UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORMN-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number:811-05088

THE AB PORTFOLIOS

(Exact name of registrant as specified in charter)

1345 Avenue of the Americas, New York, New York 10105

(Address of principal executive offices) (Zip code)

Joseph J. Mantineo

AllianceBernstein L.P.

1345 Avenue of the Americas

New York, New York 10105

(Name and address of agent for service)

Registrant’s telephone number, including area code: (800)221-5672

Date of fiscal year end: August 31, 2019

Date of reporting period: February 28, 2019

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

FEB 02.28.19

SEMI-ANNUAL REPORT

AB ALL MARKET TOTAL RETURN PORTFOLIO

Beginning January 1, 2021, as permitted by new regulations adopted by the Securities and Exchange Commission, the Fund’s annual and semi-annual shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website address to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Fund electronically at any time by contacting your financial intermediary (such as a broker-dealer or bank) or, if you are a direct investor, by calling the Fund at (800) 221 5672.

You may elect to receive all future reports in paper form free of charge. If you invest through a financial intermediary, you can contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports; if you invest directly with the Fund, you can call the Fund at (800) 221 5672. Your election to receive reports in paper form will apply to all funds held in your account with your financial intermediary or, if you invest directly, to all AB Mutual Funds you hold.

| | |

| |

| Investment Products Offered | | • Are Not FDIC Insured• May Lose Value• Are Not Bank Guaranteed |

Investors should consider the investment objectives, risks, charges and expenses of the Fund carefully before investing. For copies of our prospectus or summary prospectus, which contain this and other information, visit us online at www.abfunds.com or contact your AB representative. Please read the prospectus and/or summary prospectus carefully before investing.

This shareholder report must be preceded or accompanied by the Fund’s prospectus for individuals who are not current shareholders of the Fund.

You may obtain a description of the Fund’s proxy voting policies and procedures, and information regarding how the Fund voted proxies relating to portfolio securities during the most recent12-month period ended June 30, without charge. Simply visit AB’s website at www.abfunds.com, or go to the Securities and Exchange Commission’s (the “Commission”) website at www.sec.gov, or call AB at (800) 227 4618.

The Fund files its complete schedule of portfolio holdings with the Commission for the first and third quarters of each fiscal year as an exhibit to its reports on Form N-PORT. The Fund’s Form N-PORT reports are available on the Commission’s website at www.sec.gov. The Fund’s Forms N-PORT may also be reviewed and copied at the Commission’s Public Reference Room in Washington, DC; information on the operation of the Public Reference Room may be obtained by calling (800) SEC 0330. AB publishes full portfolio holdings for the Fund monthly at www.abfunds.com.

AllianceBernstein Investments, Inc. (ABI) is the distributor of the AB family of mutual funds. ABI is a member of FINRA and is an affiliate of AllianceBernstein L.P., the Adviser of the funds.

The [A/B] logo is a registered service mark of AllianceBernstein and AllianceBernstein® is a registered service mark used by permission of the owner, AllianceBernstein L.P.

| | |

| FROM THE PRESIDENT | |  |

Dear Shareholder,

We are pleased to provide this report for AB All Market Total Return Portfolio (the “Fund”). Please review the discussion of Fund performance, the market conditions during the reporting period and the Fund’s investment strategy.

As always, AB strives to keep clients ahead of what’s next by:

| + | | Transforming uncommon insights into uncommon knowledge with a global research scope |

| + | | Navigating markets with seasoned investment experience and sophisticated solutions |

| + | | Providing thoughtful investment insights and actionable ideas |

Whether you’re an individual investor or a multi-billion-dollar institution, we put knowledge and experience to work for you.

AB’s global research organization connects and collaborates across platforms and teams to deliver impactful insights and innovative products. Better insights lead to better opportunities—anywhere in the world.

For additional information about AB’s range of products and shareholder resources, please log on to www.abfunds.com.

Thank you for your investment in the AB Mutual Funds.

Sincerely,

Robert M. Keith

President and Chief Executive Officer, AB Mutual Funds

| | |

| |

| abfunds.com | | AB ALL MARKET TOTAL RETURN PORTFOLIO | 1 |

SEMI-ANNUAL REPORT

April 09, 2019

This report provides management’s discussion of fund performance for AB All Market Total Return Portfolio for the semi-annual reporting period ended February 28, 2019.

The Fund’s investment objective is to achieve the highest total return consistent with the Adviser’s determination of reasonable risk.

NAV RETURNS AS OF FEBRUARY 28, 2019(unaudited)

| | | | | | | | |

| | |

| | | 6 Months | | | 12 Months | |

| | |

| AB ALL MARKET TOTAL RETURN PORTFOLIO | | | | | | | | |

| | |

| Class A Shares | | | -0.54% | | | | 1.10% | |

| | |

| Class B Shares1 | | | -0.81% | | | | 0.41% | |

| | |

| Class C Shares | | | -0.89% | | | | 0.35% | |

| | |

| Advisor Class Shares2 | | | -0.40% | | | | 1.37% | |

| | |

| Class R Shares2 | | | -0.68% | | | | 0.69% | |

| | |

| Class K Shares2 | | | -0.47% | | | | 1.03% | |

| | |

| Class I Shares2 | | | -0.33% | | | | 1.35% | |

| | |

| Primary Benchmark: MSCI ACWI (net) | | | -2.92% | | | | -0.84% | |

| | |

Bloomberg Barclays Global Aggregate Bond Index

(USD hedged) | | | 2.55% | | | | 3.94% | |

| 1 | Effective January 31, 2009, Class B shares are no longer available for purchase to new investors. Please see Note A for additional information. |

| 2 | Please note that these share classes are for investors purchasing shares through accounts established under certain fee-based programs sponsored and maintained by certain broker-dealers and financial intermediaries, institutional pension plans and/or investment advisory clients of, and certain other persons associated with, the Adviser and its affiliates or the Fund. |

INVESTMENT RESULTS

The table above shows the Fund’s performance compared to its primary benchmark, the Morgan Stanley Capital International All Country World Index (“MSCI ACWI”) (net), and the Bloomberg Barclays Global Aggregate Bond Index (USD hedged), for the six- and 12-month periods ended February 28, 2019.

During both periods, all share classes of the Fund outperformed the primary benchmark and underperformed the Bloomberg Barclays Global Aggregate Bond Index (USD hedged), before sales charges. Equity markets were turbulent during both periods; the Fund’s more diversified approach, which balances exposures to equities, bonds, commodities and alternative strategies, outperformed the all-equity benchmark.

| | |

| |

| 2 | AB ALL MARKET TOTAL RETURN PORTFOLIO | | abfunds.com |

For the six-month period, equities and fixed-income assets contributed to absolute performance, while alternative strategies detracted. Security selection within equities contributed, while selection in fixed-income assets and alternative strategies detracted.

During the 12-month period, fixed-income assets contributed to absolute performance, while alternative strategies and equity holdings detracted. Overall allocations within fixed income and alternative strategies contributed. Security selection within equities contributed, while selection in fixed-income assets and alternative strategies detracted.

The Fund utilized derivatives for hedging and investment purposes in the form of futures, currency forwards, credit default swaps, interest rate swaps and written swaptions, which contributed to absolute performance for both periods, while variance swaps, purchased options and written options detracted; total return swaps, inflation swaps and purchased swaptions contributed for the six-month period, but detracted for the12-month period.

MARKET REVIEW AND INVESTMENT STRATEGY

During the six-month period ended February 28, 2019, US and non-US equities declined, although emerging-market equities posted modest gains. In the US, growth-style stocks outperformed value-style stocks, and small-cap stocks outperformed their large-cap peers. Global trade tensions and rising interest rates weighed on stock market performance. In Europe, Brexit uncertainty, Italian budget issues and German economic woes persisted. Slowing global growth was an increasing concern more broadly. Global equities plummeted at the end of 2018 amid increased volatility, but recouped some losses in January and February, as corporate earnings were above analyst estimates and many central banks shared more dovish monetary policy outlooks.

Fixed-income markets had generally positive returns. Global high yield, developed-market treasuries and investment-grade securities rallied. Emerging-market debt sectors rallied, amid positive idiosyncratic developments and a more favorable macro backdrop, particularly a more patient US Federal Reserve (the “Fed”). Developed-market treasury yield curves moved in different directions (bond yields move inversely to price). The Fed increased interest rates quarterly in 2018 and began to formally reduce its balance sheet before surprising markets with a more dovish tone at the beginning of 2019. Although the European Central Bank formally ended its bond-buying program, the bank also turned more dovish in 2019, putting credit-easing measures back on the table. Meanwhile, the People’s Bank of China started the new year by cutting its reserve requirement ratio.

| | |

| |

| abfunds.com | | AB ALL MARKET TOTAL RETURN PORTFOLIO | 3 |

The Fund’s Senior Investment Management Team (the “Team”) strives to provide the highest total return consistent with reasonable risk. The Team’s global multi-asset strategy focuses on growth and defensively managing market volatility. The Team utilizes a rigorous quantitative research toolset with fundamental expertise across all regions and markets.

INVESTMENT POLICIES

The Adviser allocates the Fund’s investments primarily among a number of asset classes, including equity securities, fixed-income securities, and a number of alternative asset classes and alternative investment strategies. The Fund pursues a global strategy, typically investing in securities of issuers located in the United States and in other countries throughout the world, including emerging-market countries. Under normal circumstances, at least 40% of the Fund’s net assets will be invested in securities of non-US issuers.

Equity securities will primarily be large-capitalization securities, but will include small- and mid-capitalization securities to a lesser extent, and will include derivatives related to equity securities. In selecting equity securities for the Fund, the Adviser will use fundamental and quantitative analysis with the goal of generating returns primarily from security selection rather than price movements in equity securities generally. Fixed-income securities include corporate and sovereign debt securities as well as interest rate derivatives and credit derivatives such as credit default swaps. Fixed-income securities also include debt securities with lower credit ratings (commonly known as “junk bonds”). In selecting fixed-income securities for the Fund, the Adviser will attempt to take advantage of inefficiencies that it believes exist in the global fixed-income markets. These inefficiencies arise from investor behavior, market complexity and the investment limitations to which investors are subject.

