UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-649

Fidelity Puritan Trust

(Exact name of registrant as specified in charter)

82 Devonshire St., Boston, Massachusetts 02109

(Address of principal executive offices) (Zip code)

Scott C. Goebel, Secretary

82 Devonshire St.

Boston, Massachusetts 02109

(Name and address of agent for service)

Registrant's telephone number, including area code: 617-563-7000

Date of fiscal year end: | August 31 |

| |

Date of reporting period: | August 31, 2012 |

Item 1. Reports to Stockholders

Fidelity®

Balanced

Fund -

Class K

Annual Report

August 31, 2012

(Fidelity Cover Art)

Contents

Performance | (Click Here) | How the fund has done over time. |

Management's Discussion of Fund Performance | (Click Here) | The Portfolio Manager's review of fund performance and strategy. |

Shareholder Expense Example | (Click Here) | An example of shareholder expenses. |

Investment Changes | (Click Here) | A summary of major shifts in the fund's investments over the past six months. |

Investments | (Click Here) | A complete list of the fund's investments with their market values. |

Financial Statements | (Click Here) | Statements of assets and liabilities, operations, and changes in net assets, as well as financial highlights. |

Notes | (Click Here) | Notes to the financial statements. |

Report of Independent Registered Public Accounting Firm | (Click Here) | |

Trustees and Officers | (Click Here) | |

Distributions | (Click Here) | |

Board Approval of Investment Advisory Contracts and Management Fees | (Click Here) | |

To view a fund's proxy voting guidelines and proxy voting record for the 12-month period ended June 30, visit http://www.fidelity.com/proxyvotingresults or visit the Securities and Exchange Commission's (SEC) web site at http://www.sec.gov. You may also call 1-800-835-5092 to request a free copy of the proxy voting guidelines.

Standard & Poor's, S&P and S&P 500 are registered service marks of The McGraw-Hill Companies, Inc. and have been licensed for use by Fidelity Distributors Corporation.

Other third party marks appearing herein are the property of their respective owners.

All other marks appearing herein are registered or unregistered trademarks or service marks of FMR LLC or an affiliated company. © 2012 FMR LLC. All rights reserved.

Annual Report

This report and the financial statements contained herein are submitted for the general information of the shareholders of the fund. This report is not authorized for distribution to prospective investors in the fund unless preceded or accompanied by an effective prospectus.

A fund files its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. Forms N-Q are available on the SEC's web site at http://www.sec.gov. A fund's Forms N-Q may be reviewed and copied at the SEC's Public Reference Room in Washington, DC. Information regarding the operation of the SEC's Public Reference Room may be obtained by calling 1-800-SEC-0330. For a complete list of a fund's portfolio holdings, view the most recent holdings listing, semiannual report, or annual report on Fidelity's web site at http://www.fidelity.com, http://www.advisor.fidelity.com, or http://www.401k.com, as applicable.

NOT FDIC INSURED • MAY LOSE VALUE • NO BANK GUARANTEE

Neither the fund nor Fidelity Distributors Corporation is a bank.

Annual Report

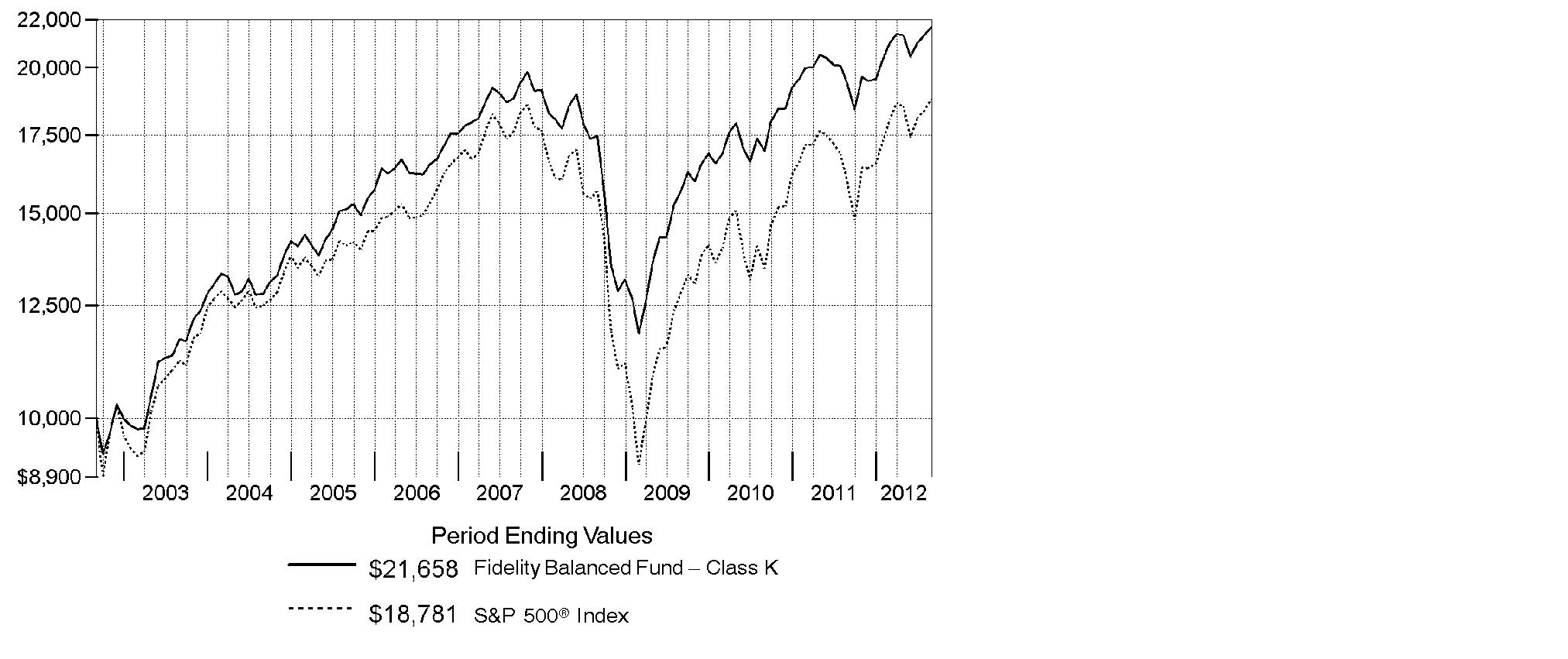

Average annual total return reflects the change in the value of an investment, assuming reinvestment of the class' distributions from dividend income and capital gains (the profits earned upon the sale of securities that have grown in value, if any) and assuming a constant rate of performance each year. The $10,000 table and the fund's returns do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. During periods of reimbursement by Fidelity, a fund's total return will be greater than it would be had the reimbursement not occurred. How a fund did yesterday is no guarantee of how it will do tomorrow.

Average Annual Total Returns

Periods ended August 31, 2012 | Past 1

year | Past 5

years | Past 10

years |

Class K A | 12.03% | 2.84% | 8.03% |

A The initial offering of Class K shares took place on May 9, 2008. Returns prior to May 9, 2008 are those of Fidelity® Balanced Fund, the original class of the fund.

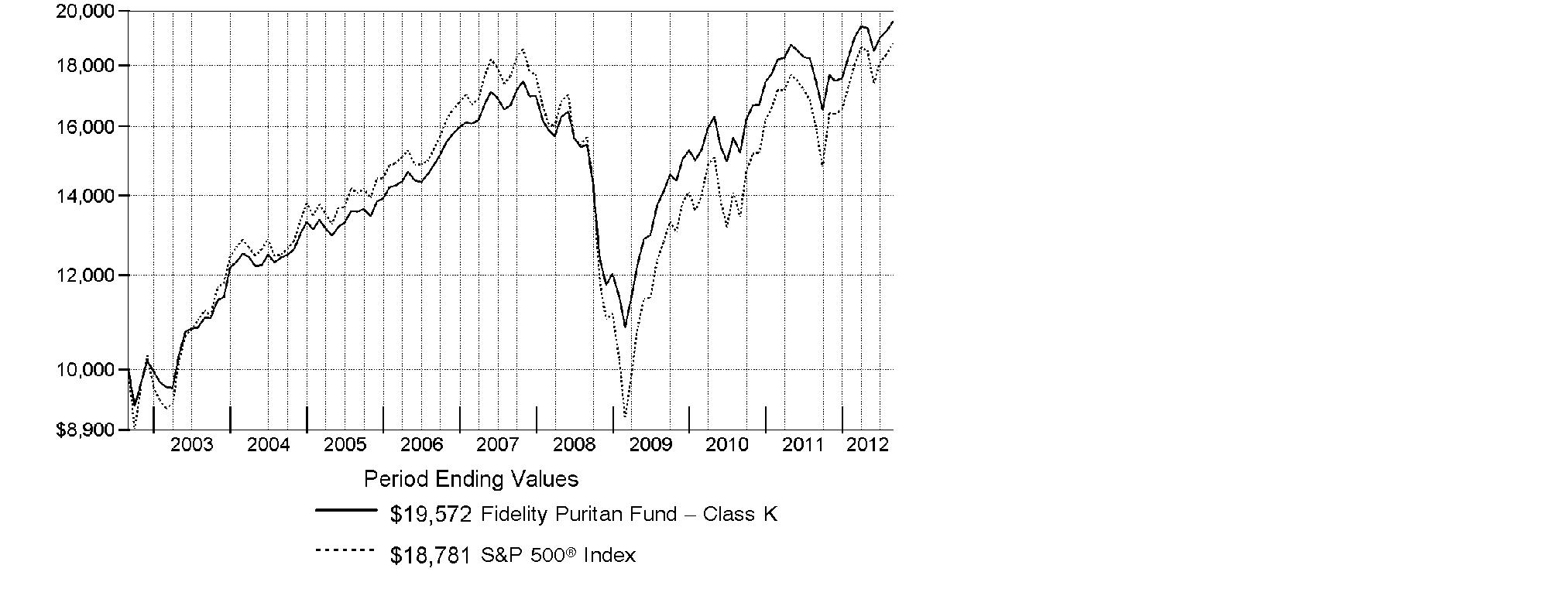

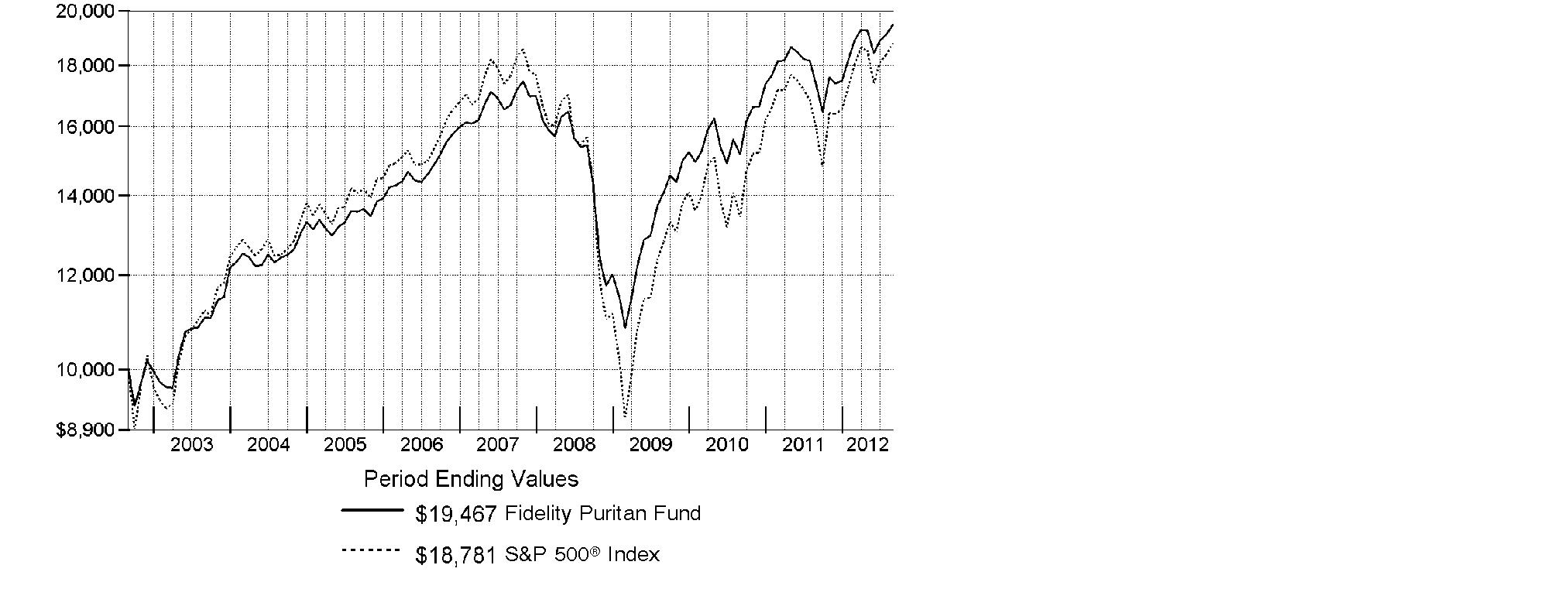

$10,000 Over 10 Years

Let's say hypothetically that $10,000 was invested in Fidelity® Balanced Fund - Class K on August 31, 2002. The chart shows how the value of your investment would have changed, and also shows how the S&P 500® Index performed over the same period. The initial offering of Class K took place on May 9, 2008. See above for additional information regarding the performance of Class K.

