UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2009

OR

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _______________ to _________________________.

Commission file number: 0-16084

CITIZENS & NORTHERN CORPORATION

(Exact name of Registrant as specified in its charter)

| PENNSYLVANIA | 23-2451943 |

| (State or other jurisdiction of | (I.R.S. Employer |

| incorporation or organization) | Identification No.) |

90-92 MAIN STREET, WELLSBORO, PA 16901

(Address of principal executive offices) (Zip code)

570-724-3411

(Registrant's telephone number including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Name of Exchange Where Registered |

| Common Stock Par Value $1.00 | The NASDAQ Stock Market LLC |

Securities registered pursuant to section 12(g) of the Act: None

Indicate by check mark whether the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (Section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes o No o

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer “and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

(Check one:) Large accelerated filer o Accelerated filer x Non-accelerated filer o Smaller reporting company o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes o No x

The aggregate market value of the registrant's common stock held by non-affiliates at June 30, 2009, the registrant’s most recently completed second fiscal quarter, was $144,560,917.

The number of shares of common stock outstanding at February 25, 2010 was 12,120,024.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s proxy statement for the annual meeting of its shareholders to be held April 20, 2010 are incorporated by reference into Parts III and IV of this report.

PART I

ITEM 1. BUSINESS

Citizens & Northern Corporation (“Corporation”) is a holding company whose principal activity is community banking. The Corporation’s principal office is located in Wellsboro, Pennsylvania. The largest subsidiary is Citizens & Northern Bank (“C&N Bank”). In 2005, the Corporation acquired Canisteo Valley Corporation and its subsidiary, First State Bank, a New York State chartered commercial bank with offices in Canisteo and South Hornell, NY. The First State Bank banking offices are located in the southern tier of New York State, in close proximity to many of the Corporation’s northern Pennsylvania branch locations. Management considers the New York State branches to be part of the same community banking operating segment as the Pennsylvania locations; however, the separate New York State charter for First State Bank has been maintained because of certain regulatory advantages. The Corporation’s other wholly-owned subsidiaries are Citizens & Northern Investment Corporation and Bucktail Life Insurance Company (“Bucktail”). Citizens & Northern Investment Corporation was formed in 1999 to engage in investment activities. Bucktail reinsures credit and mortgage life and accident and health insurance on behalf of C&N Bank.

C&N Bank is a Pennsylvania banking institution that was formed by the consolidation of Northern National Bank of Wellsboro and Citizens National Bank of Towanda on October 1, 1971. Subsequent mergers included: First National Bank of Ralston in May 1972; Sullivan County National Bank in October 1977; Farmers National Bank of Athens in January 1984; and First National Bank of East Smithfield in May 1990. On May 1, 2007, the Corporation completed its acquisition of Citizens Bancorp, Inc. (“Citizens”) for an aggregate purchase price of $28,391,000 in cash and common stock. Also, Citizens Trust Company, the banking subsidiary of Citizens, was merged with and into C&N Bank as part of the transaction. C&N Bank has held its current name since May 6, 1975, at which time C&N Bank changed its charter from a national bank to a Pennsylvania bank.

C&N Bank and First State Bank (collectively, the “Banks”) provide an extensive range of banking services, including deposit and loan products for personal and commercial customers. The Banks also maintain a trust division that provides a wide range of financial services, such as 401(k) plans, retirement planning, estate planning, estate settlements and asset management. In January 2000, C&N Bank formed a subsidiary, C&N Financial Services Corporation (“C&NFSC”). C&NFSC is a licensed insurance agency that provides insurance products to individuals and businesses. In 2001, C&NFSC added a broker-dealer division, which offers mutual funds, annuities, educational savings accounts and other investment products through registered agents. C&NFSC’s operations are not significant in relation to the total operations of the Corporation.

All phases of the Banks’ business are competitive. The Banks primarily compete in Tioga, Bradford, Sullivan, Lycoming, Potter, Cameron and McKean counties in Pennsylvania, and Steuben and Allegany counties in New York. The Banks compete with local commercial banks headquartered in our market area as well as other commercial banks with branches in our market area. Some of the banks that have branches in the Banks’ market area are larger in overall size than the Banks. With respect to lending activities and attracting deposits, the Banks also compete with savings banks, savings and loan associations, insurance companies, regulated small loan companies and credit unions. Also, the Banks compete with mutual funds for deposits. C&N Bank competes with insurance companies, investment counseling firms, mutual funds and other business firms and individuals for trust, investment management, brokerage and insurance services. The Banks are generally competitive with all financial institutions in our service area with respect to interest rates paid on time and savings deposits, service charges on deposit accounts and interest rates charged on loans. The Banks serve a diverse customer base, and are not economically dependent on any small group of customers or on any individual industry.

Major initiatives within the last 5 years included the following:

| · | expanded trust and financial services capabilities, including investment management, employee benefits and insurance services; |

| · | constructed and opened a branch facility in Jersey Shore, PA in 2005; |

| · | closed on the merger with Canisteo Valley Corporation in 2005; |

| · | constructed and opened a branch facility in Old Lycoming Township, PA, which opened in March 2006; |

| · | constructed an administration building in Wellsboro, PA, which opened in March 2006; |

| · | as described above, in May 2007, acquired Citizens Bancorp, Inc.; |

| · | implemented an overdraft privilege program in 2008; |

| · | underwent an operational process review in 2008, resulting in identification of opportunities for increases in revenue and decreases in expenses, including a net reduction in work force of 15.9%, to 297 full-time equivalent employees at December 31, 2008 from 353 at December 31, 2007 |

At December 31, 2009, C&N Bank had total assets of $1,276,365,000, total deposits of $886,937,000, net loans outstanding of $699,751,000 and 282 full-time equivalent employees. At December 31, 2009, First State Bank had total assets of $50,780,000, total deposits of $42,069,000, net loans outstanding of $13,587,000 and 11 full-time equivalent employees.

Most of the activities of the Corporation and its subsidiaries are regulated by federal or state agencies. The primary regulatory relationships are described as follows:

| · | The Corporation is a bank holding company formed under the provisions of Section 3 of the Federal Reserve Act. The Corporation is under the direct supervision of the Federal Reserve and must comply with the reporting requirements of the Federal Bank Holding Company Act. |

| · | C&N Bank is a state-chartered, nonmember bank, supervised by the Federal Deposit Insurance Corporation and the Pennsylvania Department of Banking. |

| · | Canisteo Valley Corporation is the holding company for First State Bank. The Federal Reserve is the primary regulator for Canisteo Valley Corporation. |

| · | First State Bank is a state-chartered, Federal Reserve member bank, supervised by the Federal Reserve and the New York State Department of Banking. |

| · | C&NFSC is a Pennsylvania corporation. The Pennsylvania Department of Insurance regulates C&NFSC’s insurance activities. Brokerage products are offered through a third party networking agreement between C&N Bank and UVEST Financial Services, Inc. |

| · | Bucktail is incorporated in the state of Arizona and supervised by the Arizona Department of Insurance. |

Participation in the Troubled Asset Relief Program Capital Purchase Program

On October 3, 2008, the Emergency Economic Stabilization Act (“EESA”) became law. The Troubled Asset Relief Program Capital Purchase Program (“TARP Capital Purchase Program”) was established pursuant to the EESA in order to facilitate the investment by the U.S. Department of the Treasury (“Treasury”) in senior preferred shares of qualifying banks, savings associations and certain bank and savings and loan holding companies. Pursuant to the TARP Capital Purchase Program, on January 16, 2009, the Corporation sold 26,440 shares of Series A preferred stock and a warrant to acquire 194,794 shares of common stock to the Treasury for an aggregate purchase price of $26.44 million.

