UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-5003

Blue Chip Value Fund, Inc.

(Exact name of registrant as specified in charter)

1225 17th Street, 26th Floor, Denver, Colorado 80202 |

(Address of principal executive offices) (Zip code) |

Michael P. Malloy

Drinker Biddle & Reath LLP

One Logan Square

Suite 2000

Philadelphia, Pennsylvania 19103-6996

(Name and address of agent for service)

Registrant’s Telephone Number, including Area Code: (800) 624-4190

Date of fiscal year end: December 31

Date of reporting period: January 1, 2009 - December 31, 2009

Item 1 - Reports to Stockholders

Annual Report to Stockholders December 31, 2009 |

Send Us Your E-mail Address

If you would like to receive monthly portfolio composition and characteristic updates, press releases and financial reports electronically as soon as they are available, please send an e-mail to blu@denvest.com and include your name and e-mail address. You will still receive paper copies of any required communications and reports in the mail. This service is completely voluntary and you can cancel at any time by contacting us via e-mail at blu@denvest.com or toll-free at 1-800-624-4190.

TABLE OF CONTENTS

Investment Adviser's Commentary | 2 |

Sector Diversification Chart | 4 |

Average Annual Total Returns | 4 |

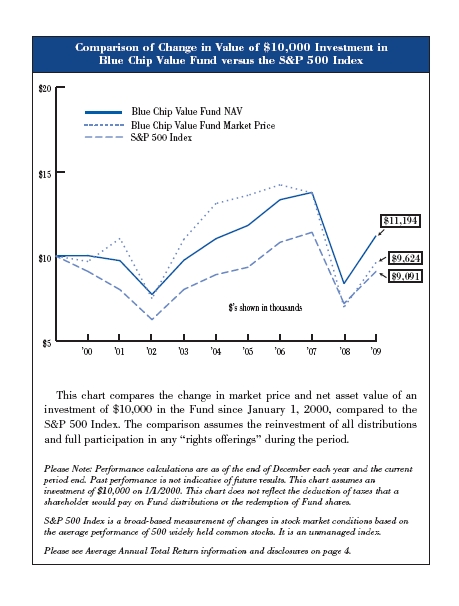

Change in Investment of $10,000 | 5 |

Performance History | 6 |

Sources of Distributions | 7 |

Dividend Reinvestment and Cash Purchase Plan | 8 |

Other Important Information | 9 |

Portfolio Management Team | 10 |

Directors and Officers | 11 |

Report of Independent Registered Public Accounting Firm | 15 |

Statement of Investments | 16 |

Country Breakdown | 19 |

Statement of Assets and Liabilities | 20 |

Statement of Operations | 21 |

Statements of Changes in Net Assets | 22 |

Statement of Cash Flows | 23 |

Financial Highlights | 24 |

Notes to Financial Statements | 26 |

1-800-624-4190 • www.blu.com | 1 |

INVESTMENT ADVISER’S COMMENTARY

| Dear Fellow Stockholders: | February 10, 2010 |

For the year ended December 31, 2009, the Blue Chip Value Fund, Inc.’s net asset value was up 33.9% while the S&P 500 Index, the Fund’s benchmark index was up 26.5% and the Fund’s peer group index, the Lipper Large Core Index was up 28.15%. The Fund’s portfolio returns benefitted from financial leverage and good stock selection.

We believe the financial crisis of 2008-2009 has abated and 2010 should be a year of economic progress and further stock market gains. Our focus continues to be on large companies we believe have strong balance sheets, good profitability and strong free cash flow.

Although it is paramount to keep looking forward, it is occasionally beneficial to stop for a moment to reflect on the past. In the decade following the turn of the 21st century, we have experienced many significant events. Among them, the shock and tragedy of 9/11, two recessions, the exposure of numerous Ponzi schemes, and the near collapse of the international banking system. Despite the challenges of the past decade, Blue Chip Value Fund’s 10-year average annual investment return (+1.13%) was better than that of the S&P 500 Index (–0.95%).

Turning to the portfolio, the stock price of Expedia, an online travel agency within the consumer cyclical sector, tripled during the year. The company’s earnings and cash flow exceeded expectations as investors appeared to recognize that, with an improved economic outlook, prospects for profits from travel booking existed. The consumer cyclical sector was the Fund’s best performing sector for the year.

Within the energy sector, Fund holding Transocean returned over 75% for the year. Transocean provides offshore drilling rigs to exploration and development companies. In late 2008, investors seemed to disregard the stability of the cash flows we thought inherent in Transocean’s long-term rig contracts and, as a result, the company’s stock price declined. During 2009, the company reported results that allowed investors to recognize the cash flows generated by these rig contracts. While energy was one of the weaker sectors of the Index, the Fund’s energy holdings outperformed relative to the S&P 500 Index.

The basic materials sector was the strongest sector in the S&P 500 Index and Fund holdings outperformed the Index led by International Paper. The company returned over 135% during 2009. During the fourth quarter of 2009, International Paper and its largest competitors announced containerboard price increases. We believe that this price increase combined with inventory replenishment, which had been at 15 year lows, should help increase company profits in 2010.

Our technology holdings performed well, up more than 44% on average for the year with none up less than 30%. However, strong performance from stocks we didn’t own, such as Apple, led the Fund’s technology holdings to underperform relative to the S&P 500 Index. We continue to monitor stock prices, free cash flow trends and expectations in this sector.

| 2 | Annual Report December 31, 2009 |

Within capital goods, Fund holding ITT Industries, an integrated manufacturer of defense, fluid and motion control products, gave updated earnings guidance for fiscal year 2010 that was slightly below investors’ expectations. The adjustment appears to be related to the timing of defense contracts as well as higher than expected raw material costs. However, the company has a history of providing conservative guidance and we anticipate that this year is no different. We are encouraged by ITT’s balance sheet and continue to believe that the company’s ability to generate free cash flow is undervalued.

Fund holding Norfolk Southern Corporation, an eastern U.S. railroad operator, lagged the transportation sector through much of the year. However, it was among our best performing stocks in the fourth quarter. Solid third-quarter results highlighted that pricing and volume improvement at the company had begun to take hold. The company continues with its cost cutting initiatives which, in our opinion, should aid its bottom line performance. Despite Norfolk’s strong fourth quarter performance, our transportation stocks modestly under-performed versus the S&P 500 Index for much of the year.

Our investment process uses an active, bottom-up stock selection process that seeks to capture the return potential of large companies that are undervalued or out of favor, but whose business appears to us to be solid or improving. Our sector weightings and portfolio positioning are driven by this fundamental research. While no major changes in the portfolio were thought necessary, we are slightly more overweight in basic materials and transportation where we continue to find companies that meet our investment criteria at attractive prices. We are slightly more underweight in capital goods stocks where we believe price expectations are more difficult to justify.

It appears to us that 2010 will be a year where company fundamentals will be much more relevant than in 2009, and we believe this environment should favor our disciplined, research-driven investment process. Thank you for your support.

Sincerely,

Todger Anderson, CFA

President, Blue Chip Value Fund, Inc.

Chairman, Denver Investment Advisors LLC

The Investment Adviser’s Commentary included in this report contains certain forward-looking statements about the factors that may affect the performance of the Fund in the future. These statements are based on Fund management’s predictions and expectations concerning certain future events and their expected impact on the Fund, such as performance of the economy as a whole and of specific industry sectors, changes in the levels of interest rates, the impact of developing world events, and other factors that may influence the future performance of the Fund. Management believes these forward-looking statements to be reasonable, although they are inherently uncertain and difficult to predict. Actual events may cause adjustments in portfolio management strategies from those currently expected to be employed.

1-800-624-4190 • www.blu.com | 3 |

Sector Diversification in Comparison to

S&P 500 as of December 31, 2009* |

| | Fund | S&P 500 |

Basic Materials | 6.6% | 3.1% |

Capital Goods | 4.5% | 7.3% |

Commercial Services | 4.8% | 2.3% |

Communications | 8.2% | 8.1% |

Consumer Cyclical | 12.9% | 12.7% |

Consumer Staples | 7.0% | 10.5% |

Energy | 10.6% | 11.1% |

Interest Rate Sensitive | 12.6% | 12.7% |

Medical/Healthcare | 10.7% | 11.8% |

REITs | 0.0% | 1.2% |

Technology | 15.1% | 13.4% |

Transportation | 3.7% | 2.1% |

Utilities | 3.1% | 3.7% |

Short-Term Investments | 0.2% | 0.0% |

*Sector diversification percentages are based on the Fund’s total investments at market value. Sector diversification is subject to change and may not be representative of future investments. |