Annual Report

Market Recap: U.S. stocks posted a strong gain for the 12 months ending August 31, 2012, overcoming losses sustained last summer and extending an uptrend that began in March 2009. The broad-based S&P 500® Index added 18.00% for the 12-month period, while the blue-chip-laden Dow Jones Industrial AverageSM and technology-heavy Nasdaq Composite® Index rose 15.86% and 20.26%, respectively. Uncertainty prevailed early on, as Greece neared insolvency and fear of debt contagion in Europe led the S&P 500® to its lowest point in more than a year, in early October. Markets reversed course that same month, and the S&P 500® rose to its largest monthly gain in two decades. Despite a rough patch in the spring, U.S. stocks pushed ahead for much of the remainder of the period, fueled by solid corporate earnings, a reviving housing market and hope for a solution in the eurozone. Elsewhere, foreign developed-markets stocks languished amid the European turmoil and as local currencies weakened versus the dollar, leaving the MSCI® EAFE® Index up just 0.10%. In the fixed-income arena, the search for yield benefited high-income securities, which returned 13.01%, according to The BofA Merrill LynchSM US High Yield Constrained Index. Higher-quality debt registered a more muted advance, with the Barclays® U.S. Aggregate Bond Index - a proxy for investment-grade debt - returning 5.78%.

Comments from Robert Stansky, Head of Fidelity's Stock Selector Large Cap Group, which manages Fidelity® Balanced Fund: For the year, the fund's Class K shares returned 12.03%, trailing the 13.34% gain of the Fidelity Balanced Hybrid Composite IndexSM, a hypothetical blend of the total returns of the S&P 500 and the Barclays® U.S. Aggregate Bond Index, using weightings of 60% and 40%, respectively. Disappointing stock selection hurt performance, although the negative impact was modestly offset by our overweighting in equities. The fund benefited the most from our fixed-income investments, including good picks and an underweighting in investment-grade bonds, and a small out-of-index allocation to high-yield bonds. Looking at individual holdings, the biggest detractor was enterprise software firm Oracle, primarily due to positioning during the first half of the period. The stock declined sharply in December, due to concern about future earnings, and we sold it by period end. Our decision to not own telecom giant and benchmark component AT&T for nearly the entire period also detracted. We were concerned about the stock's valuation. Conversely, a sizable position in Apple was the fund's top individual contributor, as the company's iPad® tablet computer and iPhone® smartphone continued to define their respective categories, helping the stock maintain its run of strong performance.

The views expressed above reflect those of the portfolio manager(s) only through the end of the period as stated on the cover of this report and do not necessarily represent the views of Fidelity or any other person in the Fidelity organization. Any such views are subject to change at any time based upon market or other conditions and Fidelity disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Fidelity fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Fidelity fund.

Annual Report

Shareholder Expense Example

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, and (2) ongoing costs, including management fees and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (March 1, 2012 to August 31, 2012).

Actual Expenses

The first line of the accompanying table for each class of the Fund provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000.00 (for example, an $8,600 account value divided by $1,000.00 = 8.6), then multiply the result by the number in the first line for a class of the Fund under the heading entitled "Expenses Paid During Period" to estimate the expenses you paid on your account during this period. A small balance maintenance fee of $12.00 that is charged once a year may apply for certain accounts with a value of less than $2,000. This fee is not included in the table below. If it was, the estimate of expenses you paid during the period would be higher, and your ending account value lower, by this amount. In addition, the Fund, as a shareholder in the underlying Fidelity Central Funds, will indirectly bear its pro-rata share of the fees and expenses incurred by the underlying Fidelity Central Funds. These fees and expenses are not included in the Fund's annualized expense ratio used to calculate the expense estimate in the table below.

Hypothetical Example for Comparison Purposes

The second line of the accompanying table for each class of the Fund provides information about hypothetical account values and hypothetical expenses based on a Class' actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Class' actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds. A small balance maintenance fee of $12.00 that is charged once a year may apply for certain accounts with a value of less than $2,000. This fee is not included in the table below. If it was, the estimate of expenses you paid during the period would be higher, and your ending account value lower, by this amount. In addition, the Fund, as a shareholder in the underlying Fidelity Central Funds, will indirectly bear its pro-rata share of the fees and expenses incurred by the underlying Fidelity Central Funds. These fees and expenses are not included in the Fund's annualized expense ratio used to calculate the expense estimate in the table below.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transaction costs. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds.

Annual Report

| Annualized

Expense Ratio | Beginning

Account Value

March 1, 2012 | Ending

Account Value

August 31, 2012 | Expenses Paid

During Period*

March 1, 2012

to August 31, 2012 |

Balanced | .59% | | | |

Actual | | $ 1,000.00 | $ 1,031.80 | $ 3.01 |

HypotheticalA | | $ 1,000.00 | $ 1,022.17 | $ 3.00 |

Class K | .47% | | | |

Actual | | $ 1,000.00 | $ 1,032.30 | $ 2.40 |

HypotheticalA | | $ 1,000.00 | $ 1,022.77 | $ 2.39 |

A 5% return per year before expenses

* Expenses are equal to each Class' annualized expense ratio, multiplied by the average account value over the period, multiplied by 184/366 (to reflect the one-half year period). The fees and expenses of the underlying Fidelity Central Funds in which the Fund invests are not included in the Fund's annualized expense ratio.

Annual Report

Investment Changes (Unaudited)

The information in the following tables is based on the combined investments of the Fund and its pro-rata share of the investments of Fidelity's fixed-income central funds. |

Top Five Stocks as of August 31, 2012 |

| % of fund's

net assets | % of fund's net assets

6 months ago |

Apple, Inc. | 5.0 | 4.3 |

QUALCOMM, Inc. | 1.6 | 1.3 |

Microsoft Corp. | 1.6 | 1.3 |

Exxon Mobil Corp. | 1.5 | 0.9 |

Procter & Gamble Co. | 1.4 | 1.4 |

| 11.1 | |

Top Five Bond Issuers as of August 31, 2012 |

(with maturities greater than one year) | % of fund's

net assets | % of fund's net assets

6 months ago |

Fannie Mae | 9.2 | 5.4 |

U.S. Treasury Obligations | 5.1 | 10.0 |

Freddie Mac | 2.7 | 2.6 |

Ginnie Mae | 2.4 | 2.1 |

Wachovia Bank Commercial Mortgage Trust | 0.4 | 0.0 |

| 19.8 | |

Top Five Market Sectors as of August 31, 2012 |

| % of fund's

net assets | % of fund's net assets

6 months ago |

Information Technology | 14.1 | 13.6 |

Financials | 13.7 | 13.3 |

Energy | 8.9 | 9.6 |

Health Care | 8.1 | 7.4 |

Consumer Staples | 7.9 | 7.4 |

Asset Allocation (% of fund's net assets) |

As of August 31, 2012 * | As of February 29, 2012 ** |

| Stocks and Equity

Futures 64.2% | | | Stocks and Equity

Futures 62.8% | |

| Bonds 34.0% | | | Bonds 34.4% | |

| Convertible

Securities 0.1% | | | Convertible

Securities 0.1% | |

| Other Investments 0.3% | | | Other Investments 0.3% | |

| Short-Term

Investments and

Net Other Assets

(Liabilities) 1.4% | |  | Short-Term

Investments and

Net Other Assets

(Liabilities) 2.4% | |

* Foreign investments | 8.9% | | ** Foreign investments | 13.1% | |

Percentages are adjusted for the effect of futures and swap contracts, if applicable. An unaudited holdings listing for the Fund, which presents direct holdings as well as the pro-rata share of any securities and other investments held indirectly through its investment in underlying non-money market Fidelity Central Funds, is available at fidelity.com. |

Percentages in the above tables are adjusted for the effect of TBA Sale Commitments. |

Annual Report

Investments August 31, 2012

Showing Percentage of Net Assets

Common Stocks - 63.7% |

| Shares | | Value (000s) |

CONSUMER DISCRETIONARY - 6.4% |

Diversified Consumer Services - 0.0% |

Weight Watchers International, Inc. (e) | 100,727 | | $ 4,812 |

Hotels, Restaurants & Leisure - 1.2% |

Arcos Dorados Holdings, Inc. | 713,097 | | 9,420 |

Domino's Pizza, Inc. | 819,931 | | 29,058 |

Dunkin' Brands Group, Inc. | 341,877 | | 9,959 |

Icahn Enterprises LP rights (a) | 290,524 | | 0 |

McDonald's Corp. | 757,421 | | 67,782 |

Starbucks Corp. | 1,086,917 | | 53,922 |

Yum! Brands, Inc. | 1,130,472 | | 72,034 |

| | 242,175 |

Internet & Catalog Retail - 0.4% |

Kayak Software Corp. (e)(f) | 203,012 | | 5,542 |

Priceline.com, Inc. (a) | 111,242 | | 67,254 |

| | 72,796 |

Media - 2.8% |

Comcast Corp. Class A | 6,618,603 | | 221,922 |

DIRECTV (a) | 1,641,196 | | 85,490 |

Legend Pictures LLC (a)(p)(q) | 8,571 | | 9,164 |

News Corp. Class A | 4,894,779 | | 114,489 |

Sirius XM Radio, Inc. (a) | 5,666,600 | | 14,336 |

The Walt Disney Co. | 2,541,497 | | 125,728 |

| | 571,129 |

Multiline Retail - 0.3% |

Dollar General Corp. (a) | 1,420,365 | | 72,538 |

Specialty Retail - 1.5% |

AutoZone, Inc. (a) | 148,441 | | 53,682 |

CarMax, Inc. (a) | 261,919 | | 8,012 |

Limited Brands, Inc. | 550,498 | | 26,754 |

Lowe's Companies, Inc. | 4,013,003 | | 114,290 |

TJX Companies, Inc. | 2,170,980 | | 99,409 |

| | 302,147 |

Textiles, Apparel & Luxury Goods - 0.2% |

Under Armour, Inc. Class A (sub. vtg.) (a)(e) | 754,878 | | 43,941 |

TOTAL CONSUMER DISCRETIONARY | | 1,309,538 |

CONSUMER STAPLES - 7.2% |

Beverages - 2.6% |

Anheuser-Busch InBev SA NV | 655,741 | | 55,169 |

Common Stocks - continued |

| Shares | | Value (000s) |

CONSUMER STAPLES - continued |

Beverages - continued |

Coca-Cola Bottling Co. CONSOLIDATED | 118,433 | | $ 8,129 |

Coca-Cola FEMSA SAB de CV sponsored ADR | 30,925 | | 3,774 |

Coca-Cola Icecek A/S | 394,435 | | 7,025 |

Companhia de Bebidas das Americas (AmBev) (PN) sponsored ADR | 164,725 | | 6,195 |