As a result of the Corporation’s participation in the TARP Capital Purchase Program, the Corporation has agreed to certain limitations on executive compensation. Additionally, on February 17, 2009, President Obama signed into law the American Recovery and Reinvestment Act of 2009 (the “ARRA”), which amended the EESA by, among other things, directing Treasury to issue regulations implementing strict limitations on compensation paid or accrued by financial institutions, like the Corporation, participating in the TARP Program. Treasury issued the applicable implementing regulations, which became effective June 15, 2009, called “TARP Standards for Compensation and Corporate Governance.” The limitations provided for in the implementing regulations are generally as follows: (1) limits on compensation that exclude incentives for senior executive officers (SEOs, as defined in the regulations) to take unnecessary and excessive risks that threaten the value of the Corporation; (2) provision for the recovery of any bonus, retention award, or incentive compensation paid to a SEO or the next twenty most highly compensated employees based on materially inaccurate statements of earnings, revenues, gains, or other criteria; (3) prohibition on making any golden parachute payments to a SEO or any of the next five most highly compensated employees; (4) prohibition on the payments or accrual of bonus, retention awards, or incentive compensation to the five most highly compensated employees of the Corporation, subject to certain exceptions for payments made in the form of restricted stock; (5) prohibitions on employee compensation plans that would encourage manipulation of earnings reported by the Corporation to enhance an employee’s compensation; (6) establishment of a compensation committee of independent directors to meet semi-annually to review employee compensation plans and the risks posed by these plans to the Corporation; (7) adoption of an excessive and luxury expenditure policy; (8) disclosure of perquisites offered to SEOs and certain highly compensated employees; (9) disclosure related to compensation consultant engagements; (10) prohibition on tax gross-ups to SEOs and certain highly compensated employees; (11) compliance with Federal securities rules and regulations regarding the submission of non-binding resolutions on SEO compensation to shareholders; and (12) establishment of the Office of the Special Master for TARP Executive Compensation (Special Master) to address the application of these rules, to TARP recipients and their employees. The implementation regulations also establish compliance reporting and recordkeeping requirements regarding the rule’s executive compensation and corporate governance standards.

A copy of the Corporation’s annual report on Form 10-K, quarterly reports on Form 10-Q, current events reports on Form 8-K, and amendments to these reports, will be furnished without charge upon written request to the Corporation’s Treasurer at P.O. Box 58, Wellsboro, PA 16901. Copies of these reports will be furnished as soon as reasonably possible, after they are filed electronically with the Securities and Exchange Commission. The information is also available through the Corporation’s web site at www.cnbankpa.com.

ITEM 1A. RISK FACTORS

The Corporation is subject to the many risks and uncertainties applicable to all banking companies, as well as risks specific to the Corporation’s geographic locations. Although the Corporation seeks to effectively manage risks, and maintains a level of equity that exceeds the banking regulatory agencies’ thresholds for being considered “well capitalized” (see Note 19 to the consolidated financial statements), management cannot predict the future and cannot eliminate the possibility of credit, operational or other losses. Accordingly, actual results may differ materially from management's expectations. Some of the Corporation’s significant risks and uncertainties are discussed below.

Credit Risk from Lending Activities - A significant source of risk is the possibility that losses will be sustained because borrowers, guarantors and related parties may fail to perform in accordance with the terms of their loan agreements. Most of the Corporation’s loans are secured, but some loans are unsecured. With respect to secured loans, the collateral securing the repayment of these loans may be insufficient to cover the obligations owed under such loans. Collateral values may be adversely affected by changes in economic, environmental and other conditions, including declines in the value of real estate, changes in interest rates, changes in monetary and fiscal policies of the federal government, wide-spread disease, terrorist activity, environmental contamination and other external events. In addition, collateral appraisals that are out of date or that do not meet industry recognized standards may create the impression that a loan is adequately collateralized when it is not. The Corporation has adopted underwriting and credit monitoring procedures and policies, including regular reviews of appraisals and borrower financial statements, that management believes are appropriate to mitigate the risk of loss. Also, as discussed further in the “Provision and Allowance for Loan Losses” section of Management’s Discussion and Analysis, the Corporation attempts to estimate the amount of losses that may be inherent in the portfolio through a quarterly evaluation process that includes several members of management and that addresses specifically identified problem loans, as well as other quantitative data and qualitative factors. Such risk management and accounting policies and procedures, however, may not prevent unexpected losses that could have a material adverse effect on the Corporation’s financial condition, results of operations or liquidity.

Interest Rate Risk - Business risk arising from changes in interest rates is an inherent factor in operating a banking organization. The Corporation’s assets are predominantly long-term, fixed rate loans and debt securities. Funding for these assets comes principally from shorter-term deposits and borrowed funds. Accordingly, there is an inherent risk of lower future earnings or decline in fair value of the Corporation’s financial instruments when interest rates change. Significant fluctuations in interest rates could have a material adverse effect on the Corporation’s financial condition, results of operations or liquidity. For additional information regarding interest rate risk, see Part II, Item 7A, "Quantitative and Qualitative Disclosures About Market Risk."

Equity Securities Risk - The Corporation’s equity securities portfolio consists of investments in stocks of banks and bank holding companies. Investments in bank stocks are subject to the risk factors affecting the banking industry, and that could cause a general market decline in the value of bank stocks. Also, losses could occur in individual stocks held by the Corporation because of specific circumstances related to each bank. These factors could have a material adverse effect on the Corporation’s financial condition, results of operations or liquidity. For additional information regarding equity securities risk, including management’s assessment of equity securities for other-than-temporary impairment as of December 31, 2008, see Part II, Item 7A, "Quantitative and Qualitative Disclosures About Market Risk."

Debt Securities Risk – As described in the Earnings Overview section of Management’s Discussion and Analysis, the Corporation’s earnings were materially impaired in 2009 and 2008 by securities losses. Much of the Corporation’s 2009 and 2008 losses from trust-preferred securities and other securities stem from the much-publicized economic problems affecting the national and international economy, which have particularly hurt the banking industry. The Corporation has exposure to the possibility of future losses from investments in a senior tranche pooled trust-preferred security, trust-preferred securities issued by individual banks, private label collateralized mortgage obligations (CMOs), and other debt securities. For additional information regarding debt securities, see Note 7 to the consolidated financial statements.

Realization of Deferred Tax Asset – The Corporation recognizes deferred tax assets and liabilities based on differences between the financial statement carrying amounts and the tax bases of assets and liabilities. At December 31, 2009, the net deferred tax asset was $22.0 million, up from a balance of approximately $16.4 million at December 31, 2008. The increase in net deferred tax asset resulted mainly from other-than-temporary impairment losses on securities for financial reporting purposes, which are not currently deductible for federal income tax reporting purposes. The net deferred tax asset balance at December 31, 2009 attributable to realized securities losses was $16.1 million, exclusive of a valuation allowance of $373,000.

The Corporation regularly reviews deferred tax assets for recoverability based on history of earnings, expectations for future earnings and expected timing of reversals of temporary differences. Realization of deferred tax assets ultimately depends on the existence of sufficient taxable income, including taxable income in prior carryback years, as well as future taxable income. Of the total deferred tax asset from realized losses on securities, a portion is from securities that, if the Corporation were to sell them, would be classified as capital losses for income tax reporting purposes. The valuation allowance at December 31, 2009 reflects the excess of the tax benefit that would be generated from selling all of the capital assets, over the amount that could be realized from available carryback and offset against capital gains generated in 2007 and 2008. Realization of the remaining $373,000 of tax benefits associated with capital assets is dependent upon realization of future capital gains. After adjustment for the valuation allowance on capital assets, management believes the recorded net deferred tax asset at December 31, 2009 is fully realizable; however, if management determines the Corporation will be unable to realize all or part of the net deferred tax asset, the Corporation would adjust the deferred tax asset, which would negatively impact earnings.

Federal Home Loan Bank of Pittsburgh Common Stock - We own common stock of the Federal Home Loan Bank of Pittsburgh, or the FHLB, in order to qualify for membership in the Federal Home Loan Bank system, which enables us to borrow funds under the Federal Home Loan Bank advance program. The carrying value and fair market value of our FHLB common stock, which is included in Other Assets in the consolidated balance sheet, was $8.6 million as of December 31, 2009. Published reports indicate that certain member banks of the Federal Home Loan Bank system may be subject to asset quality risks that could result in materially lower regulatory capital levels. In December 2008, the FHLB had notified its member banks that it had suspended dividend payments and the repurchase of capital stock until further notice is provided. In an extreme situation, it is possible that the capitalization of a Federal Home Loan Bank, including the FHLB, could be substantially diminished or reduced to zero. Consequently, given that there is no market for our FHLB common stock, we believe that there is a risk that our investment could be deemed other-than-temporarily impaired at some time in the future. If this occurs, it may adversely affect our results of operations and financial condition. If the FHLB were to cease operations, or if we were required to write-off our investment in the FHLB, our business, financial condition, liquidity, capital and results of operations may be materially adversely affected.