Average Annual Total Returns

as of December 31, 2009 |

| Return | 3 Mos. | 1-Year | 3-Year | 5-Year | 10-Year |

Blue Chip Value Fund – NAV | 4.74% | 33.92% | (5.64%) | 0.31% | 1.13% |

Blue Chip Value Fund – | | | | | |

Market Price | 2.94% | 37.97% | (12.21%) | (6.01%) | (0.39%) |

S&P 500 Index | 6.04% | 26.47% | (5.63%) | 0.42% | (0.95%) |

Past performance is no guarantee of future results. Share prices will fluctuate, so that a share may be worth more or less than its original cost when sold. Total investment return is calculated assuming a purchase of common stock on the opening of the first day and a sale on the closing of the last day of each period reported. Dividends and distributions, if any, are assumed for purposes of this calculation to be reinvested at prices obtained under the Fund’s dividend rein- vestment plan. Rights offerings, if any, are assumed for purposes of this calculation to be fully subscribed under the terms of the rights offering. Please note that the Fund’s total return shown above does not reflect the deduction of taxes that a stockholder would pay on Fund distributions or the cost of sale of Fund shares. Current performance may be higher or lower than the total return shown above. Please visit our website at www.blu.com to obtain the most recent month end returns. Generally, total investment return based on net asset value will be higher than total investment return based on market value in periods where there is an increase in the discount or a decrease in the premium of the market value to the net asset value from the beginning to the end of such periods. Conversely, total investment return based on the net asset value will be lower than total investment return based on market value in periods where there is a decrease in the discount or an increase in the premium of the market value to the net asset value from the beginning to the end of such periods. The Fund’s annualized gross expense ratio for the twelve months ended December 31, 2009 was 1.37%. |

| 4 | Annual Report December 31, 2009 |

1-800-624-4190 • www.blu.com | 5 |

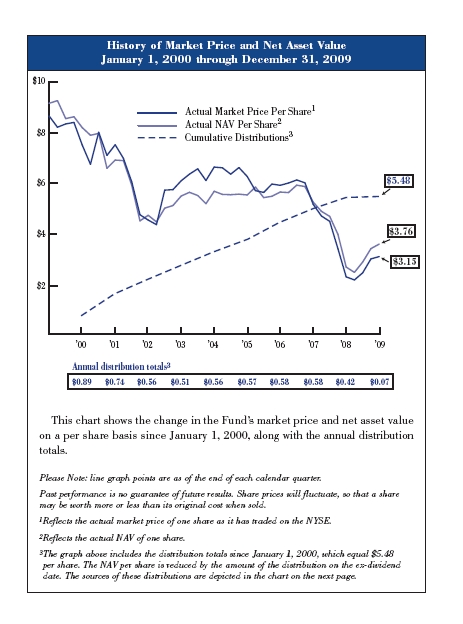

| 6 | Annual Report December 31, 2009 |

STOCKHOLDER DISTRIBUTION INFORMATION

Certain tax information regarding Blue Chip Value Fund, Inc. is required to be provided to stockholders based upon the Fund’s income and distributions to the stockholders for the calendar year ended December 31, 2009.

The following table summarizes the final sources of the 2009 reportable distributions for tax purposes.

| | Net | | Short-Term | | Long-Term | | Return | | | |

| | Investment | | Capital | | Capital | | of | | | |

| | Income | | Gain | | Gain | | Capital | | Total | |

| 4th Quarter 2008 | $ | 0.008147 | | $ | 0.000000 | | $ | 0.000000 | | $ | 0.061853 | | $ 0.07 | * |

| 1st Quarter 2009 | $ | 0.008147 | | $ | 0.000000 | | $ | 0.000000 | | $ | 0.061853 | | $ | 0.07 | |

| Total | $ | 0.016294 | | $ | 0.000000 | | $ | 0.000000 | | $ | 0.123706 | | $ | 0.14 | |

*Pursuant to Sector 852 of the Internal Revenue Code, the taxability of this distribution had been deferred until 2009.

The Fund notified stockholders by February 15, 2010 of amounts for use in preparing 2009 income tax returns.

100% of the distributions paid from net investment income and short-term capital gain qualify for the corporate dividends received deduction and meet the requirements of the tax rules regarding qualified dividend income. In addition, none of the distributions from net investment income include income derived from U.S. Treasury obligations. There were no assets invested in direct U.S. Government Obligations as of December 31, 2009.

| HISTORICAL SOURCES OF DISTRIBUTIONS | | | | | | |

| | | | | | | | | Total | | |

| | | Net | | | | | | Amount of | | Amount of |

| | | Investment | | Capital | | Return of | | Distribution | | Distribution |

| Year | | Income | | Gains | | Capital | | (Tax Basis) | | (Book Basis) |

| 2000 | | | $0.053000 | | | $0.837000 | | | $0.000000 | | | $0.89 | | | $0.89 |

| 2001 | | | $0.041200 | | | $0.362500 | | | $0.336300 | | | $0.74 | | | $0.74 |

| 2002 | | | $0.035100 | | | $0.000000 | | | $0.524900 | | | $0.56 | | | $0.56 |

| 2003 | | | $0.013600 | | | $0.000000 | | | $0.496400 | | | $0.51 | | | $0.51 |

| 2004 | | | $0.028300 | | | $0.531700 | | | $0.000000 | | | $0.56 | | | $0.56 |

| 2005 | | | $0.015000 | | | $0.112800 | | | $0.442200 | | | $0.57 | | | $0.57 |

| 2006 | | | $0.018200 | | | $0.126000 | | | $0.435800 | | | $0.58 | | | $0.58 |

| 2007 | | | $0.014600 | | | $0.211800 | | | $0.213600 | | | $0.44 | | | $0.58 |

| 2008 | | | $0.018000 | | | $0.007300 | | | $0.464700 | | | $0.49 | | | $0.42 |

| 2009 | | | $0.016294 | | | $0.000000 | | | $0.123706 | | | $0.14 | | | $0.07 |

| Totals | | | $0.253294 | | | $2.189100 | | | $3.037606 | | | $5.48 | | | $5.48 |

| % of Total | | | | | | | | | | | | | | | |

| Distribution | | | 4.62% | | | 39.95% | | | 55.43% | | 100% | | | |

1-800-624-4190 • www.blu.com | 7 |

DIVIDEND REINVESTMENT AND CASH PURCHASE PLAN

The Blue Chip Value Fund Inc.’s (the “Fund”) Dividend Reinvestment and Cash Purchase Plan (the “Plan”) offers stockholders the opportunity to reinvest the Fund’s dividends and distributions in additional shares of the Fund. A stockholder may also make additional cash investments under the Plan.

Participating stockholders will receive additional shares issued at a price equal to the net asset value per share as of the close of the New York Stock Exchange on the record date (“Net Asset Value”), unless at such time the Net Asset Value is higher than the market price of the Fund’s common stock plus brokerage commission. In this case the Fund, through BNY Mellon Shareowner Services, (the “Plan Administrator”) will attempt, generally over the next 10 business days (the “Trading Period”), to acquire shares of the Fund’s common stock in the open market at a price plus brokerage commission which is less than the Net Asset Value. In the event that prior to the time such acquisition is completed, the market price of such common stock plus commission equals or exceeds the Net Asset Value, or in the event that such market purchases are unable to be completed by the end of the Trading Period, then the balance of the distribution shall be completed by issuing additional shares at Net Asset Value. The reinvestment price is then determined by the weighted average price per share, including trading fees, of the shares issued by the Fund and/or acquired by the Plan Administrator in connection with that transaction.

Participating stockholders may also make additional cash investments (minimum $50 and maximum $10,000 per month) to acquire additional shares of the Fund. Please note, however, that these additional shares will be purchased at market value plus brokerage commission (without regard to net asset value) per share. The transaction price of shares and fractional shares acquired on the open market for each participant’s account in connection with the Plan shall be determined by the weighted average price per share, including trading fees, of the shares acquired by the Plan Administrator in connection with that transaction.

A registered stockholder may join the Plan by completing an Enrollment Form from the Plan Administrator. The Plan Administrator will hold the shares acquired through the Plan in book-entry form, unless you request share certificates. If your shares are registered with a broker, you may still be able to participate in the Fund’s Dividend Reinvestment and Cash Purchase Plan. Please contact your broker about how to reregister your shares through the Direct Registration System and to inquire if there are any fees which may be charged by the broker to your account.

The automatic reinvestment of dividends and distributions will not relieve participants of any income taxes that may be payable (or required to be withheld) on dividends or distributions, even though the stockholder does not receive the cash.

A stockholder may elect to withdraw from the Plan at any time on prior written notice, and receive future dividends and distributions in cash. There is no penalty for withdrawal from the Plan and stockholders who have withdrawn from the Plan may

| 8 | Annual Report December 31, 2009 |

rejoin in the future. In addition, you may request the Plan Administrator to sell all or a portion of your shares. When your shares are sold, you will receive the proceeds less a service charge of $15.00 and trading fees of $0.02 per share. The Plan Administrator will generally sell your shares on the day your request is received in good order, however the Plan Administrator reserves the right to take up to 5 business days to sell your shares. Shares will be aggregated by the Plan Administrator with the shares of other participants selling their shares that day and sold on the open market. A participant will receive the weighted average price minus trading fees and service charges of all liquidated shares sold by the Plan Administrator on the transaction date.

The Fund may amend the Plan at any time upon 30-days prior notice to participants.

Additional information about the Plan may be obtained from the Plan Administrator by writing to BNY Mellon Shareowner Services, 480 Washington Blvd., Jersey City, NJ 07310, by telephone at (800) 624-4190 (option #1) or by visiting the Plan Administrator at www.bnymellon.com/shareowner.