Constellation Brands, Inc. Class A (sub. vtg.) (a) | 1,476,841 | | 48,647 |

Diageo PLC sponsored ADR | 494,843 | | 54,047 |

Embotelladora Andina SA sponsored ADR | 218,222 | | 7,184 |

Molson Coors Brewing Co. Class B | 628,844 | | 28,009 |

Monster Beverage Corp. (a) | 97,800 | | 5,763 |

Pernod Ricard SA | 344,150 | | 37,084 |

Remy Cointreau SA | 176,092 | | 20,113 |

The Coca-Cola Co. | 6,784,472 | | 253,739 |

| | 534,878 |

Food & Staples Retailing - 1.0% |

CVS Caremark Corp. | 3,242,038 | | 147,675 |

Drogasil SA | 434,400 | | 4,595 |

Kroger Co. | 801,453 | | 17,856 |

Safeway, Inc. | 278,105 | | 4,352 |

Wal-Mart Stores, Inc. | 394,834 | | 28,665 |

Walgreen Co. | 386,702 | | 13,828 |

| | 216,971 |

Food Products - 0.5% |

Bunge Ltd. | 348,589 | | 22,188 |

Green Mountain Coffee Roasters, Inc. (a) | 168,876 | | 4,105 |

Mead Johnson Nutrition Co. Class A | 137,761 | | 10,102 |

Nestle SA | 338,708 | | 21,056 |

Orion Corp. | 5,168 | | 4,194 |

Pilgrims Pride Corp. | 748,200 | | 3,980 |

Unilever NV (NY Reg.) | 1,018,331 | | 35,418 |

| | 101,043 |

Household Products - 1.6% |

Colgate-Palmolive Co. | 327,533 | | 34,820 |

Procter & Gamble Co. | 4,164,463 | | 279,810 |

Spectrum Brands Holdings, Inc. | 202,786 | | 7,469 |

| | 322,099 |

Common Stocks - continued |

| Shares | | Value (000s) |

CONSUMER STAPLES - continued |

Personal Products - 0.2% |

L'Oreal SA | 256,900 | | $ 31,583 |

Nu Skin Enterprises, Inc. Class A | 281,363 | | 11,674 |

| | 43,257 |

Tobacco - 1.3% |

Altria Group, Inc. | 543,295 | | 18,450 |

British American Tobacco PLC sponsored ADR | 2,088,001 | | 218,697 |

Philip Morris International, Inc. | 200,183 | | 17,876 |

Souza Cruz SA | 477,700 | | 6,403 |

| | 261,426 |

TOTAL CONSUMER STAPLES | | 1,479,674 |

ENERGY - 7.2% |

Energy Equipment & Services - 1.6% |

Cameron International Corp. (a) | 743,991 | | 40,704 |

Ensco PLC Class A | 823,839 | | 47,264 |

Forum Energy Technologies, Inc. | 341,364 | | 8,080 |

Halliburton Co. | 746,958 | | 24,470 |

National Oilwell Varco, Inc. | 1,061,248 | | 83,626 |

Noble Corp. | 1,087,208 | | 41,466 |

Ocean Rig UDW, Inc. (United States) | 455,396 | | 7,619 |

Oceaneering International, Inc. | 220,987 | | 11,832 |

Oil States International, Inc. (a) | 101,400 | | 7,934 |

Schlumberger Ltd. | 631,524 | | 45,710 |

Vantage Drilling Co. (a) | 4,677,101 | | 7,109 |

| | 325,814 |

Oil, Gas & Consumable Fuels - 5.6% |

Anadarko Petroleum Corp. | 900,802 | | 62,399 |

Apache Corp. | 835,168 | | 71,616 |

Cheniere Energy, Inc. (a) | 193,100 | | 2,850 |

Chevron Corp. | 1,260,894 | | 141,422 |

Cobalt International Energy, Inc. (a) | 317,200 | | 7,204 |

EQT Corp. | 360,200 | | 19,436 |

Exxon Mobil Corp. | 3,618,457 | | 315,891 |

Halcon Resources Corp. (q) | 910,000 | | 6,989 |

Hess Corp. | 619,326 | | 31,295 |

HollyFrontier Corp. | 836,666 | | 33,709 |

InterOil Corp. (a)(e) | 310,031 | | 24,660 |

Marathon Oil Corp. | 2,036,593 | | 56,658 |

Marathon Petroleum Corp. | 1,189,088 | | 61,535 |

Common Stocks - continued |

| Shares | | Value (000s) |

ENERGY - continued |

Oil, Gas & Consumable Fuels - continued |

Noble Energy, Inc. | 325,965 | | $ 28,652 |

Northern Tier Energy LP Class A | 458,700 | | 8,394 |

Occidental Petroleum Corp. | 1,038,752 | | 88,304 |

Phillips 66 | 375,591 | | 15,775 |

Royal Dutch Shell PLC Class B sponsored ADR (e) | 1,233,621 | | 89,055 |

Suncor Energy, Inc. | 1,602,400 | | 50,084 |

Williams Companies, Inc. | 1,122,100 | | 36,210 |

| | 1,152,138 |

TOTAL ENERGY | | 1,477,952 |

FINANCIALS - 9.3% |

Capital Markets - 0.8% |

BlackRock, Inc. Class A | 275,742 | | 48,633 |

E*TRADE Financial Corp. (a) | 629,301 | | 5,393 |

Evercore Partners, Inc. Class A | 275,200 | | 6,797 |

ICAP PLC | 923,400 | | 4,658 |

Invesco Ltd. | 903,982 | | 21,406 |

Morgan Stanley | 1,163,200 | | 17,448 |

State Street Corp. | 563,918 | | 23,459 |

TD Ameritrade Holding Corp. | 904,736 | | 15,480 |

The Blackstone Group LP | 1,026,000 | | 13,841 |

UBS AG | 647,930 | | 7,229 |

| | 164,344 |

Commercial Banks - 2.2% |

CIT Group, Inc. (a) | 708,926 | | 26,769 |

Comerica, Inc. | 1,107,648 | | 34,016 |

Credit Agricole SA (a) | 924,624 | | 5,394 |

FirstMerit Corp. | 318,698 | | 5,000 |

Huntington Bancshares, Inc. | 4,733,054 | | 31,238 |

Lloyds Banking Group PLC (a) | 7,606,900 | | 4,014 |

M&T Bank Corp. | 314,819 | | 27,358 |

Synovus Financial Corp. (e) | 4,461,120 | | 9,279 |

U.S. Bancorp | 7,141,743 | | 238,606 |

Wells Fargo & Co. | 2,356,876 | | 80,204 |

| | 461,878 |

Consumer Finance - 1.5% |

Capital One Financial Corp. | 4,019,745 | | 227,236 |

Common Stocks - continued |

| Shares | | Value (000s) |

FINANCIALS - continued |

Consumer Finance - continued |

Discover Financial Services | 364,652 | | $ 14,123 |

SLM Corp. | 4,030,734 | | 63,484 |

| | 304,843 |

Diversified Financial Services - 1.7% |

African Bank Investments Ltd. | 692,111 | | 2,677 |

Bank of America Corp. | 3,429,996 | | 27,406 |

Citigroup, Inc. | 5,059,146 | | 150,307 |

JPMorgan Chase & Co. | 4,570,385 | | 169,744 |

NBH Holdings Corp. Class A (a)(g) | 576,500 | | 10,233 |

| | 360,367 |

Insurance - 1.9% |

ACE Ltd. | 494,636 | | 36,470 |

Amlin PLC | 1,942,409 | | 11,893 |

Berkshire Hathaway, Inc.: | | | |

Class A (a) | 234 | | 29,615 |

Class B (a) | 486,868 | | 41,062 |

Fairfax Financial Holdings Ltd. (sub. vtg.) | 71,900 | | 27,073 |

Hartford Financial Services Group, Inc. | 1,013,400 | | 18,170 |

MetLife, Inc. | 2,833,406 | | 96,704 |

Prudential Financial, Inc. | 178,800 | | 9,746 |

The Travelers Companies, Inc. | 1,037,039 | | 67,138 |

Torchmark Corp. | 494,632 | | 25,315 |

Validus Holdings Ltd. | 952,465 | | 31,917 |

| | 395,103 |

Real Estate Investment Trusts - 0.9% |

American Tower Corp. | 1,162,045 | | 81,808 |

Camden Property Trust (SBI) | 303,775 | | 21,091 |

Equity Lifestyle Properties, Inc. | 288,929 | | 19,867 |

Home Properties, Inc. | 29,800 | | 1,903 |

Japan Retail Fund Investment Corp. | 3,499 | | 5,991 |

Sun Communities, Inc. | 280,526 | | 12,851 |

The Macerich Co. | 685,541 | | 40,838 |

| | 184,349 |

Thrifts & Mortgage Finance - 0.3% |

Ocwen Financial Corp. (a) | 2,001,417 | | 51,496 |

TOTAL FINANCIALS | | 1,922,380 |

Common Stocks - continued |

| Shares | | Value (000s) |

HEALTH CARE - 7.5% |

Biotechnology - 2.3% |

Alexion Pharmaceuticals, Inc. (a) | 132,137 | | $ 14,166 |

Amgen, Inc. | 2,040,855 | | 171,269 |

Biogen Idec, Inc. (a) | 539,608 | | 79,101 |

BioMarin Pharmaceutical, Inc. (a) | 596,287 | | 22,265 |

CSL Ltd. | 293,502 | | 13,473 |

CSL Ltd. ADR | 379,200 | | 8,691 |

Gilead Sciences, Inc. (a) | 2,149,093 | | 123,981 |

Onyx Pharmaceuticals, Inc. (a) | 415,782 | | 29,903 |

Theravance, Inc. (a) | 198,850 | | 5,303 |

| | 468,152 |

Health Care Equipment & Supplies - 1.0% |

C.R. Bard, Inc. | 380,956 | | 37,376 |

Covidien PLC | 1,241,865 | | 69,607 |

Edwards Lifesciences Corp. (a) | 528,081 | | 53,922 |

Quidel Corp. (a)(e) | 1,317,147 | | 21,390 |

The Cooper Companies, Inc. | 406,065 | | 34,049 |

| | 216,344 |

Health Care Providers & Services - 1.3% |

Catamaran Corp. (a) | 165,961 | | 14,405 |

CIGNA Corp. | 816,351 | | 37,364 |

Express Scripts Holding Co. (a) | 402,065 | | 25,177 |

Henry Schein, Inc. (a) | 715,654 | | 54,969 |

McKesson Corp. | 373,348 | | 32,522 |

Omnicare, Inc. | 341,802 | | 11,068 |

UnitedHealth Group, Inc. | 1,782,107 | | 96,768 |

WellPoint, Inc. | 88,200 | | 5,281 |

| | 277,554 |

Pharmaceuticals - 2.9% |

Allergan, Inc. | 770,565 | | 66,369 |

Eli Lilly & Co. | 380,900 | | 17,106 |

GlaxoSmithKline PLC sponsored ADR | 553,190 | | 25,165 |

Merck & Co., Inc. | 2,594,840 | | 111,708 |

Optimer Pharmaceuticals, Inc. (a) | 568,104 | | 8,539 |

Pfizer, Inc. | 11,662,658 | | 278,271 |

Sanofi SA sponsored ADR | 590,703 | | 24,189 |

Valeant Pharmaceuticals International, Inc. (Canada) (a) | 1,099,375 | | 56,288 |

