As filed with the Securities and Exchange Commission on March 29, 2018

Securities Act File No. 33-12911

1940 Act Registration No. 811-5075

U.S. SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-14

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

☐ Pre-Effective Amendment No.

☐ Post-Effective Amendment No.

(Check appropriate box or boxes)

THRIVENT MUTUAL FUNDS

(Exact Name of Registrant as Specified in Charter)

625 FOURTH AVENUE SOUTH

MINNEAPOLIS, MINNESOTA 55415

(Address of Principal Executive Offices)

612-844-4198

(Area Code and Telephone Number)

MICHAEL W. KREMENAK

SECRETARY AND CHIEF LEGAL OFFICER

THRIVENT MUTUAL FUNDS

625 FOURTH AVENUE SOUTH

MINNEAPOLIS, MINNESOTA 55415

(Name and Address of Agent for Service)

Approximate Date of Proposed Public Offering: As soon as practicable after this registration statement becomes effective. It is proposed that this filing will become effective on April 30, 2018 pursuant to Rule 488 under the Securities Act of 1933.

Title of Securities Being Registered: Shares of beneficial interest, par value $.01 per share. The Registrant has registered an indefinite number of shares of beneficial interest pursuant to Section 24(f) of the Investment Company Act of 1940, as amended, and is in a continuous offering of such shares under an effective registration statement (File Nos. 33-12911 and 811-5075). No filing fee is due herewith because of reliance on Section 24(f) of the Investment Company Act of 1940, as amended.

LETTER FOR SHAREHOLDERS

Dear Shareholder:

The Board of Trustees of Thrivent Mutual Funds (the “Trust”) has scheduled special meetings of shareholders for June 21, 2018 to seek approval of the merger of Thrivent Growth and Income Plus Fund (the “Target Fund”) into Thrivent Moderately Aggressive Asset Allocation Fund (the “Acquiring Fund”). At the meeting, the shareholders of the Target Fund will be asked to consider and approve an Agreement and Plan of Reorganization (an “Agreement”) providing for its reorganization into the Acquiring Fund.

If you are not planning to attend the meeting in person, please vote before June 21 in one of the ways described below.

If the merger is approved, your investment in the Target Fund will automatically be transferred into the Acquiring Fund. We will send you a written confirmation after this takes place. This transfer is not expected to be a taxable event. (Of course, you may transfer your investment to a completely different series, which will not count as one of your permitted annual exchanges.)

Your vote counts! You may vote quickly and easily in any one of these ways:

| | ● | | Via Internet: see the instructions on the enclosed proxy card. |

| | ● | | Via Telephone: see the instructions on the enclosed proxy card. |

| | ● | | Via Mail: use the enclosed proxy card and postage-paid envelope. |

| | ● | | In person: attend the shareholder meetings on June 21 at the Thrivent Financial corporate office in Minneapolis. |

If you’d like more information about the Funds, you may order a statement of additional information to the Funds’ prospectuses, a shareholder report or the statement of additional information regarding the proposed Fund reorganizations (request the “Reorganization SAI”) by:

| | ● | | Telephone: 800-847-4836 |

| | ● | | Mail: Thrivent Mutual Funds, P.O. Box 219348, Kansas City, Missouri 64121-9348 |

| | ● | | Internet: ThriventFunds.com |

Thank you for taking this matter seriously and participating in this important process.

Sincerely,

David S. Royal

President

Thrivent Mutual Funds

Questions & Answers

For Shareholders of Thrivent Growth and Income Plus Fund

Although we recommend that you read the complete Prospectus/Proxy Statement, we have provided the following questions and answers to clarify and summarize the issues to be voted on.

Q: Why is a shareholder meeting being held?

A: A special meeting of shareholders (the “Meeting”) of Thrivent Growth and Income Plus Fund (the “Target Fund”) is being held to seek shareholder approval of a reorganization (the “Reorganization”) of the Target Fund into Thrivent Moderately Aggressive Allocation Fund (the “Acquiring Fund”). Please refer to the Prospectus/Proxy Statement for a detailed explanation of the proposed Reorganization and for a more complete description of the Acquiring Fund.

Q: Why is the Reorganization being recommended?

A: After careful consideration, the Board of Trustees (the “Board”) of Thrivent Mutual Funds (the “Trust”) has determined that the Reorganization is in the best interests of the shareholders of the Target Fund and recommends that you cast your vote “FOR” the proposed Reorganization. The Target Fund and the Acquiring Fund both invest in equity securities and debt securities in approximately the same proportion and each is a series of the Trust, an open-end management investment company registered under the Investment Company Act of 1940. Thrivent Asset Management, LLC (“Thrivent Asset Mgt.” or the “Adviser”) is the investment adviser for the Target Fund and the Acquiring Fund.

The Board believes that the Reorganization would be in the best interests of the shareholders of the Target Fund because: (i) shareholders will become shareholders of a larger combined fund with greater potential to increase asset size and achieve economies of scale; (ii) the Acquiring Fund invests in a more diversified portfolio of equity and fixed income securities; (iii) the Acquiring Fund has achieved stronger performance than the Target Fund for the one-, three- and five-year periods ended December 29, 2017, though there is no guarantee of future performance; (iv) the Adviser believes that it can most effectively manage the assets currently in the Target Fund by combining such assets with the Acquiring Fund; and (v) the Acquiring Fund has a lower gross expense ratio than the Target Fund and shareholders of the Target Fund will experience a lower net expense ratio in the Acquiring Fund following the Reorganization.

Q: Who can vote?

A: Shareholders of the Target Fund are entitled to vote.

Q: How will the Reorganization affect me?

A: Assuming shareholders approve the proposed Reorganization, the assets of the Target Fund will be combined with those of the Acquiring Fund. The Class A and Class S Shares of the Target Fund automatically would be exchanged for an equal dollar value of Class A and Class S Shares of the Acquiring Fund. Following the Reorganization, the Target Fund will dissolve.

Q: Will I have to pay any commission or other similar fee as a result of the Reorganization?

A: No. You will not pay any commissions or other similar fees as a result of the Reorganization. If you hold Class A Shares of the Target Fund, you will receive Class A Shares of the Acquiring Fund. If you hold Class S Shares of the Target Fund, you will receive Class S Shares of the Acquiring Fund.

Q: Will the total annual operating expenses that my fund investment bears increase as a result of the Reorganization?

A: No, they will likely decrease. For more information about how fund expenses may change as a result of the Reorganization, please see the comparative and pro forma table and related disclosures in the COMPARISON OF THE FUNDS—Expenses section of the Prospectus/Proxy Statement.

Q: Will I have to pay any U.S. federal income taxes as a result of the Reorganization?

A: The Reorganization is expected to be tax-free for federal income tax purposes. The Target Fund will seek an opinion of counsel to this effect. Generally, shareholders will not incur capital gains or losses on the exchange of Target Fund shares for Acquiring Fund shares as a result of the Reorganization.

Q: If shareholders of the Target Fund do not approve the Reorganization, what will happen to the Target Fund?

A: Thrivent Asset Mgt. will reassess what changes it would like to make to a Target Fund, including a possible repurposing of the Target Fund’s principal investment strategies or recommending a liquidation of the Target Fund to the Board. It may ultimately decide to make no changes.

Q: Who pays the costs of the Reorganization?

A: The expenses of the Reorganization, including the costs of the Meeting, will be paid by Thrivent Asset Mgt. or an affiliate and will not be borne by Target Fund shareholders.

Q: How can I vote?

A: Shareholders are invited to attend the Meeting and to vote in person. You may also vote by executing a proxy using one of three methods:

| | • | | By Internet: Instructions for casting your vote via the Internet can be found in the enclosed proxy voting materials. The required control number is printed on your enclosed proxy card. If this feature is used, there is no need to mail the proxy card. |

| | • | | By Telephone: Instructions for casting your vote via telephone can be found in the enclosed proxy voting materials. The toll-free number and required control number are printed on your enclosed proxy card. If this feature is used, there is no need to mail the proxy card. |

| | • | | By Mail: If you vote by mail, please indicate your voting instructions on the enclosed proxy card, date and sign the card, and return it in the envelope provided, which is addressed for your convenience and needs no postage if mailed in the United States. |

Shareholders who execute proxies by Internet, telephone or mail may revoke them at any time prior to the Meeting by filing with the Target Fund a written notice of revocation, by executing another proxy bearing a later date, by voting later by Internet or telephone or by attending the Meeting and voting in person. Merely attending the Meeting, however, will not revoke any previously submitted proxy.