Alternative investments include various instruments the returns on which are expected to have low correlation with returns on equity and fixed-income securities, such as commodities and related derivatives, real estate-related securities and inflation-indexed securities. Alternative investment strategies that may be pursued by the Fund directly or indirectly through investment in other registered investment companies include (i) long/short equity strategies through which the Fund takes long positions in certain securities in the expectation that they will increase in value and takes short positions in other securities in the expectation that they will decrease in value; (ii) strategies that consider macroeconomic and technical factors to identify and exploit opportunities across global asset classes; and (iii) event-driven strategies that invest in the securities of companies that are expected to

| | |

| |

| 4 | AB ALL MARKET TOTAL RETURN PORTFOLIO | | abfunds.com |

(continued on next page)

become the subject of major corporate events and companies in which an active role in company management has been taken or sought by a third-party investor.

The Adviser will adjust the Fund’s asset class exposure utilizing both fundamental analysis and the Adviser’s Dynamic Asset Allocation (“DAA”) approach. DAA comprises a series of analytical and forecasting tools employed by the Adviser to gauge fluctuations in the risk/return profile of various asset classes. DAA seeks to adjust the Fund’s investment exposure in changing market conditions and thereby reduce overall portfolio volatility by mitigating the effects of market fluctuations, while preserving consistent long-term return potential. For example, the Adviser may seek to reduce the Fund’s risk exposure to one or more assets classes when DAA suggests that market risks relevant to those asset classes are rising but return opportunities are declining. In addition to merely increasing or decreasing asset class exposure by buying or selling securities of that asset class, the Adviser may pursue DAA implementation for the Fund by utilizing derivatives.

The Adviser intends to utilize a variety of derivatives in its management of the Fund. As noted above, the Adviser may use derivatives to gain exposure to various asset classes, and may cause the Fund to enter into derivatives in making the adjustments called for by DAA. As a result of the use of derivatives, the Fund will frequently be leveraged, with net investment exposure substantially in excess of net assets.

While the Fund may seek to gain exposure to physical commodities traded in the commodities markets through investments in a variety of derivative instruments, the Adviser expects that the Fund will seek to gain such exposure to commodities and commodities-related instruments and derivatives primarily through investments in AB All Market Total Return Portfolio (Cayman), Ltd., a wholly-owned subsidiary of the Fund organized under the laws of the Cayman Islands (the “Subsidiary”). The Subsidiary is advised by the Adviser and has the same investment objective and substantially similar investment policies and restrictions as the Fund except that the Subsidiary, unlike the Fund, may invest, without limitation, in commodities and commodities-related instruments. The Fund will be subject to the risks associated with the commodities, derivatives and other instruments in which the Subsidiary invests, to the extent of its investment in the Subsidiary. The Fund limits its investment in the Subsidiary to no more than 25% of its total assets. Investment in the Subsidiary is expected to provide the Fund with commodity exposure within the limitations of federal tax requirements that apply to the Fund.

Currency exchange rate fluctuations can have a dramatic impact on returns. The Fund’s foreign currency exposures will come from

(continued on next page)

| | |

| |

| abfunds.com | | AB ALL MARKET TOTAL RETURN PORTFOLIO | 5 |

investment in securities priced or denominated in foreign currencies and from direct holdings in foreign currencies and currency-related derivatives. The Adviser may seek to hedge all or a portion of the currency exposure resulting from Fund investments or decide not to hedge this exposure. The Adviser may seek investment opportunities by taking long or short positions in currencies through the use of currency-related derivatives.

| | |

| |

| 6 | AB ALL MARKET TOTAL RETURN PORTFOLIO | | abfunds.com |

DISCLOSURES AND RISKS

Benchmark Disclosure

All indices are unmanaged and do not reflect fees and expenses associated with the active management of a mutual fund portfolio. The MSCI ACWI (net, free float-adjusted, market capitalization weighted) represents the equity market performance of developed and emerging markets. The Bloomberg Barclays Global Aggregate Bond Index (USD hedged) represents the performance of global investment-grade developed fixed-income markets, hedged to the US dollar. MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices, any securities or financial products. This report is not approved, reviewed or produced by MSCI. Net returns include the reinvestment of dividends after deduction of non-US withholding tax. An investor cannot invest directly in an index or average, and their results are not indicative of the performance for any specific investment, including the Fund.

A Word About Risk

Market Risk: The value of the Fund’s assets will fluctuate as the stock, bond or commodities markets fluctuate. The value of its investments may decline, sometimes rapidly and unpredictably, simply because of economic changes or other events that affect large portions of the market. It includes the risk that a particular style of investing, such as growth or value, may be underperforming the stock market generally.

Allocation Risk: The allocation of investments among different investment styles, such as equity or debt, growth or value, US or non-US securities, or diversification strategies, may have a more significant effect on the Fund’s net asset value (“NAV”) when one of these investments is performing more poorly than another.

Credit Risk: An issuer or guarantor of a fixed-income security, or the counterparty to a derivatives or other contract, may be unable or unwilling to make timely payments of interest or principal, or to otherwise honor its obligations. The issuer or guarantor may default, causing a loss of the full principal amount of a security and accrued interest. The degree of risk for a particular security may be reflected in its credit rating. There is the possibility that the credit rating of a fixed-income security may be downgraded after purchase, which may adversely affect the value of the security. Investments in fixed-income securities with lower ratings (commonly known as “junk bonds”) are subject to a higher probability that an issuer will default or fail to meet its payment obligations.

High-Yield Debt Securities Risk: Investments in fixed-income securities with lower ratings (commonly known as “junk bonds”) tend to have a higher probability that an issuer will default or fail to meet its payment obligations.

| | |

| |

| abfunds.com | | AB ALL MARKET TOTAL RETURN PORTFOLIO | 7 |

DISCLOSURES AND RISKS(continued)

These securities may be subject to greater price volatility due to such factors as specific corporate developments, interest-rate sensitivity, negative perceptions of the junk bond market generally and less secondary market liquidity.

Interest-Rate Risk: Changes in interest rates will affect the value of the Fund’s investments in fixed-income securities. When interest rates rise, the value of existing investments in fixed-income securities tends to fall and this decrease in value may not be offset by higher income from new investments. Interest-rate risk is generally greater for fixed-income securities with longer maturities or durations.

Inflation Risk: This is the risk that the value of assets or income from investments will be less in the future as inflation decreases the value of money. As inflation increases, the value of the Fund’s assets can decline as can the value of the Fund’s distributions. This risk is significantly greater for fixed-income securities with longer maturities.

Foreign (Non-US) Risk: Investments in securities of non-US issuers may involve more risk than those of US issuers. These securities may fluctuate more widely in price and may be less liquid due to adverse market, economic, political, regulatory or other factors.

Currency Risk: Fluctuations in currency exchange rates may negatively affect the value of the Fund’s investments or reduce its returns.

Emerging-Market Risk: Investments in emerging-market countries may have more risk because the markets are less developed and less liquid as well as being subject to increased economic, political, regulatory or other uncertainties.

Alternative Investments Risk: Many alternative investments can be volatile and may be illiquid. Their performance may have little correlation with the performance of equity or fixed-income markets, and they may not perform in accordance with expectations.

Capitalization Risk: Investments in small- and mid-capitalization companies may be more volatile than investments in large-capitalization companies. Investments in small-capitalization companies may have additional risks because these companies have limited product lines, markets or financial resources.

Derivatives Risk: Derivatives may be illiquid, difficult to price, and leveraged so that small changes may produce disproportionate losses for the Fund, and may be subject to counterparty risk to a greater degree than more traditional investments.

| | |

| |

| 8 | AB ALL MARKET TOTAL RETURN PORTFOLIO | | abfunds.com |

DISCLOSURES AND RISKS(continued)

Leverage Risk: To the extent the Fund uses leveraging techniques, its NAV may be more volatile because leverage tends to exaggerate the effect of changes in interest rates and any increase or decrease in the value of the Fund’s investments.

Commodity Risk: Investing in commodities and commodity-linked derivative instruments may subject the Fund to greater volatility than investments in traditional securities. The value of commodity-linked derivative instruments may be affected by overall market movements, commodity index volatility, changes in interest rates, or factors affecting a particular industry or commodity, such as drought, floods, weather, livestock disease, embargoes, tariffs and international economic, political and regulatory developments.

Subsidiary Risk: By investing in the Subsidiary, the Fund is indirectly exposed to the risks associated with the Subsidiary. The derivatives and other investments held by the Subsidiary are generally similar to those that are permitted to be held by the Fund and are subject to the same risks that apply to similar investments if held directly by the Fund. The Subsidiary is not registered under the Investment Company Act of 1940, as amended (the “1940 Act”), and, unless otherwise noted in the prospectus, is not subject to all of the investor protections of the 1940 Act. However, the Fund wholly owns and controls the Subsidiary, and the Fund and the Subsidiary are managed by the Adviser, making it unlikely the Subsidiary will take actions contrary to the interests of the Fund or its shareholders. In addition, changes in federal tax laws applicable to the Fund or interpretations thereof could limit the Fund’s ability to gain exposure to commodities investments through investments in the Subsidiary.

Short Sale Risk: The Fund is subject to short sale risk because it may engage in short sales either directly or indirectly through investment in the Underlying Portfolio. Short sales involve the risk that the Fund or Underlying Portfolio will incur a loss by subsequently buying a security at a higher price than the price at which it sold the security. The amount of such loss is theoretically unlimited, as it will be based on the increase in value of the security sold short. In contrast, the risk of loss from a long position is limited to the Fund’s or Underlying Portfolio’s investment in the security, because the price of the security cannot fall below zero. The Fund or Underlying Portfolio may not always be able to close out a short position on favorable terms.

