Table of Contents

As filed with the Securities and Exchange Commission on May 15, 2015

Securities Act File No. 333-

U.S. SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-14

REGISTRATION STATEMENT

UNDER

| THE SECURITIES ACT OF 1933 | ||||

| Pre-Effective Amendment No. | ¨ | |||

| Post-Effective Amendment No. | ¨ |

(Check appropriate box or boxes)

THRIVENT MUTUAL FUNDS

(Exact Name of Registrant as Specified in Charter)

625 FOURTH AVENUE SOUTH

MINNEAPOLIS, MINNESOTA 55415

(Address of Principal Executive Offices)

(612) 844-4198

(Area Code and Telephone Number)

MICHAEL W. KREMENAK

SECRETARY AND CHIEF LEGAL OFFICER

THRIVENT MUTUAL FUNDS

625 FOURTH AVENUE SOUTH

MINNEAPOLIS, MINNESOTA 55415

(Name and Address of Agent for Service)

Approximate Date of Proposed Public Offering: As soon as practicable after this registration statement becomes effective. It is proposed that this filing will become effective on June 15, 2015 pursuant to Rule 488 under the Securities Act of 1933.

Title of Securities Being Registered: Shares of beneficial interest, par value $.01 per share. The Registrant has registered an indefinite number of shares of beneficial interest pursuant to Section 24(f) of the Investment Company Act of 1940, as amended, and is in a continuous offering of such shares under an effective registration statement (File Nos. 33-12911 and 811-5075). No filing fee is due herewith because of reliance on Section 24(f) of the Investment Company Act of 1940, as amended.

Table of Contents

LETTER FOR SHAREHOLDERS

Dear Shareholder:

The Board of Trustees of Thrivent Mutual Funds (the “Trust”) has scheduled special meetings of shareholders for August 14, 2015 to seek approval of five mergers. At the meetings, the shareholders for each of the series of the Trust listed in the first column below (each a “Target Fund”) will be asked to consider and approve an Agreement and Plan of Reorganization (an “Agreement”) providing for its reorganization into the Trust series listed in the second column below (each an “Acquiring Fund”).

TARGET FUND | ACQUIRING FUND | |

| Thrivent Partner Small Cap Growth Fund | Thrivent Small Cap Stock Fund | |

| Thrivent Partner Small Cap Value Fund | Thrivent Small Cap Stock Fund | |

| Thrivent Mid Cap Growth Fund | Thrivent Mid Cap Stock Fund | |

| Thrivent Partner Mid Cap Value Fund | Thrivent Mid Cap Stock Fund | |

| Thrivent Natural Resources Fund | Thrivent Large Cap Stock Fund |

If you are not planning to attend the meeting in person, please vote before August 14th in one of the ways described below.

If a merger is approved, your investment in the Target Fund will automatically be transferred into the corresponding Acquiring Fund listed above. We will send you a written confirmation after this takes place. This transfer is not expected to be a taxable event.

Your vote counts! You may vote quickly and easily in any one of these ways:

| • | Via Internet: see the instructions on the enclosed proxy card. |

| • | Via Telephone: see the instructions on the enclosed proxy card. |

| • | Via Mail: use the enclosed proxy card and postage-paid envelope. |

| • | In person: attend the shareholder meetings on August 14 at the Thrivent Financial corporate office in Minneapolis. |

If you’d like more information about the Funds, you may order a statement of additional information to the Funds’ prospectuses, a shareholder report or the statement of additional information regarding the proposed Fund reorganizations (request the “Reorganization SAI”) by:

| • | Telephone: 1-800-THRIVENT (1-800-847-4836) and say “mutual funds” |

| • | Mail: Thrivent Mutual Funds, P.O. Box 219348, Kansas City, Missouri 64121-9348 |

| • | Internet: |

| • | For a copy of a prospectus, a statement of additional information, or a shareholder report: |

www.thrivent.com

| • | For a copy of this Prospectus/Proxy Statement or the Reorganization SAI: |

www.proxy-direct.com/thr-26694

Thank you for taking this matter seriously and participating in this important process.

Sincerely,

David S. Royal

President

Thrivent Mutual Funds

Table of Contents

EXPLANATORY NOTE

| This Registration Statement is organized as follows: | ||||

| Page | ||||

Thrivent Partner Small Cap Growth Fund | 3 | |||

• Questions & Answers for Shareholders of Thrivent Partner Small Cap Growth Fund | ||||

• Notice of Special Meeting of Shareholders of Thrivent Partner Small Cap Growth Fund | ||||

• Prospectus/Proxy Statement Regarding Proposed Reorganization | ||||

Thrivent Partner Small Cap Value Fund | 31 | |||

• Questions & Answers for Shareholders of Thrivent Partner Small Cap Value Fund | ||||

• Notice of Special Meeting of Shareholders of Thrivent Partner Small Cap Value Fund | ||||

• Prospectus/Proxy Statement Regarding Proposed Reorganization | ||||

Thrivent Mid Cap Growth Fund | 61 | |||

• Questions & Answers for Shareholders of Thrivent Mid Cap Growth Fund | ||||

• Notice of Special Meeting of Shareholders of Thrivent Mid Cap Growth Fund | ||||

• Prospectus/Proxy Statement Regarding Proposed Reorganization | ||||

Thrivent Partner Mid Cap Value Fund | 89 | |||

• Questions & Answers for Shareholders of Thrivent Partner Mid Cap Value Fund | ||||

• Notice of Special Meeting of Shareholders of Thrivent Partner Mid Cap Value Fund | ||||

• Prospectus/Proxy Statement Regarding Proposed Reorganization | ||||

Thrivent Natural Resources Fund | 117 | |||

• Questions & Answers for Shareholders of Thrivent Natural Resources Fund | ||||

• Notice of Special Meeting of Shareholders of Thrivent Natural Resources Fund | ||||

• Prospectus/Proxy Statement Regarding Proposed Reorganization | ||||

Statement of Additional Information Regarding the Proposed Reorganizations | ||||

Part C Information | ||||

Exhibits | ||||

- 2 -

Table of Contents

Questions & Answers

For Shareholders of Thrivent Partner Small Cap Growth Fund

Although we recommend that you read the complete Prospectus/Proxy Statement, we have provided the following questions and answers to clarify and summarize the issues to be voted on.

Q: Why is a shareholder meeting being held?

A: A special meeting of shareholders (the “Meeting”) of Thrivent Partner Small Cap Growth Fund (the “Target Fund”) is being held to seek shareholder approval of a reorganization (the “Reorganization”) of the Target Fund into Thrivent Small Cap Stock Fund (the “Acquiring Fund”). Please refer to the Prospectus/Proxy Statement for a detailed explanation of the proposed Reorganization and for a more complete description of the Acquiring Fund.

Q: Why is the Reorganization being recommended?

A: After careful consideration, the Board of Trustees (the “Board”) of Thrivent Mutual Funds (the “Trust”) has determined that the Reorganization is in the best interests of the shareholders of the Target Fund and recommends that you cast your vote “FOR” the proposed Reorganization. The Target Fund and the Acquiring Fund have substantially similar investment objectives, and each is a diversified series of the Trust, an open-end management investment company registered under the Investment Company Act of 1940. Thrivent Asset Management, LLC (“Thrivent Asset Mgt.” or the “Adviser”) is the investment adviser for the Target Fund and the Acquiring Fund.

The Board believes that the Reorganization would be in the best interests of the shareholders of the Target Fund because: (i) shareholders will become shareholders of a larger combined fund with greater potential to increase asset size and achieve economies of scale (especially given the breakpoints in the advisory fee schedule for the Acquiring Fund), whereby certain administrative costs may be spread across the combined portfolio’s larger asset base and, therefore, may increase the combined portfolio’s overall efficiency in the long term; (ii) the Acquiring Fund invests in a more diversified portfolio of equities; (iii) the Acquiring Fund has achieved stronger performance than the Target Fund for the one-year period ended December 31, 2014, which corresponds to when Matthew Finn assumed primary portfolio management responsibilities for the Acquiring Fund, though there is no guarantee of future performance; (iv) the Adviser believes that it can most effectively manage the assets currently in the Target Fund by combining such assets with the Acquiring Fund into a single mandate and under the same portfolio manager; and (v) the Acquiring Fund has lower advisory fees than the Target Fund and the Target Fund shareholders will experience a lower expense ratio in the Acquiring Fund following the Reorganization.

Q: Who can vote?

A: Shareholders of the Target Fund are entitled to vote.

Q: How will the Reorganization affect me?

A: Assuming shareholders approve the proposed Reorganization, the assets of the Target Fund will be combined with those of the Acquiring Fund. The Class A and Institutional Class Shares of the Target Fund automatically would be exchanged for an equal dollar value of Class A and Institutional Class Shares of the Acquiring Fund. Following the Reorganization, the Target Fund will dissolve.