FDIC Insurance Assessments - - During 2008 and continuing in 2009, higher levels of bank failures have dramatically increased resolution costs of the Federal Deposit Insurance Corporation, or the FDIC, and depleted the deposit insurance fund. In addition, the FDIC and the U.S. Congress have taken action to increase federal deposit insurance coverage, placing additional stress on the deposit insurance fund. In order to maintain a strong funding position and restore reserve ratios of the deposit insurance fund, the FDIC increased assessment rates of insured institutions uniformly by seven cents for every $100 of deposits beginning with the first quarter of 2009, with additional changes beginning April 1, 2009, which require riskier institutions to pay a larger share of premiums by factoring in rate adjustments based on secured liabilities and unsecured debt levels. To further support the rebuilding of the deposit insurance fund, the FDIC imposed a special assessment on each insured institution, equal to five basis points of the institution’s total assets minus Tier 1 capital as of September 30, 2009. For our banks, there was an aggregate charge of $589,000, which was recorded as a pre-tax charge during the second quarter of 2009. The FDIC has indicated that future special assessments are possible, although it has not determined the magnitude or timing of any future assessments. In December 2009, we paid a pre-payment of the FDIC’s estimated assessment total for the next three years for our banks, totaling approximately $5.5 million. This amount was included in Other Assets in the consolidated balance sheet at December 31, 2009, and will be amortized, subject to adjustments imposed by the FDIC, over the next three years.

We are generally unable to control the amount of premiums that we are required to pay for FDIC insurance. If there are additional bank or financial institution failures, we may be required to pay even higher FDIC premiums. Our expenses for 2009 were significantly and adversely affected by the increased premiums and the special assessment. These increases and assessment and any future increases in insurance premiums or additional special assessments may materially adversely affect our results of operations.

Breach of Information Security and Technology Dependence - The Corporation relies on software, communication, and information exchange on a variety of computing platforms and networks and over the Internet. Despite numerous safeguards, the Corporation cannot be certain that all of its systems are entirely free from vulnerability to attack or other technological difficulties or failures. The Corporation relies on the services of a variety of vendors to meet its data processing and communication needs. If information security is breached or other technology difficulties or failures occur, information may be lost or misappropriated, services and operations may be interrupted and the Corporation could be exposed to claims from customers. Any of these results could have a material adverse effect on the Corporation’s financial condition, results of operations or liquidity.

Limited Geographic Diversification - The Corporation grants commercial, residential and personal loans to customers primarily in the Pennsylvania Counties of Tioga, Bradford, Sullivan, Lycoming, Potter, Cameron and McKean, and in Steuben and Allegany Counties in New York State. Although the Corporation has a diversified loan portfolio, a significant portion of its debtors’ ability to honor their contracts is dependent on the local economic conditions within the region. Deterioration in economic conditions could adversely affect the quality of the Corporation's loan portfolio and the demand for its products and services, and accordingly, could have a material adverse effect on the Corporation's financial condition, results of operations or liquidity.

Growth Strategy – In recent years, the Corporation has expanded its operations by acquisitions and by building and opening new branches. The Corporation’s future financial performance will depend on its ability to execute its strategic plan and manage its future growth. Failure to execute these plans could have a material adverse effect on the Corporation’s financial condition, results of operations or liquidity.

Competition - All phases of the Corporation’s business are competitive. Some competitors are much larger in total assets and capitalization than the Corporation, have greater access to capital markets and can offer a broader array of financial services. There can be no assurance that the Corporation will be able to compete effectively in its markets. Furthermore, developments increasing the nature or level of competition could have a material adverse effect on the Corporation's financial condition, results of operations or liquidity.

Government Regulation and Monetary Policy - The Corporation and the banking industry are subject to extensive regulation and supervision under federal and state laws and regulations. The requirements and limitations imposed by such laws and regulations limit the manner in which the Corporation conducts its business, undertakes new investments and activities and obtains financing. These regulations are designed primarily for the protection of the deposit insurance funds and consumers and not to benefit the Corporation's shareholders. Financial institution regulation has been the subject of significant legislation in recent years and may be the subject of further significant legislation in the future, none of which is in the control of the Corporation. Significant new laws or changes in, or repeals of, existing laws could have a material adverse effect on the Corporation's financial condition, results of operations or liquidity. Further, federal monetary policy, particularly as implemented through the Federal Reserve System, significantly affects short-term interest rates and credit conditions, and any unfavorable change in these conditions could have a material adverse effect on the Corporation's financial condition, results of operations or liquidity.

Participation in the TARP Capital Purchase Program - Pursuant to the TARP Capital Purchase Program, on January 16, 2009, the Corporation sold 26,440 shares of Series A preferred stock and a warrant to acquire 194,794 shares of common stock to the Treasury for an aggregate purchase price of $26.44 million. As a TARP Participant, the Corporation is subject to limits on executive compensation (described in Item 1 of Form 10-K) which could limit the Corporation’s ability to attract and retain qualified management personnel. Also, because of participation in the TARP Program, the Corporation is subject to limitations on payment of dividends on common stock, which include a requirement that permission from the Treasury must be obtained to pay dividends greater than $0.24 per share (per quarter) on its common stock. Further, until January 16, 2012 (unless prior to that date, the Corporation has redeemed the preferred stock issued to the Treasury in whole or the Treasury has transferred all of the preferred stock to third parties) the Treasury’s consent is required for any repurchases of common stock, except for repurchases of shares in connection with employee benefit plans in the ordinary course of business consistent with past practice.

Bank Secrecy Act and Related Laws and Regulations - These laws and regulations have significant implications for all financial institutions. They increase due diligence requirements and reporting obligations for financial institutions, create new crimes and penalties, and require the federal banking agencies, in reviewing merger and other acquisition transactions, to consider the effectiveness of the parties to such transactions in combating money laundering activities. Even innocent noncompliance and inconsequential failure to follow the regulations could result in significant fines or other penalties, which could have a material adverse impact on the Corporation's financial condition, results of operations or liquidity.

ITEM 1B. UNRESOLVED STAFF COMMENTS

Not applicable.

ITEM 2. PROPERTIES

The Banks own each of their properties, except for the facility located at 2 East Mountain Avenue, South Williamsport, which is leased. All of the properties are in good condition. None of the owned properties are subject to encumbrance.

A listing of properties is as follows:

Main administrative offices:

| | 90-92 Main Street | or | 10 Nichols Street |

| | Wellsboro, PA 16901 | | Wellsboro, PA 16901 |

Facilities management office:

| | 13 Water Street |

| | Wellsboro, PA 16901 |

Branch offices – C&N Bank:

| | 428 S. Main Street | | 514 Main Street | | 2 East Mountain Avenue |

| | Athens, PA 18810 | | Laporte, PA 18626 | | South Williamsport, PA 17702 |

| | | | | | |

| | 10 N. Main Street | | 4534 Williamson Trail | | 41 Main Street |

| | Coudersport, PA 16915 | | Liberty, PA 16930 | | Tioga, PA 16946 |

| | | | | | |

| | 111 W. Main Street | | 1085 Main Street | | 428 Main Street |

| | Dushore, PA 18614 | | Mansfield, PA 16933 | | Towanda, PA 18848 |

| | | | | | |

| | Main Street | | RR 2 Box 3036 | | Courthouse Square |

| | East Smithfield, PA 18817 | | Monroeton, PA 18832 | | Troy, PA 16947 |

| | | | | | |

| | 104 Main Street | | 3461 Route 405 Highway | | 90-92 Main Street |

| | Elkland, PA 16920 | | Muncy, PA 17756 | | Wellsboro, PA 16901 |

| | | | | | |

| | 135 East Fourth Street | | 100 Maple Street | | 1510 Dewey Avenue |

| | Emporium, PA 15834 | | Port Allegany, PA 16743 | | Williamsport, PA 17701 |

| | | | | | |

| | 230 Railroad Street | | 24 Thompson Street | | 130 Court Street |

| | Jersey Shore, PA 17740 | | Ralston, PA 17763 | | Williamsport, PA 17701 |

| | | | | | |

| | 102 E. Main Street | | 1827 Elmira Street | | Route 6 |

| | Knoxville, PA 16928 | | Sayre, PA 18840 | | Wysox, PA 18854 |

First State Bank offices:

| | 3 Main Street | 6250 County Route 64, East Avenue Extension |

| | Canisteo, NY 14823 | Hornell, NY 14843 |

ITEM 3. LEGAL PROCEEDINGS

The Corporation and the Banks are involved in various legal proceedings incidental to their business. Management believes the aggregate liability, if any, resulting from such pending and threatened legal proceedings will not have a material adverse effect on the Corporation’s financial condition or results of operations.