Management Risk: The Fund is subject to management risk because it is an actively managed investment fund. The Adviser will apply its investment techniques and risk analyses in making investment decisions for the Fund, but there is no guarantee that its techniques will produce the intended results.

| | |

| |

| abfunds.com | | AB ALL MARKET TOTAL RETURN PORTFOLIO | 9 |

DISCLOSURES AND RISKS(continued)

These risks are fully discussed in the Fund’s prospectus. As with all investments, you may lose money by investing in the Fund.

An Important Note About Historical Performance

The investment return and principal value of an investment in the Fund will fluctuate as the prices of the individual securities in which it invests fluctuate, so that your shares, when redeemed, may be worth more or less than their original cost. Performance shown in this report represents past performance and does not guarantee future results. Current performance may be lower or higher than the performance information shown. You may obtain performance information current to the most recent month-end by visiting www.abfunds.com. The performance shown for periods prior to April 24, 2017 is based on the Fund’s prior principal strategies and may not be representative of the Fund’s performance under its current principal strategies.

All fees and expenses related to the operation of the Fund have been deducted. NAV returns do not reflect sales charges; if sales charges were reflected, the Fund’s quoted performance would be lower. SEC returns reflect the applicable sales charges for each share class: a 4.25% maximum front-end sales charge for Class A shares; the applicable contingent deferred sales charge for Class B shares (4% year 1, 3% year 2, 2% year 3, 1% year 4) and a 1%1-year contingent deferred sales charge for Class C shares. Returns for the different share classes will vary due to different expenses associated with each class. Performance assumes reinvestment of distributions and does not account for taxes.

| | |

| |

| 10 | AB ALL MARKET TOTAL RETURN PORTFOLIO | | abfunds.com |

HISTORICAL PERFORMANCE

AVERAGE ANNUAL RETURNS AS OF FEBRUARY 28, 2019(unaudited)

| | | | | | | | |

| | |

| | | NAV

Returns | | | SEC Returns

(reflects applicable

sales charges) | |

| | |

| CLASS A SHARES | | | | | | | | |

| | |

| 1 Year | | | 1.10% | | | | -3.22% | |

| | |

| 5 Years | | | 3.38% | | | | 2.48% | |

| | |

| 10 Years | | | 9.40% | | | | 8.93% | |

| | |

| CLASS B SHARES | | | | | | | | |

| | |

| 1 Year | | | 0.41% | | | | -3.59% | |

| | |

| 5 Years | | | 2.61% | | | | 2.61% | |

| | |

| 10 Years1 | | | 8.76% | | | | 8.76% | |

| | |

| CLASS C SHARES | | | | | | | | |

| | |

| 1 Year | | | 0.35% | | | | -0.65% | |

| | |

| 5 Years | | | 2.61% | | | | 2.61% | |

| | |

| 10 Years | | | 8.61% | | | | 8.61% | |

| | |

| ADVISOR CLASS SHARES2 | | | | | | | | |

| | |

| 1 Year | | | 1.37% | | | | 1.37% | |

| | |

| 5 Years | | | 3.63% | | | | 3.63% | |

| | |

| 10 Years | | | 9.71% | | | | 9.71% | |

| | |

| CLASS R SHARES2 | | | | | | | | |

| | |

| 1 Year | | | 0.69% | | | | 0.69% | |

| | |

| 5 Years | | | 2.96% | | | | 2.96% | |

| | |

| 10 Years | | | 8.98% | | | | 8.98% | |

| | |

| CLASS K SHARES2 | | | | | | | | |

| | |

| 1 Year | | | 1.03% | | | | 1.03% | |

| | |

| 5 Years | | | 3.28% | | | | 3.28% | |

| | |

| 10 Years | | | 9.32% | | | | 9.32% | |

| | |

| CLASS I SHARES2 | | | | | | | | |

| | |

| 1 Year | | | 1.35% | | | | 1.35% | |

| | |

| 5 Years | | | 3.62% | | | | 3.62% | |

| | |

| 10 Years | | | 9.69% | | | | 9.69% | |

The Fund’s current prospectus fee table shows the Fund’s total annual operating expense ratios as 1.23%, 2.00%, 1.98%, 0.98%, 1.64%, 1.33% and 1.01% for Class A, Class B, Class C, Advisor Class, Class R, Class K and Class I shares, respectively. The Financial Highlights section of this report sets forth expense ratio data for the current reporting period; the expense ratios shown above may differ from the expense ratios in the Financial Highlights section since they are based on different time periods.

| 1 | Assumes conversion of Class B shares into Class A shares after eight years. |

| 2 | These share classes are offered at NAV to eligible investors and their SEC returns are the same as their NAV returns. Please note that these share classes are for investors purchasing shares through accounts established under certain fee-based programs sponsored and maintained by certain broker-dealers and financial intermediaries, institutional pension plans and/or investment advisory clients of, and certain other persons associated with, the Adviser and its affiliates or the Fund. |

| | |

| |

| abfunds.com | | AB ALL MARKET TOTAL RETURN PORTFOLIO | 11 |

HISTORICAL PERFORMANCE(continued)

SEC AVERAGE ANNUAL RETURNS

AS OF THE MOST RECENT CALENDAR QUARTER-END

MARCH 31, 2019(unaudited)

| | | | |

| |

| | | SEC Returns

(reflects applicable

sales charges) | |

| |

| CLASS A SHARES | | | | |

| |

| 1 Year | | | -2.16% | |

| |

| 5 Years | | | 2.80% | |

| |

| 10 Years | | | 8.42% | |

| |

| CLASS B SHARES | | | | |

| |

| 1 Year | | | -2.57% | |

| |

| 5 Years | | | 2.92% | |

| |

| 10 Years1 | | | 8.25% | |

| |

| CLASS C SHARES | | | | |

| |

| 1 Year | | | 0.45% | |

| |

| 5 Years | | | 2.91% | |

| |

| 10 Years | | | 8.10% | |

| |

| ADVISOR CLASS SHARES2 | | | | |

| |

| 1 Year | | | 2.45% | |

| |

| 5 Years | | | 3.95% | |

| |

| 10 Years | | | 9.19% | |

| |

| CLASS R SHARES2 | | | | |

| |

| 1 Year | | | 1.72% | |

| |

| 5 Years | | | 3.26% | |

| |

| 10 Years | | | 8.46% | |

| |

| CLASS K SHARES2 | | | | |

| |

| 1 Year | | | 2.06% | |

| |

| 5 Years | | | 3.59% | |

| |

| 10 Years | | | 8.81% | |

| |

| CLASS I SHARES2 | | | | |

| |

| 1 Year | | | 2.35% | |

| |

| 5 Years | | | 3.92% | |

| |

| 10 Years | | | 9.16% | |

| 1 | Assumes conversion of Class B shares into Class A shares after eight years. |

| 2 | Please note that these share classes are for investors purchasing shares through accounts established under certain fee-based programs sponsored and maintained by certain broker-dealers and financial intermediaries, institutional pension plans and/or investment advisory clients of, and certain other persons associated with, the Adviser and its affiliates or the Fund. |

| | |

| |

| 12 | AB ALL MARKET TOTAL RETURN PORTFOLIO | | abfunds.com |

EXPENSE EXAMPLE

(unaudited)

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, contingent deferred sales charges on redemptions and (2) ongoing costs, including management fees; distribution(12b-1) fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period as indicated below.

Actual Expenses

The table below provides information about actual account values and actual expenses. You may use the information, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The table below also provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed annual rate of return of 5% before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds by comparing this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), or contingent deferred sales charges on redemptions. Therefore, the hypothetical example is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | |

| |

| abfunds.com | | AB ALL MARKET TOTAL RETURN PORTFOLIO | 13 |

EXPENSE EXAMPLE(continued)

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Beginning

Account

Value

September 1,

2018 | | | Ending

Account

Value

February 28,

2019 | | | Expenses

Paid

During

Period* | | | Annualized

Expense

Ratio* | | | Total

Expenses

Paid

During

Period+ | | | Total

Annualized

Expense

Ratio+ | |

| Class A | | | | | | | | | | | | | | | | |

Actual | | $ | 1,000 | | | $ | 994.60 | | | $ | 4.45 | | | | 0.90 | % | | $ | 5.09 | | | | 1.03 | % |

Hypothetical** | | $ | 1,000 | | | $ | 1,020.33 | | | $ | 4.51 | | | | 0.90 | % | | $ | 5.16 | | | | 1.03 | % |

| Class B | | | | | | | | | | | | | | | | |

Actual | | $ | 1,000 | | | $ | 991.90 | | | $ | 8.25 | | | | 1.67 | % | | $ | 8.89 | | | | 1.80 | % |

Hypothetical** | | $ | 1,000 | | | $ | 1,016.51 | | | $ | 8.35 | | | | 1.67 | % | | $ | 9.00 | | | | 1.80 | % |

| Class C | | | | | | | | | | | | | | | | |

Actual | | $ | 1,000 | | | $ | 991.10 | | | $ | 8.15 | | | | 1.65 | % | | $ | 8.79 | | | | 1.78 | % |

Hypothetical** | | $ | 1,000 | | | $ | 1,016.61 | | | $ | 8.25 | | | | 1.65 | % | | $ | 8.90 | | | | 1.78 | % |

| Advisor Class | | | | | | | | | | | | | |

Actual | | $ | 1,000 | | | $ | 996.00 | | | $ | 3.22 | | | | 0.65 | % | | $ | 3.86 | | | | 0.78 | % |

Hypothetical** | | $ | 1,000 | | | $ | 1,021.57 | | | $ | 3.26 | | | | 0.65 | % | | $ | 3.91 | | | | 0.78 | % |

| Class R | | | | | | | | | | | | | | | | |

Actual | | $ | 1,000 | | | $ | 993.20 | | | $ | 6.47 | | | | 1.31 | % | | $ | 7.12 | | | | 1.44 | % |

Hypothetical** | | $ | 1,000 | | | $ | 1,018.30 | | | $ | 6.56 | | | | 1.31 | % | | $ | 7.20 | | | | 1.44 | % |

| Class K | | | | | | | | | | | | | | | | |

Actual | | $ | 1,000 | | | $ | 995.30 | | | $ | 4.90 | | | | 0.99 | % | | $ | 5.54 | | | | 1.12 | % |

