UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-5032

BARON INVESTMENT FUNDS TRUST f/k/a BARON ASSET FUND

(Exact Name of Registrant as Specified in Charter)

767 Fifth Avenue, 49th Floor

New York, NY 10153

(Address of Principal Executive Offices) (Zip Code)

Patrick M. Patalino, General Counsel

c/o Baron Investment Funds Trust

767 Fifth Avenue, 49th Floor

New York, NY 10153

(Name and Address of Agent for Service)

(Registrant’s Telephone Number, including Area Code): 212-583-2000

Date of fiscal year end: September 30

Date of reporting period: September 30, 2022

Item 1. Report to Stockholders.

Baron Asset Fund

Baron Growth Fund

Baron Small Cap Fund

Baron Opportunity Fund

Baron Fifth Avenue Growth Fund

Baron Discovery Fund

Baron Durable Advantage Fund

Baron Funds®

Baron Investment Funds Trust

Annual Financial Report

DEAR BARON INVESTMENT FUNDS SHAREHOLDER:

In this report, you will find audited financial statements for Baron Asset Fund, Baron Growth Fund, Baron Small Cap Fund, Baron Opportunity Fund, Baron Fifth Avenue Growth Fund, Baron Discovery Fund, and Baron Durable Advantage Fund (the “Funds”) for the year ended September 30, 2022. The U.S. Securities and Exchange Commission (the “SEC”) requires mutual funds to furnish these statements semi-annually to their shareholders. We hope you find these statements informative and useful.

We thank you for choosing to join us as fellow shareholders in Baron Funds. We will continue to work hard to justify your confidence.

Sincerely,

| | | | |

| |  | |  |

Ronald Baron Chief Executive Officer November 23, 2022 | | Linda S. Martinson Chairman, President and Chief Operating Officer November 23, 2022 | | Peggy Wong Treasurer and Chief Financial Officer November 23, 2022 |

This Annual Financial Report is for the Baron Investment Funds Trust, which currently has seven series: Baron Asset Fund, Baron Growth Fund, Baron Small Cap Fund, Baron Opportunity Fund, Baron Fifth Avenue Growth Fund, Baron Discovery Fund, and Baron Durable Advantage Fund. If you are interested in Baron Select Funds, which contains the Baron Partners Fund, Baron Focused Growth Fund, Baron International Growth Fund, Baron Real Estate Fund, Baron Emerging Markets Fund, Baron Global Advantage Fund, Baron Real Estate Income Fund, Baron WealthBuilder Fund, Baron Health Care Fund, Baron FinTech Fund, Baron New Asia Fund, and Baron Technology Fund series, please visit the Funds’ website at www.BaronFunds.com or contact us at 1-800-99BARON.

The Funds’ Proxy Voting Policy is available without charge and can be found on the Funds’ website at www.BaronFunds.com, by clicking on the “Regulatory Documents” link at the bottom left corner of the homepage or by calling 1-800-99BARON and on the SEC’s website at www.sec.gov. The Funds’ most current proxy voting record, Form N-PX, is also available on the Funds’ website and on the SEC’s website.

The Funds file their complete schedules of portfolio holdings with the SEC for the first and third quarters of each fiscal year as an exhibit to their reports on Form N-PORT. The Funds’ Form N-PORT reports are available on the SEC’s website at www.sec.gov. Schedules of portfolio holdings current to the most recent quarter are also available on the Funds’ website.

Some of the comments contained in this report are based on current management expectations and are considered “forward-looking statements.” Actual future results, however, may prove to be different from our expectations. You can identify forward-looking statements by words such as “estimate,” “may,” “expect,” “should,” “could,” “believe,” “plan” and other similar terms. We cannot promise future returns and our opinions are a reflection of our best judgment at the time this report is compiled.

The views expressed in this report reflect those of BAMCO, Inc. (“BAMCO” or the “Adviser”) only through the end of the period stated in this report. The views are not intended as recommendations or investment advice to any person reading this report and are subject to change at any time without notice based on market and other conditions.

Past performance is no guarantee of future results. The investment return and principal value of an investment will fluctuate; an investor’s shares, when redeemed, may be worth more or less than their original cost. For more complete information about Baron Funds, including charges and expenses, call, write or go to www.BaronFunds.com for a prospectus or summary prospectus. Read them carefully before you invest or send money. This report is not authorized for use as an offer of sale or a solicitation of an offer to buy shares of the Funds, unless accompanied or preceded by the Funds’ current prospectus or summary prospectus.

| | |

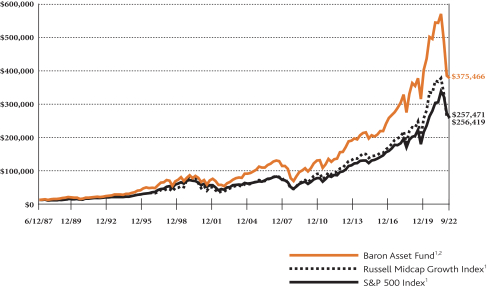

| Baron Asset Fund (Unaudited) | | September 30, 2022 |

COMPARISONOFTHECHANGEIN VALUEOF $10,000INVESTMENTIN BARON ASSET FUND† (RETAIL SHARES)

INRELATIONTOTHE RUSSELL MIDCAP GROWTH INDEXANDTHE S&P 500 INDEX

| | | | | | | | | | | | | | | | | | | | |

| AVERAGE ANNUAL TOTAL RETURNSFORTHEPERIODSENDED SEPTEMBER 30, 2022 | |

| | | One

Year | | | Three

Years | | | Five

Years | | | Ten

Years | | | Since

Inception

(June 12,

1987) | |

Baron Asset Fund — Retail Shares1, 2 | | | (30.79)% | | | | 2.14% | | | | 7.18% | | | | 10.96% | | | | 10.82% | |

Baron Asset Fund — Institutional Shares1, 2, 4 | | | (30.61)% | | | | 2.41% | | | | 7.46% | | | | 11.26% | | | | 10.93% | |

Baron Asset Fund — R6 Shares1, 2, 4 | | | (30.61)% | | | | 2.41% | | | | 7.46% | | | | 11.26% | | | | 10.93% | |

Russell Midcap Growth Index1 | | | (29.50)% | | | | 4.26% | | | | 7.62% | | | | 10.85% | | | | 9.65% | 3 |

S&P 500 Index1 | | | (15.47)% | | | | 8.16% | | | | 9.24% | | | | 11.70% | | | | 9.63% | |

| † | The Fund’s 3-year historical performance was impacted by gains from IPOs, and there is no guarantee that these results can be repeated or that the Fund’s level of participation in IPOs will be the same in the future. |

| 1 | The Russell MidcapTM Growth Index measures the performance of medium-sized U.S. companies that are classified as growth and the S&P 500 Index of 500 widely held large cap U.S. companies. The indexes and the Fund are with dividends reinvested, which positively impact the performance results. The indexes are unmanaged. The index performance is not Fund performance; one cannot invest directly into an index. |

| 2 | Past performance is not predictive of future performance. The performance data does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. The Fund’s transfer agency expenses may be reduced by expense offsets from an unaffiliated transfer agent, without which performance would have been lower. |

| 3 | For the period June 30, 1987 to September 30, 2022. |

| 4 | Performance for the Institutional Shares prior to May 29, 2009 is based on the performance of the Retail Shares. Performance for the R6 Shares prior to January 29, 2016 is based on the performance of the Institutional Shares, and prior to May 29, 2009 is based on the Retail Shares. The Retail Shares have a distribution fee, but Institutional Shares and R6 Shares do not. If the annual returns for the Institutional Shares and R6 Shares prior to May 29, 2009 did not reflect this fee, the returns would be higher. |

2

| | |

| September 30, 2022 (Unaudited) | | Baron Asset Fund |

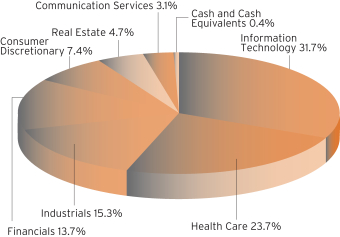

TOP TEN HOLDINGSASOF SEPTEMBER 30, 2022

| | | | |

| | | Percent of

Net Assets | |

Gartner, Inc. | | | 9.8% | |

IDEXX Laboratories, Inc. | | | 5.6% | |

Mettler-Toledo International, Inc. | | | 5.0% | |

CoStar Group, Inc. | | | 4.3% | |

Verisk Analytics, Inc. | | | 4.1% | |

FactSet Research Systems, Inc. | | | 3.8% | |

Vail Resorts, Inc. | | | 3.3% | |

ANSYS, Inc. | | | 3.2% | |

The Charles Schwab Corp. | | | 3.2% | |

Bio-Techne Corporation | | | 2.9% | |

| |

| | | | 45.2% | |

SECTOR BREAKDOWNASOF SEPTEMBER 30, 2022†

(as a percentage of net assets)

MANAGEMENT’S DISCUSSIONOF FUND PERFORMANCE

For the 12 months ended September 30, 2022, Baron Asset Fund1 declined 30.79%, while the Russell Midcap Growth Index fell 29.50% and the S&P 500 Index declined 15.47%.

Baron Asset Fund invests primarily in medium-sized growth companies for the long term, using a value-oriented purchase discipline. The Fund purchases companies that we believe have sustainable competitive advantages, strong financial characteristics, and exceptional management; and operate in industries with favorable growth characteristics.

The pandemic — and post-pandemic — market rally ended abruptly at the start of 2022. Expansionary fiscal and monetary policies and pent-up post-COVID spending desires caused demand to surge against supply constrained by supply-chain issues, shortages of housing and goods, and a tight labor market. The war in Ukraine provoked an energy crisis in Europe. China renewed COVID lockdowns, and its technology trade war with the U.S. intensified. Inflation accelerated to 40-year highs. The Federal Reserve pivoted to a more aggressive stance, embarking on a program of rate hikes in its drive to tame inflation. The highly uncertain setting led to a dramatic shift in investors’ risk tolerance and time horizons, resulting in a bear market with no immediate end in sight.

No sector contributed. Health Care, Information Technology, and Consumer Discretionary investments detracted the most.

Aspen Technology, Inc. was the top contributor. Shares of this leader in process automation software increased as organic trends improved. In addition, Aspen closed a transformative deal with industrial equipment manufacturer Emerson. We expect management to improve the growth, profitability, and cash flow of the acquired businesses by converting them to recurring revenue models while leveraging Emerson’s vast sales force to improve its own growth.