Q: Will I have to pay any commission or other similar fee as a result of the Reorganization?

A: No. You will not pay any commissions or other similar fees as a result of the Reorganization. If you hold Class A Shares of the Target Fund, you will receive Class A Shares of the Acquiring Fund. If you hold Institutional Class Shares of the Target Fund, you will receive Institutional Class Shares of the Acquiring Fund.

Table of Contents

Q: Will the total annual operating expenses that my portfolio investment bears increase as a result of the Reorganization?

A: No, they will likely decrease, and the investment management fee, which comprises a portion of the annual operating expenses, will decrease. For more information about how fund expenses may change as a result of the Reorganization, please see the comparative and pro forma table and related disclosures in the COMPARISON OF THE FUNDS—Expenses section of the Prospectus/Proxy Statement.

Q: Will I have to pay any U.S. federal income taxes as a result of the Reorganization?

A: The Reorganization is expected to be tax-free for federal income tax purposes. The Target Fund will seek an opinion of counsel to this effect. Generally, shareholders will not incur capital gains or losses on the exchange of Target Fund shares for Acquiring Fund shares as a result of the Reorganization.

Q: If shareholders of the Target Fund do not approve the Reorganization, what will happen to the Target Fund?

A: Thrivent Asset Mgt. will reassess what changes it would like to make to a Target Fund, including a possible repurposing of the Target Fund’s principal investment strategies or recommending a liquidation of the Target Fund to the Board. It may ultimately decide to make no changes.

Q: Who pays the costs of the Reorganization?

A: The expenses of the Reorganization, including the costs of the Meeting, will be paid by Thrivent Asset Mgt. or an affiliate and will not be borne by Target Fund shareholders.

Q: How can I vote?

A: Shareholders are invited to attend the Meeting and to vote in person. You may also vote by executing a proxy using one of three methods:

| • | By Internet: Instructions for casting your vote via the Internet can be found in the enclosed proxy voting materials. The required control number is printed on your enclosed proxy card. If this feature is used, there is no need to mail the proxy card. |

| • | By Telephone: Instructions for casting your vote via telephone can be found in the enclosed proxy voting materials. The toll-free number and required control number are printed on your enclosed proxy card. If this feature is used, there is no need to mail the proxy card. |

| • | By Mail: If you vote by mail, please indicate your voting instructions on the enclosed proxy card, date and sign the card, and return it in the envelope provided, which is addressed for your convenience and needs no postage if mailed in the United States. |

Shareholders who execute proxies by Internet, telephone or mail may revoke them at any time prior to the Meeting by filing with the Target Fund a written notice of revocation, by executing another proxy bearing a later date, by voting later by Internet or telephone or by attending the Meeting and voting in person. Merely attending the Meeting, however, will not revoke any previously submitted proxy.

Q: When should I vote?

A: Every vote is important and the Board encourages you to record your vote as soon as possible. Voting your proxy now will ensure that the necessary number of votes is obtained, without the time and expense required for additional proxy solicitation.

Q: Who should I call if I have questions about the proposal in the Prospectus/Proxy Statement?

A: Call 1-866-865-3843 with your questions.

- 2 -

Table of Contents

Q: How can I get more information about the Target and Acquiring Funds?

A: You may obtain (1) a prospectus, statement of additional information or annual/semiannual report for the Funds or (2) the statement of additional information regarding the Reorganization (request the “Reorganization SAI”) by:

| • | Telephone: 1-800-THRIVENT (1-800-847-4836) and say “mutual funds” |

| • | Mail: Thrivent Mutual Funds, P.O. Box 219348, Kansas City, Missouri 64121-9348 |

| • | Internet: |

| • | For a copy of a prospectus, a statement of additional information, or a shareholder report: |

www.thrivent.com

| • | For a copy of this Prospectus/Proxy Statement or the Reorganization SAI: |

www.proxy-direct.com/thr-26694

- 3 -

Table of Contents

Thrivent Partner Small Cap Growth Fund

a series of

THRIVENT MUTUAL FUNDS

625 Fourth Avenue South

Minneapolis, Minnesota 55415

(800) 847-4836

www.thrivent.com

NOTICE OF SPECIAL MEETING

OF SHAREHOLDERS

To be Held on August 14, 2015

NOTICE IS HEREBY GIVEN THAT a special meeting of shareholders (the “Meeting”) of Thrivent Partner Small Cap Growth Fund (the “Target Fund”), a series of Thrivent Mutual Funds (the “Trust”), will be held at the offices of Thrivent Financial for Lutherans, 625 Fourth Avenue South, Minneapolis, Minnesota 55415 on August 14, 2015 at 9:00 a.m. Central time for the following purposes:

| 1. | To approve an Agreement and Plan of Reorganization pursuant to which the Target Fund would (i) transfer all of its assets to Thrivent Small Cap Stock Fund (the “Acquiring Fund”), a series of the Trust, in exchange for Class A and Institutional Class Shares of the Acquiring Fund, (ii) distribute such Class A and Institutional Class Shares of the Acquiring Fund to shareholders of the Target Fund, and (iii) dissolve. |

| 2. | To transact such other business as may properly be presented at the Meeting or any adjournment thereof. |

The Board of Trustees of the Trust (the “Board”) has fixed the close of business on June 16, 2015 as the record date for the determination of shareholders entitled to notice of, and to vote at, the Meeting and all adjournments thereof.

Shareholders are invited to attend the meeting and vote in person. You may also vote by executing a proxy using one of three methods:

| • | By Internet—Instructions for casting your vote via the Internet can be found in the enclosed proxy voting materials. The required control number is printed on your enclosed proxy card. If this feature is used, there is no need to mail the proxy card. |

| • | By Telephone—Instructions for casting your vote via telephone can be found in the enclosed proxy voting materials. The toll-free number and required control number are printed on your enclosed proxy card. If this feature is used, there is no need to mail the proxy card. |

| • | By Mail—If you vote by mail, please indicate your voting instructions on the enclosed proxy card, date and sign the card, and return it in the envelope provided, which is addressed for your convenience and needs no postage if mailed in the United States. |

Shareholders who execute proxies by Internet, telephone, or mail may revoke them at any time prior to the Meeting by filing with the Target Fund a written notice of revocation, by executing another proxy bearing a later date, or by attending the Meeting and voting in person. Merely attending the Meeting, however, will not revoke any previously submitted proxy.

The Board recommends that you cast your vote FOR the proposed Reorganization as described in the Prospectus/Proxy Statement.

YOUR VOTE IS IMPORTANT

Please return your proxy card or record your voting instructions by telephone or via the Internet promptly no matter how many shares you own. In order to avoid the additional expense of further solicitation, we ask that you mail your proxy card or record your voting instructions by telephone or via the Internet promptly regardless of whether you plan to be present in person at the Meeting.

Date: , 2015

Michael W. Kremenak

Secretary

Thrivent Mutual Funds

Table of Contents

COMBINED PROSPECTUS/PROXY STATEMENT

THRIVENT PARTNER SMALL CAP GROWTH FUND

a series of

THRIVENT MUTUAL FUNDS

625 Fourth Avenue South

Minneapolis, Minnesota 55415

(800) 847-4836

, 2015

This Prospectus/Proxy Statement is furnished to you as a shareholder of Thrivent Partner Small Cap Growth Fund (the “Target Fund”), a series of Thrivent Mutual Funds (the “Trust”). A special meeting of shareholders of the Target Fund will be held on August 14, 2015 (the “Meeting”) to consider the approval of a Reorganization (the “Reorganization”) of the Target Fund into Thrivent Small Cap Stock Fund (the “Acquiring Fund”). The Board of Trustees of the Trust (the “Board”) requests that you vote your shares by completing and returning the enclosed proxy card or by recording your voting instructions by telephone or via the Internet regardless of whether you plan to be present at the Meeting in order to avoid the additional expense of further solicitation.

The Acquiring Fund and the Target Fund are sometimes referred to herein individually as a “Fund” or collectively as the “Funds.” Each of the Acquiring Fund and the Target Fund is organized as a diversified series of the Trust, an open-end management investment company registered under the Investment Company Act of 1940, as amended (the “1940 Act”).

The reorganization proposed for the Target Fund (the “Reorganization”) is not contingent upon the approval or completion of any other reorganization or merger.

This Prospectus/Proxy Statement sets forth concisely the information shareholders of the Target Fund ought to know before voting on the Reorganization. Please read it carefully and retain it for future reference.

The following documents, each having been filed with the Securities and Exchange Commission (the “SEC”), are incorporated herein by reference:

| • | The Thrivent Mutual Funds Prospectus, dated February 27, 2015 and as supplemented through the date hereof (the “Trust Prospectus”). |

| • | A Statement of Additional Information, dated , 2015, relating to this Combined Prospectus/Proxy Statement (the “Reorganization SAI”); |

| • | The Thrivent Mutual Funds Statement of Additional Information, dated February 27, 2015 and as supplemented through the date hereof (the “Trust SAI”). |

Copies of the foregoing may be obtained without charge by calling or writing the Fund as set forth below. If you wish to request the Reorganization SAI, please ask for the “Reorganization SAI.”