Q: When should I vote?

A: Every vote is important and the Board encourages you to record your vote as soon as possible. Voting your proxy now will ensure that the necessary number of votes is obtained, without the time and expense required for additional proxy solicitation.

Q: Who should I call if I have questions about the proposal in the Prospectus/Proxy Statement?

A: Call 866-865-3843 with your questions.

Q: How can I get more information about the Target and Acquiring Funds?

A: You may obtain (1) a prospectus, statement of additional information or annual/semiannual report for the Funds or (2) the statement of additional information regarding the Reorganization (request the “Reorganization SAI”) by:

| | • | | Telephone: 800-847-4836 and say “mutual funds” |

| | • | | Mail: Thrivent Mutual Funds, P.O. Box 219348, Kansas City, Missouri 64121-9348 |

| | — | For a copy of a prospectus, a statement of additional information, or a shareholder report: |

| | — | For a copy of this Prospectus/Proxy Statement or the Reorganization SAI: |

| | | www.proxy-direct.com/thr-29820 |

Thrivent Growth and Income Plus Fund

a series of

THRIVENT MUTUAL FUNDS

625 Fourth Avenue South

Minneapolis, Minnesota 55415

800-847-4836

ThriventFunds.com

NOTICE OF SPECIAL MEETING

OF SHAREHOLDERS

To be Held on June 21, 2018

NOTICE IS HEREBY GIVEN THAT a special meeting of shareholders (the “Meeting”) of Thrivent Growth and Income Plus Fund (the “Target Fund”), a series of Thrivent Mutual Funds (the “Trust”), will be held at the offices of Thrivent Financial for Lutherans, 625 Fourth Avenue South, Minneapolis, Minnesota 55415 on June 21, 2018 at 10:00 a.m. Central time for the following purposes:

| | 1. | To approve an Agreement and Plan of Reorganization pursuant to which the Target Fund would (i) transfer all of its assets to Thrivent Moderately Aggressive Allocation Fund (the “Acquiring Fund”), a series of the Trust, in exchange for Class A and Class S Shares of the Acquiring Fund, (ii) distribute such Class A and Class S Shares of the Acquiring Fund to shareholders of the Target Fund, and (iii) dissolve. |

| | 2. | To transact such other business as may properly be presented at the Meeting or any adjournment thereof. |

The Board of Trustees of the Trust (the “Board”) has fixed the close of business on April 20, 2018 as the record date for the determination of shareholders entitled to notice of, and to vote at, the Meeting and all adjournments thereof.

Shareholders are invited to attend the meeting and vote in person. You may also vote by executing a proxy using one of three methods:

| | • | | By Internet—Instructions for casting your vote via the Internet can be found in the enclosed proxy voting materials. The required control number is printed on your enclosed proxy card. If this feature is used, there is no need to mail the proxy card. |

| | • | | By Telephone—Instructions for casting your vote via telephone can be found in the enclosed proxy voting materials. The toll-free number and required control number are printed on your enclosed proxy card. If this feature is used, there is no need to mail the proxy card. |

| | • | | By Mail—If you vote by mail, please indicate your voting instructions on the enclosed proxy card, date and sign the card, and return it in the envelope provided, which is addressed for your convenience and needs no postage if mailed in the United States. |

Shareholders who execute proxies by Internet, telephone, or mail may revoke them at any time prior to the Meeting by filing with the Target Fund a written notice of revocation, by executing another proxy bearing a later date, or by attending the Meeting and voting in person. Merely attending the Meeting, however, will not revoke any previously submitted proxy.

The Board recommends that you cast your vote FOR the proposed Reorganization as described in the Prospectus/Proxy Statement.

|

YOUR VOTE IS IMPORTANT Please return your proxy card or record your voting instructions by telephone or via the Internet promptly no matter how many shares you own. In order to avoid the additional expense of further solicitation, we ask that you mail your proxy card or record your voting instructions by telephone or via the Internet promptly regardless of whether you plan to be present in person at the Meeting. |

Date: April 30, 2018

Michael W. Kremenak

Secretary

Thrivent Mutual Funds

COMBINED PROSPECTUS/PROXY STATEMENT

THRIVENT GROWTH AND INCOME PLUS FUND

a series of

THRIVENT MUTUAL FUNDS

625 Fourth Avenue South

Minneapolis, Minnesota 55415

800-847-4836

April 30, 2018

This Prospectus/Proxy Statement is furnished to you as a shareholder of Thrivent Growth and Income Plus Fund (the “Target Fund”), a series of Thrivent Mutual Funds (the “Trust”). A special meeting of shareholders of the Target Fund will be held on June 21, 2018 (the “Meeting”) to consider the approval of a Reorganization (the “Reorganization”) of the Target Fund into Thrivent Moderately Aggressive Allocation Fund (the “Acquiring Fund”). The Board of Trustees of the Trust (the “Board”) requests that you vote your shares by completing and returning the enclosed proxy card or by recording your voting instructions by telephone or via the Internet regardless of whether you plan to be present at the Meeting in order to avoid the additional expense of further solicitation.

The Acquiring Fund and the Target Fund are sometimes referred to herein individually as a “Fund” or collectively as the “Funds.” Each of the Acquiring Fund and the Target Fund is organized as a series of the Trust, an open-end management investment company registered under the Investment Company Act of 1940, as amended (the “1940 Act”). The Target Fund is a diversified company and the Acquiring Fund is non-diversified company, each as defined under the 1940 Act.

This Prospectus/Proxy Statement sets forth concisely the information shareholders of the Target Fund ought to know before voting on the Reorganization. Please read it carefully and retain it for future reference.

The following documents, each having been filed with the Securities and Exchange Commission (the “SEC”), are incorporated herein by reference:

| | • | | The Thrivent Mutual Funds Prospectuses, dated February 28, 2018 and as supplemented through the date hereof (the “Trust Prospectus”). |

| | • | | A Statement of Additional Information, dated April 30, 2018, relating to this Combined Prospectus/Proxy Statement (the “Reorganization SAI”); |

| | • | | The Thrivent Mutual Funds Statement of Additional Information, dated February 28, 2018 and as supplemented through the date hereof (the “Trust SAI”). |

Copies of the foregoing may be obtained without charge by calling or writing the Fund as set forth below. If you wish to request the Reorganization SAI, please ask for the “Reorganization SAI.”

In addition, each Fund will furnish, without charge, a copy of its most recent annual report and subsequent semi-annual report, if any, to a shareholder upon request.

Copies of each Fund’s most recent prospectus, statement of additional information, annual report and semi-annual report can be obtained at ThriventFunds.com. Requests for documents can also be made by calling 800-847-4836 or writing Thrivent Mutual Funds, P.O. Box 219348, Kansas City, Missouri 64121-9348.

The Funds file reports and other information with the SEC. Information filed by the Funds with the SEC can be reviewed and copied at the SEC’s Public Reference Room in Washington, DC or on the EDGAR database on the SEC’s internet site (https://www.sec.gov). Information on the operation of the SEC’s Public Reference Room may be obtained by calling the SEC at 202-551-8090. You can also request copies of these materials, upon payment of a duplicating fee, by electronic request at the SEC’s e-mail address (publicinfo@sec.gov) or by writing the Public Reference Section of the SEC, Washington, DC 20549-1520.

The Board knows of no business other than that discussed above that will be presented for consideration at the Meeting. If any other matter is properly presented, it is the intention of the persons named in the enclosed proxy to vote in accordance with their best judgment.

No person has been authorized to give any information or make any representation not contained in this Prospectus/Proxy Statement and, if so given or made, such information or representation must not be relied upon as having been authorized. This Prospectus/Proxy Statement does not constitute an offer to sell or a solicitation of an

1

offer to buy any securities in any jurisdiction in which, or to any person to whom, it is unlawful to make such offer or solicitation.

Neither the Securities and Exchange Commission nor any state regulator has approved or disapproved of these shares or passed upon the adequacy of this Prospectus/Proxy Statement. A representation to the contrary is a crime.

The date of this Prospectus/Proxy Statement is April 30, 2018. The Prospectus/Proxy Statement will be sent to shareholders on or around May 7, 2018.