IDEXX Laboratories, Inc. was the top detractor. Shares of this veterinary diagnostics leader declined following outsized pandemic-era gains when the veterinary industry benefited from the surge in pet adoptions and increased attentive to pet illness by people working from home. While recent results have been adversely impacted by difficult comparisons, we believe the pandemic has accelerated long-term secular trends around pet ownership and care. IDEXX’s competitive trends are outstanding, and we expect new proprietary innovations and field sales force expansion to be meaningful contributors to growth.

Although we do not know exactly when it will occur, we have little doubt the current bear market will end, as all prior bear markets have, and stock prices will eventually recover. We believe our portfolio, comprised of companies that benefit from secular growth drivers, strong competitive positions, and exceptional management teams, should perform well during a recovery. Longer term, given the significant decline in many of our companies’ shares for reasons we believe largely short term and macroeconomic in nature, we are optimistic about the long-term return potential across the portfolio. Our frequent discussions with company management indicate that business conditions have largely been untouched by the litany of investor concerns. This supports our conviction that our holdings have the potential to double in value over a five-year period.

| † | Sector levels are provided from the Global Industry Classification Standard (“GICS”), developed and exclusively owned by MSCI, Inc. and Standard & Poor’s Financial Services LLC, unless otherwise stated that they have been reclassified or classified by the Adviser. All GICS data is provided “as is” with no warranties. Individual weights may not sum to 100% due to rounding. |

| 1 | Performance information reflects results of the Retail Shares. |

3

| | |

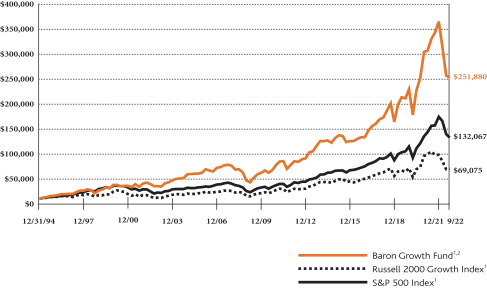

| Baron Growth Fund (Unaudited) | | September 30, 2022 |

COMPARISONOFTHECHANGEIN VALUEOF $10,000INVESTMENTIN BARON GROWTH FUND (RETAIL SHARES)

INRELATIONTOTHE RUSSELL 2000 GROWTH INDEXANDTHE S&P 500 INDEX

| | | | | | | | | | | | | | | | | | | | |

| AVERAGE ANNUAL TOTAL RETURNSFORTHEPERIODSENDED SEPTEMBER 30, 2022 | |

| | | One

Year | | | Three

Years | | | Five

Years | | | Ten

Years | | | Since

Inception

(December

31, 1994) | |

Baron Growth Fund — Retail Shares1, 2 | | | (26.31)% | | | | 6.12% | | | | 9.54% | | | | 11.02% | | | | 12.33% | |

Baron Growth Fund — Institutional Shares1, 2, 3 | | | (26.12)% | | | | 6.39% | | | | 9.81% | | | | 11.31% | | | | 12.47% | |

Baron Growth Fund — R6 Shares1, 2, 3 | | | (26.13)% | | | | 6.39% | | | | 9.81% | | | | 11.31% | | | | 12.47% | |

Russell 2000 Growth Index1 | | | (29.27)% | | | | 2.94% | | | | 3.60% | | | | 8.81% | | | | 7.21% | |

S&P 500 Index1 | | | (15.47)% | | | | 8.16% | | | | 9.24% | | | | 11.70% | | | | 9.75% | |

| 1 | The Russell 2000® Growth Index measures the performance of small-sized U.S. companies that are classified as growth and the S&P 500 Index of 500 widely held large cap U.S. companies. The indexes and the Fund are with dividends reinvested, which positively impact the performance results. The indexes are unmanaged. The index performance is not Fund performance; one cannot invest directly into an index. |

| 2 | Past performance is not predictive of future performance. The performance data does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. The Fund’s transfer agency expenses may be reduced by expense offsets from an unaffiliated transfer agent, without which performance would have been lower. |

| 3 | Performance for the Institutional Shares prior to May 29, 2009 is based on the performance of the Retail Shares. Performance for the R6 Shares prior to January 29, 2016 is based on the performance of the Institutional Shares, and prior to May 29, 2009 is based on the Retail Shares. The Retail Shares have a distribution fee, but Institutional Shares and R6 Shares do not. If the annual returns for the Institutional Shares and R6 Shares prior to May 29, 2009 did not reflect this fee, the returns would be higher. |

4

| | |

| September 30, 2022 (Unaudited) | | Baron Growth Fund |

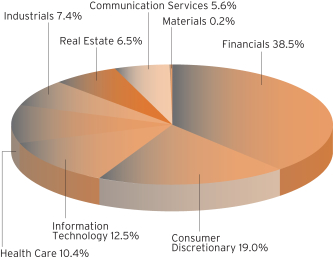

TOP TEN HOLDINGSASOF SEPTEMBER 30, 2022

| | | | |

| | | Percent of

Total Investments | |

MSCI, Inc. | | | 10.4% | |

FactSet Research Systems, Inc. | | | 7.6% | |

Vail Resorts, Inc. | | | 6.9% | |

Gartner, Inc. | | | 6.7% | |

Arch Capital Group Ltd. | | | 6.6% | |

CoStar Group, Inc. | | | 5.8% | |

Iridium Communications Inc. | | | 5.6% | |

Choice Hotels International, Inc. | | | 5.2% | |

Kinsale Capital Group, Inc. | | | 4.1% | |

Gaming and Leisure Properties, Inc. | | | 3.8% | |

| |

| | | | 62.7% | |

SECTOR BREAKDOWNASOF SEPTEMBER 30, 2022†

(as a percentage of total investments)

MANAGEMENT’S DISCUSSIONOF FUND PERFORMANCE

For the 12 months ended September 30, 2022, Baron Growth Fund1 declined 26.31%, while the Russell 2000 Growth Index fell 29.27% and the S&P 500 Index declined 15.47%.

Baron Growth Fund invests primarily in small-sized U.S. growth companies for the long term. Through independent research, we utilize an investment approach that we believe allows us to look at a business’s fundamental characteristics and beyond the current market environment. We invest based on the potential profitability of a business at what we believe are attractive valuations.

The pandemic — and post-pandemic — market rally ended abruptly at the start of 2022. Expansionary fiscal and monetary policies and pent-up post-COVID spending desires caused demand to surge against supply constrained by supply-chain issues, shortages of housing and goods, and a tight labor market. The war in Ukraine provoked an energy crisis in Europe. China renewed COVID lockdowns, and its technology trade war with the U.S. intensified. Inflation accelerated to 40-year highs. The Federal Reserve pivoted to a more aggressive stance, embarking on a program of rate hikes in its drive to tame inflation. The highly uncertain setting led to a dramatic shift in investors’ risk tolerance and time horizons, resulting in a bear market with no immediate end in sight.

Communication Services holdings contributed modestly. Consumer Discretionary, Health Care, Information Technology, and Financials investments detracted the most.

Kinsale Capital Group, Inc. was the top contributor. Shares of this specialty insurer increased on consistent quarterly results that exceeded analyst estimates. Market conditions remain favorable, with rising premium rates and more business shifting from the standard lines market to the excess and surplus lines market where Kinsale operates. We continue to own the stock because we believe Kinsale is well managed and has a long runway for growth in an attractive segment of the insurance market.

MSCI, Inc. was the top detractor. Shares of this leading provider of investment decision support tools fell in concert with the broader market rotation out of high-growth technology-related stocks. We retain long-term conviction as MSCI owns strong, “all-weather” franchises and is positioned to benefit from numerous secular tailwinds in the investment community.

The businesses in which we have invested have continued to report strong financial results despite growing concern of a slowdown. However, we recognize that the business cycle has valleys as well as peaks and we may well be headed in the former direction. That said, in the many decades we have been investors, we have never employed short-term macroeconomic forecasts to construct or manage our portfolio. We believe the $100 trillion global economy is far too complex, too interdependent, and too contingent on external factors such as geopolitics to be reliably predicted. Additionally, when such forecasts occasionally prove accurate, outcomes may already be reflected in equity prices. Instead, we focus on identifying and researching well-managed unique businesses with significant barriers to entry and compelling growth prospects, investing in them at attractive prices, and holding them for the long term.

| † | Sector levels are provided from the Global Industry Classification Standard (“GICS”), developed and exclusively owned by MSCI, Inc. and Standard & Poor’s Financial Services LLC, unless otherwise stated that they have been reclassified or classified by the Adviser. All GICS data is provided “as is” with no warranties. Individual weights may not sum to 100% due to rounding. |

| 1 | Performance information reflects results of the Retail Shares. |

5

| | |

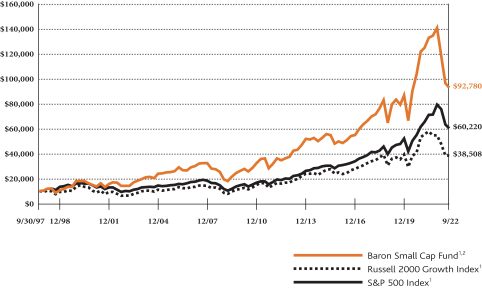

| Baron Small Cap Fund (Unaudited) | | September 30, 2022 |

COMPARISONOFTHECHANGEIN VALUEOF $10,000INVESTMENTIN BARON SMALL CAP FUND† (RETAIL SHARES)

IN RELATIONTOTHE RUSSELL 2000 GROWTH INDEXANDTHE S&P 500 INDEX

| | | | | | | | | | | | | | | | | | | | |

| AVERAGE ANNUAL TOTAL RETURNSFORTHEPERIODSENDED SEPTEMBER 30, 2022 | |

| | | One

Year | | | Three

Years | | | Five

Years | | | Ten

Years | | | Since

Inception

(September

30, 1997) | |

Baron Small Cap Fund — Retail Shares1, 2 | | | (30.93)% | | | | 5.39% | | | | 7.00% | | | | 9.85% | | | | 9.32% | |

Baron Small Cap Fund — Institutional Shares1, 2, 3 | | | (30.76)% | | | | 5.67% | | | | 7.28% | | | | 10.14% | | | | 9.47% | |

Baron Small Cap Fund — R6 Shares1, 2, 3 | | | (30.75)% | | | | 5.67% | | | | 7.28% | | | | 10.13% | | | | 9.47% | |

Russell 2000 Growth Index1 | | | (29.27)% | | | | 2.94% | | | | 3.60% | | | | 8.81% | | | | 5.54% | |