Hypothetical** | | $ | 1,000 | | | $ | 1,019.89 | | | $ | 4.96 | | | | 0.99 | % | | $ | 5.61 | | | | 1.12 | % |

| Class I | | | | | | | | | | | | | | | | |

Actual | | $ | 1,000 | | | $ | 996.70 | | | $ | 3.32 | | | | 0.67 | % | | $ | 3.96 | | | | 0.80 | % |

Hypothetical** | | $ | 1,000 | | | $ | 1,021.47 | | | $ | 3.36 | | | | 0.67 | % | | $ | 4.01 | | | | 0.80 | % |

| * | Expenses are equal to the classes’ annualized expense ratios, multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period). |

| ** | Assumes 5% annual return before expenses. |

| + | In connection with the Fund’s investments in affiliated/unaffiliated underlying portfolios, the Fund incurs no direct expenses, but bears proportionate shares of the fees and expenses (i.e., operating, administrative and investment advisory fees) of the affiliated/unaffiliated underlying portfolios. The Adviser has contractually agreed to waive its fees from the Fund in an amount equal to the Fund’s pro rata share of certain acquired fund fees and expenses of the affiliated underlying portfolios. The Fund’s total expenses are equal to the classes’ annualized expense ratio plus the Fund’s pro rata share of the weighted average expense ratio of the affiliated/unaffiliated underlying portfolios in which it invests, multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period). |

| | |

| |

| 14 | AB ALL MARKET TOTAL RETURN PORTFOLIO | | abfunds.com |

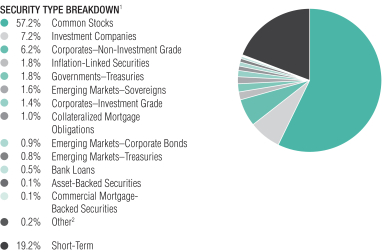

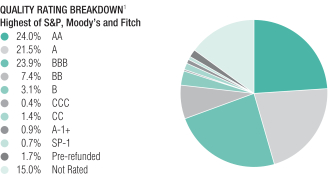

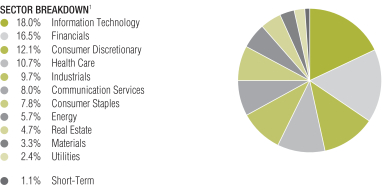

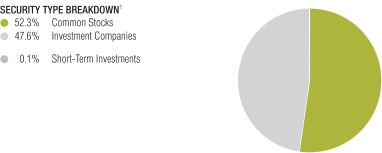

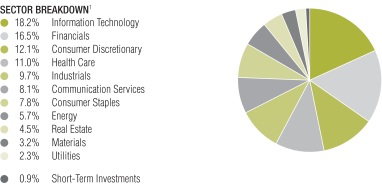

PORTFOLIO SUMMARY

February 28, 2019(unaudited)

PORTFOLIO STATISTICS

Net Assets ($mil): $724.2

| 1 | All data are as of February 28, 2019. The Fund’s security type breakdown is expressed as a percentage of total investments (excluding security lending collateral) and may vary over time. The Fund also enters into derivative transactions, which may be used for hedging or investment purposes (see “Consolidated Portfolio of Investments” section of the report for additional details). |

| 2 | “Other” represents less than 0.1% weightings in the following security types: Collateralized Loan Obligations, Local Governments–Regional Bonds, Local Governments–US Municipal Bonds, Mortgage Pass-Throughs, Options Purchased–Calls, Options Purchased–Puts, Preferred Stocks, Quasi-Sovereigns and Warrants. |

| | |

| |

| abfunds.com | | AB ALL MARKET TOTAL RETURN PORTFOLIO | 15 |

CONSOLIDATED PORTFOLIO OF INVESTMENTS

February 28, 2019(unaudited)

| | | | | | | | | | | | |

| Company | | | | | Shares | | | U.S. $ Value | |

| |

COMMON STOCKS – 56.1% | | | | | | | | | | | | |

Information Technology – 11.9% | | | | | | | | | | | | |

Communications Equipment – 0.6% | | | | | | | | | | | | |

ARRIS International PLC(a) | | | | | | | 48,100 | | | $ | 1,523,808 | |

F5 Networks, Inc.(a) | | | | | | | 633 | | | | 106,433 | |

Finisar Corp.(a) | | | | | | | 62,449 | | | | 1,529,376 | |

Juniper Networks, Inc. | | | | | | | 25,012 | | | | 677,325 | |

Telefonaktiebolaget LM Ericsson – Class B | | | | | | | 16,023 | | | | 146,053 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 3,982,995 | |

| | | | | | | | | | | | |

Electronic Equipment, Instruments & Components – 0.7% | | | | | | | | | | | | |

Amphenol Corp. – Class A | | | | | | | 45,938 | | | | 4,316,794 | |

Hitachi Ltd. | | | | | | | 9,400 | | | | 282,567 | |

IPG Photonics Corp.(a) | | | | | | | 5,148 | | | | 798,095 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 5,397,456 | |

| | | | | | | | | | | | |

IT Services – 3.6% | | | | | | | | | | | | |

Accenture PLC – Class A | | | | | | | 270 | | | | 43,573 | |

Akamai Technologies, Inc.(a) | | | | | | | 10,672 | | | | 743,411 | |

Amadeus IT Group SA – Class A | | | | | | | 13,050 | | | | 981,651 | |

Amdocs Ltd. | | | | | | | 6,967 | | | | 387,156 | |

Automatic Data Processing, Inc. | | | | | | | 16,715 | | | | 2,557,896 | |

Booz Allen Hamilton Holding Corp. | | | | | | | 29,666 | | | | 1,568,145 | |

Capgemini SE | | | | | | | 6,890 | | | | 823,548 | |

CGI, Inc.(a) | | | | | | | 5,204 | | | | 348,911 | |

Cognizant Technology Solutions Corp. – Class A | | | | | | | 34,568 | | | | 2,453,637 | |

Fidelity National Information Services, Inc. | | | | | | | 6,760 | | | | 731,094 | |

First Data Corp. – Class A(a) | | | | | | | 58,627 | | | | 1,473,883 | |

Goodman Networks, Inc.(a)(b)(c)(d) | | | | | | | 3,005 | | | | – 0 | – |

Luxoft Holding, Inc.(a) | | | | | | | 12,862 | | | | 749,726 | |

Mastercard, Inc. – Class A | | | | | | | 32,340 | | | | 7,269,061 | |

Paychex, Inc. | | | | | | | 18,510 | | | | 1,425,640 | |

Total System Services, Inc. | | | | | | | 7,890 | | | | 744,816 | |

Visa, Inc. – Class A | | | | | | | 27,188 | | | | 4,027,087 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 26,329,235 | |

| | | | | | | | | | | | |

Semiconductors & Semiconductor Equipment – 1.5% | | | | | | | | | | | | |

ASML Holding NV | | | | | | | 6,840 | | | | 1,251,286 | |

Integrated Device Technology, Inc.(a) | | | | | | | 30,794 | | | | 1,488,274 | |

Intel Corp. | | | | | | | 47,121 | | | | 2,495,528 | |

KLA-Tencor Corp. | | | | | | | 6,263 | | | | 723,343 | |

NXP Semiconductors NV | | | | | | | 9,290 | | | | 848,363 | |

Taiwan Semiconductor Manufacturing Co., Ltd. (Sponsored ADR) | | | | | | | 24,210 | | | | 945,400 | |

Texas Instruments, Inc. | | | | | | | 7,023 | | | | 742,893 | |

| | |

| |

| 16 | AB ALL MARKET TOTAL RETURN PORTFOLIO | | abfunds.com |

CONSOLIDATED PORTFOLIO OF INVESTMENTS(continued)

| | | | | | | | | | | | |

| Company | | | | | Shares | | | U.S. $ Value | |

| |

Versum Materials, Inc. | | | | | | | 31,215 | | | $ | 1,529,535 | |

Xilinx, Inc. | | | | | | | 6,750 | | | | 845,775 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 10,870,397 | |

| | | | | | | | | | | | |

Software – 4.4% | | | | | | | | | | | | |

Avaya Holdings Corp.(a) | | | | | | | 8,861 | | | | 137,257 | |

Cadence Design Systems, Inc.(a) | | | | | | | 15,303 | | | | 876,097 | |

Check Point Software Technologies Ltd.(a) | | | | | | | 12,430 | | | | 1,520,189 | |

Citrix Systems, Inc. | | | | | | | 6,685 | | | | 705,268 | |

Constellation Software, Inc./Canada | | | | | | | 1,526 | | | | 1,303,098 | |

Fortinet, Inc.(a) | | | | | | | 9,898 | | | | 859,047 | |

Gemalto NV(a) | | | | | | | 18,706 | | | | 1,083,006 | |

Microsoft Corp. | | | | | | | 131,548 | | | | 14,737,323 | |

Nice Ltd.(a) | | | | | | | 19,050 | | | | 2,246,931 | |

Oracle Corp. | | | | | | | 48,488 | | | | 2,527,679 | |

Oracle Corp. Japan | | | | | | | 18,300 | | | | 1,368,635 | |

Red Hat, Inc.(a) | | | | | | | 9,195 | | | | 1,679,007 | |

SAP SE | | | | | | | 7,021 | | | | 751,433 | |

ServiceNow, Inc.(a) | | | | | | | 1,060 | | | | 253,806 | |

Symantec Corp. | | | | | | | 32,899 | | | | 739,899 | |

VMware, Inc. – Class A | | | | | | | 4,852 | | | | 833,622 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 31,622,297 | |

| | | | | | | | | | | | |

Technology Hardware, Storage & Peripherals – 1.1% | | | | | | | | | | | | |

Apple, Inc. | | | | | | | 33,353 | | | | 5,775,072 | |

Samsung Electronics Co., Ltd. | | | | | | | 56,501 | | | | 2,261,273 | |

Travelport Worldwide Ltd. | | | | | | | 1,124 | | | | 17,669 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 8,054,014 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 86,256,394 | |

| | | | | | | | | | | | |

Financials – 9.3% | | | | | | | | | | | | |

Banks – 3.6% | | | | | | | | | | | | |

Banco do Brasil SA | | | | | | | 11,500 | | | | 154,919 | |

Bank LeumiLe-Israel BM | | | | | | | 85,600 | | | | 566,139 | |

Bank of America Corp. | | | | | | | 1,531 | | | | 44,522 | |

Bank of China Ltd. – Class A | | | | | | | 284,900 | | | | 163,589 | |

Bank of Communications Co., Ltd. – Class A | | | | | | | 59,800 | | | | 57,237 | |