| | 587,635 |

TOTAL HEALTH CARE | | 1,549,685 |

Common Stocks - continued |

| Shares | | Value (000s) |

INDUSTRIALS - 6.6% |

Aerospace & Defense - 1.9% |

Honeywell International, Inc. | 1,388,553 | | $ 81,161 |

MTU Aero Engines Holdings AG | 218,364 | | 16,664 |

Precision Castparts Corp. | 334,903 | | 53,946 |

Raytheon Co. | 683,637 | | 38,639 |

Textron, Inc. | 2,095,158 | | 55,983 |

The Boeing Co. | 899,838 | | 64,248 |

United Technologies Corp. | 1,099,534 | | 87,798 |

| | 398,439 |

Air Freight & Logistics - 0.4% |

United Parcel Service, Inc. Class B | 1,230,637 | | 90,833 |

Building Products - 0.5% |

Armstrong World Industries, Inc. | 660,746 | | 29,053 |

Owens Corning (a) | 1,469,438 | | 49,020 |

Quanex Building Products Corp. | 947,855 | | 16,587 |

| | 94,660 |

Commercial Services & Supplies - 0.2% |

Stericycle, Inc. (a) | 347,149 | | 31,771 |

Electrical Equipment - 0.4% |

Regal-Beloit Corp. | 633,339 | | 43,105 |

Roper Industries, Inc. | 350,067 | | 35,983 |

| | 79,088 |

Industrial Conglomerates - 1.8% |

Danaher Corp. | 1,396,974 | | 74,836 |

General Electric Co. | 12,219,400 | | 253,064 |

Tyco International Ltd. | 804,119 | | 45,336 |

| | 373,236 |

Machinery - 0.6% |

Caterpillar, Inc. | 205,413 | | 17,528 |

Cummins, Inc. | 441,167 | | 42,842 |

Fiat Industrial SpA | 675,197 | | 6,798 |

Illinois Tool Works, Inc. | 763,773 | | 45,284 |

| | 112,452 |

Road & Rail - 0.7% |

CSX Corp. | 1,922,124 | | 43,171 |

J.B. Hunt Transport Services, Inc. | 191,549 | | 10,045 |

Union Pacific Corp. | 807,500 | | 98,063 |

| | 151,279 |

Common Stocks - continued |

| Shares | | Value (000s) |

INDUSTRIALS - continued |

Trading Companies & Distributors - 0.1% |

W.W. Grainger, Inc. | 95,800 | | $ 19,731 |

TOTAL INDUSTRIALS | | 1,351,489 |

INFORMATION TECHNOLOGY - 13.8% |

Communications Equipment - 2.2% |

Acme Packet, Inc. (a) | 677,252 | | 12,929 |

ADTRAN, Inc. | 1,098,668 | | 22,292 |

Finisar Corp. (a) | 983,487 | | 13,513 |

Juniper Networks, Inc. (a) | 2,780,146 | | 48,486 |

NETGEAR, Inc. (a) | 322,578 | | 11,797 |

QUALCOMM, Inc. | 5,382,555 | | 330,812 |

Riverbed Technology, Inc. (a) | 616,612 | | 12,326 |

| | 452,155 |

Computers & Peripherals - 5.4% |

Apple, Inc. | 1,541,738 | | 1,025,622 |

NetApp, Inc. (a) | 157,707 | | 5,444 |

SanDisk Corp. (a) | 1,988,456 | | 81,964 |

| | 1,113,030 |

Electronic Equipment & Components - 0.3% |

Hon Hai Precision Industry Co. Ltd. (Foxconn) | 10,180,000 | | 28,884 |

Jabil Circuit, Inc. | 1,846,550 | | 42,064 |

Uni-Pixel Inc. (a) | 90,300 | | 545 |

| | 71,493 |

Internet Software & Services - 1.0% |

Dice Holdings, Inc. (a) | 965,144 | | 7,702 |

eBay, Inc. (a) | 1,081,464 | | 51,337 |

Facebook, Inc. Class A | 856,127 | | 15,479 |

Google, Inc. Class A (a) | 135,830 | | 93,056 |

Mail.ru Group Ltd.: | | | |

GDR (g) | 391,234 | | 12,821 |

GDR (Reg. S) | 195,272 | | 6,399 |

VeriSign, Inc. (a) | 337,918 | | 16,112 |

| | 202,906 |

IT Services - 0.0% |

Accenture PLC Class A | 32,270 | | 1,988 |

Semiconductors & Semiconductor Equipment - 2.3% |

Analog Devices, Inc. | 3,381,391 | | 134,376 |

ARM Holdings PLC sponsored ADR | 641,300 | | 17,469 |

Common Stocks - continued |

| Shares | | Value (000s) |

INFORMATION TECHNOLOGY - continued |

Semiconductors & Semiconductor Equipment - continued |

ASAT Holdings Ltd. (a) | 88,719 | | $ 0 |

ASML Holding NV | 501,249 | | 28,456 |

Avago Technologies Ltd. | 1,928,985 | | 70,543 |

Dialog Semiconductor PLC (a) | 384,898 | | 8,286 |

Fairchild Semiconductor International, Inc. (a) | 841,711 | | 12,222 |

International Rectifier Corp. (a) | 676,289 | | 11,774 |

Maxim Integrated Products, Inc. | 1,194,297 | | 32,413 |

Micron Technology, Inc. (a) | 7,144,995 | | 44,370 |

NXP Semiconductors NV (a) | 1,327,116 | | 30,948 |

ON Semiconductor Corp. (a) | 2,754,511 | | 17,161 |

PMC-Sierra, Inc. (a) | 2,578,085 | | 15,082 |

RF Micro Devices, Inc. (a) | 4,914,586 | | 18,430 |

Rubicon Technology, Inc. (a)(e) | 123,185 | | 1,037 |

Skyworks Solutions, Inc. (a) | 1,141,255 | | 34,763 |

| | 477,330 |

Software - 2.6% |

Check Point Software Technologies Ltd. (a) | 1,096,779 | | 50,551 |

Citrix Systems, Inc. (a) | 1,544,850 | | 120,019 |

Microsoft Corp. | 10,609,586 | | 326,987 |

Sourcefire, Inc. (a) | 158,833 | | 8,242 |

VMware, Inc. Class A (a) | 226,267 | | 20,147 |

| | 525,946 |

TOTAL INFORMATION TECHNOLOGY | | 2,844,848 |

MATERIALS - 2.0% |

Chemicals - 1.4% |

Air Products & Chemicals, Inc. | 647,168 | | 53,443 |

E.I. du Pont de Nemours & Co. | 1,381,887 | | 68,749 |

Eastman Chemical Co. | 627,953 | | 34,701 |

Ecolab, Inc. | 494,778 | | 31,681 |

LyondellBasell Industries NV Class A | 491,016 | | 23,981 |

Sherwin-Williams Co. | 299,779 | | 42,892 |

Sigma Aldrich Corp. | 389,450 | | 27,663 |

| | 283,110 |

Containers & Packaging - 0.3% |

Ball Corp. | 669,211 | | 28,221 |

Rock-Tenn Co. Class A | 470,505 | | 31,416 |

| | 59,637 |

Common Stocks - continued |

| Shares | | Value (000s) |

MATERIALS - continued |

Metals & Mining - 0.3% |

First Quantum Minerals Ltd. (e) | 1,466,705 | | $ 28,255 |

Goldcorp, Inc. | 765,897 | | 31,444 |

Turquoise Hill Resources Ltd. (a) | 1,893,665 | | 15,215 |

| | 74,914 |

TOTAL MATERIALS | | 417,661 |

TELECOMMUNICATION SERVICES - 1.5% |

Diversified Telecommunication Services - 1.2% |

AT&T, Inc. | 1,892,026 | | 69,324 |

CenturyLink, Inc. | 1,777,204 | | 75,105 |

Verizon Communications, Inc. | 2,232,168 | | 95,849 |

| | 240,278 |

Wireless Telecommunication Services - 0.3% |

SBA Communications Corp. Class A (a) | 442,894 | | 26,476 |

Sprint Nextel Corp. (a) | 9,026,777 | | 43,780 |

| | 70,256 |

TOTAL TELECOMMUNICATION SERVICES | | 310,534 |

UTILITIES - 2.2% |

Electric Utilities - 1.4% |

American Electric Power Co., Inc. | 417,924 | | 17,967 |

Duke Energy Corp. | 1,406,380 | | 91,105 |

Edison International | 1,547,007 | | 67,743 |

FirstEnergy Corp. | 1,320,436 | | 57,703 |

NextEra Energy, Inc. | 926,475 | | 62,361 |

| | 296,879 |

Gas Utilities - 0.0% |

ONEOK, Inc. | 184,456 | | 8,214 |

Independent Power Producers & Energy Traders - 0.2% |

NRG Energy, Inc. | 243,000 | | 5,186 |

The AES Corp. | 2,731,715 | | 31,114 |

| | 36,300 |

Multi-Utilities - 0.6% |

CenterPoint Energy, Inc. | 1,386,952 | | 28,280 |

NiSource, Inc. | 698,474 | | 17,001 |

Common Stocks - continued |

| Shares | | Value (000s) |

UTILITIES - continued |

Multi-Utilities - continued |

PG&E Corp. | 592,029 | | $ 25,700 |

Sempra Energy | 750,345 | | 49,673 |

| | 120,654 |

TOTAL UTILITIES | | 462,047 |

TOTAL COMMON STOCKS (Cost $10,748,046) |

13,125,808

|

Convertible Preferred Stocks - 0.0% |

| | | |

CONSUMER DISCRETIONARY - 0.0% |

Media - 0.0% |

Jumptap, Inc. Series G (q) | 893,724 | | 6,429 |

INFORMATION TECHNOLOGY - 0.0% |

Semiconductors & Semiconductor Equipment - 0.0% |

ASAT Holdings Ltd. 13.00% (a) | 2,416 | | 0 |

TOTAL CONVERTIBLE PREFERRED STOCKS (Cost $6,519) |

6,429

|

Nonconvertible Bonds - 7.4% |

| Principal Amount (000s) | | |

CONSUMER DISCRETIONARY - 0.7% |

Automobiles - 0.2% |

Daimler Finance North America LLC 1.65% 4/10/15 (g) | | $ 20,636 | | 20,903 |

Volkswagen International Finance NV 2.375% 3/22/17 (g) | | 10,000 | | 10,328 |

| | 31,231 |

Media - 0.5% |

AOL Time Warner, Inc. 7.625% 4/15/31 | | 4,975 | | 6,762 |

Comcast Corp.: | | | | |

4.65% 7/15/42 | | 5,049 | | 5,392 |

5.15% 3/1/20 | | 644 | | 767 |

6.4% 3/1/40 | | 6,097 | | 8,023 |

COX Communications, Inc. 4.625% 6/1/13 | | 3,612 | | 3,720 |

Discovery Communications LLC 3.7% 6/1/15 | | 5,116 | | 5,485 |

Nonconvertible Bonds - continued |

| Principal Amount (000s) | | Value (000s) |

CONSUMER DISCRETIONARY - continued |

Media - continued |

NBCUniversal Media LLC: | | | | |

5.15% 4/30/20 | | $ 7,276 | | $ 8,592 |

6.4% 4/30/40 | | 6,271 | | 8,138 |

News America Holdings, Inc. 7.75% 12/1/45 | | 8,630 | | 11,735 |

News America, Inc. 6.15% 2/15/41 | | 9,222 | | 11,348 |

Time Warner Cable, Inc.: | | | | |

4.5% 9/15/42 | | 5,093 | | 5,071 |

5.5% 9/1/41 | | 13,538 | | 15,346 |

6.2% 7/1/13 | | 2,729 | | 2,854 |

6.75% 7/1/18 | | 1,378 | | 1,724 |

Time Warner, Inc.: | | | | |

5.875% 11/15/16 | | 4,125 | | 4,884 |

6.2% 3/15/40 | | 3,821 | | 4,697 |

6.5% 11/15/36 | | 2,758 | | 3,449 |

| | 107,987 |

Specialty Retail - 0.0% |

Staples, Inc. 7.375% 10/1/12 | | 820 | | 824 |

TOTAL CONSUMER DISCRETIONARY | | 140,042 |