S&P 500 Index1 | | | (15.47)% | | | | 8.16% | | | | 9.24% | | | | 11.70% | | | | 7.45% | |

| �� | The Fund’s 3-year historical performance was impacted by gains from IPOs, and there is no guarantee that these results can be repeated or that the Fund’s level of participation in IPOs will be the same in the future. |

| 1 | The Russell 2000® Growth Index measures the performance of small-sized U.S. companies that are classified as growth and the S&P 500 Index of 500 widely held large cap U.S. companies. The indexes and the Fund are with dividends reinvested, which positively impact the performance results. The indexes are unmanaged. The index performance is not Fund performance; one cannot invest directly into an index. |

| 2 | Past performance is not predictive of future performance. The performance data does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. The Fund’s transfer agency expenses may be reduced by expense offsets from an unaffiliated transfer agent, without which performance would have been lower. |

| 3 | Performance for the Institutional Shares prior to May 29, 2009 is based on the performance of the Retail Shares. Performance for the R6 Shares prior to January 29, 2016 is based on the performance of the Institutional Shares, and prior to May 29, 2009 is based on the Retail Shares. The Retail Shares have a distribution fee, but Institutional Shares and R6 Shares do not. If the annual returns for the Institutional Shares and R6 Shares prior to May 29, 2009 did not reflect this fee, the returns would be higher. |

6

| | |

| September 30, 2022 (Unaudited) | | Baron Small Cap Fund |

TOP TEN HOLDINGSASOF SEPTEMBER 30, 2022

| | | | |

| | | Percent of

Net Assets | |

Gartner, Inc. | | | 6.0% | |

ASGN Incorporated | | | 4.0% | |

ICON Plc | | | 3.3% | |

Kinsale Capital Group, Inc. | | | 3.2% | |

Installed Building Products, Inc. | | | 2.9% | |

SiteOne Landscape Supply, Inc. | | | 2.8% | |

Floor & Decor Holdings, Inc. | | | 2.5% | |

Red Rock Resorts, Inc. | | | 2.4% | |

Aspen Technology, Inc. | | | 2.3% | |

BRP Group, Inc. | | | 2.1% | |

| |

| | | | 31.5% | |

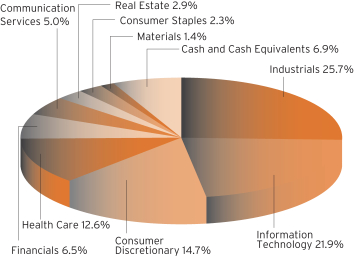

SECTOR BREAKDOWNASOF SEPTEMBER 30, 2022†

(as a percentage of net assets)

MANAGEMENT’S DISCUSSIONOF FUND PERFORMANCE

For the 12 months ended September 30, 2022, Baron Small Cap Fund1 declined 30.93%, while the Russell 2000 Growth Index fell 29.27% and the S&P 500 Index declined 15.47%.

Baron Small Cap Fund invests primarily in small-cap growth companies for the long term. The Fund invests in what we believe are well-run small-cap growth businesses that can be purchased at prices that represent a significant discount to our assessment of future value.

The pandemic — and post-pandemic — market rally ended abruptly at the start of 2022. Expansionary fiscal and monetary policies and pent-up post-COVID spending desires caused demand to surge against supply constrained by supply-chain issues, shortages of housing and goods, and a tight labor market. The war in Ukraine provoked an energy crisis in Europe. China renewed COVID lockdowns, and its technology trade war with the U.S. intensified. Inflation accelerated to 40-year highs. The Federal Reserve pivoted to a more aggressive stance, embarking on a program of rate hikes in its drive to tame inflation. The highly uncertain setting led to a dramatic shift in investors’ risk tolerance and time horizons, resulting in a bear market with no immediate end in sight.

No sector meaningfully contributed to performance. Industrials, Information Technology, and Consumer Discretionary holdings detracted the most.

Aspen Technology, Inc. was the top contributor. Shares of this leader in process automation software increased as organic trends improved. In addition, Aspen closed a transformative deal with industrial equipment manufacturer Emerson. We expect management to improve the growth, profitability, and cash flow of the acquired businesses by converting them to recurring revenue models while leveraging Emerson’s vast sales force to improve its own growth.

Vertiv Holdings, LLC was the top detractor. Shares of this provider of digital infrastructure and continuity solutions pulled back due to investor aversion to companies that had gone public via the SPAC process in addition to concerns that capital spending for data centers may be peaking. We remain shareholders. We believe Vertiv will demonstrate robust earnings power over the long term as price increases lead to substantial operating margin expansion and will execute on its strategy of long-term value creation.

With more expected hikes to come, more and more companies are reducing earnings outlooks as they anticipate a slowdown. While the market remains largely focused on near-term estimates, it is our belief that we should not adjust our long-standing and time-tested investment approach. Our long-term thesis and projections for our holdings are intact; however, they may take longer to achieve as near-term growth will be likely slower than we had expected. Still, we think the upside is unusually high, primarily because we believe the economy will stabilize and the companies we own will grow significantly. We remain invested as we are confident the tide will turn sometime before interest rates crest, even if business results are under pressure at that moment.

| † | Sector levels are provided from the Global Industry Classification Standard (“GICS”), developed and exclusively owned by MSCI, Inc. and Standard & Poor’s Financial Services LLC, unless otherwise stated that they have been reclassified or classified by the Adviser. All GICS data is provided “as is” with no warranties. Individual weights may not sum to 100% due to rounding. |

| 1 | Performance information reflects results of the Retail Shares. |

7

| | |

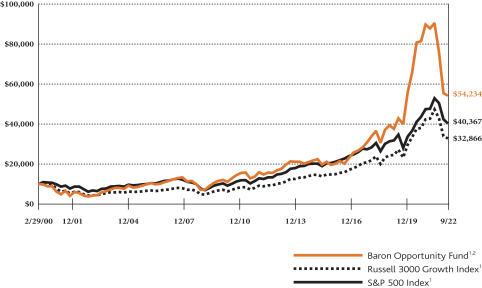

| Baron Opportunity Fund (Unaudited) | | September 30, 2022 |

COMPARISONOFTHECHANGEIN VALUEOF $10,000INVESTMENTIN BARON OPPORTUNITY FUND† (RETAIL SHARES)

INRELATIONTOTHE RUSSELL 3000 GROWTH INDEXANDTHE S&P 500 INDEX

| | | | | | | | | | | | | | | | | | | | |

| AVERAGE ANNUAL TOTAL RETURNSFORTHEPERIODSENDED SEPTEMBER 30, 2022 | |

| | | One

Year | | | Three

Years | | | Five

Years | | | Ten

Years | | | Since

Inception

(February

29, 2000) | |

Baron Opportunity Fund — Retail Shares1, 2 | | | (38.38)% | | | | 12.99% | | | | 15.23% | | | | 13.22% | | | | 7.77% | |

Baron Opportunity Fund — Institutional Shares1, 2, 3 | | | (38.23)% | | | | 13.30% | | | | 15.54% | | | | 13.52% | | | | 7.94% | |

Baron Opportunity Fund — R6 Shares1, 2, 3 | | | (38.23)% | | | | 13.28% | | | | 15.54% | | | | 13.53% | | | | 7.95% | |

Russell 3000 Growth Index1 | | | (23.01)% | | | | 10.16% | | | | 11.57% | | | | 13.36% | | | | 5.41% | |

S&P 500 Index1 | | | (15.47)% | | | | 8.16% | | | | 9.24% | | | | 11.70% | | | | 6.37% | |

| † | The Fund’s 3-, 5-, and 10-year historical performance was impacted by gains from IPOs, and there is no guarantee that these results can be repeated or that the Fund’s level of participation in IPOs will be the same in the future. |

| 1 | The Russell 3000® Growth Index measures the performance of those companies classified as growth among the largest 3,000 U.S. companies, and the S&P 500 Index of 500 widely held large cap U.S. companies. The indexes and the Fund are with dividends reinvested, which positively impact the performance results. The indexes are unmanaged. The index performance is not Fund performance; one cannot invest directly into an index. |

| 2 | Past performance is not predictive of future performance. The performance data does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. The Adviser reimburses certain Fund expenses pursuant to a contract expiring on August 29, 2033, unless renewed for another 11-year term and the Fund’s transfer agency expenses may be reduced by expense offsets from an unaffiliated transfer agent, without which performance would have been lower. |

| 3 | Performance for the Institutional Shares prior to May 29, 2009 is based on the performance of the Retail Shares. Performance for the R6 Shares prior to August 31, 2016 is based on the performance of the Institutional Shares, and prior to May 29, 2009 is based on the Retail Shares. The Retail Shares have a distribution fee, but Institutional Shares and R6 Shares do not. If the annual returns for the Institutional Shares and R6 Shares prior to May 29, 2009 did not reflect this fee, the returns would be higher. |

8

| | |

| September 30, 2022 (Unaudited) | | Baron Opportunity Fund |

TOP TEN HOLDINGSASOF SEPTEMBER 30, 2022

| | | | |

| | | Percent of

Net Assets | |

Microsoft Corporation | | | 13.2% | |

Alphabet Inc. | | | 7.9% | |

Amazon.com, Inc. | | | 6.5% | |

Tesla, Inc. | | | 5.1% | |

Gartner, Inc. | | | 4.6% | |

argenx SE | | | 4.1% | |

ZoomInfo Technologies Inc. | | | 3.2% | |

NVIDIA Corporation | | | 3.2% | |

Visa, Inc. | | | 3.0% | |

CoStar Group, Inc. | | | 2.9% | |

| |

| | | | 53.7% | |

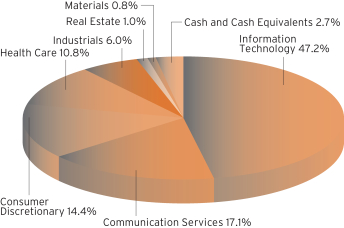

SECTOR BREAKDOWNASOF SEPTEMBER 30, 2022†

(as a percentage of net assets)

MANAGEMENT’S DISCUSSIONOF FUND PERFORMANCE

For the 12 months ended September 30, 2022, Baron Opportunity Fund1 declined 38.38%, while the Russell 3000 Growth Index fell 23.01% and the S&P 500 Index declined 15.47%.

Baron Opportunity Fund invests primarily in U.S. growth companies that we believe are driving or benefiting from innovation through development of pioneering, transformative, or technologically advanced products and services. The Fund invests in high-growth businesses of any market capitalization, selected for their capital appreciation potential.

The pandemic — and post-pandemic — market rally ended abruptly at the start of 2022. Expansionary fiscal and monetary policies and pent-up post-COVID spending desires caused demand to surge against supply constrained by supply-chain issues, shortages of housing and goods, and a tight labor market. The war in Ukraine provoked an energy crisis in Europe. China renewed COVID lockdowns, and its technology trade war with the U.S. intensified. Inflation accelerated to 40-year highs. The Federal Reserve pivoted to a more aggressive stance, embarking on a program of rate hikes in its drive to tame inflation. The highly uncertain setting led to a dramatic shift in investors’ risk tolerance and time horizons, resulting in a bear market with no immediate end in sight.

