care Technology (0.4%) | | | | | | | | |

| Computer Programs and Systems, Inc.(a) | | | 100,000 | | | | 2,469,000 | |

| | | | | | | | | |

| Hotel & Resort REITs (1.7%) | | | | | | | | |

| Sunstone Hotel Investors, Inc. | | | 1,100,000 | | | | 11,132,000 | |

| | | | | | | | | |

| Hotels, Restaurants & Leisure (1.7%) | | | | | | | | |

| Everi Holdings, Inc.(a) | | | 300,000 | | | | 4,338,000 | |

| Potbelly Corp.(a) | | | 800,000 | | | | 7,024,000 | |

| | | | | | | | 11,362,000 | |

| | | | | | | | | |

| Household Durables (3.9%) | | | | | | | | |

| Century Communities, Inc. | | | 200,000 | | | | 15,324,000 | |

| Mohawk Industries, Inc.(a) | | | 100,000 | | | | 10,316,000 | |

| | | | | | | | 25,640,000 | |

| | | | | | | | | |

| Insurance (3.3%) | | | | | | | | |

| International General Insurance Holdings, Ltd. | | | 550,000 | | | | 4,917,000 | |

| Old Republic International Corp. | | | 150,000 | | | | 3,775,500 | |

| Stewart Information Services Corp. | | | 185,000 | | | | 7,610,900 | |

| Tiptree, Inc. | | | 350,000 | | | | 5,253,500 | |

| | | | | | | | 21,556,900 | |

| | | | | | | | | |

| Life Sciences Tools & Services (0.7%) | | | | | | | | |

| Harvard Bioscience, Inc.(a) | | | 850,000 | | | | 4,666,500 | |

| | | | | | | | | |

| Machinery (3.8%) | | | | | | | | |

| Flowserve Corp. | | | 200,000 | | | | 7,430,000 | |

| Luxfer Holdings PLC | | | 175,000 | | | | 2,490,250 | |

| Shyft Group, Inc. | | | 500,000 | | | | 11,030,000 | |

| Twin Disc, Inc.(a) | | | 400,000 | | | | 4,504,000 | |

| | | | | | | | 25,454,250 | |

| | | | | | | | | |

| Media (0.4%) | | | | | | | | |

| WideOpenWest, Inc.(a) | | | 350,000 | | | | 2,954,000 | |

| The accompanying Notes to Financial Statements are an integral part of these Statements. |