Blue Hills Bancorp, Inc. | | | | | | | 42,663 | | | | 1,061,455 | |

China CITIC Bank Corp., Ltd. | | | | | | | 190,500 | | | | 186,633 | |

China Everbright Bank Co., Ltd. | | | | | | | 266,300 | | | | 168,435 | |

China Minsheng Banking Corp., Ltd. | | | | | | | 111,587 | | | | 108,973 | |

Chongqing Rural Commercial Bank Co., Ltd. – Class H | | | | | | | 281,000 | | | | 175,805 | |

Citigroup, Inc. | | | | | | | 25,644 | | | | 1,640,703 | |

DBS Group Holdings Ltd. | | | | | | | 161,200 | | | | 2,955,399 | |

DNB ASA | | | | | | | 28,577 | | | | 547,362 | |

| | |

| |

| abfunds.com | | AB ALL MARKET TOTAL RETURN PORTFOLIO | 17 |

CONSOLIDATED PORTFOLIO OF INVESTMENTS(continued)

| | | | | | | | | | | | |

| Company | | | | | Shares | | | U.S. $ Value | |

| |

Fidelity Southern Corp. | | | | | | | 4,140 | | | $ | 134,881 | |

Fifth Third Bancorp | | | | | | | 26,894 | | | | 741,737 | |

Hang Seng Bank Ltd. | | | | | | | 23,900 | | | | 591,856 | |

Industrial Bank of Korea | | | | | | | 10,544 | | | | 130,683 | |

JPMorgan Chase & Co. | | | | | | | 9,448 | | | | 985,993 | |

Jyske Bank A/S | | | | | | | 66,772 | | | | 2,614,605 | |

Mebuki Financial Group, Inc. | | | | | | | 92,900 | | | | 252,206 | |

Mitsubishi UFJ Financial Group, Inc. | | | | | | | 109,800 | | | | 569,795 | |

Oversea-Chinese Banking Corp., Ltd. | | | | | | | 22,900 | | | | 186,829 | |

PNC Financial Services Group, Inc. (The) | | | | | | | 3,790 | | | | 477,616 | |

Royal Bank of Canada | | | | | | | 25,625 | | | | 2,002,759 | |

SunTrust Banks, Inc. | | | | | | | 23,344 | | | | 1,514,325 | |

TCF Financial Corp. | | | | | | | 63,686 | | | | 1,458,409 | |

Toronto-Dominion Bank (The) | | | | | | | 29,769 | | | | 1,707,032 | |

Wells Fargo & Co. | | | | | | | 78,710 | | | | 3,926,842 | |

Westpac Banking Corp. | | | | | | | 40,870 | | | | 782,299 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 25,909,038 | |

| | | | | | | | | | | | |

Capital Markets – 3.1% | | | | | | | | | | | | |

BinckBank NV | | | | | | | 105,178 | | | | 748,804 | |

BlackRock, Inc. – Class A | | | | | | | 2,050 | | | | 908,601 | |

Cboe Global Markets, Inc. | | | | | | | 6,373 | | | | 611,234 | |

Charles Schwab Corp. (The) | | | | | | | 125,370 | | | | 5,768,274 | |

China Cinda Asset Management Co., Ltd. – Class H | | | | | | | 609,000 | | | | 176,820 | |

China Huarong Asset Management Co., Ltd.(e) | | | | | | | 806,000 | | | | 184,805 | |

CME Group, Inc. – Class A | | | | | | | 6,260 | | | | 1,138,757 | |

Daiwa Securities Group, Inc. | | | | | | | 51,200 | | | | 259,971 | |

Intercontinental Exchange, Inc. | | | | | | | 13,910 | | | | 1,073,156 | |

Investment Technology Group, Inc. | | | | | | | 33,476 | | | | 1,011,979 | |

Julius Baer Group Ltd.(a) | | | | | | | 73,878 | | | | 3,219,009 | |

Korea Investment Holdings Co., Ltd.(a) | | | | | | | 2,722 | | | | 155,753 | |

Macquarie Group Ltd. | | | | | | | 3,990 | | | | 364,306 | |

Moody’s Corp. | | | | | | | 8,630 | | | | 1,494,026 | |

NH Investment & Securities Co., Ltd.(a) | | | | | | | 12,933 | | | | 149,791 | |

Partners Group Holding AG | | | | | | | 1,150 | | | | 830,896 | |

S&P Global, Inc. | | | | | | | 10,097 | | | | 2,023,136 | |

Singapore Exchange Ltd. | | | | | | | 439,400 | | | | 2,544,550 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 22,663,868 | |

| | | | | | | | | | | | |

Consumer Finance – 0.1% | | | | | | | | | | | | |

Ally Financial, Inc. | | | | | | | 7,550 | | | | 204,530 | |

Synchrony Financial | | | | | | | 9,950 | | | | 324,469 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 528,999 | |

| | | | | | | | | | | | |

Diversified Financial Services – 0.1% | | | | | | | | | | | | |

Berkshire Hathaway, Inc. – Class B(a) | | | | | | | 841 | | | | 169,293 | |

Far East Horizon Ltd. | | | | | | | 99,000 | | | | 110,480 | |

Pargesa Holding SA | | | | | | | 8,983 | | | | 737,001 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 1,016,774 | |

| | | | | | | | | | | | |

| | |

| |

| 18 | AB ALL MARKET TOTAL RETURN PORTFOLIO | | abfunds.com |

CONSOLIDATED PORTFOLIO OF INVESTMENTS(continued)

| | | | | | | | | | | | |

| Company | | | | | Shares | | | U.S. $ Value | |

| |

Insurance – 2.4% | | | | | | | | | | | | |

Admiral Group PLC | | | | | | | 20,000 | | | $ | 579,126 | |

Aegon NV | | | | | | | 76,406 | | | | 409,964 | |

Arthur J Gallagher & Co. | | | | | | | 18,010 | | | | 1,445,843 | |

Athene Holding Ltd. – Class A(a) | | | | | | | 16,451 | | | | 732,892 | |

Direct Line Insurance Group PLC | | | | | | | 89,910 | | | | 425,045 | |

Everest Re Group Ltd. | | | | | | | 6,592 | | | | 1,490,517 | |

Fidelity National Financial, Inc. | | | | | | | 54,108 | | | | 1,898,650 | |

Japan Post Holdings Co., Ltd. | | | | | | | 24,800 | | | | 301,467 | |

Jardine Lloyd Thompson Group PLC | | | | | | | 59,396 | | | | 1,503,120 | |

Legal & General Group PLC | | | | | | | 154,943 | | | | 576,563 | |

Lincoln National Corp. | | | | | | | 11,363 | | | | 710,415 | |

Marsh & McLennan Cos., Inc. | | | | | | | 6,320 | | | | 587,886 | |

MetLife, Inc. | | | | | | | 7,435 | | | | 335,988 | |

NN Group NV | | | | | | | 45,320 | | | | 1,972,578 | |

PICC Property & Casualty Co., Ltd. – Class H | | | | | | | 152,000 | | | | 181,928 | |

Poste Italiane SpA(e) | | | | | | | 44,623 | | | | 402,299 | |

Prudential Financial, Inc. | | | | | | | 8,558 | | | | 820,284 | |

Sampo Oyj – Class A | | | | | | | 10,690 | | | | 514,293 | |

Stewart Information Services Corp. | | | | | | | 29,655 | | | | 1,273,089 | |

Swiss Re AG | | | | | | | 8,480 | | | | 838,249 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 17,000,196 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 67,118,875 | |

| | | | | | | | | | | | |

Health Care – 8.0% | | | | | | | | | | | | |

Biotechnology – 1.5% | | | | | | | | | | | | |

Amgen, Inc. | | | | | | | 3,893 | | | | 739,982 | |

Celgene Corp.(a) | | | | | | | 59,109 | | | | 4,913,140 | |

Gilead Sciences, Inc. | | | | | | | 58,760 | | | | 3,820,575 | |

Spark Therapeutics, Inc.(a) | | | | | | | 4,403 | | | | 498,860 | |

Vertex Pharmaceuticals, Inc.(a) | | | | | | | 3,080 | | | | 581,350 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 10,553,907 | |

| | | | | | | | | | | | |

Health Care Equipment & Supplies – 1.6% | | | | | | | | | | | | |

Abbott Laboratories | | | | | | | 89,869 | | | | 6,975,632 | |

Baxter International, Inc. | | | | | | | 10,858 | | | | 811,418 | |

Koninklijke Philips NV | | | | | | | 11,693 | | | | 465,290 | |

Medtronic PLC | | | | | | | 10,333 | | | | 935,137 | |

ResMed, Inc. | | | | | | | 268 | | | | 27,451 | |

Stryker Corp. | | | | | | | 1,210 | | | | 228,097 | |

West Pharmaceutical Services, Inc. | | | | | | | 18,523 | | | | 1,940,284 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 11,383,309 | |

| | | | | | | | | | | | |

Health Care Providers & Services – 1.2% | | | | | | | | | | | | |

Anthem, Inc. | | | | | | | 19,740 | | | | 5,936,410 | |

Centene Corp.(a) | | | | | | | 11,002 | | | | 669,912 | |

CVS Health Corp. | | | | | | | 774 | | | | 44,760 | |

Humana, Inc. | | | | | | | 1,186 | | | | 338,057 | |

| | |

| |

| abfunds.com | | AB ALL MARKET TOTAL RETURN PORTFOLIO | 19 |

CONSOLIDATED PORTFOLIO OF INVESTMENTS(continued)

| | | | | | | | | | | | |

| Company | | | | | Shares | | | U.S. $ Value | |

| |

McKesson Corp. | | | | | | | 5,951 | | | $ | 756,729 | |

UnitedHealth Group, Inc. | | | | | | | 3,893 | | | | 942,963 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 8,688,831 | |

| | | | | | | | | | | | |

Life Sciences Tools & Services – 0.8% | | | | | | | | | | | | |

IQVIA Holdings, Inc.(a) | | | | | | | 33,287 | | | | 4,663,509 | |

Pacific Biosciences of California, Inc.(a) | | | | | | | 103,085 | | | | 753,551 | |