OTHER IMPORTANT INFORMATION

Notice is hereby given in accordance with Section 23(c) of the Investment Company Act of 1940 that the Fund may purchase, from time to time, shares of its common stock on the open market.

How to Obtain a Copy of the Fund’s Proxy Voting Policies and Records

A description of the policies and procedures that are used by the Fund’s investment adviser to vote proxies relating to the Fund’s portfolio securities is available (1) without charge, upon request, by calling (800) 624-4190; (2) on the Fund’s website at www.blu.com and (3) on the Fund’s Form N-CSR which is available on the U.S. Securities and Exchange Commission (“SEC”) website at www.sec.gov.

Information regarding how the Fund’s investment adviser voted proxies relating to the Fund’s portfolio securities during the most recent 12-month period ended June 30 is available, (1) without charge, upon request by calling (800) 624-4190; (2) on the Fund’s website at www.blu.com and (3) on the SEC website at www.sec.gov.

Quarterly Portfolio Holdings

The Fund files its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. The Fund’s Forms N-Q are available on the SEC’s website at www.sec.gov and may be reviewed and copied at the SEC’s Public Reference Room in Washington, D.C. Information on the operation of the SEC’s Public Reference Room may be obtained by calling 1-800-SEC-0330. In addition, the Fund’s complete schedule of portfolio holdings for the first and third quarters of each fiscal year is available on the Fund’s website at www.blu.com.

1-800-624-4190 • www.blu.com | 9 |

PORTFOLIO MANAGEMENT TEAM OF BLUE CHIP VALUE FUND

Kris Herrick, CFA, Partner, Director of Value Research and Portfolio Manager, joined Denver Investments in 2000. Prior to joining the firm, he was an Equity Research Analyst with Jurika and Voyles (since 1997). He has 13 years total investment experience and has been a member of the Fund’s portfolio management team since December 1, 2003.

Mark Adelmann, CFA, CPA (Inactive), Partner and Portfolio Manager/Analyst, joined Denver Investments in 1995. He has 31 years total investment experience and has been the Fund’s portfolio manager since June 3, 2002.

Derek Anguilm, Partner and Portfolio Manager/Analyst, joined Denver Investments in 2000. Prior to joining the firm he was with EVEREN Securities (since 1999). He has 11 years total investment experience and has been a member of the Fund’s portfolio management team since December 1, 2003.

Troy Dayton, CFA, Partner and Portfolio Manager/Analyst, joined Denver Investments in 2002. Prior to joining the firm, he was an Equity Research Analyst with Jurika and Voyles (since 2001) and Dresdner RCM Global Investors (since 1998). He has 14 years total investment experience and has been a member of the Fund’s portfolio management team since December 1, 2003.

Lisa Ramirez, CFA, Vice President and Portfolio Manager/Analyst, joined Denver Investments in 1989 and started as a portfolio administrator in 1993. She became an analyst on the Mid-Cap Growth team in 1997 and joined the Value team in 2005. She has 17 years total investment experience and joined the Fund’s portfolio management team on April 30, 2009.

| 10 | Annual Report December 31, 2009 |

INFORMATION ON THE DIRECTORS AND OFFICERS OF THE FUND

The list below provides certain information about the identity and business experience of the directors and officers of the Fund.

INTERESTED DIRECTORS*

TODGER ANDERSON, CFA1

Age: 65

Position(s) Held with the Fund:

President and Director

Term of Office2 and Length of Time Served:

President since 1987. Director from 1988 to 1995 and since 1998. Term as Director expires in 2010.

Principal Occupations During the Past Five Years:

Chairman, Denver Investment Advisors LLC (since 2004);

President, Westcore Trust (since 2005);

President, Denver Investment Advisors LLC and predecessor organizations (1983-2004);

Portfolio Manager, Westcore MIDCO Growth Fund (1986-2005);

Portfolio Co-Manager, Westcore Select Fund (2001-2005).

Number of Portfolios in Fund Complex3 Overseen by Director: One

Other Directorships4 Held by Director: None

KENNETH V. PENLAND, CFA1

Age: 67

Position(s) Held with the Fund:

Chairman of the Board and Director

Term of Office2 and Length of Time Served:

Chairman of the Board and Director since 1987. Term as Director expires in 2012.

Principal Occupations During the Past Five Years:

Chairman, Denver Investment Advisors LLC and predecessor organizations (1983-2001);

President, Westcore Trust (1995-2001)

Trustee, Westcore Trust (2001-2005).

Number of Portfolios in Fund Complex3 Overseen by Director: One

Other Directorships4 Held by Director: None

1-800-624-4190 • www.blu.com | 11 |

INDEPENDENT DIRECTORS

RICHARD C. SCHULTE1

Age: 65

Position(s) Held with the Fund:

Director

Term of Office2 and Length of Time Served:

Director since 1987. Term expires in 2011.

Principal Occupations During the Past Five Years:

Private Investor;

President, Transportation Service Systems, Inc., a subsidiary of Southern Pacific Lines, Denver, Colorado (1993-1996);

Employee, Rio Grande Industries, Denver, Colorado (holding company) (1991-1993).

Number of Portfolios in Fund Complex3 Overseen by Director: One

Other Directorships4 Held by Director: None

ROBERTA M. WILSON, CFA1

Age: 66

Position(s) Held with the Fund:

Director

Term of Office2 and Length of Time Served:

Director since 1987. Term expires in 2012.

Principal Occupations During the Past Five Years:

Management consultant and coach (since 1998);

Director of Finance, Denver Board of Water Commissioners (Retired), Denver, Colorado (1985-1998).

Number of Portfolios in Fund Complex3 Overseen by Director: One

Other Directorships4 Held by Director: None

LEE W. MATHER, JR.1

Age: 66

Position(s) Held with the Fund:

Director

Term of Office2 and Length of Time Served:

Director since 2001. Term expires in 2011.

Principal Occupations During the Past Five Years:

Director, American Rivers (conservation organization) (2000-2006);

Investment Banker, Merrill Lynch & Co. (1977-2000).

Number of Portfolios in Fund Complex3 Overseen by Director: One

Other Directorships4 Held by Director: None

| 12 | Annual Report December 31, 2009 |

OFFICERS

MARK M. ADELMANN, CFA, CPA (Inactive)

Age: 52

1225 Seventeenth St.

26th Floor

Denver, Colorado 80202

Position(s) Held with the Fund:

Vice President

Term of Office2 and Length of Time Served:

Vice President since 2002.

Principal Occupations During the Past Five Years:

Vice President (since 2000) and member (since 2001), Denver Investment Advisors LLC;

Research Analyst, Denver Investment Advisors LLC (since 1995);

Portfolio management team member, Westcore Trust (since 2002).

NANCY P. O’HARA

Age: 51

One Logan Square

18th and Cherry Sts.

Philadelphia, PA 19103

Position(s) Held with the Fund:

Secretary

Term of Office2 and Length of Time Served:

Secretary since 2007.

Principal Occupations During the Past Five Years:

Counsel (since 2009) and Associate (1999-2009) of the law firm of Drinker Biddle & Reath LLP, Philadelphia, PA.

JASPER R. FRONTZ, CPA, CFA5

Age: 41

1225 Seventeenth St.

26th Floor

Denver, Colorado 80202

Position(s) Held with the Fund:

Treasurer, Chief Compliance Officer

Term of Office2 and Length of Time Served:

Treasurer since 1997, Chief Compliance Officer since 2004.

1-800-624-4190 • www.blu.com | 13 |

Principal Occupations During the Past Five Years:

Vice President, Denver Investment Advisors LLC (since 2000);

Director of Mutual Fund Administration, Denver Investment Advisors LLC (since 1997);

Fund Controller, ALPS Mutual Fund Services, Inc. (1995-1997);

Registered Representative, ALPS Distributors, Inc. (since 1995).

| NOTES |

* | These directors each may be deemed to be an “interested director” of the Fund within the meaning of the Investment Company Act of 1940 by virtue of their affiliations with the Fund’s investment adviser and their positions as officers of the Fund. |

| 1. | Each director may be contacted by writing to the director, c/o Blue Chip Value Fund, Inc., 1225 Seventeenth Street, 26th Floor, Denver, Colorado 80202, Attn: Jasper Frontz. |

| 2. | The Fund’s By-Laws provide that the Board of Directors shall consist of three classes of members. Directors are chosen for a term of three years, and the term of one class of directors expires each year. The officers of the Fund are elected by the Board of Directors and, subject to earlier termination of office, each officer holds office for one year and until his or her successor is elected and qualified. |

| 3. | The Fund complex is comprised of fifteen portfolios, the Fund, twelve Westcore Funds, the Dunham Small-Cap Value Fund and the RiverSource Partners VP Small-Cap Value Fund. |

| 4. | Includes only directorships of companies required to report to the Securities and Exchange Commission under the Securities Exchange Act of 1934 (i.e., “public companies”) or other investment companies registered under the Investment Company Act of 1940. |

| 5. | Mr. Frontz also serves as Treasurer and Chief Compliance Officer of Westcore Trust. |

| 14 | Annual Report December 31, 2009 |

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Shareholders and Board of Directors of

Blue Chip Value Fund, Inc.:

We have audited the accompanying statement of assets and liabilities of Blue Chip Value Fund, Inc. (the “Fund”), including the statement of investments, as of December 31, 2009, and the related statements of operations and cash flows for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. The Fund is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of December 31, 2009, by correspondence with the custodian. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of Blue Chip Value Fund, Inc. as of December 31, 2009, the results of its operations and its cash flows for the year then ended, the changes in its net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America.