| 12 | www.heartlandadvisors.com |

| HEARTLAND VALUE FUND | SCHEDULE OF INVESTMENTS |

| | June 30, 2023 (Unaudited) |

| | | SHARES | | | VALUE | |

| Metals & Mining (3.6%) | | | | | | | | |

| Centerra Gold, Inc. | | | 1,800,000 | | | $ | 10,800,000 | |

| Major Drilling Group | | | | | | | | |

| International, Inc. (CAD)(c)(a) | | | 1,000,000 | | | | 6,899,415 | |

| Osisko Gold Royalties, Ltd. | | | 400,000 | | | | 6,148,000 | |

| | | | | | | | 23,847,415 | |

| Oil, Gas & Consumable Fuels (2.3%) | | | | | | | | |

| Berry Corp. (Class A) | | | 1,000,000 | | | | 6,880,000 | |

| Denbury, Inc.(a) | | | 100,000 | | | | 8,626,000 | |

| | | | | | | | 15,506,000 | |

| Pharmaceuticals (2.3%) | | | | | | | | |

| Perrigo Co. PLC | | | 450,000 | | | | 15,277,500 | |

| Professional Services (2.6%) | | | | | | | | |

| Barrett Business Services, Inc. | | | 135,000 | | | | 11,772,000 | |

| Hudson Global, Inc.(a)(e) | | | 252,700 | | | | 5,440,631 | |

| | | | | | | | 17,212,631 | |

| Real Estate Management & Development (1.6%) | | | | | | | | |

| Forestar Group, Inc.(a) | | | 475,000 | | | | 10,711,250 | |

| Residential REITs (2.0%) | | | | | | | | |

BSR Real Estate Investment Trust (CAD)(c) | | | 400,300 | | | | 5,127,829 | |

| UMH Properties, Inc. | | | 500,000 | | | | 7,990,000 | |

| | | | | | | | 13,117,829 | |

| Semiconductors & Semiconductor Equipment (2.8%) | | | | | | | | |

| Photronics, Inc.(a) | | | 300,000 | | | | 7,737,000 | |

| Silicon Motion Technology Corp. (ADR) | | | 150,000 | | | | 10,779,000 | |

| | | | | | | | 18,516,000 | |

| Specialized REITs (2.0%) | | | | | | | | |

| National Storage Affiliates Trust | | | 225,000 | | | | 7,836,750 | |

| PotlatchDeltic Corp. | | | 100,000 | | | | 5,285,000 | |

| | | | | | | | 13,121,750 | |

| Specialty Retail (0.3%) | | | | | | | | |

| Envela Corp. | | | 240,388 | | | | 1,769,256 | |

| Textiles, Apparel & Luxury Goods (0.7%) | | | | | | | | |

| Carter's, Inc. | | | 60,000 | | | | 4,356,000 | |

| Trading Companies & Distributors (1.1%) | | | | | | | | |

| NOW, Inc.(a) | | | 700,000 | | | | 7,252,000 | |

| | | SHARES | | | VALUE | |

| Water Utilities (2.3%) | | | | | | |

| Consolidated Water Co., Ltd. | | | 400,000 | | | $ | 9,692,000 | |

| Pure Cycle Corp.(a) | | | 500,000 | | | | 5,500,000 | |

| | | | | | | | 15,192,000 | |

| TOTAL COMMON STOCKS | | | | | | | | |

| (Cost $518,863,264) | | | | | | $ | 642,158,684 | |

| | | INTEREST RATE | | | PAR AMOUNT | | | VALUE | |

| SHORT-TERM INVESTMENTS (3.7%) | | | | | | | | | |

| Time Deposits (3.7%) | | | | | | | | | |

| Citibank (New York) 07/03/2023(b) | | | 4.42 | % | | $ | 24,724,430 | | | $ | 24,724,430 | |

| TOTAL SHORT-TERM INVESTMENTS | | | | | |

| (Cost $24,724,430) | | | $ | 24,724,430 | |

| TOTAL INVESTMENTS - (100.6%) | | | | | |

| (Cost $543,587,694) | | | $ | 666,883,114 | |

| OTHER ASSETS AND LIABILITIES, NET - (-0.6%) | | | | (4,121,083 | ) |

| TOTAL NET ASSETS - (100.0%) | | | $ | 662,762,031 | |

| The accompanying Notes to Financial Statements are an integral part of these Statements. | |

| Semi-Annual Report | June 30, 2023 | 13 |

| HEARTLAND FUNDS | SCHEDULES OF INVESTMENTS - FOOTNOTES |

| | June 30, 2023 (Unaudited) |

| (a) | Non-income producing security. Includes securities which did not pay at least one dividend in the year preceding the date of this statement. |

| (b) | Time deposits are considered short-term obligations and are payable on demand. Interest rates change periodically on specified dates. The rate listed is the 7-day yield as of June 30, 2023. |

| (c) | Traded in a foreign country. |

| (d) | Classified as Level 2. Valued using methods determined by the Board of Directors or using systematic fair valuation model provided by an independent pricing service. See Note 3 in Notes to Financial Statements. |

| (e) | Affiliated company. See Note 10 to Notes to Financial Statements. |

Common Abbreviations:

| ADR | American Depositary Receipt. |

| Ltd. | Limited. |

| PLC | Public Limited Company is a publicly traded company which signifies that shareholders have limited liability. |

Currency Abbreviations:

| CAD | Canadian Dollar |

| AUD | Australian Dollar |

Percentages are stated as a percent of net assets.