2

TABLE OF CONTENTS

3

SUMMARY

The following is a summary of certain information contained elsewhere in this Prospectus/Proxy Statement and is qualified in its entirety by reference to the more complete information contained in this Prospectus/Proxy Statement. Shareholders should read the entire Prospectus/Proxy Statement carefully.

The Reorganization

The Board, including the trustees who are not “interested persons” (as defined in the 1940 Act) of each Fund (the “Independent Trustees”), has unanimously approved an Agreement and Plan of Reorganization (the “Reorganization Agreement”) on behalf of each Fund, subject to Target Fund shareholder approval. The Reorganization Agreement provides for:

| | • | | the transfer of all of the assets of the Target Fund to the Acquiring Fund in exchange for Class A and Class S Shares of the Acquiring Fund; |

| | • | | the distribution by the Target Fund of such Acquiring Fund Class A and Class S Shares to Target Fund shareholders; and |

| | • | | the dissolution of the Target Fund. |

When the Reorganization is complete, Target Fund shareholders will hold Acquiring Fund shares. The aggregate value of the Acquiring Fund shares a Target Fund shareholder will receive in the Reorganization will equal the aggregate value of the Target Fund shares owned by such shareholder immediately prior to the Reorganization. After the Reorganization, the Acquiring Fund will continue to operate with the investment objective and investment policies set forth in this Prospectus/Proxy Statement.

As discussed in more detail elsewhere in this Prospectus/Proxy Statement, the Board believes that the Reorganization would be in the best interests of the Target Fund’s shareholders because: (i) shareholders will become shareholders of a larger combined fund with greater potential to increase asset size and achieve economies of scale; (ii) the Acquiring Fund invests in a more diversified portfolio of equity and fixed income securities; (iii) the Acquiring Fund has achieved stronger performance than the Target Fund for the one-, three- and five-year periods ended December 29, 2017, though there is no guarantee of future performance; (iv) Thrivent Asset Management, LLC (“Thrivent Asset Mgt.” or the “Adviser”) believes that it can most effectively manage the assets currently in the Target Fund by combining such assets with the Acquiring Fund; and (v) the Acquiring Fund has a lower gross expense ratio than the Target Fund and shareholders of the Target Fund will experience a lower net expense ratio in the Acquiring Fund following the Reorganization.

In addition, the Board, when determining whether to approve the Reorganization, considered, among other things, the future growth prospects of each of the Target Fund and the Acquiring Fund, the fact that the Target Fund shareholders would not experience any diminution in shareholder services as a result of the Reorganization, and the fact that the Reorganization is expected to be a tax-free reorganization for federal income tax purposes.

Background and Reasons for the Reorganization

The Target Fund and the Acquiring Fund have similar investment objectives, but the Target Fund has an objective to seek income while the Acquiring Fund does not. The investment objective of the Target Fund is to seek long-term capital growth and income. The investment objective of the Acquiring Fund is to seek long-term capital growth.

The two Funds also have some similarities and some differences in their principal investment strategies, which are described in more detail in the COMPARISON OF FUNDS—Investment Objective and Principal Strategies section of the Prospectus/Proxy Statement. Both Funds invest in a combination of equity securities and debt securities in approximately the same proportion; the Target Fund’s target allocation is 70% equity securities and 30% debt securities and the Acquiring Fund’s target allocation is 77% equity securities and 23% debt securities. The equity securities in which the Target Fund invests are primarily income-producing, while the Acquiring Fund does not necessarily invest in income-producing equity securities. Another difference is that the Acquiring Fund invests in a combination of other funds managed by the Adviser and directly held financial instruments, but the Target Fund does not generally invest in other funds managed by the Adviser.

4

In determining whether to recommend approval of the Reorganization Agreement to Target Fund shareholders, the Board considered a number of factors, including, but not limited to: (i) the expenses and advisory fees applicable to the Funds before the proposed Reorganization and the estimated expense ratios of the combined Fund after the proposed Reorganization; (ii) the comparative investment performance of the Funds; (iii) the future growth prospects of each Fund; (iv) the terms and conditions of the Reorganization Agreement; (v) whether the Reorganization would result in the dilution of shareholder interests; (vi) the compatibility of the Funds’ investment objectives, policies, risks and restrictions; (vii) that the proposed Reorganization was expected to be a tax-free reorganization for federal income tax purposes; (viii) the compatibility of the Funds’ service features available to shareholders, including exchange privileges; and (ix) the estimated costs of the Reorganization, which would be borne by the Adviser. The Board concluded that these factors supported a determination to approve the Reorganization Agreement.

The Board has determined that the Reorganization is in the best interests of the Target Fund and that the interests of the Target Fund’s shareholders will not be diluted as a result of the Reorganization. In addition, the Board has determined that the Reorganization is in the best interests of the Acquiring Fund and that the interests of the Acquiring Fund’s shareholders will not be diluted as a result of the Reorganization.

The Board is asking shareholders of the Target Fund to approve the Reorganization at the Meeting to be held on June 21, 2018. If shareholders of the Target Fund approve the proposed Reorganization, it is expected that the closing date of the transaction (the “Closing Date”) will be after the close of business on or about June 28, 2018, but it may be at a different time as described herein. If shareholders of the Target Fund do not approve the proposed Reorganization, the Board will consider alternatives, including repurposing the Target Fund’s principal strategies.

The Board recommends that you vote “FOR” the Reorganization.

5

COMPARISON OF THE FUNDS

Investment Objective and Principal Strategies

Investment Objective. The Target Fund and the Acquiring Fund have similar investment objectives, but the Target Fund has an objective to seek income while the Acquiring Fund does not. The investment objective of the Target Fund is to seek long-term capital growth and income. The investment objective of the Acquiring Fund is to seek long-term capital growth.

Principal Strategies. Both Funds invest in a combination of equity securities and debt securities in approximately the same proportion; the Target Fund’s target allocation is 70% equity securities and 30% debt securities and the Acquiring Fund’s target allocation is 77% equity securities and 23% debt securities. While the Acquiring Fund invests in a combination of other funds managed by the Adviser and directly held financial instruments, the Target Fund does not generally invest in other funds managed by the Adviser. However, the Target Fund may invest in unaffiliated exchange-traded funds (“ETFs”) as a principal investment strategy.

The equity securities in which the Target Fund are primarily income-producing, while the Acquiring Fund does not necessarily invest in income-producing equity securities. Under normal circumstances, the Target Fund invests in real estate investment trusts (“REITs”). The Acquiring Fund does not invest in REITs as a principal investment strategy.

Both Funds invest in a variety of fixed income securities of any maturity or credit quality. Both Funds invest in in leveraged loans, which are senior secured loans that are made by banks or other lending institutions to companies that are rated below investment grade.

Both Funds can utilize derivatives (such as futures and swaps) for investment exposure or hedging purposes. The Funds may enter into standardized derivatives contracts traded on domestic or foreign securities exchanges, boards of trade, or similar entities, and non-standardized derivatives contracts traded in the over-the-counter market. In addition, both Funds have exposure to foreign securities, including those of issuers in emerging markets.

Fund Holdings. A description of the Funds’ policies and procedures with respect to the disclosure of the Funds’ portfolio securities is available on the Funds’ website.

Principal Risks

The Funds are subject to similar principal risks, with a few differences. These risks are described below. Shares of the each Fund will rise and fall in value and there is a risk that you could lose money by investing in each Fund.

Principal risks to which both Funds are subject

Allocation Risk. The Fund’s investment performance depends upon how its assets are allocated across broad asset categories and applicable sub-classes within such categories. Some broad asset categories and sub-classes may perform below expectations or the securities markets generally over short and extended periods. In particular, underperformance in the equity markets would have a material adverse effect on the Fund’s total return given its significant allocation to equity securities. Therefore, a principal risk of investing in the Fund is that the allocation strategies used and the allocation decisions made will not produce the desired results.

Credit Risk. Credit risk is the risk that an issuer of a debt security to which the Fund’s portfolio is exposed may no longer be able or willing to pay its debt. As a result of such an event, the debt security may decline in price and affect the value of the Fund.