In addition, each Fund will furnish, without charge, a copy of its most recent annual report and subsequent semi-annual report, if any, to a shareholder upon request.

Copies of each Fund’s most recent prospectus, statement of additional information, annual report and semi-annual report can be obtained at www.thrivent.com. Requests for documents can also be made by calling (800) 847-4836 or writing Thrivent Mutual Funds, P.O. Box 219348, Kansas City, Missouri 64121-9348.

The Funds file reports and other information with the SEC. Information filed by the Funds with the SEC can be reviewed and copied at the SEC’s Public Reference Room in Washington, DC or on the EDGAR database on the SEC’s internet site (http://www.sec.gov). Information on the operation of the SEC’s Public Reference Room may be obtained by calling the SEC at (202) 551-8090. You can also request copies of these materials, upon payment of a duplicating fee, by electronic request at the SEC’s e-mail address (publicinfo@sec.gov) or by writing the Public Reference Section of the SEC, Washington, DC 20549-1520.

The Board knows of no business other than that discussed above that will be presented for consideration at the Meeting. If any other matter is properly presented, it is the intention of the persons named in the enclosed proxy to vote in accordance with their best judgment.

No person has been authorized to give any information or make any representation not contained in this Prospectus/Proxy Statement and, if so given or made, such information or representation must not be relied upon as having been authorized. This Prospectus/Proxy Statement does not constitute an offer to sell or a solicitation of an offer to buy any securities in any jurisdiction in which, or to any person to whom, it is unlawful to make such offer or solicitation.

Table of Contents

Neither the Securities and Exchange Commission nor any state regulator has approved or disapproved of these shares or passed upon the adequacy of this Prospectus/Proxy Statement. A representation to the contrary is a crime.

The date of this Prospectus/Proxy Statement is , 2015. The Prospectus/Proxy Statement will be sent to shareholders on or around July 1, 2015.

- 2 -

Table of Contents

TABLE OF CONTENTS

| Page | ||||

| 1 | ||||

| 1 | ||||

| 1 | ||||

| 3 | ||||

| 3 | ||||

| 3 | ||||

| 4 | ||||

| 4 | ||||

| 5 | ||||

| 6 | ||||

The Separate Accounts and the Retirement Plans | 6 | |||

| 8 | ||||

| 9 | ||||

| 10 | ||||

| 11 | ||||

| 14 | ||||

| 14 | ||||

| 15 | ||||

| 15 | ||||

| 15 | ||||

| 16 | ||||

| 16 | ||||

Material Federal Income Tax Consequences of the Reorganization | 17 | |||

| 19 | ||||

| 19 | ||||

| 19 | ||||

| 19 | ||||

| 20 | ||||

| 20 | ||||

| 20 | ||||

| 20 | ||||

| 20 | ||||

| 20 | ||||

| 21 | ||||

| 21 | ||||

Table of Contents

The following is a summary of certain information contained elsewhere in this Prospectus/Proxy Statement and is qualified in its entirety by reference to the more complete information contained in this Prospectus/Proxy Statement. Shareholders should read the entire Prospectus/Proxy Statement carefully.

The Board, including the trustees who are not “interested persons” (as defined in the 1940 Act) of each Fund, has unanimously approved an Agreement and Plan of Reorganization (the “Reorganization Agreement”) on behalf of each Fund, subject to Target Fund shareholder approval. The Reorganization Agreement provides for:

| • | the transfer of all of the assets of the Target Fund to the Acquiring Fund in exchange for Class A and Institutional Class Shares of the Acquiring Fund; |

| • | the distribution by the Target Fund of such Acquiring Fund Class A and Institutional Class Shares to Target Fund shareholders; and |

| • | the dissolution of the Target Fund. |

When the Reorganization is complete, Target Fund shareholders will hold Acquiring Fund shares. The aggregate value of the Acquiring Fund shares a Target Fund shareholder will receive in the Reorganization will equal the aggregate value of the Target Fund shares owned by such shareholder immediately prior to the Reorganization. After the Reorganization, the Acquiring Fund will continue to operate with the investment objective and investment policies set forth in this Prospectus/Proxy Statement.

As discussed in more detail elsewhere in this Prospectus/Proxy Statement, the Board believes that the Reorganization would be in the best interests of the Target Fund’s shareholders because: (i) shareholders will become shareholders of a larger combined fund with greater potential to increase asset size and achieve economies of scale; (ii) the Acquiring Fund invests in a more diversified portfolio of equities; (iii) the Acquiring Fund has achieved stronger performance over the one-year period ended December 31, 2014 with outperformance of 2.54%, which corresponds to when Matthew Finn assumed primary portfolio management responsibilities for the Acquiring Fund; (iv) Thrivent Asset Management, LLC (“Thrivent Asset Mgt.” or the “Adviser”) believes that it can most effectively manage the assets currently in the Target Fund by combining such assets with the Acquiring Fund into a single mandate and under the same portfolio manager; and (v) Target Fund shareholders will experience a lower expense ratio in the merged Acquiring Fund.

In addition, the Board, when determining whether to approve the Reorganization, considered, among other things, the future growth prospects of each of the Target Fund and the Acquiring Fund, the fact that the Target Fund shareholders would not experience any diminution in shareholder services as a result of the Reorganization, and the fact that the Reorganization is expected to be a tax-free reorganization for federal income tax purposes.

Background and Reasons for the Reorganization

The Target Fund and the Acquiring Fund have substantially similar investment objectives. The investment objective of the Target Fund is to seek to achieve long-term growth of capital. The investment objective of the Acquiring Fund is to seek long-term capital growth.

The two Funds also have similar, although not identical, principal investment strategies, which are described in more detail in the COMPARISON OF FUNDS—Investment Objective and Principal Strategies section of the Prospectus/Proxy Statement. Under normal circumstances, both Funds invest at least 80% of their net assets (plus the amount of any borrowing for investment purposes) in securities of small companies. In the case of the Target Fund, the Adviser focuses mainly in the securities of smaller U.S. companies which have market capitalizations similar to those companies included in widely known indices such as the S&P SmallCap 600 Growth Index, the Russell 2000® Growth Index, or the small company market capitalization classifications published by Lipper, Inc. In the case of the Acquiring Fund, the Adviser focuses mainly in the securities of smaller U.S. companies which have market capitalizations similar to those companies included in widely known indices such as the S&P SmallCap 600 Index or the Russell 2000® Index.

Table of Contents

In determining whether to recommend approval of the Reorganization Agreement to Target Fund shareholders, the Board considered a number of factors, including, but not limited to: (i) the expenses and advisory fees applicable to the Funds before the proposed Reorganization and the estimated expense ratios of the combined Fund after the proposed Reorganization; (ii) the comparative investment performance of the Funds; (iii) the future growth prospects of each Fund; (iv) the terms and conditions of the Reorganization Agreement; (v) whether the Reorganization would result in the dilution of shareholder interests; (vi) the compatibility of the Funds’ investment objectives, policies, risks and restrictions; (vii) the anticipated tax consequences of the proposed Reorganization; (viii) the compatibility of the Funds’ service features available to shareholders, including exchange privileges; and (ix) the estimated costs of the Reorganization. The Board concluded that these factors supported a determination to approve the Reorganization Agreement.

The Board has determined that the Reorganization is in the best interests of the Target Fund and that the interests of the Target Fund’s shareholders will not be diluted as a result of the Reorganization. In addition, the Board has determined that the Reorganization is in the best interests of the Acquiring Fund and that the interests of the Acquiring Fund’s shareholders will not be diluted as a result of the Reorganization.

The Board is asking shareholders of the Target Fund to approve the Reorganization at the Meeting to be held on August 14, 2015. If shareholders of the Target Fund approve the proposed Reorganization, it is expected that the closing date of the transaction (the “Closing Date”) will be after the close of business on or about August 28, 2015, but it may be at a different time as described herein. If shareholders of the Target Fund do not approve the proposed Reorganization, the Board will consider alternatives, including repurposing the Target Fund’s principal strategies.

The Board recommends that you vote “FOR” the Reorganization.

- 2 -

Table of Contents

Investment Objective and Principal Strategies

Investment Objective. The Target Fund and the Acquiring Fund have substantially similar investment objectives. The investment objective of the Target Fund is to seek to achieve long-term growth of capital. The investment objective of the Acquiring Fund is to seek long-term capital growth.