Sector and Industry classifications are sourced from GICS®, The Global Industry Classification Standard (GICS®) is the exclusive intellectual property of MSCI Inc. (“MSCI”) and S&P Global Market Intelligence ("S&P"). Neither MSCI, S&P, their affiliates, nor any of their third party providers (“GICS Parties”) makes any representations or warranties, express or implied, with respect to GICS or the results to be obtained by the use thereof, and expressly disclaims all warranties, including warranties of accuracy, completeness, merchantability and fitness for a particular purpose. The GICS Parties shall not have any liability for any direct, indirect, special, punitive, consequential, or any other damages (including lost profits) even if notified of such damages.

| The accompanying Notes to Financial Statements are an integral part of these Statements. |

| 14 | www.heartlandadvisors.com |

| HEARTLAND FUNDS | STATEMENTS OF ASSETS AND LIABILITIES |

| | June 30, 2023 (Unaudited) |

| | | MID CAP VALUE FUND | | | VALUE PLUS FUND | | | VALUE FUND | |

| ASSETS: | | | | | | | | | |

| Investments in securities, at cost(a) | | $ | 455,408,327 | | | $ | 415,305,950 | | | $ | 543,587,694 | |

| Investments in securities, at value | | $ | 496,183,502 | | | $ | 440,826,096 | | | $ | 648,973,483 | |

| Investments in affiliates, at value (See Note 10) | | | - | | | | - | | | | 17,909,631 | |

| Total Investments, at value | | | 496,183,502 | | | | 440,826,096 | | | | 666,883,114 | |

| Receivable for securities sold | | | 3,954,934 | | | | 290,013 | | | | 603,299 | |

| Accrued dividends and interest | | | 658,401 | | | | 387,948 | | | | 381,231 | |

| Receivable for capital shares issued | | | 903,693 | | | | 78,373 | | | | 147,315 | |

| Prepaid expenses | | | 81,897 | | | | 33,488 | | | | 46,367 | |

| Total Assets | | | 501,782,427 | | | | 441,615,918 | | | | 668,061,326 | |

| LIABILITIES: | | | | | | | | | | | | |

| Payable for securities purchased | | | - | | | | 1,122,885 | | | | 4,358,278 | |

| Payable for capital shares redeemed | | | 375,291 | | | | 112,433 | | | | 751,913 | |

| Accrued expenses | | | | | | | | | | | | |

| Management fees | | | 27,476 | | | | 25,142 | | | | 40,469 | |

| Distribution fees - Investor Class | | | 4,757 | | | | 5,539 | | | | 7,309 | |

| Fund accounting fees | | | 19,930 | | | | 22,202 | | | | 36,193 | |

| Transfer agency fees | | | 31,619 | | | | 48,611 | | | | 34,743 | |

| Custody fees | | | 3,501 | | | | 6,645 | | | | 10,093 | |

| Audit fees | | | 12,143 | | | | 11,124 | | | | 16,643 | |

| Printing fees | | | 26,125 | | | | 69,536 | | | | 40,987 | |

| Other | | | - | | | | 40,707 | | | | 2,667 | |

| Total Liabilities | | | 500,842 | | | | 1,464,824 | | | | 5,299,295 | |

| TOTAL NET ASSETS | | $ | 501,281,585 | | | $ | 440,151,094 | | | $ | 662,762,031 | |

| | | | | | | | | | | | | |

| NET ASSETS CONSIST OF: | | | | | | | | | | | | |

| Paid-in capital | | $ | 447,669,781 | | | $ | 401,985,888 | | | $ | 509,530,808 | |

| Total distributable earnings | | | 53,611,804 | | | | 38,165,206 | | | | 153,231,223 | |