Derivatives Risk. The use of derivatives (such as futures and swaps) involves additional risks and transaction costs which could leave the Fund in a worse position than if it had not used these instruments. The use of derivatives can lead to losses because of adverse movements in the price or value of the underlying asset, index or rate, which may be magnified by certain features of the contract. Changes in the value of the derivative may not correlate as intended with the underlying asset, rate or index, and the Fund could lose much more than the original amount invested. Derivatives can be highly volatile, illiquid and difficult to value. Certain derivatives may also be subject to counterparty risk, which is that the other party in the transaction will not fulfill its contractual obligations due to its financial condition, market events, or other reasons.

6

Emerging Markets Risk. The economic and political structures of developing countries, in most cases, do not compare favorably with the U.S. or other developed countries in terms of wealth and stability, and their financial markets often lack liquidity. Fund performance will likely be negatively affected by portfolio exposure to countries in the midst of, among other things, hyperinflation, currency devaluation, trade disagreements, sudden political upheaval, or interventionist government policies. Significant buying or selling actions by a few major investors may also heighten the volatility of emerging markets. These factors make investing in emerging market countries significantly riskier than in other countries, and events in any one country could cause the Fund’s share price to decline.

Foreign Securities Risk. Foreign securities are generally more volatile than their domestic counterparts, in part because of higher political and economic risks, lack of reliable information and fluctuations in currency exchange rates. Foreign securities may also be more difficult to resell than comparable U.S. securities because the markets for foreign securities are often less liquid. Even when a foreign security increases in price in its local currency, the appreciation may be diluted by adverse changes in exchange rates when the security’s value is converted to U.S. dollars. Foreign withholding taxes also may apply and errors and delays may occur in the settlement process for foreign securities. All of these risks may be heightened for securities of issuers located in, or with significant operations in, emerging market countries.

High Yield Risk. High yield securities – commonly known as “junk bonds” – to which the Fund’s portfolio is exposed are considered predominantly speculative with respect to the issuer’s continuing ability to make principal and interest payments. If the issuer of the security is in default with respect to interest or principal payments, the value of the Fund may be negatively affected.

Interest Rate Risk. Interest rate risk is the risk that bond prices decline in value when interest rates rise for bonds that pay a fixed rate of interest. Bonds with longer durations or maturities tend to be more sensitive to changes in interest rates than bonds with shorter durations or maturities. In addition, both mortgage-backed and asset-backed securities are sensitive to changes in the repayment patterns of the underlying security. If the principal payment on the underlying asset is repaid faster or slower than the holder of the asset-backed or mortgage-backed security anticipates, the price of the security may fall, particularly if the holder must reinvest the repaid principal at lower rates or must continue to hold the security when interest rates rise. This effect may cause the value of the Fund to decline and reduce the overall return of the Fund. Changes by the Federal Reserve to monetary policies could affect interest rates and the value of some securities.

Investment Adviser Risk. The Fund is actively managed and the success of its investment strategy depends significantly on the skills of the Adviser in assessing the potential of the investments in which the Fund invests. This assessment of investments may prove incorrect, resulting in losses or poor performance, even in rising markets.

Issuer Risk. Issuer risk is the possibility that factors specific to a company to which the Fund’s portfolio is exposed will affect the market prices of the company’s securities and therefore the value of the Fund. Common stock of a company is subordinate to other securities issued by the company. If a company becomes insolvent, interests of investors owning common stock will be subordinated to the interests of other investors in, and general creditors of, the company.

Leveraged Loan Risk. Leveraged loans (also known as bank loans) are subject to the risks typically associated with debt securities. In addition, leveraged loans, which typically hold a senior position in the capital structure of a borrower, are subject to the risk that a court could subordinate such loans to presently existing or future indebtedness or take other action detrimental to the holders of leveraged loans. Leveraged loans are also subject to the risk that the value of the collateral, if any, securing a loan may decline, be insufficient to meet the obligations of the borrower, or be difficult to liquidate. Some leveraged loans are not as easily purchased or sold as publicly-traded securities and others are illiquid, which may make it more difficult for the Fund to value them or dispose of them at an acceptable price. Below investment-grade leveraged loans are typically more credit sensitive. In the event of fraud or misrepresentation, the Fund may not be protected under federal securities laws with respect to leveraged loans that may not be in the form of “securities.” The settlement period for some leveraged loans may be more than seven days.

Liquidity Risk. Liquidity is the ability to sell a security relatively quickly for a price that most closely reflects the actual value of the security. High-yield bonds and leveraged loans have a less liquid resale market. In addition, dealer inventories of bonds are at or near historic lows in relation to market size, which has the potential to decrease liquidity and increase price volatility in the fixed income markets, particularly during periods of economic or market

7

stress. As a result, the Adviser may have difficulty selling or disposing of securities quickly in certain markets or may only be able to sell the holdings at prices substantially less than what the Adviser believes they are worth.

Market Risk. Over time, securities markets generally tend to move in cycles with periods when security prices rise and periods when security prices decline. The value of the Fund’s investments may move with these cycles and, in some instances, increase or decrease more than the applicable market(s) as measured by the Fund’s benchmark index(es). The securities markets may also decline because of factors that affect a particular industry.

Mortgage-Related and Other Asset-Backed Securities Risk. The value of mortgage-related and asset-backed securities will be influenced by the factors affecting the housing market and the assets underlying such securities. As a result, during periods of declining asset value, difficult or frozen credit markets, swings in interest rates, or deteriorating economic conditions, mortgage-related and asset-backed securities may decline in value, face valuation difficulties, become more volatile and/or become illiquid.

Volatility Risk. Volatility risk is the risk that certain types of securities shift in and out of favor depending on market and economic conditions as well as investor sentiment. The value of the Fund’s shares may be affected by weak equity markets or changes in interest rate or bond yield levels. As a result, the value of the Fund’s shares may fluctuate significantly in the short term.

Additional principal risks to which only the Target Fund is subject

Convertible Securities Risk. Convertible securities are subject to the usual risks associated with debt securities, such as interest rate risk and credit risk. Convertible securities also react to changes in the value of the common stock into which they convert, and are thus subject to market risk. The Fund may also be forced to convert a convertible security at an inopportune time, which may decrease the Fund’s return.

ETF Risk. An ETF is subject to the risks of the underlying investments that it holds. In addition, for index-based ETFs, the performance of an ETF may diverge from the performance of such index (commonly known as tracking error). ETFs are subject to fees and expenses (like management fees and operating expenses) that do not apply to an index, and the Fund will indirectly bear its proportionate share of any such fees and expenses paid by the ETFs in which it invests.

Portfolio Turnover Rate Risk. The Fund may engage in active and frequent trading of portfolio securities in implementing its principal investment strategies. A high rate of portfolio turnover (100% or more) involves correspondingly greater expenses which are borne by the Fund and its shareholders and may also result in short-term capital gains taxable to shareholders.

Preferred Securities Risk. There are certain additional risks associated with investing in preferred securities, including, but not limited to, preferred securities may include provisions that permit the issuer, at its discretion, to defer or omit distributions for a stated period without any adverse consequences to the issuer; preferred securities are generally subordinated to bonds and other debt instruments in a company’s capital structure in terms of having priority to corporate income and liquidation payments, and therefore will be subject to greater credit risk than more senior debt instruments; preferred securities may be substantially less liquid than many other securities, such as common stocks or U.S. Government securities; generally, traditional preferred securities offer no voting rights with respect to the issuing company unless preferred dividends have been in arrears for a specified number of periods, at which time the preferred security holders may elect a number of directors to the issuer’s board; and in certain varying circumstances, an issuer of preferred securities may redeem the securities prior to a specified date.

Real Estate Investment Trust (“REIT”) Risk. REITs generally can be divided into three types: equity REITs, mortgage REITs, and hybrid REITs (which combine the characteristics of equity REITs and mortgage REITs). Equity REITs will be affected by changes in the values of, and income from, the properties they own, while mortgage REITs may be affected by the credit quality of the mortgage loans they hold. All REIT types may be affected by changes in interest rates. REITs are subject to additional risks, including the fact that they are dependent on specialized management skills that may affect the REITs’ abilities to generate cash flows for operating purposes and for making investor distributions. REITs may have limited diversification and are subject to the risks associated with obtaining financing for real property. As with any investment, there is a risk that REIT securities and other real estate industry investments may be overvalued at the time of purchase. In addition, a REIT can pass its income through to its investors without any tax at the entity level if it complies with various requirements under the Internal Revenue Code. There is the risk, however, that a REIT held by the Fund will fail to qualify for this tax-free pass-through treatment of its income. In addition, due to recent changes in the tax laws, certain tax benefits of REITs may not be passed through to mutual fund shareholders. By investing in REITs indirectly through the Fund, in addition to

8

bearing a proportionate share of the expenses of the Fund, you will also indirectly bear similar expenses of the REITs in which the Fund invests.