Principal Strategies. Under normal circumstances, both Funds invest at least 80% of their net assets (plus the amount of any borrowing for investment purposes) in securities of small companies. In the case of the Target Fund, the Adviser focuses mainly in the securities of smaller U.S. companies which have market capitalizations similar to those companies included in widely known indices such as the S&P SmallCap 600 Growth Index, the Russell 2000® Growth Index, or the small company market capitalization classifications published by Lipper, Inc. In the case of the Acquiring Fund, the Adviser focuses mainly in the securities of smaller companies which have market capitalizations similar to those companies included in widely known indices such as the S&P SmallCap 600 Index or the Russell 2000® Index. Should the Adviser determine that a Fund would benefit from reducing the percentage of its assets invested in securities of small companies from 80% to a lesser amount, it will notify shareholders at least 60 days prior to such a change.

Both Funds seek to achieve its investment objective by investing primarily in common stocks. The Advisers for both Funds use fundamental, quantitative, and technical investment research techniques to determine what securities to buy and sell. The Advisers look for small companies that, in their opinion:

| • | have an improving fundamental outlook; |

| • | have capable management; and |

| • | are financially sound. |

The Advisers may sell securities for a variety of reasons, such as to secure gains, limit losses, or reposition assets to more promising opportunities.

Fund Holdings. A description of the Funds’ policies and procedures with respect to the disclosure of the Funds’ portfolio securities is available on the Funds’ website.

The Funds are subject to similar principal risks. Both Funds are subject to Market Risk, Issuer Risk, Small Cap Risk, Liquidity Risk and Investment Adviser Risk. Both Funds are also subject to Volatility Risk, though each may be subject to different types of volatility risk. These risks are described below.

Principal risks to which both Funds are subject

Market Risk. Over time, securities markets generally tend to move in cycles with periods when security prices rise and periods when security prices decline. The value of the Fund’s investments may move with these cycles and, in some instances, increase or decrease more than the applicable market(s) as measured by the Fund’s benchmark index(es). The securities markets may also decline because of factors that affect a particular industry.

Issuer Risk. Issuer risk is the possibility that factors specific to a company to which the Fund’s portfolio is exposed will affect the market prices of the company’s securities and therefore the value of the Fund. Some factors affecting the performance of a company include demand for the company’s products or services, the quality of management of the company and brand recognition and loyalty. Common stock of a company is subordinate to other securities issued by the company. If a company becomes insolvent, interests of investors owning common stock will be subordinated to the interests of other investors in, and general creditors of, the company.

Small Cap Risk. Smaller, less seasoned companies often have greater price volatility, lower trading volume, and less liquidity than larger, more established companies. These companies tend to have small revenues, narrower product lines, less management depth and experience, small shares of their product or service markets, fewer financial resources, and less competitive strength than larger companies. Such companies seldom pay significant dividends that could cushion returns in a falling market.

- 3 -

Table of Contents

Liquidity Risk. Liquidity is the ability to sell a security relatively quickly for a price that most closely reflects the actual value of the security. Small capitalization stocks often have a less liquid resale market. As a result, the Fund may have difficulty selling or disposing of securities quickly in certain markets or may only be able to sell the holdings at prices substantially less than what the Fund believes they are worth.

Investment Adviser Risk. The Fund is actively managed and the success of its investment strategy depends significantly on the skills of the adviser(s) in assessing the potential of the investments in which the Fund invests. This assessment of investments may prove incorrect, resulting in losses or poor performance, even in rising markets.

Volatility Risk. Volatility risk is the risk that certain types of securities shift in and out of favor depending on market and economic conditions as well as investor sentiment.

Additional principal risks to which only the Target Fund is subject

Volatility Risk. Growth style investing includes the risk of investing in securities whose prices historically have been more volatile than other securities, especially over the short term. Stocks of growth companies historically have been more volatile than other securities, especially over the short term. Growth stock prices reflect projections of future earnings or revenues and if a company’s earnings or revenues fall short of expectations its stock price may fall dramatically.

The Board. The Board is responsible for the overall supervision of the operations of each Fund and performs the various duties imposed on the directors of investment companies by the 1940 Act and under applicable state law.

The Adviser. Thrivent Asset Mgt. is the investment adviser for each Fund. Thrivent Asset Mgt. and its investment advisory affiliate, Thrivent Financial for Lutherans (“Thrivent Financial”) have been in the investment advisory business since 1986 and managed approximately $96 billion in assets as of December 31, 2014, including approximately $41 billion in mutual fund assets. These advisory entities are located at 625 Fourth Avenue South, Minneapolis, Minnesota 55415.

The Adviser and the Trust received an exemptive order from the SEC that permits the Adviser and the Funds, with the approval of the Board, to retain one or more subadvisers for the Funds, or subsequently change a subadviser, without submitting the respective investment subadvisory agreements, or material amendments to those agreements, to a vote of the shareholders of the applicable Fund. The Adviser will notify shareholders of a Fund if there is a new subadviser for that Fund.

The Funds’ annual report to shareholders discusses the basis for the Board approving the investment advisory agreement during the period covered by the report.

Portfolio Management. David J. Lettenberger, CFA has served as portfolio manager of the Target Fund since 2014. Mr. Lettenberger has been with Thrivent Financial since 2013 and previously served as an associate portfolio manager.

Matthew D. Finn, CFA has served as lead portfolio manager of the Acquiring Fund since 2013. James M. Tinucci, CFA has served as the associate portfolio manager of the Acquiring Fund since 2015. Mr. Finn has been a portfolio manager at Thrivent Financial since 2004, when he joined the firm. Mr. Tinucci has been with Thrivent Financial since 2014, and previously held various positions at Thrivent Financial from 2007 to 2012. Prior to joining Thrivent Financial, Mr. Tinucci was a manager at Deloitte Consulting.

The Trust SAI provides information about the portfolio managers’ compensation, other accounts managed by the portfolio managers, and the portfolio managers’ ownership of shares of the Funds.

Advisory Fees. Each Fund pays an annual investment advisory fee to the Adviser. The advisory contract between the Adviser and the Fund provides for the following advisory fees for each class of shares of a Fund, expressed as an annual rate of average daily net assets:

- 4 -

Table of Contents

Target Fund

0.900% of average daily net assets up to $500 million

0.800% of average daily net assets over $500 million

Acquiring Fund

0.700% of average daily net assets up to $200 million

0.650% of average daily net assets greater than $200 million but not greater than $1 billion

0.600% of average daily net assets greater than $1 billion but not greater than $2.5 billion

0.550% of average daily net assets greater than $2.5 billion but not greater than $5 billion

0.525% of average daily net assets over $5 billion

During the twelve-months ended October 31, 2014, the contractual advisory fees for the Class A shares of the Target Fund were 0.92% of the Target Fund’s average daily net assets, and the contractual advisory fees for the Class I shares of the Target Fund were 0.90% of the Target Fund’s average daily net assets.

During the twelve-months ended October 31, 2014, the contractual advisory fees for the Class A shares of the Acquiring Fund were 0.68% of the Acquiring Fund’s average daily net assets, and the contractual advisory fees for the Class I shares of the Acquiring Fund were 0.68% of the Acquiring Fund’s average daily net assets.

For a complete description of each Fund’s advisory services, see the section of the Trust Prospectus entitled “Management” and the section of the Trust SAI entitled “Investment Adviser, Investment Subadvisers, and Fund Managers.”

12b-1 Plan. The Trust has adopted a Distribution Plan and Agreement pursuant to Rule 12b-1 under the 1940 Act (the “Rule 12b-1 Plan”) with respect to the Class A Shares of each Fund. Thrivent Investment Management Inc. (the “Distributor”), an affiliate of the Adviser, located at 625 Fourth Avenue South, Minneapolis, Minnesota 55415, serves as the distributor of each Fund. Under the Rule 12b-1 Plan, Class A Shares of each Fund pay the Distributor an aggregate fee for distribution and shareholder servicing equal to an annual rate of 0.25% of the average daily net asset value represented by such shares. Institutional Class Shares are not subject to a Rule 12b-1 Plan and the Funds do not pay any percentage of their assets attributable to Institutional Class Shares for distribution or shareholder servicing. For a complete description of these arrangements with respect to each Fund, see the section of the Class A Prospectus entitled “Shareholder Information—Rule 12b-1 Fees” and the section of the Trust SAI entitled “Underwriting and Distribution Service.” These sections are incorporated by reference herein.

Investments in the Target Fund by Certain Affiliated Funds

The Reorganization is not contingent upon the approval or completion of any other reorganization or merger. However, simultaneous with shareholders’ consideration of this Prospectus/Proxy Statement, shareholders of Thrivent Partner Small Cap Value Fund (the “Other Target Fund,” and collectively with the Target Fund, the “Target Funds”) are considering a reorganization of that fund into the Acquiring Fund. Therefore, pro forma financial and expense information presented in this Prospectus/Proxy Statement under the headings “COMPARISON OF THE FUNDS – Expenses” and “COMPARISON OF THE FUNDS – Capitalization”, and the pro forma information regarding the Acquiring and Target Funds in the Reorganization SAI (collectively, the “Pro Forma Information”), is presented on the basis of the alternate assumptions that the Reorganization involves solely the Target Fund or both of the Target Funds.