Sartorius Stedim Biotech | | | | | | | 3,475 | | | | 408,751 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 5,825,811 | |

| | | | | | | | | | | | |

Pharmaceuticals – 2.9% | | | | | | | | | | | | |

Astellas Pharma, Inc. | | | | | | | 48,800 | | | | 756,625 | |

Bausch Health Cos., Inc.(a) | | | | | | | 13,200 | | | | 313,562 | |

Bristol-Myers Squibb Co. | | | | | | | 18,510 | | | | 956,227 | |

BTG PLC(a) | | | | | | | 23,345 | | | | 257,927 | |

Eli Lilly & Co. | | | | | | | 7,958 | | | | 1,005,016 | |

Endo International PLC(a) | | | | | | | 3,078 | | | | 33,827 | |

Horizon Pharma PLC(a) | | | | | | | 1,435 | | | | 41,629 | |

Johnson & Johnson | | | | | | | 7,577 | | | | 1,035,321 | |

Merck & Co., Inc. | | | | | | | 39,418 | | | | 3,204,290 | |

Novo Nordisk A/S – Class B | | | | | | | 21,520 | | | | 1,055,031 | |

Pfizer, Inc. | | | | | | | 62,296 | | | | 2,700,532 | |

Roche Holding AG | | | | | | | 15,526 | | | | 4,308,841 | |

Sanofi | | | | | | | 11,981 | | | | 999,088 | |

UCB SA | | | | | | | 4,608 | | | | 386,061 | |

Zoetis, Inc. | | | | | | | 45,990 | | | | 4,333,637 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 21,387,614 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 57,839,472 | |

| | | | | | | | | | | | |

Consumer Discretionary – 6.8% | | | | | | | | | | | | |

Auto Components – 0.6% | | | | | | | | | | | | |

Aptiv PLC | | | | | | | 48,460 | | | | 4,027,511 | |

Atd New Holdings, Inc.(a)(b)(c) | | | | | | | 2,609 | | | | 46,962 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 4,074,473 | |

| | | | | | | | | | | | |

Automobiles – 0.0% | | | | | | | | | | | | |

BAIC Motor Corp., Ltd.(e) | | | | | | | 133,500 | | | | 84,857 | |

| | | | | | | | | | | | |

| | | |

Diversified Consumer Services – 0.8% | | | | | | | | | | | | |

H&R Block, Inc. | | | | | | | 27,729 | | | | 669,655 | |

Laureate Education, Inc. – Class A(a) | | | | | | | 3,231 | | | | 49,402 | |

Service Corp. International/US | | | | | | | 97,183 | | | | 4,017,545 | |

Sotheby’s(a) | | | | | | | 29,566 | | | | 1,297,061 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 6,033,663 | |

| | | | | | | | | | | | |

Hotels, Restaurants & Leisure – 1.8% | | | | | | | | | | | | |

Aristocrat Leisure Ltd. | | | | | | | 60,970 | | | | 1,065,019 | |

Caesars Entertainment Corp.(a) | | | | | | | 5,492 | | | | 47,341 | |

Choice Hotels International, Inc. | | | | | | | 7,129 | | | | 569,179 | |

Compass Group PLC | | | | | | | 80,008 | | | | 1,766,979 | |

| | |

| |

| 20 | AB ALL MARKET TOTAL RETURN PORTFOLIO | | abfunds.com |

CONSOLIDATED PORTFOLIO OF INVESTMENTS(continued)

| | | | | | | | | | | | |

| Company | | | | | Shares | | | U.S. $ Value | |

| |

eDreams ODIGEO SA(a) | | | | | | | 29,487 | | | $ | 93,912 | |

Las Vegas Sands Corp. | | | | | | | 29,452 | | | | 1,809,236 | |

McDonald’s Corp. | | | | | | | 6,880 | | | | 1,264,819 | |

Starbucks Corp. | | | | | | | 91,868 | | | | 6,454,646 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 13,071,131 | |

| | | | | | | | | | | | |

Household Durables – 0.1% | | | | | | | | | | | | |

Auto Trader Group PLC(e) | | | | | | | 100,510 | | | | 634,514 | |

Hovnanian Enterprises, Inc. – Class A(a) | | | | | | | 7,965 | | | | 5,393 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 639,907 | |

| | | | | | | | | | | | |

Internet & Direct Marketing Retail – 1.0% | | | | | | | | | | | | |

Amazon.com, Inc.(a) | | | | | | | 1,075 | | | | 1,762,817 | |

Booking Holdings, Inc.(a) | | | | | | | 2,742 | | | | 4,653,284 | |

Nutrisystem, Inc. | | | | | | | 28,494 | | | | 1,233,220 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 7,649,321 | |

| | | | | | | | | | | | |

Media – 0.2% | | | | | | | | | | | | |

Clear Channel Outdoor Holdings, Inc. – Class A(a) | | | | | | | 7,440 | | | | 40,771 | |

Tribune Media Co. – Class A | | | | | | | 32,438 | | | | 1,499,609 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 1,540,380 | |

| | | | | | | | | | | | |

Multiline Retail – 0.3% | | | | | | | | | | | | |

Dollar General Corp. | | | | | | | 11,400 | | | | 1,350,444 | |

Lotte Shopping Co., Ltd. | | | | | | | 801 | | | | 135,954 | |

Next PLC | | | | | | | 8,032 | | | | 541,706 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 2,028,104 | |

| | | | | | | | | | | | |

Specialty Retail – 1.7% | | | | | | | | | | | | |

AutoZone, Inc.(a) | | | | | | | 1,130 | | | | 1,061,036 | |

Home Depot, Inc. (The) | | | | | | | 12,027 | | | | 2,226,678 | |

O’Reilly Automotive, Inc.(a) | | | | | | | 2,256 | | | | 839,142 | |

Ross Stores, Inc. | | | | | | | 19,937 | | | | 1,890,626 | |

TJX Cos., Inc. (The) | | | | | | | 31,330 | | | | 1,606,916 | |

Ulta Salon Cosmetics & Fragrance, Inc.(a) | | | | | | | 14,628 | | | | 4,571,104 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 12,195,502 | |

| | | | | | | | | | | | |

Textiles, Apparel & Luxury Goods – 0.3% | | | | | | | | | | | | |

Samsonite International SA(a)(e) | | | | | | | 659,700 | | | | 1,960,490 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 49,277,828 | |

| | | | | | | | | | | | |

Industrials – 5.7% | | | | | | | | | | | | |

Aerospace & Defense – 1.3% | | | | | | | | | | | | |

Arconic, Inc. | | | | | | | 34,769 | | | | 642,879 | |

BAE Systems PLC | | | | | | | 96,250 | | | | 593,446 | |

Boeing Co. (The) | | | | | | | 4,190 | | | | 1,843,432 | |

Esterline Technologies Corp.(a) | | | | | | | 9,814 | | | | 1,194,855 | |

Harris Corp. | | | | | | | 4,660 | | | | 768,574 | |

L3 Technologies, Inc. | | | | | | | 7,382 | | | | 1,563,138 | |

| | |

| |

| abfunds.com | | AB ALL MARKET TOTAL RETURN PORTFOLIO | 21 |

CONSOLIDATED PORTFOLIO OF INVESTMENTS(continued)

| | | | | | | | | | | | |

| Company | | | | | Shares | | | U.S. $ Value | |

| |

Raytheon Co. | | | | | | | 12,120 | | | $ | 2,260,380 | |

Spirit AeroSystems Holdings, Inc. – Class A | | | | | | | 8,491 | | | | 838,911 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 9,705,615 | |

| | | | | | | | | | | | |

Air Freight & Logistics – 0.1% | | | | | | | | | | | | |

CH Robinson Worldwide, Inc. | | | | | | | 5,956 | | | | 538,303 | |

Hyundai Glovis Co., Ltd. | | | | | | | 1,068 | | | | 132,295 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 670,598 | |

| | | | | | | | | | | | |

Airlines – 0.2% | | | | | | | | | | | | |

Qantas Airways Ltd. | | | | | | | 207,000 | | | | 841,571 | |

United Continental Holdings, Inc.(a) | | | | | | | 8,070 | | | | 708,627 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 1,550,198 | |

| | | | | | | | | | | | |

Building Products – 0.8% | | | | | | | | | | | | |

Allegion PLC | | | | | | | 45,248 | | | | 4,070,510 | |

Lennox International, Inc. | | | | | | | 530 | | | | 129,983 | |

LIXIL Group Corp. | | | | | | | 18,700 | | | | 253,343 | |

USG Corp. | | | | | | | 34,497 | | | | 1,487,166 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 5,941,002 | |

| | | | | | | | | | | | |

Commercial Services & Supplies – 0.5% | | | | | | | | | | | | |

Republic Services, Inc. – Class A | | | | | | | 10,530 | | | | 825,868 | |

Secom Co., Ltd. | | | | | | | 28,400 | | | | 2,456,580 | |

Toppan Printing Co., Ltd. | | | | | | | 16,700 | | | | 266,014 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 3,548,462 | |