Sovereign Debt Risk. Sovereign debt securities are issued or guaranteed by foreign governmental entities. These investments are subject to the risk that a governmental entity may delay or refuse to pay interest or repay principal on its sovereign debt, due, for example, to cash flow problems, insufficient foreign currency reserves, political considerations, the relative size of the governmental entity’s debt position in relation to the economy or the failure to put in place economic reforms required by the International Monetary Fund or other multilateral agencies.

Additional principal risks to which only the Acquiring Fund is subject

Underlying Fund Risk. The performance of the Fund is dependent, in part, upon the performance of the underlying Funds in which the Fund invests. As a result, the Fund is subject to the same risks as those faced by the underlying Funds.

Management of the Funds

The Board. The Board has oversight responsibilities for each Fund and performs its fiduciary duties imposed on the directors of investment companies by the 1940 Act and under applicable state law.

The Adviser. Thrivent Asset Mgt. is the investment adviser for each Fund and manages each Fund on a day-to-day basis. Thrivent Asset Mgt. and its investment advisory affiliate, Thrivent Financial for Lutherans (“Thrivent Financial”) have been in the investment advisory business since 1986 and managed approximately $120.6 billion in assets as of December 31, 2017, including approximately $50.3 billion in mutual fund assets. These advisory entities are located at 625 Fourth Avenue South, Minneapolis, Minnesota 55415.

The Funds’ annual report to shareholders discusses the basis for the Board approving the investment advisory agreement during the period covered by the report.

Portfolio Management. Stephen D. Lowe, CFA has been a portfolio manager of the Target Fund since August 2013. Mark L. Simenstad, CFA, Noah J. Monsen, CFA, and Reginald L. Pfeifer, CFA have served as portfolio managers of the Target Fund since May 2015. John T. Groton, Jr., CFA has served as a portfolio manager of the Target Fund since February 2016. Mr. Lowe is Vice President of Fixed Income Mutual Funds and Separate Accounts and has been with Thrivent Financial since 1997. He has served as a portfolio manager since 2009. Mr. Simenstad is Chief Investment Strategist and has been with Thrivent Financial since 1999. Mr. Monsen has been with Thrivent Financial since 2000 and has served in an investment management capacity since 2008. Mr. Pfeifer has been with Thrivent Financial since 1990 and has served as an equity portfolio manager since 2003. Mr. Groton is the Director of Equity Research and has been with Thrivent Financial since 2007.

David C. Francis, CFA and Mark L. Simenstad, CFA have served as portfolio managers of the Acquiring Fund since June 2005. Darren M. Bagwell, CFA and Stephen D. Lowe, CFA have served as portfolio managers of the Acquiring Fund since April 2016. David S. Royal has served as a portfolio manager of the Acquiring Fund since April 2018. Mr. Francis is Vice President of Investment Equities and has been with Thrivent Financial since 2001. Mr. Simenstad is Chief Investment Strategist and has been with Thrivent Financial since 1999. Mr. Bagwell has been with Thrivent Financial since 2002 in an investment management capacity and currently is a Senior Equity Portfolio Manager. Mr. Lowe is Vice President of Fixed Income Mutual Funds and Separate Accounts and has been with Thrivent Financial since 1997. He has served as a portfolio manager since 2009. Mr. Royal is the Chief Investment Officer and has been with Thrivent Financial since 2006.

The Trust SAI provides information about the portfolio managers’ compensation, other accounts managed by the portfolio managers, and the portfolio managers’ ownership of shares of the Funds.

Advisory and Other Fees

Advisory Fees. Each Fund pays an annual investment advisory fee to the Adviser. The advisory contract between the Adviser and the Fund provides for the following advisory fees for each class of shares of a Fund, expressed as an annual rate of average daily net assets:

9

|

Target Fund |

0.650% of average daily net assets up to $250 million |

0.600% of average daily net assets over $250 million |

|

Acquiring Fund |

0.700% of average daily net assets up to $500 million |

0.675% of average daily net assets greater than $500 million up to $2 billion |

0.650% of average daily net assets greater than $2 billion up to $5 billion |

0.625% of average daily net assets greater than $5 billion up to $10 billion |

0.600% of average daily net assets over $10 billion |

During the fiscal year ended December 31, 2017, the contractual advisory fees for the Class A shares of the Target Fund were 0.65% of the Target Fund’s average daily net assets, and the contractual advisory fees for the Class S shares of the Target Fund were 0.65% of the Target Fund’s average daily net assets.

During the fiscal year ended October 31, 2017, the contractual advisory fees for the Class A shares of the Acquiring Fund were 0.68% of the Acquiring Fund’s average daily net assets, and the contractual advisory fees for the Class S shares of the Acquiring Fund were 0.68% of the Acquiring Fund’s average daily net assets. The Adviser has contractually agreed, for as long as the current fee structure is in place and through at least February 28, 2019, to waive an amount equal to any investment advisory fees indirectly incurred by the Acquiring Fund as a result of its investment in any other mutual fund for which the Adviser or an affiliate serves as investment adviser, other than Thrivent Cash Management Trust.

For a complete description of each Fund’s advisory services, see the section of the Trust Prospectus entitled “Management, Organization and Capital Structure” and the section of the Trust SAI entitled “Investment Adviser, Investment Subadvisers, and Portfolio Managers.”

12b-1 Plan. The Trust has adopted a Distribution Plan and Agreement pursuant to Rule 12b-1 under the 1940 Act (the “Rule 12b-1 Plan”) with respect to the Class A shares of each Fund. Thrivent Distributors, LLC (the “Distributor”), an affiliate of the Adviser, located at 625 Fourth Avenue South, Minneapolis, Minnesota 55415, serves as the distributor of each Fund. Under the Rule 12b-1 Plan, Class A shares of each Fund pay the Distributor an aggregate fee for distribution and shareholder servicing equal to an annual rate of 0.25% of the average daily net asset value represented by such shares. Class S shares are not subject to a Rule 12b-1 Plan and the Funds do not pay any percentage of their assets attributable to Class S shares for distribution or shareholder servicing. For a complete description of these arrangements with respect to each Fund, see the section of the Class A Prospectus entitled “Shareholder Information—Rule 12b-1 Fees” and the section of the Trust SAI entitled “Underwriting and Distribution Service.” These sections are incorporated by reference herein.

Expenses

The table below sets forth the fees and expenses that investors may pay to buy and hold shares of each of the Target Fund and the Acquiring Fund, including (i) the fees and expenses paid by the Target Fund for the twelve-month period ended December 31, 2017, (ii) the fees and expenses paid by the Acquiring Fund for the twelve-month period ended October 31, 2017, and (iii) pro forma fees and expenses for the Acquiring Fund for the twelve-month period ended October 31, 2017, assuming the Reorganization had been completed as of the beginning of such period.