No sector meaningfully contributed. Information Technology, Communication Services, and Consumer Discretionary holdings detracted the most.

ShockWave Medical, Inc. contributed the most. Shares of this medical device company increased on continued strong uptake of its minimally invasive treatment for arterial plaque despite hospital staffing shortages and other challenges. We think ShockWave has a differentiated technology serving a significant unmet need in arterial disease with potential to expand into treatment of heart valves.

Alphabet Inc. was the top detractor. Shares of the parent company of Google were down given broad weakness in digital advertising demand. We remain investors as we believe Alphabet will continue to benefit from long-term secular growth in mobile and online video advertising, accruing to its core assets of Search, YouTube, and the Google ad network. Although less significant in the current environment, Alphabet’s investments in Cloud, AI, and other bets provide additional long-term avenues for potential growth.

This continues to be a time of significant unknowns. However, we don’t have to answer the unanswerable to deliver solid investment returns. Rather, we focus our research, analysis, and investment decisions on what we can know and what matters: identifying the durable secular growth trends we believe will drive long-term economic growth and the companies with durable competitive advantages, profitable business models, and long-term-oriented managers driving or riding these trends. We establish and monitor short- and long-term price targets for holdings and target companies using projections of revenues, earnings, and free cash flow and appropriate multiples, and we buy or add to our shares at prices where we believe we can deliver substantial returns.

| † | Sector levels are provided from the Global Industry Classification Standard (“GICS”), developed and exclusively owned by MSCI, Inc. and Standard & Poor’s Financial Services LLC, unless otherwise stated that they have been reclassified or classified by the Adviser. All GICS data is provided “as is” with no warranties. Individual weights may not sum to 100% due to rounding. |

| 1 | Performance information reflects results of the Retail Shares. |

9

| | |

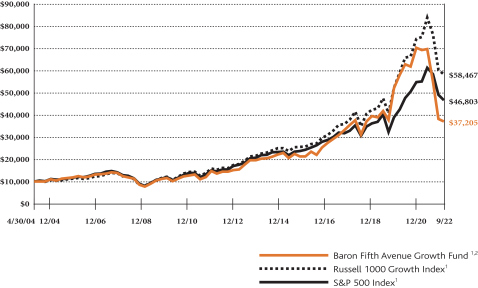

| Baron Fifth Avenue Growth Fund (Unaudited) | | September 30, 2022 |

COMPARISONOFTHECHANGEIN VALUEOF $10,000INVESTMENTIN BARON FIFTH AVENUE GROWTH FUND†

(RETAIL SHARES)INRELATIONTOTHE RUSSELL 1000 GROWTH INDEXANDTHE S&P 500 INDEX

| | | | | | | | | | | | | | | | | | | | |

| AVERAGE ANNUAL TOTAL RETURNSFORTHEPERIODSENDED SEPTEMBER 30, 2022 | |

| | | One

Year | | | Three

Years | | | Five

Years | | | Ten

Years | | | Since

Inception

(April 30,

2004) | |

Baron Fifth Avenue Growth Fund — Retail Shares1, 2 | | | (46.49)% | | | | (1.58)% | | | | 4.95% | | | | 9.97% | | | | 7.39% | |

Baron Fifth Avenue Growth Fund — Institutional Shares1, 2, 3 | | | (46.35)% | | | | (1.33)% | | | | 5.21% | | | | 10.25% | | | | 7.59% | |

Baron Fifth Avenue Growth Fund — R6 Shares1, 2, 3 | | | (46.36)% | | | | (1.33)% | | | | 5.21% | | | | 10.25% | | | | 7.59% | |

Russell 1000 Growth Index1 | | | (22.59)% | | | | 10.67% | | | | 12.17% | | | | 13.70% | | | | 10.06% | |

S&P 500 Index1 | | | (15.47)% | | | | 8.16% | | | | 9.24% | | | | 11.70% | | | | 8.74% | |

| † | The Fund’s 3-, 5-, and 10-year historical performance was impacted by gains from IPOs, and there is no guarantee that these results can be repeated or that the Fund’s level of participation in IPOs will be the same in the future. |

| 1 | The Russell 1000® Growth Index measures the performance of large-sized U.S. companies that are classified as growth and the S&P 500 Index of 500 widely held large cap U.S. companies. The indexes and the Fund are with dividends reinvested, which positively impact the performance results. The indexes are unmanaged. The index performance is not Fund performance; one cannot invest directly into an index. |

| 2 | Past performance is not predictive of future performance. The performance data does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. The Adviser reimburses certain Fund expenses pursuant to a contract expiring on August 29, 2033, unless renewed for another 11-year term and the Fund’s transfer agency expenses may be reduced by expense offsets from an unaffiliated transfer agent, without which performance would have been lower. |

| 3 | Performance for the Institutional Shares prior to May 29, 2009 is based on the performance of the Retail Shares. Performance for the R6 Shares prior to January 29, 2016 is based on the performance of the Institutional Shares, and prior to May 29, 2009 is based on the Retail Shares. The Retail Shares have a distribution fee, but Institutional Shares and R6 Shares do not. If the annual returns for the Institutional Shares and R6 Shares prior to May 29, 2009 did not reflect this fee, the returns would be higher. |

10

| | |

| September 30, 2022 (Unaudited) | | Baron Fifth Avenue Growth Fund |

TOP TEN HOLDINGSASOF SEPTEMBER 30, 2022

| | | | |

| | | Percent of

Net Assets | |

Amazon.com, Inc. | | | 9.2% | |

Alphabet Inc. | | | 7.8% | |

Mastercard Incorporated | | | 5.8% | |

Snowflake Inc. | | | 5.7% | |

Tesla, Inc. | | | 5.4% | |

ServiceNow, Inc. | | | 5.3% | |

CrowdStrike, Inc. | | | 4.9% | |

Datadog, Inc. | | | 4.1% | |

EPAM Systems, Inc. | | | 4.0% | |

NVIDIA Corporation | | | 3.9% | |

| |

| | | | 56.1% | |

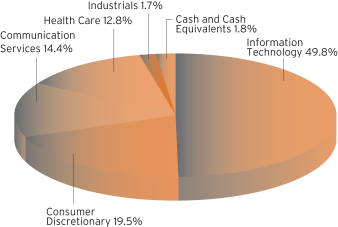

SECTOR BREAKDOWNASOF SEPTEMBER 30, 2022†

(as a percentage of net assets)

MANAGEMENT’S DISCUSSIONOF FUND PERFORMANCE

For the 12 months ended September 30, 2022, Baron Fifth Avenue Growth Fund1 declined 46.49%, while the Russell 1000 Growth Index fell 22.59% and the S&P 500 Index declined 15.47%.

Baron Fifth Avenue Growth Fund focuses on identifying and investing in what we believe are unique companies with durable competitive advantages and the ability to redeploy capital at high rates of return. The portfolio is constructed on a bottom-up basis,

with the quality of ideas and conviction level the most important determinants of the size of each investment. We expect our highest conviction businesses to have meaningful weight in the portfolio. Sector weightings are incidental to portfolio construction, and sector exposure is a result of stock selection.

The pandemic — and post-pandemic — market rally ended abruptly at the start of 2022. Expansionary fiscal and monetary policies and pent-up post-COVID spending desires caused demand to surge against supply constrained by supply-chain issues, shortages of housing and goods, and a tight labor market. The war in Ukraine provoked an energy crisis in Europe. China renewed COVID lockdowns, and its technology trade war with the U.S. intensified. Inflation accelerated to 40-year highs. The Federal Reserve pivoted to a more aggressive stance, embarking on a program of rate hikes in its drive to tame inflation. The highly uncertain setting led to a dramatic shift in investors’ risk tolerance and time horizons, resulting in a bear market with no immediate end in sight.

No sector meaningfully contributed. Information Technology, Consumer Discretionary, and Communication Services holdings detracted the most.

Argenx SE was the top contributor. Shares of this biotechnology company rose with the strong launch of Vyvgart, a treatment for generalized myasthenia gravis, an autoimmune disease that causes muscle weakness. Early sales tripled consensus estimates, and global approvals are coming earlier than guided. We remain shareholders given Vyvgart’s rare “pipeline in a product” potential to treat numerous diseases, which is what helps drugs achieve multi-blockbuster status.

Shopify Inc. was the top detractor. Shares of this cloud-based software provider offering an operating system for multi-channel commerce fell due to post-pandemic e-commerce normalization as economies reopened, competitive concerns following Amazon’s announcement of Buy with Prime, and the broader sell-off in growth stocks.

The markets seem resigned that the Federal Reserve will continue raising rates and a recession in 2023 is a foregone conclusion. Yet longer-term data continues to move in the right direction, at least as it relates to inflation. The 10-year inflation breakeven rate remains at its lowest level since early 2021, implying that the market is pricing in a 2.22% rate of inflation over the long term, just 22 bps above the Fed’s stated 2% objective.