CONSUMER STAPLES - 0.5% |

Beverages - 0.1% |

Beam, Inc.: | | | | |

1.875% 5/15/17 | | 1,331 | | 1,359 |

3.25% 5/15/22 | | 1,578 | | 1,636 |

Diageo Capital PLC 5.2% 1/30/13 | | 4,139 | | 4,219 |

FBG Finance Ltd. 5.125% 6/15/15 (g) | | 3,447 | | 3,811 |

Fortune Brands, Inc.: | | | | |

5.375% 1/15/16 | | 1,615 | | 1,840 |

5.875% 1/15/36 | | 6,416 | | 7,676 |

6.375% 6/15/14 | | 482 | | 527 |

SABMiller Holdings, Inc. 3.75% 1/15/22 (g) | | 5,490 | | 5,958 |

| | 27,026 |

Food Products - 0.0% |

Cargill, Inc. 6% 11/27/17 (g) | | 572 | | 695 |

Kraft Foods, Inc.: | | | | |

6.5% 2/9/40 | | 3,854 | | 5,316 |

6.75% 2/19/14 | | 436 | | 474 |

| | 6,485 |

Nonconvertible Bonds - continued |

| Principal Amount (000s) | | Value (000s) |

CONSUMER STAPLES - continued |

Tobacco - 0.4% |

Altria Group, Inc.: | | | | |

2.85% 8/9/22 | | $ 4,604 | | $ 4,591 |

4.25% 8/9/42 | | 4,604 | | 4,500 |

9.7% 11/10/18 | | 16,451 | | 23,620 |

Philip Morris International, Inc. 1.125% 8/21/17 | | 24,419 | | 24,374 |

Reynolds American, Inc.: | | | | |

6.75% 6/15/17 | | 3,486 | | 4,223 |

7.25% 6/15/37 | | 7,569 | | 9,708 |

| | 71,016 |

TOTAL CONSUMER STAPLES | | 104,527 |

ENERGY - 1.1% |

Energy Equipment & Services - 0.2% |

DCP Midstream LLC: | | | | |

4.75% 9/30/21 (g) | | 6,554 | | 6,949 |

5.35% 3/15/20 (g) | | 6,637 | | 7,281 |

El Paso Pipeline Partners Operating Co. LLC: | | | | |

4.1% 11/15/15 | | 7,675 | | 8,099 |

5% 10/1/21 | | 2,791 | | 3,050 |

6.5% 4/1/20 | | 1,091 | | 1,287 |

Transocean, Inc.: | | | | |

5.05% 12/15/16 | | 4,522 | | 5,009 |

6.375% 12/15/21 | | 5,971 | | 7,198 |

Weatherford International Ltd.: | | | | |

4.95% 10/15/13 | | 2,045 | | 2,130 |

5.15% 3/15/13 | | 2,673 | | 2,730 |

| | 43,733 |

Oil, Gas & Consumable Fuels - 0.9% |

Anadarko Petroleum Corp.: | | | | |

5.95% 9/15/16 | | 718 | | 830 |

6.375% 9/15/17 | | 13,514 | | 16,161 |

Canadian Natural Resources Ltd. 5.15% 2/1/13 | | 5,282 | | 5,380 |

Duke Capital LLC 6.25% 2/15/13 | | 809 | | 829 |

Duke Energy Field Services: | | | | |

5.375% 10/15/15 (g) | | 1,435 | | 1,545 |

6.45% 11/3/36 (g) | | 6,493 | | 7,497 |

El Paso Natural Gas Co. 5.95% 4/15/17 | | 1,098 | | 1,258 |

Enbridge Energy Partners LP 4.2% 9/15/21 | | 7,741 | | 8,264 |

Encana Holdings Finance Corp. 5.8% 5/1/14 | | 3,391 | | 3,644 |

Nonconvertible Bonds - continued |

| Principal Amount (000s) | | Value (000s) |

ENERGY - continued |

Oil, Gas & Consumable Fuels - continued |

Enterprise Products Operating LP: | | | | |

5.6% 10/15/14 | | $ 715 | | $ 783 |

5.65% 4/1/13 | | 563 | | 577 |

Gulfstream Natural Gas System LLC 6.95% 6/1/16 (g) | | 327 | | 382 |

Marathon Petroleum Corp. 5.125% 3/1/21 | | 4,207 | | 4,837 |

Midcontinent Express Pipeline LLC 5.45% 9/15/14 (g) | | 6,234 | | 6,430 |

Motiva Enterprises LLC 6.85% 1/15/40 (g) | | 4,294 | | 5,662 |

Nakilat, Inc. 6.067% 12/31/33 (g) | | 2,490 | | 2,944 |

Nexen, Inc. 5.2% 3/10/15 | | 1,067 | | 1,161 |

Petrobras International Finance Co. Ltd.: | | | | |

3.875% 1/27/16 | | 6,946 | | 7,293 |

7.875% 3/15/19 | | 7,382 | | 9,153 |

Petroleos Mexicanos: | | | | |

4.875% 1/24/22 (g) | | 1,430 | | 1,605 |

5.5% 1/21/21 | | 7,423 | | 8,666 |

5.5% 6/27/44 (g) | | 6,720 | | 7,308 |

6% 3/5/20 | | 952 | | 1,135 |

6.5% 6/2/41 (g) | | 8,760 | | 10,884 |

Phillips 66: | | | | |

4.3% 4/1/22 (g) | | 6,038 | | 6,580 |

5.875% 5/1/42 (g) | | 5,485 | | 6,484 |

Plains All American Pipeline LP/PAA Finance Corp.: | | | | |

3.65% 6/1/22 | | 3,381 | | 3,575 |

3.95% 9/15/15 | | 149 | | 161 |

4.25% 9/1/12 | | 718 | | 718 |

6.125% 1/15/17 | | 1,940 | | 2,301 |

Ras Laffan Liquefied Natural Gas Co. Ltd. III: | | | | |

4.5% 9/30/12 (g) | | 3,472 | | 3,472 |

5.5% 9/30/14 (g) | | 5,137 | | 5,535 |

5.832% 9/30/16 (g) | | 1,121 | | 1,222 |

6.332% 9/30/27 (g) | | 5,910 | | 6,988 |

6.75% 9/30/19 (g) | | 3,177 | | 3,939 |

Rockies Express Pipeline LLC 6.25% 7/15/13 (g) | | 3,193 | | 3,289 |

Southeast Supply Header LLC 4.85% 8/15/14 (g) | | 543 | | 571 |

Spectra Energy Capital, LLC 5.65% 3/1/20 | | 455 | | 525 |

Spectra Energy Partners, LP: | | | | |

2.95% 6/15/16 | | 1,325 | | 1,352 |

4.6% 6/15/21 | | 1,733 | | 1,882 |

Texas Eastern Transmission LP 6% 9/15/17 (g) | | 1,301 | | 1,513 |

Nonconvertible Bonds - continued |

| Principal Amount (000s) | | Value (000s) |

ENERGY - continued |

Oil, Gas & Consumable Fuels - continued |

TransCapitalInvest Ltd. 5.67% 3/5/14 (g) | | $ 4,215 | | $ 4,457 |

Western Gas Partners LP 5.375% 6/1/21 | | 7,979 | | 8,862 |

| | 177,654 |

TOTAL ENERGY | | 221,387 |

FINANCIALS - 3.2% |

Capital Markets - 0.2% |

BlackRock, Inc. 3.375% 6/1/22 | | 3,840 | | 4,063 |

Goldman Sachs Group, Inc.: | | | | |

5.95% 1/18/18 | | 4,684 | | 5,269 |

6.15% 4/1/18 | | 1,671 | | 1,900 |

Lazard Group LLC: | | | | |

6.85% 6/15/17 | | 4,528 | | 5,108 |

7.125% 5/15/15 | | 1,616 | | 1,773 |

Merrill Lynch & Co., Inc.: | | | | |

6.11% 1/29/37 | | 5,110 | | 5,138 |

6.4% 8/28/17 | | 4,179 | | 4,749 |

Morgan Stanley: | | | | |

5.5% 7/28/21 | | 7,030 | | 7,212 |

5.625% 9/23/19 | | 1,795 | | 1,858 |

5.75% 1/25/21 | | 2,403 | | 2,483 |

7.3% 5/13/19 | | 6,528 | | 7,367 |

| | 46,920 |

Commercial Banks - 0.6% |

Bank of America NA 5.3% 3/15/17 | | 8,427 | | 9,173 |

BB&T Corp. 3.95% 3/22/22 | | 6,787 | | 7,330 |

Credit Suisse New York Branch 6% 2/15/18 | | 15,195 | | 16,877 |

Discover Bank: | | | | |

7% 4/15/20 | | 3,831 | | 4,509 |

8.7% 11/18/19 | | 2,425 | | 3,070 |

Fifth Third Bancorp: | | | | |

4.5% 6/1/18 | | 584 | | 634 |

8.25% 3/1/38 | | 4,070 | | 5,690 |

Fifth Third Bank 4.75% 2/1/15 | | 951 | | 1,014 |

Fifth Third Capital Trust IV 6.5% 4/15/67 (m) | | 4,393 | | 4,393 |

HBOS PLC 6.75% 5/21/18 (g) | | 560 | | 553 |

HSBC Holdings PLC 4% 3/30/22 | | 5,850 | | 6,276 |

Huntington Bancshares, Inc. 7% 12/15/20 | | 1,908 | | 2,278 |

JPMorgan Chase Bank 6% 10/1/17 | | 2,460 | | 2,897 |

Nonconvertible Bonds - continued |

| Principal Amount (000s) | | Value (000s) |

FINANCIALS - continued |

Commercial Banks - continued |

KeyBank NA: | | | | |

5.45% 3/3/16 | | $ 2,765 | | $ 3,092 |

5.8% 7/1/14 | | 5,776 | | 6,190 |

Marshall & Ilsley Bank: | | | | |

4.85% 6/16/15 | | 3,561 | | 3,840 |

5% 1/17/17 | | 9,004 | | 10,094 |

5.25% 9/4/12 | | 2,221 | | 2,221 |

Regions Bank: | | | | |

6.45% 6/26/37 | | 9,201 | | 9,213 |

7.5% 5/15/18 | | 3,852 | | 4,488 |

Regions Financial Corp.: | | | | |

5.75% 6/15/15 | | 1,443 | | 1,533 |

7.75% 11/10/14 | | 6,740 | | 7,466 |

UnionBanCal Corp. 5.25% 12/16/13 | | 777 | | 813 |

Wachovia Corp.: | | | | |

5.625% 10/15/16 | | 3,991 | | 4,596 |

5.75% 6/15/17 | | 2,371 | | 2,830 |

Wells Fargo & Co. 3.676% 6/15/16 | | 3,236 | | 3,521 |

| | 124,591 |

Consumer Finance - 0.4% |

Capital One Financial Corp. 2.15% 3/23/15 | | 20,318 | | 20,810 |

Discover Financial Services: | | | | |

5.2% 4/27/22 | | 1,290 | | 1,372 |

6.45% 6/12/17 | | 12,103 | | 13,712 |

Ford Motor Credit Co. LLC 2.5% 1/15/16 | | 16,000 | | 16,005 |

General Electric Capital Corp. 5.625% 9/15/17 | | 15,752 | | 18,615 |

HSBC USA, Inc. 2.375% 2/13/15 | | 8,675 | | 8,889 |

| | 79,403 |

Diversified Financial Services - 0.5% |

Bank of America Corp.: | | | | |

3.875% 3/22/17 | | 7,618 | | 8,027 |

5.65% 5/1/18 | | 1,270 | | 1,419 |

5.7% 1/24/22 | | 12,760 | | 14,439 |

5.75% 12/1/17 | | 11,990 | | 13,408 |

5.875% 2/7/42 | | 5,117 | | 5,815 |

BP Capital Markets PLC: | | | | |

3.625% 5/8/14 | | 4,599 | | 4,828 |

4.5% 10/1/20 | | 961 | | 1,119 |

4.742% 3/11/21 | | 6,000 | | 7,044 |

Nonconvertible Bonds - continued |

| Principal Amount (000s) | | Value (000s) |

FINANCIALS - continued |

Diversified Financial Services - continued |

Capital One Capital V 10.25% 8/15/39 | | $ 4,813 | | $ 4,957 |

Citigroup, Inc.: | | | | |

2.25% 8/7/15 | | 5,000 | | 5,043 |

4.75% 5/19/15 | | 11,282 | | 12,112 |

6.125% 5/15/18 | | 1,701 | | 1,973 |

6.5% 8/19/13 | | 19,655 | | 20,671 |

JPMorgan Chase & Co. 3.15% 7/5/16 | | 10,650 | | 11,276 |

TECO Finance, Inc. 4% 3/15/16 | | 1,828 | | 1,982 |

| | 114,113 |

Insurance - 0.7% |

American International Group, Inc.: | | | | |

2.375% 8/24/15 | | 16,000 | | 16,028 |

4.875% 6/1/22 | | 3,000 | | 3,272 |

Aon Corp.: | | | | |

3.125% 5/27/16 | | 4,391 | | 4,638 |

3.5% 9/30/15 | | 3,180 | | 3,353 |

Axis Capital Holdings Ltd. 5.75% 12/1/14 | | 452 | | 486 |

Great-West Life & Annuity Insurance Co. 7.153% 5/16/46 (g)(m) | | 1,750 | | 1,785 |