DELOITTE & TOUCHE LLP

Denver, Colorado

February 16, 2010

1-800-624-4190 • www.blu.com | 15 |

| BLUE CHIP VALUE FUND, INC. |

| | | | | | | |

| STATEMENT OF INVESTMENTS |

| December 31, 2009 |

| | | | | | | | | Market |

| | | Shares | | | Cost | | | Value |

| COMMON STOCKS – 110.45% | | | | | | | |

| BASIC MATERIALS – 7.32% | | | | | | | |

| Forestry & Paper – 5.50% | | | | | | | |

| Ball Corp. | | 41,940 | | $ | 2,200,539 | | $ | 2,168,298 |

| International Paper Co. | | 138,600 | | | 3,349,014 | | | 3,711,708 |

| | | | | | 5,549,553 | | | 5,880,006 |

| Specialty Chemicals – 1.82% | | | | | | | |

| The Mosaic Co. | | 32,500 | | | 1,706,361 | | | 1,941,225 |

| TOTAL BASIC MATERIALS | | | | 7,255,914 | | | 7,821,231 |

| | | | | | | | | |

| CAPITAL GOODS – 5.02% | | | | | | | |

| Aerospace & Defense– 2.90% | | | | | | | | |

| General Dynamics Corp. | | 22,100 | | | 1,444,761 | | | 1,506,557 |

| Raytheon Co. | | 31,000 | | | 1,465,509 | | | 1,597,120 |

| | | | | | 2,910,270 | | | 3,103,677 |

| Industrial Products – 2.12% | | | | | | | |

| ITT Corp. | | 45,500 | | | 2,500,494 | | | 2,263,170 |

| TOTAL CAPITAL GOODS | | | | | 5,410,764 | | | 5,366,847 |

| | | | | | | | | |

| COMMERCIAL SERVICES – 5.30% | | | | | | | |

| Business Products & Services – 2.20% | | | | | | | |

| Quanta Services Inc.** | | 113,000 | | | 3,475,189 | | | 2,354,920 |

| IT Services – 1.67% | | | | | | | | |

| Computer Sciences Corp.** | | 31,050 | | | 1,630,333 | | | 1,786,307 |

| Transaction Processing – 1.43% | | | | | | | |

| The Western Union Co. | | 81,000 | | | 1,341,107 | | | 1,526,850 |

| TOTAL COMMERCIAL SERVICES | | | | 6,446,629 | | | 5,668,077 |

| | | | | | | | | |

| COMMUNICATIONS – 9.14% | | | | | | | |

| Networking – 4.76% | | | | | | | | |

| Cisco Systems Inc.** | | 212,500 | | | 5,209,726 | | | 5,087,250 |

| Telecomm Equipment & Solutions – 4.38% | | | | | | |

| Nokia Corp. – ADR (Finland) | 72,230 | | | 1,081,638 | | | 928,156 |

| QUALCOMM Inc. | | 81,200 | | | 3,667,187 | | | 3,756,312 |

| | | | | | 4,748,825 | | | 4,684,468 |

| TOTAL COMMUNICATIONS | | | | 9,958,551 | | | 9,771,718 |

| | | | | | | | | |

| CONSUMER CYCLICAL – 14.30% | | | | | | | |

| Apparel & Footwear Manufacturers – 1.93% | | | | | | |

| Nike Inc. | | 31,150 | | | 1,956,597 | | | 2,058,081 |

| Clothing & Accessories– 1.07% | | | | | | | | |

| TJX Companies Inc. | | 31,400 | | | 1,070,492 | | | 1,147,670 |

| 16 | Annual Report December 31, 2009 |

| STATEMENT OF INVESTMENTS (cont’d.) |

| | | | | | Market |

| | Shares | | Cost | | Value |

| Department Stores – 2.10% | | | | | | | |

| Macy’s Inc. | 133,700 | | $ | 2,378,598 | | $ | 2,240,812 |

| Other Consumer Services – 2.70% | | | | | | | |

| Expedia Inc.** | 112,400 | | | 3,017,526 | | | 2,889,804 |

| Publishing & Media – 2.82% | | | | | | | |

| Walt Disney Co. | 93,500 | | | 2,708,030 | | | 3,015,374 |

| Restaurants – 1.97% | | | | | | | |

| Darden Restaurants Inc. | 59,940 | | | 1,879,712 | | | 2,102,096 |

| Specialty Retail – 1.71% | | | | | | | |

| Best Buy Co. Inc | 46,300 | | | 1,992,323 | | | 1,826,998 |

| TOTAL CONSUMER CYCLICAL | | | | 15,003,278 | | | 15,280,835 |

| | | | | | | | |

| CONSUMER STAPLES – 7.75% | | | | | | | |

| Consumer Products – 2.80% | | | | | | | |

| Colgate Palmolive Co. | 36,400 | | | 2,894,135 | | | 2,990,260 |

| Food & Agricultural Products – 4.95% | | | | | | | |

| Campbell Soup Co. | 67,900 | | | 2,476,554 | | | 2,295,020 |

| Unilever N.V. (Netherlands) | 92,700 | | | 3,284,852 | | | 2,996,991 |

| | | | | 5,761,406 | | | 5,292,011 |

| TOTAL CONSUMER STAPLES | | | | 8,655,541 | | | 8,282,271 |

| | | | | | | | |

| ENERGY – 11.72% | | | | | | | |

| Exploration & Production – 4.50% | | | | | | | |

| Occidental Petroleum Corp. | 59,180 | | | 4,099,689 | | | 4,814,293 |

| Integrated Oils – 3.92% | | | | | | | |

| Exxon Mobil Corp. | 18,000 | | | 1,365,034 | | | 1,227,420 |

| Marathon Oil Corp. | 94,800 | | | 3,366,929 | | | 2,959,656 |

| | | | | 4,731,963 | | | 4,187,076 |

| Oil Services – 3.30% | | | | | | | |

| Transocean Inc. (Switzerland)** | 42,549 | | | 3,933,951 | | | 3,523,057 |

| TOTAL ENERGY | | | | 12,765,603 | | | 12,524,426 |

| | | | | | | | |

| INTEREST RATE SENSITIVE – 13.93% | | | | | | | |

| Money Center Banks – 6.13% | | | | | | | |

| Bank of America Corp. | 194,000 | | | 3,225,368 | | | 2,921,640 |

| JPMorgan Chase & Co. | 87,100 | | | 3,799,943 | | | 3,629,457 |

| | | | | 7,025,311 | | | 6,551,097 |

| Property Casualty Insurance – 3.08% | | | | | | | |

| ACE Ltd. (Switzerland)** | 38,700 | | | 2,109,636 | | | 1,950,480 |

| The Travelers Cos. Inc. | 26,900 | | | 1,295,715 | | | 1,341,234 |

| | | | | 3,405,351 | | | 3,291,714 |

| Regional Banks – 1.09% | | | | | | | |

| SunTrust Banks Inc. | 57,400 | | | 1,197,875 | | | 1,164,646 |

1-800-624-4190 • www.blu.com | 17 |

| STATEMENT OF INVESTMENTS (cont’d.) |

| | | | | | Market |

| | Shares | | Cost | | Value |

| Securities & Asset Management – 3.63% | | | | | | | |

| The Bank of New York Mellon Corp. | 38,400 | | $ | 1,257,450 | | $ | 1,074,048 |

| Invesco Ltd. | 56,200 | | | 1,370,566 | | | 1,320,138 |

| State Street Corp. | 34,200 | | | 2,116,113 | | | 1,489,068 |

| | | | | 4,744,129 | | | 3,883,254 |

| TOTAL INTEREST RATE SENSITIVE | | | | 16,372,666 | | | 14,890,711 |

| | | | | | | | |

| MEDICAL & HEALTHCARE – 11.80% | | | | | | | |

| Medical Technology – 2.71% | | | | | | | |

| Zimmer Holdings Inc.** | 49,000 | | | 3,345,140 | | | 2,896,390 |

| Pharmaceuticals – 9.09% | | | | | | | |

| Abbott Laboratories | 53,000 | | | 2,802,905 | | | 2,861,470 |

| Amgen Inc.** | 54,500 | | | 3,254,314 | | | 3,083,065 |

| Forest Laboratories Inc.** | 80,000 | | | 2,176,616 | | | 2,568,800 |

| Pfizer Inc. | 66,468 | | | 1,197,725 | | | 1,209,053 |

| | | | | 9,431,560 | | | 9,722,388 |

| TOTAL MEDICAL & HEALTHCARE | | | | 12,776,700 | | | 12,618,778 |

| | | | | | | | |

| TECHNOLOGY – 16.71% | | | | | | | |

| Computer Software – 5.60% | | | | | | | |

| Microsoft Corp. | 88,300 | | | 2,318,118 | | | 2,692,267 |

| Symantec Corp.** | 184,200 | | | 3,261,616 | | | 3,295,338 |

| | | | | 5,579,734 | | | 5,987,605 |

| PC’s & Servers – 5.38% | | | | | | | |

| Dell Inc.** | 147,200 | | | 2,262,451 | | | 2,113,792 |

| International Business Machines Corp. | 27,800 | | | 3,275,796 | | | 3,639,020 |