ITEM 4. SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS

During the fourth quarter of 2009, no matters were submitted to a vote of security holders, through the solicitation of proxies or otherwise.

PART II

ITEM 5. MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Trades of the Corporation’s stock are executed through various brokers who maintain a market in the Corporation’s stock. The Corporation’s stock is listed on the NASDAQ Capital Market with the trading symbol CZNC. As of December 31, 2009, there were 2,619 shareholders of record of the Corporation’s common stock.

The following table sets forth the high and low sales prices of the common stock during 2009 and 2008.

| | | 2009 | | | 2008 | |

| | | | | | | | | Dividend | | | | | | | | | Dividend | |

| | | | | | | | | Declared | | | | | | | | | Declared | |

| | | High | | | Low | | | Per Quarter | | | High | | | Low | | | Per Quarter | |

| First quarter | | $ | 20.94 | | | $ | 14.06 | | | $ | 0.24 | | | $ | 21.00 | | | $ | 16.85 | | | $ | 0.24 | |

| Second quarter | | | 22.46 | | | | 16.46 | | | | 0.24 | | | | 20.50 | | | | 15.82 | | | | 0.24 | |

| Third quarter | | | 22.06 | | | | 14.50 | | | | 0.24 | | | | 25.80 | | | | 16.13 | | | | 0.24 | |

| Fourth quarter | | | 15.14 | | | | 8.15 | | | | 0.00 | | | | 25.45 | | | | 17.18 | | | | 0.24 | |

In December 2009, the Corporation announced that the Board of Directors was delaying until January 2010 a decision regarding the size of the dividend on common stock to be declared for the fourth quarter of 2009. This was a departure from the Corporation’s customary practice which had been to declare a dividend for the fourth quarter of the year in mid-December, with a dividend payment date in mid- to late January. In January 2010, the Board of Directors declared a dividend of $0.08 per share on common stock, which was paid in February 2010. Since the $.08 dividend was declared in 2010, it is not included in the table above.

Future dividend payments will depend upon maintenance of a strong financial condition, future earnings and capital and regulatory requirements. Also, the Corporation, C&N Bank and First State Bank are subject to restrictions on the amount of dividends that may be paid without approval of banking regulatory authorities. These restrictions are described in Note 19 to the consolidated financial statements. Specifically, under guidance issued in 2009 by the Federal Reserve, until further notice the Corporation must consult the Federal Reserve before declaring dividends on either common or preferred stock. Further, pursuant to participation in the TARP Program, the Corporation may continue to pay dividends on its common stock, subject to the following requirements and limitations: (1) all accrued and unpaid dividends for all past dividend periods on the preferred stock issued to the Treasury must be fully paid; and (2) consent of the Treasury is required for any increase above $0.24 per quarter in the per share dividends on common shares until January 16, 2012, unless prior to that date, the Corporation has redeemed the preferred stock issued to the Treasury in whole or the Treasury has transferred all of the preferred stock to third parties.

On August 21, 2008, the Corporation announced the extension and amendment of a plan that permits the repurchase of shares of its outstanding common stock, up to an aggregate total of $10 million, through August 31, 2009. The Board of Directors authorized repurchase from time to time at prevailing market prices in open market or in privately negotiated transactions as, in management’s sole opinion, market conditions warrant and based on stock availability, price and the Corporation’s financial performance. At August 31, 2009, the stock repurchase program expired and no repurchases were made in 2009.

Pursuant to participation in the TARP Program, until January 16, 2012 (unless prior to that date, the Corporation has redeemed the preferred stock issued to the Treasury in whole or the Treasury has transferred all of the preferred stock to third parties) the Treasury’s consent is required for any repurchases of common stock, except for repurchases of shares in connection with employee benefit plans in the ordinary course of business consistent with past practice.

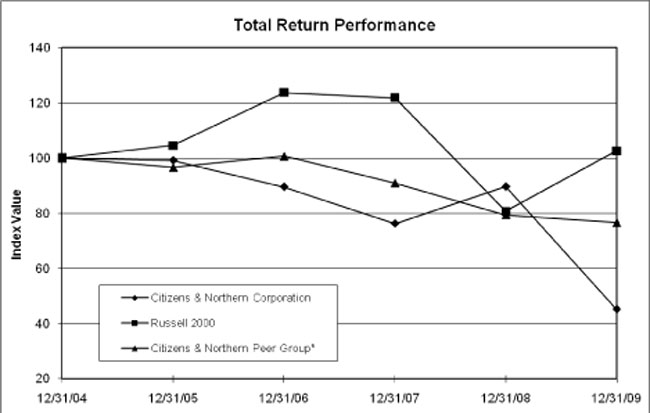

PERFORMANCE GRAPH

Set forth below is a chart comparing the Corporation’s cumulative return to stockholders against the cumulative return of the Russell 2000 and a Peer Group Index of similar banking organizations selected by the Corporation for the five-year period commencing December 31, 2004 and ended December 31, 2009. The index values are market-weighted dividend-reinvestment numbers, which measure the total return for investing $100.00 five years ago. This meets Securities & Exchange Commission requirements for showing dividend reinvestment share performance over a five-year period and measures the return to an investor for placing $100.00 into a group of bank stocks and reinvesting any and all dividends into the purchase of more of the same stock for which dividends were paid.

COMPARISON OF 5-YEAR CUMULATIVE RETURN

| Citizens & Northern Corporation |

| | | Period Ending | |

| Index | | 12/31/04 | | | 12/31/05 | | | 12/31/06 | | | 12/31/07 | | | 12/31/08 | | | 12/31/09 | |

| Citizens & Northern Corporation | | | 100.00 | | | | 99.12 | | | | 89.53 | | | | 76.17 | | | | 89.58 | | | | 45.10 | |

| Russell 2000 | | | 100.00 | | | | 104.55 | | | | 123.76 | | | | 121.82 | | | | 80.66 | | | | 102.58 | |

| Citizens & Northern Peer Group* | | | 100.00 | | | | 96.66 | | | | 100.68 | | | | 90.98 | | | | 79.39 | | | | 76.52 | |

The C&N peer group consists of banks headquartered in Pennsylvania with total assets of $500 million to $1.3 billion. This peer group consists of 1st Summit Bancorp of Johnstown, Inc., Johnstown; ACNB Corporation, Gettysburg; AmeriServ Financial, Inc., Johnstown; Bryn Mawr Bank Corporation, Bryn Mawr; CCFNB Bancorp, Inc., Bloomsburg; Citizens Financial Services, Inc., Mansfield; CNB Financial Corporation, Clearfield; Codorus Valley Bancorp, York; Comm Bancorp, Inc., Clarks Summit; Dimeco, Inc., Honesdale; DNB Financial Corporation, Downingtown; ENB Financial Corp., Ephrata; Fidelity D & D Bancorp, Inc., Dunmore; First Keystone Corporation, Berwick; FNB Bancorp, Inc., Newtown; Franklin Financial Services Corporation, Chambersburg; Kish Bancorp, Inc., Reedsville; Mid Penn Bancorp, Inc., Millersburg; Norwood Financial Corp., Honesdale; Orrstown Financial Services, Inc., Shippensburg; Penns Woods Bancorp, Inc., Williamsport; Penseco Financial Services Corporation, Scranton; QNB Corp., Quakertown; Republic First Bancorp, Inc., Philadelphia; Somerset Trust Holding Company, Somerset; Union National Financial Corporation, Lancaster; and VIST Financial Corp., Wyomissing.

The data for this graph was obtained from SNL Financial L.C.

EQUITY COMPENSATION PLAN INFORMATION

The following table sets forth information concerning the Stock Incentive Plan and Independent Directors Stock Incentive Plan, both of which have been approved by the Corporation’s shareholders. The figures shown in the table below are as of December 31, 2009.

| | | | | | | | | Number of | |

| | | Number of | | | Weighted- | | | Securities | |

| | | Securities to be | | | average | | | Remaining | |

| | | Issued Upon | | | Exercise | | | for Future | |

| | | Exercise of | | | Price of | | | Issuance Under | |

| | | Outstanding | | | Outstanding | | | Equity Compen- | |

| | | Options | | | Options | | | sation Plans | |

| Equity compensation plans | | | | | | | | | |

| approved by shareholders | | | 306,358 | | | $ | 20.53 | | | | 524,311 | |

| | | | | | | | | | | | | |

| Equity compensation plans | | | | | | | | | | | | |

| not approved by shareholders | | | 0 | | | | N/A | | | | 0 | |

More details related to the Corporation’s equity compensation plans are provided in Notes 1 and 13 to the consolidated financial statements.