10

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Class A Shares | | | Class S Shares | | | | |

| | | Actual | | | Pro Forma | | | Actual | | | Pro Forma | | | | |

| | | Target

Fund | | | Acquiring

Fund | | | Acquiring

Fund

(assuming

merger

with

Target

Fund) | | | Target

Fund | | | Acquiring

Fund | | | Acquiring

Fund

(assuming

merger

with

Target

Fund) | | | | |

Shareholder Fees (fees paid directly from your investment) | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

Maximum Sales Charge (Load) Imposed on Purchases (as a percentage of offering price) | | | 4.50 | % | | | 4.50 | % | | | 4.50 | % | | | N/A | | | | N/A | | | | N/A | | | | | |

| | | | | | | |

Maximum Deferred Sales Charge (Load) (as a percentage of net asset value at time of purchase or redemption, whichever is lower)* | | | 1.00 | % | | | 1.00 | % | | | 1.00 | % | | | N/A | | | | N/A | | | | N/A | | | | | |

| | | | | | | |

Annual Fund Operating Expenses as a Percentage of Average Net Assets (expenses that are deducted from Fund assets) | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

Management Fees | | | 0.65 | % | | | 0.68 | % | | | 0.68 | % | | | 0.65 | % | | | 0.68 | % | | | 0.68 | % | | | | |

Distribution and Service (12b-1 Fees) | | | 0.25 | % | | | 0.25 | % | | | 0.25 | % | | | None | | | | None | | | | None | | | | | |

Other Expenses | | | 0.51 | % | | | 0.15 | % | | | 0.15 | % | | | 0.55 | % | | | 0.15 | % | | | 0.15 | % | | | | |

Acquired (Underlying) Fund Fees and Expenses | | | 0.03 | % | | | 0.31 | % | | | 0.31 | % | | | 0.03 | % | | | 0.31 | % | | | 0.31 | % | | | | |

Total Annual Operating Expenses | | | 1.44 | % | | | 1.39 | % | | | 1.39 | % | | | 1.23 | % | | | 1.14 | % | | | 1.14 | % | | | | |

Less Expense Reimbursement** | | | 0.31 | % | | | 0.27 | % | | | 0.27 | % | | | 0.30 | % | | | 0.27 | % | | | 0.27 | % | | | | |

Net Annual Fund Operating Expenses | | | 1.13 | % | | | 1.12 | % | | | 1.12 | % | | | 0.93 | % | | | 0.87 | % | | | 0.87 | % | | | | |

* When you invest $1,000,000 or more, a deferred sales charge of 1% will apply to shares redeemed within one year.

** The Adviser has contractually agreed, through at least February 28, 2019, to waive a portion of the management fees associated with the Class A and Class S shares of the Thrivent Growth and Income Plus Fund in order to limit the Total Annual Fund Operating Expenses After Fee Waivers and/or Expense Reimbursements to an annual rate of 1.10% of the average daily net assets of the Class A shares and 0.90% of the average daily net assets of the Class S shares. This contractual provision, however, may be terminated before the indicated termination date upon the mutual agreement between the Independent Trustees and the Adviser.

** The Adviser has contractually agreed, for as long as the current fee structure is in place and through at least February 28, 2019, to waive an amount equal to any investment advisory fees indirectly incurred by Moderately Aggressive Allocation Fund as a result of its investment in any other mutual fund for which the Adviser or an

11

affiliate serves as investment adviser, other than Thrivent Cash Management Trust. This contractual provision may be terminated upon the mutual agreement between the Independent Trustees and the Adviser.

Example

The following example, using the actual expenses for the most recent fiscal year ends and pro forma operating expenses for the twelve-month period ended October 31, 2017, is intended to help you compare the costs of investing in the Acquiring Fund pro forma after the Reorganization with the costs of investing in each of the Target Fund and the Acquiring Fund without the Reorganization. The example assumes that you invest $10,000 in each Fund for the time period indicated and that you redeem all of your shares at the end of each period. The example also assumes that your investments have a 5% return each year and that each Fund’s operating expenses remain the same each year. Although your actual returns may be higher or lower, based on these assumptions your costs would be:

| | | | | | | | | | | | |

| | | Actual | | | Pro Forma |

| | | Target

Fund | | | Acquiring

Fund | | | Acquiring Fund

(assuming merger

with the Target

Fund) | | |

Total operating expenses for Class A Shares assuming redemption at the

end of the period | | | | | | | | | | | | |

One Year | | | $560 | | | | $559 | | | $559 | | |

Three Years | | | $856 | | | | $845 | | | $845 | | |

Five Years | | | $1,173 | | | | $1,152 | | | $1,152 | | |

Ten Years | | | $2,071 | | | | $2,021 | | | $2,021 | | |

Total operating expenses for Class S Shares assuming redemption at the

end of the period | | | | | | | | | | | | |

One Year | | | $95 | | | | $89 | | | $89 | | |

Three Years | | | $361 | | | | $335 | | | $335 | | |

Five Years | | | $647 | | | | $602 | | | $602 | | |

Ten Years | | | $1,462 | | | | $1,362 | | | $1,362 | | |

Portfolio Turnover

Each Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in Total Annual Operating Expenses or in the Example, affect the Funds’ performance. During the fiscal year ended October 31, 2017, the Acquiring Fund’s portfolio turnover rate was 103% of the average value of its portfolio. During the fiscal year ended December 31, 2017, the Target Fund’s portfolio turnover rate was 121% of the average value of its portfolio.

Purchase, Valuation, Redemption and Exchange of Shares; Dividends and Distributions

Pricing of Fund Shares. The price of a Fund’s shares is based on the Fund’s net asset value (“NAV”). Each Fund determines its NAV for a particular class of shares once daily at the close of regular trading on the New York Stock Exchange (“NYSE”), which is normally 4:00 p.m. Eastern time. If the NYSE has an unscheduled early close but certain other markets remain open until their regularly scheduled closing time, the NAV may be determined as of the regularly scheduled closing time of the NYSE. If the NYSE and/or certain other markets close early due to extraordinary circumstances (e.g., weather, terrorism, etc.), the NAV may be calculated as of the early close of the NYSE and/or certain other markets. The NAV generally will not be determined on days when, due to extraordinary circumstances, the NYSE and/or certain other markets do not open for trading. The Funds generally do not determine NAV on holidays observed by the NYSE or on any other day when the NYSE is closed. The NYSE is regularly closed on Saturdays and Sundays, New Year’s Day, Martin Luther King, Jr. Day, Presidents’ Day, Good Friday, Memorial Day, Independence Day, Labor Day, Thanksgiving Day and Christmas Day. The price at which you purchase or redeem shares of a Fund is based on the next calculation of the NAV after the Fund receives your purchase or redemption request in good order.

Each Fund determines the NAV for a particular class by dividing the total Fund assets attributable to that class, less all liabilities attributable to such class, by the total number of outstanding shares of that class. To

12

determine the NAV, the other Funds generally value their securities at current market value using readily available market prices. If market prices are not available or if the Adviser determines that they do not accurately reflect fair value for a security, the Board of Trustees has authorized the Adviser to make fair valuation determinations pursuant to policies approved by the Board of Trustees. Fair valuation of a particular security is an inherently subjective process, with no single standard to utilize when determining a security’s fair value. In each case where a security is fair valued, consideration is given to the facts and circumstances relevant to the particular situation. This consideration includes a review of various factors set forth in the pricing policies adopted by the Board of Trustees. For any portion of a Fund’s assets that are invested in other mutual funds, the NAV is calculated based upon the NAV of the mutual funds in which the Fund invests, and the prospectuses for those mutual funds explain the circumstances under which they will use fair value pricing and the effects of such a valuation.

Because many foreign markets close before the U.S. markets, significant events may occur between the close of the foreign market and the close of the U.S. markets, when the Fund’s assets are valued, that could have a material impact on the valuation of foreign securities (i.e., available price quotations for these securities may not necessarily reflect the occurrence of the significant event). The Funds, subject to oversight by the Board of Trustees, evaluate the impact of these significant events and adjust the valuation of foreign securities to reflect the fair value as of the close of the U.S. markets to the extent that the available price quotations do not, in the Adviser’s opinion, adequately reflect the occurrence of the significant events.

Please note that the Target Fund and the Acquiring Fund have identical valuation policies. As a result, there will be no material change to the value of the Target Fund’s assets because of the Reorganization.

Also, the Target Fund and the Acquiring Fund have identical policies with respect to frequent purchases and redemptions and standing allocation orders (for more information, please see Frequent Trading Policies and Monitoring Processes and Standing Allocation Order disclosures in the Acquiring Fund’s Prospectus - these disclosures are incorporated herein by reference). The Reorganization will not affect these policies.

Class A Shares. The Class A shares of each Fund are subject to an initial sales charge of up to 4.50%. The initial sales charge applicable to Class A shares of the Acquiring Fund will be waived for Class A shares acquired in the Reorganization. Any subsequent purchases of Class A shares of the Acquiring Fund, excluding Class A shares purchased through the automatic dividend reinvestment plan, after the Reorganization will be subject to an initial sales charge of up to 4.50%. The initial sales charge is reduced for investments in excess of $50,000. Purchases of Class A shares of each Fund in amounts of $1 million or more are not subject to an initial sales charge, but a contingent deferred sales charge of up to 1.00% may be imposed on certain redemptions made within one year of purchase. No contingent deferred sales charge will be imposed on Class A shares of the Target Fund in connection with the Reorganization. For additional information, please see the section entitled “Shareholder Information—Class A Shares” in the Class A Prospectus. This section is incorporated by reference herein.