Hartford Financial Services Group, Inc.: | | | | |

5.125% 4/15/22 | | 11,774 | | 12,663 |

5.375% 3/15/17 | | 287 | | 314 |

6.625% 4/15/42 | | 9,968 | | 11,222 |

Liberty Mutual Group, Inc.: | | | | |

5% 6/1/21 (g) | | 8,525 | | 8,953 |

6.5% 3/15/35 (g) | | 1,315 | | 1,412 |

Marsh & McLennan Companies, Inc. 4.8% 7/15/21 | | 4,458 | | 5,008 |

Massachusetts Mutual Life Insurance Co. 5.375% 12/1/41 (g) | | 3,576 | | 4,078 |

MetLife, Inc.: | | | | |

5% 6/15/15 | | 941 | | 1,045 |

6.75% 6/1/16 | | 5,158 | | 6,169 |

Metropolitan Life Global Funding I: | | | | |

5.125% 4/10/13 (g) | | 452 | | 464 |

5.125% 6/10/14 (g) | | 4,625 | | 4,972 |

Monumental Global Funding III 5.5% 4/22/13 (g) | | 2,585 | | 2,647 |

Northwestern Mutual Life Insurance Co. 6.063% 3/30/40 (g) | | 4,915 | | 6,329 |

Pacific Life Insurance Co. 9.25% 6/15/39 (g) | | 3,353 | | 4,566 |

Pacific LifeCorp 6% 2/10/20 (g) | | 5,390 | | 6,002 |

Nonconvertible Bonds - continued |

| Principal Amount (000s) | | Value (000s) |

FINANCIALS - continued |

Insurance - continued |

Prudential Financial, Inc.: | | | | |

3.875% 1/14/15 | | $ 5,340 | | $ 5,663 |

5.15% 1/15/13 | | 2,934 | | 2,982 |

6.2% 11/15/40 | | 2,535 | | 2,989 |

7.375% 6/15/19 | | 2,520 | | 3,173 |

Symetra Financial Corp. 6.125% 4/1/16 (g) | | 5,955 | | 6,479 |

Unum Group: | | | | |

5.625% 9/15/20 | | 3,667 | | 4,051 |

5.75% 8/15/42 | | 5,242 | | 5,405 |

7.125% 9/30/16 | | 869 | | 1,012 |

| | 137,160 |

Real Estate Investment Trusts - 0.3% |

Alexandria Real Estate Equities, Inc. 4.6% 4/1/22 | | 1,925 | | 2,029 |

AvalonBay Communities, Inc. 4.95% 3/15/13 | | 296 | | 302 |

Boston Properties, Inc. 3.85% 2/1/23 | | 4,358 | | 4,562 |

BRE Properties, Inc. 5.5% 3/15/17 | | 977 | | 1,109 |

Camden Property Trust: | | | | |

5.375% 12/15/13 | | 3,103 | | 3,257 |

5.875% 11/30/12 | | 542 | | 548 |

DDR Corp. 4.625% 7/15/22 | | 2,262 | | 2,346 |

Developers Diversified Realty Corp.: | | | | |

4.75% 4/15/18 | | 5,964 | | 6,393 |

7.5% 4/1/17 | | 4,622 | | 5,411 |

Duke Realty LP: | | | | |

4.375% 6/15/22 | | 3,546 | | 3,707 |

4.625% 5/15/13 | | 967 | | 987 |

5.4% 8/15/14 | | 771 | | 823 |

5.5% 3/1/16 | | 3,075 | | 3,372 |

6.75% 3/15/20 | | 560 | | 675 |

8.25% 8/15/19 | | 2,489 | | 3,148 |

Equity One, Inc.: | | | | |

5.375% 10/15/15 | | 948 | | 1,023 |

6% 9/15/17 | | 717 | | 798 |

6.25% 12/15/14 | | 1,000 | | 1,084 |

6.25% 1/15/17 | | 399 | | 445 |

Federal Realty Investment Trust: | | | | |

5.4% 12/1/13 | | 355 | | 373 |

5.9% 4/1/20 | | 1,860 | | 2,227 |

6.2% 1/15/17 | | 501 | | 583 |

HCP, Inc. 3.15% 8/1/22 | | 7,000 | | 6,835 |

Nonconvertible Bonds - continued |

| Principal Amount (000s) | | Value (000s) |

FINANCIALS - continued |

Real Estate Investment Trusts - continued |

Health Care REIT, Inc. 4.125% 4/1/19 | | $ 13,700 | | $ 14,415 |

HRPT Properties Trust: | | | | |

5.75% 11/1/15 | | 1,731 | | 1,818 |

6.25% 6/15/17 | | 996 | | 1,093 |

6.65% 1/15/18 | | 676 | | 750 |

Washington (REIT) 5.25% 1/15/14 | | 476 | | 497 |

| | 70,610 |

Real Estate Management & Development - 0.5% |

AMB Property LP 5.9% 8/15/13 | | 2,086 | | 2,160 |

BioMed Realty LP: | | | | |

3.85% 4/15/16 | | 7,000 | | 7,316 |

4.25% 7/15/22 | | 2,970 | | 3,100 |

6.125% 4/15/20 | | 2,467 | | 2,878 |

Brandywine Operating Partnership LP 5.7% 5/1/17 | | 129 | | 141 |

Digital Realty Trust LP: | | | | |

4.5% 7/15/15 | | 3,650 | | 3,866 |

5.25% 3/15/21 | | 4,138 | | 4,570 |

ERP Operating LP: | | | | |

4.625% 12/15/21 | | 12,970 | | 14,876 |

4.75% 7/15/20 | | 5,288 | | 5,990 |

5.5% 10/1/12 | | 382 | | 383 |

5.75% 6/15/17 | | 2,042 | | 2,406 |

Liberty Property LP: | | | | |

4.125% 6/15/22 | | 3,041 | | 3,156 |

4.75% 10/1/20 | | 7,482 | | 8,153 |

5.125% 3/2/15 | | 1,229 | | 1,320 |

5.5% 12/15/16 | | 1,772 | | 1,987 |

Mack-Cali Realty LP: | | | | |

4.5% 4/18/22 | | 1,907 | | 2,021 |

7.75% 8/15/19 | | 1,036 | | 1,273 |

Post Apartment Homes LP 6.3% 6/1/13 | | 3,079 | | 3,167 |

Prime Property Funding, Inc.: | | | | |

5.125% 6/1/15 (g) | | 2,258 | | 2,304 |

5.5% 1/15/14 (g) | | 816 | | 836 |

5.7% 4/15/17 (g) | | 1,991 | | 2,082 |

Regency Centers LP: | | | | |

4.95% 4/15/14 | | 494 | | 518 |

5.25% 8/1/15 | | 1,725 | | 1,878 |

5.875% 6/15/17 | | 877 | | 1,008 |

Nonconvertible Bonds - continued |

| Principal Amount (000s) | | Value (000s) |

FINANCIALS - continued |

Real Estate Management & Development - continued |

Simon Property Group LP: | | | | |

4.2% 2/1/15 | | $ 2,640 | | $ 2,816 |

6.75% 5/15/14 | | 5,698 | | 6,163 |

Tanger Properties LP: | | | | |

6.125% 6/1/20 | | 9,256 | | 10,984 |

6.15% 11/15/15 | | 1,254 | | 1,400 |

| | 98,752 |

TOTAL FINANCIALS | | 671,549 |

HEALTH CARE - 0.3% |

Biotechnology - 0.1% |

Amgen, Inc. 5.15% 11/15/41 | | 17,224 | | 18,836 |

Celgene Corp. 2.45% 10/15/15 | | 907 | | 939 |

| | 19,775 |

Health Care Providers & Services - 0.2% |

Aristotle Holding, Inc.: | | | | |

4.75% 11/15/21 (g) | | 10,952 | | 12,640 |

6.125% 11/15/41 (g) | | 5,466 | | 7,131 |

Coventry Health Care, Inc.: | | | | |

5.95% 3/15/17 | | 1,413 | | 1,652 |

6.3% 8/15/14 | | 2,925 | | 3,170 |

Express Scripts, Inc. 6.25% 6/15/14 | | 1,991 | | 2,175 |

Medco Health Solutions, Inc.: | | | | |

2.75% 9/15/15 | | 1,740 | | 1,820 |

4.125% 9/15/20 | | 5,031 | | 5,468 |

| | 34,056 |

Pharmaceuticals - 0.0% |

Watson Pharmaceuticals, Inc. 5% 8/15/14 | | 1,065 | | 1,133 |

TOTAL HEALTH CARE | | 54,964 |

INDUSTRIALS - 0.3% |

Aerospace & Defense - 0.1% |

BAE Systems Holdings, Inc.: | | | | |

4.95% 6/1/14 (g) | | 846 | | 892 |

6.375% 6/1/19 (g) | | 5,000 | | 5,971 |

| | 6,863 |

Nonconvertible Bonds - continued |

| Principal Amount (000s) | | Value (000s) |

INDUSTRIALS - continued |

Airlines - 0.0% |

Continental Airlines, Inc.: | | | | |

6.648% 3/15/19 | | $ 2,631 | | $ 2,775 |

6.9% 7/2/19 | | 798 | | 863 |

U.S. Airways pass-thru trust certificates: | | | | |

6.85% 1/30/18 | | 1,522 | | 1,591 |

8.36% 1/20/19 | | 1,259 | | 1,366 |

| | 6,595 |

Road & Rail - 0.2% |

Burlington Northern Santa Fe LLC: | | | | |

4.4% 3/15/42 | | 18,995 | | 20,003 |

5.05% 3/1/41 | | 8,624 | | 9,904 |

Norfolk Southern Corp. 3% 4/1/22 | | 13,653 | | 14,156 |

| | 44,063 |

TOTAL INDUSTRIALS | | 57,521 |

INFORMATION TECHNOLOGY - 0.1% |

Electronic Equipment & Components - 0.0% |

Tyco Electronics Group SA: | | | | |

5.95% 1/15/14 | | 3,694 | | 3,940 |

6% 10/1/12 | | 4,552 | | 4,570 |

6.55% 10/1/17 | | 1,119 | | 1,353 |

| | 9,863 |

Office Electronics - 0.1% |

Xerox Corp.: | | | | |

1.8679% 9/13/13 (m) | | 10,110 | | 10,180 |

4.25% 2/15/15 | | 545 | | 580 |

4.5% 5/15/21 | | 2,447 | | 2,572 |

| | 13,332 |

TOTAL INFORMATION TECHNOLOGY | | 23,195 |

MATERIALS - 0.2% |

Chemicals - 0.1% |

Dow Chemical Co. 7.6% 5/15/14 | | 10,939 | | 12,139 |

Construction Materials - 0.0% |

CRH America, Inc. 6% 9/30/16 | | 2,152 | | 2,388 |

Metals & Mining - 0.1% |

Anglo American Capital PLC 9.375% 4/8/14 (g) | | 1,278 | | 1,433 |

Nonconvertible Bonds - continued |

| Principal Amount (000s) | | Value (000s) |

MATERIALS - continued |

Metals & Mining - continued |

Corporacion Nacional del Cobre de Chile (Codelco): | | | | |

3.875% 11/3/21 (g) | | $ 6,889 | | $ 7,434 |

6.375% 11/30/12 (g) | | 1,618 | | 1,637 |

Vale Overseas Ltd.: | | | | |

4.375% 1/11/22 | | 6,000 | | 6,154 |

6.25% 1/23/17 | | 2,726 | | 3,125 |

| | 19,783 |

TOTAL MATERIALS | | 34,310 |

TELECOMMUNICATION SERVICES - 0.3% |

Diversified Telecommunication Services - 0.2% |

AT&T, Inc. 6.8% 5/15/36 | | 9,241 | | 12,642 |

BellSouth Capital Funding Corp. 7.875% 2/15/30 | | 1,158 | | 1,574 |

CenturyLink, Inc.: | | | | |

6.15% 9/15/19 | | 3,372 | | 3,671 |

6.45% 6/15/21 | | 3,263 | | 3,644 |

7.6% 9/15/39 | | 1,011 | | 1,046 |

Embarq Corp. 7.995% 6/1/36 | | 3,741 | | 4,142 |

Telefonica Emisiones SAU 5.462% 2/16/21 | | 4,994 | | 4,594 |

Verizon Communications, Inc.: | | | | |

6.1% 4/15/18 | | 2,674 | | 3,341 |

6.25% 4/1/37 | | 4,611 | | 6,123 |

| | 40,777 |

Wireless Telecommunication Services - 0.1% |

America Movil SAB de CV 3.625% 3/30/15 | | 1,082 | | 1,155 |

DIRECTV Holdings LLC/DIRECTV Financing, Inc.: | | | | |

5.15% 3/15/42 | | 3,616 | | 3,696 |

5.875% 10/1/19 | | 8,810 | | 10,362 |

6.35% 3/15/40 | | 2,500 | | 2,945 |

Vodafone Group PLC 5% 12/16/13 | | 2,696 | | 2,849 |

| | 21,007 |

TOTAL TELECOMMUNICATION SERVICES | | 61,784 |

UTILITIES - 0.7% |

Electric Utilities - 0.4% |

Ameren Illinois Co. 6.125% 11/15/17 | | 333 | | 393 |

AmerenUE 6.4% 6/15/17 | | 3,507 | | 4,209 |

Nonconvertible Bonds - continued |

| Principal Amount (000s) | | Value (000s) |

UTILITIES - continued |

Electric Utilities - continued |

Cleveland Electric Illuminating Co. 5.65% 12/15/13 | | $ 4,829 | | $ 5,092 |

Duke Capital LLC 5.668% 8/15/14 | | 2,413 | | 2,601 |

Duquesne Light Holdings, Inc.: | | | | |

5.9% 12/1/21 (g) | | 5,410 | | 6,106 |

6.4% 9/15/20 (g) | | 10,602 | | 12,253 |

Edison International 3.75% 9/15/17 | | 4,275 | | 4,571 |

Enel Finance International SA 5.7% 1/15/13 (g) | | 305 | | 308 |

FirstEnergy Corp. 7.375% 11/15/31 | | 9,223 | | 12,171 |

FirstEnergy Solutions Corp.: | | | | |

4.8% 2/15/15 | | 1,798 | | 1,920 |

6.05% 8/15/21 | | 6,625 | | 7,372 |

LG&E and KU Energy LLC: | | | | |

2.125% 11/15/15 | | 4,999 | | 5,050 |

3.75% 11/15/20 | | 984 | | 1,019 |

Nevada Power Co.: | | | | |

6.5% 5/15/18 | | 5,290 | | 6,602 |

6.5% 8/1/18 | | 1,844 | | 2,312 |

Pennsylvania Electric Co. 6.05% 9/1/17 | | 618 | | 710 |

Pepco Holdings, Inc. 2.7% 10/1/15 | | 4,728 | | 4,870 |

Sierra Pacific Power Co. 5.45% 9/1/13 | | 1,831 | | 1,909 |

| | 79,468 |

Gas Utilities - 0.0% |

Southern Natural Gas Co. 5.9% 4/1/17 (g) | | 357 | | 420 |

Southern Natural Gas Co. / Southern Natural Issuing Corp. 4.4% 6/15/21 | | 2,360 | | 2,533 |

| | 2,953 |

Independent Power Producers & Energy Traders - 0.0% |

PSEG Power LLC 2.75% 9/15/16 | | 1,703 | | 1,777 |

Multi-Utilities - 0.3% |

Dominion Resources, Inc.: | | | | |

2.7606% 9/30/66 (m) | | 13,426 | | 12,223 |

7.5% 6/30/66 (m) | | 3,828 | | 4,139 |

MidAmerican Energy Holdings, Co.: | | | | |

5.875% 10/1/12 | | 3,227 | | 3,239 |

6.5% 9/15/37 | | 3,287 | | 4,491 |

National Grid PLC 6.3% 8/1/16 | | 407 | | 470 |

NiSource Finance Corp.: | | | | |

4.45% 12/1/21 | | 2,779 | | 3,007 |

5.25% 9/15/17 | | 682 | | 786 |

Nonconvertible Bonds - continued |

| Principal Amount (000s) | | Value (000s) |

UTILITIES - continued |

Multi-Utilities - continued |

NiSource Finance Corp.: - continued | | | | |

5.25% 2/15/43 | | $ 4,557 | | $ 5,046 |

5.4% 7/15/14 | | 6,582 | | 7,075 |

5.45% 9/15/20 | | 980 | | 1,120 |

5.8% 2/1/42 | | 3,785 | | 4,503 |

6.4% 3/15/18 | | 1,557 | | 1,864 |

6.8% 1/15/19 | | 4,065 | | 4,874 |

Sempra Energy 2.3% 4/1/17 | | 7,119 | | 7,446 |

Wisconsin Energy Corp. 6.25% 5/15/67 (m) | | 3,554 | | 3,763 |

| | 64,046 |

TOTAL UTILITIES | | 148,244 |

TOTAL NONCONVERTIBLE BONDS (Cost $1,363,957) |

1,517,523

|

U.S. Government and Government Agency Obligations - 4.9% |

|

U.S. Treasury Inflation Protected Obligations - 1.0% |

U.S. Treasury Inflation-Indexed Bonds: | | | | |

0.75% 2/15/42 | | 129,548 | | 142,315 |

2.125% 2/15/41 | | 44,924 | | 66,568 |

TOTAL U.S. TREASURY INFLATION PROTECTED OBLIGATIONS | | 208,883 |

U.S. Treasury Obligations - 3.9% |

U.S. Treasury Bills, yield at date of purchase 0.1% 11/23/12 (i) | | 6,110 | | 6,109 |