| | | | | | | | | | | | |

Construction & Engineering – 0.1% | | | | | | | | | | | | |

Daelim Industrial Co., Ltd. | | | | | | | 1,826 | | | | 151,739 | |

GS Engineering & Construction Corp. | | | | | | | 4,040 | | | | 153,641 | |

Obayashi Corp. | | | | | | | 28,500 | | | | 277,799 | |

Willscot Corp.(c)(d) | | | | | | | 1,235 | | | | 12,585 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 595,764 | |

| | | | | | | | | | | | |

Consumer Cyclical - Automotive – 0.0% | | | | | | | | | | | | |

Exide Technologies(a)(b)(d)(f) | | | | | | | 2,460 | | | | 172 | |

Exide Technologies/Old(a)(b)(d)(f) | | | | | | | 1,244 | | | | 87 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 259 | |

| | | | | | | | | | | | |

Electrical Equipment – 0.0% | | | | | | | | | | | | |

Emerson Electric Co. | | | | | | | 1,156 | | | | 78,781 | |

| | | | | | | | | | | | |

| | | |

Industrial Conglomerates – 0.0% | | | | | | | | | | | | |

SK Holdings Co., Ltd. | | | | | | | 672 | | | | 162,821 | |

| | | | | | | | | | | | |

| | | |

Machinery – 0.9% | | | | | | | | | | | | |

Dover Corp. | | | | | | | 39,070 | | | | 3,537,007 | |

Kone Oyj – Class B(g) | | | | | | | 27,610 | | | | 1,348,983 | |

Mitsubishi Heavy Industries Ltd. | | | | | | | 7,500 | | | | 305,853 | |

PACCAR, Inc. | | | | | | | 11,560 | | | | 783,768 | |

Stanley Black & Decker, Inc. | | | | | | | 5,708 | | | | 755,911 | |

Weichai Power Co., Ltd. – Class H | | | | | | | 110,000 | | | | 153,146 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 6,884,668 | |

| | | | | | | | | | | | |

| | |

| |

| 22 | AB ALL MARKET TOTAL RETURN PORTFOLIO | | abfunds.com |

CONSOLIDATED PORTFOLIO OF INVESTMENTS(continued)

| | | | | | | | | | | | |

| Company | | | | | Shares | | | U.S. $ Value | |

| |

Professional Services – 1.5% | | | | | | | | | | | | |

Experian PLC | | | | | | | 31,390 | | | $ | 816,600 | |

RELX PLC | | | | | | | 153,142 | | | | 3,515,290 | |

Robert Half International, Inc. | | | | | | | 10,960 | | | | 747,362 | |

Verisk Analytics, Inc. – Class A(a) | | | | | | | 34,270 | | | | 4,332,756 | |

Wolters Kluwer NV | | | | | | | 18,190 | | | | 1,198,656 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 10,610,664 | |

| | | | | | | | | | | | |

Road & Rail – 0.1% | | | | | | | | | | | | |

ALD SA(e) | | | | | | | 43,783 | | | | 631,738 | |

| | | | | | | | | | | | |

| | | |

Trading Companies & Distributors – 0.0% | | | | | | | | | | | | |

Emeco Holdings Ltd.(a) | | | | | | | 4,397 | | | | 6,661 | |

| | | | | | | | | | | | |

| | | |

Transportation Infrastructure – 0.2% | | | | | | | | | | | | |

Airports of Thailand PCL | | | | | | | 71,900 | | | | 154,010 | |

Flughafen Zurich AG | | | | | | | 5,443 | | | | 969,046 | |

Zhejiang Expressway Co., Ltd. – Class H | | | | | | | 154,000 | | | | 160,719 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 1,283,775 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 41,671,006 | |

| | | | | | | | | | | | |

Communication Services – 5.6% | | | | | | | | | | | | |

Diversified Telecommunication Services – 0.9% | | | | | | | | | | | | |

China Communications Services Corp., Ltd. – Class H | | | | | | | 190,000 | | | | 191,144 | |

Elisa Oyj | | | | | | | 9,356 | | | | 392,582 | |

HKT Trust & HKT Ltd. – Class SS | | | | | | | 1,356,000 | | | | 2,117,846 | |

LG Uplus Corp. | | | | | | | 9,547 | | | | 127,146 | |

Nippon Telegraph & Telephone Corp. | | | | | | | 37,400 | | | | 1,616,527 | |

Spark New Zealand Ltd. | | | | | | | 102,876 | | | | 261,157 | |

Telenor ASA | | | | | | | 20,515 | | | | 400,080 | |

TELUS Corp. | | | | | | | 16,830 | | | | 611,326 | |

Verizon Communications, Inc. | | | | | | | 14,101 | | | | 802,629 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 6,520,437 | |

| | | | | | | | | | | | |

Entertainment – 0.4% | | | | | | | | | | | | |

Daiichikosho Co., Ltd. | | | | | | | 12,600 | | | | 622,567 | |

Live Nation Entertainment, Inc.(a) | | | | | | | 12,631 | | | | 714,409 | |

NCSoft Corp. | | | | | | | 353 | | | | 144,739 | |

Netflix, Inc.(a) | | | | | | | 703 | | | | 251,744 | |

Twenty-First Century Fox, Inc. – Class B | | | | | | | 12,380 | | | | 620,981 | |

Viacom, Inc. – Class B | | | | | | | 23,725 | | | | 693,245 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 3,047,685 | |

| | | | | | | | | | | | |

Interactive Media & Services – 2.2% | | | | | | | | | | | | |

Alphabet, Inc. – Class A(a) | | | | | | | 837 | | | | 942,922 | |

Alphabet, Inc. – Class C(a) | | | | | | | 9,075 | | | | 10,163,274 | |

Autohome, Inc. (ADR)(a)(g) | | | | | | | 6,560 | | | | 616,968 | |

Facebook, Inc. – Class A(a) | | | | | | | 26,740 | | | | 4,317,173 | |

Twitter, Inc.(a) | | | | | | | 3,170 | | | | 97,573 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 16,137,910 | |

| | | | | | | | | | | | |

| | |

| |

| abfunds.com | | AB ALL MARKET TOTAL RETURN PORTFOLIO | 23 |

CONSOLIDATED PORTFOLIO OF INVESTMENTS(continued)

| | | | | | | | | | | | |

| Company | | | | | Shares | | | U.S. $ Value | |

| |

Media – 1.0% | | | | | | | | | | | | |

CBS Corp. – Class B | | | | | | | 14,198 | | | $ | 712,881 | |

Charter Communications, Inc. – Class A(a) | | | | | | | 193 | | | | 66,568 | |

Comcast Corp. – Class A | | | | | | | 32,438 | | | | 1,254,377 | |

DISH Network Corp. – Class A(a) | | | | | | | 609 | | | | 19,799 | |

Multichoice Group Ltd. | | | | | | | 12,910 | | | | 96,227 | |

Naspers Ltd. – Class N | | | | | | | 12,910 | | | | 2,784,287 | |

Omnicom Group, Inc. | | | | | | | 11,130 | | | | 842,541 | |

Quebecor, Inc. – Class B | | | | | | | 40,290 | | | | 978,815 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 6,755,495 | |

| | | | | | | | | | | | |

Wireless Telecommunication Services – 1.1% | | | | | | | | | | | | |

China Mobile Ltd. | | | | | | | 124,000 | | | | 1,309,746 | |

DiGi.Com Bhd | | | | | | | 147,100 | | | | 164,233 | |

Globe Telecom, Inc. | | | | | | | 4,160 | | | | 152,620 | |

KDDI Corp. | | | | | | | 100,800 | | | | 2,436,304 | |

Millicom International Cellular SA | | | | | | | 11,028 | | | | 663,730 | |

SK Telecom Co., Ltd. | | | | | | | 603 | | | | 139,662 | |

SoftBank Group Corp. | | | | | | | 22,800 | | | | 2,115,710 | |

Sprint Corp.(a) | | | | | | | 189,563 | | | | 1,203,725 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 8,185,730 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 40,647,257 | |

| | | | | | | | | | | | |

Consumer Staples – 2.8% | | | | | | | | | | | | |

Beverages – 0.3% | | | | | | | | | | | | |

Ambev SA | | | | | | | 114,900 | | | | 527,063 | |

Coca-Cola Amatil Ltd. | | | | | | | 47,456 | | | | 268,342 | |

PepsiCo, Inc. | | | | | | | 5,830 | | | | 674,181 | |

Wuliangye Yibin Co., Ltd. – Class A | | | | | | | 75,190 | | | | 803,102 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 2,272,688 | |

| | | | | | | | | | | | |

Food & Staples Retailing – 0.9% | | | | | | | | | | | | |

Casino Guichard Perrachon SA | | | | | | | 6,020 | | | | 318,338 | |

Colruyt SA | | | | | | | 3,817 | | | | 272,247 | |

Dairy Farm International Holdings Ltd. | | | | | | | 18,300 | | | | 163,808 | |

Empire Co., Ltd. – Class A | | | | | | | 13,972 | | | | 324,575 | |

Koninklijke Ahold Delhaize NV | | | | | | | 58,444 | | | | 1,506,232 | |

Kroger Co. (The) | | | | | | | 25,720 | | | | 754,368 | |

Seven & i Holdings Co., Ltd.(g) | | | | | | | 11,100 | | | | 488,529 | |

Southeastern Grocers, Inc. Npv(a)(b)(c)(d) | | | | | | | 2,013 | | | | 71,461 | |