Class S Shares. Class S shares of each Fund are not subject to an initial sales charge or a contingent deferred sales charge. For additional information, please see the section entitled “Shareholder Information—Class S Shares” in the Class S Prospectus. This section is incorporated by reference herein.

Buying Shares. Shares of each Fund may be purchased through a shareholder’s registered representative, by mail, by telephone, by the Internet, by wire transfer, through an automatic investment plan or by exchange from other Thrivent mutual funds. For additional information regarding buying shares of each Fund and exchanging shares of each Fund, see the sections of the Trust Prospectus entitled “Shareholder Information—Buying Shares” and “Shareholder Information—Exchanging Shares Between Funds.”

Redeeming Shares. When a Fund receives a request for redemption, such Fund will redeem such shares at the next calculation of the Fund’s NAV. A Fund may postpone payment or suspend the right of redemption in unusual circumstances, as permitted by the SEC. When a shareholder purchases shares by check, electronic funds transfer (other than bank wire) or automatic investment plan and elects to redeem those shares soon after their purchase, the Fund may delay paying the redemption proceeds until the shareholder’s payment has cleared, which could take up to 10 days or more from the date of purchase. Shares may be redeemed by mail, by phone, by the Internet, by wire/ACH transfer or through a systematic withdrawal plan. For additional information regarding redeeming shares of each Fund, see the section of the Trust Prospectus entitled “Shareholder Information—Redeeming Shares.” This section is incorporated by reference herein.

13

Dividends and Distributions. Dividends of the Target Fund and the Acquiring Fund, if any, are generally declared and paid quarterly and annually, respectively. Income dividends are derived from investment income, including dividends, interest, and certain foreign currency gains received by each Fund. Capital gains distributions, if any, usually will be declared and paid in December for the prior twelve-month period ending October 31 for the Acquiring Fund and for prior twelve-month period ending December 31 for the Target Fund. Any election made by Target Fund shareholders in respect of the receipt of dividends and capital gains distributions will continue to apply to Class A and Class S Shares of the Acquiring Fund received in the Reorganization. For additional information regarding these elections see the section of the Trust Prospectus entitle “Distribution Options.” This section is incorporated by reference herein.

Capitalization

The following table sets forth the capitalization of the Target Fund as of October 31, 2017 and the Acquiring Fund as of October 31, 2017 and the pro forma capitalization of the Acquiring Fund as if the Reorganization occurred on October 31, 2017. These numbers may differ as of the Closing Date.

| | | | | | | | | | | | | | | | | | | | |

| | | Actual | | | Pro Forma | |

| | | Target Fund | | | Acquiring Fund | | | Acquiring Fund

(assuming merger with

the Target Fund) | |

Net assets | | | | | | | | | | | | | | | | | | | | |

Class A Shares | | | $73,970,412 | | | | $2,086,854,644 | | | | | | | | $2,160,825,056 | | | | | |

Class S Shares | | | $13,040,904 | | | | $389,919,959 | | | | | | | | $402,960,863 | | | | | |

Total Fund Net Assets | | | $87,011,316 | | | | $2,476,774,603 | | | | | | | | $2,563,785,919 | | | | | |

Net asset value per share | | | | | | | | | | | | | | | | | | | | |

Class A Shares | | | $10.87 | | | | $15.19 | | | | | | | | $15.19 | | | | | |

Class S Shares | | | $10.89 | | | | $15.32 | | | | | | | | $15.32 | | | | | |

Shares outstanding | | | | | | | | | | | | | | | | | | | | |

Class A Shares | | | 6,806,945 | | | | 137,421,261 | | | | | | | | 142,292,286 | | | | | |

Class S Shares | | | 1,197,625 | | | | 25,445,856 | | | | | | | | 26,296,896 | | | | | |

Total Shares Outstanding | | | 8,004,570 | | | | 162,867,117 | | | | | | | | 168,589,182 | | | | | |

The pro forma shares outstanding reflect the issuance by the Acquiring Fund of approximately 4,871,025 Class A Shares and 851,040 Class S Shares (for a total of 5,722,065 shares). Such issuance reflects the exchange of the assets of the Target Fund for newly issued Class A Shares and Class S Shares of the Acquiring Fund at the pro forma net asset value per share. The aggregate value of the Acquiring Fund shares that a Target Fund shareholder receives in the Reorganization will equal the aggregate value of the Target Fund shares owned immediately prior to the Reorganization.

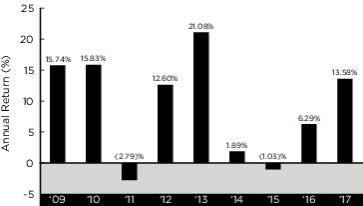

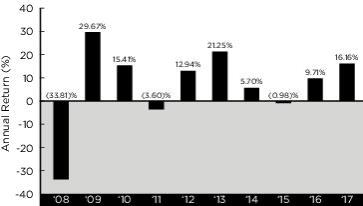

Annual Performance Information

The following chart shows the annual returns of the Target Fund since its inception and the Acquiring Fund for the past ten years. The bar charts include the effects of each Fund’s expenses, but not sales charges. If sales charges were included, returns would be lower than those shown. The table includes the effects of Fund expenses and maximum sales charges and assumes that you sold your shares at the end of the period. After-tax returns are shown only for the Class A Shares and after-tax returns for the Class S Shares will differ from those shown for the Class A Shares. The after-tax returns are calculated using the historical highest individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown and after-tax returns are not relevant to investors who hold their Fund shares through tax-deferred arrangements such as 401(k) plans or individual retirement accounts. How either Fund performed in the past (before and after taxes) is not necessarily an indication of how it will perform in the future.

14

Target Fund - Class A Shares

Acquiring Fund - Class A Shares

As a result of market activity, current performance may vary from the figures shown.

The Target Fund’s (Class A Shares) total return for the three-month period from January 1, 2018 to March 31, 2018 was [ ]%. The Acquiring Fund’s (Class A Shares) total return for the three-month period from January 1, 2018 to March 31, 2018 was [ ]%. Since its inception, the Target Fund’s (Class A Shares) highest quarterly return was 14.37% (for the quarter ended June 30, 2009) and its lowest quarterly return was -16.34% (for the quarter ended December 31, 2011). During the past 10 years, the Acquiring Fund’s (Class A Shares) highest quarterly return was 16.93% (for the quarter ended June 30, 2009) and its lowest quarterly return was -19.42% (for the quarter ended December 31, 2008).

Comparative Performance Information

As a basis for evaluating each Fund’s performance and risks, the following table shows how each Fund’s performance compares with broad-based market indices that the Adviser believes are appropriate benchmarks for such Fund. The Target Fund’s benchmarks are the MSCI World Index – USD Net Returns, which measures the performance of stock markets in developed countries throughout the world, the Bloomberg Barclays U.S. Mortgage-Backed Securities Index, which covers the mortgage-backed securities component of the Bloomberg Barclays U.S. Aggregate Bond Index, the S&P/LSTA Leveraged Loan Index, which reflects the performance of the largest facilities in the leveraged loan market, and the Bloomberg Barclays U.S. High Yield Ba/B 2% Issuer Capped Index, which represents the performance of U.S. short duration, higher-rated high yield bonds. The Acquiring Fund’s benchmarks are the S&P 500 Index, which measures the performance of 500 widely held, publicly traded stocks, the Bloomberg Barclays U.S. Aggregate Bond Index, which measures the performance of U.S. investment grade bonds,

15

and the MSCI All Country World Index ex-USA – USD Net Returns, which measures the performance of stock markets in developed and emerging markets countries throughout the world (excluding the U.S.). Further, the table includes the effects of each Fund’s expenses, but not sales charges. If sales charges were included, returns would be lower than those shown.

Average annual total returns are shown below for each Fund for the periods ended December 29, 2017 (the most recently completed calendar year prior to the date of this Prospectus/Proxy Statement). Remember that past performance of a Fund is not indicative of its future performance.