| | | | | 5,538,247 | | | 5,752,812 |

| Semiconductors – 5.73% | | | | | | | |

| Altera Corp. | 153,900 | | | 3,103,339 | | | 3,482,756 |

| Intel Corp. | 129,100 | | | 2,486,977 | | | 2,633,640 |

| | | | | 5,590,316 | | | 6,116,396 |

| TOTAL TECHNOLOGY | | | | 16,708,297 | | | 17,856,813 |

| | | | | | | | |

| TRANSPORTATION – 4.06% | | | | | | | |

| Railroads – 4.06% | | | | | | | |

| Norfolk Southern Corp. | 49,800 | | | 2,622,313 | | | 2,610,516 |

| Union Pacific Corp. | 27,100 | | | 1,672,103 | | | 1,731,690 |

| | | | | 4,294,416 | | | 4,342,206 |

| TOTAL TRANSPORTATION | | | | 4,294,416 | | | 4,342,206 |

| | | | | | | | |

| UTILITIES – 3.40% | | | | | | | |

| Independent Power – 1.31% | | | | | | | |

| PPL Corp. | 43,450 | | | 1,999,930 | | | 1,403,870 |

| 18 | Annual Report December 31, 2009 |

| STATEMENT OF INVESTMENTS (cont’d.) |

| | | | | | Market |

| | Shares | | Cost | | Value |

| Regulated Electric – 2.09% | | | | | | | |

| Edison International | 64,200 | | $ | 2,046,265 | | $ | 2,232,876 |

| TOTAL UTILITIES | | | | 4,046,195 | | | 3,636,746 |

| TOTAL COMMON STOCKS | | | | 119,694,554 | | | 118,060,659 |

| | | | | | | | |

| SHORT TERM INVESTMENTS – 0.23% | | | | | | |

| Fidelity Institutional Money Market | | | | | | | |

| Government Portfolio – Class I | | | | | | | |

| (7 Day Yield 0.05%)(1) | 247,438 | | | 247,438 | | | 247,438 |

| TOTAL SHORT TERM INVESTMENTS | | | | 247,438 | | | 247,438 |

| | | | | | | | |

| TOTAL INVESTMENTS | 110.68% | | $ | 119,941,992 | | $ | 118,308,097 |

| Liabilities in Excess of Other Assets | (10.68)% | | | | | | (11,418,283) |

| NET ASSETS | 100.00% | | | | | $ | 106,889,814 |

| | | | | | | | |

| | | | | | | | |

| **Non-dividend paying stock |

| (1) Investments in other funds are calculated at their respective net asset values as determined by those funds, in accordance with the Investment Company Act of 1940. |

| ADR – American Depositary Receipt |

| Sector and industry classifications presented herein are based on the sector and industry categorization methodology of the Investment Adviser to the Fund. |

| |

| COUNTRY BREAKDOWN |

| As of December 31, 2009 (Unaudited) |

| | | | | |

| | Market | | |

| Country | Value | | % |

| United States | $ | 108,909,413 | | 101.89% |

| Switzerland | | 5,473,537 | | 5.12% |

| Netherlands | | 2,996,991 | | 2.80% |

| Finland | | 928,156 | | 0.87% |

| Total Investments | $ | 118,308,097 | | 110.68% |

| Liabilities in Excess of Other Assets | | (11,418,283) | | (10.68%) |

| Net Assets | $ | 106,889,814 | | 100.00% |

| | | | | |

| | | | | |

| Please note the country classification is based on the company headquarters. All of the Fund’s investments are traded on U.S. exchanges. |

| | | | | |

| See accompanying notes to financial statements. |

1-800-624-4190 • www.blu.com | 19 |

| BLUE CHIP VALUE FUND, INC. |

| | | |

| STATEMENT OF ASSETS AND LIABILITIES |

| December 31, 2009 |

| | | |

| ASSETS | | |

| Investments at market value (cost $119,941,992) | $ | 118,308,097 |

| Dividends and interest receivable | | 166,673 |

| Other assets | | 18,687 |

TOTAL ASSETS | | 118,493,457 |

| | | |

| LIABILITIES | | |

| Loan payable to bank (Note 5) | | 11,465,000 |

| Interest due on loan payable to bank | | 12,283 |

| Advisory fee payable | | 57,877 |

| Administration fee payable | | 8,182 |

| Accrued Compliance Officer fees | | 4,681 |

| Accrued expenses and other liabilities | | 55,620 |

TOTAL LIABILITIES | | 11,603,643 |

| NET ASSETS | $ | 106,889,814 |

| | | |

| COMPOSITION OF NET ASSETS | | |

| Capital stock, at par | $ | 284,639 |

| Paid-in-capital | | 108,493,226 |

| Accumulated net realized loss | | (254,156) |

| Net unrealized depreciation on investments | | (1,633,895) |

| NET ASSETS | $ | 106,889,814 |

| | | |

| SHARES OF COMMON STOCK OUTSTANDING | |

(100,000,000 shares authorized at $0.01 par value) | | 28,463,912 |

| | | |

| Net asset value per share | $ | 3.76 |

| | | |

| | | |

| See accompanying notes to financial statements. |

| 20 | Annual Report December 31, 2009 |

| BLUE CHIP VALUE FUND, INC. |

| | | | | | | |

| STATEMENT OF OPERATIONS |

| For the Year Ended December 31, 2009 |

| | | | | | | |

| INCOME | | | | | | |

| Dividends (net of foreign withholding taxes of $20,980) | | $ | 1,702,783 | | | |