Sysco Corp. | | | | | | | 11,220 | | | | 757,911 | |

Walgreens Boots Alliance, Inc. | | | | | | | 10,305 | | | | 733,613 | |

Walmart, Inc. | | | | | | | 14,650 | | | | 1,450,203 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 6,841,285 | |

| | | | | | | | | | | | |

Food Products – 0.3% | | | | | | | | | | | | |

Danone SA | | | | | | | 9,315 | | | | 703,555 | |

Marine Harvest ASA(a)(g) | | | | | | | 17,245 | | | | 397,964 | |

| | |

| |

| 24 | AB ALL MARKET TOTAL RETURN PORTFOLIO | | abfunds.com |

CONSOLIDATED PORTFOLIO OF INVESTMENTS(continued)

| | | | | | | | | | | | |

| Company | | | | | Shares | | | U.S. $ Value | |

| |

Nestle Malaysia Bhd | | | | | | | 4,300 | | | $ | 156,265 | |

Salmar ASA | | | | | | | 18,950 | | | | 907,829 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 2,165,613 | |

| | | | | | | | | | | | |

Household Products – 0.3% | | | | | | | | | | | | |

Kimberly-Clark Corp. | | | | | | | 718 | | | | 83,884 | |

Procter & Gamble Co. (The) | | | | | | | 24,150 | | | | 2,379,982 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 2,463,866 | |

| | | | | | | | | | | | |

Personal Products – 0.3% | | | | | | | | | | | | |

L’Oreal SA | | | | | | | 4,942 | | | | 1,246,420 | |

Unilever PLC | | | | | | | 11,570 | | | | 615,962 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 1,862,382 | |

| | | | | | | | | | | | |

Tobacco – 0.7% | | | | | | | | | | | | |

Altria Group, Inc. | | | | | | | 15,326 | | | | 803,236 | |

British American Tobacco PLC | | | | | | | 33,424 | | | | 1,225,427 | |

Imperial Brands PLC | | | | | | | 27,900 | | | | 929,693 | |

KT&G Corp. | | | | | | | 1,770 | | | | 165,932 | |

Philip Morris International, Inc. | | | | | | | 20,256 | | | | 1,761,057 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 4,885,345 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 20,491,179 | |

| | | | | | | | | | | | |

Energy – 2.0% | | | | | | | | | | | | |

Energy Equipment & Services – 0.1% | | | | | | | | | | | | |

Helmerich & Payne, Inc. | | | | | | | 12,490 | | | | 676,958 | |

| | | | | | | | | | | | |

| | | |

Oil, Gas & Consumable Fuels – 1.9% | | | | | | | | | | | | |

Berry Petroleum Corp. | | | | | | | 9,528 | | | | 121,291 | |

BP PLC | | | | | | | 30,721 | | | | 217,790 | |

CHC Group LLC(a)(f) | | | | | | | 2,966 | | | | 148 | |

Chevron Corp. | | | | | | | 5,027 | | | | 601,129 | |

Denbury Resources, Inc.(a) | | | | | | | 2,348 | | | | 4,508 | |

Encana Corp. | | | | | | | 213,272 | | | | 1,546,214 | |

Equinor ASA | | | | | | | 39,680 | | | | 892,481 | |

Exxon Mobil Corp. | | | | | | | 3,422 | | | | 270,441 | |

Galp Energia SGPS SA | | | | | | | 9,687 | | | | 158,823 | |

Gazprom PJSC (Sponsored ADR) | | | | | | | 33,560 | | | | 158,403 | |

GS Holdings Corp. | | | | | | | 3,130 | | | | 149,060 | |

Halcon Resources Corp.(a)(g) | | | | | | | 579 | | | | 869 | |

HollyFrontier Corp. | | | | | | | 8,418 | | | | 431,002 | |

K2016470219 South Africa Ltd. – Series A(a)(b)(c)(d) | | | | | | | 465,862 | | | | – 0 | – |

K2016470219 South Africa Ltd. – Series B(a)(b)(c)(d) | | | | | | | 73,623 | | | | – 0 | – |

Kinder Morgan, Inc./DE | | | | | | | 36,500 | | | | 699,340 | |

LUKOIL PJSC (Sponsored ADR) | | | | | | | 17,354 | | | | 1,449,927 | |

Marathon Petroleum Corp. | | | | | | | 6,921 | | | | 429,171 | |

Paragon Litigation – Class A(b)(c) | | | | | | | 649 | | | | 528 | |

Paragon Litigation – Class B(b)(c) | | | | | | | 974 | | | | 34,821 | |

| | |

| |

| abfunds.com | | AB ALL MARKET TOTAL RETURN PORTFOLIO | 25 |

CONSOLIDATED PORTFOLIO OF INVESTMENTS(continued)

| | | | | | | | | | | | |

| Company | | | | | Shares | | | U.S. $ Value | |

| |

Peabody Energy Corp. | | | | | | | 1,456 | | | $ | 44,918 | |

Petroleo Brasileiro SA | | | | | | | 8,900 | | | | 70,752 | |

Phillips 66 | | | | | | | 4,780 | | | | 460,601 | |

Roan Resources, Inc.(a) | | | | | | | 99 | | | | 769 | |

Royal Dutch Shell PLC – Class B | | | | | | | 123,696 | | | | 3,880,375 | |

Tervita Corp.(a) | | | | | | | 62,228 | | | | 334,323 | |

TOTAL SA | | | | | | | 16,944 | | | | 964,430 | |

Triangle Petroleum Corp.(a) | | | | | | | 7,408 | | | | 122 | |

Valero Energy Corp. | | | | | | | 6,221 | | | | 507,385 | |

Vantage Drilling International(a)(b)(c) | | | | | | | 200 | | | | 51,200 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 13,480,821 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 14,157,779 | |

| | | | | | | | | | | | |

Materials – 1.6% | | | | | | | | | | | | |

Chemicals – 1.0% | | | | | | | | | | | | |

BASF SE | | | | | | | 33,409 | | | | 2,542,997 | |

CF Industries Holdings, Inc. | | | | | | | 8,388 | | | | 353,974 | |

Covestro AG(e) | | | | | | | 5,290 | | | | 301,198 | |

Ecolab, Inc. | | | | | | | 15,740 | | | | 2,658,643 | |

Indorama Ventures PCL | | | | | | | 90,700 | | | | 148,229 | |

Ingevity Corp.(a) | | | | | | | 2 | | | | 230 | |

Methanex Corp. | | | | | | | 4,296 | | | | 241,806 | |

Mitsubishi Chemical Holdings Corp. | | | | | | | 31,900 | | | | 235,907 | |

Sinopec Shanghai Petrochemical Co., Ltd. | | | | | | | 213,400 | | | | 175,992 | |

Sinopec Shanghai Petrochemical Co., Ltd. – Class H | | | | | | | 280,000 | | | | 141,959 | |

Sumitomo Chemical Co., Ltd. | | | | | | | 52,800 | | | | 262,534 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 7,063,469 | |

| | | | | | | | | | | | |

Containers & Packaging – 0.2% | | | | | | | | | | | | |

Bemis Co., Inc. | | | | | | | 28,467 | | | | 1,505,904 | |

RPC Group PLC | | | | | | | 11,207 | | | | 117,467 | |

Westrock Co. | | | | | | | 16 | | | | 598 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 1,623,969 | |

| | | | | | | | | | | | |

Metals & Mining – 0.3% | | | | | | | | | | | | |

Artsonig Pty Ltd.(b)(c)(d) | | | | | | | 51,133 | | | | 767 | |

BHP Group Ltd. | | | | | | | 7,580 | | | | 200,198 | |

Cia Siderurgica Nacional SA(a) | | | | | | | 56,300 | | | | 196,053 | |

Constellium NV – Class A(a) | | | | | | | 8,939 | | | | 84,563 | |

Goldcorp, Inc. | | | | | | | 142,046 | | | | 1,497,165 | |

Maanshan Iron & Steel Co., Ltd. – Class H | | | | | | | 342,000 | | | | 162,873 | |

Neenah Enterprises, Inc.(a)(b)(c)(d) | | | | | | | 10,896 | | | | 32,797 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 2,174,416 | |

| | | | | | | | | | | | |

Paper & Forest Products – 0.1% | | | | | | | | | | | | |

Mondi PLC | | | | | | | 23,549 | | | | 539,100 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 11,400,954 | |

| | | | | | | | | | | | |

| | |

| |

| 26 | AB ALL MARKET TOTAL RETURN PORTFOLIO | | abfunds.com |

CONSOLIDATED PORTFOLIO OF INVESTMENTS(continued)

| | | | | | | | | | | | |

| Company | | | | | Shares | | | U.S. $ Value | |

| |

Utilities – 1.2% | | | | | | | | | | | | |

Electric Utilities – 0.7% | | | | | | | | | | | | |

CEZ AS | | | | | | | 6,466 | | | $ | 156,653 | |

EDP – Energias de Portugal SA | | | | | | | 310,750 | | | | 1,139,365 | |

Electricite de France SA | | | | | | | 24,190 | | | | 351,198 | |

Enel SpA | | | | | | | 75,480 | | | | 456,438 | |

Exelon Corp. | | | | | | | 16,838 | | | | 818,158 | |

Manila Electric Co. | | | | | | | 23,630 | | | | 167,940 | |

Orsted A/S(e) | | | | | | | 5,920 | | | | 429,697 | |

PPL Corp. | | | | | | | 23,666 | | | | 761,335 | |

Red Electrica Corp. SA | | | | | | | 9,760 | | | | 210,866 | |

Terna Rete Elettrica Nazionale SpA | | | | | | | 63,052 | | | | 392,260 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 4,883,910 | |

| | | | | | | | | | | | |

Gas Utilities – 0.1% | | | | | | | | | | | | |

Tokyo Gas Co., Ltd. | | | | | | | 28,800 | | | | 793,928 | |

| | | | | | | | | | | | |

| | | |

Independent Power and Renewable Electricity Producers – 0.1% | | | | | | | | | | | | |

AES Corp./VA | | | | | | | 45,645 | | | | 786,463 | |

| | | | | | | | | | | | |

| | | |

Multi-Utilities – 0.2% | | | | | | | | | | | | |

Ameren Corp. | | | | | | | 9,660 | | | | 688,179 | |

CenterPoint Energy, Inc. | | | | | | | 24,008 | | | | 723,601 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 1,411,780 | |

| | | | | | | | | | | | |

Water Utilities – 0.1% | | | | | | | | | | | | |

Guangdong Investment Ltd. | | | | | | | 584,000 | | | | 1,119,472 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 8,995,553 | |

| | | | | | | | | | | | |

Real Estate – 1.2% | | | | | | | | | | | | |