Other series of the Trust for which Thrivent Asset Mgt. is the investment adviser (the “Affiliated Funds”) currently invest in the Target Funds. The Affiliated Funds are asset allocation funds investing a range of asset categories and permit Thrivent Asset Mgt. to determine whether to invest directly in securities and other investments, in addition to, or instead of, investing in other series of the Fund (including the Target Funds). Over time, Thrivent Asset Mgt. has gradually invested a larger percentage of the Affiliated Funds’ assets in direct investments and has reduced the percentage of assets invested in other series of the Trust. Thrivent Asset Mgt. expects to continue decreasing the percentage of Affiliated Funds’ assets invested in other series over time. This trend of relying more heavily on direct investments is expected to accelerate since Thrivent Asset Mgt. has proposed changes that will simplify the investment advisory fee structure of the Affiliated Funds. These changes would encourage a more streamlined approach of direct investments, while accommodating investments in other series of

- 5 -

Table of Contents

the Trust when Thrivent Asset Mgt. deems it to be advisable. As a result, the Affiliated Funds are likely to redeem their holdings (if any) out of the Target Funds irrespective of whether the Reorganization is approved. These redemptions would most likely be processed as redemptions-in-kind, with the effect that the Affiliated Funds would receive a pro rata distribution of the Target Funds’ investments. These redemptions may be substantial, relative to the size of the Target Fund(s) prior to such redemption, and are likely to occur prior to the effective date of the Reorganization. The Pro Forma Information presented in this Prospectus/Proxy Statement and the Reorganization SAI does not include any effects of such redemptions.

The table below sets forth the fees and expenses that investors may pay to buy and hold shares of each of the Target Fund and the Acquiring Fund, including (i) the fees and expenses paid by the Target Fund for the twelve-month period ended December 31, 2014, (ii) the fees and expenses paid by the Acquiring Fund for the twelve-month period ended December 31, 2014, (iii) pro forma fees and expenses for the Acquiring Fund for the twelve-month period ended December 31, 2014, assuming the Reorganization had been completed as of the beginning of such period, and (iv) pro forma fees and expenses for the Acquiring Fund for the twelve-month period ended December 31, 2014, assuming that the Target Fund and Thrivent Partner Small Cap Value Fund (collectively referred to as the “Target Funds”) all merged into the Acquiring Fund as of the beginning of such period.

| Class A Shares | Institutional Class Shares | |||||||||||||||||||||||||||||||

| Actual | Pro Forma | Pro Forma | Actual | Pro Forma | Pro Forma | |||||||||||||||||||||||||||

| Target Fund | Acquiring Fund | Acquiring Fund (assuming merger with Target Fund) | Acquiring Fund (assuming merger with Target Funds) | Target Fund | Acquiring Fund | Acquiring Fund (assuming merger with Target Fund) | Acquiring Fund (assuming merger with Target Funds) | |||||||||||||||||||||||||

Shareholder Fees (fees paid directly from your investment) | ||||||||||||||||||||||||||||||||

Maximum Sales Charge (Load) Imposed on Purchases (as a percentage of offering price) | 5.50 | % | 5.50 | % | 5.50 | % | 5.50 | % | N/A | N/A | N/A | N/A | ||||||||||||||||||||

Maximum Deferred Sales Charge (Load) (as a percentage of net asset value at time of purchase or redemption, whichever is lower)* | 1.00 | % | 1.00 | % | 1.00 | % | 1.00 | % | N/A | N/A | N/A | N/A | ||||||||||||||||||||

Annual Fund Operating Expenses as a Percentage of Average Net Assets (expenses that are deducted from Fund assets) | ||||||||||||||||||||||||||||||||

Management Fees | 0.92 | % | 0.68 | % | 0.67 | % | 0.66 | % | 0.90 | % | 0.68 | % | 0.67 | % | 0.66 | % | ||||||||||||||||

Distribution and Service (12b-1 Fees) | 0.25 | % | 0.25 | % | 0.25 | % | 0.25 | % | — | — | — | — | ||||||||||||||||||||

Other Expenses | 0.56 | % | 0.32 | % | 0.32 | % | 0.31 | % | 0.12 | % | 0.07 | % | 0.06 | % | 0.08 | % | ||||||||||||||||

Acquired (Underlying) Fund Fees and Expenses | — | 0.01 | % | 0.01 | % | 0.01 | % | — | 0.01 | % | 0.01 | % | 0.01 | % | ||||||||||||||||||

Total Annual Operating Expenses | 1.73 | % | 1.26 | % | 1.25 | % | 1.23 | % | 1.02 | % | 0.76 | % | 0.74 | % | 0.75 | % | ||||||||||||||||

Less Expense Reimbursement** | 0.43 | % | — | — | — | 0.02 | % | — | — | — | ||||||||||||||||||||||

Net Annual Fund Operating Expenses | 1.30 | % | 1.26 | % | 1.25 | % | 1.23 | % | 1.00 | % | 0.76 | % | 0.74 | % | 0.75 | % | ||||||||||||||||

- 6 -

Table of Contents

| * | When you invest $1,000,000 or more, a deferred sales charge of 1% will apply to shares redeemed within one year. |

| ** | The Adviser has contractually agreed, through at least February 28, 2016, to waive certain fees and/or reimburse certain expenses associated with the Class A shares of the Thrivent Partner Small Cap Growth Fund in order to limit the Net Annual Fund Operating Expenses (excluding Acquired (Underlying) Fund Fees and Expenses, if any) to an annual rate of 1.30% of the average daily net assets of the Class A shares. This contractual provision, however, may be terminated before the indicated termination date upon the mutual agreement between the Independent Trustees of the Fund and the Adviser. |

| ** | The Adviser has contractually agreed, through at least February 28, 2016, to waive certain fees and/or reimburse certain expenses associated with the Institutional Class shares of the Thrivent Partner Small Cap Growth Fund in order to limit the Net Annual Fund Operating Expenses (excluding Acquired (Underlying) Fund Fees and Expenses, if any) to an annual rate of 1.00% of the average daily net assets of the Institutional Class shares. This contractual provision, however, may be terminated before the indicated termination date upon the mutual agreement between the Independent Trustees of the Fund and the Adviser. |

Example

The following example, using the actual and pro forma operating expenses for the twelve-month period ended October 31, 2014, is intended to help you compare the costs of investing in the Acquiring Fund pro forma after the Reorganization with the costs of investing in each of the Target Fund and the Acquiring Fund without the Reorganization. The example assumes that you invest $10,000 in each Fund for the time period indicated and that you redeem all of your shares at the end of each period. The example also assumes that your investments have a 5% return each year and that each Fund’s operating expenses remain the same each year. Although your actual returns may be higher or lower, based on these assumptions your costs would be:

| Actual | Pro Forma | |||||||||||||||

| Target Fund | Acquiring Fund | Acquiring Fund (assuming merger with the Target Fund) | Acquiring Fund (assuming merger with the Target Funds) | |||||||||||||

Total operating expenses for Class A Shares assuming redemption at the end of the period | ||||||||||||||||

One Year | $ | 675 | $ | 671 | $ | 670 | $ | 668 | ||||||||

Three Years | $ | 1,025 | $ | 928 | $ | 925 | $ | 919 | ||||||||

Five Years | $ | 1,399 | $ | 1,204 | $ | 1,199 | $ | 1,188 | ||||||||

Ten Years | $ | 2,445 | $ | 1,989 | $ | 1,978 | $ | 1,957 | ||||||||

Total operating expenses for Institutional Class Shares assuming redemption at the end of the period | ||||||||||||||||

One Year | $ | 102 | $ | 78 | $ | 76 | $ | 77 | ||||||||

Three Years | $ | 323 | $ | 243 | $ | 237 | $ | 240 | ||||||||

Five Years | $ | 561 | $ | 422 | $ | 411 | $ | 417 | ||||||||

Ten Years | $ | 1,246 | $ | 942 | $ | 918 | $ | 930 | ||||||||

Portfolio Turnover

Each Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in Total Annual Operating Expenses or in the Example, affect the Funds’ performance. During the fiscal year ended October 31, 2014, the Acquiring Fund’s and the Target Fund’s portfolio turnover rates were 56% and 94%, respectively, of the average value of their portfolios.

- 7 -

Table of Contents

Purchase, Valuation, Redemption and Exchange of Shares; Dividends and Distributions

Pricing of Fund Shares. The price of a Fund’s shares is based on the Fund’s net asset value (“NAV”). The Funds determine their NAV once daily at the close of trading on the New York Stock Exchange (“NYSE”), which is normally 4:00 p.m. Eastern Time. The Funds do not determine NAV on holidays observed by the NYSE or on any other day when the NYSE is closed. The NYSE is regularly closed on Saturdays and Sundays, New Year’s Day, Martin Luther King, Jr. Day, Presidents Day, Good Friday, Memorial Day, Independence Day, Labor Day, Thanksgiving Day and Christmas Day.