| Interest | | | 936 | | | |

TOTAL INCOME | | | | | $ | 1,703,719 |

| | | | | | | |

| EXPENSES | | | | | | |

| Investment advisory fee (Note 4) | | | 584,387 | | | |

| Administrative services fee (Note 4) | | | 87,251 | | | |

| Interest on outstanding loan payable to bank | | | 140,027 | | | |

| Directors’ fees | | | 86,639 | | | |

| Legal fees | | | 86,032 | | | |

| Stockholder reporting | | | 75,000 | | | |

| Transfer agent fees | | | 65,000 | | | |

| Audit and tax fees | | | 29,570 | | | |

| NYSE listing fees | | | 27,023 | | | |

| Insurance and fidelity bond | | | 23,253 | | | |

| Chief Compliance Officer fees | | | 21,525 | | | |

| Custodian fees | | | 9,600 | | | |

| Other | | | 4,540 | | | |

| TOTAL EXPENSES | | | | | | 1,239,847 |

| NET INVESTMENT INCOME | | | | | | 463,872 |

| REALIZED AND UNREALIZED GAIN | | | | | | |

| ON INVESTMENTS | | | | | | |

| Net realized gain on investments | | | | | | 1,301,120 |

| Change in net unrealized appreciation or | | | | | | |

| depreciation of investments | | | | | | 24,839,041 |

| NET REALIZED AND UNREALIZED GAIN | | | | | | |

| ON INVESTMENTS | | | | | | 26,140,161 |

| NET INCREASE IN NET ASSETS | | | | | | |

| RESULTING FROM OPERATIONS | | | | | $ | 26,604,033 |

| | | | | | | |

| | | | | | | |

| See accompanying notes to financial statements. |

1-800-624-4190 • www.blu.com | 21 |

| BLUE CHIP VALUE FUND, INC. |

| | | | |

| STATEMENTS OF CHANGES IN NET ASSETS |

| | | For the | | | For the |

| | | Year Ended | | | Year Ended |

| | | December 31, | | | December 31, |

| | | 2009 | | | 2008 |

| | | | | | |

| Increase/(decrease) in net assets | | | | | |

| from operations: | | | | | |

| Net investment income | $ | 463,872 | | $ | 510,959 |

| Net realized gain on investments | | 1,301,120 | | | 248,725 |

| Change in net unrealized appreciation | | | | | |

| or depreciation of investments | | 24,839,041 | | | (58,762,315) |

| | | 26,604,033 | | | (58,002,631) |

| | | | | | |

| Decrease in net assets from distributions | | | | | |

| to stockholders from: | | | | | |

| Net investment income | | (463,872) | | | (510,959) |

| Net realized gain on investments | | — | | | (208,973) |

| Tax return of capital | | (1,529,359) | | | (11,232,334) |

| | | (1,993,231) | | | (11,952,266) |

| | | | | | |

| Increase in net assets from common | | | | | |

| stock transactions: | | | | | |

| Net asset value of common stock issued to | | | | | |

| stockholders from reinvestment of dividends | | | | | |

| (0 and 29,014 shares issued, respectively) | | — | | | 142,459 |

| | | — | | | 142,459 |

| | | | | | |

| NET INCREASE/(DECREASE) IN NET ASSETS | | 24,610,802 | | | (69,812,438) |

| | | | | | |

| NET ASSETS | | | | | |

| Beginning of year | | 82,279,012 | | | 152,091,450 |

| End of year (including undistributed net investment | | | | | |

| income of $0 and $0, respectively) | $ | 106,889,814 | | $ | 82,279,012 |

| | | | | | |

| | | | | | |

| See accompanying notes to financial statements. |

| 22 | Annual Report December 31, 2009 |

| BLUE CHIP VALUE FUND, INC. | | |

| | | |

| STATEMENT OF CASH FLOWS | | |

| For the Year Ended December 31, 2009 | | |

| | | |

| Cash Flows from Operating Activities | | |

| Net increase in net assets from operations | $ | 26,604,033 |

| Adjustments to reconcile net increase in net | | |

| assets from operations to net cash provided | | |

| by operating activities: | | |

| Purchase of investment securities | | (86,674,183) |

| Proceeds from disposition of investment securities | | 90,851,426 |

| Net sale of short-term investment securities | | 44,461 |

| Proceeds from class-action litigation settlements | | 59,833 |

| Net realized gain from securities investments | | (1,301,120) |

| Net change in unrealized depreciation | | |

| on investments | | (24,839,041) |

| Decrease in dividends and interest receivable | | 59,454 |

| Increase in other assets | | (3) |

| Increase in advisory fee payable | | 14,203 |

| Increase in interest due on loan payable to bank | | 1,391 |

| Increase in administrative fee payable | | 1,284 |

| Decrease in other accrued expenses and payables | | (26,033) |

| Net cash provided by operating activities | | 4,795,705 |

| | | |

| Cash Flows from Financing Activities | | |

| Proceeds from bank borrowing | | 6,565,000 |

| Repayment of bank borrowing | | (7,375,000) |

| Cash distributions paid | | (3,985,705) |

| Net cash used in financing activities | | (4,795,705) |

| | | |

| Net increase in cash | | 0 |

| Cash, beginning balance | | 0 |

| Cash, ending balance | | 0 |

| | | |

| Supplemental disclosure of cash flow information: | | |

| Cash paid during the period for interest from bank borrowing: $138,636. | | |

| | | |

| | | |

| See accompanying notes to financial statements. |

1-800-624-4190 • www.blu.com | 23 |

| BLUE CHIP VALUE FUND, INC. |

| |

| FINANCIAL HIGHLIGHTS |

| Per Share Data |

| (for a share outstanding throughout each period) |

| Net asset value – beginning of year |

| Investment operations(1) |

| Net investment income |

| Net gain/(loss) on investments |

| Total from investment operations |

| Distributions |

| From net investment income |

| From net realized gains on investments |

| Tax return of capital |

| Total distributions |

| Net asset value, end of year |

| |

| Per share market value, end of year |

| |

| Total investment return(2) based on: |

| Market Value |

| Net Asset Value |

| Ratios/Supplemental data: |

| Ratio of total expenses to average net assets(3) |

| Ratio of net investment income to average net assets |

| Ratio of total distributions to average net assets |

| Portfolio turnover rate(4) |

| Net assets – end of year (in thousands) |

| |

| See accompanying notes to financial statements. |

| | |

| (1) | Per share amounts calculated based on average shares outstanding during the period. |

| (2) | Total investment return is calculated assuming a purchase of common stock on the opening of the first day and a sale on the closing of the last day of each period reported. Dividends and distributions, if any, are assumed for purposes of this calculation to be reinvested at prices obtained under the Fund’s dividend reinvestment plan. Rights offerings, if any, are assumed for purposes of this calculation to be fully subscribed under the terms of the rights offering. Please note that the Fund’s total investment return does not reflect the deduction of taxes that a stockholder would pay on Fund distributions or the sale of Fund shares. Generally, total investment return based on net asset value will be higher than total investment return based on market value in periods where there is an increase in the discount or a decrease in the premium of the market value to the net asset value from the beginning to the end of such periods. Conversely, total investment return based on the net asset value will be lower than |

| 24 | Annual Report December 31, 2009 |

| | | For the year ended December 31, | | | |

| | 2009 | | | 2008 | | | 2007 | | | 2006 | | | 2005 | |

| $ | 2.89 | | $ | 5.35 | | $ | 5.73 | | $ | 5.62 | | $ | 5.76 | |

| | | | | | | | | | | | | | | |

| | 0.02 | | | 0.02 | | | 0.01 | | | 0.02 | | | 0.01 | |

| | 0.92 | | | (2.06 | ) | | 0.19 | | | 0.67 | | | 0.42 | |

| | 0.94 | | | (2.04 | ) | | 0.20 | | | 0.69 | | | 0.43 | |

| | | | | | | | | | | | | | | |

| | (0.02 | ) | | (0.02 | ) | | (0.02 | ) | | (0.02 | ) | | (0.02 | ) |

| | — | | | (0.01 | ) | | (0.21 | ) | | (0.13 | ) | | (0.11 | ) |

| | (0.05 | ) | | (0.39 | ) | | (0.35 | ) | | (0.43 | ) | | (0.44 | ) |

| | (0.07 | ) | | (0.42 | ) | | (0.58 | ) | | (0.58 | ) | | (0.57 | ) |

| $ | 3.76 | | $ | 2.89 | | $ | 5.35 | | $ | 5.73 | | $ | 5.62 | |

| | | | | | | | | | | | | | | |

| $ | 3.15 | | $ | 2.35 | | $ | 5.21 | | $ | 5.96 | | $ | 6.31 | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | 37.97 | % | | (49.27 | %) | | (3.3 | %) | | 4.6 | % | | 3.7 | % |

| | 33.92 | % | | (39.25 | %) | | 3.3 | % | | 12.9 | % | | 7.1 | % |

| | | | | | | | | | | | | | | |

| | 1.37% | (4) | | 1.38 | % | | 1.34 | % | | 1.36 | % | | 1.33 | % |

| | 0.51% | (4) | | 0.41 | % | | 0.25 | % | | 0.32 | % | | 0.21 | % |

| | 2.21 | % | | 9.51 | % | | 10.04 | % | | 10.25 | % | | 10.13 | % |

| | 86 | % | | 51 | % | | 40 | % | | 37 | % | | 41 | % |

| $ | 106,890 | | $ | 82,279 | | $ | 152,091 | | $ | 160,663 | | $ | 155,208 | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | total investment return based on market value in periods where there is a decrease in the discount or an increase in the premium of the market value to the net asset value from the beginning to the end of such periods. |

| (3) | For the years ended December 31, 2009, 2008, 2007, 2006, and 2005, the ratio of total expenses to average net assets excluding interest expense was 1.22%, 1.09%, 0.93%, 0.92% and 0.97%, respectively. |

| (4) | A portfolio turnover rate is the percentage computed by taking the lesser of purchases or sales of portfolio securities (excluding short-term investments) for the year and dividing it by the monthly average of the market value of the portfolio securities during the year. Purchases and sales of investment securities (excluding short-term securities) for the year ended December 31, 2009 were $86,674,183 and $ 90,851,426, respectively. |

1-800-624-4190 • www.blu.com | 25 |

BLUE CHIP VALUE FUND, INC.

NOTES TO FINANCIAL STATEMENTS

December 31, 2009

1. ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES

Blue Chip Value Fund, Inc. (the “Fund”) is registered under the Investment Company Act of 1940, as amended, as a diversified, closed-end management investment company.

The following is a summary of significant accounting policies followed by the Fund in the preparation of its financial statements.

Security Valuation – All securities of the Fund are valued as of the close of regular trading on the New York Stock Exchange (“NYSE”), generally 4:00 p.m. (Eastern Time), on each day that the NYSE is open. Listed securities are generally valued at the last sales price as of the close of regular trading on the NYSE. Securities traded on the National Association of Securities Dealers Automated Quotation (“NASDAQ”) are generally valued at the NASDAQ Official Closing Price (“NOCP”). In the absence of sales and NOCP, such securities are valued at the mean of the bid and asked prices.

Securities having a remaining maturity of 60 days or less are valued at amortized cost which approximates market value.

When market quotations are not readily available or when events occur that make established valuation methods unreliable, securities of the Fund may be valued at fair value determined in good faith by or under the direction of the Board of Directors. Factors which may be considered when determining the fair value of a security include (a) the fundamental data relating to the investment; (b) an evaluation of the forces which influence the market in which the security is sold, including the liquidity and depth of the market; (c) the market value at date of purchase; (d) information as to any transactions or offers with respect to the security or comparable securities; and (e) any other relevant matters.

Investment Transactions – Investment transactions are accounted for on the date the investments are purchased or sold (trade date). Realized gains and losses from investment transactions and unrealized appreciation and depreciation of investments are determined on the “specific identification” basis for both financial statement and federal income tax purposes. Dividend income is recorded on the ex-dividend date. Interest income, which includes interest earned on money market funds, is accrued and recorded daily.

| 26 | Annual Report December 31, 2009 |

Federal Income Taxes – No provision for income taxes is included in the accompanying financial statements, as the Fund intends to distribute to shareholders all taxable investment income and realized gains and otherwise comply with Subchapter M of the Internal Revenue Code applicable to regulated investment companies.