| TOTAL NET ASSETS | | $ | 501,281,585 | | | $ | 440,151,094 | | | $ | 662,762,031 | |

| | | | | | | | | | | | | |

| NET ASSET VALUE, OFFERING PRICE & REDEMPTION PRICE PER SHARE: | | | | | | | | | | | | |

| INVESTOR CLASS: | | | | | | | | | | | | |

| Net assets | | $ | 233,974,591 | | | $ | 271,833,820 | | | $ | 598,290,851 | |

| Shares outstanding | | | 17,502,099 | | | | 7,353,342 | | | | 13,925,041 | |

| NET ASSET VALUE, OFFERING PRICE & REDEMPTION PRICE PER SHARE | | $ | 13.37 | | | $ | 36.97 | | | $ | 42.97 | |

| INSTITUTIONAL CLASS: | | | | | | | | | | | | |

| Net assets | | $ | 267,306,994 | | | $ | 168,317,274 | | | $ | 64,471,180 | |

| Shares outstanding | | | 19,870,977 | | | | 4,582,618 | | | | 1,461,826 | |

| NET ASSET VALUE, OFFERING PRICE & REDEMPTION PRICE PER SHARE | | $ | 13.45 | | | $ | 36.73 | | | $ | 44.10 | |

| (a) | Includes cost of investments in affiliates of $- for the Mid Cap Value Fund, $- for the Value Plus Fund and $17,413,126 for the Value Fund. See Note 10 in the Notes to Financial Statements. |

| The accompanying Notes to Financial Statements are an integral part of these Statements. | |

| Semi-Annual Report | June 30, 2023 | 15 |

| HEARTLAND FUNDS | STATEMENTS OF OPERATIONS |

| | For the Six Months Ended June 30, 2023 (Unaudited) |

| | | MID CAP VALUE FUND | | | VALUE PLUS FUND | | | VALUE FUND | |

| INVESTMENT INCOME: | | | | | | | | | |

| Dividends(a) | | $ | 4,580,514 | | | $ | 4,957,230 | | | $ | 5,737,531 | |

| Interest | | | 132,900 | | | | 411,222 | | | | 661,335 | |

| Foreign taxes withheld | | | - | | | | (286 | ) | | | (106,147 | ) |

| Total Investment Income | | | 4,713,414 | | | | 5,368,166 | | | | 6,292,719 | |

| | | | | | | | | | | | | |

| EXPENSES: | | | | | | | | | | | | |

| Management fees | | | 1,562,681 | | | | 1,569,238 | | | | 2,447,583 | |

| Distribution fees - Investor Class | | | 274,090 | | | | 338,662 | | | | 576,638 | |

| Transfer agency fees | | | 215,945 | | | | 271,546 | | | | 237,172 | |

| Fund accounting fees | | | 68,359 | | | | 75,258 | | | | 108,321 | |

| Custodian fees | | | 10,217 | | | | 13,301 | | | | 21,348 | |

| Printing and communication fees | | | 5,832 | | | | 12,071 | | | | 8,196 | |

| Postage fees | | | 8,673 | | | | 17,371 | | | | 8,996 | |

| Legal fees | | | 27,859 | | | | 35,405 | | | | 51,803 | |

| Registration fees | | | 20,145 | | | | 23,056 | | | | 4,952 | |

| Directors’ fees | | | 40,588 | | | | 51,760 | | | | 76,373 | |

| Audit and tax fees | | | 10,945 | | | | 12,186 | | | | 9,574 | |

| Insurance fees | | | 15,129 | | | | 19,815 | | | | 29,918 | |

| Other expenses | | | 11,065 | | | | 13,054 | | | | 20,669 | |

| Total Expenses before waivers | | | 2,271,528 | | | | 2,452,723 | | | | 3,601,543 | |

| Expenses waived by investment advisor (See Note 6) | | | 222,775 | | | | - | | | | - | |

| Total Expenses after waivers | | | 2,048,753 | | | | 2,452,723 | | | | 3,601,543 | |