Each Fund determines its NAV for a particular class by dividing the total Fund assets attributable to that class, less all liabilities attributable to such class, by the total number of outstanding shares of that class. To determine the NAV, the other Funds generally value their securities at current market value using readily available market prices. If market prices are not available or if the Adviser determines that they do not accurately reflect fair value for a security, the Board has authorized the Adviser to make fair valuation determinations pursuant to policies approved by the Board. Fair valuation of a particular security is an inherently subjective process, with no single standard to utilize when determining a security’s fair value. In each case where a security is fair valued, consideration is given to the facts and circumstances relevant to the particular situation. This consideration includes a review of various factors set forth in the pricing policies adopted by the Board. For any portion of a Fund’s assets that are invested in other mutual funds, the NAV is calculated based upon the NAV of the mutual funds in which the Fund invests, and the prospectuses for those mutual funds explain the circumstances under which they will use fair value pricing and the effects of such a valuation.

Because many foreign markets close before the U.S. markets, significant events may occur between the close of the foreign market and the close of the U.S. markets, when the Fund’s assets are valued, that could have a material impact on the valuation of foreign securities (i.e., available price quotations for these securities may not necessarily reflect the occurrence of the significant event). The Funds, subject to oversight by the Board, evaluate the impact of these significant events and adjust the valuation of foreign securities to reflect the fair value as of the close of the U.S. markets to the extent that the available price quotations do not, in the Adviser’s opinion, adequately reflect the occurrence of the significant events.

Please note that the Target Fund and the Acquiring Fund have identical valuation policies. As a result, there will be no material change to the value of the Target Fund’s assets because of the Reorganization.

Also, the Target Fund and the Acquiring Fund have identical policies with respect to frequent purchases and redemptions and standing allocation orders (for more information, please see Frequent Trading Policies and Monitoring Processes and Standing Allocation Order disclosures in the Acquiring Fund’s Prospectus—these disclosures are incorporated herein by reference). The Reorganization will not affect these policies.

Class A Shares. The Class A Shares of each Fund are subject to an initial sales charge of up to 5.50%. The initial sales charge applicable to Class A Shares of the Acquiring Fund will be waived for Class A Shares acquired in the Reorganization. Any subsequent purchases of Class A Shares of the Acquiring Fund, excluding Class A Shares purchased through the automatic dividend reinvestment plan, after the Reorganization will be subject to an initial sales charge of up to 5.50%. The initial sales charge is reduced for investments in excess of $50,000. Purchases of Class A Shares of each Fund in amounts of $1 million or more are not subject to an initial sales charge, but a contingent deferred sales charge of up to 1.00% may be imposed on certain redemptions made within one year of purchase. No contingent deferred sales charge will be imposed on Class A Shares of the Target Fund in connection with the Reorganization. For additional information, please see the section entitled “Shareholder Information—Class A Shares” in the Class A Prospectus. This section is incorporated by reference herein.

Institutional Class Shares. Institutional Class Shares of each Fund are not subject to an initial sales charge or a contingent deferred sales charge. Institutional Class Shares are offered to institutions, church organizations, retirement plans sponsored by institutions and participants in various mutual fund asset allocation, fee-based investment advisory programs offered by the Distributor. For additional information, please see the section entitled “Shareholder Information—Institutional Class Shares” in the Institutional Class Prospectus. This section is incorporated by reference herein.

- 8 -

Table of Contents

Buying Shares. Shares of each Fund may be purchased through a shareholder’s registered representative, by mail, by telephone, by the Internet, by wire transfer, through an automatic investment plan or by exchange from other Thrivent mutual funds. For additional information regarding buying shares of each Fund and exchanging shares of each Fund, see the sections of the Trust Prospectus entitled “Shareholder Information—Buying Shares” and “Shareholder Information—Exchanging Shares Between Funds.”

Redeeming Shares. When a Fund receives a request for redemption, such Fund will redeem such shares at the next calculation of the Fund’s NAV. A Fund may postpone payment or suspend the right of redemption in unusual circumstances, as permitted by the SEC. When a shareholder purchases shares by check, electronic funds transfer (other than bank wire) or automatic investment plan and elects to redeem those shares soon after their purchase, the Fund may delay paying the redemption proceeds until the shareholder’s payment has cleared, which could take up to 10 days or more from the date of purchase. Shares may be redeemed by mail, by phone, by the Internet, by wire/ACH transfer or through a systematic withdrawal plan. For additional information regarding redeeming shares of each Fund, see the section of the Trust Prospectus entitled “Shareholder Information—Redeeming Shares.” This section is incorporated by reference herein.

Dividends and Distributions. Dividends of the Target Fund and the Acquiring Fund, if any, are generally declared and paid annually. Income dividends are derivative from investment income, including dividends, interest, and certain foreign currency gains received by each Fund. Capital gains distributions, if any, usually will be declared and paid in December for the prior twelve-month period ending October 31. Any election made by Target Fund shareholders in respect of the receipt of dividends and capital gains distributions will continue to apply to Class A and Institutional Class Shares of the Acquiring Fund received in the Reorganization. For additional information regarding these elections see the section of the Trust Prospectus entitle “Distribution Options.” This section is incorporated by reference herein.

The following table sets forth the capitalization of the Target Fund and the Acquiring Fund, as of October 31, 2014, and the pro forma capitalization of the Acquiring Fund as if the Reorganization occurred on that date. These numbers may differ as of the Closing Date.

| Actual | Pro Forma | |||||||||||||||

| Target Fund | Acquiring Fund | Acquiring Fund (assuming merger with the Target Fund) | Acquiring Fund (assuming merger with the Target Funds) | |||||||||||||

Net assets | ||||||||||||||||

Class A Shares | $ | 17,237,097 | $ | 259,839,518 | $ | 277,076,615 | $ | 373,393,130 | ||||||||

Institutional Class Shares | $ | 238,381 | $ | 90,790,306 | $ | 91,028,687 | $ | 251,663,893 | ||||||||

|

|

|

|

|

|

|

| |||||||||

Total Fund Net Assets | $ | 17,475,478 | $ | 350,629,824 | $ | 368,105,302 | $ | 625,057,023 | ||||||||

Net asset value per share | ||||||||||||||||

Class A Shares | $ | 15.12 | $ | 20.12 | $ | 20.12 | $ | 20.12 | ||||||||

Institutional Class Shares | $ | 15.72 | $ | 22.92 | $ | 22.92 | $ | 22.92 | ||||||||

Shares outstanding | ||||||||||||||||

Class A Shares | 1,139,712 | 12,913,722 | 13,770,385 | 18,557,203 | ||||||||||||

Institutional Class Shares | 15,165 | 3,960,533 | 3,970,932 | 10,978,287 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Total Shares Outstanding | 1,154,877 | 16,874,255 | 17,741,317 | 29,535,490 | ||||||||||||

The pro forma shares outstanding reflect the issuance by the Acquiring Fund of: i) assuming a merger with the Target Fund, approximately 856,663 Class A Shares and 10,399 Institutional Class Shares (for a total of 867,062 shares); and ii) assuming a merger with the Target Funds, approximately 5,643,481 Class A Shares and 7,017,754 Institutional Class Shares (for a total of 12,661,235 shares). In each case, such issuance reflects the exchange of the assets of the Target Fund for newly issued Class A Shares and Institutional Class Shares of the Acquiring Fund, respectively, at the pro forma net asset value per share. The aggregate value of the Acquiring Fund shares that a Target Fund shareholder receives in the Reorganization will equal the aggregate value of the Target Fund shares owned immediately prior to the Reorganization.

- 9 -

Table of Contents

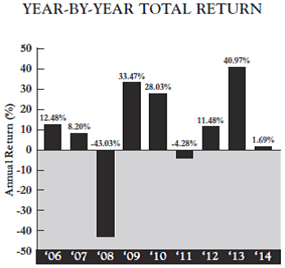

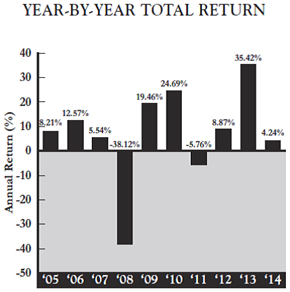

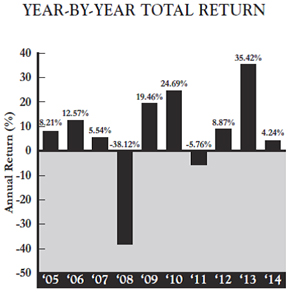

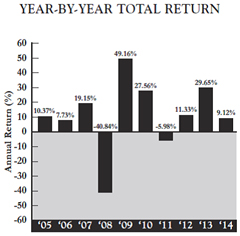

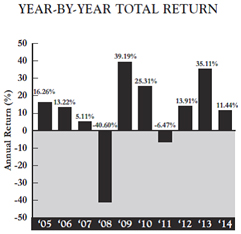

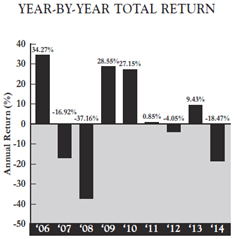

Annual Performance Information

The following chart shows the annual returns of the Target Fund since its inception and the Acquiring Fund for the past ten years. The bar charts include the effects of each Fund’s expenses, but not sales charges. If sales charges were included, returns would be lower than those shown. The table includes the effects of Fund expenses and maximum sales charges and assumes that you sold your shares at the end of the period. After-tax returns are shown only for the Class A Shares and after-tax returns for the Institutional Class Shares will differ from those shown for the Class A Shares. The after-tax returns are calculated using the historical highest individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown and after-tax returns are not relevant to investors who hold their Fund shares through tax-deferred arrangements such as 401(k) plans or individual retirement accounts. How either Fund performed in the past (before and after taxes) is not necessarily an indication of how it will perform in the future.