ITEM 6. SELECTED FINANCIAL DATA

| | | As of or for the Year Ended December 31, | | | | |

| INCOME STATEMENT (In Thousands) | | 2009 | | | 2008 | | | 2007 | | | 2006 | | | 2005 | |

| Interest and fee income | | $ | 67,976 | | | $ | 74,237 | | | $ | 70,221 | | | $ | 64,462 | | | $ | 61,108 | |

| Interest expense | | | 24,456 | | | | 31,049 | | | | 33,909 | | | | 30,774 | | | | 25,687 | |

| Net interest income | | | 43,520 | | | | 43,188 | | | | 36,312 | | | | 33,688 | | | | 35,421 | |

| Provision for loan losses | | | 680 | | | | 909 | | | | 529 | | | | 672 | | | | 2,026 | |

| Net interest income after provision for loan losses | | | 42,840 | | | | 42,279 | | | | 35,783 | | | | 33,016 | | | | 33,395 | |

| Noninterest income excluding securities (losses)/gains | | | | | | | | | | | | | | | | | | | | |

| and gains from sale of credit card loans | | | 12,669 | | | | 12,883 | | | | 10,440 | | | | 7,970 | | | | 7,636 | |

| Net impairment losses recognized in earnings from | | | | | | | | | | | | | | | | | | | | |

| available-for-sale securities | | | (85,363 | ) | | | (10,088 | ) | | | 0 | | | | 0 | | | | 0 | |

| Realized gains on available-for-sale securities | | | 1,523 | | | | 750 | | | | 127 | | | | 5,046 | | | | 1,802 | |

| Gain from sale of credit card loans | | | 0 | | | | 0 | | | | 0 | | | | 340 | | | | 1,906 | |

| Noninterest expense | | | 33,659 | | | | 33,446 | | | | 33,283 | | | | 31,614 | | | | 28,962 | |

| (Loss) income before income tax (credit) provision | | | (61,990 | ) | | | 12,378 | | | | 13,067 | | | | 14,758 | | | | 15,777 | |

| Income tax (credit) provision | | | (22,655 | ) | | | 2,319 | | | | 2,643 | | | | 2,772 | | | | 2,793 | |

| Net (loss) income | | | (39,335 | ) | | | 10,059 | | | | 10,424 | | | | 11,986 | | | | 12,984 | |

| U.S. Treasury preferred dividends | | | 1,428 | | | | 0 | | | | 0 | | | | 0 | | | | 0 | |

| Net (loss) income available to common shareholders | | $ | (40,763 | ) | | $ | 10,059 | | | $ | 10,424 | | | $ | 11,986 | | | $ | 12,984 | |

| PER COMMON SHARE: (1) | | | | | | | | | | | | | | | | | | | | |

| Basic earnings per share | | $ | (4.40 | ) | | $ | 1.12 | | | $ | 1.19 | | | $ | 1.42 | | | $ | 1.53 | |

| Diluted earnings per share | | $ | (4.40 | ) | | $ | 1.12 | | | $ | 1.19 | | | $ | 1.42 | | | $ | 1.52 | |

| Cash dividends declared per share | | $ | 0.72 | | | $ | 0.96 | | | $ | 0.96 | | | $ | 0.96 | | | $ | 0.93 | |

| Stock dividend | | None | | | None | | | | 1 | % | | | 1 | % | | | 1 | % |

| Book value per common share at period-end | | $ | 10.46 | | | $ | 13.66 | | | $ | 15.34 | | | $ | 15.51 | | | $ | 15.58 | |

| Tangible book value per common share at period-end | | $ | 9.43 | | | $ | 12.22 | | | $ | 13.85 | | | $ | 15.13 | | | $ | 15.18 | |

| Weighted average common shares outstanding - basic | | | 9,271,869 | | | | 8,961,805 | | | | 8,784,134 | | | | 8,422,495 | | | | 8,458,813 | |

| Weighted average common shares outstanding - diluted | | | 9,271,869 | | | | 8,983,300 | | | | 8,795,366 | | | | 8,448,169 | | | | 8,517,598 | |

| END OF PERIOD BALANCES (In Thousands) | | | | | | | | | | | | | | | | | | | | |

| Available-for-sale securities | | $ | 396,288 | | | $ | 419,688 | | | $ | 432,755 | | | $ | 356,665 | | | $ | 427,298 | |

| Gross loans | | | 721,603 | | | | 743,544 | | | | 735,941 | | | | 687,501 | | | | 653,299 | |

| Allowance for loan losses | | | 8,265 | | | | 7,857 | | | | 8,859 | | | | 8,201 | | | | 8,361 | |

| Total assets | | | 1,321,795 | | | | 1,281,637 | | | | 1,283,746 | | | | 1,127,368 | | | | 1,162,954 | |

| Deposits | | | 926,789 | | | | 864,057 | | | | 838,503 | | | | 760,349 | | | | 757,065 | |

| Borrowings | | | 235,471 | | | | 285,473 | | | | 300,132 | | | | 228,440 | | | | 266,939 | |

| Stockholders' equity | | | 152,410 | | | | 122,026 | | | | 137,781 | | | | 129,888 | | | | 131,968 | |

| Common stockholders' equity (stockholders' equity, | | | | | | | | | | | | | | | | | | | | |

| excluding preferred stock) | | | 126,661 | | | | 122,026 | | | | 137,781 | | | | 129,888 | | | | 131,968 | |

| AVERAGE BALANCES (In Thousands) | | | | | | | | | | | | | | | | | | | | |

| Total assets | | | 1,296,086 | | | | 1,280,924 | | | | 1,178,904 | | | | 1,134,689 | | | | 1,144,619 | |

| Earning assets | | | 1,208,280 | | | | 1,202,872 | | | | 1,090,035 | | | | 1,055,103 | | | | 1,065,189 | |

| Gross loans | | | 728,748 | | | | 743,741 | | | | 729,269 | | | | 662,714 | | | | 618,344 | |

| Deposits | | | 886,703 | | | | 847,714 | | | | 812,255 | | | | 750,982 | | | | 702,404 | |

| Stockholders' equity | | | 141,787 | | | | 130,790 | | | | 138,669 | | | | 131,082 | | | | 132,465 | |

| KEY RATIOS | | | | | | | | | | | | | | | | | | | | |

| Return on average assets | | | -3.03 | % | | | 0.79 | % | | | 0.88 | % | | | 1.06 | % | | | 1.13 | % |

| Return on average equity | | | -27.74 | % | | | 7.69 | % | | | 7.52 | % | | | 9.14 | % | | | 9.80 | % |

| Average equity to average assets | | | 10.94 | % | | | 10.21 | % | | | 11.76 | % | | | 11.55 | % | | | 11.57 | % |

| Net interest margin (2) | | | 3.84 | % | | | 3.77 | % | | | 3.51 | % | | | 3.42 | % | | | 3.62 | % |

| Efficiency (3) | | | 56.97 | % | | | 57.40 | % | | | 68.39 | % | | | 71.73 | % | | | 62.68 | % |

| Cash dividends as a % of diluted earnings per share | | NM | | | | 85.71 | % | | | 80.67 | % | | | 67.61 | % | | | 61.18 | % |

| Tier 1 leverage | | | 9.77 | % | | | 10.12 | % | | | 10.91 | % | | | 11.22 | % | | | 10.62 | % |

| Tier 1 risk-based capital | | | 16.65 | % | | | 13.99 | % | | | 15.46 | % | | | 16.51 | % | | | 16.52 | % |

| Total risk-based capital | | | 17.84 | % | | | 14.84 | % | | | 16.52 | % | | | 17.97 | % | | | 18.19 | % |

| Tangible common equity/tangible assets | | | 8.72 | % | | | 8.61 | % | | | 9.79 | % | | | 11.27 | % | | | 11.09 | % |