| NET INVESTMENT INCOME | | | 2,664,661 | | | | 2,915,443 | | | | 2,691,176 | |

| | | | | | | | | | | | | |

| REALIZED & UNREALIZED GAINS (LOSSES) ON INVESTMENTS, AND TRANSLATION OF ASSETS AND LIABILITIES IN FOREIGN CURRENCY | | |

| Net realized gains (losses) on: | | | | | | | | | | | | |

| Investments | | | 11,746,487 | | | | 9,806,176 | | | | 29,869,341 | |

| Investments - Affiliated securities (See Note 10) | | | - | | | | - | | | | (747,754 | ) |

| Foreign currency translation | | | - | | | | - | | | | (9,320 | ) |

| Net change in unrealized appreciation (depreciation) on: | | | | | | | | | | | | |

| Investments | | | 18,965,758 | | | | (12,934,072 | ) | | | (1,132,587 | ) |

| Investments - Affiliated securities (See Note 10) | | | - | | | | - | | | | 7,300,194 | |

| Foreign currency translation | | | - | | | | - | | | | 155 | |

| TOTAL REALIZED & UNREALIZED NET GAINS (LOSSES) ON INVESTMENTS, AND TRANSLATION OF ASSETS IN FOREIGN CURRENCY | | | 30,712,245 | | | | (3,127,896 | ) | | | 35,280,029 | |

| NET INCREASE (DECREASE) IN NET ASSETS RESULTING FROM OPERATIONS | | $ | 33,376,906 | | | $ | (212,453 | ) | | $ | 37,971,205 | |

| (a) | Includes $- received from affiliated issuers held by the Value Fund. See Note 10 in the Notes to Financial Statements. |

| The accompanying Notes to Financial Statements are an integral part of these Statements | |

| 16 | www.heartlandadvisors.com |

| HEARTLAND FUNDS | STATEMENTS OF CHANGES IN NET ASSETS |

| | |

| | | MID CAP VALUE FUND | | | VALUE PLUS FUND | | | VALUE FUND | |

| | | For the Six Months Ended June 30, 2023 (Unaudited) | | | For the Year Ended December 31, 2022 | | | For the Six Months Ended June 30, 2023 (Unaudited) | | | For the Year Ended December 31, 2022 | | | For the Six Months Ended June 30, 2023 (Unaudited) | | | For the Year Ended December 31, 2022 | |

| FROM INVESTMENT OPERATIONS: | | | |

| Net investment income | | $ | 2,664,661 | | | $ | 2,288,859 | | | $ | 2,915,443 | | | $ | 2,646,422 | | | $ | 2,691,176 | | | $ | 2,818,250 | |

| Net realized gains | | | 11,746,487 | | | | 13,334,014 | | | | 9,806,176 | | | | 2,656,250 | | | | 29,112,267 | | | | 5,533,353 | |

| Net change in unrealized appreciation (depreciation) | | | 18,965,758 | | | | (24,160,569 | ) | | | (12,934,072 | ) | | | (30,014,764 | ) | | | 6,167,762 | | | | (83,292,876 | ) |

| Net increase (decrease) in net assets resulting from operations | | | 33,376,906 | | | | (8,537,696 | ) | | | (212,453 | ) | | | (24,712,092 | ) | | | 37,971,205 | | | | (74,941,273 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| DISTRIBUTIONS TO SHAREHOLDERS: | | | | | | | | | | | | | | | | | | | | | | | | |

| Investor Class | | | - | | | | (10,850,257 | ) | | | - | | | | (6,022,695 | ) | | | - | | | | (16,977,738 | ) |

| Institutional Class | | | - | | | | (7,495,651 | ) | | | - | | | | (4,106,441 | ) | | | - | | | | (1,802,249 | ) |

| Total distributions to shareholders | | | - | | | | (18,345,908 | ) | | | - | | | | (10,129,136 | ) | | | - | | | | (18,779,987 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | |

CAPITAL TRANSACTIONS: | | | | | | | | | | | | | | | | | | | | | | | | |

| Investor Class | | | | | | | | | | | | | | | | | | | | | | | | |

| Proceeds from shares issued | | | 20,857,764 | | | | 19,368,233 | | | | 20,866,249 | | | | 16,429,781 | | | | 6,841,142 | | | | 8,020,563 | |

| Dividends reinvested | | | 18,372 | | | | 10,624,103 | | | | - | | | | 5,932,882 | | | | - | | | | 16,315,469 | |

| Value of shares redeemed(a) | | | (12,882,403 | ) | | | (30,403,465 | ) | | | (21,840,972 | ) | | | (41,597,246 | ) | | | (23,229,601 | ) | | | (44,083,777 | ) |

| Total Investor Class | | | 7,993,733 | | | | (411,129 | ) | | | (974,723 | ) | | | (19,234,583 | ) | | | (16,388,459 | ) | | | (19,747,745 | ) |

| Institutional Class | | | | | | | | | | | | | | | | | | | | | | | | |

| Proceeds from shares issued | | | 129,008,911 | | | | 78,440,292 | | | | 37,011,546 | | | | 47,514,874 | | | | 1,738,686 | | | | 6,385,682 | |

| Dividends reinvested | | | - | | | | 7,438,577 | | | | - | | | | 3,647,828 | | | | - | | | | 1,727,689 | |

| Value of shares redeemed(a) | | | (19,889,285 | ) | | | (16,950,884 | ) | | | (32,048,737 | ) | | | (49,326,038 | ) | | | (1,359,219 | ) | | | (6,668,167 | ) |

| Total Institutional Class | | | 109,119,626 | | | | 68,927,985 | | | | 4,962,809 | | | | 1,836,664 | | | | 379,467 | | | | 1,445,204 | |

| Net increase (decrease) in net assets derived from capital transactions | | | 117,113,359 | | | | 68,516,856 | | | | 3,988,086 | | | | (17,397,919 | ) | | | (16,008,992 | ) | | | (18,302,541 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| TOTAL INCREASE (DECREASE) IN NET ASSETS | | | 150,490,265 | | | | 41,633,252 | | | | 3,775,633 | | | | (52,239,147 | ) | | | 21,962,213 | | | | (112,023,801 | ) |

| NET ASSETS AT THE BEGINNING OF THE PERIOD | | | 350,791,320 | | | | 309,158,068 | | | | 436,375,461 | | | | 488,614,608 | | | | 640,799,818 | | | | 752,823,619 | |

| NET ASSETS AT THE END OF THE PERIOD | | $ | 501,281,585 | | | $ | 350,791,320 | | | $ | 440,151,094 | | | $ | 436,375,461 | | | $ | 662,762,031 | | | $ | 640,799,818 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

FUND SHARE TRANSACTIONS | | | | | | | | | | | | | | | | | | | | | | | | |

| Investor Class | | | | | | | | | | | | | | | | | | | | | | | | |

| Shares Issued | | | 1,616,238 | | | | 1,487,673 | | | | 565,312 | | | | 445,478 | | | | 162,904 | | | | 187,059 | |

| Reinvested Shares | | | 1,503 | | | | 869,403 | | | | - | | | | 163,485 | | | | - | | | | 409,320 | |

| Shares Redeemed | | | (1,002,353 | ) | | | (2,345,635 | ) | | | (589,804 | ) | | | (1,136,868 | ) | | | (549,936 | ) | | | (1,034,473 | ) |

| Net increase (decrease) resulting from share transactions | | | 615,388 | | | | 11,441 | | | | (24,492 | ) | | | (527,905 | ) | | | (387,032 | ) | | | (438,094 | ) |

| Institutional Class | | | | | | | | | | | | | | | | | | | | | | | | |

| Shares Issued | | | 10,018,742 | | | | 6,045,436 | | | | 975,829 | | | | 1,299,313 | | | | 40,747 | | | | 142,252 | |