U.S. Treasury Bonds 3% 5/15/42 | | 83,902 | | 89,801 |

U.S. Treasury Notes: | | | | |

0.5% 7/31/17 | | 151,500 | | 150,896 |

0.75% 6/30/17 (j) | | 40,000 | | 40,338 |

0.875% 7/31/19 | | 175,011 | | 173,712 |

U.S. Government and Government Agency Obligations - continued |

| Principal Amount (000s) | | Value (000s) |

U.S. Treasury Obligations - continued |

U.S. Treasury Notes: - continued | | | | |

1% 8/31/19 | | $ 195,000 | | $ 194,985 |

1.625% 8/15/22 | | 155,000 | | 156,017 |

TOTAL U.S. TREASURY OBLIGATIONS | | 811,858 |

TOTAL U.S. GOVERNMENT AND GOVERNMENT AGENCY OBLIGATIONS (Cost $990,501) |

1,020,741

|

U.S. Government Agency - Mortgage Securities - 8.8% |

|

Fannie Mae - 7.2% |

2.558% 6/1/36 (m) | | 181 | | 194 |

2.777% 7/1/37 (m) | | 544 | | 585 |

3% 4/1/27 to 8/1/42 | | 30,176 | | 31,504 |

3% 9/1/27 (h) | | 9,100 | | 9,603 |

3% 9/1/27 (h) | | 9,300 | | 9,814 |

3% 9/1/27 (h) | | 8,000 | | 8,442 |

3% 9/1/42 (h) | | 700 | | 726 |

3% 9/1/42 (h) | | 195,900 | | 203,280 |

3% 9/1/42 (h) | | 11,300 | | 11,726 |

3% 9/1/42 (h) | | 184,600 | | 191,554 |

3% 10/1/42 (h) | | 135,900 | | 140,487 |

3.5% 1/1/21 to 8/1/42 | | 25,483 | | 27,231 |

3.5% 9/1/27 (h) | | 4,000 | | 4,253 |

3.5% 7/1/42 | | 84 | | 90 |

3.5% 7/1/42 | | 122 | | 130 |

3.5% 8/1/42 | | 156 | | 167 |

3.5% 8/1/42 | | 144 | | 154 |

3.5% 9/1/42 (h) | | 268,800 | | 285,012 |

3.5% 9/1/42 (h) | | 3,700 | | 3,923 |

3.5% 9/1/42 (h) | | 7,300 | | 7,740 |

4% 9/1/26 to 4/1/42 | | 43,345 | | 46,757 |

4% 9/1/41 | | 132 | | 142 |

4% 9/1/42 (h) | | 77,000 | | 82,570 |

4.5% 6/1/18 to 7/1/41 | | 31,845 | | 34,882 |

4.5% 9/1/42 (h) | | 69,000 | | 74,682 |

4.5% 9/1/42 (h) | | 5,600 | | 6,061 |

5% 12/1/25 to 5/1/40 | | 35,141 | | 38,607 |

5% 9/1/42 (h) | | 1,300 | | 1,420 |

U.S. Government Agency - Mortgage Securities - continued |

| Principal Amount (000s) | | Value (000s) |

Fannie Mae - continued |

5% 9/1/42 (h) | | $ 500 | | $ 546 |

5% 9/1/42 (h) | | 52,000 | | 56,794 |

5.5% 9/1/24 to 3/1/40 | | 40,142 | | 44,126 |

5.5% 9/1/42 (h) | | 60,000 | | 65,845 |

6% 6/1/35 to 4/1/40 | | 52,455 | | 57,935 |

6% 9/1/42 (h) | | 40,000 | | 44,078 |

TOTAL FANNIE MAE | | 1,491,060 |

Freddie Mac - 0.8% |

3.454% 10/1/35 (m) | | 259 | | 278 |

3.5% 4/1/32 to 4/1/42 | | 9,965 | | 10,669 |

4% 6/1/24 to 11/1/41 | | 16,220 | | 17,650 |

4% 9/1/41 | | 870 | | 946 |

4% 9/1/42 (h) | | 23,000 | | 24,606 |

4.5% 7/1/25 to 10/1/41 | | 45,001 | | 48,942 |

5% 3/1/19 to 9/1/40 | | 29,059 | | 31,672 |

5.5% 1/1/28 to 3/1/40 | | 20,160 | | 21,973 |

6% 7/1/37 to 8/1/37 | | 1,077 | | 1,185 |

6.5% 3/1/36 | | 1,330 | | 1,504 |

TOTAL FREDDIE MAC | | 159,425 |

Ginnie Mae - 0.8% |

3% 10/1/42 (h) | | 11,300 | | 11,837 |

3.5% 11/15/41 to 3/15/42 | | 10,016 | | 10,859 |

3.5% 9/1/42 (h) | | 1,200 | | 1,299 |

4% 1/15/25 to 11/15/41 | | 28,145 | | 30,737 |

4.5% 5/15/39 to 4/15/41 | | 53,616 | | 59,455 |

5% 3/15/39 to 9/15/41 | | 24,680 | | 27,630 |

5.5% 12/15/31 to 1/15/39 | | 1,304 | | 1,460 |

6% 2/15/34 to 9/20/38 | | 13,321 | | 15,050 |

TOTAL GINNIE MAE | | 158,327 |

TOTAL U.S. GOVERNMENT AGENCY - MORTGAGE SECURITIES (Cost $1,790,231) |

1,808,812

|

Asset-Backed Securities - 0.3% |

| Principal Amount (000s) | | Value (000s) |

Accredited Mortgage Loan Trust Series 2005-1 Class M1, 0.7055% 4/25/35 (m) | | $ 1,086 | | $ 836 |

ACE Securities Corp. Home Equity Loan Trust: | | | | |

Series 2004-HE1 Class M2, 1.8855% 3/25/34 (m) | | 424 | | 346 |

Series 2005-HE2 Class M2, 0.6855% 4/25/35 (m) | | 89 | | 85 |

Advanta Business Card Master Trust Series 2006-C1 Class C1, 0.6758% 10/20/14 (m) | | 688 | | 7 |

Ally Master Owner Trust Series 2012-3 Class A2, 1.21% 6/15/17 | | 32,660 | | 32,719 |

Ameriquest Mortgage Securities, Inc. pass-thru certificates: | | | | |

Series 2003-10 Class M1, 0.9355% 12/25/33 (m) | | 85 | | 64 |

Series 2004-R2 Class M3, 0.7855% 4/25/34 (m) | | 120 | | 47 |

Series 2005-R2 Class M1, 0.6855% 4/25/35 (m) | | 2,266 | | 2,030 |

Argent Securities, Inc. pass-thru certificates: | | | | |

Series 2003-W7 Class A2, 1.0262% 3/25/34 (m) | | 53 | | 42 |

Series 2004-W11 Class M2, 0.9355% 11/25/34 (m) | | 616 | | 433 |

Series 2004-W7 Class M1, 0.7855% 5/25/34 (m) | | 1,600 | | 1,136 |

Series 2006-W4 Class A2C, 0.3955% 5/25/36 (m) | | 1,429 | | 432 |

Asset Backed Securities Corp. Home Equity Loan Trust: | | | | |

Series 2004-HE2 Class M1, 1.0605% 4/25/34 (m) | | 2,575 | | 2,120 |

Series 2006-HE2 Class M1, 0.6055% 3/25/36 (m) | | 64 | | 0* |

Axon Financial Funding Ltd. Series 2007-1 Class A1, 0.9743% 4/4/17 (d)(g)(m) | | 6,960 | | 0 |

Capital Trust Ltd. Series 2004-1: | | | | |

Class A2, 0.687% 7/20/39 (g)(m) | | 138 | | 125 |

Class B, 0.987% 7/20/39 (g)(m) | | 290 | | 130 |

Class C, 1.337% 7/20/39 (g)(m) | | 372 | | 6 |

Carrington Mortgage Loan Trust Series 2007-RFC1 Class A3, 0.3755% 12/25/36 (m) | | 1,978 | | 788 |

Citigroup Mortgage Loan Trust Series 2005-HE4 Class A2C, 0.5055% 10/25/35 (m) | | 447 | | 445 |

Countrywide Asset-Backed Certificates Trust Series 2007-4 Class A1A, 0.3662% 9/25/37 (m) | | 129 | | 128 |

Countrywide Home Loan Trust Series 2006-13 Class N, 7% 8/25/37 (g) | | 363 | | 0 |

Countrywide Home Loans, Inc.: | | | | |

Series 2004-3 Class M4, 1.2055% 4/25/34 (m) | | 175 | | 80 |

Series 2004-4 Class M2, 1.0305% 6/25/34 (m) | | 645 | | 371 |

Fannie Mae Series 2004-T5 Class AB3, 1.1466% 5/28/35 (m) | | 43 | | 27 |

Fieldstone Mortgage Investment Corp. Series 2004-3 Class M5, 2.4105% 8/25/34 (m) | | 319 | | 197 |

Asset-Backed Securities - continued |

| Principal Amount (000s) | | Value (000s) |

First Franklin Mortgage Loan Trust: | | | | |

Series 2004-FF2 Class M3, 1.0605% 3/25/34 (m) | | $ 25 | | $ 10 |

Series 2006-FF14 Class A2, 0.2955% 10/25/36 (m) | | 462 | | 457 |

Fremont Home Loan Trust Series 2005-A: | | | | |

Class M3, 0.9705% 1/25/35 (m) | | 1,041 | | 325 |

Class M4, 1.2555% 1/25/35 (m) | | 399 | | 53 |

GCO Education Loan Funding Master Trust II Series 2007-1A Class C1L, 0.8069% 2/25/47 (g)(m) | | 3,122 | | 1,284 |

GCO Slims Trust Series 2006-1A, 5.72% 3/1/22 (g) | | 624 | | 602 |

GE Business Loan Trust: | | | | |

Series 2003-1 Class A, 0.6695% 4/15/31 (g)(m) | | 216 | | 203 |

Series 2006-2A: | | | | |

Class A, 0.4195% 11/15/34 (g)(m) | | 1,457 | | 1,254 |

Class B, 0.5195% 11/15/34 (g)(m) | | 526 | | 364 |

Class C, 0.6195% 11/15/34 (g)(m) | | 874 | | 498 |

Class D, 0.9895% 11/15/34 (g)(m) | | 332 | | 103 |

Guggenheim Structured Real Estate Funding Ltd. Series 2006-3 Class C, 0.7855% 9/25/46 (g)(m) | | 1,540 | | 1,481 |

Home Equity Asset Trust: | | | | |

Series 2003-2 Class M1, 1.5555% 8/25/33 (m) | | 376 | | 293 |

Series 2003-3 Class M1, 1.5255% 8/25/33 (m) | | 745 | | 623 |

Series 2003-5 Class A2, 0.9355% 12/25/33 (m) | | 36 | | 30 |

HSI Asset Securitization Corp. Trust Series 2007-HE1 Class 2A3, 0.4255% 1/25/37 (m) | | 1,642 | | 549 |

JPMorgan Mortgage Acquisition Trust: | | | | |

Series 2006-NC2 Class M2, 0.5355% 7/25/36 (m) | | 3,185 | | 44 |

Series 2007-CH1 Class AV4, 0.3655% 11/25/36 (m) | | 1,641 | | 1,507 |

Keycorp Student Loan Trust: | | | | |

Series 1999-A Class A2, 0.7906% 12/27/29 (m) | | 570 | | 512 |

Series 2006-A Class 2C, 1.6106% 3/27/42 (m) | | 2,909 | | 138 |

Marriott Vacation Club Owner Trust Series 2006-2A: | | | | |

Class B, 5.442% 10/20/28 (g) | | 9 | | 9 |

Class C, 5.691% 10/20/28 (g) | | 4 | | 4 |

Class D, 6.01% 10/20/28 (g) | | 48 | | 49 |

MASTR Asset Backed Securities Trust Series 2007-HE1 Class M1, 0.5355% 5/25/37 (m) | | 861 | | 7 |

Meritage Mortgage Loan Trust Series 2004-1 Class M1, 0.9855% 7/25/34 (m) | | 163 | | 104 |

Merrill Lynch Mortgage Investors Trust: | | | | |

Series 2003-OPT1 Class M1, 1.2105% 7/25/34 (m) | | 506 | | 336 |

Series 2006-FM1 Class A2B, 0.3455% 4/25/37 (m) | | 1,582 | | 1,428 |

Series 2006-OPT1 Class A1A, 0.4955% 6/25/35 (m) | | 2,995 | | 2,411 |

Asset-Backed Securities - continued |

| Principal Amount (000s) | | Value (000s) |

Morgan Stanley ABS Capital I Trust: | | | | |

Series 2004-HE6 Class A2, 0.5755% 8/25/34 (m) | | $ 63 | | $ 50 |

Series 2005-NC1 Class M1, 0.6755% 1/25/35 (m) | | 439 | | 264 |

Series 2005-NC2 Class B1, 1.4055% 3/25/35 (m) | | 457 | | 54 |

National Collegiate Student Loan Trust: | | | | |

Series 2004-2 Class AIO, 9.75% 10/27/14 (o) | | 1,638 | | 21 |

Series 2006-4 Class D, 1.3355% 5/25/32 (m) | | 2,225 | | 0* |

New Century Home Equity Loan Trust Series 2005-4 Class M2, 0.7455% 9/25/35 (m) | | 1,566 | | 1,012 |

Ocala Funding LLC: | | | | |

Series 2005-1A Class A, 1.737% 3/20/10 (d)(g)(m) | | 621 | | 0 |

Series 2006-1A Class A, 1.637% 3/20/11 (d)(g)(m) | | 1,290 | | 0 |

Park Place Securities, Inc.: | | | | |

Series 2004-WCW1: | | | | |

Class M3, 1.4855% 9/25/34 (m) | | 585 | | 255 |

Class M4, 1.6855% 9/25/34 (m) | | 750 | | 170 |

Series 2005-WCH1 Class M4, 1.0655% 1/25/36 (m) | | 1,620 | | 926 |

Salomon Brothers Mortgage Securities VII, Inc. Series 2003-HE1 Class A, 1.0355% 4/25/33 (m) | | 6 | | 5 |

Saxon Asset Securities Trust Series 2004-1 Class M1, 1.0305% 3/25/35 (m) | | 1,392 | | 1,009 |

Sierra Receivables Funding Co. Series 2007-1A Class A2, 0.3968% 3/20/19 (FGIC Insured) (g)(m) | | 444 | | 434 |

SLM Private Credit Student Loan Trust Series 2004-A Class C, 1.4179% 6/15/33 (m) | | 1,396 | | 845 |

Specialty Underwriting & Residential Finance Trust Series 2006-AB2 Class N1, 5.75% 6/25/37 (g) | | 655 | | 0 |

Structured Asset Investment Loan Trust Series 2004-8 Class M5, 1.9605% 9/25/34 (m) | | 70 | | 24 |

SVO VOI Mortgage Corp. Series 2006-AA Class A, 5.28% 2/20/24 (g) | | 475 | | 487 |

Terwin Mortgage Trust Series 2003-4HE Class A1, 1.0955% 9/25/34 (m) | | 32 | | 29 |

Trapeza CDO XII Ltd./Trapeza CDO XII, Inc. Series 2007-12A Class B, 1.0196% 4/6/42 (g)(m) | | 2,177 | | 27 |

WaMu Asset Holdings Corp. Series 2006-8 Class N1, 6.048% 10/25/46 (g) | | 974 | | 0 |

Asset-Backed Securities - continued |

| Principal Amount (000s) | | Value (000s) |

Wells Fargo Home Equity Trust Series 2004-3 Class A, 4.5% 11/27/34 (g) | | $ 8 | | $ 0 |

Whinstone Capital Management Ltd. Series 1A Class B3, 2.2511% 10/25/44 (g)(m) | | 1,964 | | 1,296 |

TOTAL ASSET-BACKED SECURITIES (Cost $60,917) |

64,180

|

Collateralized Mortgage Obligations - 0.2% |

|

Private Sponsor - 0.2% |

Bayview Commercial Asset Trust Series 2006-3A, Class IO, 3.9199% 10/25/36 (g)(m)(o) | | 27,699 | | 979 |