ITEM 6. SELECTED FINANCIAL DATA, continued

NM = Not a meaningful ratio.

| (1) | All share and per share data have been restated to give effect to stock dividends and splits. |

| (2) | Rates of return on tax-exempt securities and loans are calculated on a fully-taxable equivalent basis. |

| (3) | The efficiency ratio is calculated by dividing total noninterest expense by the sum of net interest income (including income from tax-exempt securities and loans on a fully-taxable equivalent basis) and noninterest income excluding securities gains and gains from sale of credit card loans. |

ITEM 7. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Certain statements in this section and elsewhere in this Annual Report on Form 10-K are forward-looking statements. Citizens & Northern Corporation and its wholly-owned subsidiaries (collectively, the Corporation) intend such forward-looking statements to be covered by the safe harbor provisions for forward-looking statements contained in the Private Securities Reform Act of 1995. Forward-looking statements, which are not historical facts, are based on certain assumptions and describe future plans, business objectives and expectations, and are generally identifiable by the use of words such as, "should", “likely”, "expect", “plan”, "anticipate", “target”, “forecast”, and “goal”. These forward-looking statements are subject to risks and uncertainties that are difficult to predict, may be beyond management’s control and could cause results to differ materially from those expressed or implied by such forward-looking statements. Factors which could have a material, adverse impact on the operations and future prospects of the Corporation include, but are not limited to, the following:

| · | changes in monetary and fiscal policies of the Federal Reserve Board and the U.S. Government, particularly related to changes in interest rates |

| · | changes in general economic conditions |

| · | legislative or regulatory changes |

| · | downturn in demand for loan, deposit and other financial services in the Corporation’s market area |

| · | increased competition from other banks and non-bank providers of financial services |

| · | technological changes and increased technology-related costs |

| · | changes in accounting principles, or the application of generally accepted accounting principles. |

These risks and uncertainties should be considered in evaluating forward-looking statements and undue reliance should not be placed on such statements.

EARNINGS OVERVIEW

For the year ended December 31, 2009, a net loss available to common shareholders was reported of $40,763,000, or $4.40 per share, while net income was $10,059,000 ($1.12 per share – basic and diluted) in 2008 and $10,424,000 ($1.19 per share – basic and diluted) in 2007. The net loss for the year ended December 31, 2009 included the impact of after-tax other-than-temporary impairment (OTTI) charges on available-for-sale securities (adjusted for realized gains on some securities subsequently sold) of $55,849,000. In 2008, the after-tax impact of OTTI charges was $6,638,000. There were no OTTI charges in 2007.

Core Earnings is an earnings performance measurement which the Corporation’s management has defined to exclude the effects of OTTI losses on available-for-sale securities and realized gains on securities for which OTTI has previously been recognized. Core Earnings is a performance measurement that is not based on U.S. generally accepted accounting principles. Management believes Core Earnings information is meaningful for evaluating the Corporation’s operating performance, because it excludes some of the impact of market volatility as it relates to investments in pooled trust-preferred securities and other securities. More information concerning Core Earnings, including a reconciliation to the Corporation’s earnings results based on U.S. generally accepted accounting principles, is provided in the following section of Management’s Discussion and Analysis. The Corporation’s results for 2009 included positive Core Earnings available to common shareholders of $15,086,000 ($1.63 per diluted share), reduced by after-tax OTTI charges on available-for-sale securities (net of subsequent gains from selling some of the securities) of $55,849,000. In 2008, the Corporation had Core Earnings of $16,697,000 ($1.86 per diluted share), and Core Earnings for 2007 totaled $10,424,000 ($1.19 per diluted share).

Pre-tax OTTI charges totaled $85,363,000 in 2009 and $10,088,000 in 2008, with no OTTI charges in 2007. A summary of pre-tax OTTI charges is as follows:

| (In Thousands) | | 2009 | | | 2008 | | | 2007 | |

| Pooled trust preferred securities - mezzanine tranches | | $ | (73,674 | ) | | $ | (8,210 | ) | | $ | 0 | |

| Marketable equity securities (bank stocks) | | | (6,324 | ) | | | (1,878 | ) | | | 0 | |

| Trust preferred securities issued by individual institutions | | | (3,209 | ) | | | 0 | | | | 0 | |

| Collateralized mortgage obligations | | | (2,156 | ) | | | 0 | | | | 0 | |

| | | | | | | | | | | | | |

| Net impairment losses recognized in earnings | | $ | (85,363 | ) | | $ | (10,088 | ) | | $ | 0 | |

Pooled trust-preferred securities are very long-term (usually 30-year maturity) instruments, mainly issued by banks. The Corporation’s investments in pooled trust-preferred securities are each made up of companies with geographic and size diversification. Almost all of the Corporation’s pooled trust-preferred securities are composed of debt issued by banking companies, with lesser amounts issued by insurance companies and real estate investment trusts. Management evaluates the pooled trust-preferred securities for OTTI by estimating the cash flows expected to be received from each security, taking into account estimated levels of deferrals and defaults by the underlying issuers. In determining cash flows, management assumes all issuers currently deferring or in default would make no future payments, and assigns estimated future default levels for the remaining issuers in each security based on financial strength ratings assigned by a national ratings service. The Corporation’s process for evaluating pooled trust-preferred securities for OTTI is described in more detail in Note 7 to the consolidated financial statements. After the impact of the impairment charges, the Corporation’s cost basis in pooled trust-preferred securities at December 31, 2009 totaled $11.649 million, including senior tranche assets of $11.383 million and mezzanine tranche assets of $0.266 million. The estimated fair value at December 31, 2009 of pooled trust-preferred securities was $8.314 million.

As described in more detail in Notes 2 and 7 to the consolidated financial statements, the Corporation adopted new accounting principles in 2009, which resulted in the impairment of debt securities being separated into (a) the amount of the total impairment related to credit loss, which is recognized in the income statement, and (b) the amount of the total impairment related to all other factors, which is recognized in other comprehensive income. In 2009, the effect of the new principles was to increase impairment losses recognized in earnings by $3,451,000, and decrease the income tax provision by $1,173,000, resulting in a decrease in net income (larger net loss) of $2,275,000, or $0.25 per average common share.

STATEMENT REGARDING NON-GAAP FINANCIAL MEASUREMENT

This report contains supplemental financial information determined by a method other than in accordance with Accounting Principles Generally Accepted in the United States of America (“GAAP”). Management uses this non-GAAP measure in its analysis of the Corporation’s performance. This measure, Core Earnings, excludes the effects of OTTI losses on available-for-sale securities and realized gains on securities for which OTTI has previously been recognized. Management believes the presentation of this financial measure, which excludes the impact of the specified items, provides useful supplemental information that is essential to a proper understanding of the financial results of the Corporation. The Core Earnings measure provides a method to assess operating performance excluding the impact of market volatility related to investments in pooled trust-preferred securities and other securities. This disclosure should not be viewed as a substitute for results determined in accordance with GAAP, nor is it necessarily comparable to non-GAAP performance measures that may be presented by other companies.

| RECONCILIATION OF NON-GAAP MEASURE (UNAUDITED) | | | | | | | | | | | | | | | | |

| (In thousands, except per-share data) | | | | | | | | | | | | | | | | | |

| | 2009 | | | 2008 | | | 2007 | |

| | Net | | | | | | | | | | | | | | | | |

| | (Loss)/ | | | Diluted | | | Net | | | Diluted | | | Net | | | Diluted | |

| | Income | | | EPS | | | Income | | | EPS | | | Income | | | EPS | |

| Net (loss) income available to common shareholders | $ | (40,763 | ) | | $ | (4.40 | ) | | $ | 10,059 | | | $ | 1.12 | | | $ | 10,424 | | | $ | 1.19 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| Other-than-temporary impairment losses on | | | | | | | | | | | | | | | | | | | | | | | |

| available-for-sale securities | | (85,363 | ) | | | | | | | (10,088 | ) | | | | | | | 0 | | | | | |

| Realized gains on assets previously written down | | 1,308 | | | | | | | | 31 | | | | | | | | 0 | | | | | |

| Other-than-temporary impairment losses on | | | | | | | | | | | | | | | | | | | | | | | |

| available-for-sale securities, net of related gains | | (84,055 | ) | | | | | | | (10,057 | ) | | | | | | | 0 | | | | | |

| Income taxes (1) | | 28,206 | | | | | | | | 3,419 | | | | | | | | 0 | | | | | |

| Other-than-temporary impairment losses, net | | (55,849 | ) | | | | | | | (6,638 | ) | | | | | | | 0 | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| Core earnings available to common shareholders | $ | 15,086 | | | $ | 1.63 | | | $ | 16,697 | | | $ | 1.86 | | | $ | 10,424 | | | $ | 1.19 | |

(1) Income tax has been allocated to the non-core losses at 34%, adjusted for a valuation allowance of $373,000 in 2009 on deferred tax assets associated with losses from securities classified as capital assets for federal income tax reporting purposes. The valuation allowance is described in more detail in Note 15 to the consolidated financial statements.