The Fund evaluates tax positions taken (or expected to be taken) in the course of preparing the Fund’s tax returns to determine whether these positions meet a “more-likely-than-not” standard that, based on the technical merits, have a more than fifty percent likelihood of being sustained by a taxing authority upon examination. A tax position that meets the “more-likely-than-not” recognition threshold is measured to determine the amount of benefit to recognize in the financial statements.

Management of the Fund analyzes all open tax years, as defined by the Statute of Limitations, for all major jurisdictions, including federal tax authorities and certain state tax authorities. As of and during the fiscal year ended December 31, 2009, the Fund did not have a liability for any unrecognized tax benefits. The Fund files income tax returns in the U.S. federal jurisdiction and Colorado. For the years ended December 31, 2006 through December 31, 2009 for the federal jurisdiction and for the years ended December 31, 2005 through December 31, 2009, for Colorado, the Fund’s returns are still open to examination by the appropriate taxing authority.

Classification of Distributions to Shareholders – Net investment income (loss) and net realized gain (loss) may differ for financial statement and tax purposes. The character of distributions made during the year from net investment income or net realized gains may differ from its ultimate characterization for federal income tax purposes. Also, due to the timing of dividend distributions, the fiscal year in which amounts are distributed may differ from the fiscal year in which the income or realized gain was recorded by the Fund.

The tax character of the distributions paid was as follows:

| | Year Ended | | Year Ended |

| | December 31, | | December 31, |

| | 2009 | | 2008 |

| Distributions paid from: | | | | | |

| Ordinary income | $ | 463,872 | | $ | 510,959 |

| Long-term capital gain | | — | | | 208,973 |

| Tax return of capital | | 3,521,833 | | | 13,220,746 |

| Total | $ | 3,985,705 | | $ | 13,940,678 |

1-800-624-4190 • www.blu.com | 27 |

As of December 31, 2009, the components of distributable earnings on a tax basis were as follows:| | | |

| Undistributed net investment income | $ | — |

| Accumulated net realized loss | | (254,156) |

| Net unrealized depreciation | | (1,633,895) |

| Total | $ | (1,888,051) |

At December 31, 2009, the Fund had available for tax purposes unused capital loss carryovers of $254,156, expiring December 31, 2017.

The difference between book basis and tax basis is typically attributable to the tax deferral of losses on wash sales, corporate actions and post October losses.

Distributions to Stockholders – Distributions to stockholders are recorded on the ex-dividend date.

Prior to May 1, 2009, the Fund maintained a “managed distribution policy” (the “Policy”) which distributed at least 2.5% of its net asset value quarterly to its stockholders. The Fund declared and paid the first quarter distribution in April 2009. This distribution was not related to the amount of the Fund’s net investment income or net realized capital gains or losses and will be classified to conform to the tax reporting requirements of the Internal Revenue Code. If the Fund’s total distributions for the year exceed the Fund’s “current and accumulated earnings and profits,” the excess will be treated as non-taxable return of capital, reducing the stockholder’s adjusted basis in their shares.

The Fund’s Policy was suspended, as approved by the Board of Directors, at the regular meeting held May 1, 2009. The Board took this action after considering a number of factors including, but not limited to, the outlook for the overall economy, an assessment of investment opportunities, the asset size and expense ratio of the Fund and the negative impact that the policy may have on the asset level and expense ratio. The Fund will continue to pay out any net investment income and net realized capital gains on an annual basis.

The Board will continue to evaluate the Fund’s Policy and may reinstate the Policy at its discretion.

Use of Estimates – The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the amounts reported in the financial statements and disclosures made in the accompanying notes to the financial statements. Actual results could differ from those estimates.

| 28 | Annual Report December 31, 2009 |

2. FAIR VALUE MEASUREMENTS

A three-tier hierarchy has been established to measure fair value based on the extent of use of “observable inputs” as compared to “unobservable inputs” for disclosure purposes and requires additional disclosures about these valuations measurements. Inputs refer broadly to the assumptions that market participants would use in pricing a security. Observable inputs are inputs that reflect the assumptions market participants would use in pricing the security developed based on market data obtained from sources independent of the reporting entity. Unobservable inputs are inputs that reflect the reporting entity’s own assumptions about the assumptions market participants would use in pricing the security developed based on the best information available in the circumstances.

The three-tier hierarchy is summarized as follows:

Level 1 – quoted prices in active markets for identical investments.

Level 2 – other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, credit risk, etc.).

Level 3 – significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments).

The following is a summary of the inputs used as of December 31, 2009 in valuing the Fund’s assets:

| Assets: | | | Level 2 – | | | | |

| | | | | Other | | Level 3 – | | | |

| | Level 1 – | | Significant | | Significant | | | |

| Investments in | Quoted | | Observable | | Unobservable | | | |

| Securities at Value | Prices | | Inputs | | Inputs | | | Total |

| Common Stocks | $ | 118,060,659 | | $ | — | | $ | — | | $ | 118,060,659 |

| Short Term Investments | | 247,438 | | | — | | | — | | | 247,438 |

| Total | $ | 118,308,097 | | $ | — | | $ | — | | $ | 118,308,097 |

All securities of the Fund were valued using Level 1 inputs during the year ended December 31, 2009. Thus a reconciliation of assets in which significant unobservable inputs (Level 3) were used is not applicable.

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

In April 2009, FASB issued “Determining Fair Value When the Volume and Level of Activity for the Asset or Liability Have Significantly Decreased and Identifying Transactions That Are Not Orderly,” which provides additional guidance for estimating fair value in accordance with Fair Value Measurements when the volume and level of activity for the asset or liability have significantly decreased as well as guidance on identifying circumstances that indicate a transaction is not orderly.

1-800-624-4190 • www.blu.com | 29 |

Additionally, it amends the Fair Value Measurement Standard by expanding disclosure requirements for reporting entities surrounding the major categories of assets and liabilities carried at fair value. The required disclosures have been incorporated into the summary of inputs table above. Management expects the Fund’s investments to typically be classified as Level 1 and therefore applying this guidance did not have a material impact on the Fund’s financial statements.

| 3. UNREALIZED APPRECIATION AND INVESTMENTS (TAX BASIS) |

| | | |

| As of December 31, 2009: | | | |

| Gross appreciation (excess of value over tax cost) | $ | 5,238,102 | |

| Gross depreciation (excess of tax cost over value) | | (6,871,997) | |

| Net unrealized depreciation | $ | (1,633,895) | |

| Cost of investments for income tax purposes | $ | 119,941,992 | |

4. INVESTMENT ADVISORY AND ADMINISTRATION SERVICES

The Fund has an Investment Advisory Agreement with Denver Investment Advisors LLC, also doing business as Denver Investments (“Denver Investments”), whereby an investment advisory fee is paid to Denver Investments based on an annual rate of 0.65% of the Fund’s average weekly net assets up to $100,000,000 and 0.50% of the Fund’s average weekly net assets in excess of $100,000,000. The management fee is paid monthly based on the average of the net assets of the Fund computed as of the last business day the New York Stock Exchange is open each week. Certain officers and a director of the Fund are also officers of Denver Investments.

ALPS Fund Services, Inc. (“ALPS”) and Denver Investments serve as the Fund’s co-administrators. The Administrative Agreement includes the Fund’s administrative and fund accounting services. The administrative services fee is based on the current annual rate for ALPS and Denver Investments, respectively, of 0.0955% and 0.01% of the Fund’s average daily net assets up to $75,000,000, 0.05%, and 0.005% of the Fund’s average daily net assets between $75,000,000 and $125,000,000, and 0.03% and 0.005% of the Fund’s average daily net assets in excess of $125,000,000 plus certain out-of-pocket expenses. The administrative service fee is paid monthly.

The Directors have appointed a Chief Compliance Officer who is also Treasurer of the Fund and an employee of Denver Investments. The Directors agreed that the Fund would reimburse Denver Investments a portion of his compensation for his services as the Fund’s Chief Compliance Officer.

| 30 | Annual Report December 31, 2009 |

5. LOAN OUTSTANDING

The Fund has a line of credit with The Bank of New York Mellon (“BONY”) in which the Fund may borrow up to the lesser of 15% of the Fund’s total assets, $15,000,000 or the maximum amount the Fund is permitted to borrow under the Investment Company Act of 1940. For the period January 1, 2009 through February 28, 2009 the interest rate reset daily at overnight Federal Funds Rate plus 0.825%. Effective March 1, 2009, the interest rate changed to the overnight Federal Funds Rate plus 1.00% and the Fund pays an annual loan facility fee of 0.03%. The borrowings under the BONY loan are secured by a perfected security interest on all of the Fund’s assets.