Our goal remains to maximize long-term returns without taking significant risks of a permanent loss of capital. We are optimistic about the prospects of our investments and continue searching for new ideas while remaining patient and investing only when we believe companies are trading significantly below their intrinsic values.

| † | Sector levels are provided from the Global Industry Classification Standard (“GICS”), developed and exclusively owned by MSCI, Inc. and Standard & Poor’s Financial Services LLC, unless otherwise stated that they have been reclassified or classified by the Adviser. All GICS data is provided “as is” with no warranties. Individual weights may not sum to 100% due to rounding. |

| 1 | Performance information reflects results of the Retail Shares. |

11

| | |

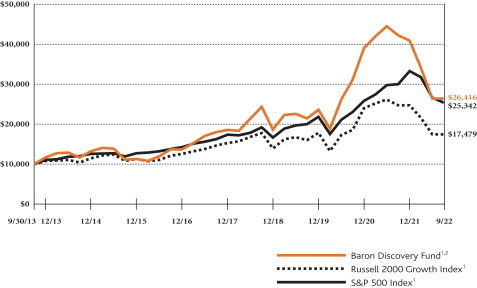

| Baron Discovery Fund (Unaudited) | | September 30, 2022 |

COMPARISONOFTHECHANGEIN VALUEOF $10,000INVESTMENTIN BARON DISCOVERY FUND† (RETAIL SHARES)

INRELATIONTOTHE RUSSELL 2000 GROWTH INDEXANDTHE S&P 500 INDEX

| | | | | | | | | | | | | | | | |

| AVERAGE ANNUAL TOTAL RETURNSFORTHEPERIODSENDED SEPTEMBER 30, 2022 | |

| | | One

Year | | | Three

Years | | | Five

Years | | | Since

Inception

(September 30,

2013) | |

Baron Discovery Fund — Retail Shares1, 2 | | | (37.47)% | | | | 7.21% | | | | 8.00% | | | | 11.40% | |

Baron Discovery Fund — Institutional Shares1, 2 | | | (37.31)% | | | | 7.51% | | | | 8.28% | | | | 11.68% | |

Baron Discovery Fund — R6 Shares1, 2, 3 | | | (37.30)% | | | | 7.51% | | | | 8.28% | | | | 11.68% | |

Russell 2000 Growth Index1 | | | (29.27)% | | | | 2.94% | | | | 3.60% | | | | 6.40% | |

S&P 500 Index1 | | | (15.47)% | | | | 8.16% | | | | 9.24% | | | | 10.88% | |

| † | The Fund’s 3- and 5-year historical performance was impacted by gains from IPOs, and there is no guarantee that these results can be repeated or that the Fund’s level of participation in IPOs will be the same in the future. |

| 1 | The Russell 2000® Growth Index measures the performance of small-sized U.S. companies that are classified as growth and the S&P 500 Index of 500 widely held large cap U.S. companies. The indexes and the Fund are with dividends reinvested, which positively impact the performance results. The indexes are unmanaged. The index performance is not Fund performance; one cannot invest directly into an index. |

| 2 | Past performance is not predictive of future performance. The performance data does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. The Adviser reimburses certain Fund expenses pursuant to a contract expiring on August 29, 2033, unless renewed for another 11-year term and the Fund’s transfer agency expenses may be reduced by expense offsets from an unaffiliated transfer agent, without which performance would have been lower. |

| 3 | Performance for the R6 Shares prior to August 31, 2016 is based on the performance of the Institutional Shares. |

12

| | |

| September 30, 2022 (Unaudited) | | Baron Discovery Fund |

TOP TEN HOLDINGSASOF SEPTEMBER 30, 2022

| | | | |

| | | Percent of

Net Assets | |

Kinsale Capital Group, Inc. | | | 5.6% | |

Axonics, Inc. | | | 3.9% | |

Boyd Gaming Corporation | | | 3.1% | |

Revance Therapeutics, Inc. | | | 3.0% | |

Rexford Industrial Realty, Inc. | | | 3.0% | |

Advanced Energy Industries, Inc. | | | 2.9% | |

Axon Enterprise, Inc. | | | 2.5% | |

Silk Road Medical, Inc. | | | 2.5% | |

Mercury Systems, Inc. | | | 2.5% | |

Floor & Decor Holdings, Inc. | | | 2.4% | |

| |

| | | | 31.4% | |

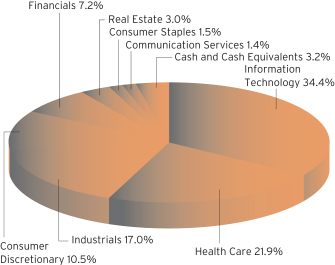

SECTOR BREAKDOWNASOF SEPTEMBER 30, 2022†

(as a percentage of net assets)

MANAGEMENT’S DISCUSSIONOF FUND PERFORMANCE

For the 12 months ended September 30, 2022, Baron Discovery Fund1 declined 37.47%, while the Russell 2000 Growth Index fell 29.27% and the S&P 500 Index declined 15.47%.

Baron Discovery Fund invests primarily in small-sized U.S. companies which at time of purchase have market capitalizations up to the largest market cap stock in the Russell 2000 Growth Index at June 30, or companies with market capitalizations up to $2.5 billion, whichever is larger.

The pandemic — and post-pandemic — market rally ended abruptly at the start of 2022. Expansionary fiscal and monetary policies and pent-up post-COVID spending desires caused demand to surge against supply constrained by supply-chain issues, shortages of housing and goods, and a tight labor market. The war in Ukraine provoked an energy crisis in Europe. China renewed COVID lockdowns, and its technology trade war with the U.S. intensified. Inflation accelerated to 40-year highs. The Federal Reserve pivoted to a more aggressive stance, embarking on a program of rate hikes in its drive to tame inflation. The highly uncertain setting led to a dramatic shift in investors’ risk tolerance and time horizons, resulting in a bear market with no immediate end in sight.

Financials holdings contributed modestly. Information Technology, Industrials, and Health Care holdings detracted the most.

Specialty insurer Kinsale Capital Group, Inc. contributed the most on consistently strong financial results. Favorable market conditions with rate increases well above loss cost trends resulted in better margins and enhanced reserve development. We believe Kinsale is well managed and has a long runway for growth in an attractive segment of the insurance market.

S4 Capital plc detracted the most. Shares of this global digital marketing services business declined in as investors reacted negatively to an accounting issue earlier in the period followed by a reduced earnings outlook due to higher costs as the company ramped hiring in its content division. We remain impressed with S4’s 25% organic top-line growth expectations as the industry struggles and believe management has concrete levers to manage costs.

Thus far, 2022 has been a challenging year for the economy and the market. In many cases, small-cap stocks are trading at or below the valuation levels we saw during the steep downturn at the start of the COVID pandemic. Investor sentiment is as pessimistic as we have ever seen since these readings started in the 1980s. It is understandable that we encounter significant investor skepticism when we say we are becoming more positive. However, we believe successful long-term investing requires a contrarian mindset. As Warren Buffett said once, be “fearful when others are greedy and greedy when others are fearful.” It is never easy to go against the crowd, and it is almost impossible to time the market bottom perfectly, but we believe that by staying the course with our competitively advantaged, emerging growth businesses, our shareholders will be rewarded when the inevitable economic recovery begins.

| † | Sector levels are provided from the Global Industry Classification Standard (“GICS”), developed and exclusively owned by MSCI, Inc. and Standard & Poor’s Financial Services LLC, unless otherwise stated that they have been reclassified or classified by the Adviser. All GICS data is provided “as is” with no warranties. Individual weights may not sum to 100% due to rounding. |

| 1 | Performance information reflects results of the Retail Shares. |

13

| | |

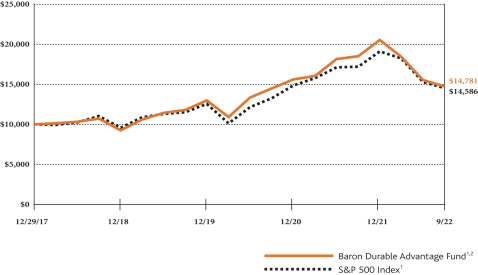

| Baron Durable Advantage Fund (Unaudited) | | September 30, 2022 |

COMPARISONOFTHECHANGEIN VALUEOF $10,000INVESTMENTIN BARON DURABLE ADVANTAGE FUND

(RETAIL SHARES)INRELATIONTOTHE S&P 500 INDEX

| | | | | | | | | | | | |

| AVERAGE ANNUAL TOTAL RETURNSFORTHEPERIODSENDED SEPTEMBER 30, 2022 | |

| | | One

Year | | | Three

Years | | | Since

Inception

(December 29,

2017) | |

Baron Durable Advantage Fund — Retail Shares1, 2 | | | (20.39)% | | | | 7.76% | | | | 8.57% | |

Baron Durable Advantage Fund — Institutional Shares1, 2 | | | (20.21)% | | | | 8.02% | | | | 8.84% | |

Baron Durable Advantage Fund — R6 Shares1, 2 | | | (20.21)% | | | | 8.00% | | | | 8.82% | |

S&P 500 Index1 | | | (15.47)% | | | | 8.16% | | | | 8.27% | |

| 1 | The S&P 500 Index measures the performance of 500 widely held large cap U.S. companies. The index and the Fund are with dividends reinvested, which positively impact the performance results. The index is unmanaged. The index performance is not Fund performance; one cannot invest directly into an index. |

| 2 | Past performance is not predictive of future performance. The performance data does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. The Adviser reimburses certain Fund expenses pursuant to a contract expiring on August 29, 2033, unless renewed for another 11-year term and the Fund’s transfer agency expenses may be reduced by expense offsets from an unaffiliated transfer agent, without which performance would have been lower. |

14

| | |

| September 30, 2022 (Unaudited) | | Baron Durable Advantage Fund |

TOP TEN HOLDINGSASOF SEPTEMBER 30, 2022

| | | | |

| | | Percent of

Net Assets | |

Microsoft Corporation | | | 7.9% | |

Amazon.com, Inc. | | | 7.1% | |

Alphabet Inc. | | | 5.3% | |

UnitedHealth Group Incorporated | | | 5.2% | |

Arch Capital Group Ltd. | | | 4.9% | |

Danaher Corporation | | | 4.8% | |

Thermo Fisher Scientific Inc. | | | 4.7% | |

Accenture plc | | | 4.6% | |

S&P Global Inc. | | | 4.3% | |

Mastercard Incorporated | | | 4.2% | |

| |

| | | | 53.0% | |

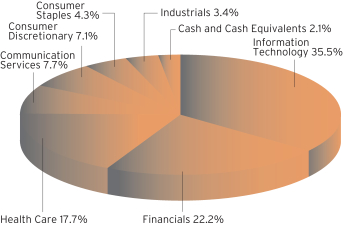

SECTOR BREAKDOWNASOF SEPTEMBER 30, 2022†

(as a percentage of net assets)

MANAGEMENT’S DISCUSSIONOF FUND PERFORMANCE

For the 12 months ended September 30, 2022, Baron Durable Advantage Fund1 declined 20.39% while the S&P 500 Index declined 15.47%.

Baron Durable Advantage Fund invests mainly in large-sized U.S. companies with competitive advantages and market capitalizations no smaller than the top 90th percentile by market capitalization of the S&P 500 Index at June 30, or companies with

market capitalizations above $10 billion, whichever is smaller. The Fund emphasizes businesses with excess free cash flow that can be returned to shareholders.

The pandemic — and post-pandemic — market rally ended abruptly at the start of 2022. Expansionary fiscal and monetary policies and pent-up post-COVID spending desires caused demand to surge against supply constrained by supply-chain issues, shortages of housing and goods, and a tight labor market. The war in Ukraine provoked an energy crisis in Europe. China renewed COVID lockdowns, and its technology trade war with the U.S. intensified. Inflation accelerated to 40-year highs. The Federal Reserve pivoted to a more aggressive stance, embarking on a program of rate hikes in its drive to tame inflation. The highly uncertain setting led to a dramatic shift in investors’ risk tolerance and time horizons, resulting in a bear market with no immediate end in sight.

No sector meaningfully contributed. Information Technology, Communication Services, and Financials holdings detracted the most.