| Reinvested Shares | | | - | | | | 605,254 | | | | - | | | | 101,300 | | | | - | | | | 42,273 | |

| Shares Redeemed | | | (1,541,962 | ) | | | (1,311,593 | ) | | | (886,008 | ) | | | (1,348,475 | ) | | | (31,110 | ) | | | (159,548 | ) |

| Net increase resulting from share transactions | | | 8,476,780 | | | | 5,339,097 | | | | 89,821 | | | | 52,138 | | | | 9,637 | | | | 24,977 | |

| (a) | Value of shares redeemed includes amounts for early redemption fees. See Note 7 in Notes to Financial Statements. |

| The accompanying Notes to Financial Statements are an integral part of these Statements. | |

| Semi-Annual Report | June 30, 2023 | 17 |

| HEARTLAND FUNDS | FINANCIAL HIGHLIGHTS |

| | |

| | | Net asset value, beginning of period | | | Net investment income (loss)(a)(b) | | | Net realized and unrealized gains (losses) | | | Total income (loss) from investment operations | | | Distributions from net investment income | | | Distributions from net realized gains on investments | | | Total distributions | | | Net asset value, end of period | |

| MID CAP VALUE FUND | | | | | | | | | | | | | | | | | | | | | | | | |

| Investor Class | | | | | | | | | | | | | | | | | | | | | | | | |

| June 30, 2023 (Unaudited) | | $ | 12.38 | | | $ | 0.08 | | | $ | 0.91 | | | $ | 0.99 | | | $ | - | | | $ | - | | | $ | - | | | $ | 13.37 | |

| December 31, 2022 | | | 13.47 | | | | 0.09 | | | | (0.50 | ) | | | (0.41 | ) | | | (0.07 | ) | | | (0.61 | ) | | | (0.68 | ) | | | 12.38 | |

| December 31, 2021 | | | 13.03 | | | | 0.14 | | | | 3.53 | | | | 3.67 | | | | (0.12 | ) | | | (3.11 | ) | | | (3.23 | ) | | | 13.47 | |

| December 31, 2020 | | | 12.24 | | | | 0.13 | | | | 0.72 | | | | 0.85 | | | | (0.06 | ) | | | - | | | | (0.06 | ) | | | 13.03 | |

| December 31, 2019 | | | 9.99 | | | | 0.11 | | | | 2.42 | | | | 2.53 | | | | (0.10 | ) | | | (0.18 | ) | | | (0.28 | ) | | | 12.24 | |

| December 31, 2018 | | | 11.99 | | | | 0.17 | | | | (1.21 | ) | | | (1.04 | ) | | | (0.13 | ) | | | (0.83 | ) | | | (0.96 | ) | | | 9.99 | |

| Institutional Class | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| June 30, 2023 (Unaudited) | | $ | 12.44 | | | $ | 0.22 | | | $ | 0.79 | | | $ | 1.01 | | | $ | - | | | $ | - | | | $ | - | | | $ | 13.45 | |

| December 31, 2022 | | | 13.53 | | | | 0.13 | | | | (0.51 | ) | | | (0.38 | ) | | | (0.10 | ) | | | (0.61 | ) | | | (0.71 | ) | | | 12.44 | |

| December 31, 2021 | | | 13.08 | | | | 0.18 | | | | 3.54 | | | | 3.72 | | | | (0.16 | ) | | | (3.11 | ) | | | (3.27 | ) | | | 13.53 | |

| December 31, 2020 | | | 12.27 | | | | 0.17 | | | | 0.71 | | | | 0.88 | | | | (0.07 | ) | | | - | | | | (0.07 | ) | | | 13.08 | |

| December 31, 2019 | | | 10.00 | | | | 0.15 | | | | 2.41 | | | | 2.56 | | | | (0.11 | ) | | | (0.18 | ) | | | (0.29 | ) | | | 12.27 | |