Bear Stearns ALT-A Trust floater Series 2005-1 Class A1, 0.7955% 1/25/35 (m) | | 1,962 | | 1,689 |

Cobalt CMBS Commercial Mortgage Trust Series 2007-C2 Class B, 5.617% 4/15/47 (m) | | 1,468 | | 616 |

COMM pass-thru certificates floater Series 2001-J2A Class A2F, 0.7385% 7/16/34 (g)(m) | | 8 | | 8 |

First Horizon Mortgage pass-thru Trust Series 2004-AR5 Class 2A1, 2.623% 10/25/34 (m) | | 1,183 | | 1,139 |

Granite Master Issuer PLC: | | | | |

floater: | | | | |

Series 2006-1A Class A5, 0.377% 12/20/54 (g)(m) | | 6,713 | | 6,545 |

Series 2006-3 Class M2, 0.517% 12/20/54 (m) | | 5,460 | | 4,750 |

Series 2006-4: | | | | |

Class B1, 0.417% 12/20/54 (m) | | 4,556 | | 4,157 |

Class M1, 0.577% 12/20/54 (m) | | 1,198 | | 1,042 |

Series 2007-1: | | | | |

Class 1B1, 0.377% 12/20/54 (m) | | 4,650 | | 4,243 |

Class 1M1, 0.537% 12/20/54 (m) | | 1,611 | | 1,402 |

Class 2M1, 0.737% 12/20/54 (m) | | 2,067 | | 1,798 |

Series 2007-2 Class 2C1, 1.098% 12/17/54 (m) | | 2,864 | | 2,162 |

sequential payer Series 2006-3 Class B2, 0.407% 12/20/54 (m) | | 5,461 | | 4,983 |

Granite Mortgages PLC floater Series 2003-3 Class 1C, 2.9051% 1/20/44 (m) | | 472 | | 374 |

JPMorgan Chase Commercial Mortgage Securities Trust Series 2007-CB18 Class A3, 5.447% 6/12/47 (m) | | 1,532 | | 1,620 |

JPMorgan Mortgage Trust sequential payer Series 2006-A5 Class 3A5, 5.6881% 8/25/36 (m) | | 1,956 | | 1,506 |

LB-UBS Commercial Mortgage Trust sequential payer Series 2006-C6 Class A4, 5.372% 9/15/39 | | 591 | | 682 |

Collateralized Mortgage Obligations - continued |

| Principal Amount (000s) | | Value (000s) |

Private Sponsor - continued |

MASTR Adjustable Rate Mortgages Trust Series 2007-3 Class 22A2, 0.4455% 5/25/47 (m) | | $ 848 | | $ 543 |

Merrill Lynch Alternative Note Asset Trust floater Series 2007-OAR1 Class A1, 0.4055% 2/25/37 (m) | | 1,476 | | 1,158 |

Opteum Mortgage Acceptance Corp. floater Series 2005-3 Class APT, 0.5255% 7/25/35 (m) | | 2,048 | | 1,665 |

RESI Finance LP/RESI Finance DE Corp. floater Series 2003-B: | | | | |

Class B5, 2.5903% 7/10/35 (g)(m) | | 1,153 | | 919 |

Class B6, 3.0903% 7/10/35 (g)(m) | | 245 | | 194 |

Residential Funding Securities Corp. floater Series 2003-RP2 Class A1, 0.6855% 6/25/33 (g)(m) | | 221 | | 212 |

Salomon Brothers Mortgage Securities VII, Inc. Series 2006-C2 Class H, 6.308% 7/18/33 (g) | | 185 | | 62 |

Sequoia Mortgage Trust floater Series 2004-6 Class A3B, 1.6169% 7/20/34 (m) | | 38 | | 33 |

Structured Asset Securities Corp. Series 2003-15A Class 4A, 5.3743% 4/25/33 (m) | | 333 | | 311 |

TBW Mortgage-Backed pass-thru certificates floater Series 2006-4 Class A3, 0.4355% 9/25/36 (m) | | 3,513 | | 3,021 |

TOTAL COLLATERALIZED MORTGAGE OBLIGATIONS (Cost $35,173) |

47,813

|

Commercial Mortgage Securities - 1.9% |

|

Asset Securitization Corp. Series 1997-D5: | | | | |

Class A6, 7.1354% 2/14/43 (m) | | 153 | | 154 |

Class PS1, 1.2297% 2/14/43 (m)(o) | | 747 | | 22 |

Banc of America Commercial Mortgage Trust: | | | | |

sequential payer: | | | | |

Series 2006-2 Class AAB, 5.7087% 5/10/45 (m) | | 1,083 | | 1,146 |

Series 2006-5: | | | | |

Class A2, 5.317% 9/10/47 | | 3,817 | | 3,838 |

Class A3, 5.39% 9/10/47 | | 1,832 | | 1,944 |

Series 2006-6 Class A3, 5.369% 10/10/45 | | 2,628 | | 2,872 |

Series 2007-4 Class A3, 5.7921% 2/10/51 (m) | | 1,291 | | 1,342 |

Series 2006-6 Class E, 5.619% 10/10/45 (g) | | 759 | | 76 |

Series 2007-3: | | | | |

Class A3, 5.6612% 6/10/49 (m) | | 2,194 | | 2,237 |

Class A4, 5.6612% 6/10/49 (m) | | 2,739 | | 3,133 |

Commercial Mortgage Securities - continued |

| Principal Amount (000s) | | Value (000s) |

Banc of America Commercial Mortgage, Inc.: | | | | |

sequential payer: | | | | |

Series 2001-1 Class A4, 5.451% 1/15/49 | | $ 2,878 | | $ 3,297 |

Series 2004-2 Class A4, 4.153% 11/10/38 | | 1,406 | | 1,445 |

Series 2005-1 Class A3, 4.877% 11/10/42 | | 469 | | 469 |

Series 2001-3 Class H, 6.562% 4/11/37 (g) | | 735 | | 735 |

Series 2005-3 Class A3B, 5.09% 7/10/43 (m) | | 4,082 | | 4,299 |

Banc of America Large Loan, Inc. floater: | | | | |

Series 2005-MIB1: | | | | |

Class C, 0.5495% 3/15/22 (g)(m) | | 564 | | 558 |

Class D, 0.5995% 3/15/22 (g)(m) | | 572 | | 564 |

Class E, 0.6395% 3/15/22 (g)(m) | | 472 | | 463 |

Class F, 0.7095% 3/15/22 (g)(m) | | 676 | | 656 |

Class G, 0.7695% 3/15/22 (g)(m) | | 438 | | 416 |

Series 2006-BIX1: | | | | |

Class D, 0.4495% 10/15/19 (g)(m) | | 115 | | 111 |

Class E, 0.4795% 10/15/19 (g)(m) | | 956 | | 903 |

Class F, 0.5495% 10/15/19 (g)(m) | | 2,868 | | 2,696 |

Class G, 0.5695% 10/15/19 (g)(m) | | 1,350 | | 1,255 |

Bayview Commercial Asset Trust: | | | | |

floater: | | | | |

Series 2003-2 Class M1, 1.0855% 12/25/33 (g)(m) | | 65 | | 47 |

Series 2004-1: | | | | |

Class A, 0.5955% 4/25/34 (g)(m) | | 1,120 | | 988 |

Class B, 2.1355% 4/25/34 (g)(m) | | 125 | | 73 |

Class M1, 0.7955% 4/25/34 (g)(m) | | 101 | | 72 |

Class M2, 1.4355% 4/25/34 (g)(m) | | 93 | | 65 |

Series 2005-2A: | | | | |

Class A1, 0.5455% 8/25/35 (g)(m) | | 1,525 | | 1,100 |

Class M1, 0.6655% 8/25/35 (g)(m) | | 83 | | 49 |

Class M2, 0.7155% 8/25/35 (g)(m) | | 137 | | 74 |

Class M3, 0.7355% 8/25/35 (g)(m) | | 76 | | 37 |

Series 2005-3A: | | | | |

Class A2, 0.6355% 11/25/35 (g)(m) | | 536 | | 421 |

Class M1, 0.6755% 11/25/35 (g)(m) | | 70 | | 40 |

Class M2, 0.7255% 11/25/35 (g)(m) | | 89 | | 48 |

Class M3, 0.7455% 11/25/35 (g)(m) | | 80 | | 41 |

Class M4, 0.8355% 11/25/35 (g)(m) | | 100 | | 47 |

Series 2005-4A: | | | | |

Class A2, 0.6255% 1/25/36 (g)(m) | | 1,392 | | 986 |

Class B1, 1.6355% 1/25/36 (g)(m) | | 120 | | 18 |

Class M1, 0.6855% 1/25/36 (g)(m) | | 449 | | 277 |

Commercial Mortgage Securities - continued |

| Principal Amount (000s) | | Value (000s) |

Bayview Commercial Asset Trust: - continued | | | | |

floater: | | | | |

Series 2005-4A: | | | | |

Class M2, 0.7055% 1/25/36 (g)(m) | | $ 135 | | $ 78 |

Class M3, 0.7355% 1/25/36 (g)(m) | | 197 | | 105 |

Class M4, 0.8455% 1/25/36 (g)(m) | | 109 | | 53 |

Class M5, 0.8855% 1/25/36 (g)(m) | | 109 | | 36 |

Class M6, 0.9355% 1/25/36 (g)(m) | | 116 | | 31 |

Series 2006-1: | | | | |

Class A2, 0.5955% 4/25/36 (g)(m) | | 215 | | 159 |

Class M1, 0.6155% 4/25/36 (g)(m) | | 77 | | 46 |

Class M2, 0.6355% 4/25/36 (g)(m) | | 81 | | 45 |

Class M3, 0.6555% 4/25/36 (g)(m) | | 70 | | 36 |

Class M4, 0.7555% 4/25/36 (g)(m) | | 40 | | 18 |

Class M5, 0.7955% 4/25/36 (g)(m) | | 39 | | 14 |

Class M6, 0.8755% 4/25/36 (g)(m) | | 77 | | 26 |

Series 2006-2A: | | | | |

Class A1, 0.4655% 7/25/36 (g)(m) | | 3,201 | | 2,257 |

Class A2, 0.5155% 7/25/36 (g)(m) | | 190 | | 135 |

Class B1, 1.1055% 7/25/36 (g)(m) | | 71 | | 10 |

Class B3, 2.9355% 7/25/36 (g)(m) | | 67 | | 2 |

Class M1, 0.5455% 7/25/36 (g)(m) | | 200 | | 65 |

Class M2, 0.5655% 7/25/36 (g)(m) | | 141 | | 42 |

Class M3, 0.5855% 7/25/36 (g)(m) | | 117 | | 26 |

Class M4, 0.6555% 7/25/36 (g)(m) | | 79 | | 17 |

Class M5, 0.7055% 7/25/36 (g)(m) | | 97 | | 19 |

Class M6, 0.7755% 7/25/36 (g)(m) | | 145 | | 23 |

Series 2006-3A: | | | | |

Class B1, 1.0355% 10/25/36 (g)(m) | | 4 | | 0* |

Class M4, 0.6655% 10/25/36 (g)(m) | | 157 | | 24 |

Class M5, 0.7155% 10/25/36 (g)(m) | | 188 | | 12 |

Class M6, 0.7955% 10/25/36 (g)(m) | | 369 | | 9 |

Series 2006-4A: | | | | |

Class A1, 0.4655% 12/25/36 (g)(m) | | 809 | | 549 |

Class A2, 0.5055% 12/25/36 (g)(m) | | 3,952 | | 1,841 |

Class B1, 0.9355% 12/25/36 (g)(m) | | 78 | | 2 |

Class M1, 0.5255% 12/25/36 (g)(m) | | 263 | | 54 |

Class M2, 0.5455% 12/25/36 (g)(m) | | 175 | | 27 |

Class M3, 0.5755% 12/25/36 (g)(m) | | 176 | | 24 |

Class M4, 0.6355% 12/25/36 (g)(m) | | 213 | | 24 |

Class M5, 0.6755% 12/25/36 (g)(m) | | 195 | | 16 |

Class M6, 0.7555% 12/25/36 (g)(m) | | 175 | | 10 |

Series 2007-1 Class A2, 0.5055% 3/25/37 (g)(m) | | 810 | | 436 |

Commercial Mortgage Securities - continued |

| Principal Amount (000s) | | Value (000s) |

Bayview Commercial Asset Trust: - continued | | | | |

floater: | | | | |

Series 2007-2A: | | | | |

Class A1, 0.5055% 7/25/37 (g)(m) | | $ 771 | | $ 434 |

Class A2, 0.5555% 7/25/37 (g)(m) | | 723 | | 240 |

Class B1, 1.8355% 7/25/37 (g)(m) | | 105 | | 1 |

Class M1, 0.6055% 7/25/37 (g)(m) | | 253 | | 66 |

Class M2, 0.6455% 7/25/37 (g)(m) | | 139 | | 17 |

Class M3, 0.7255% 7/25/37 (g)(m) | | 140 | | 14 |

Class M4, 0.8855% 7/25/37 (g)(m) | | 278 | | 22 |

Class M5, 0.9855% 7/25/37 (g)(m) | | 245 | | 17 |

Class M6, 1.2355% 7/25/37 (g)(m) | | 311 | | 16 |

Series 2007-3: | | | | |

Class A2, 0.5255% 7/25/37 (g)(m) | | 827 | | 420 |

Class B1, 1.1855% 7/25/37 (g)(m) | | 184 | | 12 |

Class B2, 1.8355% 7/25/37 (g)(m) | | 433 | | 24 |