Thrivent Partner Small Cap Growth Fund—Class A Shares

- 10 -

Table of Contents

Thrivent Small Cap Stock Fund—Class A Shares

As a result of market activity, current performance may vary from the figures shown.

The Target Fund’s (Class A Shares) total return for the three-month period from January 1, 2015 to March 31, 2015 was 7.63%. The Acquiring Fund’s (Class A Shares) total return for the three-month period from January 1, 2015 to March 31, 2015 was 3.46%. Since its inception, the Target Fund’s (Class A Shares) highest quarterly return was 22.66% (for the quarter ended June 30, 2009) and its lowest quarterly return was -26.78% (for the quarter ended December 31, 2008). During the past 10 years, the Acquiring Fund’s (Class A Shares) highest quarterly return was 18.90% (for the quarter ended September 30, 2009) and its lowest quarterly return was -24.62% (for the quarter ended December 31, 2008).

Comparative Performance Information

As a basis for evaluating each Fund’s performance and risks, the following table shows how each Fund’s performance compares with broad-based market indices that the Adviser believes are appropriate benchmarks for such Fund. The Target Fund’s benchmark is the Russell 2000® Growth Index, which is comprised of small-cap companies with a greater-than-average growth orientation. The Acquiring Fund’s benchmark is the Russell 2000® Index, which is comprised of 2000 of the smaller companies in the Russell 3000® Index. Further, the table includes the effects of each Fund’s expenses, but not sales charges. If sales charges were included, returns would be lower than those shown.

Average annual total returns are shown below for each Fund for the periods ended December 31, 2014 (the most recently completed calendar year prior to the date of this Prospectus/Proxy Statement). Remember that past performance of a Fund is not indicative of its future performance.

Average Annual Total Returns for the Period ended December 31, 2014

- 11 -

Table of Contents

| Target Fund | Acquiring Fund | |||||||||||||||||||||||

| Past 1 Year | Past 5 Years | Since Inception (6/30/2005) | Past 1 Year | Past 5 Years | Past 10 Years | |||||||||||||||||||

Applicable Fund, Class A (before taxes) | -3.91 | % | 13.11 | % | 6.62 | % | -1.48 | % | 11.29 | % | 4.96 | % | ||||||||||||

(after taxes on distributions) | -6.28 | % | 11.52 | % | 5.70 | % | -4.17 | % | 10.64 | % | 3.77 | % | ||||||||||||

(after taxes on distributions and redemptions) | -0.35 | % | 10.30 | % | 5.18 | % | 1.10 | % | 8.95 | % | 3.70 | % | ||||||||||||

Russell 2000® Growth Index (reflects no deductions for fees, expenses or taxes) | 5.60 | % | 16.80 | % | 9.42 | % | — | — | — | |||||||||||||||

Russell 2000® Index (reflects no deductions for fees, expenses or taxes) | — | — | — | 4.89 | % | 15.55 | % | 7.77 | % | |||||||||||||||

- 12 -

Table of Contents

Financial Highlights of the Acquiring Fund

| Income from Investment Operations | Less Distributions From | Ratio to Average Net Assets** | Ratios to Average Net Assets Before Expenses Waived, Credited or Paid Indirectly** | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net Asset Value, Beginning of Period | Net Investment Income/ (Loss) | Net Realized and Unrealized Gain/(Loss) on Investments(a) | Total from Investment Operations | Net Investment Income | Net Realized Gain on Investments | Total Distributions | Net Asset Value, End of Period | Total Return(b) | Net Assets, End of Period (in millions) | Expenses | Net Investment Income/ (Loss) | Expenses | Net Investment Income/ (Loss) | Portfolio Turnover Rate | ||||||||||||||||||||||||||||||||||||||||||||||

Class A Shares | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Year Ended 10/31/2014 | $ | 18.52 | ($ | 0.05 | ) | $ | 1.80 | $ | 1.75 | $ | — | ($ | 0.15 | ) | ($ | 0.15 | ) | $ | 20.12 | 9.48 | % | $ | 259.80 | 1.25 | % | (0.15 | )% | 1.25 | % | (0.15 | )% | 56 | % | |||||||||||||||||||||||||||

Year Ended 10/31/2013 | 14.28 | (0.05 | ) | 4.29 | 4.24 | — | — | — | 18.52 | 29.69 | % | 255.6 | 1.29 | % | (0.16 | )% | 1.29 | % | (0.16 | )% | 66 | % | ||||||||||||||||||||||||||||||||||||||

Year Ended 10/31/2012 | 13.35 | (0.06 | ) | 0.99 | 0.93 | — | — | — | 14.28 | 6.97 | % | 216.6 | 1.33 | % | (0.31 | )% | 1.33 | % | (0.31 | )% | 91 | % | ||||||||||||||||||||||||||||||||||||||

Year Ended 10/31/2011 | 12.56 | (0.11 | ) | 0.90 | 0.79 | — | — | — | 13.35 | 6.29 | % | 226.3 | 1.37 | % | (0.67 | )% | 1.37 | % | (0.67 | )% | 99 | % | ||||||||||||||||||||||||||||||||||||||

Year Ended 10/31/2010 | 10.26 | (0.09 | ) | 2.39 | 2.30 | — | — | — | 12.56 | 22.42 | % | 239.1 | 1.46 | % | (0.62 | )% | 1.46 | % | (0.62 | )% | 203 | % | ||||||||||||||||||||||||||||||||||||||

Institutional Class Shares | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Year Ended 10/31/2014 | 20.98 | 0.05 | 2.04 | 2.09 | — | (0.15 | ) | (0.15 | ) | 22.92 | 10.00 | % | 90.8 | 0.75 | % | 0.35 | % | 0.75 | % | 0.35 | % | 56 | % | |||||||||||||||||||||||||||||||||||||

Year Ended 10/31/2013 | 16.09 | 0.09 | 4.80 | 4.89 | — | — | — | 20.98 | 30.39 | % | 80.2 | 0.76 | % | 0.36 | % | 0.76 | % | 0.36 | % | 66 | % | |||||||||||||||||||||||||||||||||||||||

Year Ended 10/31/2012 | 14.96 | 0.05 | 1.08 | 1.13 | — | — | — | 16.09 | 7.55 | % | 63.4 | 0.77 | % | 0.26 | % | 0.77 | % | 0.26 | % | 91 | % | |||||||||||||||||||||||||||||||||||||||

Year Ended 10/31/2011 | 13.99 | 0.07 | 0.90 | 0.97 | — | — | — | 14.96 | 6.93 | % | 60.3 | 0.76 | % | (0.05 | )% | 0.76 | % | (0.05 | )% | 99 | % | |||||||||||||||||||||||||||||||||||||||

Year Ended 10/31/2010 | 11.35 | 0.02 | 2.62 | 2.64 | — | — | — | 13.99 | 23.26 | % | 68.6 | 0.78 | % | 0.05 | % | 0.78 | % | 0.05 | % | 203 | % | |||||||||||||||||||||||||||||||||||||||

| (a) | The amount shown may not correlate with the change in aggregate gains and losses of portfolio securities due to the timing of sales and redemptions of fund shares. |

| (b) | Total investment return assumes dividend reinvestment and does not reflect any deduction for applicable sales charges. Not annualized for periods less than one year. |

| * | All per share amounts have been rounded to the nearest cent. |

| ** | Computed on an annualized basis for periods less than one year |

The financial highlights for the Target Fund’s Class A Shares and Institutional Class Shares are available in the Thrivent Mutual Funds prospectus for each respective share class, dated February 27, 2015 and as supplemented through the date hereof and are incorporated herein by reference.