UnitedHealth Group Incorporated was the top contributor. Shares of this leading health insurer increased on robust earnings and guidance during the period. We believe UnitedHealth leads the industry in innovation and execution, as evidenced by its Medicare Advantage share gains, cost controls, and leadership in the shift to value-based care.

Meta Platforms, Inc. was the top detractor. Shares of the world’s largest social network fell due to broader digital advertising weakness and difficulties with advertising effectiveness as a result of Apple’s enhanced privacy features implemented in late 2021. We believe Meta will resolve these issues and utilize its leadership in mobile advertising, massive user base, and technological scale to perform well over the long term, with additional monetization opportunities ahead.

The markets seem resigned that the Federal Reserve will continue raising rates and a recession in 2023 is a foregone conclusion. Yet longer-term data continues to move in the right direction, at least as it relates to inflation. The 10-year inflation breakeven rate remains at its lowest level since early 2021, implying that the market is pricing in a 2.22% rate of inflation over the long term, just 22 bps above the Fed’s stated 2% objective.

We believe investing in great businesses at attractive valuations will enable us to earn excess risk-adjusted returns over the long term. We look for companies with strong and durable competitive advantages, track records of successful capital allocation, high returns on invested capital, and high free cash flow generation, a significant portion of which is returned to shareholders as dividends or share repurchases. We are optimistic about the prospects of the companies we own while continuing to search for new ideas.

| † | Sector levels are provided from the Global Industry Classification Standard (“GICS”), developed and exclusively owned by MSCI, Inc. and Standard & Poor’s Financial Services LLC, unless otherwise stated that they have been reclassified or classified by the Adviser. All GICS data is provided “as is” with no warranties. Individual weights may not sum to 100% due to rounding. |

| 1 | Performance information reflects results of the Retail Shares. |

15

| | |

| Baron Asset Fund | | September 30, 2022 |

STATEMENT OF NET ASSETS

| | | | | | | | | | | | |

| Shares | | | | | Cost | | | Value | |

| Common Stocks (97.49%) | |

| Communication Services (3.12%) | |

| | | | Advertising (0.90%) | |

| | 594,000 | | | The Trade Desk, Inc., Cl A1 | | $ | 11,554,017 | | | $ | 35,491,500 | |

| |

| | | | Cable & Satellite (0.38%) | |

| | 200,000 | | | Liberty Broadband

Corporation, Cl C1 | | | 14,005,757 | | | | 14,760,000 | |

| |

| | | | Interactive Media &

Services (1.84%) | |

| | 1,735,709 | | | ZoomInfo Technologies, Inc.1 | | | 43,840,818 | | | | 72,309,637 | |

| | | | | | | | | | | | |

| | Total Communication Services | | | 69,400,592 | | | | 122,561,137 | |

| | | | | | | | | | | | |

|

| Consumer Discretionary (6.73%) | |

| | | | Automobile

Manufacturers (0.36%) | | | | | | | | |

| | 425,305 | | | Rivian Automotive, Inc., Cl A1 | | | 33,173,790 | | | | 13,996,788 | |

| |

| | | | Home Improvement

Retail (0.41%) | |

| | 230,000 | | | Floor & Decor Holdings, Inc., Cl A1 | | | 20,284,647 | | | | 16,159,800 | |

| | | |

| | | | Hotels, Resorts & Cruise Lines (2.64%) | | | | | | | | |

| | 546,442 | | | Choice Hotels International, Inc. | | | 5,198,084 | | | | 59,846,328 | |

| | 543,233 | | | Hyatt Hotels Corp., Cl A1 | | | 16,817,762 | | | | 43,980,143 | |

| | | | | | | | | | | | |

| | | | 22,015,846 | | | | 103,826,471 | |

| |

| | | | Leisure Facilities (3.32%) | |

| | 603,538 | | | Vail Resorts, Inc. | | | 11,683,688 | | | | 130,146,934 | |

| | | | | | | | | | | | |

| | Total Consumer Discretionary | | | 87,157,971 | | | | 264,129,993 | |

| | | | | | | | | | | | |

|

| Financials (13.74%) | |

| | | | Asset Management &

Custody Banks (0.63%) | |

| | 237,514 | | | T. Rowe Price Group, Inc. | | | 5,729,987 | | | | 24,941,345 | |

| |

| | | | Financial Exchanges &

Data (5.71%) | |

| | 370,725 | | | FactSet Research Systems, Inc. | | | 19,898,420 | | | | 148,330,780 | |

| | 201,267 | | | MarketAxess Holdings, Inc. | | | 21,743,183 | | | | 44,779,895 | |

| | 30,000 | | | MSCI, Inc. | | | 7,783,774 | | | | 12,653,700 | |

| | 326,189 | | | Tradeweb Markets, Inc., Cl A | | | 11,978,713 | | | | 18,403,583 | |

| | | | | | | | | | | | |

| | | | 61,404,090 | | | | 224,167,958 | |

| |

| | | | Insurance Brokers (0.81%) | |

| | 158,421 | | | Willis Towers Watson plc2 | | | 19,439,430 | | | | 31,833,116 | |

| |

| | | | Investment Banking &

Brokerage (3.31%) | |

| | 1,750,936 | | | The Charles Schwab Corp. | | | 1,542,900 | | | | 125,839,770 | |

| | 19,000 | | | LPL Financial Holdings, Inc. | | | 4,376,048 | | | | 4,151,120 | |

| | | | | | | | | | | | |

| | | | 5,918,948 | | | | 129,990,890 | |

| | | | Property & Casualty

Insurance (2.56%) | |

| | 2,203,444 | | | Arch Capital Group Ltd.1,2 | | | 7,933,936 | | | | 100,344,840 | |

| |

| | | | Regional Banks (0.72%) | |

| | 216,421 | | | First Republic Bank | | | 5,518,736 | | | | 28,253,761 | |

| | | | | | | | | | | | |

| | Total Financials | | | 105,945,127 | | | | 539,531,910 | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| Shares | | | | | Cost | | | Value | |

| Common Stocks (continued) | |

|

| Health Care (23.66%) | |

| | | | Biotechnology (0.52%) | |

| | 58,366 | | | argenx SE, ADR1,2 | | $ | 18,854,201 | | | $ | 20,606,116 | |

| |

| | | | Health Care Equipment (7.73%) | |

| | 682,000 | | | DexCom, Inc.1 | | | 54,311,293 | | | | 54,928,280 | |

| | 673,630 | | | IDEXX Laboratories, Inc.1 | | | 12,186,829 | | | | 219,468,654 | |

| | 143,644 | | | Teleflex, Inc. | | | 25,017,949 | | | | 28,938,520 | |

| | | | | | | | | | | | |

| | | | 91,516,071 | | | | 303,335,454 | |

| | | | Health Care Supplies (1.45%) | |

| | 215,418 | | | The Cooper Companies, Inc. | | | 36,713,299 | | | | 56,848,810 | |

| | | |

| | | | Health Care Technology (1.93%) | | | | | | | | |

| | 459,386 | | | Veeva Systems, Inc., Cl A1 | | | 27,115,596 | | | | 75,743,564 | |

| |

| | | | Life Sciences Tools &

Services (12.03%) | |

| | 399,986 | | | Bio-Techne Corporation | | | 39,595,545 | | | | 113,596,024 | |

| | 135,000 | | | ICON plc1,2 | | | 29,220,173 | | | | 24,810,300 | |

| | 212,552 | | | Illumina, Inc.1 | | | 9,061,707 | | | | 40,552,796 | |

| | 181,117 | | | Mettler-Toledo International, Inc.1 | | | 10,795,784 | | | | 196,352,562 | |

| | 394,404 | | | West Pharmaceutical Services, Inc. | | | 17,058,063 | | | | 97,054,937 | |

| | | | | | | | | | | | |

| | | | 105,731,272 | | | | 472,366,619 | |

| | | | | | | | | | | | |

| | Total Health Care | | | 279,930,439 | | | | 928,900,563 | |

| | | | | | | | | | | | |

|

| Industrials (13.83%) | |

| | | | Environmental & Facilities

Services (1.45%) | |

| | 1,643,418 | | | Rollins, Inc. | | | 24,597,482 | | | | 56,993,736 | |

| | | |

| | | | Industrial Machinery (1.74%) | | | | | | | | |

| | 340,760 | | | IDEX Corporation | | | 24,525,881 | | | | 68,100,886 | |

| |

| | | | Research & Consulting

Services (10.64%) | |

| | 2,439,930 | | | CoStar Group, Inc.1 | | | 59,005,227 | | | | 169,941,125 | |

| | 1,438,500 | | | TransUnion | | | 77,172,718 | | | | 85,576,365 | |

| | 951,206 | | | Verisk Analytics, Inc. | | | 23,582,787 | | | | 162,209,159 | |

| | | | | | | | | | | | |

| | | | 159,760,732 | | | | 417,726,649 | |

| | | | | | | | | | | | |

| | Total Industrials | | | 208,884,095 | | | | 542,821,271 | |

| | | | | | | | | | | | |

|

| Information Technology (31.68%) | |

| | | | Application Software (13.18%) | |

| | 571,856 | | | ANSYS, Inc.1 | | | 20,310,482 | | | | 126,780,475 | |

| | 166,026 | | | Aspen Technology, Inc.1 | | | 30,241,636 | | | | 39,547,393 | |

| | 1,636,093 | | | Ceridian HCM Holding, Inc.1 | | | 64,026,866 | | | | 91,424,877 | |

| | 150,000 | | | Fair Isaac Corp.1 | | | 63,616,939 | | | | 61,801,500 | |

| | 1,421,809 | | | Guidewire Software, Inc.1 | | | 77,473,157 | | | | 87,554,998 | |

| | 65,861 | | | HubSpot, Inc.1 | | | 39,133,171 | | | | 17,790,373 | |

| | 257,192 | | | Roper Technologies, Inc. | | | 26,184,327 | | | | 92,496,531 | |

| | | | | | | | | | | | |

| | | | 320,986,578 | | | | 517,396,147 | |

| |

| | | | Data Processing &

Outsourced Services (2.07%) | |

| | 589,217 | | | Fidelity National Information Services, Inc. | | | 33,648,188 | | | | 44,527,129 | |

| | 771,076 | | | SS&C Technologies Holdings, Inc. | | | 20,933,204 | | | | 36,818,879 | |

| | | | | | | | | | | | |

| | | | 54,581,392 | | | | 81,346,008 | |

| | |

| 16 | | See Notes to Financial Statements. |

| | |

| September 30, 2022 | | Baron Asset Fund |

STATEMENT OF NET ASSETS (Continued)