2009 vs. 2008

The most significant changes in components of the Corporation's Core Earnings results for 2009, as compared to 2008, were as follows:

| | · | The interest margin increased $332,000, or 0.8%. On a fully taxable-equivalent basis, the interest margin increased $1,032,000, or 2.3%. The interest margin has been positively impacted by lower short-term market interest rates, which have reduced interest rates paid on deposits and borrowings. The interest margin has also been positively impacted by increased levels of investments and high yields on municipal bonds. The interest margin has been negatively impacted by weak consumer loan demand, as average loans outstanding have shrunk approximately $15.0 million in 2009 as compared to 2008. |

| | · | The provision for loan losses was $229,000 lower in 2009 than in 2008. The ratio of nonperforming loans (including nonaccrual loans and loans 90 days or more past due and still accruing interest) and other real estate owned, as a percentage of assets, was 0.76% at December 31, 2009, higher than the 0.69% level at December 31, 2008, but still relatively low by historical standards. |

| | · | Non-interest income decreased $214,000, or 1.7%. In 2008, non-interest income included a gain of $533,000 from redemption of restricted shares of Visa, resulting from Visa’s initial public offering. Also, in 2009, the Corporation received no dividend income on its investment in restricted stock issued by the Federal Home Loan Bank of Pittsburgh, while dividend income on this stock was $334,000 in 2008. |

| | · | Non-interest expense increased $213,000, or 0.6%. FDIC insurance assessments increased $1,784,000 in 2009, to $2,092,000 from $308,000. The higher FDIC assessments included the effects of premium increases and a special assessment of $589,000. Excluding FDIC costs, total non-interest expense was 4.7% lower in 2009 than in 2008. |

| | · | Core Earnings for 2009 were reduced by dividends on preferred stock issued to the U.S. Treasury under the TARP Capital Purchase Program of $1,428,000. |

More detailed information concerning fluctuations in the Corporation’s earnings results are provided in other sections of Management’s Discussion and Analysis.

2008 vs. 2007

Net income available to common shareholders for the year ended December 31, 2008 was $10,059,000, or $1.12 per diluted share, as compared to net income of $10,424,000, or $1.19 per diluted share, in 2007. As defined above, Core Earnings per diluted share were $1.86 in 2008, as compared to $1.19 in 2007.

The most significant changes in components of the Corporation's Core Earnings results for 2008, as compared to 2007, were as follows:

| | · | The interest margin was $6,876,000, or 18.9%, higher in 2008. The improved interest margin includes the impact of the Citizens Bancorp, Inc. acquisition, which was effective May 1, 2007. The interest margin was also positively impacted by lower market interest rates, which reduced interest rates paid on deposits and borrowings, and by higher earnings on the investment portfolio resulting from higher average total holdings of securities. |

| | · | Non-interest income increased $2,443,000, or 23.4%, in 2008 over 2007. Service charges on deposit accounts increased $1,888,000, or 73.8%, as a result of growth in deposit volumes from the Citizens Bancorp acquisition, as well as higher fees associated with a new overdraft privilege program. Also, in 2008, noninterest income included a gain of $533,000 from redemption of restricted shares of Visa, resulting from Visa’s initial public offering. |

OUTLOOK FOR 2010

As described in the “Earnings Overview” section above, the Corporation reported a net loss for 2009. Note 21 to the consolidated financial statements presents quarterly income statement data that shows there was a net loss in each of the first three quarters of 2009, primarily because of substantial securities write-downs, and positive net income of $4.242 million ($0.42 per diluted share) in the fourth quarter 2009. While management cannot guarantee there will be no additional securities losses, based on the relatively small ($0.266 million) remaining cost basis of mezzanine pooled trust-preferred securities as of December 31, 2009, we believe the vast majority of losses have been realized. Core Earnings (as defined above) results for 2009 reflect the impact of significant operational changes made in 2007 and 2008, including successful implementation of an overdraft privilege program, as well as other enhancements to noninterest revenue sources. Management also improved efficiency of various operational activities, which has resulted in significant expense reductions. In 2010, management expects the Corporation’s earnings results to continue to reflect some of the positive effects of these changes.

A major variable that affects the Corporation’s earnings is securities gains and losses. The Corporation’s 2009 and 2008 losses from trust-preferred securities and other securities stem from the much-publicized economic problems affecting the national and international economy, which have particularly hurt the banking industry. Although management believes these conditions to be cyclical, the Corporation has exposure to the possibility of future losses from investments in a senior tranche pooled trust-preferred security, trust-preferred securities issued by individual banks, bank stocks, private label collateralized mortgage obligations (CMOs), and other securities. Note 7 to the consolidated financial statements provides more detail concerning the Corporation’s investment securities.

In light of weak economic conditions, the Federal Reserve has taken actions that have driven interest rates down to very low levels by historical standards, including establishing the federal funds target rate at a range of 0% to 0.25% throughout 2009. Some recent economic reports reflect improvement in U.S. economic conditions, which could result in the Federal Reserve beginning to take actions designed to raise interest rates before the end of 2010. As described in more detail in Item 7A of this Form 10-K, the Corporation is liability sensitive, meaning that net interest income tends to increase when interest rates fall, but that net interest income tends to decrease when rates rise. One of the ways management monitors exposure to rising interest rates is by calculating the estimated impact of interest rate shocks (immediate changes in rates) at varying levels. Table XV in Item 7A presents information regarding the estimated impact of immediate interest rate shocks of 100 basis points (1%), 200 basis points and 300 basis points on net interest income and on the market value of portfolio equity.

The Corporation benefited in 2009 from a relatively low (by historical standards) provision for loan losses. Issues related to larger commercial borrowers can significantly affect the Corporation’s provision for loan losses in any particular period. Accordingly, the amount of loan loss provision for 2010 will depend substantially on the credit status of the commercial portfolio. Although management is concerned about the condition of the national economy and the potential for problems in our market area, to date the Corporation has not experienced significant deterioration in loan delinquencies, or a noticeable change in volume of activity related to troubled loans or foreclosures. The Corporation has not originated interest only mortgages, loans without documentation of the borrowers’ sources of income or net worth, or other types of subprime mortgage loans that have received negative publicity. However, if economic conditions deteriorate significantly, the Corporation may need to increase the provision for loan losses for the impact on the residential mortgage and consumer portions of the loan portfolio.

As referenced above, the Corporation implemented a new overdraft privilege program in 2008, and has recognized significant increases in non-interest income in 2008 and 2009 as compared to income from its prior overdraft process. Total revenue from overdrafts, net of waived or refunded fees and provision for charge-offs, amounted to $4,055,000 in 2009. Legislative and regulatory changes will affect the overdraft privilege program in the second half of 2010, as customers will be required to affirmatively document their consent to be assessed overdraft fees for ATM and one-time point-of-sale transactions. Also, potential legislative changes could limit the Corporation’s ability to pay overdrafts and assess fees for all these types of transactions. Management cannot currently estimate the extent of reduction in revenue that could occur in the second half of 2010 as a result of these regulatory and potential legislative changes.