-13-

Table of Contents

Thrivent Asset Mgt., 625 Fourth Avenue South, Minneapolis, Minnesota 55415, provides administrative personnel and services necessary to operate the Funds and receives an administration fee from the Funds. The custodian for the Funds is State Street Bank and Trust Company, 225 Franklin Street, Boston, Massachusetts 02110. PricewaterhouseCoopers LLP, 225 South Sixth Street, Suite 1400, Minneapolis, MN 55402, serves as the Trust’s independent registered public accounting firm.

The Trust is an open-end management investment company registered under the Investment Company Act of 1940 (the “1940 Act”) and was organized as a Massachusetts Business Trust on March 10, 1987. The Trust is made up of 26 separate series or “Funds.” Each Fund of the Trust, other than the Thrivent Asset Allocation Funds and the Thrivent Natural Resources Fund, is diversified.

The Trust is authorized to issue shares of beneficial interest, par value $.01 per share, divisible into an indefinite number of different series and classes and operates as a “series company” as provided by Rule 18f-2 under the 1940 Act.

The Declaration of Trust of the Trust, as amended through the date hereof (the “Declaration of Trust”) provides that each shareholder shall be deemed to have agreed to be bound by its terms. A vote of shareholders and the Board may amend the Declaration of Trust. The Trust may issue an unlimited number of shares in one or more series as the Board of Trustees may authorize.

Each class is subject to such investment minimums and other conditions as set forth in the Trust’s current prospectuses. Such minimums are identical the same share classes of the Target Fund and the Acquiring Fund (so, for example, the Class A Shares of both Funds have the same initial and subsequent investment minimums). The Reorganization will not affect such investment minimums and other conditions.

Differences in expenses among classes are described in the Trust’s Amended and Restated Plan Pursuant to Rule 18f-3 under the 1940 Act. Class A and Institutional Class Shares pay the expenses associated with their different distribution arrangements. Each class may, at the Trustees’ discretion, also pay a different share of other expenses, not including advisory or custodial fees or other expenses related to the management of the Trust’s assets, if these expenses are actually incurred in a different amount by that class, or if the class receives services of a different kind or to a different degree than the other class. All other expenses will be allocated to each class on the basis of the net asset value of the particular Fund.

Each class of shares has identical voting rights except that each class has exclusive voting rights on any matter submitted to shareholders relating solely to the class or where the interests of one class differ from the interests of the other class. Class A Shares have exclusive voting rights on matters involving the Rule 12b-1 Distribution Plan. Matters submitted to shareholder vote must be approved by each Fund separately except:

| • | when required otherwise by the 1940 Act; or |

| • | when the Trustees determine that the matter does not affect all Funds; then, only the shareholders of the affected Funds may vote. |

Shares are freely transferable, and holders thereof are entitled to receive dividends declared by the Board, and receive the assets of their respective Fund in the event of liquidation. The Trust generally holds shareholder meetings only when required by law or at the written request of shareholders owning at least 10% of the Trust’s outstanding shares. Shareholders may remove the Trustees from office by votes cast in person or by proxy at a shareholder meeting.

At the request of shareholders holding 10% or more of the outstanding shares of the Trust, the Trust will hold a special meeting for the purpose of considering the removal of a Trustee(s) from office, and the Trust will cooperate with and assist shareholders of record who notify the Trust that they wish to communicate with other shareholders for the purpose of obtaining signatures to request such a meeting, all pursuant to and in accordance with Section 16(c) of the 1940 Act.

- 14 -

Table of Contents

Under Massachusetts law, shareholders of a business trust may be held personally liable, under certain circumstances, for the obligations of the Trust. However, the Declaration of Trust disclaims shareholder, Trustee and/or officer liability for acts performed on behalf of the Trust or for Trust obligations that are binding only on the assets and property of the Trust. The Funds include this disclaimer in each agreement, obligation, or contract entered into or executed by the Trust or the Board. The Declaration of Trust provides for indemnification out of the Trust’s assets for all losses and expenses of any shareholder held personally liable for the obligations of the Trust. The risk of a shareholder incurring financial loss on account of shareholder liability is remote because it is limited to circumstances where the Trust itself is unable to meet its obligations.

The Trust’s organizational documents are filed as part of the Trust’s registration statement with the SEC, and shareholders may obtain copies of such documents as described on the first page of this Prospectus/Proxy Statement and in the Questions and Answers preceding this Prospectus/Proxy Statement.

Payments to Broker-Dealers and Other Financial Intermediaries

If you purchase a Fund through a broker-dealer or other financial intermediary, the Fund and its related companies may pay the intermediary for the sale of Fund shares and related services. These payments may create a conflict of interest by influencing the broker-dealer or other intermediary and your salesperson to recommend the Fund over another investment. Ask your salesperson or visit your financial intermediary’s website for more information.

INFORMATION ABOUT THE REORGANIZATION

Under the Reorganization Agreement, the Target Fund will transfer all of its assets to the Acquiring Fund in exchange for Class A and Institutional Class Shares of the Acquiring Fund. The Acquiring Fund Class A and Institutional Class Shares issued to the Target Fund will have an aggregate value equal to the aggregate value of the Target Fund’s net assets immediately prior to the Reorganization. Upon receipt by the Target Fund of Acquiring Fund Class A and Institutional Class Shares, the Target Fund will distribute such shares of the Acquiring Fund to Target Fund shareholders. Then, as soon as practicable after the Closing Date of the Reorganization, the Target Fund will dissolve under applicable state law.

The Target Fund will distribute the Acquiring Fund Class A and Institutional Class Shares received by it pro rata to Target Fund shareholders of record in exchange for their interest in Class A and Institutional Class Shares of the Target Fund. This distribution will be accomplished by opening new accounts on the books of the Acquiring Fund in the names of the Target Fund shareholders and transferring to those shareholder accounts the Acquiring Fund Class A and Institutional Class Shares received by the Target Fund. Each newly-opened account on the books of the Acquiring Fund for the previous Target Fund shareholders will represent the respective pro rata number of Acquiring Fund Class A and Institutional Class Shares due such shareholder.

Accordingly, as a result of the Reorganization, each Target Fund shareholder would own Acquiring Fund Class A and Institutional Class Shares that would have an aggregate value immediately after the Reorganization equal to the aggregate value of that shareholder’s Target Fund shares immediately prior to the Reorganization. The interests of each of the Target Fund’s shareholders will not be diluted as a result of the Reorganization. However, as a result of the Reorganization, a shareholder of the Target Fund or the Acquiring Fund will hold a reduced percentage of ownership in the larger combined fund than the shareholder did in either of the separate Funds.

No sales charge or fee of any kind will be assessed to Target Fund shareholders in connection with their receipt of Acquiring Fund Class A and Institutional Class Shares in the Reorganization.

Approval of the Reorganization will constitute approval of amendments to any of the fundamental investment restrictions of the Target Fund that might otherwise be interpreted as impeding the Reorganization, but solely for the purpose of and to the extent necessary for consummation of the Reorganization.

- 15 -

Table of Contents

Terms of the Reorganization Agreement

The following is a summary of the material terms of the Reorganization Agreement. This summary is qualified in its entirety by reference to the form of Reorganization Agreement, a form of which is attached as Appendix A to the Reorganization SAI.

Pursuant to the Reorganization Agreement, the Acquiring Fund will acquire all of the assets of the Target Fund on the Closing Date in exchange for Class A and Institutional Class Shares of the Acquiring Fund. Subject to the Target Fund’s shareholders approving the Reorganization, the Closing Date shall occur on August 28, 2015 or such other date as determined by an officer of the Fund.

On the Closing Date, the Target Fund will transfer to the Acquiring Fund all of its assets. The Acquiring Fund will in turn transfer to the Target Fund a number of its Class A and Institutional Class Shares equal in value to the value of the net assets of the Target Fund transferred to the Acquiring Fund as of the Closing Date, as determined in accordance with the valuation method described in the Acquiring Fund’s then current prospectus. In order to minimize any potential for undesirable federal income and excise tax consequences in connection with the Reorganization, the Target Fund will distribute on or before the Closing Date all or substantially all of its undistributed net investment income (including net capital gains) as of such date.

The Target Fund expects to distribute Class A and Institutional Class Shares of the Acquiring Fund received by the Target Fund to shareholders of the Target Fund promptly after the Closing Date and then dissolve.

The Acquiring Fund and the Target Fund have made certain standard representations and warranties to each other regarding their capitalization, status and conduct of business. Unless waived in accordance with the Reorganization Agreement, the obligations of the parties to the Reorganization Agreement are conditioned upon, among other things:

| • | the approval of the Reorganization by the Target Fund’s shareholders; |

| • | the absence of any rule, regulation, order, injunction or proceeding preventing or seeking to prevent the consummation of the transactions contemplated by the Reorganization Agreement; |

| • | the receipt of all necessary approvals, registrations and exemptions under federal and state laws; |

| • | the truth in all material respects as of the Closing Date of the representations and warranties of the parties and performance and compliance in all material respects with the parties’ agreements, obligations and covenants required by the Reorganization Agreement; |