| | | | | | | | | | | | |

| Shares | | | | | Cost | | | Value | |

| Common Stocks (continued) | |

|

| Information Technology (continued) | |

| |

| | | | Electronic Components (1.53%) | |

| | 900,000 | | | Amphenol Corp., Cl A | | $ | 42,881,684 | | | $ | 60,264,000 | |

| |

| | | | Internet Services &

Infrastructure (2.93%) | |

| | 592,103 | | | Verisign, Inc.1 | | | 27,318,889 | | | | 102,848,291 | |

| | 154,000 | | | Wix.com Ltd.1,2 | | | 12,246,120 | | | | 12,047,420 | |

| | | | | | | | | | | | |

| | | | 39,565,009 | | | | 114,895,711 | |

| |

| | | | IT Consulting & Other

Services (10.39%) | |

| | 60,000 | | | EPAM Systems, Inc.1 | | | 31,066,807 | | | | 21,731,400 | |

| | 1,396,323 | | | Gartner, Inc.1 | | | 30,026,819 | | | | 386,348,611 | |

| | | | | | | | | | | | |

| | | | 61,093,626 | | | | 408,080,011 | |

| | | |

| | | | Technology

Distributors (1.58%) | | | | | | | | |

| | 397,363 | | | CDW Corp. | | | 26,228,964 | | | | 62,020,417 | |

| | | | | | | | | | | | |

| | Total Information Technology | | | 545,337,253 | | | | 1,244,002,294 | |

| | | | | | | | | | | | |

|

| Real Estate (4.73%) | |

| | | | Real Estate

Services (0.93%) | |

| | 542,323 | | | CBRE Group, Inc., Cl A1 | | | 6,067,334 | | | | 36,612,226 | |

| |

| | | | Specialized REITs (3.80%) | |

| | 175,000 | | | Alexandria Real Estate Equities, Inc.4 | | | 26,236,333 | | | | 24,533,250 | |

| | 65,416 | | | Equinix, Inc. | | | 4,258,856 | | | | 37,211,238 | |

| | 306,856 | | | SBA Communications Corp. | | | 7,734,439 | | | | 87,346,560 | |

| | | | | | | | | | | | |

| | | | 38,229,628 | | | | 149,091,048 | |

| | | | | | | | | | | | |

| | Total Real Estate | | | 44,296,962 | | | | 185,703,274 | |

| | | | | | | | | | | | |

| | Total Common Stocks | | | 1,340,952,439 | | | | 3,827,650,442 | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| Private Common Stocks (0.63%) | |

| Consumer Discretionary (0.63%) | |

| | | | Internet & Direct Marketing

Retail (0.63%) | |

| | 197,613 | | | StubHub Holdings, Inc., Cl A1,3,4,6 | | | 50,000,041 | | | | 24,543,535 | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| Private Preferred Stocks (1.47%) | |

| Industrials (1.47%) | |

| | | | Aerospace & Defense (1.47%) | |

| | 96,298 | | | Space Exploration

Technologies Corp., Series N1,3,4,6 | | | 26,000,460 | | | | 57,790,702 | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| Principal Amount | | Cost | | | Value | |

| Short Term Investments (0.42%) | |

| | $16,820,449 | | | Repurchase Agreement with Fixed Income Clearing Corp., dated 9/30/2022, 0.83% due 10/3/2022; Proceeds at maturity $16,821,612; (Fully Collateralized by $19,359,800 U.S.Treasury Note, 0.375% due 12/31/2025 Market value - $17,156,858)5 | | $ | 16,820,449 | | | $ | 16,820,449 | |

| | | | | | | | | | | | |

| | Total Investments (100.01%) | | $ | 1,433,773,389 | | | | 3,926,805,128 | |

| | | | | | | | | | | | |

| | Liabilities Less Cash and Other Assets (-0.01%) | | | | (574,388 | ) |

| | | | | | | | | | | | |

| | Net Assets | | | $ | 3,926,230,740 | |

| | | | | | | | | | | | |

| Retail Shares (Equivalent to $77.43 per share

based on 23,566,345 shares outstanding) |

| | $ | 1,824,825,608 | |

| | | | | | | | | | | | |

| Institutional Shares (Equivalent to $81.71 per share

based on 24,095,119 shares outstanding) |

| | $ | 1,968,917,159 | |

| | | | | | | | | | | | |

| R6 Shares (Equivalent to $81.70 per share

based on 1,621,678 shares outstanding) |

| | $ | 132,487,973 | |

| | | | | | | | | | | | |

| % | Represents percentage of net assets. |

| 1 | Non-income producing securities. |

| 3 | At September 30, 2022, the market value of restricted and fair valued securities amounted to $82,334,237 or 2.10% of net assets. These securities are not deemed liquid. See Note 6 regarding Restricted Securities. |

| 4 | The Adviser has reclassified/classified certain securities in or out of this sub-industry. Such reclassifications/classifications are not supported by S&P or MSCI (unaudited). |

| 5 | Level 2 security. See Note 7 regarding Fair Value Measurements. |

| 6 | Level 3 security. See Note 7 regarding Fair Value Measurements. |

| ADR | American Depositary Receipt. |

All securities are Level 1, unless otherwise noted.

| | |

| See Notes to Financial Statements. | | 17 |

| | |

| Baron Growth Fund | | September 30, 2022 |

STATEMENT OF NET ASSETS

| | | | | | | | | | | | |

| Shares | | | | | Cost | | | Value | |

| Common Stocks (99.99%) | |

| Communication Services (5.60%) | |

| | | | Alternative Carriers (5.60%) | | | | | | | | |

| | 7,900,000 | | | Iridium Communications, Inc.1,4 | | $ | 48,702,979 | | | $ | 350,523,000 | |

| | | | | | | | | | | | |

| Consumer Discretionary (19.06%) | |

| | | | Casinos & Gaming (3.45%) | | | | | | | | |

| | 440,000 | | | Boyd Gaming Corporation | | | 11,056,072 | | | | 20,966,000 | |

| | 4,975,000 | | | Penn Entertainment, Inc.1 | | | 51,762,579 | | | | 136,862,250 | |

| | 1,695,000 | | | Red Rock Resorts, Inc., Cl A | | | 30,919,577 | | | | 58,070,700 | |

| | | | | | | | | | | | |

| | | | 93,738,228 | | | | 215,898,950 | |

| |

| | | | Education Services (1.08%) | |

| | 1,170,000 | | | Bright Horizons Family Solutions, Inc.1 | | | 36,788,154 | | | | 67,450,500 | |

| |

| | | | Hotels, Resorts & Cruise

Lines (7.64%) | |

| | 2,975,000 | | | Choice Hotels International, Inc.4 | | | 71,854,227 | | | | 325,822,000 | |

| | 1,250,000 | | | Marriott Vacations

Worldwide Corp. | | | 66,814,799 | | | | 152,325,000 | |

| | | | | | | | | | | | |

| | | | 138,669,026 | | | | 478,147,000 | |

| |

| | | | Leisure Facilities (6.89%) | |

| | 2,000,000 | | | Vail Resorts, Inc. | | | 56,102,209 | | | | 431,280,000 | |

| | | | | | | | | | | | |

| | Total Consumer Discretionary | | | 325,297,617 | | | | 1,192,776,450 | |

| | | | | | | | | | | | |

| Financials (38.69%) | |

| | | | Asset Management &

Custody Banks (2.62%) | |

| | 1,750,000 | | | The Carlyle Group, Inc. | | | 35,720,227 | | | | 45,220,000 | |

| | 1,900,000 | | | Cohen & Steers, Inc. | | | 41,176,154 | | | | 118,997,000 | |

| | | | | | | | | | | | |

| | | | 76,896,381 | | | | 164,217,000 | |

| |

| | | | Financial Exchanges &

Data (21.33%) | |

| | 1,200,000 | | | FactSet Research Systems, Inc. | | | 59,954,575 | | | | 480,132,000 | |

| | 945,000 | | | Morningstar, Inc. | | | 19,271,951 | | | | 200,642,400 | |

| | 1,550,000 | | | MSCI, Inc. | | | 28,720,345 | | | | 653,774,500 | |

| | | | | | | | | | | | |

| | | | 107,946,871 | | | | 1,334,548,900 | |

| |

| | | | Investment Banking &

Brokerage (0.73%) | |

| | 450,000 | | | Houlihan Lokey, Inc. | | | 19,625,873 | | | | 33,921,000 | |

| | 350,000 | | | Moelis & Co., Cl A | | | 5,215,059 | | | | 11,833,500 | |

| | | | | | | | | | | | |

| | | | 24,840,932 | | | | 45,754,500 | |

| |

| | | | Life & Health Insurance (3.00%) | |

| | 1,520,000 | | | Primerica, Inc. | | | 31,620,617 | | | | 187,644,000 | |

| |

| | | | Property & Casualty

Insurance (10.72%) | |

| | 9,120,000 | | | Arch Capital Group Ltd.1,2 | | | 28,455,005 | | | | 415,324,800 | |

| | 1,000,000 | | | Kinsale Capital Group, Inc. | | | 35,007,763 | | | | 255,420,000 | |

| | | | | | | | | | | | |

| | | | 63,462,768 | | | | 670,744,800 | |

| |

| | | | Thrifts & Mortgage

Finance (0.29%) | |

| | 520,000 | | | Essent Group Ltd.2 | | | 14,300,210 | | | | 18,132,400 | |

| | | | | | | | | | | | |

| | Total Financials | | | 319,067,779 | | | | 2,421,041,600 | |

| | | | | | | | | | | | |

| Health Care (10.46%) | |

| | | | Health Care Equipment (2.95%) | | | | | | | | |

| | 567,500 | | | IDEXX Laboratories, Inc.1 | | | 7,964,243 | | | | 184,891,500 | |

| |

| | | | Health Care Supplies (0.50%) | |

| | 1,829,564 | | | Figs, Inc., Cl A1 | | | 19,728,364 | | | | 15,093,903 | |

| | 1,147,434 | | | Neogen Corp.1 | | | 13,141,411 | | | | 16,029,653 | |

| | | | | | | | | | | | |

| | | | 32,869,775 | | | | 31,123,556 | |

| | | | | | | | | | | | |

| Shares | | | | | Cost | | | Value | |

| Common Stocks (continued) | |

| Health Care (continued) | |

| | | | Life Sciences Tools &

Services (6.73%) | |

| | 775,000 | | | Bio-Techne Corporation | | $ | 40,802,348 | | | $ | 220,100,000 | |

| | 72,000 | | | Mettler-Toledo International, Inc.1 | | | 3,293,302 | | | | 78,056,640 | |

| | 500,000 | | | West Pharmaceutical Services, Inc. | | | 17,009,688 | | | | 123,040,000 | |