Details of the loan outstanding are as follows:

| | | As of

December 31, 2009 | | | Average for the

Year Ended

December 31, 2009 | |

| Loan outstanding | $ | 11,465,000 | | $ | 10,883,918 | |

| Interest rate | | 1.11% | * | | 1.13% | |

| % of Fund's total assets | | 9.68% | | | 9.19% | |

| Amount of debt per share outstanding | $ | 0.40 | | $ | 0.38 | |

| Number of shares outstanding (in thousands) | | 28,464 | | | 28,464 | ** |

| | | | | | | |

**Annualized

**Weighted average

6. SUBSEQUENT EVENTS

Management has evaluated whether any events or transactions occurred subsequent to December 31, 2009 through February 16, 2010, the date of issuance of the Fund’s financial statements, and determined that there were no other material events or transactions that would require recognition or disclosure in the Fund’s financial statements except that effective March 1, 2010 the interest rate on the Fund’s line of credit will change to the overnight Federal Funds Rate plus 1.25%.

7. TAX DESIGNATIONS (Unaudited)

Certain tax information is provided to shareholders as required by the Internal Revenue Code or to meet a specific state’s requirement. The Fund designates the following amounts or, if subsequently determined to be different, the maximum amount allowable for its fiscal year ended December 31, 2009:

| Corporate Dividends Received Deduction | 100% | |

| Qualified Dividend Income | 100% | |

1-800-624-4190 • www.blu.com | 31 |

NOTES

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

| 32 | Annual Report December 31, 2009 |

BOARD OF DIRECTORS Kenneth V. Penland, Chairman

Todger Anderson, Director

Lee W. Mather, Jr, Director

Richard C. Schulte, Director

Roberta M. Wilson, Director OFFICERS Kenneth V. Penland, Chairman

Todger Anderson, President

Mark M. Adelmann, Vice President

Nancy P. O’Hara, Secretary

Jasper R. Frontz, Treasurer, Chief Compliance Officer Investment Adviser/Co-Administrator

Denver Investments

1225 17th Street, 26th Floor

Denver, CO 80202 Stockholder Relations

(800) 624-4190 (option #2)

e-mail: blu@denvest.com Custodian

The Bank of New York Mellon

One Wall Street

New York, NY 10286 Co-Administrator

ALPS Fund Services, Inc.

1290 Broadway, Suite 1100

Denver, CO 80203 Transfer Agent Dividend Reinvestment Plan Agent

(Questions regarding your Account)

BNY Mellon Shareowner Services

480 Washington Blvd.

Jersey City, NJ 07310

(800) 624-4190 (option #1)

www.melloninvestor.com

|

Item 2. Code of Ethics.

(a) The registrant, as of the end of the period covered by the report, has adopted a code of ethics that applies to the registrant’s principal executive officer, principal financial officer, principal accounting officer or controller, or any persons performing similar functions on behalf of the registrant.

(b) Not applicable.

(c) During the period covered by this report, no amendments were made to the provisions of the code of ethics adopted in 2(a) above.

(d) During the period covered by this report, no implicit or explicit waivers to the provisions of the code of ethics adopted in 2(a) above were granted.

(e) Not applicable.

(f) The registrant’s Code of Ethics is attached as an Exhibit hereto.

Item 3. Audit Committee Financial Expert.

The Board of Directors of the registrant has determined that the registrant has at least one “audit committee financial expert” serving on its audit committee. The Board of Directors has designated Roberta M. Wilson as the registrant’s “audit committee financial expert.” Ms. Wilson is “independent” as defined in paragraph (a)(2) of Item 3 to Form N-CSR.

Item 4. Principal Accountant Fees and Services.

(a) Audit Fees: For the registrant's fiscal years ended December 31, 2009 and December 31, 2008, the aggregate fees billed for professional services rendered by the principal accountant for the audit of the registrant's annual financial statements were $26,800 and $27,000, respectively.

(b) Audit-Related Fees: In registrant's fiscal years ended December 31, 2009 and December 31, 2008, no fees were billed for assurance and related services by the principal accountant that are reasonably related to the performance of the audit of the registrant's financial statements and are not reported under paragraph (a) of this Item.

(c) Tax Fees: For the registrant's fiscal years ended December 31, 2009 and December 31, 2008, aggregate fees of $2,770 and $2,600, respectively, were billed for professional services rendered by the principal accountant for tax compliance, tax advice, and tax planning.

(d) All Other Fees: For the registrant's fiscal year ended December 31, 2009 and December 31, 2008, no fees were billed to registrant by the principal accountant for services other than the services reported in paragraph (a) through (c) of this item.

(e) (1) Audit Committee Pre-Approval Policies and Procedures: The registrant’s Audit Committee has not adopted pre-approval policies and procedures. Instead, the Audit Committee approves on a case-by-case basis each audit or non-audit service before the engagement The Audit Committee pre-approved all of the audit and non-audit services provided by the principal accountant to the registrant in 2009 and 2008.

(e)(2) No services described in paragraphs (b) through (d) above were approved pursuant to paragraph (c)(7)(i)(C) of Rule 2-01 of Regulation S-X.

(f) Not applicable.

(g) Aggregate non-audit fees of $2,770 and $2,600 were billed by the registrant's principal accountant for services rendered to the registrant and to registrant's investment adviser for the registrant's fiscal year ended December 31, 2009 and December 31, 2008, respectively.

(h) Not applicable.

Item 5. Audit Committee of Listed Registrants.

(a) The registrant has a separately-designated standing Audit Committee established in accordance with Section 3(a)(58)(A) of the Securities Exchange Act of 1934, as amended. The committee members are: Roberta M. Wilson, Richard C. Schulte and Lee W. Mather, Jr.

(b) Not applicable.

Item 6. Investments.

(a) Schedule of Investments in securities of unaffiliated issuers as of the close of the reporting period is included as part of the Report to Stockholders filed under Item 1 of this Form N-CSR.

(b) Not applicable.

Item 7. Disclosure of Proxy Voting Policies and Procedures for Closed-End Management Investment Companies.

The registrant’s Board of Directors, at their May 2003 Board meeting, delegated to its investment adviser, Denver Investment Advisors, LLC, (“Denver Investments”) subject to the supervision of the Board, the authority to vote registrant’s proxies relating to portfolio securities and directed Denver Investments to follow and apply Denver Investments’ proxy voting policies and procedures when voting such proxies. A summary of Denver Investments’ Proxy Voting Policy which sets forth the guidelines to be utilized by Denver Investments in voting proxies for the registrant follows.

Summary of Denver Investments Proxy Voting Policy

Denver Investments, unless otherwise directed by our clients, will make reasonable attempts to research, vote and record all proxy ballots for the security positions we maintain on our clients’ behalf. To execute this responsibility to the highest standard, Denver Investments relies heavily on its subscription to RiskMetrics Group. RiskMetrics Group provides proxy research and recommendations, as well as automated voting and record keeping through its ISS Governance Services (“ISS”). Although RiskMetrics Group offers other consulting services to companies that it also makes proxy vote recommendations on, we review their policies and certain reports regarding its internal controls a minimum of once per year and will only use RiskMetrics Group’s ISS as long as we deem it independent.

We review ISS’ Proxy Voting Guidelines at least annually and follow their recommendations on most issues for shareholder vote.

In the rare instance where our portfolio research or security Analyst believes that any ISS recommendation would be to the detriment of our investment clients, we can and will override the ISS recommendation through a manual vote. The final authorization to override an ISS recommendation must be approved by the CCO or a member of the Management Committee, other than the Analyst seeking the override. A written record supporting the decision to override the ISS recommendation will be maintained.

Special considerations are made for stocks traded on foreign exchanges. Specifically, if voting will hinder or impair the liquidity of these stocks, Denver Investments will not exercise its voting rights.

For any matters subject to proxy vote for mutual funds in which Denver Investments is an affiliated party, Denver Investments will vote on behalf of clients invested in such mutual funds in accordance with ISS, with no exceptions.

Client information is automatically recorded in RiskMetric Group’s system for record keeping. RiskMetrics Group provides the necessary reports for the Blue Chip Value Fund to prepare its Form N-PX annually.

Below is a condensed version of the proxy voting recommendations contained in the ISS Proxy Voting Manual.

U.S. Proxy Voting Guidelines Concise Summary

(Digest of Selected Key Guidelines)

Copyright © 2010 by RiskMetrics Group.

The policies contained herein are a sampling of select, key proxy voting guidelines and are not exhaustive. A full listing of RiskMetrics 2010 proxy voting guidelines can be found in the Jan. 15, 2010, edition of the U.S. Proxy Voting Manual.

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording, or any information storage and retrieval system, without permission in writing from the publisher. Requests for permission to make copies of any part of this work should be sent to: RiskMetrics Group Marketing Department, One Chase Manhattan Plaza, 44th Floor, New York, NY 10005. RiskMetrics Group is a trademark used herein under license.

Routine/Miscellaneous:

Auditor Ratification

Vote FOR proposals to ratify auditors, unless any of the following apply:

- An auditor has a financial interest in or association with the company, and is therefore not independent;

- There is reason to believe that the independent auditor has rendered an opinion which is neither accurate nor indicative of the company’s financial position;

- Poor accounting practices are identified that rise to a serious level of concern, such as: fraud; misapplication of GAAP; and material weaknesses identified in Section 404 disclosures; or

- Fees for non-audit services (“Other” fees) are excessive.

Non-audit fees are excessive if:

- Non-audit (“other”) fees exceed audit fees + audit-related fees + tax compliance/preparation fees

Board of Directors:

Votes on director nominees should be determined on a CASE-BY-CASE basis.