As described in more detail in Note 22 to the consolidated financial statements, in January 2009, the Corporation issued Preferred Stock and a Warrant to purchase up to 194,794 shares of common stock at an exercise price of $20.36 per share to the United States Department of the Treasury under the TARP Program. The Corporation sold the Preferred Stock and Warrant for an aggregate price of $26,440,000. The Preferred Stock pays a cumulative dividend rate of 5% per annum for the first five years and will reset to a rate of 9% per annum after year five. Pursuant to participation in the TARP Program, the Corporation may continue to pay dividends on its common stock, subject to the following requirements and limitations: (1) all accrued and unpaid dividends for all past dividend periods on the preferred stock issued to the Treasury must be fully paid; and (2) consent of the Treasury is required for any increase over $0.24 per quarter in the per share dividends on common shares until January 16, 2012, unless prior to that date, the Corporation has redeemed the preferred stock issued to the Treasury in whole or the Treasury has transferred all of the preferred stock to third parties. Also, until January 16, 2012 (unless prior to that date, the Corporation has redeemed the preferred stock issued to the Treasury in whole or the Treasury has transferred all of the preferred stock to third parties) the Treasury’s consent is required for any repurchases of common stock, except for repurchases of shares in connection with employee benefit plans in the ordinary course of business consistent with past practice. Management is considering redemption of the Preferred Stock in 2010; however, our ability to do so is dependent upon approval from banking regulatory authorities and the Treasury.

In 2009, the Corporation issued approximately 3,090,000 shares of common stock, raising a total of $ 24,585,000, net of related offering costs. Of this total, 2,875,000 shares were issued at a price of $8.00 per share in a public offering that was completed in December 2009, and which resulted in net proceeds of $21,410,000 (included in the $24,585,000 for the year). The additional $3,175,000 was raised through issuance of shares under the Corporation’s Dividend Reinvestment Plan. Although the Corporation maintained capital ratios that exceeded regulatory requirements to be considered well capitalized throughout 2009, the additional capital provides flexibility to absorb any additional, unexpected securities losses or other economic issues that might arise. Further, management believes the additional capital increases the likelihood the Corporation will be able to repay the TARP Preferred Stock in 2010, which would reduce ongoing Preferred Stock dividend costs, and improves the Corporation’s ability to respond to any opportunities that could arise for branch or full-bank acquisitions. More information related to regulatory capital is provided in the Stockholder’s Equity and Capital Adequacy section of Management’s Discussion and Analysis.

Management estimates total capital purchases for 2010 to be approximately $1.6 million, with computer software and hardware the largest planned categories of expenditure. In comparison, total capital purchases totaled $ 1,253,000 in 2009, $998,000 in 2008 and $2,416,000 in 2007. Management does not expect capital expenditures to have a material, detrimental effect on the Corporation’s financial condition in the year ending December 31, 2010.

CRITICAL ACCOUNTING POLICIES

The presentation of financial statements in conformity with U.S. generally accepted accounting principles requires management to make estimates and assumptions that affect many of the reported amounts and disclosures. Actual results could differ from these estimates.

A material estimate that is particularly susceptible to significant change is the determination of the allowance for loan losses. Management believes that the allowance for loan losses is adequate and reasonable. The Corporation’s methodology for determining the allowance for loan losses is described in a separate section later in Management’s Discussion and Analysis. Given the very subjective nature of identifying and valuing loan losses, it is likely that well-informed individuals could make materially different assumptions, and could, therefore calculate a materially different allowance value. While management uses available information to recognize losses on loans, changes in economic conditions may necessitate revisions in future years. In addition, various regulatory agencies, as an integral part of their examination process, periodically review the Corporation’s allowance for loan losses. Such agencies may require the Corporation to recognize adjustments to the allowance based on their judgments of information available to them at the time of their examination.

Another material estimate is the calculation of fair values of the Corporation’s debt securities. For most of the Corporation’s debt securities, the Corporation receives estimated fair values of debt securities from an independent valuation service, or from brokers. In developing fair values, the valuation service and the brokers use estimates of cash flows, based on historical performance of similar instruments in similar interest rate environments. Based on experience, management is aware that estimated fair values of debt securities tend to vary among brokers and other valuation services. Accordingly, when selling debt securities, management typically obtains price quotes from more than one source.

As described in Note 6 to the consolidated financial statements, in 2008, the Corporation changed its method of valuing pooled trust-preferred securities from using price quotes received from pricing services, to a Level 3 (as described in the “FASB Accounting Standards Codification” (the “ASC”) topic 820, “Fair Value Measurements and Disclosures” ) methodology, using discounted cash flows. At both December 31, 2009 and December 31, 2008, management calculated the fair values of pooled trust-preferred securities by applying discount rates to estimated cash flows for each security. Management estimated the cash flows expected to be received from each security, taking into account estimated levels of deferrals and defaults by the underlying issuers, and used discount rates considered reflective of a market participant’s expectations regarding the extent of credit and liquidity risk inherent in the securities. Management’s estimates of cash flows and discount rates used to calculate fair values of pooled trust-preferred securities were based on sensitive assumptions, and use of different assumptions could result in calculations of fair values that would be substantially different than the amounts calculated by management.

As described in Note 7 to the consolidated financial statements, management evaluates securities for OTTI. In making that evaluation, consideration is given to (1) the length of time and the extent to which the fair value has been less than cost, (2) the financial condition and near-term prospects of the issuer, and (3) whether the Corporation intends to sell the security or more likely than not will be required to sell the security before its anticipated recovery. Management’s assessments of the likelihood and potential for recovery in value of securities are subjective and based on sensitive assumptions. Also, management’s estimates of cash flows used to evaluate other-than-temporary impairment of pooled trust-preferred securities are based on sensitive assumptions, and use of different assumptions could produce different conclusions for each security. Note 7 to the consolidated financial statements includes details concerning significant changes made at September 30, 2009, as compared to the previous four quarterly analyses, that resulted in increased amounts of estimated future defaults on pooled trust-preferred securities.

NET INTEREST MARGIN

The Corporation’s primary source of operating income is represented by the net interest margin. The net interest margin is equal to the difference between the amounts of interest income and interest expense. Tables I, II and III include information regarding the Corporation’s net interest margin in 2009, 2008 and 2007. In each of these tables, the amounts of interest income earned on tax-exempt securities and loans have been adjusted to a fully taxable-equivalent basis. Accordingly, the net interest margin amounts presented in these tables exceed the amounts presented in the consolidated financial statements. The discussion that follows is based on amounts in the tables.

2009 vs. 2008

Interest income totaled $70,874,000 in 2009, a decrease of 7.3% from 2008. Income from available-for-sale securities decreased $1,912,000 (7.7%), while interest and fees from loans decreased $3,505,000, or 6.9%. As indicated in Table II, total average available-for-sale securities (at amortized cost) in 2009 fell to $439,823,000, a decrease of $9,408,000, or 2.1% from 2008. During 2009, the Corporation increased the size of its tax-exempt municipal security portfolio, while shrinking the taxable available-for-sale securities portfolio. The Corporation’s yield on taxable securities fell in 2009 primarily because of low market interest rates, including the effects of management’s decision to limit purchases of taxable securities to investments that mature or are expected to repay a substantial portion of principal within approximately four years or less. Also, interest rates on variable-rate trust preferred securities decreased consistent with short-term global interest rates. The average rate of return on available-for-sale securities was 5.24% for 2009 and 5.55% in 2008.

The average balance of gross loans decreased 2.0% to $728,748,000 in 2009 from $743,741,000 in 2008. Due to the challenging economic environment, the Corporation experienced contraction in the balance of its mortgage and consumer loan portfolios, with slight growth in average commercial and tax-exempt loan balances. The Corporation’s yield on loans fell as rates on new loans as well as existing, variable-rate loans decreased. The average rate of return on loans was 6.54% in 2009 and 6.88% in 2008.

The average balance of interest-bearing due from banks, which in 2009 consisted primarily of balances held by the Federal Reserve, increased to $29,348,000 in 2009 from $2,385,000 in 2008. Also, the average balance of federal funds sold increased to $8,983,000 in 2009 from $5,038,000 in 2008. Although the rates of return are low, the Corporation maintained relatively high levels of these liquid assets in 2009 (as opposed to increasing long-term, available-for-sale securities at higher yields) due to management’s concern about the possibility of substantial increases in interest rates in 2010 or 2011.

Interest expense fell $6,593,000, or 21.2%, to $24,456,000 in 2009 from $31,049,000 in 2008. Table II shows that the overall cost of funds on interest-bearing liabilities fell to 2.40% in 2009 from 3.05% in 2008.

Total average deposits (interest-bearing and noninterest-bearing) increased 4.6%, to $886,703,000 in 2009 from $847,714,000 in 2008. This increase came mainly in interest checking, money market, and individual retirement accounts and is partially offset by a reduction in the balance in certificates of deposit. Consistent with substantial reductions in short-term global interest rates, the average rates incurred on deposit accounts decreased significantly in 2009 as compared to 2008.