| | | | | | | | | | | | |

| | | | 61,105,338 | | | | 421,196,640 | |

| |

| | | | Pharmaceuticals (0.28%) | |

| | 598,076 | | | Dechra Pharmaceuticals PLC (United Kingdom)2,6 | | | 18,422,044 | | | | 17,368,707 | |

| | | | | | | | | | | | |

| | Total Health Care | | | 120,361,400 | | | | 654,580,403 | |

| | | | | | | | | | | | |

| Industrials (7.11%) | |

| | | | Building Products (0.88%) | |

| | 1,250,000 | | | Trex Co., Inc.1 | | | 11,233,697 | | | | 54,925,000 | |

| |

| | | | Environmental & Facilities

Services (0.15%) | |

| | 1,200,000 | | | BrightView Holdings, Inc.1 | | | 14,780,063 | | | | 9,528,000 | |

| |

| | | | Industrial Machinery (0.21%) | |

| | 4,275,000 | | | Marel hf (Netherlands)2 | | | 18,281,670 | | | | 12,988,114 | |

| | |

| | | | Research & Consulting

Services (5.87%) | | | | | |

| | 5,275,000 | | | CoStar Group, Inc.1 | | | 22,039,585 | | | | 367,403,750 | |

| | | | | | | | | | | | |

| | Total Industrials | | | 66,335,015 | | | | 444,844,864 | |

| | | | | | | | | | | | |

| Information Technology (12.52%) | |

| | | | Application Software (5.02%) | |

| | 725,000 | | | Altair Engineering, Inc., Cl A1 | | | 11,330,019 | | | | 32,059,500 | |

| | 1,000,000 | | | ANSYS, Inc.1 | | | 22,816,668 | | | | 221,700,000 | |

| | 975,000 | | | Guidewire Software, Inc.1 | | | 29,909,124 | | | | 60,040,500 | |

| | | | | | | | | | | | |

| | | | 64,055,811 | | | | 313,800,000 | |

| |

| | | | Data Processing & Outsourced

Services (0.57%) | |

| | 750,000 | | | SS&C Technologies Holdings, Inc. | | | 5,540,901 | | | | 35,812,500 | |

| | | |

| | | | Electronic Components (0.19%) | | | | | | | | |

| | 60,000 | | | Littelfuse, Inc. | | | 6,452,400 | | | | 11,921,400 | |

| | |

| | | | IT Consulting & Other

Services (6.74%) | | | | | |

| | 1,525,000 | | | Gartner, Inc.1 | | | 21,222,737 | | | | 421,952,250 | |

| | | | | | | | | | | | |

| | Total Information Technology | | | 97,271,849 | | | | 783,486,150 | |

| | | | | | | | | | | | |

| Real Estate (6.55%) | |

| | | | Diversified REITs (0.08%) | |

| | 200,000 | | | American Assets Trust, Inc. | | | 3,350,429 | | | | 5,144,000 | |

| | | |

| | | | Office REITs (0.97%) | | | | | | | | |

| | 3,400,000 | | | Douglas Emmett, Inc. | | | 30,004,462 | | | | 60,962,000 | |

| |

| | | | Specialized REITs (5.50%) | |

| | 750,000 | | | Alexandria Real Estate

Equities, Inc.5 | | | 26,054,963 | | | | 105,142,500 | |

| | 5,400,000 | | | Gaming and Leisure

Properties, Inc. | | | 114,573,084 | | | | 238,896,000 | |

| | | | | | | | | | | | |

| | | | 140,628,047 | | | | 344,038,500 | |

| | | | | | | | | | | | |

| | Total Real Estate | | | 173,982,938 | | | | 410,144,500 | |

| | | | | | | | | | | | |

| | Total Common Stocks | | | 1,151,019,577 | | | | 6,257,396,967 | |

| | | | | | | | | | | | |

| | |

| 18 | | See Notes to Financial Statements. |

| | |

| September 30, 2022 | | Baron Growth Fund |

STATEMENT OF NET ASSETS (Continued)

| | | | | | | | | | | | |

| Shares | | | | | Cost | | | Value | |

| Private Convertible Preferred Stocks (0.50%) | |

| Industrials (0.28%) | |

| | | | Electrical Components &

Equipment (0.28%) | |

| | 59,407,006 | | | Northvolt AB (Sweden)2,3,5,7 | | $ | 9,374,989 | | | $ | 17,811,468 | |

| | | | | | | | | | | | |

|

| Materials (0.22%) | |

| | | | Fertilizers & Agricultural

Chemicals (0.22%) | | | | | | | | |

| | 341,838 | | | Farmers Business Network, Inc., Series F1,2,3,5,7 | | | 11,300,002 | | | | 10,925,143 | |

| | 80,440 | | | Farmers Business Network, Inc., Series G1,2,3,5,7 | | | 5,000,000 | | | | 2,701,175 | |

| | | | | | | | | | | | |

| | Total Materials | | | 16,300,002 | | | | 13,626,318 | |

| | | | | | | | | | | | |

| | Total Private Convertible Preferred Stocks | | | 25,674,991 | | | | 31,437,786 | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| Warrants (0.00%) | |

| Consumer Discretionary (0.00%) | |

| | | | Hotels, Resorts & Cruise

Lines (0.00%) | |

| | 96,515 | | | OneSpaWorld Holdings Ltd. Warrants, Exp 3/19/20241,2,5 | | | 0 | | | | 102,306 | |

| | | | | | | | | | | | |

| | Total Investments (100.49%) | | $ | 1,176,694,568 | | | | 6,288,937,059 | |

| | | | | | | | | | | | |

| | Liabilities Less Cash and Other Assets (-0.49%) | | | | (30,708,148 | ) |

| | | | | | | | | | | | |

| | Net Assets | | | $ | 6,258,228,911 | |

| | | | | | | | | | | | |

| Retail Shares (Equivalent to $80.38 per share

based on 25,076,918 shares outstanding) |

| | $ | 2,015,588,300 | |

| | | | | | | | | | | | |

| Institutional Shares (Equivalent to $84.34 per share

based on 48,296,135 shares outstanding) |

| | $ | 4,073,531,740 | |

| | | | | | | | | | | | |

| R6 Shares (Equivalent to $84.35 per share

based on 2,004,771 shares outstanding) |

| | $ | 169,108,871 | |

| | | | | | | | | | | | |

| % | Represents percentage of net assets. |

| 1 | Non-income producing securities. |

| 3 | At September 30, 2022, the market value of restricted and fair valued securities amounted to $31,437,786 or 0.50% of net assets. These securities are not deemed liquid. See Note 6 regarding Restricted Securities. |

| 4 | See Note 10 regarding “Affiliated” companies. |

| 5 | The Adviser has reclassified/classified certain securities in or out of this sub-industry. Such reclassifications/classifications are not supported by S&P or MSCI (unaudited). |

| 6 | Level 2 security. See Note 7 regarding Fair Value Measurements. |

| 7 | Level 3 security. See Note 7 regarding Fair Value Measurements. |

All securities are Level 1, unless otherwise noted.

| | |

| See Notes to Financial Statements. | | 19 |

| | |

| Baron Small Cap Fund | | September 30, 2022 |

STATEMENT OF NET ASSETS

| | | | | | | | | | | | |

| Shares | | | | | Cost | | | Value | |

| Common Stocks (93.07%) | |

| Communication Services (4.99%) | |

| | | | Advertising (1.14%) | |

| | 750,000 | | | The Trade Desk, Inc., Cl A1 | | $ | 2,662,500 | | | $ | 44,812,500 | |

| | | |

| | | | Cable & Satellite (1.12%) | | | | | | | | |

| | 75,000 | | | Liberty Broadband

Corporation, Cl A1 | | | 298,828 | | | | 5,595,000 | |

| | 200,000 | | | Liberty Broadband

Corporation, Cl C1 | | | 772,163 | | | | 14,760,000 | |

| | 625,000 | | | Liberty Media Corp.-Liberty SiriusXM, Cl C1 | | | 1,322,732 | | | | 23,568,750 | |

| | | | | | | | | | | | |

| | | | 2,393,723 | | | | 43,923,750 | |

| |

| | | | Movies & Entertainment (2.73%) | |

| | 1,200,000 | | | Liberty Media Corporation-Liberty Formula One, Cl C1 | | | 21,262,385 | | | | 70,200,000 | |

| | 150,000 | | | Madison Square Garden Entertainment Corp.1 | | | 2,346,185 | | | | 6,613,500 | |

| | 225,000 | | | Madison Square Garden

Sports Corp.1 | | | 8,416,556 | | | | 30,748,500 | |

| | | | | | | | | | | | |

| | | | 32,025,126 | | | | 107,562,000 | |

| | | | | | | | | | | | |

| | Total Communication Services | | | 37,081,349 | | | | 196,298,250 | |

| | | | | | | | | | | | |

|

| Consumer Discretionary (14.66%) | |

| | | | Auto Parts & Equipment (0.36%) | |

| | 3,500,000 | | | Holley, Inc.1 | | | 34,929,795 | | | | 14,175,000 | |

| |

| | | | Casinos & Gaming (3.45%) | |

| | 875,000 | | | DraftKings, Inc., Cl A1 | | | 11,187,787 | | | | 13,247,500 | |

| | 1,025,000 | | | Penn Entertainment, Inc. (formerly, Penn National Gaming, Inc.)1 | | | 18,170,393 | | | | 28,197,750 | |

| | 2,750,000 | | | Red Rock Resorts, Inc., Cl A | | | 75,439,769 | | | | 94,215,000 | |

| | | | | | | | | | | | |

| | | | 104,797,949 | | | | 135,660,250 | |

| |

| | | | Education Services (1.10%) | |

| | 750,000 | | | Bright Horizons Family

Solutions, Inc.1 | | | 29,824,721 | | | | 43,237,500 | |

| |

| | | | Home Improvement Retail (2.50%) | |

| | 1,400,000 | | | Floor & Decor Holdings, Inc., Cl A1 | | | 55,967,953 | | | | 98,364,000 | |

| |

| | | | Homebuilding (2.88%) | |

| | 1,400,000 | | | Installed Building Products, Inc. | | | 76,015,010 | | | | 113,386,000 | |

| |

| | | | Hotels, Resorts & Cruise

Lines (0.12%) | |

| | 1,000,000 | | | Membership Collective

Group, Inc., Cl A1 | | | 13,900,478 | | | | 4,720,000 | |

| |

| | | | Leisure Facilities (1.47%) | |

| | 1,000,000 | | | Planet Fitness, Inc., Cl A1 | | | 41,366,077 | | | | 57,660,000 | |

| |

| | | | Restaurants (1.68%) | |