Average Annual Total Returns for the Period ended December 29, 2017

| | | | | | | | | | | | |

| | | Target Fund | | Acquiring Fund |

| | | Past 1

Year | | Past 5

Years | | Since

Inception

(2/29/2008) | | Past 1

Year | | Past 5

Years | | Past 10

Years |

Applicable Fund, Class A (before taxes) | | 8.45% | | 7.08% | | 4.10% | | 10.95% | | 9.08% | | 5.24% |

(after taxes on distributions) | | 7.77% | | 5.67% | | 3.54% | | 9.29% | | 7.65% | | 4.28% |

(after taxes on distributions and redemptions) | | 5.13% | | 5.21% | | 3.35% | | 6.97% | | 6.81% | | 3.91% |

S&P 500 Index (reflects no deduction for fees, expenses or taxes) | | — | | — | | — | | 21.83% | | 15.79% | | 8.50% |

Bloomberg Barclays U.S. Aggregate Bond Index (reflects no deduction for fees, expenses or taxes) | | — | | — | | — | | 3.54% | | 2.10% | | 4.01% |

MSCI All Country World Index ex-USA - USD Net Returns (reflects no deduction for fees, expenses or taxes) | | — | | — | | — | | 27.19% | | 6.80% | | 1.84% |

MSCI World Index-USD Net Returns (reflects no deduction for fees, expenses or taxes) | | 22.40% | | 11.64% | | 6.03% | | — | | — | | — |

Bloomberg Barclays U.S. Mortgage-Backed Securities Index (reflects no deduction for fees, expenses or taxes) | | 2.47% | | 2.04% | | 3.71% | | — | | — | | — |

Bloomberg Barclays U.S. High Yield Ba/B 2% Issuer Capped Index (reflects no deduction for fees, expenses or taxes) | | 6.92% | | 5.45% | | 7.78% | | — | | — | | — |

S&P/LSTA Leveraged Loan Index (reflects no deduction for fees, expenses or taxes) | | 4.12% | | 4.03% | | 5.55% | | — | | — | | — |

Other Service Providers

Thrivent Asset Mgt., 625 Fourth Avenue South, Minneapolis, Minnesota 55415, provides administrative personnel and services necessary to operate the Funds and receives an administration fee from the Funds. The custodian for the Funds is State Street Bank and Trust Company, One Lincoln Street, Boston, Massachusetts 02111. PricewaterhouseCoopers LLP, 45 South Seventh Street, Suite 3400, Minneapolis, MN 55402, serves as the Trust’s independent registered public accounting firm.

Governing Law

The Trust is an open-end management investment company registered under the Investment Company Act of 1940 (the “1940 Act”) and was organized as a Massachusetts Business Trust on March 10, 1987. The Trust is made up of 25 separate series or “Funds.” Each Fund of the Trust, other than the Thrivent Asset Allocation Funds, is diversified.

The Trust is authorized to issue shares of beneficial interest, par value $.01 per share, divisible into an indefinite number of different series and classes and operates as a “series company” as provided by Rule 18f-2 under the 1940 Act.

16

The Declaration of Trust of the Trust, as amended through the date hereof (the “Declaration of Trust”) provides that each shareholder shall be deemed to have agreed to be bound by its terms. A vote of shareholders and the Board may amend the Declaration of Trust. The Trust may issue an unlimited number of shares in one or more series as the Board of Trustees may authorize.

Each class is subject to such investment minimums and other conditions as set forth in the Trust’s current prospectuses. Such minimums are identical the same share classes of the Target Fund and the Acquiring Fund (so, for example, the Class A Shares of both Funds have the same initial and subsequent investment minimums). The Reorganization will not affect such investment minimums and other conditions.

Differences in expenses among classes are described in the Trust’s Amended and Restated Plan Pursuant to Rule 18f-3 under the 1940 Act. Class A and Class S Shares pay the expenses associated with their different distribution arrangements. Each class may, at the Trustees’ discretion, also pay a different share of other expenses, not including advisory or custodial fees or other expenses related to the management of the Trust’s assets, if these expenses are actually incurred in a different amount by that class, or if the class receives services of a different kind or to a different degree than the other class. All other expenses will be allocated to each class on the basis of the net asset value of the particular Fund.

Each class of shares has identical voting rights except that each class has exclusive voting rights on any matter submitted to shareholders relating solely to the class or where the interests of one class differ from the interests of the other class. Class A Shares have exclusive voting rights on matters involving the Rule 12b-1 Distribution Plan. Matters submitted to shareholder vote must be approved by each Fund separately except:

| | • | | when required otherwise by the 1940 Act; or |

| | • | | when the Trustees determine that the matter does not affect all Funds; then, only the shareholders of the affected Funds may vote. |

Shares are freely transferable, and holders thereof are entitled to receive dividends declared by the Board, and receive the assets of their respective Fund in the event of liquidation. The Trust generally holds shareholder meetings only when required by law or at the written request of shareholders owning at least 10% of the Trust’s outstanding shares. Shareholders may remove the Trustees from office by votes cast in person or by proxy at a shareholder meeting.

At the request of shareholders holding 10% or more of the outstanding shares of the Trust, the Trust will hold a special meeting for the purpose of considering the removal of a Trustee(s) from office, and the Trust will cooperate with and assist shareholders of record who notify the Trust that they wish to communicate with other shareholders for the purpose of obtaining signatures to request such a meeting, all pursuant to and in accordance with Section 16(c) of the 1940 Act.

Under Massachusetts law, shareholders of a business trust may be held personally liable, under certain circumstances, for the obligations of the Trust. However, the Declaration of Trust disclaims shareholder, Trustee and/or officer liability for acts performed on behalf of the Trust or for Trust obligations that are binding only on the assets and property of the Trust. The Funds include this disclaimer in each agreement, obligation, or contract entered into or executed by the Trust or the Board. The Declaration of Trust provides for indemnification out of the Trust’s assets for all losses and expenses of any shareholder held personally liable for the obligations of the Trust. The risk of a shareholder incurring financial loss on account of shareholder liability is remote because it is limited to circumstances where the Trust itself is unable to meet its obligations.

The Trust’s organizational documents are filed as part of the Trust’s registration statement with the SEC, and shareholders may obtain copies of such documents as described on the first page of this Prospectus/Proxy Statement and in the Questions and Answers preceding this Prospectus/Proxy Statement.

Payments to Broker-Dealers and Other Financial Intermediaries

If you purchase a Fund through a broker-dealer or other financial intermediary, the Fund and its related companies may pay the intermediary for the sale of Fund shares and related services. These payments may create a conflict of interest by influencing the broker-dealer or other intermediary and your salesperson to recommend the

17

Fund over another investment. Ask your salesperson or visit your financial intermediary’s website for more information.

INFORMATION ABOUT THE REORGANIZATION

General

Under the Reorganization Agreement, the Target Fund will transfer all of its assets to the Acquiring Fund in exchange for Class A and Class S Shares of the Acquiring Fund. The Acquiring Fund Class A and Class S Shares issued to the Target Fund will have an aggregate value equal to the aggregate value of the Target Fund’s net assets immediately prior to the Reorganization. Upon receipt by the Target Fund of Acquiring Fund Class A and Class S Shares, the Target Fund will distribute such shares of the Acquiring Fund to Target Fund shareholders. Then, as soon as practicable after the Closing Date of the Reorganization, the Target Fund will dissolve under applicable state law.

The Target Fund will distribute the Acquiring Fund Class A and Class S Shares received by it pro rata to Target Fund shareholders of record in exchange for their interest in Class A and Class S Shares of the Target Fund. This distribution will be accomplished by opening new accounts on the books of the Acquiring Fund in the names of the Target Fund shareholders and transferring to those shareholder accounts the Acquiring Fund Class A and Class S Shares received by the Target Fund. Each newly-opened account on the books of the Acquiring Fund for the previous Target Fund shareholders will represent the respective pro rata number of Acquiring Fund Class A and Class S Shares due such shareholder.

Accordingly, as a result of the Reorganization, each Target Fund shareholder would own Acquiring Fund Class A and Class S Shares that would have an aggregate value immediately after the Reorganization equal to the aggregate value of that shareholder’s Target Fund shares immediately prior to the Reorganization. The interests of each of the Target Fund’s shareholders will not be diluted as a result of the Reorganization. However, as a result of the Reorganization, a shareholder of the Target Fund or the Acquiring Fund will hold a reduced percentage of ownership in the larger combined fund than the shareholder did in either of the separate Funds.

No sales charge or fee of any kind will be assessed to Target Fund shareholders in connection with their receipt of Acquiring Fund Class A and Class S Shares in the Reorganization.